Embed Size (px)

Citation preview

Finaccord A comparison of affinity market trends from within Germany and the UK

A comparison of affinity marketA comparison of affinity market trends from within Germany and the

UK: benchmarking best practiceUK: benchmarking best practice1st July 2009

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009

Finaccord A comparison of affinity market trends from within Germany and the UK

Agenda

Channel ComparisonsPartner Metrics

3-1213 20

Page

Partner MetricsSummary and conclusionsAny questions?

13-2021-22

23

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 2

Finaccord A comparison of affinity market trends from within Germany and the UK

Channel Comparisons

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 3

Finaccord A comparison of affinity market trends from within Germany and the UK

Definitions of generic affinity / partner distribution channelsp

Financial partners: namely, banks, building societies, credit card issuers, credit co-operatives (Germany)and savings banks (Germany).

Not-for-profit affinity groups: namely, charities, educational institutions, professional associations andtrade unions.

Non-financial commercial partners: including automotive associations, automotive dealers, automotivemanufacturers, estate agents, loyalty schemes, media entities, the Post Office, retailers, travel agents / tour

t tiliti ioperators, utilities companies.

Worksite: namely, employers.

The other generic distribution channels included in the Channel Metrics research (for which data is notshown in the following slides) are direct sales by insurance companies and financial intermediariesshown in the following slides) are direct sales by insurance companies and financial intermediaries(i.e. insurance brokers , including aggregators, and insurance agents).

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 4

Finaccord A comparison of affinity market trends from within Germany and the UK

Germany UK

Financial products investigated

Breakdown recovery insuranceCar finance and leasing contracts

Credit cardsDental insurance

Extended warranties (for cars)F l i

Breakdown recovery insuranceCar finance contracts

Cash ISAsChild Trust Funds

Credit cardsCritical illness insuranceFuneral expenses insurance

Hospital cash insuranceHOUSEHOLD INSURANCE

Investment life insuranceLegal expenses insuranceLong-term care insurance

Mortgages

Critical illness insuranceDental insurance

Extended warranties (for cars)Extended warranties (for electronic appliances)

Health / hospital cash plansHome emergency insuranceHOUSEHOLD INSURANCEMortgages

MOTOR INSURANCEPayment protection insurancePersonal accident insurancePersonal liability insurance

Personal loans / consumer financePRIVATE HEALTH INSURANCE

Interest-bearing savings depositsLife insurance

Loan payment protection insuranceMobile telephone insurance

Mortgage payment protection insuranceMortgages

MOTOR INSURANCEPrivate pension insuranceProtection life insurance

Savings accountsSavings bonds

Supplementary pension insuranceTRAVEL INSURANCE

Work incapacity insurance

MOTOR INSURANCEPersonal / stakeholder pensions

Personal accident insurancePersonal loansPet insurance

PRIVATE MEDICAL INSURANCETRAVEL INSURANCE

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009

Work incapacity insurance TRAVEL INSURANCE

5

Finaccord A comparison of affinity market trends from within Germany and the UK

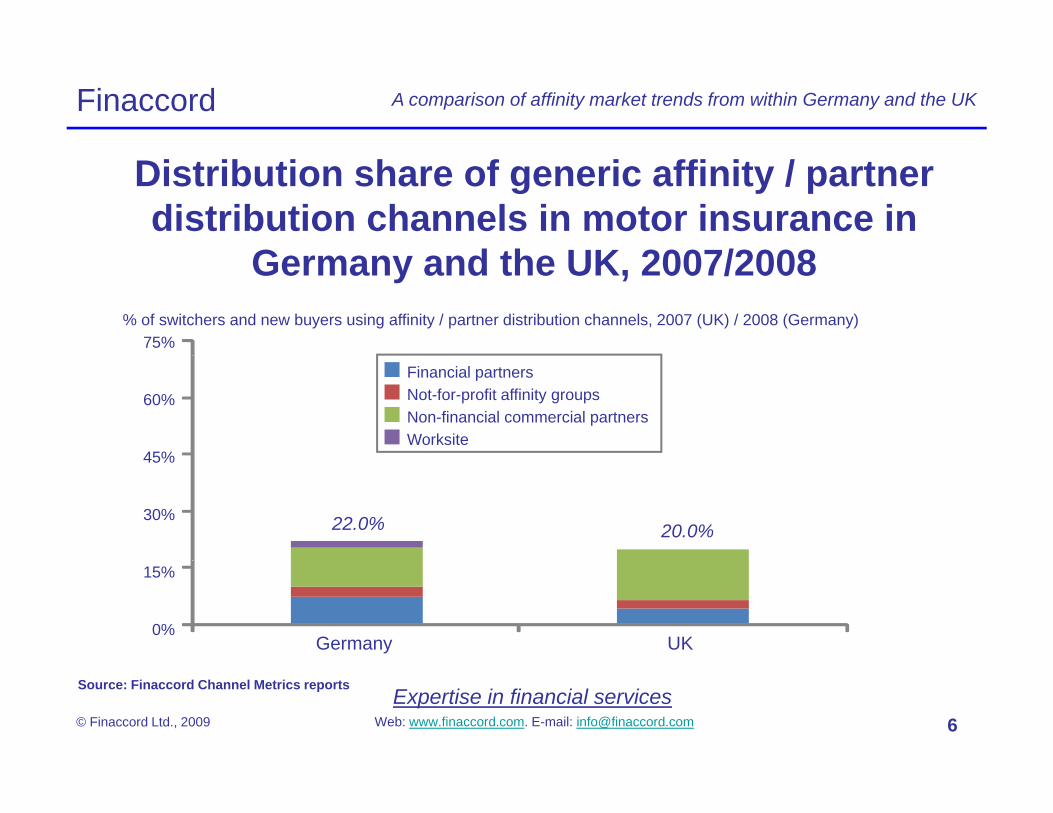

Distribution share of generic affinity / partner distribution channels in motor insurance in

G d th UK 2007/2008Germany and the UK, 2007/2008

75%% of switchers and new buyers using affinity / partner distribution channels, 2007 (UK) / 2008 (Germany)

60%

45%

Financial partnersNot-for-profit affinity groupsNon-financial commercial partnersWorksite

45%

30% 22.0% 20.0%

15%

0%Germany UK

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009

Source: Finaccord Channel Metrics reports

6

Finaccord A comparison of affinity market trends from within Germany and the UK

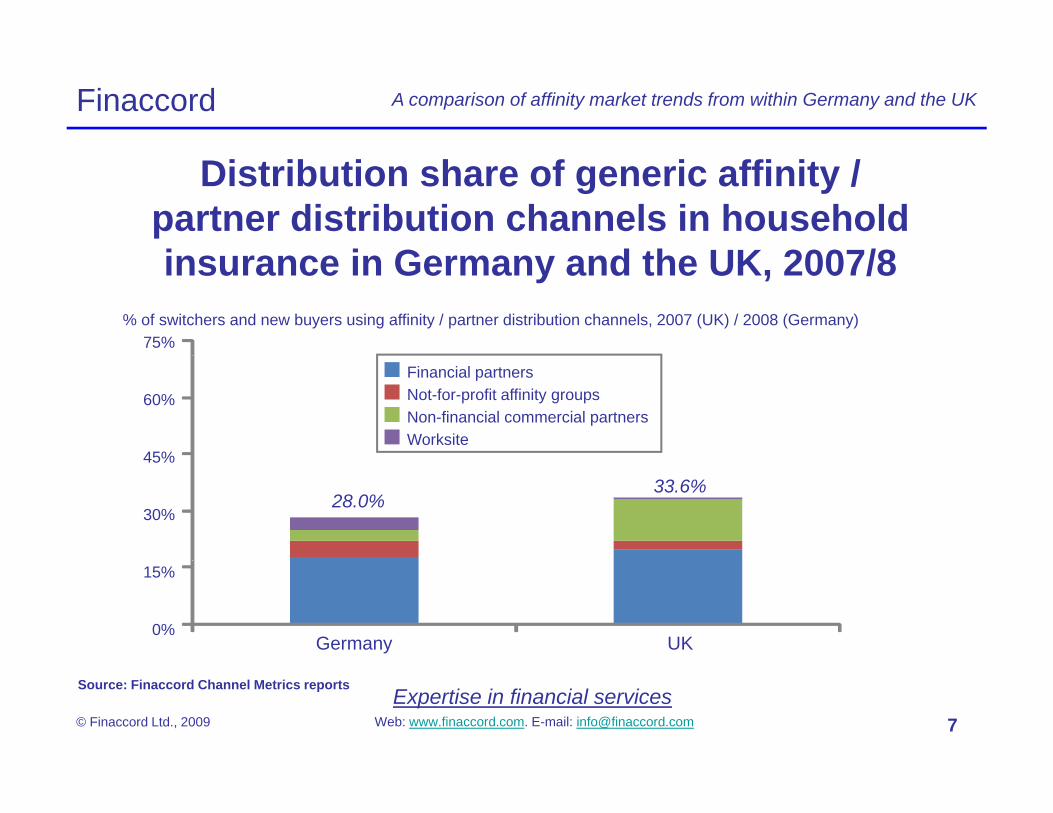

Distribution share of generic affinity / partner distribution channels in household i i G d th UK 2007/8insurance in Germany and the UK, 2007/8

75%% of switchers and new buyers using affinity / partner distribution channels, 2007 (UK) / 2008 (Germany)

60%

45%

Financial partnersNot-for-profit affinity groupsNon-financial commercial partnersWorksite

45%

30%28.0%

33.6%

15%

0%Germany UK

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 7

Source: Finaccord Channel Metrics reports

Finaccord A comparison of affinity market trends from within Germany and the UK

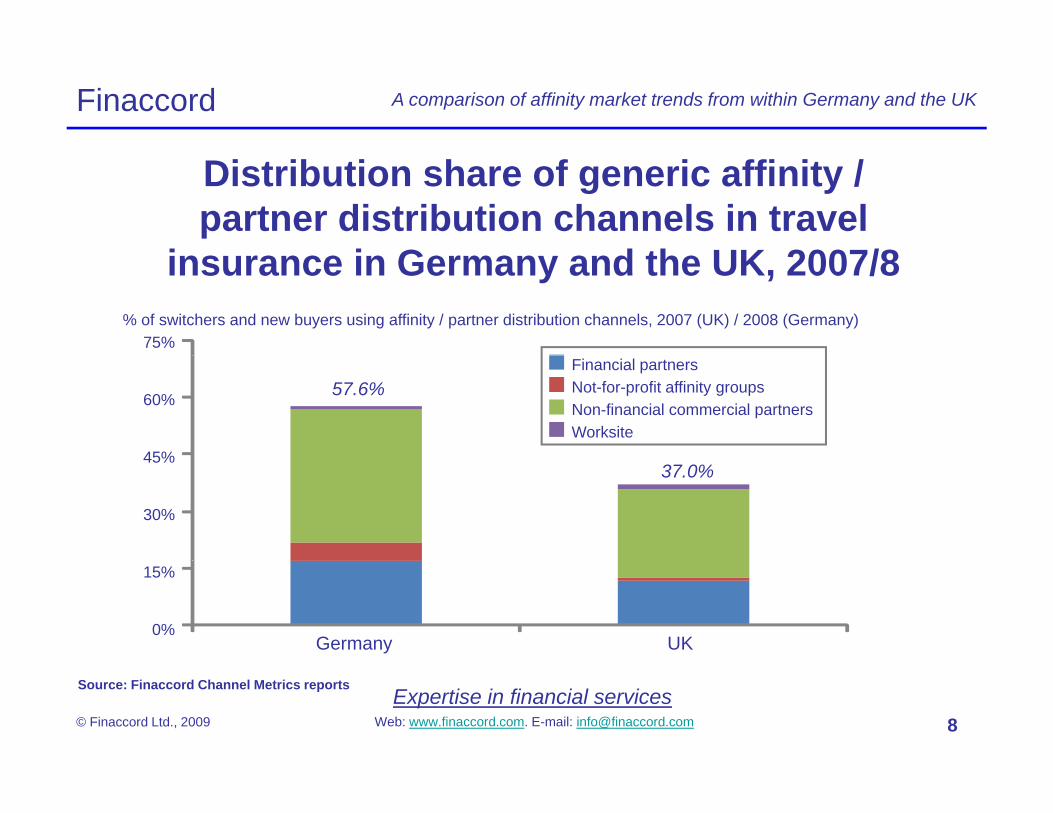

Distribution share of generic affinity / partner distribution channels in travel

i i G d th UK 2007/8insurance in Germany and the UK, 2007/8

75%% of switchers and new buyers using affinity / partner distribution channels, 2007 (UK) / 2008 (Germany)

60%

45%

57.6%Financial partnersNot-for-profit affinity groupsNon-financial commercial partnersWorksite

45%

30%

37.0%

15%

0%Germany UK

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 8

Source: Finaccord Channel Metrics reports

Finaccord A comparison of affinity market trends from within Germany and the UK

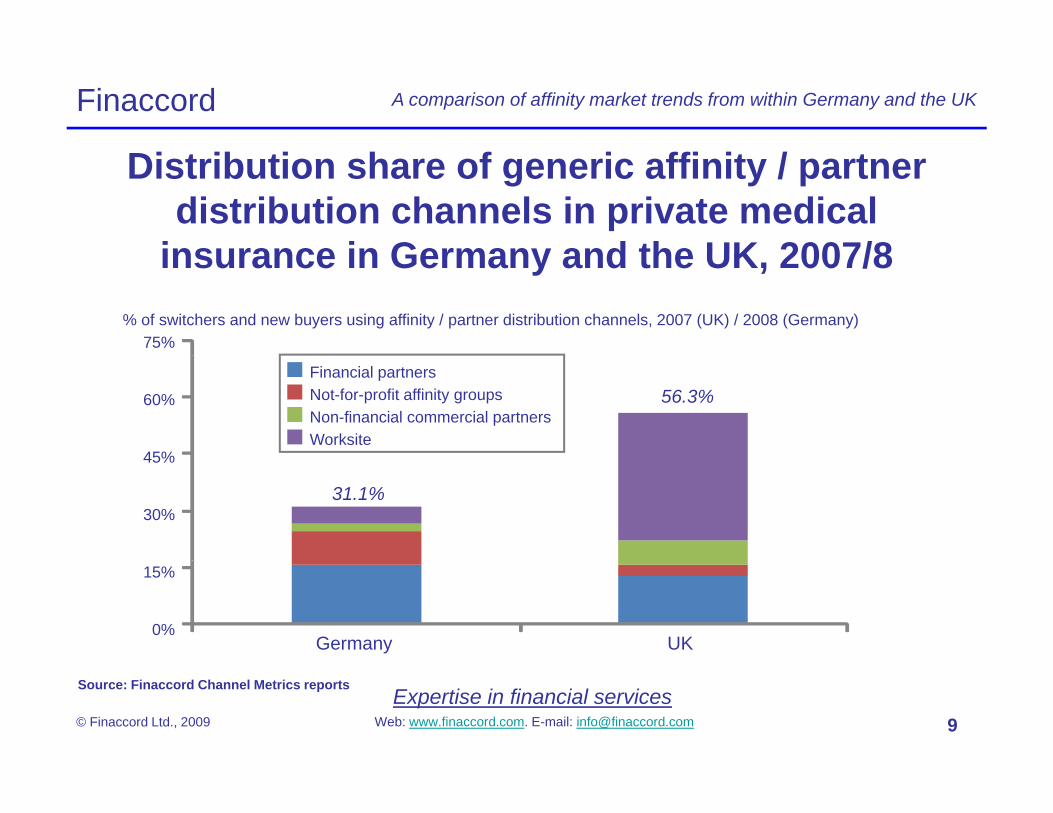

Distribution share of generic affinity / partner distribution channels in private medical

insurance in Germany and the UK 2007/8insurance in Germany and the UK, 2007/8

75%% of switchers and new buyers using affinity / partner distribution channels, 2007 (UK) / 2008 (Germany)

60%

45%

56.3%Financial partnersNot-for-profit affinity groupsNon-financial commercial partnersWorksite

45%

30%31.1%

15%

0%Germany UK

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 9

Source: Finaccord Channel Metrics reports

Finaccord A comparison of affinity market trends from within Germany and the UK

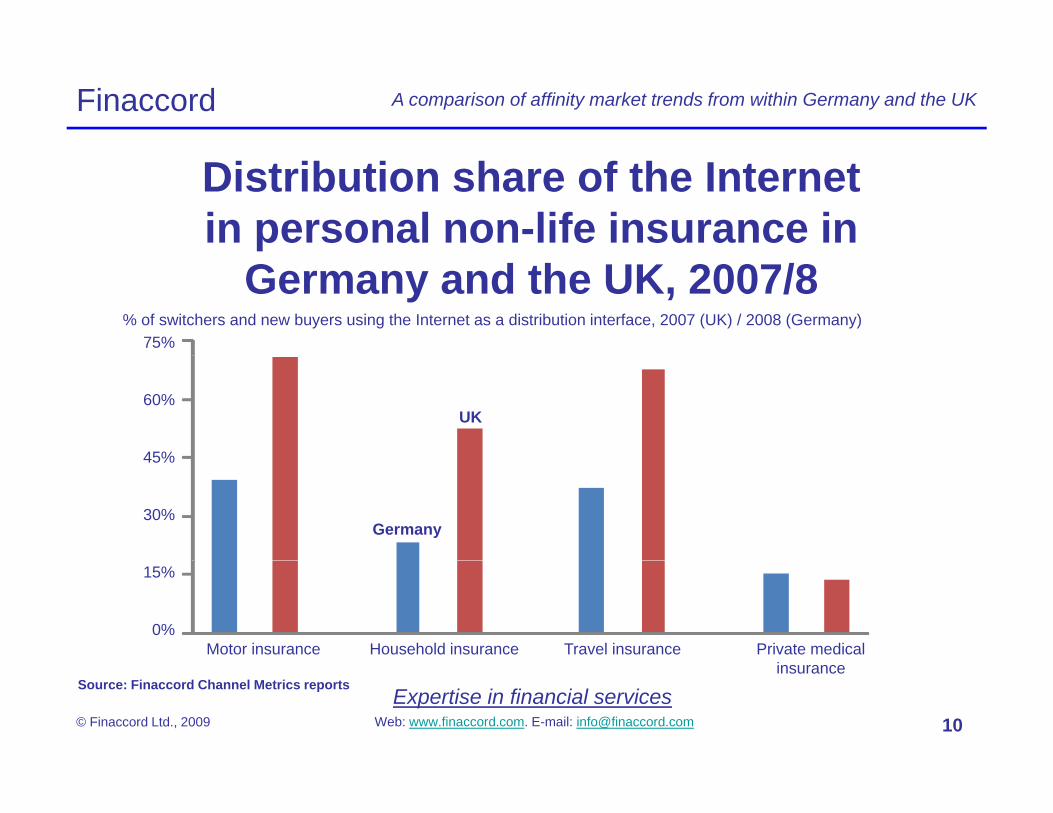

Distribution share of the Internet in personal non-life insurance in

Germany and the UK, 2007/875%

% of switchers and new buyers using the Internet as a distribution interface, 2007 (UK) / 2008 (Germany)

60%

45%

UK

45%

30%Germany

Motor insurance Household insurance Travel insurance Private medical i

15%

0%

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 10

insuranceSource: Finaccord Channel Metrics reports

Finaccord A comparison of affinity market trends from within Germany and the UK

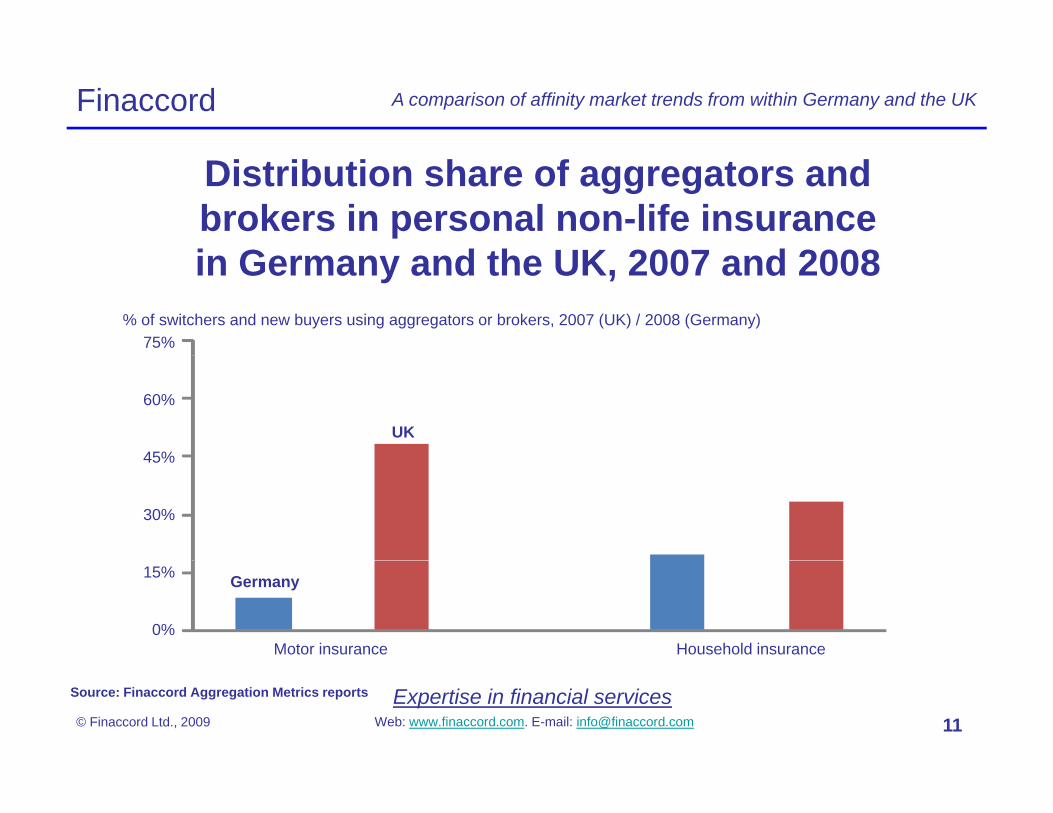

Distribution share of aggregators and brokers in personal non-life insurance i G d th UK 2007 d 2008in Germany and the UK, 2007 and 2008

75%% of switchers and new buyers using aggregators or brokers, 2007 (UK) / 2008 (Germany)

60%

45%UK

45%

30%

15%

0%Motor insurance Household insurance

Germany

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009

Source: Finaccord Aggregation Metrics reports

11

Finaccord A comparison of affinity market trends from within Germany and the UK

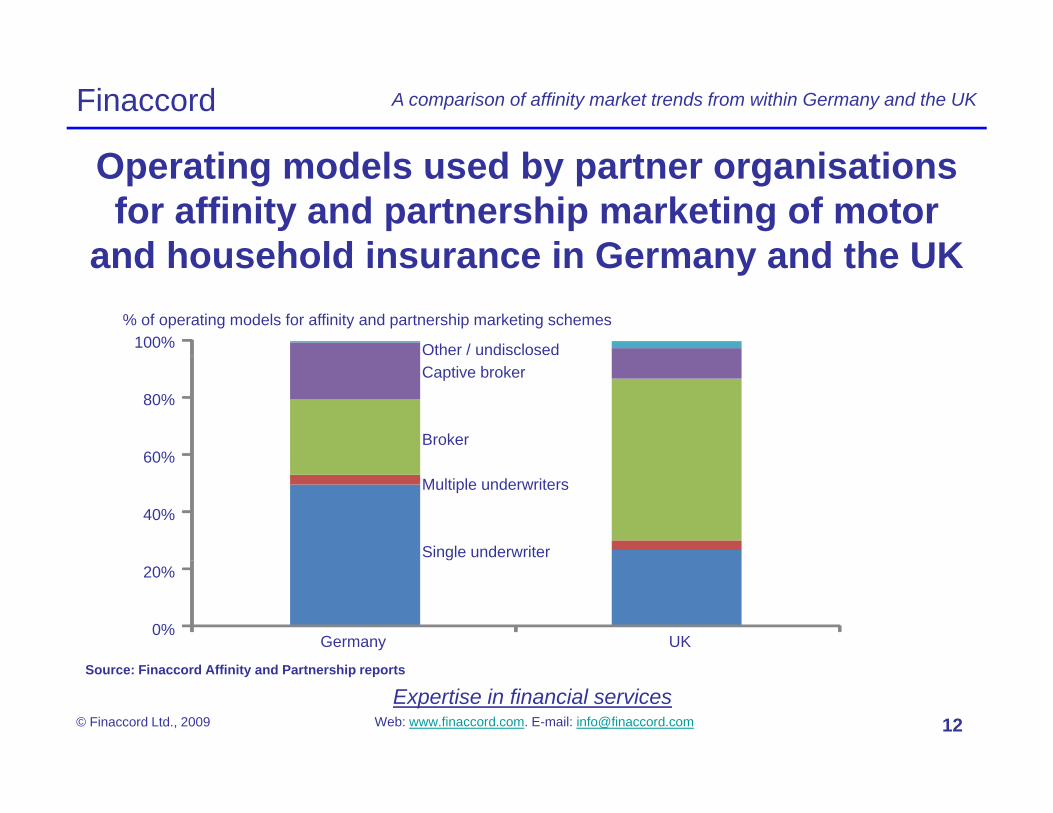

Operating models used by partner organisations for affinity and partnership marketing of motor

and household insurance in Germany and the UKand household insurance in Germany and the UK

Other / undisclosed100%% of operating models for affinity and partnership marketing schemes

Captive broker

Broker

80%

60%

Multiple underwriters

Single underwriter

60%

40%

20%

0%Germany UK

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 12

Source: Finaccord Affinity and Partnership reports

Finaccord A comparison of affinity market trends from within Germany and the UK

Partner Metrics

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 13

Finaccord A comparison of affinity market trends from within Germany and the UK

Organisations investigated in Germany, 2008/9

ADACAir Berlin

AldiAmazon

American Express

Die BahnDM Drogeriemarkt

DouglasE.ONeBay

Kaiser's TengelmannKarstadtKaufhof

LidlL'Tur

REWERossmann

RWERyanairSaturnAmerican Express

AppleAralAudiAvD

Bayern Munich

eBayEDEKAE-PlusEsso

FacebookFord

L TurLufthansa

Media MarktMercedes Benz

MTVNeckermann

SaturnSchlecker

ShellSony

Steigenberger HotelsStern

Bild ZeitungBMW

Borussia DortmundBreuninger

C&ACoop

Formula 1Frankfurter Allgemeine

Googleguenstiger.de

H&MHagebaumarkt

O2Opel

OTTO PAYBACK

Peek & CloppenburgPenny

TchiboThomas Cook

T-mobileToom

Toyota TUICoop

DER CLUB BertelsmannDeutsche Post

Deutsche TelekomDeutscher Caritas Verband

HagebaumarktHappyDigitsHornbachIhr Platz

IKEA

PennyPorscheQuelleReal

Renault

TUIVodafone

VolkswagenWelt

Yahoo!

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 14

Finaccord A comparison of affinity market trends from within Germany and the UK

Organisations investigated in the UK, 2006/7

AAAge Concern

AldiAmazon

American Express

Daily Mail / Sunday MailDaily Telegraph /

DebenhamsE.ON

Easygroup

LidlLittlewoods

Manchester United F.C.Marks & Spencer

Morrison's

RyanairSaga

Sainsbury'sShellSkyAmerican Express

AOLArgosASDA

Auto TraderB&Q

EasygroupeBay

English HeritageEsso

ExpediaFirst Choice Holidays

Morrison sMyTravel

National Trust /NectarNettoNext

SkySomerfield

Sun / News of the WorldSuperdrug

TescoTexaco

BMWBody Shopbonmarché

BootsBounty

BP

FordGoogleHalfords

HomebaseHondaIKEA

npowerO2

OrangePeugeot

Post OfficePowergen

Thomas CookThomson Holidays

Times / Sunday TimesToyota

VauxhallVirginBP

British GasBT

Chelsea F.C.csma

IKEAJet

John LewisKuoni Travel

Kwik-Fit

PowergenPrimark

QVCRAC

Renault

VirginVodafone

VolkswagenYahoo!

Yell

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 15

Finaccord A comparison of affinity market trends from within Germany and the UK

Leading five partner organisations in terms of frequency / strength of consumer relationships

Germany UK

GoogleAldi

TescoGoogle

Deutsche PostLidl

eBay

gPost Office

BTBootseBay Boots

Source: Finaccord Partner Metrics reports

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009

p

16

Finaccord A comparison of affinity market trends from within Germany and the UK

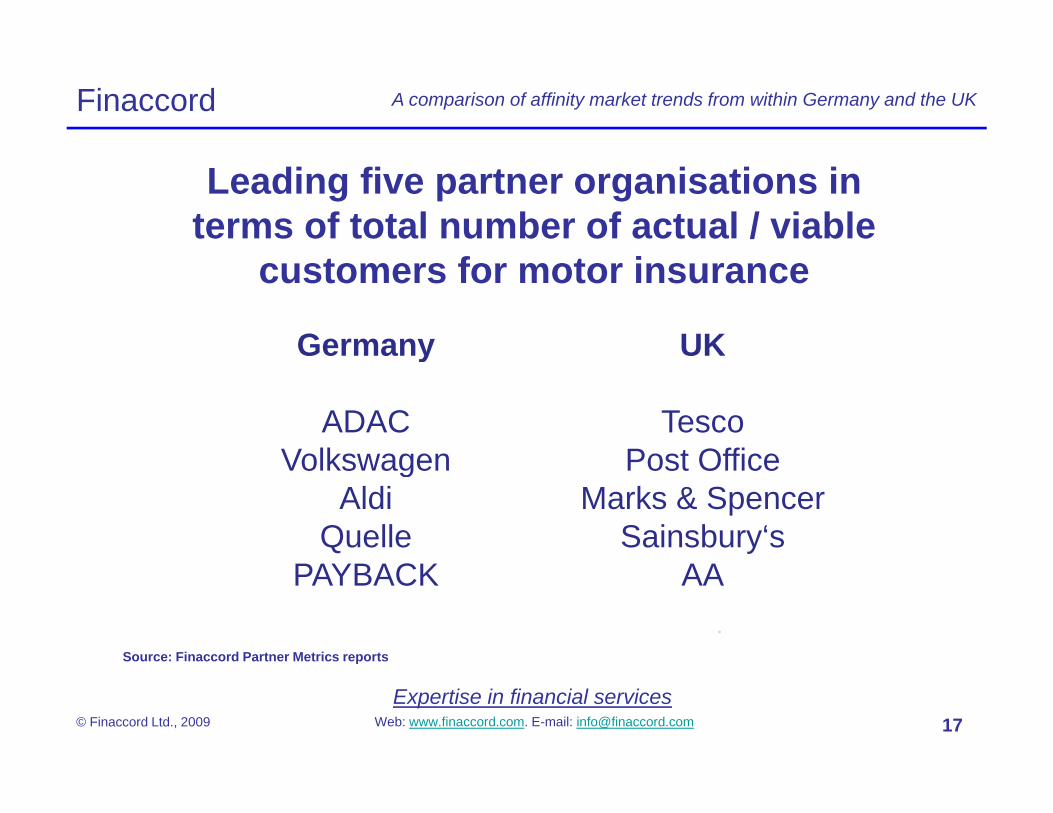

Leading five partner organisations in terms of total number of actual / viable

customers for motor insurance

Germany UKGermany

ADACVolkswagen

UK

TescoPost OfficeVolkswagen

AldiQuelle

Post OfficeMarks & Spencer

Sainsbury‘s

Source: Finaccord Partner Metrics reports

PAYBACK AA

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009

p

17

Finaccord A comparison of affinity market trends from within Germany and the UK

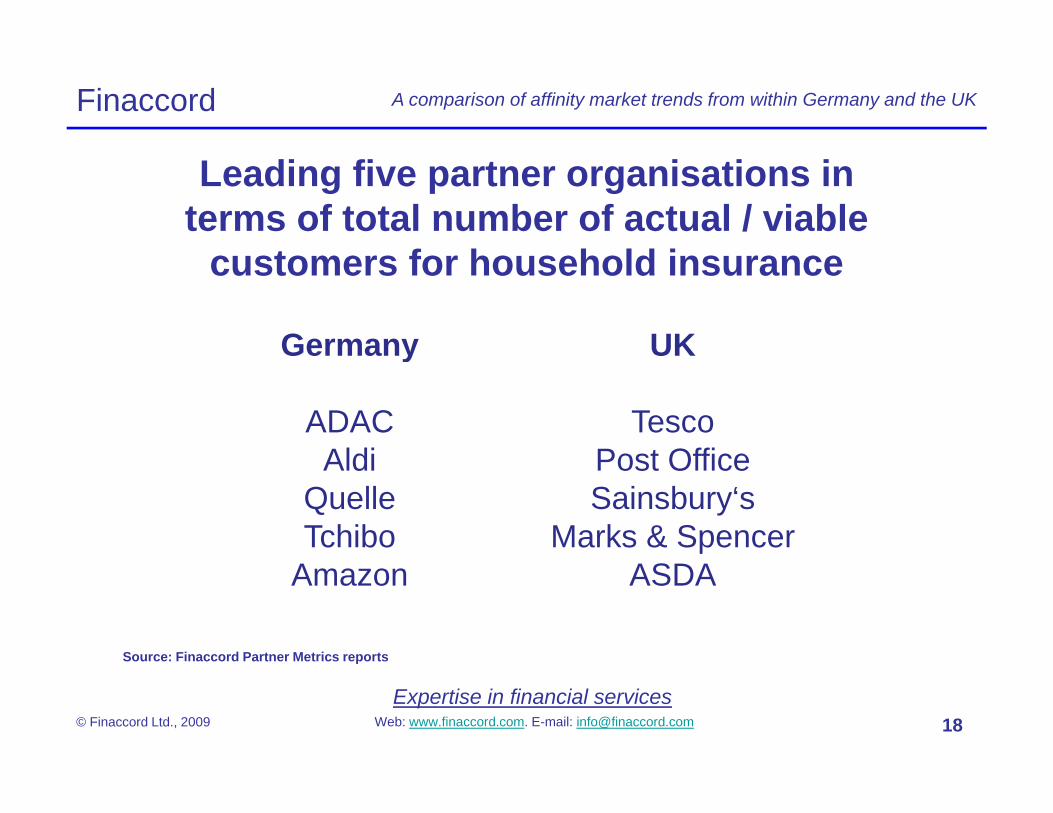

Leading five partner organisations in terms of total number of actual / viable

t f h h ld icustomers for household insurance

Germany UKGermany

ADACAldi

UK

TescoPost OfficeAldi

QuelleTchibo

Post OfficeSainsbury‘s

Marks & SpencerAmazon ASDA

Source: Finaccord Partner Metrics reports

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 18

p

Finaccord A comparison of affinity market trends from within Germany and the UK

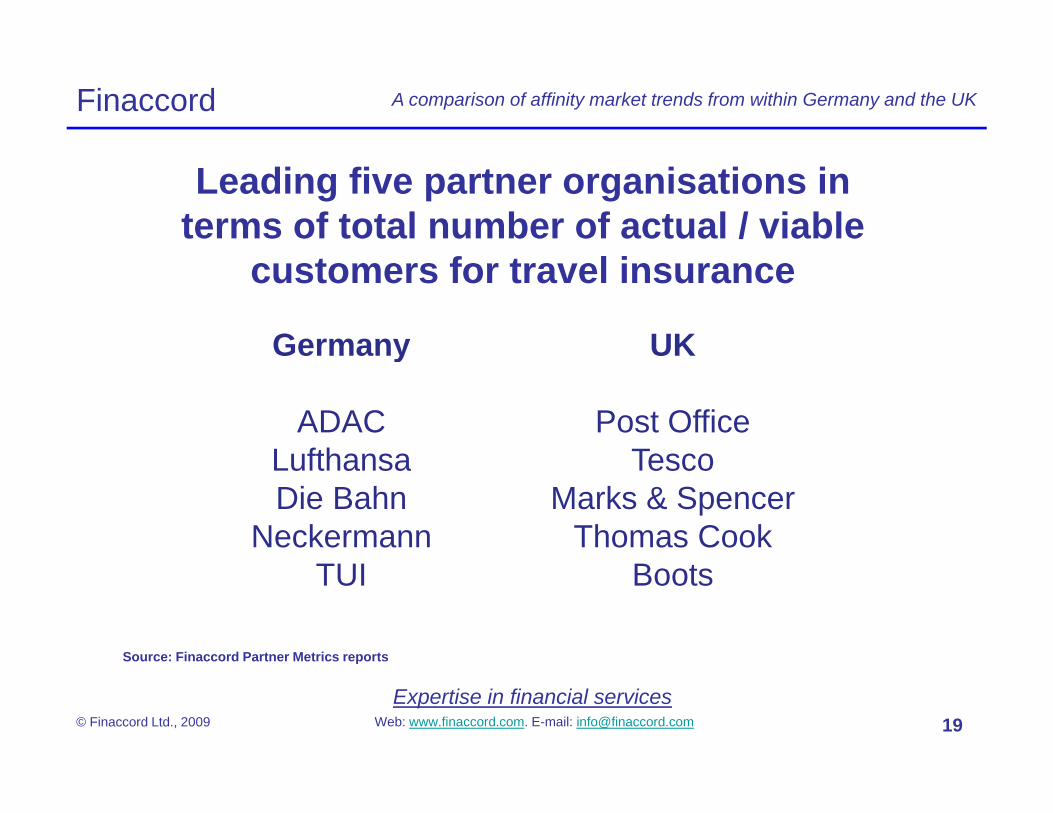

Leading five partner organisations in terms of total number of actual / viable

customers for travel insurance

Germany UKGermany

ADACLufthansa

UK

Post OfficeTescoLufthansa

Die BahnNeckermann

TescoMarks & Spencer

Thomas Cook

Source: Finaccord Partner Metrics reports

TUI Boots

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 19

p

Finaccord A comparison of affinity market trends from within Germany and the UK

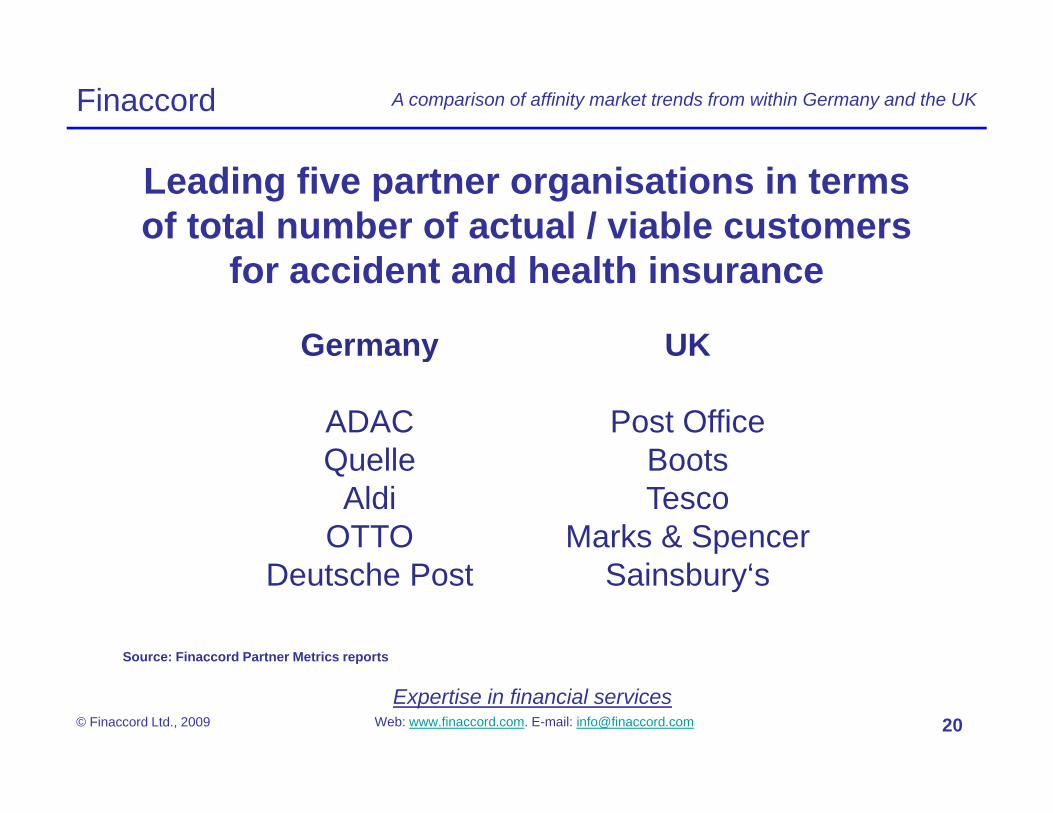

Leading five partner organisations in terms of total number of actual / viable customers

for accident and health insurance

Germany UKGermany

ADACQuelle

UK

Post OfficeBootsQuelle

AldiOTTO

BootsTesco

Marks & Spencer

Source: Finaccord Partner Metrics reports

Deutsche Post Sainsbury‘s

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 20

p

Finaccord A comparison of affinity market trends from within Germany and the UK

Summary and conclusions

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 21

Finaccord A comparison of affinity market trends from within Germany and the UK

Summary and conclusionsAffinity and partnership marketing does exist in Germany but some of itscharacteristics are different from the UK;

online distribution channels in Germany, including aggregators, are growing in

-

-importance but are still far less important than in the UK;

not all retailers will be able to have the same impact in affinity and partnershipmarketing as in the UK;

-

many major organisations in Germany (e.g. ALDI) have not yet realised theirpotential as distribution partners for financial services;

since the position of insurance agents as the traditionally dominant distributionh l i i d l d li t iti ill b il bl f ffi it

-

-channel is in gradual decline, more opportunities will become available for affinityand partnership schemes in Germany in future.

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 22

Finaccord A comparison of affinity market trends from within Germany and the UK

Any questions?

Expertise in financial servicesWeb: www.finaccord.com. E-mail: [email protected]© Finaccord Ltd., 2009 23