Embed Size (px)

Citation preview

1

Cities as Warehouses:

The Survival of Main Street Retail

in a Digital World

2

© Yellow Pages Limited 2016

1

retail (noun) /ˈrēˌtāl/ the sale of goods to the public in relatively small quantities for use or consumption rather than for resale.

2

Table of Contents

Executive Summary 4

The Evolving Landscape of Canadian Retail 8Retail’s economic contribution to the Canadian economy 9

The internet is changing everything 11

More choices, changing habits 11

Power shift towards collaboration 13

Case Study: Don Tapscott talks retail 14

Ecommerce marketplaces are dominating 17

The new competition, know it or not 19

Impact of these giant marketplace players 20

Ongoing impact of the global financial crisis 21

“Bricks and mortar” is not going away 22

What’s the future of retail? 23

The Digital Retail Customer 24Avid online researcher 25

Armed with information 26

Showroomers and webroomers 27

Seeking and using omni-channels 31

In-store preferences over online 31

Online preferences over in-store 32

Mobile is on the move 32

Big fans of free shipping 32

3

The Retailer’s Imperative 36 It’s a digital world 37

The challenges of an effective digital presence 38

Digital adoption among retailers 40

Carving out a place on the digital street 43

Blending digital and physical 44

Case Study: Frank + Oak: Building a global brand across platforms 45

The augmented retail experience 47

Case Study: Selling wine online 48

Getting started 50

The questions before us all 50

Cities as Warehouses: Multi-Local can Compete with Multi-National 52 Fight, flight … or unite? 53

Local collaboration 53

“Cities as Warehouses” 54

How does it work? 54

Multiple benefits across the retail ecosystem 55

Neighbourhoods Matter 56

Case Study: I LOVE LOCAL (HFX) Taking an “uncommon” approach to collaboration 58

Retailers as policy stakeholders 60

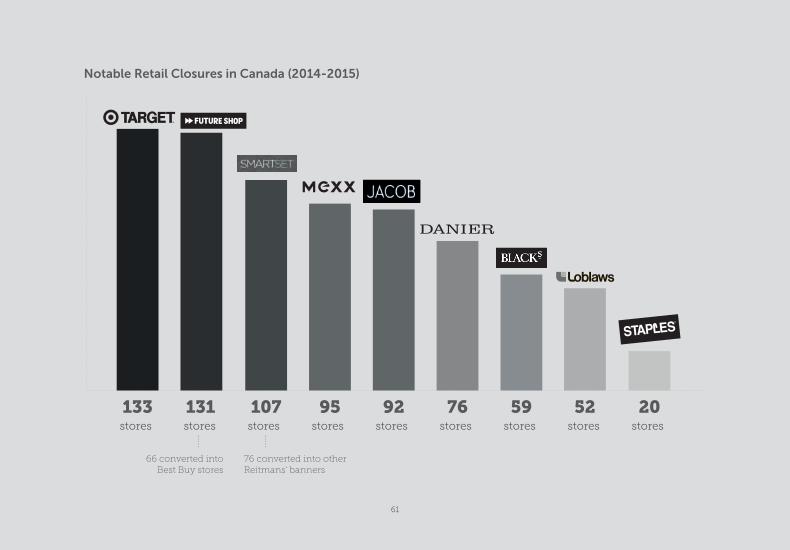

Costs of not making digital work locally 60

Reduced retail diversity 60

Significant economic impacts 62

Governments have a big stake 63

Taking the digital road forward 64

4

the Canadian consumer outpace most others consumers around the world.

And while this last factor – main street retail’s lag in digital adoption – is defining, it’s also troubling. The changing nature of retail in this country means that those local retailers not keeping up with new digital environments and habits are being left very far behind.

Three major factors have significantly impacted the traditional buyer-seller dynamic – and thus the retail experience – in Canada over the last several years. Digital lies at the heart of all of them.

1. The onset of the internet enabled real-time interplay between and among multiple participants. Interactions became digital. Supply and demand exchanges became digital. And the world became digital. This transformed traditional relationships between consumers and retailers.

2. The rise of giant ecommerce marketplaces are fundamentally re-shaping the entire retail sector. The sheer scope and well-financed strategies of these massive retailers is squeezing local retailers out of many

Executive Summary

Changing nature of retail competition

Retail in Canada is the very definition of fierce competition: it’s among the most aggressive sectors in the Canadian economic landscape. It’s woven into the Canadian fabric – and has been for centuries – but in ways that differ from other countries.

1. Retail in Canada has a significant participation from small businesses, operating at a local level;

2. The country’s proximity to the United States, plus a strong foreign retail presence within Canadian borders, creates a variety of choices for consumers, and an even more competitive market for local retailers;

3. Digital capabilities of Canadian retailers – particularly those on main streets in neighbourhoods across the country – lag considerably behind those of their global counterparts, while the digital capabilities of

5

transactions that the latter used to have with local customers.

3. Among the many effects of the global financial crisis in 2008 were changing customer habits that put a premium on savings like never before. This has translated into persistent price sensitivity among retail customers and shrinking margins for many local retailers. Widespread internet use among buyers means they seek the best prices from retailers who may or may not be local. But if it’s a deal, they’ll take it.

Each of these factors is powerful in its own right. Taken together, the cumulative effects are as profound as they are irreversible.

Retail in Canada is currently at a crossroads. The digital shopping habits of customers – who are increasingly drawn to ecommerce marketplaces – are well beyond the capacities of most main street retailers. And many smaller retailers are not prepared to take on the digital imperative required to not only compete in today’s rapidly changing economy, but to survive in it. Yet, the next step forward lies exactly in all the promises and challenges of digital.

5%

23%of retailers think customers shop in stores to speak with retail staff

of customers actually shop in stores to speak with retail staff.1

of buyers are interested in doing prior research online; retailers without a meaningful digital presence are not able to fully participate in Canada’s massive retail market – they aren’t being seen by customers.2

85%

Gap in Perceptions

1. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

2. Ibid.

Moreover, the need to close yawning gaps between buyers and sellers cannot solely be the responsibility of the retail sector alone. It must be shared by everyone in Canada’s retail ecosystem, as well as Canada’s economic stakeholders.

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

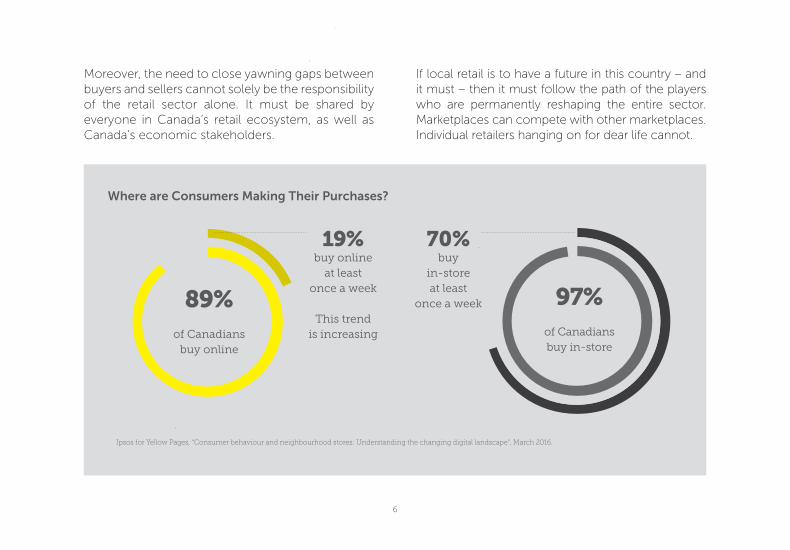

Where are Consumers Making Their Purchases?

If local retail is to have a future in this country – and it must – then it must follow the path of the players who are permanently reshaping the entire sector. Marketplaces can compete with other marketplaces. Individual retailers hanging on for dear life cannot.

6

89% of Canadians

buy online

70% buy

in-storeat least

once a week

19% buy online

at least once a week

This trendis increasing

97%

of Canadiansbuy in-store

7

This white paper further explores how the “cities as warehouses” concept may provide some needed answers to the digital gaps in Canada’s retail sector. It also outlines the need for a departure from traditional concepts of competition in retail and emphasizes the need for intra- and inter-sector collaboration to take on the unique challenges facing retail in this country.

The imperative to close the current gaps between increasingly digitized consumers and lagging local retail players is also shared by everyone in Canada’s retail ecosystem, as well as Canada’s economic stakeholders.

Digital should be used as a tool to grow Canada’s retail sector, particularly at the local level, but equally understood as a threat to its survival if not harnessed properly and collaboratively.

Equally, collaboration is a powerful solution to the challenges posed by ecommerce marketplaces and changing shopping habits.

It is both the opportunity and the challenge that lie before everyone.

Take for example, cycling. Members of a peloton compete fiercely with each other. However, by acting together, each member will almost certainly finish better than if he or she remained alone. But once dropped from the pack, it’s very hard if not impossible for retailers – like cyclists – to rejoin. They’re out of the race sooner or later. Their chances are much stronger if they work together.

The answer, in other words, lies in collaboration among local retail competitors.

And it lies in fulfilling a vision of our “cities as warehouses”. Essentially, creating, building and investing in the creation of a local digital marketplace in Canada. This would take the form of a digital destination and use geo-localization technology to recreate online the collective retail strengths of a local shopping area. This approach allows those areas – and local retailers within them – to thrive by retaining vibrant main streets with physical retail presence, but to equally compete in the face of global forces manifest in large-scale ecommerce players.

8

The Evolving Landscape

of Canadian Retail

9

Retail’s economic contribution to the Canadian economy

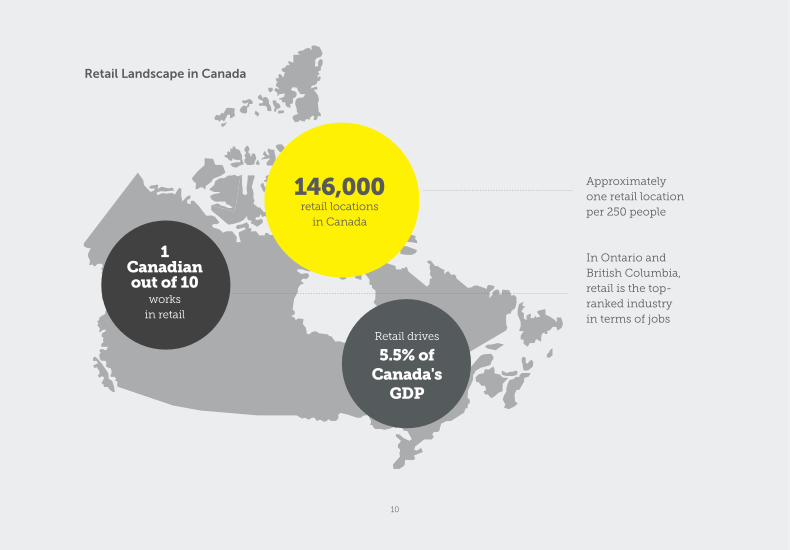

In 2015, the retail sector represented 5.5% of GDP, ranking it 11th out of 22 industries.3 Retail’s significant economic footprint is even stronger when considering jobs.

The Labour Force survey from Statistics Canada shows that retail’s total share of jobs in 2014 was 11.6%, ranking it second of all industries at the national level. In fact, retail trade is the top-ranked industry in terms of jobs in two provinces – Ontario and British Columbia – and ranks second in all other provinces.4 In total, there were approximately 146,000 retail locations across Canada.5 Meanwhile, the recent retail sales picture shows a modest year-over-year increase in 2015 to 2014.

Total retail sales in Canada in December 2015 were $43.2 billion.6

There are few segments in the Canadian economy as connected to local communities as retail. From corner shops to corporate stores, retail is of vital importance to owners, tenants, employees, customers, suppliers, neighbours and policy makers alike.

While there are no universally-accepted definitions of “local” or “neighbourhood” retail in Canada, we take it to mean any of the following:

• Independently-owned retail store(i.e. florist)

• Independently-owned franchise ofa national brand (i.e. Canadian Tire)

• Corporate retailers who havechosen to move storefronts ontomain street and integrate with theneighbourhood (i.e. lululemon)

3. Statistics Canada, “Gross domestic product at basic prices, by industry (monthly)”,www.statcan.gc.ca.

4. StatsCan figures found in RCC’s “Retail Fast Facts”, January 2016. www.retailcouncil.org. Canada’s three territories were not included in this survey.

5. Ibid.6. Retail Council of Canada, “Retail Conditions Report: Outlook 2016”,

www.retailcouncil.org. The survey was conducted during the period of February 8-12, 2016, and it includes results from 57 retailers operating almost 10,000 stores.

Retail Landscape in Canada

Retail drives 5.5% of

Canada's GDP

Approximatelyone retail locationper 250 people

146,000 retail locations

in Canada

In Ontario andBritish Columbia,retail is the top- ranked industry in terms of jobs

1Canadianout of 10

works in retail

10

11

Taking a closer look at local retail in today’s economy reveals three powerful forces fundamentally re-shaping the industry. Together, they are key parts of the big shift that is underway.

1. The internet is changing everything

Before the internet, shoppers’ retail choices were limited by what they could see and touch on the retail main street in their neighbourhood, or a short drive away.

Local retailers set the prices and stocked the shelves. This put a bias on habit. Based on experience, shoppers knew a certain retailer would (usually) have what they wanted at a price they were (usually) willing to pay. So these customers spent their money in the neighbourhood, thereby contributing to the local community’s retail vibrancy.

Retailers knew and appreciated this, and they focused on serving local customers. They also knew that customers evolved through predictable buying habits as they aged and their income levels grew. This made customer segmentation strategies fairly straightforward in the analogue economy.

The internet changed all of that.

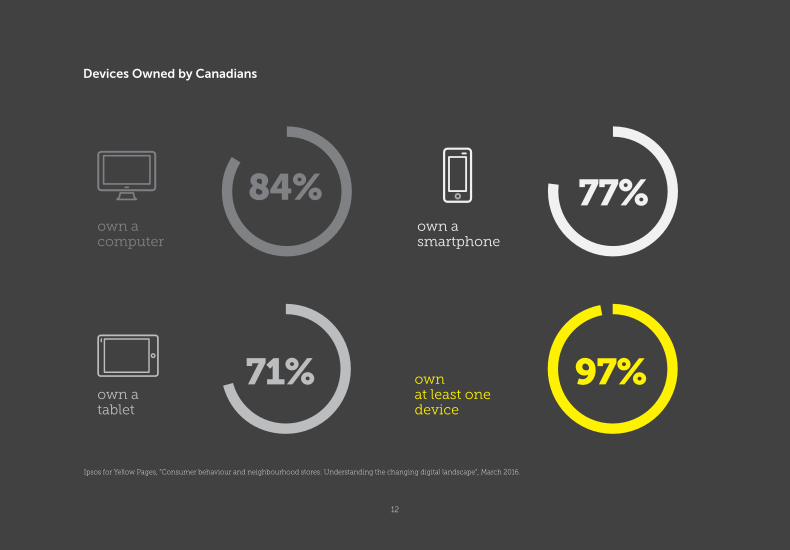

Geography is no longer a limiting, or even a defining, characteristic of the web-driven retail experience. Why should it be when the world is connected digitally and when 97% of Canadian consumers own some sort of digital device?

Consumers can just as easily browse the product list of a retailer based thousands of kilometres away as they can drop into a local store to browse the shelves.

Many Canadians do both.

More choices, changing habits

With the internet, consumers have the choice of shopping on local physical streets or on the ubiquitous “digital” street that never closes.

A confluence of websites, online search for products and price discovery and social media platforms that spread news – good and bad – at light speed around the globe are increasingly the norm in local retail. The internet connects vastly more buyers and sellers in far more ways than ever before.

own a computer

Devices Owned by Canadians

own a smartphone

own a tablet

84% 77%

71% 97%own at least one device

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

12

13

“We used to view customers as being outside our organization – we push stuff out to them. Now we can view them as being inside our business, co-innovating with you.” Don Tapscott, CEO, The Tapscott Group Inc.

Retailers across Canada now regularly reach out to customers (and potential customers) in asking them to share their shopping experiences across social networks and digital platforms.

“The use of digital goes well beyond conversion of sales. Buyers become advocates.” Gordon Stevens, President, The Uncommon Group, Halifax.

The purchasing, pricing and branding power that once rested with retailers is being shared with consumers.

It’s all about collaboration in the new digital retail world.

At the same time, customer habits are changing. Millennials, those born in the early 1980s onwards, are re-defining aspects of the entire economy by virtue of their size as a group (30% of the population) and their collective shopping habits. They are among the most educated of consumers and consistently conduct pre-purchase research online including price comparison, reviews and product comparison. Most know exactly what they plan to buy before they walk into the store. 7

Among other things, traditional, pre-internet gene-rational differences are being turned upside down. Passing on knowledge from older to younger generations is no longer the norm. Kids are teaching seniors about technology and trends, and seniors are shopping like kids across an array of physical and digital platforms. Habits are less predictable in the digital age.

Power shift towards collaboration

Using an expanding suite of digital tools, retailers and consumers are now collaborating more than ever in the retail and brand experience.

7. Yconic, “The Millennial Shopper: More social and educated than ever before”, February 2016

14

Case Study

Don Tapscott talks retail

A global digital guru, Don Tapscott has been at the forefront of innovation for many years. Author of several influential books, Don spoke with Yellow Pages about the challenges and opportunities facing local retailers in the digital economy, a phrase he coined more than 20 years ago.

What does mass collaboration mean in the digital economy for retailers?

Retail can turn consumers to producers, or what I called “prosumers” more than 20 years ago in my book The Digital Economy.

The old world of retail was an age of scale and mass – mass production, mass education, mass distribution, mass media and mass production. Owners controlled everything, and they pushed out standardized units (be they products or services) to buyers who were passive recipients of those units.

In today’s digital age, there’s much more interaction and collaboration. Some companies don’t produce anything now until the market demands it. And prosumers – customers who become producers – are creating ads for companies like Doritos.

Every retail company needs to have a digital-physical strategy. And that’s not just a website, or a website that does transactions to global market from a local store. The next step now is to go beyond that, to engage your consumer and to build communities.

In this big shift, retailers have to go beyond just focusing on their customers to engaging them.

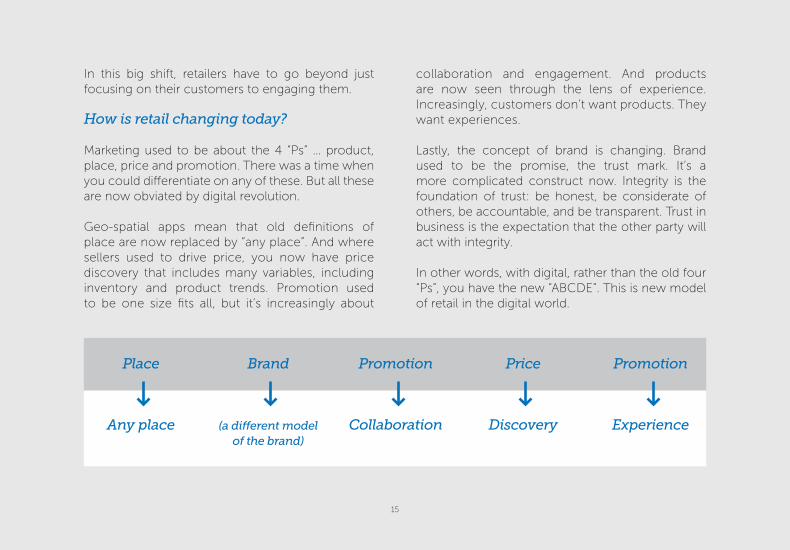

How is retail changing today?

Marketing used to be about the 4 “Ps” … product, place, price and promotion. There was a time when you could differentiate on any of these. But all these are now obviated by digital revolution.

Geo-spatial apps mean that old definitions of place are now replaced by “any place”. And where sellers used to drive price, you now have price discovery that includes many variables, including inventory and product trends. Promotion used to be one size fits all, but it’s increasingly about

collaboration and engagement. And products are now seen through the lens of experience. Increasingly, customers don’t want products. They want experiences.

Lastly, the concept of brand is changing. Brand used to be the promise, the trust mark. It’s a more complicated construct now. Integrity is the foundation of trust: be honest, be considerate of others, be accountable, and be transparent. Trust in business is the expectation that the other party will act with integrity.

In other words, with digital, rather than the old four “Ps”, you have the new “ABCDE”. This is new model of retail in the digital world.

15

Place

Any place

Brand

(a different modelof the brand)

Promotion

Collaboration

Price

Discovery

Promotion

Experience

16

give him your frequent flyer card and your entire transactional history. You just give him your driver’s licence.

In retail, and if we do this right, we can be in the halcyon age of entrepreneurship. It will be way easier to set up a business, and small companies can have all the capabilities of big companies without the main liabilities and bureaucracy.

With innovations like blockchain, customers can be inside and your talent can be outside. The world can become your HR department. The blockchain radically drops your transaction and collaboration costs. It moves companies toward network and molecular models. All of this will favour small firms.

Don Tapscott and co-author, Alex Tapscott re-cently released a new book entitled Blockchain Revolution: How the Technology Behind Bitcoin is Changing Money, Business, and the World.

* The blockchain is an online ledger of transactions that is seen and shared by multiple market participants. Bitcoin is the best-known example of blockchain, but its application does much farther than that. Retailers, banks and governments are all innovating based on blockchain technology.

Take Starbucks as the example. Starbucks is now considered “the third place”. People talk about work, home and Starbucks. That’s because they transformed the coffee experience into something you can’t get anywhere else.

What is the role of “small data” for local retailers in a world of big data for large-scale retailers? And does the blockchain* offer any opportunities for local retailers?

The blockchain revolution changes everything in retail, and it changes the data situation quite profoundly in ways that will be, in the short term, injurious to the big companies that are capturing all of our data, not the little guys where we buy things.

What if we each had our own personal identity in a black box on the blockchain? Instead of a company like Facebook owning that identity, we own it. And we only give out that information which is required, like it used to be back in the day. You get stopped by a police officer and you don’t

17

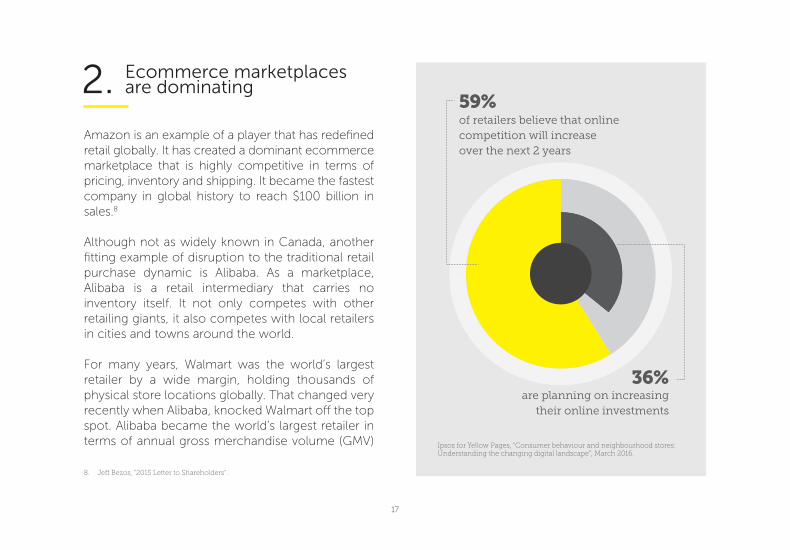

2. Ecommerce marketplacesare dominating

Amazon is an example of a player that has redefined retail globally. It has created a dominant ecommerce marketplace that is highly competitive in terms of pricing, inventory and shipping. It became the fastest company in global history to reach $100 billion in sales.8

Although not as widely known in Canada, another fitting example of disruption to the traditional retail purchase dynamic is Alibaba. As a marketplace, Alibaba is a retail intermediary that carries no inventory itself. It not only competes with other retailing giants, it also competes with local retailers in cities and towns around the world.

For many years, Walmart was the world’s largest retailer by a wide margin, holding thousands of physical store locations globally. That changed very recently when Alibaba, knocked Walmart off the top spot. Alibaba became the world’s largest retailer in terms of annual gross merchandise volume (GMV)

8. Jeff Bezos, “2015 Letter to Shareholders”.

59%of retailers believe that online competition will increase over the next 2 years

36%are planning on increasing

their online investments

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

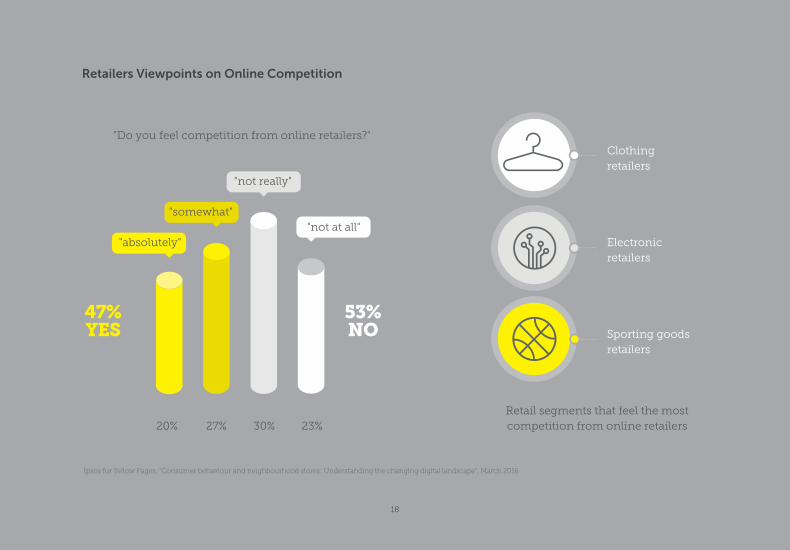

"Do you feel competition from online retailers?"

Retail segments that feel the most competition from online retailers

Retailers Viewpoints on Online Competition

Clothing retailers

Electronic retailers

Sporting goods retailers

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

"absolutely"

"somewhat"

"not really"

"not at all"

47%YES

53%NO

20% 27% 30% 23%

18

19

and sophisticated pricing algorithms, these global companies are scooping up customers and sales across Canada.

For instance, Canada is one of eBay’s most success-ful global markets, with Canadians spending more than $1 billion buying goods from the site each year. This makes eBay Canada’s second largest online retailer behind Amazon.13

Unlike ecommerce marketplaces, however, neighbour-hood retailers accustomed to competing against retailers in the same or nearby neighbourhoods can’t expand their floor space by an equally infinite amount. And they can’t hold inventories at massive scale. What inventory they do carry can only reach consumers in their immediate vicinity, further narrowing their potential markets.

At the same time, the art of pricing – a key factor mentioned earlier in driving consumer interest – has become a science. Using advanced analytics, companies such as Amazon can track and change their prices by the minute.

– $485 billion in 2015 – surpassing Walmart’s annualrevenue of $482 billion.9 Mobile accounted for 68%of Alibaba’s total GMV.10 The third largest retailerin the world, Costco, is well behind these twobehemoths, with revenues of $116 billion in 2015.11

“We used 13 years to demonstrate the power of a different business model compared with brick-and-mortar retailers.” Alibaba Group12

The new competition, know it or not

Many (if not most) Canadian retailers now directly or indirectly compete against enormous ecommerce players such as Amazon and Alibaba, whether they know it or not. This also includes large physical retailers like Walmart who are investing heavily in the Canadian ecommerce market. Armed as these players are with access to massive inventories,

13. Hollie Shaw, “eBay aims to transform shopping experience to compete with online giants Alibaba, Amazon”, Financial Post, March 28, 2016.

9. Alibaba Group, 6-K SEC Filing, April 5, 2016.10. Alibaba Group, December Quarter 2015 Results.11. Costco letter to shareholders, December 17, 2015.12. IGC Retail Analysis, “Alibaba Overtakes Walmart”, April 7, 2016.

20

by, third parties such as search engines. Often, these local retailers have to pay to be seen, through search engine marketing (SEM) campaigns, involving the promotion of a retailer website in search results through paid advertising. Even small advertising dollar investments do eventually add up for neighbourhood-level retailers.

Free or less costly options such as search engine optimization (SEO) which involves optimizing a website by keywords to affect its visibility in a search engine’s unpaid results can be wrought with challenges for local retailers. Smaller shops – unless they have very specialized inventory – can also be disadvantaged in digital search engines due to ongoing adjustments to algorithms that do not favour results with limited traffic or links.

Big retailers by contrast are well-oiled SEO and SEM machines with the resources to devote to upkeeping and adjusting campaigns as technology and digital marketing evolve.

Combine this with the shrinking profit margins experienced by many smaller retailers, and the reality of retail in the face of the rising digital competition looks stark on streets and in malls from sea to shining sea.

This means price discovery takes on a whole new definition and importance for retailers. This, while opening at 10 a.m. (if not earlier) and closing at 6 p.m. (if not later), and serving customers, staffing, cleaning, marketing and keeping up inventories.

The burden on local retailers to manage their operations in addition to competing in the digital space with dominant global players is a heavy one.

Impact of these giant marketplace players

The gravitational pull of these giant retailers means that neighbourhood retailers are now seeing an outflow of shoppers’ dollars, where once that money was kept locally.14

Single retail stores in this vast galaxy of digital – dominated by a small number of huge players – will be very challenged to capture enough digital eyeballs to maintain, let alone increase, their sales.

What’s more, the visibility in the digital space of these stores is often dependent upon, or decided

14. Shelly Banjo, “How Amazon will kill your local grocer”, Bloomberg.com, April 8, 2016.

21

Governor Stephen Poloz preparing Canadians to brace for a low dollar, higher-priced imports and rocky growth “for several years”.17

In a low-inflation economy experiencing lower-than-normal consumer spending, coupled with high debt loads18, retail consumers are very likely to continue to save whenever possible. Turning first to the internet, consumers are arming themselves with pre-purchase information online – they’re looking for the best deals – before they purchase and, regardless of emotional attachment to local, will be product and price-driven first and foremost.

“Retailers are apprehensive about the impact of the financial and world economic turmoil on consumer confidence.” Retail Council of Canada, “Retail Conditions Report: Outlook 2016”

3. Ongoing impact of the global financial crisis

The full impact of the global financial crisis in 2008-2009 was rapid and intense.

This was particularly true for a retail sector that was looking to the 2008 holiday season to boost already-flagging sales. One British analyst at the time said, the last three months of 2008 would lead into “the worst Christmas for 30 years” in terms of retail spend.15

While Canada was spared some of the economic scars suffered by other countries, the impact of that financial crisis is nonetheless still being felt here years later.

Plummeting oil prices in a resource-based national economy continue to dampen macro-economic growth in parts of Canada16, with Bank of Canada

15. Myra Butterworth, “Financial Crisis: Retailers face worse conditions for 30 years”, The Telegraph, September 30, 2008.

16. Bank of Canada, “Business Outlook Survey”, Spring 2016.

17. Barrie McKenna, “Aftermath of resource rout will be long and painful: Poloz”, The Globe and Mail, January 7, 2016.

18. TD Economics, Quarterly Economic Forecast, March 23, 2016.

22

A side effect of the retailer’s expansion into physical streets was the ability to access completely new portions of customers that they had not traditionally been able to reach online.

The online operations and business focus of the company were very targeted towards men, ages 25 to 35 and creatively inclined. What the founders discovered when opening their neighbourhood level locations was they were able to access customers through the element of discovery, having people wander in off the streets. In their physical stores, they began developing a strong customer base among men in their 40s and were surprised by how many women were also shopping in their locations.

Through their stores, they were able to quantify a substantial percentage of women purchasing menswear that they had only anecdotally been aware of in their online operations.19

“Bricks and mortar” is not going away

Despite the emergence of pure digital players in retail, the traditional bricks and mortar retail destination still offers market opportunities that can’t be found in digital.

Frank + Oak, a men’s clothing store, is one example of a retailer that took the inverse journey. The company began and grew as a pure digital retail player. Yet, in 2013, began a journey to opening physical retail locations due to customer demand. Now counting 13 locations across North America, Frank + Oak physical stores cater to an urban crowd and provide a wide variety of services under one roof.

“Our customers were always asking us to have a physical presence, because they like shopping in traditional stores. But for us it was more a question of whether we wanted to take that leap. When we decided to do it, our existing customers liked it and we were able to find a whole new set of customers.” Hicham Ratnani, Co-Founder & COO, Frank + Oak

19. Ethan Song, Co-Founder, Frank + Oak. “Digital retail heads back to the future with old-fashioned stores”, National Post, October 18, 2014.

23

Other ecommerce players have equally opened physical locations to tap new consumer markets, including Shoes.com, ClearlyContacts.ca, LXR&Co., and Etsy.com to name a few. 20

However, digital continues to attract consumer attention and dollars. It cannot be ignored and in order for physical retail locations to continue to thrive, sustaining the vibrancy of the surrounding communities, an omni-channel approach to retail in Canada should no longer be a dream or desire, but considered a real need.

Yet, despite the fact that Canadians are among the world’s most digitally-connected and engaged users21, it is estimated that Canadian retailers are two years behind their U.S. counterparts in adopting online technology.22

Two years can be a lifetime in the competitive world of retail.

20. Ibid.21. CIRA, “.CA Factbook 2015”.22. CBC News, June 2015.

What’s the future of retail?

This all leads to three very important questions when considering the present and future of local retail in Canada:

• Who is the digital retail customer and what are their habits?

• What’s the retailers’ imperative to respond to retail’s changing landscape, particularly with respect to digital technologies and ecommerce players that are re-shaping that landscape?

• How can Canada’s retail ecosystem survive in the face of unprecedented and profound change that threatens its long-term future?

24

The Digital Retail Customer

25

In Canada today, 85% of buyers have an interest in going online to research something before they buy it either online or in a store. 24

This pre-purchase is primarily motivated by price comparison, product comparison and the ability to read other consumer reviews to validate purchase choices. This pre-purchase online research is most commonly conducted for electronics, appliances, cars, games and toys. However, other categories still drive the majority of research in-store where viewing the product is considered essential, such as food, plants, and health and beauty items.25

While key drivers of in-store purchasing in small neighbourhood retailers are the ability to interact with the product and the practicality of proximity, online buyers are also driven by practicality but in a different way. They want the convenience of not having to visit the store at all and have their purchase shipped right to their door.26

23. PwC, “2015 Retail Trends”, strategyand.pwc.com.

More and more Canadians are becoming omni-shoppers. That is, they use any number of methods to research, review and purchase goods and services. They want to “move easily across channels, have many retail and product options at their fingertips, and demand full visibility into inventory and pricing.”23

In other words, they want more flexibility in how they shop, be it locally or globally. They can walk down a neighbourhood street to a local retailer, or they can click their way through the “digital” street and look at countless retailers.

Many Canadians do both. For them, choice is paramount. They like the convenience of digital and the vitality of local retail.

Avid online researcher

Canadians have a clear bias toward checking out what they can find on the “digital” street before they do any actual in-person shopping.

24. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

25. Ibid.26. Ibid.

26

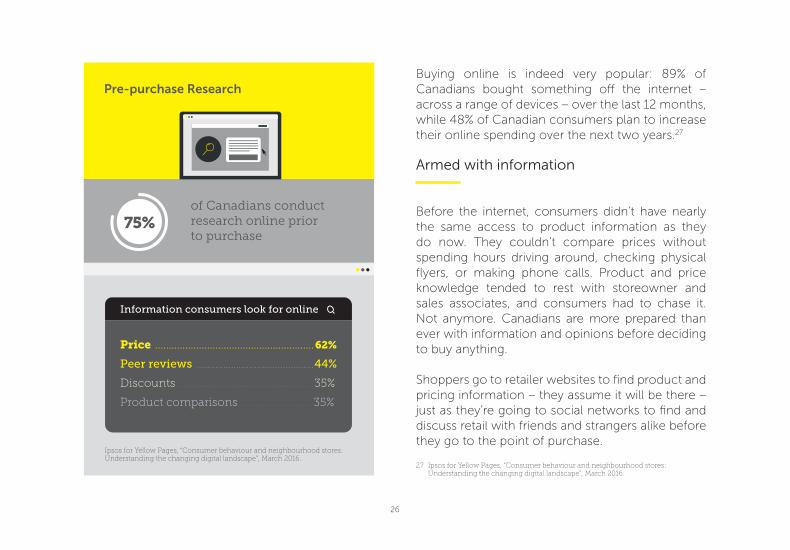

Pre-purchase ResearchBuying online is indeed very popular: 89% of Canadians bought something off the internet – across a range of devices – over the last 12 months, while 48% of Canadian consumers plan to increase their online spending over the next two years.27

Armed with information

Before the internet, consumers didn’t have nearly the same access to product information as they do now. They couldn’t compare prices without spending hours driving around, checking physical flyers, or making phone calls. Product and price knowledge tended to rest with storeowner and sales associates, and consumers had to chase it. Not anymore. Canadians are more prepared than ever with information and opinions before deciding to buy anything.

Shoppers go to retailer websites to find product and pricing information – they assume it will be there – just as they’re going to social networks to find and discuss retail with friends and strangers alike before they go to the point of purchase.

Information consumers look for online

Price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62%

Peer reviews . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44%

Discounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35%

Product comparisons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35%

of Canadians conduct research online prior to purchase

75%

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

27 Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

27

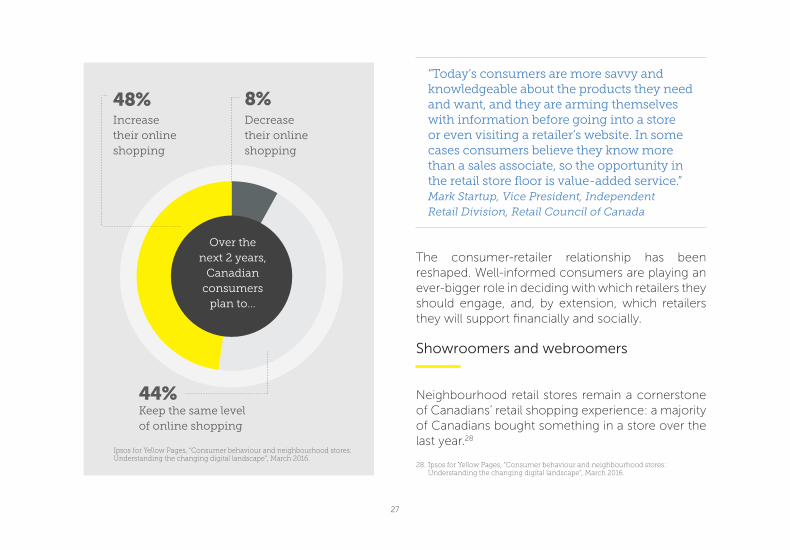

“Today’s consumers are more savvy and knowledgeable about the products they need and want, and they are arming themselves with information before going into a store or even visiting a retailer’s website. In some cases consumers believe they know more than a sales associate, so the opportunity in the retail store floor is value-added service.” Mark Startup, Vice President, Independent Retail Division, Retail Council of Canada

The consumer-retailer relationship has been reshaped. Well-informed consumers are playing an ever-bigger role in deciding with which retailers they should engage, and, by extension, which retailers they will support financially and socially.

Showroomers and webroomers

Neighbourhood retail stores remain a cornerstone of Canadians’ retail shopping experience: a majority of Canadians bought something in a store over the last year.28

28. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

48%Increase their online shopping

8%Decrease their online shopping

44%Keep the same level of online shopping

Over the next 2 years,

Canadian consumers

plan to...

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

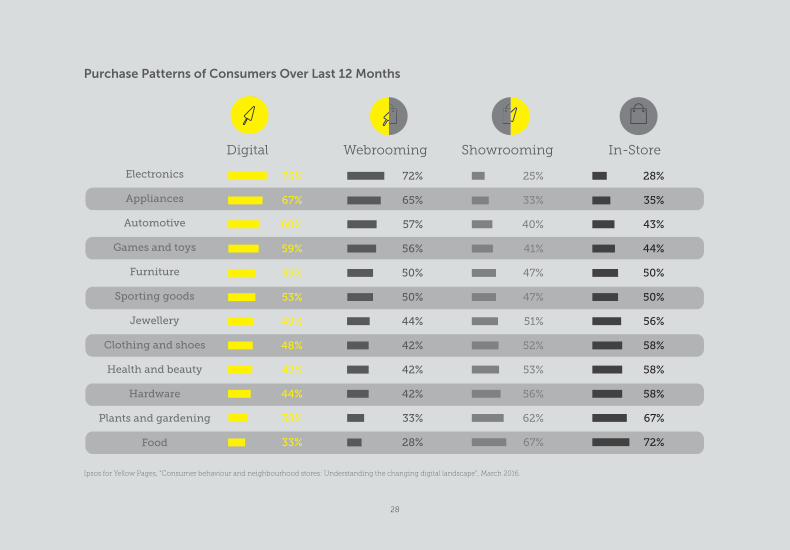

In-StoreShowroomingDigital Webrooming

Purchase Patterns of Consumers Over Last 12 Months

75% 72% 25% 28%

67% 65% 33% 35%

60% 57% 40% 43%

59% 56% 41% 44%

53% 50% 47% 50%

53% 50% 47% 50%

49% 44% 51% 56%

48% 42% 52% 58%

47% 42% 53% 58%

44% 42% 56% 58%

38% 33% 62% 67%

33% 28% 67% 72%

Electronics

Appliances

Automotive

Games and toys

Furniture

Sporting goods

Jewellery

Clothing and shoes

Health and beauty

Hardware

Plants and gardening

Food

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

28

29

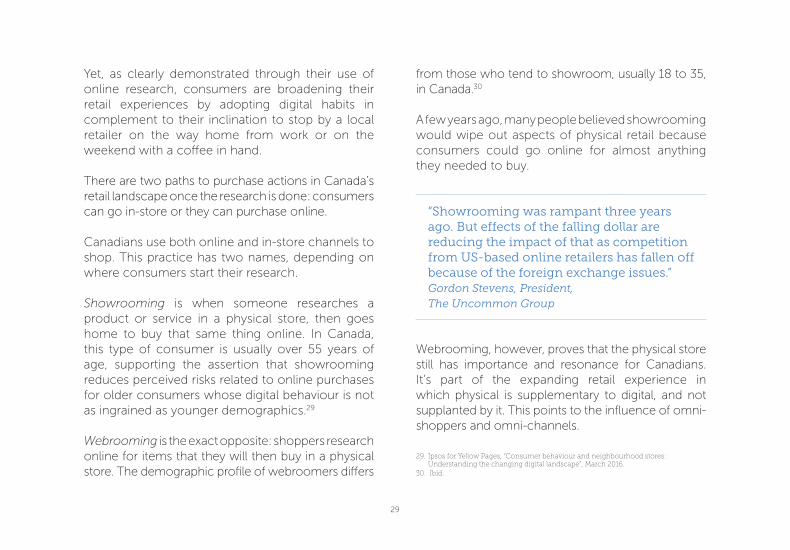

from those who tend to showroom, usually 18 to 35, in Canada.30

A few years ago, many people believed showrooming would wipe out aspects of physical retail because consumers could go online for almost anything they needed to buy.

“Showrooming was rampant three years ago. But effects of the falling dollar are reducing the impact of that as competition from US-based online retailers has fallen off because of the foreign exchange issues.” Gordon Stevens, President, The Uncommon Group

Webrooming, however, proves that the physical store still has importance and resonance for Canadians. It’s part of the expanding retail experience in which physical is supplementary to digital, and not supplanted by it. This points to the influence of omni-shoppers and omni-channels.

Yet, as clearly demonstrated through their use of online research, consumers are broadening their retail experiences by adopting digital habits in complement to their inclination to stop by a local retailer on the way home from work or on the weekend with a coffee in hand.

There are two paths to purchase actions in Canada’s retail landscape once the research is done: consumers can go in-store or they can purchase online.

Canadians use both online and in-store channels to shop. This practice has two names, depending on where consumers start their research.

Showrooming is when someone researches a product or service in a physical store, then goes home to buy that same thing online. In Canada, this type of consumer is usually over 55 years of age, supporting the assertion that showrooming reduces perceived risks related to online purchases for older consumers whose digital behaviour is not as ingrained as younger demographics.29

Webrooming is the exact opposite: shoppers research online for items that they will then buy in a physical store. The demographic profile of webroomers differs

29. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

30. Ibid.

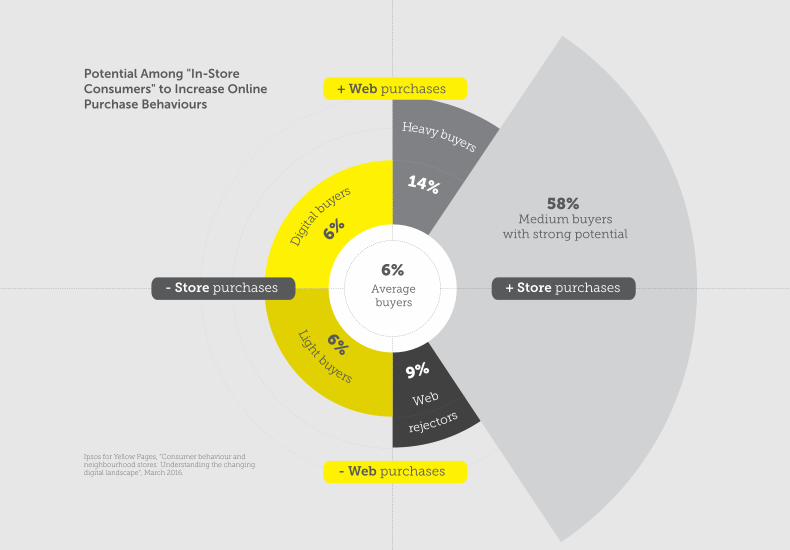

30

Averagebuyers

6%

Heavy buyers

Dig

ital b

uyers

Light buyers

rejectorsWeb

9%

6%

6%

14%58%

Medium buyerswith strong potential

+ Web purchases

- Store purchases + Store purchases

Potential Among "In-Store Consumers" to Increase Online Purchase Behaviours

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016. - Web purchases

31

“It comes down to senses. Online, you can see the imagery and the aesthetics. In the store, you can smell something, you can touch, feel a vibe. Store brings more than the visual experience. It’s broader, and it complements the online experience.” Hicham Ratnani, Co-Founder & COO, Frank + Oak.

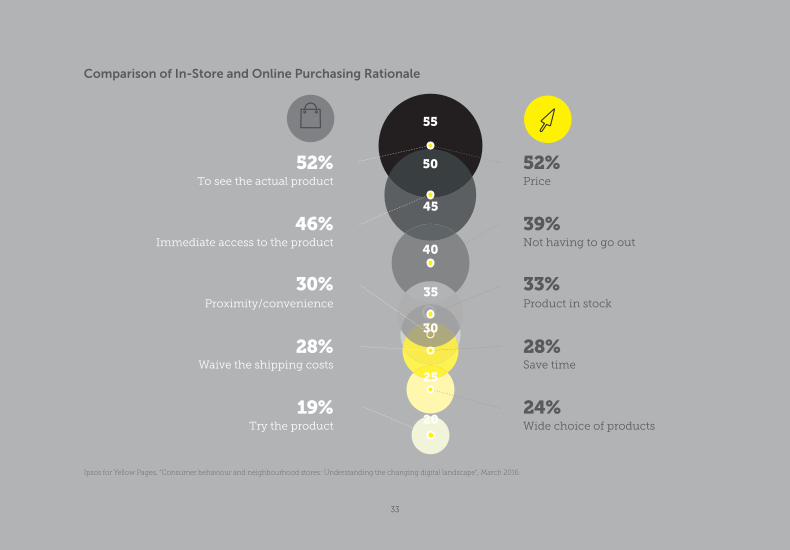

It’s perhaps not surprising, then, that food tops the list of what consumers go in-store to touch and buy, followed by health and beauty products, clothing and shoes.31

Similarly, time-pressed shoppers want to have immediate access to the product in order to buy it right then and there, after they’ve had the chance to see and touch it. Store proximity and convenience also drive the in-store decision making of customers. As well, customers avoid shipping costs when shopping locally in-store, and they can often return items more easily at a local store.

Seeking and using omni-channels

Canadians seek retailers who provide an ever-widening range of options when they are deciding whether to purchase something around the corner or across the globe.

“Customers come to us in various ways, across several digital platforms. Many check us out online several times.” John Clerides, Owner, Marquis Wine Cellars, Vancouver

Customers want and increasingly expect it all. But they have clear preferences for how and where they buy certain things.

In-store preferences over online

Canadians want to see certain products – they want to touch them – in a store. It’s an experience that’s impossible to replicate digitally.

Averagebuyers

6%

Heavy buyers

Dig

ital b

uyers

Light buyers

rejectorsWeb

9%

6%

6%

14%58%

Medium buyerswith strong potential

31. Ibid.

32

wallets, mobile devices are increasingly part of Canada’s retail ecosystem.

Canadians spend more time online with their mobile devices than with their computers: mobile accounts for 56% of all time spent on the internet in Canada, compared to 44% on desktops.33 And they are using their phones more than tablets in making purchases.

While Canadians may lag some other countries in using mobile for purchasing, we use smartphones more than anyone else to access loyalty programs: 23% of Canadians use their phones for this purpose, compared to a global figure of 16%.34 At the same time, Canadian retailers saw a 74% increase in year-over-year usage of mobile to complete transactions.35

Big fans of free shipping

Shipping is part and parcel of the online buying experience in Canada. From a customer’s perspective, free shipping is a huge driver when it comes to deciding whether to buy online or in a store.36

Online preferences over in-store

A different picture emerges when looking at what drives customers to purchase something online.

Price is the main reason why Canadians shop in the digital space.32 This is particularly true for commodity items – things you can find widely and where price is the only differentiator of note between any given seller. In these cases, being online allows buyers to quickly scan and compare pricing from their chosen location and time.

Mobile is on the move

Online shopping shrinks the time gap between urge and purchase, leading Canadians to buy an ever-widening array of goods and services from laptops, tablets and smart phones.

The use of mobile phones in retail illustrates the point. From searching on-the-go to using mobile

32. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

33. Anthony West, “Mobile is now more engaging than desktop in Canada”, October 19, 2015, www.comscore.com.

34. PwC, Total Retail 2015”, p. 17.35. Forrester, “Retail eCommerce in Canada 2015”, p. 11.36. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores:

Understanding the changing digital landscape”, March 2016.

50

55

45

40

20

35

30

25

Comparison of In-Store and Online Purchasing Rationale

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

52%Price

52%To see the actual product

39%Not having to go out

46%Immediate access to the product

33%Product in stock

30%Proximity/convenience

28%Save time

28%Waive the shipping costs

24%Wide choice of products

19%Try the product

33

34

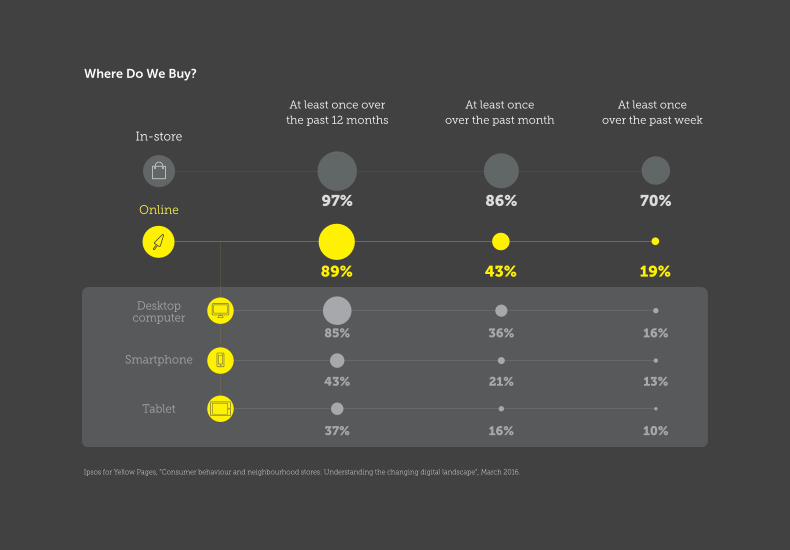

Where Do We Buy?

At least once over the past 12 months

At least onceover the past month

At least onceover the past week

In-store

Online86%

43%

70%

19%

97%

89%

85%

43%

37%

36%

21%

16%

16%

13%

10%

Desktop computer

Smartphone

Tablet

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

35

“Shipping costs for small businesses are “atrocious” and are the biggest cause of abandoned online shopping carts. The option of free shipping drives more sales than any product-price discounts.” Gordon Stevens, President, The Uncommon Group, Halifax.

Retailers, however, often have to absorb shipping costs if they want to attract online customers. The retail experience for most Canadian consumers these days boils down to two key questions they ask retailers:

• How much does it cost?

• Do you have it in stock?

Consumers answer these questions with their hearts, minds, and wallets only when they shop. Retailers have to constantly answer them in what has become a 24/7 retail world.

36

The Retailer’s Imperative

37

“If you’re a historical retailer, you had stores and now you have stores with the website attached. We are going to invert that model – we’ll be a digital commerce company with stores attached.” Brandon Stranzl, Executive Chairman, Sears Canada.39

It’s a digital world, and analogue solutions no longer work.

Retailers without a meaningful digital presence are completely missing out on opportunities to sell to an enormous consumer market that is initially seen by customers through a digital lens.

That means these retailers are, in effect, being punished by customers who may or may not know these physical retailers even exist. And that means retailers who can transition to digital are at least in position to put their best (and virtual) foot forward in being considered for a sale by information-enabled buyers.

It’s a digital world

Retail in Canada is morphing, quickly.

Driven by technology, soaring customer expecta-tions and competitors who are as likely to be based on another corner of the planet as located right across main street, the definition, execution and experience of retail in Canada is undergoing profound change.

Omni-channel marketing strategies, “click and collect” business models, online loyalty programs and mobile wallets are all now part of a rapidly expanding and increasingly sophisticated retail ecosystem in Canada.

For retailers, simply keeping up the pace of development, can be an all-consuming struggle. Some well-known retailers, such as Danier, don’t make it and wind up in liquidation.37 Others, like Sears Canada, are actively attempting turnarounds in the face of declining in-store sales.38

37. Canadian Press, “Danier Leather stores liquidating as retailer starts winding down”, www.cbc.ca, March 8, 2016.

38. Francine Kopun, “Sears Canada eyes online revamp”, Toronto Star, March 18, 2016. 39. Ibid.

38

These are not new concepts. But what is new is the expanding manner in which neighbourhood retailers have to engage and be engaging digitally given massive marketplace retail players who are using highly sophisticated digital technologies.

To capture an omni-channel shopper’s interest – to be even considered for whatever that potential customer might be inclined to buy – retailers have to have some form of meaningful, 24/7 digital presence that is integrally linked to their physical presence. And that digital presence can only be effective when the retailer includes sufficiently specific detail about their inventory, given the digital consumer's primary drivers of price and product information. Opening hours, a website and a few photos aren’t enough of a digital presence for a retailer anymore.

The imperative to provide omni-channel options firmly rests with the retailers.

Canada has become a digital nation. But main street retail in this country has not followed suit. Customers are increasingly just a short step or fast click away from going elsewhere with their purchasing dollars and, in many cases, their social media recommendations.

In other words, their retail store or market stall is being found in the brave new digital world. Their supply is finding digital demand. Choosing to be on the digital street is a choice that opens up enormous opportunities. However, visibility on the digital street, particularly for neighbourhood retailers with limited resources remains a game of catch-up.

The challenges of an effective digital presence

Retailers of various sizes all still have to do several main things very well:

1. price their goods or services competitively;

2. bring products to customers at a pace that matches market expectations;

3. attract enough customers (repeat and/or net-new customers) to maintain cash flow;

4. engage with existing and prospective customers in ways that align with both the customers’ shopping habits and the retailer’s business strategy.

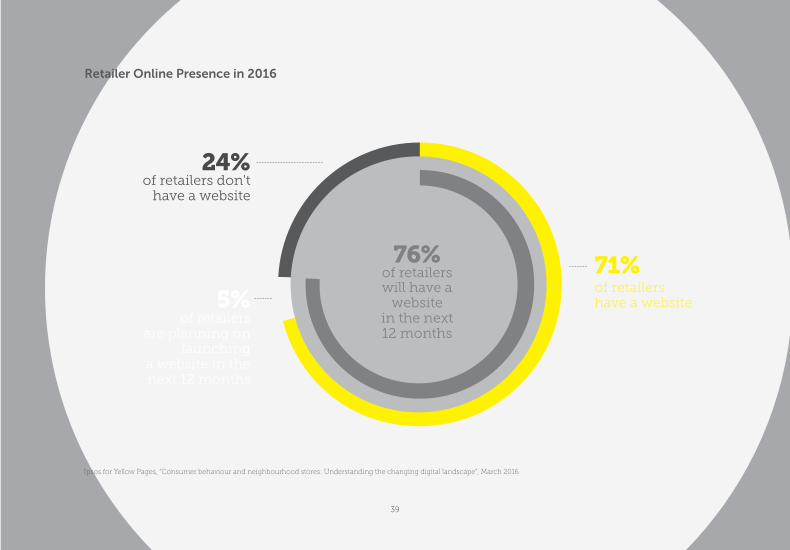

24%of retailers don't

have a website

71%of retailershave a website5%

of retailersare planning on

launchinga website in the next 12 months

76% of retailerswill have a

websitein the next 12 months

Retailer Online Presence in 2016

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

39

40

1. To what extent are neighbourhoodretailers in Canada embracing digitaltechnology?

2. Are there gaps between retailers’expectations of the promise of digitaland the expectations of their customers?

3. How can a retailer dive into digital whencompeting against massive ecommercemarketplaces?

Digital adoption among retailers

On the whole, retailers in Canada currently have an enthusiastic but limited embrace of digital. Of retailers surveyed in a recent Ipsos poll: 41

• 89% have some sort of digital presence;

• 71% have a website now, with anadditional 5% saying they will buildone within 12 months;

This leads to a variety of vital questions for retailers to ask and answer themselves, among them:

41. Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

Store traffic doesn’t matter as

much as overall customer

conversion across channels.

For multi-channel retailers,

that means the need for an

increasaingly focused, curated

and engaging brick-and-mortar

store experience that creates

maximum conversion – no

matter what channel ultimately

records the purchase. 40

40. PwC, Total Retail Survey 2016

41

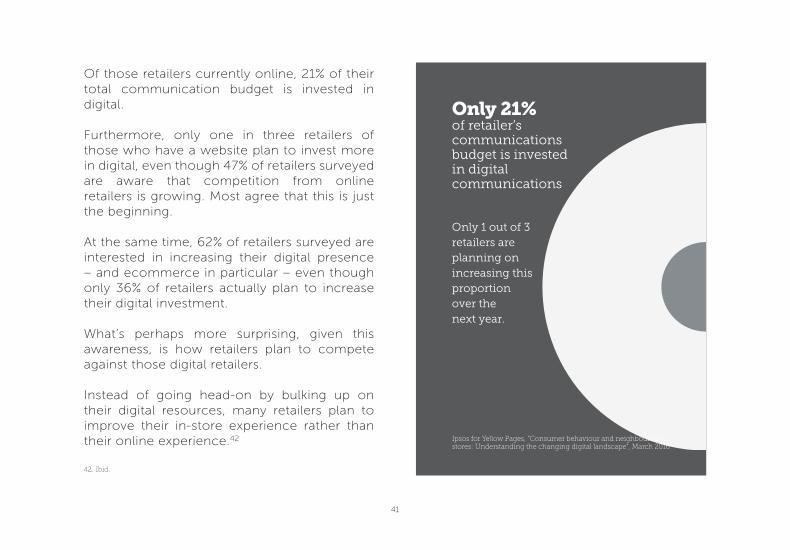

Only 21% of retailer’s communications budget is invested in digital communications

Only 1 out of 3 retailers are planning on increasing this proportion over thenext year.

Of those retailers currently online, 21% of their total communication budget is invested in digital.

Furthermore, only one in three retailers of those who have a website plan to invest more in digital, even though 47% of retailers surveyed are aware that competition from online retailers is growing. Most agree that this is just the beginning.

At the same time, 62% of retailers surveyed are interested in increasing their digital presence – and ecommerce in particular – even though only 36% of retailers actually plan to increase their digital investment.

What’s perhaps more surprising, given this awareness, is how retailers plan to compete against those digital retailers.

Instead of going head-on by bulking up on their digital resources, many retailers plan to improve their in-store experience rather than their online experience.42

42. Ibid.

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

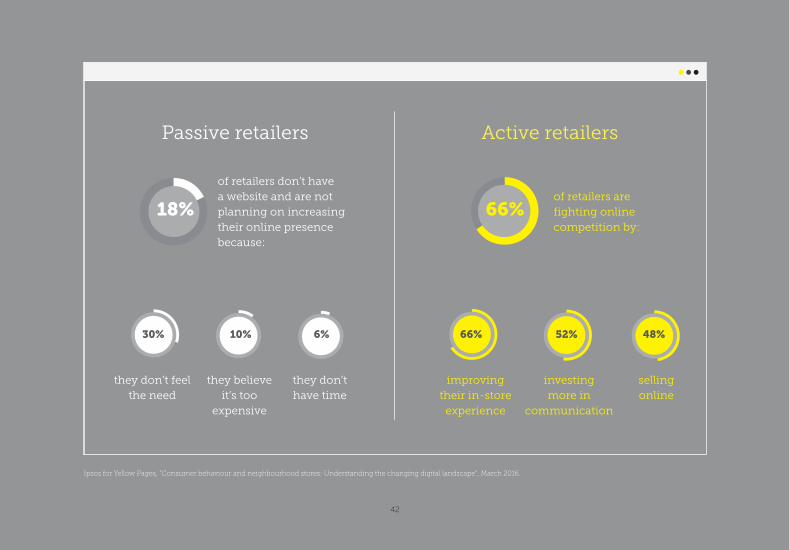

Active retailersPassive retailers

of retailers don’t havea website and are notplanning on increasingtheir online presencebecause:

of retailers arefighting online competition by:

they don’t feelthe need

improvingtheir in-store

experience

they believeit’s too

expensive

investingmore in

communication

they don’thave time

sellingonline

30% 66%

66%18%

10% 52%6% 48%

42

Ipsos for Yellow Pages, “Consumer behaviour and neighbourhood stores: Understanding the changing digital landscape”, March 2016.

43

is paramount in order to close a sale. If physical distances to obtain a product are too great, time to obtain a product too long, or if there are too many clicks required to navigate through to a given product, the likelihood of a purchase decreases. Complicated online checkout processes, for example, very often lead to abandoned baskets.43

“Many people chose their neighbourhood in order to be close to retailers, especially for things they buy daily. They don’t want to go to a mall all the time.” Chris Rickett, Manager of Entrepreneurship Services, Economic Development & Culture, City of Toronto

Simply put, buyers want easy access to sellers. Whether this translates to the location of a physical store a few minutes away or an easily navigable and accessible digital store a few quick clicks away, location – the ability to be found – is crucial.

“It’s not a sudden decision one morning to switch to digital. It’s about being where your customers are. That’s retail. Engage with your clients and give them an exceptional experience. That’s always been the case.” Mark Startup, Vice President, Independent Retail Division, Retail Council of Canada

Carving out a place on the digital street

The old expression of “location, location, location” is as true about retail as it is about real estate. Location is everything.

In the pre-internet era, retailers usually had to wait for another one to leave a prime spot on a busy street. In the internet world, however, retailers can create their own place on the digital street in complement to – or instead of – a physical location.

But it’s a very busy world, with plenty of retail options that means simplicity for the consumer

43. Andrew Meola, “Ecommerce retailers are losing their customers because of this one critical mistake”, Business Insider, March 16, 2016.

44

ecommerce site, appealing to consumers who want to read about and/or buy their fashion online.

Meanwhile, some retailers have gone the other way. These “web-to-store” retailers started off in the digital space, then opened a storefront to add to their offering.

“It’s not a question of being online or offline. It’s more a question of how you interact with your customers. We started online, and we now feel we should start to interact with our customers many different ways.” Hicham Ratnani, COO/CFO and Co-Founder, Frank + Oak

While the direction of “store-to-web” and “web-to-store” is the opposite in terms of what came first, the objective is the same – to attract and retain customers.

Traditional lines of marketing are getting blurred as retailers adopt omni-channel approaches to doing exactly that.

Blending digital and physical

Just as rapidly changing technology is increasing consumers’ choices, it’s also enabling neighbour-hood retailers to reach a vastly larger number of customers than ever before.

More and more retailers augment their physical stores with websites that can range from fairly basic “postcard” sites with store location and hours and a list of products sold, to highly interactive sites with curated content, ecommerce offerings and embedded customer reviews.

They are “store-to-web” retailers, extending their physical aisles by adopting digital technology.

Take Simons, a department store that started in 1840, as an example of “store-to-web”.

For Peter Simon, CEO of the Quebec-based retailer, having a physical presence is central to serving his customers. “We really believe in bricks and mortar because we think it’s a platform for a human connection.”44 Simons also invests in an extensive 44. Jeanne Beker, “’Bricks and mortar is a platform for human connection’”,

The Globe and Mail, March 19, 2016.

45

“We wanted to build a global brand, catering to a demographic that we think is underserved at the moment,” said Hicham Ratnani, Co-Founder & COO of Frank + Oak. “Our brand is lifestyle products, which we sell online and through our mobile app.”

Understanding their business and their customers well, Hicham and his colleagues also knew early on that they had to excel in both the digital and physical worlds to achieve their goals of becoming a global brand.

In other words, they had to offer omni-channel options to a sophisticated urban customer.

From just a few people in February 2012, Frank + Oak has grown to more than 200 employees running a dynamic website and a growing number of retail stores.

They opened their flagship store in downtown Montreal in 2015. From there they have opened 12 more stores across North America, with locations in Vancouver, Edmonton, Calgary, Toronto, Ottawa, Quebec City, Chicago, Washington and Boston.

Case Study

Frank + Oak:Building a global brand across platforms

Like many start-ups, Montreal-based menswear brand Frank + Oak started off as a small team with a big ambition – to create a lifestyle and a consumer brand for the internet generation by way of great clothing.

46

Hicham says they are methodical in their corporate growth strategy, going step by step in creating and executing on their strategy while at the same time not being afraid to take certain risks.

Above all, being a retailer in Canada – whether that’s physical, digital or both – means having an ability to handle risk.

“As an entrepreneur, you often don’t know what will happen. You often start a project and don’t have all the answers. That’s OK. It’s important to have a certain level of comfort with uncertainty and risk.”

The retail world is taking note of Frank + Oak’s successful recipe of web-to-store.

And so, too, is the fashion world.

Hicham and his colleagues recently won the Fashion Innovation Award at the Canadian Arts & Fashion Awards. This prestigious recognition is given to a company that’s innovative in its approach to creating a fashion experience through technology.

“Although a lot of shopping is done online these days, the majority is still done in retail stores,” Hicham explains. “So our goal in opening our flagship location was to be a community-oriented store where we highlight our lifestyle and create value, while being anchored in the local community.”

Hicham says they want to give their stores an urban feel.

So, the main Frank + Oak store, complete with a barber shop and a coffee shop inside, allows customers to not only experience the products but also the brand and the values of the company.

A strategic expansion into physical is growing both the Frank + Oak brand and its range of customers. They often have the same sort of buyer – such as a 28 year- old with a good job and a smartphone – across their physical and digital platforms. But the stores help bring in new types of customers.

“Our stores attract a broader demographic than our website. We have women and different ages, for example – people who wouldn’t necessarily browse our website. So the stores are opening up other possibilities.”

47

Edmonton that features huge interactive video screens that shoppers can use to design their patio or backyard with help from Oculus Rift virtual reality headsets.46

The emphasis on staff in these innovative stores is deliberate. Local shopping for certain items is still quite enjoyable for many people. And they may willingly pay a premium compared to prices available on an ecommerce marketplace to support local retailers providing unique experiences and products they can readily see and touch.

For them, sales associates with deep product knowledge are very important when it comes to in-store shopping. The changing role of the store, soaring customer expectations, and a desire to support neighbourhood businesses all put a premium on hiring talented retail employees.47

Similarly, forward-thinking retailers are leveraging digital in businesses that are traditionally more physical than digital. And they are opening new markets for themselves in so doing.

The augmented retail experience

All retailers have to get people into their store – whether it’s through a digital door and/or a physical door. An empty basket is still an empty basket.

But for retailers clinging on to traditional marketing techniques, “tried and true” won’t equate with “will always work”. Analogue solutions are losing their impact in a digital world.

From the growing use of interactive, in-store touchscreen displays45 to staff walking the sales floor with tablets, innovative retailers are blending digital with physical in creating memorable (and repeatable) shopping experiences for customers with high expectations.

Canadian Tire is investing heavily in their “clicks and bricks” business model, taking an approach the company’s Chief Technology Officer, Eugene Roman, calls a “phygital” strategy that emphasizes both physical stores and digital channels. Last year, the chain opened a 140,000 square foot store in

45. Technavio, “Global Digital Signage Market 2016-2020”, January 27, 2016.

46. Christine Wong, “Canadian Tire’s $400 million drive to shift gears as a clicks-and bricks retailer”, itbusiness.ca, April 22, 2016.

47. PwC, Total Retail 2015, p. 15

A pioneer in digital retail, John opened new markets for his company Marquis Wine Cellars when he started his first website in the mid-1990s. With over 20 years of combining online with in-store, John attracts and retains repeat customers in markets that include but also go well beyond customers in his own neighbourhood.

“Years ago you could see writing on wall,” John recounts. “Digital was going to make it so much easier to drive traffic if your customers could see you virtually. It’s also a lot faster to update your website – your virtual ads – rather than re-printing all your hard copy ads.”

John, who has maintained a physical store in Vancouver since starting his company in 1986, uses digital technology in many ways. From posting inventory updates to blogging about his upcoming in-store events, John and his team do everything possible to generate business through their website.

Case Study

Selling wine online

For decades, the sale of wine in Canada was restricted as much by geography as it was by regulations. Of-age shoppers had to be physically present to browse and buy wines, meaning the catchment area for any given wine-selling outlet was generally limited to easy driving distances. John Clerides of Vancouver had other ideas.

48

49

“The key is to reach your customers wherever they are,” says John.

It’s also about finding a good match when time-pressed retailers are looking for suppliers to help design and launch a good website.

“When starting out, you have to do your due diligence. Talk to a lot of people, map out what you want your site to look like, and benchmark it against other sites you like, regardless of what sector they’re in. Then give that idea to proper web designer, not your nephew.”

A highly-experienced digital retailer, John also has some very Canadian-sounding advice for retailers thinking they can dabble in digital with any positive effect.

“Wayne Gretzky didn’t get that good by just trying it out a few times. You have to commit.”

“Customers come to us in various ways, across several digital platforms. Many check us out online several times, but it’s hard for us to judge how often they’re checking us out. We have to be actively online, and we have to be authentic in what we’re saying.”

For John, being in a dense downtown Vancouver location has positives and negatives. The upside is that the store attracts a lot of foot and bike traffic. The downside is that car congestion can dissuade some customers from coming into Marquis as they may have a hard time parking.

By leveraging digital, Marquis is easy to find online. That means shoppers can take their time – where, when and how they want – in learning about wine and the Marquis story before choosing whether to come in personally or to shop digitally.

50

Building digital capacity now is easier and cheaper than ever before. Retailers can set up good websites for comparatively little cost. And they can work with an ever-growing array of professionals dedicated to designing, launching and running sites for and with time-pressed retailers.

“It’s not hard a process to visualize the steps ahead to make that digital transformation.” Chris Rickett, Manager of Entrepreneurship Services, Economic Development & Culture, City of Toronto

The questions before us all

Digital technology is an enabler for retailers – regardless of their size – who want to harness its power. Those who don’t are being left behind, permanently.

Getting started

Early adopters of technology in retail are thriving by engaging customers, driving sales and facilitating exchanges of goods and services in an era of profound change. They are going digital so as to meet, if not exceed, their customers’ expectations, while at the same time carving out niches for themselves in the shadow of huge ecommerce players.

“If you put as much thought and planning and resource commitment into opening an online store as you would into opening a second physical store, then you’re much more likely to succeed.” Mark Startup, Vice President, Independent Retail Division, Retail Council of Canada.

Regardless of how a retailer starts to move into the digital world, the key is getting started.

51

And what are the costs to retailers, to neighbour-hoods and to the national economy at large if, collectively, we simply stand back and allow retailers to be ploughed under – rather than thrive within – Canada’s evolving retail landscape?

So what can be done in light of massive ecommerce players permanently changing the retail sector?

What role(s) do governments have, if any, in encouraging the digital transformations on a macro level?

52

Cities as Warehouses:

Multi-Local can Compete

with Multi-National

53

Local collaboration

In looking around their own communities, many local retailers see their main competition as being across the street or around the corner. And while that may be true in many cases, the real competition today almost literally can’t be seen by just driving down main street. That’s because the real competition is found online in the form of global ecommerce marketplace players.

So, instead of only seeing competitors next door, retailers need to start seeing competitors around the world and potential allies next door.

"The most difficult part is the consultation between merchants. It’s terrible because they see themselves in competition with each other, and the more difficult the economic situation is, the more they see themselves as such, while it’s not the case. As retailers from the same neighbourhood, they are all in the same boat. " Jacques Nantel, Professor, HEC Montreal

Fight, flight … or unite?

Retail in Canada is resilient. Many retailers, some featured in this white paper, are innovative in their use of digital to create memorable customer experiences that drive sales.

But in today’s economy, it’s very difficult, if not impossible, for many neighbourhood retail-ers to fully compete against the likes of Alibaba, Amazon and eBay. Huge ecommerce players have won large swaths of the Canadian consum-er market.

It may be a question of fight or flight for many retailers facing this challenge.

But the impulse to unite may be a better choice over the near and longer terms. That’s because retailers serving local markets still offer tremendous value to their owners, employees and customers. Retailers combining their efforts to do so – with the help of digital – will magnify their impacts and efficacy.

54

As mentioned earlier, shoppers are inclined to shop locally if given the choice and if the experience is compelling and accessible.

This destination would meet all of those criteria in addition to providing the information that is the primary motivation for online shoppers in their pre-purchase research – namely price and product information, but at the local level. Therefore, merging the convenience of digital with the shared human experience of local retail under the auspices of a local digital marketplace adds to customers’ choices in an era when choice is paramount.

This digital aggregation (local digital marketplace) is mirrored by a physical aggregation of inventories in small urban-based warehouses (stores). These stores and the corresponding inventory and pricing information can be geo-localized based on the shopper – thus providing the buyer with the best and closest option for price and product – effectively levelling the playing field of giant ecommerce players.

“Cities as Warehouses”

The answer may be found in creating a local digital marketplace in Canada: a digital destination where retailers showcase their inventory and that enables consumers to geo-localize based on location.

This “cities as warehouses” approach – recreates in digital all the retail strengths of a local shopping area. And it allows entire localities to compete against large ecommerce players.

How does it work?

Using geo-localization technology, a “cities as ware-houses” concept would feature a collection of local retailers and their respective inventories and prices online in one aggregated, easy-to-navigate digital destination. The scope of this would be Canadian but could be segmented at a national, regional, city or neighbourhood level.

55

traffic and online transactions, they simply need to upload their information and inventory to be visible and present;

• Preserves the consumer option of convenience and accessibility and never needing to even visit a store, while driving dollars to the local retailer and complementing their physical presence;

• Sellers are co-located with their buyers, and through a local digital marketplace, customers will increasingly come to know they can find a growing array of products and services in locally-based meta warehouses.

Retail competition would still be fierce within each local marketplace – as it should be.

However, taking a “power in numbers” approach starts to put local retailers on a more even ground with massive ecommerce marketplaces. They are stronger together in this way than in constantly competing with each other and the large-scale ecommerce marketplaces at the same time.

“ The technology battle is over; the next retail battle is logistical. Even though solutions like Amazon Fulfillment are interesting for large manufacturers, they aren’t appropriate for small retailers. However, developing a logistical capacity locally and making available shared inventory...that is a HUGE opportunity. ” Jacques Nantel, professor, HEC Montreal

Multiple benefits across the retail ecosystem

There are many benefits to this approach from the retailers’ perspective:

• It gives local retailers greater visibility in the eyes of shoppers who search online;

• Lower barrier to entry in digital for each retailer as the digital destination already exists and is the epicenter for consumer

56

Urban-based millennials (and many others) are inclined to walk or ride (more so than drive) to local stores where they can see, touch and buy things, while also getting access to knowledgeable staff for questions that couldn’t be answered online in their pre-purchase research. This favours the ongoing vibrancy of local retail. Taking steps to turn entire communities in digital retail destinations and the storefronts collectively forming “warehouses” for the inventory in the digital marketplace, will do exactly that.

Neighbourhoods Matter

The “cities as warehouses” vision is imbued with the understanding that thriving, vibrant neigh-bourhoods are important. And neighbourhoods –defined many ways across Canada – are central to the shopping experience of millions of Canadians, particularly those living in dense, urban settings. In cities big and small, residents have strong emotional attachments to their neighbourhood.

Similarly, this approach creates many benefits for governments:

• It stimulates urban revitalization by highlighting local retailers offering good products at good prices;

• It helps maintain (and possibly expand) the local employment base;

• It fosters a culture of collaboration that can have several positive, echo effects on other aspects of community vibrancy.

Moving completely from a physical store to the digital space (i.e. the former front of house sales associate position is eliminated in favour of consumer-driven online sales) also ultimately reduces the overall number of jobs.

Embracing the “cities as warehouses” concept creates and secures local jobs by enabling both physical and digital presences to co-exist.

57

That’s because the first instinct of local residents in such cases is to shop within their immediate neighbourhood for many staples. They venture beyond the neighbourhood only when their desired items or services cannot be found locally, or simply because they want the experience of going elsewhere for the day.

“Toronto is a city made up of neighborhoods that give Toronto its unique identity. The backbone of those neighbourhoods tends to be the main streets with vibrant retail strips.” Chris Rickett, Manager of Entrepreneurship Services, Economic Development & Culture, City of Toronto

Increasingly, the allure of neighbourhood retail is found in expressions of the digital-retail nexus: shoppers use digital to search prices and products, and they go into local stores they can see online to purchase them.

West End Vancouver is a good example. It’s a very dense, urban setting with a moderate climate conducive to walking and cycling. It has an abundance of unique and chain-based retailers, creating a combination of diversity and proximity that leads many – if not most – residents to support neighbourhood retail.

“Residents in our neighbourhood may go out of the West End for some things, but there’s high convenience in high density. So they shop locally while they’re out.” Stephen Regan, Executive Director, West End BIA

In Toronto’s Little Italy, many people identify themselves as living first and foremost in Little Italy. As a result, in this neighbourhood you find several retailers catering to not only the predominant local cultural community – Italian, in this case – but also to people who live within walking and biking distance from local stores.

58

For Gordon, all three traits are important in his day-to-day job as the President of the Uncommon Group, owner and operator of Uncommon Grounds coffee and baked goods, Sugah! Confectionery and Rum Runners Rum Cake.

They also infuse his collaborative approach to helping run “I Love Local (HFX)”, a community initiative that brings dozens of local retailers together digitally and physically to support and strengthen Halifax as “an exciting and vibrant place to shop, eat and live”, as their website says.

“Halifax has a successful buy-local culture,” explains Gordon. “We have a long history of buying locally, and many retailers are quick to adapt and collaborate. We have 75 businesses working together in ‘I Love Local’, attracting thousands of people.”

Gordon and his colleagues use digital technology to attract a broad range of shoppers. The entire “I Love Local” campaign is run on social media, with no spending on traditional ad spends.

Case Study

I LOVE LOCAL (HFX)Taking an “uncommon” approach to collaboration

@ilovelocalhfx : The Twitter handle for Halifax-based retailer Gordon Stevens paints a precise picture of his approach to business – “serial entrepreneur, community supporter, family first”.

59

there’s a huge opportunity, through digital, to get these people into your store.”

“I Love Local” organizers understand that digital has changed the way most people, including tourists, shop these days. Many – if not most – people come into stores knowing what they want to buy, and are thus doing less browsing.

In Gordon’s experience, that might mean fewer shoppers walking through the door, but higher conversion rates.

“There’s a huge disadvantage to retailers who haven’t transformed to digital, as so much search is now happening on phones before people come into stores and while they’re in those stores.”

The key is to be found by shoppers who are increasingly turning to their smartphones and laptops before heading out the door.

In the case of “I Love Local”, collaboration turns that digital attention into transactions.

Making heavy use of Twitter is a big part of their campaign.

@ilovelocalhfx has more than 20,000 followers. And through the combined efforts of the campaign’s retail members, they’ve tweeted an astonishing 155,000 tweets since joining Twitter in August 2010. That’s an average of 75 tweets per day, far more than any given retailer could muster by itself.

The members of “I Love Local” capture the attention of tourists in particular by acting together through a targeted and dynamic social media campaign that highlights the depth and breadth of the retail shopping experience in Halifax.