Embed Size (px)

Citation preview

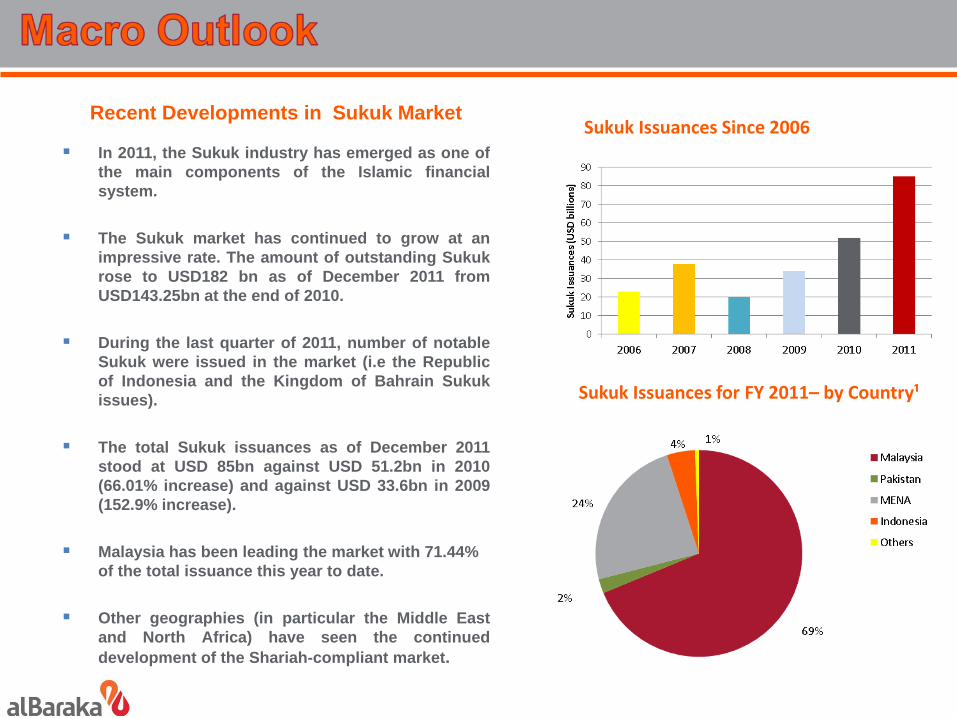

Recent Developments in Sukuk Market

In 2011, the Sukuk industry has emerged as one ofthe main components of the Islamic financialsystem.

The Sukuk market has continued to grow at animpressive rate. The amount of outstanding Sukukrose to USD182 bn as of December 2011 fromUSD143.25bn at the end of 2010.

During the last quarter of 2011, number of notableSukuk were issued in the market (i.e the Republicof Indonesia and the Kingdom of Bahrain Sukukissues).

The total Sukuk issuances as of December 2011stood at USD 85bn against USD 51.2bn in 2010(66.01% increase) and against USD 33.6bn in 2009(152.9% increase).

Malaysia has been leading the market with 71.44% of the total issuance this year to date.

Other geographies (in particular the Middle Eastand North Africa) have seen the continueddevelopment of the Shariah-compliant market.

Sukuk Issuances Since 2006

Sukuk Issuances for FY 2011– by Country¹

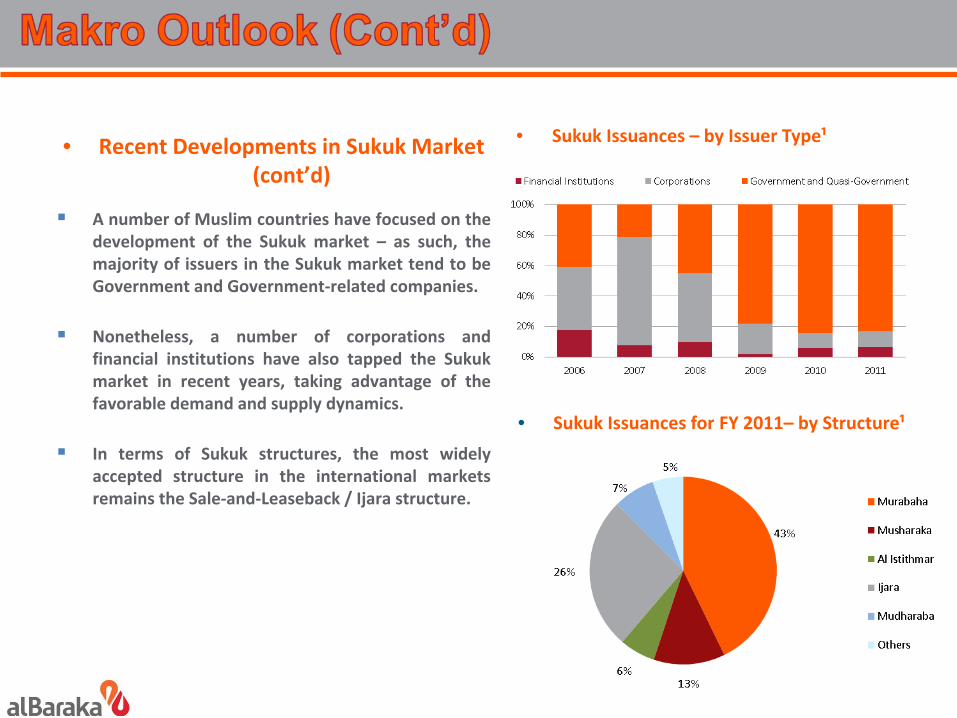

• Recent Developments in Sukuk Market (cont’d)

A number of Muslim countries have focused on thedevelopment of the Sukuk market – as such, themajority of issuers in the Sukuk market tend to beGovernment and Government-related companies.

Nonetheless, a number of corporations andfinancial institutions have also tapped the Sukukmarket in recent years, taking advantage of thefavorable demand and supply dynamics.

In terms of Sukuk structures, the most widelyaccepted structure in the international marketsremains the Sale-and-Leaseback / Ijara structure.

• Sukuk Issuances – by Issuer Type¹

• Sukuk Issuances for FY 2011– by Structure¹

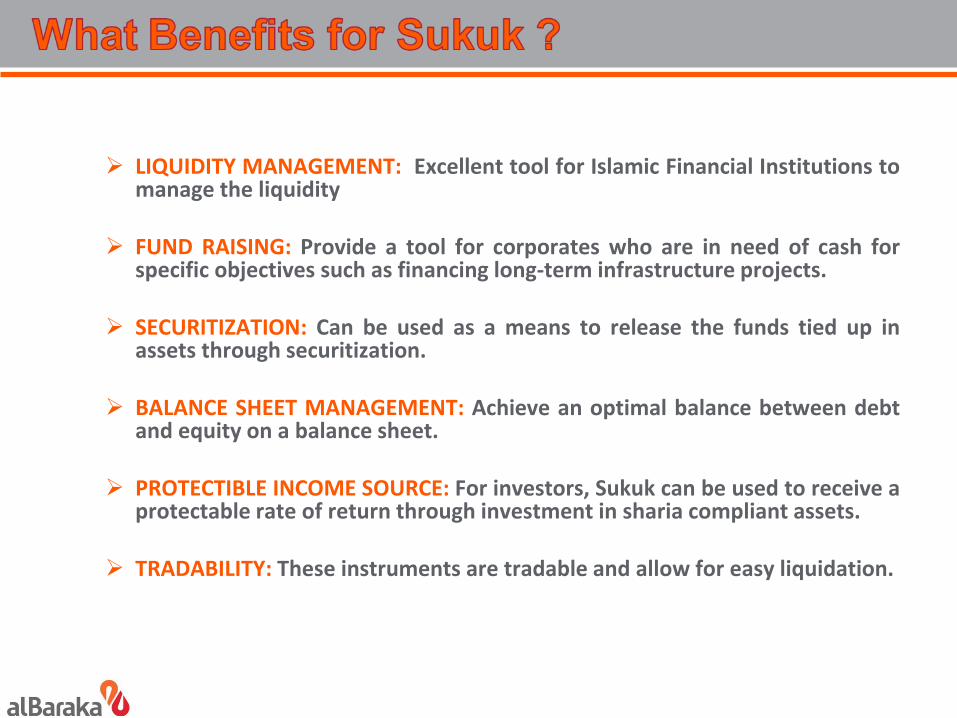

LIQUIDITY MANAGEMENT: Excellent tool for Islamic Financial Institutions tomanage the liquidity

FUND RAISING: Provide a tool for corporates who are in need of cash forspecific objectives such as financing long-term infrastructure projects.

SECURITIZATION: Can be used as a means to release the funds tied up inassets through securitization.

BALANCE SHEET MANAGEMENT: Achieve an optimal balance between debtand equity on a balance sheet.

PROTECTIBLE INCOME SOURCE: For investors, Sukuk can be used to receive aprotectable rate of return through investment in sharia compliant assets.

TRADABILITY: These instruments are tradable and allow for easy liquidation.

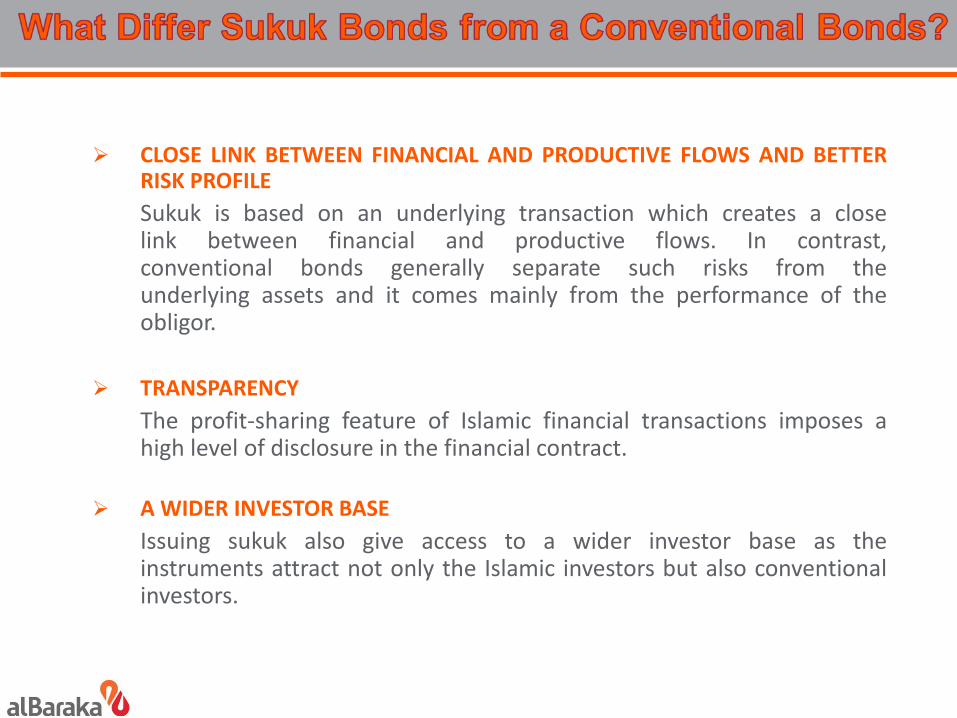

CLOSE LINK BETWEEN FINANCIAL AND PRODUCTIVE FLOWS AND BETTERRISK PROFILESukuk is based on an underlying transaction which creates a closelink between financial and productive flows. In contrast,conventional bonds generally separate such risks from theunderlying assets and it comes mainly from the performance of theobligor.

TRANSPARENCYThe profit-sharing feature of Islamic financial transactions imposes ahigh level of disclosure in the financial contract.

A WIDER INVESTOR BASEIssuing sukuk also give access to a wider investor base as theinstruments attract not only the Islamic investors but also conventionalinvestors.

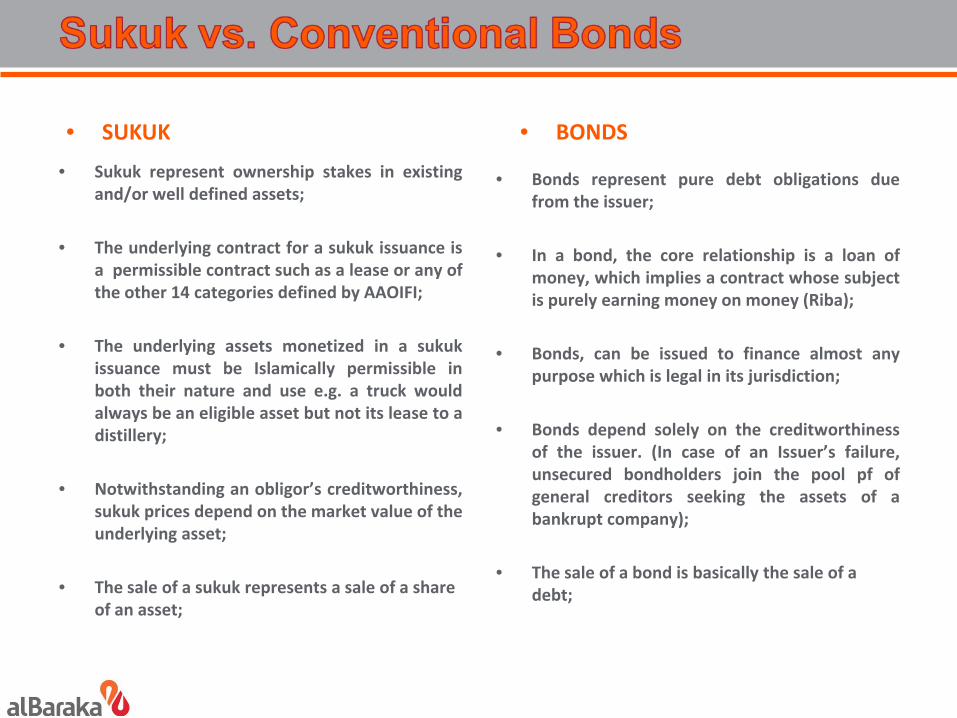

• SUKUK

• Sukuk represent ownership stakes in existingand/or well defined assets;

• The underlying contract for a sukuk issuance isa permissible contract such as a lease or any ofthe other 14 categories defined by AAOIFI;

• The underlying assets monetized in a sukukissuance must be Islamically permissible inboth their nature and use e.g. a truck wouldalways be an eligible asset but not its lease to adistillery;

• Notwithstanding an obligor’s creditworthiness,sukuk prices depend on the market value of theunderlying asset;

• The sale of a sukuk represents a sale of a share of an asset;

• BONDS

• Bonds represent pure debt obligations duefrom the issuer;

• In a bond, the core relationship is a loan ofmoney, which implies a contract whose subjectis purely earning money on money (Riba);

• Bonds, can be issued to finance almost anypurpose which is legal in its jurisdiction;

• Bonds depend solely on the creditworthinessof the issuer. (In case of an Issuer’s failure,unsecured bondholders join the pool pf ofgeneral creditors seeking the assets of abankrupt company);

• The sale of a bond is basically the sale of a debt;

Since there is a lack of savings in Turkey, the need for foreign fundsbecomes more crucial. Islamic Finance Industry and the global SukukMarkets are growing steadily despite the ongoing challenging globaleconomic environment. Turkey should also get its stake from thismarket.

An alternative way of borrowing for the Turkish Treasury and mayserve as a short-term liquidity instrument for Participation Banks.

A good source of long term funding for Pariticipation Banks thatwould ease maturity mismatch problem and will also support thegrowth of the sector.

A very suitable funding solution for the Project financing needs ofTurkish Corporates.

THE STRATEGY OF THE GOVERNMENT TO ATTRACT THE FUNDS FROM THE GULF: In 2003, the Government announced its interest in implementing a legal framework for the Issuance of Sukuk al Ijara to attract the direct investments from the Gulf.

SUKUK COMMUNIQUE OF THE CMB: The first piece of legislation directly related to Sukuk came years later. On April 1st, 2010, a communiqué (“Sukuk communiqué”) prepared by Capital Markets Board (CMB) was published in Official Gazette and came into effect. The Sukuk communiqué includes provisions about certificates and Special Purpose Vehicle (SPV) instruments. These certificates are basically called “lease certificates” as the Sukuk communiqué is based on ijara Sukuk.

FINANCE BILL IN FEBRUARY 2011: The Finance Bill 2011 in February includes tax neutrality measures for Sukuk Al-Ijara thus paving the way for a spate of corporate Sukuk issuances in Turkey. Elimination of the obstacles before Sukuk offerings under Turkish legal and tax systems have been targeted by the aforementioned regulations. Under the Finance Bill a number of amendment has been done in «Income Tax Law, Corporate Tax Law, VAT Law, Stamp Duty Law and Charges Law» to eliminate the tax obstacles in front of Sukuk Issues in Turkey.

A LIMITED LEGAL FRAMEWORK: The existing legislation sounds limited in enabling the corporates to make use of different sukuk structures such as Mudaraba, Musharaka, Salam or Istithna.

KUVEYT TURK PARTICIPATION BANK: After its debut sukuk for $100 with 3-yearterm in 2010, the Bank issued a $350 million sukuk carrying a profit rate of 5.875percent. Gulf investors accounted for nearly 70 percent of final subscribers.

BANK ASYA: Instead of complying with the existing legislation, Bank Asya usedthe classical off-shore SPV model and the Bank has completed roadshows byOctober 2011 for a potential five-year sukuk of up to $300 million. However, theBank postponed its planned sukuk issue due to negative international marketdevelopments.

TÜRKİYE FİNANS: The Bank is planning to issue its debut Sukuk by early 2013.

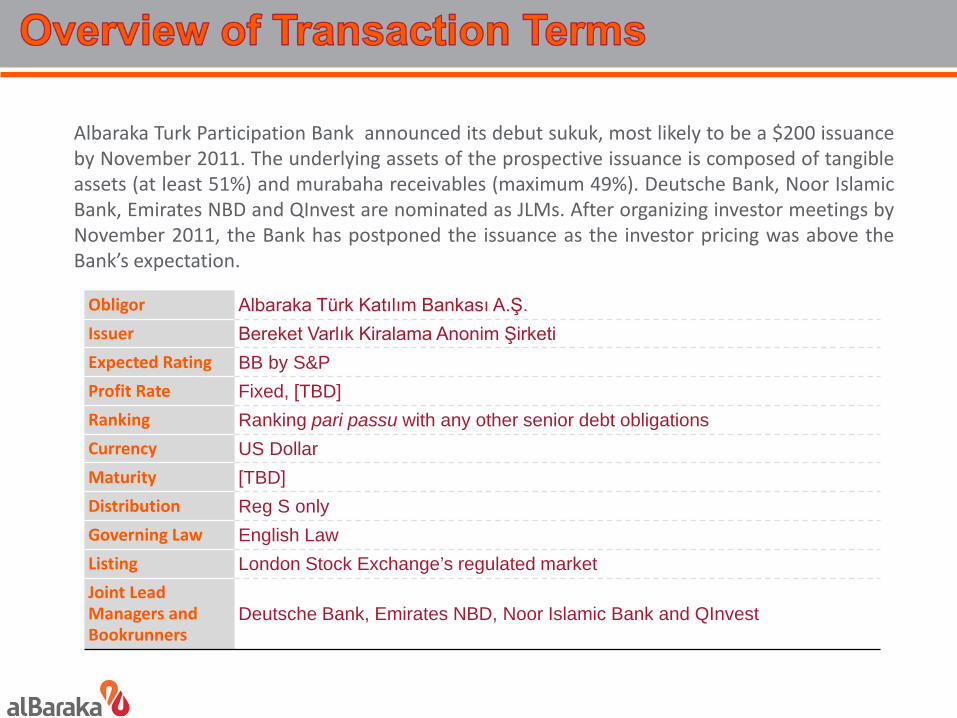

Obligor Albaraka Türk Katılım Bankası A.Ş.Issuer Bereket Varlık Kiralama Anonim ŞirketiExpected Rating BB by S&PProfit Rate Fixed, [TBD]Ranking Ranking pari passu with any other senior debt obligationsCurrency US DollarMaturity [TBD]Distribution Reg S onlyGoverning Law English LawListing London Stock Exchange’s regulated marketJoint Lead Managers and Bookrunners

Deutsche Bank, Emirates NBD, Noor Islamic Bank and QInvest

Albaraka Turk Participation Bank announced its debut sukuk, most likely to be a $200 issuanceby November 2011. The underlying assets of the prospective issuance is composed of tangibleassets (at least 51%) and murabaha receivables (maximum 49%). Deutsche Bank, Noor IslamicBank, Emirates NBD and QInvest are nominated as JLMs. After organizing investor meetings byNovember 2011, the Bank has postponed the issuance as the investor pricing was above theBank’s expectation.

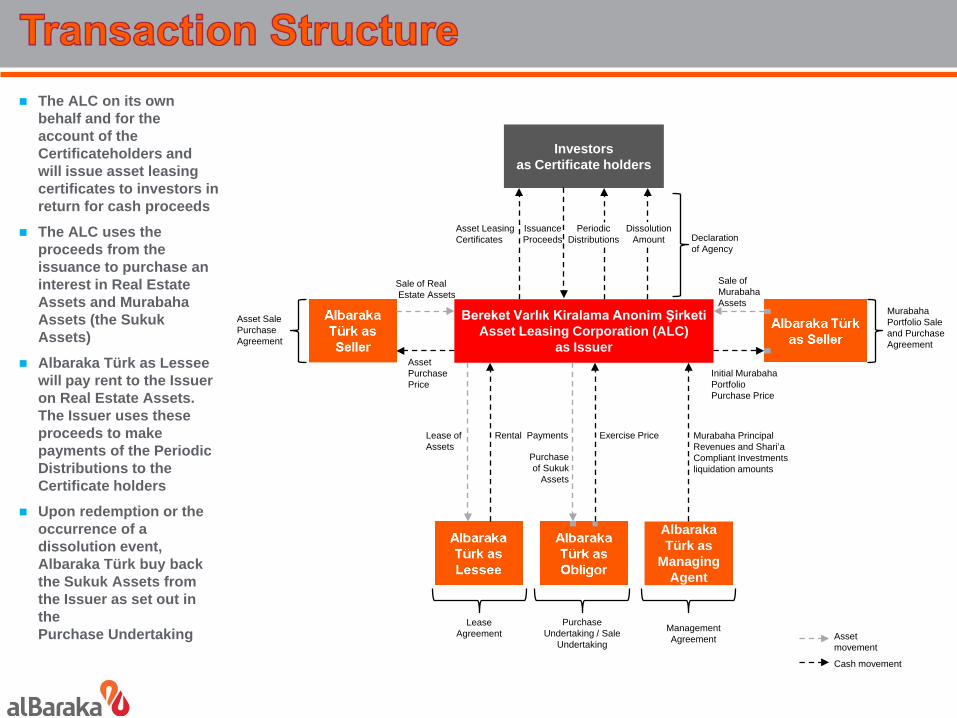

The ALC on its own behalf and for the account of the Certificateholders and will issue asset leasing certificates to investors in return for cash proceeds

The ALC uses the proceeds from the issuance to purchase an interest in Real Estate Assets and Murabaha Assets (the Sukuk Assets)

Albaraka Türk as Lessee will pay rent to the Issuer on Real Estate Assets. The Issuer uses these proceeds to make payments of the Periodic Distributions to the Certificate holders

Upon redemption or the occurrence of a dissolution event, Albaraka Türk buy back the Sukuk Assets from the Issuer as set out in the Purchase Undertaking

Albaraka Türk as

Managing Agent

Investors as Certificate holders

Asset Leasing Certificates

Issuance Proceeds

Periodic Distributions

Dissolution Amount Declaration

of Agency

Sale of RealEstate Assets

Asset Purchase Price

Sale of Murabaha Assets

Initial Murabaha Portfolio Purchase Price

Murabaha Portfolio Sale and Purchase Agreement

Bereket Varlık Kiralama Anonim ŞirketiAsset Leasing Corporation (ALC)

as Issuer

Murabaha Principal Revenues and Shari’a Compliant Investments liquidation amounts

Exercise PriceRental Payments

Purchase of Sukuk

Assets

Lease of Assets

Lease Agreement

Purchase Undertaking / Sale

Undertaking

Management Agreement

Asset Sale Purchase Agreement

Asset movement

Cash movement

RATING CHALLENGE FOR TURKISH CORPORATES: Turkey, which is rated BB, Ba2and BB+ by the three major rating agencies, slightly below investment grade, hasnot seriously underperformed Gulf credits. Its CDS are tighter than unratedDubai and BBB-rated Bahrain, though wider than AA-rated Abu Dhabi and Qatar.The Financials institutions having ratings below investment grade will not be ableto attract investors at a reasonable price. Investors and traders in Far East areespecially too much concerned about the obligor ratings.

LACK OF UNDERLYING ASSETS: As the Sukuk communiqué is based on ijara Sukuk, the Banks either use the real estate or non real estate ijara assets to issue lease certificates. However, the Banks have limited real estate and leasing portfolio. As result, the issue size would be limited due to the lack of underlying assets.

SECONDARY MARKET: Also, the profile of sukuk investors favors a hold-to-maturity investment makes secondary market trading of Islamic bonds lessliquid.

Not only Turkey but UK Treasury, French Ministry of Finance and Japan Bank for International Cooperation are waiting for the «positive market conditions» to attract investments by Sukuk issuance.

In 2004, a €100 million Sukuk, structured as a Sukuk Al Ijara, was issued in the federal state of Saxony-Anhalt in Germany. Sukuk Bonds of Turkish Treasury would attract investors from GCC and Malaysia more than any other western state would attract.

The Turkish government announced in January 2012 that it plans to issue a sovereign sukuk this year, using legislation already in place.

DIVERSIFICATION OF LONG TERM FUNDING SOURCES: The participation Banks have limitedsource of funding when compared to conventional Banks. To eliminate this obstacle whichalso provoques a disadvantage for PBs in the market, issuance of lease certificates wouldincrease the long-term borrowing capabilities of the PBs. This may also help the PBs tobetter manage the liabilities.

SOVEREIGN SUKUK AS A REMEDY FOR SHORT-TERM LIQUIDITY MANAGEMENT: The LeaseCertificates issued by the Turkish Treasury in TRL would serve as an isntrument for shortterm borrowings of PBs from the Central Bank. This instrument will support the ParticipationBanks in Turkey to widen their investment portfolios and to facilitate them a more efficientand effective liquidity management by deepening the market for Participation Banks.

ALTERNATIVE SOURCE FOR THE EXPANDING PRIVATE PENSION FUNDS (PPFs): There is aconsiderable demand for sharia-compliant private pension fund in Turkey. However, PPFs arehave limited source to enhance their business in this area. As a result, issuance of leasecertificates in TRL will fill this gap in the sector.

REDEFINITION OF THE “ASSET”: The asset is defined by the CMB Communiqué as “All sorts ofgoods which are movable or not movable and intangible assets to be purchased or leasedby the Asset Leasing Corporation.(Art. 3.L.)” In order for PBs and the non-Bank corporatesto increase their issuance possibilities, the definition should be further extended toinclude the “Murabaha and similar receivables.

PAVING THE WAY FOR HEAD-LEASE / SUB-LEASE STRUCTURE: Classical “Sale & Leaseback”model is the only structure proposed by the CMB Communiqué. However, Head-lease (50to 100 years) / Sublease (3-5-7 yaears) would be an other option to enable thestructuring. To prevent any tax burden, the tax exemption should also be recognized tothe HL/SL Structure.

REDEFINITION OF THE ORIGINATING INSTITUTION: The Art. 3.E. Of the CMB Communiquérequires that the Originating Institution should be a Joint Stock Company which is anobstacle in front of prospective issuances by the State-owned Institutions.

AMENDMENT TO THE LEASING LAW: According to the Art. 18 of the Leasing Law (nr. 3226),the assets subject to the Lease Agreement can solely be transferred to another leasingcompany if only there is an article in the Lease Agreement allowing the subject transfer.An amendment should be done in the Leasing Law to annul this prohibition in order forPBs and Leasing Companies to profit from their Leasing portfolio while determining theunderlying assets for their issuance.