Embed Size (px)

Citation preview

1

Geo Factsheetwww.curriculum-press.co.uk Number 308

Growth economies of Africa: Angola & Mozambique

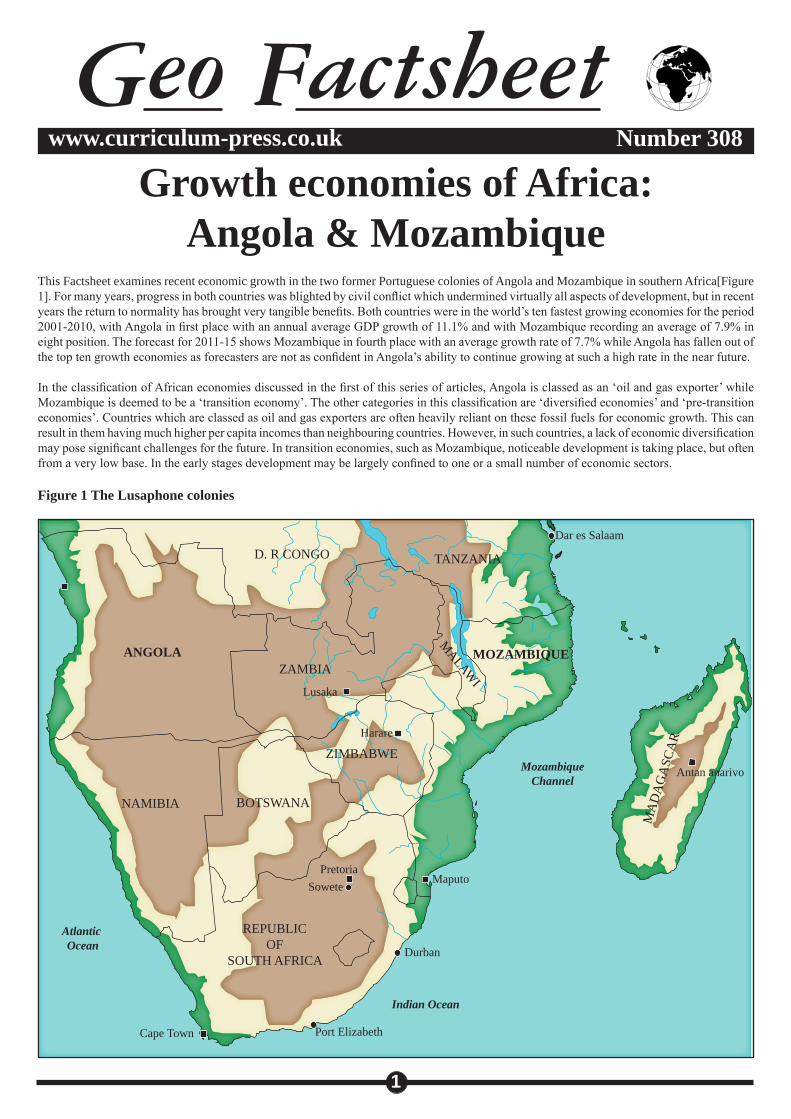

This Factsheet examines recent economic growth in the two former Portuguese colonies of Angola and Mozambique in southern Africa[Figure 1]. For many years, progress in both countries was blighted by civil conflict which undermined virtually all aspects of development, but in recent years the return to normality has brought very tangible benefits. Both countries were in the world’s ten fastest growing economies for the period 2001-2010, with Angola in first place with an annual average GDP growth of 11.1% and with Mozambique recording an average of 7.9% in eight position. The forecast for 2011-15 shows Mozambique in fourth place with an average growth rate of 7.7% while Angola has fallen out of the top ten growth economies as forecasters are not as confident in Angola’s ability to continue growing at such a high rate in the near future.

In the classification of African economies discussed in the first of this series of articles, Angola is classed as an ‘oil and gas exporter’ while Mozambique is deemed to be a ‘transition economy’. The other categories in this classification are ‘diversified economies’ and ‘pre-transition economies’. Countries which are classed as oil and gas exporters are often heavily reliant on these fossil fuels for economic growth. This can result in them having much higher per capita incomes than neighbouring countries. However, in such countries, a lack of economic diversification may pose significant challenges for the future. In transition economies, such as Mozambique, noticeable development is taking place, but often from a very low base. In the early stages development may be largely confined to one or a small number of economic sectors.

Figure 1 The Lusaphone colonies

ANGOLAZAMBIA

NAMIBIA BOTSWANA

REPUBLICOF

SOUTH AFRICA

MA

DA

GA

SCA

R

ZIMBABWE

MOZAMBIQUE

TANZANIAD. R CONGO

MALAW

I

Maputo

Durban

Port ElizabethCape Town

SowetePretoria

Harare

Dar es Salaam

Antan anarivo

Lusaka

Indian Ocean

Atlantic Ocean

MozambiqueChannel

2

Growth economies of Africa: Angola & Mozambique Geo Factsheet 308

Angola: an ‘oil and gas exporter’Angolan gas to fuel Europe’s homes as BP plant gears upHeadline in the Daily Telegraph, Friday April 26, 2013This recent newspaper article reported that BP planned to invest $15 billion in Angola over the next decade. This British company is a partner in the development of a major LNG [liquefied natural gas] project in Angola. At peak production of 5.2 million tonnes of LNG and natural gas liquids, Angola LNG should ship more than 70 cargoes a year. This plant would be the only new LNG facility in the world to start shipping this year.

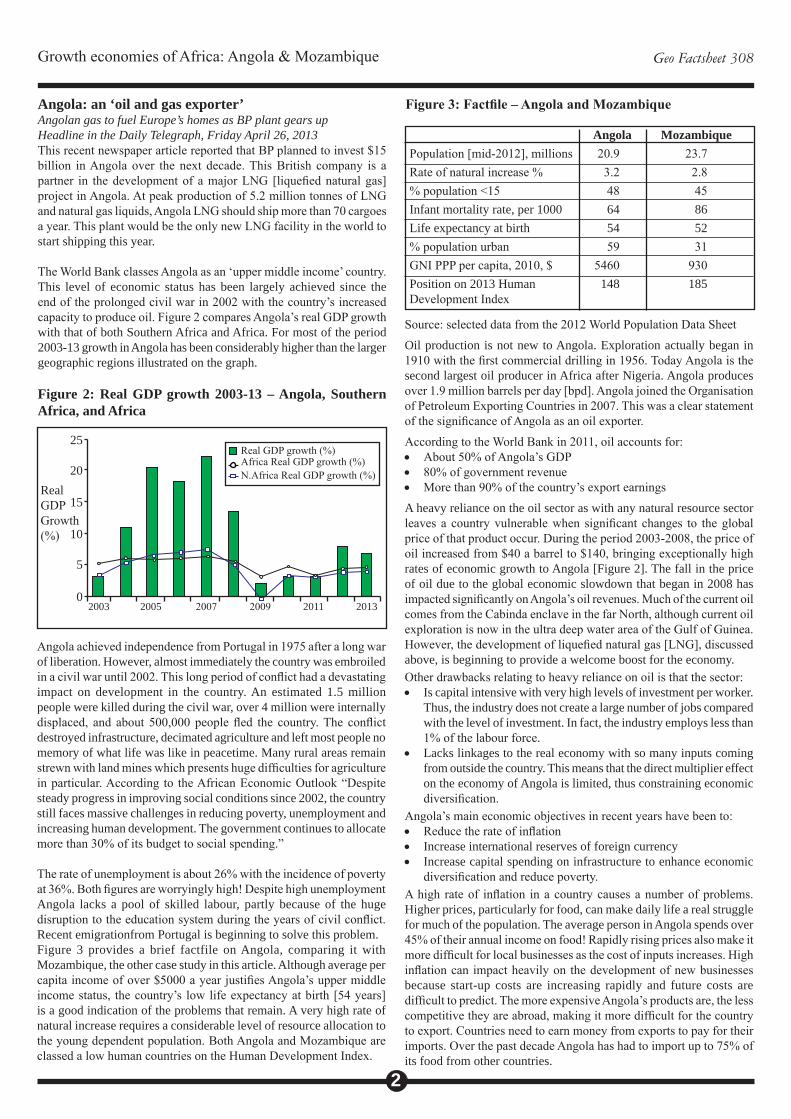

The World Bank classes Angola as an ‘upper middle income’ country. This level of economic status has been largely achieved since the end of the prolonged civil war in 2002 with the country’s increased capacity to produce oil. Figure 2 compares Angola’s real GDP growth with that of both Southern Africa and Africa. For most of the period 2003-13 growth in Angola has been considerably higher than the larger geographic regions illustrated on the graph.

Figure 2: Real GDP growth 2003-13 – Angola, Southern Africa, and Africa

2003 2005 2007 2009 2011 20130

5

10

15

20

25

Real GDPGrowth (%)

Real GDP growth (%)Africa Real GDP growth (%)N.Africa Real GDP growth (%)

Angola achieved independence from Portugal in 1975 after a long war of liberation. However, almost immediately the country was embroiled in a civil war until 2002. This long period of conflict had a devastating impact on development in the country. An estimated 1.5 million people were killed during the civil war, over 4 million were internally displaced, and about 500,000 people fled the country. The conflict destroyed infrastructure, decimated agriculture and left most people no memory of what life was like in peacetime. Many rural areas remain strewn with land mines which presents huge difficulties for agriculture in particular. According to the African Economic Outlook “Despite steady progress in improving social conditions since 2002, the country still faces massive challenges in reducing poverty, unemployment and increasing human development. The government continues to allocate more than 30% of its budget to social spending.”

The rate of unemployment is about 26% with the incidence of poverty at 36%. Both figures are worryingly high! Despite high unemployment Angola lacks a pool of skilled labour, partly because of the huge disruption to the education system during the years of civil conflict. Recent emigrationfrom Portugal is beginning to solve this problem.Figure 3 provides a brief factfile on Angola, comparing it with Mozambique, the other case study in this article. Although average per capita income of over $5000 a year justifies Angola’s upper middle income status, the country’s low life expectancy at birth [54 years] is a good indication of the problems that remain. A very high rate of natural increase requires a considerable level of resource allocation to the young dependent population. Both Angola and Mozambique are classed a low human countries on the Human Development Index.

Source: selected data from the 2012 World Population Data SheetOil production is not new to Angola. Exploration actually began in 1910 with the first commercial drilling in 1956. Today Angola is the second largest oil producer in Africa after Nigeria. Angola produces over 1.9 million barrels per day [bpd]. Angola joined the Organisation of Petroleum Exporting Countries in 2007. This was a clear statement of the significance of Angola as an oil exporter.According to the World Bank in 2011, oil accounts for:• About 50% of Angola’s GDP• 80% of government revenue• More than 90% of the country’s export earningsA heavy reliance on the oil sector as with any natural resource sector leaves a country vulnerable when significant changes to the global price of that product occur. During the period 2003-2008, the price of oil increased from $40 a barrel to $140, bringing exceptionally high rates of economic growth to Angola [Figure 2]. The fall in the price of oil due to the global economic slowdown that began in 2008 has impacted significantly on Angola’s oil revenues. Much of the current oil comes from the Cabinda enclave in the far North, although current oil exploration is now in the ultra deep water area of the Gulf of Guinea. However, the development of liquefied natural gas [LNG], discussed above, is beginning to provide a welcome boost for the economy.Other drawbacks relating to heavy reliance on oil is that the sector:• Is capital intensive with very high levels of investment per worker.

Thus, the industry does not create a large number of jobs compared with the level of investment. In fact, the industry employs less than 1% of the labour force.

• Lacks linkages to the real economy with so many inputs coming from outside the country. This means that the direct multiplier effect on the economy of Angola is limited, thus constraining economic diversification.

Angola’s main economic objectives in recent years have been to:• Reduce the rate of inflation• Increase international reserves of foreign currency• Increase capital spending on infrastructure to enhance economic

diversification and reduce poverty.A high rate of inflation in a country causes a number of problems. Higher prices, particularly for food, can make daily life a real struggle for much of the population. The average person in Angola spends over 45% of their annual income on food! Rapidly rising prices also make it more difficult for local businesses as the cost of inputs increases. High inflation can impact heavily on the development of new businesses because start-up costs are increasing rapidly and future costs are difficult to predict. The more expensive Angola’s products are, the less competitive they are abroad, making it more difficult for the country to export. Countries need to earn money from exports to pay for their imports. Over the past decade Angola has had to import up to 75% of its food from other countries.

Angola MozambiquePopulation [mid-2012], millions 20.9 23.7Rate of natural increase % 3.2 2.8% population <15 48 45Infant mortality rate, per 1000 64 86Life expectancy at birth 54 52% population urban 59 31GNI PPP per capita, 2010, $ 5460 930Position on 2013 Human 148 185Development Index

Figure 3: Factfile – Angola and Mozambique

Growth economies of Africa: Angola & Mozambique Geo Factsheet 308

3

In 2009, the Angolan government signed a Stand-By Arrangement [SBA] program with the International Monetary Fund [IMF] to the value of $1.4 billion. The SBA program is designed to improve all the main elements of Angola’s financial system. This will provide the country with greater economic strength as the development process goes forward and makes the country more attractive to a wider range of foreign direct investment. However, corruption is an obstacle to foreign investment and internal development. Transparency International, an NGO that investigates government fraud, ranks Angola 168th out of 178 countries in its corruption perception index.

Nowhere is Angola’s high level of economic growth more evident than in Luanda, the capital city. A very high level of construction is transforming the city. The concentration of economic opportunity in Luanda has resulted in considerable rural-urban migration. However, the relative security of living in the capital city in times of conflict has also been a factor in the concentration of population. Approximately 30% of Angolans live in Luanda. Almost 60% of the population live in the country’s urban areas as a whole.

Luanda, the capital, has also attracted a significant number of foreign workers which has put considerable pressure on accommodation and associated services. As a result prices have risen to extortionate levels in some cases. The divide between the rich and the poor in the capital city has never been more extreme. Two-thirds of Luanda’s five million people live in shanty-town poverty.

Currently Chinese investment in the form of soft loans and FDI is fuelling Angolan Development . Officials in Luanda estimate that there are currently 100,000 Chinese workers in the country, involved in a wide range of vital infrastructural projects.

The world’s major financial ratings agencies can have a significant impact on a country’s economic reputation. In 2011, Standard and Poor increased Angola’s sovereign debt rating to BB- because of the country’s improved revenue and current account balance. This was a welcome development for Angola, but in a global context its rating was still three levels below Standard and Poor’s lowest investment-grade rating.

Diversification of the economy beyond hydrocarbons is now the key strategy as well as using the profits from oil to rebuild the country’s infrastructure.

Mozambique: a ‘transition economy’Mozambique is another African country where civil war over a long period had a massive impact in undermining development. The civil war began in 1977, two years after the war of independence, and lasted until 1992. About one million people died in the fighting and from starvation as a result of the conflict. Five million people were displaced during the civil war.

However, since multi-party elections in 1994 the country has achieved impressive rates of economic growth. A combination of political stability, economic reforms and development aid transformed Mozambique’s fortunes although considerable development problems still remain. In 2012 Mozambique still depended on foreign assistance for 40% of its annual budget, a very high figure indeed, and over half the population live below the poverty line. Poverty reduction has stagnated in recent years due mainly to the inability to generate enough new jobs and increase productivity in agriculture. Official development assistance [ODA] is believed to have peaked and will decrease in the future as the economy of Mozambique develops.

The government has recently introduced a range of pro-poor measures in an attempt to tackle the poverty problem and avert civil unrest. Fuel and other emergency subsidies were introduced in 2010 to calm social unrest. These have since been partially phased out in an attempt to balance the budget.

Figure 4 compares annual GDP growth in Mozambique with Southern Africa and Africa for the period 2003-2013. In every single year growth of GDP in Mozambique was higher than in Africa as a whole, and only in 2007 was growth higher [marginally] in Southern Africa compared to Mozambique. The gap has been at its greatest in recent years.

Figure 4: Real GDP growth 2003-13 – Mozambique, Southern Africa, and Africa

20030

2

4

6

8

10

2005 2007 2009 2011 2013

Real GDPGrowth(%)

Real GDP growth (%)Africa Real GDP growth (%)S.Africa Real GDP growth (%)

The economy is based largely on agriculture with about 80% of the population employed in this sector. Most are engaged in small-scale subsistence farming. However, Mozambique is richly endowed with natural resources and a high level of foreign direct investment [FDI] in this sector in recent years has begun to transform the economy. Such a significant level of investment bodes well for the economic future of the country.

Mozambique is an energy giant in the making2011 marked the first export of coal for about 20 years. This shipment of 35,000 tonnes came from the Brazilian company Vale’s $1.7 billion Moatize open cast mine in Tete province. This mine is considered to be one of the world’s largest untapped coal deposits. These coal reserves comprise approximately 30% thermal and 70% higher value metallurgical coal. Production at the mine is projected to reach 11 million tonnes in 2014, rising to 26 million tonnes per year at its peak. Considerable investment in the rail network will be required to reach these targets. The three main logistical corridors for coal exports terminate at the ports of Maputo, Beira and Nacala. It is not surprising that the transport and communications sector is the second largest contributor to GDP after the extractive industries as development in one sector necessitates development in the other.

The overall capacity of Maputo’s seaport is being expanded from 100 million to 700 million tonnes per year with a new coal terminal at Maputo and Nacala’s seaport container terminal is undergoing substantial improvement. Investment in the main airports and road links has also been given priority.

According to the African Development Bank “Coal export earnings from the first mining mega-projects that began operations in 2011, coupled with strong performances in the financial services and transport and communications and construction sectors lifted real GDP growth. The resumption of strong FDI inflows, mostly in extractive industries, strong agricultural growth and infrastructure investment are expected to lead to high real growth in 2012 and 2013.”

4

Growth economies of Africa: Angola & Mozambique Geo Factsheet 308

Recent gas discoveries in Mozambique have been quoted as being the world’s largest in a decade by Bloomberg News. These offshore fields may hold enough gas to meet global consumption for more than two years. If the recent estimates prove to be correct, Mozambique’s natural gas reserves will place it 4th in the world after Russia, Iran and Qatar. The scale of Mozambique’s reserves of natural gas justifies the construction of a large LNG plant in the country according to the African Economic Outlook 2012. The LNG processing plant is being constructed via FDI by Vale, a Brasilian TNC. Gas could provide fertilisers and also gas for domestic use.

In spite of recent developments, the country’s export base remains narrow. In 2010 half of all exports by value consisted of aluminium. Only 15 products had an export value of more than $1 million. Coal exports will soon overtake those of aluminium. Plans to produce LNG could see this product contributing to exports by the end of the decade. Imports include machinery, vehicles, fuel and consumer durables. These arrive mainly from South Africa, Asia and Europe. Europe is the destination for just over half of Mozambique’s exports. The volume of intra-regional trade is relatively low at about one-fifth of GDP. This is likely to increase in the future with the consolidation of SADC[ Southern African Development Community] free trade tariffs which were initiated in 2008. Figure 5 shows the geographical extent of SADC. This economic organisation of 15 countries states that its objectives are to “achieve development, peace, security, economic growth, and to alleviate poverty through regional integration.” Mozambique has preferential access to EU markets under the EU/SADC Economic Partnership agreement signed in 2009.

Figure 5: Map of the Southern African Development Community

Unemployment is a significant problem with the overall unemployment rate standing at 27%. A high rate of population growth [2.8%] results in an additional 300,000 people entering the labour market every year. The capital-intensive nature of much FDI has done little to reduce unemployment. The formal sector is largely urban based and overall it only accounts for about 35% of all employment. Thus, many young people entering the labour market have little choice but to find marginal jobs in the informal sector. Mozambique is estimated to have the lowest education level among its adult population in the world at 1.2 years of formal education.

Although indicators of education are improving net attendance for secondary school is still only 20%. It is thus not surprising that the labour force has low levels of skill presenting difficulties for prospective

employers and also presenting obstacles to the government’s aim of promoting a culture of entrepreneurship with the development of small and medium-sized enterprises.

Climate change posed an increasing challenge for the future. A 2010 World Bank Report entitled ‘Mozambique: Economics of Adaptation to Climate Change’ concluded that the impact of climate change over the next four decades would result in a:• 2-4% decrease in yields of major crops• Reduction in energy supply of 1.4%

The Mozambique government is preparing a Strategic Program for Climate Resilience under the Pilot Program on Climate Resilience [PPCR]. Mozambique is one of three African pilot countries for PPCR which is supported by the World Bank and the African Development Bank. Mozambique is making efforts to reduce deforestation as part of this program as well as implementing drought-mitigating measures in the Limpopo basin in the south of the country and water conservation measures in the central province of Tete.

ConclusionA combination of the end of internal conflict, economic reform and natural resource endowment has prompted high rates of economic growth in both Angola and Mozambique in recent years. In many ways the future looks promising for both countries, but there remain significant obstacles too overcome. Income inequality is high on the list of major problems because of its potential to generate social unrest which could severely damage economic development.

Research QuestionsUsing evidence from this Factsheet (see Figure 3) and further reading compare the present and future prospect of Angola with that of Mozambique.

GuidelinesResearch population dividend, resources, growth rates, other key statistics such as GNP per capita and HDI.

Further readingAfrican Business July 2013 ‘A special report on lusaphone AfricaThe Africa Report 2013African Business December 2012 ‘The Brazilian Connection’

Acknowledgements; This Geo Factsheet was researched and written by Paul Guinness, a well known authorCurriculum Press, Bank House, 105 King Street, Wellington, TF1 1NUGeopress Factsheets may be copied free of charge by teaching staff or students, provided that their school is a registered subscriber.No part of these Factsheets may be reproduced, stored in a retrieval system, or transmitted, in any other form or by any other means, without the prior permission of the publisher. ISSN 1351-5136

South Africa

Angola

Tanzania

D.R. Congo

Zambia

Nambia

Botswana

Mad

agas

car

Zimbabwe Moz

ambi

que

Malaw

i

Seychelles

Mauritius

Swaziland

Lesotho

![Geography GEOG3geography-groby.weebly.com/uploads/4/3/3/7/43370205/aqa-geog3-qp... · Out of town shopping centre sales Neighbourhood ... retailing and other services. [10 marks]](https://img.pdfslide.net/doc/110x75/5a9eca9c7f8b9a76178bddc2/geography-geog3geography-groby-of-town-shopping-centre-sales-neighbourhood-.jpg)