Embed Size (px)

Citation preview

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 1/40

Bank Investors: Who Were They, Who AreThey and What Are They Looking For

Lisa Schultz

Managing Director, Equity Capital Markets & Syndicate, U.S.,

Stifel Nicolaus Weisel

11:30 AM - 12:20 AM

Anton Schutz

President & Chief Investment Officer, Mendon Capital Advisors

Corporation and Founder, New Ground Capital

On Demand Passcode: CAMELBACK Twitter Hashtag: #AOBA13Wireless Passcode: AOBA2013

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 2/40

I. Evolution of the Bank Market

II. What Investors Are Currently Looking For

III. Bank Investors Today

IV. Shareholder Activism

V. Positioning For The Future

Presentation Outline

Stifel, Nicolaus & Company, Incorporated and Thomas Weisel Partners LLC are affiliated broker-dealer subsidiaries of StifelFinancial Corp. which are collectively referred to herein under the marketing name Stifel Nicolaus Weisel, representing the firm’sinvestment banking services. This document has been prepared by the investment banking division and is not a product of StifelResearch. The information and statistical data contained herein have been obtained from sources that Stifel Nicolaus Weiselbelieves are reliable, but Stifel Nicolaus Weisel makes no representation or warranty as to the accuracy or completeness of any suchinformation or data and expressly disclaims any and all liability relating to or resulting from your use of these materials. Theinformation and data contained herein are current only as of the date(s) indicated, and Stifel Nicolaus Weisel has no intention,obligation, or duty to update these materials after such date(s). These materials do not constitute an offer to sell or the solicitation ofan offer to buy any securities. Stifel Nicolaus may be a market-maker in certain of these securities, and Stifel Nicolaus Weisel mayhave provided investment banking services to certain of the companies listed herein. Stifel Nicolaus, Thomas Weisel Partners,and/or their respective officers, directors, employees, and affiliates may at any time hold a long or short position in any of thesesecurities and may from time-to-time purchase or sell such securities. These materials may not be distributed without StifelNicolaus Weisel’s prior written consent.

Copyright 2013 Stifel, Nicolaus & Company, Incorporated

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 3/40

I. Evolution of the Bank Market

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 4/40

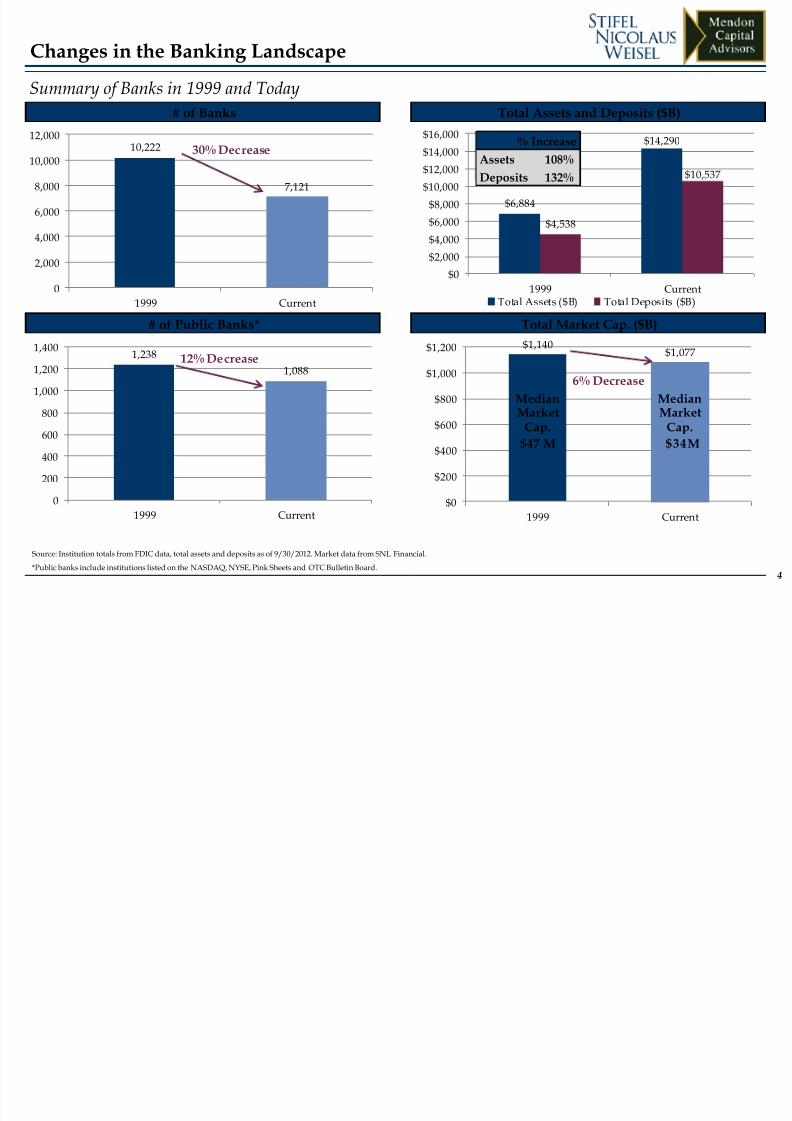

$6,884

$14,290

$4,538

$10,537

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000$16,000

1999 CurrentTotal Assets ($B) Total Deposits ($B)

4

Source: Institution totals from FDIC data, total assets and deposits as of 9/30/2012. Market data from SNL Financial.

*Public banks include institutions listed on the NASDAQ, NYSE, Pink Sheets and OTC Bulletin Board.

Summary of Banks in 1999 and Today

Changes in the Banking Landscape

# of Banks Total Assets and Deposits ($B)

# of Public Banks* Total Market Cap. ($B)

1,238

1,088

0

200

400

600

800

1,000

1,200

1,400

1999 Current

12% Decrease$1,140

$1,077

$0

$200

$400

$600

$800

$1,000

$1,200

1999 Current

Median

MarketCap.

$47 M

Median

MarketCap.

$34M

6% Decrease

% Increase

Assets 108%

Deposits 132%

10,222

7,121

0

2,000

4,000

6,000

8,000

10,000

12,000

1999 Current

30% Decrease

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 5/40

5

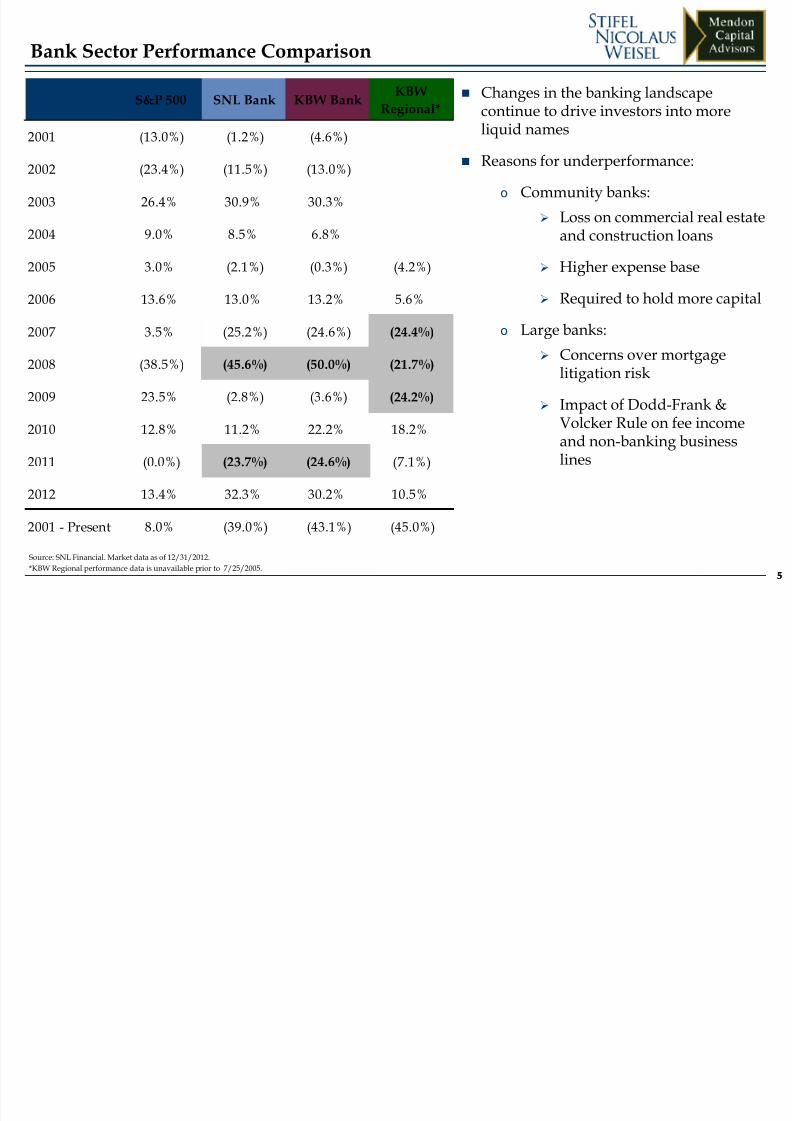

Bank Sector Performance Comparison

5

Source: SNL Financial. Market data as of 12/31/2012.

*KBW Regional performance data is unavailable prior to 7/25/2005.

S&P 500 SNL Bank KBW BankKBW

Regional*

2001 (13.0%) (1.2%) (4.6%)

2002 (23.4%) (11.5%) (13.0%)

2003 26.4% 30.9% 30.3%

2004 9.0% 8.5% 6.8%

2005 3.0% (2.1%) (0.3%) (4.2%)

2006 13.6% 13.0% 13.2% 5.6%

2007 3.5% (25.2%) (24.6%) (24.4%)

2008 (38.5%) (45.6%) (50.0%) (21.7%)

2009 23.5% (2.8%) (3.6%) (24.2%)

2010 12.8% 11.2% 22.2% 18.2%

2011 (0.0%) (23.7%) (24.6%) (7.1%)

2012 13.4% 32.3% 30.2% 10.5%

2001 - Present 8.0% (39.0%) (43.1%) (45.0%)

Changes in the banking landscapecontinue to drive investors into more

liquid names Reasons for underperformance:

o Community banks:

Loss on commercial real estateand construction loans

Higher expense base

Required to hold more capital

o Large banks:

Concerns over mortgagelitigation risk

Impact of Dodd-Frank &Volcker Rule on fee incomeand non-banking businesslines

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 6/40

6

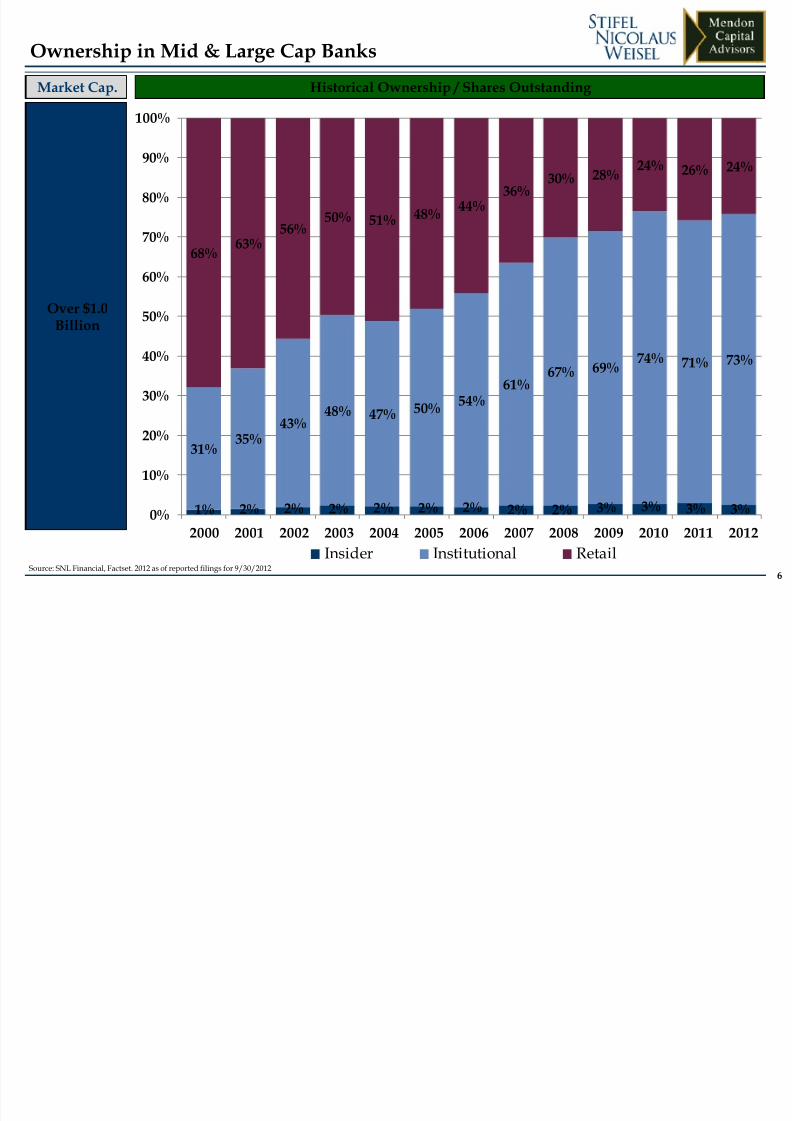

Ownership in Mid & Large Cap Banks

Source: SNL Financial, Factset. 2012 as of reported filings for 9/30/2012.

Over $1.0Billion

Market Cap. Historical Ownership / Shares Outstanding

1% 2% 2% 2% 2% 2% 2% 2% 2% 3% 3% 3% 3%

31% 35%

43% 48% 47% 50%

54%61%

67% 69% 74% 71% 73%

68% 63%

56%50% 51% 48%

44%36%

30% 28% 24% 26% 24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Insider Institutional Retail

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 7/407

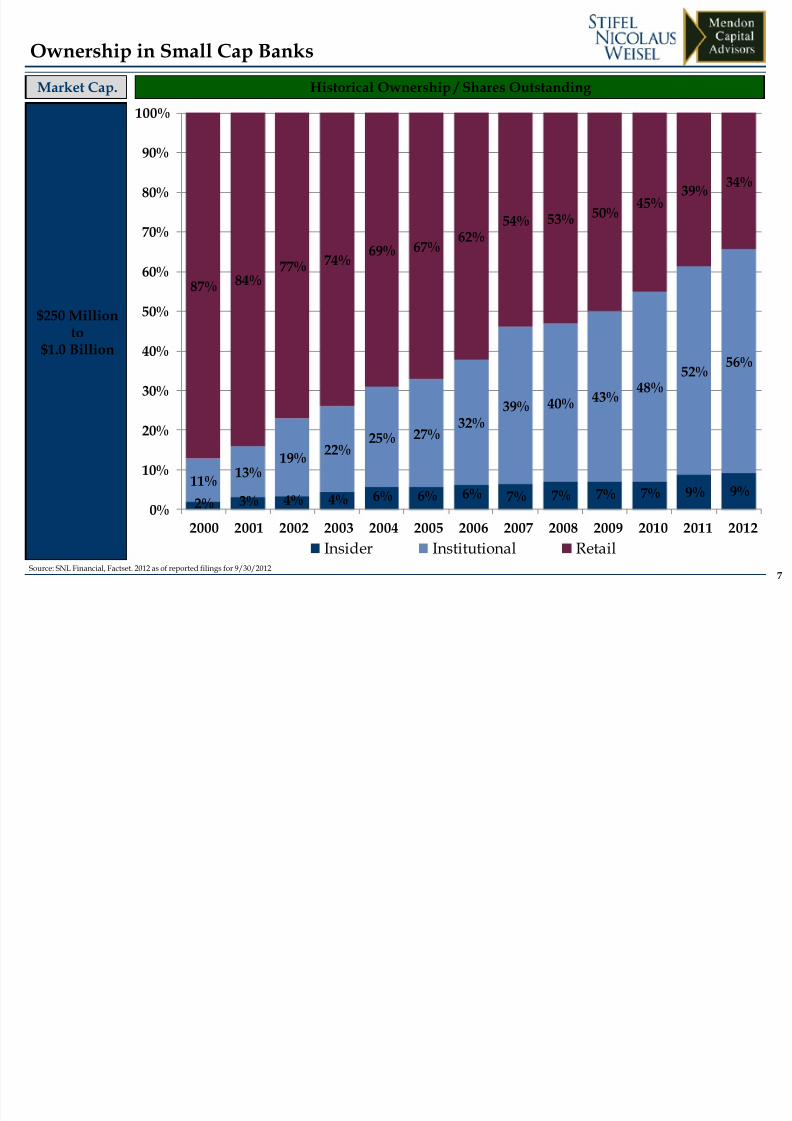

Ownership in Small Cap Banks

Market Cap.

$250 Millionto

$1.0 Billion

Historical Ownership / Shares Outstanding

2% 3% 4% 4% 6% 6% 6% 7% 7% 7% 7% 9% 9%11%

13%19%

22%25% 27%

32%39% 40% 43%

48%52%

56%

87% 84%77% 74%

69% 67% 62%

54% 53% 50% 45%

39% 34%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Insider Institutional RetailSource: SNL Financial, Factset. 2012 as of reported filings for 9/30/2012.

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 8/408

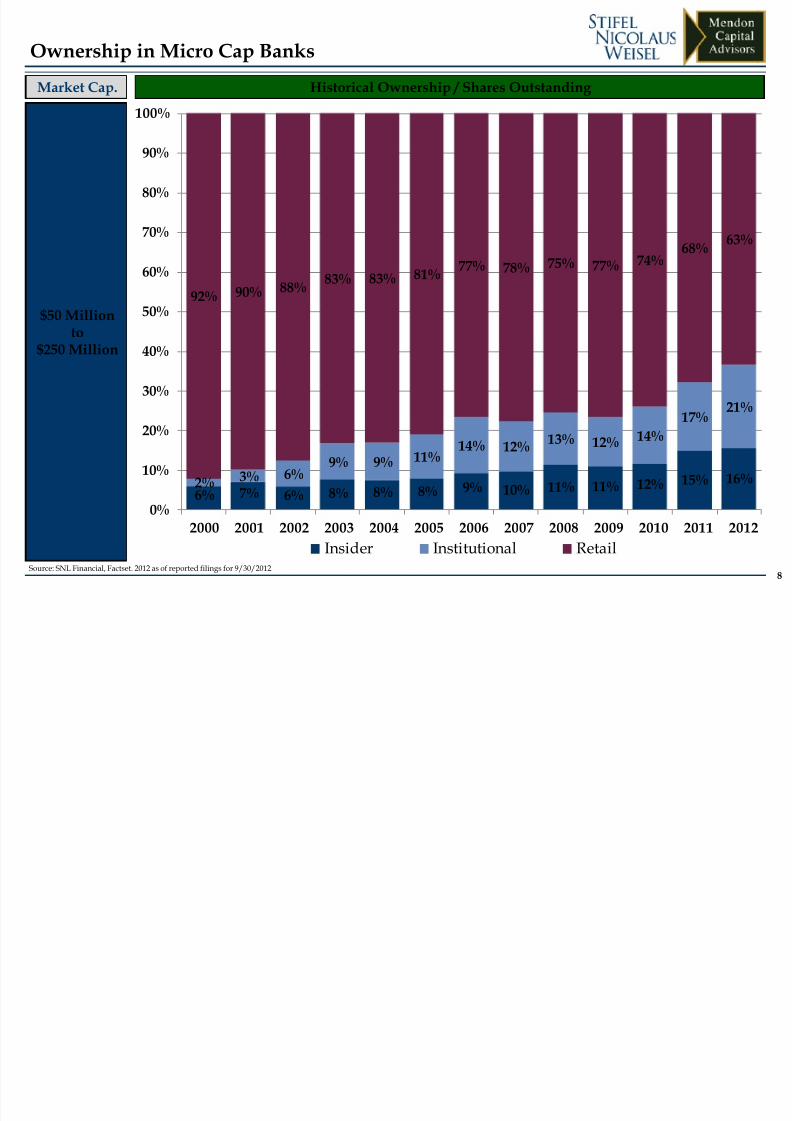

Ownership in Micro Cap Banks

Market Cap.

$50 Millionto

$250 Million

Historical Ownership / Shares Outstanding

6% 7% 6% 8% 8% 8% 9% 10% 11% 11% 12% 15% 16%2% 3% 6%9% 9% 11%

14% 12% 13% 12% 14%

17% 21%

92% 90% 88% 83% 83% 81% 77% 78% 75% 77% 74%

68% 63%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Insider Institutional RetailSource: SNL Financial, Factset. 2012 as of reported filings for 9/30/2012.

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 9/409

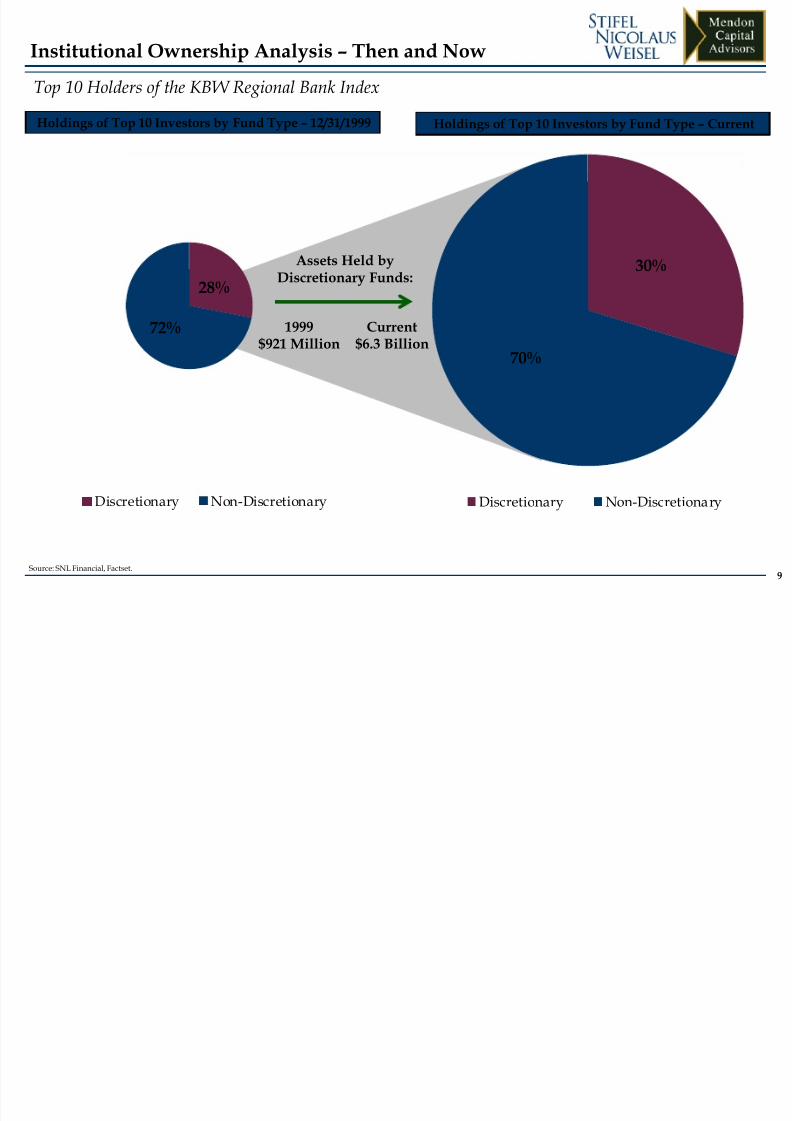

Institutional Ownership Analysis – Then and Now

Source: SNL Financial, Factset.

Holdings of Top 10 Investors by Fund Type – 12/31/1999 Holdings of Top 10 Investors by Fund Type – Current

Top 10 Holders of the KBW Regional Bank Index

30%

70%

Discretionary Non-Discretionary

28%

72%

Discretionary Non-Discretionary

1999$921 Million

Assets Held by

Discretionary Funds:

Current$6.3 Billion

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 10/4010

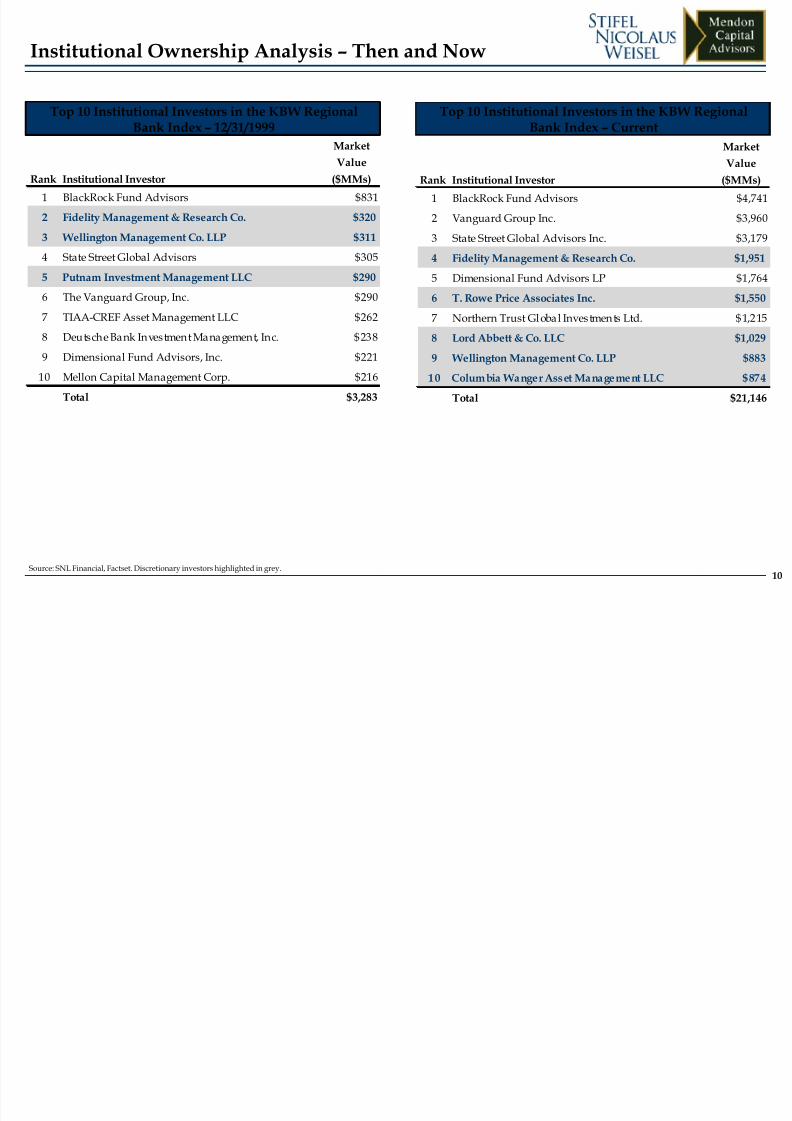

Institutional Ownership Analysis – Then and Now

Top 10 Institutional Investors in the KBW RegionalBank Index – 12/31/1999

Top 10 Institutional Investors in the KBW RegionalBank Index – Current

Source: SNL Financial, Factset. Discretionary investors highlighted in grey.

Rank Institutional Investor

Market

Value

($MMs)

1 BlackRock Fund Advisors $831

2 Fidelity Management & Research Co. $320

3 Wellington Management Co. LLP $311

4 State Street Global Advisors $305

5 Putnam Investment Management LLC $290

6 The Vanguard Group, Inc. $290

7 TIAA-CREF Asset Management LLC $262

8 Deutsche Bank Investment Management, Inc. $238

9 Dimensional Fund Advisors, Inc. $221

10 Mellon Capital Management Corp. $216

Total $3,283

Rank Institutional Investor

Market

Value

($MMs)

1 BlackRock Fund Advisors $4,741

2 Vanguard Group Inc. $3,960

3 State Street Global Advisors Inc. $3,179

4 Fidelity Management & Research Co. $1,951

5 Dimensional Fund Advisors LP $1,764

6 T. Rowe Price Associates Inc. $1,550

7 Northern Trust Global Investments Ltd. $1,215

8 Lord Abbett & Co. LLC $1,029

9 Wellington Management Co. LLP $883

10 Columbia Wanger Asset Management LLC $874

Total $21,146

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 11/4011

BlackRock Fund Advisors

TIAA-CREF

JPMorgan Asset

Management

The Banc Funds Co.

Fidelity Management

AllianceBernstein

Putnam Investment Mgmt.

Deutsche Bank Investment

Management

Columbia Management

Investor Movement Since the Beginning of 2000

KBW BankIndex

KBWRegional

Bank Index

Buying Maintaining Selling

Vanguard Group

State Street

Wellington Management

T. Rowe Price

Dodge & Cox

Invesco Advisors

Capital World Investors

Sandler Asset Management

BlackRock Fund Advisors Vanguard Group

State Street

Fidelity Management

Dimensional Fund Advisors

T. Rowe Price

Lord Abbett

Sandler Asset Management

Wellington Management TIAA-CREF

The Banc Funds Co.

Deutsche Bank InvestmentManagement

Putnam Investment Mgmt.

Mellon Capital

Source: FactSet.

DedicatedBank StockInvestors

That HaveGone Away

Tontine Asset Management Synovus Asset Management Keefe Managers

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 12/4012

Public Float Soaked Up by Index Funds

Bank ownership trends mirror those of the broader market in the sense that more money is being

managed through non-discretionary funds (ETFs and passively managed index funds)

ETFs and Index Funds have grown in popularity as investors look for lower cost investment alternatives

in a stock market that has been relatively unchanged since the beginning of 2000. Contributing to this

phenomenon have been:

High levels of stock market volatility, including the 2009 “flash crash”

Underperformance by some of the higher profile active managers (Bill Miller and others)

Access, liquidity and specialization of ETFs relative to traditional mutual funds

Current liquidity in bank stocks is diminished as public float is further reduced by shares held by index

funds

Price/valuation impacted by a higher liquidity discount applied by investors

Changes in stock ownership impacted more and more by computers/models, not fundamental

valuation techniques applied by real-life portfolio managers, which on occasion leads to over-

corrections based on technical indicators

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 13/4013

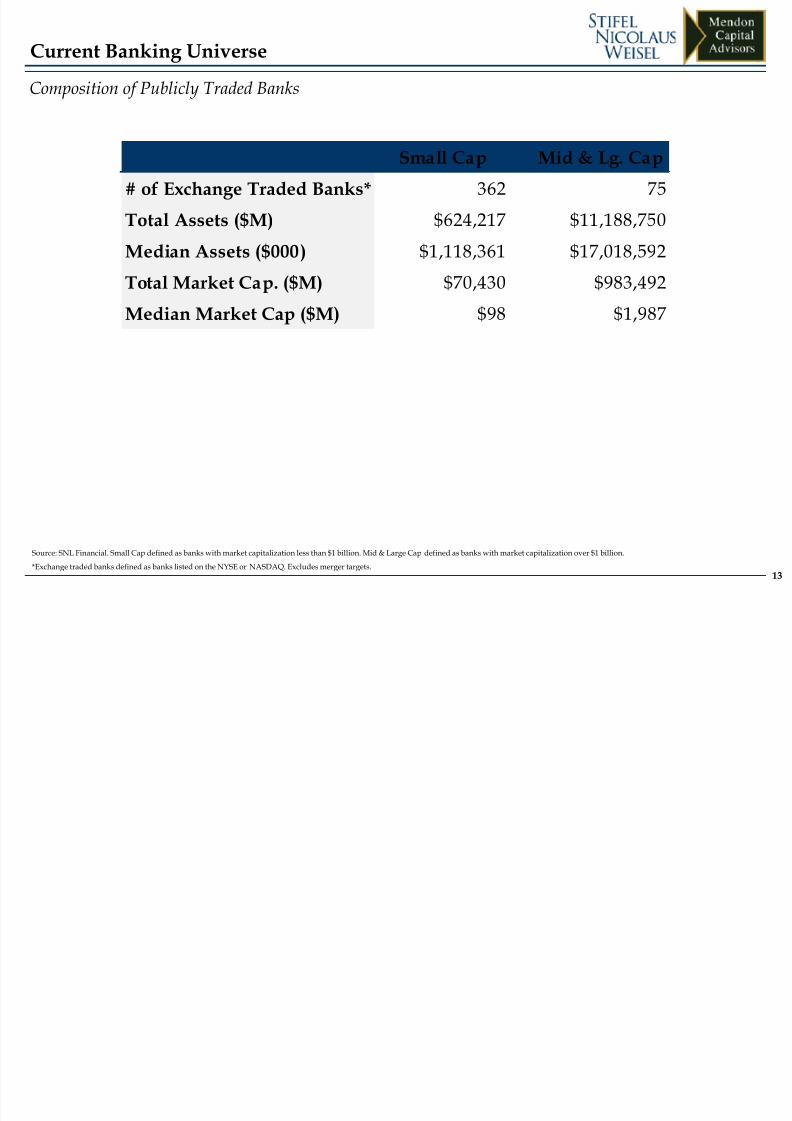

Source: SNL Financial. Small Cap defined as banks with market capitalization less than $1 billion. Mid & Large Cap defined as banks with market capitalization over $1 billion.*Exchange traded banks defined as banks listed on the NYSE or NASDAQ. Excludes merger targets.

Composition of Publicly Traded Banks

Current Banking Universe

Small Cap Mid & Lg. Cap

# of Exchange Traded Banks* 362 75

Total Assets ($M) $624,217 $11,188,750

Median Assets ($000) $1,118,361 $17,018,592

Total Market Cap. ($M) $70,430 $983,492

Median Market Cap ($M) $98 $1,987

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 14/40

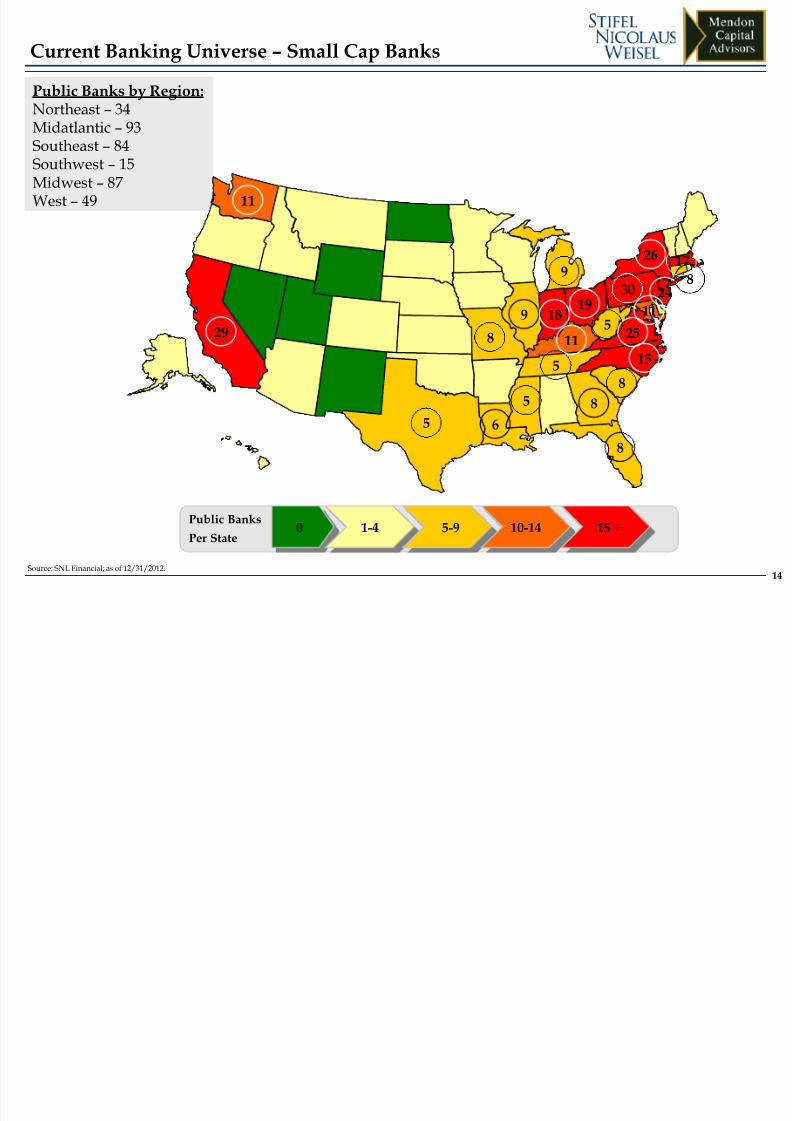

Public Banks by Region:Northeast – 34Midatlantic – 93Southeast – 84Southwest – 15Midwest – 87West – 49

Source: SNL Financial; as of 12/31/2012.

29

8

9

Public Banks

Per State0 1-4 5-9 10-14 15 +

Current Banking Universe – Small Cap Banks

18

11

6

11

15

248

19

26

25

11

14

8

17

8

5

30

85

5

5

9

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 15/40

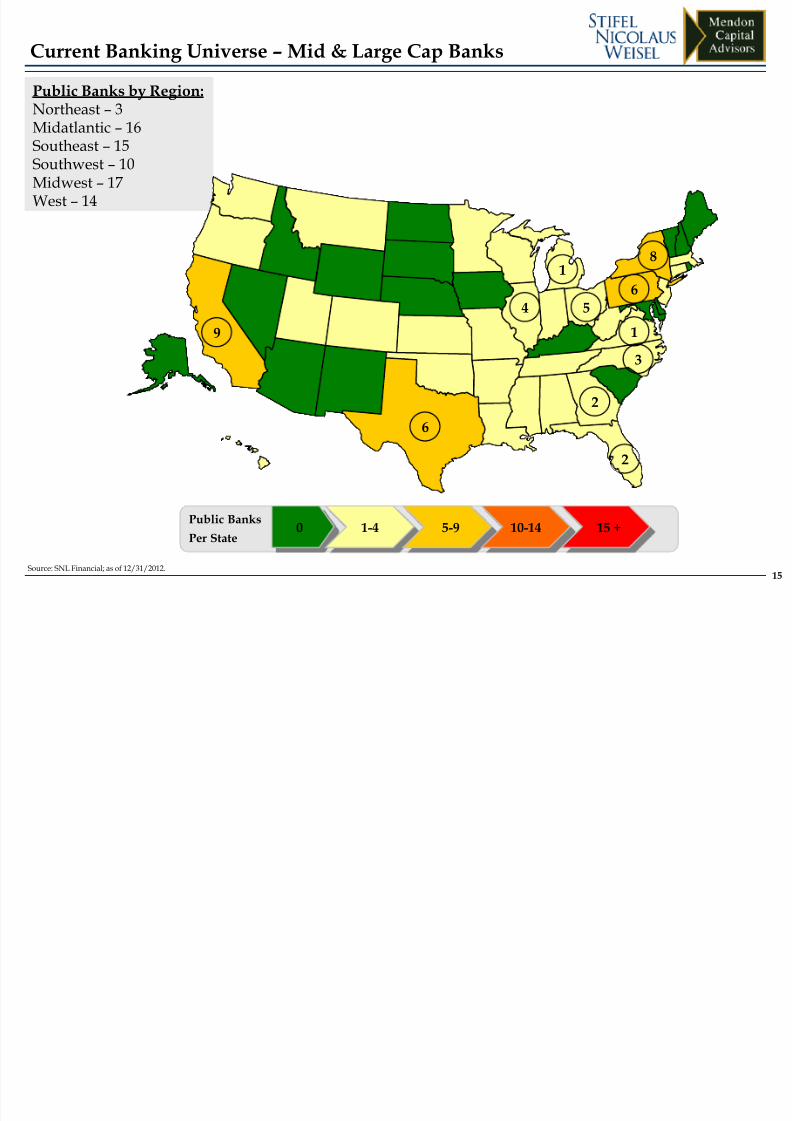

Public Banks by Region:Northeast – 3Midatlantic – 16Southeast – 15Southwest – 10Midwest – 17West – 14

Source: SNL Financial; as of 12/31/2012.

Public Banks

Per State0 1-4 5-9 10-14 15 +

Current Banking Universe – Mid & Large Cap Banks

15

9

8

6

6

1

54

1

2

3

2

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 16/40

II. What Investors Are Currently Looking For

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 17/40

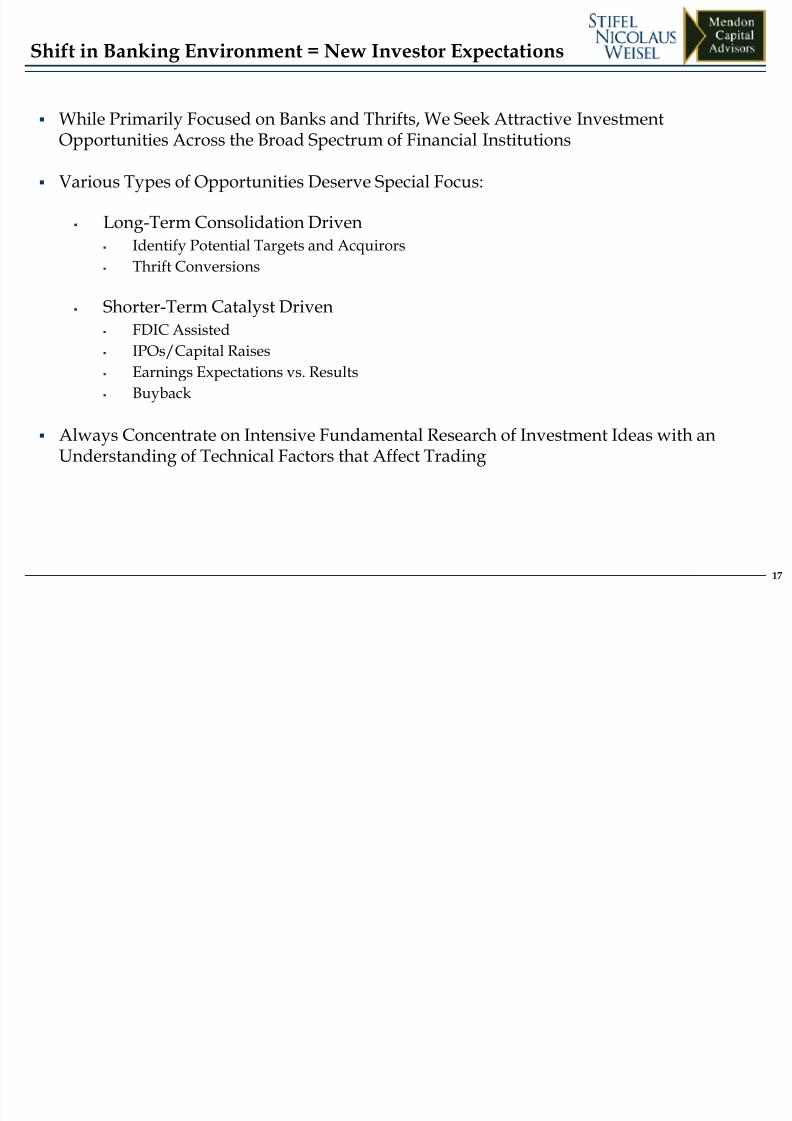

17

Shift in Banking Environment = New Investor Expectations

While Primarily Focused on Banks and Thrifts, We Seek Attractive Investment

Opportunities Across the Broad Spectrum of Financial Institutions

Various Types of Opportunities Deserve Special Focus:

Long-Term Consolidation Driven Identify Potential Targets and Acquirors

Thrift Conversions

Shorter-Term Catalyst Driven FDIC Assisted

IPOs/Capital Raises

Earnings Expectations vs. Results

Buyback

Always Concentrate on Intensive Fundamental Research of Investment Ideas with anUnderstanding of Technical Factors that Affect Trading

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 18/40

18

Three-Step Discipline:

Idea Generation

•Daily review forvaluation anomalies

•Map and model M&Apossibilities

•Analyst road trips:

several per year peranalyst

• Industry conferencesthroughout the year

• In-house managementvisits

•Daily industry news

•Filter sell-side ideas,IPOs, capital offerings

Investment Decision

•Analyst presents ideaand thesis to PM andHead Trader

•Team discussions toensure all key factorsknown and analyzed

•PM makes final call;analysts have discretionin PM’s absence

Position Monitoring

•Analyst maintainsresponsibility forinvestment thesis

•Monitor daily changes inprice and volume; newsupdates

•Regular discussions withcompany management

•Special focus aroundearnings releases, 10-Qreleases and headlinenews

Investment Process

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 19/40

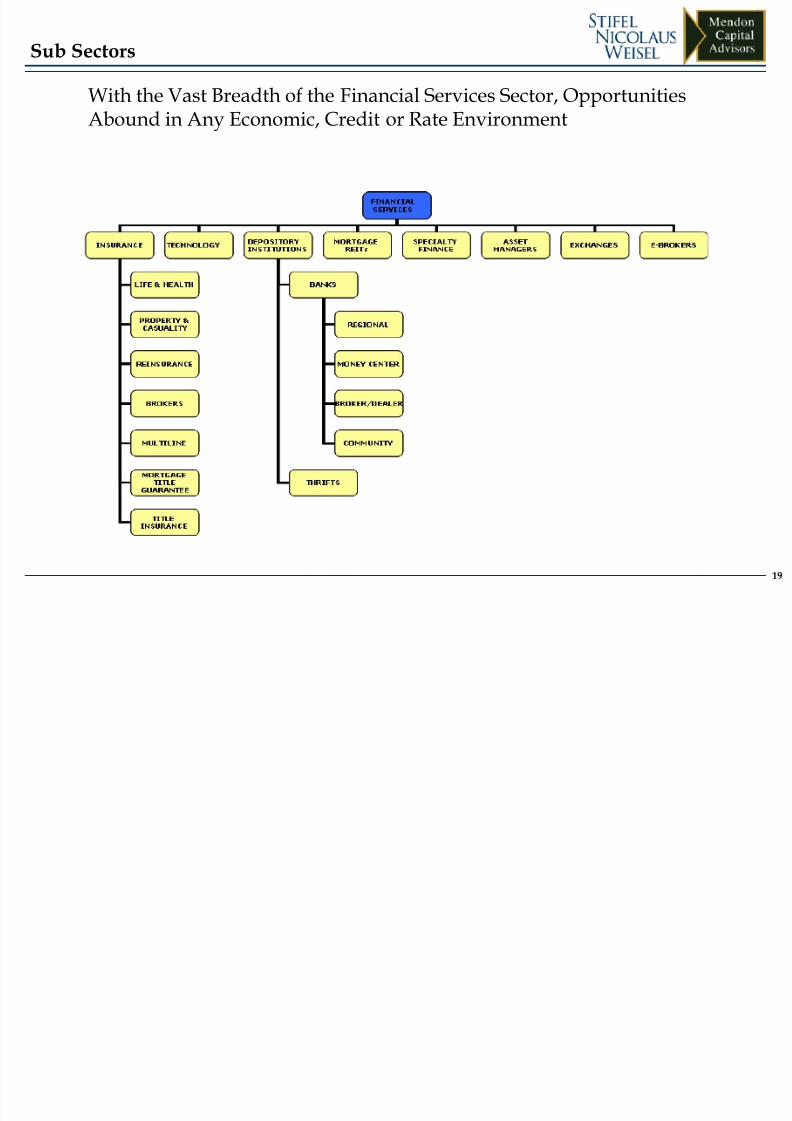

19

Sub Sectors

With the Vast Breadth of the Financial Services Sector, OpportunitiesAbound in Any Economic, Credit or Rate Environment

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 20/40

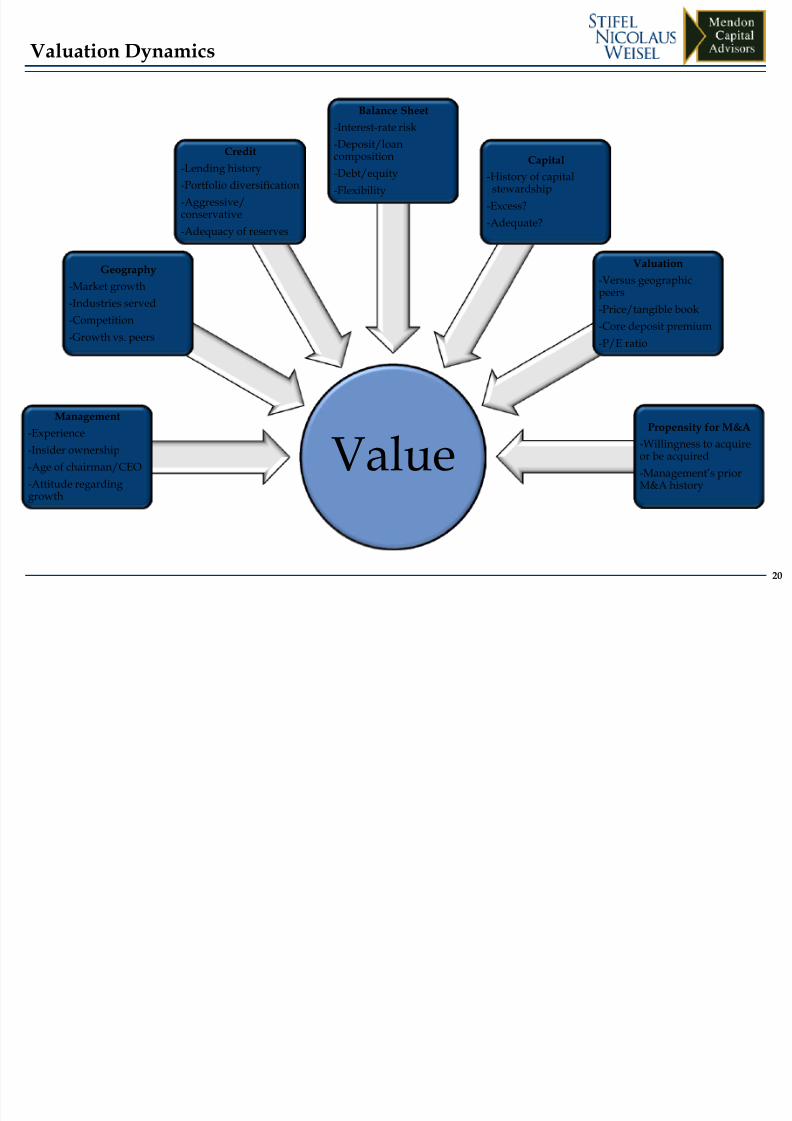

20

Valuation Dynamics

ValueManagement

-Experience

-Insider ownership

-Age of chairman/CEO

-Attitude regardinggrowth

Geography

-Market growth

-Industries served

-Competition

-Growth vs. peers

Credit

-Lending history

-Portfolio diversification

-Aggressive/conservative

-Adequacy of reserves

Balance Sheet

-Interest-rate risk

-Deposit/loancomposition

-Debt/equity

-Flexibility

Capital

-History of capitalstewardship

-Excess?

-Adequate?

Valuation

-Versus geographicpeers

-Price/tangible book

-Core deposit premium

-P/E ratio

Propensity for M&A

-Willingness to acquireor be acquired

-Management’s priorM&A history

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 21/40

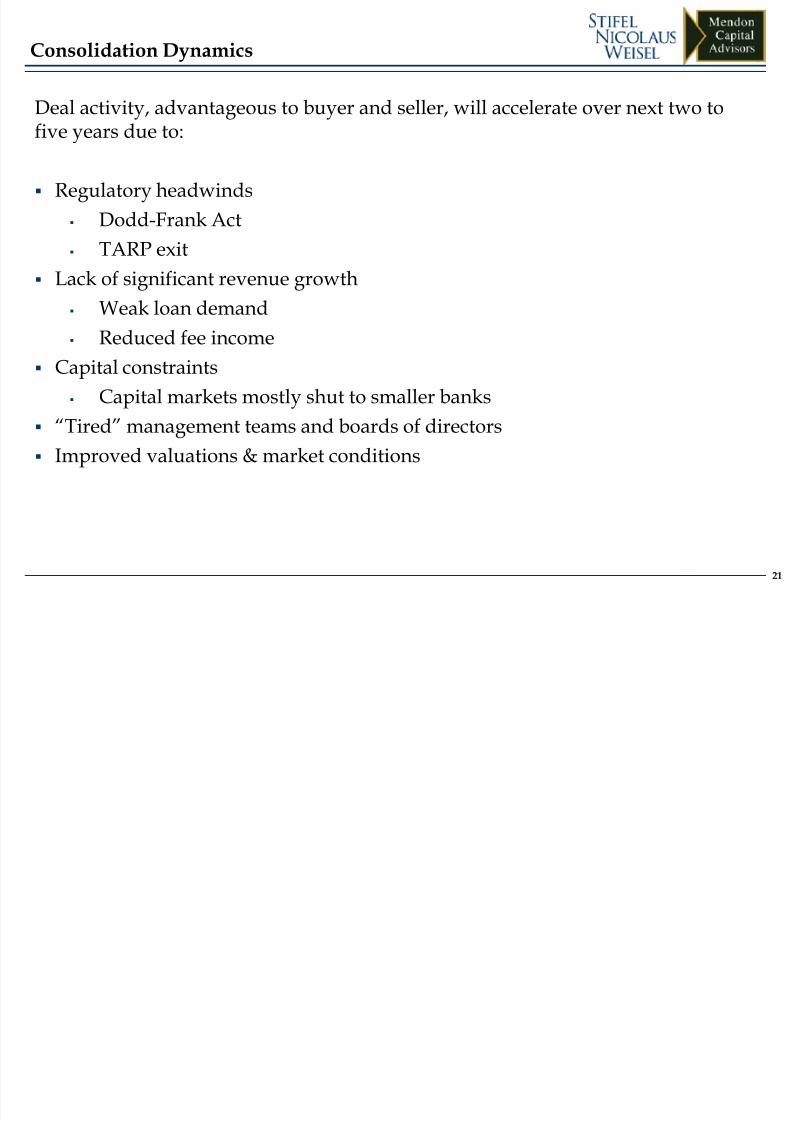

Deal activity, advantageous to buyer and seller, will accelerate over next two to

five years due to:

Regulatory headwinds

Dodd-Frank Act

TARP exit

Lack of significant revenue growth Weak loan demand

Reduced fee income

Capital constraints

Capital markets mostly shut to smaller banks

“Tired” management teams and boards of directors

Improved valuations & market conditions

21

Consolidation Dynamics

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 22/40

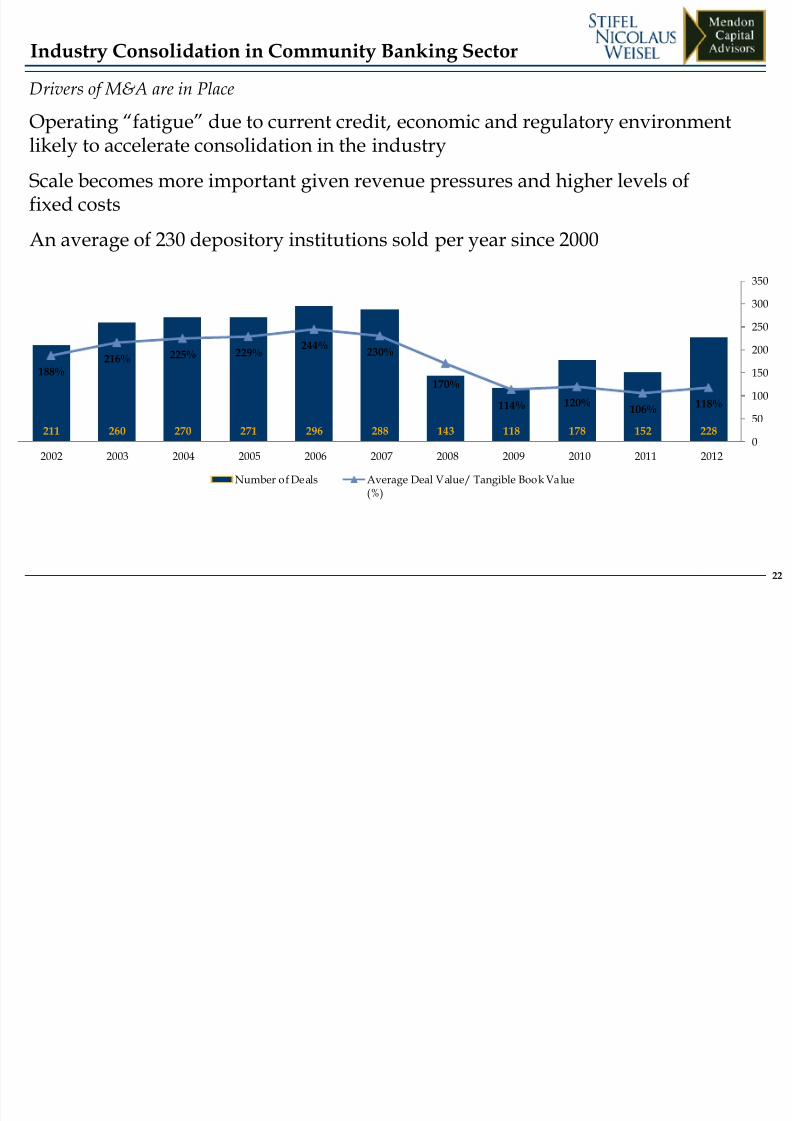

22

Drivers of M&A are in Place

Operating “fatigue” due to current credit, economic and regulatory environment

likely to accelerate consolidation in the industry

Scale becomes more important given revenue pressures and higher levels offixed costs

An average of 230 depository institutions sold per year since 2000

211 260 270 271 296 288 143 118 178 152 228

188%216% 225% 229%

244%230%

170%

114% 120%106%

118%

0

50

100

150

200

250

300

350

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Number of Deals Average Deal Value/ Tangible Book Value(%)

Industry Consolidation in Community Banking Sector

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 23/40

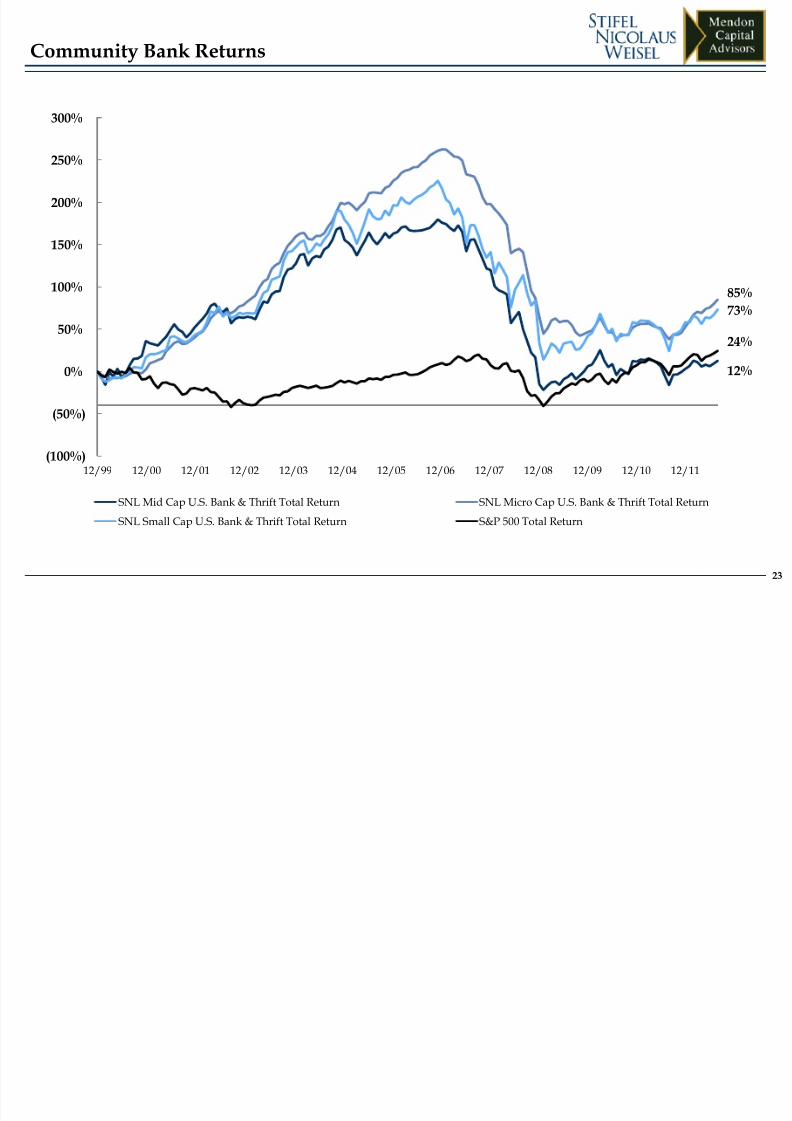

23

Community Bank Returns

12%

85%

73%

24%

(100%)

(50%)

0%

50%

100%

150%

200%

250%

300%

12/99 12/00 12/01 12/02 12/03 12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11

SNL Mid Cap U.S. Bank & Thrift Total Return SNL Micro Cap U.S. Bank & Thrift Total Return

SNL Small Cap U.S. Bank & Thrift Total Return S&P 500 Total Return

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 24/40

24

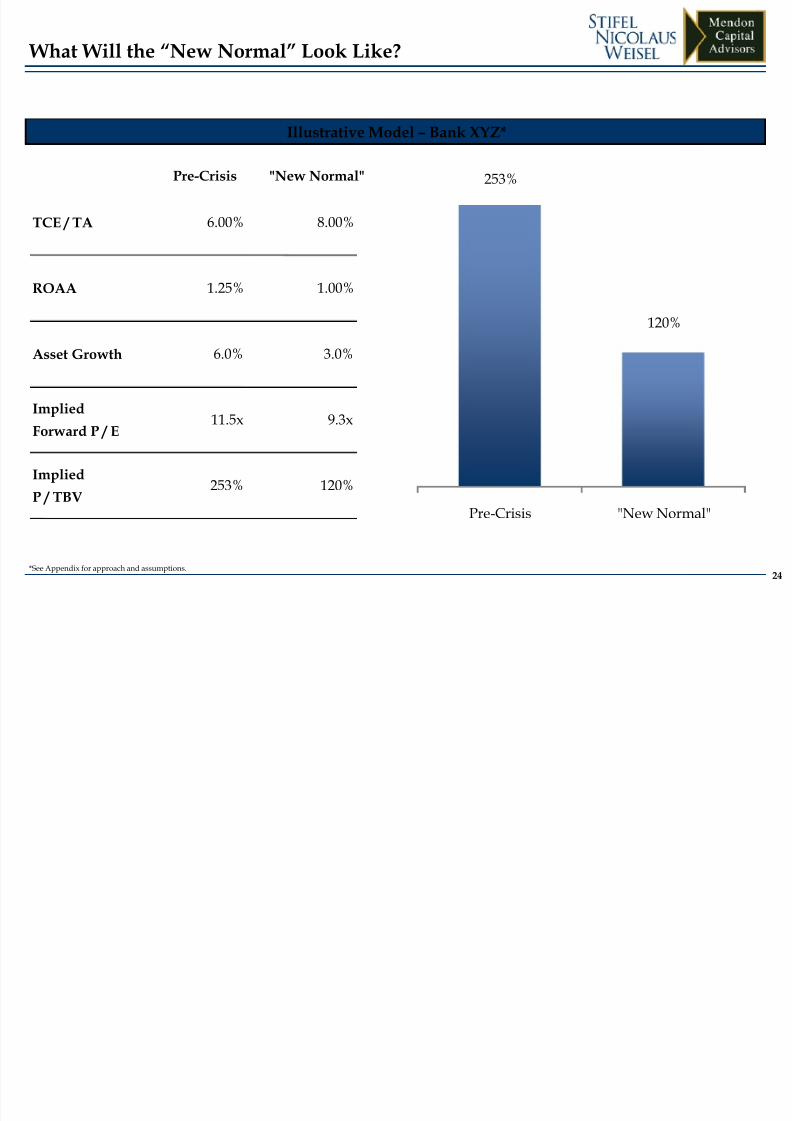

Illustrative Model – Bank XYZ*

Pre-Crisis "New Normal"

TCE / TA 6.00% 8.00%

ROAA 1.25% 1.00%

Asset Growth 6.0% 3.0%

Implied

Forward P / E 11.5x 9.3x

Implied

P / TBV253% 120%

253%

120%

Pre - Crisis "New Normal"

What Will the “New Normal” Look Like?

*See Appendix for approach and assumptions.

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 25/40

III. Bank Investors Today

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 26/40

26

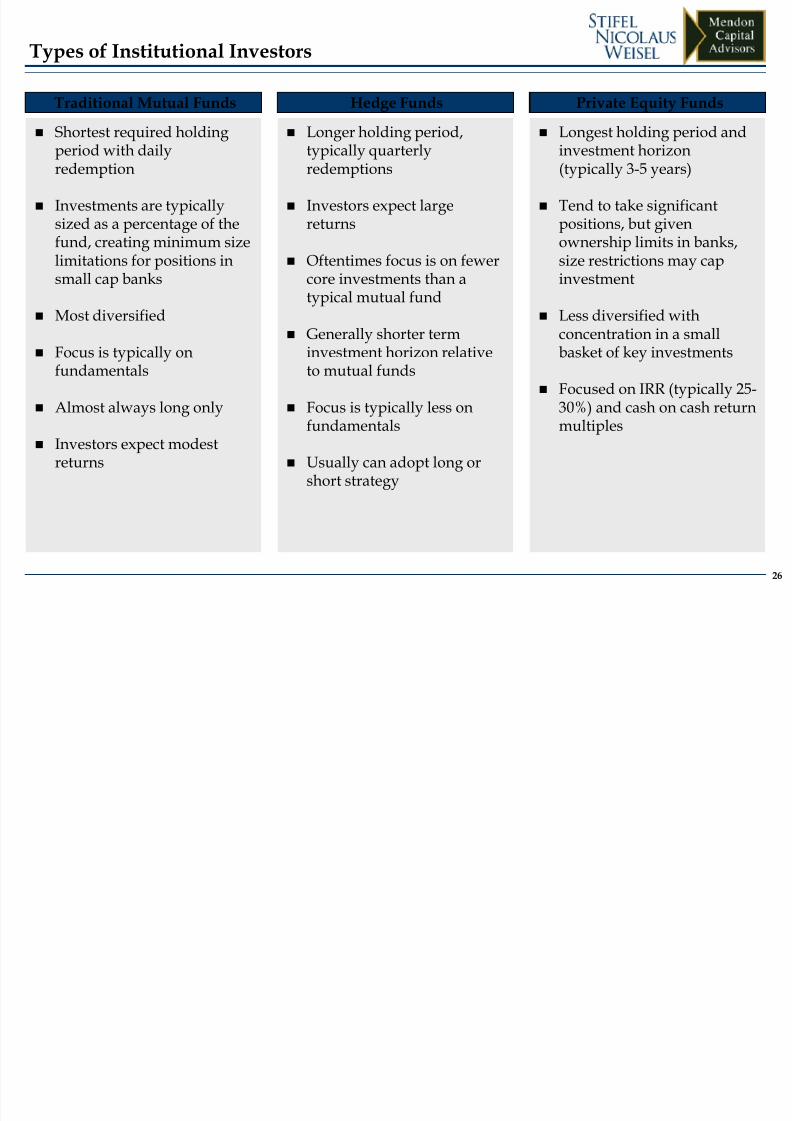

Traditional Mutual Funds Private Equity FundsHedge Funds

Shortest required holdingperiod with dailyredemption

Investments are typicallysized as a percentage of thefund, creating minimum sizelimitations for positions in

small cap banks

Most diversified

Focus is typically onfundamentals

Almost always long only

Investors expect modestreturns

Longer holding period,typically quarterlyredemptions

Investors expect largereturns

Oftentimes focus is on fewer

core investments than atypical mutual fund

Generally shorter terminvestment horizon relativeto mutual funds

Focus is typically less onfundamentals

Usually can adopt long orshort strategy

Longest holding period andinvestment horizon(typically 3-5 years)

Tend to take significantpositions, but givenownership limits in banks,size restrictions may cap

investment

Less diversified withconcentration in a smallbasket of key investments

Focused on IRR (typically 25-30%) and cash on cash returnmultiples

Types of Institutional Investors

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 27/40

27

Largest Holders By Number Of Banks HeldLargest Holders By Dollar Value of Position

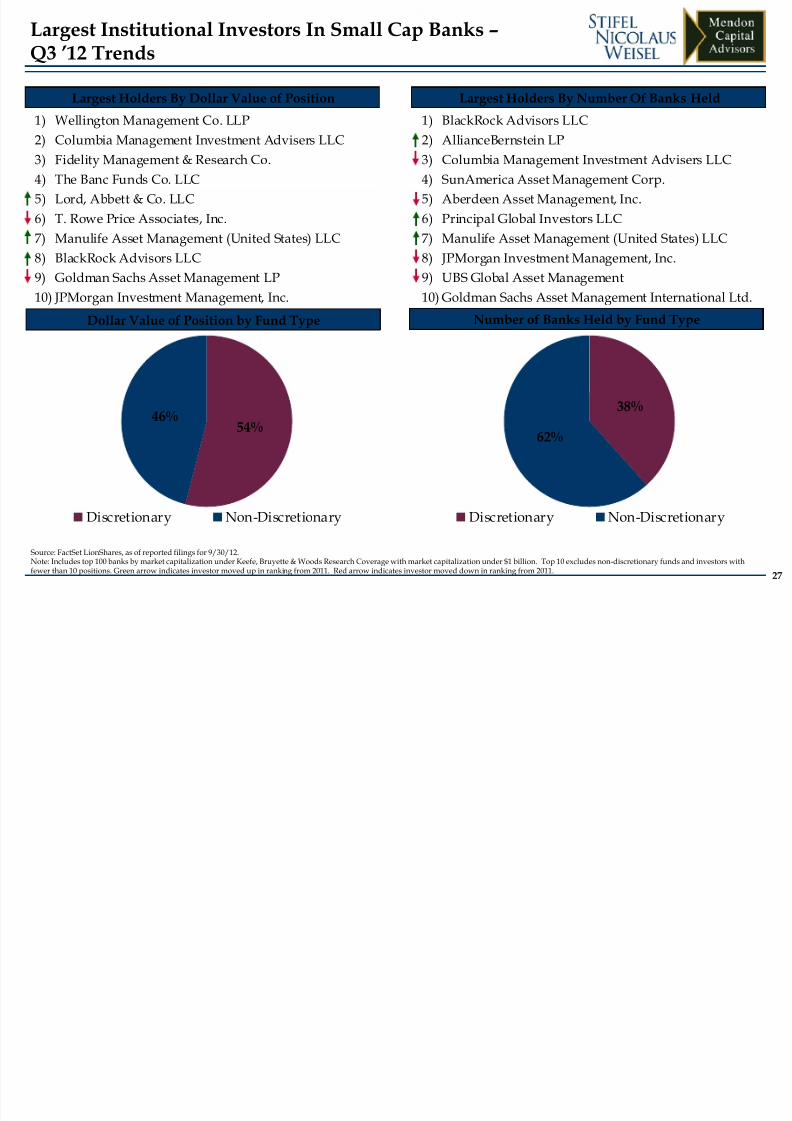

Source: FactSet LionShares, as of reported filings for 9/30/12.Note: Includes top 100 banks by market capitalization under Keefe, Bruyette & Woods Research Coverage with market capitalization under $1 billion. Top 10 excludes non-discretionary funds and investors withfewer than 10 positions. Green arrow indicates investor moved up in ranking from 2011. Red arrow indicates investor moved down in ranking from 2011.

Largest Institutional Investors In Small Cap Banks –Q3 ’12 Trends

1) BlackRock Advisors LLC

2) AllianceBernstein LP3) Columbia Management Investment Advisers LLC

4) SunAmerica Asset Management Corp.

5) Aberdeen Asset Management, Inc.

6) Principal Global Investors LLC

7) Manulife Asset Management (United States) LLC

8) JPMorgan Investment Management, Inc.

9) UBS Global Asset Management10) Goldman Sachs Asset Management International Ltd.

1) Wellington Management Co. LLP

2) Columbia Management Investment Advisers LLC3) Fidelity Management & Research Co.

4) The Banc Funds Co. LLC

5) Lord, Abbett & Co. LLC

6) T. Rowe Price Associates, Inc.

7) Manulife Asset Management (United States) LLC

8) BlackRock Advisors LLC

9) Goldman Sachs Asset Management LP10) JPMorgan Investment Management, Inc.

Dollar Value of Position by Fund Type Number of Banks Held by Fund Type

54%46%

Discretionary Non-Discretionary

38%

62%

Discretionary Non-Discretionary

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 28/40

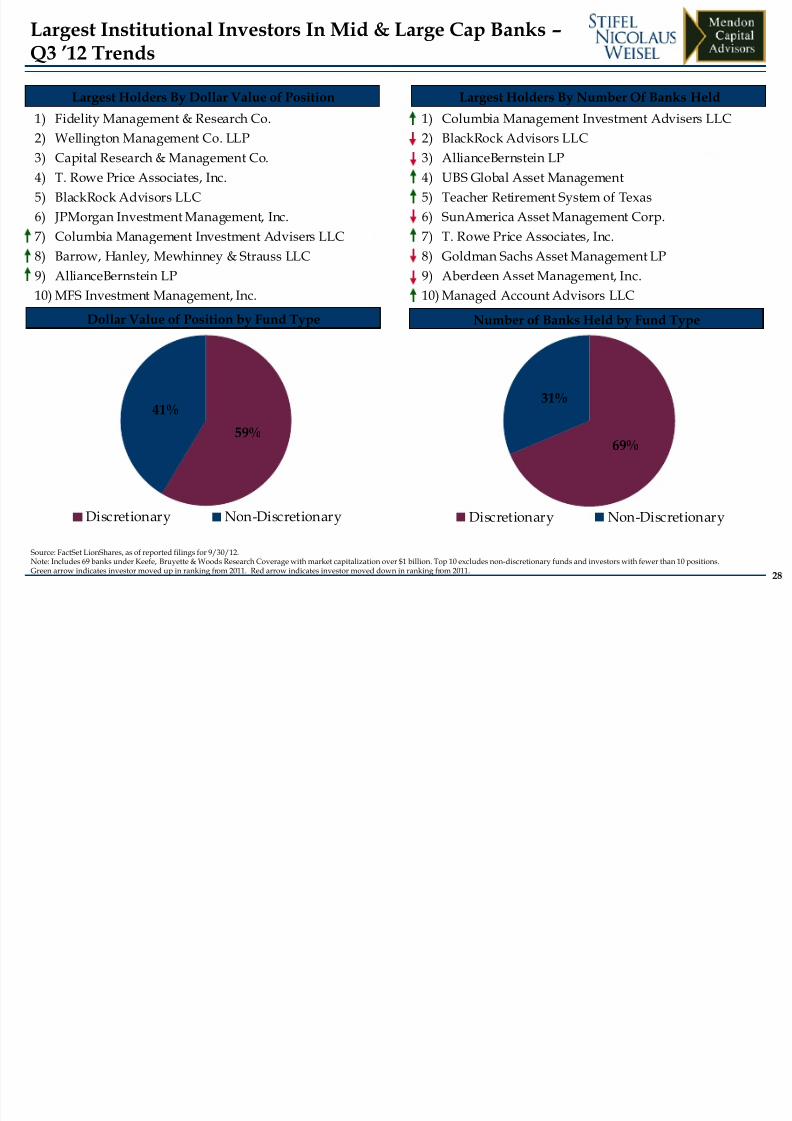

1) Columbia Management Investment Advisers LLC

2) BlackRock Advisors LLC3) AllianceBernstein LP

4) UBS Global Asset Management

5) Teacher Retirement System of Texas

6) SunAmerica Asset Management Corp.

7) T. Rowe Price Associates, Inc.

8) Goldman Sachs Asset Management LP

9) Aberdeen Asset Management, Inc.10) Managed Account Advisors LLC

28

Largest Holders By Number Of Banks HeldLargest Holders By Dollar Value of Position

Source: FactSet LionShares, as of reported filings for 9/30/12.Note: Includes 69 banks under Keefe, Bruyette & Woods Research Coverage with market capitalization over $1 billion. Top 10 excludes non-discretionary funds and investors with fewer than 10 positions.Green arrow indicates investor moved up in ranking from 2011. Red arrow indicates investor moved down in ranking from 2011.

1) Fidelity Management & Research Co.

2) Wellington Management Co. LLP3) Capital Research & Management Co.

4) T. Rowe Price Associates, Inc.

5) BlackRock Advisors LLC

6) JPMorgan Investment Management, Inc.

7) Columbia Management Investment Advisers LLC

8) Barrow, Hanley, Mewhinney & Strauss LLC

9) AllianceBernstein LP10) MFS Investment Management, Inc.

Dollar Value of Position by Fund Type Number of Banks Held by Fund Type

59%

41%

Discretionary Non-Discretionary

69%

31%

Discretionary Non-Discretionary

Largest Institutional Investors In Mid & Large Cap Banks –Q3 ’12 Trends

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 29/40

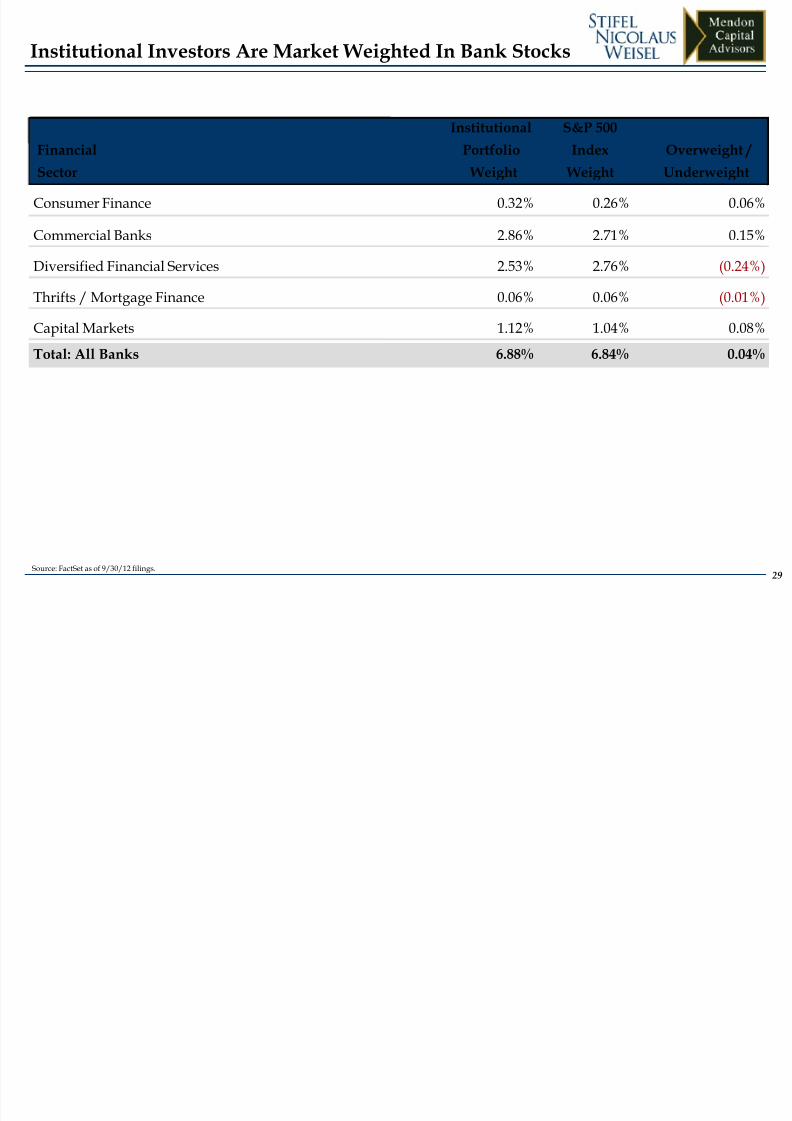

29Source: FactSet as of 9/30/12 filings.

Institutional Investors Are Market Weighted In Bank Stocks

Financial

Sector

Institutional

Portfolio

Weight

S&P 500

Index

Weight

Overweight /

Underweight

Consumer Finance 0.32% 0.26% 0.06%

Commercial Banks 2.86% 2.71% 0.15%

Diversified Financial Services 2.53% 2.76% (0.24%)

Thrifts / Mortgage Finance 0.06% 0.06% (0.01%)

Capital Markets 1.12% 1.04% 0.08%

Total: All Banks 6.88% 6.84% 0.04%

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 30/40

30

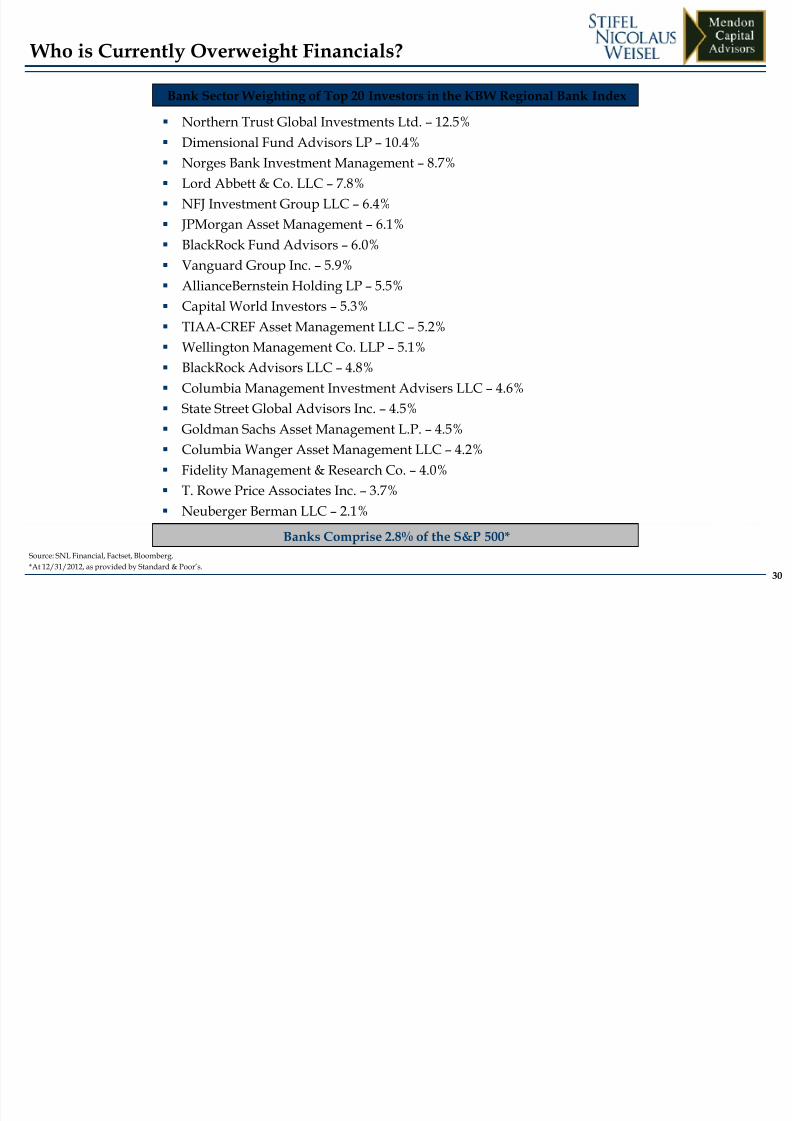

Who is Currently Overweight Financials?

Source: SNL Financial, Factset, Bloomberg.*At 12/31/2012, as provided by Standard & Poor’s.

Northern Trust Global Investments Ltd. – 12.5%

Dimensional Fund Advisors LP – 10.4% Norges Bank Investment Management – 8.7%

Lord Abbett & Co. LLC – 7.8%

NFJ Investment Group LLC – 6.4%

JPMorgan Asset Management – 6.1%

BlackRock Fund Advisors – 6.0%

Vanguard Group Inc. – 5.9%

AllianceBernstein Holding LP – 5.5%

Capital World Investors – 5.3%

TIAA-CREF Asset Management LLC – 5.2%

Wellington Management Co. LLP – 5.1%

BlackRock Advisors LLC – 4.8%

Columbia Management Investment Advisers LLC – 4.6%

State Street Global Advisors Inc. – 4.5%

Goldman Sachs Asset Management L.P. – 4.5%

Columbia Wanger Asset Management LLC – 4.2%

Fidelity Management & Research Co. – 4.0%

T. Rowe Price Associates Inc. – 3.7%

Neuberger Berman LLC – 2.1%

Banks Comprise 2.8% of the S&P 500*

Bank Sector Weighting of Top 20 Investors in the KBW Regional Bank Index

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 31/40

IV. Shareholder Activism

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 32/40

32

Objectives and Trends in Shareholder Activism

Maximize shareholder value

Force sale of company or assets

Drive change in management / board

Push for return of capital (distribute cash)

Highlight need for changes in fundamentalperformance (refocus business strategy)

Corporate governance reform

Activist Objectives Reasons for Increasing Shareholder Activism Increasing number of activist funds, including

traditionally passive institutional investors

More market liquidity

Ease of information dissemination

Success of past campaigns

Erosion of traditional takeover defenses

Political and public support for shareholderrights

Overview of Shareholder Activism

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 33/40

33

$0.1$0.1$0.2

$0.2$0.3

$0.5

$0.8

$1.2

$1.4

$1.7

$2.1

$1.5$1.6

$1.7$1.7

$1.8

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

3 Q ' 1 2

The Rise of Activist Hedge Funds

Most mutual funds and older LBO funds are barred frommaking unsolicited bids by clauses in their fundpartnership agreements

o Pension funds demanded this out of fear of adversepublicity

However, hedge funds are not bound by such restrictions

o Hedge funds are becoming a force in nearly everypublic takeover because of the amount of capital at

their disposalo This activism requires attention and warrants

careful preparation as for responding to a hostiletakeover bid. In fact, some of the attacks aredesigned to facilitate a takeover or to force a sale ofthe target

o Diligent planning and a proactive approach arecritical. Failure to prepare reduces a company’sability to control its own destiny

While the number of proxy fights has remained relativelyflat, the percentage of dissident victories (includingoutright sales, partial victories and settlements) haveincreased steadily

o Corporate control contests are increasingly votingcontests with a large public relations component

o Companies need to focus on a variety of constituentinterests including governance policies, social issues

and traditional Wall Street metrics

Growth in the Hedge Fund Industry’s AUM

($ in trillions)

The Activist Hedge Fund

Overview of Shareholder Activism

Source: Barclay Hedge Alternative Investment Database.

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 34/40

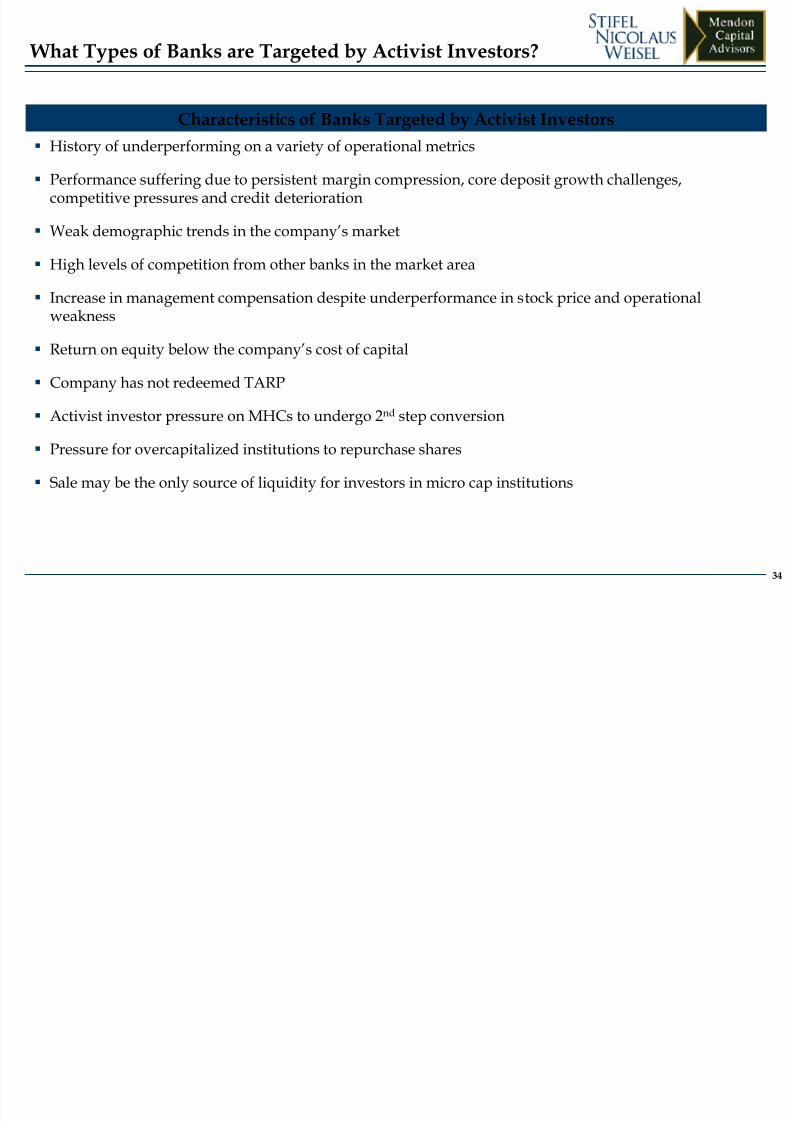

Characteristics of Banks Targeted by Activist Investors

History of underperforming on a variety of operational metrics

Performance suffering due to persistent margin compression, core deposit growth challenges,competitive pressures and credit deterioration

Weak demographic trends in the company’s market

High levels of competition from other banks in the market area

Increase in management compensation despite underperformance in stock price and operationalweakness

Return on equity below the company’s cost of capital

Company has not redeemed TARP

Activist investor pressure on MHCs to undergo 2nd

step conversion

Pressure for overcapitalized institutions to repurchase shares

Sale may be the only source of liquidity for investors in micro cap institutions

What Types of Banks are Targeted by Activist Investors?

34

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 35/40

V. Positioning For The Future

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

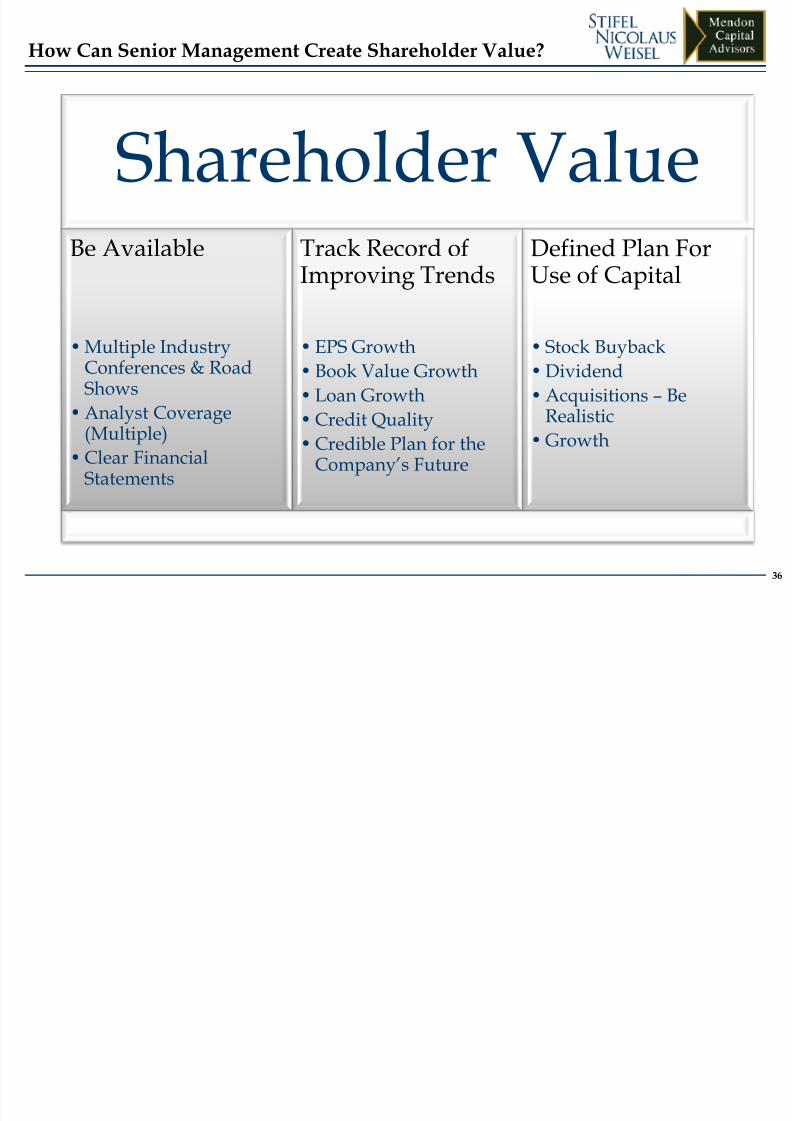

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 36/40

36

How Can Senior Management Create Shareholder Value?

Shareholder ValueBe Available

•Multiple IndustryConferences & RoadShows

•

Analyst Coverage(Multiple)

•Clear FinancialStatements

Track Record of

Improving Trends

• EPS Growth

• Book Value Growth

• Loan Growth

• Credit Quality• Credible Plan for the

Company’s Future

Defined Plan For

Use of Capital

• Stock Buyback

• Dividend

• Acquisitions – Be

Realistic• Growth

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 37/40

Return of Excess Capital: Best Options for Shareholders

Our research suggests shareholders are most likely to benefit from a large, sustainable increase in a

bank’s common dividend Performance is driven by investor perception of a stable dividend at a higher rate as well as the

strong probability for further future increases

Highest stock price impact occurred through increasing common dividends but maintaining apayout ratio less than 20%, leading to a 9.7% Bank Index outperformance

Tax changes for 2013 will negatively impact dividends as drivers of stock multiples

Stock repurchase programs have been the second most beneficial option for bank to return excesscapital

Banks that repurchased greater than 7.50% of their float outperformed their peer group index,confirming the positive effect large scale buy backs have on EPS

Least beneficial method of returning excess capital to shareholders is special dividends, as they haveprovided minimal share price outperformance in the 12 months following the declaration

Underperformance due to the one-time nature of this type of capital distribution

– Company management is perceived to view opportunities to internally return excess capitalas limited

Special dividends be beneficial and lead to stock price outperformance provided they are declaredunder the appropriate set of circumstances and to the shareholder base

Source: Stifel Nicolaus Research.

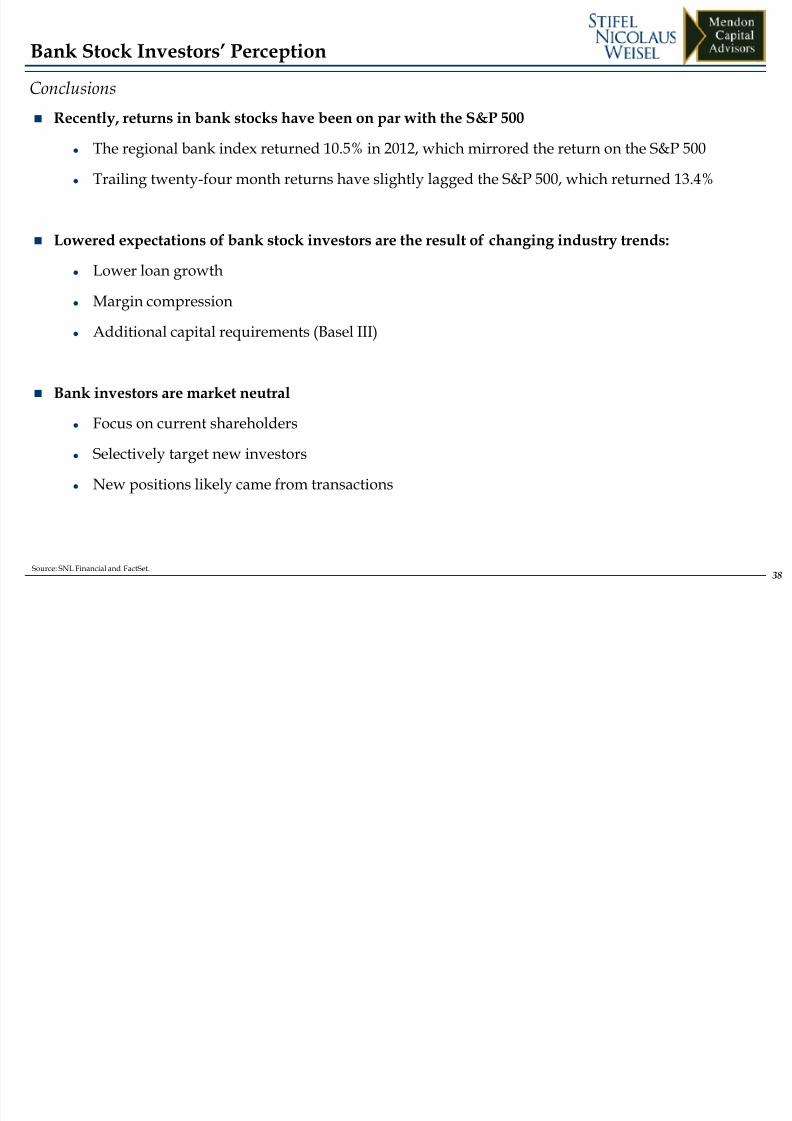

Bank Stock Investors’ Perception

37

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 38/40

Source: SNL Financial and FactSet.

Conclusions

Recently, returns in bank stocks have been on par with the S&P 500

The regional bank index returned 10.5% in 2012, which mirrored the return on the S&P 500

Trailing twenty-four month returns have slightly lagged the S&P 500, which returned 13.4%

Lowered expectations of bank stock investors are the result of changing industry trends:

Lower loan growth

Margin compression

Additional capital requirements (Basel III)

Bank investors are market neutral

Focus on current shareholders

Selectively target new investors

New positions likely came from transactions

Bank Stock Investors’ Perception

38

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 39/40

Appendix

8/12/2019 1130 Sun Bank Investors Who Were They Who Are They and What Are They Looking For

http://slidepdf.com/reader/full/1130-sun-bank-investors-who-were-they-who-are-they-and-what-are-they-looking 40/40

Illustrative Model – Bank XYZ

Approach and Assumptions

Illustrative, bottoms up valuation approach which depicts how the theoretical value of a bank and impliedmultiples are impacted by changes in assumptions in terms of profitability, asset growth and required capital

― By projecting an earnings stream based on an assumed ROAA and asset growth rate, one is able to calculatea dividend stream in relation to the excess capital generated above a certain TCE requirement. Thisdividend stream is then discounted back at the assumed cost of capital (assuming the dividend is a growingannuity) to arrive at the implied valuation of the bank. From that point, one can arrive at the implied

pricing multiples.

What Will the “New Normal” Look Like?