Embed Size (px)

Citation preview

industry analysis

Indian Aviation Industry

Submitted by- Ashish Otwal Rajput(14) Sajjin (46) Shivam Patel (48) Subin Suresh(53) Syed abu jafar B.K (61)

Report

Indian Aviation Industry

An Overview

India is the 9th largest aviation market in the world with a size of around US$ 16 billion and is poised to be the 3rd biggest by 2020. India aviation industry promises huge growth potential due to large and growing middle class population, rapid economic growth, higher disposable incomes, rising aspirations of the middle class and overall low penetration levels.

Civil aviation industry in India is experiencing a new era of expansion driven by factors such as low cost carriers, modern airports, and foreign direct investments in domestic airlines, cutting edge information technology interventions and growing emphasis on regional connectivity. Civil aviation sector has been growing steadily registering a growth of 13.8% during the last 10 years. The air transport in India has attracted FDI of over US$ 569 million from April 2000 to February 2015.

The Indian airports have a combined capacity to cater to 220.04 million passengers and 4.63 million tonnes cargo per annum and handled 168.92 million passengers and 2.28 million tonnes cargo in 2013-14. As per estimates, passenger traffic at Indian Airports is expected to increase to 450 million by 2020 from 159.3 million in 2012-2013.

Looking at future air transportation requirements and desire to become a global player in developing/commercializing aerospace technologies, India is rapidly building capabilities to emerge as a preferred destination for manufacturing of aerospace components.

Over the next decades, India undoubtedly has the potential to become a significant part of the global aerospace supply chain as India offers cost advantages of between 15 to 25 per cent in manufacturing, together with its large procurement appetite. Robust technical and engineering capabilities backed by top-notch scientific and technical institutes are other positive offerings on the table.

Market Size

During January-August 2016, domestic air passenger traffic rose 23.14 per cent to 64.47 million from 52.36 million during the same period in 2015. Passenger traffic during FY 2015-16 increased at a rate of 21.3 per cent to 85.57 million from 70.54 million in the FY 2014-15.

In July 2016, total aircraft movements at all Indian airports stood at 168,400, which was 14.3 per cent higher than July 2015. International aircraft movements increased by 8.2 per cent to 32,830 in July 2016 from 30,330 in July 2015. Domestic aircraft movements increased by 15.8 per cent to 135,570 in July 2016 from 117,050 in July 2015.

Indian domestic air traffic is expected to cross 100 million passengers by FY2017, compared to 81 million passengers in 2015, as per Centre for Asia Pacific Aviation (CAPA).

India is among the five fastest-growing aviation markets globally with 275 million new passengers. The airlines operating in India are projected to record a collective operating profit of Rs 8,100 crore (US$ 1.29 billion) in fiscal year 2016, according to Crisil Ltd.

Growth Rate

Reasons for Growth rate:

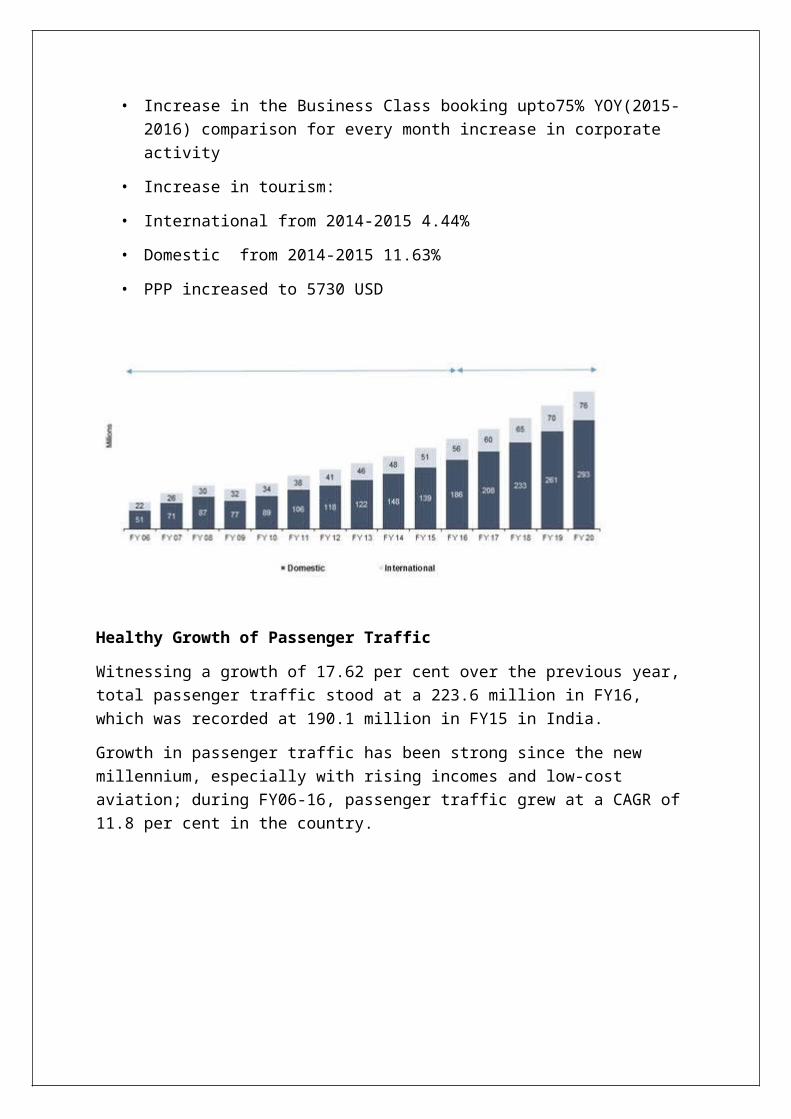

• Increase in the Business Class booking upto75% YOY(2015-2016) comparison for every month increase in corporate activity

• Increase in tourism:

• International from 2014-2015 4.44%

• Domestic from 2014-2015 11.63%

• PPP increased to 5730 USD

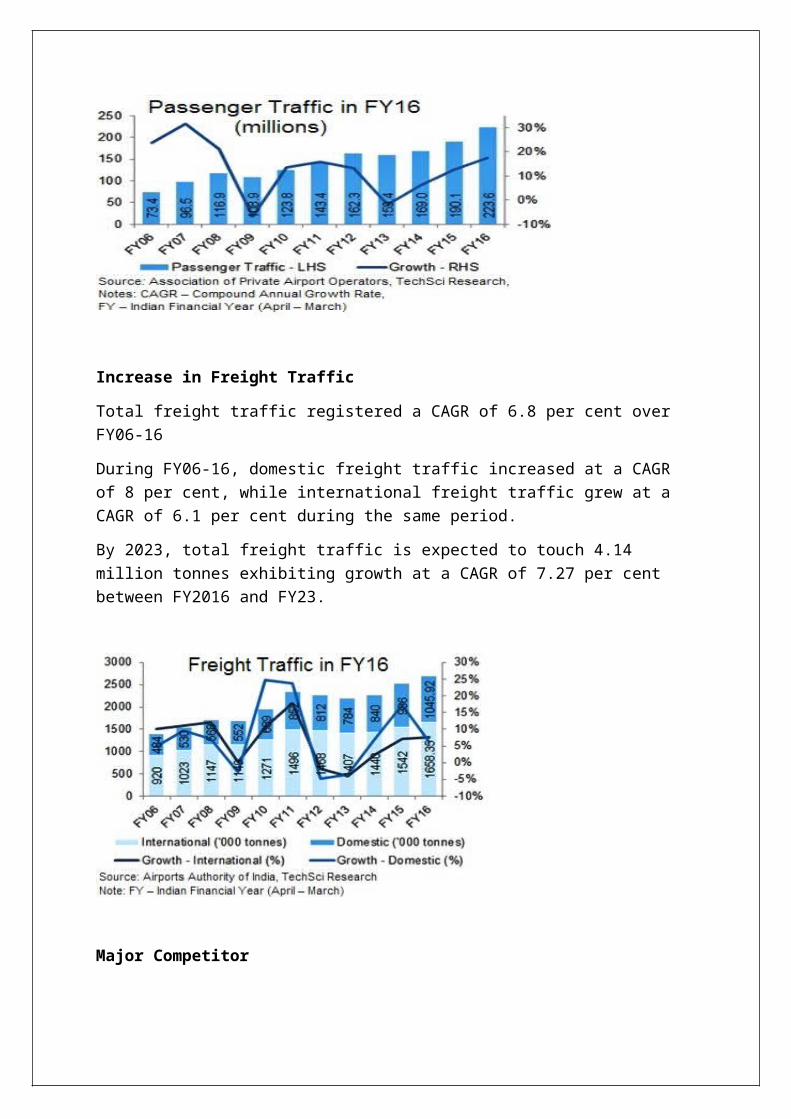

Healthy Growth of Passenger Traffic

Witnessing a growth of 17.62 per cent over the previous year, total passenger traffic stood at a 223.6 million in FY16, which was recorded at 190.1 million in FY15 in India.

Growth in passenger traffic has been strong since the new millennium, especially with rising incomes and low-cost aviation; during FY06-16, passenger traffic grew at a CAGR of 11.8 per cent in the country.

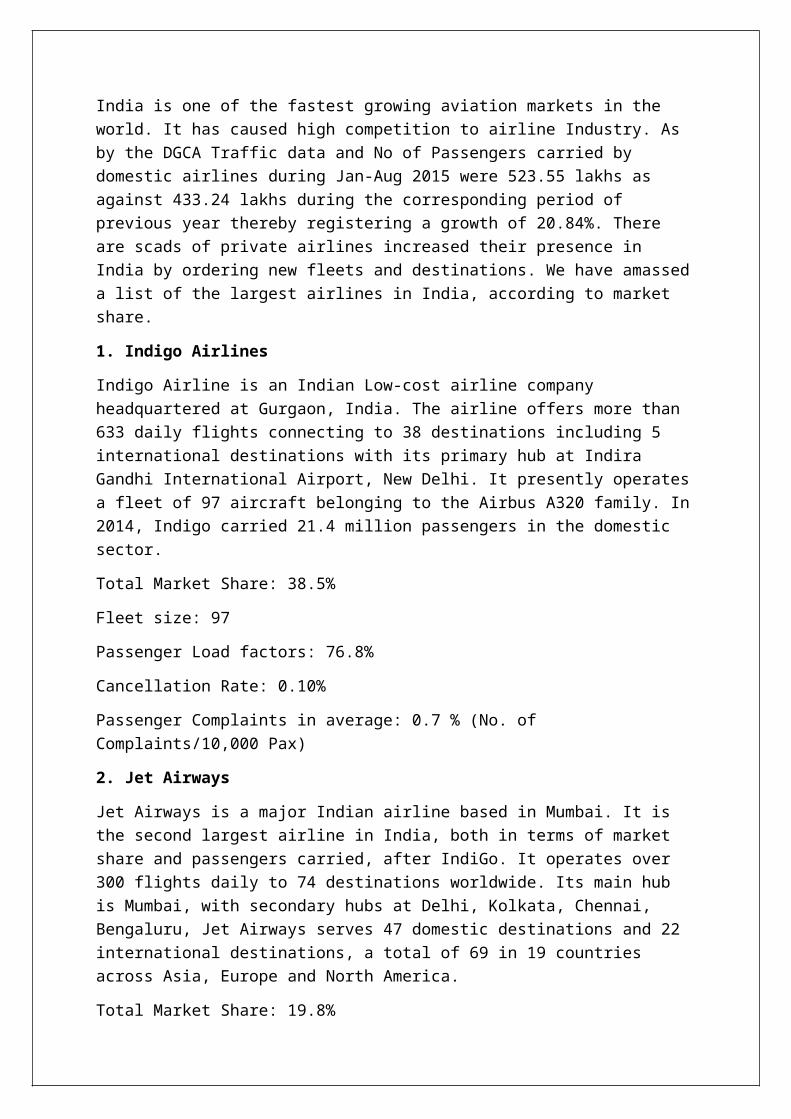

Increase in Freight Traffic

Total freight traffic registered a CAGR of 6.8 per cent over FY06-16

During FY06-16, domestic freight traffic increased at a CAGR of 8 per cent, while international freight traffic grew at a CAGR of 6.1 per cent during the same period.

By 2023, total freight traffic is expected to touch 4.14 million tonnes exhibiting growth at a CAGR of 7.27 per cent between FY2016 and FY23.

Major Competitor

India is one of the fastest growing aviation markets in the world. It has caused high competition to airline Industry. As by the DGCA Traffic data and No of Passengers carried by domestic airlines during Jan-Aug 2015 were 523.55 lakhs as against 433.24 lakhs during the corresponding period of previous year thereby registering a growth of 20.84%. There are

scads of private airlines increased their presence in India by ordering new fleets and destinations. We have amassed a list of the largest airlines in India, according to market share.

1. Indigo Airlines

Indigo Airline is an Indian Low-cost airline company headquartered at Gurgaon, India. The airline offers more than 633 daily flights connecting to 38 destinations including 5 international destinations with its primary hub at Indira Gandhi International Airport, New Delhi. It presently operates a fleet of 97 aircraft belonging to the Airbus A320 family. In 2014, Indigo carried 21.4 million passengers in the domestic sector.

Total Market Share: 38.5%

Fleet size: 97

Passenger Load factors: 76.8%

Cancellation Rate: 0.10%

Passenger Complaints in average: 0.7 % (No. of Complaints/10,000 Pax)

2. Jet Airways

Jet Airways is a major Indian airline based in Mumbai. It is the second largest airline in India, both in terms of market share and passengers carried, after IndiGo. It operates over 300 flights daily to 74 destinations worldwide. Its main hub is Mumbai, with secondary hubs at Delhi, Kolkata, Chennai, Bengaluru, Jet Airways serves 47 domestic destinations and 22 international destinations, a total of 69 in 19 countries across Asia, Europe and North America.

Total Market Share: 19.8%

Fleet size: 116

Passenger Load factors: 80.8%

Cancellations: 0.96%

Passenger Complaints in average: 1.4 % (No. of Complaints/10,000 Pax)

3. Air India

Air India is the flag carrier airline of India owned by Air India Limited (AIL), a Government of India enterprise. It is the third largest airline in India (after Indigo and Jet Airways) in domestic market share, and operates a fleet of Airbus and Boeing aircraft serving various domestic and international airports. It is headquartered at the Indian Airlines House in New Delhi

Total Market Share: 16.4%

Fleet Size: 108 (excluding subsidiaries)

Passenger Load factors: 79.3%

Cancellations: 1.20%

Passenger Complaints (average):1.7 % (No. of Complaints/10,000 Pax)

4. Spice Jet

Spice Jet is an Indian low-cost airline headquartered in Gurgaon, India. It is the country’s fourth largest airline by number of passenger carried with market share of 12.3% as of July 2015. The airline operates more than 270 daily flights to 41 destinations, including 34 Indian and 7 international cities

Total Market Share: 12.3%

Fleet size: 34

Passenger Load factors: 92.1%

Cancellations: 0.70%

Passenger Complaints (average):1.4% (No. of Complaints/10,000 Pax)

5. Go Air

Go Air is an Indian Low cost carrier based in Mumbai. It commenced operations in November 2005. It is the aviation foray of the Wadia Group. As of January 2014, it is the fifth largest airline in India by market share. It operates domestic passenger services to 22 cities with over 140 daily flights and approximately 975 weekly flights. Its hubs are at Chhatrapati Shivaji International Airport, Mumbai

Total Market Share: 8.2%

Fleet size: 19

Passenger Load factors: 75.6%

Cancellations: 0.44%

Passenger Complaints (Average): 1.3 %(No. of Complaints/10,000 Pax)

Industry Life Cycle

Introductory Stage:-

• 1910: The first Indian, or maybe even Asian, to have an airplane is the young Maharaja of Patiala, Bhupinder Singh. Commercial aviation came in the year 1911.

• JRD Tata launches India’s first scheduled airline in 1932. Tata Airlines flies 160,000 miles, carries 155 passengers and 10.71 tones of mail.

• 1946: Tata Airlines changes its name to Air India.

Growth Phase:-

• Legislation comes into force to nationalize the entire airline industry in India in 1953.

• East West Airlines becomes the first national level private airline to operate in the country after 37 years in 1990. Domestic Passenger traffic Compound Annual Growth Rate (CAGR) – 10.1% (FY 2006-16).

• International Passenger traffic CAGR – 8.8% (FY 2006-16).

• Total freight compared to International air freight traffic CAGR in Domestic Sector – 7.6% (FY 2006-16) and in International Sector 4.8% (FY 2006-16)

• India has more than 86 scheduled international airlines constituted of 5 Indian carriers and 81 Foreign carriers. Currently India has air connectivity with 55 countries through more than 300 routes.

• Passenger traffic is growing at 20% per annum in the last 2 years.

Porter 5 Force

New entrants’ threat- Low

• This industry requires a huge capital and without a strong customer base there will be little to no profit in the first few years.

• There are two aspects that do however raise the threat level.

• First, there are extremely low switching costs.

• Second, there are no proprietary products or services involved.

Customers/buyers bargaining power- High

• The airline industry is made up of two groups of buyers.

• First, there are individual flyers. They buy plane tickets for a number of reasons that can be personal or business related. This group is extremely diverse; most people in developed countries have purchased a plane ticket by themselves.

• The other group of They can do this through the specific airline or through the second group of buyers; travel agencies and online portals. This buyer group works as a middle man between the airlines and the flyers.

Bargaining power held by suppliers-Low

• Most firms have long term contracts with their suppliers. Planes are such high capital products that firms probably make long term loan agreements and have more favorable credit terms when they don’t switch companies.

• The top two manufacturers in the world currently are Boeing and Airbus(Odell,Mark).

Threat of substitute products- high

• There are substitutes in the airline industry. Consumers can choose other form of transportation such as a car, bus, train, or boat to get to their destination. There is however a cost to switch.

• Over this the main competitor for this industry is online chat industry.

• The fixed costs are extremely high in this industry. This makes it hard to leave the industry because they are probably in long term loan agreements in order to stay in business. The products involved or the planes are highly complex which also heightens the competition.

Industry Rivalry- Moderate

• Existing firms can and will use their high capital to retaliate against newer firms with whatever means necessary such as skimming pricing technique , better services, low or no cancellation charges, etc.

• The fixed costs are extremely high in this industry. This makes it hard to leave the industry because they are probably in long term loan agreements in order to stay in business. The products involved or the planes are highly complex which also heightens the competition.

About Indigo

IndiGo is India’s largest passenger airline with a market share of 40.3% as of December, 2016. We primarily operate in India’s domestic air travel market as a low-cost carrier with focus on our three pillars – offering low fares, being on-time and delivering a courteous and hassle-free experience. IndiGo has become synonymous with being on-time.

Since our inception in August 2006, we have grown from a carrier with one plane to a fleet of 126 aircraft today. A single aircraft type, high operational reliability and an award winning service make us one of the most reliable airlines in the world. We currently operate flights connecting to 43 destinations – 37 domestic and 6 international.

The Preferred Airline

IndiGo is not only the most efficient low fare operator domestically but is also comparable with global low cost airlines. We are constantly enhancing our engagement with our passengers to augment their travel experience. From multichannel direct sales (including online flight booking, call centers and airport counters), to online flight status checking, an

exclusive IndiGo app for Android, we have transformed air travel in India. Today, we are India’s most preferred airline. At IndiGo, low fares come with high quality.

Great Place to Work

Being courteous and hassle free starts with being a hassle-free place to work. A highly engaged and motivated workforce leads to higher levels of customer service. Our state-of-the-art ‘ifly’ facility is designed to deliver a real-time training experience to all our new recruits. This training facility is considered to be one the best aviation training facilities in India. With our people-friendly culture at the heart of all we do, we continuously help the company staff find work-life balance. No wonder IndiGo was chosen AON Best Employer India 2016 and one of “India’s Best Companies to Work for” 8 years in a row.

IndiGoReach

Our Corporate Social Responsibility (CSR) initiative IndiGoReach focuses on three broad themes: Children and education, women empowerment and environment. We work towards upliftment of communities not just around us but also far-flung areas on the country. After all, India’s holistic progress is rooted in the collective aspirations of its people.

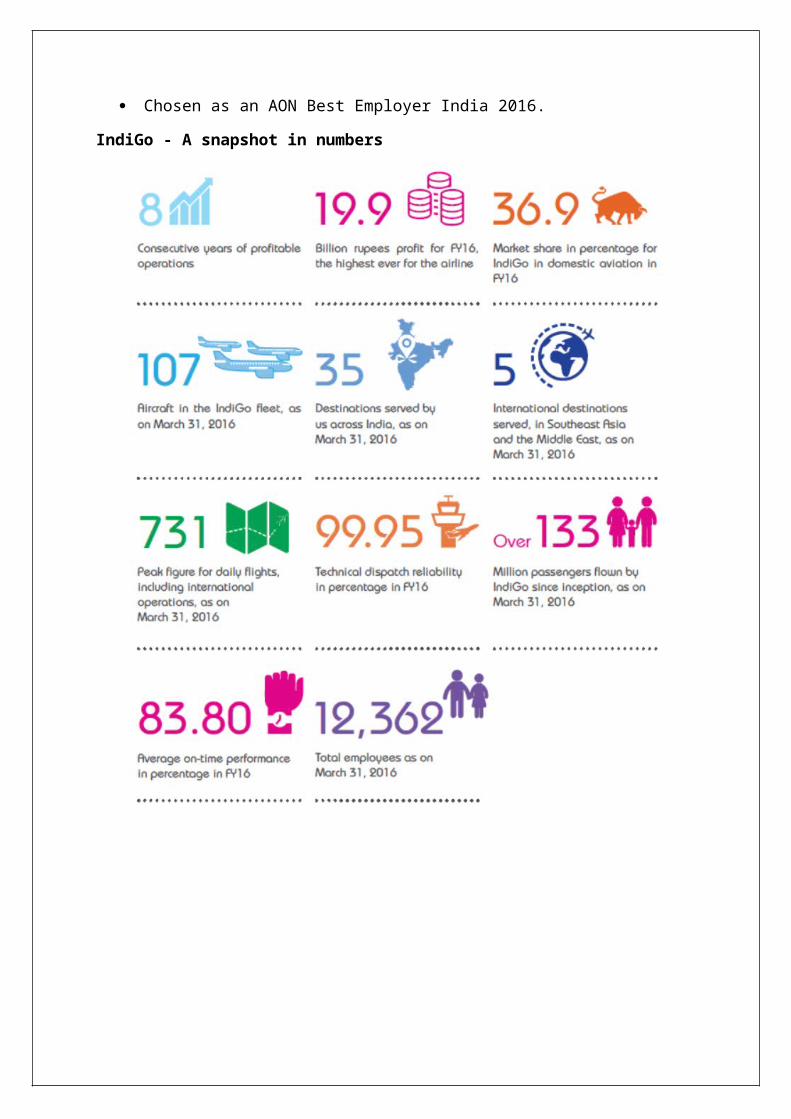

Facts and Figures

8 consecutive years of profitable operations

Market share of 38.3% as of December, 2016

Fleet of 126 aircraft including 14 new generation A320neos

"Great Place to Work for in India” 8 years in a row

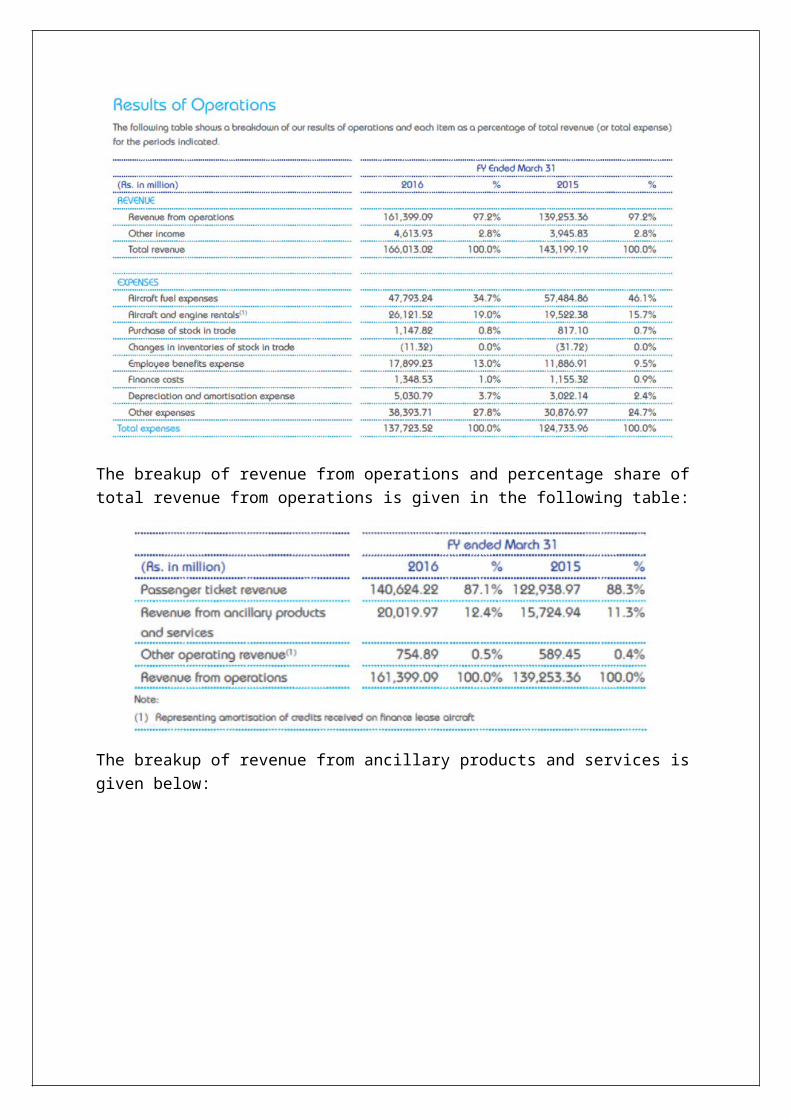

Results of Operations

Highlights

Successfully completed its Initial Public Offering and got listed on domestic bourses, namely, BSE Limited and the National Stock Exchange of India Limited; raised Rs. 30.17 billion.

Declared 8th consecutive year of profitability with highest ever yearly profit. Got delivery of 3 new generation fuelefficient A320Neo. Added 3 new destinations, Dimapur, Udaipur and Dehradun, making it a total of 35

domestic destinations. Chosen as an AON Best Employer India 2016.

IndiGo - A snapshot in numbers

The breakup of revenue from operations and percentage share of total revenue from operations is given in the following table:

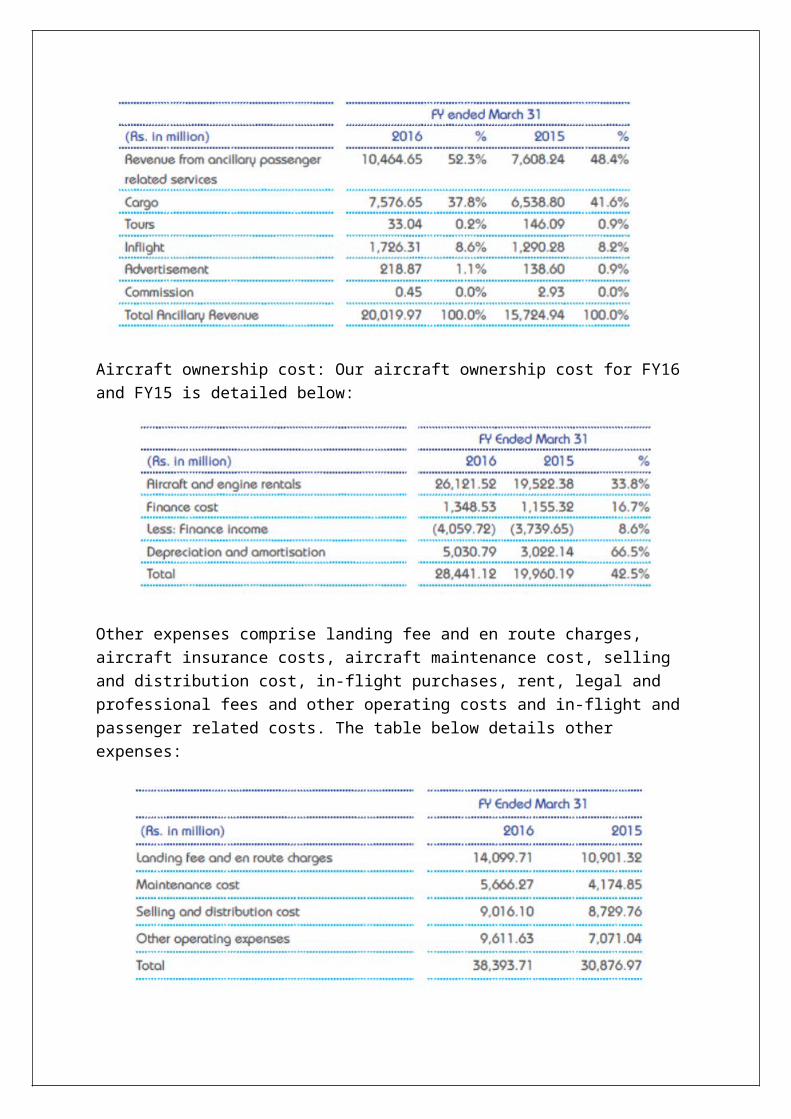

The breakup of revenue from ancillary products and services is given below:

Aircraft ownership cost: Our aircraft ownership cost for FY16 and FY15 is detailed below:

Other expenses comprise landing fee and en route charges, aircraft insurance costs, aircraft maintenance cost, selling and distribution cost, in-flight purchases, rent, legal and professional fees and other operating costs and in-flight and passenger related costs. The table below details other expenses:

Current assets increased by 76.8% from Rs. 31,680.13 million as of March 31, 2015, to Rs. 56,007.86 million as of March 31, 2016

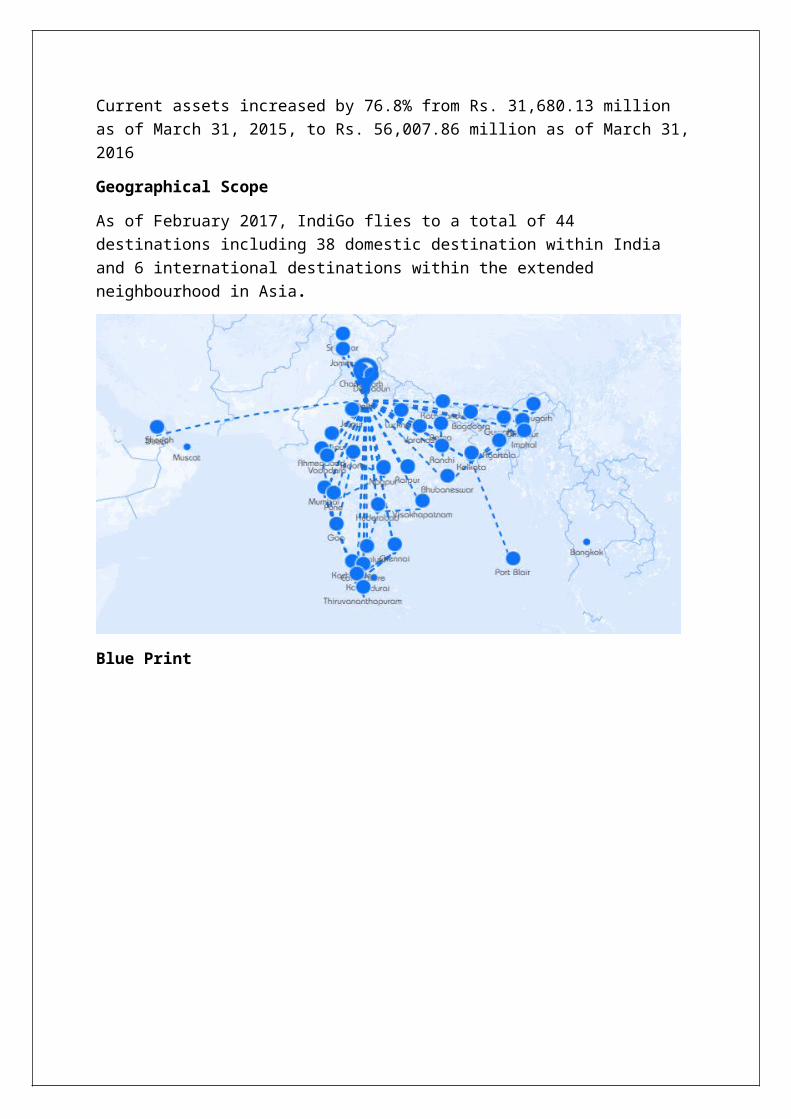

Geographical Scope

As of February 2017, IndiGo flies to a total of 44 destinations including 38 domestic destination within India and 6 international destinations within the extended neighbourhood in Asia.

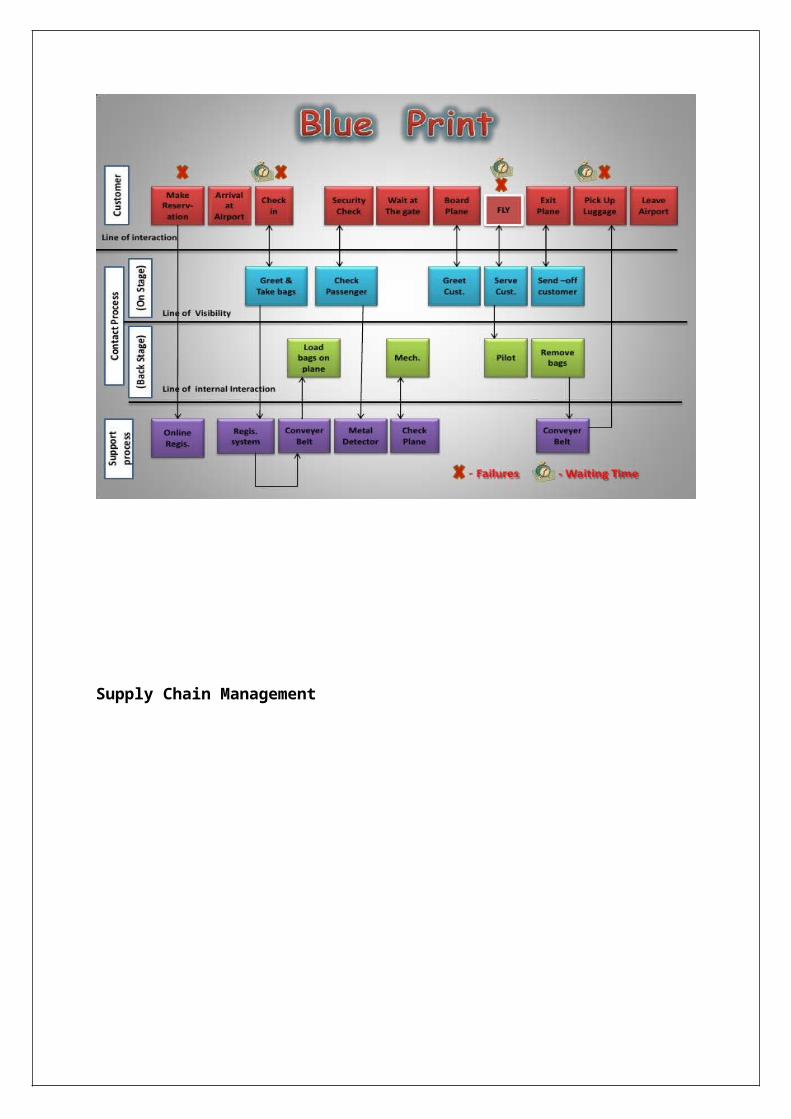

Blue Print

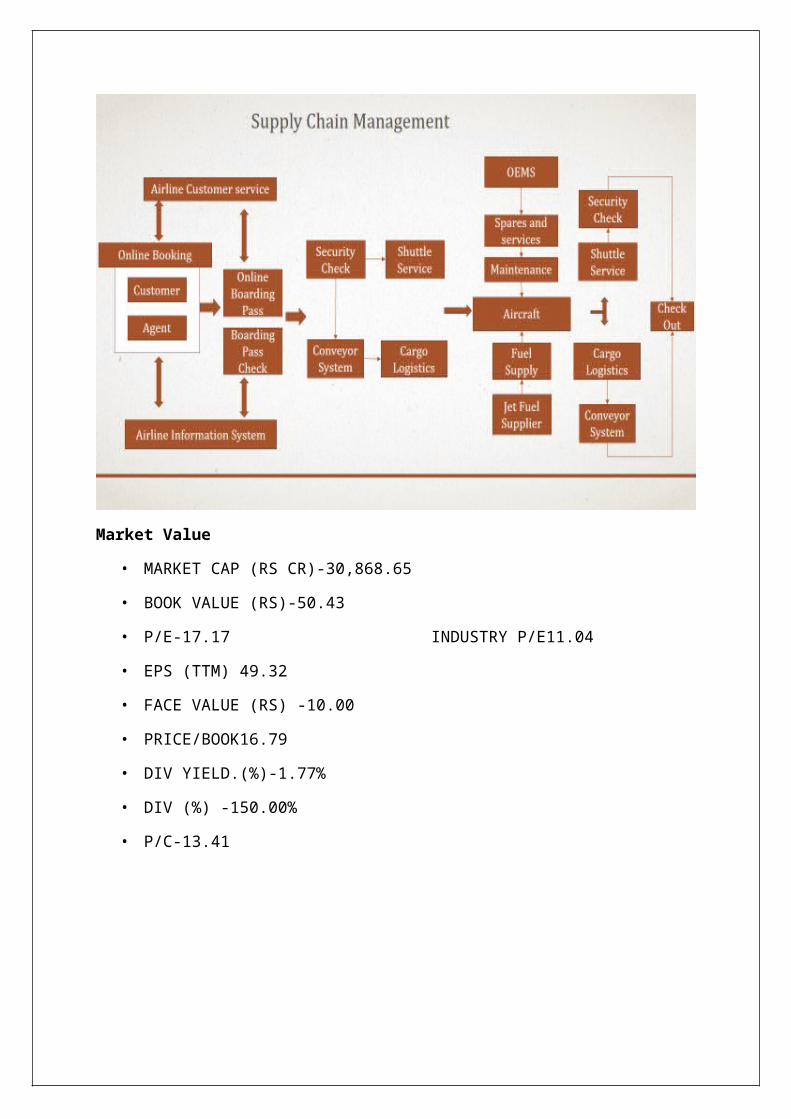

Supply Chain Management

Market Value

• MARKET CAP (RS CR)-30,868.65

• BOOK VALUE (RS)-50.43

• P/E-17.17 INDUSTRY P/E11.04

• EPS (TTM) 49.32

• FACE VALUE (RS) -10.00

• PRICE/BOOK16.79

• DIV YIELD.(%)-1.77%

• DIV (%) -150.00%

• P/C-13.41

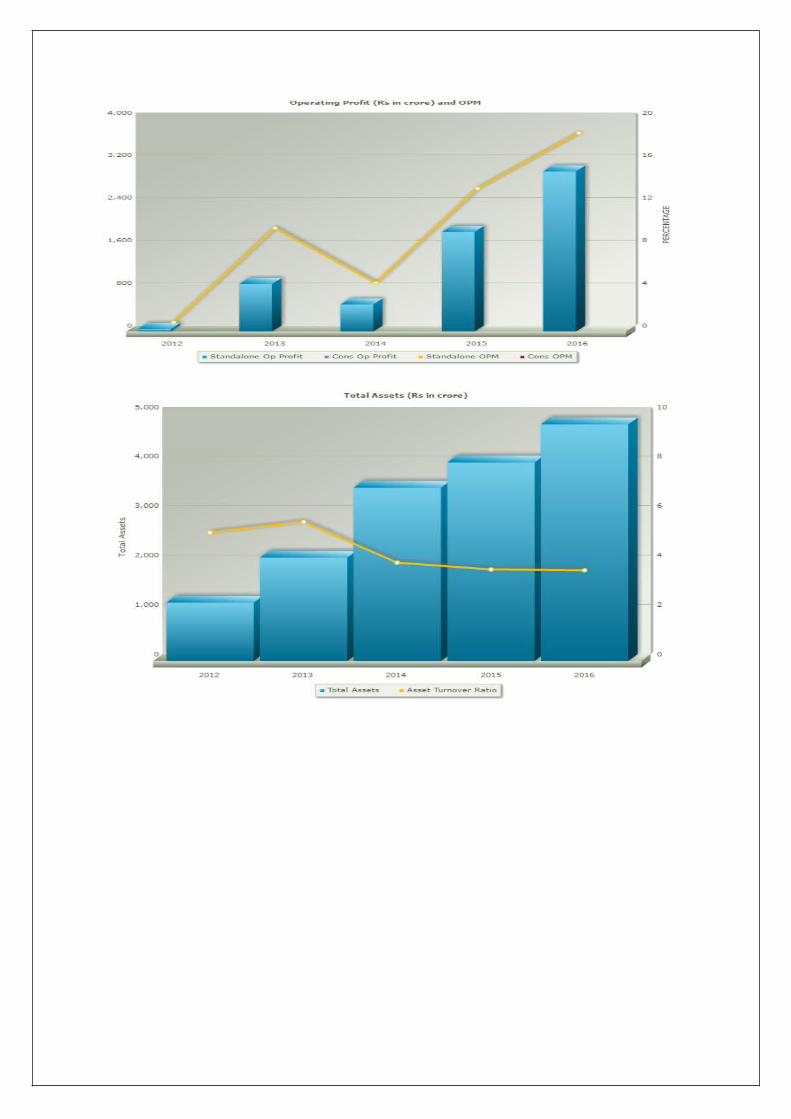

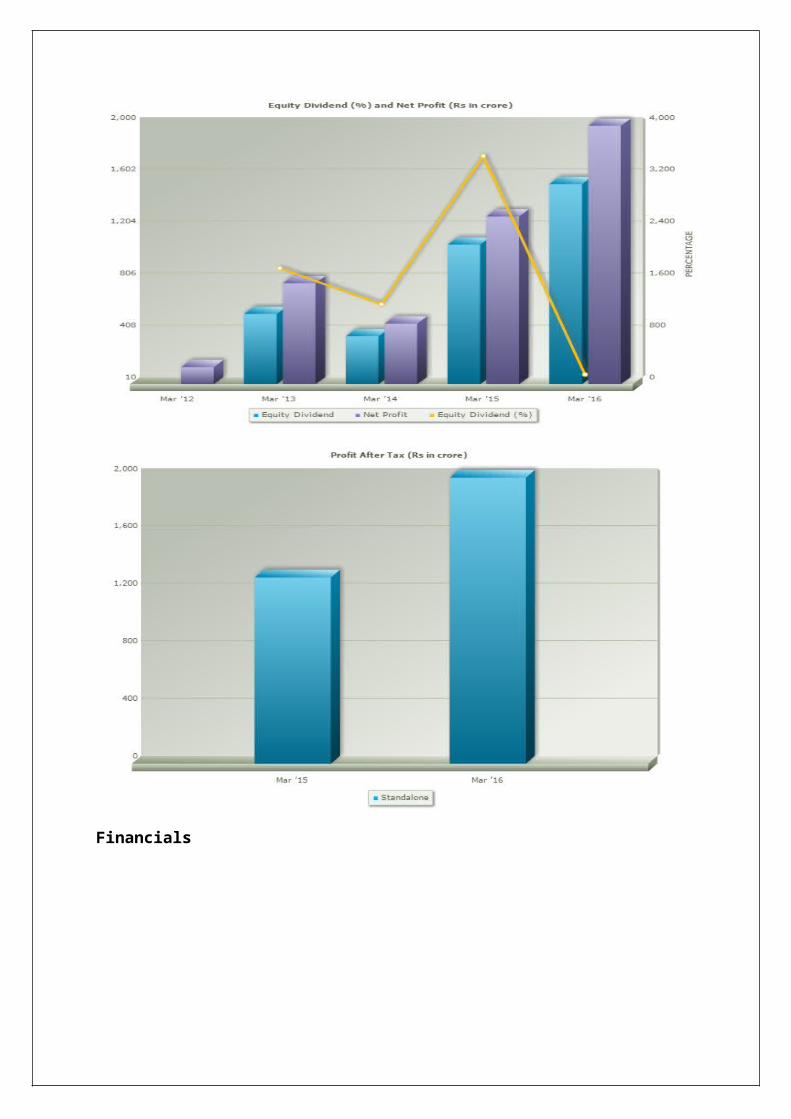

Financials

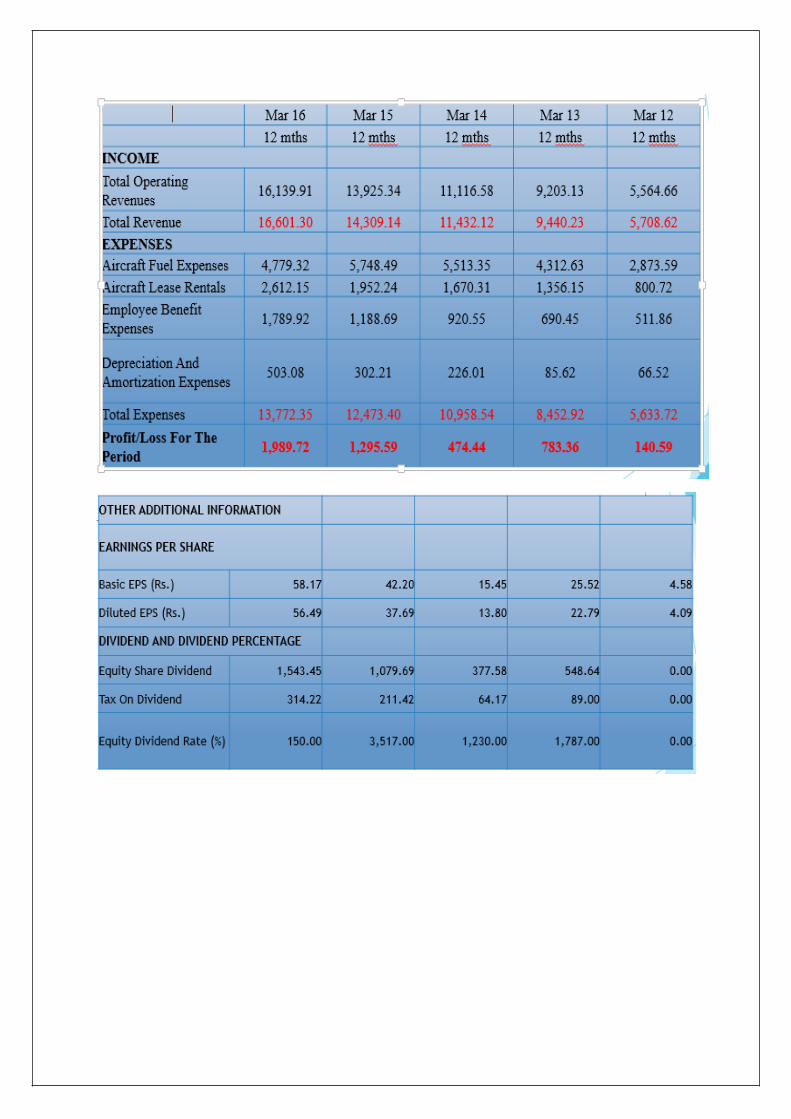

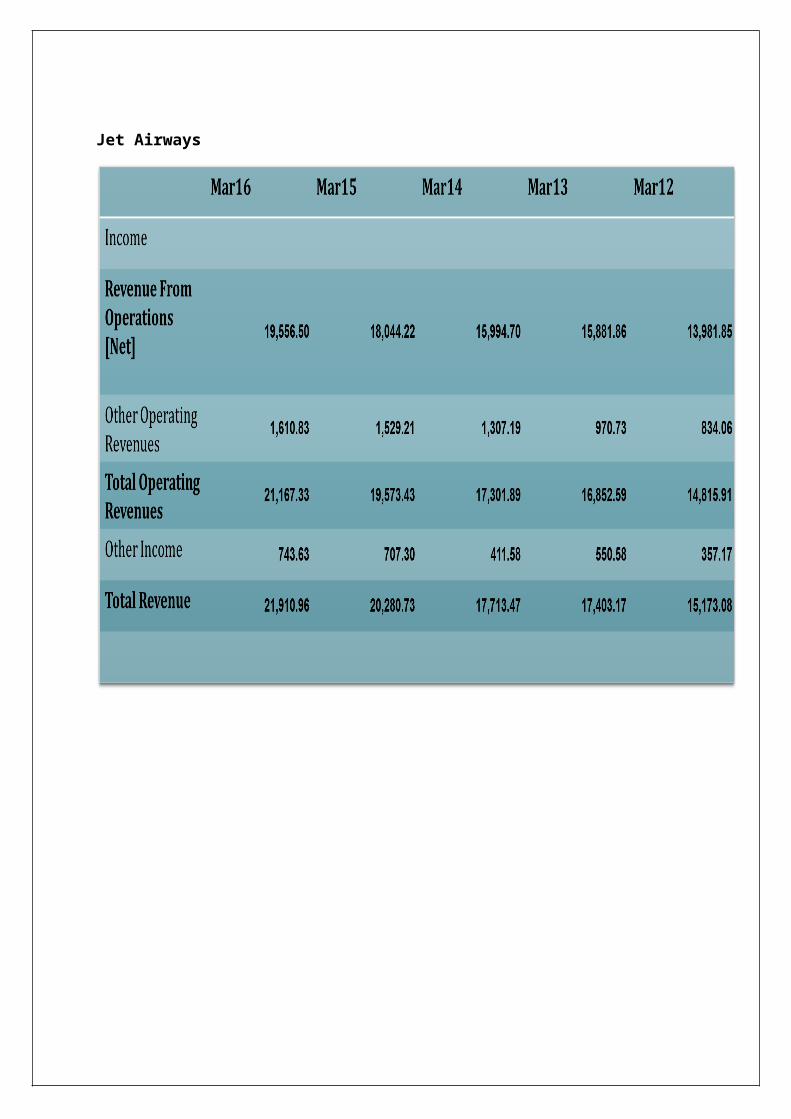

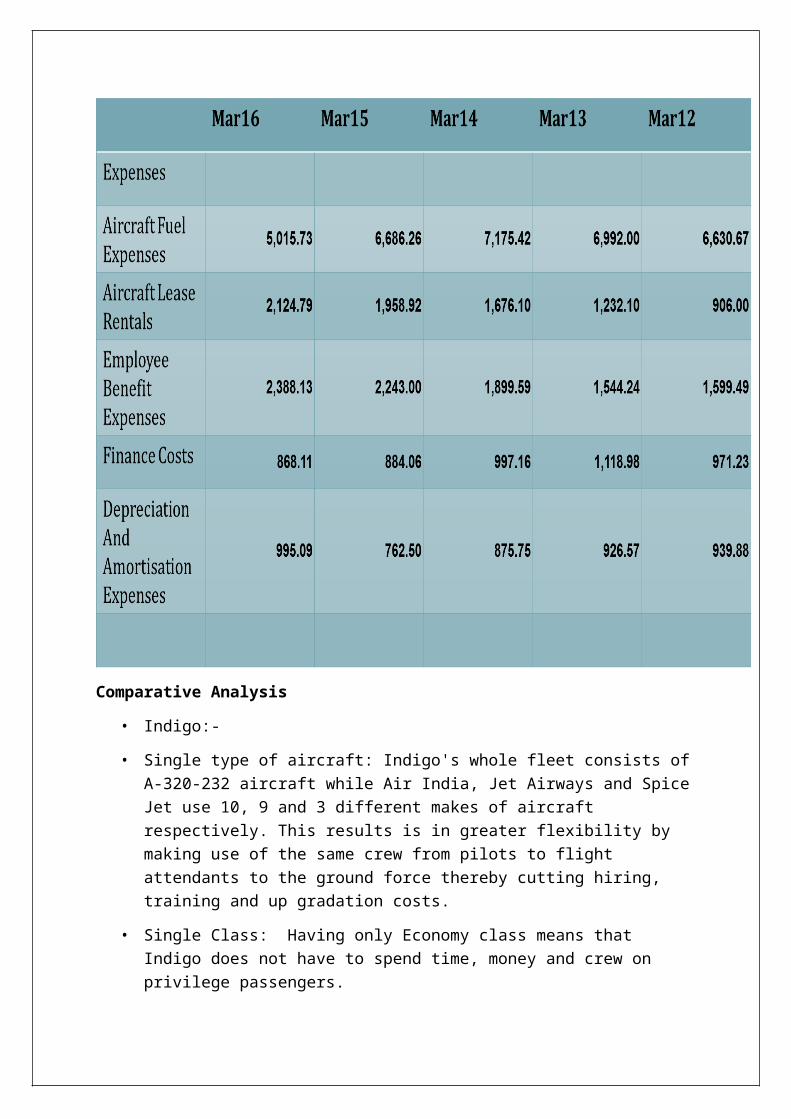

Jet Airways

Comparative Analysis

• Indigo:-

• Single type of aircraft: Indigo's whole fleet consists of A-320-232 aircraft while Air India, Jet Airways and Spice Jet use 10, 9 and 3 different makes of aircraft respectively. This results is in greater flexibility by making use of the same crew from pilots to flight attendants to the ground force thereby cutting hiring, training and up gradation costs.

• Single Class: Having only Economy class means that Indigo does not have to spend time, money and crew on privilege passengers.

• Fuel: Domestic fuel taxes can be as high as 30 per cent along with an 8.2 per cent excise duty. As a result, fuel for Indian airlines accounts for about 45 per cent of total operating costs, Indigo's aircraft try to save fuel by using software to optimize flight planning for minimum fuel burning routes and altitudes and also by making use of latest fuel saving technology.

The company is also involved in Fuel hedging after the government allowed it in 2007.

• Route Planning: Indigo operates over a lesser number of destinations than its competitors but with a higher frequency

• all Indigo's destinations are connected to at least two cities while most are connected to 3 or more destinations. Indigo can keep its aircraft in the air for a longer period of time and save up on airport charges.

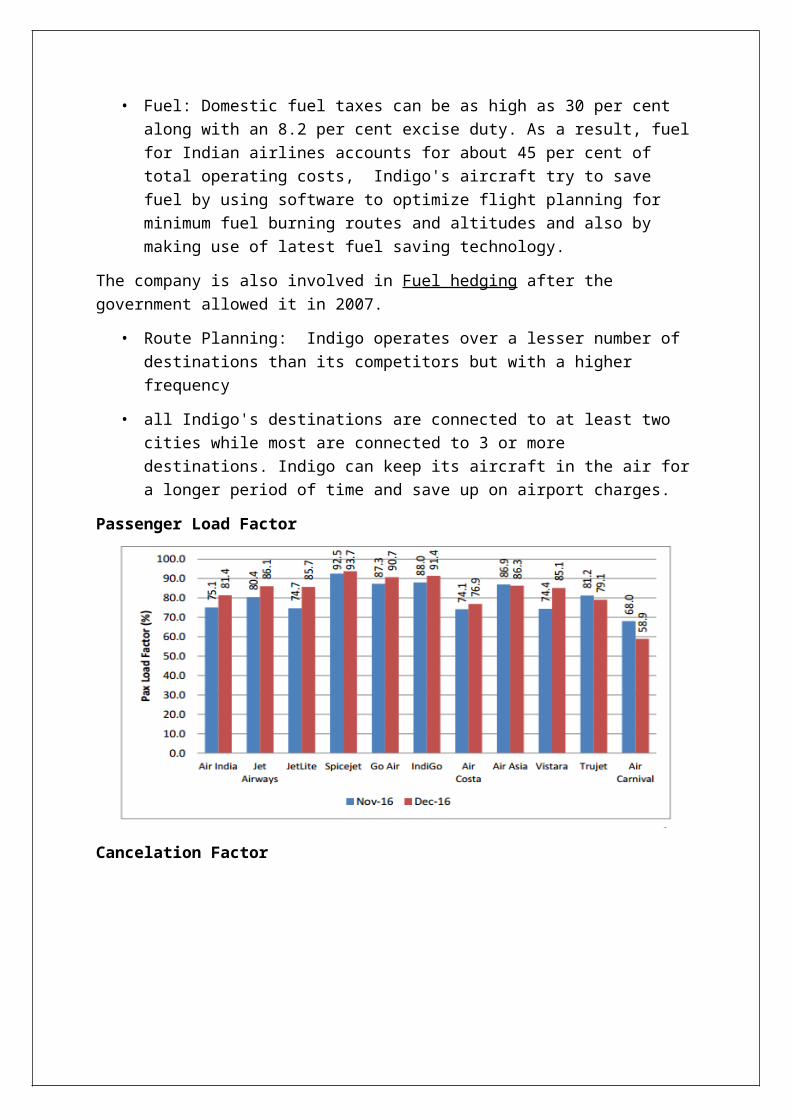

Passenger Load Factor

Cancelation Factor

Jet Airways

• Posted a profit Rs. 467.11 Crore

• Reasons for this is the turn in focus on cost and revenue quality, productivity and efficiency .

• Reasons are as follows:-

• Decrease in oil price.

• Appointment of Mr Ball as CEO( known arund as turnaround expert)

• Bringing of LCC carrirs under the brand Jetlite and Jet Konnect

• Shifting its hubs to Abu Dhabi and Amsterdam from Brussels, increasing short haul international flights and depending on codeshare agreements with Etihad's partners to ferry its passengers forward.

• Re-negotiating maintenance and engineering contracts (

It reworked the rotation of aircraft for maintenance checks, and increased utilisation of planes by two hours a day.

• The airline ensured that the cheapest buckets of its inventory was sold on its own website.

Problems

• About 24 of Jet's 75 narrow bodied planes have ages ranging from 8-15 years.

• The airline has a directly employed workforce of 15,000 people and it has an additional 6,000-7,000 on contract. This gives the airline a high employee to aircraft ratio of slightly less than 200:1

• . In 2009, Jet had to cancel hundreds of flights as pilots reported sick en masse, protesting the sacking of two colleagues.

Concentration Ratio

• In economics, a concentration ratio is a measure of the total output produced in an industry by a given number of firms in the industry

• Top companies- indigo(38.5%), jet airways(17.6%), air India(15.5%), Spicejet(12.3%), go air, air India express, jetlite airways, air asia

• In terms of Passenger Load Factor (PLF) -- an indicator of filled seats -- SpiceJet was on top with 91.1%, followed by GoAir (86.3%), IndiGo (85.1%), AirAsia (82.7%) and Air Costa (82.1%). Among other airlines, the PLF of Jet Airways was at 79.1% while that of JetLite and Air India stood at 77% and 75.7% respectively.

• Indigo(38.5%),

• Jet airways(17.6%),

• Air India(15.5%),

• Spicejet(12.3%)

• 38.5+17.6+15.5+12.3=83.9% or 84%

• The Herfindahl index (also known as Herfindahl–Hirschman Index, or HHI) is a measure of the size of firms in relation to the industry and an indicator of the amount of competition among them.

• Calculation-

• Herfindahl index= ∑ ( market share n ) x

• (0.385)2+(0.176)2+(0.155)2+(0.123)2

• 0.1482+0.0309+0.0240+0.0151=21.82% (high concentration)

• A high four firm concentration ratio and HHI above the 1,800 benchmark, indicates a high degree of concentration within the industry. This type of market concentration can be defined as a tight oligopoly, where India‘s four firms hold more than 60% of the market share.

Government Initiative

Government agencies project that around 500 brownfield and greenfield airports would be required by 2020. The private sector is being encouraged to become actively involved in the construction of airports through different Public Private Partnership models, with substantial state support in terms of financing, concessional land allotment, tax holidays and other incentives.In the Union Budget 2016-17, the government introduced various proposals for Maintenance, Repair and Overhaul (MRO) operations for airplanes. These include customs and excise duty exemption for tools and tool-kits used in MRO works. The government has also scrapped the one-year restriction for utilisation of duty free parts apart from allowing import of unserviceable parts by MROs for providing exchange. As per revised norms, the foreign aircraft brought in to India for MRO work would now be permitted to stay up to six months or as extended by aviation regulator Directorate General of Civil Aviation (DGCA). Such foreign aircraft would also be henceforth permitted to carry passengers in the flights at the start and end of its period of stay in India.Some major initiatives undertaken by the government are:

The Ministry of Civil Aviation has finalised and put forward for approval to the Union Cabinet, the new aviation policy, which includes proposals such as allowing new airlines to fly abroad, introduction of more regional flights and a new formula for granting bilateral flying rights.

The Indian Space Research Organisation (ISRO) has signed a memorandum of understanding (MoU) with the Airports Authority of India (AAI), aimed at providing space technology for construction of airports.

The Government of India is planning to boost regional connectivity by setting up 50 new airports over the next three years, out of which at least 10 would be operational by 2017.

Airports Authority of India (AAI) plans to develop city-side infrastructure at 13 regional airports across India, with help from private players for building of hotels, carparks and other facilities, and thereby boost its non-aeronautical revenues.

Directorate General of Civil Aviation (DGCA), India's aviation regulator, has signed an agreement with United States Technical Development Agency (USTDA) for India

Aviation Safety Technical Assistance Phase II, aimed at bringing in systemic improvements in the area of operation, airworthiness and licensing.

The Government of India has given site clearance to Delhi Mumbai Industrial Corridor and Development Corporation (DMICDC) for setting up of a Greenfield Airport for public use near Bhiwadi in Alwar district of Rajasthan and has granted 'in-principle' approval to 13 other greenfield airport projects.

The Airports Authority of India (AAI) plans to revive and operationalise around 50 airports in India over the next 10 years to improve regional and remote air connectivity.

Gujarat is expected to get a second international airport at Dholera. The state government has formed Dholera International Airport Co. Ltd. and is obtaining approvals from the union government.

The Directorate General of Civil Aviation (DGCA) has given its approval to Air India’s maintenance, repair and overhaul (MRO) unit.

The Government of India has decided to award airports in Kolkata, Chennai, Jaipur and Ahmedabad on management contract. AAI has issued the ‘Request for Qualification’ document for these four airports.

Strategic Industry Mapping

Conclusion

India’s aviation industry is largely untapped with huge growth opportunities, considering that air transport is still expensive for majority of the country’s population, of which nearly 40 per cent is the upwardly mobile middle class.

The industry stakeholders should engage and collaborate with policy makers to implement efficient and rational decisions that would boost India’s civil aviation industry.

With the right policies and relentless focus on quality, cost and passenger interest, India would be well placed to achieve its vision of becoming the third-largest aviation market by 2020 and the largest by 2030.

Sources

http://www.ibef.org/industry/indian-aviation.aspx

http://www.india-aviation.in/pages/view/38/an_overview.html

http://www.india-briefing.com/news/india-growing-aviation-sector-13204.html/

http://www.makeinindia.com/sector/aviation

https://home.kpmg.com/in/en/home/media/press-releases/2016/03/aviation-report-march.html

http://jetlinemarvel.net/2015/09/24/top-10-airlines-in-india-2015/

http://www.business-standard.com/article/companies/india-aviation-report-says-country-to-become-third-largest-aviation-market-by-2020-116031700265_1.html