Embed Size (px)

Citation preview

A guide to establishing presence in India

2018

2 Doing Business in India

ContentsSection Page

Foreword 3

Introduction 5

Countryprofile 6

KeyeconomicindicatorsofIndia 8

Keysectors:Anoverview 11

Politicalandlegalsystem 14

Foreigninvestment 15

Finance 19

Businessentities 23

Labour 25

Accountingandreportingrequirements 27

Directtax 30

Indirecttax 39

TransferpricinginIndia 41

Glossaryofabbreviations 45

Doing Business in India 3

Foreword

WithGDPgrowthof7.1percentandFDIinflowofUSD60bnin2016-17,IndiaisboththefastestgrowingeconomyandthelargestrecipientofFDI,globally.

Overthelastfewyears,thegovernmenthasdeliveredlandmarkstructural reforms which are expected to further propel this growth.ThislistincludestheGoodsandServicesTax(GST),whichintegratesIndiaintoasinglemarketandremovesaspate of complex indirect taxes; a competition among India’s 29statestoimprovetheir‘EaseofDoingBusiness’;the‘Indiastack’,whichleveragesthenewbiometricidentification(Aadhaar)andmobilepenetrationofabillionplusIndiansfordigital financial transactions; and a sudden withdrawal of all high denomination currency notes along with strengthened legislationandenforcementtotacklecorruptionandunaccountedmoney.

Theperiodbetween31March2015and2017sawanumberof reforms coming together within the ambit of financial regulationsinthecountry.TheIndianequivalentof‘SOX’documentationandauditorattestationofcontrols(ICFR),IndianIFRS(IndAS)andmandatoryrotationofexternalauditorsaresomeofthekeyreformsthatwillalignIndia’spracticestothebestintheworld.

There has never been a time in history where so much has happenedinIndia.AtGrantThorntoninIndia,wearedelightedto be at the forefront of helping shape a more vibrant India workingwiththegovernment,theleadersofIndiaInc.,andglobal companies that want to maximise this amazing opportunity.

Vishesh C. ChandiokChiefExecutiveOfficerGrant Thornton India LLP

PrimeMinisterNarendraModiwonalandslidemandateinMay2014−asingleparty government was formed for the first timein30years−onthepromiseofmakingIndiagreatjustlikehehadpreviouslytransformedhishomestate,Gujarat.

4 Doing Business in India

Doing Business in India 5

Introduction

ThisisaninterestingtimefortheIndianeconomy.Ratedasoneofthemoststableeconomies,Indiacontinuestoshineamidstglobalgloom.LedbytheModigovernment,anumberofeconomic,financialandinstitutional,reformsincluding the reforms leading to ease of doing business acrossstates,havebeenimplemented.Indiaclaimingthe100thspotinWorldBank’srecentlyreleasedEaseofDoingBusinessrankingsisatestimonytothisfact.Thisalsomarksthebiggestimprovementrecordedamong190countriesintheWorldBank’s‘DoingBusiness2018-Reformingtocreatejobs’report.Strictmonetaryactiontakenbythegovernmenttobringbackunaccountedmoneyintothesystempavesthewayforeconomicgrowthbackedwithdigitisation.Bankingregulationsincludingthemovetoreplacehigh-valuecurrencynoteswithnewhigherdenominationsin2016didcontributetowardsmakingtheeconomymorerobustandcompliant.Thegovernment has also notified the final regulations related to the insolvency resolution process under the Insolvency and BankruptcyCode2016.ThelawaimstoimprovetheeaseofdoingbusinessinIndiabyfacilitatingsmootherandtime-bound settlement of insolvency and faster turnaround of businesses,apartfromcreatingadatabaseofserialdefaulters.

InitiativessuchasMakeinIndiacampaign,improvingtheeaseofdoingbusinessinIndiaandStartupIndia,StandupIndiawillfurtherpavethewayforgrowth.Additionally,thegovernment’sDigitalIndiainitiativeandopeningofbankaccountsformassesviaJanDhanYojnahavebeenawelcomechange.

Thegovernmenthasstartedseveraldevelopmentschemes,which,inthelongerrun,willmakethecountrystrongerandmorestable.Inadditiontothis,thepropertymarket,whichwaslargelyconsideredfragmentedandunorganised,isnowregulatedbytheenactmentoftheRealEstateRegulationAct(popularlyknownasRERA).AllthestateshadtoimplementtherulesundertheRERAby01May2017tomaketheregulationarealityacrossthecountry.Thishasbeensupplementedbyinsolvencyandbankruptcylaws,amendmentintheBenami(aterminHindulawwhichmeans‘made,held,done,ortransactedinthenameofanotherperson’)TransactionsAct,arbitrationandconciliationlaws,andcorporategovernancelaws.

Whilethecountryisnowworkingtowardsthedevelopmentof100smartcities,spreadingfinancialinclusiontoallwillempoweralargesectionofthepopulation.

However,thebiggestmovebythegovernmentisitsenactmentofalegislationtointroduceanationalvalue-addedtax(namedGoodsandServicesTax)witheffectfromJuly2017,replacingthecurrentmultitudeofcentral,stateandlocallevies.TheGSTregime will create a much more integrated and productive economyinthelongerrun.Sofarthereisa50percentriseinthenumberofindirecttaxpayerssincetheintroductionofGST.

Aftertwoquarters,theIndianeconomyissettoshine.TheEconomicSurvey2017-18broughtoutbythegovernmentinJanuary2018forecastsagrowthrateof7to7.5percentfor2018-19.

TheInternationalMonetaryFund(IMF)alsoexpectsIndia’sGDPtogrowmorethan7percentthisyear,makingIndiatheworld’sfastest-growinglargeeconomy.Amidstslowingglobalgrowth,Indiaremainsabrightspotamongemergingeconomies.TheforecastbyIMFfactorsinthewaveofreformsthatthecountryiswitnessing.AscorroboratedbytheWorldEconomicForum’s(WEF)GlobalCompetitivenessIndexfor2017-18,Indiaranked40thonimprovingbusinessenvironmentandinnovation.Followingthecentre’smove,statestooareeyeing significant share of foreign investments demonstrating bothcooperativeandcompetitivefederalism.AllofthistrulyispoisedtounlockthepotentialforgrowthinIndiaandbuildamorevibranteconomy,andweatGrantThorntoninIndiaareallsettogrowingtogetherwithIndia.Wehopethisguidewill support your growth plans of either setting up base or expandinginIndia.Welookforwardtobeingyourgrowthadvisersinthelandofemergingopportunities.

This guide is intended to serve as a primer for companies planningtoentertheIndianmarkettotapsignificantopportunitiesinvarioussectors.Itaimstoprovidebusinessinformationonthecountry’slegal,accountingandtaxationframework.

6 Doing Business in India

Country profile

India has emerged as a key investment destination globally. The U.S. Department of Commerce has identified India as one of the world’s top 10 ‘big emerging markets’.

According to the World Investment Report 2017 published by the UNCTAD, India continues to be among the top 10 countries in terms of FDI inflows globally and the fourth in the developing Asian region.

India’s FDI inflow for the period April-December 2017 remained fairly stable at USD 35.94 bn as compared to USD 35.84 bn in the corresponding period April-December 2016.

India’s FDI inflow in 2016-17 was in excess of USD 60 bn, a new all-time high surpassing the inflows of USD 55.6 bn in 2015-16.

Summary OutlinedbelowarekeyfactsandstatisticsthatmakeIndiaafavourable business destination worldwide:• A growing middle class • An abundant supply of raw material• Anextensiverailandroadnetwork• World’slargestworkingpopulationintheagegroupof25-45

years • LargepoolofskilledEnglish-speakingmanpower• Lower labour cost and hence reduced cost of

manufacturing,especiallyincomparisontonon-Asiancountries

• Geographicallocation,whichmakesIndiaclosertomarketsincludingtheMiddleEast,SouthAsiaandEurope

Main ports of entry: Chennai,JawaharLalNehru,Kandla,Kochi,Mormugao,Kolkata,Mumbai,Paradip,Tuticorin,Ennore,VishakhapatnamandNewMangalore1

Major international airports: Chennai,NewDelhi,Mumbai,Hyderabad,Kolkata,Bengaluru,Goa and Thiruvananthapuram

Doing Business in India 7

Geographical locationIndiaformsanaturalsubcontinentwiththeHimalayanmountainrangetothenorth,andtheIndianOcean,theArabianSeaandtheBayofBengaltothesouth,westandeast,respectively.ThecountryisborderedbyPakistanonthenorthwest,China,BhutanandNepalonthenortheast,andBangladeshandMyanmarontheeast.Nearthecountry’ssoutherntip,acrossthePalkStrait,liesSriLanka.

Indiahasalandfrontierofover15,000kilometres,stretchingfromtheHimalayasinthenorthtothePalkStraitsinthesouth,andfromtheArabianSeaintheWesttotheBayofBengalintheeast.Ithasalongcoastlinespanningover7,000kilometres.The climate varies from tropical in the south to temperate in the north.

Population and standard of livingIndia is the second most populated country in the world withapopulationof1.324bn(WorldBank,2016estimates).Accordingtothe2011populationcensus,thereare35citiesinIndiawithapopulationofmorethanamillion,withMumbai,DelhiandKolkatahavingapopulationover10million.Around70percentofthecountry’spopulationresidesinruralandsemi-ruralareas.OneofthemainreasonsthatIndiaisconsideredasanattractive,high-growthmarketisitslargepoolofuntappedanduppermiddleclasspopulation.Also,the standard of living in metropolitan cities of the country is comparabletothebestinotherdevelopingnations.

Asperestimates,250mnpeoplearesettojoinIndia’sworkforceby2030.Withasignificantchunkofpopulationshiftingintotheworkingagegroup,thereisacorrespondingincreaseindisposableincomeandconsumptiondemand.Infact,itisestimatedthatIndiawillhave247,800newmillionairesby2025.

DiversityIndiaisrichinhistory,culture,religionanddiversity.Thereare22officiallyrecognisedlanguagesspokeninIndiaacrossits29statesand7unionterritories.Indiaissecularthroughitsconstitutionwithpeoplefromallfaithsresidinghere,includingHindus,Muslims,Sikhs,Christians,BuddhistsandJains.

EducationThe education system in India is considered as one of the best globally.Thesystemcomprisespublicandprivateschools,universitiesandotherinstitutionsforhigherlearning(MBA,PhD,MScetc.).Theseinstitutionsarecommittedtoimpartexcellentacademicandvocationaltraining,andencourageparticipationinsportsandotherextra-curricularactivities.ThecurrentliteracyrateinIndiastandsat74.04percent.The country offers quality education comparable to global standardsinthefieldsoffinance,consulting,literature,computerengineering&programming,science&technology,medicine,dentistryandbusinessmanagementandadministration.TheIndianInstitutesofTechnology(IITs)andIndianInstitutesofManagement(IIMs)arerecognisedworld-overaspremierhighereducationalinstitutions.

CurrencyTheIndianRupee(INR)istheofficialcurrencyoftheRepublicofIndia.TheReserveBankofIndia(RBI)isthenationalandsolecurrency-issuingauthorityinthecountry.Theexchangerateoftherupeeismainlymarketdetermined.TheRBItakesakeeninterestinthefinancialmarketsofthecountryandothercountriesgloballytodeterminesuitablemonetary,regulatoryandothermeasures.ThecurrentRBIreferencerateforINRtoUSD1is66.76(04May2018).

Key economic statisticsIndia’s economic policies are designed to attract significant capitalinflowsinthecountryonasustainedbasis,andencouragetechnologicalcollaborationwithforeignfirms.Policyinitiativestakenoverthepastfewyearshaveresultedin significant inflow of foreign investment in all areas of the economy,exceptthepublicsector.

Sources: WorldBank,indexmundi.com,Ministryofcommerceandindustry,PIB,India

1MinistryofShipping:http://shipping.gov.in/writereaddata/l892s/27963559-Perspectiveplans.pdf

India is a union of states with a parliamentary system of government Statistics (2016)

Population 1.324bn

Area 3.29mnsquarekilometres

GDP(current) USD2,263.79bn

GDP – per capita USD1,709.39

Exports(April2017-March2018) USD302.84bn

Imports(April2017-March2018) USD459.67bn

Literacy rate 74.04%(Census2011)

Life expectancy 68.35years

Urbanpopulation 33%

Local currency Indianrupee(INR)

8 Doing Business in India

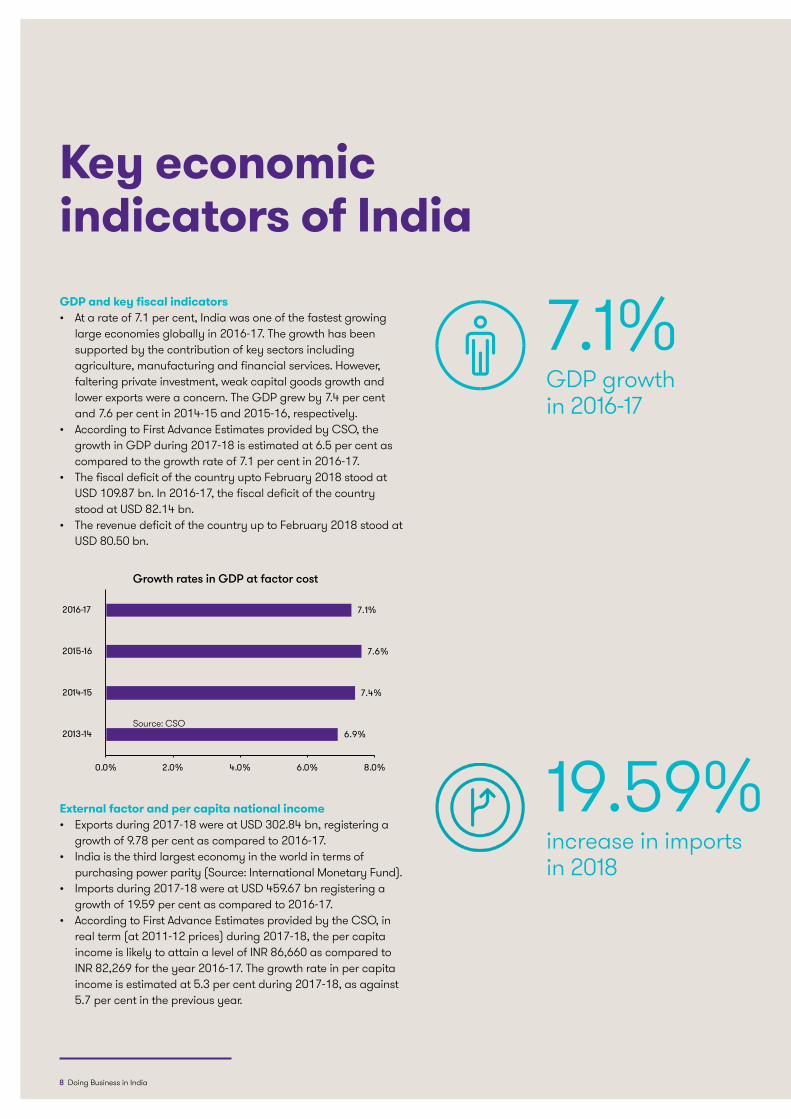

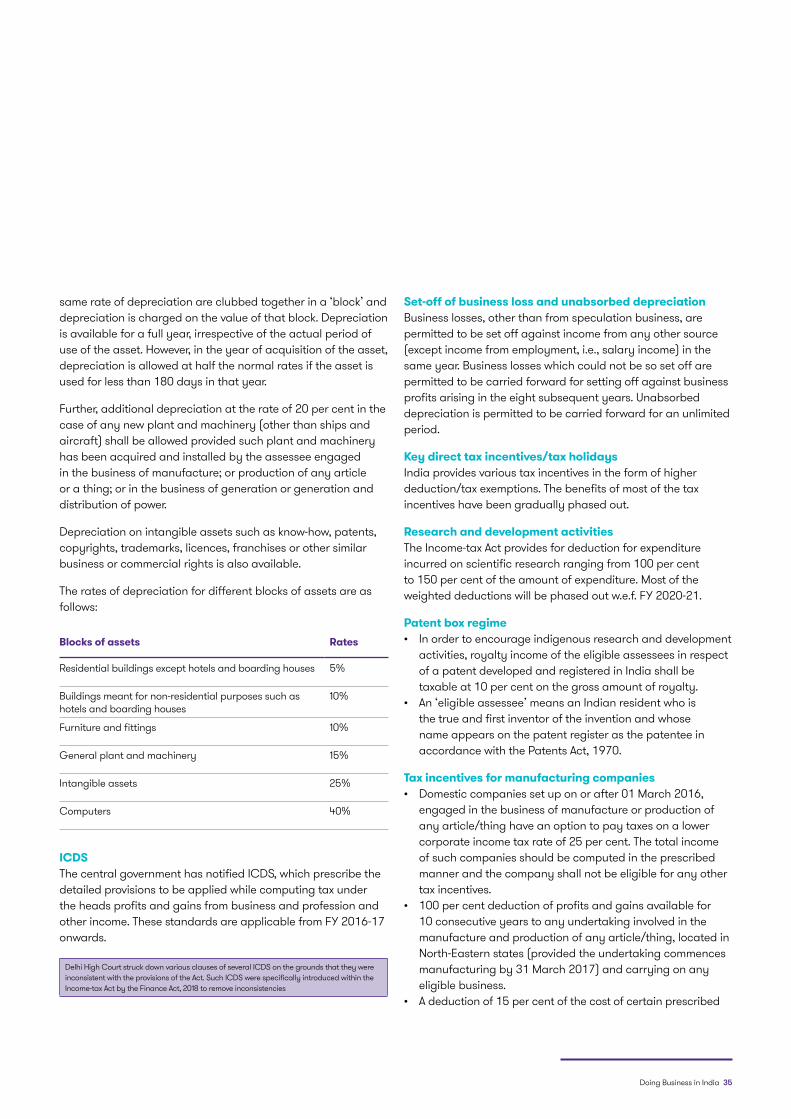

Key economic indicators of IndiaGDP and key fiscal indicators• Atarateof7.1percent,Indiawasoneofthefastestgrowing

largeeconomiesgloballyin2016-17.Thegrowthhasbeensupportedbythecontributionofkeysectorsincludingagriculture,manufacturingandfinancialservices.However,falteringprivateinvestment,weakcapitalgoodsgrowthandlowerexportswereaconcern.TheGDPgrewby7.4percentand7.6percentin2014-15and2015-16,respectively.

• AccordingtoFirstAdvanceEstimatesprovidedbyCSO,thegrowthinGDPduring2017-18isestimatedat6.5percentascomparedtothegrowthrateof7.1percentin2016-17.

• ThefiscaldeficitofthecountryuptoFebruary2018stoodatUSD109.87bn.In2016-17,thefiscaldeficitofthecountrystoodatUSD82.14bn.

• TherevenuedeficitofthecountryuptoFebruary2018stoodatUSD80.50bn.

External factor and per capita national income• Exportsduring2017-18wereatUSD302.84bn,registeringa

growthof9.78percentascomparedto2016-17.• India is the third largest economy in the world in terms of

purchasingpowerparity(Source:InternationalMonetaryFund).• Importsduring2017-18wereatUSD459.67bnregisteringa

growthof19.59percentascomparedto2016-17.• AccordingtoFirstAdvanceEstimatesprovidedbytheCSO,in

realterm(at2011-12prices)during2017-18,thepercapitaincomeislikelytoattainalevelofINR86,660ascomparedtoINR82,269fortheyear2016-17.Thegrowthrateinpercapitaincomeisestimatedat5.3percentduring2017-18,asagainst5.7percentinthepreviousyear.

Growth rates in GDP at factor cost

Source:CSO

7.1%GDP growth in2016-17

19.59%increase in imports in2018

6.9%

7.4%

7.6%

7.1%

0.0% 2.0% 4.0% 6.0% 8.0%

2013-14

2014-15

2015-16

2016-17

Doing Business in India 9

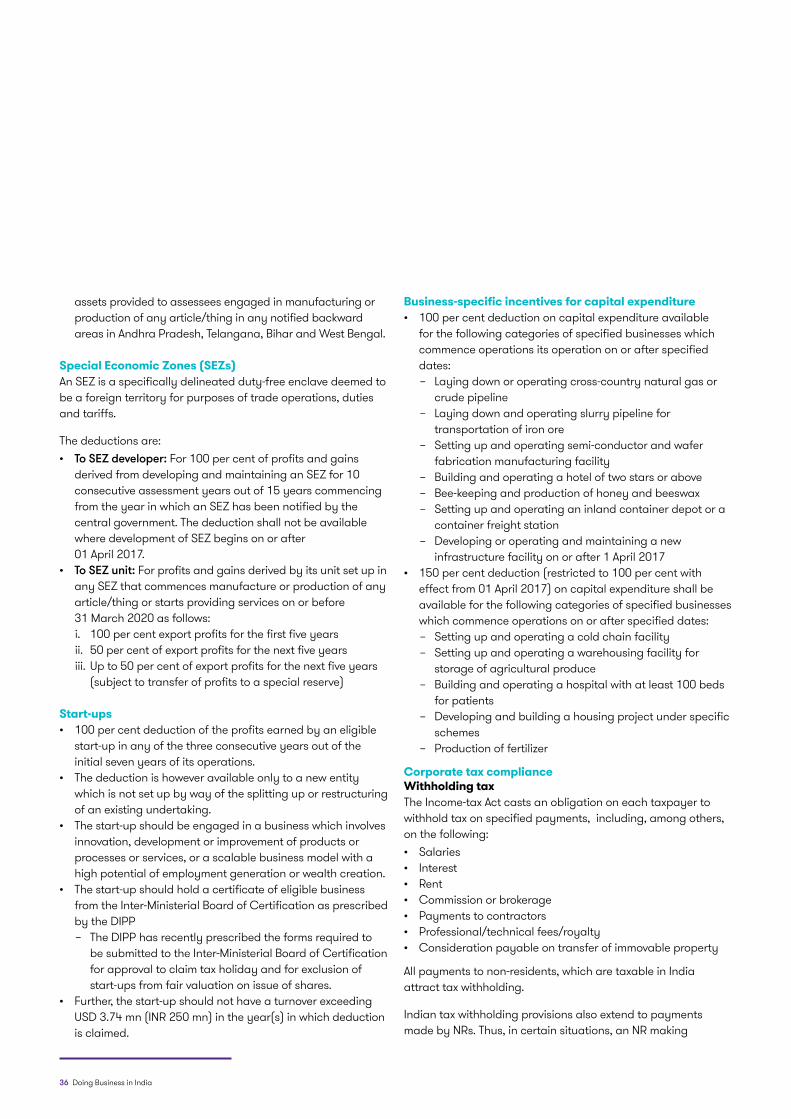

Money and credit• AsrecordedinFebruary2018,thegrossbankcreditforFY

2017-18stoodatINR73,737bn(USD1,131.98bn).(Source:RBI)

• ThegrossfixedcapitalformationaveragedUSD82.14bnduringtheperiod2001-17.Inthefourthquarterof2017,itreachedanall-timehighofINR10,519.30bn(USD161.49bn).(Source:MinistryofStatisticsandProgrammeImplementation)

• India’scurrentaccountdeficitstoodat2percentoftheGDPinthethirdquarterof2017-18ascomparedto1.4percentoftheGDPinthesameperiodayearago.(Source:RBI)

• ExternaldebtinIndiaincreasedtoUSD485.8bninthefirstquarteroftheyear2017-18,recordinganincreaseofUSD13.96bnoveritslevelatend-March2017.(Source:RBI)

• IndianforeignreservetouchedUSD424.36bnason30March2018.TheForeignCurrencyAssets(FCAs),whichformamajorityofthecountry’sforeignexchangereserves,stoodatUSD399.12bn,whilegoldreservesstoodatUSD21.61bn.(Source:RBI)

• Indiabecametheninthlargest(accordingtoWorldInvestmentReport,2017)recipientofFDIin2016intheworld,grossingUSD55.46bnfollowingaseriesofreformsbythegovernment,ascomparedtoUSD44bnin2015.(Source:WorldInvestmentReport2016bytheUnitedNationsConferenceforTradeandDevelopment)

• PMModi’sdemonetisationdrivecontinuestopushelectronictransactions.Goingforward,thiswillalsospurthegrowthoffintechcompanies.

Source:OfficeoftheEconomicAdvisor,GovernmentofIndia;DepartmentOfIndustrialPolicy&Promotion(DIPP)

9thlargest recipient ofFDIin2016globally

112.5

113.9

109.7

111.6116

160.0

165.0

170.0

175.0

180.0

185.0

190.0

2013-14 2014-15 2015-16 2016-17 Mar-18

Wholesale Price Index: Base year 2011-12 Key fiscal indicators (per cent of GDP)

4.7

4.13.9

3.5

3.23.12.9 2.8

2.11.9

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2013-14 2014-15 2015-16 2016-17 (RE) 2017-18 (BE)

Key fiscal indicators (per cent of GDP)

Series 1 Series 2

10 Doing Business in India

Doing Business in India 11

Key sectors: An overview

Thegovernment’sMakeinIndiacampaignhasputmanufacturingattheforefront.Thesectorencompassesanumberofsub-sectorssuchasmetalsandmining,industrialmanufacturing,chemicals,engineering,telecomandautomotive,amongothers.Itisexpectedthatmanufacturingwillcontributesignificantlytothecountry’sgrowthinthecomingdecade.

India is the seventh largest producer of automobiles in the worldandthefourthlargestmarketbyvolume.Thesectorcontributes7.1percenttotheGDPandemploys19mnpeople.Around31percentofsmallcarssoldgloballyaremanufacturedinIndia.Indiaistheworld’slargestmotorcyclemanufacturer.Thetwo-wheelerssegmentcontributes81per

centmarketshareandleadsthemarketonaccountofhugedomesticdemandfromtheyouthandthemiddleclassbuyer.Thus,theautomotivesectoranditsmanufacturingremainsastrongsectorofgrowthforthecountry.

India is also a prominent auto exporter and fifth largest manufacturer of commercial vehicles and the second largest manufactureroftwo-wheelersworldwide.Theexpandingeconomic activity has started to have an impact on the commercialvehiclesegment.Itisexpectedtoregisteradouble-digitgrowthinthenextoneyear.SomeofthekeyforeignplayersareSuzuki,Honda,Nissan,Piaggio,Volkswagen,Renault,Hyundai,GeneralMotors,BMW,FordandToyota.

TheoverallIndianhealthcaremarketiswortharoundUSD100bnandisexpectedtogrowtoUSD280bnby2020,ataCAGRof22.9percent.Healthcaredelivery,whichincludeshospitals,nursinghomesanddiagnosticscentres,andpharmaceuticals,constitutes65percentoftheoverallmarket.ThehealthcareInformationTechnology(IT)market,whichisvaluedatUSD1bncurrently,isexpectedtogrow1.5timesby2020.

TheIndianmedicaltourismindustry,currentlypeggedatUSD3bnperannum,withtouristarrivalsestimatedat230,000,isexpectedtoreachUSD6bnby2018,withthenumberofmedicaltouristssettodoubleoverthenextfouryears.HospitalsanddiagnosticcentresattractedFDIworthUSD3.59bnbetweenApril2000andMarch2016,accordingto data released by the Department of Industrial Policy & Promotion(DIPP).India’suniversalhealthplanthataimstoofferguaranteed benefits to a sixth of the world’s population will cost anestimatedINR1.6tn(USD23.72bn)overthenextfouryears.

TheIndianpharmaceuticalindustryisestimatedtobeUSD30bn,growingataCAGRof16.5percentduringthelastfiveyears(FY2011-16).Indiacontinuestobeamongthelargest producers and exporters of generic drug formulations intheworld,accountingforaround20percentoftotalglobalgenericdrugexports.However,exports,particularlytoregulatedmarkets,havebeenaffectedonaccountofthecontinualUSFDAalertsonIndianmanufacturingstandardsand

facilitiesandtheUSaloneaccountsforabout40percentofIndia’sdrugexports.Theextensionofpricingcontrolonmoreand more essential drugs is also discouraging multinational companiesfromintroducingpatenteddrugsinIndia.However,effortsarebeingtakentopromotelocalmanufacturingandreducing dependence on imports of API from China through thenewbulkdrugpolicytobeinitiated,andthestrongMakeinIndiapushinthesector.

ThemedicaltechnologysectorwasvaluedatUSD6.3bnin2013atendconsumerpricesandisgrowingat10-12percentperyear.Currently,theIndianmedicaldevicesindustryrepresentsjustover1.3percentoftheglobalmedicaldevicemarket.TheIndianmedicaldevicesindustryconsistsofsmallandmediumcompaniesprimarilyfocusingtheirR&Deffortsand manufacturing capabilities on affordable medical devices such as disposables and medical suppliers – which come underlowpriced,highvolumemarketsegments.Requirementsofhighendmedicalequipment–nearly75percent−aremetbyimports.Thecountry’sMakeInIndiainitiativeisbeingimplementedthrougha‘policypush’toencouragelocalmanufacturing and shift from an import dependent to an export-orientedmarket.TheimplementationoftheMedicalDevicesBill2016,alongoutstandinginitiativewhichattemptsto carve out the medical technology sector from pharma will be agamechanger.

Manufacturing and automotive

Healthcare

12 Doing Business in India

India is the world’s largest sourcing destination for the IT industry,accountingforapproximately67percentoftheUSD124-130bnmarket.Theindustryhasaworkforceofabout10mn.Moreimportantly,theindustryhasledtheeconomictransformation of the country and altered the perception of Indiaintheglobaleconomy.TheITindustryhasalsocreatedsignificantdemandintheIndianeducationsector,especiallyforengineeringandcomputerscience.

TheIndianITandITeSindustryisdividedintofourmajorsegments−ITservices,BusinessProcessManagement(BPM),softwareproductsandengineeringservices,andhardware.TheIndianITsectorisexpectedtogrowatarateof12-14percentforFY2016-17inconstantcurrencyterms.ThesectorisalsoexpectedtotripleitscurrentannualrevenuetoreachUSD350bnbyFY2025.

TheIndianM&Eindustryisasunrisesectorfortheeconomyandismakinghighgrowthstrides.ThissectorisexpectedtogrowataCompoundAnnualGrowthRate(CAGR)of14.3percenttotouchINR2.26tn(USD33.7bn)by2020,whilerevenuesfromadvertisingareexpectedtogrowat15.9percenttoINR994bn(USD15.5bn).Indiaisoneofthehighestspendingandfastestgrowingadvertisingmarketsglobally.Thecountry’sexpenditureonadvertisinggrewmorethan12percentin2016,andacceleratedfurtherin2017,ontheback

ofpopularsportingeventsliketheT20WorldCup,theIndianPremierLeague(IPL)andthemediablitzonstateelections.Thetelevisionsegment,whichcontinuestogetthehighestshareofspending,isexpectedtogrowby12.5percentin2017,ledbyincreasedspendingbypackagedconsumergoodsbrandsande-commercecompanies.

ThegovernmentofIndiahassupportedtheM&Eindustry’sgrowth through various initiatives such as digitising the cable distributionsectortoattractgreaterinstitutionalfunding,increasingFDIlimitfrom74percentto100percentincableandDTHsatelliteplatforms,andgrantingindustrystatustothefilmindustryforeasyaccesstoinstitutionalfinance.Also,thegovernment launched the Digital India programme to provide several government services to the people using IT and to integratethegovernmentdepartmentsandthepeopleofIndia.TheadoptionofkeytechnologiesacrosssectorsspurredbytheDigital India Initiative could help boost India’s Gross Domestic Product(GDP)byUSD550bntoUSD1trillionby2025.Thegovernment’sDigitalIndiaandMakeinIndiainitiativesdominatedtheIndianITindustryin2015andalsoboostedthestart-uprevolutioninthecountry.

The Indian retail and consumer industry is broadly segregatedintourbanandruralmarkets,attractingplayersfromacrosstheworld.Thesectorgrewatanannualrateof5.7percentbetween2005and2015.AnnualgrowthintheIndianconsumptionmarketisestimatedtobe6.7percentduring2015to2020and7.1percentduring2021to2025.Themaximumconsumerspendingislikelytooccurinthefood,housing,consumerdurables,andtransportandcommunicationsectors.Indiawillbeaninterestingarenainthenextfewyearsforglobalretailers.Withnewlargeformatmallsprovidinganchorspacetomanyinternationalfashionretailers,theconsumerwillbenefitfromaplethoraofchoices.Further,the current and expected real estate correction along with

economicreformssuchasGSTandinfrastructuredevelopmentschemes will also offer the brands an added incentive to stay investedinIndia.

TheGovernmentofIndiahasallowed100percentFDIunderthe automatic route in online retail of goods and services throughthemarketplacemodel,therebyprovidingclarityontheexistingbusinessesofe-commercecompaniesoperatinginIndia.Manystategovernments,corporateandeducationalorganisationsareworkingtowardsprovidingtrainingandeducationtocreateaskilledworkforceof500millionpeopleby2022.UnionCabinetreformslikeimplementationoftheGSTandSeventhPayCommissionareexpectedtogiveaboosttotheconsumerdurablesectorinIndiaduringFY2017-18.

Technology, Media and Entertainment (M&E)

Consumer products

Doing Business in India 13

Housingisoneofthebasicneedsofthepopulation.Thesectornot only employs the second most number of people directly andindirectlyinthecountry,butalsosupportsaround250ancillaryindustries.Thesectorcontributesmorethan6percenttothecountry’sGDP.However,thereisahugedemand-supply gap in the housing segment with a projected need of around18mnaffordablehousingunits.Andovertheyears,thesectorhasremainedlargelyunorganised,whichhassignificantlyimpactedtheperceptionofthesector.Withinthelastcoupleofyears,thegovernmenthasinitiatedvariousreforms−‘Housingforallby2022’scheme,creationof100

smartcities,relaxationsinFDInormstoattractinvestments&REITsregime.Apartfromthis,governmenthasfinallybeenabletoenactRERAandawardinfrastructurestatustoaffordablehousingsegment.

The plethora of these reforms not only have the ability to change the landscape of the sector in terms of bringing in muchneededtransparencyandaccountability,butalsoattract significant amount of investments for the sector – both overseas&domestic.

DemonetisationdrivebytheIndiangovernmentin2016,aimedatdrivingthecountrytowardsacashlesseconomy,isreflectiveoftherapidlychangingscenariointhecountry.This,alongwithmanymorepolicychangesandreforms,providesfinancialservicesafirmstanding.WhilethereareconcernsrelatedtohighlevelsofNon-PerformingAssets(NPAs)withbanksandotherfinancialinstitutions,thereisasilverlining.RBI,alongwiththegovernment,hastakenanumberofinitiativesforenhancing the accessibility and financial inclusion of all in the country.BankaccountpenetrationinIndiaincreasedfrom35percentin2011to53percentin2014.WithinitiativessuchasJanDhanYojana,thenumberofunbankedpopulationwithoutanybankaccountsinIndiacamedowncomedown

toaround233mnbytheendof2015,reflectingadropof58percentoverthelastfouryears.Asrecordedin2015,Indiahadatotalof1,440mndepositbankaccountsand1,170mnsavingbankaccountsin2015.Thecountryalsohasaround144mnofborroweraccounts.Withrisinglevelsofdigitisationandtechnologyadoption,thefinancialservicessectorisexpectedtodeepenitspenetrationandreachinthecountry.Consequently,theIndianbankingindustryhasthepotentialtobecomefifthlargestbytheendofFY2020andthefifthlargestbytheendofFY2025.

Real estate and construction

Financial services

14 Doing Business in India

Indiaisthelargestdemocracyintheworld.Itisestimatedthatthecountrytodayhasmorethan200politicalparties.Onefeature of the political parties in India is the dominant role playedbytheirleaders.Therearebothnationalandregionalparties,oneofwhichistheIndianNationalCongress(INC)whichhasbeenledmainlybytheNehru-Gandhifamilysincetheindependenceofthecountry.Tocompeteonanationallevel,manypoliticalpartiesformalliances.ThetwomainalliancesinthecountryareNationalDemocraticAlliance(NDA),acoalitionledbytheBharatiyaJanataParty(BJP),andUnitedProgressiveAlliance(UPA),acoalitionledbytheINC.

Structure of the governmentIndiaisthelargestmulti-partydemocracyintheworld.Itis a sovereign socialist secular democratic republic with a parliamentarysystemofgovernment,andaconstitution.TheConstitution of India provides for a parliamentary form of governmentwhich,althoughhascertainunitaryfeatures,isfederalinstructure.ThecounciloftheParliamentoftheUnionconsistsoftwolegislativehouses−theRajyaSabha(UpperHouse),whichrepresentsthestatesoftheIndianfederation,andtheLokSabha(LowerHouse),whichrepresentsthepeopleofIndiaasawhole.Atpresent,thecountryisaunionof29statesandsevenUnionTerritories(UTs).Eachstateisgovernedby a government comprising elected representatives of the public.

The central and state governments comprise a council of ministersheadedbyaPrimeMinisterandaChiefMinister,respectively.TheheadofthestateisthePresidentofIndia,whiletheheadofthegovernmentisthePrimeMinister.ThePrimeMinisterandtheChiefMinisterareusuallytheheadsofthepoliticalpartiesthatareelectedbythepeople.TheyhavesupportofallthemajoritymembersintheParliament.Electionsforthestate,centreandUTsareheldaftereveryfiveyears.

NewDelhiisthenationalcapitalofIndia.TheseatofthecentralgovernmentisNewDelhi.AlltheotherStategovernmentshaveprimaryresponsibilityformatterssuchaslawandorder,education,healthandagriculture.Currently,ShriNarendraModiisthePrimeMinisterofIndia.IndiaisamemberofmajorinternationalorganisationsincludingSouthAsianAssociationforRegionalCooperation(SAARC),Brazil,Russia,India,ChinaandSouthAfrica(BRICS),andtheCommonwealthofNations,amongothers.

Judiciary and lawIndiahasawell-established,independentjudicialsystem.TheSupremeCourtofIndiaisbasedinNewDelhi.Ineachstate,thereisaHighCourtinitscapitalcity.Thestatesalsohaveseveraldistrictcourts.

IndiaderivesmostofitsjudicialframeworkfromtheEnglishlegalsystem.ThemaingoaloftheIndianlawistoprotectthepromotionofbusinessentities,provideahealthyindustrialandsocialenvironmentandensurerobustlabourprotection.Till1991,manytradebarrierswereinplacesoastopromotethelocalindustry,butsince1991manybarriershavebeenliftedtopromotetheinfluxofforeigninvestorsinthecountry.

Political and legal system

Source:GrantThorntonDealTracker

Introduction

Doing Business in India 15

Foreign investment

IntroductionForeigninvestorskeentosetupoperationsinIndiaarerequiredtocomply,interalia,withtheforeignexchangecontrollawsofthecountry,particularlytheconsolidatedFDIPolicy,issuedbythegovernmentofIndiafromtimetotime.Accordingly,theCompaniesAct2013,ForeignExchangeManagementAct,1999(FEMA)andtheregulationsthereundergovernthesetting-upofincorporatedentities(jointventuresorwholly-ownedsubsidiaries)andofunincorporatedentities(branch,liaisonorprojectoffices).

FDI policyIn recognition of the important role played by FDI in acceleratingtheeconomicgrowthofthecountry,thegovernment initiated a slew of economic and financial reforms in1991.Indiaisnowusheringinthesecondgenerationreformsaimed at furthering the integration of the Indian economy with theglobaleconomy.

FDIisallowedinmostsectors,includingtheservicessector,throughthe‘automaticroute’withoutrequiringanyprior

governmentapproval.Ontheotherhand,inafewsectors,the existing and notified sectoral policy does not permit FDI beyondaceilingoritissubjecttocertainspecifiedconditions.

FDI can be brought in after obtaining an approval from the government.TheapprovingauthorityusedtobetheFIPBwhichusedtofunctionundertheMinistryofFinance.ThegovernmenthasabolishedFIPBwitheffectfromMay2017.Newproposalsfor FDI under approval route are now directly handled by the concernedministries.Towardsthisend,theDIPPhasissuedthe‘StandardOperatingProcedures’(SOP)forprocessingFDIproposals.ThisSOPclearlylaysdowntheproceduretosubmittheonlineapplicationthroughtheFIPBportal(nowknownastheForeignInvestmentFacilitationPortal).

The table below gives an indicative summary of the sectoral FDI policy:

FDI policy parameter Sectors

Automatic route FDIupto100percentpermittedundertheautomaticrouteinmostservices,manufacturing,infrastructuresectorandservices,B2Btrading,SingleBrandRetailTrading(SBRT)

Approval route FDIintheseactivitiesispermittedonlywithpriorgovernmentapproval,e.g.,non-operatingholdingcompanies,broadcastingcontentservices(FMradio)andprintmedia(newspaperandperiodicals)

Sectoralcapsand FDIlinkedconditions

FDIincertainsectorsissubjecttosectoralcapssuchasinsurance(49percent),defenceindustrysubjecttoindustrialLicense(49percent),multibrandretailtrading(51percent)andairlines(49percent)

Further,FDIincertainsectorsissubjecttospecifiedconditions−wholesaletrading,singlebrandretailtrading,e-commerce,constructiondevelopment−townships,housingandbuilt-upinfrastructureetc.

FDIlinkedconditions

FDIinthesesectorsissubjecttospecifiedconditions−floriculture,horticulture,apicultureandcultivationofvegetablesandmushroomsundercontrolledconditions,wholesaletrading,singlebrandretailtrading,e-commerce,constructiondevelopment−townships,housingandbuilt-upinfrastructure,printmediaandasset reconstruction companies

16 Doing Business in India

FDI is not permitted in the following sectors:• Lotterybusinessincludinggovernment/privatelottery,online

lotteries,etc.• Gamblingandbettingincludingcasinos,etc.• Agriculture(excludingplantations−tea/coffee/rubber/

cardamom/palmoiltree/oliveoiltree)• Activities/sectorsnotopentoprivatesectorinvestment,e.g.,

atomicenergyandrailways(exceptmassrapidtransportsystems)

• Business of chit fund• Nidhicompany• TradinginTransferableDevelopmentRights(TDRs)• Realestatebusiness,orconstructionoffarmhouses(subject

tocertainexceptions)• Manufacturingofcigars,cheroots,cigarillosandcigarettes,

tobacco or tobacco substitutesForeign technology collaboration in any form including licensingforfranchise,trademark,brandnameandmanagementcontractisalsoprohibitedforlotterybusiness,gamblingandbettingactivities.

TomakeIndiaanattractivedestinationforforeigninvestors,theFDIpolicyallowsrepatriationofallprofits,dividends,royalty,andknow-howpayments,freely.

Exchange controlsFEMAreplacedtheForeignExchangeRegulationAct,1973tofacilitateexternaltradeandpayments,andtopromoteorderlydevelopmentandmaintenanceoftheforeignexchangemarketinIndia.

Asperthecurrentforeignexchangecontrolregulations,transactions are divided into current account and capital accounttransactions.Capitalaccounttransactionrefertosuchatransactionwhichalterstheassetsorliabilities,includingcontingentliabilities,outsideIndia,ofapersonresidentinIndia,orassetsorliabilitiesinIndiaofapersonresidentoutsideIndia.Thus,investmentbyabodycorporateoran entity in India and investment therein by a person resident outsideIndiaarecapitalaccounttransactions.

Currentaccounttransactions,ontheotherhand,aretransactionsotherthancapitalaccounttransactions.Suchtransactionscomprise,forinstance,paymentsdueinconnectionwithforeigntrade,othercurrentbusinessservices,

andshort-termbankingandcreditfacilities,intheordinarycourseofbusiness.Broadlyspeaking,currentaccounttransactionsarepermitted,unlessspecificallybarred,andcapitalaccounttransactionsareprohibited,unlessspecificallypermitted.

Capital instrumentsFEMA,readwithrelevantregulationsgoverningFDI,provide,interalia,thatIndiancompaniescanissueequityshares,fullyandmandatorilyconvertibledebentures,fullyandmandatorilyconvertiblepreferencesharesandwarrants(issuedinaccordancewiththeregulationsissuedbySEBI),subjecttothepricingguidelines/valuationnormsandreportingrequirements,toforeigninvestorssubjecttocertainprescribedrequirements.The FDI policy allows optionality clauses in equity shares and compulsorilyandmandatorilyconvertiblepreferenceshares/debenturesissuedtonon-residentinvestorsundertheFDIschemesubjecttocertainconditions.Thepolicyprovidesthatshareswithcall/putoptionsmaybeissuedtonon-residentinvestorsprovidedthenon-residentinvestorisnotguaranteedanyassuredexitpriceatthetimeofmakingtheinvestment.

Generalpermissionisalsoavailableforissuingshares/preferencesharesagainstlumpsumtechnicalknow-howfee,royaltydueforpayment,subjecttoentryroute,sectoralcapandpricingguidelines,andcompliancewithapplicabletaxlaws.Recently,thegovernmentalsoallowedcompaniestoissueequity shares against any other funds payable by the investee company(subjecttobonafidesbeingsatisfiedregardinglegitimacyofdues),remittanceofwhichdoesnotrequirepriorpermissionofthegovernmentorRBIunderFEMAoranyrules/regulationsframedordirectionsissuedthereunder.

Foreign currency loansIntermsoftheFEMAandtherelevantregulationsgoverningExternalCommercialBorrowings(ECBs),IndiancompaniesoperatingincertainspecificsectorsarepermittedtoavailECBfromcertaincategoriesofnon-residentlenderswithaspecifiedminimumaveragematurityperiodforspecifiedenduser,under the general permission or specific permission route as applicable.Importantly,optionallyconvertibleandredeemableinstrumentslikeredeemablepreferenceshares,optionallyconvertible shares and debentures also need to comply with theECBregulations.

Doing Business in India 17

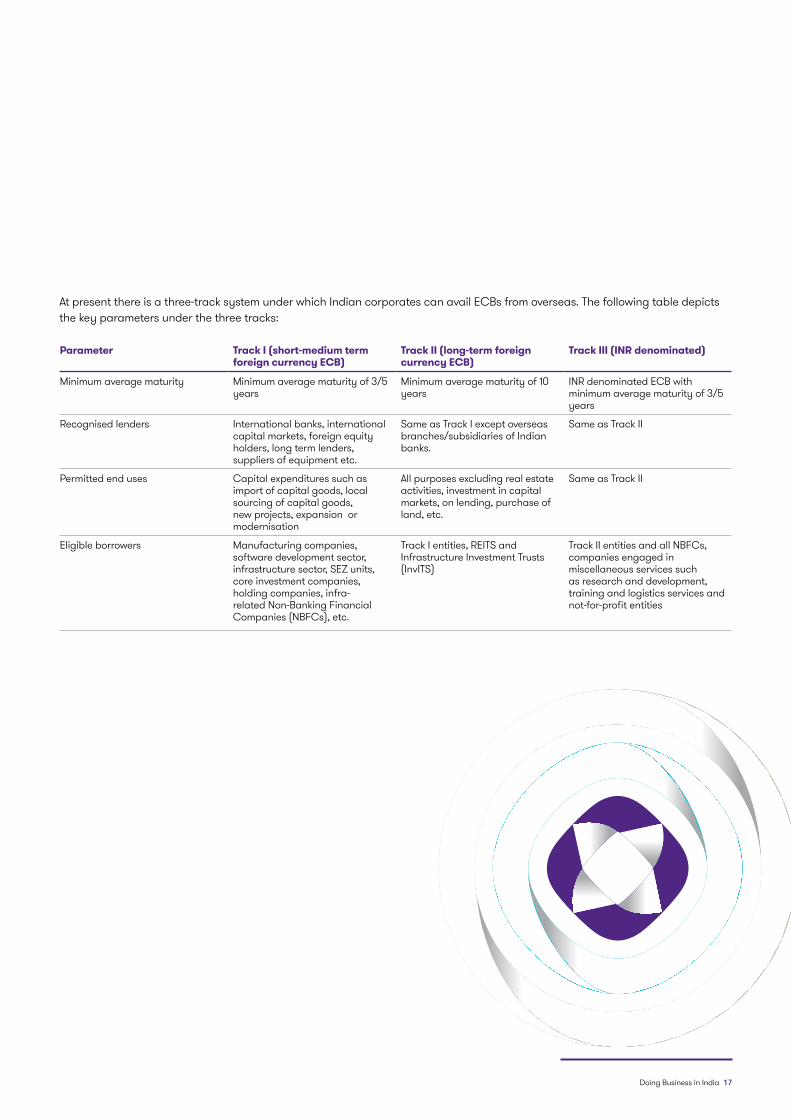

Atpresentthereisathree-tracksystemunderwhichIndiancorporatescanavailECBsfromoverseas.Thefollowingtabledepictsthekeyparametersunderthethreetracks:

Parameter Track I (short-medium term foreign currency ECB)

Track II (long-term foreign currency ECB)

Track III (INR denominated)

Minimumaveragematurity Minimumaveragematurityof3/5years

Minimumaveragematurityof10years

INRdenominatedECBwithminimumaveragematurityof3/5years

Recognisedlenders Internationalbanks,internationalcapitalmarkets,foreignequityholders,longtermlenders,suppliersofequipmentetc.

SameasTrackIexceptoverseasbranches/subsidiariesofIndianbanks.

SameasTrackII

Permitted end uses Capital expenditures such as importofcapitalgoods,localsourcingofcapitalgoods,newprojects,expansionormodernisation

All purposes excluding real estate activities,investmentincapitalmarkets,onlending,purchaseofland,etc.

SameasTrackII

Eligibleborrowers Manufacturingcompanies,softwaredevelopmentsector,infrastructuresector,SEZunits,coreinvestmentcompanies,holdingcompanies,infra-relatedNon-BankingFinancialCompanies(NBFCs),etc.

TrackIentities,REITSandInfrastructure Investment Trusts (InvITS)

TrackIIentitiesandallNBFCs,companies engaged in miscellaneous services such asresearchanddevelopment,training and logistics services and not-for-profitentities

18 Doing Business in India

Import/export controls Overtheyears,Indiantradepolicyhasundergonefundamentalshiftstocorrectthepreviousanti-importbias,throughthewithdrawalofquantitativerestrictions,reductionandrationalisationoftariffs,liberalisationinthetradeandpaymentsregime,improvementinaccesstoexportincentives,andestablishmentofarealisticandmarket-basedexchangerate.

ExportandimportofgoodsandservicesfromIndiaareallowedunderFEMA,readwiththeForeignExchangeManagement(CurrentAccount)Rulesasamendedfromtimetotime.The said export and import regulations stipulate guidelines pertaining to settlement and payment of export and import transactions,realisationofproceeds,advancereceiptsandpaymentswrittenoffandlimitspermissibleforthem.

The export regulations also set out the obligations for Indian exporters of goods such as submission of certain prescribed declarationsalongwithsupportingdocuments.Whilenoformsareprescribedforexportofservices,neverthelesstheexportproceeds are required to be realised within a stipulated time period(currentlyninemonths).

Similarly,theimportregulationsprovidethemanneranddocumentsrequiredtobefollowedbypersons,firmsandcompaniesformakingpaymentstowardsimportsintoIndia.Further,thesaidregulationsprovidethetimelineswithinwhich remittances against imports should be completed or an approvalbesoughtfromtheAD/RBIpriortotheexpirationoftheduedate.

Overseas direct investmentIndianparties(companyincorporatedinIndiaorabodycreated under an act of Parliament or a partnership firm registeredundertheIndianPartnershipAct1932oraLimitedLiabilityPartnership(LLP)incorporatedundertheLLPAct,2008)areeligibletoundertake‘overseasdirectinvestment’outsideIndiasignifyingalong-terminterestintheforeignentity(jointventureorwhollyownedsubsidiary).

AnIndianpartycanmakeoverseasdirectinvestmentundertheautomatic route in any bonafide activity up to the prescribed limitofitsnetworth(currently400percentofnetworth).Itmaybenotedthatrealestateandbankingbusinessaretheprohibitedsectorsforoverseasdirectinvestment.Overseasinvestment in the financial services sector is subject to specified conditionsincludingasatisfactorytrackrecordoftheinvestingparty,andthepriorapprovaloftheconcernedfinancialregulatorinIndia.

The regulations also prescribe provisions with respect to aspectssuchasissuanceofguarantee,ongoingcomplianceandreportingrequirementsandconditionsfordisinvestment.

Doing Business in India 19

Finance

Introduction

Indian financial services sector

ThefinancialsectorinIndiaisintrinsicallystrong,operationallysundry and exhibits competence and flexibility besides being sensitivetoIndia’seconomicaimsofdevelopingamarketoriented,industriousandviableeconomy.Thesectorcanbebroadly classified into two categories:

The organised sector:Comprisesprivate,publicandforeignownedcommercialandcooperativebanks,whichareknownasscheduledbanks,andinsurancesector.

The conventional sector:Comprisesindividualorfamily-ownedmoneylendersandNBFCs.

The force of liberalisation has transformed the structure of the financialsector.Therehavebeensignificantbankingreformsinthecountrysincetheliberalisationoftheeconomy.Thesereformshaveattractedforeignplayersinthebankingandfinancialsector.

TheRBIpolicyratesheavilyinfluencetheIndianfinancialservices.ThecurrentRBIratesason07March2018arebankrate:6.25percent;reporate:6percent;reversereporate:5.75percent.ThereserveratiosareCRR:4percentandSLR:19.5percent.

The Indian financial sector has the following broad categories:

Sr. No. Categories

1 Commercialandretailbanks

2 WhiteLabelAutomatedTellerMachine(WLA)

3 Paymentbanks/wallets

4 NBFC

5 HousingFinanceCompanies(HFC)

6 MicrofinanceInstitutions(MFIs)

7 Insurance companies

8 Capitalmarkets

9 Pension funds

10 Mutualfunds

11 PrivateequityandVentureCapital(VC)funds

12 AssetReconstructionCompanies(ARCs)

13 REIT/InvITfund

14 Angelorstart-upfund

20 Doing Business in India

ThebankingsectorisdominatedbyscheduledcommercialbankswhichincludePSUbanks,privatebanksandforeignbanks.Commercialbanksdealinalltypesofcommercialbankingbusinessesincludingcashmanagementsystem,AutomatedTellerMachines(ATMs),creditcards,termandworkingcapitalloans,housingandconsumerfinanceandpurchaseandsaleofforeigncurrencies.Manyfinancialinstitutions are becoming dynamic and entering new domains withinbankingsuchashomeloansfinance,carandretailbanking,etc.andhaveseparatedepartmentsforofferinginvestmentandstructuringservices.

In2016,inanendeavourtopromoteacashlesseconomy,thegovernment announced demonetisation of existing currency notesthroughtheRBI.ThedemonetisationprocessisexpectedtohaveapositiveimpactontheIndianeconomy,channelisingidlemoneythroughlegitimatebankingchannels.Hence,growingdepositsinthebanksmayresultinloweringtheinterestrates,furtherdroppingthelendingratesaswell.Thiswouldfurtherhelpinpromotingretailactivitiesintheeconomy.

WLAATMsset-up,ownedandoperatedbynon-bankentitiesarecalledWLAs.TheyprovidebankingservicestothecustomersofbanksinIndiabasedonthecards(debit/credit/prepaid)issuedbybanks.TheUnionCabinethasapproved100percentFDIundertheautomaticroutefornon-bankentitiesthatoperateWLA,subjecttocertainconditionsasprescribed.

Payment banks/walletsPaymentsbanksareanewmodelofbanksconceptualisedbytheRBIforfinancialinclusionbyproviding(i)smallsavingsaccountsand(ii)payments/remittanceservicestomigrantlabourworkforce,lowincomehouseholds,smallbusinesses,otherunorganisedsectorentitiesandotherusers.Theyreachcustomers mainly through the mobile phones rather than conventionalbanks.PaymentsbanksaregovernedbythefinalguidelinesreleasedbytheRBIforpaymentsbankson27November2015.

AirtelhaslaunchedIndia’sfirstlivepaymentsbank.Further,withpaymentsbanksusingsmartphonesandbiometricsystem(AadhaarCardenabledbankaccounts),theuseofcurrencycirculationintheseareastoowilldecreasedrastically.

NBFCsNBFCsarefinancialinstitutionsthatprovidecertaintypesofbankingservices,butdonotholdafullbankinglicence.NBFCsunder their criteria are permitted to offer substitutes to the

bankingservicessuchasloansandcreditfacilities,etc.Theyaregenerallyengagedinnon-fundbasedactivitiesthatkeepthem outside the scope of traditional oversight required under bankingregulations.

TheNBFCsectorinIndiahasundergoneasignificanttransformationoverthepastfewyears,withNBFCloansexpanding16.6percentintheyear,twiceasfastasthe8.8percentcreditgrowthacrossthebankingsectoronanaggregatelevel.

HFCThemandateoftheRBIistopromotehousingfinanceinstitutionstoimprove/strengthenthecreditdeliverynetworkforhousingfinanceinthecountry.HFCsareexpectedtoregulate the housing finance system of the country to prevent the affairs of any housing finance institution being conducted in a manner detrimental to the interest of the depositors or in a manner prejudicial to the interest of the housing finance institutions.

The biggest highlight of the government was to bring housing loansofuptoINR5mnunderaffordablehousingandINR2.8mninurbanandINR2.5mninothercentresunderprioritysectorlending.ThedecisionoftheRBItoincreaseLoanToValue(LTV)ratioto90percentforloansuptoINR3mnorlesswasanotherpositivesteptoenableHFCstolendmoretotheLow-andModerate-Income(LMI)group.

MFIThePrimeMinisterofIndiahaslaunchedtheMicroUnitDevelopmentandRefinanceAgency(MUDRA)tofundandpromoteMFIs,whichwouldinturnprovideloanstosmallandvulnerablesectionsofthebusinesscommunity.MFIsare the pivotal overseas organisations in each country that makeindividualmicrocreditloansdirectlytovillagers,microentrepreneurs,impoverishedwomenandpoorfamilies.Asadedicatedcreditdeliverychannelforvastunbanked/under-bankedsegments,NBFC-MFIshavebeenplayingasignificantroleintakingforwardthefinancialinclusionagendaofthegovernmentofIndia.

Insurance companiesTheInsuranceRegulatoryandDevelopmentAuthorityofIndia(IRDA),aspartofitsendeavourtoincreaseinsurancesectorgrowth,hasallowedanewdistributionavenuecalledthe‘pointofsale’person,whowillbeallowedtosellsimplestandardisedinsuranceproductsinthenon-lifeandhealthinsurancesegments,whicharelargelypre-underwritten.Therelaxation

Doing Business in India 21

intheFDIlimitto49percentintheinsurancesectorandpermissionforoffshorereinsurancetoentertheIndianmarketswouldassistIndiabecomethelargestinsurancemarketintheworld.OverfivereinsurancelicenceshavebeengrantedinIndiatopromotethereinsurancebusinessactivities.

ThegrossmarketsizeofIndia’sinsurancesectorisprojectedtotouchUSD350-400bnby2020,withtheIndianinsuranceindustry planning to increase the penetration level in the marketfromthecurrent3.9percentto5percentby2020.

Capital marketsTheIndiancapitalmarketcomprisesequity,debt,foreignexchange,derivativemarketsandfuturesmarketsincommodities.Further,inapotentialmovetoencourageforeigninvestmentintothedebtmarkets,theRBIreleasedadraftcircularon16May2016proposingtoexpandthebasketofpermissibleinstrumentsforForeignPortfolioInvestors(FPI)toincludeunlisteddebtsecuritiesaswell.

AccordingtotheDIPP,thetotalFDIinvestmentsIndiareceivedinFY2016-17wasUSD60.08bn.FPIs’netinvestmentsstoodatUSD8.58bninMarch2017,themaingrowthdriverforFPIsbeingtheequitymarket.

Pension fundsPensionfundsarecreatedbyanemployertomakecontributionsoffundssetasideforaworker’sfuturebenefit.WiththepassagepassageofthePensionFundRegulatoryandDevelopmentAuthority(PFRDA)Act2013,theinvestmentcorpusinIndia’spensionsectorisexpectedtocrossUSD1trillionby2025.Foreigninvestmentinthepensionsectorispermittedupto49percent.

Mutual fundsMutualfundsarepopularinIndia,becausetheyoffertheability to easily invest in increasingly complicated financial markets.Alargepartofthesuccessofmutualfundsistheadvantagestheyofferintermsofdiversification,professionalmanagementandliquidity.

Afterthetighteningofregulation,andwithrisingincomes,IndianowhasseveralfundhouseswithrecordAssetsUnderManagement(AUM)ofoverINR13,000bnatlastcount,andseverallakhunitholders.

Other sources of financePrivate equity and VC fundsInIndia,VCisregulatedbySEBI.Aventurecapitalmaybesetup by a company or a trust after a certificate of registration isgrantedbySEBI.AVCcanraisemoneyfromanyIndianorNon-ResidentIndian(NRI).Recently,SEBIproposedtoenhancetheinvestmentlimitforVentureCapitalFunds(VCFs)from10percentto25percentinoffshoreventurecapitalundertakingswithanIndianconnection.

Overthelastfewyears,Indiahasemergedasthethirdlargestbaseforstart-upsintheworld,aftertheUSandtheUK.Oneofthemostcommonwaysastart-upraisesmoneyforitsseedcapitalandfurtherfundingisbyventurecapital.AlternativeInvestmentFunds(AIF)refertoanyprivatelypooledinvestmentthatmaybefromIndianorforeignsourcesknownas‘privateplacement’.

In2015,theRBInotifiedaregulationwhichallowedforeigninvestmentandsimplifiedtheprocedureforinvestmentinAIFs.ThismovehasbeenapplaudedbytheAIFindustry,whichisrelativelynewinIndia.Withafreshinflowofforeigninvestment,therewillbeacceleratedgrowthindomesticAIFs,whichyieldbetter returns to investors as well as better investments for new andemergingbusinesses,socialventuresandinfrastructure.

ARCsARCshavebeencreatedtobringaboutasystemforrecoveringNPAsfromthebooksofsecuredlendersandunlockingthevalueofNPAs.Tohelptackletheissueofdecliningassetqualityofbanks,100percentFDIisallowedinARCsundertheautomaticroute.

REITs/InvIT fund REITorInVITisanalternatefund-raisingmechanismofferedtocapital-intensiveindustriesforcompaniesthatownincome-producingrealestateorinfrastructure.Assuch,theunitholdersofaREIT/InvITearnashareoftheincomeproducedthroughrealestateinvestment,withoutactuallyhavingtogooutandbuyorfinanceproperty.SEBIrelaxedtherulesforREITandInvITbyallowingthemtoinvestmoreinunder-constructionprojects,rationalisedunitholderconsentonrelatedpartytransactionsandremovedrestrictionsonSpecialPurpose

22 Doing Business in India

Vehicles(SPVs)toinvestinotherSPVsholdingtheassets.

Angel or start-up fund Angel investors are experienced entrepreneurs who have beenthroughthesamephaseandunderstandwhatittakestocreateabigcompanyfromanidea.Therearearound280investorsthatareapartofthisnetwork.Themainsectorsthatprominentlyinvolveangelinvestmentaree-commerce,

informationtechnology,healthcare,agricultureandthemobilesegmentofthetelecommunicationssector.

Doing Business in India 23

Business entities

IntroductionA foreign company has the following business entity options through which it can establish its presence in India:

These forms of business entities are discussed in detail as follows:

Unincorporatedentities • LiaisonOffice(LO)• BranchOffice(BO)• Projectoffice• Partnershipfirm

Incorporated entities • LLP• Limitedcompanypublic/private

LO Aforeigncompany(abodycorporateincorporatedoutsideIndia,includingafirmorotherassociationofindividuals)mayestablishitsLOinIndiabymakinganapplicationtotheAuthorisedDealerBank(ADBank)iftheprincipalbusinessoftheentityresidentoutsideIndiafallsundersectorswhere100percentFDIispermittedintermsoftheFDIpolicy.Incertaincases,theapplicationistobemadetotheRBIandprocessedinconsultationwiththegovernment,forinstance,wheretheapplicantisanNGOandwhentheapplicantisfromcertainspecified countries and setting up the LO in specified states in Indiaetc.

An LO is suitable for a foreign company which wishes to set up a representative office as a first step to explore and understand thebusinessandinvestmentclimateinthecountry.Thisofficeserves as a communication channel between the parent companyoverseasanditspresent/prospectivecustomersinIndia.TheLOcanalsobesetuptoestablishbusinesscontactsorgathermarketintelligencetopromotetheproductsorservicesoftheoverseasparentcompany.TheLOcannotundertakeanybusinessactivityorearnanyincomeinIndia.

BOAforeigncompanymayestablishitsBOinIndiabymakinganapplicationitsADbankinmostcases.TheBOshouldbeengagedintheactivityinwhichtheparententityisengaged,andpermissibleactivitiesforaBOincludeexporting/importinggoods,renderingprofessionalorconsultancyservices,undertakingresearchwork,promotingtechnicalorfinancialcollaborations,representingtheparentcompanyinIndiaandactingasbuying/sellingagentinIndia,renderinginformationtechnologyservicesandrenderingtechnicalsupport.

ABOisnotpermittedtoundertakeanymanufacturingactivityinthecountryexceptwheretheBOisset-upinaspecialeconomiczone.

Project officeA foreign company may open a project office in India without priorapprovalfromtheRBI,providedithassecuredacontractfrom an Indian company to execute a project in India and mettheprescribedconditions.Oncetheprojectexecutioniscompleted,asperthetermsofthecontractsawarded,theprojectofficewouldhavetobecloseddown.

24 Doing Business in India

Partnership firmsUnderthecurrentFDIpolicyandtheForeignExchangeManagementLaw,foreigninvestmentintoIndianpartnershipfirms(otherthanbynon-residentIndiansorpersonsofIndianorigin)requirespriorpermissionfromtheRBI.Apartnershipisanassociationoftwoormorepersonstocarryonasco-ownersofabusinessforprofit.Eachpartnerofapartnershiphasunlimitedliability.

LLPsAnLLPisahybridbetweenapartnershipfirmandacompany.Itisaseparatelegalentity,liabletothefullextentofitsassets,with the liability of the partners being limited to their agreed contributionintheLLP.ForeigninvestmentintoanLLPispermittedundertheautomaticroute(withoutrequiringpriorapproval)inthosesectorsinwhich100percentFDIisallowed.However,itshouldbenotedthatLLPsarenotpermittedtoraiseECBs.

An LLP is governed as per the LLP agreement between the partners,andintheabsenceofsuchagreementtheLLPwouldbegovernedbytheframeworkprovidedintheLimitedLiabilityPartnershipAct,2008.ThisActdescribesthemattersrelatingto mutual rights and duties of partners of the LLP and of the limitedliabilitypartnershipanditspartners.Importantly,theActmakesitmandatorytohavetwodesignatedindividualpartners,atleastoneofwhomshouldberesidinginIndia.

Any existing private company or existing unlisted public company can be converted into LLP by complying with therelevantprovisionsoftheLLPAct,2008.Taxneutralityconditionshavebeenstipulatedforsuchconversion.

Limited companyAlimitedcompanyisanincorporatedentity,whichisaseparatelegalentitydistinctfromitsmembers/shareholders.Asmentionedabove,foreigninvestmentinIndiaisgovernedbytheFDIpolicyofthegovernmentaswellastheForeignExchangeManagementLaw.Asperthecurrentpolicy,allcompaniesin India have to be incorporated under the provisions of the CompaniesAct,2013.

WitheffectfromMay2015,theminimumcapitalrequirementforcompanieshasbeendoneawaywith.

Private company: A minimum of two members and two directors are needed to establish a private company with at leastonedirectorbeingresidentinIndia.

Public company: A public company can be incorporated with minimum three directors and seven members with at least one directorbeingresidentinIndia.

Foreign investors while deciding to set up an entity in India as aprivatevis-à-visapubliccompanyconsiderseveralfactorssuch as:• While a private company can provide for restrictions on

transfer of its shares by inserting suitable clauses in the ArticlesofAssociation,nosuchrestrictionscanbeputontransferofsharesinapubliccompany,whicharefreelytransferable.

• A private company as the name suggests cannot invite publictosubscribeitssecurities.

• The compliances applicable to a private company under theCompaniesAct2013arefewerascomparedtothoseapplicabletoapubliccompany,suchasformationofvariousgovernancecommittees,secretarialaudits,appointment of independent directors and ceilings of managerialremuneration.

Doing Business in India 25

Labour

Employment contractIndia has adopted various measures to regulate the conditions underwhichfixed-termemploymentcontractsarewritten,appliedandinterpreted.LabourisaconcurrenttopicintheIndianConstitution−itissubjecttolegislationfrombothstateandcentralgovernments.TheIndianContractsAct,1872definestheterm‘contract’asanagreementlegallyenforceablebylaw.Theremustbealawfulofferandalawfulacceptancetoresultinanagreement.

Customary working hours and holidaysThenormalworkinghoursinafactoryperdayareeight.TheusualworkinghoursinIndiaare9amto5:30pmor9:30amto6pm.Incaseofcorporates,itissevenhoursperday,sixdaysaweek.Indiansubsidiariesofmultinationalcorporationsusuallyfollowafiveday,eighthourperdayweek.Normally,10daysofcasualleaveand20-30daysofprivilegeleaveisallowedinayear.MayDay,whichisknownastheInternationalWorkersDay,iscelebratedeveryyearon01MayinIndia.

Minimum wageTherearelawsinIndiaforworkersinmostsectorstoreceiveaminimumwage.Itisoneofthemostimportantaspectsofstartinganewlineofworkorrunninganorganisationsuccessfully.ThelawwhichenforcestheemployerstopaythesetminimumwagesinIndiaisknownastheMinimumWagesAct,1948.ThemaingoalofthisActistopreventtheexploitationofaworker.

Work permits for foreign workersAforeignnationalcomingtoIndiatoworkisrequiredtogetanemploymentvisa.Employmentvisasareusuallygrantedforoneyearorthetermoftheemployment/projectcontractandthetimeperiodcanbeextendedonceinIndia.Allforeigners(includingforeignersofIndianorigin)visitingIndiaonlong-termvisas(Student,Medical,ResearchandEmploymentVisaofmorethan180days)arerequiredtogetthemselvesregisteredwiththeForeignersRegionalRegistrationOfficer(FRRO).TheFRROregistrationprocesshasrecentlybeendigitalisedwiththeintroductionofane-FRROportalwithanaimtoprovidefaceless,cashlessandpaperlessservicetoforeignnationals.

PersonsofIndianOrigin(PIOs)whofallwithinacertaincategory,asspecified,whohavemigratedfromIndiaandacquiredcitizenshipofaforeigncountryotherthanPakistanand Bangladesh are eligible to avail the Overseas Citizen of India(OCI)statusaslongastheirhomecountriesallowdualcitizenshipinsomeformortheotherundertheirlocallaws.

Persons registered as OCI do not have the right to vote or the eligibilitytocontestforelectionstopublic/governmentoffices,etc.RegisteredOCIsshallbeentitledtothefollowingbenefits:• Multipleentry,multi-purposelife-longvisatovisitIndia• Exemptionfromreportingtopoliceauthoritiesforanylength

of stay in India• ParitywithNRIsinfinancial,economicandeducational

fields,exceptintheacquisitionofagriculturalorplantationproperties

A person registered as OCI for five years is eligible to apply for Indiancitizenshipifhe/shehasbeenresidinginIndiaforoneyearoutofthefiveyearsbeforemakingtherequest.

Social securitySocialsecurityisvalidonlyforthoseindividualswhoareemployedintheorganisedsector.TheEmployees’StateInsuranceSchemeprovidesmedicalcareandotherbenefitsforemployeesorlabourersearninglessthanUSD300amonth(INR21,000).

TheEmployees’ProvidentFundOrganisation(EPFO)isastatutorybodyundertheMinistryofLabourandEmployment,GovernmentofIndia,whichadministerssocialsecurityregulationsinIndia.Itismandatoryforallemployerswhoemploymorethan20peopletoapplythefundforthebenefitoftheirworkers.Itcoversallthepensionsandthesurvivorbenefitsintheeventofanyemployee’sdeath.Allemployeesarerequiredtocontribute12percentoftheirsalarytoEPFO.(VideFinanceAct,2018,reducedrateof8percentapplicableforwomenemployeesforfirstthreeyearsoftheiremployment).Thisisautomaticallydeductedbytheemployer.Employeesearnatax-freeinterestoncontributionsmadetothefund.EvenforeignorinternationalworkerswhoareemployedinIndiaaresubjecttothetermsofthisfund.Recently,theFinanceMinistryallowedEPFOtoinvest15percentofitscorpusinexchangetradedfunds.

Indiaalsohasasocialsecurityagreement,whichisabilateralagreementbetweentwogovernments.ThisagreementservestoprotecttheinterestsofIndiancitizensworkinginthefollowingcountries:• Australia• Austria• Belgium• CzechRepublic• Canada• Denmark• France

26 Doing Business in India

• Finland• Germany• Hungary• Japan• RepublicofKorea• Luxembourg• Netherlands• Norway• Portugal• SwissConfederation• Sweden

Sickness and pension arrangementsIt is compulsory for an employer to provide medical facilities toitsworkforcebycontributingtowardsEmployees’StateInsuranceSchemeasapplicable.

TheemployercontributestowardsaProvidentFundSchemeand a certain portion of the contribution is appropriated towardsaPensionScheme,whichprovidespensionbenefitstotheemployeesandtheirfamilymembers.Workersarealsoentitled to gratuity on completion of five years of continuous service.However,contributiontowardsaProvidentFundSchemeisnotrequiredifthenumberofemployeesinthatorganisationdoesnotexceed20.

Trade unionsThe trade unions in India are generally divided on political lines.Tradeunionshavestruggledhardtoachieveanadequatemeasureofprotectionagainstexploitation.Thetradeunionsworktoprotecttheinterestoftheworkersanddiscusskeyworkplace-relatedissueswiththemanagementsuchaswagesandbenefits.

ThesixmajorCentralTradeUnions(CTU)inIndiaaretheUnitedTradeUnionCongress(UTUC),BhartiyaMazdoorSangh(BMS),HindMazdoorSang(HMS),AllIndiaTradeUnionCongress(AITUC),CentreofIndianTradeUnions(CITU)andtheIndianNationalTradeUnionCongress(INTUC).Atradeunionwillbe recognised if it functions for more than a year after its registration.Incaseanorganisationhasmorethanoneunion,forittoberecognised,itmusthaveatleast15percentofworkersasitsmembers.

Source:MinistryofLabourandEmployment,MinistryofOverseasIndianAffairs

Doing Business in India 27

Accounting, reporting and audit requirementsSummaryInIndia,accounting,reportingandauditingrequirementsofbusiness entities are primarily governed by the regulations issuedbytheInstituteofCharteredAccountantsofIndia(ICAI),theSecuritiesandExchangeBoardofIndia(SEBI),theMinistryofCorporateAffairs(MCA)andtheCentralBoardofDirectTaxes(CBDT).

The ICAI has issued accounting standards that are applicable toallentitiesengagedincommercial,industrialorbusinessactivities.Thelegalrecognitiontothesestandardshasbeen given by the central government by notification of the standardsundertheCompaniesAct,2013(2013Act).The2013ActisanactoftheParliamentofIndiawhichgovernstheincorporationofacompany,mannerofconductingtheaffairsofacompany,responsibilitiesofitsboardofdirectorsandotherprovisionsincludingwindingup.Italsoprescribesthefinancial reporting and auditing requirements to be followed by all companies including foreign companies as defined in the 2013Act.

ThecompanieslistedonarecognisedstockexchangeinIndiaaregovernedbyrulesandregulationsissuedbytheSEBIfromtimetotime.Inaddition,thereisindustry-specificguidancerelating to financial reporting issued by the relevant authorities suchastheRBI.

Thefollowingsub-sectionsdiscusssomeofthecommonrequirements:

Records to be maintainedEverycompanyshouldfollowaccrualbasisofaccounting.The2013Actrequiresthattherecordscanalsobemaintainedinelectronic mode in the prescribed manner and are required to beretainedforaminimumperiodofeightyears.Further,thecentral government has the power to direct the company to retainthestatutorybooksforlongerperiods,incertaincases.

Preparation of financial statementsEverycompanyisrequiredtopreparebothseparateandconsolidated financial statements on an annual basis in accordancewiththeaccountingframeworkapplicabletothecompany.Further,alistedcompanyisalsorequiredtopublishquarterlyorhalfyearly,asthecasemaybe,interimfinancialinformation,subjectedtoreview,intheformatsprescribedbySEBIwithintheprescribedtimelines.

Contents of financial statementsThe2013Actlaysdowntheformatforpresentationoffinancialstatementsofcompaniesexceptinsurance,bankingandelectricity companies and other classes of companies for which formoffinancialstatementsisspecifiedbythegoverningact.Financialstatementscomprisebalancesheet,statementofprofitandloss,cashflowstatement,astatementofchangesinequity(ifapplicable)andrelatednotes.

ConsolidationThe 2013 Act mandates the preparation of consolidated financial statements if a company has one or more subsidiaries unless the following conditions complied with:• Itisawholly-ownedsubsidiaryorpartiallyownedsubsidiary

ofanothercompanyandallitsothermembers,includingthosenototherwiseentitledtovote,havebeenintimatedinwriting and they do not object to the fact that company is notpresentingconsolidatedfinancialstatements.

• Its securities are neither listed nor in the process of listing on anystockexchange,inIndiaoroutsideIndia.

• Its ultimate or any intermediary holding company files consolidated financial statements with the registrar which are in compliance with the applicable accounting standards.

Audit of financial statementsEverycompanyinIndia,irrespectiveofitssize,musthaveitsfinancial statements audited by a Chartered Accountant in practice(memberoftheICAI).Theauditsarerequiredtobeconducted in accordance with the auditing standards issued by the ICAI and notified by the central government under the 2013Act.Inaddition,theIncome-taxAct,1961mandatesaudits of taxpayers meeting certain specified thresholds to be conductedbyaCharteredAccountantinpractice(memberoftheICAI).

Auditing standardsTheStandardsofAuditingissuedbytheICAIaresubstantiallysimilar to the auditing standards issued by the International AuditingandAssuranceStandardsBoard(IAASB)oftheInternationalFederationofAccountants(IFAC).

Reporting on internal financial controlsIncaseofalistedcompany,directorsarerequiredtolaydowninternal financial controls to be followed by the company and report annually whether such internal financial controls wereadequateandoperatingeffectively.Incaseofother

28 Doing Business in India

companies,directorsarerequiredtoreportwhethersuchinternalfinancialcontrolswereadequate.

Incaseofallcompanies,auditorsarerequiredtoreportwhether internal financial controls over financial reporting in relation to separate and consolidated financial statements wereadequateinoperatingeffectively.

The2013Actdoesnotprescribeaninternalcontrolframeworkforthepurposeofreportingbyauditorsanddirectors.

Mandatory firm rotationToreducetherisksofexcessivelong-termfamiliarity,the2013Act prohibits auditor appointment for a period of more than five consecutiveyears(inthecaseofindividualasanauditor)or10consecutiveyears(inthecaseofanauditfirmasanauditor)bylistedandcertainotherclassofcompanies.Individual/auditfirm as an auditor that has completed the above prescribed period of appointment is eligible for appointment as auditors afteraperiodoffiveyearsfromthecompletionoftheabove-mentionedperiod.

Inspection of recordsThebooksofaccountsandotherrecordsareopentoinspectionbyanydirector,RegistrarofCompaniesandothergovernment authorities such as those involved with excise and salestax.

Accounting yearUnderthe2013Act,companiesarerequiredtoadoptauniformfinancialyearendingon31Marchunlessspecificallypermittedbytheauthorities.Similarly,theaccountingyearmustendon31Marcheveryyearforincome-taxpurposes.

Filing of financial statements/resultsAcompanyisrequiredtoholdanAnnualGeneralMeeting(AGM)withinsixmonthsoftheendofthefinancialyear,andfilingofthefinancialstatementswiththeRegistrarofCompaniesisrequiredwithin30daysoftheAGM.Further,listedcompaniesalsoneedtofiletheaudited(orreviewed,asapplicable)financialresultswiththestockexchangewithin60daysincaseofannualperiodsand45daysincaseofquarterlyperiodsexceptlastquarter.

Language in which business records are required to be maintainedThereisnoprescribedlanguageformaintenanceofbooksandbusinessrecords.ItcanbemaintainedinanyIndianlanguage.CompaniesgenerallymaintaintheiraccountsinEnglish.

Maintenanceofaccountingrecordsinaforeigncurrencyandpresentationoffinancialstatements.

Theaccountingrecords,whetherelectronicormanual,havetobekeptinIndiancurrency.However,theforeigncurrencyamountsmayalsobedisclosed.

Accounting frameworkThe2013Actprescribestwoaccountingframeworks:IndianAccountingStandards(IndAS),whicharebasedonInternationalFinancialReportingStandards(IFRS)asissuedbytheInternationalAccountingStandardsBoardwithcertaincarve-outs,mandatoryforcertainclassofcompanies,andstandardsthataresubstantiallydifferentfromIndAS.Companies are required to determine the relevant accounting frameworkaspertheapplicablelaw.Further,companymayirrevocablyopttoprepareIndAScompliantfinancialstatementsfortheaccountingperiodsbeginningonorafter01April2015.

TheMCAhasnotified39IndAS,whicharebasedonIFRSwithcertaincarve-outs.IndASareapplicabletocompaniesinthemannerspecifiedintheroadmapissuedbytheMCA.ThefollowingistheroadmapformandatoryadoptionofIndASbyallcompaniesotherthaninsurancecompanies,bankingcompaniesandNBFCs:• TheapplicabilityofIndASismademandatoryunderPhase

IforcompanieswhosenetworthisINR5bnormoreforaccountingperiodsbeginningonorafter01April2016,withcomparativesfortheperiodending31March2016orthereafter.

• UnderPhaseII,IndASaremademandatoryforaccountingperiodsbeginningonorafter01April2017,withcomparativesbeginningforperiodending31March2017orthereafterforcompanieshavingnetworthmorethanINR2.5bn,butlessthanINR5bn.

• UnderbothPhaseIandPhaseII,IndASwouldbemandatorily applicable to companies whose equity and debt securities are listed or are in the process of listing on anystockexchangeinIndiaoroutsideIndia,aswellastotheholding,subsidiary,jointventureorassociatecompaniesofthecompaniescoveredabove.

Separateroadmapshavebeenissuedforbanks,insurancecompaniesandNBFCstotransitiontoIndAS;theearliestperiodisaccountingperiodbeginningonorafter01April2018.

ROC filingTheMCArequiresfilingoffinancialstatementswiththe

Doing Business in India 29

RegistrarofCompanies,usingtheeXtensibleBusinessReportingLanguage(XBRL)taxonomy,forthefollowingcompanies:• all companies listed in India and their Indian subsidiaries;• allcompanieshavingapaidupcapitalofINR50mnand

above; and• allcompanieshavingaturnoverofINR1bnandabove.

All the remaining companies are required to fill the prescribed forms.

TheXBRLdocumentsoffinancialstatementsarerequiredtobecertifiedbyaCharteredAccountantorCompanySecretaryorCostAccountantinwholetimepractice.

Income Computation and Disclosure Standards (ICDS)In view of the significant developments in convergence with IFRS,ICDSwerenotifiedundertheIncome-taxAct,whichare,inprinciple,closertotheexistingIndianGAAPthantheIFRS-basedIndAS.Thesestandardsareeffectivefromthecurrentfinancialyear(2016-17)itselfandarerequiredtobefollowedby all taxpayers following the mercantile system of accounting for the purpose of computation of income from business and ‘otherincome’chargeabletotax.

30 Doing Business in India

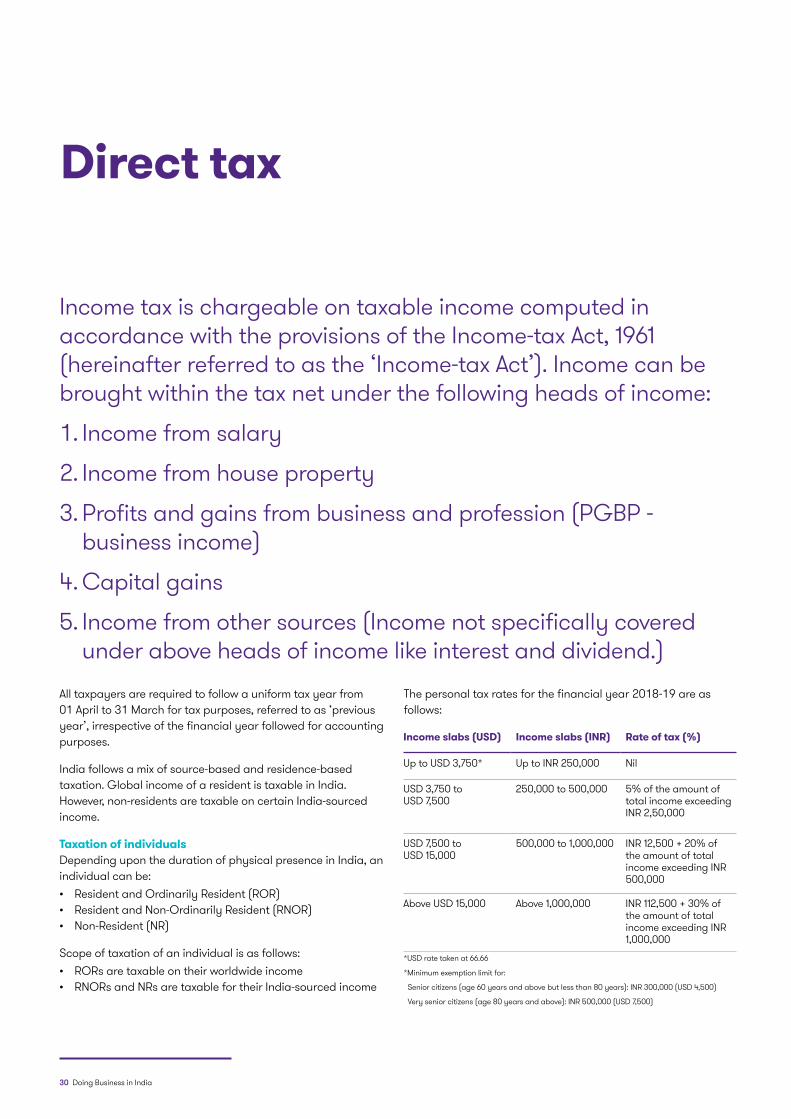

Direct tax

Income tax is chargeable on taxable income computed in accordancewiththeprovisionsoftheIncome-taxAct,1961(hereinafterreferredtoasthe‘Income-taxAct’).Incomecanbebrought within the tax net under the following heads of income:

1.Income from salary

2.Income from house property

3.Profitsandgainsfrombusinessandprofession(PGBP-businessincome)

4.Capital gains

5.Incomefromothersources(Incomenotspecificallycoveredunderaboveheadsofincomelikeinterestanddividend.)

All taxpayers are required to follow a uniform tax year from 01Aprilto31Marchfortaxpurposes,referredtoas‘previousyear’,irrespectiveofthefinancialyearfollowedforaccountingpurposes.

Indiafollowsamixofsource-basedandresidence-basedtaxation.GlobalincomeofaresidentistaxableinIndia.However,non-residentsaretaxableoncertainIndia-sourcedincome.

Taxation of individualsDependinguponthedurationofphysicalpresenceinIndia,anindividual can be:• ResidentandOrdinarilyResident(ROR)• ResidentandNon-OrdinarilyResident(RNOR)• Non-Resident(NR)

Scopeoftaxationofanindividualisasfollows:• RORsaretaxableontheirworldwideincome• RNORsandNRsaretaxablefortheirIndia-sourcedincome

Thepersonaltaxratesforthefinancialyear2018-19areasfollows:

Income slabs (USD) Income slabs (INR) Rate of tax (%)

UptoUSD3,750* UptoINR250,000 Nil

USD3,750to USD7,500

250,000to500,000 5%oftheamountoftotal income exceeding INR2,50,000

USD7,500to USD15,000

500,000to1,000,000 INR12,500+20%ofthe amount of total incomeexceedingINR500,000

AboveUSD15,000 Above1,000,000 INR112,500+30%ofthe amount of total incomeexceedingINR1,000,000

*Minimumexemptionlimitfor:

Seniorcitizens(age60yearsandabovebutlessthan80years):INR300,000(USD4,500)

Veryseniorcitizens(age80yearsandabove):INR500,000(USD7,500)

*USDratetakenat66.66

Doing Business in India 31

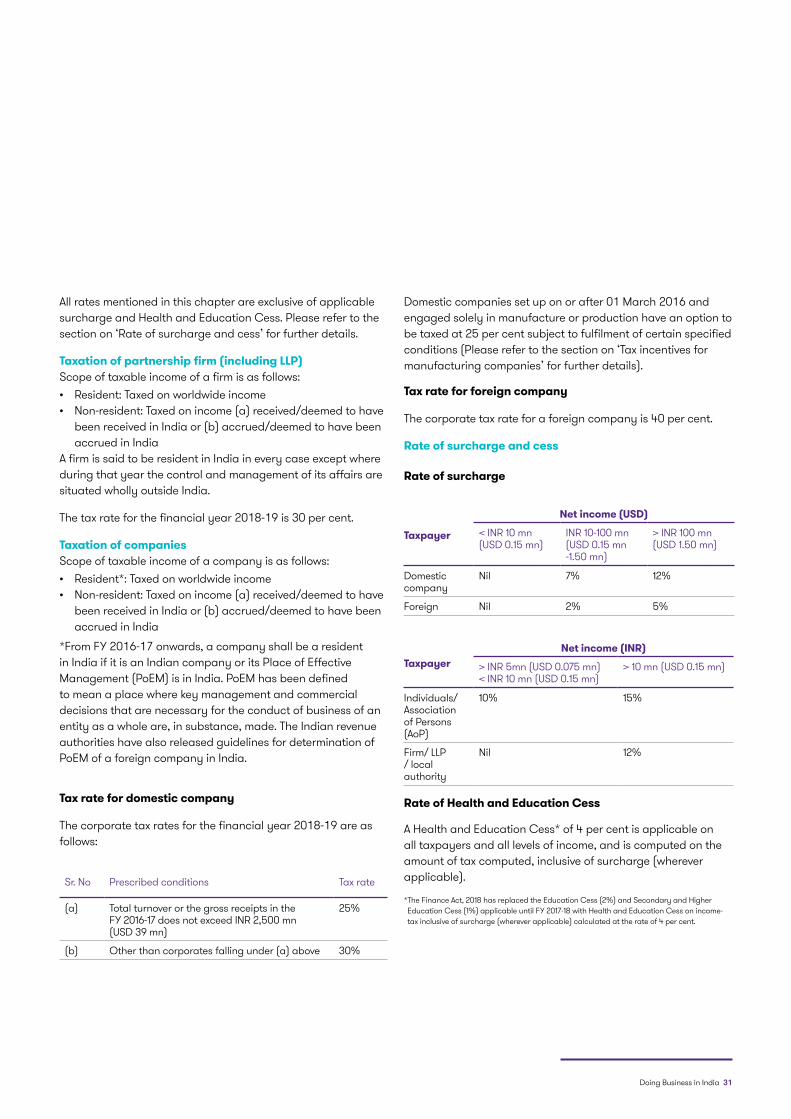

All rates mentioned in this chapter are exclusive of applicable surchargeandHealthandEducationCess.Pleaserefertothesectionon‘Rateofsurchargeandcess’forfurtherdetails.

Taxation of partnership firm (including LLP)Scopeoftaxableincomeofafirmisasfollows:• Resident:Taxedonworldwideincome• Non-resident:Taxedonincome(a)received/deemedtohave

beenreceivedinIndiaor(b)accrued/deemedtohavebeenaccrued in India

A firm is said to be resident in India in every case except where during that year the control and management of its affairs are situatedwhollyoutsideIndia.

Thetaxrateforthefinancialyear2018-19is30percent.

Taxation of companiesScopeoftaxableincomeofacompanyisasfollows:• Resident*:Taxedonworldwideincome• Non-resident:Taxedonincome(a)received/deemedtohave

beenreceivedinIndiaor(b)accrued/deemedtohavebeenaccrued in India

*FromFY2016-17onwards,acompanyshallbearesidentinIndiaifitisanIndiancompanyoritsPlaceofEffectiveManagement(PoEM)isinIndia.PoEMhasbeendefinedtomeanaplacewherekeymanagementandcommercialdecisions that are necessary for the conduct of business of an entityasawholeare,insubstance,made.TheIndianrevenueauthorities have also released guidelines for determination of PoEMofaforeigncompanyinIndia.

Tax rate for domestic company

Thecorporatetaxratesforthefinancialyear2018-19areasfollows:

Sr.No Prescribed conditions Tax rate

(a) Total turnover or the gross receipts in the FY2016-17doesnotexceedINR2,500mn (USD39mn)

25%

(b) Otherthancorporatesfallingunder(a)above 30%

Domesticcompaniessetuponorafter01March2016andengaged solely in manufacture or production have an option to betaxedat25percentsubjecttofulfilmentofcertainspecifiedconditions(Pleaserefertothesectionon‘Taxincentivesformanufacturingcompanies’forfurtherdetails).

Tax rate for foreign company

Thecorporatetaxrateforaforeigncompanyis40percent.

Rate of surcharge and cess

Rate of surcharge

Taxpayer

Net income (USD)

<INR10mn (USD0.15mn)

INR10-100mn(USD0.15mn-1.50mn)

>INR100mn(USD1.50mn)

Domestic company

Nil 7% 12%

Foreign Nil 2% 5%

TaxpayerNet income (INR)

>INR5mn(USD0.075mn) <INR10mn(USD0.15mn)

>10mn(USD0.15mn)

Individuals/Association of Persons (AoP)

10% 15%

Firm/LLP/localauthority

Nil 12%

Rate of Health and Education Cess

AHealthandEducationCess*of4percentisapplicableonalltaxpayersandalllevelsofincome,andiscomputedontheamountoftaxcomputed,inclusiveofsurcharge(whereverapplicable).

*TheFinanceAct,2018hasreplacedtheEducationCess(2%)andSecondaryandHigherEducationCess(1%)applicableuntilFY2017-18withHealthandEducationCessonincome-taxinclusiveofsurcharge(whereverapplicable)calculatedattherateof4percent.

32 Doing Business in India

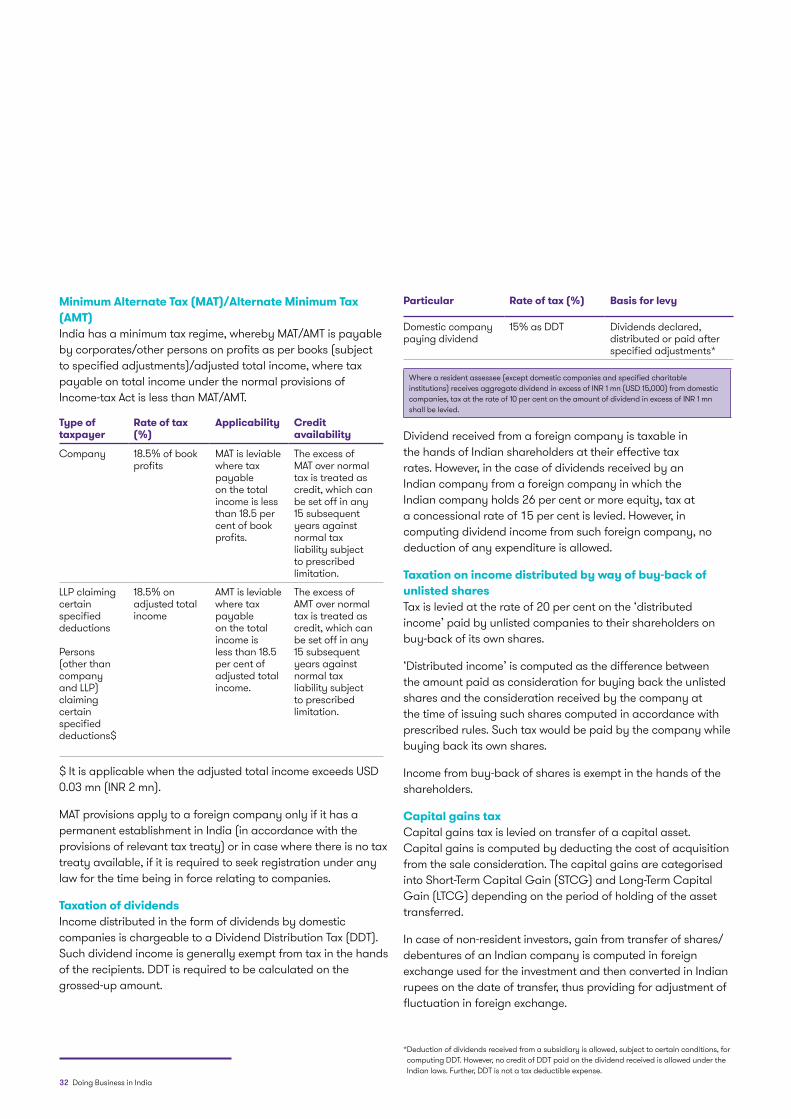

Minimum Alternate Tax (MAT)/Alternate Minimum Tax (AMT)Indiahasaminimumtaxregime,wherebyMAT/AMTispayablebycorporates/otherpersonsonprofitsasperbooks(subjecttospecifiedadjustments)/adjustedtotalincome,wheretaxpayable on total income under the normal provisions of Income-taxActislessthanMAT/AMT.

Type of taxpayer

Rate of tax (%)

Applicability Credit availability

Company 18.5%ofbookprofits

MATisleviablewhere tax payable on the total income is less than18.5percentofbookprofits.

The excess of MATovernormaltax is treated as credit,whichcanbesetoffinany15subsequentyears against normal tax liability subject to prescribed limitation.

LLP claiming certain specifieddeductions

Persons (otherthancompany andLLP)claiming certain specifieddeductions$

18.5%onadjusted total income

AMTisleviablewhere tax payable on the total income is lessthan18.5per cent of adjusted total income.

The excess of AMTovernormaltax is treated as credit,whichcanbesetoffinany15subsequentyears against normal tax liability subject to prescribed limitation.

$ItisapplicablewhentheadjustedtotalincomeexceedsUSD0.03mn(INR2mn).

MATprovisionsapplytoaforeigncompanyonlyifithasapermanentestablishmentinIndia(inaccordancewiththeprovisionsofrelevanttaxtreaty)orincasewherethereisnotaxtreatyavailable,ifitisrequiredtoseekregistrationunderanylawforthetimebeinginforcerelatingtocompanies.

Taxation of dividendsIncome distributed in the form of dividends by domestic companiesischargeabletoaDividendDistributionTax(DDT).Suchdividendincomeisgenerallyexemptfromtaxinthehandsoftherecipients.DDTisrequiredtobecalculatedonthegrossed-upamount.

*Deductionofdividendsreceivedfromasubsidiaryisallowed,subjecttocertainconditions,forcomputingDDT.However,nocreditofDDTpaidonthedividendreceivedisallowedundertheIndianlaws.Further,DDTisnotataxdeductibleexpense.

Particular Rate of tax (%) Basis for levy

Domestic company paying dividend

15%asDDT Dividendsdeclared,distributed or paid after specifiedadjustments*

Wherearesidentassessee(exceptdomesticcompaniesandspecifiedcharitableinstitutions)receivesaggregatedividendinexcessofINR1mn(USD15,000)fromdomesticcompanies,taxattherateof10percentontheamountofdividendinexcessofINR1mnshallbelevied.

Dividend received from a foreign company is taxable in the hands of Indian shareholders at their effective tax rates.However,inthecaseofdividendsreceivedbyanIndian company from a foreign company in which the Indiancompanyholds26percentormoreequity,taxataconcessionalrateof15percentislevied.However,incomputingdividendincomefromsuchforeigncompany,nodeductionofanyexpenditureisallowed.

Taxation on income distributed by way of buy-back of unlisted sharesTaxisleviedattherateof20percentonthe‘distributedincome’ paid by unlisted companies to their shareholders on buy-backofitsownshares.

‘Distributedincome’iscomputedasthedifferencebetweentheamountpaidasconsiderationforbuyingbacktheunlistedshares and the consideration received by the company at the time of issuing such shares computed in accordance with prescribedrules.Suchtaxwouldbepaidbythecompanywhilebuyingbackitsownshares.

Incomefrombuy-backofsharesisexemptinthehandsoftheshareholders.

Capital gains taxCapitalgainstaxisleviedontransferofacapitalasset.Capital gains is computed by deducting the cost of acquisition fromthesaleconsideration.ThecapitalgainsarecategorisedintoShort-TermCapitalGain(STCG)andLong-TermCapitalGain(LTCG)dependingontheperiodofholdingoftheassettransferred.

Incaseofnon-residentinvestors,gainfromtransferofshares/debentures of an Indian company is computed in foreign exchange used for the investment and then converted in Indian rupeesonthedateoftransfer,thusprovidingforadjustmentoffluctuationinforeignexchange.

Doing Business in India 33

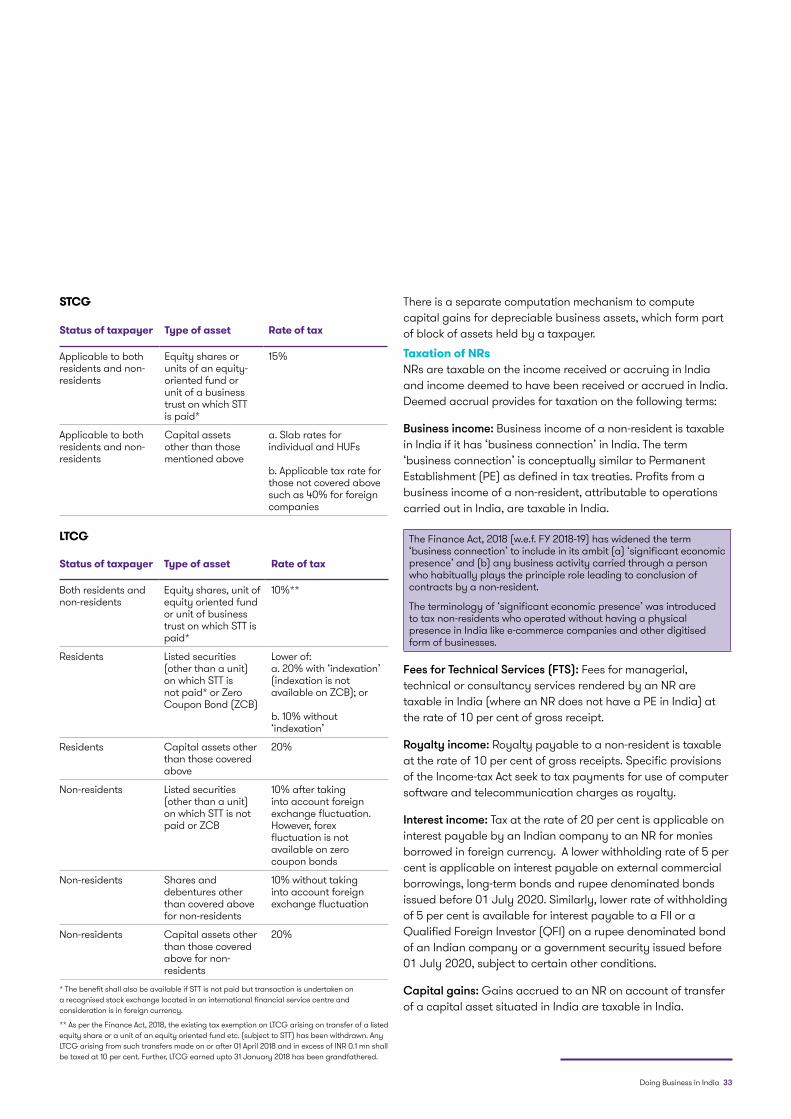

STCG

Status of taxpayer Type of asset Rate of tax

Applicable to both residentsandnon-residents

Equitysharesorunitsofanequity-oriented fund or unit of a business trustonwhichSTTispaid*

15%

Applicable to both residentsandnon-residents

Capital assets other than those mentioned above

a.SlabratesforindividualandHUFs b.Applicabletaxrateforthose not covered above suchas40%forforeigncompanies

LTCG

Status of taxpayer Type of asset Rate of tax

Both residents and non-residents

Equityshares,unitofequity oriented fund or unit of business trustonwhichSTTispaid*

10%**

Residents Listed securities (otherthanaunit)onwhichSTTisnotpaid*orZeroCouponBond(ZCB)

Lower of: a.20%with‘indexation’(indexationisnotavailableonZCB);or b.10%without‘indexation’

Residents Capital assets other than those covered above

20%

Non-residents Listed securities (otherthanaunit)onwhichSTTisnotpaidorZCB

10%aftertakinginto account foreign exchangefluctuation.However,forexfluctuationisnotavailable on zero coupon bonds

Non-residents Sharesanddebentures other than covered above fornon-residents

10%withouttakinginto account foreign exchangefluctuation

Non-residents Capital assets other than those covered abovefornon-residents

20%

*ThebenefitshallalsobeavailableifSTTisnotpaidbuttransactionisundertakenonarecognisedstockexchangelocatedinaninternationalfinancialservicecentreandconsiderationisinforeigncurrency.

**AspertheFinanceAct,2018,theexistingtaxexemptiononLTCGarisingontransferofalistedequityshareoraunitofanequityorientedfundetc.(subjecttoSTT)hasbeenwithdrawn.AnyLTCGarisingfromsuchtransfersmadeonorafter01April2018andinexcessofINR0.1mnshallbetaxedat10percent.Further,LTCGearnedupto31January2018hasbeengrandfathered.

There is a separate computation mechanism to compute capitalgainsfordepreciablebusinessassets,whichformpartofblockofassetsheldbyataxpayer.

Taxation of NRsNRsaretaxableontheincomereceivedoraccruinginIndiaandincomedeemedtohavebeenreceivedoraccruedinIndia.Deemed accrual provides for taxation on the following terms:

Business income: Businessincomeofanon-residentistaxableinIndiaifithas‘businessconnection’inIndia.Theterm‘businessconnection’isconceptuallysimilartoPermanentEstablishment(PE)asdefinedintaxtreaties.Profitsfromabusinessincomeofanon-resident,attributabletooperationscarriedoutinIndia,aretaxableinIndia.

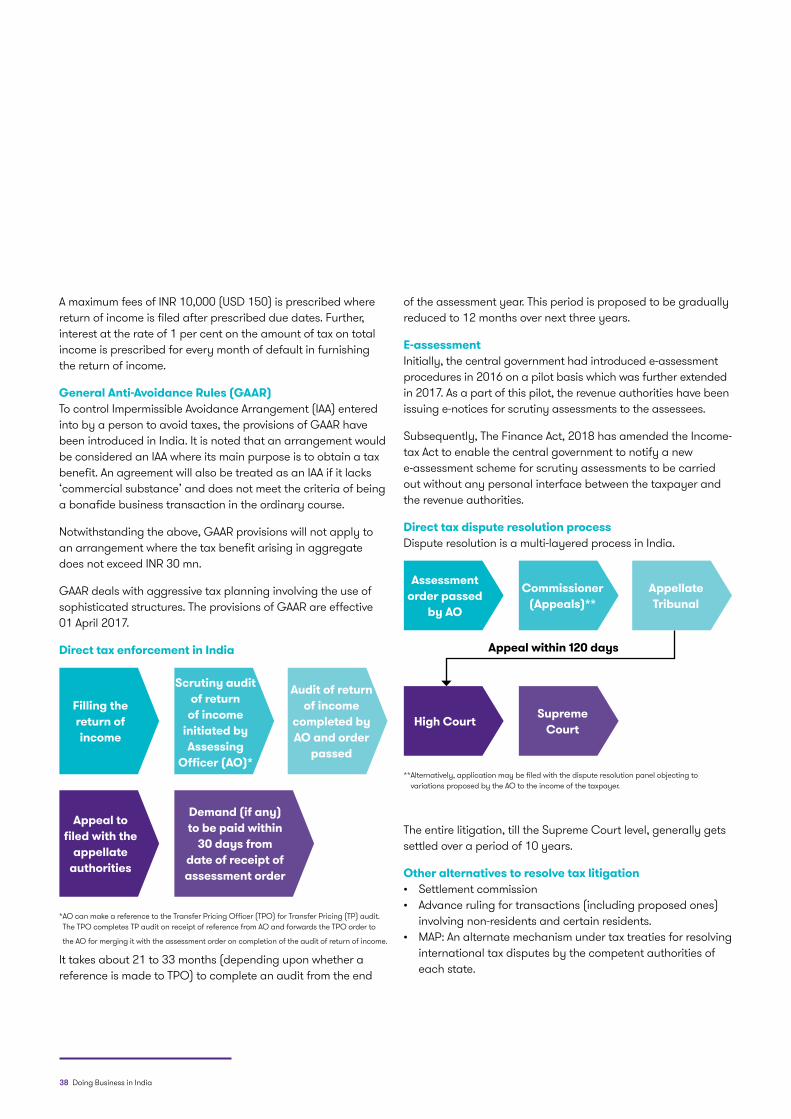

TheFinanceAct,2018(w.e.f.FY2018-19)haswidenedtheterm‘businessconnection’toincludeinitsambit(a)‘significanteconomicpresence’and(b)anybusinessactivitycarriedthroughapersonwho habitually plays the principle role leading to conclusion of contractsbyanon-resident.