Embed Size (px)

Citation preview

© 2009 Grants Central Station

Financial Literacy & Bookkeeping

1

presents the

Fundamental Five Nonprofit Training Series

Grants Central Station

November 16, 2010

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Mahalo to our Sponsors!

Office of Hawaiian Affairs – Community Based Economic Development Grant

Tri-Isle Resource Conservation & Development – Fiscal Sponsor

County of Maui Department of Health & Human Concerns - Volunteer Services

Our Board: Anna K. Ribucan, Richard Kehoe, Keith Wolter, Faye Cummings, Susie Thieman

2

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Today’s Speaker

Robert S. Kawahara, CPA Managing Member, Kawahara & Company, CPAs, LLC Vice President, Ronald A. Kawahara & Co., CPA’s, Inc. Treasurer, Maui Humane Society Treasurer, Lahaina Intermediate School Educational

Foundation Treasurer, Rotary Club of Kahului Treasurer, Angus McKelvey for State House Committee Director, Hawaii Association of Certified Public Accountants Director, Hawaii Association of Public Accountants, Maui

Chapter Supervisory Committee Chairperson, Maui County Federal

Credit Union

3

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Agenda

4

8:30 am Welcome & Introductions

8:45 am Financial Literacy 101 for Nonprofits

9:45 am Break & Network

10:00 am In & Out of Form 990

10:30 am Current Issues Affecting Nonprofits

11:00 am Break & Network

11:15 am Review

11:30 am Panel

12:15 pm Closing Remarks, Conclusion

© 2009 Grants Central Station

Who’s in attendance??

5

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Today’s Objective

Establish your baseline knowledge of financial literacy with regards to nonprofit organizations

Establish which areas of financial literacy that you need to work on

Obtain information regarding current issues affecting nonprofits

6

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Financial Literacy

Class Participation

7

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Financial Literacy

The ability to read, analyze, manage and write about the financial conditions that affect material financial health. It includes the ability to discern financial choices, discuss money and financial issues without (or despite) discomfort, plan for the future, and respond competently to events that affect everyday financial decisions, including events in the general economy.1

1Goodbye to Complacency Financial Literacy Education in the U.S. 2000-2005

8

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Let’s break it down

The ability to read, analyze, manage and write about the financial conditions that affect material financial health. . .

How do I gain that ability? Foundation, Foundation, Foundation

9

© 2009 Grants Central Stationwww.GrantsCentralStation.org

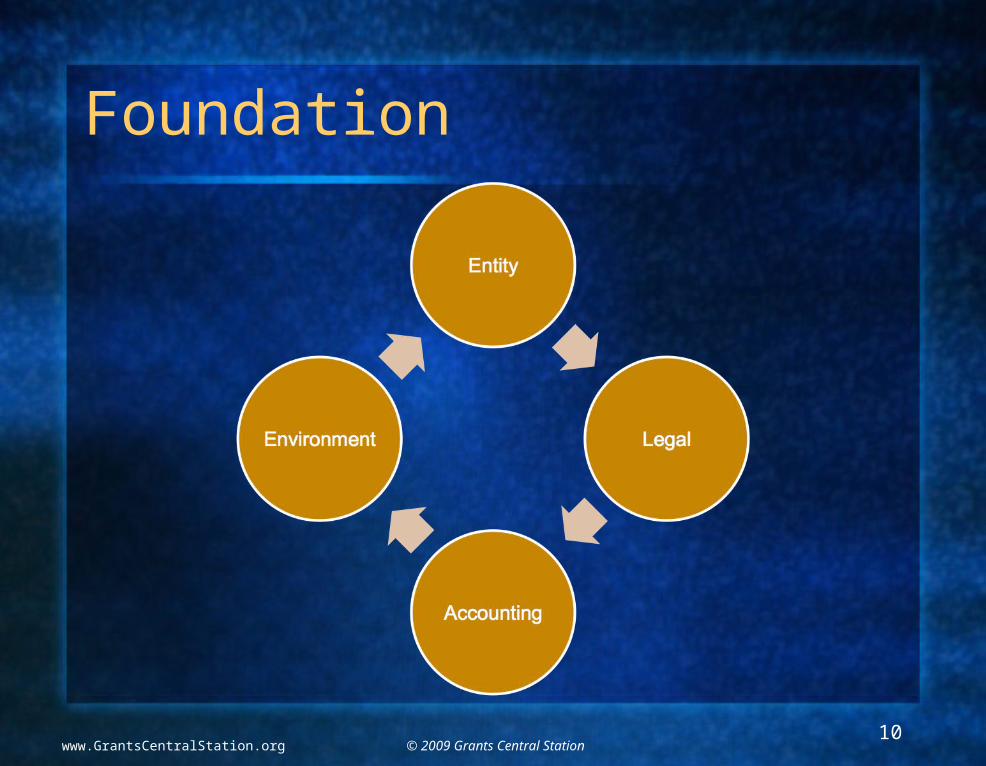

Foundation

10

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Foundation - Entity

Gain an understanding of: Mission Statement What type of nonprofit Employees Organizational Chart Funding Sources Programs

11

© 2009 Grants Central Stationwww.GrantsCentralStation.org

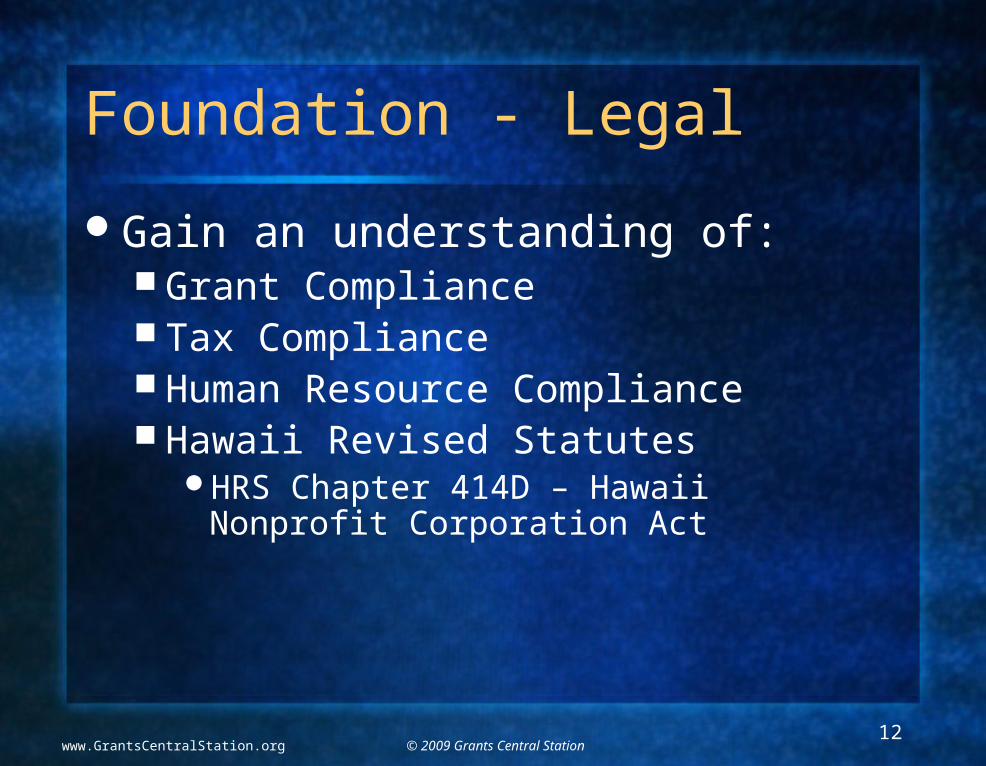

Foundation - Legal

Gain an understanding of: Grant Compliance Tax Compliance Human Resource Compliance Hawaii Revised Statutes

HRS Chapter 414D – Hawaii Nonprofit Corporation Act

12

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Foundation - Environment

Gain an understanding of: Resources Available Who are your Competitors Who are you Servicing Marketing

13

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Foundation - Accounting

Financial StatementsInternal ControlBookkeepingRecordkeepingBudgetBasis of AccountingNonprofit accounting differences

14

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Financial Statements

Statement of Financial PositionStatement of ActivitiesStatement of Functional ExpensesStatement of Cash FlowsNotes to Financial Statements

15

© 2009 Grants Central Stationwww.GrantsCentralStation.org

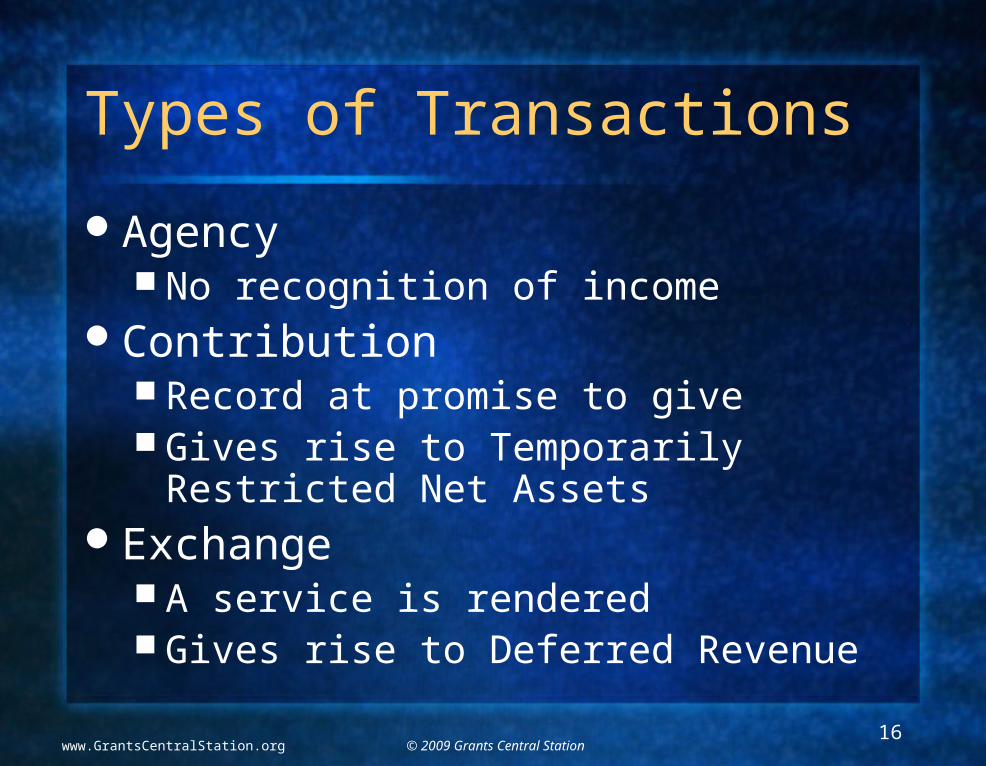

Types of Transactions

Agency No recognition of income

Contribution Record at promise to give Gives rise to Temporarily Restricted Net

AssetsExchange

A service is rendered Gives rise to Deferred Revenue

16

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Using Financial Statements

Vs. Budget Vs. Prior Period Historical vs. Projection Financial Ratios

Revenue Ratios Identify % of revenue stream

Defensive Interval Identify how many months the organization could operate

Program Service Expense Recommend minimum 65%

17

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Internal Controls

Why do we need Internal ControlsWhat is Fraud?

Black’s Law Dictionary fraud is defined as follows: “b Law. Any deliberate misrepresentation of the truth or a fact used to take money, rights, or other privilege or property away from a person or persons.”

18

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Fraud

3 Categories of fraud Corruption Asset Misappropriation Fraudulent Statements

Conditions present when fraud occurs Incentive Opportunity Rationalization

19

© 2009 Grants Central Stationwww.GrantsCentralStation.org

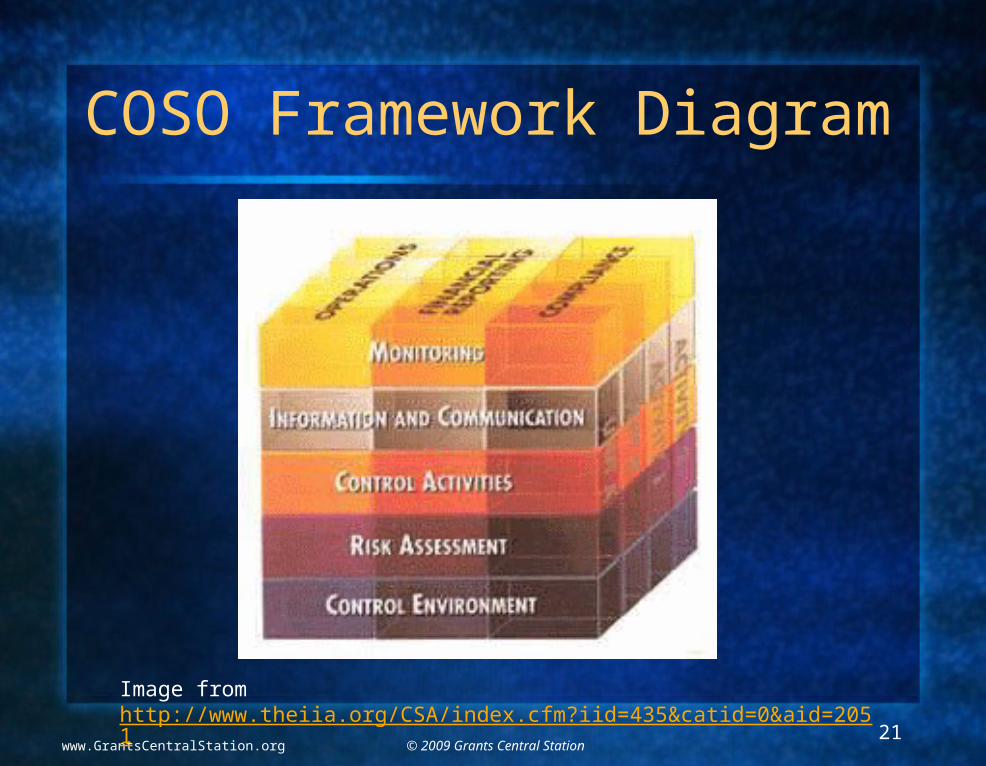

Internal Control

5 Components of Internal Control Control Environment Risk Assessment Control Activities Information and Communication Monitoring

3 Objective of Internal Control Operations Financial Reporting Compliance

20

© 2009 Grants Central Stationwww.GrantsCentralStation.org

COSO Framework Diagram

21

Image from http://www.theiia.org/CSA/index.cfm?iid=435&catid=0&aid=2051

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Internal Control

COSO defines internal control as a process, effected by an entity’s board of directors, management and other personnel. This process is designed to provide reasonable assurance regarding the achievement of objectives in effectiveness and efficiency of operations, reliability of financial reporting, and compliance with applicable laws and regulations.

Internal control is a process. It is a means to an end, not an end in itself.

Internal control is not merely documented by policy manuals and forms. Rather, it is put in by people at every level of an organization.

Internal control can provide only reasonable assurance, not absolute assurance, to an entity’s management and board.

Internal control is geared to the achievement of objectives in one or more separate but overlapping categories.

22

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Question

Can internal controls prevent fraud?What is the relationship between

principle based vs. rules with regards to polices and procedures

List types of Fraud to Internal Control

23

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Bookkeeping

Basis of Accounting Cash Tax Modified Accrual

Fund AccountingGAAP

Generally Accepted Accounting Principles

24

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Recordkeeping

Elements of a good recordkeeping systemOrganizedPermanent FileRelevantLeverage available software

Quickbooks MIP MAS 90

25

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Budgets

How many of you do a budget?Why do a budget?How effective has it been?

26

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Audits

What is an audit? An audit is a formalized process designed to

obtain reasonable assurance that a financial statement(s) is free of any material misstatements whether caused by errors, frauds, and/or direct legal acts with respect to the management assertions embodied in the financial statement(s).

27

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Audit

Financial Statement AuditSingle Audit

28

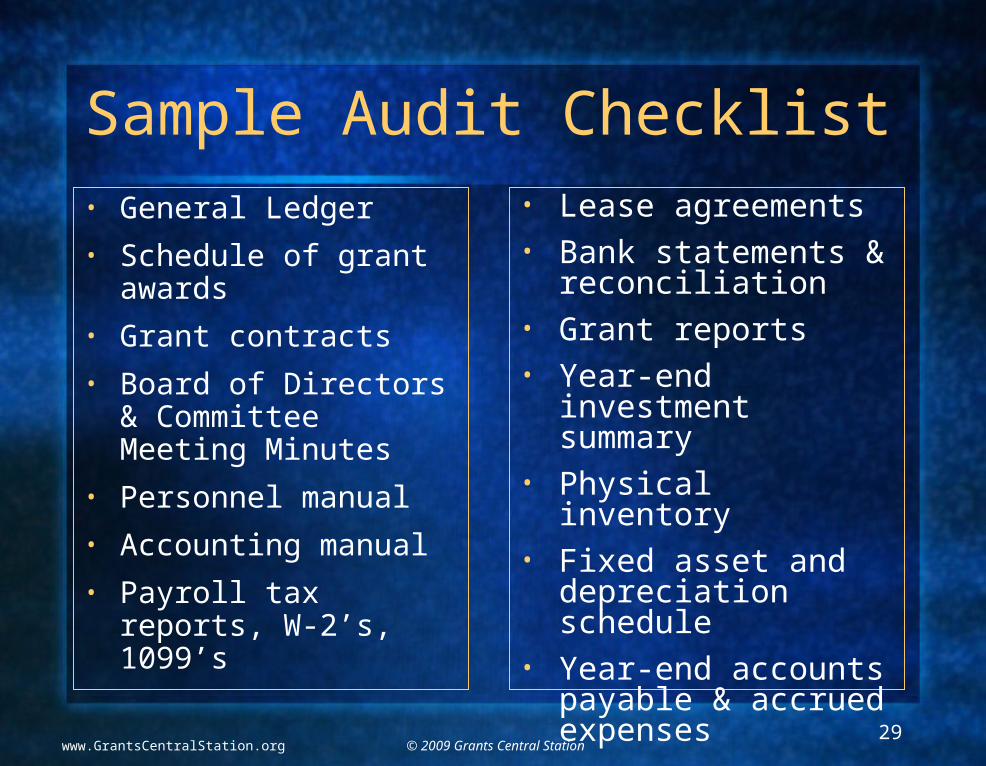

© 2009 Grants Central Stationwww.GrantsCentralStation.org29

Sample Audit Checklist• General Ledger

• Schedule of grant awards

• Grant contracts

• Board of Directors & Committee Meeting Minutes

• Personnel manual

• Accounting manual

• Payroll tax reports, W-2’s, 1099’s

• Lease agreements • Bank statements &

reconciliation• Grant reports• Year-end investment

summary • Physical inventory • Fixed asset and

depreciation schedule • Year-end accounts

payable & accrued expenses

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Question

Who is responsible for the financial statements of an organization?

30

© 2009 Grants Central Stationwww.GrantsCentralStation.org

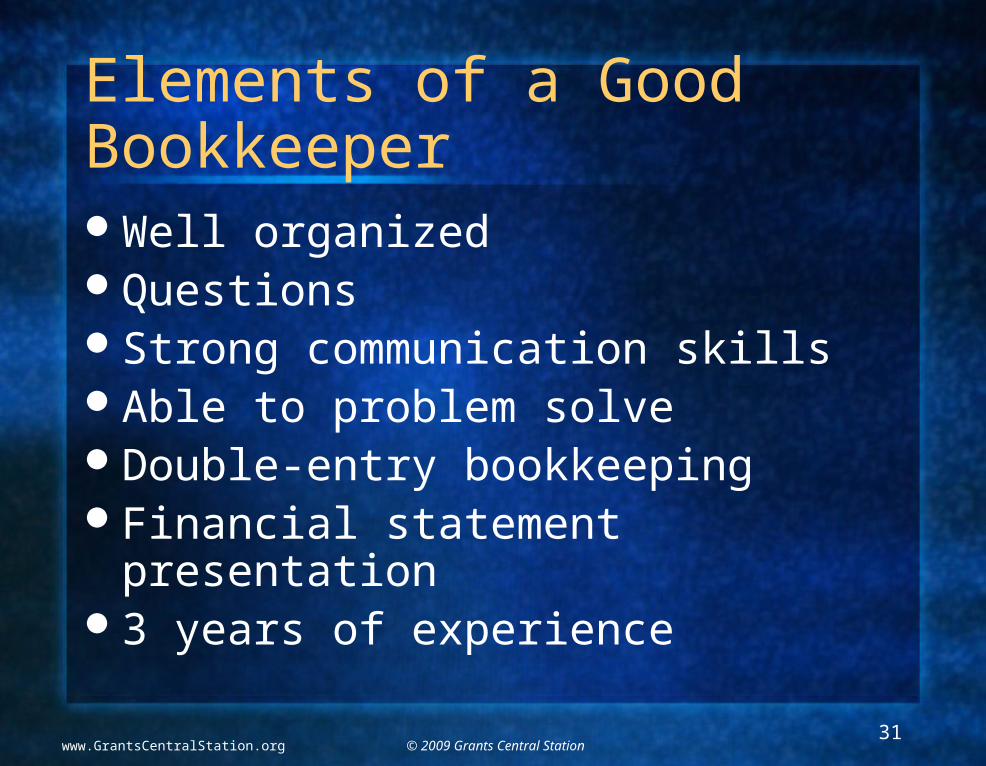

Elements of a Good Bookkeeper

Well organizedQuestionsStrong communication skillsAble to problem solveDouble-entry bookkeepingFinancial statement presentation3 years of experience

31

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Question

Who does the bookkeeper work for?Who does the accountant work for?Who does the auditor report to?

32

© 2009 Grants Central Station33

BREAK

15 minutes

© 2009 Grants Central Stationwww.GrantsCentralStation.org34

More Free Workshops!

Oct 27 Volunteer Management

Nov 16 Financial Literacy & Bookkeeping

Dec 7 Strategic Planning

Jan 11 Board Development & Training

Feb 22 Legal & Insurance Issues

Mar 8 Fundraising & Development

Apr Grant Strategy & Writing

Upcoming Fundamental Five workshops from Grants Central Station

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Form 990

Why the fuss all of a sudden? In 2008, the Form 990 was completely

redesigned by the IRSLast revision 1979

The purpose was to:Increase transparencyGood governanceReduced burden (total opposite)

Replaced with increased accountability

35

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Form 990

It’s not all that bad . . . The Form 990 is a publicly disclosed

document. Provides organizations the opportunity to:

Tell the organization’s story by effectively stating its mission and program service accomplishments

Market and development tool

36

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Form 990

Types of Form 990 Form 990

Return of Organization Exempt from Income Tax

Form 990-EZShort Form of Organization Exempt from

Income Tax Form 990-N

Electronic Notice (e-postcard)Churches are exempt

37

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Form 990 FAQs

All nonprofit organizations can file a Form 990, but not all nonprofit organizations can file a Form 990-N

Unlike most income tax returns that are quantitative in nature, Form 990 is heavily qualitative

38

© 2009 Grants Central Stationwww.GrantsCentralStation.org

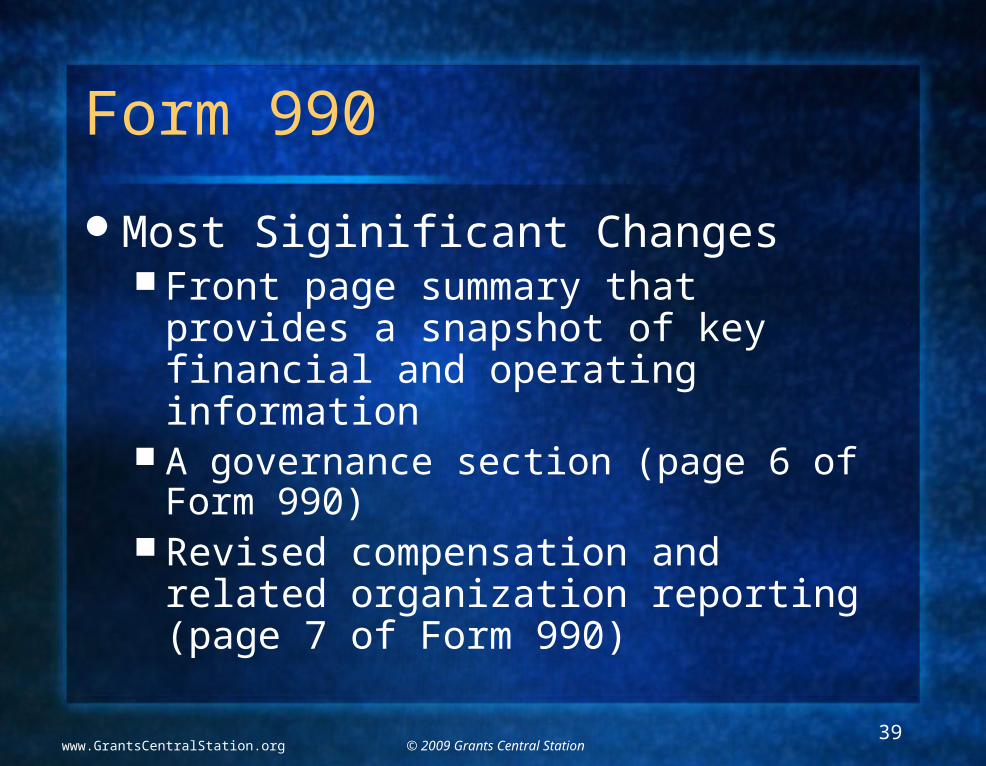

Form 990

Most Siginificant Changes Front page summary that provides a

snapshot of key financial and operating information

A governance section (page 6 of Form 990) Revised compensation and related

organization reporting (page 7 of Form 990)

39

© 2009 Grants Central Stationwww.GrantsCentralStation.org

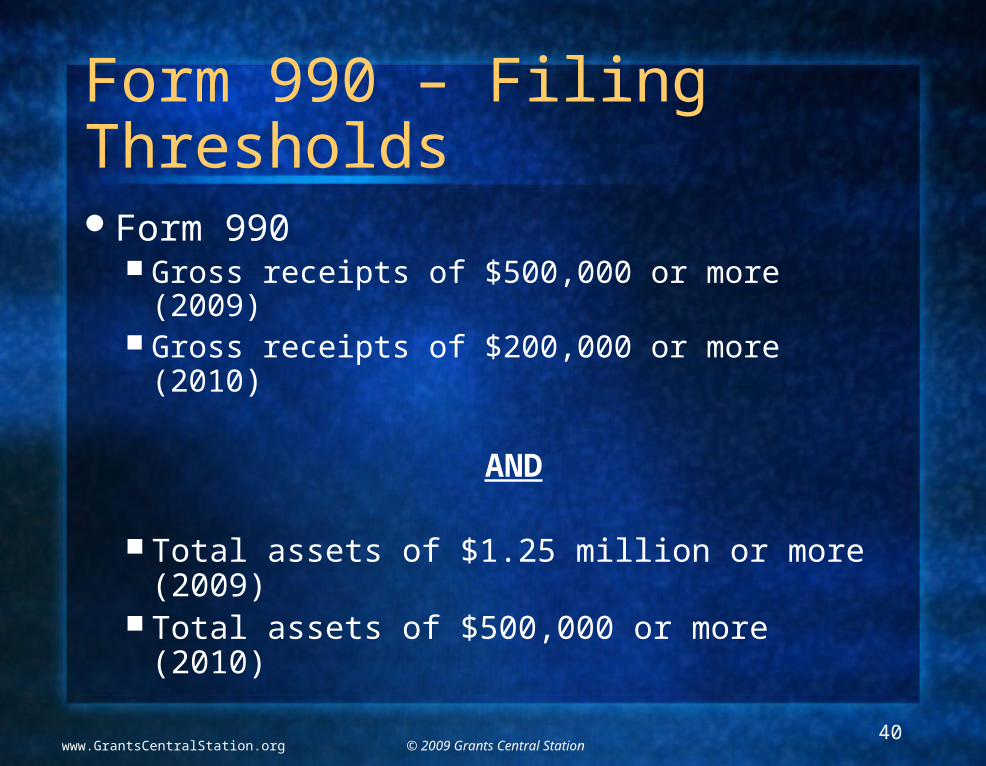

Form 990 – Filing Thresholds

Form 990 Gross receipts of $500,000 or more (2009) Gross receipts of $200,000 or more (2010)

AND

Total assets of $1.25 million or more (2009)

Total assets of $500,000 or more (2010)

40

© 2009 Grants Central Stationwww.GrantsCentralStation.org

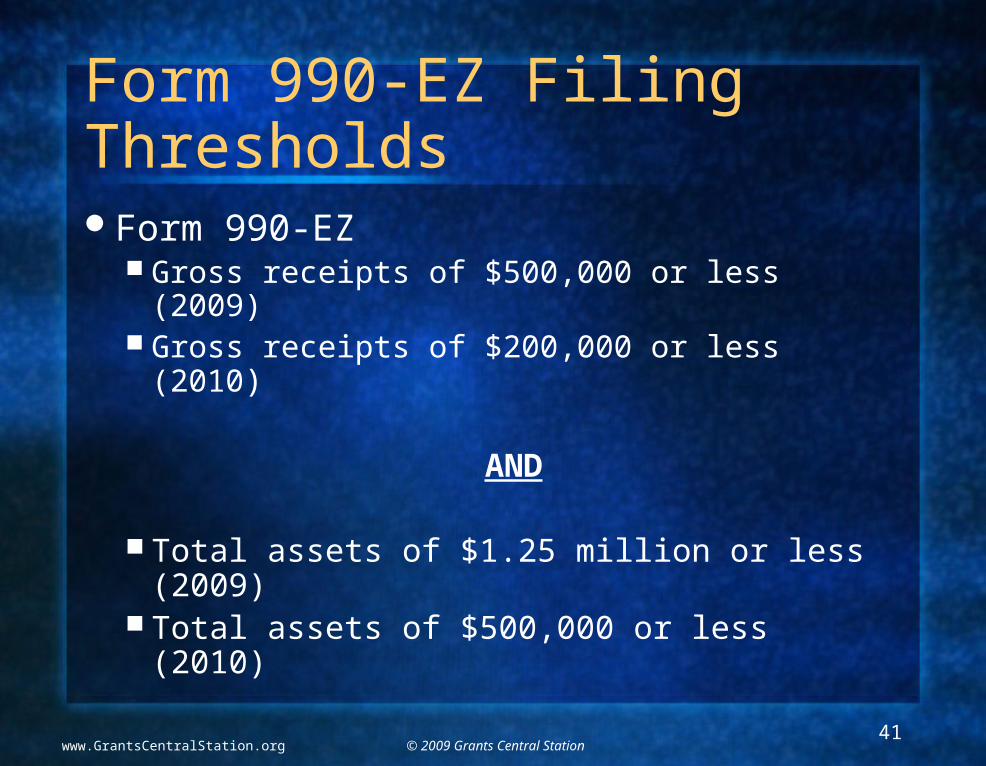

Form 990-EZ Filing Thresholds

Form 990-EZ Gross receipts of $500,000 or less (2009) Gross receipts of $200,000 or less (2010)

AND

Total assets of $1.25 million or less (2009) Total assets of $500,000 or less (2010)

41

© 2009 Grants Central Stationwww.GrantsCentralStation.org

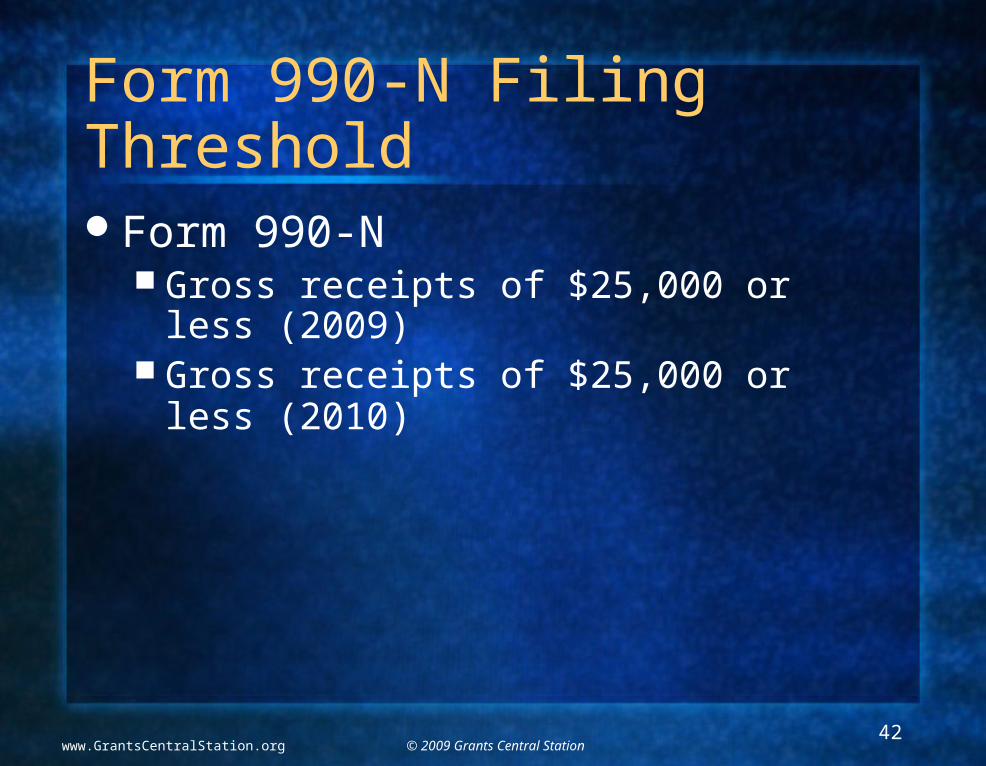

Form 990-N Filing Threshold

Form 990-N Gross receipts of $25,000 or less (2009) Gross receipts of $25,000 or less (2010)

42

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Question

Are there any other IRS filing that a nonprofit must file?

43

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Answer

Yes, besides the Form 990 or equivalent a nonprofit must still file: Payroll returns Unrelated business income tax return

(UBIT) return: Form 990-T

44

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Form 990-T

Exempt Organization Business Income Tax Return To report unrelated trade or business income. An unrelated trade or business is any trade or

business, the conduct of which is not substantially related to the exercise or performance by the organization of its exempt purpose.

The fact that an organization needs or uses the profits from a business activity to support its program services has no bearing on the determination of whether the activity is unrelated.

45

© 2009 Grants Central Stationwww.GrantsCentralStation.org

UBTI

Unrelated Business Taxable Income See IRS Publication 598 – “Tax on

Unrelated Business Income of Exempt Organizations”

There are a lot of exceptions to the rule and is considered to be a fairly “gray” area with a lot of room for interpretation.

Be conservative and remember your fiduciary responsibility

46

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Form N70-NP

State of Hawaii – Exempt Organization Business Income Tax Return

By the way, the State of Hawaii wants their cut too.

47

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Questions on UBTI

48

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Current Issues Affecting Nonprofits

Hawaii’s Charity RegistrationGeneral Excise TaxSarbanes-Oxley Act of 2002Concentration of Funds

49

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Hawaii’s Charity Registration

Chapter 467B, HRS requires charities that solicit contributions to register with the Attorney General unless exempted from the registration requirement.

Effective January 1, 2009Purpose is to protect donors from fraud

and promote donor confidence in and an accountable transparent charitable sector.

50

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Hawaii’s Charity Registration

Covers your traditional nonprofits as well as any other organization that employs a charitable appeal as the basis of any solicitation or an appeal that has a tendency to suggest there is a charitable purpose to the solicitiation

51

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Hawaii’s Charity Registration

A grant received from the government, or another 501(c)(3) charity or private foundation is not a contribution.

Membership dues and assessments are also not deemed to be contributions.

52

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Hawaii’s Charity Registration

Filing requirements: Annual filing Audited financial statements if the charity

has gross revenues over $500,000, or where the charity prepares an audited financial statement pursuant to a requirement by a governmental authority or third party.

FeesFrom $10.00 to $750.00

53

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Hawaii’s Charity Registration

Exempt from requirements: Churches PTAs Hospitals Government or instrumentality of any state or the

United States Charities with less than $25,000 annually, and does

not compensate person responsible for solicitations Prohibits charities from contracting with un-

registered professional solicitors and professional fundraising counsels.

54

© 2009 Grants Central Stationwww.GrantsCentralStation.org

General Excise Tax

Form G-6, Application for Exemption from General Excise Taxes

If you don’t file the form all forms of revenue are taxable.

55

© 2009 Grants Central Stationwww.GrantsCentralStation.org

General Excise Tax

Tax Information Release (TIR) No. 2010-05

Act 155, Session Laws of Hawaii 2010, Relating to General Excise Tax; The General Excise Tax Protection Act

Two Sections Denial of General Excise Tax Benefits Trust Fund Liability

Prospective July 1, 2010

56

© 2009 Grants Central Stationwww.GrantsCentralStation.org

General Excise Tax

Denial of General Excise Tax Benefits Obtain a GET License File annual reconciliation

If Form G-49, is not filed within 12 months from the due date for the return, the business may lose the benefit

57

© 2009 Grants Central Stationwww.GrantsCentralStation.org

General Excise Tax

Trust Fund Liability Creates liability for certain key individuals

involved in the financial management of taxpayer

Liability is prospective from July 1, 2010

58

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Sarbanes-Oxley Act of 2002

Two provisions that affect nonprofits It is illegal for any corporate entity to

punish whistleblowers or retaliate against any employee who reports suspected cases of fraud or abuse

It is a crime to alter, cover up, falsify, or destroy any document that may be relevant to an official investigation

The Act has many practices that may become best practices for governance of nonprofits

59

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Concentration of Funds

Today’s economic climate will force many nonprofits to reevaluate their past reliance on funding sources

Specifically, nonprofits that do little fundraising due to grant awards

60

© 2009 Grants Central Station61

BREAK

15 minutes

© 2009 Grants Central Stationwww.GrantsCentralStation.org62

More Free Workshops!

Oct 27 Volunteer Management

Nov 16 Financial Literacy & Bookkeeping

Dec 7 Strategic Planning

Jan 11 Board Development & Training

Feb 22 Legal & Insurance Issues

Mar 8 Fundraising & Development

Apr Grant Strategy & Writing

Upcoming Fundamental Five workshops from Grants Central Station

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Resources

Internal Revenue Service (IRS)Tax information for Charities &

NonprofitsPublication 526, Charitable

ContributionsPublication 557, Tax-Exempt Status for

Your OrganizationPublication 598, Tax on Unrelated

Business Income of Exempt Organizations

63

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Resources

State of Hawaii Tax Facts

Tax Facts No. 96-1, General Excise vs. Sales Tax Tax Facts No. 98-3, Tax Issues for Hawaii Nonprofit

Organizations Tax Information Releases

TIR No. 89-13, Application for Exemption from the General Excise Taxes for Nonprofit Organizations

TIR No. 91-2, Taxability of Gross Proceeds Received by a Nonprofit Organization from the Sale of Donated Services or Tangible Personal Property

TIR No. 91-4, Hawaii Tax Obligations of Nonprofit Organizations

64

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Resources

Accounting Generally Accepted Accounting Principles Financial Accounting Standards Board

(FASB) Accounting Standards Codification AICPA Audit and Accounting Guide, Not-

for-Profit Entities Amazon.com

Wealth of material on nonprofit financial management

65

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Review Section 1

Section 1: What is your Organization’s basis of

accounting? When is your Organization’s fiscal year

end? Does your Organization prepare compliant

financial statements?

66

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Review Section 2

Section 2: What type of Form 990 does my

Organization file? Does our Organization have Unrelated

Business Taxable Income (UBTI)? I will read my Organization’s Form 990 and

I will look at another relevant organization’s Form 990 on Guidestar

67

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Review Section 3

Section 3 I will check to see if my Organization has a

GET number I will check to see if my Organization has

filed it’s G-6 exemption I will check to see if my Organization is

current with registration with the DCCA

68

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Panel

Robert KawaharaMark MoserKerry Cullins

69

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Mark Moser

Mr. Moser was most recently the Director of Finance for the Ritz Carlton Kapalua. Prior to that, he was the Director of Finance for the Washington Dulles Airport Marriott. He holds a bachelors of science in Business Administration with Distinction, from the George Mason University in Virginia. He has been a licensed Certified Public Accountant since 1992

70

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Kerry Cullins

Kerry Cullins moved to Maui in 1996 and founded Maui Bookkeeping Consultants in 2001. Maui Bookkeeping Consultants services a wide variety of clients including restaurants, contractors, non-profit organizations, retail, realtors and more. Kerry is the president of the company and specializes in consulting, training and forensic bookkeeping as well as overseeing the day to day operations. Kerry has worked with many different non-profit organizations in professional and voluntary roles by helping to set up and clean up bookkeeping systems, organize silent auctions and acting as Treasurer.

71

© 2009 Grants Central Stationwww.GrantsCentralStation.org

Panel

Robert Kawahara

Mark Moser

Kerry Cullins

72

© 2009 Grants Central Station73

Wrap-Up

© 2009 Grants Central Stationwww.GrantsCentralStation.org74

Test Your Knowledge

Our funder (and we!) want to know how effective this workshop was for you.

This 5-minute Post-Workshop Quiz helps us gauge your progress and our success.

Mahalo.

© 2009 Grants Central Stationwww.GrantsCentralStation.org75

Help Us Serve You Better!

Please take 5 more minutes to complete the Workshop Evaluation so that we can improve this and future offerings

from Grants Central Station

Mahalo.

© 2009 Grants Central Stationwww.GrantsCentralStation.org76

More Free Workshops!

Oct 27 Volunteer Management

Nov 16 Financial Literacy & Bookkeeping

Dec 7 Strategic Planning

Jan 11 Board Development & Training

Feb 22 Legal & Insurance Issues

Mar 8 Fundraising & Development

Apr Grant Strategy & Writing

Upcoming Fundamental Five workshops from Grants Central Station

© 2009 Grants Central Stationwww.GrantsCentralStation.org77

Questions?

Robert Kawahara, CPAKawahara & Company, CPAs, LLC(808) [email protected]

© 2009 Grants Central Station78

Mahalo

For More Information or to Register for an Upcoming Workshop on Lana`i or Moloka`i

Leslie Mullens (808) 875-0500 or [email protected]

Grants Central Station

www.GrantsCentralStation.org