Embed Size (px)

DESCRIPTION

world issue

Citation preview

(08

1H[W�*UHDW�(XURSHDQ�(FRQRPLF�'LVDVWHU

E\�0DUWLQ�$��$UPVWURQJ

7here is a huge debate fer-menting over the future ofEurope. In Britain, this de-

bate is also heating up as the infa-mous date of 1999 moves closer toour focus. Many argue that Europemust pull together to fight off therising tide of trade around theglobe. A united Europe is seen asthe answer to keeping the Marxistfoundation of socialism alive. Tosome observers this appears as aclose parallel when Rome trieddesperately to fend off the inva-sions of barbarians that alsoproved fruitless in the final histori-cal analysis.

The one sales pitch that hasbeen used to sell this reviveddream of a united Europe is noneother than the currency. It has beenpointed out that if one begins inLondon with a 100 pounds, aftertraveling around Europe exchang-ing the currency in every port, when

Issue #7 July 1996 Copyright Princeton Economic Institue all rights reserved214 Carnegie Center,Princeton NJ 08540 609-987-9522 Annual Subscription US$49.95

you return to London you will haveonly 60 pounds left after spendingnothing.

While this argument appears toinvoke much common sense abouthow inefficient currency transac-tions might be between nations, atthe same time, it fails to deal withthe reality behind creating a singlecurrency. The proponents of a sin-gle currency for Europe often pointto the success of the United States,albeit behind closed doors and faraway from the public eye, as thejustification behind a single cur-rency. Many fund managers andmultinational corporations also hailthe move to a single currency asthe future for Europe simply be-cause they are finding it extremelydifficult to cope with the rising vola-tility in foreign exchange.

Nonetheless, Europe does notquite understand the United Statesmodel of a single currency. Europelooks at the US and sees one singlecurrency as being extremely effi-cient with a by-product of consis-tently lower unemployment as onegoal. However, it is in fact a singlecurrency policy that is actually partof the internal problems that arecausing much concern within boththe United States and Canada.

It is of vital importance that weunderstand the benefits as well asthe nasty side-effects of a singlecurrency for Europe as a whole andin that context US and Canada doserve as an excellent model to ex-plore for answers. Prior to 1927 thecentral banking system in the USwas established in 1913 with 12INDEPENDENT branches. Eachbranch maintained its own sepa-rate discount rate. This is very im-portant to understand. It was notuncommon to find rates at 7% inCalifornia and 3% in New York.This is far too often a point totallylost in history, but it is paramount intrying to define whether or not EMUwill succeed or fail for Europe.

The central banking systemknown as the Federal Reserveemerged as a solution out of thedisaster of the financial Panic of1907. The Federal Reserve was

formed in 1913 because the evi-dence revealed in the investiga-tions by Congress discovered thateven though a single currency hadexist ed in the US since 1792, theregional capital flows within the USwere often to blame for numerousfinancial panics - 1907 being theprimary Panic that drew the atten-tion of government to this problem.

The differences on a regionalbasis within the US economy as awhole were the source of Panicsdue to cash flow problems on anationwide scale. Even today, thedifferences between the localeconomies in Texas and New Yorkare staggering. We call this theTexas/New York arbitrage. WhenTexas is booming, New York is inthe depths of a recession and viceversa. The New York economy ismore financial and business re-lated today while Texas is morecommodity oriented with farmingand oil production. Therefore,when inflation is running high,Texas booms at the expense ofNew York.

This is the same regional capitalflow problem is silently tearing Can-ada apart. When real estate wasbooming in 1987 in the Eastern re-gions of Canada, interest ratescontinued to rise in an attempt tostop the speculation. However,while there might have been a realestate boom in the East, the risinginterest rates policies were drivingfarmers into bankruptcy in Alberta.

The Panic of 1907 followed onthe heels of the Great San Fran-cisco Earthquake. The claims wereobviously on the West Coast but allthe insurance companies were ofthe East Coast. As capital flowedfrom East to West, shortages inmoney supply emerged amongNew York banks that culminated inbank failures.

A single currency does not nec-essarily make things great. In fact,there is more to the issue of a stableeconomy than merely a single cur-rency.

The regional cash flow problemswere initially resolved between

1913 and 1927. However, a verysignificant development took placein 1927 that would forever alter thecourse of our economic destiny forthe entire century.

By the mid 1920s, it was noticedthat there were significant prob-lems emerging on a cash flow basisinternationally. In a power strugglewithin the US Federal Reserve, theNew York branch managed to con-vince the government that thesame system of regional cash flowmanagement should be extendedto the international level. The NewYork Fed won the battle againstChicago who warned that changingthe focus would undermine the do-mestic policy objectives of thebank. In the end, the entire powerof the Fed was shifted into a singlenationwide system where one in-terest rates policy would be usedthus abandoning the original mis-sion of the the Federal Reserve asthe guardian of domestic cash flowproblems.

1927 this marked the beginningof the very first G4 effort at influenc-ing international cash flows. Thediscount rate in the US wasusurped into a single rate. The firstaction was to lower US interestrates in an attempt to divert capitalback to Europe. The manipulationbackfired because it gave cre-dence to rumor that there was aproblem with the escalating debt inEurope. As the cash flows into theUS intensified, the Fed moved intoa state of panic. Capital poured intothe US driving the stock market updramatically - doubling between1927 and 1929 despite the Fedraising interest rates from 3% to6%.

The post-1927 economy has re-mained on the international re-gional focus rather than on theoriginal intent of domestic regionalcapital flow management. This iswhere our modern problems of re-gional disparities emerged. Theone-size-fits- all approach to inter-est rate policy is now increasing thetensions between regions withinmost nations. It is this very issuethat is tearing apart Canada pittingone province against another.

Providing Economic & Market Analysis Worldwide

2

This theory that a single cur-rency for Europe is NOT the an-swer. It will not solve the vast dis-parities between the economies ofEurope but in fact will be a meansof exporting deflationary policies atwork in Germany to other nationssuch as Britain. What EMU must beabout is more than a single cur-rency. While a single currency willease some risk problems for busi-ness associated with currency, itposes significant dangers thatwould breed resentment betweenmember states.

If EMU were to adopt a singlecurrency, it must NOT, under anycircumstances, lead to a singlemonetary policy that would imposea one-size-fits-all approach. Thebasic sovereignty over establishinglocal interest rates must reside witheach state. Allowing this vital powerto be usurp into a single rate willundermine the entire framework ofEurope much in the same manneras is taking place in Canada oreven the United States.

The individual nations of Europehave distinctly different economiesas is the case among the 50 US

states. When US auto manufactur-ers lost market share to the Japa-nese and European cars, the econ-omy of Michigan was devastated.When IBM was forced to restruc-ture, Massachusetts was devas-tated. When oil prices fell sharply,million dollar homes in Texas fell to$100,000. Regional problems existtoday as they did prior to 1913. IfEurope follows-through with itsone-size-fits-all plans for EMU, itvery well may lead to the worsteconomic disaster in the economichistory of Europe.

Copyright PEI July 1996 All Rights Reserved

3

9LHZ�)URP�$PHULFD

E\�0DUWLQ�$��$UPVWURQJ

7he political scene is aboutto go completely nuts aswe approach mid to late

August. At the Republican conven-tion, rumor has it that Buchanan willnot get an opportunity to speak.Amazingly, there is yet another 3rdParty movement going by the nameof the US Tax Payer’s Party whojust so happen to be holding theirconvention across the street fromthe Republicans in San Diego. Thestart date will be Friday, August16th coinciding with the end of theRepublican convention. The rumorpart is that Buchanan is going tostage a protest on national TV andwalk across the road to assume thenomination of this new 3rd Party.The US Tax Payers Party is on theballot in 28 States. AlthoughBuchanan running as yet another3rd Party candidate may not standa chance of winning, combined withPerot, the US political scene is go-ing to start looking like some Euro-pean nations with multi-party frag-mentation. This is likely going tomean that Clinton will win rathereasily as our computer models hadforecast.

Yet the second party of our long-term Presidential forecast for theUS remains quite provocative. AClinton victory in 1996 will meanthe end of the Democratic Party.Clinton should be the last Demo-cratic President to hold office!While this might appear to be apartisan statement, it is not! Thereare two factors taking shape herein the US political scene that aresimply not addressed by the mediaor many politicians for that matter.

1)DEMOGRAPHICS: If we lookat the great socialistic movement ofthe 20th century, we see that itactually reached a peak with thefirst election of Roosevelt. That firstelection marked the highest con-centration of Democratic power inthe Senate and the House. Whilethe Democrats managed to retain

control of Capital Hill for 40 yearsor so, they did so with a steadilydeclining majority. If we analysisthe generational cycle, we find thatthe bulk of the support for theDemocrats tends to be concen-trated within the elderly and lowincome minorities. As we lookahead, the elderly generation of theNew Deal will die off as we movebeyond 2000. This shift from onegeneration to the next will be pro-found. The Democrats have neverbothered to build much of a coali-tion among the middle class whoremain the bulk of the independentvoters. Consequently, the mostconservative groups among votersare not the elderly or low incomeminorities. As we move beyond2000, the Democratic Party beginsto fade in its support.

2) CORRUPTION: There is littledoubt that Clinton and his wife areperhaps the most corrupt couple tohave ever held the office of Presi-dent. Hillary is clearly guilty of justabout everything under the sunfrom laundering funds via cattle fu-tures and land deals to obstructionof justice in dealing with the Con-gress. Since the IndependentProsecutor Ken Star is holding offon filing any charges against theClintons unti l after the election, anew possibility arises. There is areasonable chance that during thefirst half of 1997 Clinton may resignor at least standby and try to defendHillary. In any event, the post-elec-tion period may become far moreinteresting than the pre-electionspeculation. This could be one fac-tor that drives the dollar to a newlow against many Europeans earlynext year.

ECONOMY:

The US economy appears tohave reached a temporary top as ofMay 1996. The back-dated statis-tics will continue to be strong rais-ing the serious possibility of a ratehike by the Fed come August. Thismay have a profound impact upon

the share market as well as bondmarkets in the US and elsewhere.If the US 30 year bonds close below10801 at the end of July on a near-est futures basis, then there will bea risk that a rate rise is possible inAugust causing the second legdown in the stock market prior toLabor Day.

SOCIAL SECURITY:

Thanks to Clinton’s clever trickswith the funding of the nationaldebt, there is a real risk that SocialSecurity will move into deficit nextyear - not 2010 as previous fore-cast by the government. This willhelp to add to the confusion of in-flation and market behaviour nextyear promising to make 1997 ayear to remember.

TAX REFORM

The Flat Tax is dead. Long livethe Consumption Tax. If the Re-publicans do manage to hold Capi-tal Hill (A BIG IF), then we shouldexpect a compromise plan toemerge from Armey- Archer. Theplan will be replacing the incometax with a national sales tax whilebusiness will still be taxed on anincome basis. Reforms in the busi-ness tax may also include the abol-ishment of worldwide income.

Congress is clearly concernedabout the Internet and the emer-gence of a new quasi-electronicform of money. They know that taxreform is going to be necessary butat the same time they also knowthat money, as we know it, mayalso be changing. There are someon Capital Hill who do envision theday where cash will be abolishedand all transactions will be takingplace with some sort of a debt-card.This will answer the prayers of thetax collector and perhaps begin the21st century on a completely newset of rules.

Providing Economic & Market Analysis Worldwide

4

3ULQFHWRQ�(FRQRPLFV������/RQGRQ�6HPLQDU

E\�%UXFH�$OOHQ([HFXWLYH�'LUHFWRU�8QLWHG�.LQJGRP�0LGGOH�(DVW

Professor, Sir Alan Walters,the former economic adviser toMargaret Thatcher was the guestspeaker at our London seminar inJune. He is also a member of TheReferendum Party set up by SirJames Goldsmith to contest thenext UK elections on the issue ofBritish sovereignty in Europe andthe right of the electorate to ex-press a direct view by referendum.He spoke on the subject of theEuropean Monetary Union (EMU)and the single European currencyas well as broader issues. From hisbackground at the heart of Britishpolitics in the 1980’s he provided aninsight into the lead up to the Euro-pean position today and a thought-ful analysis of economic and politi-cal motives currently at work. Pro-fessor Walters speech, included inthe video of the London Seminar, issummarized below.

0RQHWDU\�8QLRQ�YHUVXV6LQJOH�&XUUHQF\

There is a great distinction be-tween a monetary union and a sin-gle currency, though in economicterms broadly speaking they arethe same. Hong Kong and the USare an example of monetary unionwith the exchange rate fixed at 7.8.Interest rates in Hong Kong movebased on those of the US. And theGerman, French and Benelux cur-rencies are effectively in monetaryunion within the European Ex-change Rate Mechanism (ERM)with very little movements in theirparities. You get all the economicbenefits of a single currency with-out the need to create one due tofixed rates.

Economically, it doesn’t matterwhether you have a single currencybut politically it matters a greatdeal. Because once you have asingle currency you have lockedyourself in and thrown away thekey.

The Gold Standard from 1870through 1931 is cited by some as acase for a single currency but thatwas a monetary union, gold itselfdid not circulate to any degree. Sothat allowed Britain to get out of thestandard at various times such asin 1913. Britain went back into thestandard at $4.85 in 1925, went intoa great slump in 1926 and essen-tially stayed in it until coming off thegold standard in 1931. The USwent off in 1933 and the Frenchheld on until 1936.

Monetary Union and Inflation

The economic argument formonetary union was that all coun-tries would have the same inflationrate; Britain joining the ERM wouldborrow the Bundesbank’s credibil-ity, control the French and gang upon the Germans. There was enor-mous political pressure to join.However, there is no reason to be-lieve that monetary union or even acommon currency will result incommon inflation rates. Hong Konghas had inflation rates spread 5%above those of the US over thesame period. The central point isthat you would have the same infla-tion but only for tradeable goods.Non-tradeable goods such as realestate can be very different. TheUS itself is an example with priceinflation different in different areas.

Optimum Currency Area

A single currency for Europe hasnever been rationally arguedthrough. To argue for this youwould have to prove Europe is anoptimum currency area - all econo-mies reacting broadly in the sameway to monetary policies and mov-ing in concert. Now Europe doesnot react this way. Even the US

does not react this way but there isa great mobility of resources andlabor in the US against minimalmovement in Europe. There arestrains in the US - when oil goes upits good for Texas but the EastCoast cries. In Europe thosestrains would be two or three fold.It will be very difficult . Countries willwant to break out of the straightjacket.

Conclusion

It is likely therefore that Europewill have Monetary Union but not acommon currency beginning in1999. Kohl is in a hurry; he wantsthis established before the 1998German elections when he is likelyto retire.

0LVVLQJ�.RUHDQV

Direct investment in the UK hasincreased for a third year running torecord levels. Although the largestnumber of projects still come fromthe US, Germany has moved to thenumber two position. More than1500 German companies nowhave an operation in the UK, andinvestment from other Europeancountries is increasing. Britain re-mains the favored destination fordirect investment into the Euro-pean Union accounting for 38% ofall investment last year. The wellpublicized investment by Korea’sLG Group of £1.5 billion creating6,000 jobs has created euphoria inthe Welsh valleys around the cho-sen site. A government grant of£200 million no doubt helped inattracting this Korean investment tothis region along with the presenceof existing successful Korean ven-tures. However, stable and lowtaxation and liberal labor regula-tions remain major factors in at-tracting inward investment.

A meeting of twenty eminenteconomists recently debated em-ployment issues under the aus-pices of Southbank University’sEuropean Institute in London.

Copyright PEI July 1996 All Rights Reserved

5

Could regulation and non-wagecosts such as welfare and sever-ance be responsible for Europe’shigh and persistent unemploy-ment? The unanimous decision bythe economists was “No”! How-ever, it was noted that a viciouscircle of the public sector providingalternative jobs or compensationtriggers increased governmentspending, higher taxes or interestrates or both and that the extremelyhigh severance pay rules in Spaincould contribute to that country’s22% unemployment. No Korean in-dustrialists were observed in theaudience.

%DLO�RXW�QRZ���%DLO�RXWODWHU���

The exclusion of pension liabili-ties from the Maastricht criteriajudging qualification for the Euro-pean single currency does not ap-pear to be causing too much con-cern. Unfortunately, if they were in-cluded, it is unlikely any countrywould come close to qualification.Apart from Britain, Ireland and Hol-land, pensions for the expandingranks of the elderly are funded notby past contributions but by taxfrom the dwindling ranks of theyoung employed. Unfunded liabili-ties as a proportion of national in-come run at 69% in France, 122%in Germany and 107% in Italy.Members of the currency unionwould be jointly liable to bail out theproblems with tax payers money.Euro interest rates could gothrough the roof as each of the 400million citizens of the European Un-ion would be saddled with $50,000in debt. It is a compelling argumentfor Britain to bail out now ratherthan bail out Europe later.

7D[�+ROLGD\V

Brussels has finally acknow-ledged that it would appear to becontradictory to remove currencydistortions in free trade within theEU while leaving taxation distor-tions in place. There are very largedifferences in tax systems, taxrages and tax bases between

member states which significantlyfrustrate free trade. A "Communi-cation on direct taxation” is due tobe released by the Commissionthis summer with proposals for har-monisation perhaps a little bit be-hind the drive for harmonisation ofcurrencies and subject to very littlepromotion in public. Tax, however,sits right in the door of governmentswhilst differences in foreign ex-change can be blamed on specula-tors.

Reform of Value Added Taxation(VAT) is also under discussion.Three proposals put out by single

market commissioner Mario Montiwere to make businesses pay forBAT on cross border transactionsin the country of origin, bring allBAT rates to the same level (toavoid low tax countries having and"unfair” advantage) and to “mod-ernize” and standardize the scopeof VAT as who would pay and whowould be exempt. No doubt therewill be opportunity for a little reve-nue raising. It has been suggestedVAT should be added to the ticketprice of all aircraft travel within theEU. Good news for holiday resortsin Thailand, but not in Spain!

Providing Economic & Market Analysis Worldwide

6

0HJDORPDQLD�"

E\�+DUU\�*URHUQHUW([HFXWLYH�'LUHFWRU&RQWLQHQWDO�(XURSH

Telekom Germany has plannedto issue the first portion of 500 mil-lion shares (par value 5.00 DM) inNovember as part of the privatiza-tion program. The second allot-ment is scheduled for 1998. With abalance sheet of 160 billion DM($105 bln), sales of 66 billion DM($43 bln) and a profit of 5.8 billion($3.8 bln) for 1995 it appears to bean interesting investment - at leastinitially. The issue price is esti-mated between 25 and 30 DM - thesale shall fetch about 15 billion DM($10 bln).

Deutsche Bank, Dresdner Bankand Goldman Sachs as lead under-writers need to be successful, oth-erwise the second portion in 1998wont sell. 60% of the shares shall

be placed in Germany, 20% in theUS and 20% in the UK and Europe.

60% of the total of 15 billion forGermany means a capital require-ment of 9 billion. This is a decentamount for the German Stock-Ex-changes. In 1995 a total of 20 com-panies went public and they alto-gether raised just a total of 8.3 bil-lion. In the rest of the world, irre-spective of the fact that Telekom isnumber three on this planet, theinstitutions do hold a lot of telecom-munications shares like AT&T,NTT and BT not mentioning thesmall companies. I doubt that anysubscriber of the new issues ofNTT or BT is happy with his invest-ments - only AT&T has performedwell. Those who place and issueshares look always with optimisminto the future. They estimate thegrowth rate for telecommunicationat 15% p.a. worldwide for the next

decade. For the domestic marketthe forecast hovers around 7%.

What is worth knowing aboutTelekom? Their debt is more than120 billion DM ($79 bln) and theypay more than 8 billion ($5.2) oninterest. Telekom used to be part ofthe government. The German civilworkforce has the same reputationas other civil work forces in anyother country. Telekom also has ahuge obligation on old pensionschemes and has not yet experi-enced competition in its core mar-ket. It was also exempt from reve-nue tax until 1996.

7KH�WLS�RI�WKH�LFHEHUJ

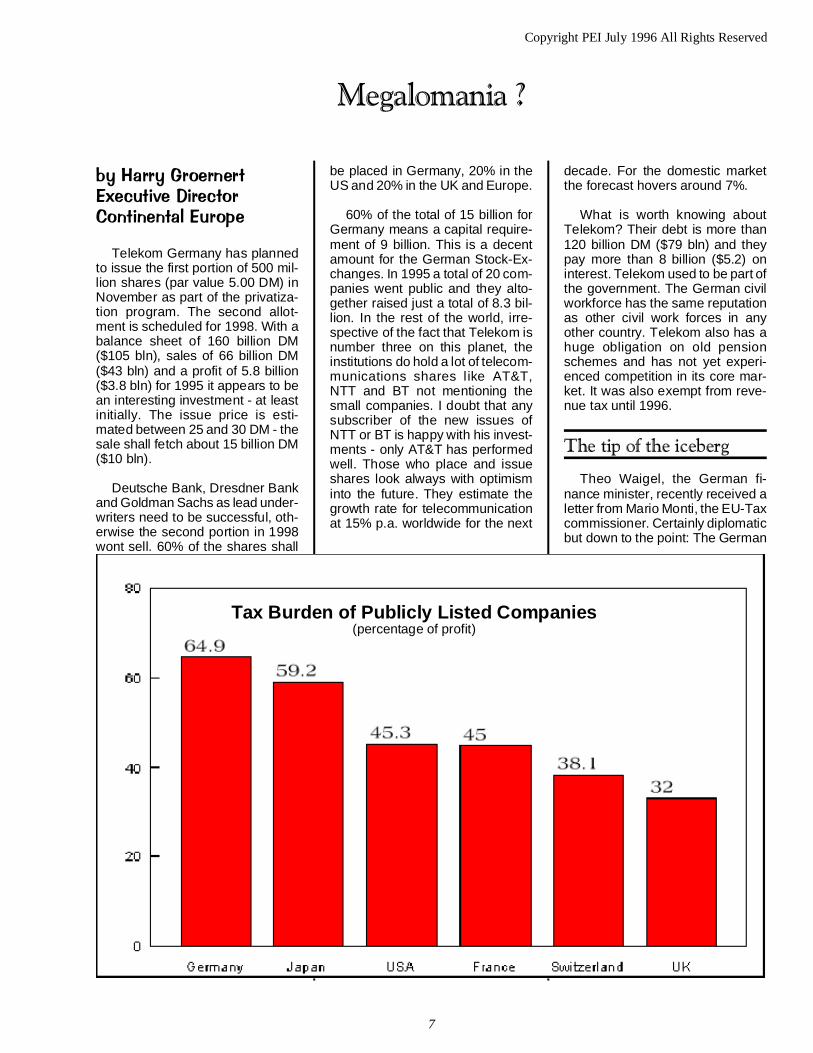

Theo Waigel, the German fi-nance minister, recently received aletter from Mario Monti, the EU-Taxcommissioner. Certainly diplomaticbut down to the point: The German

Tax Burden of Publicly Listed Companies(percentage of profit)

Copyright PEI July 1996 All Rights Reserved

7

corporation income tax (Körper-schaftssteuer) is against some ba-sic rules of the Maastricht treaty. Ithinders and restricts free capitalflow.

Tax burden of publicly listedcompanies, percentage of profit

That is not all. Germany now hastotal of 1500 companies with op-erations in the UK, the tax-haven ofEurope. Why, because businessesare voting with their wallets andinvesting abroad in order to avoidtaxes. It is as simple as that. Aslong as politicians do not learn thelessons of history they are con-demned to repeat the misery. TakeMunich as an example. A referen-dum voted with 50.6% for threenew tunnels in Munich. Three dayslater it was obvious that this wouldcost some money. The city councilvoted and decided for an increasein trade taxes. They call it the “Tun-nel-Strafsteuer” (tunnel penaltytax). What is going to happen? Anydecision upon location will be influ-enced more by the local taxes thanby economic parameters and themunicipalities will get less incomein the end.

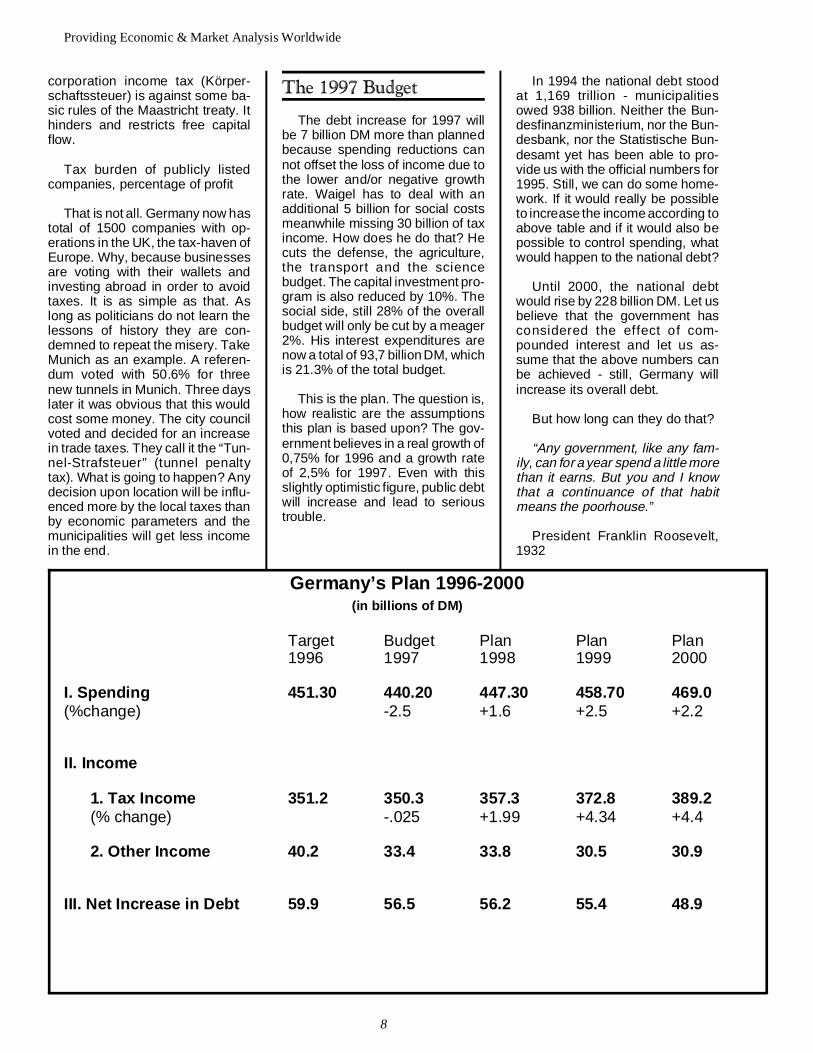

7KH������%XGJHW

The debt increase for 1997 willbe 7 billion DM more than plannedbecause spending reductions cannot offset the loss of income due tothe lower and/or negative growthrate. Waigel has to deal with anadditional 5 billion for social costsmeanwhile missing 30 billion of taxincome. How does he do that? Hecuts the defense, the agriculture,the transport and the sciencebudget. The capital investment pro-gram is also reduced by 10%. Thesocial side, still 28% of the overallbudget will only be cut by a meager2%. His interest expenditures arenow a total of 93,7 billion DM, whichis 21.3% of the total budget.

This is the plan. The question is,how realistic are the assumptionsthis plan is based upon? The gov-ernment believes in a real growth of0,75% for 1996 and a growth rateof 2,5% for 1997. Even with thisslightly optimistic figure, public debtwill increase and lead to serioustrouble.

In 1994 the national debt stoodat 1,169 trillion - municipalitiesowed 938 billion. Neither the Bun-desfinanzministerium, nor the Bun-desbank, nor the Statistische Bun-desamt yet has been able to pro-vide us with the official numbers for1995. Still, we can do some home-work. If it would really be possibleto increase the income according toabove table and if it would also bepossible to control spending, whatwould happen to the national debt?

Until 2000, the national debtwould rise by 228 billion DM. Let usbelieve that the government hasconsidered the effect of com-pounded interest and let us as-sume that the above numbers canbe achieved - still, Germany willincrease its overall debt.

But how long can they do that?

“Any government, like any fam-ily, can for a year spend a little morethan it earns. But you and I knowthat a continuance of that habitmeans the poorhouse.”

President Franklin Roosevelt,1932

Germany’s Plan 1996-2000(in billions of DM)

Target Budget Plan Plan Plan1996 1997 1998 1999 2000

I. Spending 451.30 440.20 447.30 458.70 469.0(%change) -2.5 +1.6 +2.5 +2.2

II. Income

1. Tax Income 351.2 350.3 357.3 372.8 389.2 (% change) -.025 +1.99 +4.34 +4.4

2. Other Income 40.2 33.4 33.8 30.5 30.9

III. Net Increase in Debt 59.9 56.5 56.2 55.4 48.9

Providing Economic & Market Analysis Worldwide

8

7KH�(PHUJLQJ�0DUNHW�RI�5XVVLD

E\�'DQD�6FKQHLGHU'LUHFWRU�RI�5XVVLDQ6WXGLHV

,nvesting in Russia is arisky undertaking. The po-litical environment is by no

means shatter-proof. Although therecent elections boosted stabilityand confidence in the fledgling de-mocracy and emerging market, thehealth of President Yeltsin loomslarge. Speculation is in the newsabout who would assume control ifthe president were incapacitated.Alexander Lebed, who won 15% ofthe vote in the final presidential bal-lot, has been appointed as SecurityChief and is presently seen as alikely candidate. The CommunistParty acknowledged defeat butvowed to press their agendathrough their majority in the Duma.This could hold up confirmation ofYeltsin’s Prime Minister and othergovernment officials as well asmarket and economic reform legis-lation. The most pressing issue istaxation as the IMF has held upover US$ 300 million in a loan dis-bursement until Russia acts on im-proving collection that is down over60% than projected for the first halfof 1996. So Yeltsin’s victory, al-though preferred, does not dis-place concern about political andeconomic stability in Russia.

:K\�5XVVLDQ�,QYHVWPHQW

Investing in Russia is undeni-ably appealing. The vast amountof natural resources has investorsanxious. Statistics reported fromthe State Geological Committeeshow why: Russia has 13% of theworld’s proven oil reserves; 12% ofthe coal; 35% of the gas re-sources; and a large chunk of theworld’s diamonds, timber, iron ore,gold, and rare metals. It has beenestimated that only about 10% of

these resources are under devel-opment/production.

Russia ranks sixth in terms ofpopulation (148 million) and exhib-its one of the most product starvedof consumer markets. The Ministryof Economics reported that in 1995,foreign investors put the most capi-tal into the trade and public servicesector to total 17% or US$ 471.9million. Banking and finance camein with 14.3% (US$ 386.6 million);the food sector received 10% (US$282.9 million); oil and gas industryat 9.4% (US$ 199 million); con-struction sector received 7% (US$199 million); and the chemical andmachine production both stood at5.9% (US$ 166 million and 165 mil-lion respectively). For the 1995 to-tal, foreign investment is estimatedat US$ 2.5 billion (Rbl 1,032 billion)of which direct investment was US$1.88 billion (Rbl 652.8 billion). How-ever, over US$ 890 million (Rbl155.5 billion) was received viacredits in trade, banking accountsand international financial organi-zations.

7KH�5XVVLDQ�(TXLW\0DUNHW

By mid-1995, over 70 ex-changes had been registered.Several main exchanges have de-veloped in Russia - St. Petersburg,Moscow, Yekaterinburg, Vladivos-tok, and No vosibirsk. T heRFCSCM (Russian FederationCommission on Securities and theCapital Market) oversees the ex-changes and investment instru-ments; issuance, trading, and re-porting systems and enforces mar-ket rules. The RFCS is modeledafter the US SEC but by no meansdoes the Russian counterpart en-joy its seemingly broad powers asenabling legislation, mechanisms,and agencies still need to develop.

The RFCS was established bypresidential decree in November of1994 after a large portion of priva-tization had already begun. Thelate arrival of this vital agency wasin part responsible for the fraud andinefficiency that affected the execu-tion of the privatization schemes.Consequently, the role of the RFCSis complicated by correcting prob-lems that were incurred in the pastcouple of years while trying to fore-see and headoff problems of to-morrow.

Rossiyskiy Kredit Bank Re-search cited that some 40 millionshareholders appeared by July of1994 after the process to privatizeover 16,000 large-scale enter-prises via a voucher system startedin October of 1992. More share-holders were added as the numberof privatized enterprises reachedover 100,000 by the end of 1994.Additionally, estimates of marketcapitalization for top 100 Russiancompanies as of April 1996 was atUS$ 13,935.48 (million).

The Rossiyskiy Kredit Bank re-ports that over 98% of activity inRussian stocks takes place in theover-the-counter market. Withinthe entire OTC market, there is thedeveloping electronic trading sys-tem - the Russian Trading SystemPORTAL - RTS/PORTAL. POR-TAL is the portalelectronic tradingsystem set up in the Spring of 1995that reports trading prices and vol-umes

Many professional associationshave developed in each exchangeloction. The PAUFOR is an inde-pendent professional associationof broker-dealers in Moscow. Cur-rently, PAUFOR consists of over 90members and is evolving toward awell recognized, self regulating andtraining organization. Members ofPAUFOR gain access to partici-pate in the electronic trading sys-tem through PORTAL.

Copyright PEI July 1996 All Rights Reserved

9

This screen based systemgreatly improved the transparencyof th e market. Members ofPAUFOR have committed to issu-ing firm bid and ask quotations tobe posted daily on the PORTAL. Itis the most accurate and up to datesource on market activity. TheRTS reports of pricing are out at12:00, 15:00, and 18:00 Moscowtime. It is expected that that theRTS/PORTAL system will be ex-panded nationwide to incorporateother exchanges in a similar fash-ion to the NASDAQ.

Outside of PORTAL, the systemto obtain timely and accurate mar-ket data is undeveloped. Manymarket players still telephone oneanother for bid and ask quotations.A cottage industry of independentbusiness has sprung up to fill thisvoid - providing not only currentprice information but badly neededcompany and sector research.Several of these businesses haveestablished indices. The price in-formation, method of inclusion, orweighting/calculation is not univer-sally established and is subject tochange frequently since this mar-ket is quite thin.

Currently, the Moscow Timeshas an index of the top 50 compa-nies and is emerging as the widelyaccepted index. Other privatebusiness calculate "Blue Chip"company indices or have createdother indices by sector, such as oiland non-ferrous metals. The repu-tation and credibility of these com-panies promote the index and notan industry recognized accuracy ormethodology.

Although the RFCS, PAUFOR,and the electronic trading systemPORTAL have helped the marketsystem to be a more open, trans-parent, and regulated market - anindependent and reliable registrysystem is not yet fully developedand organized. Manipulation, in-sider trading, and outright fraud,particularly outside of Moscow, isnot uncommon as estimates listover 400 share registrars. Manyshares are maintained by book en-tries written in by independent issu-

ers and registrars without over-sight. Realistically, the laws on thebooks are not enforced nor is abody set up to clearly supportregulation. Without a verifiableregistry system in place, foreign in-vestors will remain on the sidelineswhen it comes to the domestic eq-uity market.

The pursuit of ADR’s (AmericanDepository Receipts) by large Rus-sian corporations through Westernfinancial institutions is an attempt toacquire foreign shareholders in anotherwise unsecured and high riskenvironment. The huge govern-ment demand for capital as well asthe embattled economy has madeit very difficult for Russian businessto secure domestic share holders.Any capital looking for work is cur-rently put toward buying up the gov-ernment debt offering due to thehigh yield and short-term maturity.Sector giants such as LUKoil haveused ADR’s to get their shares tothe international marketplace.ADR’s are appealing to those in-vestors who are impatient for Rus-sia’s system to evolve. ADR’s aredollar based in their pricing andinterest and dividends are paid in

dollars. Clearing and settlement isalso operated by US standards soinconsistent and murky locallaws/custody and shareholderrights are by-passed. However,ADRs are vulnerable to currencyexchange rates as reflected inprice.

(OHFWLRQ�6XPPDU\

The July 3rd Russian Presiden-tial elections have concluded,firmly placing Yeltsin at the helmwith 53.82 percent of the vote. Thechallenger Zyuganov received40.31 percent. Yeltsin’s margin ofvictory was 10 million votes, or13.5%, over the 30.11 million votescast for Zyuganov. Out of Russia’s108.6 million voters, 68 percentmade it to the polls casting a totalof 73.9 million votes as reported bythe Central Electoral Commission.The turnout was 1% lower than thatof the June 16th first round dispel-ling fears of low voter turnout thatwould favor the communists. Theshowing bolstered Yeltsin’s claimto a popular mandate for continuedreforms under his leadership.

Providing Economic & Market Analysis Worldwide

10

+RQJ�.RQJ�8SGDWH

E\�&UDLJ�+��6WHSKHQ&KLHI�$QDO\VW+RQJ�.RQJ�%UDQFK

Ask investors why they invest inAsia and invariably the first two rea-sons will be strong economicgrowth and political stability, par-ticularly in comparison to alterna-tive emerging markets. While thelatter has largely been achievedwithout the shackles of democracy,and elections are typically a onehorse race, it has provided a de-gree of certainty where the politicaland economic systems are inextri-cably linked. However now we areseeing that this is being increas-ingly challenged as many of theleaders are nearing the end of theirtenures whether it be the British inHong Kong, Suharto in Indonesia,or Lee in Singapore. In China thereis the perennial rumor mill on DengXiaoping’s imminent demise - over-night an offspring of Deng on theboard is no longer a guarantee toguanxi. Positions of privilege likenepotism and monopoly rights arelikely to be threatened from the ex-colonial hongs in Hong Kong to the"first family" business empires ofPresident Suharto in Indonesia.Clearly the changing economic/po-litical landscape is one investorsmust prepare for.

China - soft landing likely

China’s half year report card wasmostly positive as further signsemerged that inflation and eco-nomic growth have been broughtunder control and it looks likely thatthere will be a further loosening inmonetary policy later in this year.The only black spot was a weaken-ing in exports. Gross domesticproduct rose 9.8 per cent in the sixmonths of June to 2.97 trillion yuan(about US$356 billion) which, afterGDP growth of 10.2 percent in thefirst quarter, shows that growth inthe second quarter slowed toaround 9.4 percent. Inflationarypressures continue to ease with the

retail price index showing an aver-age rate of 7.1 percent in the firstsix months. China is well on coursefor its 10 per cent inflation target forthe whole year and single figuresremain within reach.

There was a fall in exports by 8.2per cent to $64.06 billion in the firsthalf which was attributed to risingwages and a strengthening cur-rency, although it is expected thatthere was some reallocation of ex-ports to the stronger domestic sec-tor. Imports rose 11.6 per cent to$63.8 billion and the half year tradesurplus fell to just US$880 million.A sharply lower trade surplus forthe full year is forecast after a sur-plus of $16.9 billion last year. How-ever, increases in fixed asset in-vestment and consumption shouldcompensate for the traditionallystrong export sector. China’s fixedasset investment grew 19.9 percent in the first half after a largeincrease in the second quarter asausterity measures were graduallyrelaxed. Contracted foreign invest-ment jumped sharply in the first halfof this year as investors rushed tosign contracts before the tariff ex-emption for imported equipmentexpired on April 1st. The value ofcontracted foreign investment grew a robust 46.3 per cent toUS$45.6 bill ion in the first sixmonths. The May cut in interestrates is helping consumption toplay a larger role in driving theeconomy - retail sales rose a robust19.5 per cent in June year-on-yearas consumers see sustained dis-posable income growth.

Looking ahead China is ex-pected to see further loosening ofmonetary policy by the end of theyear according to remarks made byChina’s Central Bank Governor DaiXianglong. Despite May’s cut of anaverage of 75 basis points, due tothe continuing low levels of infla-tion, positive real interest rates ofaround 4 per cent allow scope forfurther cuts. It was also hinted thatthe People’ s Ba nk of China

(PBOC) was considering a cut inthe reserve requirement’s forbanks from 13 per cent to 10 percent. Although Mr. Dai said thismove would be offset by a similarreduction in loans that the PBOCgave the banks, the multiplier effectwould clearly make the move ex-pansionary. The surplus credit willbe directed at the cash starvedstate enterprises which remain apriority. Statistics showed thatlosses at state-owned enterpriseswere up 51.6 per cent to 41.6 billionyuan in the first half and about 45per cent remain in the red. It is alsoexpected that the cut in reserverequirements will help developChina’s capital markets as banksare able to invest excess cash intreasury and enterprise bonds.

Will China devalue yuan?

China’s weakening balance ofpayments and sluggish exports,taken with a looser monetary policyare likely to see attention focusingon the possibility of a yuan devalu-ation. While as expected officialshave denied any such plans,speculation is increasing on themost opportune timing of such amove. Pragmatism suggests it isunlikely to happen prior to the han-dover of Hong Kong next July tomaintain confidence. China’sstrong foreign currency positionand relatively low inflation rateshould reduce the negative impactof devaluation, while the movewould likely benefit both econo-mies. Two way trade would get aboost and as we saw during theprevious yuan devaluation in1993/94 hot mainland money willbe attracted into the currencyhedge offered by the Hong Kongproperty market. In the past fewmonths it is estimated that morethan $5.4billion worth of mainlandbacked investment has been madein the local property market. Thosestocks with costs in yuan and reve-nues in foreign currency wouldbenefit and vice versa.

Copyright PEI July 1996 All Rights Reserved

11

$XVWUDOLDQ�*RYHUQPHQW��(FRQRP\

E\�1LJHO�.LUZDQ

%XGJHW��%ODFN�+ROH�EORZV�RXW�WR�$����ELOOLRQ

Th e federal governmen t’ s1995/96 underlying (net of pro-ceeds of asset sales) budget defi-cit, inherited from the previous La-bor government, has blown-out toapproximately A$10 billion. Thishas strengthened the Treasurer’sjustification to bring down a budgetin August with expected massivecuts and rationalization of federalprograms. The government nowdoesn’t expect an underlying bal-anced budget for at least 3 years -the life of the current parliament.The Prime Minister however stillexpects to be able to deliver on thebulk of the coalition’s promises dur-ing this term of office.

The deficit revelations havetaken the heat off the governmenton several fronts. Treasurer PeterCostello faced an embarrassingback down over an attempt to im-pose federal sales tax on state, ter-ritory and local governments. Thestate premiers emerged with a one-off drop in federal allocations whichwere hastily passed on to the tax-payer via the raising of severalstate taxes. Meanwhile troubleprone Foreign Minister AlexanderDowner had to first admit to mis-leading parliament over variousAsian governments’ protests at theaxing of the soft loan aid schemefor importing Australian productsinto developing countries, then par-tially back down on axing thescheme due to those protests. Hisperformance has been widely seento have damaged Australia’s stand-ing in the Asian region and a diplo-matic appointment somewhere inAfrica is probably awaiting his nextmishap.

:RUOG·V�ODUJHVW�]LQF�PLQHWR�JR�DKHDG

RTZ-CRA subsidiary CenturyZinc has announced it intends todevelop its north Queensland mineafter resolution of disputes over theproject with local aboriginal com-munities. The mine is also impor-tant for Pasminco which needs therelatively clean ore from the area tosatisfy new government environ-mental standards imposed upon itssmelters in the Netherlands. Theproject proceeding is seen as a vic-tory for the framework set by thecontroversial yet popular Austra-lian Native Title Act. This agree-ment acknowledges a principle thatindigenous peoples whose ances-tors formally occupied lands overwhich pastoral leases have sincebeen granted by the Crown, have aright to negotiate compensationfrom but not to veto a mining projecton that land. This is an issue not asyet tested by the courts and affect-ing huge tracts of Western Austra-lia, the Northern Territory andQueensland where, although na-tive title has been extinguished bythe Crown grant ing pastoralleases, there are remnant commonlaw rights enjoyed by the descen-dant aboriginal inhabitants. Any at-tempt by a state or territory govern-ment to extinguish these commonlaw rights would contravene theFederal Racial Discrimination Actand suggestions of suspending theAct have provoked widespreadprotest.

&RPPRQZHDOWK�%DQNIORDW�UDLVHV����ELOOLRQ

The federal government justmanaged to get its remaining 50%share of the Commonwealth Bankof Australia floated before the localshare market gave way in sympa-thy with Wall Street’s decline. Pri-vate investors heavily oversub-scribed the float and offshore insti-tutions bid strongly to nudge outmany of the local institutions in

Australia’s largest ever float andthe largest worldwide this year. Un-fortunately the approximate $4bil-lion proceeds of the float will be puttowards covering the budget deficitas were the earlier proceeds of theQantas Airways float. The floatleaves only the Queensland StateGovernment as the owner of a in-surance and financial institution.That government recently thwartedthe takeover of the state’s largestprivate bank in order to effect areverse takeover of it by the gov-ernment owned insurance andbuilding society and developmentbank. It then hopes to graduallyprivatise the combined institutionby selling down its share while atthe same time preserving a majorstate based bank-assurancegroup. While politically perhaps awinner this type of political interfer-ence in the market place has beenwidely condemned around thecountry by governments and busi-ness alike.

This follows on from the NationalParty dominated Queensland gov-ernment decision to ax a power lineto connect the state to the nationalelectricity grid which it is estimatedwill save the state’s consumers$700 million over the next fiveyears. Rural based Queenslandwhile developing exceedingly wellon the back of mining and tourismhas always exhibited a quirkysense of sovereignty and this issueis but the latest. Many predict abattle to free up the state’s monop-oly controls over the marketing ofsugar - its major agricultural export- to be next.

&ORVHU�$XVWUDOLD��1HZ=HDODQG�HFRQRPLF�WLHV

The Federal Government andthe New Zealand Governmenthave announced the formation of acommon aviation market betweenthe two countries following on fromAir New Zealand’s intention to pur-chase TNT’s 50% of Ansett Austra-

Providing Economic & Market Analysis Worldwide

12

lia. This will allow both countries’carriers to operate domesticallywithin the other and eventuallyshould lead to common customsand immigration controls at interna-tional ports. Ansett Australia will re-main under the control of 50%shareholder News Ltd and owner-ship of Ansett New Zealand will beassumed 100% by News, 50% ofAnsett International will be placedwith Australian institutions. Al-though Air Zealand is 20% ownedby Qantas Airways the two carriersare fierce competitors and the com-bined Air New Zealand/Ansettgroup should pose as a strongerdomestic and international com-petitor in Australasia and the fastgrowing Asia Pacific market. Al-ready the largest airline in SouthEast Asia, Qantas is set to benefitagain from the new worldwide alli-ance it recently helped to match-make between 25% shareholderBritish Airways and Qantas’ U.S.ally American Airlines. Buildingupon the decade old Closer Eco-nomic Relations (C ER) free tradeagreement between Australia andNew Zealand, the Australian gov-ernment recently announced therecognition of all New Zealandregulatory standards for productsto be sold within Australia. In whatis now the most open free tradezone in the world the extensioncomes only a few years after similaragreements were finally put inplace between the AustralianStates and Territories. No politicalor monetary union is seriously con-sidered between the two countrieseven though a place is reserved forNew Zealand in the Australian Con-stitution. The relative ease at whichinternational confederative agree-ments can be brought about as op-posed to drawn-out federal/statenegotiations perhaps explains whyfrom an economic perspective (andleaving aside sport) New Zealan-ders are glad they never joined theCommonwealth!

(QTXLU\�LQWR�WKH)LQDQFLDO�6\VWHP�%DQN�0HUJHUV

The Chairman of the Committeeof Inquiry into the Australian Finan-cial System covering the regulatorycompliance roles of the ReserveBank of Australia (RBA), the Insur-ance and Superannuation Com-mission (ISC), the Australian Con-sumer & Competition Commission(ACCC), the Australian FinancialInstitutions Commission (AFIC -non-bank financial institutions),and the Foreign Investment Re-view Board (FIRB) has alreadyhinted that big bank mergers are agood thing. Also the Chairman ofthe ACCC has hinted at a morerelaxed attitude to big bank merg-ers. Already the bets are on Na-tional Australia Bank (NAB), whichemerged from the ’80s relativelyunscathed and has just announceda $2billion profit for the 2nd year ina row, having a go at one of the bigbank losers of the ’80s Westpac orpossibly ANZ Bank. NAB has beenvoracious in swallowing regionalbanks in the Republic of Ireland,Scotland, the north of England,New Zealand, and Michigan USA.Its weakest domestic markets arein New South Wales, Queenslandand Western Australia and withWestpac strongest in these statesit is a logical acquisition, howeverANZ Bank owns UK’s Grindlayswhich has a strong Asian presenceand which would also complimentNAB’s existing market coverage.The rationalization of regionalbanks which has been taking placefor some time could also providesome prize pickings for the big 4 toeither expand through or dilute thebalance sheet with in defense. Thisscenario could turn the Queens-land government’s state based in-stitution into a prize victim for amuch larger predator!

The big insurance companiescan’t be left out of the picture either.AMP was once aligned with West-pac and National Mutual with ANZ.Paul Keating said no to any merg-ers and National Mutual was takenover by the French insurer AXA.Colonial Mutual successfully bid forState Bank of NSW and AMP hasnow entered the home loan market.Watch this space.

0HGLD���IRUHLJQRZQHUVKLS�DQGFURVV�PHGLD�UXOHV�FRXOGEH�UHOD[HG

Ever since the former Labor gov-ernment changed the rules for Aus-tralian citizenship specifica lly in or-der to deny Rupert Murdoch dualcitizenship the media foreign own-ership and cross-media rules havebecome a bigger and more com-plex farce as politicians sought tothwart then court Murdoch andKerry Packer, and court then thwartthe likes of Canadians ConradBlack and Tsi Asper. There arestrong signs that the rules areabout to be done away with and thiscould see some major media as-sets put into play. Despite the factthat they are currently suing oneanother Rupert Murdoch and KerryPacker would likely emerge as thebig winners controlling the majorityof Australia’s newspapers, televi-sion and satellite/cable assets -these two usually have the ability toput aside their differences in orderto do a much bigger deal together.Though Seven Network Australiarecently won control of MGM/UAusing Kirk Kerkorian’s money, don’tbe surprised if Rupert Murdochends up in there somehow - healready has 15% of Seven.

$�ORRN�LQWR�WKH�IXWXUHIRU�&OLQWRQ�DQG�WKH'HPRFUDWV"

Former Commonwealth Secre-tary of the Treasury and NationalParty Senator for Queensland JohnStone wrote in the Australian Fi-nancial Review that exit polls at theMarch 2 Australian federal electionrevealed:

- More blue-collar workersvoted coalition (47%) than Labor(39%);

- Compared to the previous fed-eral election (1993) there was a16% drop in Labor’s vote amongtrade union members;

Copyright PEI July 1996 All Rights Reserved

13

- For probably the first time ever,more Catholic voters (48%) opteddirectly for the coalition than forLabor (37%);

-The "bush" (rural areas),which has always been more favor-able to the coalition but where La-bor previously held many seats,swung violently further against La-bor; on mainland Australia Labornow only holds two seats outsidethe major cities;

- Of the 57 House of Repre-sentatives seats in the outlyingstates , (other than New SouthWales, Victoria & ACT - the Syd-ney, Melbourne, Canberra axis)Labor now holds only 10 (3 in Tas-mania).

Since Stone’s article was pub-lished several other commentatorsincluding former Labor leader andGovernor-General Bill Haydenhave since essentially drawn simi-lar conclusions to Stone on theabove and also the strong vote forseveral populist candidates openlyopposed to traditional small "l" lib-eral causes such as so-called "gay"rights, feminism, multiculturalism,aboriginal rights, and green politics- that with the Labor Party’s eternaldrive to capture these minority con-stituencies it rightly or wrongly hasbeen seen to be hijacked by themand this has proved a real turn-offin Labor’s own heartland whereyouth unemployment is as high as30%. Shades of the current state ofthe Democratic Party in the U.S.?

Providing Economic & Market Analysis Worldwide

14

+HOPV�%XUWRQ��)RUFLQJ�WKH�:RUOG�WR�7RH�

WKH�86�/LQH%\�&KULV�4XLJOH\

The Cuban Liberty and Demo-cratic Solidarity Act (LIBERTAD),better know as the Helms-BurtonAct, was passed into US law thispast March. The law was designedto tighten the existing US embargoagainst Cuba and prepare a contin-gency plan for the US to aid a tran-sitional democratic government inCuba. Two controversial sectionsof the legislation have caused asharp reaction from US tradingpartners. Titles III and IV allow forlegal action against foreign firmsoperating on or profiting form con-fiscated US property in Cuba. Spe-cifically, Title III “Makes any personthat traffics in property confiscatedby the Cuban Government on orafter January 1. 1959 liable formoney damages to any US na-tional who owns the claim to suchproperty.” Title IV “Directs the Sec-retary of State to deny a visa to, andthe Attorney General to excludeform the United States, aliens (in-cluding their spouses, minor chil-dren, or agents) involved in theconfiscation of property, or the traf-ficking in confiscated property,owned by a US national.”

The bill is trying to hammer thefinal nail into the coffin of Cuba’scentrally planned economy. Cubalost the aid it had been receivingfrom the Soviet Union and EasternBloc nations after those communistregimes began to fall. However, Fi-del Castro began to relax restric-tions on foreign investment and for-eign money started pouring in, tak-ing the place of Soviet aid. Cana-dian companies have committedmore than C$ 250 million to invest-ments in Cuba and two way tradebe tween Cana da and Cu baamounted to C$ 576 million lastyear. European Union (EU) na-tions, led by Spain’s $62.4 million

in direct investment, accounted for45% of Cuba’s total trade in 1994.This new found money is, in theeyes of the US government, help-ing to keep Castro propped up asdictator.

The bill would never have madeit out of Congress much less beensigned by President Clinton had itnot been for Cuba’s downing of twoUS civilian aircraft flying near Cu-ban air space back in February.The Administration, the Stare De-partment and many Congressmenwere initially against Helms-Bur-ton, but this is an election year inthe US and no one - not the Presi-dent, not Congress - wanted to ap-pear soft on Cuba. Therefore, inorder to show the Cuban-Americancommunities in the key electionstates of New Jersey and Floridathat politicians were ‘getting tough’with Cuba, the legislation sailedthrough Congress and was imme-diately signed by Clinton. Almost asquickly, the EU, Canada and Mex-ico announced plans to retaliateagainst Helms-Burton.

The United States recognizes anestimated $1.8 billion in claimsagainst Cuba. Under Helms-Bur-ton, over 40 US companies andthousands of Cuban-Americanswould be allowed to file suitsagainst foreign firms. Already,many companies and former Cu-ban citizens are readying claims.However, Bill Clinton exercised hispresidential option to suspend TitleIII for six months - stopping anyclaims from being filed until at leastFebruary of 1997. But, this actionby Clinton did little to stem thegrowing controversy over a law thathas been assailed by critics in theUS and abroad.

,QWHUQDWLRQDO�5HDFWLRQ�

All of the United States’ tradingpartners have spoken up aboutHelms-Burton. And from the EU toVietnam, not one has sided with theUS. The EU is preparing sanctionsthat include publishing lists of UScompanies that file suits underHelms-Burton, requiring US busi-ness travelers to obtain visas fortravel through the EU, imposingtrade sanctions on items not cov-ered by the World Trade Organiza-tions (WTO) such as telecommuni-cations and aviation. The EU is alsopreparing a case against the USlaw that it will bring before theWTO.

The United Kingdom, Italy,Spain and France have all indi-cated that in addition to any EUsanctions they will impose sanc-tions of their own. These sanctionswould include legislation orderingtheir home companies to ignoreany US legal moves and allowinghome companies to sue US sub-sidiaries in order to ‘claw-back’ anymoney awarded by US judges.Canada and Mexico have both an-nounced retaliatory measures simi-lar to the European Union’s. Thetwo countries also will launch anappeal to the law through Nafta.

Canada has been one of themost outspoken on the issue. Be-sides having a large stake in tradeand investment with Cuba, the Ca-nadians have domestic politics ontheir minds, too. Canadian officialsdon’t want their electorate to per-ceive them as backing down to theUS over Helms-Burton. Canadianspecial interest groups and mem-bers of the opposition have ac-cused the ruling Liberals of not be-ing ‘aggressive enough’ in counter-ing the US law.

Canada is looking at this contro-versy as an opportunity to assertitself in front of the world. In anarticle from the Financial Times,

Copyright PEI July 1996 All Rights Reserved

15

Bernard Simon writes “[Helms-Bur-ton] has given Canadians a chanceto satisfy two basic cravings: tostand up to the big bully across theborder, and to be noticed by therest of the world for somethingother than Mounties, maple syrupand ice hockey.”

5HDOLWLHV�RI+HOPV�%XUWRQ

Just the threat of US actions un-der Helms-Burton has already de-terred trade with Cuba. As soon asthe bill became law, some busi-nesses either pulled out or scaledback their Cuban operations. Ce-mex, A Mexican cement maker isconsidering a complete withdrawaland ING Group NV, a Dutch bank,is pulling financing for Cuba’s sugarcrop. Officials at Canadian banksannounced that they were scalingback their credit to businesses op-erating Cuba. American Expressannounced that it was pulling thecredit of two Dutch firms operatingin Cuba amid concerns overHelms-Burton. Colombian airlineAeoroRepublica announced that itwas pulling its twice weekly flightsto Cuba over fears of US sanctions.

Title III can be either suspendedor invoked every six months. Thatfact alone makes the decision toinvest in Cuba very difficult. It wouldnot be wise for a company to investin Cuba with the possibility of facinga lawsuit every six months. Compa-nies that are going ahead with in-vestment plans are doing so cau-tiously. Canadian-based WiltonHotels is planning a large invest-ment in resorts in Cuba and ownerWalter Berukoff said, “We’ve beenvery careful not to deal in expropri-ated US properties. We have nodesire to upset the Americans.”

5LJKW�LGHD��ZURQJ�ODZ

US companies and nationalshave a legitimate claim on landconfiscated by Castro. However,the main issue for the US’s tradingpartners is not protection of prop-erty rights or contract sanctity.

Their concern is manly over the USmethod of using extraterritorial leg-islation to unilaterally enforce itsown foreign policy objectives. Withsimilar US legislation designed tocurb international trade with Iranand Libya already being voted on inCongress, it is important not to letthe US set a precedent with Helms-Burton. The European Commis-sion has stated that “extraterritorialapplication of unilateral sanctionscreates an unacceptable burdenfor the international business com-munity.” This sentiment has beenechoed by foreign trade ministersall over the world.

US business,which seeminglystands to benefitfrom the law, hasalso spoken outagainst the legisla-tion. A letter to Clin-ton from the USChamber of Com-merce and fourother trade groupssaid that the legis-lation will only hurtUS businesses.Their letter said“We believe that if[He lms -Bu r ton ]were to become ef-fective, it woulddrive a wedge be-tween the UnitedS ta te s and ourdemocratic all iesthat would signifi-cantly hinder multi-lateral efforts to en-courage democ-racy in Cuba.”

In prac ti ce,Helms-Burton willnever work. If TitleIII is ever allowedto take effect, it willimme dia tel y b erendered ineffec-ti ve by counter-measures from UStrading partners.Any settlementsawarded by UScourts, if they areever even paid, willbe lost through

counter-suits in other countries. Asfor Title IV, harassing internationalbusiness travelers by telling themwhere they can and cannot go doesabsolutely nothing to exert pres-sure on Castro’s regime. If the USreally wants to force change inCuba it needs to be done on amultilateral level with the full coop-eration of the world’s largest trad-ing blocs. Anything else will onlyhinder further improvements inworld trade and do absolutely noth-ing to change the situation in Cuba.

Providing Economic & Market Analysis Worldwide

16

:RUOG�&DSLWDO�0DUNHW�5HYLHZ86�672&.�0$5.(7

So far our computer model fore-cast is running perfectly on sched-ule. The precise high came on May23rd, 1996 with the Dow reachingthe 5800 level. The key weekly sup-port basis the S&P 500 NearestFutures rested at 64760 and oncethat area was penetrated, the cor-rection process was confirmed.

Overall, we expect to see the USshare market decline a bit further.Primary support lies at the 59800level followed by 57300-56100.This is about the extent that we seefor the correction as a whole. Whilefrom a point perspective this ap-pears to be major, the 1990 correc-tion was far more significant on apercentage basis. If the 1996 cor-rection were to match that of 1990in percentage movement terms,then we would need to see the S&P500 futures decline down to the54600 zone.

Timing continues to be a bigquestion for this correction. About90% of the total decline should becompleted by the end of August.We do see that the final low for thiscorrection is due in August, Octo-ber/November, March 1997 orMay/June 1997. If we see the57300-56100 level during mid tolate August, then either the correc-tion is over, or we will see a moresignificant correction if the Augustlow is penetrated at any time be-yond August. This would open thedoor for a decline down to the50300 level. An August low only inthe 59800 area would tend to implythat the balance of the move downto 57300-56100 might not comeuntil early next year in a slower,more choppy style move. Ouryearly models do show that if atyear-end the S&P 500 futurescloses below 59260, then clearly a1997 low should be expected.

35(&,286�0(7$/6�

Gold and silver remain captive towhat appears to be the inevitablestart of IMF gold sales. While we donot see this fundamental as long-term bearish, we do expect to seeit help keep a negative undertonefor perhaps as much as the next 6months. Silver remains the bigproblem. While many call this thepoor man’s gold, it its more like thepoor man’s opium that creates vi-sions of unrealistic grandeur. Thesilver/gold ratio still appears poisedto make new highs or at least in thenear-term retest the 100:1 level.The primary resistance remains atthe 82.84-84.80:1 zone. A monthlyclosing above 84.80:1 will signalthat silver could completely fallapart. Vital support basis NY spotremains at the $4.50 and $4.29 lev-els. If silver declines and holds$4.50 during mid August, thenthere will be some hope that thedecline is over. However, if silverpenetrates the $4.29 level, thencaution should be employed. Silvermight yet decline under $3.50 dur-ing early 1997 before any hope ofa bull market emerges. Gold, on theother hand, has reasonable sup-port at the $368 area followed by$341. We do not expect to see newlows in gold under any circum-stances.

86�'2//$5

While our long-term models con-tinue to suggest that the dollar isgoing to rally dramatically into2003, we do see that the potentialfor one more dollar low does existduring the first half of 1997 againstmost major European continentalcurrencies, with the noted excep-tion of the pound and the Japaneseyen. Only a monthly closing for thedollar above 15840 on the Dmarkwould suggest that this forecast iswrong and that the dollar low is inplace. Otherwise, a monthly clos-ing below 13985 for the dollar vsDmark would suggest that this fore-

cast is correct and that an appropri-ate hedge position is warranted.

The dollar/yen is a differentstory. Here the dollar low is in placeon a long-term basis and the overalldecline should continue taking thedollar up to 12500 or 14500 levelover the next two years. Nonethe-less, resistance stands at the11300 level and a failure to moveabove that level by Septemberwould also raise the possibility thata retest of support at the 10489-10315 level is likely. A monthlyclosing below 10315 would thenraise the potential for a very sharpdecline back to the 10065 area or9755 at worst.

86����<($5�%21'6

Here the primary monthly clos-ing support remains at the 10801level. A monthly closing beneaththis area will signal that a sharpdecline to the 10100-10200 area ispossible. If July closes below10801, then we should expect apossible rate hike by the Fed duringAugust.

1,..(,

The Japanese share market hasmost likely reached a temporarytop in June. Here we see that amonthly closing below 21170 willsignal that a correction is underwayonce again. The bulk of support liesat the 19628 and 18896 levels. Amonthly c losing below 18896would warn that a retest of long-term support is possible taking thismarket back to the 15292 zone.

&$1$'$�76(

The Canadian share market ba-sis the TSE reached a high duringMay at 52490. Here we see that acorrection back to the 48182 to44867 level is likely. A monthlyclosing below 44867 would warn

Copyright PEI July 1996 All Rights Reserved

17

that a much more serious decline ispossible where a sharp drop to the39307 level is likely. We do see thata year-end closing below 43300would warn that the overall correc-tion could extend into early 1997before reversing to the upside fornew highs going into mid 1998.

/21'21�)7

Th e Br i ti sh share marketreached a high in during the weekof April 15th. Vital support lies at the36552-36474 level basis the cash.A weekly closing below 36474 willsignal that a sharp correction isnow possible. Additional supportlies at the 34334 area. A monthlyclosing below 34334 would thenwarn of a drop back to retest long-term support at the 29388-29250zone. A year-end closing below34808 would warn that the overallcorrection could extend into early1997. We do have a panic cycledue in November so we should ex-pect to see some sharply highervolatility at that time. Key targets fora low appear to be August and Oc-tober. New lows below beyond Oc-tober would then raise the possibil-ity that a low in February orApril/May of next year .

*(50$1�'$;

The German share market basisthe DAX futures reached a high theweek of June 24th. Vital supporthere begins at the 24875 and2275 0 levels. A weekly andmonthly closing below 22750would warn that a correction is pos-sible where we see long- term sup-port forming at the 21450 and20185 levels. A September closingbelow 24515 would also warn thata retest of long-term support in the20925 area would be possible overthe next 6 or 10-12 months. Yearlymodels show that only a year-endclosing below 23270 would raisethe possibility of extending the cor-rection into early 1997.

)5(1&+�&$&���

The French share market basisthe CAC 40 futures has underper-formed most other world sharemarkets. Here the major high tookplace back in February 1994. Majorresistance continues to stand at the22380 level followed by 22620-22765. Here we see that 1996 mustclose at least above 20252 in orderto hold on to any hope that a retestof resistance is possible in themonths ahead. A closing below20252 will leave the possibility thata penetration of the 1995 low coulddevelop in early 1997. Major year-end closing support lies at the17968 area. Should 1996 close be-low this level at year-end, then adrop back to the 15750 area will bepossible next year.

6:,66�0$5.(7,1'(;

The Swiss share market basisthe nearest futures has been by farthe strongest European market.There is a potential for a July highto form if we see a weekly closingbelow the 35435 area. This will im-mediately warn that a correctioninto October is possible testing atleast the 31650 zone. A weeklyclosing below 31360 will signal thatan overall correction back to the27690 or at worst 25450-24400area will become possible.

3(,*RYHUQPHQW%RQG�:DWFK

Government debt continues toescalate despite the fact that defi-cits may bee declining in some na-tions like the US. The US situationis reaching the critical point. Wesee 1996 as the absolute bottom inthe outright deficit numbers as re-ported by government. Keep inmind that the deficit would be about$50 billion higher if it were not forthe Social Security funds beingused to offset the general expendi-ture deficit.

As reported previously, the Clin-ton debt crisis is the key factor that

is causing a rise in volatility for allbond markets globally. Clinton’sshifting of the national debt from40% financed short-term to 70% isnot merely alarming, it is outrightdangerous! In fact, 33% of the en-tire national debt is now funded 1year or less. Consequently, as thedeficit appears to be declining,there is a major shift in where themoney is going. Revenues nowamount to about $100 billion morethan is actually spent on defenseand social programs combined.This excess revenue is being ab-sorbed by interest expenditures. Asa result of the Clinton Deficit Re-duction Plan, interest expendituresare rising faster than ever before inhistory! While total expenditure for1994 was up 4.5%, interest expen-ditures rose 11.5% for the sameperiod. We are now moving into anexponential growth rate in interestexpenditures in all governmentsaround the globe.

We strongly advise that fixed in-come investment should be re-stricted to 90 days or less. Do notinvest in long-term bonds of anynation at this time. This holds truein Europe as well.

LATEST ADDITION TOPEI BLACK LIST

The fiscal corruption in the NDPgovernment of British Columbia inCanada is beyond all belief. Thishighly socialistic political party isabout as Marxist as you can get.The budget surplus they claimedexisted going into the elections hasamazingly turned into a deficit fol-lowing their victory. The politicalcorruption on an idealogical levelwithin the NDP is moving countertrend to the rest of the world. Withthe vast majority of Provincial debtin Canada moving to reform, thereis absolutely no reason to buy BCbonds. We strongly recommendthat BC bonds should be sold andinvestment in fixed income shiftedto short-term debt issues of nomore than 6 months in Canada atthis time. Both BC and federal debtissues of Canada are at serious riskof declining due to the rising ques-tion of direction.

Providing Economic & Market Analysis Worldwide

18

:RUOG�(FRQRPLF�5HYLHZ

E\�+DO�/XGZLJ'LUHFWRU�3(,�86

81,7('�67$7(6

CONSUMER PRICES: US con-sumer prices rose 0.3 percent lastmonth and 2.9 percent in the yearto May, indicating faster economicgrowth is putting only modest up-ward pressure on inflation.

In the first five months of thisyear, prices rose at an annual rateof 4.1 percent against 2.8 percentfor 1995 as a whole. But the accel-eration may not be sustained, as itlargely reflected a jump in energycosts. Oil prices have since fallenfrom peaks reached earlier thisyear.

Excluding the volatile food andenergy components, "core" con-sumer prices rose 0.2 percent lastmonth and 2.7 percent in the yearto May.

CONSUMER CONFIDENCE:US consumer confidence fell unex-pectedly in June but remainedhigher than in June last year, fig-ures indicated.

The Conference Board, a USbusiness group based in New York,said its confidence index had fallento 97.6 against 103.5 in May. Thissurprised Wall Street economistswho had predicted little change,given recent reports of rapid em-ployment growth and buoyant retailspending.

Some analysts said the declinewas consistent with projections ofslower economic growth in the sec-ond half of this year after a robustsecond quarter. But it may havejust reflected the volatility of theindex, which has fluctuated be-tween 88 and 105 in the past six

months. Historically a reading of90 to 100 has indicated steady eco-nomic growth.

EXISTING HOME SALES: USfigures showed a 1.4 percent rise insales of existing homes in May overApril, higher than most analystshad expected.

GOVERNMENT DEVELOP-MENT AID: The US slipped lastyear into fourth place behind Ja-pan, France and Germany as aprovider of government develop-ment aid, and the total declined to$59bn, the Organization for Eco-nomic Cooperation and Develop-ment (OECD) reported.

Japan remained by far the larg-est official aid donor last year with$14.5bn, according to the OECD’sdevelopment assistance commit-tee. Helped partly by the strengthof their currencies in relation to thedollar, France and Germany over-took the US to arrive in second andthird place with $8.4bn and $7.5bnrespectively.

US official aid fell by $2.6bn -- 28percent in real terms -- to $7.3bn,partly because of delays in approv-ing its 1995-96 budget but also be-cause of cuts in food assistanceand in those peacekeeping expen-ditures which qualify as aid. Lastyear the US devoted 0.1 percent ofgross national product to govern-ment aid programs, its lowest levelsince the second world war.

UNEMPLOYMENT: The LaborDepartment said non-farm payrollemployment rose 348,000 lastmonth, nearly twice the increaseexpected by economists. Figuresfor April were revised to show again of 163,000 rather 2l,000 asreported previously.

The employment gains lastmonth were broadly based, withlarge increases in many service in-dustries. But the jobless rate,which is based on a survey of

households rather than compa-nies, rose modestly to 5.6 percentagainst 5.4 percent in April, reflect-ing an increase in the number ofpeople seeking work.

LEADING INDICATORS: TheUS index of leading indicators rosefor the third consecutive month inApril, suggesting the economy willgrow robustly in coming months.

The leading index is designed topredict changes in economic activ-ity six to nine months in advance.The recent string of increases wasthe longest since autumn 1993,when the index gave advancewarning of a surge in economicgrowth in 1994 -- a surge thatprompted the Fed to tighten mone-tary policy aggressively. The indexrose 0.3 percent in April, followinga revised 0.3 percent gain in Marchand a 1.3 percent leap in February.

PURCHASING MANAGERS’INDEX: Purchasing managers re-ported a surge in an index measur-ing price pressures in manufactur-ing industry, and the CommerceDepartment announced a largerthan expected gain in new con-struction spending.

The overall purchasing manag-ers’ index fell slightly last month to49.3 percent, against 50.1 percentin April. most economists had ex-pected the index to rise modestly,reflecting a mild expansion ofmanufacturing output.

The "prices paid" componentrose to 50.8 percent from 40.1 per-cent in April, mainly because of in-creases in prices of agriculturalproducts. This followed ninemonths in which price pressures,as measured by purchasing man-agers, had appeared to ease.

CONSTRUCTION SPENDING:The Commerce Department saidconstruction spending rose 1 per-cent in April to a seasonally ad-justed annual rate of $551.7 bn. In

Copyright PEI July 1996 All Rights Reserved

19

the first four months, constructionspending averaged 5 percenthigher than in the same period lastyear.

81,7('�.,1*'20

RETAIL SALES: Retail salesfell last month for the first time sinceJanuary, raising doubts about thestrong recovery in consumerspending promised by the chancel-lor this year. The surprisingly weakfigures disappointed the City ofLondon, which had expected astrong rise in sales in line with morebuoyant survey evidence. But thedata appeared to provide furthervindication of the chancellor of theexchequer’s quarter-point interestrate cut on June 6.

Retail sales fell a seasonally ad-justed 0.1 percent between Apriland May and were 2.0 percenthigher in May than the same monthlast year, the Office for NationalStatistics said.

MANUFACTURING OUTPUT:Manufacturing activity experiencedits biggest decline for more than 31/2 years last month as factoriesreined in output and cut jobs in theface of declining order books and abuild-up of unsold goods. Compa-nies making plant and machineryraised output only fractionally whileproducers of components cut out-put sharply, according to themonthly survey by the CharteredInstitute of Purchasing and Supply.

But weakness in these two ar-eas was intensified for the first timethis year by a sharp slowdown inoutput and demand for consumergoods. Although the consumergoods sector remained the strong-est area of the economy, its poorperformance last month contrastswith the buoyant conditions earlierthis year. It suggests that con-sumer demand, which the govern-ment expects to rebound stronglyin 1996, may still be fragile.

CONSUMER CREDIT: Con-sumer credit recorded its biggestrise for 7 1/2 years last month, pro-viding a strong signal that the re-

covery in consumer spending isgathering pace. After taking ac-count of seasonal movements,co nsumers b or ro wed a netL1.01bn ($1.53 bn) from banks andother lenders in April, comparedwith L722m in March, the Bank ofEngland said. The increase, whichfar exceeded City of London expec-tations, was the highest rise sincecurrent official records began inApril 1993. The Bank said otherunofficial estimates indicated it wasthe largest increase since autumn1988.

IMPORTS: The level of importssucked into the UK economy hasrisen sharply in recent months,suggesting that overall demand inthe economy remains reasonablyhealthy. However, the rise in im-ports may also trigger concernsthat the UK’s trade deficit could de-teriorate in the months ahead, re-versing the healthy picture seen inprevious years.

Although exports performed rea-sonably well during the spring,some economists are starting tofear that the imbalance betweenimports and exports could widenfurther in the months ahead. A hintof emerging problems in the exportsector came after the EngineeringEmployers Federation said that ex-port order books were now weak-ening. This has occurred eventhough the engineering sector hashitherto weathered the downturnbetter than many other manufactur-ing industries.

Measured overall, the Office forNational Statistics said that theUK’s overall deficit in goods withthe rest of the world was a season-ally adjusted BP1.3bn ($1.98bn) inApril -- the most recent month forwhich data is available. This wasalmost dou ble the previou smonth’s deficit of BP765m.

OECD OUTLOOK: The Organi-zation for Economic Cooperationand Development said in its latestEconomic Outlook that the UK willbe one of the fastest growing Euro-pean countries over the next twoyears. Growth is at present belowtrend but activity will accelerate this