Embed Size (px)

DESCRIPTION

Agriculture sector in India contributes 16% of GDP & 10% of export earnings. Agricultural Development in India has led to exports of agricultural products worth US$ 22 Billion by 2014. More statistics here.

Citation preview

1 1

Agriculture

For updated information, please visit www.ibef.org

AUGUST

2012

2 2

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Green Revolution, Rallis India

Opportunities

Useful information

For updated information, please visit www.ibef.org

Agriculture AUGUST

2012

3 3

Agriculture

For updated information, please visit www.ibef.org ADVANTAGE INDIA

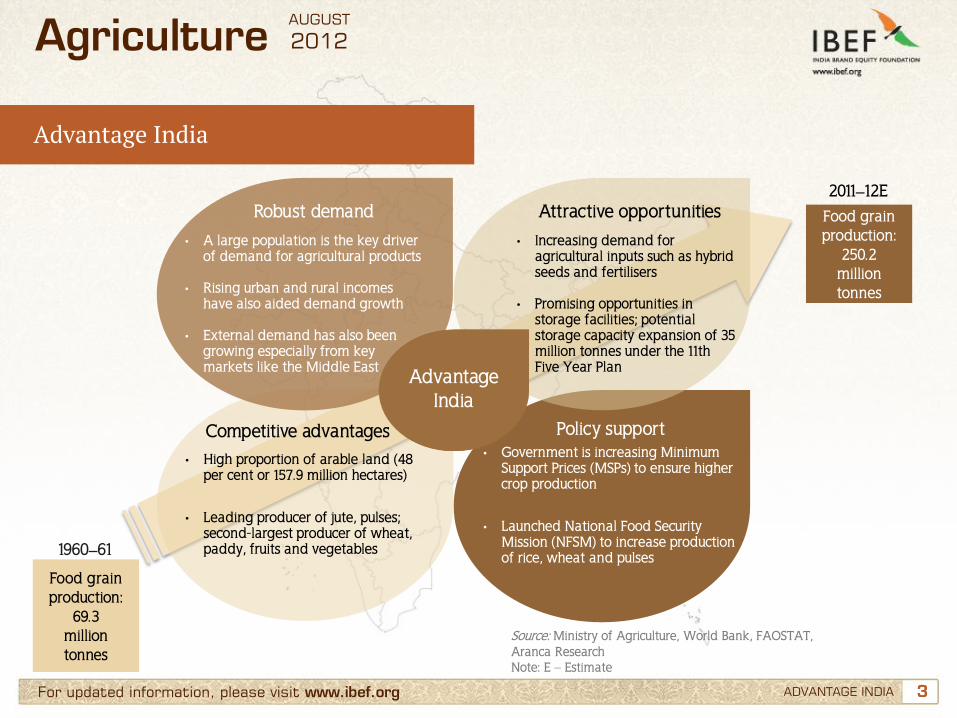

Advantage India

AUGUST

2012

Advantage India

• A large population is the key driver of demand for agricultural products

• Rising urban and rural incomes have also aided demand growth

• External demand has also been growing especially from key markets like the Middle East

• Increasing demand for agricultural inputs such as hybrid seeds and fertilisers

• Promising opportunities in

storage facilities; potential storage capacity expansion of 35 million tonnes under the 11th Five Year Plan

• High proportion of arable land (48 per cent or 157.9 million hectares)

• Leading producer of jute, pulses; second-largest producer of wheat, paddy, fruits and vegetables

• Government is increasing Minimum Support Prices (MSPs) to ensure higher crop production

• Launched National Food Security Mission (NFSM) to increase production of rice, wheat and pulses

Food grain production:

250.2 million tonnes

2011–12E

Food grain production:

69.3 million tonnes

1960–61

Source: Ministry of Agriculture, World Bank, FAOSTAT, Aranca Research Note: E – Estimate

Robust demand Attractive opportunities

Competitive advantages Policy support

4 4

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Green Revolution, Rallis India

Opportunities

Useful information

For updated information, please visit www.ibef.org

Agriculture AUGUST

2012

5 5

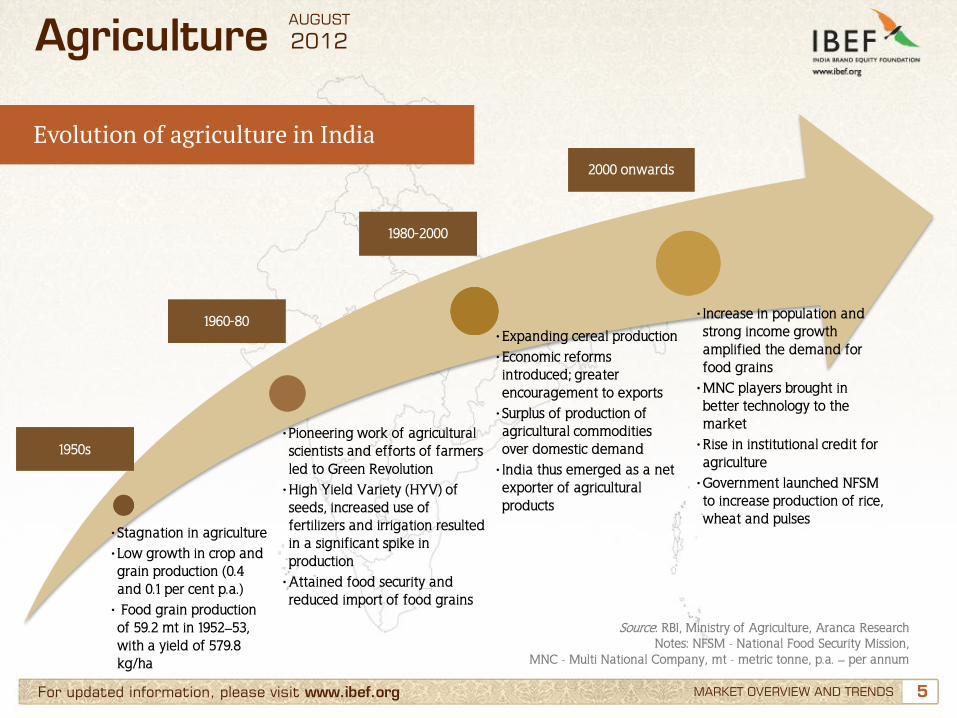

• Stagnation in agriculture • Low growth in crop and grain production (0.4 and 0.1 per cent p.a.)

• Food grain production of 59.2 mt in 1952–53, with a yield of 579.8 kg/ha

• Pioneering work of agricultural scientists and efforts of farmers led to Green Revolution

• High Yield Variety (HYV) of seeds, increased use of fertilizers and irrigation resulted in a significant spike in production

• Attained food security and reduced import of food grains

• Expanding cereal production • Economic reforms introduced; greater encouragement to exports

• Surplus of production of agricultural commodities over domestic demand

• India thus emerged as a net exporter of agricultural products

• Increase in population and strong income growth amplified the demand for food grains

• MNC players brought in better technology to the market

• Rise in institutional credit for agriculture

• Government launched NFSM to increase production of rice, wheat and pulses

For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Evolution of agriculture in India

Source: RBI, Ministry of Agriculture, Aranca Research Notes: NFSM - National Food Security Mission,

MNC - Multi National Company, mt - metric tonne, p.a. – per annum

Agriculture

1950s

1960-80

1980-2000

2000 onwards

AUGUST

2012

6 6 For updated information, please visit www.ibef.org

Growth in agriculture … (1/2)

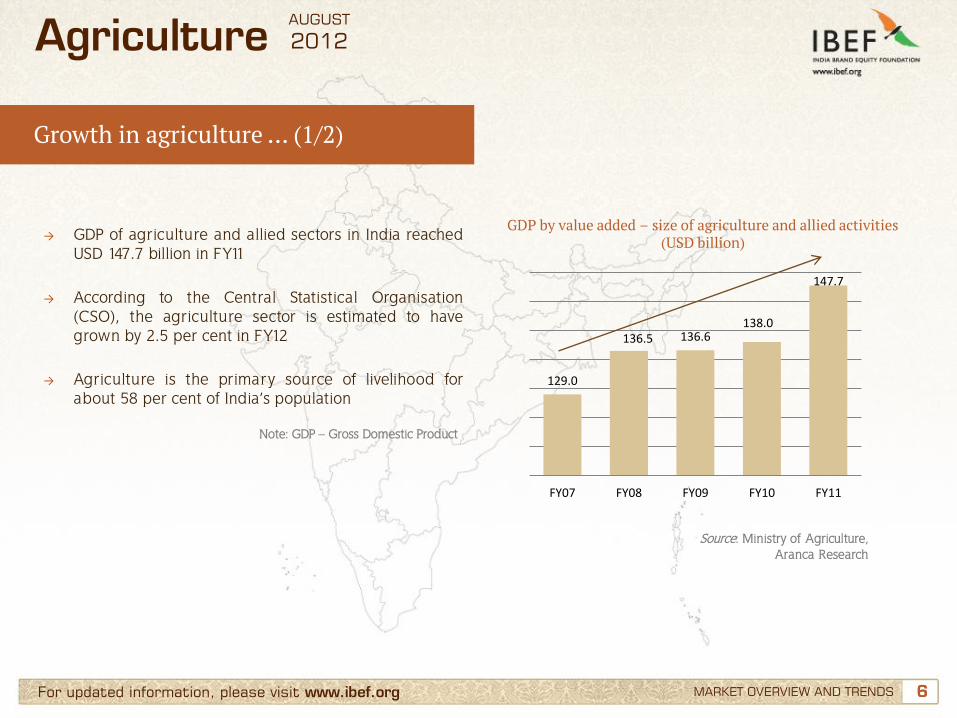

→ GDP of agriculture and allied sectors in India reached USD 147.7 billion in FY11

→ According to the Central Statistical Organisation (CSO), the agriculture sector is estimated to have grown by 2.5 per cent in FY12

→ Agriculture is the primary source of livelihood for

about 58 per cent of India’s population

GDP by value added – size of agriculture and allied activities (USD billion)

Source: Ministry of Agriculture, Aranca Research

Note: GDP – Gross Domestic Product

MARKET OVERVIEW AND TRENDS

Agriculture

129.0

136.5 136.6 138.0

147.7

FY07 FY08 FY09 FY10 FY11

AUGUST

2012

7 7 For updated information, please visit www.ibef.org

Growth in agriculture … (2/2)

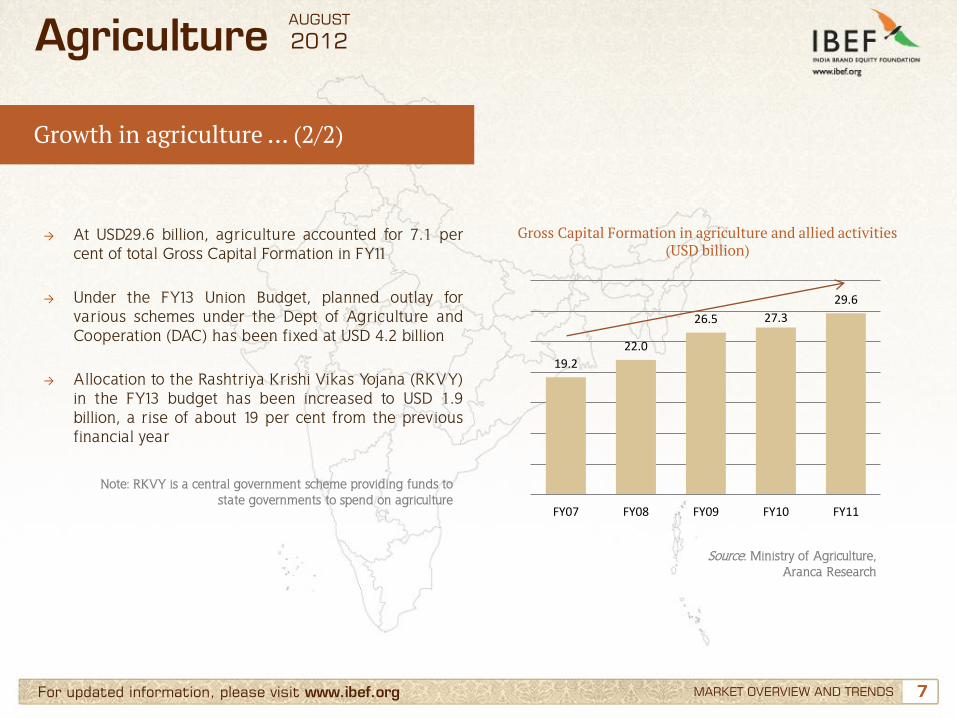

→ At USD29.6 billion, agriculture accounted for 7.1 per cent of total Gross Capital Formation in FY11

→ Under the FY13 Union Budget, planned outlay for various schemes under the Dept of Agriculture and Cooperation (DAC) has been fixed at USD 4.2 billion

→ Allocation to the Rashtriya Krishi Vikas Yojana (RKVY) in the FY13 budget has been increased to USD 1.9 billion, a rise of about 19 per cent from the previous financial year

Gross Capital Formation in agriculture and allied activities (USD billion)

Source: Ministry of Agriculture, Aranca Research

MARKET OVERVIEW AND TRENDS

Agriculture

19.2

22.0

26.5 27.3

29.6

FY07 FY08 FY09 FY10 FY11

Note: RKVY is a central government scheme providing funds to state governments to spend on agriculture

AUGUST

2012

8 8 For updated information, please visit www.ibef.org

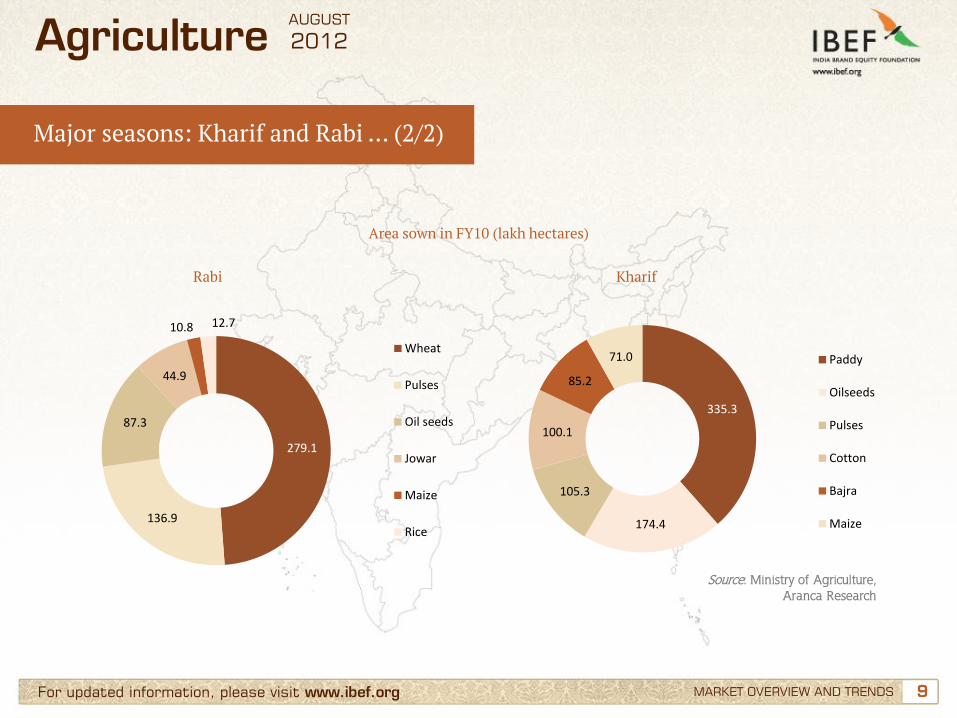

Major seasons: Kharif and Rabi … (1/2)

MARKET OVERVIEW AND TRENDS

Agriculture

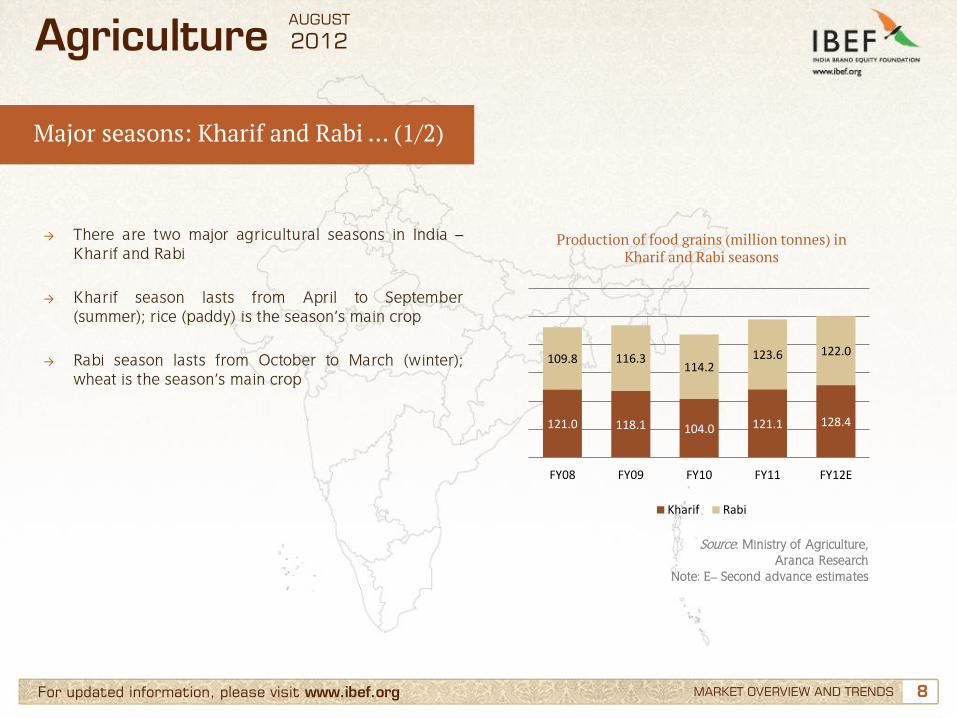

→ There are two major agricultural seasons in India – Kharif and Rabi

→ Kharif season lasts from April to September

(summer); rice (paddy) is the season’s main crop → Rabi season lasts from October to March (winter);

wheat is the season’s main crop

Production of food grains (million tonnes) in Kharif and Rabi seasons

Source: Ministry of Agriculture, Aranca Research

Note: E– Second advance estimates

121.0 118.1 104.0 121.1 128.4

109.8 116.3 114.2

123.6 122.0

FY08 FY09 FY10 FY11 FY12E

Kharif Rabi

AUGUST

2012

9 9 For updated information, please visit www.ibef.org

Major seasons: Kharif and Rabi … (2/2)

Area sown in FY10 (lakh hectares)

Source: Ministry of Agriculture, Aranca Research

MARKET OVERVIEW AND TRENDS

Agriculture

Rabi

279.1

136.9

87.3

44.9

10.8 12.7

Wheat

Pulses

Oil seeds

Jowar

Maize

Rice

Kharif

335.3

174.4

105.3

100.1

85.2

71.0 Paddy

Oilseeds

Pulses

Cotton

Bajra

Maize

AUGUST

2012

10 10 For updated information, please visit www.ibef.org

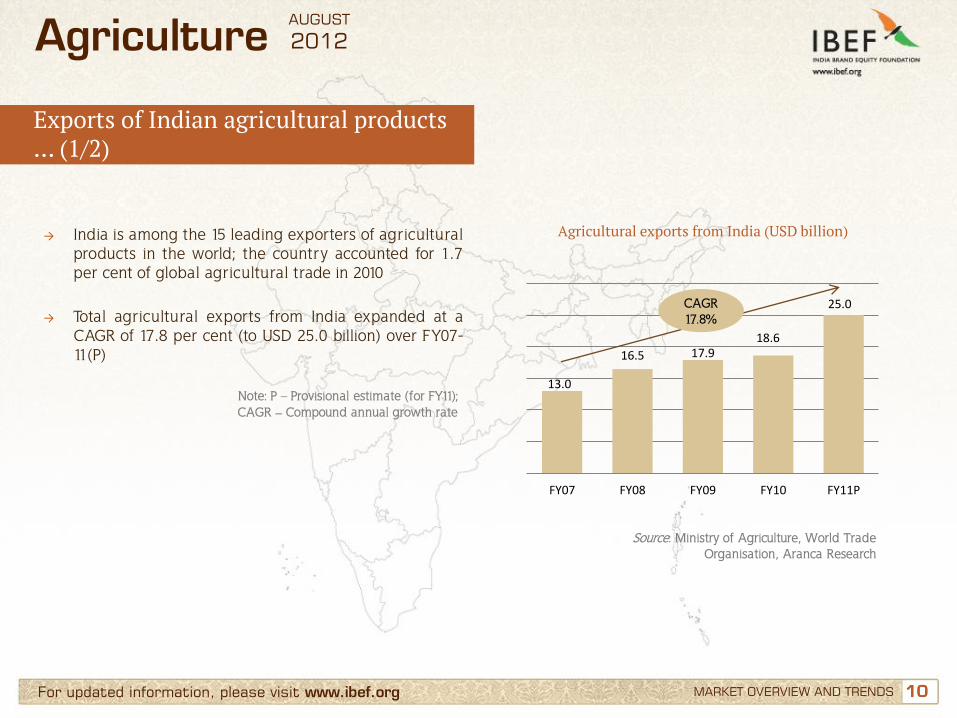

Exports of Indian agricultural products … (1/2)

MARKET OVERVIEW AND TRENDS

Agriculture

→ India is among the 15 leading exporters of agricultural products in the world; the country accounted for 1.7 per cent of global agricultural trade in 2010

→ Total agricultural exports from India expanded at a

CAGR of 17.8 per cent (to USD 25.0 billion) over FY07-11(P)

Agricultural exports from India (USD billion)

Source: Ministry of Agriculture, World Trade Organisation, Aranca Research

Note: P – Provisional estimate (for FY11); CAGR – Compound annual growth rate

13.0

16.5 17.9 18.6

25.0

FY07 FY08 FY09 FY10 FY11P

CAGR 17.8%

AUGUST

2012

11 11 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Agriculture

→ India exported cotton worth USD2.7 billion in FY11(P) accounting for nearly 11% of total agricultural exports

→ Oil meals and rice were the next largest export items

in terms of value; each accounted for about 9% of total agricultural exports in FY11(P)

→ As part of a conscious strategy, the government

monitors the flow of exports of agricultural products depending on domestic demand and availability

Key agricultural and allied sector exports from India in FY11(P) (USD billion)

Source: Ministry of Agriculture, Aranca Research

*includes meat preparations; **includes products made from paper/ wood

Exports of Indian agricultural products … (2/2)

Note: P – Provisional Estimate

2.7

2.3 2.3

1.8

1.6 1.6

0.7 0.7 0.5 0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

AUGUST

2012

12

Karnataka - largest producer of maize 3.01 million tonnes

West Bengal - largest producer of rice

14.34 million tonnes

Uttar Pradesh - largest producer of wheat

14.34 million tonnes

Gujarat - largest producer of cotton 7.99 million bales

Madhya Pradesh - largest producer of pulses 4.30 million tonnes

Punjab and Haryana were the key states of green revolution and

continue to be large producers of food grains

Assam is India’s largest producer of tea

Source: Department of Agriculture & Cooperation; Note: All figures as of 2009-10

Agriculture

Key agricultural states and their contributions

AUGUST

2012

13 13

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Green Revolution, Rallis India

Opportunities

Useful information

For updated information, please visit www.ibef.org

Agriculture AUGUST

2012

14 14 For updated information, please visit www.ibef.org GROWTH DRIVERS

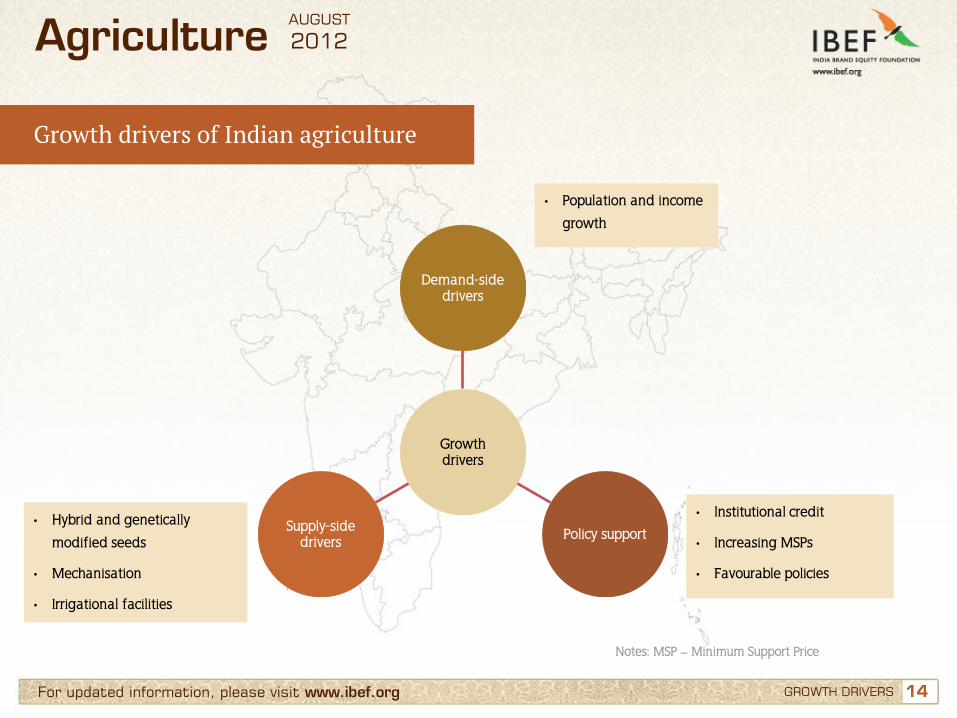

Growth drivers of Indian agriculture

Agriculture

Growth drivers

Demand-side drivers

Policy support Supply-side drivers

• Hybrid and genetically

modified seeds

• Mechanisation

• Irrigational facilities

• Institutional credit

• Increasing MSPs

• Favourable policies

• Population and income

growth

Notes: MSP – Minimum Support Price

AUGUST

2012

15 15 For updated information, please visit www.ibef.org

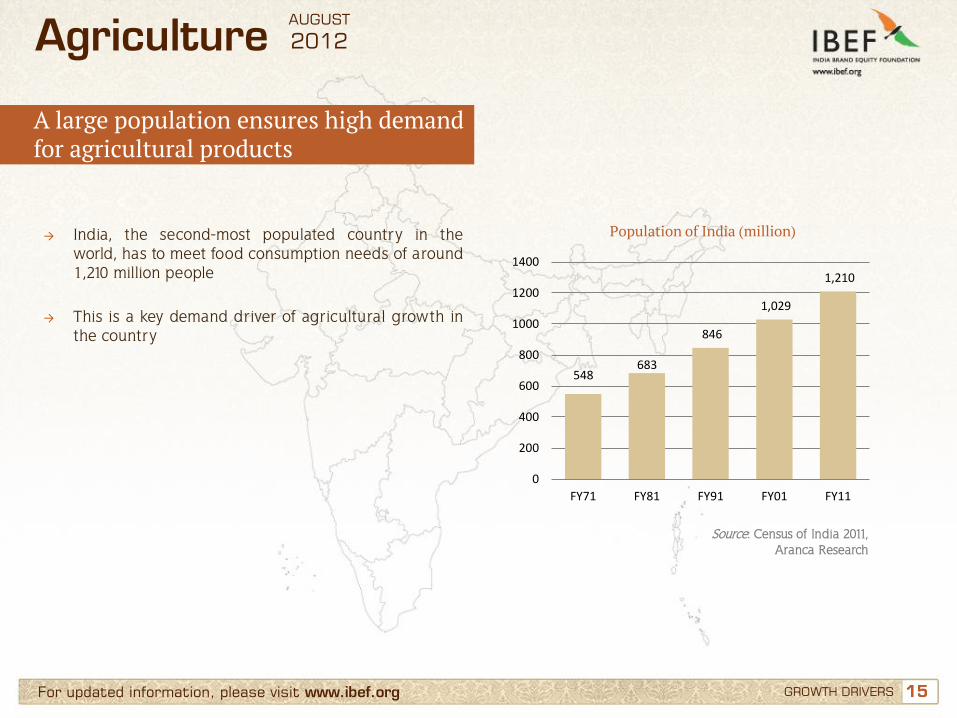

A large population ensures high demand for agricultural products

GROWTH DRIVERS

Agriculture

→ India, the second-most populated country in the world, has to meet food consumption needs of around 1,210 million people

→ This is a key demand driver of agricultural growth in

the country

Population of India (million)

Source: Census of India 2011, Aranca Research

548 683

846

1,029

1,210

0

200

400

600

800

1000

1200

1400

FY71 FY81 FY91 FY01 FY11

AUGUST

2012

16 16 For updated information, please visit www.ibef.org

Income growth also driving agriculture demand

GROWTH DRIVERS

Agriculture

→ Domestic demand for agricultural and allied products has not only been rising due to rising population, but also as a result of greater consumption by a wealthier population

→ Over FY07-11, India’s per capita income increased at a CAGR of 14.3 per cent (to USD1,111)

→ Indian agriculture has also benefitted from rising external demand and the sector’s wider participation in the global economy

Per capita income at factor cost (USD)

Source: Central Statistical Organisation, Aranca Research

650

746

849

961

1,111

0

200

400

600

800

1,000

1,200

FY07 FY08 FY09 FY10 FY11

CAGR 14.3%

AUGUST

2012

17 17 For updated information, please visit www.ibef.org

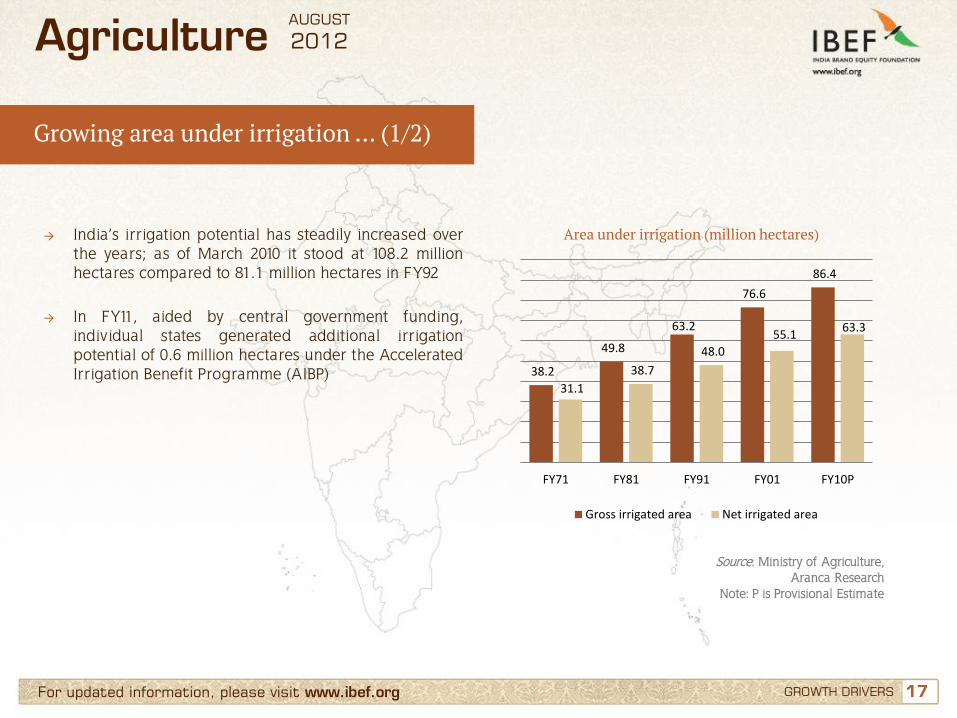

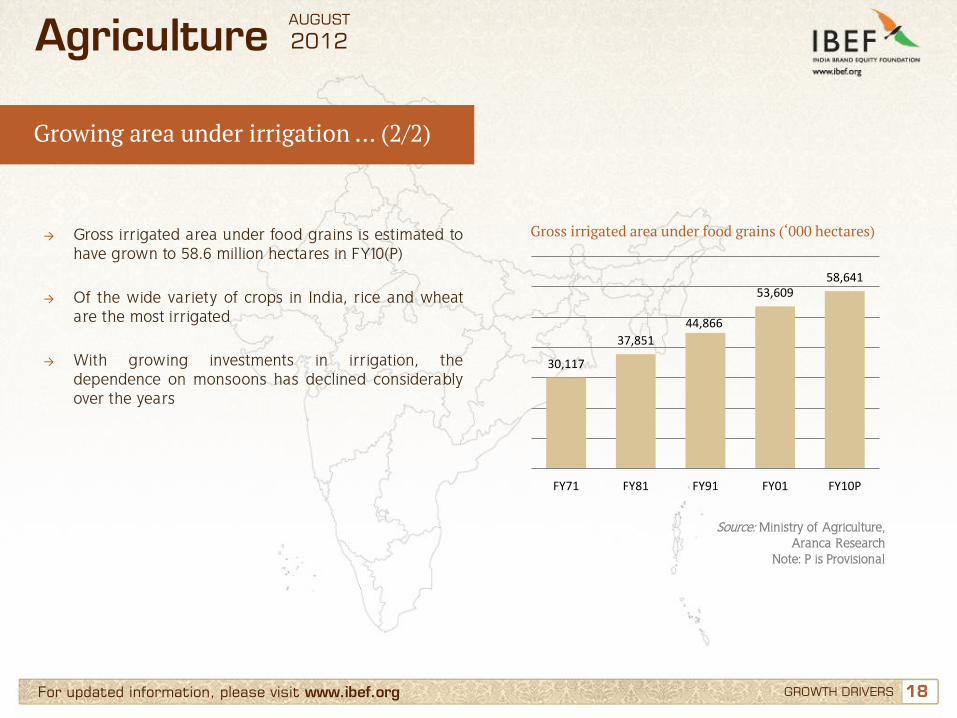

Growing area under irrigation … (1/2)

GROWTH DRIVERS

Agriculture

→ India’s irrigation potential has steadily increased over the years; as of March 2010 it stood at 108.2 million hectares compared to 81.1 million hectares in FY92

→ In FY11, aided by central government funding, individual states generated additional irrigation potential of 0.6 million hectares under the Accelerated Irrigation Benefit Programme (AIBP)

Area under irrigation (million hectares)

Source: Ministry of Agriculture, Aranca Research

Note: P is Provisional Estimate

38.2

49.8

63.2

76.6

86.4

31.1

38.7

48.0

55.1 63.3

FY71 FY81 FY91 FY01 FY10P

Gross irrigated area Net irrigated area

AUGUST

2012

18 18 For updated information, please visit www.ibef.org

Growing area under irrigation … (2/2)

GROWTH DRIVERS

Agriculture

→ Gross irrigated area under food grains is estimated to have grown to 58.6 million hectares in FY10(P)

→ Of the wide variety of crops in India, rice and wheat

are the most irrigated → With growing investments in irrigation, the

dependence on monsoons has declined considerably over the years

Gross irrigated area under food grains (‘000 hectares)

Source: Ministry of Agriculture, Aranca Research

Note: P is Provisional

30,117

37,851

44,866

53,609 58,641

FY71 FY81 FY91 FY01 FY10P

AUGUST

2012

19 19 For updated information, please visit www.ibef.org

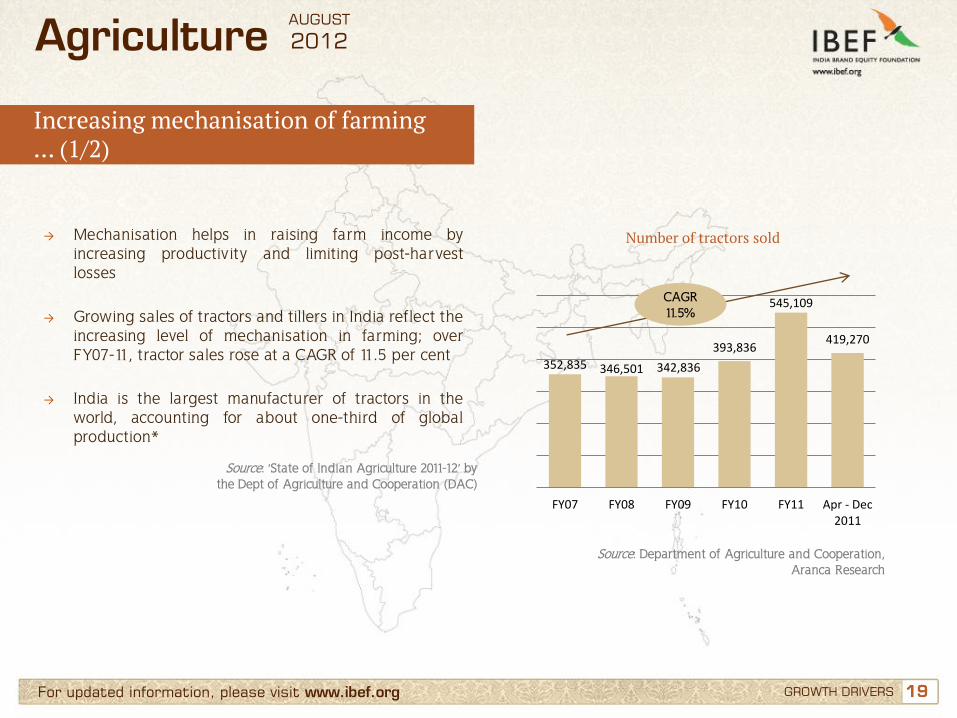

Increasing mechanisation of farming … (1/2)

GROWTH DRIVERS

Agriculture

→ Mechanisation helps in raising farm income by increasing productivity and limiting post-harvest losses

→ Growing sales of tractors and tillers in India reflect the

increasing level of mechanisation in farming; over FY07-11, tractor sales rose at a CAGR of 11.5 per cent

→ India is the largest manufacturer of tractors in the

world, accounting for about one-third of global production*

Number of tractors sold

Source: Department of Agriculture and Cooperation, Aranca Research

352,835 346,501 342,836

393,836

545,109

419,270

FY07 FY08 FY09 FY10 FY11 Apr - Dec2011

CAGR 11.5%

Source: ‘State of Indian Agriculture 2011-12’ by the Dept of Agriculture and Cooperation (DAC)

AUGUST

2012

20 20 For updated information, please visit www.ibef.org GROWTH DRIVERS

Agriculture

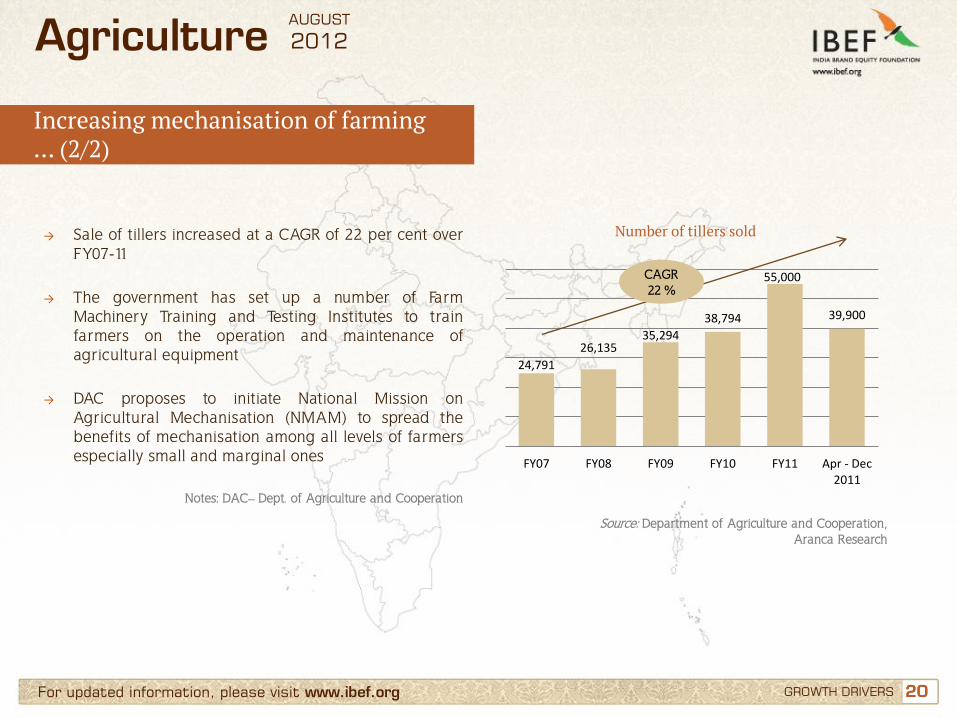

→ Sale of tillers increased at a CAGR of 22 per cent over FY07-11

→ The government has set up a number of Farm

Machinery Training and Testing Institutes to train farmers on the operation and maintenance of agricultural equipment

→ DAC proposes to initiate National Mission on

Agricultural Mechanisation (NMAM) to spread the benefits of mechanisation among all levels of farmers especially small and marginal ones

Number of tillers sold

Source: Department of Agriculture and Cooperation, Aranca Research

Increasing mechanisation of farming … (2/2)

Notes: DAC– Dept. of Agriculture and Cooperation

24,791

26,135 35,294

38,794

55,000

39,900

FY07 FY08 FY09 FY10 FY11 Apr - Dec2011

CAGR 22 %

AUGUST

2012

21 21 For updated information, please visit www.ibef.org

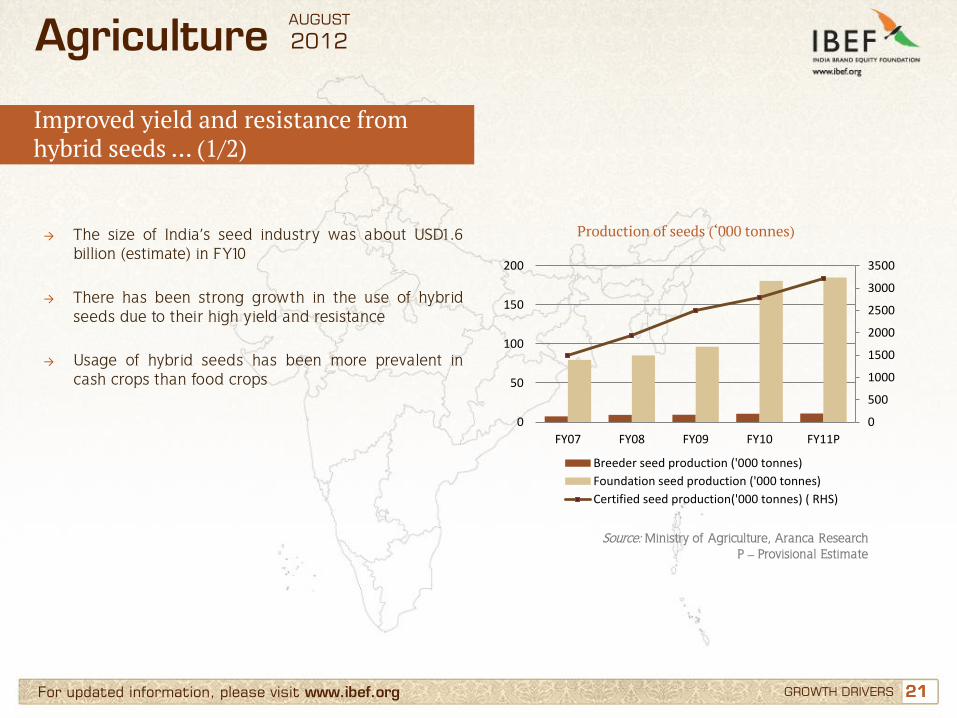

Improved yield and resistance from hybrid seeds … (1/2)

GROWTH DRIVERS

Agriculture

→ The size of India’s seed industry was about USD1.6 billion (estimate) in FY10

→ There has been strong growth in the use of hybrid

seeds due to their high yield and resistance → Usage of hybrid seeds has been more prevalent in

cash crops than food crops

Production of seeds (‘000 tonnes)

Source: Ministry of Agriculture, Aranca Research P – Provisional Estimate

0

500

1000

1500

2000

2500

3000

3500

0

50

100

150

200

FY07 FY08 FY09 FY10 FY11P

Breeder seed production ('000 tonnes)

Foundation seed production ('000 tonnes)

Certified seed production('000 tonnes) ( RHS)

AUGUST

2012

22 22 For updated information, please visit www.ibef.org

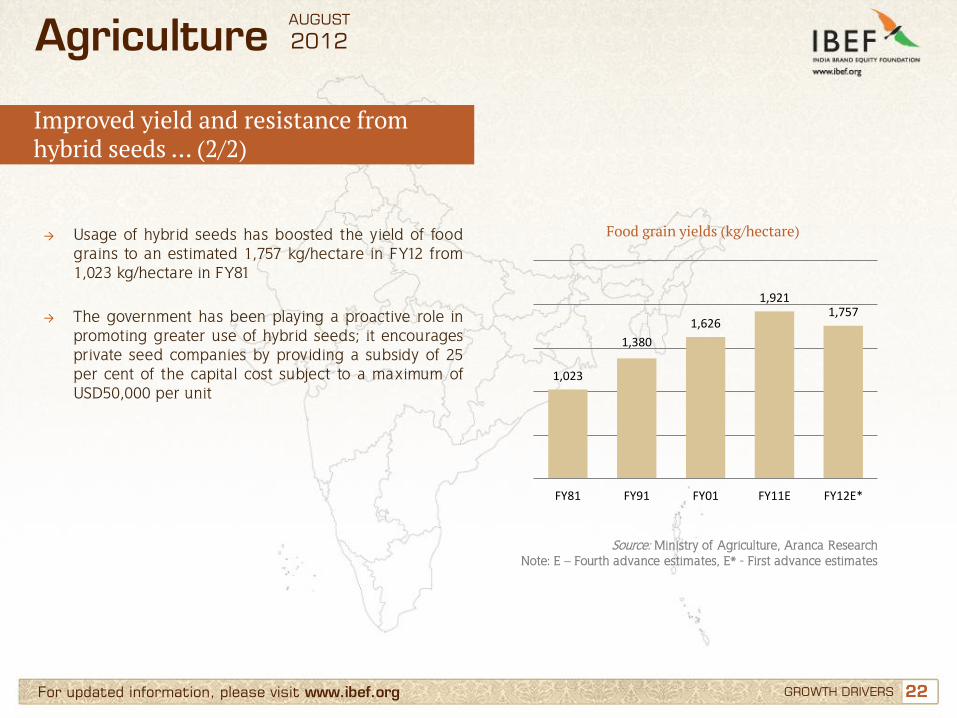

Improved yield and resistance from hybrid seeds … (2/2)

GROWTH DRIVERS

Agriculture

→ Usage of hybrid seeds has boosted the yield of food grains to an estimated 1,757 kg/hectare in FY12 from 1,023 kg/hectare in FY81

→ The government has been playing a proactive role in

promoting greater use of hybrid seeds; it encourages private seed companies by providing a subsidy of 25 per cent of the capital cost subject to a maximum of USD50,000 per unit

Food grain yields (kg/hectare)

Source: Ministry of Agriculture, Aranca Research Note: E – Fourth advance estimates, E* - First advance estimates

1,023

1,380

1,626

1,921 1,757

FY81 FY91 FY01 FY11E FY12E*

AUGUST

2012

23 23 For updated information, please visit www.ibef.org

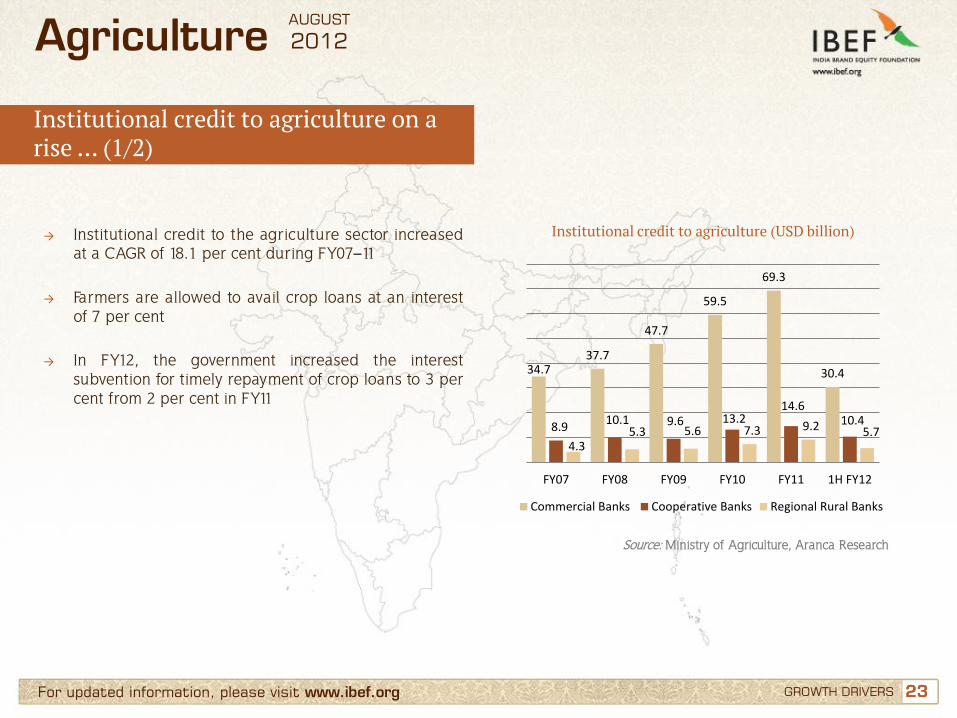

Institutional credit to agriculture on a rise … (1/2)

GROWTH DRIVERS

Agriculture

→ Institutional credit to the agriculture sector increased at a CAGR of 18.1 per cent during FY07–11

→ Farmers are allowed to avail crop loans at an interest of 7 per cent

→ In FY12, the government increased the interest subvention for timely repayment of crop loans to 3 per cent from 2 per cent in FY11

Institutional credit to agriculture (USD billion)

Source: Ministry of Agriculture, Aranca Research

34.7 37.7

47.7

59.5

69.3

30.4

8.9 10.1 9.6 13.2

14.6 10.4

4.3 5.3 5.6 7.3 9.2 5.7

FY07 FY08 FY09 FY10 FY11 1H FY12

Commercial Banks Cooperative Banks Regional Rural Banks

AUGUST

2012

24 24 For updated information, please visit www.ibef.org GROWTH DRIVERS

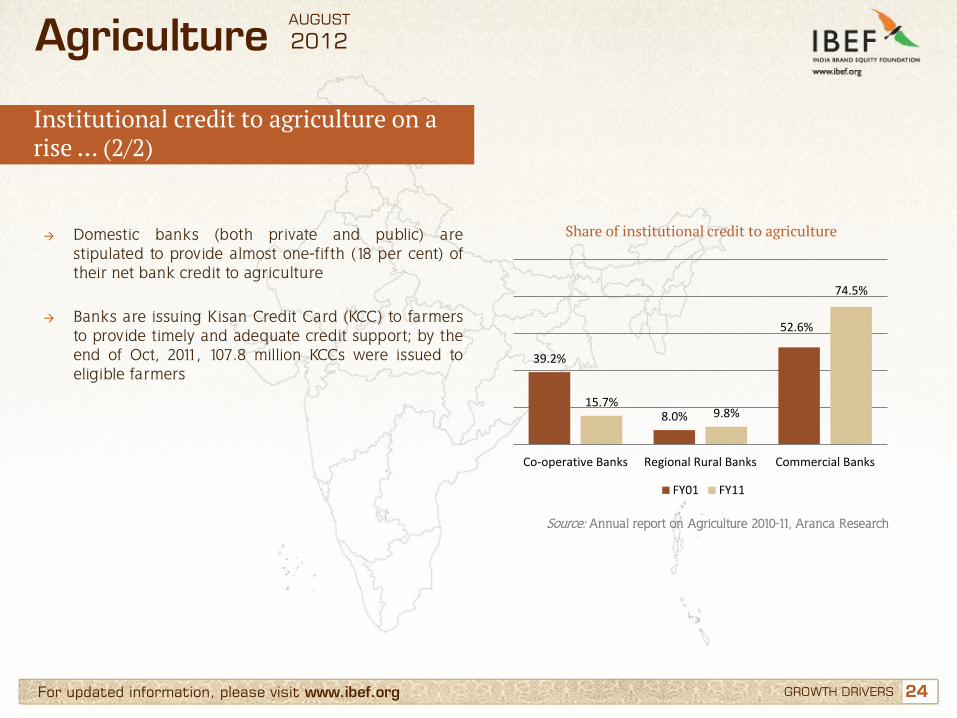

Agriculture

→ Domestic banks (both private and public) are stipulated to provide almost one-fifth (18 per cent) of their net bank credit to agriculture

→ Banks are issuing Kisan Credit Card (KCC) to farmers

to provide timely and adequate credit support; by the end of Oct, 2011, 107.8 million KCCs were issued to eligible farmers

Share of institutional credit to agriculture

Source: Annual report on Agriculture 2010-11, Aranca Research

Institutional credit to agriculture on a rise … (2/2)

39.2%

8.0%

52.6%

15.7% 9.8%

74.5%

Co-operative Banks Regional Rural Banks Commercial Banks

FY01 FY11

AUGUST

2012

25 25 For updated information, please visit www.ibef.org

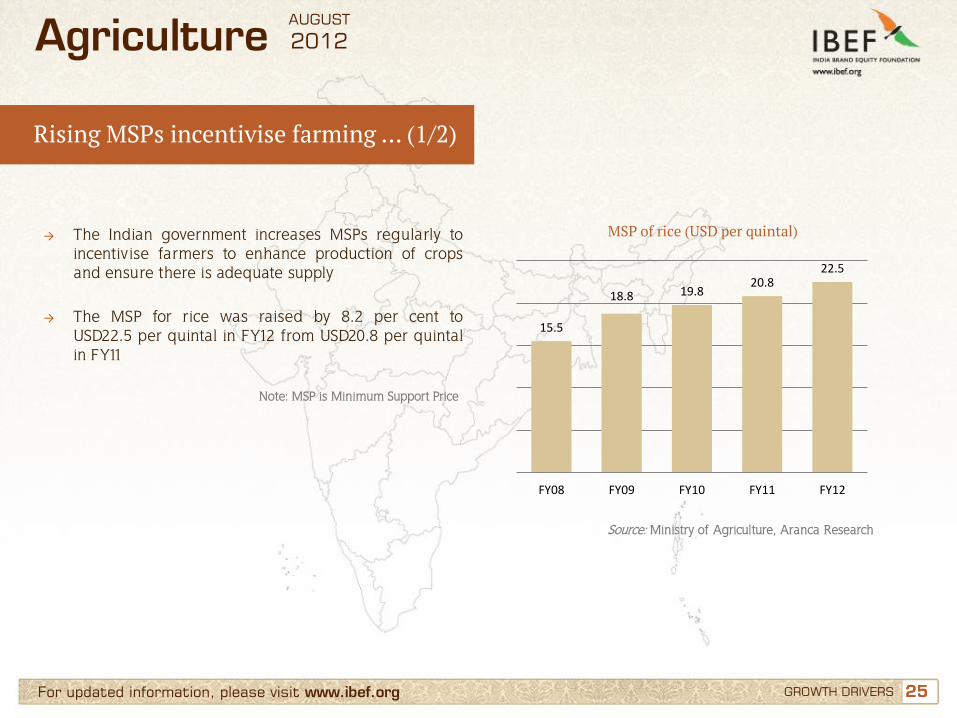

Rising MSPs incentivise farming … (1/2)

GROWTH DRIVERS

Agriculture

→ The Indian government increases MSPs regularly to incentivise farmers to enhance production of crops and ensure there is adequate supply

→ The MSP for rice was raised by 8.2 per cent to

USD22.5 per quintal in FY12 from USD20.8 per quintal in FY11

MSP of rice (USD per quintal)

Source: Ministry of Agriculture, Aranca Research

Note: MSP is Minimum Support Price

15.5

18.8 19.8 20.8

22.5

FY08 FY09 FY10 FY11 FY12

AUGUST

2012

26 26 For updated information, please visit www.ibef.org

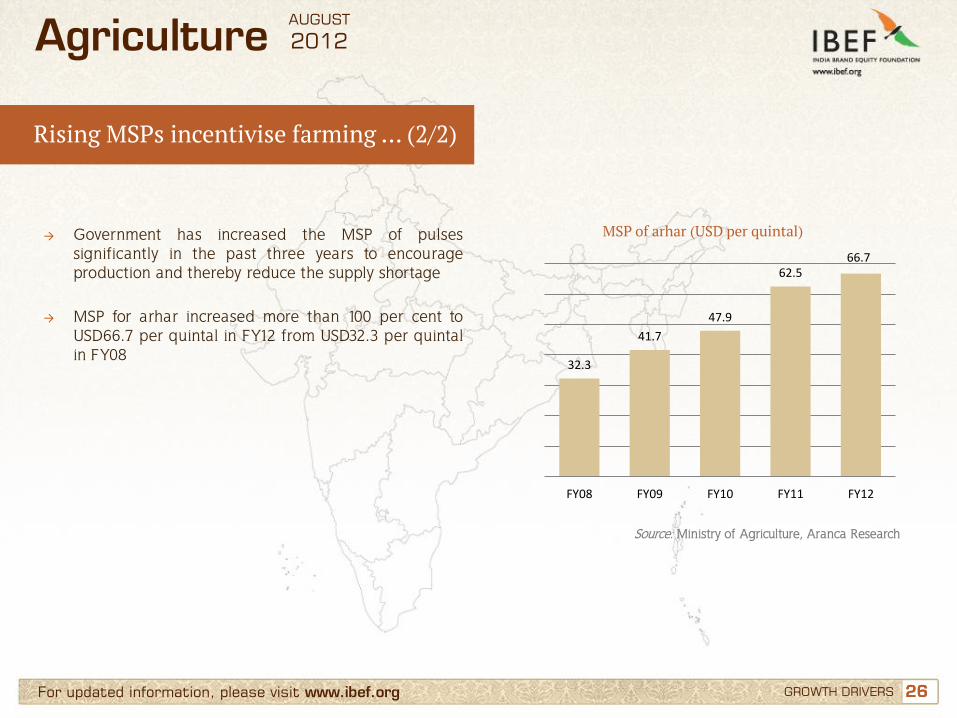

Rising MSPs incentivise farming … (2/2)

GROWTH DRIVERS

Agriculture

→ Government has increased the MSP of pulses significantly in the past three years to encourage production and thereby reduce the supply shortage

→ MSP for arhar increased more than 100 per cent to

USD66.7 per quintal in FY12 from USD32.3 per quintal in FY08

MSP of arhar (USD per quintal)

Source: Ministry of Agriculture, Aranca Research

32.3

41.7

47.9

62.5 66.7

FY08 FY09 FY10 FY11 FY12

AUGUST

2012

27 27 For updated information, please visit www.ibef.org

Favourable policies are supporting the sector growth … (1/2)

GROWTH DRIVERS

Agriculture

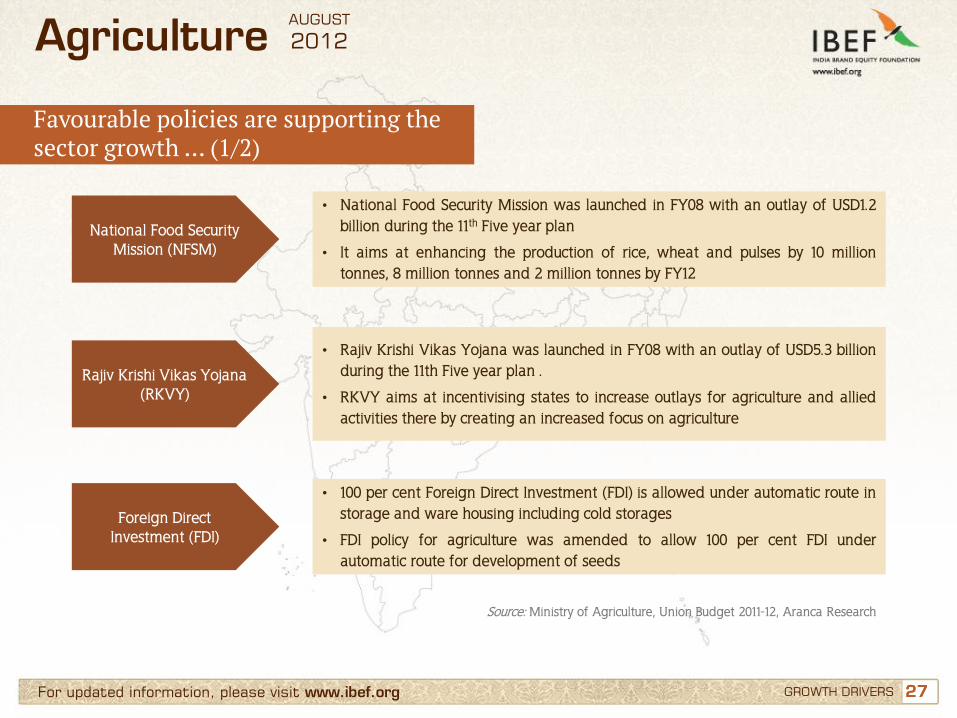

National Food Security Mission (NFSM)

• National Food Security Mission was launched in FY08 with an outlay of USD1.2 billion during the 11th Five year plan

• It aims at enhancing the production of rice, wheat and pulses by 10 million tonnes, 8 million tonnes and 2 million tonnes by FY12

Rajiv Krishi Vikas Yojana (RKVY)

• Rajiv Krishi Vikas Yojana was launched in FY08 with an outlay of USD5.3 billion during the 11th Five year plan .

• RKVY aims at incentivising states to increase outlays for agriculture and allied activities there by creating an increased focus on agriculture

Foreign Direct Investment (FDI)

• 100 per cent Foreign Direct Investment (FDI) is allowed under automatic route in storage and ware housing including cold storages

• FDI policy for agriculture was amended to allow 100 per cent FDI under automatic route for development of seeds

Source: Ministry of Agriculture, Union Budget 2011-12, Aranca Research

AUGUST

2012

28 28 For updated information, please visit www.ibef.org

Favourable policies are supporting the sector growth … (2/2)

GROWTH DRIVERS

Agriculture

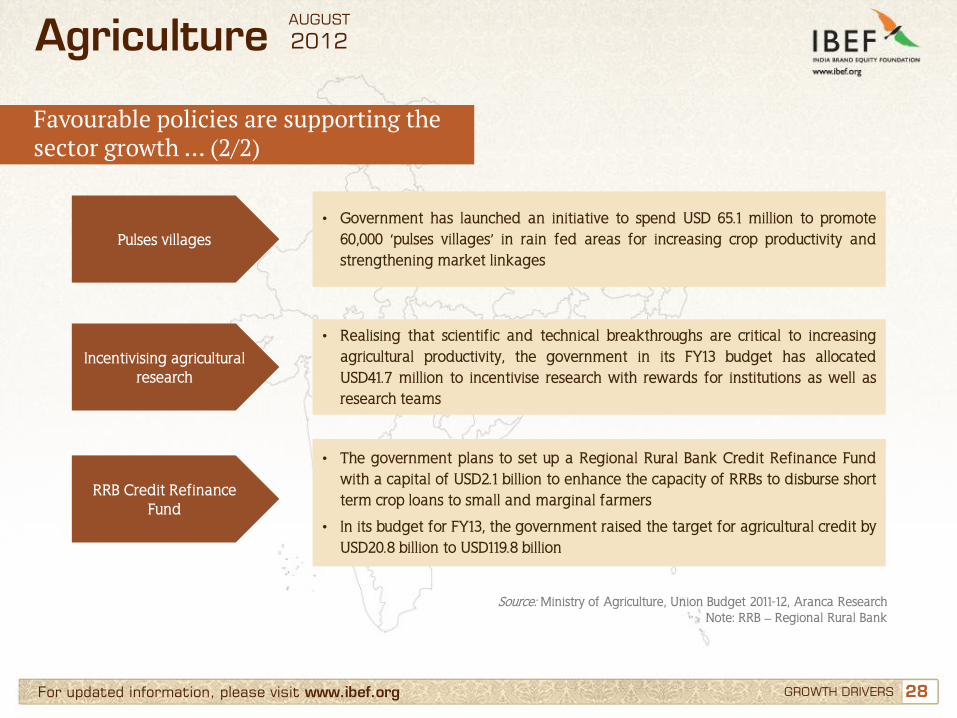

• Government has launched an initiative to spend USD 65.1 million to promote 60,000 ‘pulses villages’ in rain fed areas for increasing crop productivity and strengthening market linkages

Source: Ministry of Agriculture, Union Budget 2011-12, Aranca Research Note: RRB – Regional Rural Bank

• Realising that scientific and technical breakthroughs are critical to increasing agricultural productivity, the government in its FY13 budget has allocated USD41.7 million to incentivise research with rewards for institutions as well as research teams

Pulses villages

Incentivising agricultural research

• The government plans to set up a Regional Rural Bank Credit Refinance Fund with a capital of USD2.1 billion to enhance the capacity of RRBs to disburse short term crop loans to small and marginal farmers

• In its budget for FY13, the government raised the target for agricultural credit by USD20.8 billion to USD119.8 billion

RRB Credit Refinance Fund

AUGUST

2012

29 29

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Green revolution, Rallis India

Opportunities

Useful information

For updated information, please visit www.ibef.org

Agriculture AUGUST

2012

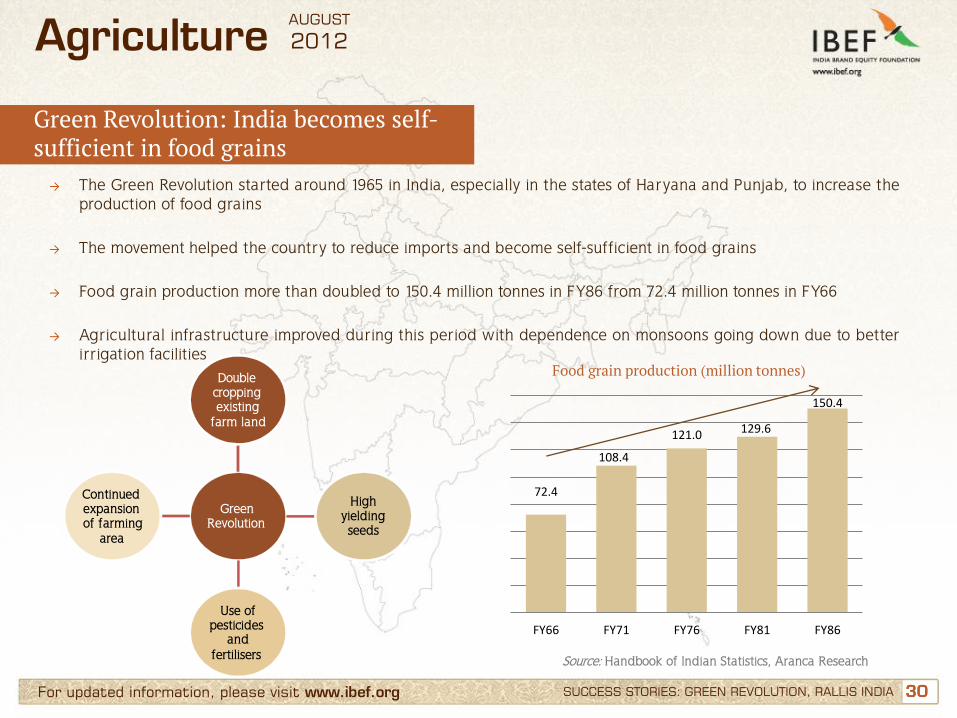

30 30 For updated information, please visit www.ibef.org SUCCESS STORIES: GREEN REVOLUTION, RALLIS INDIA

Green Revolution: India becomes self-sufficient in food grains

Agriculture

→ The Green Revolution started around 1965 in India, especially in the states of Haryana and Punjab, to increase the production of food grains

→ The movement helped the country to reduce imports and become self-sufficient in food grains

→ Food grain production more than doubled to 150.4 million tonnes in FY86 from 72.4 million tonnes in FY66 → Agricultural infrastructure improved during this period with dependence on monsoons going down due to better

irrigation facilities

Green Revolution

Double cropping existing

farm land

High yielding seeds

Use of pesticides

and fertilisers

Continued expansion of farming

area

Food grain production (million tonnes)

Source: Handbook of Indian Statistics, Aranca Research

72.4

108.4

121.0 129.6

150.4

FY66 FY71 FY76 FY81 FY86

AUGUST

2012

31 31 For updated information, please visit www.ibef.org

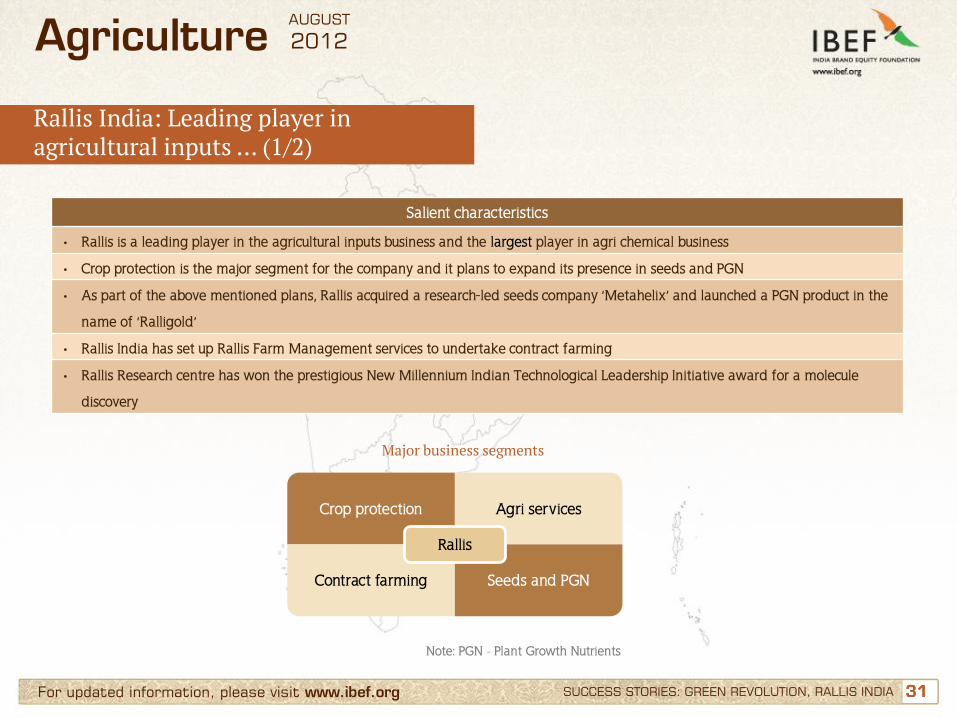

Rallis India: Leading player in agricultural inputs … (1/2)

Agriculture

Note: PGN - Plant Growth Nutrients

Major business segments

Crop protection Agri services

Contract farming Seeds and PGN

Rallis

Salient characteristics

• Rallis is a leading player in the agricultural inputs business and the largest player in agri chemical business

• Crop protection is the major segment for the company and it plans to expand its presence in seeds and PGN

• As part of the above mentioned plans, Rallis acquired a research-led seeds company ‘Metahelix’ and launched a PGN product in the

name of ‘Ralligold’

• Rallis India has set up Rallis Farm Management services to undertake contract farming

• Rallis Research centre has won the prestigious New Millennium Indian Technological Leadership Initiative award for a molecule

discovery

SUCCESS STORIES: GREEN REVOLUTION, RALLIS INDIA

AUGUST

2012

32 32 For updated information, please visit www.ibef.org

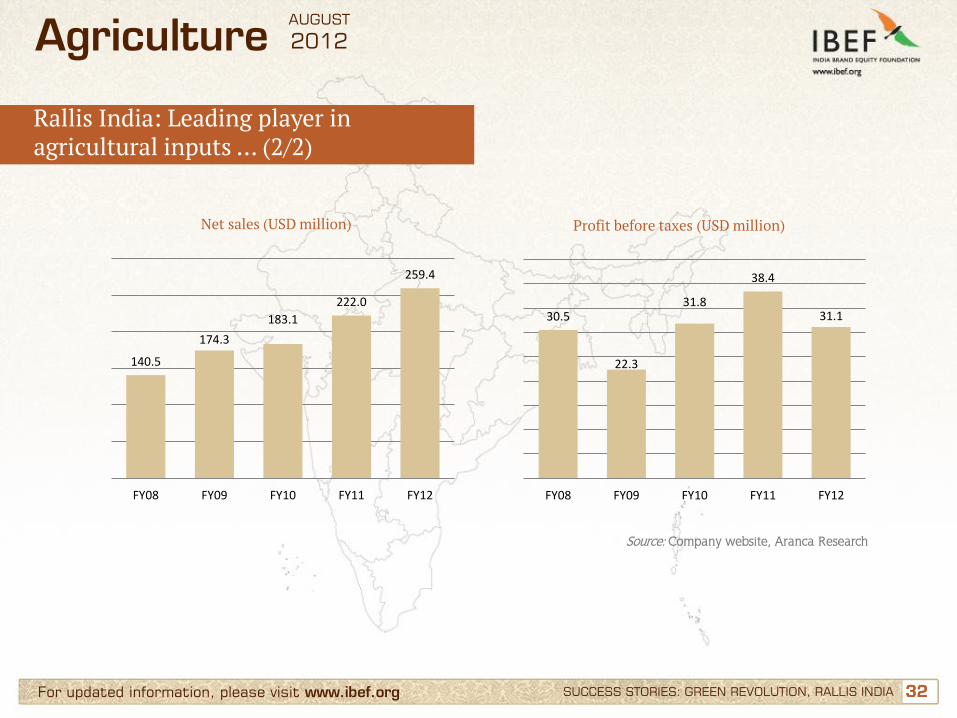

Rallis India: Leading player in agricultural inputs … (2/2)

Agriculture

Net sales (USD million) Profit before taxes (USD million)

Source: Company website, Aranca Research

SUCCESS STORIES: GREEN REVOLUTION, RALLIS INDIA

140.5

174.3

183.1

222.0

259.4

FY08 FY09 FY10 FY11 FY12

30.5

22.3

31.8

38.4

31.1

FY08 FY09 FY10 FY11 FY12

AUGUST

2012

33 33

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Green Revolution, Rallis India

Opportunities

Useful information

For updated information, please visit www.ibef.org

Agriculture AUGUST

2012

34 34 For updated information, please visit www.ibef.org OPPORTUNITIES

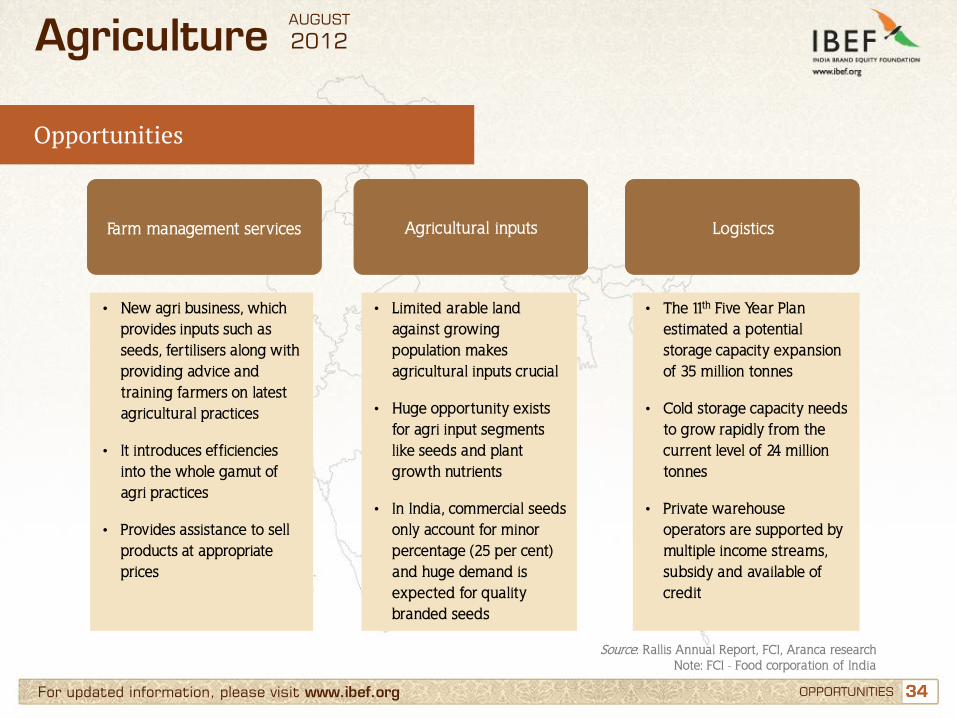

Opportunities

Source: Rallis Annual Report, FCI, Aranca research Note: FCI - Food corporation of India

Agriculture

• New agri business, which provides inputs such as seeds, fertilisers along with providing advice and training farmers on latest agricultural practices

• It introduces efficiencies into the whole gamut of agri practices

• Provides assistance to sell products at appropriate prices

• Limited arable land against growing population makes agricultural inputs crucial

• Huge opportunity exists for agri input segments like seeds and plant growth nutrients

• In India, commercial seeds only account for minor percentage (25 per cent) and huge demand is expected for quality branded seeds

• The 11th Five Year Plan estimated a potential storage capacity expansion of 35 million tonnes

• Cold storage capacity needs to grow rapidly from the current level of 24 million tonnes

• Private warehouse operators are supported by multiple income streams, subsidy and available of credit

Farm management services

Agricultural inputs

Logistics

AUGUST

2012

35

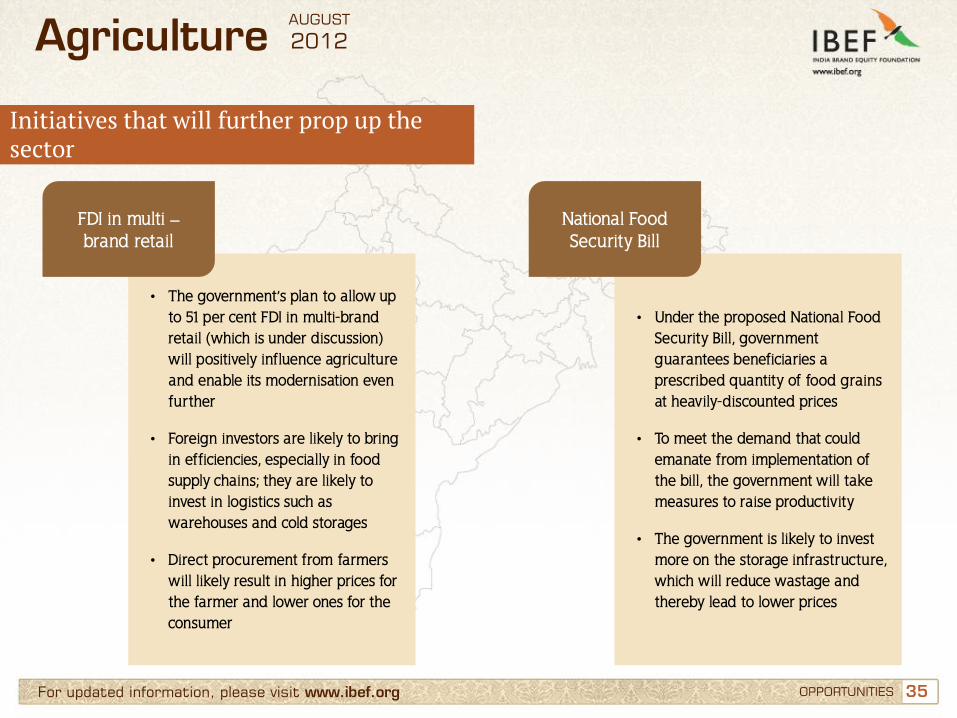

Initiatives that will further prop up the sector

Agriculture

• The government’s plan to allow up to 51 per cent FDI in multi-brand retail (which is under discussion) will positively influence agriculture and enable its modernisation even further

• Foreign investors are likely to bring in efficiencies, especially in food supply chains; they are likely to invest in logistics such as warehouses and cold storages

• Direct procurement from farmers will likely result in higher prices for the farmer and lower ones for the consumer

• Under the proposed National Food Security Bill, government guarantees beneficiaries a prescribed quantity of food grains at heavily-discounted prices

• To meet the demand that could emanate from implementation of the bill, the government will take measures to raise productivity

• The government is likely to invest more on the storage infrastructure, which will reduce wastage and thereby lead to lower prices

FDI in multi – brand retail

National Food Security Bill

For updated information, please visit www.ibef.org OPPORTUNITIES

AUGUST

2012

36 36

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: Green Revolution, Rallis India

Opportunities

Useful information

For updated information, please visit www.ibef.org

Agriculture AUGUST

2012

37 37 For updated information, please visit www.ibef.org USEFUL INFORMATION

Industry Associations … (1/2)

Autonomous Bodies • National Institute of Agricultural Extension Management

Rajendranagar, Hyderabad–500 030, Andhra Pradesh Phone: 040-24016702 to 706 Fax: 040-24015388

• National Institute of Agricultural Marketing (NIAM) Bambala, Kota Road Jaipur–302033, Rajasthan Phone: 0141-2770027 Fax: 0141-2771938, 2770027

Boards • Central Insecticides Board and Registration Committee Machinary Store Building, N.H.IV Faridabad Phone: 0129 -2413002 • Coconut Development Board Kera Bhavan, SRVHS Road, Kochi Kerala–682011

Phone: 0484-2376265, 2377267, 2376553 Fax: 0484-2377902

Agriculture AUGUST

2012

38 38 For updated information, please visit www.ibef.org

Industry Associations … (2/2)

• National Dairy Development Board (NDDB) PB No 40, Anand–388 001 Phone: 02692-260148/260149/260160 Fax: 02692-260157

• National Horticulture Board (NHB)

Ministry of Agriculture, Government of India 85, Institutional Area, Sector-18 Gurgaon–122015, Haryana

• National Oilseeds and Vegetable Oils Development Board

(NOVOD) 86, Institutional Area, Sector-18 Gurgaon–122015, Haryana

Councils • Indian Council of Agricultural Research (ICAR)

Krishi Bhavan, New Delhi 110 114 Phone: 91-11-25846010

USEFUL INFORMATION

Agriculture AUGUST

2012

39 39 For updated information, please visit www.ibef.org

Glossary

→ AIBP: Accelerated Irrigation Benefit Programme → Breeder seeds : Seeds move from germplasm ( research) stage to breeder stage

→ CAGR: Compound annual growth rate

→ Certified/quality seeds : Foundation seeds are further multiplied to get certified seeds, which are sold to farmers → FMTTI : Farm Machinery Training and Testing Institutes

→ Foundation seeds : Breeder seeds are multiplied as foundation seeds

→ FY: Indian financial year (April to March)– FY12 implies April 2011 to March 2012

→ KCC: Kisan Credit card

→ MSP : Minimum Support Prices

→ NFSM : National Food security mission

→ NMAM: National Mission on Agricultural Mechanisation → PGN : Plant Growth Nutrients

→ RKVY : Rashtriya Krushi Vikas Yojana is a central government scheme providing funds to state governments to spend on

agriculture

→ USD: US Dollar– Conversion rate used: USD 1 = INR 48

→ Wherever applicable, numbers have been rounded off to the nearest whole number

USEFUL INFORMATION

Agriculture AUGUST

2012

40

India Brand Equity Foundation (IBEF) engaged Aranca to prepare this presentation and the same has been prepared by Aranca in consultation with IBEF. All rights reserved. All copyright in this presentation and related works is solely and exclusively owned by IBEF. The same may not be reproduced, wholly or in part in any material form (including photocopying or storing it in any medium by electronic means and whether or not transiently or incidentally to some other use of this presentation), modified or in any manner communicated to any third party except with the written approval of IBEF. This presentation is for information purposes only. While due care has been taken during the compilation of this

presentation to ensure that the information is accurate to the best of Aranca and IBEF’s knowledge and belief, the content is not to be construed in any manner whatsoever as a substitute for professional advice. Aranca and IBEF neither recommend nor endorse any specific products or services that may have been mentioned in this presentation and nor do they assume any liability or responsibility for the outcome of decisions taken as a result of any reliance placed on this presentation. Neither Aranca nor IBEF shall be liable for any direct or indirect damages that may arise due to any act or omission on the part of the user due to any reliance placed or guidance taken from any portion of this presentation.

Disclaimer

For updated information, please visit www.ibef.org DISCLAIMER

Agriculture AUGUST

2012

![Department of Agriculture and Cooperation, Ministry of ......Department of Agriculture and Cooperation, Ministry of Agriculture, Government of India, New Delhi [2] National Agricultural](https://img.pdfslide.net/doc/110x75/5f89066a747baa1cb15eb13b/department-of-agriculture-and-cooperation-ministry-of-department-of-agriculture.jpg)