Embed Size (px)

DESCRIPTION

Â

Citation preview

Front Cover: The Bougainvillea, locally known as Puti Tai Nobio, is the Territorial Flower for Guam. It is a thorny,year-round plant of many colors - such as red, pink, purple, orange, white or mixed. The name when translated means"It hurts not to have a boyfriend". It is easily grown through cuttings.

COMPREHENSIVE ANNUAL FINANCIAL REPORT For The Fiscal Year Ended September 30, 2014

Edward J. B. Calvo

Governor of Guam

Anthony C. Blaz Director of Administration

Kathrine B. Kakigi, CPA

Financial Manager

Prepared By: The Division of Accounts

P.O. Box 884 Hagatna, Guam 96932 Location: 2nd Floor, Manuel F.L. Guerrero Building

212 Aspinall Avenue, Hagatna (671) 475-1260/1169

2014 Table of Contents

INTRODUCTORY SECTION

Letter of Transmittal .................................................................................................................................................................................... i Certificate of Achievement for Excellence in Financial Reporting ....................................................................................... xiii Organizational Chart ............................................................................................................................................................................... xiv Elected Officials .......................................................................................................................................................................................... xv

FINANCIAL SECTION

Independent Auditor’s Report ................................................................................................................................................................1 Management’s Discussion & Analysis (Unaudited) ........................................................................................................................4 Basic Financial Statements

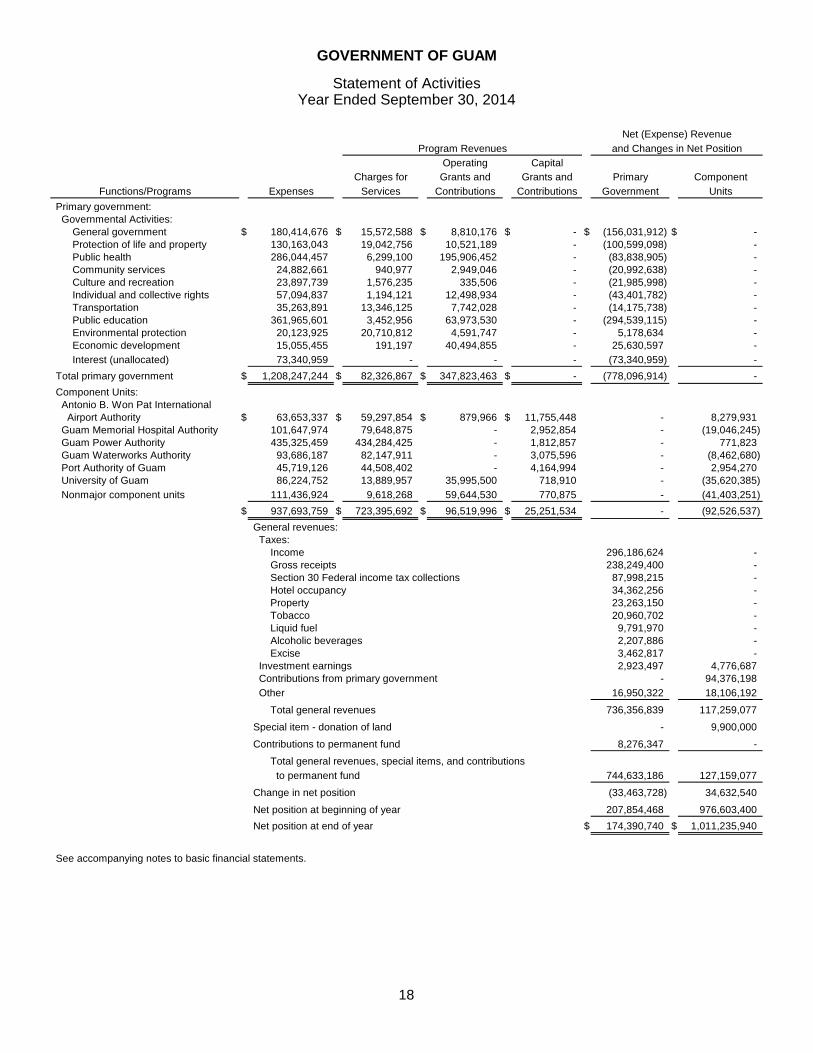

Government-wide Financial Statements Statement of Net Assets ............................................................................................................................................................ 16 Statement of Activities .............................................................................................................................................................. 18

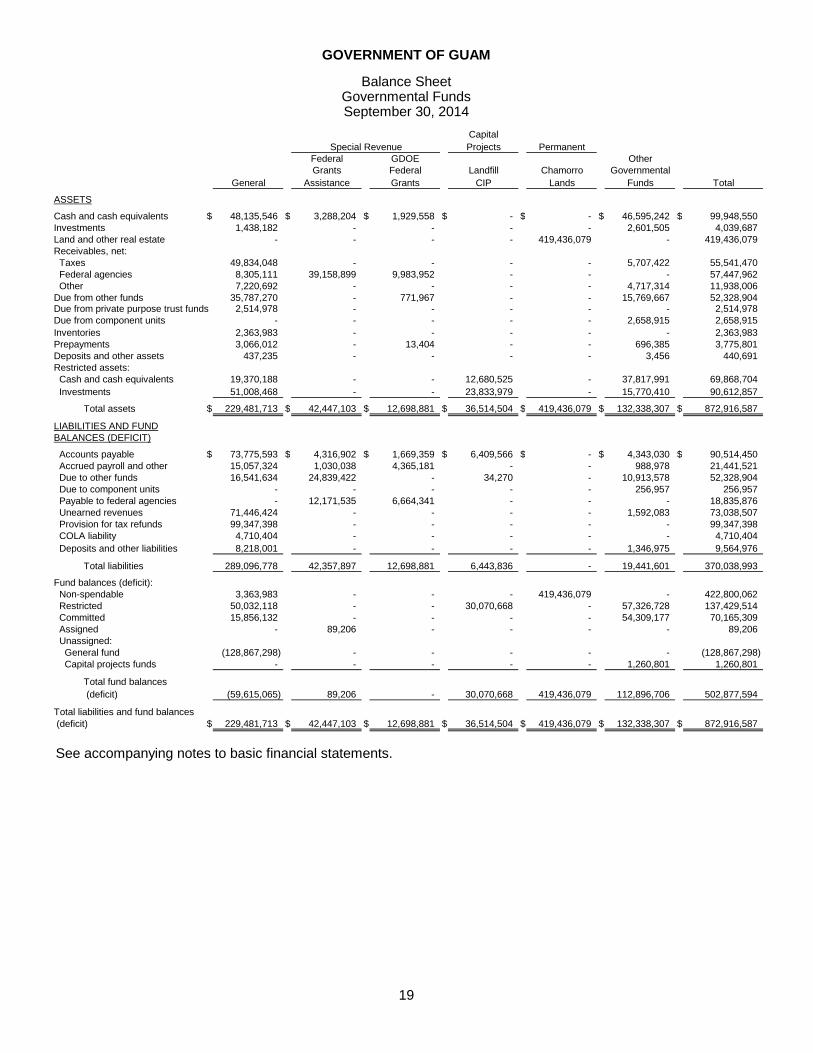

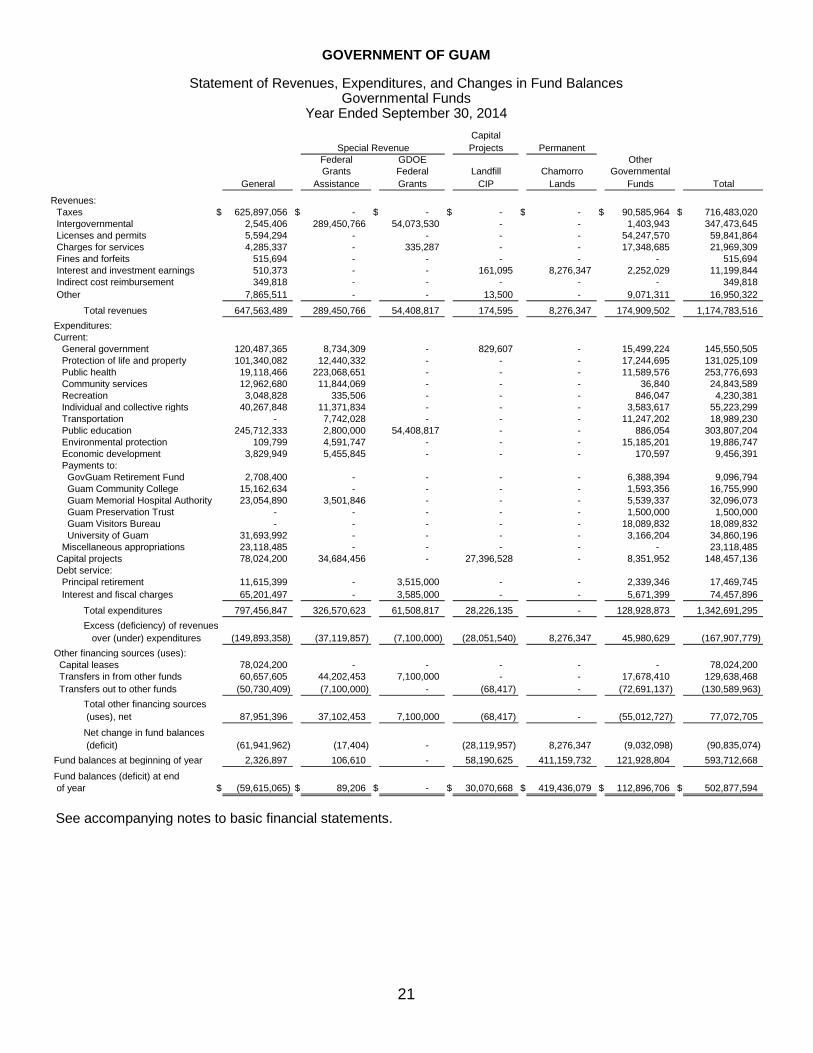

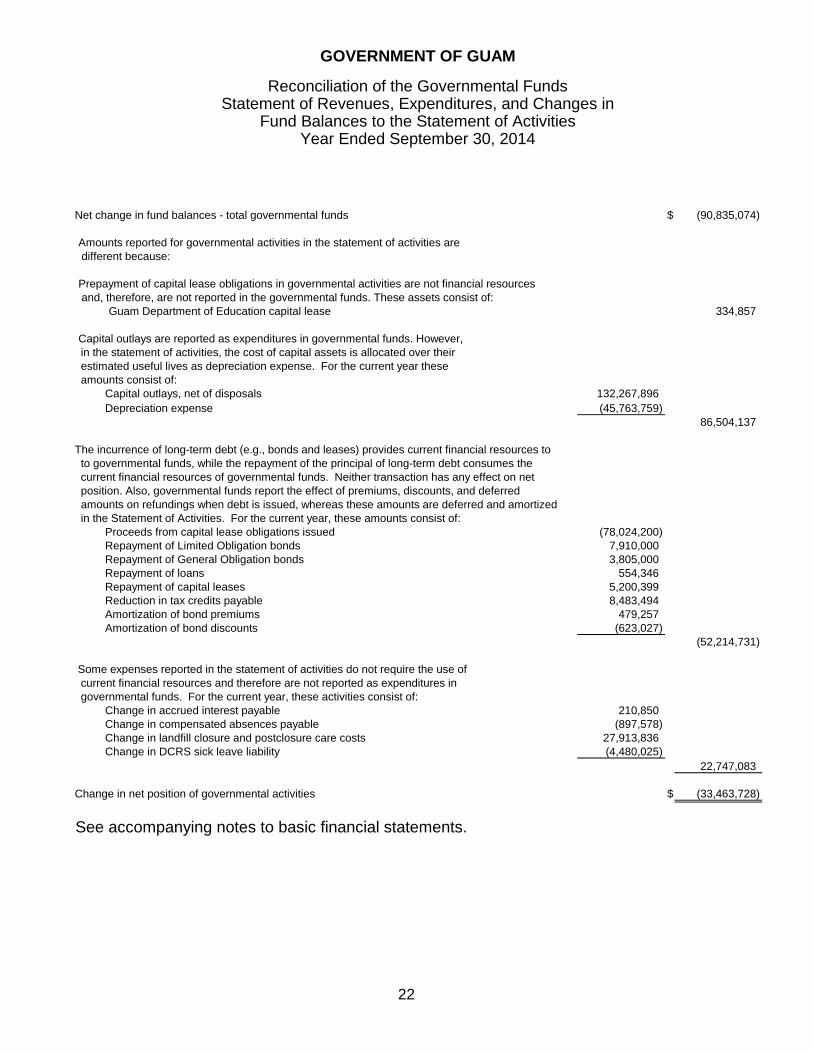

Government Fund Financial Statements Balance Sheet ................................................................................................................................................................................ 19 Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position ...................... 20 Statement of Revenues, Expenditures, and Changes in Fund Balances (Deficits) .......................................... 21 Reconciliation of the Governmental Funds Statement of Revenues, Expenditures, and

Changes in Fund Balances to the Statement of Activities .................................................................................... 22 Fiduciary Fund Financial Statements

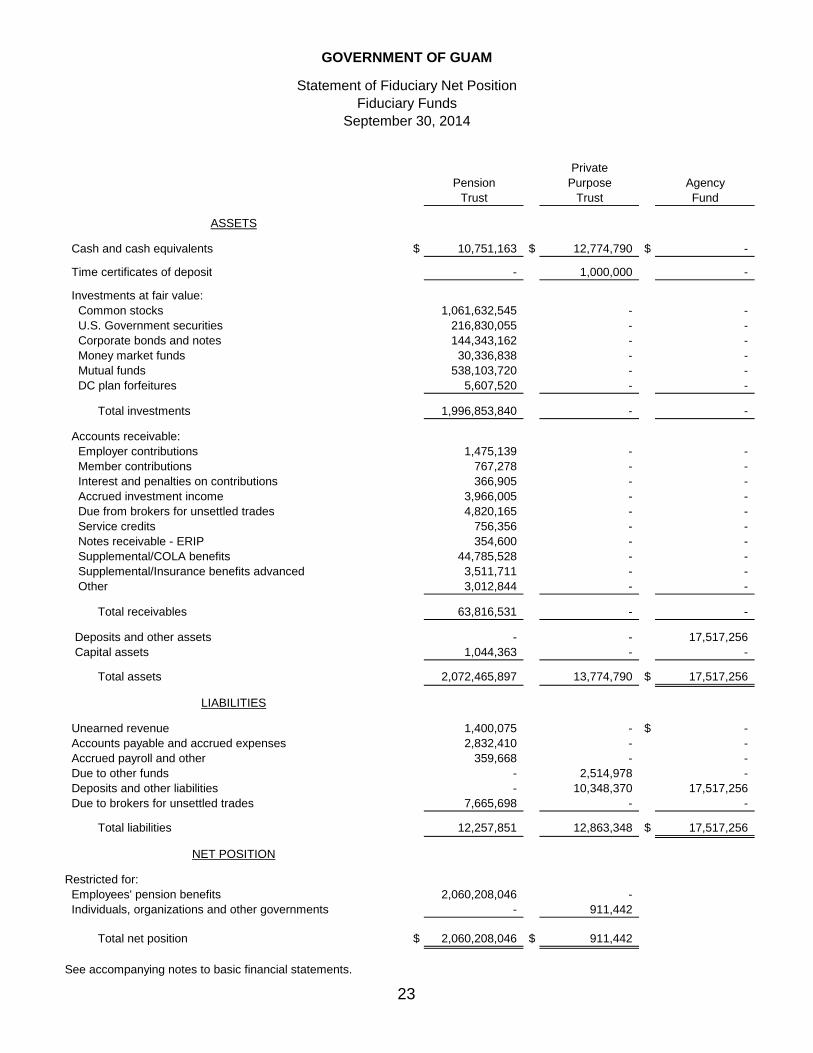

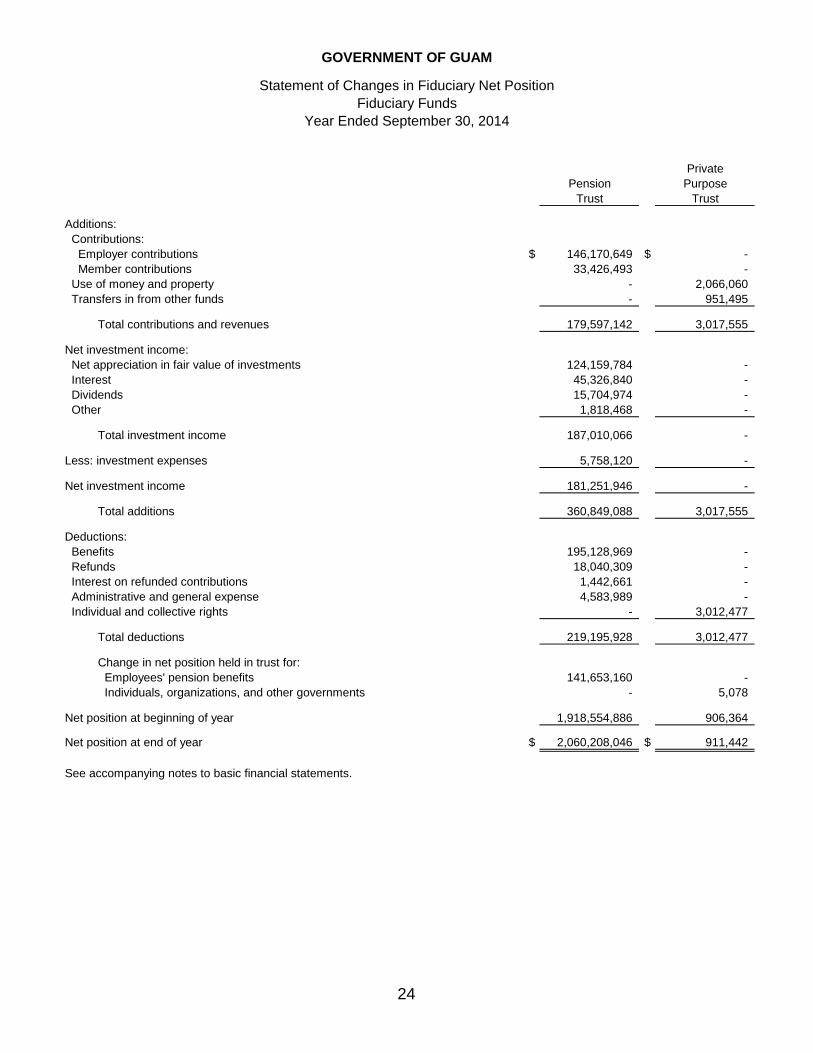

Statement of Fiduciary Net Position .................................................................................................................................... 23 Statement of Changes in Fiduciary Net Position ............................................................................................................ 24

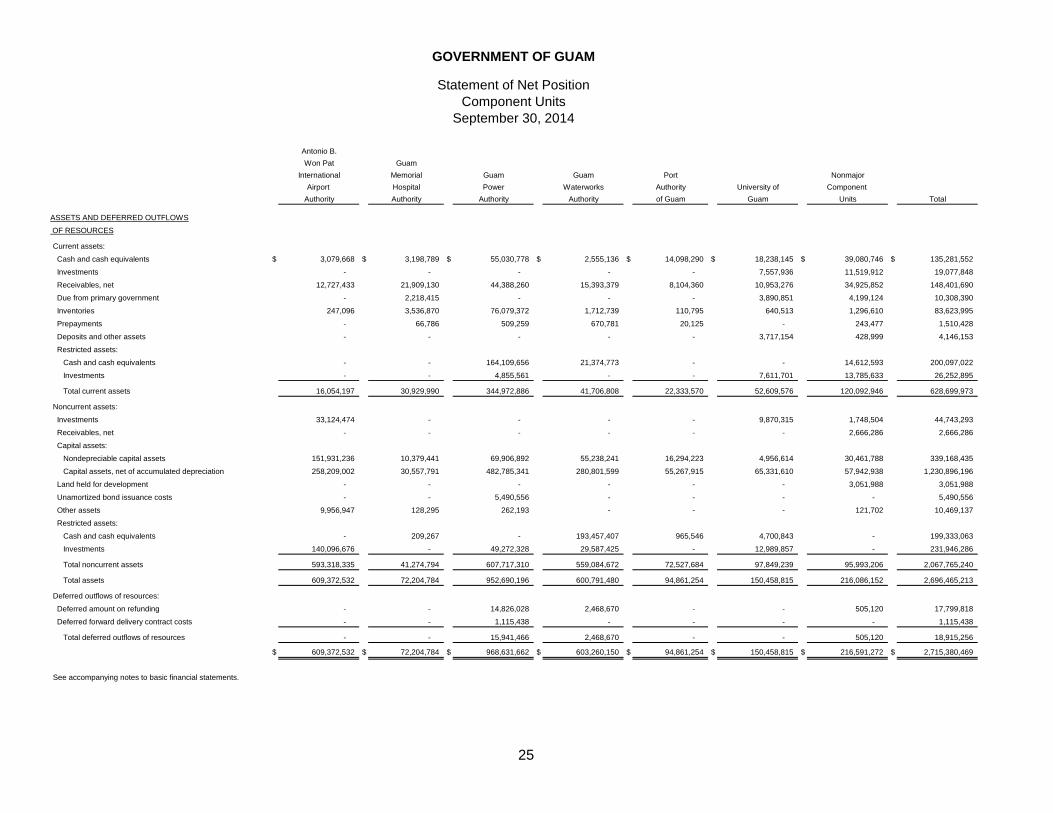

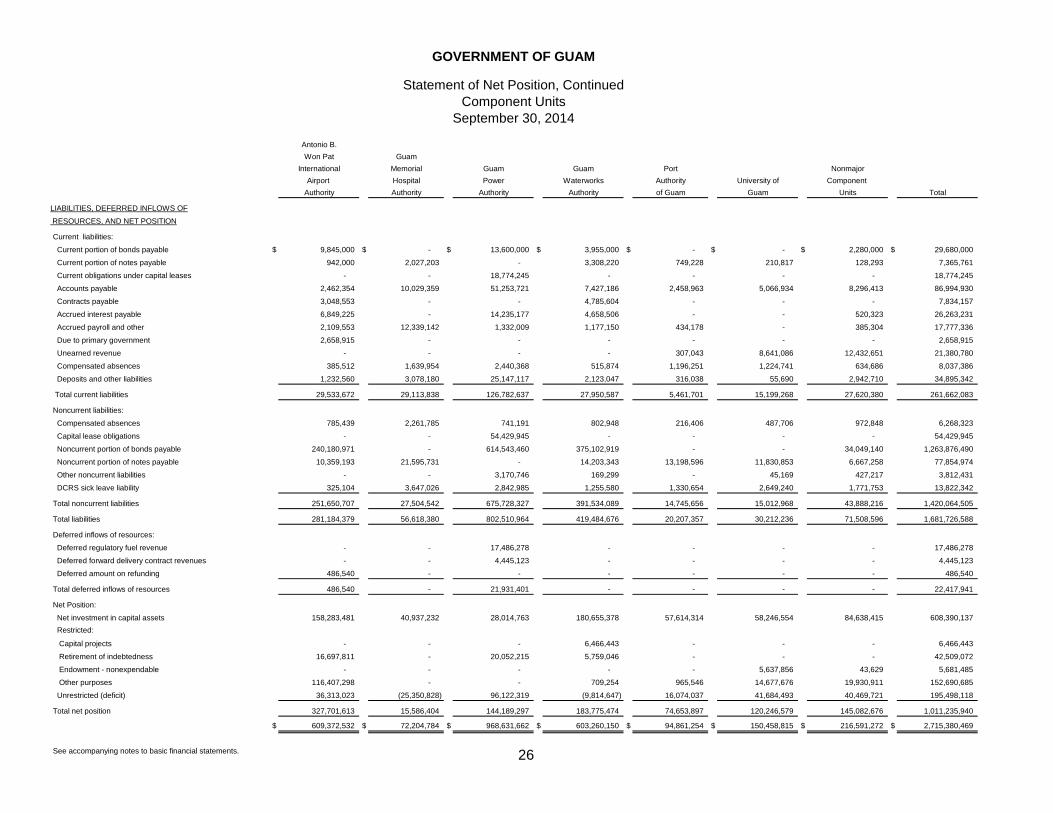

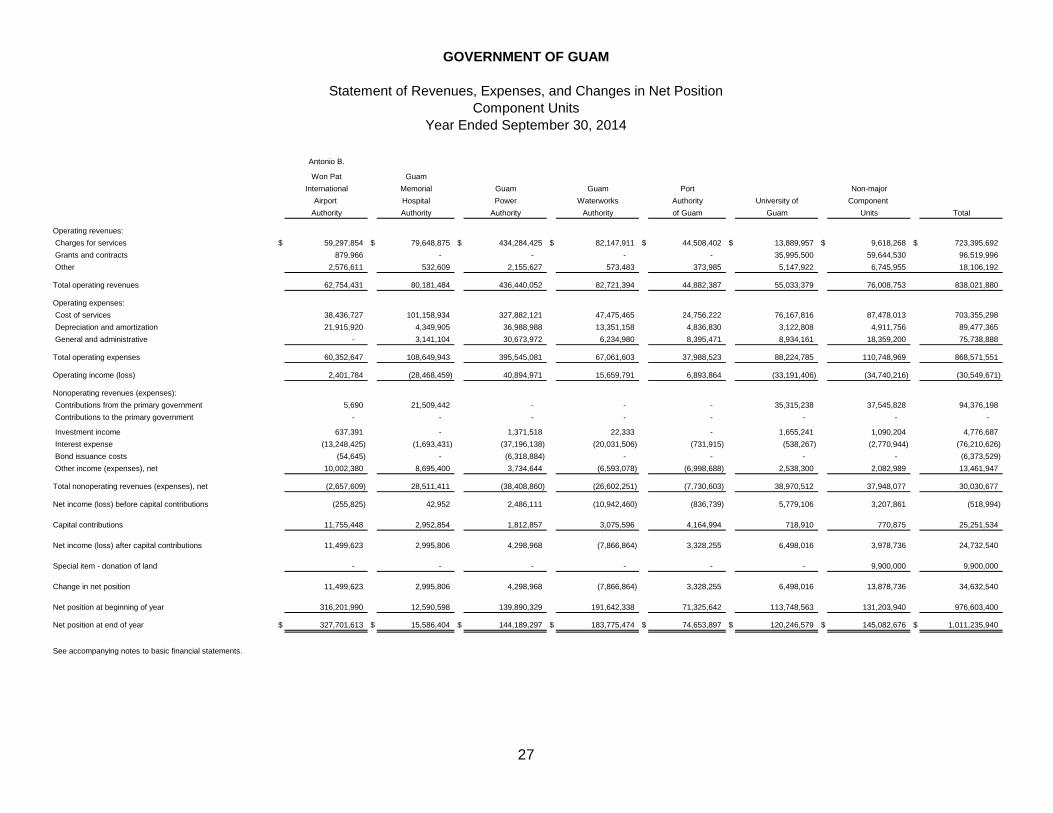

Discretely Presented Component Unit Financial Statements Statement of Net Position ........................................................................................................................................................ 25 Statement of Revenues, Expenses, and Changes in Net Position ............................................................................. 26

Notes to the Basic Financial Statements .................................................................................................................................. 28 Required Supplementary Information- Other than Management’s Discussion and Analysis

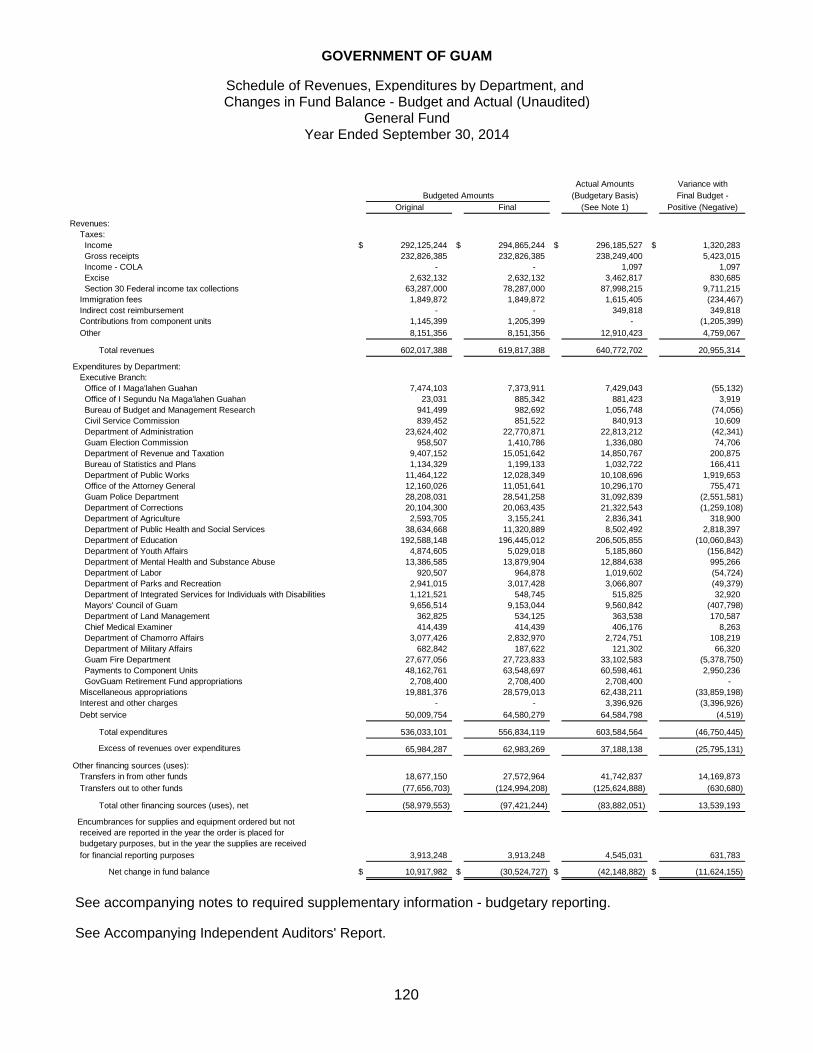

Schedule of Revenues, Expenditures, and Changes in Fund Balance (Deficit) - Budget and Actual- General Fund (Unaudited) .................................................................................................................................................... 120

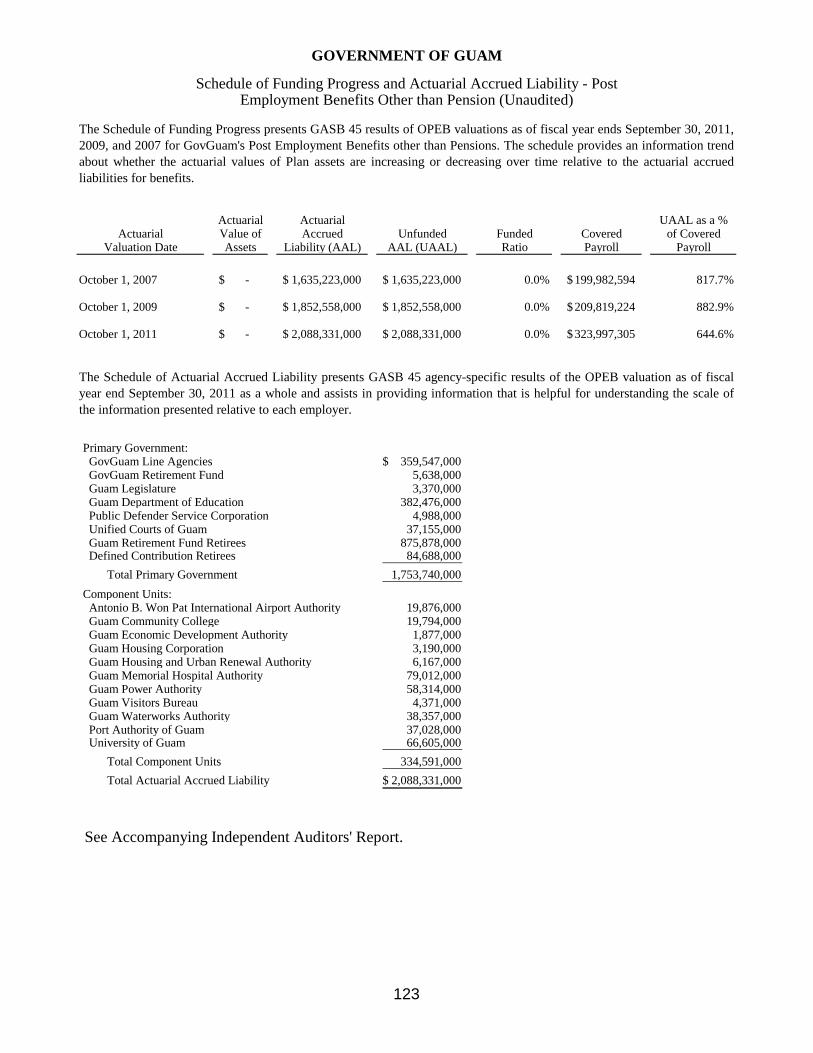

Notes to the Required Supplementary Information- Budgetary Reporting ........................................................... 121 Schedule of Funding Programs and Unfunded Actuarial Accrued Liability (Unaudited) ................................. 123

Other Supplementary Information General Fund

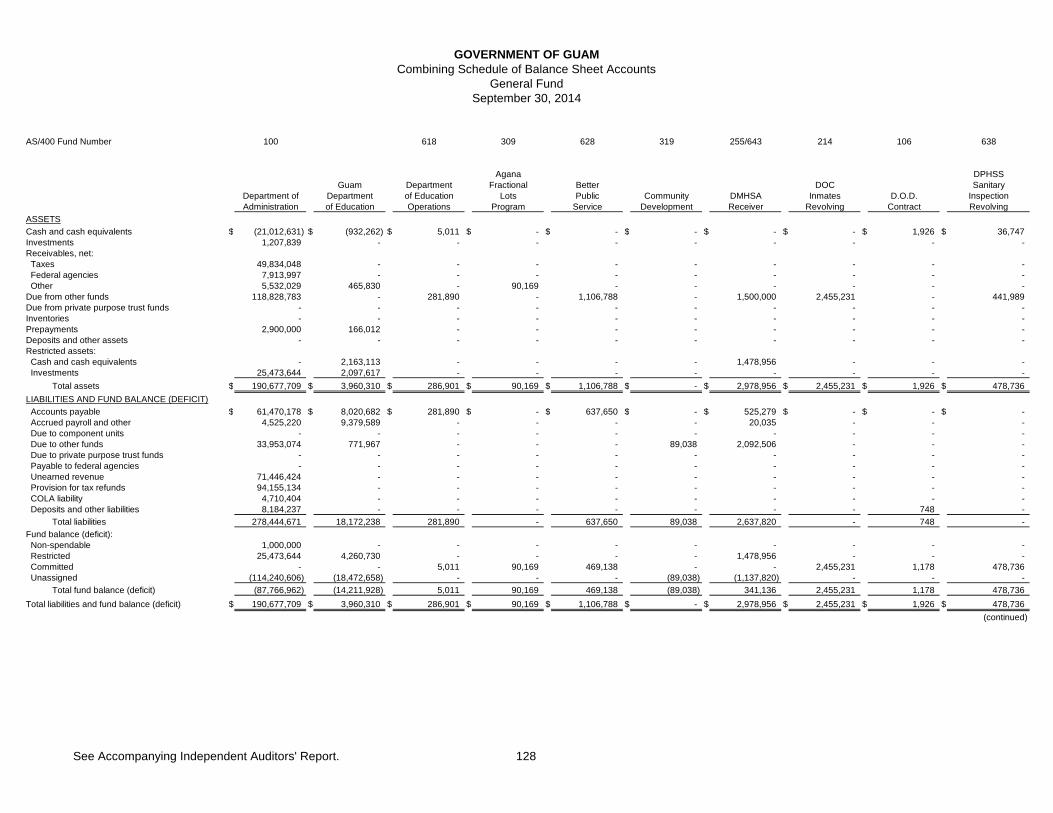

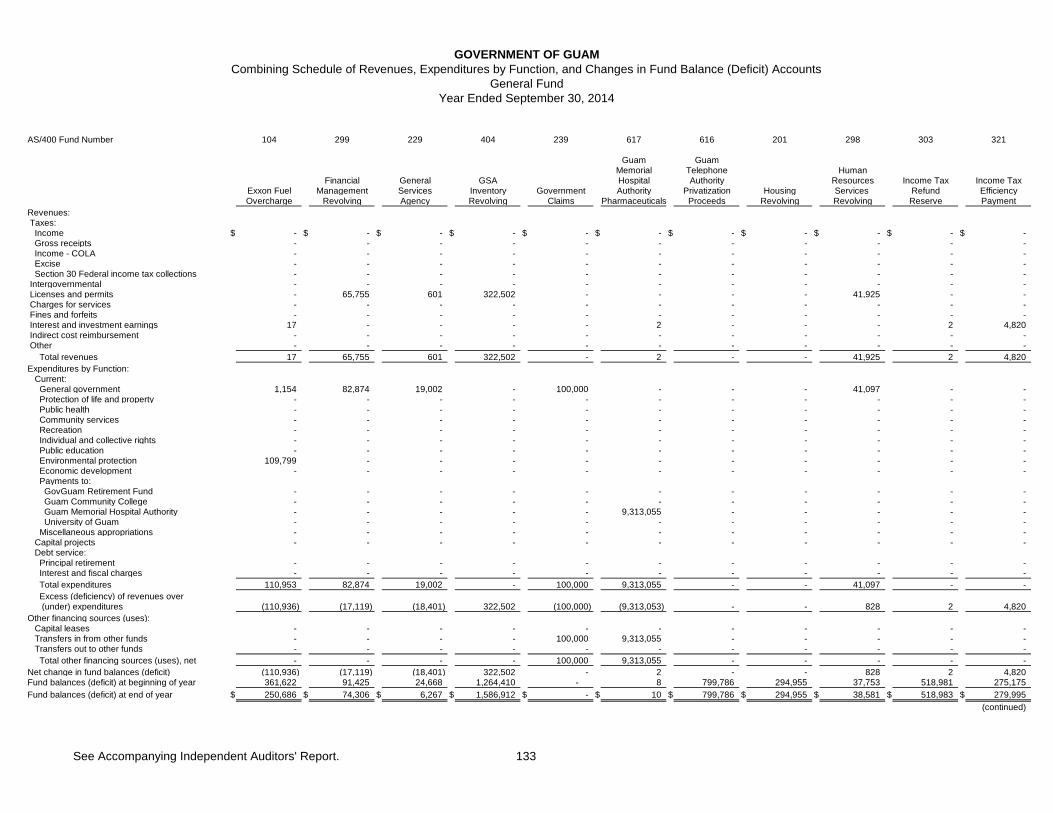

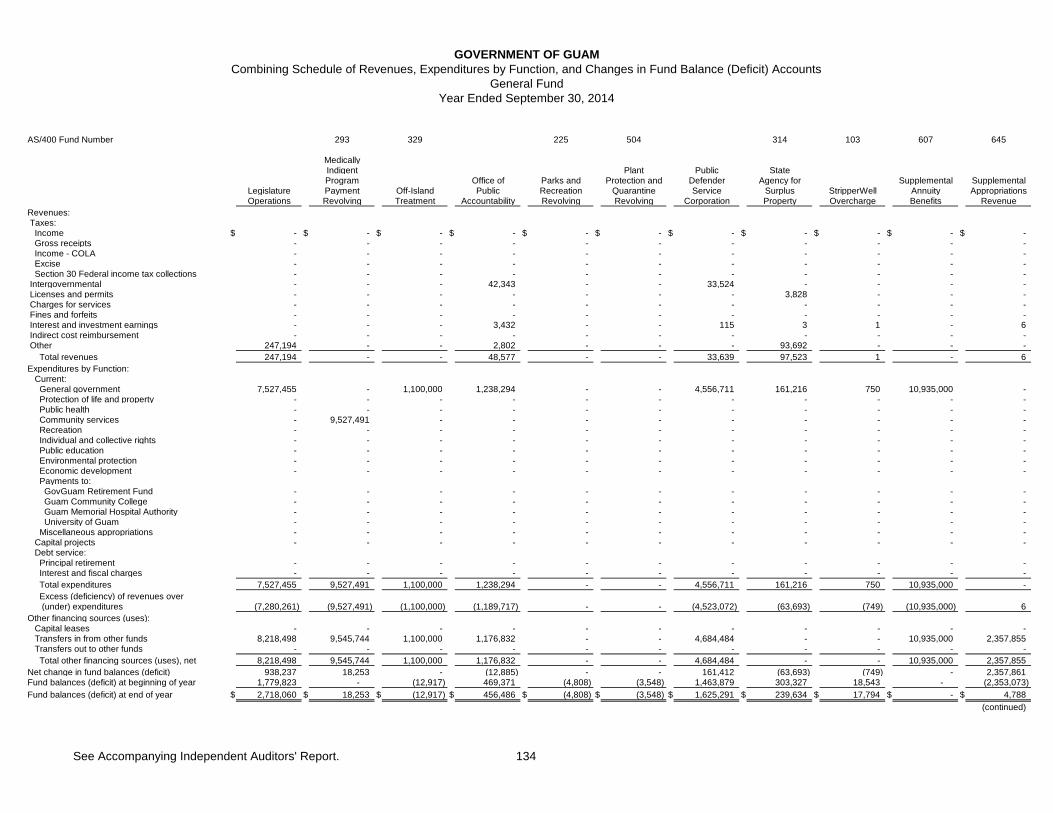

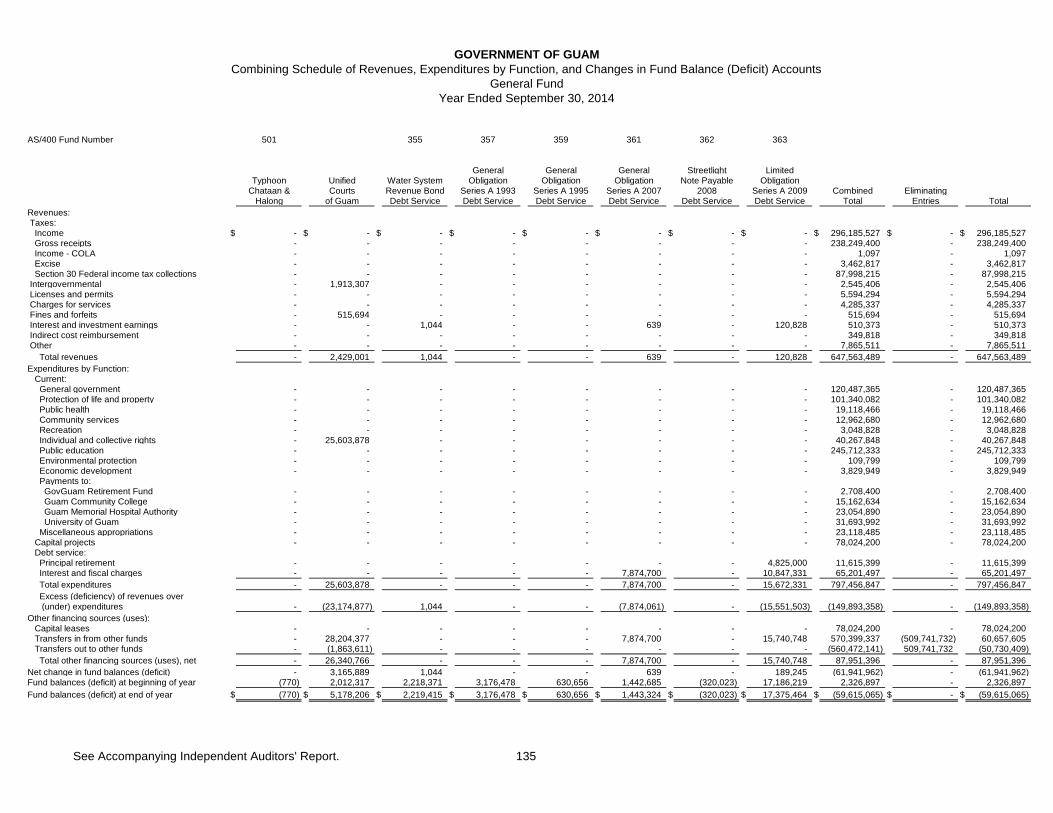

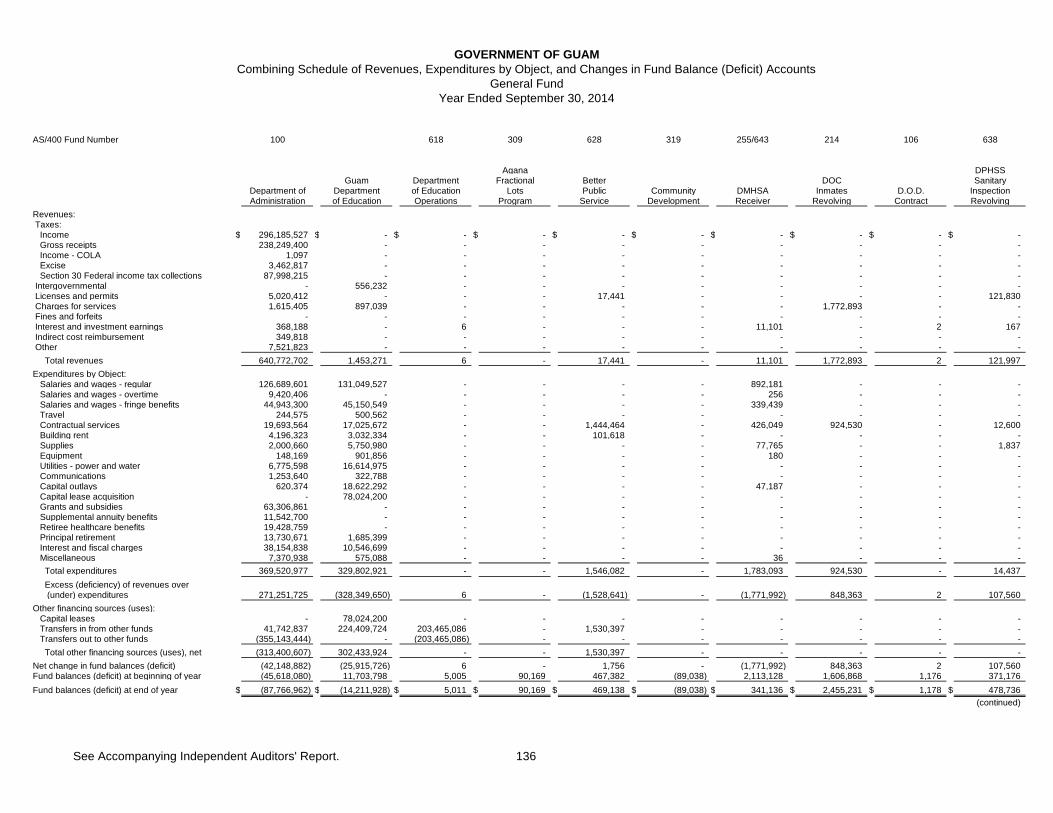

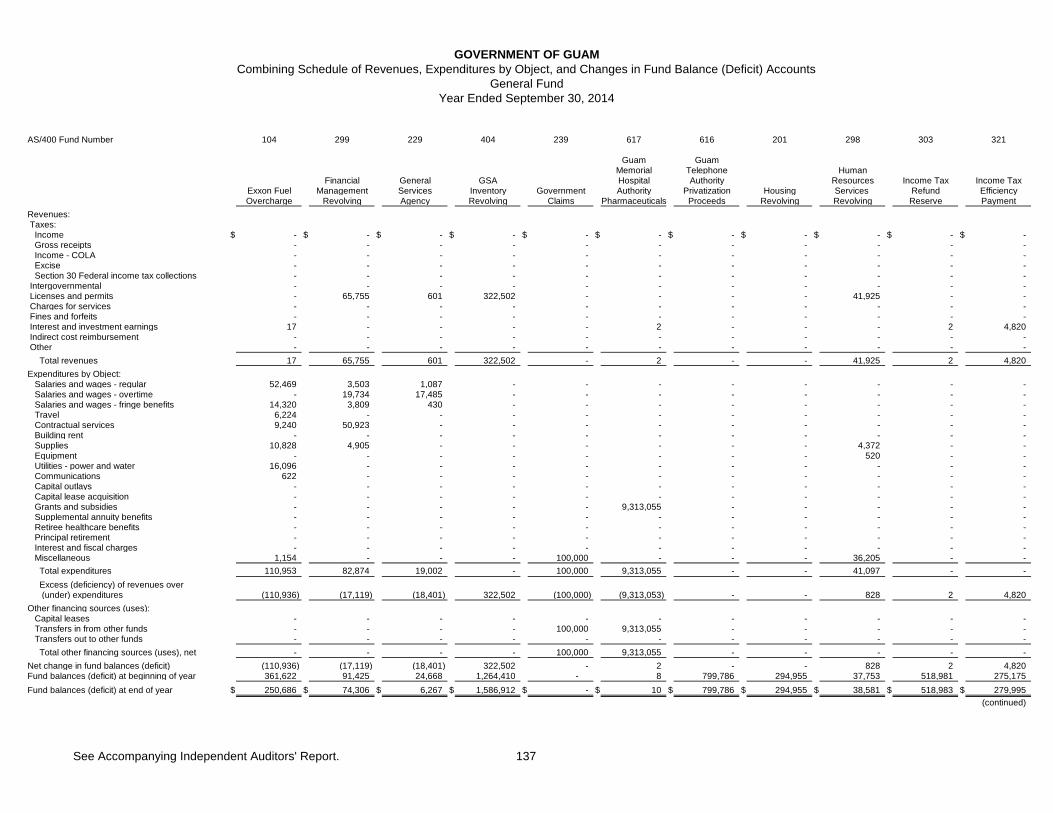

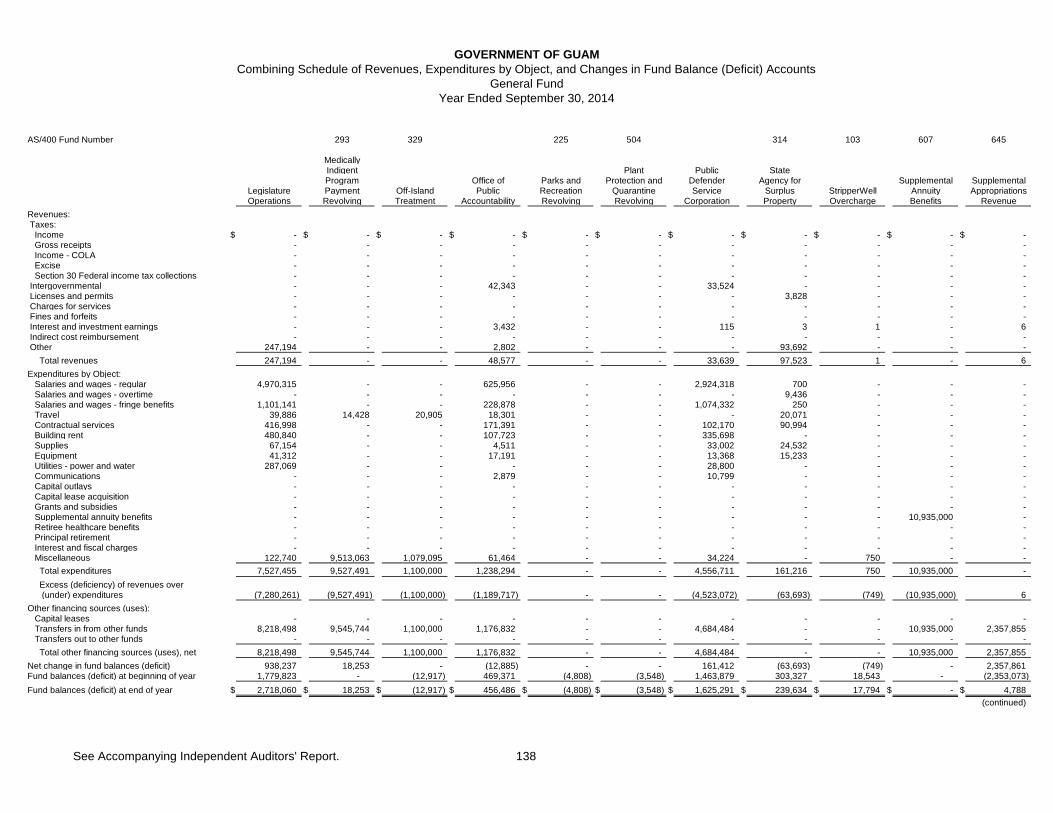

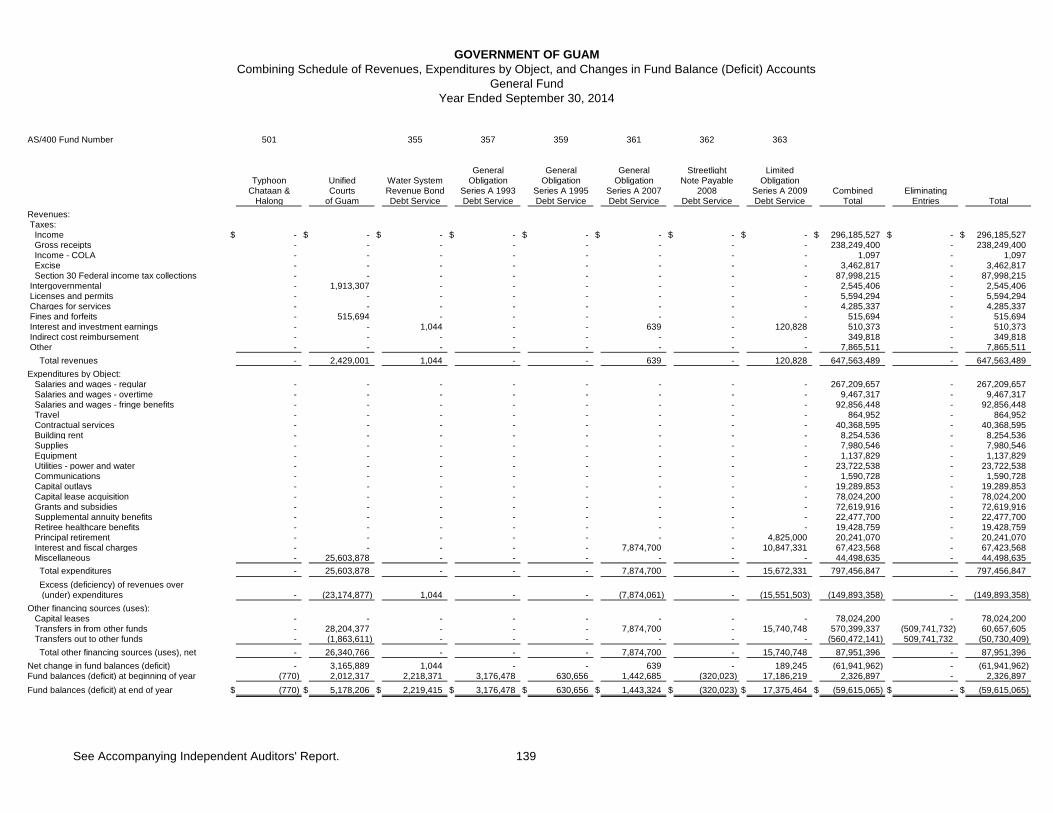

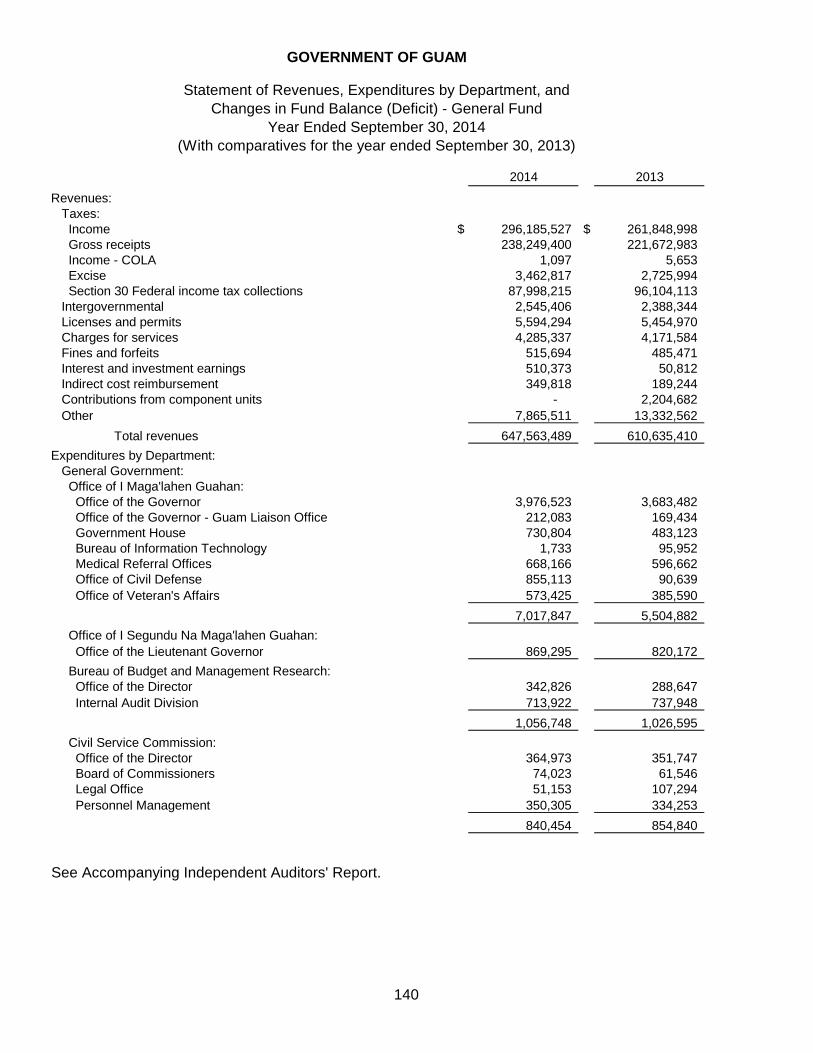

Narrative ...................................................................................................................................................................................... 125 Combining Schedule of Balance Sheet Accounts ......................................................................................................... 128 Combining Schedule of Revenue, Expenditures by Function, and Changes in Fund Balance (Deficit) Accounts .................................................................................................................................................... 132 Combining Schedule of Revenue, Expenditures by Object, and Changes in Fund Balance (Deficit) Accounts .................................................................................................................................................... 136 Statement of Revenues, Expenditures by Department, and Changes in Fund Balance (Deficit) – General Fund (Department of Administration) ............................................................................................................................ 140 Statement of Revenues, Expenditures by Department, and Changes in Fund Balance (Deficit) – Budget and Actual - General Fund (Department of Administration).................................................................................. 148

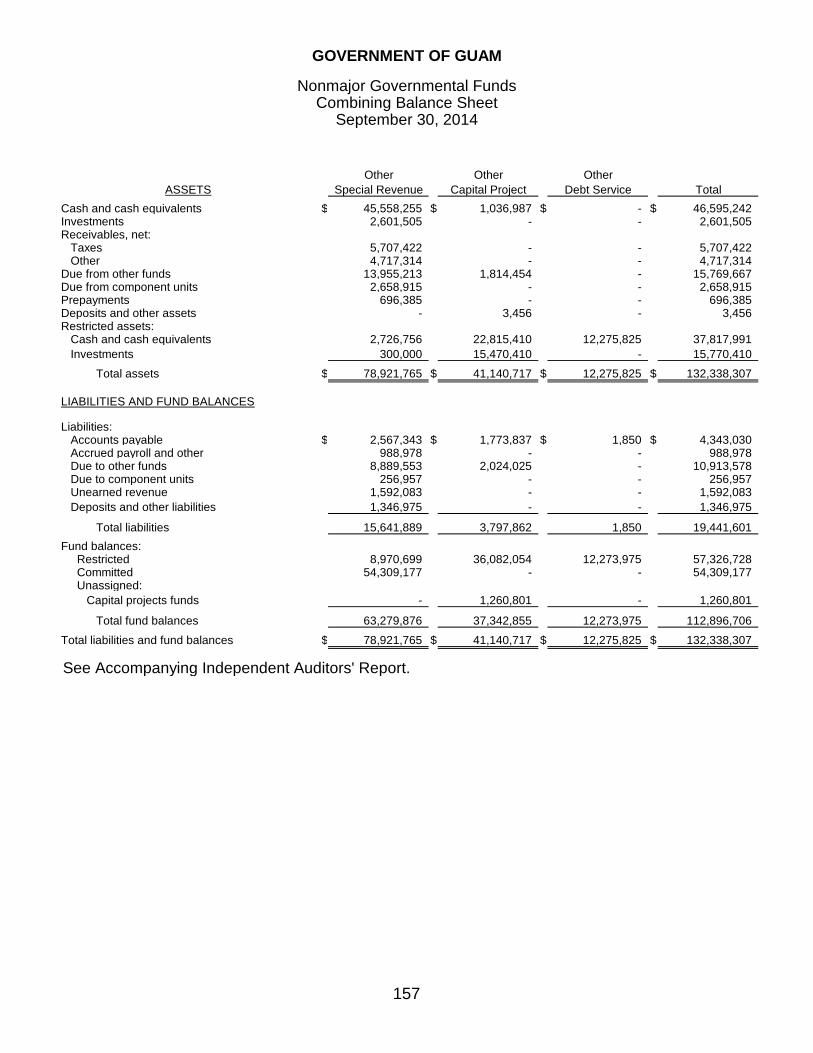

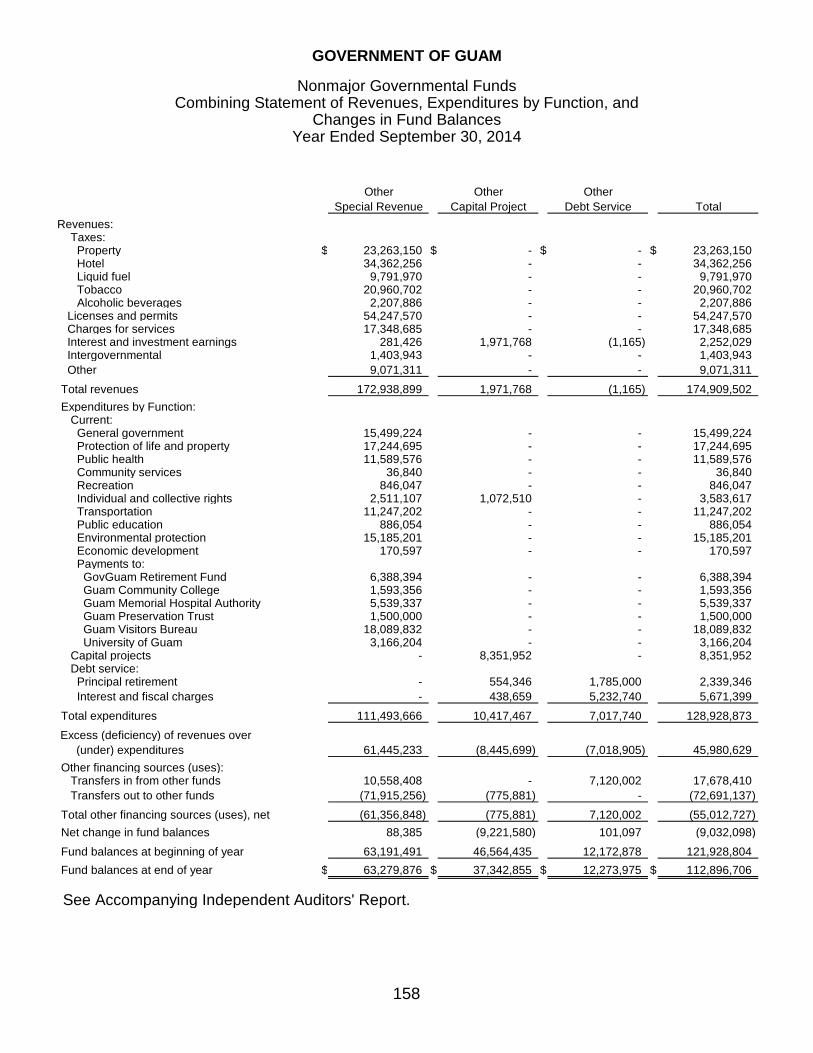

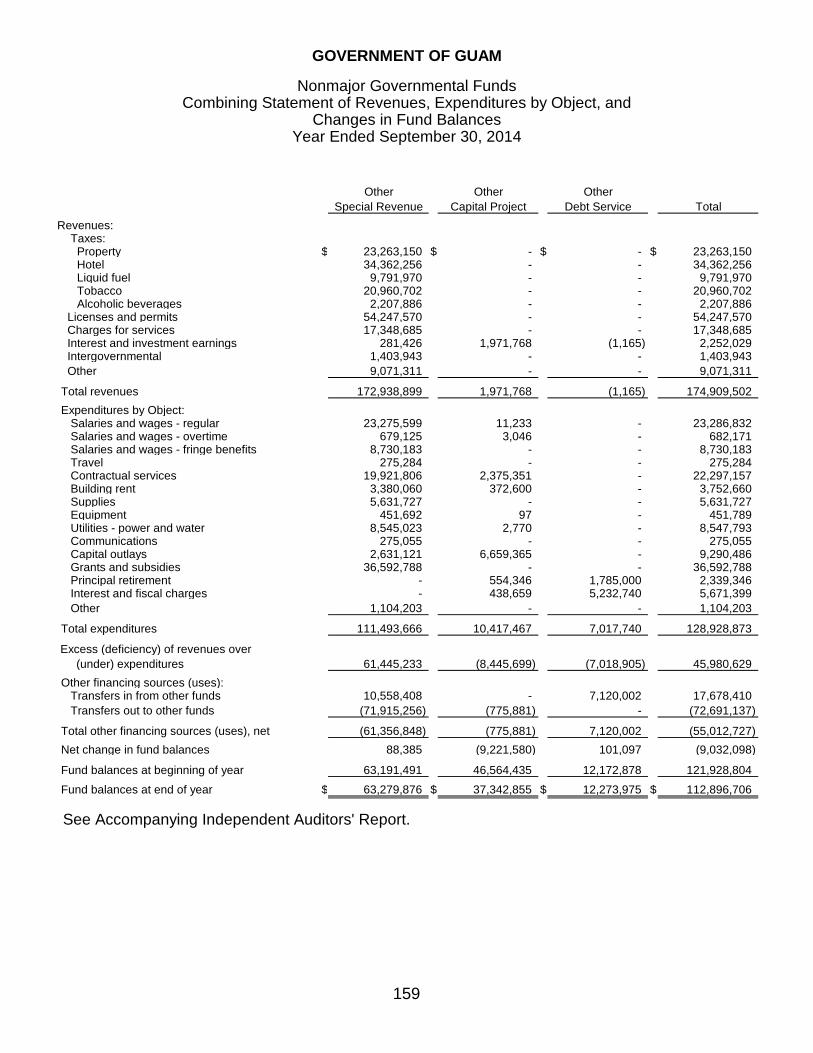

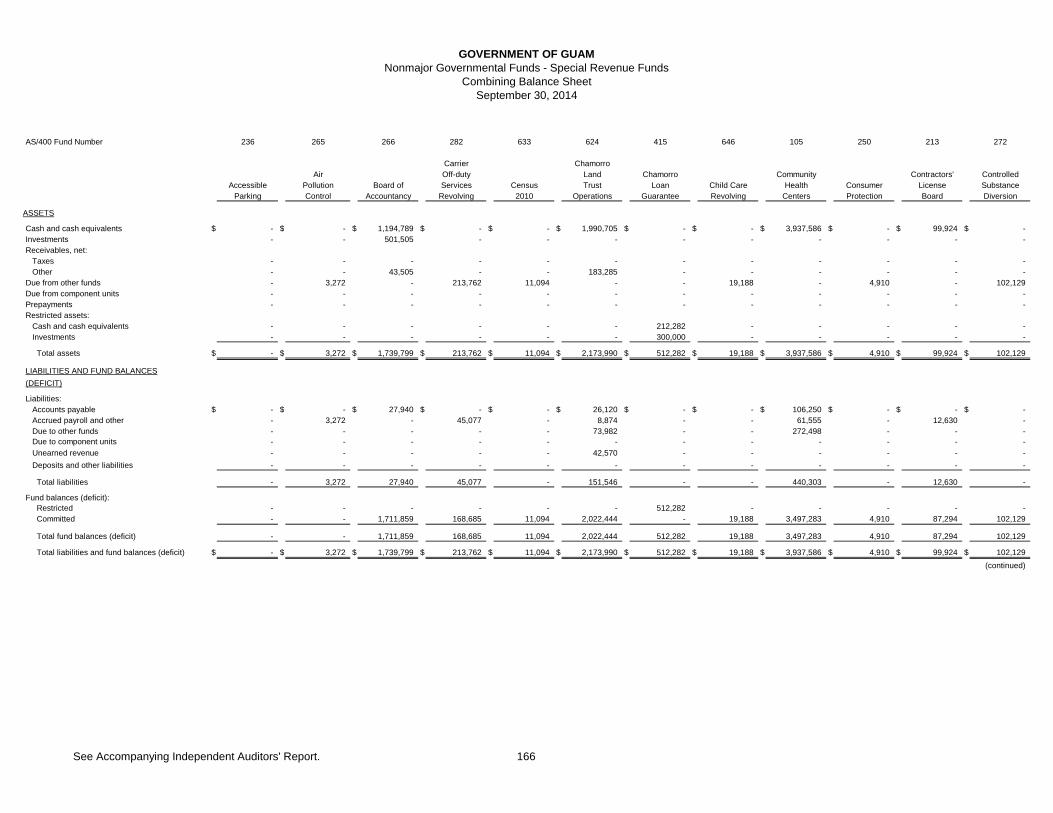

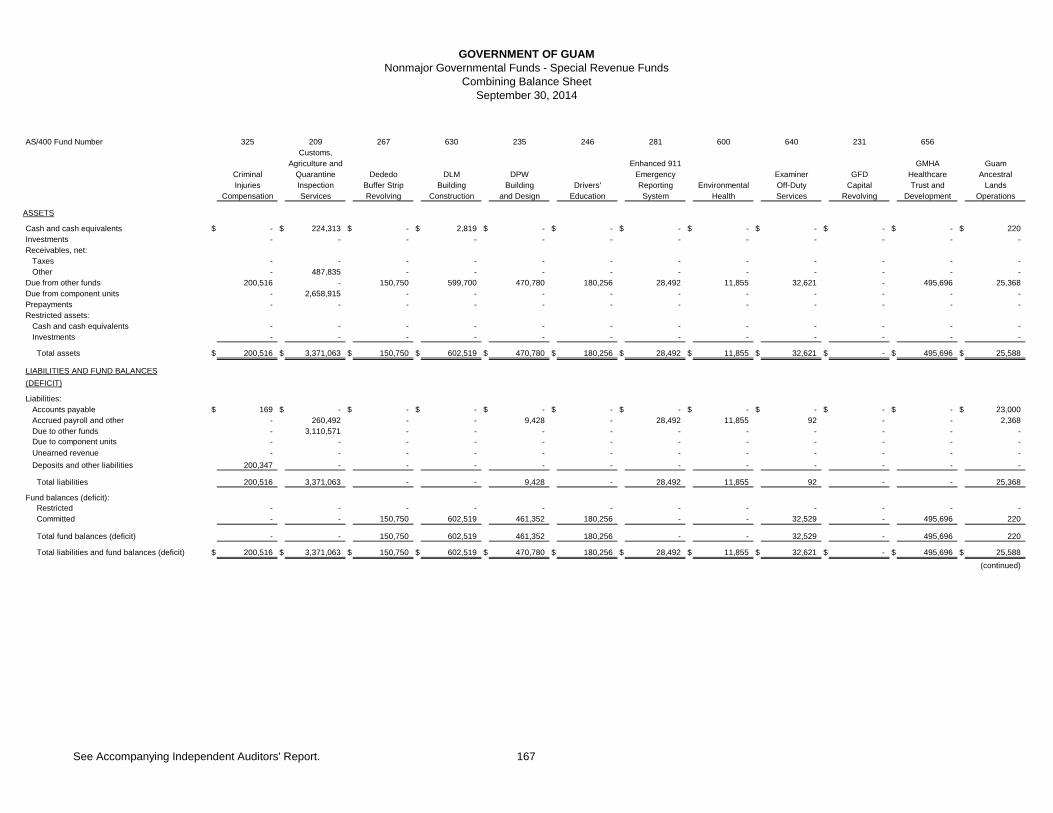

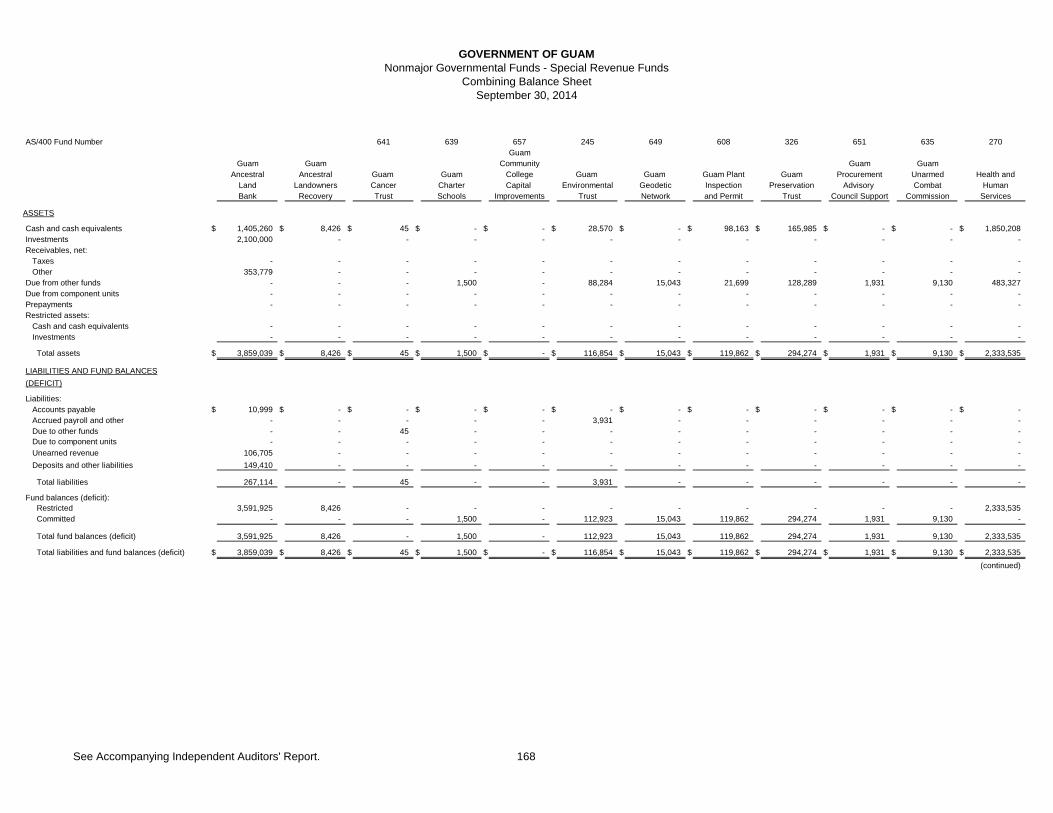

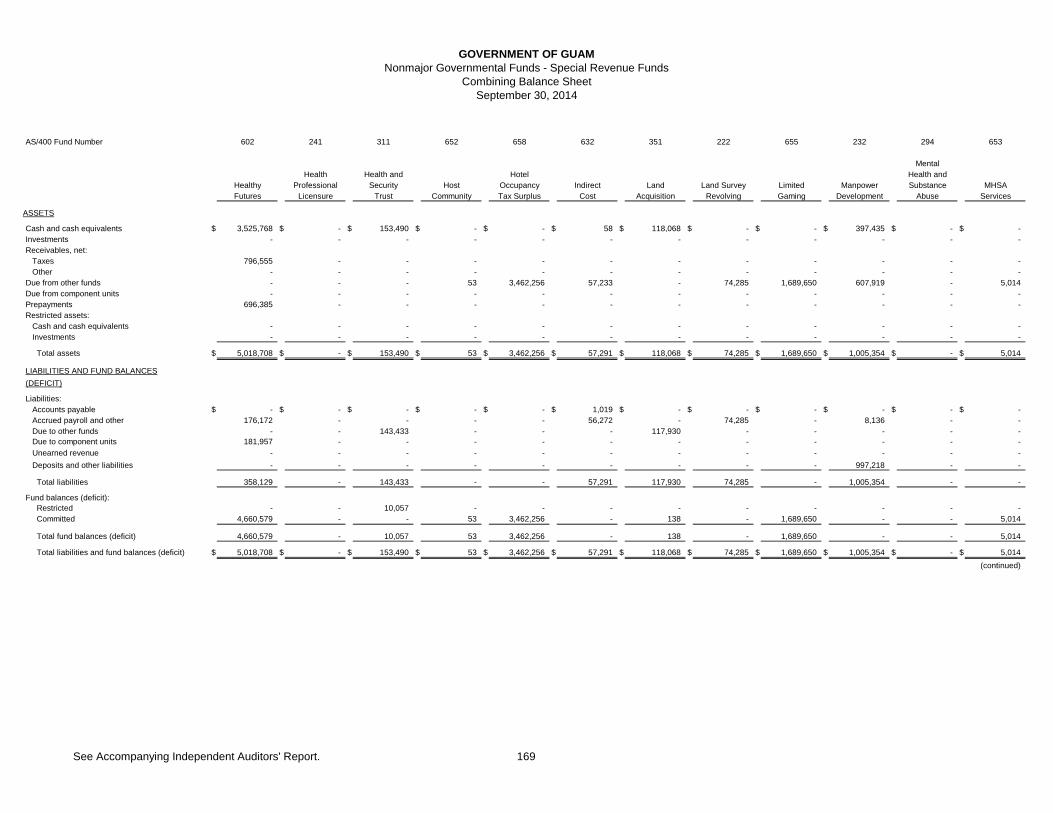

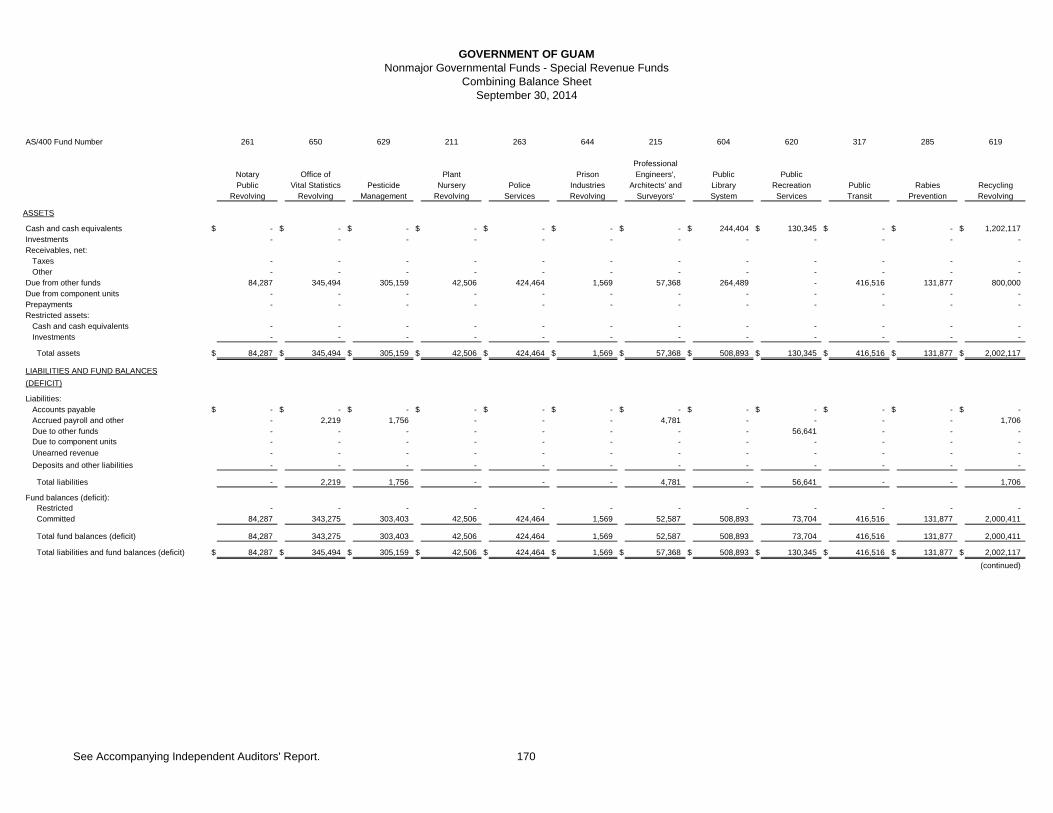

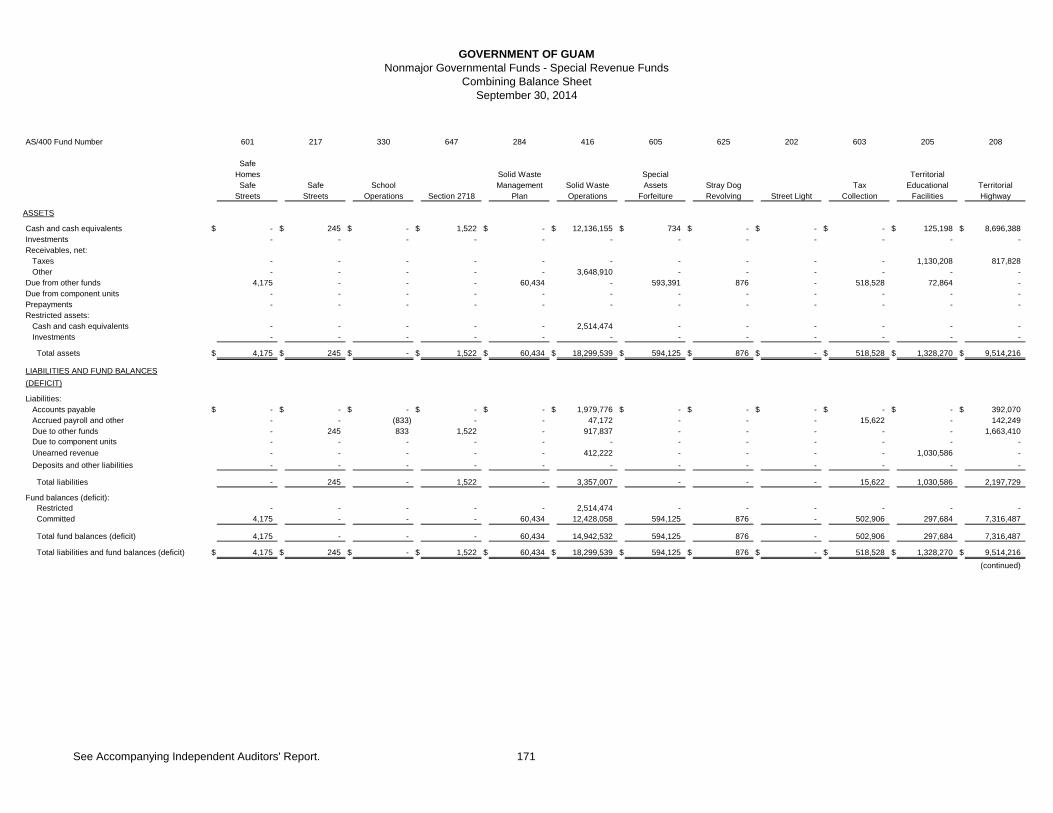

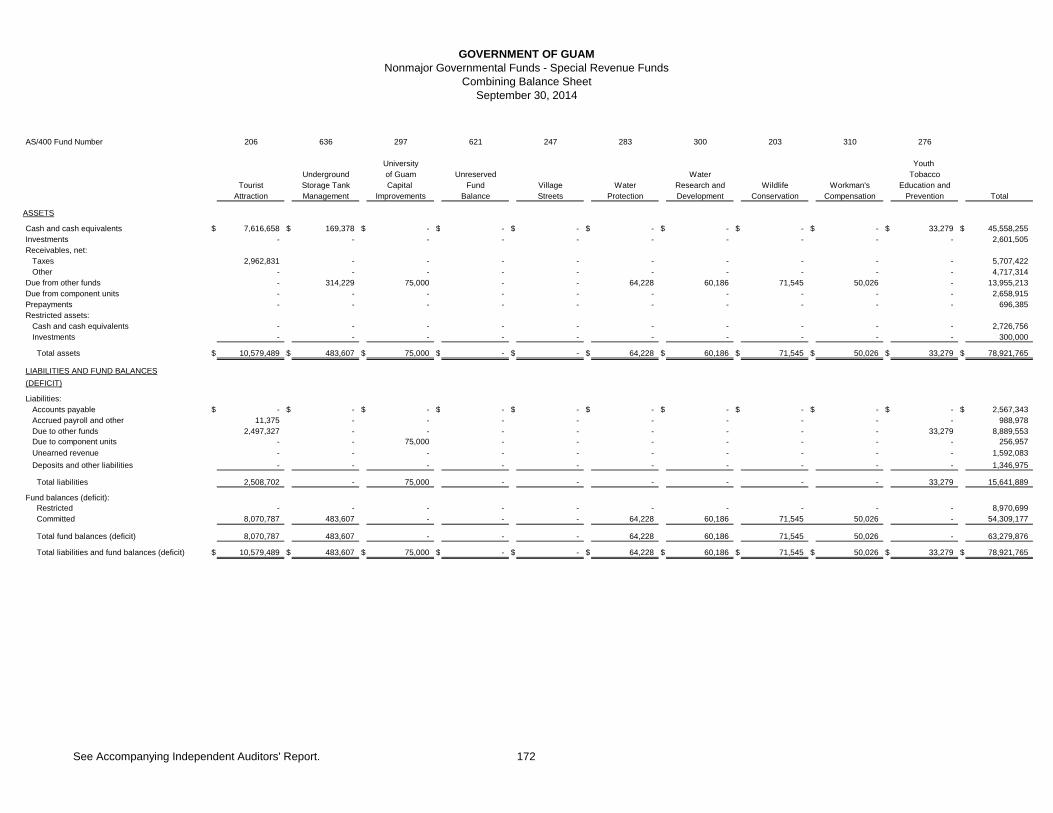

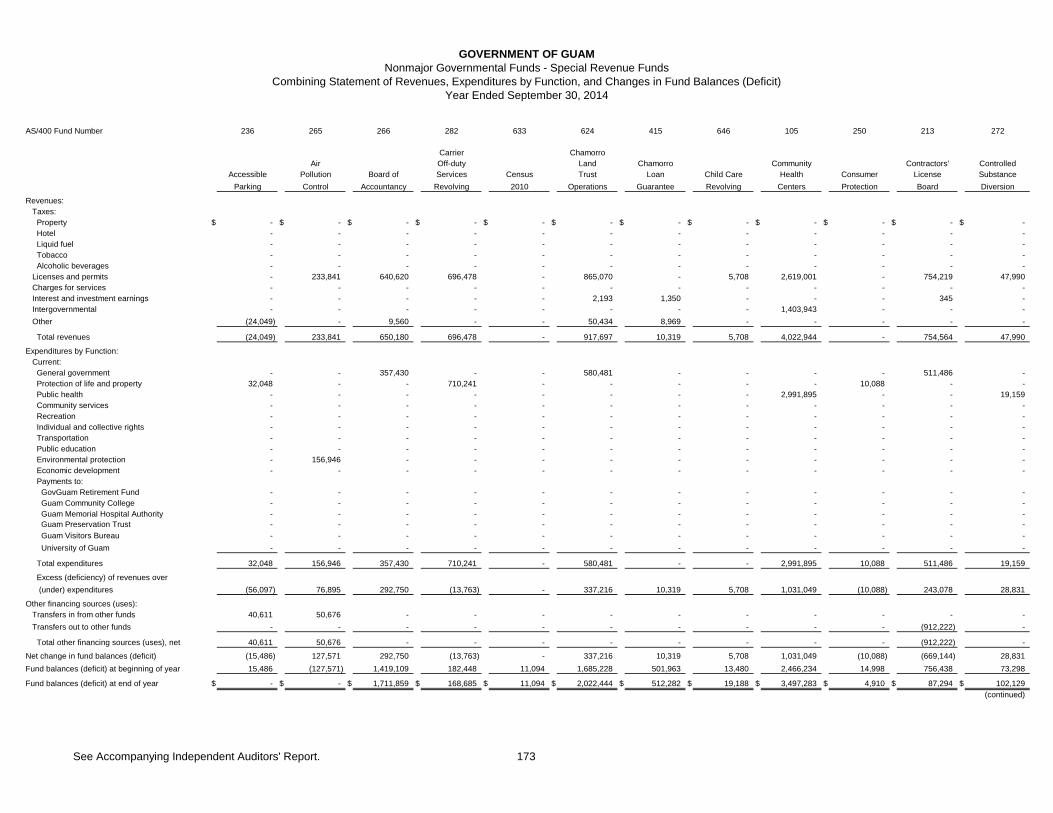

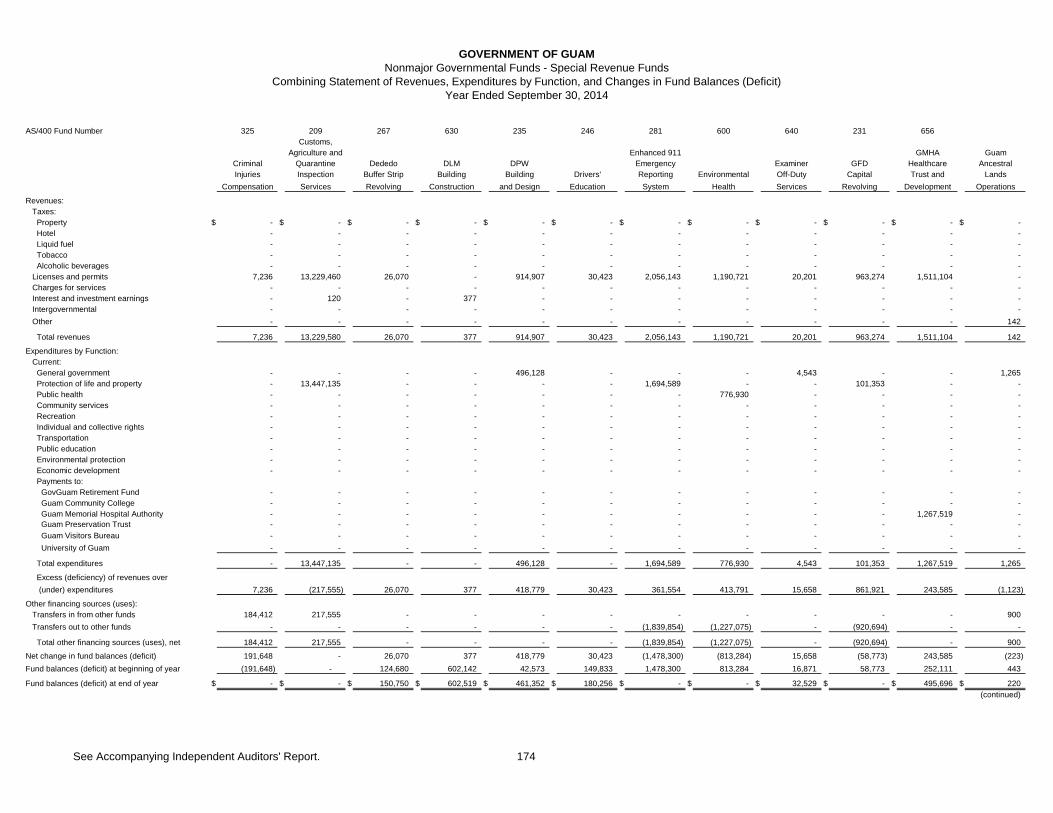

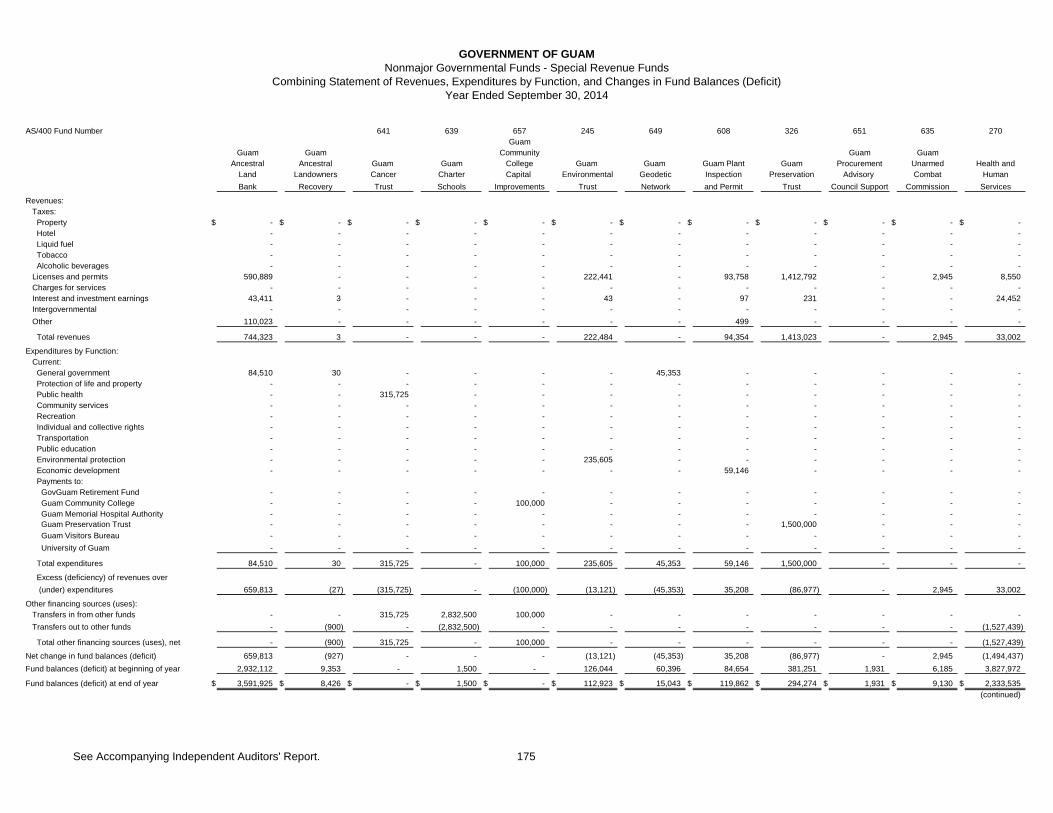

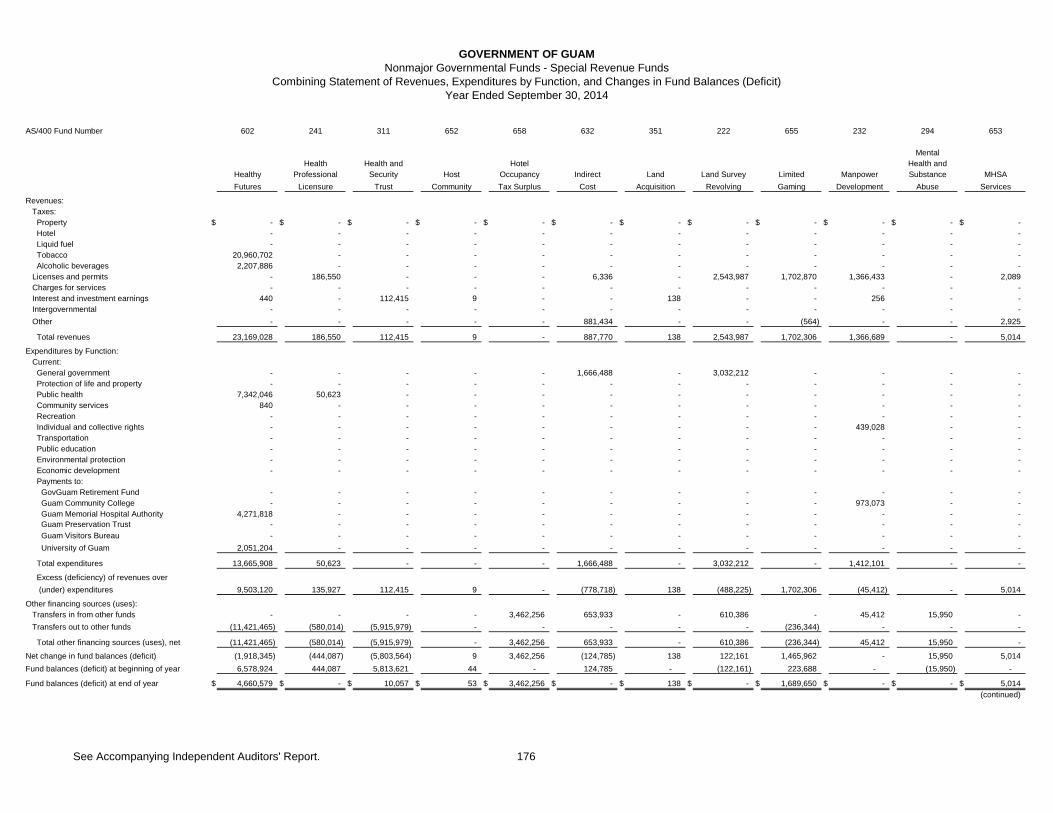

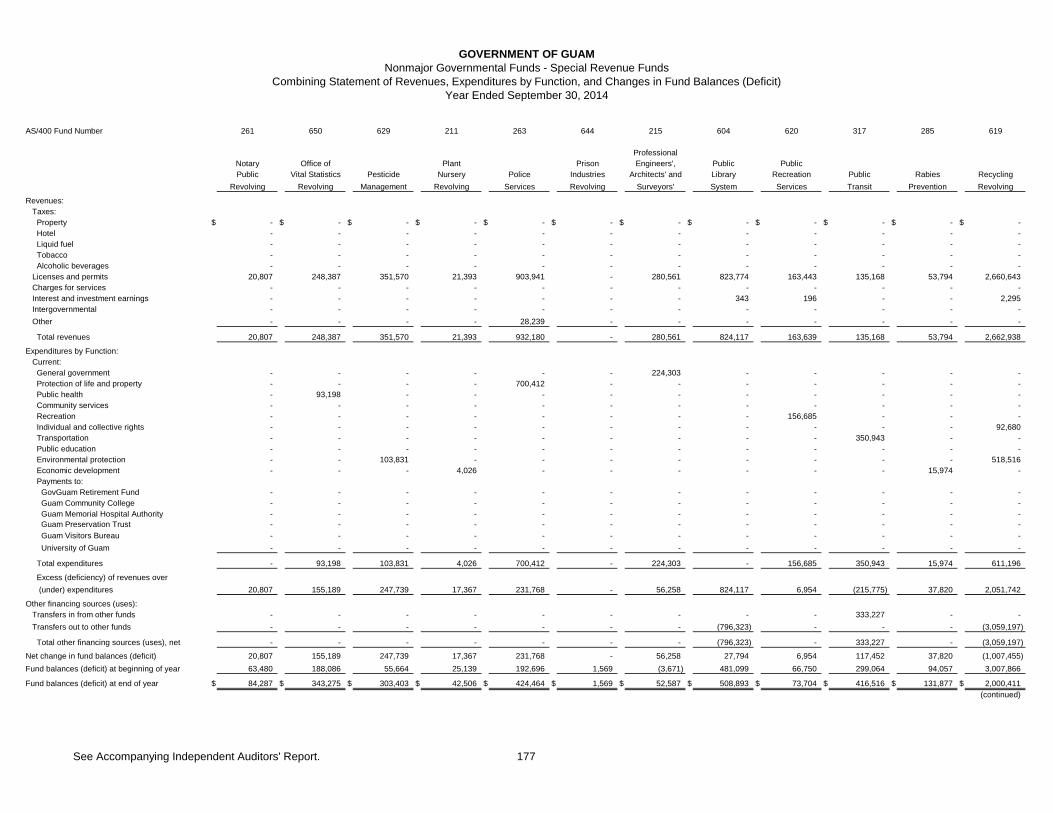

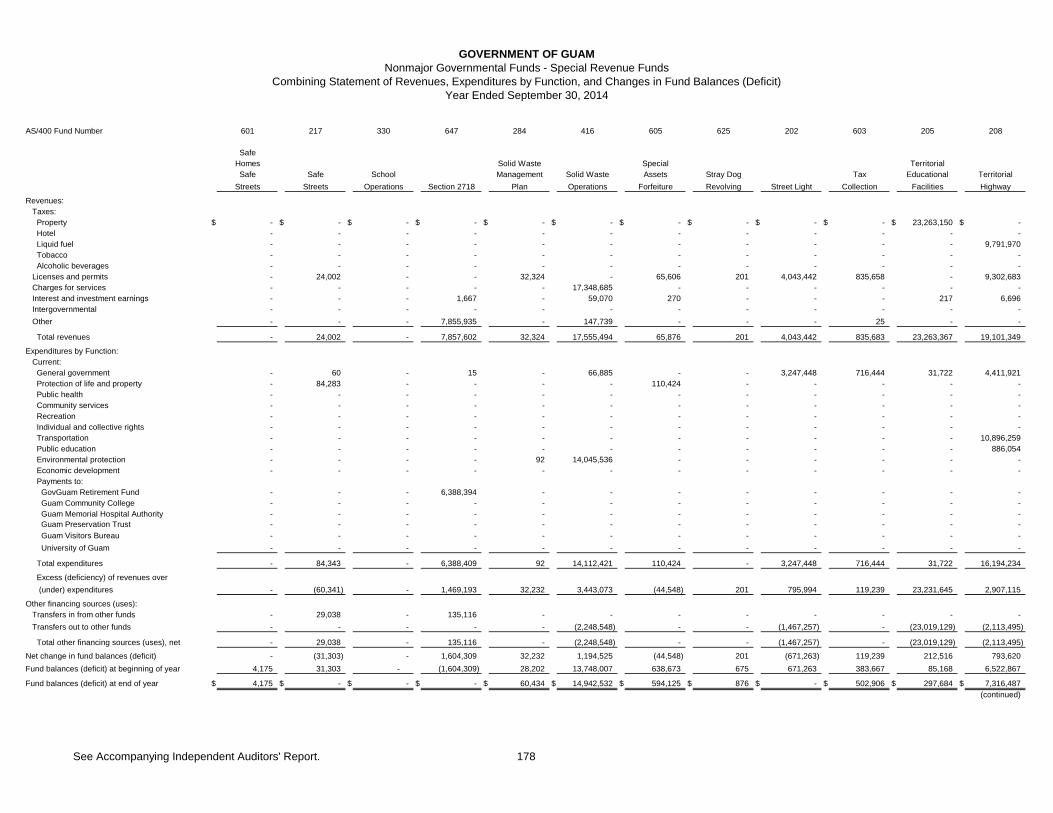

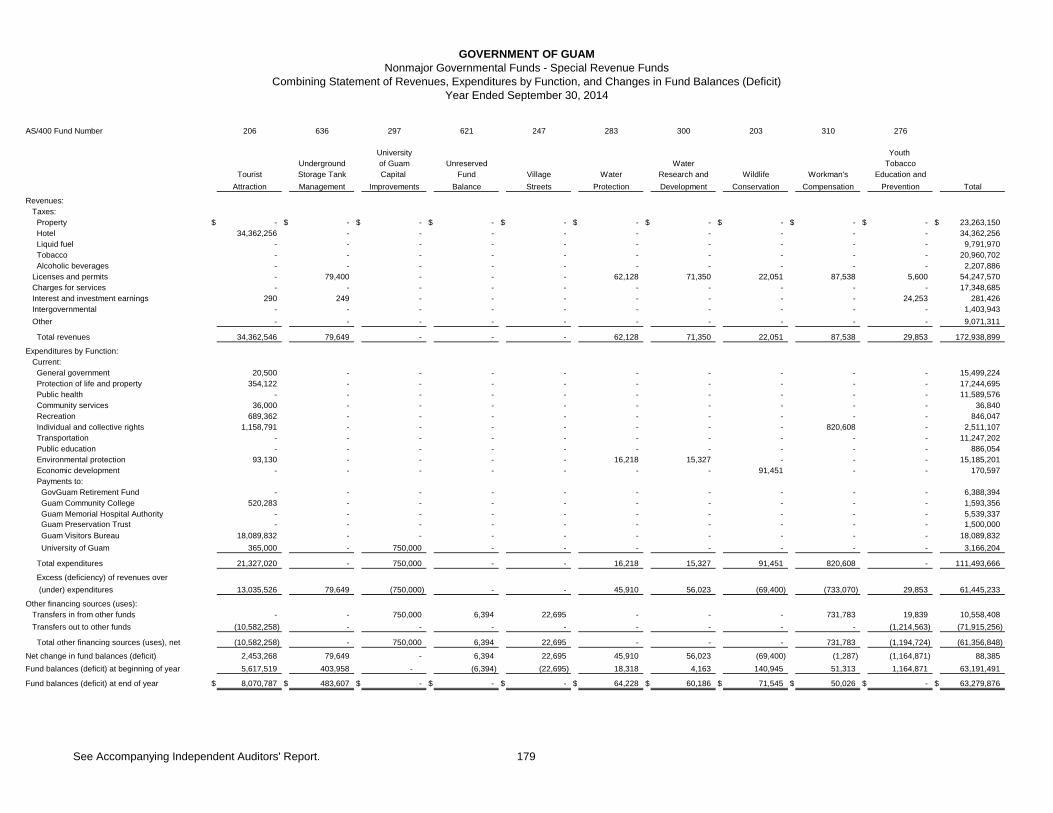

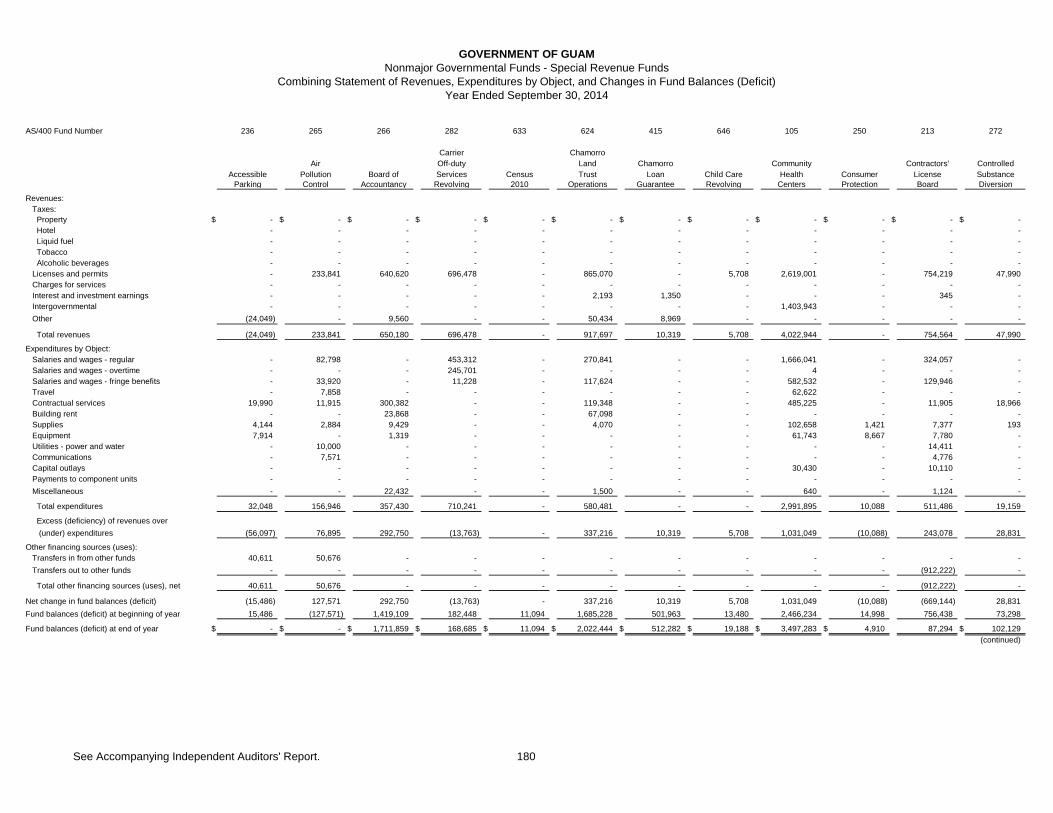

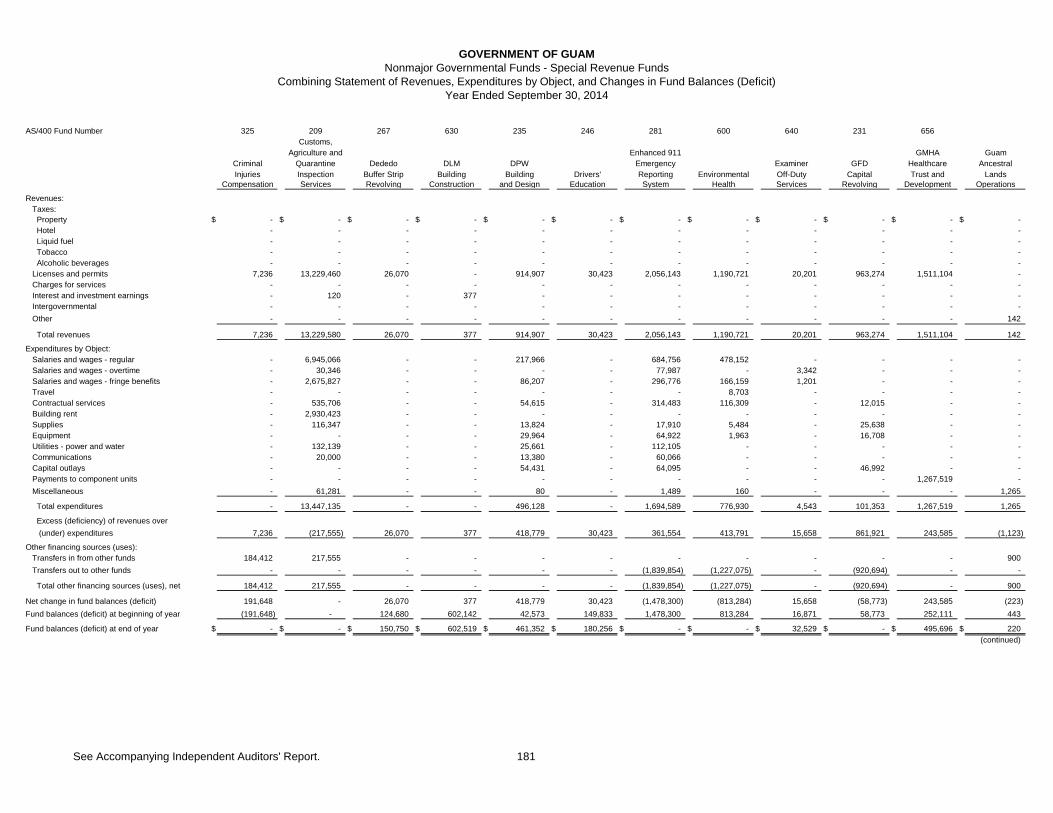

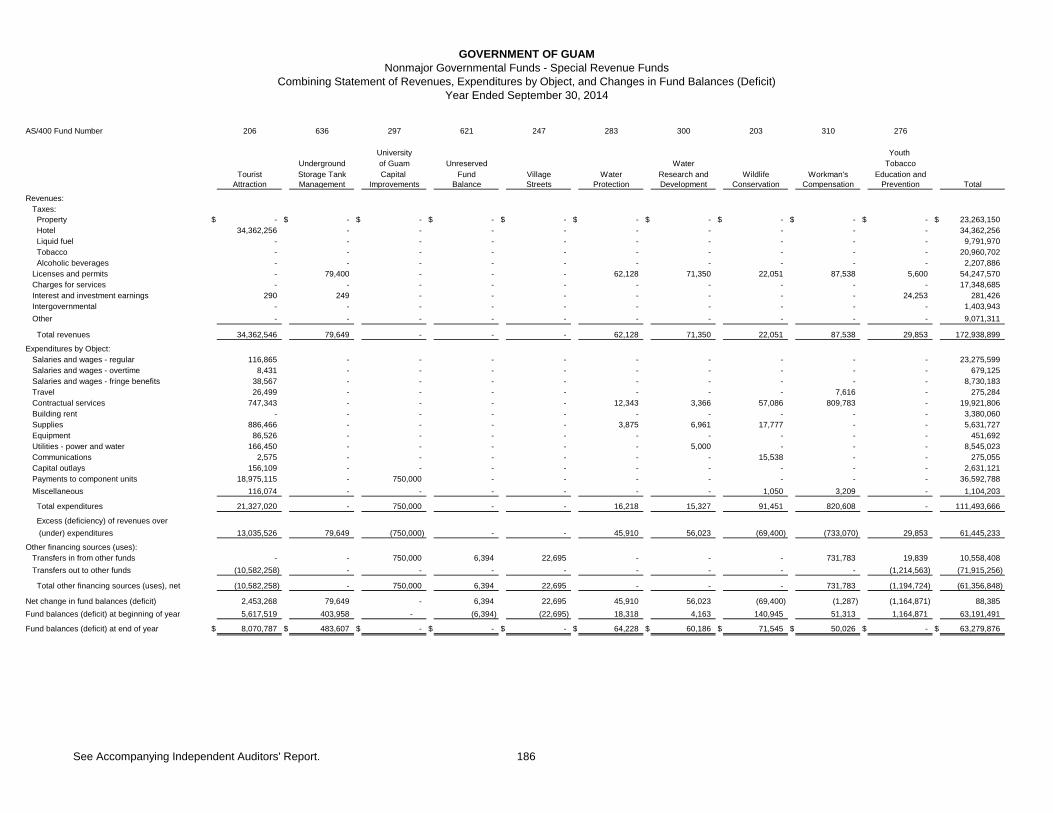

Nonmajor Governmental Funds Narrative ...................................................................................................................................................................................... 156 Combining Balance Sheet Accounts – Nonmajor Governmental Funds ............................................................. 157 Combining Statement of Revenue, Expenditures by Function, and Changes in Fund Balances – Nonmajor Governmental Funds .................................................................................................................. 158 Combining Schedule of Revenue, Expenditures by Object, and Changes in Fund Balances – Nonmajor Governmental Funds .................................................................................................................. 159

2014 Table of Contents

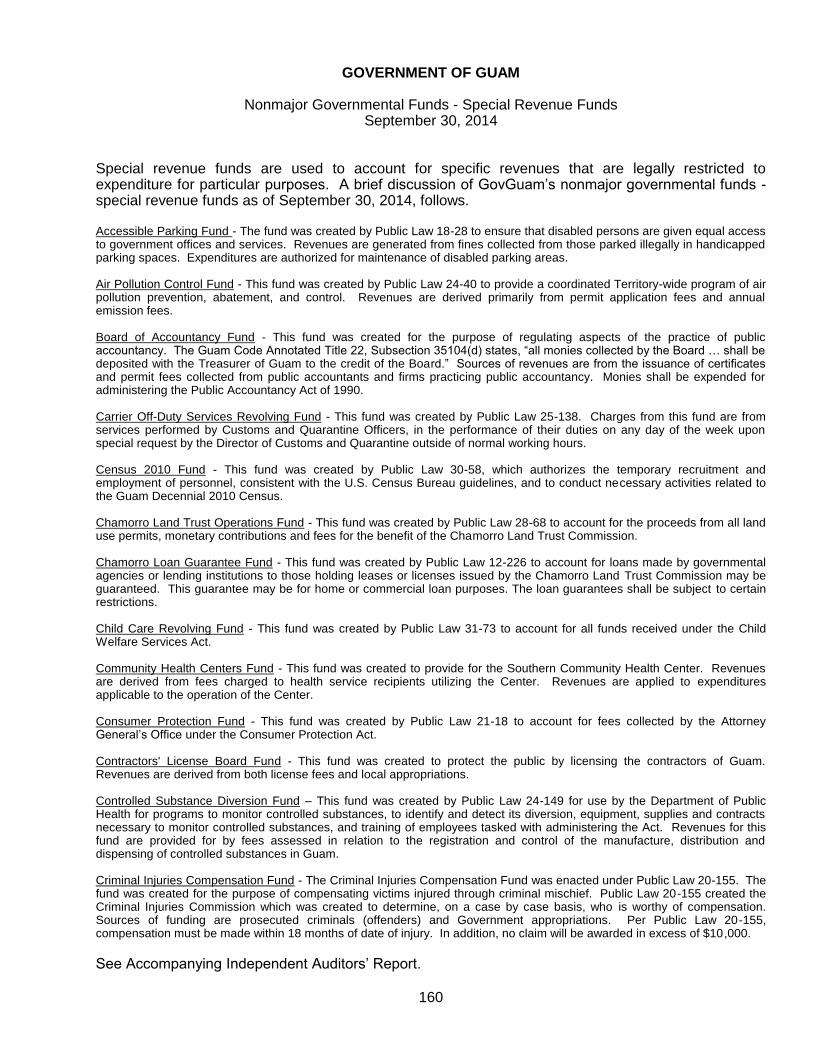

Nonmajor Governmental Funds – Special Revenue Funds

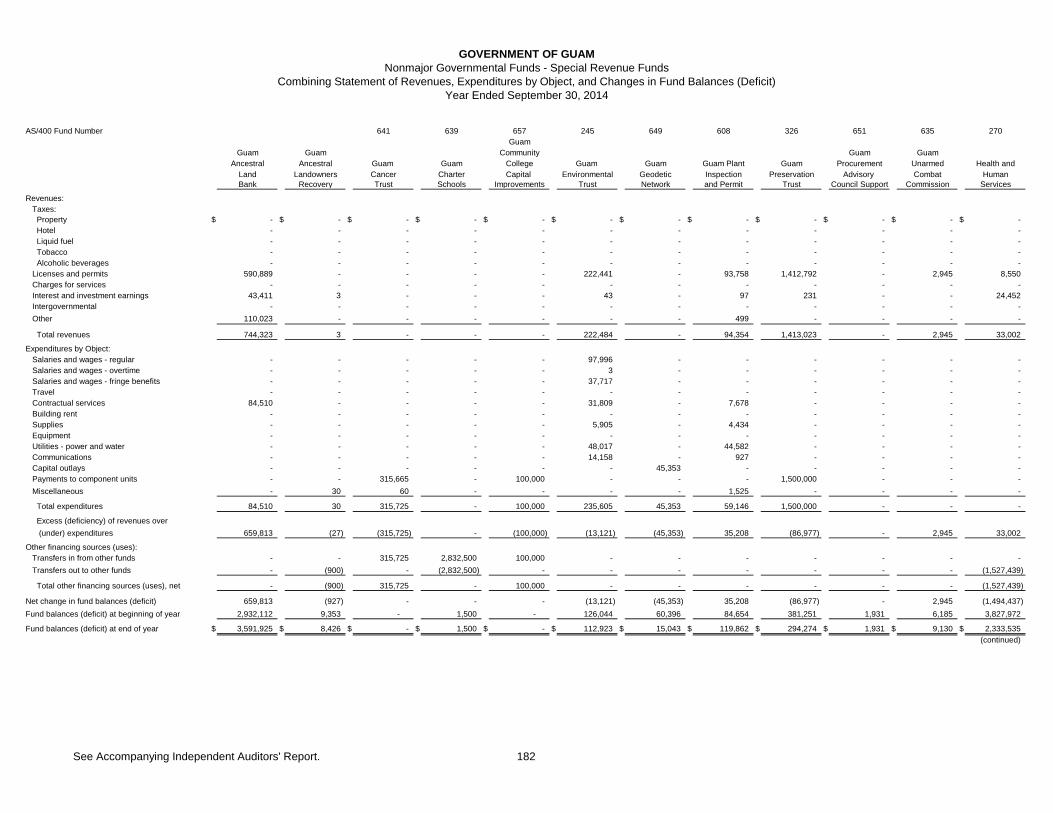

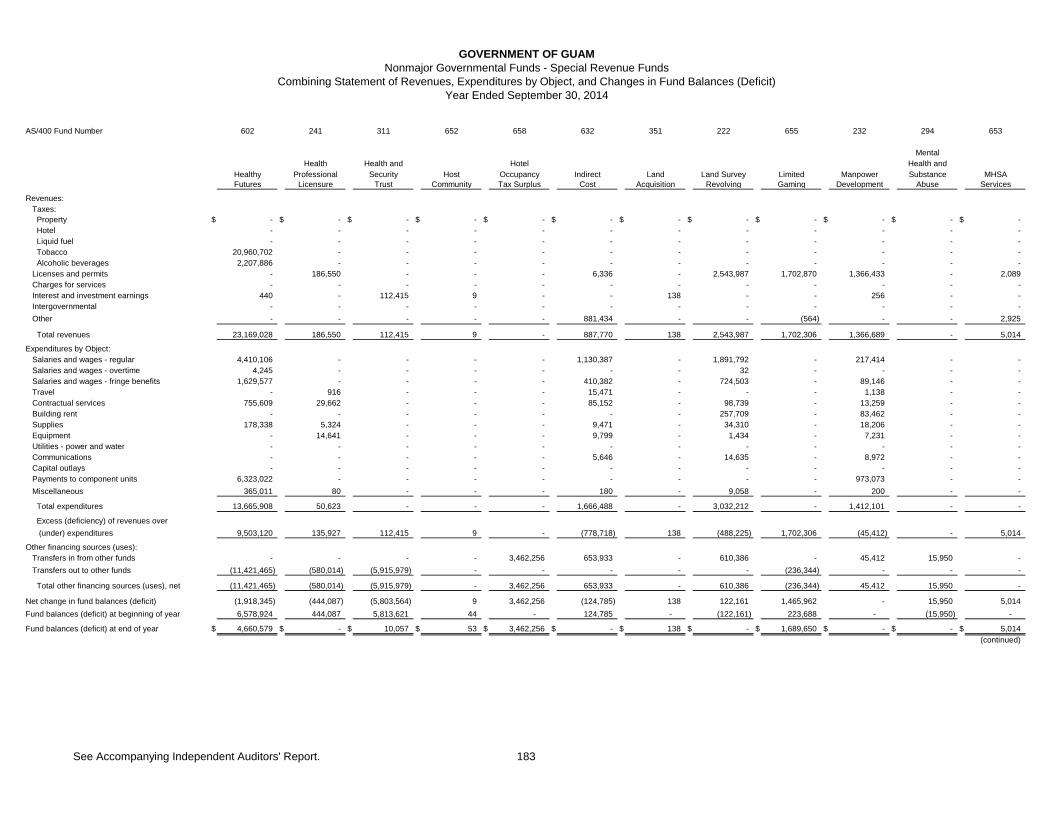

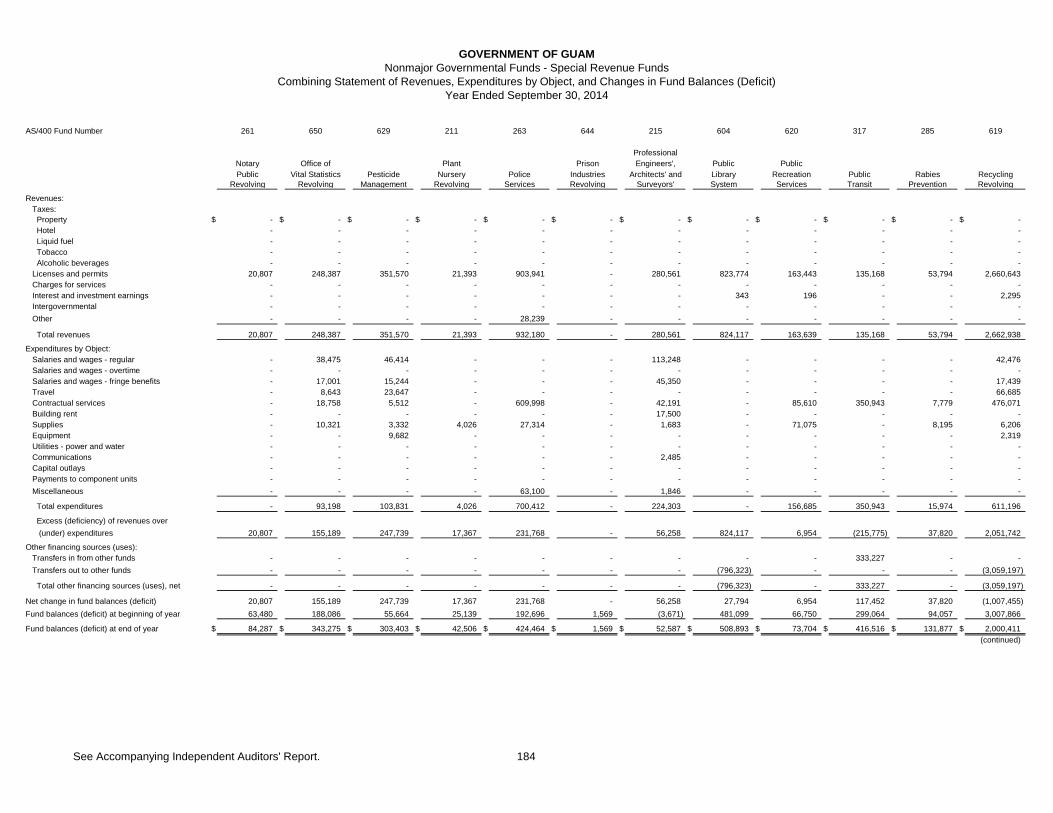

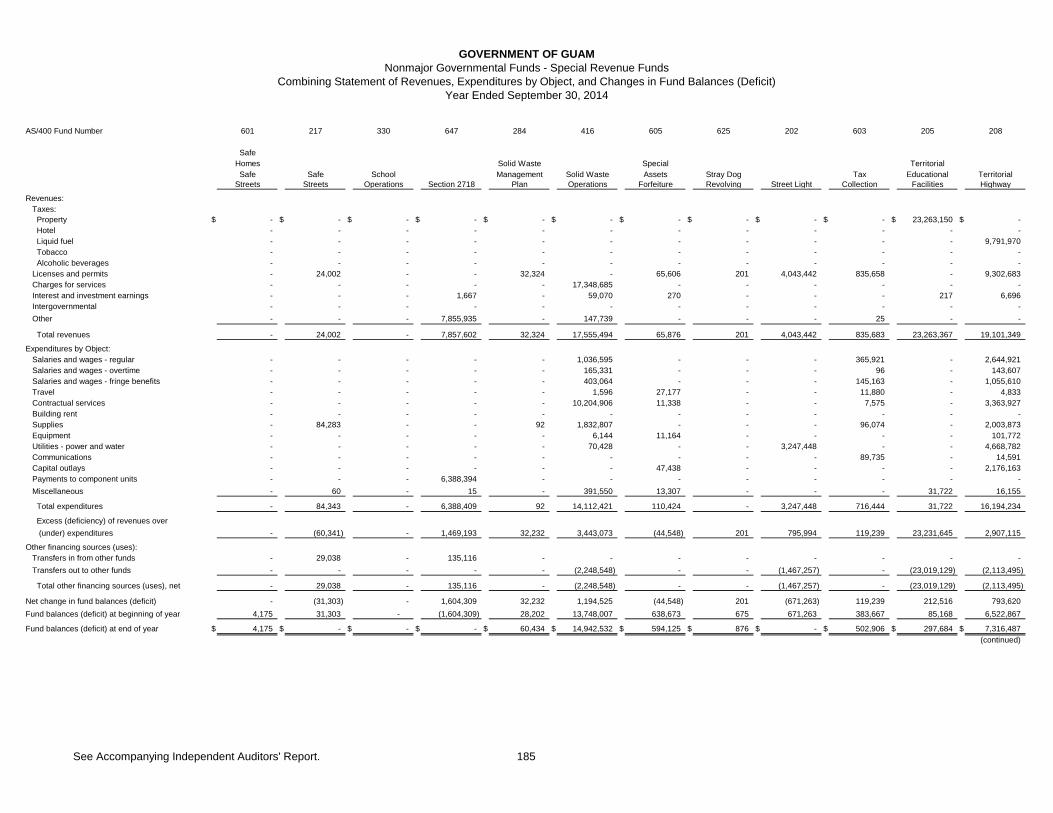

Narrative ...................................................................................................................................................................................... 160 Combining Balance Sheet ...................................................................................................................................................... 166 Combining Statement of Revenue, Expenditures by Function, and Changes in Fund Balance (Deficit) ........................................................................................................................................................................ 173 Combining Schedule of Revenue, Expenditures by Object, and Changes in Fund Balances (Deficit) .... 180

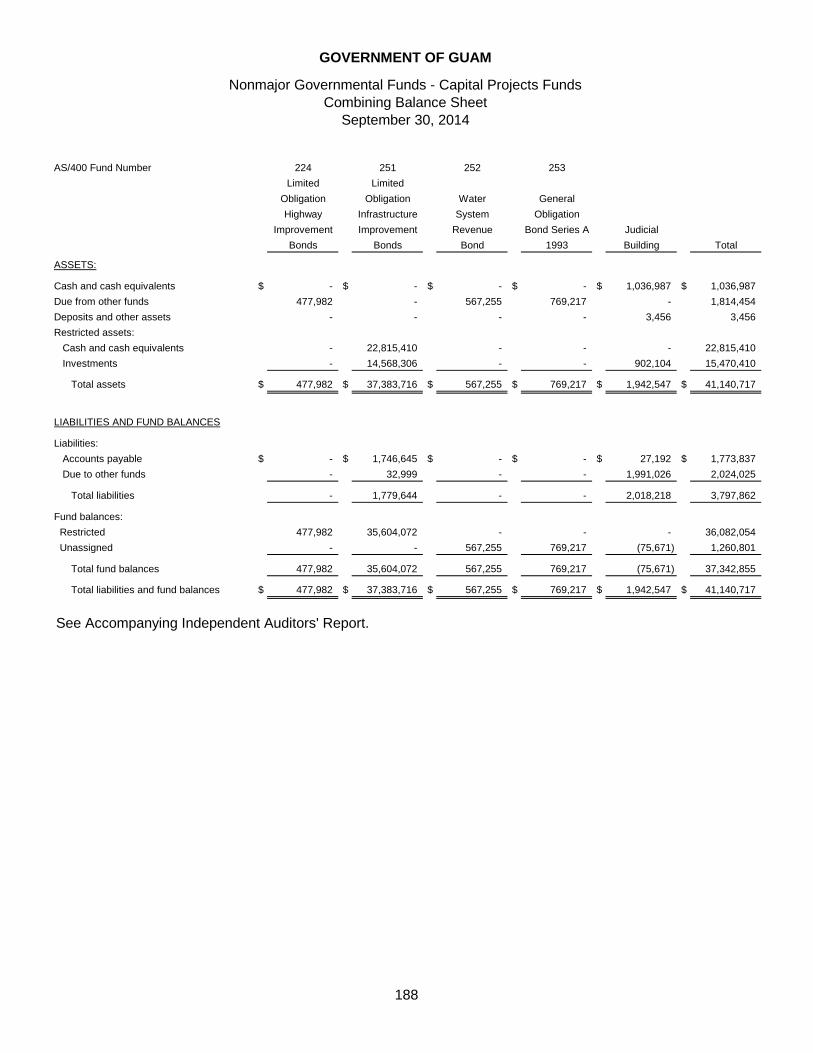

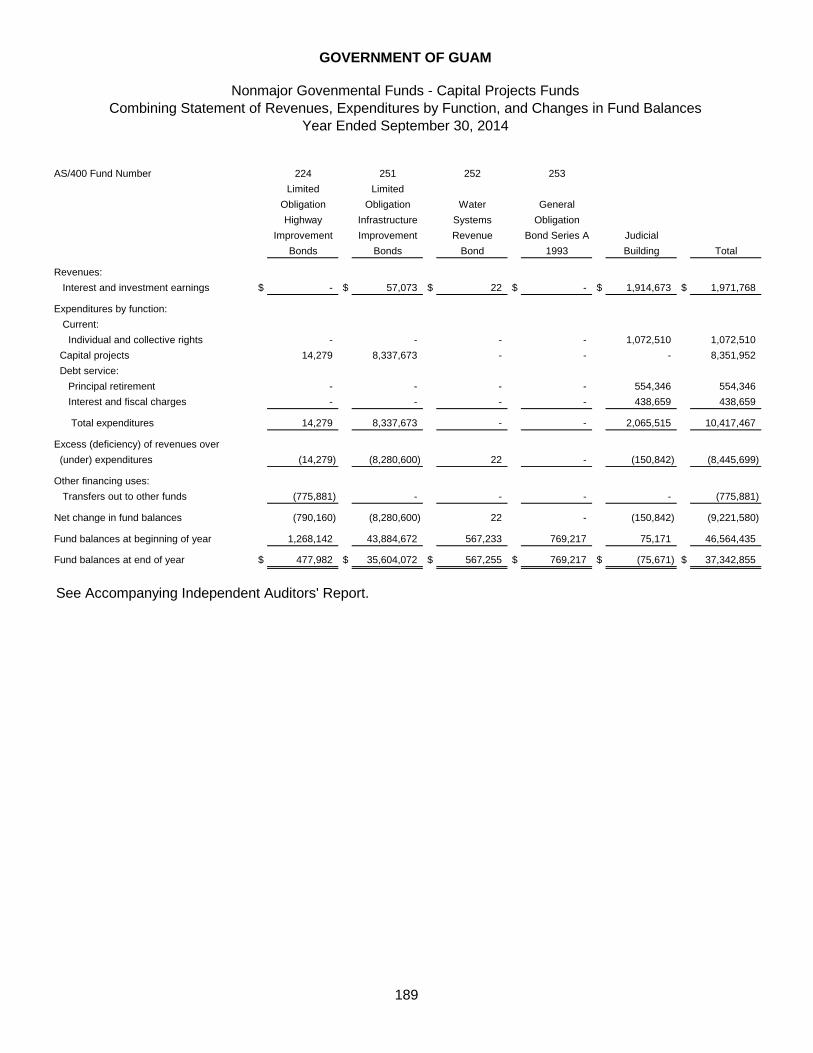

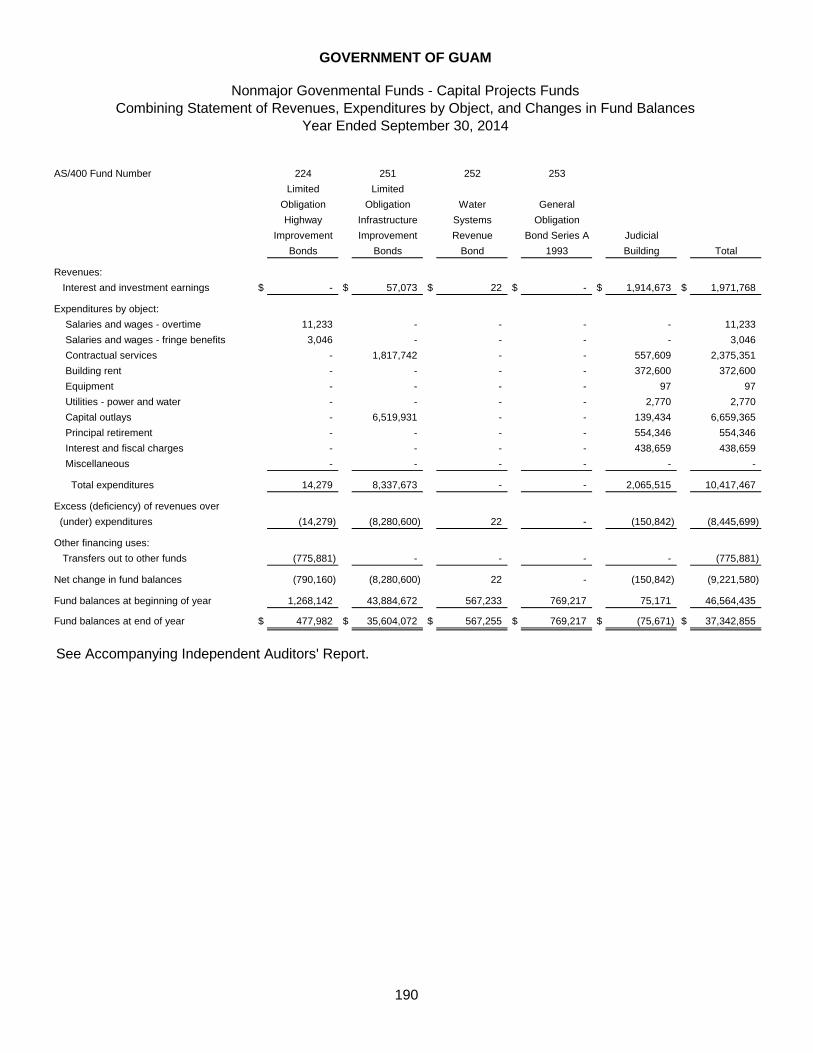

Nonmajor Governmental Funds – Capital Projects Funds Narrative ...................................................................................................................................................................................... 187 Combining Balance Sheet ...................................................................................................................................................... 188 Combining Statement of Revenue, Expenditures by Function, and Changes in Fund Balances ........................................................................................................................................................................................ 189 Combining Schedule of Revenue, Expenditures by Object, and Changes in Fund Balances ...................... 190

Nonmajor Governmental Funds – Debt Service Funds Narrative ...................................................................................................................................................................................... 191

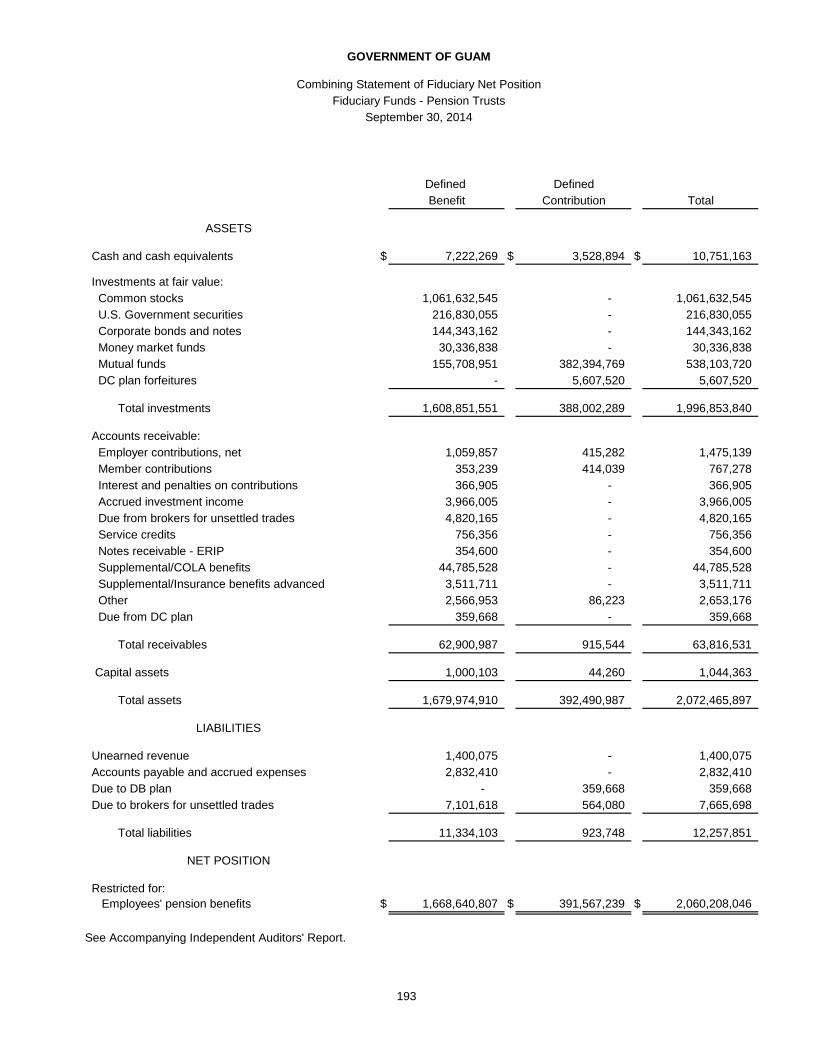

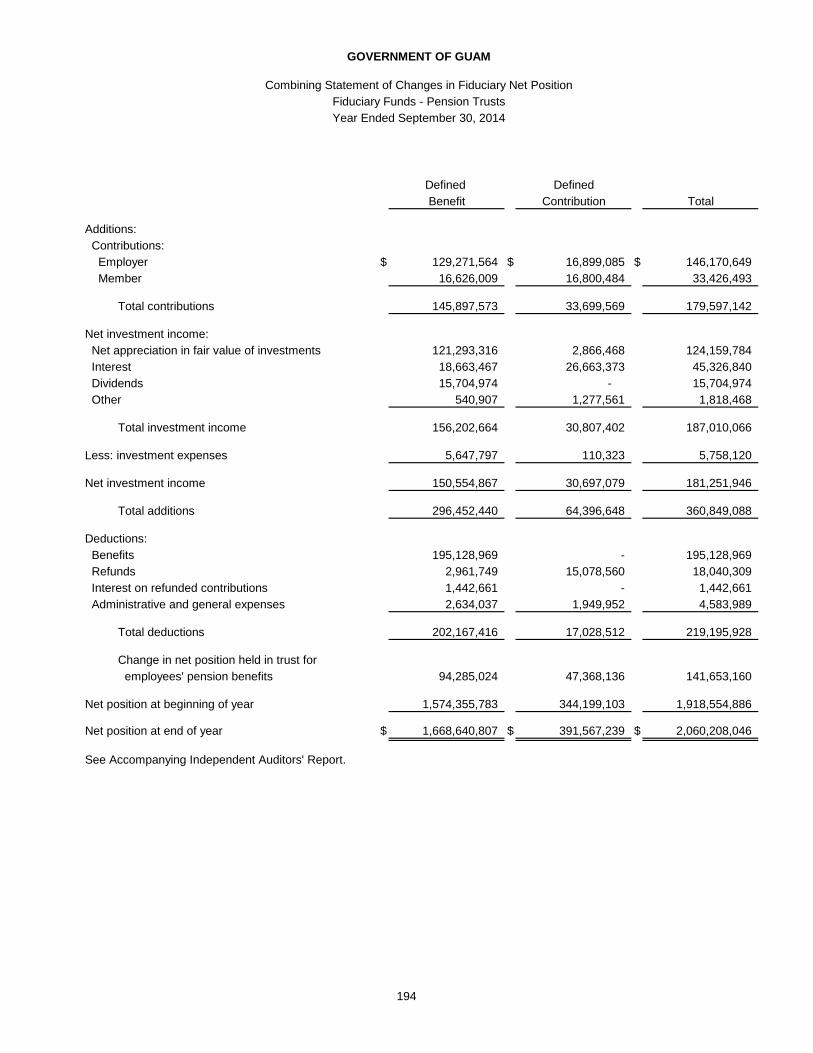

Fiduciary Funds – Pension Trusts Narrative ...................................................................................................................................................................................... 192 Combining Statement of Fiduciary Net Assets ............................................................................................................. 193 Combining Statement of Changes in Fiduciary Net Assets ..................................................................................... 194

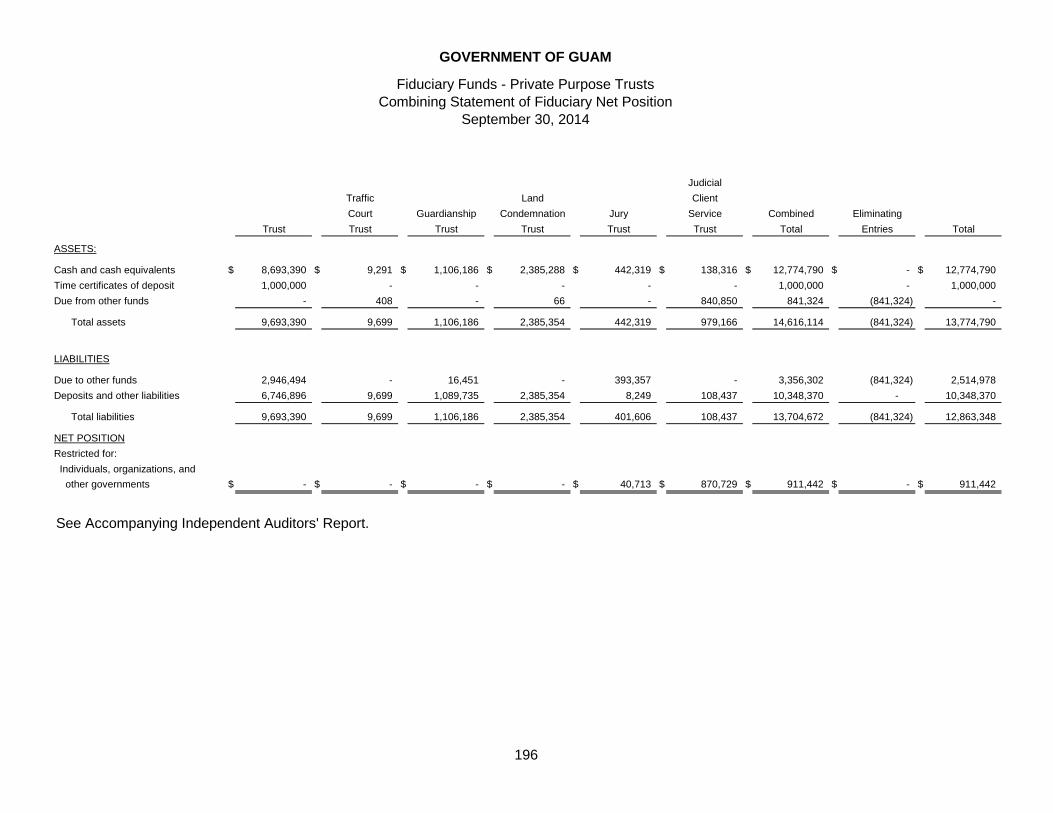

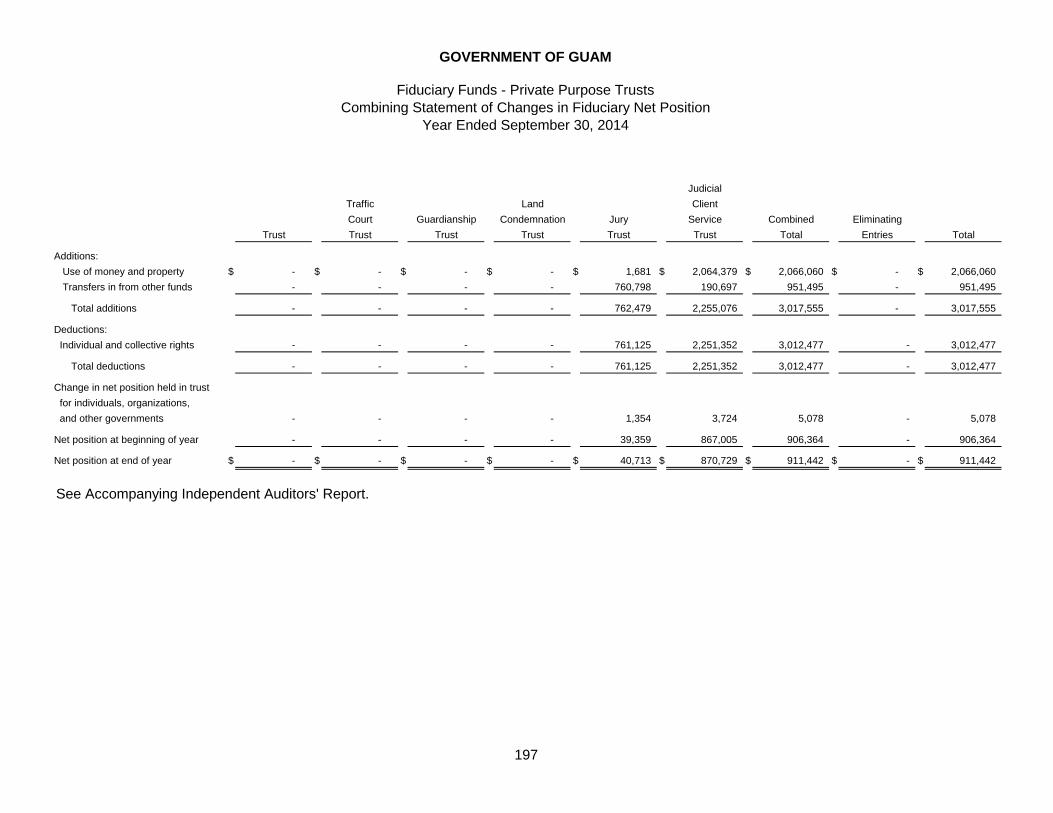

Fiduciary Funds – Private Purpose Trusts Narrative ...................................................................................................................................................................................... 195 Combining Statement of Fiduciary Net Assets ............................................................................................................. 196 Combining Statement of Changes in Fiduciary Net Assets ...................................................................................... 197

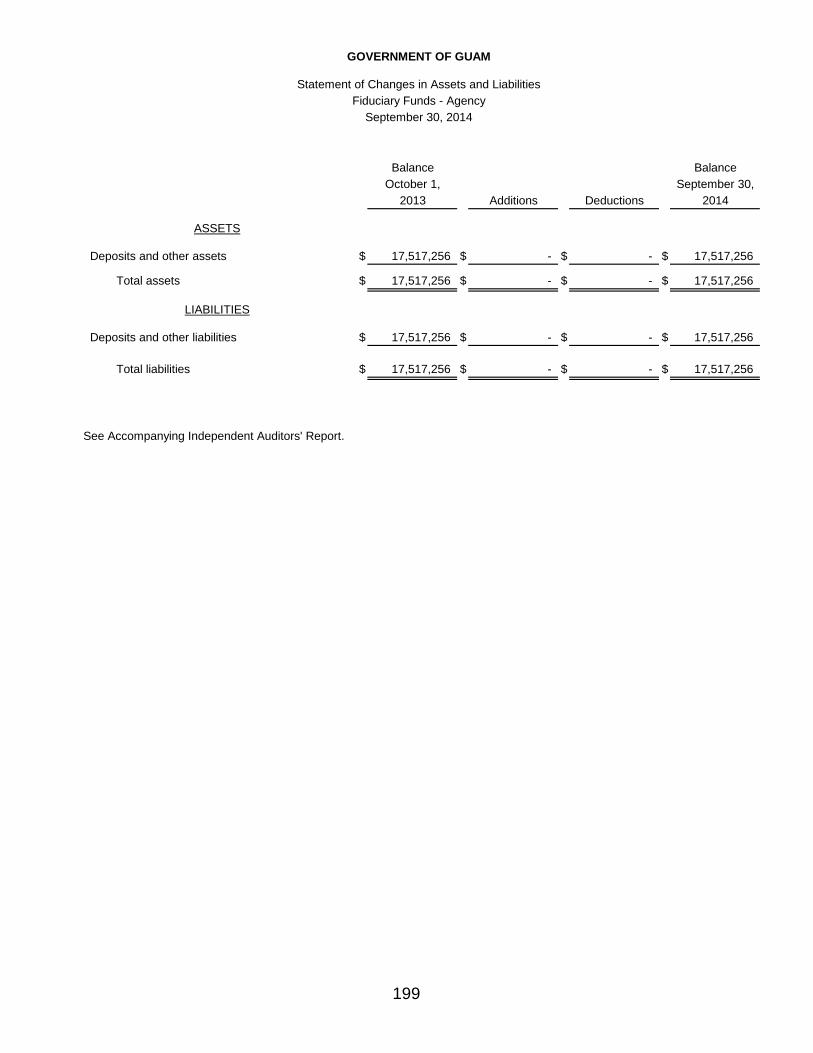

Fiduciary Funds – Agency Narrative ...................................................................................................................................................................................... 198 Statement of Changes in Assets and Liabilities ............................................................................................................ 199

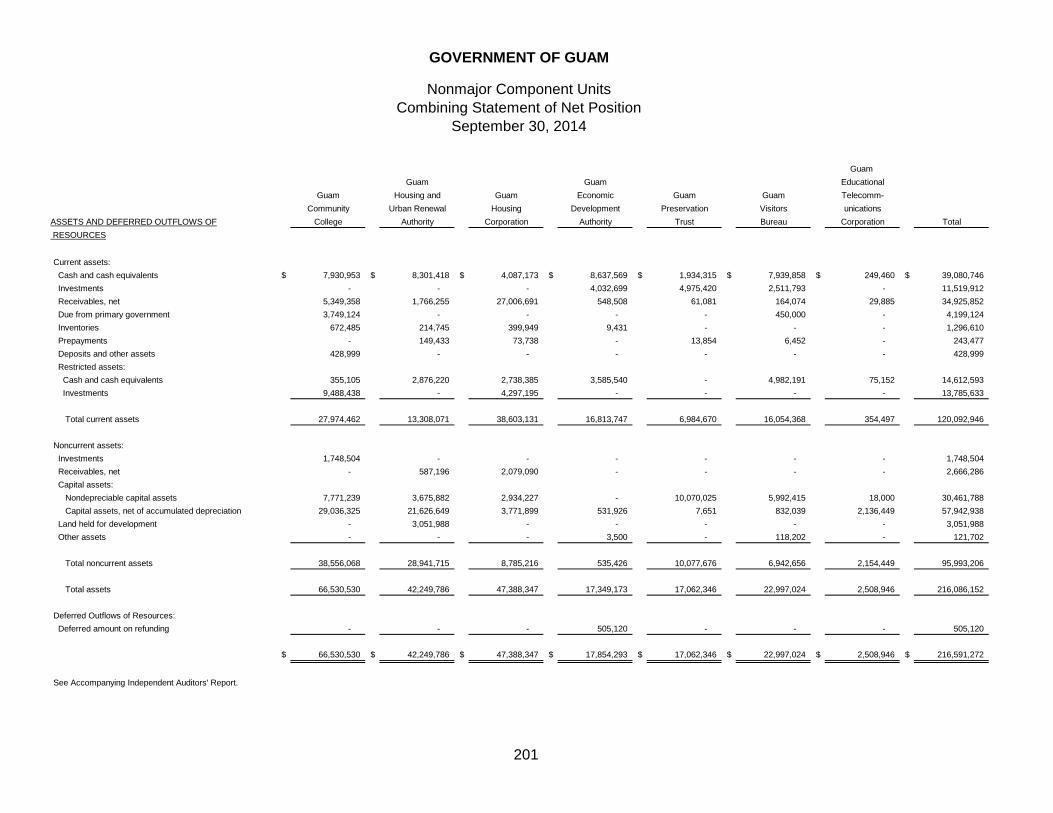

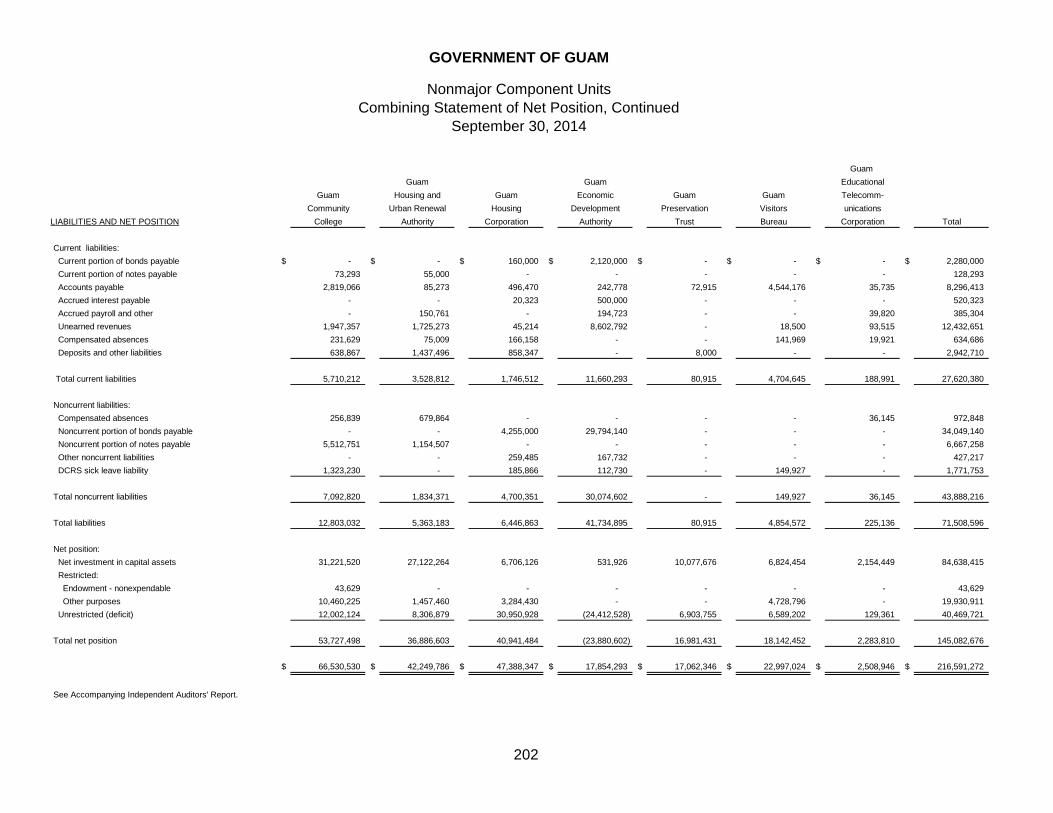

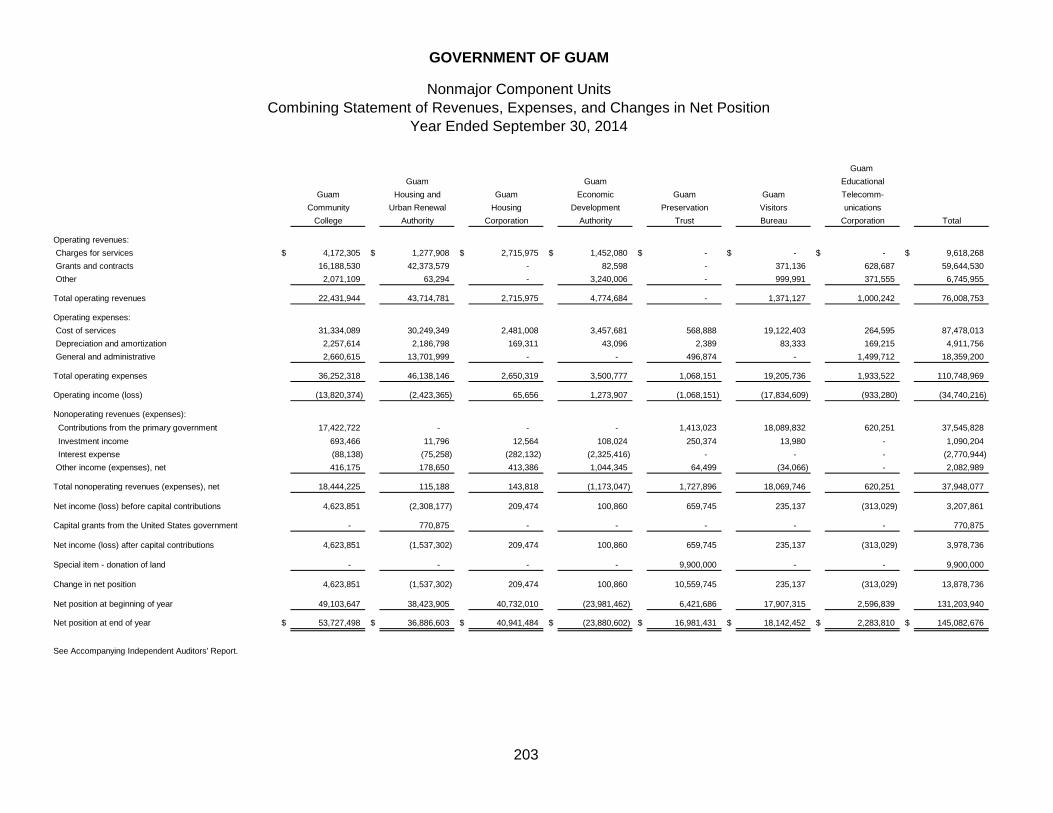

Nonmajor Component Units Narrative ...................................................................................................................................................................................... 200 Combining Statement of Net Assets (Deficiency) ....................................................................................................... 201 Combining Statement of Changes in Net Assets (Deficiency) ................................................................................ 203

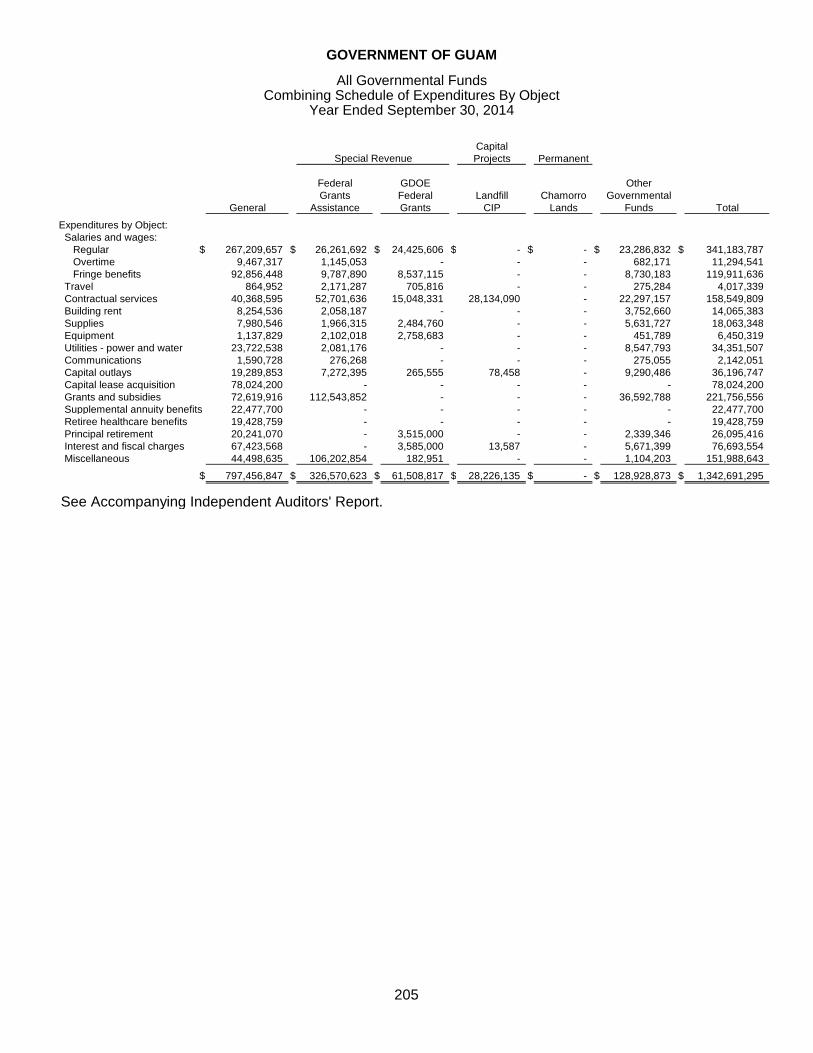

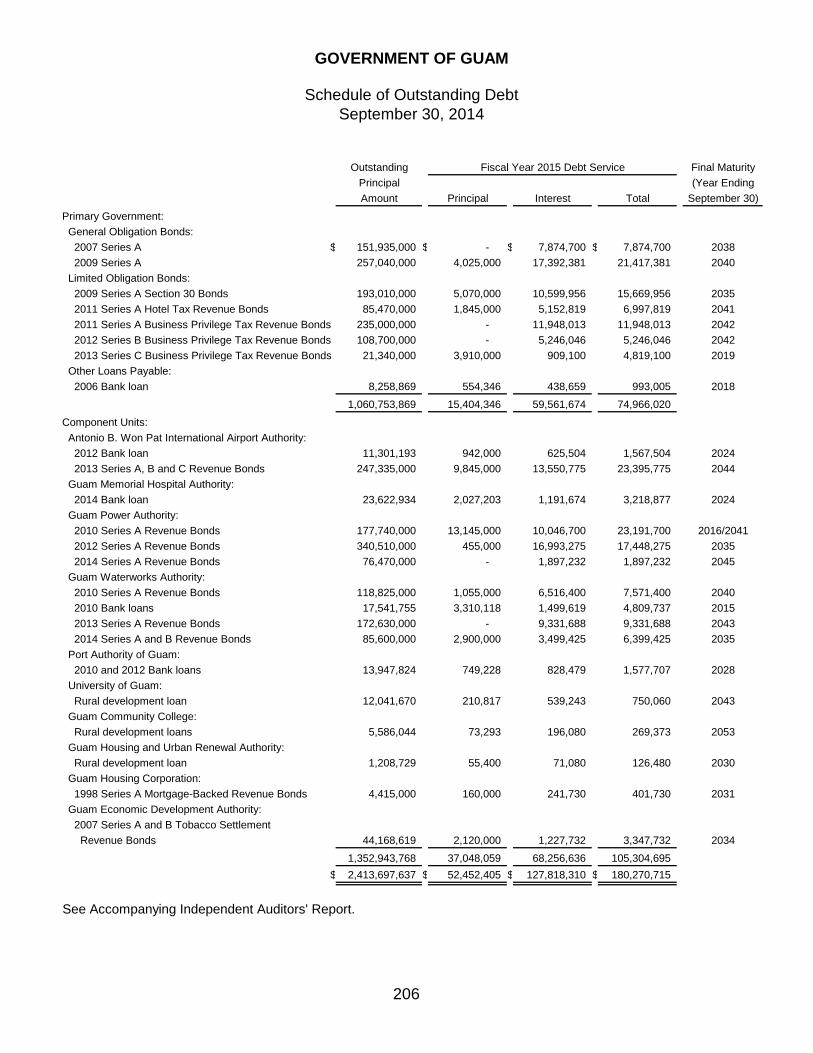

Other Information Narrative ...................................................................................................................................................................................... 204 Combining Schedule of Expenditures By Object – All Governmental Funds ................................................... 205 Schedule of Outstanding Debt – Primary Government and Component Units ............................................... 206

STATISTICAL SECTION

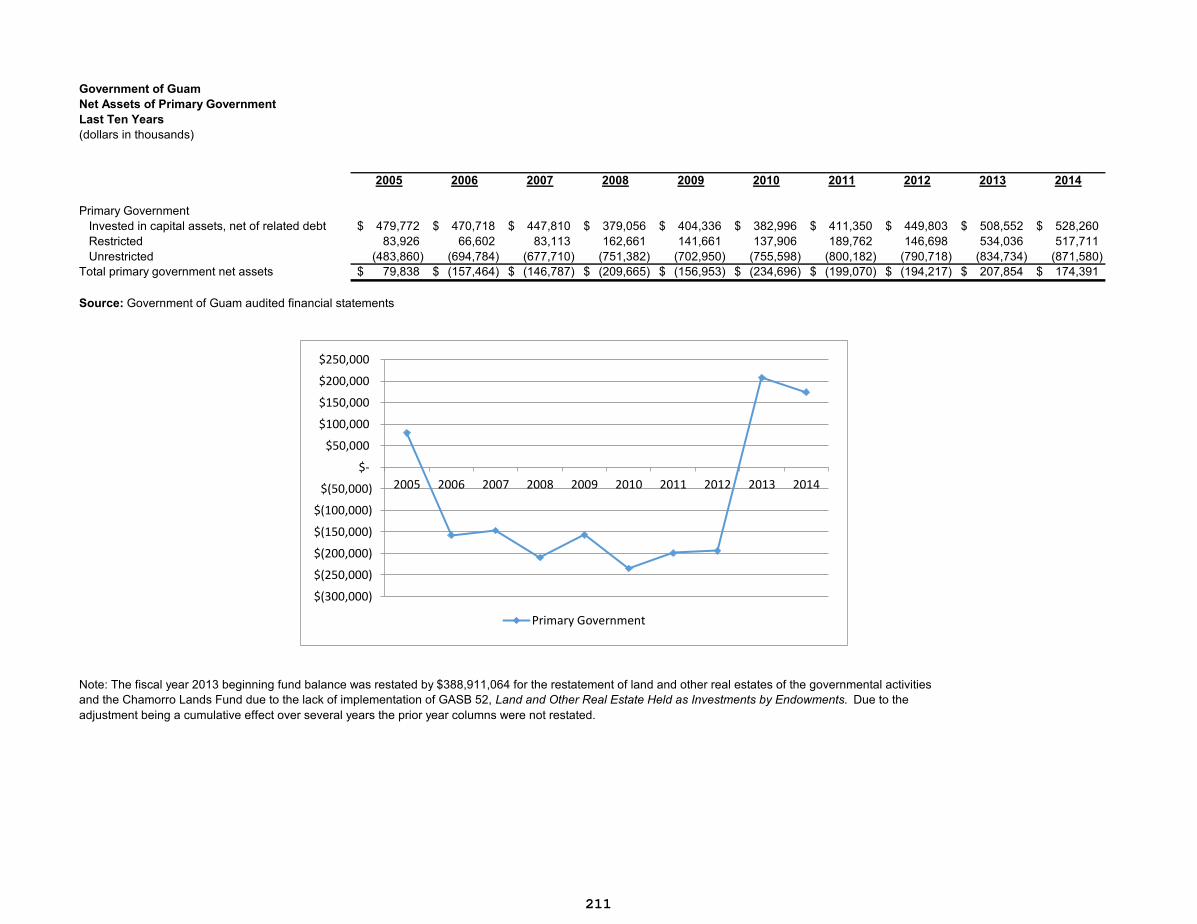

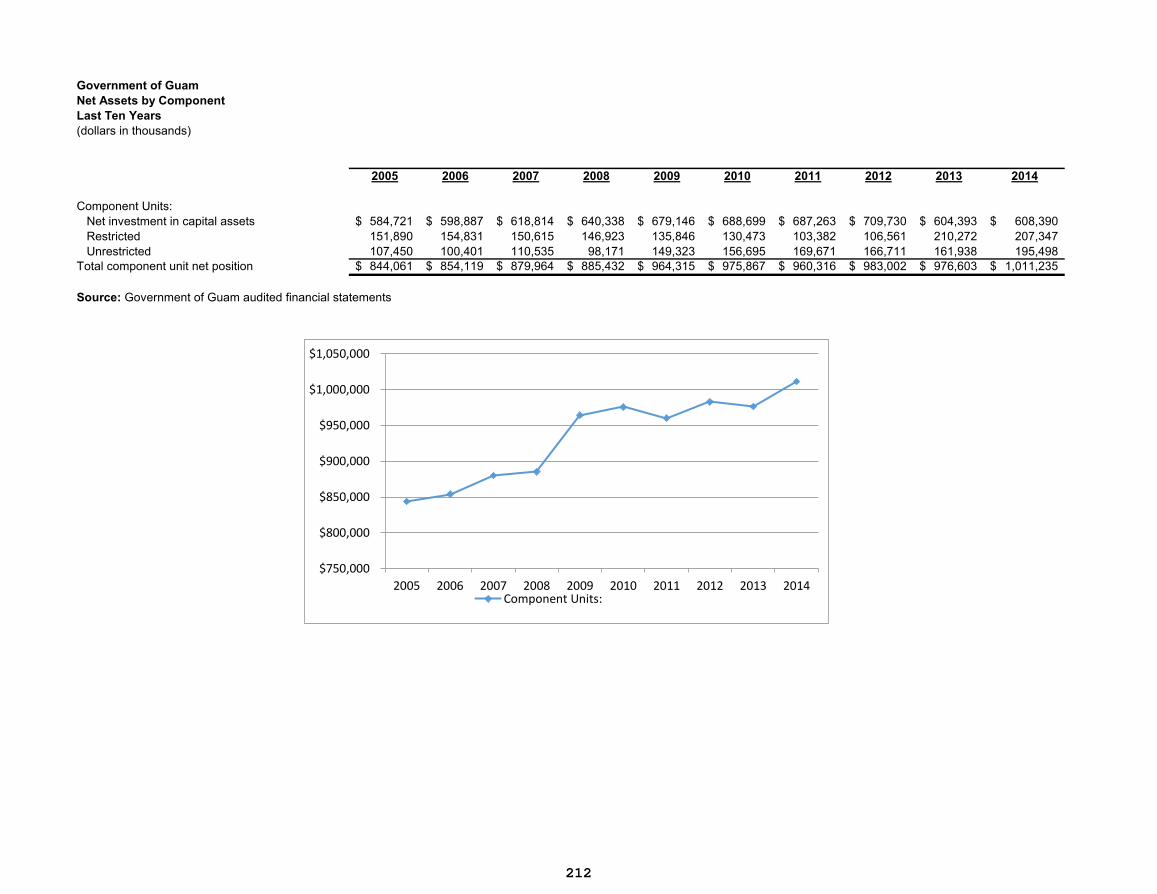

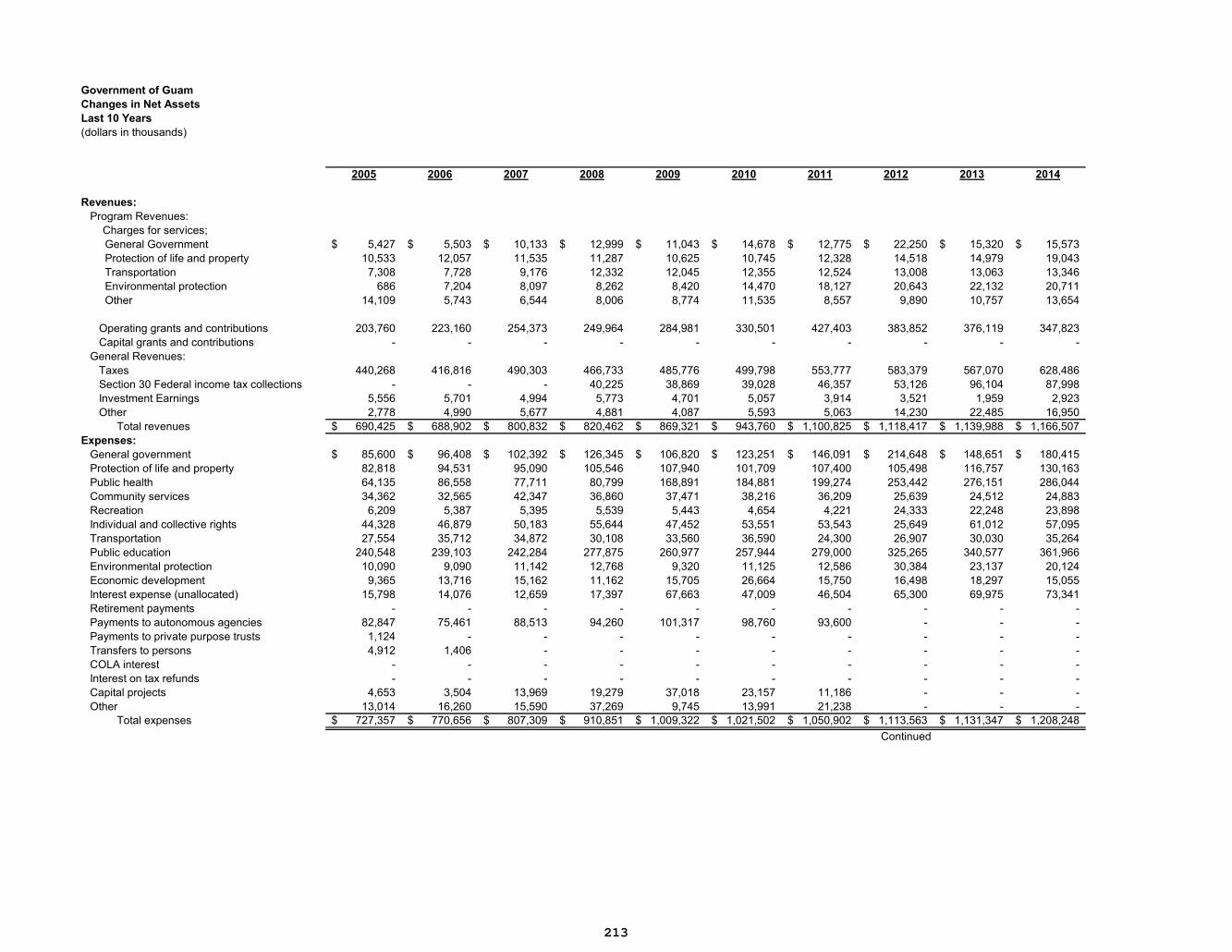

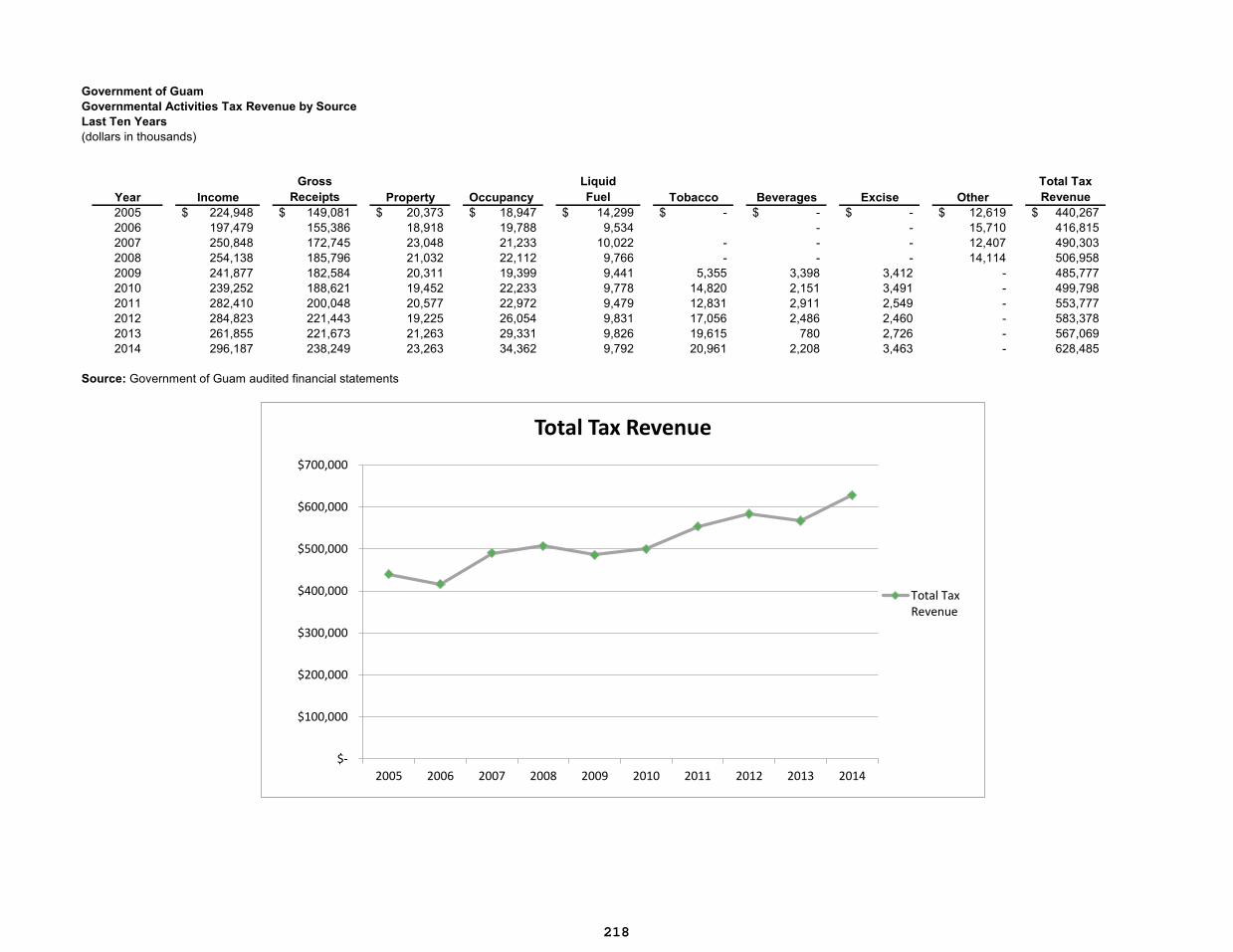

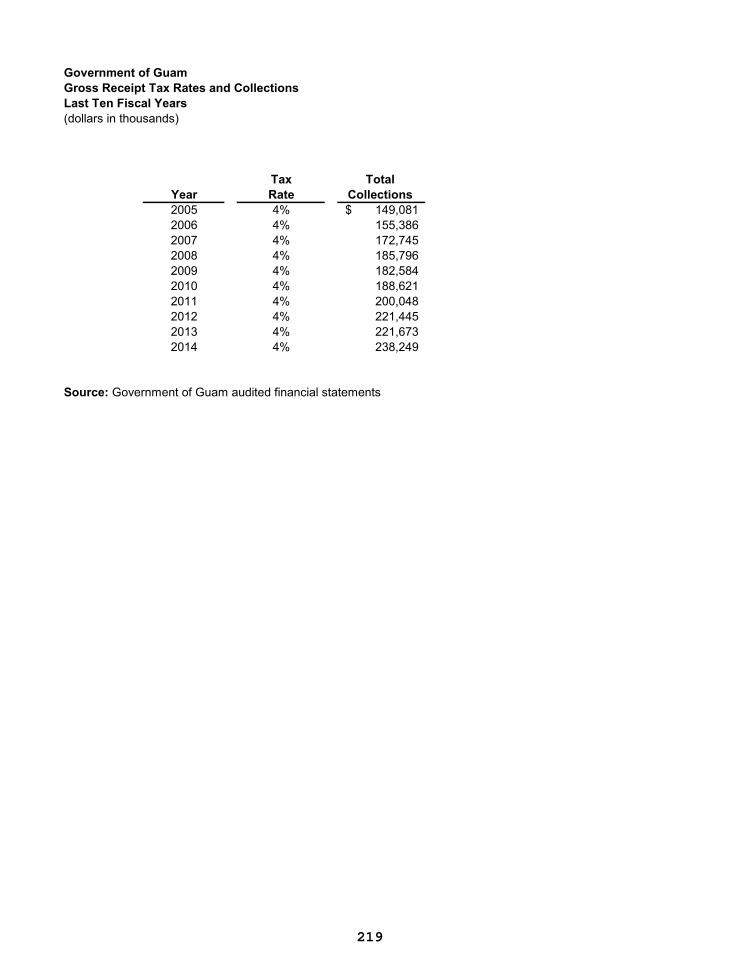

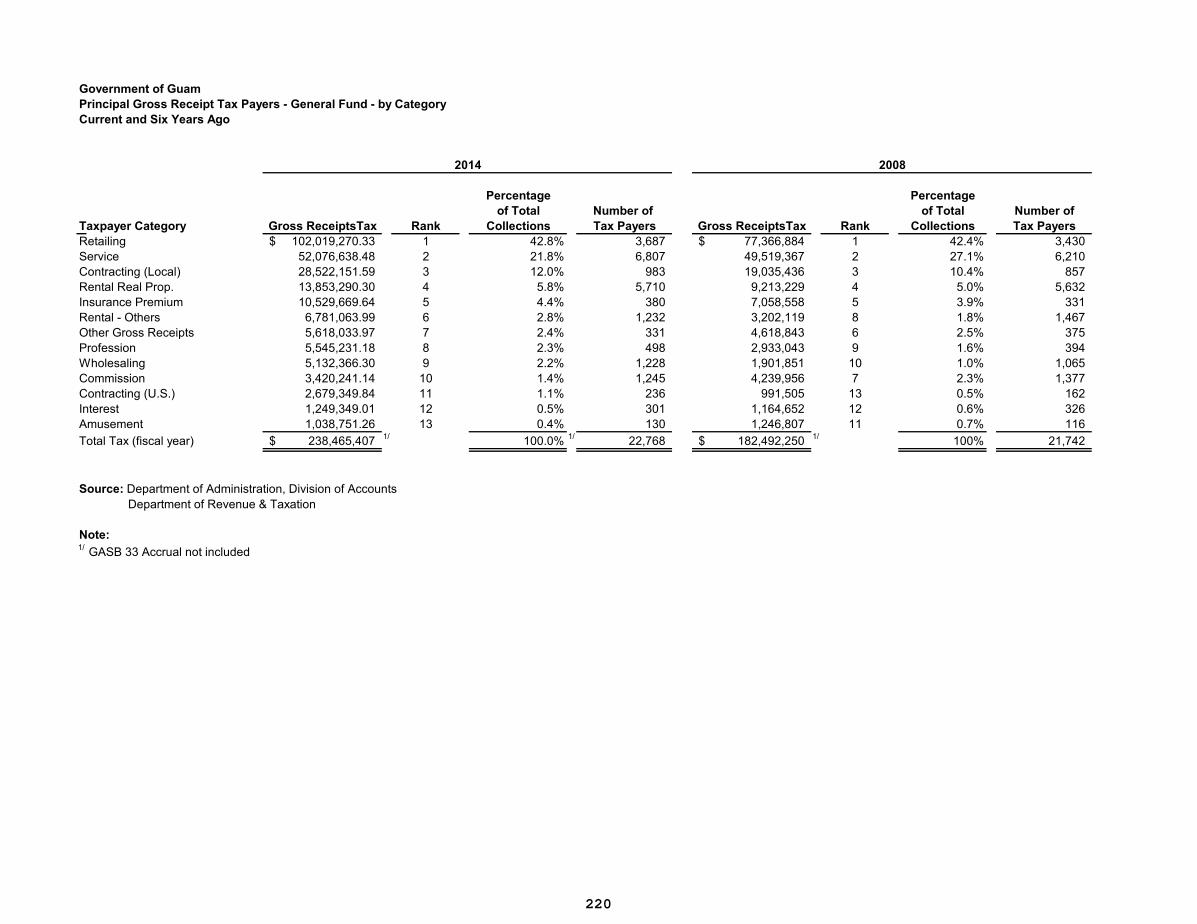

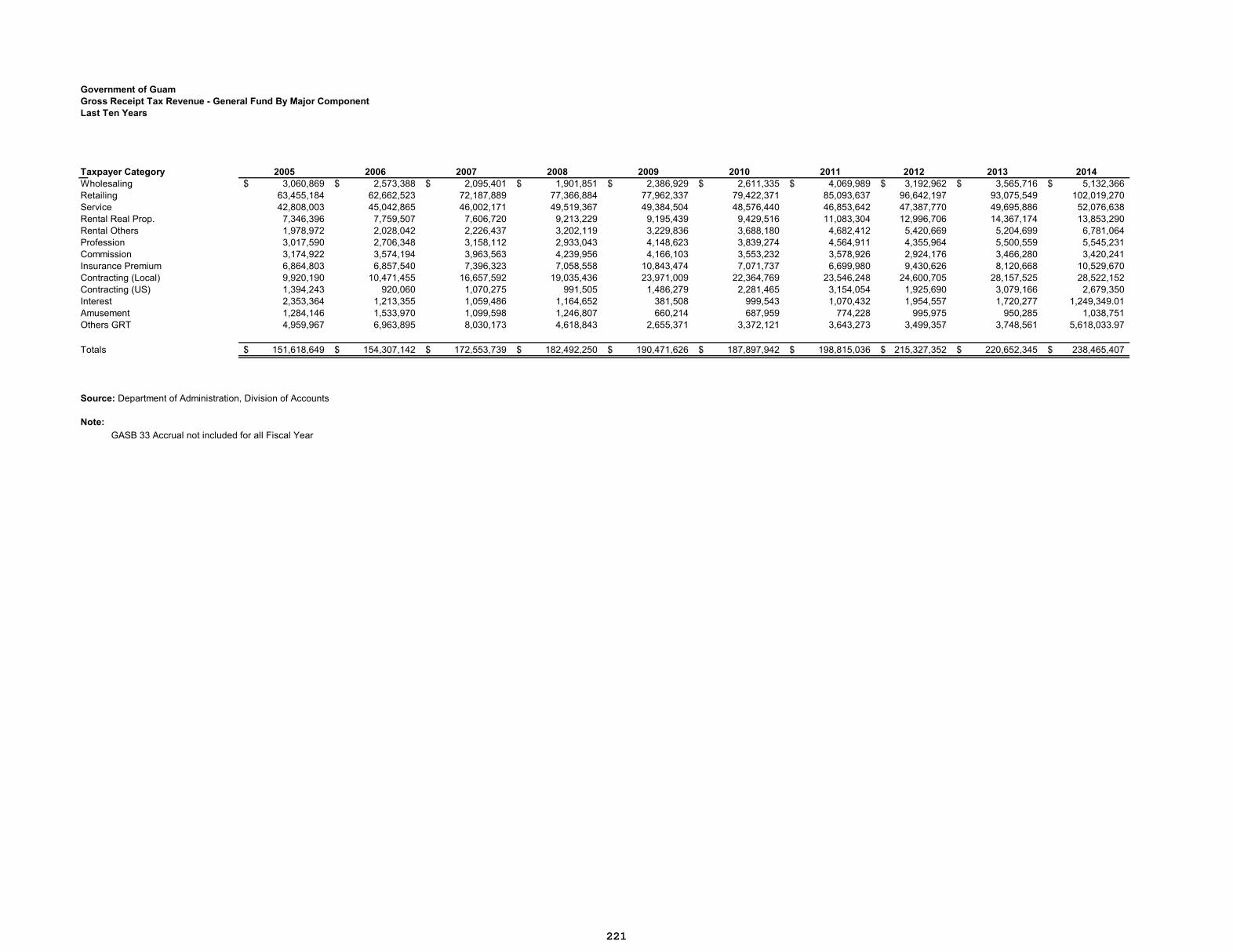

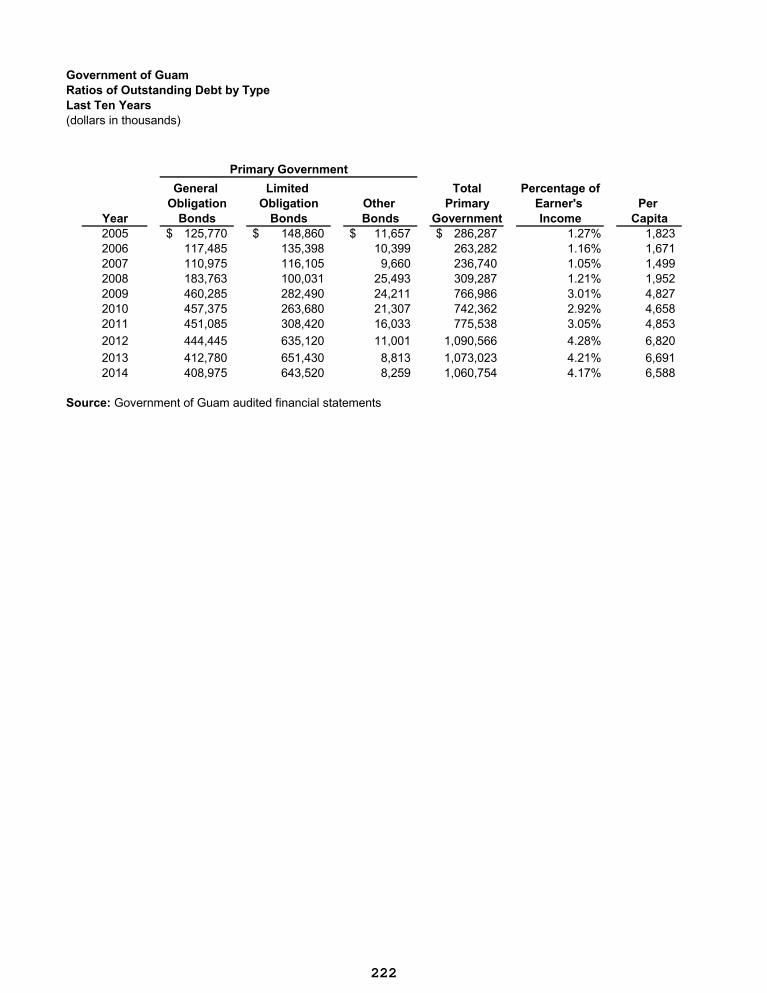

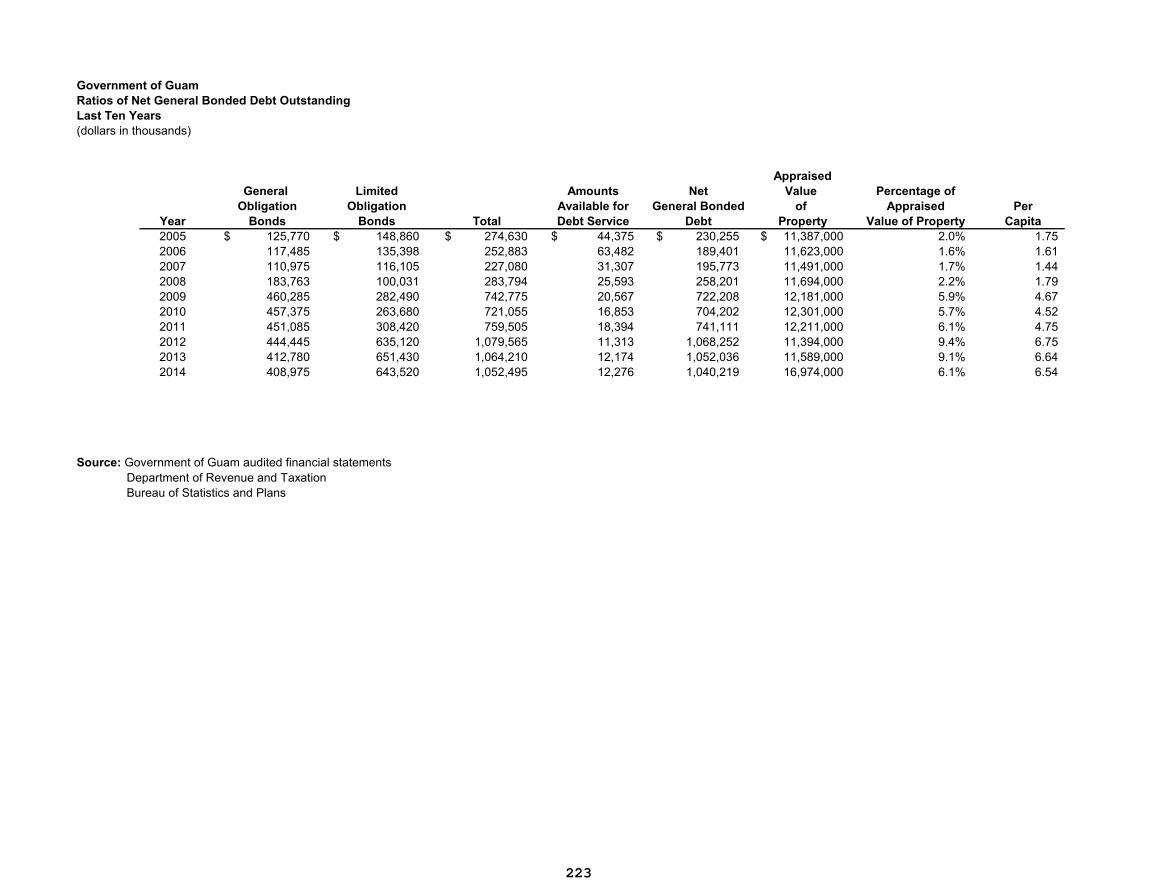

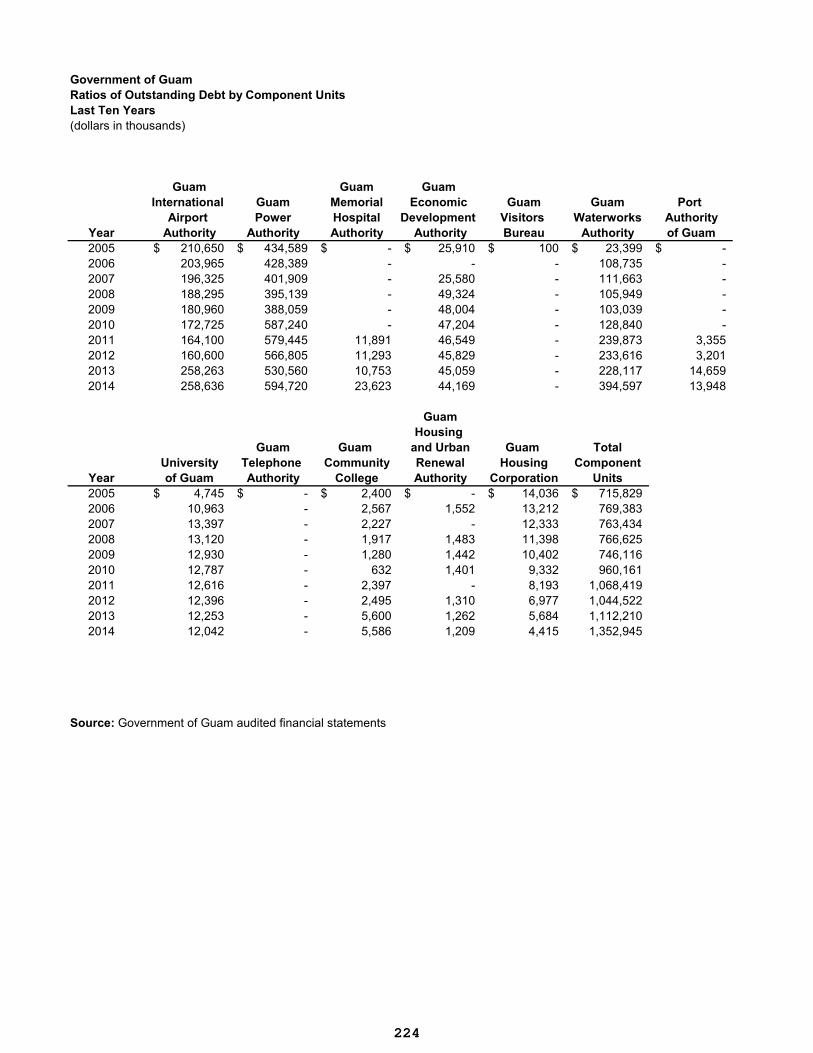

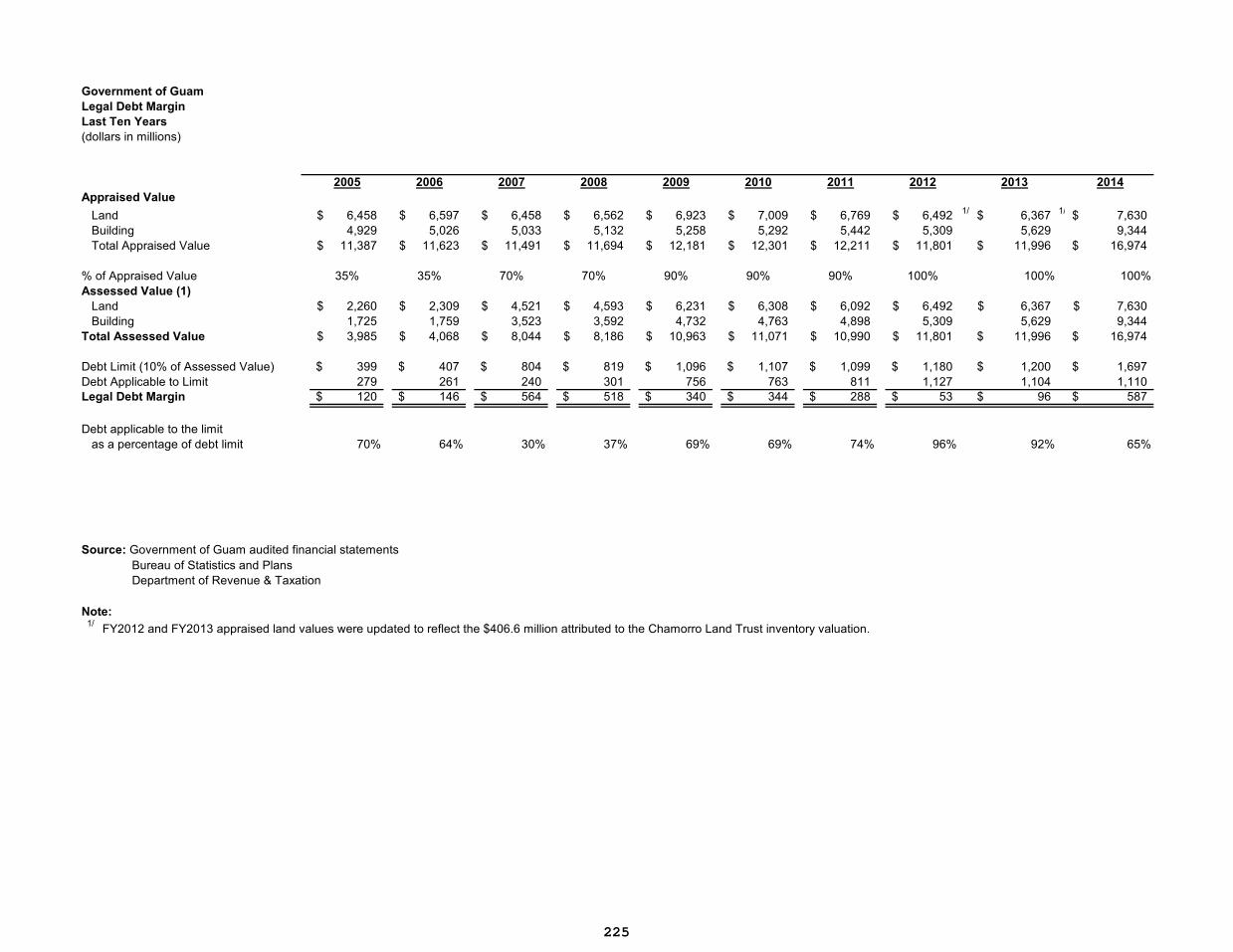

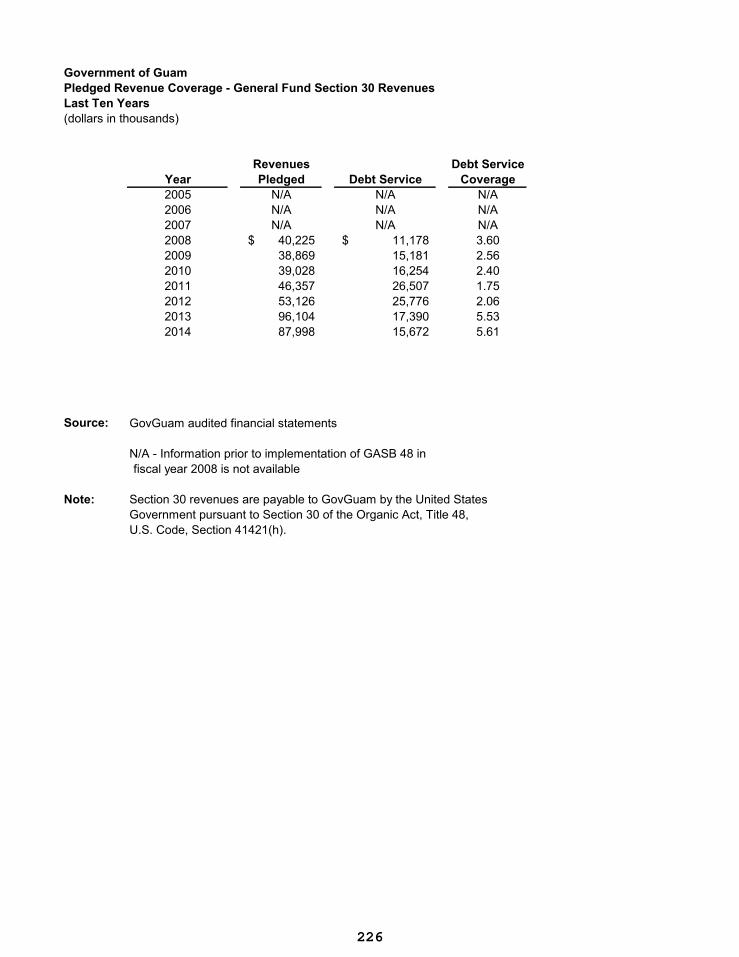

Net Assets of Primary Government................................................................................................................................................. 211 Net Assets by Component ................................................................................................................................................................... 212 Changes in Net Assets ........................................................................................................................................................................... 213 Fund Balances of Governmental Funds ......................................................................................................................................... 215 Changes in Fund Balances of Governmental Funds ................................................................................................................. 216 Governmental Activities Tax Revenue by Source ..................................................................................................................... 218 Property Tax Levies and Collections .............................................................................................................................................. 219 Principal Gross Receipt Tax Payers – General Fund – by Category ................................................................................... 220 Gross Receipt Tax Revenue – General Fund by Major Component .................................................................................... 221 Ratios of Outstanding Debt by Type ............................................................................................................................................... 222 Ratios of Net General Bonded Debt Outstanding ...................................................................................................................... 223 Ratio of Outstanding Debt by Component Units ........................................................................................................................ 224 Legal Debt Margin .................................................................................................................................................................................. 225 Pledged Revenue Coverage – General Fund Section 30 Revenues .................................................................................... 226

2014 Table of Contents

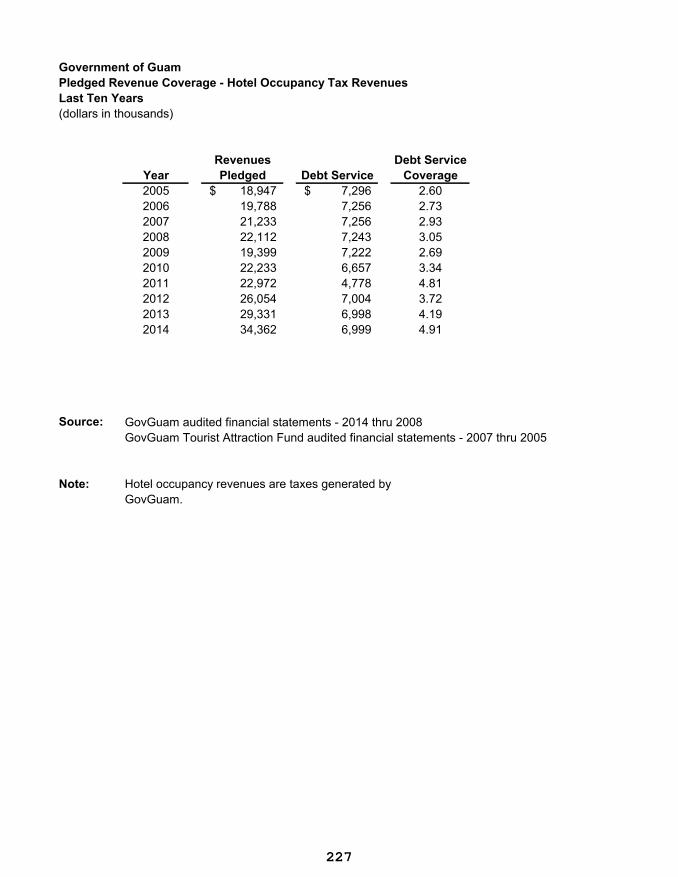

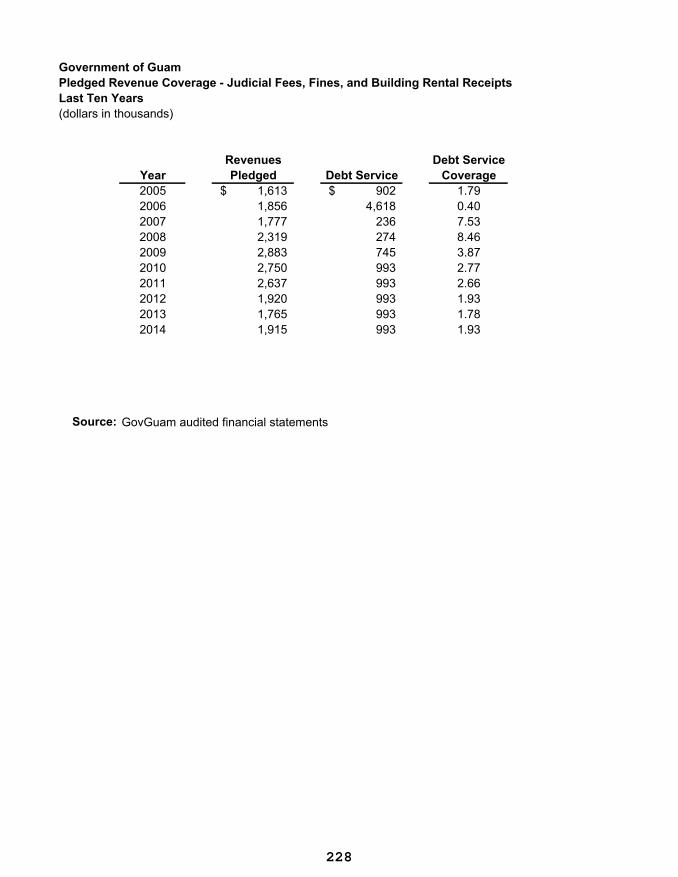

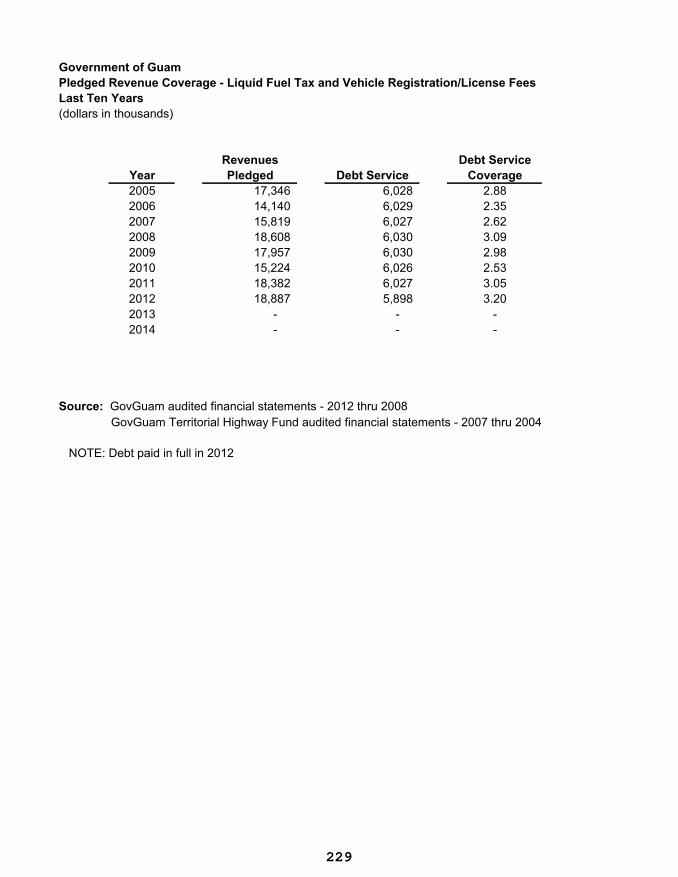

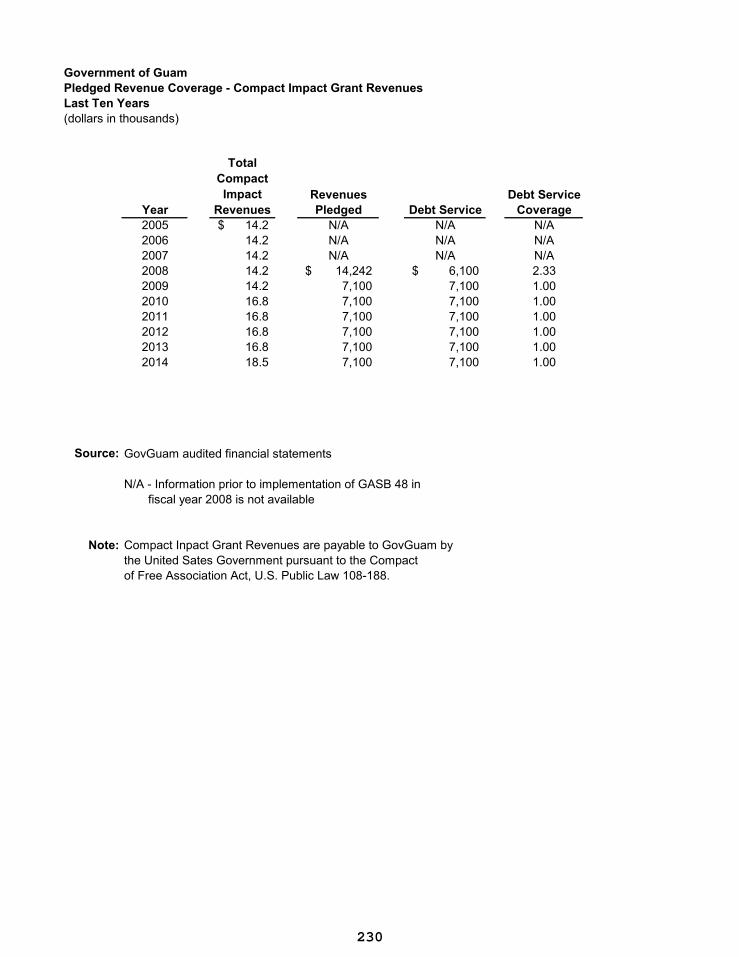

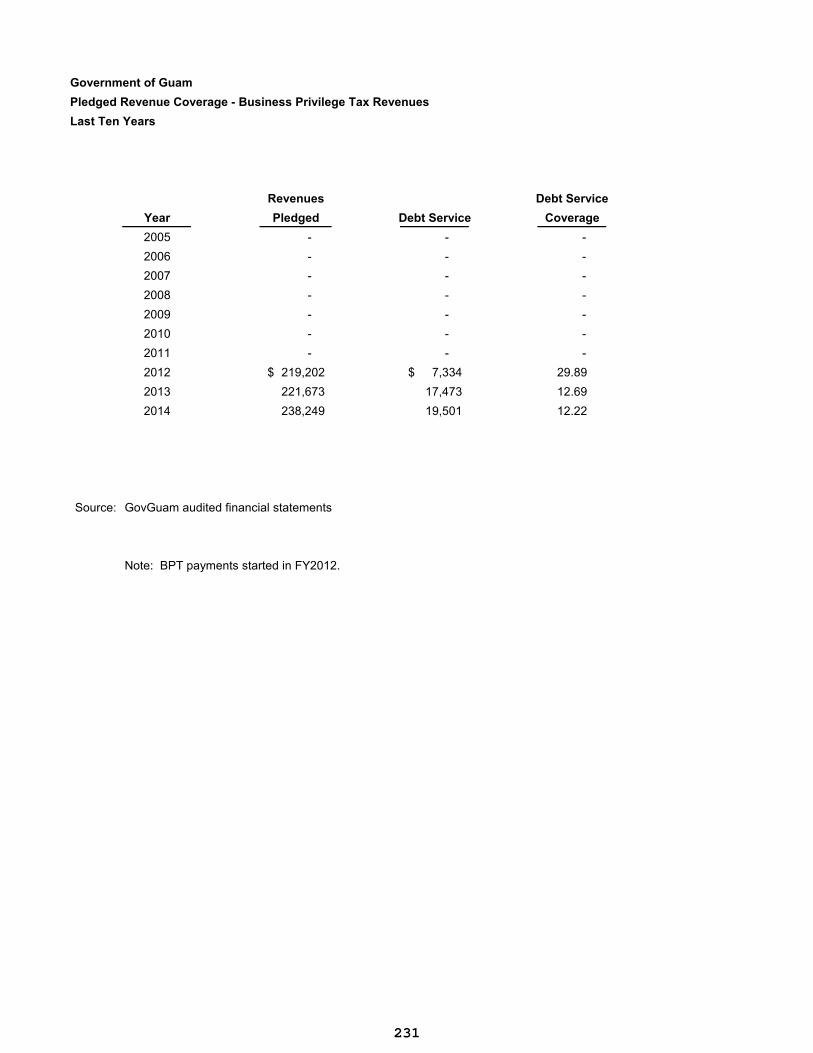

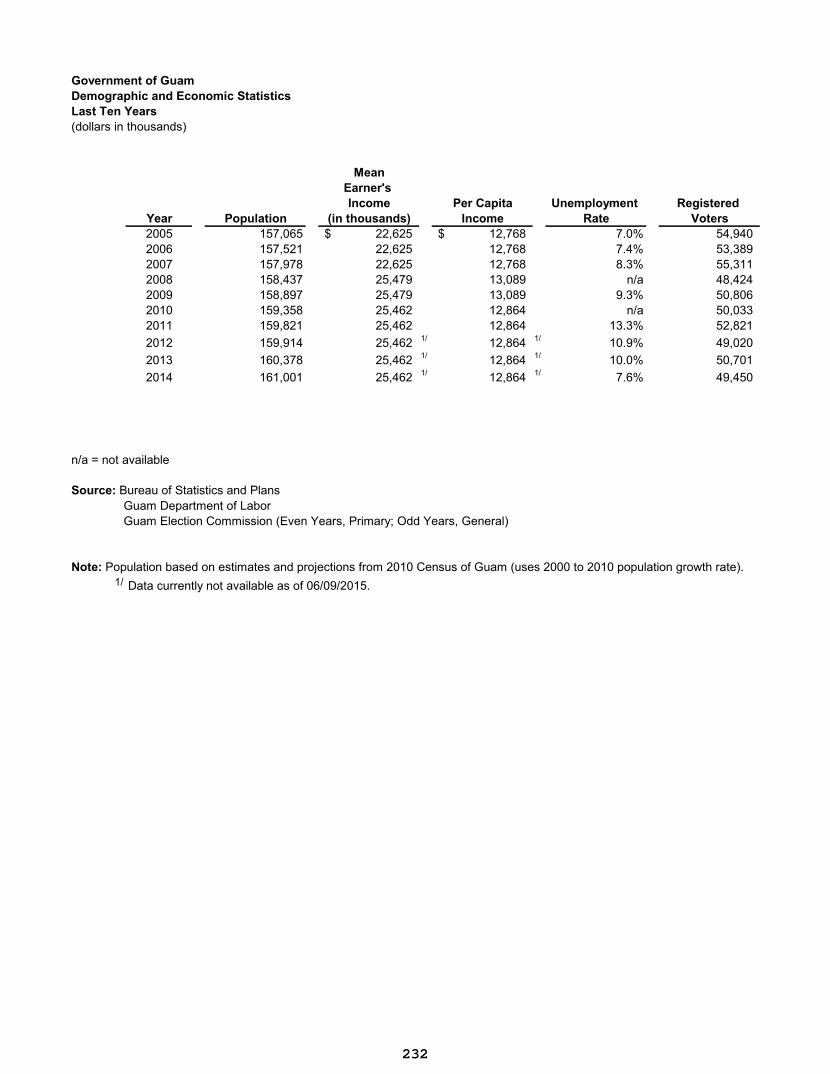

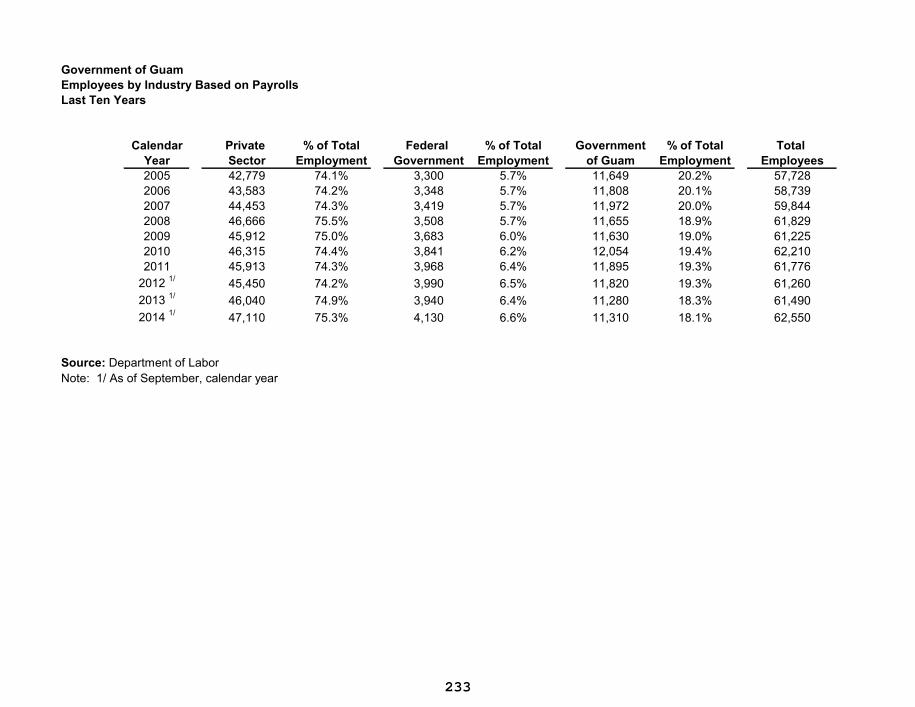

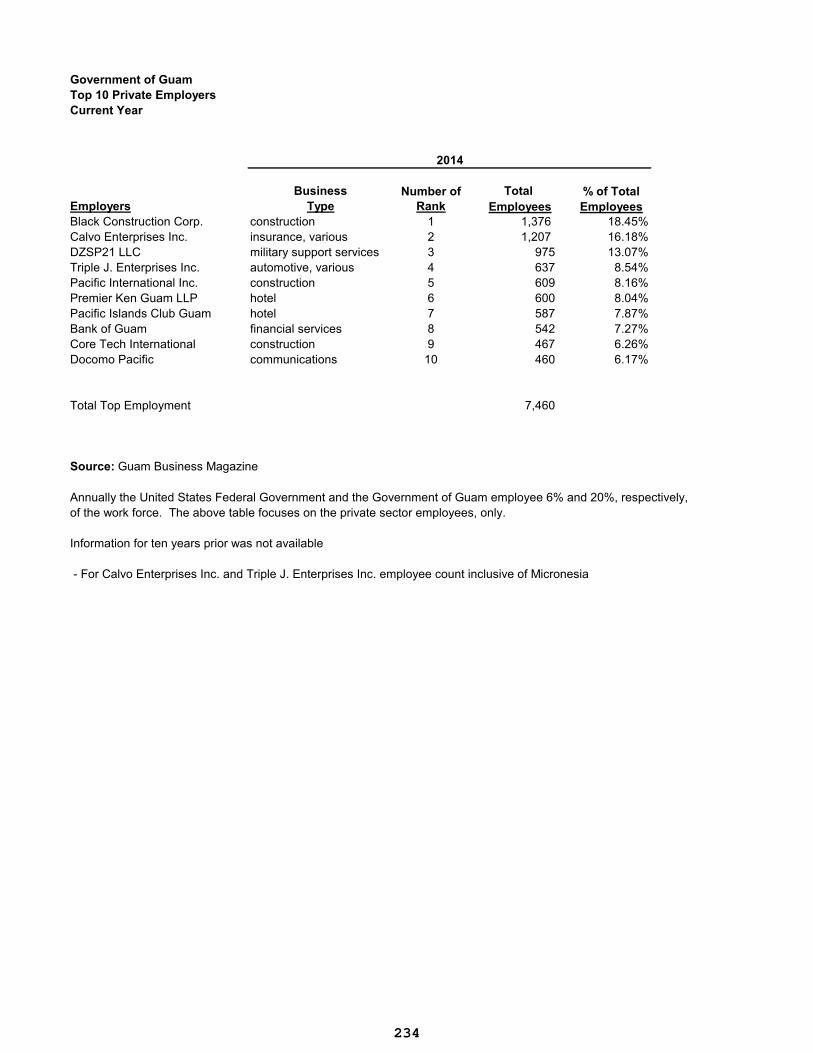

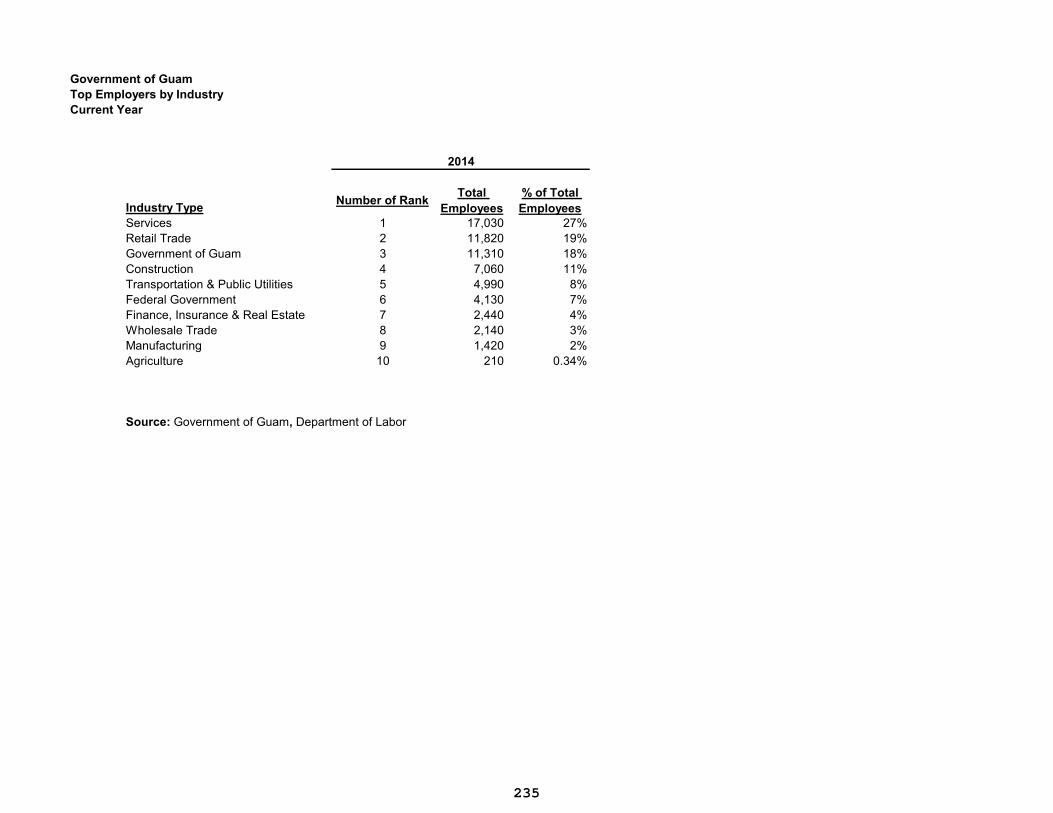

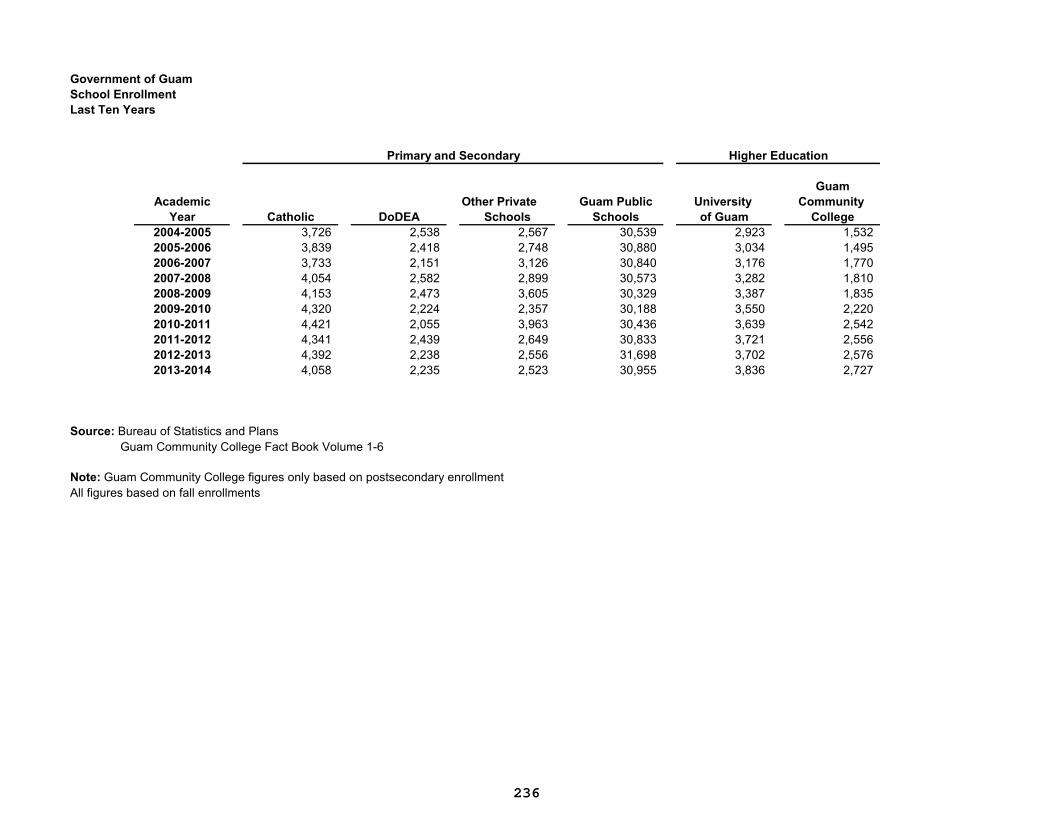

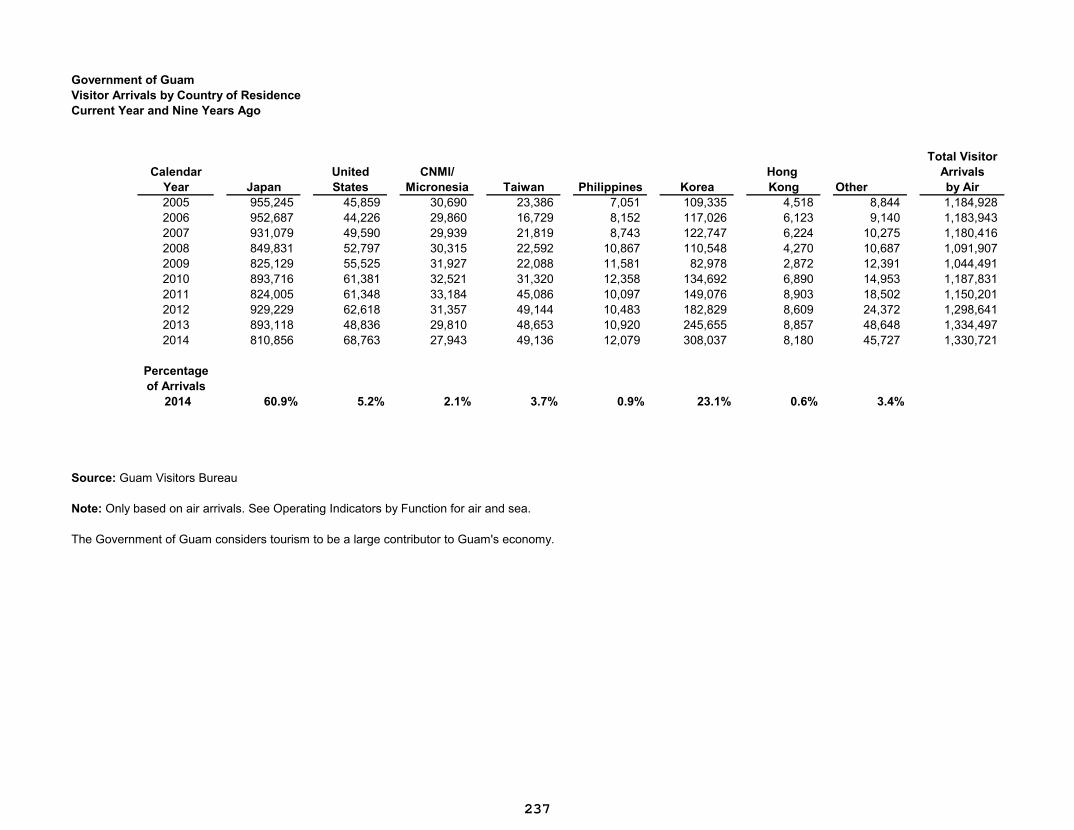

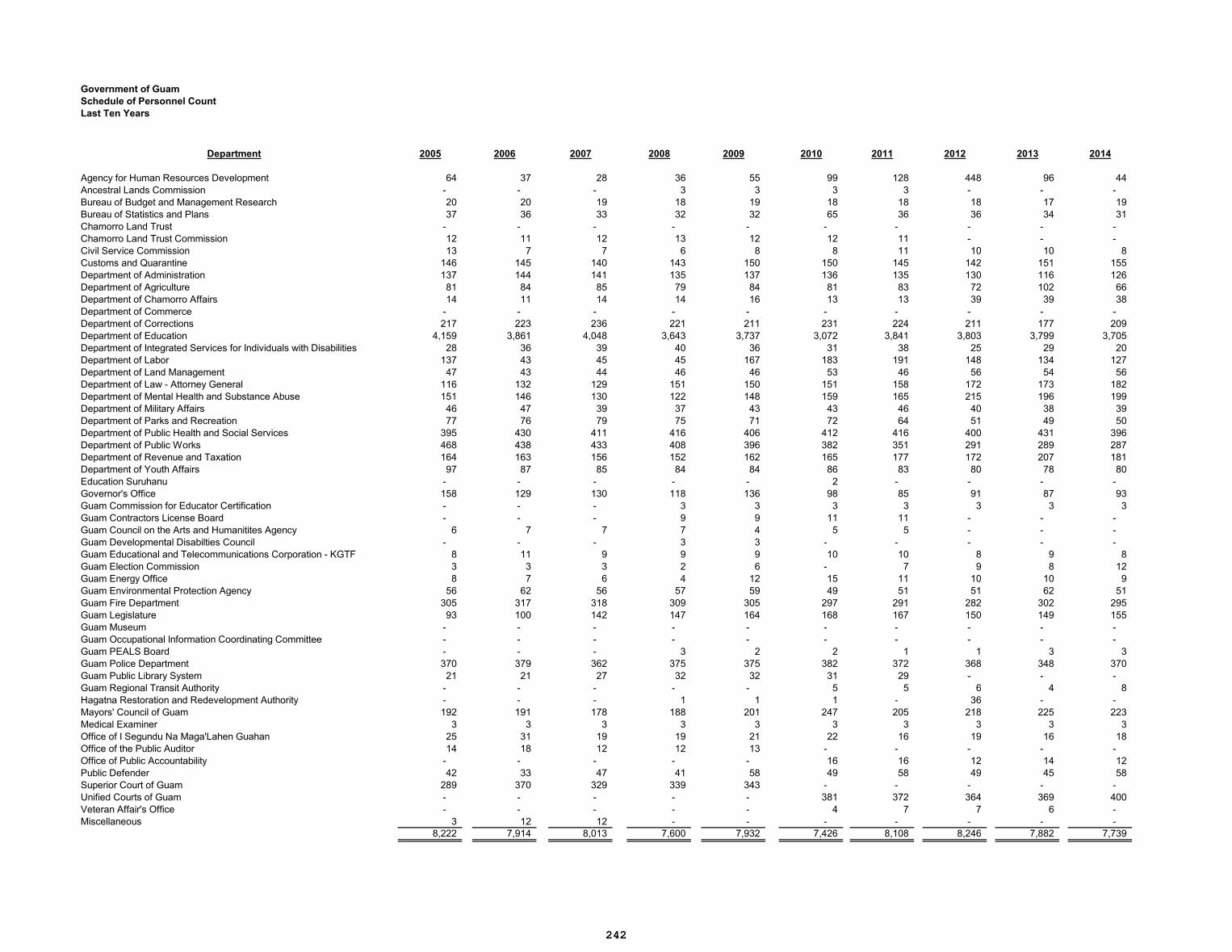

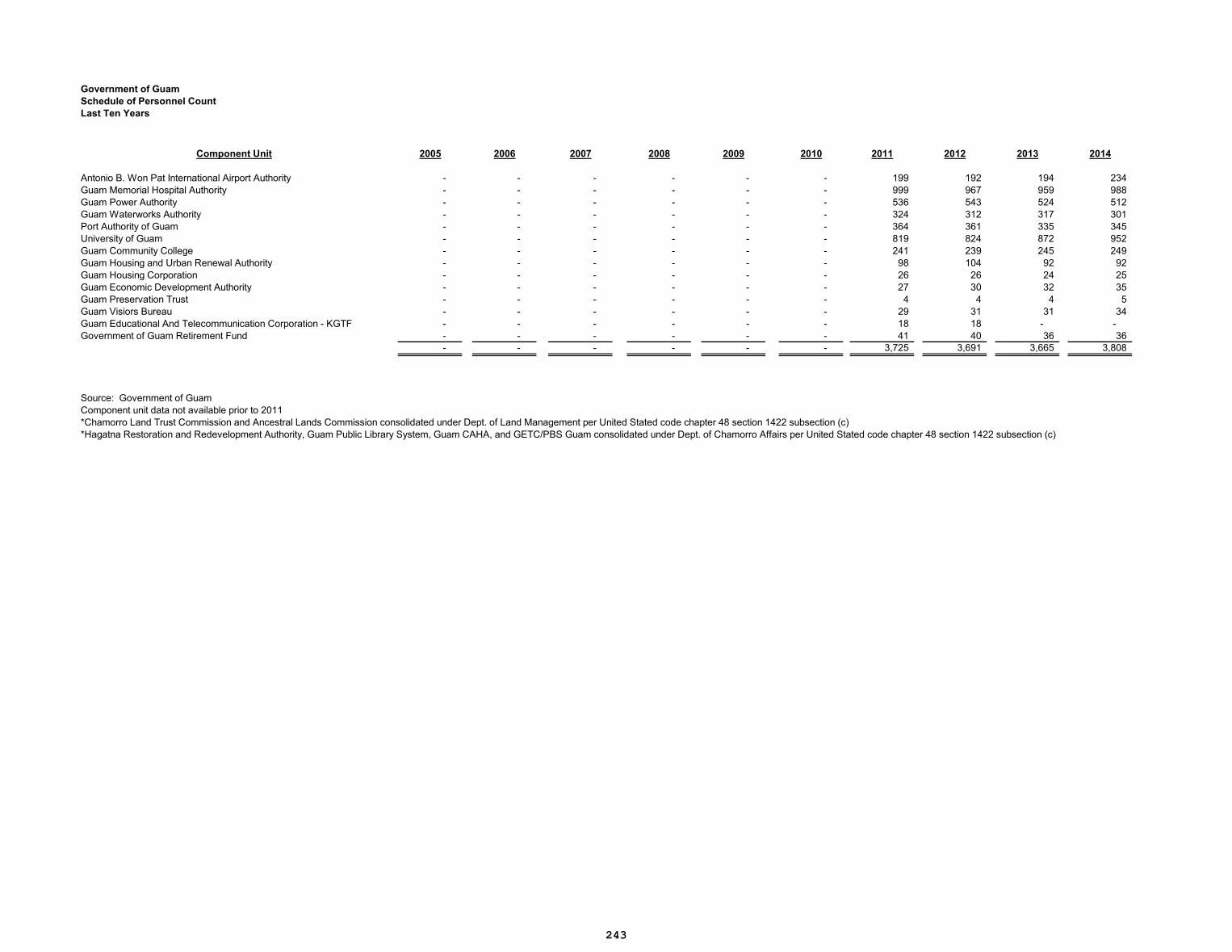

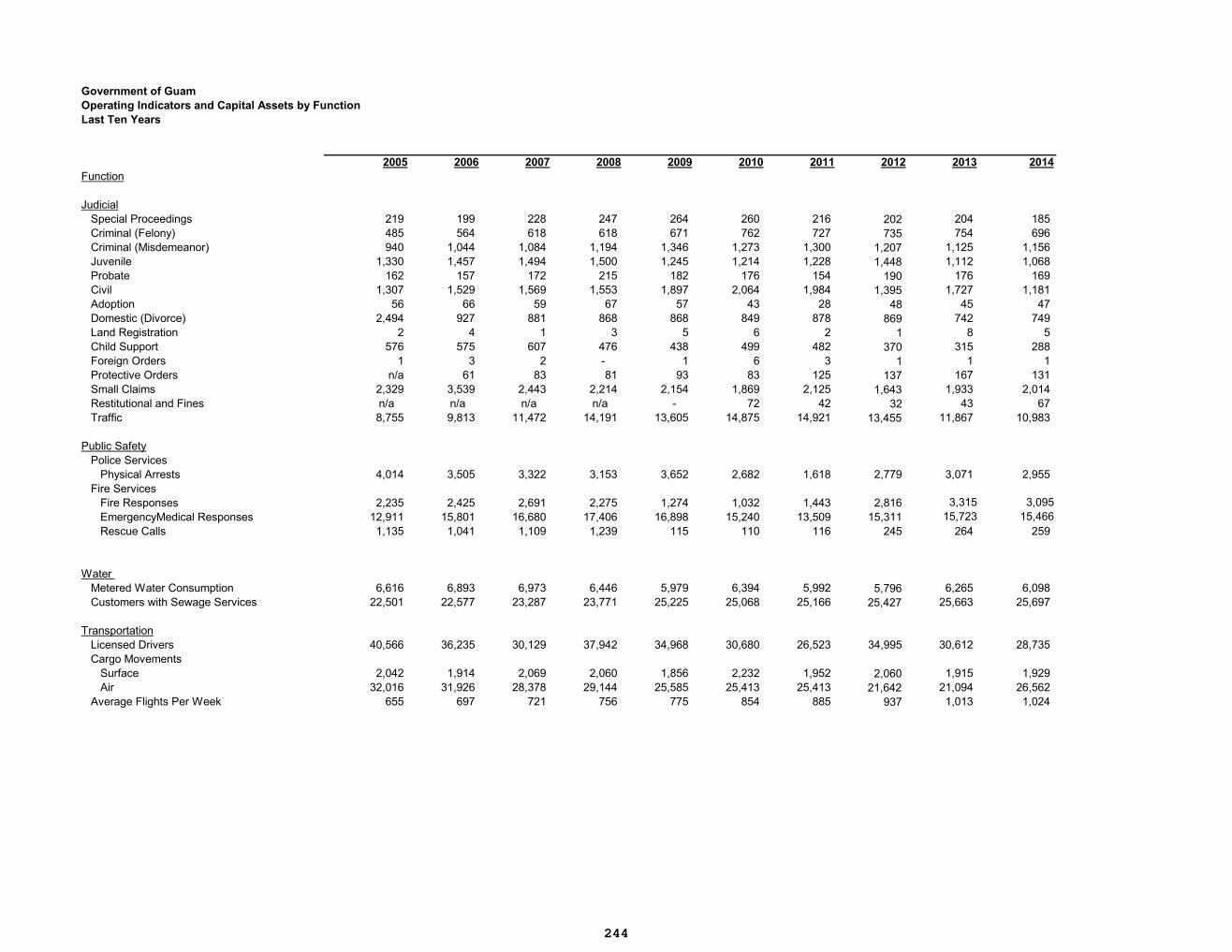

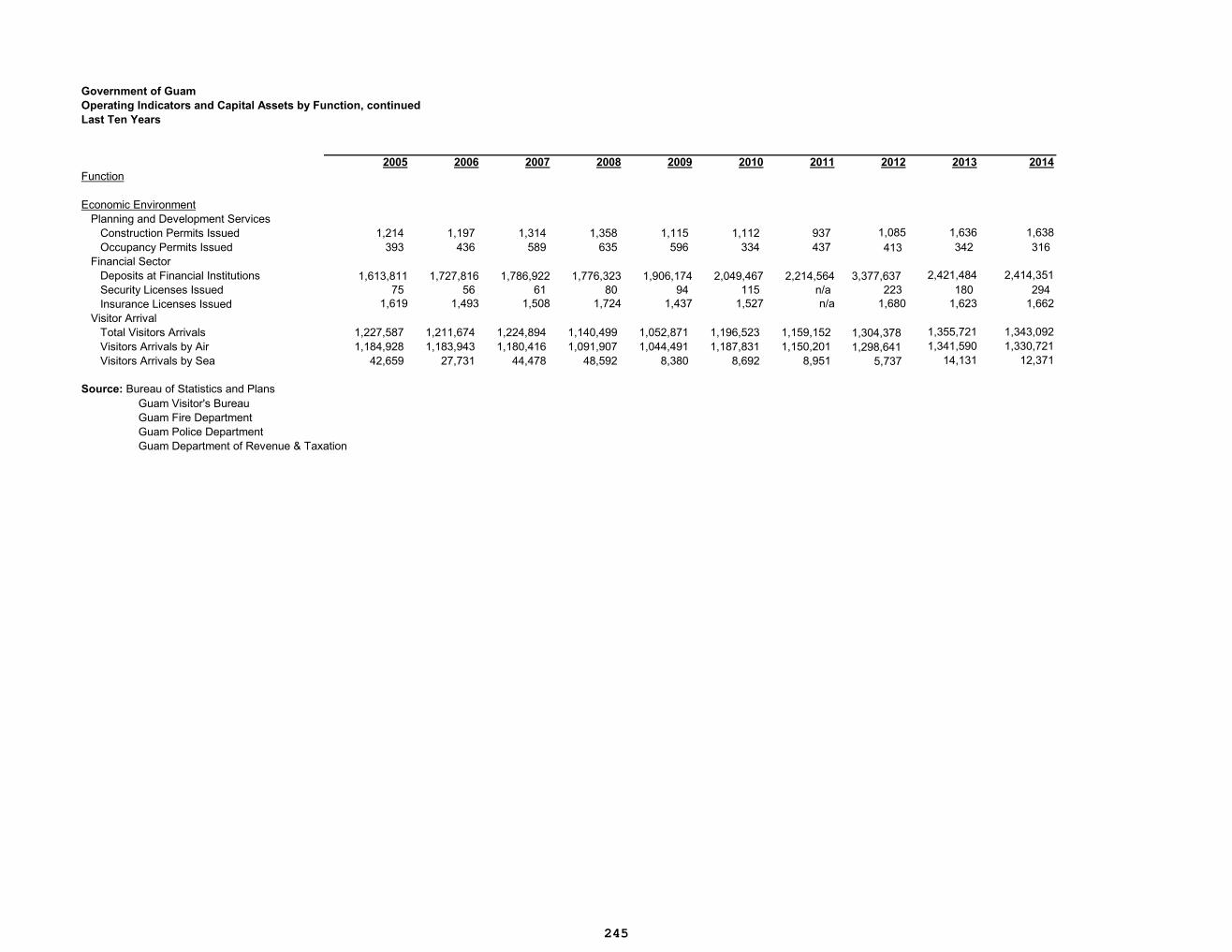

Pledged Revenue Coverage – Hotel Occupancy Tax Revenues............................................................................................ 227 Pledged Revenue Coverage – Judicial Fees, Fines and Building Rental Receipts ......................................................... 228 Pledged Revenue Coverage – Liquid Fuel Tax and Vehicle Registration / License Fees .......................................... 229 Pledged Revenue Coverage – Compact Impact Grant Revenues ........................................................................................ 230 Pledged Revenue Coverage – Business Privilege Tax Revenues......................................................................................... 231 Demographic and Economic Statistics .......................................................................................................................................... 232 Employees by Industry Based on Payrolls ................................................................................................................................... 233 Top 10 Private Employers .................................................................................................................................................................. 234 Top Employers by Industry ................................................................................................................................................................ 235 School Enrollment .................................................................................................................................................................................. 236 Visitor Arrivals by Country of Residence ..................................................................................................................................... 237 Primary Reason for Trip to Guam – Visitors Only .................................................................................................................... 238 Average Visitor Expenditures by Market ..................................................................................................................................... 240 Tourism Indicators ................................................................................................................................................................................ 241 Military Expenditures ........................................................................................................................................................................... 242 Schedule of Personnel Count ............................................................................................................................................................. 243 Operating Indicators and Capital Assets by Function ............................................................................................................. 245 Capital Assets by Function .................................................................................................................................................................. 247 Value Added by Industry ..................................................................................................................................................................... 248 Pledged Revenue Coverage – General Fund Provision for Tax Refunds.......................................................................... 249 Guam Facts ................................................................................................................................................................................................ 251

Government of Guam

July 1, 2014

The Honorable Edward J. B. Calvo

Governor of Guam

Ricardo J. Bordallo Governor’s Complex

Adelup, Guam 96910

Dear Governor Calvo:

We are pleased to transmit the Comprehensive Annual Financial Report (CAFR) of the

Government of Guam (GovGuam) for the fiscal year ended September 30, 2013, inclusive of the

Independent Auditors’ Report. The Division of Accounts, Department of Administration, prepares

the CAFR in conformance with the principles and standards for financial reporting set forth by the

Governmental Accounting Standards Board (GASB).

Responsibility for both the accuracy of the data and the completeness and fairness of the

presentation, including all disclosures, rests with management. Management is also responsible

for establishing and maintaining an internal control structure designed to ensure that the assets of

GovGuam are protected from loss, theft or misuse and to ensure that adequate accounting data is

compiled to allow for the preparation of financial statements in conformity with generally accepted

accounting principles. The internal control structure is designed to provide reasonable, but not

absolute, assurance that these objectives are met. We believe that the data, as presented, is accurate

in all material respects; that its presentation fairly shows the financial position and the results of

the government’s operations as measured by the financial activity of its various funds; and that the

included disclosures will provide the reader with an understanding of the government’s financial

affairs.

Management provides a narrative introduction, overview, and analysis to accompany the Basic

Financial Statements in the form of a Management’s Discussion & Analysis (MD&A). This letter

of transmittal is designed to complement the MD&A and should be read in conjunction with

it. The MD&A can be found immediately following the report of the independent auditors.

Our CAFR is divided into the following sections:

The Introductory Section includes this transmittal letter and information about the principal

officials and organizational structure of the Government of Guam.

i

Letter of Transmittal, continued

The Financial Section is prepared in accordance with the GASB 34 requirements by including

the MD&A, the Basic Financial Statements including notes and the Required Supplementary

Information. The Basic Financial Statements include the government-wide financial statements

that present an overview of the GovGuam’s entire financial operations and the fund financial

statements that present the financial information of each of the GovGuam’s major funds, as well

as non-major governmental, fiduciary and other funds. Also included in this section is the

Independent Auditors’ Report on the basic financial statements.

The Statistical Section includes tables containing historical financial trend data, revenue capacity,

debt capacity, demographic and economic information and operating information of Guam that are

of interest to potential investors in our bonds and to other readers.

Government of Guam Profile:

The diversely populated island of Guam is the southernmost island in the Marianas, located in the

Western Pacific Ocean. Covering 214 square miles, Guam is the biggest, most populated and well

developed land of the Mariana Islands as well as the Micronesian Region. Its geographic location

is 13.28° N and 144.47° E. The island’s close proximity to the equator brings warm weathers with

a daytime temperature average at 82°F and nighttime at 65-75°F, which is very appealing to

tourists.

Guam is an organized, unincorporated U.S. territory under the jurisdiction of the Office of Insular

Affairs, US Department of Interior. In past years, the island was ruled by Spain, ceased by the

U.S. in 1898, captured by Japan in 1941, and then recaptured by the U.S. in 1944. Six (6) years

after U.S. Military rule, Congress signed the Organic Act of Guam to establish the local

government of Guam. Like the U.S., Guam is administered through three branches: the executive,

legislative and judicial.

The executive branch is headed by the governor and lieutenant governor who are both elected by

popular vote for a four-year term. The governor and lieutenant governor may only serve for two

consecutive terms. After, they must wait one whole term before running for office again.

The island also holds a unicameral Legislature seating fifteen (15) elected senators. Like the

governor and lieutenant governor, the members are elected by popular vote; senators serve for two

years but may serve consecutively. The people of Guam also elect one non-voting delegate to the

U.S. House of Representatives.

The judicial branch consists of the Federal District Court, Supreme Court of Guam and Territorial

Superior Court. For the Federal District Court, a judge is appointed by the President. Judges for

the Supreme Court of Guam, which hears appeals from the Superior court, are appointed by the

ii

Letter of Transmittal, continued

Governor. Lastly, the judges for the Territorial Superior Court are appointed for eight-year terms

by the Governor.

Local Economy:

As of September 2014 Guam experienced an unemployment rate of 7.6 percent, 1.4 percentage

points lower than the June 2014 figure of 9.0 percent. Compared to the September 2013 percentage

of 10.0, the rate decreased 2.4 percentage points. For September 2014, the unemployment number

was 5,390 – reflecting a decrease of 1,770 in comparison to September 2013.

According to the Government of Guam’s Department of Labor September 2014 Current

Employment Report, initial statistics display an overall increase of private sector jobs by 440 in

the fourth quarter of fiscal year 2014. More importantly, in comparison to the fourth quarter of

fiscal year 2013, fiscal year 2014 ended reflecting a 740-job increase. Also throughout the fiscal

year the construction industry showed an increase of 160 jobs as compared to fiscal year 2013.

Retail jobs, hotel employment, and other services showed an overall year growth of 260, 210, and

230 jobs in their respective orders.

In FY2014, Guam’s tourism industry increased by 0.3% for a total of 1,341,171 as compared to

FY2013 1,337,665 visitors. Japan showed a historically low of arrivals-825K but was counter

measured with Korea’s increase from 233K in FY2013 to 293K in FY2014. The increase in

Korean tourists can be attributed to flight services originating from Incheon by United Airlines

and four flights a week from Busan by Korean Air. To further facilitate the positive growth in

Korean arrivals, Jin Air will be upgrading from a Boeing 737 to a Boeing 777 giving an additional

170 seating capacity. Furthermore, Jeju Air will begin flights from Busan as the upward rise in

travelers is expected to continue through FY2015. Overall FY2014 represents a new plateau

record of 1,341,171 arrivals as Guam continues to push the boundaries in diversifying market

segments. (GVB report)

According to the U.S. Department of State, United States and China now hold an agreement to

increase the tourist, student, and exchange visitor visas from one year to 10 years, the Guam

Visitors Bureau remains optimistic as Guam aggressively pursues the Chinese market segment.

According to former GVB General Manager Karl Pangelinan, “…this visa extension will definitely

help ease the travel process for visitors and provide more jobs and opportunities for our people.”

To further supplement the growth in the Chinese traveler, Dynamic Airways has started in June

2014 direct flights from Beijing occurring every five days. The flights will bring in an influx of

235 expected visitors. The Chinese market plays a crucial role in the Tourism 2020 diversification

plan, as Guam attains a share of the 200 million outbound travelers expected by 2017.

Russia remains a promising market as it surpassed its target arrival of 12,500 arrivals with a year

ending 18,291 visitors. Fiscal year 2014, displayed an amazing 198.2 percent growth compared

iii

Letter of Transmittal, continued

to FY2013’s 6,134 travelers. Taiwan, Guam’s third largest Asian source market, brought in 50K,

while China markets brought in 14K visitors. (GVB report)

Major Initiatives

HOT Bond

Hagatña Projects: Since 2013 a number of the HOT Bond projects have seen tremendous

progress. The Guam Chamorro and Educational Facility (GCEF), commonly known as the

Guam Museum, is currently in its hard construction phase with Inland Builders as the

contractor for the project. Although the project was initially estimated to be completed in

December of 2014, the contractor has revised the estimated completion date on or around

May 2015 due to a number of issues to include various archaeological finds consisting of

artifacts, portions of historical structures, as well as human remains among other issues.

Along with the hard construction, other elements for the GCEF are currently in their

contracting phase. These include the facility’s security systems, lighting, procurement of

the exhibit fabrication, and $200K budgeted for local artists to add their work to the

museum. Even with all these elements, the project still remains within its initial budget of

$27M. Also within the capital of Hagatña, the crosswalk between the Skinner Plaza and

Chamorro Village is currently in its design phase with LYON Associates as the contracted

designer. With the passage of PL 32-56, $2M was transferred to the Guam Fishermen’s

Cooperative Association in 2014 to begin major renovations of their current facility

adjacent to the Chamorro Village.

Park Projects: Working in conjunction with the Department of Parks and Recreation,

improvements to several of Guam’s public parks have begun their construction phase with

an NTP issued to Reliable builders in June 2014. The Parks and Scenic Overlooks

Improvement Project includes Cetti Bay Point Overlook, East Agana Pinic Shelters

(Trinchera Beach Park), Fadi’an Point Overlook, Pedro C. Santos Memorial Park, Umatac

Bay Overlook, Fleet Admiral Chester W. Nimitz Beach Park, Teguhan Bay Beach Park

(Fish Eye), along with the re-design and construction of the Senator Angel L.G. Santos

Memorial Park (former Latte’ Stone Park). Estimated completion of this project is within

a year of NTP. As for the Hagatña Tennis Courts and Pool, scoping work continues along

with the guidance of DPR in order to determine the balance between their respective needs

and $150K budget for each.

Village Projects: The Scenic Informational and Highway Signs Project, which included

Village Monument Signs for each village, issued an NTP to Maeda Pacific Corporation in

June of 2013. In order to design the monuments for each village, Maeda worked closely

with the Mayors Council and each individual mayor to tailor the design of each monument

in order to showcase those features that makes each village unique. While this project has

iv

Letter of Transmittal, continued

been ongoing, its completion is highly anticipated for November of 2014. As $50K was

budgeted for improvements to the Mangilao Public Market, these funds were approved to

be transferred to the Mangilao Mayor’s Office in order to maximize the use of the funds.

As for Umatac and Malesso, the Magellan Monument and Malesso Bell Tower Project

design contract was awarded to Setiadi Architects wherein, given the historic nature of

these two landmarks, extensive work in historical research, design and construction moving

forward required guidance and a close partnership with Guam Preservation Trust. With the

design of the Farmers’ Cooperative Association of Guam and Relocation of the Dededo

Flea Market Facility completed by Architects Laguana in 2013, bid, award, and

construction of the project by Mega United has broken ground in August of 2014. With

construction budgeted for $3M and construction completion estimated for summer 2015,

local farmers, vendors, shoppers and tourist will come together in a new 7 acre facility

nestled on the corner of Marine Corps Drive and Santa Monica Avenue in Dededo.

Tumon Projects: Due to its highly environmentally sensitive nature, the San Vitores

Flooding Mitigation Project with its $11.5M budget began its scoping phase in July of 2013

with the guidance, collaboration and advice of a number of local residents, engineering

professionals, and government regulatory agencies. This project proceeded to its design

phase in February of 2014. Design is ongoing and is estimated to be complete and

submitted for public and government review in February of 2015. Lighting and Electrical

Improvements for the Governor Joseph Flores Memorial Park saw a re-issue of an

Invitation for Bids as previous 2012 bid results exceeded the $400K budgeted for the

project. Bids for the re-issue of this project were received in March of 2014 and are under

review. As with the Hagatña pedestrian safety crosswalks, LYON and Associates is also

in the process of designing the improvements to those crosswalks and other pedestrian

safety features along the Pleasure Island area of Tumon. With this, enhanced safety and

aesthetical features will characterize the highest tourist densely populated area of the

island.

Military Buildup

In a visit to Guam, Robert Work Deputy Secretary of the Department of Defense mentioned,

“there’s momentum to move forward with plans for the military buildup on Guam.” Work further

added, “By February 2015, the draft Supplemental Environmental Impact Statement for the

buildup will be released and there will be no more changes to the plan.” Guam exhibits a crucial

role in the U.S. military’s “rebalance” in the Asia Pacific Region. Work’s visit immediately came

after DOD submitted the buildup master plan to Congress

Some of the projects that reinforce the buildup plans include the $53.7 million contract award for

the construction of the aircraft maintenance hangar at Andersen Air Force Base, Guam. The

v

Letter of Transmittal, continued

project will feature a hangar bay, maintenance area, and section for administration and operations

according to the Naval Facilities Engineering Command Pacific. The construction project began

in fiscal year 2014 with a scheduled completion date by December 2016. Adding to the

infrastructure improvement is the $62 million, 1303 Guam Pipeline military construction project

that was awarded on June 6, 2014. The project will create a 15.7-mile fuel pipeline, with an

estimated completion date by June 2016.

In the April 2014 draft environmental impact statement, issues relating to the relocation of the

marines firing range was addressed along with the displacement of local residents. The draft held

that instead of the proposed firing range being held on Guamanian ancestral lands the range will

be relocated within Andersen Air Force Base. Furthermore, housing construction for military

personnel and families will occur under federal owned land so as to avoid displacement of local

residents. For Mark Calvo, director of the Government of Guam Military Buildup Office the April

2014 draft EIS release shows, “Our concerns were heard, and they’re adapting. This is a major

milestone in moving forward with the relocation of Marines to Guam.”

Water and Waste Management System

With the Layon Landfill currently in full operations much progress has been made in the closure

of the Ordot dump for FY2014. The two phase approach in the closure has currently seen phase

one completions of temporary leachate storage pond construction, scattered waste consolidation,

western channel relocation, leachate storage tank construction, and construction of gas collection

wells. As our solid waste management made headway into the closure of Ordot dump, Guam

Waterworks Authority saved ratepayers 14 million in the refinancing of the 2005 bond. According

to Simon Sanchez, chairman of the Consolidated Commission on Utilities, “They really view

Guam’s bonds as good value they’re going to get repaid triple tax exempt so all in all everybody

got a benefit the bond holders are happy and they got a reliable investment and most importantly

Guam’s ratepayers are going to save $14 million in the coming years.”

Modernized Schools

After a long anticipated wait, Untalan Middle School finally opened its doors for the new 2014

school year. The middle school had undergone major modernizations in order to revitalize the

crumbling infrastructure. The administration worked relentlessly as the modernization project

became a major initiative that the Governor held close and personal to his heart. In a statement

release by Governor Eddie Baza Calvo, “We stuck to our guns and took the long journey today.

Now the kids have a new school. I’m so proud.”

To alleviate overcrowding in the islands’ public high schools, the new Tiyan High School opened

for the 2014 academic year. Tiyan High stands as the first new high school since 2008, and will

most especially lessen the overcrowding that has plagued George Washington High School for

vi

Letter of Transmittal, continued

two decades. Ultimately there was a need to alleviate overcrowding in our central and northern

public high schools, and so the administration along with fellow supporters held steadfast to the

mission and persevered despite all opposition. To sum the accomplishment, in a public release

Governor Calvo exclaimed, “Happy Birthday to Tiyan High School!”

Highway System

Guam is currently undergoing several capital projects in an effort to improve the highway system.

Currently there are four ongoing project-1) Route 1/8 Intersection Improvements and Agana

Bridge Replacement, 2) Route 17 Rehabilitation and Widening, Phase 2A, 3) Route 25/26

Intersection Improvement, 4) Replacement of Welded Petroleum Distribution Piping and

Appurtenances. The route 1/8 intersection improvement and Agana bridge replacement represent

a major project holding a cost of $16.4 million. Most importantly, the completion of these projects

would mean compliance with federal highway regulations.

Jose D. Leon Guerrero Commercial Port

In preparation of the ongoing military buildup the Port Authority of Guam has undergone major

renovations as to avoid becoming a potential chokepoint for the importing of construction

materials as the military undergoes critical infrastructure projects. According to Joanne Brown,

Port Authority of Guam General Manager, “the Port’s facilities, with federal funding, have

improved significantly…” Furthermore Brown added, “I don’t see the Port of Guam as a

chokepoint.” The Port Authority of Guam has currently completed Phase I-A, which holds for the

enlargement of the break-bulk laydown area, updating of the CFS Building, construction of new

gate complex, utilities renovation, and security upgrades. Overall the total cost of the Port’s

modernization is expected to cost about $260 million with a project length spanning 30 years.

Long-term Financial Planning:

As the government of Guam continues to reevaluate funding sources in an effort to improve critical

government services, a major source of revenue has been the revaluation of property tax. The last

appraisal conducted was 20 years ago and with the large increase in values the Territorial

Education Facilities Fund will largely benefit. According to Governor Calvo, “By updating our

real property tax codes and conducting revaluations and appraisals, we may be able to increase

education funding without significantly decreasing support for other essential government

services.” Furthermore, in a news release Department of Revenue and Taxation Director, John

Camacho commented on the 2014 property tax collections saying, “the department’s assessment

pegs about $32 million in revenue from the new property values – a nearly $10 million increase

from previous years.”

vii

Letter of Transmittal, continued

Keeping to the Guam Visitors Bureau Tourism 2020 strategic plan of creating a world class resort

destination, showcasing five star amenities and activities many initiatives have taken place

throughout fiscal year 2014. Some of the initiatives include the establishment of a Visitor Safety

Officer program, development of an online Tourism Academy, portfolio diversification, and also

efforts in promoting MICE business in the off-season. More importantly, the plan holds the unique

Chamorro culture as a focal point for visitors’ experience. For Mark Baldyga, Chairman of the

Board for Guam Visitors Bureau the Tourism 2020 strategic plan will mean, “…thousands of new

job opportunities for our people and significantly increased revenue for the Government of Guam.”

In a news release by the Washington Post, the Obama administration has decided that the

Affordable Care Act stipulations do not apply to the territories. According to the Department of

Health and Human Services the Public Health Service Act (PHS Act) clearly holds that the

territories do not meet the definition of “state”. The news comes to much relief for the territories,

as the federal government would not provide any subsidies and there was no individual mandate

requiring residents to get coverage. Without the federal subsidies the coverage plans of the

territories will be rather costly placing a large financial burden on the local governments.

Awards:

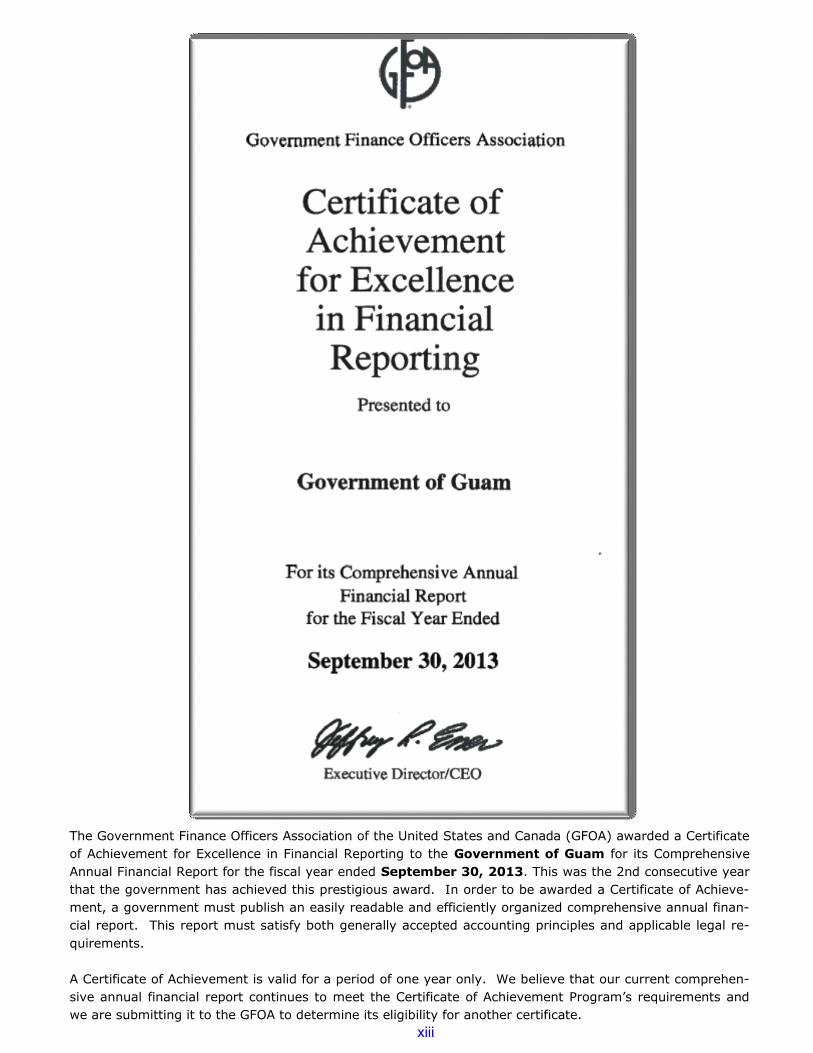

The Government Finance Officers Association of the United States and Canada (GFOA) awarded

a Certificate of Achievement for Excellence in Financial Reporting to Government of Guam for

its comprehensive annual financial report for the fiscal year ended September 30, 2013.

In order to be awarded a Certificate of Achievement, a government must publish an easily readable

and efficiently organized comprehensive annual financial report. This report must satisfy both

generally accepted accounting principles and applicable legal requirements. A Certificate of

Achievement is valid for a period of one year only.

Acknowledgements:

The Department of Administration is pleased to have completed the third Comprehensive Annual

Financial Report. The context of the report points to the marked improvement of the General

Fund’s financial posture and the overall improvement in this government’s ability to be

accountable and fiscally responsible for taxpayers’ money. We have improved our financial

reporting capabilities and made great strides in our cash management efforts. Governor, your

continued leadership, guidance and fiscal policies have culminated in the completion of this third

Comprehensive Annual Financial Report, yet another monumental financial achievement that we

are all proud of.

The Comprehensive Annual Financial Report is being submitted to the Government Finance

Officers Association of the United States and Canada (GFOA) for participation in its Certificate

viii

Government of Guam Letter of Transmittal, continued

of Achievement in Financial Reporting Program. We believe it will meet the programrequirements to be awarded the Certificate of Achievement in Financial Reporting.

Assisting us in the preparation and review of this Comprehensive Annual Financial Reportincludes staff of the Division of Accounts, Department of Administration and other departmentswith staff that process financial transactions, or otherwise contribute to the information, presentedin this report.

Sincerely,

Anthony C. BlazDirector, Department of Administration

I$athrine 3. Ka1gi “

Financial Manager, Department of Administration

ix

Letter of Transmittal, continued

Sources:

“China Tourism Market Update: Throwing open the Eastern gate” by Thomas Johnson

http://www.guambusinessmagazine.com/?p=2985

“Deputy SecDef highlights Guam in U.S. military buildup plan” by Gaynor Dumat-ol Daleno

http://archive.militarytimes.com/article/20140820/NEWS05/308200060/Deputy-SecDef-

highlights-Guam-U-S-military-buildup-plan

“Feds OK China visa extension” by Jasmine Stole

http://mvguam.com/local/news/37848-feds-ok-china-visa-extension.html#.VX4jpGc9J9B

“HISTORIC NEWS: Guam cracks open floodgates to China tourist market” by Phillip Leon

Guerrero

http://governor.guam.gov/2014/05/09/historic-news-guam-cracks-open-floodgates-china-

tourist-market/

Guam Visitors Bureau FY 2014 Financial Highlights, Office of Public Accountability Guam

http://www.opaguam.org/sites/default/files/gvb_fy14_highlights.pdf

Guam Transportation Program, Ongoing Projects

http://www.guamtransportationprogram.com/projects/ongoing

Guam Department of Labor, September 2014 Current Employment Report

http://bls.guam.gov/wp-content/uploads/bsk-pdf-manager/14_CES_SEP2014.PDF

Guam Visitors Bureau, 2014 GVB Annual Report

https://www.guamvisitorsbureau.com/research-and-reports/reports/annual-report

Diego, Mendiola, Real Property Assistant Manager, Guam Economic Development Authority.

HOT BONDS interview.

x

Letter of Transmittal, continued

Port Authority of Guam FY2014 Financial Highlights, Office of Public Accountability Guam

http://www.opaguam.org/sites/default/files/pag_hl14_0.pdf

GDOE preparing for opening of new Tiyan High School by Louella Losinio

http://mvguam.com/local/news/34647-gdoe-preparing-for-opening-of-new-tiyan-high-

school-.html?tmpl=component&print=1&layout=default&page=#.VX9blmc9J9A

THE FULL STORY: about the long journey to Untalan Middle School’s return to a modern

campus by Phillip Leon Guerrero

http://governor.guam.gov/2014/08/13/full-story-long-journey-untalan-middle-schools-

return-modern-campus/

Hard-fought victory: Guam has first new high school since 2008 by Phillip Leon Guerrero

http://governor.guam.gov/2014/08/14/hard-fought-victory-guam-high-school-2008/

Quarterly Report of the Receiver, Civil Case No. 02-00022 United States of America v.

Government of Guam, Guam Solid Waste Authority, Prepared for: U.S. District Court of Guam,

Submitted by: GBB Solid Waste Management Consultants Receiver, October 9, 2014

http://www.guamsolidwastereceiver.org/pdf/Tab1-Quarterly-Report-of-the-Receiver.pdf

The administration just took Obamacare away from the territories, from The Washington Post by

Jason Millman

http://www.washingtonpost.com/blogs/wonkblog/wp/2014/07/17/the-administration-just-

took-obamacare-away-from-the-territories/

Dept. of Health & Human Services, Letter to Commissioner Gregory R. Francis, Office of the

Lieutenant Governor, Division of Banking & Insurance, St. Croix Office

http://www.cms.gov/CCIIO/Resources/Letters/Downloads/letter-to-Francis.pdf

Reevaluation of real property is paying dividends, KUAM news by Ken Quintanilla

http://www.kuam.com/global/story.asp?s=29348309

xi

Letter of Transmittal, continued

“GWA, GEDA refinance 2005 bond” KUAM news article by Sabrina Salas Matanane

http://www.kuam.com/story/26087987/2014/07/23/gwa-geda-refinance-2005-bond

“Contract awarded for hangar on Guam to support Marine squadrons” Stars and Stripes article

http://www.stripes.com/news/contract-awarded-for-hangar-on-guam-to-support-marine-

squadrons-1.282217

“DLA Energy Pacific breaks ground on Guam pipeline” by Christopher Goulait Defense

Logistics Agency Energy

http://www.andersen.af.mil/news/story.asp?id=123414603

“Navy Hails Gains in Plan to Move Marines to Guam” by Richard Sisk

http://www.military.com/daily-news/2014/04/18/navy-hails-gains-in-plan-to-move-

marines-to-guam.html

“The Unemployment Situation on Guam: December 2014” by Bureau of Labor Statistics,

Department of Labor, Government of Guam

http://bls.guam.gov/unemployment-situation-on-guam/

xii

The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate

of Achievement for Excellence in Financial Reporting to the Government of Guam for its Comprehensive

Annual Financial Report for the fiscal year ended September 30, 2013. This was the 2nd consecutive year

that the government has achieved this prestigious award. In order to be awarded a Certificate of Achieve-

ment, a government must publish an easily readable and efficiently organized comprehensive annual finan-

cial report. This report must satisfy both generally accepted accounting principles and applicable legal re-

quirements.

A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehen-

sive annual financial report continues to meet the Certificate of Achievement Program’s requirements and

we are submitting it to the GFOA to determine its eligibility for another certificate.

xiii

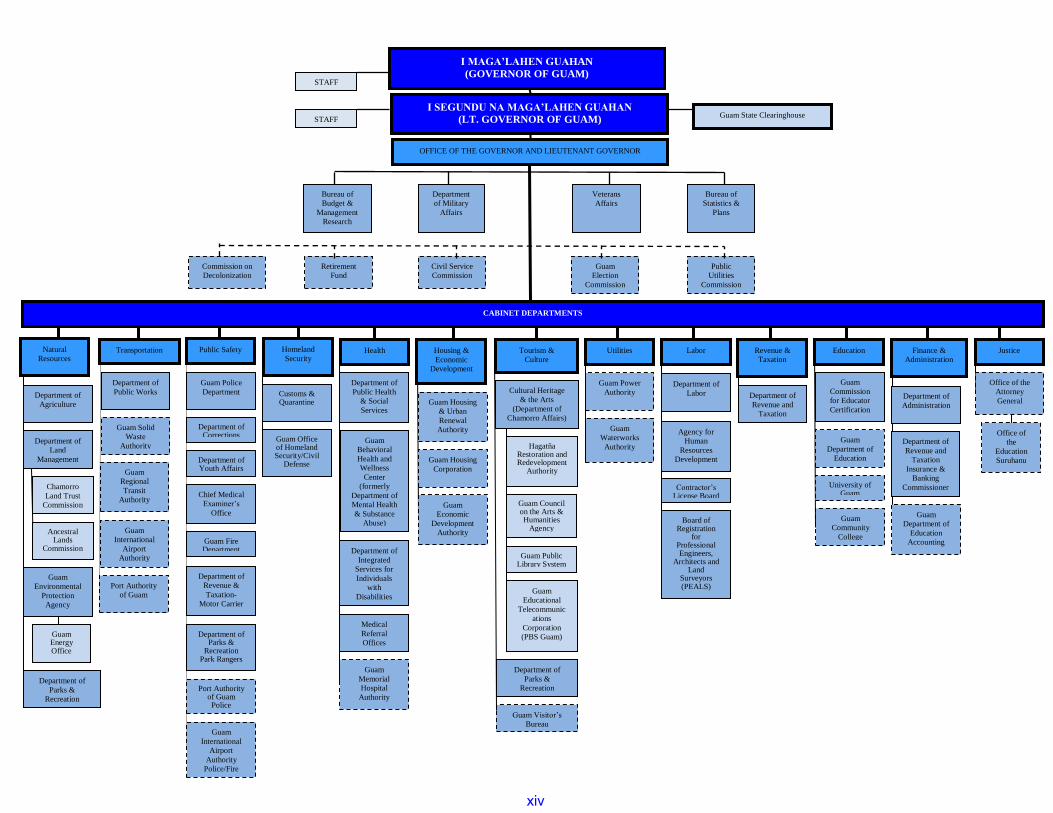

OFFICE OF THE GOVERNOR AND LIEUTENANT GOVERNOR

I SEGUNDU NA MAGA’LAHEN GUAHAN

(LT. GOVERNOR OF GUAM) Guam State Clearinghouse

STAFF

STAFF

Guam

Waterworks

Authority

Guam Power

Authority

Medical

Referral

Offices

Department of

Public Health

& Social

Services

Guam

Behavioral

Health and

Wellness

Center

(formerly

Department of

Mental Health

& Substance

Abuse)

Department of

Integrated

Services for

Individuals

with

Disabilities

Guam

Memorial

Hospital

Authority

Guam Office of Homeland Security/Civil

Defense

Customs & Quarantine

Department of

Agriculture

Department of

Land

Management

Department of

Parks &

Recreation

Commission on

Decolonization

Retirement

Fund

Civil Service

Commission

Guam

Election

Commission

Public

Utilities

Commission

Department

of Military

Affairs

Bureau of

Budget &

Management

Research

Veterans

Affairs

Bureau of

Statistics &

Plans

Department of

Parks &

Recreation

Historic

Preservation

Transportation Public Safety Homeland

Security

Health

Guam Visitor’s

Bureau

Ancestral Lands

Commission

Chamorro

Land Trust

Commission

Guam

Environmental

Protection

Agency

Guam Energy Office

Guam Police

Department

Department of Corrections

Department of Youth Affairs

Chief Medical

Examiner’s

Office

Guam Fire Department

Department of

Revenue &

Taxation-

Motor Carrier

Department of Parks &

Recreation Park Rangers

Port Authority of Guam Police

Guam

International

Airport

Authority

Police/Fire

Department of

Public Works

Guam Solid

Waste

Authority

Guam

Regional

Transit

Authority

Guam

International

Airport

Authority

Port Authority

of Guam

Hagatña Restoration and Redevelopment

Authority

Guam Council on the Arts & Humanities

Agency

Guam

Educational

Telecommunic

ations

Corporation

(PBS Guam)

Guam Public Library System

Cultural Heritage

& the Arts

(Department of

Chamorro Affairs)

Guam Housing

& Urban

Renewal

Authority

Guam Housing

Corporation

Guam

Economic

Development

Authority

Housing &

Economic

Development

Department of

Labor

Agency for

Human

Resources

Development

Contractor’s License Board

Board of Registration

for Professional Engineers,

Architects and Land

Surveyors (PEALS)

Department of

Revenue and

Taxation

Guam

Department of

Education

University of Guam

Guam

Commission

for Educator

Certification

Guam

Community

College

Department of

Administration

Guam

Department of

Education

Accounting

Department of

Revenue and

Taxation

Insurance &

Banking

Commissioner

Finance &

Administration

Office of

the

Education

Suruhanu

Office of the

Attorney

General

Tourism &

Culture

Utilities Labor Revenue &

Taxation

Education Justice

CABINET DEPARTMENTS

Guam Solid

Waste

Authority

I MAGA’LAHEN GUAHAN

(GOVERNOR OF GUAM)

Natural

Resources

xiv

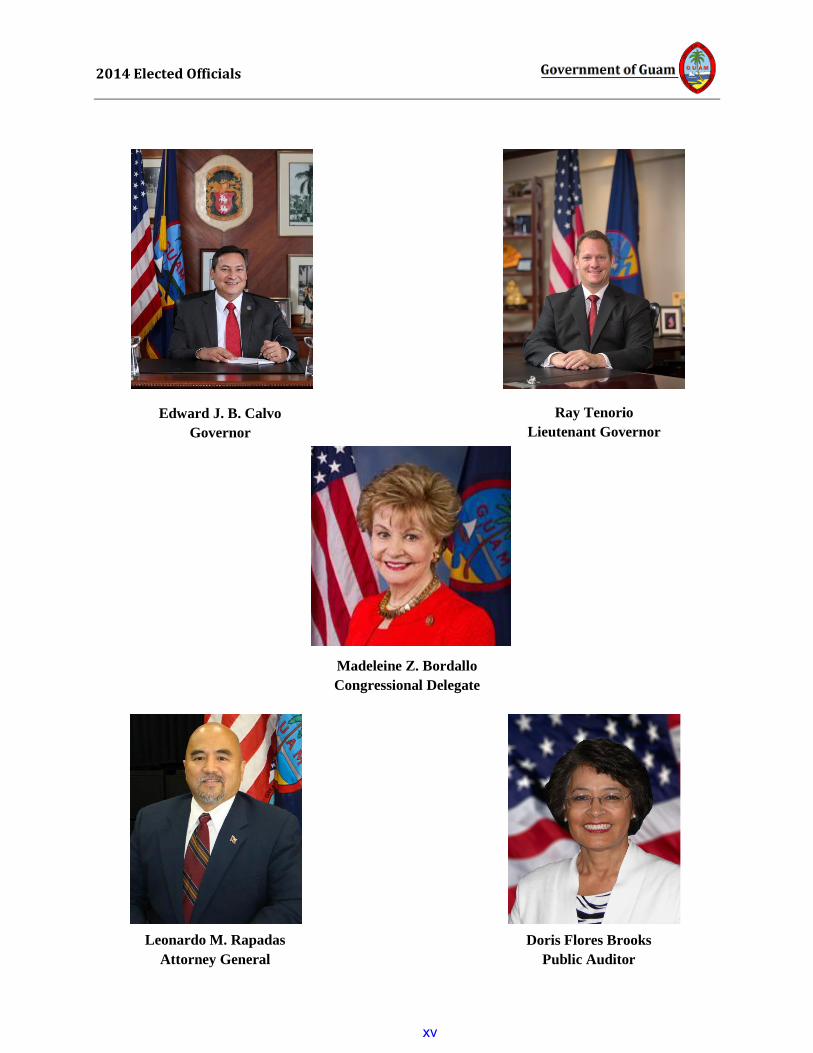

2014 Elected Officials

Ray Tenorio

Lieutenant Governor

Edward J. B. Calvo

Governor

Madeleine Z. Bordallo

Congressional Delegate

Leonardo M. Rapadas

Attorney General

Doris Flores Brooks

Public Auditor

xv

2014 Elected Officials

32nd Guam Legislature

Judith T. Won Pat (D)

Speaker

Benjamin J. F. Cruz (D)

Vice-Speaker

Tina R. Muña Barnes (D)

Legislative Secretary

Rory J. Respicio (D)

Majority Leader

Thomas C. Ada (D)

Assistant Majority Leader

Dennis G. Rodriguez, Jr. (D)

Majority Whip

Michael F.Q. San Nicolas (D) Frank B. Aguon, Jr. (D) Vicente C. Pangelinan (D)

xvi

2014 Elected Officials

32nd Guam Legislature

V. Anthony Ada (R)

Minority Leader

Aline A. Yamashita, PhD (R) Christopher M. Duenas (R)

Assistant Minority Leader

Brant McCreadie (R) Michael Limtiaco (R) Thomas Morrison (R)

xvii

1

INDEPENDENT AUDITORS' REPORT Honorable Eddie Baza Calvo Governor Government of Guam: Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information of the Government of Guam (GovGuam) as of and for the year ended September 30, 2014, and the related notes to the financial statements, which collectively comprise GovGuam’s basic financial statements as set forth in Section III of the foregoing table of contents. Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors' Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We did not audit the financial statements of the GovGuam Retirement Fund, which represents 93%, 95% and 67%, respectively, of the assets, net position/fund balances and revenues of the aggregate remaining fund information, and the Antonio B. Won Pat International Airport Authority, the Guam Housing and Urban Renewal Authority, the Guam Housing Corporation, and the Guam Preservation Trust, which represent 26%, 42% and 13%, respectively, of the assets and deferred outflows, net position and operating revenues of GovGuam’s discretely presented component units. Those statements were audited by other auditors whose reports have been furnished to us, and our opinion, insofar as it relates to the amounts included for the GovGuam Retirement Fund, the Antonio B. Won Pat International Airport Authority, the Guam Housing and Urban Renewal Authority, the Guam Housing Corporation, and the Guam Preservation Trust, is based solely on the reports of the other auditors. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

Deloitte & Touche LLP 361 South Marine Corps Drive Tamuning, GU 96913-3911 USA Tel: (671) 646-3884 Fax: (671) 649-4932 www.deloitte.com

2

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, based on our audit and the reports of other auditors, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information of the Government of Guam as of September 30, 2014, and the respective changes in financial position for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis-of-Matter Implementation of New Accounting Standards As discussed in note 1, the Government of Guam implemented Governmental Accounting Standards Board (GASB) Statement No. 67, Financial Reporting for Pension Plans. The effects of implementation of GASB 67 are presented in Note 16. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the Management’s Discussion and Analysis on pages 4 through 15 as well as the Schedule of Revenues, Expenditures, and changes in Deficit - Budget and Actual - General Fund and notes thereto, on pages 120 through 122, and the Schedule of Funding Progress, on page 123, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise GovGuam's basic financial statements. The Other Supplementary Information, as set forth in Section V of the foregoing table of contents, is presented for purposes of additional analysis and is not a required part of the basic financial statements.

3

The Other Supplementary Information is the responsibility of management. The additional information on pages 128 through 139 and 148 through 206 as well as the 2014 information on pages 140 through 147 were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America by us and other auditors. In our opinion, based on our audit, the procedures performed as described above, and the reports of the other auditors, the additional information on pages 128 through 139 and 148 through 206 as well as the 2014 information on pages 140 through 147 is fairly stated, in all material respects, in relation to the basic financial statements as a whole. The 2013 information on pages 140 through 147 has not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on it. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated June 29, 2015, on our consideration of GovGuam’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering GovGuam’s internal control over financial reporting and compliance. June 29, 2015

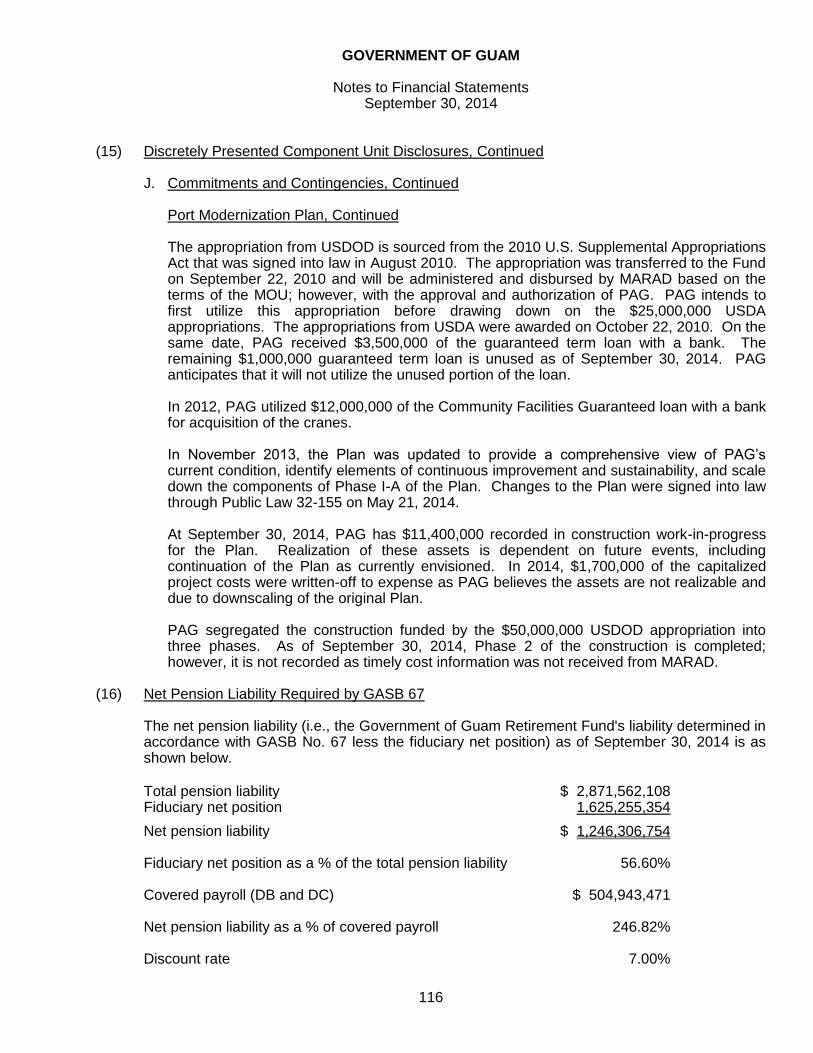

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

4

Our discussion and analysis of the Government of Guam (“GovGuam”) financial performance provides an overview of GovGuam’s financial activities for the fiscal year ended September 30, 2014. Please read it in conjunction with GovGuam’s financial statements, which follow this section. Fiscal year 2013 comparative information has been included, where appropriate. FINANCIAL HIGHLIGHTS For the fiscal year ended September 30, 2014, GovGuam’s total net position decreased by $33.5

million (or 16.1%) from a net position of $207.9 million in the prior year to a net position of $174.4 million.

During fiscal year 2014, GovGuam’s expenses for governmental activities were $1.2 billion and were funded in part by $430.2 million in program revenues and $736.3 million in taxes and other general revenues. Expenses were up from fiscal year 2014 by $76.9 million (or 6.8%) whereas revenues were up from fiscal year 2013 by $26.5 million (or 2.33%).

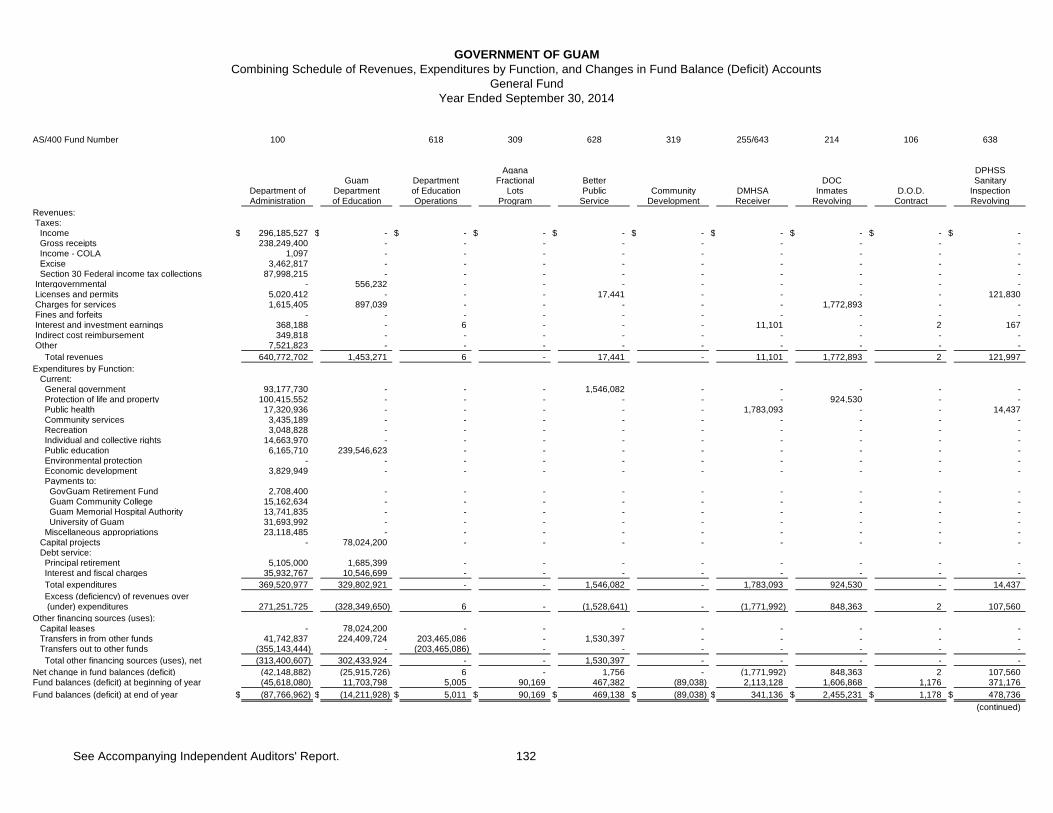

For the fiscal year ended September 30, 2014, the General Fund reported expenditures (including transfers out) of $848.2 million, an increase of $156.4 million (or 22.6%) from fiscal year 2013 expenditures and transfers out of $691.8 million. The majority of the deficit can be directly attributed to Guam Department of Education’s (GDOE) capital expenditure outlays of $21 million, PL 29-105 unfunded law enforcement payments of $24 million, and $8.6 million attributable to unreimbursed debt service from the Guam Solid Waste Authority under the federal receivership. These expenditures were outside of our direct control.

At September 30, 2014, the General Fund reported a cumulative fund deficiency of $59.6 million, which is a decrease of $61.9 million from the prior year fund balance of $2.3 million. The unfunded expenditures, GDOE’s capital outlays, and the unreimbursed debt service have negatively affected the General Fund’s fund deficiency.

OVERVIEW OF THE FINANCIAL STATEMENTS This discussion and analysis is intended to serve as an introduction to GovGuam’s basic financial statements. GovGuam’s basic financial statements comprise three components: 1) governmental-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains additional required supplementary information in the form of a budgetary schedule, which is prepared on the budgetary basis of accounting, and other optional supplementary information, in addition to the basic financial statements themselves, which includes combining statements for governmental funds and component units. Government-Wide Financial Statements The government-wide statements report information about GovGuam as a whole using accounting methods similar to those used by private-sector companies. The statement of net position includes all of the government’s assets and liabilities. All of the current year’s revenues and expenses are accounted for in the statement of activities regardless of when cash is received or paid. The two government-wide statements report GovGuam’s net position and how that has changed. Net position - the difference between GovGuam’s assets and liabilities - is one way to measure GovGuam’s financial health or position. Over time, increases or decreases in GovGuam’s net position is an indicator of whether its financial

health is improving or deteriorating, respectively.

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

5

To assess the overall health of GovGuam, additional non-financial factors such as changes in

GovGuam’s tax base, the condition of GovGuam’s roads and infrastructure, and the quality of services also need to be considered.

The government-wide financial statements of GovGuam are divided into two categories: Primary government - this grouping comprises governmental activities, which includes most of

GovGuam’s basic services such as education, public safety, health, finance, judiciary, and general administration. Local sourced tax revenues and other federal grants finance most activities of the primary government.

Discretely presented component units - GovGuam includes numerous other entities in its report. Although legally separate, these “component units” are important because GovGuam is financially accountable for them.

Fund Financial Statements The fund financial statements provide more detailed information about GovGuam’s most significant funds - not GovGuam as a whole. Funds are accounting devices that GovGuam uses to keep track of specific sources of funding and spending for particular purposes. Some funds are required by enabling legislation.

GovGuam establishes other funds to control and manage money for particular purposes (like Solid

Waste Operations Fund) or to show that it is properly using certain grants (like federal grants reported in the Federal Grants Fund).

GovGuam has two kinds of funds: Governmental funds - Most of GovGuam’s basic services are reported in governmental funds,

which focus on how money flows into and out of those funds and the balances left at year-end that are available for spending. These funds are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of GovGuam’s general government operations and the basic services it provides. Governmental fund information helps determine whether there are more or fewer financial resources that can be spent in the near future to finance GovGuam’s programs.

Fiduciary funds - GovGuam is the trustee, or fiduciary, for other assets that because of trust

arrangement, can be used only for the trust beneficiaries. GovGuam is responsible for ensuring that the assets reported in these funds are used for their intended purposes. All of GovGuam’s fiduciary activities are reported in a separate statement of fiduciary net assets and a statement of change in fiduciary net assets. We exclude these activities from GovGuam’s government-wide financial statements because GovGuam cannot use these assets to finance its operations.

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

6

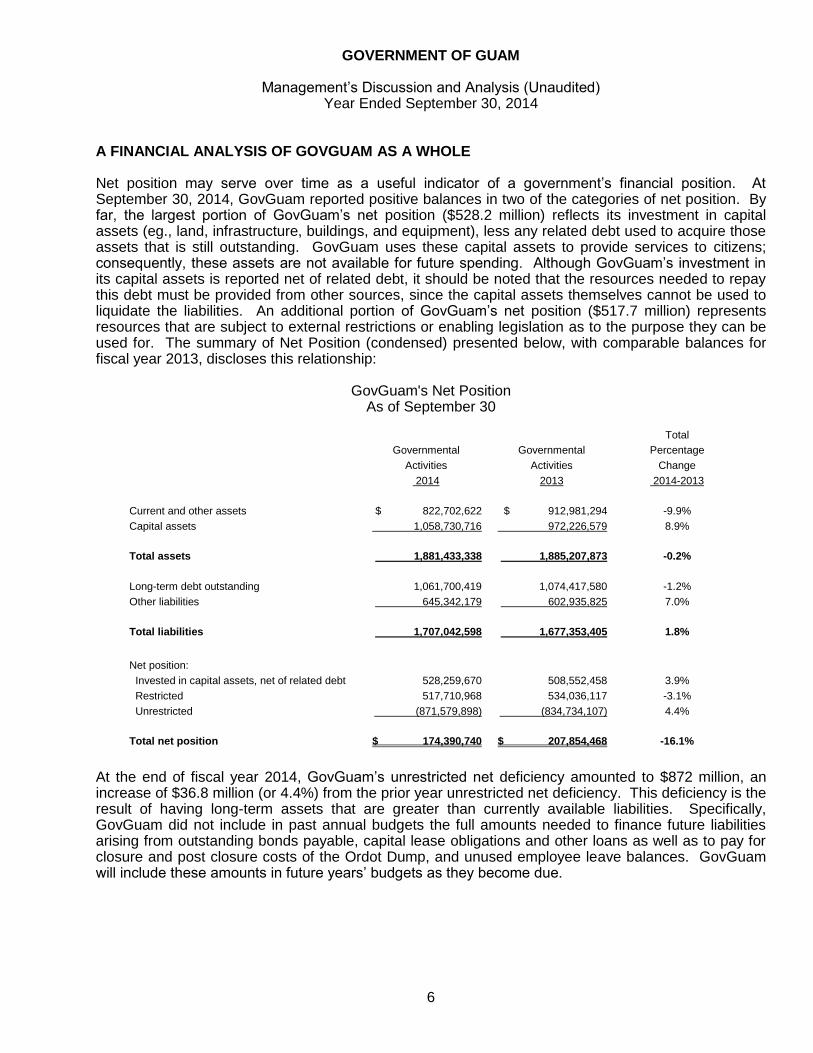

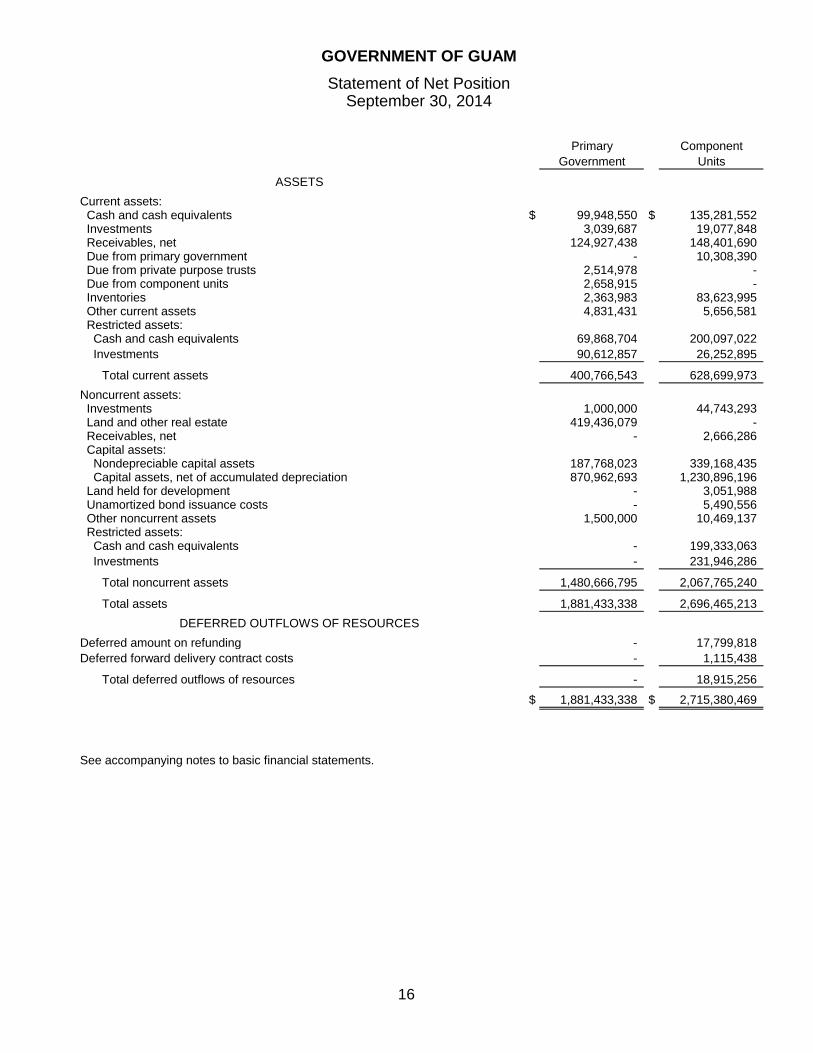

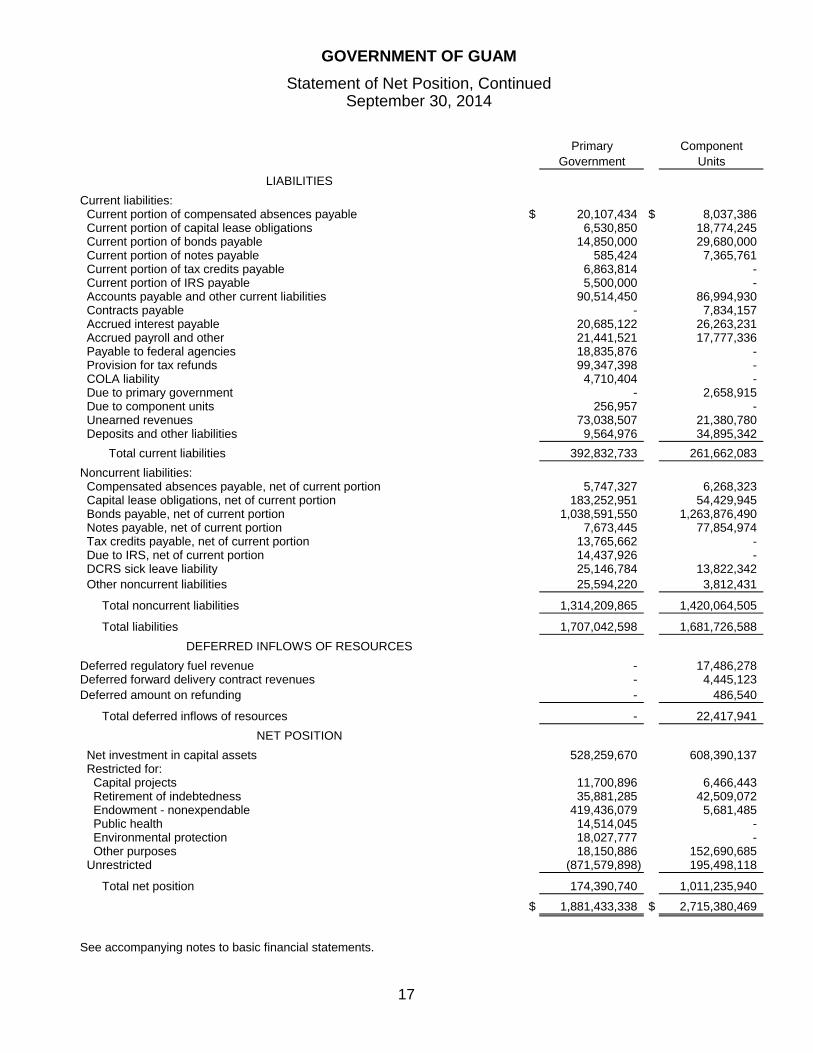

A FINANCIAL ANALYSIS OF GOVGUAM AS A WHOLE Net position may serve over time as a useful indicator of a government’s financial position. At September 30, 2014, GovGuam reported positive balances in two of the categories of net position. By far, the largest portion of GovGuam’s net position ($528.2 million) reflects its investment in capital assets (eg., land, infrastructure, buildings, and equipment), less any related debt used to acquire those assets that is still outstanding. GovGuam uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although GovGuam’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate the liabilities. An additional portion of GovGuam’s net position ($517.7 million) represents resources that are subject to external restrictions or enabling legislation as to the purpose they can be used for. The summary of Net Position (condensed) presented below, with comparable balances for fiscal year 2013, discloses this relationship:

GovGuam's Net Position

As of September 30

Total

Governmental Governmental Percentage

Activities Activities Change

2014 2013 2014-2013

Current and other assets $ 822,702,622 $ 912,981,294 -9.9%

Capital assets 1,058,730,716 972,226,579 8.9%

Total assets 1,881,433,338 1,885,207,873 -0.2%

Long-term debt outstanding 1,061,700,419 1,074,417,580 -1.2%

Other liabilities 645,342,179 602,935,825 7.0%

Total liabilities 1,707,042,598 1,677,353,405 1.8%

Net position:

Invested in capital assets, net of related debt 528,259,670 508,552,458 3.9%

Restricted 517,710,968 534,036,117 -3.1%

Unrestricted (871,579,898) (834,734,107) 4.4%

Total net position $ 174,390,740 $ 207,854,468 -16.1%

At the end of fiscal year 2014, GovGuam’s unrestricted net deficiency amounted to $872 million, an increase of $36.8 million (or 4.4%) from the prior year unrestricted net deficiency. This deficiency is the result of having long-term assets that are greater than currently available liabilities. Specifically, GovGuam did not include in past annual budgets the full amounts needed to finance future liabilities arising from outstanding bonds payable, capital lease obligations and other loans as well as to pay for closure and post closure costs of the Ordot Dump, and unused employee leave balances. GovGuam will include these amounts in future years’ budgets as they become due.

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

7

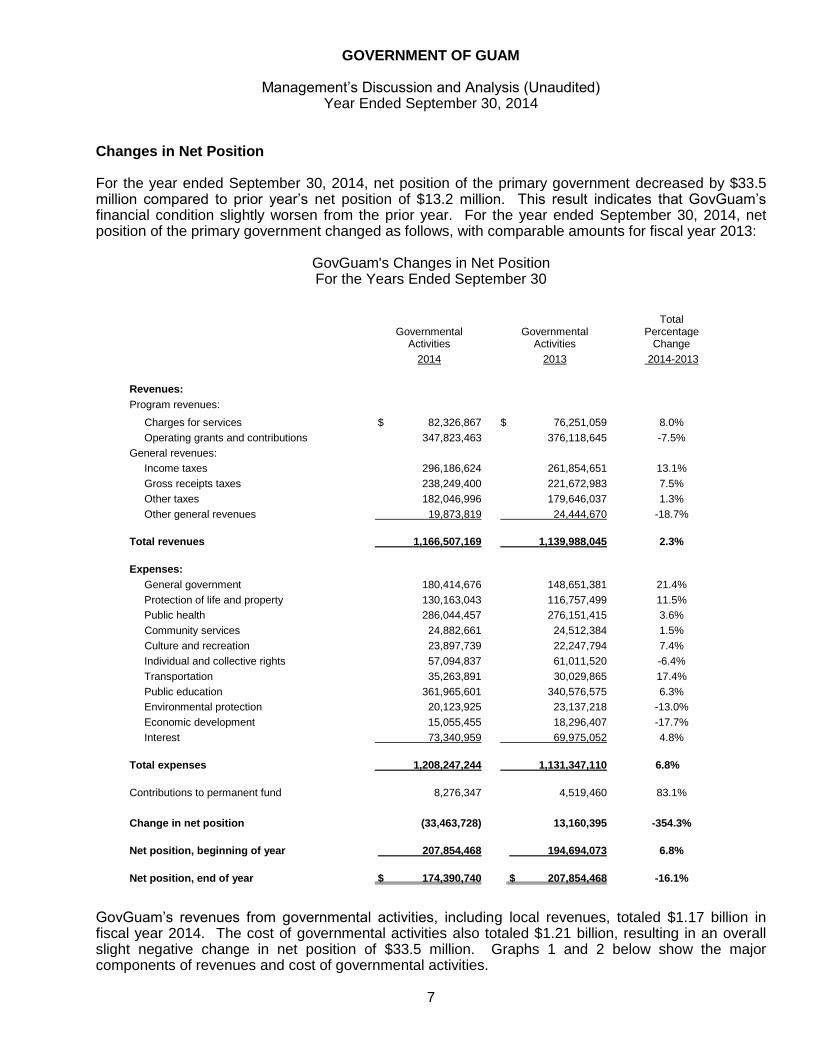

Changes in Net Position For the year ended September 30, 2014, net position of the primary government decreased by $33.5 million compared to prior year’s net position of $13.2 million. This result indicates that GovGuam’s financial condition slightly worsen from the prior year. For the year ended September 30, 2014, net position of the primary government changed as follows, with comparable amounts for fiscal year 2013:

GovGuam's Changes in Net Position For the Years Ended September 30

Governmental

Governmental

Total

Percentage Activities Activities Change

2014 2013 2014-2013

Revenues:

Program revenues:

Charges for services $ 82,326,867 $ 76,251,059 8.0%

Operating grants and contributions 347,823,463 376,118,645 -7.5%

General revenues:

Income taxes 296,186,624 261,854,651 13.1%

Gross receipts taxes 238,249,400 221,672,983 7.5%

Other taxes 182,046,996 179,646,037 1.3%

Other general revenues 19,873,819 24,444,670 -18.7%

Total revenues 1,166,507,169 1,139,988,045 2.3%

Expenses:

General government 180,414,676 148,651,381 21.4%

Protection of life and property 130,163,043 116,757,499 11.5%

Public health 286,044,457 276,151,415 3.6%

Community services 24,882,661 24,512,384 1.5%

Culture and recreation 23,897,739 22,247,794 7.4%

Individual and collective rights 57,094,837 61,011,520 -6.4%

Transportation 35,263,891 30,029,865 17.4%

Public education 361,965,601 340,576,575 6.3%

Environmental protection 20,123,925 23,137,218 -13.0%

Economic development 15,055,455 18,296,407 -17.7%

Interest 73,340,959 69,975,052 4.8%

Total expenses 1,208,247,244 1,131,347,110 6.8%

Contributions to permanent fund 8,276,347 4,519,460 83.1%

Change in net position (33,463,728) 13,160,395 -354.3%

Net position, beginning of year 207,854,468 194,694,073 6.8%

Net position, end of year $ 174,390,740 $ 207,854,468 -16.1%

GovGuam’s revenues from governmental activities, including local revenues, totaled $1.17 billion in fiscal year 2014. The cost of governmental activities also totaled $1.21 billion, resulting in an overall slight negative change in net position of $33.5 million. Graphs 1 and 2 below show the major components of revenues and cost of governmental activities.

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

8

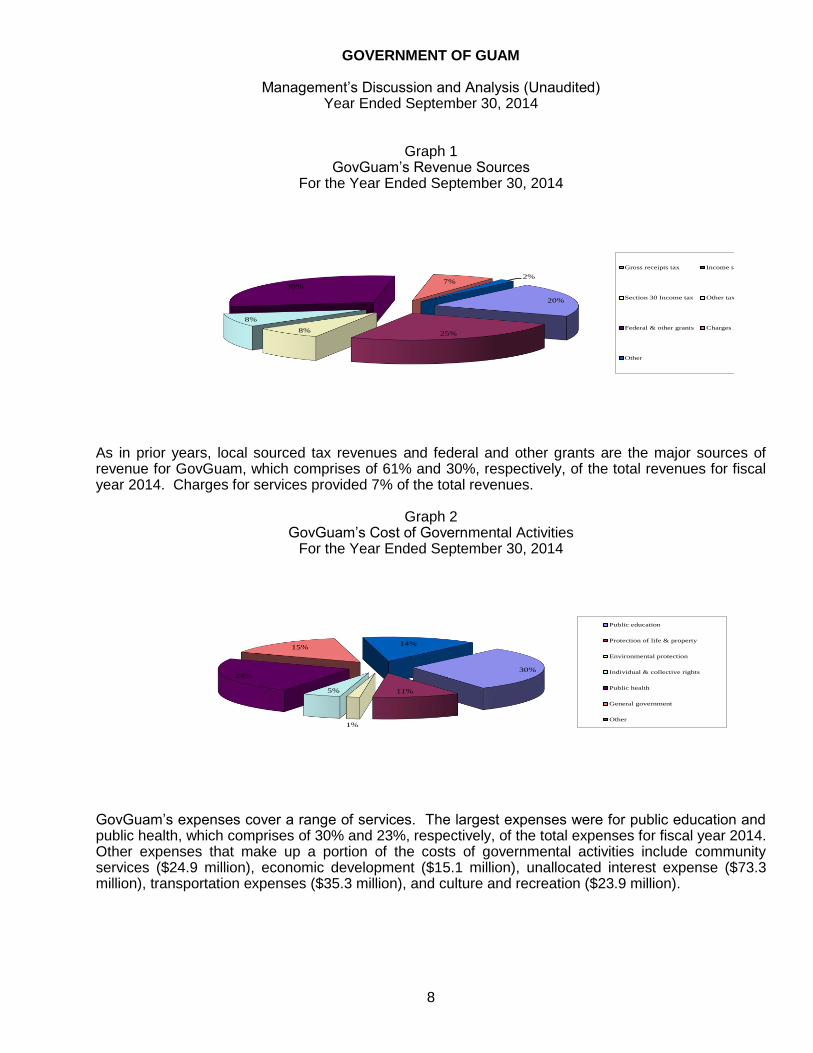

Graph 1 GovGuam’s Revenue Sources

For the Year Ended September 30, 2014

20%

25%8%

8%

30%7%

2%

Gross receipts tax Income tax

Section 30 Income tax Other taxes

Federal & other grants Charges for services

Other

As in prior years, local sourced tax revenues and federal and other grants are the major sources of revenue for GovGuam, which comprises of 61% and 30%, respectively, of the total revenues for fiscal year 2014. Charges for services provided 7% of the total revenues.

Graph 2 GovGuam’s Cost of Governmental Activities

For the Year Ended September 30, 2014

30%

11%

1%

5%

24%

15%14%

Public education

Protection of life & property

Environmental protection

Individual & collective rights

Public health

General government

Other

GovGuam’s expenses cover a range of services. The largest expenses were for public education and public health, which comprises of 30% and 23%, respectively, of the total expenses for fiscal year 2014. Other expenses that make up a portion of the costs of governmental activities include community services ($24.9 million), economic development ($15.1 million), unallocated interest expense ($73.3 million), transportation expenses ($35.3 million), and culture and recreation ($23.9 million).

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

9

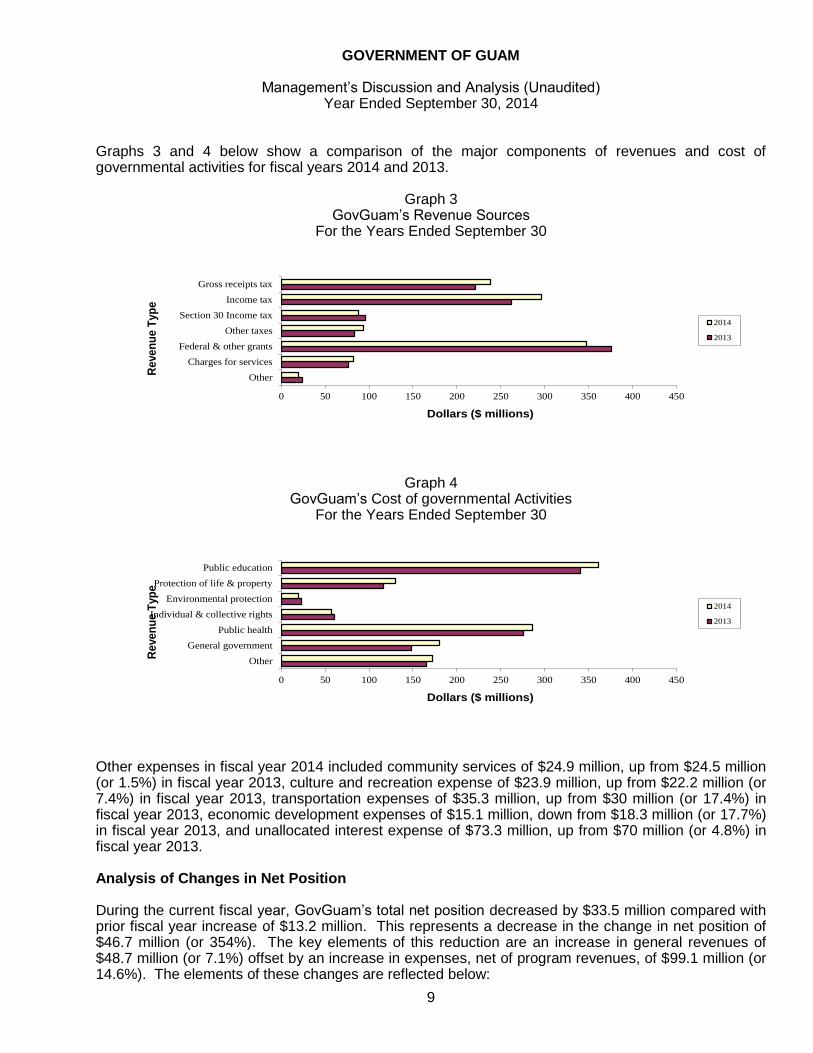

Graphs 3 and 4 below show a comparison of the major components of revenues and cost of governmental activities for fiscal years 2014 and 2013.

Graph 3 GovGuam’s Revenue Sources

For the Years Ended September 30

0 50 100 150 200 250 300 350 400 450

Other

Charges for services

Federal & other grants

Other taxes

Section 30 Income tax

Income tax

Gross receipts tax

Dollars ($ millions)

Re

ve

nu

e T

yp

e

2014

2013

Graph 4 GovGuam’s Cost of governmental Activities

For the Years Ended September 30

0 50 100 150 200 250 300 350 400 450

Other

General government

Public health

Individual & collective rights

Environmental protection

Protection of life & property

Public education

Dollars ($ millions)

Re

ve

nu

e T

yp

e

2014

2013

Other expenses in fiscal year 2014 included community services of $24.9 million, up from $24.5 million (or 1.5%) in fiscal year 2013, culture and recreation expense of $23.9 million, up from $22.2 million (or 7.4%) in fiscal year 2013, transportation expenses of $35.3 million, up from $30 million (or 17.4%) in fiscal year 2013, economic development expenses of $15.1 million, down from $18.3 million (or 17.7%) in fiscal year 2013, and unallocated interest expense of $73.3 million, up from $70 million (or 4.8%) in fiscal year 2013. Analysis of Changes in Net Position During the current fiscal year, GovGuam’s total net position decreased by $33.5 million compared with prior fiscal year increase of $13.2 million. This represents a decrease in the change in net position of $46.7 million (or 354%). The key elements of this reduction are an increase in general revenues of $48.7 million (or 7.1%) offset by an increase in expenses, net of program revenues, of $99.1 million (or 14.6%). The elements of these changes are reflected below:

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

10

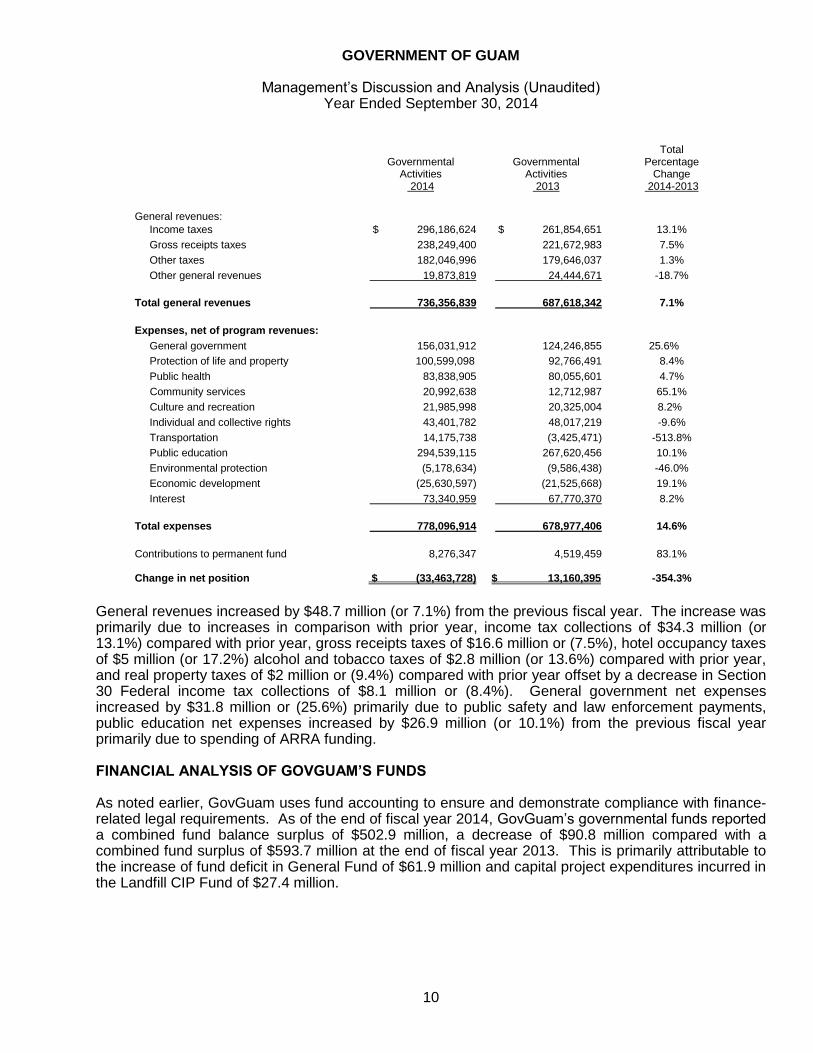

Governmental

Activities

Governmental

Activities

Total Percentage

Change 2014 2013 2014-2013

General revenues:

Income taxes $ 296,186,624 $ 261,854,651 13.1%

Gross receipts taxes 238,249,400 221,672,983 7.5%

Other taxes 182,046,996 179,646,037 1.3%

Other general revenues 19,873,819 24,444,671 -18.7%

Total general revenues 736,356,839 687,618,342 7.1%

Expenses, net of program revenues:

General government 156,031,912 124,246,855 25.6%

Protection of life and property 100,599,098 92,766,491 8.4%

Public health 83,838,905 80,055,601 4.7%

Community services 20,992,638 12,712,987 65.1%

Culture and recreation 21,985,998 20,325,004 8.2%

Individual and collective rights 43,401,782 48,017,219 -9.6%

Transportation 14,175,738 (3,425,471) -513.8%

Public education 294,539,115 267,620,456 10.1%

Environmental protection (5,178,634) (9,586,438) -46.0%

Economic development (25,630,597) (21,525,668) 19.1%

Interest 73,340,959 67,770,370 8.2%

Total expenses 778,096,914 678,977,406 14.6%

Contributions to permanent fund 8,276,347 4,519,459 83.1% Change in net position $ (33,463,728) $ 13,160,395 -354.3%

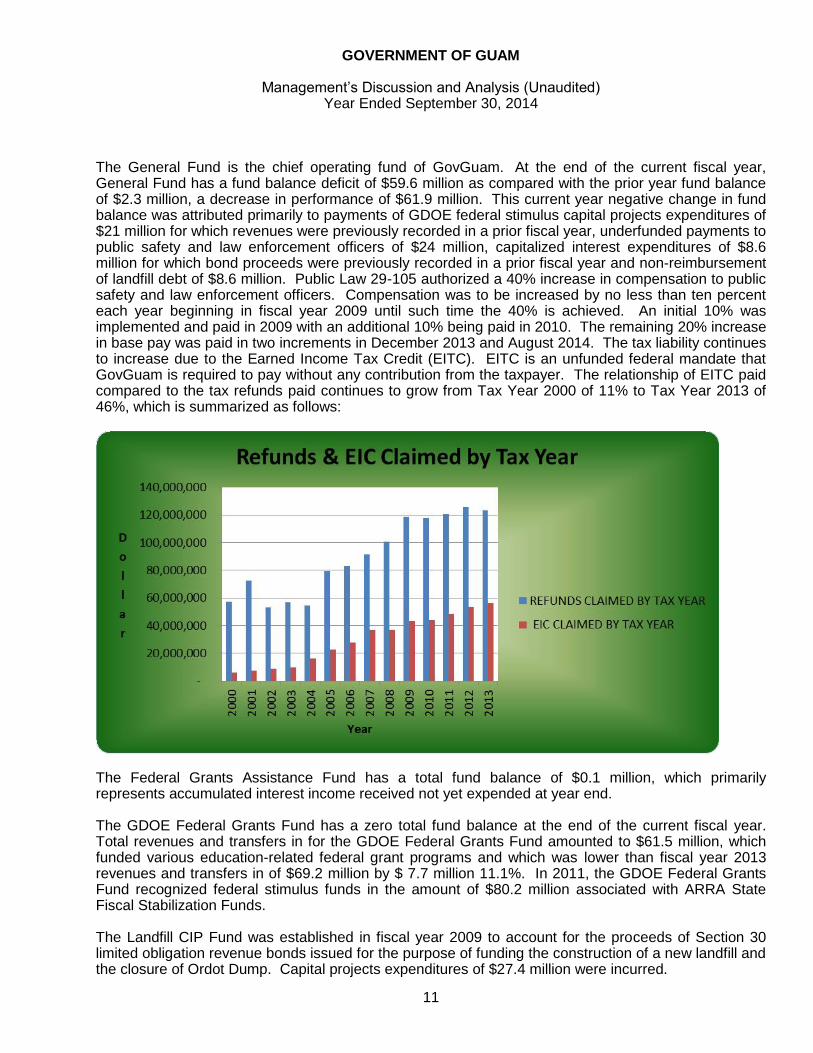

General revenues increased by $48.7 million (or 7.1%) from the previous fiscal year. The increase was primarily due to increases in comparison with prior year, income tax collections of $34.3 million (or 13.1%) compared with prior year, gross receipts taxes of $16.6 million or (7.5%), hotel occupancy taxes of $5 million (or 17.2%) alcohol and tobacco taxes of $2.8 million (or 13.6%) compared with prior year, and real property taxes of $2 million or (9.4%) compared with prior year offset by a decrease in Section 30 Federal income tax collections of $8.1 million or (8.4%). General government net expenses increased by $31.8 million or (25.6%) primarily due to public safety and law enforcement payments, public education net expenses increased by $26.9 million (or 10.1%) from the previous fiscal year primarily due to spending of ARRA funding. FINANCIAL ANALYSIS OF GOVGUAM’S FUNDS As noted earlier, GovGuam uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. As of the end of fiscal year 2014, GovGuam’s governmental funds reported a combined fund balance surplus of $502.9 million, a decrease of $90.8 million compared with a combined fund surplus of $593.7 million at the end of fiscal year 2013. This is primarily attributable to the increase of fund deficit in General Fund of $61.9 million and capital project expenditures incurred in the Landfill CIP Fund of $27.4 million.

GOVERNMENT OF GUAM

Management’s Discussion and Analysis (Unaudited) Year Ended September 30, 2014

11