Embed Size (px)

Citation preview

2

Solar PV Manufacturing

A White Paper by EAI

3

Solar PV Manufacturing

A White Paper by EAI

Preface

These are exciting times in the solar PV sector. The rapidly falling PV system prices, the ever

increasing coal and oil prices, and the furious pace of PV production capacity addition

happening worldwide and ambitious governmental missions, have set the stage for an

exponential growth the of solar PV. The implication of these developments for the Indian solar

PV manufacturing sector is significant too.

This paper evaluates the diversification opportunities for Indian corporates keen on entering

the solar PV manufacturing sector. This includes both crystalline silicon and thin film

technologies.

The white paper is divided into threesections. The first section examines the global market

dynamics of the solar PV sector and the opportunities and challenges for this sector. This

section also provides an introduction to the prominent technologies used in solar PV.

In the second section, the different parts of the crystalline silicon solar PV value chain are

analysed (for both crystalline and thin films), with a view to provide insights on manufacturing

opportunities available in these segments. The status of India for each of these segments is

provided too. This section should help the reader in comparing the key industry dynamics

worldwide and in India for various elements of the value chain.

The third section provides the highlights and summary and also provides a framework to

enable Indian companies to decide on investing in solar PV manufacturing in India.

This report was prepared by Energy Alternatives India (EAI), a leader in the Indian renewable

energy consulting and research sector, with a specialised focus on solar. Our solar division is

one of the few teams in India that has prior expertise in having worked on all the segments

within the solar PV value chain.

The report was last updated in December 2011.

Narasimhan Santhanam

Cofounder and Director

EAI - Energy Alternatives India @ www.eai.in

[email protected], Mob: +91-98413-48117

4

Solar PV Manufacturing

A White Paper by EAI

5

Solar PV Manufacturing

A White Paper by EAI

Table of Contents

SECTION 1 – PV STATUS AND TRENDS 7

INTRODUCTION 9

Global Solar PV Installation Scenario 9

Global PV Manufacturing Scenario 12

PV Technologies 13

Key Differences between Crystalline Silicon and Thin Film Technology 14

Market Share of Different Technologies 15

Key Takeaways 16

SECTION 2 – INDIA SOLAR PV MANUFACTURING 17

KEY DRIVERS 19

MANUFACTURING OPTIONS 21

CRYSTALLINE SILICON 21

POLYSILICON 23

Major Factors Influencing Profitability 24

Global Market Scenario 24

Indian Scenario 25

Future Outlook 25

Conclusion 26

INGOT AND WAFER 27

Major Factors Influencing Profitability 28

Global Market Scenario 29

Indian Scenario 29

Future Outlook 29

Conclusion 30

CELLS 31

Major Factors Influencing Profitability 32

Global Market Scenario 32

Indian Scenario 32

Future Outlook 33

6

Solar PV Manufacturing

A White Paper by EAI

Conclusion 34

MODULES 35

Major Factors Influencing Profitability 36

Global Market Scenario 36

Indian Scenario 36

Future Outlook 37

Conclusion 39

CRYSTALLINE SILICON VALUE CHAIN COMPARISON 40

MANUFACTURING OPTIONS 41

THIN FILM PV 41

AMORPHOUS SILICON (A-SI) 43

Major Factors Influencing Profitability 43

Global Market Scenario 43

Indian Scenario 44

Future Outlook 44

Conclusion 45

CADMIUM TELLURIDE (CDTE) 46

Major Factors Influencing Profitability 46

Global Market Scenario 46

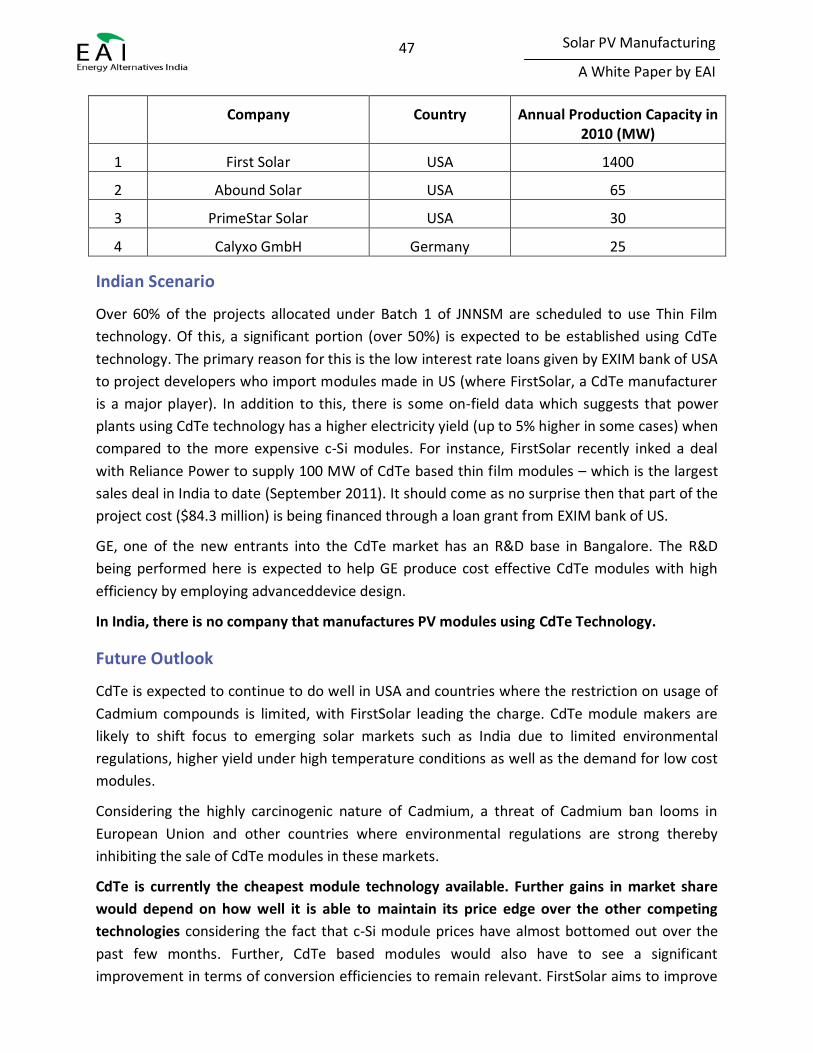

Indian Scenario 47

Future Outlook 47

Conclusion 48

COPPER INDIUM GALLIUM (DI)SELINIDE (CIGS) 49

Major Factors Influencing Profitability 49

Global Market Scenario 49

Indian Scenario 50

Future Outlook 50

Conclusion 50

THIN FILMS COMPARISON 51

SECTION 3 – SUITABLE PV MANUFACTURING OPPORTUNITY 53

7

Solar PV Manufacturing

A White Paper by EAI

Section 1 – PV Status and Trends

8

Solar PV Manufacturing

A White Paper by EAI

9

Solar PV Manufacturing

A White Paper by EAI

Introduction

Solar PV manufacturing is a very dynamic sector that has seen long term growth amidst lots of

demand shortages as well as excess production capacities. From being a technology intensive

sector based in Europe and USA, solar PV manufacturing has become more of a commoditized

business and has moved to lower cost production bases in China and other far-east Asian

countries. This shift in PV manufacturing has resulted in huge capacity expansions which have

led to significant drop in the price of solar PV systems. This cost reduction in turn has

accelerated the adaption of solar PV not only in rich countries like Germany, but also in

resource constrained countries in Africa.

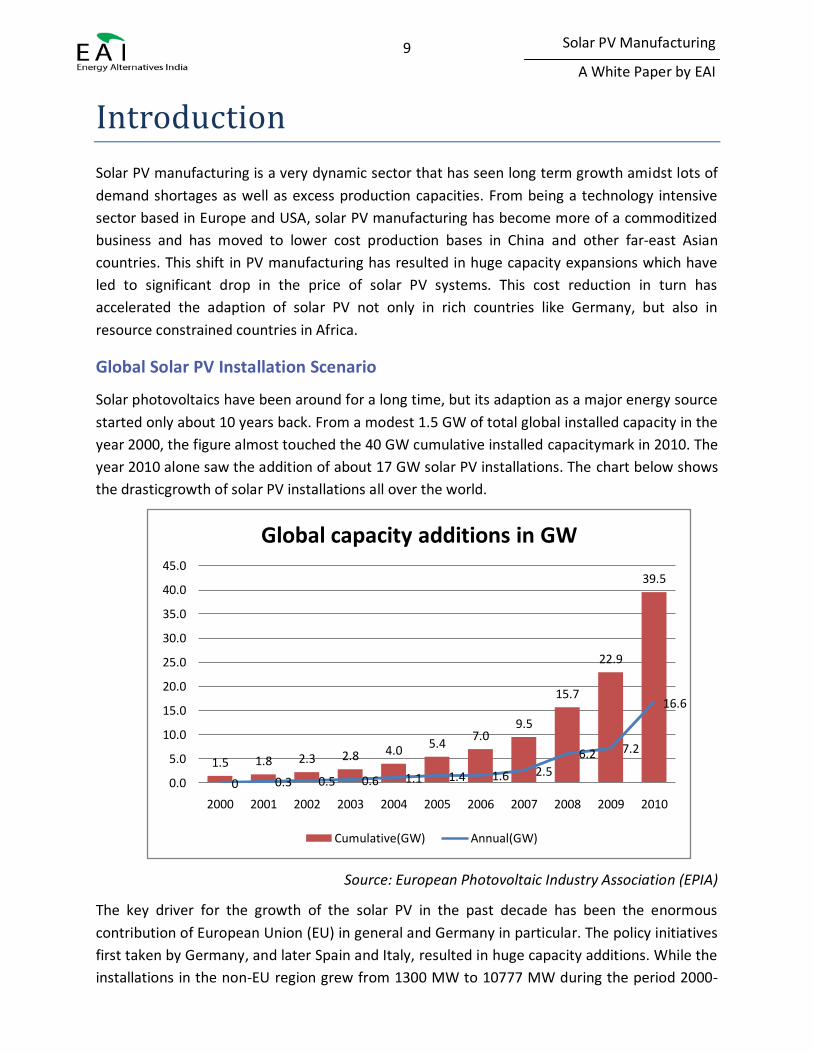

Global Solar PV Installation Scenario

Solar photovoltaics have been around for a long time, but its adaption as a major energy source

started only about 10 years back. From a modest 1.5 GW of total global installed capacity in the

year 2000, the figure almost touched the 40 GW cumulative installed capacitymark in 2010. The

year 2010 alone saw the addition of about 17 GW solar PV installations. The chart below shows

the drasticgrowth of solar PV installations all over the world.

Source: European Photovoltaic Industry Association (EPIA)

The key driver for the growth of the solar PV in the past decade has been the enormous

contribution of European Union (EU) in general and Germany in particular. The policy initiatives

first taken by Germany, and later Spain and Italy, resulted in huge capacity additions. While the

installations in the non-EU region grew from 1300 MW to 10777 MW during the period 2000-

1.5 1.8 2.3 2.8 4.05.4

7.09.5

15.7

22.9

39.5

0 0.3 0.5 0.6 1.1 1.4 1.6 2.5

6.2 7.2

16.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Global capacity additions in GW

Cumulative(GW) Annual(GW)

10

Solar PV Manufacturing

A White Paper by EAI

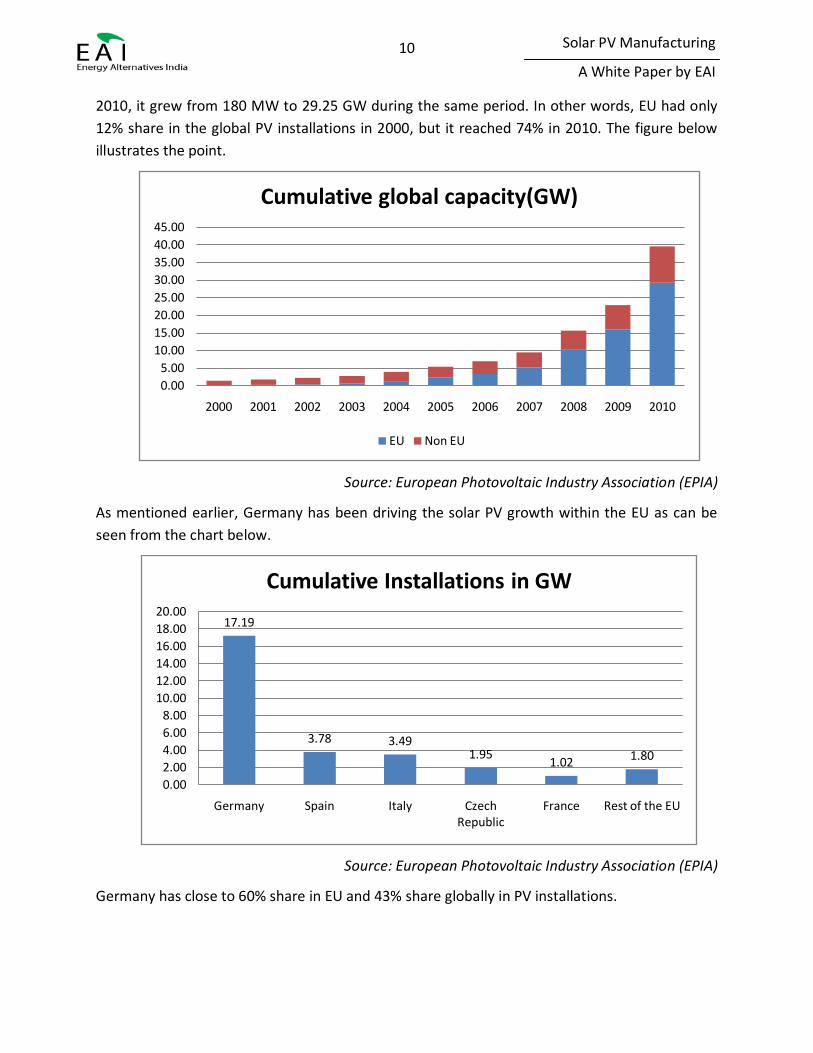

2010, it grew from 180 MW to 29.25 GW during the same period. In other words, EU had only

12% share in the global PV installations in 2000, but it reached 74% in 2010. The figure below

illustrates the point.

Source: European Photovoltaic Industry Association (EPIA)

As mentioned earlier, Germany has been driving the solar PV growth within the EU as can be

seen from the chart below.

Source: European Photovoltaic Industry Association (EPIA)

Germany has close to 60% share in EU and 43% share globally in PV installations.

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Cumulative global capacity(GW)

EU Non EU

17.19

3.78 3.491.95

1.021.80

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

Germany Spain Italy Czech Republic

France Rest of the EU

Cumulative Installations in GW

11

Solar PV Manufacturing

A White Paper by EAI

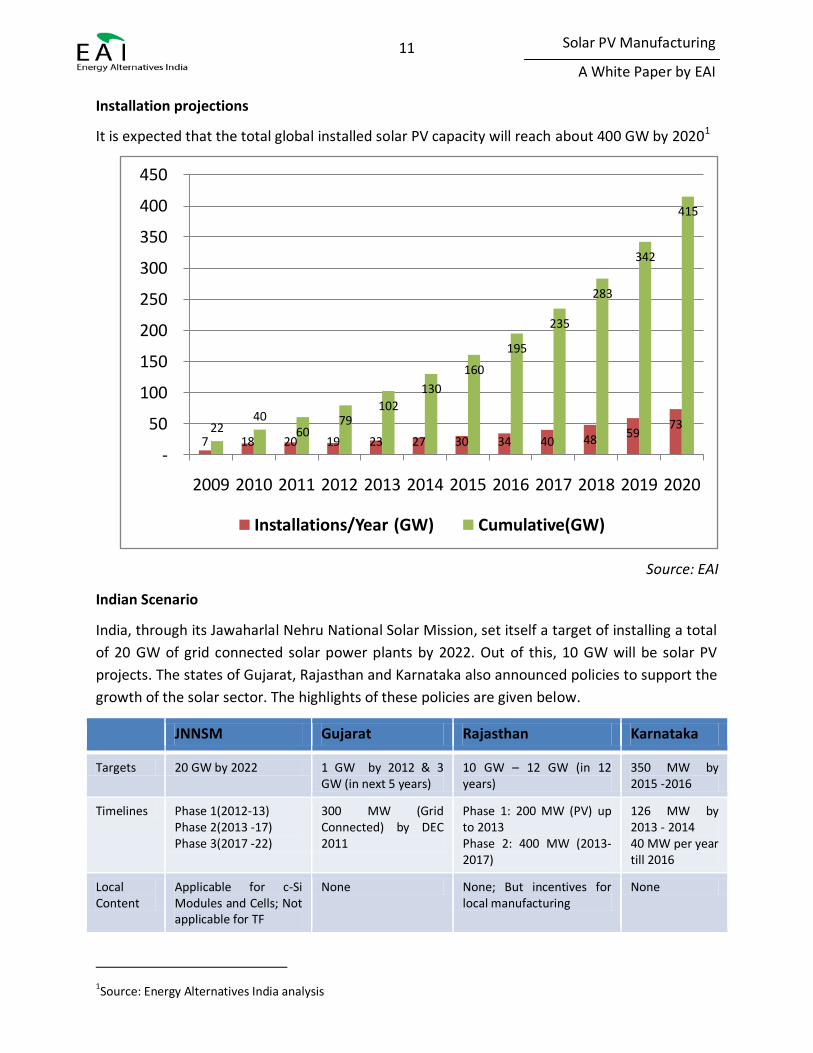

Installation projections

It is expected that the total global installed solar PV capacity will reach about 400 GW by 20201

Source: EAI

Indian Scenario

India, through its Jawaharlal Nehru National Solar Mission, set itself a target of installing a total

of 20 GW of grid connected solar power plants by 2022. Out of this, 10 GW will be solar PV

projects. The states of Gujarat, Rajasthan and Karnataka also announced policies to support the

growth of the solar sector. The highlights of these policies are given below.

JNNSM Gujarat Rajasthan Karnataka

Targets 20 GW by 2022 1 GW by 2012 & 3 GW (in next 5 years)

10 GW – 12 GW (in 12 years)

350 MW by 2015 -2016

Timelines Phase 1(2012-13) Phase 2(2013 -17) Phase 3(2017 -22)

300 MW (Grid Connected) by DEC 2011

Phase 1: 200 MW (PV) up to 2013 Phase 2: 400 MW (2013-2017)

126 MW by 2013 - 2014 40 MW per year till 2016

Local Content

Applicable for c-Si Modules and Cells; Not applicable for TF

None None; But incentives for local manufacturing

None

1Source: Energy Alternatives India analysis

7 18 20 19 23 27 30 34 40 4859

732240

6079

102

130

160

195

235

283

342

415

-

50

100

150

200

250

300

350

400

450

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Installations/Year (GW) Cumulative(GW)

12

Solar PV Manufacturing

A White Paper by EAI

Feed-in-

Tariff

Reverse Bidding :

Round 1 -Solar PV

Rs. 10.9 - 12.75/kWh

Rs. 15/kW (1st 12

years)

Rs. 5/kWh (13th

to

25th

year)

Reverse Bidding Rates: Up to 200 MW.

Rs. 14.50 /kWh

(max)

Current

Status

Phase 1 : 150 MW PV

allotted; 300 MW by

end of 2011

PPAs signed for about

1200 MW

Allotment in progress Allotment in

progress

Source: Various state policies, EAI

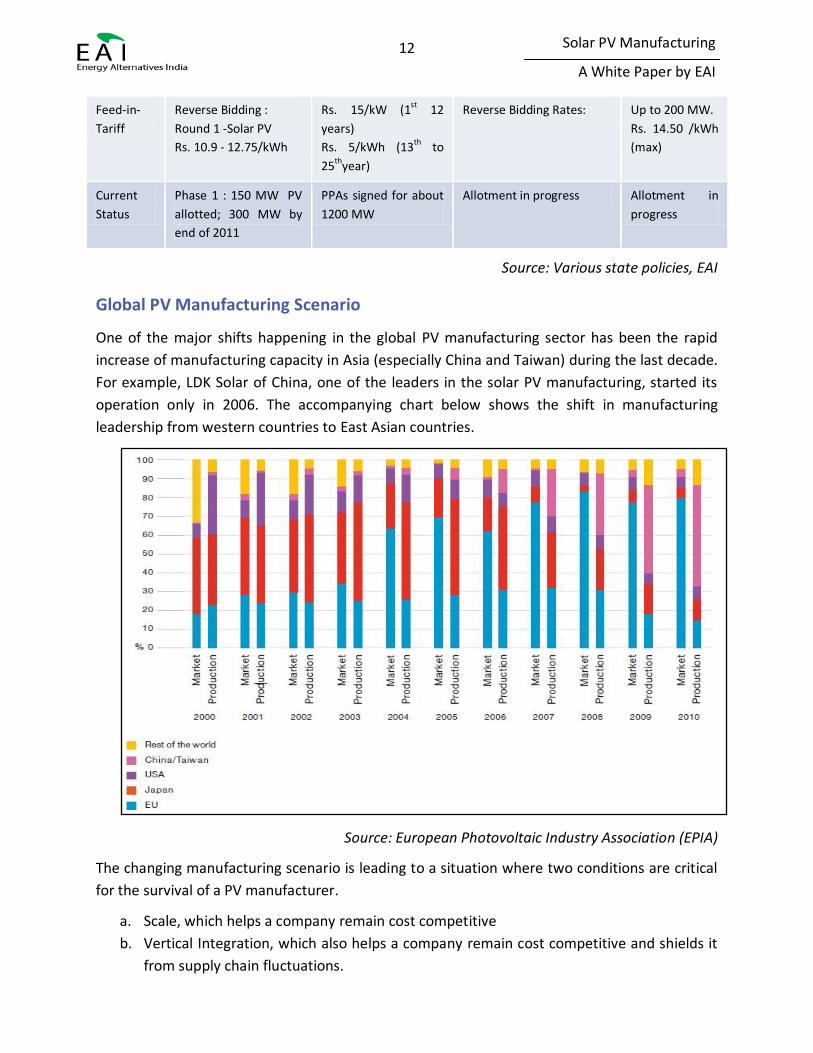

Global PV Manufacturing Scenario

One of the major shifts happening in the global PV manufacturing sector has been the rapid

increase of manufacturing capacity in Asia (especially China and Taiwan) during the last decade.

For example, LDK Solar of China, one of the leaders in the solar PV manufacturing, started its

operation only in 2006. The accompanying chart below shows the shift in manufacturing

leadership from western countries to East Asian countries.

Source: European Photovoltaic Industry Association (EPIA)

The changing manufacturing scenario is leading to a situation where two conditions are critical

for the survival of a PV manufacturer.

a. Scale, which helps a company remain cost competitive

b. Vertical Integration, which also helps a company remain cost competitive and shields it

from supply chain fluctuations.

13

Solar PV Manufacturing

A White Paper by EAI

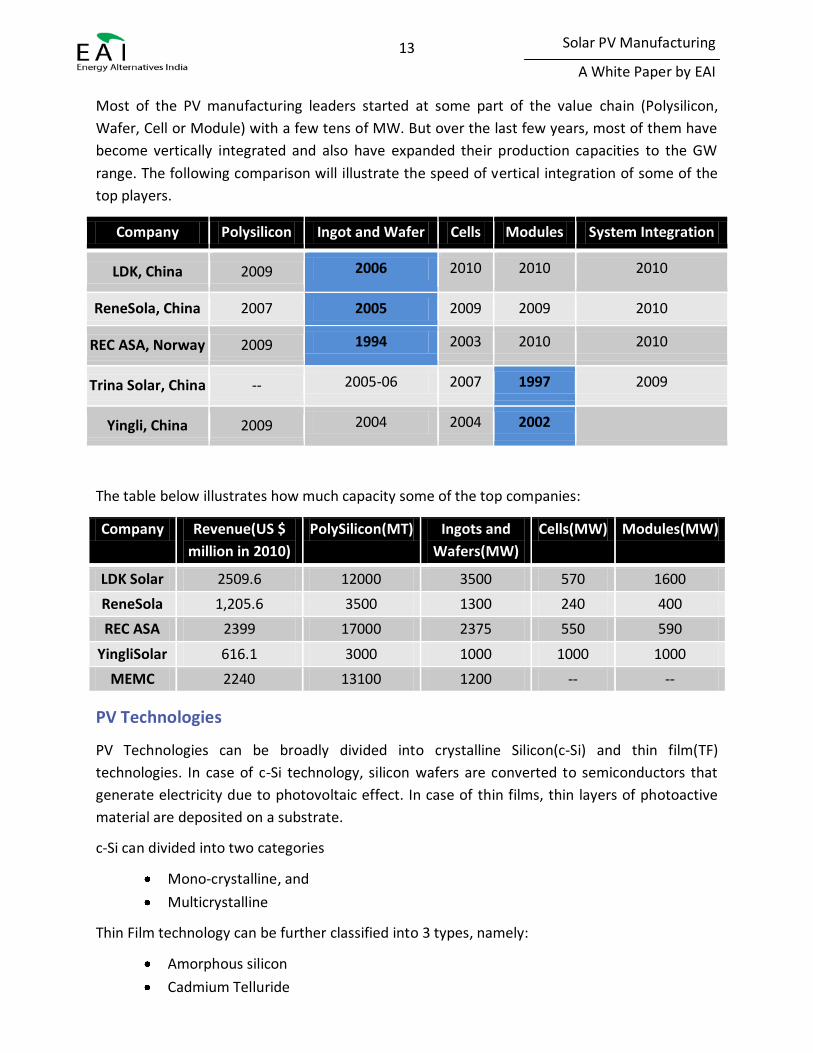

Most of the PV manufacturing leaders started at some part of the value chain (Polysilicon,

Wafer, Cell or Module) with a few tens of MW. But over the last few years, most of them have

become vertically integrated and also have expanded their production capacities to the GW

range. The following comparison will illustrate the speed of vertical integration of some of the

top players.

Company Polysilicon Ingot and Wafer Cells Modules System Integration

LDK, China 2009 2006 2010 2010 2010

ReneSola, China 2007 2005 2009 2009 2010

REC ASA, Norway 2009 1994 2003 2010 2010

Trina Solar, China -- 2005-06 2007 1997 2009

Yingli, China 2009 2004 2004 2002

The table below illustrates how much capacity some of the top companies:

Company Revenue(US $

million in 2010)

PolySilicon(MT) Ingots and

Wafers(MW)

Cells(MW) Modules(MW)

LDK Solar 2509.6 12000 3500 570 1600

ReneSola 1,205.6 3500 1300 240 400

REC ASA 2399 17000 2375 550 590

YingliSolar 616.1 3000 1000 1000 1000

MEMC 2240 13100 1200 -- --

PV Technologies

PV Technologies can be broadly divided into crystalline Silicon(c-Si) and thin film(TF)

technologies. In case of c-Si technology, silicon wafers are converted to semiconductors that

generate electricity due to photovoltaic effect. In case of thin films, thin layers of photoactive

material are deposited on a substrate.

c-Si can divided into two categories

Mono-crystalline, and

Multicrystalline

Thin Film technology can be further classified into 3 types, namely:

Amorphous silicon

Cadmium Telluride

14

Solar PV Manufacturing

A White Paper by EAI

Cadmium Indium Gallium (di)selinide

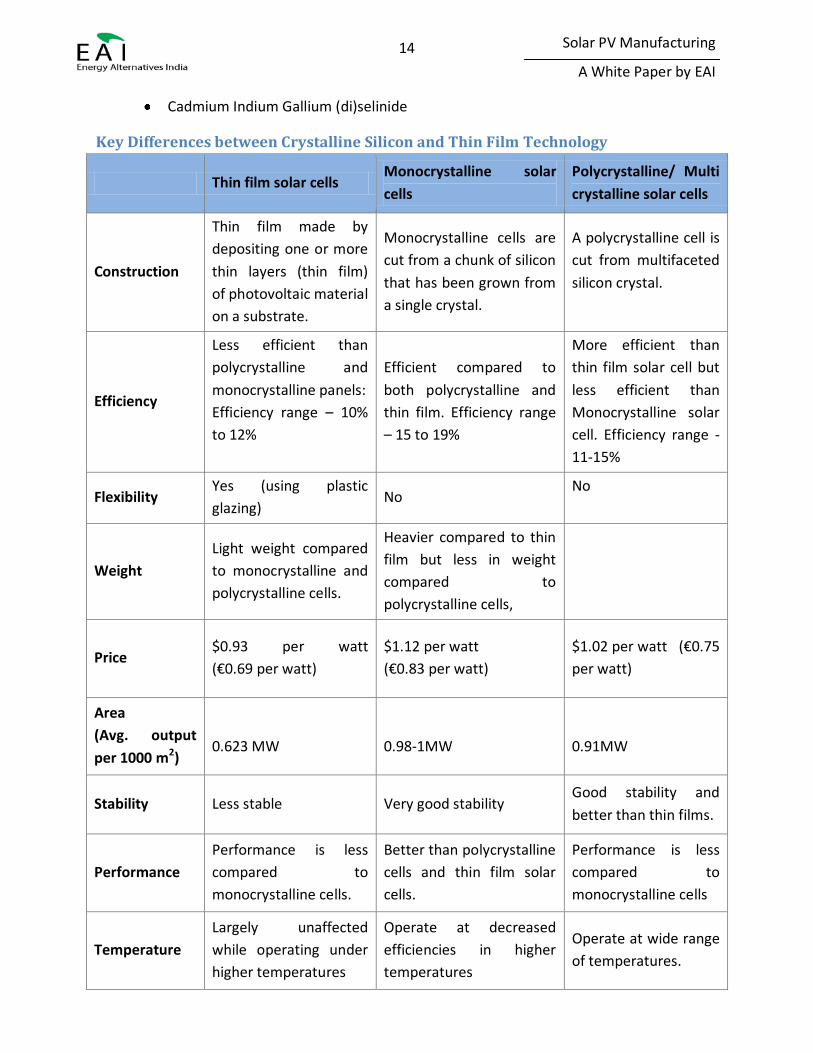

Key Differences between Crystalline Silicon and Thin Film Technology

Thin film solar cells Monocrystalline solar

cells

Polycrystalline/ Multi

crystalline solar cells

Construction

Thin film made by

depositing one or more

thin layers (thin film)

of photovoltaic material

on a substrate.

Monocrystalline cells are

cut from a chunk of silicon

that has been grown from

a single crystal.

A polycrystalline cell is

cut from multifaceted

silicon crystal.

Efficiency

Less efficient than

polycrystalline and

monocrystalline panels:

Efficiency range – 10%

to 12%

Efficient compared to

both polycrystalline and

thin film. Efficiency range

– 15 to 19%

More efficient than

thin film solar cell but

less efficient than

Monocrystalline solar

cell. Efficiency range -

11-15%

Flexibility Yes (using plastic

glazing) No

No

Weight

Light weight compared

to monocrystalline and

polycrystalline cells.

Heavier compared to thin

film but less in weight

compared to

polycrystalline cells,

Price $0.93 per watt

(€0.69 per watt)

$1.12 per watt

(€0.83 per watt)

$1.02 per watt (€0.75

per watt)

Area

(Avg. output

per 1000 m2)

0.623 MW

0.98-1MW

0.91MW

Stability Less stable Very good stability Good stability and

better than thin films.

Performance

Performance is less

compared to

monocrystalline cells.

Better than polycrystalline

cells and thin film solar

cells.

Performance is less

compared to

monocrystalline cells

Temperature

Largely unaffected

while operating under

higher temperatures

Operate at decreased

efficiencies in higher

temperatures

Operate at wide range

of temperatures.

15

Solar PV Manufacturing

A White Paper by EAI

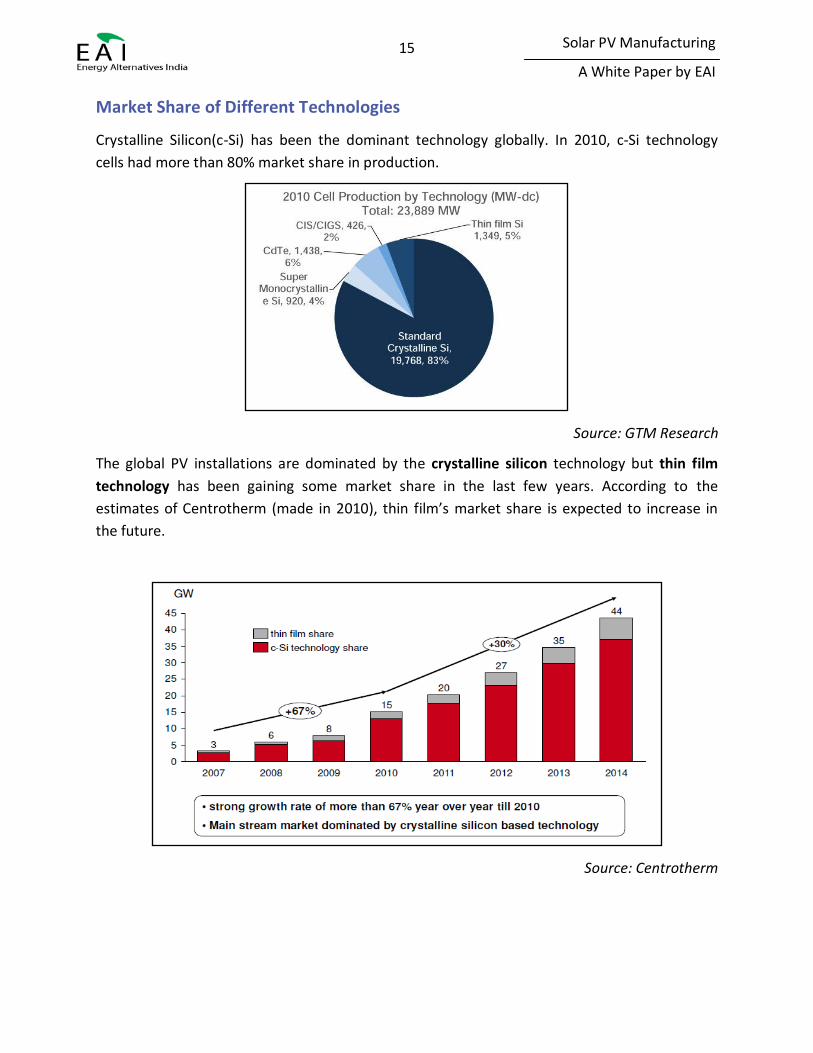

Market Share of Different Technologies

Crystalline Silicon(c-Si) has been the dominant technology globally. In 2010, c-Si technology

cells had more than 80% market share in production.

Source: GTM Research

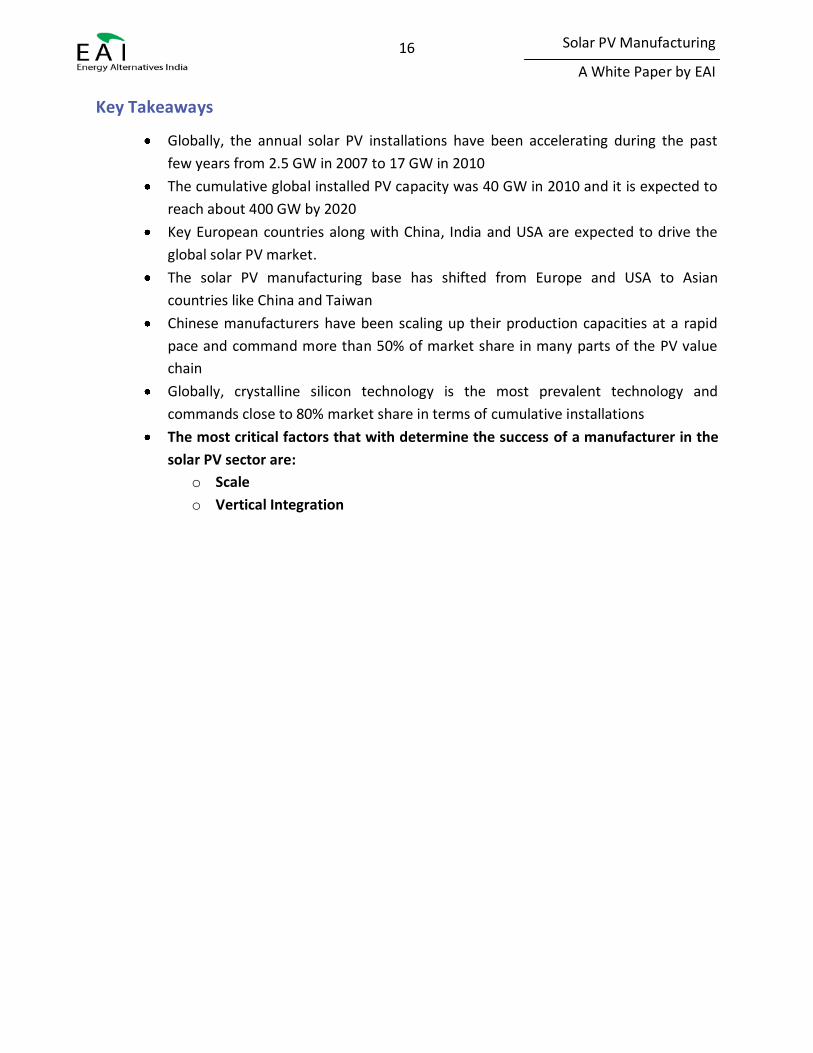

The global PV installations are dominated by the crystalline silicon technology but thin film

technology has been gaining some market share in the last few years. According to the

estimates of Centrotherm (made in 2010), thin film’s market share is expected to increase in

the future.

Source: Centrotherm

16

Solar PV Manufacturing

A White Paper by EAI

Key Takeaways

Globally, the annual solar PV installations have been accelerating during the past

few years from 2.5 GW in 2007 to 17 GW in 2010

The cumulative global installed PV capacity was 40 GW in 2010 and it is expected to

reach about 400 GW by 2020

Key European countries along with China, India and USA are expected to drive the

global solar PV market.

The solar PV manufacturing base has shifted from Europe and USA to Asian

countries like China and Taiwan

Chinese manufacturers have been scaling up their production capacities at a rapid

pace and command more than 50% of market share in many parts of the PV value

chain

Globally, crystalline silicon technology is the most prevalent technology and

commands close to 80% market share in terms of cumulative installations

The most critical factors that with determine the success of a manufacturer in the

solar PV sector are:

o Scale

o Vertical Integration

17

Solar PV Manufacturing

A White Paper by EAI

Section 2 –India Solar PV Manufacturing

18

Solar PV Manufacturing

A White Paper by EAI

19

Solar PV Manufacturing

A White Paper by EAI

Key Drivers

Market

The solar PV segment in India is expected to achieve very high growth rates over the course of

the next few years. While currently, India contributes relatively little by way of manufacturing

in solar PV value chain; this contribution is expected to increase significantly. It has been

predicted that even under the worst case scenario, India would see installations of about 500

MW in 2012.

Drivers for PV Manufacturing in India

The following are drivers for accelerated investments in the solar PV manufacturing ecosystem

Increasing demand for solar power

Domestic content requirements

Requirement of technology tailored to Indian conditions

Priority sector lending

Avoiding the volatility of foreign currency borrowing

Growing Demand

The recent announcement of winners revealed something that was totally unexpected – Solar

has almost attained grid parity in India. The lowest quoted price under the reverse bidding was

Rs. 7.49 per kWh(15 cents per kWh),suggesting that the capital cost for solar has gone down

significantly – falling from the previous high of about Rs. 14 Crore per MW to possibly Rs. 9

Crore per MW. With solar coming within the reach of the common man, it is highly likely that

the levels of capacity addition will be far higher than expected. Considering the future

exponential increase in demand, local manufacturers can be assured of good off take

Domestic Content Requirements

The National Solar Mission currently mandates that for power plants using c-Si technology, both

the c-Si cells and modules would have to be manufactured in India. States such as Rajasthan

have started providing incentives to manufacturers who are involved further upstream i.e.

they provide incentives for manufacturers producing everything from wafers to modules. With

states having taken this initiative, it is very likely that the National Solar Mission would follow

suit.

It is also likely that the domestic content requirements would be enforced on other

technologies (Thin Films, CPV etc.). The likely reason that it has not been enforced currently is

to ensure that technology transfer takes place from abroad. When domestic

20

Solar PV Manufacturing

A White Paper by EAI

manufacturers/suppliers start to exhibit significant expertise in this area, it is likely that the

domestic requirements would be enforced.

Requirement of Tailored Technology

Most of the PV technology in use today is tailored to the western markets and their climatic

conditions. This is the reason why thin film modules are performing better in India owing to

their lower temperature coefficients. With sufficient R&D, factors like temperature degradation

can be lowered to better suit the hotter Indian climate. For instance, currently, CdTe based

modules offer lower temperature coefficients (-0.25% per K) compared to others but the use of

carcinogenic materials may limit its potential. With significant R&D, other technologies such as

c-Si and CIGS could be adapted to achieve similar performance levels.

These minor improvements in technical characteristics would result in modules that perform

better under Indian scenarios, thus providing higher kWh/kW yields. This would act as the USP

for indigenous modules leading to higher demand provided the product is marketed properly.

Priority Sector Lending

Presently, most of the modules used are thin films imported from abroad (primarily USA). The

drivers for this are two fold

No domestic content requirement for thin film modules under the National Solar

Mission

Availability of financing at low interest rates from foreign institutions (i.e. EXIM Bank,

OPIC etc.)

Low interest rates are can significantly impact projected costs and returns. It is likely that the

government would learn from this and offer low interest rate loans to both Indian developers

and domestic manufacturers to meet the increased demand that this would create (a la China).

Avoiding Volatility in Foreign Borrowing

The problem with importing modules is that they are all charged at international rates (read:

Dollars). With the Rupee currently depreciating rapidly, it would make more sense to not hedge

it against the dollar or other foreign currencies. This provides a significant reason for

developers to source modules manufactured locally.

21

Solar PV Manufacturing

A White Paper by EAI

Manufacturing Options Crystalline Silicon

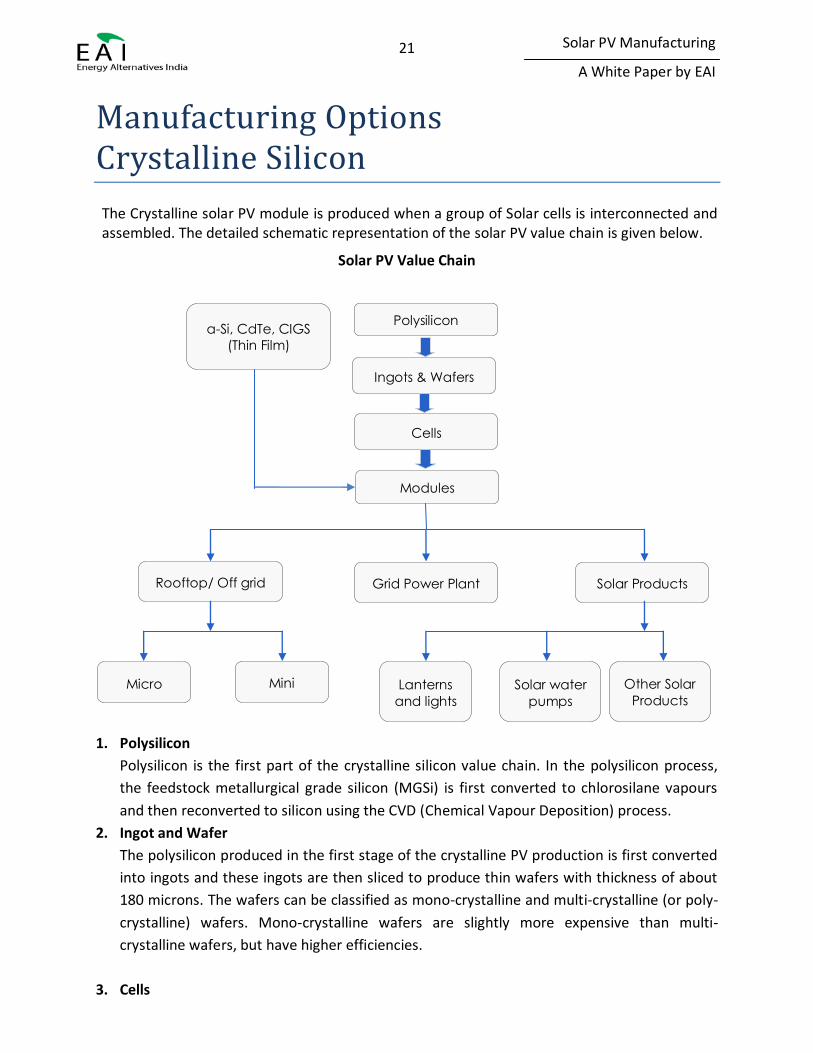

The Crystalline solar PV module is produced when a group of Solar cells is interconnected and assembled. The detailed schematic representation of the solar PV value chain is given below.

Solar PV Value Chain

1. Polysilicon

Polysilicon is the first part of the crystalline silicon value chain. In the polysilicon process,

the feedstock metallurgical grade silicon (MGSi) is first converted to chlorosilane vapours

and then reconverted to silicon using the CVD (Chemical Vapour Deposition) process.

2. Ingot and Wafer

The polysilicon produced in the first stage of the crystalline PV production is first converted

into ingots and these ingots are then sliced to produce thin wafers with thickness of about

180 microns. The wafers can be classified as mono-crystalline and multi-crystalline (or poly-

crystalline) wafers. Mono-crystalline wafers are slightly more expensive than multi-

crystalline wafers, but have higher efficiencies.

3. Cells

Polysilicon

Ingots & Wafers

Cells

Modules

Rooftop/ Off grid Grid Power Plant Solar Products

Micro Mini Lanterns

and lights

Solar water

pumps

Other Solar

Products

a-Si, CdTe, CIGS

(Thin Film)

22

Solar PV Manufacturing

A White Paper by EAI

The silicon wafer is converted to a photovoltaic material in the cell manufacturing process.

The material used and the production process determines the output cell efficiencies. The c-

Si silicon cells available in the market have efficiencies upto 25% as of August 2011.

4. Modules

The solar PV module is the end product which is used to generate power for 20-25 years.

The PV module production is essentially an assembly process wherein cells are

interconnected and laminated to give the requisite power rating. The efficiency of the

module depends on the type of cell used and will be 2-3% points less than the efficiency of

the cells used.

23

Solar PV Manufacturing

A White Paper by EAI

Polysilicon

Polysilicon is a common feedstock for both the solar industry and the electronics industry. The

level of purity of the polysilicon determines how it is classified. Solar grade polysilicon has a

purity level of 99.999999% (6N) whereas semiconductor/electronics grade polysilicon has a

purity level of 99.999999999 % (9N). According to WackerChemie, the polysilicon market in

2010 was €6.8 Billion out of which solar sector constitutes 75% and semiconductor market

constitutes the rest. The polysilicon demand in the solar sector has been growing at 30%

annually while the same for the semiconductor sector has been growing at an annual growth

rate of 6%2.

As mentioned earlier, polysilicon is produced from Metallurgical Grade Silicon (MGSi) using the

CVD process. The commercially popular production technologies are

o TCS Siemens using hydrochlorination

o TCS Siemens using chlorination & converters

o Silane Siemens

o SilaneFluidizedBed Reactor

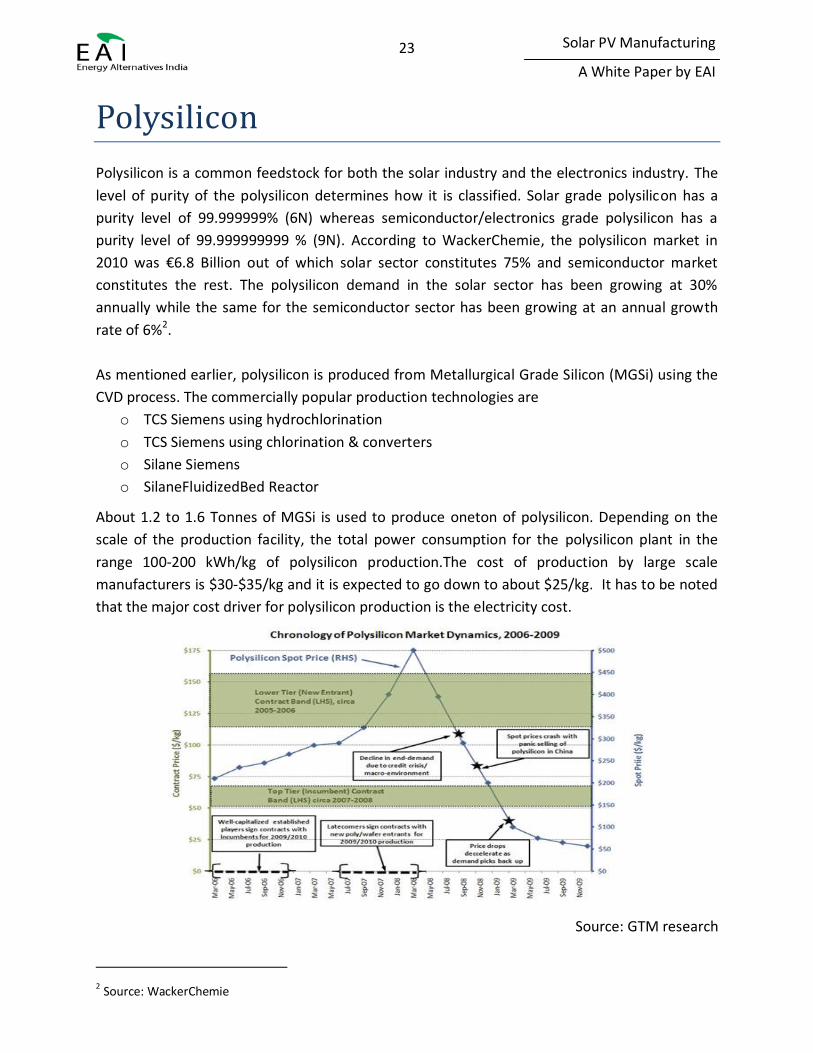

About 1.2 to 1.6 Tonnes of MGSi is used to produce oneton of polysilicon. Depending on the

scale of the production facility, the total power consumption for the polysilicon plant in the

range 100-200 kWh/kg of polysilicon production.The cost of production by large scale

manufacturers is $30-$35/kg and it is expected to go down to about $25/kg. It has to be noted

that the major cost driver for polysilicon production is the electricity cost.

Source: GTM research

2 Source: WackerChemie

24

Solar PV Manufacturing

A White Paper by EAI

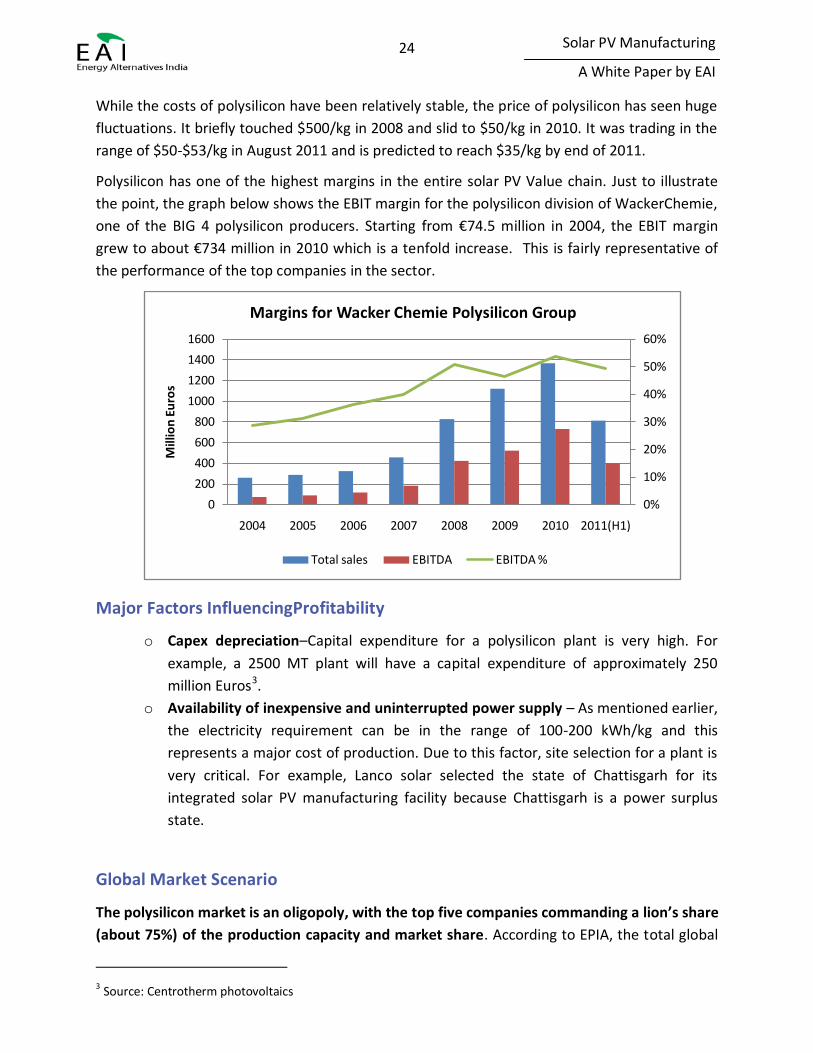

While the costs of polysilicon have been relatively stable, the price of polysilicon has seen huge

fluctuations. It briefly touched $500/kg in 2008 and slid to $50/kg in 2010. It was trading in the

range of $50-$53/kg in August 2011 and is predicted to reach $35/kg by end of 2011.

Polysilicon has one of the highest margins in the entire solar PV Value chain. Just to illustrate

the point, the graph below shows the EBIT margin for the polysilicon division of WackerChemie,

one of the BIG 4 polysilicon producers. Starting from €74.5 million in 2004, the EBIT margin

grew to about €734 million in 2010 which is a tenfold increase. This is fairly representative of

the performance of the top companies in the sector.

Major Factors InfluencingProfitability

o Capex depreciation–Capital expenditure for a polysilicon plant is very high. For

example, a 2500 MT plant will have a capital expenditure of approximately 250

million Euros3.

o Availability of inexpensive and uninterrupted power supply – As mentioned earlier,

the electricity requirement can be in the range of 100-200 kWh/kg and this

represents a major cost of production. Due to this factor, site selection for a plant is

very critical. For example, Lanco solar selected the state of Chattisgarh for its

integrated solar PV manufacturing facility because Chattisgarh is a power surplus

state.

Global Market Scenario

The polysilicon market is an oligopoly, with the top five companies commanding a lion’s share

(about 75%) of the production capacity and market share. According to EPIA, the total global

3 Source: Centrotherm photovoltaics

0%

10%

20%

30%

40%

50%

60%

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008 2009 2010 2011(H1)

Mill

ion

Eu

ros

Margins for Wacker Chemie Polysilicon Group

Total sales EBITDA EBITDA %

25

Solar PV Manufacturing

A White Paper by EAI

polysilicon production capacity was 350,000 MT in 2010 which is expected to rise to 370,000

MT in 2011. Among the top 10 companies, five companies (Hemlock, WackerChemie, OCI,

Tokuyama, Daqo) are pure play Polysilicon producers, but are mostly present in other chemicals

production. Three players (GCL, MEMC, M.Seteck) also produce wafers a well. Two other

companies (LDK, REC) are fully integrated with their presence in all parts of the crystalline

silicon PV value chain.

Indian Scenario

Currently, no Indian manufacturer makes polysilicon on a large scale. However, to meet the

large scale uptake of solar PV installations projected under JNNSM, about 15,000 tons per

annum of polysilicon production would be required assuming domestic content requirements

stipulated by JNNSM might be extended beyond cell/module to wafer/polysilicon.

Large scale production of polysilicon in India would also depend on how the issue of

uninterrupted power supply with very little voltage fluctuations is addressed as this is a critical

factor that affects cost of production of polysilicon. In addition, polysilicon production, being a

capital intensive process would require low interest rate loans (which is currently hard to

procure within the country).

Companies such Lanco Solar, BHEL and Birla Surya have announced their plans to set up

polysilicon plants in India. LancoSolar’s plant is expected to produce 11 N (semiconductor

grade) polysilicon, while BHEL’s tie up with BEL is expected to result in an integrated

manufacturing facilitythat produces 10,000 tons of polysilicon per annum.

Future Outlook

Due to the increase in the total production capacity, it is expected the polysilicon market will change drastically. Some of the expected changes are

Polysilicon spot price expected to drop to $35/kg and more by end of 2011.

Cost of production to drop to $20/kg.

However, there are other factors that might actually counteract the above trends. These

include:

Purity becomes important. More and more customers are demanding 9N purity polysilicon

because, higher the purity of the polysilicon, higher the efficiencies that can be achieved at

the module level.

Shortage of metallurgical grade silicon. Centrotherm Photovoltaics AG expects that the

MGSi production capacity will face difficulty in keeping pace with the polysilicon demand.

This could lead to a shortage of MGSi in 2014. In this scenario, the polysilicon price is likely

to go up.

Upgraded Metallurgical Silicon (UMG) gaining market share. With the advancements in

production technology, some of the companies are betting that they will be able to produce

26

Solar PV Manufacturing

A White Paper by EAI

UMG at less than $15/kg at quality levels comparable to those of polysilicon. Some of them

expect to capture about 30% market share by 20164

Conclusion

Polysilicon industry is going through a phase of massive capacity expansion by the entrenched

incumbents. This capacity addition, while creates bigger barriers to entry for newer players,

also leads to economies of scale and price reduction. This price reduction is passed through in

the value chain and will result in lower PV module prices.

For a company evaluating polysilicon manufacturing opportunity, it is important to

ensure the following:

a. Production capacity should be substantially large as this results in low polysilicon

price which in turn ensures that the product is cost competitive in the global market

against the offerings from the entrenched market giants

b. Ensuring cheap and uninterrupted power supply is a critical factor for successas

price of electricity forms a major chunk (26%)of production cost while

uninterrupted power ensures efficient polysilicon production

c. Along the c-Si value chain, CAPEX depreciation is highest for polysilicon (45%). Thus

access to low cost of capital should be ensured to remain cost competitive

4 Source: Photon International

27

Solar PV Manufacturing

A White Paper by EAI

Ingot and Wafer

Multicrystalline modules dominated in the c-Si space with a 68% market share as against 32%

market share for monocrystalline modules in 20105. However, with the increasing demand for

high efficiency PV modules, it is likely that mono-crystalline technology will become more

prominent in the near future.

Production of Ingots and Wafers are typically done together in the same plant, even though

there are companies that specialize in the manufacturing of either ingots or wafers. The most

common commercial wafer production technologies are

Czochralski crystallization production process – For Mono-crystalline Ingot

manufacturing

Bricking/solidification - Multi-crystalline Ingot manufacturing

Wafer slicing(using wire saws) – For shaping and slicing the ingots into thin wafers

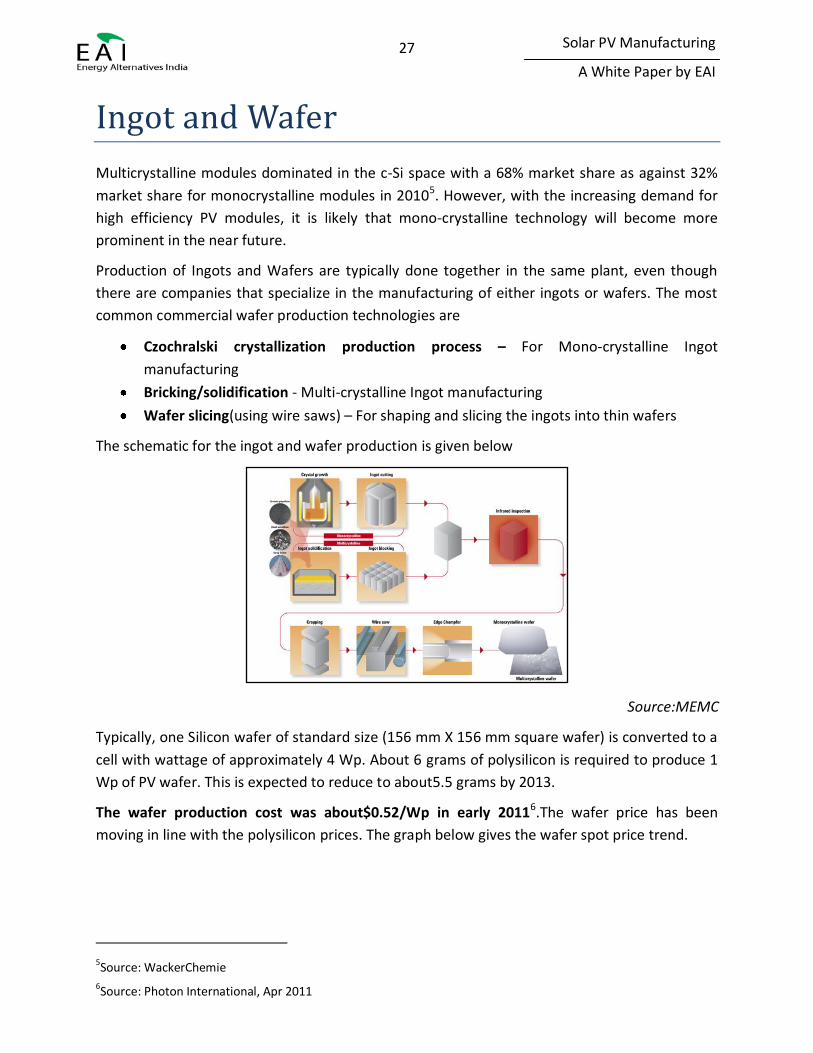

The schematic for the ingot and wafer production is given below

Source:MEMC

Typically, one Silicon wafer of standard size (156 mm X 156 mm square wafer) is converted to a

cell with wattage of approximately 4 Wp. About 6 grams of polysilicon is required to produce 1

Wp of PV wafer. This is expected to reduce to about5.5 grams by 2013.

The wafer production cost was about$0.52/Wp in early 20116.The wafer price has been

moving in line with the polysilicon prices. The graph below gives the wafer spot price trend.

5Source: WackerChemie

6Source: Photon International, Apr 2011

28

Solar PV Manufacturing

A White Paper by EAI

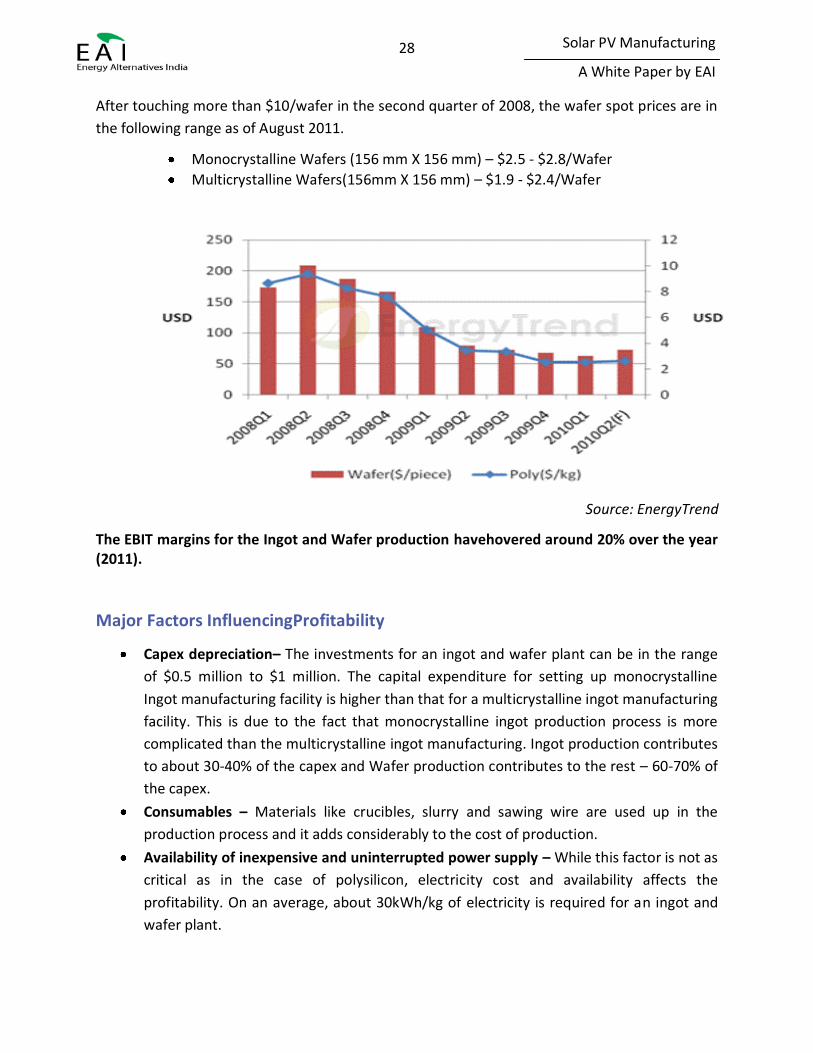

After touching more than $10/wafer in the second quarter of 2008, the wafer spot prices are in

the following range as of August 2011.

Monocrystalline Wafers (156 mm X 156 mm) – $2.5 - $2.8/Wafer

Multicrystalline Wafers(156mm X 156 mm) – $1.9 - $2.4/Wafer

Source: EnergyTrend

The EBIT margins for the Ingot and Wafer production havehovered around 20% over the year (2011).

Major Factors InfluencingProfitability

Capex depreciation– The investments for an ingot and wafer plant can be in the range

of $0.5 million to $1 million. The capital expenditure for setting up monocrystalline

Ingot manufacturing facility is higher than that for a multicrystalline ingot manufacturing

facility. This is due to the fact that monocrystalline ingot production process is more

complicated than the multicrystalline ingot manufacturing. Ingot production contributes

to about 30-40% of the capex and Wafer production contributes to the rest – 60-70% of

the capex.

Consumables – Materials like crucibles, slurry and sawing wire are used up in the

production process and it adds considerably to the cost of production.

Availability of inexpensive and uninterrupted power supply – While this factor is not as

critical as in the case of polysilicon, electricity cost and availability affects the

profitability. On an average, about 30kWh/kg of electricity is required for an ingot and

wafer plant.

29

Solar PV Manufacturing

A White Paper by EAI

Global Market Scenario

According to EPIA, the total global production capacity was between 30-35 GW in 2010. Out of

this, more than 55% capacity is in China. Of the top 10 Wafer manufacturers, twocompanies

(Pillar-Spain, Green Energy Technology-Taiwan) are independent wafer manufacturers.

Twocompanies (GCL Poly, MEMC) produce polysilicon as well, whereas onecompany (Trina

Solar) is fully integrated except for polysiliconproduction. Five companies (LDK Solar,

Solarworld, REC, Renesola, Yingli) are fully integrated.

Indian Scenario

Currently, there are no Indian companies that manufacture c-Si waferson a large scale. It is

estimated that an annual production of about 2000 MW would be required to meet the

proposed installation capacities under the National Solar Mission.

About 60% of the cost of production of wafers can be attributed to the raw materials used

(including polysilicon). The fact that polysilicon cannot be sourced locally is a major source of

concern that discourages setting up of wafer manufacturing units within the country. Thus

scaling up the domestic polysilicon production would be required for proliferation of wafer

manufacturing units. Failing to do this, companies would have to resort to setting up integrated

manufacturing units (i.e. producing both polysilicon and wafer) to ensure that they remain cost

competitive.

As mentioned earlier, Lanco Solar and Birla Surya have announced plans to set up integrated c-

Si PV plants. Carborundum Universal (part of Murugappa Group) had also announced its

intention to enter this segment. The fully integrated Lanco Solar production line is expected to

produce about 250 MW of wafers per year catering to both the monocrystalline as well as

multicrystalline markets.

Future Outlook

Globally, many cell manufacturers are backward integrating by getting into wafer production. It

is expected that standalone wafer manufacturing companies will find it difficult to compete and

will disappear. It is also expected that mono-crystalline wafers will become more popular

because of the increasing requirement for higher efficiency modules.

The price of wafers will also keep reducing in tandem with the polysilicon prices. The price

drops are expected to be so large that some of the big name wafer manufacturers are

contemplating a complete shutdown of their wafer manufacturing facilities. For instance, one

of the big name wafer manufacturer – REC shutdown their multicrystalline solar wafer plant in

Glomfjord, Norway (775 MW production capacity) in October 2011, followed by the temporary

closure of part of its 650 MW multicrystalline wafer facility in Herøya, Norway(expected to be

closed in December 2011) citing a 30% drop in wafer prices over the year.

30

Solar PV Manufacturing

A White Paper by EAI

Other wafer manufacturers, like ReneSola, are striving to achieve cost of production of less

than $0.2/Wp by end of 2011 to counteract the bottoming wafer prices. The cost reductions are

expected to be achieved using more efficient manufacturing processes (reducing the amount of

electricity required for production and reducing waste) as well as lowering wafer thickness

using advanced sawing techniques over the next few years.

It is worth noting that wafer inventory levels have continued to decrease over the year. This can

be attributed to the fact that small and medium scale manufacturers are ceasing production

while the global wafer demand is met almost entirely by the inventory backlog that the large

scale manufacturers currently have. This suggests that the wafer price is expected to be

relatively stable for the immediate futurethereby ensuring that the EBIT margins remain fairly

stable.

Conclusion

With the improved manufacturing processes that reduce material losses, reduce electricity

consumption and improve the utilization of consumables, the prices of wafers are expected to

go down further. Together with the drop in polysilicon prices, this wafer price drop will

contribute to c-Si PV system price drop.

For a new entrant to the sector, the following key things need to be kept in mind.

a. It will be challenging for a stand-alone wafer manufacturer. After establishing the

ingot and wafer business, it might become imperative to vertically integrate either

forward cell manufacturing or backward to polysilicon manufacturing (or both)

b. Scale of the installation is critical, which will help to

i. Reduce the production cost

ii. Have a better bargaining power in sourcing polysilicon and selling wafers

c. Cheap and uninterrupted power supply is another critical success driver

31

Solar PV Manufacturing

A White Paper by EAI

Cells

The solar cell manufacturing process has three main stages

After removing any surface damages, the silicon wafers are first treated with a dopant

(typically phosphorous) to create a photoactive p/n junction.

An anti-reflective coating is applied to the front side of the wafer to increase the

absorption of sunlight by the cells.

In the next stage known as metallization, narrow contact fingers and two or three wider

strips (“bus bars”) perpendicular to the contact fingers are printed on the front side. On

the back side, bus bars are applied and the back surface is imprinted with Aluminium.

The wafer is then dried and thermally fired (“sintered”) to ensure good electrical contact with

the Silicon.

Excluding the feedstock (Wafer), the processing cost for cells is in the range of $0.25/Wp –

$0.4/Wp. Another major cost in cell manufacturing is the R&D expense incurred on

continuously improving the solar cell efficiencies.

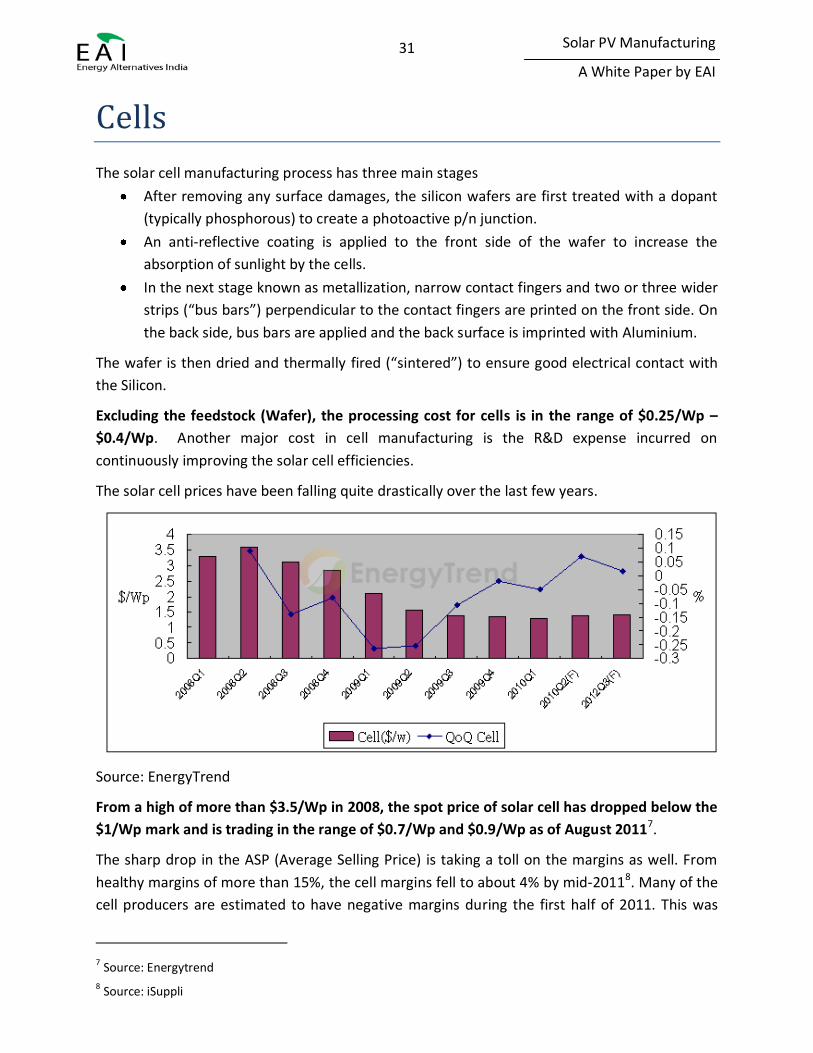

The solar cell prices have been falling quite drastically over the last few years.

Source: EnergyTrend

From a high of more than $3.5/Wp in 2008, the spot price of solar cell has dropped below the

$1/Wp mark and is trading in the range of $0.7/Wp and $0.9/Wp as of August 20117.

The sharp drop in the ASP (Average Selling Price) is taking a toll on the margins as well. From

healthy margins of more than 15%, the cell margins fell to about 4% by mid-20118. Many of the

cell producers are estimated to have negative margins during the first half of 2011. This was

7 Source: Energytrend

8 Source: iSuppli

32

Solar PV Manufacturing

A White Paper by EAI

caused by excess inventory in the supply chain that led to sharp price cutting by the cell

manufacturers in order to liquidate their stock.

Major Factors InfluencingProfitability

Capexdepreciation– The cost of setting up a solar cell plant comes to about $1

million/MW.

Materials–The Ag (Silver) andAl (Aluminum) paste used in the production process.

Process media (Phosphorous oxy chloride, other acids, gases like nitrogen, argon,

ammonia, etc.) contribute significantly to the cost.

R&D– As mentioned earlier, the demand for higher cell efficiencies is relentless. R&D

plays a key role in improving cell efficiency.

Global Market Scenario

In 2010, the total cell capacity was close to 30 GW, out of which more than 50% capacity was in

China9. Of the top 10 Cell manufacturers, two companies(JA Solar, Gintech) make only cells

whereas five companies(Suntech, Q-Cells, Motech, Sharp, Kyocera) make cells and modules.

Onecompany (Trina Solar) is present in wafers, cells and module manufacturing, whereas

another company (Yingli Solar) is fully integrated. First Solar, which is among the top 10, is a

CdTe Thin Film manufacturer.

Indian Scenario

The growth in solar cell manufacturing in India has largely been due to the inclusion of domestic

content requirements under the National Solar Missions which states that for solar PV projects

using c-Si technology, both the cells and modules would have to be manufactured within the

country.

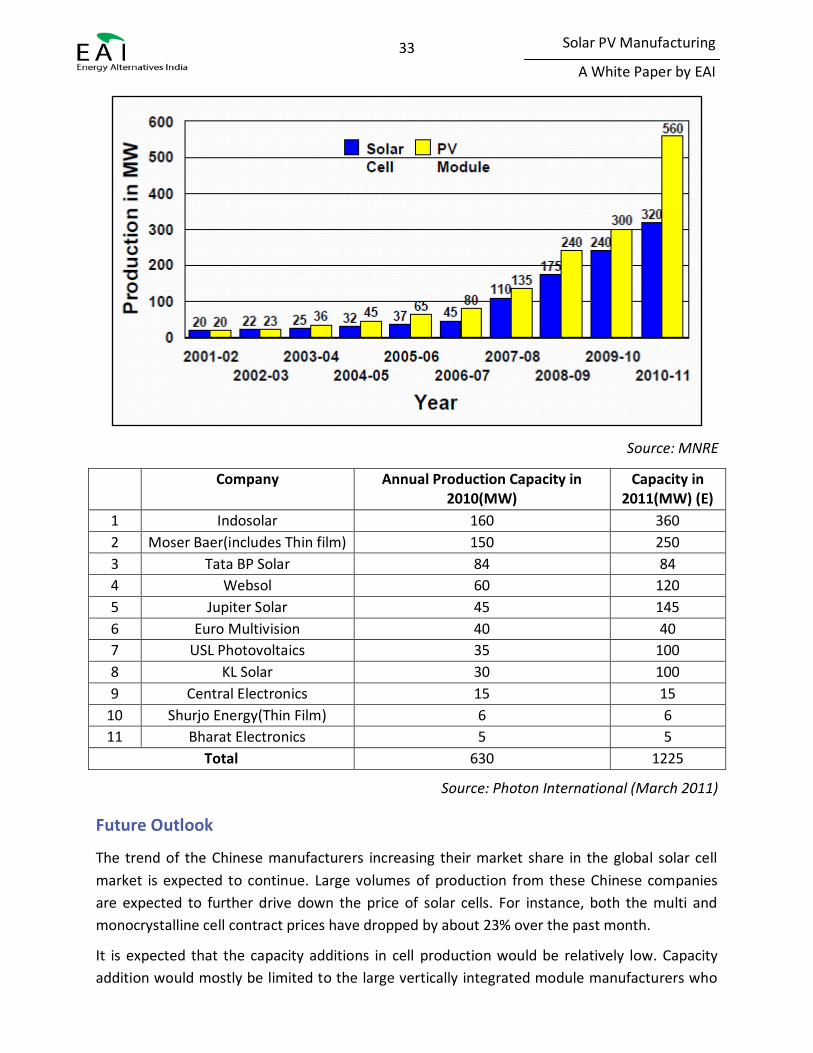

Cell production in India started with about 20 MW of production capacity in 2001-02. This

number has grown to over 700 MW with about 320 MW of capacity being added in 2010-11.

Significant capacity additions took place between 2009 and 2011 coinciding with the

announcement of the National Solar Mission Guidelines.

Currently, there are over 10 companies manufacturing cells in India; the combined cell

production capacity is over 600 MW. The installed cell production capacity is expected to

double by yearend or early next year considering the fact that at least 500MW of solar capacity

is scheduled to be set up over the course of the next few years (of which 350 MW is scheduled

to come up under JNNSM which mandates a domestic content requirement).

9 Source: EPIA

33

Solar PV Manufacturing

A White Paper by EAI

Source: MNRE

Company Annual Production Capacity in 2010(MW)

Capacity in 2011(MW) (E)

1 Indosolar 160 360

2 Moser Baer(includes Thin film) 150 250

3 Tata BP Solar 84 84

4 Websol 60 120

5 Jupiter Solar 45 145

6 Euro Multivision 40 40

7 USL Photovoltaics 35 100

8 KL Solar 30 100

9 Central Electronics 15 15

10 Shurjo Energy(Thin Film) 6 6

11 Bharat Electronics 5 5

Total 630 1225

Source: Photon International (March 2011)

Future Outlook

The trend of the Chinese manufacturers increasing their market share in the global solar cell

market is expected to continue. Large volumes of production from these Chinese companies

are expected to further drive down the price of solar cells. For instance, both the multi and

monocrystalline cell contract prices have dropped by about 23% over the past month.

It is expected that the capacity additions in cell production would be relatively low. Capacity

addition would mostly be limited to the large vertically integrated module manufacturers who

34

Solar PV Manufacturing

A White Paper by EAI

are looking to source a significant portion of their cells in-house so that they can stem the

thinning profit margins in the module manufacturing business. Cell manufacturers would need

to provide cells with higher efficiencies through better cell design to hope to compete in the

market as seen in the case of the high efficiency cells offered by SunPower.

From a production of about 30GW(including Thin Films) in 2010, the announced production

capacities for 2011 will be close to 50 GW10. In a market where the total PV installation is

expected to be only 22 GW (for 2011), the cell capacity is more than double the demand.

Conclusion

The year 2010 saw record production of PV cells – about 30 GW, whereas the total global PV

installation for the year was less than 20GW. This huge supply-demand gap is expected to

continue in the near future and will lead to further reduction of cell and module prices.

The following points will influence the success of a newcomer to cell manufacturing industry.

Cells are getting increasingly commoditized, and the best way to differentiate a

product from the competition is to produce higher efficiency cells. This makes it

critical to invest in Research and Development (R&D) - both for process

improvements and for material usage.

In order to remain competitive, it is highly recommended that the new entrant plans

for vertical integration once the cell manufacturing business is stabilized.

10 Source: iSuppli

35

Solar PV Manufacturing

A White Paper by EAI

Modules

Module production is a fairly standardized assembly process wherein cells are interconnected,

encapsulated, laminated and framed to produce the final product. The efficiency of the cell

drops a few percentage points due to the encapsulation of the interconnected cells.

PV cells contribute to about 70% of the total cost of a module and hence, the price of module

moves in tandem with the cell price. As seen in the previous sections, prices have been falling in

all parts of the value chain and this trend is reflected at the PV module level. The price trend

can be seen in the figure below.

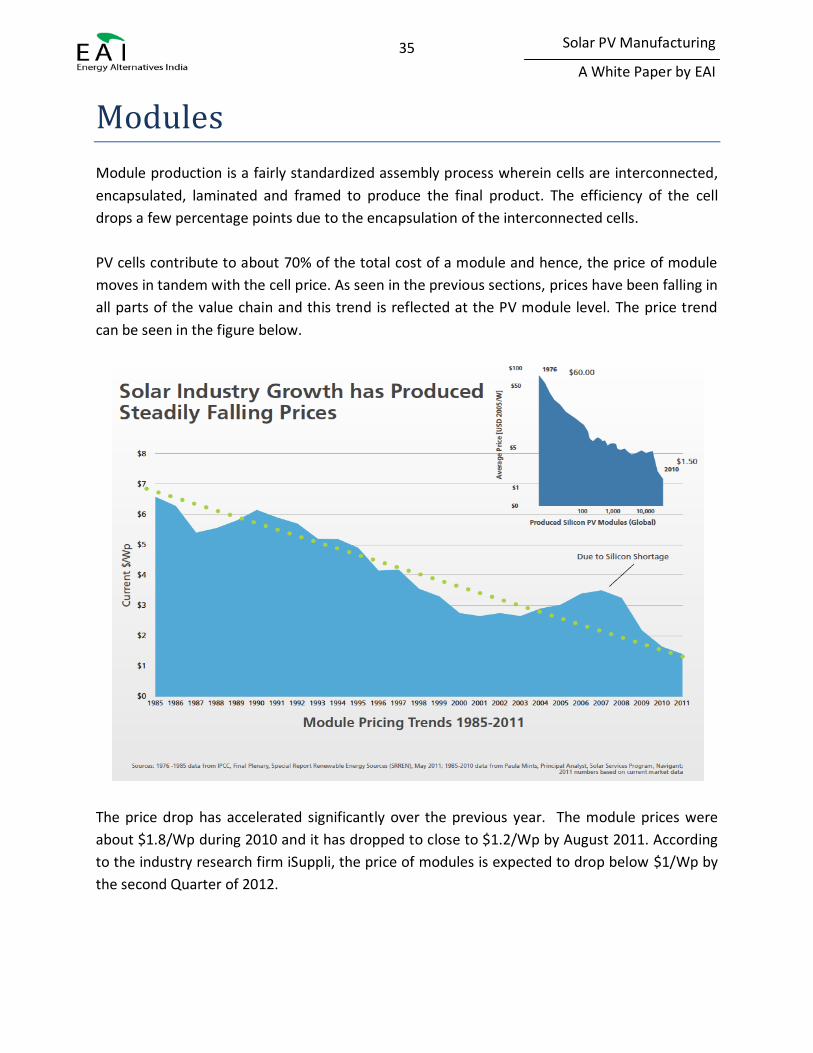

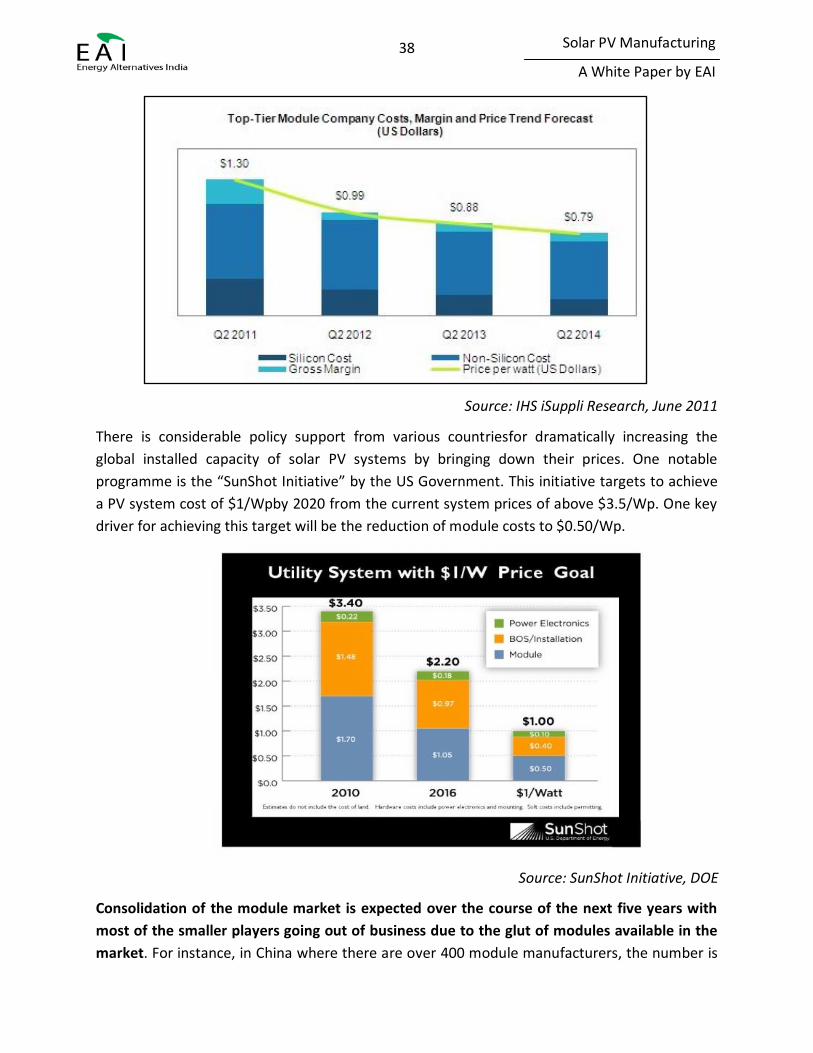

The price drop has accelerated significantly over the previous year. The module prices were

about $1.8/Wp during 2010 and it has dropped to close to $1.2/Wp by August 2011. According

to the industry research firm iSuppli, the price of modules is expected to drop below $1/Wp by

the second Quarter of 2012.

36

Solar PV Manufacturing

A White Paper by EAI

Major Factors InfluencingProfitability

Since module production is an assembly process, the only major factor that affects the

profitability of the module making is the material cost. As mentioned earlier, cells constitute

about 70% of the total cost and another 10-15% cost is constituted by other materials like

encapsulant, backsheet, glass, frame, etc.

Global Market Scenario

The module sector has very low barriers to entry because

a. The capital costs for setting up a module assembly unit is low(typically $50,000/MW)

b. Very low technology risk because the production process is an assembly process

c. Standardized production process

Due to this, there are several manufacturers of solar PV modules all over the world and the

sector is highly fragmented. Many of the top companies are integrated forward and/or

backward. Some companies like Q-Cells, MEMC, etc. do contract manufacturing for cell

companies. According to reports, there are over 400 module manufacturers in China with

varying capacities. Given below is the list of the top 15 Solar PV module manufacturers in 2010.

Source: GTM Research

Indian Scenario

The solar module manufacturing process is largely an assembly process. Due to the low

technological as well as capital requirements in this sector, India has seen an explosive growth

37

Solar PV Manufacturing

A White Paper by EAI

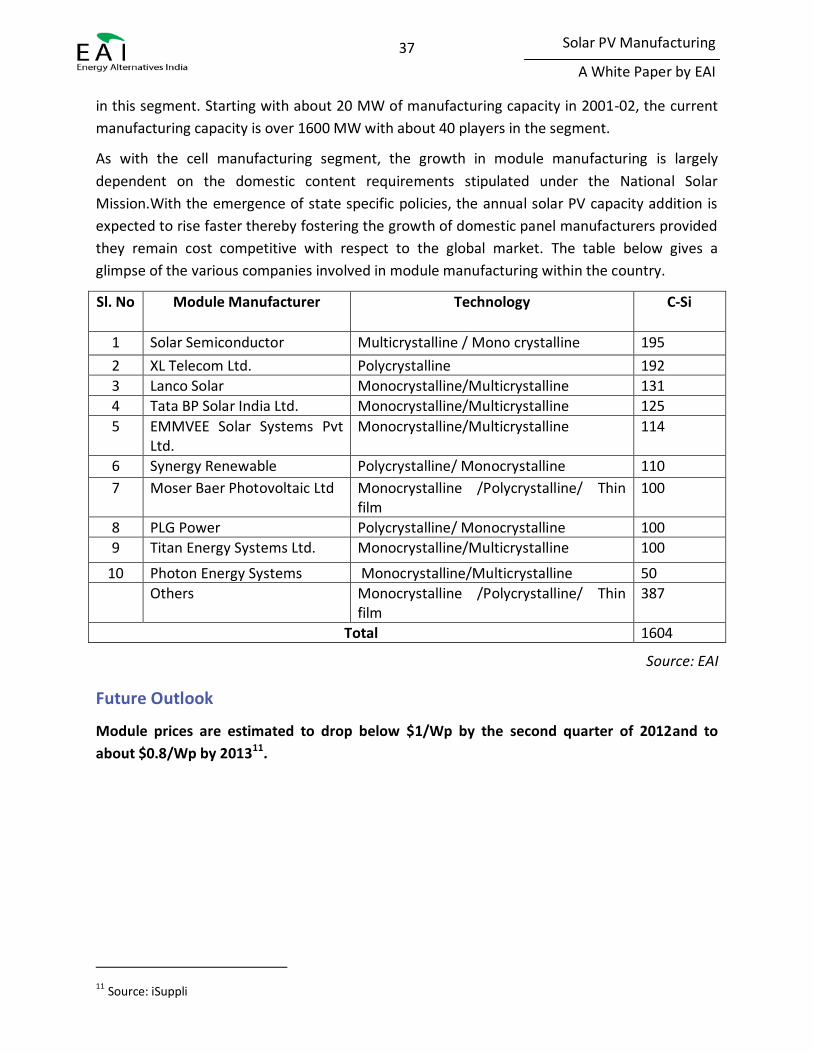

in this segment. Starting with about 20 MW of manufacturing capacity in 2001-02, the current

manufacturing capacity is over 1600 MW with about 40 players in the segment.

As with the cell manufacturing segment, the growth in module manufacturing is largely

dependent on the domestic content requirements stipulated under the National Solar

Mission.With the emergence of state specific policies, the annual solar PV capacity addition is

expected to rise faster thereby fostering the growth of domestic panel manufacturers provided

they remain cost competitive with respect to the global market. The table below gives a

glimpse of the various companies involved in module manufacturing within the country.

Sl. No Module Manufacturer Technology C-Si

1 Solar Semiconductor Multicrystalline / Mono crystalline 195

2 XL Telecom Ltd. Polycrystalline 192

3 Lanco Solar Monocrystalline/Multicrystalline 131

4 Tata BP Solar India Ltd. Monocrystalline/Multicrystalline 125

5 EMMVEE Solar Systems Pvt Ltd.

Monocrystalline/Multicrystalline 114

6 Synergy Renewable Polycrystalline/ Monocrystalline 110

7 Moser Baer Photovoltaic Ltd Monocrystalline /Polycrystalline/ Thin film

100

8 PLG Power Polycrystalline/ Monocrystalline 100

9 Titan Energy Systems Ltd. Monocrystalline/Multicrystalline 100

10 Photon Energy Systems Monocrystalline/Multicrystalline 50

Others Monocrystalline /Polycrystalline/ Thin film

387

Total 1604

Source: EAI

Future Outlook

Module prices are estimated to drop below $1/Wp by the second quarter of 2012and to

about $0.8/Wp by 201311.

11 Source: iSuppli

38

Solar PV Manufacturing

A White Paper by EAI

Source: IHS iSuppli Research, June 2011

There is considerable policy support from various countriesfor dramatically increasing the

global installed capacity of solar PV systems by bringing down their prices. One notable

programme is the “SunShot Initiative” by the US Government. This initiative targets to achieve

a PV system cost of $1/Wpby 2020 from the current system prices of above $3.5/Wp. One key

driver for achieving this target will be the reduction of module costs to $0.50/Wp.

Source: SunShot Initiative, DOE

Consolidation of the module market is expected over the course of the next five years with

most of the smaller players going out of business due to the glut of modules available in the

market. For instance, in China where there are over 400 module manufacturers, the number is

39

Solar PV Manufacturing

A White Paper by EAI

set to reduce to about 15 by 2016-17 fuelled mainly by the cutthroat pricing wars amongst the

various Chinese panel makers.

Conclusion

Module making is one sector that is highly dependent on what happens upstream (polysilicon,

ingots and wafers, cells) on the cost front and the efficiency front. As seen earlier, the module

prices have been falling drastically, thereby increasing the solar PV penetration.

For an investor contemplating entry into this sector, there are several considerations

that include

o Module manufacturing is an assembly process and has the lowest capital

expenditure requirement. This means that the barriers of entry to this sector are

very low.

o The minimum size of a module manufacturing can be about 10 MW or lower.

However, higher plant sizes can help in decreasing the cost of production.

o Working capital required is relatively high for module manufacturing.

o More and more module manufacturers are investing in to branding in order to

differentiate their modules from the competition.

40

Solar PV Manufacturing

A White Paper by EAI

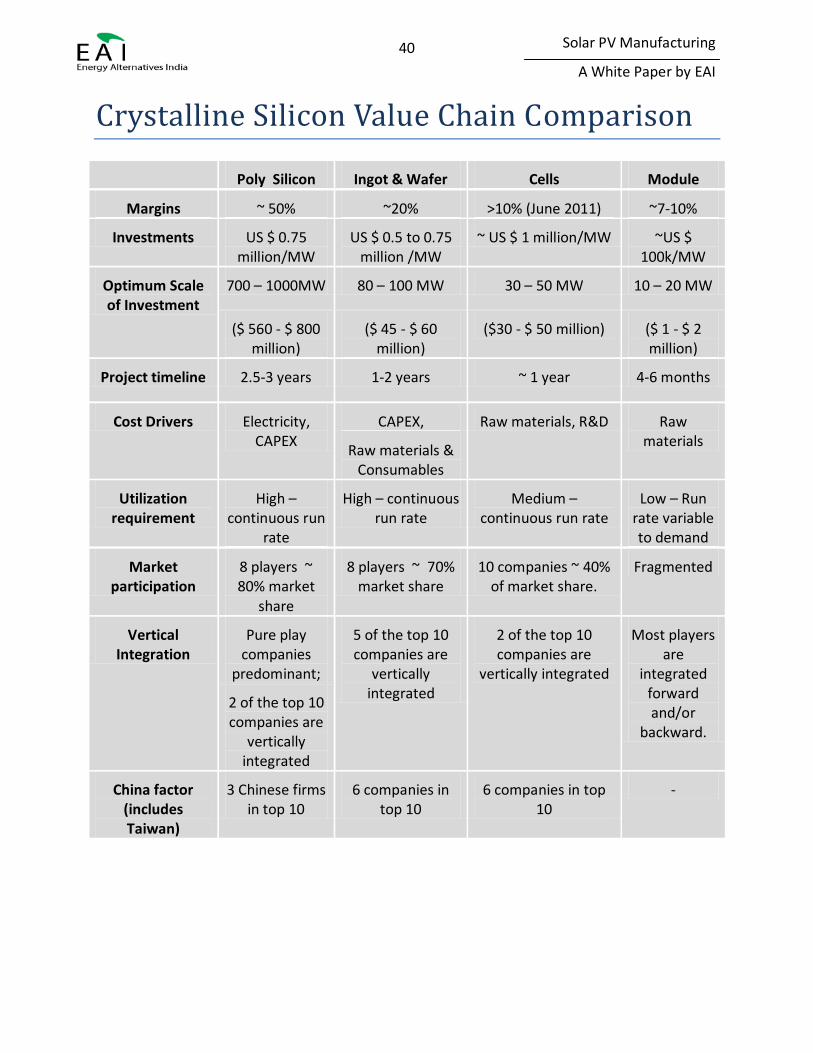

Crystalline Silicon Value Chain Comparison

Poly Silicon Ingot & Wafer Cells Module

Margins ~ 50% ~20% >10% (June 2011) ~7-10%

Investments US $ 0.75 million/MW

US $ 0.5 to 0.75 million /MW

~ US $ 1 million/MW ~US $ 100k/MW

Optimum Scale of Investment

700 – 1000MW 80 – 100 MW 30 – 50 MW 10 – 20 MW

($ 560 - $ 800 million)

($ 45 - $ 60 million)

($30 - $ 50 million) ($ 1 - $ 2 million)

Project timeline 2.5-3 years 1-2 years ~ 1 year 4-6 months

Cost Drivers Electricity, CAPEX

CAPEX, Raw materials, R&D Raw materials

Raw materials & Consumables

Utilization requirement

High – continuous run

rate

High – continuous run rate

Medium – continuous run rate

Low – Run rate variable to demand

Market participation

8 players ~ 80% market

share

8 players ~ 70% market share

10 companies ~ 40% of market share.

Fragmented

Vertical Integration

Pure play companies

predominant;

5 of the top 10 companies are

vertically integrated

2 of the top 10 companies are

vertically integrated

Most players are

integrated forward and/or

backward.

2 of the top 10 companies are

vertically integrated

China factor (includes Taiwan)

3 Chinese firms in top 10

6 companies in top 10

6 companies in top 10

-

41

Solar PV Manufacturing

A White Paper by EAI

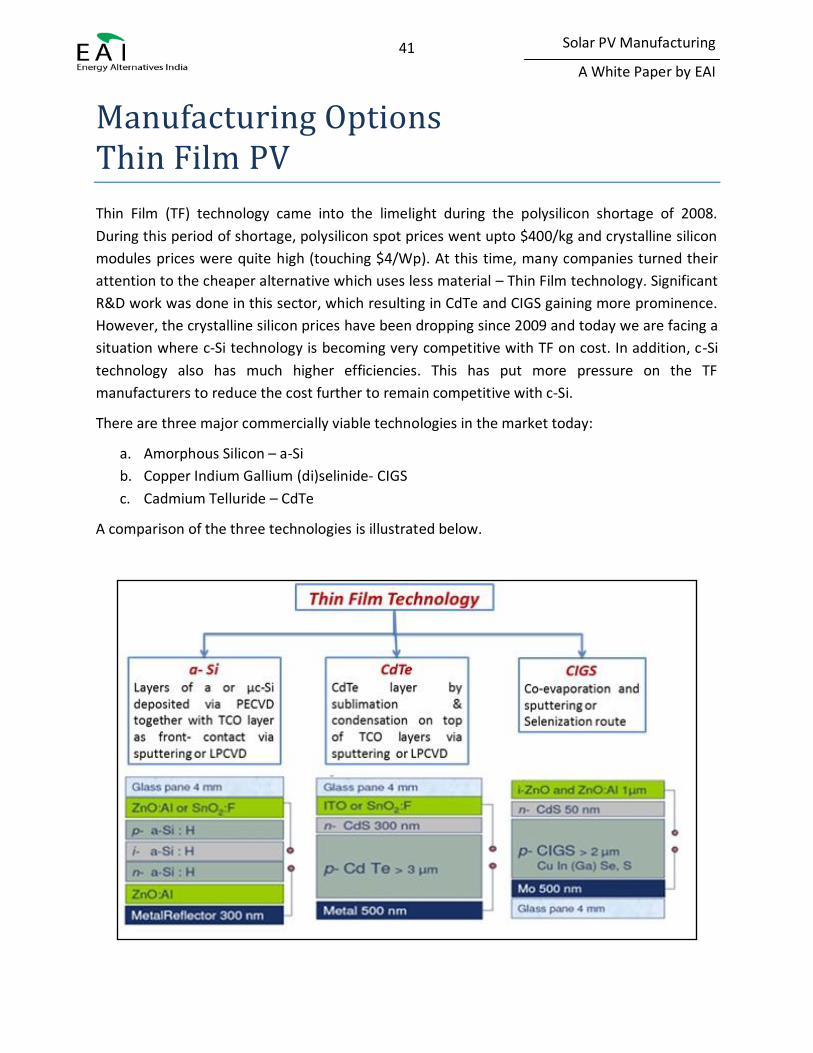

Manufacturing Options Thin Film PV

Thin Film (TF) technology came into the limelight during the polysilicon shortage of 2008.

During this period of shortage, polysilicon spot prices went upto $400/kg and crystalline silicon

modules prices were quite high (touching $4/Wp). At this time, many companies turned their

attention to the cheaper alternative which uses less material – Thin Film technology. Significant

R&D work was done in this sector, which resulting in CdTe and CIGS gaining more prominence.

However, the crystalline silicon prices have been dropping since 2009 and today we are facing a

situation where c-Si technology is becoming very competitive with TF on cost. In addition, c-Si

technology also has much higher efficiencies. This has put more pressure on the TF

manufacturers to reduce the cost further to remain competitive with c-Si.

There are three major commercially viable technologies in the market today:

a. Amorphous Silicon – a-Si

b. Copper Indium Gallium (di)selinide- CIGS

c. Cadmium Telluride – CdTe

A comparison of the three technologies is illustrated below.

42

Solar PV Manufacturing

A White Paper by EAI

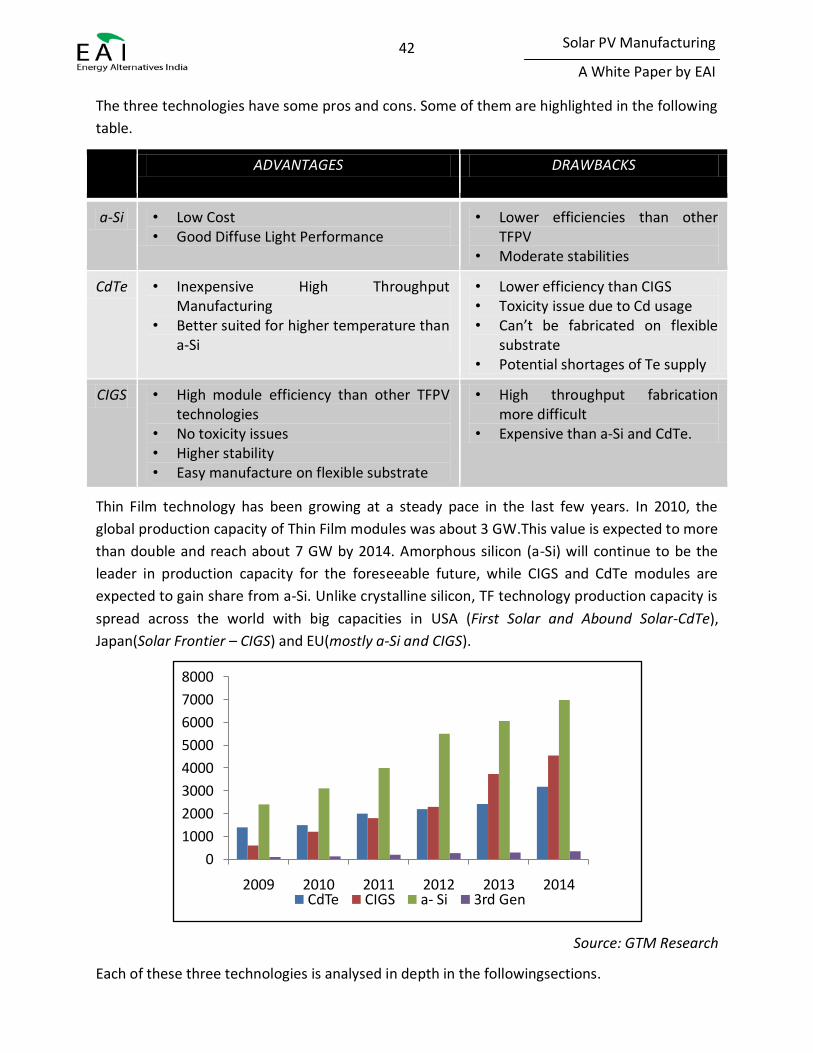

The three technologies have some pros and cons. Some of them are highlighted in the following

table.

ADVANTAGES DRAWBACKS

a-Si • Low Cost • Good Diffuse Light Performance

• Lower efficiencies than other TFPV

• Moderate stabilities

CdTe • Inexpensive High Throughput Manufacturing

• Better suited for higher temperature than a-Si

• Lower efficiency than CIGS • Toxicity issue due to Cd usage • Can’t be fabricated on flexible

substrate • Potential shortages of Te supply

CIGS • High module efficiency than other TFPV technologies

• No toxicity issues • Higher stability • Easy manufacture on flexible substrate

• High throughput fabrication more difficult

• Expensive than a-Si and CdTe.

Thin Film technology has been growing at a steady pace in the last few years. In 2010, the

global production capacity of Thin Film modules was about 3 GW.This value is expected to more

than double and reach about 7 GW by 2014. Amorphous silicon (a-Si) will continue to be the

leader in production capacity for the foreseeable future, while CIGS and CdTe modules are

expected to gain share from a-Si. Unlike crystalline silicon, TF technology production capacity is

spread across the world with big capacities in USA (First Solar and Abound Solar-CdTe),

Japan(Solar Frontier – CIGS) and EU(mostly a-Si and CIGS).

Source: GTM Research

Each of these three technologies is analysed in depth in the followingsections.

0

1000

2000

3000

4000

5000

6000

7000

8000

2009 2010 2011 2012 2013 2014CdTe CIGS a- Si 3rd Gen

43

Solar PV Manufacturing

A White Paper by EAI

Amorphous silicon (a-Si)

This is the only TF technology that uses silicon as its raw material. The manufacturing process

for amorphous silicon photovoltaic modules uses an amorphous silicon deposition approach. In

this approach, tin oxide-glass plates are coated with amorphous silicon in a single vacuum

chamber. The overall manufacturing sequence is:

1. Glass preparation (seams and washes) 2. Deposition of tin oxide & laser scribing of tin oxide 3. Deposition of a-Si & laser scribing of a-Si 4. Sputter deposition of Al & laser scribing of Al 5. Encapsulation and testing

Micromorph-Si is manufactured using two types of silicon namely amorphous and

microcrystalline. These modules tend to offer higher efficiencies than traditional a-Si modules.

The higher efficiency however does not result in a higher price tag. Thus, these modules have a

higher market share compared to traditional a-Si modules.

The cost of the amorphous silicon module is about $1.1 per Wp. Many of the thin film

equipment vendors like Oerlikon are targeting a cost of production of less than $1 per

Wp.The price of a-Si modules is about $1.2/Wp.

Major Factors InfluencingProfitability

About 60% of the cost is due to the materials and process media used. These include

Amorphous silicon

Process gas

Substrate

Encapsulant

Junction box

Global Market Scenario

a-Si technology is the leader among thethree different technologies due to the fact that it the

oldest of all technologies. However, due to the limited potential to improve a-Si technology,

other technologies like CdTe and CIGS are catching up. Some of the prominent a-Si TF

companies are given below.

Company Country Actual

Production in

2010(MW)

1 Sharp Solar Japan 195

2 Trony Solar China 138

44

Solar PV Manufacturing

A White Paper by EAI

3 Uni-Solar USA 120

4 NexPower China 85

5 Kaneka Solartech Co. Ltd Japan 58

Total 596

Source: GTM Research

Indian Scenario

a-Si has been gaining significant market share in India. In fact the largest solar PV power plant in

India – a 30 MW installation commissioned in October 2011, by Moser Baer in Gujarat uses a-Si

modules manufactured by Moser Baer themselves. Further, Moser Baer expects to have a total

of 100 MW of installed capacity in operation by year end, all of which would use a-Si modules.

In India, Moser Baerand HHV are the only players in the a-Si manufacturing segment. Moser

Baer has an annual a-Si production capacity of 50 MW, while HHV has a capacity of 10

MW.HHV is expected to expand its production capacity to 500 MW over the next five years. It is

worth noting that HHV is the first Indian company to have developed both the technology as

well as the equipment for setting up a thin film module manufacturing facility.In addition, they

are the only indigenous vendor for thin film manufacturing equipment.

Future Outlook

The major challenge for the growth of a-Si is the limitation in efficiency, which is estimated to

be limited to 10%. Variants like Micromorph silicon could become more prevalent, but the

future is unclear. The recent exit of the top a-Si manufacturing vendor, Applied Materials, has

raised questions about the future growth of this technology.

Though this may have come as a blow, there are other big names keeping a-Si alive. For

example, DuPont (known in the industry as anencapsulant manufacturer) has started churning

out a-Si modules through its subsidiary DuPont Apollo who have their capacity sold out for

2011. Like other thin film manufacturers they too are focusing on emerging markets. For

instance, in the second half of 2011, DuPont Apollo signed an agreement to supply an Indian

company – Wipro EcoEnergy with a-Si modules while also coming up with a proposal to setup a

10 MW power plant in Gujarat using their a-Si modules.

Due to the physical properties (primarily flexibility) of a-Si modules, such as those using tandem

junctions, the future could be in off-grid applications such as solar powered cars and BIPV. The

market is currently prime for investors to gain a first mover advantage.

45

Solar PV Manufacturing

A White Paper by EAI

Conclusion

While a-Si will continue to maintain its market leadership in the thin film segment for the next

few years, it is only a matter of time before CdTe or CIGS overtake a-Si Technology.

The key things a new entrant to the a-Si market should keep in mind are the following:

The limitation on efficiency increase needs to be counteracted by lowering the cost

of production.

Unlike the other technologies, the raw material – Si, is neither toxic nor a rare earth

metal. This eliminates the availability of raw material risk.

46

Solar PV Manufacturing

A White Paper by EAI

Cadmium Telluride (CdTe)

Cadmium Telluride is a technology which is predominantly driven by just one major company –

First Solar. CdTe modules are currently the cheapest TF modules available in the market with

cell efficiencies(12-17%) higher than a-Si but comparable to CIGS. CdTe technology is however

considered risky by many because of its usage of Cadmium, a carcinogen, as one of its raw

materials.

Manufacturing of CdTe thin film solar cell involves a set of physical and chemical procedures in

which the layers are sequentially deposited onto a substrate in a back wall configuration which

means that light is incident on the larger bandgap material.

The most common structure is glass-TCO-CdS-CdTe-BC where

TCO is the front contact, a transparent conducting oxide which is exposed to light The CdS film represents the n-semiconductor, transmitting a large part of the sunlight

into the absorber p-CdTe semiconductor. The sequence ends with a metallic back-contact (BC). Prior to BC deposition, the CdTe

layer is submitted to heat treatment in the presence of CdCl2, which deeply affects the properties of the CdTe layer and is essential to achieve high efficiency.

The cost of CdTe module is about $0.85/Wp. As it currently stands, the cost of production is

about $0.75/Wp.However, First Solar claims to have lower production costs because of its

scale. First Solar production capacity is about 1.4GW.

The price of CdTe modules is less than $1/Wp making it the cheapest TF technology.

Major Factors Influencing Profitability

A big part of the cost is due to the materials and process media used. These include

Active material : Cadmium Telluride

Cadmium Sulfide

Substrate

Encapsulant

Junction box

Global Market Scenario

First Solar is the biggest Thin Film module manufacturer in the world and till recently, it had

production capacities higher than the top c-Si manufacturing firm – Suntech. First Solar is

followed by Abound Solar which ranks second in terms of annual production capacity. GE has

entered CdTe production in a big way through investments in its recently acquired subsidiary –

Primestar Solar.

47

Solar PV Manufacturing

A White Paper by EAI

Company Country Annual Production Capacity in 2010 (MW)

1 First Solar USA 1400

2 Abound Solar USA 65

3 PrimeStar Solar USA 30

4 Calyxo GmbH Germany 25

Indian Scenario

Over 60% of the projects allocated under Batch 1 of JNNSM are scheduled to use Thin Film

technology. Of this, a significant portion (over 50%) is expected to be established using CdTe

technology. The primary reason for this is the low interest rate loans given by EXIM bank of USA

to project developers who import modules made in US (where FirstSolar, a CdTe manufacturer

is a major player). In addition to this, there is some on-field data which suggests that power

plants using CdTe technology has a higher electricity yield (up to 5% higher in some cases) when

compared to the more expensive c-Si modules. For instance, FirstSolar recently inked a deal

with Reliance Power to supply 100 MW of CdTe based thin film modules – which is the largest

sales deal in India to date (September 2011). It should come as no surprise then that part of the

project cost ($84.3 million) is being financed through a loan grant from EXIM bank of US.

GE, one of the new entrants into the CdTe market has an R&D base in Bangalore. The R&D

being performed here is expected to help GE produce cost effective CdTe modules with high

efficiency by employing advanceddevice design.

In India, there is no company that manufactures PV modules using CdTe Technology.

Future Outlook

CdTe is expected to continue to do well in USA and countries where the restriction on usage of

Cadmium compounds is limited, with FirstSolar leading the charge. CdTe module makers are

likely to shift focus to emerging solar markets such as India due to limited environmental

regulations, higher yield under high temperature conditions as well as the demand for low cost

modules.

Considering the highly carcinogenic nature of Cadmium, a threat of Cadmium ban looms in

European Union and other countries where environmental regulations are strong thereby

inhibiting the sale of CdTe modules in these markets.

CdTe is currently the cheapest module technology available. Further gains in market share

would depend on how well it is able to maintain its price edge over the other competing

technologies considering the fact that c-Si module prices have almost bottomed out over the

past few months. Further, CdTe based modules would also have to see a significant

improvement in terms of conversion efficiencies to remain relevant. FirstSolar aims to improve

48

Solar PV Manufacturing

A White Paper by EAI

CdTe module conversion efficiencies to between 13.5% and 14.5% by 2014 making it highly

competitive.

Conclusion

CdTe has grown remarkably in the past few years, driven mainly by First Solar and possibly will

be driven by Abound and GE in the future. CdTe will have the advantages as the cheapest TF

technology and also good efficiencies. However questions on the toxicity of Cadmium remain.

For a new entrant into CdTe, the following challenges need to be overcome to be a successful

player in this segment.

Access to production technology that can lead to low cost production

Sufficient scale to remain competitive with the entrenched incumbents

Overcome the perception problem related to cadmium toxicity

49

Solar PV Manufacturing

A White Paper by EAI

Copper Indium Gallium (di)selinide (CIGS)

CIGS cells have reached higher efficiencies and do not use any toxic material like Cadmium in its

production. These cells operate similarly to conventional crystalline silicon solar cells. When

light hits the cell it is absorbed in the CIGS the photovoltaic characteristics of the material lead

to electricity generation. The basic steps involved in the manufacturing process are given in the

flowchart below.

1. Glass preparation 2. Sputter deposition of molybdenum 3. Molybdenum conductor patterning 4. Compound formation to create CIGS 5. Sputter deposition of the zinc oxide transparent conductor 6. Zinc oxide deposition 7. Encapsulation 8. Testing

CIGS being the newest technology of all TF technologies, it is still more expensive than others

and there is significant potential for cost reduction. The cost of CIGS production is about $1.2-

$1.3/Wp whereas the price is about $1.4/Wp.

Major Factors InfluencingProfitability

Most of the cost is due to materials like

Active material – Copper, Indium, Gallium Selenium)

Cadmium Sulfide

Substrate

Encapsulant

Junction box

Global Market Scenario

Solar Frontier (Japan) dominates the production capacity with a total of close to 800 MW

capacity. Other companies include

o Global Solar Energy – total production capacity - 75 MW (USA)

o Miasole – total production capacity - 60 MW (USA)

o Nanosolar (US)

o Avancis(Shell Solar) (Germany)

In September 2011, the CIGS market played host to one of the most high profile solar module

manufacturer collapse in recent times. Solyndra, a CIGS manufacturer producing innovative

cylindrical CIGS modules recently went under in spite of a $500 million loan guarantee from the

50

Solar PV Manufacturing

A White Paper by EAI

US Government. The reason cited for this collapse is that the modules produced by Solyndra

could not compete in terms of price with the crystalline modules offered by the Chinese

module makers.

Indian Scenario

CIGS technology has started to make its foray into India. Solar Frontier, one of the largest

CIGS/CIS manufacturers in the world made an announcement in September 2011, that it had

closed deals to supply CIS modules to projects in India under the National Solar Mission and the

Gujarat State Policy totalling 30 MW.

Shurjo Energy has a production capacity of 7MW with plans to increase production capacity

to 100 MW in the near future12. No other company has a CIGS production facility in India.

Future Outlook

While CIGS has the potential to increase efficiencies, it has to reduce its cost base in order to

remain competitive with the c-Si technology. With the exit of equipment vendor VEECO,

question remains on the long term success of the CIGS technology. On the flipside, equipment

manufacturers such as Centrotherm are putting significant efforts into CIGS R&D to ensure that

their equipment guarantees high performance CIGS modules which can compete in the global

market.

The installed production capacity expanded to 439 MW in 2010. It is expected that the

production capacity would increase by close to 200% in 2011 to about 1.3 GW. Some experts

say that the production capacity addition by year end to could be as a high 2.2 GW. This

would help put CIGS in a more favourable position in the market in hopes that the large

volumes of production would drive down prices.

Conclusion

With higher efficiency potential, if CIGS can reduce costs, CIGS will get more market

penetration.

For a new entrant into CIGS, the following points are critical

- CIGS technology is still evolving and the production technology is yet to be standardized.

This presents both a challenge and opportunity.

- CIGS has to find a way to remain cost competitive with the other technologies.

- The opportunity is that the scope for increasing efficiencies is much higher relative to

the other technologies.

- As we have mentioned for others, scale is important in case of CIGS as well.

12Source: Shurjo Energy

51

Solar PV Manufacturing

A White Paper by EAI

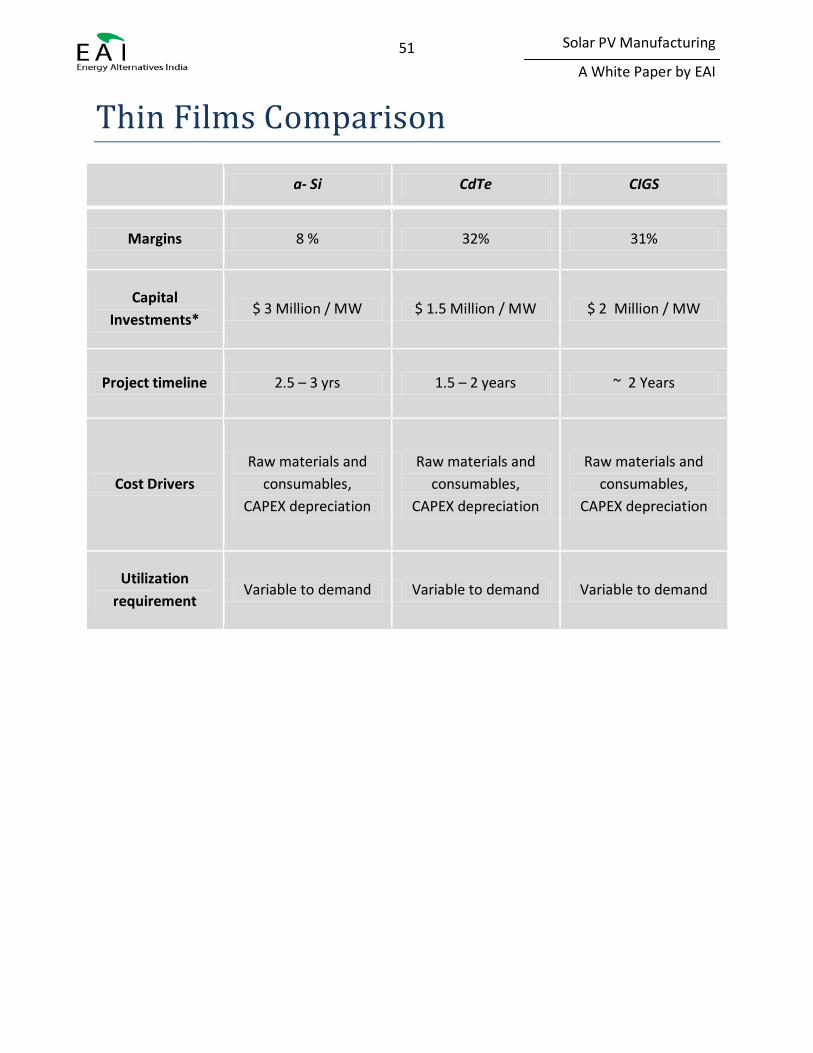

Thin Films Comparison

a- Si CdTe CIGS

Margins 8 % 32% 31%

Capital

Investments* $ 3 Million / MW $ 1.5 Million / MW $ 2 Million / MW

Project timeline 2.5 – 3 yrs 1.5 – 2 years ~ 2 Years

Cost Drivers

Raw materials and

consumables,

CAPEX depreciation

Raw materials and

consumables,

CAPEX depreciation

Raw materials and

consumables,

CAPEX depreciation

Utilization

requirement Variable to demand Variable to demand Variable to demand

52

Solar PV Manufacturing

A White Paper by EAI

53

Solar PV Manufacturing

A White Paper by EAI

Section 3 – Suitable PV Manufacturing Opportunity

54

Solar PV Manufacturing

A White Paper by EAI

55

Solar PV Manufacturing

A White Paper by EAI

Summary

The previous two sections provided the global and Indian trends in solar PV, the rationale for

having a local solar PV manufacturing ecosystem in India and the key characteristics of each

stage of the value chain.

The following points emerge:

The growth of solar PV is expected to be aggressive worldwide, and in India, for the

foreseeable future.

India has few or no companies operating in the upstream portions of the solar PV

manufacturing value chain.

China is fast becoming the manufacturing hub for all manufacturing segments in solar

PV, and will provide stiff competition from its low cost products, a result of the high

scales at which Chinese companies operate.

The different manufacturing segments along the value chain display strikingly different

characteristics on key parameters such as capital costs, profit margins and the key

drivers for success.

Choosing the Right Manufacturing Option for Your Company

Based on inputs and insights in this document, how does a corporate decide whether or not to

invest in manufacturing, and if they decide to invest, which segment of the value chain should

they invest in?

EAI has provided a simple, preliminary framework to enable such decision-making. This

framework, comprising four parameters, provides a quick checklist for your company to

eliminate/shortlist options.

For companies looking forward to venturing into the solar manufacturing business, the right

choice however would depend on:

Aspirations

o Is your company targeting global leadership or Indian?

o What are the profit margins that your company is targeting?

Constraints

o How much capital is your company willing to invest?

o How comfortable is your company to work in tech driven domains?

With these questions in mind, the following matrix aims to take your evaluation to the next

stage.

56

Solar PV Manufacturing

A White Paper by EAI

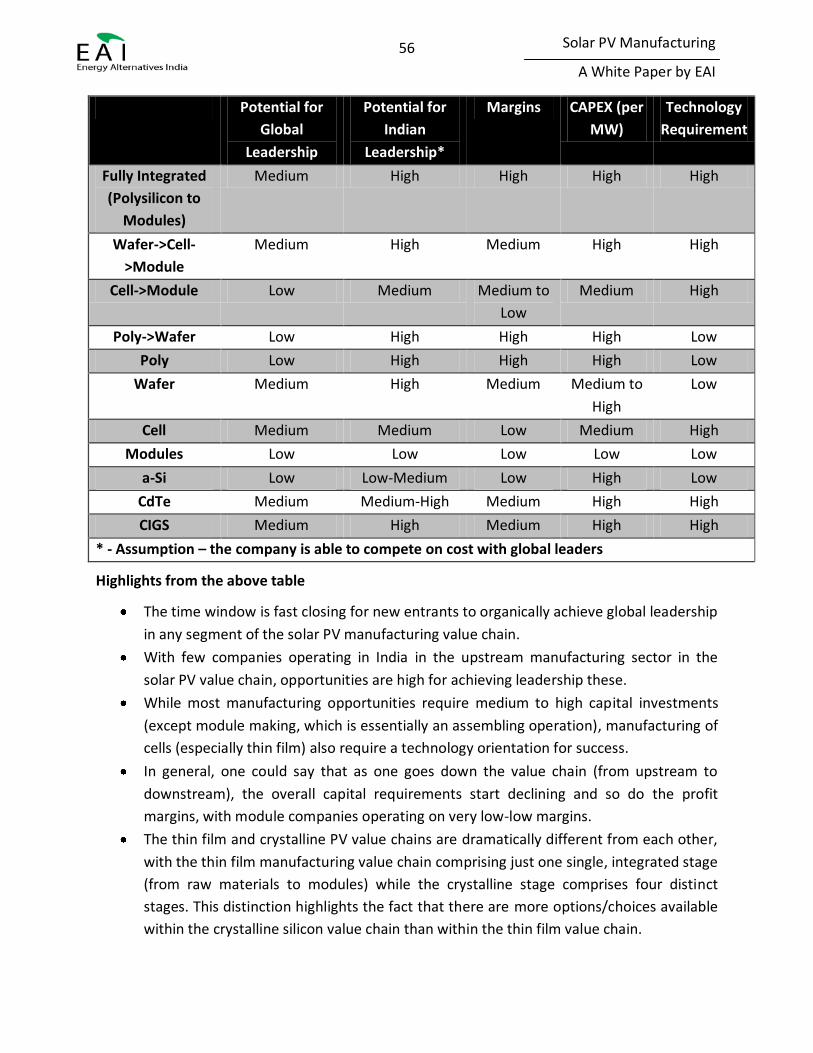

Potential for

Global

Leadership

Potential for

Indian

Leadership*

Margins CAPEX (per

MW)

Technology

Requirement

Fully Integrated

(Polysilicon to

Modules)

Medium High High High High

Wafer->Cell-

>Module

Medium High Medium High High

Cell->Module Low Medium Medium to

Low

Medium High

Poly->Wafer Low High High High Low

Poly Low High High High Low

Wafer Medium High Medium Medium to

High

Low

Cell Medium Medium Low Medium High

Modules Low Low Low Low Low

a-Si Low Low-Medium Low High Low

CdTe Medium Medium-High Medium High High

CIGS Medium High Medium High High

* - Assumption – the company is able to compete on cost with global leaders

Highlights from the above table

The time window is fast closing for new entrants to organically achieve global leadership

in any segment of the solar PV manufacturing value chain.

With few companies operating in India in the upstream manufacturing sector in the

solar PV value chain, opportunities are high for achieving leadership these.

While most manufacturing opportunities require medium to high capital investments

(except module making, which is essentially an assembling operation), manufacturing of

cells (especially thin film) also require a technology orientation for success.

In general, one could say that as one goes down the value chain (from upstream to

downstream), the overall capital requirements start declining and so do the profit

margins, with module companies operating on very low-low margins.

The thin film and crystalline PV value chains are dramatically different from each other,

with the thin film manufacturing value chain comprising just one single, integrated stage

(from raw materials to modules) while the crystalline stage comprises four distinct

stages. This distinction highlights the fact that there are more options/choices available

within the crystalline silicon value chain than within the thin film value chain.

57

Solar PV Manufacturing

A White Paper by EAI

EAI - Assisting Your Company for Attractive

Manufacturing Opportunities in Solar PV

EAI offers intelligence on the overall manufacturing opportunities in

Solar PV upstream – Polysilicon, Ingots and Wafers

Solar PV downstream – Cells and Modules

Thin Film manufacturing

Components – sub-components for cells and modules, chemicals and other

consumables

Balance of systems – inverters, monitoring systems

Equipment and machineries – Furnaces, wafer cutting tools, cell production line, module

production line

Identifying the most attractive opportunities for your company

Understanding your company’s aspirations in the context of solar energy sector

Understanding your company’s manufacturing competencies

Evaluating the fit between your aspirations + competencies and the available

opportunities

Clearly identifying the attractive opportunities appropriate for your company

Feasibility study for shortlisted opportunities

Demand and supply analysis