Embed Size (px)

Citation preview

Leveraging Your Accounting Partner and Deltek for Maintaining DCAA ComplianceTed Rose

President & CEO

Rose Financial Services, LLC

Biography

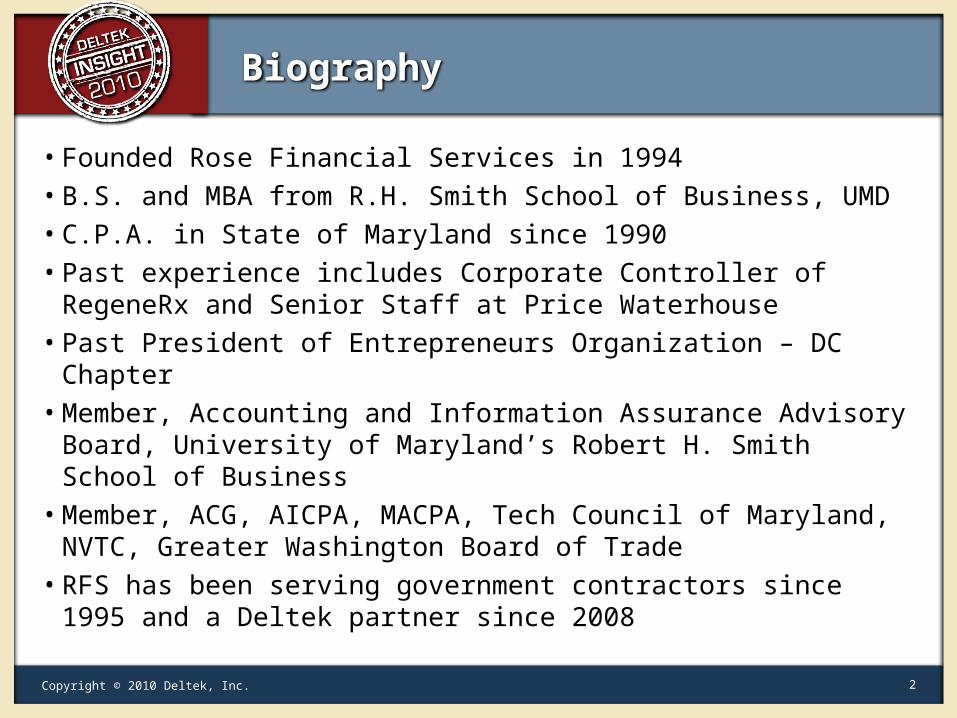

• Founded Rose Financial Services in 1994• B.S. and MBA from R.H. Smith School of Business, UMD• C.P.A. in State of Maryland since 1990• Past experience includes Corporate Controller of RegeneRx and

Senior Staff at Price Waterhouse• Past President of Entrepreneurs Organization – DC Chapter• Member, Accounting and Information Assurance Advisory Board,

University of Maryland’s Robert H. Smith School of Business• Member, ACG, AICPA, MACPA, Tech Council of Maryland,

NVTC, Greater Washington Board of Trade• RFS has been serving government contractors since 1995 and a

Deltek partner since 2008

Copyright © 2010 Deltek, Inc. 2

Agenda

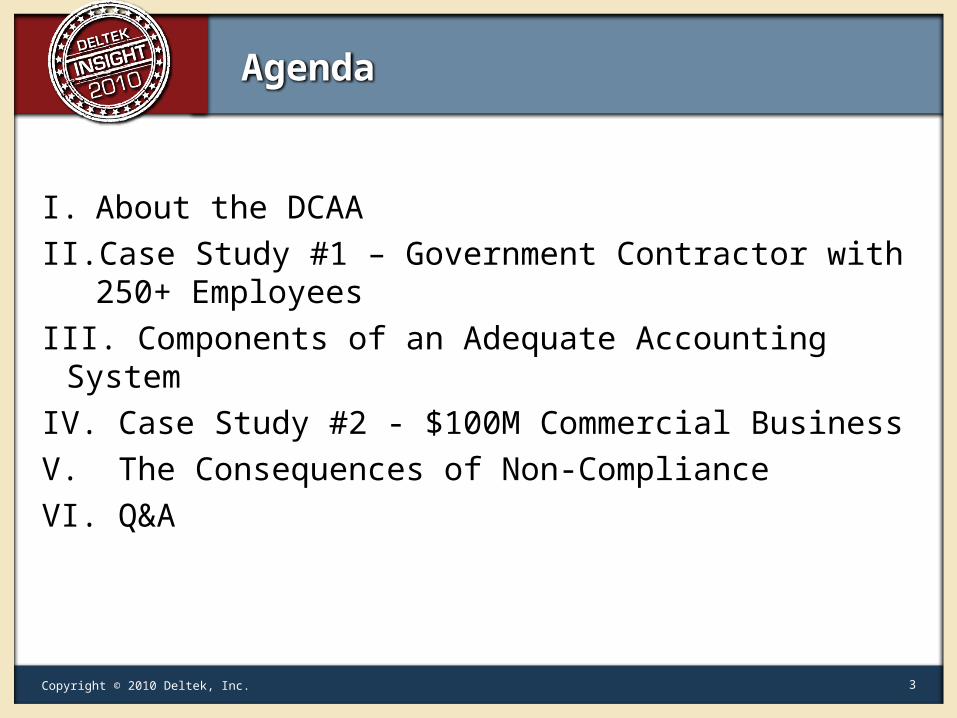

I. About the DCAA

II. Case Study #1 – Government Contractor with 250+ Employees

III. Components of an Adequate Accounting System

IV. Case Study #2 - $100M Commercial Business

V. The Consequences of Non-Compliance

VI. Q&A

Copyright © 2010 Deltek, Inc. 3

About the Defense Contract Audit Agency (DCAA)

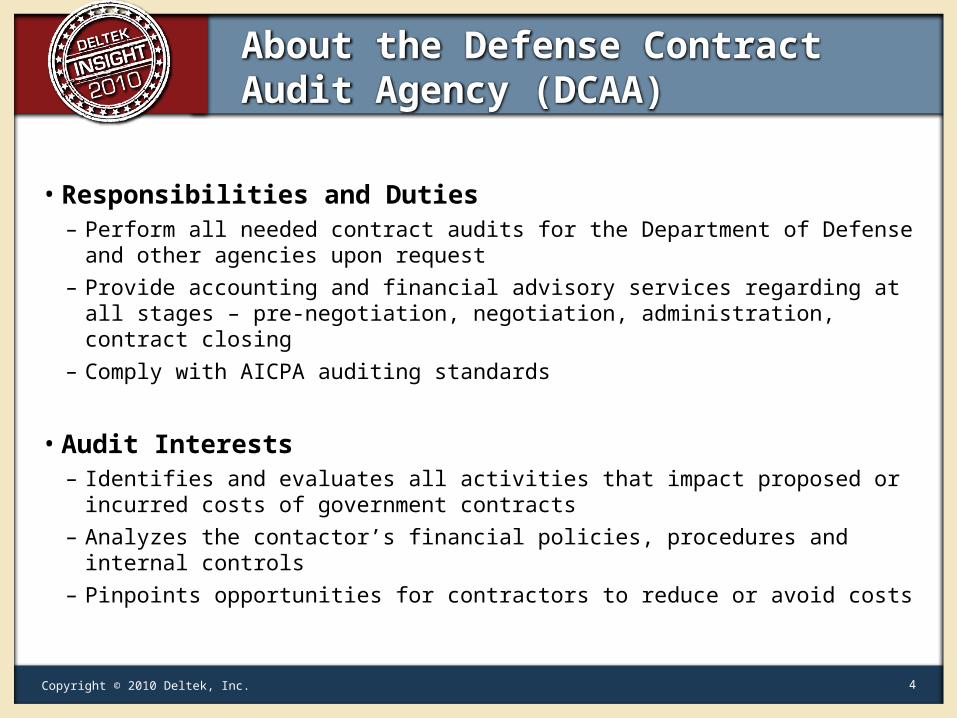

• Responsibilities and Duties– Perform all needed contract audits for the Department of Defense and

other agencies upon request

– Provide accounting and financial advisory services regarding at all stages – pre-negotiation, negotiation, administration, contract closing

– Comply with AICPA auditing standards

• Audit Interests– Identifies and evaluates all activities that impact proposed or incurred

costs of government contracts

– Analyzes the contactor’s financial policies, procedures and internal controls

– Pinpoints opportunities for contractors to reduce or avoid costs

Copyright © 2010 Deltek, Inc. 4

About the DCAA (cont.)

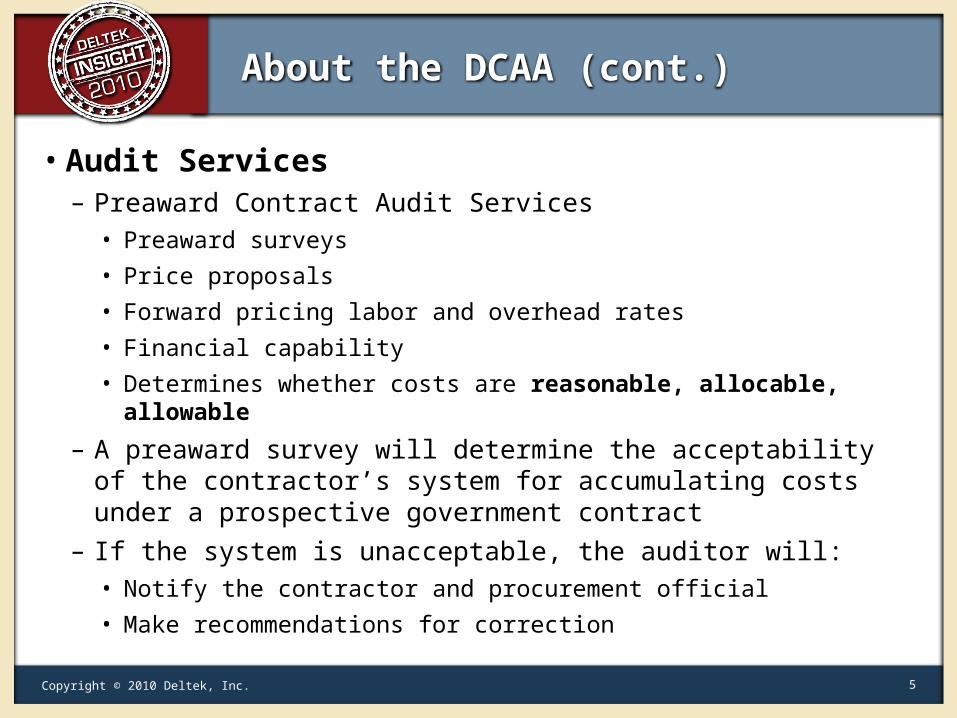

• Audit Services– Preaward Contract Audit Services

• Preaward surveys

• Price proposals

• Forward pricing labor and overhead rates

• Financial capability

• Determines whether costs are reasonable, allocable, allowable

– A preaward survey will determine the acceptability of the contractor’s system for accumulating costs under a prospective government contract

– If the system is unacceptable, the auditor will:• Notify the contractor and procurement official

• Make recommendations for correction

Copyright © 2010 Deltek, Inc. 5

About the DCAA (cont.)

– Postaward Contract Audit Services• Incurred costs/annual overhead rates

• Truth in Negotiation Act compliance

• Claims

• CAS compliance and adequacy

– Other• Internal Control System Audits

• Negotiation Assistance

Copyright © 2010 Deltek, Inc. 6

Case Study #1 - Government Contractor – 250+ employees

1) Turnover at the Controller/CFO level

2) Late and/or inadequate submissions to DCAA

3) Ineffective proposal process

4) Incomplete system conversion to Deltek

5) Overly complicated indirect rate structure and allocations

Copyright © 2010 Deltek, Inc. 7

Turnover at the Controller/CFO Level

• Inadequate Accounting System Oversight– Lack of expertise/knowledge of government-specific rules and

regulations internally

– Loss of historical knowledge• Four CFOs in 2 ½ year period

– Reliance on inadequate consultants• Addressing symptoms instead of causes

• Limited Internal Controls in place– Accounting manual was in place but not being followed

– Processes were not effective and efficient

– Lacking proper level of supervision, testing and monitoring

– Problems not being fixed in a timely manner

Copyright © 2010 Deltek, Inc. 8

Late and/or Inadequate Submissions to DCAA

• Indirect rates and reconciliations• Contract close-out packages• Incurred Cost Submissions (ICE)• Provisional rate requests• Inadequate responses to audit questions

Copyright © 2010 Deltek, Inc. 9

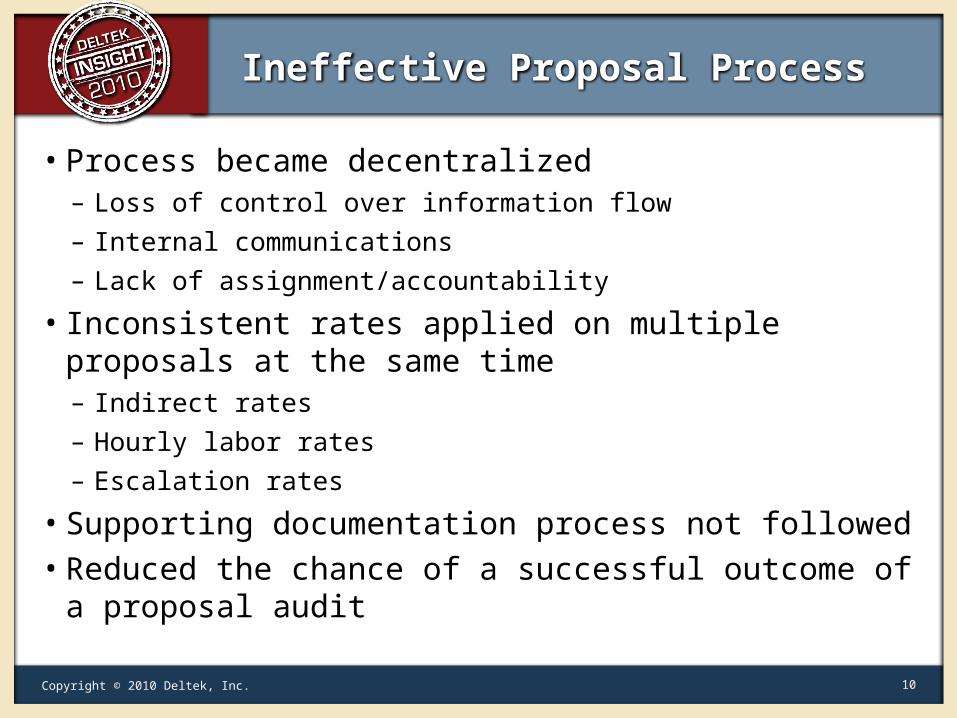

Ineffective Proposal Process

• Process became decentralized– Loss of control over information flow

– Internal communications

– Lack of assignment/accountability

• Inconsistent rates applied on multiple proposals at the same time– Indirect rates

– Hourly labor rates

– Escalation rates

• Supporting documentation process not followed• Reduced the chance of a successful outcome of a proposal

audit

Copyright © 2010 Deltek, Inc. 10

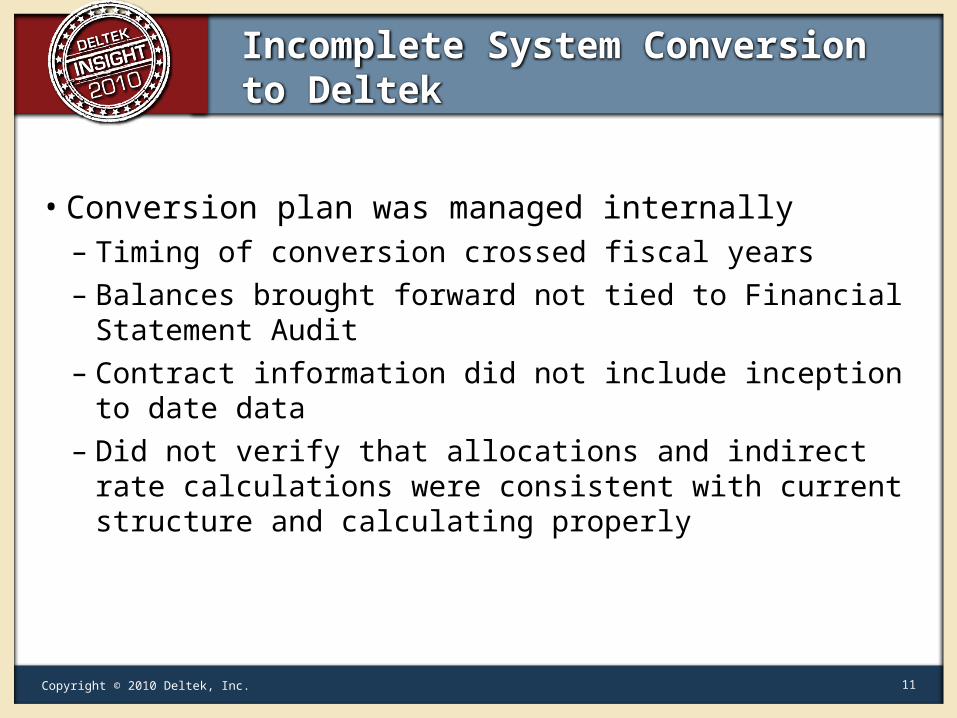

Incomplete System Conversion to Deltek

• Conversion plan was managed internally– Timing of conversion crossed fiscal years

– Balances brought forward not tied to Financial Statement Audit

– Contract information did not include inception to date data

– Did not verify that allocations and indirect rate calculations were consistent with current structure and calculating properly

Copyright © 2010 Deltek, Inc. 11

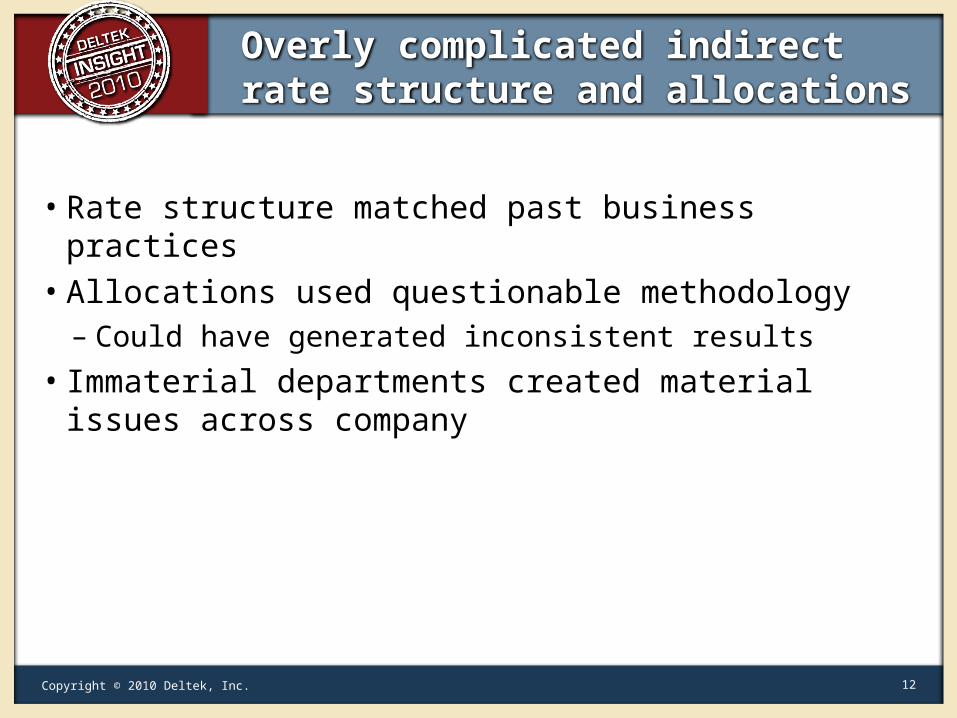

Overly complicated indirect rate structure and allocations

• Rate structure matched past business practices• Allocations used questionable methodology

– Could have generated inconsistent results

• Immaterial departments created material issues across company

Copyright © 2010 Deltek, Inc. 12

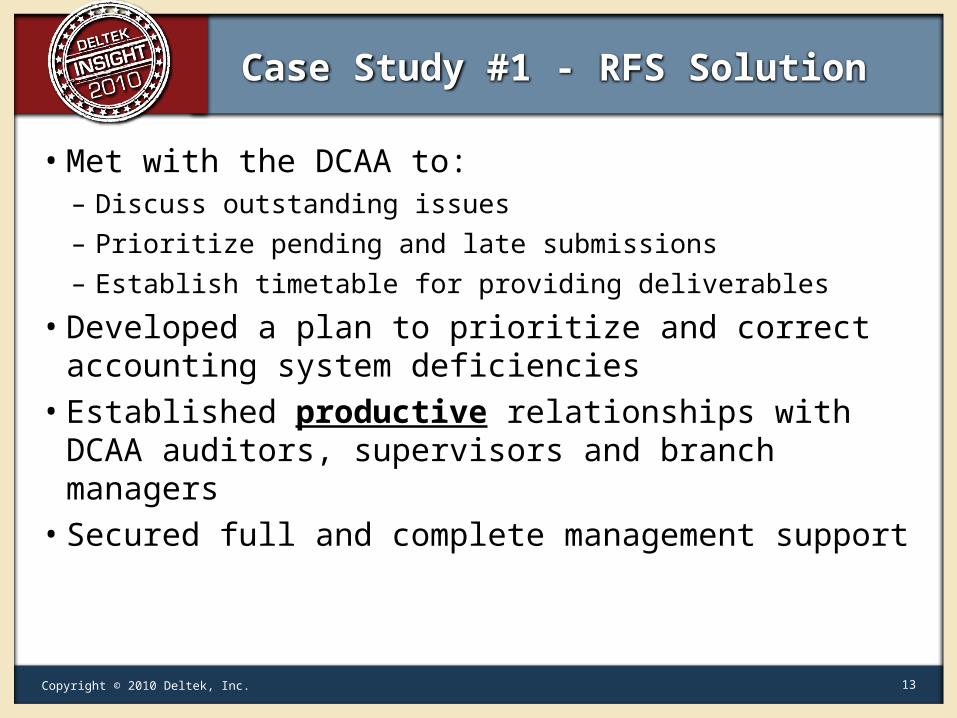

Case Study #1 - RFS Solution

• Met with the DCAA to:– Discuss outstanding issues

– Prioritize pending and late submissions

– Establish timetable for providing deliverables

• Developed a plan to prioritize and correct accounting system deficiencies

• Established productive relationships with DCAA auditors, supervisors and branch managers

• Secured full and complete management support

Copyright © 2010 Deltek, Inc. 13

Case Study #1 - RFS Solution (cont.)

• Worked with the DCAA to:

– Pull back two proposals under audit and resubmit them with accurate and consistent rates

– Allow the company to remain on direct bill

– Hold back possible issuance of a Flash Report

Copyright © 2010 Deltek, Inc. 14

Copyright © 2010 Deltek, Inc. 15

Case Study #1 – RFS and Deltek GCS Premier

• DCAA auditors are familiar with Deltek GCS Premier– Able to rely on the functionality of the system

– DCAA Auditors know what reports to view

• Deltek GCS Premier was able to produce the Indirect Rate Calculations as a standard part of the program

• The DCAA tested the Indirect Rate Calculation, but was able to rely on the monthly rate calculations generated by Deltek GCS Premier

Components of an Adequate Accounting System

• Deltek was developed with Generally Accepted Accounting Principles (GAAP), Federal Acquisition Regulations (FAR), and Cost Accounting Standards (CAS) in mind. Thus, making the DCAA audit process seamless and efficient

if used properly. • General accounting system components:

– Financial reporting

– Management reporting

– Tax reporting

– Government Cost Accounting Standards

Copyright © 2010 Deltek, Inc. 16

Components of an Adequate Accounting System (cont.)

• Government Cost Accounting Standards Require:– Proper segregation of direct from indirect costs

– Identification and accumulation of direct costs by contract (i.e. job reports which support billings)

– Logical and consistent method to allocate indirect costs to intermediate and final cost objectives

– Accumulation of costs under general ledger control

– Interim determination of costs charged to a contract through routine posting of books of account

– Exclusion from cost charged to government contracts of amounts which are unallowable per FAR

– Identification of costs by contract line item

– Segregation of pre-production from production costs

Copyright © 2010 Deltek, Inc. 17

What Makes Deltek GCS Premier Great for Government Contractors?

• Deltek GCS Premier contains a Contracts module and preset Indirect Rate Calculations

• The Billings and Contracts modules link together so the DCAA can rely on the system’s functionality

• The integration of Deltek T&E and payroll to Deltek GCS Premier is a strong control point that the DCAA has tested and documented as adequate

Copyright © 2010 Deltek, Inc. 18

Critical Components – Books & Records

• Chart of Accounts• General Ledger• Job Cost Ledger• Subsidiary Ledger• Financial Statements

Copyright © 2010 Deltek, Inc. 19

Critical Components – Books & Records (cont.)

• Labor– Segregation of responsibilities

– Evident and reasonable procedures

– Continual verification of control maintenance

– Constant reminders of controls to employees

• Timekeeping– Restriction of access to employee timesheets

– Accuracy

– Verifiable audit trail that collects initial entries and subsequent changes

Copyright © 2010 Deltek, Inc. 20

Critical Components – Internal Controls

• The purpose of employing internal controls is to mitigate risk

• Internal controls include:– Separation of authority between key accounting functions

• i.e. payroll vs. timekeeping, billing function vs. accounts receivable

– Written policies and procedures

– Application of general controls• i.e. passwords, restricting system access

– Physical controls• i.e. locks, safeguarding assets

Copyright © 2010 Deltek, Inc. 21

Critical Components – Unallowable Costs

• A method is needed to identify and separate unallowable costs (i.e. General Ledger account numbers, accounting review process and policies for employees)

• Types of unallowable costs include: – Costs for amortization, expensing, write-off or write-down of goodwill

– Public relations and advertising costs

– Bad debts

– Contributions or donations

– Interest costs

– Entertainment costs

– Lobbying and political activity costs

– Losses on other contracts

– Certain taxes including federal income

Copyright © 2010 Deltek, Inc. 22

Case Study #2 - $100 Mil Commercial Business

1) Commercial business 95% commercial – one relatively small fixed price government

contract Not subject to CAS previously

2) Limited government contracting experience at the CFO level Limited familiarity with FAR’s Misunderstanding of DCAA’s communications and processes

Copyright © 2010 Deltek, Inc. 23

Case Study #2 - $100 Mil Commercial Business (cont.)

3) Inadequate submissions to DCAA Responses not appropriate for the government agency

environment Multiple attempts

4) Ineffective proposal process Geared for commercial proposals

5) Accounting system Not set up to accommodate government structure

Copyright © 2010 Deltek, Inc. 24

Case Study #2 – RFS Solution

• RFS redesigned the accounting system to support government cost accounting standards while maintaining commercial flexibility

• RFS set up an exit interview with the DCAA to discuss prior disclosure statement submissions and the accompanying issues

• The DCAA allowed the third submission to be pulled back at request of Contracting Officer

• Disclosure statement was rewritten using RFS-designed CAS compliant accounting system

• After resubmission, the Company’s Accounting System was deemed “adequate”

Copyright © 2010 Deltek, Inc. 25

Potential Consequences of Inadequate System/Non-Compliance

• Loss of potential award• Removal from direct bill• Suspension of voucher approvals and payments• Flash Report issued to other DCAA auditors/agencies• Legal Troubles

– Defective Pricing

Copyright © 2010 Deltek, Inc. 26

Potential Consequences of Inadequate System/Non-Compliance (cont.)

• Loss of Revenue– Propose too low or accept lower rates (i.e. ceilings) due to inaccurate

or non-current information

– Weaker negotiating position

– Disallowed Costs

– Time spent attending to issues

• Proposal rejections– Government or Prime “Moves On” to next contractor

• Damage to Relationships/Reputation in Marketplace

Copyright © 2010 Deltek, Inc. 27

Questions?

Ted Rose

President & CEO

Rose Financial Services

301.527.1130 x204

Copyright © 2010 Deltek, Inc. 28