Embed Size (px)

Citation preview

The impact of freezing UK energy prices

Ropemaker Place, 25 Ropemaker Street,London EC2Y 9LY / T: +44 (0)20 3100 2000www.liberum.com

Liberum Capital Limited is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales No. 5912554

January 2014

Peter Atherton Research+44 (0) 20 3100 [email protected]

Mulu Sun Research+44 (0) 20 3100 [email protected]

This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

Background and contents

Labour leader Ed Miliband pledged at the party’s conference on September 24th, 2013 to freeze UK gas and electricity bills for 20 months if it wins a May 2015 general election. In this presentation made at a Cornwall Energy conference in London on January 23, 2014, Liberum Utilities analyst Peter Atherton reviews the impact of that commitment. His colleague Mulu Sun contributed to the presentation.

Centrica & SSE 3MSCI UK Utils vs. Euro ex-UK Utils (five years before Ed Miliband speech) 5MSCI UK Utils 6MSCI UK Utils - Relative performance since Miliband speech 7One-year share price performance before Miliband speech 8Share price performance since Miliband speech 9Centrica – lost market cap (£m, absolute) 10SSE – lost market cap (£m, absolute) 12Centrica & SSE – combined lost market cap (£m, absolute) 13Centrica & SSE – combined lost market cap (£m, relative to FTSE100) 14MSCI UK Utils – lost market cap 15Why so damaging? 16How will this play out if Labour is ahead in the polls? 17The Affordability Crisis 18

2This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

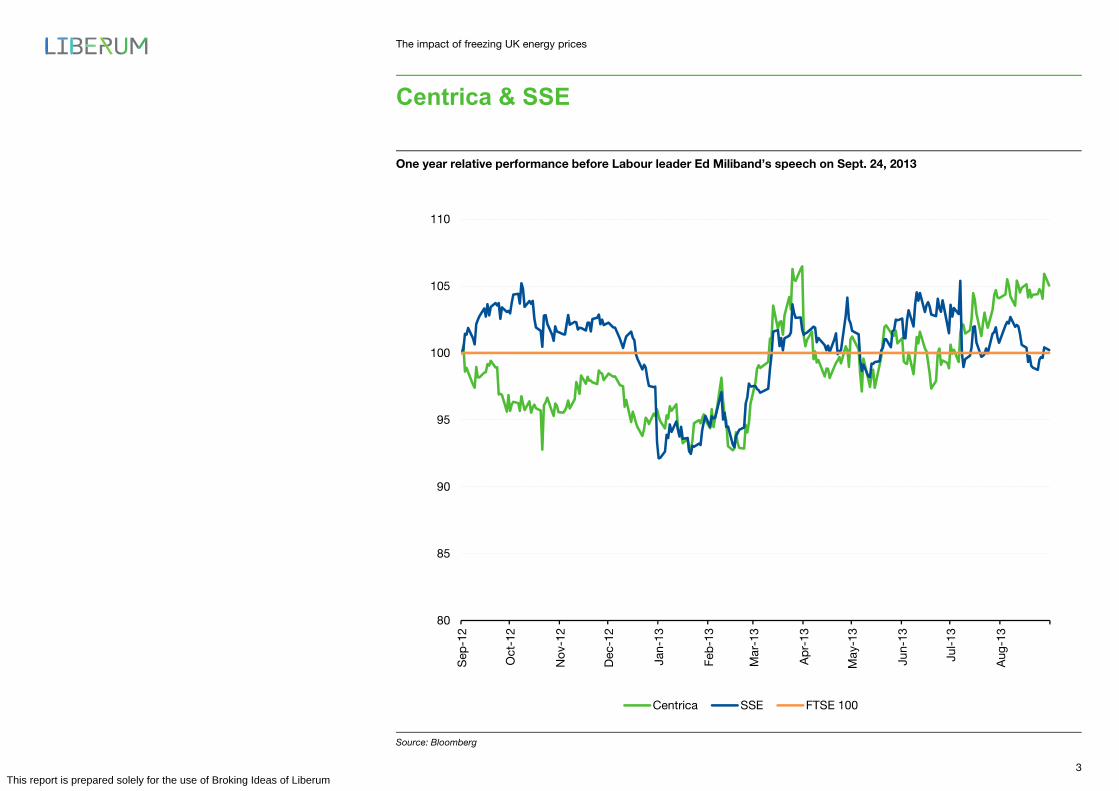

Centrica & SSE

One year relative performance before Labour leader Ed Miliband’s speech on Sept. 24, 2013

Source: Bloomberg

80

85

90

95

100

105

110

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Ap

r-13

May

-13

Jun-

13

Jul-

13

Aug

-13

Centrica SSE FTSE 100

3This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

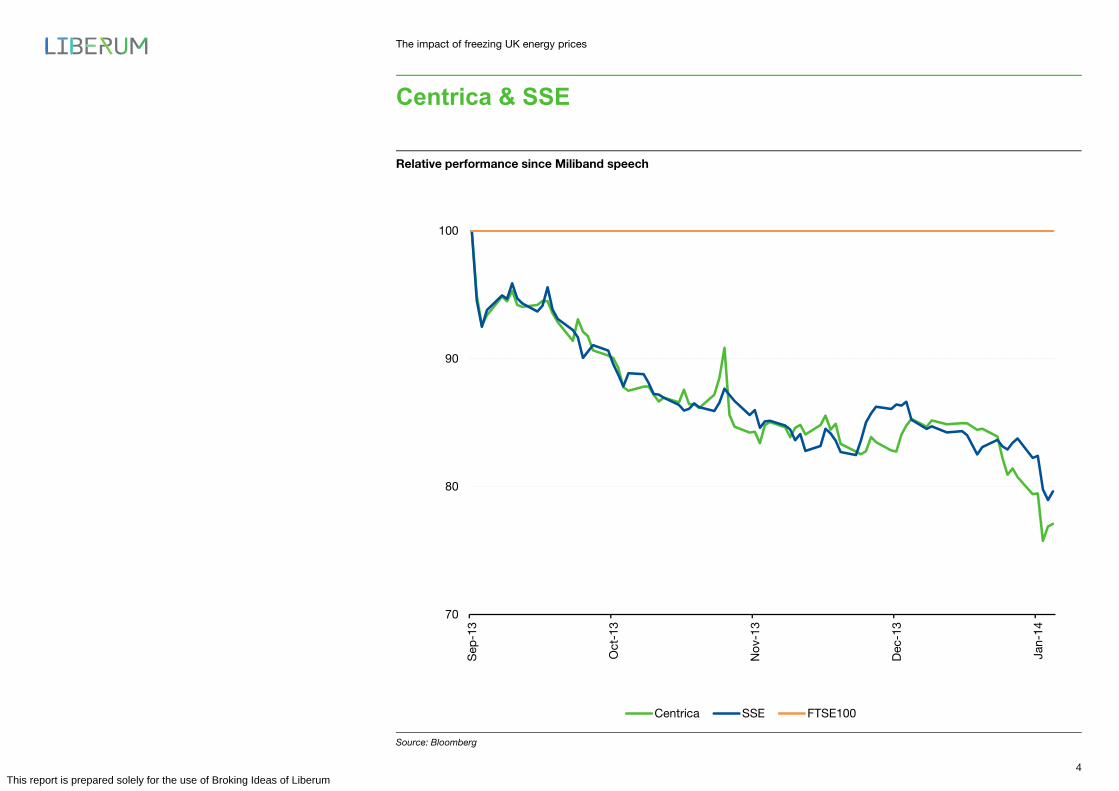

Centrica & SSE

Relative performance since Miliband speech

Source: Bloomberg

70

80

90

100

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Centrica SSE FTSE100

4This report is prepared solely for the use of Broking Ideas of Liberum

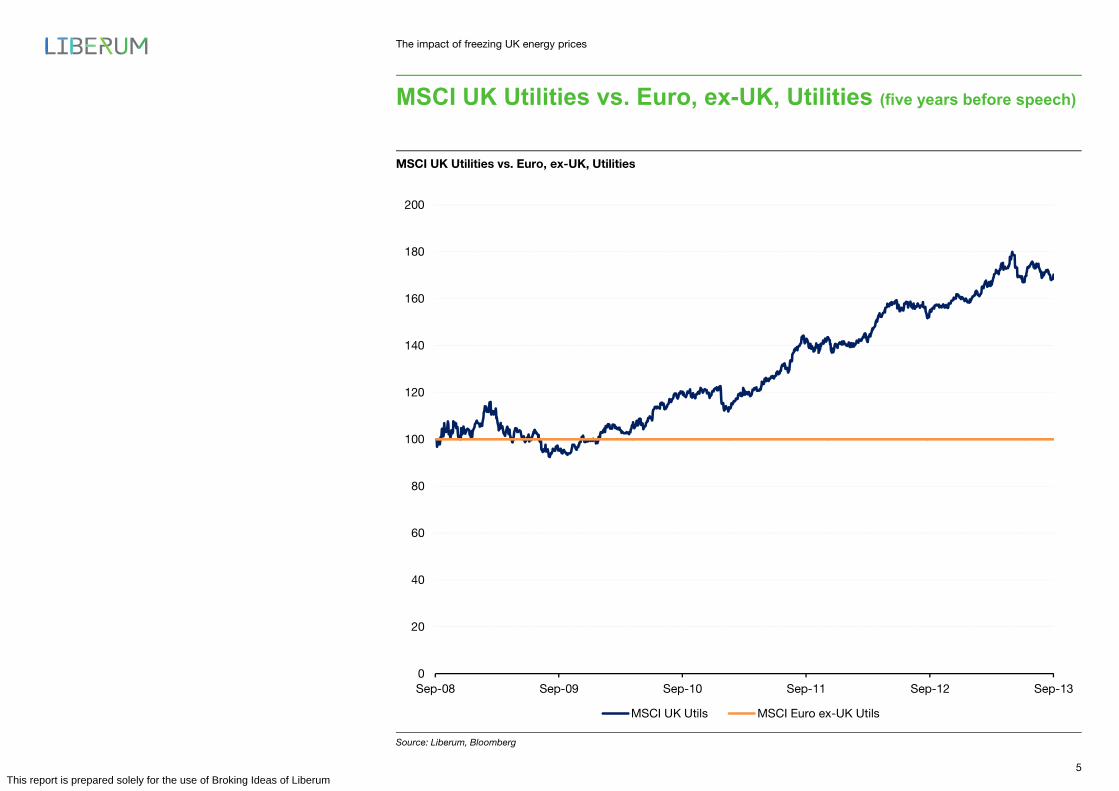

The impact of freezing UK energy prices

MSCI UK Utilities vs. Euro, ex-UK, Utilities (five years before speech)

MSCI UK Utilities vs. Euro, ex-UK, Utilities

Source: Liberum, Bloomberg

0

20

40

60

80

100

120

140

160

180

200

Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13

MSCI UK Utils MSCI Euro ex-UK Utils

5This report is prepared solely for the use of Broking Ideas of Liberum

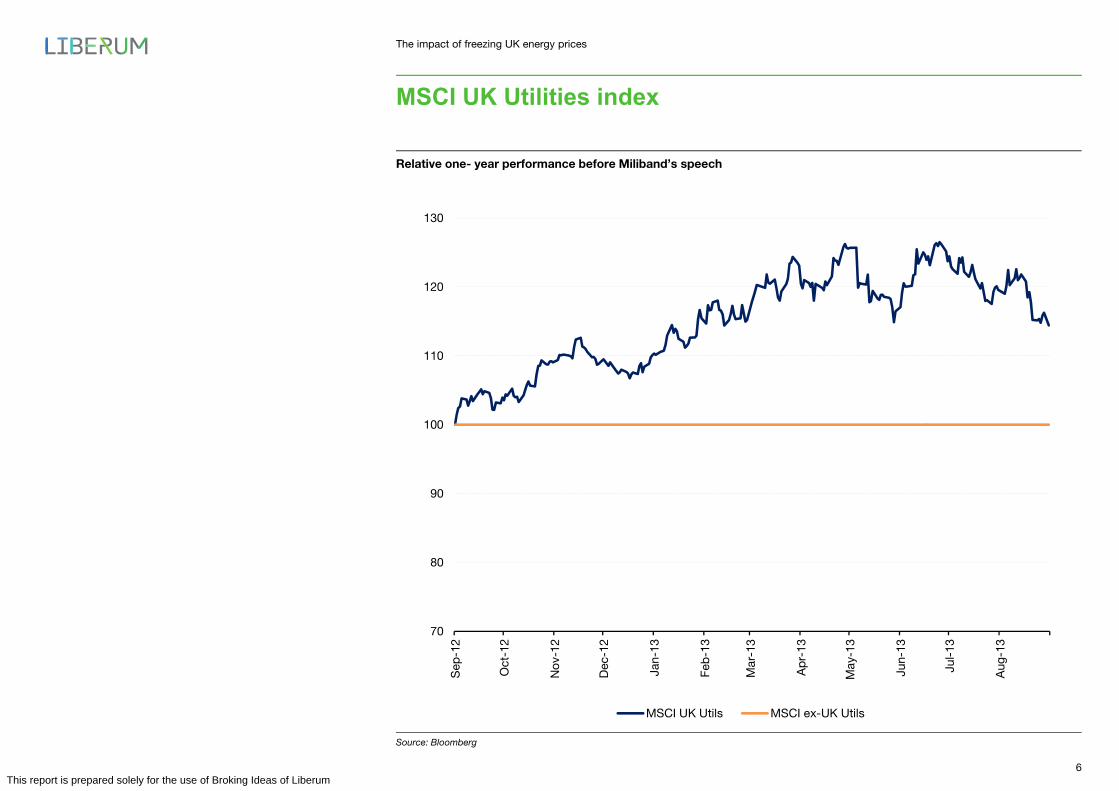

The impact of freezing UK energy prices

MSCI UK Utilities index

Relative one- year performance before Miliband’s speech

Source: Bloomberg

70

80

90

100

110

120

130

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Ap

r-13

May

-13

Jun-

13

Jul-

13

Aug

-13

MSCI UK Utils MSCI ex-UK Utils

6This report is prepared solely for the use of Broking Ideas of Liberum

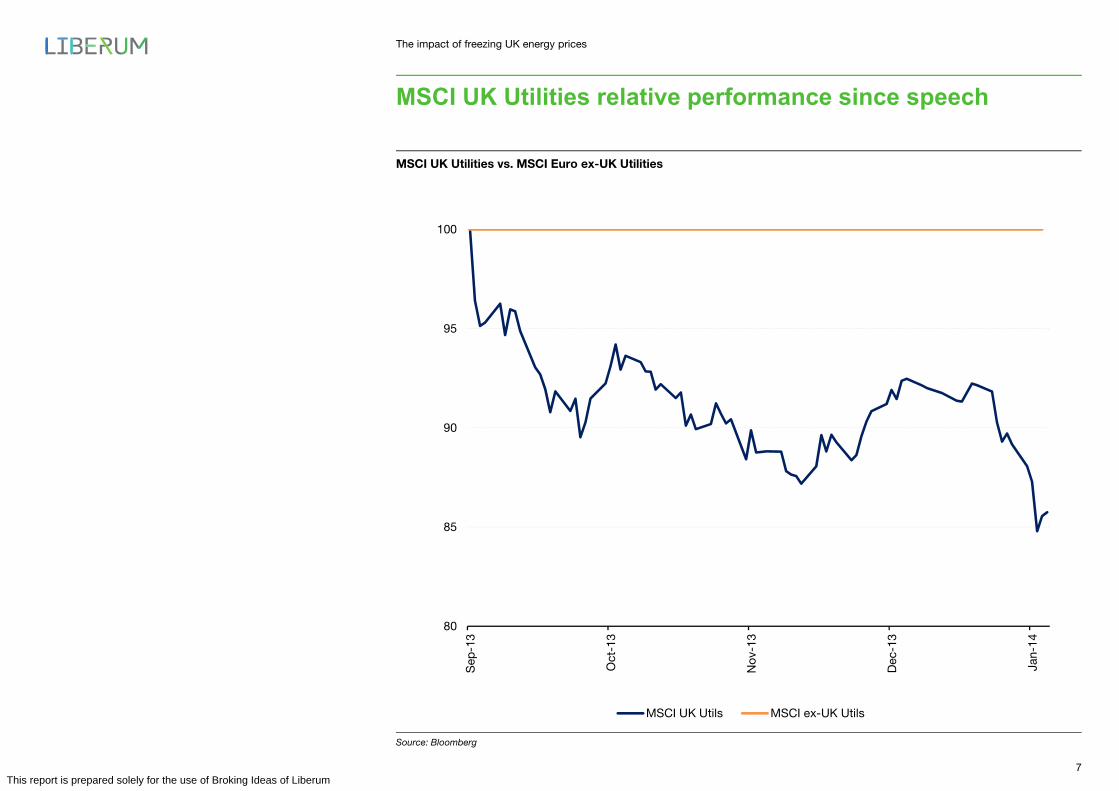

The impact of freezing UK energy prices

MSCI UK Utilities relative performance since speech

MSCI UK Utilities vs. MSCI Euro ex-UK Utilities

Source: Bloomberg

80

85

90

95

100

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

MSCI UK Utils MSCI ex-UK Utils

7This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

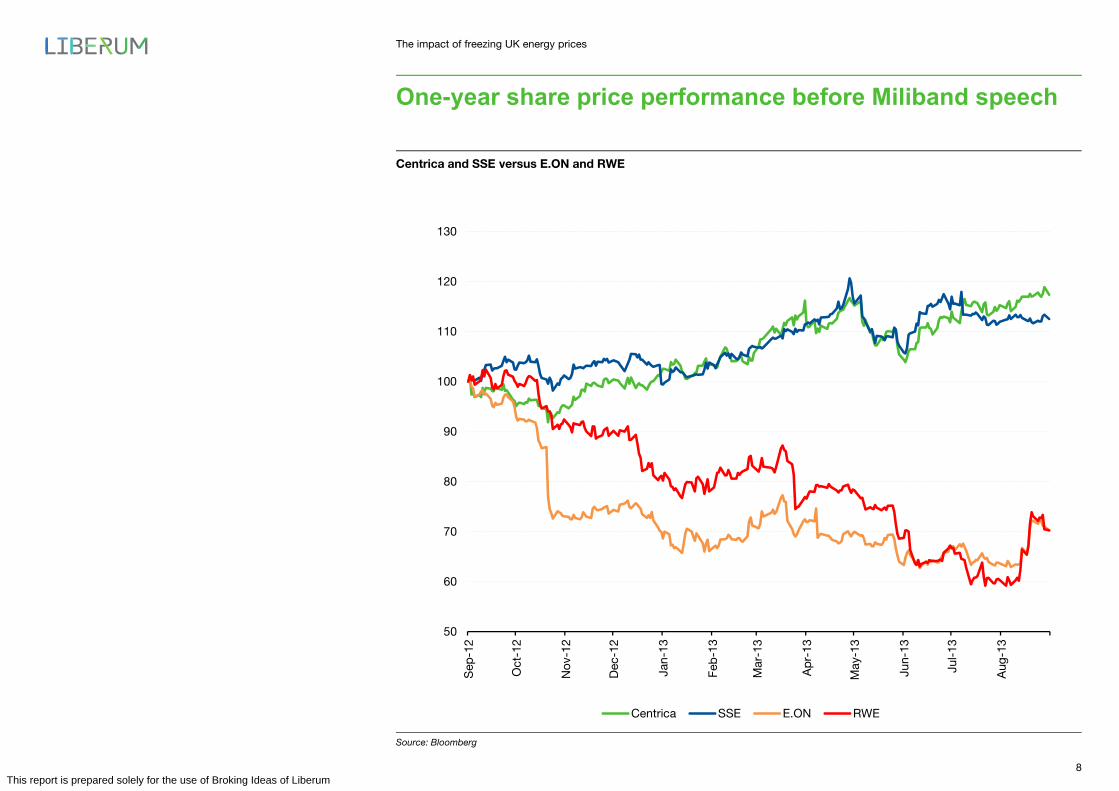

One-year share price performance before Miliband speech

Centrica and SSE versus E.ON and RWE

Source: Bloomberg

50

60

70

80

90

100

110

120

130

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Ap

r-13

May

-13

Jun-

13

Jul-

13

Aug

-13

Centrica SSE E.ON RWE

8This report is prepared solely for the use of Broking Ideas of Liberum

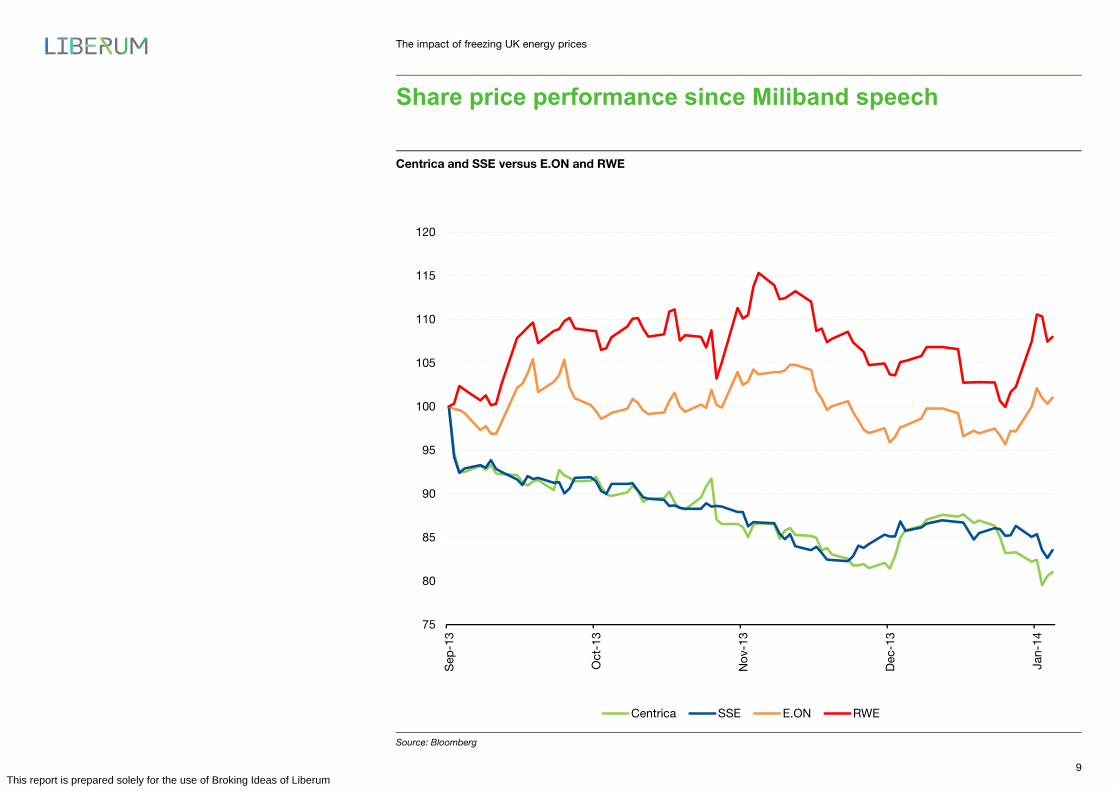

The impact of freezing UK energy prices

Share price performance since Miliband speech

Centrica and SSE versus E.ON and RWE

Source: Bloomberg

75

80

85

90

95

100

105

110

115

120

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Centrica SSE E.ON RWE

9This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

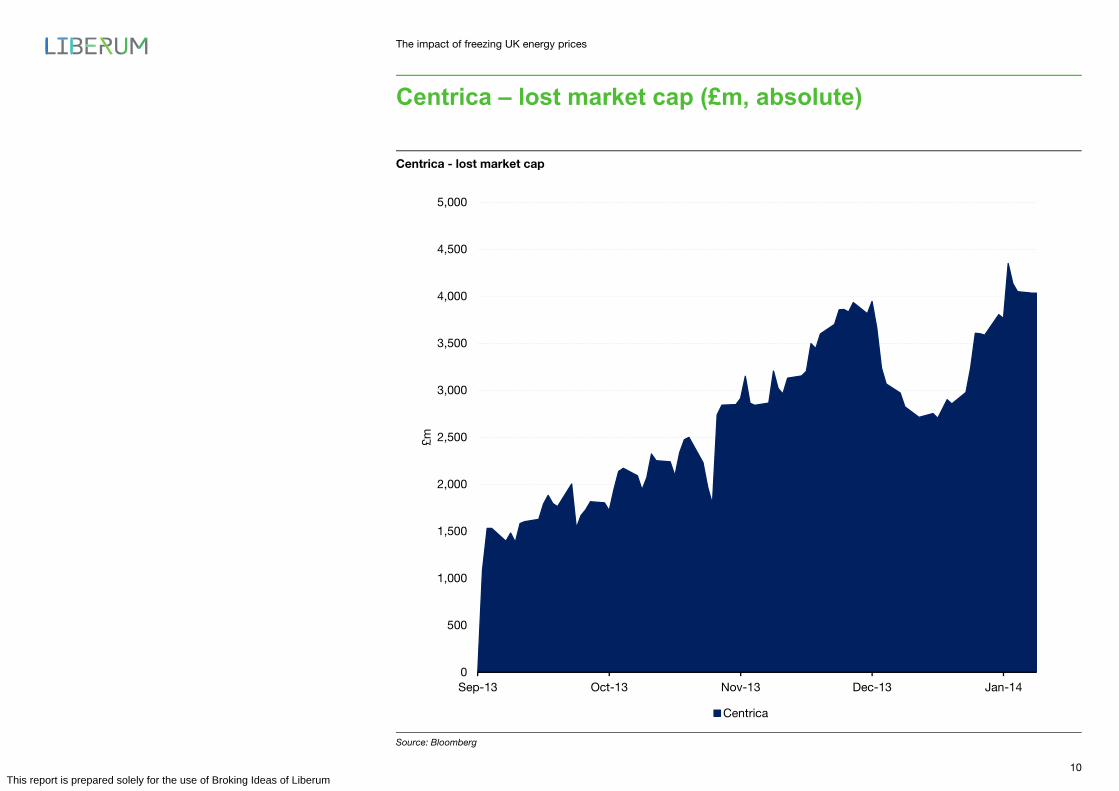

Centrica – lost market cap (£m, absolute)

Centrica - lost market cap

Source: Bloomberg

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

£m

Centrica

10This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

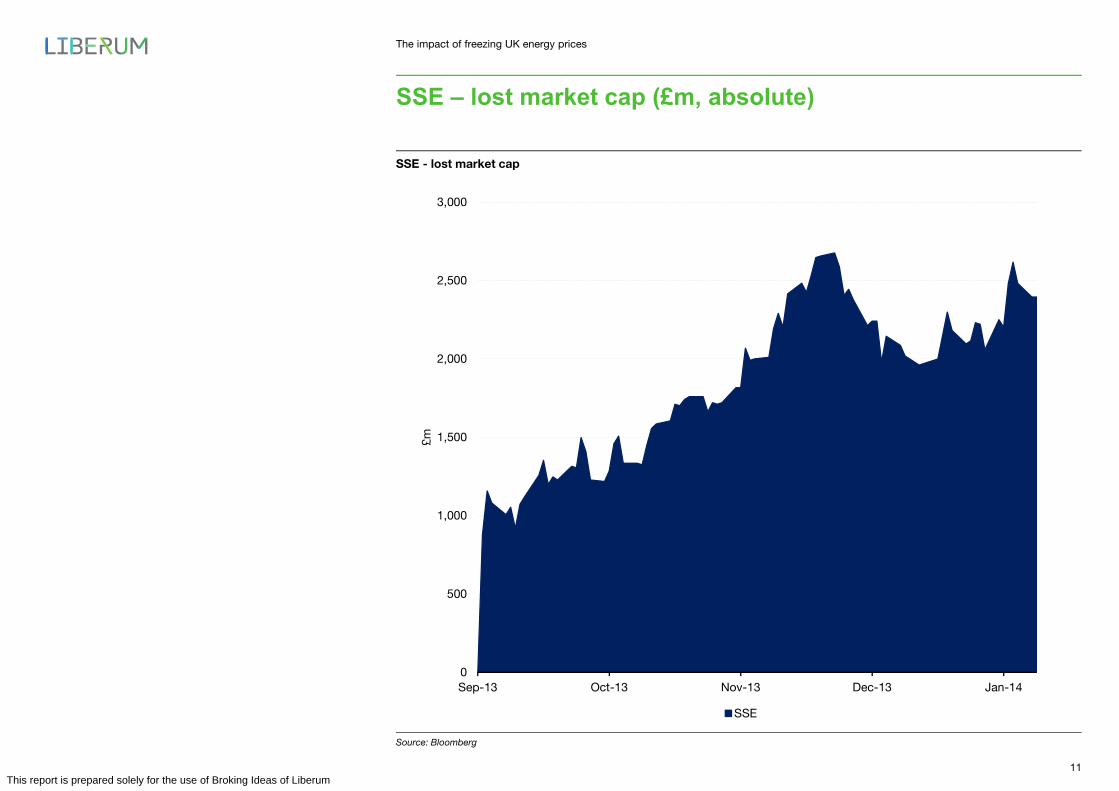

SSE – lost market cap (£m, absolute)

SSE - lost market cap

Source: Bloomberg

0

500

1,000

1,500

2,000

2,500

3,000

Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

£m

SSE

11This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

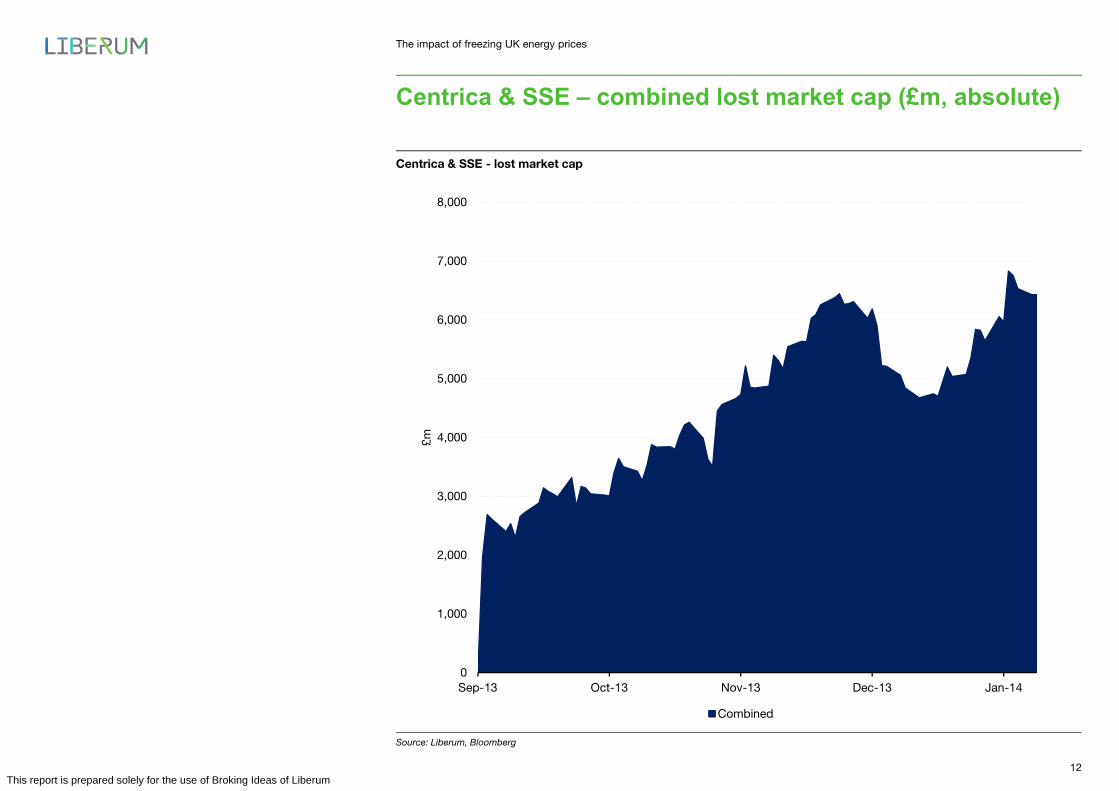

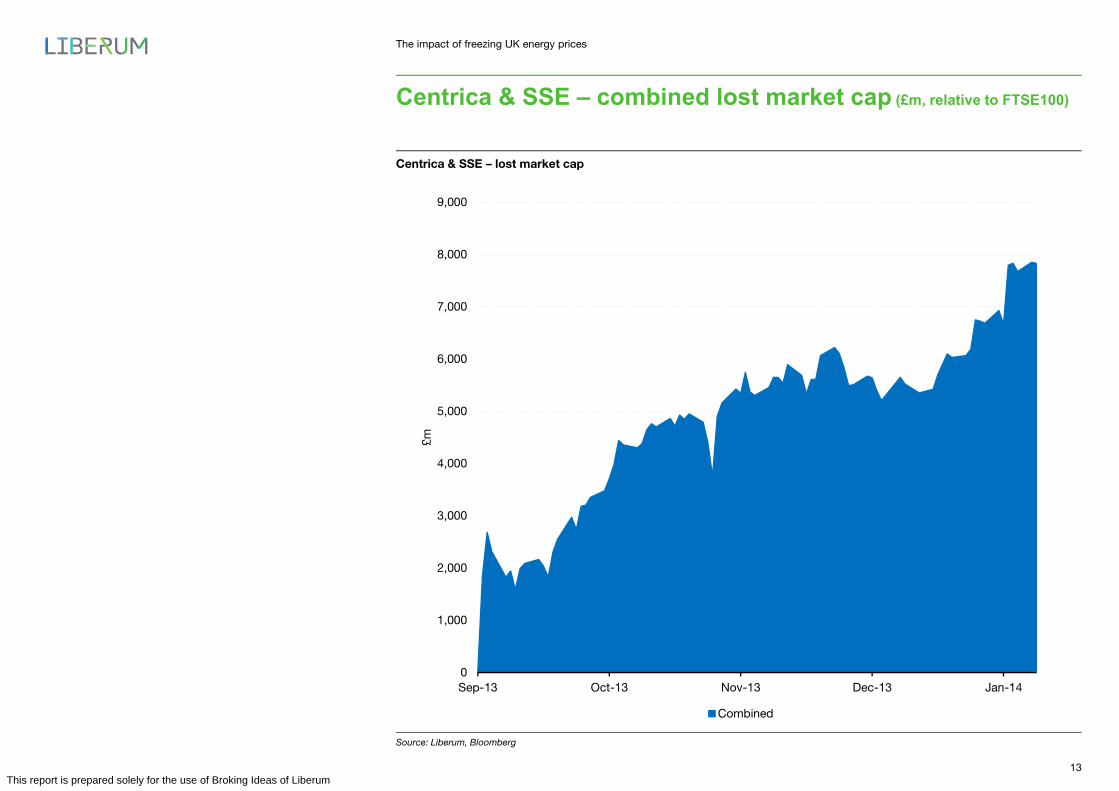

Centrica & SSE – combined lost market cap (£m, absolute)

Centrica & SSE - lost market cap

Source: Liberum, Bloomberg

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

£m

Combined

12This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

Centrica & SSE – combined lost market cap (£m, relative to FTSE100)

Centrica & SSE – lost market cap

Source: Liberum, Bloomberg

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

£m

Combined

13This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

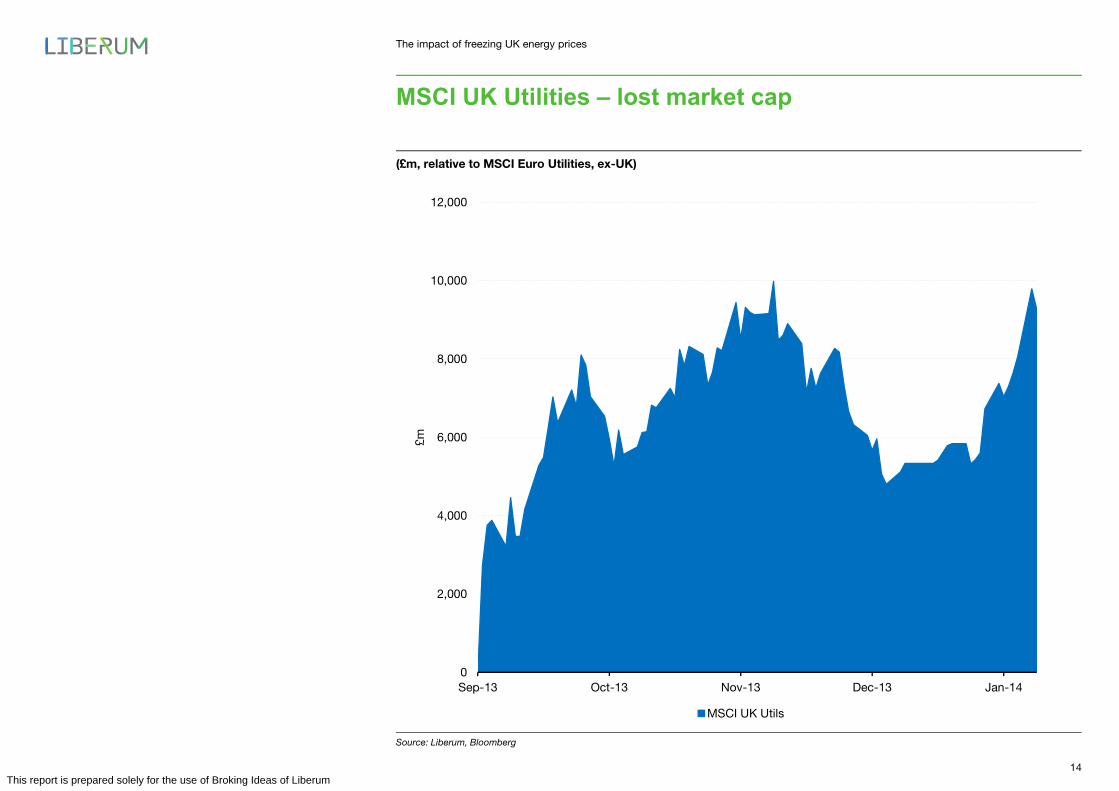

MSCI UK Utilities – lost market cap

(£m, relative to MSCI Euro Utilities, ex-UK)

Source: Liberum, Bloomberg

0

2,000

4,000

6,000

8,000

10,000

12,000

Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

£m

MSCI UK Utils

14This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

Why was the speech so damaging?

• The compact between industry & policy makers has been broken

• Labour effectively wants supply businesses to suck policy-driven cost increases for two years

• Returns on investment are entirely dependent on public policy – so investors need to trust politicians

• Specific threat to supply companies…

• …but risk has increased across the sector. Who is next?

• The ‘Everest’ scale of required investment lies ahead, not behind

• The cost of capital must have increased

• Experience from Europe holds few comforts for investors

• Can investors trust politicians to defend both higher prices AND higher profits that naturally flow from the £200bn+ required investment?

15This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

How will this play out if Labour is ahead in the polls?

• Supply companies will seek to reduce their risk exposure to a freeze

• Inevitably they will have to try and fix volumes and price ahead of 2015/16

• This is very likely to push up wholesale gas and power prices…

• ….just as world energy prices could be falling

• Would expose independent suppliers to potentially ruinous risk

• So costs to consumers are very likely to be higher than they otherwise would be

16This report is prepared solely for the use of Broking Ideas of Liberum

The impact of freezing UK energy prices

The Affordability Crisis

• UK government policy, with all-party support, is consciously and specifically designed to increase the unit cost of energy

• Policy makers forecast that unit cost increases will be offset by energy efficiency gains

• Policy makers expect the world to face rising fossil fuel and/or carbon prices over the coming decades

• Therefore UK/EU energy policy will, in the long run, deliver lower-cost energy compared with a fossil-fuel based system

• So policy makers think the affordability crises will resolve itself in the long term. But…

• …policy makers recognise that costs to consumers may rise during the transition phase

• Very big risk that assumptions on energy efficiency and world prices prove to be wrong

• Therefore affordability crises might last a lot longer than expected and/or not resolve itself in the long term

• In reality there are only two potential solutions:a. Rebalance energy policy to reduce cost pressures or… b. Convince the British public that these costs are a price worth paying

Everything else is kicking the can down the road

17This report is prepared solely for the use of Broking Ideas of Liberum

Disclaimer

The impact of freezing UK energy prices

This material is the commercial property of Liberum and may not be disclosed or distributed to any third party without the express permission of Liberum. You shall not remove or modify any disclaimer or copyright or trademark notice contained in any Material. If you have received this material in error, please immediately notify the sender and destroy the material.This Material is for information only and it should not be regarded as an offer to sell or a solicitation of an offer to buy. It is based on current public information and/or from sources which Liberum believes to be reliable, but the accuracy, completeness, timeliness or correct sequencing of the information included herein cannot be guaranteed. Neither Liberum nor any source will be liable for the accuracy of, or availability of, such information or will have any duty to verify, correct, complete or update any material. Neither Liberum nor any source will be liable for any loss, cost, claim or damage (including direct, indirect or consequential damages or lost profits) arising out of or otherwise relating to any material or the use or access to or unavailability of any material. Any information or opinions contained herein are subject to change without notice. Unless stated otherwise, this material is not investment research or a research recommendation for the purposes of FCA rules or a research report under U.S. securities laws. It is provided on the understanding that Liberum is not acting in a fiduciary capacity and it is not a personal recommendation to you. The securities referred to may not be suitable for you and this material should not be relied upon in substitution for the exercise of independent judgement.Liberum and/or its officers, directors and employees may have or take positions in securities of companies mentioned in this communication (or in any related investment) and may from time to time dispose of any such positions. Liberum may act as a market maker in the securities of companies discussed in this communication (or in any related investments), may sell them or buy them from customers on a principal basis, and may also provide corporate finance or underwriting services for or relating to those companies, for which it is remunerated.

United Kingdom and the rest of Europe: This material has been prepared and issued by Liberum. Liberum is a trading name of Liberum Capital Limited, who are authorised and regulated by the Financial Conduct Authority (FCA) and a member of the London Stock Exchange. Ropemaker Place, Level 12, 25 Ropemaker Street, London EC2Y 9LY.Tel +44 (0)20 3100 2000 Fax +44 (0)20 3100 2299United States: This communication is distributed to US institutional investors by Liberum Inc, which is a member of FINRA & SIPC. 441 Lexington Avenue (15th Floor), New York, NY 10017, Tel +1 212 596 4800 Fax +1 212 596 4898.

18This report is prepared solely for the use of Broking Ideas of Liberum

![Benediktinerinnen- bzw. Birgittenkloster Altomünster · st. virgilii primus, confirmatus a. 1473 in ecclesia st. Jodoci in Lanczhuet, dedit [sic!] presentem liberum [sic!] ad monasterium](https://img.pdfslide.net/doc/110x75/5e1dc84bf5ad0c5f391c5128/benediktinerinnen-bzw-birgittenkloster-altomnster-st-virgilii-primus-confirmatus.jpg)