Embed Size (px)

Citation preview

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 4

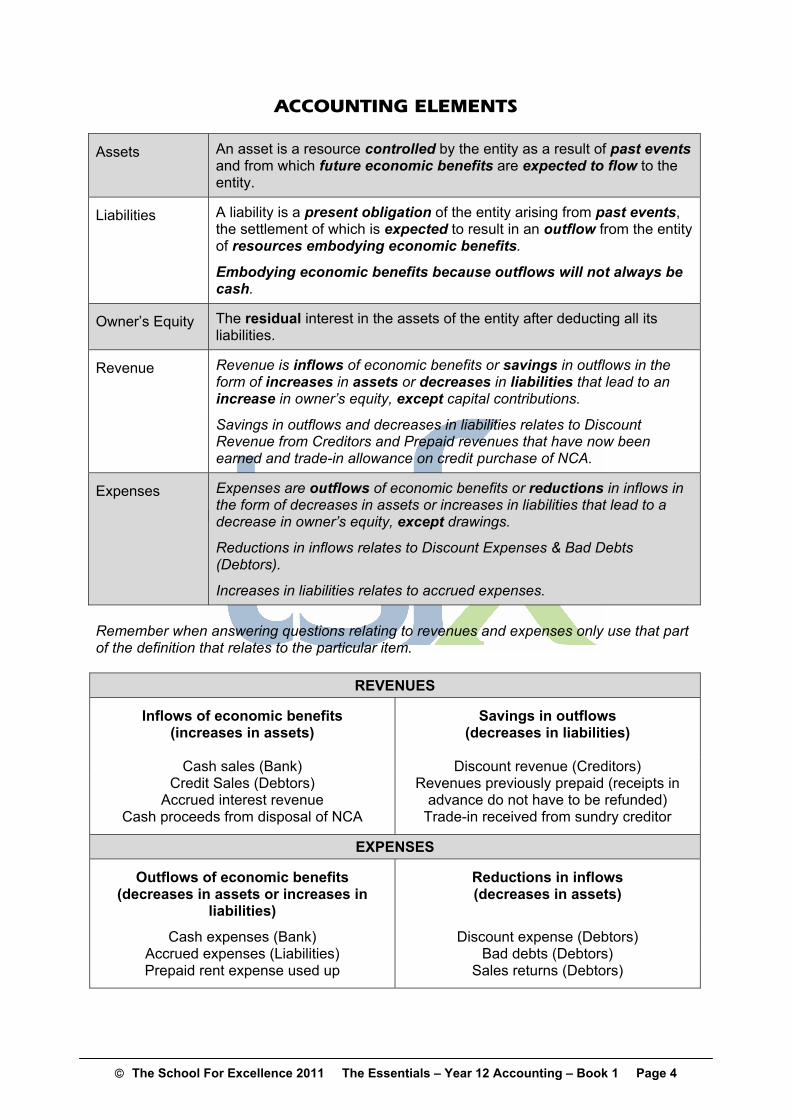

ACCOUNTING ELEMENTS

Assets

An asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity.

Liabilities

A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

Embodying economic benefits because outflows will not always be cash.

Owner’s Equity

The residual interest in the assets of the entity after deducting all its liabilities.

Revenue

Revenue is inflows of economic benefits or savings in outflows in the form of increases in assets or decreases in liabilities that lead to an increase in owner’s equity, except capital contributions.

Savings in outflows and decreases in liabilities relates to Discount Revenue from Creditors and Prepaid revenues that have now been earned and trade-in allowance on credit purchase of NCA.

Expenses

Expenses are outflows of economic benefits or reductions in inflows in the form of decreases in assets or increases in liabilities that lead to a decrease in owner’s equity, except drawings.

Reductions in inflows relates to Discount Expenses & Bad Debts (Debtors).

Increases in liabilities relates to accrued expenses.

Remember when answering questions relating to revenues and expenses only use that part of the definition that relates to the particular item.

REVENUES

Inflows of economic benefits (increases in assets)

Savings in outflows (decreases in liabilities)

Cash sales (Bank) Discount revenue (Creditors) Credit Sales (Debtors)

Accrued interest revenue Cash proceeds from disposal of NCA

Revenues previously prepaid (receipts in advance do not have to be refunded)

Trade-in received from sundry creditor

EXPENSES

Outflows of economic benefits (decreases in assets or increases in

liabilities)

Reductions in inflows (decreases in assets)

Cash expenses (Bank) Discount expense (Debtors) Accrued expenses (Liabilities) Bad debts (Debtors) Prepaid rent expense used up Sales returns (Debtors)

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 5

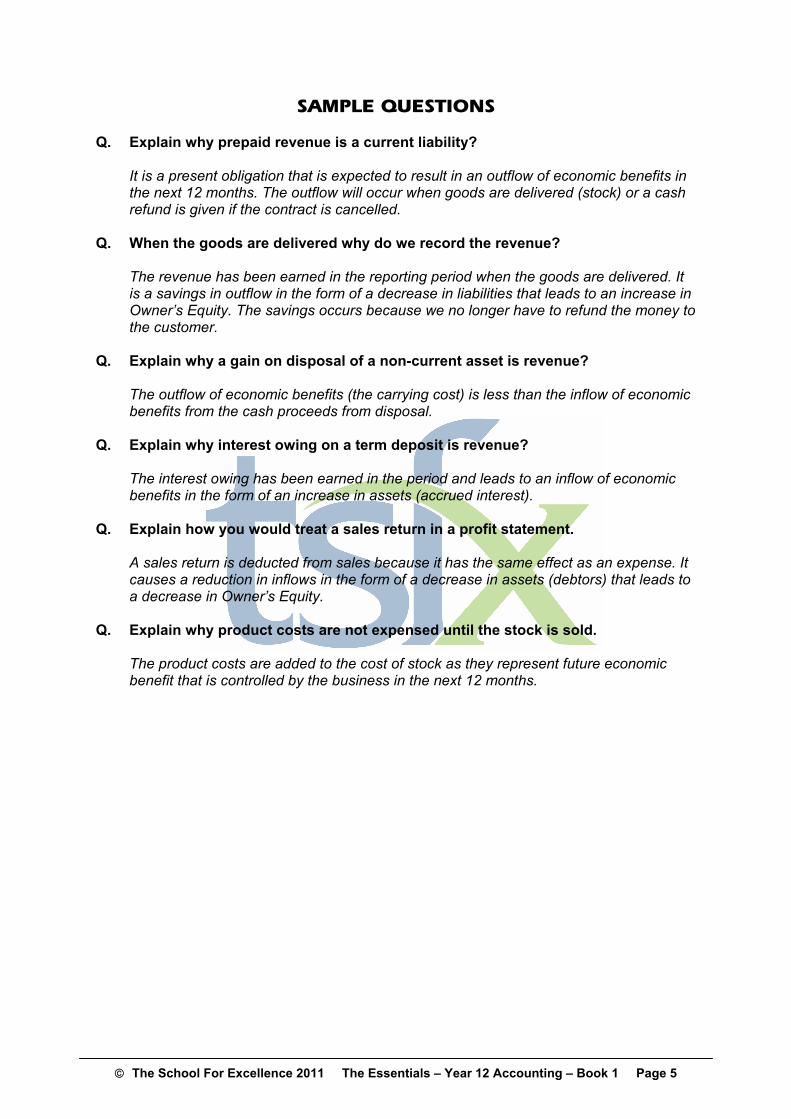

SAMPLE QUESTIONS Q. Explain why prepaid revenue is a current liability?

It is a present obligation that is expected to result in an outflow of economic benefits in the next 12 months. The outflow will occur when goods are delivered (stock) or a cash refund is given if the contract is cancelled.

Q. When the goods are delivered why do we record the revenue?

The revenue has been earned in the reporting period when the goods are delivered. It is a savings in outflow in the form of a decrease in liabilities that leads to an increase in Owner’s Equity. The savings occurs because we no longer have to refund the money to the customer.

Q. Explain why a gain on disposal of a non-current asset is revenue?

The outflow of economic benefits (the carrying cost) is less than the inflow of economic benefits from the cash proceeds from disposal.

Q. Explain why interest owing on a term deposit is revenue?

The interest owing has been earned in the period and leads to an inflow of economic benefits in the form of an increase in assets (accrued interest).

Q. Explain how you would treat a sales return in a profit statement.

A sales return is deducted from sales because it has the same effect as an expense. It causes a reduction in inflows in the form of a decrease in assets (debtors) that leads to a decrease in Owner’s Equity.

Q. Explain why product costs are not expensed until the stock is sold.

The product costs are added to the cost of stock as they represent future economic benefit that is controlled by the business in the next 12 months.

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 6

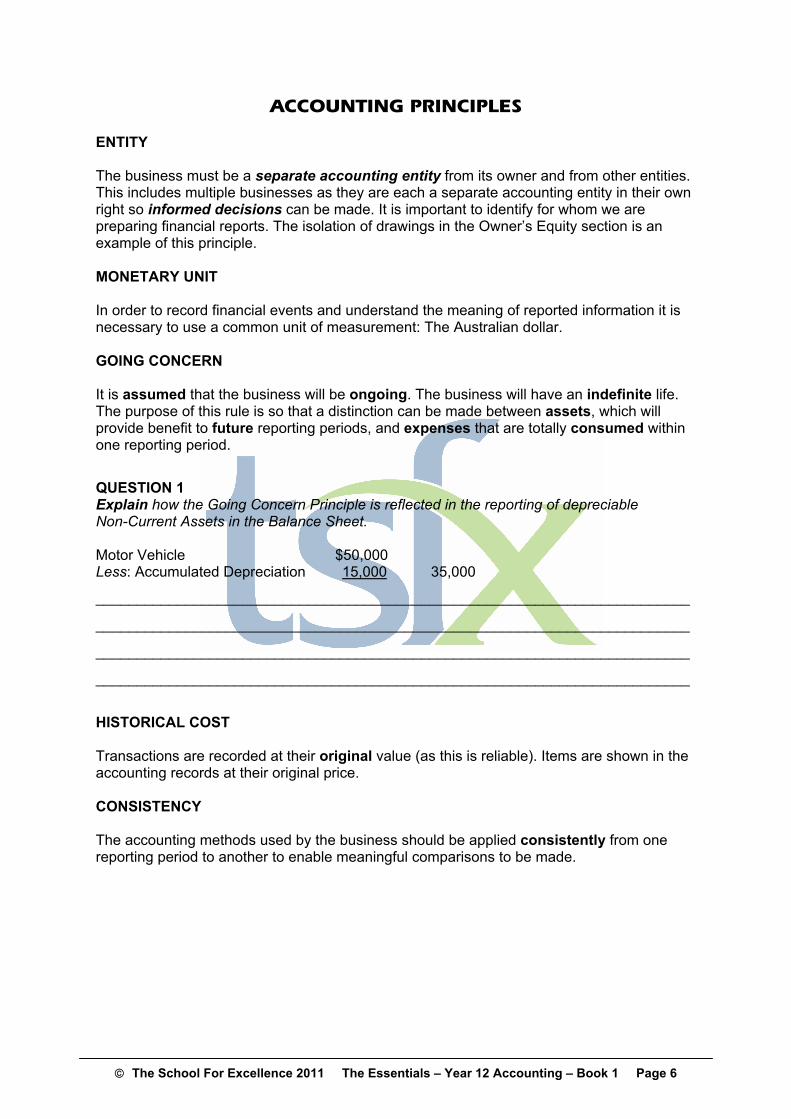

ACCOUNTING PRINCIPLES ENTITY The business must be a separate accounting entity from its owner and from other entities. This includes multiple businesses as they are each a separate accounting entity in their own right so informed decisions can be made. It is important to identify for whom we are preparing financial reports. The isolation of drawings in the Owner’s Equity section is an example of this principle. MONETARY UNIT In order to record financial events and understand the meaning of reported information it is necessary to use a common unit of measurement: The Australian dollar. GOING CONCERN It is assumed that the business will be ongoing. The business will have an indefinite life. The purpose of this rule is so that a distinction can be made between assets, which will provide benefit to future reporting periods, and expenses that are totally consumed within one reporting period.

QUESTION 1 Explain how the Going Concern Principle is reflected in the reporting of depreciable Non-Current Assets in the Balance Sheet. Motor Vehicle $50,000 Less: Accumulated Depreciation 15,000 35,000

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

HISTORICAL COST Transactions are recorded at their original value (as this is reliable). Items are shown in the accounting records at their original price. CONSISTENCY The accounting methods used by the business should be applied consistently from one reporting period to another to enable meaningful comparisons to be made.

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 7

QUESTION 2 The owner wants to change the depreciation % on his assets to reduce his expenses in the next period. Explain why this is breaching an accounting principle.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

CONSERVATISM It is acknowledged that gains will not be recognised until earned and losses will be recognised as soon as they are likely to occur. This will avoid overstating assets and revenue and understating liabilities/expenses.

QUESTION 3 The stock on hand of $28000 could be sold for $60000. The owner wants to record this revenue and related profit in this reporting period. Explain why is this not an acceptable accounting practice?

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

QUESTION 4 Explain why the application of the “lower of cost and net realisable value” is using the principle of Conservatism.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

QUESTION 5 Explain why treating a deposit as prepaid revenue is an example of Conservatism.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 8

REPORTING PERIOD The ongoing life of a business is broken into regular intervals of time for the preparation of accounting reports. Profit is calculated by matching revenue earned against expenses incurred in a particular reporting period for the purposes of decision-making.

QUESTION 6 The owner has recommended to the accountant that he should not worry about including any interest revenue as it will not be received from the bank until the next reporting period. Explain why the owner is incorrect.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

QUALITATIVE CHARACTERISTICS RELEVANCE To be useful, information must be relevant to the decision-making needs of users. Information has the quality of relevance when it influences the economic decisions of users by helping them evaluate past, present or future events or confirming, or correcting their past evaluation. The relevance of information is affected by its nature and materiality. Information is material if its omission or misstatement could influence the economic decisions of users taken on the basis of the financial report. Materiality provides a cut-off point which information must have if it is to be useful.

QUESTION 7 Identify and explain a qualitative characteristic that would assist with the decision to add $0.20 delivery cost to a particular stock item or treat the total cost of $400 as a Period Cost.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 9

QUESTION 8 Explain why the use of net realisable value is an acceptable accounting practice even though there is not verifiable evidence.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

RELIABILITY Reports must reflect what they say without bias or undue influence. This is achieved when reports are prepared from verifiable evidence, such as source documents. UNDERSTANDABILITY An essential quality of the information provided in financial reports is that it is readily understandable by users. For this purpose, users are assumed to have a reasonable knowledge of business, economic activities and accounting, and a willingness to study the information with reasonable diligence. However, information about complex matters should be included in the financial report because of its relevance to the economic decision-making needs of users, and should not be excluded merely on the grounds that it may be too difficult for certain users to understand. The business is currently facing a law suit for selling genetically modified seeds to unsuspecting customers. The lawyer estimates potential damages at $100,000. The owner believes that this should be ignored until the case is resolved. He also believes that the issue is too confusing for investors and other users of the financial information.

QUESTION 9 Explain with reference to two qualitative characteristics why this information should be reported. Can you also identify an Accounting Principle that would apply to this situation?

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 10

COMPARABILITY For reports to be useful there is a need to use similar accounting methods, both over time and between different businesses in order to effectively compare results when making decisions. The measurement and display of the financial effect of like transactions and other events must be carried out in a consistent way throughout an entity and over time and in a consistent way for different entities.

QUESTION 10 Explain the link between the Accounting Principle of Consistency and the Qualitative Characteristic of Comparability.

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

To answer questions on Principles, Elements and Qualitative characteristics use the IDL approach. IDENTIFY the principle / characteristic / item. DEFINE in textbook terms. LINK to the specifics of the question, i.e. answer the question!

LINKS between Principles and Qualitative Characteristics:

PRINCIPLES QUALITATIVE CHARACTERISTICS

Historical Cost Reliability

Consistency Comparability

Going Concern Relevance/Understandability

Reporting Period Relevance

Accounting Entity Relevance

Conservatism Relevance

Monetary Understandability

Principles relate to the recording of financial information and Qualitative characteristics relate to the reporting of information.

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 11

UNIT 4 ACCOUNTING Do students need to be able to calculate financial indicators/ratios for analysis and interpretation in the November examination? In order for students to best answer analysis questions in the November examination, they should have an understanding of what the financial indicators listed below involve and the formulas attached to them. Students will be expected to know how financial indicators are calculated, but in the examination setting students will not be expected to make those calculations. DO NOT ASSUME THAT RATIO FORMULAS WILL BE PROVIDED IN THE EXAM

Recording of the GST in the Statement of Cash Flows for the purchase of a non-current asset: The GST will be reported as an operating outflow. For example, if a motor vehicle

were purchased for $20 000 cash, with GST of $2000. The $20 000 would be an investing outflow, with the $2000 GST being reported as an operating outflow.

In a Budgeted Statement of Cash Flows how are prepayments, payments of an expense, repayment of a loan and payment of interest treated? When preparing cash budgets, the distinction should be made between the payments

of an expense and the prepayment of an expense. Distinction should also be made between the repayment of a loan and the payment of interest on the loan.

How are sales and purchase returns treated? To be consistent with the First-In, First-Out (FIFO) assumption, sales returns should be

recorded at the most recent cost price. The cost of purchase returns will be identified as the FIFO assumption only applies to

the selling of stock.

Sundry Debtors or Sundry Creditors are not part of the Debtor/Creditor Control system so they do not require an additional entry into a Subsidiary Ledger.

SECTION 2:

SALES & PURCHASE RETURNS

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 12

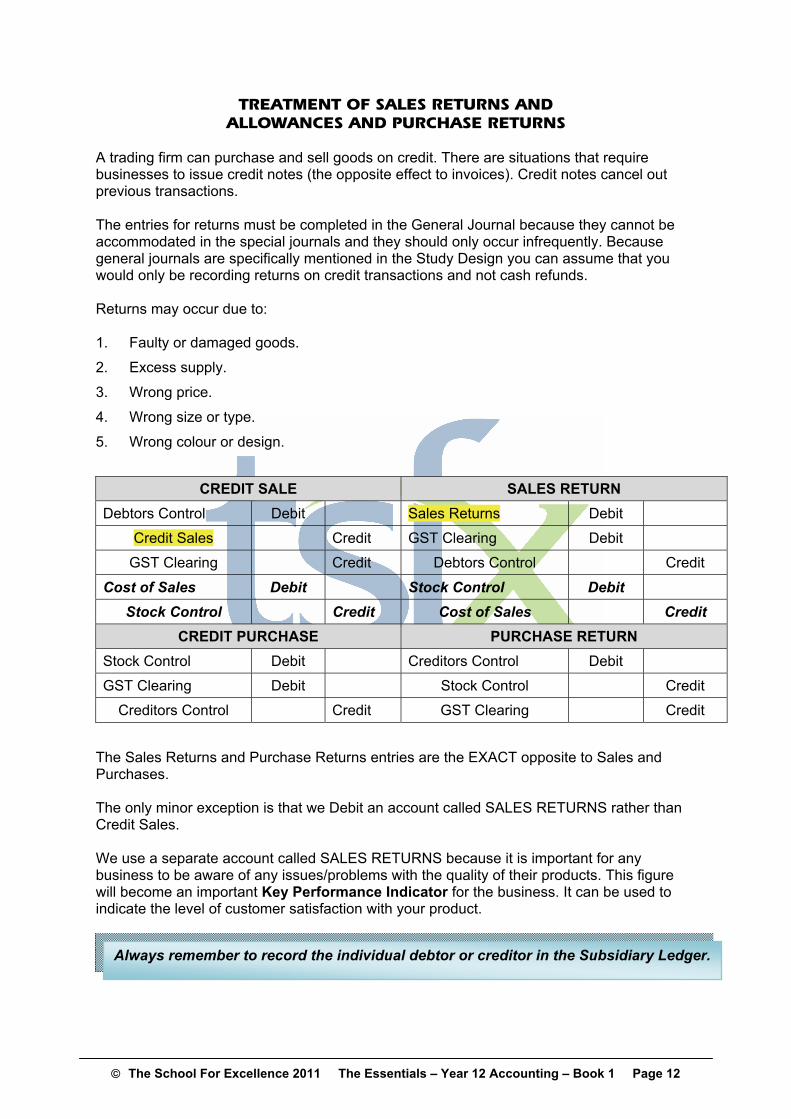

TREATMENT OF SALES RETURNS AND ALLOWANCES AND PURCHASE RETURNS

A trading firm can purchase and sell goods on credit. There are situations that require businesses to issue credit notes (the opposite effect to invoices). Credit notes cancel out previous transactions. The entries for returns must be completed in the General Journal because they cannot be accommodated in the special journals and they should only occur infrequently. Because general journals are specifically mentioned in the Study Design you can assume that you would only be recording returns on credit transactions and not cash refunds. Returns may occur due to: 1. Faulty or damaged goods.

2. Excess supply.

3. Wrong price.

4. Wrong size or type.

5. Wrong colour or design.

CREDIT SALE SALES RETURN

Debtors Control Debit Sales Returns Debit

Credit Sales Credit GST Clearing Debit

GST Clearing Credit Debtors Control Credit

Cost of Sales Debit Stock Control Debit

Stock Control Credit Cost of Sales Credit

CREDIT PURCHASE PURCHASE RETURN

Stock Control Debit Creditors Control Debit

GST Clearing Debit Stock Control Credit

Creditors Control Credit GST Clearing Credit

The Sales Returns and Purchase Returns entries are the EXACT opposite to Sales and Purchases. The only minor exception is that we Debit an account called SALES RETURNS rather than Credit Sales. We use a separate account called SALES RETURNS because it is important for any business to be aware of any issues/problems with the quality of their products. This figure will become an important Key Performance Indicator for the business. It can be used to indicate the level of customer satisfaction with your product.

Always remember to record the individual debtor or creditor in the Subsidiary Ledger.

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 13

PROFORMA LEDGERS

DEBTORS CONTROL

Date Cross Reference $ Date Cross Reference $

Sales/GST Clearing Sales Returns/GST clearing

Bank/Discount Expense

Bad Debts

SALES

Date Cross Reference $ Date Cross Reference $

Debtors Control

SALES RETURNS

Date Cross Reference $ Date Cross Reference $

Debtors Control

STOCK CONTROL

Date Cross Reference $ Date Cross Reference $

Creditors Control Creditors Control (purchase return)

Cost of Sales (sales return)

Cost of Sales

Cost of Sales

CREDITORS CONTROL

Date Cross Reference $ Date Cross Reference $

Bank/Discount Revenue

Stock Control/GST (purchase ret) Stock Control/GST clearing

GST CLEARING

Date Cross Reference $ Date Cross Reference $

Creditors Control Creditors Control (purchase ret)

Bank Bank

Debtors Control (sales return) Debtors Control

The words in brackets are for instructional purpose only. Do not show these in your

ledgers!

COST OF SALES

Date Cross Reference $ Date Cross Reference $

Stock Control Stock Control (sales return)

Stock Control

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 14

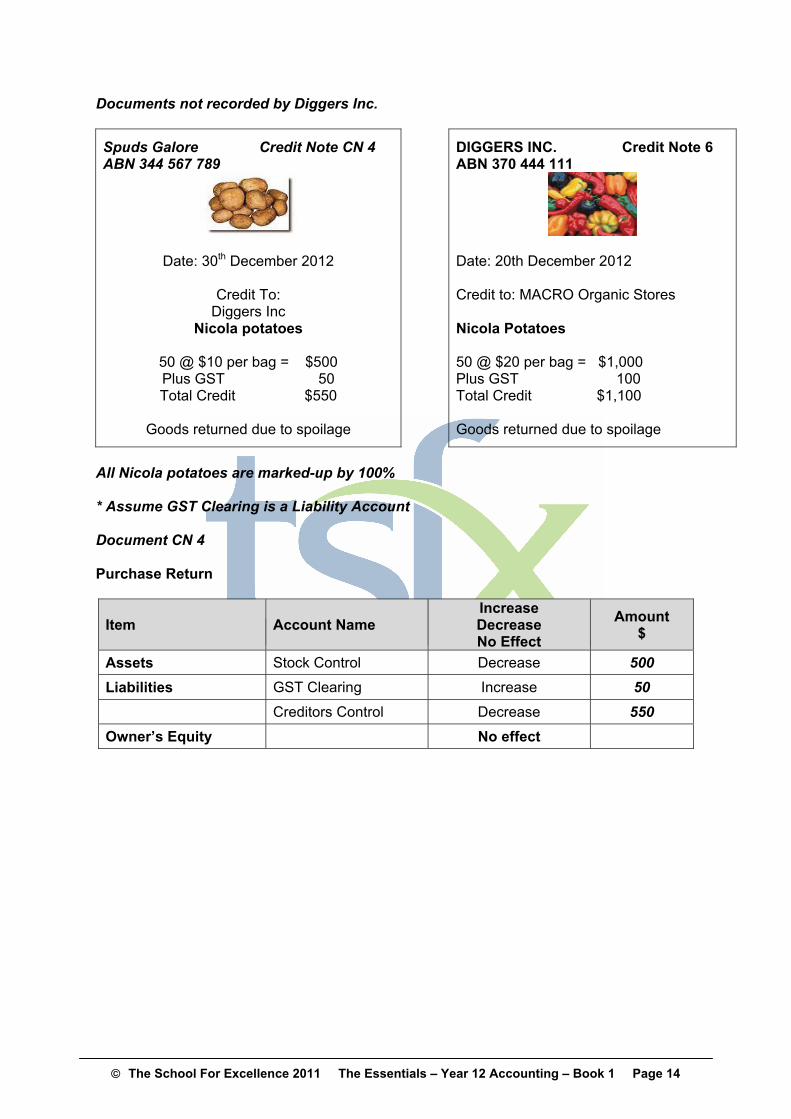

Documents not recorded by Diggers Inc.

Spuds Galore Credit Note CN 4 ABN 344 567 789

Date: 30th December 2012

Credit To: Diggers Inc

Nicola potatoes

50 @ $10 per bag = $500 Plus GST 50 Total Credit $550

Goods returned due to spoilage

DIGGERS INC. Credit Note 6 ABN 370 444 111

Date: 20th December 2012 Credit to: MACRO Organic Stores Nicola Potatoes 50 @ $20 per bag = $1,000 Plus GST 100 Total Credit $1,100 Goods returned due to spoilage

All Nicola potatoes are marked-up by 100% * Assume GST Clearing is a Liability Account Document CN 4 Purchase Return

Item Account Name Increase Decrease No Effect

Amount $

Assets Stock Control Decrease 500

Liabilities GST Clearing Increase 50

Creditors Control Decrease 550

Owner’s Equity No effect

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 15

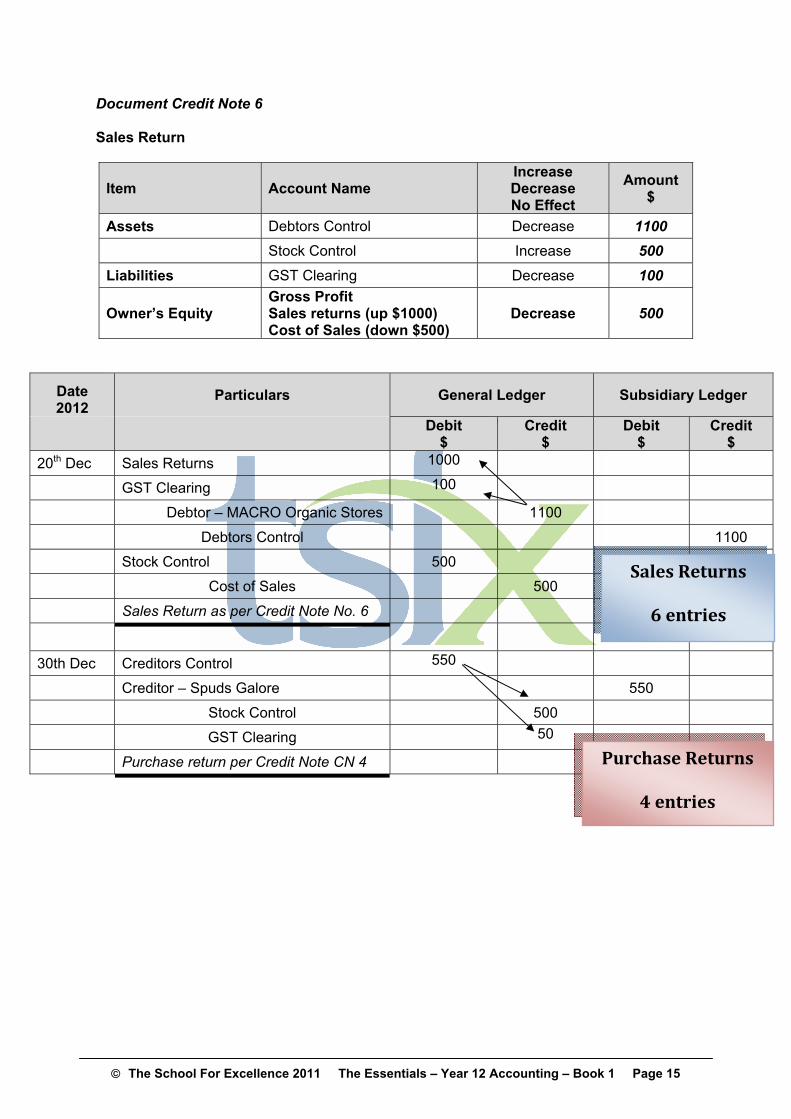

Document Credit Note 6 Sales Return

Item Account Name Increase Decrease No Effect

Amount $

Assets Debtors Control Decrease 1100

Stock Control Increase 500

Liabilities GST Clearing Decrease 100

Owner’s Equity Gross Profit Sales returns (up $1000) Cost of Sales (down $500)

Decrease 500

Date 2012

Particulars General Ledger Subsidiary Ledger

Debit

$ Credit

$ Debit

$ Credit

$

20th Dec Sales Returns 1000

GST Clearing 100

Debtor – MACRO Organic Stores 1100

Debtors Control 1100

Stock Control 500

Cost of Sales 500

Sales Return as per Credit Note No. 6

30th Dec Creditors Control 550

Creditor – Spuds Galore 550

Stock Control 500

GST Clearing 50

Purchase return per Credit Note CN 4

Purchase Returns

4 entries

Sales Returns

6 entries

The School For Excellence 2011 The Essentials – Year 12 Accounting – Book 1 Page 16

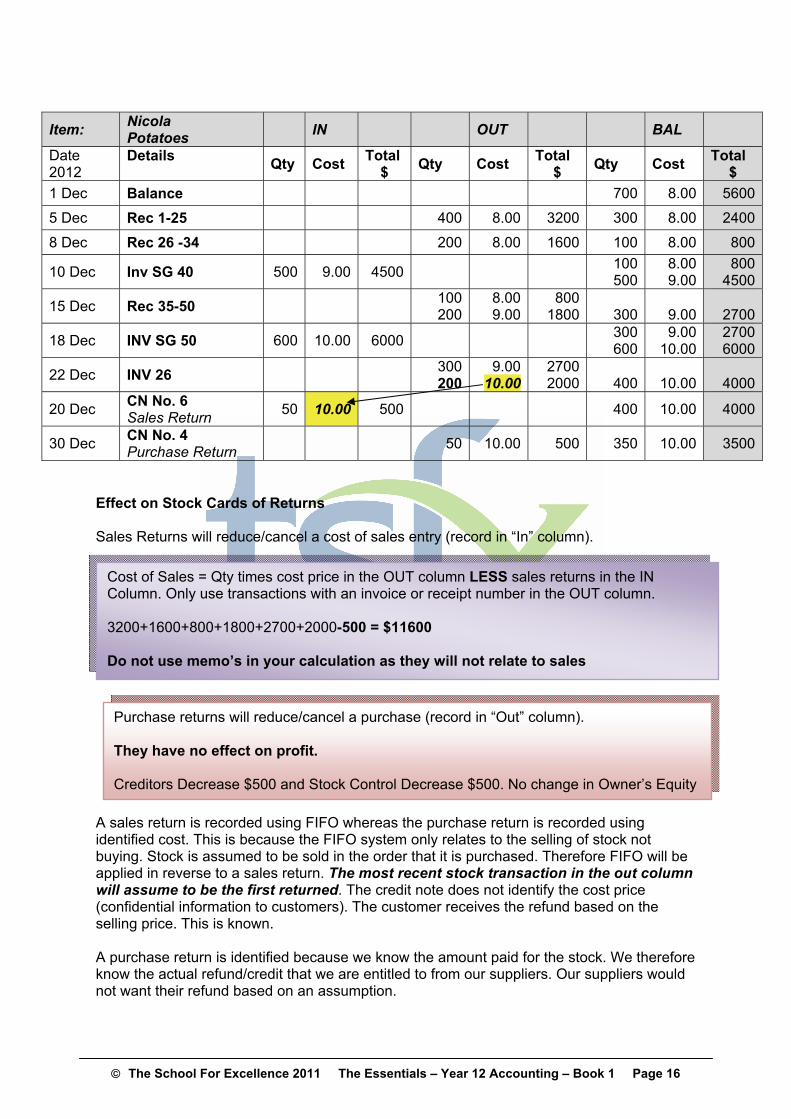

Item: Nicola Potatoes

IN OUT BAL

Date 2012

Details

Qty Cost Total

$ Qty Cost

Total $

Qty Cost Total

$

1 Dec Balance 700 8.00 5600

5 Dec Rec 1-25 400 8.00 3200 300 8.00 2400

8 Dec Rec 26 -34 200 8.00 1600 100 8.00 800

10 Dec Inv SG 40 500 9.00 4500 100 500

8.009.00

8004500

15 Dec Rec 35-50 100200

8.009.00

800 1800

300 9.00 2700

18 Dec INV SG 50 600 10.00 6000 300 600

9.0010.00

27006000

22 Dec INV 26 300200

9.0010.00

2700 2000

400 10.00 4000

20 Dec CN No. 6 Sales Return

50 10.00 500 400 10.00 4000

30 Dec CN No. 4 Purchase Return

50 10.00 500 350 10.00 3500

Effect on Stock Cards of Returns Sales Returns will reduce/cancel a cost of sales entry (record in “In” column). A sales return is recorded using FIFO whereas the purchase return is recorded using identified cost. This is because the FIFO system only relates to the selling of stock not buying. Stock is assumed to be sold in the order that it is purchased. Therefore FIFO will be applied in reverse to a sales return. The most recent stock transaction in the out column will assume to be the first returned. The credit note does not identify the cost price (confidential information to customers). The customer receives the refund based on the selling price. This is known. A purchase return is identified because we know the amount paid for the stock. We therefore know the actual refund/credit that we are entitled to from our suppliers. Our suppliers would not want their refund based on an assumption.

Cost of Sales = Qty times cost price in the OUT column LESS sales returns in the IN Column. Only use transactions with an invoice or receipt number in the OUT column. 3200+1600+800+1800+2700+2000-500 = $11600 Do not use memo’s in your calculation as they will not relate to sales

Purchase returns will reduce/cancel a purchase (record in “Out” column). They have no effect on profit. Creditors Decrease $500 and Stock Control Decrease $500. No change in Owner’s Equity

![[Specialist] 2010 TSFX Exam 2](https://img.pdfslide.net/doc/110x75/577c849a1a28abe054b999cf/specialist-2010-tsfx-exam-2.jpg)