Embed Size (px)

Citation preview

1

LEXINGTON PARK

ROTARY

FINANCIAL

LITERACY

PRESENTATION

(Financial Survival

Skills)

LEXINGTON PARK

ROTARY

FINANCIAL

LITERACY

PRESENTATION

(Financial Survival

Skills)

2

What Is ROTARY?

• Rotary is a worldwide organization of business and professional leaders that provides humanitarian service, encourages high ethical standards in all vocations, and helps build goodwill and peace in the world. Approximately 1.2 million Rotarians belong to more than 32,000 clubs in more than 200 countries.

3

What Is ROTARY?

• Lexington Park Rotary Club– Chartered May 7, 1960– Have 100 members– Meet Mondays at J.T. Daugherty Center (12 Noon)– Provide financial support for scholarships, charity and

international projects– Community Service: Dictionary Project, Christmas In

April, Four-Way Speech Contest and Financial Literacy– Fund Raising Projects:

• Oyster Festival• River Concert Series• Golf Tournament

4

Disclaimer

The information and material presented herein are provided for information purposes only. This is not an offer to buy or sell securities, investment products or other financial instruments, nor to constitute any advice or recommendations with respect to securities, investment products or other financial instruments.

5

Topics

• Personal Budgeting• Emergency Fund• Debt Management• Insurance• Tuition Assistance• Income Taxes• Investments• Retirement Planning• Financial Publications and Websites

6

Personal Budgeting

7

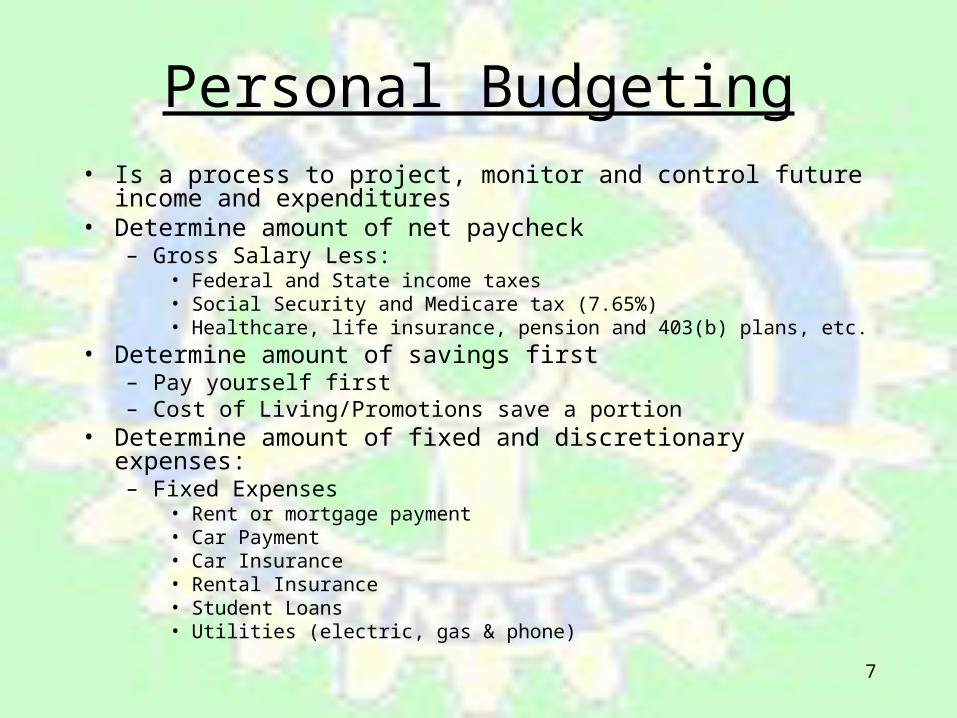

Personal Budgeting• Is a process to project, monitor and control future income and

expenditures• Determine amount of net paycheck

– Gross Salary Less:• Federal and State income taxes• Social Security and Medicare tax (7.65%)• Healthcare, life insurance, pension and 403(b) plans, etc.

• Determine amount of savings first– Pay yourself first– Cost of Living/Promotions save a portion

• Determine amount of fixed and discretionary expenses:– Fixed Expenses

• Rent or mortgage payment• Car Payment• Car Insurance• Rental Insurance• Student Loans• Utilities (electric, gas & phone)

8

Personal Budgeting

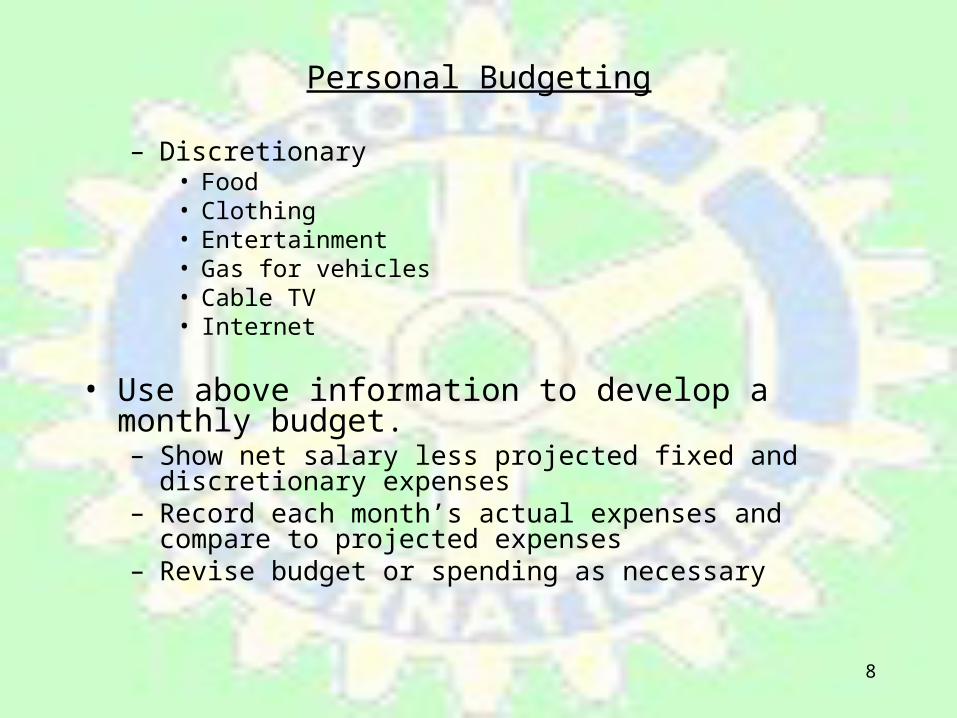

– Discretionary• Food• Clothing• Entertainment• Gas for vehicles• Cable TV• Internet

• Use above information to develop a monthly budget.– Show net salary less projected fixed and discretionary expenses– Record each month’s actual expenses and compare to projected

expenses– Revise budget or spending as necessary

9

Emergency Fund

10

Emergency Fund

• Should cover 3-6 months of living expenses• Should have funds to cover unexpected

events– Household replacements– Medical expenses– Temporary illness not covered by sick leave or

disability policy

• Part of your Savings Program

11

Debt Management

12

-- Paying the minimum balance on a credit card

results in the payment of monthly interest but very

little principal.

CreditCards

Debt Management

CreditCard Cost

13

CreditCards

Debt Management

CreditCard Cost

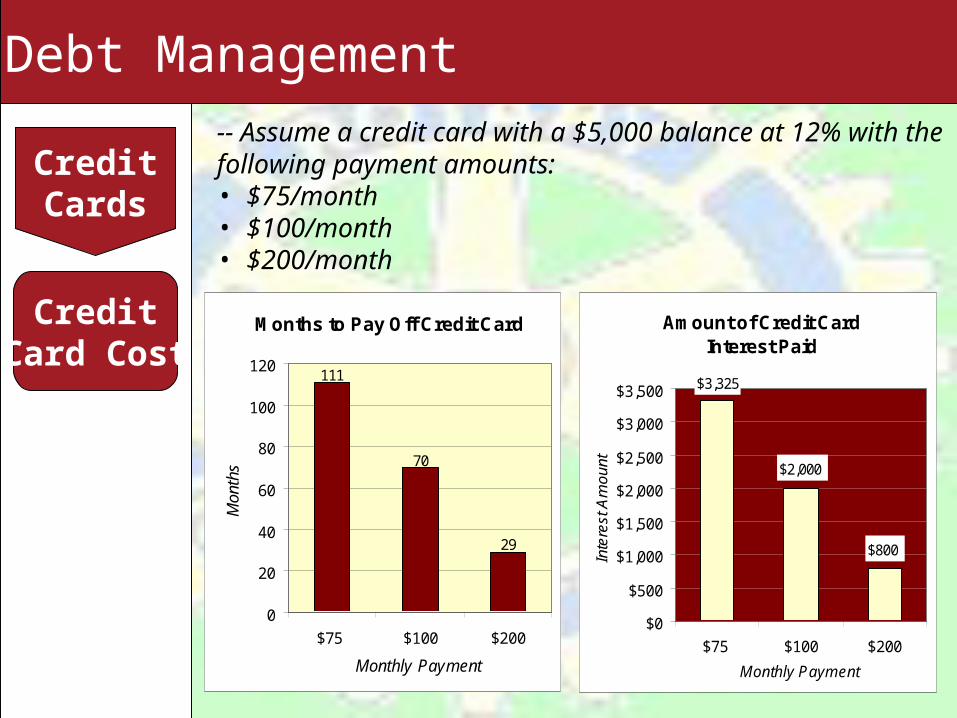

-- Assume a credit card with a $5,000 balance at 12% with the following payment amounts:• $75/month• $100/month• $200/month

Months to Pay Off Credit Card

111

70

29

0

20

40

60

80

100

120

$75 $100 $200

Monthly Payment

Mon

ths

Amount of Credit CardInterest Paid

$3,325

$800

$2,000

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$75 $100 $200

Monthly Payment

Inte

rest

Am

ount

14

Debt Management – Credit Cards

• Call credit card companies and negotiate a lower rate

• Develop a plan to pay off credit card debt• In most cases, Pay off highest interest rate credit

card first or pay off small credit card balances• Transfer balances to a lower rate credit card• Cancel unused credit cards• Only maintain several credit cards• Maintain a high credit score

15

Credit Score

• Should know your credit score– Impacts your loan interest rates

– Impacts your insurance costs

• Credit Score Components– 35% payment history

– 30% amounts owed

– 15% length of credit history

– 10% new credit accounts

– 10% types of credit used

Credit Score

• Obtain copies of your credit reports from Equifax, Experian and TransUnion– Go to www.annualcreditreport.com for free

reports– Can get free copy every 12 months– Review reports to insure they are correct

17

Insurance

18

Life Insurance

• Life Insurance is a must if your death would cause hardship for someone you want to protect

• Stages of Life Insurance Needs:– Little need – young single person– Greater need – spouse/children

19

Term Insurance

• Pays a predetermined sum if insured dies during specified time period

• Is pure insurance with no cash value• Most companies provide term life insurance but is

usually not transferable• Is inexpensive for young people• Provides large death benefit at lowest cost• Excellent choice for temporary insurance• Is available at level face amount

20

Whole Life Insurance

• Provides life-time protection

• Has a savings component

• Has a cash value– Can be used for a loan– Can be surrendered and receive cash

• Payment options– Premiums are level for life– Premiums are paid for a specified period

21

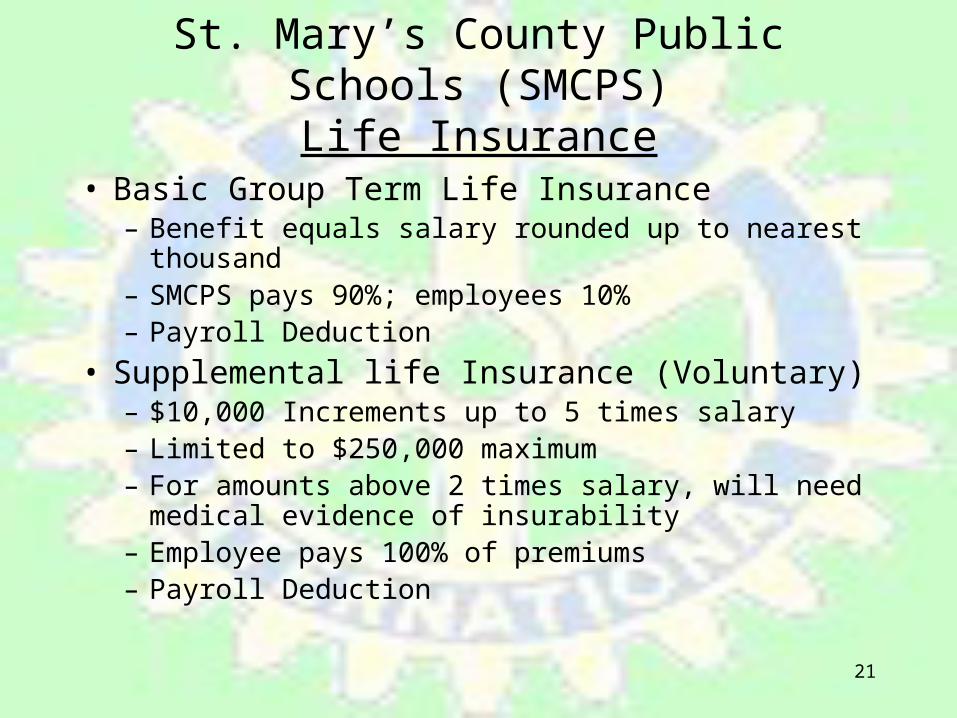

St. Mary’s County Public Schools (SMCPS)Life Insurance

• Basic Group Term Life Insurance– Benefit equals salary rounded up to nearest thousand– SMCPS pays 90%; employees 10%– Payroll Deduction

• Supplemental life Insurance (Voluntary)– $10,000 Increments up to 5 times salary– Limited to $250,000 maximum– For amounts above 2 times salary, will need medical

evidence of insurability– Employee pays 100% of premiums– Payroll Deduction

22

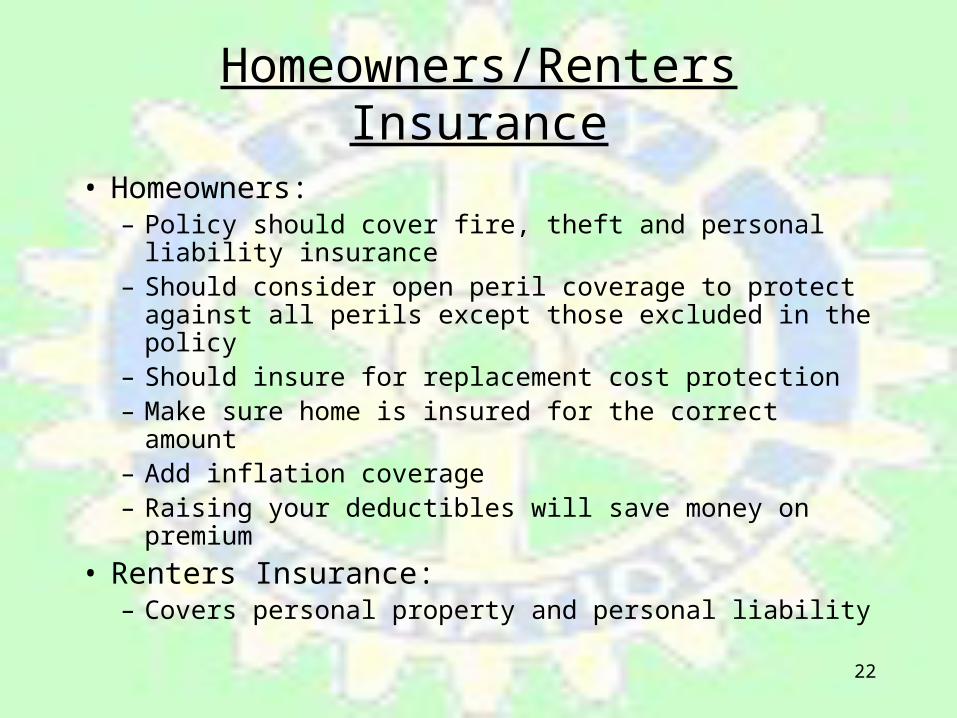

Homeowners/Renters Insurance

• Homeowners:– Policy should cover fire, theft and personal liability

insurance– Should consider open peril coverage to protect against

all perils except those excluded in the policy– Should insure for replacement cost protection– Make sure home is insured for the correct amount– Add inflation coverage– Raising your deductibles will save money on premium

• Renters Insurance:– Covers personal property and personal liability

23

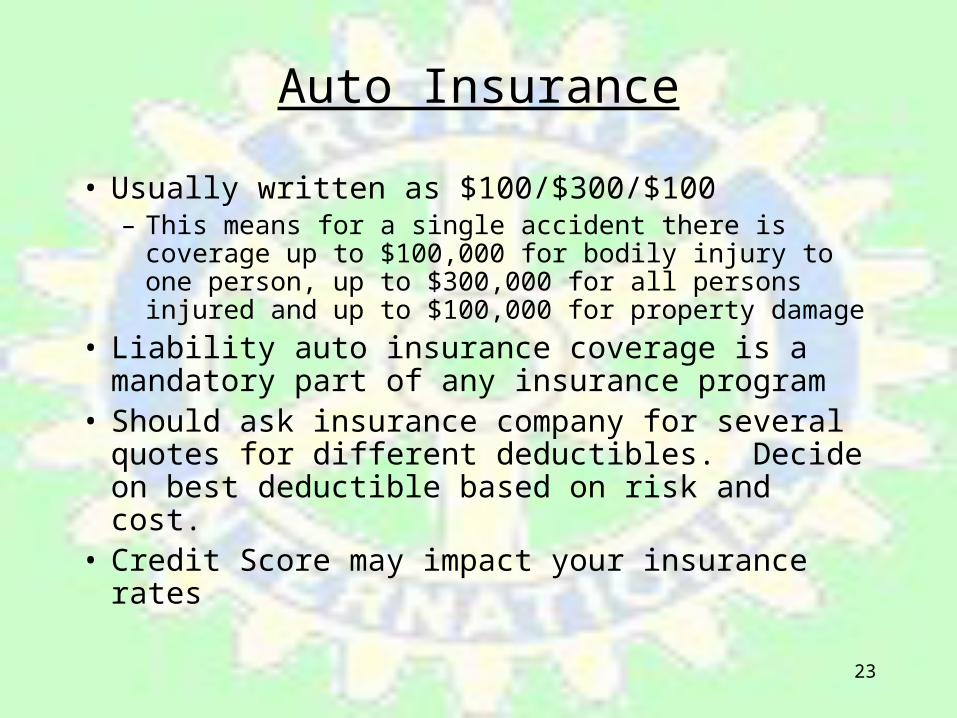

Auto Insurance

• Usually written as $100/$300/$100– This means for a single accident there is coverage up to

$100,000 for bodily injury to one person, up to $300,000 for all persons injured and up to $100,000 for property damage

• Liability auto insurance coverage is a mandatory part of any insurance program

• Should ask insurance company for several quotes for different deductibles. Decide on best deductible based on risk and cost.

• Credit Score may impact your insurance rates

24

Tuition Assistance

25

Tuition Assistance

• $2,300 Tuition reimbursement (2008-2009)

26

Income Taxes

27

Income Taxes

• For 2008, Teachers classroom unreimbursed qualified expenditures– Can deduct up to $250 to Adjusted Gross Income– Can deduct amount in excess of $250 on

Schedule A as an itemized deduction subject to 2% of AGI

– Examples: books, supplies and supplemental material used in the classroom

28

Income Taxes

• Interest paid during the year for qualified education loans may be deductible depending on income level.

• College tuition deduction to adjusted gross income or use life long learning credit per family– The deduction or credit will depend on income

levels

29

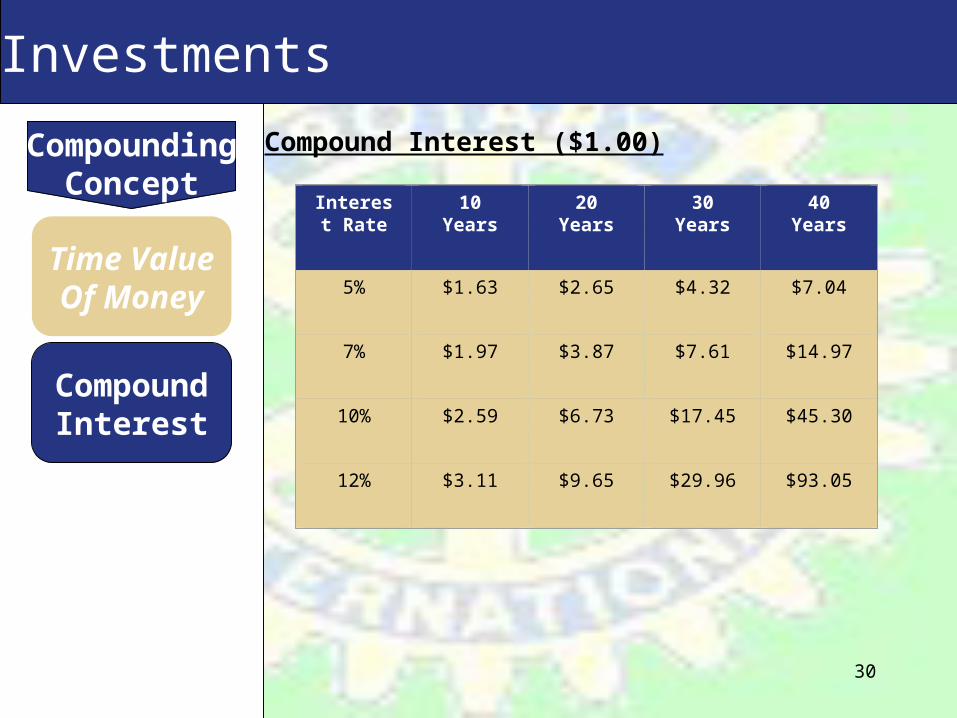

Investments

30

Investments

CompoundingConcept

Time ValueOf Money

CompoundInterest

Compound Interest ($1.00)

Interest Rate

10 Years 20 Years 30 Years 40 Years

5% $1.63 $2.65 $4.32 $7.04

7% $1.97 $3.87 $7.61 $14.97

10% $2.59 $6.73 $17.45 $45.30

12% $3.11 $9.65 $29.96 $93.05

31

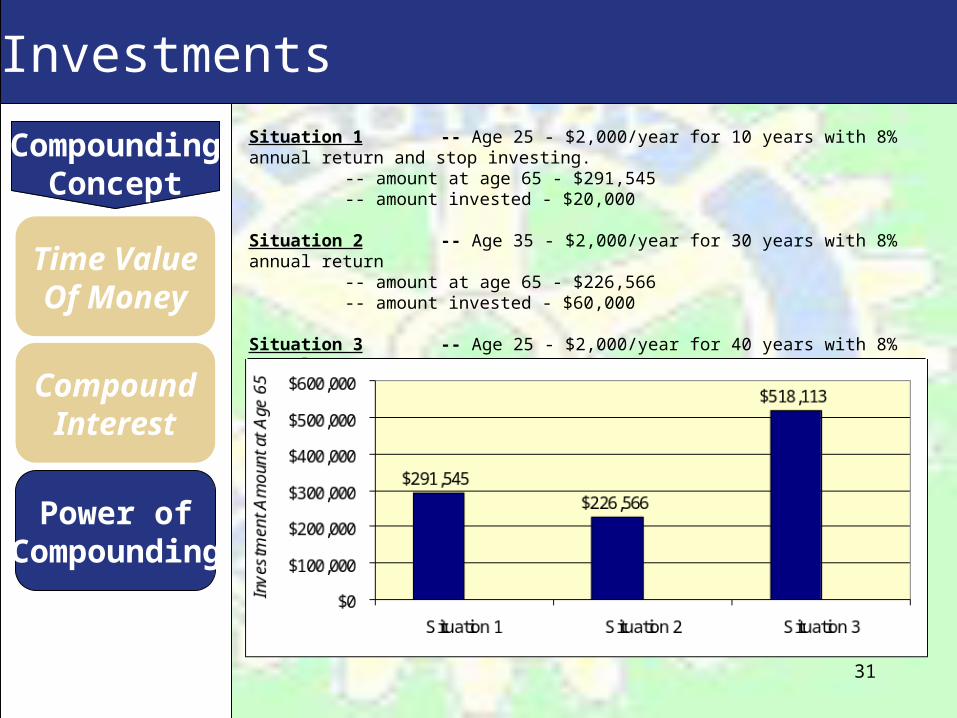

Investments

CompoundingConcept

Time ValueOf Money

CompoundInterest

Power ofCompounding

Situation 1 -- Age 25 - $2,000/year for 10 years with 8% annual return and stop investing.-- amount at age 65 - $291,545-- amount invested - $20,000

Situation 2 -- Age 35 - $2,000/year for 30 years with 8% annual return-- amount at age 65 - $226,566-- amount invested - $60,000

Situation 3 -- Age 25 - $2,000/year for 40 years with 8% annual return-- amount at age 65 - $518,113-- amount invested - $80,000

32

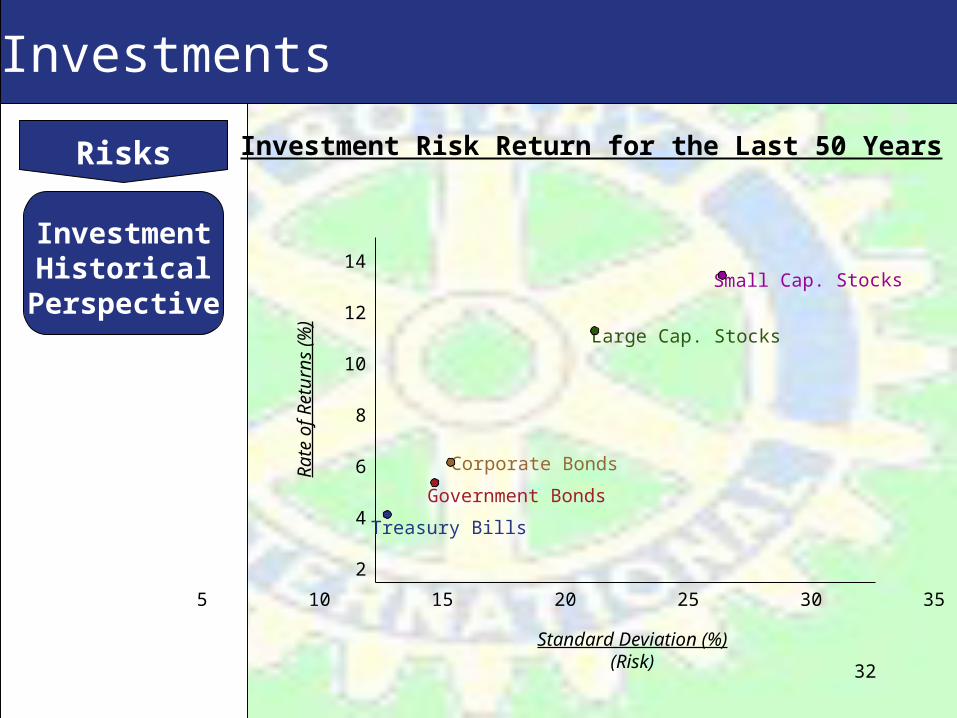

Investments

Risks

InvestmentHistorical

Perspective

Investment Risk Return for the Last 50 Years

Rat

e o

f R

etu

rns

(%)

14

12

10

8

6

4

2

Standard Deviation (%)(Risk)

5 10 15 20 25 30 35 40

Treasury Bills

Corporate Bonds

Government Bonds

Small Cap. Stocks

Large Cap. Stocks

33

Long View on Investing

• Historical study of assets over the past 200 years by Dr. Siegel, Professor of Finance, The Wharton School:

• $1 invested in the following assets 200 years ago would be worth today:– Gold $28– T-Bills $4,455– Bonds with interest reinvested $13,975– Common Stocks with dividends reinvested $8,800,000

• Over the last 90 years, using 25 year rolling periods, annual investment returns would be:– 30 day T-Bills 3.89%– 20 year Treasuries 5.3%– Large Company stocks 11%– Small Company stocks 12%

34

Retirement Planning

35

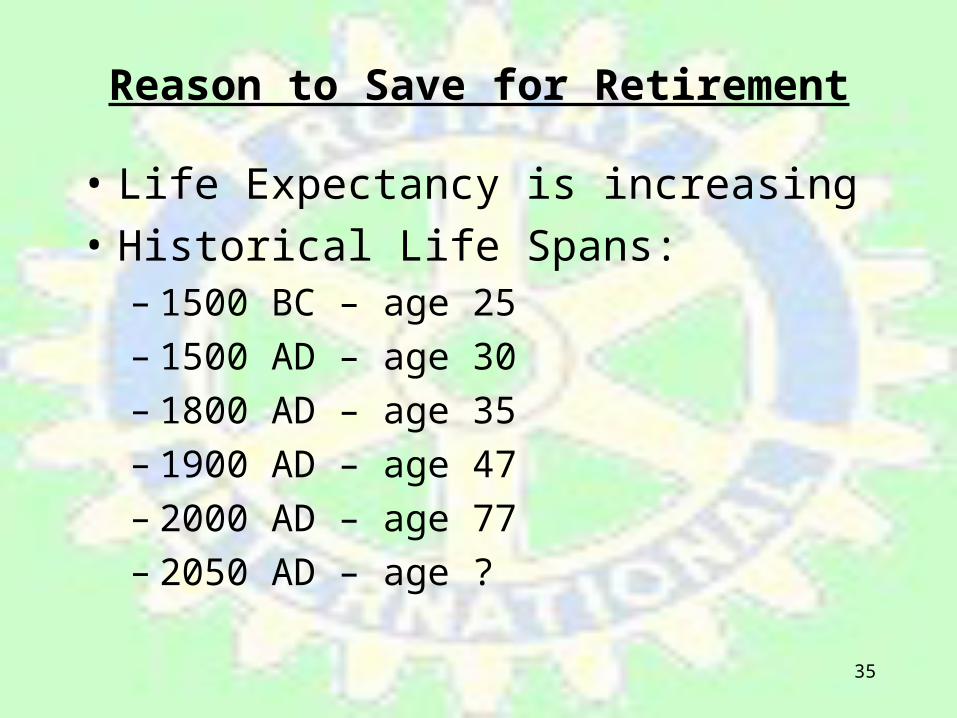

Reason to Save for Retirement

• Life Expectancy is increasing

• Historical Life Spans:– 1500 BC – age 25– 1500 AD – age 30– 1800 AD – age 35– 1900 AD – age 47– 2000 AD – age 77– 2050 AD – age ?

36

Retirement Planning

Inflation -- Is an increase in the general level of prices

-- Wages, salaries and retirement plans may not increase at the inflation rate

-- Retirement planning should reflect inflation as a factor

-- Inflation erodes buying power

2003

37

Retirement Planning

Inflation

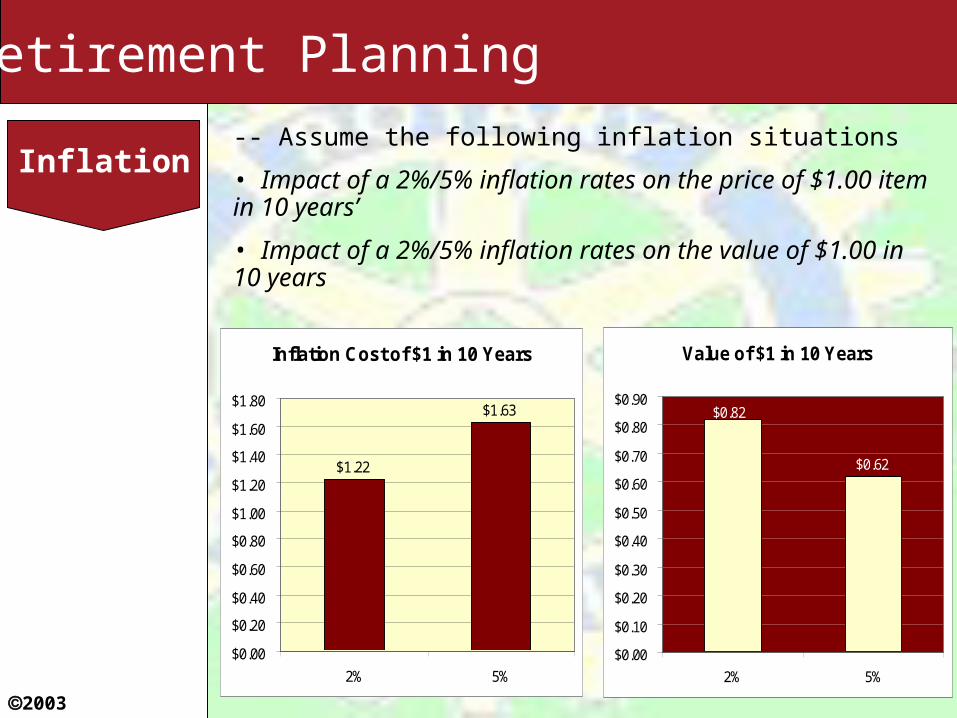

Inflation Cost of $1 in 10 Years

$1.22

$1.63

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

2% 5%

Value of $1 in 10 Years

$0.62

$0.82

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

2% 5%

-- Assume the following inflation situations

• Impact of a 2%/5% inflation rates on the price of $1.00 item in 10 years’

• Impact of a 2%/5% inflation rates on the value of $1.00 in 10 years

2003

38

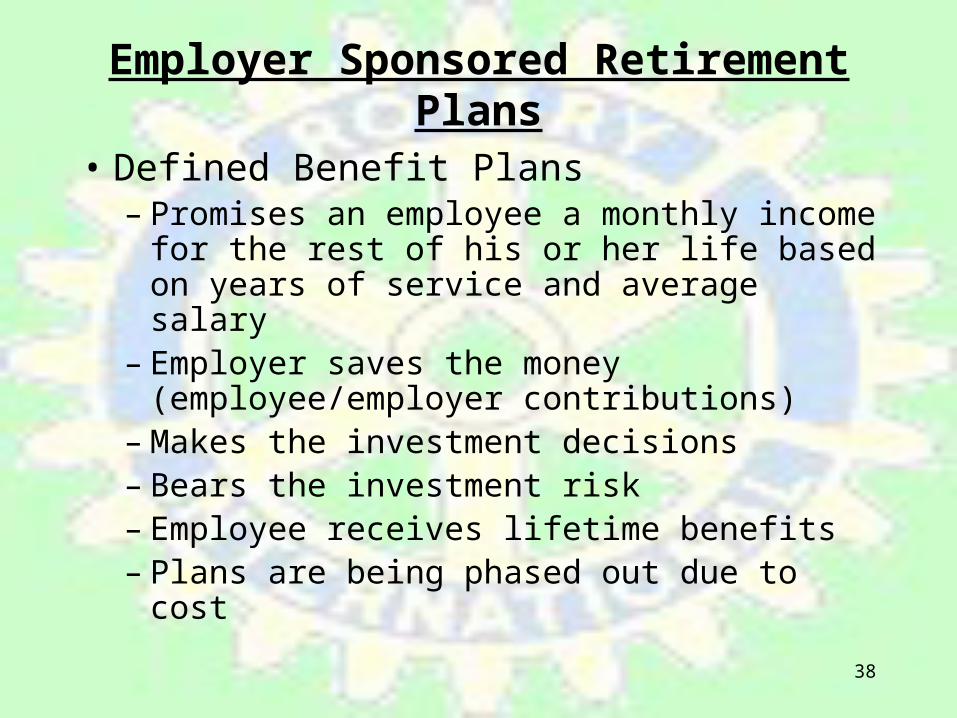

Employer Sponsored Retirement Plans

• Defined Benefit Plans– Promises an employee a monthly income for

the rest of his or her life based on years of service and average salary

– Employer saves the money (employee/employer contributions)

– Makes the investment decisions– Bears the investment risk– Employee receives lifetime benefits– Plans are being phased out due to cost

39

Employer Sponsored Retirement Plans

• Defined Contribution Plans– 401(k) and 403(b) are examples– There is no promise to the employee except any amount

of employer contribution– Employee determines contribution amount and makes

investment decisions– Employee has investment risk– Retirement check will be based on employer/employee

contribution and investment decisions– Employee contributions should contribute at least the

employer match (it is free money)– Since individuals are living longer, should contribute

more than the employer matching amount

40

Retirement Options• Maryland State Retirement Agency (MSRA) Program

– Defined Benefit Plan– Eligible and Required to participate– 4% of salary is deducted for retirement– All contributions belong to employee– After five years of creditable service, employee is vested or

eligible for benefits• Tax-Sheltered Annuity (TSA) – 403(b) Plan

– Defined Contribution Plan– Voluntary plan but essential– Defer a portion of salary on a pre-tax basis– SMCPS offers an opportunity to participate in a Plan– Can set aside up to $16,500 per year (2009)– Payroll Deduction

41

Retirement Contributions Tax Savings

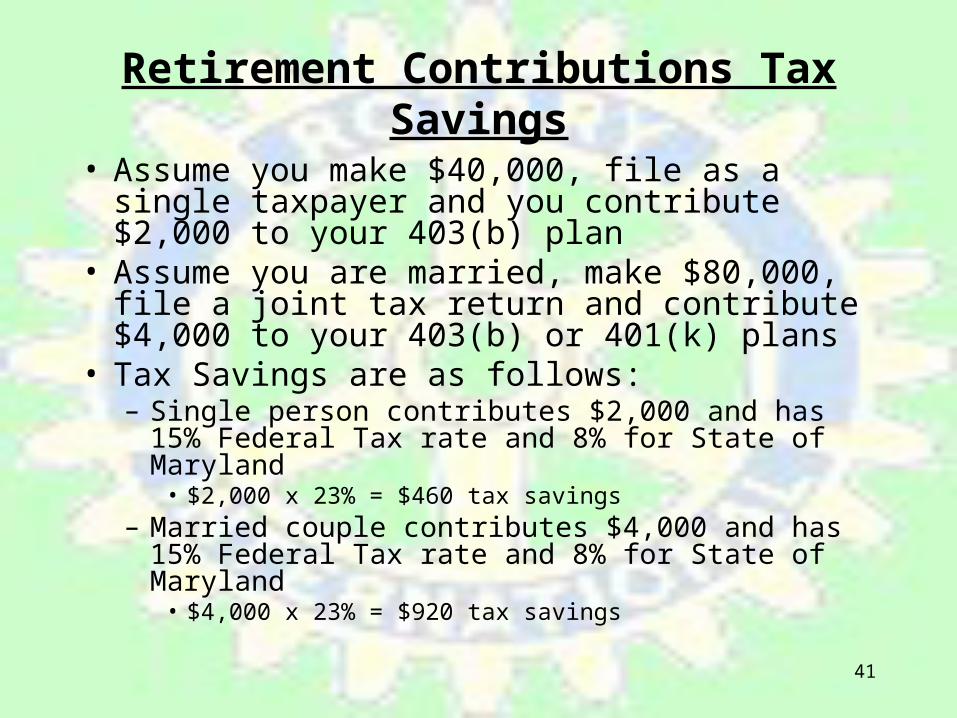

• Assume you make $40,000, file as a single taxpayer and you contribute $2,000 to your 403(b) plan

• Assume you are married, make $80,000, file a joint tax return and contribute $4,000 to your 403(b) or 401(k) plans

• Tax Savings are as follows:– Single person contributes $2,000 and has 15% Federal

Tax rate and 8% for State of Maryland• $2,000 x 23% = $460 tax savings

– Married couple contributes $4,000 and has 15% Federal Tax rate and 8% for State of Maryland

• $4,000 x 23% = $920 tax savings

42

Points To Remember

• Pay yourself first.

• Create an emergency fund.

• Know your Credit Score and its impact.

• Insurance is to reduce your liability costs.

• Understand compound interest concept.

• Need to do retirement investment early in your career.

43

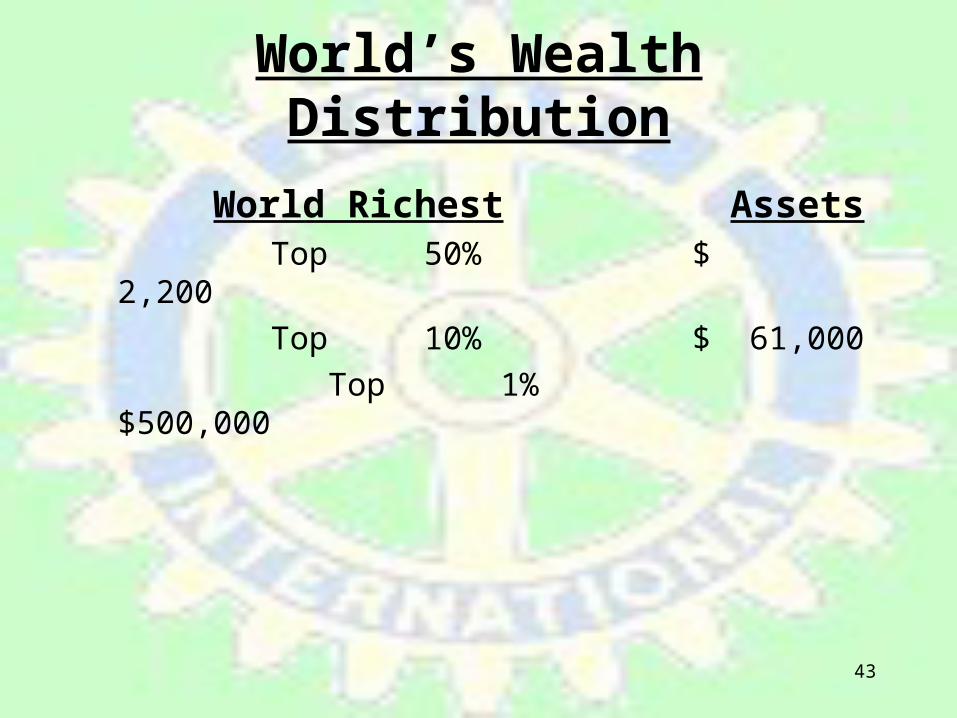

World’s Wealth Distribution

World Richest Assets Top 50% $ 2,200

Top 10% $ 61,000

Top 1% $500,000

44

Rotary Financial Literacy

Questions?