Embed Size (px)

Citation preview

WORD COUNTNumber of Pages: 23

Number of Words: 4500

Word count is exclusive of the followings:

Cover Page

Content Page

Citation and Referencing

Conclusion

Gantt Chant

Tables

Graphs

Titles/Headings

Accounting 2 Page 1

TABLE OF CONTENTS

3.1: THE PURPOSE AND NATURE OF THE BUDGETING PROCESS................3

3.2: SELECT APPROPRIATE BUDGETING METHODS..........................................5

3.3: PREPARE BUDGETS ACCORDING TO THE CHOSEN BUDGETING

METHOD............................................................................................................................6

3.4: Glentruan Furniture Ltd CASH BUDGET FOR 2012............................................16

4.1: CACULATE VARIANCES, IDENTIFY POSSIBILE CASUE AND

RECOMMEND CORRECTIVE ACTION.....................................................................18

4.2 Reconciliation of Budgeted and Actual Profit:............................................................19

4.3 RECOMMENDATION FOR BUISNESS RELATIONSHIP.....................................22

4.0: REFERENCES........................................................................................................23

Accounting 2 Page 2

3.1: THE PURPOSE AND NATURE OF THE BUDGETING PROCESS

Nowadays, budgeting is considered as the preparation for any company to forecast the

costs, plan for an organisation’s outgoing exenses, revenues that the organisation can

list the objectives and strategies for a specific time period. A good Preparation of

budgeting can give GT Furniture many profits to ensure the achievement of the

oranisation’s ojectives; which will be explained in the informations below:

3.1.1 To aid the planning of actual operations

In GT Furniture, budgeting helps them to analyse the problems then the manager can

find the way to develop and solve it. In general, the costs and the revenue always

change so GT Furniture can plan; track and control the spending to forces management

to look ahead and reach the objectives

3.1.2 To communicate plans to various responsibility centre managers

The communication plays an important role of distribution in GT Furniture. Preparing a

budgeting to analyse and develop the business can help employees and managers

clearly know about their responsibilities in work. Furthermore, it also ensure that each

person affected by the plans then they can be supposed to be doing; GT Furniture’s

employee can communicate with their managers in correctly and receive the feedback

from managers as supporting.

3.1.3 To co-ordinate the activities of the organisation

After leading the responsibilities, objectives bugedting also create the co-ordination

between managers and subordinates or between departments in GT Furniture. These

actions can be made to ensure maximum tintergration of effort towards common goals

(Learning Media 2010)

For example, the branch of GT Furniture will calculate the number of product in the store

then budget to analyse the production requirements to ensure the objective achievement

and minise the risk. Then, the budgeting will be sent to sale centre of GT Furniture to

define product needed such as table, wood chair. Looking on the budgeting, the

manager can analyse the customer demand to take the right decisions in producing

goods.

3.1.4 To control activities

The uniform activities are very important in the organisation that helps manager and

employee can control the work and easy to solve the problems occur. Having a

budgeting it means they can list exactly the work for all department in GT Furniture such

as the objective in sale department in May is 1000 Wood tables and chairs. The

Accounting 2 Page 3

manager can control activities relate to budgeting of department to ensure they can

achieve the goals in business.

3.1.5 To evaluate the performance of managers

The managers also relate to the income revenue, the costs or payment after a business

quarter to analyse the effective of plan or the current budgeting then they can change

and make the decisions to improve and develop the sale for GT Furniture. Furthermore,

budgeting can help managers to forecast the risk; which can occur in their business and

evaluate the situation of the company.

Besides, to control and provide a suitable plan for organisation the manager and GT

Furniture must also choose right budget methods to have good result in their business.

3.1.6 Incremental Budgeting

Nowadays, Incremental Budgeting is quite common to use in many organisation. This

budgeting method is related to take the figures in last year about inflation, or planned

increases in sales price and costs. The budget is prepared by taking the current period's

budget or actual performance as a base, with incremental amounts then being added for

the new budget period. Therefore in a few particular cases, the manager can have a

common misapprehension about Incremental budgeting that the big disavantages in this

budget is does not to allow for inflation but sometimes it has.

3.1.7 Zero Base Budgeting

In this method the manager will identify the activities to analyse the activity expenses,

the purpose, classify different methods to achieve the objectives, establish the

performance measures for the activity and evaluate, asseses the activity at different

levels. After that, the manager also sees and analyse the process in detail base on the

figures calculated by started from zero base at period year.

Accounting 2 Page 4

3.2: SELECT APPROPRIATE BUDGETING METHODS

To having right plans and developing the business and minimise the risk calculation in

accounting the organisation must choose the right budget methods for manager can

control any activity that has a financial impact. There are 2 budgeting methods; which

will be explained in the next paragraphs:

3.2.1 Incremental Budgeting:

It is a method to identify the targets in estimates based on the actual operating results of

the previous period and acjested for growth rate and expected inflation rate. Thus, this

method is clear, easy to understand and easy to use, built relatively stable, enabling,

sustainable basis for the managerment of the operating units in all activities.

3.2.2 Zero Base Budgeting

Zero base budgeting is a budgeting method that helps manager to prepare estimates of

their expenses for a period time. Nitto Jokaso can use this method to minise the risks

during the producing in manufacture. The manager or director can see in figures at

activities; which started from a buget base of zero to analyse the budget cycle then have

a right view in all expenses and justify them to save and reduce wasting expense to

minimise it. However, if the unit will use this method to assess in detail the cost effective

operation of the unit, ending the imbalance between workload and implementation costs,

and help unit selection is the most optimal way to achieve its objectives.

The benefits of this budgeting are organisation can remove inefficient or obsolete

operations because the calculation will be started in the end of the period bugeting.

Furthermore, the manager will clearly analyse budgeting to reduce the costs. Besides, it

provides a budgeting and planning tool for management to control the money flow which

be prepared and pay for the material and other variable costs. Then, it can increase

motivations for employee to set the target.

Accounting 2 Page 5

3.3: PREPARE BUDGETS ACCORDING TO THE CHOSEN BUDGETING METHOD

In the recent year, the company developed new product line using of latest technology

are AP and SG. The manager must ensure to prepare the budgets for control and

forecast the activity base on producing goods and minimise the risk in manufacture to

have best profits.

As the managers know, they have to prepare and calculate the budget in sale,

production, direct materials usage, direct material and purchase, direct labor, factory

overhead, selling and Amin, master budget and Cash Flow to show the director and

explain how the company can run the process effectively. The budget will be shown in

next information belows:

3.3.1 The Sales Budget of company

The sale budget will be set to forecast the number of product will be sold in the period

time. For example, Nitto Jokaso often recieve orders from Japan to procduce Jo Kenso.

The manager must care about number of Jo Kenso in warehouse and manage them by

calculating the number of goods will be produced each day. The order will be transfered

in 7 – 10 days so the director must ensure and have right budget at a right time to supply

it for their customer.

Base on the case study, we can calculate the revenue of each model for the year 2013:

Sales revenues = Sales volume (unit) x Sales prices ($/unit)

Sales revenue Model AP = 8,500 x 400 = 3,400,000

Sales revenue Model SG = 1,600 x 560 = 896,000

We can calculate the total revenues for two models:

Total revenues = sales revenue Model AP + sales revenue Model SG

= 3,400,000 + 896,000 = 4,296,0000

After calculating the sale budget is shown by the table below:

Details Model AP Model SG Total

Sales volume (unit) 8,500 1,600

Sales prices ($/unit) £400 £560

Sales revenue ($) £3,400,000 £896,000 £4,296,0003.3.2 The Production Budget

Accounting 2 Page 6

Production budget help a company to forecast how much the product will be produced to

supply the customer and then it relates to other budget such as labor budget, material

budget and expense budget; which impact on the producing goods in Nitto Jokaso. For

example, the company will produce 100-150 Jo Kenso to supply the order from Japan so

the manager must know exactly the quantity of product will be made in the manufacture

to ensure supply enough goods for customer in the right time.

As the manager can see in the calculation, the production budget will be calculated by

Budgeted production in units = Forecast sales in units + Ending inventory required in units – Beginning inventory in units=> Budgeted production in units Model AP = 8,500 + 1,870 – 170 = 10.200

=> Budgeted production in units Model SG = 1,600 + 90 – 85 = 1,650

The Production Budget of Nitto Jokaso:

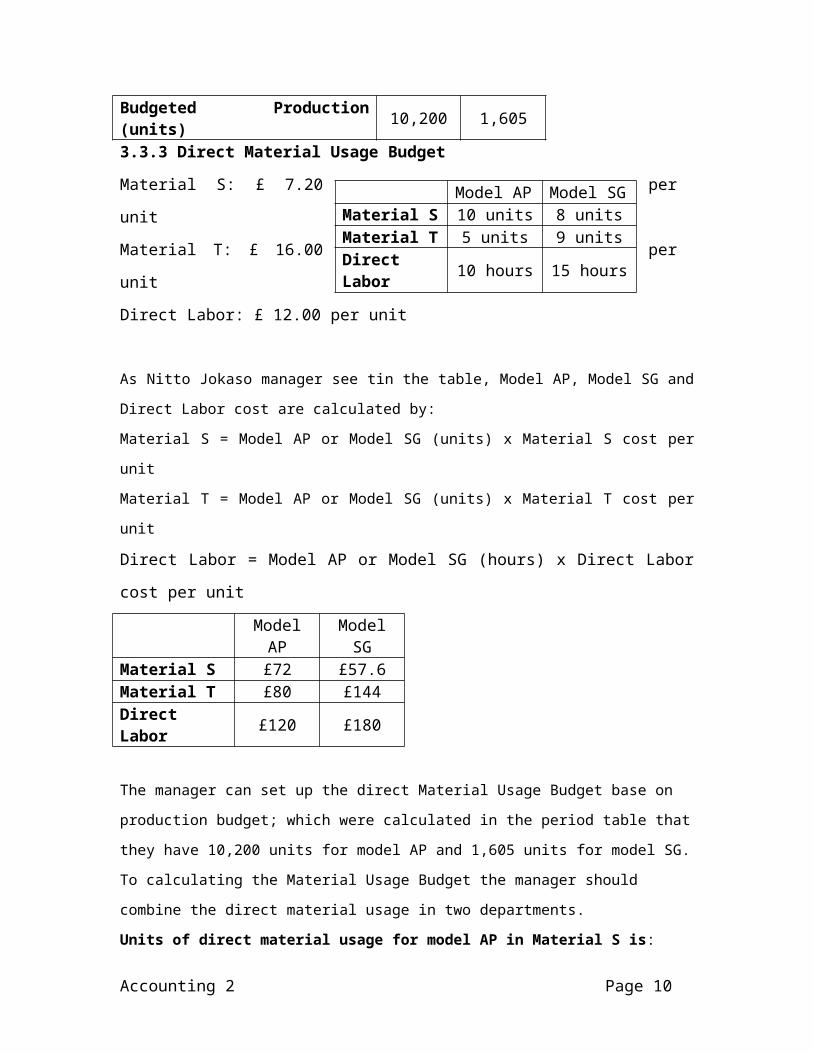

Model AP Model SGForecast Sales (units) 8,500 1,600Ending Inventory Required (units) 1,870 90Beginning Inventory (units) 170 85Budgeted Production (units) 10,200 1,6053.3.3 Direct Material Usage Budget

Material S: £ 7.20 per unit

Material T: £ 16.00 per unit

Direct Labor: £ 12.00 per unit

As Nitto Jokaso manager see tin the table, Model AP, Model SG and Direct Labor cost

are calculated by:

Material S = Model AP or Model SG (units) x Material S cost per unit

Material T = Model AP or Model SG (units) x Material T cost per unit

Direct Labor = Model AP or Model SG (hours) x Direct Labor cost per unit

Model AP Model SGMaterial S £72 £57.6Material T £80 £144Direct Labor £120 £180

The manager can set up the direct Material Usage Budget base on production budget;

which were calculated in the period table that they have 10,200 units for model AP and

Accounting 2 Page 7

Model AP Model SG Material S 10 units 8 unitsMaterial T 5 units 9 unitsDirect Labor 10 hours 15 hours

1,605 units for model SG. To calculating the Material Usage Budget the manager should

combine the direct material usage in two departments.

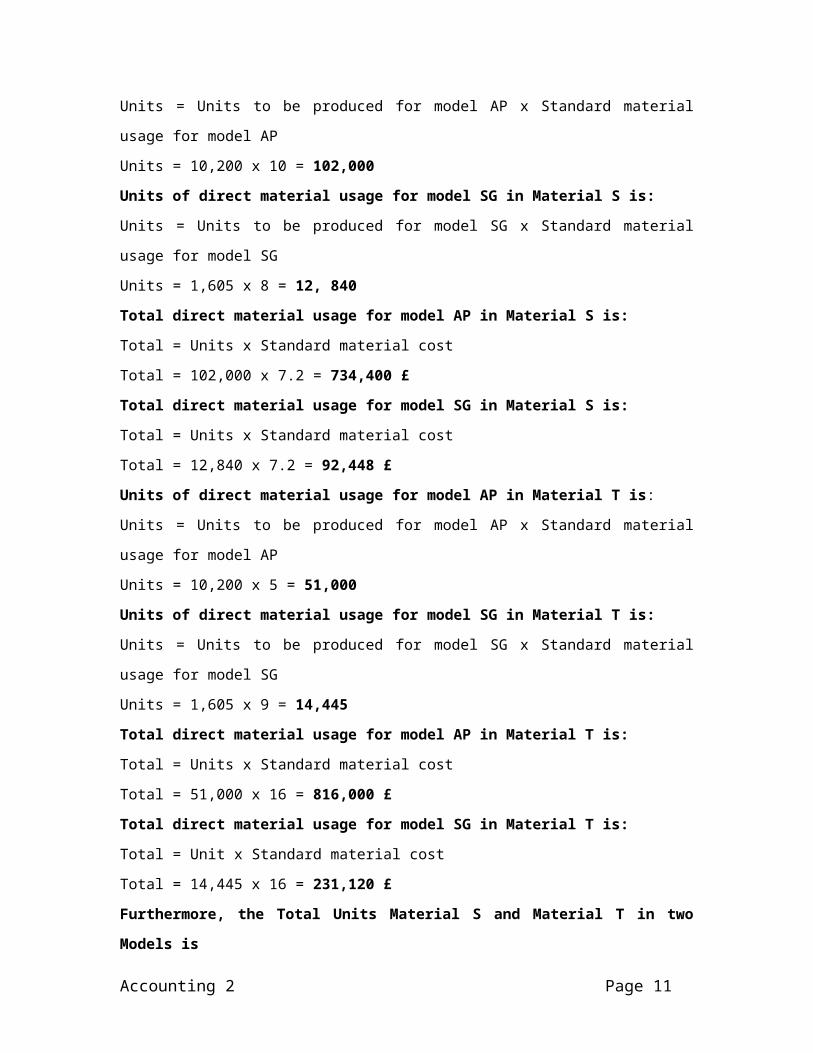

Units of direct material usage for model AP in Material S is:

Units = Units to be produced for model AP x Standard material usage for model AP

Units = 10,200 x 10 = 102,000Units of direct material usage for model SG in Material S is:Units = Units to be produced for model SG x Standard material usage for model SG

Units = 1,605 x 8 = 12, 840Total direct material usage for model AP in Material S is:Total = Units x Standard material cost

Total = 102,000 x 7.2 = 734,400 £Total direct material usage for model SG in Material S is:Total = Units x Standard material cost

Total = 12,840 x 7.2 = 92,448 £Units of direct material usage for model AP in Material T is:

Units = Units to be produced for model AP x Standard material usage for model AP

Units = 10,200 x 5 = 51,000Units of direct material usage for model SG in Material T is:Units = Units to be produced for model SG x Standard material usage for model SG

Units = 1,605 x 9 = 14,445Total direct material usage for model AP in Material T is:Total = Units x Standard material cost

Total = 51,000 x 16 = 816,000 £Total direct material usage for model SG in Material T is:Total = Unit x Standard material cost

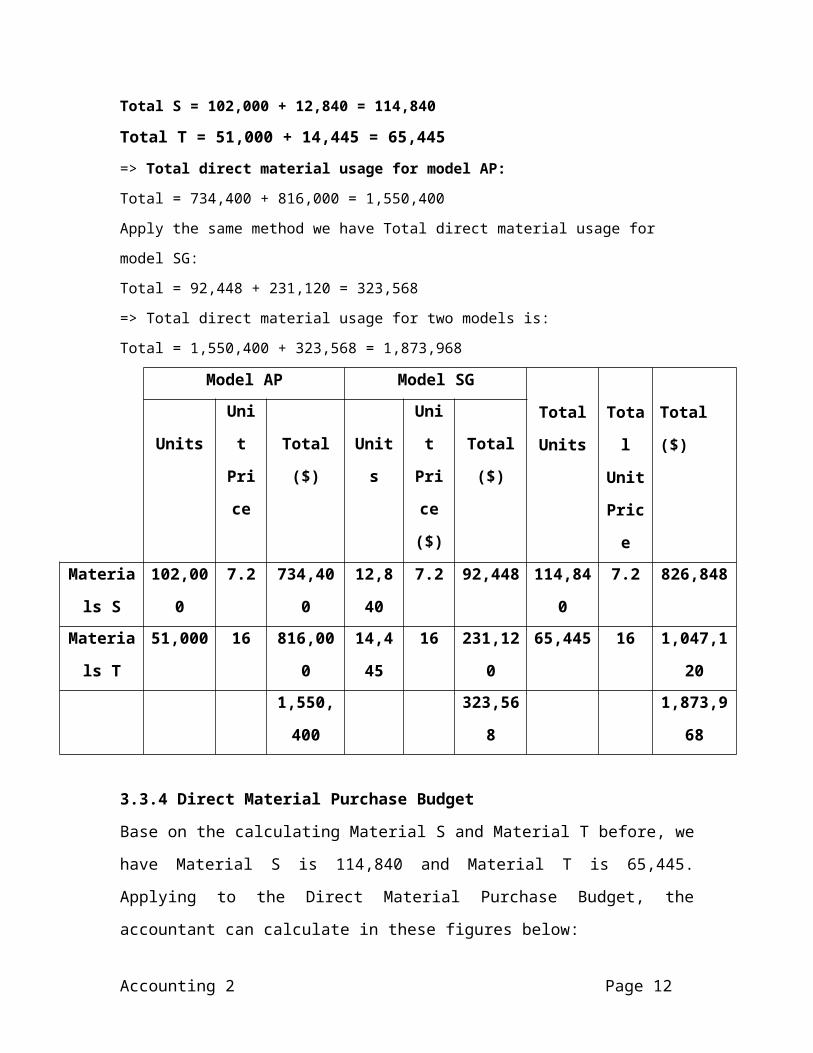

Total = 14,445 x 16 = 231,120 £Furthermore, the Total Units Material S and Material T in two Models isTotal S = 102,000 + 12,840 = 114,840

Total T = 51,000 + 14,445 = 65,445

=> Total direct material usage for model AP:Total = 734,400 + 816,000 = 1,550,400

Apply the same method we have Total direct material usage for model SG:

Total = 92,448 + 231,120 = 323,568

=> Total direct material usage for two models is:

Accounting 2 Page 8

Total = 1,550,400 + 323,568 = 1,873,968

Model AP Model SG

Total

Units

Total

Unit

Price

Total ($)

Units

Unit

Price Total ($) Units

Unit

Price

($)

Total

($)

Materials

S

102,000 7.2 734,400 12,840 7.2 92,448 114,840 7.2 826,848

Materials

T

51,000 16 816,000 14,445 16 231,120 65,445 16 1,047,120

1,550,400 323,568 1,873,968

3.3.4 Direct Material Purchase Budget

Base on the calculating Material S and Material T before, we have Material S is 114,840

and Material T is 65,445. Applying to the Direct Material Purchase Budget, the

accountant can calculate in these figures below:

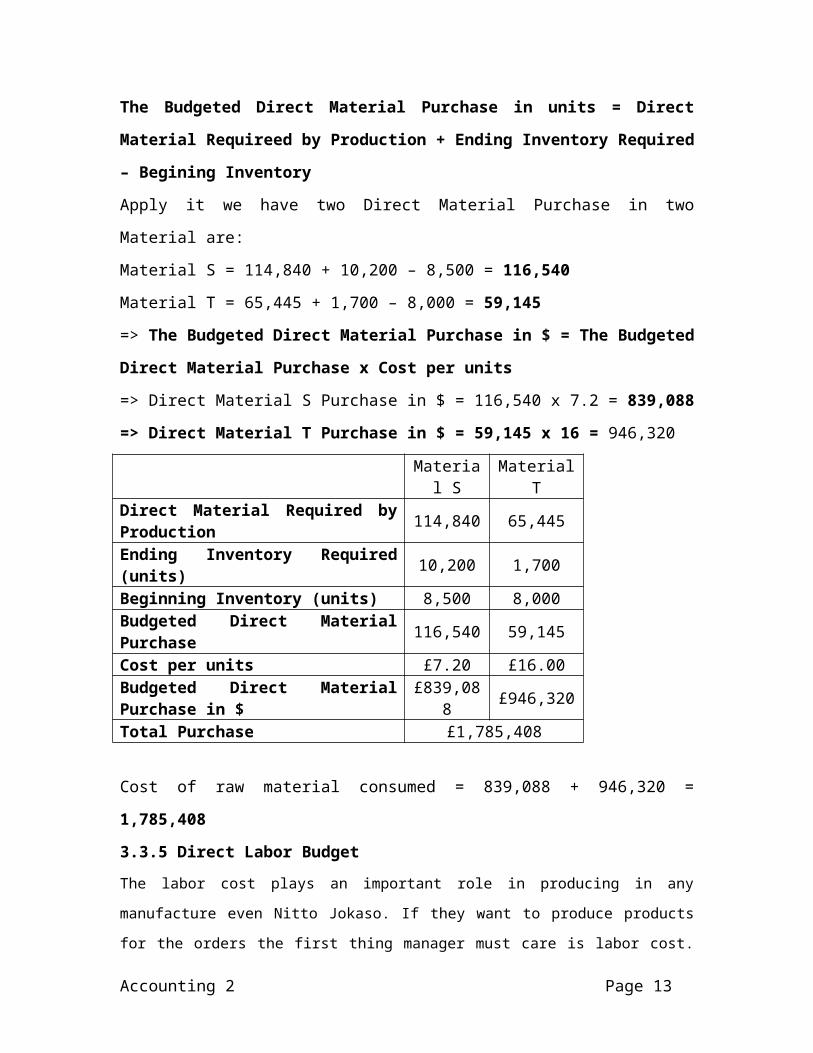

The Budgeted Direct Material Purchase in units = Direct Material Requireed by

Production + Ending Inventory Required – Begining Inventory

Apply it we have two Direct Material Purchase in two Material are:

Material S = 114,840 + 10,200 – 8,500 = 116,540

Material T = 65,445 + 1,700 – 8,000 = 59,145

=> The Budgeted Direct Material Purchase in $ = The Budgeted Direct Material

Purchase x Cost per units

=> Direct Material S Purchase in $ = 116,540 x 7.2 = 839,088

=> Direct Material T Purchase in $ = 59,145 x 16 = 946,320

Material S Material TDirect Material Required by Production 114,840 65,445Ending Inventory Required (units) 10,200 1,700Beginning Inventory (units) 8,500 8,000Budgeted Direct Material Purchase 116,540 59,145Cost per units £7.20 £16.00Budgeted Direct Material Purchase in $ £839,088 £946,320Total Purchase £1,785,408

Accounting 2 Page 9

Cost of raw material consumed = 839,088 + 946,320 = 1,785,408

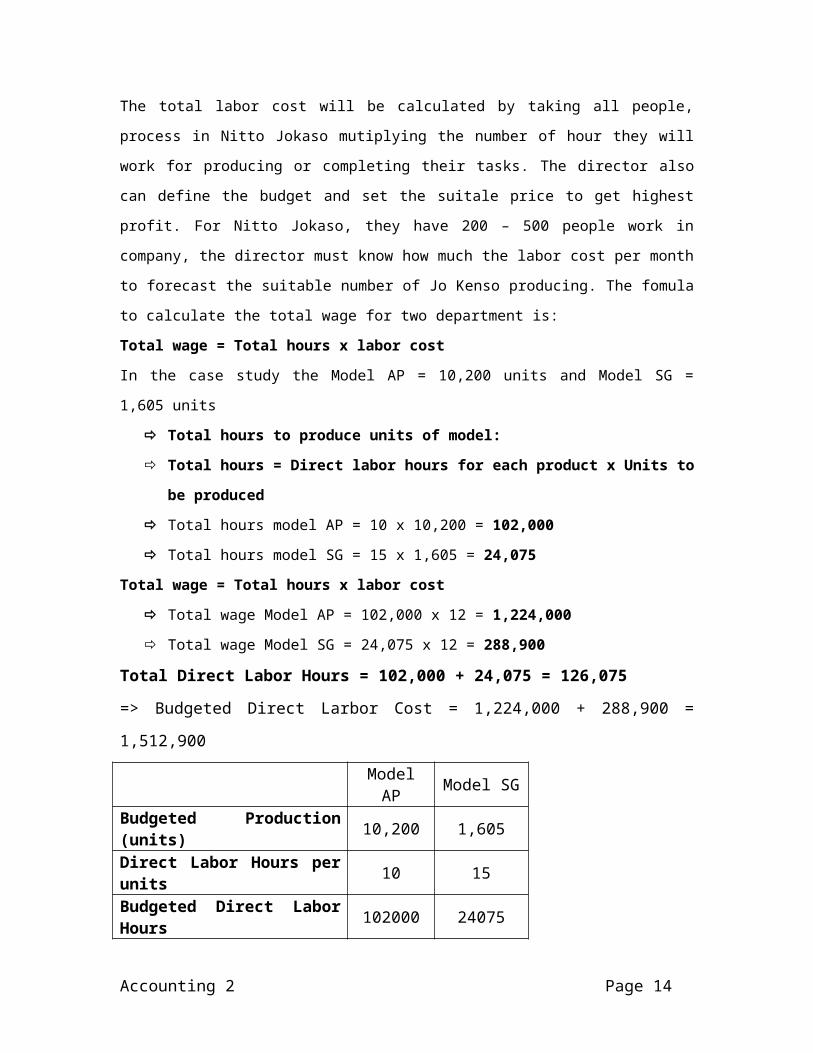

3.3.5 Direct Labor Budget

The labor cost plays an important role in producing in any manufacture even Nitto

Jokaso. If they want to produce products for the orders the first thing manager must care

is labor cost. The total labor cost will be calculated by taking all people, process in Nitto

Jokaso mutiplying the number of hour they will work for producing or completing their

tasks. The director also can define the budget and set the suitale price to get highest

profit. For Nitto Jokaso, they have 200 – 500 people work in company, the director must

know how much the labor cost per month to forecast the suitable number of Jo Kenso

producing. The fomula to calculate the total wage for two department is:

Total wage = Total hours x labor costIn the case study the Model AP = 10,200 units and Model SG = 1,605 units

Total hours to produce units of model: Total hours = Direct labor hours for each product x Units to be produced Total hours model AP = 10 x 10,200 = 102,000 Total hours model SG = 15 x 1,605 = 24,075

Total wage = Total hours x labor cost Total wage Model AP = 102,000 x 12 = 1,224,000 Total wage Model SG = 24,075 x 12 = 288,900

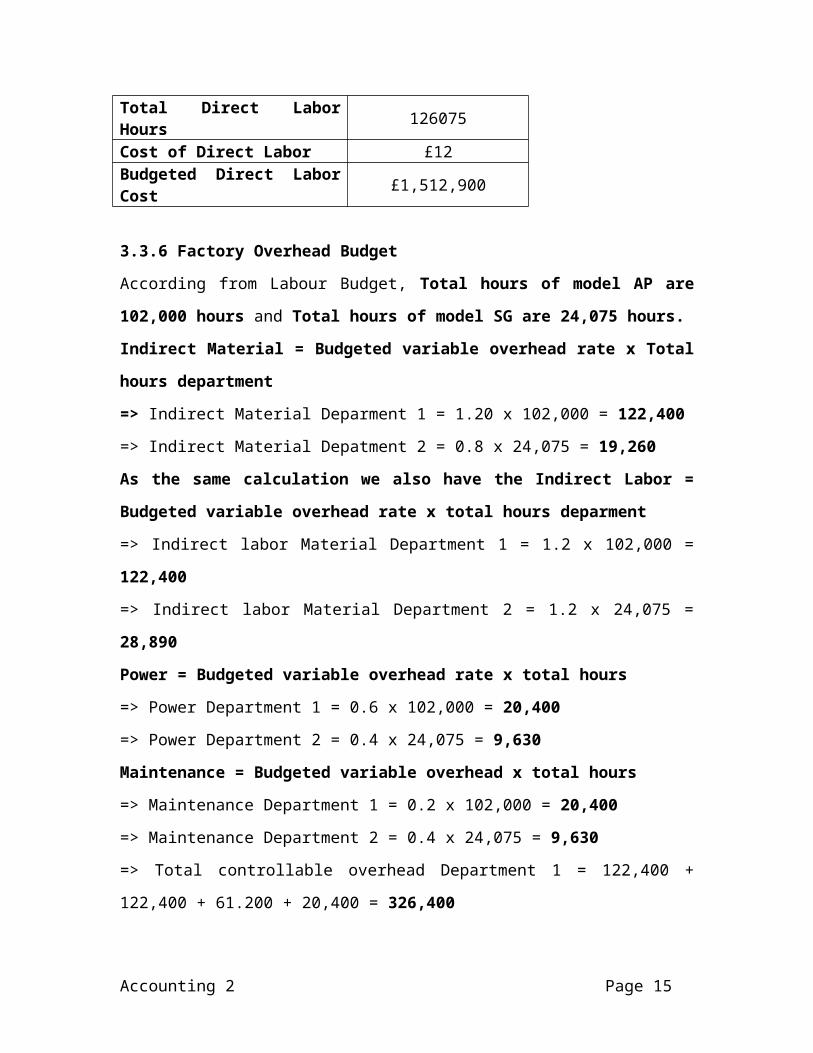

Total Direct Labor Hours = 102,000 + 24,075 = 126,075

=> Budgeted Direct Larbor Cost = 1,224,000 + 288,900 = 1,512,900

Model AP Model SGBudgeted Production (units) 10,200 1,605Direct Labor Hours per units 10 15Budgeted Direct Labor Hours 102000 24075Total Direct Labor Hours 126075Cost of Direct Labor £12Budgeted Direct Labor Cost £1,512,900

3.3.6 Factory Overhead Budget

According from Labour Budget, Total hours of model AP are 102,000 hours and Total

hours of model SG are 24,075 hours.

Indirect Material = Budgeted variable overhead rate x Total hours department

=> Indirect Material Deparment 1 = 1.20 x 102,000 = 122,400

Accounting 2 Page 10

=> Indirect Material Depatment 2 = 0.8 x 24,075 = 19,260

As the same calculation we also have the Indirect Labor = Budgeted variable

overhead rate x total hours deparment

=> Indirect labor Material Department 1 = 1.2 x 102,000 = 122,400

=> Indirect labor Material Department 2 = 1.2 x 24,075 = 28,890

Power = Budgeted variable overhead rate x total hours

=> Power Department 1 = 0.6 x 102,000 = 20,400

=> Power Department 2 = 0.4 x 24,075 = 9,630

Maintenance = Budgeted variable overhead x total hours

=> Maintenance Department 1 = 0.2 x 102,000 = 20,400

=> Maintenance Department 2 = 0.4 x 24,075 = 9,630

=> Total controllable overhead Department 1 = 122,400 + 122,400 + 61.200 + 20,400 =

326,400

=> Total controllable overhead Department 2 = 19,260 + 28,890 + 9,630 + 9,630 =

67,410

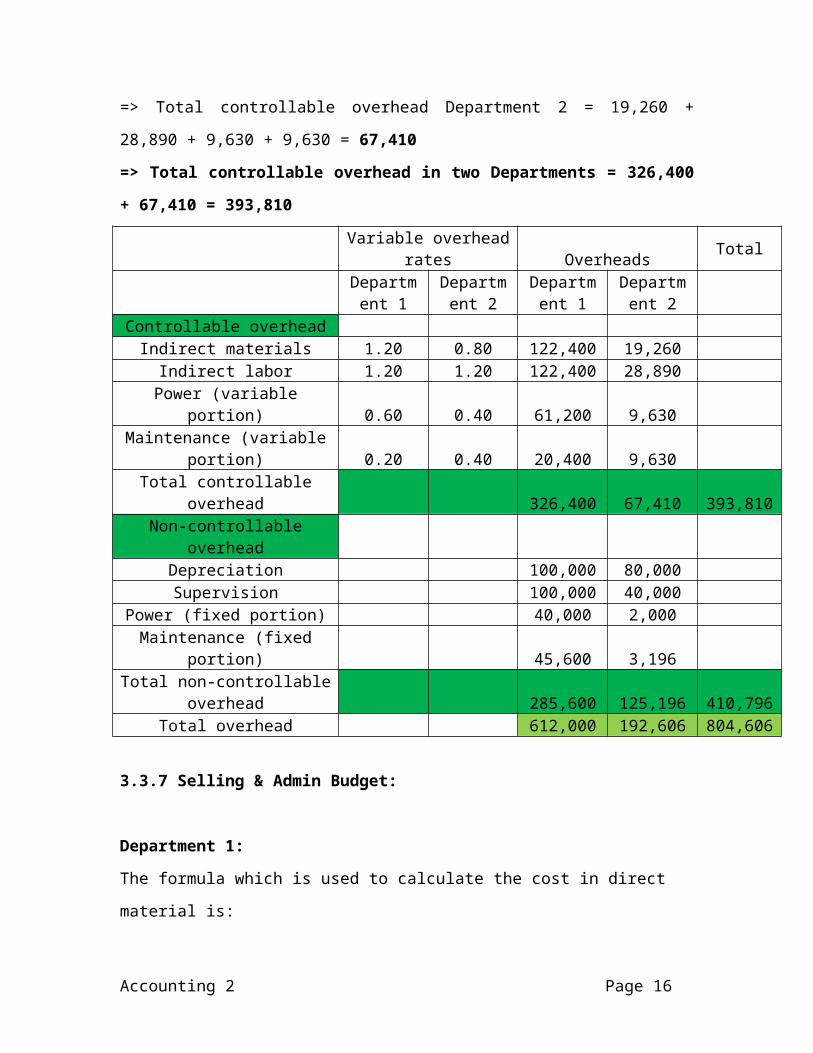

=> Total controllable overhead in two Departments = 326,400 + 67,410 = 393,810

Variable overhead rates Overheads TotalDepartment

1Department

2Department

1Department

2Controllable overhead

Indirect materials 1.20 0.80 122,400 19,260Indirect labor 1.20 1.20 122,400 28,890

Power (variable portion) 0.60 0.40 61,200 9,630Maintenance (variable portion) 0.20 0.40 20,400 9,630

Total controllable overhead 326,400 67,410 393,810Non-controllable overhead

Depreciation 100,000 80,000Supervision 100,000 40,000

Power (fixed portion) 40,000 2,000Maintenance (fixed portion) 45,600 3,196

Total non-controllable overhead 285,600 125,196 410,796Total overhead 612,000 192,606 804,606

3.3.7 Selling & Admin Budget:

Department 1:

Accounting 2 Page 11

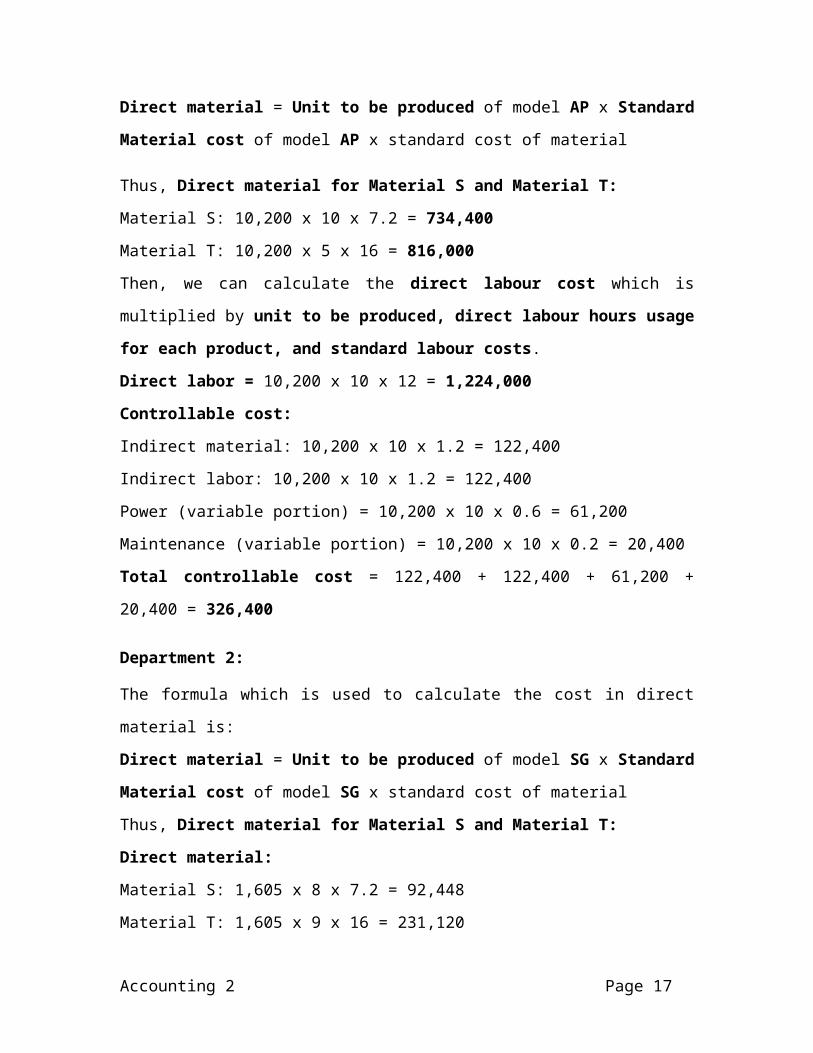

The formula which is used to calculate the cost in direct material is:

Direct material = Unit to be produced of model AP x Standard Material cost of

model AP x standard cost of material

Thus, Direct material for Material S and Material T:

Material S: 10,200 x 10 x 7.2 = 734,400

Material T: 10,200 x 5 x 16 = 816,000

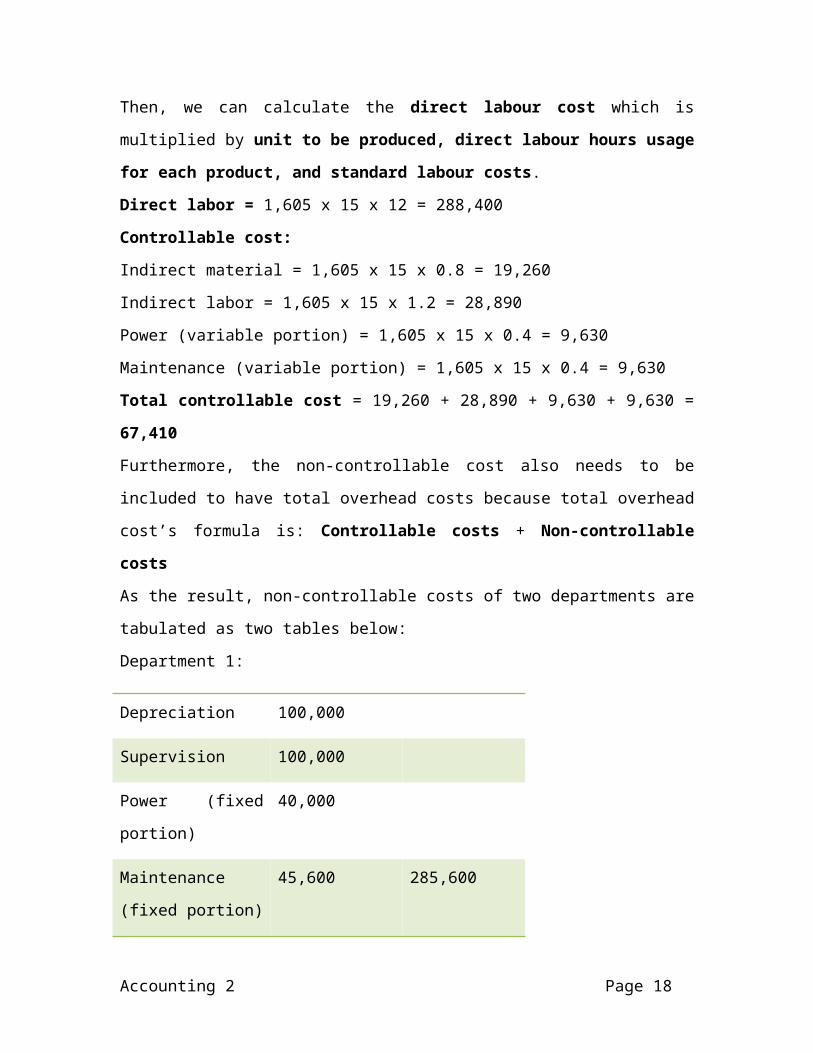

Then, we can calculate the direct labour cost which is multiplied by unit to be

produced, direct labour hours usage for each product, and standard labour costs.

Direct labor = 10,200 x 10 x 12 = 1,224,000

Controllable cost:

Indirect material: 10,200 x 10 x 1.2 = 122,400

Indirect labor: 10,200 x 10 x 1.2 = 122,400

Power (variable portion) = 10,200 x 10 x 0.6 = 61,200

Maintenance (variable portion) = 10,200 x 10 x 0.2 = 20,400

Total controllable cost = 122,400 + 122,400 + 61,200 + 20,400 = 326,400

Department 2:

The formula which is used to calculate the cost in direct material is:

Direct material = Unit to be produced of model SG x Standard Material cost of

model SG x standard cost of material

Thus, Direct material for Material S and Material T:

Direct material:

Material S: 1,605 x 8 x 7.2 = 92,448

Material T: 1,605 x 9 x 16 = 231,120

Then, we can calculate the direct labour cost which is multiplied by unit to be

produced, direct labour hours usage for each product, and standard labour costs.

Direct labor = 1,605 x 15 x 12 = 288,400

Controllable cost:

Indirect material = 1,605 x 15 x 0.8 = 19,260

Indirect labor = 1,605 x 15 x 1.2 = 28,890

Power (variable portion) = 1,605 x 15 x 0.4 = 9,630

Accounting 2 Page 12

Maintenance (variable portion) = 1,605 x 15 x 0.4 = 9,630

Total controllable cost = 19,260 + 28,890 + 9,630 + 9,630 = 67,410

Furthermore, the non-controllable cost also needs to be included to have total overhead

costs because total overhead cost’s formula is: Controllable costs + Non-controllable

costs

As the result, non-controllable costs of two departments are tabulated as two tables

below:

Department 1:

Depreciation 100,000

Supervision 100,000

Power (fixed portion) 40,000

Maintenance (fixed

portion)

45,600 285,600

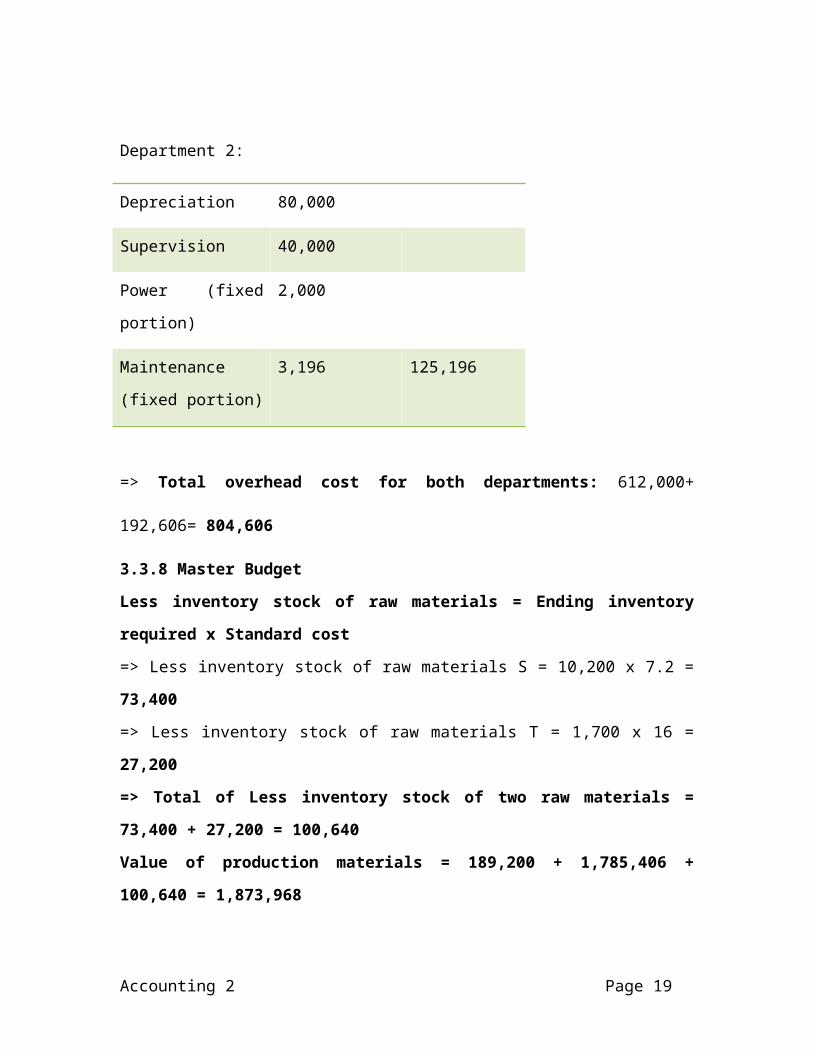

Department 2:

Depreciation 80,000

Supervision 40,000

Power (fixed portion) 2,000

Maintenance (fixed

portion)

3,196 125,196

=> Total overhead cost for both departments: 612,000+ 192,606= 804,606

3.3.8 Master Budget

Less inventory stock of raw materials = Ending inventory required x Standard cost

=> Less inventory stock of raw materials S = 10,200 x 7.2 = 73,400

Accounting 2 Page 13

=> Less inventory stock of raw materials T = 1,700 x 16 = 27,200

=> Total of Less inventory stock of two raw materials = 73,400 + 27,200 = 100,640

Value of production materials = 189,200 + 1,785,406 + 100,640 = 1,873,968

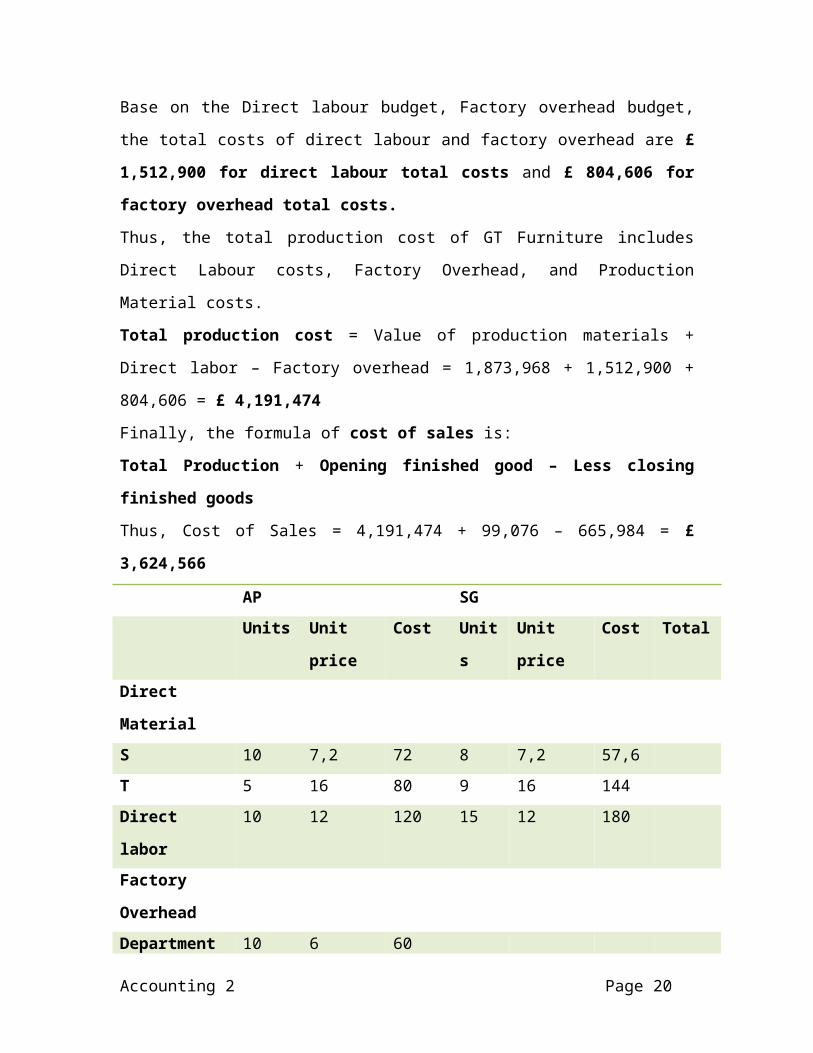

Base on the Direct labour budget, Factory overhead budget, the total costs of direct

labour and factory overhead are £ 1,512,900 for direct labour total costs and £ 804,606

for factory overhead total costs.

Thus, the total production cost of GT Furniture includes Direct Labour costs, Factory

Overhead, and Production Material costs.

Total production cost = Value of production materials + Direct labor – Factory

overhead = 1,873,968 + 1,512,900 + 804,606 = £ 4,191,474

Finally, the formula of cost of sales is:

Total Production + Opening finished good – Less closing finished goods

Thus, Cost of Sales = 4,191,474 + 99,076 – 665,984 = £ 3,624,566

AP SG

Units Unit price Cost Units Unit price Cost Total

Direct Material

S 10 7,2 72 8 7,2 57,6

T 5 16 80 9 16 144

Direct labor 10 12 120 15 12 180

Factory

Overhead

Department 1 10 6 60

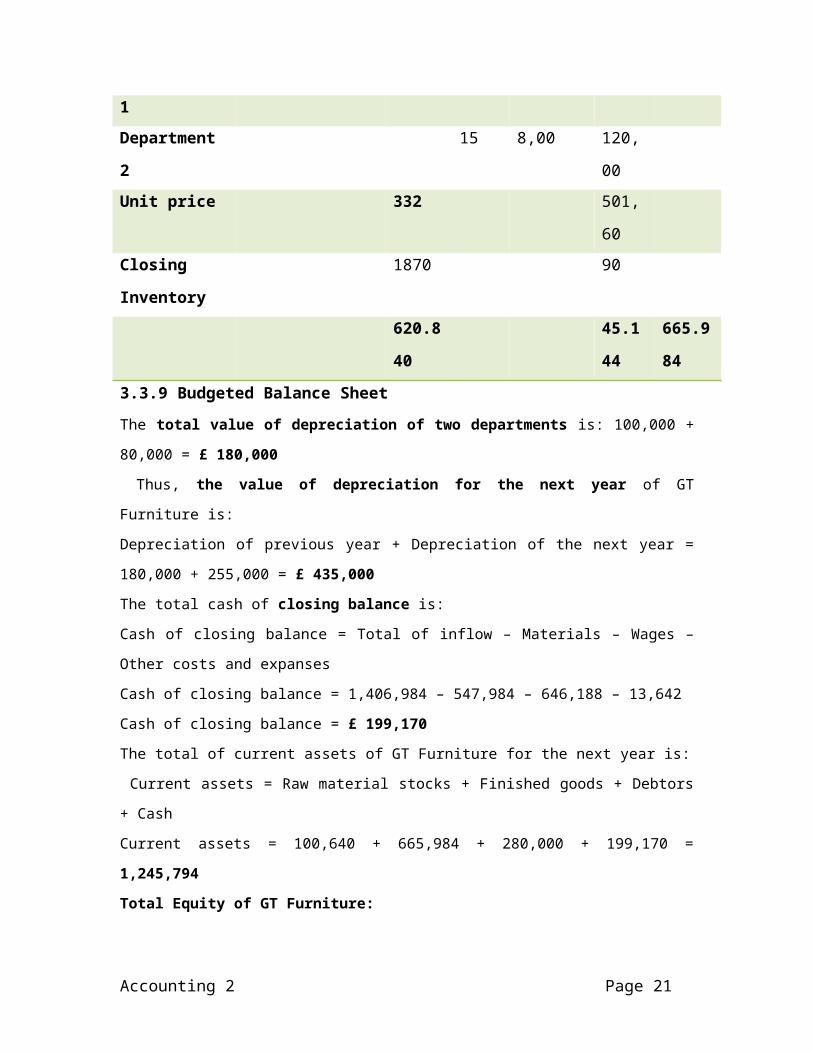

Department 2 15 8,00 120,00

Unit price 332 501,60

Closing

Inventory

1870 90

620.840 45.144 665.984

3.3.9 Budgeted Balance Sheet

The total value of depreciation of two departments is: 100,000 + 80,000 = £ 180,000

Thus, the value of depreciation for the next year of GT Furniture is:

Accounting 2 Page 14

Depreciation of previous year + Depreciation of the next year = 180,000 + 255,000 = £ 435,000The total cash of closing balance is:

Cash of closing balance = Total of inflow – Materials – Wages – Other costs and

expanses

Cash of closing balance = 1,406,984 – 547,984 – 646,188 – 13,642

Cash of closing balance = £ 199,170The total of current assets of GT Furniture for the next year is:

Current assets = Raw material stocks + Finished goods + Debtors + Cash

Current assets = 100,640 + 665,984 + 280,000 + 199,170 = 1,245,794

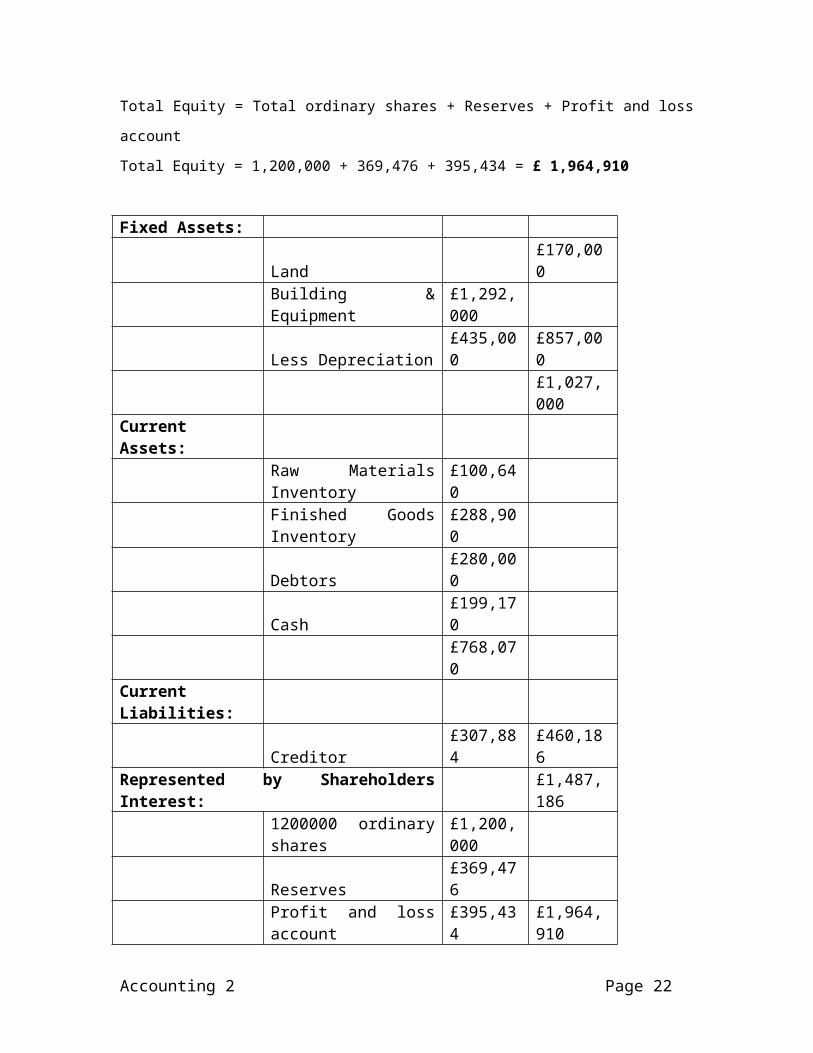

Total Equity of GT Furniture: Total Equity = Total ordinary shares + Reserves + Profit and loss account

Total Equity = 1,200,000 + 369,476 + 395,434 = £ 1,964,910

Fixed Assets: Land £170,000 Building & Equipment £1,292,000 Less Depreciation £435,000 £857,000 £1,027,000Current Assets: Raw Materials Inventory £100,640

Finished Goods Inventory £288,900

Debtors £280,000 Cash £199,170 £768,070 Current Liabilities: Creditor £307,884 £460,186Represented by Shareholders Interest: £1,487,186 1200000 ordinary shares £1,200,000 Reserves £369,476 Profit and loss account £395,434 £1,964,910

Accounting 2 Page 15

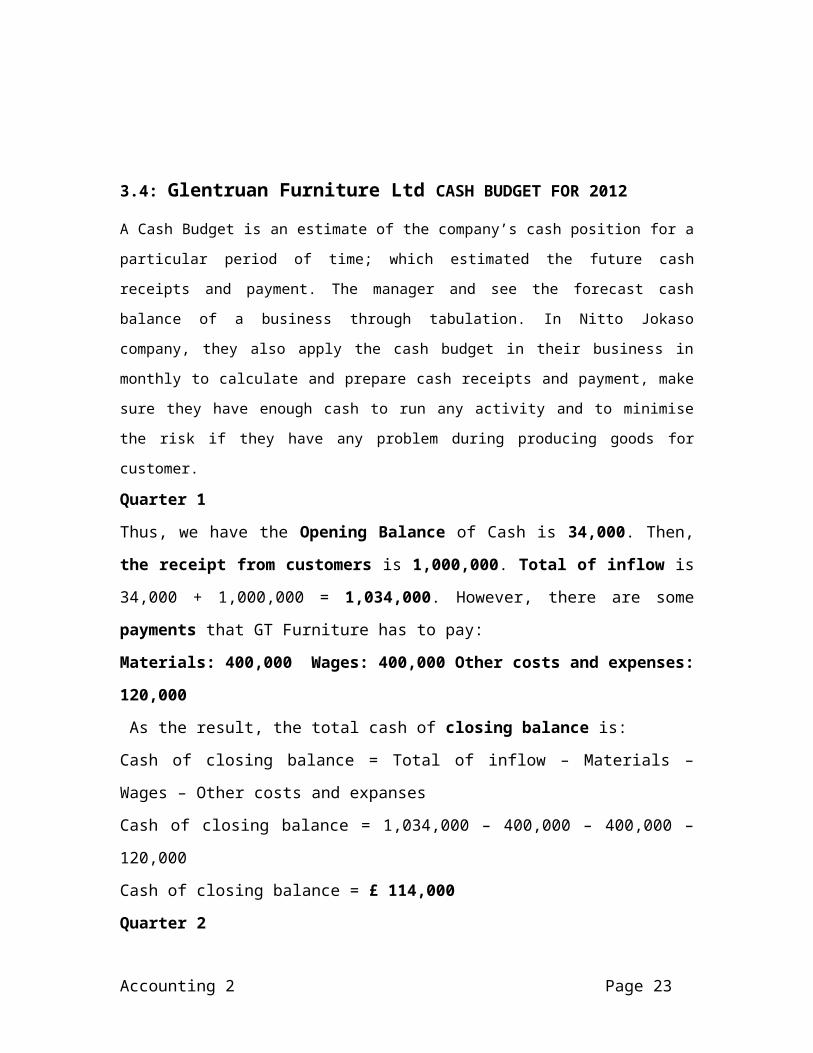

3.4: Glentruan Furniture Ltd CASH BUDGET FOR 2012

A Cash Budget is an estimate of the company’s cash position for a particular period of

time; which estimated the future cash receipts and payment. The manager and see the

forecast cash balance of a business through tabulation. In Nitto Jokaso company, they

also apply the cash budget in their business in monthly to calculate and prepare cash

receipts and payment, make sure they have enough cash to run any activity and to

minimise the risk if they have any problem during producing goods for customer.

Quarter 1

Thus, we have the Opening Balance of Cash is 34,000. Then, the receipt from

customers is 1,000,000. Total of inflow is 34,000 + 1,000,000 = 1,034,000. However,

there are some payments that GT Furniture has to pay:

Materials: 400,000 Wages: 400,000 Other costs and expenses: 120,000

As the result, the total cash of closing balance is:

Cash of closing balance = Total of inflow – Materials – Wages – Other costs and

expanses

Cash of closing balance = 1,034,000 – 400,000 – 400,000 – 120,000

Cash of closing balance = £ 114,000

Quarter 2

Because of cash of previous quarter’s Closing Balance is also cash of next quarter’s

Opening Balance, the Opening Balance for Quarter 2 is 114,000. Then, the receipt

from customers is 1,200,000. Total of inflow is 114,000 + 1,200,000 = 1,314,000.

However, there are some payments that GT Furniture has to pay:

Materials: 480,000 Wages: 440,000 Other costs and expenses: 100,000

As the result, the total cash of closing balance is:

Cash of closing balance = Total of inflow – Materials – Wages – Other costs and

expanses

Cash of closing balance = 1,314,000 – 480,000 – 440,000 – 100,000

Cash of closing balance = £ 294,000

Accounting 2 Page 16

Quarter 3

As the same formula, the Opening Balance for Quarter 2 is 294,000. Then, the receipt

from customers is 1,120,000. Total of inflow is 294,000 + 1,120,000 = 1,414,000.

However, there are some payments that GT Furniture has to pay:

Materials: 440,000 Wages: 480,000 Other costs and expenses: 72,016

As the result, the total cash of closing balance is:

Cash of closing balance = Total of inflow – Materials – Wages – Other costs and

expanses

Cash of closing balance = 1,414,000 – 440,000 – 480,000 – 72,016

Cash of closing balance = £ 421,984

Quarter 4

As the same formula, the Opening Balance for Quarter 2 is 421,984. Then, the receipt

from customers is 985,000. Total of inflow is 421,984 + 985,000 = 1,406,984.

However, there are some payments that GT Furniture has to pay:

Materials: 547,984 Wages: 646,188 Other costs and expenses: 13,642

As the result, the total cash of closing balance is:

Cash of closing balance = Total of inflow – Materials – Wages – Other costs and

expanses

Cash of closing balance = 1,406,984 – 547,984 – 646,188 – 13,642

Cash of closing balance = £ 199,170

Quarter 1 Quarter 2 Quarter 3 Quarter 4 TotalOpening balance 34,000 114,000 294,000 421,984 863,984Receipts from customers 1,000,000 1,200,000 1,120,000 985,000 4,305,000

1,034,000 1,314,000 1,414,000 1,406,984 4,339,000Payments: Materials 400,000 480,000 440,000 547,984 1,867,984Payments for wages 400,000 440,000 480,000 646,188 1,966,188Other costs and expenses 120,000 100,000 72,016 13,642 305,658

920,000 1,020,000 992,016 1,207,814 4,139,830Closing Balance 114,000 294,000 421,984 199,170 1,029,154

Closing balance each quarter = Opening balance – Payment. The current closing balance

will be the next opening balance for next quarter.

Accounting 2 Page 17

To Developing the company more effective Glentruan Furniture can also apply the

Expense and Capital Budget in their business.

These are two budgets; which Nitto Jokaso should prepare during the business. As we

have been already known they often have the meeting with our supplier, customer,

upgrading or fixing the facilities and the bills. It is also relate to expense and budgeting

so the manager must know about it. For Nitto Jokaso the meeting cost does not more

than 15% total cost to ensure they have the profit for developing business. Capital

Budget is planned for controling the total cost in Nitto Jokaso, it helps manager and

director fix the price, cost for any activity and take the right decisions to achieve the

objectives or have good result in monthly and yearly.

4.1: CACULATE VARIANCES, IDENTIFY POSSIBILE CASUE AND RECOMMEND CORRECTIVE ACTION

This is the calculation variance of company to identify the possible causes then manager

can make the solution for budget.

4.1.1 Direct Material Variances:

Material Price Variances: (SP – AP) x AQ

A = (£10 - £11)*19,000Kg = -19,000 (Adverse)

B = (£15 - £14)*10,100Kg = 10,100 (Favorable)

=> Total Material Price Variances = (-19,000) + 10,100 = -8,900(Adverse)

Material Usage Variances: (SQ – AQ) x SP

The standard quantity of each material

A = 2*9,000 = 18,000Kg

B = 1*9,000 = 9,000Kg

A = (18,000 – 19,000)*£10 = -10,000 (Adverse)

B = (9,000 – 10,100)*£15 = -16,500 (Adverse)

=> Total Material Usage Variances = (-10,000) + (-16,500) = -26,500(Adverse)

4.1.2 Direct Labor Variances:

Labor Rate Variances = (£9 - £9.60)*28,500 = -17,100 (Adverse)

Labor Efficiency Variances = (27,000 – 28,500)*£9 = -13,500 (Adverse)

4.1.3 Overheads Variances:

Accounting 2 Page 18

Variable Overheads = (AH x SR) – Actual Cost =28,500 x £2 – 52,000 = 5000

(Favorable)

Standard Hour = 9,000 x 3 = 27,000

Overheads Efficiency Variances = (SH – AH) x SR = £2*(27,000 -28,500) = -3000

(Adverse)

Total Variances: Material A 29000 AMaterial B 6400 ALabor 30600 AVariable Overhead 2000 F

4.1.4 Sale Variance:

Sales margin price = (AP – BP) x AQ = (£90 - £88) x 9,000 = £18,000 (Favorable)

Sales margin volume = (AQ – BQ) x SM = (9,000 -10,000) x £20 = £20,000 (Adverse)

Total Sales = Sales margin price + Sales margin volume = £2,000 (Adverse)

4.2 Reconciliation of Budgeted and Actual Profit:

$ $ $ $

Budgeted net profit

80 000

Sales variances

Sales margin price

18 000 F

Sales margin volume

20 000 A 2 000 A

Direct cost variance

Material Price: Material A 19 000 A

Material B 10 100 F 8 900 A

Usage: Material A 10 000 A

Material B 16 500 A 26 500 A 35 400 A

Labour Rate

17 100 A

Accounting 2 Page 19

Efficiency

13 500 A 30 600 A

Manufacturing in overhead variances

Fixed Overhead expenditure

4 000 F

Variable Overhead expenditure

5 000 F

Variable Overhead efficiency

3 000 A 6000 F 62 000 A

Actual profit

18 000As the manager can see in the table, the Reconciliation of budget and actual profit can

show how business run and the impact of Actual Price (Cost) and Standard Price (Cost)

to company actual profit. According to the table, manager can see about Sales variances,

Direct cost variance, Labour variances and the Overhead variances.

4.2.1 Sales Variances

manager calculate Sales Variances = Sales margin price + Sales margin volume

= 18,000 + (-20,000) = -2,000 (Adverse)

4.2.2 Direct Cost Variances

Direct Cost Variances = Total Material Price + Total Material Usage

= (-8,900) + (-26,500) = -35,400(Adverse)

4.2.3 Direct Labor Variances

Direct Labor Variances = Labor Rate Variances + Labor Efficiency Variances

= (-17,100) + (-13,500) = -30,600(Adverse)

4.2.4 Manufacturing in Overhead Variances

Manufacturing in Overhead Variances = Fixed Overhead expenditure + Variable

Overhead expenditure + Variable Overhead efficiency

= 4,000 + 5000 + (-3,000) = 6,000 (Favorable)

The Budget net profit given is 80,000 then manager can calculate the total Actual Profit

by Budget net profit + Sales Variances + Direct Cost Variances + Direct Labor Variances

+ Manufacturing in Overhead Variances

= 80,000 + (-2,000) + (-35,400) + (-30,600) + 6,000 = 18,000

Accounting 2 Page 20

It can be easily to see that the company must improve their business and try to save the

cost because there are many adverse costs for the organisation. It relates and influences

the actual profit as we can see. To improve it the manager can reference the informations

below:

Sales Variances: the manager must forecast the number of prodcut can be sold in actual;

which relate to Sales margin volume. If the quantity of product sold more units that

expected they will be recieved more sales volume variance. In this case, the quantity is

lower than the customer demand.

Direct Cost Variances: It includes the Material Price and Material Usage in Variances.

The manager can have other relationships with suppliers to have good price for their

material. Furthermore, the usage must be calculated and forecasted to ensure the product

will be produced enough to supply the customer orders. If not, the organisation will

losses their business and profit.

Direct Labor Varinaces: The labor rate and labor efficiency are very important to produce

the product. If the manager cannot forecast the labor rate, they will not have enouch labor

resources to produce goods and loss the labor efficiency. For this case, the manager must

calculate and forecast the number of employee, their work performance to improve the

labor perfomance in organisation.

Accounting 2 Page 21

4.3 RECOMMENDATION FOR BUISNESS RELATIONSHIP

To: Board of Manager

From: Management Accountant

Date: 5 April 2014

Subject: Report for reponsibility center of Nitto Jokaso Ltd

Executive summary:

The report is the result from the research through all responsibility center of company. It

will highlight all information to help manager get the overview

Method of research:

This report has been completed from finding a various responsibility center include cost

center, revenue center and profit center.

Cost Center: This center is about company cost; which the manager can relate to take

the decisions about the cost. Furthermore they also have overall the costs to minimise and

control them.

Revenue Center: This is very important to relate the final profit center. Basing on the

revuenue center, manager will clearly know how to develop and improve their business.

Profit Center: Is the overall view for manager taking the decisions and plans to

maximise the profit for company.

Recommendation

The responsibility centers are identifiable segment within company for each individual. It

include revenue center, cost center, profit center and investment center

This report research finding designed to the responsibility center of Nitto Jokaso Ltd.

Accounting 2 Page 22

4.0: REFERENCES

Accaglobal (2010) Comparing budgeting techiques [Online] available from:

<http://www.accaglobal.com/gb/en/student/acca-qual-student-journey/qual-

resource/acca-qualification/f5/technical-articles/comparing-budgeting-

techniques.html>

Businessdictionary (2012) Sales volume variance [Online] available from:

<http://www.businessdictionary.com/definition/sales-volume-variance.html>

Dummies (2012) Choosing a budget method [Online] available from:

<http://www.dummies.com/how-to/content/choosing-a-budget-method.html>

Ketoanthue (2010) Finance management for organisation [Online] available from:

<http://www.ketoanthue.vn/index.php/cac-tin-kiem-toan-da-dang/1779-quan-ly-

tai-chinh-don-vi-su-nghiep-va-nhung-van-de-dat-ra-hien-nay.html>

Shell-livewire (2014) Accounts and finance budgeting, type of budgeting [Online]

available from:

<http://www.shell-livewire.org/home/business-library/accounts-and-finance/

budgeting/types-of-budgeting/>

Accounting 2 Page 23