Embed Size (px)

Citation preview

Advanced Taxation Republic of Ireland 2nd Year Examination August 2014 Exam Paper, Solutions & Examiner’s Report

Advanced Taxation (ROI) August 2014 2nd Year Paper

2

NOTES TO USERS ABOUT THESE SOLUTIONS

The solutions in this document are published by Accounting Technicians Ireland. They are intended to provide guidance to students and their teachers regarding possible answers to questions in our examinations. Although they are published by us, we do not necessarily endorse these solutions or agree with the views expressed by their authors. There are often many possible approaches to the solution of questions in professional examinations. It should not be assumed that the approach adopted in these solutions is the ideal or the one preferred by us. Alternative answers will be marked on their own merits. This publication is intended to serve as an educational aid. For this reason, the published solutions will often be significantly longer than would be expected of a candidate in an examination. This will be particularly the case where discursive answers are involved. This publication is copyright 2014 and may not be reproduced without permission of Accounting Technicians Ireland. © Accounting Technicians Ireland, 2014.

Advanced Taxation (ROI) August 2014 2nd Year Paper

3 A2014 Adv. Taxation (ROI)

Accounting Technicians Ireland

2nd Year Examination: Autumn 2014 Paper

Paper: ADVANCED TAXATION (Republic of Ireland)

Thursday 14th August 2014 – 2.30 p.m. to 5.30 p.m.

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY For candidates answering in accordance with the law and practice of the Republic of Ireland. Candidates should answer the paper in accordance with the appropriate provisions up to and including the Finance Act, 2013. The provisions of the Finance Act (No 2), 2013 should be ignored. Allowances and rates of taxation, to be used by candidates, are set out in a separate booklet supplied with the examination paper. Answer ALL THREE QUESTIONS in Section A, and ANY TWO of the FOUR questions in Section B. If more than TWO questions are answered in Section B, then only the first two questions, in the order filed, will be corrected. Candidates should allocate their time carefully. All workings should be shown. All figures should be labelled as appropriate e.g. €s, units, etc. Answers should be illustrated with examples, where appropriate. Question 1 begins on Page 2 overleaf. The following insert is included with this paper. Tax Reference Material (ROI)

Advanced Taxation (ROI) August 2014 2nd Year Paper

4 A2014 Adv. Taxation (ROI)

SECTION A

Answer QUESTION 1 and QUESTION 2 and QUESTION 3 (Compulsory) in this Section QUESTION 1 (Compulsory) Brian aged 43 and John aged 38 entered into a civil partnership in 2011. They are both medical professionals. Brian has his own GP practice and John works part-time for the HSE as he stays at home three days a week to look after their daughter Penny. Brian had started his own GP practice on the 1st May 2011 and his profits have been as follows:- € Year ended 30th April 2012 90,000 Year ended 30th April 2013 75,000 Brian purchased the following assets for use in his GP surgery: Date Details Cost (€) 1/5/2011 Computer system 10,000 1/5/2011 Motor vehicle emissions 140g/km 25% private use 35,000 1/5/2011 Office furniture 5,000 1/7/2012 Medical equipment 20,000 Details of Brian’s other income and outgoings for 2013 are as follows:- € Deposit interest received from AIB plc 2,640 Rental income from Spanish property 9,500 Annual maintenance payment to ex-spouse Siobhan 15,000 Retirement annuity – annual premium 9,500 Permanent health insurance 950 John works two days a week for the HSE. His salary for 2013 was €26,000 (PAYE deducted €2,000). John’s only other income was a dividend from an Irish company of €600 gross. Required: Calculate Brian and John’s Income tax for 2013. You may assume that they have elected for separate assessment. Total 20 Marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

5 A2014 Adv. Taxation (ROI)

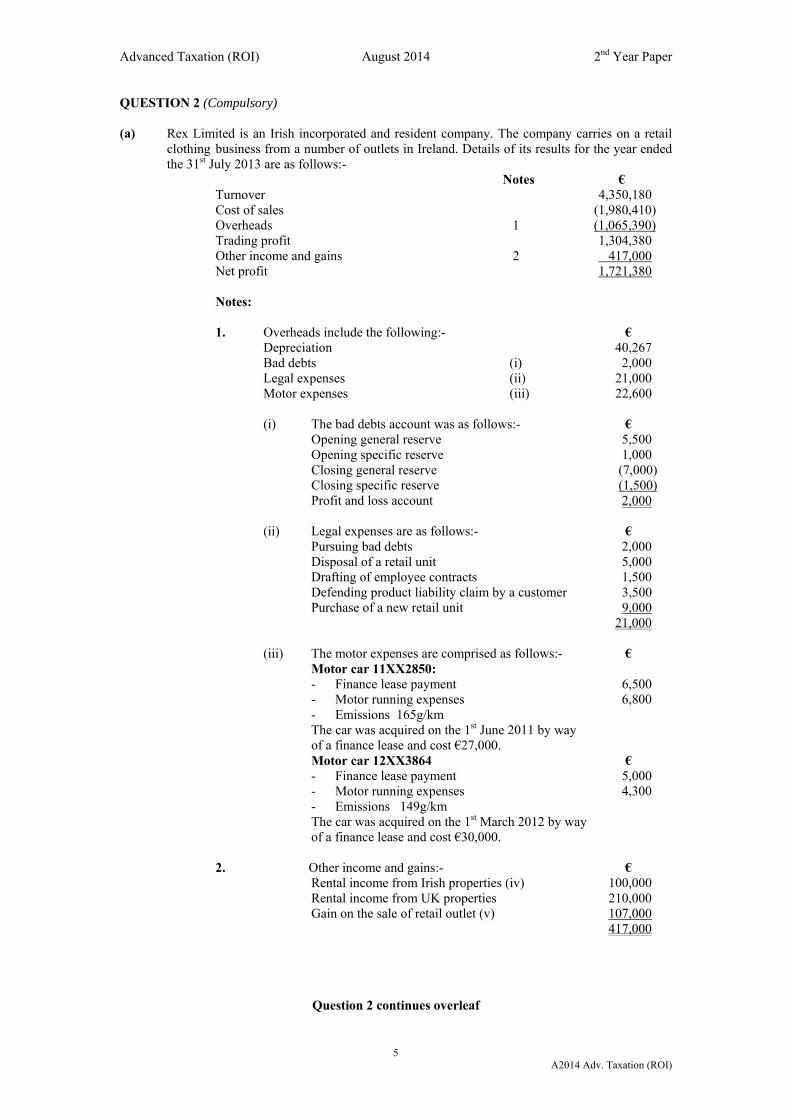

QUESTION 2 (Compulsory) (a) Rex Limited is an Irish incorporated and resident company. The company carries on a retail

clothing business from a number of outlets in Ireland. Details of its results for the year ended the 31st July 2013 are as follows:-

Notes € Turnover 4,350,180 Cost of sales (1,980,410) Overheads 1 (1,065,390) Trading profit 1,304,380 Other income and gains 2 417,000 Net profit 1,721,380 Notes: 1. Overheads include the following:- € Depreciation 40,267 Bad debts (i) 2,000 Legal expenses (ii) 21,000 Motor expenses (iii) 22,600 (i) The bad debts account was as follows:- € Opening general reserve 5,500 Opening specific reserve 1,000 Closing general reserve (7,000) Closing specific reserve (1,500) Profit and loss account 2,000 (ii) Legal expenses are as follows:- € Pursuing bad debts 2,000 Disposal of a retail unit 5,000 Drafting of employee contracts 1,500 Defending product liability claim by a customer 3,500 Purchase of a new retail unit 9,000 21,000 (iii) The motor expenses are comprised as follows:- € Motor car 11XX2850:

- Finance lease payment 6,500 - Motor running expenses 6,800 - Emissions 165g/km The car was acquired on the 1st June 2011 by way of a finance lease and cost €27,000. Motor car 12XX3864 € - Finance lease payment 5,000 - Motor running expenses 4,300 - Emissions 149g/km The car was acquired on the 1st March 2012 by way of a finance lease and cost €30,000.

2. Other income and gains:- € Rental income from Irish properties (iv) 100,000 Rental income from UK properties 210,000 Gain on the sale of retail outlet (v) 107,000

417,000

Question 2 continues overleaf

Advanced Taxation (ROI) August 2014 2nd Year Paper

6 A2014 Adv. Taxation (ROI)

QUESTION 2 (Cont’d)

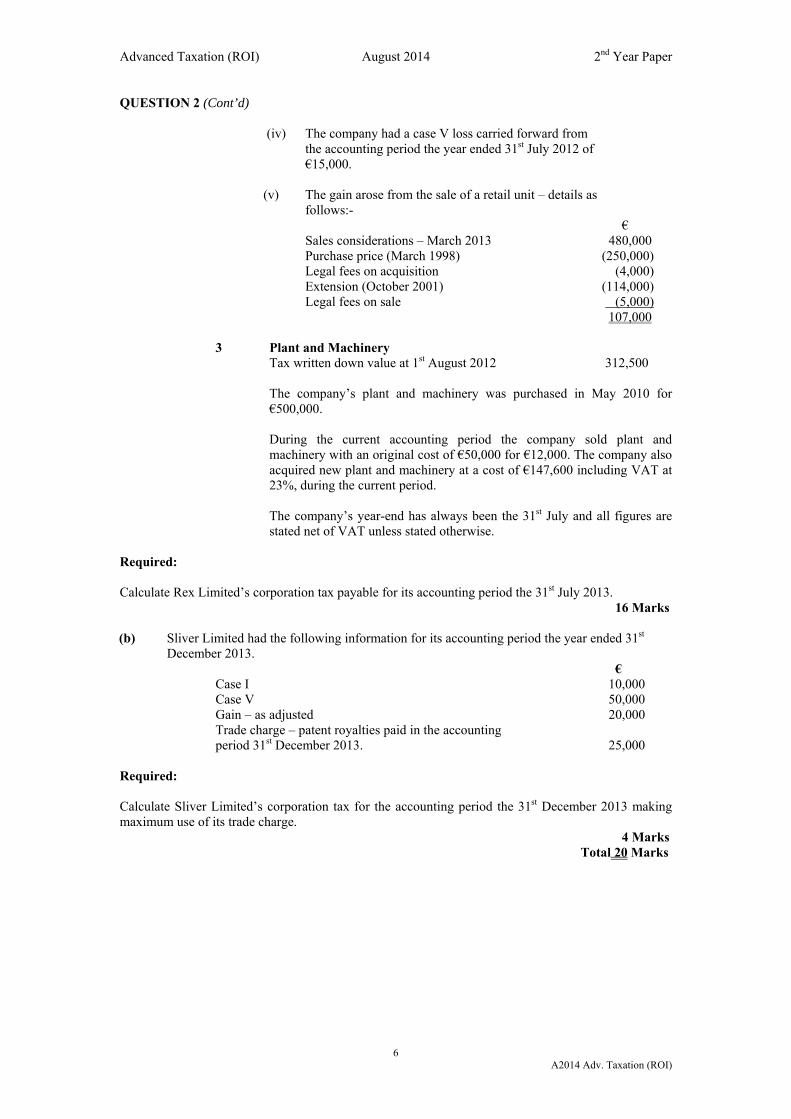

(iv) The company had a case V loss carried forward from the accounting period the year ended 31st July 2012 of €15,000.

(v) The gain arose from the sale of a retail unit – details as follows:- € Sales considerations – March 2013 480,000 Purchase price (March 1998) (250,000) Legal fees on acquisition (4,000) Extension (October 2001) (114,000) Legal fees on sale (5,000) 107,000

3 Plant and Machinery Tax written down value at 1st August 2012 312,500 The company’s plant and machinery was purchased in May 2010 for

€500,000. During the current accounting period the company sold plant and

machinery with an original cost of €50,000 for €12,000. The company also acquired new plant and machinery at a cost of €147,600 including VAT at 23%, during the current period.

The company’s year-end has always been the 31st July and all figures are

stated net of VAT unless stated otherwise.

Required:

Calculate Rex Limited’s corporation tax payable for its accounting period the 31st July 2013. 16 Marks

(b) Sliver Limited had the following information for its accounting period the year ended 31st

December 2013. € Case I 10,000 Case V 50,000 Gain – as adjusted 20,000 Trade charge – patent royalties paid in the accounting period 31st December 2013. 25,000

Required: Calculate Sliver Limited’s corporation tax for the accounting period the 31st December 2013 making maximum use of its trade charge. 4 Marks

Total 20 Marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

7 A2014 Adv. Taxation (ROI)

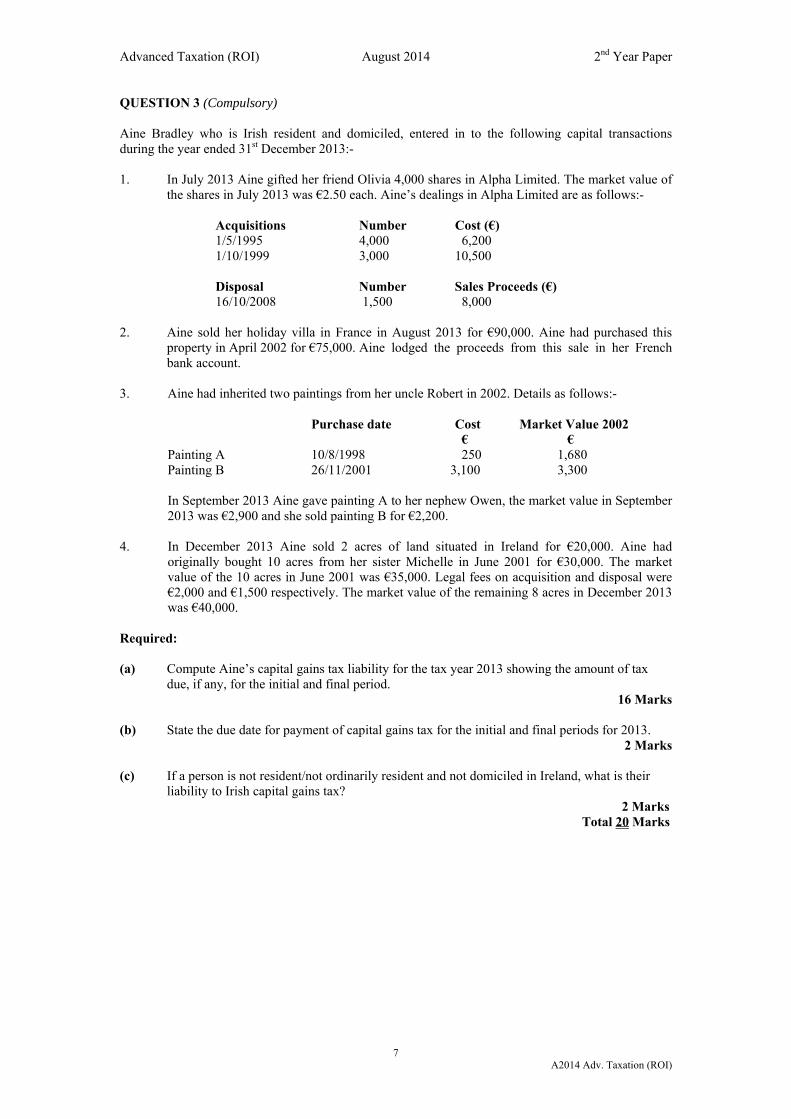

QUESTION 3 (Compulsory) Aine Bradley who is Irish resident and domiciled, entered in to the following capital transactions during the year ended 31st December 2013:- 1. In July 2013 Aine gifted her friend Olivia 4,000 shares in Alpha Limited. The market value of

the shares in July 2013 was €2.50 each. Aine’s dealings in Alpha Limited are as follows:- Acquisitions Number Cost (€) 1/5/1995 4,000 6,200 1/10/1999 3,000 10,500 Disposal Number Sales Proceeds (€) 16/10/2008 1,500 8,000 2. Aine sold her holiday villa in France in August 2013 for €90,000. Aine had purchased this

property in April 2002 for €75,000. Aine lodged the proceeds from this sale in her French bank account.

3. Aine had inherited two paintings from her uncle Robert in 2002. Details as follows:- Purchase date Cost Market Value 2002 € € Painting A 10/8/1998 250 1,680 Painting B 26/11/2001 3,100 3,300

In September 2013 Aine gave painting A to her nephew Owen, the market value in September 2013 was €2,900 and she sold painting B for €2,200.

4. In December 2013 Aine sold 2 acres of land situated in Ireland for €20,000. Aine had

originally bought 10 acres from her sister Michelle in June 2001 for €30,000. The market value of the 10 acres in June 2001 was €35,000. Legal fees on acquisition and disposal were €2,000 and €1,500 respectively. The market value of the remaining 8 acres in December 2013 was €40,000.

Required: (a) Compute Aine’s capital gains tax liability for the tax year 2013 showing the amount of tax

due, if any, for the initial and final period. 16 Marks

(b) State the due date for payment of capital gains tax for the initial and final periods for 2013.

2 Marks (c) If a person is not resident/not ordinarily resident and not domiciled in Ireland, what is their

liability to Irish capital gains tax? 2 Marks

Total 20 Marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

8 A2014 Adv. Taxation (ROI)

SECTION B

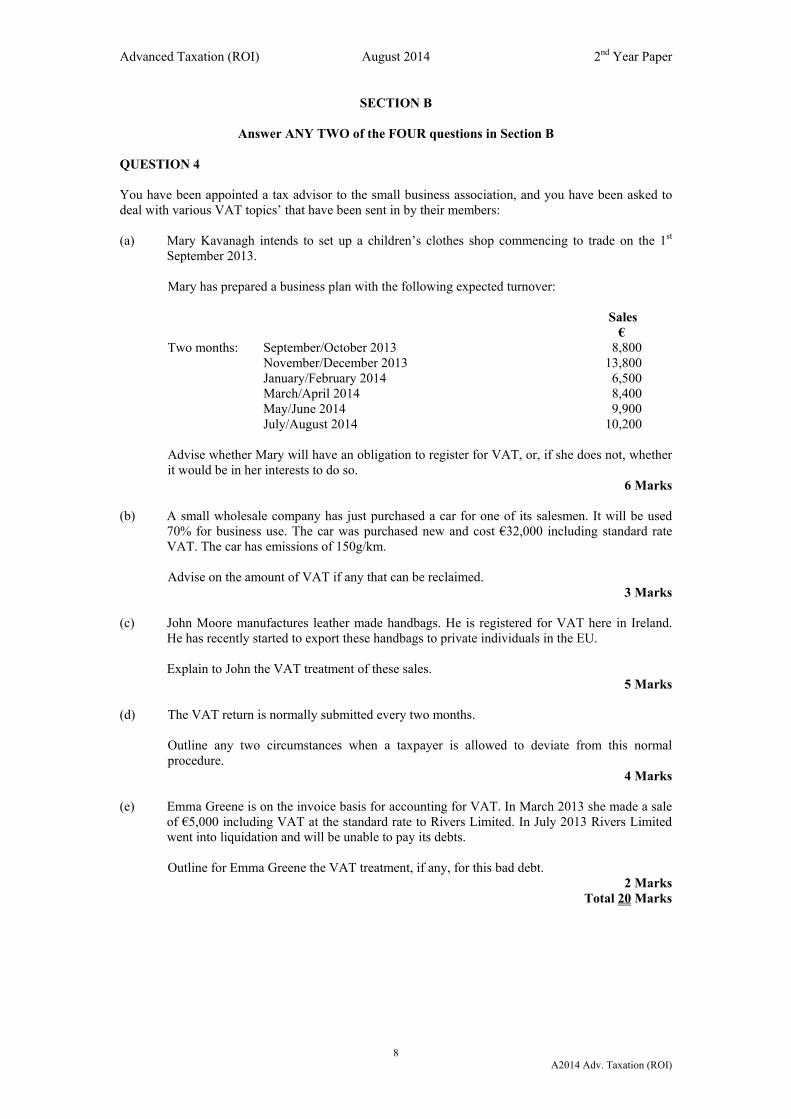

Answer ANY TWO of the FOUR questions in Section B QUESTION 4 You have been appointed a tax advisor to the small business association, and you have been asked to deal with various VAT topics’ that have been sent in by their members: (a) Mary Kavanagh intends to set up a children’s clothes shop commencing to trade on the 1st

September 2013. Mary has prepared a business plan with the following expected turnover: Sales € Two months: September/October 2013 8,800 November/December 2013 13,800 January/February 2014 6,500 March/April 2014 8,400 May/June 2014 9,900 July/August 2014 10,200

Advise whether Mary will have an obligation to register for VAT, or, if she does not, whether it would be in her interests to do so.

6 Marks (b) A small wholesale company has just purchased a car for one of its salesmen. It will be used

70% for business use. The car was purchased new and cost €32,000 including standard rate VAT. The car has emissions of 150g/km.

Advise on the amount of VAT if any that can be reclaimed.

3 Marks (c) John Moore manufactures leather made handbags. He is registered for VAT here in Ireland.

He has recently started to export these handbags to private individuals in the EU.

Explain to John the VAT treatment of these sales. 5 Marks

(d) The VAT return is normally submitted every two months.

Outline any two circumstances when a taxpayer is allowed to deviate from this normal procedure.

4 Marks (e) Emma Greene is on the invoice basis for accounting for VAT. In March 2013 she made a sale

of €5,000 including VAT at the standard rate to Rivers Limited. In July 2013 Rivers Limited went into liquidation and will be unable to pay its debts.

Outline for Emma Greene the VAT treatment, if any, for this bad debt.

2 Marks Total 20 Marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

9 A2014 Adv. Taxation (ROI)

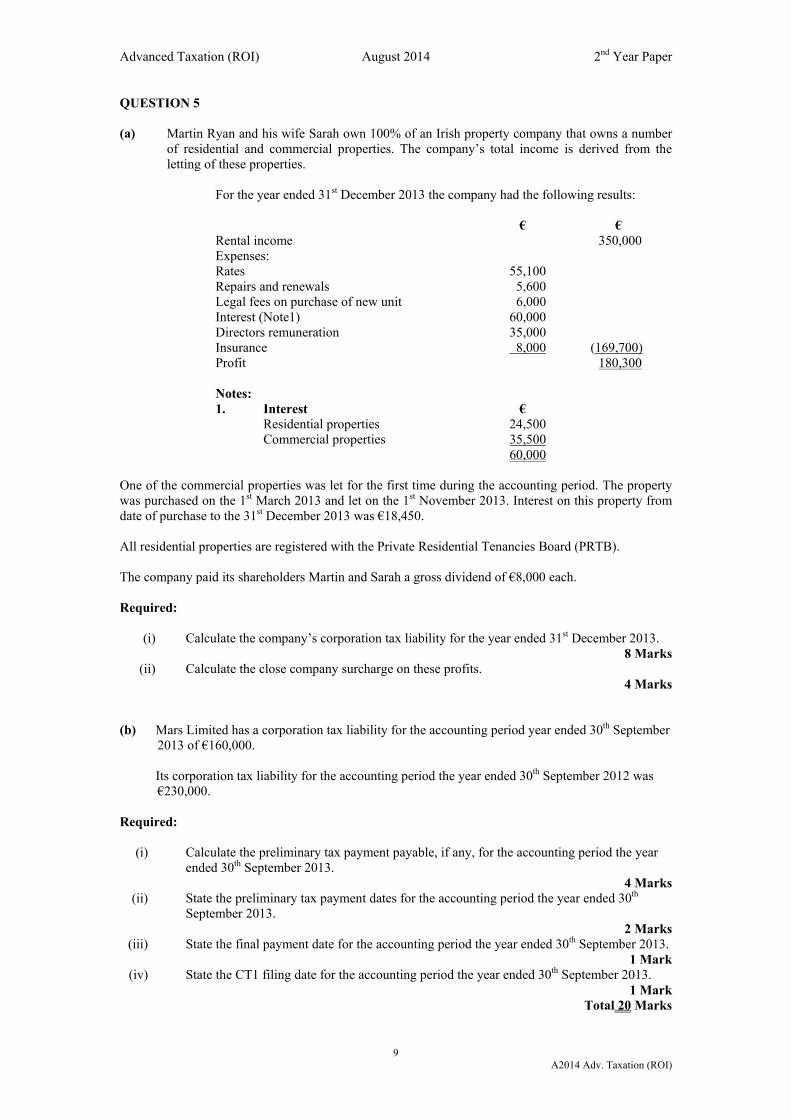

QUESTION 5 (a) Martin Ryan and his wife Sarah own 100% of an Irish property company that owns a number

of residential and commercial properties. The company’s total income is derived from the letting of these properties.

For the year ended 31st December 2013 the company had the following results: € € Rental income 350,000 Expenses: Rates 55,100 Repairs and renewals 5,600 Legal fees on purchase of new unit 6,000 Interest (Note1) 60,000 Directors remuneration 35,000 Insurance 8,000 (169,700) Profit 180,300 Notes: 1. Interest € Residential properties 24,500 Commercial properties 35,500 60,000 One of the commercial properties was let for the first time during the accounting period. The property was purchased on the 1st March 2013 and let on the 1st November 2013. Interest on this property from date of purchase to the 31st December 2013 was €18,450. All residential properties are registered with the Private Residential Tenancies Board (PRTB). The company paid its shareholders Martin and Sarah a gross dividend of €8,000 each. Required:

(i) Calculate the company’s corporation tax liability for the year ended 31st December 2013. 8 Marks

(ii) Calculate the close company surcharge on these profits. 4 Marks (b) Mars Limited has a corporation tax liability for the accounting period year ended 30th September

2013 of €160,000. Its corporation tax liability for the accounting period the year ended 30th September 2012 was

€230,000. Required:

(i) Calculate the preliminary tax payment payable, if any, for the accounting period the year ended 30th September 2013.

4 Marks (ii) State the preliminary tax payment dates for the accounting period the year ended 30th

September 2013. 2 Marks (iii) State the final payment date for the accounting period the year ended 30th September 2013.

1 Mark (iv) State the CT1 filing date for the accounting period the year ended 30th September 2013. 1 Mark

Total 20 Marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

10 A2014 Adv. Taxation (ROI)

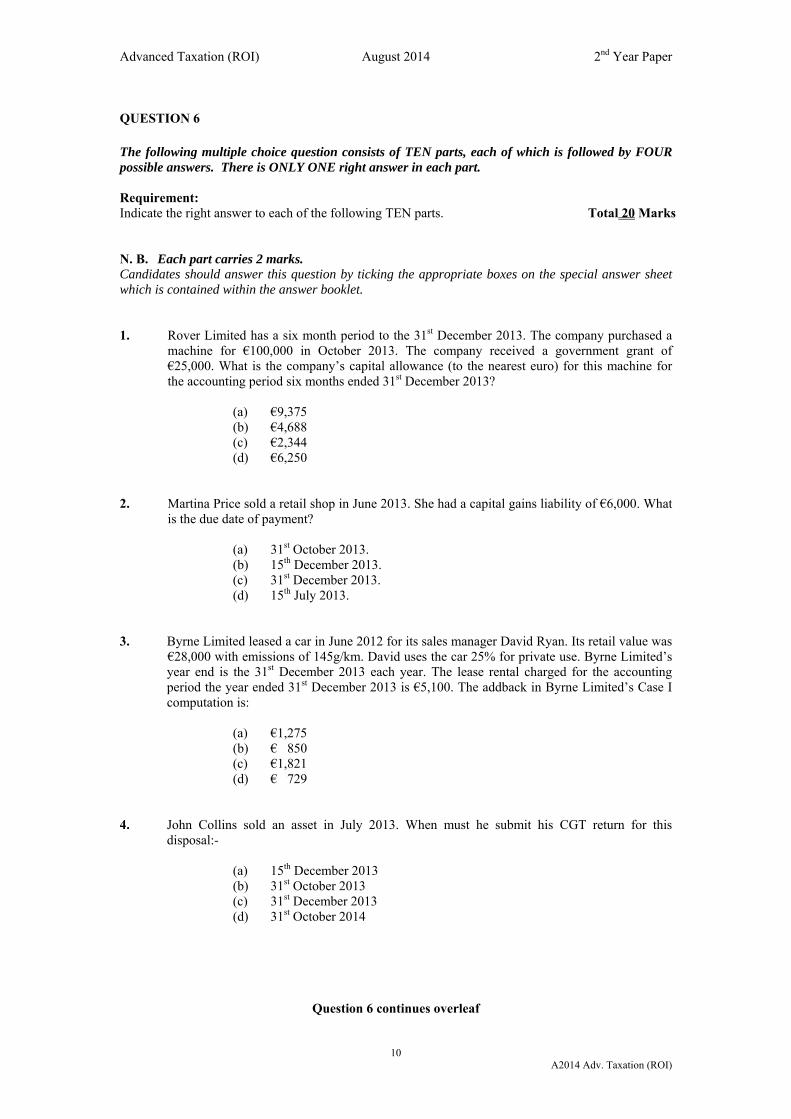

QUESTION 6 The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible answers. There is ONLY ONE right answer in each part. Requirement: Indicate the right answer to each of the following TEN parts. Total 20 Marks N. B. Each part carries 2 marks. Candidates should answer this question by ticking the appropriate boxes on the special answer sheet which is contained within the answer booklet. 1. Rover Limited has a six month period to the 31st December 2013. The company purchased a

machine for €100,000 in October 2013. The company received a government grant of €25,000. What is the company’s capital allowance (to the nearest euro) for this machine for the accounting period six months ended 31st December 2013?

(a) €9,375 (b) €4,688 (c) €2,344 (d) €6,250

2. Martina Price sold a retail shop in June 2013. She had a capital gains liability of €6,000. What

is the due date of payment?

(a) 31st October 2013. (b) 15th December 2013. (c) 31st December 2013. (d) 15th July 2013.

3. Byrne Limited leased a car in June 2012 for its sales manager David Ryan. Its retail value was

€28,000 with emissions of 145g/km. David uses the car 25% for private use. Byrne Limited’s year end is the 31st December 2013 each year. The lease rental charged for the accounting period the year ended 31st December 2013 is €5,100. The addback in Byrne Limited’s Case I computation is:

(a) €1,275 (b) € 850 (c) €1,821 (d) € 729

4. John Collins sold an asset in July 2013. When must he submit his CGT return for this

disposal:-

(a) 15th December 2013 (b) 31st October 2013 (c) 31st December 2013 (d) 31st October 2014

Question 6 continues overleaf

Advanced Taxation (ROI) August 2014 2nd Year Paper

11 A2014 Adv. Taxation (ROI)

QUESTION 6 (Cont’d)

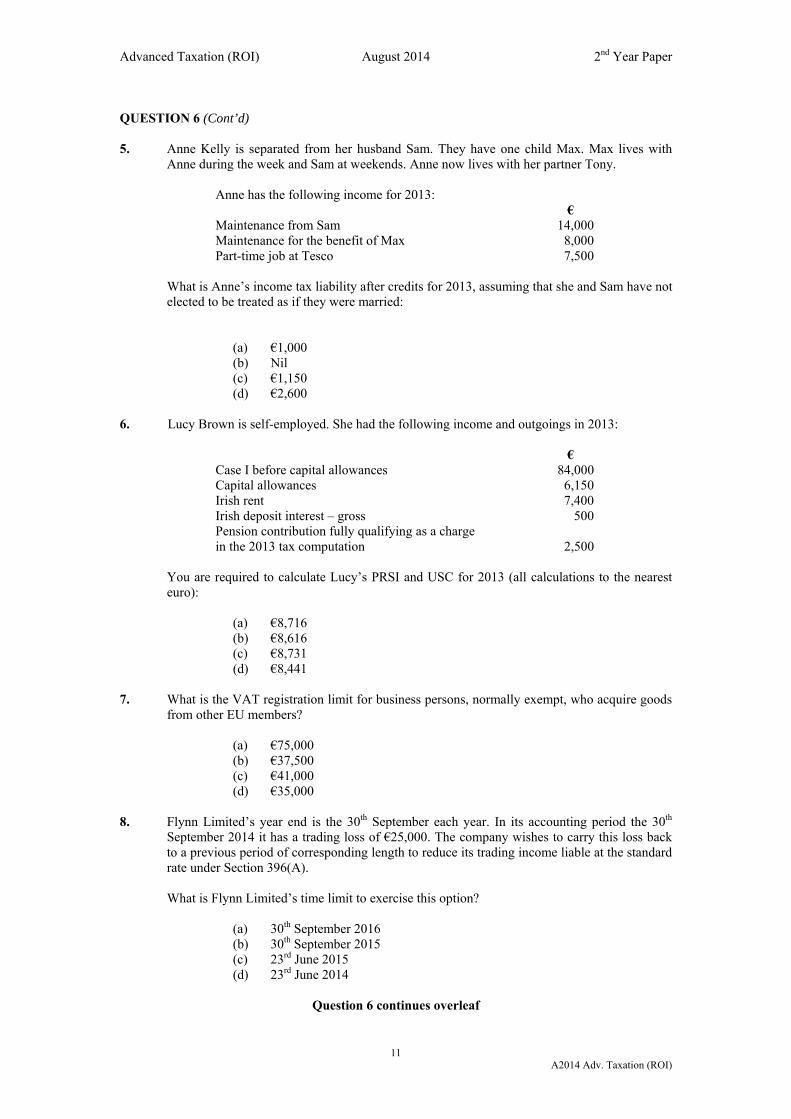

5. Anne Kelly is separated from her husband Sam. They have one child Max. Max lives with

Anne during the week and Sam at weekends. Anne now lives with her partner Tony. Anne has the following income for 2013: € Maintenance from Sam 14,000 Maintenance for the benefit of Max 8,000 Part-time job at Tesco 7,500

What is Anne’s income tax liability after credits for 2013, assuming that she and Sam have not elected to be treated as if they were married:

(a) €1,000 (b) Nil (c) €1,150 (d) €2,600

6. Lucy Brown is self-employed. She had the following income and outgoings in 2013: € Case I before capital allowances 84,000 Capital allowances 6,150 Irish rent 7,400 Irish deposit interest – gross 500 Pension contribution fully qualifying as a charge in the 2013 tax computation 2,500 You are required to calculate Lucy’s PRSI and USC for 2013 (all calculations to the nearest

euro):

(a) €8,716 (b) €8,616 (c) €8,731 (d) €8,441

7. What is the VAT registration limit for business persons, normally exempt, who acquire goods

from other EU members?

(a) €75,000 (b) €37,500 (c) €41,000 (d) €35,000

8. Flynn Limited’s year end is the 30th September each year. In its accounting period the 30th

September 2014 it has a trading loss of €25,000. The company wishes to carry this loss back to a previous period of corresponding length to reduce its trading income liable at the standard rate under Section 396(A).

What is Flynn Limited’s time limit to exercise this option?

(a) 30th September 2016 (b) 30th September 2015 (c) 23rd June 2015 (d) 23rd June 2014

Question 6 continues overleaf

Advanced Taxation (ROI) August 2014 2nd Year Paper

12 A2014 Adv. Taxation (ROI)

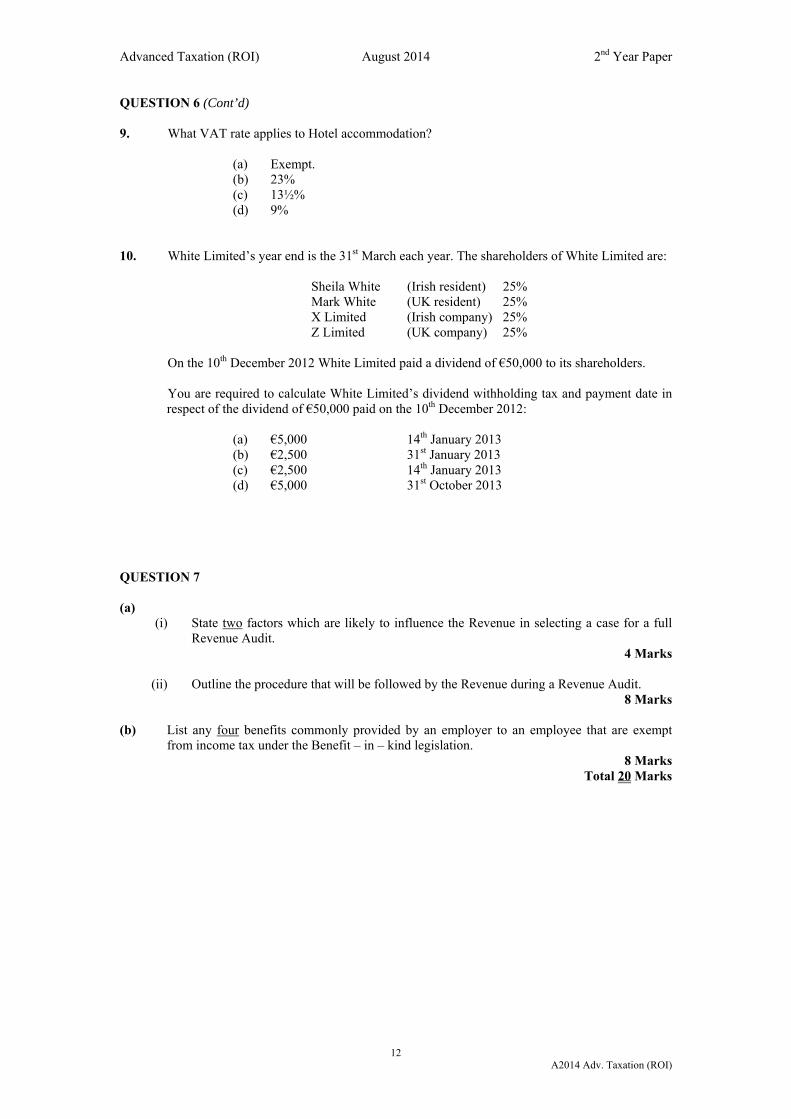

QUESTION 6 (Cont’d) 9. What VAT rate applies to Hotel accommodation?

(a) Exempt. (b) 23% (c) 13½% (d) 9%

10. White Limited’s year end is the 31st March each year. The shareholders of White Limited are: Sheila White (Irish resident) 25% Mark White (UK resident) 25% X Limited (Irish company) 25% Z Limited (UK company) 25% On the 10th December 2012 White Limited paid a dividend of €50,000 to its shareholders.

You are required to calculate White Limited’s dividend withholding tax and payment date in respect of the dividend of €50,000 paid on the 10th December 2012:

(a) €5,000 14th January 2013 (b) €2,500 31st January 2013 (c) €2,500 14th January 2013 (d) €5,000 31st October 2013

QUESTION 7 (a)

(i) State two factors which are likely to influence the Revenue in selecting a case for a full Revenue Audit.

4 Marks

(ii) Outline the procedure that will be followed by the Revenue during a Revenue Audit. 8 Marks

(b) List any four benefits commonly provided by an employer to an employee that are exempt

from income tax under the Benefit – in – kind legislation. 8 Marks

Total 20 Marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

13 A2014 Adv. Taxation (ROI)

2nd Year Examination: August 2014

Advanced Taxation ROI

Suggested Solutions and

Examiner’s Comments

Students please note: These are suggested solutions only; alternative answers may also be deemed to be correct and will be marked on their own merits.

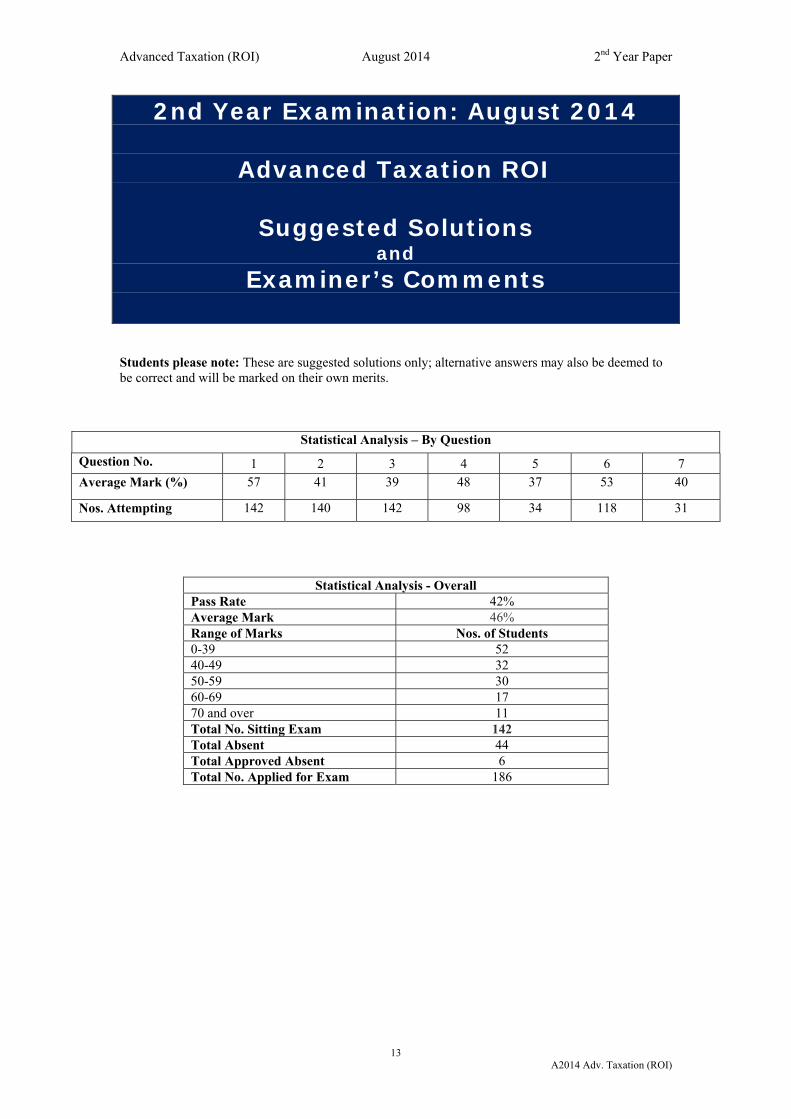

Statistical Analysis – By Question

Question No. 1 2 3 4 5 6 7 Average Mark (%) 57 41 39 48 37 53 40

Nos. Attempting 142 140 142 98 34 118 31

Statistical Analysis - Overall Pass Rate 42% Average Mark 46% Range of Marks Nos. of Students 0-39 52 40-49 32 50-59 30 60-69 17 70 and over 11 Total No. Sitting Exam 142 Total Absent 44 Total Approved Absent 6 Total No. Applied for Exam 186

Advanced Taxation (ROI) August 2014 2nd Year Paper

14 A2014 Adv. Taxation (ROI)

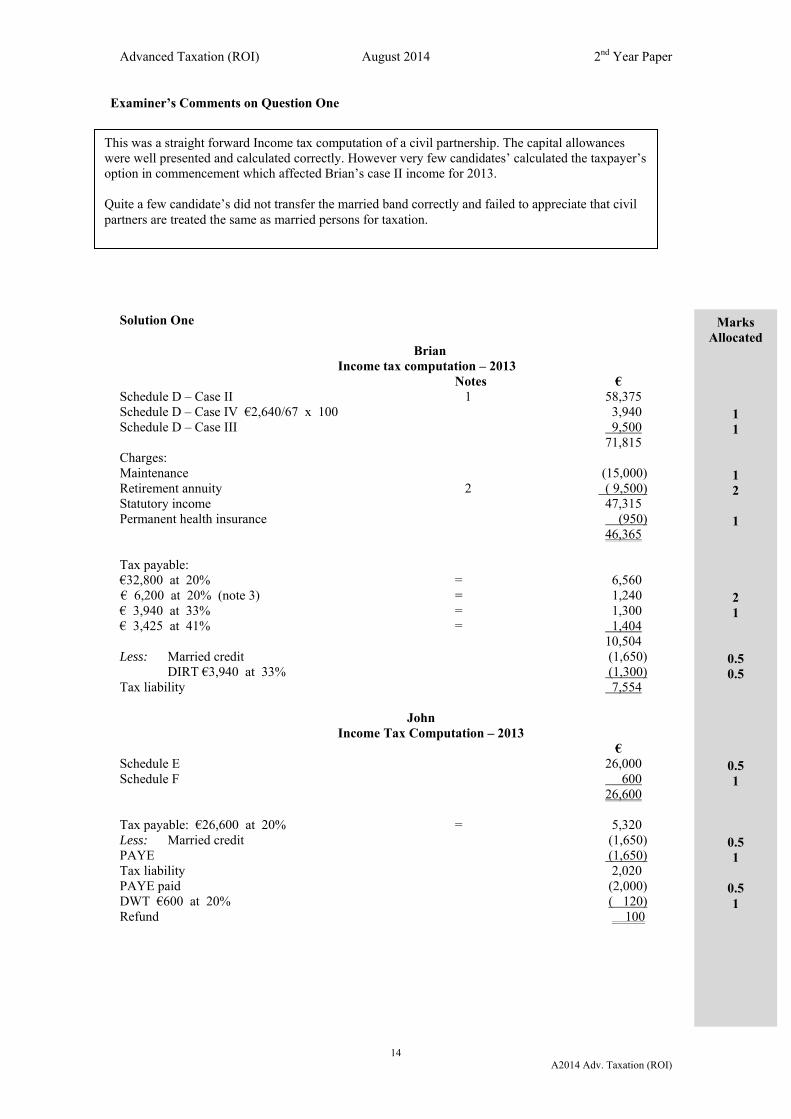

Examiner’s Comments on Question One

Solution One

Brian Income tax computation – 2013 Notes € Schedule D – Case II 1 58,375 Schedule D – Case IV €2,640/67 x 100 3,940 Schedule D – Case III 9,500 71,815 Charges: Maintenance (15,000) Retirement annuity 2 ( 9,500) Statutory income 47,315 Permanent health insurance (950) 46,365 Tax payable: €32,800 at 20% = 6,560 € 6,200 at 20% (note 3) = 1,240

€ 3,940 at 33% = 1,300 € 3,425 at 41% = 1,404 10,504 Less: Married credit (1,650) DIRT €3,940 at 33% (1,300) Tax liability 7,554 John Income Tax Computation – 2013 € Schedule E 26,000 Schedule F 600 26,600 Tax payable: €26,600 at 20% = 5,320 Less: Married credit (1,650) PAYE (1,650) Tax liability 2,020 PAYE paid (2,000) DWT €600 at 20% ( 120) Refund 100

This was a straight forward Income tax computation of a civil partnership. The capital allowances were well presented and calculated correctly. However very few candidates’ calculated the taxpayer’s option in commencement which affected Brian’s case II income for 2013. Quite a few candidate’s did not transfer the married band correctly and failed to appreciate that civil partners are treated the same as married persons for taxation.

Marks Allocated

1 1

1 2

1

2 1

0.5 0.5

0.5 1

0.5 1

0.5 1

Advanced Taxation (ROI) August 2014 2nd Year Paper

15 A2014 Adv. Taxation (ROI)

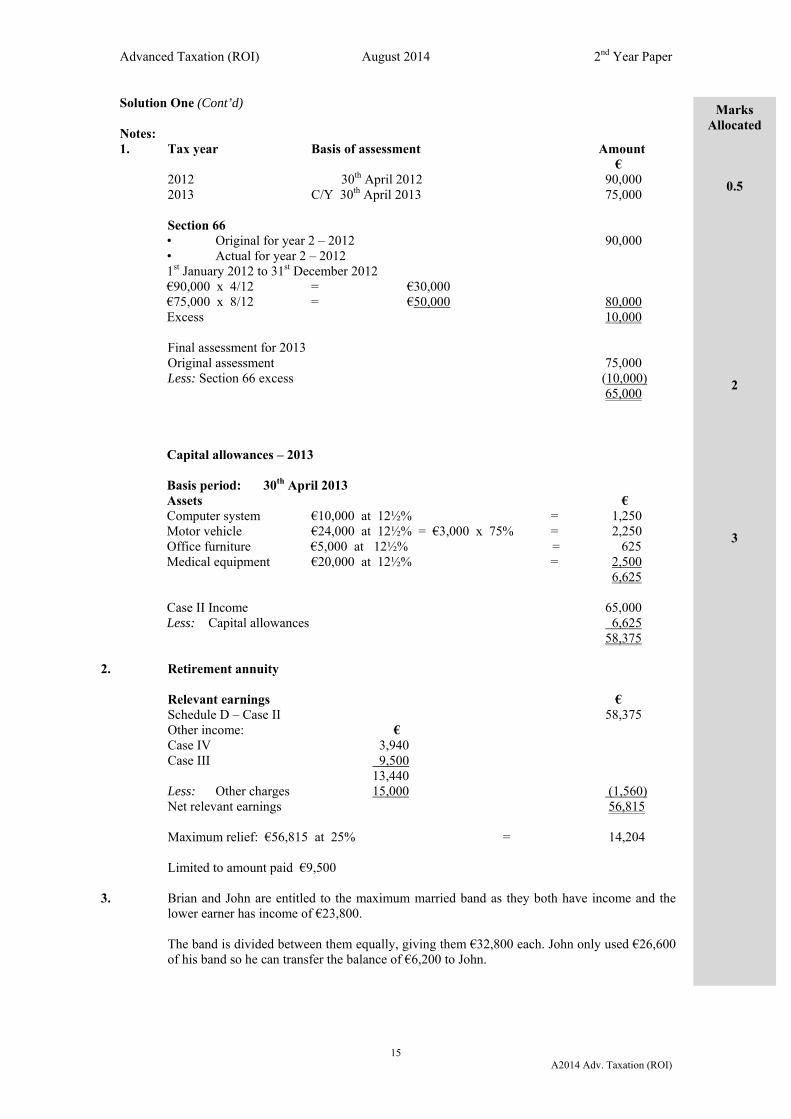

Solution One (Cont’d) Notes: 1. Tax year Basis of assessment Amount € 2012 30th April 2012 90,000 2013 C/Y 30th April 2013 75,000 Section 66

• Original for year 2 – 2012 90,000 • Actual for year 2 – 2012 1st January 2012 to 31st December 2012 €90,000 x 4/12 = €30,000 €75,000 x 8/12 = €50,000 80,000 Excess 10,000

Final assessment for 2013 Original assessment 75,000 Less: Section 66 excess (10,000) 65,000

Capital allowances – 2013 Basis period: 30th April 2013 Assets € Computer system €10,000 at 12½% = 1,250 Motor vehicle €24,000 at 12½% = €3,000 x 75% = 2,250 Office furniture €5,000 at 12½% = 625 Medical equipment €20,000 at 12½% = 2,500 6,625 Case II Income 65,000 Less: Capital allowances 6,625 58,375

2. Retirement annuity Relevant earnings € Schedule D – Case II 58,375 Other income: € Case IV 3,940 Case III 9,500 13,440 Less: Other charges 15,000 (1,560) Net relevant earnings 56,815 Maximum relief: €56,815 at 25% = 14,204 Limited to amount paid €9,500 3. Brian and John are entitled to the maximum married band as they both have income and the

lower earner has income of €23,800.

The band is divided between them equally, giving them €32,800 each. John only used €26,600 of his band so he can transfer the balance of €6,200 to John.

Marks Allocated

0.5

2

3

Advanced Taxation (ROI) August 2014 2nd Year Paper

16 A2014 Adv. Taxation (ROI)

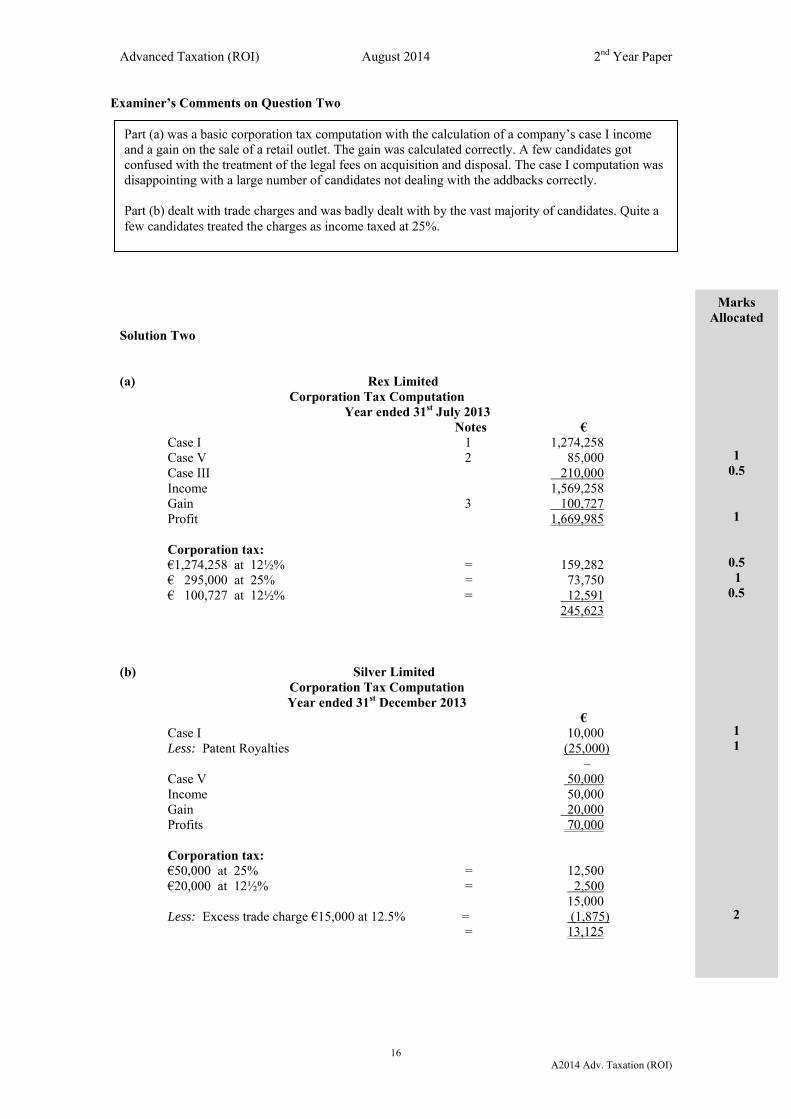

Examiner’s Comments on Question Two

Solution Two

(a) Rex Limited

Corporation Tax Computation Year ended 31st July 2013 Notes € Case I 1 1,274,258 Case V 2 85,000 Case III 210,000 Income 1,569,258 Gain 3 100,727 Profit 1,669,985 Corporation tax: €1,274,258 at 12½% = 159,282 € 295,000 at 25% = 73,750 € 100,727 at 12½% = 12,591 245,623 (b) Silver Limited

Corporation Tax Computation Year ended 31st December 2013

€ Case I 10,000 Less: Patent Royalties (25,000) ‒ Case V 50,000 Income 50,000 Gain 20,000 Profits 70,000 Corporation tax: €50,000 at 25% = 12,500 €20,000 at 12½% = 2,500 15,000 Less: Excess trade charge €15,000 at 12.5% = (1,875) = 13,125

Part (a) was a basic corporation tax computation with the calculation of a company’s case I income and a gain on the sale of a retail outlet. The gain was calculated correctly. A few candidates got confused with the treatment of the legal fees on acquisition and disposal. The case I computation was disappointing with a large number of candidates not dealing with the addbacks correctly. Part (b) dealt with trade charges and was badly dealt with by the vast majority of candidates. Quite a few candidates treated the charges as income taxed at 25%.

Marks Allocated

1 0.5

1

0.5 1 0.5

1 1

2

Advanced Taxation (ROI) August 2014 2nd Year Paper

17 A2014 Adv. Taxation (ROI)

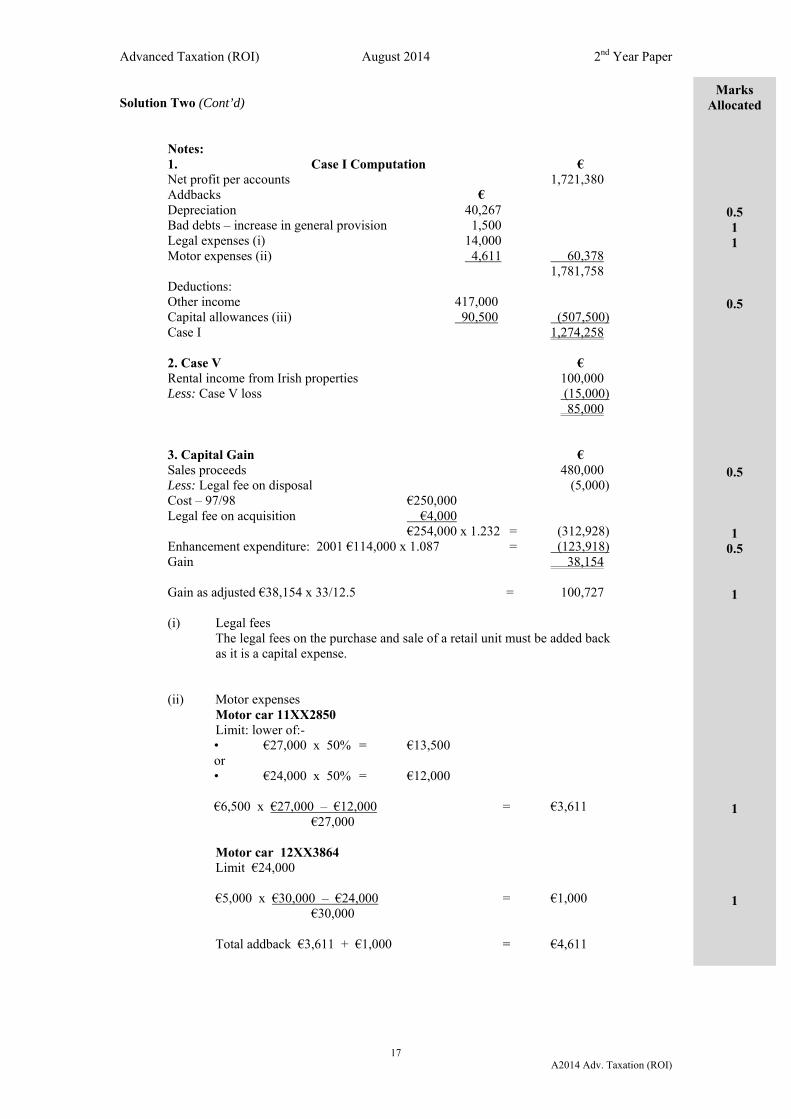

Solution Two (Cont’d) Notes: 1. Case I Computation € Net profit per accounts 1,721,380 Addbacks € Depreciation 40,267 Bad debts – increase in general provision 1,500 Legal expenses (i) 14,000 Motor expenses (ii) 4,611 60,378 1,781,758 Deductions:

Other income 417,000 Capital allowances (iii) 90,500 (507,500) Case I 1,274,258 2. Case V € Rental income from Irish properties 100,000 Less: Case V loss (15,000) 85,000

3. Capital Gain € Sales proceeds 480,000 Less: Legal fee on disposal (5,000) Cost – 97/98 €250,000 Legal fee on acquisition €4,000 €254,000 x 1.232 = (312,928) Enhancement expenditure: 2001 €114,000 x 1.087 = (123,918) Gain 38,154 Gain as adjusted €38,154 x 33/12.5 = 100,727 (i) Legal fees The legal fees on the purchase and sale of a retail unit must be added back as it is a capital expense. (ii) Motor expenses Motor car 11XX2850 Limit: lower of:-

• €27,000 x 50% = €13,500 or • €24,000 x 50% = €12,000

€6,500 x €27,000 ‒ €12,000 = €3,611

€27,000

Motor car 12XX3864 Limit €24,000

€5,000 x €30,000 ‒ €24,000 = €1,000

€30,000

Total addback €3,611 + €1,000 = €4,611

Marks Allocated

0.5 1 1

0.5

0.5

1 0.5

1

1

1

Advanced Taxation (ROI) August 2014 2nd Year Paper

18 A2014 Adv. Taxation (ROI)

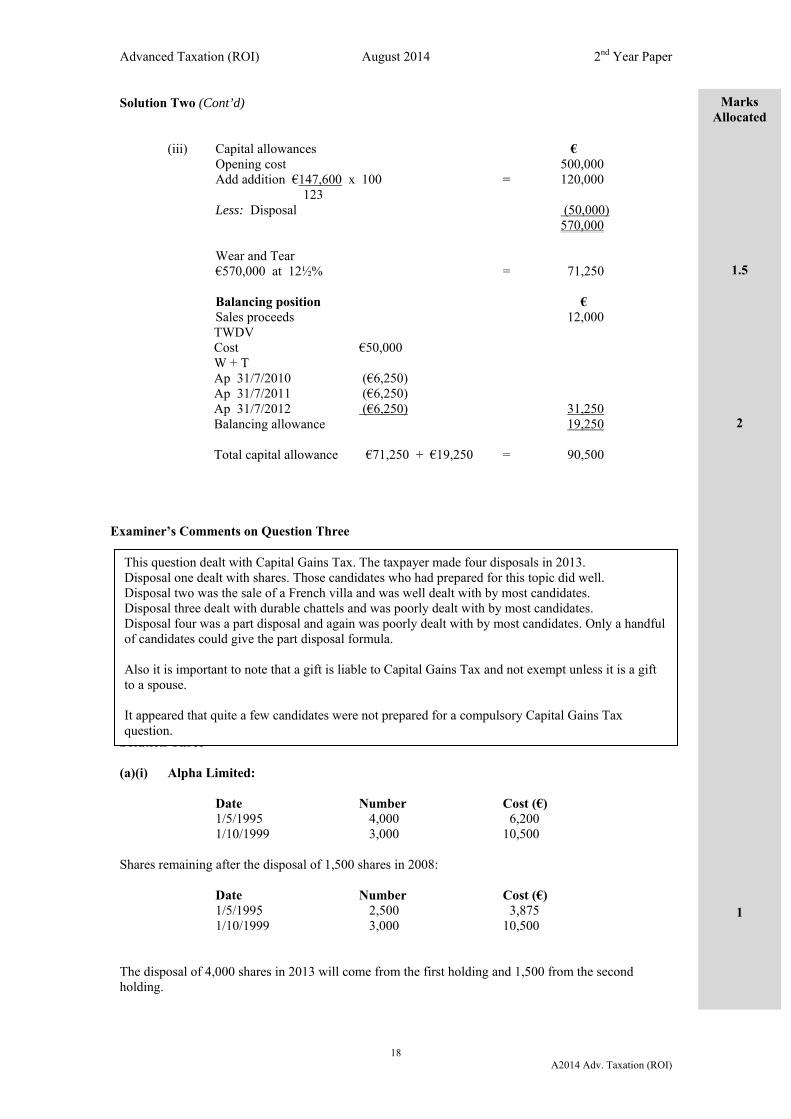

Solution Two (Cont’d)

(iii) Capital allowances € Opening cost 500,000 Add addition €147,600 x 100 = 120,000 123 Less: Disposal (50,000) 570,000 Wear and Tear €570,000 at 12½% = 71,250 Balancing position € Sales proceeds 12,000

TWDV Cost €50,000 W + T Ap 31/7/2010 (€6,250) Ap 31/7/2011 (€6,250) Ap 31/7/2012 (€6,250) 31,250 Balancing allowance 19,250 Total capital allowance €71,250 + €19,250 = 90,500

Examiner’s Comments on Question Three

Solution Three (a)(i) Alpha Limited: Date Number Cost (€) 1/5/1995 4,000 6,200 1/10/1999 3,000 10,500 Shares remaining after the disposal of 1,500 shares in 2008: Date Number Cost (€) 1/5/1995 2,500 3,875 1/10/1999 3,000 10,500 The disposal of 4,000 shares in 2013 will come from the first holding and 1,500 from the second holding.

This question dealt with Capital Gains Tax. The taxpayer made four disposals in 2013. Disposal one dealt with shares. Those candidates who had prepared for this topic did well. Disposal two was the sale of a French villa and was well dealt with by most candidates. Disposal three dealt with durable chattels and was poorly dealt with by most candidates. Disposal four was a part disposal and again was poorly dealt with by most candidates. Only a handful of candidates could give the part disposal formula. Also it is important to note that a gift is liable to Capital Gains Tax and not exempt unless it is a gift to a spouse. It appeared that quite a few candidates were not prepared for a compulsory Capital Gains Tax question.

Marks Allocated

1.5

2

1

Advanced Taxation (ROI) August 2014 2nd Year Paper

19 A2014 Adv. Taxation (ROI)

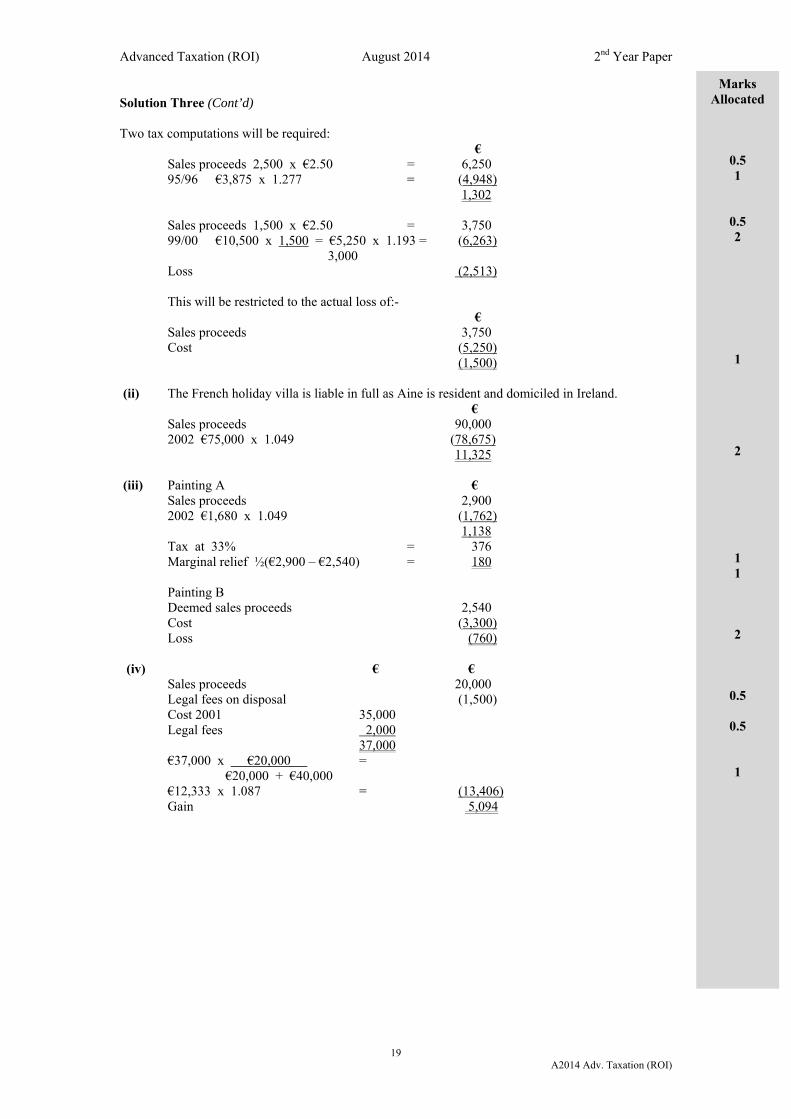

Solution Three (Cont’d) Two tax computations will be required: €

Sales proceeds 2,500 x €2.50 = 6,250 95/96 €3,875 x 1.277 = (4,948)

1,302 Sales proceeds 1,500 x €2.50 = 3,750 99/00 €10,500 x 1,500 = €5,250 x 1.193 = (6,263) 3,000 Loss (2,513) This will be restricted to the actual loss of:- € Sales proceeds 3,750 Cost (5,250) (1,500) (ii) The French holiday villa is liable in full as Aine is resident and domiciled in Ireland. € Sales proceeds 90,000 2002 €75,000 x 1.049 (78,675) 11,325 (iii) Painting A € Sales proceeds 2,900 2002 €1,680 x 1.049 (1,762) 1,138 Tax at 33% = 376 Marginal relief ½(€2,900 ‒ €2,540) = 180 Painting B Deemed sales proceeds 2,540 Cost (3,300) Loss (760) (iv) € € Sales proceeds 20,000 Legal fees on disposal (1,500) Cost 2001 35,000 Legal fees 2,000 37,000 €37,000 x €20,000 = €20,000 + €40,000 €12,333 x 1.087 = (13,406) Gain 5,094

Marks Allocated

0.5 1

0.5 2

1

2

1 1

2

0.5

0.5

1

Advanced Taxation (ROI) August 2014 2nd Year Paper

20 A2014 Adv. Taxation (ROI)

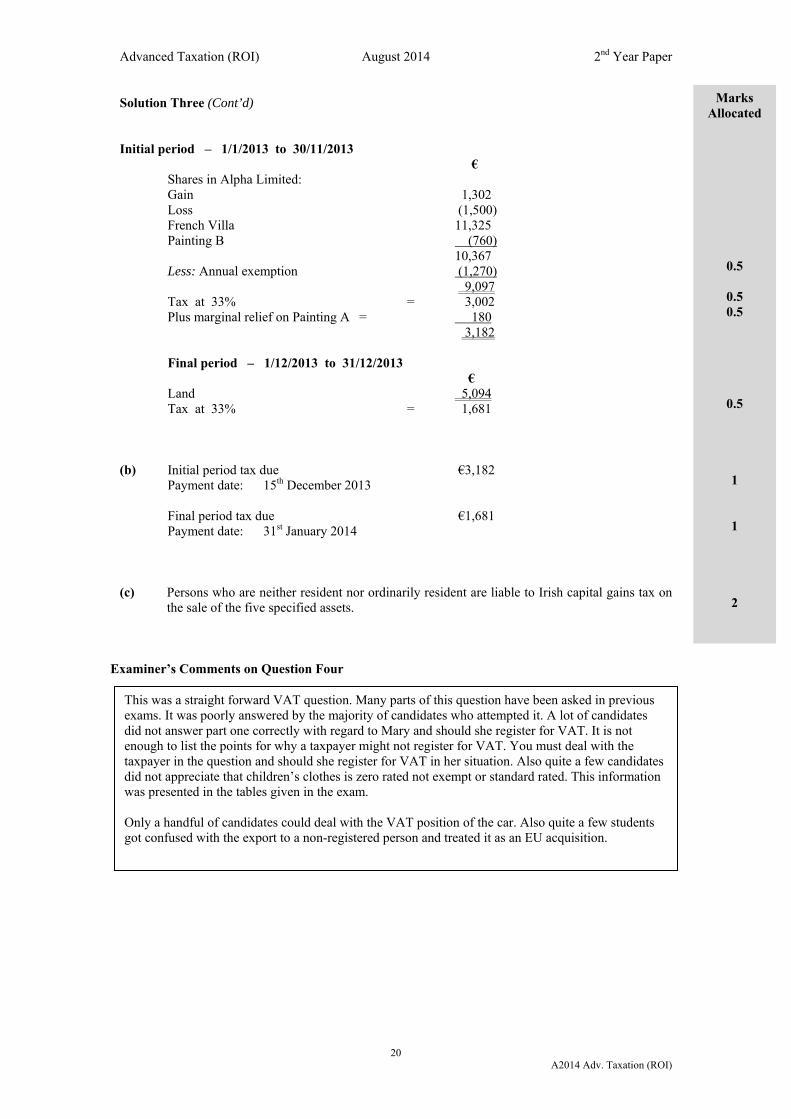

Solution Three (Cont’d) Initial period ‒ 1/1/2013 to 30/11/2013 € Shares in Alpha Limited: Gain 1,302 Loss (1,500) French Villa 11,325 Painting B (760) 10,367 Less: Annual exemption (1,270) 9,097 Tax at 33% = 3,002 Plus marginal relief on Painting A = 180 3,182 Final period ‒ 1/12/2013 to 31/12/2013 € Land 5,094 Tax at 33% = 1,681 (b) Initial period tax due €3,182 Payment date: 15th December 2013 Final period tax due €1,681 Payment date: 31st January 2014 (c) Persons who are neither resident nor ordinarily resident are liable to Irish capital gains tax on

the sale of the five specified assets.

Examiner’s Comments on Question Four

This was a straight forward VAT question. Many parts of this question have been asked in previous exams. It was poorly answered by the majority of candidates who attempted it. A lot of candidates did not answer part one correctly with regard to Mary and should she register for VAT. It is not enough to list the points for why a taxpayer might not register for VAT. You must deal with the taxpayer in the question and should she register for VAT in her situation. Also quite a few candidates did not appreciate that children’s clothes is zero rated not exempt or standard rated. This information was presented in the tables given in the exam. Only a handful of candidates could deal with the VAT position of the car. Also quite a few students got confused with the export to a non-registered person and treated it as an EU acquisition.

Marks Allocated

0.5

0.5 0.5

0.5

1

1

2

Advanced Taxation (ROI) August 2014 2nd Year Paper

21 A2014 Adv. Taxation (ROI)

Solution Four (a) There is an obligation to register for VAT, if a trader’s turnover from the sale of goods is, or is

likely, in any continuous period of 12 months, to exceed €75,000 per annum.

To establish if Mary is required to register for VAT it is necessary to review her VAT exclusive turnover. The projected turnover for the 12 month period to 31st August 2014 is as follows:

Two months ending € October 2013 8,800 December 2013 13,800 February 2014 6,500 April 2014 8,400 June 2014 9,900 August 2014 10,200 57,600 As Mary’s turnover is below €75,000 she is not obliged to register for VAT. However given that she has zero rated sales it would be in her interests to register.

She would have to charge VAT on her sales but it would be the zero rate and she would be able to reclaim VAT on her purchases like fixtures, telephone, light and heat etc.

(b) From the 1st January 2009 it is possible for a business that buys a category A, B or C car and

uses that car at least 60% for business to reclaim 20% of the VAT charged. €32,000 is the VAT inclusive cost. The VAT is €5,984 (€32,000/123 x 23). The taxpayer will

be able to claim 20% of this, €1,197 as an input credit. (c) As John is VAT registered and the customers are EU private individuals John must charge

Irish VAT as the place of supply is Ireland where the transport begins. However all EU countries have a registration limit for distance sellers. If John makes a supply

in excess of the threshold of the relevant country, John must register for VAT in that country and charge that country’s VAT rate when making the supply. VAT is now charged where the transportation ends.

Example John supplies €40,000 worth of handbags to non-registered customers in Germany in the year

to the 30th June 2013. What is the VAT position? Solution The registration limit for distance sales in Germany is €100,000. As John has not exceeded

this he does not have to register for VAT in Germany and he charges Irish VAT on these sales. (d) A number of alternatives to the usual bi-monthly return are available: (i) Taxpayers in a permanent repayment position may be permitted to furnish monthly returns. (ii) The Collector General may authorise taxable persons to file an annual VAT return. In the case

of all traders, an application may be made to the Collector General to account for VAT payable on an annual basis. In order to avail of this treatment, the taxable person is obliged to set up a direct debit facility and make a monthly payment on account to the Collector General.

Once the annual VAT return is filed, the balance of VAT payable, if any, must be paid by the 19th day of the month immediately following the annual accounting period. Where the balancing payment is in excess of 20% of the tax payable for the year then the Revenue

Marks Allocated

1

2

1

2

2

1

2.5

2.5

2 marks each, (Max 4 marks)

Advanced Taxation (ROI) August 2014 2nd Year Paper

22 A2014 Adv. Taxation (ROI)

Solution Four (Cont’d) Commissioners may charge interest on the balance outstanding. The interest will be charged from a date 6 months prior to the submission date. This measure is to ensure that a taxable person does not postpone payment of what may be a substantial VAT liability until the end of the accounting period.

(iii) Four monthly returns are available to traders who have a total VAT liability of between

€3,000 and €14,400 per annum. The filing date is the 19th day of the month following the quarterly period (23rd if using ROS).

(iv) Bi-annual returns are available to traders who have a total VAT liability of less that €3,000 per

annum. The filing date is the 19th day of the month following the six month period. (23rd if using ROS).

The question only requires two of the above. (e) Relief for the VAT on a bad debt is possible where a debtor defaults and fails to pay the

accountable person. Emma Greene, accounts for VAT on the invoice basis so has already accounted for VAT

when the sale was made. Where the Revenue is satisfied that every effort has been made to collect the outstanding debt

they will allow Emma to reduce the VAT liability in the period the debt is written off.

Examiner’s Comments on Question Five

Solution Five (a) (i) Corporation Tax Computation Year ended 31st December 2013 Notes € Case V 1 207,185 Corporation tax €207,185 at 25% = €51,796

This question was dealt with satisfactorily. The main problem was in part (b) where most candidates failed to note that it was a large company for corporation tax purposes. This meant they had the wrong preliminary tax requirements.

Marks Allocated

2

2

Advanced Taxation (ROI) August 2014 2nd Year Paper

23 A2014 Adv. Taxation (ROI)

Solution Five (Cont’d) Notes: 1. Case V Computation € € Rent received 350,000 Less: Expenses Rates 55,100 Repairs and renewals 5,600 Interest (working 1) 39,115 Directors remuneration 35,000 Insurance 8,000 (142,815) 207,185 Workings: 1. Residential properties €24,500 at 75% = 18,375 Commercial properties €35,500 ‒ €18,450 = 17,050 New commercial property €18,450 x 2/10 = 3,690 39,115

2. The legal fees on the purchase of the new unit are a capital expense and not allowed.

(ii) Close company surcharge:

€ Case V income 207,185 Less: Corporation tax (51,796) Distribution (16,000) Undistributed Estate Income 139,389 Surcharge at 20% = 27,878 (b) (i) 1st Installment 45% of expected liability: €160,000 x 45% = 72,000 or 50% of previous liability: €230,000 x 50% = 115,000 Pay = 72,000 2nd Installment €160,000 x 90% = 144,000 Less: €72,000 paid = 72,000 payable (ii) Preliminary tax payment dates: 1st Installment: 23rd March 2013 2nd Installment: 23rd August 2013 (iii) Final payment date is: 23rd June 2014 (iv) CTI filing date is: 23rd June 2014

Marks Allocated

0.5 0.5

0.5 0.5

1 1 1

1

1 2 2

1

1

1

1 1

1

1

Advanced Taxation (ROI) August 2014 2nd Year Paper

24 A2014 Adv. Taxation (ROI)

Examiner’s Comments on Question Six

Solution Six 1. (b) €100,000 ‒ €25,000 = €75,000 x 12½% x 6/12 = €4,688 2. (b) 3. (d) €5,100 x €28,000 ‒ €24,000 = €729 €28,000 4. (d) 5. (c) Income tax computation € Case IV 14,000 Schedule E 7,500 21,500 €21,500 at 20% = 4,300 Less: Single credit (1,650) PAYE credit €7,500 at 20% (1,500) Tax liability 1,150 6. (a) Case I €84,000 ‒ €6,150 77,850 Case V 7,400 Case IV 500 85,750 PRSI at 4% = 3,430 Case I 77,850 Case V 7,400 85,250 USC: €10,036 at 2% = 201 € 5,980 at 4% = 239 €69,234 at 7% = 4,846 5,286 Total €3,430 + €5,286 = €8,716 7. (c) 8. (a) 9. (d) 10. (c) €50,000 x 25% = €12,500 €12,500 x 20% = € 2,500

The multi-choice question was answered satisfactorily.

Marks Allocated

Each part carries 2 marks

Advanced Taxation (ROI) August 2014 2nd Year Paper

25 A2014 Adv. Taxation (ROI)

Examiner’s Comments on Question Seven

Solution Seven (a) (i) Revenue uses three methods of selection. These are:

Screening tax returns The vast majority of audit cases are selected in this way. Screening involves examining the returns made by a variety of taxpayers and reviewing their tax compliance history. The figures in the returns and accounts are then analysed in the light of trends and patterns in the particular business or profession and evaluated against other available information. Officers who screen cases seek to minimise the possibility of selecting taxpayers whose tax affairs are likely to be in order. Projects on business sectors: From time to time, projects are conducted to examine tax compliance levels in particular trades or professions. The returns for a large number of taxpayers in a particular sector are screened in detail and a proportion of these selected for audit. Random selection This is in addition to the first two methods. It means that all taxpayers have a possibility of being audited. Each year, a small proportion of audit cases are selected using this method.

(ii) Typically, an audit involves a series of steps. The sequences of these steps are as follows:-

1. On arrival, the auditor identifies himself or herself to you and explains the purpose of

the audit. An indication of the length of time he or she expects to spend on your premises is also given.

2. You are given an opportunity to disclose to the auditor all inaccuracies in your tax return. By making such a disclosure you ensure speedier conclusion of the audit with maximum reduction in penalties and you avoid having your name published in the annual list of tax defaulters.

3. To get a better understanding of your business, the auditor may ask you questions about your book-keeping and how your business operates. The auditor then commences to examine your books and records to verify that the figures have been correctly calculated and that the tax returns and/or declarations for the different taxes are correct.

4. If the auditor finds the returns to be largely correct as is often the case you will be told as soon as this becomes clear. The auditor is not concerned with pursuing immaterial adjustments. He or she will let you know in writing that no adjustments arise

5. If the auditor finds that adjustments are required, he or she will quantify the adjustments and the additional tax. The details of how the additional tax arises will be discussed with you and you will be notified in writing. You will be given time to consider the proposed adjustments, and if you wish, to take independent tax advice.

This was a two part question. Part (a) on revenue audit was answered satisfactorily. In part (b) I asked for four exempt BIK. A lot of candidates did not read the question correctly and listed four BIK that would be liable to Income Tax under Schedule E like the motor vehicle and a preferential loan.

Marks Allocated

2

2

1

1

1

1

1

Advanced Taxation (ROI) August 2014 2nd Year Paper

26 A2014 Adv. Taxation (ROI)

Solution Seven (Cont’d)

6. In addition to tax, interest at the rate specified by law, will normally be payable. If

the additional tax is of a material amount and can be shown as arising due to fraud or neglect on your part, penalties will also be payable. The auditor will explain to you how interest and penalties are calculated.

7. At the final interview, the auditor will ask for your agreement to the total settlement figure. This figure will include tax, interest and, if they arise, penalties. If the total settlement figure exceeds €30,000 (including interest and any penalties) and you did not make a full voluntary disclosure, details of the settlement will be included in the annual list of tax defaulters published by the Revenue Commissioners.

8. Once agreed, the full amount should be paid to the auditor who will issue you with a receipt.

(b) Benefits received by employees that are exempt from income tax:

(1) The provision of living accommodation for an employee (other than a director), who is required to live on the business premises, provided that the accommodation is necessary for the employee to carry out their duties, or the accommodation has been provided as part of the office of employment prior to 1948.

(2) The provision of canteen meals, which are provided for all staff generally. (3) The cost of providing a monthly/annual bus or rail pass. (4) Security services/assets are exempt where there is a risk to the personal safety of the

employee/director while carrying out the duties of employment. (5) The provision of a new bicycle and related safety equipment subject to a maximum

value of €1,000. (6) Where an employee uses a car that is considered to be in a ‘car pool’. (7) Where an employee uses a business asset mainly for business but there is some

private use, but the private use is considered to be entirely incidental. (8) Qualifying removal or relocation expenses, that is those expenses incurred directly as

a result of the change of residence necessary to take up employment. The question only requires four benefits.

Marks Allocated

1

1

1

2 marks each, (Max 8 marks)