Embed Size (px)

Citation preview

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 1/89

CONTENTS

CHAPTERS

PAGE NO.S

(1.) BASIC INTRODUCTION AND DEFINITIONS ………………….02 TO 05

(2.) RESIDENTIAL STATUS AND SCOPE OF TOTAL INCOME…. 06 TO 10

(3.) INCOMES EXEMPT FROM TAX ………………………………. . 11 TO 16

(4.) HEADS OF INCOME……………………………………………… 17 TO 17

(5.) INCOME FROM SALARY ………………………………………...18 TO 41

(6.) INCOME FROM HOUSE PROPERTY …………………………..42 TO 52

(7.) PROFITS AND GAINS OF BUSINESS OR PROFESSION ….…53 TO 61

(8.) CAPITAL GAINS……………………………………………..……..62 TO 78

(9.) INCOME FROM OTHER SOURCES ...…………………….….… 79 TO 83

(10.) DEDUCTIONS UNDER CHAPTER VI-A …………………………84 TO 89

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 2/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

CH-1

BASIC INTRODUCTION AND DEFINITIONS

Those taxes, the final incidence or burden of which is borne by the person paying

the tax, are known as “ DIRECT TAXES” , for e.g.: Income Tax, whereas, those taxes, thefinal incidence of which is passed to someone else by the person paying the tax, are called

as “ INDIRECT TAXES ”, for e.g.: SALES TAX, EXCISE DUTY, CUSTOMS DUTY,

SERVICE TAX, etc.All taxes, whether direct or indirect are levied by the government, hence, are finally

to be deposited with the government. Those Indirect taxes, which are paid to the

government first and recovered from others later, are called “DUTIES” , for e.g.: Excise

Duty, Customs Duty, etc. whereas, those which are collected first and later on deposited

with the government, are known as “TAXES” for e.g.: Service Tax, Sales Tax, etc. as theyare collected from customers first and later on deposited on with the government.

Therefore, one can say that all duties are necessarily indirect taxes, but all indirect taxes arenot duties.

INCOME TAX ACT, 1961

‘Income Tax’ is a tax charged on income earned during the year, i.e. it is an annualcharge on income. It is payable on a yearly basis. “Constitution” is the Parent Law and all

the Acts enacted in India are subject to the overall framework of the constitution of India

and norms laid down therein. Constitution of India has empowered the ‘CentralGovernment’ of India to levy tax on income and by virtue of this power; the CentralGovernment has enacted Income Tax Act, 1961, by replacing the earlier act called Income

Tax Act, 1922.

According to Section 1 of the Income Tax Act, 1961, the act is to be called as“Income Tax Act, 1961” and it extends to the whole of India. It came into force with effect

from 01st April, 1962. It is implemented and administered through the rules laid down in

the act, circulars issued by the Central Board of Direct Taxes (CBDT) and High Court /Supreme Court decisions on various issues.

Section 2 of the Income Tax Act, 1961 defines various terms and expressions used in

the act, but before that one must understand certain terminologies used in these definitions.

(a.) “MEANS”: When a definition uses a term “means”, then the definition is self

explanatory and exhaustive. It implies that the term so defined means only what is

defined therein and nothing beyond that. For e.g.: Definition of “Assessment Year”.

(b.) “INCLUDES”: When an exhaustive definition is not possible or Legislature wants

to widen the scope of the definition, it uses the term “includes”, in order to give an

2

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 3/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

inclusive definition or an illustrative definition. For e.g.: Definition of “Income” or

definition of “Person”.

(c.) “MEANS AND INCLUDES”: When Legislature intends to define a term and also

include certain items, it includes both the terms “means and includes”. For e.g.:

definition of “Assessee”.

DEFINITIONS

[A.] “ASSESSEE”:Section 2 (7) of the act, defines the term “assessee” to mean a Person by whom any tax or any other sum of money is payable under the act and includes :

(i.) Every person in respect of whom, any proceeding under the act has been taken

up, whether in respect of assessment of his own income or income of any

other person,(ii.) A person who is deemed to be an assessee under any provision of the act. For

e.g.: Representative assessee, Agent of Non-Resident, etc.(iii.) A person who is deemed to be ‘an assessee in default’ under any provision of

the act. For e.g.: An employer who fails to deduct tax at source from salary

paid by him to his employee.

[B.] “PERSON”: As per Section 2 (31), Person includes :-

(i.) An Individual,(ii.) A Hindu Undivided Family (H.U.F.),

(iii.) A Company,(iv.) A Firm,(v.) An Association of Persons (A.O.P.) (e.g.:‘Navjeevan Co.Op. Housing

Society’ is an A.O.P.) or Body of Individuals (B.O.I.), whether incorporated

or not,(vi.) A Local Authority (e.g.: MUMBAI MUNICIPAL CORPORATION)

(vii.) Every Artificial Juridical Person not falling in any of the above (e.g.

UNIVERSITY OF MUMBAI)

The term ‘Person’ has been defined in an inclusive manner. If one observes the

definitions of the terms “assessee” and “person” both, then one will find that every

‘assessee’ is necessarily a ‘person’, but every ‘person’ need not necessarily be an‘assessee’.

The term ‘Association of Persons (A.O.P.)’ or ‘Body of Individuals (B.O.I.)’ hasnot been defined anywhere in the Act, but in general sense would mean coming together of

more than one person or more than one individual for some common purpose or goal.

There are mainly two basic differences between an AOP and BOI. An AOP can be formed

by two or more persons, wherein the term ‘person’ would mean the same as defined by

3

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 4/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

section 2(31) and on the other hand BOI can be formed by two or more ‘individuals’ only.

And second difference is that an AOP is formed for the purpose or desire to earn income,

whereas such intention is not necessary in case of BOI, BOI may be for non-incomeearning purposes also. For e.g.: Legal Heirs of a deceased person, coming together to

receive income from the estate/property belonging to the deceased, will be said to have

formed Body of Individuals.

[C.] “ASSESSMENT”: The term assessment has not been defined by the act, but itwould mean evaluating or computing the income and determining the income tax

liability of an assessee. According to Section 2 (8) of the act, the term ‘assessment’,

includes ‘reassessment’. Therefore, one can say that ‘Assessment’ is quantification

of Income and Income Tax Liability of an assessee.

[D.] “PREVIOUS YEAR” (P.Y.): The financial year in which the income is earned is

known as Previous Year (and the year in which it is taxed is known as assessmentyear). Income Tax Act, has defined the term in Section 3 as ‘The financial year,

immediately preceding the assessment year’. For e.g.: For the Assessment Year 2010-2011, Previous Year would be 2009-2010 i.e. the Financial Year beginning

on 01st April, 2009 and ending on 31st March, 2010.

But for a Business or a Profession newly set up, the very first Previous Year would begin on the date on which business/profession is set up. For e.g.: If a business

is set up on 17th October, 2009, then first previous year would begin on 17th October,

2009 and end on 31st March, 2010 and thereafter, it would begin on 01st April every

year and end on 31st March, of the next year.Upto Assessment Year 1988-89, assessees were allowed to follow any year as

their previous year, but from Assessment Year 1989-90 onwards this liberty waswithdrawn and now all assesses are required to follow ‘Financial Year’ as their Previous Year.

[E.] “ASSESSMENT YEAR” (A.Y.): Assessment Year has been defined by Section2 (9), to mean ‘A Financial Year, which immediately succeeds the relevant Previous

Year’. For e.g.: For Financial Year 2009-2010, Assessment Year will be 2010-2011.

Income of one financial year is taxed in the next year, which is known as ‘Assessment

Year’.

[F.] “INCOME”: The term ‘Income’ has been defined by Section 2 (24) of the act in a nillustrative manner. According to Section 2 (24), ‘income’ includes;

(a.) Profits and Gains,(b.) Dividend, [Though the term ‘income’ includes ‘dividend’, certain dividends are

exempt from income tax under section 10(34)]

(c.) Voluntary contributions received by Charitable or Religious Trust or Institution,

4

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 5/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

(d.) Value of any perquisite, Profit in lieu of salary, Special Allowance or any other

benefit received by an employee from his employer,

(e.) Export Incentive (e.g.: Duty Drawback),(f.) Any Interest, Salary, Bonus, Commission or remuneration received by a partner of

a firm from the firm,

(g.) Capital Gains,(h.) Winnings from Lotteries, Crossword Puzzles, Card Games, Races including Horse

Races, any other game of any sort or from Gambling or Betting of any nature,

(i.) Any sum received by the assessee from his employees towards Welfare Fund,Provident Fund, Superannuation Fund, etc.

(j.) Any sum received under KEYMAN INSURANCE POICY including any Bonus if

any, on such policy,

(k.)Non-Compete Fees, Compensation for not sharing any intangible asset such asKnow-how, Patent, Trademark, etc.

(l.) Any sum referred to in section 56 (2)(v).

# Points to be noted:

(1.) Income from ‘Illegal activities’ is also an income and hence, is taxable.(2.) Income need not be in ‘cash’, it may even be in ‘kind’.

(3.) Gifts of personal nature is not an income. For e.g.: Gifts received on

Birthday or on occasion of Marriage or Festival gifts, etc. But giftsreceived in the course of profession is an income. For e.g.: Gift received by

a doctor from his patient in addition to his professional fees for conducting

a successful operation is an income and is taxable, or an award or trophy

received by a sportsman like cricketer is also an income chargeable to tax.(4.) Income includes ‘Loss’ also, as loss is a negative income.

(5.) ‘Pin money’ (an amount received by wife from her husband towardshousehold expenses, or for her personal expenses, etc.) is not treated asincome of wife.

5

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 6/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

CH-2

RESIDENTIAL STATUS AND SCOPE OF TOTAL INCOME

(SECTION 6)

The incidence of tax of an assessee depends upon his residential status. Therefore,

residential status of an assessee plays an important role. Residential Status is to be

determined on a year to year basis, as it may change every year, a person may be Resident in one year and Non-Resident in the other year. Residential status is different from

citizenship/nationality.

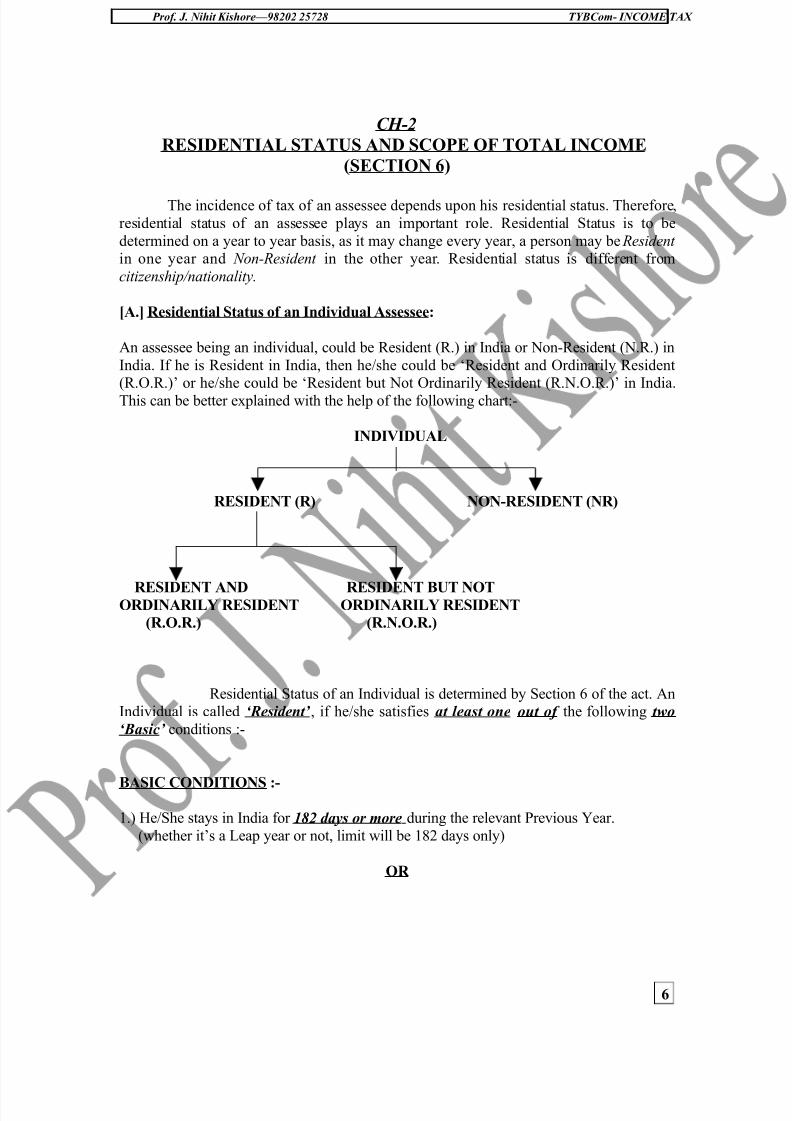

[A.] Residential Status of an Individual Assessee:

An assessee being an individual, could be Resident (R.) in India or Non-Resident (N.R.) in

India. If he is Resident in India, then he/she could be ‘Resident and Ordinarily Resident(R.O.R.)’ or he/she could be ‘Resident but Not Ordinarily Resident (R.N.O.R.)’ in India.

This can be better explained with the help of the following chart:-

INDIVIDUAL

RESIDENT (R) NON-RESIDENT (NR)

RESIDENT AND RESIDENT BUT NOTORDINARILY RESIDENT ORDINARILY RESIDENT

(R.O.R.) (R.N.O.R.)

Residential Status of an Individual is determined by Section 6 of the act. AnIndividual is called ‘Resident’ , if he/she satisfies at least one out of the following two

‘Basic’ conditions :-

BASIC CONDITIONS :-

1.) He/She stays in India for 182 days or more during the relevant Previous Year.

(whether it’s a Leap year or not, limit will be 182 days only)

OR

6

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 7/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

2.) (a.) He/She is in India for 60 days or more during the relevant Previous Year (whether

it’s a Leap year or not, limit will be 60 days only)

and

(b.) He/She is in India for 365 days or more during the last four Previous Years,

immediately preceding the relevant previous year.

EXCEPTIONS TO THE ABOVE CONDITIONS :- In the following two cases, the

second basic condition as given above is not applicable :-

1.) An Indian Citizen, who leaves India during the previous year, for the purpose of

employment (employment includes job, business or profession also) outside India or

leaves India for employment as a crew member of an Indian Ship.2.) An Indian Citizen or a person of Indian origin, who stays abroad, but comes to India

for a visit during the relevant Previous Year. (A person is said to be of Indian Origin if

he himself or any of his/her parents or grandparents were born in undivided India,

where unndivided India would mean India, Pakistan and Bangladesh of toady’s time).

Residential Status is to be determined on a year to year basis, as it may changeevery year. A person who satisfies either of the two basic conditions mentioned above, will

be treated as a Resident for that Previous Year and person who does not satisfy both the

basic conditions will be treated as Non-Resident (N.R.) for that Previous Year. But in caseof two exceptions, the second basic condition is not applicable at all, hence, such persons

will be Resident only if he/she satisfies the first basic condition of ‘182 days or more’

during the relevant Previous Year, else, he/she will be a Non-Resident for that Previous

Year.

ADDITIONAL CONDITIONS : Under Section 6(6), a Resident, is called as ‘OrdinarilyResident (ROR)’ in India, if both the additional conditions mentioned below are satisfied,

otherwise he/she will be treated as ‘Not Ordinarily Resident (RNOR)’ in India :-

1.) He has been Resident in India (based on two basic conditions mentioned above) in at

least 2 out of last 10 Previous Years immediately preceding the relevant Previous

Year.

AND

2.) He/She has been in India for a period of 730 days or more during the last 7 Previous

Years, immediately preceding the relevant Previous Year.

Therefore, we can say that

R.O.R. : An Assessee, who satisfies at least one of the two basic conditions plus both

the Additional conditions.

R.N.O.R. : An Assessee, who satisfies at least one of the two basic conditions and does

7

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 8/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

not satisfy either both or anyone of the Additional conditions.

N.R. : An Assessee, who does not satisfy any of the basic conditions.

Note :

1.) The Date of entering India, as well as the date of leaving India, shall be counted as

stay in India. Where, stay in India is not for the whole day, then physical presence

shall be counted on hourly basis.2.) Stay outside the soil (land) of India, but within the territorial waters of India,

shall also be treated as stay in India. (Territorial Water limits of India = water

limit upto a distance of 20 Nautical Miles from the land of India). For e.g.: Stay in

a Boat moored or anchored within territorial waters of India.3.) February month has 29 days in case of a leap year. (Leap year is that year, which is

divisible by ‘four’ for e.g.: 2008, 2004, 2000, 1996, 1992, 1988, etc.).

4.) There can not be different residential status for different source of income falling

within the same Previous Year i.e. if an assessee is Non-Resident for one income,then he is Non-Resident for all the incomes within the same year, as residential

status is to be determined for a particular year and not for a particular income.5.) A person may be resident in more than one country in the same year. There are

365/366 days in a year. A person may become resident in India by staying for 182

days in India and for rest of the year he may stay in another country and may become resident of that country also. So, it would be wrong to say that a person

who is resident in India is non-resident in all other countries.

6.) Stay in India need not be continuous.

7.) Stay need not be at the same place in India, it could be at any place or places of India.

SCOPE OF TOTAL INCOME:

As we discussed at the beginning of this chapter, that the tax incidence of anassesee, depends upon his/her residential status, let us now understand the tax implication

of an income of an assessee under different residential status, namely, Resident and

Ordinarily Resident (R.O.R.), Resident but not Ordinarily Resident (R.N.O.R.) and Non--Resident (N.R.). This can be better explained with the help of the following table:-

Particulars R.O.R. R.N.O.R. N.R.1.) INDIAN INCOME Taxable Taxable Taxable

2.) FOREIGN INCOME :

a.) Income from Business controlled from

India or a Profession set up in India

Taxable Taxable Not Taxable

b.) Other Foreign Incomes Taxable Not

Taxabl

Not Taxable

8

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 9/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

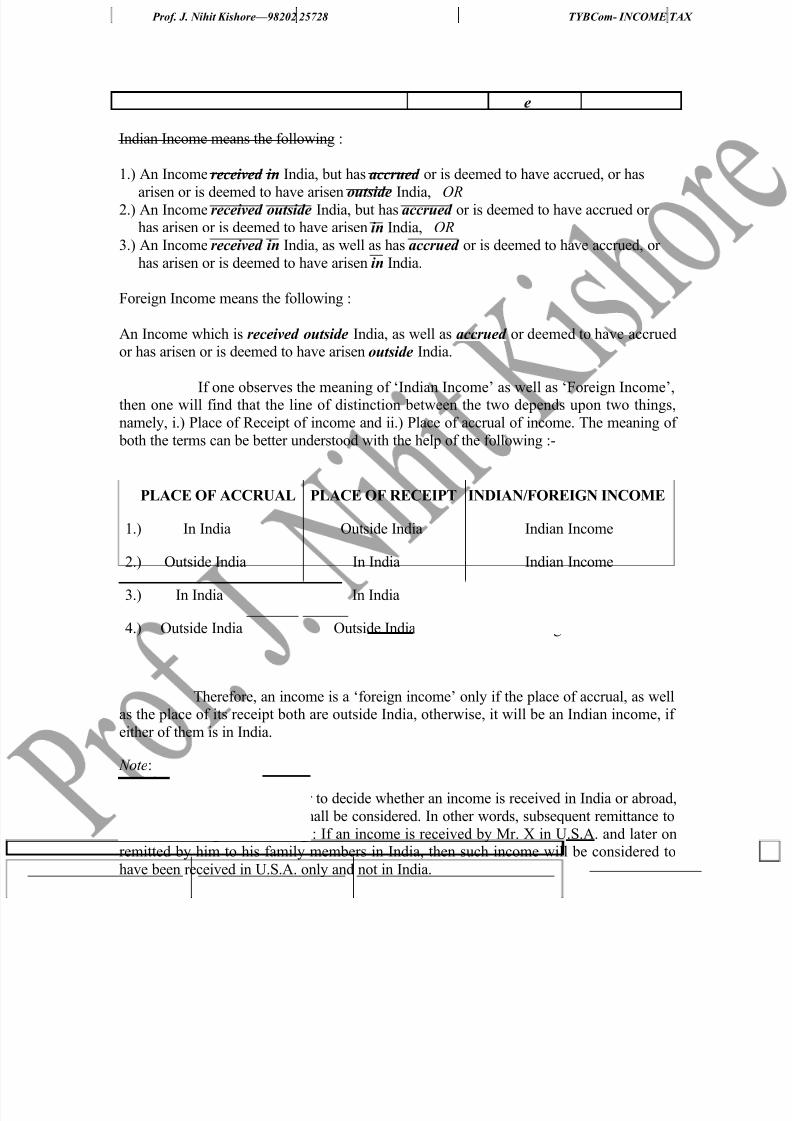

e

Indian Income means the following :

1.) An Income received in India, but has accrued or is deemed to have accrued, or has

arisen or is deemed to have arisen outside India, OR2.) An Income received outside India, but has accrued or is deemed to have accrued or

has arisen or is deemed to have arisen in India, OR

3.) An Income received in India, as well as has accrued or is deemed to have accrued, or

has arisen or is deemed to have arisen in India.

Foreign Income means the following :

An Income which is received outside India, as well as accrued or deemed to have accruedor has arisen or is deemed to have arisen outside India.

If one observes the meaning of ‘Indian Income’ as well as ‘Foreign Income’,then one will find that the line of distinction between the two depends upon two things,

namely, i.) Place of Receipt of income and ii.) Place of accrual of income. The meaning of

both the terms can be better understood with the help of the following :-

PLACE OF ACCRUAL PLACE OF RECEIPT INDIAN/FOREIGN INCOME

1.) In India Outside India Indian Income

2.) Outside India In India Indian Income

3.) In India In India Indian Income

4.) Outside India Outside India Foreign Income

Therefore, an income is a ‘foreign income’ only if the place of accrual, as wellas the place of its receipt both are outside India, otherwise, it will be an Indian income, if

either of them is in India.

Note:

A.) Receipt of Income: In order to decide whether an income is received in India or abroad,

only the first place of receipt shall be considered. In other words, subsequent remittance to

India shall be ignored. For e.g.: If an income is received by Mr. X in U.S.A. and later onremitted by him to his family members in India, then such income will be considered to

have been received in U.S.A. only and not in India.

9

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 10/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

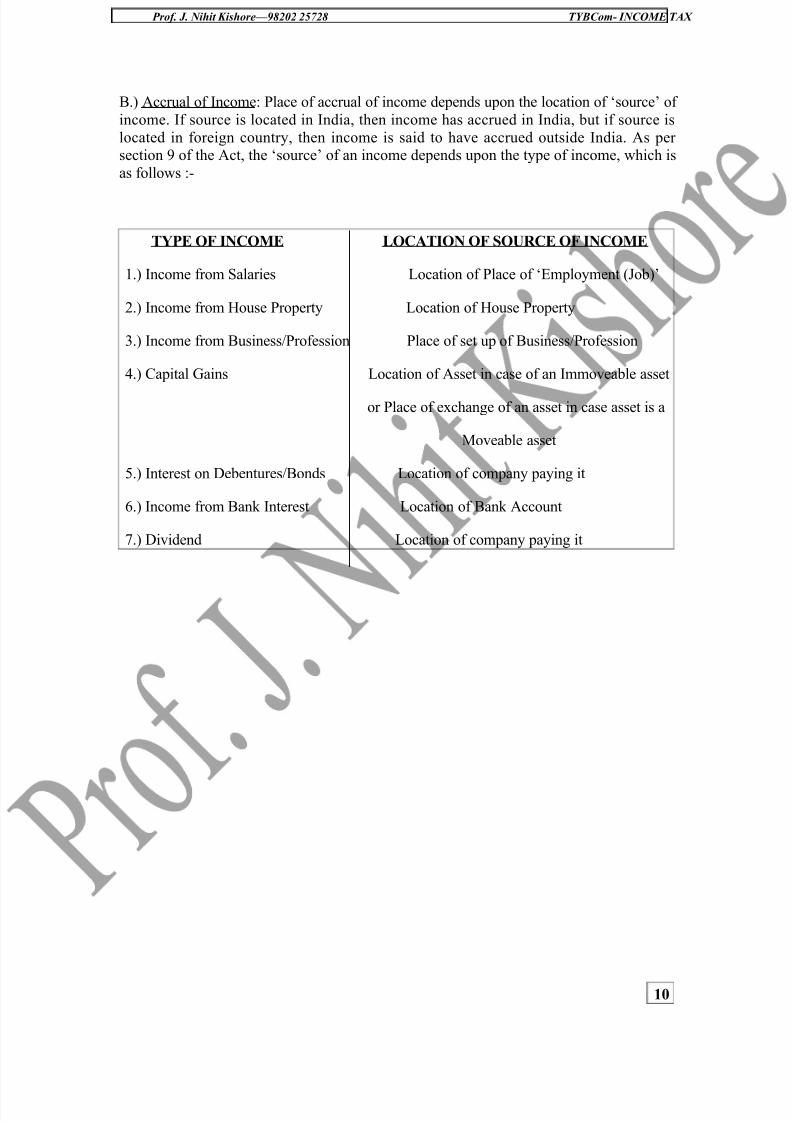

B.) Accrual of Income: Place of accrual of income depends upon the location of ‘source’ of

income. If source is located in India, then income has accrued in India, but if source is

located in foreign country, then income is said to have accrued outside India. As per section 9 of the Act, the ‘source’ of an income depends upon the type of income, which is

as follows :-

TYPE OF INCOME LOCATION OF SOURCE OF INCOME

1.) Income from Salaries Location of Place of ‘Employment (Job)’

2.) Income from House Property Location of House Property

3.) Income from Business/Profession Place of set up of Business/Profession

4.) Capital Gains Location of Asset in case of an Immoveable asset

or Place of exchange of an asset in case asset is a

Moveable asset

5.) Interest on Debentures/Bonds Location of company paying it

6.) Income from Bank Interest Location of Bank Account

7.) Dividend Location of company paying it

10

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 11/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

CH-3

EXEMPT INCOME

(SECTION 10)

Section 10 o the Income Tax Act, deals with incomes, which do not form part

of an assessee’s total income. In other words Section 10 exempts certain incomes from

chargeability to tax. The following are the incomes which are exempted under section 10:-

[1.] Section 10(1): Agricultural Income: Under this section “Agricultural Income” from

“an Agricultural land” in India is exempt from tax. However, Agricultural Income from

Agricultural Land outside India is not exempt, even Agricultural Income from a Non-Agricultural Land in India or an urban land in India is fully taxable.

[2.] Section 10(2): Share of a member in the income of a Hindu Undivided Family

(H.U.F.): Share in income of HUF received by an individual being a member of that HUF

is exempt in the hands of that individual under this section. Under Income Tax Act, HUF is

an ‘Assessee’, separate from its members and being an assessee, it pays income tax on its

own income separately. If a member of HUF also has to pay tax on his share in the profitsof the HUF, which are already taxed in the hands of HUF, then it would amount to double

taxation. The same income would be taxed twice. Therefore, section 10 (2), exempts such

income in the hands of member of HUF.

[3.] Section 10(2A): Share of a Partner in the profits of the Partnership Firm: Just like

HUF in the above case, Partnership Firm is also an ‘Assessee’ separate from its partnersand has to pay tax on its profits. If partners also have to pay tax on their share in the profits

of the firm, then it would amount to double taxation. Section 10 (2A), therefore, exempts

the share of partners in the profits of the firm received by the partner. (Only share of profitis exempt and not any other remuneration like salary, bonus, commission, interest on

capital, received by partner from the firm).

[4.] Section 10(3): Casual Income: Exemption under this section is now no more availablewith effect from Assessment Year 2003-2004.

[5.] Section 10(5): Amount received as ‘Leave Travel Concession’: Will be separatelydealt with in the Chapter on ‘Income from Salaries’.

[6.] Section 10(7): Allowances or Perquisites received by a Citizen of India being an

employee of Government of India: received outside India from Government of India for services rendered outside India, are fully exempt from tax in India under section 10 (7). But

Salary received by such an Indian Citizen from Government of India for services rendered

outside India, though accrued as well as received outside India, is however, deemed to haveaccrued in India and is accordingly taxable in India.

11

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 12/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

[7.] Section 10(10): Amount received as ‘Gratuity’: Will be separately dealt with in the

Chapter on ‘Income from Salaries’.

[8.] Section 10(10A): Amount received as ‘Commuted Pension’: Will be separately

dealt with in the Chapter on ‘Income from Salaries’.

[9.] Section 10(10AA): Amount received as ‘Leave Salary’: Will be separately dealt

with in the Chapter on ‘Income from Salaries’.

[10.] Section 10(10B): Amount received as ‘Retrenchment Compensation’: Will be

separately dealt with in the Chapter on ‘Income from Salaries’.

[11.] Section 10(10C):Compensation received under ‘Voluntary Retirement Scheme’:

Will be separately dealt with in the Chapter on ‘Income from Salaries’.

[12.] Section 10(10CC): Tax on Non-Monetary Perquisites paid by Employer: If tax on

non-monetary or non-cash perquisites received by an employee is paid by his employer,then such tax shall not be added in the income of that employee, as it is exempt from tax in

his hands under section 10 (10CC) with effect from Assessment Year 2003-2004. Such taxas is paid by the employer shall not be allowed to the employer as a deduction on account

of business expenditure under section 40. (Here, exemption is available only on tax paid by

employer on non-monetary perquisites and not on tax paid by him on monetary or cash perquisites).

[13.] Section 10(10D): Maturity Proceeds of a ‘Life Insurance Policy’: Any sum

received by a Policyholder or his Legal Heirs as a maturity proceeds of a Life Insurance policy or any Bonus on such policy from an Insurance Company is fully exempt from tax

in the hands of either a Policyholder or his Legal Heirs under section 10 (10D).However, maturity proceeds of a ‘Keyman Insurance policy’ or any Bonus onsuch policy is not exempt from tax. (For meaning of ‘Keyman Insurance policy’ and its

taxability, refer to Chapter – I )

With effect from Assessment Year 2004-2005, this exemption is not applicableon maturity proceeds of that Life Insurance policy or any Bonus thereon, whose ‘Annual

Premium’ exceeds 20 % of the ‘Sum Assured’, provided policy was issued on or after 01st

April, 2003 (i.e. issued from the day one of the Previous Year 2003-2004, which pertains to

Assessment Year 2004-2005).

[14.] Section 10(11) / (12):Receipts from ‘Provident Fund’: Will be separately dealt with

in the Chapter on ‘Income from Salaries’.

[15.] Section 10(13):Receipts from ‘An Approved Superannuation Fund’: When an

employee retires from his service, due to his retirement age or his ill health or due to hisincapacitation to work more or due to his death, he or his family members would receive an

amount from ‘Superannuation Fund’. Any amount received from an approved

‘Superannuation Fund’ is exempt from tax under section 10 (13), whether received by an

12

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 13/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

employee at the time of his retirement or by his family members or his legal heirs at the

time of his death.

[16.] Section 10(13A):Amount received as ‘House Rent Allowance’ (H.R.A.): An

amount of fixed monthly allowance received by an employee from his employer, towards

paying rent of a house is exempt from tax in the hands of that employee subject to the leastof the followings:- (Balance H.R.A. received will thus be taxable in his hands)

a) Actual H.R.A. received by the employee from his employer for that many num ber

of months for which the house was rented by him. (If House was rented only for three months during the year, then H.R.A. of only three months only shall be

considered here and not for the whole year) OR

b) 50 % of the salary, if rented house is situated at Chennai, Delhi, Mumbai or Kolkata

or 40 % of salary if rented house is situated at any other place other than Chennai,Delhi, Mumbai or Kolkata [Here, ‘Salary’ would mean ‘Basic Salary’ plus

‘Dearness Allowance (D.A.)’ only if D.A. forms part of Retirement Benefits

otherwise only ‘Basic Salary’] OR

c) Excess of rent paid over 10 % of Salary [Here also, the term ‘Salary’ would mean‘Basic Salary’ plus ‘Dearness Allowance (D.A.)’ only if D.A. forms part of

Retirement Benefits otherwise only ‘Basic Salary’]

In (b) and (c) above ‘Basic Salary and D.A.’ of only that many months shall be

considered during which the house was rented and not ‘Basic Salary and D.A.’ of thewhole year.

If an employee resides in his ‘own house’ or he does not pay any rent for the house

where he resides, then answer to point (c) above will be NIL and therefore, the least of (a),

(b) and (c) will also be NIL and nothing will be exempt under section 10 (13A). As a resultof this entire amount received by employee as H.R.A. will become taxable in his hands as a

Salary.

[17.] Section 10(14): ‘Special Allowance’ received: Will be separately dealt with in the

Chapter on ‘Income from Salaries’.

[18.] Section 10(15): Interest on certain securities: Interest received from 7 % Capital

Investment Bonds, notified ‘Relief Bonds’ , Gold Deposit Bonds, notified bonds issued by

‘Local Authority’ and interest received from following notified bonds, securities or

certificates are fully exempt from tax under section 10 (15):-

National Defence Gold Bonds,

National Plan Certificates,

National Plan Savings Certificates, 12 Year National Savings Annuity Certificates,

Treasury Savings Deposit Certificates,

10.5 % Tax Free Bonds issued by HUDCO,

10.5 % Tax Free Bonds issued by National Hydroelectric Power Corporation,

9.25 % Tax Free Bonds issued by Rural electrification Corporation Ltd. (RECL),

N.R.I. Bonds (Second series) issued by State Bank of India,

13

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 14/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

N.R.I. Bonds-1988 issued by State Bank of India,

Special Bearer Bonds,

Post Office Cash Certificates,

Post Office Savings Account,

Post Office Cumulative Time Deposits (CTD),

Special Deposit Schemes, etc. Gold deposit Bonds issued under Gold deposit Scheme, 1999 and notified by

Central Government,

Bonds issued by Local Authority and notified by Central Government,

Notified Bonds.

[19.] Section 10(16): Educational Scholarships: Educational Scholarship received by an

assessee, being a student from any person including Government, to meet the ‘cost of

education’ is fully exempt from tax in the hands of the recipient assessee under section 10

(16). Here, ‘cost of education’ does not mean only ‘Tuition Fees’, but also any other incidental expenses to acquire education. The term ‘Education’ is not restricted to only

those courses leading to a degree. Educational Scholarship is awarded to meet the cost of

education and will be exempt from tax under this section, even if it is not entirely spent for meeting the cost of education.

[20.] Section 10(17): Daily Allowances received by MPs / MLAs / MLCs: DailyAllowances received by Members of Parliament (M.P.s), Members of Legislative

Assembly (M.L.A.s) or Members of Legislative Council (M.L.C.s) is fully exempt from tax

under section 10 (17).

But Salary received by MPs / MLAs / MLCs is not exempt, it is taxable. Though, it iscalled as ‘Salary’, it is always taxable as ‘Income from Other Sources’ and not as ‘Income

from Salary’, as MPs / MLAs / MLCs are not employees of Government.

[21.] Section 10(17A): Awards: Any award received by an assessee whether in cash or in

kind, issued to him in ‘Public Interest’ by ‘Central / State Government’ or by any body /

Institution / organization approved by Central / State Government is fully exempt from taxin the hands of the recipient assessee under section 10 (17A).

But if an award is received from any individual or any private organization then

exemption under section 10 (17A) is not available on such award. Also, if an award isreceived by an employee from his employer, then it will be taxable and taxable as a

‘Salary’ income.

Few examples of such exempt awards are:-

• Sir C. V. Raman Award,

• Sir Jagdish Chandra Bose Award,

• Ramon Magsaysay Award,

• Pope John XIII Award,

• Kennedy International Award,

• Bhartiya Janpith Award,

• National Award for Films,

14

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 15/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

• Dr. Rajendra Prasad Award,

• Cash reward for passing Hindi Examinations, etc.

[22.] Section 10(32): Income of Minor Child: Minor Child is not taxable in respect of his / her own income. Minor Child’s income is taxable in the hands of either of his parents,

by virtue of section 64(1A) on ‘Clubbing of Income’. That parent in whose income, the

income of Minor Child is included / clubbed, is entitled to this exemption under section10(32).

Exemption under section 10(32) is restricted to actual income of Minor Child

clubbed in the hands of that parent or Rs. 1,500/- per Minor Child, whichever is lower.(Here, Minor Child includes a ‘Step Child’ as well as an ‘Adopted Child’, but does not

include an ‘Illegal Child’ or a child born as a result of an illegal marriage.) There is no

restriction on the number of minor children, but exemption will be restricted to Rs. 1,500/- per minor child, per annum.

[23.] Section 10(33): Capital Gain on transfer of Units of US-64 of UTI: Any Capital

Gain arising on transfer of units of US-64 Scheme of Unit Trust of India (U.T.I.) on or after

01st

April, 2002 shall be exempt by virtue of section 10(33), provided units of US-64 wereheld as Capital Asset.

[24.] Section 10(34): Dividend from a ‘Domestic Company’: Any amount received by an

assessee as a Dividend or as an Interim Dividend from shares (whether equity shares or

preference shares) of an ‘Indian Company’ (whether Public Company or a PrivateCompany) is fully exempt from tax by virtue of section 10(34) [earlier this exemption was

covered by section 10(33)]. It would be worth to note here that under section 10(34) what

is exempt from tax is dividend from an Indian domestic company. Therefore, dividend

received from a Foreign Company or from a Co.-Operative Society will not be exempt. Itwill always be taxable and will be taxable as ‘Income from Other Sources’.

[25.] Section 10(35): Income from ‘Units of a Mutual Fund’: Any income, other thanCapital Gains received by an assessee from units of a Mutual Fund, including units of Unit

Trust Of India (U.T.I.), is exempt from tax under section 10(35). [Earlier it was covered by

Section 10(33)].

[26.] Section 10 (36): Long Term Capital Gains on transfer of eligible Equity Shares:

Long Term Capital Gain arising on transfer of eligible equity shares shall be exempt fromtax by virtue of section 10(36), provided such eligible equity shares were acquired on or

after 01st March, 2003, but before 01st March, 2004 and held for a period of 12 months

before their transfer and sold through a recognized Stock Exchange in India. An ‘Eligible

equity share’ would mean either (1.) An equity share acquired by way of a Public Issue(I.P.O.) on or after 01st March, 2003 but before 01st March, 2004, or (2.) An Equity share of

a company, which is listed as on 01st March, 2003 as a BSE-500 INDEX companies on

Mumbai Stock Exchange.

[27.] Section 10(37): Income from Capital Gain on Transfer of Agricultural Land:

Only in the case of an assessee being an Individual or a Hindu Undivided Family, anyCapital Gain arising on transfer of an Agricultural Land situated in a specified area and

15

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 16/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

used by that individual or his/her parents or by HUF for agricultural purposes, shall be

exempt from its chargeability to Income Tax under section 10(37), provided impugned

Agricultural Land was compulsorily acquired by Government under any Law in force or sale consideration of such Agricultural Land was determined by Reserve Bank of India

(RBI) or by Central Government. This exemption was being introduced with effect from

Assessment Year 2005-2006 and exempts only those Capital Gains, which have arisen onsale consideration received on or after 01st April, 2004.

[28.] Section 10(38): Long Term Capital Gain on transfer of Listed Securities: AnyLong Term Capital Gain (Only Long Term Capital Gains and not Short Term Capital

Gains) arising on transfer of Equity Shares listed on a Recognized Stock Exchange in

India, or Equity Oriented Units of Mutual Fund shall be exempt by virtue of Section

10(38), provided such sale transaction attracts Securities Transaction Tax (S.T.T.). Section10(38) has been introduced with effect from Assessment Year 2005-2006.

Examination Hint: Important sections from examination point of view are – Section

10(1), 10(2), 10(2A), 10(5), 10(10), 10(10A), 10(10AA), 10(11) / (12), 10(13A),10(14), 10(34), 10(35), and 10(38).

16

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 17/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

CH-4

HEADS OF INCOME

(SECTION 14)

For the purpose of computing total income of an assessee and income taxthereon, section 14 of the act requires all the incomes of an asseessee to be classified under

the following five heads of income:-

(1.) Income from Salaries,

(2.) Income from House Properties,

(3.) Profits and Gains of Business or Profession,

(4.) Capital Gains and

(5.) Income from Other Sources.

Total of incomes under all the five heads of income is known as Gross TotalIncome (G.T.I.) and in the following chapters, we shall discuss all the five heads

individually with the help of practical illustrations.

Expenditure incurred in relation to exempt income: Section 14A: Deductibility of an

actual expenditure incurred to earn an income, depends upon the head of income under

which that income is chargeable to tax, which is discussed with each head of incomeseparately. For e.g.: For an income chargeable to tax under the head Profits and Gains of

Business or Profession, all actual expenditures incurred to earn that income shall beallowed to be deducted, whereas for an income chargeable to tax under the head incomefrom House Properties, all actual expenditures are not allowed to be deducted, but certain

percentage of such income is allowed to be deducted.

But Section 14A of the act requires that under no circumstances, expenditureincurred to earn an exempt income shall be allowed to be deducted. For e.g.: Dividend

from an Indian Company is exempt by virtue of section 10 (34). Any expenditure incurred

to earn such dividend income shall be ineligible as to its deductibility from other taxableincome by virtue of section 14A.

17

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 18/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

CH-5

INCOME FROM SALARIES

(SECTION 15 TO SECTION 17)

In earlier chapter we discussed that there are five heads of income. Now in thischapter, we shall discuss the first head of income i.e. income from ‘Salaries’. To a common

man or a layman, the term ‘salary’ would mean a fixed monthly remuneration received

from employer for work done, but from Income Tax Act point of view the term ‘salary’would mean ‘salary’ as defined under section 17 (1). Under section 17 (1), the term ‘salary’

has been specifically defined in an inclusive manner.

Section 15 of the act talks about the chargeability of an item to tax under this

head as ‘salary’. It explains the basis of charge. According to section 15 the followings are

chargeable to tax under this head:-(a.) Any salary due to an employee, whether received by him or not – this means that

salary is taxable even if not received by employee, but has become due to him.(b.)Any salary received by an employee, whether due or not – this means that salary is

taxable even if it has not become due to him but has been received by him. For e.g.:

Advance Salary.(c.) ‘Arrears of Salary’ – Earlier year’s salary, which has now become due to him and

now received by him.

In other words, any amount due to or received by an employee from his employer

or his ex-employer and coming within the purview of the meaning of the term ‘salary’, asdefined under section 17 (1) is chargeable to tax under the head ‘salary’.

Now a question arises is that what is the definition of the term ‘salary’ as given

by section 17 (1)? But before we jump to the definition, let us understand certain essential

norms of the salary income. In order to understand the meaning of the term salary, one has

to keep in mind the following norms. These norms will simplify the understanding of thedefinition of the term salary.

(a.) Existence of Employer-Employee Relationship or Master-Servant

Relationship: In order to charge an income under this head there must exist an

employer-employee or master-servant relationship between the person liable to pay

and person entitled to receive remuneration. An employer-employee or master-

servant relationship is in contrast to Contractor-Contractee relationship or Principal-Agent relationship. Servant works under direct control and supervision of

his master unlike an agent who controls and supervises his work on his own and

therefore an agent’s remuneration is known as ‘commission’ and is chargeable totax under the head ‘Profits and gains of Business or Profession’ unlike ‘salary

income’ in the hands of a servant or an employee.

(b.) Every person who is employed need not be an Employee: Every person who isan employee, is necessarily employed by another, but every person who is

18

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 19/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

employed by another need not be an employee. For e.g.: A Lawyer employed to

file a legal suit or a Doctor employed to operate a patient are though employed by

their clients to carry out some work are not their employees.

(c.) Only Individuals can have a salary income: Only an Individual assessee can

have employer-employee relationship with the other. Therefore, only individuals

can have salary income unlike partnership firm or a company.(d.) Any payment received from employer: Once employer-employee relationship is

established then any payment received by an employee from his employer is a

salary like fees, commission received from employer. On the other hand, if sameremuneration is received from any other person for the same work, then its not an

income from salary. For e.g.: A Professor who is an employee of XYZ College,

receives a payment for setting/correcting examination papers. – If received from

college, then ‘Salary income’, but if received from University, then ‘Income fromother sources’.

(e.) “Salary” v/s “Wages”: “Salary” and “Wages” are conceptually not different from

each other; both are paid for work done. Normally, Salary is paid for non-manual

work, whereas “Wages” are paid for manual work. Wages are normally, paid ondaily basis whereas salary is normally paid on monthly basis. Income Tax Act

views no difference between salary and wages, both are taxed at the same rate andare taxed under the same head as ‘income from salary’.

(f.) Salary from past / prospective employer : Salary from past employer or ex-

employer is taxable just like salary from present employer, though employer-employee relationship is no more in existence. For e.g.: Pension, Termination

Bonus, etc. Salary from future or prospective employer is also taxable just like

salary from present employer, though employer-employee relationship is yet to be

developed. For e.g.: Join-in Bonus.

(g.) Additional Salary : Salary received in addition to normal salary though not

contracted before, between employer and employee, is also taxable. For e.g.:Overtime salary.

(h.) Net of Tax Salary : If an employee is being offered a Net of tax salary, then what is

taxable in the hands of employee is not only the salary, but also the tax paid on it

by his employer, whether tax is paid by employer voluntarily or under contract or agreement. Tax paid by employer is treated as a perquisite in the hands of the

employee under section 17(2). For e.g.: If an employee is being paid a tax free

salary of Rs. 2,21,000/- and tax paid by the employer on this salary is Rs. 29,000/-

then what is taxable as salary in the hands of employee is not only Rs. 2,21,000/- but Rs. 2,50,000/- i.e. Rs. 2,21,000/- + Rs. 29,000/- of tax paid.

(i.) Salary of M.P. / M.L.A. / M.L.C.: Remuneration to Member of Parliament

(M.P.), Member of Legislative Assembly (M.L.A.) or Member of LegislativeCouncil (M.L.C.) is paid by Government and is called salary. Even though it is

called as salary it is not taxable as salary but is taxable as income from other

sources as there is no employer-employee relationship between Government andM.P./M.L.A./M.L.C. on the other hand.

(n.) Salary of a Partner of a Partnership Firm: Salary, Bonus, Commission or any

other remuneration by whatever name called, other than interest on capital

received by a partner from partnership firm is not taxable as salary, but is taxable

19

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 20/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

as ‘Profits and Gains of Business or Profession’. It is basically not a salary in its

real nature, but is just an appropriation of profits of the firm and again no partner

can be called as an employee of the firm.

(o.) Salary to a Director of a Company: Every director of a company is not

necessarily an employee of the company. He may or may not be an employee.

If as per the agreement with the employer company he is an employee of thecompany then his remuneration will be taxable as ‘salary’, but if he is not an

employee of the company, then his remuneration will be taxable either as ‘Profits

and Gains of Business or Profession’ or as ‘Income from other sources’. Even if aDirector is an employee of a company, if he receives any commission from his

employer company for arranging any loan for the company or for his standing as a

guarantor of his company for the loan taken by his company, such commission or

fees as is received by him will not taxable as ‘salary’, but will be taxable as‘income from other sources’.

(p.) Method of Accounting: Salary is taxable on ‘due’ or ‘receipt’ basis, whichever

is earlier. Method of Accounting followed by assessee is irrelevant. Salary once

taxed on due basis will not be taxed again on receipt basis and similarly, salaryonce taxed on receipt basis will not be taxed again on due basis. In other words,

there will be no double taxation of the same salary.

(q.) Pension: Monthly or periodical Pension received by the assessee after his

Retirement, is taxable as salary till he/she is alive. Same Pension received by the

Family members/Legal Heirs of the assessee upon death of the assessee is taxablein the hands of his/her family members or legal heirs as ‘Family Pension’ and is

taxable as ‘income from other sources’ under section 56 and not as ‘salary’.

(r.) Advance against salary: As we discussed earlier in point (p.) above, salary is

taxable on due or receipt basis whichever is earlier, salary received in advancewill be taxable on receipt basis. For e.g.: Salary for the month of April, 2009 is

if received in March, 2009 then it will be taxable as salary of the year 2008-2009,though it should have been normally taxable in the year 2009-2010.One must understand here that ‘Advance Salary’ is different from ‘Advance

against salary’. Advance Salary is taxable on receipt basis, whereas ‘Advance

against salary’ is not an income only, hence is not taxable, as it is like a loan takenagainst security of salary.

(s.) Salary in ‘Kind’: Salary is taxable whether received in ‘Cash’ or in ‘Kind’. For

e.g.: If 25 Kg. of Rice is received as a salary then market value of rice will be

taxable as salary.

(t.) Arrears of Salary: Arrears of salary is earlier year’s salary which is now being

received by the employee. In other words, arrears of salary is that salary which

was never due to employee earlier, but has now become due and is now beingreceived by him. It is taxable only on receipt basis in the year of receipt just like

Bonus or Commission or Leave Salary and not on due basis. It is taxable as

‘income from salary’ only. Arrears of salary may arise due to ‘revision in pay-- scale with retrospective effect’ or due to ‘court’s order to increase the pay with

retrospective effect’.

(u.) Grade of Salary: When a candidate applies for a job or employment, he/she is

offered a salary in a particular Grade/Scale. For e.g.: Salary is in the Grade of

20

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 21/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

Rs.12,000 – 1000 – 18,000 : this means that he/she is appointed at a monthly

salary of Rs. 12,000/- and it will be increased by Rs. 1,000/- p.m. at the end of

every year, till his/her monthly salary reaches Rs. 18,000/- p.m. and thereafter there will be no increment in the salary. His first year salary will be Rs. 12,000/-

per month and second year salary will be Rs. 13,000/- per month if he continues

his job. Thereafter, it will be increased to Rs. 14,000/- per month in the thirdyear of his service and so on till monthly salary reaches the level of Rs. 18,000/-

(v.) Salary from UNITED NATIONS ORGANIZATION: Salary received from

United Nations Organization (U.N.O.) or any other Allowances or Perquisites or Pension received from U.N.O. is not taxable at all.

Year of Chargeability of Salary: Salary is chargeable to tax in that year in whicheither it has become due or it is received, whichever year is earlier. This rule of

chargeability is however subject to certain exceptions like Bonus, Commission, Arrears

of Salary, Leave Salary are chargeable to tax as salary only on receipt basis i.e. only in

that year in which these are actually received and not in the year in which they have become due.

Place of Accrual of Salary: Salary is deemed to accrue or arise at the place where

services are rendered. Under section 9(1) of the act, Salary for services rendered in

India are deemed to accrue or arise in India. There is only one exception to this rule.Salary received by an Indian Citizen from Government of India for services rendered

outside India is deemed to have accrued or arisen in India (even though services are not

rendered in India). But all perquisites and allowances received by such person from

Government of India outside India are exempt from tax under section 10(7).

Definition of Salary: Let us now understand the meaning of the term ‘Salary’ asdefined by section 17 (1) of the act. Section 17 (1) defines the term ‘Salary’ in an

inclusive manner and it includes eight items. According to it Salary includes:-

1) Wages,

2) Pension or Annuity [After claiming exemption U/S 10 (10A)],

3) Gratuity [After claiming exemption U/S 10 (10)],

4) Fees, Commission, Perquisites, Profits in lieu of or in addition to salary or wages,

5) Advance Salary,

6) Leave Salary [After claiming exemption U/S 10 (10AA)],7) Balance to the credit of Employee’s ‘Recognized Provident Fund’ [After

claiming exemption U/S 10 (11)],

8) Transferred balance to the credit of Employee’s ‘Recognized Provident FundAccount’ (R.P.F. A/C) (transferred from employee’s R.P.F. A/C with previous

employer to employee’s R.P.F. A/C with current employer) [After claiming

exemption U/S 10 (12)].

21

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 22/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

Let us now understand the meaning of certain terminologies included in the

above eight items as well as exemption from tax under section 10 available on few of theseeight items.

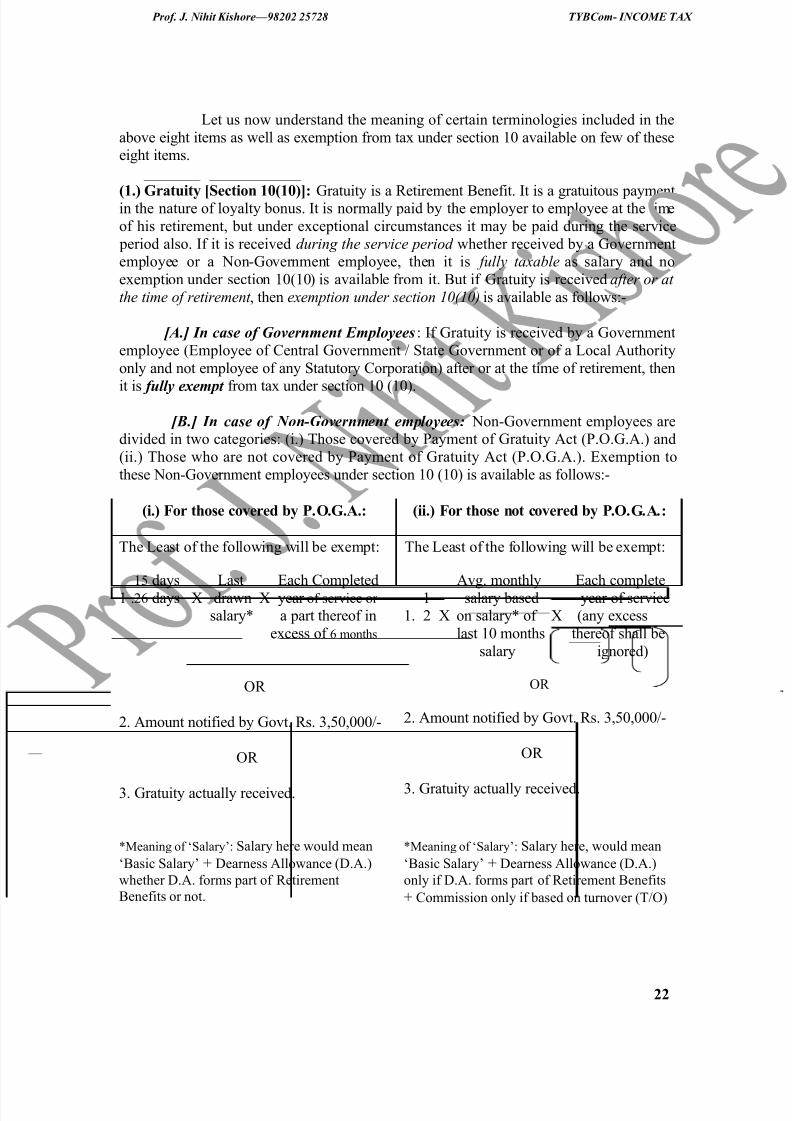

(1.) Gratuity [Section 10(10)]: Gratuity is a Retirement Benefit. It is a gratuitous paymentin the nature of loyalty bonus. It is normally paid by the employer to employee at the time

of his retirement, but under exceptional circumstances it may be paid during the service

period also. If it is received during the service period whether received by a Governmentemployee or a Non-Government employee, then it is fully taxable as salary and no

exemption under section 10(10) is available from it. But if Gratuity is received after or at

the time of retirement , then exemption under section 10(10) is available as follows:-

[A.] In case of Government Employees: If Gratuity is received by a Government

employee (Employee of Central Government / State Government or of a Local Authority

only and not employee of any Statutory Corporation) after or at the time of retirement, then

it is fully exempt from tax under section 10 (10).

[B.] In case of Non-Government employees: Non-Government employees aredivided in two categories: (i.) Those covered by Payment of Gratuity Act (P.O.G.A.) and

(ii.) Those who are not covered by Payment of Gratuity Act (P.O.G.A.). Exemption to

these Non-Government employees under section 10 (10) is available as follows:-

(i.) For those covered by P.O.G.A.: (ii.) For those not covered by P.O.G.A.:

The Least of the following will be exempt: The Least of the following will be exempt:

15 days Last Each Completed1 .26 days X drawn X year of service or

salary* a part thereof in

excess of 6 months

OR

2. Amount notified by Govt. Rs. 3,50,000/-

OR

3. Gratuity actually received.

Avg. monthly Each complete1 salary based year of service1. 2 X on salary* of X (any excess

last 10 months thereof shall be

salary ignored)

OR

2. Amount notified by Govt. Rs. 3,50,000/-

OR

3. Gratuity actually received.

*Meaning of ‘Salary’: Salary here would mean

‘Basic Salary’ + Dearness Allowance (D.A.)

whether D.A. forms part of Retirement

Benefits or not.

*Meaning of ‘Salary’: Salary here, would mean

‘Basic Salary’ + Dearness Allowance (D.A.)

only if D.A. forms part of Retirement Benefits

+ Commission only if based on turnover (T/O)

22

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 23/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

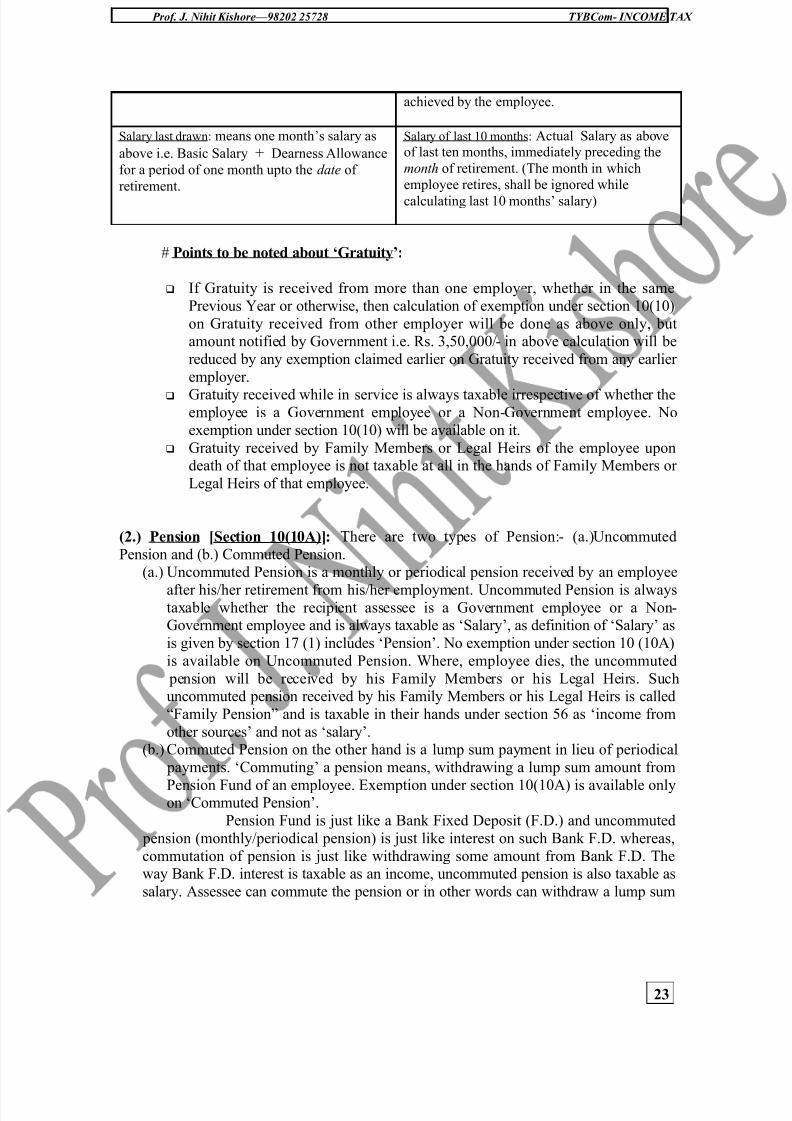

achieved by the employee.

Salary last drawn: means one month’s salary as

above i.e. Basic Salary + Dearness Allowance

for a period of one month upto the date of

retirement.

Salary of last 10 months: Actual Salary as aboveof last ten months, immediately preceding the

month of retirement. (The month in which

employee retires, shall be ignored while

calculating last 10 months’ salary)

# Points to be noted about ‘Gratuity’:

If Gratuity is received from more than one employer, whether in the same

Previous Year or otherwise, then calculation of exemption under section 10(10)

on Gratuity received from other employer will be done as above only, butamount notified by Government i.e. Rs. 3,50,000/- in above calculation will be

reduced by any exemption claimed earlier on Gratuity received from any earlier

employer. Gratuity received while in service is always taxable irrespective of whether the

employee is a Government employee or a Non-Government employee. No

exemption under section 10(10) will be available on it. Gratuity received by Family Members or Legal Heirs of the employee upon

death of that employee is not taxable at all in the hands of Family Members or

Legal Heirs of that employee.

(2.) Pension [Section 10(10A)]: There are two types of Pension:- (a.)Uncommuted

Pension and (b.) Commuted Pension.(a.) Uncommuted Pension is a monthly or periodical pension received by an employee

after his/her retirement from his/her employment. Uncommuted Pension is alwaystaxable whether the recipient assessee is a Government employee or a Non-Government employee and is always taxable as ‘Salary’, as definition of ‘Salary’ as

is given by section 17 (1) includes ‘Pension’. No exemption under section 10 (10A)

is available on Uncommuted Pension. Where, employee dies, the uncommuted

pension will be received by his Family Members or his Legal Heirs. Suchuncommuted pension received by his Family Members or his Legal Heirs is called

“Family Pension” and is taxable in their hands under section 56 as ‘income from

other sources’ and not as ‘salary’.(b.) Commuted Pension on the other hand is a lump sum payment in lieu of periodical

payments. ‘Commuting’ a pension means, withdrawing a lump sum amount from

Pension Fund of an employee. Exemption under section 10(10A) is available onlyon ‘Commuted Pension’.

Pension Fund is just like a Bank Fixed Deposit (F.D.) and uncommuted

pension (monthly/periodical pension) is just like interest on such Bank F.D. whereas,

commutation of pension is just like withdrawing some amount from Bank F.D. Theway Bank F.D. interest is taxable as an income, uncommuted pension is also taxable as

salary. Assessee can commute the pension or in other words can withdraw a lump sum

23

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 24/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

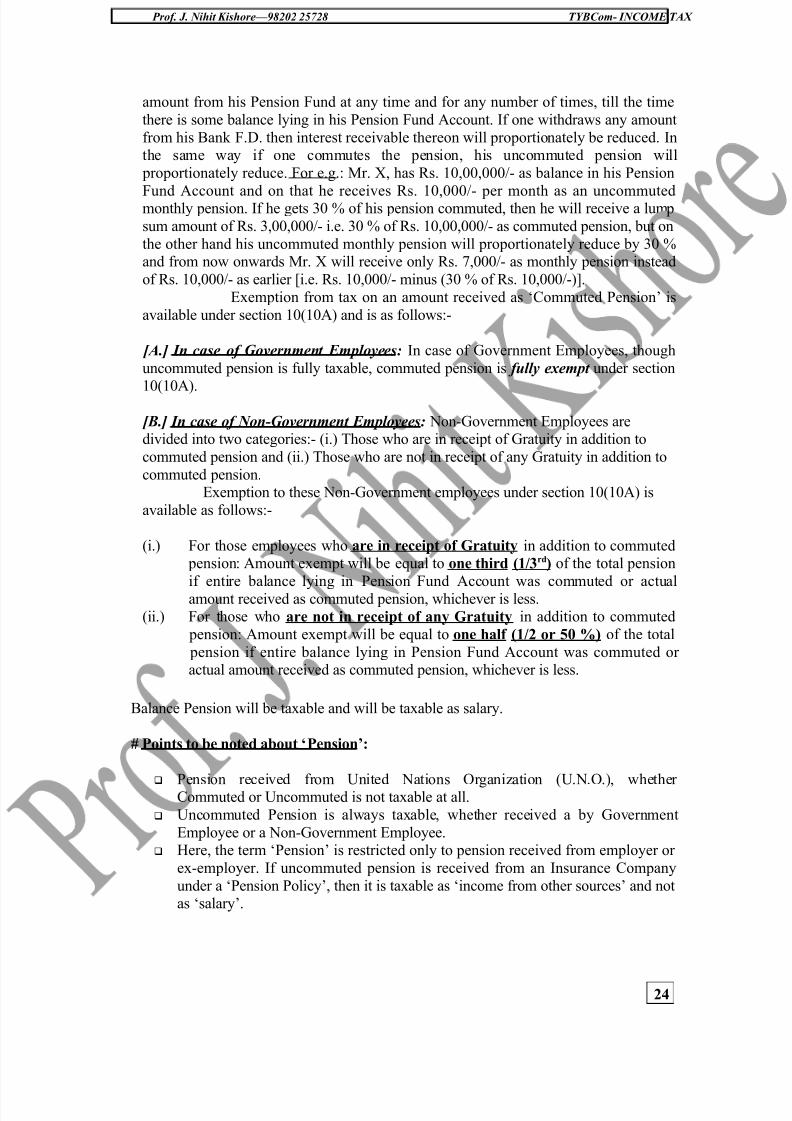

amount from his Pension Fund at any time and for any number of times, till the time

there is some balance lying in his Pension Fund Account. If one withdraws any amount

from his Bank F.D. then interest receivable thereon will proportionately be reduced. Inthe same way if one commutes the pension, his uncommuted pension will

proportionately reduce. For e.g.: Mr. X, has Rs. 10,00,000/- as balance in his Pension

Fund Account and on that he receives Rs. 10,000/- per month as an uncommutedmonthly pension. If he gets 30 % of his pension commuted, then he will receive a lum p

sum amount of Rs. 3,00,000/- i.e. 30 % of Rs. 10,00,000/- as commuted pension, but on

the other hand his uncommuted monthly pension will proportionately reduce by 30 %and from now onwards Mr. X will receive only Rs. 7,000/- as monthly pension instead

of Rs. 10,000/- as earlier [i.e. Rs. 10,000/- minus (30 % of Rs. 10,000/-)].

Exemption from tax on an amount received as ‘Commuted Pension’ is

available under section 10(10A) and is as follows:-

[A.] In case of Government Employees: In case of Government Employees, though

uncommuted pension is fully taxable, commuted pension is fully exempt under section

10(10A).

[B.] In case of Non-Government Employees: Non-Government Employees aredivided into two categories:- (i.) Those who are in receipt of Gratuity in addition to

commuted pension and (ii.) Those who are not in receipt of any Gratuity in addition to

commuted pension.Exemption to these Non-Government employees under section 10(10A) is

available as follows:-

(i.) For those employees who are in receipt of Gratuity in addition to commuted pension: Amount exempt will be equal to one third (1/3rd) of the total pension

if entire balance lying in Pension Fund Account was commuted or actualamount received as commuted pension, whichever is less.(ii.) For those who are not in receipt of any Gratuity in addition to commuted

pension: Amount exempt will be equal to one half (1/2 or 50 %) of the total

pension if entire balance lying in Pension Fund Account was commuted or actual amount received as commuted pension, whichever is less.

Balance Pension will be taxable and will be taxable as salary.

# Points to be noted about ‘Pension’:

Pension received from United Nations Organization (U.N.O.), whether Commuted or Uncommuted is not taxable at all.

Uncommuted Pension is always taxable, whether received a by Government

Employee or a Non-Government Employee. Here, the term ‘Pension’ is restricted only to pension received from employer or

ex-employer. If uncommuted pension is received from an Insurance Company

under a ‘Pension Policy’, then it is taxable as ‘income from other sources’ and notas ‘salary’.

24

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 25/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

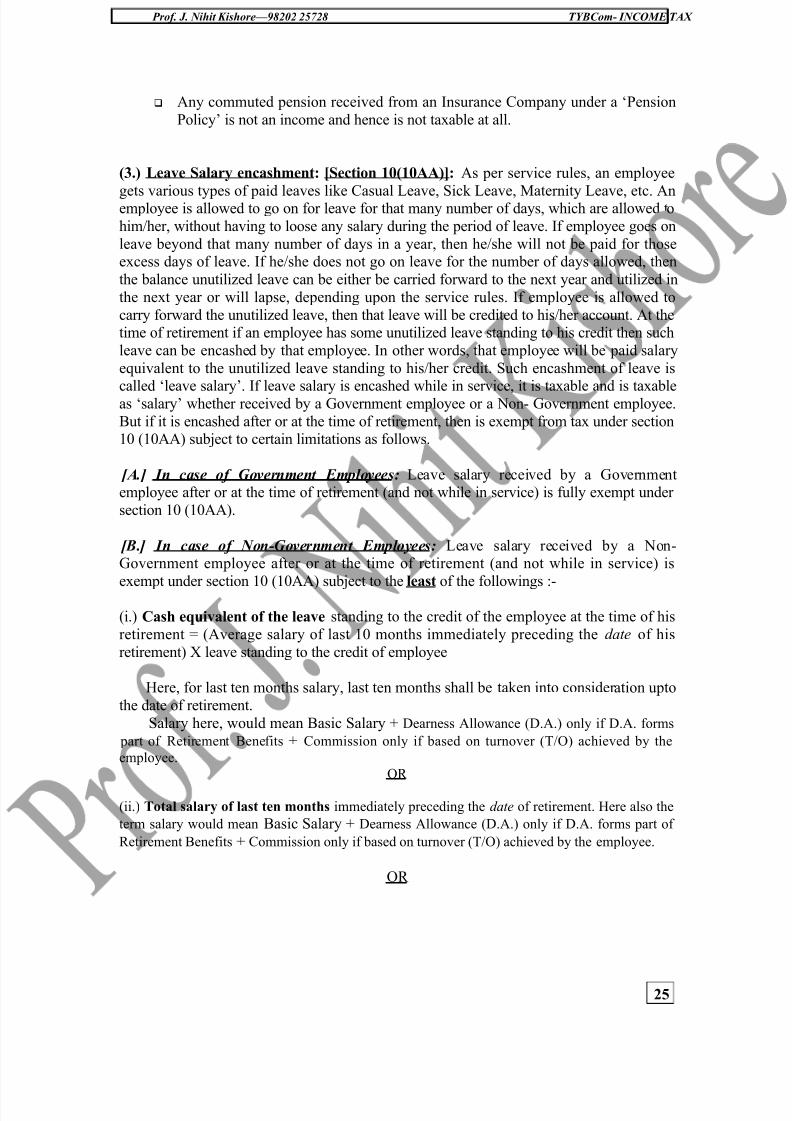

Any commuted pension received from an Insurance Company under a ‘Pension

Policy’ is not an income and hence is not taxable at all.

(3.) Leave Salary encashment: [Section 10(10AA)]: As per service rules, an employee

gets various types of paid leaves like Casual Leave, Sick Leave, Maternity Leave, etc. Anemployee is allowed to go on for leave for that many number of days, which are allowed to

him/her, without having to loose any salary during the period of leave. If employee goes on

leave beyond that many number of days in a year, then he/she will not be paid for thoseexcess days of leave. If he/she does not go on leave for the number of days allowed, then

the balance unutilized leave can be either be carried forward to the next year and utilized in

the next year or will lapse, depending upon the service rules. If employee is allowed to

carry forward the unutilized leave, then that leave will be credited to his/her account. At thetime of retirement if an employee has some unutilized leave standing to his credit then such

leave can be encashed by that employee. In other words, that employee will be paid salary

equivalent to the unutilized leave standing to his/her credit. Such encashment of leave is

called ‘leave salary’. If leave salary is encashed while in service, it is taxable and is taxableas ‘salary’ whether received by a Government employee or a Non- Government employee.

But if it is encashed after or at the time of retirement, then is exempt from tax under section10 (10AA) subject to certain limitations as follows.

[A.] In case of Government Employees: Leave salary received by a Governmentemployee after or at the time of retirement (and not while in service) is fully exempt under

section 10 (10AA).

[B.] In case of Non-Government Employees: Leave salary received by a Non-Government employee after or at the time of retirement (and not while in service) is

exempt under section 10 (10AA) subject to the least of the followings :-

(i.) Cash equivalent of the leave standing to the credit of the employee at the time of his

retirement = (Average salary of last 10 months immediately preceding the date of his

retirement) X leave standing to the credit of employee

Here, for last ten months salary, last ten months shall be taken into consideration upto

the date of retirement.

Salary here, would mean Basic Salary + Dearness Allowance (D.A.) only if D.A. forms

part of Retirement Benefits + Commission only if based on turnover (T/O) achieved by the

employee.

OR

(ii.) Total salary of last ten months immediately preceding the date of retirement. Here also the

term salary would mean Basic Salary + Dearness Allowance (D.A.) only if D.A. forms part of

Retirement Benefits + Commission only if based on turnover (T/O) achieved by the employee.

OR

25

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 26/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

(iii.) Actual amount received as Leave salary encashment.

OR

(iv.) Amount notified by Government which presently is Rs. 3,00,000/-

Whichever is less will be exempt and balance will be taxable as salary.

# Points to be noted about ‘Leave Salary’:

Leave salary received during the service is always taxable, whether received by a

Government employee or a Non-Government employee. Leave salary received at the time of or after the retirement is taxable only in the

case of Non-Government employees, subject to availability of exemption under

section 10 (10A). If Leave salary is received from more than one employer, whether in the same

previous year or in different previous years, then amount of exemption will becalculated as above only, but the amount notified by Government i.e. Rs. 3,00,000/-

will be reduced by any exemption already claimed earlier, if any on Leave salaryreceived from any previous employer.

Leave salary received by Legal Heirs or Family Members of an employee upon

death of employee, (whether Government employee or a Non-Governmentemployee) is not taxable at all in the hands of Legal Heirs or Family Members of

that employee.

(4.) Retrenchment Compensation: [Section 10(10B)]:If an employee is retrenched or

removed by his employer, then employer may have to compensate him for earlytermination of his employment, under Industrial Disputes Act, 1947. Such compensation isexempt in the hands of that employee at the least of the followings:-

(i.) Amount calculated as per provisions of Industrial Disputes Act, 1947. OR (ii.) Amount actually received as Retrenchment Compensation. OR

(iii.) Amount notified by Government which is Rs 5,00,000/-.

Whichever is less will be exempt under section 10(10B) and balance will be taxable

and taxable as ‘salary’.

# Points to be noted about ‘Retrenchment Compensation’:

If Retrenchment Compensation is received from more than one employer,

whether in one previous year or in different previous years, then exemption will

be calculated as above only, but the amount notified by Government i.e. Rs.5,00,000/- will be reduced by the amount of exemption claimed earlier, if any

on Retrenchment Compensation received from any earlier employer.

26

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 27/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

If amount calculated as per provisions of Industrial Disputes Act, 1947 is not

given in the exam, then exemption amount shall be lower of Actual amount

received or amount notified by Government.

(5.) Compensation received under ‘Voluntary Retirement Scheme’ (V.R.S.):[Section 10(10C)]: An amount received by an employee from his employer upon

his/her retiring voluntarily from employment which is known ‘Voluntary Retirement

Scheme (V.R.S.)’ or ‘Voluntary Separation Scheme’ compensation is exempt from taxunder section 10(10C) subject to the least of the followings:-

(i.) Amount actually received as V.R.S. Compensation OR

(ii.) Amount notified by Government which is Rs. 5,00,000/-

(iii.) Amount calculated as per prescribed guidelines of the scheme, which shall not

exceed the lower of the followings:

(a.) Three months salary for each completed year of service. OR

(b.) Actual salary for balance months of service left.Here, salary would mean last drawn (Basic salary + Dearness Allowance).

Exemption under section 10(10C) is once in a life-time exemption. In other words,

once it is claimed by an assessee, it can not be claimed again by that assessee in any

other assessment year.

(6.) Tax on Non-Monetary Perquisites paid by Employer: [Section 10(10CC)]: If tax

on non-monetary or non-cash perquisites received by an employee is paid by his employer,

then such tax shall not be added in the income of that employee, as it is exempt from tax inhis hands under section 10(10CC) with effect from Assessment Year 2003-2004. Such tax

as is paid by the employer shall not be allowed to the employer as a deduction on accountof business expenditure under section 40. (Here, exemption is available only on tax paid byemployer on non-monetary perquisites and not on tax paid by him on monetary or cash

perquisites).

(7.) Value of any Leave Travel Concession: [Section 10(5)]: An employee may receive

Leave Travel Concession or Passage money from his present employer or his ex-employer

for himself and his family members in connection with his proceeding (journey) to any

place in India (journey must be at any place in India only and not outside India, otherwiseexemption under section 10(5) will not be available). Journey may be performed while in

service or after retirement. Exemption under section 10(5) is available with respect to only

two journeys performed in a block of four calendar years (Calendar year and not financialyear i.e. year beginning on 01st January and ending on 31st December), where four years’

block is predefined by the act as beginning from 1982 and ending on 1985 and so on, like

1986-1989, 1990-1993, 1994-1997, 1998-2001, 2002-2005. This means that exemptionunder section 10(5) is available only two times in a block of four calendar years.

Exemption under section 10(5) will be the least of the following:-

(i.) Actual amount of Leave Travel Concession or Passage money received. OR

27

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 28/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

(ii.) Amount spent for the purpose. OR

(iii.) Amount prescribed for exemption by Central Board of Direct Taxes (CBDT)

in this behalf.

# Points to be noted about ‘Leave Travel Concession’:

Exemption under section 10(5) is available irrespective of whether L.T.C. was

received while in service or after retirement.

No distinction is made between Government employee or Non-Governmentemployee.

In order to claim exemption, journey shall be performed at any place within India

only, otherwise exemption will not be available.

Exemption is available for L.T.C. of employee as well as of his Family members.

Family members for this purpose means spouse and two children (whether

dependent or not) and dependent parents, brothers and sisters. Exemption is

available with respect to only shortest route to the destination, though employee

may adopt any other route, other than the shortest route. In any case exemption shall be restricted to the actual expenditure incurred.

Exemption is available only in respect of traveling expenses i.e. for Air Fare, RailFare, Bus Fare or Fare of Recognized Public transport System only. Any other

expenses, though may have been incurred by employee and reimbursed by

employer are not entitled for exemption. For e.g.: Hotel Accommodation charges,Food charges, Lodging and Boarding charges, Auto-Rickshaw charges, Scooter

charges, etc.

(8.) Provident Funds (P.F.): [Section 10(11)]: Provident Fund (P.F.) is a retirement

benefit scheme. Under this, a fixed sum is deducted from employee’s salary as his

contribution and generally, employer also contributes a similar sum as his contribution.Such funds are then invested in interest yielding securities and they earn interest on it. So, a balance in employee’s P.F. A/c comprises of four elements, viz. (i.) Employee’s own

contribution, (ii.) Interest on Employee’s own contribution, (iii.) Employer’s contribution,

and (iv.) Interest on Employer’s contribution. The balance in employee’s P.F. A/c is paid tohim at the time of his retirement or is transferred to his new P.F. A/c with a new employer,

if he/she takes up a new employment with a new employer. P.F. Scheme is developed by

Government, basically to promote compulsory savings.Basically, there are four types of Provident Fund Accounts, namely, (i.) Statutory

Provident Fund (SPF), (ii.) Recognized Provident Fund (R.P.F.), (iii.) Unrecognized

Provident Fund (U.R.P.F.) and (iv.) Public Provident Fund (P.P.F.). Recognized Provident

Fund is a Provident Fund, which is recognized by Commissioner of Income Tax (C.I.T.),whereas, Unrecognized Provident Fund is a Provident Fund, which is not so recognized by

Commissioner of Income Tax (C.I.T.). Its only an employer and an employee who can

contribute to SAF/RPF/URPF and not an outsider. Central Government has also establisheda scheme called Public Provident Fund (P.P.F.), which is a P.F. Scheme open to general

public at large. Any person, whether Salaried or Self-employed can participate in the PPF

Scheme, by opening a PPF A/c with State Bank of India or any of its subsidiaries or any

28

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 29/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

Nationalised Bank. Even a salaried employee, who already maintains a SPF/RPF/URPF

A/c may open a PPF A/c in addition to that. In order to maintain a PPF A/c, one has to

compulsorily contribute a minimum of Rs. 500/- every year to the scheme or more than Rs.500/- in multiples of Rs. 5/- but maximum Rs. 70,000/- in a year. Funds of PPF are

invested in some interest yielding securities. PPF A/c of the accountholder is credited with

a predetermined rate of interest every year on balance lying in the account (current rate of interest is 8 % per annum). Accumulated balance in PPF A/c is repaid together with

interest, after 15 years of maturity period, unless account is extended by accountholder.

SPF/RPF/URPF A/c balance comprises of four things as discussed earlier i.e.contribution of employer and employee and interest thereon, whereas PPF A/c balance can

comprise of only two things, namely (i.) Contribution of Accountholder and (ii.) Interest on

accountholder’s contribution, it cannot a have contribution from employer and accordingly,

question of interest on employer’s contribution does not arise.

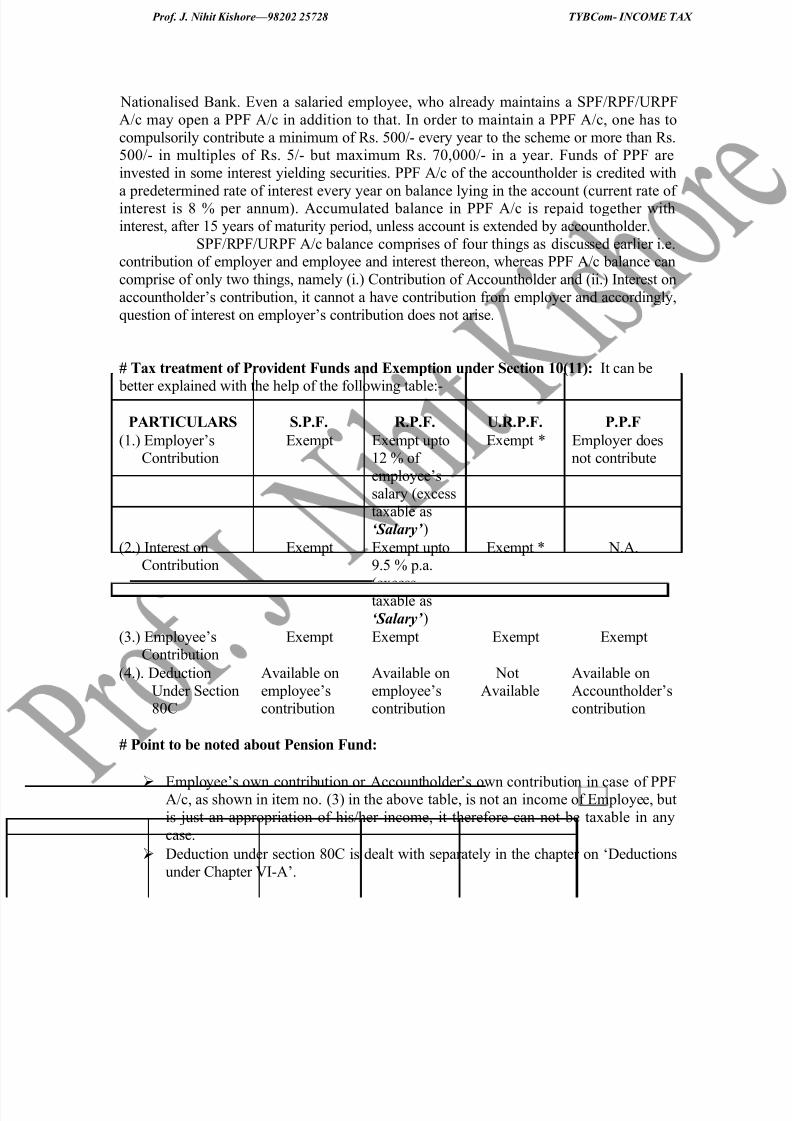

# Tax treatment of Provident Funds and Exemption under Section 10(11): It can be

better explained with the help of the following table:-

PARTICULARS S.P.F. R.P.F. U.R.P.F. P.P.F

(1.) Employer’sContribution

Exempt Exempt upto12 % of

employee’s

salary (excess

taxable as

‘Salary’ )

Exempt * Employer doesnot contribute

(2.) Interest onContribution

Exempt Exempt upto9.5 % p.a.

(excesstaxable as

‘Salary’ )

Exempt * N.A.

(3.) Employee’sContribution

Exempt Exempt Exempt Exempt

(4.). Deduction

Under Section80C

Available on

employee’scontribution

Available on

employee’scontribution

Not

Available

Available on

Accountholder’scontribution

# Point to be noted about Pension Fund:

Employee’s own contribution or Accountholder’s own contribution in case of PPFA/c, as shown in item no. (3) in the above table, is not an income of Employee, but

is just an appropriation of his/her income, it therefore can not be taxable in any

case.

Deduction under section 80C is dealt with separately in the chapter on ‘Deductions

under Chapter VI-A’.

29

5/14/2018 42 Tybcom Five Heads Theory 89 Pgs(1) - slidepdf.com

http://slidepdf.com/reader/full/42-tybcom-five-heads-theory-89-pgs1 30/89

Prof. J. Nihit Kishore—98202 25728 TYBCom- INCOME TAX

* Employer’s contribution to URPF is exempt in the hands of employee at the time

of contribution, but it becomes taxable as ‘salary’, when balance in URPF A/c isrepaid back to employee.

* Interest on contribution to URPF is exempt in the hands of employee at the time it

is credited to the account, but it becomes taxable as ‘salary’, when balance in URPF

A/c is repaid back to employee. The term Salary shall mean Basic Salary + D.A. forming part of retirement benefits

+ Commission based on fixed Turnover achieved by the employee. [Basic + DA(R)

+ Commn.(T/O)]

(9.) Approved Superannuation Fund (S.A.F.): [Section 10(13)]: Just like Recognized