Embed Size (px)

Citation preview

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Alternative Data

Transforming SME Finance

John Owens & Lisa Wilhelm

SME Finance Forum Webinar

June 12, 2017 (updated June 19, 2017)

Washington DC

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

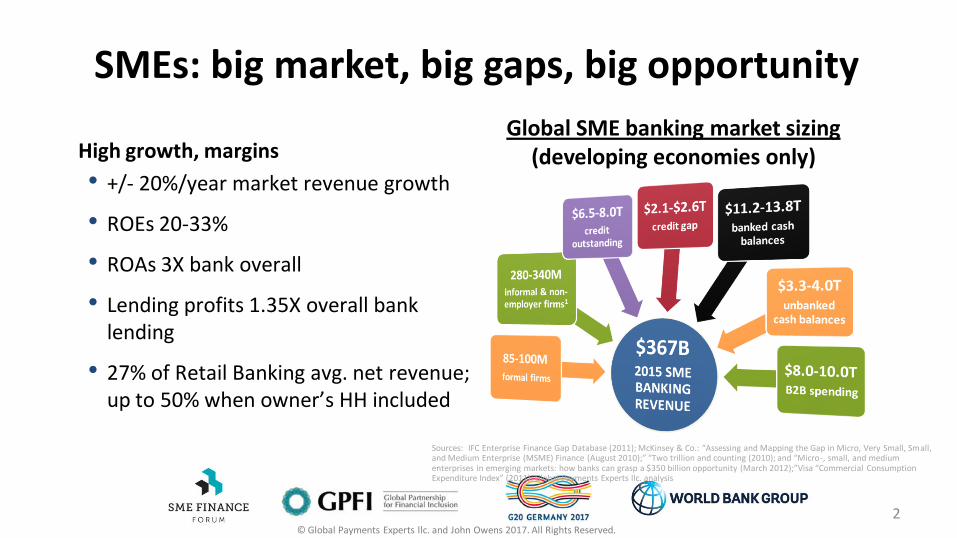

SMEs: big market, big gaps, big opportunity

High growth, margins

• +/- 20%/year market revenue growth

• ROEs 20-33%

• ROAs 3X bank overall

• Lending profits 1.35X overall bank lending

• 27% of Retail Banking avg. net revenue; up to 50% when owner’s HH included

Global SME banking market sizing (developing economies only)

Sources: IFC Enterprise Finance Gap Database (2011); McKinsey & Co.: “Assessing and Mapping the Gap in Micro, Very Small, Small, and Medium Enterprise (MSME) Finance (August 2010);” “Two trillion and counting (2010); and “Micro-, small, and medium enterprises in emerging markets: how banks can grasp a $350 billion opportunity (March 2012);”Visa “Commercial Consumption Expenditure Index” (2011); Global Payments Experts llc. analysis

2

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

The credit gap challenges Credit executives worry about adverse selection; top executives worry they won’t earn sufficient returns above their 10-15% cost of capital

1. IFC (October 2013). “Closing the Credit Gap for Formal and Informal Micro, Small, and Medium Enterprises.”

SME DEMAND-SIDE ISSUES

High risk

BANK SUPPLY-SIDE ISSUES

High cost

Informality

Difficult to reach, dispersed

Difficult requirements

High costs/interest

Cumbersome, slow applications

Low revenue/account

Low business, financial literacy

INFORMATION OPACITY

DEVELOPING MARKET SME CREDIT GAP

200-245 million MSMEs1 $2.1-2.6 trillion1

Fear of decline

3

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

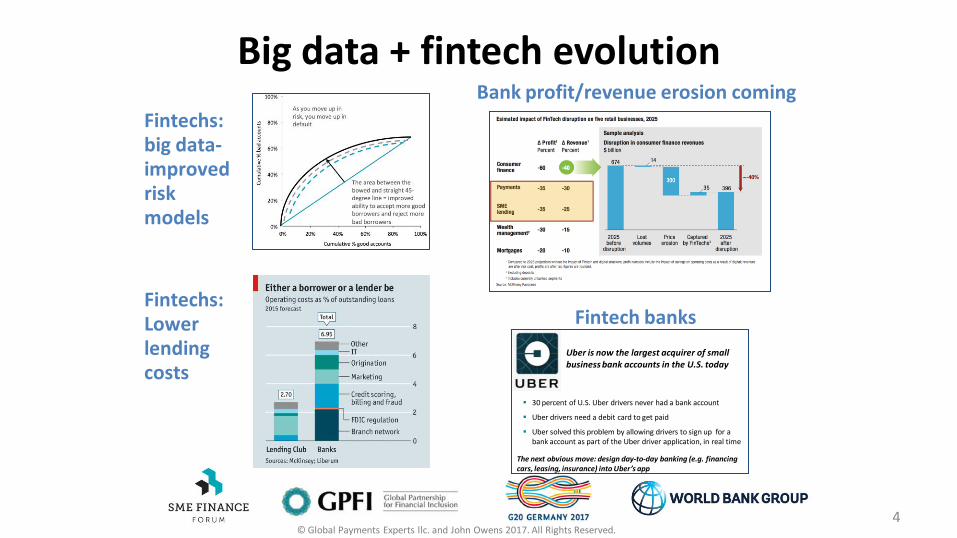

Big data + fintech evolution

4

Bank profit/revenue erosion coming

Fintech banks

30 percent of U.S. Uber drivers never had a bank account

Uber drivers need a debit card to get paid

Uber solved this problem by allowing drivers to sign up for a bank account as part of the Uber driver application, in real time

Uber is now the largest acquirer of small business bank accounts in the U.S. today

The next obvious move: design day-to-day banking (e.g. financing cars, leasing, insurance) into Uber’s app

Fintechs: Lower lending costs

Fintechs: big data-improved risk models

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

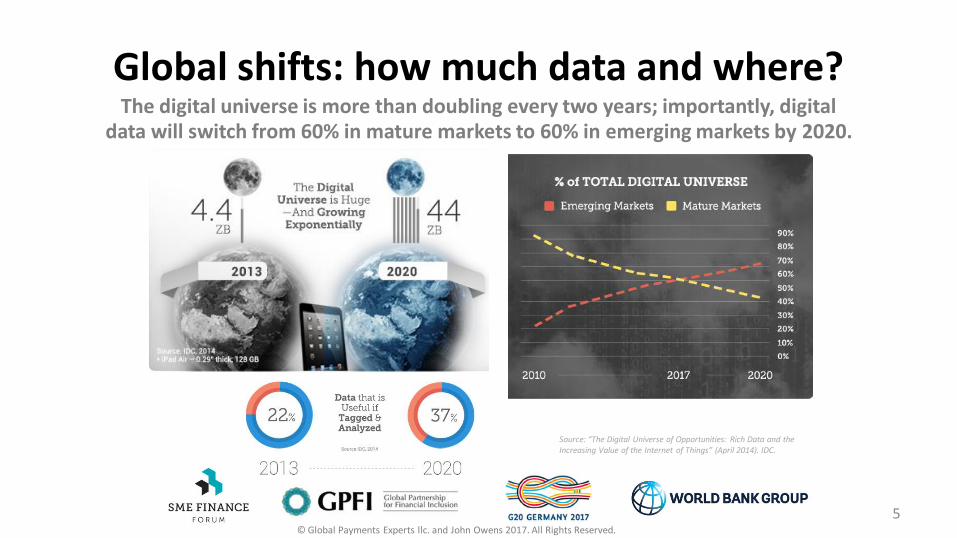

Global shifts: how much data and where? The digital universe is more than doubling every two years; importantly, digital

data will switch from 60% in mature markets to 60% in emerging markets by 2020.

Source: “The Digital Universe of Opportunities: Rich Data and the Increasing Value of the Internet of Things” (April 2014). IDC.

5

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

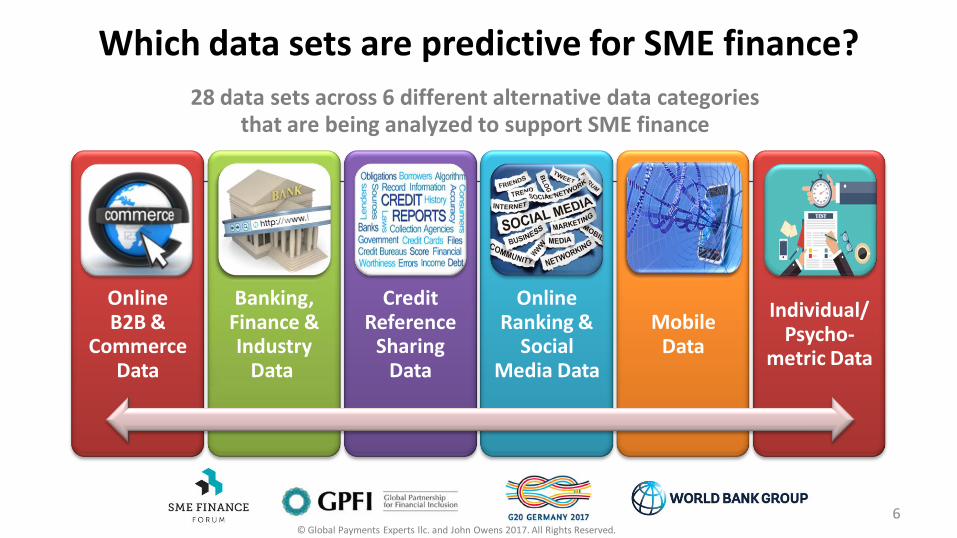

Which data sets are predictive for SME finance?

28 data sets across 6 different alternative data categories that are being analyzed to support SME finance

Online B2B &

Commerce Data

Banking, Finance & Industry

Data

Credit Reference

Sharing Data

Online Ranking &

Social Media Data

Mobile Data

Individual/ Psycho-

metric Data

6

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Fintech transforming the SME lending status quo A rapidly growing crop of technology-focused SME lenders are putting customer needs, big data, and advanced analytics at the center of their business models.

P2P SME lenders Supply/trade financing Online balance

sheet SME lenders

Online invoice financing

7

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Global SME ‘operating systems’ moving online Every time SMEs use cloud-based services, make digital payments, browse the internet, use their mobile phones, engage in social media, buy or sell electronically, ship packages, and manage their receivables, payables, and recordkeeping online, they create and deepen the digital footprints they leave behind.

Payment acceptance + much more

Making payments Cloud accounting + much more

8

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Emerging digital SME lending ecosystem New analytic firms help lenders analyze big data; telco, bank, and technology firm

convergence is fueling new mobile data-lending and financial services; and new loan broker marketplaces help SMEs make sense of their growing lending options.

Big data analytics Mobile data lending graduating to SMEs

SME loan broker marketplaces

9

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

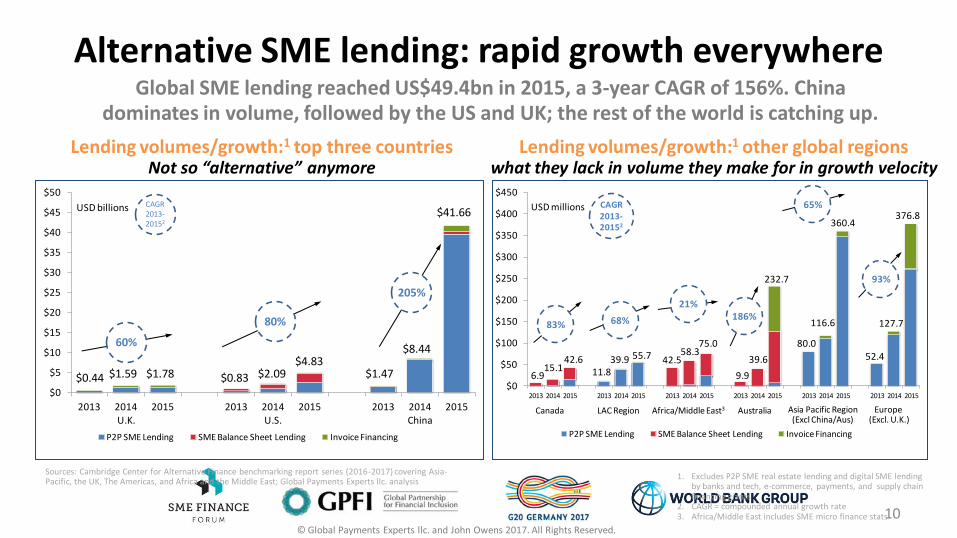

Alternative SME lending: rapid growth everywhere Global SME lending reached US$49.4bn in 2015, a 3-year CAGR of 156%. China

dominates in volume, followed by the US and UK; the rest of the world is catching up.

10

1. Excludes P2P SME real estate lending and digital SME lending by banks and tech, e-commerce, payments, and supply chain financing giants

2. CAGR = compounded annual growth rate 3. Africa/Middle East includes SME micro finance stats

Sources: Cambridge Center for Alternative Finance benchmarking report series (2016-2017) covering Asia-Pacific, the UK, The Americas, and Africa and the Middle East; Global Payments Experts llc. analysis

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2013 2014 2015 2013 2014 2015 2013 2014 2015 2013 2014 2015 2013 2014 2015 2013 2014 2015

P2P SME Lending SME Balance Sheet Lending Invoice Financing

6.915.1

42.6

127.7

52.4

376.8USD millions

83%

CAGR 2013-20152

Canada LAC Region Australia Asia Pacific Region(Excl China/Aus)

Europe (Excl. U.K.)

11.839.9 55.7

68%

9.9

39.6

232.7

186%

80.0

116.6

360.4

65%

93%

42.558.3

75.0

21%

Africa/Middle East3

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

2013 2014 U.K.

2015 2013 2014 U.S.

2015 2013 2014 China

2015

P2P SME Lending SME Balance Sheet Lending Invoice Financing

$0.44 $1.59 $1.78 $0.83 $2.09$4.83

$1.47

$8.44

$41.66USD billions

60%

80%

205%

CAGR 2013-20152

Lending volumes/growth:1 other global regions what they lack in volume they make for in growth velocity

Lending volumes/growth:1 top three countries Not so “alternative” anymore

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

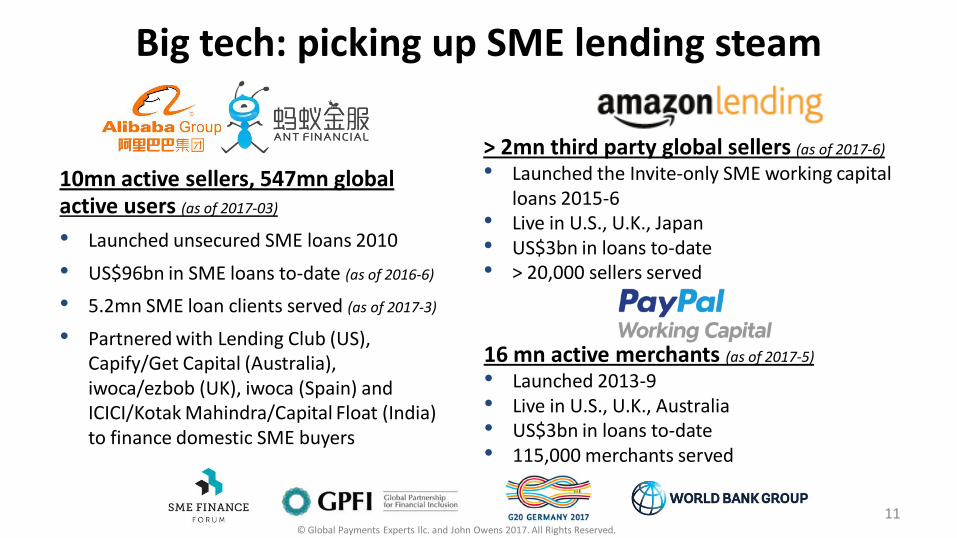

Big tech: picking up SME lending steam

11

> 2mn third party global sellers (as of 2017-6)

• Launched the Invite-only SME working capital loans 2015-6

• Live in U.S., U.K., Japan • US$3bn in loans to-date • > 20,000 sellers served

16 mn active merchants (as of 2017-5)

• Launched 2013-9 • Live in U.S., U.K., Australia • US$3bn in loans to-date • 115,000 merchants served

10mn active sellers, 547mn global active users (as of 2017-03)

• Launched unsecured SME loans 2010

• US$96bn in SME loans to-date (as of 2016-6)

• 5.2mn SME loan clients served (as of 2017-3)

• Partnered with Lending Club (US), Capify/Get Capital (Australia), iwoca/ezbob (UK), iwoca (Spain) and ICICI/Kotak Mahindra/Capital Float (India) to finance domestic SME buyers

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

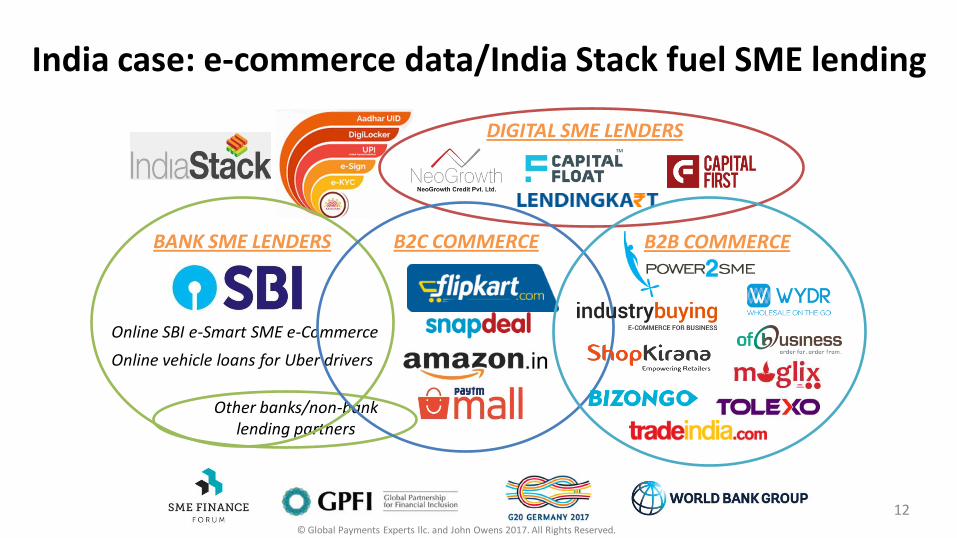

India case: e-commerce data/India Stack fuel SME lending

Other banks/non-bank lending partners

DIGITAL SME LENDERS

Online SBI e-Smart SME e-Commerce

Online vehicle loans for Uber drivers

B2C COMMERCE B2B COMMERCE BANK SME LENDERS

12

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

09.09.15

• New digital data platforms allow for expanded supply/trade and invoice finance to smaller firms on a more cost-effective basis.

• This is happening more and more in countries and markets where SMEs are able to move their accounting and B2B relationships online and to digital platforms.

Digital data & supply chain financing

13

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

09.09.15

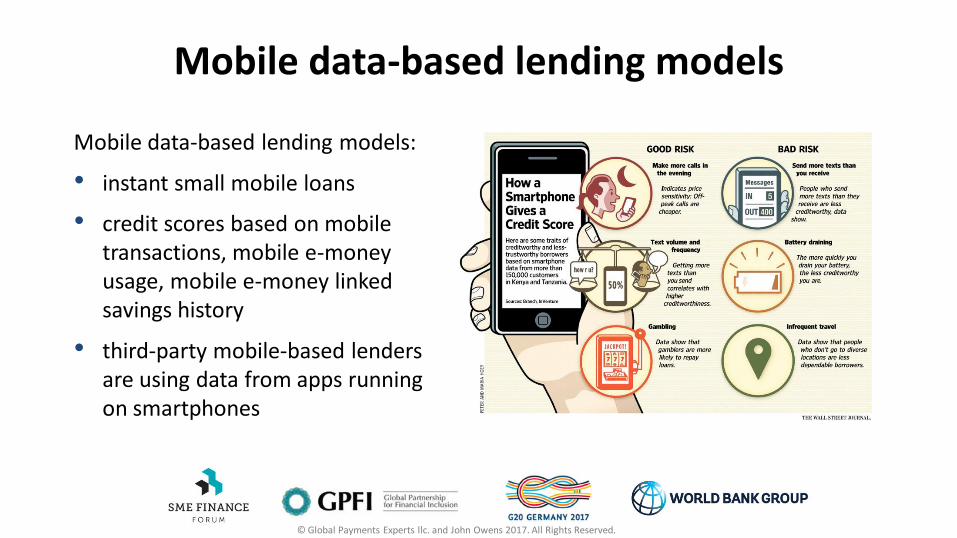

Mobile data-based lending models:

• instant small mobile loans

• credit scores based on mobile transactions, mobile e-money usage, mobile e-money linked savings history

• third-party mobile-based lenders are using data from apps running on smartphones

Mobile data-based lending models

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

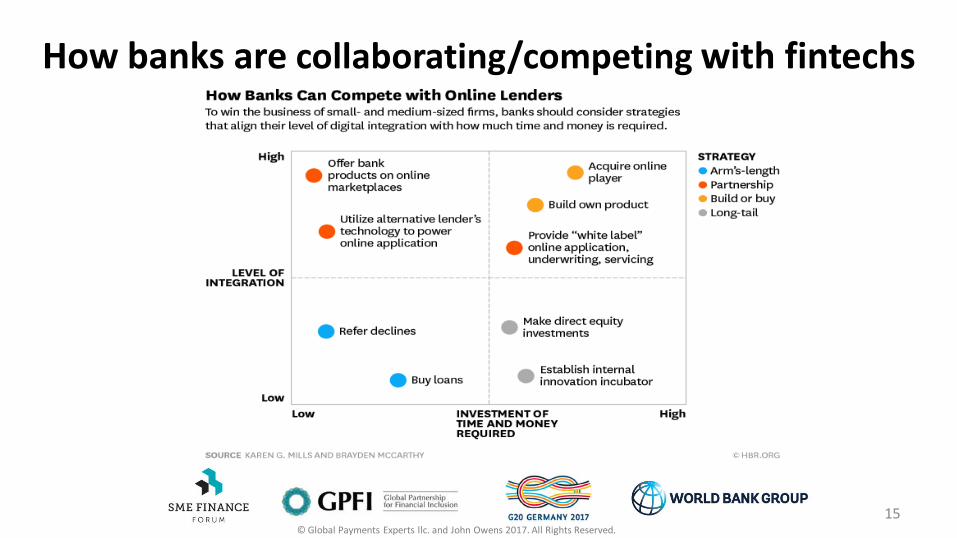

How banks are collaborating/competing with fintechs

15

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Fintech and banks 2017: more friend than foe

Advantage: banks • Captive, large customer base/positive

selection in applicant mix

• Brand

• Distribution coverage

• Valuable, “free” internal data (but underutilized)

• Low cost, stable source of funds

• Regulatory certainty (mostly)

16

Advantage: fintechs • Customer service oriented

• Simple and often friction-free applications

• More credit data sources

• Enhanced risk models

• Underwriting costs

• Pricing for risk

• Less regulation in many markets (but the future is uncertain)

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

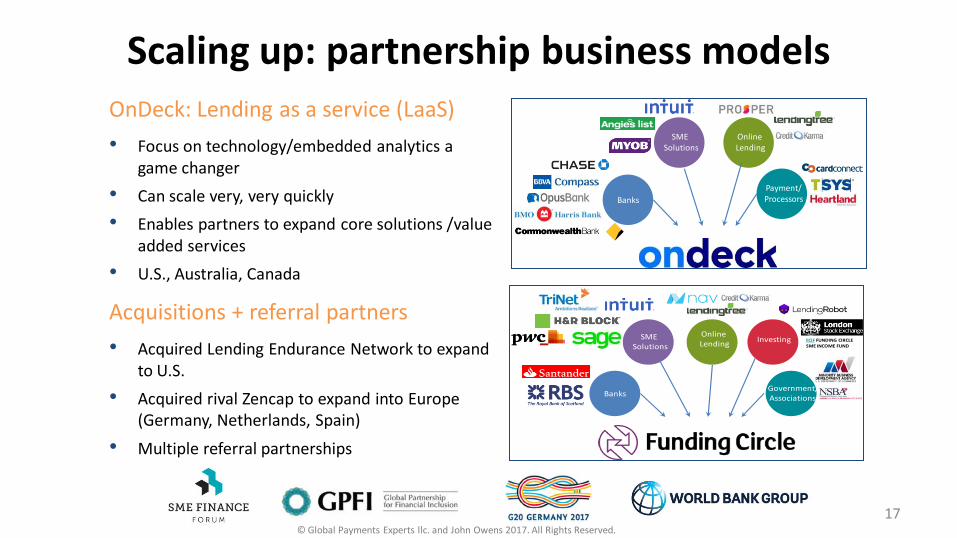

Scaling up: partnership business models

17

Banks

SME Solutions

Online Lending

Government/Associations

Investing FCIF FUNDING CIRCLE SME INCOME FUND

OnDeck: Lending as a service (LaaS)

• Focus on technology/embedded analytics a game changer

• Can scale very, very quickly

• Enables partners to expand core solutions /value added services

• U.S., Australia, Canada

Acquisitions + referral partners

• Acquired Lending Endurance Network to expand to U.S.

• Acquired rival Zencap to expand into Europe (Germany, Netherlands, Spain)

• Multiple referral partnerships

Banks

SME Solutions

Online Lending

Payment/Processors

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

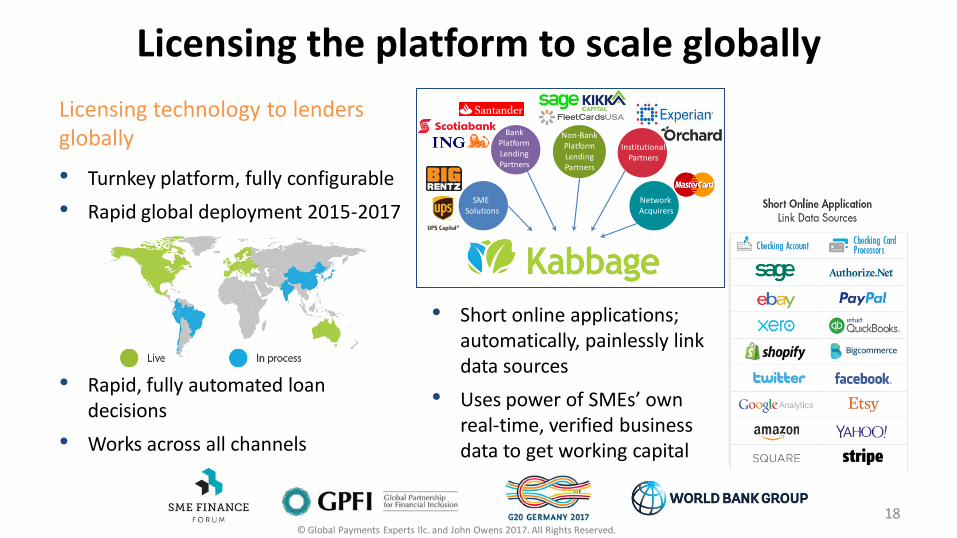

Licensing the platform to scale globally

18

Licensing technology to lenders globally

• Turnkey platform, fully configurable

• Rapid global deployment 2015-2017

• Rapid, fully automated loan decisions

• Works across all channels

• Short online applications; automatically, painlessly link data sources

• Uses power of SMEs’ own real-time, verified business data to get working capital

SME Solutions

Non-Bank Platform LendingPartners

Network Acquirers

Institutional Partners

Bank Platform LendingPartners

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

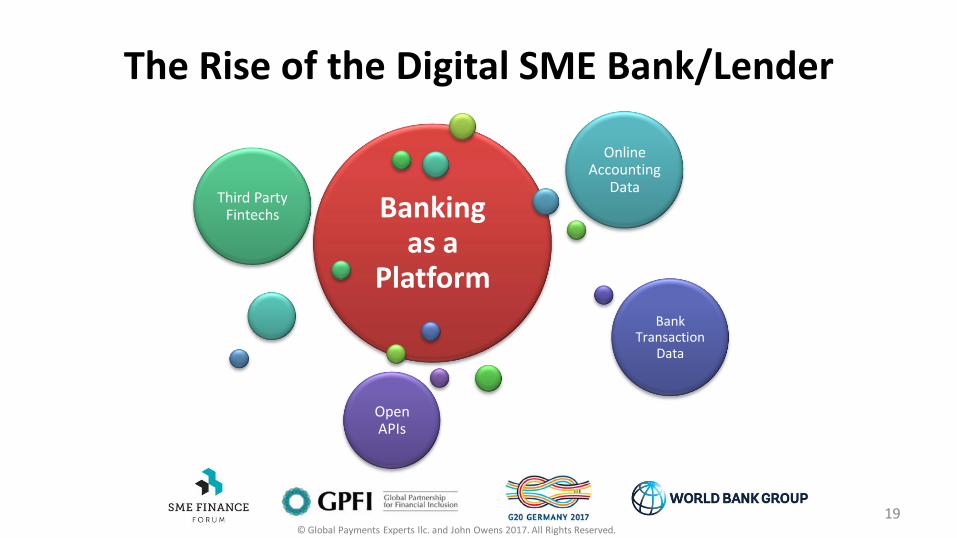

The Rise of the Digital SME Bank/Lender

Banking as a

Platform

Third Party Fintechs

Online Accounting

Data

Bank Transaction

Data

Open APIs

19

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Alternative Data: Policy Issues and Challenges

• Data privacy and consumer protection issues

• Opt-in vs opt-out models

• Credit reporting sharing and access

• Cyber security

• Transparency & disclosure

• Balancing integrity, innovation and marketplace competition

20

© Global Payments Experts llc. and John Owens 2017. All Rights Reserved.

Thanks

@jvowens

@wilhelminc

21