Embed Size (px)

Citation preview

Presenter logo Here

Tax Tips, Tools and Traps

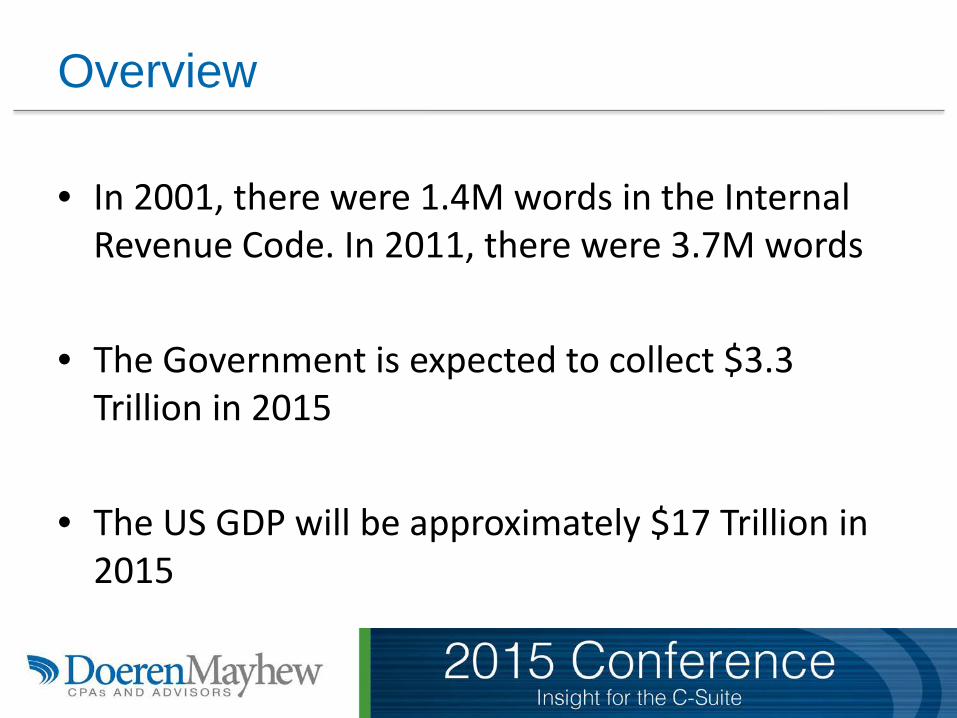

Presenter Logo here Overview

• In 2001, there were 1.4M words in the Internal Revenue Code. In 2011, there were 3.7M words

• The Government is expected to collect $3.3 Trillion in 2015

• The US GDP will be approximately $17 Trillion in 2015

Presenter Logo here Overview (continued)

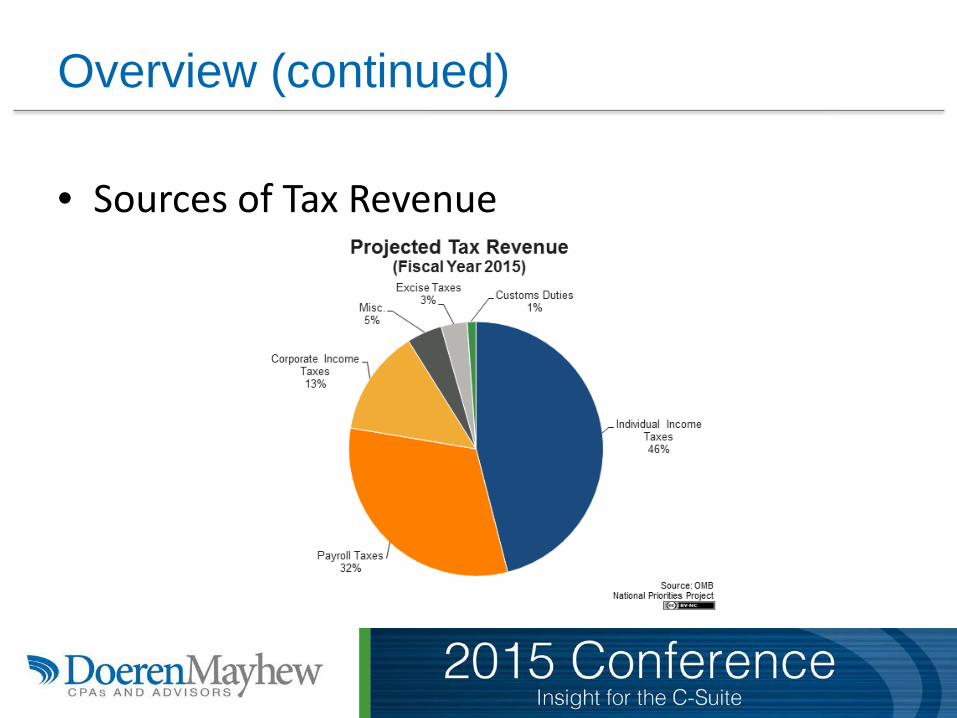

• Sources of Tax Revenue

Presenter Logo here Overview (continued)

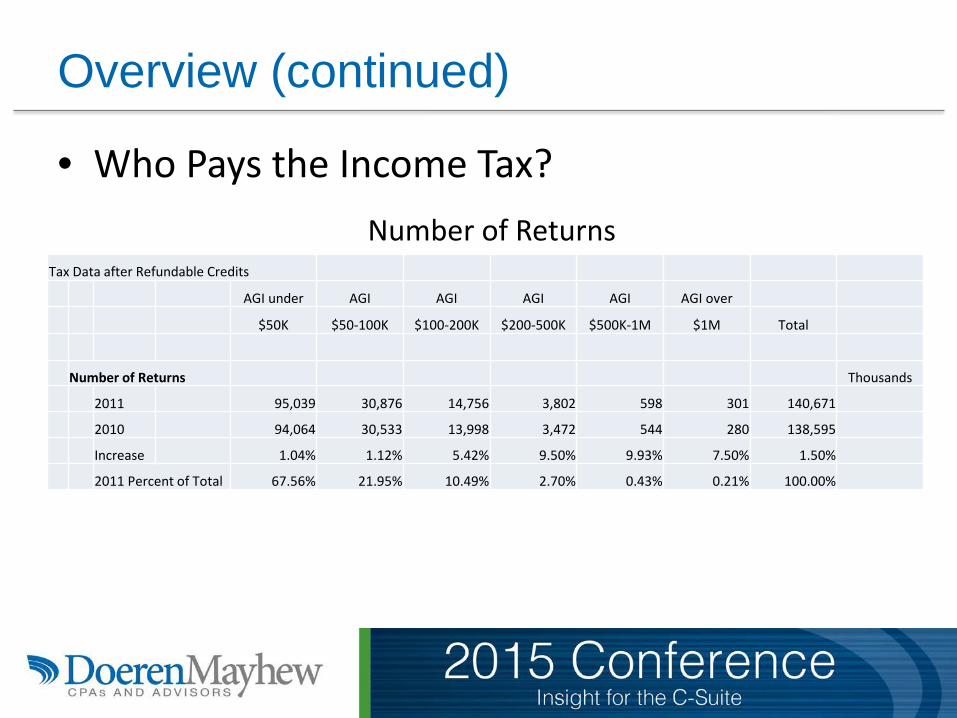

• Who Pays the Income Tax?

Tax Data after Refundable Credits

AGI under AGI AGI AGI AGI AGI over

$50K $50-100K $100-200K $200-500K $500K-1M $1M Total

Number of Returns Thousands

2011 95,039 30,876 14,756 3,802 598 301 140,671

2010 94,064 30,533 13,998 3,472 544 280 138,595

Increase 1.04% 1.12% 5.42% 9.50% 9.93% 7.50% 1.50%

2011 Percent of Total 67.56% 21.95% 10.49% 2.70% 0.43% 0.21% 100.00%

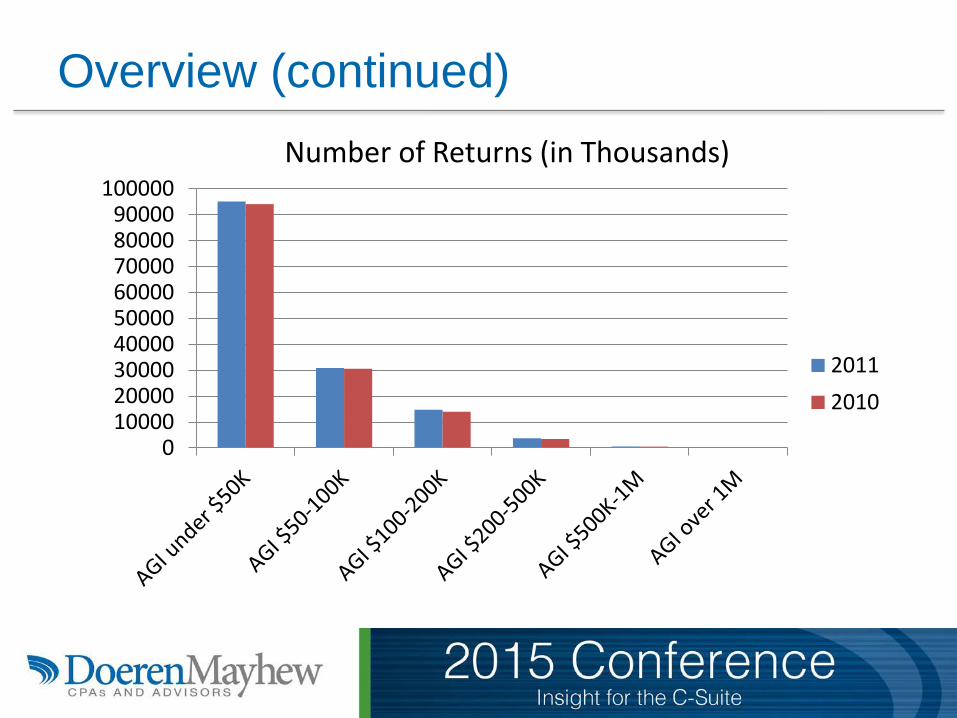

Number of Returns

Presenter Logo here Overview (continued)

0100002000030000400005000060000700008000090000

100000

20112010

Number of Returns (in Thousands)

Presenter Logo here Overview (continued)

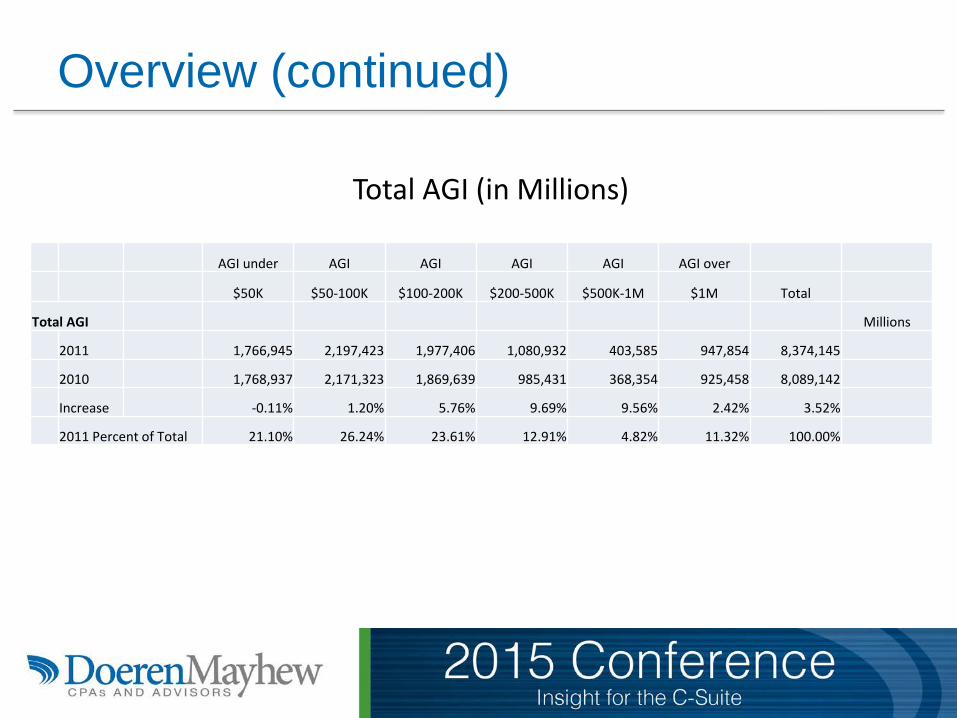

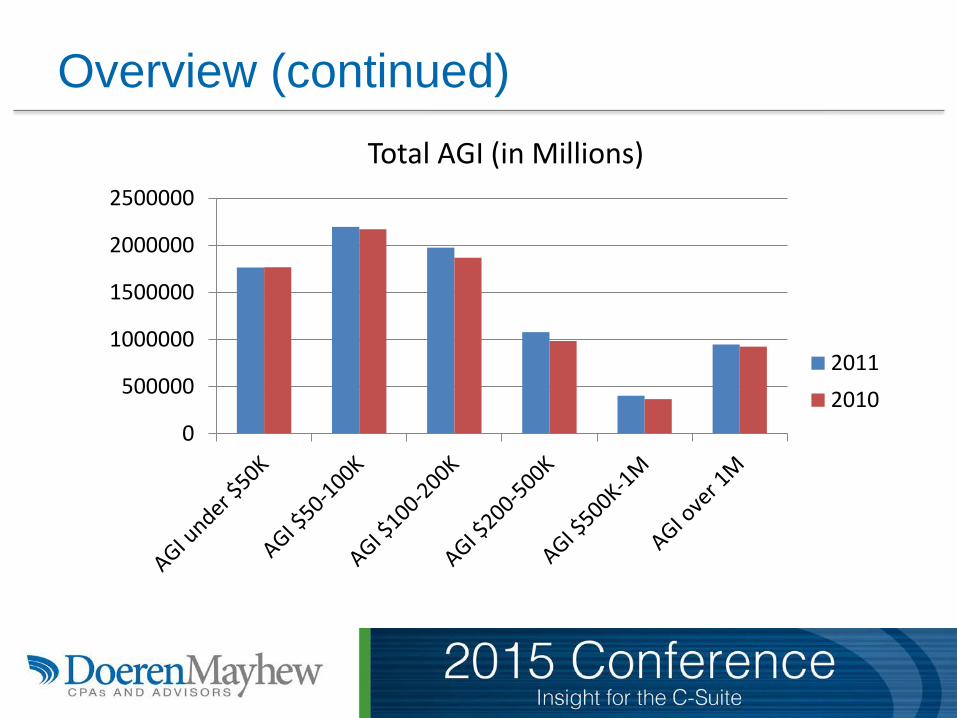

AGI under AGI AGI AGI AGI AGI over

$50K $50-100K $100-200K $200-500K $500K-1M $1M Total

Total AGI Millions

2011 1,766,945 2,197,423 1,977,406 1,080,932 403,585 947,854 8,374,145

2010 1,768,937 2,171,323 1,869,639 985,431 368,354 925,458 8,089,142

Increase -0.11% 1.20% 5.76% 9.69% 9.56% 2.42% 3.52%

2011 Percent of Total 21.10% 26.24% 23.61% 12.91% 4.82% 11.32% 100.00%

Total AGI (in Millions)

Presenter Logo here Overview (continued)

0

500000

1000000

1500000

2000000

2500000

20112010

Total AGI (in Millions)

Presenter Logo here Overview (continued)

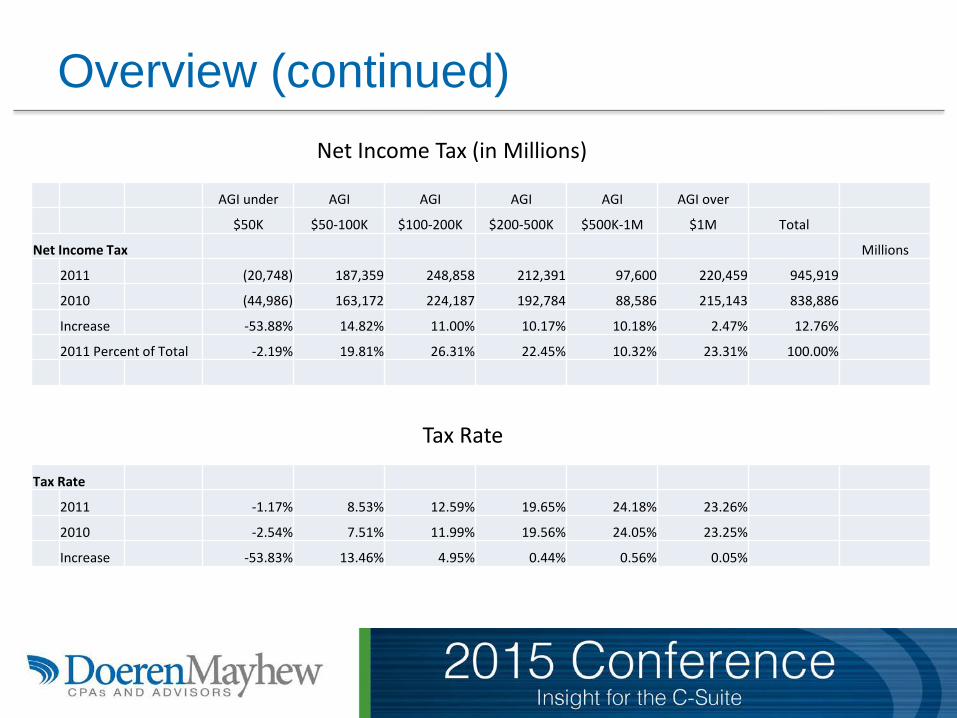

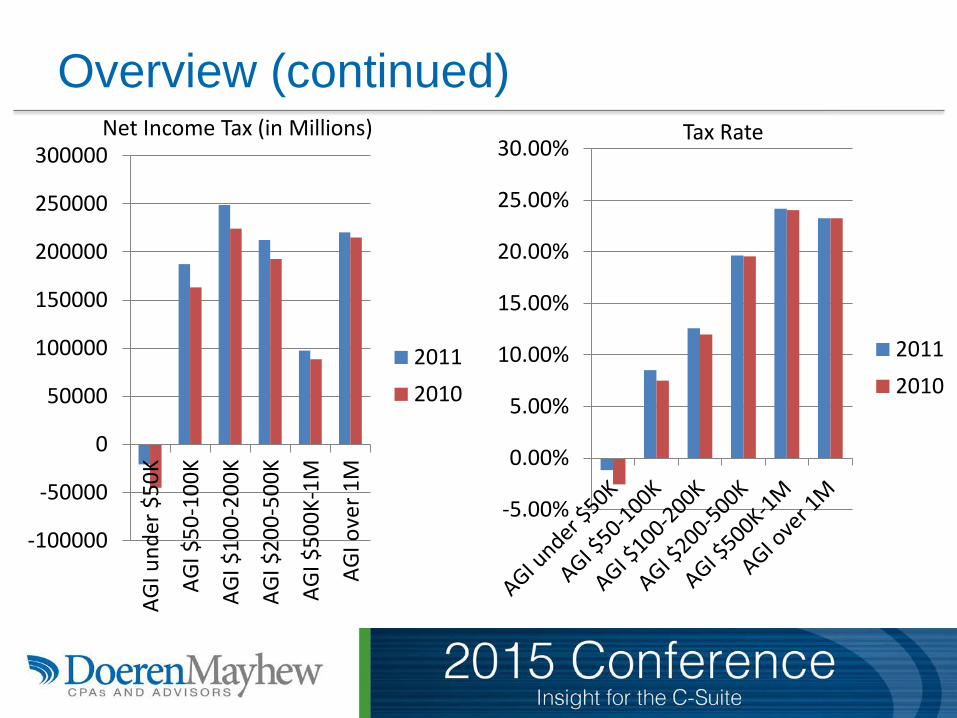

AGI under AGI AGI AGI AGI AGI over

$50K $50-100K $100-200K $200-500K $500K-1M $1M Total

Net Income Tax Millions

2011 (20,748) 187,359 248,858 212,391 97,600 220,459 945,919

2010 (44,986) 163,172 224,187 192,784 88,586 215,143 838,886

Increase -53.88% 14.82% 11.00% 10.17% 10.18% 2.47% 12.76%

2011 Percent of Total -2.19% 19.81% 26.31% 22.45% 10.32% 23.31% 100.00%

Net Income Tax (in Millions)

Tax Rate

2011 -1.17% 8.53% 12.59% 19.65% 24.18% 23.26%

2010 -2.54% 7.51% 11.99% 19.56% 24.05% 23.25%

Increase -53.83% 13.46% 4.95% 0.44% 0.56% 0.05%

Tax Rate

Presenter Logo here Overview (continued)

-100000

-50000

0

50000

100000

150000

200000

250000

300000AG

I und

er $

50K

AGI $

50-1

00K

AGI $

100-

200K

AGI $

200-

500K

AGI $

500K

-1M

AGI o

ver 1

M20112010

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

20112010

Tax Rate Net Income Tax (in Millions)

Presenter Logo here

Year End Tax Extender Legislation for Individuals • Sales Tax Deduction through 2014 • Higher Education Deduction through 2014 with

an AGI limit • Exclusion of Mortgage Debt Cancellation through

2014 for up to $2M

Presenter Logo here

Year End Tax Extender Legislation for Individuals (continued)

• Mortgage Insurance Premium deductions through 2014 with an AGI limit

• Exclusion of Charitable Distributions from IRA’s through 2014 up to $100K

Presenter Logo here

Year End Tax Extender Legislation for Individuals (continued)

• The extender package did not address the Pease Limitation that was brought back in 2013 that reduces the value of itemized deductions by 3% for every dollar above $305K up to 80%. The limit does not impact medical expenses, investment interest expenses, casualty losses, and gambling losses.

Presenter Logo here

Year End Tax Extender Legislation for Businesses • Good news on Bonus Depreciation since the 50

percent deduction was extended through 2014.

• Same for Section 179 with a $500K expensing election with a $2M phase out investment limitation. After 2015, the deduction reverts again to $25K.

Presenter Logo here

Year End Tax Extender Legislation for Businesses (continued)

• Improvements to Qualified Leasehold Property have beneficial recovery options that are often overlooked

• The R&D credit was extended through 2014.

• 100% Exclusion for Gain on Qualified Small Business Stock was extended through 2014 for stock acquired after September 2010 and before 2015.

Presenter Logo here

Year End Tax Extender Legislation for Businesses (continued)

• The Work Opportunity Credit was extended through

2014. Generally, this is $2,400 tax credit against the first year wages of a newly-hired veteran.

• The Built-in Gains Tax Reduced Recognition Period for S Corporations was extended through 2014. Generally, the recognition period is 10 years; however, it is only 5 years for asset dispositions occurring in 2011-2014.

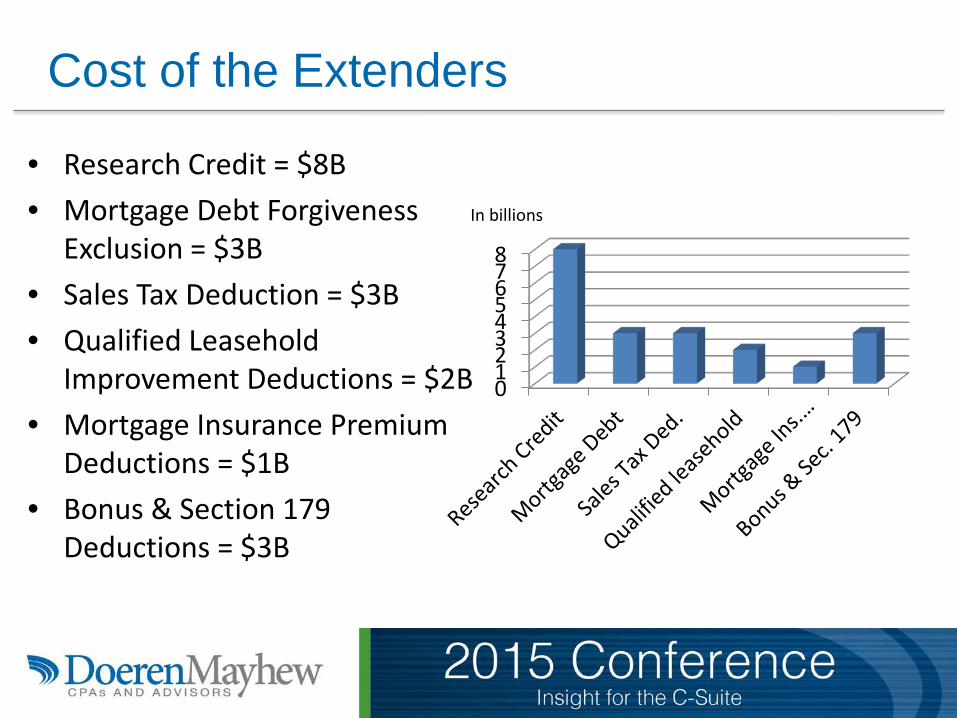

Presenter Logo here Cost of the Extenders

• Research Credit = $8B • Mortgage Debt Forgiveness

Exclusion = $3B • Sales Tax Deduction = $3B • Qualified Leasehold

Improvement Deductions = $2B • Mortgage Insurance Premium

Deductions = $1B • Bonus & Section 179

Deductions = $3B

012345678

In billions

Presenter Logo here The President’s Proposals for Individuals

• Make permanent the Earned Income and related credits based on AGI limitations – cost is $154B

• Expand the Earned Income Credit to childless workers – cost is $60B

• IRA Auto Enrollment – cost is $15B

Presenter Logo here

The President’s Proposals for Individuals (continued)

• Limit the benefit from itemized deductions to 28 percent – increased revenue is $598B

• Reform Estate Tax by reducing the exclusions, increasing the tax rates, and reforming some tax strategies that have been utilized in the past – increased revenue is $131B

Presenter Logo here

The President’s Proposals for Individuals (continued)

• Increased IRS enforcement funding – increased revenue is $75B

• Ensure that the tax rate of any household earning more than $1M is at least 30 percent – increased revenue of $53B

Presenter Logo here

The President’s Proposals for Individuals (continued)

• Restrict the benefit that can be deferred in retirement plans (i.e., limit not just the contribution, but also the earnings of the accounts) – increased revenue is $34B

• Tax a Carried Interest as compensation for investment partnerships – increased revenue is $14B

Presenter Logo here The President’s Proposals for Businesses

• Lower the corporate tax rate to 28 percent for

most corporations and 25 percent for manufacturing – unfortunately this is just a goal as the revenue reduction must be offset by tax increases related to the reduction of “loopholes”.

• Make the Research Credit permanent – cost is $108B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Make permanent the exclusion for investments in Small Business Stocks – cost is $9B

• Increase employer’s FUTA wage base from $7K to $15K – increased revenue is $74B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Change the revenue recognition of derivatives investments to mark-to-market and characterize gains as ordinary income – increased revenue is $19B

• Impose self-employment tax on professional service income generated by S corporations – increased revenue is $38B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Make permanent the Section 179 expensing election – cost is $57B

• Defer interest on foreign investments in offshore businesses until profits are repatriated – increased revenue is $43B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Change the computational method for realizing a Foreign Tax Credit as well as the definition of creditable taxes (the latter would mainly impact E&P companies) – increased revenue is $85B

• Expand the definition of subpart F to include excess profits obtained from IP migrations to low tax jurisdictions – increased revenue is $26B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Restrict deductions related to debt financing of US subsidiaries (earnings stripping) – increased revenue is $49B

• Expand the definition of subpart F to include sales of digital goods and services – increased revenue is $12B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Expand the definition of subpart F by narrowing the application of the manufacturing exception to those foreign subsidiaries that actually make the product (i.e., contract and toll manufacturing arrangement would no longer qualify for the exception) – increased revenue of $25B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Strengthen the anti-inversion provisions of Section 7874 – increased revenue of $17B

• Repeal the LIFO election for inventory – increased revenue of $83B

• Limit the Like-Kind exchange deferral to $1M – increased revenue of $18B

Presenter Logo here

The President’s Proposals for Businesses (continued)

• Require the amortization of intangible drilling costs, eliminate percentage depletion, and exclude use of the DPAD for the extraction industry

• There is an expansion and extension of a number of green energy incentives.

Presenter Logo here

THANK YOU