Embed Size (px)

Citation preview

An ISO 9001:2008 Certified Company

AEROTROPOLISA CASE STUDY OF BENGALURU

January 2015

A Report By Strategic Advisory Group

CONTACT US

USAChicago: 300 N. LaSalle Street, Suite 1850, Chicago, IL 60654|T: +1 312 920 0290

INDIABengaluru: First Floor, West Wing, DuParc Trinity, #17, M G Road, Bengaluru - 560 001|T: +91 80 4062 0100Mumbai: Acme Plaza, Unit No.501, 5th floor, Andheri Kurla Road, Andheri (East), Mumbai - 400 059|T: +91 022 4215 3060Chennai: Penthouse Suite-1, Apeejay Business Centre, Apeejay House, 3rd Floor, 39/12, Haddows Road, Nungambakkam, Chennai - 600 006|T: +91 44 3915 9351/ 6665 9351Hyderabad: 2nd Floor, N.N.R Arcade, Plot 13, Road No.10, Banjara Hills, Hyderabad - 500 034|T: +91 40 3378 2100 Pune: Level 6, Pentagon P-2, Magarpatta City, Hadapsar, Pune - 411 013|T: +91 20 4014 7855

CHINAShanghai: Unit 1207, No. 546, Changing Road, Changing District, Shanghai - 200 042|T: +86 21 3255 6366Beijing: No. 91 Jian Guo Road,16F Gemdale Plaza Tower A, Chaoyang District, Beijing 100022, PRC|T: (8610) 5920 8108

SRI LANKAColombo: Colombo World Trade Centre - Fort, Level 26, East Tower, Echelon Square, Colombo, 00100

Executive Summary

•

•

•

•

•

•

•

AEROTROPOLIS2 3

• For centuries, civilizations have flourished around transportation hubs

like rivers, sea ports, railroads and highways. In the 21st century,

airports are becoming the main drivers of city growth.

• ‘Airport City’ and ‘Aerotropolis’ are the two models for an airport centric

development. An airport city has the terminal building with its retail and

business facilities representing the urban square and its office,

hospitality, convention facilities and other uses within the airport fence

analogous to the CBD of a city. An aerotropolis is a form of urban

development with an airport city at the centre and aviation-linked

businesses agglomerating around it.

• In India, post the economic liberalization in 1991, in keeping with the

global benchmarks, private sector partners got involved in airport

infrastructure development. They adopted either the airport city concept

or the aerotropolis concept while developing new airports.

• So far, aerotropolis concept has been incorporated in greenfield airports

of Bengaluru, Hyderabad and Kochi and airport city concept has been

incorporated in the expansion/upgradation of Delhi and Mumbai

airports.

• Factors influencing the development of an aerotropolis are location,

regional connectivity, infrastructure, regional economy, operational

capacity, governance and real estate demand.

• Post a detailed analysis of the Kempegowda International Airport (KIA)

and the area under the jurisdiction of Bengaluru Airport Area Planning

Authority (BIAAPA), on the above mentioned parameters and

benchmarking it against aerotropolis regions around the world, the

following observations were made:

Bengaluru has the potential to develop into an aerotropolis

due to its strong economic growth, location advantage,

favourable demographics, airport’s growing operational

capacity, improving infrastructure and availability of large

land area for future growth.

Kempegowda International Airport (KIA) is advantageously located

within the region with shortest distance to all other airports in

South India.

The announcement of the Chennai - Bengaluru, Bengaluru -

Mumbai Industrial corridor is likely to improve its connectivity to

major ports and will increase its catchment area due to the growth

of new industrial area along this belt.

Intra-city connectivity is limited only to road. Travel time to the

airport from key economic hubs is still 60-90 minutes. However,

planned projects like Peripheral Ring Road and Metro Rail

connectivity are likely to reduce travel time over the next 5 years.

Like other established Aerotropoli, Bengaluru has a strong

economic base. Currently the Government of Karnataka is

promoting various business parks in the vicinity of the KIA and

close to 500,000 new jobs are anticipated to be created by 2025.

Currently, KIA is far behind in its operational capacity compared to

benchmark aerotropolis regions. However, at the current rate of

growth, the airport will reach annual passenger capacity of 50

million per annum, the average passenger capacity of benchmark

airports, by 2030. The airport also has sufficient land to handle

this increase in capacity.

In terms of governance, Bengaluru has adopted the hybrid form

that combines the best of market driven, hierarchical and network

driven approach.

Although real estate development in the study region is in a

nascent stage, but with activity in government promoted

economic hubs gaining traction, this region is likely to emerge as

the future real estate hotspot of Bengaluru.

• Based on the above observations, we conclude that BIAAPA region

may be India’s first aerotropolis in the making.

CONTENTS PAGE

Executive Summary 3Introduction 4 Factors Influencing Aerotropolis Development 10Real Estate Developments at KIA, Bengaluru 21Conclusion 27

Glossary 28Authors 29About Vestian 30

Introduction

Incheon International Airport (ICN), South Korea

JIT Manufacturing Flex Tech

Industrial Park

Industrial Park

Medical &Wellness Clusters

Research/Technology

Park

Distribution Centre

BondedWarehouse District

AirportCity

Hote

l

Hote

lBu

sines

s Offi

ce

Busin

ess O

ffice

AirCargo

Retail/wholesaleMerchandise

Marts

Hotel &Entertainment District

Business Park

ExibitionComplex

Residential

Airport Expressway (Aerolane)

Airport Expressway (Aerolane)

Airport Expressway (Aerolane)

Airpo

rt Ex

pres

sway

Train

(Aer

otra

in)Air

port

Expr

essw

ay Tr

ain (A

erot

rain)

Logistics Park& Free Trade Zone

Airport Expressway (Aerolane)Flow-Thru & E-Fullfillment

Facilities

Adap

tatio

n of

con

cept

map

cre

ated

by

John

D. K

asar

da

Figure 2: Schematic Diagram Of The Airport City And The Aerotropolis Region

Transportation hubs – Seaports, railroads & highways have been focal points around

which cities developed. In the 21st century Airports are taking on this role.

• For centuries, civilizations flourished around transportation hubs with

cities developing around seaports, railroads and highways. In the 19th

century, introduction of railways, led to transformation in city scape

with core trading and business activities centered in and around

railway stations. By the 20th century, highways came into prominence,

connecting cities and shifting commercial activities along the region;

thus leading to sub-urbanisation.

• In the speed-driven and globally connected economy of the 21st

century, airports are fast becoming the main drivers of city’s growth.

The role of an airport today is not just limited to a

transportation hub that facilitates movement of people and cargo, but

has evolved into that of an anchor that is crucial to the development of

a city. ‘Aerotropolis’, a term coined by Dr. John D Kasarda, is used to

describe such developments. Aerotropoli are likely to become import-

ant features in the globalized world providing companies with fast

access to suppliers, customers and enterprise partners1.

DEFENCE AIRPORTS

1909 Onwards(in USA & Europe)

1935 Onwards(in N. America & Europe)

2003 Onwards(in India2)

Post 2000 (around the world)

Located in defencebases and

catering to militaryand defence

affairs

CIVILIAN AIRPORTS

Located in suburbanareas involved in

passenger & cargomovement

PRIVATE AIRPORTS

Developed under publicprivate partnership

as greenfield3

or brownfield4

airports

AIRPORT CITY & AEROTROPOLIS

Located in peripheral region of a city &

operating as business enterprise incorporating

various non - aeronautical services

Figure 1: Evolution Of Airports

• Historically airports were funded and developed by governments of

nations across Europe and North America, to use aircrafts for military

combat purposes, especially during the period between World War I

(WWI) & World War II (WWII). Both aircraft technology & production

witnessed great advancements during this period.

• After WWII, commercial aviation became popular, using ex-military

aircraft and cargo airbuses. Defense airstrips then gave way to

airports and private funding started flowing in, to develop terminal

buildings and other passenger/cargo facilities within airports.

• Today airports are much more than just a medium/machinery to

facilitate commutation domestically or across international borders.

With aviation-enabled firms agglomerating around airports, creating

‘economies of speed’, airports are shaping up as business hubs,

integrating various non-aeronautical services with aeronautical

business, leading to the development of new business models such

as ‘airport city’ and ‘aerotropolis’.

AEROTROPOLIS6 7

An aerotropolis is an urban development with an airport at the center with aviation-linked

businesses agglomerating around it.• The airport city is a model where the terminal building with its retail

use is equated to that of an urban square and the office, hospitality,

convention facilities, etc., are spread around the terminal building as

part of the airport’s public - access property; synonymous to the Ce

ntral Business District (CBD) concept thereby creating a city-like

environment within the airport property.

• The development of an airport city may lead to the agglomeration of

various businesses like:

Valuable or perishable cargo that is hugely dependent on short

transit time and protection from pilferage, which will otherwise

obliterate the value of the product.

Aviation related research & technology development centres

requiring location proximity to airports.

Logistics companies and warehouses to facilitate transportation

and distribution of air cargo.

Various service-related businesses that reinforce the system

like retail, hotels & entertainments centres, commercial offices

as well a residential developments.

This urban development centered, around an airport city, with

an agglomeration of airport dependent businesses and

associated mixed use residential developments is defined as an

aerotropolis.

• Most of the greenfield airport projects across the world are adopting

the ‘aerotropolis’ model while existing brownfield developments are

innovating and refurbishing their existing infrastructure to incorporate

the airport city model to increase the non-aeronautical revenues and

derive lucrative returns of an otherwise capital intensive airport

venture.

• Key examples of aerotropoli around the world include:

Memphis International Airport - Memphis, Tennessee and Dallas-Fort

Worth International Airport (DFW), Texas, USA are prime examples of

market driven aerotropoli that have developed due to the need for

fastest possible networking to transport cargo. Incheon, South Korea

and Dubai World Central, United Arab Emirates (UAE) are greenfield

airports that are hierarchy-driven with top down governance approach

with the government being the key decision-maker. Fraport in

Frankfurt, Germany has developed due to its regional economy as a

financial capital while Schipol, Amsterdam is a key example of an

airport city operating on private sector principles.

1 John D. Kasarda, 2010, ‘Global Airport Cities’, Insight Media, www.GlobalAirportCities.com2Private sector participation in airport development was allowed post the amendment of Airport Authority of India Act, 1994 in 2003. However, private sector participation has been prevalent in airport development

in other countries around the world even prior to 2003.3 Greenfield Airports are airports built from scratch on an undeveloped site.4 Brownfield Airports refer to existing airports that are upgraded. These projects impose restrictions due to existing developments.

AEROTROPOLIS8 9

132Total number of

operationalairports under AAI

3 Greenfield airports

developed with privatepartners till 2014

2 Brownfield airports

expanded/upgraded withprivate partners

15New greenfield airports

approved

200Low cost airports

announced in Tier ll, lllcities by over next 20 years

25International

airports

Overview Of Airport Development In India • Since economic liberalization in 1991, Indian aviation industry has

transformed from being a state owned industry to one that is

dominated by privately owned full services airlines and low-cost

carriers.The adoption of open skies policy post 1991 has added to the

overall growth in air-traffic. Between 2006 and 2013, total air

passenger traffic grew by about 65% from 96 million to 159 million

passengers in the country.

• Mumbai, Delhi, Bengaluru, Hyderabad, Chennai, Kolkata and Cochin

airports account for 70% of the total passenger traffic in India. Delhi

and Mumbai collectively amount to 40% of the total passenger traffic

and are the two busiest airports in India.

• With increasing air traffic the infrastructure of the existing airports

encountered capacity constraint and necessitated modernisation and

upgradation. To bring a quick turnaround, the GoI and AAI have taken

the following steps:

The AAI Act has been amended to allow airport privatization.

Adopted the Public Private Partnership (PPP) model for

development of greenfield airports and modernization of

existing airports.

Allowed 100% FDI in greenfield airports under the automatic

route and 100% FDI for expansion/upgradation of existing

airports subject to FIPB approval for funding beyond 74%.

• In line with global advances in airport development, airports across

India are being modernized and upgraded incorporating the

characteristics of the airport city and aerotropolis models. A

comparative matrix of the operational capacity and future

development possibilities is prepared to understand the airports’

potential to develop into an aerotropolis.

• Delhi, Mumbai and Chennai lose out on the opportunity to develop

into aerotropoli due to the location of their airport in suburban areas

with no scope for future expansion. However, airport city model may

be incorporated in these airports. Hyderabad and Cochin have

sufficient land due to their peripheral location, but are lower in

capacity compared to Bengaluru. Bengaluru has sufficient operational

capacity as well as location advantage both in terms of regional

connectivity and land availability.

• Therefore, we have taken the case of KIA, Bengaluru for the study.

Economic liberalization has given a prominent role to private airlines that has resulted in an

increase in air traffic. Today, modernization of airports is done largely under PPP model. ParticularsIndira Gandhi

International Airport, Delhi

Delhi International Airport Pvt. Ltd.

Suburban

National Capital

6,300

36.9

10

21.80

60

100

2.2

No

High

Chattrapati Shivaji International Airport,

Mumabi

Mumbai International Airport Ltd.

Suburban

Financial Capital

2,900

32.2

7

19.10

30

50

0.15

No

Very High

Chennai International Airport,

Chennai

AAI

Suburban

Port City

1,283

12.89

6

7.60

23

25

0.29

No

Moderate

Owner/Operator

Location

USP

Area (in acres)

Total Passengers (in millions) 2013-14

Growth Rate (in %)

Market Share (in %)1

Handling Capacity (pax p. a. in millions)

Scope For Expansion (pax p. a. in millions)

Availability Of Land For Aerotropolis Development(outside airport fence)

Real Estate Cost

Cargo Handling Capacity(in million tons)

Kempegowda International Airport,

Bengaluru

BIAL/GVK

Peripheral

IT Capital

4,000

12.9

8

8.00

20

50

0.36

Yes

Moderate

Rajiv Gandhi International Airport,

Hyderabad

GMR HyderabadInter. Airport Ltd.

Peripheral

Emerging Metropolis

5,500

8.7

7

5.00

12

40

0.15

Yes

Low

Cochin International Airport,

Cochin

Cochin International Airport Ltd.

Peripheral

Port City

2,460

5.4

10

3.00

9

20

0.15

Yes

Low

Table 1: Snapshot Of Key Modern Airports In India

Source: Vestian Research 2014

1 Percentage of passenger traffic in respective airport over total air passenger traffic

Indira Gandhi International Airport, Delhi

Kempegowda International Airport (KIA), Bengaluru

Kempegowda International Airport- An Aerotropolis In Making

AEROTROPOLIS12 13

Figure 4: Factors Influencing Aerotropolis Development

Factors Influencing Aerotropolis Development

Location, Connectivity& Infrastructure

• Regional location• Regional connectivity• Location of the airport in the city• Distance from CBD• Connectivity to CBD & other economic hubs within the city• Infrastructure projects that will improve connectivity to the airport• Airport infrastructure

Economic Drivers

• Target Industries in the region• Number of jobs created in the region• Number of direct employees at the airport• Incentives for setting up business in the region

Operational Capacity

• Passenger traffic• Cargo landed weight• Number of passenger airlines• Total aircraft operations• Capacity (arrivals/departures per hour)• Airlines that have made airport their hub

Governance

• Ownership structure• Key decision-makers• Key stakeholders

Real Estate

• Commercial• Residential• Retail• Hospitality• Healthcare• Education

Location, connectivity & infrastructure, regional economy, operational capacity, governance

and real estate demand are the factors crucial for the development of an aerotropolis.

Location, Connectivity & Infrastructure• Airport cities world over have developed on urban fringes as the

development requires large tracts of land both for immediate use and

future expansion.

• Location on urban fringes necessitates high-speed connectivity to the

city for the movement of both passengers and cargo. This has led to

the development of infrastructure such as airport expressway links,

high speed rail links and dedicated freight corridors.

Regional Economy• Regional economy and airports share a close link. High tech industries

(firms specializing in Information and Communication Technologies)

generally locate their facilities within the airport fence as high-tech

professionals are likely to travel by air at least 60% more frequently

than other professionals. Proximity to the airport also gives these

businesses high visibility for their brands.

• Airports and its immediate environs attract non service components of

the economy. New economy products such as micro-electronics,

pharmaceuticals, aerospace components, medical devices and other

high value-to-weight, time sensitive products account for 80% of

international air cargo.

• Therefore, cities with high-tech and new economy products as their

primary economic drivers will witness the agglomeration of these

industries in the aerotropolis regions.

Operational Capacity• Growing dependence on the airport for passenger and cargo movement

has necessitated the need to increase operational capacities of

airports. Higher passenger and cargo traffic in turn results in better

airport infrastructure, increased demand for hotels, retail and other

real estate development.

Governance• An aerotropolis region is spread across multiple jurisdictions, and a

successful aerotropolis region requires coordinated investments in

land use and infrastructure development in order to benefit the

businesses located in the region.

• Four types of governance structures defined and are -

Market driven, where individual firms locate close to the airports

to maximize economic benefits, thereby creating RE demand.

This involves multiple agencies for governing various

jurisdiction. Key example is Memphis International Airport

Tennesee, USA.

Hierarchy - driven, where governance is driven through top -

down directives. Key examples are Incheon International

Airport,Seoul; Dubai World Central, United Arab Emirates (UAE).

Network - driven, where decisions are arrived at based on

consultation with stakeholders. Key example is Schiphol,

Amsterdam.

Hybrid - This incorporates the most suitable aspects of the

above three structures.

Real Estate• With more airports going the privatization route, revenue from

non-aeronautical services is becoming important in order to keep the

airports profitable.

• Recent studies sampling airports all over the world suggest a

correlation between an airport development and proliferation of

supportive real estate in the adjoining region.

Figure 5: Airport City & Aerotropolis Locations Worldwide

Study Area: BIAAPA Region• The Kempegowda International Airport (KIA) was conceptualized in

the year 1994 and Karnataka State Industrial Infrastructure

Development Corporation (KSIIDC) was appointed as the nodal

agency. The greenfield airport is developed in Devanahalli, 35 km

from Bengaluru city.

• The greenfield airport is developed on a Public Private Partnership

(PPP) Model and opened for public in May 2008.

• KIA property is spread across approximately 3,880 acres of land.

About 2,000 acres are developed as part of Phase I. Approximately

450 acres are available for real estate development.

• The area under the jurisdiction of the Bengaluru International Airport

Area Planning Authority (BIAAPA) is considered as the study area. It

covers an area of 985 sqkm.

• In this section, we undertake an in-depth study of KIA and BIAAPA

region and then compare it with established aerotropolis regions

around the world to understand if the region has the potential to

develop as an aerotropolis.

Benchmark aerotropolis regions include

• Memphis International Airport (MEM) - Memphis, Tennessee, USA

• Dallas-Fort Worth International Airport (DFW) - Texas, USA

• Hong Kong International Airport (HKIA) - Hong Kong, China

• Incheon International Airport (ICN) - Seoul, South Korea

• Fraport (FRA) - Frankfurt, Germany

• Schiphol Amsterdam Airport (AMS) - Amsterdam, The Netherlands

Dallas Fortworth International Airport (DFW)

Memphis International Airport (MEM)

Frankfurt Am Main Airport (FRA)

Amsterdam Schiphol Airport (AMS)

Hong Kong International Airport (HKIA)

Kempegowda International Airport (KIA)

Incheon International Airport (ICN)

Operational Aerotropolis

Developing Aerotropolis

Operational Airport City

Developing Airport City

Benchmark Aerotropolis

Case Study KIA

DODDABALLAPUR

HOSKOTE

KANAKAPURA

RAMANAGARAM

MAGADI

BENGALURUCITY

STUDY AREA

ANEKAL

NELAMANGALAKIA

Figure 3: Map Of Study Area, Bengaluru• Regional economic conditions play a major role in creating real estate

demand within the airport cities.

• Round the clock activities in an airport are gradually transforming these

transportation hubs into viable retail, hospitality, business & industrial

destinations.

N

AEROTROPOLIS14 15

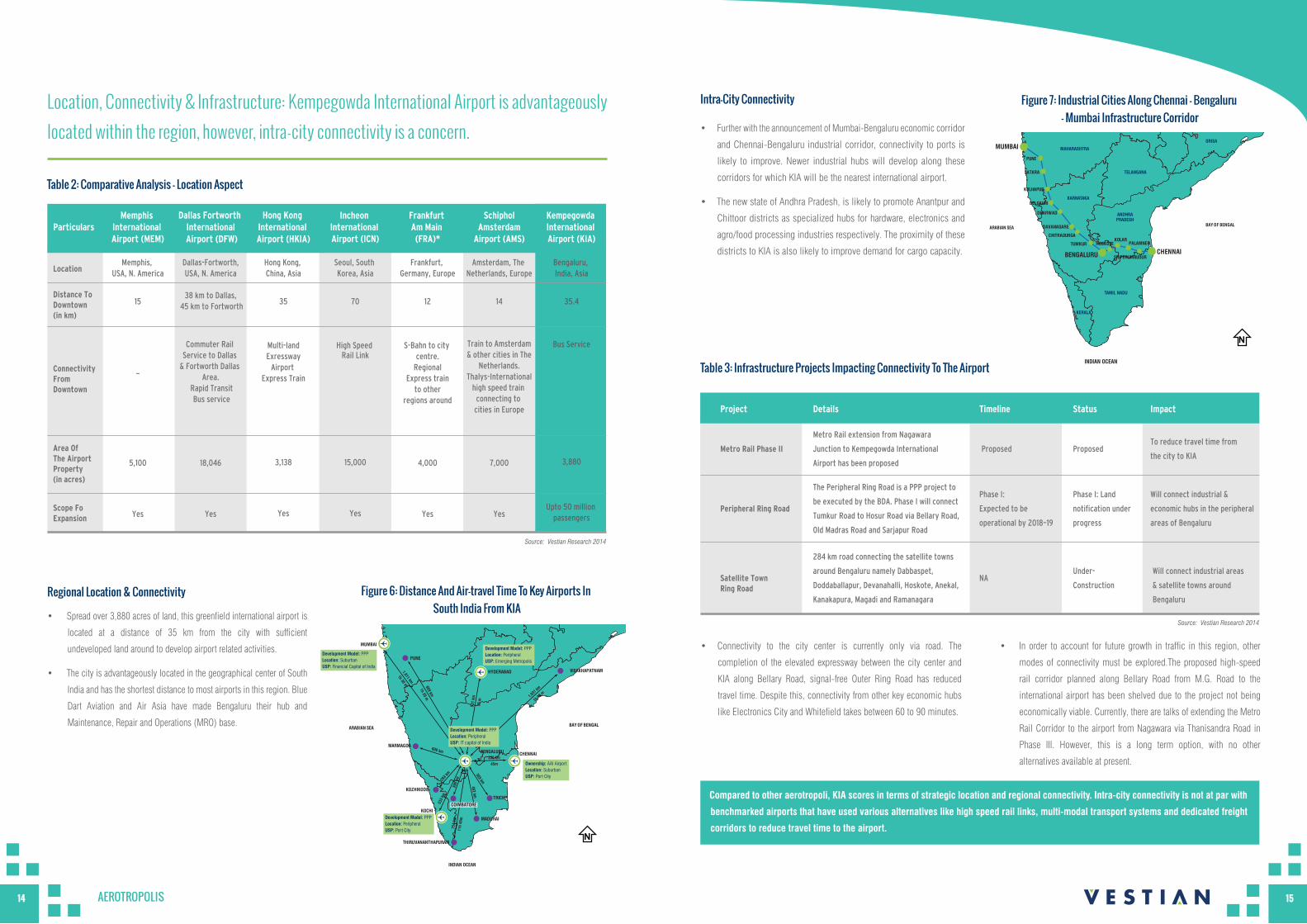

• Further with the announcement of Mumbai-Bengaluru economic corridor

and Chennai-Bengaluru industrial corridor, connectivity to ports is

likely to improve. Newer industrial hubs will develop along these

corridors for which KIA will be the nearest international airport.

• The new state of Andhra Pradesh, is likely to promote Anantpur and

Chittoor districts as specialized hubs for hardware, electronics and

agro/food processing industries respectively. The proximity of these

districts to KIA is also likely to improve demand for cargo capacity.

Table 2: Comparative Analysis - Location Aspect

• Spread over 3,880 acres of land, this greenfield international airport is

located at a distance of 35 km from the city with sufficient

undeveloped land around to develop airport related activities.

• The city is advantageously located in the geographical center of South

India and has the shortest distance to most airports in this region. Blue

Dart Aviation and Air Asia have made Bengaluru their hub and

Maintenance, Repair and Operations (MRO) base.

Regional Location & Connectivity

Intra-City ConnectivityLocation, Connectivity & Infrastructure: Kempegowda International Airport is advantageously

located within the region, however, intra-city connectivity is a concern.

ParticularsMemphis

International Airport (MEM)

Dallas Fortworth International

Airport (DFW)

Hong Kong International Airport (HKIA)

LocationMemphis,

USA, N. America

15

_

5,100

Yes

Dallas-Fortworth,USA, N. America

38 km to Dallas, 45 km to Fortworth

Commuter Rail Service to Dallas

& Fortworth Dallas Area.

Rapid Transit Bus service

18,046

Yes

Hong Kong, China, Asia

35

Multi-landExressway

Airport Express Train

3,138

Yes

Distance To Downtown (in km)

Connectivity From Downtown

Area Of The AirportProperty (in acres)

Scope FoExpansion

Frankfurt Am Main (FRA)*

Incheon International Airport (ICN)

SchipholAmsterdam

Airport (AMS)

Kempegowda International Airport (KIA)

Frankfurt, Germany, Europe

12

S-Bahn to city centre.

Regional Express train

to other regions around

4,000

Yes

Seoul, South Korea, Asia

70

High Speed Rail Link

15,000

Yes

Amsterdam, The Netherlands, Europe

14

Train to Amsterdam & other cities in The

Netherlands. Thalys-International

high speed train connecting to cities in Europe

7,000

Yes

Bengaluru, India, Asia

35.4

Bus Service

3,880

Upto 50 million passengers

Compared to other aerotropoli, KIA scores in terms of strategic location and regional connectivity. Intra-city connectivity is not at par with

benchmarked airports that have used various alternatives like high speed rail links, multi-modal transport systems and dedicated freight

corridors to reduce travel time to the airport.

• Connectivity to the city center is currently only via road. The

completion of the elevated expressway between the city center and

KIA along Bellary Road, signal-free Outer Ring Road has reduced

travel time. Despite this, connectivity from other key economic hubs

like Electronics City and Whitefield takes between 60 to 90 minutes.

• In order to account for future growth in traffic in this region, other

modes of connectivity must be explored.The proposed high-speed

rail corridor planned along Bellary Road from M.G. Road to the

international airport has been shelved due to the project not being

economically viable. Currently, there are talks of extending the Metro

Rail Corridor to the airport from Nagawara via Thanisandra Road in

Phase III. However, this is a long term option, with no other

alternatives available at present.

Figure 6: Distance And Air-travel Time To Key Airports In South India From KIA

THIRUVANANTHAPURAM

CHENNAI

MADURAI

TRICHY

KOZHIKODE

KOCHI

MARMAGOA

VISAKHAPATNAM

BAY OF BENGAL

INDIAN OCEAN

ARABIAN SEA

BENGALURU

MUMBAI

PUNE

869 km

1h 20 m

531

km55

m

608 km

393 k

m

396

km

369 km

462 km

338 km

45m

754

km11

h 45

m

533

km

1,031

km

1h 30

m

1,011 km

1h 30 m

HYDERABAD

Development Model: PPPLocation: SuburbanUSP: Financial Capital of India

Development Model: PPPLocation: PeripheralUSP: Emerging Metropolis

Development Model: PPPLocation: PeripheralUSP: Port City

Development Model: PPPLocation: PeripheralUSP: IT capital of India

Ownership: AAI AirportLocation: SuburbanUSP: Port City

COIMBATORE

Figure 7: Industrial Cities Along Chennai – Bengaluru – Mumbai Infrastructure Corridor

CHENNAI

BAY OF BENGALARABIAN SEA

MUMBAI

PUNE

SATARA

KOLHAPUR

BELGAUM

DHARWAD

DAVANAGARE

CHITRADURGA

TUMKUR

BENGALURU SRIPERUMBUDUR

HOSKOTEKOLAR

PALAMNER

INDIAN OCEAN

TELANGANA

ORISA

ANDHRAPRADESH

KARNATAKA

TAMIL NADU

KERALA

MAHARASHTRA

Table 3: Infrastructure Projects Impacting Connectivity To The Airport

DetailsProject Timeline Status Impact

Metro Rail extension from Nagawara

Junction to Kempegowda International

Airport has been proposed

The Peripheral Ring Road is a PPP project to

be executed by the BDA. Phase I will connect

Tumkur Road to Hosur Road via Bellary Road,

Old Madras Road and Sarjapur Road

284 km road connecting the satellite towns

around Bengaluru namely Dabbaspet,

Doddaballapur, Devanahalli, Hoskote, Anekal,

Kanakapura, Magadi and Ramanagara

Metro Rail Phase II Proposed ProposedTo reduce travel time from

the city to KIA

Peripheral Ring Road

Phase I:

Expected to be

operational by 2018–19

Phase I: Land

notification under

progress

Will connect industrial &

economic hubs in the peripheral

areas of Bengaluru

Will connect industrial areas

& satellite towns around

Bengaluru

Under-

ConstructionSatellite Town Ring Road

NA

Source: Vestian Research 2014

Source: Vestian Research 2014

N

N

Table 5: Government Promoted Economic Hubs In Bengaluru

Particulars

Location

Devanahalli Business Park

Devanahalli -

Adjacent to KIA

414

KSIIDC

Fresh EOI invited

in August 2011 to

develop the project

on a PPP basis.

Design for the

convention center

within has

been finalized

_

250,000

Aerospace Park

South of KIA

1,000

KIADB

Wipro,

Starrag Heckert,

Amada and

TE operational

BEML, AIMIL,

Dynamatic

Technologies,

Sunshine Aerospace,

Centum Electronics

20,000

Logistic Parks

Balepura

near

Devanahalli

150

KSIIDC

Land

aqusition

is underway

_

10,000

HardwarePark

Bagalur

Village

941

KIADB

Shell

Technologies’

facility (1.5million

sqft) is under

construction.

Foundation stone

laid for the financial

city on 50 acres to

be developed by IFIC

Bangalore Bio-Tech

labs, Shell

Technology,

Moser Baer

40,000

IT/BT Park

Bagalur

Village

1,028

KIADB

Land alloted to

companies like

TCS & Cognizant

Sunlux Technology

150,000

IT Investment Region (ITIR)

Muddenahalli,

Kaniverayanapura,

Chikkaballapur

12,000

KEONICS

Land acquisition

underway for 2,200

acres of Phase I.

55 companies

including Infosys,

Wipro, TCS,

Cognizant have

signed up MOUs

1.2 million

Integrated Textile Park

Doddaballapur

Road

469

KIADB

Operational

Gokuldas Images,

Madura Garments,

Raymonds, Bombay

Rayon Fashion

15,000

Area (in acres)

Agency

Status

Companies That Have Been Alloted Land

Employment Generation By 2025

AEROTROPOLIS16 17

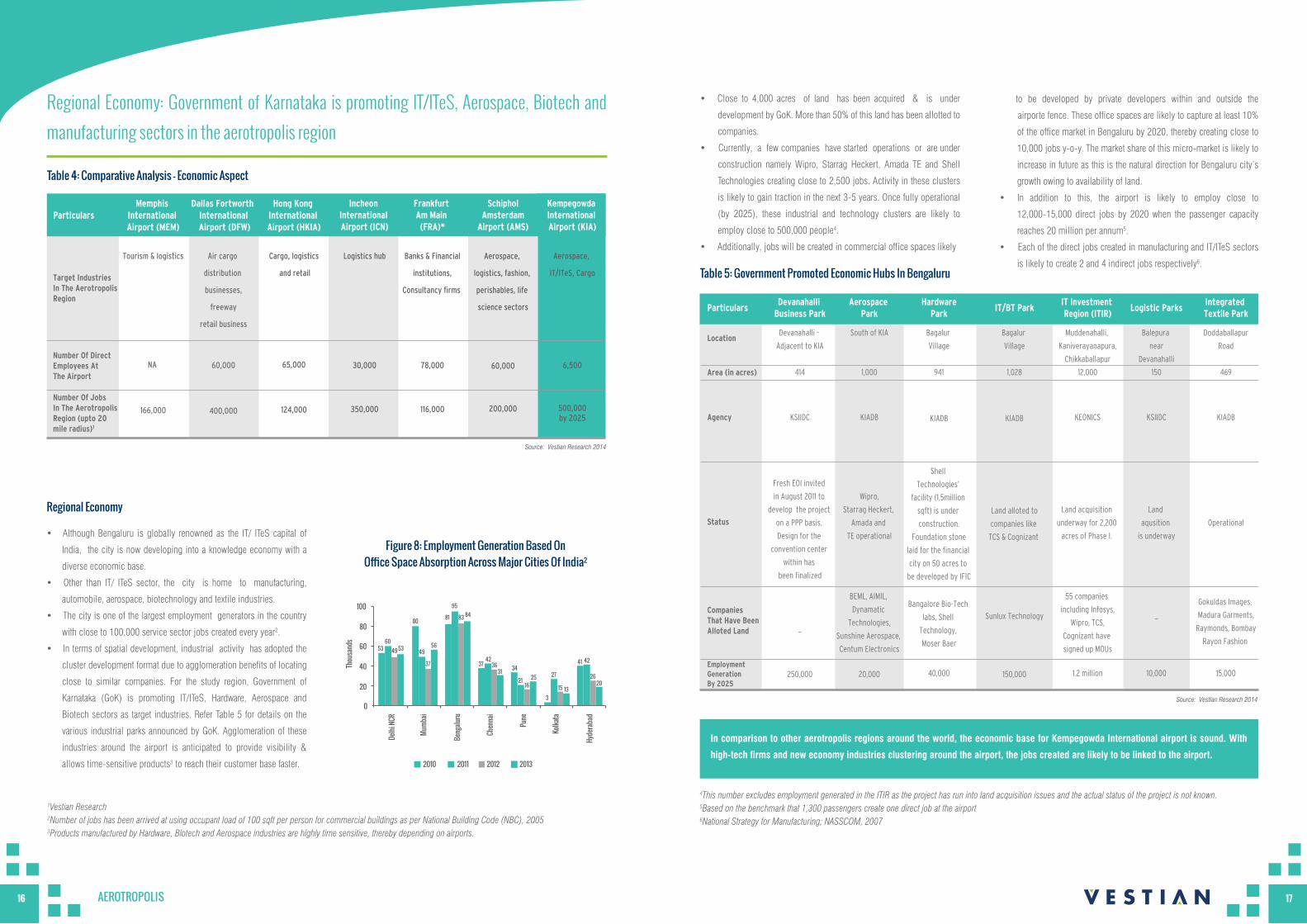

• Although Bengaluru is globally renowned as the IT/ ITeS capital of

India, the city is now developing into a knowledge economy with a

diverse economic base.

• Other than IT/ ITeS sector, the city is home to manufacturing,

automobile, aerospace, biotechnology and textile industries.

• The city is one of the largest employment generators in the country

with close to 100,000 service sector jobs created every year2.

• In terms of spatial development, industrial activity has adopted the

cluster development format due to agglomeration benefits of locating

close to similar companies. For the study region, Government of

Karnataka (GoK) is promoting IT/ITeS, Hardware, Aerospace and

Biotech sectors as target industries. Refer Table 5 for details on the

various industrial parks announced by GoK. Agglomeration of these

industries around the airport is anticipated to provide visibility &

allows time-sensitive products3 to reach their customer base faster.

• Close to 4,000 acres of land has been acquired & is under

development by GoK. More than 50% of this land has been allotted to

companies.

• Currently, a few companies have started operations or are under

construction namely Wipro, Starrag Heckert, Amada TE and Shell

Technologies creating close to 2,500 jobs. Activity in these clusters

is likely to gain traction in the next 3-5 years. Once fully operational

(by 2025), these industrial and technology clusters are likely to

employ close to 500,000 people4.

• Additionally, jobs will be created in commercial office spaces likely

1Vestian Research2Number of jobs has been arrived at using occupant load of 100 sqft per person for commercial buildings as per National Building Code (NBC), 20053Products manufactured by Hardware, Biotech and Aerospace industries are highly time sensitive, thereby depending on airports.

4This number excludes employment generated in the ITIR as the project has run into land acquisition issues and the actual status of the project is not known.5Based on the benchmark that 1,300 passengers create one direct job at the airport6National Strategy for Manufacturing; NASSCOM, 2007

0

20

Delhi

NCR

Thou

sand

s

Mumb

ai

Beng

aluru

Chen

nai

Pune

Kolka

ta

Hyde

raba

d

40

60

80

100

20122010 2011 2013

53

80

4956

81

95

83

37

15 13

41 42

2620

27

3

2116

2534

4236

31

84

37

6049 53

Figure 8: Employment Generation Based OnOffice Space Absorption Across Major Cities Of India2

to be developed by private developers within and outside the

airporte fence. These office spaces are likely to capture at least 10%

of the office market in Bengaluru by 2020, thereby creating close to

10,000 jobs y-o-y. The market share of this micro-market is likely to

increase in future as this is the natural direction for Bengaluru city’s

growth owing to availability of land.

• In addition to this, the airport is likely to employ close to

12,000-15,000 direct jobs by 2020 when the passenger capacity

reaches 20 million per annum5.

• Each of the direct jobs created in manufacturing and IT/ITeS sectors

is likely to create 2 and 4 indirect jobs respectively6.

Table 4: Comparative Analysis – Economic Aspect

Regional Economy: Government of Karnataka is promoting IT/ITeS, Aerospace, Biotech and

manufacturing sectors in the aerotropolis region

ParticularsMemphis

International Airport (MEM)

Dallas Fortworth International

Airport (DFW)

Hong Kong International Airport (HKIA)

Tourism & logistics

NA

166,000

Air cargo

distribution

businesses,

freeway

retail business

60,000

400,000

Cargo, logistics

and retail

65,000

124,000

Target Industries In The AerotropolisRegion

Number Of Direct Employees At The Airport

Number Of JobsIn The Aerotropolis Region (upto 20 mile radius)1

Frankfurt Am Main (FRA)*

Incheon International Airport (ICN)

SchipholAmsterdam

Airport (AMS)

Kempegowda International Airport (KIA)

Logistics hub

30,000

350,000

Banks & Financial

institutions,

Consultancy firms

78,000

116,000

Aerospace,

logistics, fashion,

perishables, life

science sectors

60,000

200,000

Aerospace,

IT/ITeS, Cargo

6,500

500,000by 2025

In comparison to other aerotropolis regions around the world, the economic base for Kempegowda International airport is sound. With

high-tech firms and new economy industries clustering around the airport, the jobs created are likely to be linked to the airport.

Regional Economy

Source: Vestian Research 2014

Source: Vestian Research 2014

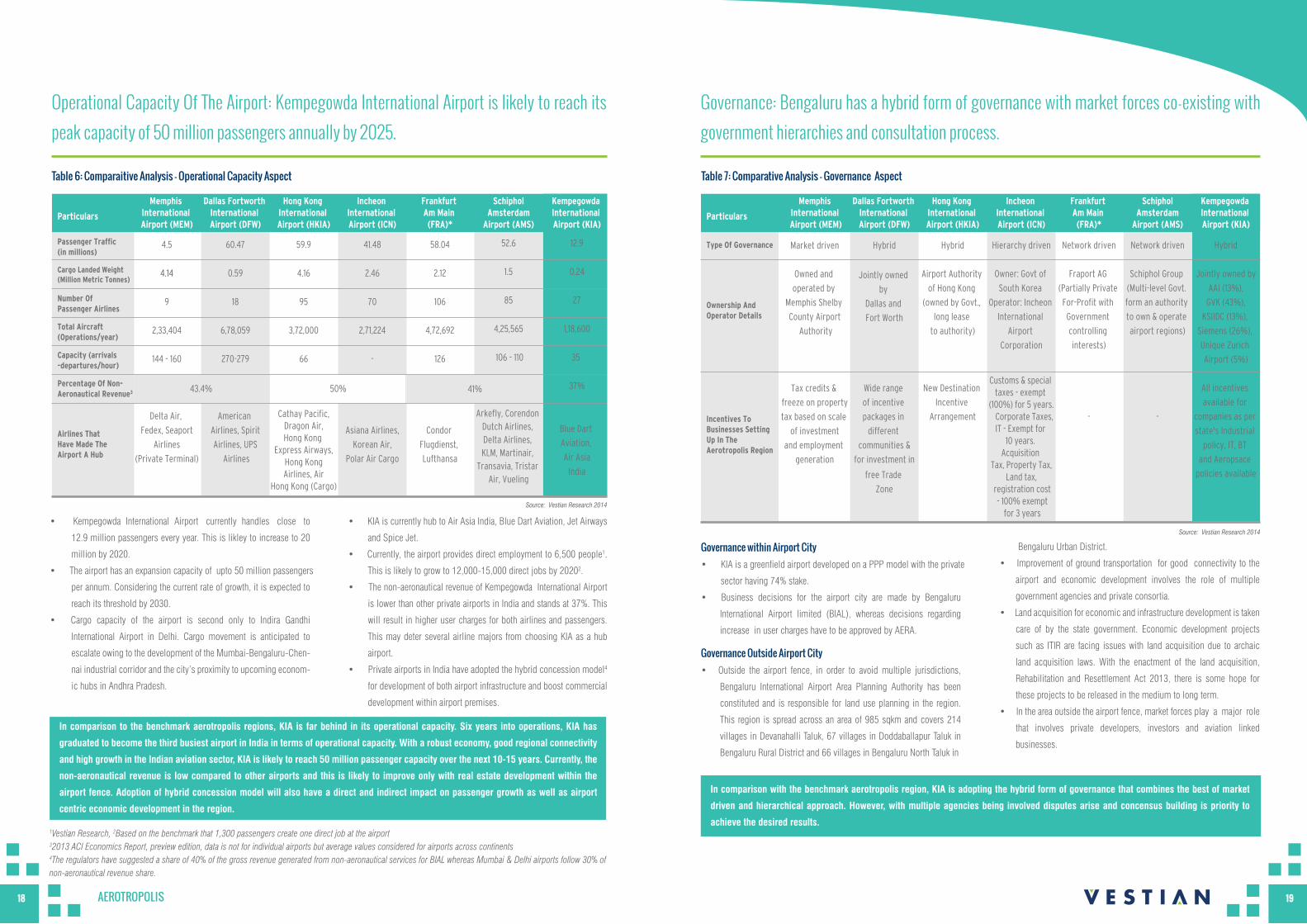

In comparison to the benchmark aerotropolis regions, KIA is far behind in its operational capacity. Six years into operations, KIA has

graduated to become the third busiest airport in India in terms of operational capacity. With a robust economy, good regional connectivity

and high growth in the Indian aviation sector, KIA is likely to reach 50 million passenger capacity over the next 10-15 years. Currently, the

non-aeronautical revenue is low compared to other airports and this is likely to improve only with real estate development within the

airport fence. Adoption of hybrid concession model will also have a direct and indirect impact on passenger growth as well as airport

centric economic development in the region.

AEROTROPOLIS18 19

Operational Capacity Of The Airport: Kempegowda International Airport is likely to reach its

peak capacity of 50 million passengers annually by 2025.

Particulars

Memphis International Airport (MEM)

Dallas Fortworth International Airport (DFW)

Hong Kong International Airport (HKIA)

Incheon International Airport (ICN)

Frankfurt Am Main (FRA)*

SchipholAmsterdam

Airport (AMS)

Kempegowda International Airport (KIA)

Passenger Traffic(in millions)

Cargo Landed Weight (Million Metric Tonnes)

Number Of Passenger Airlines

Total Aircraft (Operations/year)

Capacity (arrivals-departures/hour)

Percentage Of Non-Aeronautical Revenue3

Airlines ThatHave Made The Airport A Hub

4.5

4.14

9

2,33,404

144 - 160

Delta Air,

Fedex, Seaport

Airlines

(Private Terminal)

60.47

0.59

18

6,78,059

270-279

American

Airlines, Spirit

Airlines, UPS

Airlines

59.9

4.16

95

3,72,000

66

Cathay Pacific,Dragon Air,Hong Kong

Express Airways, Hong Kong Airlines, Air

Hong Kong (Cargo)

41.48

2.46

70

2,71,224

-

Asiana Airlines,

Korean Air,

Polar Air Cargo

58.04

2.12

106

4,72,692

126

Condor

Flugdienst,

Lufthansa

52.6

1.5

85

4,25,565

106 - 110

Arkefly, Corendon Dutch Airlines, Delta Airlines, KLM, Martinair,

Transavia, Tristar Air, Vueling

12.9

0.24

27

1,18,600

35

37%

Blue Dart

Aviation,

Air Asia

India

43.4% 41%50%

Table 6: Comparaitive Analysis - Operational Capacity Aspect

Governance: Bengaluru has a hybrid form of governance with market forces co-existing with

government hierarchies and consultation process.

Particulars

Memphis International Airport (MEM)

Dallas Fortworth International Airport (DFW)

Hong Kong International Airport (HKIA)

Incheon International Airport (ICN)

Frankfurt Am Main (FRA)*

SchipholAmsterdam

Airport (AMS)

Kempegowda International Airport (KIA)

Type Of Governance

Ownership And Operator Details

Incentives To Businesses Setting Up In The Aerotropolis Region

Market driven

Owned and

operated by

Memphis Shelby

County Airport

Authority

Tax credits &

freeze on property

tax based on scale

of investment

and employment

generation

Hybrid

Jointly owned

by

Dallas and

Fort Worth

Wide range

of incentive

packages in

different

communities &

for investment in

free Trade

Zone

Hybrid

Airport Authority

of Hong Kong

(owned by Govt.,

long lease

to authority)

New Destination

Incentive

Arrangement

Hierarchy driven

Owner: Govt of

South Korea

Operator: Incheon

International

Airport

Corporation

Customs & special taxes - exempt

(100%) for 5 years. Corporate Taxes,

IT - Exempt for 10 years.

Acquisition Tax, Property Tax,

Land tax, registration cost - 100% exempt

for 3 years

Network driven

Fraport AG

(Partially Private

For-Profit with

Government

controlling

interests)

-

Network driven

Schiphol Group

(Multi-level Govt.

form an authority

to own & operate

airport regions)

-

Hybrid

Jointly owned by

AAI (13%),

GVK (43%),

KSIIDC (13%),

Siemens (26%),

Unique Zurich

Airport (5%)

All incentives

available for

companies as per

state's Industrial

policy, IT, BT

and Aeropsace

policies available

Table 7: Comparative Analysis - Governance Aspect

In comparison with the benchmark aerotropolis region, KIA is adopting the hybrid form of governance that combines the best of market

driven and hierarchical approach. However, with multiple agencies being involved disputes arise and concensus building is priority to

achieve the desired results.

Governance within Airport City• KIA is a greenfield airport developed on a PPP model with the private

sector having 74% stake.

• Business decisions for the airport city are made by Bengaluru

International Airport limited (BIAL), whereas decisions regarding

increase in user charges have to be approved by AERA.

Governance Outside Airport City• Outside the airport fence, in order to avoid multiple jurisdictions,

Bengaluru International Airport Area Planning Authority has been

constituted and is responsible for land use planning in the region.

This region is spread across an area of 985 sqkm and covers 214

villages in Devanahalli Taluk, 67 villages in Doddaballapur Taluk in

Bengaluru Rural District and 66 villages in Bengaluru North Taluk in

Bengaluru Urban District.

• Improvement of ground transportation for good connectivity to the

airport and economic development involves the role of multiple

government agencies and private consortia.

• Land acquisition for economic and infrastructure development is taken

care of by the state government. Economic development projects

such as ITIR are facing issues with land acquisition due to archaic

land acquisition laws. With the enactment of the land acquisition,

Rehabilitation and Resettlement Act 2013, there is some hope for

these projects to be released in the medium to long term.

• In the area outside the airport fence, market forces play a major role

that involves private developers, investors and aviation linked

businesses.

Source: Vestian Research 2014

Source: Vestian Research 2014

1Vestian Research, 2Based on the benchmark that 1,300 passengers create one direct job at the airport32013 ACI Economics Report, preview edition, data is not for individual airports but average values considered for airports across continents4The regulators have suggested a share of 40% of the gross revenue generated from non-aeronautical services for BIAL whereas Mumbai & Delhi airports follow 30% of non-aeronautical revenue share.

• Kempegowda International Airport currently handles close to

12.9 million passengers every year. This is likley to increase to 20

million by 2020.

• The airport has an expansion capacity of upto 50 million passengers

per annum. Considering the current rate of growth, it is expected to

reach its threshold by 2030.

• Cargo capacity of the airport is second only to Indira Gandhi

International Airport in Delhi. Cargo movement is anticipated to

escalate owing to the development of the Mumbai-Bengaluru-Chen-

nai industrial corridor and the city’s proximity to upcoming econom-

ic hubs in Andhra Pradesh.

• KIA is currently hub to Air Asia India, Blue Dart Aviation, Jet Airways

and Spice Jet.

• Currently, the airport provides direct employment to 6,500 people1.

This is likely to grow to 12,000-15,000 direct jobs by 20202.

• The non-aeronautical revenue of Kempegowda International Airport

is lower than other private airports in India and stands at 37%. This

will result in higher user charges for both airlines and passengers.

This may deter several airline majors from choosing KIA as a hub

airport.

• Private airports in India have adopted the hybrid concession model4

for development of both airport infrastructure and boost commercial

development within airport premises.

Schiphol Amsterdam Airport (AMS), The Netherlands

Real Estate Developments at KempegowdaInternational Airport, Bengaluru

AEROTROPOLIS22 23

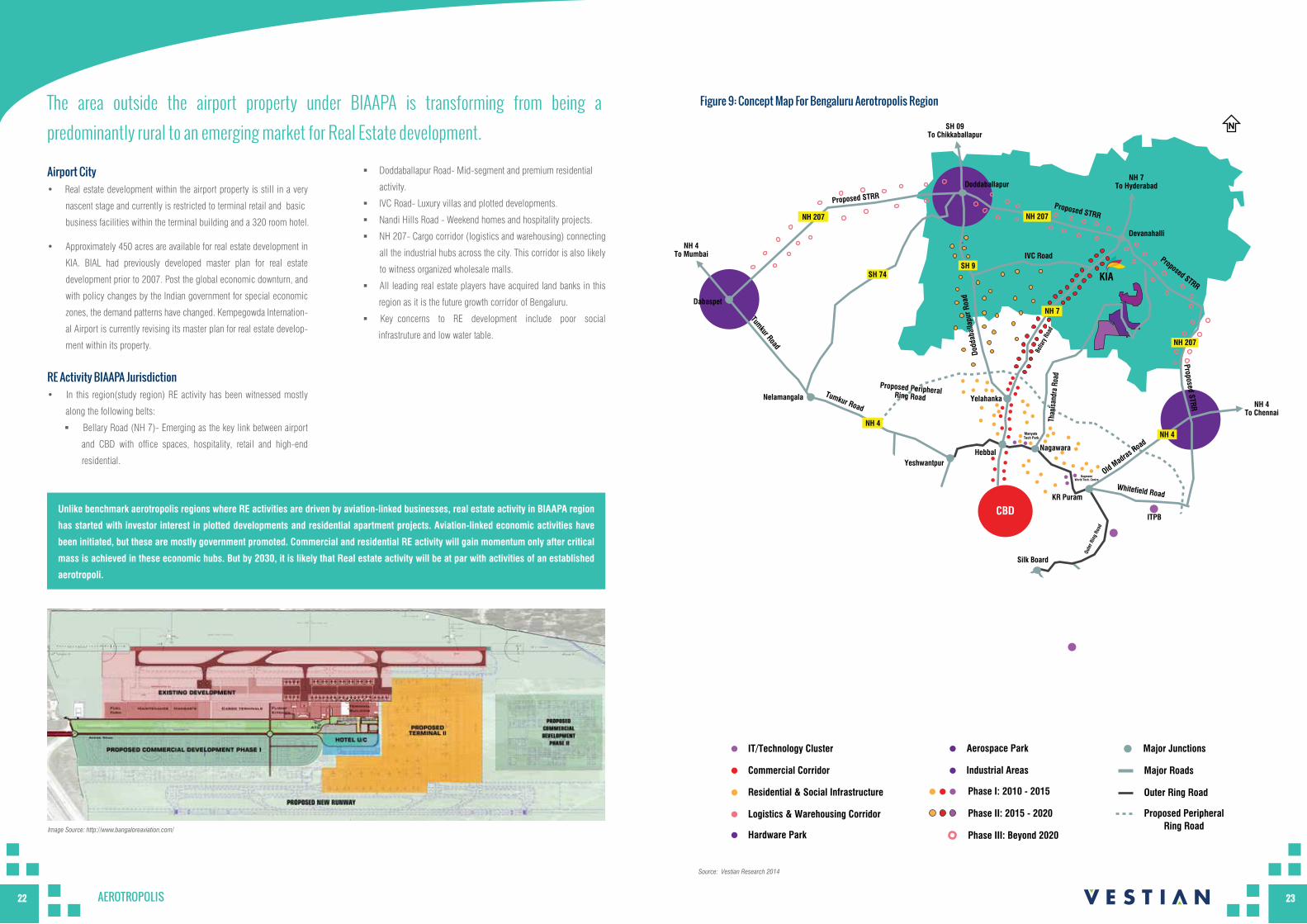

The area outside the airport property under BIAAPA is transforming from being a

predominantly rural to an emerging market for Real Estate development.

Airport City• Real estate development within the airport property is still in a very

nascent stage and currently is restricted to terminal retail and basic

business facilities within the terminal building and a 320 room hotel.

• Approximately 450 acres are available for real estate development in

KIA. BIAL had previously developed master plan for real estate

development prior to 2007. Post the global economic downturn, and

with policy changes by the Indian government for special economic

zones, the demand patterns have changed. Kempegowda Internation-

al Airport is currently revising its master plan for real estate develop-

ment within its property.

RE Activity BIAAPA Jurisdiction• In this region(study region) RE activity has been witnessed mostly

along the following belts:

Bellary Road (NH 7)- Emerging as the key link between airport

and CBD with office spaces, hospitality, retail and high-end

residential.

Unlike benchmark aerotropolis regions where RE activities are driven by aviation-linked businesses, real estate activity in BIAAPA region

has started with investor interest in plotted developments and residential apartment projects. Aviation-linked economic activities have

been initiated, but these are mostly government promoted. Commercial and residential RE activity will gain momentum only after critical

mass is achieved in these economic hubs. But by 2030, it is likely that Real estate activity will be at par with activities of an established

aerotropoli.

Figure 9: Concept Map For Bengaluru Aerotropolis Region

KR Puram

ITPB

Whitefield Road

NH 4

NH 7

Devanahalli

Doddaballapur

NICE

Roa

d

Hebbal

Yelahanka

Manyata Tech Park

BagmaneWorld Tech. Centre

N

SH 9SH 74

NH 207

NH 207

Nelamangala

Dabaspet

NH 7To Hosur

SH 17 NH 209SH 87

SH 35To Attibele

NH 4To Chennai

Sarjapur Road

IVC Road

Silk Board

Yeshwantpur

ElectronicsCity

SH 85

KIA

NH 207

CBD

Nagawara

SH 35

NH 7

SH 87Bannerghatta

NH 209To Coimbatore

SH 17To Mysore

SH 85To Magadi

NH 4To Mumbai

SH 09To Chikkaballapur

NH 7To Hyderabad

Proposed Peripheral

Ring Road

Proposed PeripheralRing Road

Proposed STRRProposed STRR

Proposed STRR

Proposed STRR

Oute

r Rin

g Ro

ad

Oute

r Rin

g Ro

ad

Old Madras Road

Tumkur Road

Dodd

abal

lapu

r Roa

d

Tumkur Road

Bella

ry R

oad

Than

isan

dra

Road

NH 4

IT/Technology Cluster

Commercial Corridor

Residential & Social Infrastructure

Logistics & Warehousing Corridor

Hardware Park

Aerospace Park

Industrial Areas

Source: Vestian Research 2014

Phase I: 2010 - 2015

Phase II: 2015 - 2020

Phase III: Beyond 2020

Major Junctions

Major Roads

Outer Ring Road

Proposed PeripheralRing Road

Doddaballapur Road- Mid-segment and premium residential

activity.

IVC Road- Luxury villas and plotted developments.

Nandi Hills Road - Weekend homes and hospitality projects.

NH 207- Cargo corridor (logistics and warehousing) connecting

all the industrial hubs across the city. This corridor is also likely

to witness organized wholesale malls.

All leading real estate players have acquired land banks in this

region as it is the future growth corridor of Bengaluru.

Key concerns to RE development include poor social

infrastruture and low water table.

Image Source: http://www.bangaloreaviation.com/

AEROTROPOLIS24 25

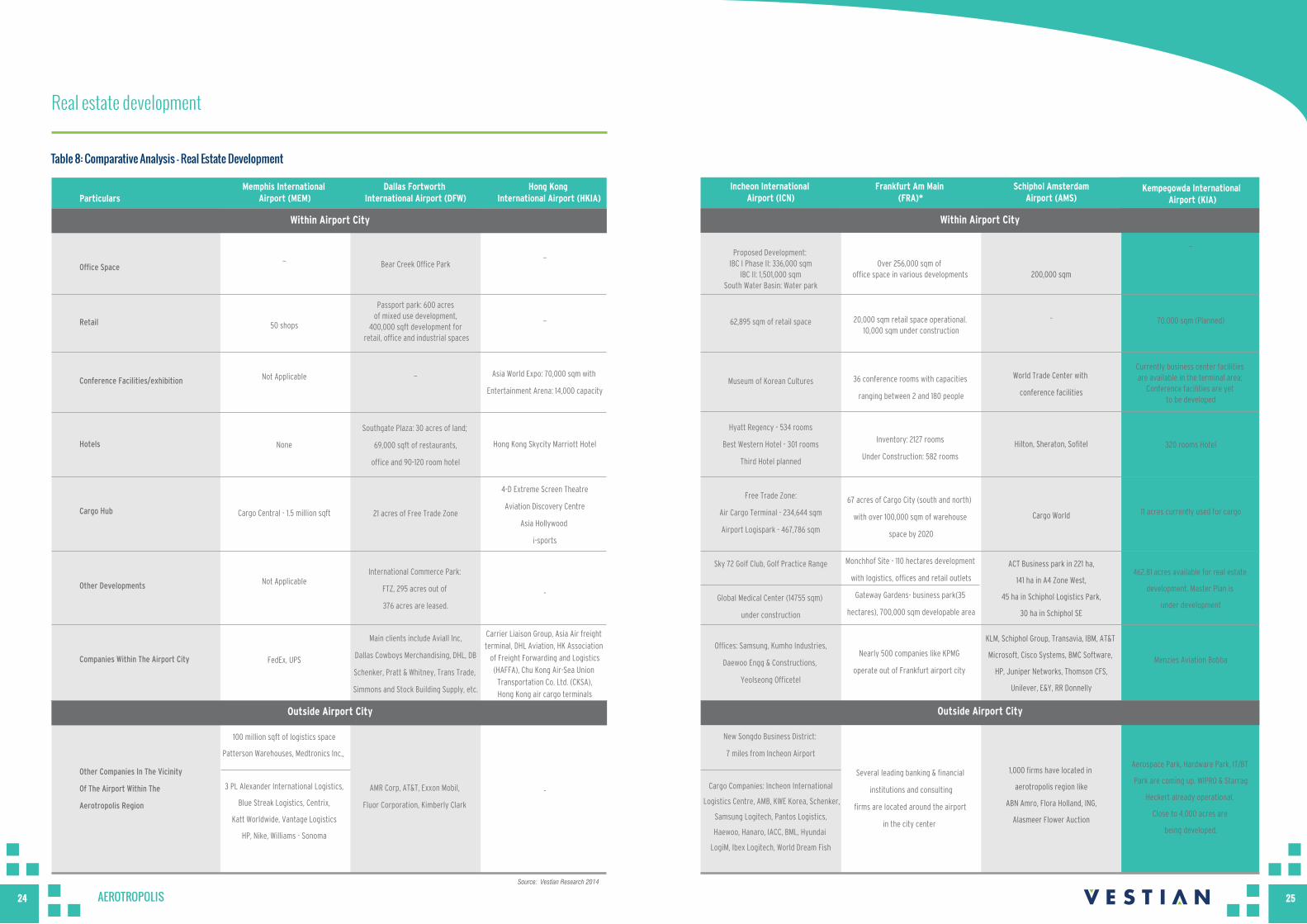

ParticularsMemphis International

Airport (MEM)Dallas Fortworth

International Airport (DFW)Hong Kong

International Airport (HKIA)Incheon International

Airport (ICN)Frankfurt Am Main

(FRA)*Schiphol Amsterdam

Airport (AMS)

Proposed Development: IBC I Phase II: 336,000 sqm

IBC II: 1,501,000 sqmSouth Water Basin: Water park

62,895 sqm of retail space

Museum of Korean Cultures

Hyatt Regency - 534 rooms

Best Western Hotel - 301 rooms

Third Hotel planned

Free Trade Zone:

Air Cargo Terminal - 234,644 sqm

Airport Logispark - 467,786 sqm

Sky 72 Golf Club, Golf Practice Range

Global Medical Center (14755 sqm)

under construction

Offices: Samsung, Kumho Industries,

Daewoo Engg & Constructions,

Yeolseong Officetel

New Songdo Business District:

7 miles from Incheon Airport

Cargo Companies: Incheon International

Logistics Centre, AMB, KWE Korea, Schenker,

Samsung Logitech, Pantos Logistics,

Haewoo, Hanaro, IACC, BML, Hyundai

LogiM, Ibex Logitech, World Dream Fish

Over 256,000 sqm of office space in various developments

20,000 sqm retail space operational. 10,000 sqm under construction

36 conference rooms with capacities

ranging between 2 and 180 people

Inventory: 2127 rooms

Under Construction: 582 rooms

67 acres of Cargo City (south and north)

with over 100,000 sqm of warehouse

space by 2020

Monchhof Site - 110 hectares development

with logistics, offices and retail outlets

Gateway Gardens- business park(35

hectares), 700,000 sqm developable area

Nearly 500 companies like KPMG

operate out of Frankfurt airport city

Several leading banking & financial

institutions and consulting

firms are located around the airport

in the city center

200,000 sqm

-

World Trade Center with

conference facilities

Hilton, Sheraton, Sofitel

Cargo World

ACT Business park in 221 ha,

141 ha in A4 Zone West,

45 ha in Schiphol Logistics Park,

30 ha in Schiphol SE

KLM, Schiphol Group, Transavia, IBM, AT&T

Microsoft, Cisco Systems, BMC Software,

HP, Juniper Networks, Thomson CFS,

Unilever, E&Y, RR Donnelly

Do

1,000 firms have located in

aerotropolis region like

ABN Amro, Flora Holland, ING,

Alasmeer Flower Auction

_

70,000 sqm (Planned)

Currently business center facilities are available in the terminal area;

Conference facilities are yet to be developed

320 rooms Hotel

11 acres currently used for cargo

462.81 acres available for real estate

development. Master Plan is

under development

Menzies Aviation Bobba

Aerospace Park, Hardware Park, IT/BT

Park are coming up. WIPRO & Starrag

Heckert already operational.

Close to 4,000 acres are

being developed.

Bear Creek Office Park

Passport park: 600 acres of mixed use development,

400,000 sqft development for retail, office and industrial spaces

_

Southgate Plaza: 30 acres of land;

69,000 sqft of restaurants,

office and 90-120 room hotel

21 acres of Free Trade Zone

International Commerce Park:

FTZ, 295 acres out of

376 acres are leased.

Main clients include Aviall Inc,

Dallas Cowboys Merchandising, DHL, DB

Schenker, Pratt & Whitney, Trans Trade,

Simmons and Stock Building Supply, etc.

AMR Corp, AT&T, Exxon Mobil,

Fluor Corporation, Kimberly Clark

_

50 shops

Not Applicable

None

Cargo Central - 1.5 million sqft

Not Applicable

FedEx, UPS

100 million sqft of logistics space

Patterson Warehouses, Medtronics Inc.,

3 PL Alexander International Logistics,

Blue Streak Logistics, Centrix,

Katt Worldwide, Vantage Logistics

HP, Nike, Williams - Sonoma

_

_

Asia World Expo: 70,000 sqm with

Entertainment Arena: 14,000 capacity

Hong Kong Skycity Marriott Hotel

4-D Extreme Screen Theatre

Aviation Discovery Centre

Asia Hollywood

i-sports

-

Carrier Liaison Group, Asia Air freight

terminal, DHL Aviation, HK Association

of Freight Forwarding and Logistics

(HAFFA), Chu Kong Air-Sea Union

Transportation Co. Ltd. (CKSA),

Hong Kong air cargo terminals

-

Kempegowda International Airport (KIA)

Office Space

Retail

Hotels

Cargo Hub

Other Developments

Companies Within The Airport City

Other Companies In The Vicinity

Of The Airport Within The

Aerotropolis Region

Conference Facilities/exhibition

Table 8: Comparative Analysis – Real Estate Development

Real estate development

Outside Airport City

Within Airport City Within Airport City

Outside Airport City

Source: Vestian Research 2014

ConclusionSWOT analysis for aerotropolis around Kempegowda International Airport

STRENGTHS• Greenfield airport with hundreds of acres available for expansion and

development.

• The city has a diverse economic base.

• Growing air-passenger traffic.

• Private sector participation in the development of the airport has

provided funding for developing state of the art airport infrastructure.

• Government is promoting economic activities in the study area.

• Bengaluru city has the highest absorption of commercial office space

on account of consistent demand from corporates to set up

operations in the city.

• Land & leasing costs are also low compared to the other metropolitan

cities of India, thereby increasing its attractiveness.

• Planned development of the study area under a separate planning

authority with plenty of land available to develop business parks,

industrial & cargo clusters.

• Reduced travel time to the airport due to the commissioning of the

Bellary Road Elevated Expressway.

WEAKNESSES• Slow pace of real estate development within the airport city.

• Non-aeronautical revenue is currently low as compared to other

aerotropoli.

Aerotropolis Development

Possibility

An aerotropolis can develop around Kempegowda International Airport, Bengaluru. The region and KIA score

in terms of location, regional economy, airport infrastructure, availability of land for future growth, operational

capacity and governance.

Scale Of Development

Compared to aerotropolis regions around the world, Bengaluru aerotropolis may be smaller in

extent and regional impact owing to the presence of other greenfield airports like GMR Rajiv

Gandhi International Airport, Hyderabad & Kochi International Airport, Kochi in the vicinity.

The size of the economy is also smaller as compared to benchmarked aerotropoli.

Timeline ForDevelopment

The development may take longer than in benchmarked aerotropolis regions due to the slow pace of

infrastructure development. Relevant parameters such as funding for capital intensive projects, land

acquisition issues and shortage of water may pose a challenge.

Thrust Areas Key aspects that call for immediate action include - improving connectivity and reducing

travel time between the airport and the city, as well as to the key economic hubs. This region

also requires contionuous support of the GoK.

• High landing charges.

• Land acquisition issues associated with ITIR region.

• Low ground water levels which can dampen prospects in the long run.

• Rail link is still in talks - no other means of transportation to reduce

travel time.

• Land acquisition issues in the proposed government initiatives around

the airport.

OPPORTUNITIES• Shortest connecting distance to all airports in south India - therefore

opportunity to develop into a MRO hub.

• Region falls on the proposed Mumbai - Bengaluru - Chennai

infrastructure corridor.

THREATS• Competition from other airports in the vicinity like Hyderabad’s GMR

International Airport and Chennai International Airport.

AEROTROPOLIS26 27

Glossary

AEROTROPOLIS28 29

AcknowledgmentThe Vestian Strategic Advisory team would like to take this opportunity to

extend our gratitude towards all those who have helped us in our

endeavour to produce this report. We would like to especially thank Dhara

Shah, Shailendra H C, Abilash Sudarshan, Krishna Chaitanya, Abhijit Aich

and Romita Banerjee for extending their valuable support & cooperation.

Our sincere thanks to Kantharaju C, Corporate Communications Team for

designing the report.

DisclaimerThis report contains information available to the public at various public

domains and has been extracted by Vestian Global Workplace Services

from such public domains. Vestian accepts no responsibility if this should

prove not to be accurate. No warranty or representation, expressed or

implied is made to the accuracy or completeness of the information

contained herein, and the same is submitted subject to errors, omissions,

change of price, rental or other conditions and withdrawal without notice.

Amrita Datta

Sr. Manager, Strategic Advisory [email protected] | +91 80 4062 0100

As a part of Strategic Advisory Group, Amrita is responsible for

consultancy assignments, topical research papers and property market

updates. She has over 8 years of experience in the real estate sector and

has worked on a wide spectrum of research papers and customized reports

for various clients across all key real estate segments. She is a

management honours graduate from Assam University, Silchar.

Gorakh Jhunjhunwala, MRICS

VP, Strategic Advisory [email protected] | +91 80 4062 0100

Gorakh serves as Vice President and heads the Strategic Advisory Group.

He guides the team and is responsible for research output as well as client

assignments. With over 11 years of work experience in investments,

consulting and advisory domain, he has executed and delivered

assignments across asset classes. Gorakh pursued his master’s degree

from Indian Institute of Technology, Delhi and holds a bachelor’s degree in

Architecture.

Authors

IT Information Technology

ITeS Information Technology enabled Services

INR Indian Rupee

BDA Bengaluru Development Authority

FDI Foreign Direct Investment

BIAL Bengaluru International Airport Limited

ORR Outer Ring Road

GDP Gross Domestic Product

AAI Airport Authority Of India

FIPB Foreign Investment Promotion Board

FTZ Free Trade Zone

GoK Government Of Karnataka

USP Unique Selling Proposition

y-o-y Year-on-Year

SEZ Special Economic Zone

CBD Central Business District

GoI Government of India

AERA Airport Economic & Regulatory Authority

PPP Public Private Partnership

EOI Expression Of Interest

NH National Highway

SH State Highway

KIADB Karnataka Industrial Areas Development Board

KSIIDC Karnataka State Industrial & Infrastructure

Development Corporation

KIA Kempegowda International Airport

ITIR Information Technology Investment Region

IVC Inter Village Connective

CBD Central Business District

IFCI Industrial Finance Corporation Of India

MOU Memorandum Of Understanding

BIAAPA Bengaluru International Airport Area Planning Autority

Pax. Pa Passenger Per Annum

PPP Public Private Partnership

MRO Maintenance Repair Operations

Shwetha H Pai

Director, Strategic Advisory [email protected] | +91 80 4062 0100

Shwetha has over 9 years of experience in real estate research and

consultancy. As an account manager for key residential focus clients at

Vestian, she is responsible for developing and implementing customized

research, corporate strategy & project conceptualization. A qualified urban

planner from the School of Planning & Architecture (SPA), New Delhi, she

has worked in both Indian and US markets.

AEROTROPOLIS30 31

Bangalore:Whitefield &Electronic City

About Vestian

Vestian Reports

Vestian Global Workplace Services, is an ISO 9001:2008 certified

contemporary workplace solutions firm that specializes in providing

occupier focused solutions for commercial, residential, industrial, retail

and hospitality sectors. Our service portfolio includes Strategic Advisory,

Retail Business Solutions, Transaction Advisory, Integrated Service

Delivery, Project Services and Facilities Management Services.

We measure key deliverables of our business and align it to the clients’

strategic business goals. Our commitment to achieve excellence and

consistency in our service delivery models has helped us attain high

standards of quality and raised the bar for the industry.

Our experienced team has the required expertise and exposure in different

sectors. Combining global best practices and local knowledge, the team

provides an integrated solution for all real estate requirements. Moreover,

the belief in our corporate philosophy - Delivering Measurable Results -

helps us in providing solutions in keeping with global delivery standard.

Strategic AdvisoryVestian Global Workplace Services’ Strategic Advisory Group is the

research arm of Vestian. They align business strategies of corporate clients

with their real estate portfolio strategy. Property market intelligence,

economic, urban & space planning principles and analytical methods all

come together to provide strategic insights to real estate occupiers. This

approach guarantees recommendations that are thorough and meets not

only the needs of today, but of the future as well. We primarily cater to

Developers, Builders, Investors and Occupiers. Our studies span a

spectrum of sectors such as commercial, residential, industrial,

educational & hospitality.

Transaction AdvisoryVestian’s competent Transaction team provides an array of services

focused on optimizing workplace solutions that enhance the client’s real

Bangalore:Residential Market Report

Chennai:OMR & GST Road

Bangalore:Outer Ring Road

Bangalore:Retail Real EstateMarket Report

Bangalore:Real EstateMarket Report

Michael SilverChairman, Vestian

Michael serves as Chairman and is responsible for strategic oversight. He

is a recognized leader in the field of workplace services. He has

established and led the growth of a large occupier focused services

corporation.

In 2006, he received the Ernst & Young "Entrepreneur of the Year" Award.

He is also an active member of the YPO (Young Presidents' Organization)

and WPO (World Presidents' Organization).

Shrinivas Rao, MRICSCEO - Asia Pacific, Vestian

Shrinivas serves as Chief Executive Officer for Asia Pacific arm of Vestian.

With over 22 years of experience in working with global clients India, he is

well-versed in delivering solutions that work in India's very challenging

workplace services markets. Amongst the pioneers of professional

workplace consulting services in India, he successfully established and

led operations of three multinational corporations in India. He is widely

recognized as a "change leader", known for his keen insights into

workplace services trends and innovative structuring services.

Management

estate portfolio. We handle varied workplace related transactions such as

purchase, lease, disposal, lease management, lease renegotiations and

restructuring. We provide solutions that are aligned to the business

objectives of our clients.

Retail Business SolutionsVestian Retail Business Solutions is the full-service retail arm of Vestian.

We work with each client to understand their objectives and associated

risks, establish achievable goals, develop and implement effective

solutions. Vestian Retail Business Solutions provides end-to-end services,

which include Retailer Expansion Strategy, Real Estate Services, Occupier

Representation, Retail Concept Development & Consulting, and Retail

Project Management.

Project ServicesThe Vestian Project Services team is a one-stop solution for clients opting

for Project Management solutions.

We operate on 3 different models-Project Consulting, Integrated Service

Delivery & Workplace Strategy to deliver functional facilities that meet the

clients’ space requirements. We deliver consistent, reliable and viable

solutions for local and international markets. Our delivery process involves

preparation of design documents, co-ordination with architects &

consultants for design, finalization of vendor, supervision of the project

and project closure.

Facilities Management ServicesVestian’s F acilties Management Services team helps clients focus on

their core business activities. We act on behalf of the client to preserve and

prolong the life cycle of the asset, while generating income. We, effective-

ly oversee property performance and maintenance following international

best practices, using high end technology and precision processes. We

manage the administration of residential, commercial, retail and/or

industrial real estate.