Embed Size (px)

Citation preview

Fast Forward to Growth Seizing opportunities in high-growth markets

1

Foreword 3

Executive summary 5

A wake-up call 9

Locating demand: The search for growth 13

New players, new rules: 26 The new shape of competition

Rethinking capabilities: The roadmap to success 33Sizing the future: Assessing where and when to act 35

Shaping the future: Seeding tomorrow’s growth 43

Seizing the future: Operating at speed and scale 54

Conclusion: Windows to the future 65

Methodology: Income and consumption forecasting 67

References 69

Contents

2

3

ForewordThe search for growth opportunities in emerging economies is no longer a matter of choice; it has become a necessity. With short-term growth difficult to find in developed markets, emerging markets must be considered as more than an optional, longer-term bet.

But making bets on the future, whether short-term or long-term, is an especially difficult challenge amid the persistent uncertainty, complexity and volatility in the global marketplace. In my conversations with clients around the world, I am struck by how today’s business executives often find themselves struggling to prioritize their investments across the diverse set of growth markets in emerging economies. The questions I hear in boardrooms vary widely: Why aren’t we making profits in China yet? Is it too late to enter Brazil? How can we move faster to establish a foothold in Africa? The questions highlight a key factor in strategic growth planning: the importance of getting your timing right.

Planning an effective global growth strategy across time horizons demands significant investments of time, effort and resources to assess market potential accurately and to build the requisite capabilities for success. Putting off such investments, waiting to see how markets evolve, is tempting in today’s economic environment, and it may be the right decision.

But this presents executives with a critical paradox: ongoing global economic change may lead businesses to shy away from action in the very markets that hold the key to faster growth. The longer firms hesitate, the greater the risk of missing out on opportunities, and the more challenging the competitive environment they will face when they eventually take action.

I see two underlying factors at play.

First, regardless of when and how growth returns to developed markets, the future map of global demand will look very different from that of

previous decades. Fundamental shifts in income and demography are reshaping the landscape of global consumption. Predicting where and when the related market opportunities will arise is difficult enough; understanding how to grasp them is even harder.

Second, I see a new constellation of competition being formed out of the market turbulence of recent years. This is due partly to the new economic and political relationships that are being forged, particularly between emerging economies. But I also see transformation in how businesses operate. The downturn has spurred improvements in the efficiency of global operations. New technologies and reconfigured operating models are allowing companies to create value more effectively and to build more direct and intimate connections with their customers. And these new business models, practices and capabilities draw from a more diverse pool of global players, characterized by important differences in strategic priorities, governance and culture.

It is in the context of this dramatically altered landscape of opportunity and competition that this report, the work of the Accenture Institute for High Performance, calls for an urgent reassessment of the strategies and capabilities that will be central to achieving high performance in tomorrow’s global marketplace. Business leaders cannot allow change and uncertainty to paralyze their decision making. We hope you find the report insightful and stimulating and its recommendations both useful and actionable.

Mark Spelman

Global Head of StrategyAccenture

Mark Spelman

4

1 We analyzed household income data across 64 countries (see Methodology on page 67 for details) which together accounted for more than 90 percent of global GDP in 2010. The income of the emerging-market households in our analysis will jump by more than US$8.5 trillion between 2010 and 2020.

5

In the current global economic environment, executives fear that prospects for growth in many markets are patchy and vulnerable. With this fear comes a renewed search for pockets of growth in the global economy. We surveyed nearly 600 business leaders worldwide and found that 80 percent are focused primarily on high-growth markets in emerging economies to chart a more compelling path for the future. And with good reason. Household incomes in emerging economies will jump by more than US$8.5 trillion between 2010 and 2020—nearly 60 percent of the global increase over this period, in real terms.1 As these incomes grow, so will consumption and demand.

But many executives are not confident that their organizations are up to the task. Forty percent do not believe that their companies possess the strategic and operational capabilities to fully grasp the opportunities in emerging economies. The same proportion worry that they do not fully understand the competitive dynamics they will face. These doubts are not misplaced—and may be exacerbated by the emergence of a rapidly intensifying competitive landscape, populated by new players with new capabilities. High-growth emerging markets are a fast-moving target. Companies must build powerful new capabilities to address this new reality.

Tracking the income surgeThe pace of income growth in emerging economies can be bewildering. Many companies have been impatiently awaiting the promise of profitability in emerging economies. But as our detailed analysis of household incomes shows, the real growth in consumption

is yet to come. For example, many companies are pinning their hopes on China, the world’s most populous nation and one of its largest and fastest-growing economies. Currently, 27 other economies—including Poland, Colombia and Turkey—have a greater number of households with an annual income above US$30,000. But over the next decade, China will rapidly accelerate up the ranks, leaving only three economies with a greater number of households earning US$30,000 and above: the United States, Japan and Germany. This pace of change is not restricted to China: Mexican households in this income band are expected to boost their income by an additional US$340 billion by 2020, an increase higher than that expected in Germany. And in a richer income segment, households with an annual income of more than US$50,000, Turkey will see a total increase of US$380 billion, the highest of any emerging economy. As these examples demonstrate, the varying degree and speed of change across these markets make the size and timing of opportunities difficult to grasp.

Mapping the competitive terrainCompanies seeking their fortunes in high-growth markets face a challenging competitive landscape. As competitors jostle for position, firms targeting these markets will confront domestic players with strong local knowledge and intimate customer relationships; established multinationals with global scale that have improved their efficiency in response to the downturn; and a further potent breed, growing multinationals from emerging economies. The competitive landscape is characterized by a combination of scale advantages, strong brands,

low-cost capabilities and deep local knowledge, as well as an increased role of relationships and government support. In this environment, with its wide range of players and broad variety of capabilities, many companies will face a challenge in pressing home their own competitive advantage.

The opportunity paradoxOur research uncovers a paradox: on one hand, there is strong affirmation that firms see continued growth coming from emerging economies. On the other hand, they feel that the windows of opportunity to secure their company’s share of these markets may be shrinking. The point is underlined by our survey finding that 73 percent of respondents believe they need to accelerate their efforts, or may already be too late, to build satisfactory market share in these high-growth markets.

Our research supports this imperative to accelerate action in seeking opportunities in high-growth markets. In an uncertain economic environment, there is a strong temptation for companies to watch and wait, or even to retrench or withdraw from some markets until the global economic environment becomes clearer. In fact, many organizations have significant reserves of cash that could be used for expansion. But they continue to hesitate. A strategy of “wait and see” may be effective, as long as it is based on a realistic assessment of the options, opportunities and risks involved. More likely, however, hesitation in today’s global competitive environment may be the most dangerous choice of all. High-growth markets offer many opportunities, but the explosion in demand is matched by ever-intensifying competition.

Executive summary

6

Faced with the risk of squandering these opportunities, what can companies do to accelerate their efforts and avoid missing the boat? What are the specific capabilities they need to build in order to compete effectively and claim their share of future growth?

Opening windows of opportunityIn our research we found that successful companies in high-growth markets think differently about the capabilities critical for growth and prioritize their investments in different ways. Specifically, these “successful globalizers”—companies with a track record of successful performance in emerging economies, that are confident and committed about their future prospects in these markets—excel in three areas. They are better able to size the future—they possess the ability to accurately size, time and prioritize demand opportunities around the world. They are better able to shape the future—they possess the insights and capabilities to cultivate and protect future demand opportunities around the world. And they are better able to seize the future—they display the operational agility and flexibility to adapt and reorient the company to grasp opportunities across growth markets. Companies can take specific actions today to improve their capabilities in each of these areas:

1. Sizing the future: Where and when to investOur research suggests that successful companies in high-growth markets adopt new approaches to assessing potential market opportunity. They take a more dynamic view that incorporates foresight and flexibility into strategic planning.

They are more adept at examining global opportunities through multiple lenses. This allows them to aggregate seemingly disparate markets and uncover business cases that would otherwise have remained untapped. Witness companies that have successfully targeted diaspora communities scattered across the world, or specific high-potential customer segments, such as those in water-scarce areas, rural communities or

newly-empowered female populations. In this way, successful globalizers develop a more complete and realistic understanding of the markets in which they intend to operate.

Second, in a rapidly-changing environment, these companies understand better than their competitors the importance of planning over time horizons, allowing them to sequence and prioritize their investments. Our research, conducted in partnership with Oxford Economics, illustrates the importance of identifying where different markets will sit in terms of their consumption of specific products and services. How close are they to reaching a point where demand rapidly takes off? How close are they to market maturity? What are the opportunities of different markets over different time horizons?

This deep understanding of their target markets allows successful globalizers to become masters of strategic positioning: to be not only where opportunities are today, but where they will be tomorrow. Through their superior ability to discern the size, location and timing of opportunities, these companies make more informed decisions and trade-offs around where and when to invest, and remain several moves ahead of the competition.

To become masters of strategic positioning, companies can:

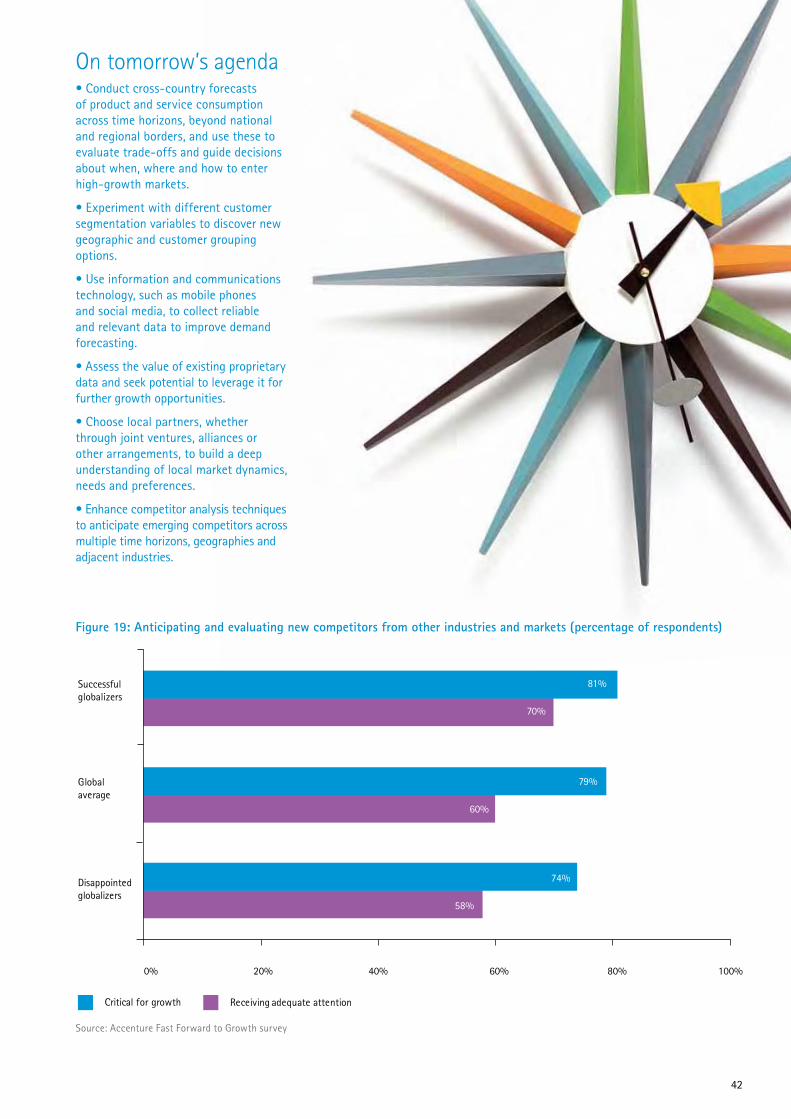

• Conduct cross-country forecasts of product and service consumption across time horizons, beyond national and regional borders, and use these to evaluate trade-offs and guide decisions about when, where and how to enter high-growth markets. Some markets may offer immediate opportunities, while others may be poised for more significant growth in the longer term.

• Experiment with different customer segmentation variables to uncover new geographic and demographic groups. Discovering segments that cut across country borders may unearth business cases beyond those that focus exclusively on country-level segmentation. Procter & Gamble has designed razors, shampoos and cleansing products specifically designed for consumers in water-scarce areas.

• Use information and communications technology (ICT) such as mobile phones and social media to collect reliable and relevant data, improve demand forecasting, and overcome data scarcity. Coca-Cola has 22 million consumers following it through social media, and the ensuing dialogue has given Coca-Cola valuable ideas for new beverages and other products.

• Leverage existing proprietary data for further growth opportunities: the Mexican retailer Grupo Elektra built one of the country’s largest networks of banking branches based on data from a credit service it launched for retail customers.

• Choose local partners—whether through joint ventures, alliances or other arrangements—to gain a deep understanding of local market dynamics, needs and preferences.

• Enhance competitor analysis techniques to anticipate emerging competitors across multiple time horizons, from different geographies and adjacent industries.

2. Shaping the future: Cultivating new marketsWhile some companies may feel they are too late to secure their position in high-growth markets, our research shows that successful globalizers do not simply accept that windows of opportunity are shrinking. Instead, they open new windows of opportunity by discovering new demand and seeding future opportunities.

In an environment where attaining market share is challenging, successful companies have identified the opportunity to grow the size of the overall opportunity, not just their share. They understand how to extend the frontiers of opportunity, often through targeted partnerships and collaboration with local stakeholders.

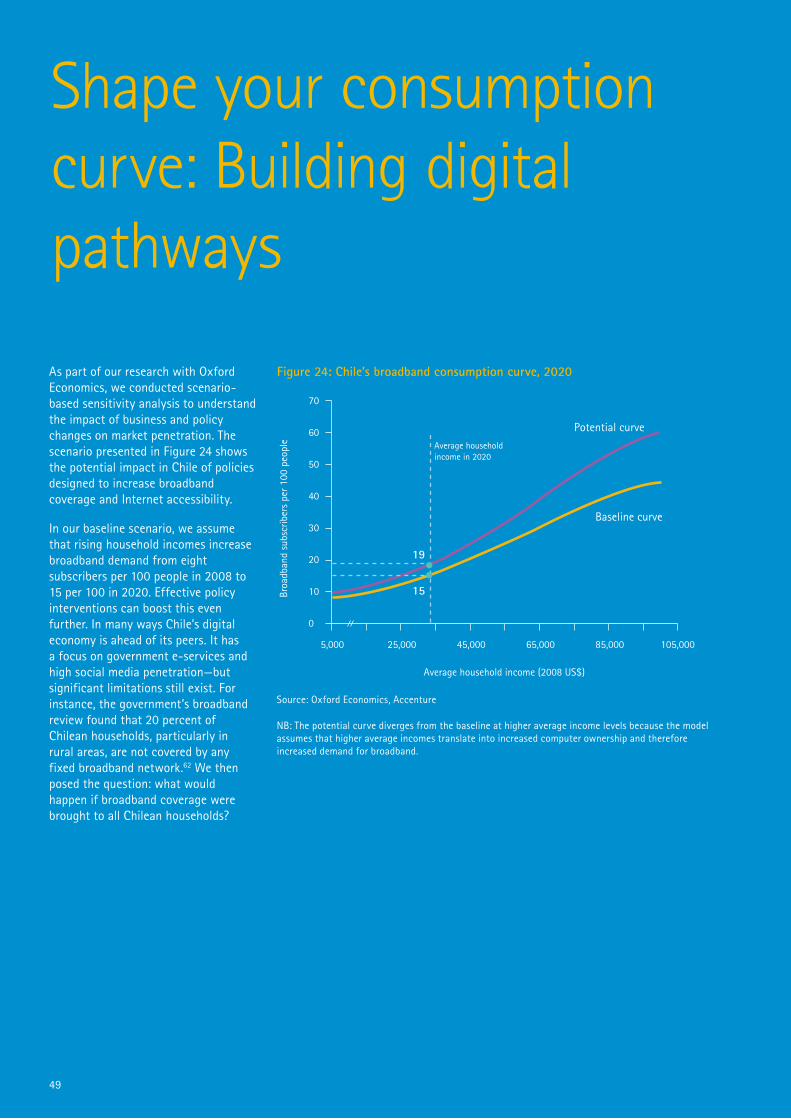

Our research demonstrates the impact, in real consumption opportunities, that can be achieved when businesses invest in generating future demand. For example, our analysis examines how demand can be measurably increased through improvements in infrastructure, education and health care.

7

To achieve a better understanding of how they can push open new windows of opportunity, companies can:

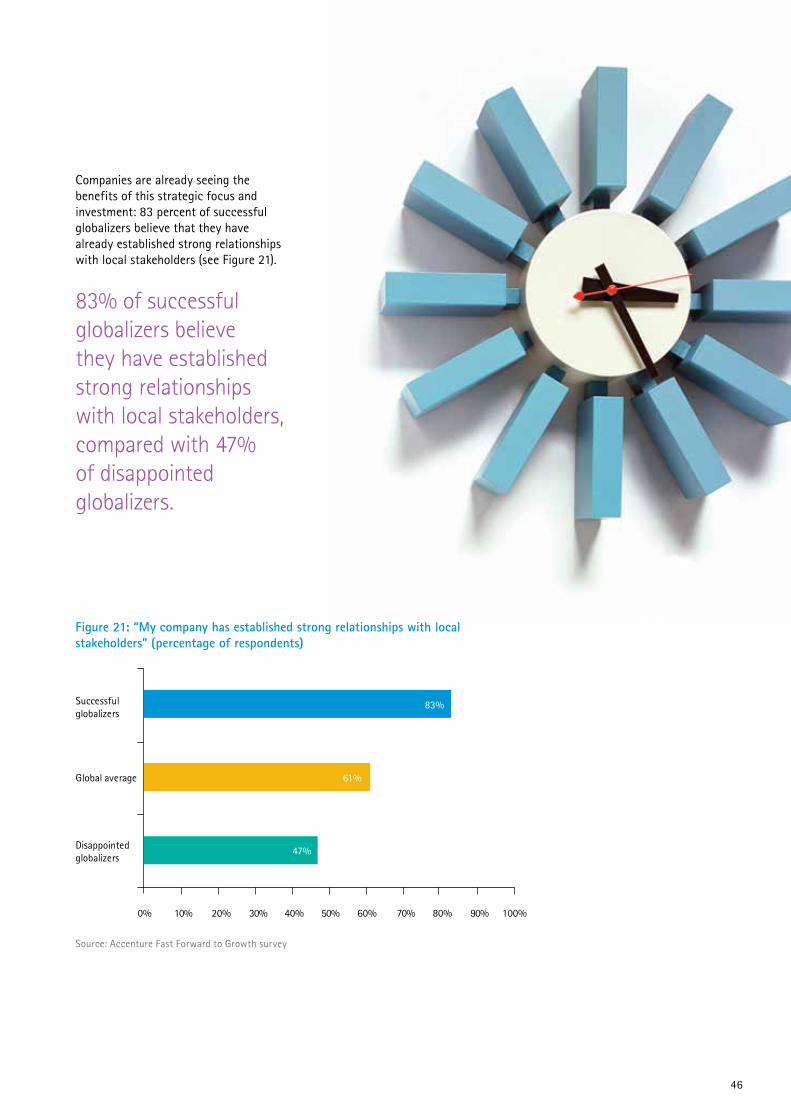

• Identify and map key stakeholders, local and global, and build trusted relationships.

• Assess the strength of relationships with government agencies, industry regulators and local communities. These relationships can help obtain a license to operate, ease the policy environment, and improve access to scarce resources. Executives may be surprised at the extent of common interests held by these stakeholders.

• Innovate to fulfill unmet needs, and involve local consumers in innovation and design. Vodafone and Safaricom’s M-PESA money transfer platform was designed to address a particular need in Kenyan society, to send money to family at home. The service has grown quickly, achieving 14 million registered users within four years, and has simultaneously brought an entirely new business model to markets across the world.

• Evaluate local and global leadership’s understanding of social and economic factors that influence demand, and promote the social and economic development of local communities. Companies successful in emerging markets engage national and local governments to help create the conditions needed for their businesses to prosper. GSK, a leading pharmaceutical and healthcare products company, reduced the price of its patented medicines in the world’s poorest countries, providing social benefits and opening up new markets.

3. Seizing the future: The operational agility to grasp new opportunities Successful companies infuse their organizations with the strategic, operational and cultural agility to grasp new opportunities. Identifying opportunities is one thing, but rapidly mobilizing the organization to attain them is another. In order to achieve this, they prioritize and invest in distinctive capabilities that boost operational agility and flexibility. These capabilities are not just instrumental in helping

companies to grasp the opportunities of today, but will play a fundamental role in shaping the markets of tomorrow.

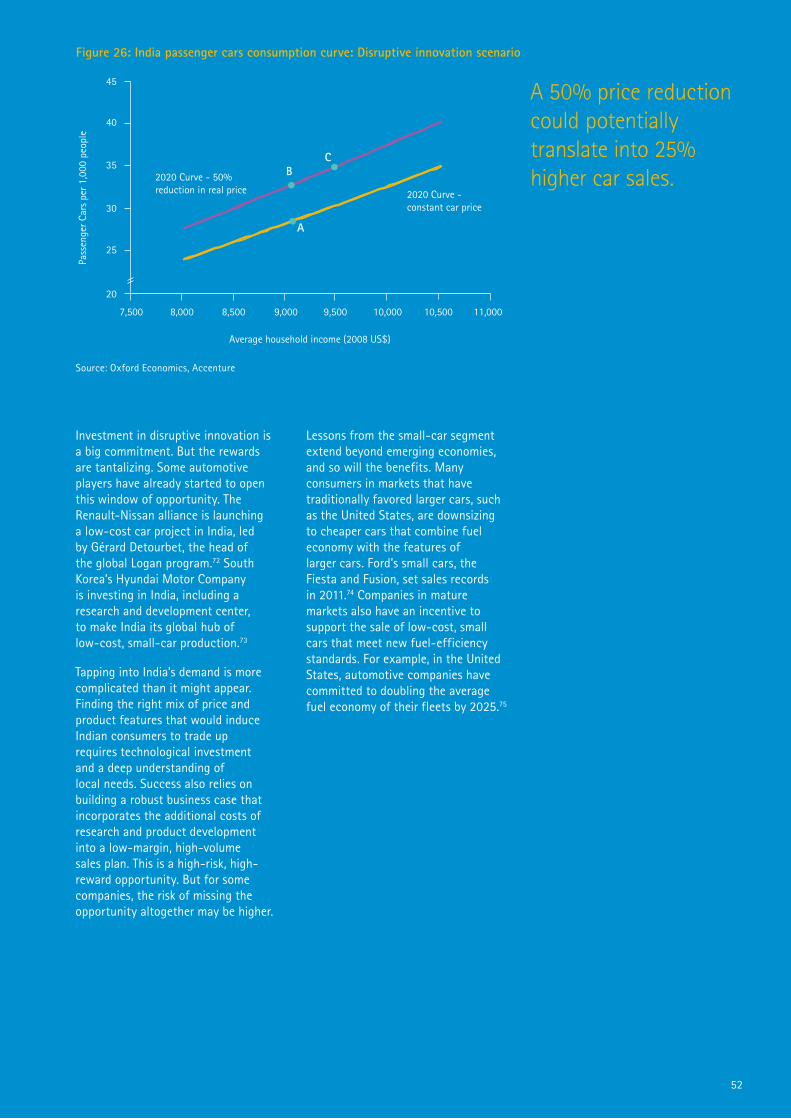

For example, our analysis shows how the power of disruptive innovation can transform industry dynamics, improving the accessibility of consumer products and creating markets. In the automotive sector, for example, process redesign and low-cost materials have dramatically broadened the accessibility of passenger cars to new customers. New pockets of demand have opened up for those companies with the agility and efficiency to design low-price business models. Successful globalizers are pushing the boundaries of what is possible: they understand that business performance and the bottom line will only become more important in geographic growth plans. They understand that operating at speed and scale will play an ever greater role in determining the winners and losers of the next phase of global competition.

To achieve operational agility and seize new opportunities, companies can:

• Explore partnership and acquisition options to boost reach, capability and speed; and continually reassess and evolve ownership and governance structures as circumstances change. The flexibility of Starbucks in managing a range of business models and partnerships has been instrumental to its success in China, which the company now regards as its “second home market.”

• Develop systems to rapidly redeploy people, capital and ideas around the global organization. In expanding its global footprint, Tata Communications designed a wholly new international operating model to incorporate local leadership expertise into its global operations.

• Encourage experimentation—incubate, fund and protect new ideas. The success of Indian pharmaceutical companies demonstrates the importance of innovation, and the benefits of scaling new ideas across the global organization.

• Assess the leadership team and how its skills and experience align with growth plans. Nestlé is relaunching its

International Development Program, giving future leaders experience in foreign markets within the company’s business units across the globe.

No business decisions are simple in today’s environment of prolonged global economic uncertainty. But a game of “wait and see” purely due to a lack of understanding or preparedness poses the risk of missing the boat. This report uncovers the key dynamics at play and details specific actions that companies can take to build the capabilities for success in the high-growth markets of the future.

The researchAccenture’s Institute for High Performance has conducted thorough research to investigate the keys for success in today’s competitive high-growth markets. The main elements of research include:

• Household income analysis, in collaboration with Oxford Economics. We created five standard bands of annual household income and, for each of 64 countries, estimated the number of households falling into each band in 2010, 2015 and in 2020. All forecasts are measured in real terms, and at market exchange rates.

• Industry consumption curves, in collaboration with Oxford Economics. This research forecasts the evolution of consumption for a select group of industries across the world. It also includes scenario-based sensitivity analysis to assess the impact of changes in the business and policy environment.

• A survey of 588 business leaders, across 85 countries and 22 industries, conducted by the Economist Intelligence Unit. Business leaders were asked about their perceptions of the competitive landscape, their company’s plans for growth and the capabilities important for success in these markets.

• Conversations with clients and experts across industries and extensive secondary research, including company case studies and analysis of greenfield and M&A investment data.

8

9

A wake-up call

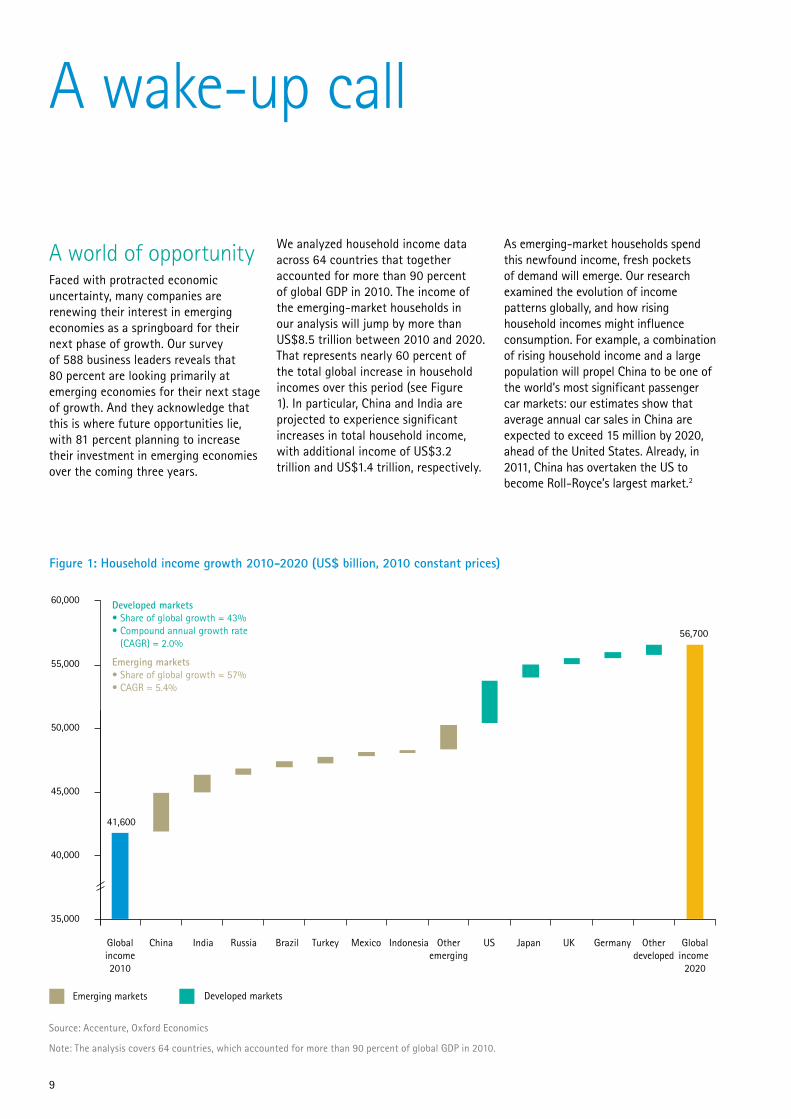

A world of opportunityFaced with protracted economic uncertainty, many companies are renewing their interest in emerging economies as a springboard for their next phase of growth. Our survey of 588 business leaders reveals that 80 percent are looking primarily at emerging economies for their next stage of growth. And they acknowledge that this is where future opportunities lie, with 81 percent planning to increase their investment in emerging economies over the coming three years.

We analyzed household income data across 64 countries that together accounted for more than 90 percent of global GDP in 2010. The income of the emerging-market households in our analysis will jump by more than US$8.5 trillion between 2010 and 2020. That represents nearly 60 percent of the total global increase in household incomes over this period (see Figure 1). In particular, China and India are projected to experience significant increases in total household income, with additional income of US$3.2 trillion and US$1.4 trillion, respectively.

As emerging-market households spend this newfound income, fresh pockets of demand will emerge. Our research examined the evolution of income patterns globally, and how rising household incomes might influence consumption. For example, a combination of rising household income and a large population will propel China to be one of the world’s most significant passenger car markets: our estimates show that average annual car sales in China are expected to exceed 15 million by 2020, ahead of the United States. Already, in 2011, China has overtaken the US to become Roll-Royce’s largest market.2

Figure 1: Household income growth 2010-2020 (US$ billion, 2010 constant prices)

35,000

40,000

45,000

50,000

55,000

60,000

Globalincome2010

China India Russia Brazil Turkey Mexico Indonesia Otheremerging

US Japan UK Germany Otherdeveloped

Globalincome

2020

Developed markets• Share of global growth = 43%• Compound annual growth rate (CAGR) = 2.0%

Emerging markets• Share of global growth = 57%• CAGR = 5.4%

41,600

56,700

Emerging markets Developed markets

Source: Accenture, Oxford Economics

Note: The analysis covers 64 countries, which accounted for more than 90 percent of global GDP in 2010.

“Emerging markets,” however, is a nebulous term that obscures the diversity and complexity across those markets. South Korea, India and Vietnam are often cited as high-potential “emerging markets” to watch. Yet average household income in these markets diverges significantly; approximately US$35,400, US$5,800 and US$3,300, respectively, in 2010. The value of comparing a “typical” consumer across these countries is questionable, even when factoring in cultural differences.

Headline numbers can also mislead. China, for example, is the world’s most populous country and home to one of the world’s largest and fastest-growing economies. Yet in 2010 it had fewer households with annual incomes above US$30,000 than many other smaller “emerging” economies, including Colombia, South Africa and Argentina. While attention is focused on the BRIC economies, we project that by 2020 Turkey will be home to an additional 4.7 million households in this income bracket, on a par with expected growth levels in Brazil. Mexico will also undergo rapid growth in its consumer-market potential: there will be an additional 3.3 million households in this segment over the decade to 2020. With so much variation and rapid change, the size and timing of opportunities can be challenging to grasp.

The temptation to hesitateBusinesses are understandably hesitant to prioritize their investments in these diverse, unfamiliar, but potentially lucrative markets. Each brings unique opportunities, challenges and operating environments. The temptation to hesitate is aggravated by continued global economic uncertainty, sluggishness in developed markets and increasingly tempered near-term growth prospects in emerging markets.

The instinctive response of many companies will be to watch and wait, or even to retrench or withdraw from some geographic locations. Yet our research demonstrates that in today’s global competitive environment, hesitation

may be the most dangerous choice of all. The economic downturn has had a profound impact, dramatically reshaping the global competitive landscape. High-growth markets present many opportunities, but these opportunities are being rapidly snapped up by a new breed of players from emerging economies, as well as multinationals that have entrenched themselves in these markets during previous phases of globalization. The longer they wait, the more challenging competitive environment they will face when eventually taking action.

The risk of missing the boatCompanies turning their attention to high-growth markets must act quickly and definitively to carve out their position. Firms entering and expanding in high-growth markets can expect to face a range of competitors with powerful strengths: from low-cost players to global giants, from locally networked incumbents to masters of global scale and efficiency. In this environment, hesitation risks squandering opportunities. The longer the hesitation, the greater the odds that more nimble and prepared players will position themselves for these lucrative growth opportunities.

The mobile telecoms market in Latin America, for example, is often predicted to be one of the world’s fastest-growing telecoms markets over the next five years (See “América Móvil and Telefónica: Seizing opportunities ahead of the pack,” page 12). The market for value-added services such as mobile data is not yet established in much of Latin America. Penetration rates remain very low in many countries, and rapid increases in demand may be far off. These facts have not stopped Mexico’s América Móvil and Spain’s Telefónica from expanding rapidly across these smaller markets, acquiring local providers and gaining access to the infrastructure essential for growth when demand does take off. Companies looking to enter these nascent markets will face not only domestic players, but also two Fortune Global 500 multinationals with established products, infrastructure, relationships and brands.

The growth prospects are clear. But it is also clear that many companies will feel locked out of the opportunity to become serious players in the market, even before it has taken off.

This pattern is repeating itself in different industries and locations around the world. In some cases, the risk of being locked out of markets threatens deep and long-term consequences. The CEO of a large Chinese railway equipment manufacturer explained that the financial crisis weakened the ability of European and North American banks to finance large railway contracts demanded in Asia’s emerging economies. Chinese enterprises and banks partnered to fill the void. The CEO is confident that his company’s products rival the quality of multinational competitors and will anchor rapid sales expansion in Asia: exports for the first half of 2009 increased by 60 percent over the same period in the previous year.3 The prospect of being locked out of such long-term contracts around the world should be a sobering thought for many companies.

The intensity of competition is not all that has changed. The diversity of competitors, and of their competitive advantages, brings new challenges. In this report, we bring to light the fundamental shifts in the global business landscape that the downturn has wrought. We make clear the new challenges companies face in determining the optimal location and timing of opportunities, and the risk of delaying action in the face of aggressive competition.

The opportunity paradoxOur global business survey uncovered a paradox: on one hand, companies see continued growth coming from emerging economies. On the other, they feel that their windows of opportunity may be shrinking. Our survey findings underscored the point: 73 percent of respondents believe they need to accelerate their efforts to build satisfactory market share in these high-growth markets—or that it may already be too late.

10

Wanted: Action and confidenceEven while companies feel they are missing out on opportunities, uncertainty may lead them to hesitate about investing in high-growth markets. In fact, many companies have healthy cash reserves that could be used for expansion. Cash holdings for American nonfinancial companies in June 2011 exceeded US$1.9 trillion, the highest in half a century.4

The volatile economic environment drives uncertainty and hesitation, but our research uncovers deeper concerns. We found that many business leaders are not confident about their own company’s ability to succeed in high-growth markets.

• 40 percent do not believe that their company possesses the strategic and operational capabilities to fully grasp the opportunities in emerging economies.

• The same proportion acknowledge that they do not fully understand the competitive dynamics they will face.

• Nearly one-third do not even believe that their company has a clear strategy for high-growth markets.

With almost three-quarters of business leaders believing that they need to accelerate their efforts in high-growth markets, it is critical to understand the dynamics that constrain their progress.

Many companies may not appreciate the degree of change in the business landscape since the downturn.

On the demand side, companies have not adjusted their methods to locate and measure demand and fully evaluate potential opportunities: their tools are often inappropriate, or even outdated and irrelevant.

On the supply side, companies underestimate the diversity of players and capabilities they will encounter in the competitive landscape. Next, we explore these demand and supply dynamics.

73% of companies feel they need to accelerate efforts or may already be too late to build satisfactory market share in high-growth markets.

11

12

Latin America is projected to be the fastest-growing telecoms market over the next five years. Demand is growing at unprecedented rates: penetration reached a high of 89 percent this year.5 As penetration rates rise, so do opportunities for lucrative “value-added” services. Almost one-third of all new phones in Latin America by 2014 are expected to be smartphones. The number of mobile data plan subscribers is expected to more than double this year, a sizable opportunity in a continent of nearly 600 million people.6

The market is dominated by two global telecoms giants, each looking for growth to offset a decline in its traditional revenue base: América Móvil, which is looking for growth in mobile, broadband and pay TV to offset declining revenue in fixed-line services since the market was liberalized and opened up to competition, and Telefónica, which is looking to broaden its footprint beyond Europe, an intensely saturated and competitive market.7

These two companies are the dominant players in most key Latin American markets. In Mexico, Telcel—América Móvil’s mobile arm—holds 72 percent of the market, but Telefónica is closing fast. In the last quarter of 2010, the two companies accounted for 90 percent of the one million new connections: Telcel took 30 percent, but Telefónica took 61 percent. And in Brazil, América Móvil’s Claro brand is a key player in the market, along with Vivo, acquired by Telefónica in 2007.8

The strategies América Móvil and Telefónica use to build their presence are revealing. América Móvil has for many years been buying up smaller operators around Latin America, taking control of fixed-line infrastructure and

increasing its customer base. In recent years, Telefónica has built on long-standing relationships in the region, strengthening its presence through sizable acquisitions of established players such as Vivo.

As other telecoms players look to high-growth markets in Latin America, they are faced not only with smaller domestic incumbents but also with two Fortune Global 500 multinationals with global reach and scale, combined with local presence and understanding across the region. Breaking through this incumbency poses new and challenging questions to potential entrants.

América Móvil and Telefónica are already jostling for position in new services, including mobile data, broadband and pay TV. Telefónica recently rebranded its operations across Latin America, bringing together fixed line, mobile, broadband and TV under the Movistar brand.

When Latin America’s markets begin their inevitable acceleration—broadband penetration rates are still hovering at around 15 percent in most of these countries—América Móvil and Telefónica will be at the forefront of new opportunities.9 They are identifying and snapping up opportunities almost before they appear.

América Móvil and Telefónica: Seizing opportunities ahead of the pack

13

Locating demand: The search for growth

Between 2011 and 2016, approximately 60 percent of global economic growth is forecast to come from emerging economies,10 despite an expected near-term slowdown in key high-growth markets such as China and India. The triad economies of the United States, Europe and Japan continue to experience persistently high unemployment and public debt levels. Many developed economies have seen their economic growth forecasts downgraded in recent months and companies struggle to locate the next sources of growth in these markets. In many emerging economies, in contrast, unemployment is falling and governments hold significant reserves. Many companies in these markets may not even have felt the impact of the downturn.

Levels of consumption and demand for goods and services in emerging economies will increase as incomes grow. But with enormous differences in the size and growth rates of demand, along with a variety of customer preferences, it is difficult to accurately assess and forecast growth opportunities.

A fast-moving targetWe have conducted an extensive analysis, in collaboration with Oxford Economics, of household incomes and their evolution over the coming decade. According to our analysis, China lags behind 27 other economies, including Poland, Turkey and Colombia, in the number of households with an annual income greater than US$30,000. This comes as no surprise to companies eagerly and impatiently awaiting

profitability in China. But over the next decade, China will rapidly move up the ranks, leaving only three economies with a greater number of households earning US$30,000 and above: the United States, Japan and Germany. In 2010, the number of Chinese households in this income bracket was almost twice that in Thailand—but by 2020, there will be more than thirteen times as many. Our analysis highlights the dynamics shaping global demand opportunities through 2020 (see “In focus: Household buying power,” page 18). Specifically, we illustrate how US$15 trillion of additional household income will be dispersed around the world across distinct income segments. The stories that emerge reveal where “high growth” may be found.

Attachment to outdated labelsIncome levels and the speed of change are difficult to keep up with and translate into investment decisions. Commentators are quick to embrace labels such as BRIC (Brazil, Russia, India and China), MINT (Mexico, Indonesia, Nigeria and Turkey) and CIVETS (Colombia, Indonesia, Vietnam, Egypt, Turkey and South Africa). But the dramatic speed at which the demand landscape is changing brings into question the value of these terms. Over the next three years, in real terms, India’s economy will grow at a rate twice as fast as that of Russia. China will grow twice as fast as Brazil. And there are significant structural differences: while India’s growth has been fueled primarily by domestic demand (private consumption accounts

for 56 percent of India’s economy, compared with 34 percent in China),11 China’s economy is largely built on investment and export growth, and Russia is heavily dependent on its natural resources: oil, fuel and gas accounted for 69 percent of exports in 2010.12 These fundamental differences illustrate the dangers of relying upon such country groupings for detailed analysis and comparisons. Looking outside the BRICs, Vietnam, Peru and Angola are all forecast to grow more quickly than Russia. It becomes clear that even the accuracy of the terms “emerging markets” and “high-growth markets” is debatable.

Economic groupings and macroeconomic terminology help describe important global trends. But when a company plans its own global strategy, it needs a far more granular analysis—one that looks beneath headline figures and provides a more accurate picture of the true size and pace of growth in demand around the world.

The dangers of generalizationLabeling groups of countries can also lead companies to overlook important differences among unfamiliar markets. For decades, the African continent has borne the brunt of such generalizations. In 2010, Nigeria had a per capita GDP of US$1,300, lower than the sub-Saharan Africa average (see Figure 2).13 Nigeria’s total household income was approximately US$200 billion—lower than South Africa’s, despite a population three times as large.14

14

However, Nigeria’s consumer-market potential will soon outstrip that of other African economies it lags behind today. By 2020, 7.8 million additional households are expected to have an income level of US$5,000 and above, with 12 percent of these earning more than US$30,000. This translates into US$130 billion of additional household income and an increase far greater than other African economies (see Figure 3). The income growth is also greater than that in burgeoning Asian economies, such as Malaysia and Thailand. The key driver of Nigeria’s rapid economic growth, and incomes, is the country’s expected fast population growth.

The misleading “middle class”Hyperbole and imprecise terminology hamper the sizing of high-growth market opportunities. Take the much vaunted “emerging middle class.” This consumer segment is variously estimated to include anywhere between 500 million and 2 billion people. Some forecasts claim that it could double over the next two decades.15 However,

“middle class” is a loosely defined term and differs across markets. In some cases it is merely the middle of the income distribution. In others, it refers to a specific level of income. Either way, a middle-class household in India is unlikely to afford the deluxe refrigerator, high-end TV, smartphone and sport utility vehicle of a middle-class American family. These large discrepancies and ambiguities in the definition of “middle class” matter for companies trying to find the most attractive markets for their products and services.

Redrawing bordersCompanies must take into account the most appropriate geographic units in strategic planning. For example, it may make sense to plan in terms of regions and cities rather than countries and continents. In China, for example, there are significant variations across provinces in income, demographics, religion, language and geography. By delving more deeply into their assessment of China and other large emerging markets, companies can create a more accurate picture of where

the greatest opportunities lie. Some might be surprised at what they find. Significant opportunities exist in cities that many multinationals haven’t even heard of. Zhengzhou is a prime example. The capital of Henan province in China, Zhengzhou by 2020 will have a bigger economy than Sweden, Hong Kong or Israel.16 And Surat, in the Indian state of Gujarat, is forecast to be home to nearly 8 million people by 2020, more than the whole of Paraguay or Norway.17

One example of a company that has followed a city expansion approach is Xiang Piaopiao Food (XPP), which entered the Chinese beverage market in 2005 with a milk tea product. The market at the time was concentrated in Tier 1 and Tier 2 cities, but XPP avoided the high entry costs associated with these markets by focusing on 600 smaller cities, using traditional channels of local distributors. The company has achieved compound annual growth of more than 100 percent, with total sales from smaller cities and towns typically accounting for 75 to 80 percent of total sales in each province.18

Figure 2: GDP per capita, 2010 (US$ at 2010 prices and market exchange rates)

0

1,000

2,000

3,000

4,000

5,000

7,000

6,000

SouthAfrica

Egypt Ghana Nigeria Kenya

Sub-SaharanAfrica average

8,000

Source: Oxford Economics

Figure 3: Change in total income for households with annual income of US$5,000 and above, 2010-2020 (US$ billion, constant 2010 prices)

Source: Oxford Economics

0

100

80

60

40

20

SouthAfrica

Egypt GhanaNigeria Kenya

120

140

Thailand Malaysia

15

Understand the “unknown-knowns” A large number of external factors can cause consumer spending to diverge from expectations. One such factor is change in the distribution of income, something that is receiving increased attention from opinion formers and policymakers around the world. China, for example, has made reducing income inequality a priority in its 12th Five-Year Plan.

In South Africa, greater income equality is also an explicit policy goal. We modelled what would happen if South Africa’s Gini coefficient fell from 58 to 51, still a high co-efficient by global standards (see Figure 4). The impact of this reduction in income inequality would be to expand by 7 million the number of households with annual incomes of between US$5,000 and US$50,000. Understanding shifts in the distribution of income allows companies to measure market potential more accurately. This can mean the difference between making a decision to enter a market or not. Or

it might mean that companies need to accelerate entry plans as demand for their product picks up sooner than they had expected. This example illustrates how changes in external factors may have an unexpected but significant impact on market opportunities and strategic planning.

Spotting opportunity—creating demandA clear awareness of income trends is a crucial first step toward developing an accurate map of current and future demand. Understanding the point at which consumption of a product will pick up, accelerate and mature should be a central part of planning market entry and expansion. Accurately assessing market maturity across different locations can offer critical insights into how those markets can best be aligned for strategic planning purposes. To illustrate, we have estimated the global relationship between household income levels and market penetration for select products and services (see “In focus: Consumption curves,” page 23).

Figure 4. South Africa income inequality scenarios: Number of households, 2020 (million)

1

2

3

4

5

6

7

US$0-US$5,000 US$50,000+

Baseline income inequality Reduced income inequality

0

US$5,000-US$15,000 US$15,000-US$30,000 US$30,000-US$50,000

Source: Accenture, Oxford Economics

16

17

18

In focus: Household buying power

While high-growth markets offer attractive consumer opportunities, diverse and rapidly evolving income patterns often pose significant strategic planning challenges. In collaboration with Oxford Economics, we forecast the evolution of household incomes across 64 economies.19

Our forecasts are measured in real terms at constant 2010 prices to avoid the potential distorting effect of inflation over time. We compare income levels across countries using market exchange rates, rather than purchasing power parities (PPP). We believe this avoids the upward bias of PPP measures and corresponds more closely to the actual size of revenue opportunity for businesses. Even with our conservative methodology, the stories that emerge are striking.

Between 2010 and 2020, the number of households in the 64 countries we studied is forecast to jump by 124 million—87 percent will be in emerging economies—translating into US$15 trillion of additional household income by 2020. Emerging economies will account for 57 percent of this increase in income.

19

The emerging consumers

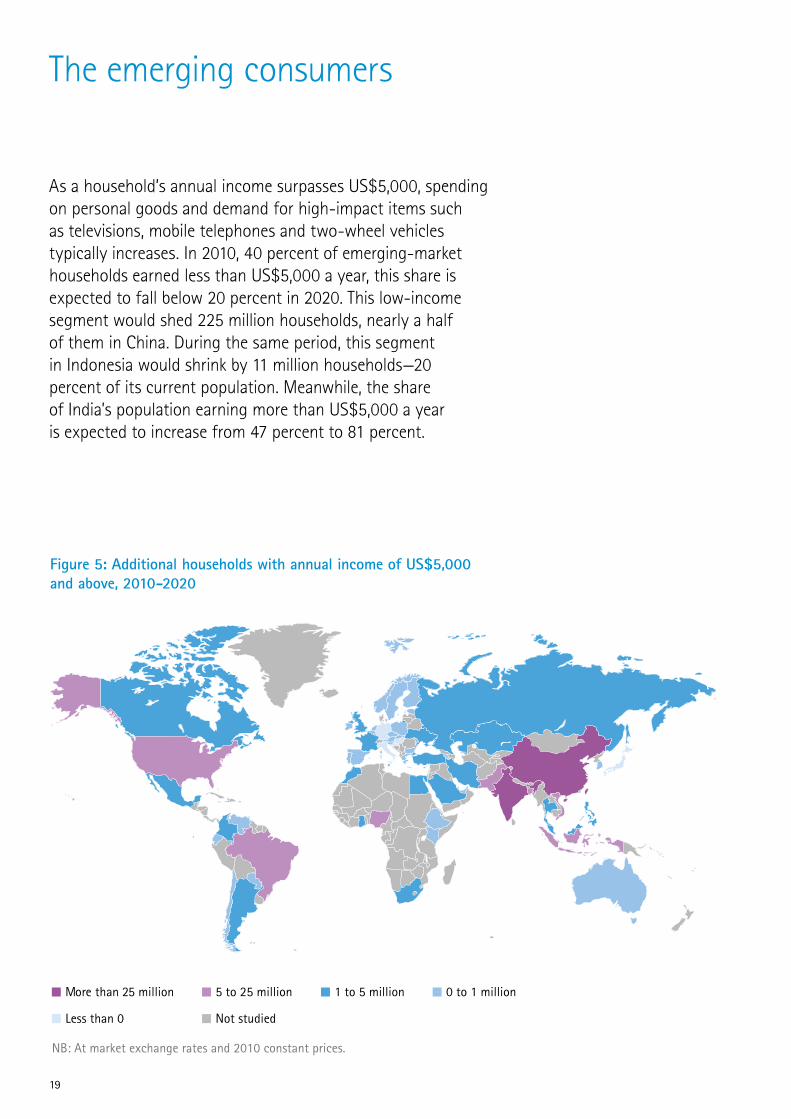

Figure 5: Additional households with annual income of US$5,000 and above, 2010-2020

More than 25 million

NB: At market exchange rates and 2010 constant prices.

5 to 25 million 1 to 5 million 0 to 1 million

Less than 0 Not studied

As a household’s annual income surpasses US$5,000, spending on personal goods and demand for high-impact items such as televisions, mobile telephones and two-wheel vehicles typically increases. In 2010, 40 percent of emerging-market households earned less than US$5,000 a year, this share is expected to fall below 20 percent in 2020. This low-income segment would shed 225 million households, nearly a half of them in China. During the same period, this segment in Indonesia would shrink by 11 million households—20 percent of its current population. Meanwhile, the share of India’s population earning more than US$5,000 a year is expected to increase from 47 percent to 81 percent.

20

The great leap

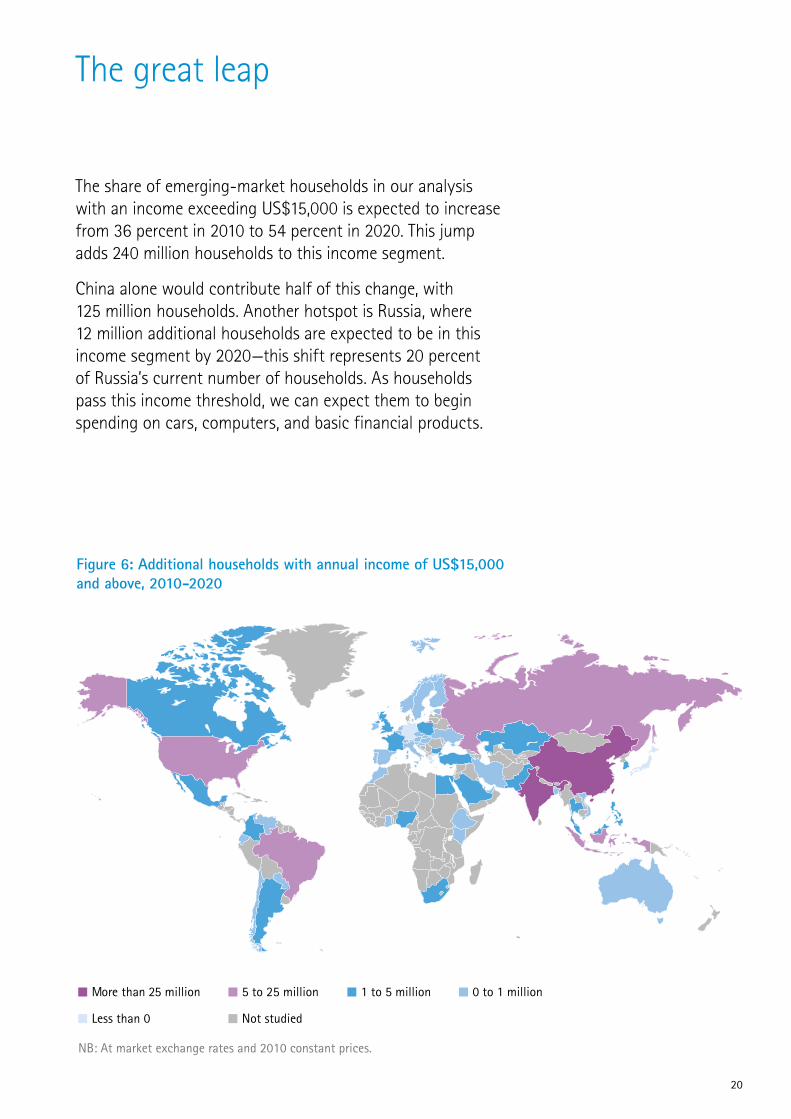

Figure 6: Additional households with annual income of US$15,000 and above, 2010-2020

More than 25 million

NB: At market exchange rates and 2010 constant prices.

5 to 25 million 1 to 5 million 0 to 1 million

Less than 0 Not studied

The share of emerging-market households in our analysis with an income exceeding US$15,000 is expected to increase from 36 percent in 2010 to 54 percent in 2020. This jump adds 240 million households to this income segment.

China alone would contribute half of this change, with 125 million households. Another hotspot is Russia, where 12 million additional households are expected to be in this income segment by 2020—this shift represents 20 percent of Russia’s current number of households. As households pass this income threshold, we can expect them to begin spending on cars, computers, and basic financial products.

21

Multiple consumer hubs

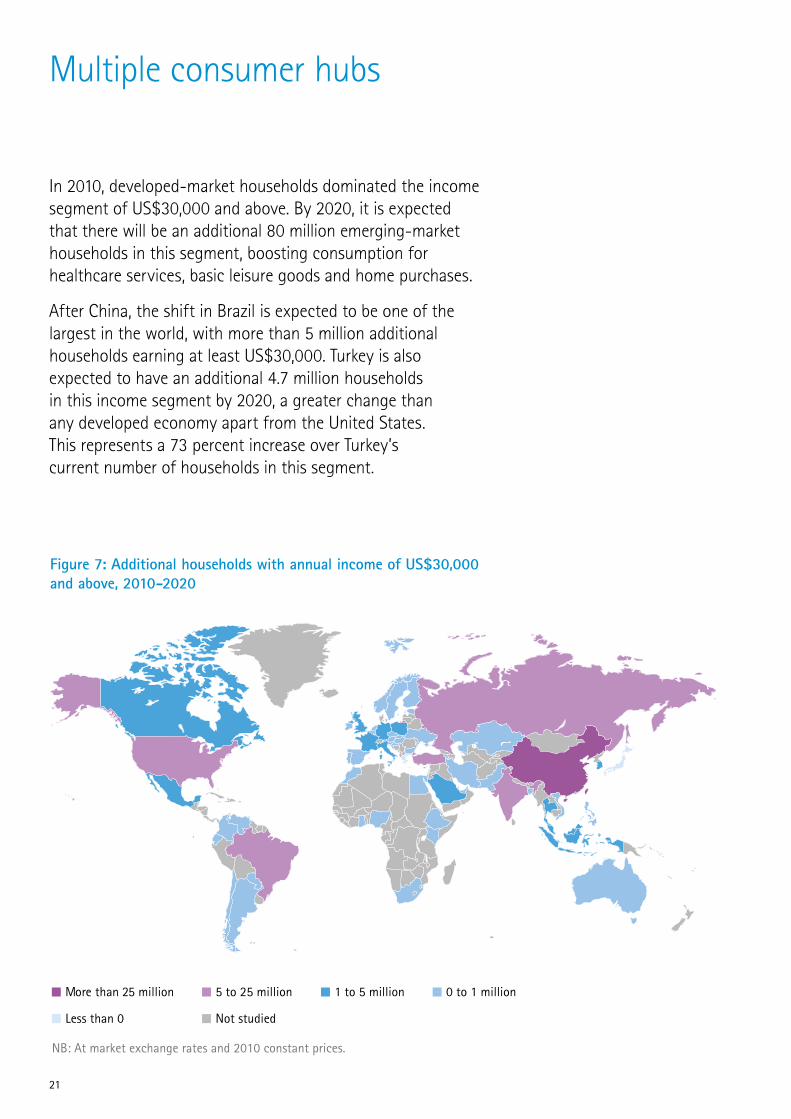

Figure 7: Additional households with annual income of US$30,000 and above, 2010-2020

More than 25 million

NB: At market exchange rates and 2010 constant prices.

5 to 25 million 1 to 5 million 0 to 1 million

Less than 0 Not studied

In 2010, developed-market households dominated the income segment of US$30,000 and above. By 2020, it is expected that there will be an additional 80 million emerging-market households in this segment, boosting consumption for healthcare services, basic leisure goods and home purchases.

After China, the shift in Brazil is expected to be one of the largest in the world, with more than 5 million additional households earning at least US$30,000. Turkey is also expected to have an additional 4.7 million households in this income segment by 2020, a greater change than any developed economy apart from the United States. This represents a 73 percent increase over Turkey’s current number of households in this segment.

22

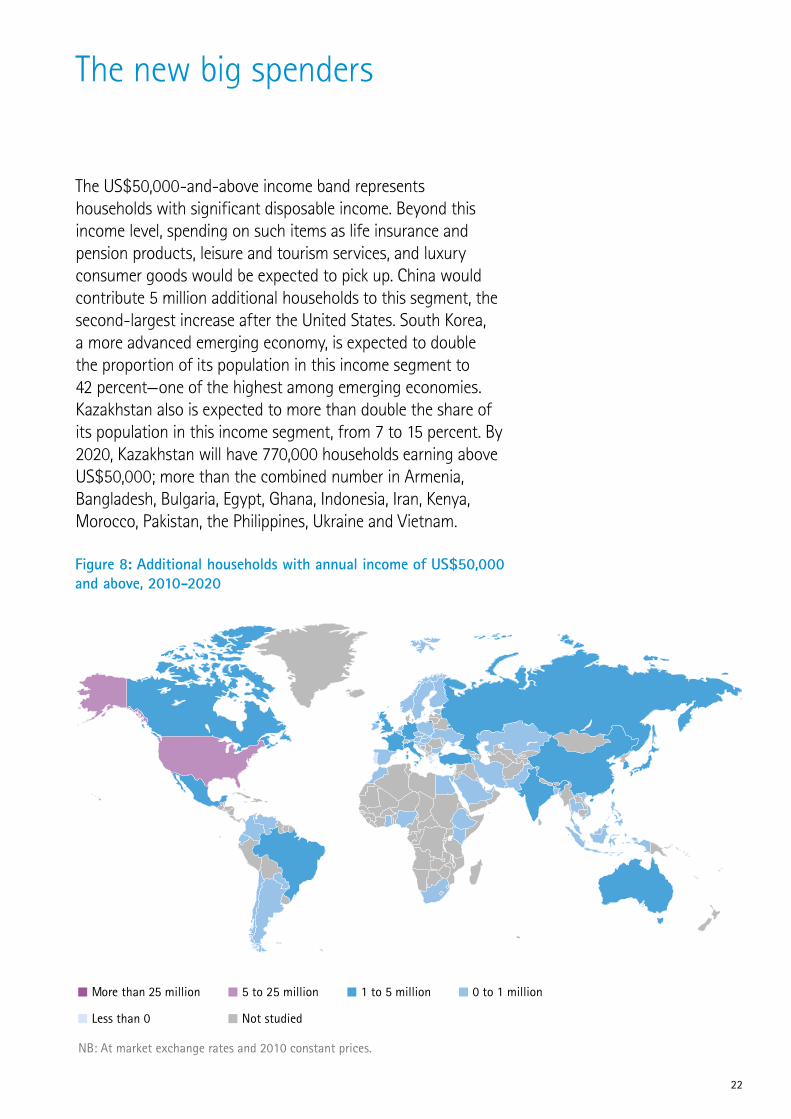

The new big spenders

Figure 8: Additional households with annual income of US$50,000 and above, 2010-2020

More than 25 million

NB: At market exchange rates and 2010 constant prices.

5 to 25 million 1 to 5 million 0 to 1 million

Less than 0 Not studied

The US$50,000-and-above income band represents households with significant disposable income. Beyond this income level, spending on such items as life insurance and pension products, leisure and tourism services, and luxury consumer goods would be expected to pick up. China would contribute 5 million additional households to this segment, the second-largest increase after the United States. South Korea, a more advanced emerging economy, is expected to double the proportion of its population in this income segment to 42 percent—one of the highest among emerging economies. Kazakhstan also is expected to more than double the share of its population in this income segment, from 7 to 15 percent. By 2020, Kazakhstan will have 770,000 households earning above US$50,000; more than the combined number in Armenia, Bangladesh, Bulgaria, Egypt, Ghana, Indonesia, Iran, Kenya, Morocco, Pakistan, the Philippines, Ukraine and Vietnam.

23

In focus: Consumption curves

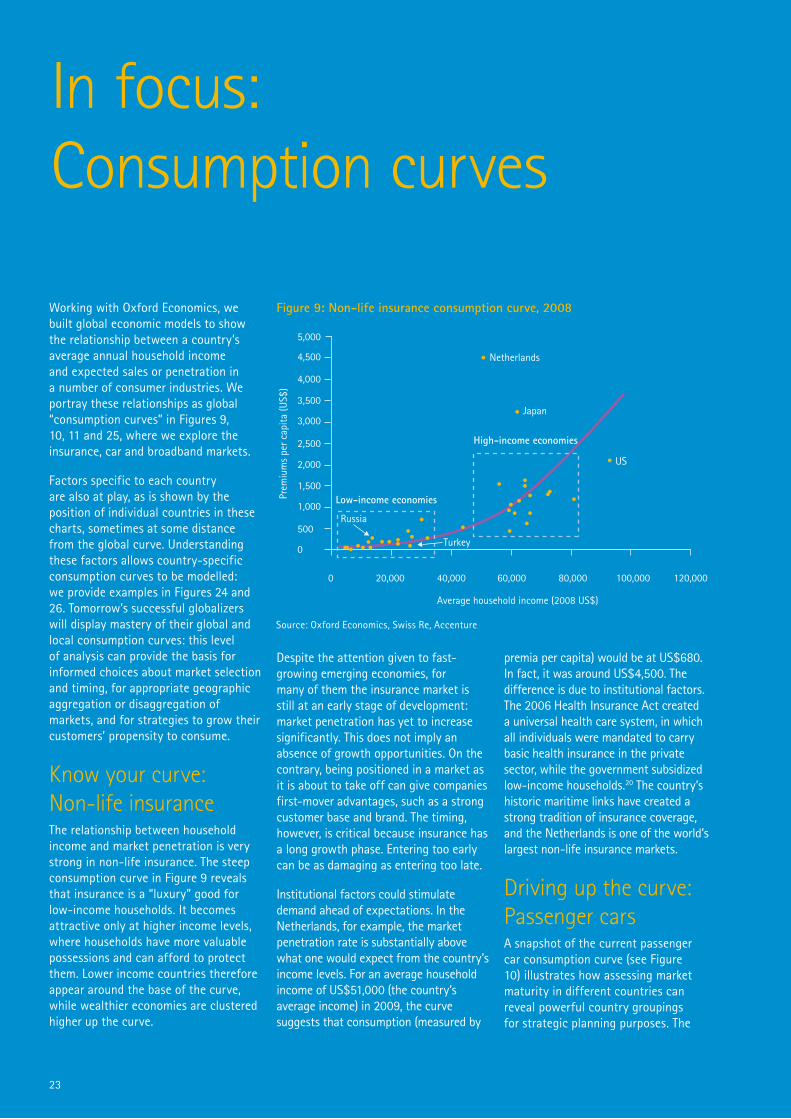

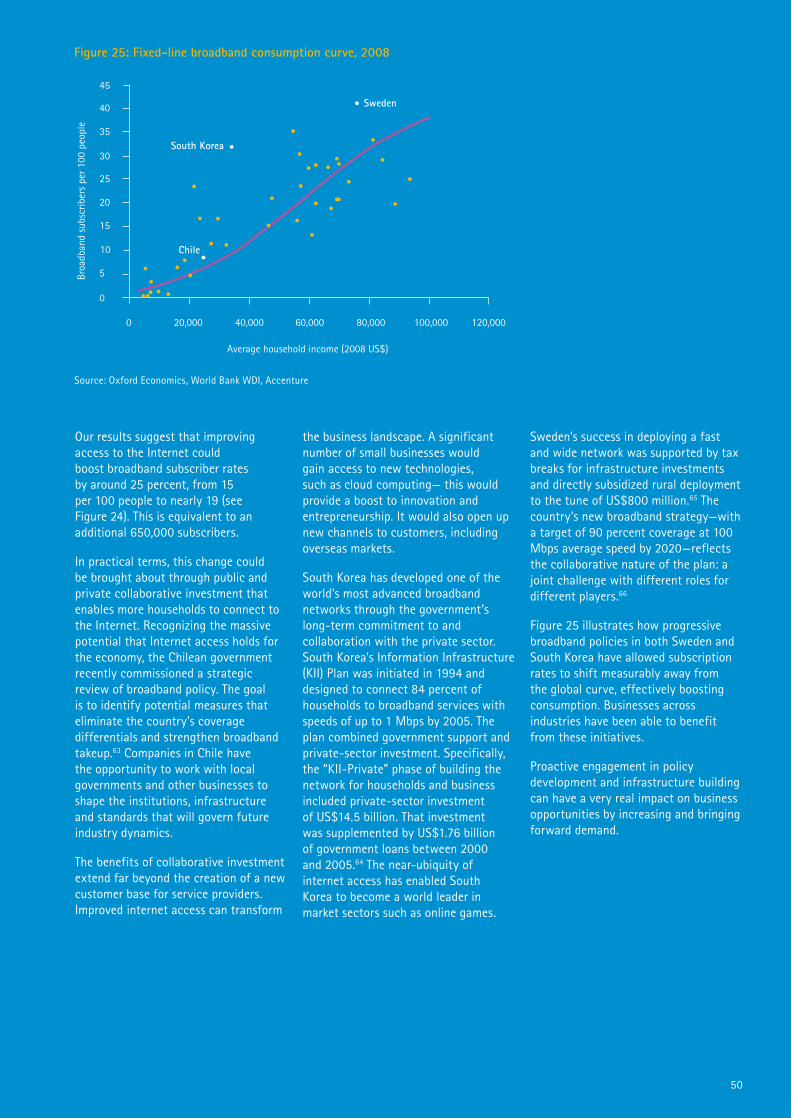

Working with Oxford Economics, we built global economic models to show the relationship between a country’s average annual household income and expected sales or penetration in a number of consumer industries. We portray these relationships as global “consumption curves” in Figures 9, 10, 11 and 25, where we explore the insurance, car and broadband markets.

Factors specific to each country are also at play, as is shown by the position of individual countries in these charts, sometimes at some distance from the global curve. Understanding these factors allows country-specific consumption curves to be modelled: we provide examples in Figures 24 and 26. Tomorrow’s successful globalizers will display mastery of their global and local consumption curves: this level of analysis can provide the basis for informed choices about market selection and timing, for appropriate geographic aggregation or disaggregation of markets, and for strategies to grow their customers’ propensity to consume.

Know your curve: Non-life insuranceThe relationship between household income and market penetration is very strong in non-life insurance. The steep consumption curve in Figure 9 reveals that insurance is a “luxury” good for low-income households. It becomes attractive only at higher income levels, where households have more valuable possessions and can afford to protect them. Lower income countries therefore appear around the base of the curve, while wealthier economies are clustered higher up the curve.

Despite the attention given to fast-growing emerging economies, for many of them the insurance market is still at an early stage of development: market penetration has yet to increase significantly. This does not imply an absence of growth opportunities. On the contrary, being positioned in a market as it is about to take off can give companies first-mover advantages, such as a strong customer base and brand. The timing, however, is critical because insurance has a long growth phase. Entering too early can be as damaging as entering too late.

Institutional factors could stimulate demand ahead of expectations. In the Netherlands, for example, the market penetration rate is substantially above what one would expect from the country’s income levels. For an average household income of US$51,000 (the country’s average income) in 2009, the curve suggests that consumption (measured by

premia per capita) would be at US$680. In fact, it was around US$4,500. The difference is due to institutional factors. The 2006 Health Insurance Act created a universal health care system, in which all individuals were mandated to carry basic health insurance in the private sector, while the government subsidized low-income households.20 The country’s historic maritime links have created a strong tradition of insurance coverage, and the Netherlands is one of the world’s largest non-life insurance markets.

Driving up the curve: Passenger carsA snapshot of the current passenger car consumption curve (see Figure 10) illustrates how assessing market maturity in different countries can reveal powerful country groupings for strategic planning purposes. The

Prem

ium

s pe

r cap

ita (U

S$)

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

0 20,000 40,000 60,000 80,000 100,000 120,000

High-income economies

Low-income economies

Average household income (2008 US$)

Japan

Netherlands

US

Russia

Turkey

Figure 9: Non-life insurance consumption curve, 2008

Source: Oxford Economics, Swiss Re, Accenture

Figure 10: Passenger cars consumption curve, 2008

Source: Oxford Economics, World Bank WDI, Accenture

Cars

per

1,0

00 p

eopl

e

700

600

500

400

300

200

100

0

0 20,000 40,000 60,000 80,000 100,000 120,000

Emerging phase

Average household income (2008 US$)

Rapid-growth phase

Maturing phase Illustrative consumption figures

Cars per 1,000 people

China 27Thailand 54Turkey 92Mexico 181Slovakia 272Croatia 346United States 451

US

China

Russia

Figure 11: Passenger cars: Expected change in car penetration, 2008-2020

Source: Oxford Economics, World Bank WDI, Accenture

Cars

per

1,0

00 p

eopl

e

600

500

400

300

200

100

0

0 10,000 20,000 30,000 60,000 70,000 80,000

Average household income (2008 US$)

Illustrative consumption growth: change 2008-2020

Cars per Average 1,000 people sales, annual

Slovakia 99 160,000China 94 15,030,000 Turkey 82 1,120,000Mexico 54 2,200,000Thailand 45 560,000Croatia 28 110,000

40,000

Thailand

50,000

Slovakia

Croatia

Turkey

Mexico

2008 2020

24

car markets in Mexico, Slovakia and Turkey appear to be at similar growth phases—rapidly growing markets with car purchase penetration increasing faster than income growth. A “maturing” cluster of markets is also apparent further up the curve: in these countries, a change in income will induce a proportionally smaller change in demand.

Companies can use these patterns and groupings to identify potential targets, similarities and synergies. For example, many countries that are approaching the “rapid growth” phase are also significant automotive manufacturing hubs. Mexico, Slovakia and Turkey are fast becoming hotspots for auto parts production and assembly21 and are attracting considerable investment.22 These markets

and their major trading partners may promise lucrative opportunities for the automotive sector, as well as for ancillary products and services.

In maturing car markets, the next wave of growth may be in electric or hybrid vehicles. Although these vehicles still make up only a small proportion of total car sales, by aggregating similar markets, companies may uncover sufficient scale to build a profitable cross-country business case.

The greatest value in consumption curves is their ability to forecast over time. By comparing market dynamics across time horizons and geographies, companies can paint more accurate pictures of where and when opportunities will arise. These comparisons anchor a more effective

prioritization of investments across target markets. For example, in 2008, the Thai market had not yet taken off. But between 2008 and 2020, the car stock is expected to nearly double to 103 cars per 1,000 people, and annual sales will average 560,000 cars (see Figure 11). By the same token, Turkey is further up the consumption curve and expects a much larger increase in consumption earlier in the decade. Penetration is expected to increase by an additional 82 cars per 1,000 people—equivalent to annual car sales of 1.12 million. These examples illustrate the value of more granular analysis: some companies may need to prioritize today’s investment dollars between building a longer-term position in Thailand and betting on Turkey’s more immediate window of opportunity.

25

26

New players, new rules: The new shape of competition

This chapter looks at the important dynamics reshaping the global competitive landscape: the key players and new competitive pressures that make it more difficult for companies to access growth opportunities. We introduce the players in this new phase of global competition and then look at how they are changing the rules of the game.

New playersInternationalization has never been a simple journey. The ability to become relevant and respond to local needs in new markets has always been a fundamental challenge. A major obstacle is the strength of incumbents, with their deep local-level relationships, acute knowledge of local needs and preferences, and enviable customer loyalty. Business school case studies and media coverage are littered with praise for companies that have managed to effectively tailor their offerings to local markets. By the same token, companies unable to recognize and adapt to local circumstances are criticized.

But companies looking to enter high-growth markets today face a more complex incumbency challenge than ever before. High-growth markets have spurred growing levels of investment and corporate activity over recent years.

Many economies have actively courted foreign investment, and governments compete against one another to attract firms from around the world. The impact on local competitive dynamics has been dramatic.

Multiple layers of incumbencyFirst, companies must compete against strong local knowledge and the relationships that domestic players enjoy. Second, many can expect to face Western multinationals that have expended significant effort to become locally entrenched. These multinational players possess the scale and efficiency of global enterprises, some possess strong brands, and most have become leaner and more competitive in response to economic troubles in their home countries. Finally, companies entering new markets will also face multinationals from emerging economies that can leverage scale advantages with low-cost capabilities and, in some cases, government support and funding. Most companies are rightly daunted by the prospect of having to take share from these incumbents. It is no wonder that some firms feel they are already too late to enter these markets (For an example of how to respond to these pressures, see “Cencosud: Retail relations,” page 30).

27

Emerging giantsAlready 117 companies from emerging economies are in the Fortune Global 500, a six-fold increase since 2000. This trend appears to be accelerating. Twenty-two emerging-market multinationals replaced their developed market peers on the list in 2011 (see Figure 12). The emerging-market companies are also quickly moving up the ranks. In 2011, 70 percent of the Fortune Global 500 fastest-growing companies (by revenue) were from emerging markets.

Companies based in emerging economies often have an advantage in entering and expanding in high-growth markets. For example, they may be more familiar with serving low-income customer groups or operating amid infrastructure deficiencies. The size of the prize is evident, and the success stories are only increasing. China’s fast-growing Chery, an automotive company, launched its mini car, QQ, in nearly 80 countries, most of them emerging economies. Chery is particularly successful in Brazil. In the first half of 2011, Chery’s exports to Brazil reached 18,000 units, a quarter of its exports.23 The company has recently built a plant in Brazil to

meet the demand there and from other South American countries. Embraer, the Brazilian commercial plane manufacturer, reports record profits through sales of mid-size jets suitable for regional travel between emerging economies. SABMiller, a leading global brewer with roots in South Africa, recently built a brewery in South Sudan. The company’s deep experience in emerging economies—it operates in 17 African countries—gave it the confidence to enter this unserved market, despite South Sudan’s severe infrastructure barriers.

These examples of success in high-growth markets by companies from emerging economies exemplify a broader transformation in the global business landscape: the sharp increase in business activity between emerging economies since the beginning of the downturn. China has displaced the United States as Brazil’s largest trading partner. China has also become India’s biggest trading partner, and the two countries have agreed to a US$100 billion bilateral trade target by 2015. But the story isn’t just about China. India’s exports to Brazil increased more than tenfold from 2000 to 2010 and exceed those of Latin American economies such as Mexico. “The journey to multidirectional trade”

(see page 31) details this important shift and how rapidly intra-emerging market (“E2E”) trade has grown in just the past ten years to transform the global competitive landscape. As emerging economies increasingly dominate global trade and investment flows, it is only a matter of time before the world sees a new global map of talent, innovation and industry standards.

Seasoned global playersNotwithstanding the importance of competitors from emerging economies, it would be wrong to assume that they will dominate the next era of competition. Some of the best examples of success in high-growth markets have been multinationals based in developed markets. With a well-established presence in emerging economies, these companies are well positioned to combine their superior global scale and efficiency with their local knowledge and responsiveness. Many solidified their position during the downturn as their gains in emerging economies made up for the pain felt at home. For example, Figure 13 illustrates how, through its presence in emerging economies, Unilever sustained growth during the downturn despite shrinking

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011

Developed Emerging

95

405

91

409

78

422

70

430

60

440

47

453

117

383

Source: Fortune Global 500, Accenture analysis

Figure 12: Fortune Global 500

28

38.4

-2.28.1 44.3

0

5

10

15

20

25

30

35

40

45

50

Total revenue, 2005

2005-2010 change in

revenue from developed

markets

2005-2010 change in

revenue from emerging

markets

Total revenue, 2010

60%

40%

58%

42%

56%

44%

53%

47%

51%

49%

47%

53%

2005 2006 2007 2008 2009 2010

Developed markets Emerging markets

Source: Unilever company reports

Figure 13: Unilever revenue growth breakdown (€ billion)

Source: Unilever company reports

Figure 14: Composition of Unilever’s revenue (percentage share)

revenue from developed markets. In 2010, for the first time, the majority of Unilever’s revenue was from emerging economies (see Figure 14). The company plans to increase this share to 75 percent by 2020.24

Companies such as Tesco in South Korea or Coca-Cola in Brazil have shown that being a foreign or “Western” company is certainly no disadvantage. These companies possess strong competitive advantages. Their established brand presence positions them well to attract talent and customers. They can also draw upon their regional and global networks and mechanisms to better identify and rapidly act on local opportunities. What matters for high performance is not a company’s country of origin; it is the company’s strategic and operational capabilities for success.

Combining forcesCompanies also have a greater appetite for cross-border partnerships across emerging- and developed-market economies, built through joint ventures, acquisitions and other models. These complementary capabilities, assets and strengths can create a formidable competitive force. Tata Motors’

acquisition of Jaguar and Land Rover created a company with a range of high- and low-value offerings well positioned to compete at the opposite ends of the same market. With these offerings, Tata Motors can also cater to markets around the world at different stages of development.

Such ventures can leverage their complementary strengths to rapidly build market share in home markets and form a springboard for global success. Some companies have used partnerships to develop entirely new offerings: Vodafone and Safaricom’s M-PESA money-transfer service acquired 14 million registered customers within four years (see “M-PESA: Creating new markets through innovation,” page 44).

New rulesAs the key players in global markets change, so do the pressures that shape the rules of competition. The location of a company’s headquarters matters less than its ability to grasp opportunities while others watch and wait.

The following three trends are increasingly shaping the competitive landscape.

Capital, credit and corporate governance: The freedom to invest for the long term

Constraints on capital investment and difficulties securing credit have hampered growth efforts in the wake of the downturn. Firms backed by state capital and sovereign wealth funds, meanwhile, have benefited in this environment as they have been able to access investment capital largely unconstrained by the pressures on global capital markets.

Consider the example of sovereign wealth funds in the Middle East, which have approximately US$1.7 trillion in assets under management.25 In 2010, as funds across the Middle East sought to diversify and invest in new high-growth markets, 49 percent of their investments were directed toward the Asia Pacific region—a significant leap compared with the 7 percent invested in the region from 2000 to 2008.26

Many of the fast movers into high-growth markets have been those that have had the freedom to take a longer-term investment perspective. Ownership and governance structures

29

play a role here, as certain models are less beholden to short-term shareholder demands. This freedom provides a distinct advantage in tasks such as product development or market planning. Of China’s 54 businesses in the Fortune Global 500, 41 are state-owned. While the total number of state-owned enterprises in China fell from 159,000 in 2003 to 114,500 in 2010, the total assets of those under central government control rose from RMB 3 trillion (US$473 billion) to RMB 20 trillion (US$3,150 billion).27 And though many of Brazil’s large companies are publicly listed, most of them are family-owned. The majority of India’s giant conglomerates still hold family names, and family members serve on boards.

Access and preferential treatment: The importance of relationshipsMore and more, relationships are shaping access to new market opportunities: business-to-business, business-to-government, government-to-government, as well as cross-sector relationships with civil society and non-governmental organizations (NGOs).

The resources and extractives sector is a case in point. Mining rights and access to natural resources are carefully controlled by host governments and are often granted to state-backed companies on the basis of high-level governmental agreements. In exchange for rights to extract more than 11 million tons of copper and 620,000 tons of cobalt in the Democratic Republic of Congo, China has agreed to build hundreds of clinics, hospitals and schools, two hydro-electric dams, 3,300km of road and 3,000km of railway there.28 As long-term investment deals brokered by governments seeking foreign expertise erect barriers to later entrants, the path to new opportunities for many companies may be blocked.

In other industries, access to opportunities may depend on cultivating relationships with the right partners. In the banking sector, acquisitions and joint ventures are a common route to entry. Banking has traditionally been an industry where market share is

difficult to steal. Africa, for example, was emerging as a compelling growth opportunity for global banks just as the financial crisis struck. Since then, companies less affected by the downturn have taken advantage of Africa’s more open playing field and snapped up the most lucrative partnerships and acquisitions. For example, the Industrial and Commercial Bank of China recently acquired 20 percent of South Africa’s Standard Bank and formed a commercial partnership for corporate banking services.29 And Bank of China partnered with Togo-based Ecobank, which operates widely across Africa, to facilitate trade and investments between Africa and Asia. Snapping up the most promising partners is a key advantage to moving fast in this sector.

Global efficiency and local responsiveness: Dual imperatives, not a trade-offThe most astute competitors in today’s fast-evolving opportunities combine global efficiency and scale with local relevance and responsiveness. For example, while Coca-Cola benefits from its global scale and brand, its local market understanding allows the company to offer 15 varieties of Fanta in Mexico.30 Such success requires a carefully designed international operating model: deep local market insights, such as preferences around packaging and the local palate, combined with flexible sales and distribution strategies that can respond to the local retail infrastructure.

Many companies grounded in efficiency advantages have built more targeted offerings to appeal to specific consumer groups. Players such as China’s Haier, Taiwan’s HTC and South Korea’s Samsung and LG have moved beyond their initial low-cost offerings to design products and services for a variety of income levels, cultural tastes and preferences. Haier has driven international expansion by tailoring its products to local markets: in China’s rural Sichuan province, Haier sells washing machines specifically designed and labeled to wash “clothes, sweet potatoes and peanuts.” In Africa, its

high-capacity machines are equipped to wash traditional gowns. And when LG expanded into the Indian market with a television set featuring on-screen display in the regional languages of Hindi, Tamil and Bengali, the “Sampoorna” sold more than 100,000 sets in the first year of its launch.31

With opportunity and competition difficult to evaluate and predict, companies often hesitate to invest. It is not surprising that the majority of businesses believe they need to accelerate their efforts to build market share—or that it may be already too late. As companies wait, they fear that the windows of opportunity are shrinking. They know the opportunities lie in high-growth markets. They know they need to accelerate their efforts. But what exactly should they be doing? What are the capabilities they need to build in order to succeed in high-growth markets? The following chapters seek to answer these questions.

30

Cencosud in Latin America established, through a focus on strong relationships, a regional foothold that is daunting to potential competitors. For supermarkets, chances of success are strongly influenced by access to the infrastructure and ecosystems that support their business. Appropriate real estate, and effective supplier and distribution networks, can make or break a venture. The right local-level relationships are critical because control over real estate and supply chains can sit in a small number of hands in high-growth markets. In an industry where market share really counts, relationships can provide the access needed to unlock opportunity and to establish a leading presence.

Cencosud has long been one of the key players in its home market of Chile, and the company is building on its domestic position to expand across Latin America. In stepping up its regional expansion, the company

looked to acquire well-entrenched players in high-growth markets, such as the Wong Group in Peru, thereby gaining access to established infrastructure and relationships. These acquisitions—13 in just 10 years—have enabled the company to expand rapidly across the region, driving year-on-year growth of more than 25 percent. Cencosud is now the leading or No. 2 supermarket retailer in three of the four countries in which it operates.32

Cencosud’s competitive position is raising the stakes for other retailers attempting to gain a foothold in these high-growth markets. New entrants, whether regional or global retailers, will be pitted against Cencosud’s mastery of local knowledge and relationships.

Cencosud: Retail relations

31

A new map of global trade and investment is emerging. The dominance of developed economies is being challenged, and the last ten years alone have seen a sharp transformation in the dynamics of global trade. The implications are far reaching, not least in giving a clue as to where the future hubs of opportunity and competition will lie.

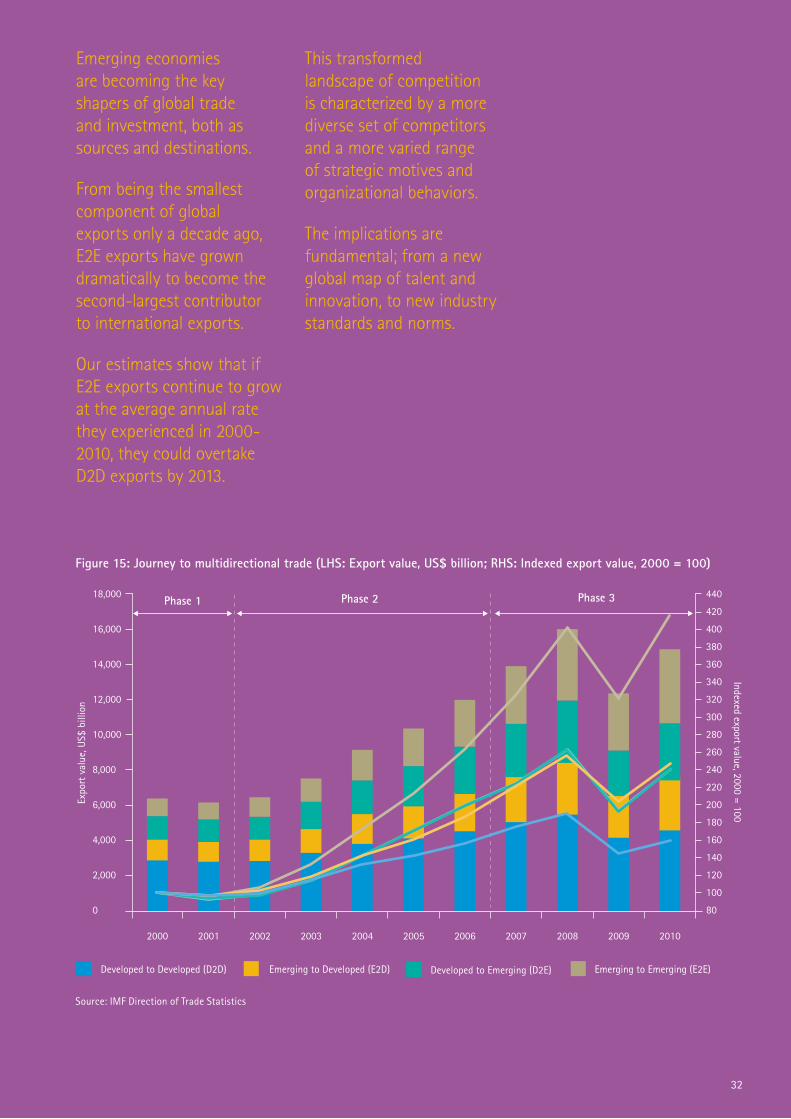

The journey to multidirectional trade over the past decade has three distinct phases (see Figure 15).

Phase 1Before 2002, the majority of global trade took place between developed economies. For example, just ten years ago, 47 percent of world exports excluded emerging economies completely. Exports between emerging economies accounted for just 15 percent of total exports in 2000. Emerging economies were largely perceived as sources of raw materials. The triad economies of the United States, Japan and the European Union determined the norms and rules of business. However, China’s accession to the World Trade Organization in 2001 marked a turning point, opening up China’s vast potential as an exporter, particularly of manufactured goods, to the rest of the world.

Phase 2From 2002 to 2006, E2E exports averaged 25 percent annual growth. By 2003, they overtook exports from developed to emerging economies, and by 2006 E2E exports overtook those from emerging to developed economies. Exports between developed economies remained the dominant component of global trade. But their relative share declined during this period, from 53 percent in 2002 to 38 percent by 2006.

Phase 3The third phase, heralded by the global downturn, is still under way. It is characterized by the resilience of exports between emerging economies. E2E exports have grown from the smallest component of global trade to the second-largest contributor to international exports, just behind D2D (developed market to developed market) exports. Our estimates suggest that if E2E exports continue to grow at the average annual rate they experienced from 2000 to 2010, they could overtake D2D exports by 2013.

The journey to multidirectional trade

32

Figure 15: Journey to multidirectional trade (LHS: Export value, US$ billion; RHS: Indexed export value, 2000 = 100)

Source: IMF Direction of Trade Statistics

80

100

120

140

160

180

200

220

240

260

280

300

320

340

360

380

400

420

440

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Indexed export value, 2000 = 100

Expo

rt v

alue

, US$

bill

ion

Phase 1 Phase 2 Phase 3

Developed to Developed (D2D) Emerging to Developed (E2D) Developed to Emerging (D2E) Emerging to Emerging (E2E)

Emerging economies are becoming the key shapers of global trade and investment, both as sources and destinations.

From being the smallest component of global exports only a decade ago, E2E exports have grown dramatically to become the second-largest contributor to international exports.

Our estimates show that if E2E exports continue to grow at the average annual rate they experienced in 2000-2010, they could overtake D2D exports by 2013.

This transformed landscape of competition is characterized by a more diverse set of competitors and a more varied range of strategic motives and organizational behaviors.

The implications are fundamental; from a new global map of talent and innovation, to new industry standards and norms.

33

Rethinking capabilities: The roadmap to success

Business leaders realize that they need to step up their search for growth—and that old approaches will not be suitable for the new competitive landscape. Some 57 percent of respondents to our survey acknowledge that they need to “reassess” or “fundamentally rethink” their approaches and capabilities to compete and win in high-growth markets.

Moreover, our research unearthed key differences between successful and unsuccessful companies in high-growth markets. Successful companies think differently about the capabilities critical for growth and prioritize investments in different ways.

In our research, we were keen to understand the perceptions and the actions of two particular sample groups:

Successful globalizers We looked at companies that have had a track record of successful performance during recent years and are also confident and committed about their future growth in high-growth markets. Specifically, they are defined by the following characteristics, based on their responses to our survey:

• They are primarily looking at emerging economies for their next stage of growth.

• They are planning to increase investment in their target high-growth markets over the next three years.

• They believe they have an accurate understanding of the size of opportunities in emerging economies.

• They believe they fully understand the competitive dynamics that they face in these markets.

• They believe they possess the strategic and operational capabilities to fully grasp those opportunities.

• In the past three years, their company revenue and profits in high-growth markets have developed in line with, or faster than, their expectations.

In 2010, 61 percent of these successful globalizers experienced global revenue growth of 5 percent or more.