Embed Size (px)

Citation preview

May 2014

Certified Pre-Owned Vehicles:

Accelerating Forward

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 2

© 2014 NADA Used Card Guide

TABLE OF CONTENTS

The Genesis of Certified Pre-Owned ........................................................................................... 2

Consumer & Dealer Sentiment Aligned ....................................................................................... 3

Late Model Supply Helping to Drive CPO Sales ........................................................................... 4

CPO Premiums: Consumer Expectations vs. Actual .................................................................... 6

Conclusion .................................................................................................................................... 7

At NADA Used Car Guide ............................................................................................................. 9

Certified Pre-Owned Vehicles: Accelerating Forward

The Genesis of Certified Pre-Owned

It might come as a surprise to many consumers that manufacturer-sponsored certified

pre-owned (CPO) used vehicle programs have been around for the better part of 20

years now. Conceived as a means to protect residual values and address the large

number of off-lease vehicles hitting the used market, manufacturers promoted CPO

vehicles as a cost-effective alternative to purchasing new.

Manufacturers encouraged consumer demand for certified vehicles by reconditioning

them to like-new standards and extending bumper-to

-bumper and powertrain warranties to reduce repair

cost fears. In short, CPO gave consumers a third

option for auto purchases in addition to new and

used: superior used.

After growing rapidly through its infancy stage at the

beginning of the 2000s, CPO sales experienced just

incremental gains in the years that followed.

Hindered by higher costs and limited awareness, CPO

sales increased by only 200,000 units from 2003 to

2011 and deliveries consistently fell between 1.5-1.7

million units over the period.

0.5

0.7

1.3

1.51.6 1.6 1.6

1.7 1.7

1.51.6

1.71.8

2.1

0.0

0.5

1.0

1.5

2.0

2.5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ce

rtif

ied

Pre

-Ow

ne

d S

ale

s (m

illio

ns)

Calendar Year

Manufacturer Certified Pre-Owned Vehicle Sales

Source: Autodata

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 3

© 2014 NADA Used Card Guide

CPO sales began to take off in 2012, however, due in

part to recovering auto demand in general as well as

increased awareness of, and consideration for, CPO

units among the more value-conscious post-recession

consumer.

CPO sales reached an all-time high of 2.1 million units

in 2013, up 15% from 2012’s figure of 1.8 million.

With both late model supply and consumer

awareness growing, sales are on pace to hit another

record this year. In fact, CPO sales through April

stood at nearly 750,000 units, up 11% on a prior-year

basis and well ahead of the 3% rise in both new and

used vehicle sales.

To get a better understanding of certified pre-owned sales trends and what’s fueling

growth, May’s edition of NADA Perspective reviews consumer and dealer sentiment

toward CPO vehicles, how manufacturer sales have unfolded, and CPO pricing trends.

Consumer & Dealer Sentiment Aligned

Certified pre-owned vehicles benefit consumers and dealers in a variety of ways.

Consumers are able to purchase a fully reconditioned used vehicle with warranty

coverage similar to a new one, but at a much lower price. These attributes form the

basis of CPO’s value proposition for consumers. AutoTrader.com’s 2013 study, Certified

Pre-Owned: Understanding the Customer, revealed that the number one reason why

perspective CPO buyers consider buying certified is because of peace of mind. This point

goes hand-in-hand with the second most cited reason, CPO’s attractive extended

warranty coverage.

AutoTrader.com also points out that new vehicle affordability and economic concerns

are major reasons driving buyers to CPO units. Another benefit is access to low rate

financing as most manufacturers offer reduced interest rates as an incentive to buy CPO

vehicles. This increases affordability and offsets a portion of their higher upfront costs.

As for dealers, CPO sales support current and future profitability and strengthen

customer loyalty. Since a CPO vehicle is under warranty, consumers are more apt to

return to their original dealer for maintenance and repairs than go to an independent

repair shop.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2007 2008 2009 2010 2011 2012 2013 2014

Nu

mb

er

of

Pag

es

Calendar Year

Google Search Results for "Certified Pre-Owned Car"The number of pages returned for the phrase "certified pre-owned car" by calendar year.

Source: Google

+109% since 2011

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 4

© 2014 NADA Used Card Guide

This increases service and parts business and presents the dealer with an extended

audition to leave a favorable impression so the customer keeps coming back – whether

for service or another vehicle purchase – after the warranty has expired. Further, data

shows that certified vehicles remain on dealer lots for far less time than non-certified

ones. Dealers have consistently reported in NADA surveys that CPO vehicles sell 1–2

weeks faster than otherwise; this not only increases throughput, but also reduces the

amount of money dealers have to allocate to floor plan expenses.

Late Model Supply Helping to Drive CPO Sales

The sharp increase in CPO demand that has occurred over the past two years has come

at an opportune time for manufacturers. After years of declines stemming from the

falloff in new vehicle sales during the recession, late-model supply – or the primary pool

from which CPO vehicles are derived – finally started growing again in 2013.

Per NADA Used Car Guide’s used vehicle supply forecast, late-model supply is expected

to grow by 8% in 2014 and another 9% in 2015;

combined, the 17% increase in used supply through

2015 will act as an additional catalyst supporting a

continued increase in CPO sales.

Brands experiencing the largest increases in late-

model supply have also realized some of the biggest

gains in CPO sales. For example, NADA estimates that

late-model supply for Kia and Subaru grew by 17%

and 13% in 2013, respectively, figures exceeded only

by VW’s 20% rise. Kia and Subaru were also at the top

of the non-luxury CPO sales growth leaderboard last

year, as deliveries for the two increased by 72% and

45%, respectively. As for VW, CPO sales rose by a

more modest 9% in 2013.

So far in 2014, 12 of the 15 mainstream brands

reviewed have reported gains in CPO sales on a prior-

year basis. Sales for the top three performers Kia,

Subaru and Hyundai are up by 44%, 37%, and 26%,

respectively. Not coincidentally, NADA estimates that

late-model supply will grow the most for Kia and

Hyundai this year, while supply growth for Subaru is

expected to be among the industry leaders.

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

An

nu

al C

han

ge

Annual Change in Mainstream Brand Used Vehicle SupplyVehicles to 5 years in age

CY 2013 CY 2014 CY 2015

Source: NADA Used Car Guide

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

An

nu

al C

han

ge

Annual Change in Luxury Brand Used Vehicle SupplyVehicles to 5 years in age

CY 2013 CY 2014 CY 2015

Source: NADA Used Car Guide

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 5

© 2014 NADA Used Card Guide

Late-model supply for luxury brand Land Rover is

expected to grow more than any other premium

nameplate this year and so far the brand’s year-to-

date CPO sales improvement of 66% is ahead of other

luxury makes. Following closely behind, CPO

deliveries for Jaguar and Infiniti are up by a combined

average of 61%, while Lincoln has increased CPO

sales by 20% year-to-date. It will be interesting to see

if Lincoln can maintain its solid CPO performance as

NADA expects that late-model supply for the brand

will rise by a relatively mild 5% this year.

BMW, Mercedes-Benz and Audi have grown CPO

sales by 14% apiece and NADA estimates that supply

for the group will increase by respective figures of

8%, 11% and 15% over the course of the year.

Certified growth for Lexus and Acura has lagged other

luxury brands, with sales for the two up by 3% and

2%, respectively.

NADA expects used supply to be flat in 2014 for

Lexus, which is likely playing a role in holding back

CPO sales growth. It should be noted that while

growth has been mild, more than 24,000 Lexus CPO

vehicles have been sold so far this year, third most among luxury brands. Things should

improve for Lexus in 2015, as NADA estimates that late-model supply will be 8.4%

higher than this year’s expected level.

0

50

100

150

200

250

300

350

400

Un

its

Sold

(Th

ou

san

ds)

Mainstream Brand CPO SalesCalendar Years 2011 - 2013

2011 2012 2013

Source: Autodata

0

20

40

60

80

100

120

Un

its

Sold

(Th

ou

san

ds)

Luxury Brand CPO SalesCalendar Years 2011 - 2013

2011 2012 2013

Source: Autodata

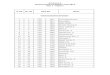

Mainstream Brand CPO Retail Sales

2013 v. 2014, YTD

Make 2013 YTD 2014 YTD % Change

Buick 9,055 11,175 23%

Chevrolet 83,582 93,017 11%

Chrysler 8,285 9,036 9%

Dodge 18,311 21,531 18%

Ford 62,390 77,672 24%

GMC 16,258 20,471 26%

Honda 78,567 77,980 -1%

Hyundai 23,953 30,278 26%

Jeep 12,433 15,658 26%

Kia 9,625 13,830 44%

Mazda 11,518 13,533 17%

Nissan 36,858 43,783 19%

Subaru 10,320 14,150 37%

Toyota 120,220 115,598 -4%

Volkswagen 31,988 29,393 -8%

Source: Autodata

Luxury Brand CPO Retail Sales2013 v. 2014, YTD

Make 2013 YTD 2014 YTD % Change

Acura 13,116 13,439 2%

Audi 12,311 14,016 14%

BMW 26,314 30,011 14%

Cadillac 6,316 6,705 6%

Infiniti 3,629 5,802 60%

Jaguar 1,172 1,894 62%

Land Rover 2,258 3,750 66%

Lexus 23,388 24,186 3%

Lincoln 6,741 8,099 20%

Mercedes-Benz 33,091 37,716 14%

Porsche 3,260 3,672 13%

Volvo 3,786 4,037 7%

Source: Autodata

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 6

© 2014 NADA Used Card Guide

CPO Premiums: Consumer Expectations vs. Actual

Certified pre-owned vehicles cost more than their non-certified counterparts because of

the expenses associated with a comprehensive inspection, repairs required to meet

manufacturer certification standards (e.g., worn tires replaced, cracked windshield

repaired, worn brake pads replaced, etc.) and the bumper-to-bumper extended

warranty. Most CPO programs also include roadside assistance and a free vehicle history

report, and some include free scheduled maintenance (e.g., oil changes, tire rotations,

etc.).

Results from AutoTrader.com’s 2013 CPO study showed that many consumers are still

unfamiliar with all that goes into certifying a used vehicle. More than a third of new car

shoppers were unaware that a certified vehicle was fully inspected and 45% didn’t

realize that a CPO vehicle came with an extended warranty. Used car shopper inspection

and warranty awareness wasn’t any better, as 32% and 46%, respectively, were

unfamiliar with these program aspects.

Consumer unfamiliarity with CPO benefits can largely explain why sizable percentages of

shoppers are unwilling to pay a premium for a CPO vehicle. AutoTrader.com data shows

that while 62% of new car buyers are willing to pay a CPO premium, just 34% of used car

shoppers are.

But while premium willingness is non-existent for some, the amount that agreeable

shoppers are prepared to pay has doubled. In AutoTrader.com’s 2011 CPO survey, the

average acceptable CPO premium for new and used car shoppers was $1,245 and

$1,292, respectively, but these amounts jumped to $2,940 and $2,163 in the 2013

survey.

A review of CPO sales data indicates that premiums

are predominantly well below the consumer

thresholds derived from AutoTrader.com’s latest

report. Records collected by NADA from mainstream

and luxury manufacturers show that 75% of CPO

transactions carried premiums ranging from $500-

$2,000; this disparity implies that CPO’s value

proposition actually exceeds consumer expectations.

As far as the differences in CPO prices are concerned,

NADA concludes that prices are dictated by four

primary factors – vehicle brand, age, price and the

competitiveness of a given manufacturer’s CPO

0

100

200

300

400

500

600

Vo

lum

e

CPO Premium

NADA Analysis: Distribution of CPO PremiumsThe CPO premium relative to a non-certified retail transation price.

Source: NADA Used Car Guide

75% of transactions have a CPO premium ranging between $500 - $2,000.

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 7

© 2014 NADA Used Card Guide

program (i.e., length of warranty, mileage allowance,

etc.). Correspondingly, these factors and CPO sales

data form the basis of NADA’s certified pre-owned

value methodology and dictate the CPO values found

in NADA’s Official Used Car Guide®.

Generally speaking, CPO values are greatest for

newer and more expensive models backed by

programs that extend bumper-to-bumper and

powertrain warranties out the furthest, while values

are lower for older, less expensive and less

competitive programs.

Currently, NADA’s used vehicle certified pre-owned

premiums range from an average of $1,532 for 2008 model year vehicles to $1,737 for

2014 vehicles*; mainstream brand CPO values range from an average of $1,166 to

$1,371, while luxury values range from $1,992 to $2,381.

At the brand level and specific to three-year old 2011 model year vehicles, Ford’s CPO

value average of $1,486 topped other mainstream CPO values, but was followed closely

by GMC’s average of $1,424. With respective figures of $1,284 and $1,222, Toyota and

Chevrolet CPO premiums are a bit further down the line, while Scion, Suzuki and SMART

each carry CPO premiums below

$900. As for luxury brands,

Mercedes’ average premium of

$2,909 is currently $300 higher

than second-place Porsche’s

$2,605 average, while Acura’s

$1,525 figure is the lowest of the

group.

Conclusion

With demand and supply now

moving solidly in the right

direction, CPO vehicle sales

should achieve meaningful

growth over the next few years.

$0

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$2,000

$2,250

$2,500

$2,750

2008 2009 2010 2011 2012 2013 2014

CP

O V

alu

e

Model Year

NADA Official Used Car Guide Certified Pre-Owned ValuesAverage CPO value by model year and vehicle type

Luxury Mainstream Total

Source: NADA Used Car Guide

*Note: 2008 MY averages are higher due to

changes in Brand mix.

$1,525

$1,650

$1,709

$1,855

$1,870

$1,878

$2,018

$2,068

$2,161

$2,175

$2,605

$2,909

$0 $1,000 $2,000 $3,000 $4,000

ACURA

INFINITI

VOLVO

LINCOLN

CADILLAC

AUDI

BMW

LAND ROVER

JAGUAR

LEXUS

PORSCHE

MERCEDES-BENZ

NADA CPO Values: Luxury Brands2011 model year vehicles

Source: NADA Used Car Guide

$750

$844

$883

$949

$987

$993

$1,050

$1,064

$1,067

$1,083

$1,132

$1,134

$1,148

$1,175

$1,182

$1,190

$1,222

$1,284

$1,424

$1,486

$0 $500 $1,000 $1,500 $2,000

SMART

SUZUKI

SCION

MITSUBISHI

MAZDA

KIA

MINI

HONDA

VOLKSWAGEN

CHRYSLER

JEEP

HYUNDAI

BUICK

SUBARU

DODGE

NISSAN

CHEVROLET

TOYOTA

GMC LIGHT DUTY

FORD

NADA CPO Values: Mainstream Brands2011 model year vehicles

Source: NADA Used Car Guide

*Note that of the 37 brands with CPO programs, 13 cover vehicles from the 2008 model year or newer and 21 from the 2009 model year and up; as a result,

differences in brand mix (i.e., fewer CPO-eligible mainstream vehicles for the ’08 model year) will influence model year averages.

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 8

© 2014 NADA Used Card Guide

To ensure this opportunity is maximized, manufacturers will need to enhance marketing

efforts to clearly outline to consumers all that certification entails. The substantial

benefits associated with buying CPO – the rigorous reconditioning, extended warranty

coverage and peace of mind that the vehicle is backed by the factory and its dealer

partners – should make the task less challenging.

Having a better understanding of CPO premiums should help support certified

consideration as well, especially since CPO premiums deemed tolerable by consumers

are above current sales levels. In addition, consumers who currently believe they can’t

afford a CPO vehicle might reconsider if they had a realistic idea as to what the

additional cost would be and the relative value of benefits for which they would be

paying.

Given that certified pre-owned sales account for roughly 13% of all used vehicle sales at

franchised dealerships, there is huge potential for CPO growth moving forward. In the

end, cultivating consumer familiarity and understanding will play a lead role in dictating

how quickly and how high CPO sales grow.

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 9

© 2014 NADA Used Card Guide

AT NADA USED CAR GUIDE

Financial Industry, Accounting, Legal, OEM Captive Steve Stafford 800.248.6232 x7275 [email protected]

Director, Sales and Customer Service Dan Ruddy 800.248.6232 x4707 [email protected]

Credit Unions, Fleet, Lease, Rental Industry, Government Doug Ott 800.248.6232 x4710 [email protected]

Automotive OEMs Stu Zalud 800.248.6232 x4636 [email protected]

Automotive Dealers, Auctions, Insurance Jim Dodd 800.248.6232 x7115 [email protected]

PR Manager Allyson Toolan 800.248.6232 x7165 [email protected]

Business Development Manager James Gibson 800.248.6232 x7136 [email protected]

What’s New

Available on iPhone, iPad and Android devices, the recently enhanced NADA MarketValues is

the fastest, easiest and most cost-efficient way to make smart vehicle decisions on the go. This

native app allows you to get your NADA values anywhere, anytime without an Internet

connection. Subscriptions start at $50 per month and when you download NADA

MarketValues from Google Play or the Apple Store for $1.99, you’ll receive a FREE 30-day trial!

On the Road

Dan Ruddy and Larry Dixon are attending the 18th Annual Non-Prime Auto Financing Conference on May 28—30 in Fort Worth,

Texas. Larry is speaking on a panel titled “Optimizing Collateral Values in Auto Financing” on Thursday, May 29 at 4:00 p.m.

Mike Stanton and Jim Dodd are attending the NIADA Convention and Expo from June 23—26 in Las Vegas, where NADA Used Car

Guide is co-sponsoring the National Quality Dealer Awards. Stop by booth 414 to see Jim.

About NADA Used Car Guide

Since 1933, NADA Used Car Guide has earned its reputation as the leading provider of vehicle valuation

products, services and information to businesses throughout the United States and worldwide. NADA’s

editorial team collects and analyzes over one million combined automotive and truck wholesale and

retail transactions per month. Its guidebooks, auction data, analysis, and data solutions offer

automotive/truck, finance, insurance and government professionals the timely information and reliable

solutions they need to make better business decisions. Visit nada.com/b2b to learn more.

Perspective | May 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 10

© 2014 NADA Used Card Guide

NADA CONSULTING SERVICES

NADA’s market intelligence team leverages a database of nearly 200 million automotive transactions and more than

100 economic and automotive market-related series to describe the factors driving current trends to help industry

stakeholders make more informed decisions. Analyzing data at both wholesale and retail levels, the team continuously

provides content that is both useful and usable to the automotive industry, financial institutions, businesses and

consumers.

Complemented by NADA’s analytics team, which maintains and advances NADA’s internal forecasting models and

develops customized forecasting solutions for automotive clients, the market intelligence team is responsible for

publishing white papers, special reports and the Used Car & Truck Blog. Throughout every piece of content, the team

strives to go beyond what is happening in the automotive industry to confidently answer why it is happening and how it

will impact the market in the future.

Senior Director, Vehicle Analysis & Analytics Jonathan Banks 800.248.6232 x4709 [email protected]

Senior Manager, Market Intelligence Larry Dixon 800.248.6232 x4713 [email protected]

Automotive Analyst David Paris 800.248.6232 x7044 [email protected]

Automotive Analyst Joseph Choi 800.248.6232 x4706 [email protected]

ADDITIONAL RESOURCES

Connect with NADA

White Papers NADA’s white papers and special reports aim to inform industry stakeholders on current and expected used vehicle price movement to better maximize today’s opportunities and manage tomorrow’s risk.

Used Car & Truck Blog Written and managed by the Market Intelligence team, the Used Car & Truck Blog analyzes market data, lends insight into industry trends and highlights relevant events.

NADA Perspective

Leveraging data from various industry

sources and NADA’s analysts, NADA

Perspective takes a deep dive into a

range of industry trends to determine

why they are happening and what to

expect in the future.

Guidelines Updated monthly with a robust data set from various industry sources and NADA’s own proprietary analytical tool, Guidelines provides the insight needed to make decisions in today’s market.

Read our Blog

nada.com/usedcar

Follow Us on Twitter

@NADAUsedCarGde

Find Us on Facebook

Facebook.com/NADAUsedCarGuide

Watch Us on YouTube

Youtube.com/NADAUsedCarGuide

Disclaimer: NADA Used Car Guide makes no representations about future performance or results based on the data and the contents available in this report (“Guidelines”). Guidelines is provided for informational purposes only and is provided AS IS without warranty or guarantee of any kind. By accessing Guidel ines via email or the NADA website, you agree not to reprint, reproduce, or distribute Guidelines without the express written permission of NADA Used Car Guide.