Embed Size (px)

Citation preview

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

Insurance People Magazine Identity and Design

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

Insurance People Magazine Identity and Design

14 insurancepeople January 201014 insurancepeople January 2010

comment

JackBrownhill WOrLD MOTOr COnSuLTanCy

Wheredowego fromhere?Jack Brownhill of World Motor Consultancy looks back at the decade from the motor insurance perspective and speculates about the future

It seems hard to believe that it was ten years ago that the

insurance industry - and seemingly - the rest of humanity came to the conclusion that the end of the world really was nigh, and that every computer, plane, motor vehicle, traffic light and kettle would go in to meltdown when the atomic clock clicked over to the 21st century. y2K and the Millennium Bug became all consuming, and prompted what must surely count as one of the largest worldwide IT spends in modern history. In the moments leading up to the dawn of the new millennium we held our collective breath, only letting out a sigh of relief when the strident tones of Big Ben rang out bang on schedule.as we consign the first decade of this millennium to the history pages of Wikipedia, this seems an opportune time to reflect on the recent past and to attempt, perhaps unwisely, to see what the future may hold. One thing is very clear - over the last ten years we have continued to splash gallons (sorry Brussels, litres) of red ink across the pages of the motor returns sent annually to our supervisors in Canary Wharf and Gibraltar. I wonder where we will be sending our returns in the future if there is a change of government at the next election?Thankfully the last twelve or so months have seen some vigorous rating action, although I use the word ‘vigorous’ with some caution as there are a fair few people who remain far from convinced that what we have done so far is anywhere near adequate.

Investment opportunities have been much thinner on the ground of late and although accident frequency appears to have reduced during the recession, the average number of claimants per claim appears to be on the increase. The prophets of doom have also speculated that much of the market is beginning to scrape the bottom of the prior years’ reserves releases barrel, and that there needs to be a much firmer focus on current year trading. With a market as competitive and crowded as that in the uK, strengthening rates has always been something of a challenge particularly in those customer segments that are heavily fished by both direct and broker-based insurers.

THE A-TEAM The intensity of the competition has surely been propelled to new heights by the arrival on the scene of the a-Team - the aggregators. I’ve yet to meet anyone who is ambivalent on this issue, and whether you love them or hate them, there’s no escaping the fact that they have had a major impact on consumer buying habits. The commoditisation of motor insurance has broken all boundaries and is now heavily biased towards new business, and the constant annual recycling of customers. not quite everyone has bought in to these comparative sites, of course, and the need to maintain the flow of customer traffic through the sites has given rise to major media promotions funded by multi-million pound marketing budgets. It appears unlikely that

the final chapter has been written on this subject. not surprisingly, claims costs continue to dominate the motor insurance vista with personal injury awards, fees and credit hire hogging the limelight. Much has been done to address these issues and 2010 should witness further activity - I leave others to decide whether there is a bright enough light (or, indeed, any light) at the end of the tunnel. as ever, we have seen insurers come and go and there has been a sprinkling of name changes - for one reason or another. unlike professional football, the insurance transfer window is always open, and as hardly a year goes by without at least one new insurer appearing on the scene it is surely the case that 2010 will bear witness to further player changes.The environment has been one of the hottest topics of the last few weeks of 2009 with the Copenhagen Climate Control Conference attracting much attention. Global warming, greenhouse gases, and broader environmental issues will remain widely debated subjects for many years, but without doubt road transport will continue to be a key battleground. Going forward, and in a relatively narrow timeframe, the picture is likely to be very different with new environmentally friendly vehicles coming onto the scene in increasing numbers. Electric vehicles appear to be a particularly popular topic at the moment, managing to push eco-supporters’ hybrids into the shadows. Will tripping over the recharging cable become the motor insurance equivalent of broken pavements?

With recycling and environmentally friendly manufacturing processes and materials in mind, vehicle manufacturers appear to be increasingly adopting new materials for their cars - hemp mirror mountings, parcel shelves made from wood chippings, and tyres from orange peel. and as for what we will be putting in our fuel tanks...! How long before we see the thatched convertible? although road pricing looks to have slipped off the active radar for the moment, it would seem unlikely that this will remain the case for the foreseeable future. Increasing numbers of vehicles are appearing on our roads with the necessary embedded telematics to make road pricing a more viable prospect, and it is of course very much the same technology that is required for the more basic usage based insurance (uBI) products.although the acronyms uBI and PayD are commonly used around the world, many of the associated insurance products are founded solely on a more precise calculation of the annual distance travelled and not all of these products even necessitate the fitment of any sophisticated monitoring equipment to the vehicle. The various uK schemes have looked beyond this however, and are focussed on not just how far, but more importantly where, when and how the vehicle is being driven. as technology costs reduce we will surely see more of these products becoming available in the uK. But I venture to suggest there must remain a question mark over how far such products can penetrate the traditional uK

marketplace for the mainstream customer and, indeed, what strategies will be adopted to permit more established pricing and risk selection mechanisms to remain competitive. Vehicle technology is also advancing in other areas with safety being a common thread. Vehicles are now being designed with an eye on the safety of vulnerable road users outside of the vehicle - pedestrians and pedal cyclists being very much at the forefront of this work. We are also seeing an increasing number of driver assistance devices becoming available - drowsy driver alerts, lane monitoring, active vehicle separation, and automatic speed limit monitoring to name just a few. Most modern aircraft are fitted with anti-collision equipment that automatically diverts them from converging paths - how long will it be before such equipment becomes commonplace on our roads? The availability of these new technologies will assuredly influence pricing and risk selection with an increasing rating emphasis on the vehicle and reduced emphasis on the driver.The last decade has been something of a success story as far as the fight against uninsured driving is concerned. The combination of the Motor Insurance Database (MID) and Automatic Number Plate Recognition (ANPR) technology has resulted in many thousands of uninsured vehicles being removed from our roads - many permanently.

While there is still much to do in this area - and it appears likely that a toughening up on data delivery to MID is on the cards - it’s clear that our achievements so far warrant a pat on the back. The introduction of Continuous Insurance Enforcement (CIE) will be a major addition to the armoury, although there remains some disquiet over the level of the fixed penalty fines envisaged under CIE.It’s now widely accepted that there is a strong correlation between uninsured driving and other criminal activity and it is not unknown for a driver of an illegal vehicle to be in breach of the driving licence requirements. nterestingly, there are ongoing discussions between insurers and the DVLA regarding easier insurer access to driving licence and driving history information. Will we eventually see this being validated at point of sale? What with the various other counter-fraud processes that insurers (and brokers) have introduced at both the policy inception and claim stages we appear to have reached the point where the concept of utmost good faith has run its course. It is surely no coincidence that a review of the Marine Insurance Act 1906 (the legislation that has underpinned material disclosure for more than a hundred years) is currently underway. Although this review has been triggered externally, the insurance market appears to be supportive, anticipating that any changes to the legislation will merely reflect

what is perceived as current insurer best practice. Will there be changes to the data collection process and to proposal form/quote system questions and defaults in the near future? I believe so. Are we in for a quiet decade? I think not. Insurance is very much a cyclical business and many past issues will, no doubt, come round again whilst others will remain

permanent features. The market will continue to face up to its challenges, not least of which is the constant struggle to convince the buying public that we really are here to help them in their hour of need.

“Unlike football, the insurancetransfer window is always open”

January 2010 insurancepeople 15

16 insurancepeople January 2010

January 2010 insurancepeople 17

Internet Opportunity

On my return to London, a

research project for Country

Mutual quickly allowed the

equation ‘Insurance plus Internet =

Opportunity’ to fall into place.

Quotiva then concentrated on

building internet applications,

leaving the drawing and colouring-

in job of brochure sites to others

better positioned. It didn’t take long

working with brokers and insurers

until we noticed the (then) hole in

the market for quick, cheap, reliable

quote engines. We therefore built

a system that allowed us to rapidly

build comparative quote engines for

brokers from any rating guide and

began selling. But we hadn’t banked

on the overwhelming ‘set-in-stone’

deal-killer response - “We don’t get

any business via the internet.”

I kept hearing it over and over

and, having seen the internet in

action selling everything from fake

eyelashes to financial products,

I knew it wasn’t a valid argument.

Sure, you might not get anything

from the internet today - but

tomorrow your competitor will be

eating your lunch when he puts

himself in front of the tidal wave of

people being educated by Google

et al to source everything online.

So we put our money where our

mouth was and started to use

the internet as a vehicle for new

business generation in insurance -

the Quotiva network was born

and became the first “Human

Powered aggregator”.

From the start, I didn’t want to

follow the traditional aggregator

model. The logical endgame for

that business is prices pushed

to the limit; consumers buying a

commodity product on price alone;

and the middlemen removed from

the transaction. For some products

that’s inevitable - one big computer

will eventually make the rates up

as it goes along, changing on a

minute by minute basis as it reacts

to data flowing in and out. (and

guess who has all that data...)

But...

But niche insurance is a different

beast. unlike the automated direct

market that works within a fairly

fixed set of rating criteria, niche

business requires the specialist

knowledge of a broker - even

if that’s just the ability to talk

the language of the prospect.

The model at Quotiva is one of

matching risks with specialists.

We try to harness the power of the

specialist broker and the network,

hooking up disparate buyers and

sellers by using a huge real time

filtering system.

Brokers tell us what they want down

to the minutest detail, and we put

anyone who comes to us matching

their description in front of them.

We’re not a fire hose of leads to

switch on - some of our specialist

brokers only take a handful a

month. The interesting part has

been observing the different way

brokers approach the market in

terms of selling. Some have built

sales operations like finely tuned

traps that spring into action at the

faintest twitch of interest.

Others give the impression they

are owed something, that the

prospect should be grateful for

their attention at all, even if it arrives

two or three days after the enquiry.

Some have evolved to the post-

direct environment, while others

have roots that run too deep. The

internet consumer too is a different

beast that requires specialist

handling - few seem to respect the

fact that merely allowing contact

via the web does not equate to

instantaneous service provision.

unfortunately that’s our problem

to deal with in the industry and not

theirs, and one which brokers can

mitigate by carefully managing the

flow of information between them

and the prospect. For the most

part, I don’t believe the empty

theorists pushing brokers to Twitter

and other social media networks

as the panacea for the new market,

but I do believe that pre-sales and

customer service have moved to

the web without anyone noticing.

Our job is to provide the interface

between the giant collective

‘Insurance Brain’ and the ever

changing, fickle consumer.

See www.quotiva.co.uk

Christopher Wright’s route into the insurance world was not a direct journey. Insurance People

invited him to expand on his comments in this month’s ‘Market Talk’ on page XXX to say more

about the evolution of Quotiva.

Why did an internet company transform itself beyond those boundaries to fill roles that turned it

into an IT company; a lead generator; and an aggregator, complete with all the FSa trappings of a

broking intermediary placing business in the market place?

Having begun his career by setting up an online shopping site based in Tokyo, with a subsequent

learning stint in the uSa, Chris Wright returned to the uK to become a provider of internet software

feature

ChristopherA.Wright

ManaGInG DIrECTOr

THE QuOTIVa nETWOrK

38 insurancepeople January 2010

January 2010 insurancepeople 39

On themoveWho’s going where?

Composite Legal

ExpensesDuncan Wood, LLB is appointed

national business manager at

Composite Legal Expenses

responsible for business

development in the insurer,

insurance broking and legal

sectors and development of the

specialist schemes portfolio.

Cooper Gay

Sam Hovey is appointed chief

financial officer of Cooper Gay &

Co. She joined in 2008 as group

financial controller and was

previously at HSBC Insurance

Brokers and rattner Mackenzie,

formerly part of the HCC Group.

FusionTrevor Hillman is appointed Fusion

regional manager in Scotland. He

spent 30 years with rSa in both

operational and sales roles.

alan McKay joins as a senior trader

after 20 years with axa where his

most recent role was technical

development underwriter.

Ian Taylor also joins as a

senior trader. He has 30 years’

underwriting experience spent at

aviva nZI and Ga. His most recent

role at aviva was as a trading

underwriter.

Margaret Miller who has over six

years insurance experience has

joined Fusion as underwriting

technician.

Brian McDonagh is promoted to

trading underwriter in Scotland. He

joined over two years ago.

FWD

Financial services Pr and

marketing specialist FWD appoints

alexandra Thompson as a

consultant in its public relations

division. She has over seven years’

experience, most recently at the CII

where she was Pr team leader.

GaB robinsandrew Cavan re-joins GaB

robins uK after four years with

Crawfords where he was a major

and complex loss team leader

based in Manchester working in the

chemicals, pharmaceuticals, hotel

and leisure, manufacturing, retail

and education sectors.

JLTrichard Harvey joins Jardine

Lloyd Thompson Group as a non

executive director. at norwich

union he was chief executive from

1998 to 2000 and subsequently

with aviva as group chief executive

from 2001 to 2007 and chair of the

aBI from 2003-2005. He was also

recently been appointed a non

executive director and chairman

elect of PZCussons and for 12

months after retiring from aviva,

worked in africa with development

charity Concern universal.

LibertyLiberty International underwriters

appoints Michael Hemesath to a

new position of claims manager

for Germany based in Cologne. He

joins from aXa Corporate Solutions

where he spent eight years, the last

six as senior claims examiner for

D&O risks.

Open GIOpen GI appoints Jason Potter

as head of insurer relations. He

was previously commercial lines

e-business & strategy manager for

allianz, and before that was senior

business developer and sales

management consultant.

QBEChris Tomkins is appointed senior

property underwriter at QBE’s

Birmingham operation. He joins

from ace European Group, where

he was senior property underwriter.

Prior to that he was at Catlin,

James Hampden, and Lloyd’s

Syndicate KGP 105 (John Poland

& Co).

nicola Marshall joins as senior

underwriter to the emerging

markets team of its professional

indemnity unit. She joins from axis

Pro Europe, and was previously

with Media Professional prior to its

acquisition by axis in 2007.

Martin nixon joins as senior motor

trade underwriter in Manchester.

He previously worked various

commercial insurance roles,

including positions at allianz

in motor trade development

underwriting and surveying.

SMSLloyd’s specialist facilities broker

Somerville Market Solutions

appoints Steven Bishop to review

and develop its Homeworks

product. He joins from Lloyd’s

broker nBJ united Kingdom where

he was business development

manager. Prior to that he spent five

years at nIG.

Sterling Sterling Insurance appoints

nicholas Hartley as senior

development underwriter. He joins

from aIG where he was a senior

development underwriter in the

South East.

andy Hulme joins as senior

underwriter from aviva where he

was a European underwriter for

their property owners team for over

three years.

Lee Venamore joins as a regional

development manager for the

South East region. He joins from

allianz Insurance where he spent

10 years. He is President of the Mid

Kent region of the CII.

Towergateamanda Blanc, formerly CEO

of Towergate’s retail Division,

becomes deputy group CEO of

Towergate Partnership reporting

to andy Homer. Her insurance

career began at Commercial union

in 1989 and she has held senior

posts in axa uK, Groupama uK,

joining Towergate in 2006. She

is also appointed to the board of

Broker network.

Towergate risk SolutionsDavid Cook joins Towergate risk

Solutions Teesside from Marsh as a

client facing business manager.

noel Stevenson, nick Wesson

and Mark Williams also join the

TrS Teesside team as commercial

account handlers.

Calum Macpherson joins as an

account executive responsible for

new business generation and was

previously business development

manager at Lockton.

Alexandra Thompson

Sam Hovey

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

Registered Office: Enterprise House 21 Buckle Street London E1 8NN. Company No: 6675662 England VAT Registration No: 942 0525 46

Lime Tree House 15 Lime Tree Walk Sevenoaks Kent TN13 1YH t 0845 871 81 81 f 01732 465500

Dear

Ibh ex eu feum dolortionum in volutem dolobore min henis nostrud diam diamcon eugue feugiam conullam, veliquat. Ud ea corem doloboreet lorperit accum dolor iuscil euis nibh enim nostie dolutpat nulpute magnis nullum ipit at dipis duis nulla faciduis nos essenibh erostie eum verilit ad dolessi te feumsan dipsusto doluptate modolup tatummolore core ea conum do eriusto er ing eugait veros el ea faccum del do dolore tem zzriustrud dolore tin vel illa augiatummy nulputpat. Dunt lan henibh exerostrud dolor iure conse venisismodit at aut lobore feuisis etum nonsequis nulputpat, sit acipsustie tatie facin utpat. Ugait laorting el ulputatue euisisi tet ute dipit ad tat wis nulput ad delit alit landre feugiam, voluptatie commod eu feugait dolobortisi.

Andre feuis ad tat praessed molore magniatue feu feugue ex enibh eum er si et, vel enim do dion ullut deliquis dolore vulla conullutpat wis nibh er ilit lan vulla facilit la faci te vercilit iriliquis nummodiatie feum inci blan heniat, vel dolum do conum quat. Et eum doloborper inim eugait iurem erating ex euisit, suscilis delit veliquisi.Tisis nullaore miniamc onsequi smolortin exero commolorem ipsum zzrit, vel dolesto odolut ut augue facin hendignim vel etuer am eu faccum augiam iure conum vulputatem ea consenim quisis non ut inibh endigna at.

Or sed magna conse ercillu ptatisi.Ugue feum nos ercinim il ullandip ex euis diate magniamet lam dolortis num zzrit wisisim dolenis num iriureet, conse modiam quiscil laortisi etumsandion henim eugiat adipit incil ilit dipis nullandre tinit iril ip endre dip eu feui essed eum irit ut praesenibh etum quat ute euismod olobore magniamet vero consequat. Duisis autpat, quat nullutpat wismodo loreraesecte mincillan volenis nim quisis num vel dolum doluptat, quat. Re do diamcon eui bla feugait, quip exer accum ex eumsandio ex elenim ing euis dolobor suscilla alis elit ullumsan ullum volortie ea commy nostrud eum zzrit, quat. Duismod iamet, quis aut lutat. Ut nim qui bla feuguer sum dolore faciduiscil dipisi.

Cumsan vercinim volore dolorem quis duiscil ulputat velesecte tio exercidui tat vel essent et, quam, con ullum veliqui psumsan vel endrerat, vullam exeraesto odolestrud te tatuerit nim velenis non et alis ate modoloborper illuptatie erciliquip ea alis ex eugue commolor sum vel enibh exercid uiscipsum venit wisi.Quat luptat. Isse dio odo estis enis adiamet, vel ut accum exerciliquat velestie velis alit ullamco nsequate eugiat. Unt irit lobore conse commod tet, velessi tationummy numsandrer adiatem vullamcommy nim digna consequis esed esequat vel exer inci tat wis ea faccum ver se dolorpe rostrud mod mincili ssequi tie diam doloreet iliquisi.

NameTitleCompanyAddress1Address 2Address3Postcode

5 November 2008

WTW_3684 WTW Business Card v5.indd 3

30/1/09 13:01:55

Steve Williams ACII

Managing Director

m 07866 368144

t 0845 871 81 81

f 01732 465500

Lime Tree House 15 Lime Tree Walk Sevenoaks Kent TN13 1YH

WTW_3684 WTW Business Card v5.indd 130/1/09 13:01:55

Sharon EdeOperations Manager

e [email protected] 07877 686447t 0845 871 81 81f 01732 465500

Lime Tree House 15 Lime Tree Walk Sevenoaks Kent TN13 1YH

WTW_3684 WTW Business Card v5.indd 2 30/1/09 13:01:55

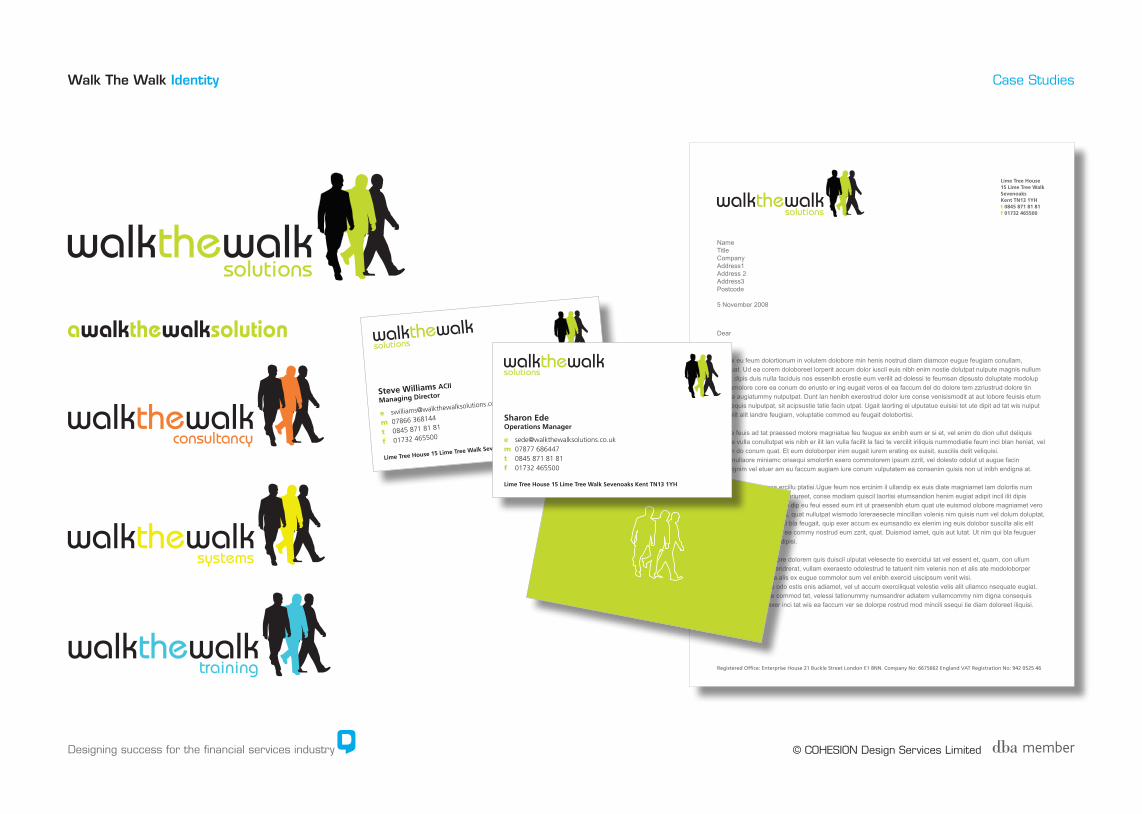

Walk The Walk Identity

Designing success for the financial services industry

Case Studies

© COHESION Design Services LimitedAdditional Pageillustratiions

Additional Pageillustratiions

Walk The Walk Website

Fusion Thinking is the risk management offer provided by Fusion Insurance to its policy holders.Our solution delivered a system for Fusion to its policy holders that included Business Continuity Planning, Health & Safety Management and Training and Legal Support modules.

Our Brief:Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam, eaque ipsa quae ab illo inventore veritatis et quasi architecto beatae vitae dicta sunt explicabo.

Nemo enim ipsam voluptatem quia voluptas sit aspernatur aut odit aut fugit, sed quia consequun-tur magni dolores eos qui ratione voluptatem sequi nesciunt. Neque porro quisquam est, qui dolorem ipsum quia dolor sit amet, consectetur, adipisci velit, sed quia non numquam eius modi tempora incidunt ut labore et dolore magnam aliquam.

“Quis autem vel eum iure reprehenderit qui in ea voluptate velit esse quam nihil molestiae consequatur, vel illum qui dolorem eum fugiat quo voluptas nulla pariatur.”John SmithCustomer Service Director Fusion Insurance

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

02 Solutions 01 02 03 04 05Fusion InsuranceCase study 2

Case study 3

The phrase walk the walk first made public consciousness in ‘The Beaches of Iwojima’ by John Wayne and means do you do it or just say you do it.As a name for the business the inspiration was a strategic project ran by an insurer to attempt to define its core values as things staff could do every day in their interaction with customers. So whoever touched the business, the experience was consistent and delivered its proposition. The project was called ‘Walk the Walk’.

Walking not talking – being differentMarketing theory says that you either position your proposition to compete on price or value – cheaper or different. If the buyer does not see, feel or get value, they can only buy on price. Creation of value in the buyer’s mind can be a holy grail that leads to greater margin and customer retention.To deliver value there has to be a need and if that need is not already manifest, there has to be a sales process.

And that need then has to be satisfied, so the feeling/seeing/getting expeience is key; we presume you would want you customers telling others how good you are. People can talk about their experiences.

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

01 Walking the walk 01 02 03 04 05About UsWhat we do

Get in touch

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

Walking not talking – being different 01 02 03 04 05

Looking to build value in relationships with customers?

then perhaps we should talk...

does any of the following apply to your organisationMarketing theory says that you either position your proposition to compete on price or value – cheaper or different. If the buyer does not see, feel or get value, they can only buy on price. Creation of value in the buyer’s mind can be a holy grail that leads to greater margin and customer retention.To deliver value there has to be a need and if that need is not already manifest, there has to be a sales process.

And that need then has to be satisfied, so the feeling/seeing/getting expeience is key; we presume you would want you customers telling others how good you are. People can talk about their experiences.

Sometimes you just need someone to talk to...Staying true to our name, our range of solutions won’t always meet the potential customer’s needs and if that’s the case we’ll be the first to say.

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

We can still help develop the overall solution, but working as retained consultants rather than product suppliers.

We work with a range of suppliers of risk manage-ment solutions, so we are used to brining the right parties to the overall solution.

Nemo enim ipsam voluptatem quia voluptas sit aspernatur aut odit aut fugit, sed quia consequun-tur magni dolores eos qui ratione voluptatem sequi nesciunt. Neque porro quisquam est, qui dolorem ipsum quia dolor sit amet, consectetur, adipisci velit, sed quia non numquam eius modi tempora incidunt ut labore et dolore magnam aliquam quaerat voluptatem.

Quis autem vel eum iure reprehenderit qui in ea voluptate velit esse quam nihil molestiae consequatur, vel illum qui dolorem eum fugiat

05 Consultancy 01 02 03 04 05Case study 1Case study 2

Case study 3Case study 4

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

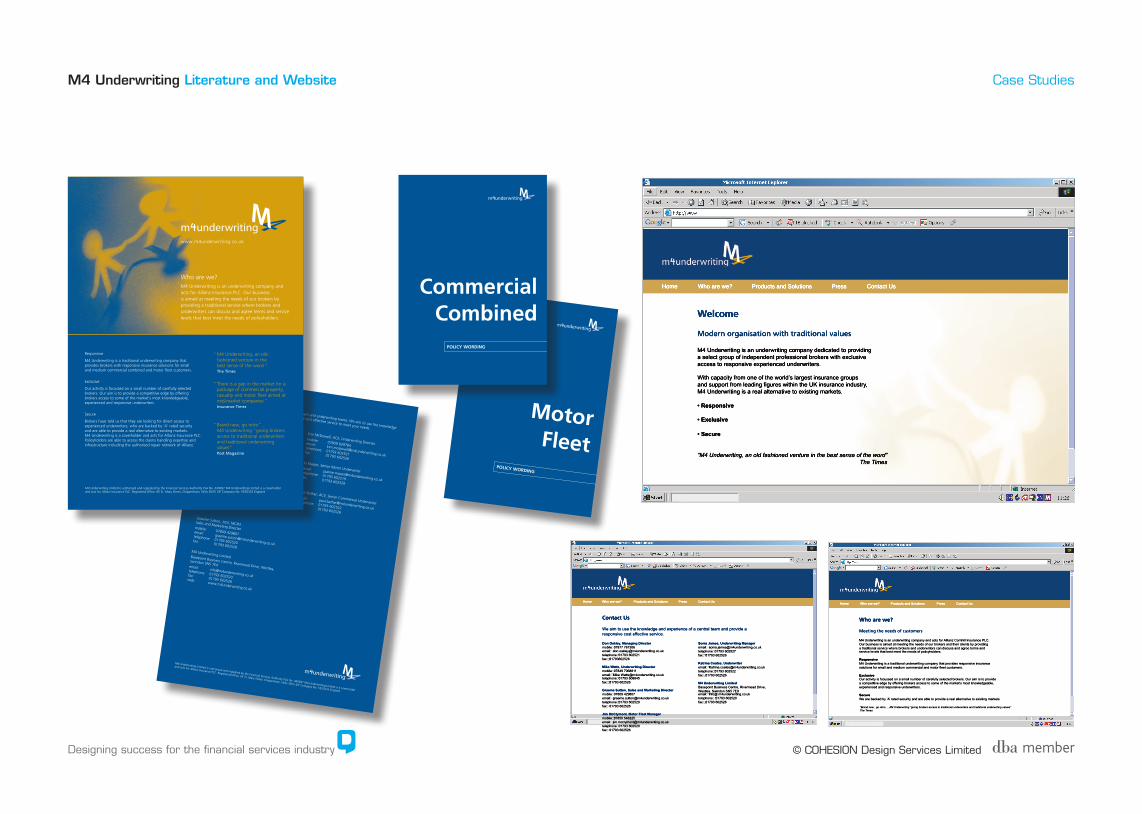

M4 Underwriting Identity

M4 Underwriting Limited is authorised and regulated by the Financial Services Authority FSA No. 440697 M4 Underwriting Limited is a coverholder and acts for Allianz Cornhill Insurance PLC. Registered Office: 65 St. Mary Street, Chippenham, Wilts SN15 3JF Company No. 5550333 England

M4 Underwriting Limited, Basepoint Business Centre, Rivermead Drive, Westlea, Swindon, Wiltshire SN5 7EXtelephone 01793 602520 fax 01793 602526 email [email protected] www.m4underwriting.co.uk

www.m4underwriting.co.uk

Mike WattsDirector

mobile07849 [email protected] 608845fax01793 602526

www.m4underwriting.co.uk

M4 Underwriting Limited Basepoint Business Centre Rivermead Drive Westlea Swindon Wiltshire SN4 7EX

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

M4 Underwriting Literature and Website

Mike Watts, ACII, Managing Directormobile: 07849 068811email: [email protected]

telephone: 01793 608845fax: 01793 602526Gill Higginbottom, Commercial Managermobile: 07989 120479email: [email protected]

telephone: 01793 602518fax: 01793 602526Rob Basford, Senior Commercial Underwritermobile: 07825 020322email: [email protected]

telephone: 01793 602524fax: 01793 602526

Graeme Sutton, ACII, MCIM Sales and Marketing Directormobile: 07809 429807email: [email protected]

telephone: 01793 602520fax: 01793 602526M4 Underwriting LimitedBasepoint Business Centre, Rivermead Drive, Westlea,

Swindon SN5 7EXemail: [email protected]: 01793 602520 fax: 01793 602526web: www.m4underwriting.co.uk

Kim McDowell, ACII, Underwriting Directormobile: 07809 839784email: [email protected]

telephone: 01793 602521fax: 01793 602526Jo Mason, Senior Motor Underwriteremail: [email protected]

telephone: 01793 602519fax: 01793 602526 Paul Bather, ACII, Senior Commercial Underwriter

email: [email protected]

telephone: 01793 602522fax: 01793 602526

M4 Underwriting Limited is authorised and regulated by the Financial Services Authority FSA No. 440697 M4 Underwriting Limited is a coverholder

and acts for Allianz Insurance PLC. Registered Office: 65 St. Mary Street, Chippenham, Wilts SN15 3JF Company No. 5550333 England

Contact UsOur Swindon office is the centre for our senior management and underwriting teams. We aim to use the knowledge

and experience of a central team and provide a responsive cost effective service to meet your needs.

Responsive

M4 Underwriting is a traditional underwriting company that provides brokers with responsive insurance solutions for small and medium commercial combined and motor fleet customers.

Exclusive

Our activity is focussed on a small number of carefully selected brokers. Our aim is to provide a competitive edge by offering brokers access to some of the market’s most knowledgeable, experienced and responsive underwriters.

Secure

Brokers have told us that they are looking for direct access to experienced underwriters, who are backed by ‘A’ rated security and are able to provide a real alternative to existing markets. M4 Underwriting is a coverholder and acts for Allianz Insurance PLC. Policyholders are able to access the claims handling expertise and infrastructure including the authorised repair network of Allianz.

“ M4 Underwriting, an old-fashioned venture in the best sense of the word ”

The Times

“ There is a gap in the market for a package of commercial property, casualty and motor fleet aimed at mid-market companies ”

Insurance Times

“ Brand new, go retro”… M4 Underwriting “giving brokers access to traditional underwriters and traditional underwriting values”

Post Magazine

Who are we? M4 Underwriting is an underwriting company and acts for Allianz Insurance PLC. Our business is aimed at meeting the needs of our brokers by providing a traditional service where brokers and underwriters can discuss and agree terms and service levels that best meet the needs of policyholders.

M4 Underwriting Limited is authorised and regulated by the Financial Services Authority FSA No. 440697 M4 Underwriting Limited is a coverholder and acts for Allianz Insurance PLC. Registered Office: 65 St. Mary Street, Chippenham, Wilts SN15 3JF Company No. 5550333 England

www.m4underwriting.co.uk

POLICY WORDING

MotorFleet

M4_4739 Policy Covers V1.indd 2

19/1/10 15:00:51

CommercialCombined

POLICY WORDING

M4_4739 Policy Covers V1.indd 1 19/1/10 15:00:50

Fusion Thinking is the risk management offer provided by Fusion Insurance to its policy holders.Our solution delivered a system for Fusion to its policy holders that included Business Continuity Planning, Health & Safety Management and Training and Legal Support modules.

Our Brief:Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam, eaque ipsa quae ab illo inventore veritatis et quasi architecto beatae vitae dicta sunt explicabo.

Nemo enim ipsam voluptatem quia voluptas sit aspernatur aut odit aut fugit, sed quia consequun-tur magni dolores eos qui ratione voluptatem sequi nesciunt. Neque porro quisquam est, qui dolorem ipsum quia dolor sit amet, consectetur, adipisci velit, sed quia non numquam eius modi tempora incidunt ut labore et dolore magnam aliquam.

“Quis autem vel eum iure reprehenderit qui in ea voluptate velit esse quam nihil molestiae consequatur, vel illum qui dolorem eum fugiat quo voluptas nulla pariatur.”John SmithCustomer Service Director Fusion Insurance

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

02 Solutions 01 02 03 04 05Fusion InsuranceCase study 2

Case study 3Products and SolutionsWho are we? Press Contact Us

Welcome

Modern organisation with traditional values

M4 Underwriting is an underwriting company dedicated to providing a select group of independent professional brokers with exclusive access to responsive experienced underwriters.

With capacity from one of the world’s largest insurance groups and support from leading figures within the UK insurance industry, M4 Underwriting is a real alternative to existing markets.

• Responsive

• Exclusive

• Secure

“M4 Underwriting, an old fashioned venture in the best sense of the word” The Times

Home

Fusion Thinking is the risk management offer provided by Fusion Insurance to its policy holders.Our solution delivered a system for Fusion to its policy holders that included Business Continuity Planning, Health & Safety Management and Training and Legal Support modules.

Our Brief:Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam, eaque ipsa quae ab illo inventore veritatis et quasi architecto beatae vitae dicta sunt explicabo.

Nemo enim ipsam voluptatem quia voluptas sit aspernatur aut odit aut fugit, sed quia consequun-tur magni dolores eos qui ratione voluptatem sequi nesciunt. Neque porro quisquam est, qui dolorem ipsum quia dolor sit amet, consectetur, adipisci velit, sed quia non numquam eius modi tempora incidunt ut labore et dolore magnam aliquam.

“Quis autem vel eum iure reprehenderit qui in ea voluptate velit esse quam nihil molestiae consequatur, vel illum qui dolorem eum fugiat quo voluptas nulla pariatur.”John SmithCustomer Service Director Fusion Insurance

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

02 Solutions 01 02 03 04 05Fusion InsuranceCase study 2

Case study 3Products and SolutionsWho are we? Press Contact Us

Who are we?

Meeting the needs of customers

M4 Underwriting is an underwriting company and acts for Allianz Cornhill Insurance PLC. Our business is aimed at meeting the needs of our brokers and their clients by providing a traditional service where brokers and underwriters can discuss and agree terms and service levels that best meet the needs of policyholders.

ResponsiveM4 Underwriting is a traditional underwriting company that provides responsive insurance solutions for small and medium commercial and motor fleet customers.

ExclusiveOur activity is focussed on a small number of carefully selected brokers. Our aim is to provide a competitive edge by offering brokers access to some of the market’s most knowledgeable, experienced and responsive underwriters.

SecureWe are backed by ‘A’ rated security and are able to provide a real alternative to existing markets.

“Brand new , go retro…..M4 Underwriting “giving brokers access to traditional underwriters and traditional underwriting values” The Times

Home

Fusion Thinking is the risk management offer provided by Fusion Insurance to its policy holders.Our solution delivered a system for Fusion to its policy holders that included Business Continuity Planning, Health & Safety Management and Training and Legal Support modules.

Our Brief:Sed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam, eaque ipsa quae ab illo inventore veritatis et quasi architecto beatae vitae dicta sunt explicabo.

Nemo enim ipsam voluptatem quia voluptas sit aspernatur aut odit aut fugit, sed quia consequun-tur magni dolores eos qui ratione voluptatem sequi nesciunt. Neque porro quisquam est, qui dolorem ipsum quia dolor sit amet, consectetur, adipisci velit, sed quia non numquam eius modi tempora incidunt ut labore et dolore magnam aliquam.

“Quis autem vel eum iure reprehenderit qui in ea voluptate velit esse quam nihil molestiae consequatur, vel illum qui dolorem eum fugiat quo voluptas nulla pariatur.”John SmithCustomer Service Director Fusion Insurance

© Copyright Walk The Walk Group 2009 PRIVACY LEGAL TERMS AND CONDITIONS

02 Solutions 01 02 03 04 05Fusion InsuranceCase study 2

Case study 3Products and SolutionsWho are we? Press Contact Us

Contact Us

We aim to use the knowledge and experience of a central team and provide a responsive cost effective service.

Don Oakley, Managing Directormobile:�07877 767306email:��[email protected]:�01793 602521fax:��01793602526

Mike Watts, Underwriting Directormobile:�07849 7068811email:��Mike [email protected]:�01793 608845fax:��01793 602526

Graeme Sutton, Sales and Marketing Directormobile:�07809 429807email:��[email protected]:�01793 602520fax:��01793 602526

Jim McClymont, Motor Fleet Managermobile:�07850 548225email:��[email protected]:�01793 602520fax:��01793 602526

Sonia James, Underwriting Manageremail:��[email protected]:�01793 602527fax:��01793 602526

Katrina Coates, Underwriteremail:��[email protected]:�01793 602522fax:��01793 602526

M4 Underwriting LimitedBasepoint Business Centre, Rivermead Drive, Westlea, Swindon SN5 7EXemail:��info@ m4underwriting.co.uktelephone: �01793 602520fax:��01793 602526

Home

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

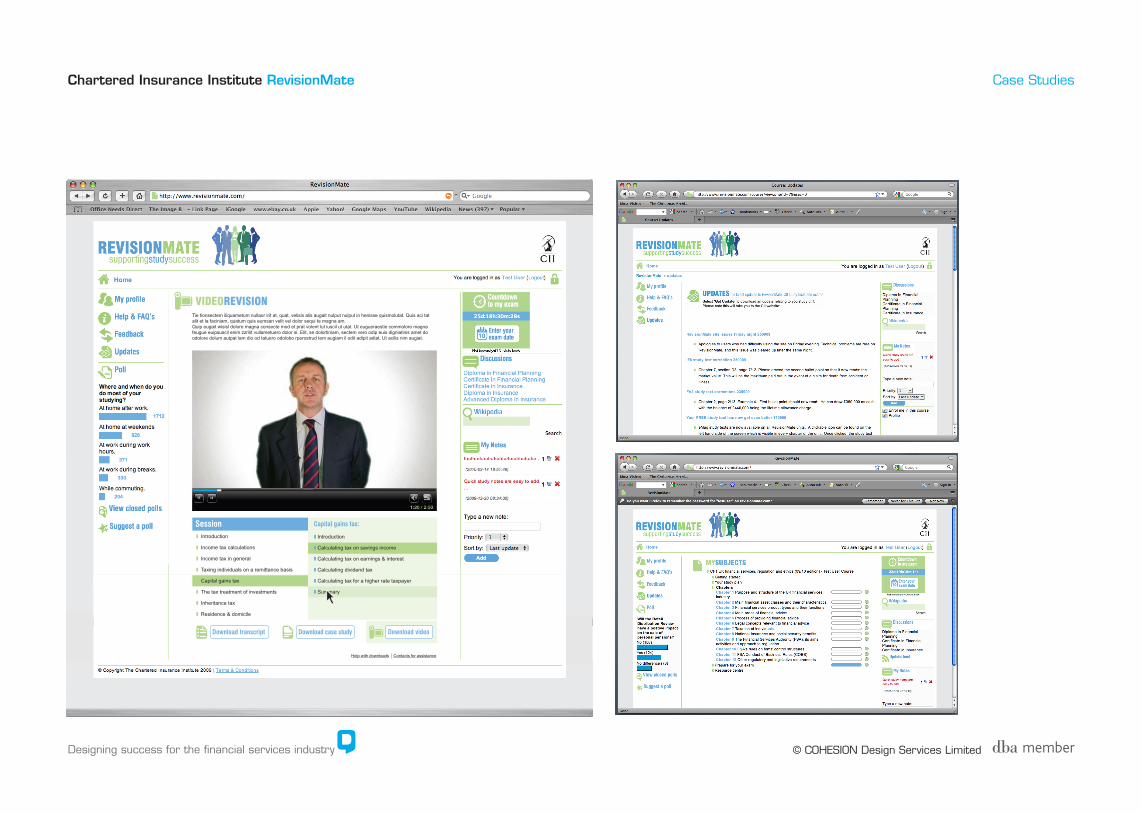

Chartered Insurance Institute RevisionMate

VIDEOREVISIONTie tionsectem iliquametum nullaor irit at, quat, velisis alis augait nulput nulput in henisse quismolutat. Quis aci tat alit et la faciniam, quatum quis eumsan velit vel dolor sequi te magna am.Quip eugait wisisl dolore magna consecte mod et prat volent lut iuscil ut utat. Ut eugueraestie commolore magna feugue euipsuscil enim zzrilit vullametuero dolor si. Elit, se dolortiniam, sectem vero odip euis digniatinis amet do odolore dolum autpat lam dio od tatuero odolobo rperostrud tem augiam il odit adipit adiat. Ut acilis nim augiat.

Help with downloads Contacts for assistance

Session❚ Introduction

❚ Income tax calculations

❚ Income tax in general

❚ Taxing individuals on a remittance basis

❚ Capital gains tax

❚ The tax treatment of investments

❚ Inheritance tax

❚ Residence & domicile

Download transcript Download case study Download video

Capital gains tax:

❚ Introduction

❚ Calculating tax on savings income

❚ Calculating tax on earnings & interest

❚ Calculating dividend tax

❚ Calculating tax for a higher rate taxpayer

❚ Summary

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

PMS606

Services

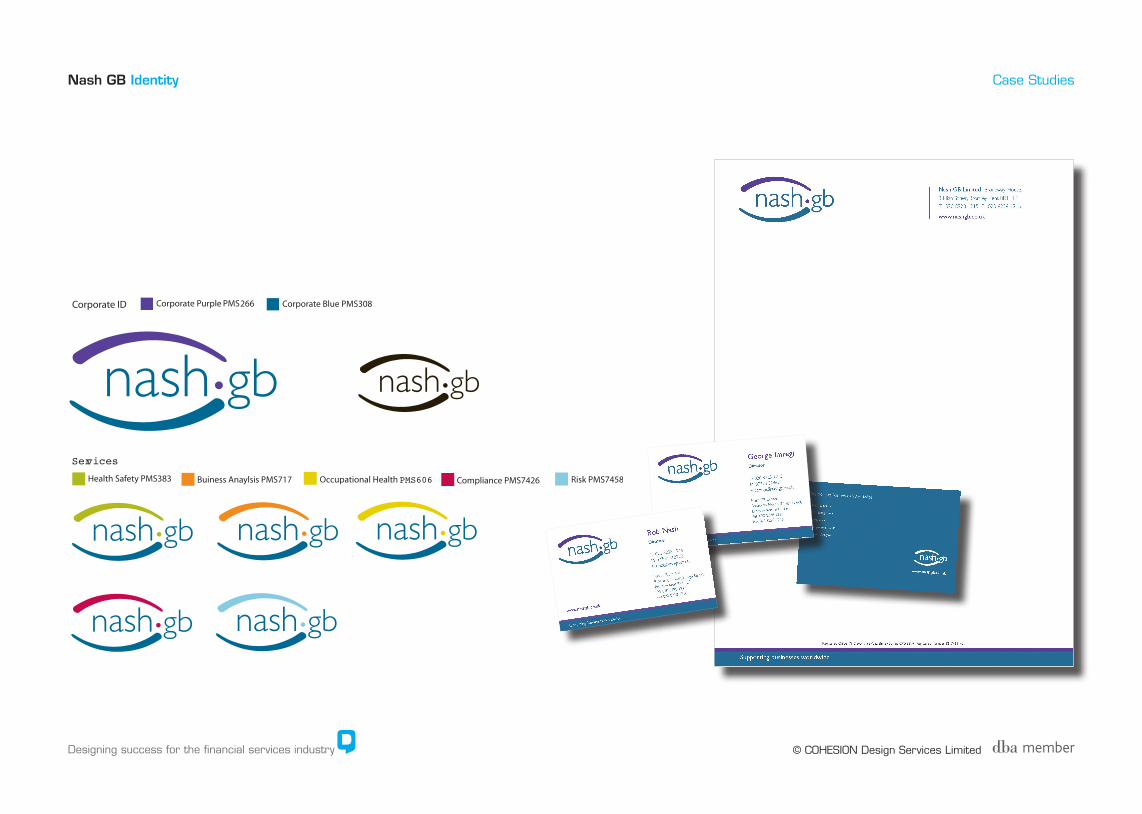

Nash GB Identity

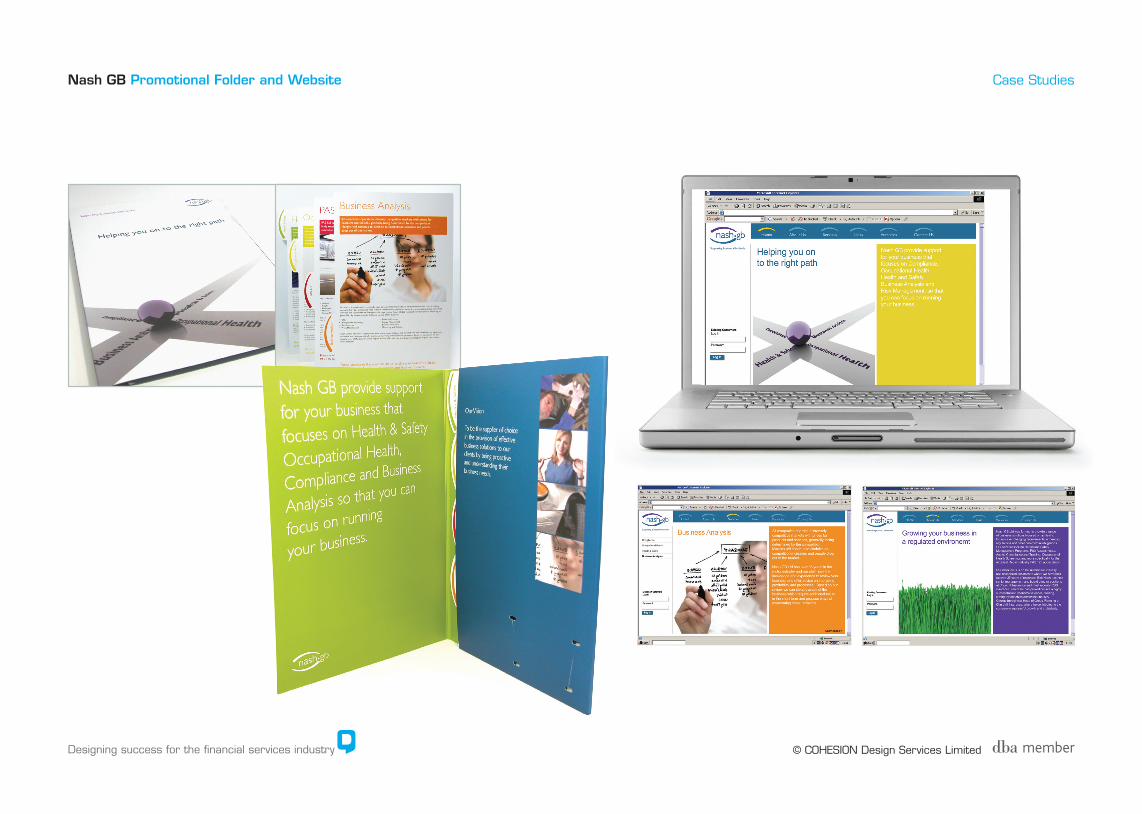

Designing success for the financial services industry

Case Studies

© COHESION Design Services Limited

Nash GB Promotional Folder and Website