Embed Size (px)

Citation preview

HRIS Needs Analysis and cost estimations

“Failing to plan is planning to fail.” (Alge & Upright 2009, p.80)

“Use the right tool for the job,” the old saying goes, “and to use the right tool you have to know what job you’re trying to do.”

(Meade 2003, p.84)

2

Do you need one?

3

Australian Defence Force

ADF some time ago flagged its intention to replace the HR systems with a wider solution. In December 2009, chief information officer Greg Farr told ZDNet.com.au that the department expected to ditch the "far from perfect" HR systems in 2009 in a tender worth around $400 million. (LeMay 2009)

http://www.abc.net.au/pm/content/2010/s2815919.htm

4

Payroll implementation

“Behind every successful HRMS implementation, there was a thorough needs analysis". You can quote me on that! I cannot back that statement up statistically, however, after over 25 years in the business and 10 years of listening to IHRIM (International Association for Human Resources Information Management) members share "war stories", I am totally convinced that the amount of time spent on a thorough needs analysis before purchasing and implementing a new HRMS is the best barometer for predicting the success or failure of the project.” (Doran 2010)

5

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

6

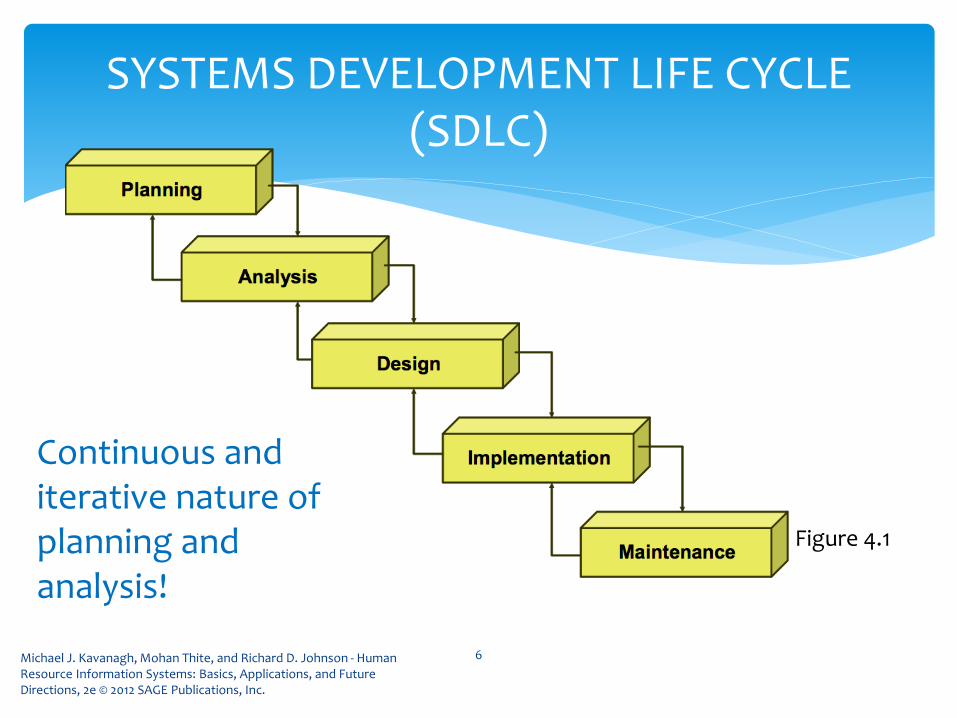

SYSTEMS DEVELOPMENT LIFE CYCLE (SDLC)

Continuous and iterative nature of planning and analysis!

Figure 4.1

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Planning

Long-range

Short-range

Analysis

Needs Analysis

Gap Analysis

7

SDLC: Overview

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Design

“Blue print” for the system

Vendor selection

Implementation

Build, test and readied to “go live”

Maintenance

Corrective, adaptive, perfective & preventative

8

SDLC OVERVIEW

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Needs: long-range planning

Strategic

“Big picture”

Phase containment

Needs: short range planning

Operational

Specific projects and programs

9

SDLC: Planning

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

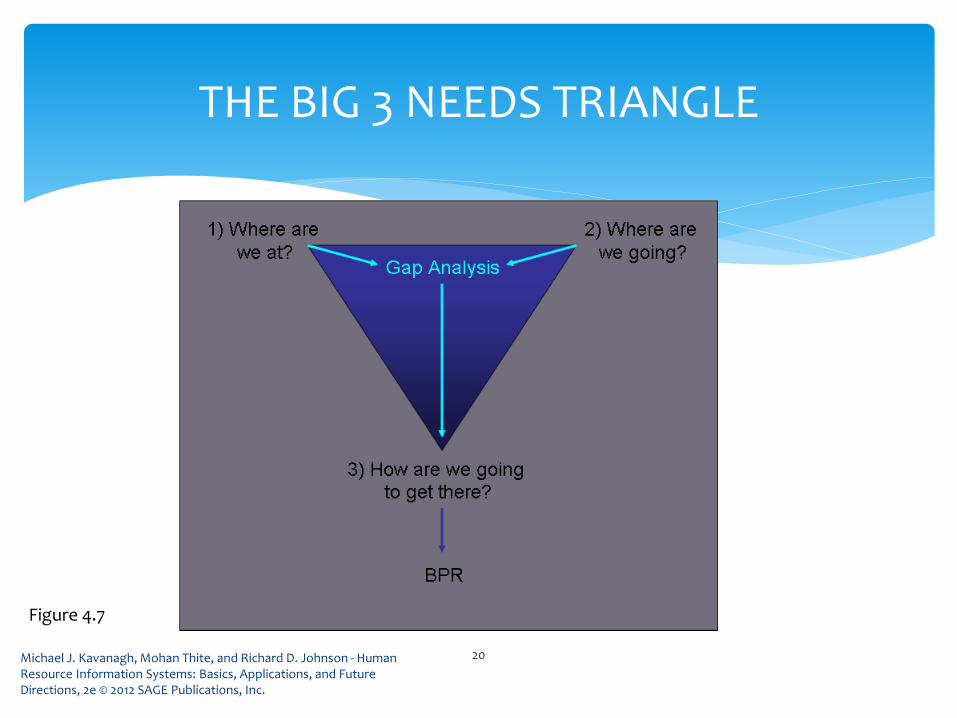

Where are we now?

Where are we going?

How are we going to get there?

Revise and revisit these questions

On a regular basis!

10

THE BIG 3

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Dissect and document current capabilities

Identify and prioritize needs

Conduct A gap analysis

Review the feasibility analysis

Determine usefulness of gap analysis in developing RFP for vendors

11

ANALYSIS

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Current analysis

Use combination of methods:

Interviews

Focus groups

Surveys and online tools

Organizational archives

12

ANALYSIS: WHERE ARE WE NOW?

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Who to ask:

HR functional experts

Job experts

Technical experts

End users

Top management

Consultants and other business partners

13

ANALYSIS: WHERE ARE WE NOW?

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Heart of the needs analysis

Business requirements definition

Point at which organization determines and documents its current and future needs

Often used interchangeably with needs analysis

Prioritize business and system needs

14

ANALYSIS: WHERE WE NEED TO GO

Where are we going?

Strategic vision: To transform the University’s way of doing business into a

flexible and user-centric portfolio of applications that integrates all Purdue enterprise data, information and processes

Helped identify needs in detail and select best system

Resulted in SAP-HCM

15

Purdue University

16

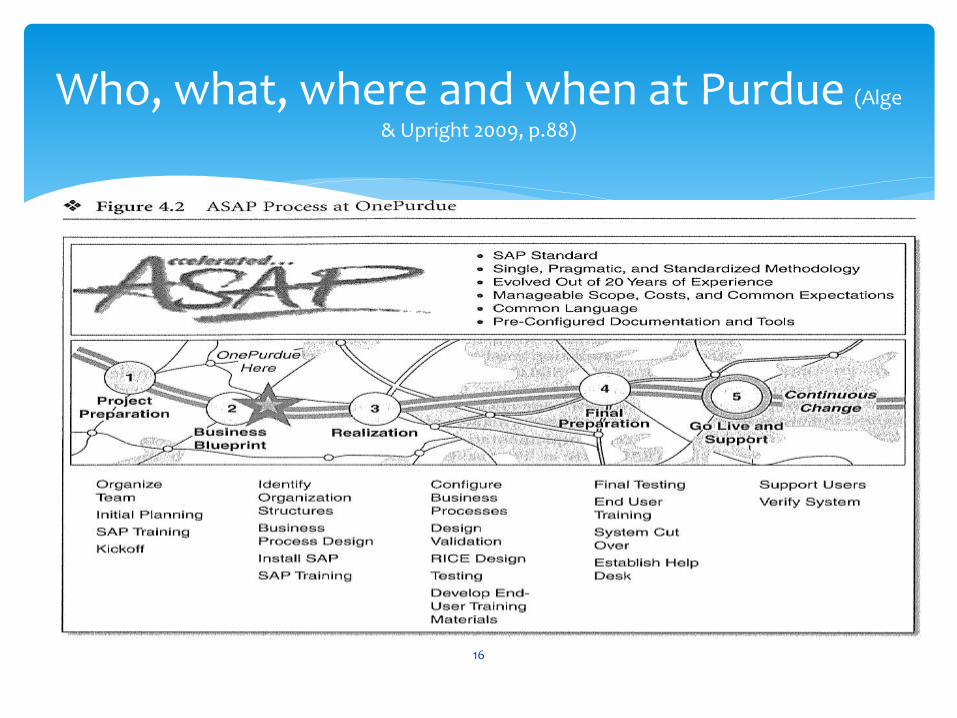

Who, what, where and when at Purdue (Alge

& Upright 2009, p.88)

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

http://www.erp.com/attachments/4074_Accelerated%20SAP%20Implementations.pdf

17

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

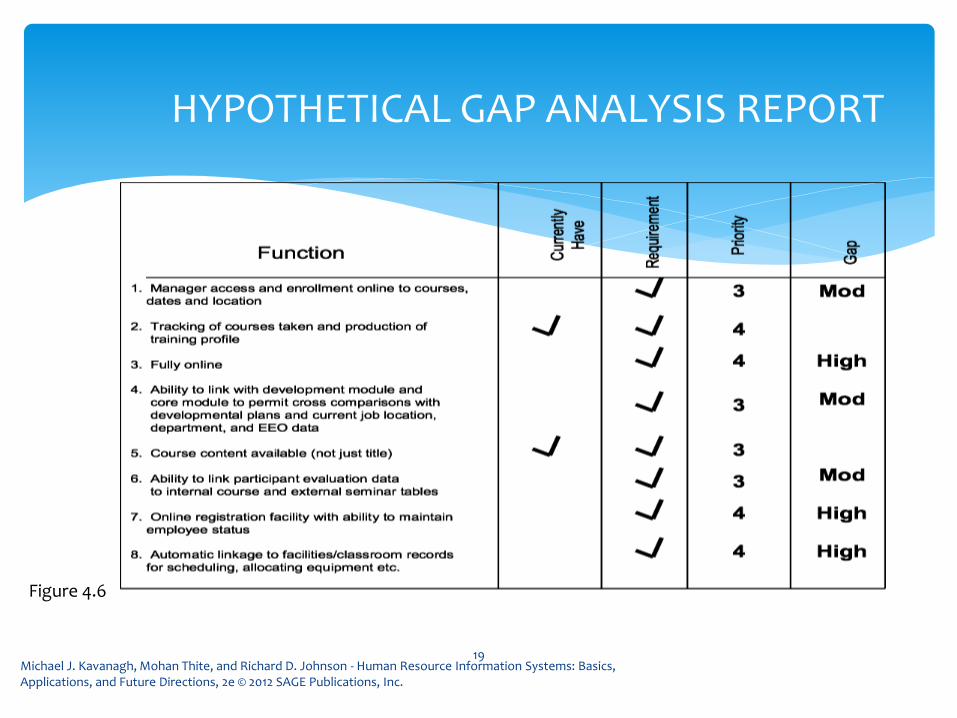

Culmination of the needs analysis.

Compares current state of hris with desired state of hris

What important needs are not being met

What important needs are being met

Important decision making tool for HRIS project leaders.

18

GAP ANALYSIS

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

19

HYPOTHETICAL GAP ANALYSIS REPORT

Figure 4.6

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

20

THE BIG 3 NEEDS TRIANGLE

Figure 4.7

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

Who should determine what our needs are going forward?

How can we ensure that all of our needs are identified?

How do we limit the scope to the things we truly need?

Is it feasible at this point to implement a system that can meet our critical needs?

21

NEEDS ANALYSIS: CRITICAL QUESTIONS

Basically a Project Management activity

Stipulate objectives, activities, time-frame, costs, required resources and staff, information collection methodology

Will help encourage management of project viability

22

Develop a NA Plan

Typically, 2 reports emerge from the NA process

Long, technical, operational document, to guide system development or selection/purchase

Summary version, to trigger action from top management

23

Develop the HRIS Strategy

Finally, a critical review of the whole process

As a guideline for any future modifications, or for a new purchase in future years

an analysis of which activities worked well and which didn’t

a phase possibly ignored by many organisations (many don’t even do NA’s!)

Discuss alternatives

24

Evaluate the NA Effort

There’s no one right way for NA. Every organization is unique.

Even a token attempt at NA can save a lot of time, money, effort and heartache.

25

Conclusion

Lect part 2

Cost Justifying HRIS

Investments

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

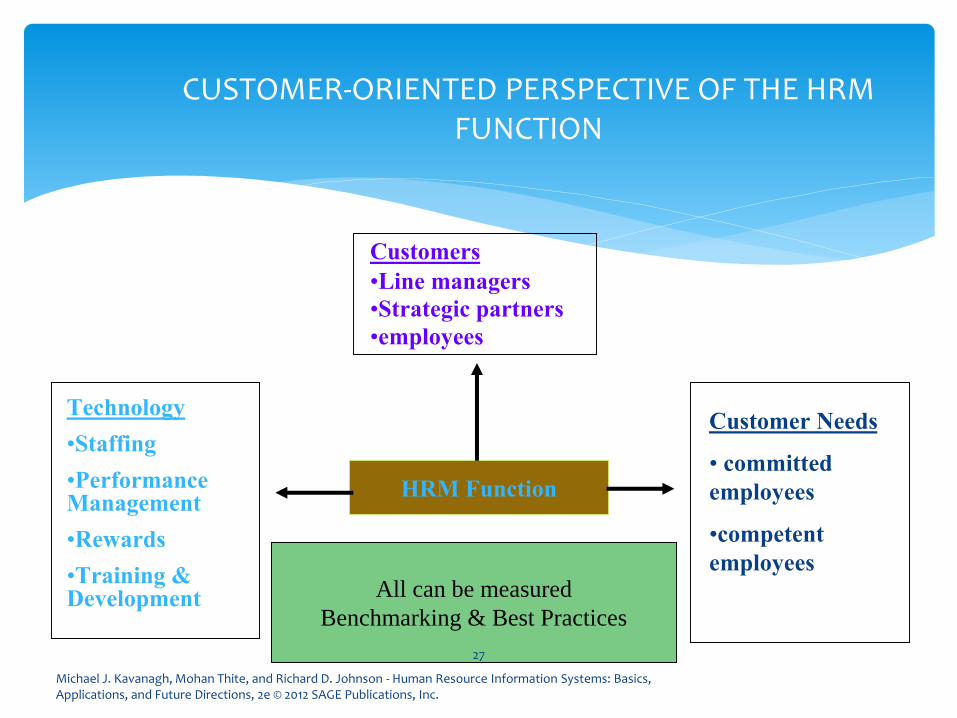

CUSTOMER-ORIENTED PERSPECTIVE OF THE HRM FUNCTION

Customers

•Line managers

•Strategic partners

•employees

HRM Function

Technology

•Staffing

•Performance Management

•Rewards

•Training & Development

Customer Needs

• committed

employees

•competent

employeesAll can be measured

Benchmarking & Best Practices

27

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

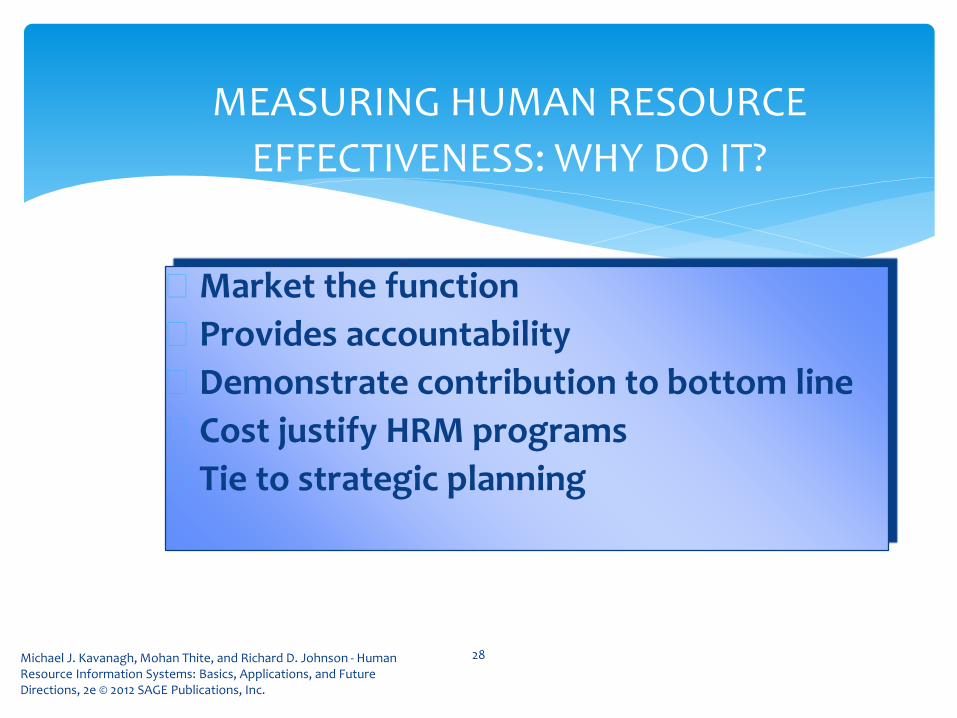

MEASURING HUMAN RESOURCE

EFFECTIVENESS: WHY DO IT?

Market the function

Provides accountability

Demonstrate contribution to bottom line

Cost justify HRM programs

Tie to strategic planning

28

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

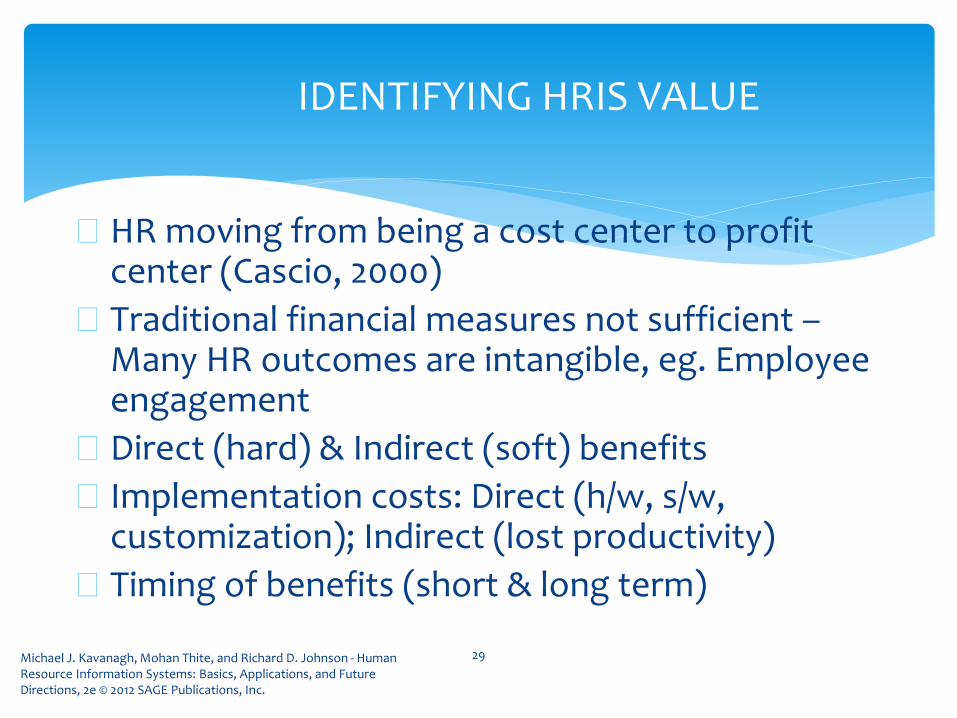

IDENTIFYING HRIS VALUE

HR moving from being a cost center to profit center (Cascio, 2000)

Traditional financial measures not sufficient –Many HR outcomes are intangible, eg. Employee engagement

Direct (hard) & Indirect (soft) benefits

Implementation costs: Direct (h/w, s/w, customization); Indirect (lost productivity)

Timing of benefits (short & long term)

29

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

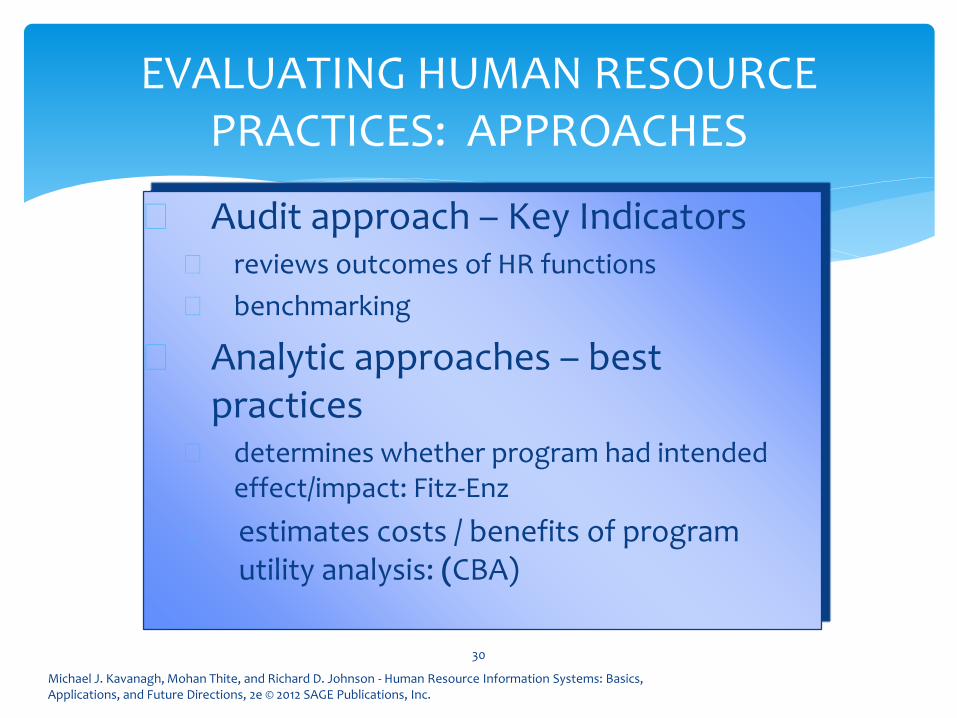

EVALUATING HUMAN RESOURCE PRACTICES: APPROACHES

Audit approach – Key Indicators reviews outcomes of HR functions

benchmarking

Analytic approaches – best practices

determines whether program had intended effect/impact: Fitz-Enz

estimates costs / benefits of programutility analysis: (CBA)

30

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

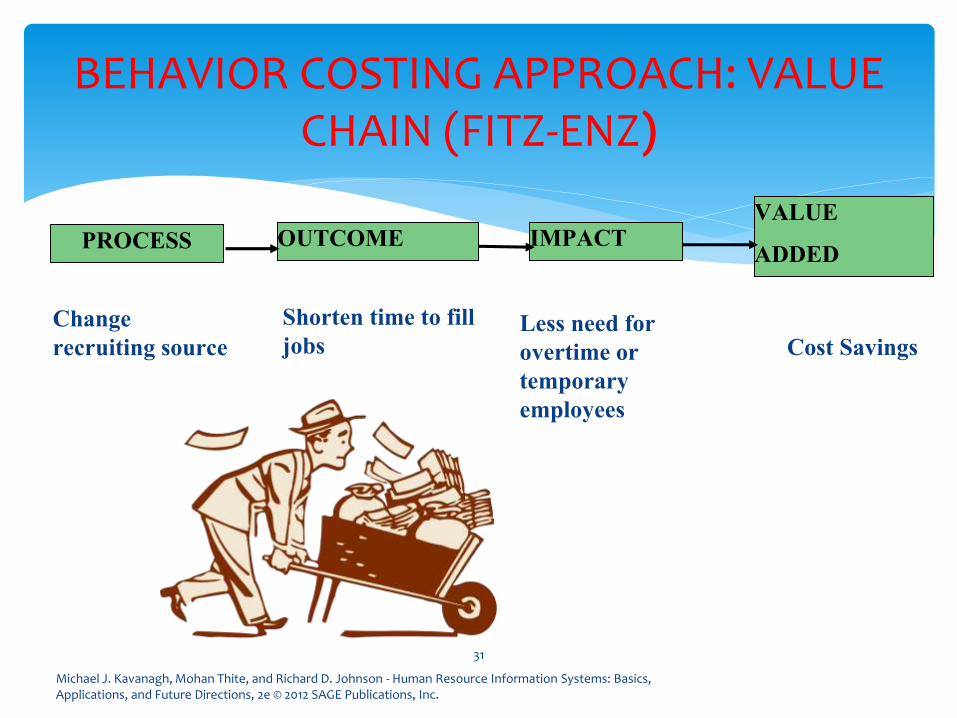

BEHAVIOR COSTING APPROACH: VALUE CHAIN (FITZ-ENZ)

PROCESS

Change

recruiting source

OUTCOME IMPACTVALUE

ADDED

Shorten time to fill

jobsLess need for

overtime or

temporary

employees

Cost Savings

31

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

HRIS COST BENEFIT ANALYSIS

Language of business is dollars & HR should learn this language

HRIS CBA: Comparison of projected costs & benefits

Covers full suit of HRIS functionality (transactional/ traditional/ transformational)

HR Metrics: (Table 6.1, Ch.6) Absence rate/ Cost per hire/ Healthcare costs/ HR Expense factor/ Human capital ROI & value added/ training costs/ turnover costs/ OHS costs…

Compare costs/ value within & outside

32

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

JUSTIFYING HRIS COSTS

Risk Avoidance strategies (Y2K)

Organization Enhancement Strategies: Increased revenue or reduced costs due to new/ improved HRIS

Evolution: Manual to automation; web applications; further improvements will have incremental not radical benefits; Value add is seen as more important than cost reduction but how to measure it?

33

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

GUIDELINES TO SUCCESSFUL CBA

Table 7.1

Objective is improving organisational effectiveness

Be honest with yourself – open mind

Focus on functionality not products

Estimate benefits first & costs later

Know your business

Develop the best estimate possible

Separate CBA from justifying final decision34

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

HRIS CBA INVESTMENT ANALYSIS

Requires three basic pieces of information (1) sources of costs and benefits,

(2) an estimated dollar value for each cost and benefit item, and

(3) the time when the organization will incur each cost and receive each benefit.

35

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

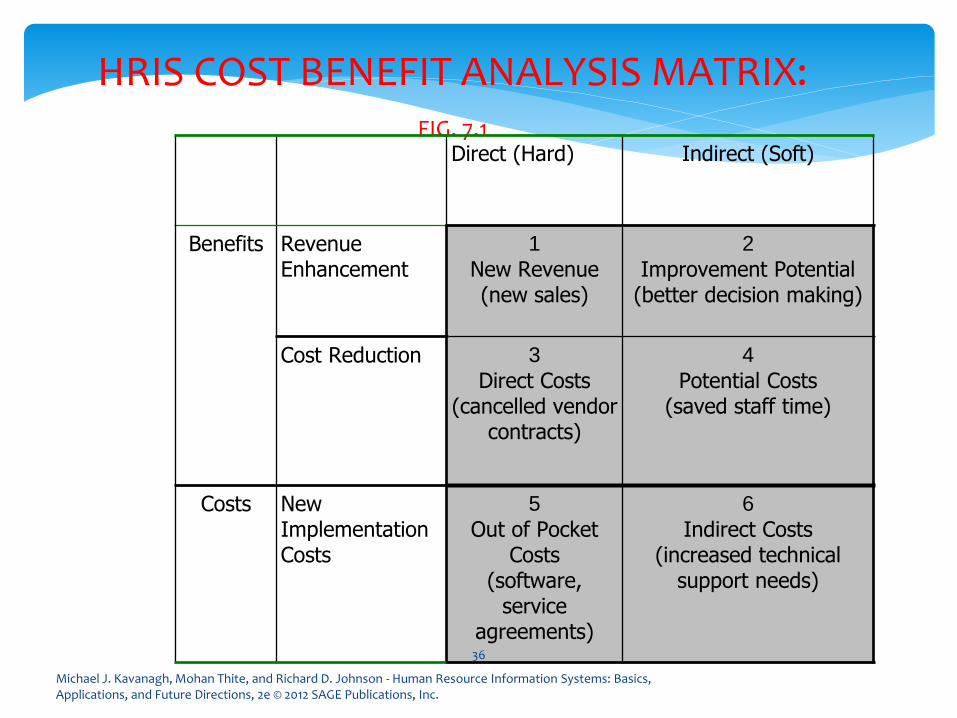

HRIS COST BENEFIT ANALYSIS MATRIX: FIG. 7.1

Direct (Hard) Indirect (Soft)

Benefits Revenue Enhancement

1

New Revenue(new sales)

2

Improvement Potential(better decision making)

Cost Reduction 3

Direct Costs(cancelled vendor

contracts)

4

Potential Costs(saved staff time)

Costs New Implementation Costs

5

Out of Pocket Costs

(software, service

agreements)

6

Indirect Costs(increased technical

support needs)

36

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

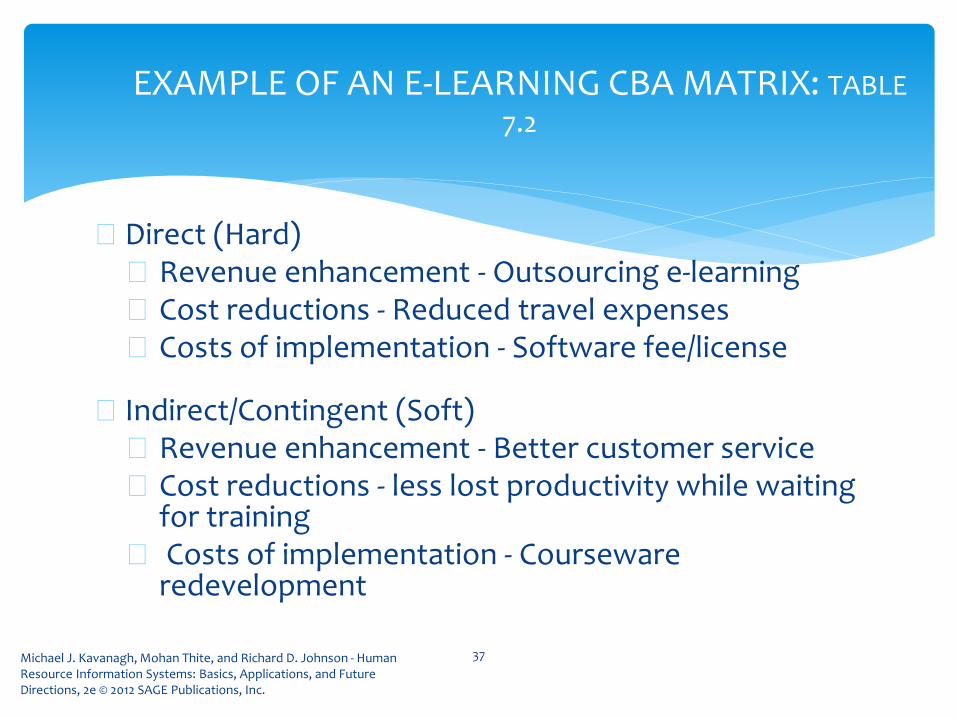

EXAMPLE OF AN E-LEARNING CBA MATRIX: TABLE

7.2

Direct (Hard) Revenue enhancement - Outsourcing e-learning Cost reductions - Reduced travel expenses Costs of implementation - Software fee/license

Indirect/Contingent (Soft) Revenue enhancement - Better customer service Cost reductions - less lost productivity while waiting

for training Costs of implementation - Courseware

redevelopment

37

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

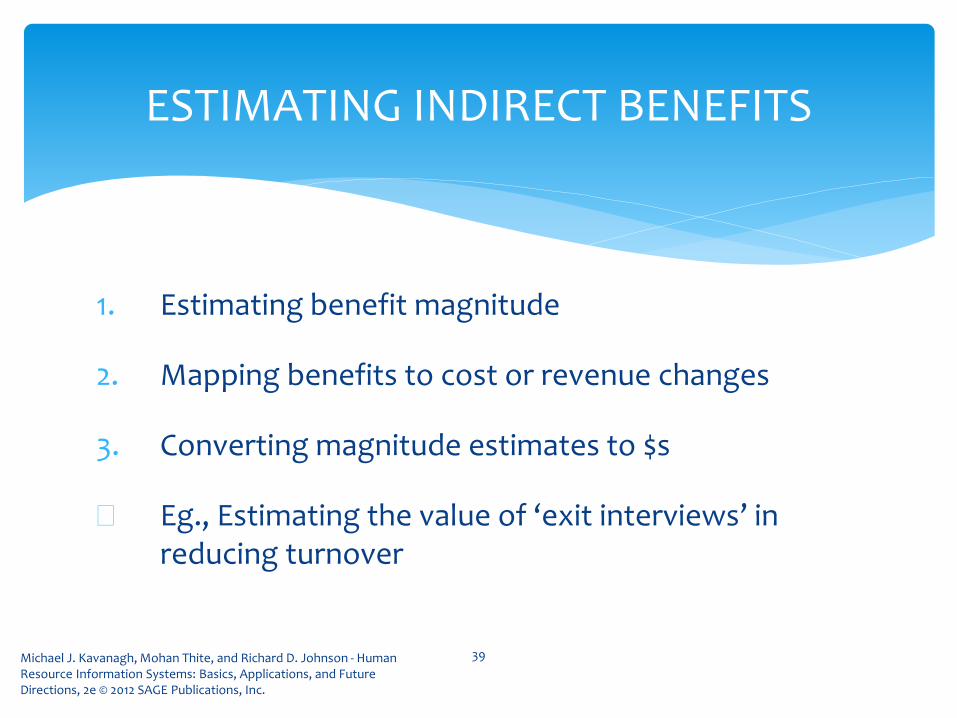

ESTIMATING INDIRECT BENEFITS

1. Estimating benefit magnitude

2. Mapping benefits to cost or revenue changes

3. Converting magnitude estimates to $s

Eg., Estimating the value of ‘exit interviews’ in reducing turnover

39

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

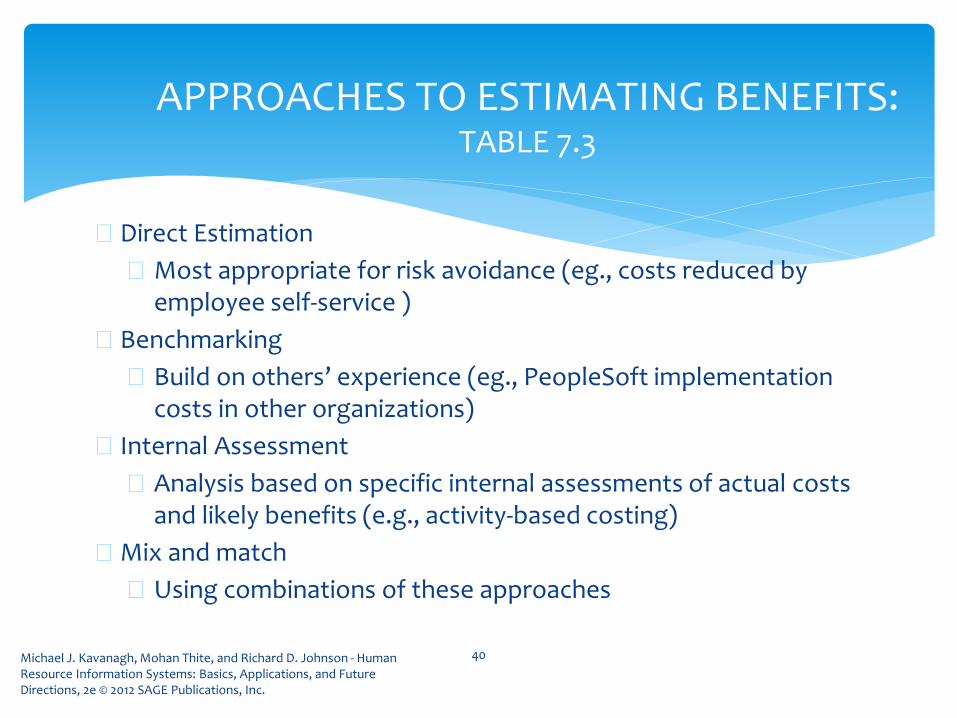

APPROACHES TO ESTIMATING BENEFITS: TABLE 7.3

Direct Estimation

Most appropriate for risk avoidance (eg., costs reduced by employee self-service )

Benchmarking

Build on others’ experience (eg., PeopleSoft implementation costs in other organizations)

Internal Assessment

Analysis based on specific internal assessments of actual costs and likely benefits (e.g., activity-based costing)

Mix and match

Using combinations of these approaches

40

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

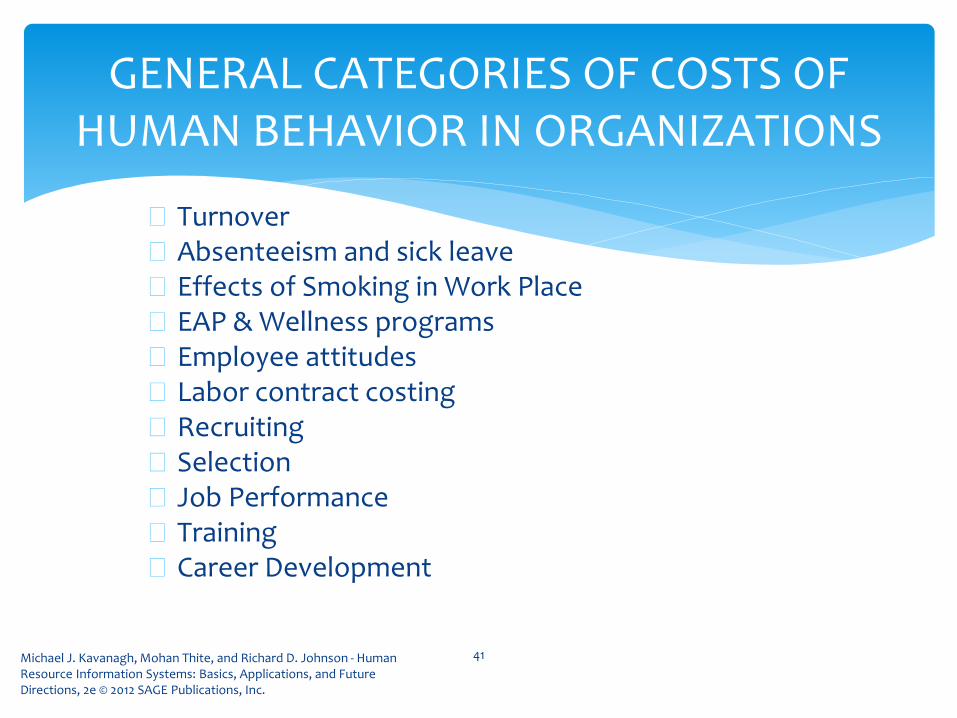

GENERAL CATEGORIES OF COSTS OF HUMAN BEHAVIOR IN ORGANIZATIONS

Turnover Absenteeism and sick leave Effects of Smoking in Work Place EAP & Wellness programs Employee attitudes Labor contract costing Recruiting Selection Job Performance Training Career Development

41

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

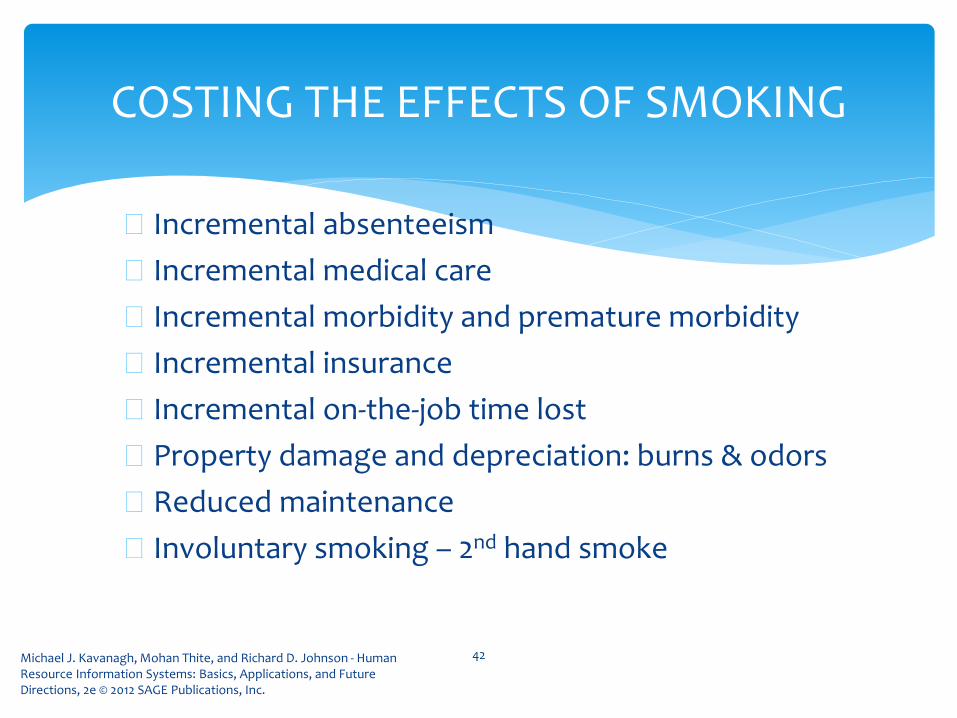

COSTING THE EFFECTS OF SMOKING

Incremental absenteeism

Incremental medical care

Incremental morbidity and premature morbidity

Incremental insurance

Incremental on-the-job time lost

Property damage and depreciation: burns & odors

Reduced maintenance

Involuntary smoking – 2nd hand smoke

42

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

COSTING EMPLOYEE TURNOVER

3 components of costing employee turnover

Separation costs

Replacement costs

Training costs

43

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

SEPARATION COSTS

The four components of separation costs are as follows:

Exit Interview Interviewers time

Termination time

Administrative Functions Related to Termination Removal of employee from payroll

Termination of employee benefits

Turn-in of company equipment

Separation Pay Severance packages

44

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

REPLACEMENT COSTS

Replacement costs consist of eight components as follows:

Communication of job availability

Pre-employment administrative functions

Entrance interviews

Testing

Staff meetings

Travel and moving expenses

Post employement acquisition and dissemination of information

Medical examination45

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

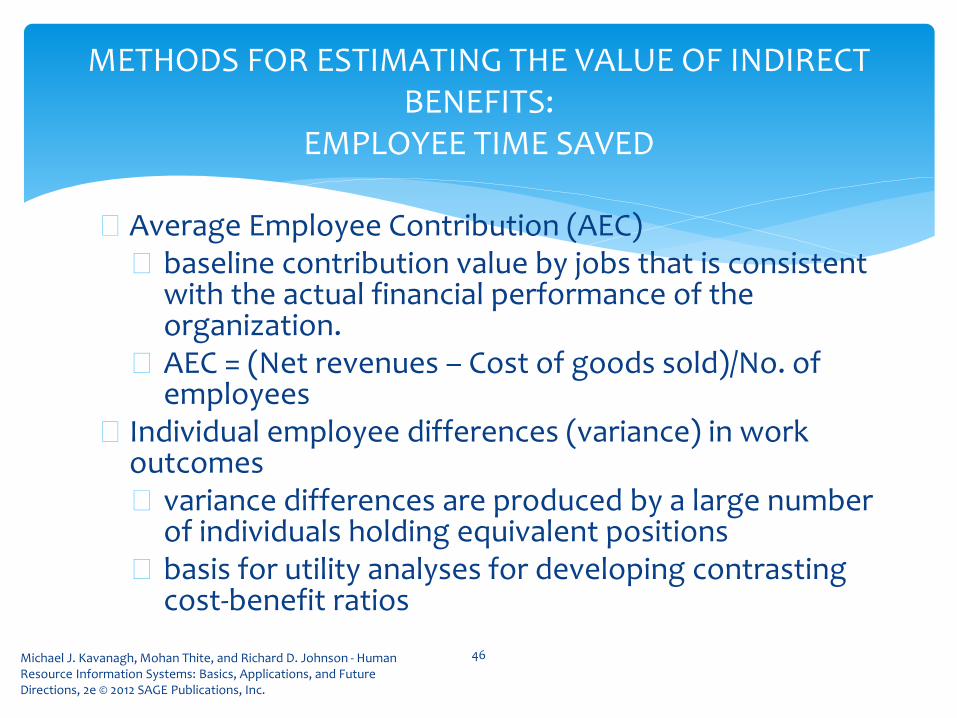

METHODS FOR ESTIMATING THE VALUE OF INDIRECT BENEFITS:

EMPLOYEE TIME SAVED

Average Employee Contribution (AEC) baseline contribution value by jobs that is consistent

with the actual financial performance of the organization.

AEC = (Net revenues – Cost of goods sold)/No. of employees

Individual employee differences (variance) in work outcomes variance differences are produced by a large number

of individuals holding equivalent positions basis for utility analyses for developing contrasting

cost-benefit ratios

46

Michael J. Kavanagh, Mohan Thite, and Richard D. Johnson - Human Resource Information Systems: Basics, Applications, and Future Directions, 2e © 2012 SAGE Publications, Inc.

THREE COMMON PROBLEMS IN DEVELOPING AN HRIS CBA

it ignores HR’s more strategic role in improving organizational effectiveness

in many instances items listed as direct cost reductions are actually indirect cost reductions

be sure that value estimates assigned to time saved are reasonable

47