Embed Size (px)

Citation preview

8-1

ADJUSTMENTS

CHAPTER 8CHAPTER 8

8-2

Adjustments Adjustments

? When are adjustments

finished?

!At the end of the

accounting period, usually the end of a

month

8-3

Accruals

Adjustments

Defferals

Defferrals and AccrualsDefferrals and Accruals

Not mentioned

postponement of expenses and revenues

paid or received before

8-4

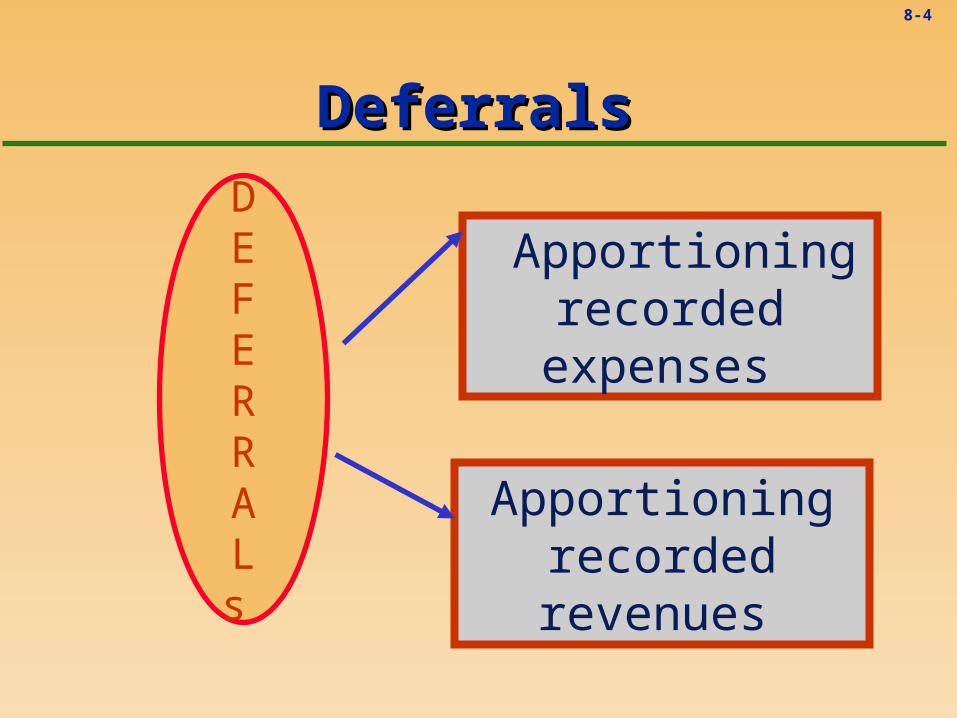

DeferralsDeferrals

Apportioning recorded revenues

Apportioning recorded expenses

DEFERRALs

8-5

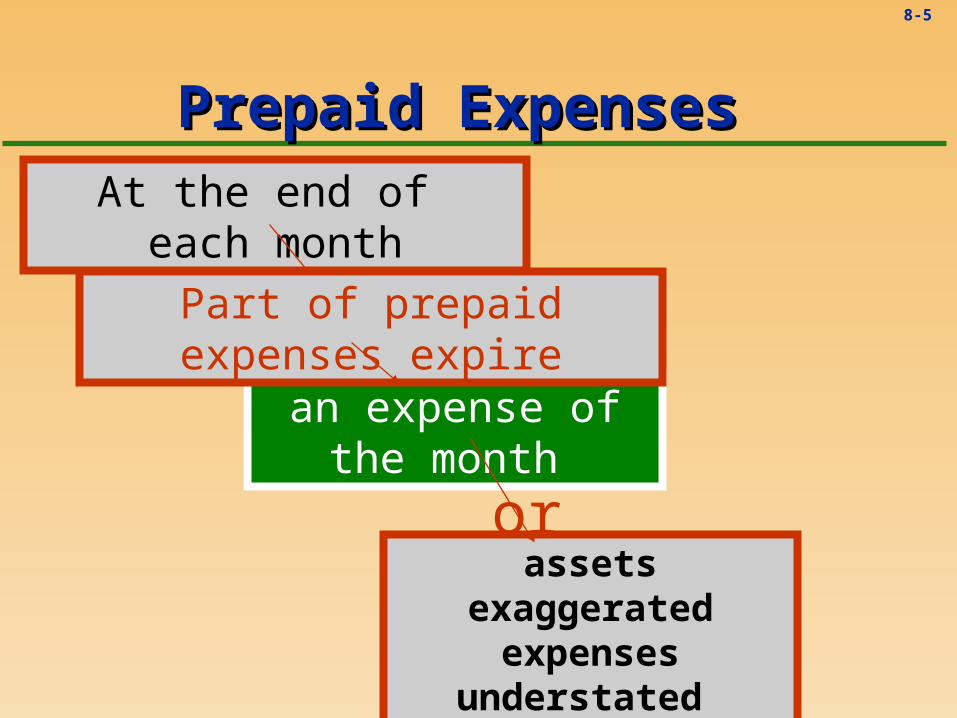

an expense of the month

Prepaid ExpensesPrepaid Expenses At the end of each month

Part of prepaid expenses expire

assets exaggerated expenses understated

or

8-6

Examples Examples

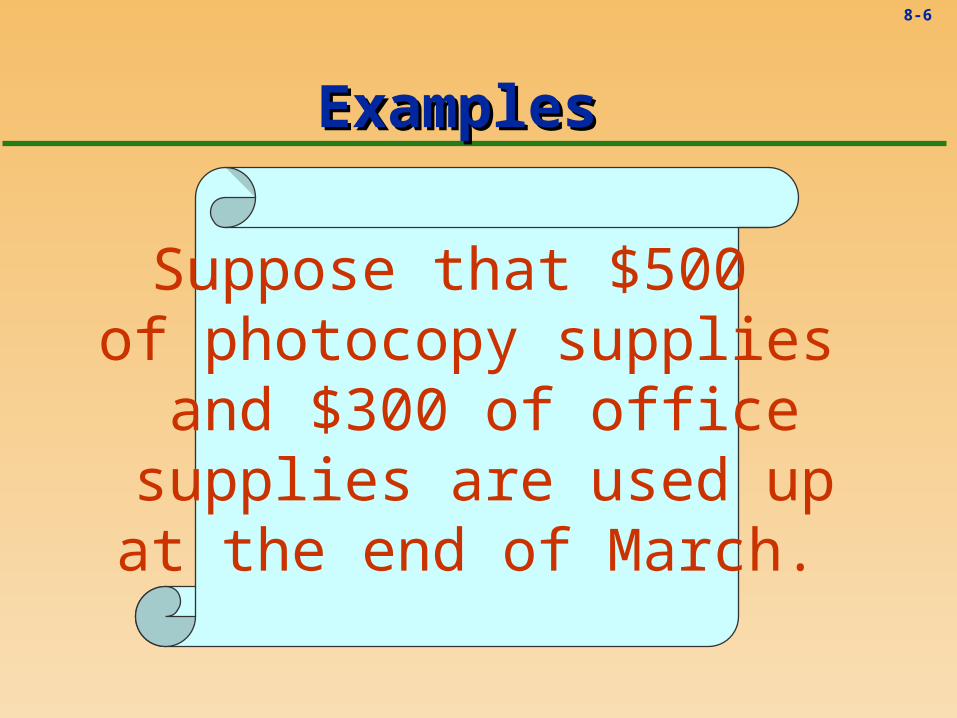

Suppose that $500 of photocopy supplies

and $300 of office supplies are used up at the end of March.

8-7

Analysis of ExampleAnalysis of Example

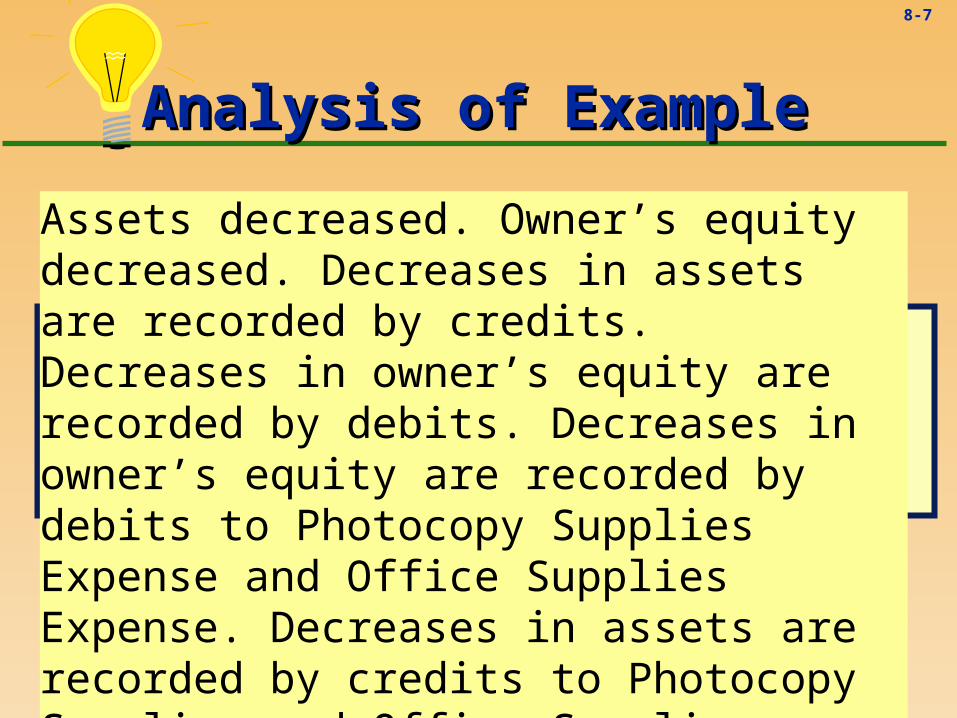

Assets decreased. Owner’s equity decreased. Decreases in assets are recorded by credits. Decreases in owner’s equity are recorded by debits. Decreases in owner’s equity are recorded by debits to Photocopy Supplies Expense and Office Supplies Expense. Decreases in assets are recorded by credits to Photocopy Supplies and Office Supplies.

8-8

8-9

Dr. Photocopy Supplies Expense $500

Cr.Photocopy Supplies $500

Entries for the exampleEntries for the example

Dr. Office Supplies Expense $300

Cr. Office Supplies $300

8-10

ExampelsExampels

On March 6, George Ross Photocopy Company paid

$4,800 for a year’s rent in advance.

8-11

Asset decreased. Owner’s equity decreased. Decreases in assets are recorded by credits. Decreases in owner’s equity are recorded by debits. Decrease in owner’s equity is recorded by a debit to Rent Expense. Decrease in assets is recorded by a credit to Prepaid Rent.

AnalysisAnalysis

8-12

Dr. Rent Expense $400

Cr. Prepaid Rent $400

Entries for the exampleEntries for the example

8-13

ExampleExample

George Ross Photocopy Company

paid $4,800 for a year’s rent

in advance.

8-14

Analysis of transactionAnalysis of transaction

Asset decreased. Owner’s equity decreased. Decreases in assets are recorded by credits.

Decreases in owner’s equity are recorded by debits.

Decrease in owner’s equity is recorded by a debit to Rent

Expense. Decrease in assets is recorded by a credit to Prepaid

Rent.

8-15

Dr. Rent Expense $400 Cr.Prepaid Rent $400

ENTRIESENTRIES

8-16

EXAMPLEEXAMPLE

On March 8, the agency paid

$600 for a one-year insurance policy.

As each day of the month passed,

a part of the expenditure

expired.

8-17

Assets decreased. Owner’s equity decreased. Decreases in assets are recorded by credits. Decreases in owner’s equity are

recorded by debits. Decrease in owner’s equity is recorded by ad debit to Insurance Expense. Decrease in asset is recorded by a

credit to Prepaid Insurance.

Analysis of TransactionAnalysis of Transaction

8-18

Dr. Insurance Expense $50 Cr. Prepaid Insurance $50

EntriesEntries

8-19

Unearned revenue is liability

It indicates that thecompany should pay money or service

Unearned RevenuesUnearned Revenues

8-20

IllustrationIllustration

On March 14, George’s agency received $1,300 as an advance fee for copying works to be

done for an advertisement agency. Suppose that $500 of the copying

works was finished

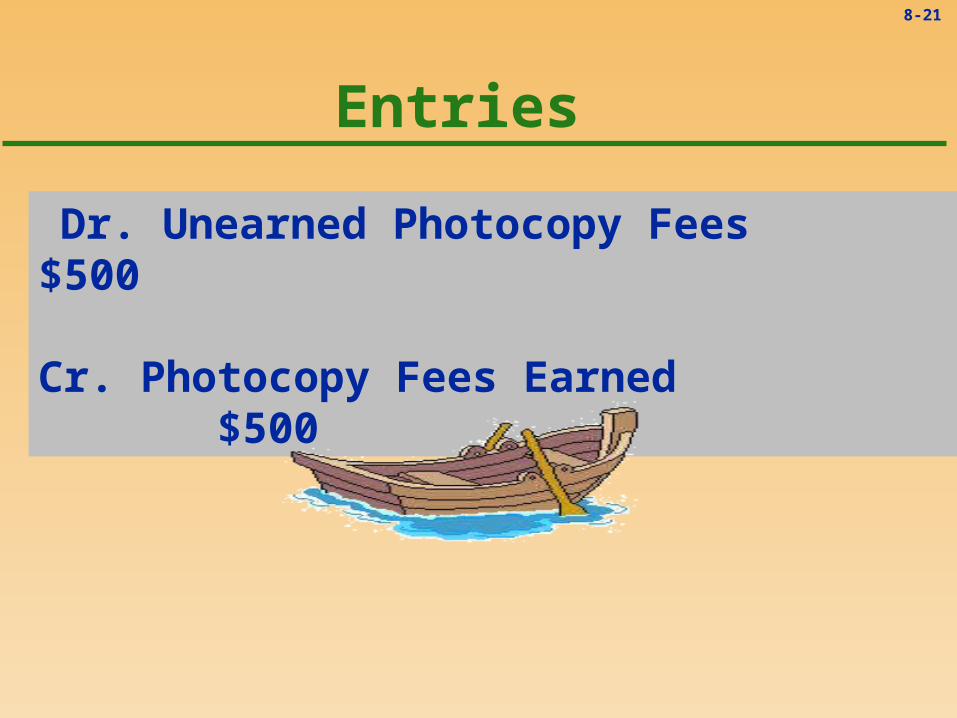

8-21

Entries

Dr. Unearned Photocopy Fees $500

Cr. Photocopy Fees Earned $500

8-22

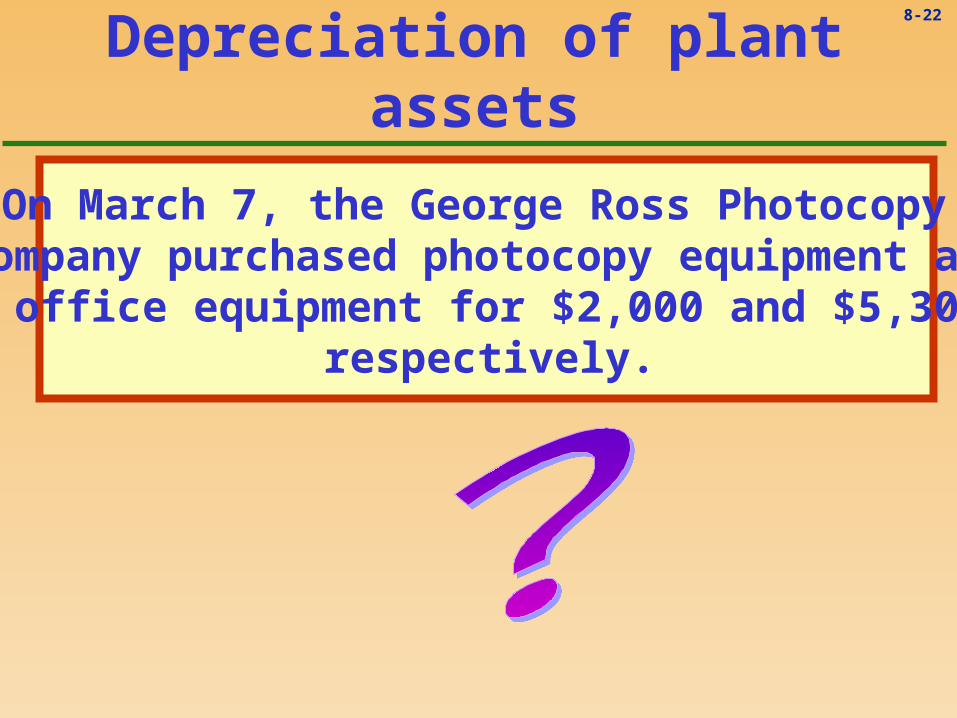

Depreciation of plant assets

On March 7, the George Ross Photocopy Company purchased photocopy equipment and

office equipment for $2,000 and $5,300 respectively.

8-23

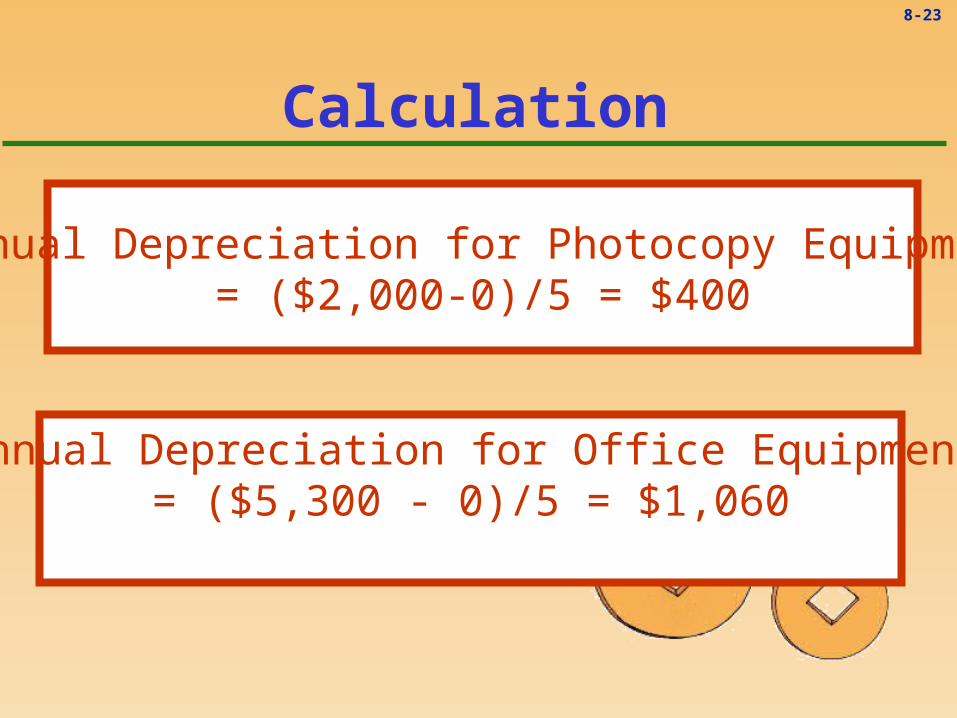

Calculation

Annual Depreciation for Photocopy Equipment= ($2,000-0)/5 = $400

Annual Depreciation for Office Equipment = ($5,300 - 0)/5 = $1,060

8-24

WE ARE SAILING RIGHT ALONG!!