Embed Size (px)

Citation preview

23 - 1Copyright 2003 Pearson Education Canada Inc.

CHAPTER 23Assurance Services:

Attest Engagements

23 - 2Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports

GAAS identifies “special audit-based

engagements”for which

a public accountant may be engaged.

23 - 3Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::financial information other than financial information other than

financial statementsfinancial statementsAn auditor may be engaged to report on a specific aspect of the financial statements,e.g., sales, accounts receivable, costs of acapital project.

accountsreceivable

23 - 4Copyright 2003 Pearson Education Canada Inc.

An auditor may be engaged to report on a specific aspect of the financial statements,e.g., sales, accounts receivable, costs of a capital project.

Materiality must be defined in terms of theelement/account/item rather than the overallfinancial statements.

Special ReportsSpecial Reports::financial information other than financial information other than

financial statementsfinancial statements

23 - 5Copyright 2003 Pearson Education Canada Inc.

Materiality must be defined in terms of theelement/account/item rather than the overall financial statements.

The auditor should comply with the general and examination standards of GAAS.

Special ReportsSpecial Reports::financial information other than financial information other than

financial statementsfinancial statements

23 - 6Copyright 2003 Pearson Education Canada Inc.

Introductory Paragraph- audit performed- any relevant portions of any agreements

statutes,etc. - basis of accounting if other than GAAP- any lack of consistent application or

interpretation- responsibilities of management and auditor

Special ReportsSpecial Reports::financial information other than financial information other than

financial statementsfinancial statements

23 - 7Copyright 2003 Pearson Education Canada Inc.

Introductory Paragraph

Scope Paragraph- similar but refers to financial information

Special ReportsSpecial Reports::financial information other than financial information other than

financial statementsfinancial statements

23 - 8Copyright 2003 Pearson Education Canada Inc.

Introductory Paragraph

Scope Paragraph

Opinion Paragraph- whether information is presented fairly in

accordance with accounting basis and any interpretations

Special ReportsSpecial Reports::financial information other than financial information other than

financial statementsfinancial statements

23 - 9Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Applying specified auditing Applying specified auditing

proceduresproceduresClient specifies audit procedures to be applied and form of report.

Distribution of report is normally restricted

23 - 10Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Applying specified auditing Applying specified auditing

proceduresproceduresClient specifies audit procedures to be applied and form of report.

Distribution of report is normally restricted.

The public accountant should comply with the general and first examination standard of GAAS.

23 - 11Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Applying specified auditing Applying specified auditing

proceduresprocedures

Report specifies:

- financial information

- procedures

- factual results of the procedures

- audit not performed - disclaimer

- any restrictions

23 - 12Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::compliance with agreements, compliance with agreements,

statutes, regulationsstatutes, regulations

In this type of engagement, the auditor determines whether a client is in compliancewith accounting and reporting requirementsin contract, statutes, regulations, e.g., a debtcovenant.

23 - 13Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::compliance with agreements, compliance with agreements,

statutes, regulationsstatutes, regulations

In this type of engagement, the auditor determines whether a client is in compliancewith accounting and reporting requirementsin contract, statutes, regulations, e.g., a debtcovenant.

The auditor should comply with the general and examination standards of GAAS.

23 - 14Copyright 2003 Pearson Education Canada Inc.

Introductory Paragraph- compliance is as audited- relevant provisions of agreement, statute or

regulation and any interpretations- any lack of consistent interpretation- responsibilities of management and auditor

Special ReportsSpecial Reports:: compliance with agreements, compliance with agreements,

statutes, regulationsstatutes, regulations

23 - 15Copyright 2003 Pearson Education Canada Inc.

Introductory Paragraph

Scope Paragraph- similar but refers to compliance with

relevant agreement, statute, regulation

Special ReportsSpecial Reports:: compliance with agreements, compliance with agreements,

statutes, regulationsstatutes, regulations

23 - 16Copyright 2003 Pearson Education Canada Inc.

Introductory Paragraph

Scope Paragraph

Opinion Paragraph- whether entity has complied with the

established criteria

Special ReportsSpecial Reports:: compliance with agreements, compliance with agreements,

statutes, regulationsstatutes, regulations

23 - 17Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Opinion on control procedures at Opinion on control procedures at

a service organizationa service organization

Service organizations may providecustodial, data-processing, or assetmanagement services

23 - 18Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Opinion on control procedures at Opinion on control procedures at

a service organizationa service organizationTypes of engagements:

1. design and existence of control procedures at point in time

2. design, effective operation and continuity of control procedures during a period of time

23 - 19Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Opinion on control procedures at Opinion on control procedures at

a service organizationa service organization

Service auditor should comply with the general standard, and the first and third examination standards.

23 - 20Copyright 2003 Pearson Education Canada Inc.

Special ReportsSpecial Reports::Opinion on control procedures at Opinion on control procedures at

a service organizationa service organizationSteps:

1. plan scope2. review design of internal control3. perform tests of control4. evaluate results5. obtain written management representation6. prepare report

23 - 21Copyright 2003 Pearson Education Canada Inc.

What is a What is a ReviewReview of of Financial Statements?Financial Statements?

23 - 22Copyright 2003 Pearson Education Canada Inc.

What is a What is a ReviewReview of of Financial Statements?Financial Statements?

A review is an engagement in which theaccountant expresses limited assurance as a result of a few auditing procedures.

23 - 23Copyright 2003 Pearson Education Canada Inc.

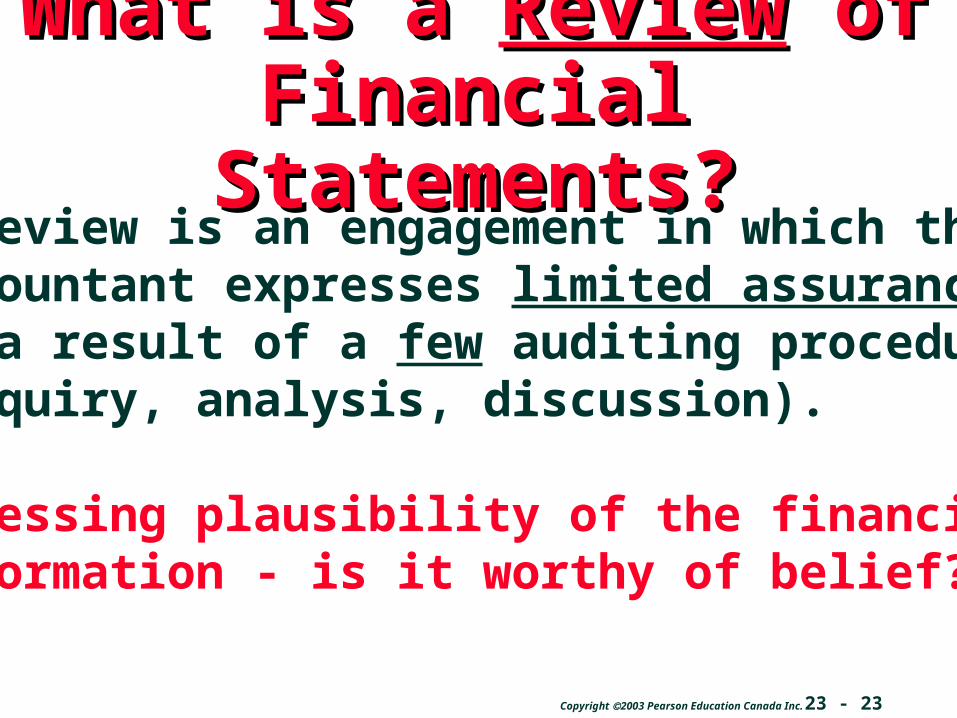

What is a What is a ReviewReview of of Financial Statements?Financial Statements?

A review is an engagement in which theaccountant expresses limited assurance as a result of a few auditing procedures(enquiry, analysis, discussion).

Assessing plausibility of the financialinformation - is it worthy of belief?

23 - 24Copyright 2003 Pearson Education Canada Inc.

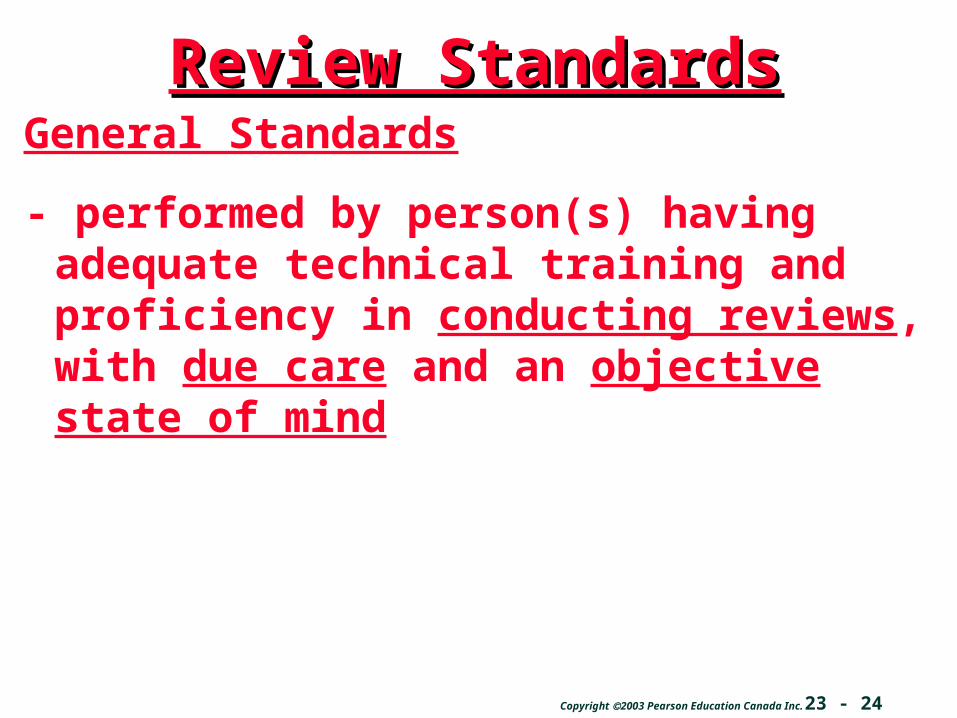

Review StandardsReview StandardsGeneral Standards

- performed by person(s) having adequate technical training and proficiency in conducting reviews, with due care and an objective state of mind

23 - 25Copyright 2003 Pearson Education Canada Inc.

Review StandardsReview StandardsGeneral Standards

Review Standards

- adequate planning, proper execution and proper supervision

- possess sufficient knowledge of the business for intelligent enquiry and assessment of information

- assess whether information is plausible using- enquiry, analysis, discussion- additional procedures if necessary

23 - 26Copyright 2003 Pearson Education Canada Inc.

Review StandardsReview StandardsGeneral Standards

Review Standards

Reporting Standards

- indicate scope, clearly indicate nature of review and distinguish from an audit

- indicate whether anything causes you not to believe information is in accordance with criteria or no assurance- explain any reservations and, if determinable, their effect

23 - 27Copyright 2003 Pearson Education Canada Inc.

Review ProceduresReview Procedures- gain sufficient knowledge of accounting principles and practices of the client and the industry

ACE

23 - 28Copyright 2003 Pearson Education Canada Inc.

Review ProceduresReview Procedures- gain sufficient knowledge of accounting principles and practices of the client and the industry- enquire of management/other personnel to determine fairness of statements and management integrity EXAMPLES: - accounting practices - actions at board and share- holder meetings - accounting methods used

23 - 29Copyright 2003 Pearson Education Canada Inc.

Review ProceduresReview Procedures- gain sufficient knowledge of accounting principles and practices of the client and the industry- enquire of management/other personnel to determine fairness of statements and management integrity - perform analytical procedures to identify unusual items and relationships

23 - 30Copyright 2003 Pearson Education Canada Inc.

Review ProceduresReview Procedures- gain sufficient knowledge of accounting principles and practices of the client and the industry- enquire of management/client personnel to determine fairness of statements and management integrity - perform analytical procedures to identify unusual items and relationships- discuss with management/client personnel the results of analytical procedures, the financial statements, and other matters

23 - 31Copyright 2003 Pearson Education Canada Inc.

Is an Engagement Letter RequiredIs an Engagement Letter Requiredon a Review Engagement?on a Review Engagement?

23 - 32Copyright 2003 Pearson Education Canada Inc.

Is an Engagement Letter RequiredIs an Engagement Letter Requiredon a Review Engagement?on a Review Engagement?

NO!But it is strongly advised as But it is strongly advised as

agreement as to nature and extent of agreement as to nature and extent of services is requiredservices is required

23 - 33Copyright 2003 Pearson Education Canada Inc.

What Should an Engagement What Should an Engagement Letter Cover?Letter Cover?

23 - 34Copyright 2003 Pearson Education Canada Inc.

What Should an Engagement What Should an Engagement Letter Cover?Letter Cover?

- public accountant’s services- client’s responsibilities- audit not to be performed; no opinion to be

expressed- any restrictions on distribution- each page of financial statements should be

marked “unaudited”- expected content of the report - engagement can’t be relied on to detect

fraud, error or other irregularities- statements don’t satisfy any statutory

requirements (if applicable)

23 - 35Copyright 2003 Pearson Education Canada Inc.

Is a Representation Letter Required Is a Representation Letter Required on a Review Engagement?on a Review Engagement?

23 - 36Copyright 2003 Pearson Education Canada Inc.

Is a Representation Letter Required Is a Representation Letter Required on a Review Engagement?on a Review Engagement?

NO!

But it is strongly advisedBut it is strongly advised

23 - 37Copyright 2003 Pearson Education Canada Inc.

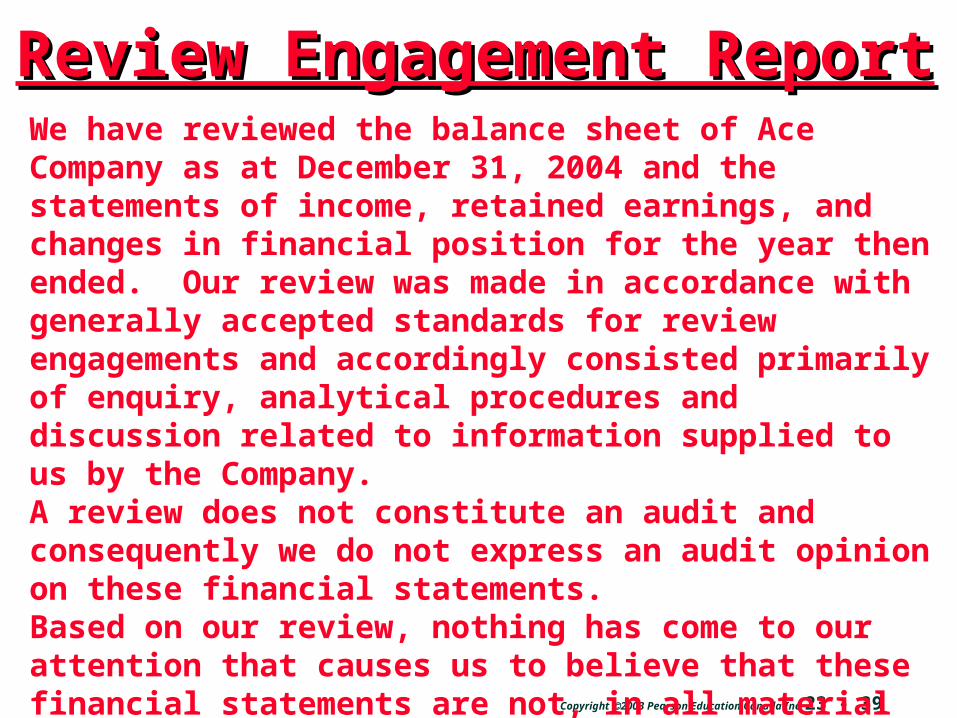

Review Engagement ReportReview Engagement ReportWe have reviewed the balance sheet of Ace Company as at December 31, 2004 and the statements of income, retained earnings, and changes in financial position for the year then ended. Our review was made in accordance with generally accepted standards for review engagements and accordingly consisted primarily of enquiry, analytical procedures and discussion related to information supplied to us by the Company.

23 - 38Copyright 2003 Pearson Education Canada Inc.

Review Engagement ReportReview Engagement ReportWe have reviewed the balance sheet of Ace Company as at December 31, 2004 and the statements of income, retained earnings, and changes in financial position for the year then ended. Our review was made in accordance with generally accepted standards for review engagements and accordingly consisted primarily of enquiry, analytical procedures and discussion related to information supplied to us by the Company.

A review does not constitute an audit and consequently we do not express an audit opinion on these financial statements.

23 - 39Copyright 2003 Pearson Education Canada Inc.

Review Engagement ReportReview Engagement ReportWe have reviewed the balance sheet of Ace Company as at December 31, 2004 and the statements of income, retained earnings, and changes in financial position for the year then ended. Our review was made in accordance with generally accepted standards for review engagements and accordingly consisted primarily of enquiry, analytical procedures and discussion related to information supplied to us by the Company.A review does not constitute an audit and consequently we do not express an audit opinion on these financial statements.Based on our review, nothing has come to our attention that causes us to believe that these financial statements are not, in all material respects, in accordance with generally accepted accounting principles.

23 - 40Copyright 2003 Pearson Education Canada Inc.

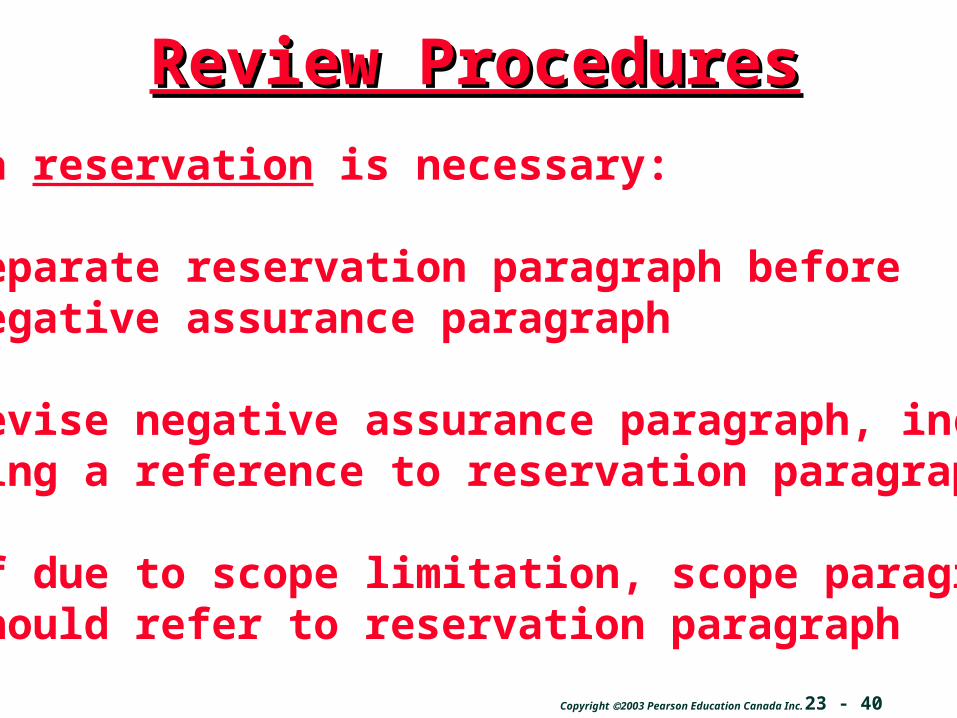

Review ProceduresReview Procedures

If a reservation is necessary:

- separate reservation paragraph before negative assurance paragraph

- revise negative assurance paragraph, inclu- ding a reference to reservation paragraph

- if due to scope limitation, scope paragraph should refer to reservation paragraph

23 - 41Copyright 2003 Pearson Education Canada Inc.

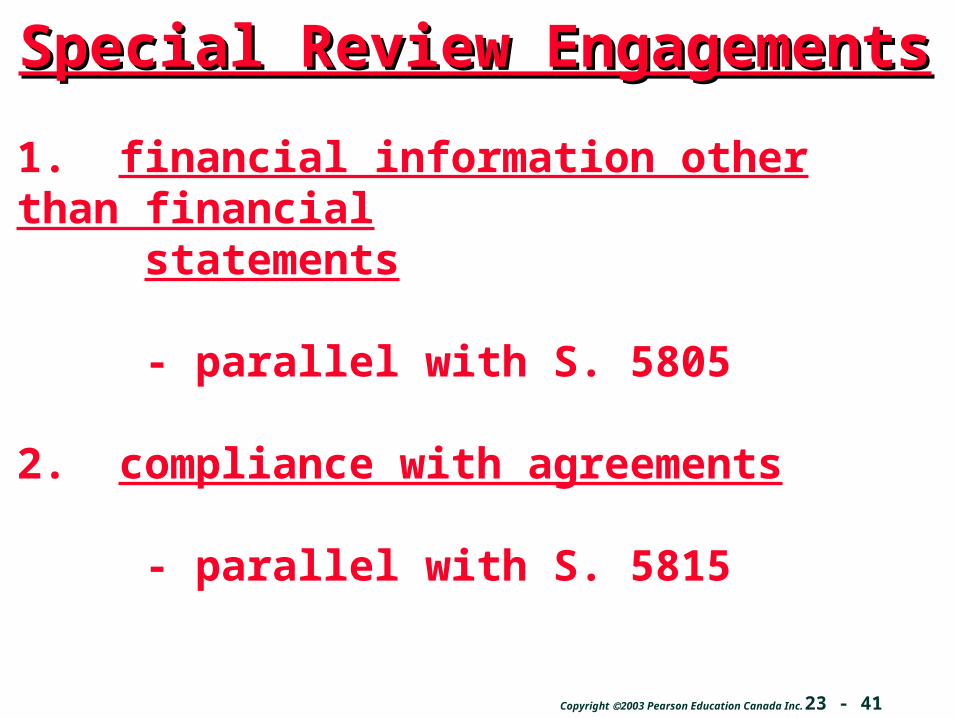

Special Review EngagementsSpecial Review Engagements

1. financial information other than financial statements

- parallel with S. 5805

2. compliance with agreements

- parallel with S. 5815

23 - 42Copyright 2003 Pearson Education Canada Inc.

What is a What is a compilationcompilation??

23 - 43Copyright 2003 Pearson Education Canada Inc.

What is a What is a compilationcompilation??In a compilation engagement, the publicaccountant prepares the client’s finan-cial statements without expressing anyassurance on the statements.

assurance

23 - 44Copyright 2003 Pearson Education Canada Inc.

Compilation ProceduresCompilation Procedures - assemble the information and ensure it is arithmetically correct

23 - 45Copyright 2003 Pearson Education Canada Inc.

Compilation ProceduresCompilation Procedures- assemble the information and ensure it is arithmetically correct- before issuing the report, read the compiled statements and consider whether such statements appear obviously false or misleading

23 - 46Copyright 2003 Pearson Education Canada Inc.

Should an Engagement Letter and a Should an Engagement Letter and a Representation Letter be Obtained Representation Letter be Obtained

on a Compilation Engagement?on a Compilation Engagement?

23 - 47Copyright 2003 Pearson Education Canada Inc.

Should an Engagement Letter and a Should an Engagement Letter and a Representation Letter be Obtained Representation Letter be Obtained

on a Compilation Engagement?on a Compilation Engagement?

YES!

It is It is alwaysalways advised to do so advised to do so

23 - 48Copyright 2003 Pearson Education Canada Inc.

Notice to ReaderNotice to Reader

We have compiled the balance sheet of Ace Company as at December 31, 2004 and the statements of income, retained earnings, and changes in financial position for the year then ended from information provided by management.

23 - 49Copyright 2003 Pearson Education Canada Inc.

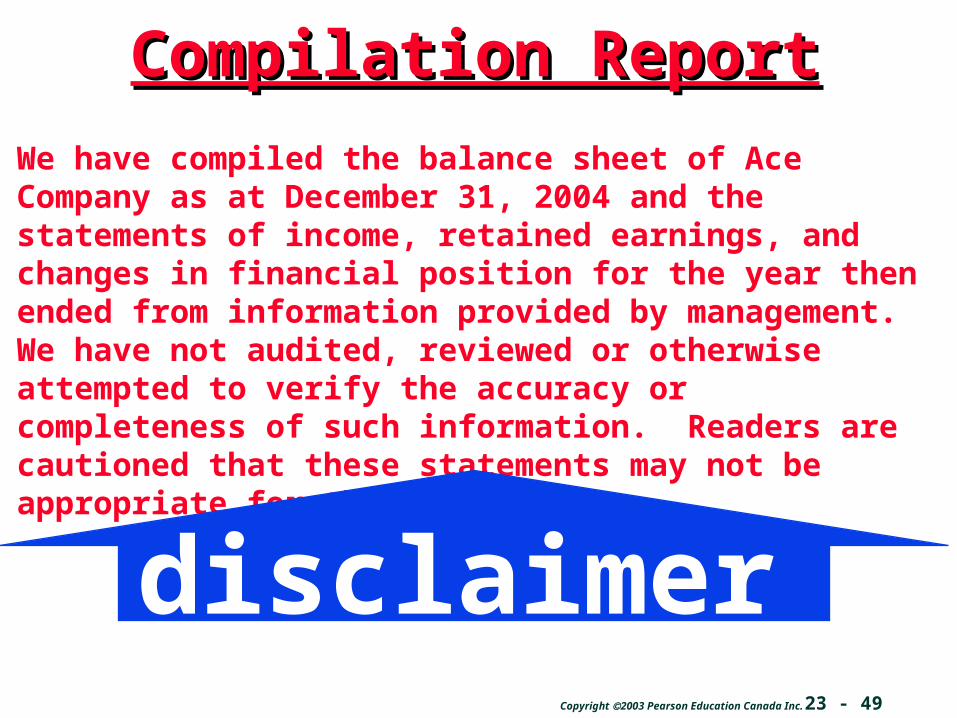

Compilation ReportCompilation Report

We have compiled the balance sheet of Ace Company as at December 31, 2004 and the statements of income, retained earnings, and changes in financial position for the year then ended from information provided by management. We have not audited, reviewed or otherwise attempted to verify the accuracy or completeness of such information. Readers are cautioned that these statements may not be appropriate for their purposes.

disclaimer

23 - 50Copyright 2003 Pearson Education Canada Inc.

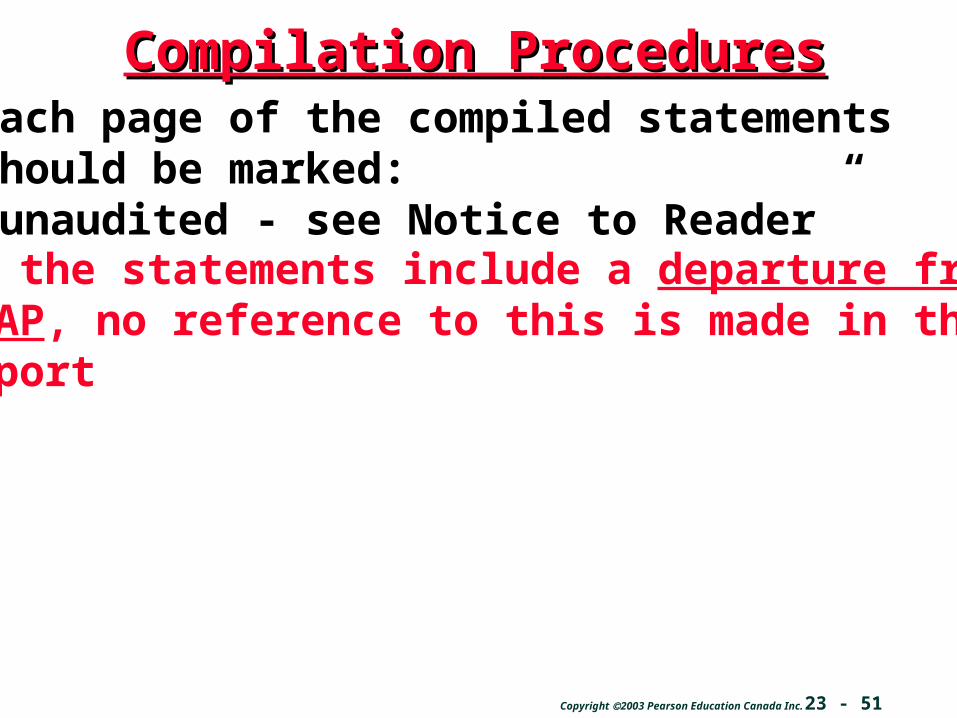

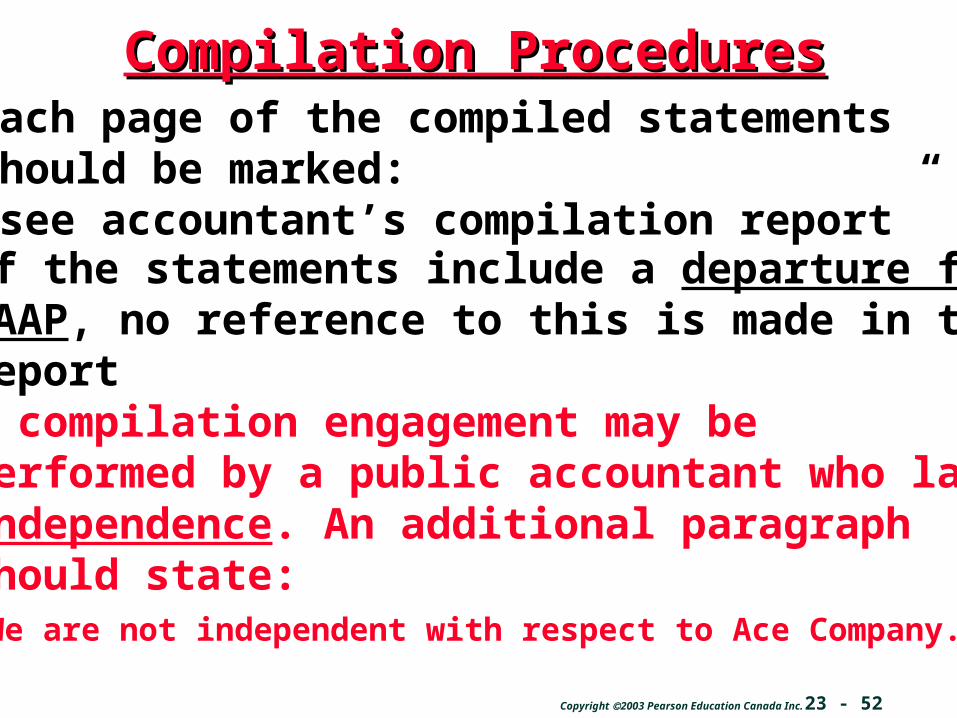

Compilation ProceduresCompilation Procedures

- each page of the compiled statements should be marked: “unaudited - see Notice to Reader”

why?

23 - 51Copyright 2003 Pearson Education Canada Inc.

Compilation ProceduresCompilation Procedures

- if the statements include a departure from GAAP, no reference to this is made in the report

- each page of the compiled statements should be marked: “unaudited - see Notice to Reader”

23 - 52Copyright 2003 Pearson Education Canada Inc.

Compilation ProceduresCompilation Procedures

- if the statements include a departure from GAAP, no reference to this is made in the report- a compilation engagement may be performed by a public accountant who lacks independence. An additional paragraph should state: “We are not independent with respect to Ace Company.”

- each page of the compiled statements should be marked: “see accountant’s compilation report”

23 - 53Copyright 2003 Pearson Education Canada Inc.

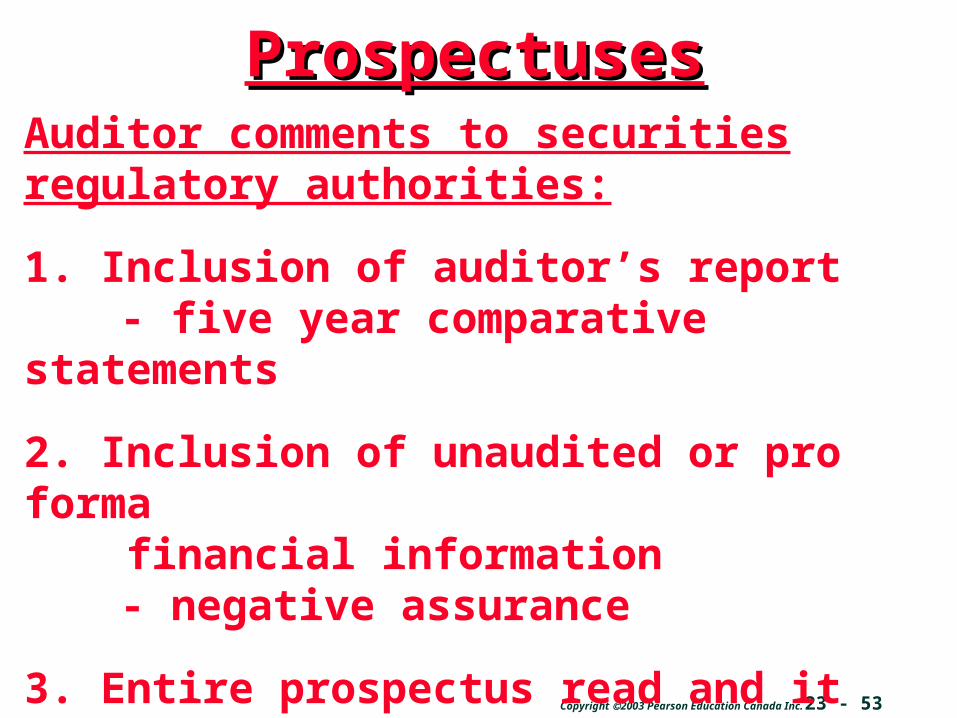

ProspectusesProspectusesAuditor comments to securities regulatory authorities:

1. Inclusion of auditor’s report- five year comparative statements

2. Inclusion of unaudited or pro forma financial information

- negative assurance

3. Entire prospectus read and it contains no misrepresentations

23 - 54Copyright 2003 Pearson Education Canada Inc.

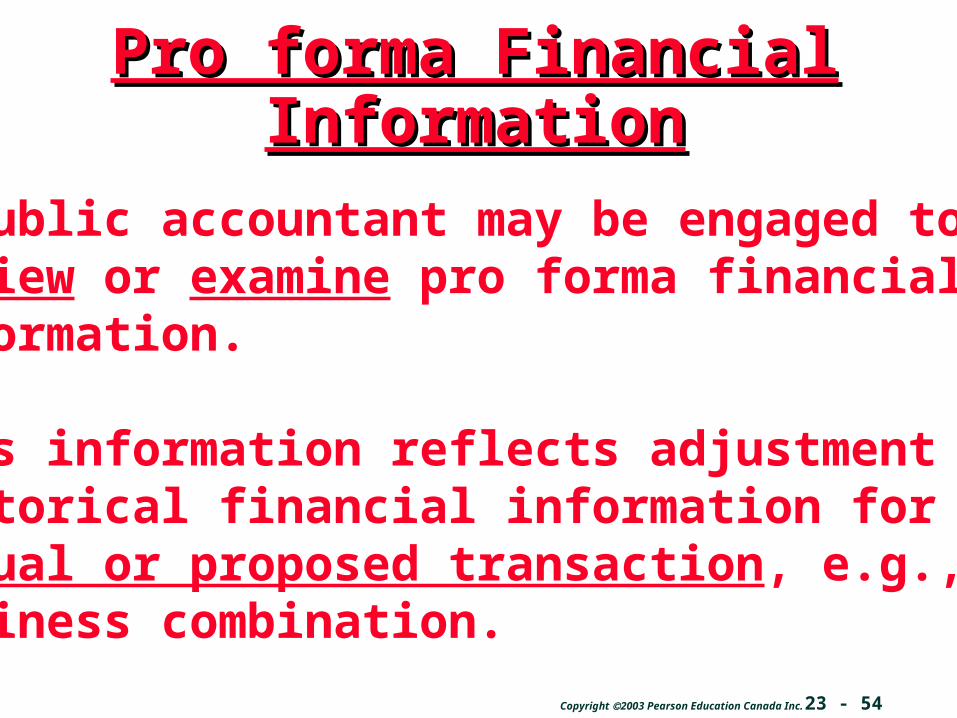

Pro forma Financial Pro forma Financial InformationInformation

A public accountant may be engaged toreview or examine pro forma financial information.

This information reflects adjustment of historical financial information for anactual or proposed transaction, e.g., abusiness combination.

23 - 55Copyright 2003 Pearson Education Canada Inc.

Pro forma Financial Pro forma Financial InformationInformation

The resulting review report indicatesthat the engagement was less in scope than an examination and provides negative assurance.

23 - 56Copyright 2003 Pearson Education Canada Inc.

Pro forma Financial Pro forma Financial InformationInformation

The resulting review report indicatesthat the engagement was less in scope than an examination and provides negative assurance.

The resulting examination report in-cludes an opinion regarding the reason-ableness of management’s assumptions.

23 - 57Copyright 2003 Pearson Education Canada Inc.

Letters for UnderwritersLetters for Underwriters

When an audit client issues new securities, the underwriters will request a “comfort” letter from the auditor regarding information in the prospectus that is not covered in the accountant’s report.

23 - 58Copyright 2003 Pearson Education Canada Inc.

Letters for UnderwritersLetters for UnderwritersWhen an audit client issues new securities, the underwriters will request a “comfort” letter from the auditor regarding information in the prospectus that is not covered in the accountant’s report.

The auditor’s letter will include:- positive assurance regarding the audit and auditor independence- negative assurance or summary information on other information in the prospectus

23 - 59Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsA public accountant may be asked by a client of another accountant:- to report on certain actual or hypothetical transactions

23 - 60Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsA public accountant may be asked by a clientof another accountant:- to report on certain actual or hypothetical transactions- the type of opinion which would be rendered based on certain facts

opinion?

23 - 61Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsA public accountant may be asked by a client of another accountant:- to report on certain actual or hypothetical transactions- the type of opinion which would be rendered based on certain facts- the appropriate application of accounting principles to hypothetical situations

23 - 62Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsA public accountant may be asked by a client of another accountant:- to report on certain actual or hypothetical transactions- the type of opinion which would be rendered based on certain facts- the appropriate application of accounting principles to hypothetical situations- the appropriate application of auditing of review standards

23 - 63Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsIn completing this type of engagement, a public accountant must:- get permission from the client

23 - 64Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsIn completing this type of engagement, a public accountant must:- get permission from the client- contact the client’s current accountant/auditor (predecessor/successor rules are applicable)

23 - 65Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsIn completing this type of engagement, a public accountant must:- obtain the client’s permission- contact the client’s current accountant/auditor (predecessor/successor rules are applicable)- get a written statement of all relevant facts and assumptions

23 - 66Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsIn completing this type of engagement, a public accountant must:- obtain the client’s permission- contact the client’s current accountant/auditor (predecessor/successor rules are applicable)- get a written statement of all relevant facts and assumptions- comply with the general standard, and the first and third examination standards of GAAS

23 - 67Copyright 2003 Pearson Education Canada Inc.

Application of accounting Application of accounting principles, auditing standards, principles, auditing standards,

review standardsreview standardsIn completing this type of engagement, a public accountant must:- obtain the client’s permission- contact the client’s current accountant/auditor (predecessor/successor rules are applicable)- get a written statement of all relevant facts and assumptions- comply with the general standard, and the first and third examination standards of GAAS- report in writing

23 - 68Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

How does a forecast

differ from a projection?

23 - 69Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

A forecast is a prediction of a company’s future financial position and results.A projection considers the effects of one ormore hypotheses.

23 - 70Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

A forecast is a prediction of a company’s future financial position and results.

A projection considers the effects of one ormore hypotheses.

A public accountant may be engaged to compile or examine these reports.

23 - 71Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

Professional standards- adequate technical training and proficiency

in auditing- due care- adequate planning and supervision- obtain sufficient evidence- document important matters

23 - 72Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and ProjectionsFinancial Forecasts and Projections

Contents of engagement letter:- form of forecast- time period covered- management to comply with CICA accounting

standards and any relevant securities requirements

- management is responsible for the forecast- management is responsible for assumptions being

reasonable- any need for accountant to have access to outside

specialists and third party reports- form and content of report- no responsibility to update

23 - 73Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

- a public accountant should not be associated with these reports if the assumptions are not disclosed

criticallyimportant

23 - 74Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

- a public accountant should not be associated with these reports if the assumptions are not disclosed- forecasts may be for general OR limited use, BUT projections are for limited use ONLY

23 - 75Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

- forecasts may be for general OR limited use, BUT projections are for limited use ONLY- the compilation report expresses no assurance, the examination report provides assurance regarding reasonableness of assumptions

23 - 76Copyright 2003 Pearson Education Canada Inc.

Financial Forecasts and Financial Forecasts and ProjectionsProjections

Both the compilation and examinationreports end with the following:

Since this forecast is based on assumptions regarding futureevents, actual results will vary from the information presentedand the variations may be material...

23 - 77Copyright 2003 Pearson Education Canada Inc.

What is an What is an attestationattestation engagement? engagement?

23 - 78Copyright 2003 Pearson Education Canada Inc.

What is an What is an attestationattestation engagement? engagement?

In an attestation engagement, the publicaccountant forms an opinion regarding the reliability of someone’s assertionusing appropriate criteria.

examples?

23 - 79Copyright 2003 Pearson Education Canada Inc.

What is a What is a direct reportingdirect reporting engagement?engagement?

An engagement where the auditordirectly expresses a conclusion on the evaluation using appropriate criteria.

There are 15 professional standardswhich are somewhat similar to GAAS,and are categorized into general,performance, and reporting standards.

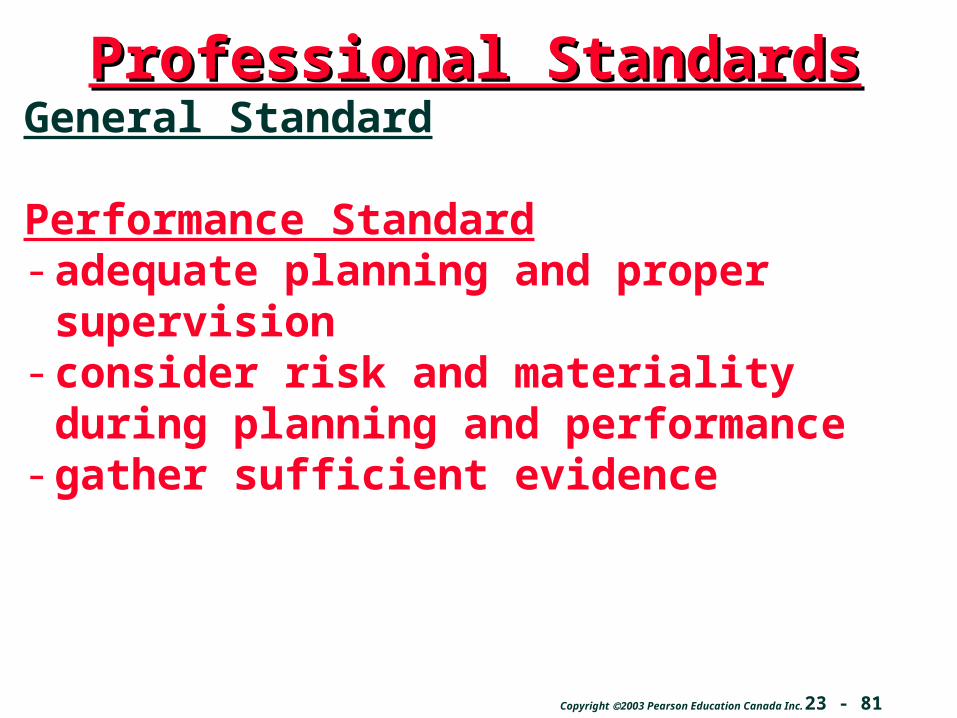

23 - 80Copyright 2003 Pearson Education Canada Inc.

General Standard- ensure engagement can be completed in

accordance with assurance standards- adequate proficiency- collectively possess adequate knowledge of

the subject matter- due care- objective statement of mind

Professional StandardsProfessional Standards

23 - 81Copyright 2003 Pearson Education Canada Inc.

General Standard

Performance Standard- adequate planning and proper supervision- consider risk and materiality during

planning and performance- gather sufficient evidence

Professional StandardsProfessional Standards

23 - 82Copyright 2003 Pearson Education Canada Inc.

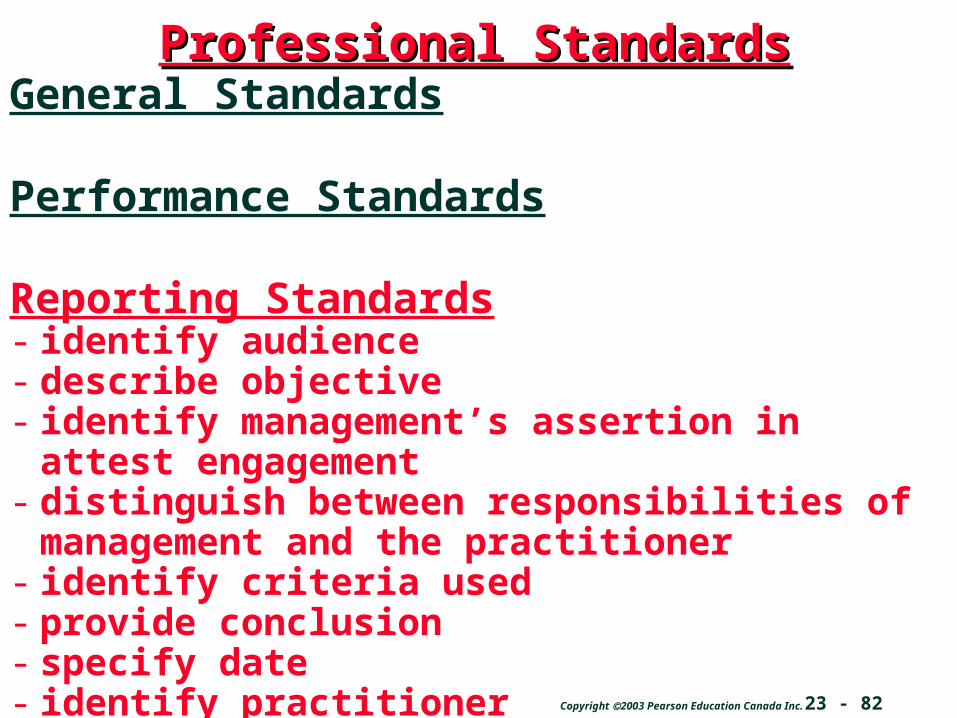

General Standards

Performance Standards

Reporting Standards- identify audience- describe objective- identify management’s assertion in attest

engagement- distinguish between responsibilities of

management and the practitioner- identify criteria used- provide conclusion- specify date- identify practitioner- identify place

Professional StandardsProfessional Standards