Embed Size (px)

DESCRIPTION

Accounting Hot Topics – Hotter than the Summer of 2012. Welcome. Kyle Hansen Audit Manager. Greg Steiner Audit Partner. Tim Engeldinger Audit Managing Director. Today’s Agenda. Proposed Revenue Recognition Standard Disclosures about an Employer’s Participation in a Multiemployer Plan - PowerPoint PPT Presentation

Citation preview

© Grant Thornton LLP. All rights reserved.

Accounting Hot Topics – Hotter than the Summer of 2012

© Grant Thornton LLP. All rights reserved.

Welcome

Tim EngeldingerAudit Managing

Director

Greg SteinerAudit Partner

Kyle HansenAudit Manager

© Grant Thornton LLP. All rights reserved.

Today’s Agenda

• Proposed Revenue Recognition Standard

• Disclosures about an Employer’s Participation in a Multiemployer Plan

• Presentation of Comprehensive Income

• Variable Interest Entities

• Proposed Leasing Standard

© Grant Thornton LLP. All rights reserved.

Proposed Revenue Recognition Standard

• Overview

• Proposed revenue recognition model

• Other issues

• Next steps

© Grant Thornton LLP. All rights reserved.

Overview

• Original exposure draft issued in June 2010

• Almost 1,000 comment letters received

• Revised exposure draft issued in November 2011

• Comment period ended in March 2012

• Target date for final standard 1st half of 2013

• Effective date – TBD, but no sooner than January 1, 2015• One year delayed effective date for private companies

© Grant Thornton LLP. All rights reserved.

Overview – continued

• Core principle: An entity shall recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration the entity expects to be entitled in exchange for those goods or services (ED par. 3)

• Goal: Standardizing revenue recognition reporting across industries while retaining many current construction industry practices

© Grant Thornton LLP. All rights reserved.

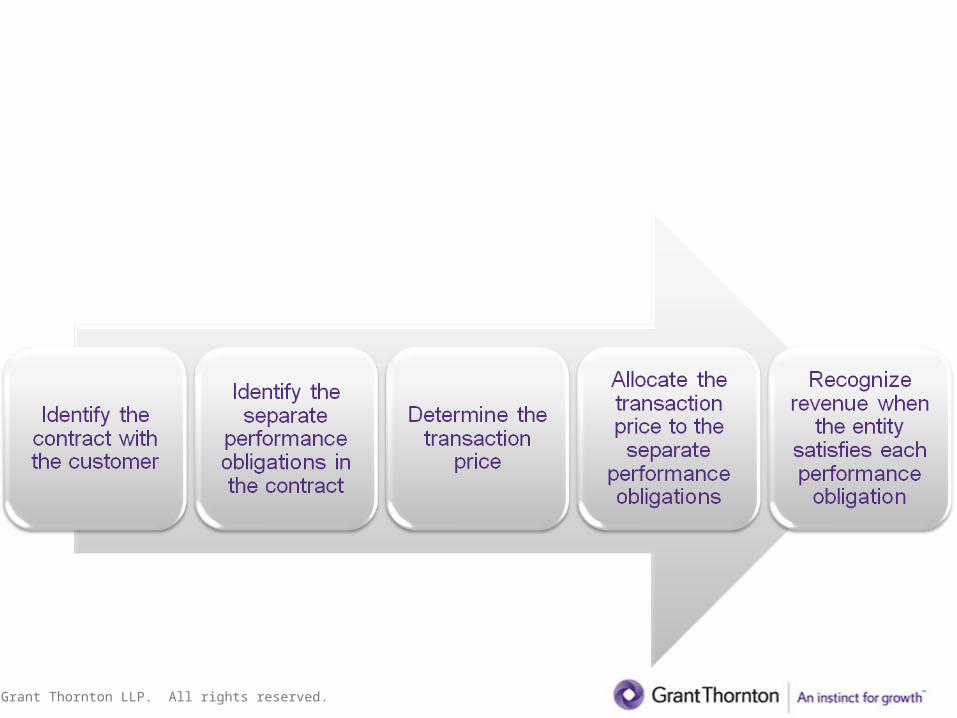

Proposed revenue recognition model

5 steps to apply the core principle

© Grant Thornton LLP. All rights reserved.

Proposed revenue recognition model – continued

Step 2 – Identify the separate performance obligations• Goods or services are highly interrelated and vendor provides

a service of integrating the goods or services into a combined item

• The vendor must significantly modify or customize the bundle of goods or services to fulfill the contract

If both of the above conditions exist, the bundle of goods or services are accounted for as a single performance obligation

© Grant Thornton LLP. All rights reserved.

Proposed revenue recognition model – continued

Step 3 – Determine the transaction price

Transaction price: The transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties (ED para. 50).

© Grant Thornton LLP. All rights reserved.

Proposed revenue recognition model – continued

Step 3 – Determine the transaction price

• Unapproved change orders, potential incentive payments and claims– Proposed standard allows these estimates to be

determined using either a probability-weighted approach or “most likely” estimates

– Most construction companies will utilize “most likely” approach for these estimates

Update the estimates each reporting period

© Grant Thornton LLP. All rights reserved.

Proposed revenue recognition model – continued

Step 5 – Recognize revenue

• Recognize revenue by measuring progress toward completion• Objective is to faithfully depict the entity’s performance (that

is, the pattern of transfer)– Output methods – direct measurements of customer value

such as milestones reached or units produced– Input methods – based on vendor’s efforts such as costs

incurred, labor hours, or time lapsed• If unable to reasonably measure progress, but expect to

recover costs – recognize revenue to the extent of costs incurred

© Grant Thornton LLP. All rights reserved.

Other issues

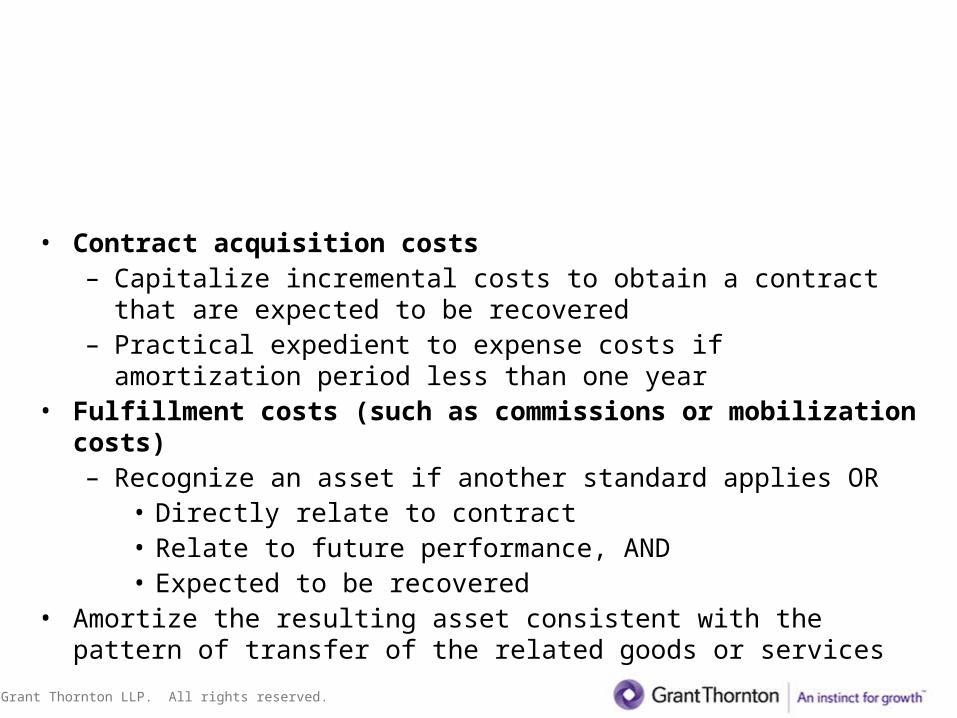

Contract costs

• Contract acquisition costs– Capitalize incremental costs to obtain a contract that are

expected to be recovered– Practical expedient to expense costs if amortization period

less than one year• Fulfillment costs (such as commissions or mobilization

costs)– Recognize an asset if another standard applies OR

• Directly relate to contract• Relate to future performance, AND• Expected to be recovered

• Amortize the resulting asset consistent with the pattern of transfer of the related goods or services

© Grant Thornton LLP. All rights reserved.

Next steps

• Redeliberations ongoing through December 2012 – recent discussions on:– Identifying separate performance obligations– Satisfying performance obligations– Constraining revenue– Collectibility– Time value of money

• Target date for final standard is first half of 2013• Retrospective transition method proposed with limited practical

expedients• Effective date – TBD, but no sooner than January 1, 2015

– One year delayed effective date for private companies

© Grant Thornton LLP. All rights reserved.

Next steps – continued

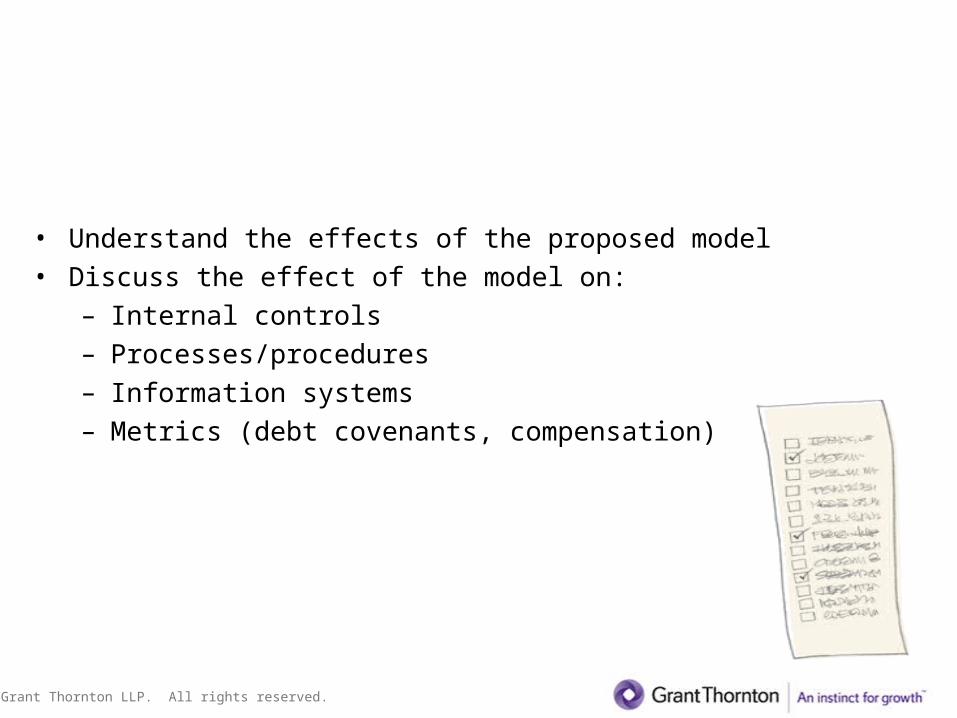

What should companies be doing now?

• Understand the effects of the proposed model• Discuss the effect of the model on:

– Internal controls– Processes/procedures– Information systems– Metrics (debt covenants, compensation)

© Grant Thornton LLP. All rights reserved.

Today’s Agenda

• Proposed Revenue Recognition Standard

• Disclosures about an Employer’s Participation in a Mulitemployer Plan

• Presentation of Comprehensive Income

• Variable Interest Entities

• Proposed Leasing Standard

© Grant Thornton LLP. All rights reserved.

Disclosures about an Employer’s Participation in a Multiemployer Plan (ASU 2011-09)

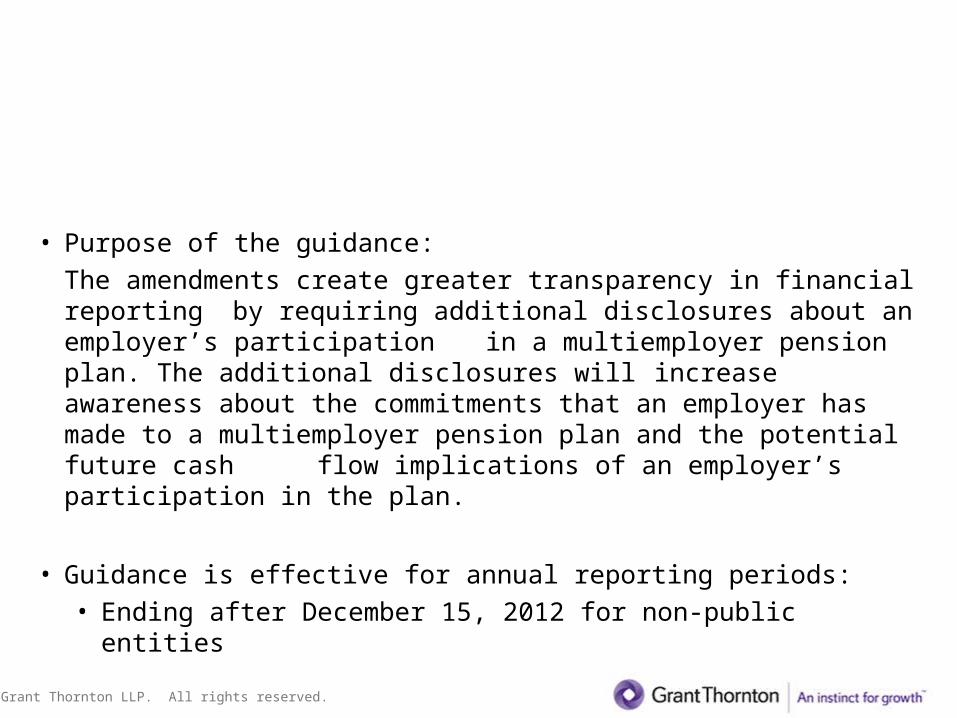

• Purpose of the guidance:The amendments create greater transparency in financial reporting by requiring additional disclosures about an employer’s participation in a multiemployer pension plan. The additional disclosures will increase awareness about the commitments that an employer has made to a multiemployer pension plan and the potential future cash flow implications of an employer’s participation in the plan.

• Guidance is effective for annual reporting periods:• Ending after December 15, 2012 for non-public entities

© Grant Thornton LLP. All rights reserved.

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

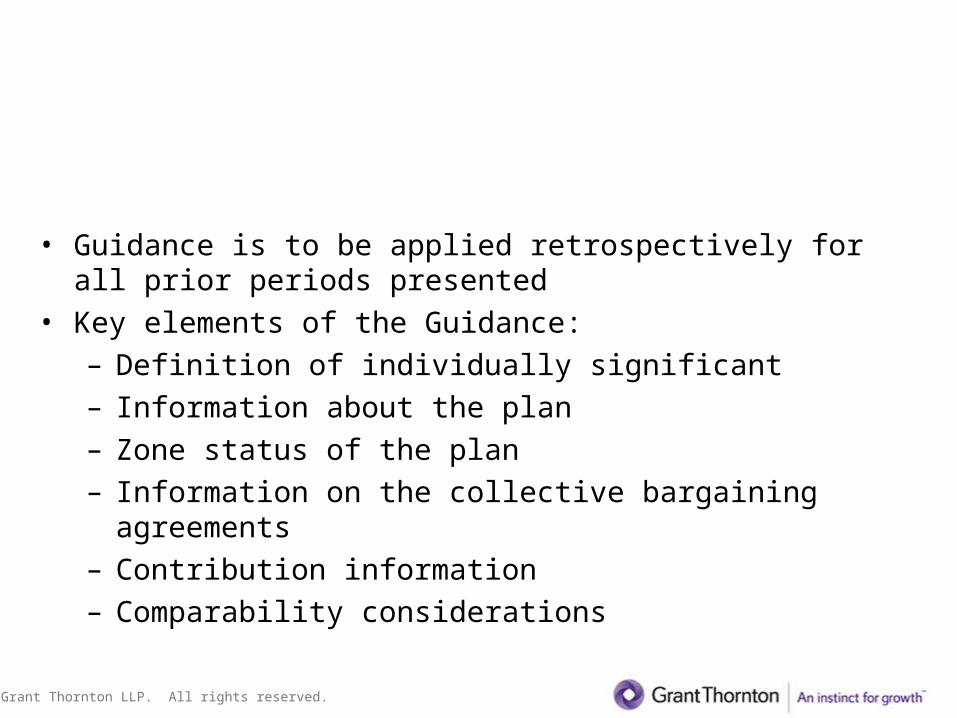

• Guidance is to be applied retrospectively for all prior periods presented

• Key elements of the Guidance:– Definition of individually significant– Information about the plan– Zone status of the plan– Information on the collective bargaining agreements– Contribution information– Comparability considerations

© Grant Thornton LLP. All rights reserved.

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

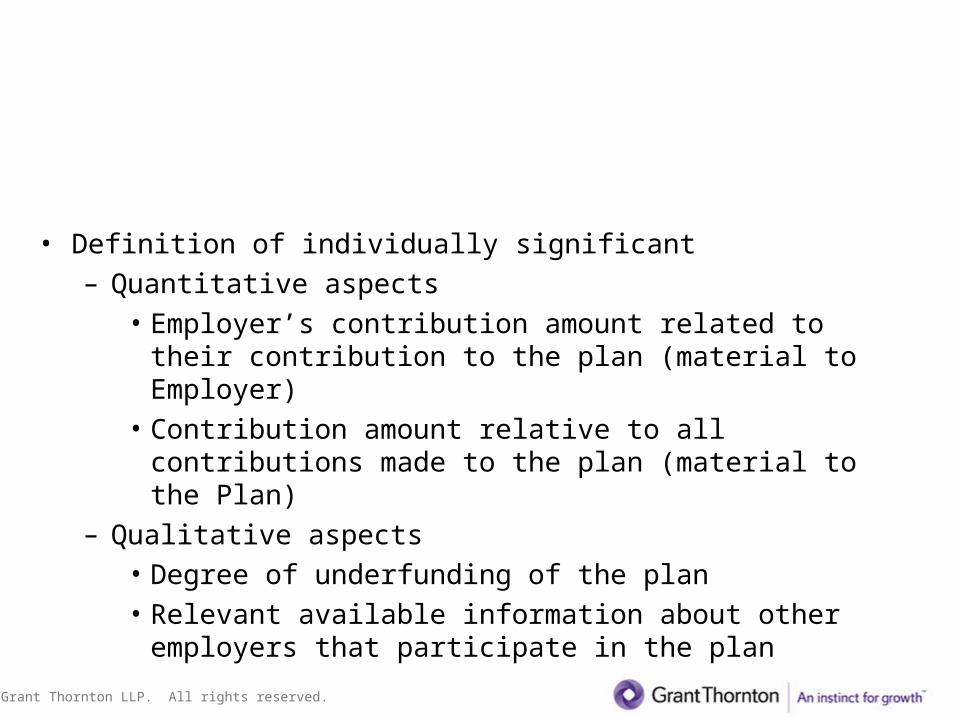

• Definition of individually significant– Quantitative aspects

• Employer’s contribution amount related to their contribution to the plan (material to Employer)

• Contribution amount relative to all contributions made to the plan (material to the Plan)

– Qualitative aspects• Degree of underfunding of the plan• Relevant available information about other

employers that participate in the plan

© Grant Thornton LLP. All rights reserved.

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

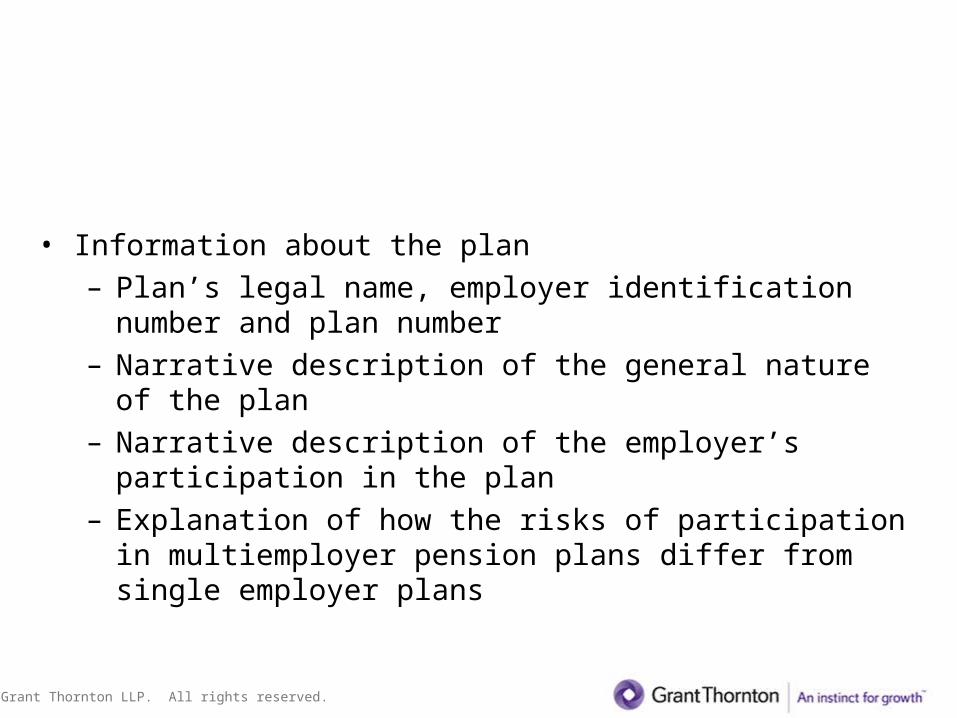

• Information about the plan– Plan’s legal name, employer identification number

and plan number– Narrative description of the general nature of the

plan– Narrative description of the employer’s participation

in the plan– Explanation of how the risks of participation in

multiemployer pension plans differ from single employer plans

© Grant Thornton LLP. All rights reserved.

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

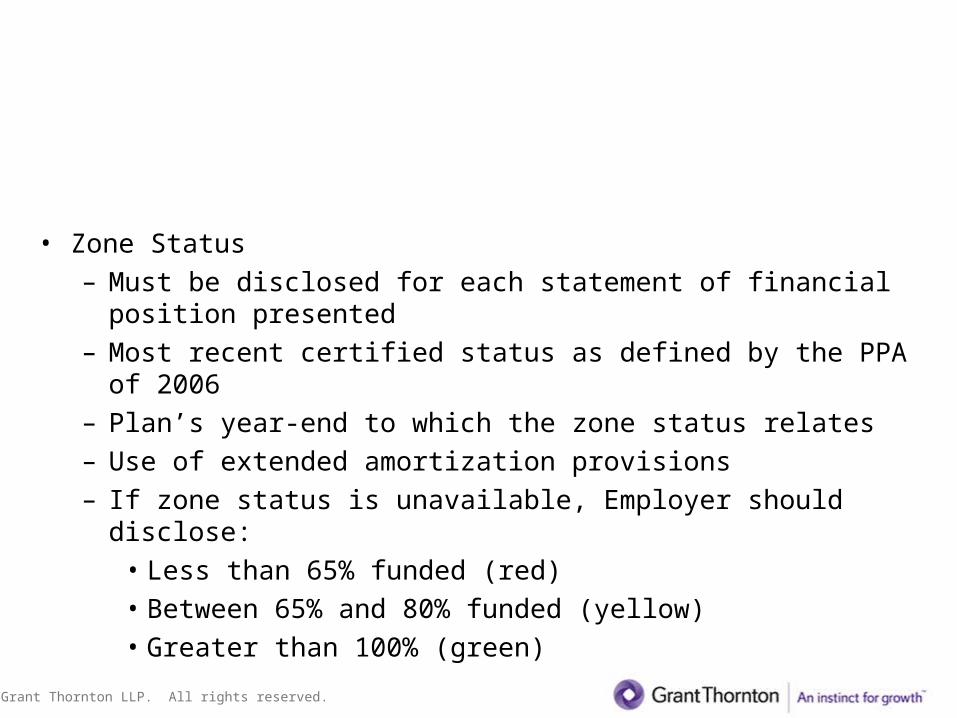

• Zone Status– Must be disclosed for each statement of financial

position presented– Most recent certified status as defined by the PPA of

2006– Plan’s year-end to which the zone status relates– Use of extended amortization provisions – If zone status is unavailable, Employer should disclose:

• Less than 65% funded (red)• Between 65% and 80% funded (yellow)• Greater than 100% (green)

© Grant Thornton LLP. All rights reserved.

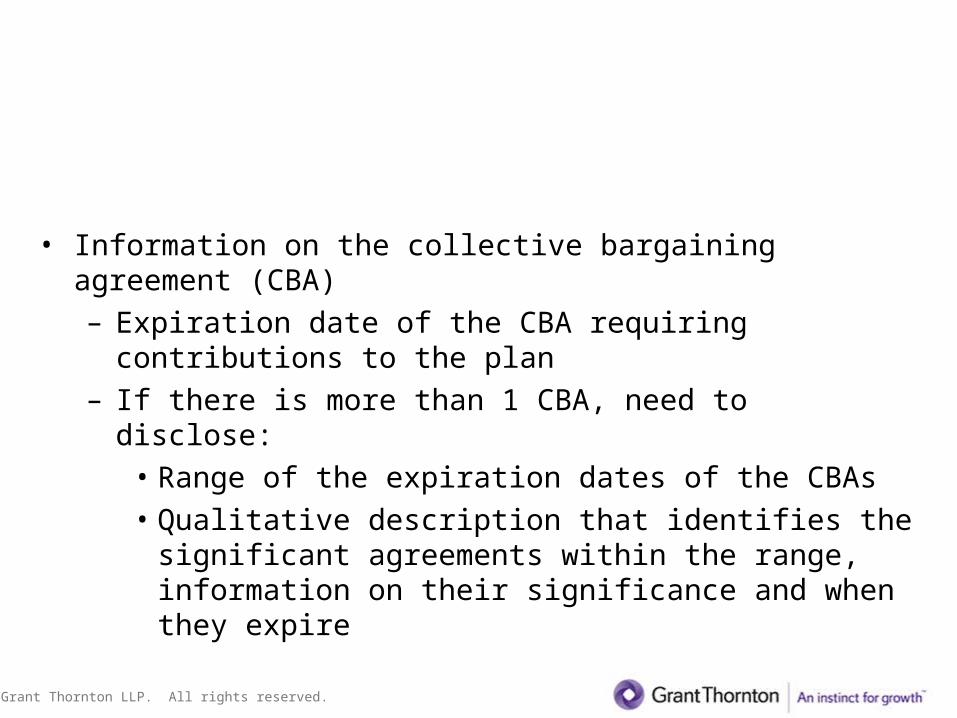

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

• Information on the collective bargaining agreement (CBA)– Expiration date of the CBA requiring contributions to

the plan– If there is more than 1 CBA, need to disclose:

• Range of the expiration dates of the CBAs• Qualitative description that identifies the

significant agreements within the range, information on their significance and when they expire

© Grant Thornton LLP. All rights reserved.

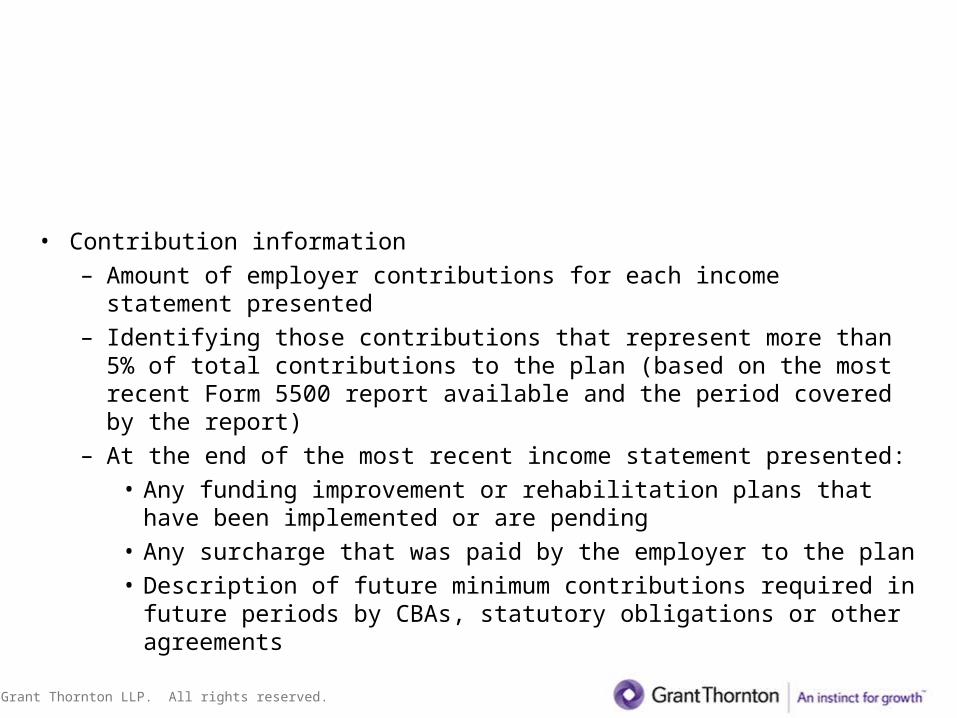

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

• Contribution information– Amount of employer contributions for each income statement

presented– Identifying those contributions that represent more than 5% of

total contributions to the plan (based on the most recent Form 5500 report available and the period covered by the report)

– At the end of the most recent income statement presented:• Any funding improvement or rehabilitation plans that have

been implemented or are pending• Any surcharge that was paid by the employer to the plan• Description of future minimum contributions required in

future periods by CBAs, statutory obligations or other agreements

© Grant Thornton LLP. All rights reserved.

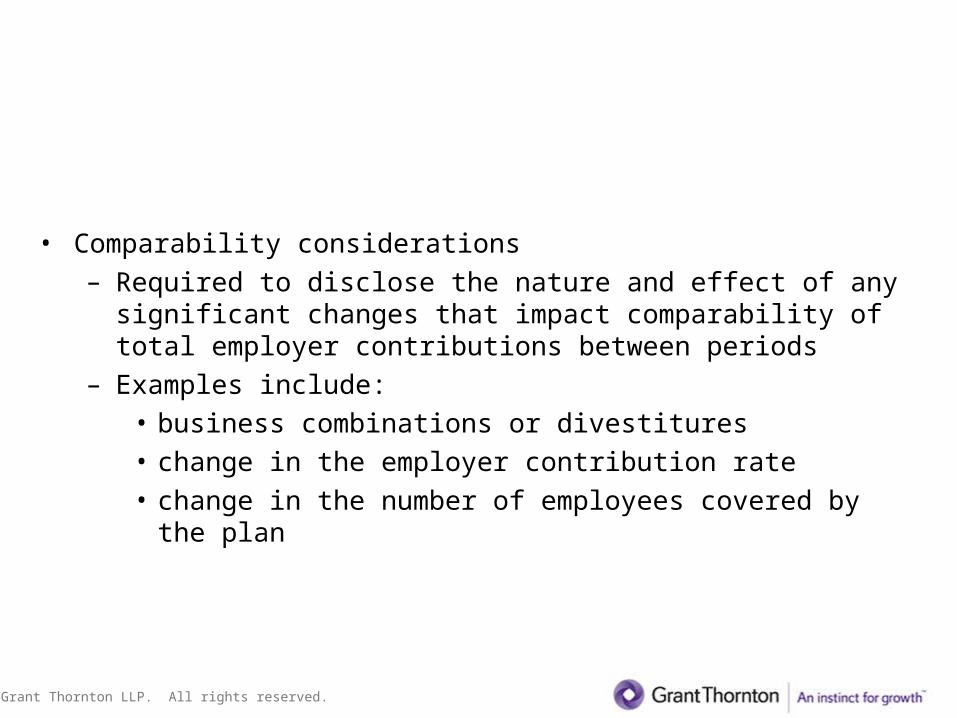

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

• Comparability considerations– Required to disclose the nature and effect of any

significant changes that impact comparability of total employer contributions between periods

– Examples include:• business combinations or divestitures• change in the employer contribution rate• change in the number of employees covered by the plan

© Grant Thornton LLP. All rights reserved.

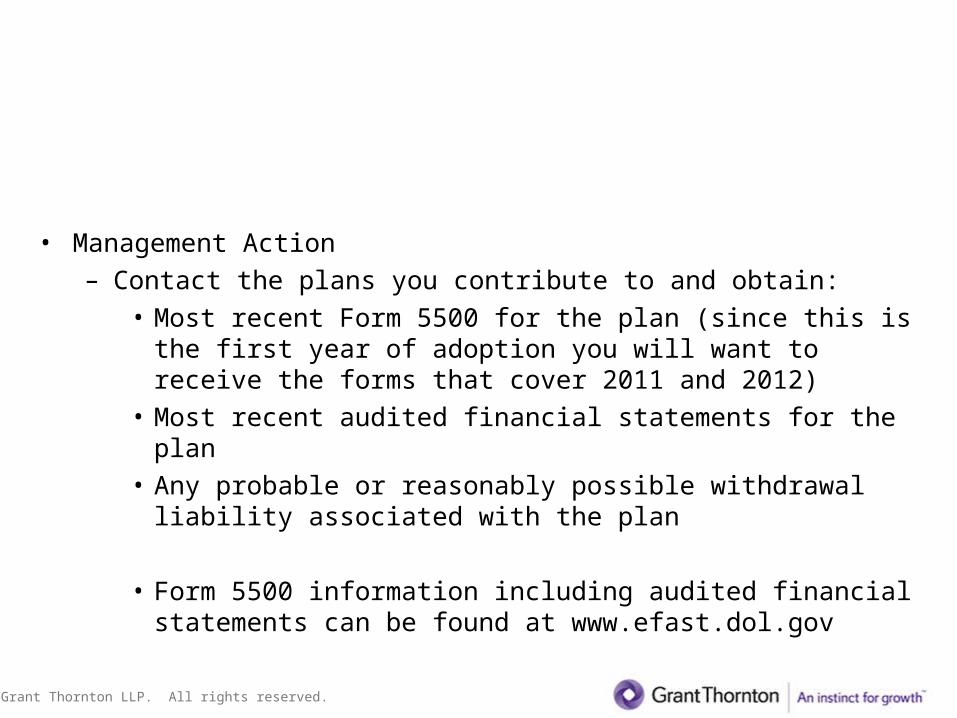

Disclosures about an Employer’s Participation in a Multiemployer Plan – continued

• Management Action– Contact the plans you contribute to and obtain:

• Most recent Form 5500 for the plan (since this is the first year of adoption you will want to receive the forms that cover 2011 and 2012)

• Most recent audited financial statements for the plan• Any probable or reasonably possible withdrawal

liability associated with the plan

• Form 5500 information including audited financial statements can be found at www.efast.dol.gov

© Grant Thornton LLP. All rights reserved.

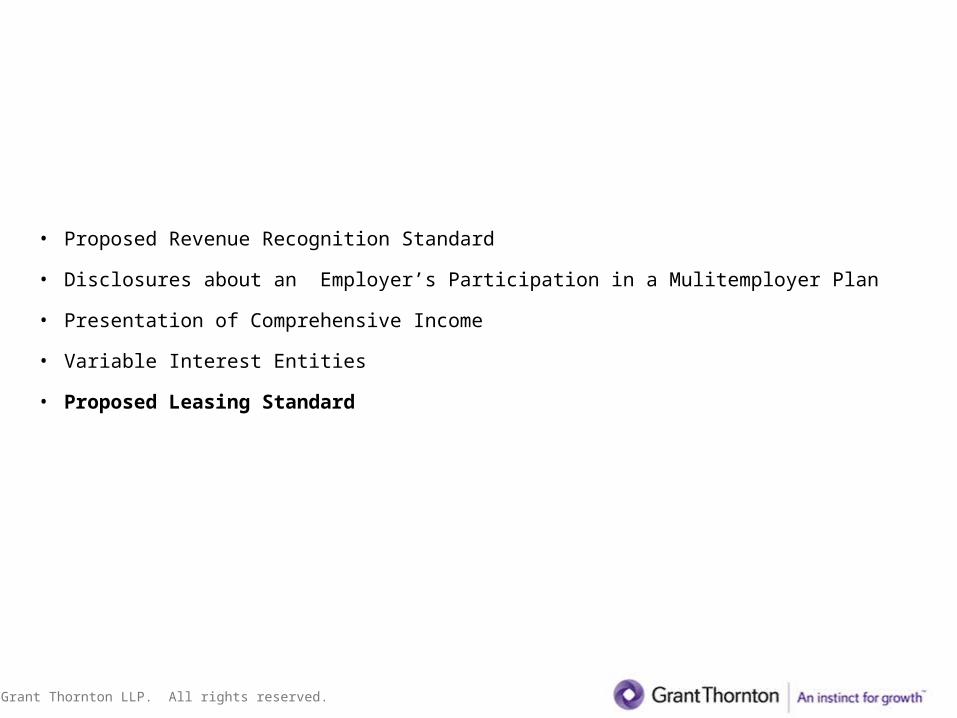

Today’s Agenda

• Proposed Revenue Recognition Standard

• Disclosures about an Employer’s Participation in a Mulitemployer Plan

• Presentation of Comprehensive Income

• Variable Interest Entities

• Proposed Leasing Standard

© Grant Thornton LLP. All rights reserved.

Presentation of Comprehensive Income (ASU 2011-05)

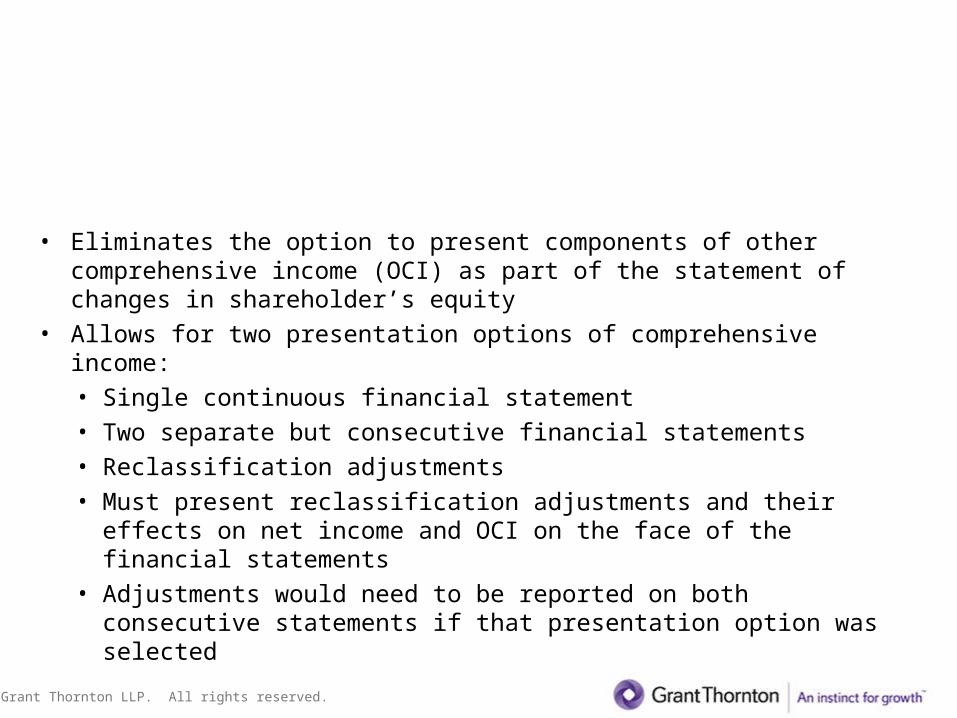

• Eliminates the option to present components of other comprehensive income (OCI) as part of the statement of changes in shareholder’s equity

• Allows for two presentation options of comprehensive income:• Single continuous financial statement• Two separate but consecutive financial statements• Reclassification adjustments• Must present reclassification adjustments and their effects

on net income and OCI on the face of the financial statements

• Adjustments would need to be reported on both consecutive statements if that presentation option was selected

© Grant Thornton LLP. All rights reserved.

Presentation of Comprehensive Income – continued

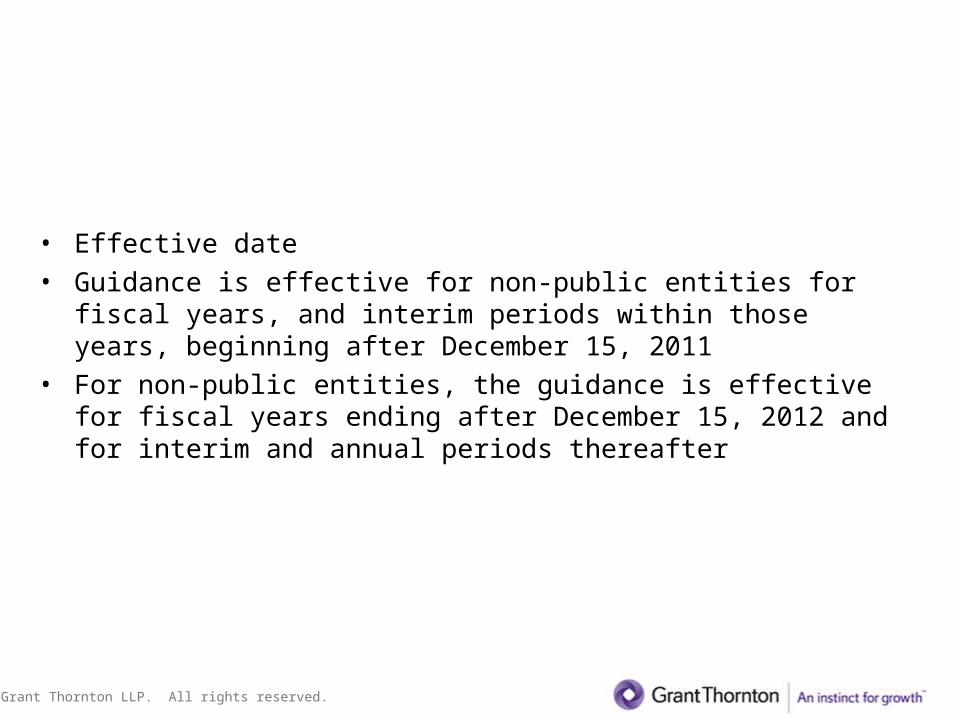

• Effective date• Guidance is effective for non-public entities for fiscal years,

and interim periods within those years, beginning after December 15, 2011

• For non-public entities, the guidance is effective for fiscal years ending after December 15, 2012 and for interim and annual periods thereafter

© Grant Thornton LLP. All rights reserved.

Today’s Agenda

• Proposed Revenue Recognition Standard

• Disclosures about an Employer’s Participation in a Mulitemployer Plan

• Presentation of Comprehensive Income

• Variable Interest Entities

• Proposed Leasing Standard

© Grant Thornton LLP. All rights reserved.

Variable Interest Entities (VIEs)

Key Concepts

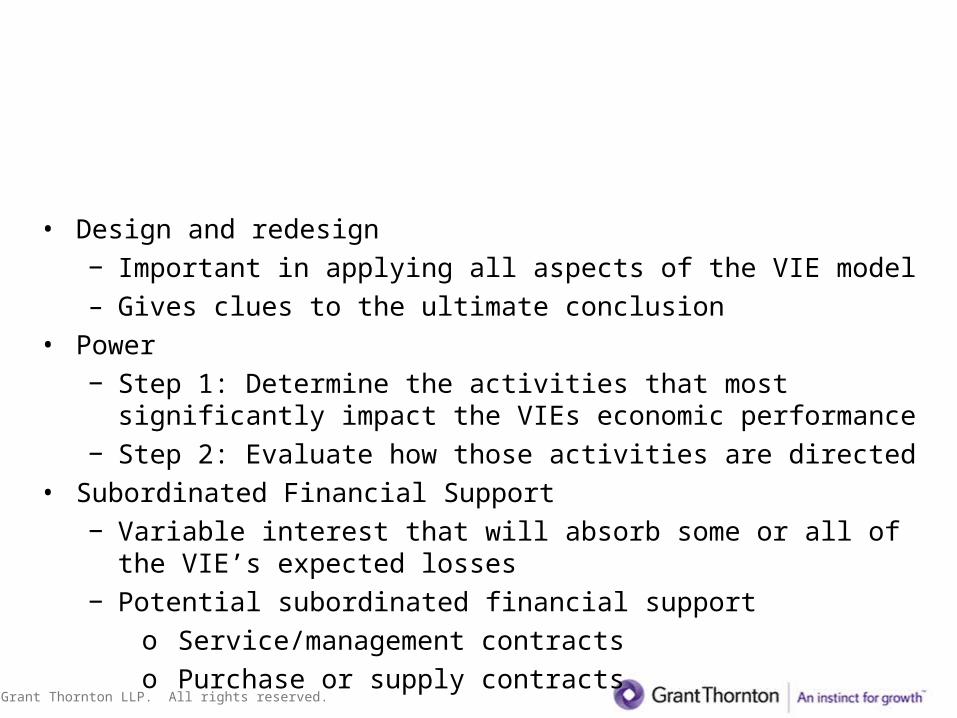

• Design and redesign− Important in applying all aspects of the VIE model– Gives clues to the ultimate conclusion

• Power− Step 1: Determine the activities that most significantly

impact the VIEs economic performance− Step 2: Evaluate how those activities are directed

• Subordinated Financial Support− Variable interest that will absorb some or all of the VIE’s

expected losses− Potential subordinated financial support

o Service/management contractso Purchase or supply contracts

© Grant Thornton LLP. All rights reserved.

Variable Interest Entities – continued

Variable Interests

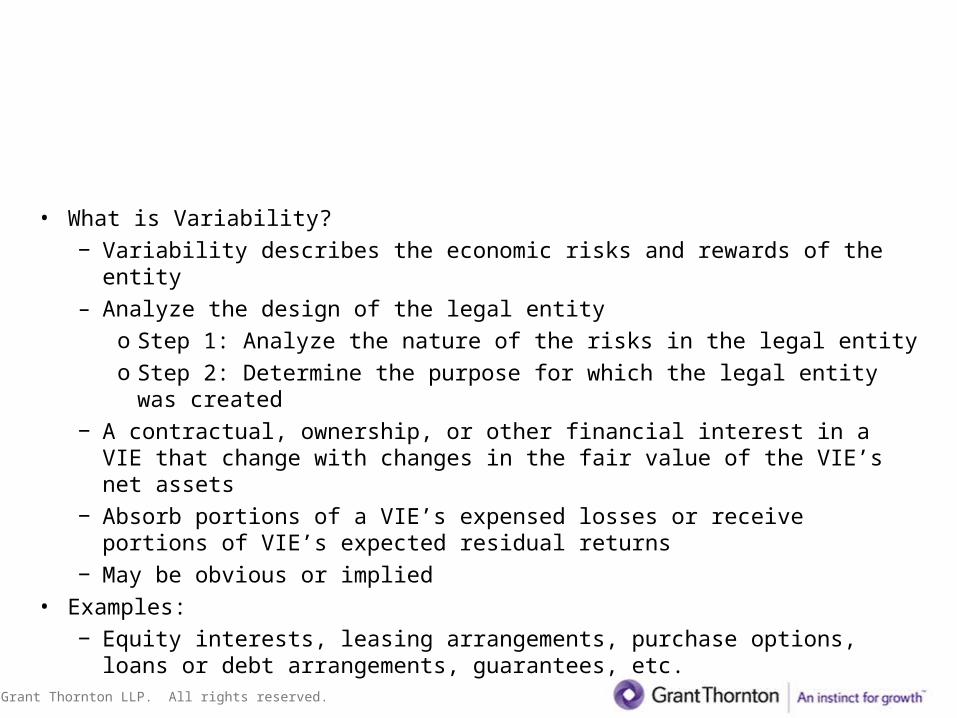

• What is Variability?− Variability describes the economic risks and rewards of the entity– Analyze the design of the legal entity

o Step 1: Analyze the nature of the risks in the legal entityo Step 2: Determine the purpose for which the legal entity was

created − A contractual, ownership, or other financial interest in a VIE that

change with changes in the fair value of the VIE’s net assets − Absorb portions of a VIE’s expensed losses or receive portions of

VIE’s expected residual returns− May be obvious or implied

• Examples:− Equity interests, leasing arrangements, purchase options, loans

or debt arrangements, guarantees, etc.

© Grant Thornton LLP. All rights reserved.

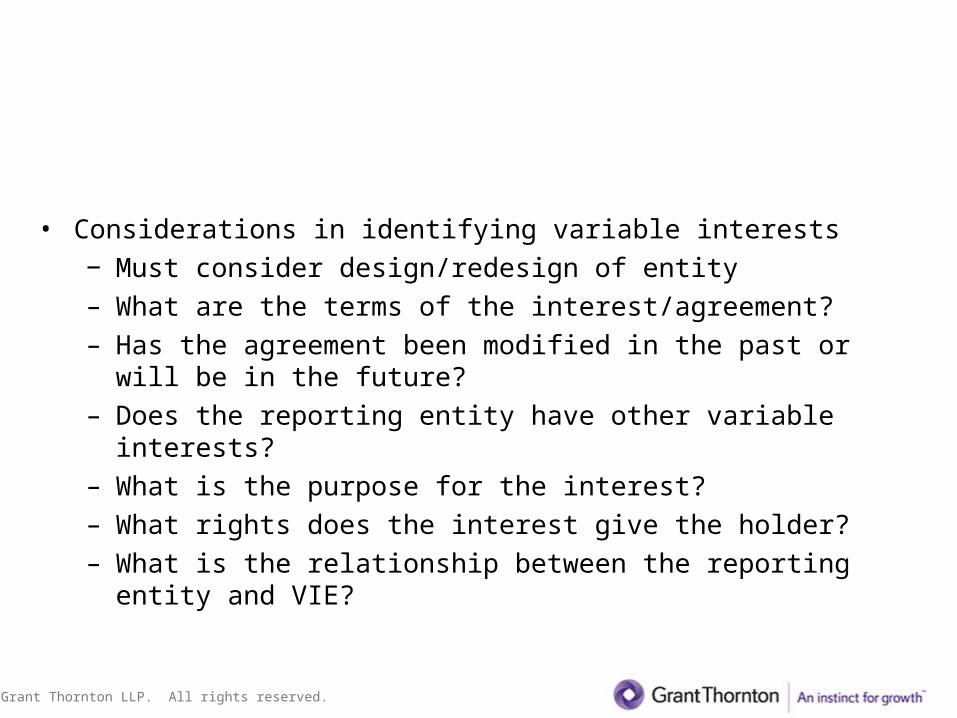

Variable Interest Entities – continued

Variable Interests

• Considerations in identifying variable interests− Must consider design/redesign of entity– What are the terms of the interest/agreement?– Has the agreement been modified in the past or will be in

the future?– Does the reporting entity have other variable interests?– What is the purpose for the interest?– What rights does the interest give the holder?– What is the relationship between the reporting entity and

VIE?

© Grant Thornton LLP. All rights reserved.

Variable Interest Entities – continued

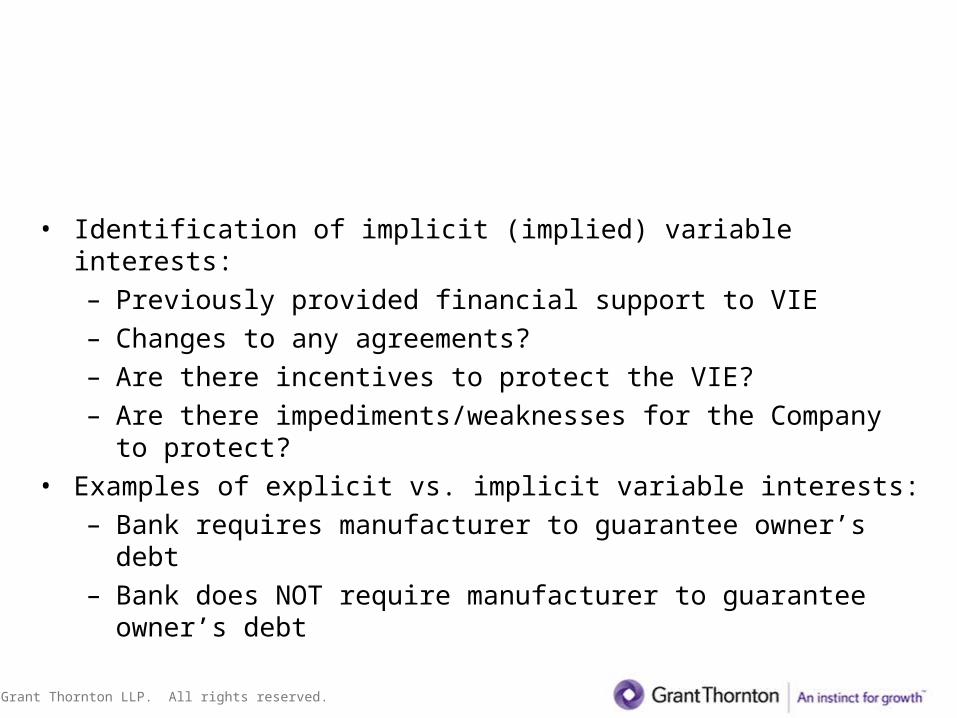

Variable Interests

• Identification of implicit (implied) variable interests:– Previously provided financial support to VIE– Changes to any agreements?– Are there incentives to protect the VIE?– Are there impediments/weaknesses for the Company to

protect?• Examples of explicit vs. implicit variable interests:

– Bank requires manufacturer to guarantee owner’s debt– Bank does NOT require manufacturer to guarantee

owner’s debt

© Grant Thornton LLP. All rights reserved.

Variable Interest Entities – continued

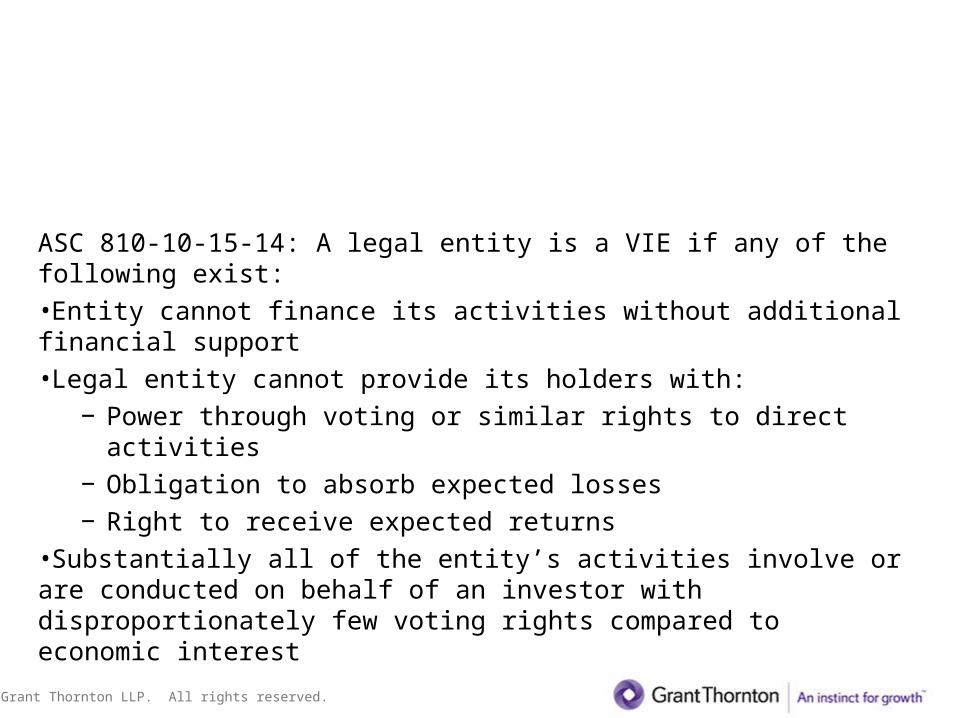

What is a Variable Interest Entity or VIE?

ASC 810-10-15-14: A legal entity is a VIE if any of the following exist:•Entity cannot finance its activities without additional financial support•Legal entity cannot provide its holders with:

− Power through voting or similar rights to direct activities

− Obligation to absorb expected losses − Right to receive expected returns

•Substantially all of the entity’s activities involve or are conducted on behalf of an investor with disproportionately few voting rights compared to economic interest

© Grant Thornton LLP. All rights reserved.

Variable Interest Entities – continued

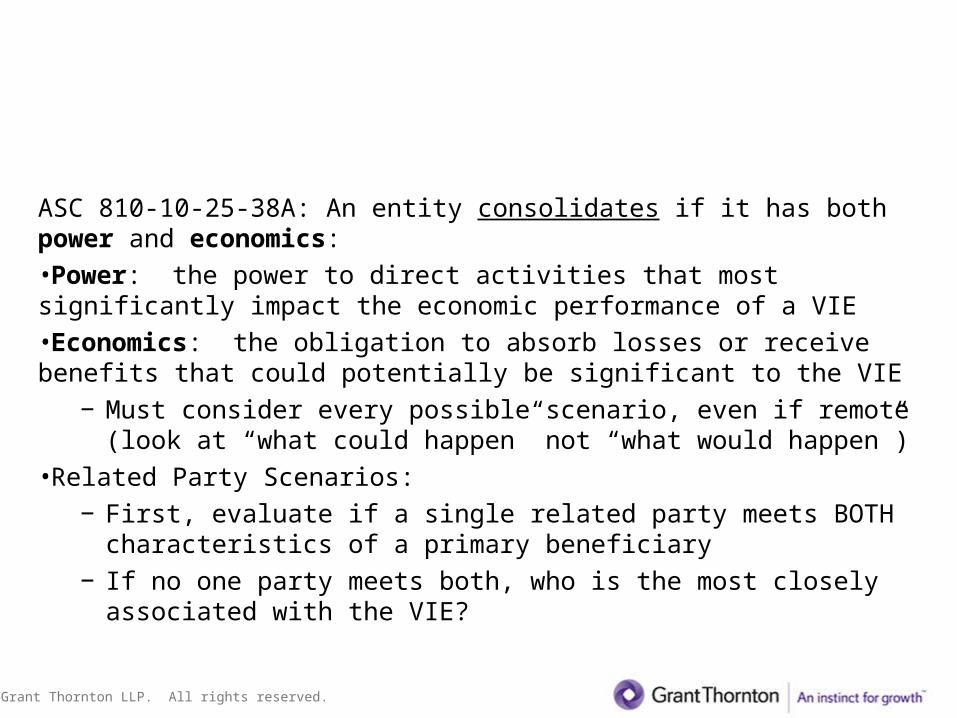

Determining the Primary Beneficiary of a VIE:

ASC 810-10-25-38A: An entity consolidates if it has both power and economics:•Power: the power to direct activities that most significantly impact the economic performance of a VIE•Economics: the obligation to absorb losses or receive benefits that could potentially be significant to the VIE

− Must consider every possible scenario, even if remote (look at “what could happen” not “what would happen”)

•Related Party Scenarios:− First, evaluate if a single related party meets BOTH

characteristics of a primary beneficiary− If no one party meets both, who is the most closely

associated with the VIE?

© Grant Thornton LLP. All rights reserved.

Variable Interest Entities – continued

Recap of Variable Interest Entities:

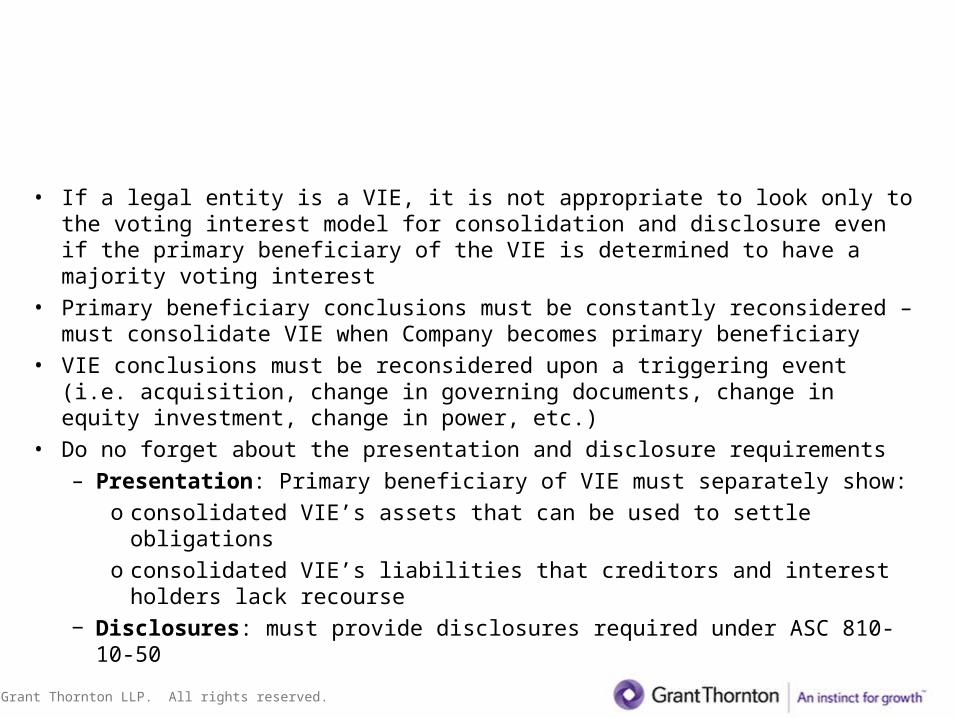

• If a legal entity is a VIE, it is not appropriate to look only to the voting interest model for consolidation and disclosure even if the primary beneficiary of the VIE is determined to have a majority voting interest

• Primary beneficiary conclusions must be constantly reconsidered – must consolidate VIE when Company becomes primary beneficiary

• VIE conclusions must be reconsidered upon a triggering event (i.e. acquisition, change in governing documents, change in equity investment, change in power, etc.)

• Do no forget about the presentation and disclosure requirements– Presentation: Primary beneficiary of VIE must separately show:

o consolidated VIE’s assets that can be used to settle obligationso consolidated VIE’s liabilities that creditors and interest holders

lack recourse− Disclosures: must provide disclosures required under ASC 810-

10-50

© Grant Thornton LLP. All rights reserved.

Today’s Agenda

• Proposed Revenue Recognition Standard

• Disclosures about an Employer’s Participation in a Mulitemployer Plan

• Presentation of Comprehensive Income

• Variable Interest Entities

• Proposed Leasing Standard

© Grant Thornton LLP. All rights reserved.

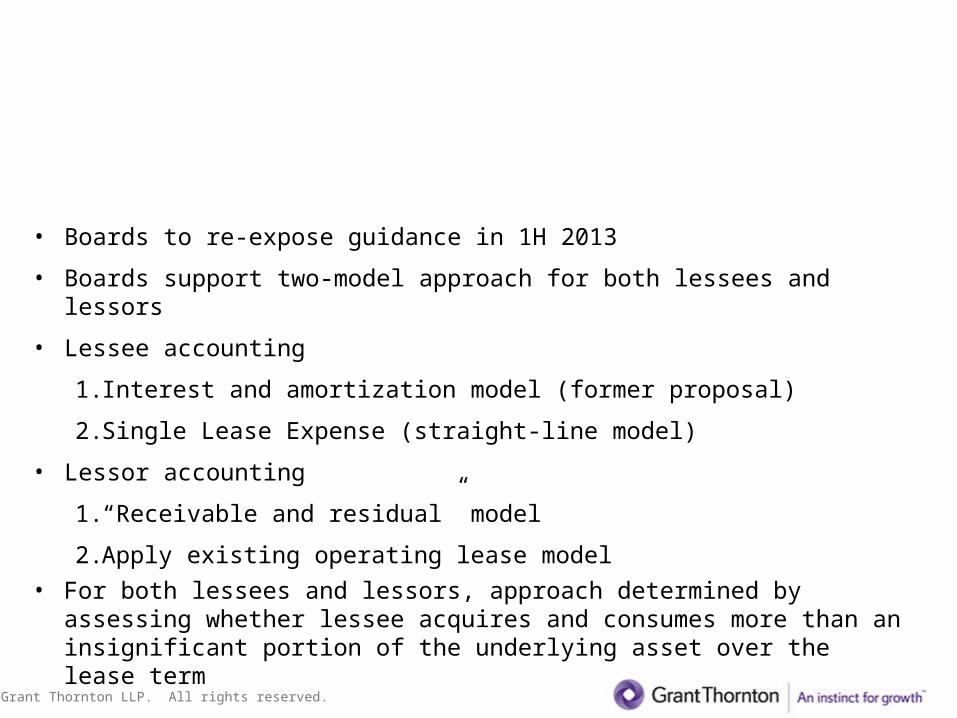

Proposed Leasing Standard

• Boards to re-expose guidance in 1H 2013

• Boards support two-model approach for both lessees and lessors

• Lessee accounting

1. Interest and amortization model (former proposal)

2. Single Lease Expense (straight-line model)

• Lessor accounting

1. “Receivable and residual” model

2. Apply existing operating lease model• For both lessees and lessors, approach determined by

assessing whether lessee acquires and consumes more than an insignificant portion of the underlying asset over the lease term

© Grant Thornton LLP. All rights reserved.

Are there any questions?

Thank You!