Embed Size (px)

DESCRIPTION

General information, legal framework, tax framework, application: SOPARFI Financial Holding Company

Citation preview

WWW.IASFID.LU INFO@IASFID.LU

IAS FIDUCIAIRE S.À R.L.

WWW.IASFID.LU INFO@IASFID.LU

IAS FIDUCIAIRE S.À R.L.

SOPARFI Financial Holding Company

Financial Engineering in Luxembourg

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

• General information

• Legal framework

• Tax framework

• Application

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

General information

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Société de PARticipations Financières – Financial Holding Company

• Optimizing the administration of groups of companies

• Double tax treaties Luxemburg

• Excercise of all administrative activities associated with their investments

• With the management of the investment portfolio related activities:

e.g. provision of financial advisory services and financing activities

• All directly and indirectly related business activities

• Business permit for commercial activities

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Legal Framework

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

• No legal definition or special legal status

• Legal forms

– Public limited company (S.A.)

– Private limited company (S.à r.l.)

– Partnership limited by shares (S.C.A.)

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

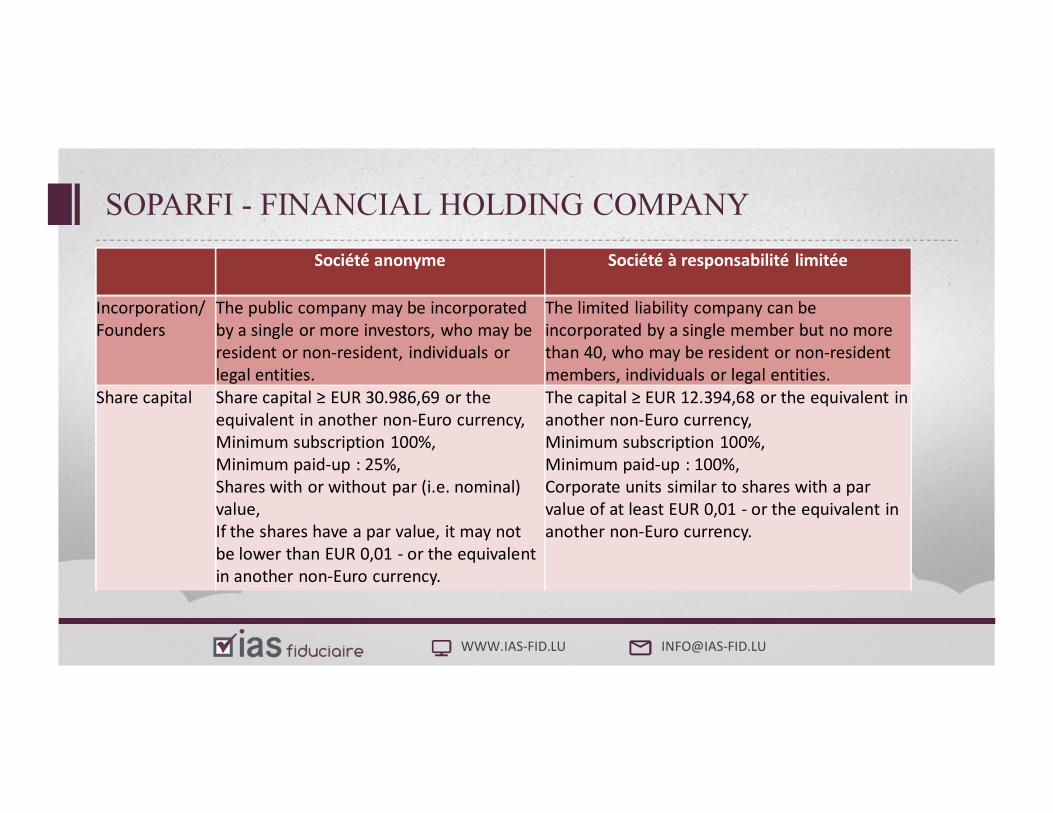

Société anonyme Société à responsabilité limitée

Incorporation/

Founders

The public company may be incorporated

by a single or more investors, who may be

resident or nonresident, individuals or

legal entities.

The limited liability company can be

incorporated by a single member but no more

than 40, who may be resident or nonresident

members, individuals or legal entities.

Share capital Share capital ≥ EUR 30.986,69 or the

equivalent in another nonEuro currency,

Minimum subscription 100%,

Minimum paidup : 25%,

Shares with or without par (i.e. nominal)

value,

If the shares have a par value, it may not

be lower than EUR 0,01 or the equivalent

in another nonEuro currency.

The capital ≥ EUR 12.394,68 or the equivalent in

another nonEuro currency,

Minimum subscription 100%,

Minimum paidup : 100%,

Corporate units similar to shares with a par

value of at least EUR 0,01 or the equivalent in

another nonEuro currency.

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

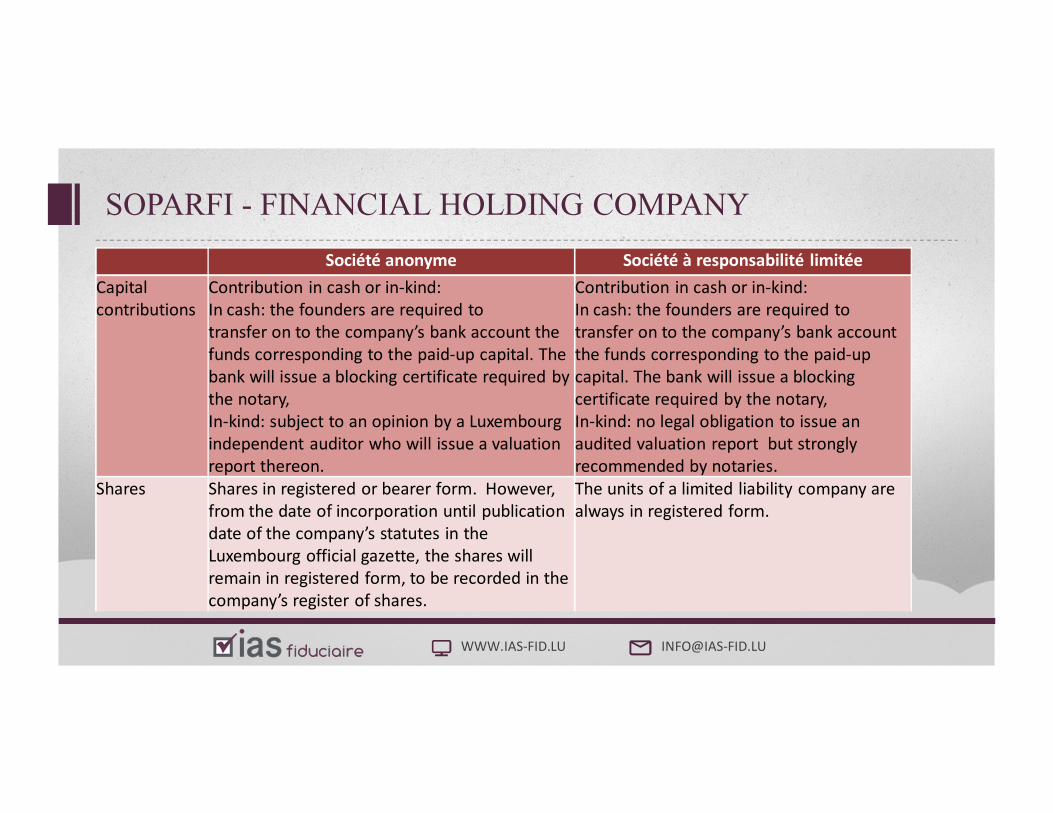

Société anonyme Société à responsabilité limitée

Capital

contributions

Contribution in cash or inkind:

In cash: the founders are required to

transfer on to the company’s bank account the

funds corresponding to the paidup capital. The

bank will issue a blocking certificate required by

the notary,

Inkind: subject to an opinion by a Luxembourg

independent auditor who will issue a valuation

report thereon.

Contribution in cash or inkind:

In cash: the founders are required to

transfer on to the company’s bank account

the funds corresponding to the paidup

capital. The bank will issue a blocking

certificate required by the notary,

Inkind: no legal obligation to issue an

audited valuation report but strongly

recommended by notaries.

Shares Shares in registered or bearer form. However,

from the date of incorporation until publication

date of the company’s statutes in the

Luxembourg official gazette, the shares will

remain in registered form, to be recorded in the

company’s register of shares.

The units of a limited liability company are

always in registered form.

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

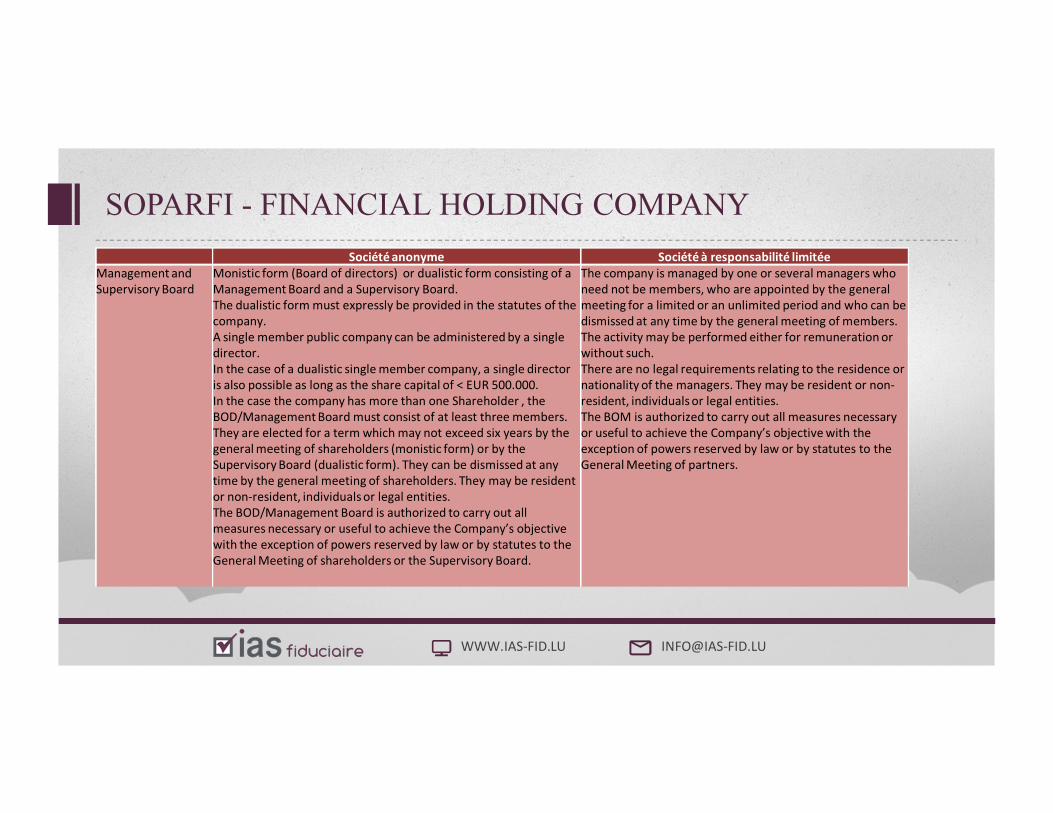

Société anonyme Société à responsabilité limitée

Management and

Supervisory Board

Monistic form (Board of directors) or dualistic form consisting of a

Management Board and a Supervisory Board.

The dualistic form must expressly be provided in the statutes of the

company.

A single member public company can be administered by a single

director.

In the case of a dualistic single member company, a single director

is also possible as long as the share capital of < EUR 500.000.

In the case the company has more than one Shareholder , the

BOD/Management Board must consist of at least three members.

They are elected for a term which may not exceed six years by the

general meeting of shareholders (monistic form) or by the

Supervisory Board (dualistic form). They can be dismissed at any

time by the general meeting of shareholders. They may be resident

or nonresident, individuals or legal entities.

The BOD/Management Board is authorized to carry out all

measures necessary or useful to achieve the Company’s objective

with the exception of powers reserved by law or by statutes to the

General Meeting of shareholders or the Supervisory Board.

The company is managed by one or several managers who

need not be members, who are appointed by the general

meeting for a limited or an unlimited period and who can be

dismissed at any time by the general meeting of members.

The activity may be performed either for remuneration or

without such.

There are no legal requirements relating to the residence or

nationality of the managers. They may be resident or non

resident, individuals or legal entities.

The BOM is authorized to carry out all measures necessary

or useful to achieve the Company’s objective with the

exception of powers reserved by law or by statutes to the

General Meeting of partners.

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Société anonyme Société à responsabilité limitée

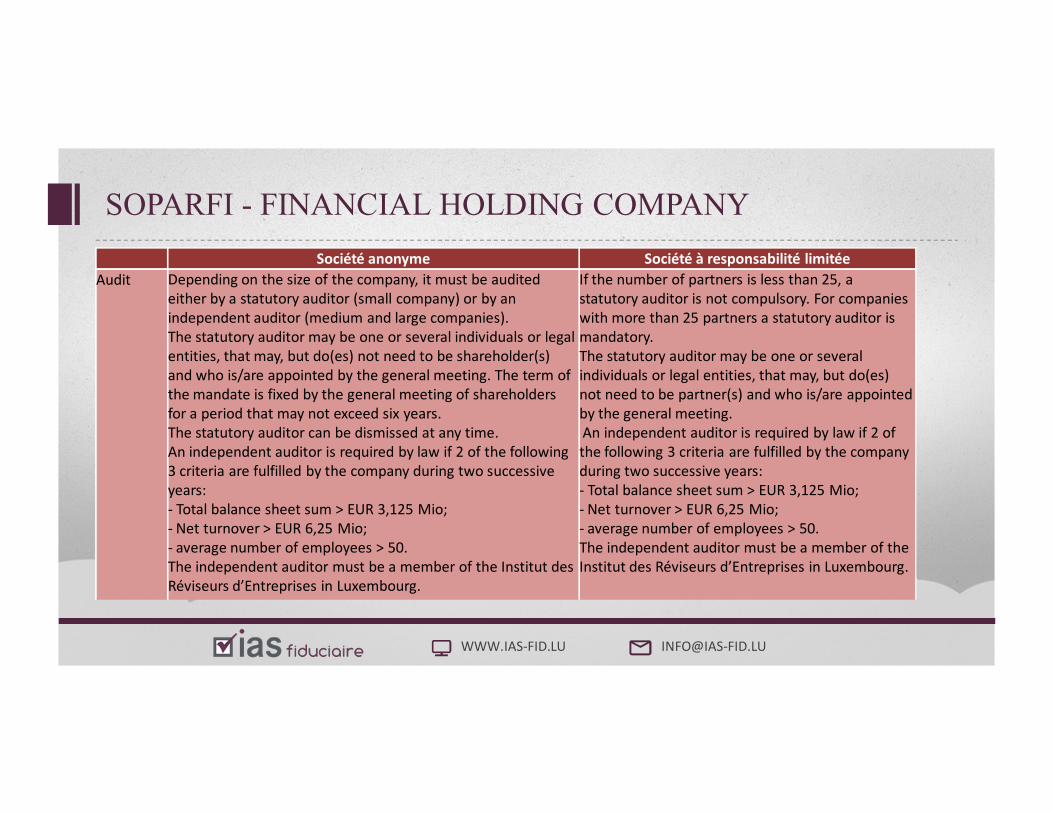

Audit Depending on the size of the company, it must be audited

either by a statutory auditor (small company) or by an

independent auditor (medium and large companies).

The statutory auditor may be one or several individuals or legal

entities, that may, but do(es) not need to be shareholder(s)

and who is/are appointed by the general meeting. The term of

the mandate is fixed by the general meeting of shareholders

for a period that may not exceed six years.

The statutory auditor can be dismissed at any time.

An independent auditor is required by law if 2 of the following

3 criteria are fulfilled by the company during two successive

years:

Total balance sheet sum > EUR 3,125 Mio;

Net turnover > EUR 6,25 Mio;

average number of employees > 50.

The independent auditor must be a member of the Institut des

Réviseurs d’Entreprises in Luxembourg.

If the number of partners is less than 25, a

statutory auditor is not compulsory. For companies

with more than 25 partners a statutory auditor is

mandatory.

The statutory auditor may be one or several

individuals or legal entities, that may, but do(es)

not need to be partner(s) and who is/are appointed

by the general meeting.

An independent auditor is required by law if 2 of

the following 3 criteria are fulfilled by the company

during two successive years:

Total balance sheet sum > EUR 3,125 Mio;

Net turnover > EUR 6,25 Mio;

average number of employees > 50.

The independent auditor must be a member of the

Institut des Réviseurs d’Entreprises in Luxembourg.

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Société anonyme Société à responsabilité limitée

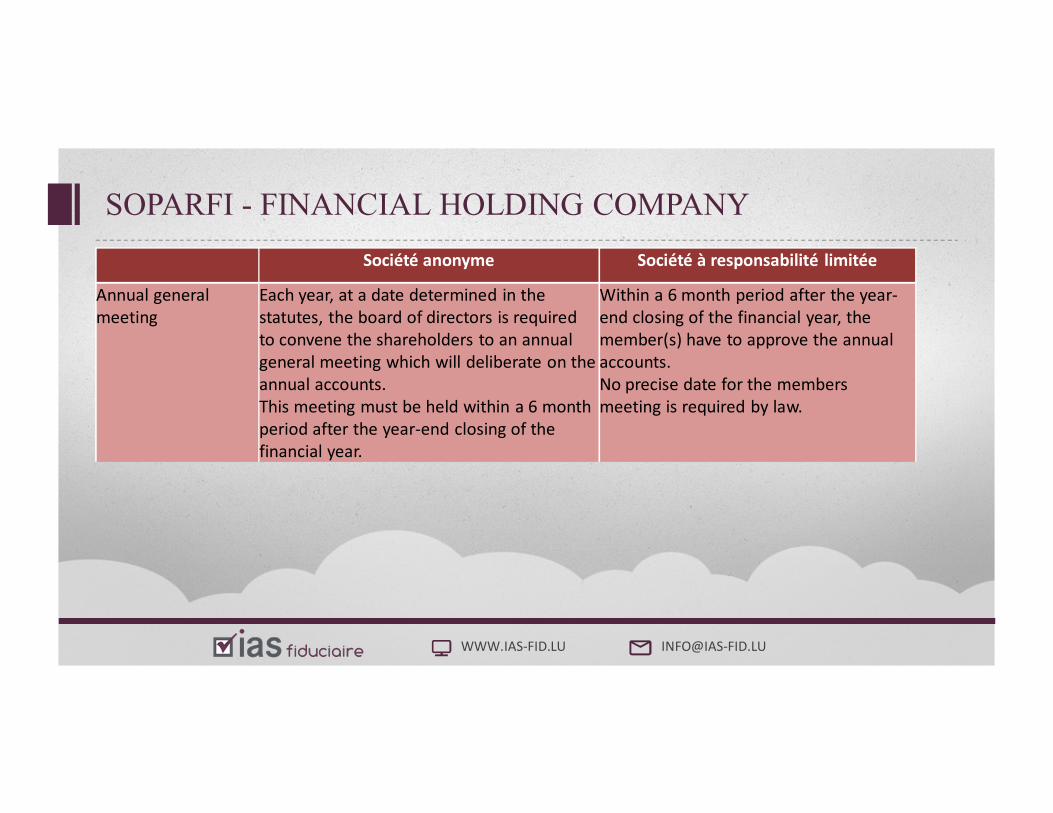

Annual general

meeting

Each year, at a date determined in the

statutes, the board of directors is required

to convene the shareholders to an annual

general meeting which will deliberate on the

annual accounts.

This meeting must be held within a 6 month

period after the yearend closing of the

financial year.

Within a 6 month period after the year

end closing of the financial year, the

member(s) have to approve the annual

accounts.

No precise date for the members

meeting is required by law.

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

• Commercial and accounting law:

– Law of 10 August 1915 concerning commercial companies

– Accounting Law of 19 December 2002

– Grand Ducal Regulation of 10 June 2009

– Accounting Law of 10 December 2010

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

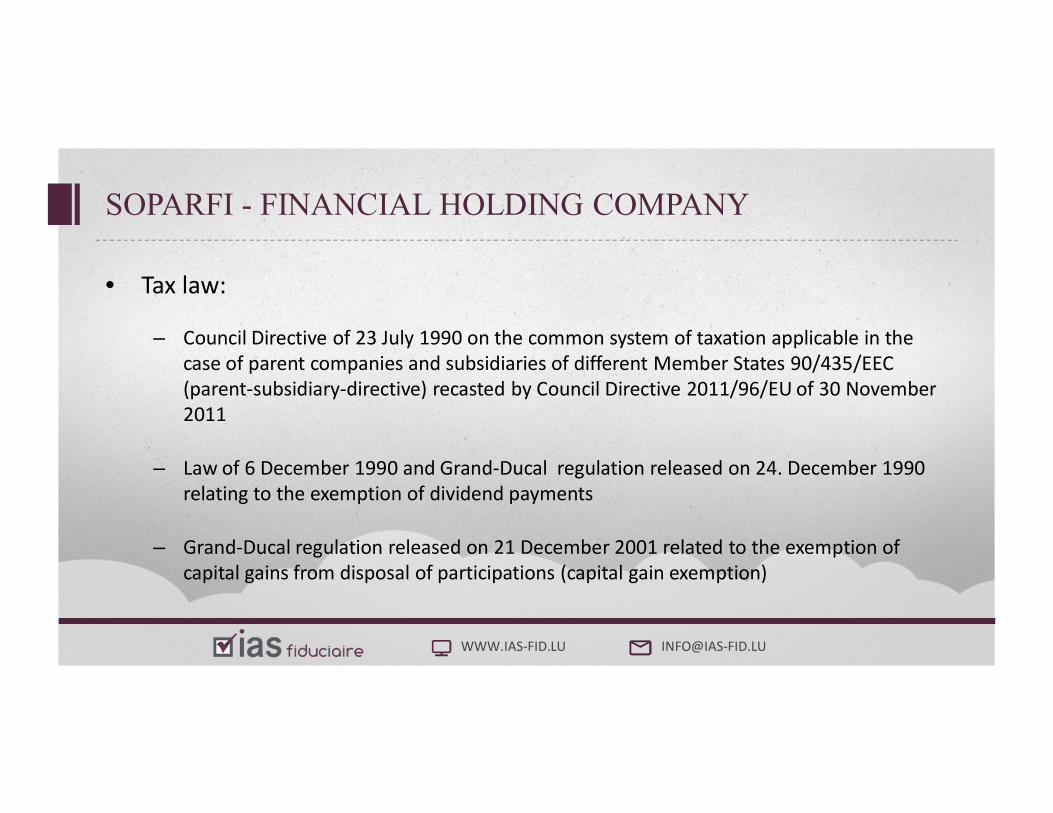

• Tax law:

– Council Directive of 23 July 1990 on the common system of taxation applicable in the

case of parent companies and subsidiaries of different Member States 90/435/EEC

(parentsubsidiarydirective) recasted by Council Directive 2011/96/EU of 30 November

2011

– Law of 6 December 1990 and GrandDucal regulation released on 24. December 1990

relating to the exemption of dividend payments

– GrandDucal regulation released on 21 December 2001 related to the exemption of

capital gains from disposal of participations (capital gain exemption)

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Tax framework

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

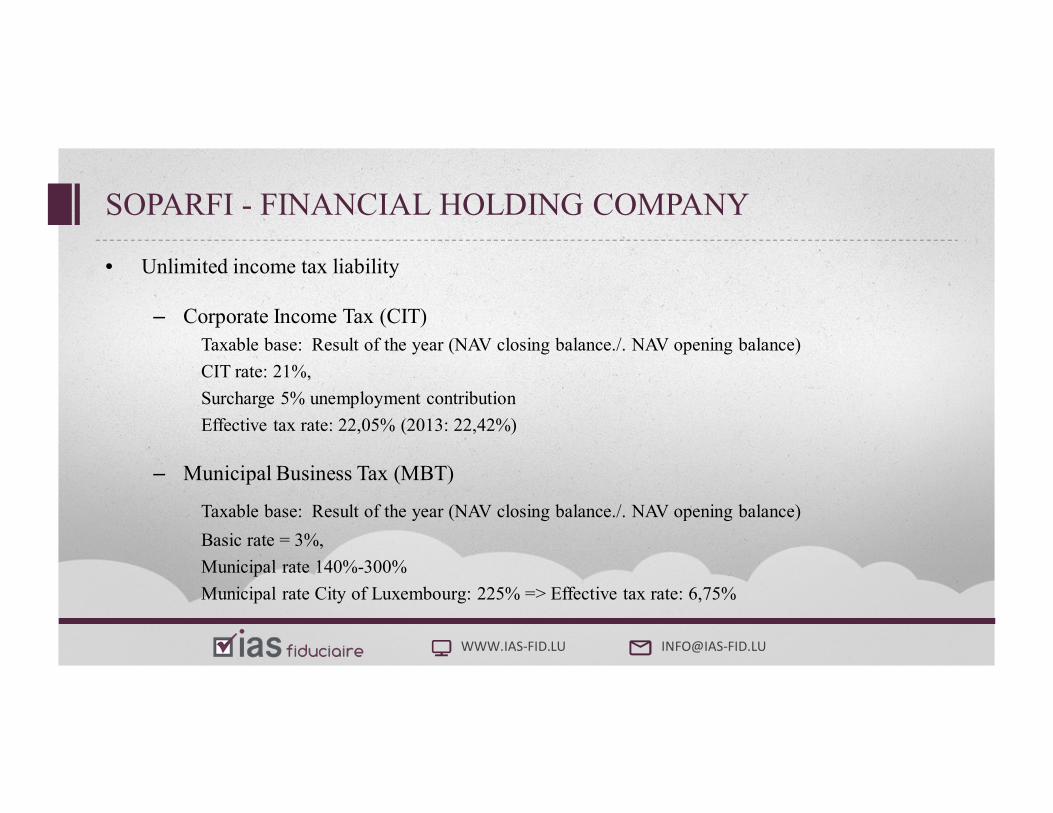

• Unlimited income tax liability

– Corporate Income Tax (CIT)Taxable base: Result of the year (NAV closing balance./. NAV opening balance)

CIT rate: 21%,

Surcharge 5% unemployment contribution

Effective tax rate: 22,05% (2013: 22,42%)

– Municipal Business Tax (MBT)

Taxable base: Result of the year (NAV closing balance./. NAV opening balance)

Basic rate = 3%,

Municipal rate 140%-300%

Municipal rate City of Luxembourg: 225% => Effective tax rate: 6,75%

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

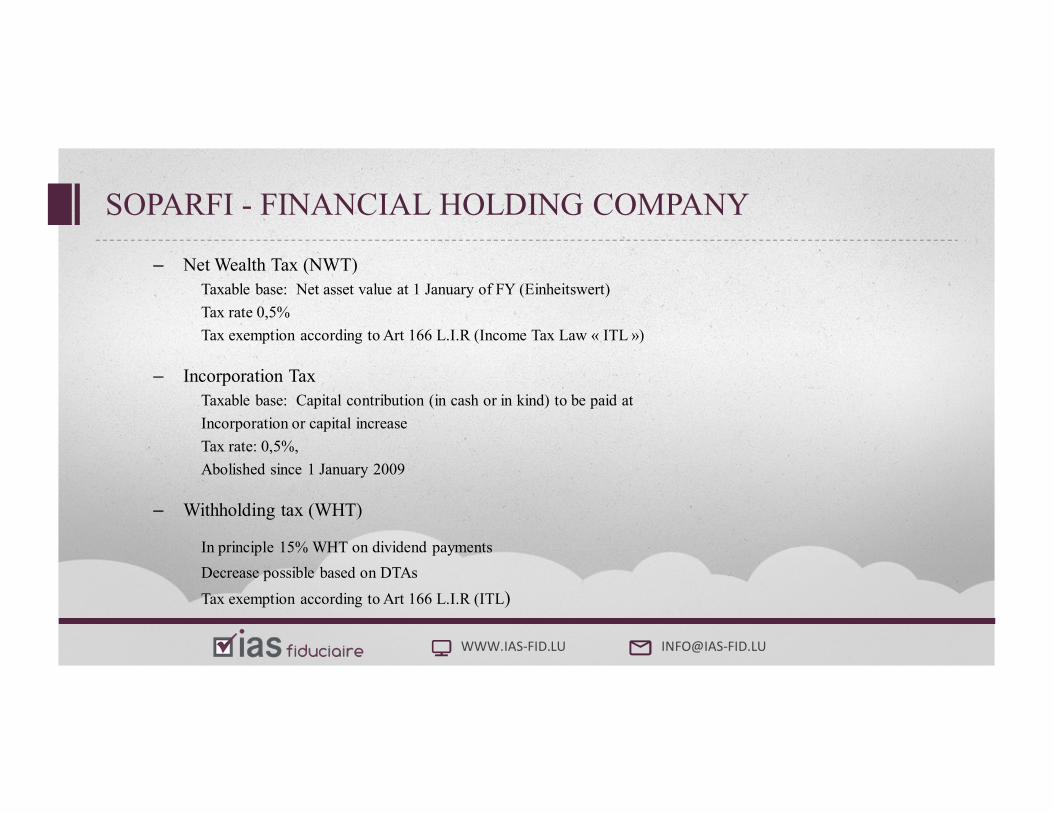

– Net Wealth Tax (NWT)Taxable base: Net asset value at 1 January of FY (Einheitswert)

Tax rate 0,5%

Tax exemption according to Art 166 L.I.R (Income Tax Law « ITL »)

– Incorporation TaxTaxable base: Capital contribution (in cash or in kind) to be paid at

Incorporation or capital increase

Tax rate: 0,5%,

Abolished since 1 January 2009

– Withholding tax (WHT)

In principle 15% WHT on dividend payments

Decrease possible based on DTAs

Tax exemption according to Art 166 L.I.R (ITL)

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Tax exemption on dividend payments

According to Art. 166 L.I.R. dividends payed by a Luxemburg or foreign company to a Luxemburg

SOPARFI are exempt from CIT and MBT if the following conditions are met:

– Participation ≥ 10% or purchase price ≥ EUR 1.200.000

– At date of dividend payment the participation must be hold at least for 12 months

– Distributing subsidiary is• A fully taxable corporate entity resident in Luxembourg

• A foreign fully taxable corporate entity which is subject to a foreign tax corresponding to Luxembourg CIT (Luxembourg tax authorities generally consider a tax rate ≥ 11% as comparable)

• A company residend in an EU country outside Luxembourg applying the Council directive of 23 July 1990

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Tax exemption on capital gains

The Grand-Ducal regulation of 21 December 2001 extended the application of Art 166 L.I.R.

to capital gains from disposal of participations. Capital gains from disposal of participations

are exempt from CIT and MBT if the following conditions are met:

– Participation ≥ 10% or purchase price ≥ EUR 6.000.000

– At date of disposal the participation must be hold at least for 12 months

– The subsidiary is a fully taxable corporate entity registered in Luxembourg or a foreignfully taxable corporate entity which is subject to a foreign tax corresponding to Luxembourg CIT (Luxembourg tax authorities generally consider a tax rate ≥ 11% as comparable)

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Tax exemption on NWT

The net asset value of a participation is exempt from NWT if the following conditions are met:

– Participation ≥ 10% or purchase price ≥ EUR 1.200.000

– The subsidiary is• A fully taxable corporate entity resident in Luxembourg

• A foreign fully taxable corporate entity which is subject to a foreign tax corresponding to Luxembourg CIT (Luxembourg tax authorities generally consider a tax rate ≥ 11% as comparable)

• A company residend in an EU country outside Luxembourg applying the Council directive of 23 July 1990

No holding period of participation is defined by law

If the SOPARFI financed the purchase of the participation by a loan this amount is not exempt from NWT

=> net on disposal of fixed assets approach

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Thin Capitalization Rules

– No statutory role in Luxembourg tax law regarding an debt-equity ratio

– Practice: 85/15 debt-equity ratio accepted by Luxmbourg tax authorities

– Within this limit, interest on debt paid or accrued tax is exempt from withholding tax

– Should this ratio be exceeded, tax autorties may qualify a part of the shareholder’s loan as equity. Related interest payments would then be recast as hidden dividend payment.

– No restriction of debt-equity ratio relating to liabilities to external parties

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Tax exemptions in a nutshell

– Net wealth tax

– Dividend payments

– Capital gains from disposal of participation

– Witholding tax

– Liquidation proceeds

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Application

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Characteristics

– Unregulated Vehicle

– No investment and investors restrictions

– No risk spreading requirements

– Vehicle quickly set-up, designed for pure participation taking in qualifying subsidiaries

– Flexible financing policy (however: thin capitalization rules)

– Frequently used by PE Funds because of limited incorporation expenses and operating costs

– Application of double tax treaties

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

Characteristics

– Flexible dividend distribution policy realizable by flexible financingstructuring or by implementing hybride financialinstruments/mezzanine capital

– Flexible dividend distribution by (interim) dividend payments withinthe limits of Art 72-2 of Law of 10 August 1915 concerningcommercial companies

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

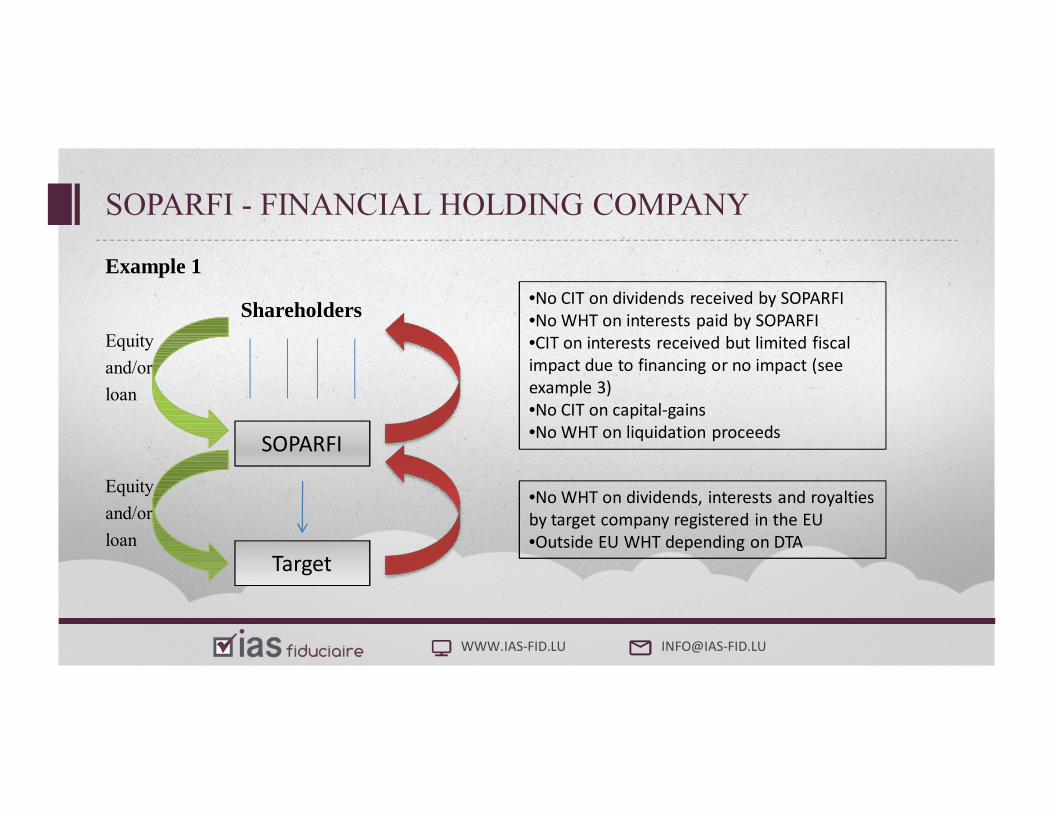

SOPARFI

Target

Example 1

ShareholdersEquity

and/or

loan

Equity

and/or

loan

•No CIT on dividends received by SOPARFI•No WHT on interests paid by SOPARFI •CIT on interests received but limited fiscal impact due to financing or no impact (seeexample 3)•No CIT on capitalgains•No WHT on liquidation proceeds

•No WHT on dividends, interests and royalties by target company registered in the EU•Outside EU WHT depending on DTA

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

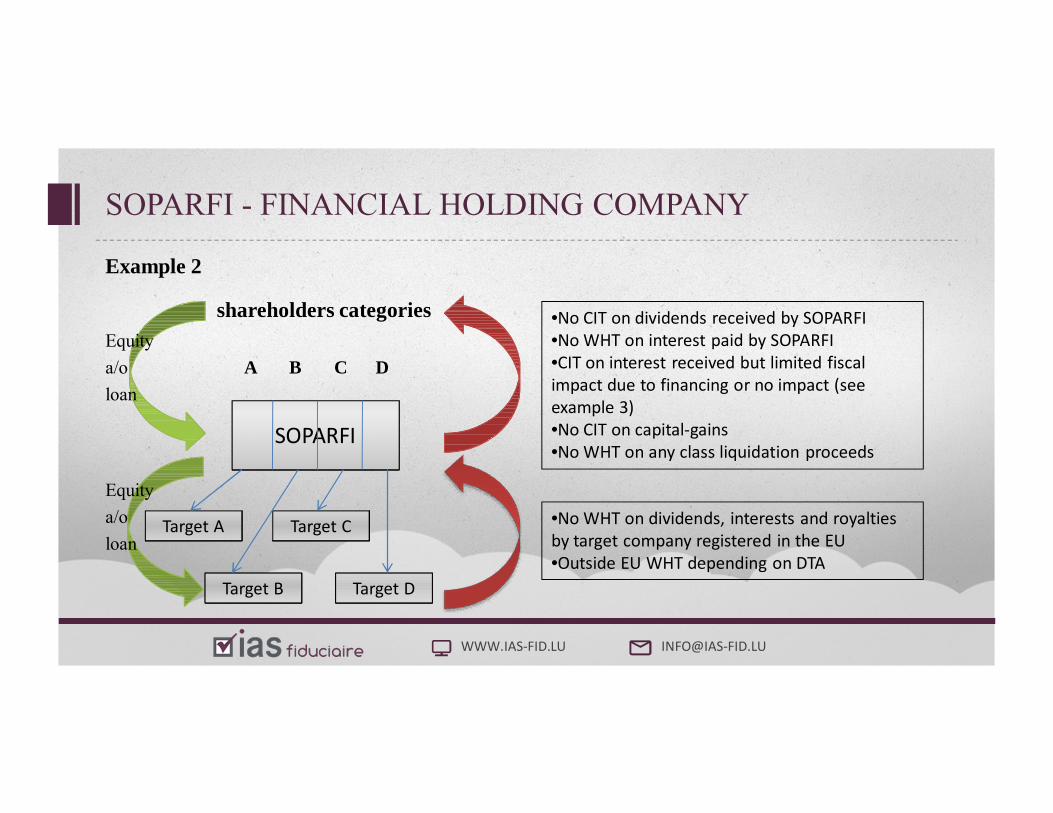

SOPARFI

Target A

Target B

Target C

Target D

•No CIT on dividends received by SOPARFI•No WHT on interest paid by SOPARFI •CIT on interest received but limited fiscal impact due to financing or no impact (seeexample 3)•No CIT on capitalgains•No WHT on any class liquidation proceeds

Example 2

shareholders categoriesEquity

a/o A B C D

loan

Equity

a/o

loan•No WHT on dividends, interests and royalties by target company registered in the EU•Outside EU WHT depending on DTA

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

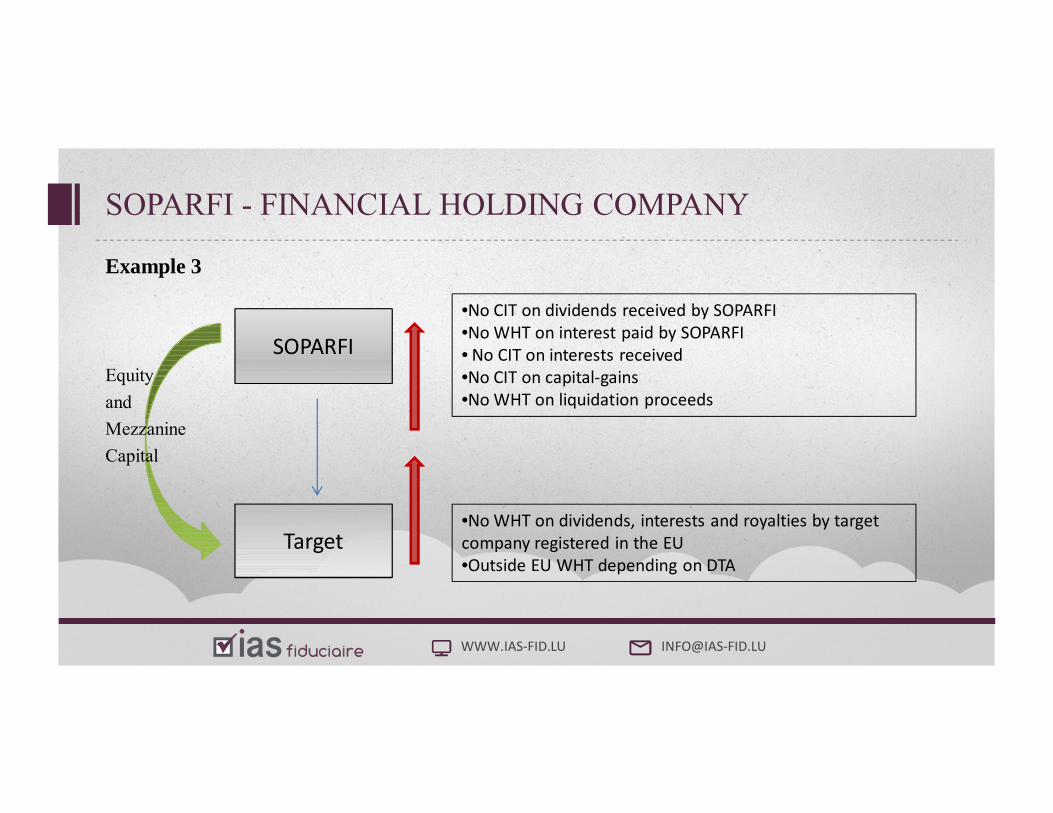

SOPARFI

Target

Example 3

Equity

and

Mezzanine

Capital

•No CIT on dividends received by SOPARFI

•No WHT on interest paid by SOPARFI

• No CIT on interests received

•No CIT on capitalgains

•No WHT on liquidation proceeds

•No WHT on dividends, interests and royalties by target

company registered in the EU

•Outside EU WHT depending on DTA

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

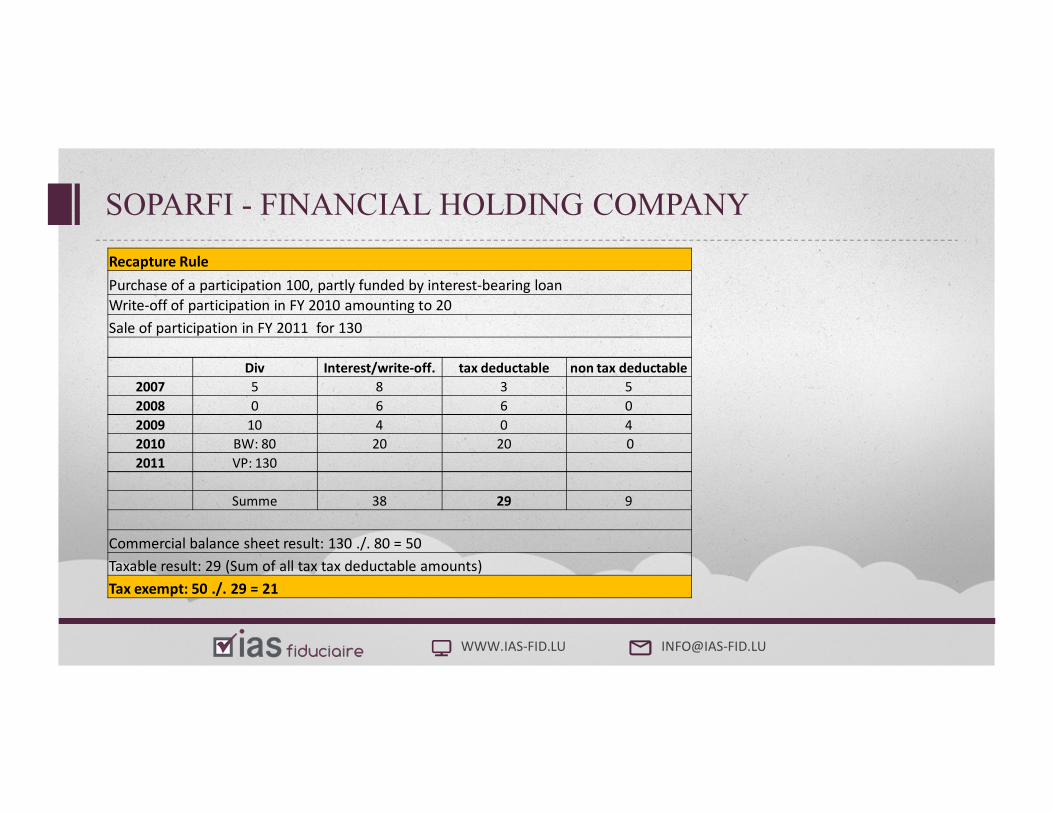

Recapture Rule

Purchase of a participation 100, partly funded by interestbearing loan

Writeoff of participation in FY 2010 amounting to 20

Sale of participation in FY 2011 for 130

Div Interest/writeoff. tax deductable non tax deductable

2007 5 8 3 5

2008 0 6 6 0

2009 10 4 0 4

2010 BW: 80 20 20 0

2011 VP: 130

Summe 38 29 9

Commercial balance sheet result: 130 ./. 80 = 50

Taxable result: 29 (Sum of all tax tax deductable amounts)

Tax exempt: 50 ./. 29 = 21

WWW.IASFID.LU INFO@IASFID.LU

SOPARFI - FINANCIAL HOLDING COMPANY

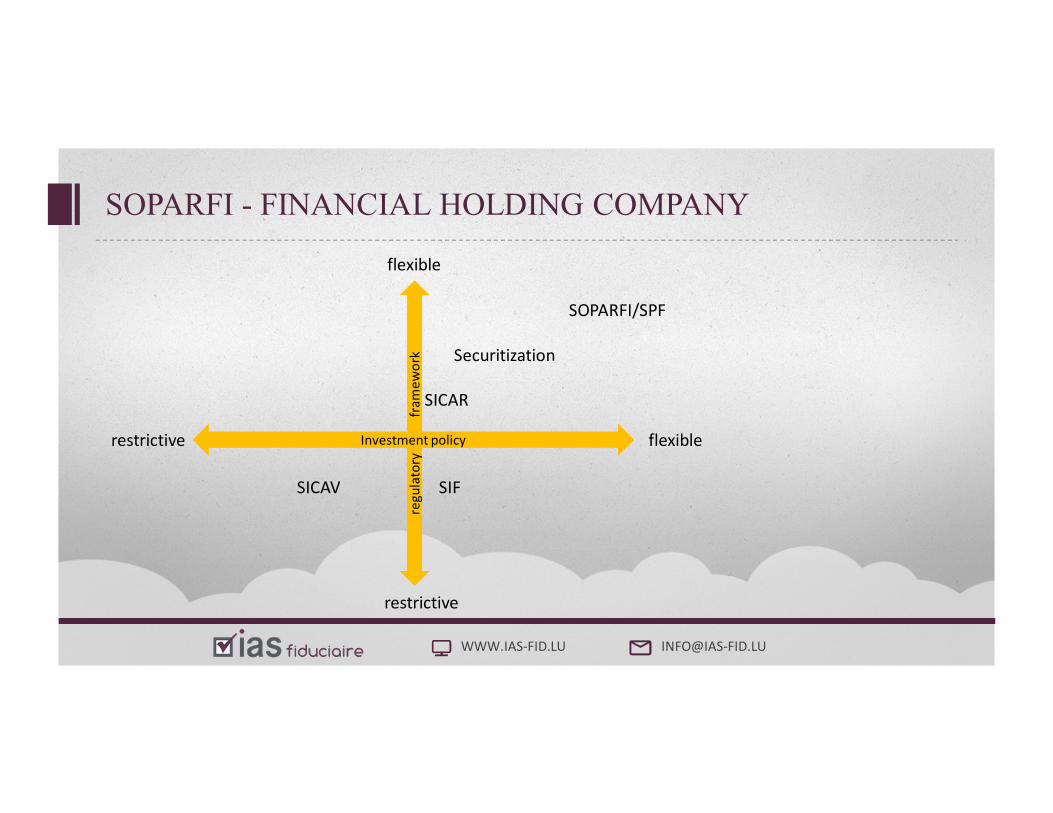

reg

ula

tory

fra

me

wo

rk

Investment policy

restrictive

flexible

restrictive flexible

SICAV SIF

SICAR

Securitization

SOPARFI/SPF

WWW.IASFID.LU INFO@IASFID.LU

QUESTIONS & ANSWERS

Q&A

WWW.IASFID.LU INFO@IASFID.LU

CONTACT US:

www.iasfid.lu

info@iasfid.lu

IAS Fiduciaire S.à r.l.54, route de MondorfL-3260 Bettembourg

Tel.: + 352 275 101 40

Fax: + 352 275 101 41