Embed Size (px)

Citation preview

PROJECT REPORTON

INITIAL PUBLIC OFFERING

INITIAL PUBLIC OFFERING

SUBMITTED TO:- Mrs. Deepika Dhall SUBMITTED BY:- ARUN GULERIA

MBA Sem. IV

ARUN GULERIA [email protected]

1

LOVELY PROFESSIONAL UNIVERSITY LOVELY INSTITUTE OF MANAGEMENT (LIM)

ACKNOWLEDGEMENT

In order to make my project I acknowledge a special thanks to all those people without

whose supports it would not be possible for me to complete for me to complete my report.

First of all I really thankful to my Lovely Professional University because of them I

could achieve the target. I express my sincere thanks to my project guide Mrs. Deepika Dhall

who had guide to me throughout my project.

Also I would like to express my inner feeling for all the people for co-operating and

helping me throughout the project.

Last but not the least I am thankful to my parents and friends who have provided me with

their constant support throughout this project.

Arun

Guleria

ARUN GULERIA [email protected]

2

INDEXS.No. PARTICULAR Page No.

1. ACKNOWLEDGEMENT (i)

2. EXECUTIVE SUMMARY 4

3. LITERATURE REVIEW: Kenji and Smith (2009) Sherman and Jagannathan (2009)

Kaneko and Pettway (2008) Biasis and Faugeron-Crouzet (2007) Wilhelm (2007) Summary of previous research

567789

7. IPO – AN INTRODUCTION 10

8. SIGNIFICANCE OF IPO 12

9. KINDS OF PUBLIC OFFERINGS 13

10. ANALYZING AN IPO INVESTMENT 17

12. IPO INVESTMENT STRATEGIES 19

13. PRICING OF AN IPO 21

14. UNDERPRICING AND OVERPRICING OF IPO’S 22

15. PRINCIPAL STEPS IN AN IPO 23

16. BOOK-BUILDING PROCESS 27

17. PLAYERS IN IPO 33

18 HDIL’s IPO VALUATION 37

19. FINDING 49

20. SUGGESTIONS 50

21. IPO GLOSSARY 51

22. BIBLIOGRAPHY 54

ARUN GULERIA [email protected]

3

EXECUTIVE SUMMARY

As we all know IPO – INITIAL PUBLIC OFFERING is the hottest topic in the current industry, mainly because of India being a developing country and lot of growth in various sectors which leads a country to ultimate success. And when we talk about country’s growth which is dependent on the kind of work and how much importance to which sector is given. And when we say or talk about industries growth which leads the economy of country has to be balanced and given proper finance so as to reach the levels to fulfill the needs of the society. And industries which have massive outflow of work and a big portfolio then its very difficult for any company to work with limited finance and this is where IPO plays an important role.

This report talks about how IPO helps in raising fund for the companies going public, what are its pros and cons, and also it gives us detailed idea why companies go public. How and what are the steps taken by the companies before going for any IPO and also the role of (SEBI) Securities and Exchange Board of India the BSE and NSE , what are primary and secondary markets and also the important terms related to IPO. It gives us idea of how IPO is driven in the market and what are various factors taken into consideration before going for an IPO. And it also tells us how we can more or less judge a good IPO. Then we all know that scams have always been a part of any sector you go in for which are covered in it and also few recommendations are given for the same. It also gives us some idea about what are the expenses that a company undertakes during an IPO.

IPO has been one of the most important generators of funds for the small companies making them big and given a new vision in past and it is still continuing its work and also for many coming years.

ARUN GULERIA [email protected]

4

LITERATURE REVIEW

This section describes five key studies that have researched different forms of going public. This chapter also provides a brief account of a study which analyzed spreads, in addition to outlining a study which analyzed the impact of Internet technology on investment banking.

1. Kenji and Smith (2009)Kenji and Smith (2004) study the benefits and drawbacks of auctions versus book building as a method of IPO issuance in Japan. Their reason for choosing Japan as a test environment was due to the fact that book building has been a legal way of going public in Japan since 1997. Previously, auctioning was the only way that a company could go public in Japan. In their research, Kenji and Smith use the total issue cost as a percentage of the value of the issue to measure the benefits and drawbacks of the different methods of going public.

The data that is used in this paper is a sample of 484 IPOs by companies that are listed on the JASDAQ or JASDAQ-OTC markets during a five-year period from 1995 to 1999. This included 321 auction IPOs and 163 book built IPOs. However, due to varying market conditions during the years spanning from 1995 to 1999, the research has been divided into two different sections. The first uses all the data from the whole sample period, whereas the second section uses data only from the years 1996 through 1998, when the market was characterized by very stable market conditions. This provides a fairly similar setting for both auctions (January 1996 - September 1997) and book built (October 1997 - December 1998) IPO data sets. Firm data that is used include: sales revenue, equity to book value, shares outstanding, firm age, as well as number of employees. Issue data includes offering date, number of shares issued, amount raised, offer price, first after market price, and other offering details. Total issue cost in their research is defined as the first aftermarket price instead of actual issue price.

During the whole period, the total issue cost against the aftermarket price in book built IPOs is an average of 28,04%, whereas the auction priced cost is only 8,17%. However, the second sample (1996-1998) notes values of 15,3% and 7% respectively. The data demonstrates that the book building method provides more flexibility, making small issues appear to be more feasible, and decreasing the cost of going public for larger companies.

The empirical analysis demonstrates that under the auctions-only system, issuers are older and larger than book built issuers. The analysis also reveals that underpricing is a substitute cost for lower fees, thus when all else being equal, increased underpricing reduces the fee as a percentage of the aftermarket price. The method used for analysis in Kenji’s and Smith’s study was regression analysis, with reliance on previously identified variables.

When analyzing total issue cost and issue size, it was found that issuer age, sales revenue, and equity to book value are not significantly related to the total cost of auctioned IPOs. In the book built issues, the percentage cost is less for large issuers with established track records.

ARUN GULERIA [email protected]

5

In the study, the difference in equally-weighted average issue cost compares what the issue cost would have been in both book building and auction scenarios for any given company individually. Kenji and Smith found that auctioning reduces mean total issue cost by an average of 6% of the first aftermarket price. Additionally, they predicted that pricing through the auction method is projected to have resulted in lower total costs at least in 82,5% of the subsample.

In conclusion, Kenji and Smith found that under the auction method, high quality issuers had a limited ability to distinguish themselves from low quality issuers. Furthermore, the research found that small and risky firms, as a group, incur higher costs with book building, whereas larger and better-established issuers realize savings with this particular method. Overall in this sample of Japanese IPOs, the average total issue cost, measured as a percentage of the initial aftermarket price, was significantly higher in the book building regime than in the auction regime. However, it was found that aggregate underpricing would have been lower under the book building, on the basis of either the full sample, or the subsample.

2. Sherman and Jagannathan (2009)In their study Sherman and Jagannathan identify the underlying reason for the relative unpopularity of auctions as a means of going public. This study appears to be the most comprehensive endeavor in terms of attempting to holistically identify the reasons auctions have not been as attractive as other means of going public. Their research studies international trends in auctions use. Here, the evidence overwhelmingly indicates that auctions have been tried in over 20 countries but are rarely used today. “In other words, out of more than 45 countries, we have not been able to find even one country in which auctions are currently the dominant method.” (Sherman and Jagannathan 2005, 14)

Sherman and Jagannathan delve into commonly used stereotypical explanations for why auctions are not used. The two most common notions are (1) auctions are not used because they are still experimental and unproven, and (2) issuers are pressured into book building due to higher fees. Nonetheless, through international research, it was proven that even in markets where auctions have been used for a long time, there was a decline in their use as soon as book building or some other method became available. For the second issue, the authors found that competition in the market would drive down prices of book building issues. Additionally, other research has shown that fixed price offers lead to even lower spreads, compared to auctions.

In their study Sherman and Jagannathan find that on a global scale initial returns are not the most important aspect of the issue for the issuer. This was evident from data collected on IPOs in Singapore, where both auctions and fixed price offers were available. In this case, statistics revealed that the fixed price method was chosen as the dominant means of going public, although auctions consistently provided lower underpricing.

Finally, the study also deemed whether any perceivable effect can be distinguished from adding modern Internet technologies to enable bidding for the IPO auction. The results illustrate that the median return for Open IPOs is 2%, which is excellent. However, the research points out that there are significant outliers in the group. In conclusion, Sherman and Jagannathan find that

ARUN GULERIA [email protected]

6

auctions have been tried and tested in many markets, but have lost popularity due to poor control on the part of the issuer in terms of the price and effort that are applied. They also identify that auctions provide lower underpricing. This would imply that issuers are not only looking to optimize underpricing, but are moreover interested in other attributes of the issue. “Without some way of screening out free-riders and the unsure participation of serious investors, IPO auctions are too risky for both issuers and investors.”

3. Kaneko and Pettway (2008)Kaneko and Pettway attempt to provide an answer to the question “Does book building provide a better mechanism for issuing firms than auctions?” Similar to Kenji and Smith (2004), the Japanese market is used to test the assumption. The Japanese auction process uses price discriminating auctions, instead of a fixed price or market-clearing price as in the Open IPO process.

The empirical research in Kaneko and Pettway (2003) is broken up into three parts.Firstly the descriptive statistics are analyzed, which demonstrate that book building had significantly higher initial returns than auction priced IPOs. In the following part, the auctioned priced and book built IPOs are analyzed separately through regression analysis. In this section seven independent variables17 are tested to uncover which variables have the most impact on underpricing. In the test of auctioned IPOs, it was found that market volatility of daily index returns one month prior to the issue is the most significant factor affecting underpricing. When the same regressions were run on the book built IPOs, it was found that market change three months prior to the IPO was the most significant factor affecting underpricing.

In the third part of Kaneko’s and Pettway’s research, regression analysis was run on both sets of data, however controlling for the different firm specific characteristics. There, it was also found that book built IPOs are underpriced significantly more than auction priced IPOs. When the book built and auctioned priced IPOs were analyzed for effects of hot and cold markets, it was found that book built IPOs are still much more frequently underpriced.

In conclusion, Kaneko and Pettway found that under all conditions and while controlling firm specific characteristics, book built IPOs were much more frequently underpriced in comparison to auctioned IPOs.

4. Biasis and Faugeron-Crouzet (2007)In their research, Biasis and Faugeron-Crouzet analyze different types of IPO auctions. They study uniform price auctions, fixed price offerings, internet-based Open IPO mechanisms, and auctions such as Mise en Vente in France. These were analyzed within a uniform theoretical model. (Biasis and Faugeron-Crouzet 2002, 13-17). In fixed price offers, Biasis and Faugeron-Crouzet found high initial returns. High returns were left both to institutional investors as well as small-uninformed investors, because of a lack of adjustment for price and demand. For uniform

ARUN GULERIA [email protected]

7

price auctions, underpricing was also evident, however with less underpricing than with fixed price offers.

The Mise en Vente auction is an auction type IPO procedure that is commonly used in France. This auction has a fixed market clearing price and pro rata allocation. The highest market clearing bids do not set the market-clearing price, instead it is set by a Bourse official, based on the function of demand. It is noted that an explicit algorithm that maps demand into price does not set the pricing in such cases.

The research found that for an optimal IPO auction, the IPO price must be set in a manner, which reflects the information held by investors. If this is not done as in fixed price auctions, underpricing is bound to be pervasive, whereas information gathering of the value of the stock during the IPO process is bound to be insignificant. Biasis Faugeron-Crouzet viewed the Open IPO process as a true Dutch auction when it in fact was not. An Open IPO process is a so-called ´Dirty Dutch´ auction as coined by Sherman (1999). Much like the Mise en Vente, the fixed market-clearing price is not set at the highest possible level, but instead it is marked down and set by the issuing company and the underwriter based on their own perception of the function of demand.

Their study moreover identifies the problem of translating, i.e., mapping demand into prices and into explicit computerized rules, which occur in Mise en Vente and in Book building. The authors also highlight the importance of established relationships between bidders and underwriters. Finally, according to Biasis and Faugeron-Crouzet an established relationship can enhance the ability to extract information from investors.

5. Wilhelm (2007)Wilhelm’s research dwells into the issue of how the Internet has affected investment banking that has relied on relationship based production technology to date. The methodology applied in this study is based on previous research relating to investment banking. The author does not conduct his own empirical study; instead, he identifies a list of anomalies that other studies have found indicative of the phenomenon that investment banking, as we know it, could be changing.

Indications of the change in traditional investment banking according to the author are that there has been a decline in the size of underwriter syndicates and there are fewer or more dominant intermediaries in the securities underwriting business (Pichler and Wilhelm 2001, 2256).

The second observation was made on the point of low-cost communication and data processing, which might lead to a “direct marketing” business model. For example Wit Capital, a subsidiary of Goldman Sachs, seeks to identify affinity groups through data mining for a given firm’s offering.

ARUN GULERIA [email protected]

8

In sum, the study forecasts that new technologies will complement traditional technologies, rather than replace them, as has been witnessed with Wit Capital and W.R.Hambrecht’s Open IPO.

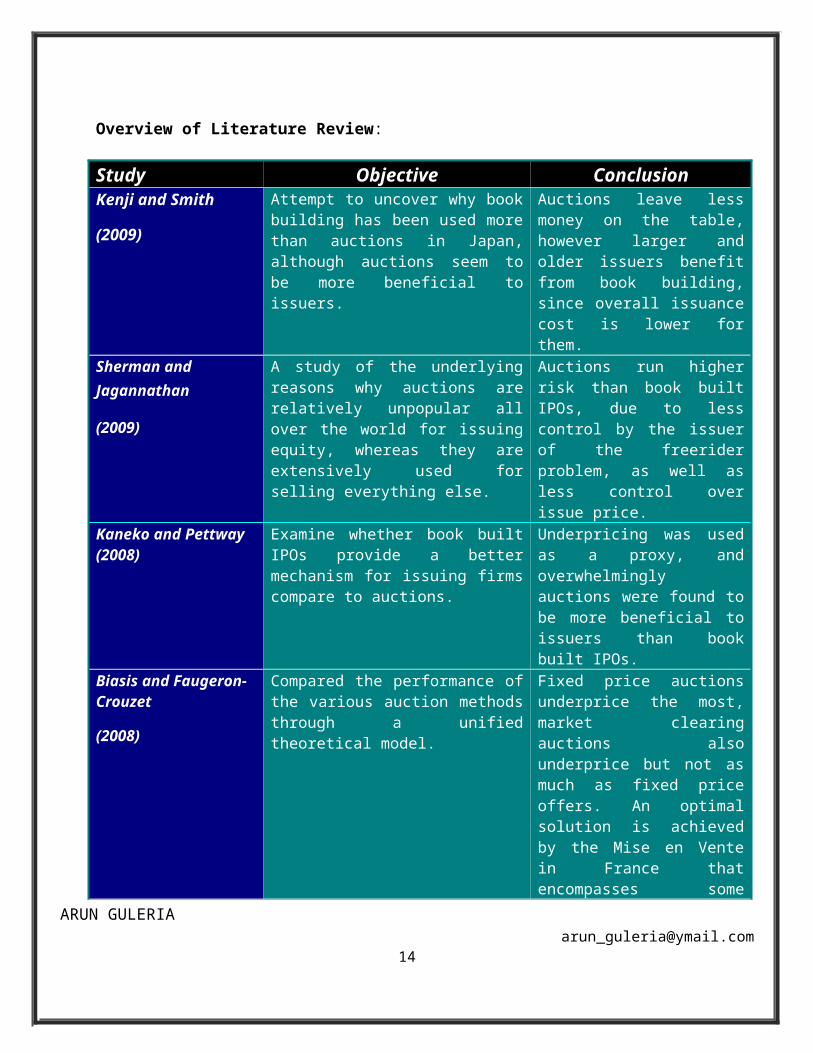

6. Summary of previous researchBelow is a table summarizing the findings of the five key studies in the field:

Overview of Literature Review:

Study Objective ConclusionKenji and Smith

(2009)

Attempt to uncover why book building has been used more than auctions in Japan, although auctions seem to be more beneficial to issuers.

Auctions leave less money on the table, however larger and older issuers benefit from book building, since overall issuance cost is lower for them.

Sherman and Jagannathan

(2009)

A study of the underlying reasons why auctions are relatively unpopular all over the world for issuing equity, whereas they are extensively used for selling everything else.

Auctions run higher risk than book built IPOs, due to less control by the issuer of the freerider problem, as well as less control over issue price.

Kaneko and Pettway (2008)

Examine whether book built IPOs provide a better mechanism for issuing firms compare to auctions.

Underpricing was used as a proxy, and overwhelmingly auctions were found to be more beneficial to issuers than book built IPOs.

Biasis and Faugeron- Crouzet

(2008)

Compared the performance of the various auction methods through a unified theoretical model.

Fixed price auctions underprice the most, market clearing auctions also underprice but not as much as fixed price offers. An optimal solution is achieved by the Mise en Vente in France that encompasses some characteristics of the book built offers.

Wilhelm

(2007)

Questions whether new communication technologies could impact traditional relationship based production technology that has been used until now in investment banking.

Results indicate that there is potential for the traditional relationship based production technology to be enhanced by Internet technologies, especially in issuing IPOs

ARUN GULERIA [email protected]

9

INITIAL PUBLIC OFFERING (IPO)

The first public offering of equity shares or convertible securities by a company, which is

followed by the listing of a company’s shares on a stock exchange, is known as an ‘Initial

Public Offering’. In other words, it refers to the first sale of a company’s common shares to

investors on a public stock exchange, with an intention to raise new capital.

The most important objective of an IPO is to raise capital for the company. It helps a company

to tap a wide range of investors who would provide large volumes of capital to the company for

future growth and development. A company going for an IPO stands to make a lot of money

from the sale of its shares which it tries to anticipate how to use for further expansion and

development. The company is not required to repay the capital and the new shareholders get a

right to future profits distributed by the company.

Companies fall into two broad categories: Private and Public .

A privately held company has fewer shareholders and its owners don't have to disclose much

information about the company. When a privately held corporation needs additional capital, it

can borrow cash or sell stock to raise needed funds. Often "going public" is the best choice for a

growing business. Compared to the costs of borrowing large sums of money for ten years or

more, the costs of an initial public offering are small. The capital raised never has to be repaid.

When a company sells its stock publicly, there is also the possibility for appreciation of the share

price due to market factors not directly related to the company. Anybody can go out and

incorporate a company: just put in some money, file the right legal documents and follow the

reporting rules of jurisdiction such as Indian Companies Act 1956. It usually isn't possible to buy

shares in a private company. One can approach the owners about investing, but they're not

obligated to sell you anything. Public companies, on the other hand, have sold at least a portion

ARUN GULERIA [email protected]

10

of themselves to the public and trade on a stock exchange. This is why doing an IPO is also

referred to as "going public."

Why go public??

Before deciding whether one should complete an IPO, it is important to consider the

positive and negative effects that going public may have on their mind. Typically, companies go

public to raise and to provide liquidity for their shareholders. But there can be other benefits.

Going public raises cash and usually a lot of it. Being publicly traded also opens many financial

doors:

Because of the increased scrutiny, public companies can usually get better rates when

they issue debt.

As long as there is market demand, a public company can always issue more stock. Thus,

mergers and acquisitions are easier to do because stock can be issued as part of the deal.

Trading in the open markets means liquidity. This makes it possible to implement things

like employee stock ownership plans, which help to attract top talent.

Going public can also boost a company’s reputation which in turn, can help the company

to expand in the marketplace.

ARUN GULERIA [email protected]

11

SIGNIFICANCE OF IPO

Investing in IPO has its own set of advantages and disadvantages. Where on one hand, high

element of risk is involved, if successful, it can even result in a higher rate of return. The rule is:

Higher the risk, higher the returns.

The company issues an IPO with its own set of management objectives and the investor looks for

investment keeping in mind his own objectives. Both have a lot of risk involved. But then

investment also comes with an advantage for both the company and the investors.

The significance of investing in IPO can be studied from 2 viewpoints – for the company and for

the investors. This is discussed in detail as follows:

SIGNIFICANCE TO THE COMPANY:

When a privately held corporation needs additional capital, it can borrow cash or sell stock to

raise needed funds. Or else, it may decide to “go public”. "Going Public" is the best choice for a

growing business for the following reasons:

The costs of an initial public offering are small as compared to the costs of borrowing

large sums of money for ten years or more,

The capital raised never has to be repaid.

When a company sells its stock publicly, there is also the possibility for appreciation of

the share price due to market factors not directly related to the company.

It allows a company to tap a wide pool of investors to provide it with large volumes of

capital for future growth.

ARUN GULERIA [email protected]

12

SIGNIFICANCE TO THE SHAREHOLDERS:

The investors often see IPO as an easy way to make money. One of the most attractive features

of an IPO is that the shares offered are usually priced very low and the company’s stock prices

can increase significantly during the day the shares are offered. This is seen as a good

opportunity by ‘speculative investors’ looking to notch out some short-term profit. The

‘speculative investors’ are interested only in the short-term potential rather than long-term gains.

Primary Market And Secondary Market

When shares are bought in an IPO it is termed primary market. The primary market does not involve the stock exchanges. A company that plans an IPO contacts an investment banker who will in turn called on securities dealers to help sell the new stock issue.

This process of selling the new stock issues to prospective investors in the primary market is called underwriting.

When an investor buys shares from another investor at an agreed prevailing market price, it is called as buying from the secondary market.

The secondary market involves the stock exchanges and it is regulated by a regulatory authority. In India, the secondary and primary markets are governed by the Security and Exchange Board of India (SEBI).

Kinds of Public Offerings:

1. Primary offering : - New shares are sold to raise cash for the company.

2. Secondary offering : - Existing shares (owned by VCs or firm founders) are sold, no new cash goes to company. A single offering may include both of these initial public offering.

ARUN GULERIA [email protected]

13

THE RISK FACTOR

Investing in IPO is often seen as an easy way of investing, but it is highly risky and many

investment advisers advise against it unless you are particularly experienced and knowledgeable.

The risk factor can be attributed to the following reasons:

UNPREDICTABLE:

The Unpredictable nature of the IPO’s is one of the major reasons that investors advise

against investing in IPO’s. Shares are initially offered at a low price, but they see

significant changes in their prices during the day. It might rise significantly during the

day, but then it may fall steeply the next day.

NO PAST TRACK RECORD OF THE COMPANY:

No past track record of the company adds further to the dilemma of the shareholders as to

whether to invest in the IPO or not. With no past track record, it becomes a difficult

choice for the investors to decide whether to invest in a particular IPO or not, as there is

basis to decide whether the investment will be profitable or not.

POTENTIAL OF STOCK MARKET :

Returns from investing in IPO are not guaranteed. The Stock Market is highly volatile.

Stock Market fluctuations widely affect not only the individuals and household, but the

economy as a whole. The volatility of the stock market makes it difficult to predict how

the shares will perform over a period of time as the profit and risk potential of the IPO

depends upon the state of the stock market at that particular time.

ARUN GULERIA [email protected]

15

RISK ASSESSMENT:

The possibility of buying stock in a promising start-up company and finding the next

success story has intrigued many investors. But before taking the big step, it is essential

to understand some of the challenges, basic risks and potential rewards associated with

investing in an IPO.

This has made Risk Assessment an important part of Investment Analysis. Higher the

desired returns, higher would be the risk involved. Therefore, a thorough analysis of risk

associated with the investment should be done before any consideration.

For investing in an IPO, it is essential not only to know about the working of an IPO, but

we also need to know about the company in which we are planning to invest. Hence, it is

imperative to know:

The fundamentals of the business

The policies and the objectives of the business

Their products and services

Their competitors

Their share in the current market

The scope of their issue being successful

It would be highly risky to invest without having this basic knowledge about the company.

ARUN GULERIA [email protected]

16

There are 3 kinds of risks involved in investing in IPO:

BUSINESS RISK :

It is important to note whether the company has sound business and management

policies, which are consistent with the standard norms. Researching business risk

involves examining the business model of the company.

FINANCIAL RISK:

Is this company solvent with sufficient capital to suffer short-term business setbacks? The

liquidity position of the company also needs to be considered. Researching financial risk

involves examining the corporation's financial statements, capital structure, and other

financial data.

MARKET RISK:

It would beneficial to check out the demand for the IPO in the market, i.e., the appeal of

the IPO to other investors in the market. Hence, researching market risk involves

examining the appeal of the corporation to current and future market conditions.

ARUN GULERIA [email protected]

17

ANALYSING AN IPO INVESTMENT

POTENTIAL INVESTORS AND THEIR OBJECTIVES:

Initial Public Offering is a cheap way of raising capital, but all the same it is not considered as

the best way of investing for the investor. Before investing, the investor must do a proper

analysis of the risks to be taken and the returns expected. He must be clear about the benefits he

hope to derive from the investment. The investor must be clear about the objective he has for

investing, whether it is long-term capital growth or short-term capital gains.

The potential investors and their objectives could be categorized as:

INCOME INVESTOR:

An ‘income investor’ is the one who is looking for steadily rising profits that will be

distributed to shareholders regularly. For this, he needs to examine the company's

potential for profits and its dividend policy.

GROWTH INVESTOR:

A ‘growth investor’ is the one who is looking for potential steady increase in profits that

are reinvested for further expansion. For this he needs to evaluate the company's growth

plan, earnings and potential for retained earnings.

SPECULATOR:

ARUN GULERIA [email protected]

18

A ‘speculator’ looks for short-term capital gains. For this he needs to look for potential of

an early market breakthrough or discovery that will send the price up quickly with little

care about a rapid decline.

INVESTOR RESEARCH:

It is imperative to properly analyze the IPO the investor is planning to invest into. He needs to

do a thorough research at his end and try to figure out if the objective of the company match his

own personal objectives or not. The unpredictable nature of IPO’s and volatility of the stock

market adds greatly to the risk factor. So, it is advisable that the investor does his homework,

before investing.

The investor should know about the following:

BUSINESS OPERATIONS:

What are the objectives of the business?

What are its management policies?

What is the scope for growth?

What is the turnover of the labour force?

Would the company have long-term stability?

FINANCIAL OPERATIONS :

What is the company’s credit history?

What is the company’s liquidity position?

Are there any defaults on debts?

Company’s expenditure in comparison to competitors.

Company’s ability to pay-off its debts.

What are the projected earnings of the company

MARKETING OPERATIONS :

ARUN GULERIA [email protected]

19

Who are the potential investors?

What is the scope for success of the IPO?

What is the appeal of the IPO for the other investors?

What are the products and services offered by the company?

Who are the strongest competitors of the company?

IPO INVESTMENT STRATEGIES

Investing in IPOs is much different than investing in seasoned stocks. This is because there is

limited information and research on IPOs, prior to the offering. And immediately following the

offering, research opinions emanating from the underwriters are invariably positive.

There are some of the strategies that can be considered before investing in the IPO:

UNDERSTAND THE WORKING OF IPO:

The first and foremost step is to understand the working of an IPO and the basics of an

investment process. Other investment options could also be considered depending upon

the objective of the investor.

GATHER KNOWLEDGE:

It would be beneficial to gather as much knowledge as possible about the IPO market, the

company offering it, the demand for it and any offer being planned by a competitor.

INVESTIGATE BEFORE INVESTING :

ARUN GULERIA [email protected]

20

The prospectus of the company can serve as a good option for finding all the details of

the company. It gives out the objectives and principles of the management and will also

cover the risks.

KNOW YOUR BROKER:

This is a crucial step as the broker would be the one who would majorly handle your

money. IPO allocations are controlled by underwriters. The first step to getting IPO

allocations is getting a broker who underwrites a lot of deals.

MEASURE THE RISK INVOLVED:

IPO investments have a high degree of risk involved. It is therefore, essential to measure

the risks and take the decision accordingly.

INVEST AT YOUR OWN RISK:

Finally, after the homework is done, and the big step needs to be taken. All that can be

suggested is to ‘invest at your own risk’. Do not take a risk greater than your capacity.

ARUN GULERIA [email protected]

21

PRICING OF AN IPO

The pricing of an IPO is a very critical aspect and has a direct impact on the success or failure of

the IPO issue. There are many factors that need to be considered while pricing an IPO and an

attempt should be made to reach an IPO price that is low enough to generate interest in the

market and at the same time, it should be high enough to raise sufficient capital for the company.

The process for determining an optimal price for the IPO involves the underwriters arranging

share purchase commitments from leading institutional investors.

PROCESS:

Once the final prospectus is printed and distributed to investors, company management meets

with their investment bank to choose the final offering price and size. The investment bank tries

to fix an appropriate price for the IPO depending upon the demand expected and the capital

requirements of the company.

The pricing of an IPO is a delicate balancing act as the investment firms try to strike a balance

between the company and the investors. The lead underwriter has the responsibility to ensure

smooth trading of the company’s stock. The underwriter is legally allowed to support the price

of a newly issued stock by either buying them in the market or by selling them short.

ARUN GULERIA [email protected]

22

IPO PRICING DIFFERENCES:

It is generally noted, that there is a large difference between the price at the time of issue of an

Initial Public Offering (IPO) and the price when they start trading in the secondary market.

These pricing disparities occur mostly when an IPO is considered “hot”, or in other words, when

it appeals to a large number of investors. An IPO is “hot” when the demand for it far exceeds the

supply.

This imbalance between demand and supply causes a dramatic rise in the price of each share in

the first day itself, during the early hours of trading.

UNDERPRICING AND OVERPRICING OF IPO’s

UNDERPRICING:

The pricing of an IPO at less than its market value is referred to as ‘Underpricing’. In other

words, it is the difference between the offer price and the price of the first trade.

Historically, IPO’s have always been ‘underpriced’. Underpriced IPO helps to generate

additional interest in the stock when it first becomes publicly traded. This might result in

significant gains for investors who have been allocated shares at the offering price. However,

underpricing also results in loss of significant amount of capital that could have been raised had

the shares been offered at the higher price.

OVERPRICING:

The pricing of an IPO at more than its market value is referred to as ‘Overpricing’. Even

“overpricing” of shares is not as healthy option. If the stock is offered at a higher price than what

the market is willing to pay, then it is likely to become difficult for the underwriters to fulfill

their commitment to sell shares. Furthermore, even if the underwriters are successful in selling

ARUN GULERIA [email protected]

23

all the issued shares and the stock falls in value on the first day itself of trading, then it is likely

to lose its marketability and hence, even more of its value.

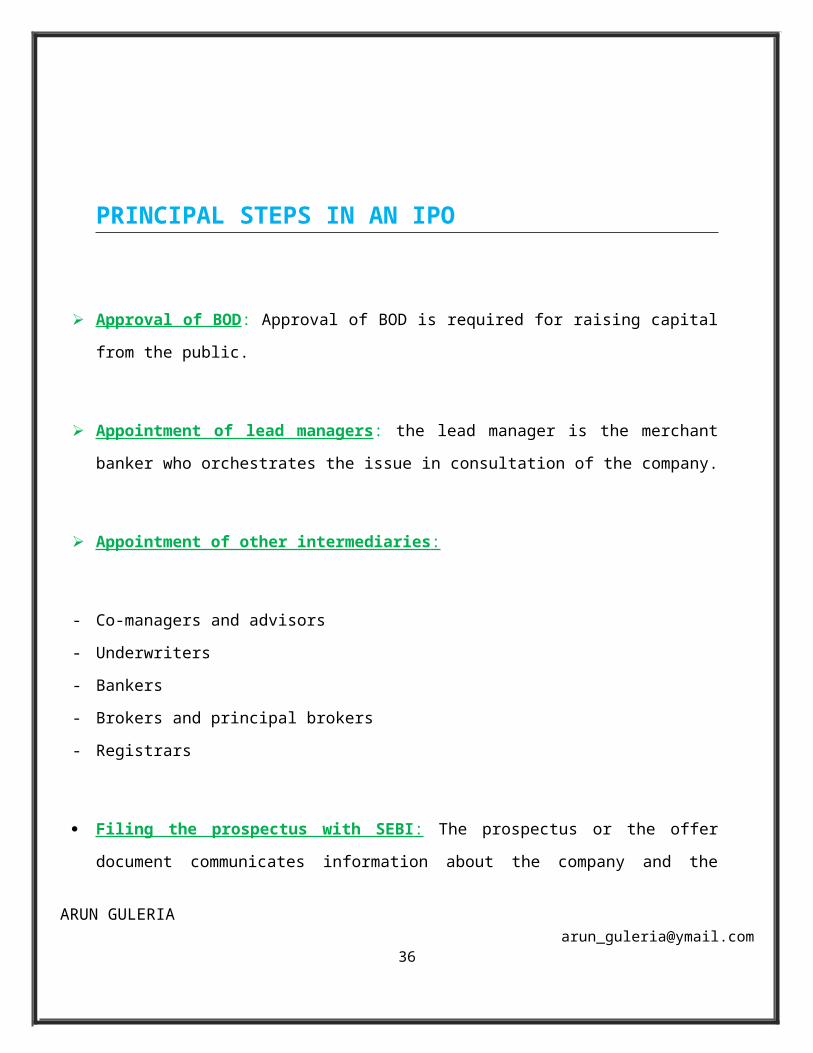

PRINCIPAL STEPS IN AN IPO

Approval of BOD : Approval of BOD is required for raising capital from the public.

Appointment of lead managers : the lead manager is the merchant banker who orchestrates the

issue in consultation of the company.

Appointment of other intermediaries :

- Co-managers and advisors

- Underwriters

- Bankers

- Brokers and principal brokers

- Registrars

ARUN GULERIA [email protected]

24

Filing the prospectus with SEBI : The prospectus or the offer document communicates

information about the company and the proposed security issue to the investing public. All the

companies seeking to make a public issue have to file their offer document with SEBI. If SEBI

or public does not communicate its observations within 21 days from the filing of the offer

document, the company can proceed with its public issue.

Filing of the prospectus with the registrar of the companies : once the prospectus have been

approved by the concerned stock exchanges and the consent obtained from the bankers, auditors,

registrar, underwriters and others, the prospectus signed by the directors, must be filed with the

registrar of companies, with the required documents as per the companies act 1956.

Printing and dispatch of prospectus : After the prospectus is filed with the registrar of

companies, the company should print the prospectus. The quantity in which prospectus is printed

should be sufficient to meet requirements. They should be send to the stock exchanges and

brokers so they receive them atleast 21 days before the first announcement is made in the news

papers.

Filing of initial listing application : Within 10 days of filing the prospectus, the initial listing

application must be made to the concerned stock exchanges with the listing fees.

Promotion of the issue : The promotional campaign typically commences with the filing of the

prospectus with the registrar of the companies and ends with the release of the statutory

announcement of the issue.

Statutory announcement : The issue must be made after seeking approval of the stock

exchange. This must be published atleast 10 days before the opening of the subscription list.

ARUN GULERIA [email protected]

25

Collections of applications : The Statutory announcement specifies when the subscription would

open, when it would close, and the banks where the applications can be made. During the period

the subscription is kept open, the bankers will collect the applications on behalf of the company.

Processing of applications : Scrutinizing of the applications is done.

Establishing the liability of the underwriters : If the issue is undersubscribed, the liability of

the underwriters has to be established.

Allotment of shares : Proportionate system of allotment is to be followed.

Listing of the issue : The detail listing application should be submitted to the concerned stock

exchange along with the listing agreement and the listing fee. The allotment formalities should

be completed within 30 days.

Book building is the process of price discovery (Basic concept)

The company does not come out with a fixed price for its shares; instead, it indicates a price

band that mentions the lowest (referred to as the floor) and the highest (the cap) prices at which a

share can be sold.

Bids are then invited for the shares. Each investor states how many shares s/he wants and what

s/he is willing to pay for those shares (depending on the price band). The actual price is then

discovered based on these bids. As we continue with the series, we will explain the process in

detail.

ARUN GULERIA [email protected]

26

According to the book building process, three classes of investors can bid for the shares:

1. Qualified Institutional Buyers: Mutual funds and Foreign Institutional Investors.

2. Retail investors: Anyone who bids for shares under Rs 50,000 is a retail investor.

3. High net worth individuals and employees of the company.

Allotment is the process whereby those who apply are given (allotted) shares. The bids are first

allotted to the different categories and the over-subscription (more shares applied for than shares

available) in each category is determined. Retail investors and high net worth individuals get

allotments on a proportional basis.

Example 1:

Assuming you are a retail investor and have applied for 200 shares in the issue, and the

issue is over-subscribed five times in the retail category, you qualify to get 40 shares (200

shares/5). Sometimes, the over-subscription is huge or the issue is priced so high that you can't

really bid for too many shares before the Rs 50,000 limit is reached. In such cases, allotments are

made on the basis of a lottery.

Example 2:

Say, a retail investor has applied for five shares in an issue, and the retail category has

been over-subscribed 10 times. The investor is entitled to half a share. Since that isn't possible, it

may then be decided that every 1 in 2 retail investors will get allotment. The investors are then

selected by lottery and the issue allotted on a proportional basis. That is why there is no way you

can be sure of getting an allotment.

ARUN GULERIA [email protected]

27

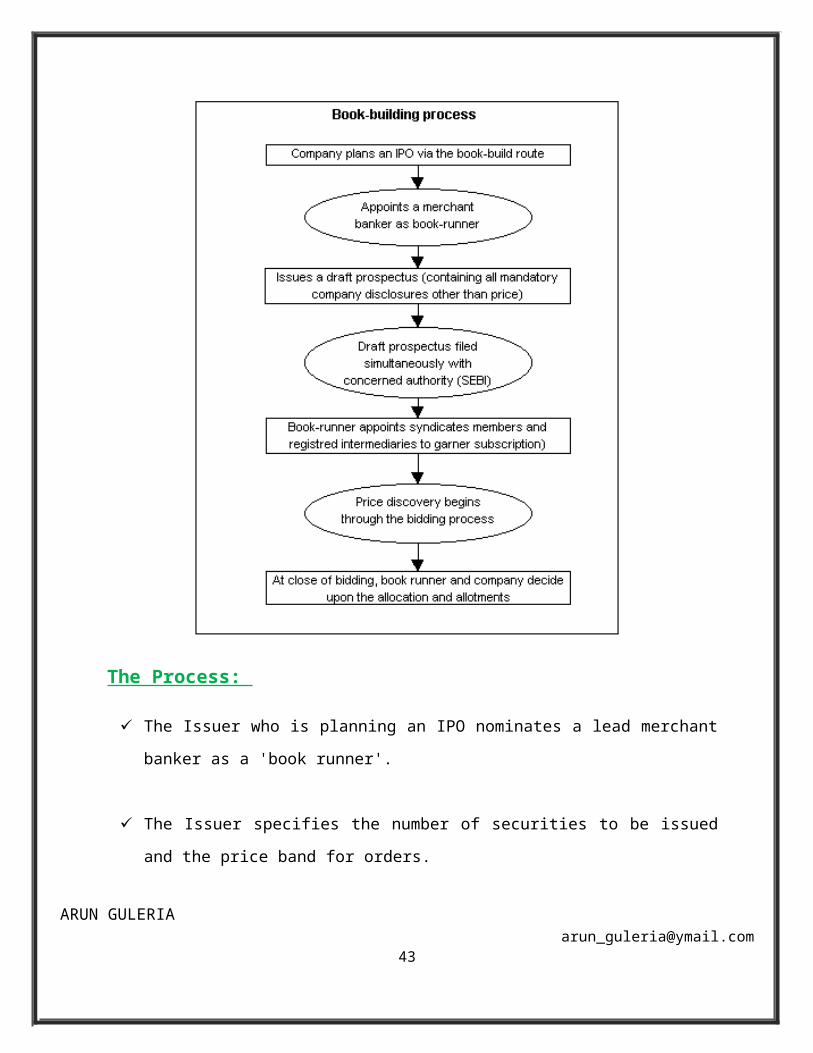

BOOK BUILDING PROCESS

Book Building is basically a capital issuance process used in Initial Public Offer (IPO) which

aids price and demand discovery. It is a process used for marketing a public offer of equity

shares of a company. It is a mechanism where, during the period for which the book for the IPO

is open, bids are collected from investors at various prices, which are above or equal to the floor

price. The process aims at tapping both wholesale and retail investors. The offer/issue price is

then determined after the bid closing date based on certain evaluation criteria.

ARUN GULERIA [email protected]

28

The Process:

The Issuer who is planning an IPO nominates a lead merchant banker as a 'book runner'.

The Issuer specifies the number of securities to be issued and the price band for orders.

The Issuer also appoints syndicate members with whom orders can be placed by the

investors.

ARUN GULERIA [email protected]

29

Investors place their order with a syndicate member who inputs the orders into the

'electronic book'. This process is called 'bidding' and is similar to open auction.

A Book should remain open for a minimum of 5 days.

Bids cannot be entered less than the floor price.

Bids can be revised by the bidder before the issue closes.

On the close of the book building period the 'book runner evaluates the bids on the basis

of the evaluation criteria which may include -

Price Aggression

Investor quality

Earliness of bids, etc.

The book runner the company concludes the final price at which it is willing to issue the

stock and allocation of securities.

Generally, the numbers of shares are fixed; the issue size gets frozen based on the price

per share discovered through the book building process.

Allocation of securities is made to the successful bidders.

Book Building is a good concept and represents a capital market which is in the process

of maturing.

Book-building is all about letting the company know the price at which you are willing to buy

the stock and getting an allotment at a price that a majority of the investors are willing to pay.

The price discovery is made depending on the demand for the stock.

The price that you can suggest is subject to a certain minimum price level, called the floor price.

For instance, the floor price fixed for the Maruti's initial public offering was Rs 115, which

means that the price you are willing to pay should be at or above Rs 115.

ARUN GULERIA [email protected]

30

In some cases, as in Biocon, the price band (minimum and maximum price) at which you can

apply is specified. A price band of Rs 270 to Rs 315 means that you can apply at a floor price of

Rs 270 and a ceiling of Rs 315.

If you are not still very comfortable fixing a price, do not worry. You, as a retail investor, have

the option of applying at the cut-off price. That is, you can just agree to pick up the shares at the

final price fixed. This way, you do not run the risk of not getting an allotment because you have

bid at a lower price. If you bid at the cut-off price and the price is revised upwards, then the

managers to the offer may reduce the number of shares allotted to keep it within the payment

already made. You can get the application forms from the nearest offices of the lead managers to

the offer or from the corporate or the registered office of the company.

How is the price fixed?

All the applications received till the last date are analysed and a final offer price, known as the

cut-off price is arrived at. The final price is the equilibrium price or the highest price at which all

the shares on offer can be sold smoothly.

If your price is less than the final price, you will not get allotment. If your price is higher than the

final price, the amount in excess of the final price is refunded if you get allotment. If you do not

get allotment, you should get your full refund of your money in 15 days after the final allotment

is made. If you do not get your money or allotment in a month's time, you can demand interest at

15 per cent per annum on the money due.

How are shares allocated?

As per regulations, at least 25 per cent of the shares on offer should be set aside for retail

investors. Fifty per cent of the offer is for qualified institutional investors. Qualified

Institutional Bidders (QIB) are specified under the regulation and allotment to this class is

made at the discretion of the company based on certain criteria.

ARUN GULERIA [email protected]

31

QIBs can be mutual funds, foreign institutional investors, banks or insurance companies.

If any of these categories is under-subscribed, say, the retail portion is not adequately

subscribed, then that portion can be allocated among the other two categories at the

discretion of the management. For instance, in an offer for two lakh shares, around 50,000

shares (or generally 25 per cent of the offer) are reserved for retail investors. But if the bids

from this category are received are only for 40,000 shares, then 10,000 shares can be

allocated either to the QIBs or non-institutional investors.

The allotment of shares is made on a pro-rata basis. Consider this illustration: An offer is

made for two lakh shares and is oversubscribed by times times, that is, bids are received for

six lakh shares. The minimum allotment is 100 shares. 1,500 applicants have applied for 100

shares each; and 200 applicants have bid for 500 shares each. The shares would be allotted in

the following manner:

Shares are segregated into various categories depending on the number of shares applied

for. In the above illustration, all investors who applied for 100 shares will fall in category A

and those for 500 shares in category B and so on.

The total number of shares to be allotted in category A will be 50,000 (100*1500*1/3).

That is, the number of shares applied for (100)* number of applications received (1500)*

oversubscription ratio (1/3). Category B will be allotted 33,300 shares in a similar manner.

Shares allotted to each applicant in category A should be 33 shares (100*1/3). That is,

shares applied by each applicant in the category multiplied by the oversubscription ratio. As,

the minimum allotment lot is 100 shares, it is rounded off to the nearest minimum lot.

Therefore, 500 applicants will get 100 shares each in category A — total shares allotted to

the category (50,000) divided by the minimum lot size (100).

ARUN GULERIA [email protected]

32

In category B, each applicant should be allotted 167 shares (500/3). But it is rounded off

to 200 shares each. Therefore, 167 applicants out of 200 (33300/200) would get an allotment

of 200 shares each in category B.

The final allotment is made by drawing a lot from each category. If you are lucky you

may get allotment in the final draw.

The shares are listed and trading commences within seven working days of finalisation of

the basis of allotment. You can check the daily status of the bids received, the price bid for

and the response form various categories in the Web sites of stock exchanges. This will give

you an idea of the demand for the stock and a chance to change your mind. After seeing the

response, if you feel you have bid at a higher or a lower price, you can always change the bid

price and submit a revision form.

The traditional method of doing IPOs is the fixed price offering. Here, the issuer and the

merchant banker agree on an "issue price" - e.g. Rs.100. Then one have the choice of filling

in an application form at this price and subscribing to the issue. Extensive research has

revealed that the fixed price offering is a poor way of doing IPOs. Fixed price offerings, all

over the world, suffer from `IPO underpricing'. In India, on average, the fixed-price seems to

be around 50% below the price at first listing; i.e. the issuer obtains 50% lower issue

proceeds as compared to what might have been the case. This average masks a steady stream

of dubious IPOs who get an issue price which is much higher than the price at first listing.

Hence fixed price offerings are weak in two directions: dubious issues get overpriced and

good issues get underpriced, with a prevalence of underpricing on average.

What is needed is a way to engage in serious price discovery in setting the price at the IPO. No

issuer knows the true price of his shares; no merchant banker knows the true price of the shares;

it is only the market that knows this price. In that case, can we just ask the market to pick the

price at the IPO?

ARUN GULERIA [email protected]

33

Imagine a process where an issuer only releases a prospectus, announces the number of shares

that are up for sale, with no price indicated. People from all over India would bid to buy shares in

prices and quantities that they think fit. This would yield a price. Such a procedure should

innately obtain an issue price which is very close to the price at first listing -- the hallmark of a

healthy IPO market.

Recently, in India, there had been issue from Hughes Software Solutions which was a milestone

in our growth from fixed price offerings to true price discovery IPOs. While the HSS issue has

many positive and fascinating features, the design adopted was still riddled with flaws, and we

can do much better.

Documents Required:

A company coming out with a public issue has to come out with an Offer Document/

Prospectus.

An offer document is the document that contains all the information you need about the

company. It will tell you why the company is coming is out with a public issue, its financials

and how the issue will be priced.

The Draft Offer Document is the offer document in the draft stage. Any company making a

public issue is required to file the draft offer document with the Securities and Exchange

Board of India, the market regulator.

If SEBI demands any changes, they have to be made. Once the changes are made, it is filed

with the Registrar of Companies or the Stock Exchange. It must be filed with SEBI at least

21 days before the company files it with the RoC/ Stock Exchange. During this period, you

can check it out on the SEBI Web site.

ARUN GULERIA [email protected]

34

Red Herring Prospectus is just like the above, except that it will have all the information as

a draft offer document; it will, however, not have the details of the price or the number of

shares being offered or the amount of issue. That is because the Red Herring Prospectus is

used in book building issues only, where the details of the final price are known only after

bidding is concluded.

Players:

Co-managers and advisors

Underwriters

Lead managers

Bankers

Brokers and principal brokers

Registrars

Stock exchanges.

ARUN GULERIA [email protected]

35

ABOUT HDIL:

HOUSING DEVELOPMENT AND INFRASTRUCTURE LIMITED (HDIL) is a part of

the Wadhawan Group (formerly known as the Dheeraj Group), which has been involved in real

estate development in the Mumbai Metropolitan Region for almost three decades.

Since 1996, HDIL has been satisfying the diverse needs of scores of home seekers in Mumbai

Metropolitan region. Their business focuses on real estate development, including construction

and development of residential projects, commercial, retail and slum rehabilitation projects.

A sincere study of the market and a strong feeling to meet the needs of the lower and the middle

income group prompted HDIL to help these people tide over difficult times and harrowing

experiences of buying a home.

HDIL had acted pro-actively in identifying the intricate needs of its residents and offered them

just what they needed. It provided and still provides all services under one roof through tie-ups

with banks and HFC’s.

With numerous projects to its credit and lakhs of happy and satisfied home buyers, HDIL has

carved a niche for itself in the real estate industry and has made its mark in the hearts of millions

of people.

HDIL’s Board of Directors :

In tune with its efforts to evolve into a professionally managed Corporate Structure, HDIL has

broaden its Board composition by inducting people of high standing from the banking industry,

legal and the audit profession as Independent Directors.

ARUN GULERIA [email protected]

37

The Company now has an ideal mix of Executive and Independent Directors, which gives it an

advantage of expertise of various fields in effective management and consistent growth.

MISSION:

HDIL is committed to creating microstructures, megastructures and infrastructure for the nation

and creating value for our customers, investors, employees & society at large.

Their mission is to be an icon in Infrastructure & Real Estate Development, defining:

QUALITY – Conforming to standards

MARKMANSHIP – Par Excellence

CUSTOMER SATISFACTION – Their Motto to deliver the best at all time

FINANCE:

Finance for buying flats in any of the HDIL projects can be obtained through any one of the

following Housing Finance Companies:

HDFC

LIC

GIC

Dewan Housing Finance Corporation Limited

VYSYA Bank Housing Finance

Housing Development and Infrastructure Ltd – IPO

HDIL IPO - opened for subscription on 28 June, 2007 and closed on July 03, 2007.

ARUN GULERIA

About the Company:

Since 1978, HDIL has been satisfying the diverse needs of scores of home seekers in Mumbai,

the commercial capital of India and Bangalore. It was not just the intention of doing business by

being responsible for marketing affordable homes; the very inclination was to give the best to the

home seeker fraternity at large.

Issue Details :

Issue of Equity Shares# 30,000,000 Equity Shares of which

Employee Reservation Portion# 600,000 Equity Shares

Net Issue# 29,400,000 Equity Shares Of which:

Qualified Institutional Buyers (QIBs) Portion At least 17,640,000 Equity Shares* of which

Available for Mutual Funds only 882,000 Equity Shares*

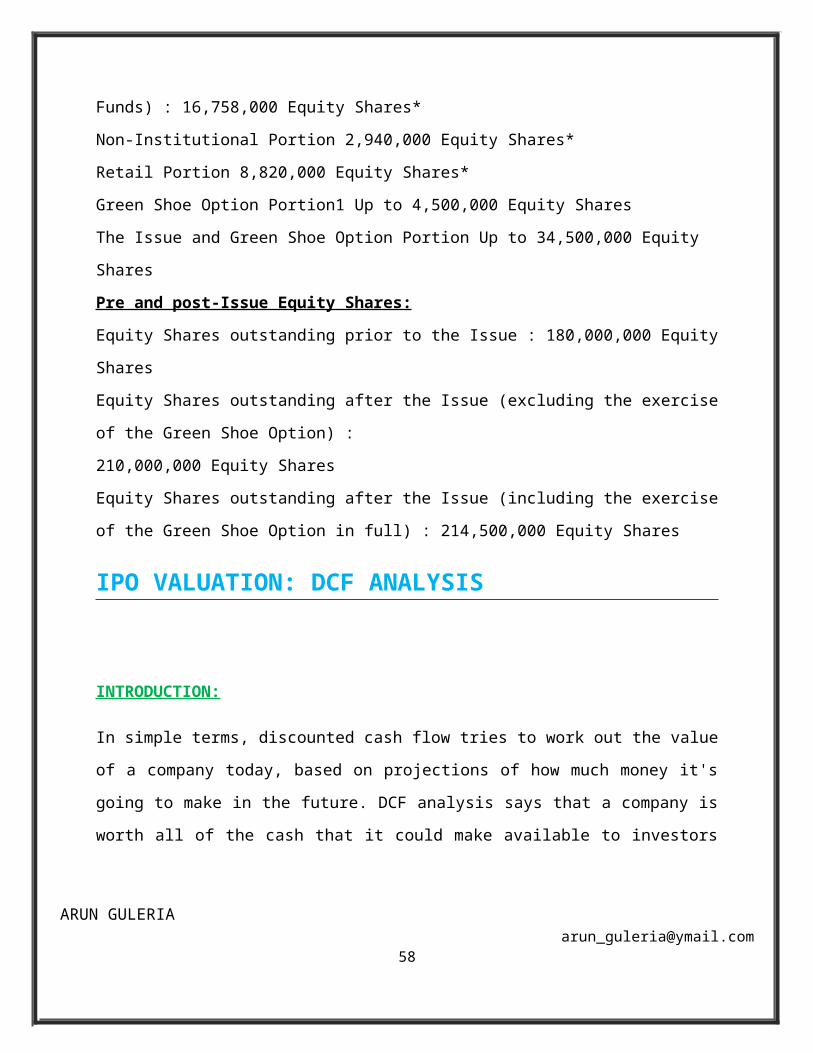

Balance of QIB Portion (available for QIBs including Mutual Funds) : 16,758,000 Equity

Shares*

Non-Institutional Portion 2,940,000 Equity Shares*

Retail Portion 8,820,000 Equity Shares*

Green Shoe Option Portion1 Up to 4,500,000 Equity Shares

The Issue and Green Shoe Option Portion Up to 34,500,000 Equity Shares

Pre and post-Issue Equity Shares:

Equity Shares outstanding prior to the Issue : 180,000,000 Equity Shares

Equity Shares outstanding after the Issue (excluding the exercise of the Green Shoe Option) :

210,000,000 Equity Shares

Equity Shares outstanding after the Issue (including the exercise of the Green Shoe Option in

full) : 214,500,000 Equity Shares

IPO VALUATION: DCF ANALYSIS

ARUN GULERIA [email protected]

39

INTRODUCTION:

In simple terms, discounted cash flow tries to work out the value of a company today, based on

projections of how much money it's going to make in the future. DCF analysis says that a

company is worth all of the cash that it could make available to investors in the future. It is

described as "discounted" cash flow because cash in the future is worth less than cash today.

For example, let's say someone asked you to choose between receiving Rs100 today and

receiving Rs100 in a year. Chances are you would take the money today, knowing that you could

invest that Rs100 now and have more than Rs100 in a year's time. If you turn that thinking on its

head, you are saying that the amount that you'd have in one year is worth Rs100 today - or the

discounted value is Rs100. Make the same calculation for all the cash you expect a company to

produce in the future and you have a good measure of the company’s revenue. There are several

tried and true approaches to discounted cash flow analysis; we will use the free cash flow to

firm approach commonly used by Street analysts to determine the "fair value" of companies.

The Forecast Period:

The table below shows good guidelines to use when determining a company's excess return

period/forecast period:

Company Competitive PositionExcess Return/Forecast

Period

Slow-growing company; operates in

highly competitive, low margin industry 1 year

Solid company; operates with advantage

such as strong marketing channels,

recognizable brand name, or regulatory

5 years

ARUN GULERIA [email protected]

40

advantage

Outstanding growth company; operates

with very high barriers to entry, dominant

market position or prospects

10 years

How far in the future should we forecast? Let's assume that the company is keeping itself busy

meeting the demand for its Infrastructure development. Thanks to strong marketing channels and

upgraded technology and HDIL has been satisfying the diverse needs of scores of home seekers

in Mumbai Metropolitan region. Their business focuses on real estate development, including

construction and development of residential projects, commercial, retail and slum rehabilitation

projects. There is enough demand for Infrastructure development to maintain five years of strong

growth, but after that the market will be saturated as new competitors enter the market. So, from

the above table, we will project cash flows for the next five years of business.

Growth Rate:

HDIL is expected to grow at to have CAGR of 42 %( source: Emkay Research). We take fixed

growth rate of 42% for DCF valuation for coming 5 years.

Reinvestment Rate:

If we relax the assumption that the only source of equity is retained earnings, the growth in net

income can be different from the growth in earnings per share. Intuitively, note that a firm can

grow net income significantly by issuing new equity to fund new projects while earnings per

share stagnate. To derive the relationship between net income growth and fundamentals, we need

a measure of how investment that goes beyond retained earnings. One way to obtain such a

measure is to estimate directly how much equity the firm reinvests back into its businesses in the

form of net capital expenditures and investments in working capital.

ARUN GULERIA [email protected]

41

Equity Reinvestment Rate = Growth Rate / ROE

= 42/76

= 55.26 %

Forecasting Free Cash Flows:

Free cash flow is the cash that flows through a company in the course of a quarter or a year once

all cash expenses have been taken out. Free cash flow represents the actual amount of cash that a

company has left from its operations that could be used to pursue opportunities that enhance

shareholder value - for example, developing new products, paying dividends to investors or

doing share buybacks.

Free cash flow = EBIT (1-tax) – [EBIT (1-tax) × Reinvestment Rate]

EBIT (1-tax) nth year = EBIT (1-tax) n-1 year × (1 + growth rate)

Rs in mn

Current Year

2008 2009 2010 2011 2012

ARUN GULERIA [email protected]

42

Expected Growth Rate - 42% 42% 42% 42% 42%

EBIT (1-tax) 6181 8777 12463 17698 25131 35686

Equity Reinvestment Rate - 55.26% 55.26% 55.26% 55.26% 55.26%

FCFE - 22185 30394 41639 57046 78153

eA wide variety of methods can be used to determine discount rates, but in most cases, these

calculations resemble art more than science. Still, it is better to be generally correct than

precisely incorrect, so it is worth your while to use a rigorous method to estimate the discount

rate. A good strategy is to apply the concepts of the weighted average cost of capital (WACC).

The WACC is essentially a blend of the cost of equity and the after-tax cost of debt.

Cost of Equity (Re):

Unlike debt, which the company must pay at a set rate of interest, equity does not have a

concrete price that the company must pay. But that doesn't mean that there is no cost of equity.

Equity shareholders expect to obtain a certain return on their equity investment in a company.

From the company's perspective, the equity holders' required rate of return is a cost, because if

the company does not deliver this expected return, shareholders will simply sell their shares,

causing the price to drop. Therefore, the cost of equity is basically what it costs the company to

maintain a share price that is satisfactory (at least in theory) to investors. The most commonly

accepted method for calculating cost of equity comes from the Nobel Prize-winning capital asset

pricing model (CAPM), where:

Cost of Equity = RF + Beta (Rm-Rf)

Rf - Risk-Free Rate - This is the amount obtained from investing in securities considered free

from credit risk, such as government bonds from developed countries. The interest rate of

government bonds is frequently used as a proxy for the risk-free rate.

ARUN GULERIA [email protected]

43

ß - Beta - This measures how much a company's share price moves against the market as a

whole. A beta of one, for instance, indicates that the company moves in line with the market. If

the beta is in excess of one, the share is exaggerating the market's movements; less than one

means the share is more stable.We take Beta of comparable firm i.e Unitech which is having beta

of 1.1

(Rm – Rf) Equity Market Risk Premium - The equity market risk premium (EMRP) represents

the returns investors expect, over and above the risk-free rate, to compensate them for taking

extra risk by investing in the stock market. In other words, it is the difference between the risk-

free rate and the market rate.

Cost of Debt (Rd):

As companies benefit from the tax deductions available on interest paid, the net cost of the debt

is actually the interest paid less the tax savings resulting from the tax-deductible interest

payment. Therefore, the after-tax cost of debt is Rd (1 - corporate tax rate).

Weighted Average Cost Of Capital (WACC):

The WACC is the weighted average of the cost of equity and the cost of debt based on the

proportion of debt and equity in the company's capital structure. The proportion of debt is

represented by D/V, a ratio comparing the company's debt to the company's total value (equity +

debt). The proportion of equity is represented by E/V, a ratio comparing the company's equity to

the company's total value (equity + debt). The WACC is represented by the following formula:

WACC = Cost of Equity + Cost of Debt

= E/V x Re + Rd x (1 - corporate tax rate) x D/V.

ARUN GULERIA [email protected]

44

E/V 0.66 Rf 7.44

Corporate tax 30% Beta 1.1

D/V 0.34 Rm 13.5

Cost of Debt Cost of Equity

D/V x (1 - corporate tax rate) E/V x [Rf + Beta (Rm-Rf)]

0.34 [1-0.30] 0.66 [7.44 + 1.1 x 6]

WACC = Cost of Debt + Cost of Equity = 9.5%

Present Value:

The present value of a single or multiple future payments (known as cash flows) is the nominal

amounts of money to change hands at some future date, discounted to account for the time value

of money, and other factors such as investment risk. A given amount of money is always more

valuable sooner than later since this enables one to take advantage of investment opportunities.

Present values are therefore smaller than corresponding future values.

When future cash flow of the company is divided by the discount rate we get the present value of

that predicted years cash flow.

Present Value n = Predicted cash flow n / (1+ discount rate)n

Where, n = year

Rs in mn

2008 2009 2010 2011 2012

ARUN GULERIA [email protected]

45

Free Cash Flow 3927 5576 7918 11243 15965

Discount rate 1.095 (1.095)² (1.095)³ (1.095)4 (1.095)5

Present value 3586 4650 6030 7820 10141

TERMINAL VALUE

Perpetuity Growth Model:

The Perpetuity Growth Model accounts for the value of free cash flows that continues

into perpetuity in the future, growing at an assumed constant rate. Here, the projected free cash

flow in the first year beyond the projection horizon (N+1) is used.

We have assumed perpetuity growth rate for HDIL as 6%

Beyond 2012 HDIL is expected to grow at 6% p.a i.e. at its perpetuity rate, hence net income for

the year 2013 will be:

Net income of 2012 × (1+ perpetuity growth rate)

= 35686 × (1+0.06)

= Rs. 37827 mn

ARUN GULERIA [email protected]

46

Reinvestment rate after 2012 (Terminal Point):

Reinvestment rate = Perpetuity Growth rate / Return on Equity

Here, return on equity is rate at which company expect to get returns on its investments after

terminal point i.e. 2012.

Return on equity will drop to the stable period cost of capital of 9.5%.

Reinvestment rate (terminal point) = 6/9.5

= 63%

Free cash flow = EBIT (1-tax) – [EBIT (1-tax) x Reinvestment Rate]

Therefore,

Free cash flow 2013 = 37827 – [37827 x 52%]

= Rs. 13936 mn

Gordon Growth Model:

There are several ways to estimate a terminal value of cash flows, but one well-worn method is

to value the company as a perpetuity using the Gordon Growth Model. The model uses this

formula:

Free cash flow of the year after the terminal year

ARUN GULERIA [email protected]

47

(Discount Rate –Perpetuity Growth Rate)

The formula simplifies the practical problem of projecting cash flows far into the future.

Therefore,

Terminal Value = 13936 × 100 9.5 – 6

= Rs 146099 mn

Present value of = 146099 / (1.095)6

Terminal year

= Rs. 84754 mn

Calculating Total Enterprise Value:

Total Enterprise = Sum of Present value for 5 years + Present valueOf Terminal Year + Cash – Debt

= 32228 + 84754 + 1949 - 3756

= Rs. 115175 mn

Fair value = Rs 115175 mn

Number of outstanding shares = 214 mn

Fair value of the HDIL per share = Rs 538

ARUN GULERIA [email protected]

48

SENSITIVITY ANALYSIS

Sensitivity analysis is the investigation of how the projected performance varies along with

changes in the key assumptions on which the projections are based.

The sensitivity analysis of the above DCF model can be done as follows:

Discount Rate

Perpetuity Growth

Rate

HDIL IPO

Particulars Figures

Issue of Equity shares 30,000,000

Equity Shares outstanding prior to the

Issue

180,000,000

Equity Shares outstanding after the

Issue

210,000,000

Price Band Rs. 430 to Rs.500

Issue Price Rs. 500

Listing Price Rs. 538

3 Days High Rs.634

3 Days Low Rs.535

ARUN GULERIA [email protected]

49

9% 9.5% 10%

5.5% 596 592 585

6% 533 538 537

6.5% 469 483 489

Close Price (26th July 2007) Rs. 621

DCF Valuation Rs. 538

NSE Data

Date Prev Close Open High Low CloseTotal Trd Qty Turnover in Lacs

24-Jul-09 500 538.6 575.95 535 559.35 28590806 160030.8

25-Jul-09 559.35 549.4 587.4 545.3 580.1 8552244 48465.14

26-Jul-09 580.1 585.6 634.3 585.6 621.4 9125757 55976.88

It can be seen that per share value of the HDIL comes to Rs. 538 and the listing price is Rs.538. Close Price as of 26th July 2007 is Rs.621. Hence it is buying opportunity of the investors.

HDIL IPO NEWS TRIVIA:

According to CLSA, HDIL IPO had been priced at a 20-30% discount to its forward

NPV. The IPO is good but the only concern here is the fall in retail demand for

property because of high interest rates.

The HDIL IPO had performed pretty well.

It had been subscribed by 6.6 times (oversubscribed 5.6 times).

Retail category has been subscribed by only 1.59 times (oversubscribed by 0.59

times).ARUN GULERIA

Institutional investor category in the HDIL IPO had been subscribed by over 10.13

times (oversubscribed 9.13 times)

The High Networth Individual category had been subscribed by 1.78 times

(oversubscription ratio: 0.78 times).

ARUN GULERIA [email protected]

51

FINDING

According to my study the investment done in the securities by the investors is mainly

done only by the image of the company but not on the basis of the fundamental

analysis.

EPS is the money that is left over after a company pays all of its debt so, higher the

EPS the better it is.

A low P/E is generally considered good because it may mean that the stock price has

not risen to reflect its earning power. A high P/E, on the other may reflect an

overpriced stock or decreasing earnings.

A Beta of 1 indicates that the Security’s price will move with the market. A Beta of

less than 1 means that security will be less volatile than the market. A Beta of greater

than 1 indicates that the security price will be more volatile than the market.

According to my study most probably, listing price is more compare to allotment

price.

According to my study, compare to year 2005 (61) and 2006 (85), in this year there

are more IPO listed in the year 2007 (110).

ARUN GULERIA [email protected]

52

SUGGESTIONS

The investment in IPO can prove too risky because the investor does not know

anything about the company because it is listed first time in the market so its

performance cannot be measure.

On the other hand it can be said that the higher the risk higher the returns earned.

So we can say that the though risky if investment is done then it can give higher

returns as well.

For example- we can take the example of Reliance power. The

Investors invested in huge amounts with the faith that they will get

good returns but nothing happened so when the IPO got listed. So

one should think and invest in IPO

Primary market is more volatile than the secondary market because all the

companies are listed for the first time in the market so nothing can be said about its

performance.

If higher risk is taken, it is always rewarded with the higher returns. So higher the

risk the more the returns rewarded for it.

“We can fairly predict the future, but can’t make it happen as it is.”

ARUN GULERIA [email protected]

53

IPO GLOSSARY

A

Allocation This is the amount of stock in an initial public offering (IPO) granted by the underwriter to an investor.

Aftermarket Trading in the IPO subsequent to its offering is called the aftermarket.

B

Board of Directors The composition of the Board of Directors is particularly critical for an IPO. Typically, a board is composed of inside and outside directors.

Broken IPOs If an IPO trades below its IPO price in the aftermarket, it is said to be a broken IPO.

C

Calendar This refers to upcoming IPOs and secondary offerings. Brokerage houses have equity calendars, bond calendars and municipal calendars.

Clearing Price The price at which all shares of an IPO can be sold to investors in a Dutch Auction. Sometimes referred to as the “market clearing price”.

ARUN GULERIA [email protected]

54

F

First Day Close The closing price at the end of the first day of trading reflects not only how well the lead manager priced and placed the deal, but what the near-term trading is likely to be.

Float When a company is publicly traded, a distinction is made between the total number of shares outstanding and the number of shares in circulation, referred to as the float. The float consists of the company's shares held by the general public.

G

Green Shoe A typical underwriting agreement allows the underwriters to buy up to an additional 15% of shares at the offering price for a period of several weeks after the offering. This option is also called the overallotment and is exercised when the IPO is oversubscribed and trading above its offer price. The term comes from the Green Shoe Company, which was the first to have this option.

H

Hot Issue When there is significantly more demand than supply for an IPO it is said to be a hot issue.

I

Initial Public Offering This is the event of a company first selling its shares to the public.

Insiders Management, directors and significant stockholders are regarded as insiders because they are privy to information about the operations of a company not known to the general public.

IPO Price Individual investors often ask why the price at which an IPO starts trading is different from its offer price. This occurs because the offer price is set by the underwriters before

ARUN GULERIA [email protected]

55

the stock starts trading. Once the stock starts trading, the price is determined by actual supply and demand and can be higher or lower.

IPO Research Prior to the offering, the underwriters involved in the IPO are prohibited from issuing research or recommendations for forty days. Following the IPO, the underwriter is allowed to issue a research report

M-N

Market Capitalization The total market value of a firm. It is defined as the product of the company's stock price per share and the total number of shares outstanding

Market Value The market value of a company is determined by multiplying the number of shares outstanding by the current price of the stock.

O

Offering Price This is the price at which the IPO is first sold to the public. It is set by the lead manager, usually after the close of stock market trading the night before the shares are distributed to IPO buyers. In the case of some foreign IPOs, the pricing occurs over the weekend.

Oversubscribed When a deal has more orders than there are shares available it is said to be oversubscribed.

P

Preliminary Prospectus This is the offering document printed by the company containing a description of the business, discussion of strategy, presentation of historical financial statements, explanation of recent financial results, management and their backgrounds and ownership.

Proceeds Companies go public to raise money. The money raised is referred to as proceeds.

ARUN GULERIA [email protected]

56

R

Red Herring This is the term of art for the preliminary prospectus. It gets its name from the printed red disclaimer on the left side of the prospectus.

U-V

Underwriter This is a brokerage firm that raises money for companies using public equity and debt markets. Underwriters are financial intermediaries that buy stock or bonds from an issuer and then sell these securities to the public.

Venture Capital Funding acquired during the pre-IPO process of raising money for companies. It is done only by accredited investors.

ARUN GULERIA [email protected]

57

BIBLIOGRAPHY

BOOKS1. Berenson Mark and Levine David (2000), “Basic Business Statistics, Concepts and

Applications”, Prentice Hall.

2. Branscomb Anne Wells (2004), “Who Owns Information”, Basic Books.

3. Grinblatt Mark, Titman Sheridan (2008), “Financial markets and Corporate Strategy”, McGraw-Hill.

4. Shapiro Carl and Varian Hal R. (2009), “Information Rules: A Strategy Guide to the Network Economy”, Harvard Business School Press.

5. Udayan Gupta (2006), “Done Deals: Venture capitalists tell their stories”, Harvard Business School Press.

INTERNET www.ipohome.com/hie-gerieooie/htm

www.essortment.com/gteorerui-100%dkfjdkei.pdf

www.investopedia.com/reserchpaper.froee-heofdvl%fkldks/