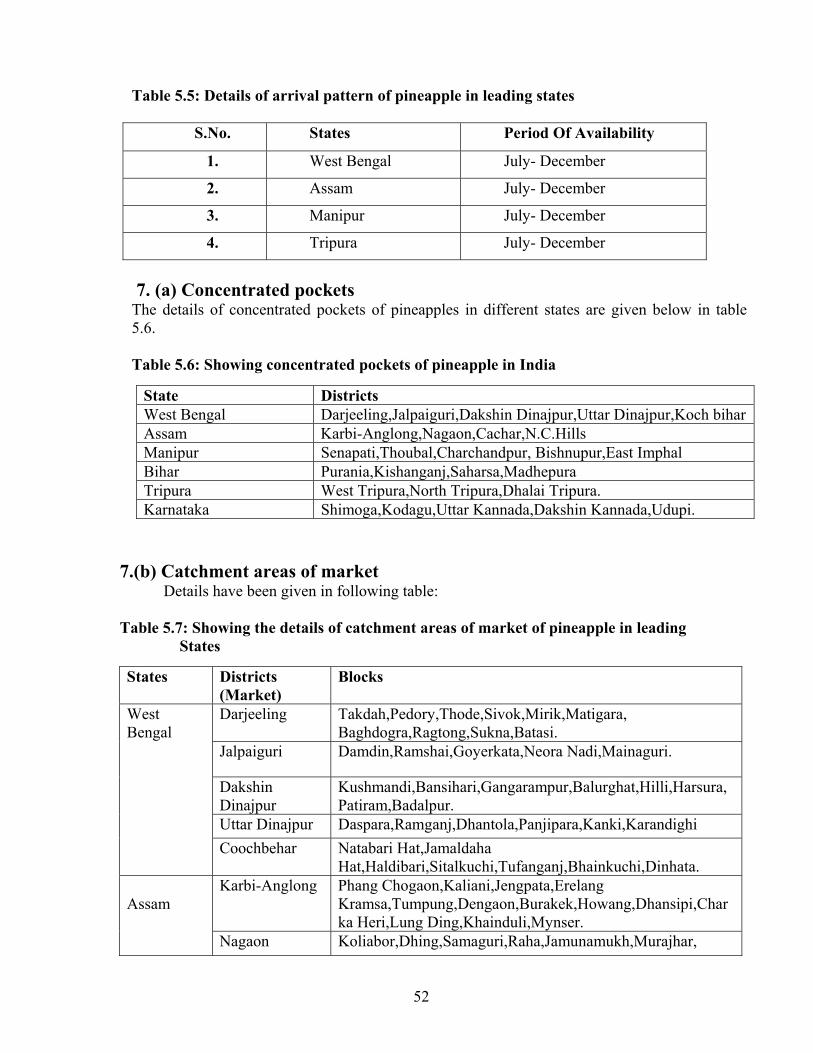

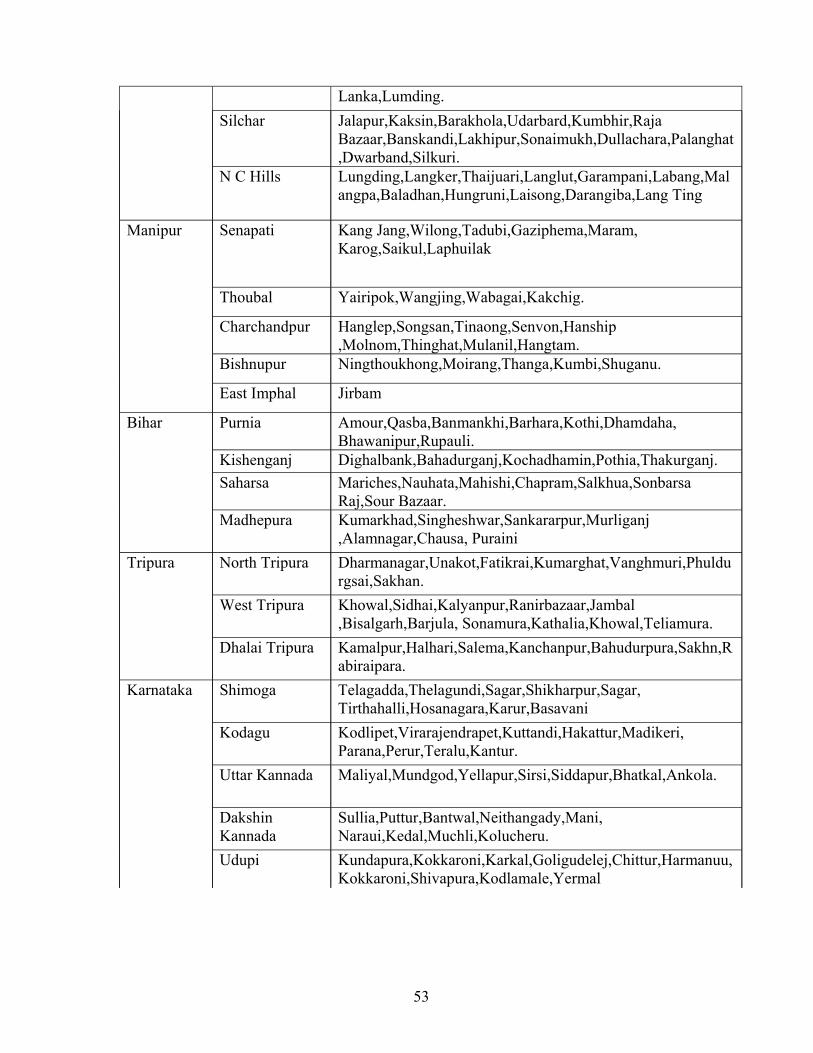

Embed Size (px)

Citation preview

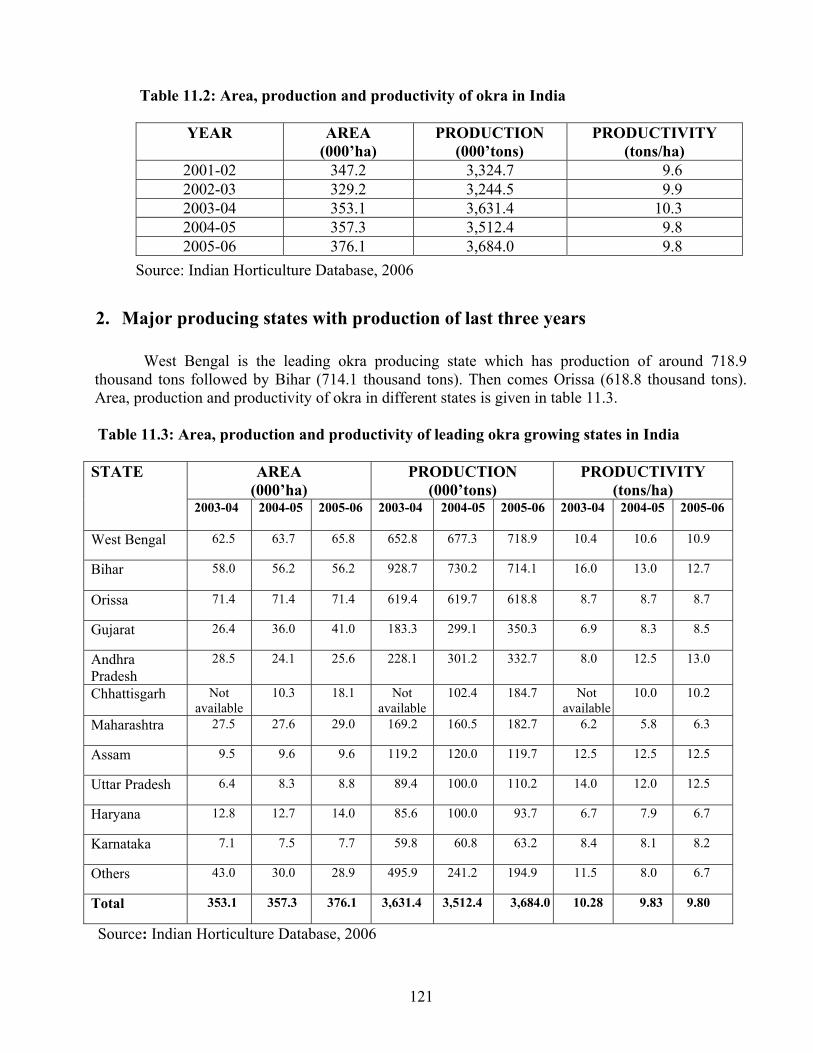

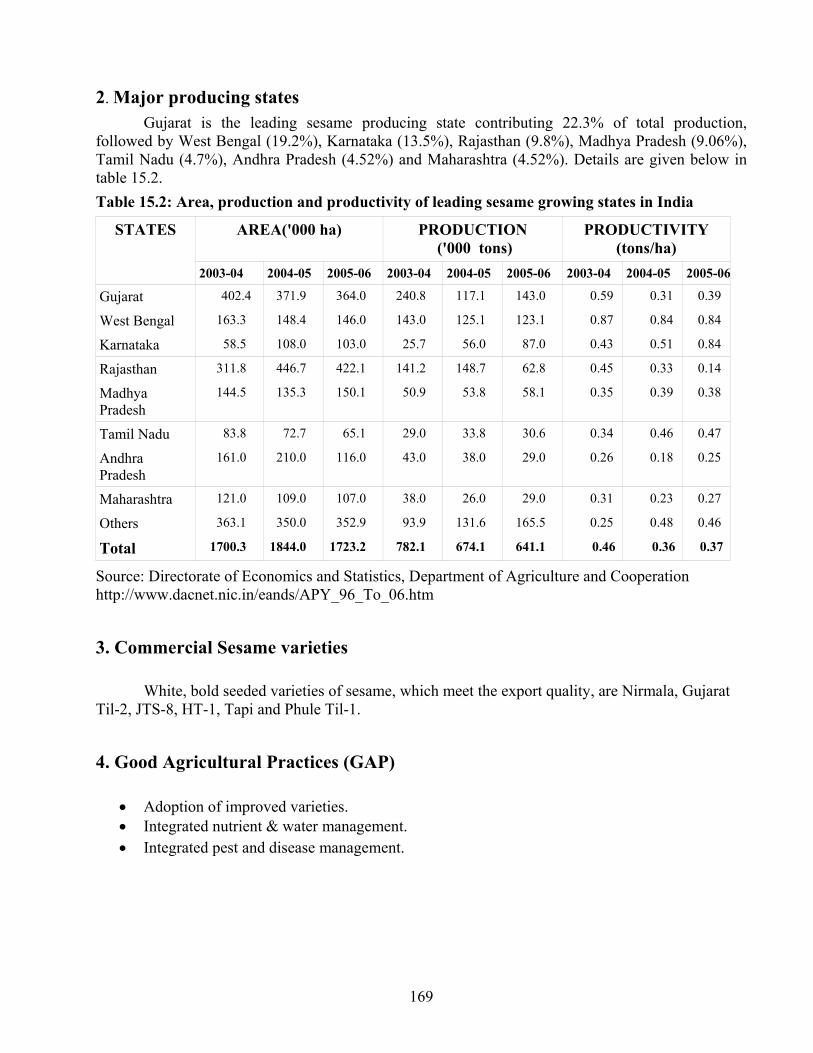

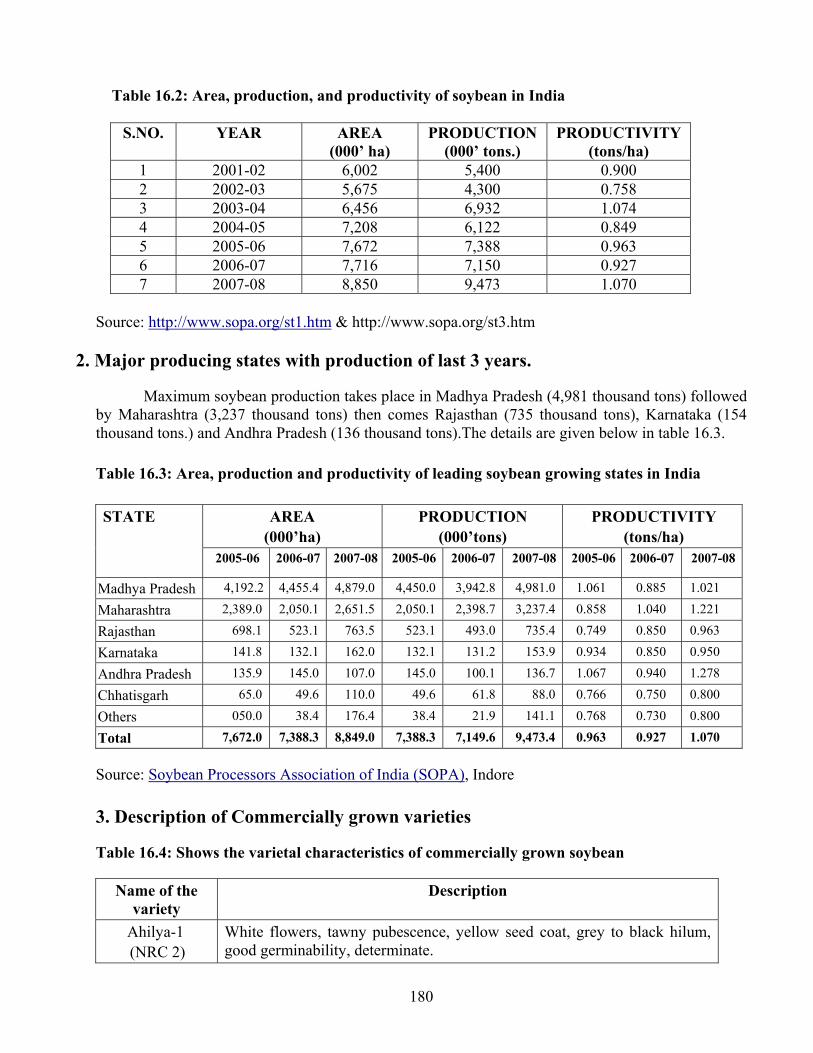

1

CHAPTER - 1

INTRODUCTION

Agriculture, including crop and Animal Husbandry, fisheries, forestry and agro processing constitutes the very basis of socio economic lives of India. It is one of the world’s largest agrarian economies, as the agriculture sector contributed about 18% of the country’s GDP (during 2006-07), 10.7% of the total export in 2006-07 and also provides employment to around 58% of the total work force. Agriculture also plays a critical role as it is essential to meet not only the food and nutritional security to the people and provide livelihood and income in the rural areas, but also to meet the requirement of raw material / inputs for the agro based industries in the domestic front.

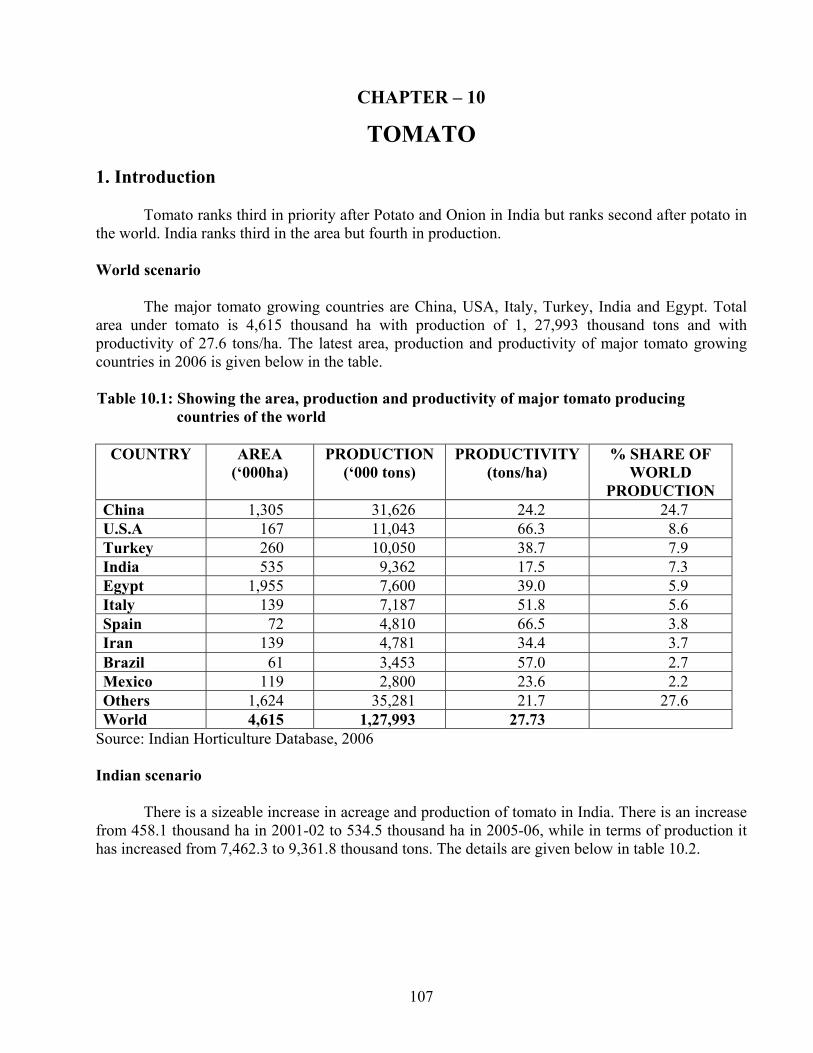

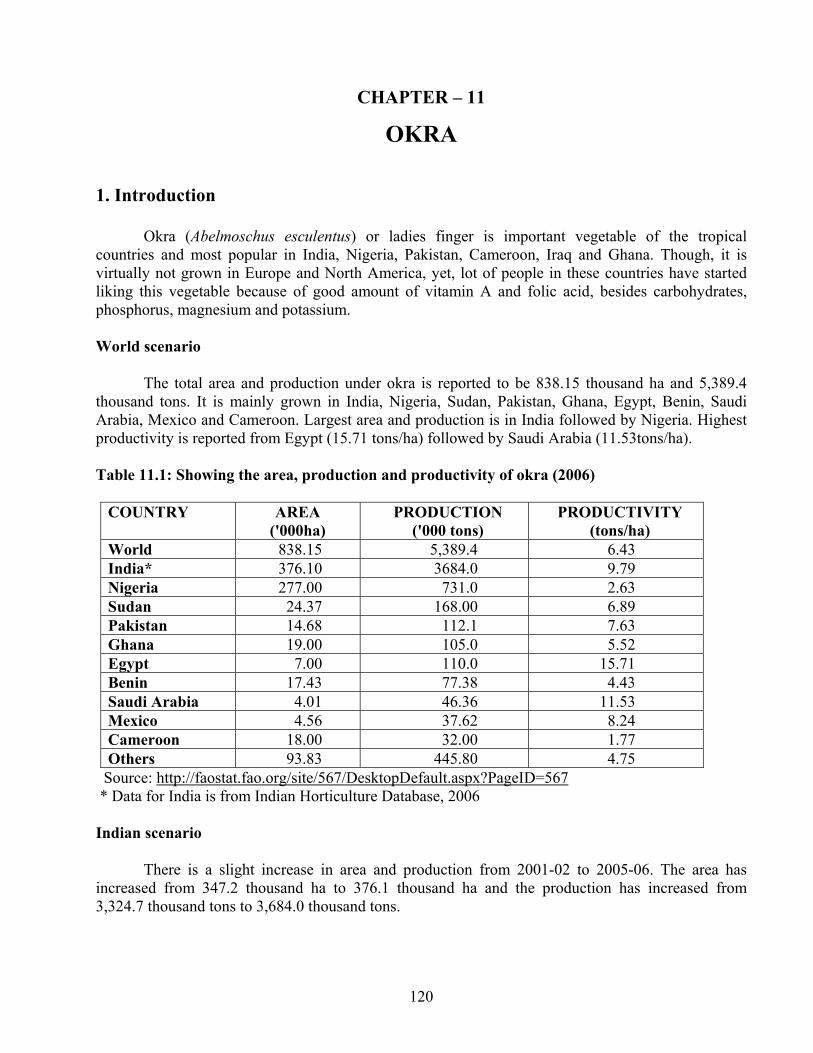

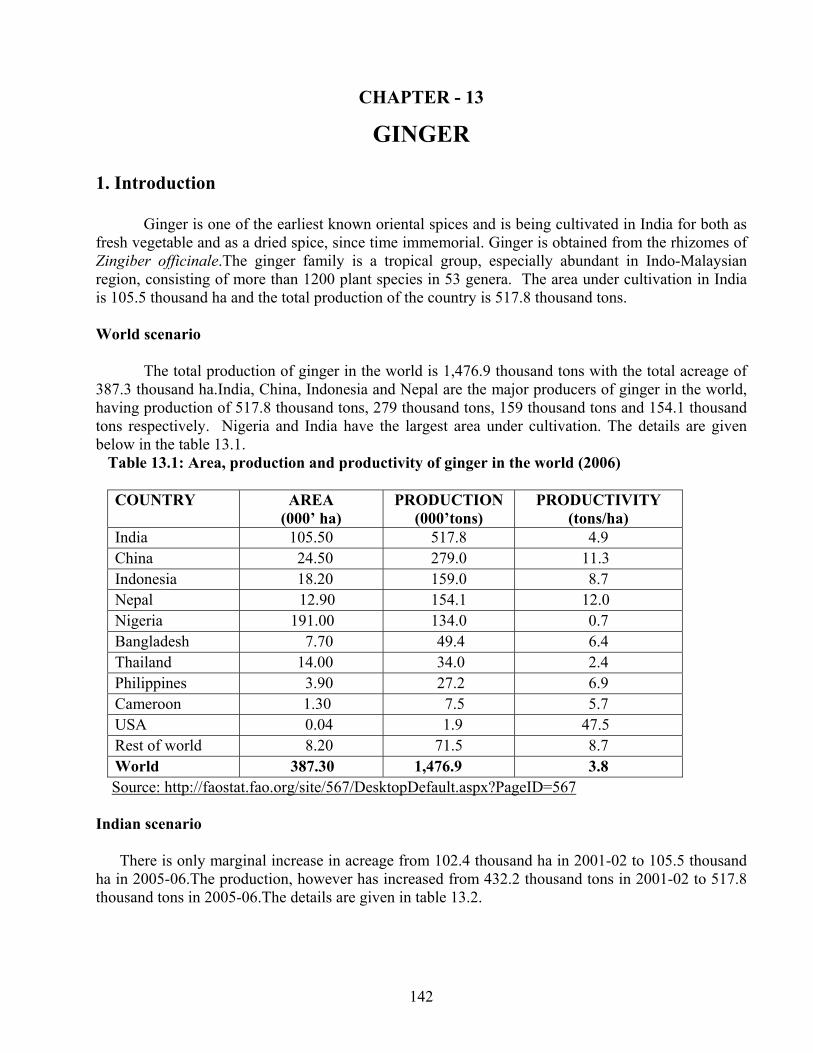

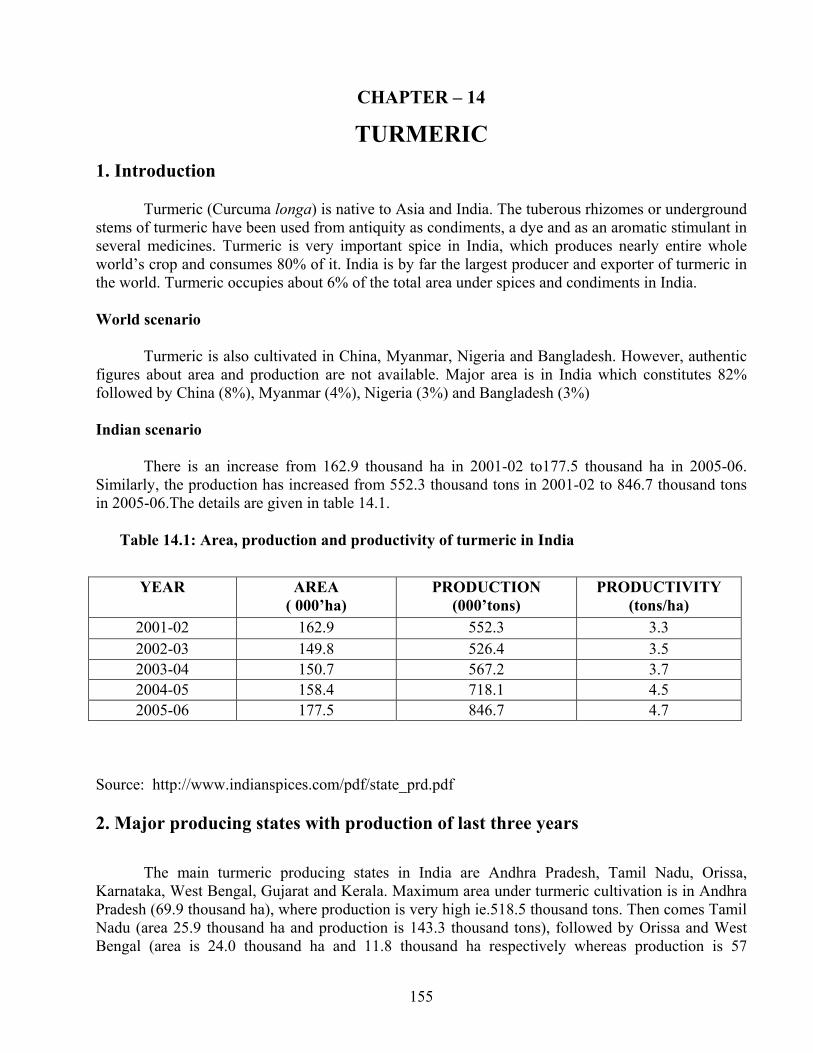

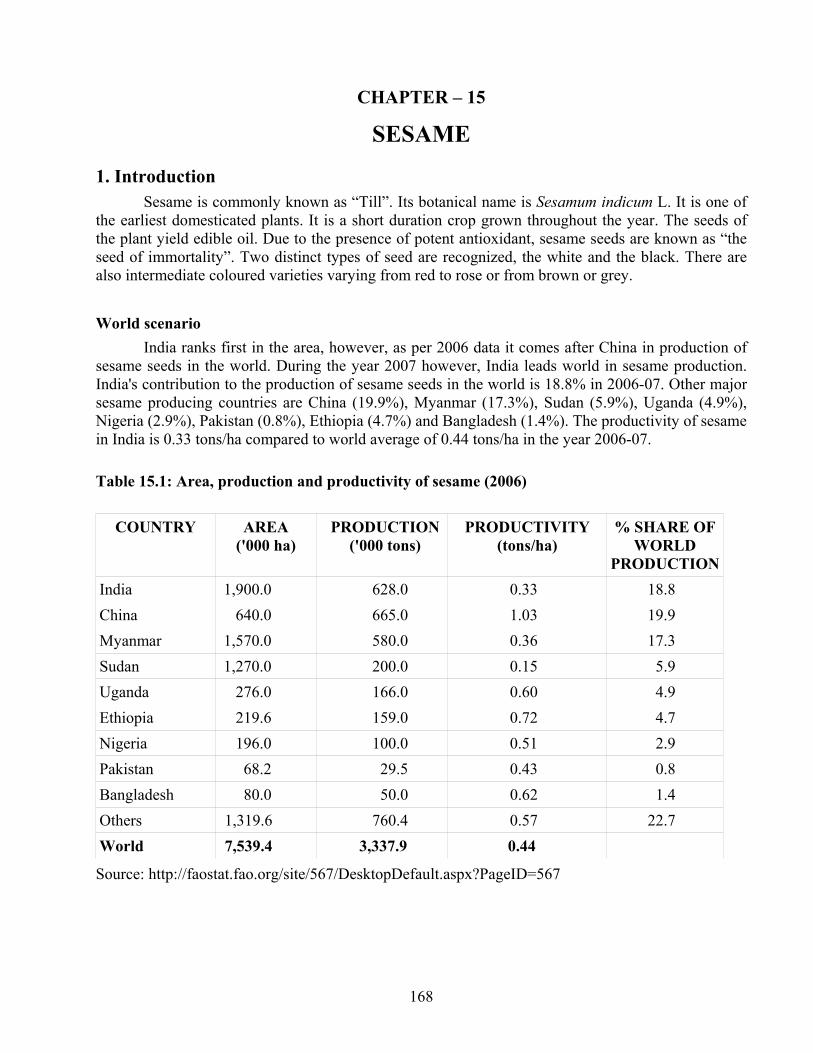

The total geographic area of the country is 328.7 m ha. extended over a large range of vertical and horizontal coordinates makes it to witness a wide variability in climatic conditions and varied range of soil characteristics. The diversified climatic and soil characteristics have helped the country in producing various types of fruits and vegetables, spices and other agricultural crops based on their suitability to the specific environment. This also gives the country opportunities to produce a wide range of varieties of a particular crop with specific characteristics and taste. India is the second largest producer of fruits and vegetables. Maximum production of ginger, turmeric and sesame takes place in India. India is also second largest producer of cotton in the world. However, India is still lagging behind in the productivity of many crops compared to the global scenario. A lot of effort is required for increasing the productivity, developing allied activities and building appropriate infrastructure in rural areas to be self-reliant in food and agricultural products as well as to generate surplus to facilitate more returns through export.

Government is giving lot of emphasis on agriculture sector for increasing the production and productivity of agriculture commodities for achieving an impressive growth in the agriculture front under the GDP. A number of new initiatives like Technology Mission for Integrated Development of Horticulture in the North Eastern States (TMNE), National Horticulture Mission (NHM), National Food Security Mission (NFSM), Macro management in Agriculture (MMA), Rastriya Krishi Vikash Yojana (RKVY), National Project on Organic Farming (NPOF), National Project on Management of Soil Health and Fertility (NPMSHF) etc. indicate the intensive approach in this direction. The success of these programmes will definitely lead to significant rise in agriculture production at the end of XI plan. The surplus production after meeting the domestic requirement will help to promote export and will have a great impact on Indian economy.

In a World Bank report submitted to the Agriculture Ministry, it has been highlighted that despite leading producer of fruits & vegetables in the world, India’s export is poor due to high delivery costs, fragmented supply chain and poor logistics with poor quality standards. India’s share in global export of vegetables remained at 1.7% and that of fruits at 0.5%. The inability to compete abroad presently may lead to the inability to compete at home in future as the multinational companies will be dominating the domestic market availing quality products at competitive prices from other countries.

Country is also lacking in appropriate technology & infrastructure in many aspects of modern storage and shipping methods, post harvest handling, value addition etc. The situation is further restricted due to complicated export regulations and procedures. An exporter faces enormous difficulties to equip himself on various parameters of export like regulatory, quality

2

standards, global export opportunities, tariffs on exports, production scenario & availability, present export trend etc. for developing gainful strategic approach in a competitive mode.

In view of above, Government of India, Ministry of Agriculture (Trade Division),

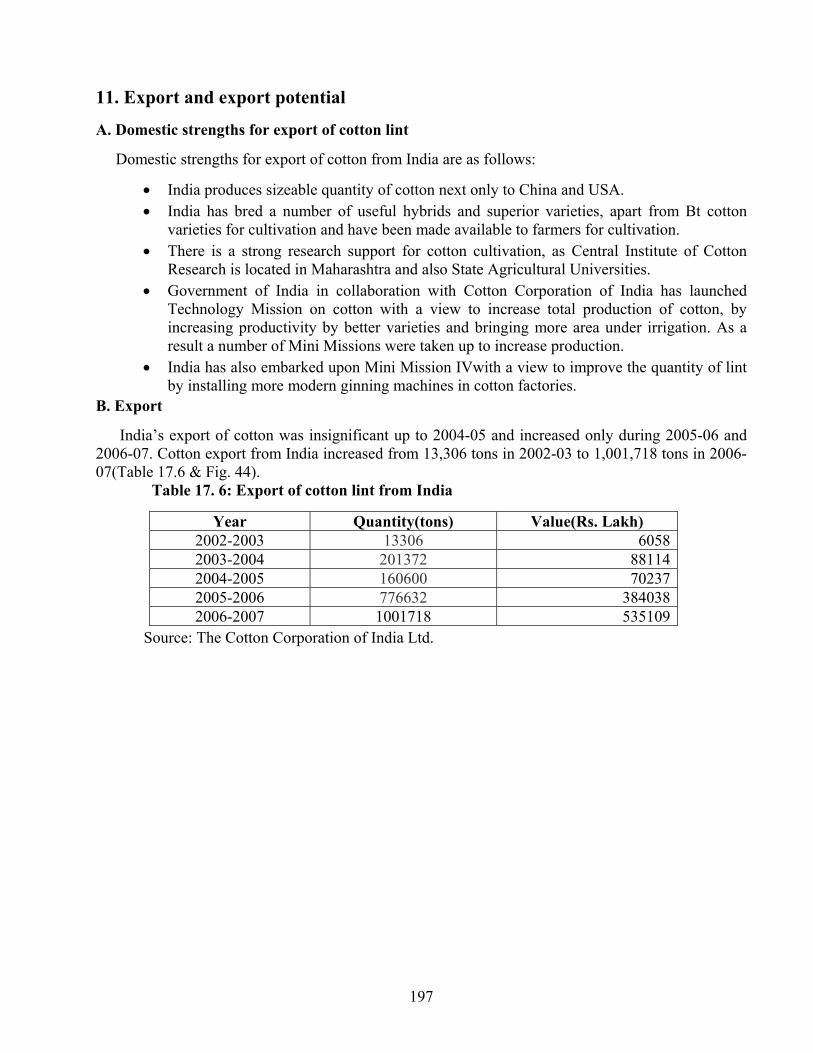

sanctioned a project to NAFED entitled “Market Intelligence study of selected crops having export potential” at a total cost of 82.0 lakhs. The crops for the present study have been identified on the basis of trade volumes and importance of the commodity in relation to production. The selected crops are mango, grapes, pomegranates, litchi, pineapple, banana and aonla among fruits; tomato, green chillies, okra and onion among vegetables; ginger and turmeric among spices; and sesame, soyameal and cotton among commercial crops/products.

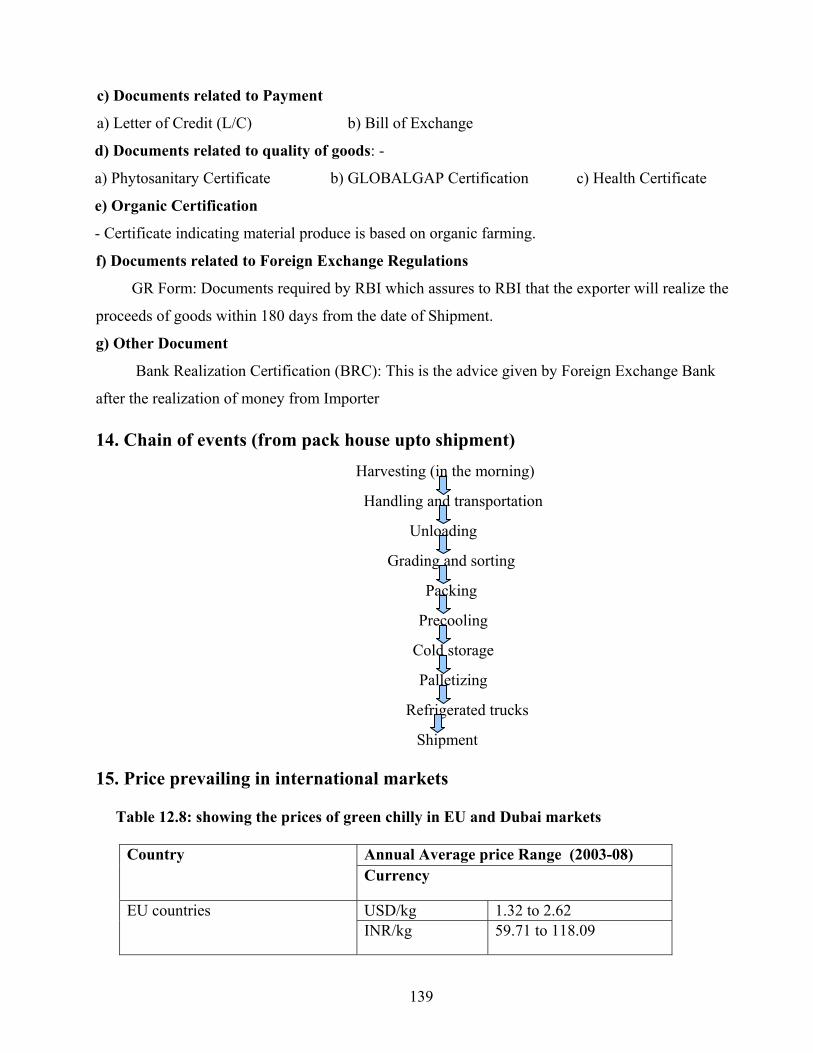

At present, India's export volumes of fruits and vegetables in general and other selected crops are 74, 69,086 tons (2006-07). The value of these exports in US dollar terms comes to 2.85 billion compared to 113.94 billion US dollars of world exports. This constitutes only 2.5% of world export value, whereas India's production is 10.9% of total world production for these specific crops.

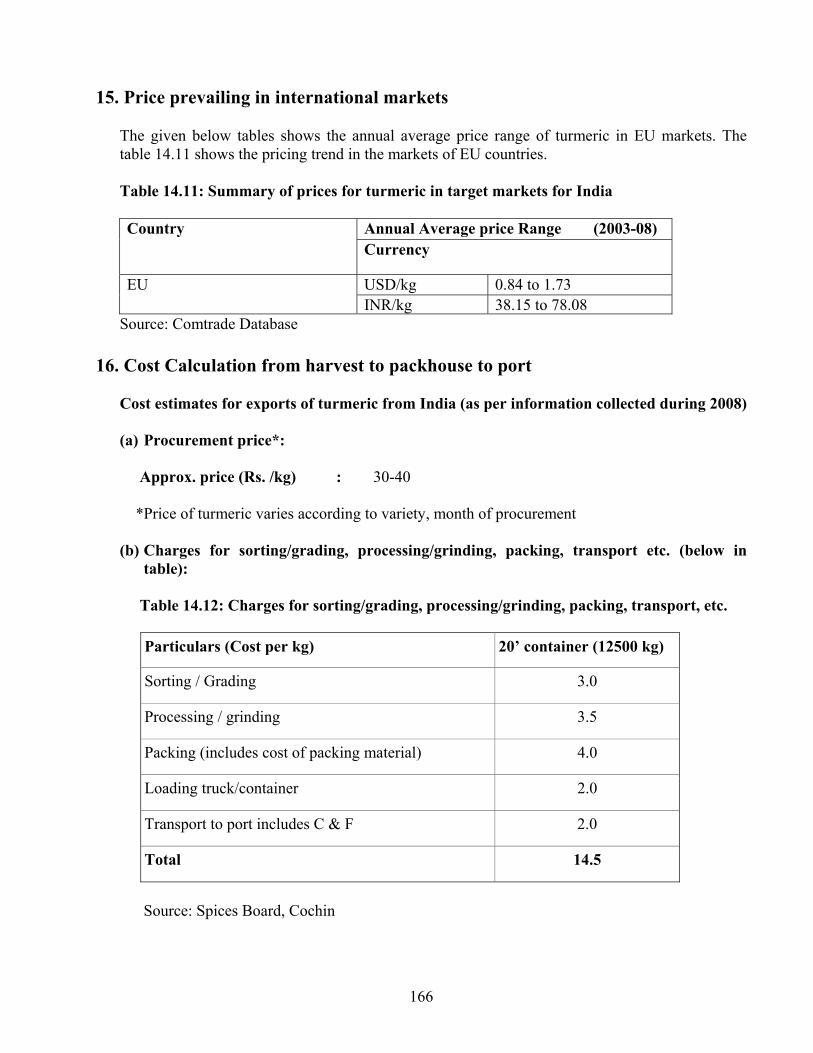

The emphasis in this study has been given on the compilation of information on quality standards, permissible residue limits for various pesticides and fungicides in crops being studied, information on packing requirements, present exports trends, competing countries, opportunities existing for exports, present strengths, availability of infrastructure etc. This information at one place will help in promoting export in the countries / markets of GCC, EU, ASEAN, Australia, etc.

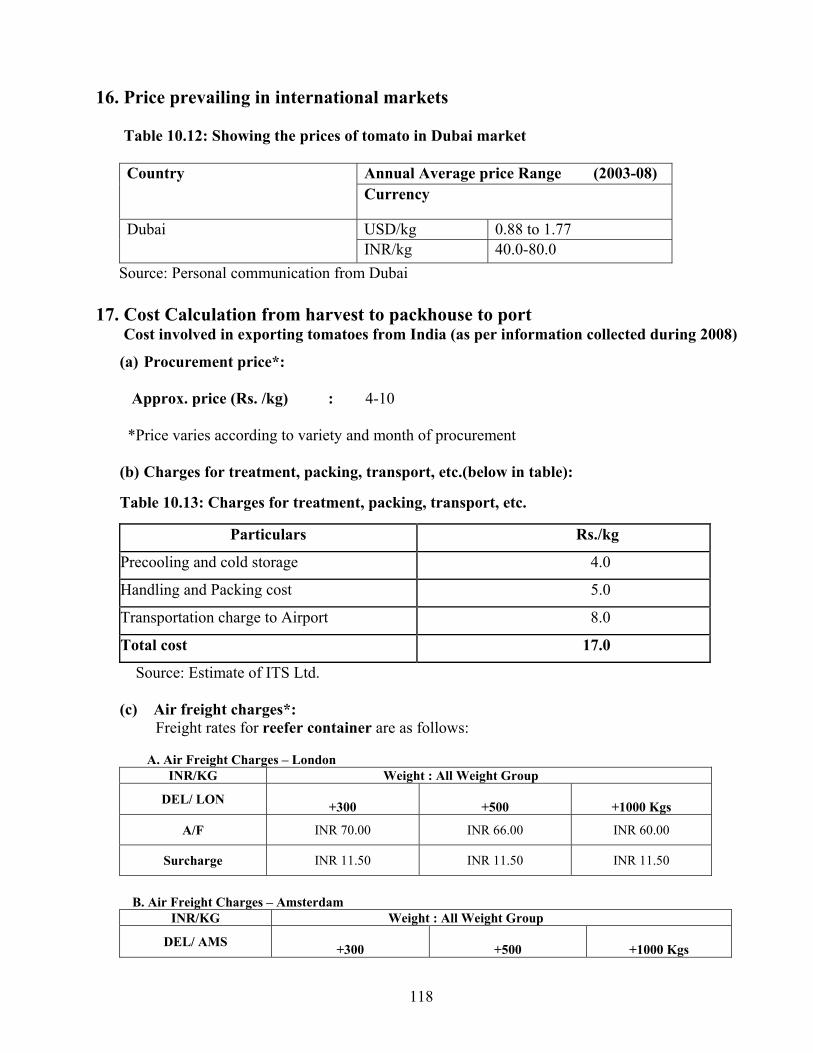

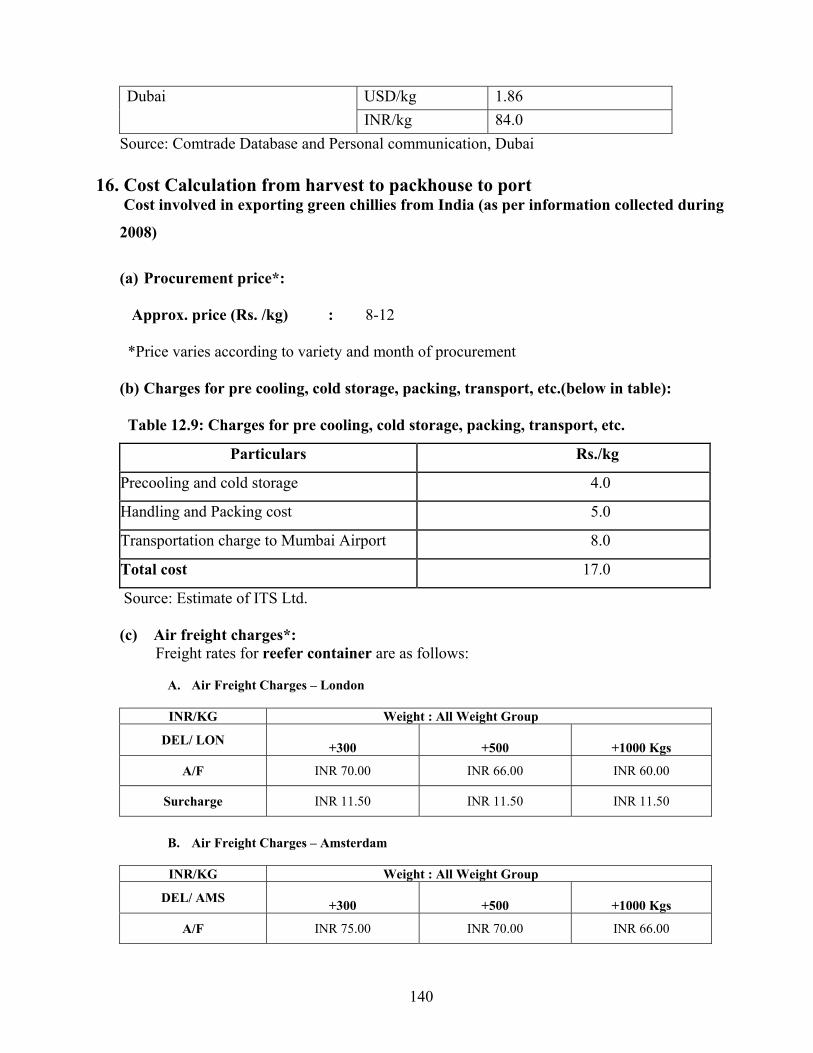

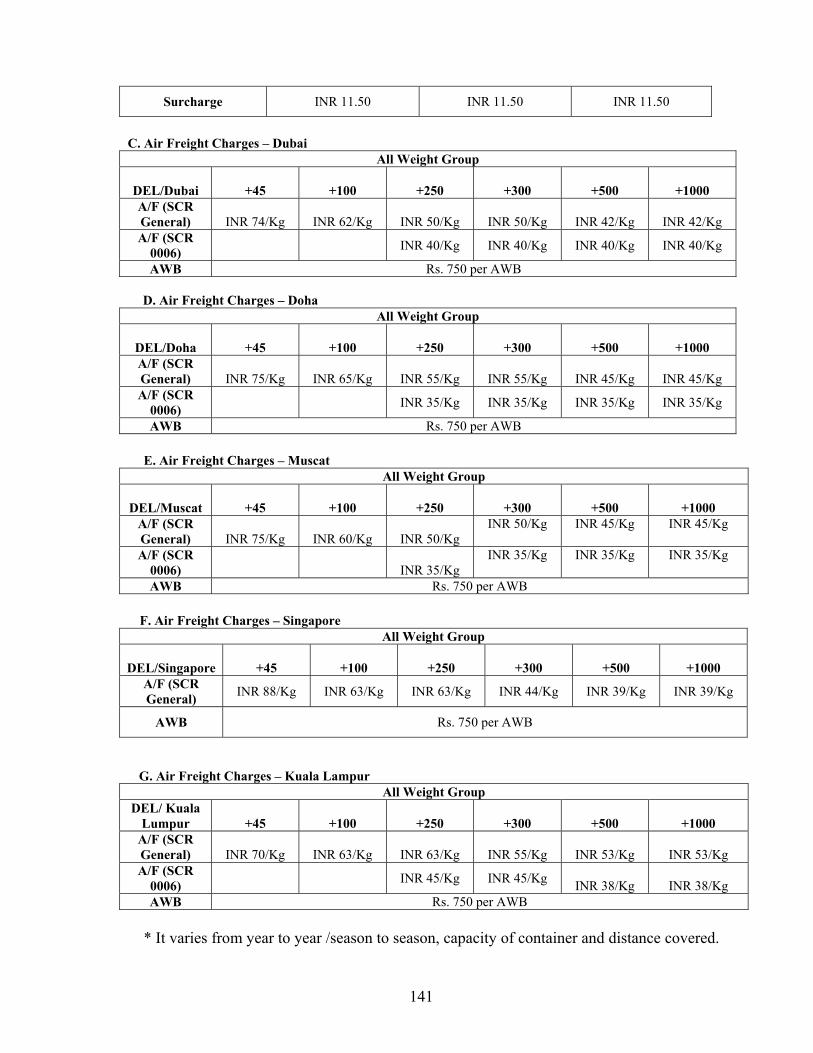

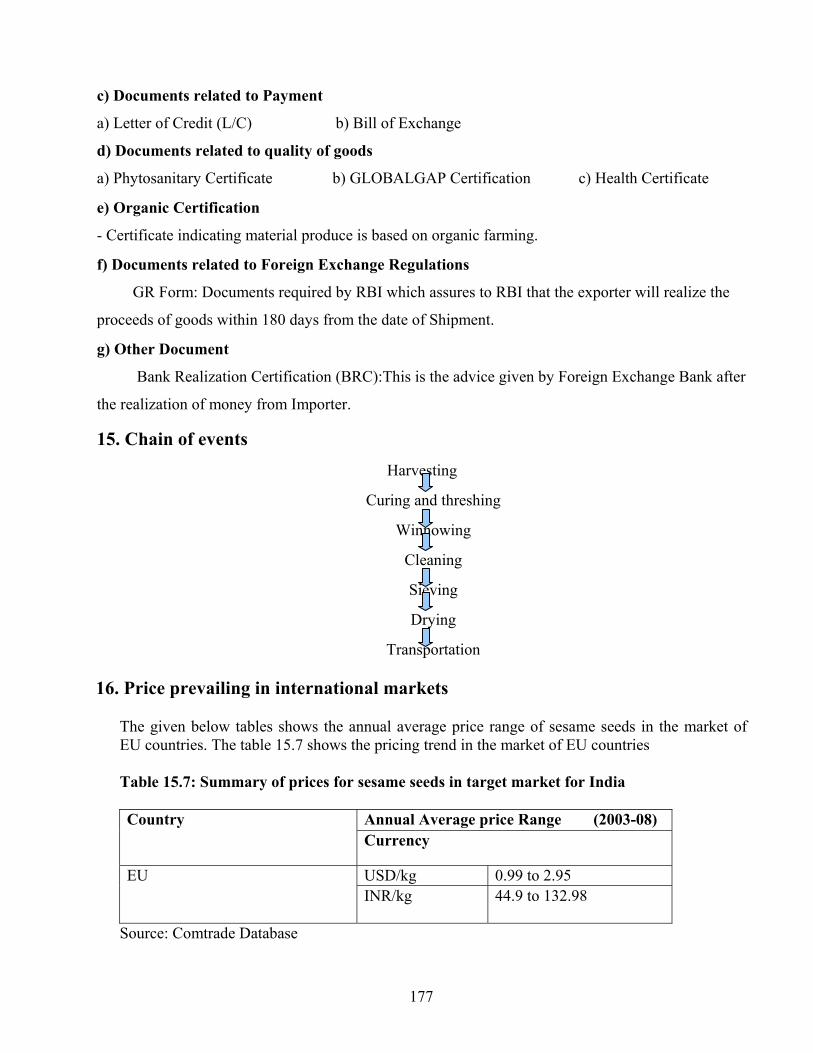

The study has also focused on capacity building of various stake holders in various aspects of production and export process, right from the producers to the exporters with the objective to place the country in a leading position in the global market. The ultimate objective is to establish a National database which can pool information from promotional agencies associated with export and import activities in selected countries/ markets for the access of different user agencies. A URL namely marketagri.com has been created which is providing relevant information to the producer and exporter so as to design the production programme in an appropriate manner.

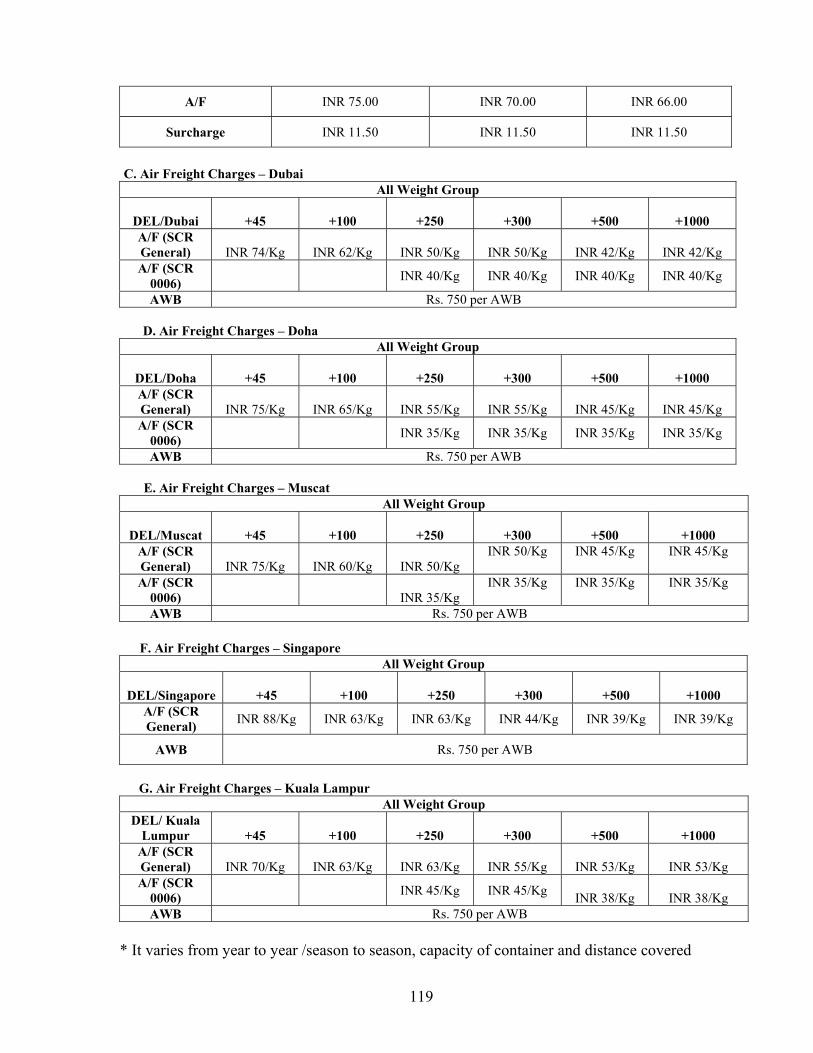

Looking into the large set of information/content generated and to place it in a presentable form for the easy access of the user agencies, the report of the study “Market Intelligence study of selected crops having export potential” has been split in to four volumes as enlisted below: (a) Volume I – Main Report – Covering all the deliverables outlined in the study including the suggestions and recommendations based on the detailed reports (separate volumes on profiles of selected crops, export analysis and tariffs & non tariff protocols). (b) Volume II – Domestic Market Research – Covering profiles of selected crops namely mango, grapes, pomegranates, litchi, pineapple, banana, aonla, tomato, green chillies, okra, onion, ginger, turmeric, sesame, soyameal and cotton. (c) Volume III – In four sections namely A,B,C and D on International Market Research- Covering opportunities, analysis and competitiveness in EU, GCC, ASEAN, Australia, China and Korea (d) Volume IV – In three sections namely A, B and C on International Market Research – Covering World Trade scenario, tariff duties and non-tariff protocols of different countries.

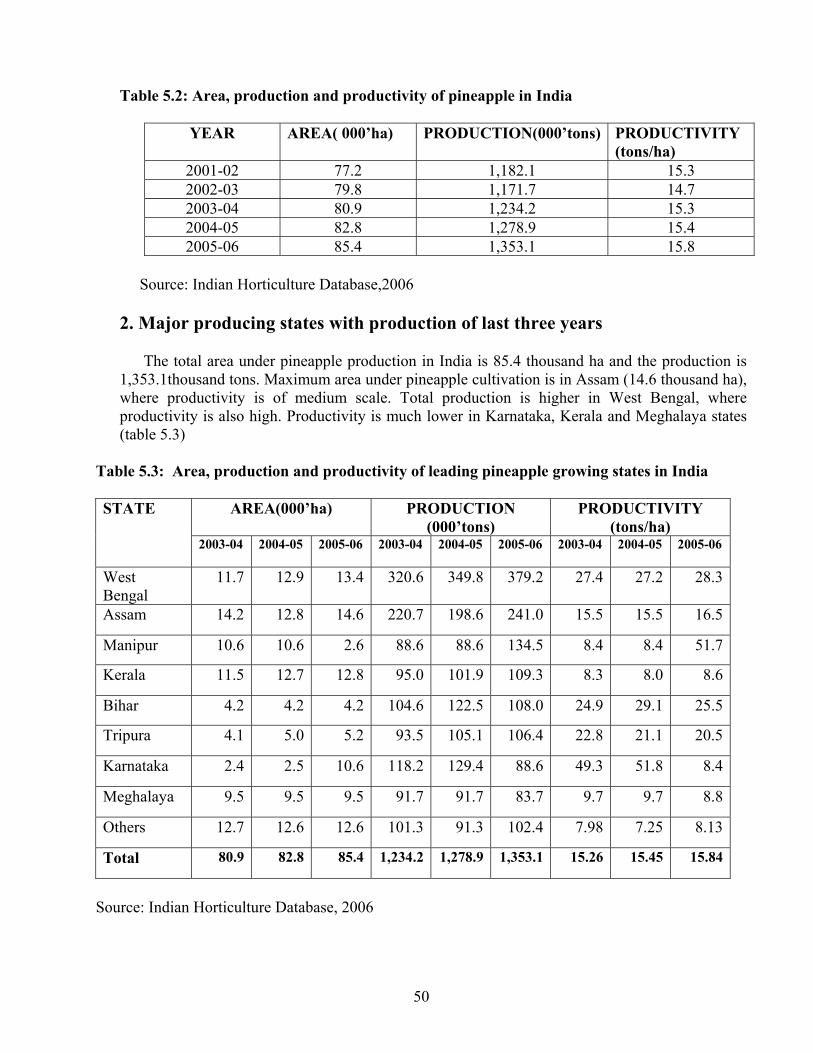

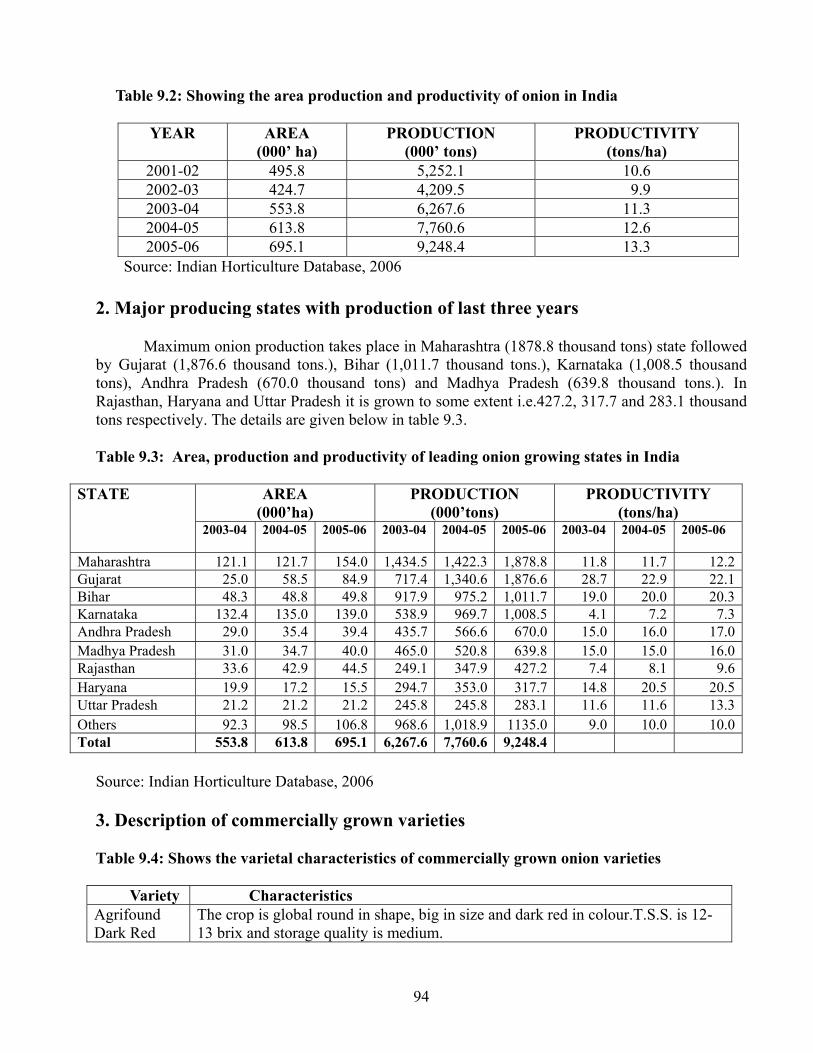

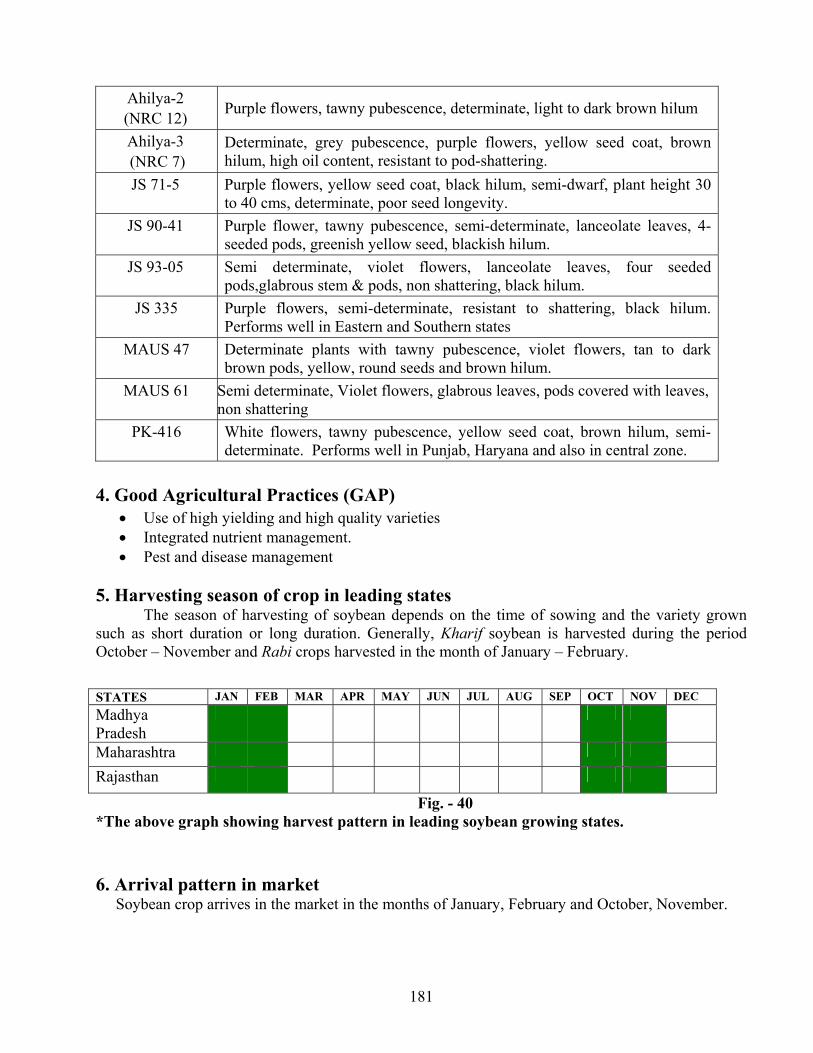

One of the important components of the study is to know the export potential of a particular crop on which, the information on the area, production & productivity, consumption,

3

post harvest losses procuring markets and surplus production is pre-requisite. Therefore, domestic market research was conducted on fruits (mango, grapes, pomegranate, pineapple, litchi, banana & aonla) vegetables (onion, tomato, okra and green chilly), spices (ginger and turmeric), sesame seeds, soyameal and cotton.

Information, thus collected, has been incorporated in various crop profiles. These profiles essentially provide information on production, local consumption, procurement, various aspects of marketing and export. These profiles are first of kind write-ups on these crops having commercial angle.

The information collected on the crops mentioned above is primarily on acreage under cultivation, total production and productivity per hectare area, area under crop in different states, production and productivity there in, description of few export worthy varieties, harvesting season, arrival pattern in markets etc. Also in this collected information are details of concentrated pockets of cultivation and catchment areas of markets and Mandies.

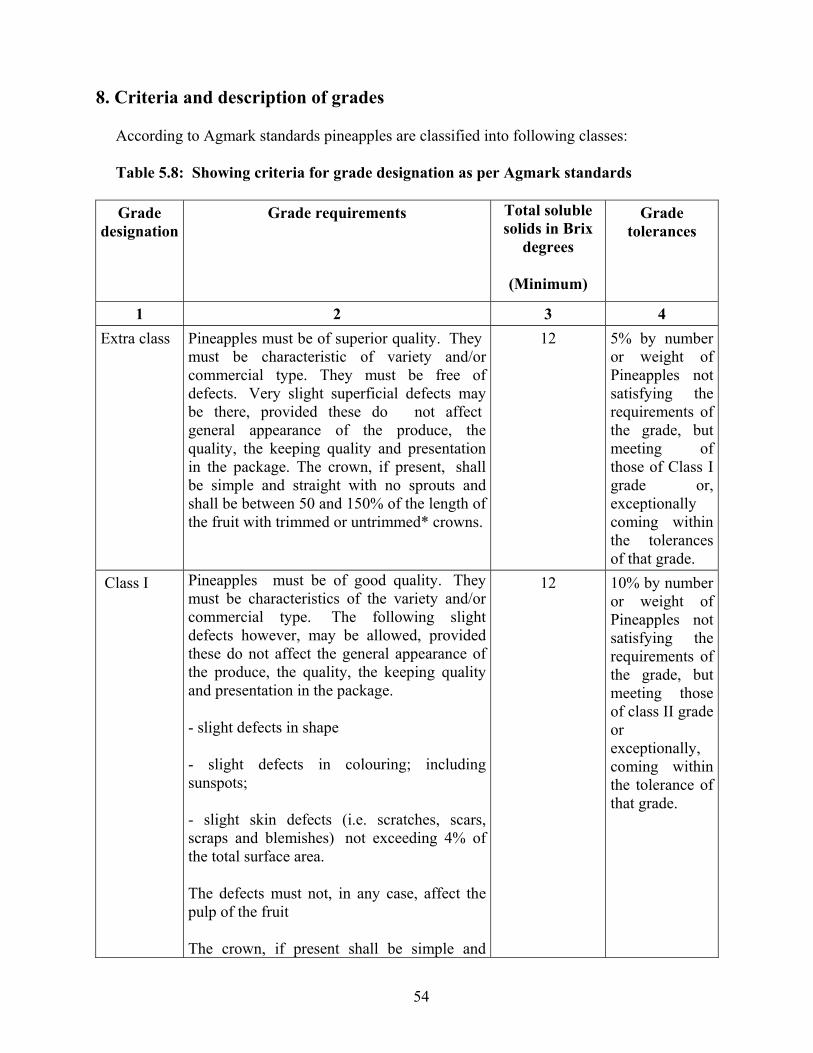

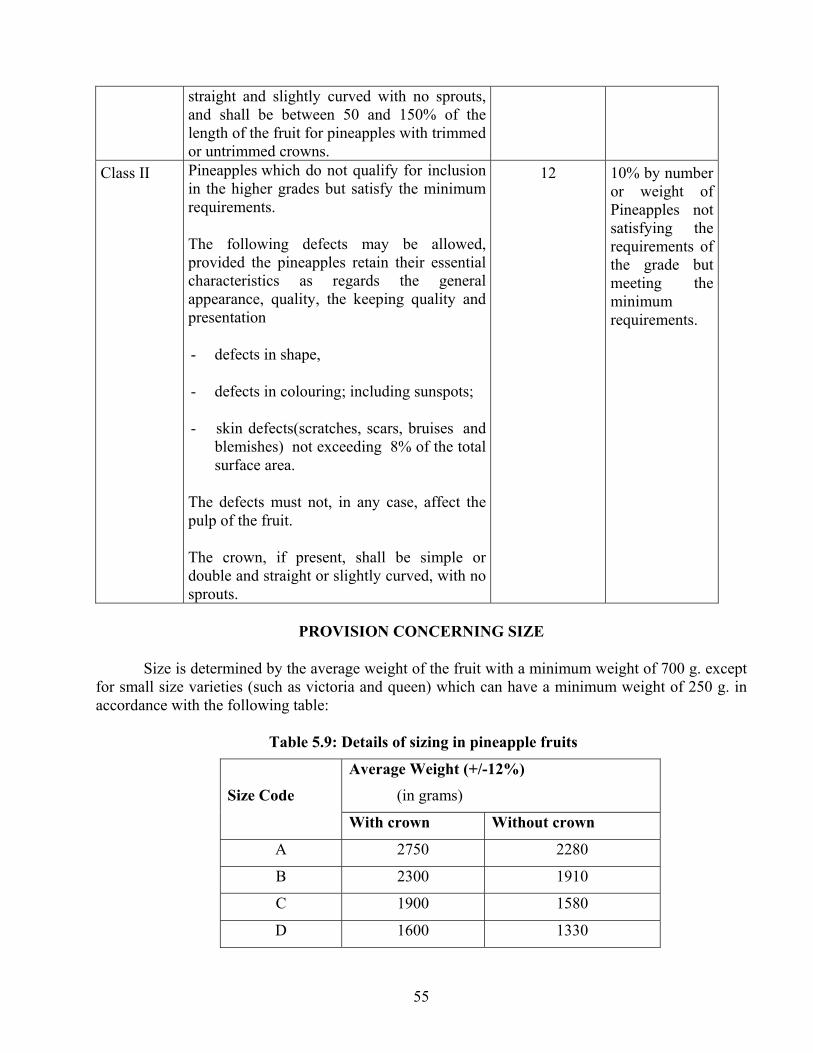

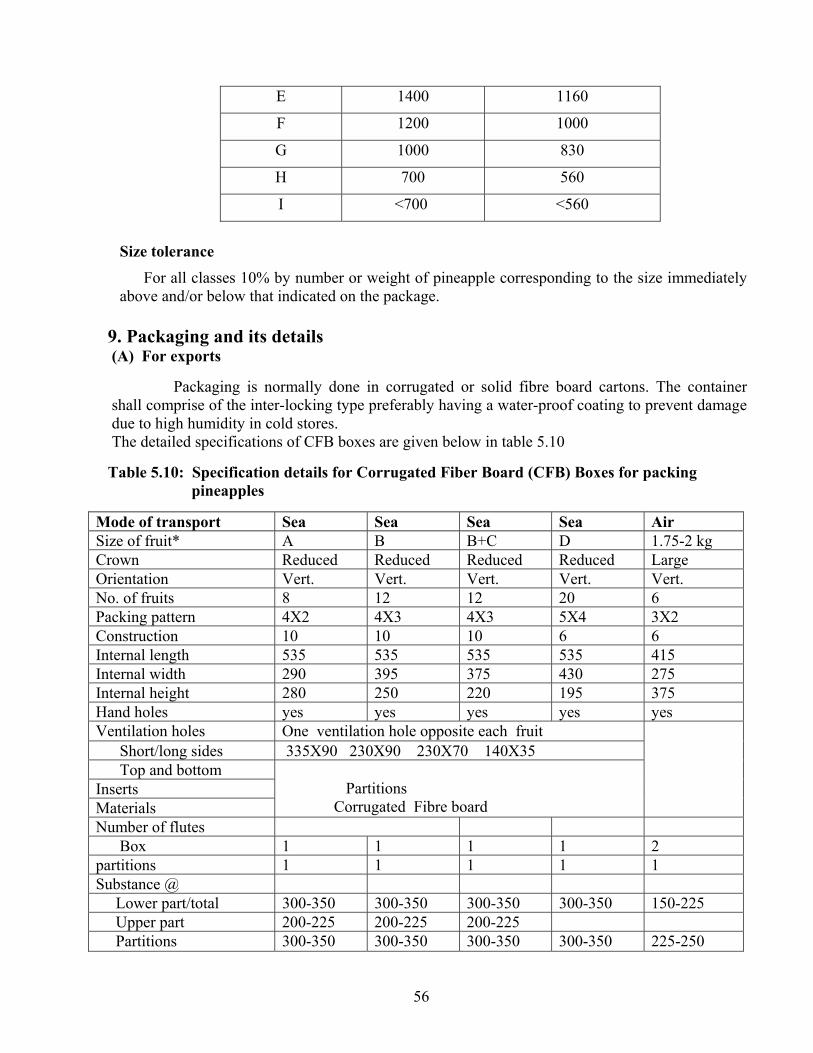

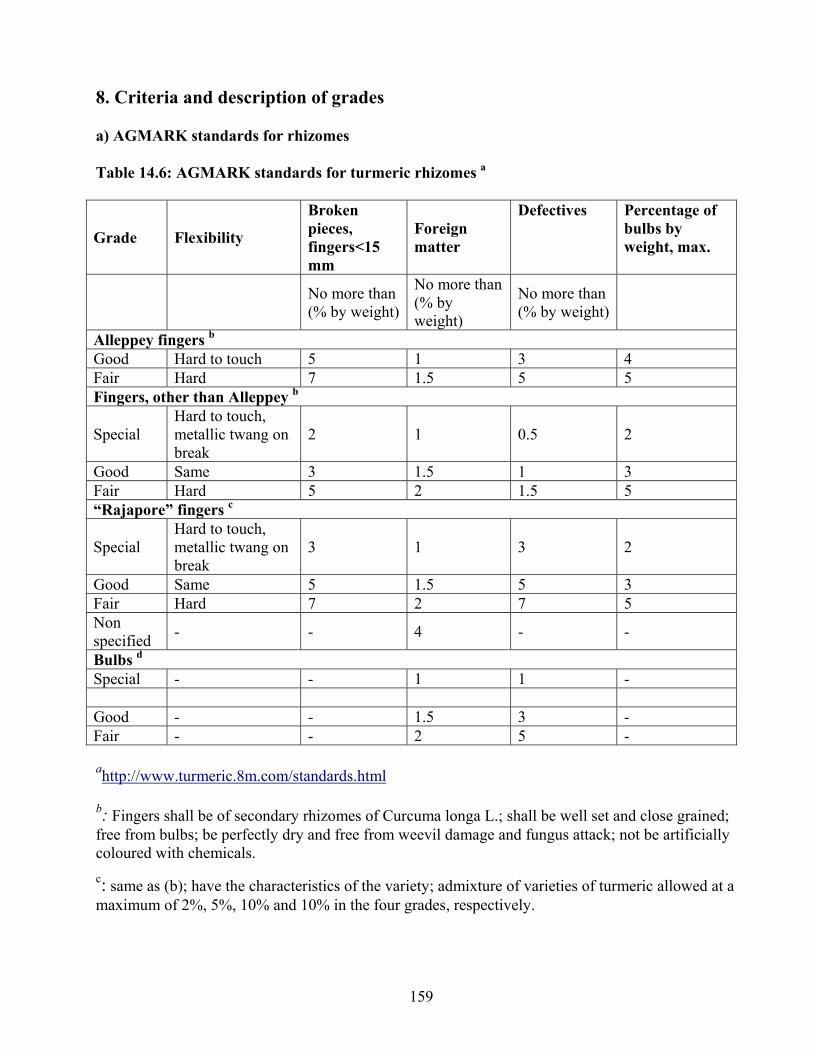

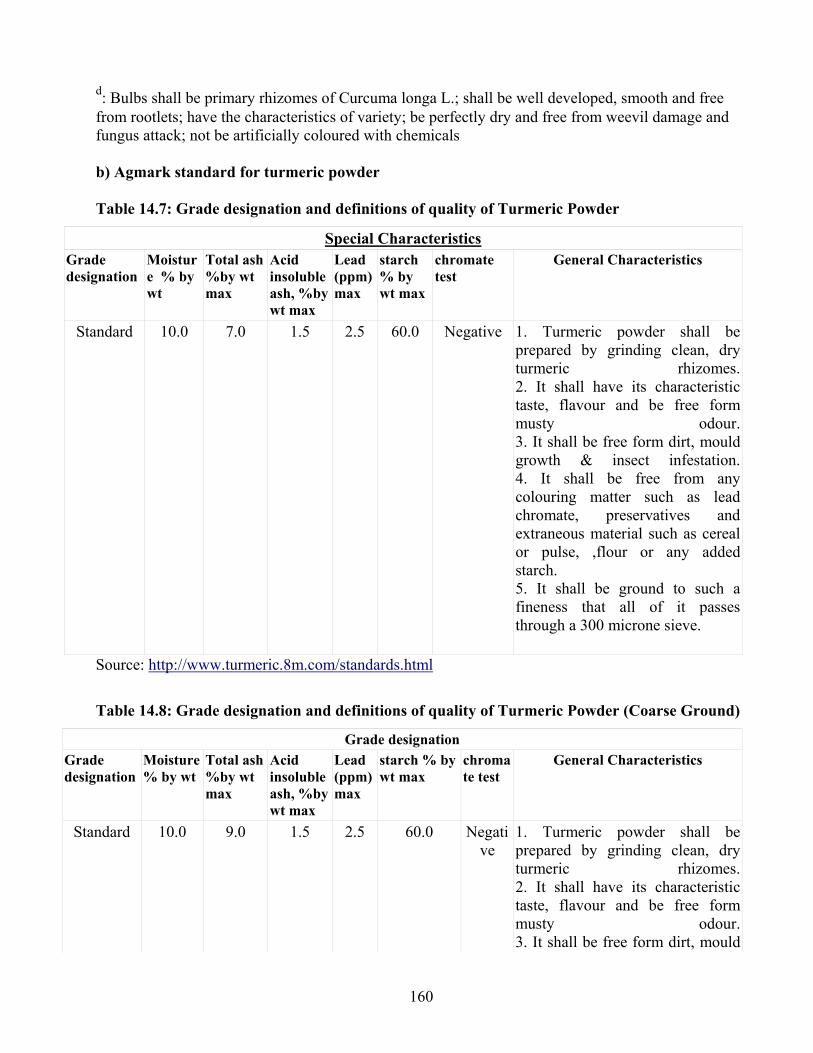

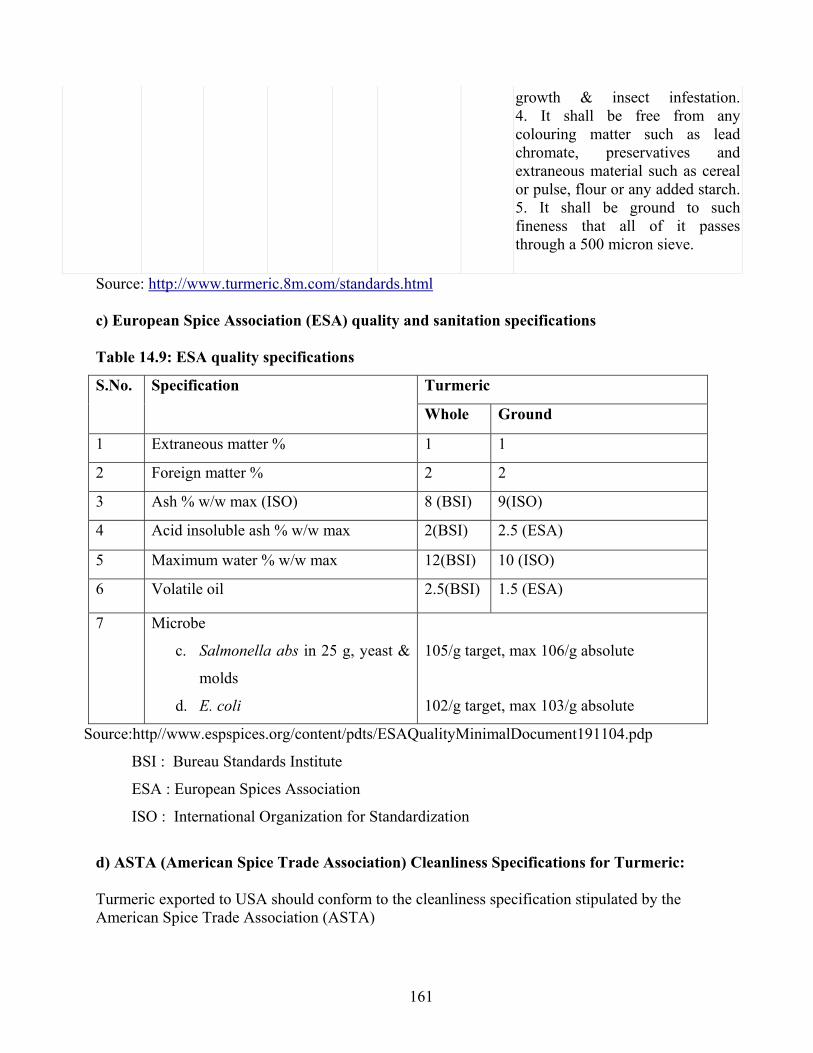

In addition, the information on Agmark, description of grades and standards, packaging

for export, export and export potential (including domestic strengths and measures for enhancing exports), prices prevailing in international markets, procurement prices, storage details, documents required for exports, chain of events from harvest to shipment, expenses likely to be incurred on post-harvest handling, treatment, transport to port and freight charges ( by air or sea as the case may be) have also been given in the profiles.

In nutshell, profiles contain all the information required for export purposes. The crop profiles have been prepared for following commodities: (a) Fruits

• Mango • Grapes • Pomegranate • Pineapple • Litchi • Banana • Aonla.

(b) Vegetables

• Onion • Tomato • Okra • Green Chilly.

(c) Spices

• Ginger • Turmeric

(d) Commercial crops

• Sesame seeds • Soyameal • Cotton.

4

CHAPTER- 2

MANGO

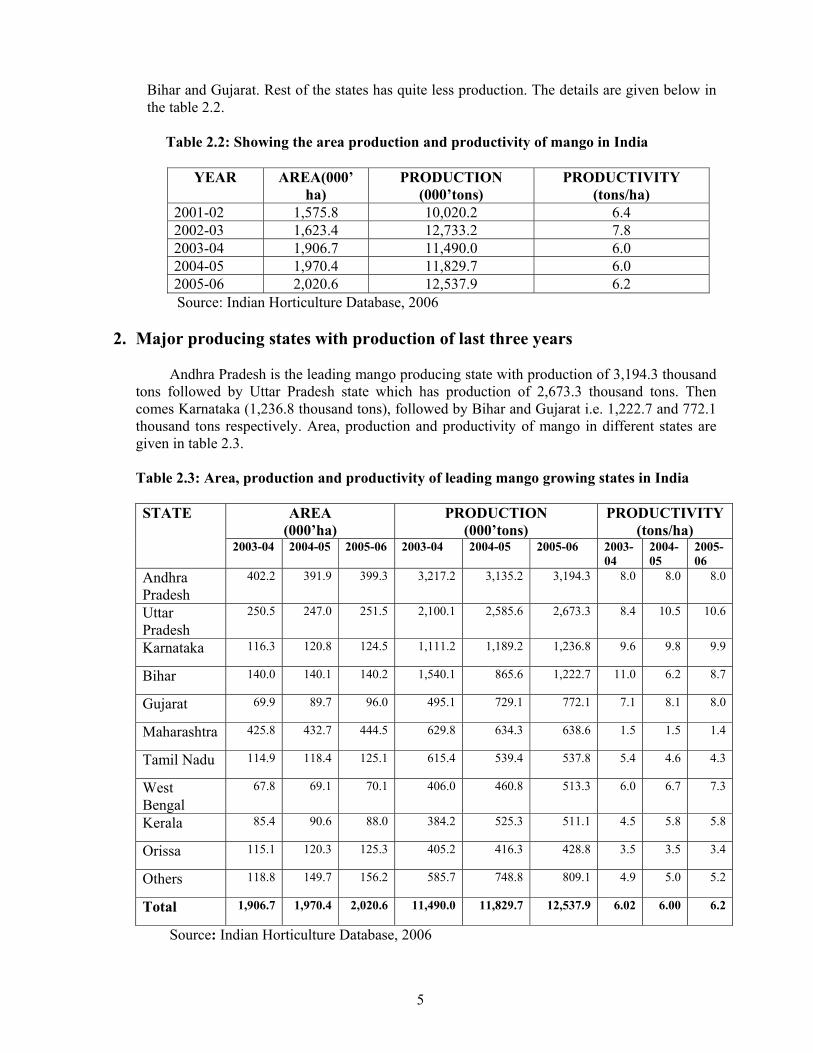

1. Introduction

Mango (Mangifera indica Linn) is the most important fruit of India and is known as “King of fruits”. The fruit is cultivated in the largest area i.e. 2,021 thousand ha and the production is around 12.5 million tons, contributing 40.1% of the total world production of mango. The main mango producing states in India are Andhra Pradesh (25%), Uttar Pradesh (21%), Karnataka (9.8%), Bihar (9.7%), Gujarat (6.1%) and Maharashtra (5.09%)

Total export of mangoes from India is 79.06 thousand tons, valuing Rs. 141.9 crores during 2006-07. India exports mango to over 50 countries worldwide. India’s exports to UAE, Saudi Arabia, Qatar, Bahrain, UK, Kuwait, Singapore, Malaysia and Bangladesh together account for 97% of total exports of fresh mangoes from India.

World scenario

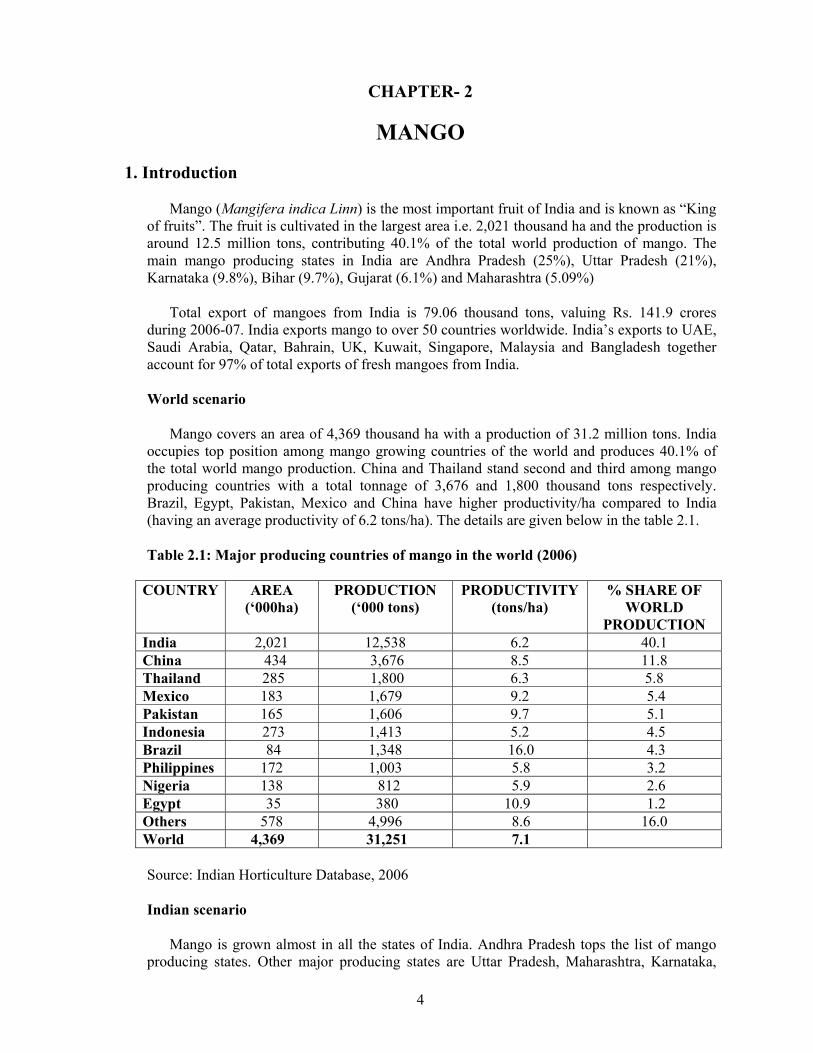

Mango covers an area of 4,369 thousand ha with a production of 31.2 million tons. India occupies top position among mango growing countries of the world and produces 40.1% of the total world mango production. China and Thailand stand second and third among mango producing countries with a total tonnage of 3,676 and 1,800 thousand tons respectively. Brazil, Egypt, Pakistan, Mexico and China have higher productivity/ha compared to India (having an average productivity of 6.2 tons/ha). The details are given below in the table 2.1.

Table 2.1: Major producing countries of mango in the world (2006)

COUNTRY AREA (‘000ha)

PRODUCTION (‘000 tons)

PRODUCTIVITY (tons/ha)

% SHARE OF WORLD

PRODUCTION India 2,021 12,538 6.2 40.1 China 434 3,676 8.5 11.8 Thailand 285 1,800 6.3 5.8 Mexico 183 1,679 9.2 5.4 Pakistan 165 1,606 9.7 5.1 Indonesia 273 1,413 5.2 4.5 Brazil 84 1,348 16.0 4.3 Philippines 172 1,003 5.8 3.2 Nigeria 138 812 5.9 2.6 Egypt 35 380 10.9 1.2 Others 578 4,996 8.6 16.0 World 4,369 31,251 7.1

Source: Indian Horticulture Database, 2006

Indian scenario

Mango is grown almost in all the states of India. Andhra Pradesh tops the list of mango producing states. Other major producing states are Uttar Pradesh, Maharashtra, Karnataka,

5

Bihar and Gujarat. Rest of the states has quite less production. The details are given below in the table 2.2.

Table 2.2: Showing the area production and productivity of mango in India

YEAR AREA(000’ ha)

PRODUCTION (000’tons)

PRODUCTIVITY (tons/ha)

2001-02 1,575.8 10,020.2 6.4 2002-03 1,623.4 12,733.2 7.8 2003-04 1,906.7 11,490.0 6.0 2004-05 1,970.4 11,829.7 6.0 2005-06 2,020.6 12,537.9 6.2

Source: Indian Horticulture Database, 2006

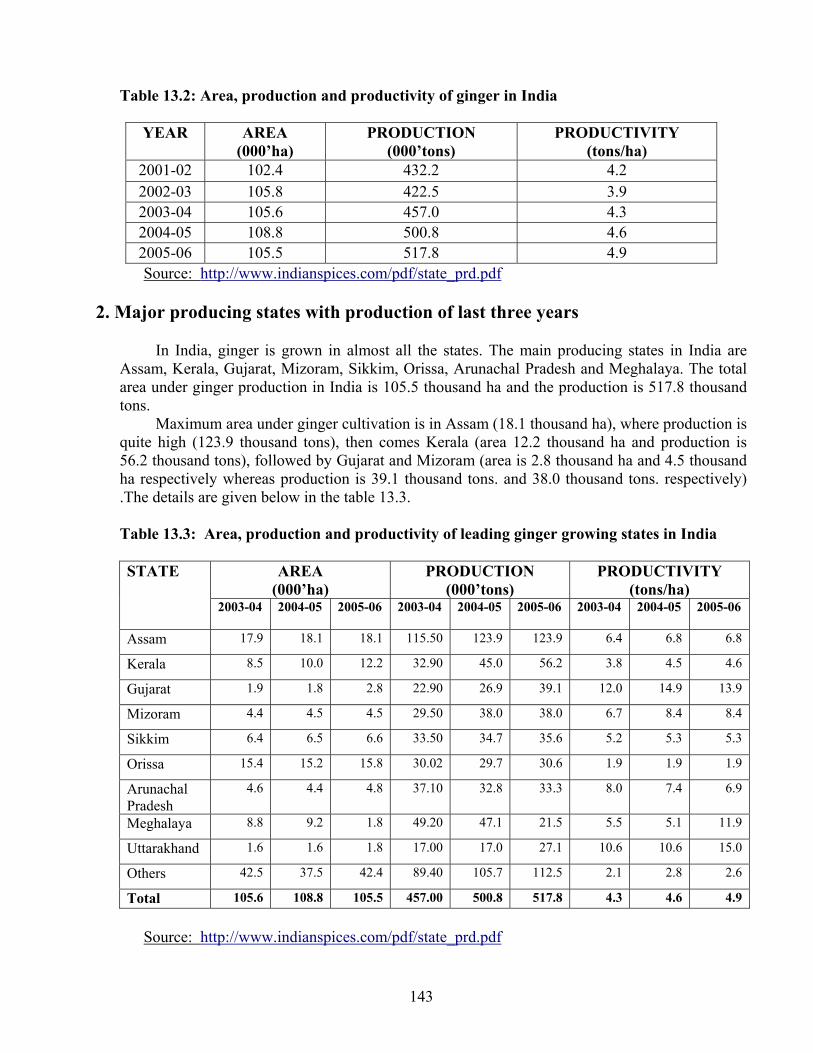

2. Major producing states with production of last three years

Andhra Pradesh is the leading mango producing state with production of 3,194.3 thousand tons followed by Uttar Pradesh state which has production of 2,673.3 thousand tons. Then comes Karnataka (1,236.8 thousand tons), followed by Bihar and Gujarat i.e. 1,222.7 and 772.1 thousand tons respectively. Area, production and productivity of mango in different states are given in table 2.3.

Table 2.3: Area, production and productivity of leading mango growing states in India

AREA (000’ha)

PRODUCTION (000’tons)

PRODUCTIVITY (tons/ha)

STATE

2003-04

2004-05 2005-06 2003-04 2004-05 2005-06 2003-04

2004-05

2005-06

Andhra Pradesh

402.2 391.9 399.3 3,217.2 3,135.2 3,194.3 8.0 8.0 8.0

Uttar Pradesh

250.5 247.0 251.5 2,100.1 2,585.6 2,673.3 8.4 10.5 10.6

Karnataka 116.3 120.8 124.5 1,111.2 1,189.2 1,236.8 9.6 9.8 9.9

Bihar 140.0 140.1 140.2 1,540.1 865.6 1,222.7 11.0 6.2 8.7

Gujarat 69.9 89.7 96.0 495.1 729.1 772.1 7.1 8.1 8.0

Maharashtra 425.8 432.7 444.5 629.8 634.3 638.6 1.5 1.5 1.4

Tamil Nadu 114.9 118.4 125.1 615.4 539.4 537.8 5.4 4.6 4.3

West Bengal

67.8 69.1 70.1 406.0 460.8 513.3 6.0 6.7 7.3

Kerala 85.4 90.6 88.0 384.2 525.3 511.1 4.5 5.8 5.8

Orissa 115.1 120.3 125.3 405.2 416.3 428.8 3.5 3.5 3.4

Others 118.8 149.7 156.2 585.7 748.8 809.1 4.9 5.0 5.2

Total 1,906.7 1,970.4 2,020.6 11,490.0 11,829.7 12,537.9 6.02 6.00 6.2

Source: Indian Horticulture Database, 2006

6

3. Description of commercially grown varieties

There are near about 30 varieties of mangoes which are grown commercially. Some of the most important varieties have been listed below in the table 2.4.

Table 2.4: Shows the varietal characteristics of commercially grown mangoes

Variety Characteristics Alphonso This variety is medium in size, ovate oblique in shape and orange

yellow in colour. The pulp is yellow to orange in colour. It is soft, firm and fibreless. It is a mid-season variety.

Banganpalli The flesh is firm to meaty, fibreless. Fruit is large in size and obliquely oval in shape. The colour of fruit is golden yellow. Good keeping quality and a mid season variety.

Chausa Fruit is large in size, ovate to oval oblique in shape and light yellow in colour. It is a late variety.

Dashehri Fruit size is medium, shape is oblong to oblong-oblique and fruit colour is yellow. The pulp is firm and fibreless and a mid season variety.

Langra Fruit is of medium size, ovate shape and lettuce green in colour.The lemon-yellow flesh is juicy and flavourful. It is scarcely fibrous, a mid season variety.

Totapuri Fruit size is medium to large, shape is oblong with necked base and colour is golden yellow. Flesh is cadmium yellow and fibreless, a mid season variety.

Kesar Fruits are medium sized, flesh is sweet and fibreless. Colour is apricot yellow with red blush, an early season variety.

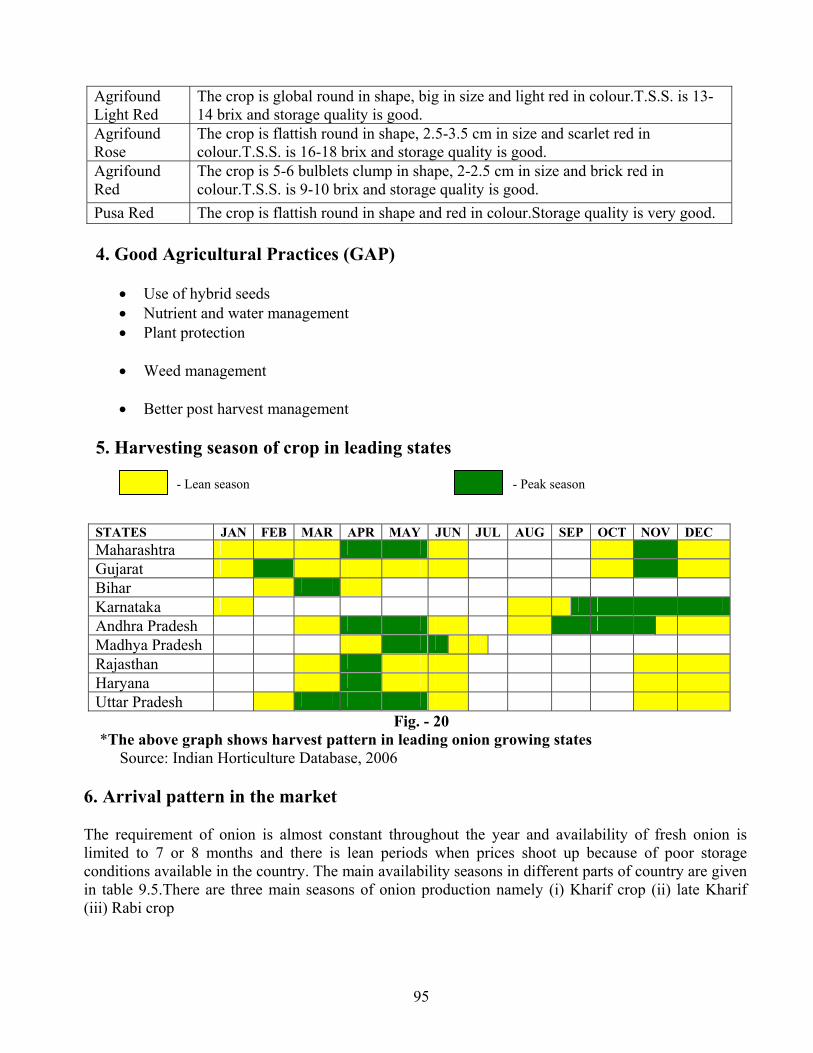

4. Good Agricultural Practices (GAP)

• Adoption of improved cultivars. • Adoption of high density planting in cultivars • Regulating flowering and increasing intensity of flowering. • Pruning malformed mango shoots at bearing stage • Alternate bearing needs to be managed by reducing fruiting during a year by adoption

of pruning and thinning practices. • Providing life saving irrigation at the critical stage of fruit growth etc. • Integrated nutrient and water management. • Management of spongy tissue through sod mulching. • Integrated pest and disease management practices and timely control of pests and

diseases, especially mango hopper, mango mealy bug and sprays of Bavistin at fruit development stage especially after rains.

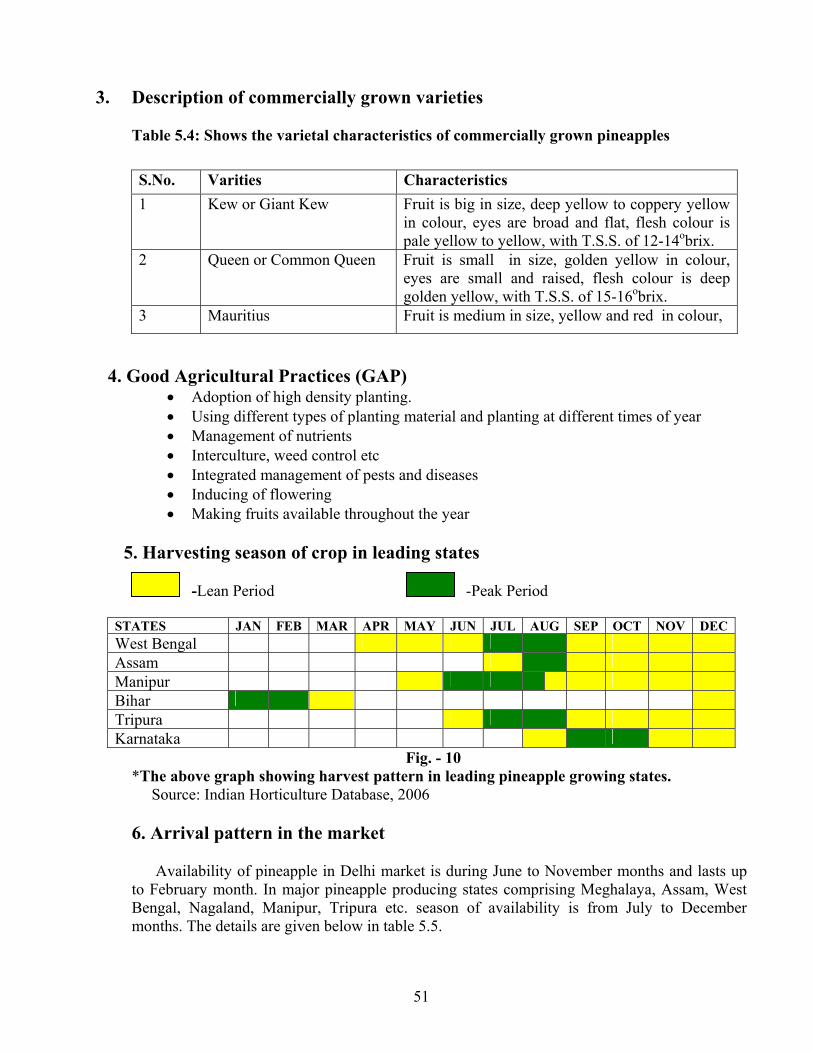

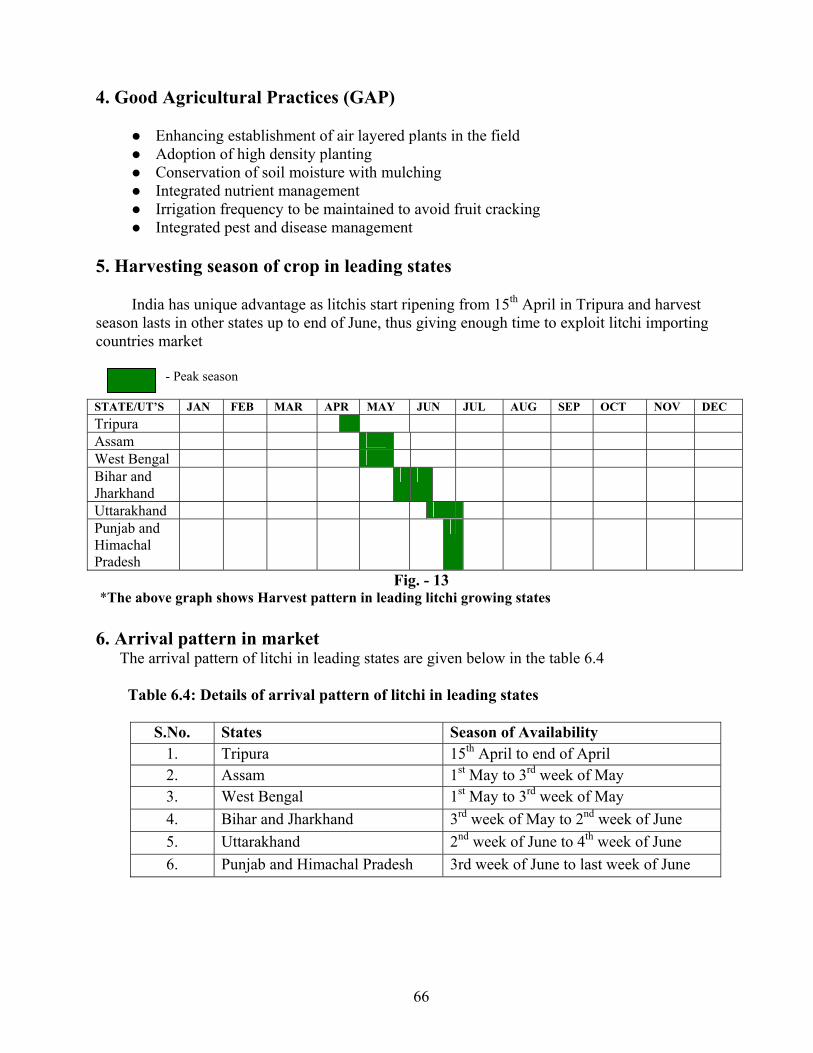

5. Harvesting season of crop in leading states

- Lean season - Peak season

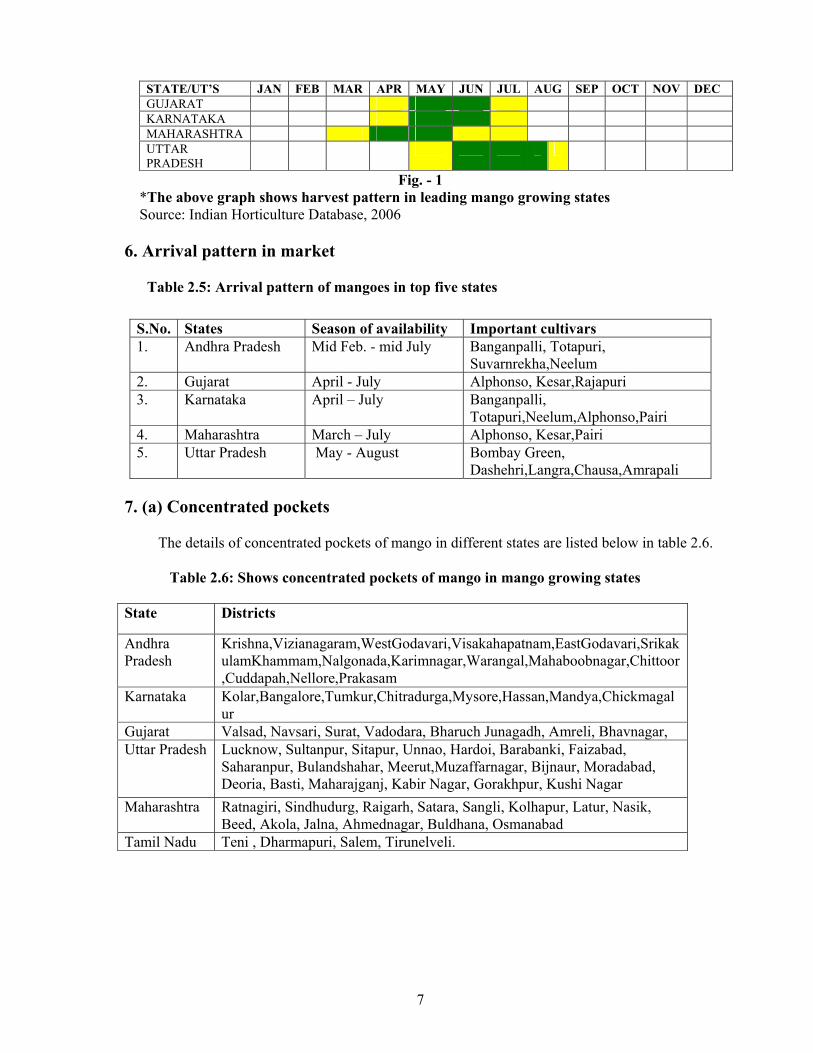

STATE/UT’S JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC ANDHRA PRADESH

7

STATE/UT’S JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC GUJARAT KARNATAKA MAHARASHTRA UTTAR PRADESH

Fig. - 1 *The above graph shows harvest pattern in leading mango growing states Source: Indian Horticulture Database, 2006

6. Arrival pattern in market

Table 2.5: Arrival pattern of mangoes in top five states

7. (a) Concentrated pockets

The details of concentrated pockets of mango in different states are listed below in table 2.6.

Table 2.6: Shows concentrated pockets of mango in mango growing states

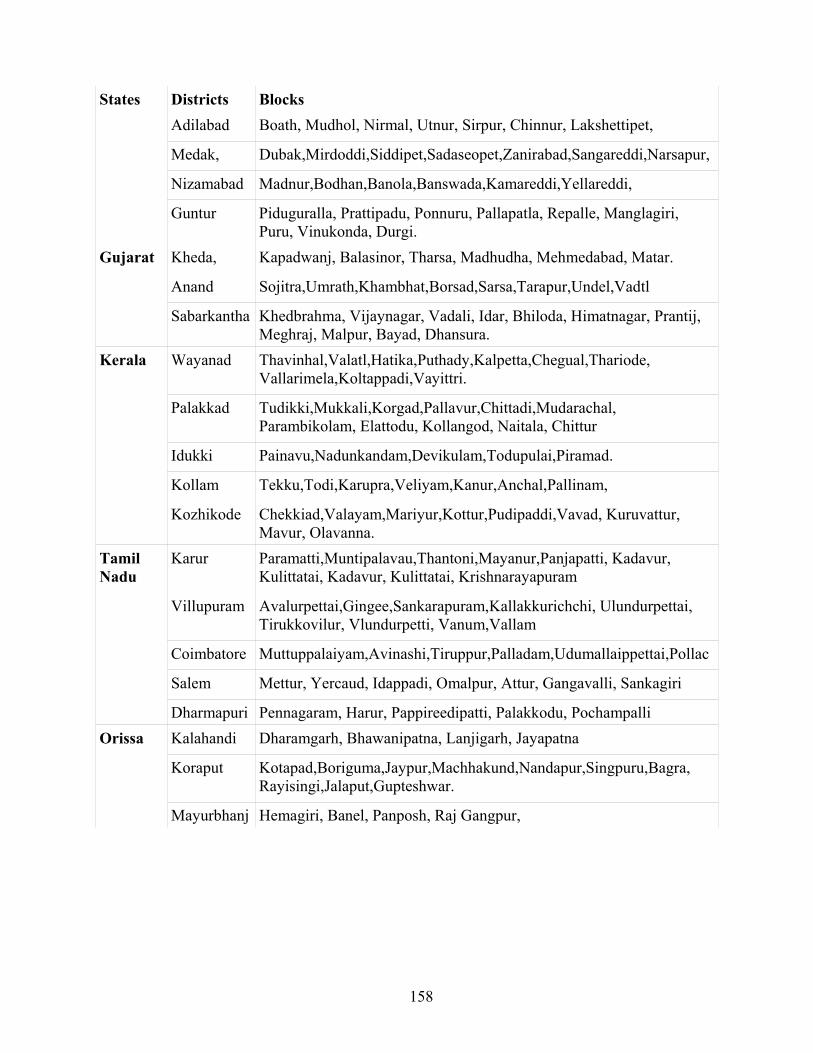

State Districts

Andhra Pradesh

Krishna,Vizianagaram,WestGodavari,Visakahapatnam,EastGodavari,SrikakulamKhammam,Nalgonada,Karimnagar,Warangal,Mahaboobnagar,Chittoor,Cuddapah,Nellore,Prakasam

Karnataka Kolar,Bangalore,Tumkur,Chitradurga,Mysore,Hassan,Mandya,Chickmagalur

Gujarat Valsad, Navsari, Surat, Vadodara, Bharuch Junagadh, Amreli, Bhavnagar, Uttar Pradesh Lucknow, Sultanpur, Sitapur, Unnao, Hardoi, Barabanki, Faizabad,

Saharanpur, Bulandshahar, Meerut,Muzaffarnagar, Bijnaur, Moradabad, Deoria, Basti, Maharajganj, Kabir Nagar, Gorakhpur, Kushi Nagar

Maharashtra Ratnagiri, Sindhudurg, Raigarh, Satara, Sangli, Kolhapur, Latur, Nasik, Beed, Akola, Jalna, Ahmednagar, Buldhana, Osmanabad

Tamil Nadu Teni , Dharmapuri, Salem, Tirunelveli.

S.No. States Season of availability Important cultivars 1. Andhra Pradesh Mid Feb. - mid July Banganpalli, Totapuri,

Suvarnrekha,Neelum 2. Gujarat April - July Alphonso, Kesar,Rajapuri 3. Karnataka April – July Banganpalli,

Totapuri,Neelum,Alphonso,Pairi 4. Maharashtra March – July Alphonso, Kesar,Pairi 5. Uttar Pradesh May - August Bombay Green,

Dashehri,Langra,Chausa,Amrapali

8

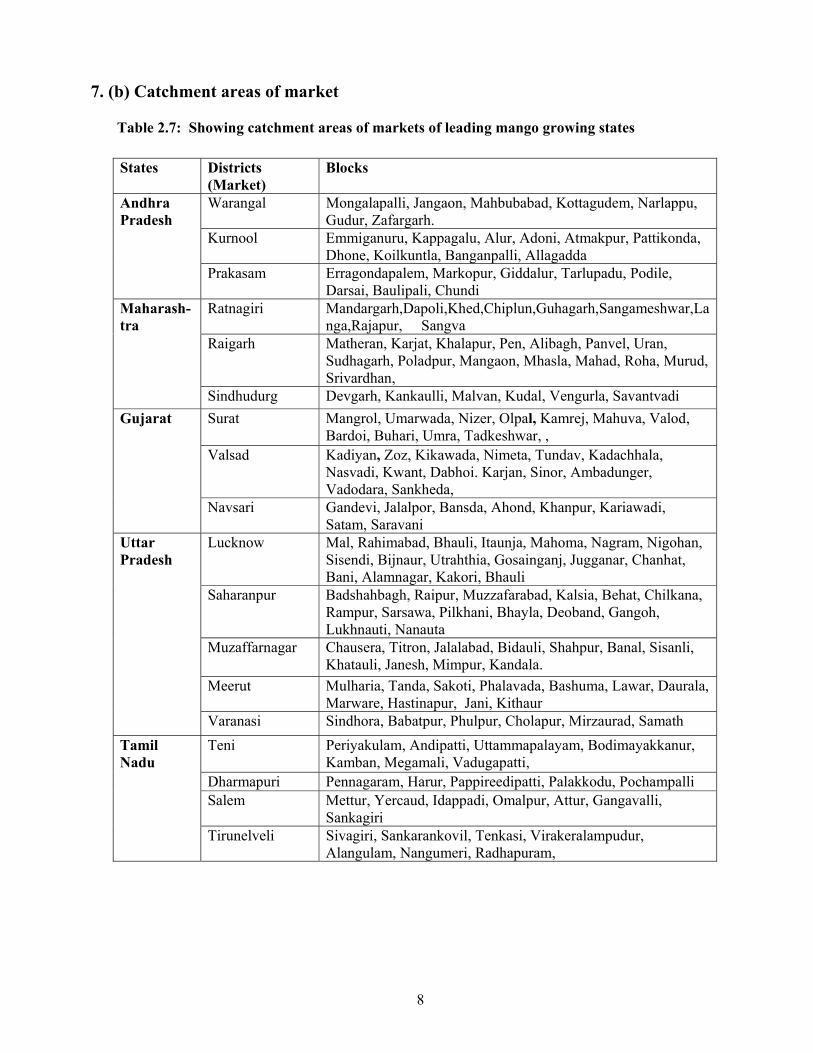

7. (b) Catchment areas of market

Table 2.7: Showing catchment areas of markets of leading mango growing states

States Districts (Market)

Blocks

Warangal Mongalapalli, Jangaon, Mahbubabad, Kottagudem, Narlappu, Gudur, Zafargarh.

Kurnool Emmiganuru, Kappagalu, Alur, Adoni, Atmakpur, Pattikonda, Dhone, Koilkuntla, Banganpalli, Allagadda

Andhra Pradesh

Prakasam Erragondapalem, Markopur, Giddalur, Tarlupadu, Podile, Darsai, Baulipali, Chundi

Ratnagiri Mandargarh,Dapoli,Khed,Chiplun,Guhagarh,Sangameshwar,Langa,Rajapur, Sangva

Raigarh Matheran, Karjat, Khalapur, Pen, Alibagh, Panvel, Uran, Sudhagarh, Poladpur, Mangaon, Mhasla, Mahad, Roha, Murud, Srivardhan,

Maharash-tra

Sindhudurg Devgarh, Kankaulli, Malvan, Kudal, Vengurla, Savantvadi Surat Mangrol, Umarwada, Nizer, Olpal, Kamrej, Mahuva, Valod,

Bardoi, Buhari, Umra, Tadkeshwar, , Valsad Kadiyan, Zoz, Kikawada, Nimeta, Tundav, Kadachhala,

Nasvadi, Kwant, Dabhoi. Karjan, Sinor, Ambadunger, Vadodara, Sankheda,

Gujarat

Navsari Gandevi, Jalalpor, Bansda, Ahond, Khanpur, Kariawadi, Satam, Saravani

Lucknow Mal, Rahimabad, Bhauli, Itaunja, Mahoma, Nagram, Nigohan, Sisendi, Bijnaur, Utrahthia, Gosainganj, Jugganar, Chanhat, Bani, Alamnagar, Kakori, Bhauli

Saharanpur Badshahbagh, Raipur, Muzzafarabad, Kalsia, Behat, Chilkana, Rampur, Sarsawa, Pilkhani, Bhayla, Deoband, Gangoh, Lukhnauti, Nanauta

Muzaffarnagar Chausera, Titron, Jalalabad, Bidauli, Shahpur, Banal, Sisanli, Khatauli, Janesh, Mimpur, Kandala.

Meerut Mulharia, Tanda, Sakoti, Phalavada, Bashuma, Lawar, Daurala, Marware, Hastinapur, Jani, Kithaur

Uttar Pradesh

Varanasi Sindhora, Babatpur, Phulpur, Cholapur, Mirzaurad, Samath Teni Periyakulam, Andipatti, Uttammapalayam, Bodimayakkanur,

Kamban, Megamali, Vadugapatti, Dharmapuri Pennagaram, Harur, Pappireedipatti, Palakkodu, Pochampalli Salem Mettur, Yercaud, Idappadi, Omalpur, Attur, Gangavalli,

Sankagiri

Tamil Nadu

Tirunelveli Sivagiri, Sankarankovil, Tenkasi, Virakeralampudur, Alangulam, Nangumeri, Radhapuram,

9

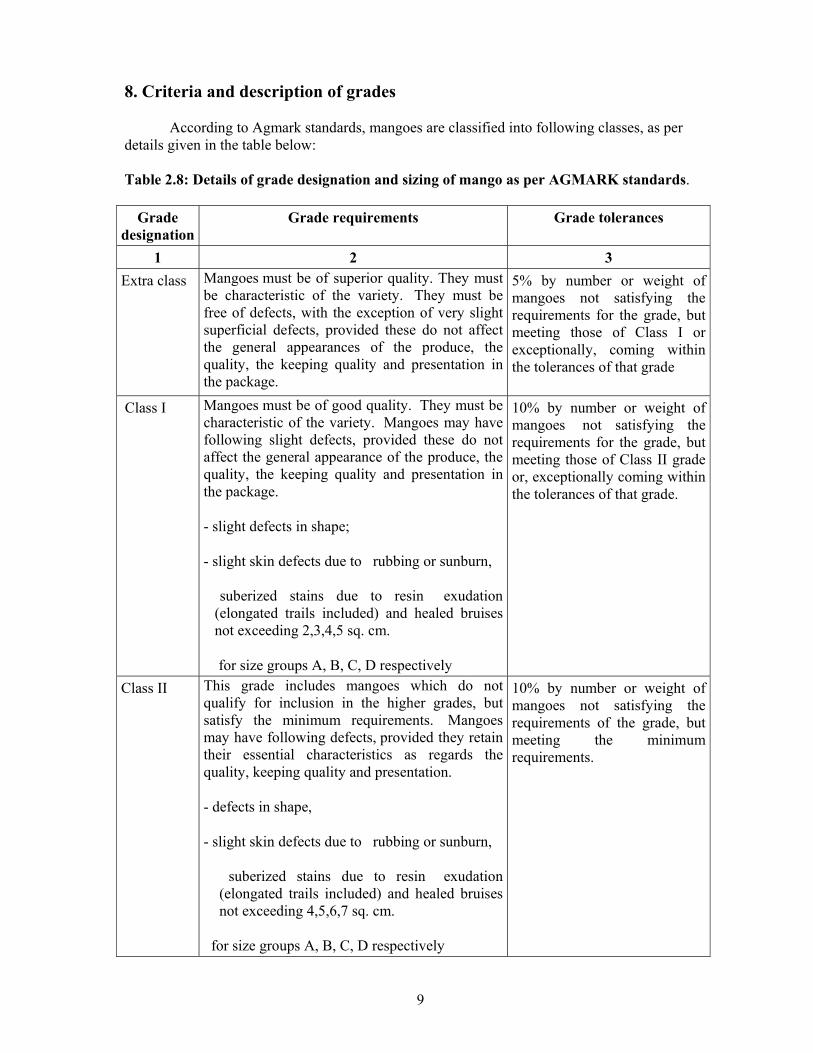

8. Criteria and description of grades According to Agmark standards, mangoes are classified into following classes, as per

details given in the table below:

Table 2.8: Details of grade designation and sizing of mango as per AGMARK standards.

Grade designation

Grade requirements Grade tolerances

1 2 3 Extra class Mangoes must be of superior quality. They must

be characteristic of the variety. They must be free of defects, with the exception of very slight superficial defects, provided these do not affect the general appearances of the produce, the quality, the keeping quality and presentation in the package.

5% by number or weight of mangoes not satisfying the requirements for the grade, but meeting those of Class I or exceptionally, coming within the tolerances of that grade

Class I Mangoes must be of good quality. They must be characteristic of the variety. Mangoes may have following slight defects, provided these do not affect the general appearance of the produce, the quality, the keeping quality and presentation in the package.

- slight defects in shape;

- slight skin defects due to rubbing or sunburn,

suberized stains due to resin exudation (elongated trails included) and healed bruises not exceeding 2,3,4,5 sq. cm.

for size groups A, B, C, D respectively

10% by number or weight of mangoes not satisfying the requirements for the grade, but meeting those of Class II grade or, exceptionally coming within the tolerances of that grade.

Class II This grade includes mangoes which do not qualify for inclusion in the higher grades, but satisfy the minimum requirements. Mangoes may have following defects, provided they retain their essential characteristics as regards the quality, keeping quality and presentation.

- defects in shape,

- slight skin defects due to rubbing or sunburn,

suberized stains due to resin exudation (elongated trails included) and healed bruises not exceeding 4,5,6,7 sq. cm.

for size groups A, B, C, D respectively

10% by number or weight of mangoes not satisfying the requirements of the grade, but meeting the minimum requirements.

10

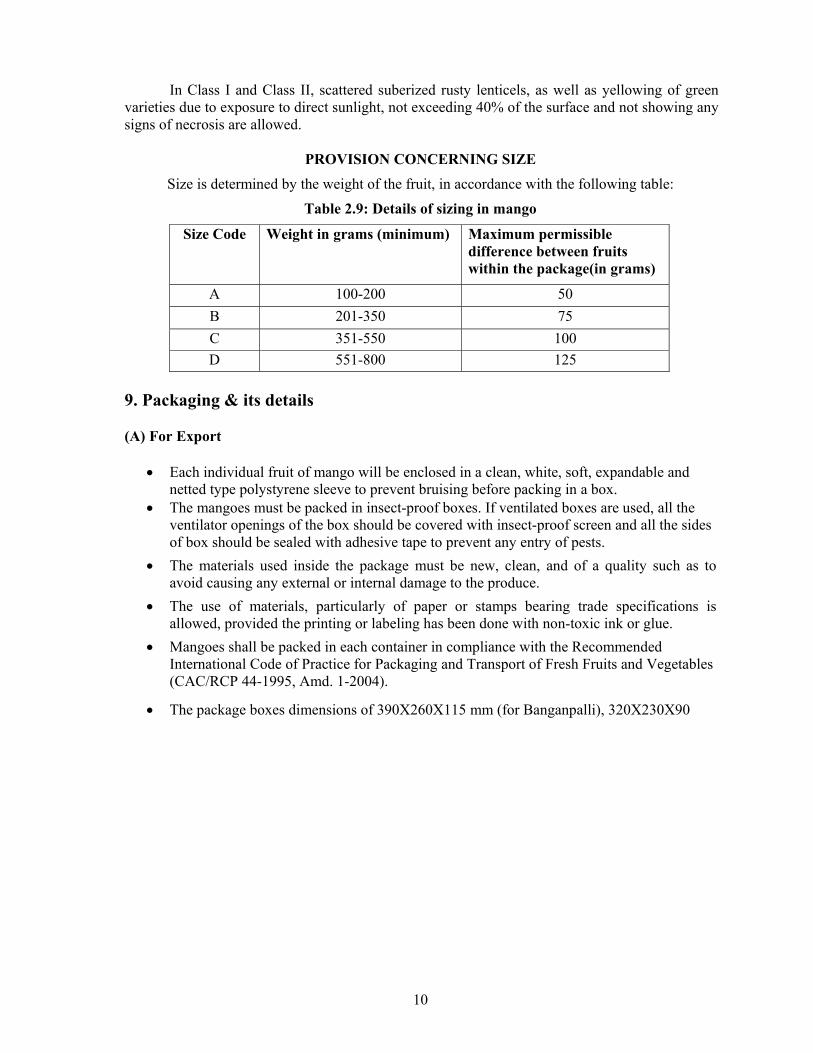

In Class I and Class II, scattered suberized rusty lenticels, as well as yellowing of green varieties due to exposure to direct sunlight, not exceeding 40% of the surface and not showing any signs of necrosis are allowed.

PROVISION CONCERNING SIZE

Size is determined by the weight of the fruit, in accordance with the following table:

Table 2.9: Details of sizing in mango

Size Code Weight in grams (minimum) Maximum permissible difference between fruits within the package(in grams)

A 100-200 50 B 201-350 75 C 351-550 100 D 551-800 125

9. Packaging & its details

(A) For Export

• Each individual fruit of mango will be enclosed in a clean, white, soft, expandable and netted type polystyrene sleeve to prevent bruising before packing in a box.

• The mangoes must be packed in insect-proof boxes. If ventilated boxes are used, all the ventilator openings of the box should be covered with insect-proof screen and all the sides of box should be sealed with adhesive tape to prevent any entry of pests.

• The materials used inside the package must be new, clean, and of a quality such as to avoid causing any external or internal damage to the produce.

• The use of materials, particularly of paper or stamps bearing trade specifications is allowed, provided the printing or labeling has been done with non-toxic ink or glue.

• Mangoes shall be packed in each container in compliance with the Recommended International Code of Practice for Packaging and Transport of Fresh Fruits and Vegetables (CAC/RCP 44-1995, Amd. 1-2004).

• The package boxes dimensions of 390X260X115 mm (for Banganpalli), 320X230X90

11

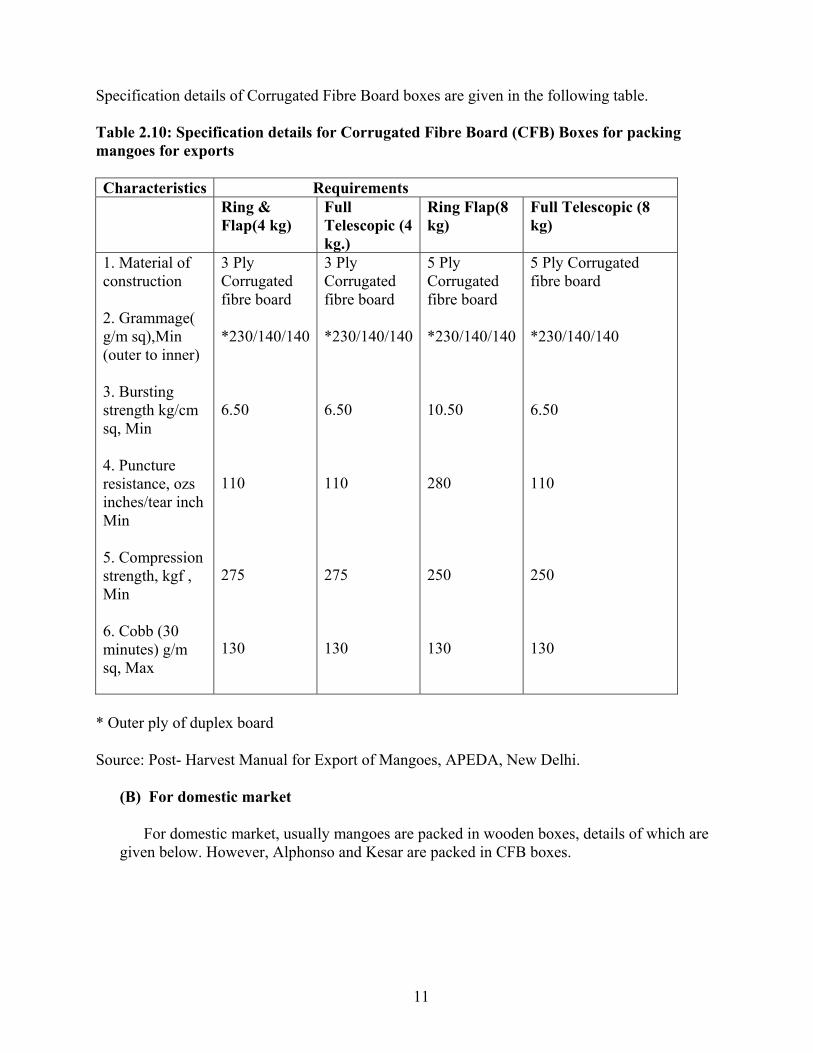

Specification details of Corrugated Fibre Board boxes are given in the following table. Table 2.10: Specification details for Corrugated Fibre Board (CFB) Boxes for packing mangoes for exports Characteristics Requirements Ring &

Flap(4 kg) Full Telescopic (4 kg.)

Ring Flap(8 kg)

Full Telescopic (8 kg)

1. Material of construction

2. Grammage( g/m sq),Min (outer to inner)

3. Bursting strength kg/cm sq, Min

4. Puncture resistance, ozs inches/tear inch Min

5. Compression strength, kgf , Min

6. Cobb (30 minutes) g/m sq, Max

3 Ply Corrugated fibre board

*230/140/140 6.50 110 275 130

3 Ply Corrugated fibre board

*230/140/140 6.50 110 275 130

5 Ply Corrugated fibre board

*230/140/140 10.50 280 250 130

5 Ply Corrugated fibre board

*230/140/140 6.50 110 250 130

* Outer ply of duplex board

Source: Post- Harvest Manual for Export of Mangoes, APEDA, New Delhi.

(B) For domestic market

For domestic market, usually mangoes are packed in wooden boxes, details of which are given below. However, Alphonso and Kesar are packed in CFB boxes.

12

Table 2.11: Specifications of wooden boxes for domestic marketing

Type of Carton Inner Dimension(cm)

Capacity (kgs)

Wooden crates

45X30X30 (Ratnagiri)

21.6X21.6X42 (Malihabad )

16-18

10-11

10. Distribution of produce from primary to terminal market

• Mangoes grown in different parts of the country are transported to the big cities for marketing.

• The fruits produced in Andhra Pradesh and Tamil Nadu find markets in Nagpur, Bombay, and Calcutta.

• The important wholesale mango markets in India are Calcutta, Delhi, Bombay, Madras, Ahmedabad, Pune and Nagpur.

• Mangoes for these big markets are usually collected at the central places in all the mango-growing areas, e.g., in Uttar Pradesh, Lucknow and Varanasi; in Gujarat, Gandevi, Gadat and Amalsar talukas; and in Maharashtra, Ratnagiri and Vengurla.

• Delhi and Bombay are the most important markets for despatch of mangoes. At Delhi all the mangoes are assembled at Sabzimandi, Ashoka market, and at Bombay at Crawford and Byculla markets for distribution.

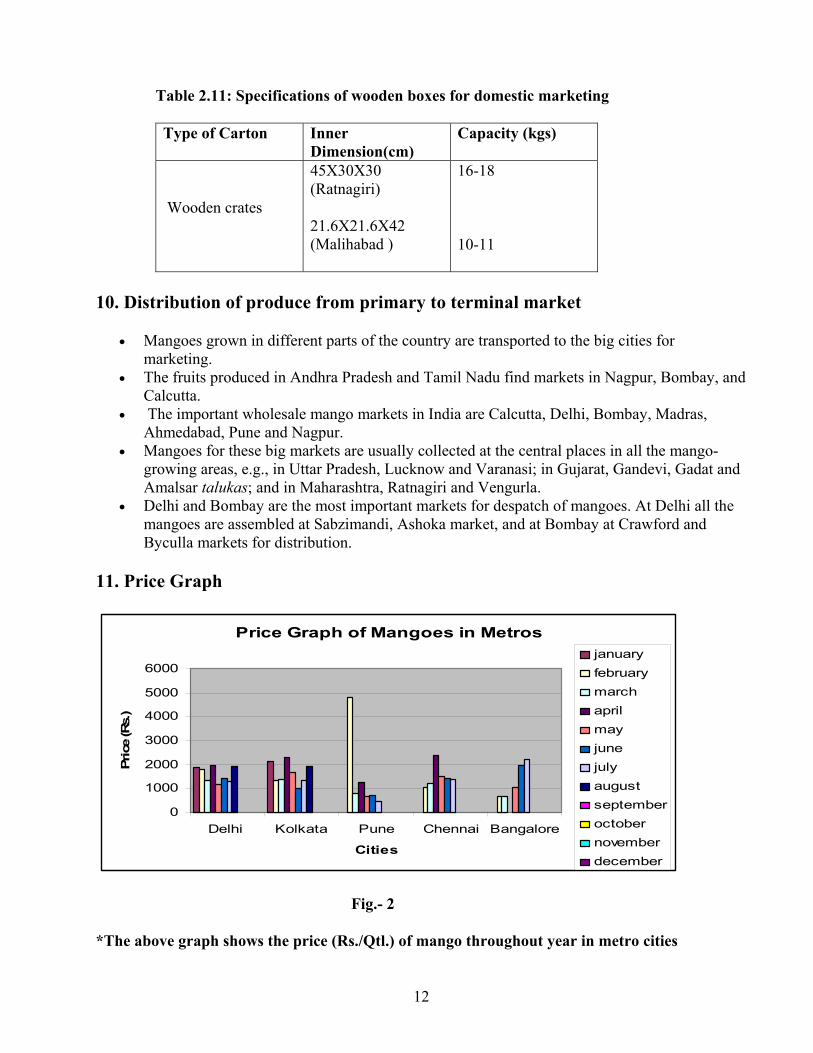

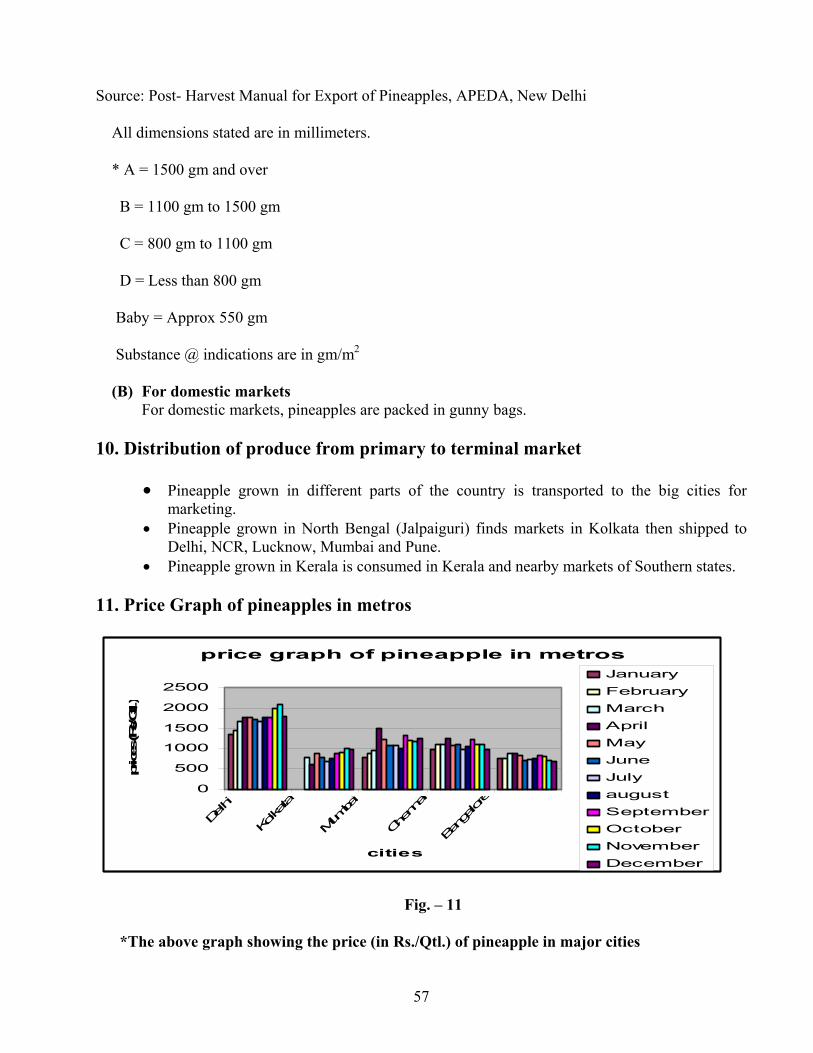

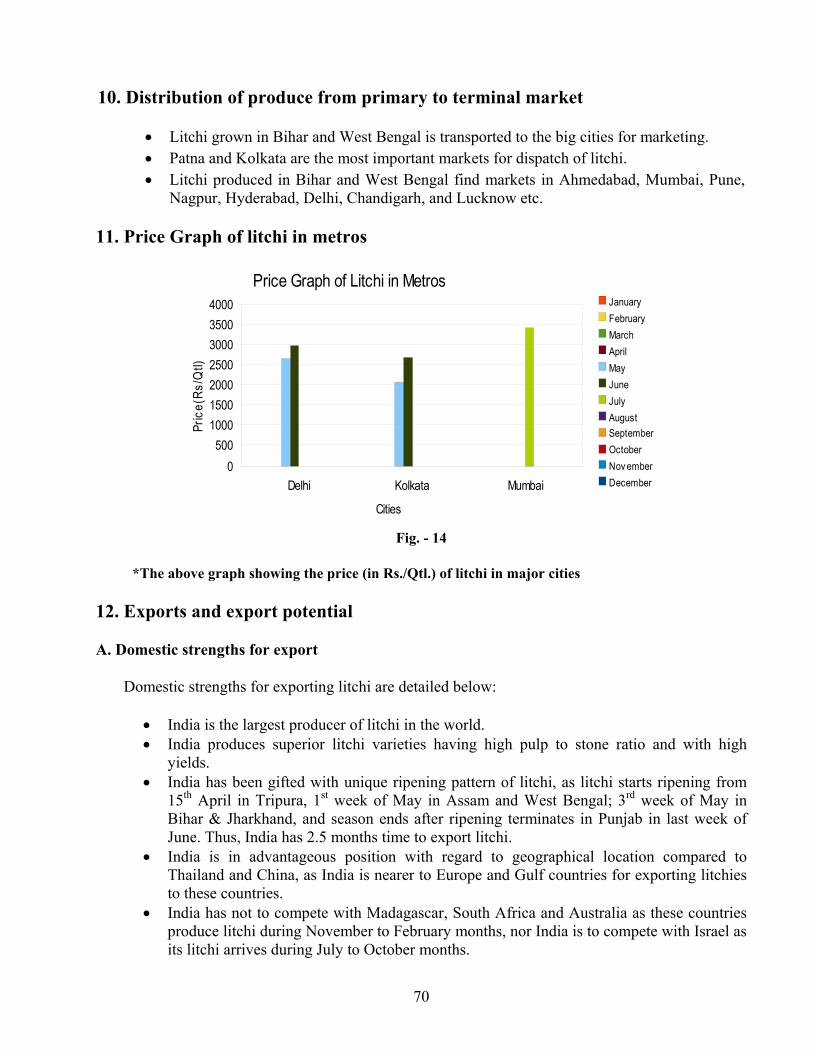

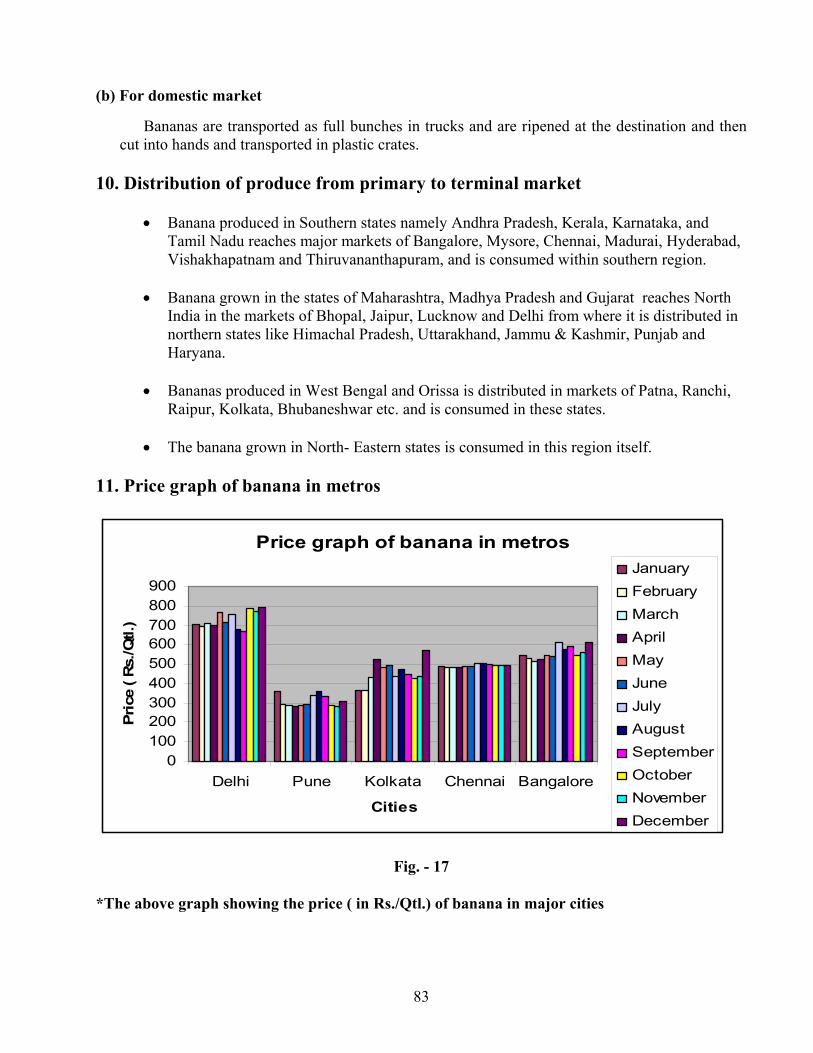

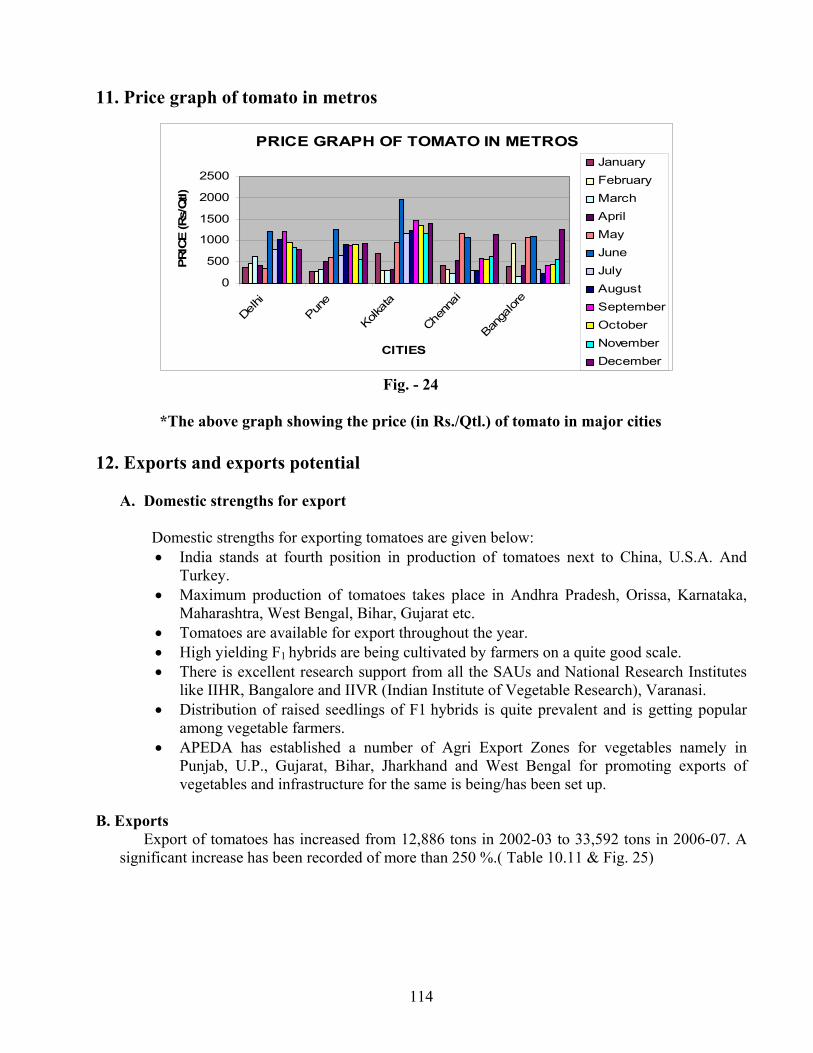

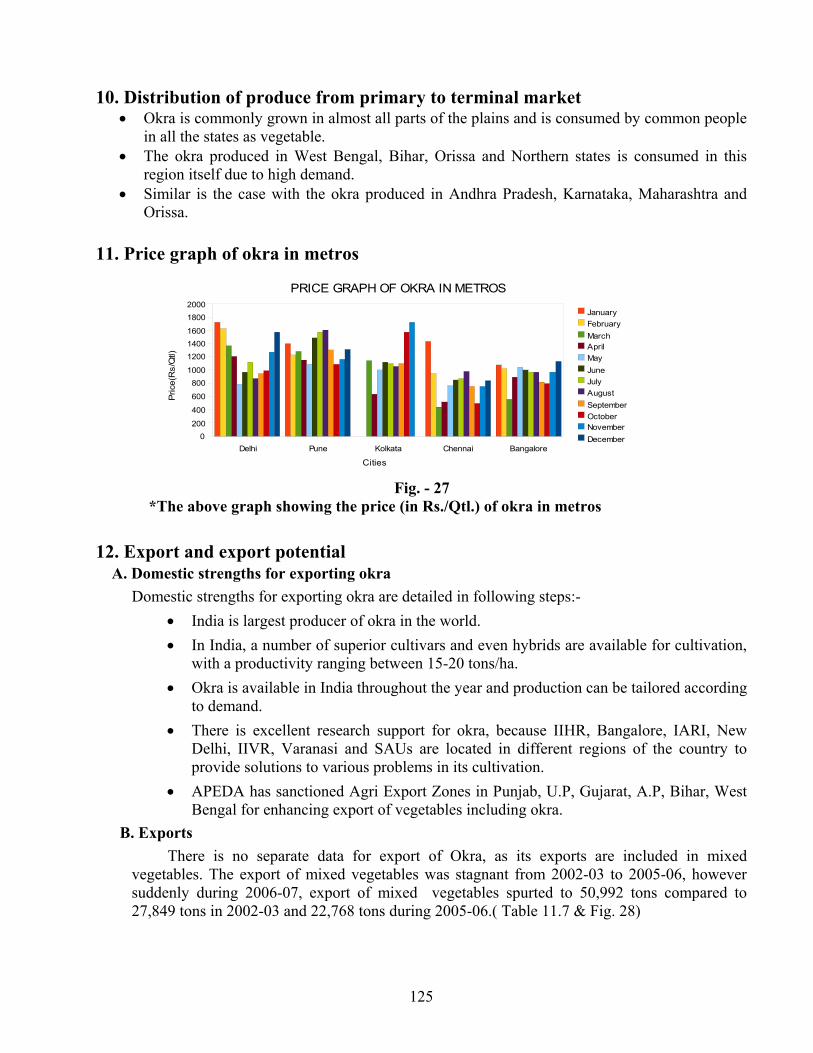

11. Price Graph

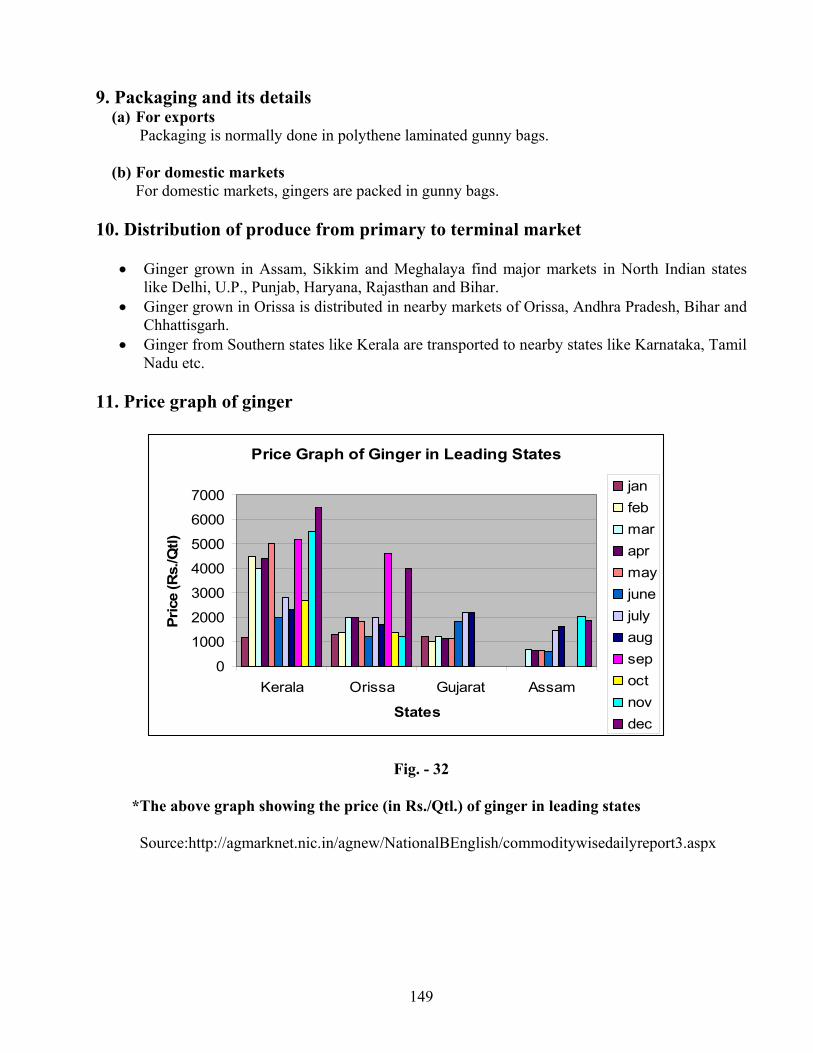

Price Graph of Mangoes in Metros

0

1000

2000

3000

4000

5000

6000

Delhi Kolkata Pune Chennai Bangalore

Cities

Pric

e (R

s.)

januaryfebruarymarchaprilmayjunejulyaugustseptemberoctobernovemberdecember

Fig.- 2

*The above graph shows the price (Rs./Qtl.) of mango throughout year in metro cities

13

12. Exports and export potential

A. Domestic strengths for exporting mango

Domestic strengths for exporting mango from India are listed below:

• India occupies top position in total production among mango growing countries of the world. • India cultivates a wide variety of mangoes; some of them are very colourful and attractive

with par excellence edible quality. • Mangoes are cultivated with sizeable production in almost all the states i.e. Andhra Pradesh,

Uttar Pradesh, Maharashtra, Gujarat, Tamil Nadu etc. • Transfer of technology for cultivation of mango is easy as in many states; farmers have

formed associations/cooperatives. • In Maharashtra state mango growers are quite innovative. • Agri Export Zones for facilitating exports have been established in almost all mango growing

areas. • Packhouses on modern lines have been provided in all mango exporting regions i.e. in

Ratnagiri and Sindhudurg in Maharashtra and in Navsari and Borsad in Gujarat for Alphonso variety; in Latur and Aurangabad for Kesar mango; in Saharanpur and Malihabad in U.P. for Dashehari and Chausa mangoes.

• Facilities for facilitating mango exports like Post-harvest Management Centre have been established at Malihabad and Saharanpur. Similarly a mango Export Facility Centre has been established at Ratnagiri.

• Mango farmers of Alphonso and Kesar are already being trained in GLOBALGAP requirements.

• Mango growers of Saharanpur have already branded their product as “NAWAB” mango. • Facilities for Vapour Heat Treatment and irradiation for eliminating fruit fly have already

been set up. • India is in advantageous position, as it is nearer to Middle East countries compared to

Australia, Kenya etc. main suppliers in Middle East.

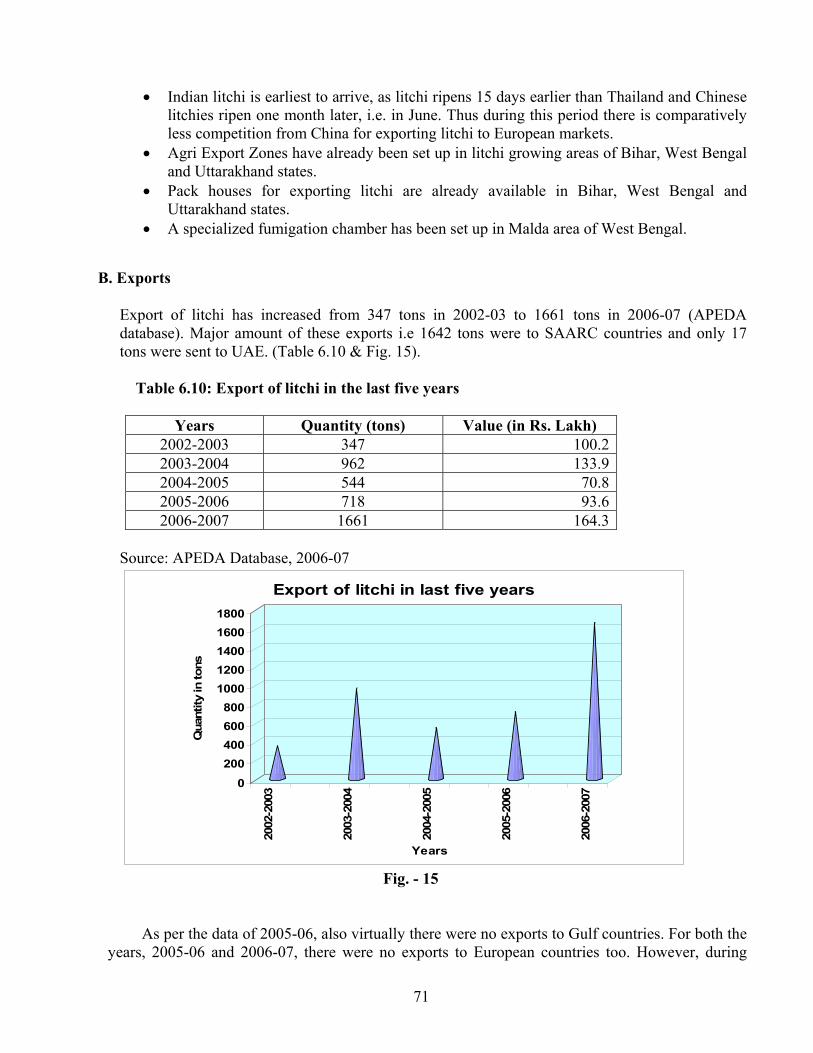

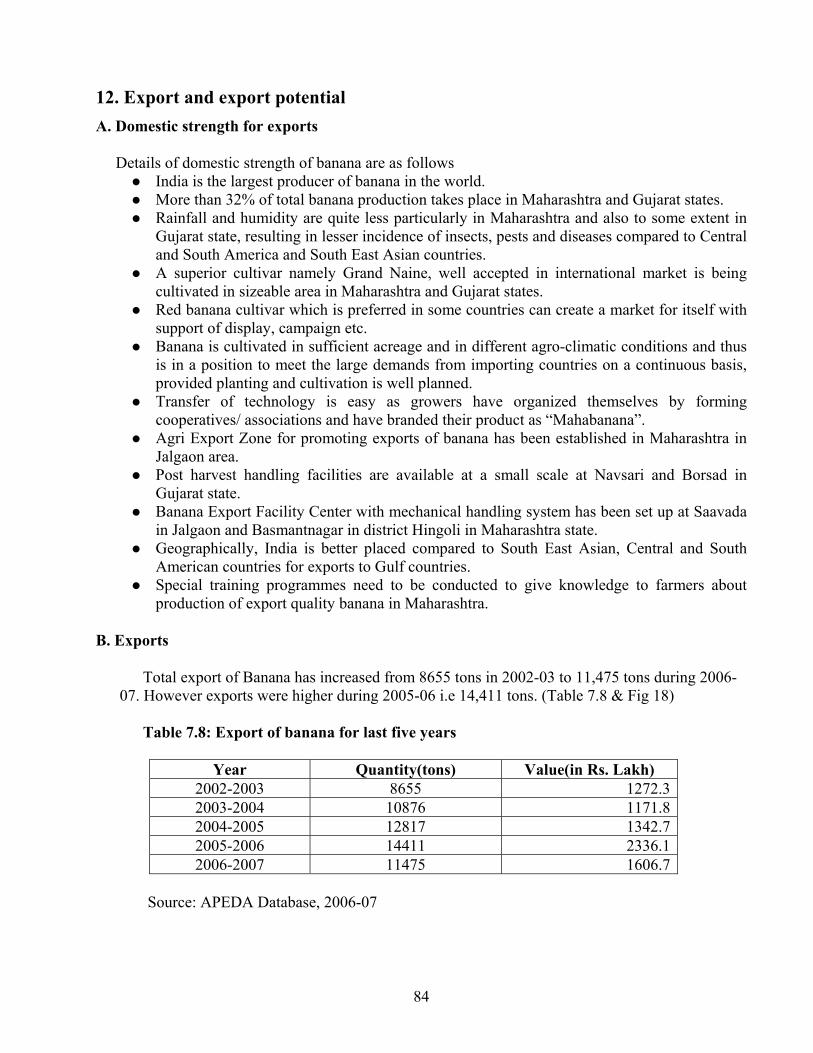

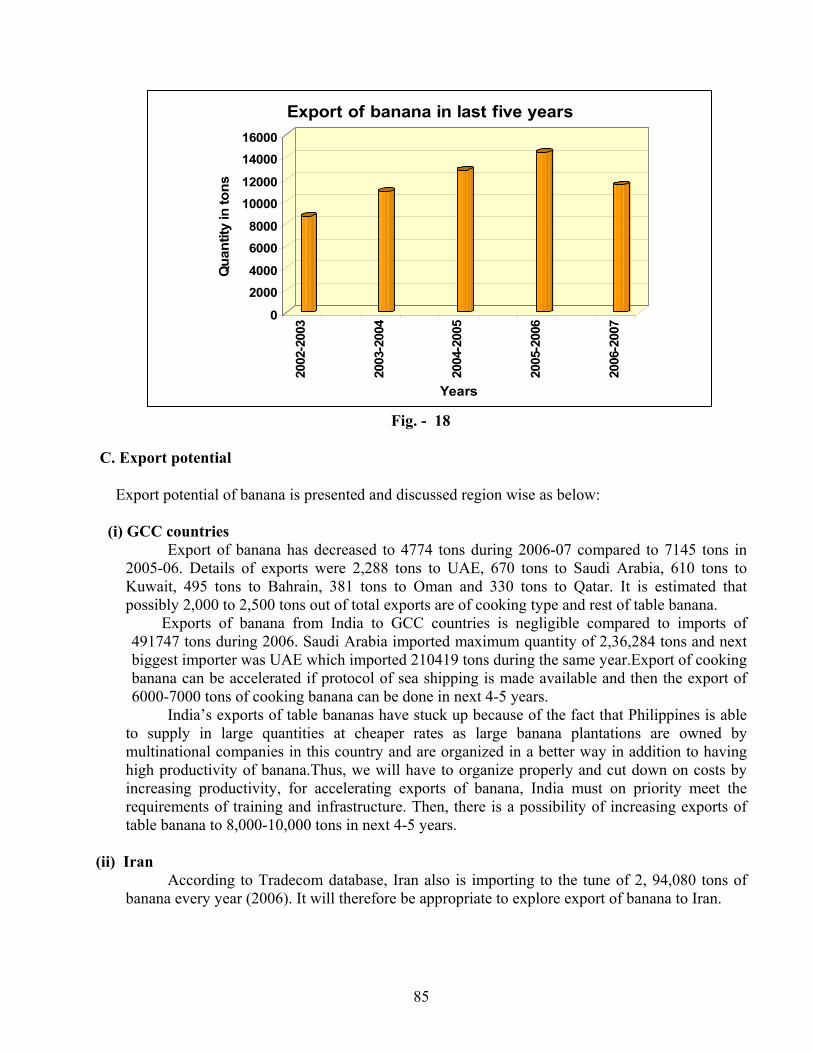

B. Exports

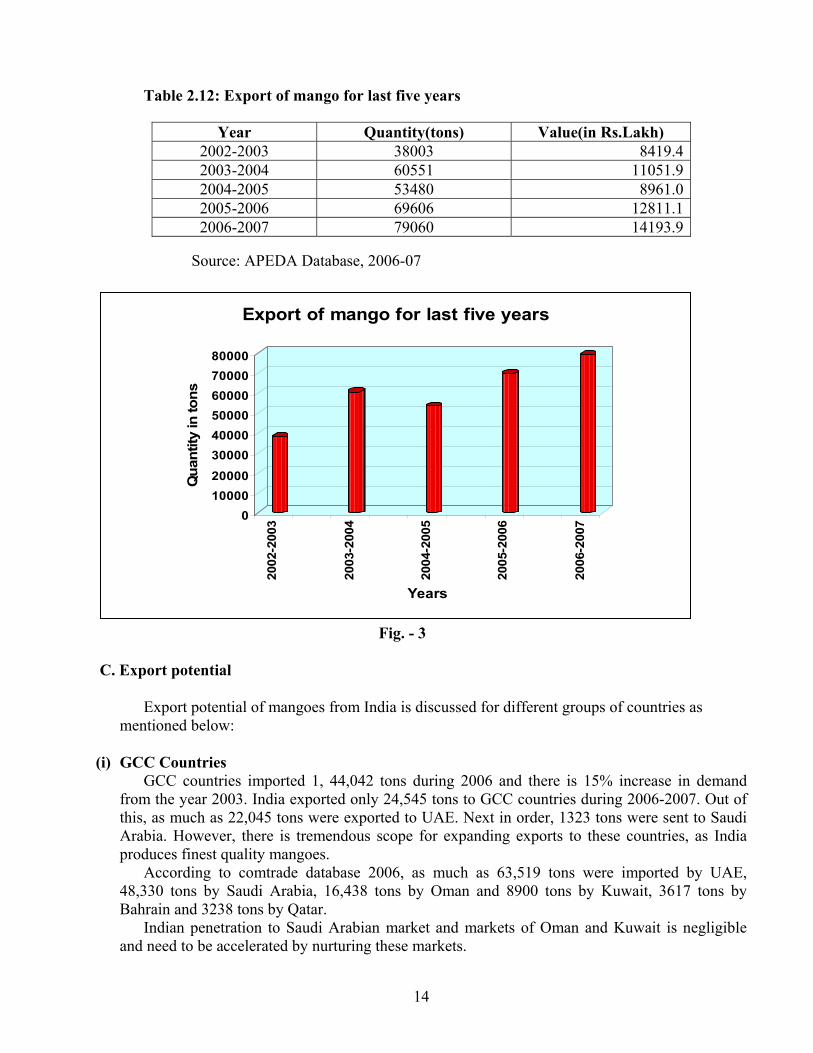

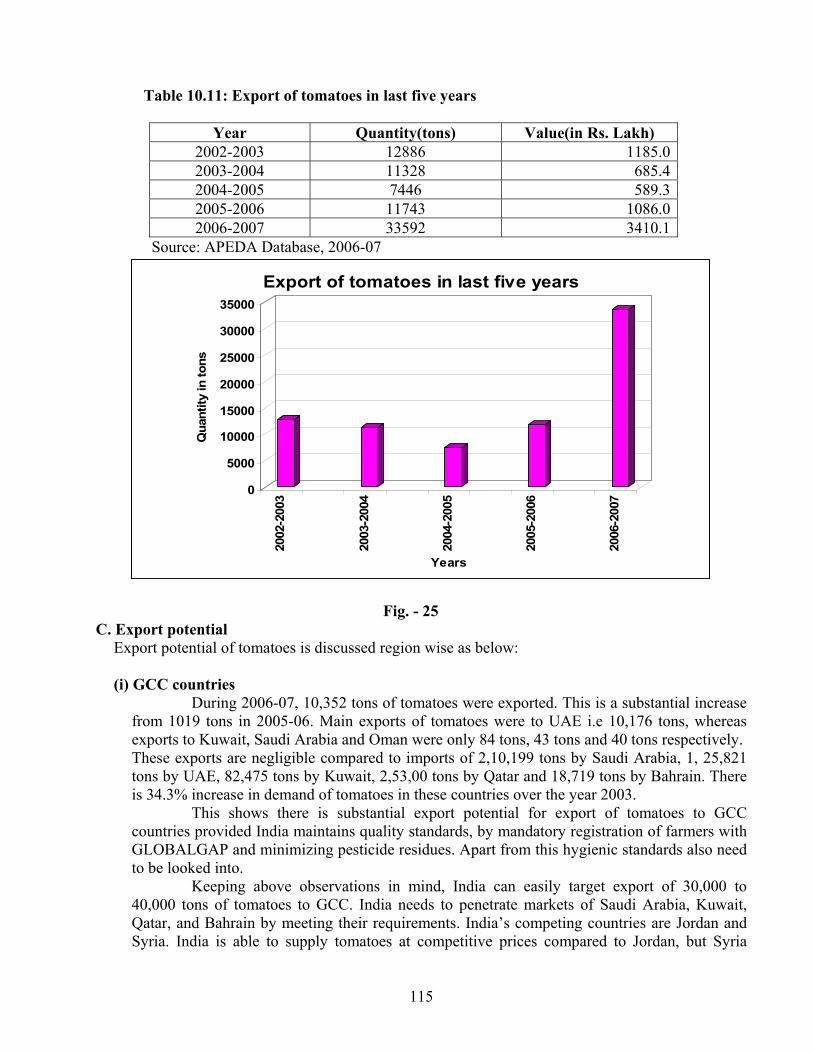

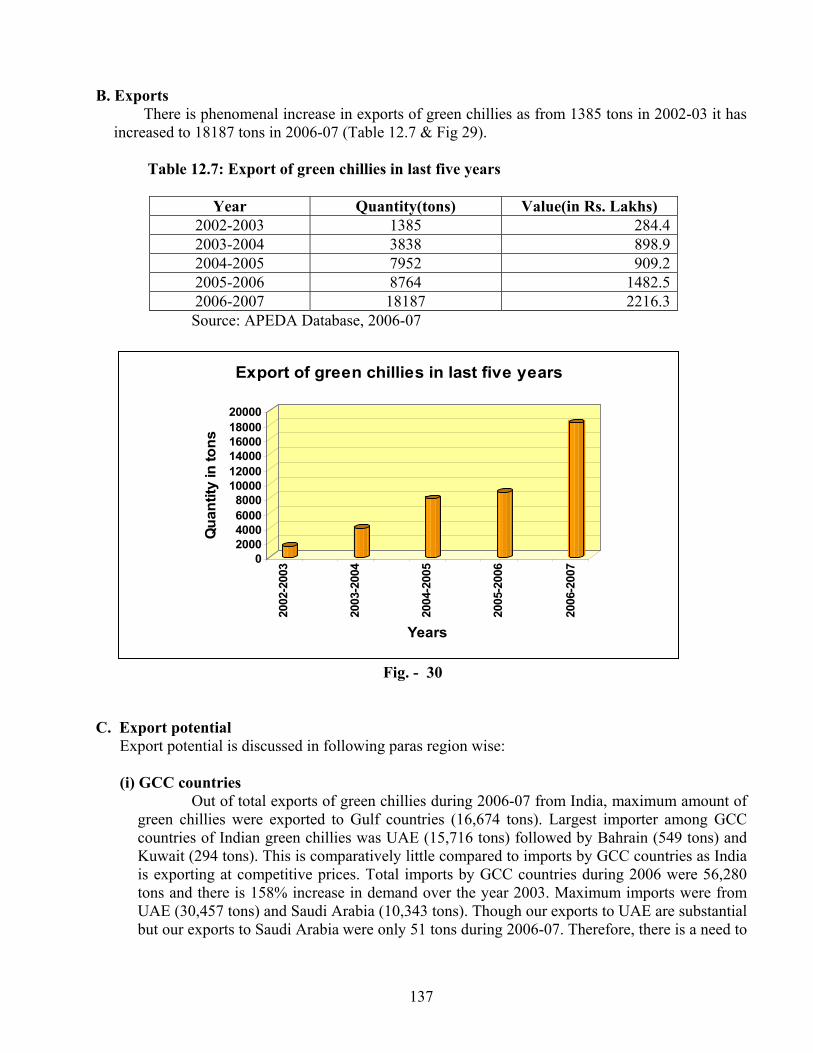

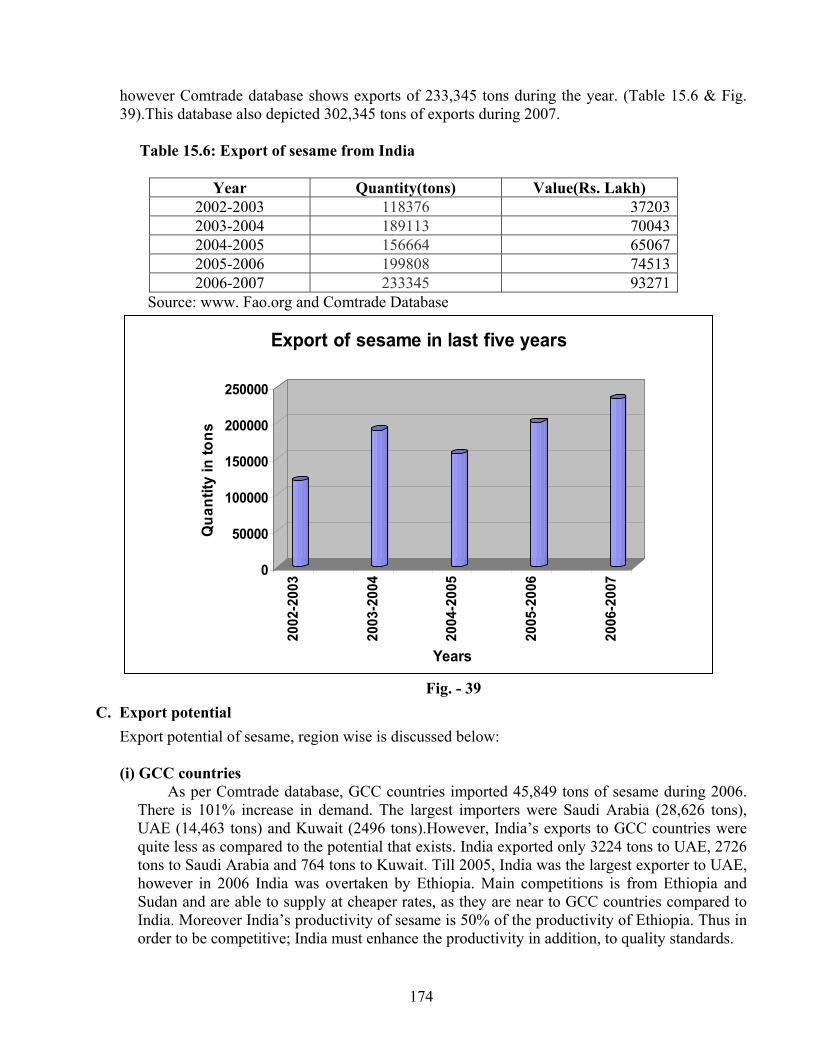

Export of mango has increased from 38,003 tons in 2002-2003 to 79,060 tons 2006-2007, a 107% increase in the last five years. (Table 2.12 & Fig. 3). This is a phenomenal growth.

As per APEDA database of 2006-2007, major portion of exports (50,942 tons) has gone to

SAARC countries and only 24,545 tons have been exported to GCC countries. For EU countries still lesser quantity i.e. 2658 tons has been exported.

14

Table 2.12: Export of mango for last five years

Source: APEDA Database, 2006-07

01000020000300004000050000600007000080000

Qua

ntity

in to

ns

2002

-200

3

2003

-200

4

2004

-200

5

2005

-200

6

2006

-200

7Years

Export of mango for last five years

Fig. - 3

C. Export potential

Export potential of mangoes from India is discussed for different groups of countries as mentioned below:

(i) GCC Countries GCC countries imported 1, 44,042 tons during 2006 and there is 15% increase in demand from the year 2003. India exported only 24,545 tons to GCC countries during 2006-2007. Out of this, as much as 22,045 tons were exported to UAE. Next in order, 1323 tons were sent to Saudi Arabia. However, there is tremendous scope for expanding exports to these countries, as India produces finest quality mangoes. According to comtrade database 2006, as much as 63,519 tons were imported by UAE, 48,330 tons by Saudi Arabia, 16,438 tons by Oman and 8900 tons by Kuwait, 3617 tons by Bahrain and 3238 tons by Qatar. Indian penetration to Saudi Arabian market and markets of Oman and Kuwait is negligible and need to be accelerated by nurturing these markets.

Year Quantity(tons) Value(in Rs.Lakh) 2002-2003 38003 8419.42003-2004 60551 11051.92004-2005 53480 8961.02005-2006 69606 12811.12006-2007 79060 14193.9

15

India's total exports are substantial during March – April months and reduce significantly during May onwards because of competition from Pakistan. India must explore reducing costs Kesar variety of mango which is much more acceptable by increased productivity and make available through reefer containers,. We must target at least 40,000 to 50,000 tons of exports to GCC countries in next 4-5 years period of the total imports of 1,44,042 tons.

(ii) EU countries

EU countries import mangoes varying from 2, 50,000 tons to 3, 00,000 tons every year. There is 31% increase in demand from the year 2003. However, during 2006-07, only 2519 tons were exported from India. Out of this, maximum quantity was exported to UK (1883 tons). India is not able to penetrate other EU countries in a significant way. The exports to EU countries so far, are more or less consistent. The main reason for the absence of upsurge of export of mangoes to EU is supply of mangoes by countries like Brazil, Peru, and Israel etc. at cheaper rates. Thus, India must lower the cost of production by increasing productivity. Apart from above, the other reason is that the EU market has become used to appreciate only coloured mangoes. Consumers at times pay higher price for these coloured mangoes. Even superior edible quality of Indian mangoes does not get much attention before coloured mangoes like Tommy Atkins, Kent and Haden. Realising this, Research Institutes in India have bred coloured varieties like Arka Anmol, Arka Puneet, Pusa Arunima, Ambika etc. However, their commercial productivity, acceptability in EU markets etc should be assessed on priority within definite time framework. The above mentioned coloured varieties are not only attractive but have very good edible quality.

(iii) ASEAN countries

ASEAN countries are importing mangoes to the tune of 50,327tons (2006). Major importers are Malaysia (23,521 tons), Singapore (16,027 tons). Vietnam (7212 tons), Indonesia (1103), and Thailand (262 tons). However exports of mango from India to ASEAN countries are only 332 tons to Malaysia and 230 tons to Singapore and 20 tons to Vietnam during 2006-2007. This is negligible as compared to what is potential; however, Thailand is able to supply mangoes at much cheaper price to Malaysia and Singapore, the main importers. Therefore, the strategy for India may be to make available cheaper mangoes like Totapuri (Banglora) in Malaysian market on one hand and campaign for quality and having red blush varieties like Suvarnrekha, Kesar and Alphonso varieties on the other hand for Singapore market. Market for high quality mangoes will have to be nurtured. For competing with Thailand, variety like Totapuri (Banglora) need to be explored and require to be exported from Eastern Port of Andhra Pradesh to save on logistic costs. Side by side India must reduce the cost of production by increasing the productivity. Perhaps with this strategy, we may target a volume of 6000-8000 tons of mango in next 4-5 years.

(iv) Hong Kong

Hong Kong is a centre for trade for fruits and vegetables and imported up to 42,422 tons and exported 19,988 tons of mangoes during the year 2006. The prices prevailing in Hong Kong market are also quite high. However, India has exported only 49 tons during 2006.Therefore; concerted campaign needs to be launched for our quality mangoes in this market.

16

(v) Pacific Rim countries and China Pacific Rim countries comprise Australia, Japan, Korea etc. and potential for exports of mangoes to these countries is given below: (a) Australia

Australia imported only 810 tons during 2006. However, Australia has very strict regulations for entry of Indian mangoes in their country. Australia has put mangoes from India under Import Risk Analysis (IRA). By this, Australia is to identify and classify potential quarantine risks and develop policies to manage them. Provisional IRA has been released, but still one cannot export mangoes to Australia, till it is totally finalized. At present, Indo-Australian agreement is under negotiation, and export of mangoes should be covered in the agreement. There should be no difficulty, as India has already standardized irradiation treatment for eliminating fruit fly, which is acceptable to Australia.

(b) South Korea

South Korea has imported 1235 tons of mangoes during 2006. At present South Korea has high duties on imported mangoes, however, India is likely to finalize Free Trade Agreement with Korea soon and it is hoped that export of mangoes to S. Korea will begin.

(c) Japan

According to comtrade database, Japan imported 12586 tons of mangoes in 2006. Japan has a requirement of Vapour Heat Treatment (VHT) for eliminating fruit fly. India has already established facilities for VHT treatment and exported 74 tons during 2006. However, even then export of mangoes has not accelerated to Japan, which needs to be taken up.

(d) China

China has only moderate import duties on export of mangoes to China under Asia Pacific Trade Agreement. Some amount of mangoes has already been exported to China. There is good scope of exporting mangoes to China, as it imported to the tune of 23,763 tons during 2006 (comtrade database). India is in a position to fulfill all the requirements of importing country from plant protection, quarantine and hygienic angles.

(e) U.S.A and Canada

According to comtrade database, USA imported 2, 98,088 tons of mangoes and Canada imported 42,161 tons during the year 2006. India did not export any mangoes to U.S.A during 2006 but exported 75 tons to Canada during the year (2006). MOU has been signed between USA and India for export of mangoes to USA. India has already provided irradiation facilities at a number of locations. There should be no further difficulty in exporting mangoes both to U.S.A. and Canada.

D. Measures for enhancing competitiveness for exporting mangoes

Following measures need to be adopted for enhancing competitiveness:

17

• Protocol for CA and MA storage for sea shipping needs to be perfected suiting to all exportable varieties of mango, so that shelf life can be extended and we can compete with Thailand in South East Asia.

• Similarly, if sea shipping protocol is perfected, India can stand competitively with Australia, Kenya etc. for exporting to Middle East countries and can effectively enter EU market.

• Main emphasis needs to be laid on cost reduction by increasing productivity per hectare which is very low, so that India can compete with Pakistan and other countries which supply mangoes at lower price.

13. Storage Temperature : 13°C ± 0.5°C

Relative Humidity : 90 – 95 %

Storage Period : 3 - 7 weeks

Freezing Point : -1°C

Mango has sensitivity to refrigeration, freezing and ethylene exposure.

14. Documents required for exports a) Documents related to goods

a) Invoice b) Packing List c) Certificate of origin

b) Documents related to shipment

a) Mate Receipt b) Shipping Bill c) Bill of handing d) Airway Bill

c) Documents related to Payment

a) Letter of Credit (L/C) b) Bill of Exchange

d) Documents related to quality of goods

a) Phytosanitary Certificate b) GLOBALGAP Certification c) Health Certificate

e) Organic Certification

- Certificate indicating material produce is based on organic farming.

f) Documents related to Foreign Exchange Regulations

GR Form: Documents required by RBI which assures to RBI that the exporter will realize the

proceeds of goods within 180 days from the date of Shipment.

g) Other Document

Bank Realization Certification (BRC): This is the advice given by Foreign Exchange Bank

after the realization of money from Importer.

18

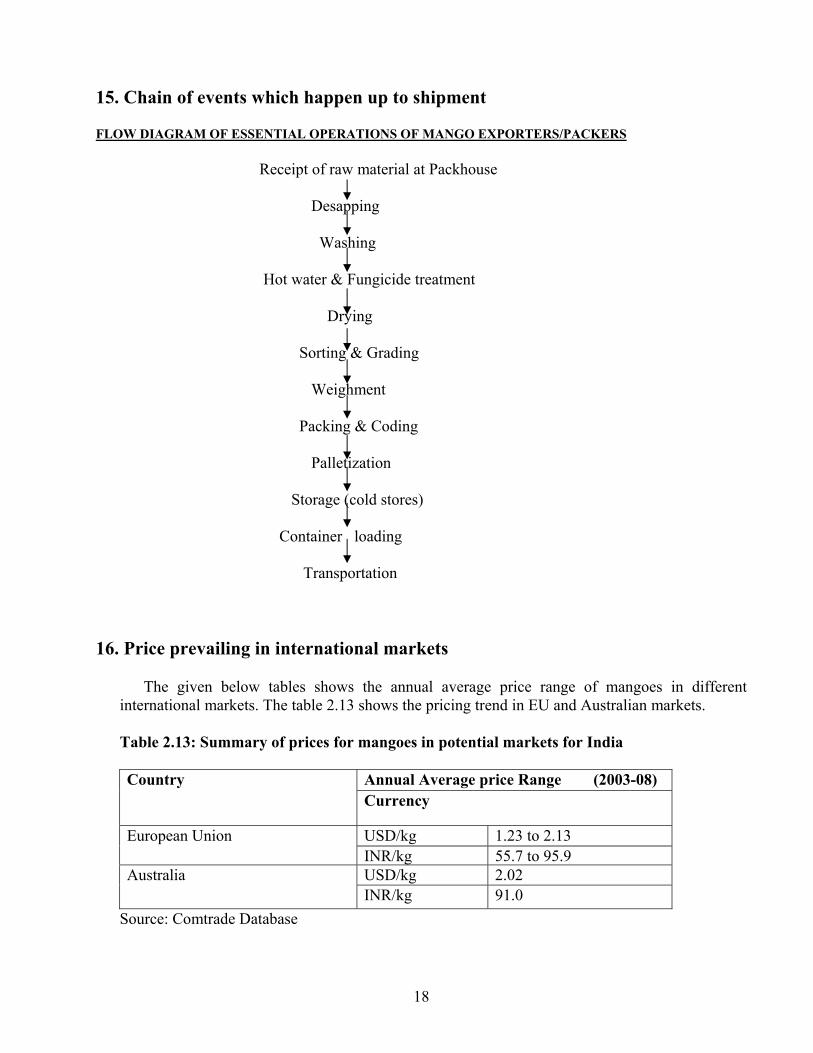

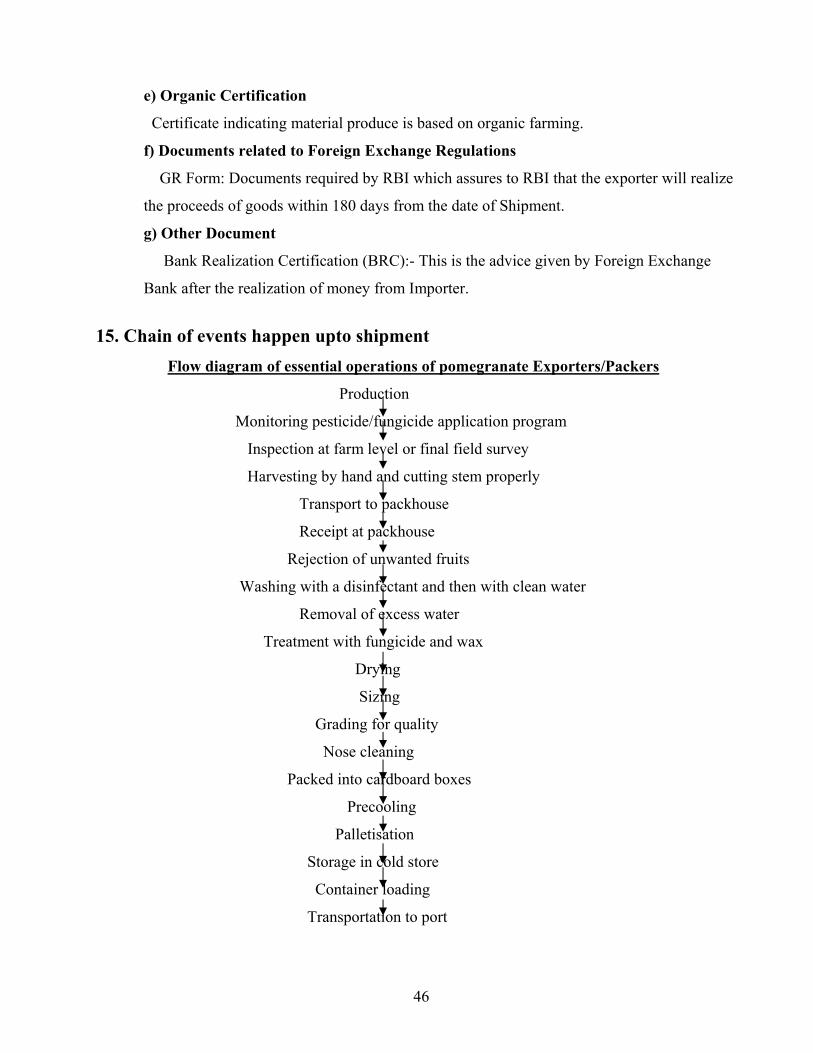

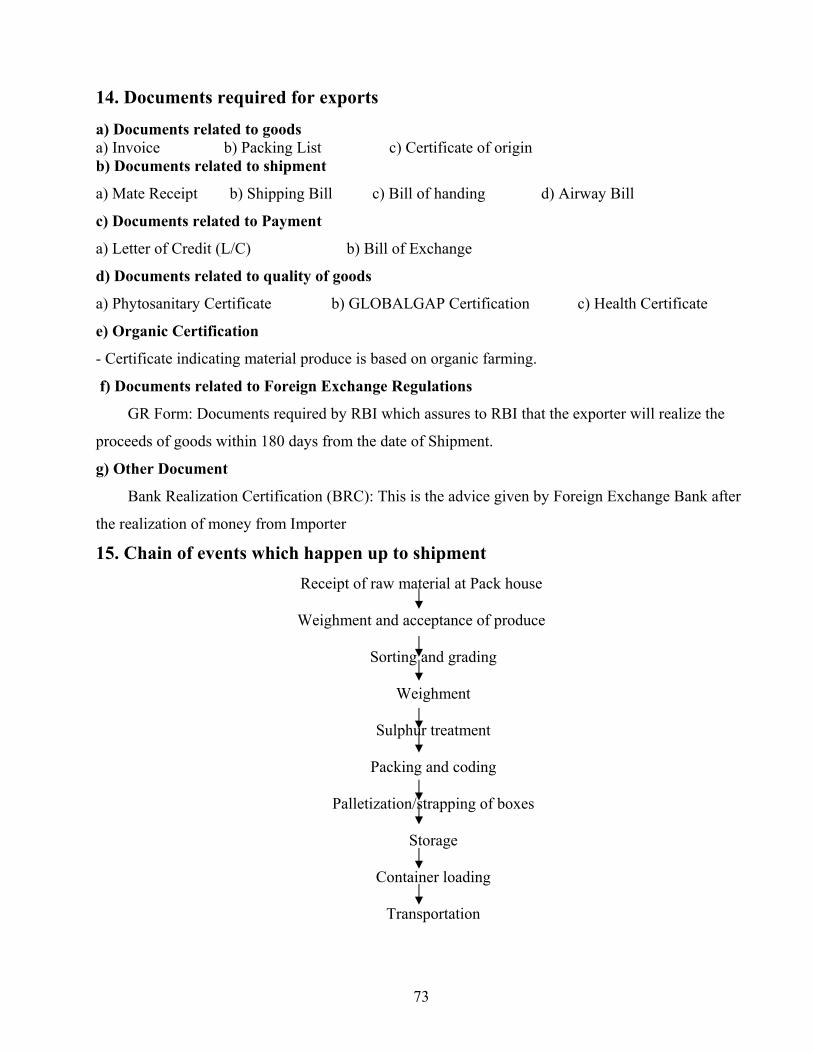

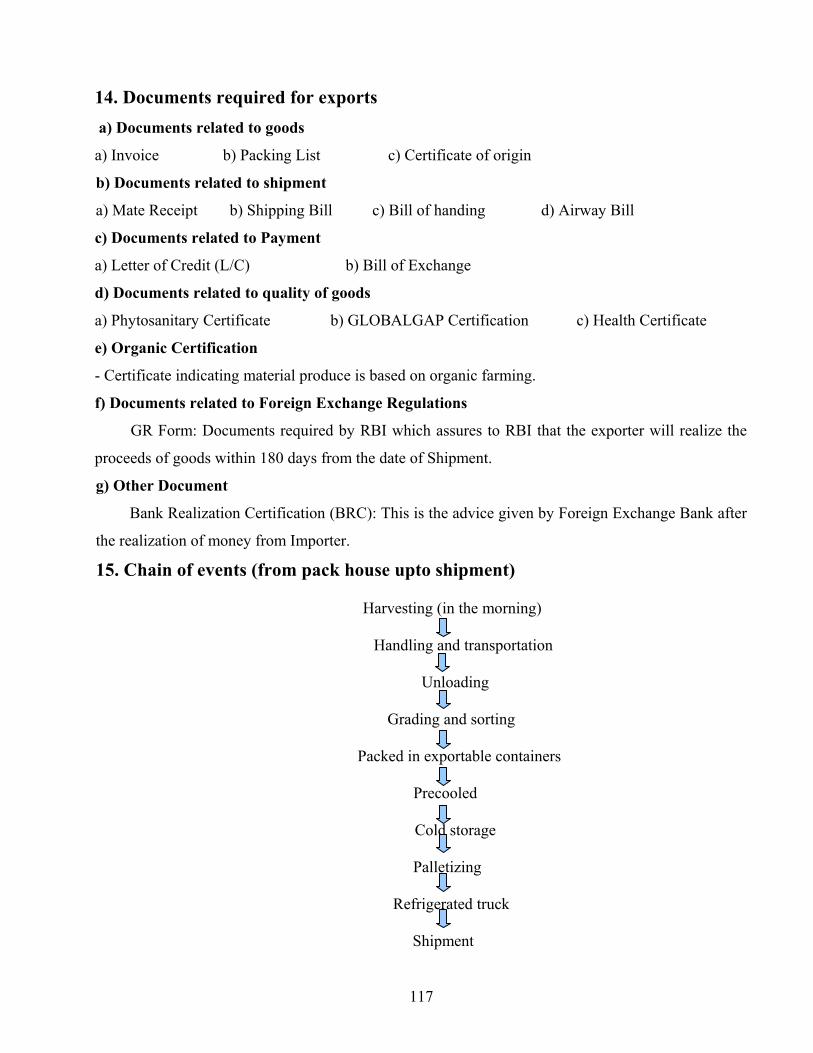

15. Chain of events which happen up to shipment

FLOW DIAGRAM OF ESSENTIAL OPERATIONS OF MANGO EXPORTERS/PACKERS Receipt of raw material at Packhouse Desapping Washing Hot water & Fungicide treatment Drying Sorting & Grading Weighment Packing & Coding Palletization Storage (cold stores) Container loading Transportation

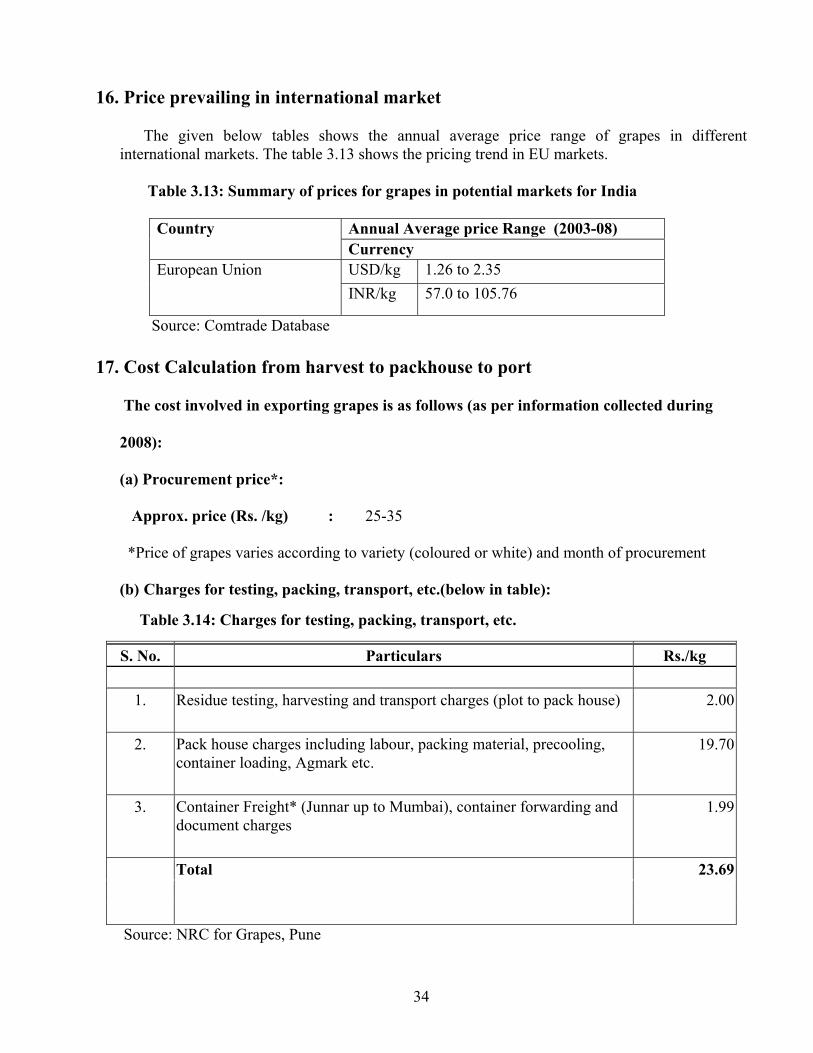

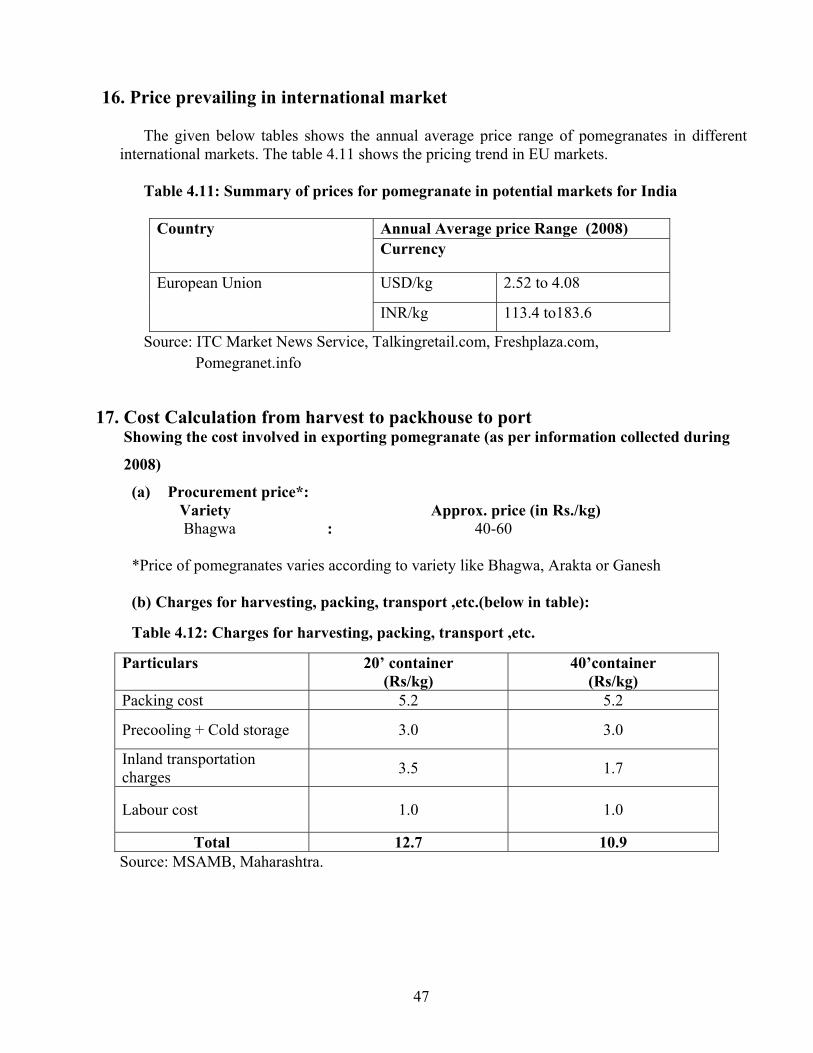

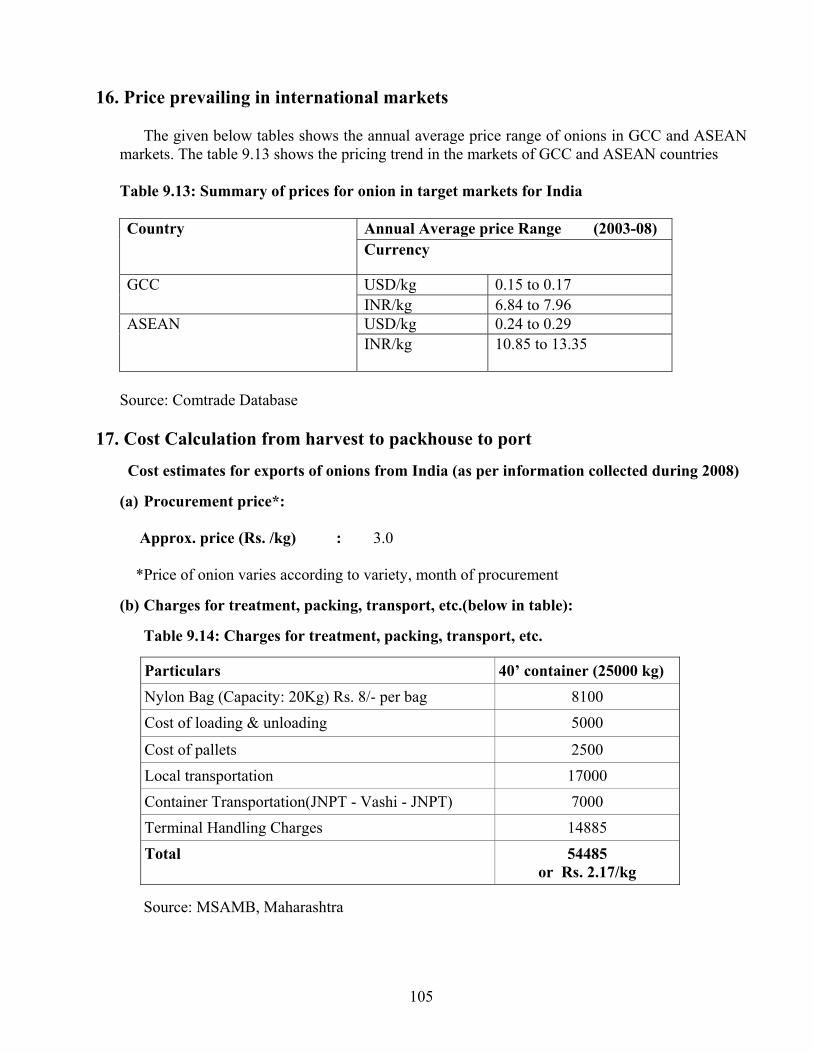

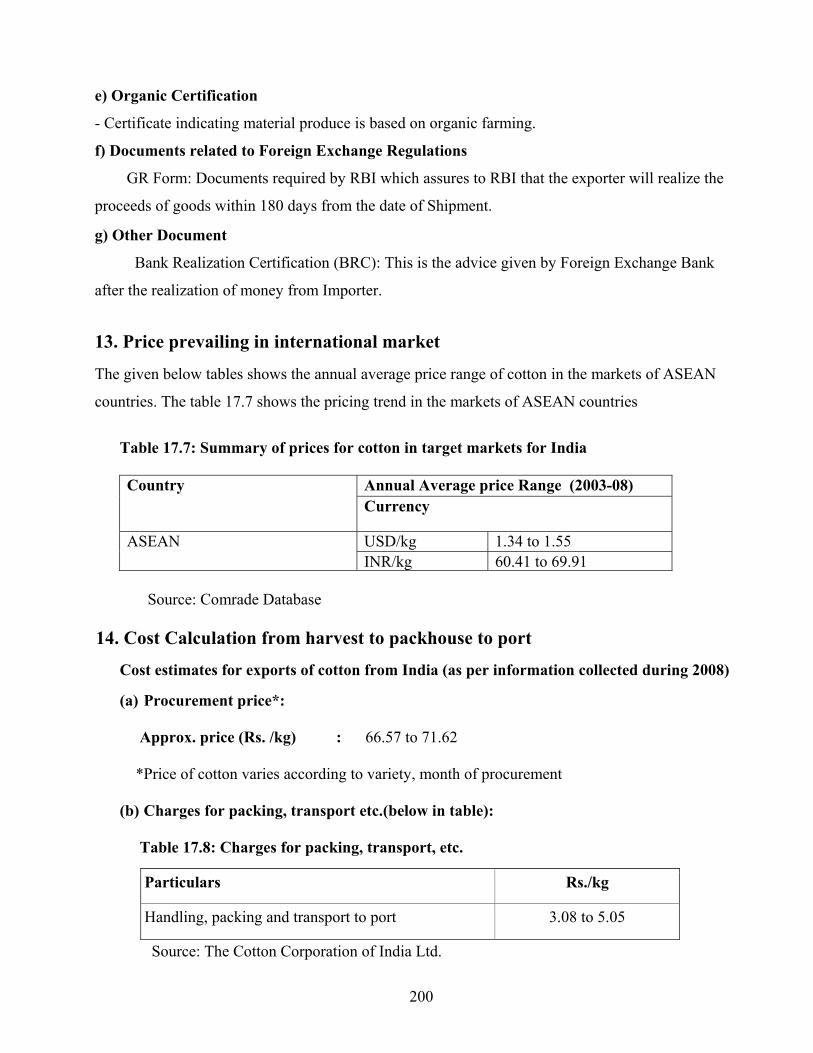

16. Price prevailing in international markets

The given below tables shows the annual average price range of mangoes in different international markets. The table 2.13 shows the pricing trend in EU and Australian markets.

Table 2.13: Summary of prices for mangoes in potential markets for India

Annual Average price Range (2003-08) Country Currency

USD/kg 1.23 to 2.13 European Union INR/kg 55.7 to 95.9 USD/kg 2.02 Australia INR/kg 91.0

Source: Comtrade Database

19

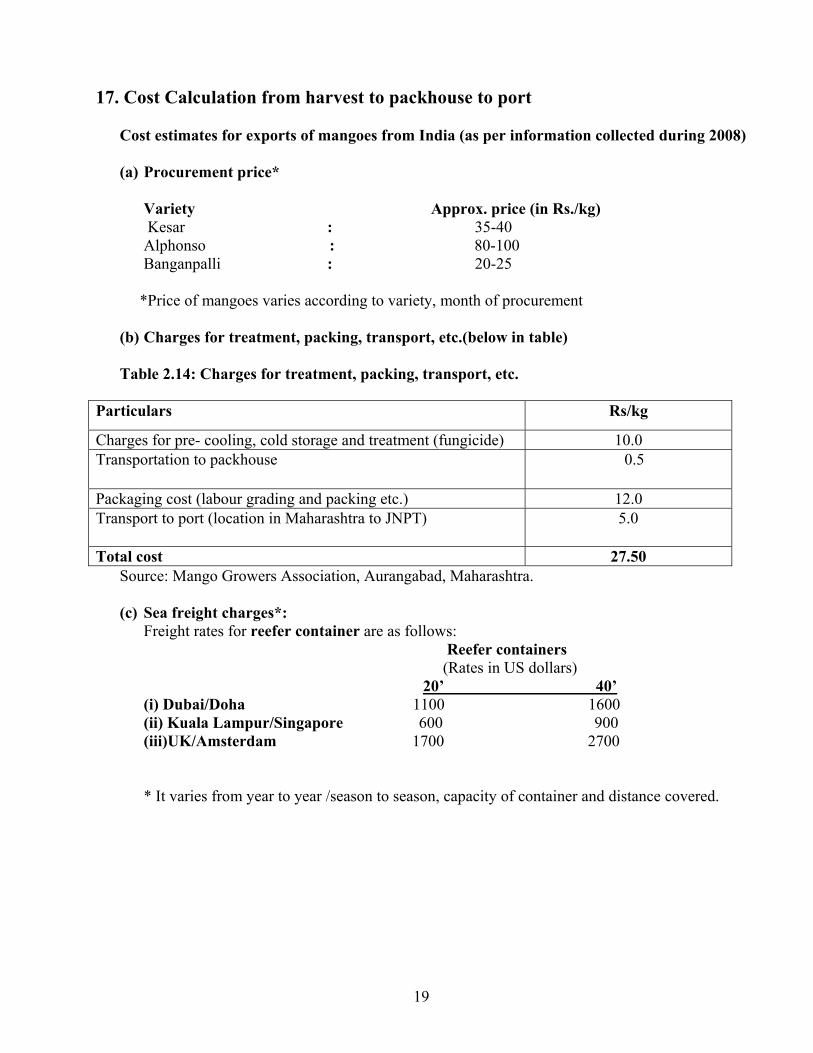

17. Cost Calculation from harvest to packhouse to port

Cost estimates for exports of mangoes from India (as per information collected during 2008)

(a) Procurement price*

Variety Approx. price (in Rs./kg) Kesar : 35-40 Alphonso : 80-100 Banganpalli : 20-25

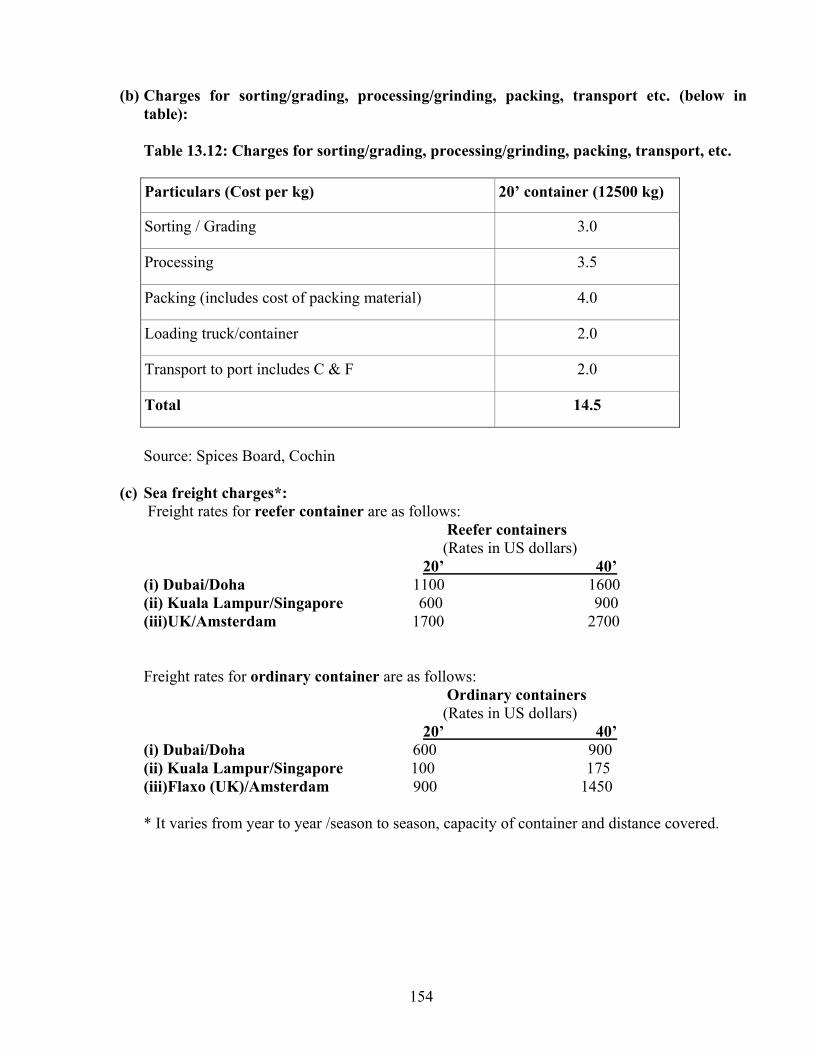

*Price of mangoes varies according to variety, month of procurement (b) Charges for treatment, packing, transport, etc.(below in table) Table 2.14: Charges for treatment, packing, transport, etc.

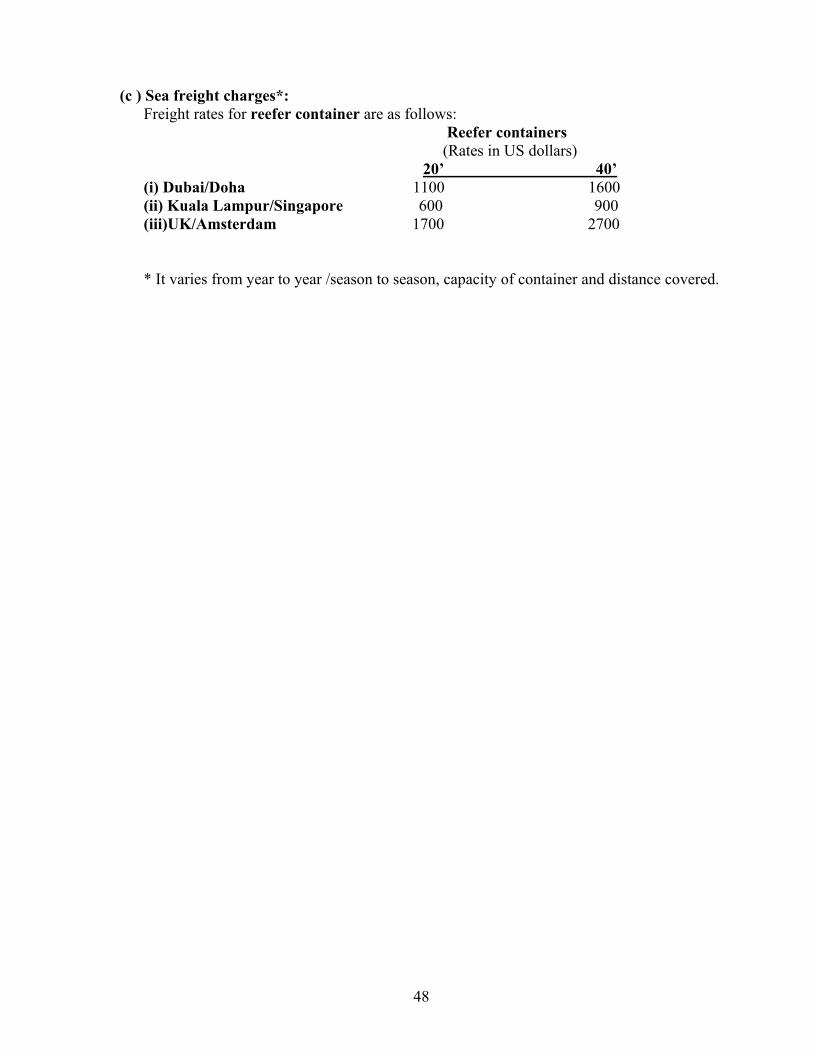

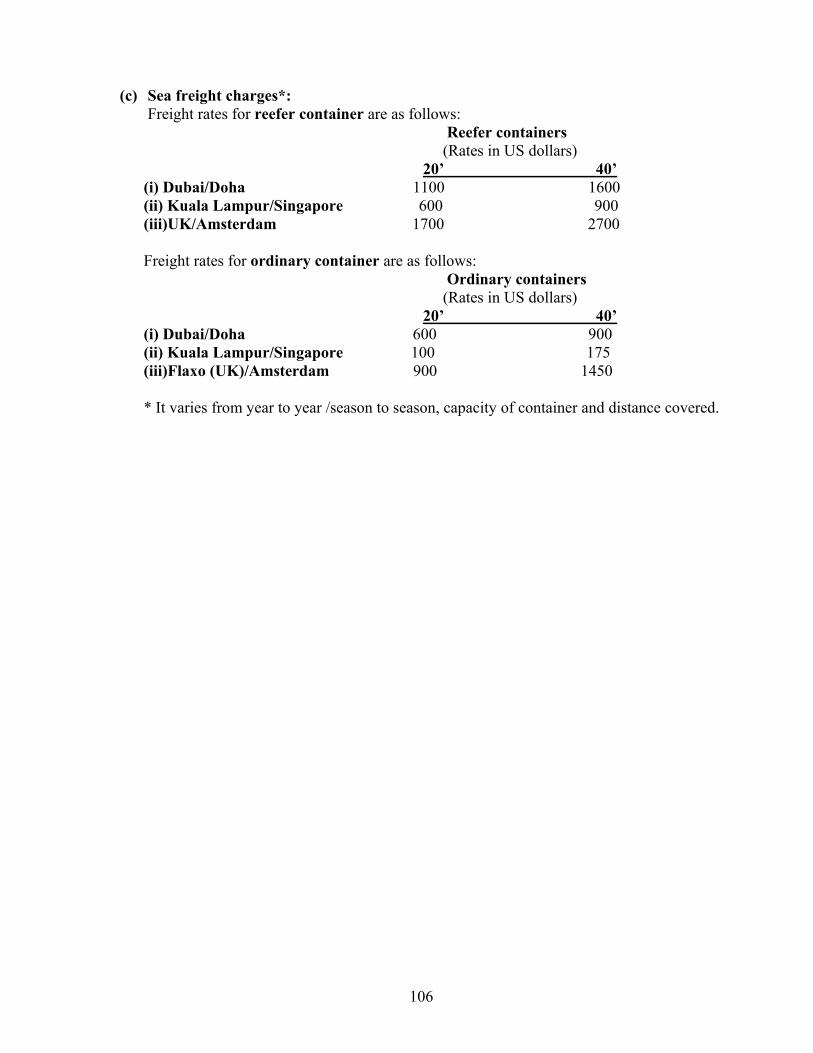

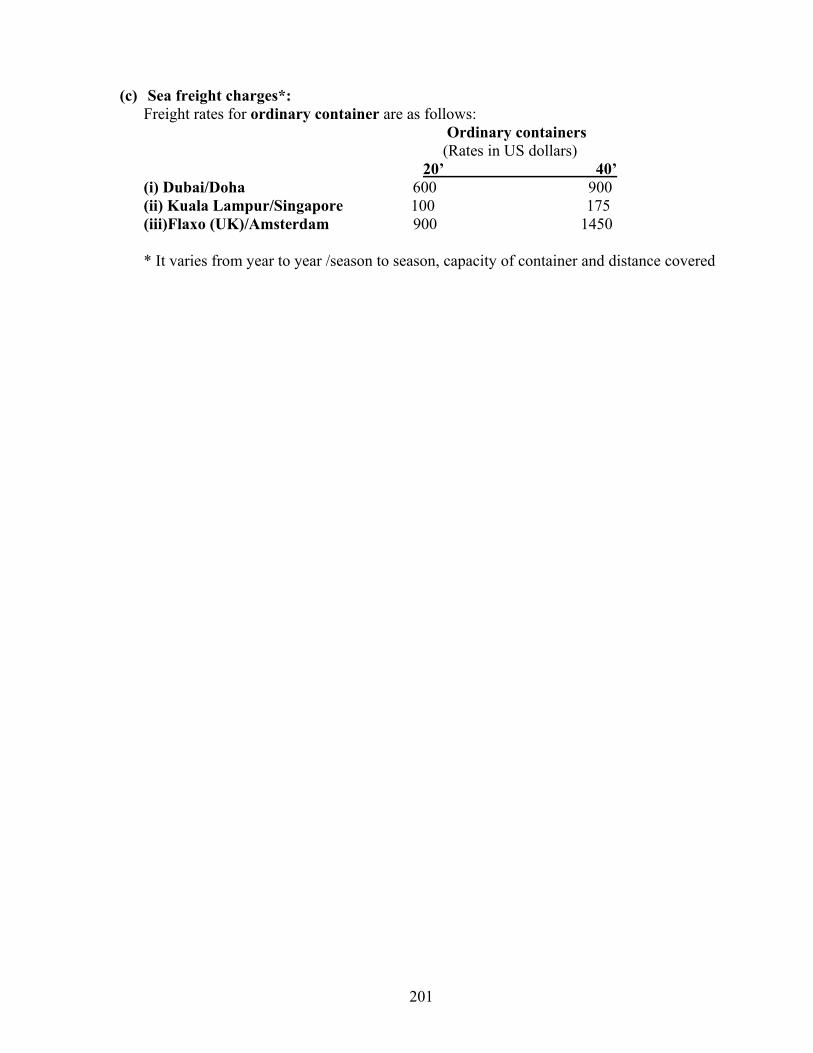

Source: Mango Growers Association, Aurangabad, Maharashtra. (c) Sea freight charges*:

Freight rates for reefer container are as follows: Reefer containers (Rates in US dollars) 20’ 40’

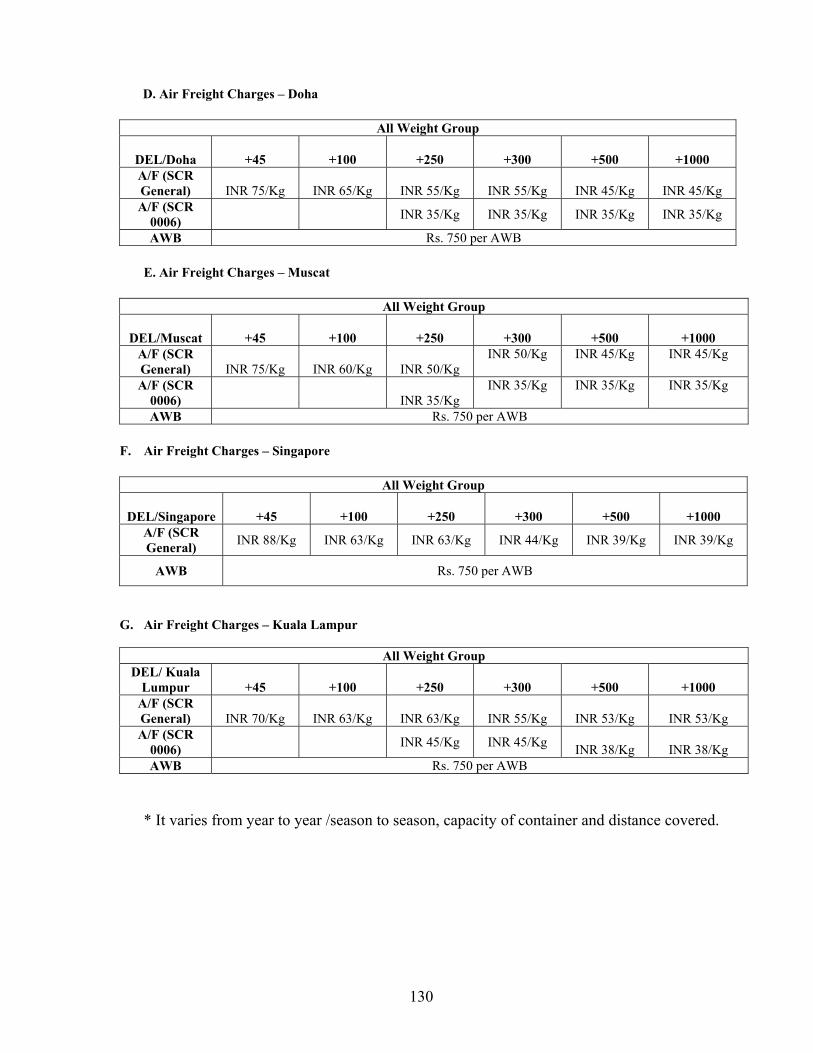

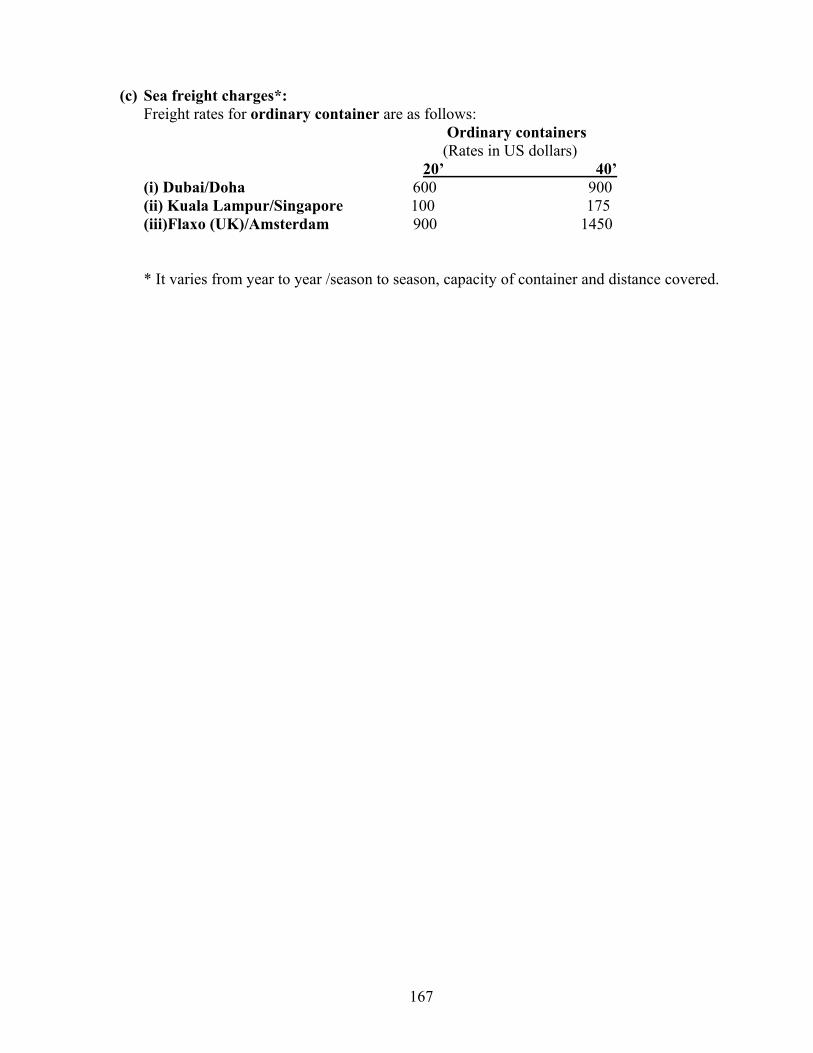

(i) Dubai/Doha 1100 1600 (ii) Kuala Lampur/Singapore 600 900 (iii)UK/Amsterdam 1700 2700 * It varies from year to year /season to season, capacity of container and distance covered.

Particulars Rs/kg

Charges for pre- cooling, cold storage and treatment (fungicide) 10.0 Transportation to packhouse 0.5

Packaging cost (labour grading and packing etc.) 12.0 Transport to port (location in Maharashtra to JNPT) 5.0

Total cost 27.50

20

CHAPTER- 3

GRAPES

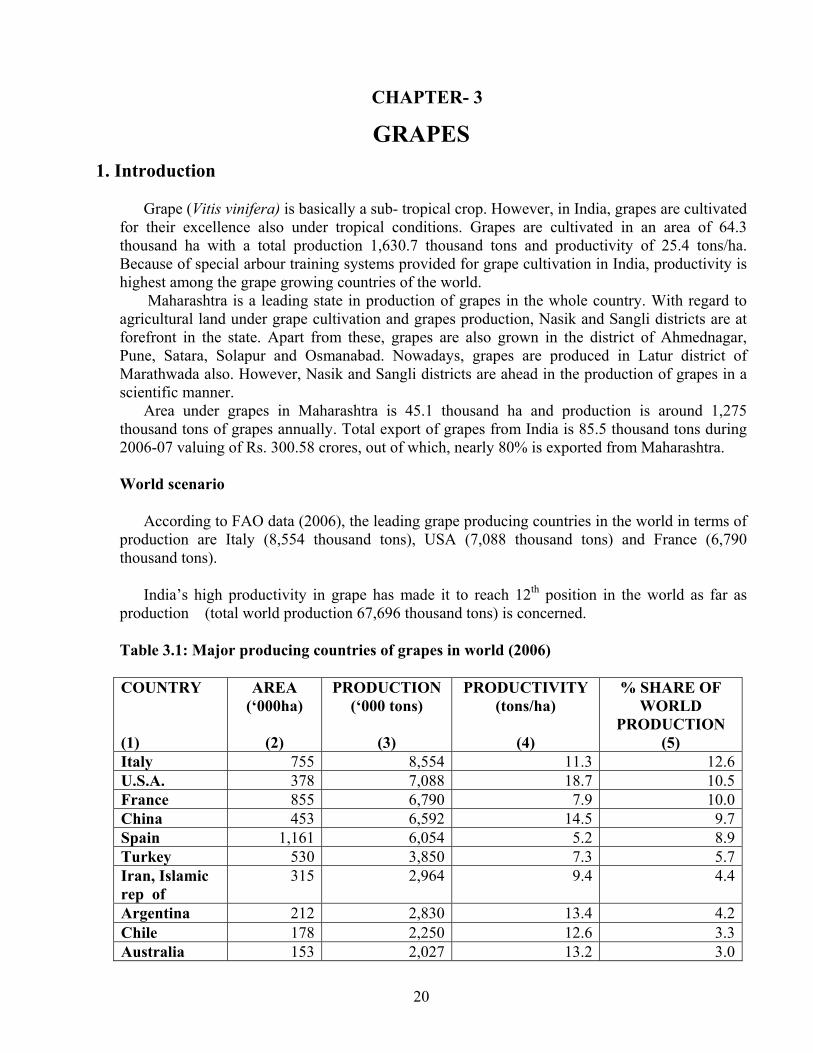

1. Introduction Grape (Vitis vinifera) is basically a sub- tropical crop. However, in India, grapes are cultivated

for their excellence also under tropical conditions. Grapes are cultivated in an area of 64.3 thousand ha with a total production 1,630.7 thousand tons and productivity of 25.4 tons/ha. Because of special arbour training systems provided for grape cultivation in India, productivity is highest among the grape growing countries of the world.

Maharashtra is a leading state in production of grapes in the whole country. With regard to agricultural land under grape cultivation and grapes production, Nasik and Sangli districts are at forefront in the state. Apart from these, grapes are also grown in the district of Ahmednagar, Pune, Satara, Solapur and Osmanabad. Nowadays, grapes are produced in Latur district of Marathwada also. However, Nasik and Sangli districts are ahead in the production of grapes in a scientific manner.

Area under grapes in Maharashtra is 45.1 thousand ha and production is around 1,275 thousand tons of grapes annually. Total export of grapes from India is 85.5 thousand tons during 2006-07 valuing of Rs. 300.58 crores, out of which, nearly 80% is exported from Maharashtra.

World scenario

According to FAO data (2006), the leading grape producing countries in the world in terms of production are Italy (8,554 thousand tons), USA (7,088 thousand tons) and France (6,790 thousand tons).

India’s high productivity in grape has made it to reach 12th position in the world as far as production (total world production 67,696 thousand tons) is concerned.

Table 3.1: Major producing countries of grapes in world (2006)

COUNTRY (1)

AREA (‘000ha)

(2)

PRODUCTION (‘000 tons)

(3)

PRODUCTIVITY (tons/ha)

(4)

% SHARE OF WORLD

PRODUCTION (5)

Italy 755 8,554 11.3 12.6U.S.A. 378 7,088 18.7 10.5France 855 6,790 7.9 10.0China 453 6,592 14.5 9.7Spain 1,161 6,054 5.2 8.9Turkey 530 3,850 7.3 5.7Iran, Islamic rep of

315 2,964 9.4 4.4

Argentina 212 2,830 13.4 4.2Chile 178 2,250 12.6 3.3Australia 153 2,027 13.2 3.0

21

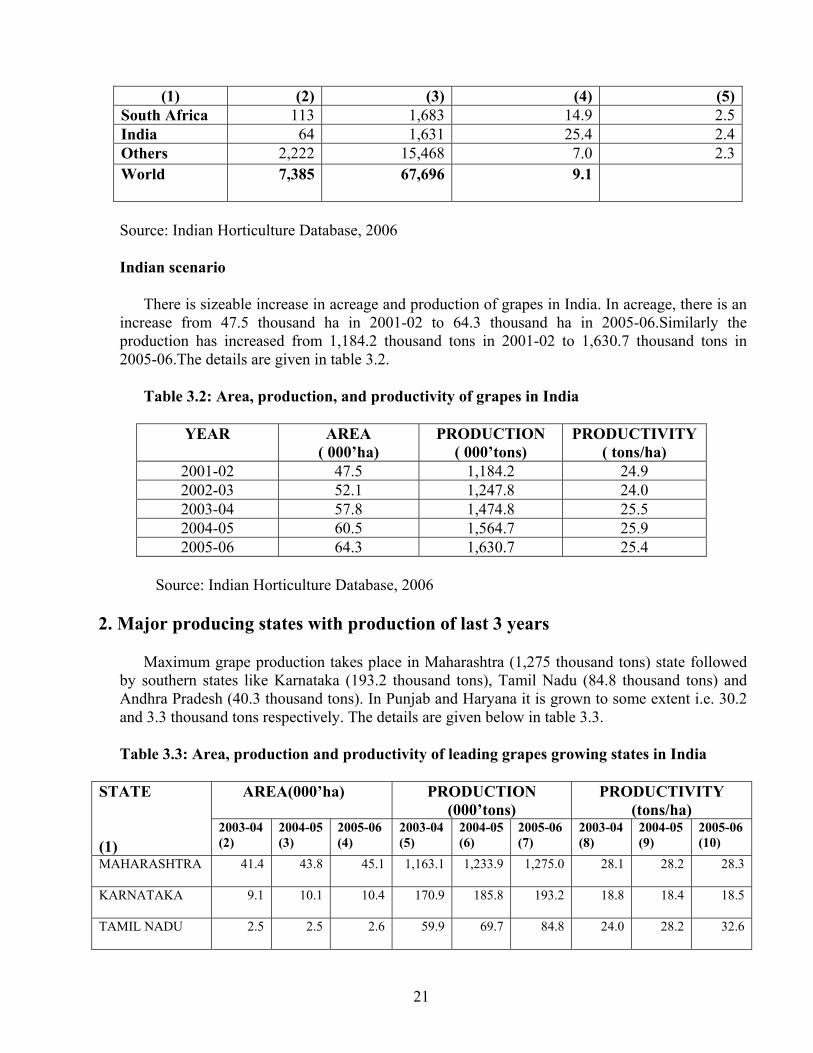

(1) (2) (3) (4) (5)South Africa 113 1,683 14.9 2.5India 64 1,631 25.4 2.4Others 2,222 15,468 7.0 2.3World 7,385

67,696 9.1

Source: Indian Horticulture Database, 2006

Indian scenario

There is sizeable increase in acreage and production of grapes in India. In acreage, there is an increase from 47.5 thousand ha in 2001-02 to 64.3 thousand ha in 2005-06.Similarly the production has increased from 1,184.2 thousand tons in 2001-02 to 1,630.7 thousand tons in 2005-06.The details are given in table 3.2.

Table 3.2: Area, production, and productivity of grapes in India

YEAR AREA ( 000’ha)

PRODUCTION ( 000’tons)

PRODUCTIVITY ( tons/ha)

2001-02 47.5 1,184.2 24.9 2002-03 52.1 1,247.8 24.0 2003-04 57.8 1,474.8 25.5 2004-05 60.5 1,564.7 25.9 2005-06 64.3 1,630.7 25.4

Source: Indian Horticulture Database, 2006

2. Major producing states with production of last 3 years

Maximum grape production takes place in Maharashtra (1,275 thousand tons) state followed by southern states like Karnataka (193.2 thousand tons), Tamil Nadu (84.8 thousand tons) and Andhra Pradesh (40.3 thousand tons). In Punjab and Haryana it is grown to some extent i.e. 30.2 and 3.3 thousand tons respectively. The details are given below in table 3.3.

Table 3.3: Area, production and productivity of leading grapes growing states in India

AREA(000’ha) PRODUCTION (000’tons)

PRODUCTIVITY (tons/ha)

STATE (1)

2003-04 (2)

2004-05 (3)

2005-06 (4)

2003-04 (5)

2004-05(6)

2005-06 (7)

2003-04 (8)

2004-05 (9)

2005-06 (10)

MAHARASHTRA 41.4

43.8 45.1 1,163.1 1,233.9 1,275.0 28.1 28.2 28.3

KARNATAKA 9.1

10.1 10.4 170.9 185.8 193.2 18.8 18.4 18.5

TAMIL NADU 2.5

2.5 2.6 59.9 69.7 84.8 24.0 28.2 32.6

22

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

ANDHRA PRADESH

1.8 1.9 1.9 35.0 37.8 40.3 19.4 22.0 21.2

PUNJAB 1.2 1.2 1.1 33.7 32.3 30.2 28.1 27.0 27.0

HARYANA 0.9 0.1 0.1 8.5 1.4 3.3 9.4 10.5 33.0

MADHYA PRADESH

0.1 0.1 0.1 2.3 2.4 2.6 23.0 25.0 25.0

OTHERS 0.8

0.9 2.9 1.4 1.4 1.2 2.5 1.9 0.9

Total 57.8

60.5 64.3 1,474.8 1,564.7 1,630.7 25.5 25.8 25.3

Source: Indian Horticulture Database, 2006

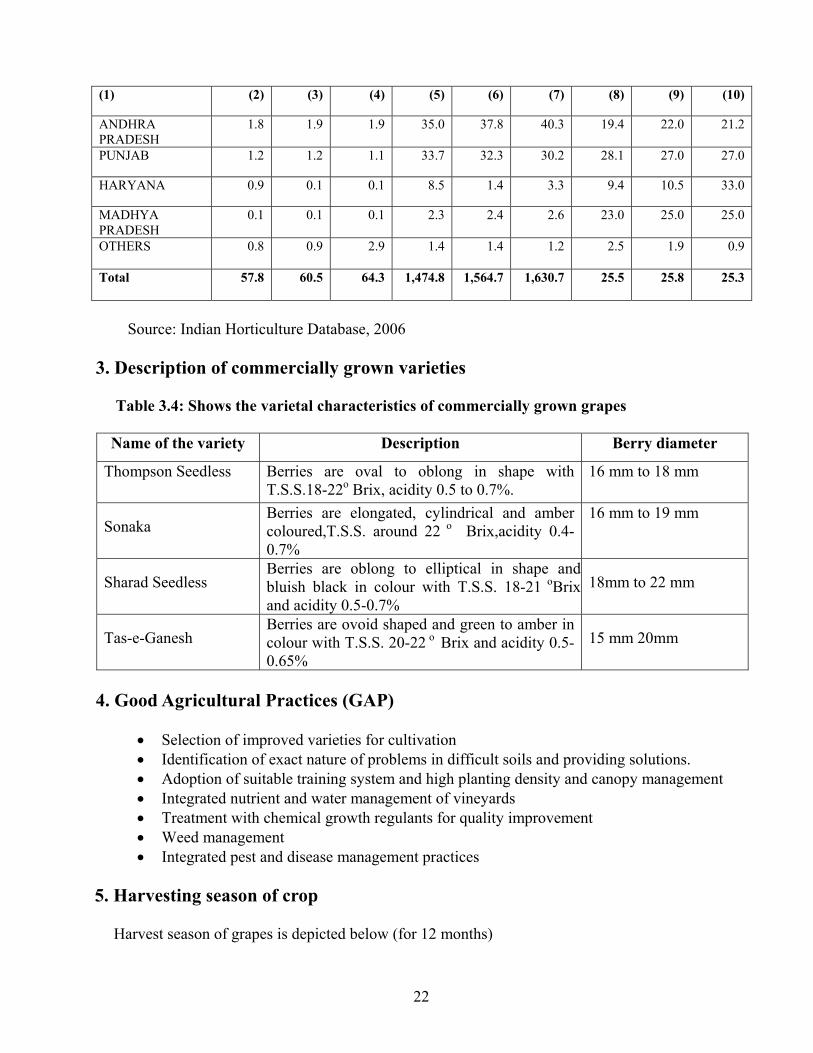

3. Description of commercially grown varieties Table 3.4: Shows the varietal characteristics of commercially grown grapes

Name of the variety Description Berry diameter

Thompson Seedless Berries are oval to oblong in shape with T.S.S.18-22o Brix, acidity 0.5 to 0.7%.

16 mm to 18 mm

Sonaka Berries are elongated, cylindrical and amber coloured,T.S.S. around 22 o Brix,acidity 0.4-0.7%

16 mm to 19 mm

Sharad Seedless Berries are oblong to elliptical in shape and bluish black in colour with T.S.S. 18-21 oBrix and acidity 0.5-0.7%

18mm to 22 mm

Tas-e-Ganesh Berries are ovoid shaped and green to amber in colour with T.S.S. 20-22 o Brix and acidity 0.5-0.65%

15 mm 20mm

4. Good Agricultural Practices (GAP)

• Selection of improved varieties for cultivation • Identification of exact nature of problems in difficult soils and providing solutions. • Adoption of suitable training system and high planting density and canopy management • Integrated nutrient and water management of vineyards • Treatment with chemical growth regulants for quality improvement • Weed management • Integrated pest and disease management practices

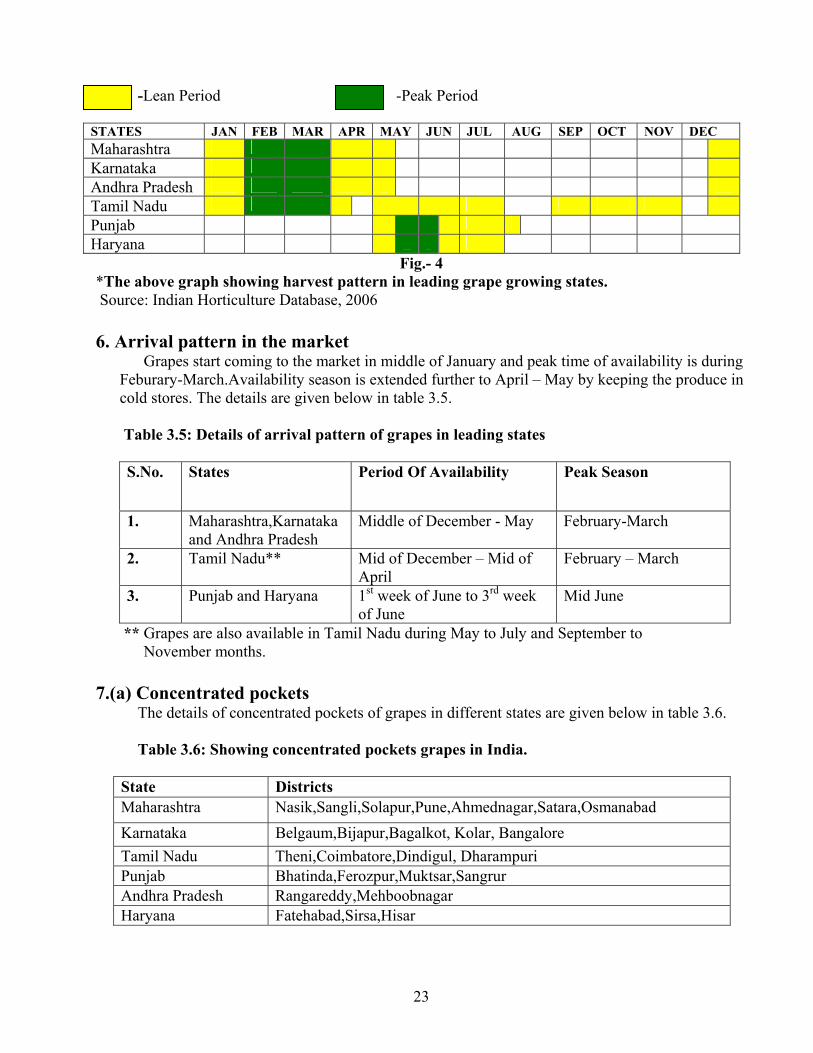

5. Harvesting season of crop

Harvest season of grapes is depicted below (for 12 months)

23

-Lean Period -Peak Period

STATES JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Maharashtra Karnataka Andhra Pradesh Tamil Nadu Punjab Haryana

Fig.- 4 *The above graph showing harvest pattern in leading grape growing states. Source: Indian Horticulture Database, 2006 6. Arrival pattern in the market

Grapes start coming to the market in middle of January and peak time of availability is during Feburary-March.Availability season is extended further to April – May by keeping the produce in cold stores. The details are given below in table 3.5.

Table 3.5: Details of arrival pattern of grapes in leading states

S.No. States Period Of Availability Peak Season

1. Maharashtra,Karnataka and Andhra Pradesh

Middle of December - May February-March

2. Tamil Nadu** Mid of December – Mid of April

February – March

3. Punjab and Haryana 1st week of June to 3rd week of June

Mid June

** Grapes are also available in Tamil Nadu during May to July and September to November months. 7.(a) Concentrated pockets

The details of concentrated pockets of grapes in different states are given below in table 3.6. Table 3.6: Showing concentrated pockets grapes in India.

State Districts Maharashtra Nasik,Sangli,Solapur,Pune,Ahmednagar,Satara,Osmanabad Karnataka Belgaum,Bijapur,Bagalkot, Kolar, Bangalore Tamil Nadu Theni,Coimbatore,Dindigul, Dharampuri Punjab Bhatinda,Ferozpur,Muktsar,Sangrur Andhra Pradesh Rangareddy,Mehboobnagar Haryana Fatehabad,Sirsa,Hisar

24

7.(b) Catchment areas of market

Table 3.7: Showing the details of catchment areas of market of grapes in leading states

States Districts (Market)

Blocks

Solapur Karmala,Barsi,Madha,Mohol,Mangalwedha,Sangole,Malsiras,Pandharpur,Akalkot.

Nashik Kalvan,Peint,Igatpuri,Sinnar,Niphad,Yeola,Nandgaon, Satana,Furgana,Dindori,Melgaon,

Sangli Atpadi,Khanapur,Islampur,Shirala,Valva,Tasgaon,Kavathe, Mahankal,Jath, Miraj

Ahmednagar Srirampur,Sangamner,Akola,Rahusi,Nevasa,Parner,Pathardi, Srigonda,Karjat

Pune Junnar,Ambegaon,Ghod,Rajgurunagar,Wadgaonsirur,Mulshi, Welhe,Purandhar,Bhor,Baramati,Indapur,Daund,Saswad.

Maharashtra

Satara Mahabaleshwar,Khandala,Wai,Phaltan,Koregaon,Khata,Patan, Karad,Vadug.

Bijapur Indi,Sindgi,Basavna Bagevadi,Muddebihal,Tikota. Belgaum Athni,Arkali,Chikodi,Mukeri,Bailhongal,Ramdurg,Khauapur. Bagalkot Jamkhandi,Mudhol,Hungund,Badami. Kolar Bagepalli,Gauribidanur,Gudibanda,ChikBallapur,Mulbagal,

Malur,Bangarapet

Karnataka

Bangalore Amekal,Sonnenahalti,Kannur,Bagalur,Nagarur,Marangondahalli,Haralur,Mantapa,Solurur,Chandapur.

Rangareddy Marpali,Vikarabad,Tandur,Pargi,Ibranimpatan,Shahabad, Doma,Maisaram,Miryan,Nancherla.

Andhra Pradesh

Mehbubnagar

Kollur,Keshampat,Mughalgidda,Karnul,Wanparti,Atmakur,Gadwall,Alampur,Kolhapur,Achampet,Kondangol.

Theni Periyakulam, Andipatti, Uttammapalayam, Bodimayakkanur, Kamban, Megamali, Vadugapatti,

Coimbatore Muttuppalaiyam,Avinashi,Tiruppur,Palladam,Udumallaippettai, Pollachi,Valparai.

Tamil Nadu

Dindigul Palani,Kodaikkanal,Oddanchatran,Vedasandur,Naltam, Nilakkotai,Palaiyan

Bhatinda Rampura Phul,Talwani Sabo,Bhagra,Jalal,Nathana, Bandi,Jaisinghwala,Shergarh,Sangat,Malkana,Lahri,Teona.

Ferozpur Zira,Fazilla,Abohar,Jalalbad,Fatehgarh,Panjeke,Ladhuka, Lakhawall,Ramsara,Wahabwala.

Punjab

Muktsar Kanianwali,Malaut,Baruwali,Sotha,Doda,Bhadar,AbulKharana,Bhagu,Waring,Khera

Fatehabad Ratiya,Tohana,Badalgarh,Bhattu,Sampla,Pirthala,Samiyana,Kharihajan,Bhattukalan

Sirsa Fatehpur,Dabwali,Ellenabad,Banwala,SalamKhera,Nathohar,Mangla,Jamal,Gushalyana.

Haryana

Hisar Bithmara,Adampur,Narnaund,Hansi,Budak,Mangal, Umra,Sultanpur,Babal,Baria,Agroha,Kanoh,Khedar,Budak.

25

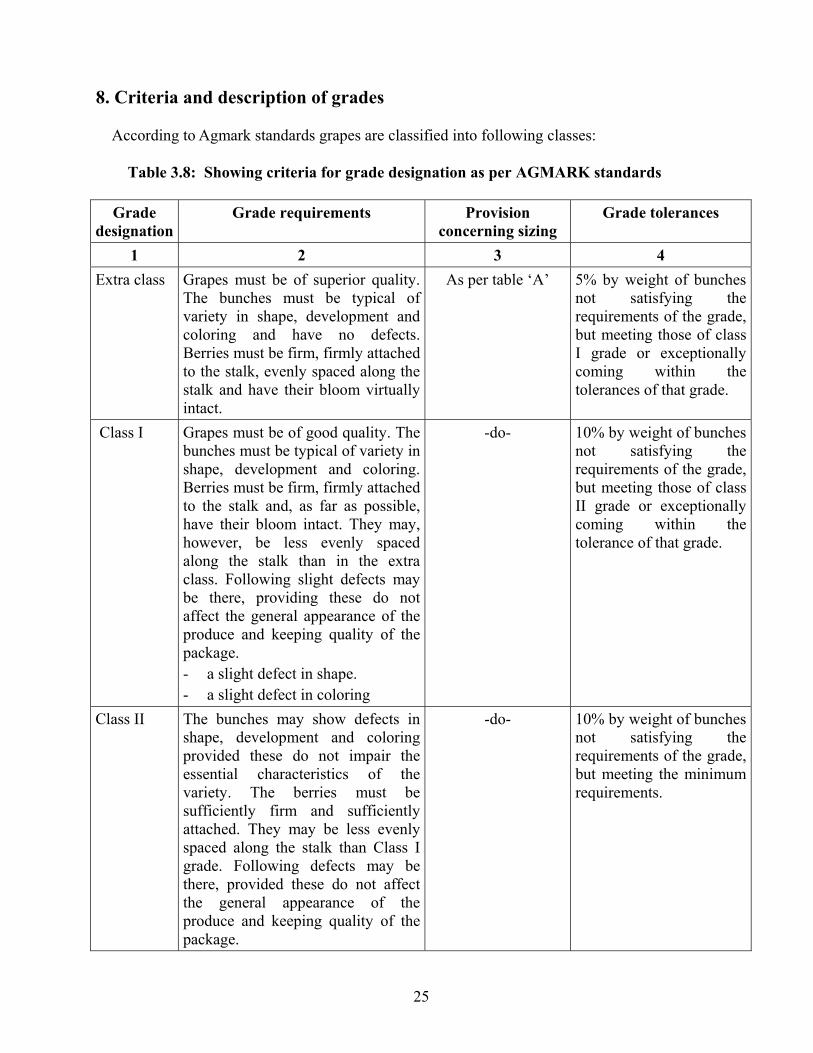

8. Criteria and description of grades According to Agmark standards grapes are classified into following classes:

Table 3.8: Showing criteria for grade designation as per AGMARK standards

Grade designation

Grade requirements Provision concerning sizing

Grade tolerances

1 2 3 4 Extra class Grapes must be of superior quality.

The bunches must be typical of variety in shape, development and coloring and have no defects. Berries must be firm, firmly attached to the stalk, evenly spaced along the stalk and have their bloom virtually intact.

As per table ‘A’ 5% by weight of bunches not satisfying the requirements of the grade, but meeting those of class I grade or exceptionally coming within the tolerances of that grade.

Class I Grapes must be of good quality. The bunches must be typical of variety in shape, development and coloring. Berries must be firm, firmly attached to the stalk and, as far as possible, have their bloom intact. They may, however, be less evenly spaced along the stalk than in the extra class. Following slight defects may be there, providing these do not affect the general appearance of the produce and keeping quality of the package. - a slight defect in shape. - a slight defect in coloring

-do- 10% by weight of bunches not satisfying the requirements of the grade, but meeting those of class II grade or exceptionally coming within the tolerance of that grade.

Class II The bunches may show defects in shape, development and coloring provided these do not impair the essential characteristics of the variety. The berries must be sufficiently firm and sufficiently attached. They may be less evenly spaced along the stalk than Class I grade. Following defects may be there, provided these do not affect the general appearance of the produce and keeping quality of the package.

-do- 10% by weight of bunches not satisfying the requirements of the grade, but meeting the minimum requirements.

26

- defects in shape - defects in coloring - slight sun scorch affecting the

skin only, - slight bruising, - slight skin defects

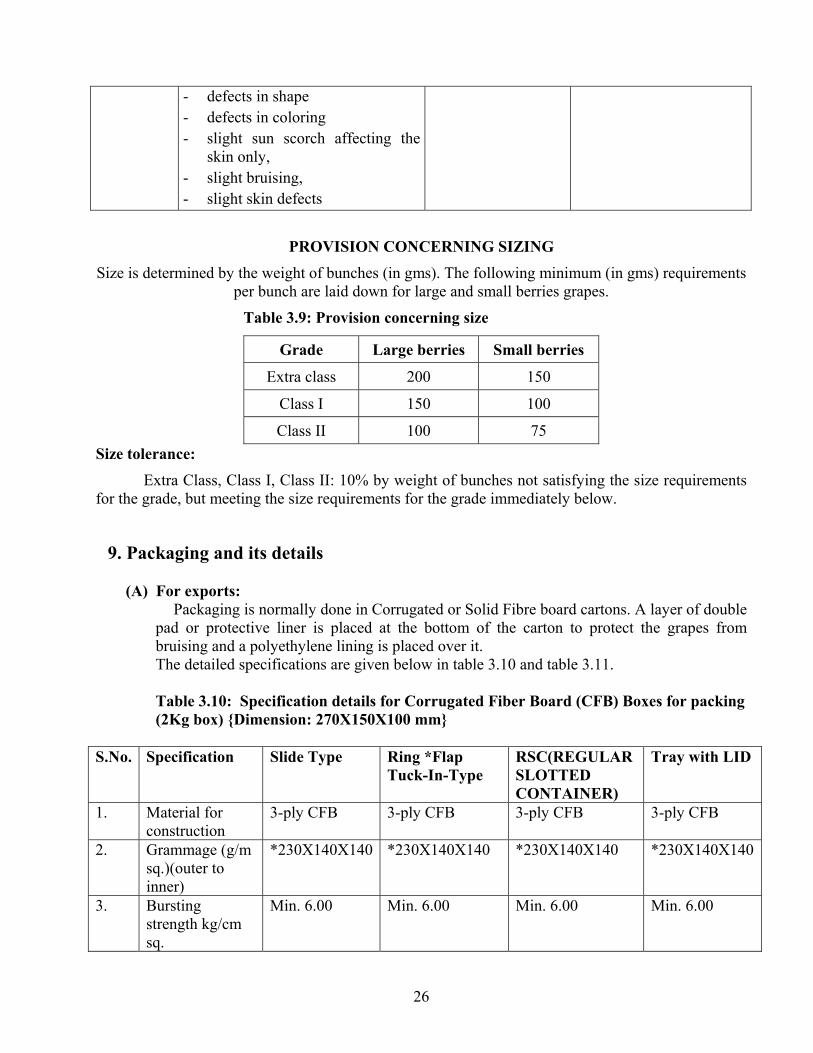

PROVISION CONCERNING SIZING

Size is determined by the weight of bunches (in gms). The following minimum (in gms) requirements per bunch are laid down for large and small berries grapes.

Table 3.9: Provision concerning size

Grade Large berries Small berries

Extra class 200 150

Class I 150 100

Class II 100 75 Size tolerance:

Extra Class, Class I, Class II: 10% by weight of bunches not satisfying the size requirements for the grade, but meeting the size requirements for the grade immediately below.

9. Packaging and its details

(A) For exports: Packaging is normally done in Corrugated or Solid Fibre board cartons. A layer of double pad or protective liner is placed at the bottom of the carton to protect the grapes from bruising and a polyethylene lining is placed over it. The detailed specifications are given below in table 3.10 and table 3.11.

Table 3.10: Specification details for Corrugated Fiber Board (CFB) Boxes for packing (2Kg box) {Dimension: 270X150X100 mm}

S.No. Specification Slide Type Ring *Flap Tuck-In-Type

RSC(REGULAR SLOTTED CONTAINER)

Tray with LID

1. Material for construction

3-ply CFB 3-ply CFB 3-ply CFB 3-ply CFB

2. Grammage (g/m sq.)(outer to inner)

*230X140X140 *230X140X140 *230X140X140 *230X140X140

3. Bursting strength kg/cm sq.

Min. 6.00 Min. 6.00 Min. 6.00 Min. 6.00

27

4. Puncture resistance inches/teat inch

Min.10.00 Min.10.00 Min.10.00 Min.10.00

5. Compression strength Kg.

Min.225 Min.225 Min.225 Min.225

6. Cobb (30 minutes g/m sq.)

Min.130 Min.130 Min.130 Min.130

Source: Post- Harvest Manual for Export of Grapes, APEDA, New Delhi.

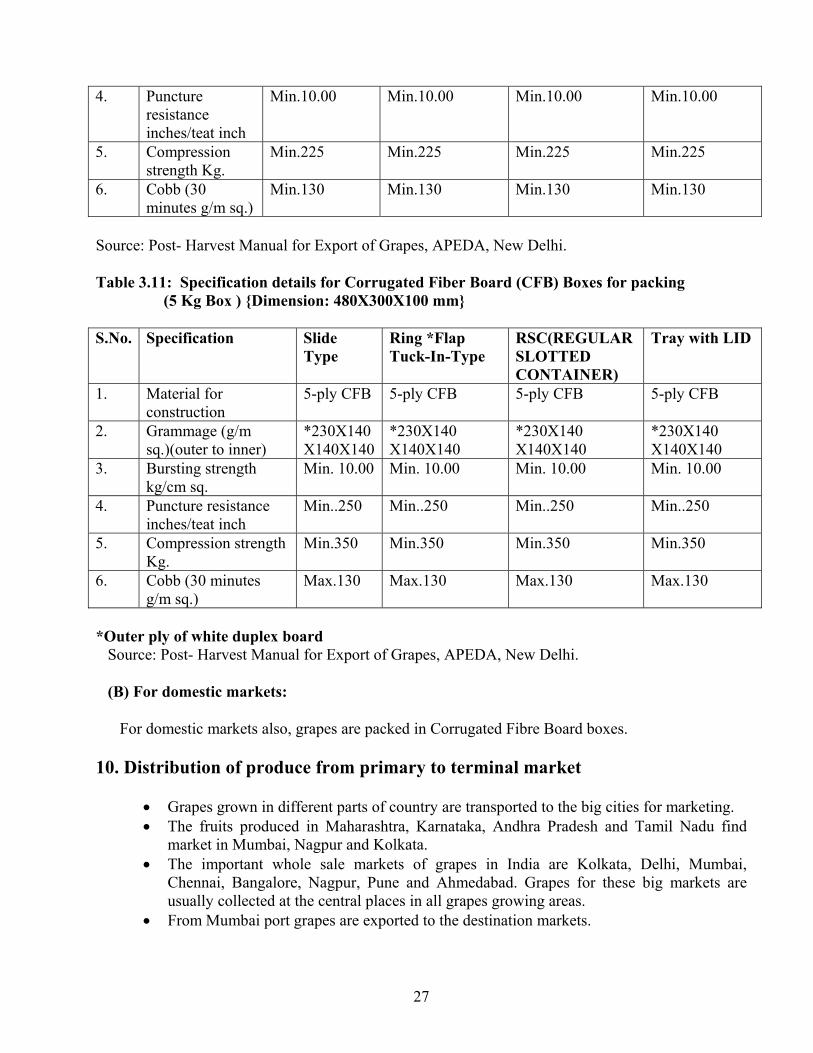

Table 3.11: Specification details for Corrugated Fiber Board (CFB) Boxes for packing (5 Kg Box ) {Dimension: 480X300X100 mm} S.No. Specification Slide

Type Ring *Flap Tuck-In-Type

RSC(REGULAR SLOTTED CONTAINER)

Tray with LID

1. Material for construction

5-ply CFB 5-ply CFB 5-ply CFB 5-ply CFB

2. Grammage (g/m sq.)(outer to inner)

*230X140 X140X140

*230X140 X140X140

*230X140 X140X140

*230X140 X140X140

3. Bursting strength kg/cm sq.

Min. 10.00 Min. 10.00 Min. 10.00 Min. 10.00

4. Puncture resistance inches/teat inch

Min..250 Min..250 Min..250 Min..250

5. Compression strength Kg.

Min.350 Min.350 Min.350 Min.350

6. Cobb (30 minutes g/m sq.)

Max.130 Max.130 Max.130 Max.130

*Outer ply of white duplex board

Source: Post- Harvest Manual for Export of Grapes, APEDA, New Delhi.

(B) For domestic markets:

For domestic markets also, grapes are packed in Corrugated Fibre Board boxes.

10. Distribution of produce from primary to terminal market

• Grapes grown in different parts of country are transported to the big cities for marketing. • The fruits produced in Maharashtra, Karnataka, Andhra Pradesh and Tamil Nadu find

market in Mumbai, Nagpur and Kolkata. • The important whole sale markets of grapes in India are Kolkata, Delhi, Mumbai,

Chennai, Bangalore, Nagpur, Pune and Ahmedabad. Grapes for these big markets are usually collected at the central places in all grapes growing areas.

• From Mumbai port grapes are exported to the destination markets.

28

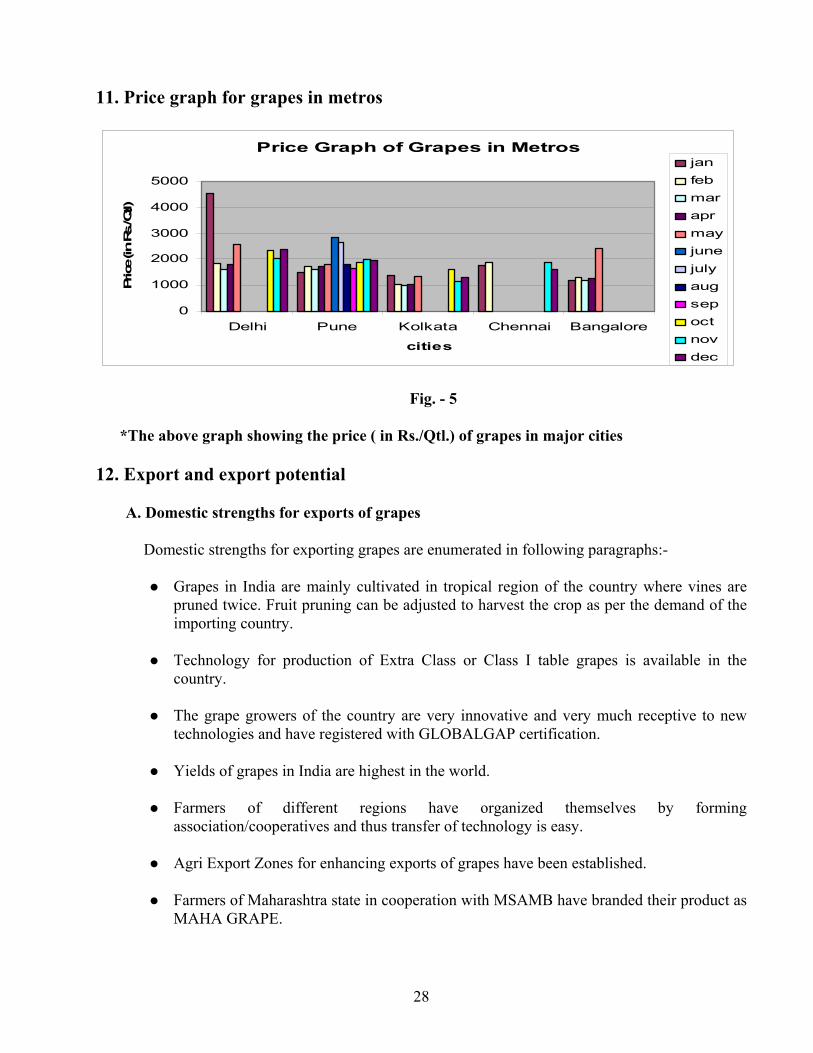

11. Price graph for grapes in metros

Price Graph of Grapes in Metros

0

1000

2000

3000

4000

5000

Delhi Pune Kolkata Chennai Bangalore

cities

Price (in

Rs./Q

tl)

janfebmaraprmayjunejulyaugsepoctnovdec

Fig. - 5

*The above graph showing the price ( in Rs./Qtl.) of grapes in major cities

12. Export and export potential

A. Domestic strengths for exports of grapes

Domestic strengths for exporting grapes are enumerated in following paragraphs:-

Grapes in India are mainly cultivated in tropical region of the country where vines are pruned twice. Fruit pruning can be adjusted to harvest the crop as per the demand of the importing country.

Technology for production of Extra Class or Class I table grapes is available in the country.

The grape growers of the country are very innovative and very much receptive to new technologies and have registered with GLOBALGAP certification.

Yields of grapes in India are highest in the world.

Farmers of different regions have organized themselves by forming association/cooperatives and thus transfer of technology is easy.

Agri Export Zones for enhancing exports of grapes have been established.

Farmers of Maharashtra state in cooperation with MSAMB have branded their product as MAHA GRAPE.

29

The grape cultivators have research support from NRC for grapes, Pune, IIHR, Bangalore and State Agricultural Universities.

Grape growers in cooperation with MSAMB and APEDA have set up modern packhouses for handling and packing of grapes for exports.

APEDA has already set up a residue analysis laboratory at Pune for grape growing area of Maharashtra in order to cater to phytosanitary requirements of importing countries.

Geographically India is at an advantageous position as compared to Chile, South Africa and Israel for exporting grapes to South East Asian countries like Hong Kong, Singapore etc.

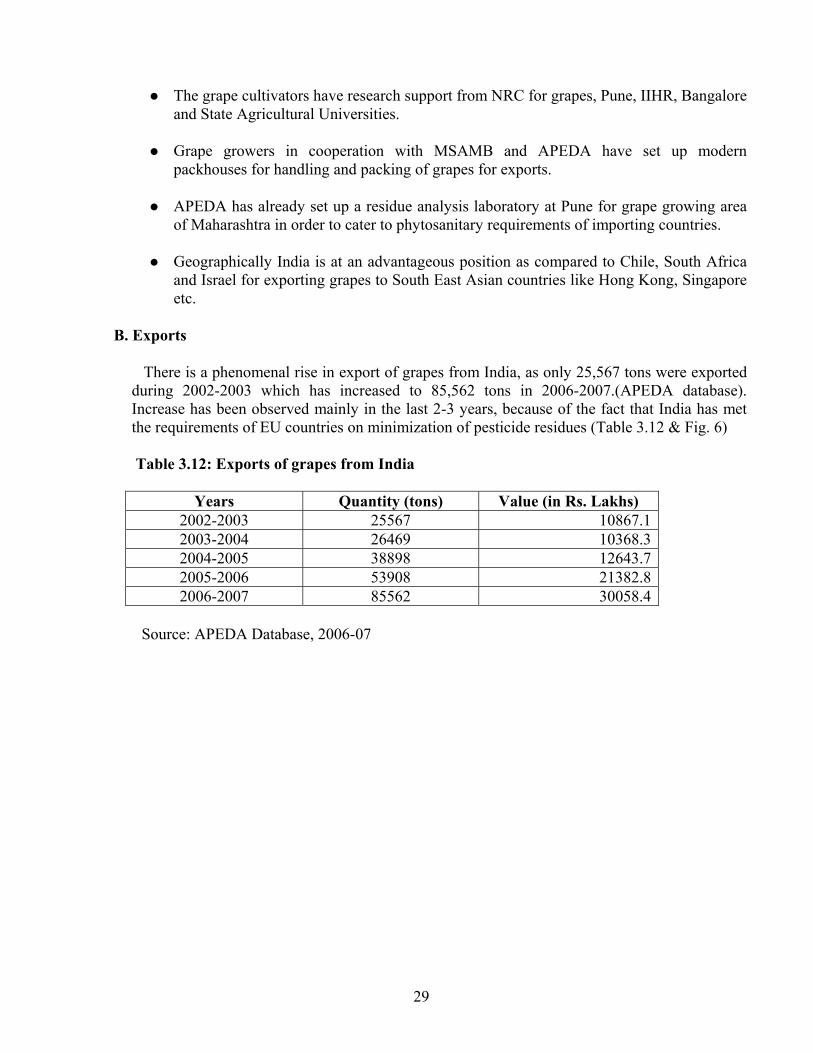

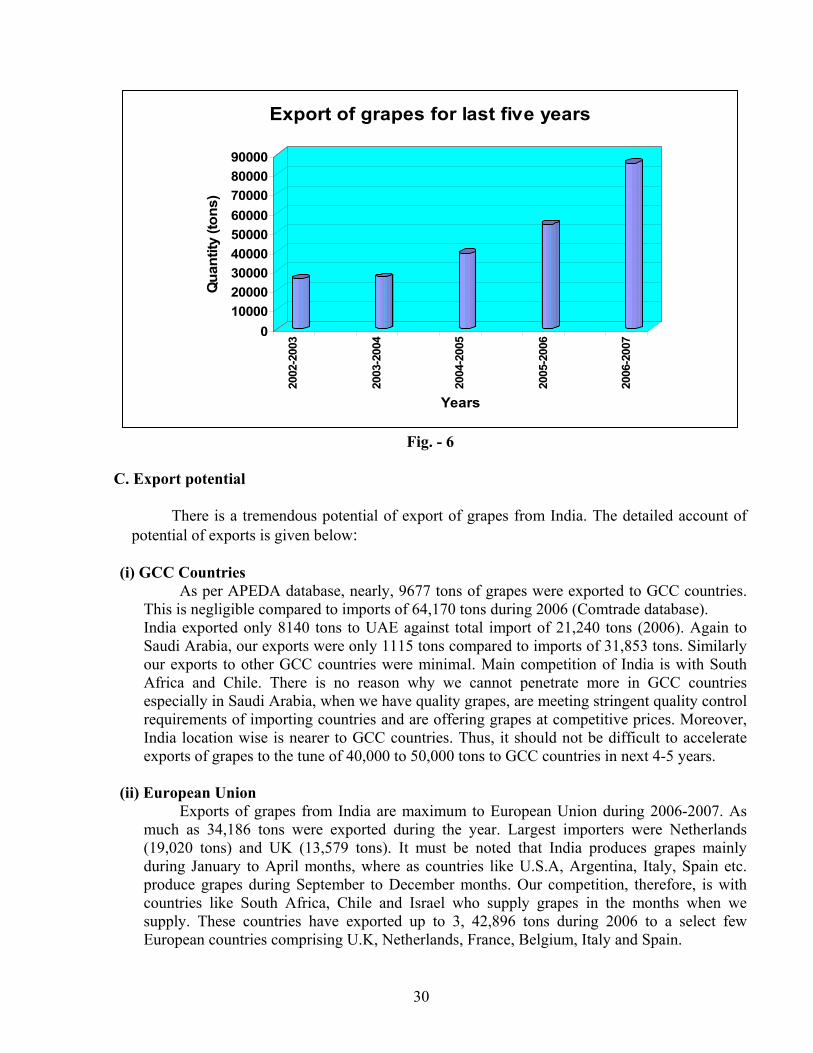

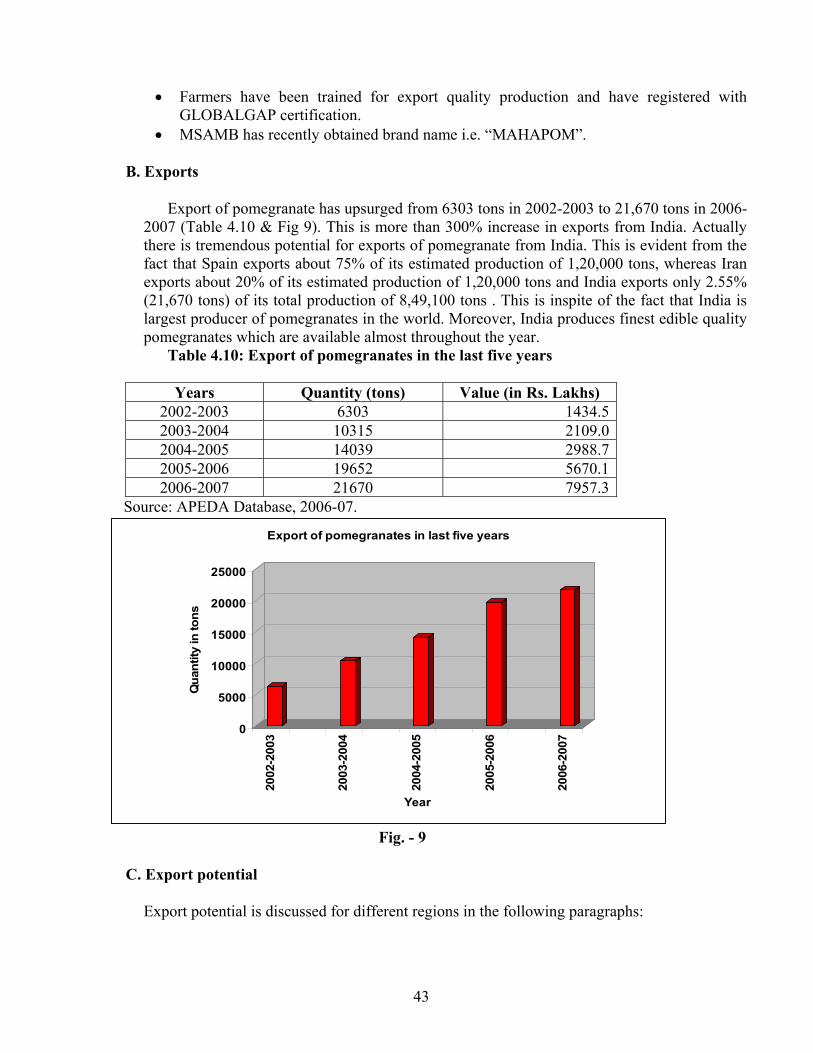

B. Exports

There is a phenomenal rise in export of grapes from India, as only 25,567 tons were exported during 2002-2003 which has increased to 85,562 tons in 2006-2007.(APEDA database). Increase has been observed mainly in the last 2-3 years, because of the fact that India has met the requirements of EU countries on minimization of pesticide residues (Table 3.12 & Fig. 6)

Table 3.12: Exports of grapes from India

Years Quantity (tons) Value (in Rs. Lakhs) 2002-2003 25567 10867.1 2003-2004 26469 10368.3 2004-2005 38898 12643.7 2005-2006 53908 21382.8 2006-2007 85562 30058.4

Source: APEDA Database, 2006-07

30

0100002000030000400005000060000700008000090000

Qua

ntity

(ton

s)

2002

-200

3

2003

-200

4

2004

-200

5

2005

-200

6

2006

-200

7

Years

Export of grapes for last five years

Fig. - 6

C. Export potential

There is a tremendous potential of export of grapes from India. The detailed account of potential of exports is given below:

(i) GCC Countries As per APEDA database, nearly, 9677 tons of grapes were exported to GCC countries.

This is negligible compared to imports of 64,170 tons during 2006 (Comtrade database). India exported only 8140 tons to UAE against total import of 21,240 tons (2006). Again to Saudi Arabia, our exports were only 1115 tons compared to imports of 31,853 tons. Similarly our exports to other GCC countries were minimal. Main competition of India is with South Africa and Chile. There is no reason why we cannot penetrate more in GCC countries especially in Saudi Arabia, when we have quality grapes, are meeting stringent quality control requirements of importing countries and are offering grapes at competitive prices. Moreover, India location wise is nearer to GCC countries. Thus, it should not be difficult to accelerate exports of grapes to the tune of 40,000 to 50,000 tons to GCC countries in next 4-5 years.

(ii) European Union

Exports of grapes from India are maximum to European Union during 2006-2007. As much as 34,186 tons were exported during the year. Largest importers were Netherlands (19,020 tons) and UK (13,579 tons). It must be noted that India produces grapes mainly during January to April months, where as countries like U.S.A, Argentina, Italy, Spain etc. produce grapes during September to December months. Our competition, therefore, is with countries like South Africa, Chile and Israel who supply grapes in the months when we supply. These countries have exported up to 3, 42,896 tons during 2006 to a select few European countries comprising U.K, Netherlands, France, Belgium, Italy and Spain.

31

Since India is meeting quality requirements including pesticide residues of all the importing countries in EU and supplying grapes at competitive prices, there is no reason why we cannot penetrate in the markets of Belgium, Germany, Spain and have larger share of imports in Netherlands and UK. Thus, it should not be difficult to meet the targets of export of 20 to 25 % of total imports of EU i.e. 3, 42,896 tons of grapes in this season in next 4-5 years.

Russian Federation imports as much as 3, 20,677 tons in addition to imports of Ukraine to the tune of 55,168 tons. Therefore, India must make concentrated efforts to accelerate export of grapes to these countries also.

(iii) ASEAN countries

ASEAN countries import grapes to the tune of 1,04,477 tons. The demand for grapes has increased by 50% from the year 2003. The main importers are Indonesia (26,366 tons), Philippines (14,748 tons), Singapore (12,166 tons) and Vietnam (11,025 tons). Main competitors with India for export of grapes to these countries are U.S.A, Australia, China and South Africa. Out of total quantity of 1,04,477 tons, approx 40,000-50,000 tons are supplied by U.S.A , 17,000 to 20,000 tons by Australia and 10,000- 11,000 tons by China and South Africa each. However, supplies from U.S.A and China are during September to December months and thus India’s competition is with South Africa, Chile and Australia. India can easily compete with these countries, as India location wise is closer to ASEAN countries compared to South Africa and Chile. Moreover, India is supplying grapes at competitive prices.

At present, India has exported only 196 tons to Malaysia, 93 tons to Singapore, 78 tons to Thailand, 34 tons to Indonesia and 13 tons Vietnam during 2006. These export volumes are negligible compared to the potential that exists. Moreover because of free trade agreements with Thailand and Singapore (likely to be signed very soon), exports of grapes are likely to accelerate, as even otherwise import duties of the order of 5-7% only are imposed by Malaysia, Philippines and Indonesia. Thus, in next 4-5 years time, target of export of 10,000-15,000 is not difficult to meet as India is producing quality grapes and is able to meet quality requirements. India must campaign aggressively and nurture these markets.

(iv) Hong Kong

Hong Kong is a trade hub and imported up to 91,517 tons and exported up to 46,868 tons during 2006. However, India exported only 156 tons during 2006.There is excellent potential and also possibility of realizing higher prices in Hong Kong market. India must make aggressive campaign and nurture the market.

(v) Pacific Rim countries and China

Pacific Rim countries comprising South Korea, Japan and Australia are also importing grapes to the extent of 17,921, 9949 and 4759 tons respectively. At present India is not exporting any quantity of grapes to these countries.

It is expected that with the signing of Free Trade Agreement with South Korea, export of grapes should initiate. Similarly with China, grape export should be explored as China has imported 46,021 tons of grapes during 2006. India and China are participants in Asia Pacific Trade Agreement.

32

D. Measures for enhancing competitiveness for exporting grapes

Following measures need to be adopted for enhancing competitiveness for exporting grapes.

Competition of India is with countries like Chile, South Africa and Israel, which produce quality grapes. Therefore, India must maintain superior quality free from pesticide residues etc. for keeping up momentum of exports.

There is huge demand of grapes in Hong Kong, Singapore, Malaysia etc., India needs to exploit this opportunity, by holding fruit shows, exhibitions and buyer- seller meets frequently.

India needs to enhance its competitiveness by making grapes available during Ramzan period in Middle East countries and in Malaysia, Indonesia etc, by altering pruning time for fruiting.

India can further enhance its competitiveness by economizing on logistics by exporting from eastern port to South East Asian countries and by intensifying production in Andhra Pradesh.

Similarly, grapes can be made available during Christmas period by changing pruning time for fruiting.

13. Storage

Temperature : 0 ± 0.5o C Relative Humidity : 93 ± 2 % Storage period : 3-8 weeks Freezing point : -1o C

14. Documents required for exports

a) Documents related to goods: -

a) Invoice b) Packing List c) Certificate of origin

b) Documents related to shipment: -

a) Mate Receipt b) Shipping Bill c) Bill of handing d) Airway Bill

c) Documents related to Payment: -

a) Letter of Credit (L/C) b) Bill of Exchange

33

d) Documents related to quality of goods: -

a) Phytosanitary Certificate b) GLOBALGAP Certification c) Health Certificate

e) Organic Certification: -

- Certificate indicating material produce is based on organic farming.

f) Documents related to Foreign Exchange Regulations: -

GR Form: Documents required by RBI which assures to RBI that the exporter will realize

the proceeds of goods within 180 days from the date of Shipment.

g) Other Document:

Bank Realization Certification (BRC): This is the advice given by Foreign Exchange Bank

after the realization of money from Importer.

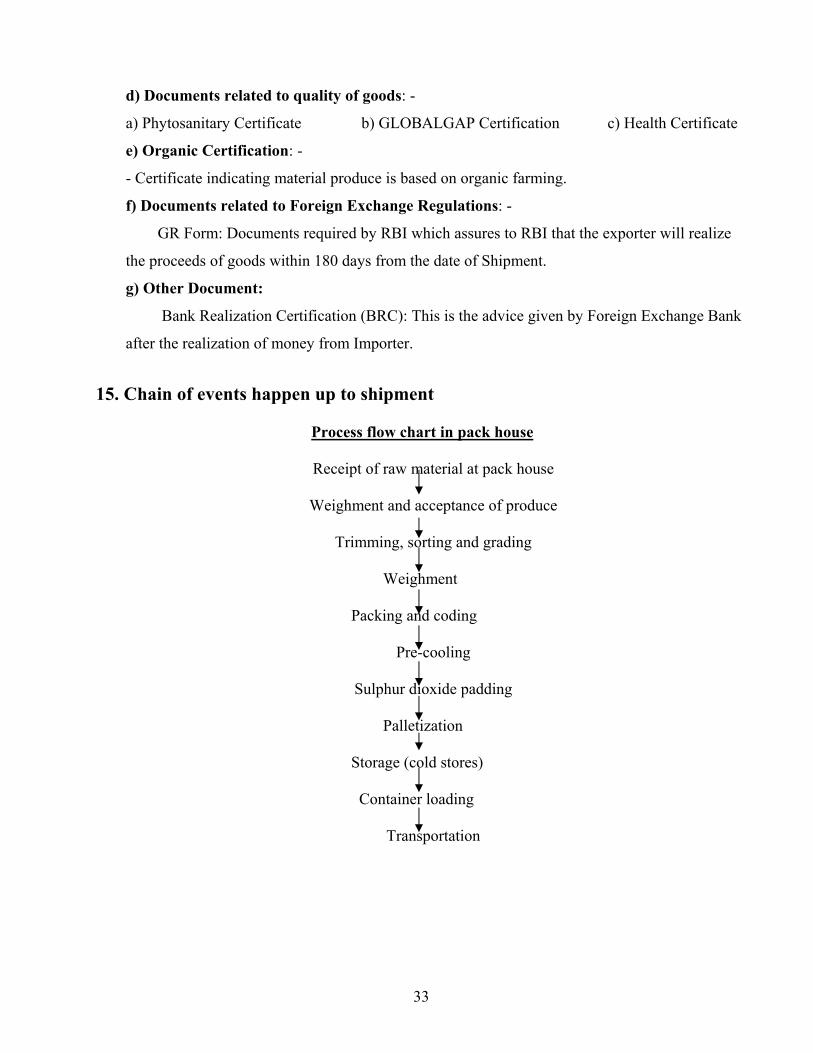

15. Chain of events happen up to shipment Process flow chart in pack house

Receipt of raw material at pack house

Weighment and acceptance of produce

Trimming, sorting and grading

Weighment

Packing and coding

Pre-cooling

Sulphur dioxide padding

Palletization

Storage (cold stores)

Container loading

Transportation

34

16. Price prevailing in international market

The given below tables shows the annual average price range of grapes in different international markets. The table 3.13 shows the pricing trend in EU markets.

Table 3.13: Summary of prices for grapes in potential markets for India

Annual Average price Range (2003-08) Country Currency USD/kg 1.26 to 2.35 European Union

INR/kg 57.0 to 105.76

Source: Comtrade Database 17. Cost Calculation from harvest to packhouse to port

The cost involved in exporting grapes is as follows (as per information collected during

2008):

(a) Procurement price*:

Approx. price (Rs. /kg) : 25-35 *Price of grapes varies according to variety (coloured or white) and month of procurement (b) Charges for testing, packing, transport, etc.(below in table): Table 3.14: Charges for testing, packing, transport, etc.

S. No. Particulars Rs./kg

1. Residue testing, harvesting and transport charges (plot to pack house) 2.00

2. Pack house charges including labour, packing material, precooling, container loading, Agmark etc.

19.70

3. Container Freight* (Junnar up to Mumbai), container forwarding and document charges

1.99

Total 23.69

Source: NRC for Grapes, Pune

35

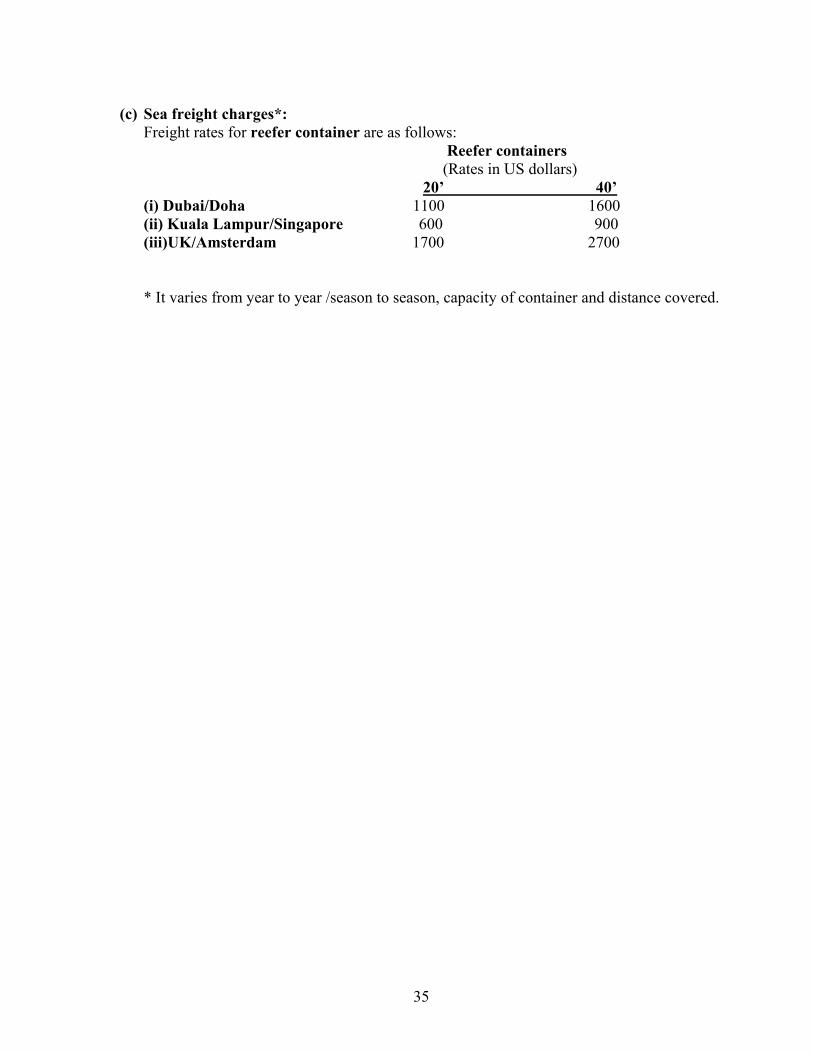

(c) Sea freight charges*:

Freight rates for reefer container are as follows: Reefer containers (Rates in US dollars) 20’ 40’

(i) Dubai/Doha 1100 1600 (ii) Kuala Lampur/Singapore 600 900 (iii)UK/Amsterdam 1700 2700

* It varies from year to year /season to season, capacity of container and distance covered.

36

CHAPTER - 4 POMEGRANATE

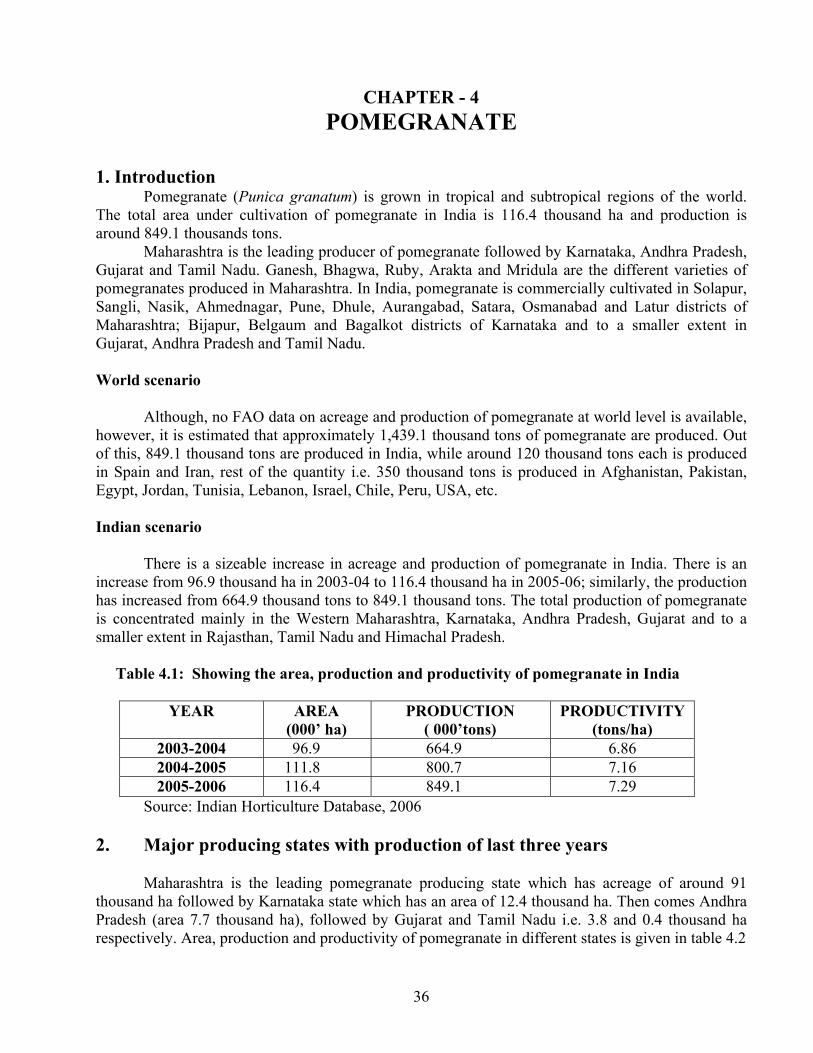

1. Introduction

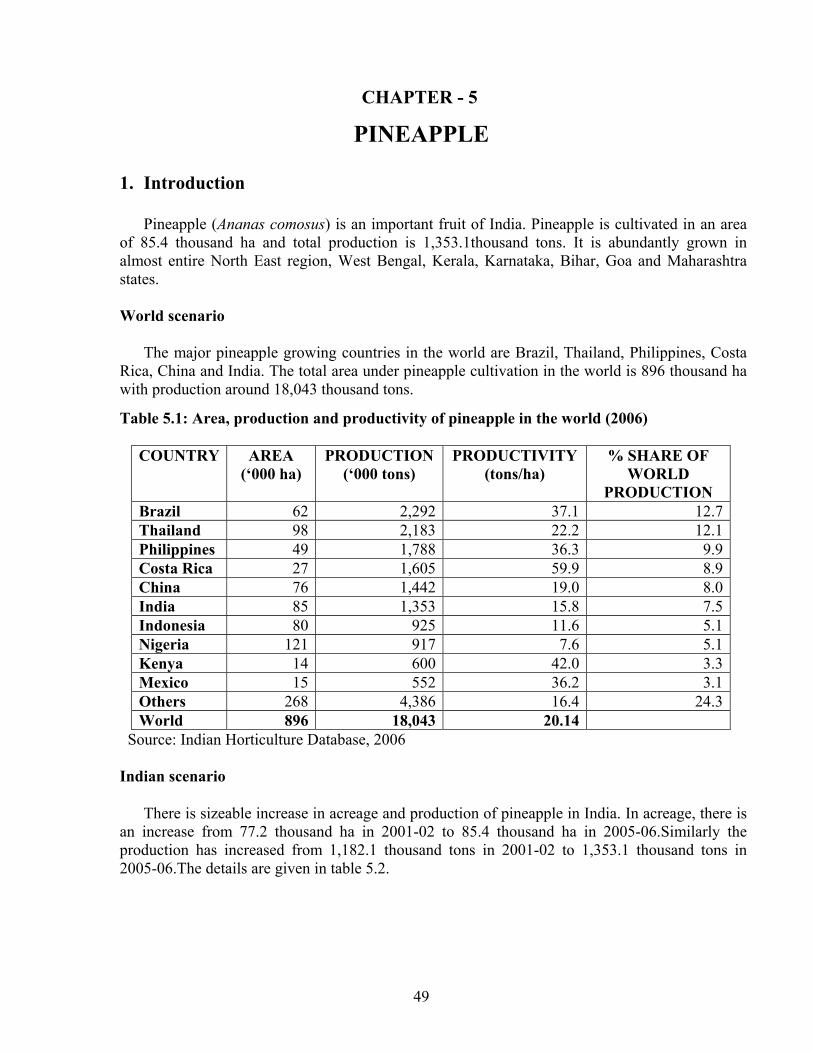

Pomegranate (Punica granatum) is grown in tropical and subtropical regions of the world. The total area under cultivation of pomegranate in India is 116.4 thousand ha and production is around 849.1 thousands tons.

Maharashtra is the leading producer of pomegranate followed by Karnataka, Andhra Pradesh, Gujarat and Tamil Nadu. Ganesh, Bhagwa, Ruby, Arakta and Mridula are the different varieties of pomegranates produced in Maharashtra. In India, pomegranate is commercially cultivated in Solapur, Sangli, Nasik, Ahmednagar, Pune, Dhule, Aurangabad, Satara, Osmanabad and Latur districts of Maharashtra; Bijapur, Belgaum and Bagalkot districts of Karnataka and to a smaller extent in Gujarat, Andhra Pradesh and Tamil Nadu. World scenario

Although, no FAO data on acreage and production of pomegranate at world level is available, however, it is estimated that approximately 1,439.1 thousand tons of pomegranate are produced. Out of this, 849.1 thousand tons are produced in India, while around 120 thousand tons each is produced in Spain and Iran, rest of the quantity i.e. 350 thousand tons is produced in Afghanistan, Pakistan, Egypt, Jordan, Tunisia, Lebanon, Israel, Chile, Peru, USA, etc.

Indian scenario

There is a sizeable increase in acreage and production of pomegranate in India. There is an increase from 96.9 thousand ha in 2003-04 to 116.4 thousand ha in 2005-06; similarly, the production has increased from 664.9 thousand tons to 849.1 thousand tons. The total production of pomegranate is concentrated mainly in the Western Maharashtra, Karnataka, Andhra Pradesh, Gujarat and to a smaller extent in Rajasthan, Tamil Nadu and Himachal Pradesh. Table 4.1: Showing the area, production and productivity of pomegranate in India

YEAR AREA (000’ ha)

PRODUCTION ( 000’tons)

PRODUCTIVITY (tons/ha)

2003-2004 96.9 664.9 6.86 2004-2005 111.8 800.7 7.16 2005-2006 116.4 849.1 7.29

Source: Indian Horticulture Database, 2006 2. Major producing states with production of last three years Maharashtra is the leading pomegranate producing state which has acreage of around 91 thousand ha followed by Karnataka state which has an area of 12.4 thousand ha. Then comes Andhra Pradesh (area 7.7 thousand ha), followed by Gujarat and Tamil Nadu i.e. 3.8 and 0.4 thousand ha respectively. Area, production and productivity of pomegranate in different states is given in table 4.2

37

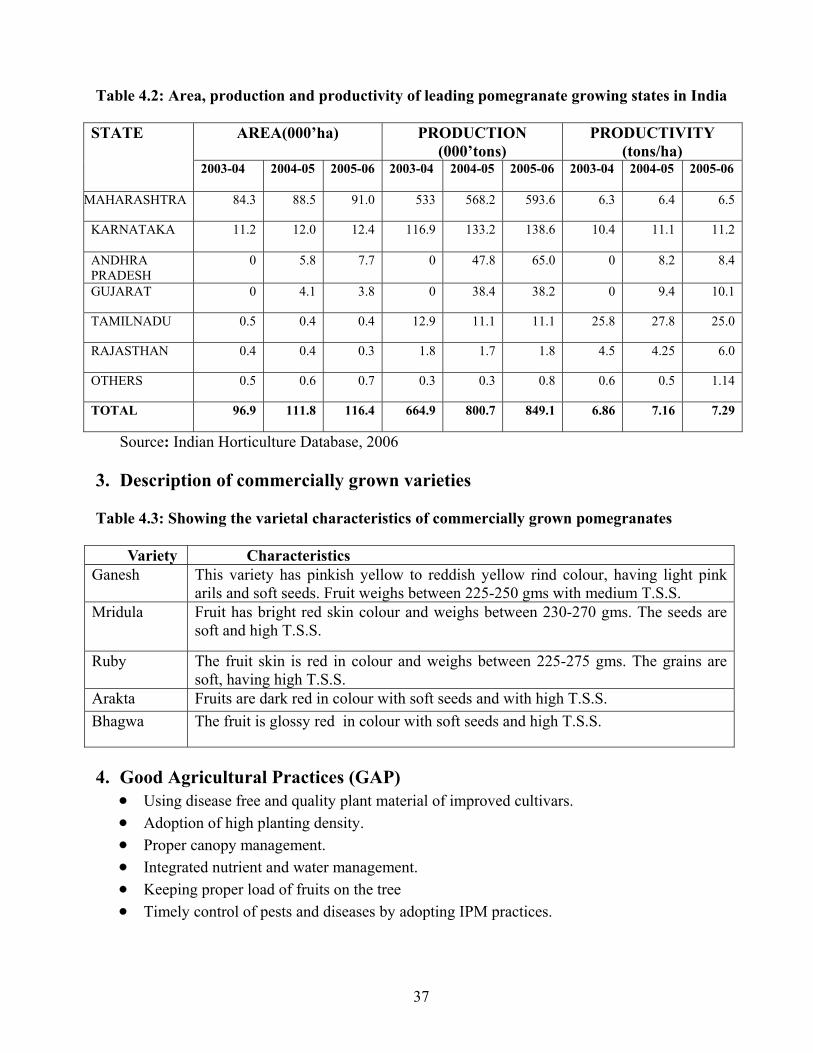

Table 4.2: Area, production and productivity of leading pomegranate growing states in India

AREA(000’ha) PRODUCTION (000’tons)

PRODUCTIVITY (tons/ha)

STATE

2003-04

2004-05 2005-06 2003-04 2004-05 2005-06 2003-04 2004-05 2005-06

MAHARASHTRA 84.3 88.5 91.0 533 568.2 593.6 6.3 6.4 6.5

KARNATAKA 11.2 12.0 12.4 116.9 133.2 138.6 10.4 11.1 11.2

ANDHRA PRADESH

0 5.8 7.7 0 47.8 65.0 0 8.2 8.4

GUJARAT 0 4.1 3.8 0 38.4 38.2 0 9.4 10.1

TAMILNADU 0.5 0.4 0.4 12.9 11.1 11.1 25.8 27.8 25.0

RAJASTHAN 0.4 0.4 0.3 1.8 1.7 1.8 4.5 4.25 6.0

OTHERS 0.5 0.6 0.7 0.3 0.3 0.8 0.6 0.5 1.14

TOTAL 96.9 111.8 116.4 664.9 800.7 849.1 6.86 7.16 7.29

Source: Indian Horticulture Database, 2006

3. Description of commercially grown varieties Table 4.3: Showing the varietal characteristics of commercially grown pomegranates Variety Characteristics Ganesh This variety has pinkish yellow to reddish yellow rind colour, having light pink

arils and soft seeds. Fruit weighs between 225-250 gms with medium T.S.S. Mridula Fruit has bright red skin colour and weighs between 230-270 gms. The seeds are

soft and high T.S.S.

Ruby The fruit skin is red in colour and weighs between 225-275 gms. The grains are soft, having high T.S.S.

Arakta Fruits are dark red in colour with soft seeds and with high T.S.S. Bhagwa The fruit is glossy red in colour with soft seeds and high T.S.S.

4. Good Agricultural Practices (GAP)

• Using disease free and quality plant material of improved cultivars. • Adoption of high planting density. • Proper canopy management. • Integrated nutrient and water management. • Keeping proper load of fruits on the tree • Timely control of pests and diseases by adopting IPM practices.

38

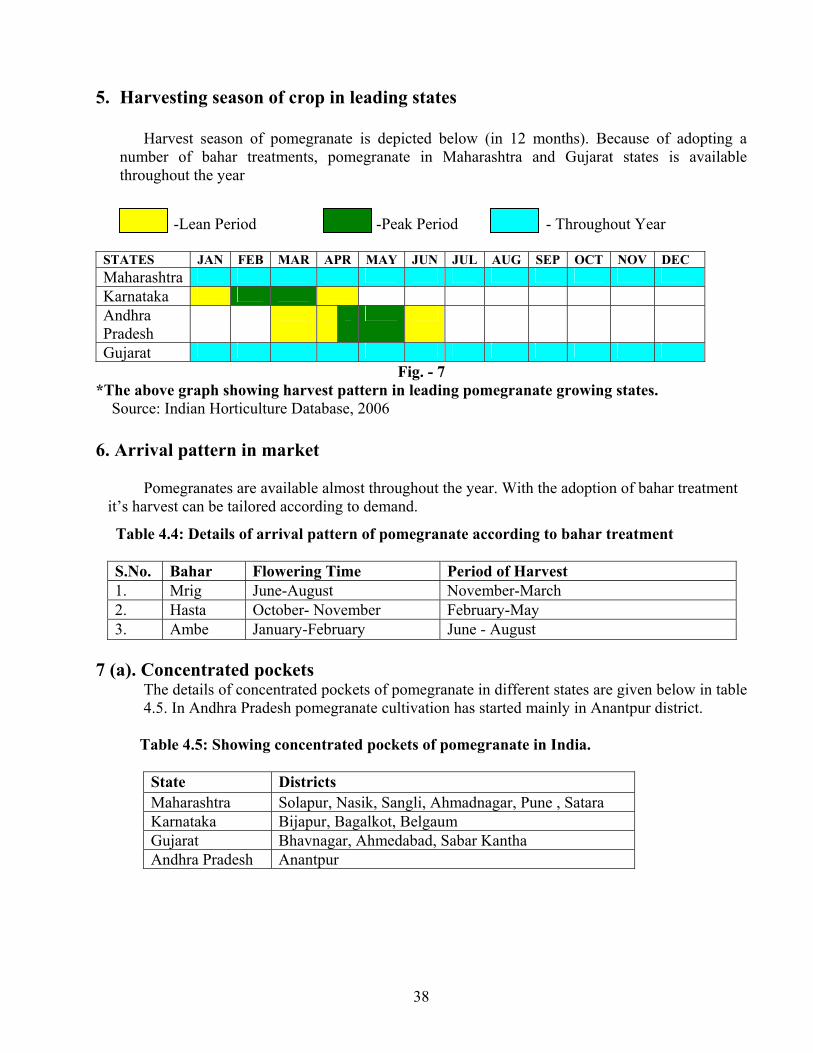

5. Harvesting season of crop in leading states

Harvest season of pomegranate is depicted below (in 12 months). Because of adopting a number of bahar treatments, pomegranate in Maharashtra and Gujarat states is available throughout the year

-Lean Period -Peak Period - Throughout Year

STATES JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Maharashtra Karnataka Andhra Pradesh

Gujarat Fig. - 7

*The above graph showing harvest pattern in leading pomegranate growing states. Source: Indian Horticulture Database, 2006 6. Arrival pattern in market

Pomegranates are available almost throughout the year. With the adoption of bahar treatment it’s harvest can be tailored according to demand.

Table 4.4: Details of arrival pattern of pomegranate according to bahar treatment S.No. Bahar Flowering Time Period of Harvest 1. Mrig June-August November-March 2. Hasta October- November February-May 3. Ambe January-February June - August

7 (a). Concentrated pockets

The details of concentrated pockets of pomegranate in different states are given below in table 4.5. In Andhra Pradesh pomegranate cultivation has started mainly in Anantpur district.

Table 4.5: Showing concentrated pockets of pomegranate in India.

State Districts Maharashtra Solapur, Nasik, Sangli, Ahmadnagar, Pune , Satara Karnataka Bijapur, Bagalkot, Belgaum Gujarat Bhavnagar, Ahmedabad, Sabar Kantha Andhra Pradesh Anantpur

39

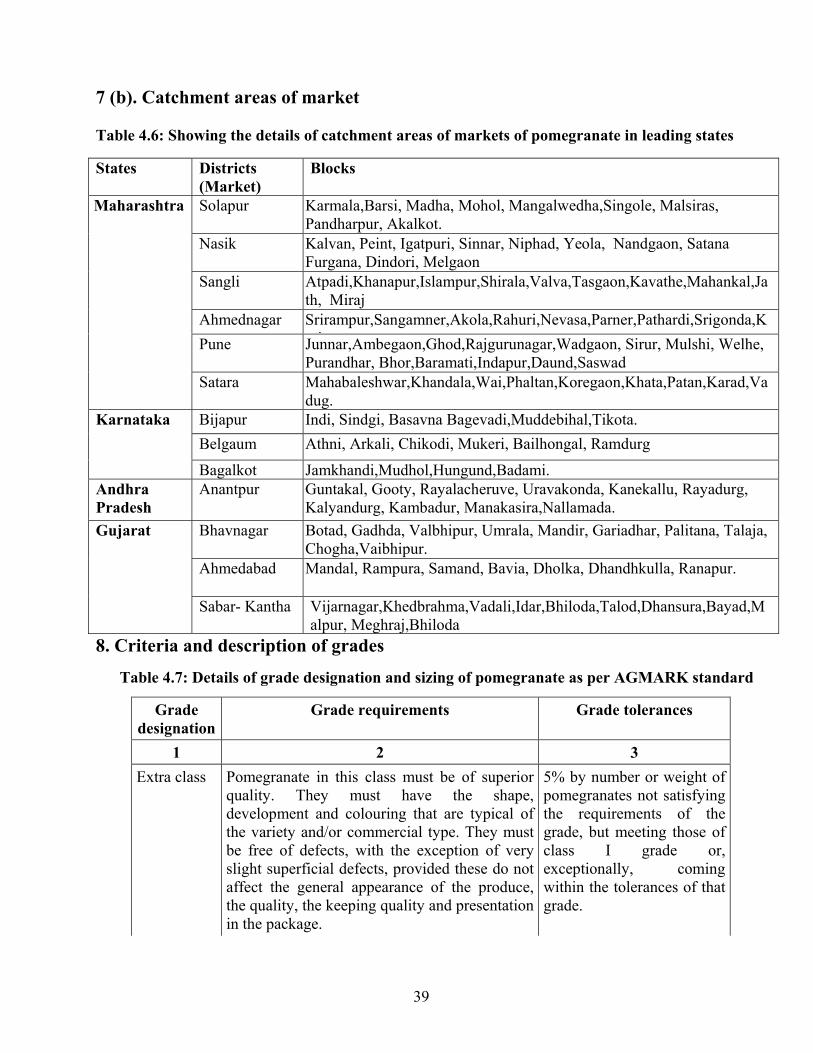

7 (b). Catchment areas of market Table 4.6: Showing the details of catchment areas of markets of pomegranate in leading states

8. Criteria and description of grades

Table 4.7: Details of grade designation and sizing of pomegranate as per AGMARK standard

Grade designation

Grade requirements Grade tolerances

1 2 3 Extra class Pomegranate in this class must be of superior

quality. They must have the shape, development and colouring that are typical of the variety and/or commercial type. They must be free of defects, with the exception of very slight superficial defects, provided these do not affect the general appearance of the produce, the quality, the keeping quality and presentation in the package.

5% by number or weight of pomegranates not satisfying the requirements of the grade, but meeting those of class I grade or, exceptionally, coming within the tolerances of that grade.

States Districts (Market)

Blocks

Solapur Karmala,Barsi, Madha, Mohol, Mangalwedha,Singole, Malsiras, Pandharpur, Akalkot.

Nasik Kalvan, Peint, Igatpuri, Sinnar, Niphad, Yeola, Nandgaon, Satana Furgana, Dindori, Melgaon

Sangli Atpadi,Khanapur,Islampur,Shirala,Valva,Tasgaon,Kavathe,Mahankal,Jath, Miraj

Ahmednagar Srirampur,Sangamner,Akola,Rahuri,Nevasa,Parner,Pathardi,Srigonda,Kj tPune Junnar,Ambegaon,Ghod,Rajgurunagar,Wadgaon, Sirur, Mulshi, Welhe,

Purandhar, Bhor,Baramati,Indapur,Daund,Saswad

Maharashtra

Satara Mahabaleshwar,Khandala,Wai,Phaltan,Koregaon,Khata,Patan,Karad,Vadug.

Bijapur Indi, Sindgi, Basavna Bagevadi,Muddebihal,Tikota. Belgaum Athni, Arkali, Chikodi, Mukeri, Bailhongal, Ramdurg

Karnataka

Bagalkot Jamkhandi,Mudhol,Hungund,Badami. Andhra Pradesh

Anantpur Guntakal, Gooty, Rayalacheruve, Uravakonda, Kanekallu, Rayadurg, Kalyandurg, Kambadur, Manakasira,Nallamada.

Bhavnagar Botad, Gadhda, Valbhipur, Umrala, Mandir, Gariadhar, Palitana, Talaja, Chogha,Vaibhipur.

Ahmedabad Mandal, Rampura, Samand, Bavia, Dholka, Dhandhkulla, Ranapur.

Gujarat

Sabar- Kantha Vijarnagar,Khedbrahma,Vadali,Idar,Bhiloda,Talod,Dhansura,Bayad,Malpur, Meghraj,Bhiloda

40

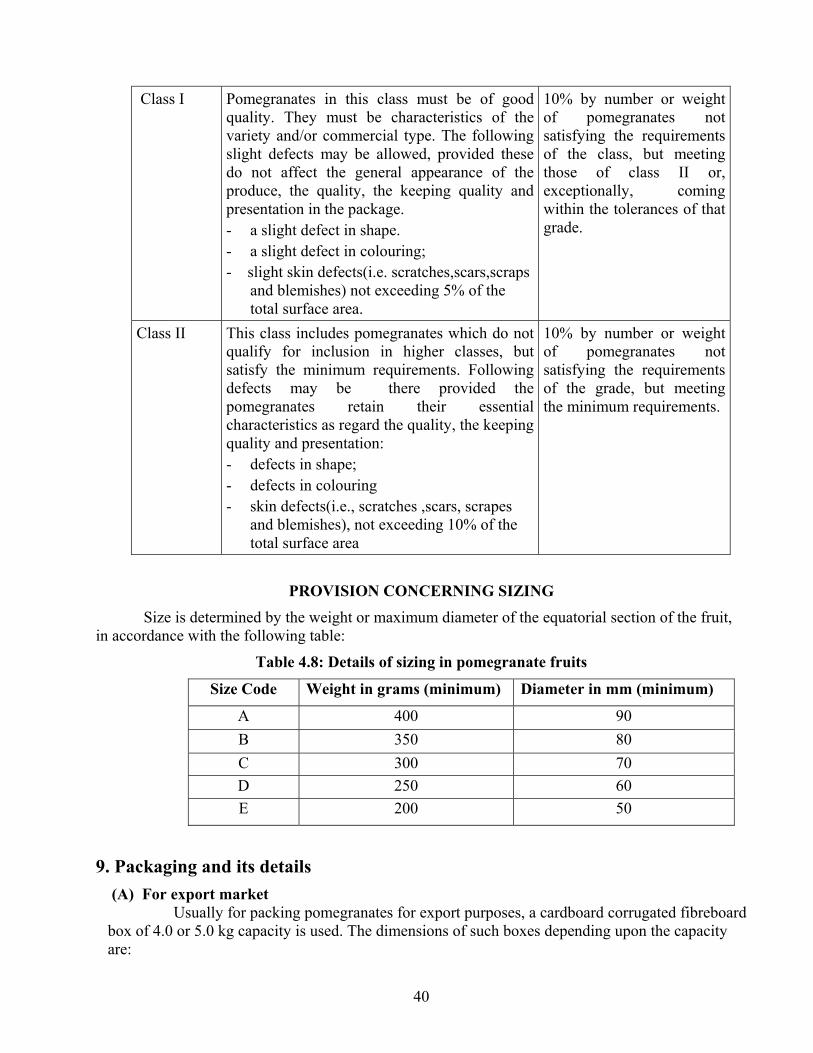

Class I Pomegranates in this class must be of good quality. They must be characteristics of the variety and/or commercial type. The following slight defects may be allowed, provided these do not affect the general appearance of the produce, the quality, the keeping quality and presentation in the package. - a slight defect in shape. - a slight defect in colouring; - slight skin defects(i.e. scratches,scars,scraps

and blemishes) not exceeding 5% of the total surface area.

10% by number or weight of pomegranates not satisfying the requirements of the class, but meeting those of class II or, exceptionally, coming within the tolerances of that grade.

Class II This class includes pomegranates which do not qualify for inclusion in higher classes, but satisfy the minimum requirements. Following defects may be there provided the pomegranates retain their essential characteristics as regard the quality, the keeping quality and presentation: - defects in shape; - defects in colouring - skin defects(i.e., scratches ,scars, scrapes

and blemishes), not exceeding 10% of the total surface area

10% by number or weight of pomegranates not satisfying the requirements of the grade, but meeting the minimum requirements.

PROVISION CONCERNING SIZING

Size is determined by the weight or maximum diameter of the equatorial section of the fruit, in accordance with the following table:

Table 4.8: Details of sizing in pomegranate fruits

Size Code Weight in grams (minimum) Diameter in mm (minimum)

A 400 90 B 350 80 C 300 70 D 250 60 E 200 50

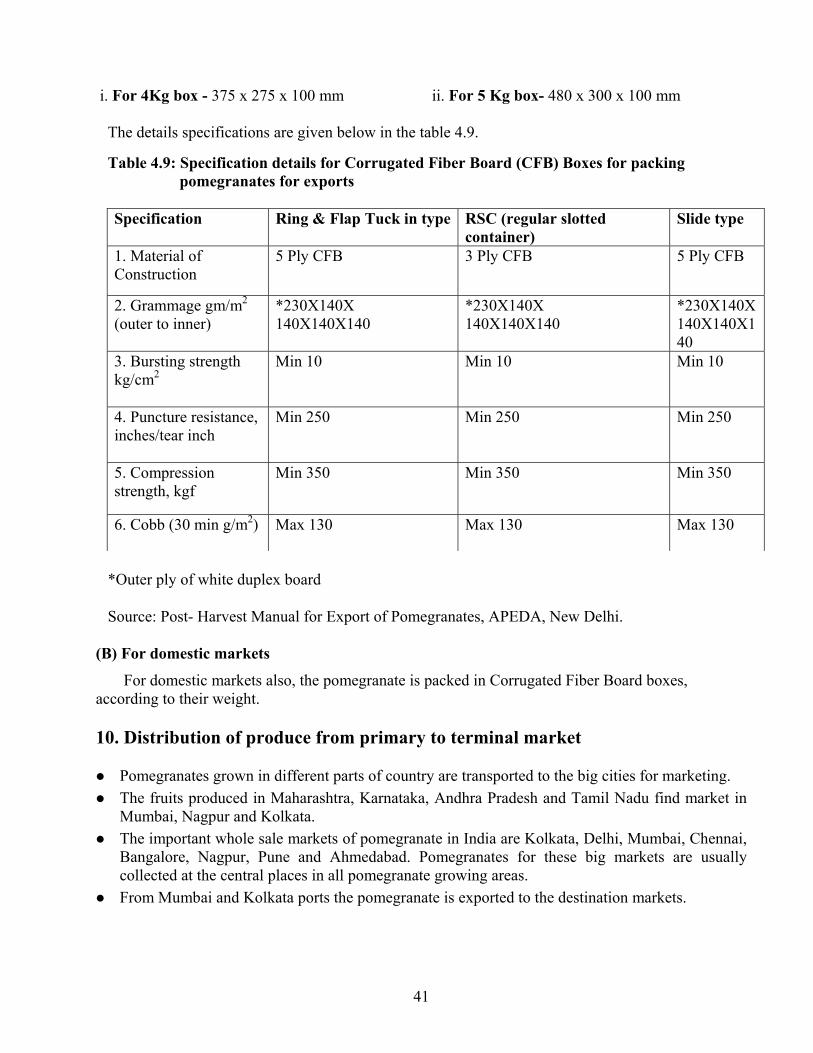

9. Packaging and its details

(A) For export market Usually for packing pomegranates for export purposes, a cardboard corrugated fibreboard box of 4.0 or 5.0 kg capacity is used. The dimensions of such boxes depending upon the capacity are:

41

i. For 4Kg box - 375 x 275 x 100 mm ii. For 5 Kg box- 480 x 300 x 100 mm The details specifications are given below in the table 4.9.

Table 4.9: Specification details for Corrugated Fiber Board (CFB) Boxes for packing pomegranates for exports

*Outer ply of white duplex board

Source: Post- Harvest Manual for Export of Pomegranates, APEDA, New Delhi.

(B) For domestic markets

For domestic markets also, the pomegranate is packed in Corrugated Fiber Board boxes, according to their weight.

10. Distribution of produce from primary to terminal market

Pomegranates grown in different parts of country are transported to the big cities for marketing. The fruits produced in Maharashtra, Karnataka, Andhra Pradesh and Tamil Nadu find market in

Mumbai, Nagpur and Kolkata. The important whole sale markets of pomegranate in India are Kolkata, Delhi, Mumbai, Chennai,

Bangalore, Nagpur, Pune and Ahmedabad. Pomegranates for these big markets are usually collected at the central places in all pomegranate growing areas.

From Mumbai and Kolkata ports the pomegranate is exported to the destination markets.

Specification Ring & Flap Tuck in type RSC (regular slotted container)

Slide type

1. Material of Construction

5 Ply CFB 3 Ply CFB 5 Ply CFB

2. Grammage gm/m2 (outer to inner)

*230X140X 140X140X140

*230X140X 140X140X140

*230X140X 140X140X140

3. Bursting strength kg/cm2

Min 10

Min 10

Min 10

4. Puncture resistance, inches/tear inch

Min 250

Min 250

Min 250

5. Compression strength, kgf

Min 350

Min 350

Min 350

6. Cobb (30 min g/m2) Max 130 Max 130 Max 130

42

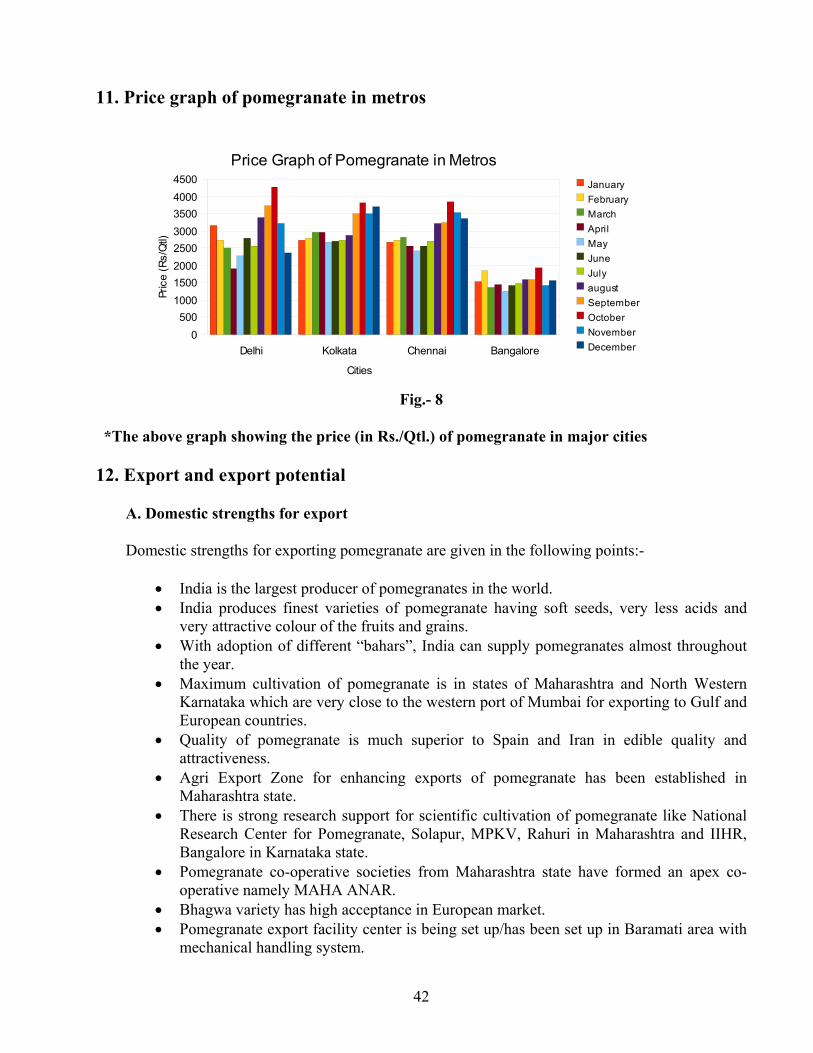

11. Price graph of pomegranate in metros

Fig.- 8

*The above graph showing the price (in Rs./Qtl.) of pomegranate in major cities

12. Export and export potential

A. Domestic strengths for export

Domestic strengths for exporting pomegranate are given in the following points:-

• India is the largest producer of pomegranates in the world. • India produces finest varieties of pomegranate having soft seeds, very less acids and