Embed Size (px)

Citation preview

3700 West Sam Houston Parkway South, Suite 250, Houston, Texas 77042(713) 260-9000 (800) 262-6631 (713) 260-9050(Fax)

Scott Frakes, Regional Vice PresidentScott Wynant, Executive Vice President

October 2011

2

Capstone Profile• Founded in 1987, Capstone is in its 25th year of providing investment

management services.

• Capstone is an independent investment advisor headquartered in Houston, Texas.

• Capstone manages $3.8 billion in equity, bond and balanced accounts with clients nationwide.*

• Clients include:– Corporations − Individuals– Foundations − Health Care Organizations– Pension Plans − Public Funds– Unions − Insurance Companies

• Capstone provides proven disciplined investment processes that have been in place since inception of the firm.

• Capstone employs a team approach to management which results in consistency among client accounts.

• Capstone offers high quality portfolios customized via the following solutions:

Theta Growth (Income Oriented Equity)

Fixed Income

Non-Taxable Fixed Income

Current Income Portfolio (Income Oriented Fixed Income)

Balanced

Core Equity Large Cap Growth

Global Equity Income

* Capstone Financial Services, Inc. and it’s subsidiary companies.

Capstone Houston Headquarters

3

4

What are Retirees Thinking

• Their expectations are higher

• They’re going to be in retirement longer

• They’ll be responsible for more

• Their family situations are more complex

5

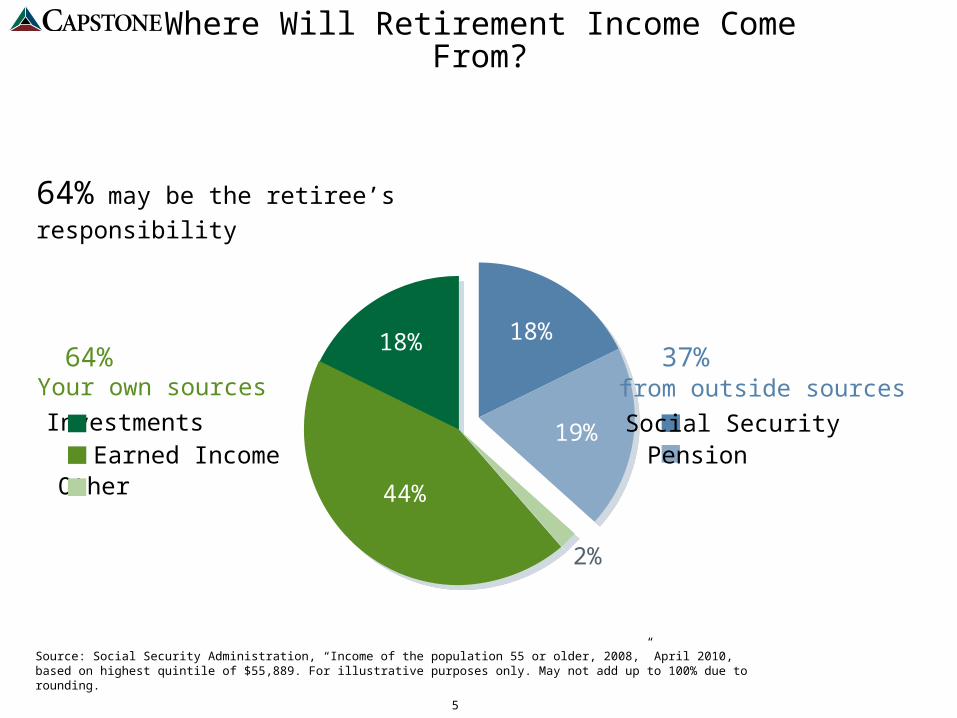

Where Will Retirement Income Come From?

Source: Social Security Administration, “Income of the population 55 or older, 2008,” April 2010, based on highest quintile of $55,889. For illustrative purposes only. May not add up to 100% due to rounding.

64% may be the retiree’s responsibility

18%64%

2%

44%

InvestmentsEarned Income

Other

Your own sources37%

18%

19% Social SecurityPension

from outside sources

6

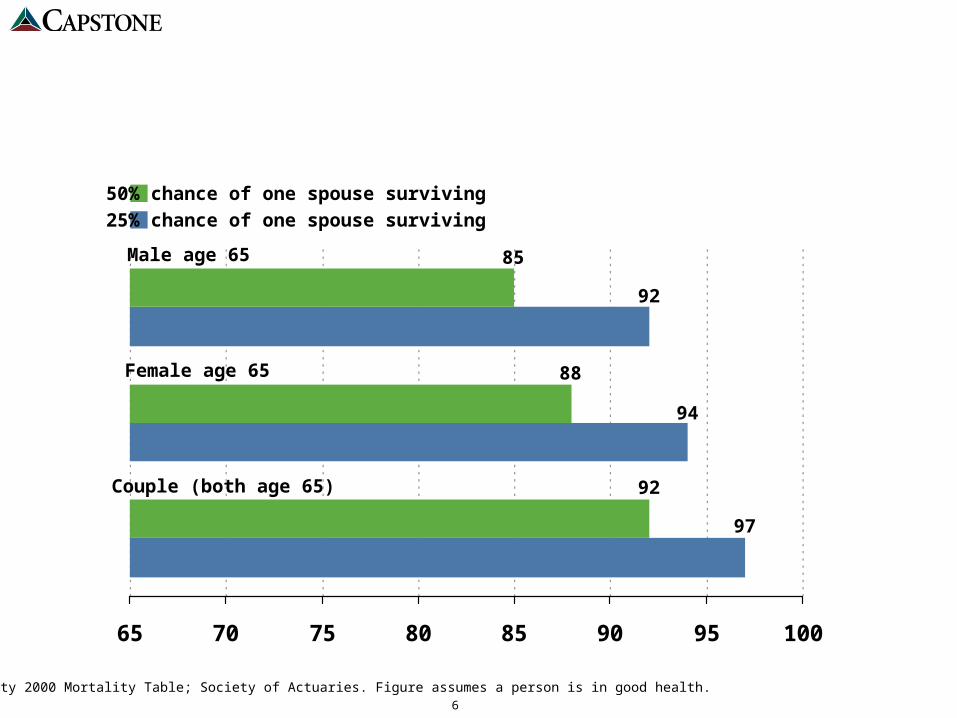

Source: Annuity 2000 Mortality Table; Society of Actuaries. Figure assumes a person is in good health.

65 70 75 80 85 90 95 100

50% chance of one spouse surviving

25% chance of one spouse surviving

Male age 65

Female age 65

Couple (both age 65)

85

92

88

94

92

97

7

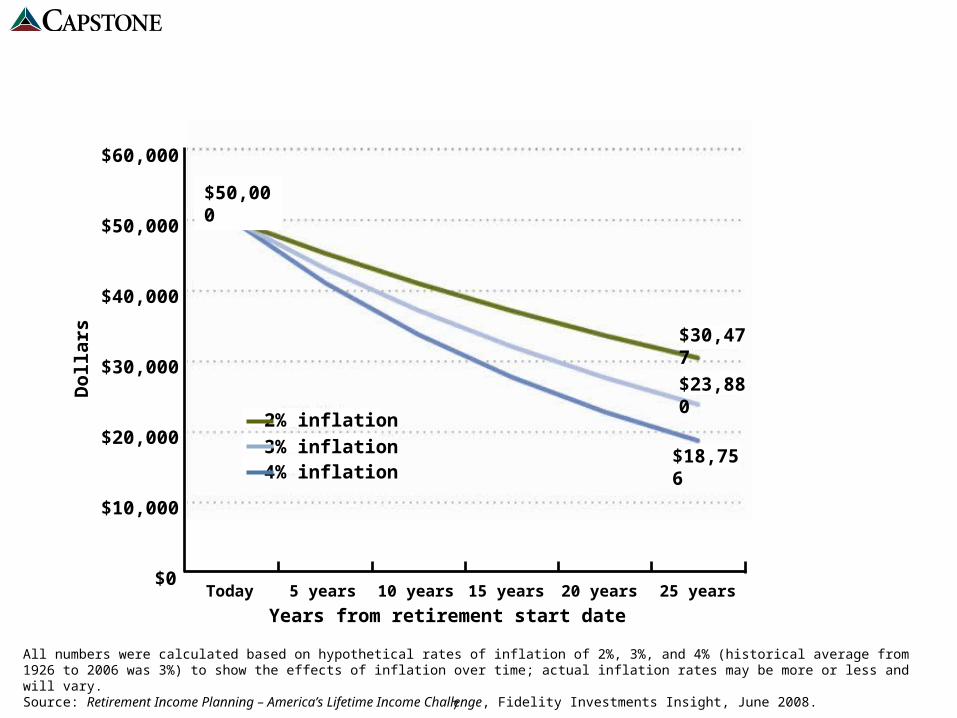

All numbers were calculated based on hypothetical rates of inflation of 2%, 3%, and 4% (historical average from 1926 to 2006 was 3%) to show the effects of inflation over time; actual inflation rates may be more or less and will vary.Source: Retirement Income Planning – America’s Lifetime Income Challenge, Fidelity Investments Insight, June 2008.

Dol

lars

$60,000

$50,000

$40,000

$30,000

$20,000

$10,000

$0Today 5 years 10 years 15 years 20 years 25 years

Years from retirement start date

$50,000

$18,756

$23,880

$30,477

2% inflation

3% inflation4% inflation

8

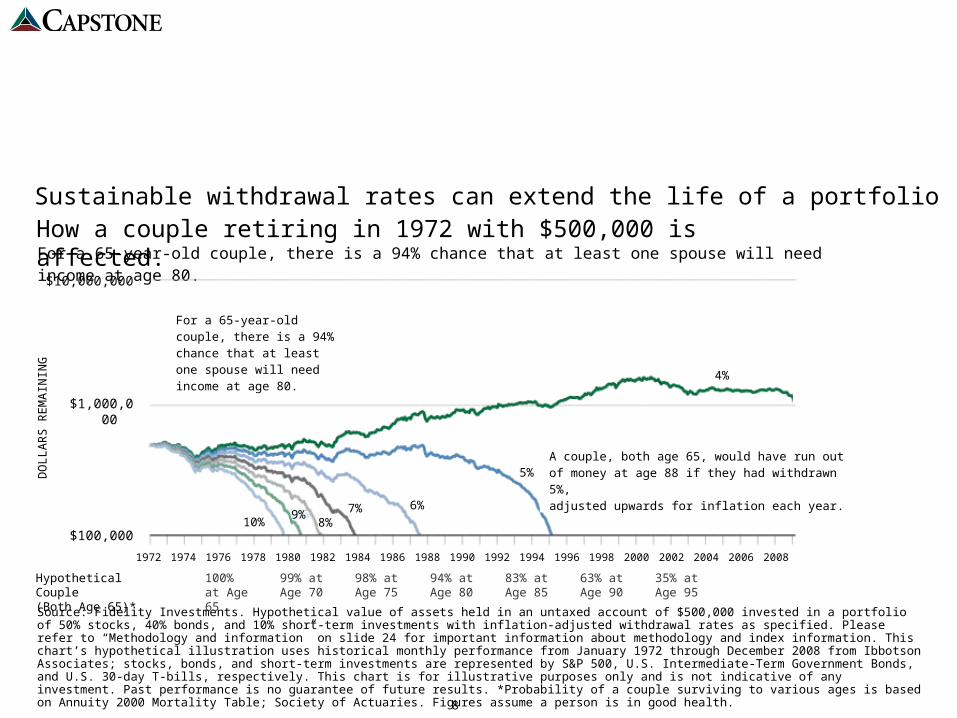

Sustainable withdrawal rates can extend the life of a portfolioHow a couple retiring in 1972 with $500,000 is affected.For a 65-year-old couple, there is a 94% chance that at least one spouse will need income at age 80.

Source: Fidelity Investments. Hypothetical value of assets held in an untaxed account of $500,000 invested in a portfolio of 50% stocks, 40% bonds, and 10% short-term investments with inflation-adjusted withdrawal rates as specified. Please refer to “Methodology and information” on slide 24 for important information about methodology and index information. This chart’s hypothetical illustration uses historical monthly performance from January 1972 through December 2008 from Ibbotson Associates; stocks, bonds, and short-term investments are represented by S&P 500, U.S. Intermediate-Term Government Bonds, and U.S. 30-day T-bills, respectively. This chart is for illustrative purposes only and is not indicative of any investment. Past performance is no guarantee of future results. *Probability of a couple surviving to various ages is based on Annuity 2000 Mortality Table; Society of Actuaries. Figures assume a person is in good health.

4%

5%

6%7%8%

9%

100% at Age 65

99% at Age 70

98% at Age 75

94% at Age 80

83% at Age 85

63% at Age 90

35% at Age 95

A couple, both age 65, would have run out of money at age 88 if they had withdrawn 5%,adjusted upwards for inflation each year.

$100,000

DO

LL

AR

S R

EM

AIN

ING

$1,000,000

Hypothetical Couple(Both Age 65)*

$10,000,000

For a 65-year-old couple, there is a 94% chance that at least one spouse will need income at age 80.

1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

10%

9

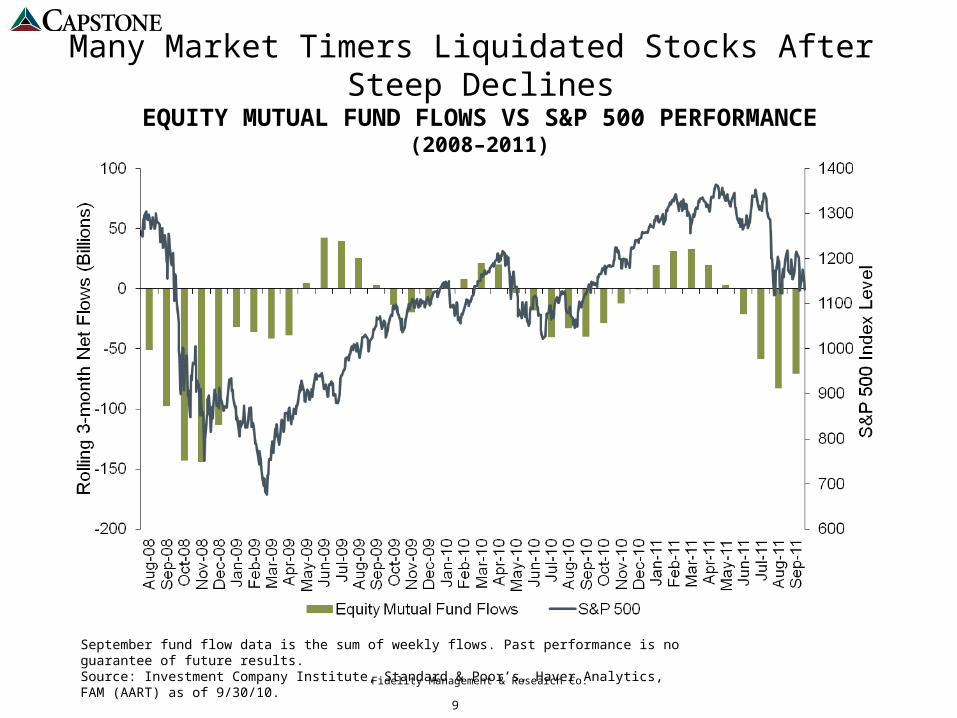

Many Market Timers Liquidated Stocks After Steep Declines

Fidelity Management & Research Co.

September fund flow data is the sum of weekly flows. Past performance is no guarantee of future results. Source: Investment Company Institute, Standard & Poor’s, Haver Analytics, FAM (AART) as of 9/30/10.

EQUITY MUTUAL FUND FLOWS VS S&P 500 PERFORMANCE(2008–2011)

10

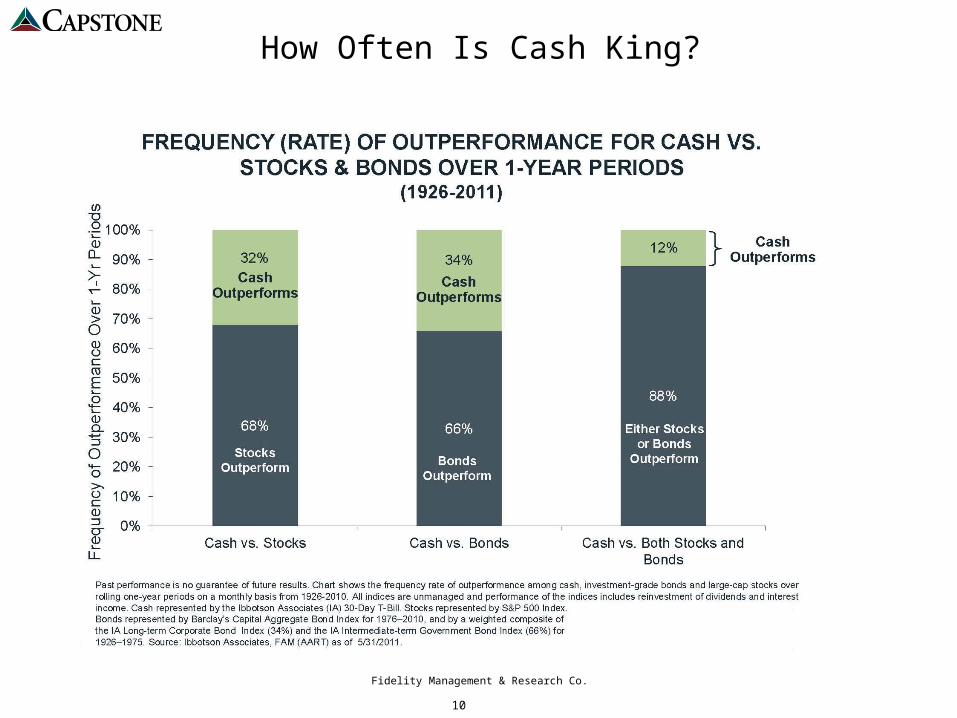

How Often Is Cash King?

Fidelity Management & Research Co.

11

Source: FactSet

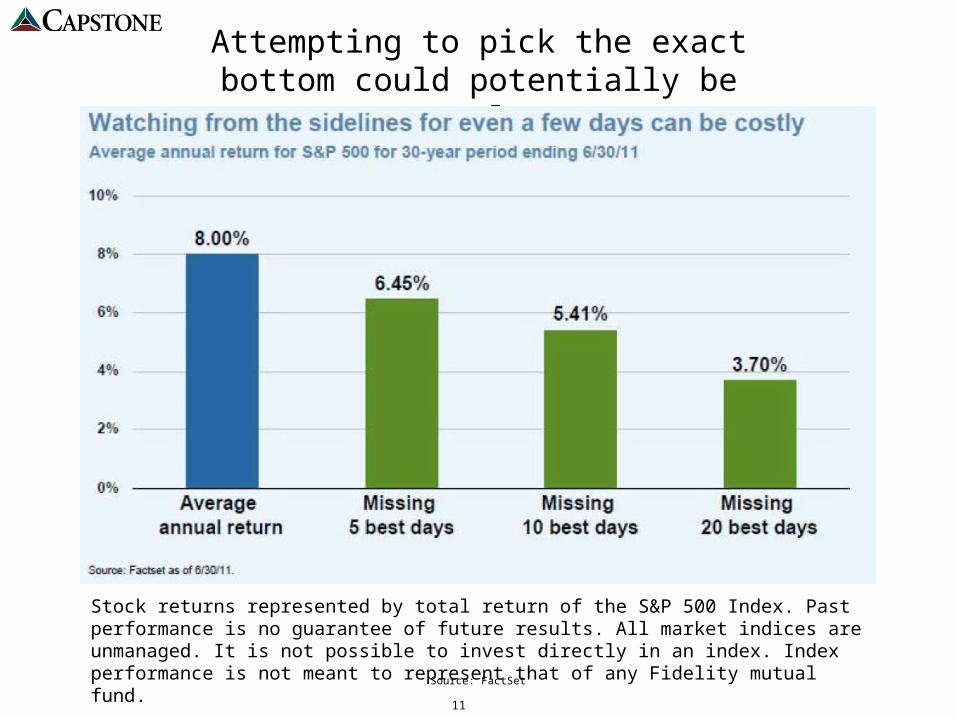

Attempting to pick the exact bottom could potentially be costly.

Stock returns represented by total return of the S&P 500 Index. Past performance is no guarantee of future results. All market indices are unmanaged. It is not possible to invest directly in an index. Index performance is not meant to represent that of any Fidelity mutual fund.

12

Current Income Portfolio “CIP”

13

Investment Profile

Current Income Portfolio seeks to:

• Provide the highest current yields available on investment grade, coupon

and dividend-paying, U.S. investments;

• Utilize a high degree of issuer diversification and asset allocation strategic

management;

• Establish a defined investment horizon to safeguard investment principal;

• Maintain the highest possible absolute returns/cash flow.

14

Current Income Portfolio invests in:

• One to fifteen year investment grade corporates;

• U.S. Agencies (with call and step-up provisions);

• Corporate inflation protection (floating rate) securities;

• Seasoned mortgage-backed securities; and

• Listed preferred stocks.

Investment Profile

15

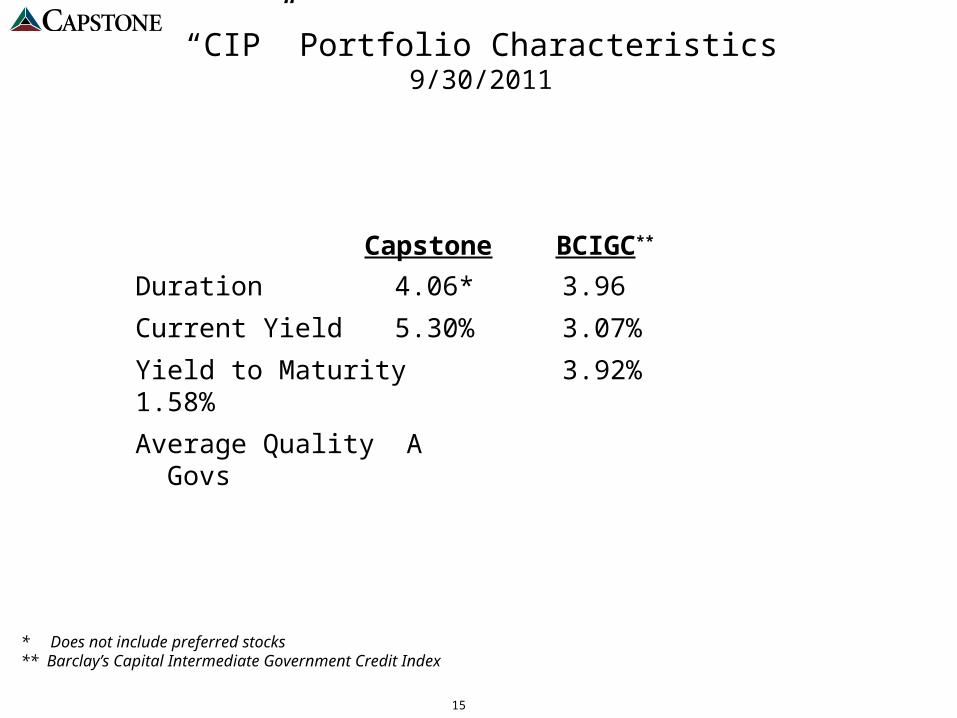

“CIP” Portfolio Characteristics9/30/2011

* Does not include preferred stocks** Barclay’s Capital Intermediate Government Credit Index

Capstone BCIGC**

Duration 4.06* 3.96

Current Yield 5.30% 3.07%

Yield to Maturity 3.92% 1.58%

Average Quality A Govs

16

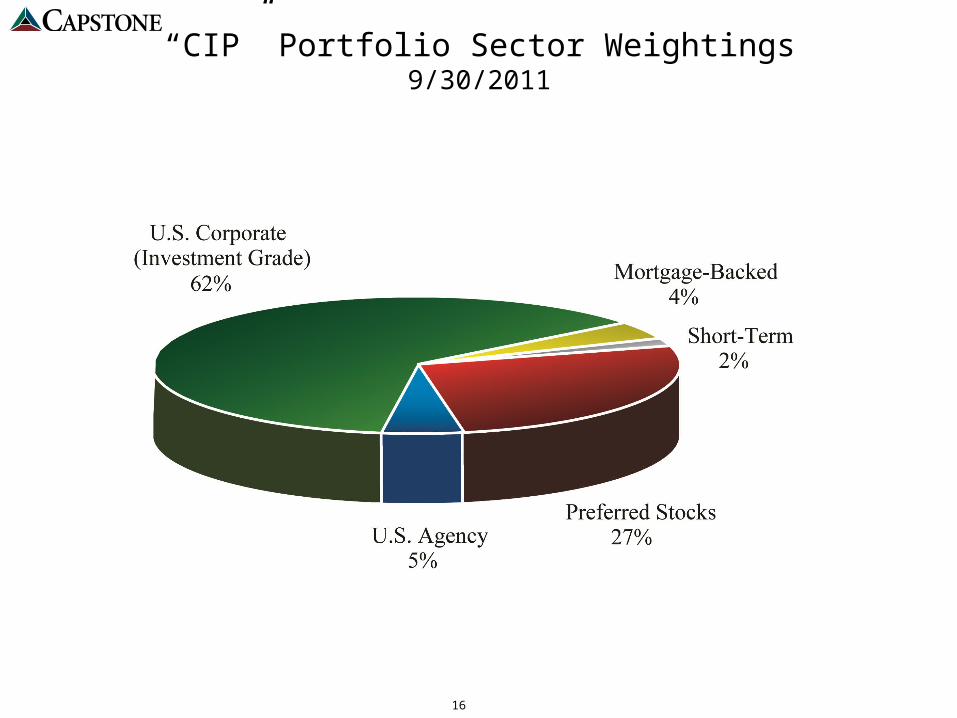

“CIP” Portfolio Sector Weightings9/30/2011

17

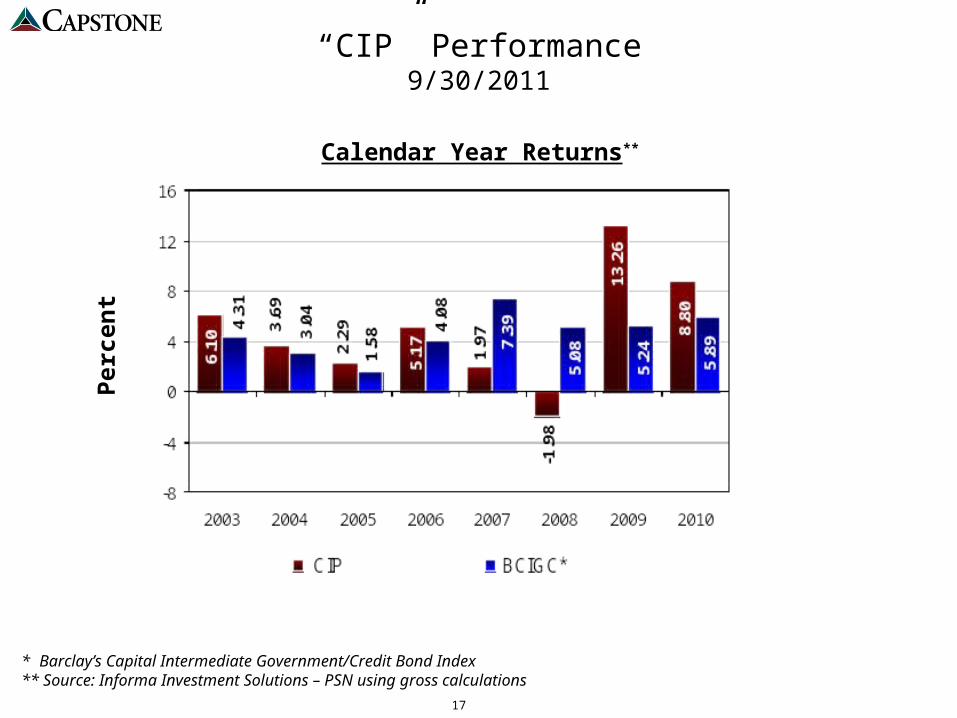

“CIP” Performance9/30/2011

* Barclay’s Capital Intermediate Government/Credit Bond Index** Source: Informa Investment Solutions – PSN using gross calculations

Per

cent

Calendar Year Returns**

18

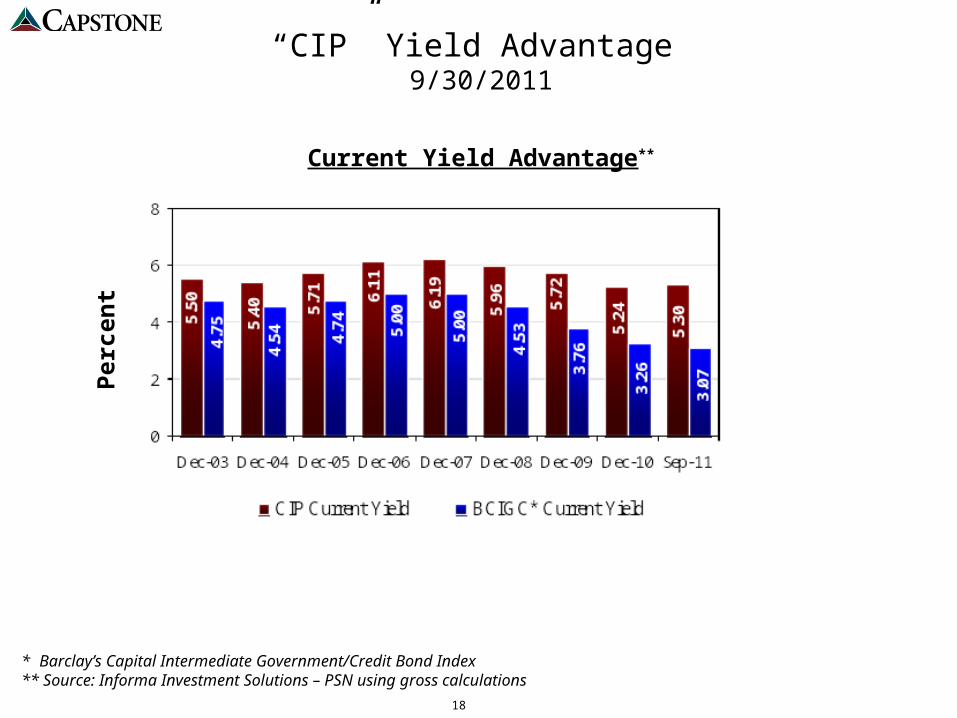

“CIP” Yield Advantage 9/30/2011

Per

cent

Current Yield Advantage**

* Barclay’s Capital Intermediate Government/Credit Bond Index** Source: Informa Investment Solutions – PSN using gross calculations

19

Global Equity Income

20

Global Equity Income Goals And Strategy

Objective:

Seeks to generate current income and long-term growth of capital.

The Global Equity Income Strategy offers investors a privately managed stock portfolio designed to provide dividend income, the potential for long-term capital appreciation and exposure to International Markets.

Investment Universe

S&P 1500S&P ADR

21

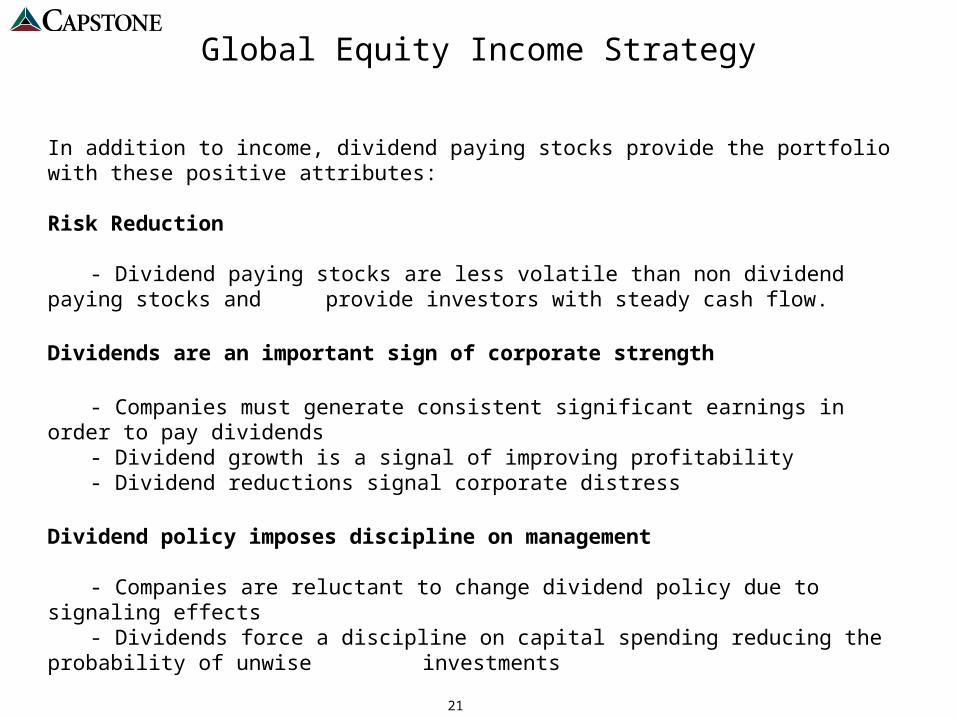

Global Equity Income Strategy

In addition to income, dividend paying stocks provide the portfolio with these positive attributes:

Risk Reduction

- Dividend paying stocks are less volatile than non dividend paying stocks and provide investors with steady cash flow.

Dividends are an important sign of corporate strength

- Companies must generate consistent significant earnings in order to pay dividends- Dividend growth is a signal of improving profitability- Dividend reductions signal corporate distress

Dividend policy imposes discipline on management

- Companies are reluctant to change dividend policy due to signaling effects- Dividends force a discipline on capital spending reducing the probability of unwise investments

22

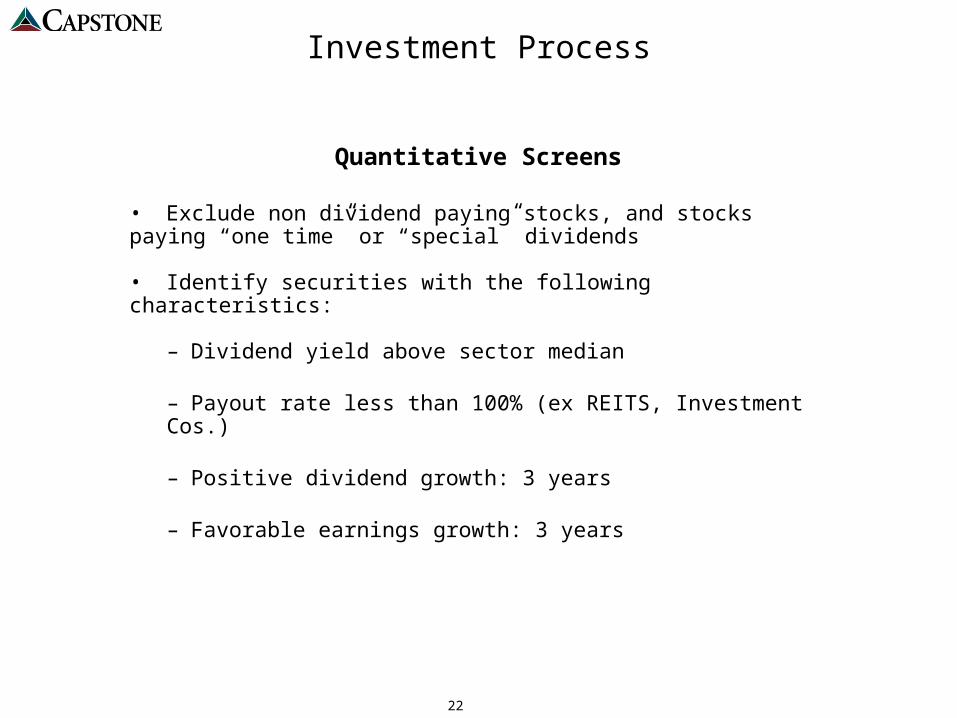

Investment Process

• Exclude non dividend paying stocks, and stocks paying “one time” or “special” dividends • Identify securities with the following characteristics:

– Dividend yield above sector median

– Payout rate less than 100% (ex REITS, Investment Cos.)

– Positive dividend growth: 3 years

– Favorable earnings growth: 3 years

Quantitative Screens

23

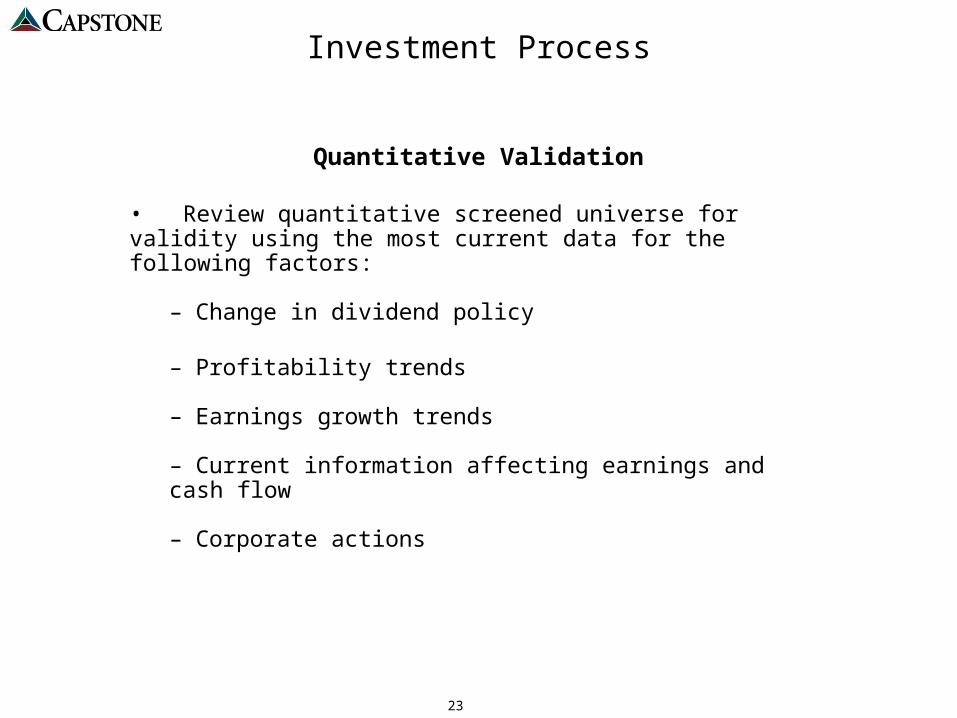

Investment Process

• Review quantitative screened universe for validity using the most current data for the following factors:

– Change in dividend policy

– Profitability trends – Earnings growth trends – Current information affecting earnings and cash flow – Corporate actions

Quantitative Validation

24

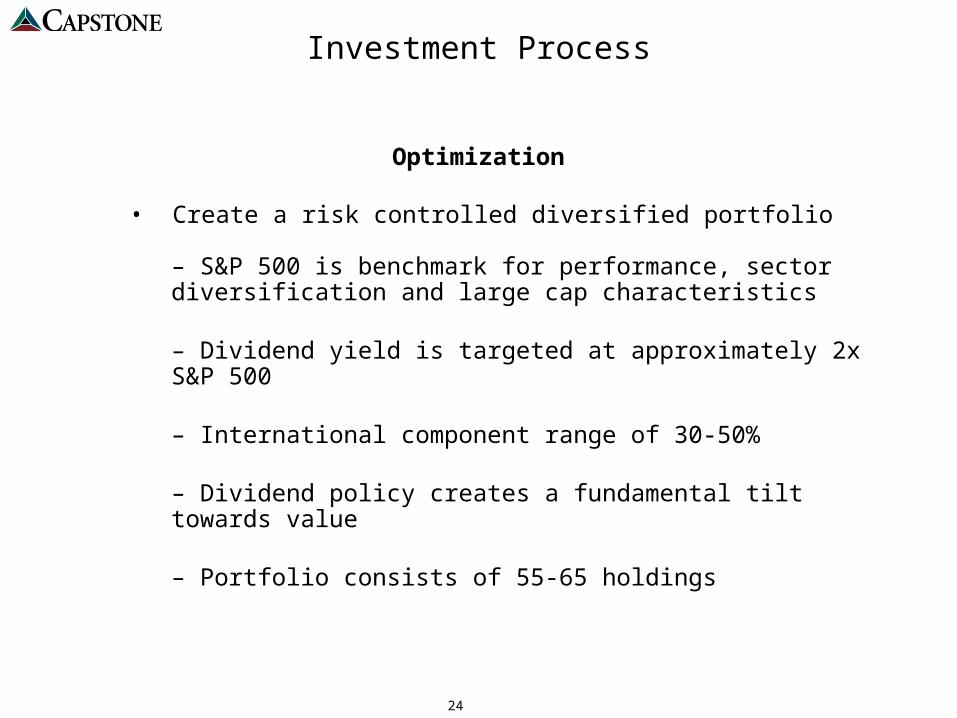

Investment Process

• Create a risk controlled diversified portfolio

– S&P 500 is benchmark for performance, sector diversification and large cap characteristics

– Dividend yield is targeted at approximately 2x S&P 500

– International component range of 30-50%

– Dividend policy creates a fundamental tilt towards value

– Portfolio consists of 55-65 holdings

Optimization

25

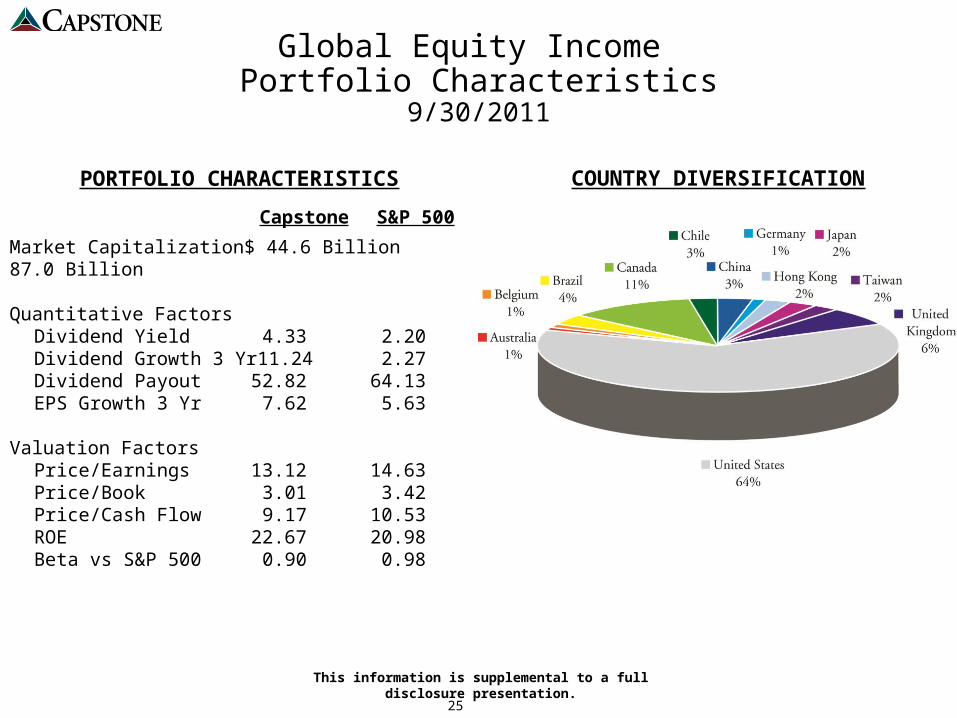

Global Equity Income Portfolio Characteristics

9/30/2011

This information is supplemental to a full disclosure presentation.

COUNTRY DIVERSIFICATION

Market Capitalization $ 44.6 Billion $ 87.0 Billion

Quantitative FactorsDividend Yield 4.33 2.20Dividend Growth 3 Yr 11.24 2.27Dividend Payout 52.82 64.13EPS Growth 3 Yr 7.62 5.63

Valuation FactorsPrice/Earnings 13.12 14.63Price/Book 3.01 3.42Price/Cash Flow 9.17 10.53ROE 22.67 20.98Beta vs S&P 500 0.90 0.98

PORTFOLIO CHARACTERISTICS

Capstone S&P 500

26

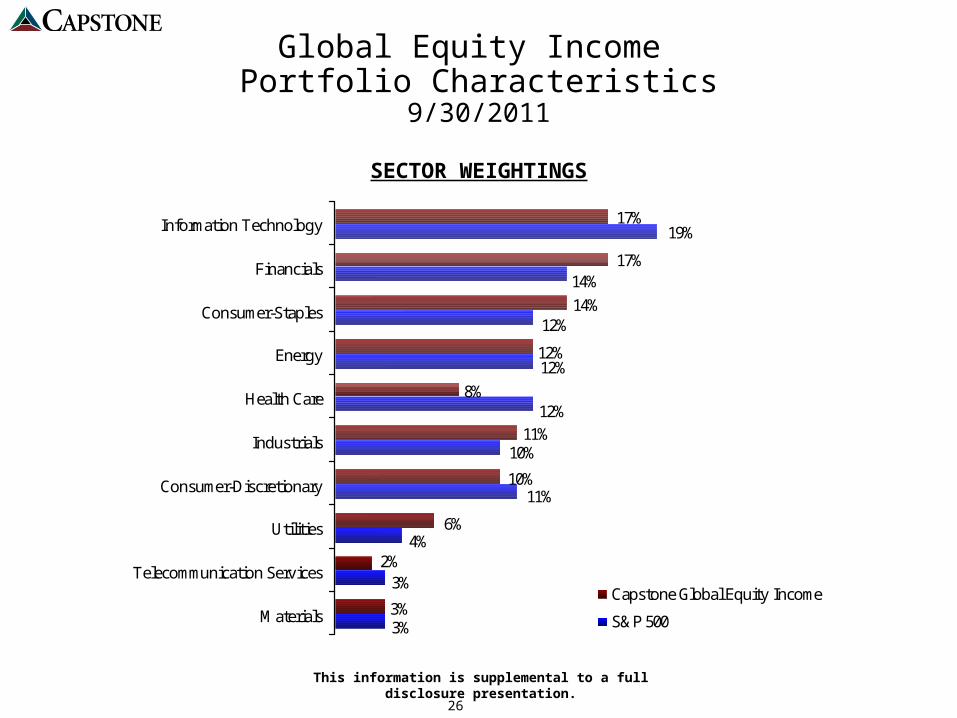

Global Equity Income Portfolio Characteristics

9/30/2011

SECTOR WEIGHTINGS

3%

10%

11%

19%

4%

3%

12%

12%

12%

3%

14%

2%

17%

14%

6%

10%

12%

17%

11%

8%

Materials

Telecommunication Services

Utilities

Consumer-Discretionary

Industrials

Health Care

Energy

Consumer-Staples

Financials

Information Technology

Capstone Global Equity Income

S&P 500

This information is supplemental to a full disclosure presentation.

27

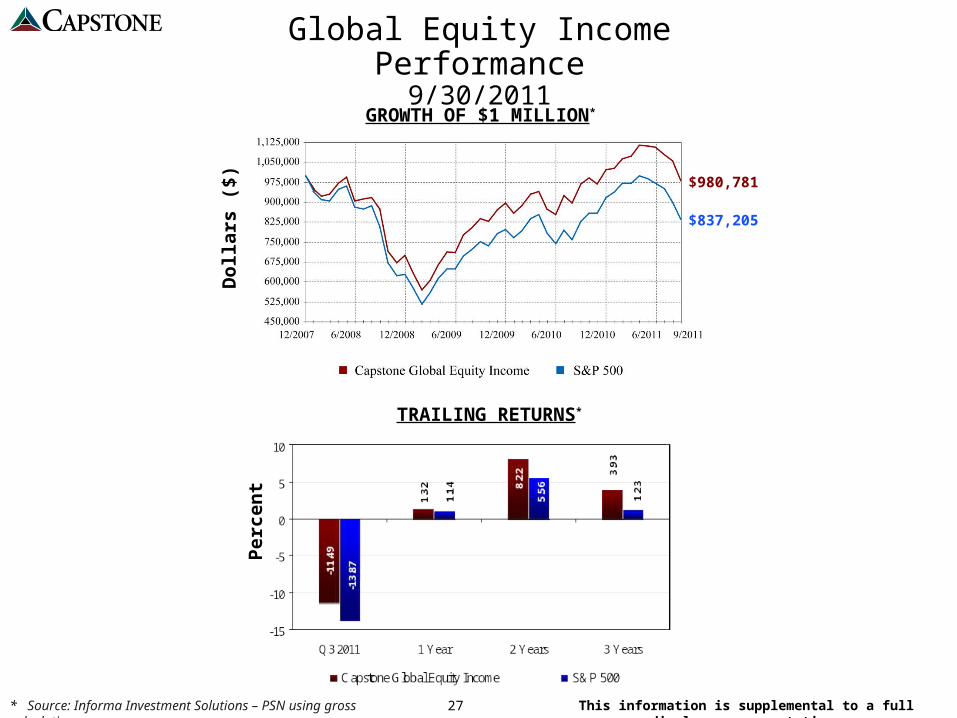

Global Equity Income Performance9/30/2011

* Source: Informa Investment Solutions – PSN using gross calculations

GROWTH OF $1 MILLION*

Per

cen

t

$837,205

$980,781

Dol

lars

($)

TRAILING RETURNS*

This information is supplemental to a full disclosure presentation.

28

Why Capstone ?

• Disciplined Investment Process

• Consistently Applied Investment Process

• Customization

• Active Client Communications

29

30

The States Compared To The Rest Of The World

3700 West Sam Houston Parkway South, Suite 250Houston, Texas 77042

(713) 260-9000 / (800) 262-6631www.capstonefinancial.com

©2011