Embed Size (px)

DESCRIPTION

Citation preview

Masco IR Presentation May 2013

Safe Harbor Statement

2

Written and oral statements made in this presentation that reflect our views about our future performance constitute "forward-looking statements" under the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “believe,” “anticipate,” “appear,” “may,” “will,” “should,” “intend,” “plan,” “estimate,” “expect,” “assume,” “seek,” “forecast,” and similar references to future periods. These views involve risks and uncertainties that are difficult to predict and, accordingly, our actual results may differ materially from the results discussed in our forward-looking statements. We caution you against relying on any of these forward-looking statements. Our future performance may be affected by our reliance on new home construction and home improvement, our reliance on key customers, the cost and availability of raw materials, uncertainty in the international economy, shifts in consumer preferences and purchasing practices, our ability to improve our underperforming businesses, and our ability to maintain our competitive position in our industries. These and other factors are discussed in detail in Item 1A, “Risk Factors” in our Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and in other filings we make with the Securities and Exchange Commission. Our forward-looking statements in this presentation speak only as of the date of this presentation. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. Unless required by law, we undertake no obligation to update publicly any forward-looking statements as a result of new information, future events or otherwise.

Certain of the financial and statistical data included in this presentation and the related

materials are non-GAAP financial measures as defined under Regulation G. The Company believes that non-GAAP performance measures and ratios used in managing the business may provide attendees of this presentation with additional meaningful comparisons between current results and results in prior periods. Non-GAAP performance measures and ratios should be viewed in addition to, and not as an alternative for, the Company's reported results under accounting principles generally accepted in the United States. Additional information about the Company is contained in the Company's filings with the SEC and is available on Masco’s web site, www.masco.com.

I N V E S T M E N T T H E S I S

Strong Fundamentals - Positioned for Growth

3

The strengths

The growth

The strategy

The company

Masco at a Glance

Revenue % renovation vs. new construction 73%

Employees 30,000

Market capitalization >$6.0B

Dividend yield 2.9%

Revenue $7.5B

Cumulative free cash flow last 3 years ~$1B

4

2012

Cash at 12/31/2012 $1.4B

Masco – Strong Brands with Industry Leading Positions

Business Segment

Cabinets and Related Products

Plumbing Products

Installation and Other Services

Decorative Architectural Products

$0.9B

$3.0B

$1.2B

$1.8B

Revenue 2012 % of Total

38%

24%

12%

16%

$7.5B 100% Total company

5

Other Specialty Products $0.6B 7%

R&R% vs. NC NA% vs. Int’l

82% 59%

99% 100%

69% 92%

16% 100%

75% 75%

73% 80%

R&R = % of sales to repair and remodel channels NC = % of sales to new construction channels NA = % of sales within North America Int’l = % of sales outside North America

Masco – Unique Scope and Scale

6

manufacturer of faucets in the world Largest

non-commodity supplier to The Home Depot Largest

supplier to Lowe’s Kitchen and Bath segment Largest

supplier of architectural coatings to the U.S. DIY market Largest

installer of insulation products for the new home construction market Largest

We believe we are the……

I N V E S T M E N T T H E S I S

Strong Fundamentals - Positioned for Growth

7

The strengths

The growth

The strategy

The company

Masco’s Strategic Initiatives

8

Positioned for Growth

• Leverage brands

• Innovative products Expand market leadership

• Total cost productivity

• Drive lean benefits Reduce costs

• Return Cabinets to profitability

• Drive profitability and growth in Installation

Improve underperforming businesses

1

2

3

• Debt reduction

• Strong liquidity Strengthen Balance Sheet

4

1 . E X P A N D M A R K E T L E A D E R S H I P

Key Brands Gaining Share since 2010

Examples Gaining Share

• Delta®, Peerless®, and Brizo® brands in U.S.

• International plumbing growth with Hansgrohe

• Decorative Architectural: Behr® #1 DIY Paint at The Home Depot, Direct to Pro® service growth, Kilz Pro line

• Other Specialty: Milgard® windows outperforming market, UK growing share

• Masco Contractor Services gaining share with insulation, retrofit and commercial channels

9

• Merillat® and Quality® cabinet brands gaining share with builders

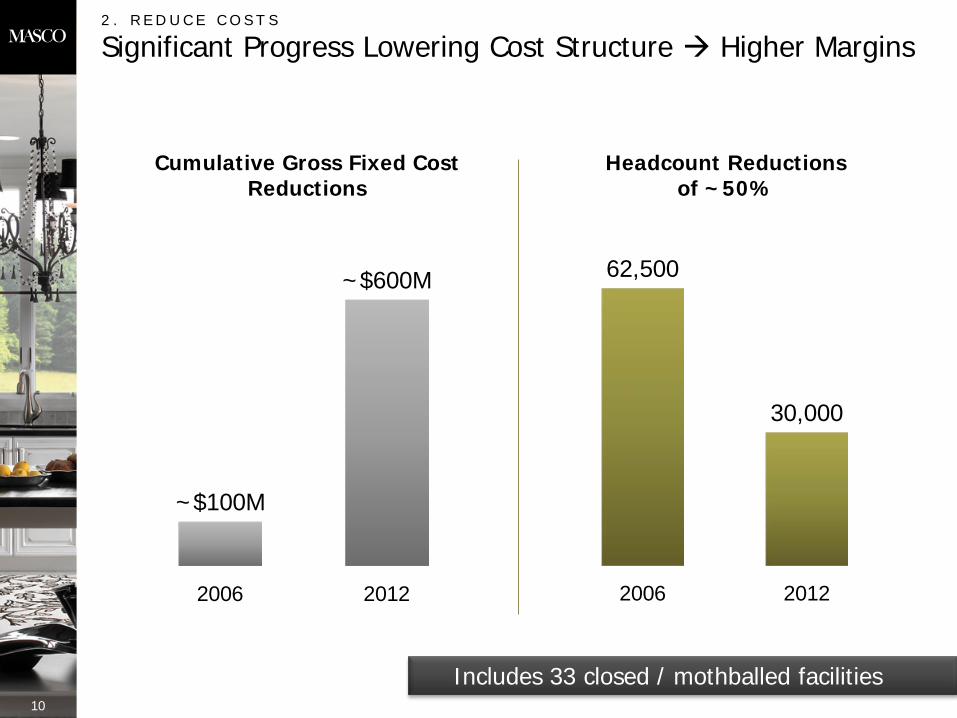

2 . R E D U C E C O S T S

Significant Progress Lowering Cost Structure Higher Margins

Cumulative Gross Fixed Cost Reductions

Headcount Reductions of ~50%

~$100M

~$600M

2006 2012

62,500

30,000

2006 2012

Includes 33 closed / mothballed facilities 10

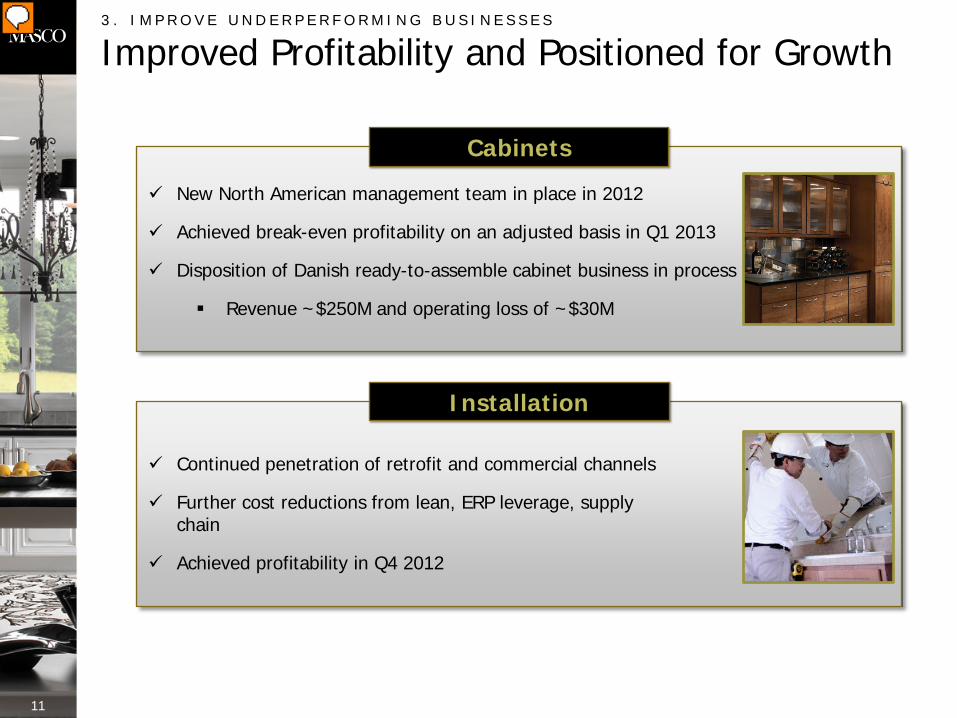

3 . I M P R O V E U N D E R P E R F O R M I N G B U S I N E S S E S

Improved Profitability and Positioned for Growth

Cabinets

New North American management team in place in 2012

Achieved break-even profitability on an adjusted basis in Q1 2013

Disposition of Danish ready-to-assemble cabinet business in process

Revenue ~$250M and operating loss of ~$30M

Installation

Continued penetration of retrofit and commercial channels

Further cost reductions from lean, ERP leverage, supply chain

Achieved profitability in Q4 2012

11

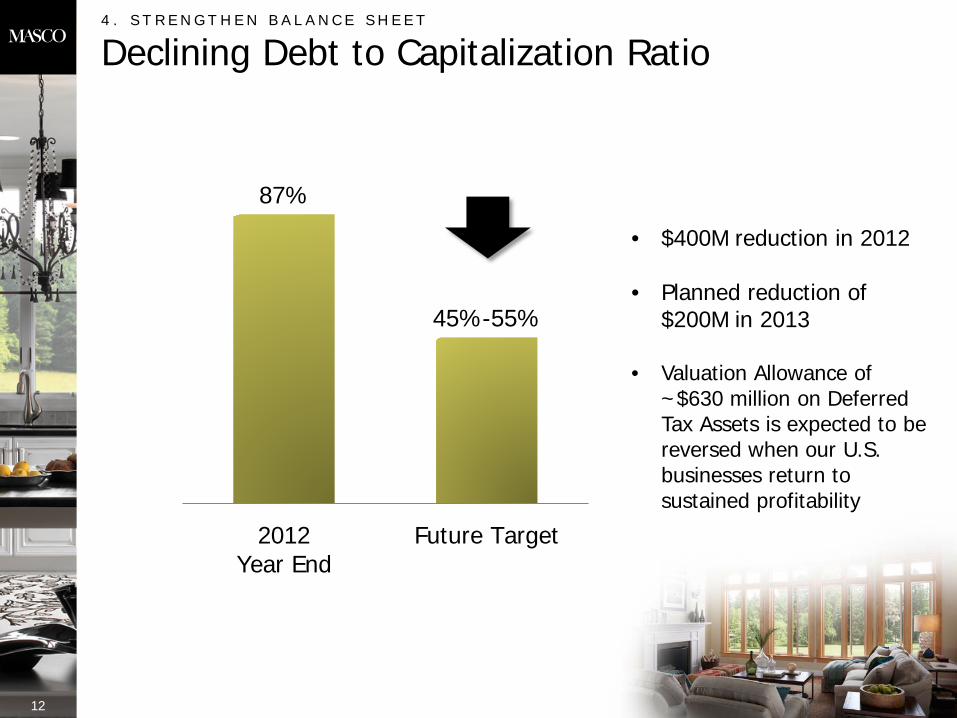

4 . S T R E N G T H E N B A L A N C E S H E E T

Declining Debt to Capitalization Ratio

12

87%

45%-55%

2012Year End

Future Target

• $400M reduction in 2012 • Planned reduction of

$200M in 2013 • Valuation Allowance of

~$630 million on Deferred Tax Assets is expected to be reversed when our U.S. businesses return to sustained profitability

I N V E S T M E N T T H E S I S

Strong Fundamentals - Positioned for Growth

13

The strengths

The growth

The strategy

The company

Broad distribution 3

Industry innovator 2

Market-leading brands 1

Masco Business System 4

Strong financial position 5

Key Strengths we are Leveraging

14

S T R E N G T H 1 : M A R K E T L E A D I N G B R A N D S

Unparalleled Brand Strength

15

Installation & Other Services

Plumbing Products

Cabinets & Related Products

Decorative Architectural Products

Other Specialty Products

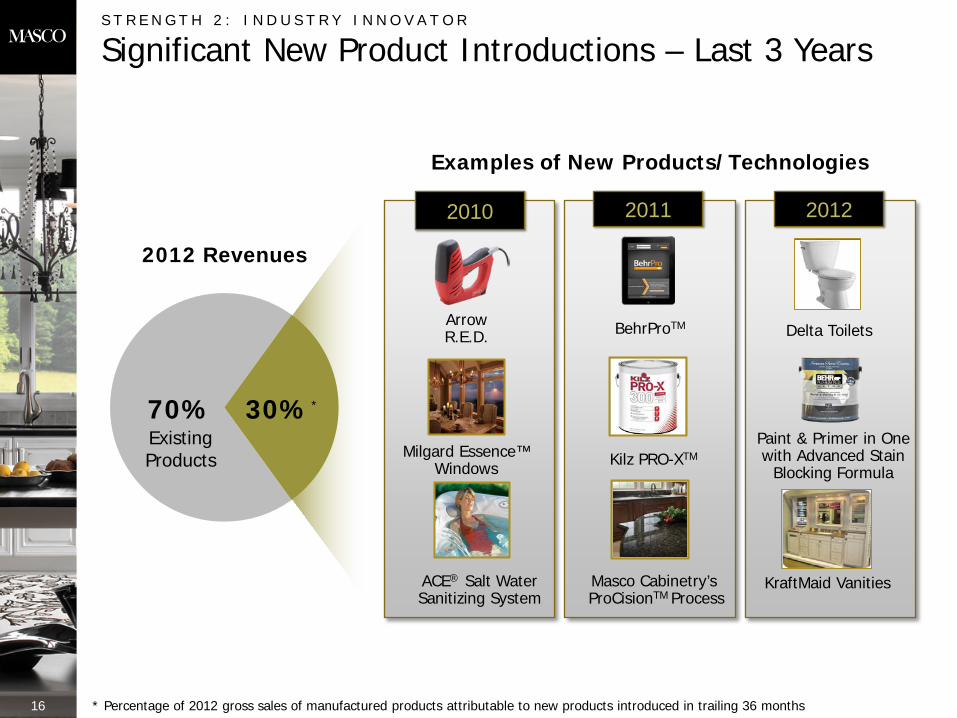

S T R E N G T H 2 : I N D U S T R Y I N N O V A T O R

Significant New Product Introductions – Last 3 Years

30%*

Examples of New Products/Technologies

Existing Products

2012 2011 2010

70% Milgard Essence™

Windows

Arrow R.E.D.

ACE® Salt Water Sanitizing System

2012 Revenues

16

BehrProTM

Masco Cabinetry’s ProCisionTM Process

* Percentage of 2012 gross sales of manufactured products attributable to new products introduced in trailing 36 months

Kilz PRO-XTM

Delta Toilets

Paint & Primer in One with Advanced Stain

Blocking Formula

KraftMaid Vanities

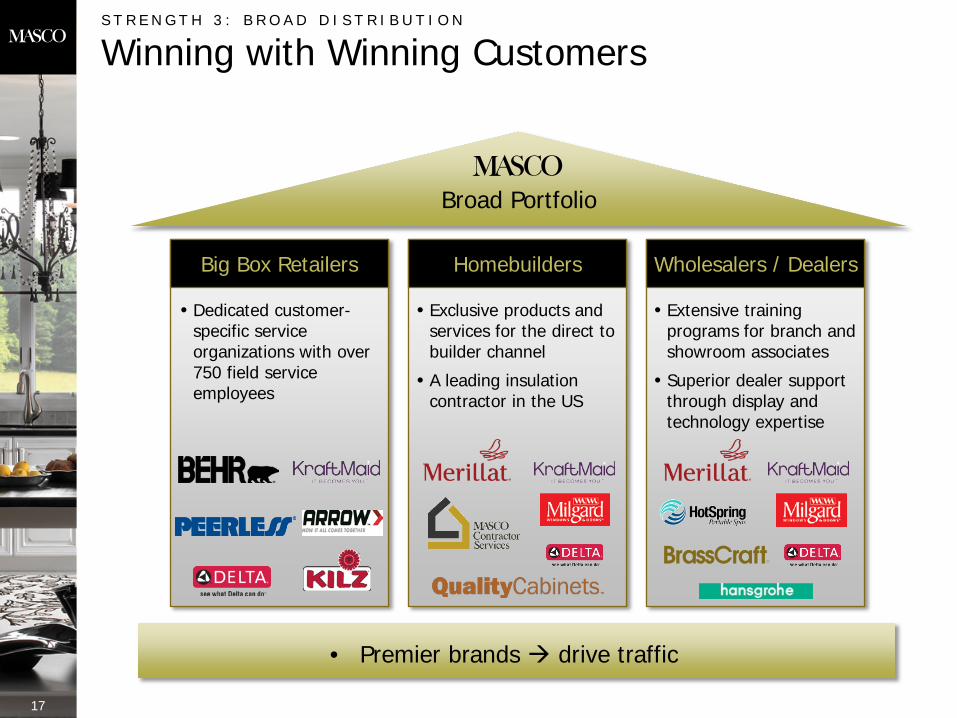

S T R E N G T H 3 : B R O A D D I S T R I B U T I O N

Winning with Winning Customers

Broad Portfolio

Big Box Retailers Homebuilders Wholesalers / Dealers

• Exclusive products and services for the direct to builder channel

• A leading insulation contractor in the US

• Dedicated customer-specific service organizations with over 750 field service employees

• Extensive training programs for branch and showroom associates

• Superior dealer support through display and technology expertise

• Premier brands drive traffic

17

Customer focus

Lean Quality Talent

Innovation

S T R E N G T H 4 : M A S C O B U S I N E S S S Y S T E M S

A Continuous Improvement Culture – At the Center of Our Success

18

MBS

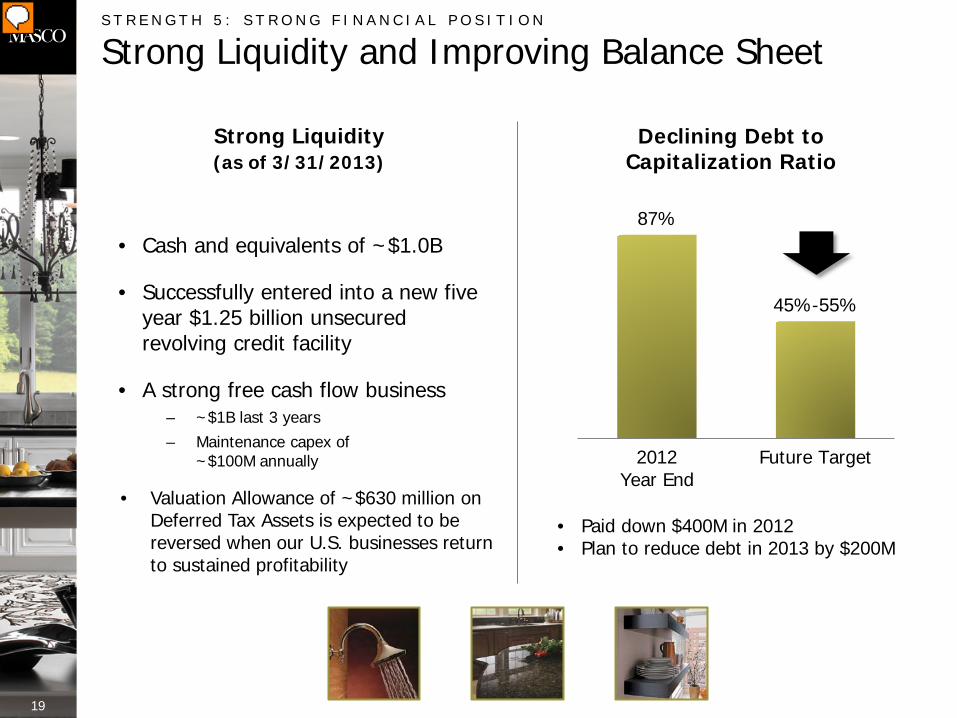

S T R E N G T H 5 : S T R O N G F I N A N C I A L P O S I T I O N

Strong Liquidity and Improving Balance Sheet

Strong Liquidity (as of 3/31/2013)

• Cash and equivalents of ~$1.0B

• Successfully entered into a new five year $1.25 billion unsecured revolving credit facility

• A strong free cash flow business – ~$1B last 3 years – Maintenance capex of

~$100M annually

19

• Paid down $400M in 2012 • Plan to reduce debt in 2013 by $200M

Declining Debt to Capitalization Ratio

87%

45%-55%

2012Year End

Future Target

• Valuation Allowance of ~$630 million on Deferred Tax Assets is expected to be reversed when our U.S. businesses return to sustained profitability

I N V E S T M E N T T H E S I S

Strong Fundamentals - Positioned for Growth

20

The strengths

The growth

The strategy

The company

Positioned for Growth

21

Leveraged to the recovery

Continued brand leverage and share expansion

Continued cost position improvement

Disciplined capital deployment

1

2

3

4

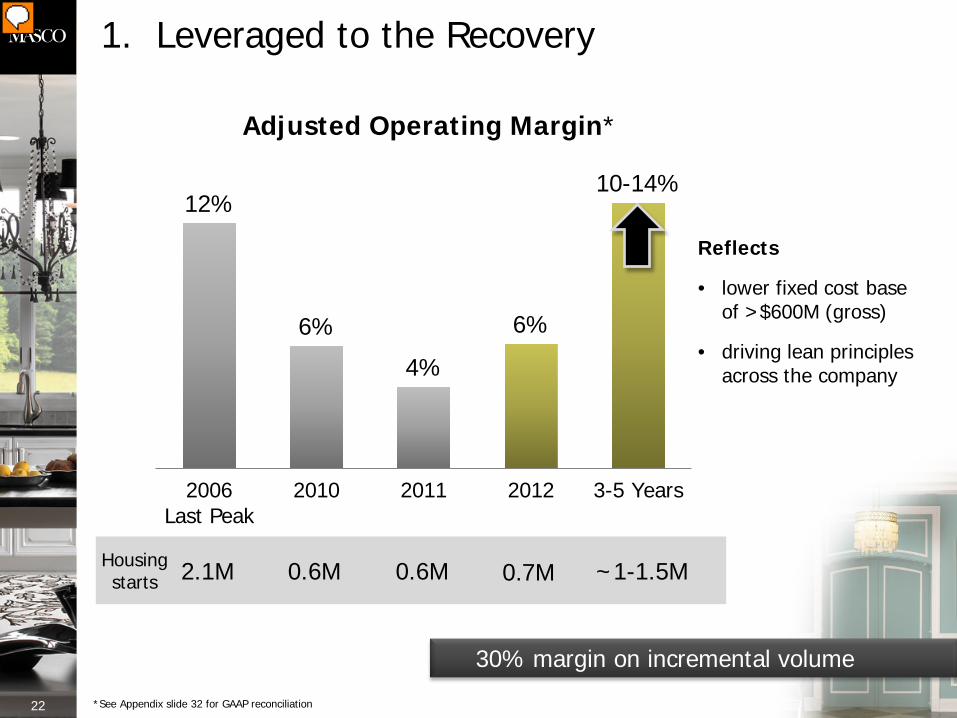

1. Leveraged to the Recovery

12%

6%

4%

6%

10-14%

2006Last Peak

2010 2011 2012 3-5 Years

Adjusted Operating Margin*

22

Reflects

• lower fixed cost base of >$600M (gross)

• driving lean principles across the company

30% margin on incremental volume

Housing starts 2.1M 0.6M 0.6M ~1-1.5M

*See Appendix slide 32 for GAAP reconciliation

0.7M

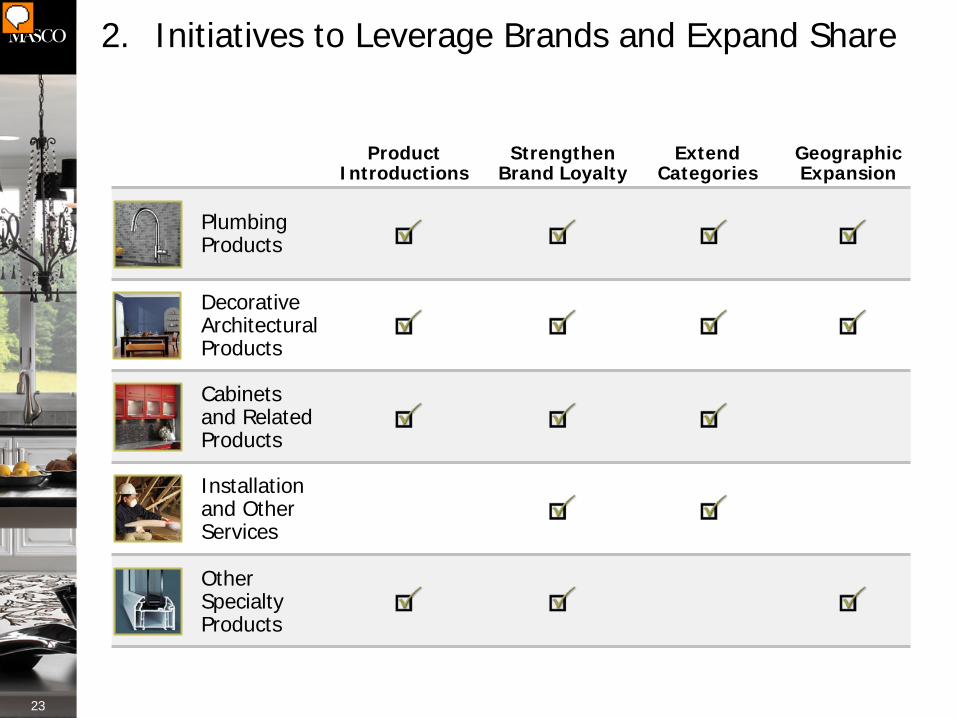

2. Initiatives to Leverage Brands and Expand Share

Geographic Expansion

Cabinets and Related Products

Plumbing Products

Installation and Other Services

Decorative Architectural Products

Other Specialty Products

Product Introductions

Extend Categories

Strengthen Brand Loyalty

23

3. Continue to Improve Cost Position

~$195M* of Total Cost Productivity

in 2012

24 * Gross

Sourcing

Lean Initiatives

Driven by: Driven by:

Distribution & Logistics

Actions Taken In Prior Years

• Plant Closures • Headcount

Reductions • System

Implementations

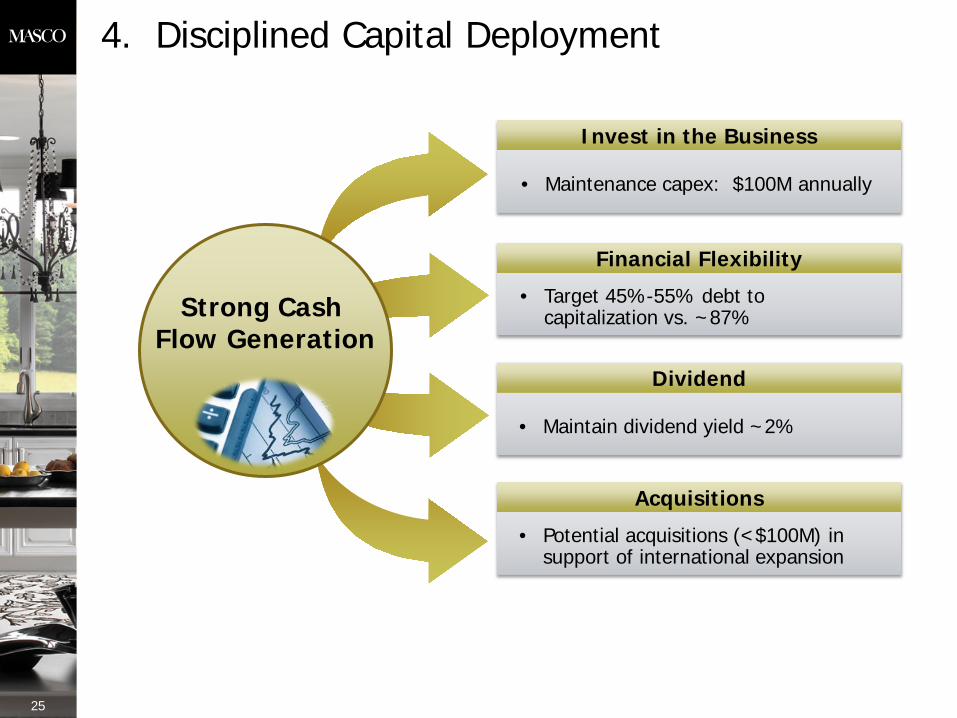

4. Disciplined Capital Deployment

Invest in the Business

• Maintenance capex: $100M annually

Strong Cash Flow Generation

Financial Flexibility

• Target 45%-55% debt to capitalization vs. ~87%

Dividend

• Maintain dividend yield ~2%

Acquisitions

• Potential acquisitions (<$100M) in support of international expansion

25

Delivering on 2013 Priorities

Investment in strategic growth initiatives

Geographic expansion

Total cost productivity

Reduce debt by ~$200M

Cabinet profit improvement

Profitably grow Installation

Grow share of key brands

26

Successfully launch new products and programs

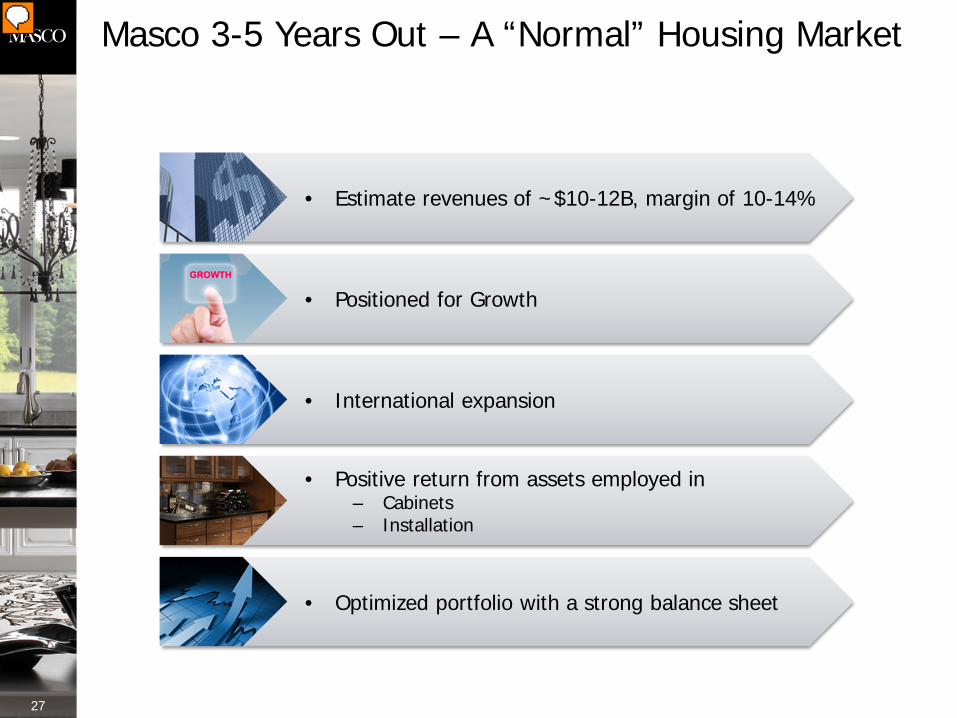

Masco 3-5 Years Out – A “Normal” Housing Market

27

• Estimate revenues of ~$10-12B, margin of 10-14%

• Positioned for Growth

• Optimized portfolio with a strong balance sheet

• International expansion

• Positive return from assets employed in – Cabinets – Installation

W H Y I N V E S T I N M A S C O

Strong Fundamentals - Positioned for Growth

28

Executing initiatives to improve performance • Continuing to reduce fixed costs, expand share and

improve underperformers The Strategy

Building on market-leading positions • Best brands, innovative products, lean practices,

strong financial position The Strengths

Well-positioned for growth • Lower cost structure higher margins, leveraged

to recovery The Growth

Appendix

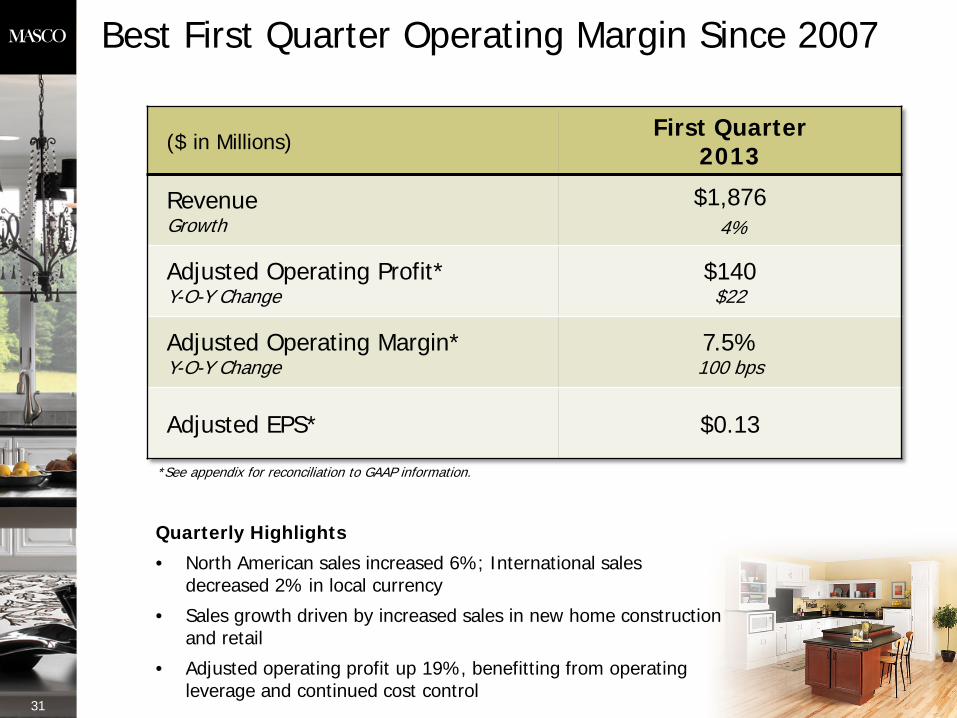

Best First Quarter Operating Margin Since 2007

31

($ in Millions) First Quarter

2013

Revenue Growth

$1,876 4%

Adjusted Operating Profit* Y-O-Y Change

$140 $22

Adjusted Operating Margin* Y-O-Y Change

7.5% 100 bps

Adjusted EPS* $0.13

Quarterly Highlights

• North American sales increased 6%; International sales decreased 2% in local currency

• Sales growth driven by increased sales in new home construction and retail

• Adjusted operating profit up 19%, benefitting from operating leverage and continued cost control

*See appendix for reconciliation to GAAP information.

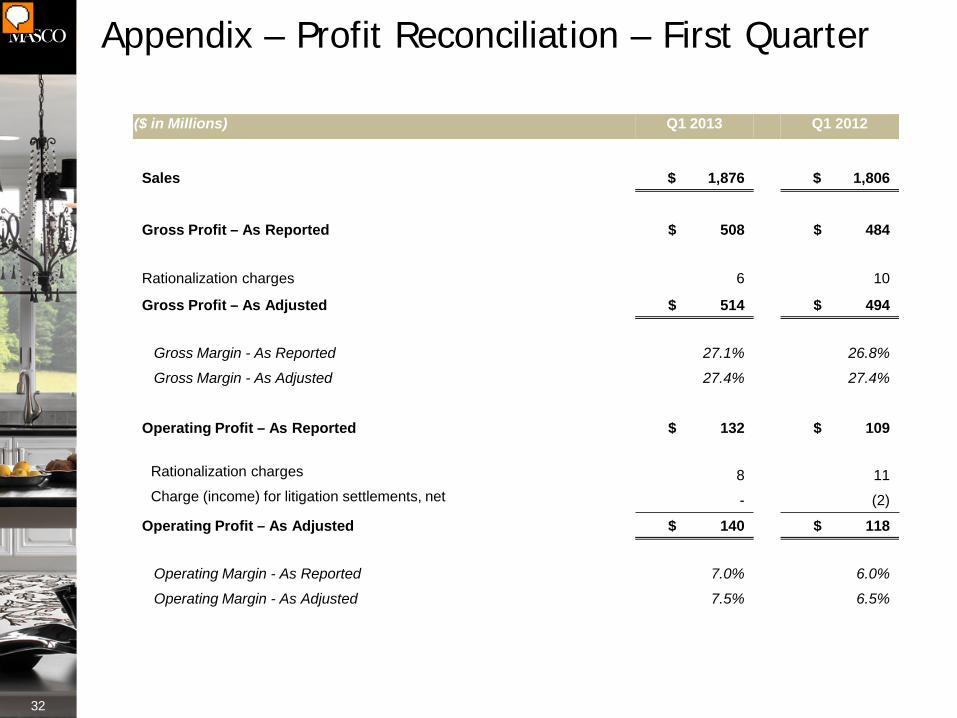

Appendix – Profit Reconciliation – First Quarter

32

($ in Millions) Q1 2013 Q1 2012

Sales $ 1,876 $ 1,806

Gross Profit – As Reported $ 508 $ 484 Rationalization charges 6 10

Gross Profit – As Adjusted $ 514 $ 494 Gross Margin - As Reported 27.1% 26.8%

Gross Margin - As Adjusted 27.4% 27.4%

Operating Profit – As Reported $ 132 $ 109

Rationalization charges 8 11 Charge (income) for litigation settlements, net - (2)

Operating Profit – As Adjusted $ 140 $ 118 Operating Margin - As Reported 7.0% 6.0%

Operating Margin - As Adjusted 7.5% 6.5%

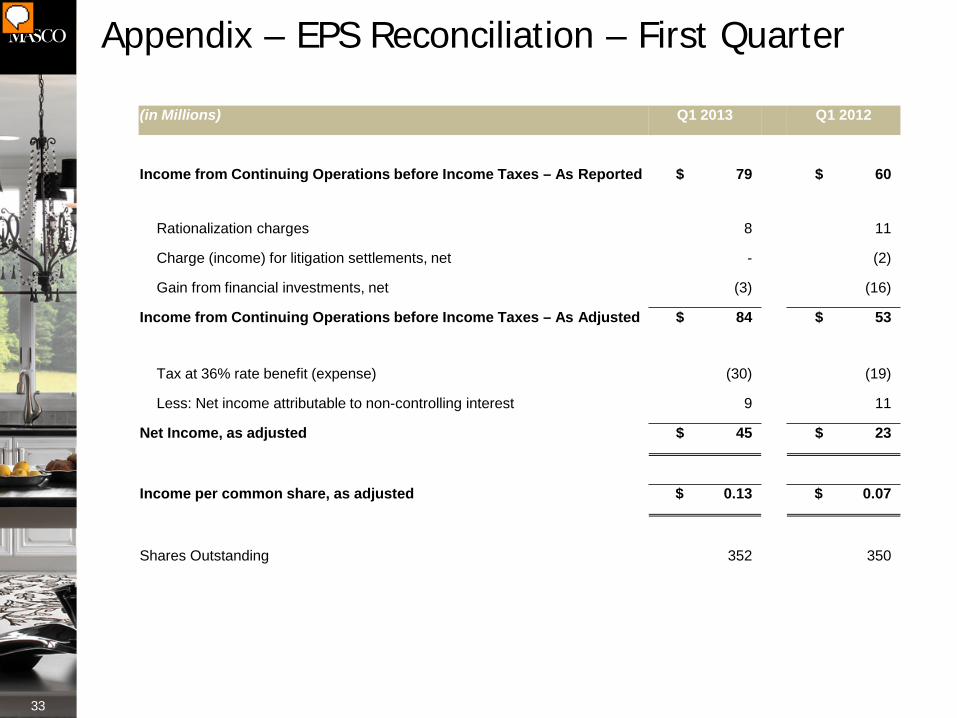

Appendix – EPS Reconciliation – First Quarter

33

(in Millions) Q1 2013 Q1 2012

Income from Continuing Operations before Income Taxes – As Reported $ 79 $ 60

Rationalization charges 8 11

Charge (income) for litigation settlements, net - (2)

Gain from financial investments, net (3) (16)

Income from Continuing Operations before Income Taxes – As Adjusted $ 84 $ 53

Tax at 36% rate benefit (expense) (30) (19)

Less: Net income attributable to non-controlling interest 9 11

Net Income, as adjusted $ 45 $ 23

Income per common share, as adjusted $ 0.13 $ 0.07

Shares Outstanding 352 350

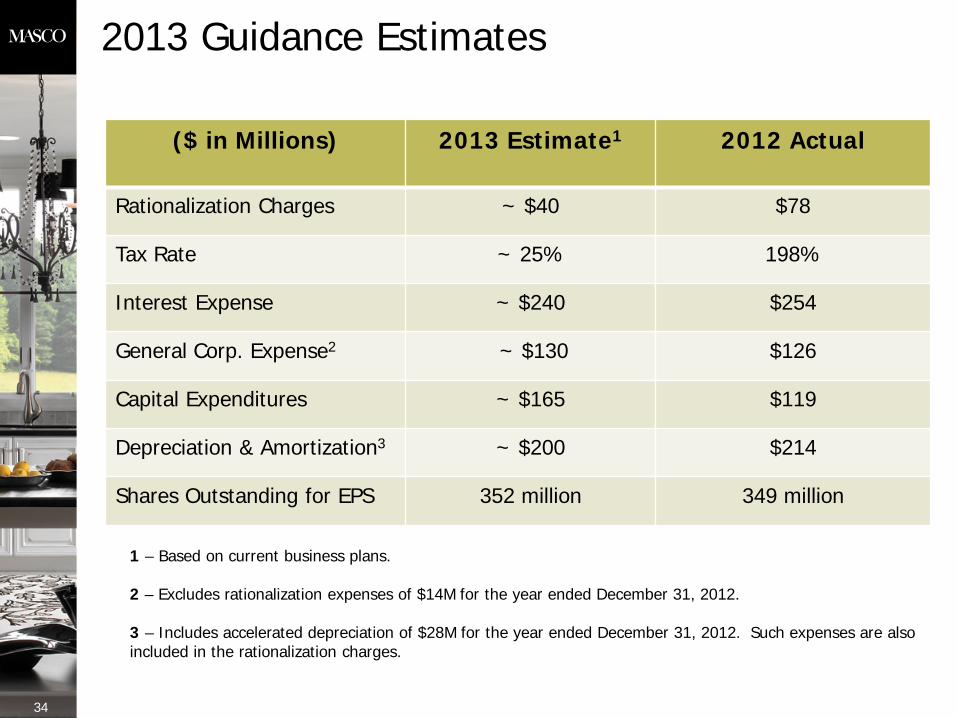

($ in Millions) 2013 Estimate1

2012 Actual

Rationalization Charges ~ $40 $78

Tax Rate ~ 25% 198%

Interest Expense ~ $240 $254

General Corp. Expense2 ~ $130 $126

Capital Expenditures ~ $165 $119

Depreciation & Amortization3 ~ $200 $214

Shares Outstanding for EPS 352 million 349 million

2013 Guidance Estimates

1 – Based on current business plans. 2 – Excludes rationalization expenses of $14M for the year ended December 31, 2012. 3 – Includes accelerated depreciation of $28M for the year ended December 31, 2012. Such expenses are also included in the rationalization charges.

34

Segment Mix Full Year 2012

Business Segment

Cabinets and Related Products

Plumbing Products

Installation and Other Services

Decorative Architectural Products

$0.9B

$3.0B

$1.2B

$1.8B

Revenue 2012 % of Total

40%

24%

12%

16%

$7.5B 100% Total company

35

Other Specialty Products $0.6B 8%

R&R% vs. NC NA% vs. Int’l

82% 59%

99% 100%

69% 92%

16% 100%

75% 75%

73% 80%

R&R = % of sales to repair and remodel channels NC = % of sales to new construction channels NA = % of sales within North America Int’l = % of sales outside North America

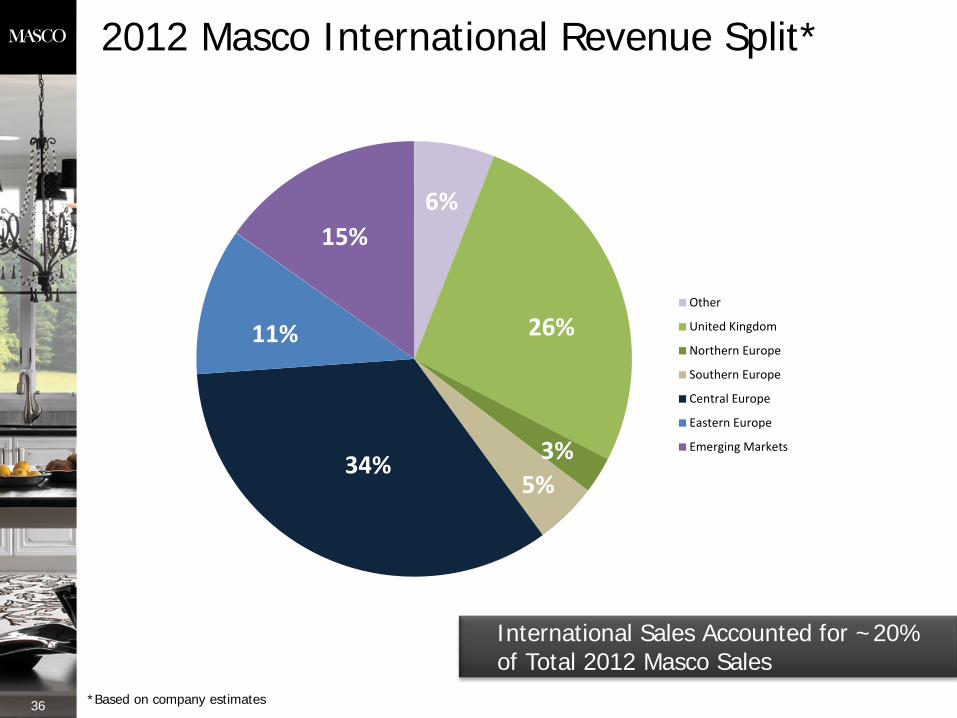

2012 Masco International Revenue Split*

36 *Based on company estimates

International Sales Accounted for ~20% of Total 2012 Masco Sales

6%

26%

3% 5%

34%

11%

15%

Other

United Kingdom

Northern Europe

Southern Europe

Central Europe

Eastern Europe

Emerging Markets