Embed Size (px)

Citation preview

Page 1 of 28

Introduction

When two or more companies carrying on similar business go

into liquidation and a new company is formed to take over their

business, it is called amalgamation. In other words, amalgamation

refers to the formation of a new company by taking over the business

of two or more existing companies doing similar type of business. In

amalgamation, two or more companies are liquidated and a new

company is formed to take over the business of liquidating companies.

The companies which go into liquidation are called vendor or

amalgamating companies where as the new company which is formed

to take over the business of liquidating companies is called purchasing

or amalgamated or transferee company. The main aim of

amalgamation is to minimize the possibility of cut-throat competition

and to secure the advantages of large scale production.

Before we proceed to know, What is Amalgamation? First let's

understand the meaning of two terms viz., 'amalgamating companies'

and 'amalgamated company'. The meaning of these terms is as follows:

1. Amalgamating companies are those two or more companies which

willingly unite (combine) to carry on their business activities

jointly.

2. Amalgamated company is a newly formed union (alliance) of two

or more amalgamating companies. It has a separate legal existence

with a new unique name.

Now let's discuss the meaning of amalgamation with some

examples.

Page 2 of 28

To amalgamate means to unite or combine or blend. It is an act

or process in which two or more things fuse together to form a new

potent thing.

Amalgamation is an emerging trend of today's business world. It

results in the formation of a new, strong, stable and large company. It

also results in the growth and expansion of this newly formed

company.

During amalgamation, two or more companies willingly come

together to cooperate with each other and diversify (expand) their

business activities.

After amalgamation, two or more companies dissolve

(disintegrate) and lose their individual legal status (existence), hence

they no longer exist anymore. However, they again re-establish

themselves, but now jointly, by forming a new company having a

unique name.

Thus, amalgamation results in the formation of a new (separate)

company which has a unique name, logo, identity and existence.

The management of amalgamated company is led (directed) by

members of two or more companies getting amalgamated.

Page 3 of 28

DEFINITION of 'Amalgamation'

The combination of one or more companies into a new entity.

An amalgamation is distinct from a merger because neither of the

combining companies survives as a legal entity. Rather, a completely

new entity is formed to house the combined assets and liabilities of

both companies.

Amalgamation is defined as a simple arrangement or

reconstruction of business. It is a process that involves combining of

two or more companies as either absorption or as blend. Two or more

companies can either be absorbed by an entirely new firm or a

subsidiary powered by one of the basic firm. In such cases all the

shareholders of the absorbed company automatically become the

shareholders of the ruling company as the amalgamating company

loses its existence. All the assets and liabilities are also transferred to

the new entity.

Amalgamation has given different forms to different actions in

due course of the merger taking place. It can either be classified in the

nature of merger or in the nature of purchase. If the process takes place

in the nature of merger then the all assets, liabilities, and shareholders

holding not less than 90% of equity shares are automatically

transferred to the new company or the holding company by virtue of

the amalgamation.

When amalgamation takes place in nature of purchase then the

assets and liabilities of the company are taken over by the ruling

company. All the properties and characteristics of amalgamating

company should vest with the other company. Even the shareholders

Page 4 of 28

holding shares not less than 75% should transfer their shares to the

transferee company. In such a case any company does not purchase the

business resulting in a takeover, the transferor company does not

completely lose its existence.

Page 5 of 28

Features Of Amalgamation

* Two or more existing companies are liquidated.

* A new company is formed to take over the business of liquidating

companies.

* The nature of business of existing companies is similar.

* Liquidating companies are called vendor companies and the new

company is called purchasing company.

* Generally, purchase consideration is discharged by the issue of

equity shares of purchasing company.

"Amalgamation" is Dissolution of one or more Companies and

Transfer of Business to Another Entity. Companies which come

together are Known as "Amalgamating companies" or" Transferor

Companies" , Companies which the Transferor companies get

amalgamated into is "Amalgamated Company"

Amalagamation includes Absorbtion.Absorbtion is Aquisition of

business of Existing company.

AS 14 doesn't Cover parent subsidiary relationship where one

company Acquires control over other without impinging the Legal

independent Status of other company.It is Dealt with under AS21.

AS 14 brings Concept of Amalgamation under two broad categories.

First Amalgamation in nature of “Merger” , Under this category

there is Genuine pooling of

o Not merely Assets and Liabilities of the Amalgamating companies

o But also the interest of Shareholders and business of the

companies.

Page 6 of 28

Second is Amalgamation in Nature of “Purchase” .

o A mode by which one company acquires another company and

o As a consequence the shareholders of company which acquired

normally do not continue to possess interest in equity of the

combined company in an identical proportion to that held by them

in liquidated company. Also the business of company which

acquired is not necessarily intended to be continued.

AS 14 gives 5 Specific conditions on fulfillment of which

Amalgamation is treated as merger.

Page 7 of 28

Five Conditions

1. All the ASSETS and liabilities of transferor company become

assets and liabilities of transferee company.

2. Shareholders of SC holding not less than 90 % of “Face value” of

equity shares become shareholders of PC by virtue of

“Amalgamation” . For purpose of computing 90% , Following

shares are not be considered

a. Shares held by PC in SC

b. Shares held by One or more subsidiaries of PC in SC

c. Nominees of PC in SC

3. The Consideration Paid to Equity shareholders of SC is in form of

Equity shares of PC , Except cash may be paid for Partial shares.

4. Business of is intended to be continued on after amalgamation by

PC and

5. Assets and liabilities of SC are incorporated in financial statements

of the PC at book values except to ensure uniform accounting

policies.

AS 14 provides two methods of accounting for AS 14 ,Which are

Pooling of Interest method for Amalgamation in nature of Merger

Purchase method of Amalgamation in nature of purchase.

Page 8 of 28

Salient features of Pooling of interest method.

1. In preparing the financial statements of PC the Assets and

Liabilities of SC should be recorded at their existing values and

in the same form as on date of amalgamation. The balance of

P&L account should be aggregated with corresponding balance

of PC .

2. If at time of amalgamation , transferee and transferor company

were to have conflict of accounting policies , Such conflict is

resolved and brought in line with policy adopted by PC .

3. The Difference between amount recorded as Share capital issued

and amount of capital of SC should be adjusted in reserves .

Accordingly No goodwill or Capital reserve will Arise.

Salient features of Purchase method.

1. The Assets and Liabilities of SC are incorporated in financial

statements of PC at existing values . Alternatively the purchase

consideration should be allocated to individual indentifiable assets

and liabilities on basis of fair values.

2. Identity of Non statutory reserves of SC is not preserved . Hence

such reserves should not be included in financial statements of PC

3. If purchase consideration is more than net assets of PC , then the

difference is credited to goodwill, Alternatively if Purchase

consideration is less than Net assets of PC the difference is credited

to Capital reserve.

4. Goodwill arising out of Amalgamation should be amortized over its

useful life not exceeding period of Five years.

Page 9 of 28

5. Where the requirements of relevant statute demands “Statutory

reserve” of SC to be recorded in financial statements of PC . While

crediting the statutory reserve the debit needs to be given to

“Amalgamation adjustment A/c” . The Account should be disclosed

under “Misc expenditure .

Impact on AS 4 – Amalgamation after balance sheet date.

Where Amalgamation happens after Balance sheet date , the

Impact cannot be shown as part of Financial statements and hence

needs to be disclosed in directors report.

Page 10 of 28

Accounting for amalgamations

A. Computation of Purchase consideration

Net assets Method

Assets taken over at fair values - XXXX

Less : Liabilities taken over at agreed amounts -XXXX

_____

Net Assets / Purchase Consideration XXXX

=====

Payments

Aggregate of shares paid to various shareholders.

Page 11 of 28

B. Transferor Company accounting.

Tranfer to realization account :

Realization A/C Dr

To Assets

Liabilities A/C Dr

To Realization

Purchase consideration .

Due entry :

Transferee Company Dr

To Realisation

Payment entry

Shares in transferee company Dr

Bank Dr

To transferee company

Page 12 of 28

Sale of Assets Not taken over

Bank Dr

To Assets (Book value)

To Realisation ( Profit)

Settlement of Liabilities Not taken over

Liabilities Dr

To Bank

To Realisation

Realisation Expenses

a. Incurred by transferor company

Realisation A/C Dr

To Bank

b. Incurred by transferor company and reimbursed by transferee

company

Transferee Company A/C Dr

To Bank

Bank Dr

To Transferee company

Page 13 of 28

c. Incurred by Transferee company

No Entries

Amount Due to equity share holders.

Equity share capital Dr

Reserves Dr

To Shareholders

Transfer of Balance of realization

Realsisation A/C Dr

To Shareholders

Settlement to Shareholders by transfer of Consideration received.

Share holders A/C Dr

T o Shares in Purchasing company

To Bank

Transferee Company Accounting

1. Accounting should be done as per AS 14

2. Accounting should be done as per Mode of Amalgamation.

Purchase method

Due Entry for Business Consideration

Business Purchase Dr

To Liquidator of transferor company

Page 14 of 28

Incorporation of Assets and liabilities taken over

Assets

Assets A/C Dr

Goodwill Dr

To Liabilities

To Business Purchase

To Capital reserve

Discharge of Purchase consideration

Liquidator of transferor company A/C Dr

To Share capital

To Securities premium

To Bank

Others

Cancellation of Intercompany Owings.

Creditors Dr

To Debtors

Elimination of Unrealized Profits on goods sold by one company to

another and remaining unsold as of date of amalgamation

Goodwill /Capital reserve Dr

To Stock Reserve

Page 15 of 28

Realisation Expenses

Goodwill/Capital reserve Dr

To bank

Contra entry for statutory reserve of which liability is not yet fulfilled

Amalgamation adjustment Dr

To Statutory reserve

Page 16 of 28

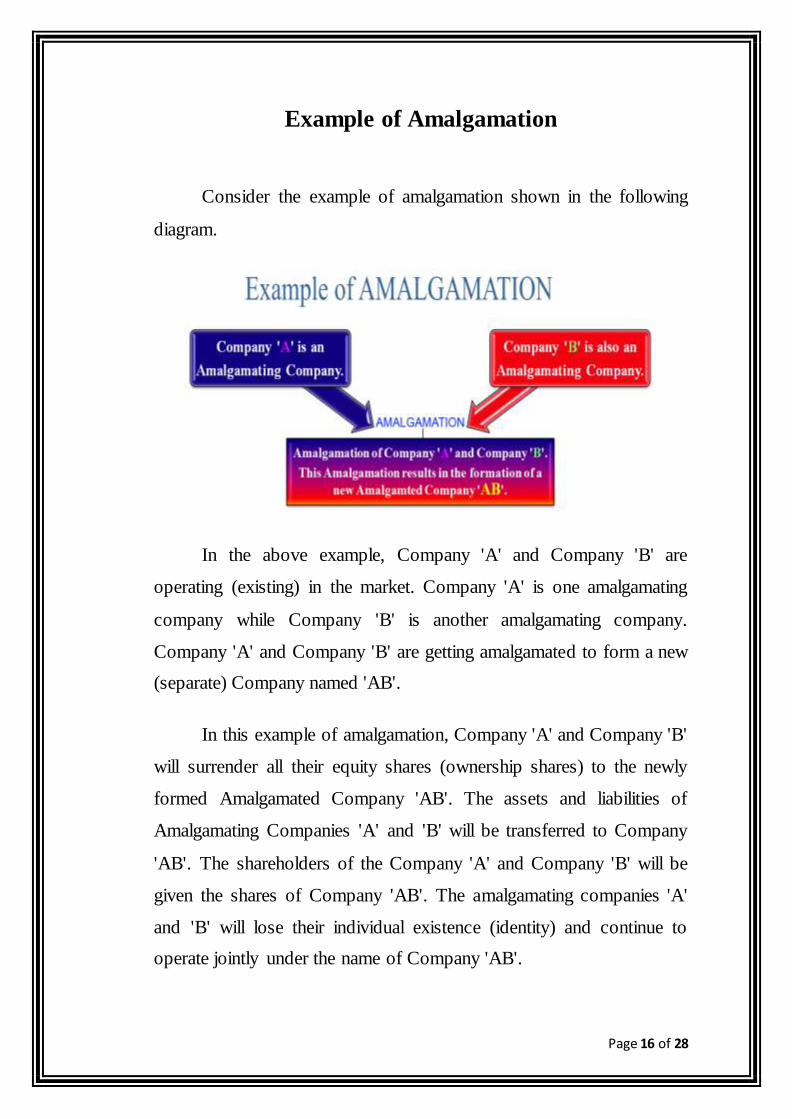

Example of Amalgamation

Consider the example of amalgamation shown in the following

diagram.

In the above example, Company 'A' and Company 'B' are

operating (existing) in the market. Company 'A' is one amalgamating

company while Company 'B' is another amalgamating company.

Company 'A' and Company 'B' are getting amalgamated to form a new

(separate) Company named 'AB'.

In this example of amalgamation, Company 'A' and Company 'B'

will surrender all their equity shares (ownership shares) to the newly

formed Amalgamated Company 'AB'. The assets and liabilities of

Amalgamating Companies 'A' and 'B' will be transferred to Company

'AB'. The shareholders of the Company 'A' and Company 'B' will be

given the shares of Company 'AB'. The amalgamating companies 'A'

and 'B' will lose their individual existence (identity) and continue to

operate jointly under the name of Company 'AB'.

Page 17 of 28

Two good examples of amalgamations are as follows:

1. Maruti Motors operating in India and Suzuki based in Japan

amalgamated to form a new company called Maruti Suzuki (India)

Limited.

2. Tata Sons operating in India and AIA Group based in Hong Kong

amalgamated to form a new company called TATA AIG Life

Insurance.

Page 18 of 28

Maruti suzuki

Maruti Suzuki India Limited is an automobile manufacturer in

India. It is a subsidiary of Japanese automobile and motorcycle

manufacturer Suzuki. As of November 2012, it had a market share of

37% of the Indian passenger car markets. Maruti Suzuki manufactures

and sells a complete range of cars from the entry level Maruti 800,

Alto, to the hatchback Ritz, Celerio, , A-Star, Swift, Wagon R, Zen and

sedans DZire, Ciaz, Kizashi and SX4, in the 'C' segment Eeco, Omni,

Multi Purpose vehicle Suzuki Ertiga and Sports Utility vehicle Grand

Vitara.

The company's headquarters are at No 1, Nelson Mandela Road,

New Delhi. In February 2012, the company sold its ten millionth

vehicle in India.

Joint venture related issues

Relationship between the Government of India, under the United

Front (India) coalition and Suzuki Motor Corporation over the joint

venture was a point of heated debate in the Indian media until Suzuki

Motor Corporation gained the controlling stake. This highly profitable

joint venture that had a near monopolistic trade in the Indian

automobile market and the nature of the partnership built up till then

was the underlying reason for most issues. The success of the joint

venture led Suzuki to increase its equity from 26% to 40% in 1987, and

further to 50% in 1992. In 1982 both the venture partners had entered

into an agreement to nominate their candidate for the post of Managing

Director and every Managing Director will have a tenure of five years

Page 19 of 28

R.C. Bhargava was the initial managing director of the company since

the inception of the joint venture. Till today he is regarded as

instrumental for the success of Maruti Suzuki. Joining in 1982 he held

several key positions in the company before heading the company as

Managing Director. Currently he is on the Board of Directors. After

completing his five-year tenure, Mr. Bhargava later assumed the office

of Part-Time Chairman. The Government nominated Mr. S.S.L.N.

Bhaskarudu as the Managing Director on 27 August 1997. Mr.

Bhaskarudu had joined Maruti Suzuki in 1983 after spending 21 years

in the Public sector undertaking Bharat Heavy Electricals Limited as

General Manager. In 1987 he was promoted as Chief General

Manager. In 1988 he was named Director, Productions and Projects.

The next year (1989) he was named Director of Materials and in 1993

he became Joint Managing Director.

Suzuki did not attend the Annual General Meeting of the Board

with the reason of it being called on a short notice. Later Suzuki Motor

Corporation went on record to state that Bhaskarudu was

"incompetent" and wanted someone else. However, the Ministry of

Industries, Government of India refuted the charges. Media stated from

the Maruti Suzuki sources that Bhaskarudu was interested to indigenise

most of components for the models including gear boxes especially for

Maruti 800. Suzuki also felt that Bhaskarudu was a proxy for the

Government and would not let it increase its stake in the venture.[21] If

Maruti Suzuki would have been able to indigenise gear boxes then

Maruti Suzuki would have been able to manufacture all the models

without the technical assistance from Suzuki. Till today the issue of

localization of gear boxes is highlighted in the press.

Page 20 of 28

Manufacturing facilities

Maruti Suzuki has two manufacturing facilities in India. Both

manufacturing facilities have a combined production capacity of

14,50,000 vehicles annually. During a recent meeting of the Gujarat

chief minister with Suzuki Motor Corp chairman & CEO Osamu

Suzuki,the Chairman had said that the work on car manufacturing plant

at Mandal near Ahmedabad would be started soon. Maruti Suzuki to

set up second plant in Gujarat; acquires 600 acres.

The Gurgaon manufacturing facility has three fully integrated

manufacturing plants and is spread over 300 acres (1.2 km2). All three

plants have an installed capacity of 350,000 vehicles annually but

productivity improvements have enabled it to manufacture 900,000

vehicles annually. The Gurgaon facilities also manufacture 240,000 K-

Series engines annually. The entire facility is equipped with more than

150 robots, out of which 71 have been developed in-house. The

Gurgaon Facilities manufactures the 800, Alto, WagonR, Estilo, Omni,

Gypsy, Ertiga, Ritz and Eeco.

The Manesar manufacturing plant was inaugurated in February

2007 and is spread over 600 acres (2.4 km2). Initially it had a

production capacity of 100,000 vehicles annually but this was

increased to 300,000 vehicles annually in October 2008. The

production capacity was further increased by 250,000 vehicles taking

total production capacity to 550,000 vehicles annually. The Manesar

Plant produces the A-star, Swift, Swift DZire, SX4, Ritz and Celerio.

Page 21 of 28

On 25 June 2012, Haryana State Industries and Infrastructure

Development Corporation demanded Maruti Suzuki to pay an

additional Rs 235 crore for enhanced land acquisition for its Haryana

plant expansion. The agency reminded Maruti that failure to pay the

amount would lead to further proceedings and vacating the enhanced

land acquisition.

Industrial relations

Since its founding in 1983, Maruti Udyog Limited experienced

problems with its labour force. The Indian labour it hired readily

accepted Japanese work culture and the modern manufacturing

process. In 1997, there was a change in ownership, and Maruti became

predominantly government controlled. Shortly thereafter, conflict

between the United Front Government and Suzuki started. Labour

unrest started under management of Indian central government. In

2000, a major industrial relations issue began and employees of Maruti

went on an indefinite strike, demanding among other things, major

revisions to their wages, incentives and pensions.

Employees used slowdown in October 2000, to press a revision

to their incentive-linked pay. In parallel, after elections and a new

central government led by NDA alliance, India pursued a

disinvestments policy. Along with many other government owned

companies, the new administration proposed to sell part of its stake in

Maruti Suzuki in a public offering. The worker's union opposed this

sell-off plan on the grounds that the company will lose a major

business advantage of being subsidised by the Government, and the

Page 22 of 28

union has better protection while the company remains in control of the

government.

The standoff between the union and the management continued

through 2001. The management refused union demands citing

increased competition and lower margins. The central government

prevailed and privatized Maruti in 2002. Suzuki became the majority

owner of Maruti Udyog Limited.

Manesar violence

On 18 July 2012, Maruti's Manesar plant was hit by violence as

workers at one of its auto factories attacked supervisors and started a

fire that killed a company official and injured 100 managers, including

two Japanese expatriates. The violent mob also injured nine policemen.

The company's General Manager of Human Resources had both arms

and legs broken by his attackers, unable to leave the building that was

set ablaze, and was charred to death. The incident is the worst-ever for

Suzuki since the company began operations in India in 1983.

Since April 2012, the Manesar union had demanded a three-fold

increase in basic salary, a monthly conveyance allowance of 10,000, a

laundry allowance of 3,000, a gift with every new car launch, and a

house for every worker who wants one or cheaper home loans for those

who want to build their own houses.Initial reports claimed wage

dispute and a union spokesman alleged the incident may be caste-

related.[35][36] According to the Maruti Suzuki Workers Union a

supervisor had abused and made discriminatory comments to a low-

caste worker.[37] These claims were denied by the company and the

police.[33] The supervisor alleged was found to belong to a tribal

Page 23 of 28

heritage and outside of Hindu caste system; further, the numerous

workers involved in violence were not affiliated with caste either.

Maruti said the unrest began, not over wage discussions, but after the

workers' union demanded the reinstatement of a worker who had been

suspended for beating a supervisor.[34] The workers claim harsh

working conditions and extensive hiring of low-paid contract workers

which are paid about $126 a month, about half the minimum wage of

permanent employees. Maruti employees currently earn allowances in

addition to their base wage. Company executives denied harsh

conditions and claim they hired entry-level workers on contracts and

made them permanent as they gained experience. It was also claimed

that bouncers were deployed by the company.

Page 24 of 28

Amalgamation of Firms

Amalgamation of Firms When two or more firms merge into one

firm and makes a new firm, then this is called amalgamation of firms.

For accounting point of view this definition is so important because if

one firm purchases other firm, then this is not called amalgamation but

if both firms decide to join or integrate then this is called

amalgamation. For Example, Suppose A and B firm decide to close

their business and start the business with the name of AB firm after

joining with each other then this is called amalgamation of A and B

firm. Steps for closing the accounts of old firm at the time of

amalgamation of firms When two firm amalgamate with each other, at

this time we treat following accounting in the books of old firms so

that all doubt solves.

1st: Revaluation of Assets and Liabilities All entries same as at

the time of admission and retirement

2nd: Transferring reserve to old partners capital account into

their old ratio

3rd: Treatment of Goodwill We evaluate the goodwill according

to the condition of agreement and then goodwill will open with agreed

value int the books

4th: Treatment of Assets and liabilities not taken by new firm If

assets and liabilities are not taken by new firm, then these item will

transfer to the capital accounts of partners of old firm and we close

these accounts Treatment of assets and liabilities taken by new firm In

the books of old partners a For closing the account of assets New Firms

Page 25 of 28

Account Debit Assets Account Credit at revalued value b For closing

the accounts of liabilities Liabilities Account Debit New Firm Account

Credit 6th Closing the accounts of partners capital Partner's capital

account Debit New Firms Account Credit In the books of new firm

Assets Account Debit Liabilities Account Credit Partner's capital

Account Credit

Accounting of jewellery business There is boom in jewellery

business. Due to increasing the value of gold jewellery business is

giving high rate of return to business man. Because of my background

is related to this business so, I am writing and telling you the technique

of how to make and maintain the accounts of jewellery business. It is

very simple to record of jewellery business but it is very harmful to

make any mistake in these type of accounts. Because 10 gram's

quantity's value is approximately Rs. 10000 so be careful while doing

the accounts of jewellery business. When we purchase gold, it will our

raw material. So it will deal as stock, it should valued on cost. Then

you should regular passing the voucher entry of purchasing of gold. In

cash book if you purchase on cash, if you purchase on credit, then your

duty is also to maintain the accounts of your creditors also. Because

this is our current liabilities, we should know how much amount, we

will have to pay to our creditors. In manual accounting, we just make

journal or day book, ledger after this we should find out our profit or

loss from manufacturing, trading and profit and loss account after this

we also must make balance sheet.

Steps for maintaining branch accounting 1 In that type of

branches, it is necessary to make bank account in the name of head

office so that amount got from cash sale can be deposited in head

Page 26 of 28

office bank account. 2 All miscellaneous expenses is given by head

office accountant to branch accountant on impress or advance system

of cash book. 3 All salaries, rent, advertising and other expenses must

be paid by head office. 4 Head office can send goods to branch on cost

price or invoice price. 5 It is necessary for branch to make the list of

debtors if branch has all to sell the goods on credit. It is duty of branch

accountant to send branch debtors list to head office weekly or

monthly. 6 These branches can make memorandums in different

registers. On these memorandums and registers head office can make

branch account For making branch account in head office, we open

each branch account in head office with given branch name.

Accounting treatment of web-publishing profession If you have

your own website, web blog, or any blog and you are earning more

than tax limit in India. I am providing you the full tutorial of

accounting treatment of web publishing profession. For this I am

making income and expenditure account In vertical form which is

accepted by Income tax department.

Page 27 of 28

CONCLUSION

Amalgamtion can also be defined as “Amalgamation takes place

when two or more comapanies combine into one company, the

shareholders in the amalgamting companies becoming substantially the

shareholders in the amalgamted company.”

In more common way, Amalgamtion would mean the two

business entities joining together to make totally new business entity or

to allow one business entity to survive absorbing the other one.

Amalgamation or merger is also a method of reconstruction. In

amalgamation, two or more companies are fused into one by merger or

by one taking over the other. When two companies are merged and are

so joined as to form third company or one is absorbed into other or

blended with another, the amalgamating company loses its identity.

There may be amalgamation either by transfer of two or more

undertakings to a new company or by the transfer of one or more

undertakings to an existing company. An amalgamation may be

defined as an arrangement whereby the assets of the two companies

which has as its share holders all, or substantially all the share holders

of the two companies

A consolidation is a combination of two or more companies into

a new company. In this form of merge, all the existing companies,

which combine, go into a new company. In this form of merger, all the

existing companies, which combine, go into liquidation and form a

new company with a different entity. The entity of the existing

company is lost and their assets and liabilities are taking over by the

new corporation or company.

Page 28 of 28

BIBLIOGRAPHY

http://www.svtuition.org/2008/12/steps-for-closing-accounts-of-

old-firm.html

http://www.examrace.com/Study-

Material/Commerce/Accounting-and-Audit/Amalgamation-of-

Firms.html

http://www.goodreturns.in/news/2013/02/08/maruti-suzuki-

scheme-amalgamation-159664.html

en.wikipedia.org/wiki/Amalgamation

www.investopedia.com/terms/a/amalgamation.asp