Embed Size (px)

DESCRIPTION

Continuum Development Coorporation | Concept Book

Citation preview

Continuum Development Corporation /// Concept Book //

A New Way to Stay //

/// Continuum Development Corporation LLC

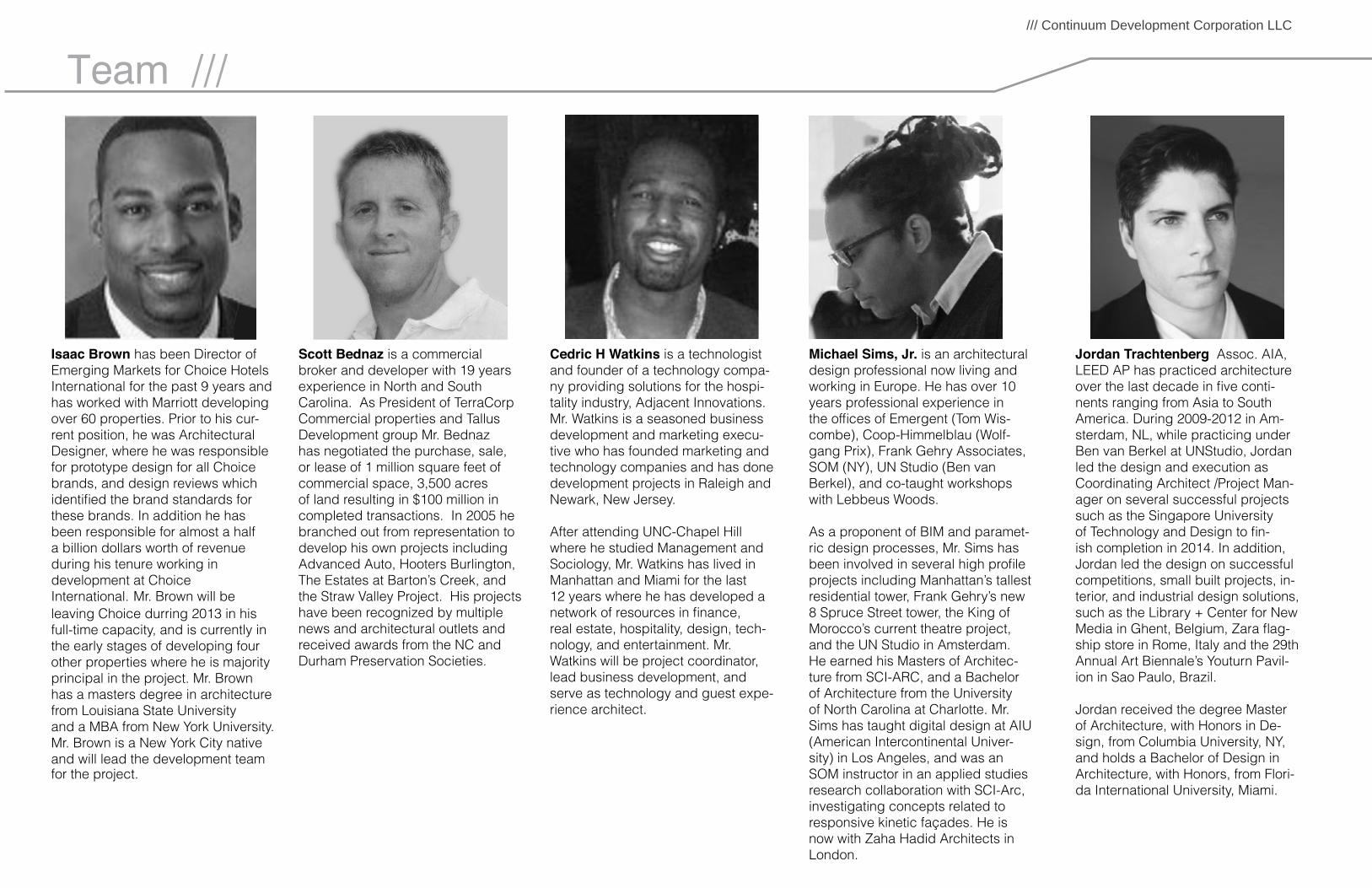

Scott Bednaz is a commercial broker and developer with 19 years experience in North and South Carolina. As President of TerraCorp Commercial properties and Tallus Development group Mr. Bednaz has negotiated the purchase, sale, or lease of 1 million square feet of commercial space, 3,500 acres of land resulting in $100 million in completed transactions. In 2005 he branched out from representation to develop his own projects including Advanced Auto, Hooters Burlington, The Estates at Barton’s Creek, and the Straw Valley Project. His projects have been recognized by multiple news and architectural outlets and received awards from the NC and Durham Preservation Societies.

Isaac Brown has been Director of Emerging Markets for Choice HotelsInternational for the past 9 years and has worked with Marriott developing over 60 properties. Prior to his cur-rent position, he was Architectural Designer, where he was responsible for prototype design for all Choice brands, and design reviews which

Mr. Brown will be

these brands. In addition he has been responsible for almost a half a billion dollars worth of revenue during his tenure working in development at Choice International.leaving Choice durring 2013 in his full-time capacity, and is currently in the early stages of developing four other properties where he is majority principal in the project. Mr. Brownhas a masters degree in architecture from Louisiana State Universityand a MBA from New York University. Mr. Brown is a New York City native and will lead the development team for the project.

Cedric H Watkins is a technologist and founder of a technology compa-ny providing solutions for the hospi-tality industry, Adjacent Innovations. Mr. Watkins is a seasoned business development and marketing execu-tive who has founded marketing and technology companies and has done development projects in Raleigh and Newark, New Jersey.

After attending UNC-Chapel Hill where he studied Management andSociology, Mr. Watkins has lived in Manhattan and Miami for the last12 years where he has developed a

real estate, hospitality, design, tech-nology, and entertainment. Mr.Watkins will be project coordinator, lead business development, andserve as technology and guest expe-rience architect.

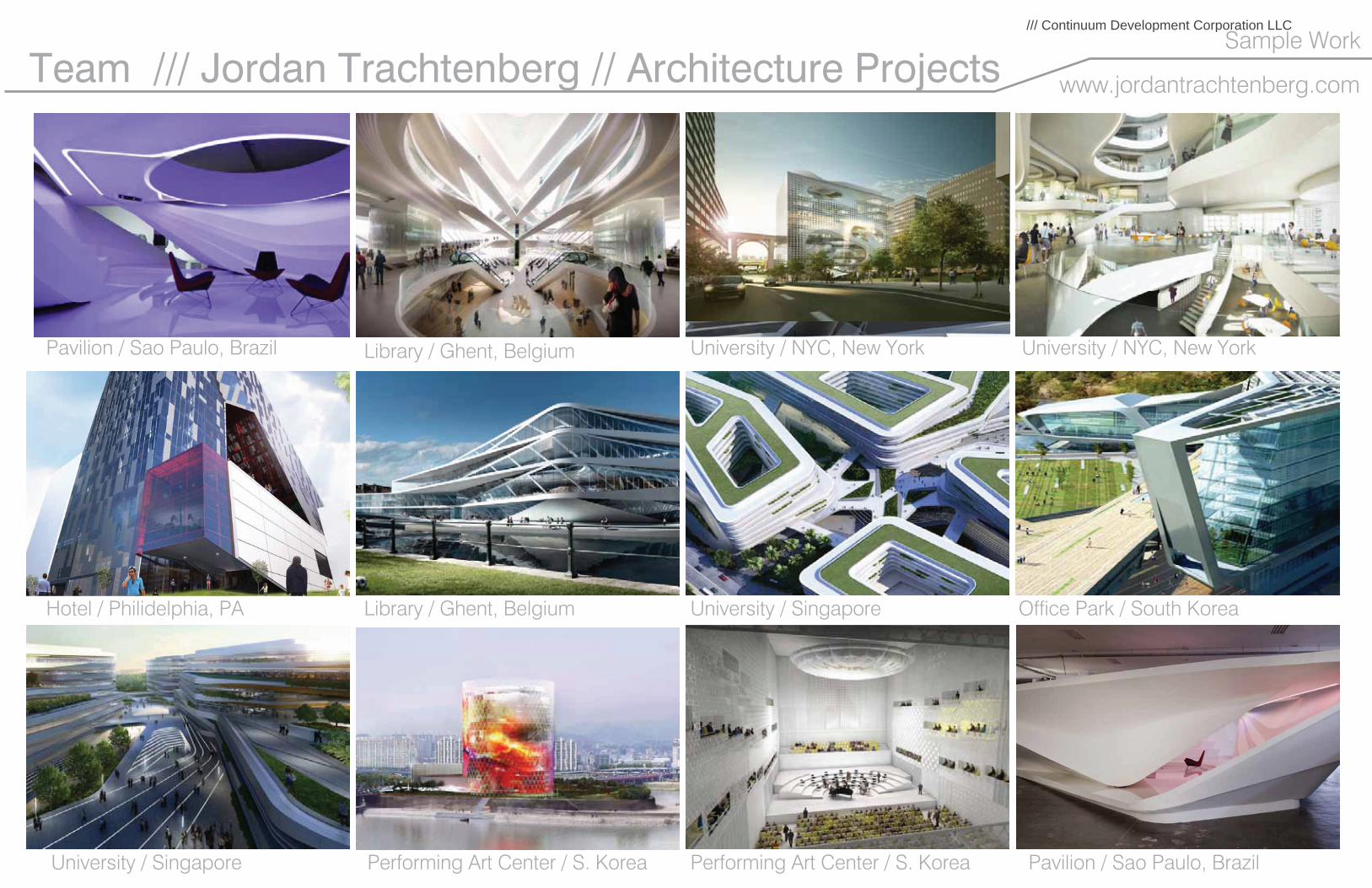

Jordan Trachtenberg Assoc. AIA, LEED AP has practiced architecture

-nents ranging from Asia to South America. During 2009-2012 in Am-sterdam, NL, while practicing under Ben van Berkel at UNStudio, Jordan led the design and execution as Coordinating Architect /Project Man-ager on several successful projects such as the Singapore University

-ish completion in 2014. In addition, Jordan led the design on successful competitions, small built projects, in-terior, and industrial design solutions, such as the Library + Center for New

-ship store in Rome, Italy and the 29th Annual Art Biennale’s Youturn Pavil-ion in Sao Paulo, Brazil.

Jordan received the degree Master of Architecture, with Honors in De-sign, from Columbia University, NY, and holds a Bachelor of Design in Architecture, with Honors, from Flori-da International University, Miami.

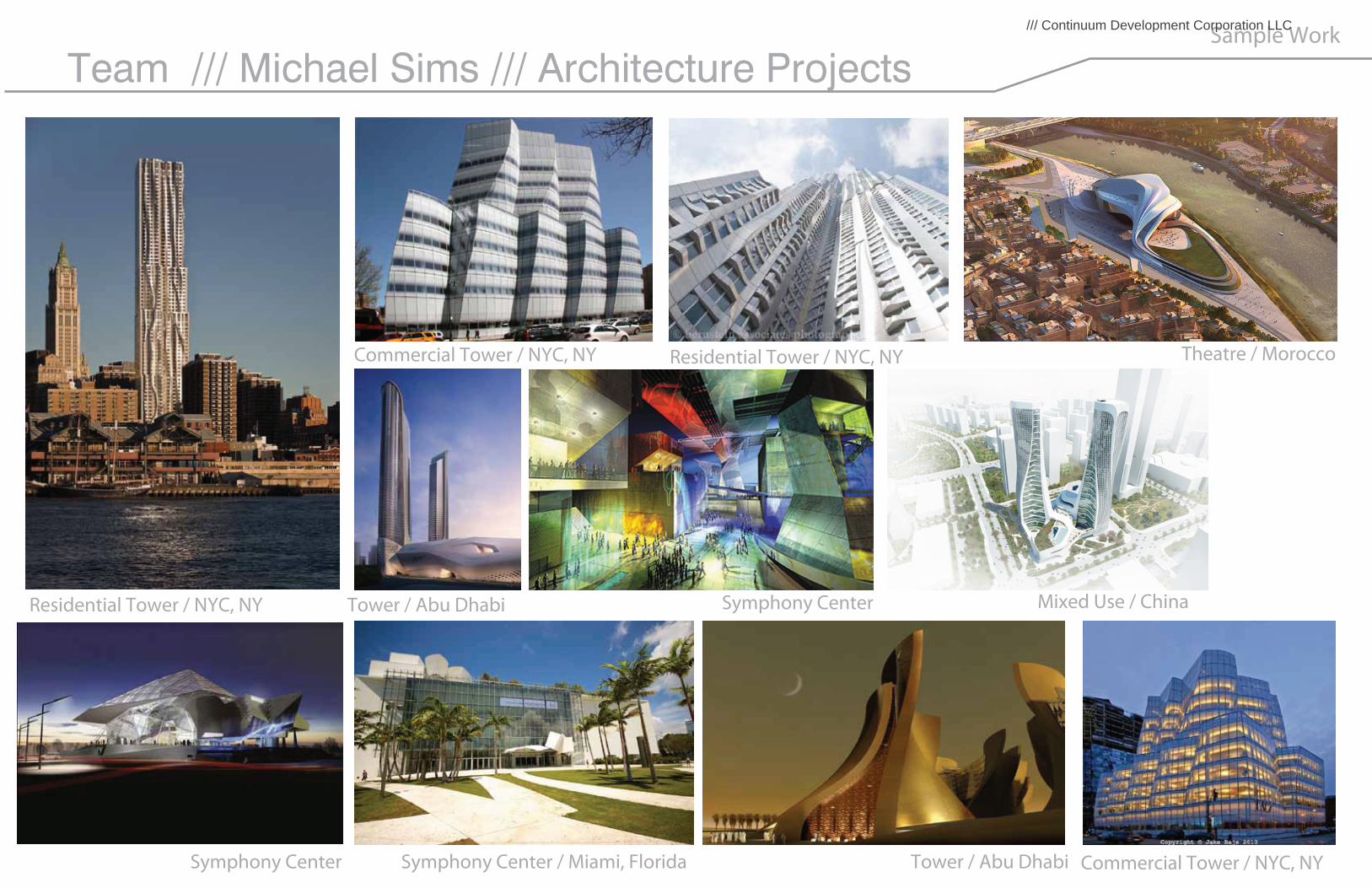

Michael Sims, Jr. is an architectural design professional now living and working in Europe. He has over 10 years professional experience in

-combe), Coop-Himmelblau (Wolf-gang Prix), Frank Gehry Associates, SOM (NY), UN Studio (Ben van Berkel), and co-taught workshops with Lebbeus Woods.

As a proponent of BIM and paramet-ric design processes, Mr. Sims has

projects including Manhattan’s tallest residential tower, Frank Gehry’s new 8 Spruce Street tower, the King of Morocco’s current theatre project, and the UN Studio in Amsterdam. He earned his Masters of Architec-ture from SCI-ARC, and a Bachelor of Architecture from the University of North Carolina at Charlotte. Mr. Sims has taught digital design at AIU (American Intercontinental Univer-sity) in Los Angeles, and was an SOM instructor in an applied studies research collaboration with SCI-Arc, investigating concepts related to responsive kinetic façades. He is now with Zaha Hadid Architects in London.

Team /// /// Continuum Development Corporation LLC

Team /// Jordan Trachtenberg // Architecture Projects Sample Work

www.jordantrachtenberg.com

Pavilion / Sao Paulo, Brazil University / NYC, New York University / NYC, New York

Hotel / Philidelphia, PA Library / Ghent, Belgium

Library / Ghent, Belgium

University / Singapore

University / Singapore Performing Art Center / S. Korea Performing Art Center / S. Korea

Office Park / South Korea

Pavilion / Sao Paulo, Brazil

/// Continuum Development Corporation LLC

Team /// Michael Sims /// Architecture Projects

Residential Tower / NYC, NY

Residential Tower / NYC, NY

Mixed Use / ChinaTower / Abu Dhabi

Tower / Abu DhabiSymphony Center / Miami, Florida

Theatre / Morocco

Symphony Center

Symphony Center

Commercial Tower / NYC, NY

Commercial Tower / NYC, NY

Sample Work /// Continuum Development Corporation LLC

Light House ///

A New Way to Stay // Concept Design Book

/// Continuum Development Corporation LLC

The Concept /// Past + Present + Future

With its rich cultural history and well deserved reputation for some of the best weather in the world and establishing the idea of “living the life of luxury”, Mi-ami is undoubtedly a world-class city, yet it is lacking in one area. With such a legacy, the current version of the luxury experience with thousand dollar bottles at packed clubs, celebrity dj’s, and laser light shows are not doing this legacy justice. In a city like Miami where money does not ensure access, the true defini-tion of luxury must include access to the best of the life of luxury, which includes service, entertainment and socializing with like natured individuals.

Experiencing luxury in the manner and style in which you desire is the para-mount of living the life of luxury. The manner, frequency, and consistency in which the Lighthouse lifestyle of luxury will provide this paramount experi-ence to our guests and residents creates a lifestyle and residential environment unique and incomparable to anywhere in the world. Living in the state of luxury requires not only access, but also convenience. Having access to the best of the life of luxury is the current standard for experiencing luxury. Having those things brought to your doorstep is “living in the state of luxury”, which is life at The Lighthouse.

With Miami being one of the hottest travel destinations and condo markets in the world and the hotel market being one of the few markets experiencing in-creased tourism and higher rates for both occupancy and average daily rates, the opportunity to leverage both of these facts and capitalizing on Miami’s current lack of quality live music and entertainment makes this opportunity unique and one-of-a-kind. The Lighthouse brings together the culture of The City and ap-preciation for creation, music, and performance with the Miami lifestyle of luxury and celebrity, and infused with the universal spirit of the true appreciation of “the party scene”. This unique combination will make The Lighthouse a true destina-tion experience for the few fortunate enough to experience it during their stay or for the truly fortunate who call it home.

/// Continuum Development Corporation LLC

The Concept /// Past + Present + Future

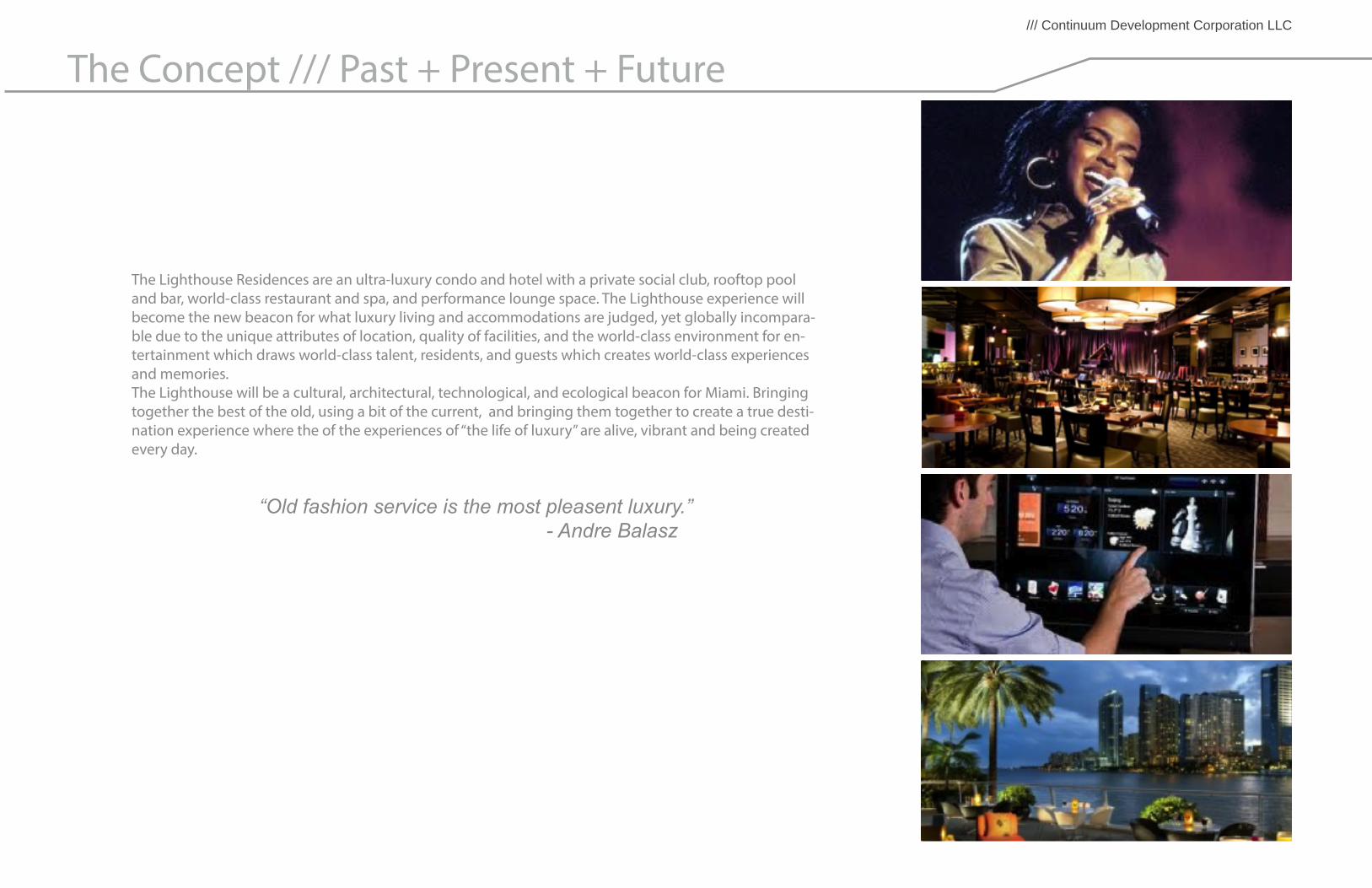

The Lighthouse Residences are an ultra-luxury condo and hotel with a private social club, rooftop pool and bar, world-class restaurant and spa, and performance lounge space. The Lighthouse experience will become the new beacon for what luxury living and accommodations are judged, yet globally incompara-ble due to the unique attributes of location, quality of facilities, and the world-class environment for en-tertainment which draws world-class talent, residents, and guests which creates world-class experiences and memories. The Lighthouse will be a cultural, architectural, technological, and ecological beacon for Miami. Bringing together the best of the old, using a bit of the current, and bringing them together to create a true desti-nation experience where the of the experiences of “the life of luxury” are alive, vibrant and being created every day.

“Old fashion service is the most pleasent luxury.” - Andre Balasz

/// Continuum Development Corporation LLC

Design Model / /

/// Continuum Development Corporation LLC

Design Strategies ///

Vertical Landscape - Minimum Site Coverage - Iconic

Urban Social Landscape - Max Site Coverage

Vertical to LateralOur design philosophy is flexible in its concept. Depending on each site in context we adapt the design model to both vertical and horizontal typologies. This promotes a true understanding of our site, its surroundings, and how to best integrate the design model.

/// Continuum Development Corporation LLC

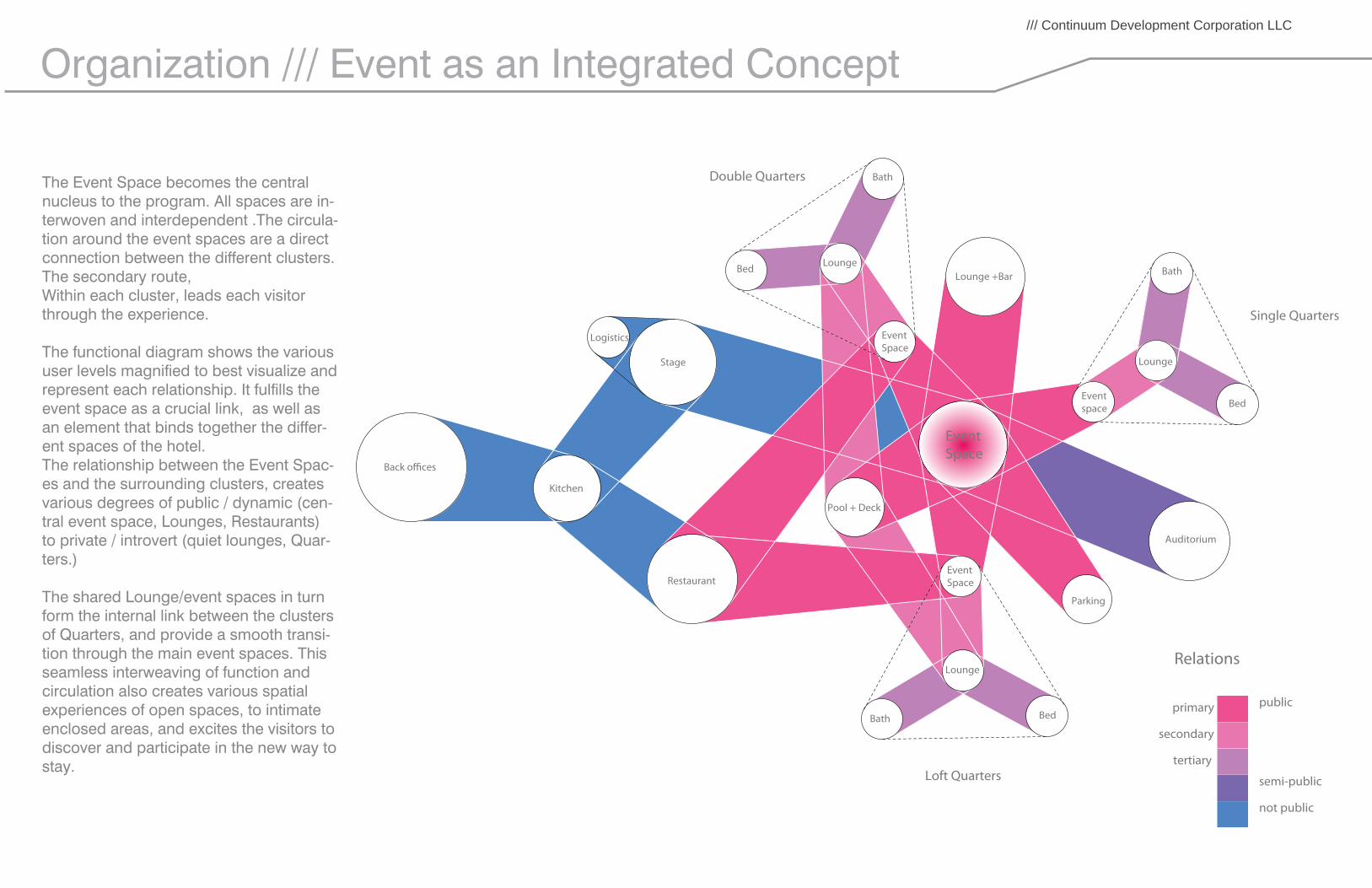

Organization /// Event as an Integrated Concept

EventSpace

Auditorium

Restaurant

Pool + Deck

EventSpace

Bed

Bath

EventSpace

Eventspace

Bath

Bath

Bed

Bed

Lounge

Back o�ces

Stage

Logistics

Kitchen

Lounge +Bar

Parking

Lounge

Lounge

Relations

publicprimary

secondary

tertiary

semi-public

not publicDouble Quarters

Loft Quarters

Single Quarters

21

EventSpace

Auditorium

Restaurant

Pool + Deck

EventSpace

Bed

Bath

EventSpace

Eventspace

Bath

Bath

Bed

Bed

Lounge

Back o�ces

Stage

Logistics

Kitchen

Lounge +Bar

Parking

Lounge

Lounge

Relations

publicprimary

secondary

tertiary

semi-public

not publicDouble Quarters

Loft Quarters

Single Quarters

21

The Event Space becomes the central nucleus to the program. All spaces are in-terwoven and interdependent .The circula-tion around the event spaces are a direct connection between the different clusters. The secondary route,Within each cluster, leads each visitor through the experience.

The functional diagram shows the various user levels magnified to best visualize and represent each relationship. It fulfills the event space as a crucial link, as well as an element that binds together the differ-ent spaces of the hotel.The relationship between the Event Spac-es and the surrounding clusters, creates various degrees of public / dynamic (cen-tral event space, Lounges, Restaurants) to private / introvert (quiet lounges, Quar-ters.)

The shared Lounge/event spaces in turn form the internal link between the clusters of Quarters, and provide a smooth transi-tion through the main event spaces. This seamless interweaving of function and circulation also creates various spatial experiences of open spaces, to intimate enclosed areas, and excites the visitors to discover and participate in the new way to stay.

/// Continuum Development Corporation LLC

Design Strategy / /

/// Continuum Development Corporation LLC

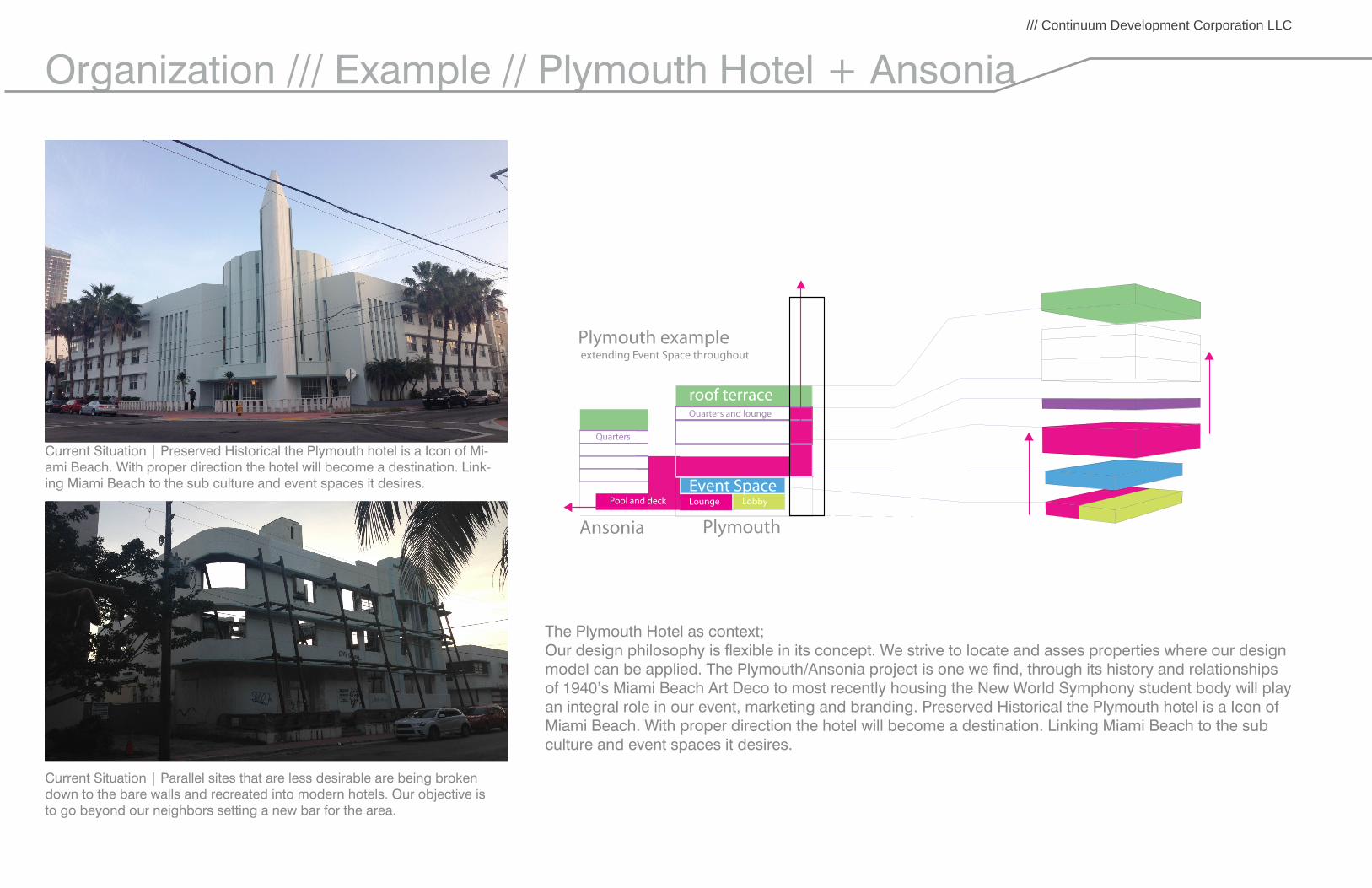

Organization /// Example // Plymouth Hotel + Ansonia

The Plymouth Hotel as context; Our design philosophy is flexible in its concept. We strive to locate and asses properties where our design model can be applied. The Plymouth/Ansonia project is one we find, through its history and relationships of 1940’s Miami Beach Art Deco to most recently housing the New World Symphony student body will play an integral role in our event, marketing and branding. Preserved Historical the Plymouth hotel is a Icon of Miami Beach. With proper direction the hotel will become a destination. Linking Miami Beach to the sub culture and event spaces it desires.

Current Situation | Preserved Historical the Plymouth hotel is a Icon of Mi-ami Beach. With proper direction the hotel will become a destination. Link-ing Miami Beach to the sub culture and event spaces it desires.

Current Situation | Parallel sites that are less desirable are being broken down to the bare walls and recreated into modern hotels. Our objective is to go beyond our neighbors setting a new bar for the area.

Organization /// Example // Plymouth Hotel + Ansonia

The Plymouth Hotel as context; erties where our design ory and relationships

of 1940’s Miami Beach Art Deco to most recently housing the New World Symphony student body will play an integral role in our event, marketing and branding. Preserved Historical the Plymouth hotel is an icon of Miami Beach. With proper direction the hotel will become a destination. Linking Miami Beach to the sub culture and event spaces it desires.

Current Situation | Preserved Historical the Plymouth hotel is a Icon of Mi-ami Beach. With proper direction the hotel will become a desitation. Linking Miami Beach to the sub culture and event spaces it desires.

Current Situation | Parralel sites that are less desierable are being broken down to the bare walls and recreated into moder hotels. Our objective is to go beyond our neighbors stting a new bar for the area.

Plymouth example

Plymouth Ansonia

roof terraceQuarters and lounge

Quarters

Event SpaceLoungePool and deck Lobby

extending Event Space throughout

/// Continuum Development Corporation LLC

/// Continuum Development Corporation LLC

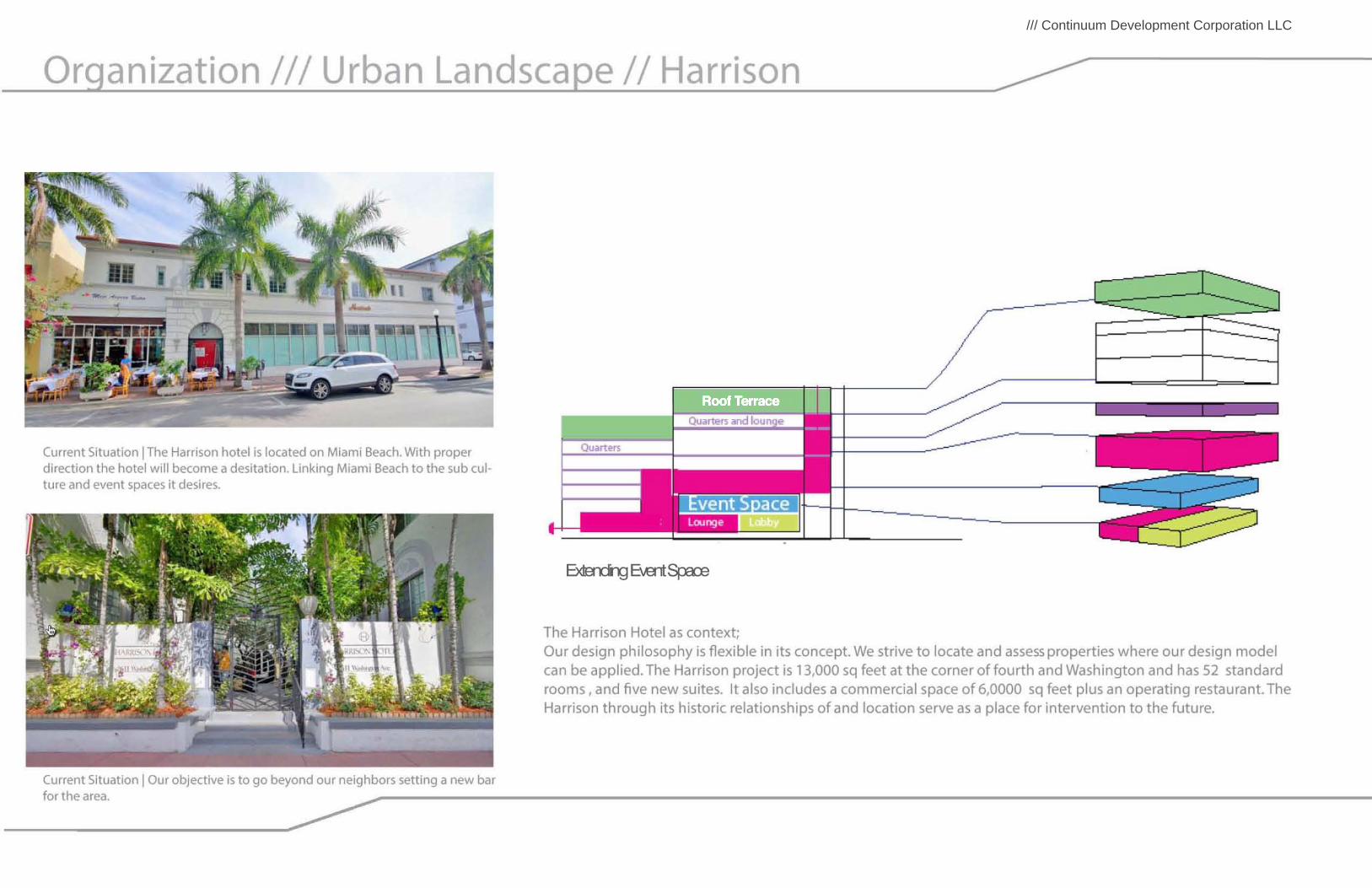

Organization /// Vertical Landscape // Site Context

Parking

150 Condo

150 Hotel

RestaurantCommercial Lobby

Event

EventBar/Social

The Design philosophy applied to this site in Edgewater, centrally located between Mid-Town, South Beach and Downtown offers an ideal proximity to tap into the optimal demo-graphic applying a mixed use programmatic approach amplifies the ability to tap into mul-tiple revenue streams.

/// Continuum Development Corporation LLC

Roof Terrace

/// Continuum Development Corporation LLC

Tr iangle House ///

A New Way to Stay // Concept Design Book

/// Continuum Development Corporation LLC

The Concept /// Past + Present + Future

The Triangle House Resort & Spa is a luxury, full service “inner-suburban” resort and conference center, with an emphasis on world-class facilities and service made comfortable with some south-ern hospitality. The project is an architectural, technological, and ecological showpiece for the “New North Carolina” which is building its reputation from the RDU/Triangle area, based of world-class universities, research and industry, mild seasonal weather, and a quality of life paralleled by very few places in the country.

The Triangle House Resort & Spa will have a focus on hosting small to medium sized university and corporate meetings and conferences. We will capitalize on the triangle’s geography and ex-istent conference business and area attractions by providing the areas only world-class banquet and meeting spaces with conference focused facilities and guest-facing technologies. The Tri-angle House will continue the areas rich traditions of producing and showcasing world-class and local talent in the event lounge space.

The hotel will tell this rich history through art, and help create new chapters with Artist-in- residen-cy programs and providing a venue for the creation and expression for the wealth of talent in our area.

The areas legendary universities and athletic programs will be steady drivers of business, includ-ing conferences, graduations, game-days, and other events. Banquet facilities, performance lounge, spa, retail and bar will also bring steady visibility, traffic, and revenue. The hotel will of-fer memberships to the private social club, which provides access to the wine bar and rooftop lounge, fitness facilities, preferential considerations for restaurant reservations, event tickets, facili-ties access, and discounts on hotel rooms.

Designed by world-class architects and expertly appointed, Triangle House blends world-class hospitality with a collection of exquisite condominium residences located in the heart of the RTP area. Residents will enjoy access to Triangle House’s superlative services and offerings in addi-tion to an array of enviable building amenities. The Residences at Triangle House represents the ultimate in

/// Continuum Development Corporation LLC

The Concept /// Past + Present + Future

The property will be a hospitable and conducive environment for gathering, celebrating, work-ing, creating, and relaxation, with a staff that exudes sincere hospitality and professionalism, without the stuffiness.

The property will carry a mystique and demand reminiscent of what the Morgan Hotels had when they first opened. Where people wanted to stay there because it was the place to be in that area, where you experienced the newest trends, and you never know who would also be-ing staying there. With a spa, pool, fantastic restaurants, rooftop and lobby bars, and the hot-test club and live music venue in the area, a guest has no reason to leave the property. We will create this experience, and enable the guests to take some of the it with them, with our “Take it with You” program, which allows the guests to purchase anything they experienced at the hotel (bed, sheets, furniture, TV, food, art, etc).

Additional property amenities will include a library to access and showcase research and the pursuit of knowledge. A place for people to study, work, and research, utilizing mobile kiosks linked to university libraries, with printing, creation, and business center facilities available.

/// Continuum Development Corporation LLC

Design Model / /

/// Continuum Development Corporation LLC

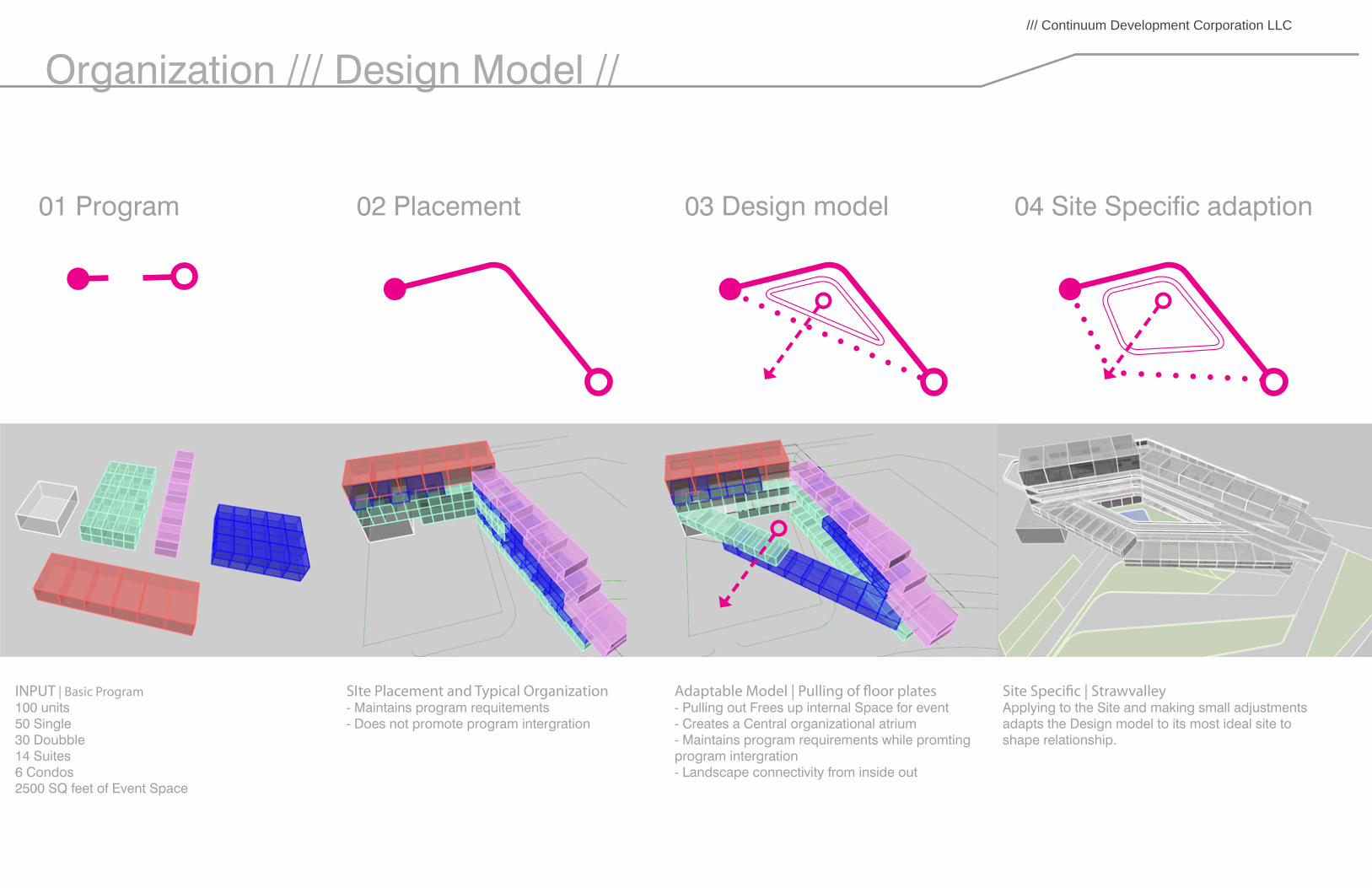

Organization /// Design Model //

INPUT | Basic Program 100 units50 Single30 Doubble14 Suites6 Condos 2500 SQ feet of Event Space

01 Program 02 Placement 03 Design model 04 Site Specific adaption

SIte Placement and Typical Organization- Maintains program requitements - Does not promote program intergration

Adaptable Model | Pulling of floor plates- Pulling out Frees up internal Space for event- Creates a Central organizational atrium - Maintains program requirements while promting program intergration- Landscape connectivity from inside out

Site Specific | StrawvalleyApplying to the Site and making small adjustments adapts the Design model to its most ideal site to shape relationship.

/// Continuum Development Corporation LLC

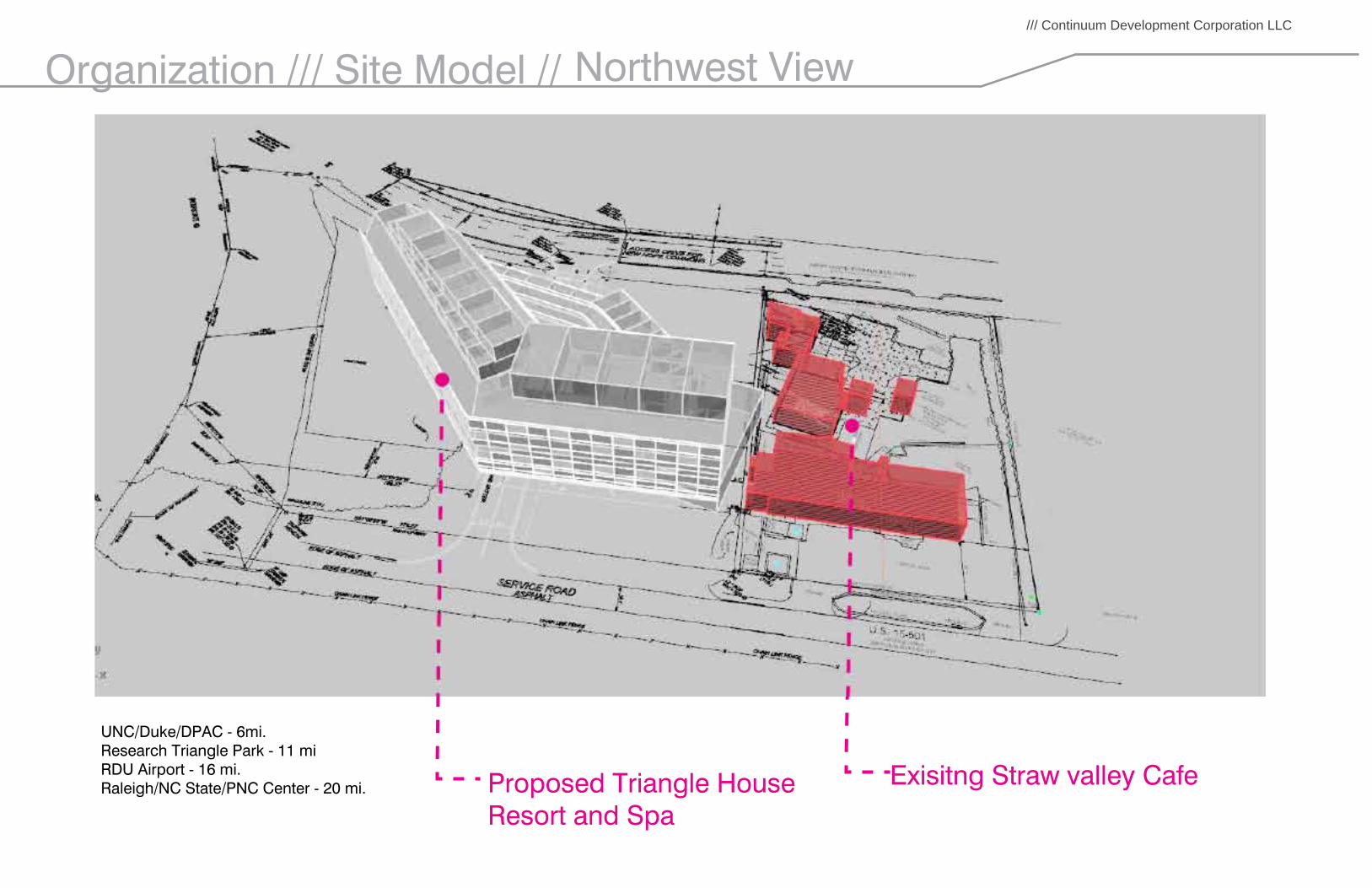

Organization /// Site Model //

UNC/Duke/DPAC - 6mi.Research Triangle Park - 11 miRDU Airport - 16 mi.Raleigh/NC State/PNC Center - 20 mi.

Northwest View

North West

Exisitng Straw valley CafeProposed Triangle House Resort and Spa

/// Continuum Development Corporation LLC

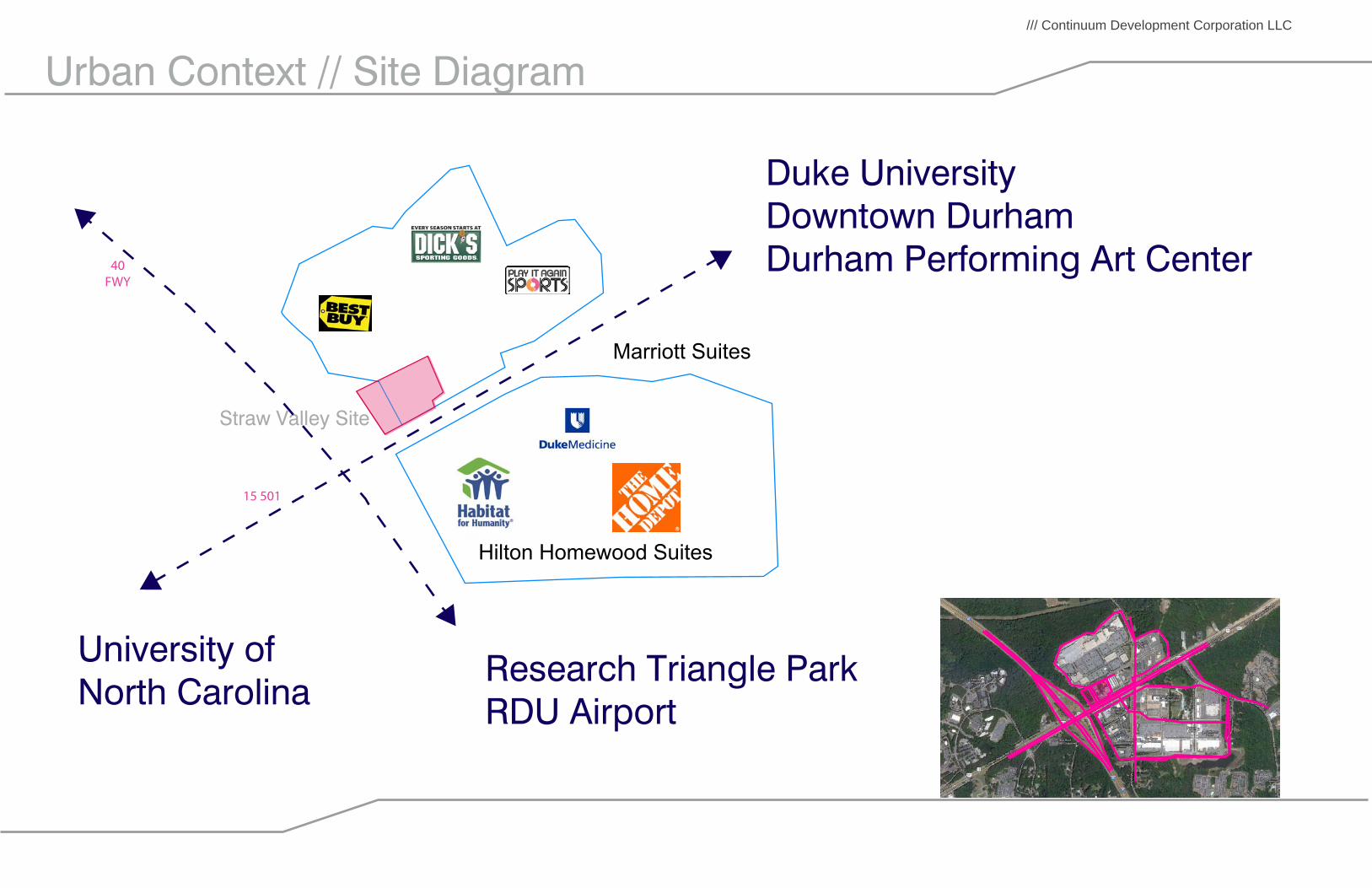

Urban Context // Site Diagram

Straw Valley Site

40FWY

Marriott Suites

Hilton Homewood Suites

15 501

University ofNorth Carolina

Duke University Downtown DurhamDurham Performing Art Center

Research Triangle ParkRDU Airport

/// Continuum Development Corporation LLC

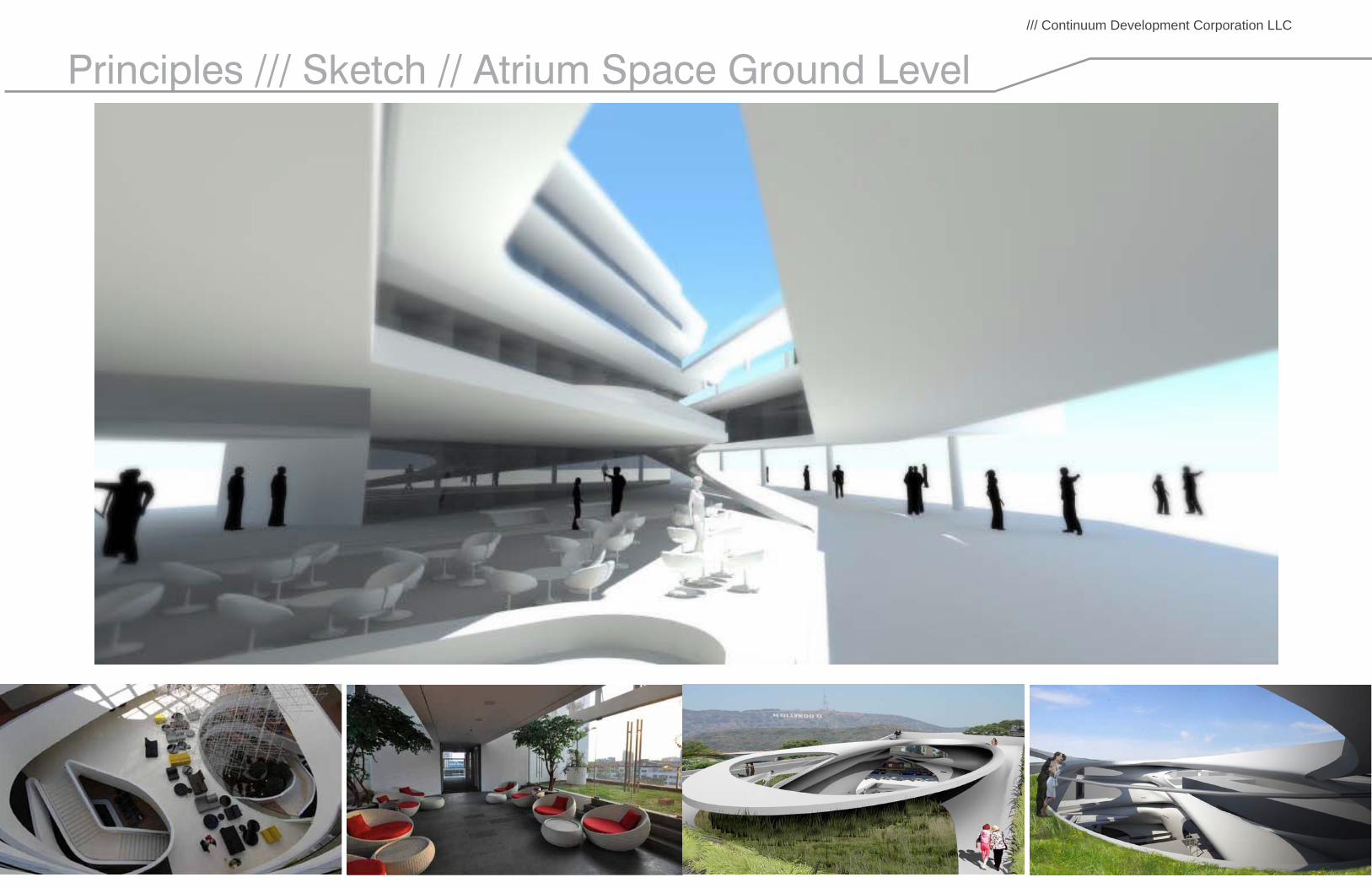

Principles /// Sketch // Atrium Space Ground Level/// Continuum Development Corporation LLC

Principles /// Sketch // Atrium Space Pool Level/// Continuum Development Corporation LLC

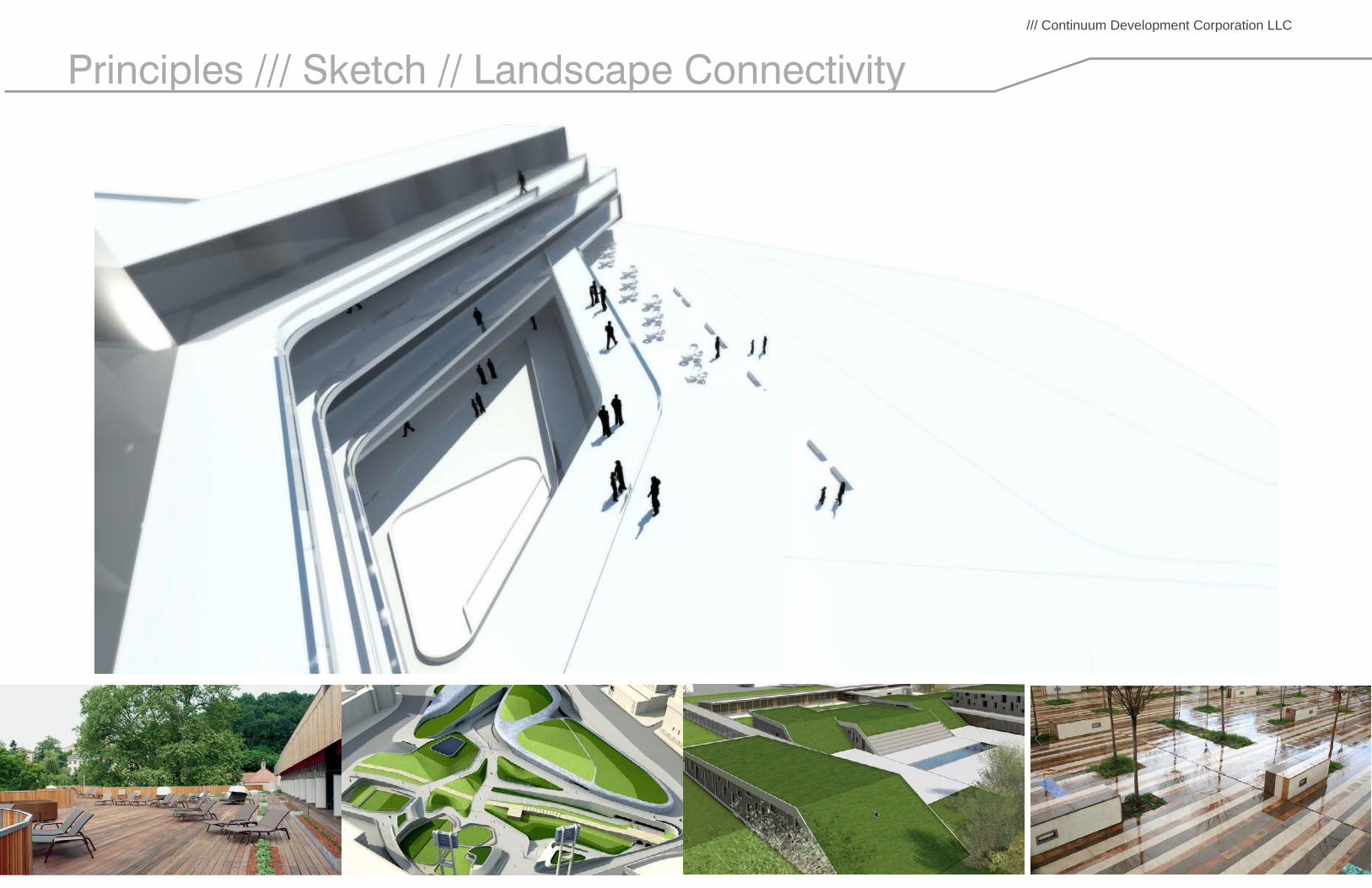

Principles /// Sketch // Landscape Connectivity/// Continuum Development Corporation LLC

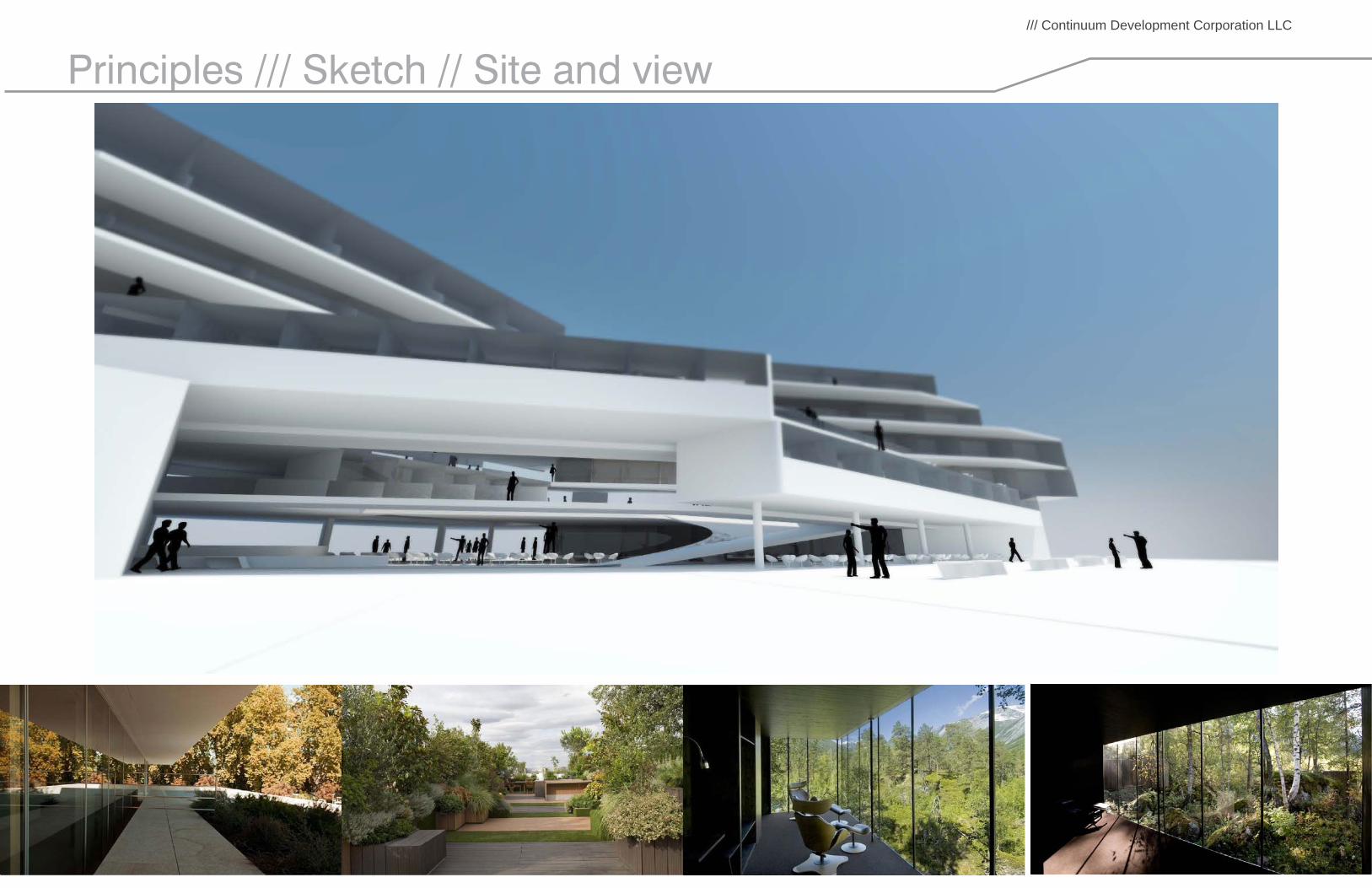

Principles /// Sketch // Site and view/// Continuum Development Corporation LLC

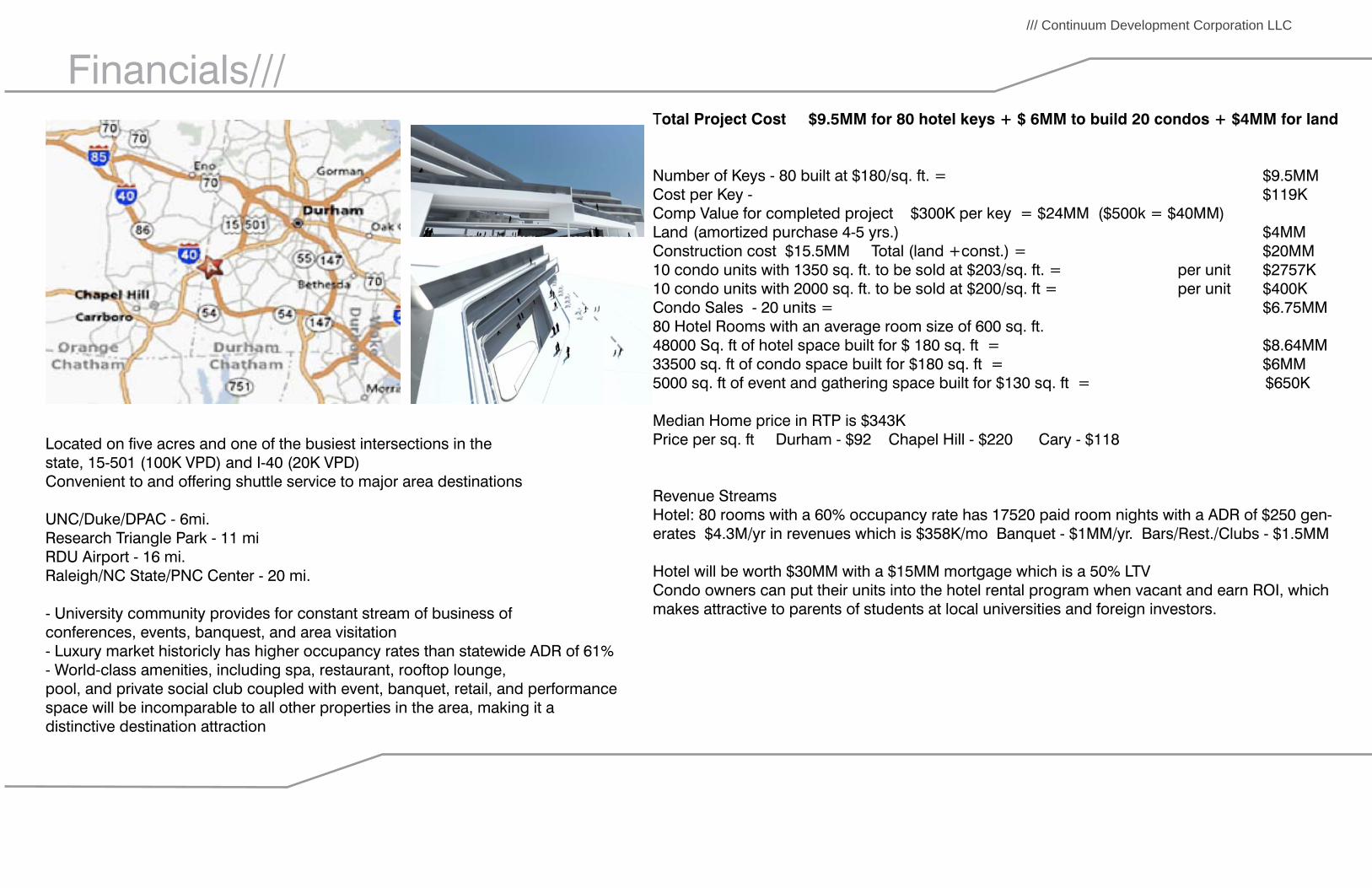

Financials/// Total Project Cost $9.5MM for 80 hotel keys + $ 6MM to build 20 condos + $4MM for land

Number of Keys - 80 built at $180/sq. ft. = $9.5MM Cost per Key - $119KComp Value for completed project $300K per key = $24MM ($500k = $40MM)Land (amortized purchase 4-5 yrs.) $4MMConstruction cost $15.5MM Total (land +const.) = $20MM10 condo units with 1350 sq. ft. to be sold at $203/sq. ft. = per unit $2757K 10 condo units with 2000 sq. ft. to be sold at $200/sq. ft = per unit $400K Condo Sales - 20 units = $6.75MM80 Hotel Rooms with an average room size of 600 sq. ft. 48000 Sq. ft of hotel space built for $ 180 sq. ft = $8.64MM33500 sq. ft of condo space built for $180 sq. ft = $6MM5000 sq. ft of event and gathering space built for $130 sq. ft = $650K

Median Home price in RTP is $343KPrice per sq. ft Durham - $92 Chapel Hill - $220 Cary - $118

Revenue StreamsHotel: 80 rooms with a 60% occupancy rate has 17520 paid room nights with a ADR of $250 gen-erates $4.3M/yr in revenues which is $358K/mo Banquet - $1MM/yr. Bars/Rest./Clubs - $1.5MM

Hotel will be worth $30MM with a $15MM mortgage which is a 50% LTVCondo owners can put their units into the hotel rental program when vacant and earn ROI, which makes attractive to parents of students at local universities and foreign investors.

Located on five acres and one of the busiest intersections in thestate, 15-501 (100K VPD) and I-40 (20K VPD)Convenient to and offering shuttle service to major area destinations

UNC/Duke/DPAC - 6mi.Research Triangle Park - 11 miRDU Airport - 16 mi.Raleigh/NC State/PNC Center - 20 mi.

- University community provides for constant stream of business ofconferences, events, banquest, and area visitation- Luxury market historicly has higher occupancy rates than statewide ADR of 61%- World-class amenities, including spa, restaurant, rooftop lounge,pool, and private social club coupled with event, banquet, retail, and performance space will be incomparable to all other properties in the area, making it adistinctive destination attraction

/// Continuum Development Corporation LLC

Contexual References / /

/// Continuum Development Corporation LLC

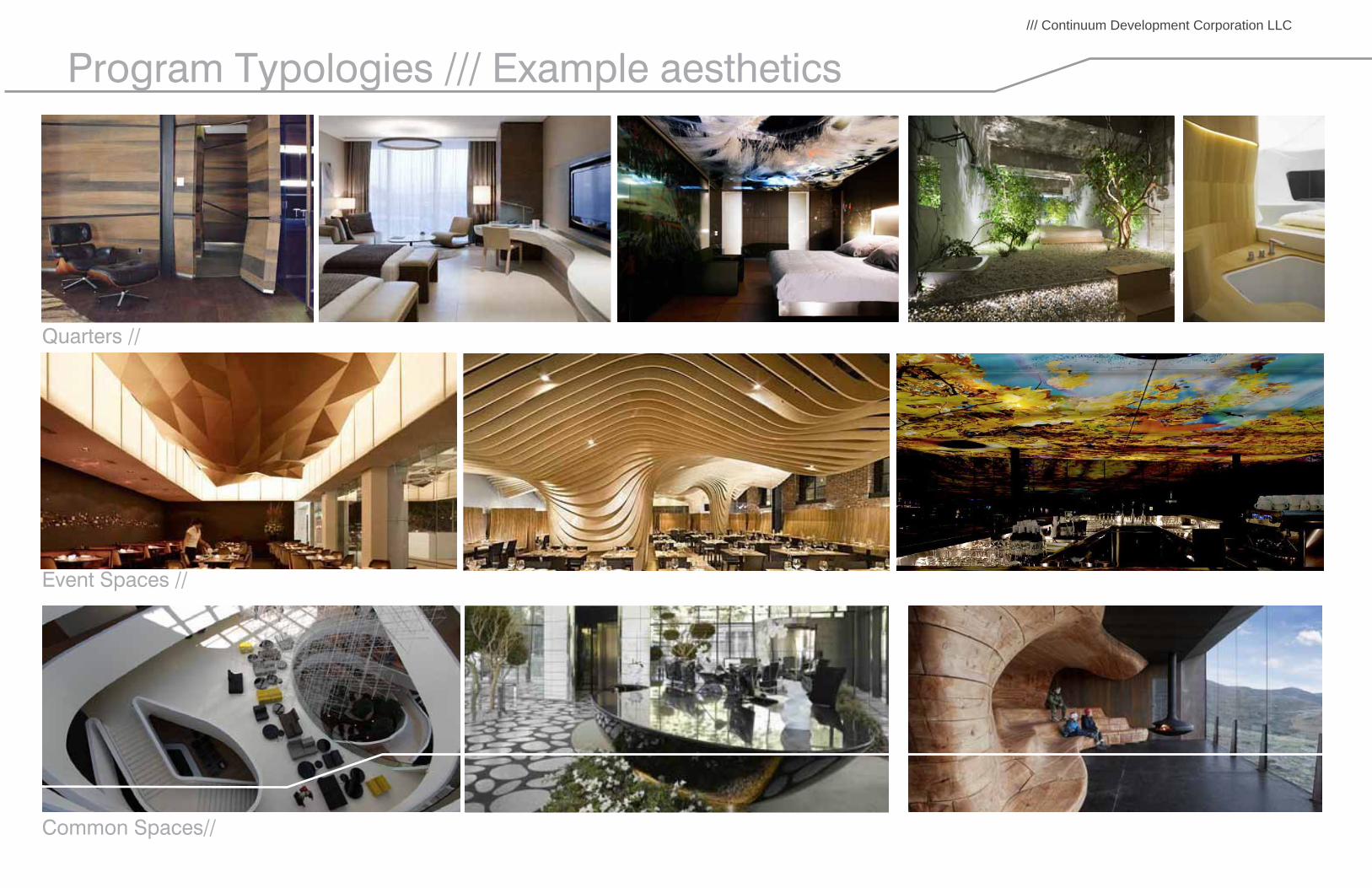

Program Typologies /// Example aesthetics

Quarters //

Event Spaces //

Common Spaces//

/// Continuum Development Corporation LLC

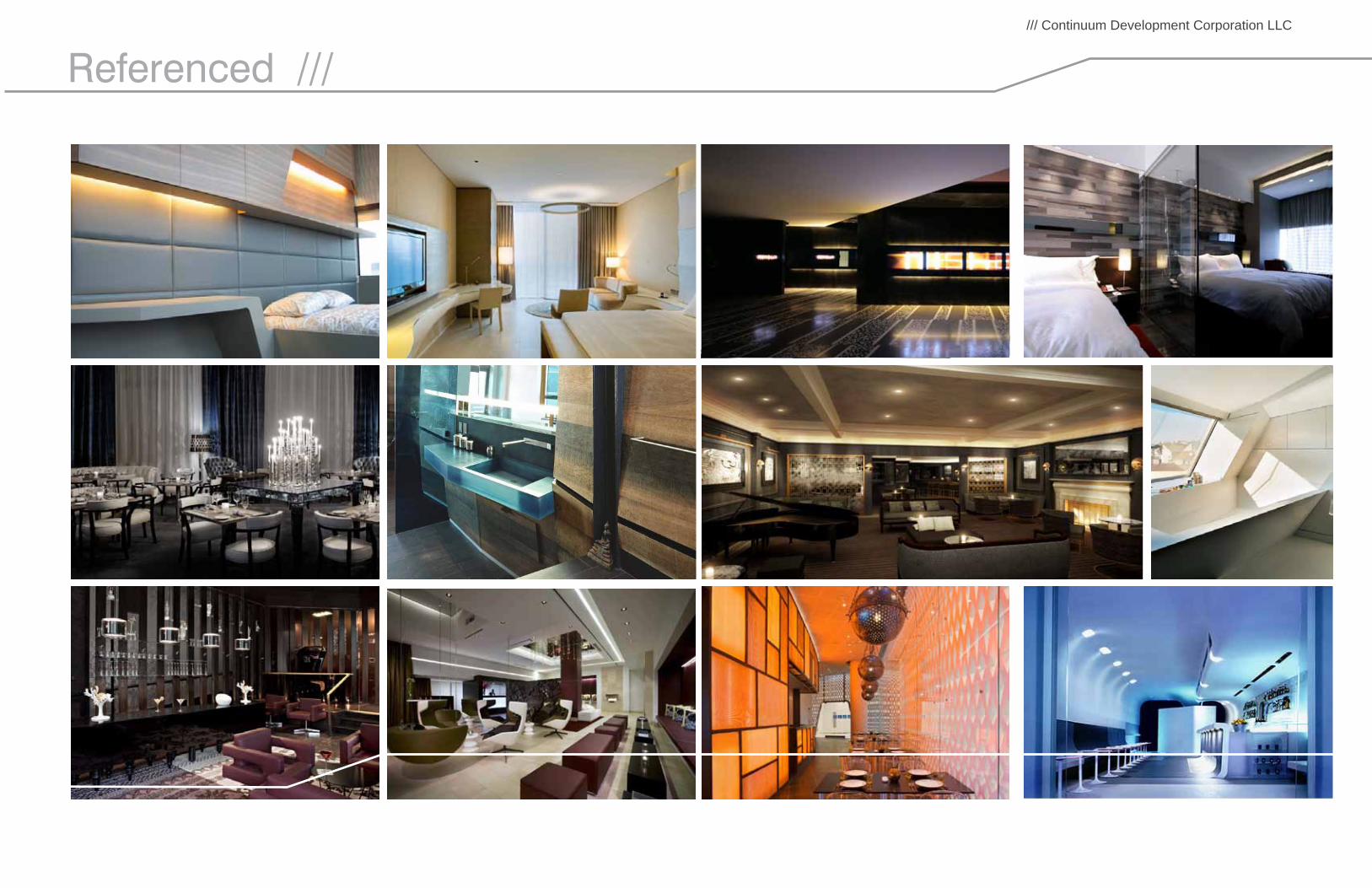

Referenced /// /// Continuum Development Corporation LLC

Details /// Technology + Space + FunctionalityEach square foot is thought about in detail. How to maximize interactivity, comfort and usability

/// Continuum Development Corporation LLC

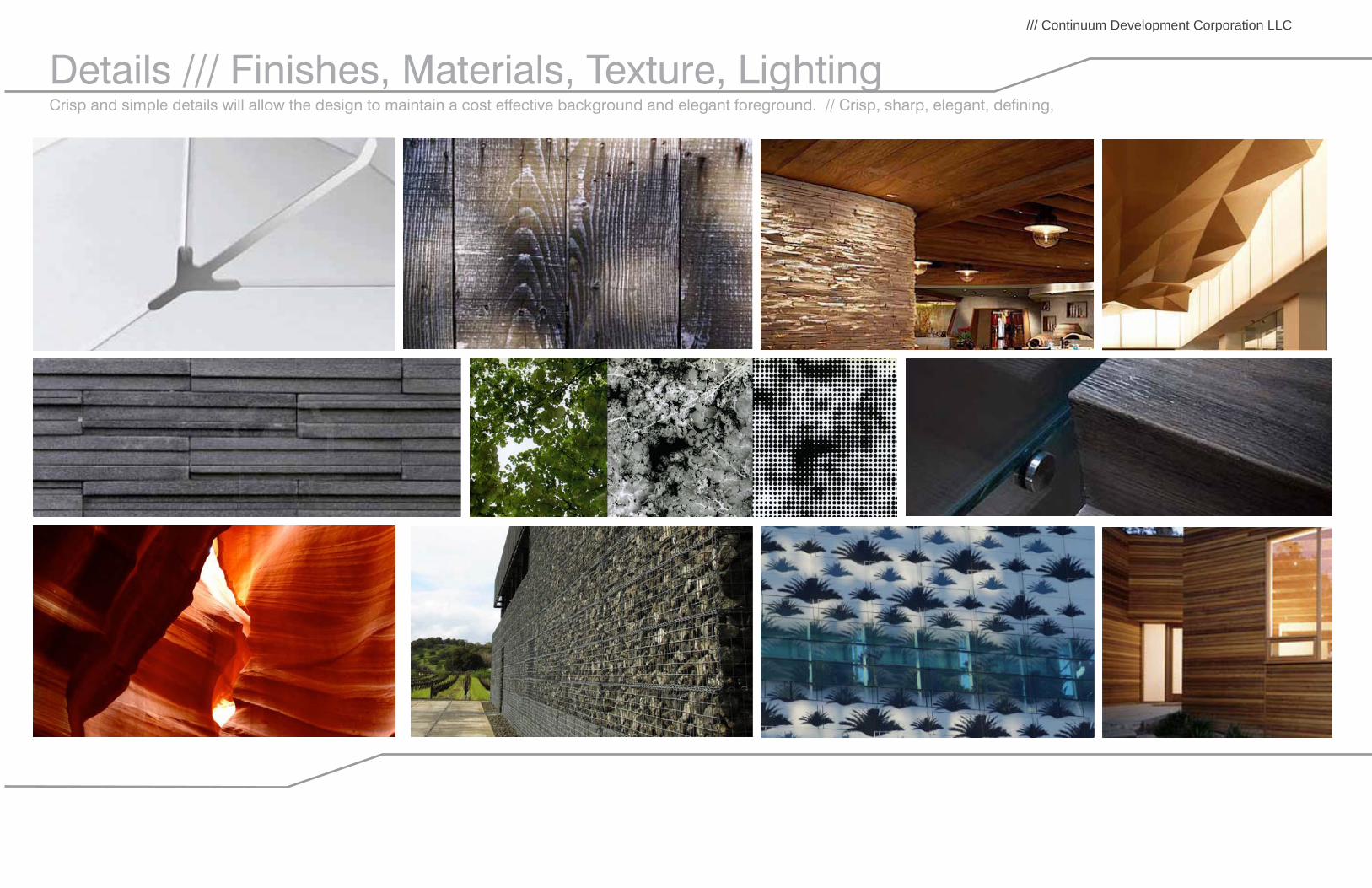

Details /// Finishes, Materials, Texture, LightingCrisp and simple details will allow the design to maintain a cost effective background and elegant foreground. // Crisp, sharp, elegant, defining,

/// Continuum Development Corporation LLC

Financials / /

/// Continuum Development Corporation LLC

/// Continuum Development Corporation LLC

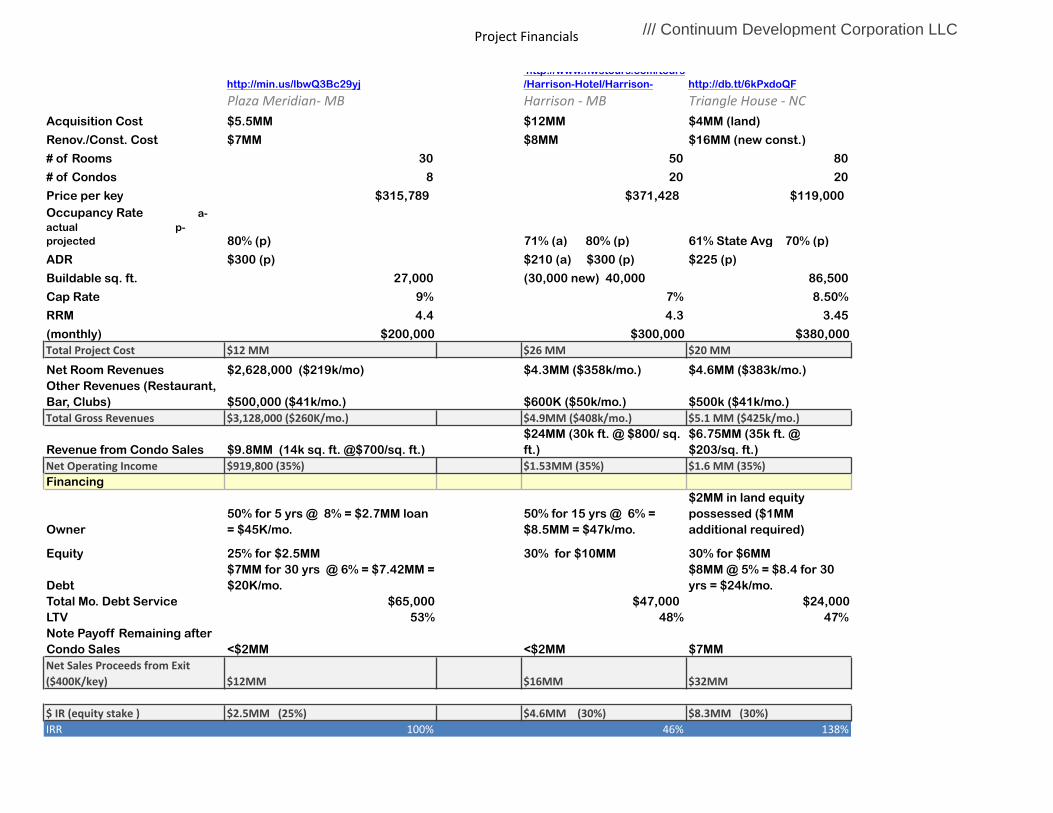

Project Financials

http://min.us/lbwQ3Bc29yj http://www.nwstours.com/tours/Harrison-Hotel/Harrison- http://db.tt/6kPxdoQF

Plaza Meridian-‐ MB Harrison -‐ MB Triangle House -‐ NCAcquisition Cost $5.5MM $12MM $4MM (land)

Renov./Const. Cost $7MM $8MM $16MM (new const.)

# of Rooms 30 50 80

# of Condos 8 20 20

Price per key $315,789 $371,428 $119,000Occupancy Rate a- actual p- projected 80% (p) 71% (a) 80% (p) 61% State Avg 70% (p)

ADR $300 (p) $210 (a) $300 (p) $225 (p)

Buildable sq. ft. 27,000 (30,000 new) 40,000 86,500

Cap Rate 9% 7% 8.50%

RRM 4.4 4.3 3.45Net Cash after Debt Service (monthly) $200,000 $300,000 $380,000 Total Project Cost $12 MM $26 MM $20 MM

Net Room Revenues $2,628,000 ($219k/mo) $4.3MM ($358k/mo.) $4.6MM ($383k/mo.)Other Revenues (Restaurant, Bar, Clubs) $500,000 ($41k/mo.) $600K ($50k/mo.) $500k ($41k/mo.)Total Gross Revenues $3,128,000 ($260K/mo.) $4.9MM ($408k/mo.) $5.1 MM ($425k/mo.)

Revenue from Condo Sales $9.8MM (14k sq. ft. @$700/sq. ft.)$24MM (30k ft. @ $800/ sq. ft.)

$6.75MM (35k ft. @ $203/sq. ft.)

Net Operating Income $919,800 (35%) $1.53MM (35%) $1.6 MM (35%)Financing

Owner50% for 5 yrs @ 8% = $2.7MM loan = $45K/mo.

50% for 15 yrs @ 6% = $8.5MM = $47k/mo.

$2MM in land equity possessed ($1MM additional required)

Equity 25% for $2.5MM 30% for $10MM 30% for $6MM

Debt$7MM for 30 yrs @ 6% = $7.42MM = $20K/mo.

$8MM @ 5% = $8.4 for 30 yrs = $24k/mo.

Total Mo. Debt Service $65,000 $47,000 $24,000 LTV 53% 48% 47%Note Payoff Remaining after Condo Sales <$2MM <$2MM $7MMNet Sales Proceeds from Exit ($400K/key) $12MM $16MM $32MM

$ IR (equity stake ) $2.5MM (25%) $4.6MM (30%) $8.3MM (30%)IRR 100% 46% 138%

/// Continuum Development Corporation LLC

Appendix Miami / /

/// Continuum Development Corporation LLC

What’s inn fashion

Downtown and Brickell hotel projects now rival Miami Beach stalwarts

November 03, 2012 By Alexander Britell

As the greater Miami condominium market sees an unprecedented sales spree, the area’s hotel sector has experienced similar gains. And it’s not just the traditional vacation destination of Miami Beach that is thriving; downtown Miami is also reaping the benefits.

The growth of downtown Miami’s hotel sector in the last two to three years has transformed an area once home to economy hotels into a legitimate competitor to Miami Beach and given Miami-Dade County not one, but two robust hotel markets.

The volume of hotel transactions in greater Miami rose 154 percent in 2011 compared to the previous year, according to a report from Jones Lang LaSalle Hotels.

In Miami Beach, rows of aging Art Deco classics and forgotten boutiques, from the former Peter Miller (now the Lennox) Hotel to Vikram Chatwal’s Dream South Beach, have been overhauled in recent years, helping to move forward a resurgence that began with the work of frontiersmen like André Balazs and Ian Schrager in the 1990s and early 2000s.

“By the end of this year, the market will probably move to 2008 levels, which is pretty impressive,” said Bo Ashbel, who oversees the hospitality group at Aztec Group, a Miami-based investment banking firm. “The average daily rate has been very, very strong, and so far through July, the revenue per available room rose 8.9 percent.”

Ashbel brokered the sale of the Fontainebleau Miami Beach in 2005, three years before it unveiled $1 billion in renovations. While the Morris Lapidus–designed resort underwent a series of financial troubles during the downturn, it was the hotel’s 2008 debut that reinforced Miami Beach as a destination.

The Fontainebleau was one of the first of a series of city hotels that are either being completely demolished and built up anew (like Sam Nazarian’s SLS South Beach) or overhauled (like the Menin Group’s Shelborne South Beach).

A number of big players have made an entry into Miami in the last two years, highlighted by a group of Starwood affiliates that purchased the Gansevoort South Beach on Collins Avenue, rebranding it as the Perry South Beach. Starwood plans a $100 million renovation project that is slated for completion in 2013.

/// Continuum Development Corporation LLC

And in April, Man-Co purchased the Miami Beach Best Western for $50 million.

The total sales volume in 2011 was $557 million.

So it’s only natural that the two hotels largely responsible for bringing hotel hype back to Miami Beach in the 1990s — the aforementioned Schrager’s Delano and the Raleigh, which represented Balazs’s first foray into South Beach, were both put on the block this summer. The Raleigh reportedly sold to David Edelstein, the developer of W South Beach, and his partners for about $55 million in August; the Delano is still for sale.

“The Miami Beach hotel market has been extremely active,” said Lori Schumacher, a partner in the hotel practice at Miami law firm Bilzin Sumberg Baena Price & Axelrod. “Miami is a gateway city, so everyone wants to be there. And there’s limited supply, so the top hotels that are being snatched up are beachfront properties and the boutique luxury hotels.”

And as Miami Beach has regained its status as a vacation destination — and a continued investment target — downtown Miami has become a hospitality hub, too, from the Viceroy Miami and JW Marriott Marquis to the newly opened, eco-conscious Hampton Inn in Brickell.

Laurence Dubey, the general manager at the Viceroy, came to downtown Miami three years ago when the city’s downtown was, for all intents and purposes, a ghost town.

“You’ve really seen growth in the downtown Brickell area that competes 100 percent with Miami Beach,” Dubey said. “Before, everyone would be referred to a hotel on the beach. Now with the Kimpton, the Four Seasons, the Marriott and us, [there are] luxury hotels that actually wanted to be based in downtown Brickell.”

Brickell-downtown Miami is now the second-best-performing hotel submarket in Miami-Dade County (after Miami Beach), according to Ashbel.

“Some can argue that probably the best hotels in Dade County are in Brickell and downtown,” he said. “There’s a great deal of interest and a great deal of demand in staying in Brickell — I think [Miami and Miami Beach] complement each other.”

As Miami-‐Dade real estate and hotel markets boom, more players want in October 30, 2012 By: Steve Gara

According to a Miami Herald report, Miami real estate is headed upward and more players are wanting in. Case in point: A Miami-based private equity firm, with capital from Turkey, Brazil

/// Continuum Development Corporation LLC

and Peru, is snapping up prime South Florida real estate, including the historic Surf Club in Surfside.

Fort Capital focuses on prime, often waterfront, real estate, typically in distress or in need of a change. The firm bought most of the Capri South Beach and repositioned the Miami Beach condominium. It acquired The Strand restaurant in South Beach and the nearby Pelican Parking garage, and earlier this year added the Millennium at Bay Harbor condominium to its portfolio.

In another instance, the trailblazing Delano, which revitalized the destination in 1995 and is now being marketed for sale after an $11 million renovation, is flanked by the historic National Hotel, in the midst of a major restoration, and the Philippe Starck-designed SLS, formerly the Ritz Plaza, which opened in June after eight years and about $85 million.

“Miami is a hot market now, so it’s hard to get a hotel,” said Keith Menin, principal of Menin Hotels, which is developing the latest — but certainly not last — addition to the busy scene. The company’s 87-room Gale South Beach & Regent Hotel at 1690 Collins Ave. is set to open in early December, more than a year after finishing most of the renovations on the family-owned Shelborne just up the road.

After a recession-fueled pause, when visitor numbers dropped and financing dried up, Miami-Dade is in the throes of a hotel buying-and-building boom. Or, more appropriately, a re-building boom.

Local investment is following a national trend.

Shelling out billions

According to a recent report from Bjorn Hanson, a dean at the Preston Robert Tisch Center for Hospitality, Tourism and Sports Management at New York University, the lodging industry is expected to shell out a projected $5 billion this year on upgrades after curtailing spending since 2009.

Improvements could include everything from redesigned lobbies to better technology in rooms and meeting areas and more appealing fitness centers and restaurants, according to the report, which notes that the expected spending boost is due to vastly improved occupancy numbers and average daily rates.

In Miami, industry experts say robust tourism numbers, the scarcity of available land and the willingness of banks to lend money again are drawing waves of investors who see hotels in the destination as a must for their portfolios. Potential buyers include private equity firms, real estate investment trusts, major brands and some foreign investors.

“Miami is improving faster than a lot of the other markets, and it is a major, major market,” said Suzanne Amaducci-Adams, head of the hospitality group at the Bilzin Sumberg law firm. “So everybody wants to be here.”

/// Continuum Development Corporation LLC

Through September, hotels in Miami-Dade were more than 76 percent full, a small gain over the first nine months of 2011 despite a dip during the summer. But room rates have continued to climb, up nearly 7 percent to almost $163. And hotels countywide are making more revenue per available room; that figure grew about 8 percent to more than $124.55 through September.

Observers say the area is also gaining stature internationally because of the growth of arts and culture, as well as its ability to attract business from places including Russia and Asia in addition to Latin America.

“We really are just maturing and becoming a much more sophisticated global destination, and that’s really what is driving this,” Amaducci-Adams said.

Hotel transactions volume is expected to reach $650 million in the county this year, a 13 percent increase over 2011, according to brokerage Jones Lang LaSalle Hotels. And that figure doesn’t includes the hundreds of millions more being poured into upgrades at properties including the Perry Hotel South Beach (formerly Gansevoort Miami Beach) and Trump Doral Golf Resort & Spa, which mogul Donald Trump says he’s spending $200 million to fix up after he bought it for $150 million earlier this year.

Like the Doral and a few sites near Miami International Airport, a sliver of the current action is happening on the mainland. Only a Hampton Inn has gone up in the downtown Miami or Brickell area since the JW Marriott Marquis opened in late 2010, capping a decade that saw the arrival of the Mandarin Oriental, Four Seasons, JW Marriott, Conrad, Viceroy and Epic.

Hotel upgrades

Now, the stalwart InterContinental Miami is about to wrap up a $30 million upgrade and the former Continental Bayside Hotel is undergoing a renovation that is expected to finish in early 2013, when the property at 146 Biscayne Blvd. will become the first hotel in the budget-friendly b2 brand.

But the bulk of the investment action is happening in Miami Beach, which still commands the highest room rates.

Gregory Rumpel, managing director of Jones Lang LaSalle Hotels in Miami, calls it “a truckload of cash” that will reinvigorate the remainingproperties in disrepair to push rates even higher when all the projects are done.

“Once we get these derelict buildings renovated and repositioned, I think it really helps the image, improves the vibe,” he said. “It creates more velocity, more activity.”

Like Menin’s Gale, many projects are resurrections of dilapidated, decades-old buildings that are historically significant. Because most of the popular areas for hotels lie within protected historic districts, any changes are subject to tough standards and approval.

/// Continuum Development Corporation LLC

“It would be a lot cheaper for developers to come in and knock down these buildings, but you can’t,” said Max Comess, a director in the hotel group at commercial real estate investment banking firm HFF. “And the trade-off is that you have some really amazing architecturally significant buildings to work with. I think that’s what makes Miami so appealing, not only to investors: It’s really like you’re staying in a museum.”

Restoration

Kobi Karp Architecture and Interior Design, a Miami firm, is working on a handful of such projects on the beach, including the restoration and addition of new buildings at the Surf Club in Surfside, which will include a condo-hotel; the transformation of a complex of decrepit buildings into boutique hotels in the Collins Park neighborhood of Miami Beach and the Hotel Versailles in Miami Beach.

The firm’s principal, Kobi Karp, said the volume of hotel restoration projects has increased in the last couple of years.

“They are challenging, but they’re also inspirational because you get to work with a history and a story that was there before you,” he said.

Comess is marketing the Haddon Hall hotel at 1500 Collins Ave. and adjacent apartments to potential buyers. That traditional South Beach area has been on the front end of development, with renovated properties on Ocean Drive and Collins Avenue including Hotel Breakwater, Dream South Beach, Room Mate Waldorf Towers, the Surfcomber and the Shelborne all coming online last year.

After a summer soft opening, the SLS at 1701 Collins Ave. holds its official grand opening event in early November, when the renovated and newly branded James Royal Palm also opens and the Ritz-Carlton, South Beach finishes a $10 million room refresh.

Many projects are still in the pipeline, including the transformation of the Continental Oceanfront South Beach Hotel at 1825 Collins Ave., which is scheduled to open next year as B South Beach.

The Chetrit Group, a New York-based developer that bought the Tides at 1220 Ocean Dr. last year and made it part of the hip King & Grove brand, is behind the planned restoration of the Collins Park buildings and the Hotel Versailles. The group is also planning an extension of the Tides as well as a project at the empty Fairwind Hotel at 10th Street and Collins Avenue.

Often finding themselves priced out of the heart of South Beach — or simply without anything to buy there at any price — investors are also looking north for opportunities.

New York-based Sydell Group, which owns the NoMad Hotel in Manhattan and developed the Ace hotels there and in Palm Springs, had five cities in mind when executives decided to start an upscale hostel concept. They found the first location off the beaten path in Miami Beach at the old Indian Creek Hotel, 2727 Indian Creek Dr., some 10 blocks north of the heart of South Beach

/// Continuum Development Corporation LLC

buzz. After buying the hotel for $12 million in January and putting about $8 million into upgrades, the company will launch the new 65-room Freehand with a soft open in December.

Sydell Group CEO Andrew Zobler said the goal was to create a place with an affordable price point that would attract youth and energy — distance from the South Beach action notwithstanding.

“I really like the location. I think a lot of our audience are going to ride bicycles,” he said. “The beach is not that big a place. You can pop from one place to the next on a bicycle. I think a lot of the energy is moving up the beach.”

More buzz

At the Lifestyle/Boutique Hotel Development Conference at the Fontainebleau Miami Beach earlier this month, a panel of industry experts agreed that the south doesn’t have a monopoly on buzz.

“South Beach is starting to creep up to this part of the beach as well,” said Patrick Goddard, president and chief operating officer of Trust Hospitality.

The popular W South Beach, at 22nd Street, and Perry at 24th have already pushed the hip factor far north of Lincoln Road, and the upcoming Edition at 29th Avenue is expected to do the same when it opens late next year.

Marriott announced two years ago that it was buying the old Seville Beach Hotel to become an Edition, a chic and exclusive new brand formed in partnership with hotelier Ian Schrager. The Miami Beach location will be the only one in the United States when it opens.

Jay Coldren, Marriott International’s vice president of lifestyle brands, said at the hotel conference that the company’s investment in the Edition is unusual — Marriott does not typically own the hotels it operates — and a sign of Miami’s significance in the world.

“We’re really serious about this market, the future of this market and what it means to the global positioning of the brand,” he said.

Slightly north of the Edition, the Saxony hotel at 3201 Collins Ave. is coming back to life courtesy of Argentine developer Alan Faena. And the old Cadillac Hotel at 3925 Collins Ave., now the Courtyard Miami Beach Oceanfront, changed hands late last year for $95 million. New owner Hersha Hospitality Trust is adding a tower with another 93 rooms to the property, scheduled for completion by the end of 2013.

Hersha, a Philadelphia company that also has property in New York, Boston, Washington, D.C., Philadelphia and California, had been eyeing Miami for years before making the purchase. Back during the height of the real estate market, said CFO Ashish Parikh, prices were prohibitive.

/// Continuum Development Corporation LLC

“The market obviously went into a freefall,” he said. “At that point we really didn’t know where Miami was going to shake out. As we looked at the trajectory, we thought last year Miami was shaping up to have a nice long run — and it seems like that’s coming to fruition.”

Comess, of HFF, predicts a “wave” effect that started with reconstruction of oceanfront hotels and will move inland to properties across from the beach, then farther away from the water in Miami Beach, followed by downtown Miami, Coconut Grove and Coral Gables.

A fall newsletter from hospitality consulting firm HVS Miami suggests investors should consider looking beyond Miami-Dade to the Fort Lauderdale area, Florida Keys and West Palm Beach. While Broward has seen some investment, the volume is far less than its southern neighbor.

Other markets

“Statistics show that Miami is not the only hotel market in South Florida illustrating strong performance indicators,” the HVS report says. “Investors could benefit from widening their ‘gateway city myopia.’ ”

But for those who are set on Miami-Dade, Comess said, Miami Beach could start to get too pricey.

“The premium’s obviously on the beach, and that’s the first place everyone wants to be,” he said. “But as pricing gets ridiculous on the beach and exceeds peak levels, both guests and investors will start coming inland to find more attractive deals in terms of places to stay.”

Some of the most talked-about future projects are planned for the mainland, though specifics are far from clear. Genting Group, the Malaysian company that bought the Miami Herald building for $236 million last year, had initially said it planned a 5,000-room resort complex with a casino. But after state legislators failed to approve expanded gaming, the company has said it plans to scale the project down.

Swire Properties plans to include a 265-room hotel in its $1.05 billion Brickell CitiCentre project, and developer Craig Robins has said his $312 million vision for the Design District includes a hotel.

And the market is clamoring for more select-service hotels such as Courtyard by Marriott, said Ezra Katz, chairman of real estate investment banking firm Aztec Group. In Miami-Dade, at least two Aloft hotels from Starwood are on the books for early 2013, in the Brickell area and Doral.

The Miami International Airport area also has potential for future development, Katz said.

“It’s a very healthy market, and that airport generates a lot of traffic,” he said. “You may not get rich, but you won’t get poor.”

/// Continuum Development Corporation LLC

The South Florida hospitality industry, of course, is wary of boom-and-bust cycles after recovering from the impact of the Sept. 11, 2001 terrorist attacks and the recent worldwide recession. Industry players say there doesn’t appear to be a bubble in the making but warn about the unexpected.

Outside influence

Peter Zalewski, a principal with Bal Harbour-based consultancy Condo Vultures, said added inventory could be an initial drag on occupancy and pricing. And, he pointed out, hotels are especially vulnerable to outside events.

“We’re one international incident away from the whole scene changing,” he said.

In this post-recession phase, tourism boosters and visitors alike are enjoying the progress.

Interior designer Colette Anderson, visiting from the Atlanta area recently as part of the lodging conference held at the Fontainebleau, toured the new SLS with a group and “took 100,000 pictures.”

“It’s just quite fascinating that there’s a big construction boom down here in South Beach,” she said.

The constant redevelopment helps to keep interest fresh in Miami, especially as northerners are making their winter vacation plans, said Chanize Thorpe, editor of the Condé Nast site HotelChatter.com.

“You’ve got these kind of classic hotels that are reinventing themselves,” she said. “I think that’s one of the reasons why people will continually be interested in what’s going on.”

/// Continuum Development Corporation LLC

Articles from recapping the

2012 Lifestyle/Boutique Hotel Development Conference

Booming Boutique Business Meets in Miami

Beach

Oct 19, 2012 7:06 AM, By Ed Watkins

South Florida Leads the Way Back in Boutique/Lifestyle Segment

Jason Pomeranc of Commune Hotels believes in some cases branding can be a negative in

obtaining financing.

It‟s no surprise to anyone that the boutique and lifestyle segments of the hotel industry are doing

well. And based on strong operating performance in the sector, interest in the product has gained

a lot of ground in recent years from developers, operators, lenders and even traditional brand

companies. And nowhere is that trend more evident than in Miami, and in its Miami Beach

submarket, one of two epicenters (Manhattan is the other) of the boutique and lifestyle hotel

industry.

As Jay Coldren, vice president of lifestyle brands at Marriott, said during an opening panel at this

week‟s Lifestyle/Boutique Hotel Development Conference, “If you‟re serious about this

segment, you must be in Miami.”

Lodging Hospitality, in conjunction with HVS Hotel Management, sponsors LBHDC, which is

being held at the Fontainebleau Hotel in Miami Beach. The School of Hospitality Management

at Michigan State University is the conference‟s academic sponsor.

New data from STR shows the strength of the Miami area markets. Year-to-date through August

occupancy for Miami was 77.7%, while RevPAR increased a whopping 8.2%. And perhaps most

promising is the news that ADR has almost fully recovered to pre-recession levels, a process that

took 48 months.

The success of the lifestyle/boutique segment is having an effect throughout the industry. All

hotels, but especially lifestyle and boutique properties, need to become “more experiential and

sensory, said Marriott‟s Coldren. “The alternative is to perish.”

/// Continuum Development Corporation LLC

An example of how this segment has grown is seen in the financing arena. While many believe

it‟s difficult for non-branded hotels to attract debt or equity financing, Jason Pomeranc of

Commune Hotels said a brand can actually be a negative for a boutique hotel seeking financing,

particularly in some high-rate markets like New York City.

“With some products and in some markets it‟s warranted [to affiliate with a brand], but lenders

and institutions are starting to see in certain sectors you can do without brands and be better off,”

said Pomeranc. Commune includes a JdV Collection and the Thompson-brand hotels. He said

the company is also developing a new value-oriented, design-driven chain that will compete with

boutiques in lower price segments.

Marriott‟s Jay Coldren says all hotels need to take on some of the

characteristics of boutique hotels.

Nor surprisingly, Coldren of Marriott had a different opinion. In explaining the rationale for

Marriott‟s soft-brand Autograph Collection, he said, “People are looking for the ability to

function independently in the lifestyle segment but also to have a floor to their risk. By plugging

into our [reservations system] but maintaining the independent integrity of these hotels gives

lenders a lot more comfort and the financing comes a lot easier.”

The boutique segment is a beneficiary to what Denihan Hospitality President David Duncan

called a “raindrop recovery. Recovery very specifically depends on where you are,” he said,

adding that while nationwide about 35% of jobs lost in the downturn have returned, in New York

City 135% of jobs have returned. Denihan has 16 hotels under two brands (Affinia and James)

and a collection of independent properties. “That‟s why we focus on the top five to 10 markets

and in the center cities of those markets.”

Every industry conference panel focused on the boutique segment seems obligated to define the

word boutique, and this one was no different. While terms like “luxury finishes,” and

“individualized experiences” were cited by some panelists, Trust Hospitality President & COO

Patrick Goddard may have had the most insightful take on the topic.

“In many ways, a consumer‟s lodging decision is a form of self-expression,” he said. “That‟s the

way consumers buy certain brands of cars, clothing or shoes. The ways they choose a restaurant

or a hotel are reflections of themselves. So when we‟re creating a brand identity or voice, we

look at the target demographic and think about what they want in their experience.”

“Lifestyle” may be an even harder term to pin down. As Coldren said, “Every consumer product

on the market seems to have a „lifestyle‟ bent to it, right down to „lifestyle tires.‟” And as

moderator Jeff Higley of Smith Travel Research noted, the notion of a lifestyle product is really

not new in the hotel industry. “Even Knights Inn was developed decades ago as a lifestyle hotel

because it catered to the lifestyle of truckers,” he said.

/// Continuum Development Corporation LLC

Independent and Boutique Hotels Gain

Mainstream Acceptance

by Eric Stoessel October 19th, 2012

What Ian Schrager and Bill Kimpton started 25 years ago on opposite ends of the country in

gateway cities like San Francisco and New York has now met in the middle. Independent

boutique hotels can work — and thrive — in cities like Milwaukee, and developers at the fourth

annual Lifestyle/Boutique Hotel Development Conference in Miami this week talked about

projects in faraway places like Montana, Kentucky and Tennessee.

The segment has reached mainstream acceptance by consumers, investors and even the hotel

franchise companies.

Jay Coldren, vice president of lifestyle brands for Marriott International, said it‟s because of a

generational — and transformational — shift happening as Gen Y consumers and their

preference for lifestyle hotels take over buying power from the Baby Boomers in the next five

years.

Coldren heads Marriott‟s fast-growing Autograph Collection, a pseudo-brand allowing owners

more independence, yet a connection to the powerful Marriott system. Other hotel franchise

companies have similar offerings, like Choice‟s Ascend Collection, and more will follow in the

next five years, said Jeff Low, CEO and founder of Stash Hotel Rewards.

Investors and lenders are also taking notice. Neil Shah, president and chief operating officer of

Hersha Hospitality Trust, said in some markets independents have recovered faster than their

branded-counterparts and are trading at similar or even premium levels, in part because they are

unencumbered of a franchise or management contract. He also added that during the last cycle

there were many lenders who were only interested in branded properties. “Not anymore,” he said

during a general session at the Fontainebleau Thursday. “That‟s changing. More investors are

interested in independents.”

The general acceptance of the segment and success stories like the Iron Horse in Milwaukee

have helped open the door to new development in secondary markets. Patrick Goddard, president

of Trust Hospitality, said his company even targets some of those non-gateway cities. “There are

different prices, investments and it may be harder to get financing, but it can be done,” he said.

When this conference began three years ago we talked about the “burgeoning” lifestyle and

boutique segments. They‟re now booming.

Related Topics: General |

/// Continuum Development Corporation LLC

Independent Hoteliers Share Best Practices

Oct 23, 2012 9:03 AM, By Eric Stoessel

Jeff Low, founder and CEO of Stash Hotel Rewards, said one of the biggest challenges facing

independent hotel owners and operators is their “isolation.” They have no “idea bank” to draw

from.

At last week‟s Lifestyle/Boutique Hotel Development Conference at the Fontainebleau in Miami,

a panel of independent hoteliers traded best practices and shared similar stories of the challenges

they face competing in a branded world. The panel — titled, „Independents‟ Day‟ — was

moderated by Paramount Lodging Advisors Associate Michael Kitchen, and also included

Stash‟s Low, Clarendon Hotel Owner and General Manager Ben Bethel, Gemstone Resorts

Principal Jeff McIntyre and Cambean Hospitality President Brian Scheinblum.

“What‟s cool about being an independent is the customer tells us what we should be doing, not

the brand,” said McIntyre. “We‟re in the business of making memories.”

Being nimble and capable of reacting quickly to problems and market situations was the

consensus advantage independents have. “We can do what we want when we want,” said

Scheinblum, whose Cambean Hospitality owns and operates four small boutique hotels in South

Beach.

Online travel agencies were the biggest challenge facing independents, the panel agreed.

“Independents have twice the bookings from OTAs,” said Low. “Think about that, there‟s so

much money going out. Meanwhile you‟re calking your window to save money and you‟ve got

an entire wall missing. A lot independent players just aren‟t aware …

“If OTAs are like crack, then flash sales are like meth. Either way, your teeth fall out.”

Stash Rewards has approximately 200 hotel partners taking advantage of its loyalty program for

independents that helps offset franchised chains‟ hugely successful rewards programs.

During the downturn, Scheinblum said, there were many hotels probably “borderline losing

money on every single room they sold through OTAs” because of the reduced rates and high

commissions.

“Capture and keep,” said McIntyre of the strategy after bringing in a customer through an OTA

booking. “We don‟t just look at the 24% (cost), but (OTAs) are also a search engine to us. Many

customers look at pricing and product offerings and then book at the hotel‟s website. There is a

billboard effect.”

/// Continuum Development Corporation LLC

He also said OTAs could be a “great tool” for distressed properties, which Gemstone often is

brought on to manage. “As independents, those channels can‟t be ignored.”

Like the OTAs, where franchise partners often get better margins through brand-negotiated rates,

procurement was another area of concern for the independent hotelier. Low said he‟s heard from

his hotel partners that margins they‟re paying for purchasing products can be 25%, while the rate

is as low as 17% for at least one of the large franchise companies.

Bethel, the owner and general manager of the Clarendon, said he‟s ordered products direct from

Amazon.com and also recommended alibaba.com for sourcing and shipping direct from factories

around the world.

Bethel, who had no prior hotel experience, said he‟s not afraid to call other owners and

properties he respects to ask for advice. It was his only education after maxing out credit cards

and using home equity loans to buy the dilapidated building in Phoenix two weeks after he first

considered the idea.

At the Clarendon, he doesn‟t see an ROI in having a sales staff and doesn‟t employ a director of

sales. Instead, he heavily incents his front-desk staff with 20% to 50% commissions for every

room upgrade, early check-in or additional pool pass sold, meaning they can make up to $80,000

per year on their $10/hour salary. “Our front desk staff is so important, not just for loyalty

building, but to increase revenue,” he said.

Even more outside the box, Bethel charged guests for his property taxes during the downturn to

stay afloat when he couldn‟t even make his debt service. A 5% property tax fee was included on

all folios and also listed as a surcharge at all online sites. “We brought in $90,000 initially and it

enabled us to catch up,” he said. “It‟s not what I wanted to do, but at the time was something I

thought was a great idea when we were having problems making ends meet.”

Be Strong If You Want to Finance a Boutique

Hotel

Oct 24, 2012 6:44 AM, By Ed Watkins

Cash Flow Is the Most Important Ingredient

A panel on lending to boutiques said strong and stable cash flow is the most important element in

securing financing.

In the final analysis, finding financing for a transaction involving a boutique or lifestyle hotel

isn‟t much different than for a more traditional branded property. Most speakers on the topic at

last week‟s Lifestyle/Boutique Hotel Development Conference in Miami agreed it‟s all a matter

/// Continuum Development Corporation LLC

of strength: a strong story, strong sponsorship and management and, perhaps above all, strong

cash flow.

“In putting together the capital stack for a boutique property, the first questions to come up are

what is the cash flow, how stable is it, how does it compare to the peak of the market and how

much more room is there to grow,” said Frank Nardozza, chairman & CEO of REH Capital

Partners, who spoke on a panel titled „The Boutique Lending Landscape.‟ “If we can articulate

the cash flow, we can then get the interest of capital, both debt and equity.”

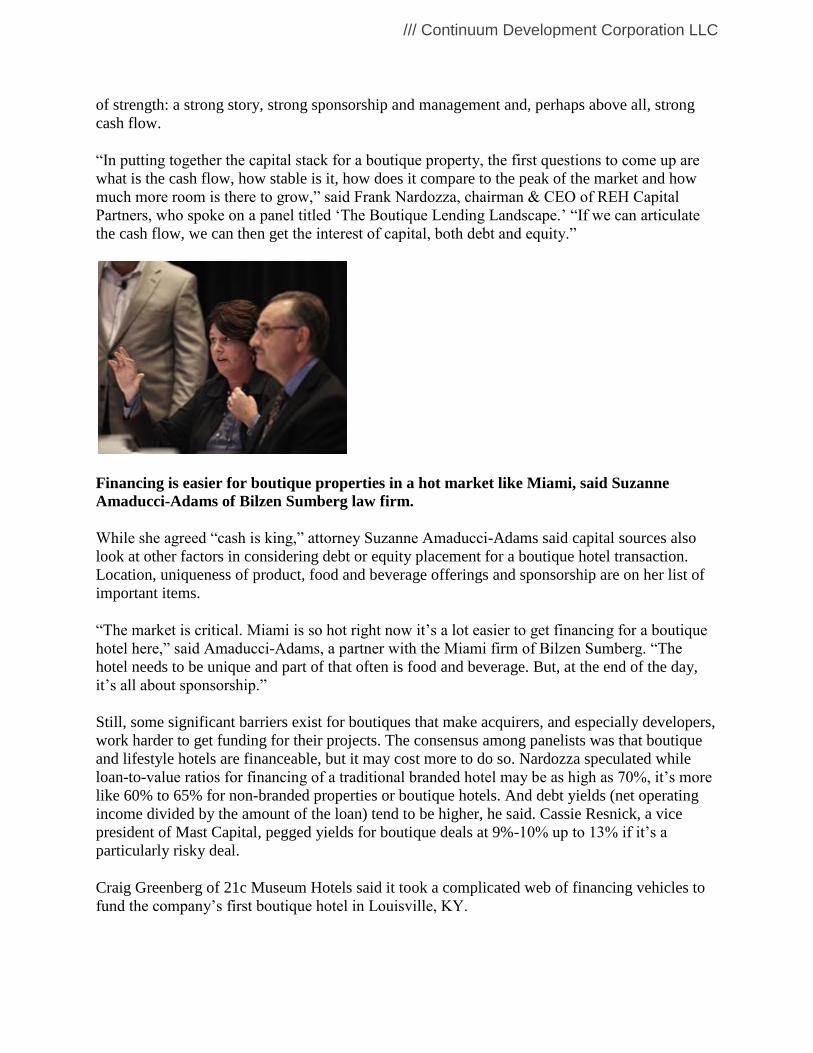

Financing is easier for boutique properties in a hot market like Miami, said Suzanne

Amaducci-Adams of Bilzen Sumberg law firm.

While she agreed “cash is king,” attorney Suzanne Amaducci-Adams said capital sources also

look at other factors in considering debt or equity placement for a boutique hotel transaction.

Location, uniqueness of product, food and beverage offerings and sponsorship are on her list of

important items.

“The market is critical. Miami is so hot right now it‟s a lot easier to get financing for a boutique

hotel here,” said Amaducci-Adams, a partner with the Miami firm of Bilzen Sumberg. “The

hotel needs to be unique and part of that often is food and beverage. But, at the end of the day,

it‟s all about sponsorship.”

Still, some significant barriers exist for boutiques that make acquirers, and especially developers,

work harder to get funding for their projects. The consensus among panelists was that boutique

and lifestyle hotels are financeable, but it may cost more to do so. Nardozza speculated while

loan-to-value ratios for financing of a traditional branded hotel may be as high as 70%, it‟s more

like 60% to 65% for non-branded properties or boutique hotels. And debt yields (net operating

income divided by the amount of the loan) tend to be higher, he said. Cassie Resnick, a vice

president of Mast Capital, pegged yields for boutique deals at 9%-10% up to 13% if it‟s a

particularly risky deal.

Craig Greenberg of 21c Museum Hotels said it took a complicated web of financing vehicles to

fund the company‟s first boutique hotel in Louisville, KY.

/// Continuum Development Corporation LLC

Another panel at the conference tackled the problem of how to overcome the often-negative

perception lenders have about unbranded and independent boutique hotels. Craig Greenberg,

president of 21c Museum Hotels, acknowledged the issue is especially critical in the markets in

which his firm operates. The company has a successful property open in Louisville, KY, with

another to open next month in Cincinnati, followed by one in northwest Arkansas.

“It‟s definitely more challenging, especially in smaller or medium-sized cities, to get money,”

said Greenberg, who showed the audience an elaborate chart outlining the variety of funding

sources—a mix of tax credits, rebates, grants, equity and traditional recourse bank loans—used

to develop the first 21c. “In that kind of environment, it usually takes a perfect story to put

together a financing package.”

Oliver Striker, a director at UBS Investment Bank, agreed, saying his firm, which provides both

CMBS financing and direct investment, takes a “holistic approach” to evaluating financing

proposals, both from traditional hotels and also boutique and lifestyle properties. While he said

location is a primary factor, it‟s not the only one.

“Gateway cities with high barriers of entry and depth of demand are obviously preferred,” he

said, “but sponsorship is also crucial, especially the depth of experience they have in the sector.

It‟s also important the sponsor has skin in the game, because it forces them to keep their eyes on

the ball.”

Despite these caveats, speakers on both panels believe financing for boutique and lifestyle

products, both branded and non-branded, is becoming more mainstream.

“Because real cash flows are showing up on the bottom lines of boutique hotels, there is more

receptivity in the lending community to funding and capitalizing [these products],” said

Nardozza. “It‟s a more familiar product to guests and a more familiar product to the capital

markets.”

/// Continuum Development Corporation LLC

Appendix N.C. / /

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

2012 North Carolina Lodging Report

A Publication of the North Carolina Division of Tourism, Film and Sports Development

January 2013

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

2012 North Carolina Lodging Report

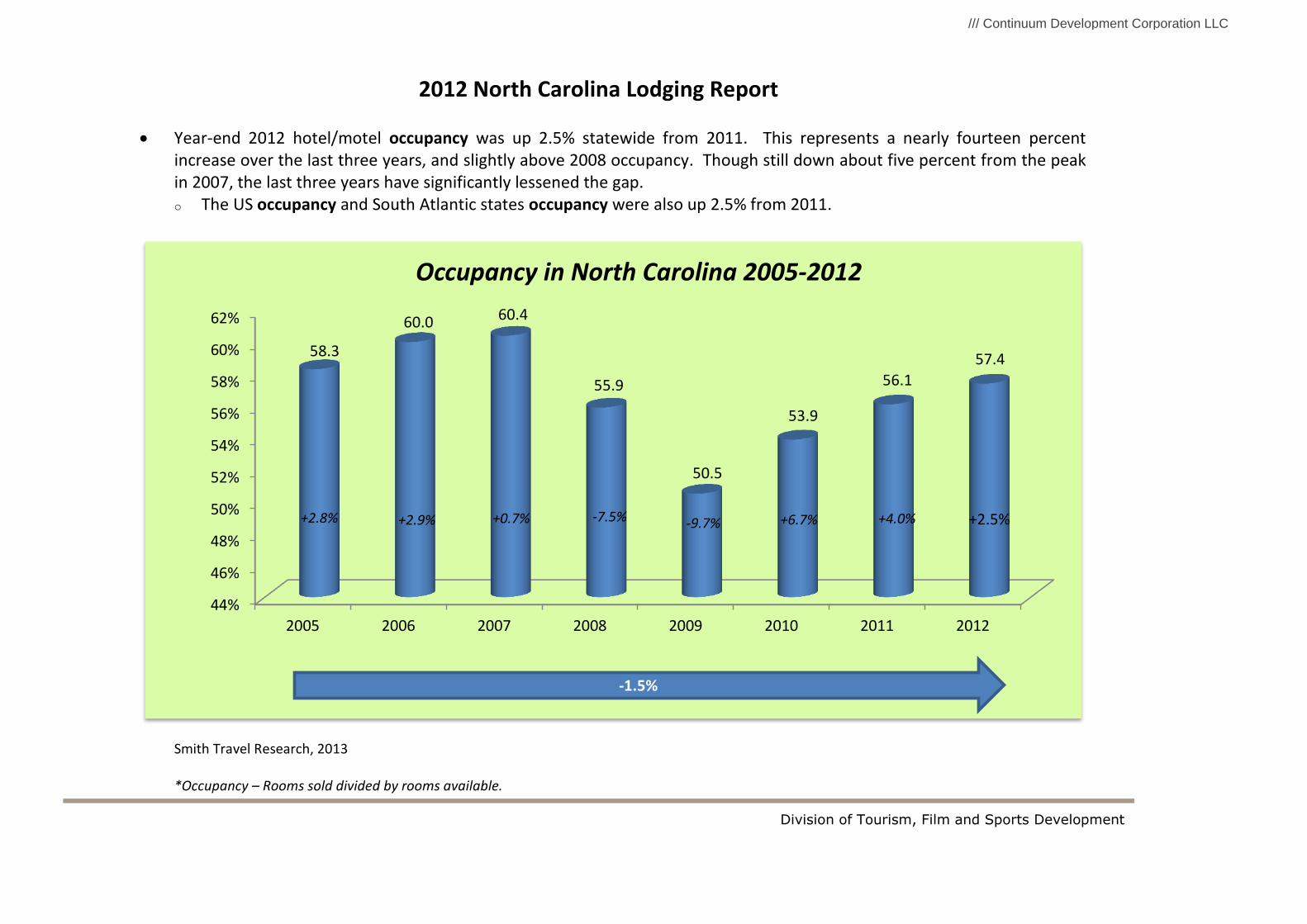

Year-end 2012 hotel/motel occupancy was up 2.5% statewide from 2011. This represents a nearly fourteen percent increase over the last three years, and slightly above 2008 occupancy. Though still down about five percent from the peak in 2007, the last three years have significantly lessened the gap. o The US occupancy and South Atlantic states occupancy were also up 2.5% from 2011.

Smith Travel Research, 2013 *Occupancy – Rooms sold divided by rooms available.

44%

46%

48%

50%

52%

54%

56%

58%

60%

62%

2005 2006 2007 2008 2009 2010 2011 2012

58.3

60.0 60.4

55.9

50.5

53.9

56.1

57.4

Occupancy in North Carolina 2005-2012

+2.9% +0.7% -7.5% +2.8%

-1.5%

-9.7% +6.7% +4.0% +2.5%

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

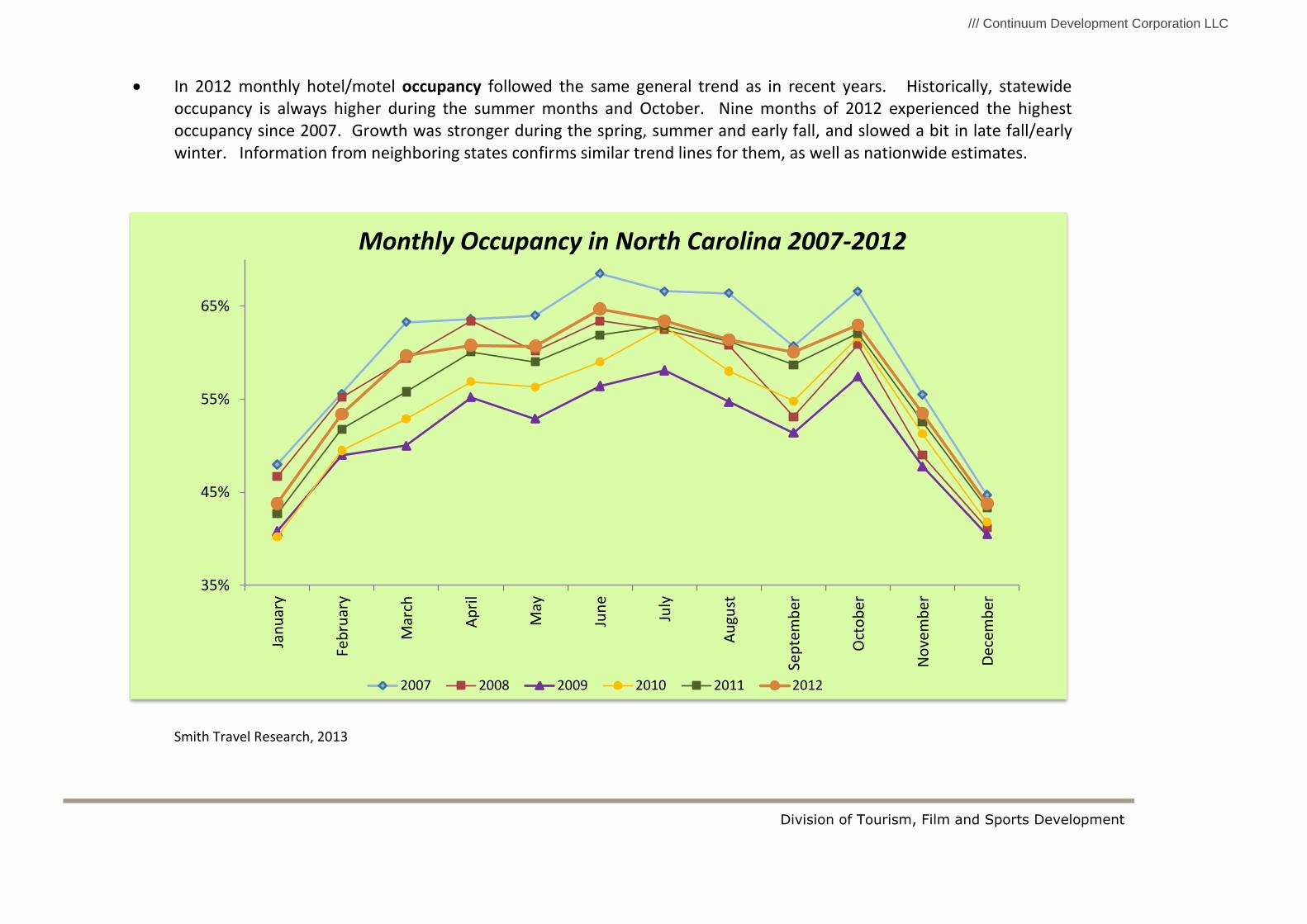

In 2012 monthly hotel/motel occupancy followed the same general trend as in recent years. Historically, statewide occupancy is always higher during the summer months and October. Nine months of 2012 experienced the highest occupancy since 2007. Growth was stronger during the spring, summer and early fall, and slowed a bit in late fall/early winter. Information from neighboring states confirms similar trend lines for them, as well as nationwide estimates.

Smith Travel Research, 2013

35%

45%

55%

65%

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gust

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Monthly Occupancy in North Carolina 2007-2012

2007 2008 2009 2010 2011 2012

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

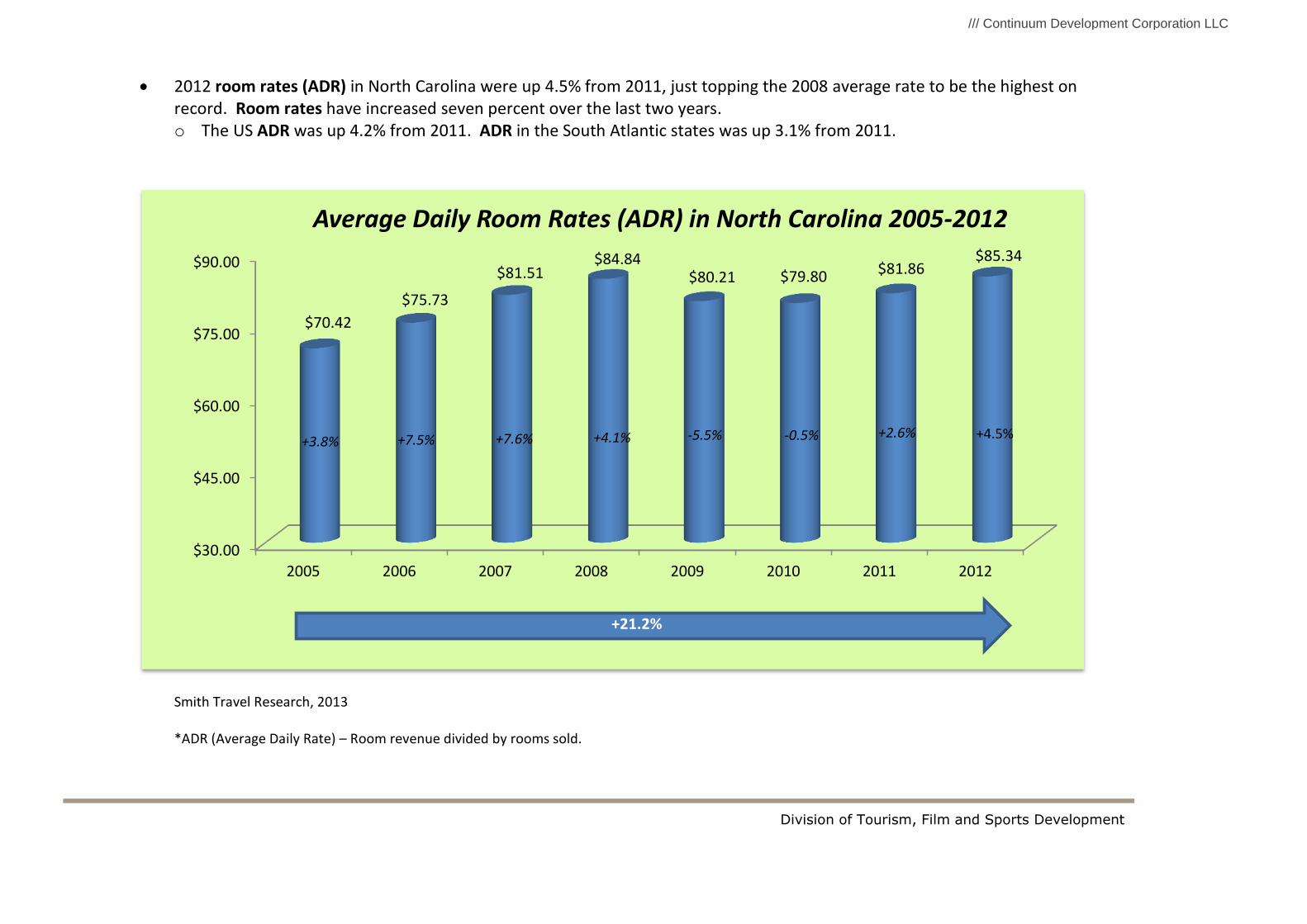

2012 room rates (ADR) in North Carolina were up 4.5% from 2011, just topping the 2008 average rate to be the highest on record. Room rates have increased seven percent over the last two years. o The US ADR was up 4.2% from 2011. ADR in the South Atlantic states was up 3.1% from 2011.

Smith Travel Research, 2013 *ADR (Average Daily Rate) – Room revenue divided by rooms sold.

$30.00

$45.00

$60.00

$75.00

$90.00

2005 2006 2007 2008 2009 2010 2011 2012

$70.42

$75.73

$81.51 $84.84

$80.21 $79.80 $81.86 $85.34

Average Daily Room Rates (ADR) in North Carolina 2005-2012

+7.5% +7.6% +4.1% +3.8%

+21.2%

-5.5% -0.5% +2.6% +4.5%

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

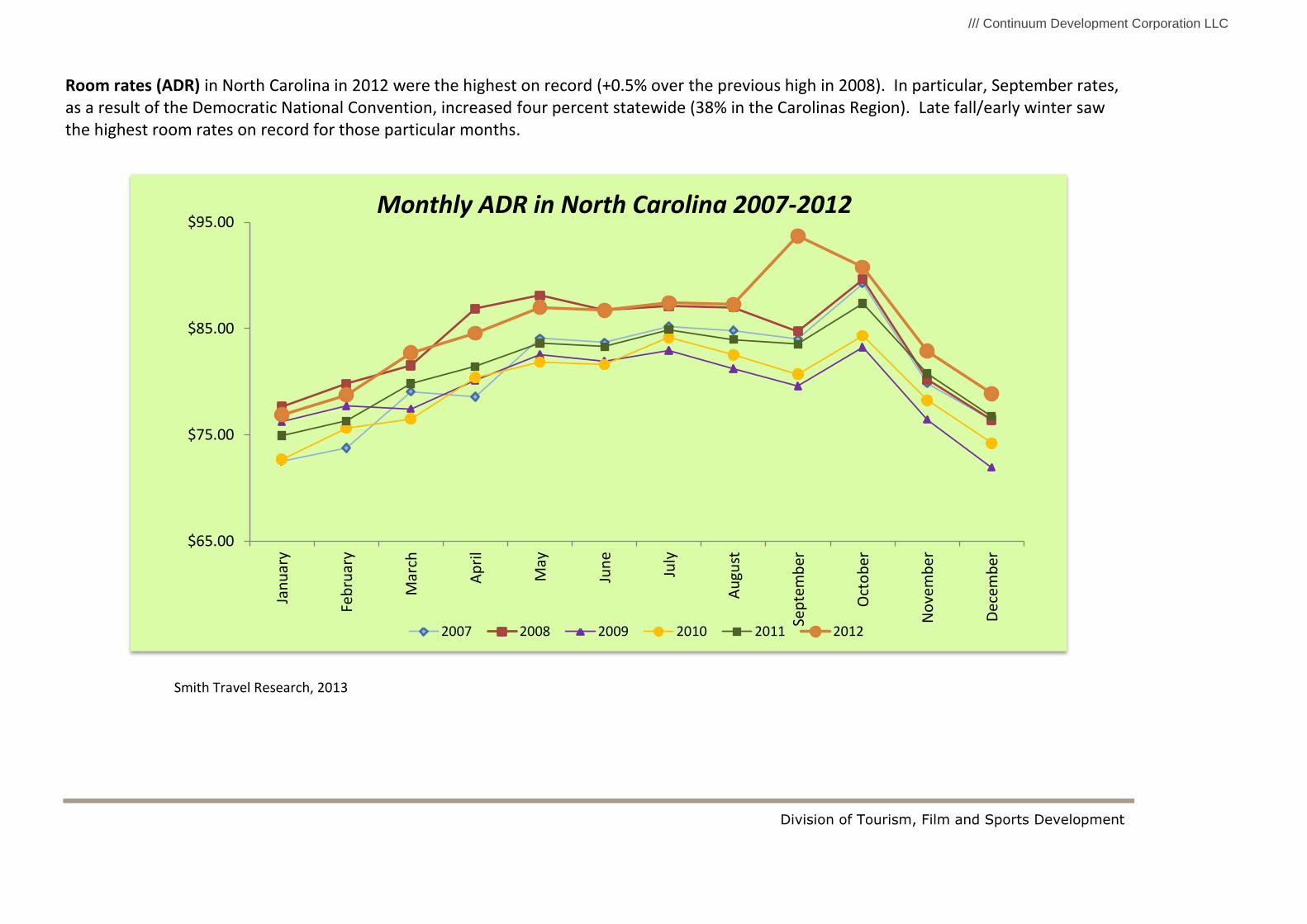

Room rates (ADR) in North Carolina in 2012 were the highest on record (+0.5% over the previous high in 2008). In particular, September rates, as a result of the Democratic National Convention, increased four percent statewide (38% in the Carolinas Region). Late fall/early winter saw the highest room rates on record for those particular months.

Smith Travel Research, 2013

$65.00

$75.00

$85.00

$95.00

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gust

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Monthly ADR in North Carolina 2007-2012

2007 2008 2009 2010 2011 2012

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

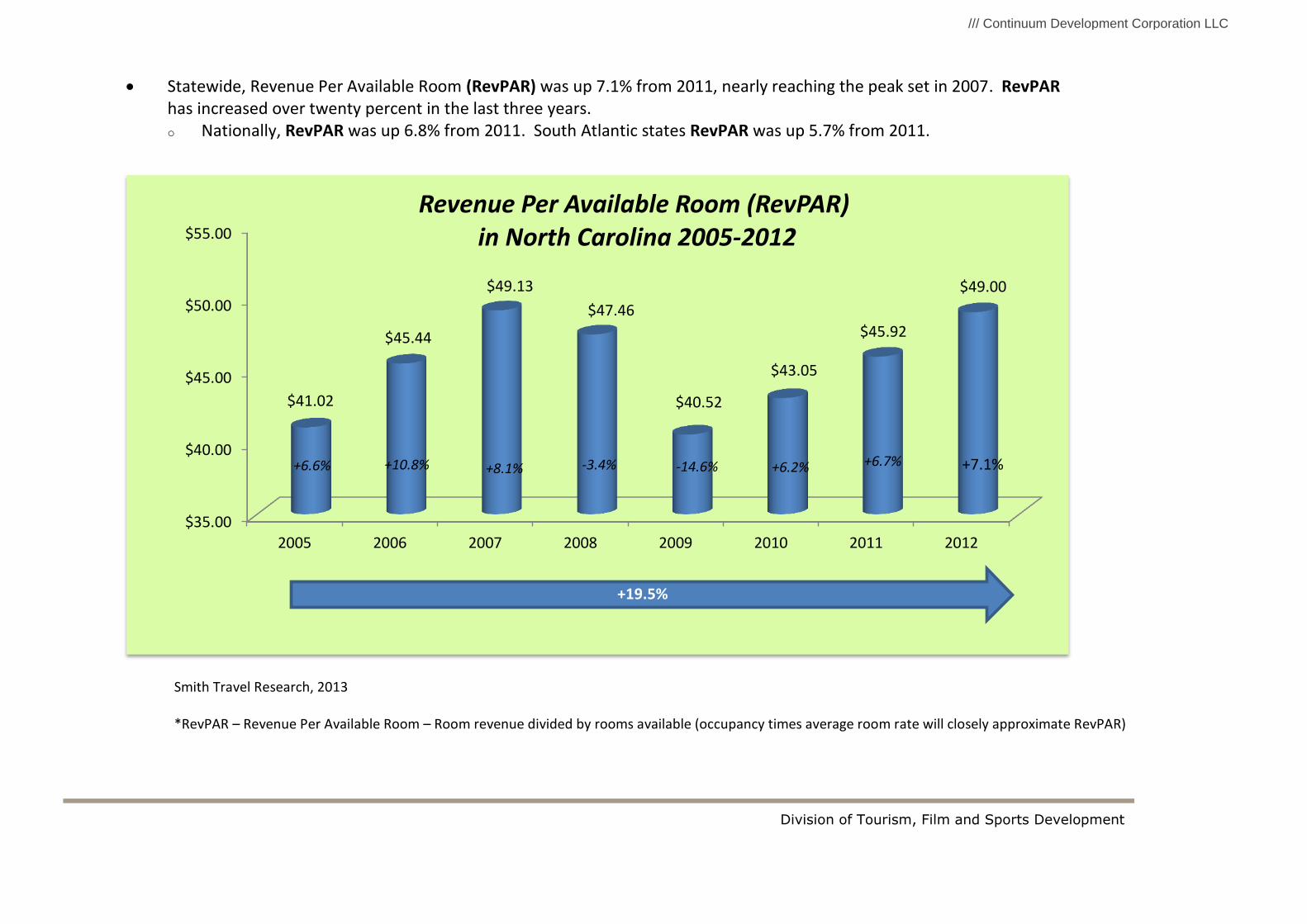

Statewide, Revenue Per Available Room (RevPAR) was up 7.1% from 2011, nearly reaching the peak set in 2007. RevPAR has increased over twenty percent in the last three years. o Nationally, RevPAR was up 6.8% from 2011. South Atlantic states RevPAR was up 5.7% from 2011.

Smith Travel Research, 2013 *RevPAR – Revenue Per Available Room – Room revenue divided by rooms available (occupancy times average room rate will closely approximate RevPAR)

$35.00

$40.00

$45.00

$50.00

$55.00

2005 2006 2007 2008 2009 2010 2011 2012

$41.02

$45.44

$49.13

$47.46

$40.52

$43.05

$45.92

$49.00

Revenue Per Available Room (RevPAR) in North Carolina 2005-2012

+10.8% +8.1% -3.4% +6.6%

+19.5%

-14.6% +6.2% +6.7% +7.1%

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

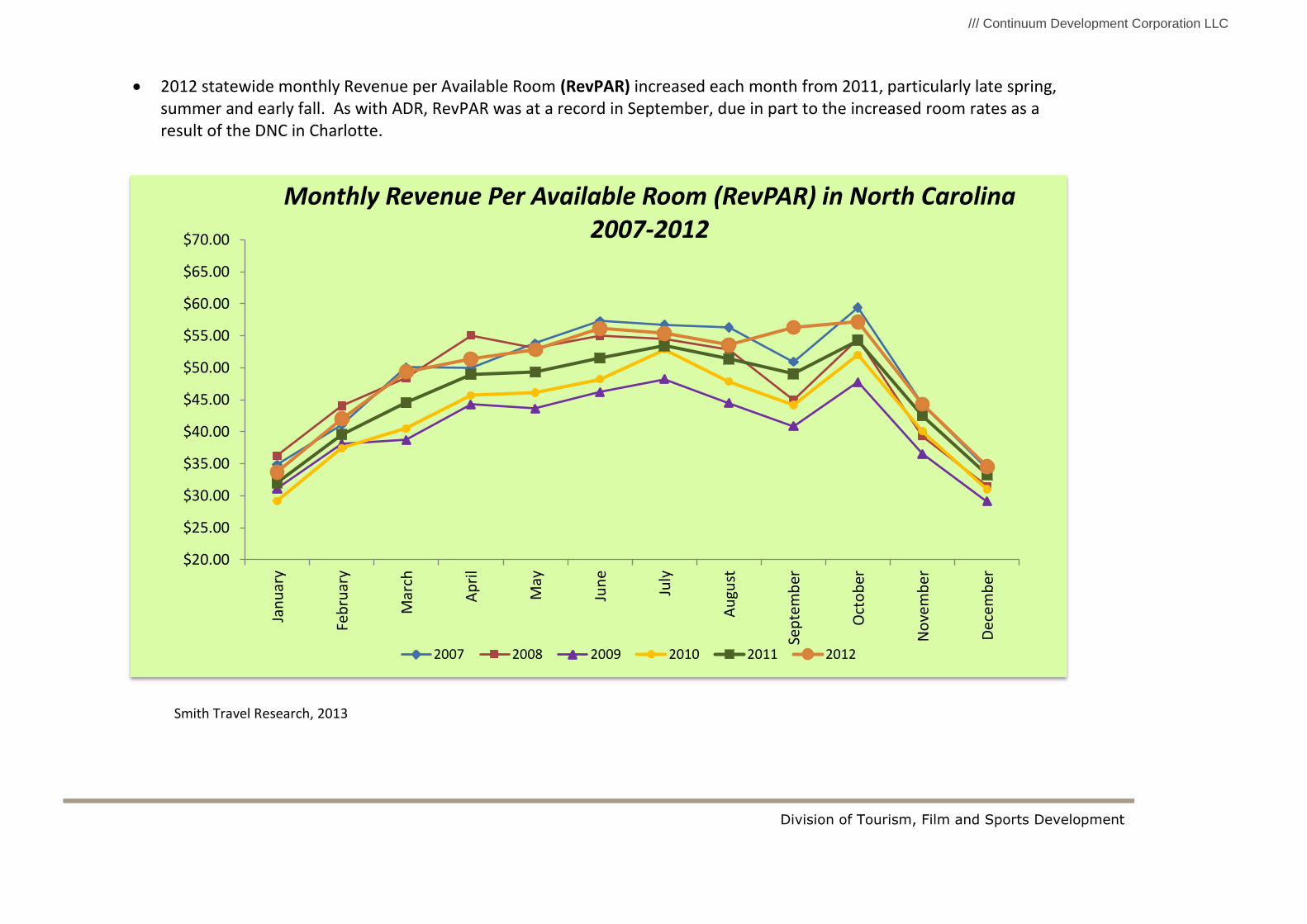

2012 statewide monthly Revenue per Available Room (RevPAR) increased each month from 2011, particularly late spring, summer and early fall. As with ADR, RevPAR was at a record in September, due in part to the increased room rates as a result of the DNC in Charlotte.

Smith Travel Research, 2013

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

$65.00

$70.00

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gust

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Monthly Revenue Per Available Room (RevPAR) in North Carolina 2007-2012

2007 2008 2009 2010 2011 2012

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

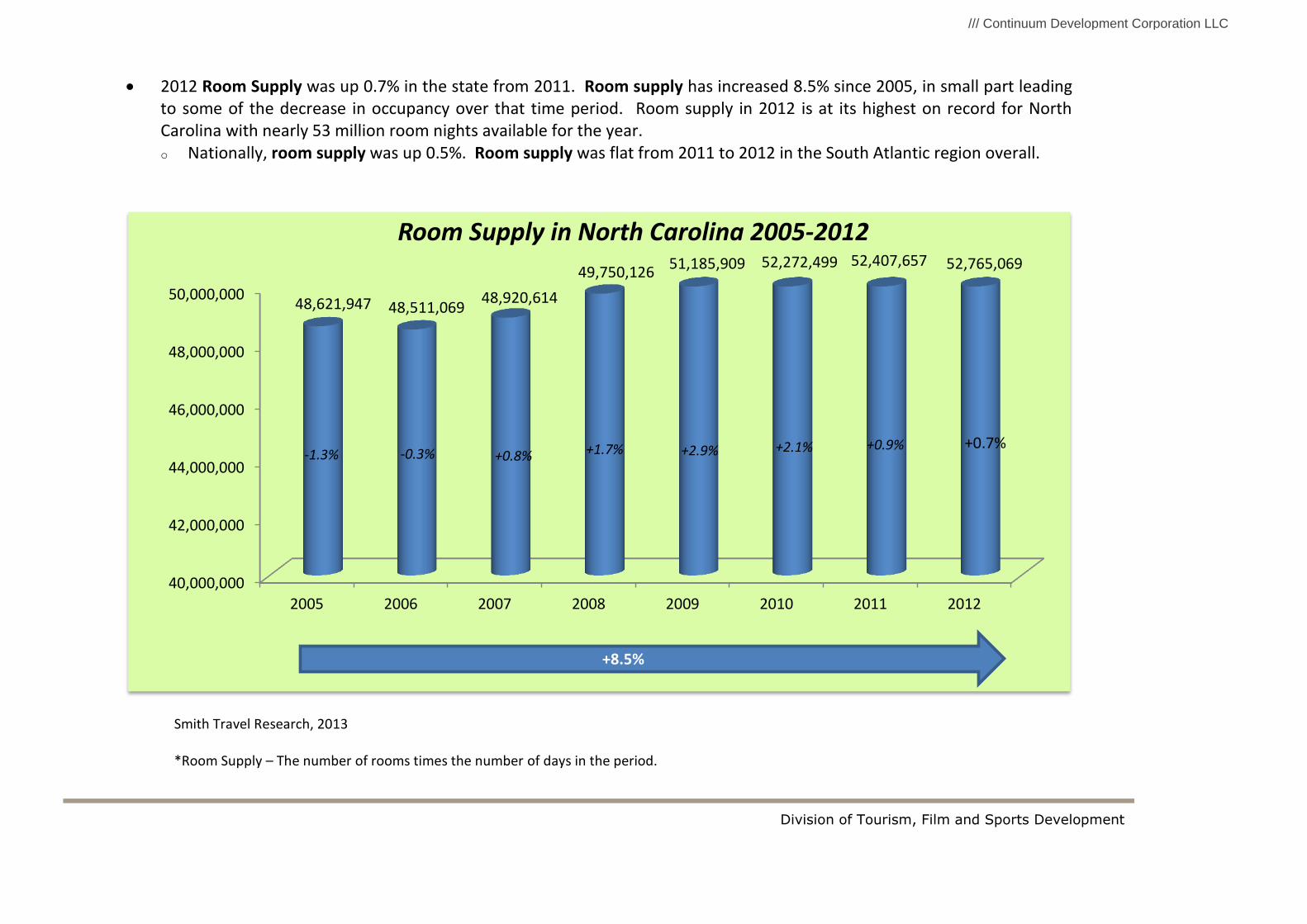

2012 Room Supply was up 0.7% in the state from 2011. Room supply has increased 8.5% since 2005, in small part leading to some of the decrease in occupancy over that time period. Room supply in 2012 is at its highest on record for North Carolina with nearly 53 million room nights available for the year. o Nationally, room supply was up 0.5%. Room supply was flat from 2011 to 2012 in the South Atlantic region overall.

Smith Travel Research, 2013 *Room Supply – The number of rooms times the number of days in the period.

40,000,000

42,000,000

44,000,000

46,000,000

48,000,000

50,000,000

2005 2006 2007 2008 2009 2010 2011 2012

48,621,947 48,511,069 48,920,614

49,750,126 51,185,909 52,272,499 52,407,657 52,765,069

Room Supply in North Carolina 2005-2012

-0.3% +0.8% +1.7% -1.3%

+8.5%

+2.9% +2.1% +0.9% +0.7%

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

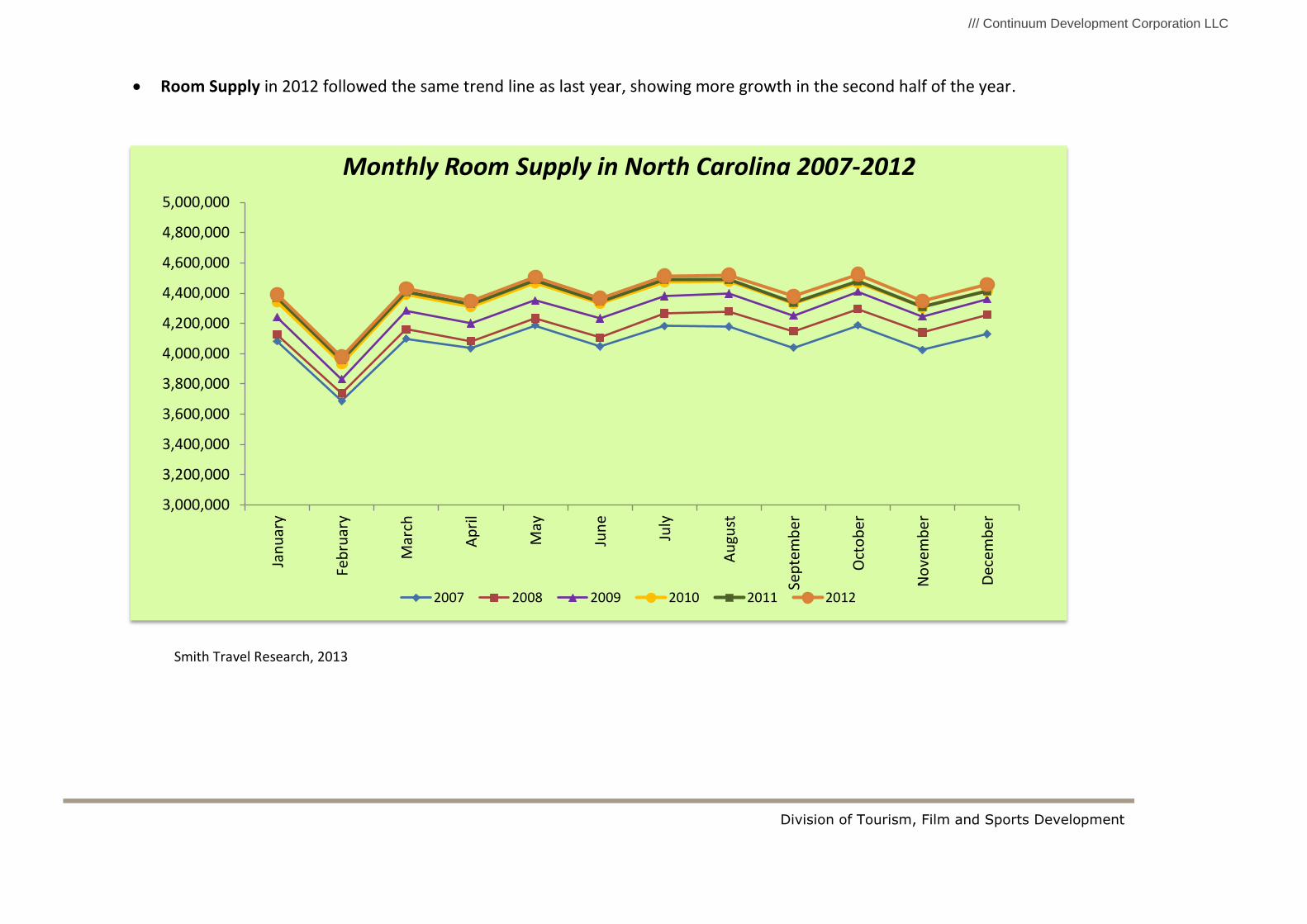

Room Supply in 2012 followed the same trend line as last year, showing more growth in the second half of the year.

Smith Travel Research, 2013

3,000,000

3,200,000

3,400,000

3,600,000

3,800,000

4,000,000

4,200,000

4,400,000

4,600,000

4,800,000

5,000,000

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gust

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Monthly Room Supply in North Carolina 2007-2012

2007 2008 2009 2010 2011 2012

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

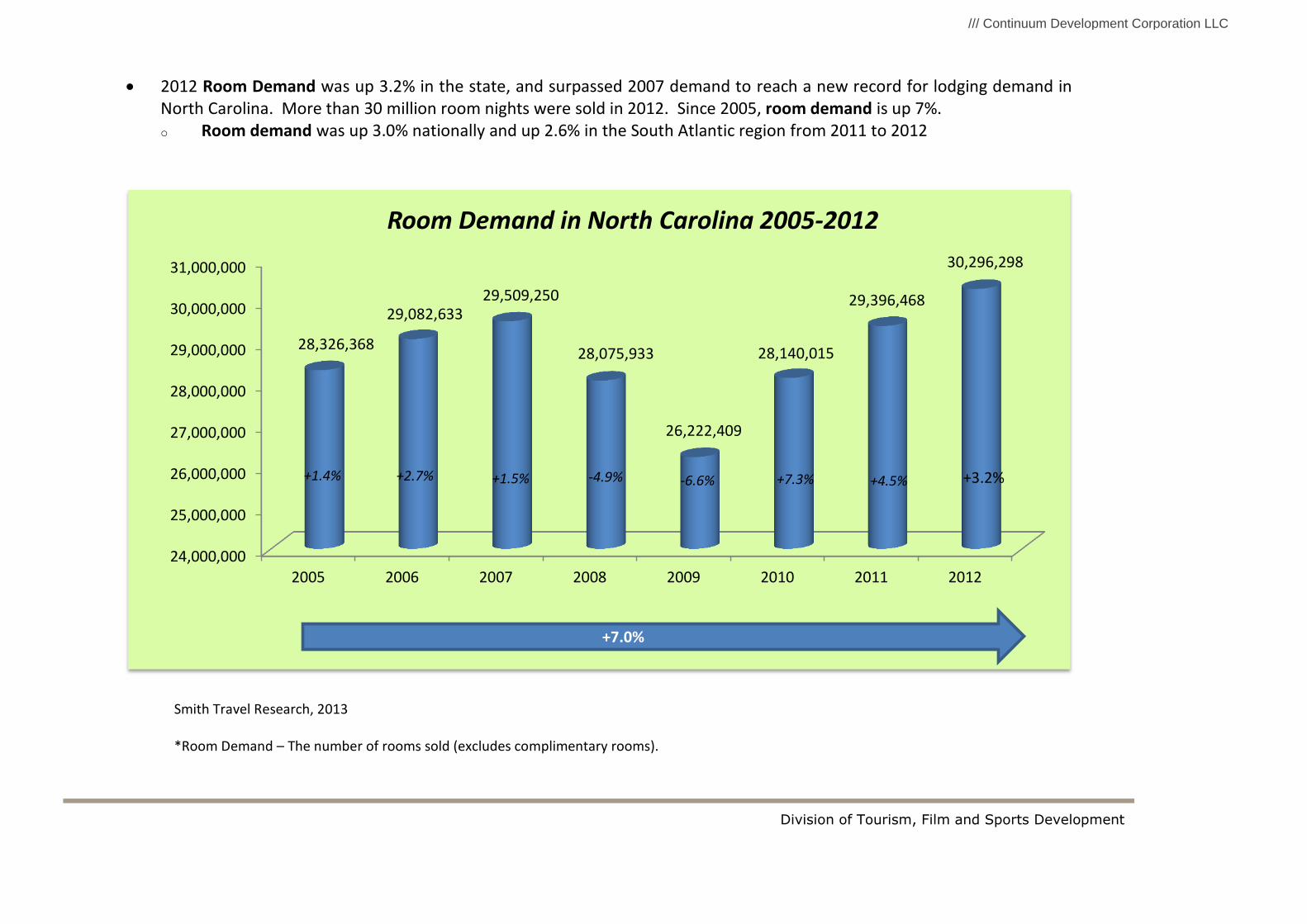

2012 Room Demand was up 3.2% in the state, and surpassed 2007 demand to reach a new record for lodging demand in North Carolina. More than 30 million room nights were sold in 2012. Since 2005, room demand is up 7%. o Room demand was up 3.0% nationally and up 2.6% in the South Atlantic region from 2011 to 2012

Smith Travel Research, 2013 *Room Demand – The number of rooms sold (excludes complimentary rooms).

24,000,000

25,000,000

26,000,000

27,000,000

28,000,000

29,000,000

30,000,000

31,000,000

2005 2006 2007 2008 2009 2010 2011 2012

28,326,368

29,082,633 29,509,250

28,075,933

26,222,409

28,140,015

29,396,468

30,296,298

Room Demand in North Carolina 2005-2012

+2.7% +1.5% -4.9% +1.4%

+7.0%

-6.6% +7.3% +4.5% +3.2%

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

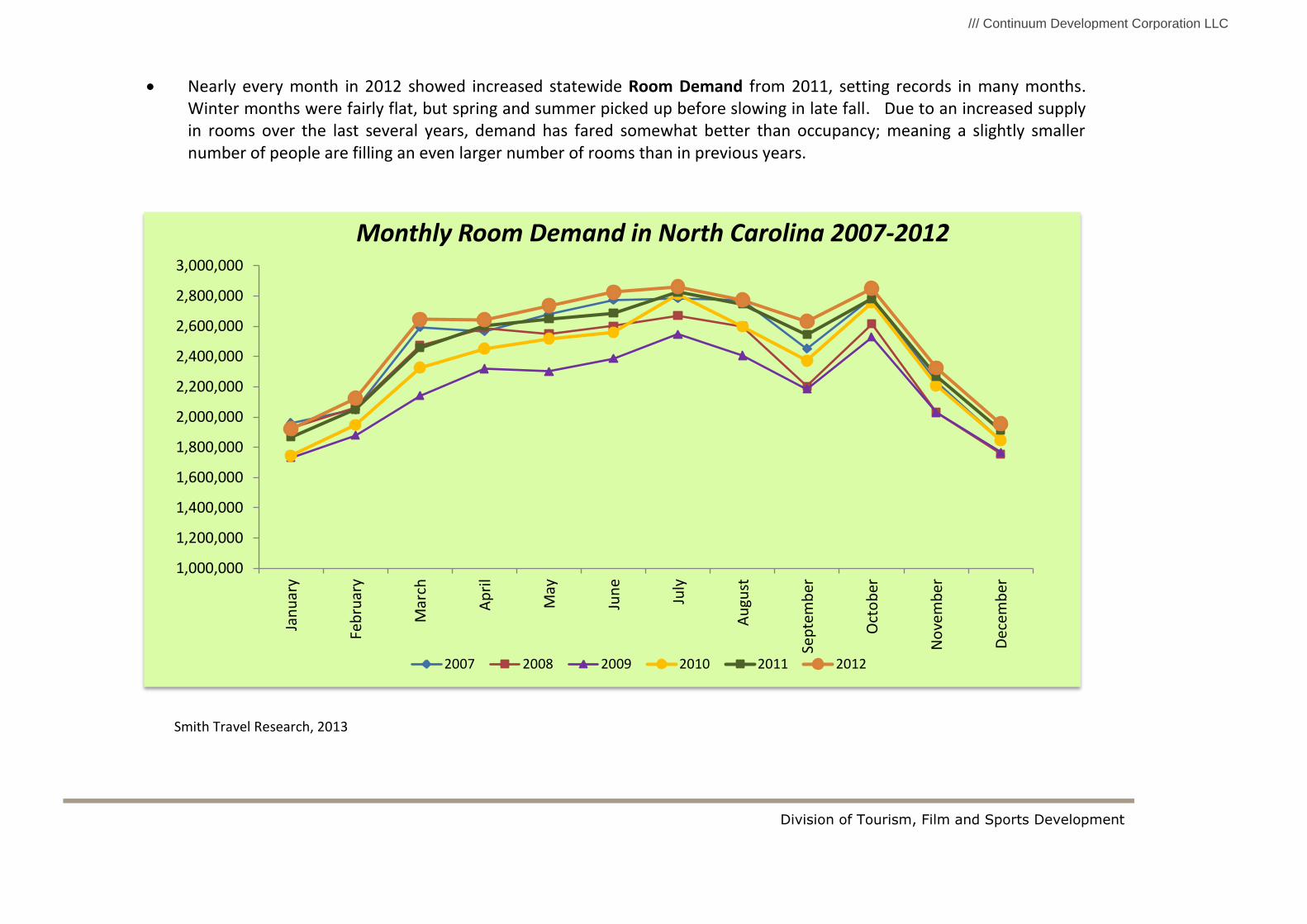

Nearly every month in 2012 showed increased statewide Room Demand from 2011, setting records in many months. Winter months were fairly flat, but spring and summer picked up before slowing in late fall. Due to an increased supply in rooms over the last several years, demand has fared somewhat better than occupancy; meaning a slightly smaller number of people are filling an even larger number of rooms than in previous years.

Smith Travel Research, 2013

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gust

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Monthly Room Demand in North Carolina 2007-2012

2007 2008 2009 2010 2011 2012

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

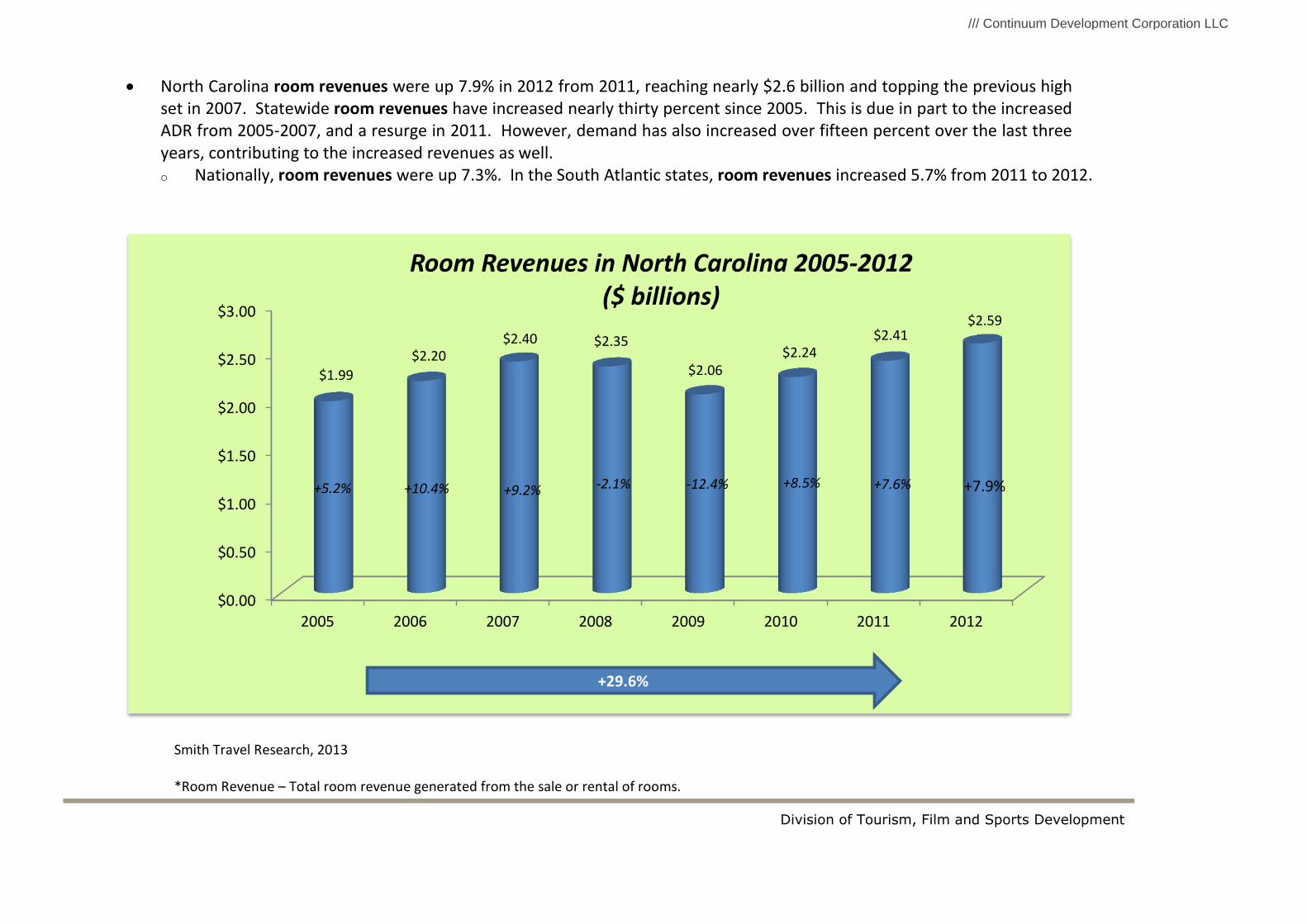

North Carolina room revenues were up 7.9% in 2012 from 2011, reaching nearly $2.6 billion and topping the previous high set in 2007. Statewide room revenues have increased nearly thirty percent since 2005. This is due in part to the increased ADR from 2005-2007, and a resurge in 2011. However, demand has also increased over fifteen percent over the last three years, contributing to the increased revenues as well. o Nationally, room revenues were up 7.3%. In the South Atlantic states, room revenues increased 5.7% from 2011 to 2012.

Smith Travel Research, 2013 *Room Revenue – Total room revenue generated from the sale or rental of rooms.

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2005 2006 2007 2008 2009 2010 2011 2012

$1.99

$2.20 $2.40 $2.35

$2.06 $2.24

$2.41 $2.59

Room Revenues in North Carolina 2005-2012 ($ billions)

+10.4% +9.2% -2.1% +5.2%

+29.6%

-12.4% +8.5% +7.6% +7.9%

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

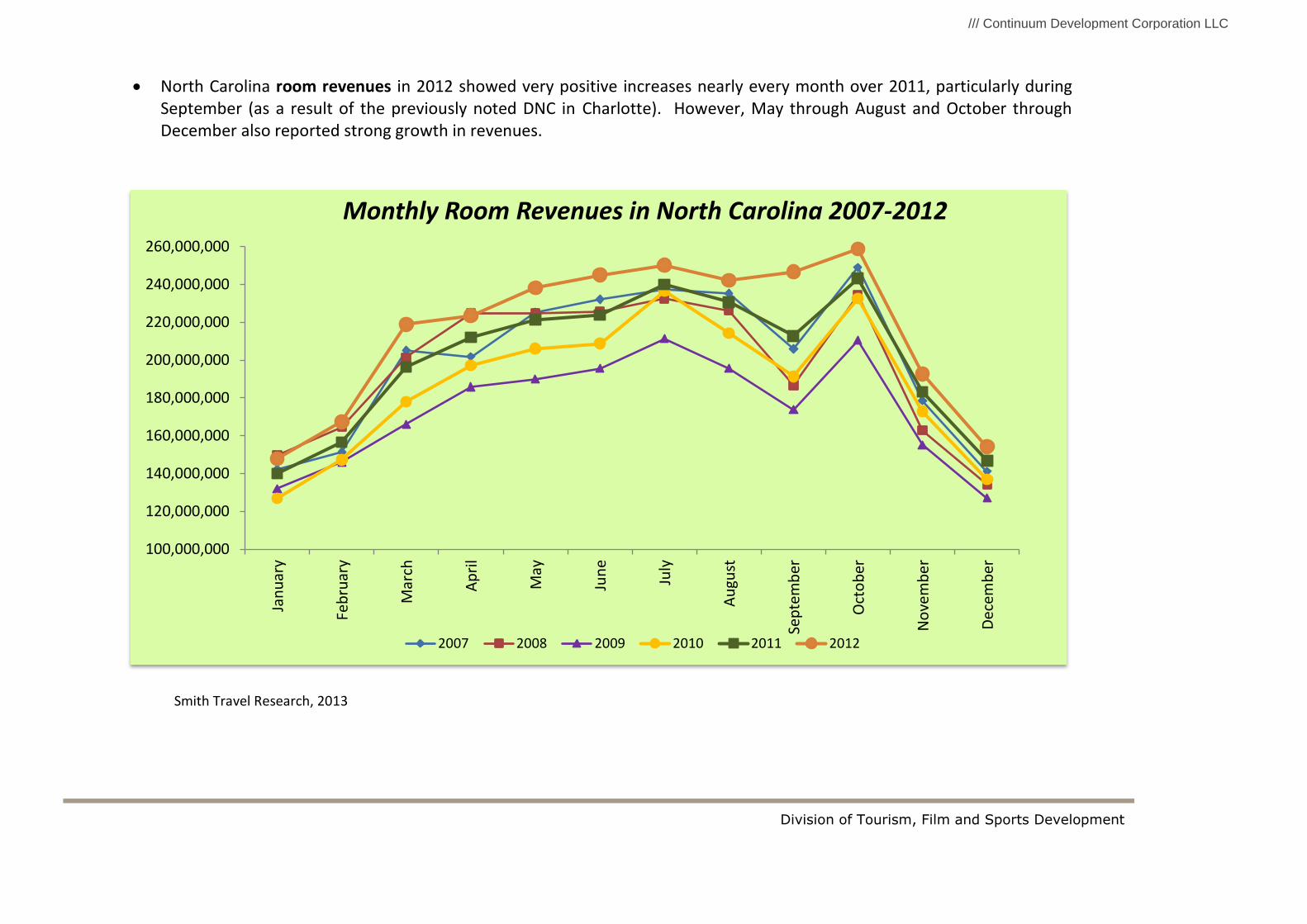

North Carolina room revenues in 2012 showed very positive increases nearly every month over 2011, particularly during September (as a result of the previously noted DNC in Charlotte). However, May through August and October through December also reported strong growth in revenues.

Smith Travel Research, 2013

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

240,000,000

260,000,000

Jan

uar

y

Feb

ruar

y

Mar

ch

Ap

ril

May

Jun

e

July

Au

gust

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Monthly Room Revenues in North Carolina 2007-2012

2007 2008 2009 2010 2011 2012

/// Continuum Development Corporation LLC

Division of Tourism, Film and Sports Development

Methodology

While virtually every chain in the United States provides STR with data on almost all of their properties, there are still some hotels that don't submit data. However, every year STR examines guidebook listings and hotel directories for information on hotels that don't provide data. STR calls each hotel in their database every year to obtain "published" rates for multiple categories. Based on this information all hotels are grouped - those that report data and those that don't - into groupings based off of price level and geographic proximity. They then estimate the non-respondents based off of nearby hotels with similar price levels.

Glossary

ADR (Average Daily Rate)

Revenue (Room Revenue)

Room revenue divided by rooms sold.

Total room revenue generated from the sale or rental of rooms.

Affiliation Date

RevPAR - Revenue Per Available Room

Date the property affiliated with current chain/flag

Room revenue divided by rooms available (occupancy times average room rate will closely approximate RevPAR).

Census (Properties and Rooms)

The number of properties and rooms that exist (universe)

Sample % (Rooms)

The % of rooms STR receives data from. Calculated as (Sample

Change in Rooms

Rooms/Census Rooms) * "100".

Indicator of whether or not an individual hotel has had added or deleted rooms.

Standard Historical TREND

Exchange Rate

Data on selected properties or segments starting in 1997.

The factor used to convert revenue from U.S. Dollars to the local currency.

The exchange rate data is obtained from Oanda.com. Any aggregated number

STR Code

in the report (YTD, Running 3 month, Running 12 month) uses the exchange

Smith Travel Research's proprietary numbering system. Each hotel in the

rate of each relative month when calculating the data.

lodging census has a unique STR code.

Demand (Rooms Sold)

Supply (Rooms Available)

The number of rooms sold (excludes complimentary rooms).

The number of rooms times the number of days in the period.

Full Historical TREND

Twelve Month Moving Average

Data on selected properties or segments starting in 1987.

The value of any given month is computed by taking the value of that month

and the values of the eleven preceding months, adding them together and

Occupancy

dividing by twelve.

Rooms sold divided by rooms available.

Year to Date

Open Date

Average or sum of values starting January 1 of the given year.

Date the property opened

Percent Change

Amount of growth, up, flat, or down from the same period last year (month, ytd, three months, twelve months). Calculated as ((TY-LY)/LY) * "100".

/// Continuum Development Corporation LLC

Investing in secondary markets is lucrative

19 February 2013

By Aik Hong Tan

HotelNewsNow.com columnist

Story Highlights

With interest rates remaining at historic low levels, cash-on-cash yield investing in

secondary markets can be lucrative with the appropriate level of leverage.

The key to successful investments in secondary markets is the existence of diverse and

sustainable demand generators.

The number of demand drivers in secondary markets is more targeted than in major

markets.

As the industry recovery continues to gain momentum, opportunities for investors abound.

Whether it’s a full-service property in New York, San Francisco or Miami, a select service hotel

in Pittsburgh or Raleigh, North Carolina, or a limited-service asset in Frisco, Texas, or Pueblo,

Colorado, there is no shortage of capital waiting to get off the sidelines and back in the game.

With real estate investment trusts, sovereign funds and institutional capital chasing deals in the

major markets, yields are being driven down to the range of 3% to 5%. The situation is quite

different in the secondary markets, where capitalization rates are ranging from 8.5% up to as

high as 12%. As a result, with interest rates remaining at historic low levels, cash-on-cash yield

investing in secondary markets can be

lucrative with the appropriate level of

leverage.

With that said, to be successful, an investor must pay special attention to specific issues that are

unique to any secondary-market deal.

Demand First and foremost, as with deals of any kind, careful study and understanding of demand

generators in the market are crucial. The number and nature of demand drivers in secondary

markets tends to be fewer and more targeted than in major markets such as New York or Los

Angeles.

/// Continuum Development Corporation LLC

It is important to understand the dynamics that draw travelers to the area. Sometimes it can be a

single landmark such as a college or military base. In these cases, it is essential to realize that

even one single event, like the closure of the military base, can have a major impact on demand.

In other cases, factors such as the construction or major refurbishment of a factory might bring