Embed Size (px)

Citation preview

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20071

BUSINESS UPDATE AND HALF YEAR RESULTS ANNOUNCEMENTHALF YEAR ENDED 31 DECEMBER 2007

25 February 2008David Clarke Chief Executive OfficerTim Dodd Chief Financial Officer

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20072

Agenda

1.1. Current SituationCurrent Situation2. First Half Business Review3. Financial Performance4. Balance Sheet, Funding and Liquidity5. Summary6. Appendix

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20073

What Happened?

� Allco was committed to a growth strategy and was making financial commitments to acquire assets, build funds and grow its organisation.

� Subsequent dislocation in global credit markets and associated volatility in equity markets significantly impacted Allco’s operations, financial position and outlook.

� Shareholders and investors lost confidence in Allco:� Concern regarding related party transactions.� Falling share price.� Margin calls on substantial shareholder.� Continued short selling of AFG shares.� Focus on debt levels and complexity of business.

� Fund investors have not proceeded with stated commitments at this time.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20074

What Happened? (cont.)

� Market capitalisation trigger enabled banks to review all seniorfacilities:� We are not in breach of financial covenants.� There have been no default or late interest payments.

� Constructive discussions with banks continue regarding restructuring terms and conditions of facilities.

� Anticipate successful outcome of these negotiations.

� We did not anticipate all these things occurring simultaneously. Led to insufficient liquidity to deal with these events.

� These events have led to management commencing an aggressive business restructuring program to ensure viability and rehabilitate the business.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20075

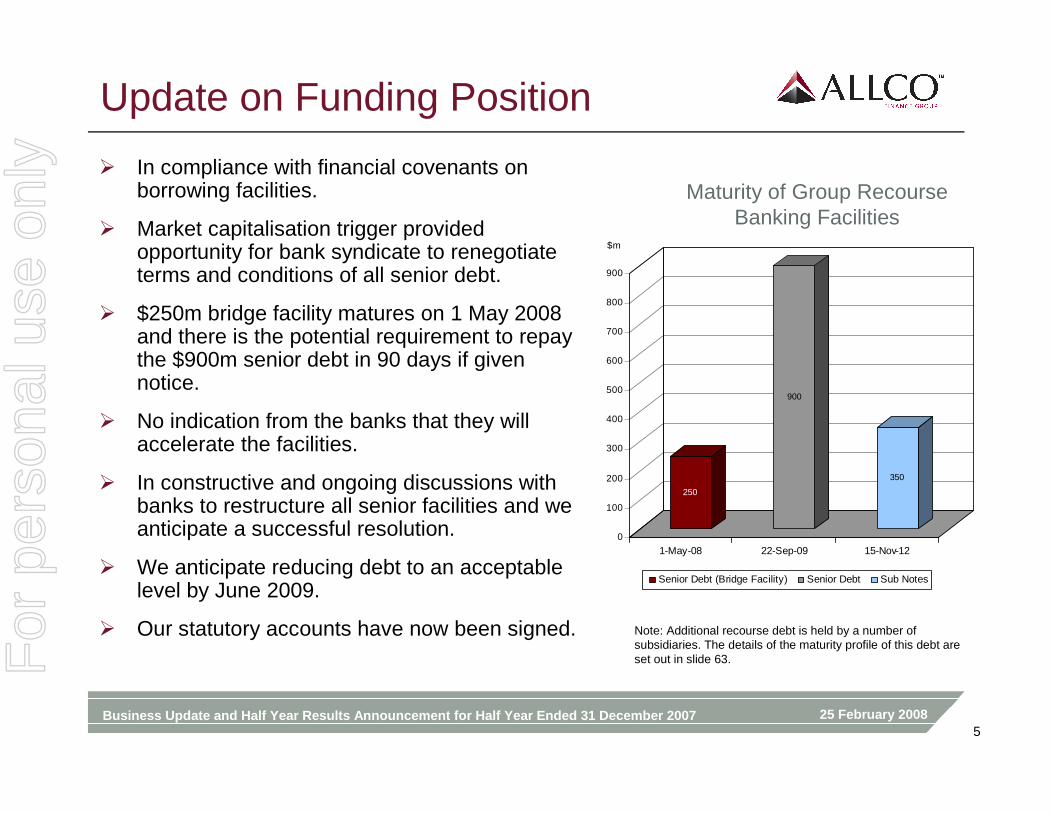

Update on Funding Position

� In compliance with financial covenants on borrowing facilities.

� Market capitalisation trigger provided opportunity for bank syndicate to renegotiate terms and conditions of all senior debt.

� $250m bridge facility matures on 1 May 2008 and there is the potential requirement to repay the $900m senior debt in 90 days if given notice.

� No indication from the banks that they will accelerate the facilities.

� In constructive and ongoing discussions with banks to restructure all senior facilities and we anticipate a successful resolution.

� We anticipate reducing debt to an acceptable level by June 2009.

� Our statutory accounts have now been signed.

Maturity of Group Recourse Banking Facilities

250

900

350

0

100

200

300

400

500

600

700

800

900

$m

1-May-08 22-Sep-09 15-Nov-12

Senior Debt (Bridge Facility) Senior Debt Sub Notes

Note: Additional recourse debt is held by a number of subsidiaries. The details of the maturity profile of this debt are set out in slide 63.F

or p

erso

nal u

se o

nly

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20076

What are we Doing?� We are developing a business restructuring program to focus on core activities:

� Focus on Aviation, Shipping, Rail and Real Estate.

� Through the orderly sale and wind-back of involvement:

� Exiting capital intensive Infrastructure business.

� Exiting Financial Assets which aren’t consistent with our focus on real assets.

� Sale of non-core assets to reduce debt.

� Implement measures designed to reduce the gap between net tangible assets of listed real estate funds and their trading prices.

� Active discussions with parties interested in acquiring selective non-core assets and / or businesses.

� Agreed transaction with Industry Funds Management to dispose of our interest in the Consolidated Edison portfolio of power stations which will result in a pre-tax loss of $72.1m in second half of FY08. No further financial commitment.

� No interim dividend to be paid and no full year dividend currently anticipated.

� Repositioned business requires significantly less headcount:� Core businesses will continue to be appropriately resourced.

� Continue to explore options that would strengthen financial position and enhance value of core businesses.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20077

Business Model Going Forward� Allco will continue to be an alternative asset manager focused on “real

assets”:� Focus on our core asset classes of Aviation, Shipping, Rail and Real Estate.

� Assets Allco invests in complement investment portfolios comprised of traditional and other alternative investments.

� Continued access to debt funding in our core asset classes.

� Continued strong demand from our operating clients for our core assets, which remain critical to their business.

� Board and Management remain confident in the business model and the ability to restore financial stability and build value over time.

� Progress has been made in building a funds management platform and we will continue to build on our capabilities:� Focus on investor requirements rather than on product design in creating funds.� Simplify investment propositions, structure and terms.� Remunerate fund managers based on fund performance.� Through co-investment of funds, align interests of Allco with investors.

� The leadership team is absolutely committed to rebuilding Allco.For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20078

Agenda

1. Current Situation

2.2. First Half Business ReviewFirst Half Business Review3. Financial Performance 4. Balance Sheet, Funding and Liquidity5. Summary6. Appendix

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 20079

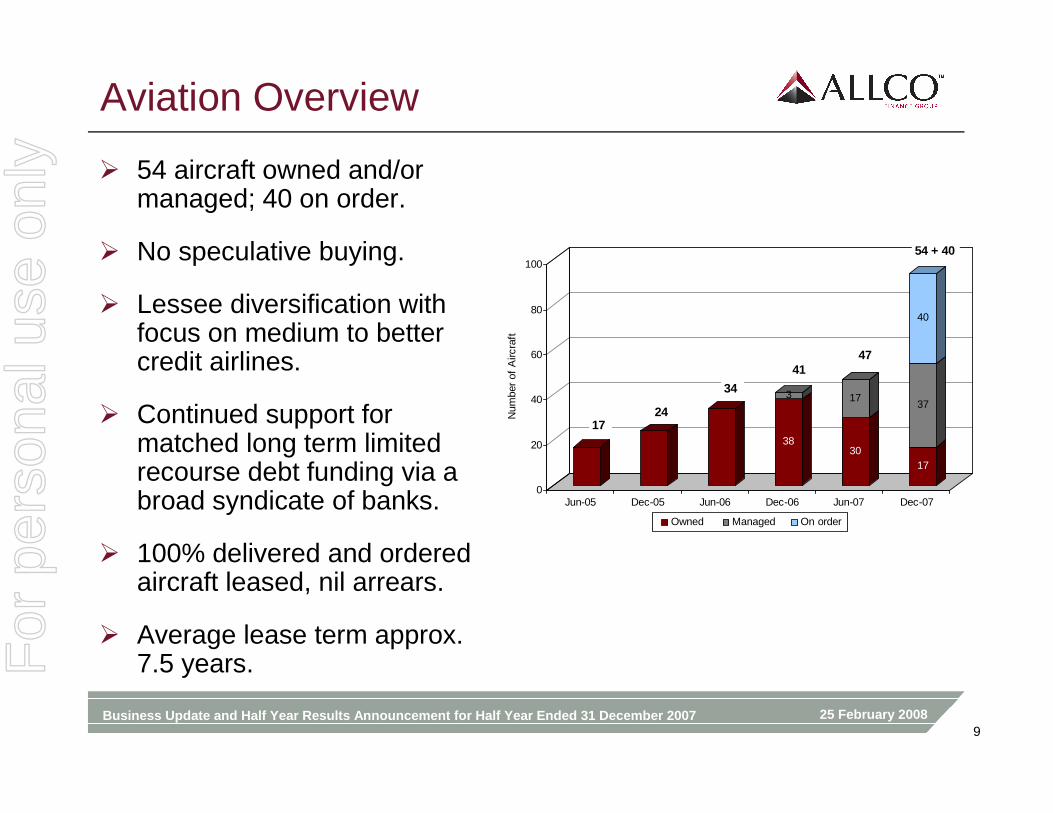

Aviation Overview

� 54 aircraft owned and/or managed; 40 on order.

� No speculative buying.

� Lessee diversification with focus on medium to better credit airlines.

� Continued support for matched long term limited recourse debt funding via a broad syndicate of banks.

� 100% delivered and ordered aircraft leased, nil arrears.

� Average lease term approx. 7.5 years.

38

3

30

17

17

37

40

0

20

40

60

80

100

Num

ber

of A

ircra

ftJun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Owned Managed On order

1724

34

54 + 40

4741

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200710

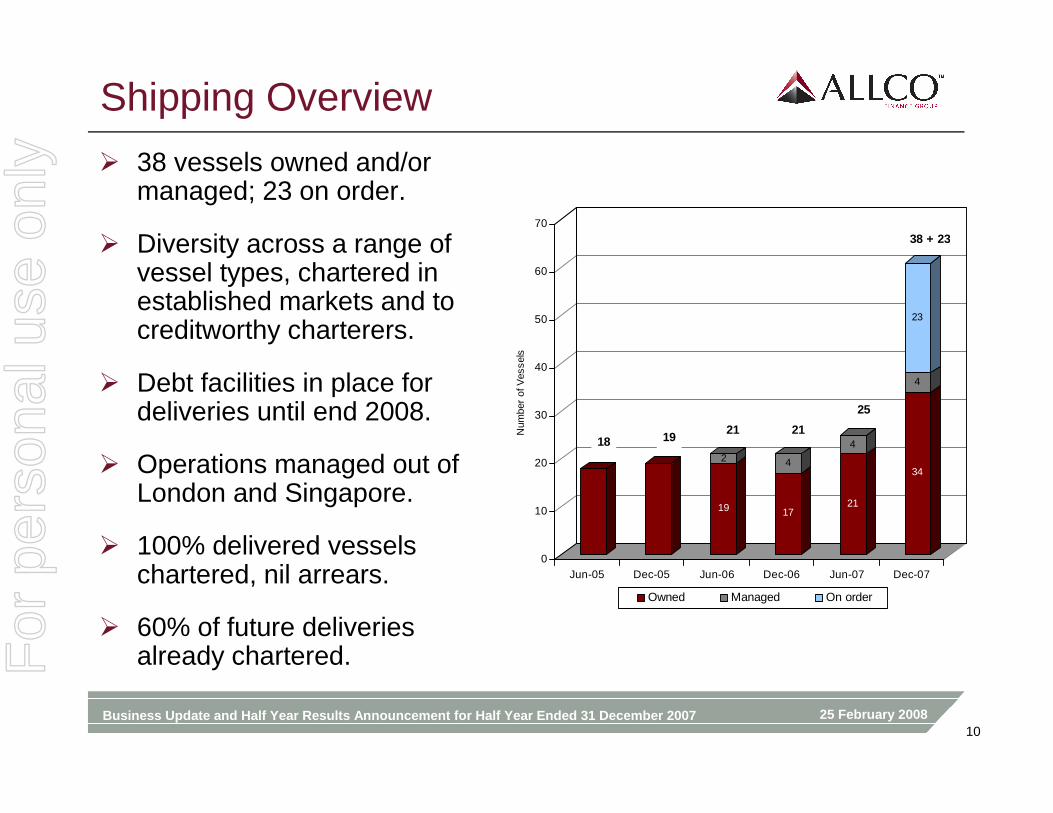

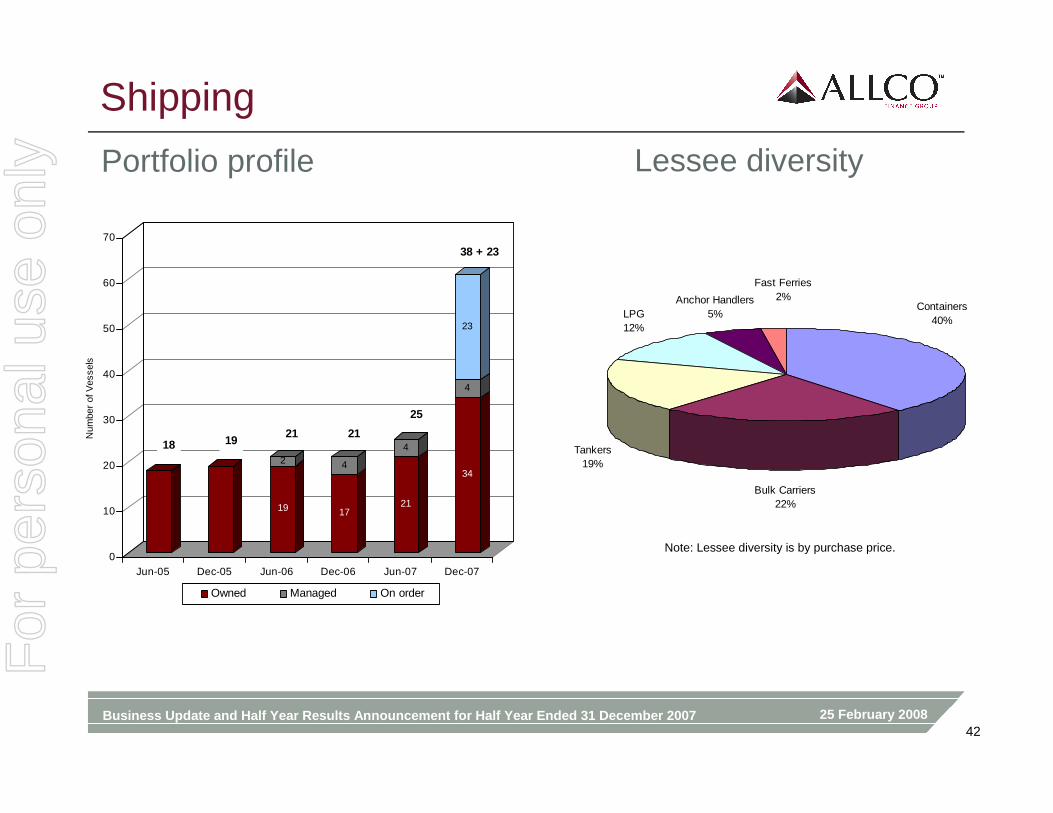

Shipping Overview

� 38 vessels owned and/or managed; 23 on order.

� Diversity across a range of vessel types, chartered in established markets and to creditworthy charterers.

� Debt facilities in place for deliveries until end 2008.

� Operations managed out of London and Singapore.

� 100% delivered vessels chartered, nil arrears.

� 60% of future deliveries already chartered.

19

2

17

4

21

4

34

4

23

0

10

20

30

40

50

60

70

Num

ber

of V

esse

ls

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Owned Managed On order

21 21

38 + 23

25

18 19

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200711

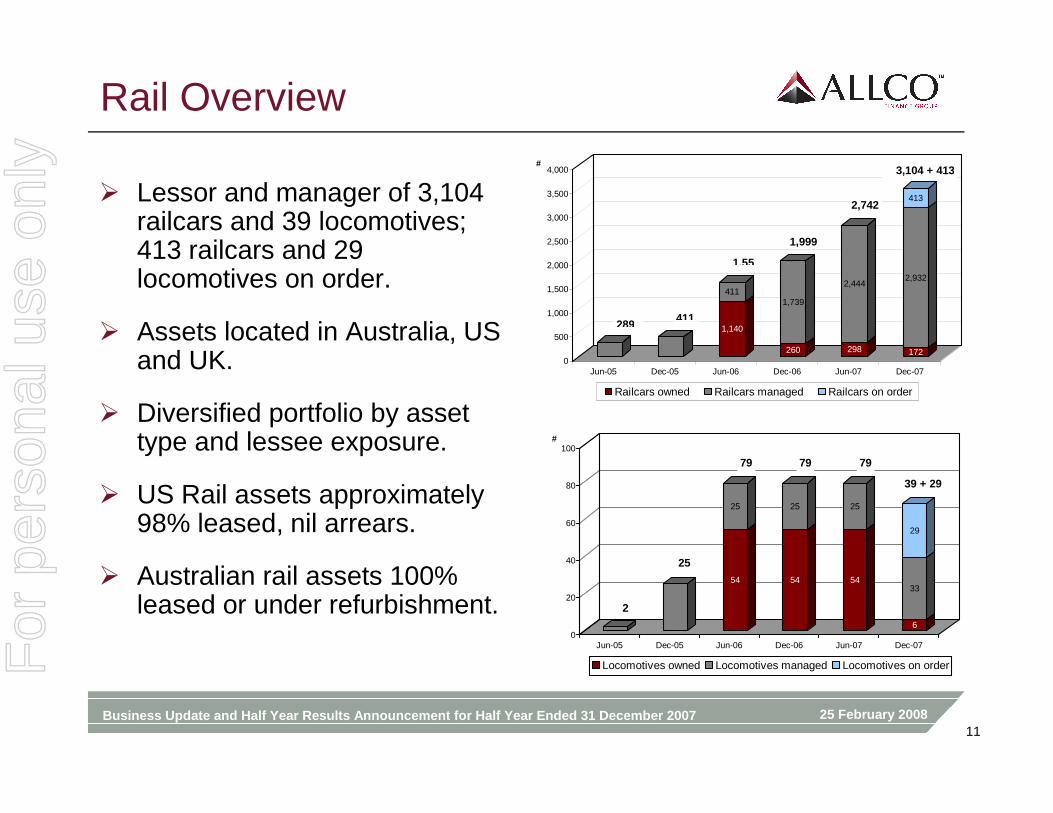

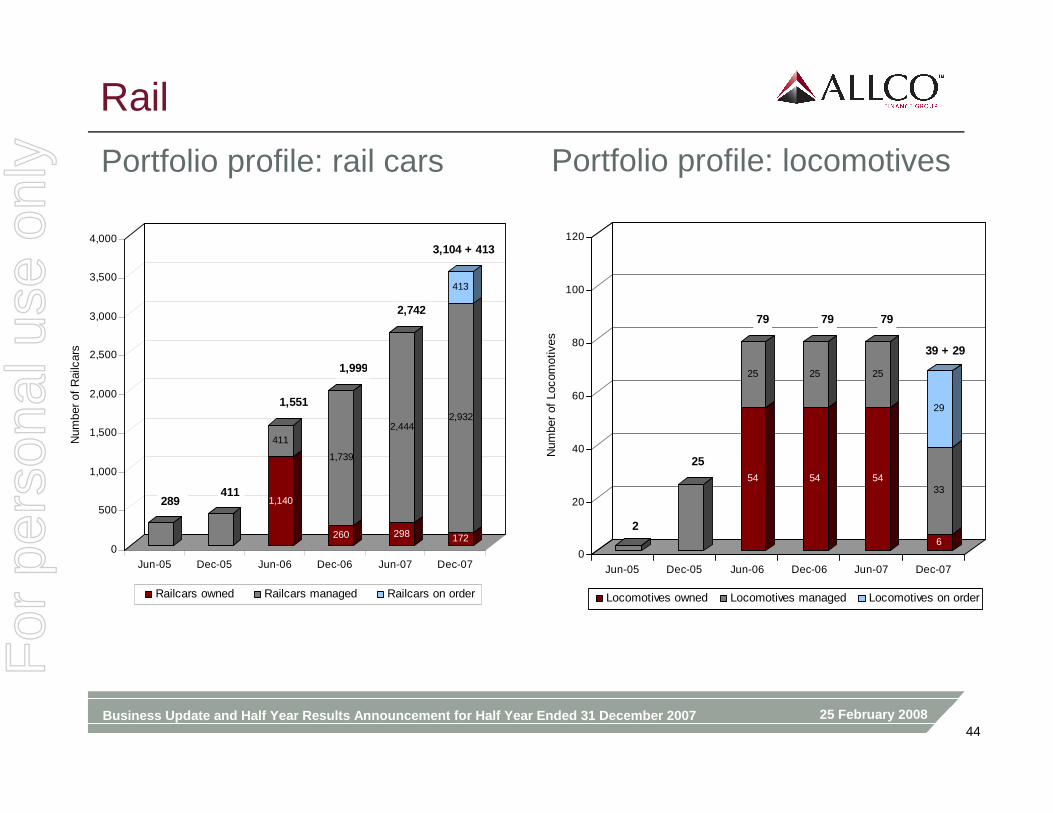

Rail Overview

� Lessor and manager of 3,104 railcars and 39 locomotives; 413 railcars and 29 locomotives on order.

� Assets located in Australia, US and UK.

� Diversified portfolio by asset type and lessee exposure.

� US Rail assets approximately 98% leased, nil arrears.

� Australian rail assets 100% leased or under refurbishment.

1,140

411

260

1,739

298

2,444

172

2,932

413

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000#

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Railcars owned Railcars managed Railcars on order

3,104 + 413

289 411

1,55

1,999

2,742

54

25

54

25

54

25

6

33

29

0

20

40

60

80

100#

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Locomotives owned Locomotives managed Locomotives on order

39 + 29

2

25

79 79 79

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200712

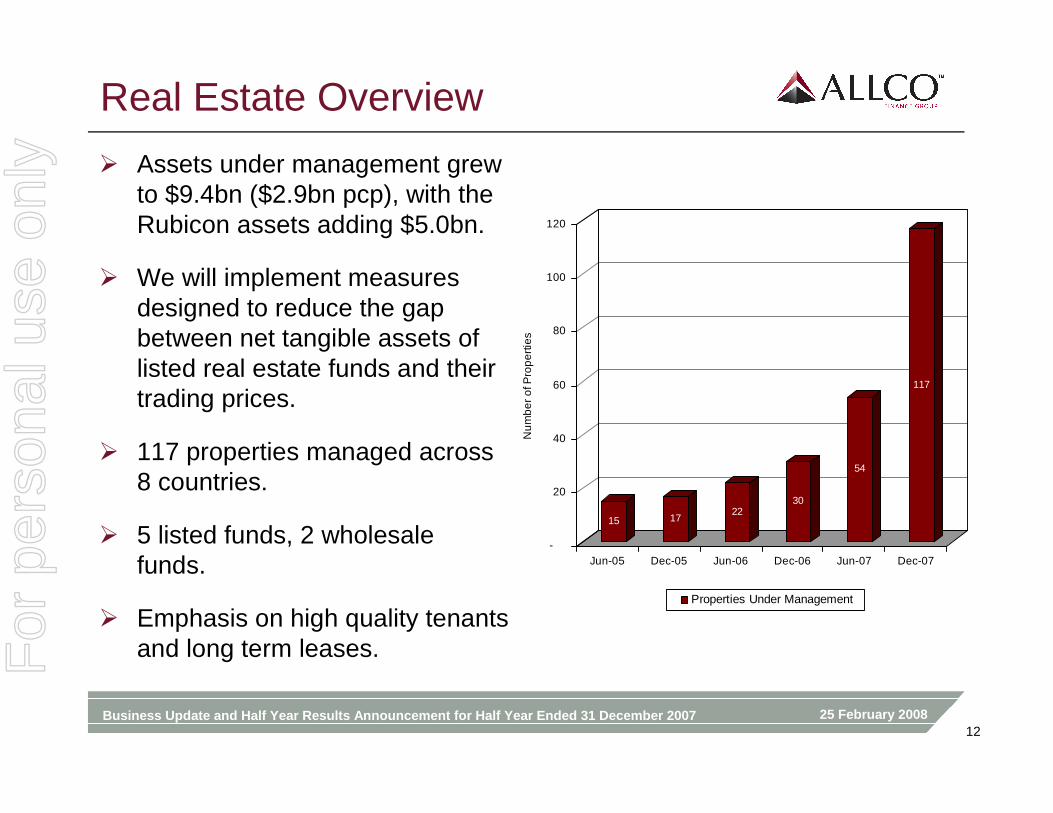

Real Estate Overview

� Assets under management grew to $9.4bn ($2.9bn pcp), with the Rubicon assets adding $5.0bn.

� We will implement measures designed to reduce the gap between net tangible assets of listed real estate funds and their trading prices.

� 117 properties managed across 8 countries.

� 5 listed funds, 2 wholesale funds.

� Emphasis on high quality tenants and long term leases.

15 1722

30

54

117

-

20

40

60

80

100

120

Nu

mb

er o

f Pro

per

ties

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Properties Under Management

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200713

Agenda

1. Current Situation2. First Half Business Review

3.3. Financial PerformanceFinancial Performance4. Balance Sheet, Funding and Liquidity5. Summary6. Appendix

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200714

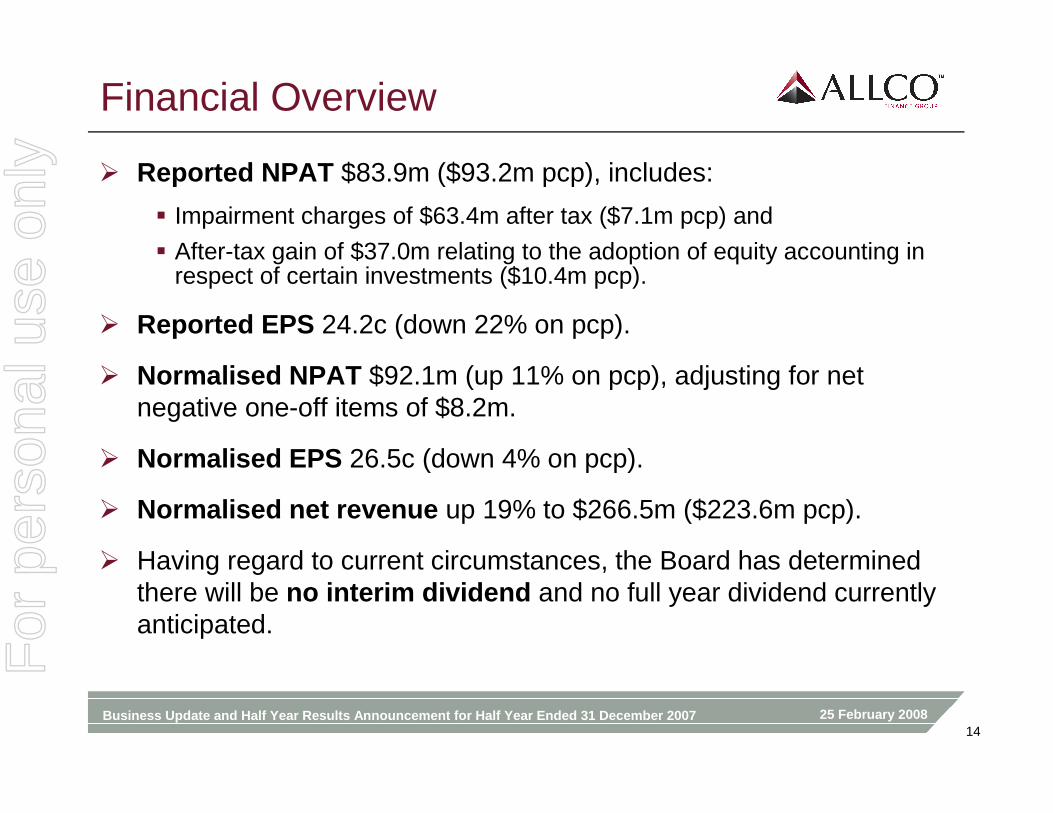

Financial Overview

� Reported NPAT $83.9m ($93.2m pcp), includes:

� Impairment charges of $63.4m after tax ($7.1m pcp) and

� After-tax gain of $37.0m relating to the adoption of equity accounting in respect of certain investments ($10.4m pcp).

� Reported EPS 24.2c (down 22% on pcp).

� Normalised NPAT $92.1m (up 11% on pcp), adjusting for net negative one-off items of $8.2m.

� Normalised EPS 26.5c (down 4% on pcp).

� Normalised net revenue up 19% to $266.5m ($223.6m pcp).

� Having regard to current circumstances, the Board has determinedthere will be no interim dividend and no full year dividend currently anticipated.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200715

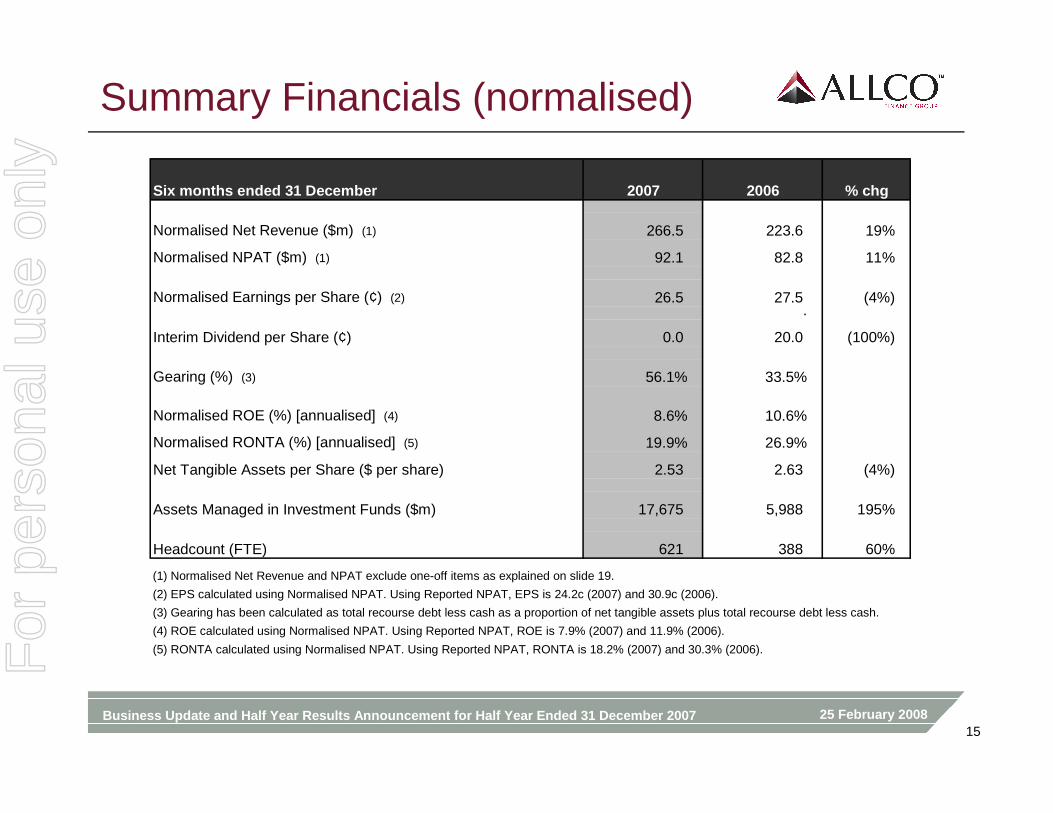

Summary Financials (normalised)

Six months ended 31 December 2007 2006 % chg

Normalised Net Revenue ($m) (1) 266.5 223.6 19%

Normalised NPAT ($m) (1) 92.1 82.8 11%

Normalised Earnings per Share (¢) (2) 26.5 27.5 (4%).

Interim Dividend per Share (¢) 0.0 20.0 (100%)

Gearing (%) (3) 56.1% 33.5%

Normalised ROE (%) [annualised] (4) 8.6% 10.6%

Normalised RONTA (%) [annualised] (5) 19.9% 26.9%

Net Tangible Assets per Share ($ per share) 2.53 2.63 (4%)

Assets Managed in Investment Funds ($m) 17,675 5,988 195%

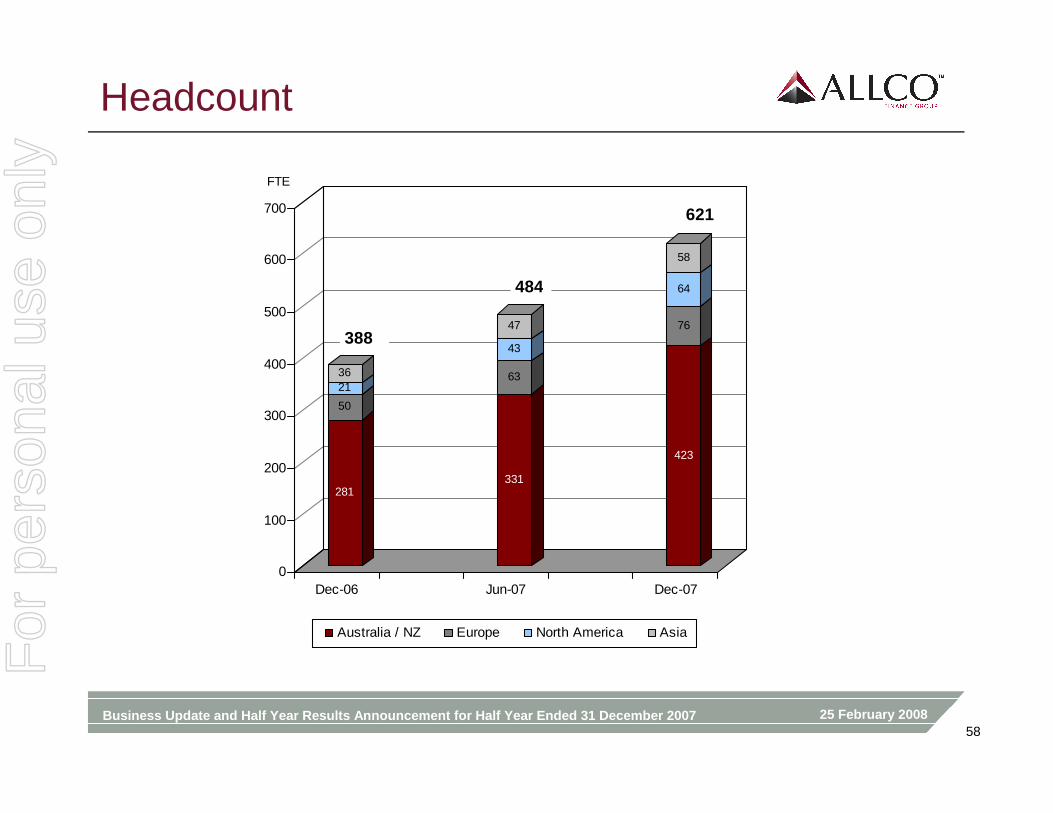

Headcount (FTE) 621 388 60%

(1) Normalised Net Revenue and NPAT exclude one-off items as explained on slide 19.

(2) EPS calculated using Normalised NPAT. Using Reported NPAT, EPS is 24.2c (2007) and 30.9c (2006).

(3) Gearing has been calculated as total recourse debt less cash as a proportion of net tangible assets plus total recourse debt less cash.

(4) ROE calculated using Normalised NPAT. Using Reported NPAT, ROE is 7.9% (2007) and 11.9% (2006).

(5) RONTA calculated using Normalised NPAT. Using Reported NPAT, RONTA is 18.2% (2007) and 30.3% (2006).For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200716

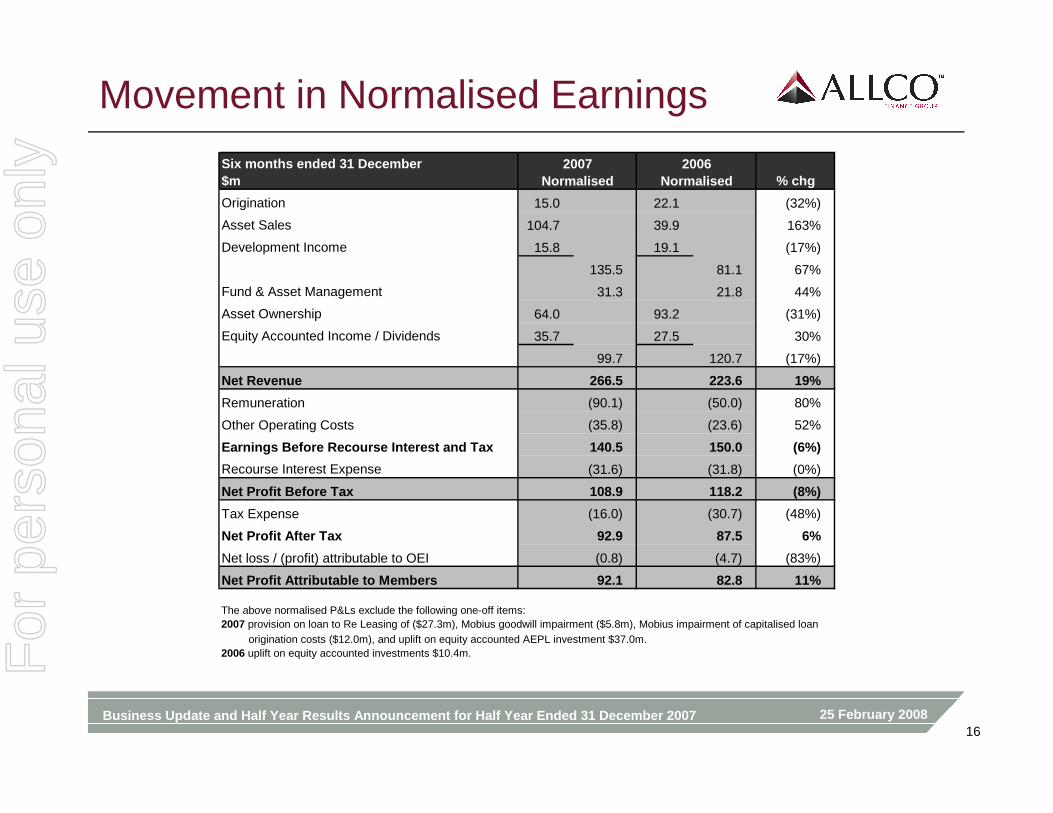

Movement in Normalised Earnings

Six months ended 31 December$m % chg

Origination 15.0 22.1 (32%)

Asset Sales 104.7 39.9 163%

Development Income 15.8 19.1 (17%)

135.5 81.1 67%

Fund & Asset Management 31.3 21.8 44%

Asset Ownership 64.0 93.2 (31%)

Equity Accounted Income / Dividends 35.7 27.5 30%

99.7 120.7 (17%)

Net Revenue 266.5 223.6 19%

Remuneration (90.1) (50.0) 80%

Other Operating Costs (35.8) (23.6) 52%

Earnings Before Recourse Interest and Tax 140.5 150.0 (6%)

Recourse Interest Expense (31.6) (31.8) (0%)

Net Profit Before Tax 108.9 118.2 (8%)

Tax Expense (16.0) (30.7) (48%)

Net Profit After Tax 92.9 87.5 6%

Net loss / (profit) attributable to OEI (0.8) (4.7) (83%)

Net Profit Attributable to Members 92.1 82.8 11%

The above normalised P&Ls exclude the following one-off items:2007 provision on loan to Re Leasing of ($27.3m), Mobius goodwill impairment ($5.8m), Mobius impairment of capitalised loan origination costs ($12.0m), and uplift on equity accounted AEPL investment $37.0m.2006 uplift on equity accounted investments $10.4m.

2007Normalised

2006Normalised

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200717

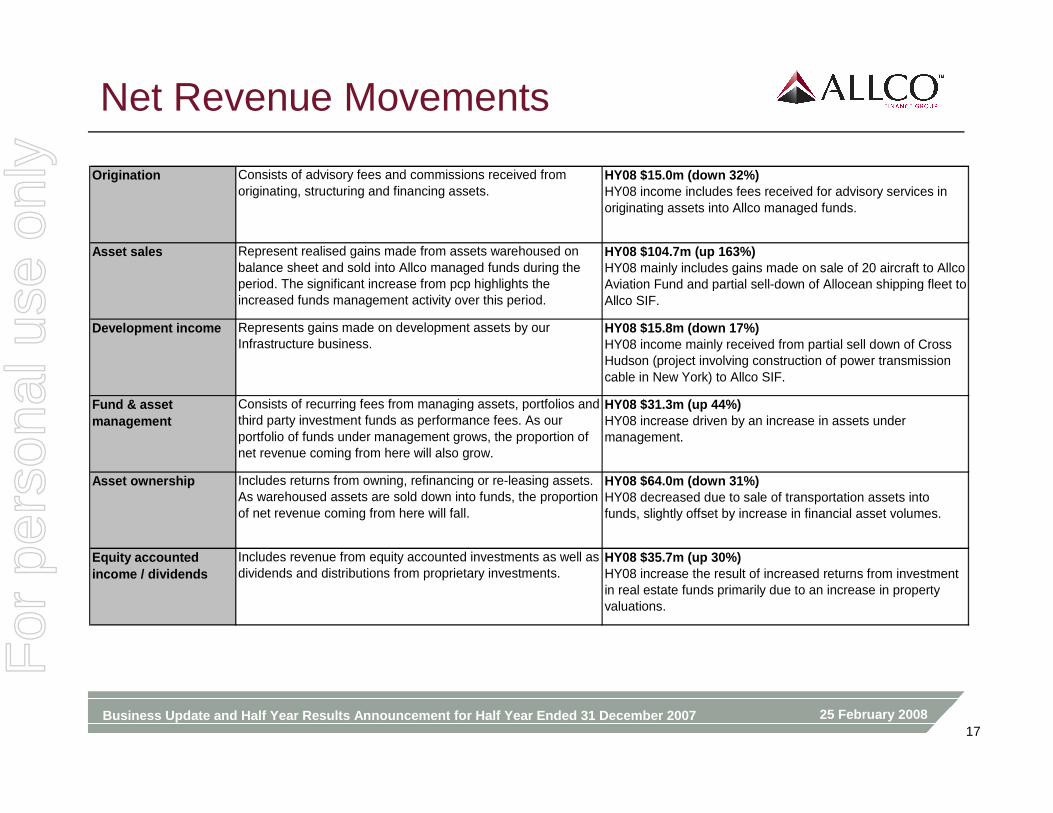

Net Revenue Movements

Origination Consists of advisory fees and commissions received from originating, structuring and financing assets.

HY08 $15.0m (down 32%)HY08 income includes fees received for advisory services in originating assets into Allco managed funds.

Asset sales Represent realised gains made from assets warehoused on balance sheet and sold into Allco managed funds during the period. The significant increase from pcp highlights the increased funds management activity over this period.

HY08 $104.7m (up 163%)HY08 mainly includes gains made on sale of 20 aircraft to Allco Aviation Fund and partial sell-down of Allocean shipping fleet to Allco SIF.

Development income Represents gains made on development assets by our Infrastructure business.

HY08 $15.8m (down 17%)HY08 income mainly received from partial sell down of Cross Hudson (project involving construction of power transmission cable in New York) to Allco SIF.

Fund & asset management

Consists of recurring fees from managing assets, portfolios and third party investment funds as performance fees. As our portfolio of funds under management grows, the proportion of net revenue coming from here will also grow.

HY08 $31.3m (up 44%)HY08 increase driven by an increase in assets under management.

Asset ownership Includes returns from owning, refinancing or re-leasing assets. As warehoused assets are sold down into funds, the proportion of net revenue coming from here will fall.

HY08 $64.0m (down 31%)HY08 decreased due to sale of transportation assets into funds, slightly offset by increase in financial asset volumes.

Equity accounted income / dividends

Includes revenue from equity accounted investments as well as dividends and distributions from proprietary investments.

HY08 $35.7m (up 30%)HY08 increase the result of increased returns from investment in real estate funds primarily due to an increase in property valuations.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200718

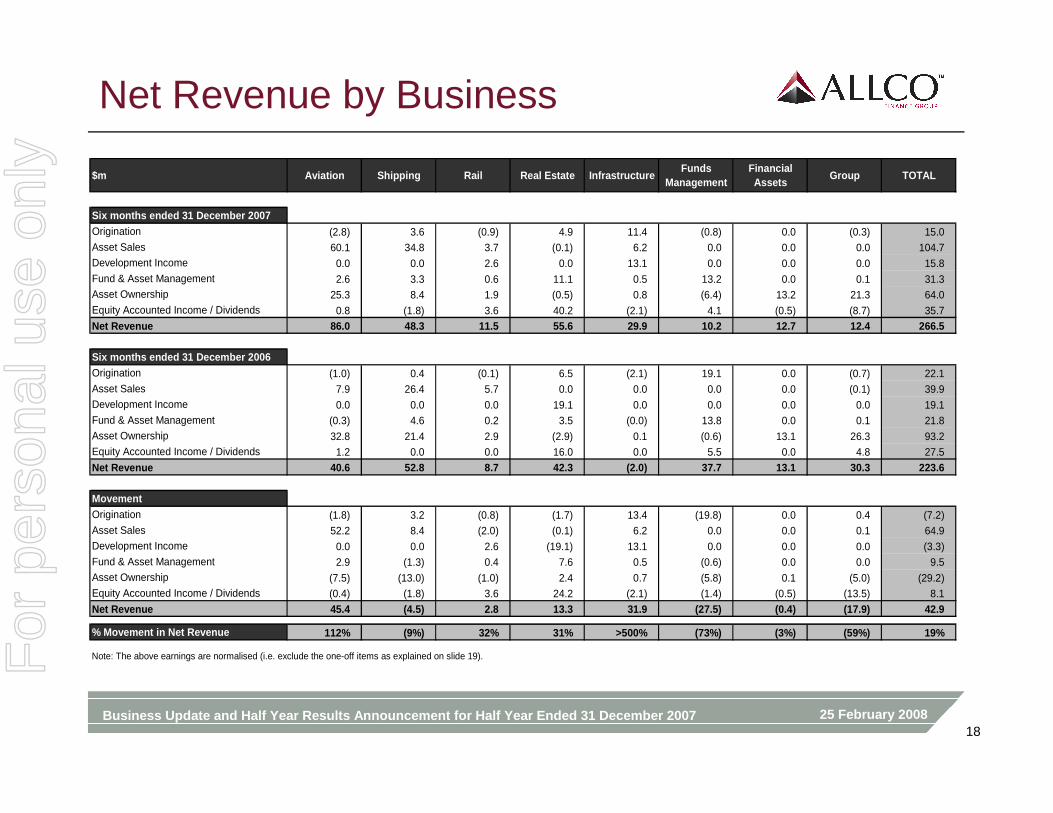

Net Revenue by Business

$m Aviation Shipping Rail Real Estate InfrastructureFunds

ManagementFinancial Assets

Group TOTAL

Six months ended 31 December 2007Origination (2.8) 3.6 (0.9) 4.9 11.4 (0.8) 0.0 (0.3) 15.0Asset Sales 60.1 34.8 3.7 (0.1) 6.2 0.0 0.0 0.0 104.7Development Income 0.0 0.0 2.6 0.0 13.1 0.0 0.0 0.0 15.8Fund & Asset Management 2.6 3.3 0.6 11.1 0.5 13.2 0.0 0.1 31.3Asset Ownership 25.3 8.4 1.9 (0.5) 0.8 (6.4) 13.2 21.3 64.0Equity Accounted Income / Dividends 0.8 (1.8) 3.6 40.2 (2.1) 4.1 (0.5) (8.7) 35.7Net Revenue 86.0 48.3 11.5 55.6 29.9 10.2 12.7 12.4 266.5

Six months ended 31 December 2006Origination (1.0) 0.4 (0.1) 6.5 (2.1) 19.1 0.0 (0.7) 22.1Asset Sales 7.9 26.4 5.7 0.0 0.0 0.0 0.0 (0.1) 39.9Development Income 0.0 0.0 0.0 19.1 0.0 0.0 0.0 0.0 19.1Fund & Asset Management (0.3) 4.6 0.2 3.5 (0.0) 13.8 0.0 0.1 21.8Asset Ownership 32.8 21.4 2.9 (2.9) 0.1 (0.6) 13.1 26.3 93.2Equity Accounted Income / Dividends 1.2 0.0 0.0 16.0 0.0 5.5 0.0 4.8 27.5

Net Revenue 40.6 52.8 8.7 42.3 (2.0) 37.7 13.1 30.3 223.6

MovementOrigination (1.8) 3.2 (0.8) (1.7) 13.4 (19.8) 0.0 0.4 (7.2)Asset Sales 52.2 8.4 (2.0) (0.1) 6.2 0.0 0.0 0.1 64.9Development Income 0.0 0.0 2.6 (19.1) 13.1 0.0 0.0 0.0 (3.3)Fund & Asset Management 2.9 (1.3) 0.4 7.6 0.5 (0.6) 0.0 0.0 9.5Asset Ownership (7.5) (13.0) (1.0) 2.4 0.7 (5.8) 0.1 (5.0) (29.2)Equity Accounted Income / Dividends (0.4) (1.8) 3.6 24.2 (2.1) (1.4) (0.5) (13.5) 8.1

Net Revenue 45.4 (4.5) 2.8 13.3 31.9 (27.5) (0.4) (17.9) 42.9

% Movement in Net Revenue 112% (9%) 32% 31% >500% (73%) (3%) (59%) 19%

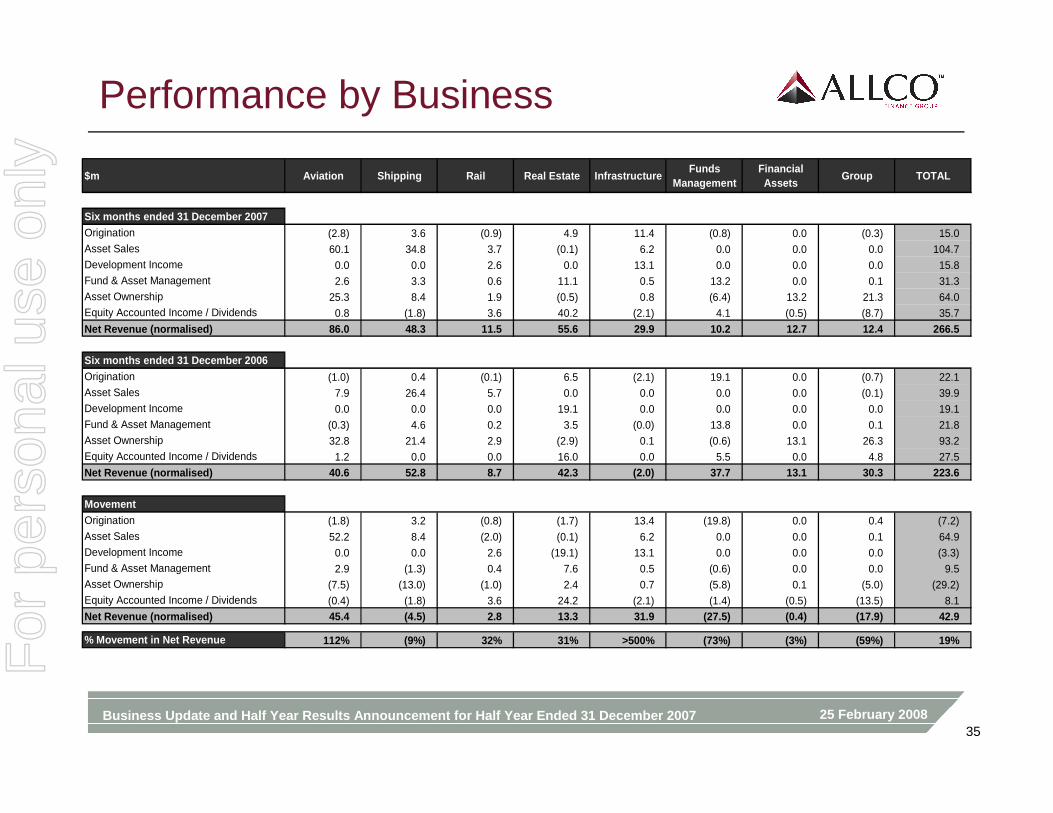

Note: The above earnings are normalised (i.e. exclude the one-off items as explained on slide 19).For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200719

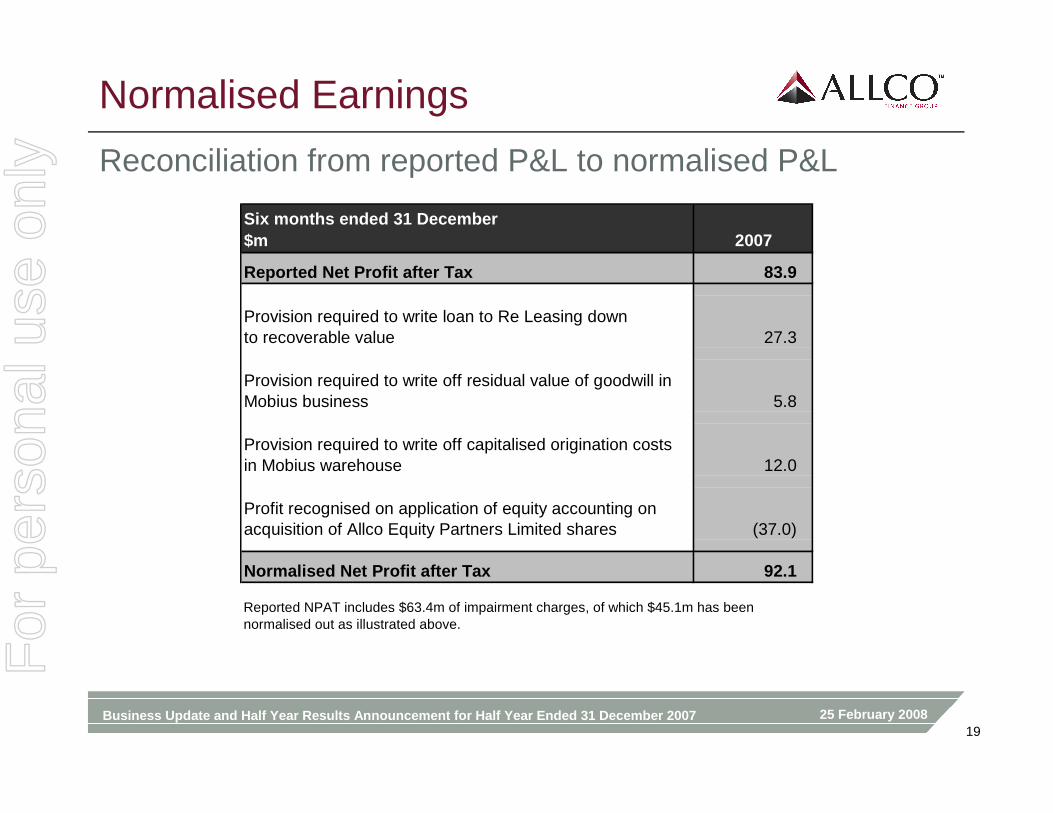

Normalised Earnings

Reconciliation from reported P&L to normalised P&L

Six months ended 31 December$m 2007

Reported Net Profit after Tax 83.9

Provision required to write loan to Re Leasing downto recoverable value 27.3

Provision required to write off residual value of goodwill in Mobius business 5.8

Provision required to write off capitalised origination costs in Mobius warehouse 12.0

Profit recognised on application of equity accounting on acquisition of Allco Equity Partners Limited shares (37.0)

Normalised Net Profit after Tax 92.1

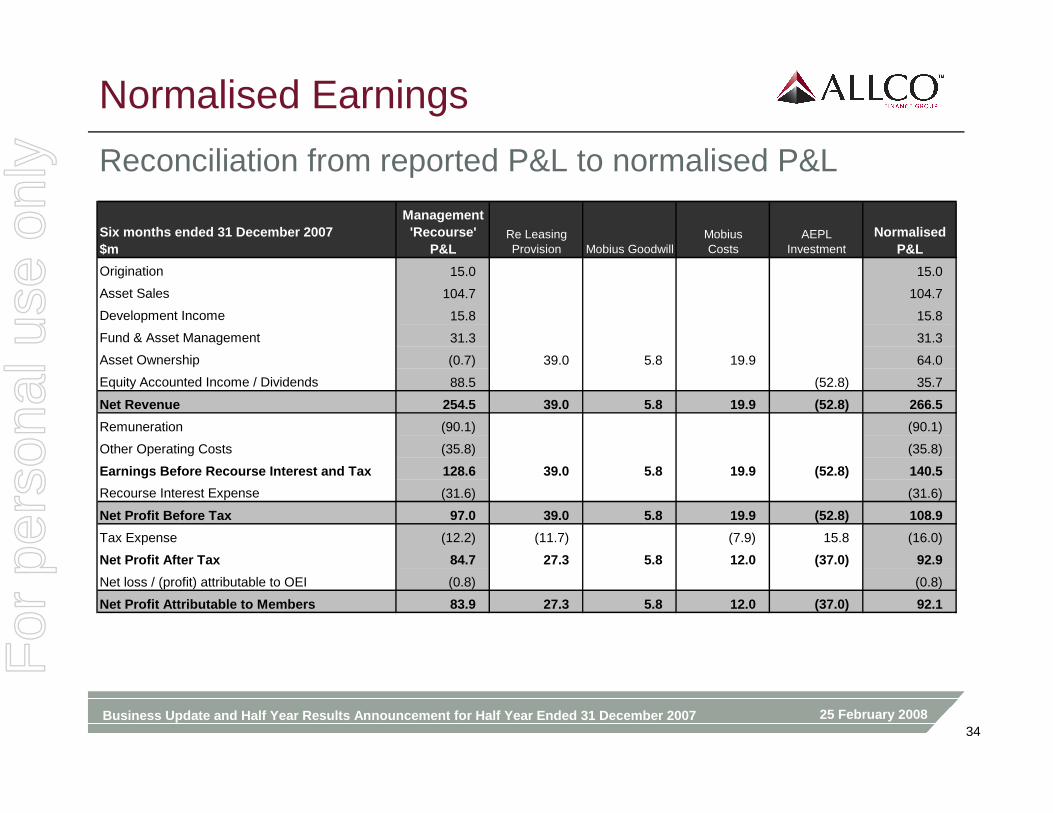

Reported NPAT includes $63.4m of impairment charges, of which $45.1m has been normalised out as illustrated above.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200720

Agenda

1. Current Situation2. First Half Business Review3. Financial Performance

4.4. Balance Sheet, Funding and LiquidityBalance Sheet, Funding and Liquidity5. Summary6. Appendix

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200721

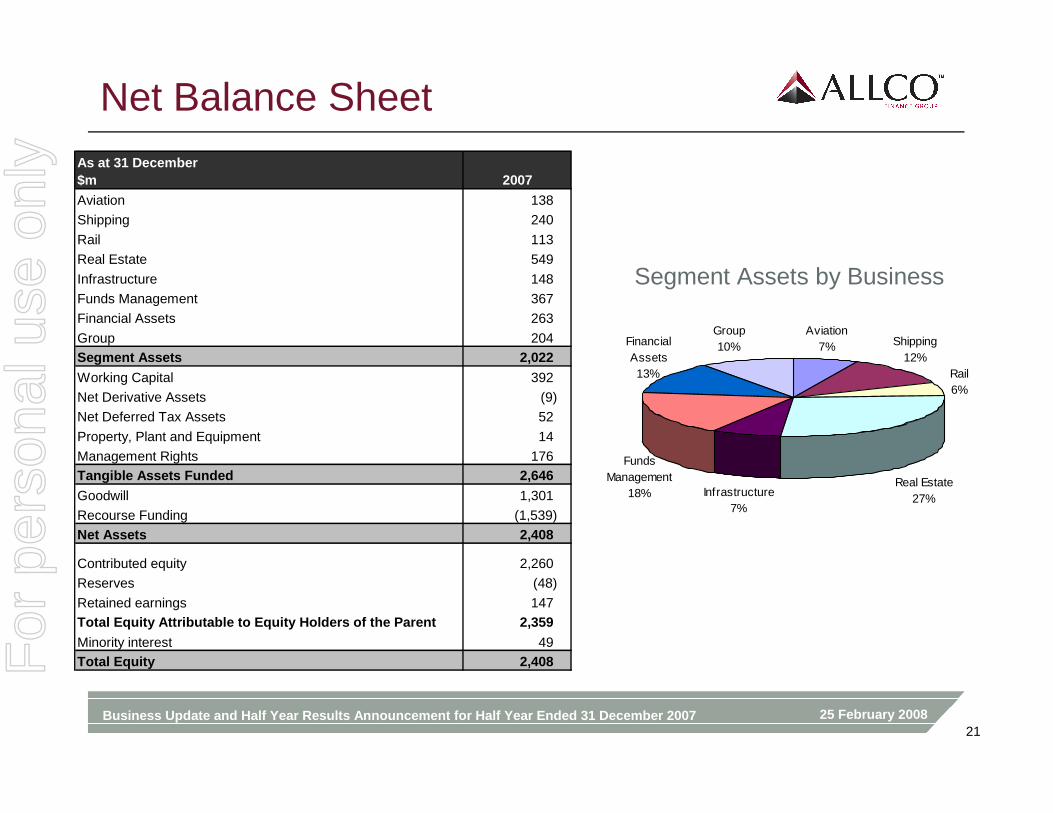

Net Balance SheetAs at 31 December$m 2007

Aviation 138

Shipping 240

Rail 113

Real Estate 549

Infrastructure 148

Funds Management 367

Financial Assets 263

Group 204 Segment Assets 2,022

Working Capital 392

Net Derivative Assets (9)

Net Deferred Tax Assets 52

Property, Plant and Equipment 14

Management Rights 176 Tangible Assets Funded 2,646

Goodwill 1,301

Recourse Funding (1,539)Net Assets 2,408

Contributed equity 2,260

Reserves (48)

Retained earnings 147 Total Equity Attributable to Equity Holders of the Parent 2,359

Minority interest 49 Total Equity 2,408

Group10%

Real Estate27%Infrastructure

7%

Rail6%

Aviation7% Shipping

12%Financial Assets13%

Funds Management

18%

Segment Assets by Business

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200722

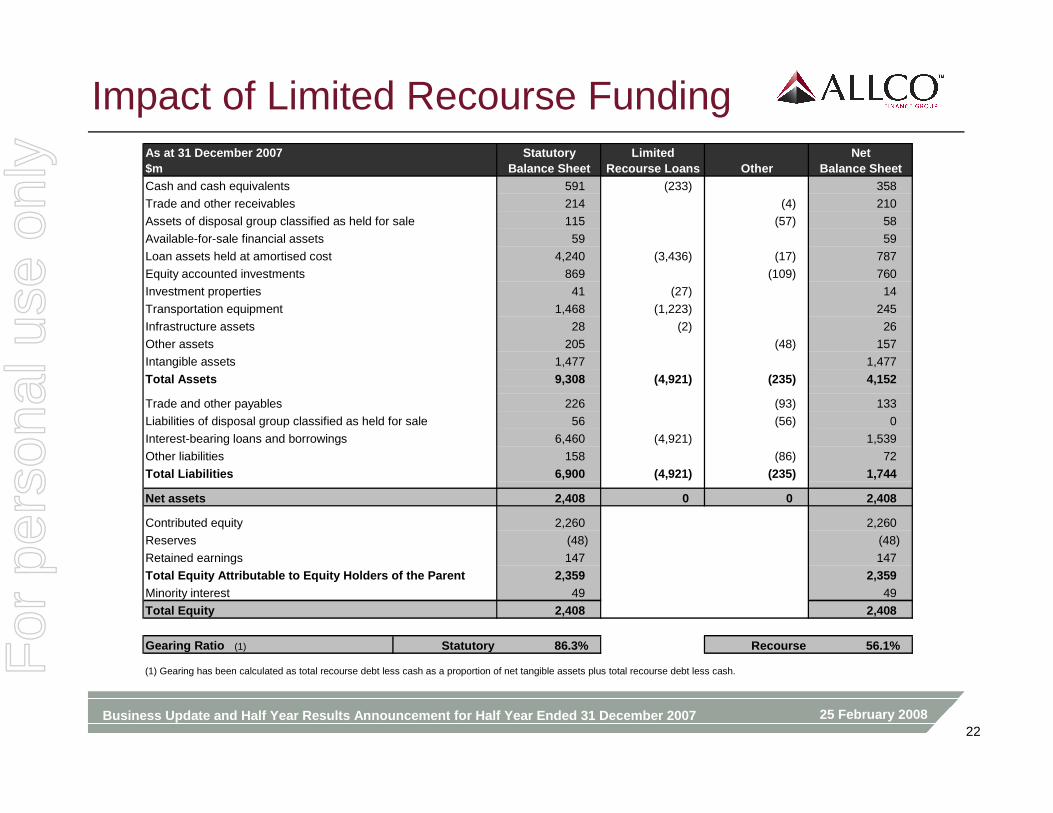

Impact of Limited Recourse FundingAs at 31 December 2007$m

StatutoryBalance Sheet

Limited Recourse Loans Other

NetBalance Sheet

Cash and cash equivalents 591 (233) 358

Trade and other receivables 214 (4) 210

Assets of disposal group classified as held for sale 115 (57) 58

Available-for-sale financial assets 59 59

Loan assets held at amortised cost 4,240 (3,436) (17) 787

Equity accounted investments 869 (109) 760

Investment properties 41 (27) 14

Transportation equipment 1,468 (1,223) 245

Infrastructure assets 28 (2) 26

Other assets 205 (48) 157

Intangible assets 1,477 1,477

Total Assets 9,308 (4,921) (235) 4,152

Trade and other payables 226 (93) 133

Liabilities of disposal group classified as held for sale 56 (56) 0

Interest-bearing loans and borrowings 6,460 (4,921) 1,539

Other liabilities 158 (86) 72

Total Liabilities 6,900 (4,921) (235) 1,744

Net assets 2,408 0 0 2,408

Contributed equity 2,260 2,260

Reserves (48) (48)

Retained earnings 147 147

Total Equity Attributable to Equity Holders of the Parent 2,359 2,359 Minority interest 49 49

Total Equity 2,408 2,408

Gearing Ratio (1) Statutory 86.3% Recourse 56.1%

(1) Gearing has been calculated as total recourse debt less cash as a proportion of net tangible assets plus total recourse debt less cash.For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200723

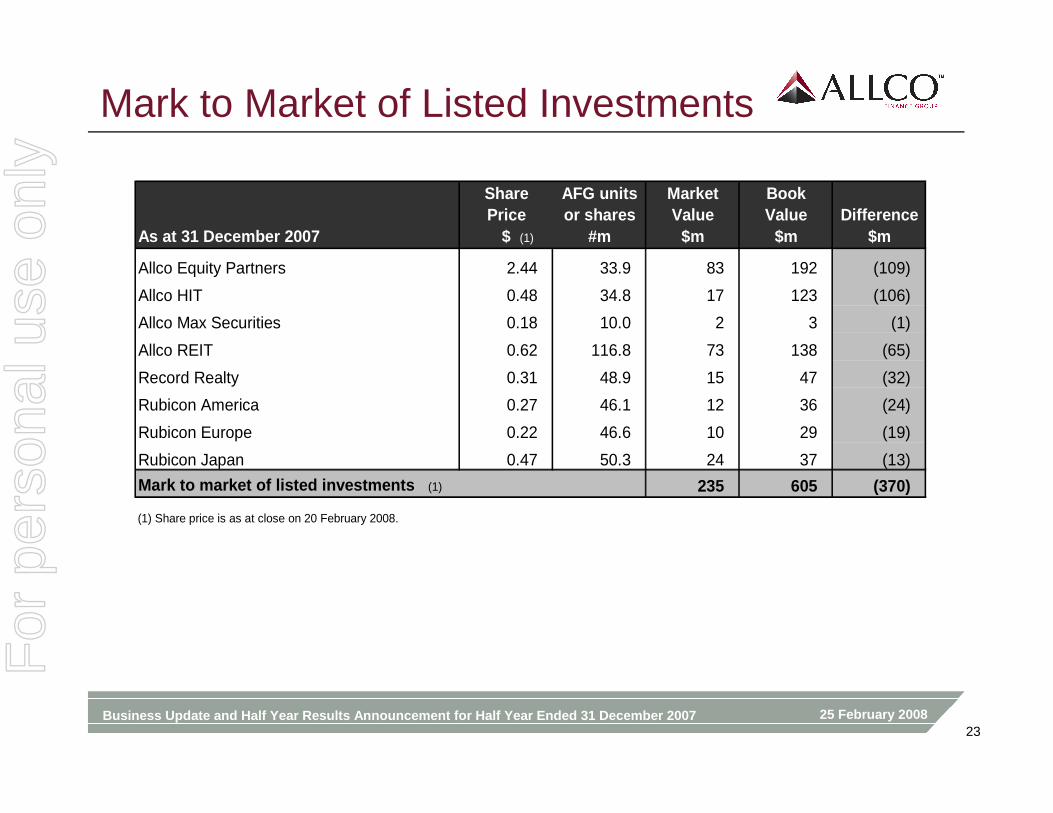

Mark to Market of Listed Investments

As at 31 December 2007

SharePrice

$ (1)

AFG unitsor shares

#m

MarketValue

$m

BookValue

$mDifference

$m

Allco Equity Partners 2.44 33.9 83 192 (109)

Allco HIT 0.48 34.8 17 123 (106)

Allco Max Securities 0.18 10.0 2 3 (1)

Allco REIT 0.62 116.8 73 138 (65)

Record Realty 0.31 48.9 15 47 (32)

Rubicon America 0.27 46.1 12 36 (24)

Rubicon Europe 0.22 46.6 10 29 (19)

Rubicon Japan 0.47 50.3 24 37 (13)

Mark to market of listed investments (1) 235 605 (370)

(1) Share price is as at close on 20 February 2008.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200724

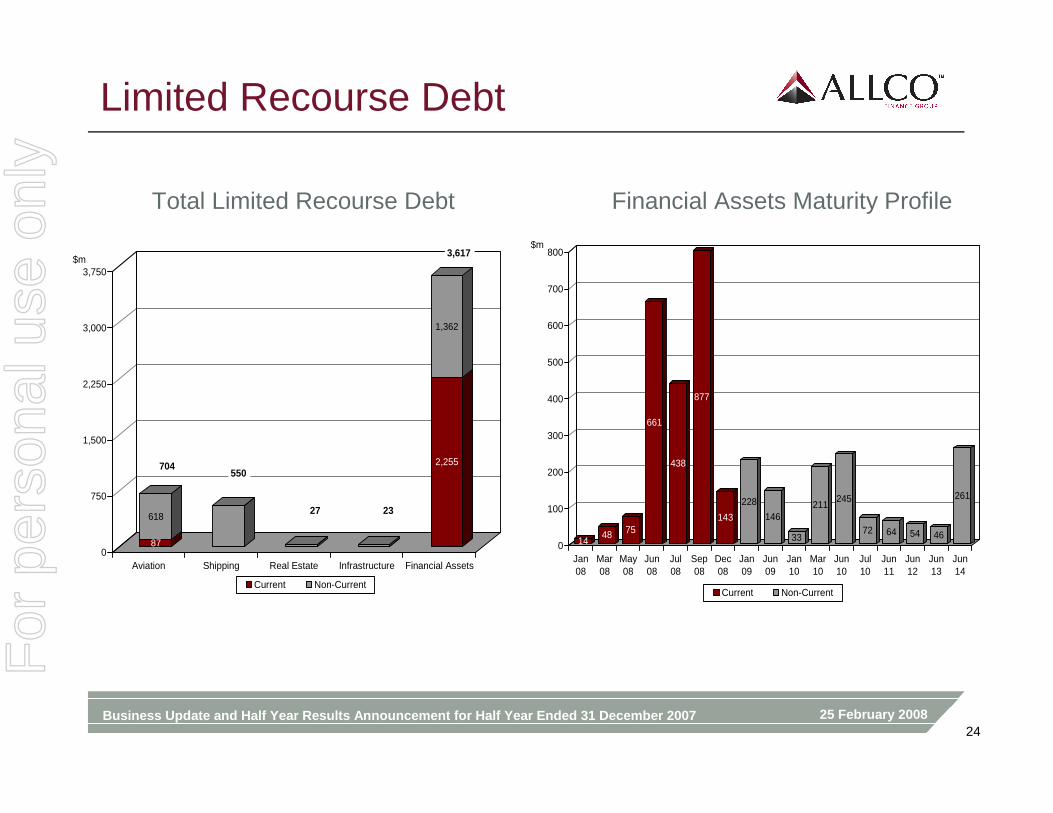

Limited Recourse Debt

Total Limited Recourse Debt Financial Assets Maturity Profile

87

618

2,255

1,362

0

750

1,500

2,250

3,000

3,750$m

Aviation Shipping Real Estate Infrastructure Financial Assets

Current Non-Current

704550

27 23

3,617

1448 75

661

438

877

143

228

146

33

211245

72 64 54 46

261

0

100

200

300

400

500

600

700

800$m

Jan08

Mar08

May08

Jun08

Jul08

Sep08

Dec08

Jan09

Jun09

Jan10

Mar10

Jun10

Jul10

Jun11

Jun12

Jun13

Jun14

Current Non-Current

For

per

sona

l use

onl

y

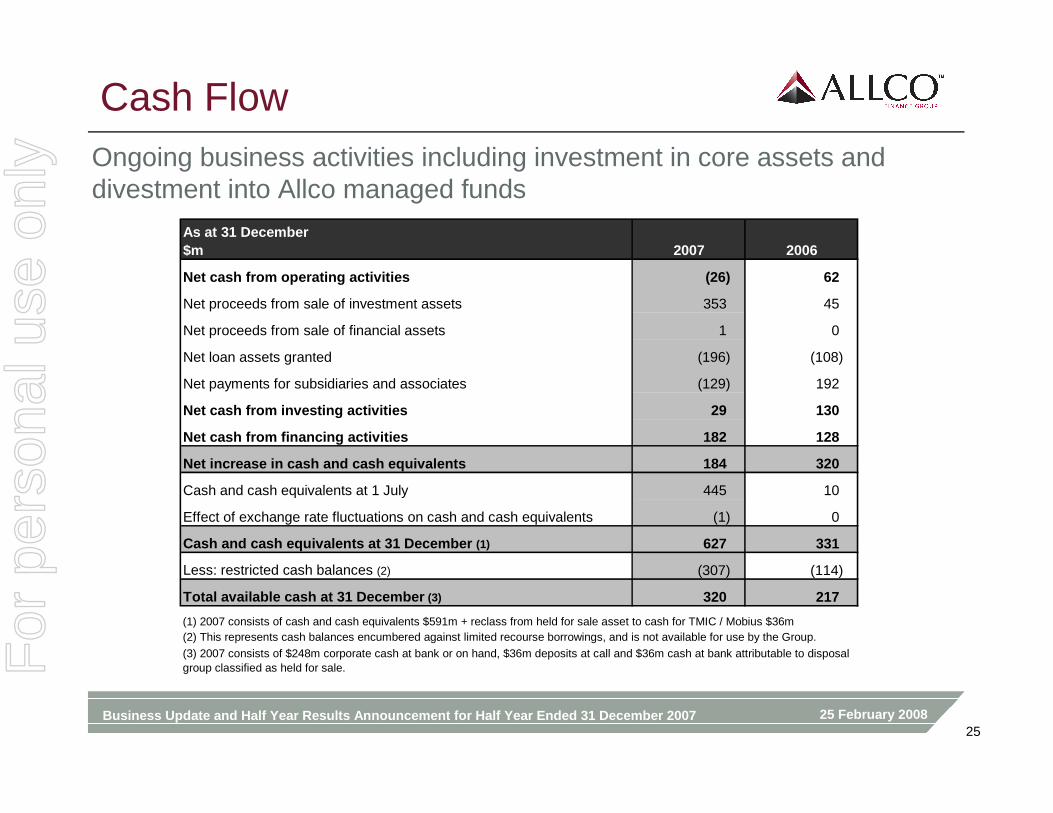

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200725

Cash FlowOngoing business activities including investment in core assets and divestment into Allco managed funds

As at 31 December$m 2007 2006

Net cash from operating activities (26) 62

Net proceeds from sale of investment assets 353 45

Net proceeds from sale of financial assets 1 0

Net loan assets granted (196) (108)

Net payments for subsidiaries and associates (129) 192

Net cash from investing activities 29 130

Net cash from financing activities 182 128

Net increase in cash and cash equivalents 184 320

Cash and cash equivalents at 1 July 445 10

Effect of exchange rate fluctuations on cash and cash equivalents (1) 0

Cash and cash equivalents at 31 December (1) 627 331

Less: restricted cash balances (2) (307) (114)

Total available cash at 31 December (3) 320 217

(1) 2007 consists of cash and cash equivalents $591m + reclass from held for sale asset to cash for TMIC / Mobius $36m(2) This represents cash balances encumbered against limited recourse borrowings, and is not available for use by the Group.

(3) 2007 consists of $248m corporate cash at bank or on hand, $36m deposits at call and $36m cash at bank attributable to disposal group classified as held for sale.For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200726

Agenda

1. Current Situation2. First Half Business Review3. Financial Performance 4. Balance Sheet, Funding and Liquidity

5.5. SummarySummary6. Appendix

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200727

Summary

� Complete the development of and implement the business restructuring program:� Focus on our core asset classes of Aviation, Shipping, Rail and Real Estate.

� Exit the businesses of Infrastructure and Financial Assets, through an orderly program to sell and wind-back involvement in these activities.

� Undertake a targeted sale of non-core assets to reduce debt.

� Implement measures designed to reduce the gap between net tangible assets of listed real estate funds and their trading prices.

� Successfully restructure our senior banking facilities with support of our banks.

� Anticipate to have our debt at an acceptable level by June 2009.

� Build value from refocused operations.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200728

BUSINESS UPDATE AND HALF YEAR RESULTS ANNOUNCEMENTHALF YEAR ENDED 31 DECEMBER 2007

THANK YOU

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200729

Agenda

1. Current Situation2. First Half Business Review3. Financial Performance 4. Balance Sheet, Funding and Liquidity5. Summary

6.6. AppendixAppendix

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200730

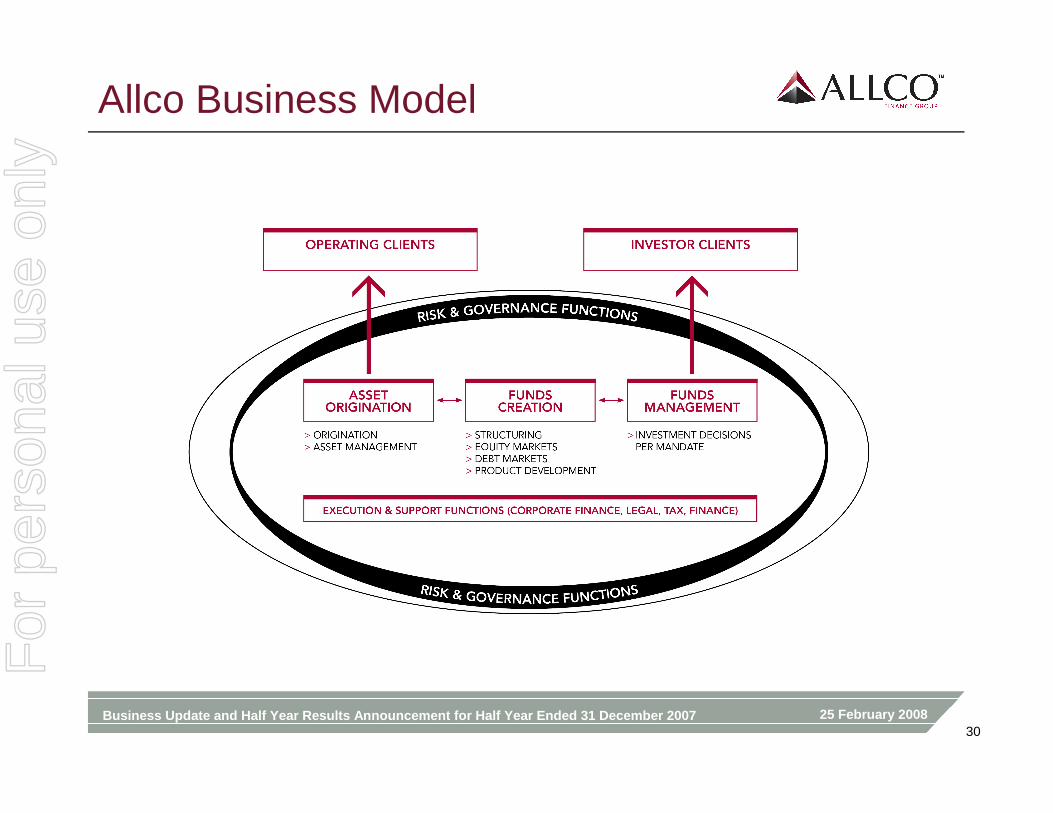

Allco Business Model

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200731

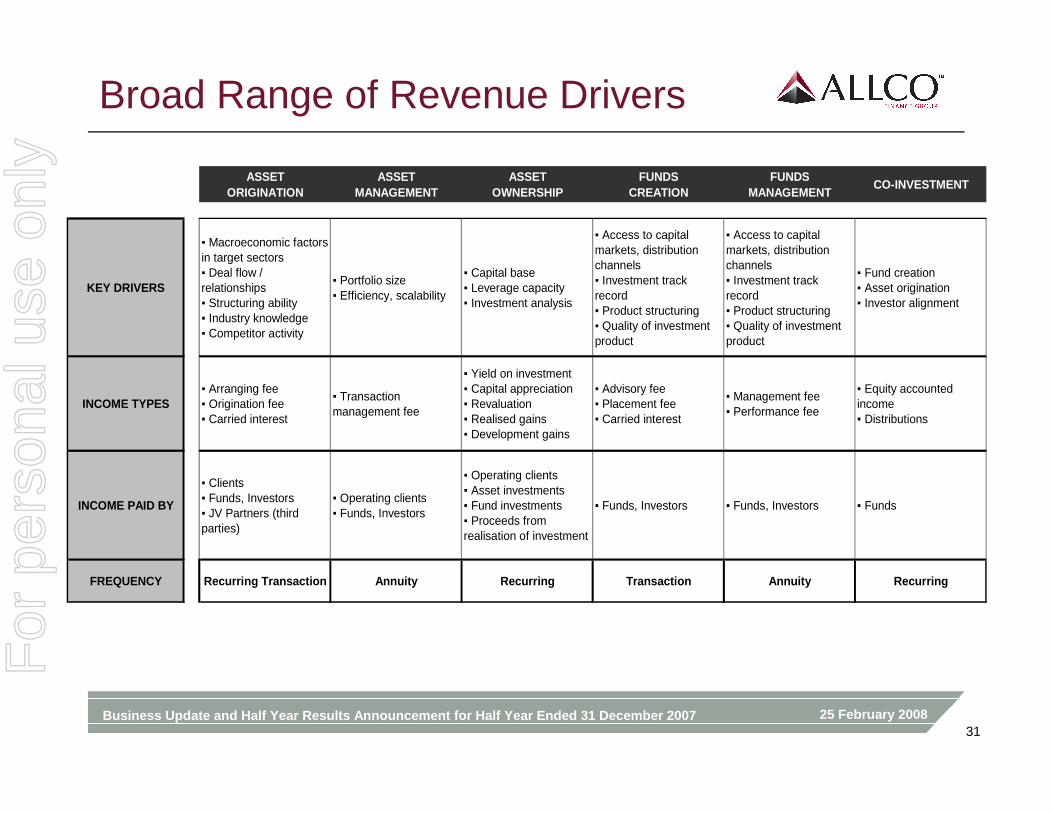

Broad Range of Revenue Drivers

ASSETORIGINATION

ASSETMANAGEMENT

ASSETOWNERSHIP

FUNDSCREATION

FUNDSMANAGEMENT

CO-INVESTMENT

KEY DRIVERS

▪ Macroeconomic factors in target sectors▪ Deal flow / relationships▪ Structuring ability▪ Industry knowledge▪ Competitor activity

▪ Portfolio size▪ Efficiency, scalability

▪ Capital base▪ Leverage capacity▪ Investment analysis

▪ Access to capital markets, distribution channels▪ Investment track record▪ Product structuring▪ Quality of investment product

▪ Access to capital markets, distribution channels▪ Investment track record▪ Product structuring▪ Quality of investment product

▪ Fund creation▪ Asset origination▪ Investor alignment

INCOME TYPES▪ Arranging fee▪ Origination fee▪ Carried interest

▪ Transaction management fee

▪ Yield on investment▪ Capital appreciation▪ Revaluation▪ Realised gains▪ Development gains

▪ Advisory fee▪ Placement fee▪ Carried interest

▪ Management fee▪ Performance fee

▪ Equity accounted income▪ Distributions

INCOME PAID BY

▪ Clients▪ Funds, Investors▪ JV Partners (third parties)

▪ Operating clients▪ Funds, Investors

▪ Operating clients▪ Asset investments▪ Fund investments▪ Proceeds from realisation of investment

▪ Funds, Investors ▪ Funds, Investors ▪ Funds

FREQUENCY Recurring Transaction Annuity Recurring Trans action Annuity Recurring

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200732

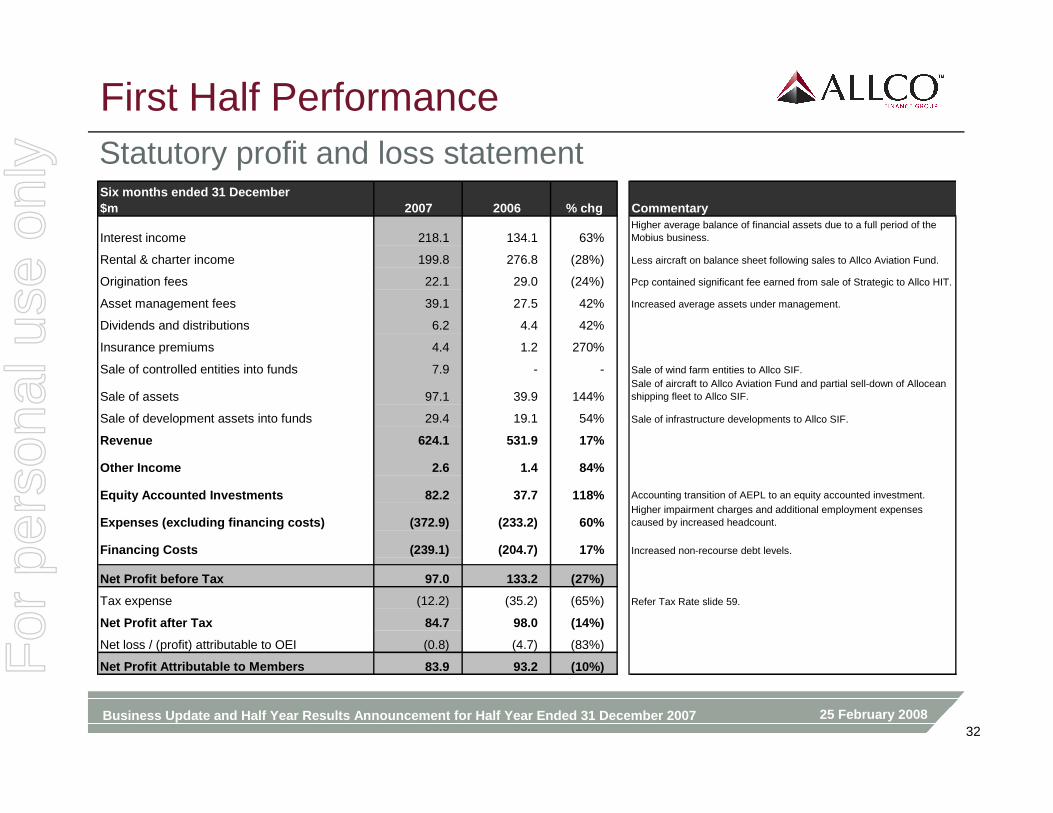

First Half PerformanceStatutory profit and loss statementSix months ended 31 December$m 2007 2006 % chg Commentary

Interest income 218.1 134.1 63%Higher average balance of financial assets due to a full period of the Mobius business.

Rental & charter income 199.8 276.8 (28%) Less aircraft on balance sheet following sales to Allco Aviation Fund.

Origination fees 22.1 29.0 (24%) Pcp contained significant fee earned from sale of Strategic to Allco HIT.

Asset management fees 39.1 27.5 42% Increased average assets under management.

Dividends and distributions 6.2 4.4 42%

Insurance premiums 4.4 1.2 270%

Sale of controlled entities into funds 7.9 - - Sale of wind farm entities to Allco SIF.

Sale of assets 97.1 39.9 144%Sale of aircraft to Allco Aviation Fund and partial sell-down of Allocean shipping fleet to Allco SIF.

Sale of development assets into funds 29.4 19.1 54% Sale of infrastructure developments to Allco SIF.

Revenue 624.1 531.9 17%

Other Income 2.6 1.4 84%

Equity Accounted Investments 82.2 37.7 118% Accounting transition of AEPL to an equity accounted investment.

Expenses (excluding financing costs) (372.9) (233.2) 6 0%Higher impairment charges and additional employment expenses caused by increased headcount.

Financing Costs (239.1) (204.7) 17% Increased non-recourse debt levels.

Net Profit before Tax 97.0 133.2 (27%)

Tax expense (12.2) (35.2) (65%) Refer Tax Rate slide 59.

Net Profit after Tax 84.7 98.0 (14%)

Net loss / (profit) attributable to OEI (0.8) (4.7) (83%)

Net Profit Attributable to Members 83.9 93.2 (10%)For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200733

First Half Performance

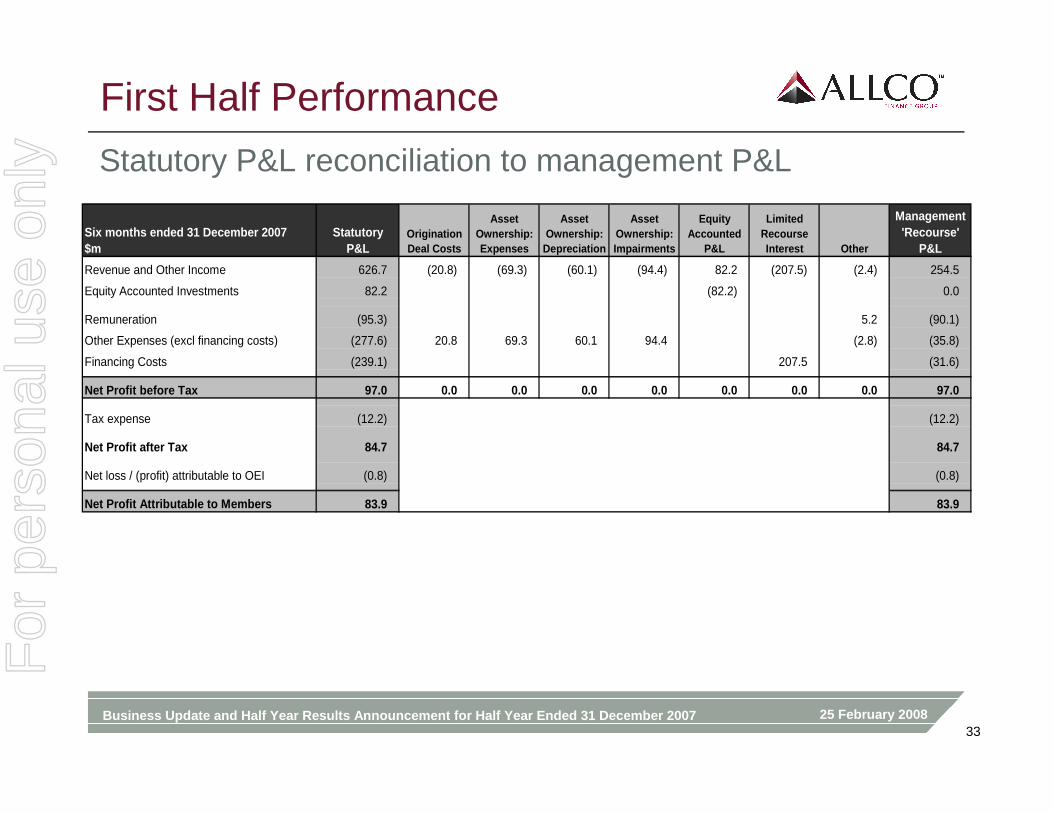

Statutory P&L reconciliation to management P&L

Six months ended 31 December 2007$m

StatutoryP&L

Origination Deal Costs

Asset Ownership: Expenses

Asset Ownership:

Depreciation

Asset Ownership: Impairments

Equity Accounted

P&L

Limited Recourse Interest Other

Management'Recourse'

P&L

Revenue and Other Income 626.7 (20.8) (69.3) (60.1) (94.4) 82.2 (207.5) (2.4) 254.5

Equity Accounted Investments 82.2 (82.2) 0.0

Remuneration (95.3) 5.2 (90.1)

Other Expenses (excl financing costs) (277.6) 20.8 69.3 60.1 94.4 (2.8) (35.8)

Financing Costs (239.1) 207.5 (31.6)

Net Profit before Tax 97.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 97.0

Tax expense (12.2) (12.2)

Net Profit after Tax 84.7 84.7

Net loss / (profit) attributable to OEI (0.8) (0.8)

Net Profit Attributable to Members 83.9 83.9

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200734

Normalised Earnings

Reconciliation from reported P&L to normalised P&L

Six months ended 31 December 2007$m

Management'Recourse'

P&LRe Leasing Provision Mobius Goodwill

MobiusCosts

AEPL Investment

NormalisedP&L

Origination 15.0 15.0

Asset Sales 104.7 104.7

Development Income 15.8 15.8

Fund & Asset Management 31.3 31.3

Asset Ownership (0.7) 39.0 5.8 19.9 64.0

Equity Accounted Income / Dividends 88.5 (52.8) 35.7

Net Revenue 254.5 39.0 5.8 19.9 (52.8) 266.5

Remuneration (90.1) (90.1)

Other Operating Costs (35.8) (35.8)

Earnings Before Recourse Interest and Tax 128.6 39.0 5 .8 19.9 (52.8) 140.5

Recourse Interest Expense (31.6) (31.6)

Net Profit Before Tax 97.0 39.0 5.8 19.9 (52.8) 108.9

Tax Expense (12.2) (11.7) (7.9) 15.8 (16.0)

Net Profit After Tax 84.7 27.3 5.8 12.0 (37.0) 92.9

Net loss / (profit) attributable to OEI (0.8) (0.8)

Net Profit Attributable to Members 83.9 27.3 5.8 12.0 (3 7.0) 92.1

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200735

Performance by Business

$m Aviation Shipping Rail Real Estate InfrastructureFunds

ManagementFinancial Assets

Group TOTAL

Six months ended 31 December 2007Origination (2.8) 3.6 (0.9) 4.9 11.4 (0.8) 0.0 (0.3) 15.0Asset Sales 60.1 34.8 3.7 (0.1) 6.2 0.0 0.0 0.0 104.7Development Income 0.0 0.0 2.6 0.0 13.1 0.0 0.0 0.0 15.8Fund & Asset Management 2.6 3.3 0.6 11.1 0.5 13.2 0.0 0.1 31.3Asset Ownership 25.3 8.4 1.9 (0.5) 0.8 (6.4) 13.2 21.3 64.0Equity Accounted Income / Dividends 0.8 (1.8) 3.6 40.2 (2.1) 4.1 (0.5) (8.7) 35.7

Net Revenue (normalised) 86.0 48.3 11.5 55.6 29.9 10.2 12. 7 12.4 266.5

Six months ended 31 December 2006Origination (1.0) 0.4 (0.1) 6.5 (2.1) 19.1 0.0 (0.7) 22.1Asset Sales 7.9 26.4 5.7 0.0 0.0 0.0 0.0 (0.1) 39.9Development Income 0.0 0.0 0.0 19.1 0.0 0.0 0.0 0.0 19.1Fund & Asset Management (0.3) 4.6 0.2 3.5 (0.0) 13.8 0.0 0.1 21.8Asset Ownership 32.8 21.4 2.9 (2.9) 0.1 (0.6) 13.1 26.3 93.2Equity Accounted Income / Dividends 1.2 0.0 0.0 16.0 0.0 5.5 0.0 4.8 27.5Net Revenue (normalised) 40.6 52.8 8.7 42.3 (2.0) 37.7 13. 1 30.3 223.6

MovementOrigination (1.8) 3.2 (0.8) (1.7) 13.4 (19.8) 0.0 0.4 (7.2)Asset Sales 52.2 8.4 (2.0) (0.1) 6.2 0.0 0.0 0.1 64.9Development Income 0.0 0.0 2.6 (19.1) 13.1 0.0 0.0 0.0 (3.3)Fund & Asset Management 2.9 (1.3) 0.4 7.6 0.5 (0.6) 0.0 0.0 9.5Asset Ownership (7.5) (13.0) (1.0) 2.4 0.7 (5.8) 0.1 (5.0) (29.2)Equity Accounted Income / Dividends (0.4) (1.8) 3.6 24.2 (2.1) (1.4) (0.5) (13.5) 8.1Net Revenue (normalised) 45.4 (4.5) 2.8 13.3 31.9 (27.5) ( 0.4) (17.9) 42.9

% Movement in Net Revenue 112% (9%) 32% 31% >500% (73%) (3%) (59%) 19%For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200736

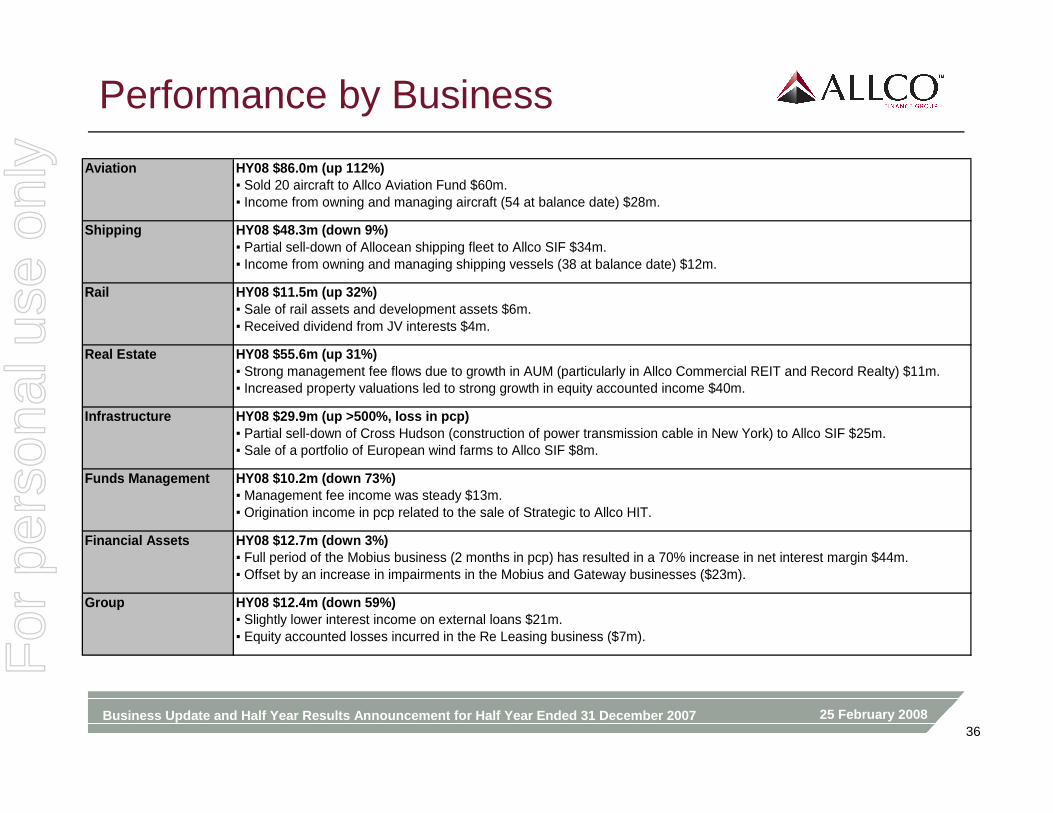

Performance by Business

Aviation HY08 $86.0m (up 112%)▪ Sold 20 aircraft to Allco Aviation Fund $60m.▪ Income from owning and managing aircraft (54 at balance date) $28m.

Shipping HY08 $48.3m (down 9%)▪ Partial sell-down of Allocean shipping fleet to Allco SIF $34m.▪ Income from owning and managing shipping vessels (38 at balance date) $12m.

Rail HY08 $11.5m (up 32%)▪ Sale of rail assets and development assets $6m.▪ Received dividend from JV interests $4m.

Real Estate HY08 $55.6m (up 31%)▪ Strong management fee flows due to growth in AUM (particularly in Allco Commercial REIT and Record Realty) $11m.▪ Increased property valuations led to strong growth in equity accounted income $40m.

Infrastructure HY08 $29.9m (up >500%, loss in pcp)▪ Partial sell-down of Cross Hudson (construction of power transmission cable in New York) to Allco SIF $25m.▪ Sale of a portfolio of European wind farms to Allco SIF $8m.

Funds Management HY08 $10.2m (down 73%)▪ Management fee income was steady $13m.▪ Origination income in pcp related to the sale of Strategic to Allco HIT.

Financial Assets HY08 $12.7m (down 3%)▪ Full period of the Mobius business (2 months in pcp) has resulted in a 70% increase in net interest margin $44m.▪ Offset by an increase in impairments in the Mobius and Gateway businesses ($23m).

Group HY08 $12.4m (down 59%)▪ Slightly lower interest income on external loans $21m.▪ Equity accounted losses incurred in the Re Leasing business ($7m).

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200737

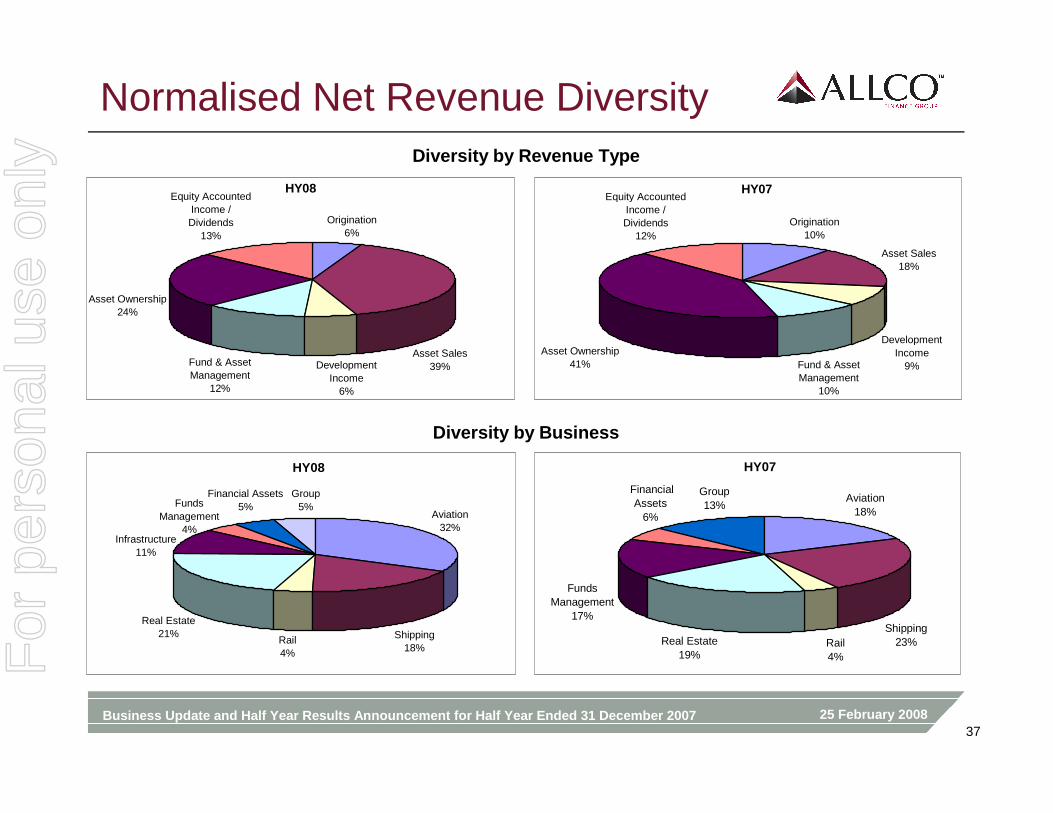

Normalised Net Revenue DiversityDiversity by Revenue Type

Diversity by Business

HY08

Origination6%

Development Income

6%

Fund & Asset Management

12%

Equity Accounted Income / Dividends

13%

Asset Ownership24%

Asset Sales39%

Origination10%

Asset Sales18%

Equity Accounted Income / Dividends

12%

Asset Ownership41% Fund & Asset

Management10%

Development Income

9%

HY07

Shipping18%

Rail4%

Real Estate21%

Group5%

Financial Assets5%

Infrastructure11%

Aviation32%

FundsManagement

4%

HY08

Aviation18%

Real Estate19%

Funds Management

17%

Group13%

Rail4%

Shipping23%

Financial Assets

6%

HY07

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200738

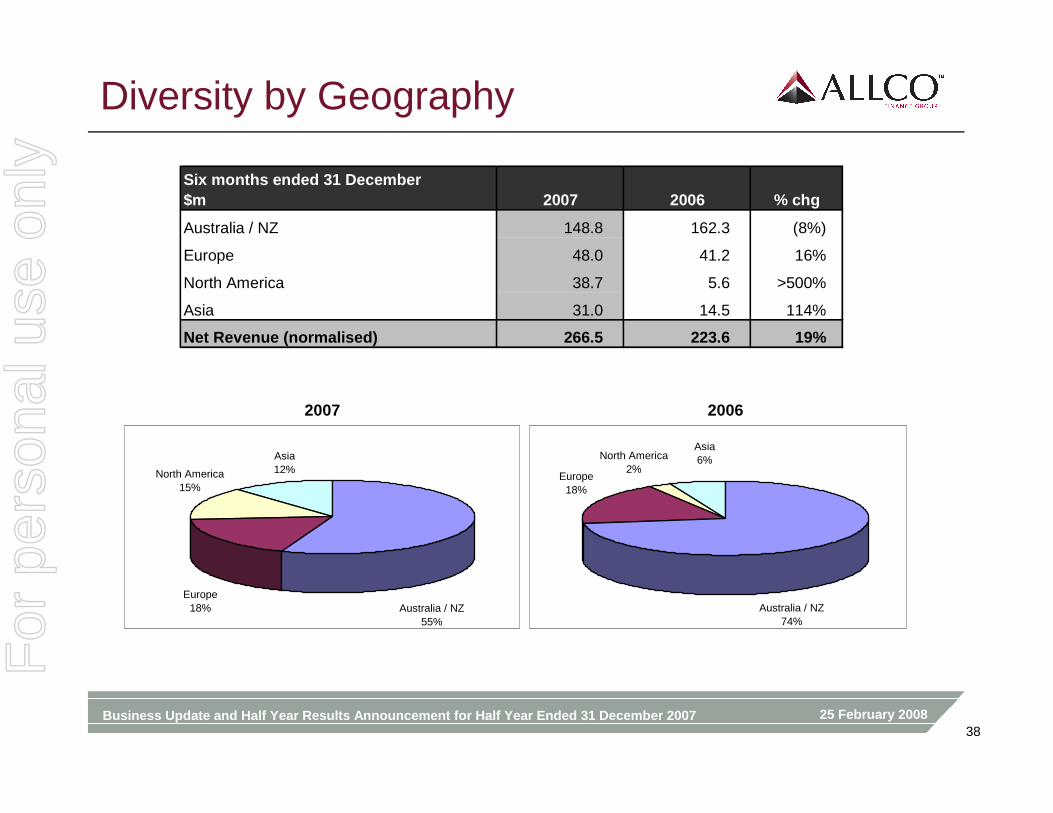

Diversity by Geography

2007 2006

Asia12%

Australia / NZ55%

North America15%

Europe18% Australia / NZ

74%

Europe18%

Asia6%North America

2%

Six months ended 31 December$m 2007 2006 % chg

Australia / NZ 148.8 162.3 (8%)

Europe 48.0 41.2 16%

North America 38.7 5.6 >500%

Asia 31.0 14.5 114%

Net Revenue (normalised) 266.5 223.6 19%

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200739

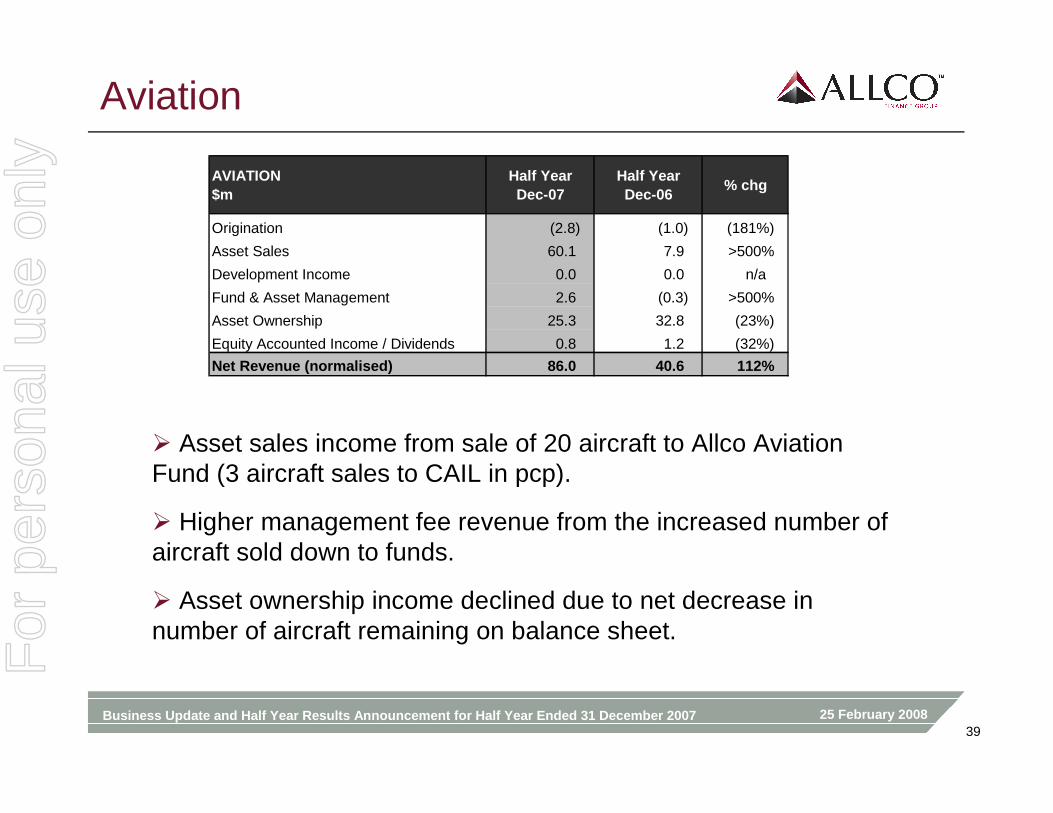

Aviation

� Asset sales income from sale of 20 aircraft to Allco Aviation Fund (3 aircraft sales to CAIL in pcp).

� Higher management fee revenue from the increased number of aircraft sold down to funds.

� Asset ownership income declined due to net decrease in number of aircraft remaining on balance sheet.

AVIATION$m

Half YearDec-07

Half YearDec-06

% chg

Origination (2.8) (1.0) (181%)

Asset Sales 60.1 7.9 >500%

Development Income 0.0 0.0 n/a

Fund & Asset Management 2.6 (0.3) >500%

Asset Ownership 25.3 32.8 (23%)

Equity Accounted Income / Dividends 0.8 1.2 (32%)

Net Revenue (normalised) 86.0 40.6 112%

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200740

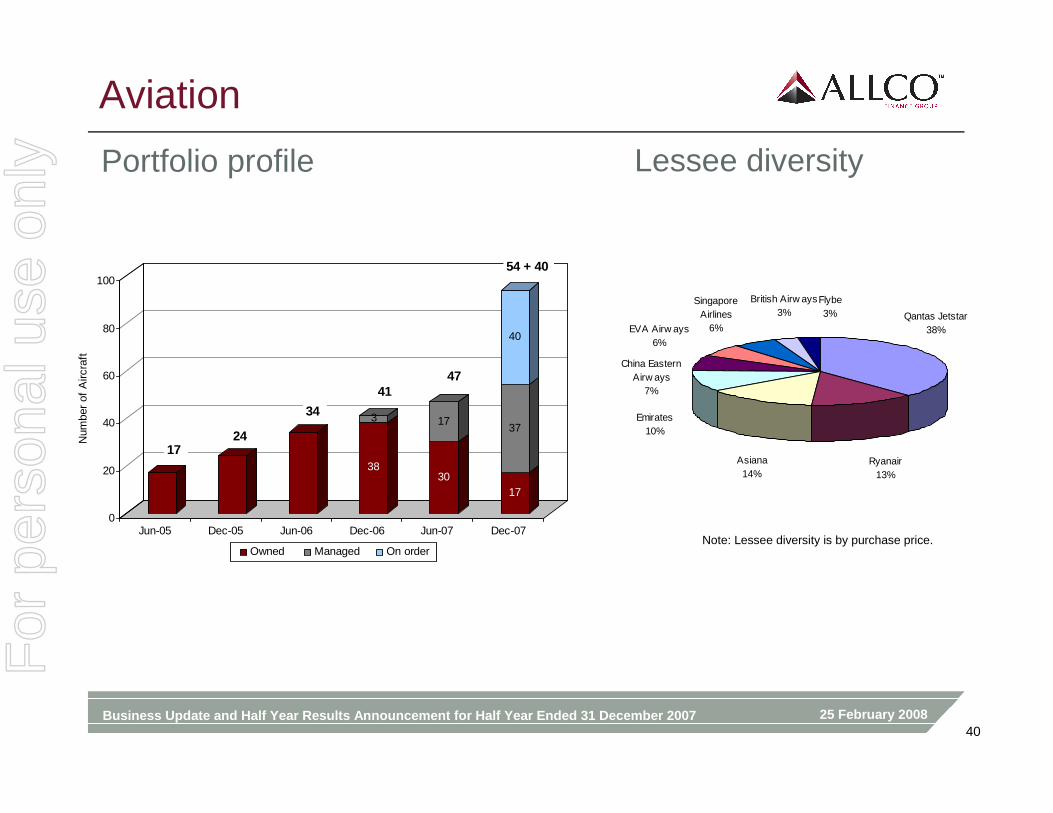

Aviation

Portfolio profile Lessee diversity

Note: Lessee diversity is by purchase price.

Ryanair13%

Asiana14%

Qantas Jetstar38%

Emirates10%

EVA Airw ays6%

China Eastern Airw ays

7%

Flybe3%

British Airw ays3%

Singapore Airlines

6%

38

3

30

17

17

37

40

0

20

40

60

80

100

Num

ber

of A

ircra

ft

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Owned Managed On order

1724

34

54 + 40

4741

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200741

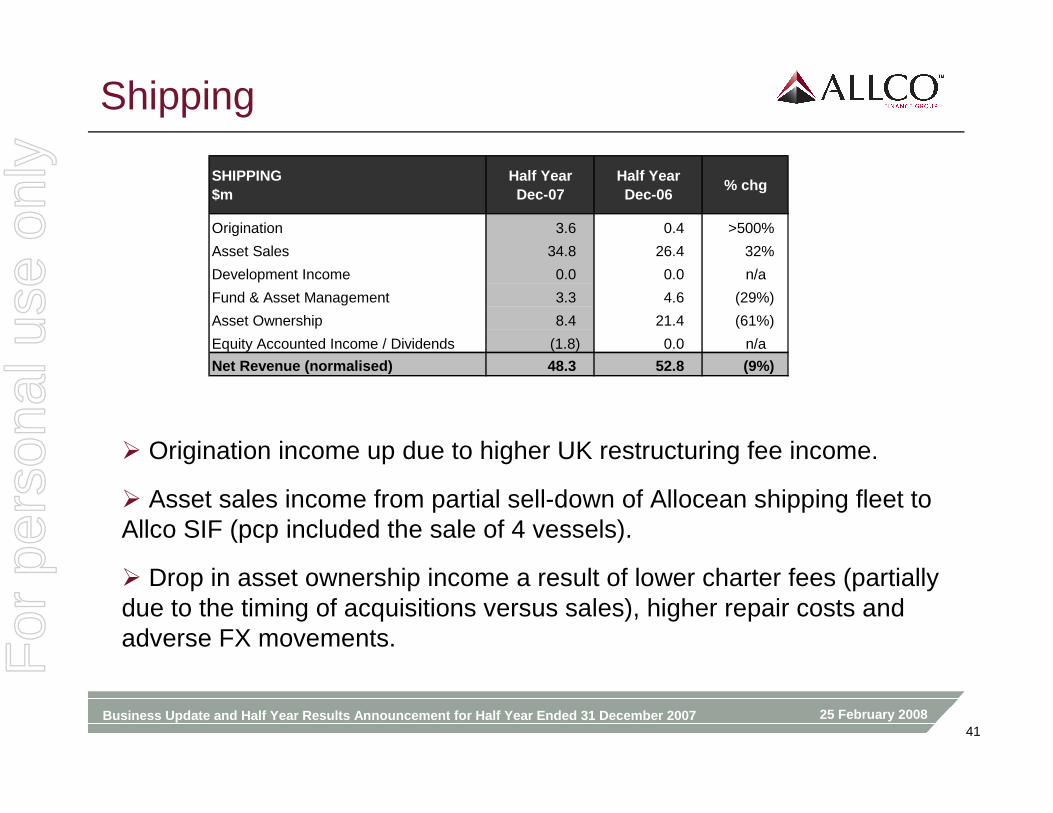

Shipping

� Origination income up due to higher UK restructuring fee income.

� Asset sales income from partial sell-down of Allocean shipping fleet to Allco SIF (pcp included the sale of 4 vessels).

� Drop in asset ownership income a result of lower charter fees (partially due to the timing of acquisitions versus sales), higher repair costs andadverse FX movements.

SHIPPING$m

Half YearDec-07

Half YearDec-06

% chg

Origination 3.6 0.4 >500%

Asset Sales 34.8 26.4 32%

Development Income 0.0 0.0 n/a

Fund & Asset Management 3.3 4.6 (29%)

Asset Ownership 8.4 21.4 (61%)

Equity Accounted Income / Dividends (1.8) 0.0 n/a

Net Revenue (normalised) 48.3 52.8 (9%)

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200742

Shipping

Portfolio profile Lessee diversity

Anchor Handlers5%

Fast Ferries2%

LPG12%

Containers40%

Tankers19%

Bulk Carriers22%

Note: Lessee diversity is by purchase price.

19

2

17

4

21

4

34

4

23

0

10

20

30

40

50

60

70

Num

ber

of V

esse

ls

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Owned Managed On order

21 21

38 + 23

25

18 19

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200743

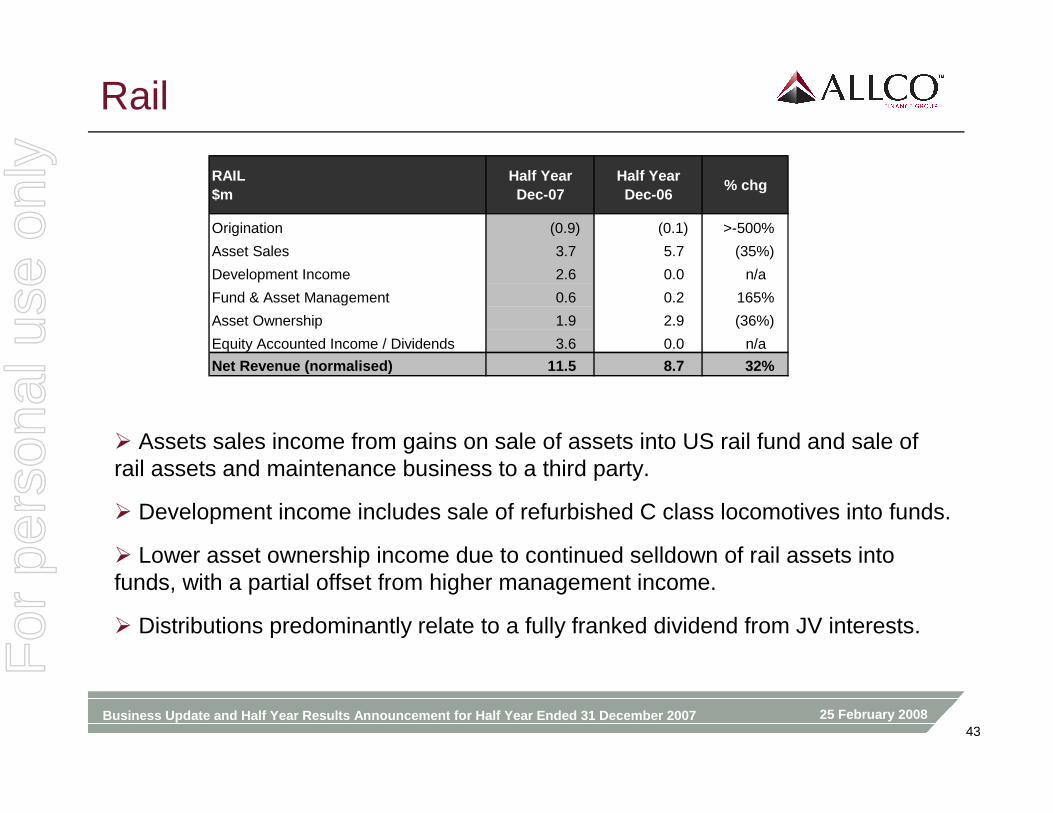

Rail

� Assets sales income from gains on sale of assets into US rail fund and sale of rail assets and maintenance business to a third party.

� Development income includes sale of refurbished C class locomotives into funds.

� Lower asset ownership income due to continued selldown of rail assets into funds, with a partial offset from higher management income.

� Distributions predominantly relate to a fully franked dividend from JV interests.

RAIL$m

Half YearDec-07

Half YearDec-06

% chg

Origination (0.9) (0.1) >-500%

Asset Sales 3.7 5.7 (35%)

Development Income 2.6 0.0 n/a

Fund & Asset Management 0.6 0.2 165%

Asset Ownership 1.9 2.9 (36%)

Equity Accounted Income / Dividends 3.6 0.0 n/a

Net Revenue (normalised) 11.5 8.7 32%

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200744

Rail

Portfolio profile: rail cars Portfolio profile: locomotives

1,140

411

260

1,739

298

2,444

172

2,932

413

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Num

ber

of R

ailc

ars

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Railcars owned Railcars managed Railcars on order

3,104 + 413

289411

1,551

1,999

2,742

54

25

54

25

54

25

6

33

29

0

20

40

60

80

100

120

Num

ber

of L

ocom

otiv

es

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Locomotives owned Locomotives managed Locomotives on order

39 + 29

2

25

79 79 79

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200745

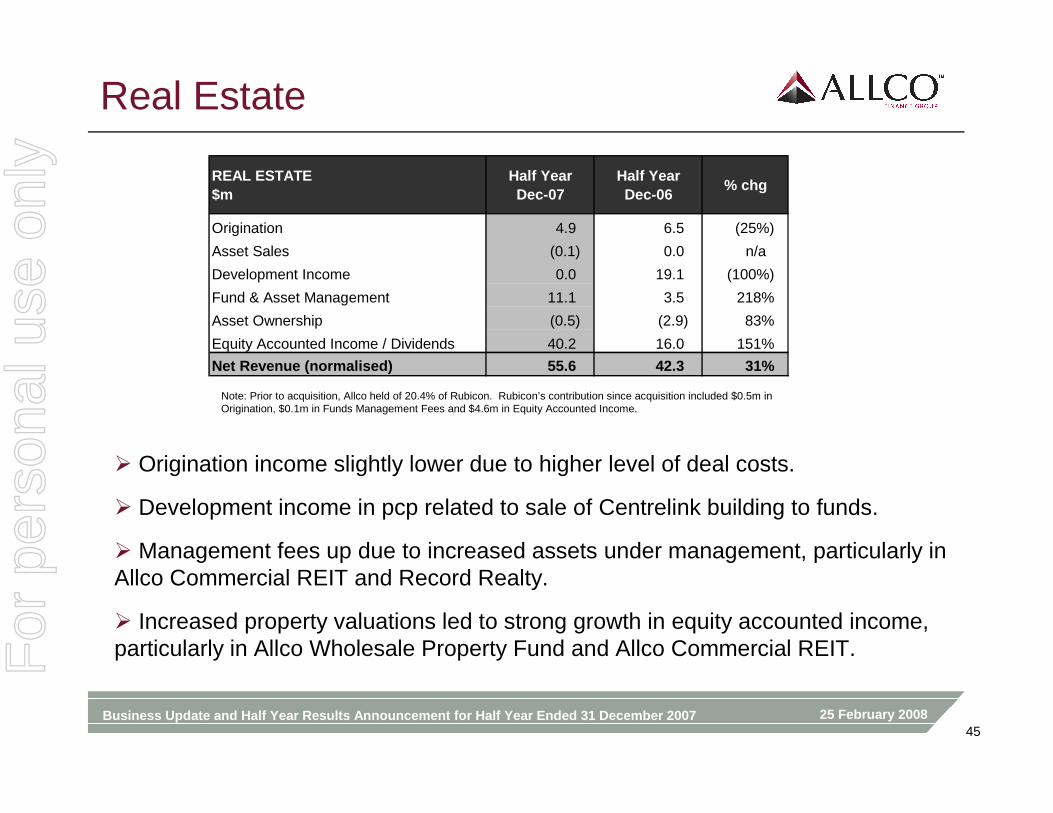

Real Estate

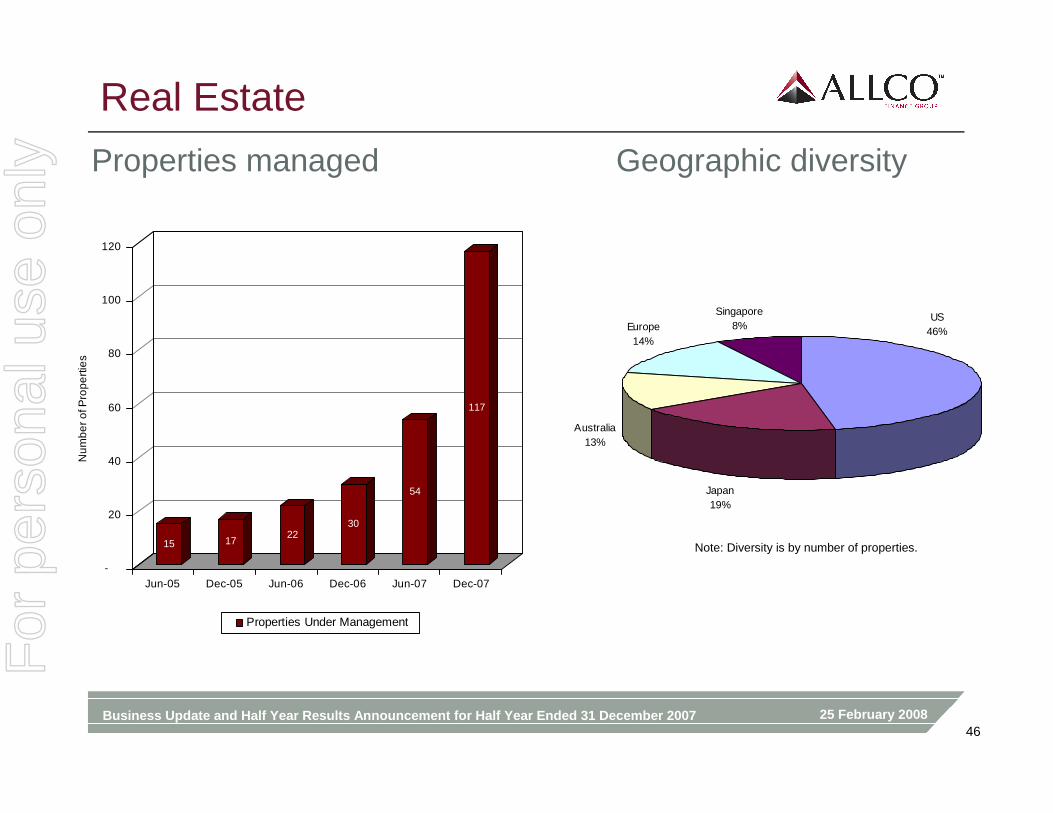

� Origination income slightly lower due to higher level of deal costs.

� Development income in pcp related to sale of Centrelink building to funds.

� Management fees up due to increased assets under management, particularly in Allco Commercial REIT and Record Realty.

� Increased property valuations led to strong growth in equity accounted income, particularly in Allco Wholesale Property Fund and Allco Commercial REIT.

Note: Prior to acquisition, Allco held of 20.4% of Rubicon. Rubicon’s contribution since acquisition included $0.5m in Origination, $0.1m in Funds Management Fees and $4.6m in Equity Accounted Income.

REAL ESTATE$m

Half YearDec-07

Half YearDec-06

% chg

Origination 4.9 6.5 (25%)

Asset Sales (0.1) 0.0 n/a

Development Income 0.0 19.1 (100%)

Fund & Asset Management 11.1 3.5 218%

Asset Ownership (0.5) (2.9) 83%

Equity Accounted Income / Dividends 40.2 16.0 151%

Net Revenue (normalised) 55.6 42.3 31%

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200746

Real Estate

Properties managed Geographic diversity

Singapore8%Europe

14%

US46%

Australia13%

Japan19%

Note: Diversity is by number of properties.15 1722

30

54

117

-

20

40

60

80

100

120

Num

ber o

f Pro

perti

es

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07

Properties Under Management

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200747

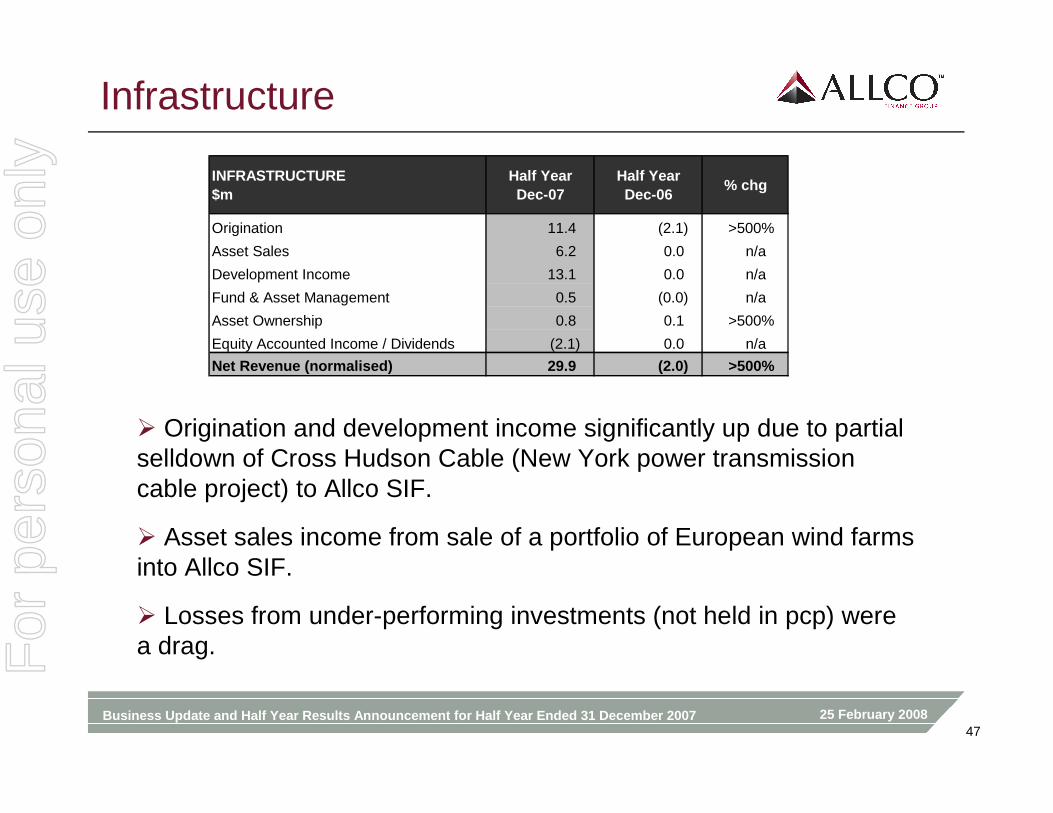

Infrastructure

� Origination and development income significantly up due to partial selldown of Cross Hudson Cable (New York power transmission cable project) to Allco SIF.

� Asset sales income from sale of a portfolio of European wind farms into Allco SIF.

� Losses from under-performing investments (not held in pcp) were a drag.

INFRASTRUCTURE$m

Half YearDec-07

Half YearDec-06

% chg

Origination 11.4 (2.1) >500%

Asset Sales 6.2 0.0 n/a

Development Income 13.1 0.0 n/a

Fund & Asset Management 0.5 (0.0) n/a

Asset Ownership 0.8 0.1 >500%

Equity Accounted Income / Dividends (2.1) 0.0 n/a

Net Revenue (normalised) 29.9 (2.0) >500%

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200748

Infrastructure

� Focus on energy generation and related assets. Core investments in power generation (gas-fired and renewable) and transmission.

� Value creation: carbon footprint and generation constrained markets.

� Gas-fired generation:� Cross Hudson Cable. Development of a transmission cable between New

Jersey and New York in partnership with Cavallo.

� Wind Energy:� Development of 2,000 MW in Tehachapi, California, as well as other US,

European, and Asia Pacific pipeline (1,500MW).

� 50MW of European & US wind projects in construction with commercial operation in FY08.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200749

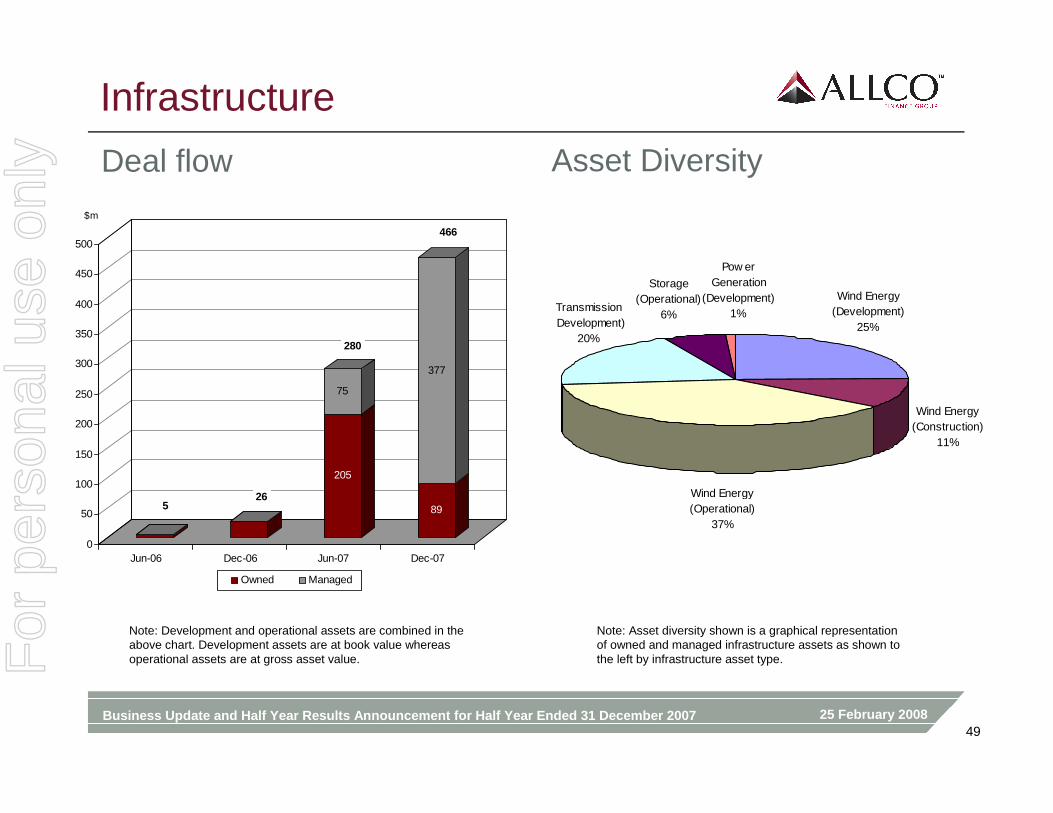

Infrastructure

Deal flow Asset Diversity

Note: Development and operational assets are combined in the above chart. Development assets are at book value whereas operational assets are at gross asset value.

Note: Asset diversity shown is a graphical representation of owned and managed infrastructure assets as shown to the left by infrastructure asset type.

Pow er Generation

(Development)1%

Storage (Operational)

6%

Wind Energy (Construction)

11%

Wind Energy (Operational)

37%

Wind Energy (Development)

25%

Transmission (Development)

20%

205

75

89

377

0

50

100

150

200

250

300

350

400

450

500

$m

Jun-06 Dec-06 Jun-07 Dec-07

Owned Managed

26

280

466

5

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200750

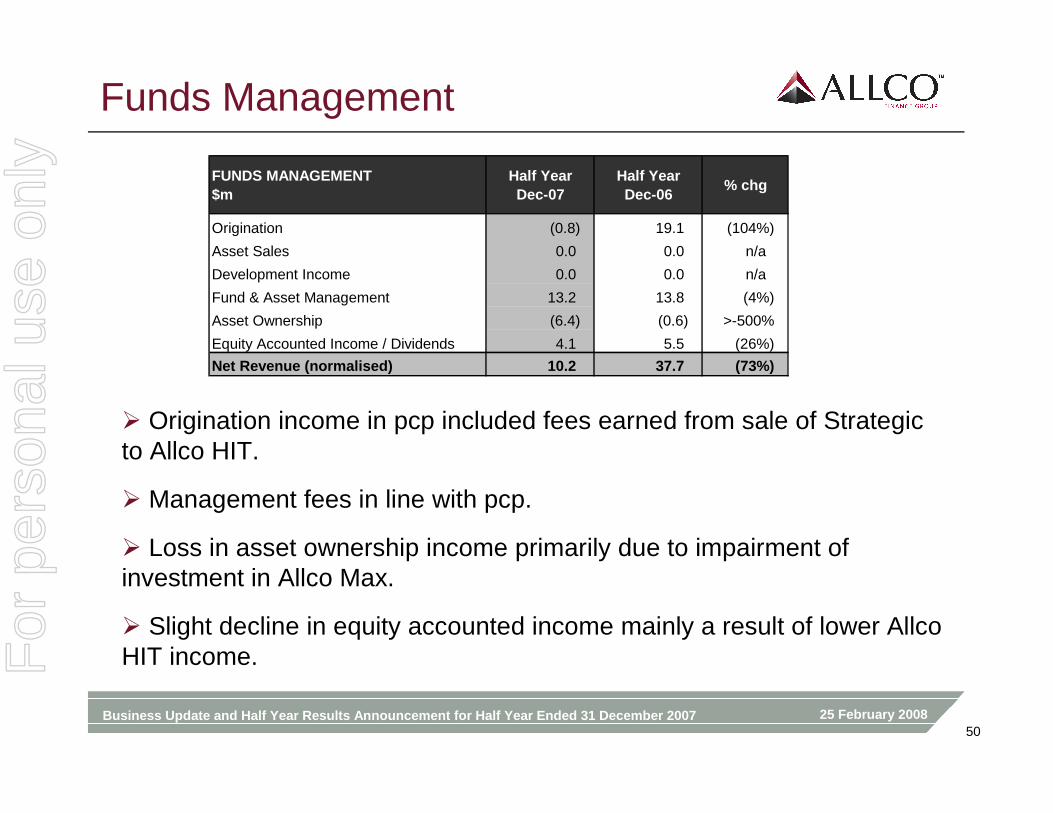

Funds Management

� Origination income in pcp included fees earned from sale of Strategic to Allco HIT.

� Management fees in line with pcp.

� Loss in asset ownership income primarily due to impairment of investment in Allco Max.

� Slight decline in equity accounted income mainly a result of lower Allco HIT income.

FUNDS MANAGEMENT$m

Half YearDec-07

Half YearDec-06

% chg

Origination (0.8) 19.1 (104%)

Asset Sales 0.0 0.0 n/a

Development Income 0.0 0.0 n/a

Fund & Asset Management 13.2 13.8 (4%)

Asset Ownership (6.4) (0.6) >-500%

Equity Accounted Income / Dividends 4.1 5.5 (26%)

Net Revenue (normalised) 10.2 37.7 (73%)

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200751

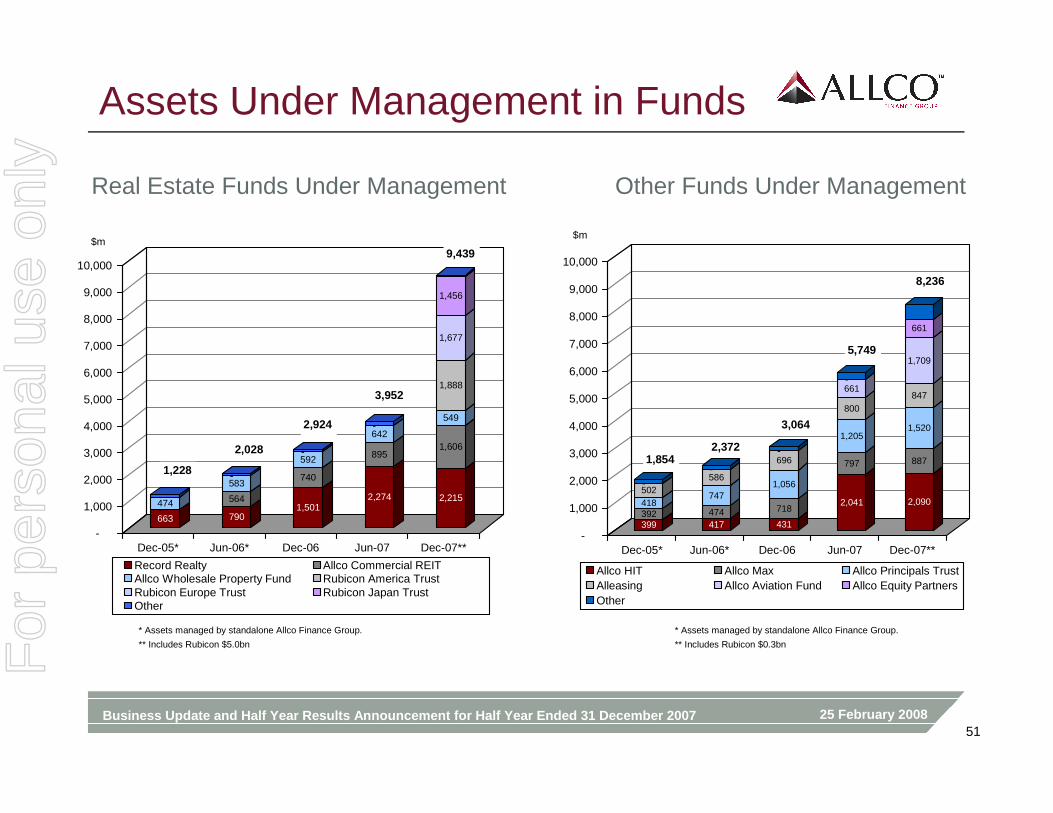

Assets Under Management in Funds

* Assets managed by standalone Allco Finance Group. * Assets managed by standalone Allco Finance Group.

** Includes Rubicon $5.0bn ** Includes Rubicon $0.3bn

663-474---

790

564

583---

1,501

740

592---

2,274

895

642---

2,215

1,606

549

1,888

1,677

1,456

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

$m

Dec-05* Jun-06* Dec-06 Jun-07 Dec-07**

Record Realty Allco Commercial REITAllco Wholesale Property Fund Rubicon America TrustRubicon Europe Trust Rubicon Japan TrustOther

399392418502--

417474

747

586--

431

718

1,056

696--

2,041

797

1,205

800

661-

2,090

887

1,520

847

1,709

661

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

$m

Dec-05* Jun-06* Dec-06 Jun-07 Dec-07**

Allco HIT Allco Max Allco Principals TrustAlleasing Allco Aviation Fund Allco Equity PartnersOther

1,8542,372

3,064

5,749

8,236

1,228

2,028

2,924

3,952

9,439

Real Estate Funds Under Management Other Funds Under Management

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200752

Assets Under Management in Funds

* Assets managed by standalone Allco Finance Group. * Assets managed by standalone Allco Finance Group.

** Includes Rubicon listed $5.0bn and unlisted $0.3bn ** Includes Rubicon real estate $5.0bn and diversified $0.3bn

1,454

1,628

2,245

2,155

3,390

2,598

6,007

3,694

12,480

5,195

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

$m

Dec-05* Jun-06* Dec-06 Jun-07 Dec-07**

Listed Unlisted

1,228

1,436

418--

2,028

1,625

747--

2,924

1,944

1,120--

3,952

3,728

1,285

736-

9,439

3,931

1,812

1,832

661

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

$m

Dec-05* Jun-06* Dec-06 Jun-07 Dec-07**

Real Estate Financial AssetsDiversified Infrastructure & TransportPrivate Equity

3,082

4,400

5,988

9,701

17,675

3,082

4,400

5,988

9,701

17,675

Listed vs. Unlisted Funds Fund by Type

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200753

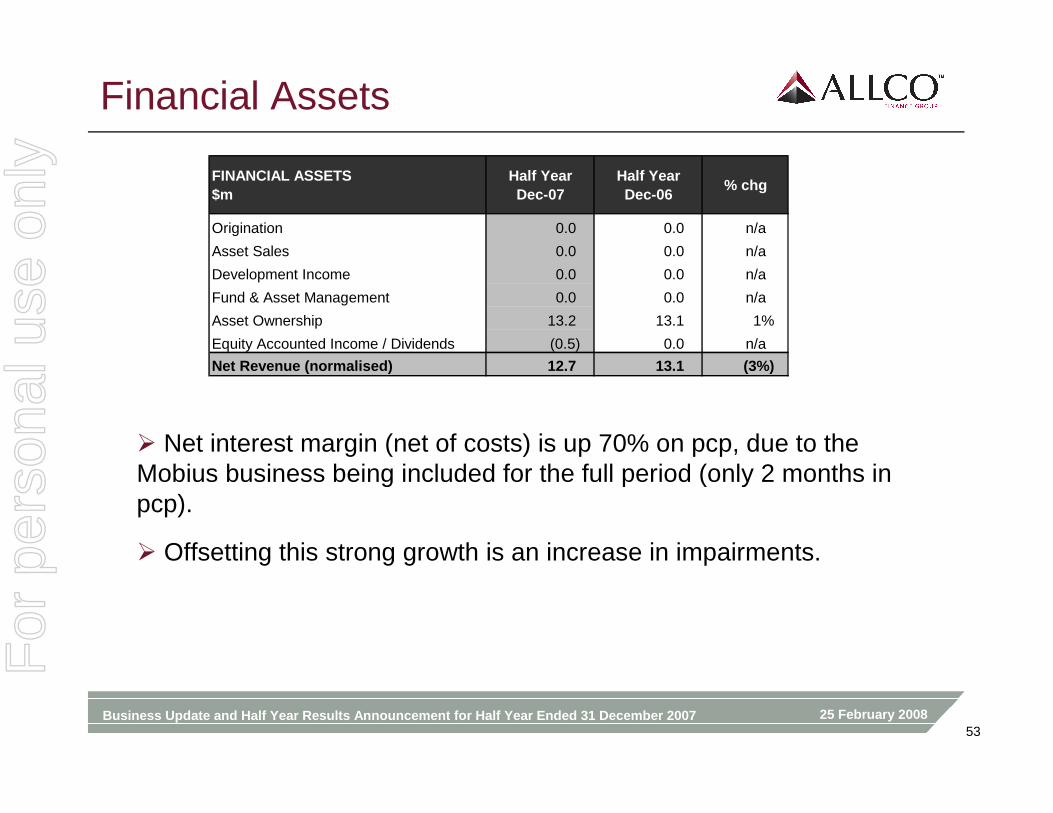

Financial Assets

� Net interest margin (net of costs) is up 70% on pcp, due to theMobius business being included for the full period (only 2 months in pcp).

� Offsetting this strong growth is an increase in impairments.

FINANCIAL ASSETS$m

Half YearDec-07

Half YearDec-06

% chg

Origination 0.0 0.0 n/a

Asset Sales 0.0 0.0 n/a

Development Income 0.0 0.0 n/a

Fund & Asset Management 0.0 0.0 n/a

Asset Ownership 13.2 13.1 1%

Equity Accounted Income / Dividends (0.5) 0.0 n/a

Net Revenue (normalised) 12.7 13.1 (3%)

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200754

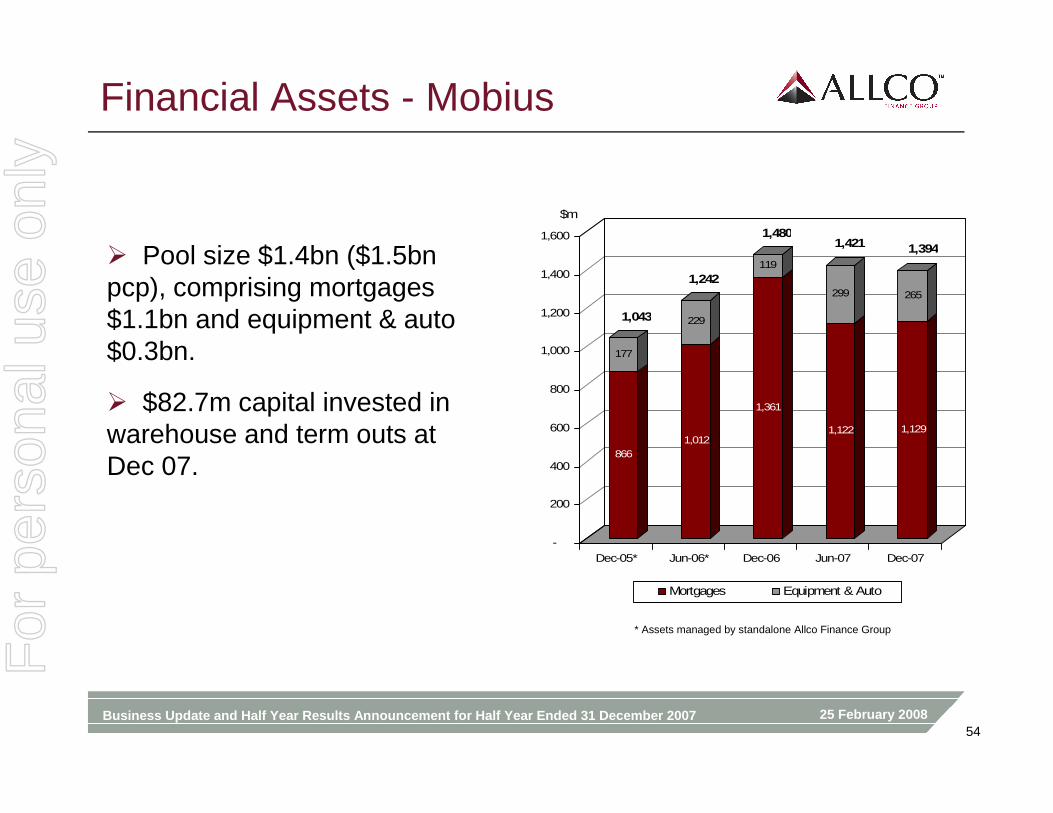

Financial Assets - Mobius

� Pool size $1.4bn ($1.5bn pcp), comprising mortgages $1.1bn and equipment & auto $0.3bn.

� $82.7m capital invested in warehouse and term outs at Dec 07.

* Assets managed by standalone Allco Finance Group

866

177

1,012

229

1,361

119

1,122

299

1,129

265

-

200

400

600

800

1,000

1,200

1,400

1,600

$m

Dec-05* Jun-06* Dec-06 Jun-07 Dec-07

Mortgages Equipment & Auto

1,043

1,242

1,4801,421 1,394

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200755

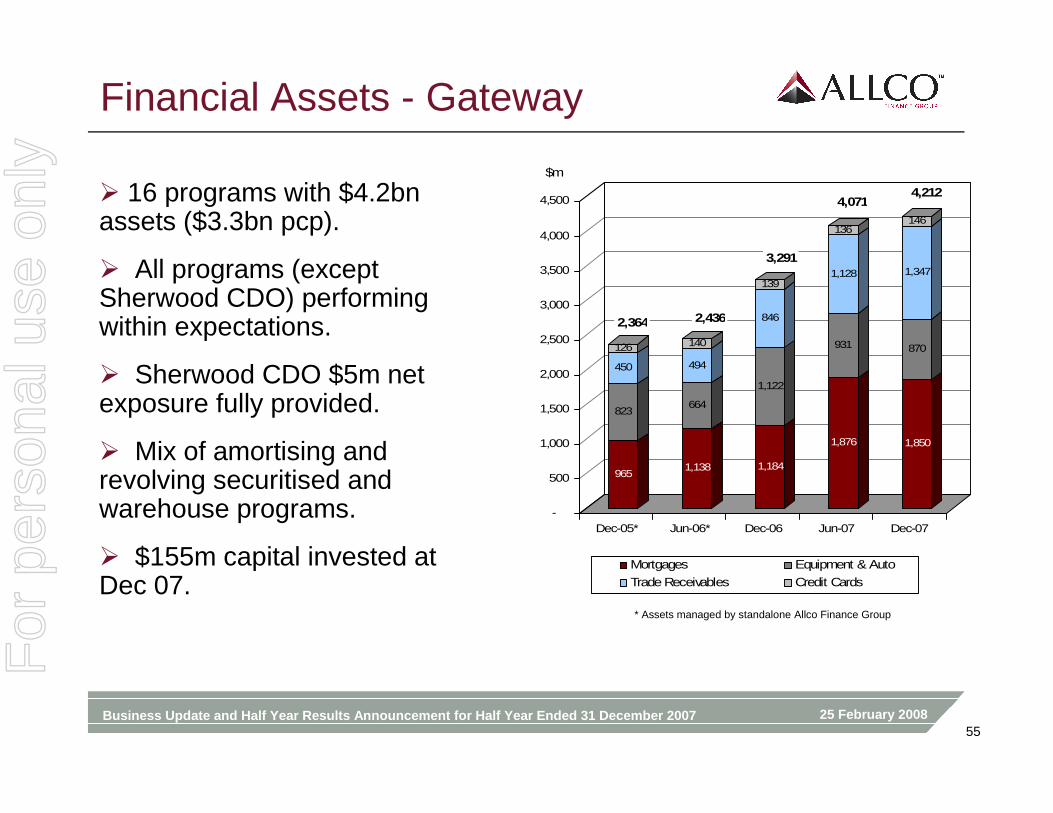

Financial Assets - Gateway

� 16 programs with $4.2bn assets ($3.3bn pcp).

� All programs (except Sherwood CDO) performing within expectations.

� Sherwood CDO $5m net exposure fully provided.

� Mix of amortising and revolving securitised and warehouse programs.

� $155m capital invested at Dec 07.

* Assets managed by standalone Allco Finance Group

965

823

450

126

1,138

664

494

140

1,184

1,122

846

139

1,876

931

1,128

136

1,850

870

1,347

146

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

$m

Dec-05* Jun-06* Dec-06 Jun-07 Dec-07

Mortgages Equipment & Auto

Trade Receivables Credit Cards

2,364 2,436

3,291

4,0714,212

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200756

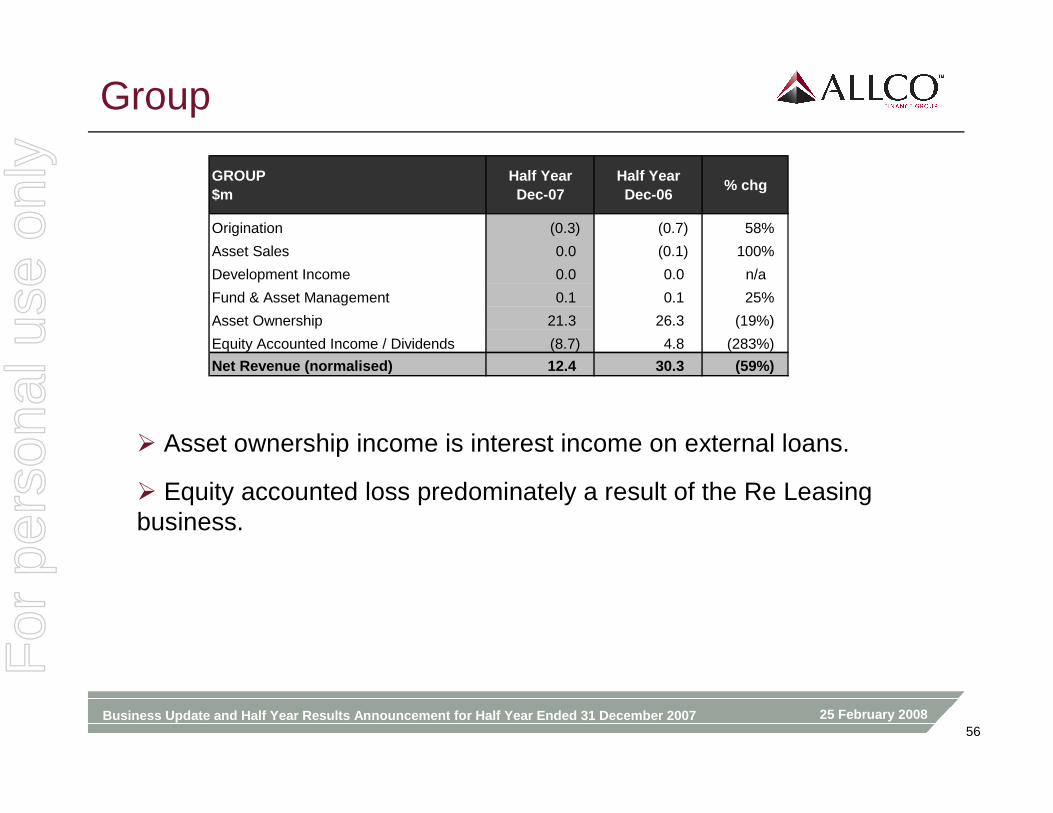

Group

� Asset ownership income is interest income on external loans.

� Equity accounted loss predominately a result of the Re Leasing business.

GROUP$m

Half YearDec-07

Half YearDec-06

% chg

Origination (0.3) (0.7) 58%

Asset Sales 0.0 (0.1) 100%

Development Income 0.0 0.0 n/a

Fund & Asset Management 0.1 0.1 25%

Asset Ownership 21.3 26.3 (19%)

Equity Accounted Income / Dividends (8.7) 4.8 (283%)

Net Revenue (normalised) 12.4 30.3 (59%)

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200757

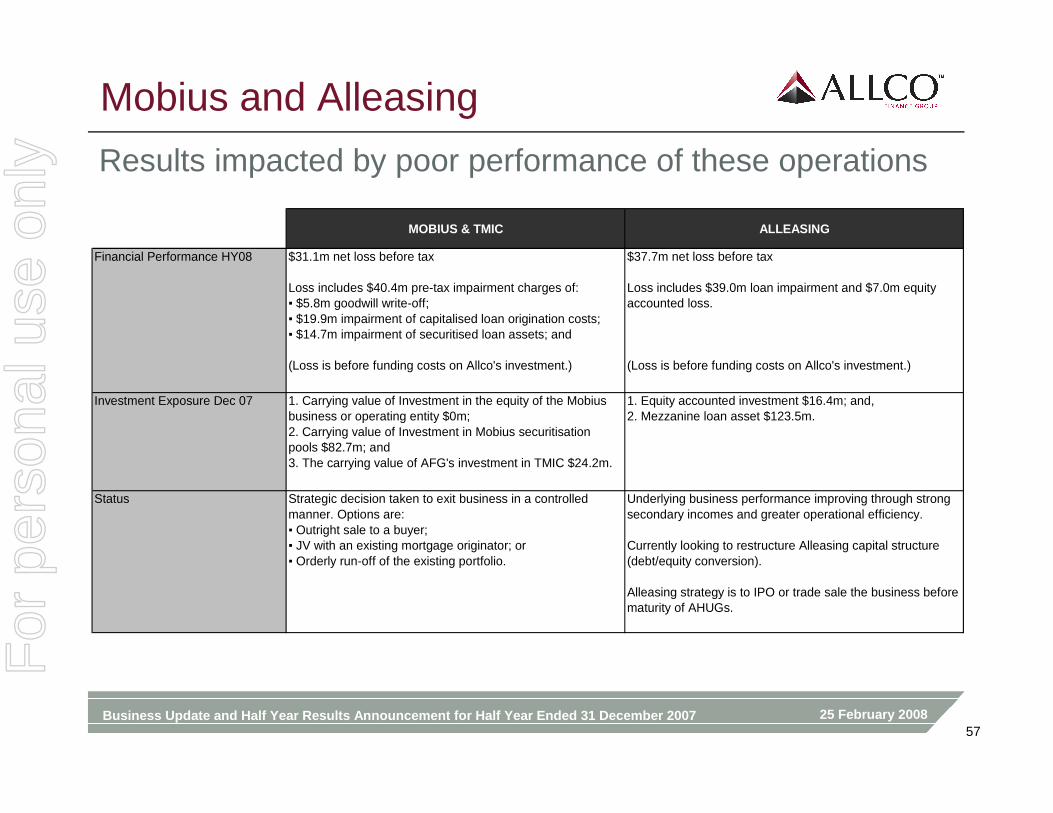

Mobius and Alleasing

Results impacted by poor performance of these operations

MOBIUS & TMIC ALLEASING

Financial Performance HY08 $31.1m net loss before tax

Loss includes $40.4m pre-tax impairment charges of:▪ $5.8m goodwill write-off;▪ $19.9m impairment of capitalised loan origination costs;▪ $14.7m impairment of securitised loan assets; and

(Loss is before funding costs on Allco's investment.)

$37.7m net loss before tax

Loss includes $39.0m loan impairment and $7.0m equity accounted loss.

(Loss is before funding costs on Allco's investment.)

Investment Exposure Dec 07 1. Carrying value of Investment in the equity of the Mobius business or operating entity $0m;2. Carrying value of Investment in Mobius securitisation pools $82.7m; and3. The carrying value of AFG's investment in TMIC $24.2m.

1. Equity accounted investment $16.4m; and,2. Mezzanine loan asset $123.5m.

Status Strategic decision taken to exit business in a controlled manner. Options are:▪ Outright sale to a buyer;▪ JV with an existing mortgage originator; or▪ Orderly run-off of the existing portfolio.

Underlying business performance improving through strong secondary incomes and greater operational efficiency.

Currently looking to restructure Alleasing capital structure (debt/equity conversion).

Alleasing strategy is to IPO or trade sale the business before maturity of AHUGs.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200758

Headcount

281

50

2136

331

63

43

47

423

76

64

58

0

100

200

300

400

500

600

700

FTE

Dec-06 Jun-07 Dec-07

Australia / NZ Europe North America Asia

388

484

621

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200759

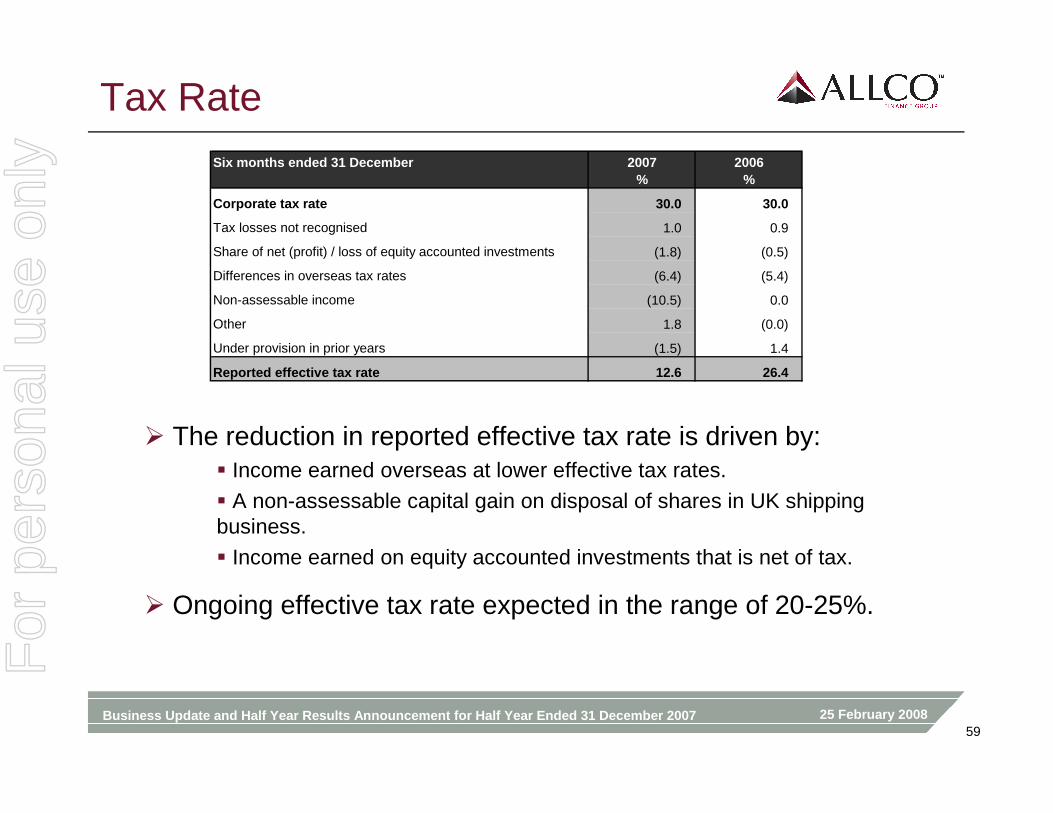

Tax Rate

� The reduction in reported effective tax rate is driven by:� Income earned overseas at lower effective tax rates.

� A non-assessable capital gain on disposal of shares in UK shipping business.

� Income earned on equity accounted investments that is net of tax.

� Ongoing effective tax rate expected in the range of 20-25%.

Six months ended 31 December 2007%

2006%

Corporate tax rate 30.0 30.0

Tax losses not recognised 1.0 0.9

Share of net (profit) / loss of equity accounted investments (1.8) (0.5)

Differences in overseas tax rates (6.4) (5.4)

Non-assessable income (10.5) 0.0

Other 1.8 (0.0)

Under provision in prior years (1.5) 1.4

Reported effective tax rate 12.6 26.4

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200760

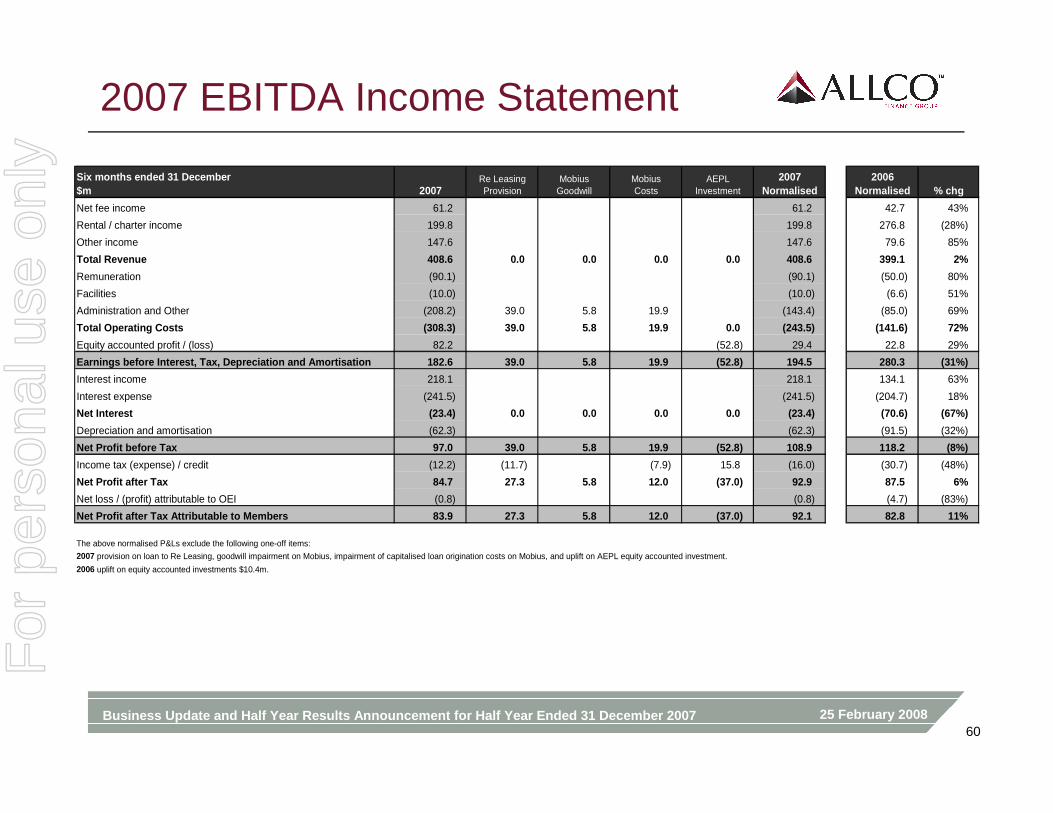

2007 EBITDA Income Statement

Six months ended 31 December$m 2007

Re LeasingProvision

MobiusGoodwill

MobiusCosts

AEPLInvestment

2007 Normalised

2006 Normalised % chg

Net fee income 61.2 61.2 42.7 43%

Rental / charter income 199.8 199.8 276.8 (28%)

Other income 147.6 147.6 79.6 85%

Total Revenue 408.6 0.0 0.0 0.0 0.0 408.6 399.1 2%

Remuneration (90.1) (90.1) (50.0) 80%

Facilities (10.0) (10.0) (6.6) 51%

Administration and Other (208.2) 39.0 5.8 19.9 (143.4) (85.0) 69%

Total Operating Costs (308.3) 39.0 5.8 19.9 0.0 (243.5) (141.6) 72%

Equity accounted profit / (loss) 82.2 (52.8) 29.4 22.8 29%

Earnings before Interest, Tax, Depreciation and Amo rtisation 182.6 39.0 5.8 19.9 (52.8) 194.5 280.3 (31% )

Interest income 218.1 218.1 134.1 63%

Interest expense (241.5) (241.5) (204.7) 18%

Net Interest (23.4) 0.0 0.0 0.0 0.0 (23.4) (70.6) (67%)

Depreciation and amortisation (62.3) (62.3) (91.5) (32%)

Net Profit before Tax 97.0 39.0 5.8 19.9 (52.8) 108.9 118.2 (8%)

Income tax (expense) / credit (12.2) (11.7) (7.9) 15.8 (16.0) (30.7) (48%)

Net Profit after Tax 84.7 27.3 5.8 12.0 (37.0) 92.9 87.5 6%

Net loss / (profit) attributable to OEI (0.8) (0.8) (4.7) (83%)

Net Profit after Tax Attributable to Members 83.9 27 .3 5.8 12.0 (37.0) 92.1 82.8 11%

The above normalised P&Ls exclude the following one-off items:

2007 provision on loan to Re Leasing, goodwill impairment on Mobius, impairment of capitalised loan origination costs on Mobius, and uplift on AEPL equity accounted investment.

2006 uplift on equity accounted investments $10.4m.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200761

Recourse vs. Limited Recourse Debt

� Assets acquired by Allco typically include elements of limited recourse debt – that is, debt which has recourse to the assets it finances. Allco’s exposure is limited to its investment in these vehicles.

� Asset finance debt continues to be available.

� Debt terms are directly factored into asset valuations and bids.

� Refinance gains are not factored into base case economics.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200762

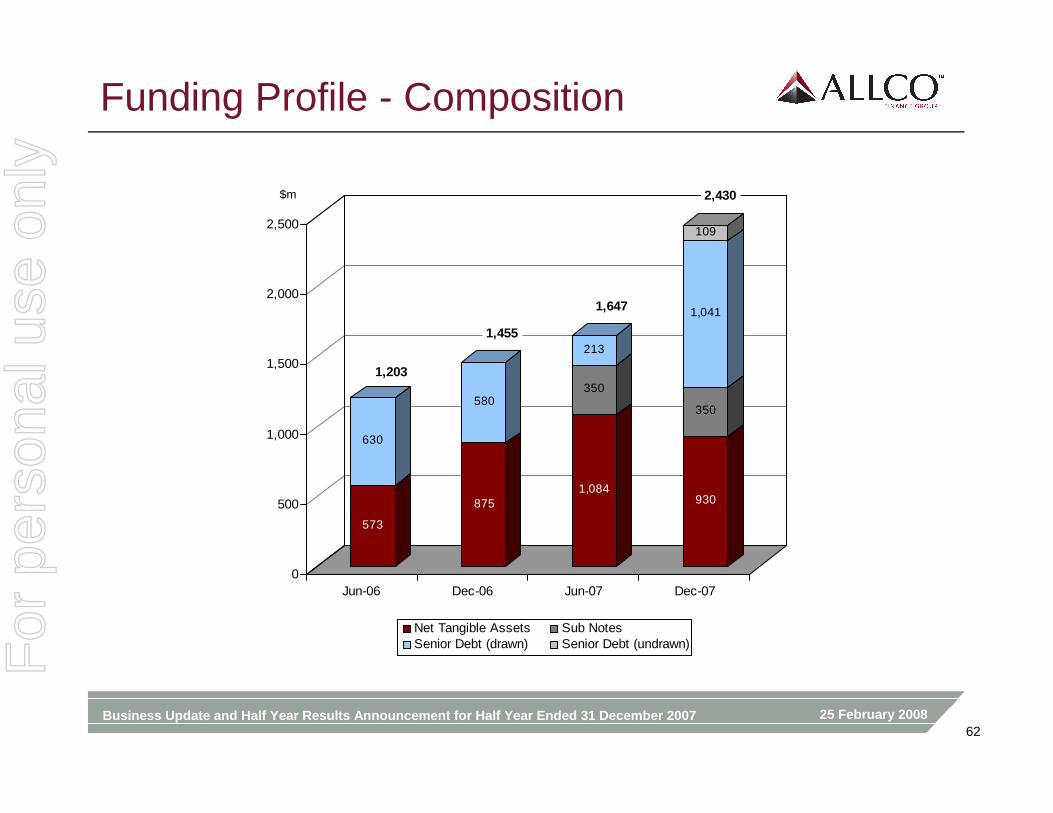

Funding Profile - Composition

573

630

875

580

1,084

350

213

930

350

1,041

109

0

500

1,000

1,500

2,000

2,500

$m

Jun-06 Dec-06 Jun-07 Dec-07

Net Tangible Assets Sub NotesSenior Debt (drawn) Senior Debt (undrawn)

1,203

1,455

1,647

2,430

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200763

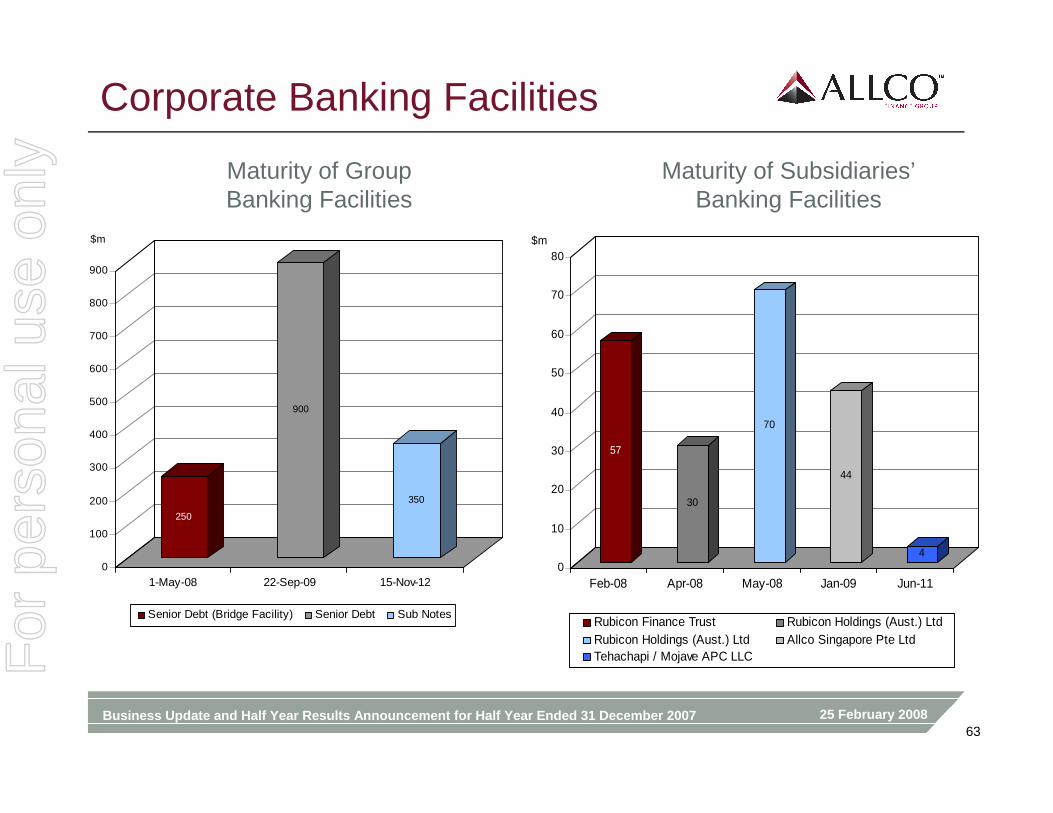

Corporate Banking Facilities

57

30

70

44

40

10

20

30

40

50

60

70

80$m

Feb-08 Apr-08 May-08 Jan-09 Jun-11

Rubicon Finance Trust Rubicon Holdings (Aust.) LtdRubicon Holdings (Aust.) Ltd Allco Singapore Pte LtdTehachapi / Mojave APC LLC

Maturity of Group Banking Facilities

Maturity of Subsidiaries’Banking Facilities

250

900

350

0

100

200

300

400

500

600

700

800

900

$m

1-May-08 22-Sep-09 15-Nov-12

Senior Debt (Bridge Facility) Senior Debt Sub Notes

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200764

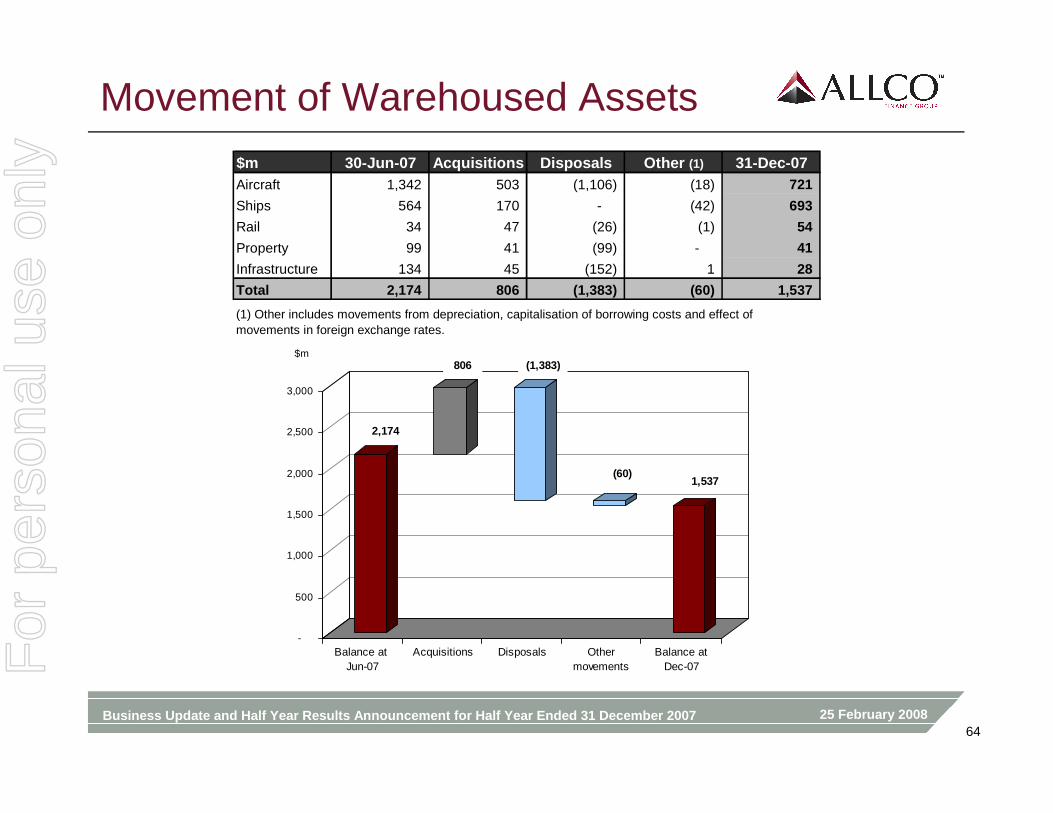

Movement of Warehoused Assets

-

500

1,000

1,500

2,000

2,500

3,000

$m

Balance at Jun-07

Acquisitions Disposals Othermovements

Balance atDec-07

806 (1,383)

(60)1,537

2,174

$m 30-Jun-07 Acquisitions Disposals Other (1) 31-Dec-07Aircraft 1,342 503 (1,106) (18) 721

Ships 564 170 - (42) 693

Rail 34 47 (26) (1) 54

Property 99 41 (99) - 41

Infrastructure 134 45 (152) 1 28

Total 2,174 806 (1,383) (60) 1,537

(1) Other includes movements from depreciation, capitalisation of borrowing costs and effect of movements in foreign exchange rates.

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200765

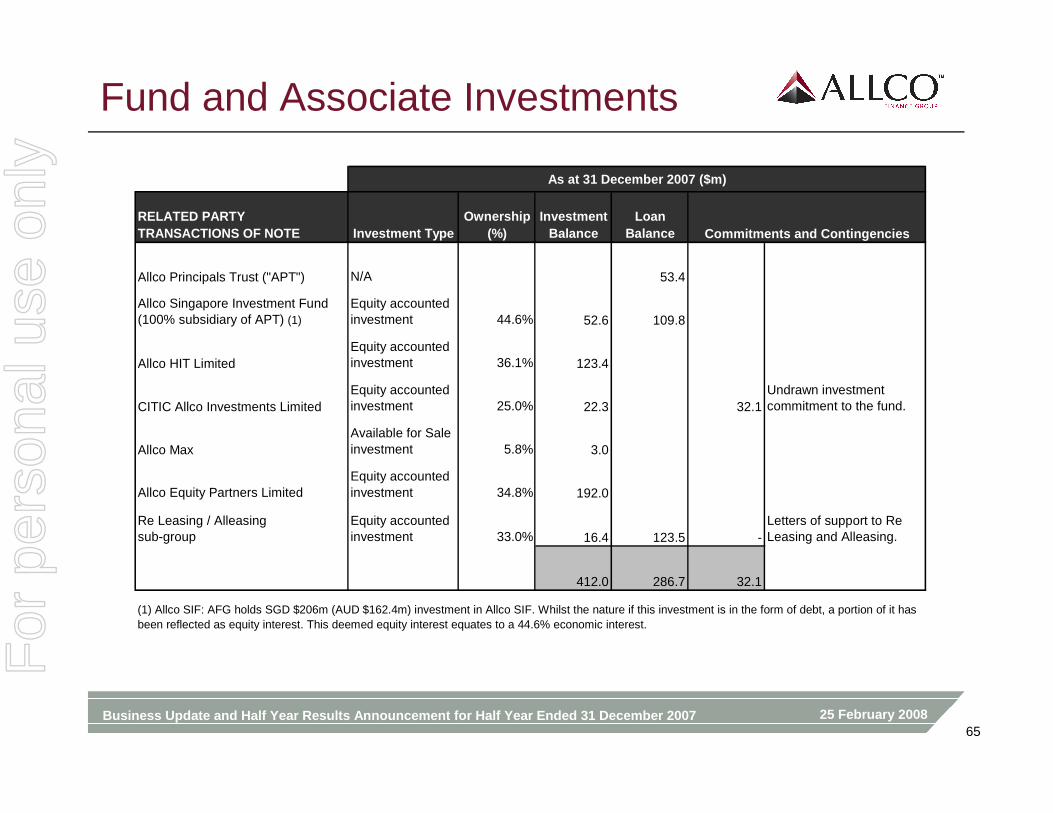

Fund and Associate Investments

As at 31 December 2007 ($m)

RELATED PARTYTRANSACTIONS OF NOTE Investment Type

Ownership (%)

InvestmentBalance

LoanBalance

Allco Principals Trust ("APT") N/A 53.4

Allco Singapore Investment Fund(100% subsidiary of APT) (1)

Equity accounted investment 44.6% 52.6 109.8

Allco HIT LimitedEquity accounted investment 36.1% 123.4

CITIC Allco Investments LimitedEquity accounted investment 25.0% 22.3 32.1

Undrawn investment commitment to the fund.

Allco MaxAvailable for Sale investment 5.8% 3.0

Allco Equity Partners LimitedEquity accounted investment 34.8% 192.0

Re Leasing / Alleasingsub-group

Equity accounted investment 33.0% 16.4 123.5 -

Letters of support to Re Leasing and Alleasing.

412.0 286.7 32.1

(1) Allco SIF: AFG holds SGD $206m (AUD $162.4m) investment in Allco SIF. Whilst the nature if this investment is in the form of debt, a portion of it has been reflected as equity interest. This deemed equity interest equates to a 44.6% economic interest.

Commitments and Contingencies

For

per

sona

l use

onl

y

25 February 2008Business Update and Half Year Results Announcement for Half Year Ended 31 December 200766

Important NoticeThe material above is a presentation of general background information about Allco’s activities current at the date of the presentation, 25 February 2008. It is information given in summary form and does not purport to be complete.

This presentation is not an offer or invitation for subscription or purchase of or a recommendation of securities. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice, when deciding if an investment is appropriate.

Information, including forecast financial information, in this presentation should not be considered as a recommendation in relation to holding, purchasing or selling shares, securities or other instruments in Allco. Due care and attention has been used in the preparation of forecast information. However, actual results may vary from forecasts and any variation may be materially positive or negative. Forecasts by their very nature, are subject to uncertainty and contingencies many of which are outside the control of Allco. Past performance is not a reliable indication of future performance.

The information in this presentation remains subject to change without notice. Circumstances may change and the contents of this presentation may become outdated as a result.

For

per

sona

l use

onl

y