Embed Size (px)

Citation preview

AMERICAN ARBITRATION ASSOCIATION CONSTRUCTION INDUSTRY ARBITRATIONTRIBUNAL: AWARD IN THE MATTER OF THE ARBITRATION BETWEEN PHILIP MORRISINTERNATIONAL FINANCE CORPORATION and OVERSEAS PRIVATE INVESTMENTCORPORATION (Inconvertibility Claim in the Dominican Republic)Source: International Legal Materials, Vol. 27, No. 2 (MARCH 1988), pp. 487-491Published by: American Society of International LawStable URL: http://www.jstor.org/stable/20693206 .

Accessed: 12/06/2014 12:52

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

American Society of International Law is collaborating with JSTOR to digitize, preserve and extend access toInternational Legal Materials.

http://www.jstor.org

This content downloaded from 185.44.79.22 on Thu, 12 Jun 2014 12:52:44 PMAll use subject to JSTOR Terms and Conditions

487

AMERICAN ARBITRATION ASSOCIATION CONSTRUCTION INDUSTRY ARBITRATION TRIBUNAL:

AWARD IN THE MATTER OF THE ARBITRATION BETWEEN PHILIP MORRIS INTERNATIONAL FINANCE CORPORATION

and OVERSEAS PRIVATE INVESTMENT CORPORATION*

(Inconvertibility Claim in the Dominican Republic) [December 3, 1987]

+Cite as 27 I.L.M. 487 (1988)+

I.L.M. Content Summary

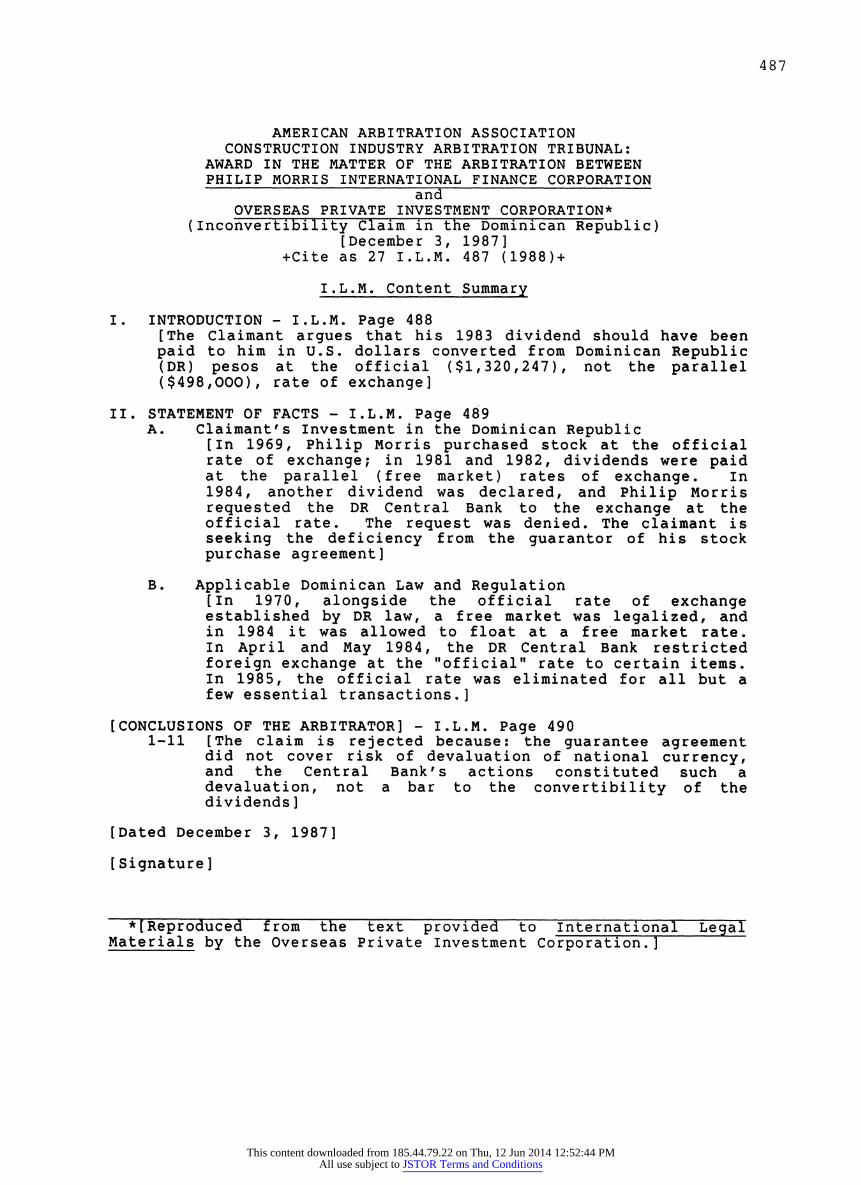

I. INTRODUCTION - I.L.M. Page 488 [The Claimant argues that his 1983 dividend should have been

paid to him in U.S. dollars converted from Dominican Republic (DR) pesos at the official ($1,320,247), not the parallel ($498,000), rate of exchange]

II. STATEMENT OF FACTS - I.L.M. Page 489 A. Claimant's Investment in the Dominican Republic

[In 1969, Philip Morris purchased stock at the official rate of exchange; in 1981 and 1982, dividends were paid at the parallel (free market) rates of exchange. In 1984, another dividend was declared, and Philip Morris requested the DR Central Bank to the exchange at the official rate. The request was denied. The claimant is seeking the deficiency from the guarantor of his stock purchase agreement]

B. Applicable Dominican Law and Regulation [In 1970, alongside the official rate of exchange established by DR law, a free market was legalized, and in 1984 it was allowed to float at a free market rate. In April and May 1984, the DR Central Bank restricted foreign exchange at the "official" rate to certain items. In 1985, the official rate was eliminated for all but a few essential transactions.]

[CONCLUSIONS OF THE ARBITRATOR] - I.L.M. Page 490 1-11 [The claim is rejected because: the guarantee agreement

did not cover risk of devaluation of national currency, and the Central Bank's actions constituted such a devaluation, not a bar to the convertibility of the dividends]

[Dated December 3, 1987]

[Signature]

*[Reproduced from t??? text provided to International Legal Materials by the Overseas Private Investment Corporation.]

This content downloaded from 185.44.79.22 on Thu, 12 Jun 2014 12:52:44 PMAll use subject to JSTOR Terms and Conditions

488

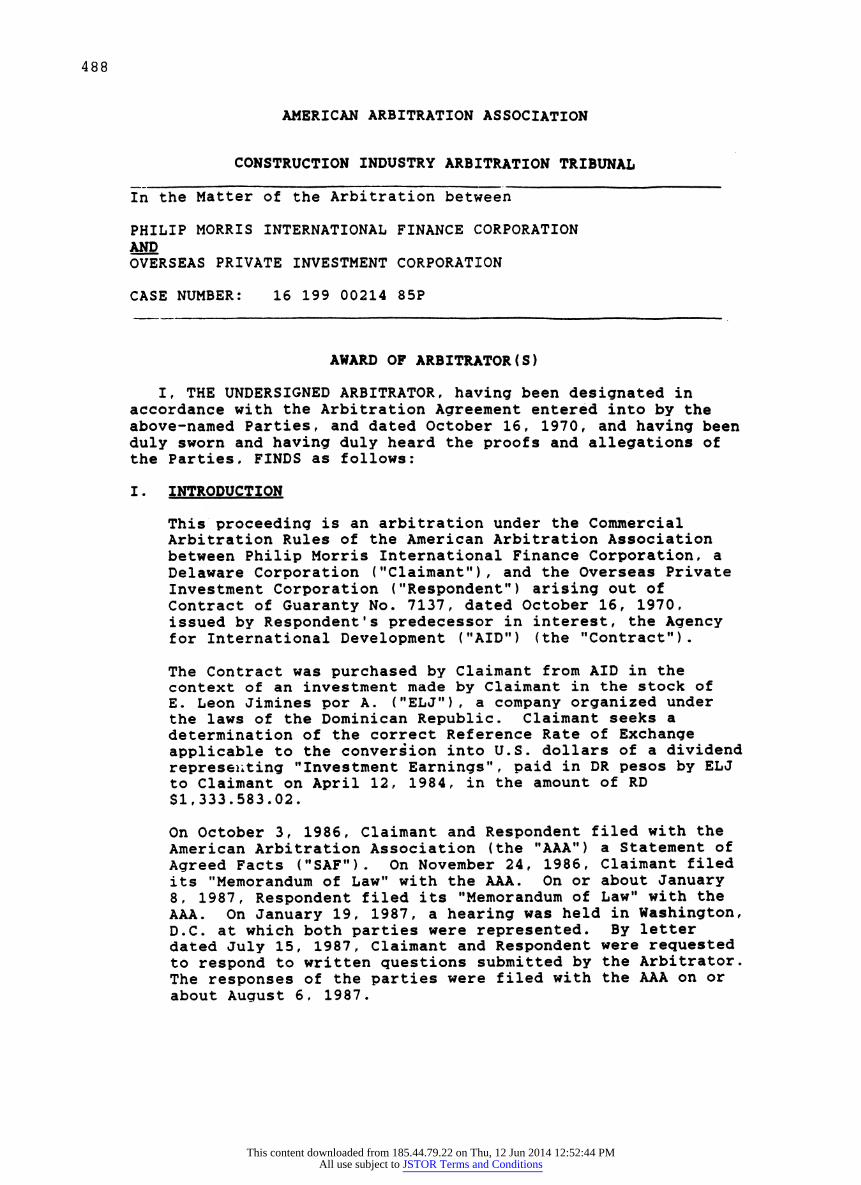

AMERICAN ARBITRATION ASSOCIATION

CONSTRUCTION INDUSTRY ARBITRATION TRIBUNAL

In the Matter of the Arbitration between

PHILIP MORRIS INTERNATIONAL FINANCE CORPORATION AND OVERSEAS PRIVATE INVESTMENT CORPORATION

CASE NUMBER: 16 199 00214 85P

AWARD OF ARBITRATOR(S)

I, THE UNDERSIGNED ARBITRATOR, having been designated in accordance with the Arbitration Agreement entered into by the above-named Parties, and dated October 16, 1970, and having been duly sworn and having duly heard the proofs and allegations of the Parties, FINDS as follows:

I. INTRODUCTION

This proceeding is an arbitration under the Commercial Arbitration Rules of the American Arbitration Association between Philip Morris International Finance Corporation, a Delaware Corporation ("Claimant"), and the Overseas Private Investment Corporation ("Respondent") arising out of Contract of Guaranty No. 7137, dated October 16, 1970, issued by Respondent's predecessor in interest, the Agency for International Development ("AID") (the "Contract").

The Contract was purchased by Claimant from AID in the context of an investment made by Claimant in the stock of E. Leon Jimines por A. ("ELJ"), a company organized under

the laws of the Dominican Republic. Claimant seeks a determination of the correct Reference Rate of Exchange applicable to the conversion into U.S. dollars of a dividend representing "Investment Earnings", paid in DR pesos by ELJ to Claimant on April 12, 1984, in the amount of RD 31,333.583.02.

On October 3, 1986, Claimant and Respondent filed with the American Arbitration Association (the "AAA") a Statement of Agreed Facts ("SAF"). On November 24, 1986, Claimant filed its "Memorandum of Law" with the AAA. On or about January 8, 1987, Respondent filed its "Memorandum of Law" with the AAA. On January 19, 1987, a hearing was held in Washington, D.C. at which both parties were represented. By letter dated July 15, 1987, Claimant and Respondent were requested to respond to written questions submitted by the Arbitrator. The responses of the parties were filed with the AAA on or about August 6, 1987.

This content downloaded from 185.44.79.22 on Thu, 12 Jun 2014 12:52:44 PMAll use subject to JSTOR Terms and Conditions

STATEMENT OF FACTS

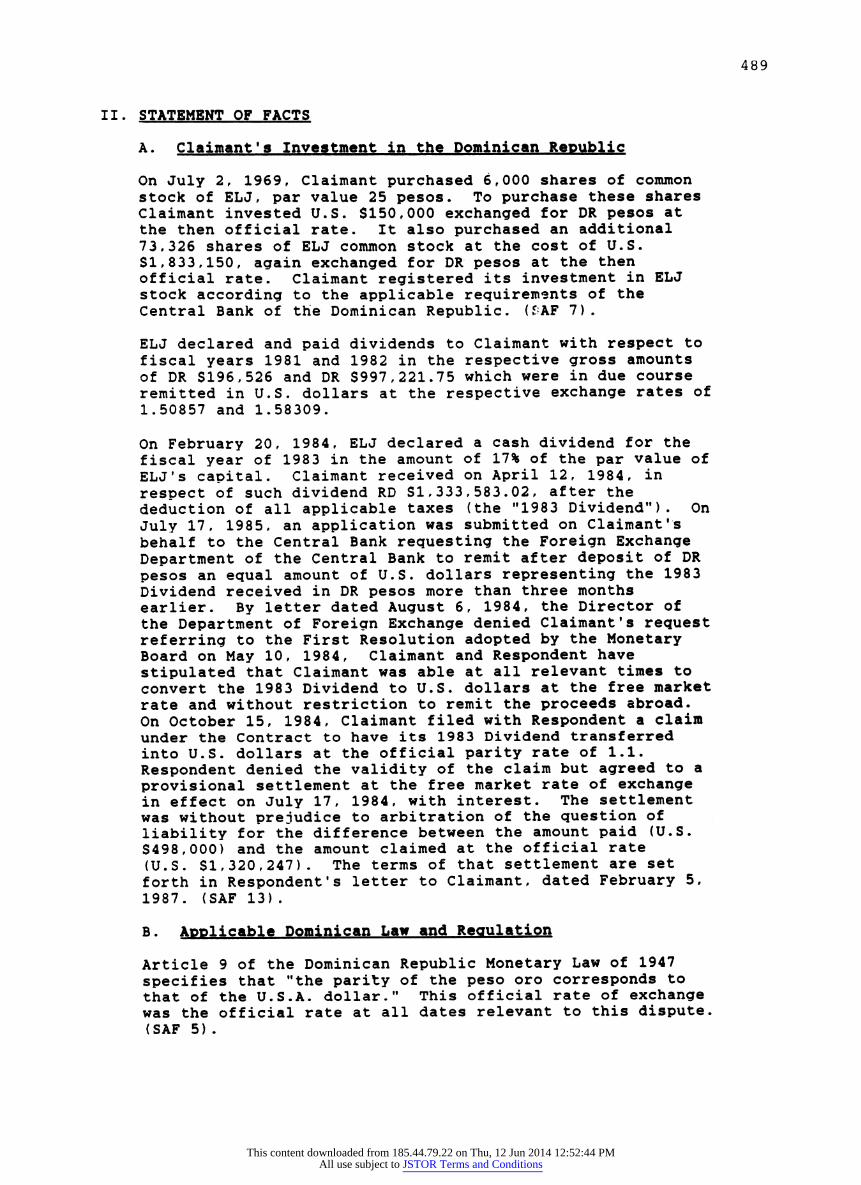

A. Claimant's Investment in the Dominican Republic

On July 2, 1969, Claimant purchased 6,000 shares of common stock of ELJ, par value 25 pesos. To purchase these shares Claimant invested U.S. $150,000 exchanged for DR pesos at the then official rate. It also purchased an additional 73,326 shares of ELJ common stock at the cost of U.S. $1,833,150, again exchanged for DR pesos at the then official rate. Claimant registered its investment in ELJ stock according to the applicable requirements of the Central Bank of the Dominican Republic. (ikF 7).

ELJ declared and paid dividends to Claimant with respect to fiscal years 1981 and 1982 in the respective gross amounts of DR $196,526 and DR $997,221.75 which were in due course remitted in U.S. dollars at the respective exchange rates of 1.50857 and 1.58309.

On February 20, 1984, ELJ declared a cash dividend for the fiscal year of 1983 in the amount of 17% of the par value of ELJ*s capital. Claimant received on April 12, 1984, in respect of such dividend RD SI, 333,583.02, after the deduction of all applicable taxes (the "1983 Dividend"). On July 17, 1985, an application was submitted on Claimant's behalf to the Central Bank requesting the Foreign Exchange Department of the Central Bank to remit after deposit of DR pesos an equal amount of U.S. dollars representing the 1983 Dividend received in DR pesos more than three months earlier. By letter dated August 6, 1984, the Director of the Department of Foreign Exchange denied Claimant's request referring to the First Resolution adopted by the Monetary Board on May 10, 1984, Claimant and Respondent have stipulated that Claimant was able at all relevant times to convert the 1983 Dividend to U.S. dollars at the free market rate and without restriction to remit the proceeds abroad. On October 15, 1984, Claimant filed with Respondent a claim under the Contract to have its 1983 Dividend transferred

into U.S. dollars at the official parity rate of 1.1. Respondent denied the validity of the claim but agreed to a

provisional settlement at the free market rate of exchange in effect on July 17, 1984, with interest. The settlement was without prejudice to arbitration of the question of liability for the difference between the amount paid (U.S. $498,000) and the amount claimed at the official rate (U.S. $1,320,247). The terms of that settlement are set forth in Respondent's letter to Claimant, dated February 5, 1987. (SAF 13).

B. Applicable Dominican Law and Regulation

Article 9 of the Dominican Republic Monetary Law of 1947 specifies that "the parity of the peso oro corresponds to that of the U.S.A. dollar." This official rate of exchange was the official rate at all dates relevant to this dispute. (SAF 5) .

This content downloaded from 185.44.79.22 on Thu, 12 Jun 2014 12:52:44 PMAll use subject to JSTOR Terms and Conditions

490

Commencing in 1970 a parallel foreign exchange market was tolerated by the Dominican authorities. In 1978, the Central Bank began limiting the categories of imports for which the official exchange rate would be made available, thereby shifting all other transactions to the depreciated parallel foreign exchange market. In 1982, the Central Bank formally recognized the parallel foreign exchange market as

legal. In 1984, the parallel markets was allowed to float at a free market rate. (SAF 11).

On April 17, 1984, the Monetary Board of the Central Bank adopted a Second Resolution which provided in relevant part that foreign exchange of the national banking system would be provided by the Central Bank only for the following items :

"a) payments for the remittance of overdue dividends relating to foreign investments registered under Law No. 861 of June 22, 1978, for which the applications for foreign exchange have been received on the date hereof by the Central Bank and found in order in accordance with the internal procedures in force in the matter ..." (translation provided)

On May 10, 1984, the Monetary Board of the Central Bank adopted a First Resolution amending its earlier resolution and providing in relevant part that the Central Bank would grant foreign exchange at official parity for specified items including:

"a) overdue payments for remittance of dividends and repatriation of capital, relative to foreign investments registered pursuant to Law No. 861, dated July 22, 1978, for which applications for foreign exchange have been received by the Central Bank as of April 17, 1984, and found in order, in accordance with the internal

procedures in effect in the matter and for which the Pesos in support of these applications have been deposited at the Central Bank before April 17, 1984." (translation provided)

In 1985, the Monetary Board of the Central Bank unified the official and free exchange rates by eliminating the official

*

rate for all but a few essential transactions and transferring almost all transactions to the free market rate.

Based upon the terms of the Contract, the applicable legislation, regulation and practice in the Dominican Republic at the dates relevant to this dispute, the

Stipulation of Facts submitted by the parties and their respective "Memoranda of Law" the Arbitrator hereby concludes as follows:

1. The Contract provided Claimant with insurance in the covered amount against inconvertibility of its Investment Earnings arising from its investment in ELJ.

This content downloaded from 185.44.79.22 on Thu, 12 Jun 2014 12:52:44 PMAll use subject to JSTOR Terms and Conditions

491

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

The dividend received by Claimant with respect to ELJ's fiscal year 1983 qualified as Investment Earnings.

The Contract did not guarantee Claimant against devaluation of the DR peso in relation to the U.S. dollar.

The progressive limitation of the cases in which foreign exchange of the national banking system would be provided at the official rate by the Central Bank of the Dominican Republic acting through its Monetary Board, as last evidenced for the purposes of this dispute by the Monetary Board's Second Resolution of May 10, 1984, was a legitimate exercise of sovereign power and constituted a devaluation of the national currency to those values applicable in the parallel market for those transactions not qualifying for application of the official rate.

Claimant was free at all times relevant to this dispute to transfer its 1983 Dividend received from ELJ into U.S. dollars at the free market rate of exchange and to remit the same abroad.

Claimant's 1983 Dividend was not, therefore, inconvertible and was remittable at the depreciated free

market rate.

In those circumstances, Claimant's demand for the difference between the amount received from Respondent and the amount which would have been received had such amount been determined at the official rate was invalid and is rejected. The risk of devaluation was not covered by the Contract, and there existed no barrier to remittance at the Insured Investment Earnings of ELJ.

The settlement by Respondent was not required by the Contract and may have been improperly made.

The administrative fees and expenses of the American Arbitration Association shall be borne equally by the parties. Said fees and expenses shall be paid as directed by the Association.

Fees for the remuneration of the Arbitrator shall be borne equally by the parties. Said fees shall be paid as directed by the Association.

This Award is in full settlement of all claims submitted to this Arbitration.

This content downloaded from 185.44.79.22 on Thu, 12 Jun 2014 12:52:44 PMAll use subject to JSTOR Terms and Conditions