Embed Size (px)

DESCRIPTION

Analysis of Working Capital Requirements in Construction- Real Estate Sector

Citation preview

Analysis of Working Capital requirements in Construction-Real Estate Sector

FINAL PROJECT REPORT ON

ANALYSIS OF WORKING CAPITAL REQUIREMENT IN CONSTRUCTION - REAL ESTATE SECTOR

SUBMITTED IN PARTIAL FULFILLMENT OF

MASTER OF MANAGEMENT STUDIES

(M.M.S.) 2012 – 2014

UNDER THE SUPERVISION OF:

CA. AJIT JOSHI

BY

YOGITA M. PAWAR

ROLL NO 34

M.M.S.2012 – 2014

PTVA’s INSTITUTE OF MANAGEMENT

VILE PARLE (EAST)

MUMBAI.

1

Analysis of Working Capital requirements in Construction-Real Estate Sector

CERTIFICATE

2

Analysis of Working Capital requirements in Construction-Real Estate Sector

DECLARATION

I, Ms. Yogita Pawar MMS Student of Parle Tilak Vidyalaya Association’s Institute of Management, hereby declare that I have completed the project titled ‘Analysis of working capital requirement in construction-real estate sector’ during the academic year 2014.

The report work is original and the information/data and the references included in the report are true to the best of my knowledge. Due credit is extended on the work of Literature/Secondary Survey by endorsing it in the Bibliography as per the prescribed format.

Signature of the Student with Date

Name of Student

Yogita M. Pawar

M.M.S Finance (2012-2014)

Roll No: 34

3

Analysis of Working Capital requirements in Construction-Real Estate Sector

ACKNOWLEDGEMENT

I would like to express my gratitude to few people who have been instrumental in making this

project a success. With a pleasure I take the opportunity to express my sincere thanks and

obligation to my esteemed guide CA. Ajit Joshi. It is because his able and mature guidance and

co-operation without which it would not have been possible for me to complete my project.

I am thankful to Mr. Milind Joshi for his unconditional support and constant guidance which

helped me tremendously in giving the right direction and in successfully completing this

project.Without their care and consideration this report would not have been completed.

I have tried my best to present the information as clearly as possible using basic terms that I hope

will be comprehend by the wildest spectrum of researchers, analysts and students for further

studies.

Finally, I gratefully acknowledge the support, encouragement & patience of my family, and as

always, nothing in my life would be possible without God, Thank You!

4

Analysis of Working Capital requirements in Construction-Real Estate Sector

TABLE OF CONTENTS

SR.NO Particulars Page No

1 Introduction 8

1.1 Working capital management 8

1.2 The need for working capital in construction sector 9

1.3 The importance of working capital management in construction sector

10

1.4 Profile of companies under the study 12-13

2 Literature Review 14-17

3 Objective Of The Study 18

4 Research Methodology 19

5 Data analysis of 5 companies 20

5.1 Ratio Analysis 20-29

5.2 Analysis of the liquidity position by Motaal’s Comprehensive test 30-31

6 Limitation of the study 32

7 Conclusion 33-34

8 Bibliography 35

5

Analysis of Working Capital requirements in Construction-Real Estate Sector

LIST OF GRAPHS

Graph No Particulars Page No.

1 Current Ratio 20

2 Quick Ratio 22

3 Working Capital Turnover Ratio 24

4 Inventory Turnover Ratio 25

5 Total Assets Turnover Ratio 27

6 Fixed assets turnover ratio 28

6

Analysis of Working Capital requirements in Construction-Real Estate Sector

EXECUTIVE SUMMARY

Working capital policy is an important issue in any organization because without the proper

management of working capital components it will be difficult for the organizations to run its

operations smoothly. Working capital management is significant due to the fact that it plays a

vital role in keeping the wheels of the business running.

This project emphasis on study on working capital requirements with reference to five

construction- real estate sector companies. The study is done on five companies DLF Ltd,

Unitech, Ansal API, Sobha developers and Parsvnath developers over the period of five years

from 2009-2013. The determinants that may have effect on working capital derived from the

ratio analysis.

The importance of efficient working capital management (WCM) is indisputable. Moreover, the

adequate and timely flow of inventory is imperative for the success and growth of any company.

This project is an attempt to study in depth ratio analysis of Indian Construction- real estate

companies and its impact on working capital efficiency.

In this project a study on the liquidity position of five Indian construction- real estate companies

has been done to know the liquidity position of the companies. Analysis is done through

Motaal’s Liquidity test.

7

Analysis of Working Capital requirements in Construction-Real Estate Sector

1. INTRODUCTION

1.1 Working Capital Management

Working capital may be regarded as life blood of a business. Working Capital is the amount of

capital that a business has available to meet the day to day cash requirements of its operations. It

is concerned with the problem arise in attempting to manage the current assets, the current

liabilities and the inter relationship that exist between them. Working Capital is the difference

between resources in cash or readily convertible into cash and organizational commitments for

which cash will soon be required or within one year without undergoing a diminution in value

and without disrupting the operation of the firm. It also refers to the amount of current Assets

that exceeds current Liabilities.

Working Capital refers to that part of the firm capital, which is required for financing Short-

Term or Current Assets such as Cash, Marketable Securities, Debtors and Inventories. Working

Capital is also known as Revolving or Circulating Capital or Short Term Capital. The goal of

working capital management is to manage the firm’s current assets and current liabilities in such

way that the satisfactory level of working capital is mentioned. The current should be large

enough to cover its current liabilities in order

to ensure a reasonable margin of the safety.

Capital required for a business can be classifies under two main categories:

Fixed Capital

Working Capital

Every business needs funds for two purposes for its establishments and to carry out day to day

operations. Long term funds are required to create production facilities through purchase of fixed

assets such as plant and machinery, land and building, furniture etc. Investments in these assets

are representing that part of firm’s capital which is blocked on a permanent or fixed basis and is

called fixed capital. Funds are also needed for short term purposes for the purchasing of raw

materials, payments of wages and other day to day expenses etc. These funds are known as

working capital. In simple words, Working capital refers to that part of the firm’s capital which

8

Analysis of Working Capital requirements in Construction-Real Estate Sector

is required for financing short term or current assets such as cash, marketable securities, debtors

and inventories

1.2 The need for Working Capital in Construction Sector

The need for working capital cannot be over emphasized. Every business needs some amount of

working capital. The need for working capital arises due to the time gap between production and

realization of cash from sales. There is an operating cycle involved in the sales and realization of

cash.

Construction is an essential part of any country’s infrastructure and industrial development. The

Indian construction sector is an integral part of the economy and a conduit for a substantial part

of India’s development investment. Forecasting working capital along with cash requirements is

essential for all construction contractors during the tendering stage since cash flow at the

beginning of the project is a major cause of construction companies’ failure. In the contracting

business, construction firms are generally more concerned with short-term financial strategies

than the long term ones. Working capital management is the central issue of all short-term

financial concerns.

Factors requiring consideration while estimating working capital in construction projects:

The average credit period expected to be allowed by suppliers

Total costs incurred on material, wages.

The length of time for which raw material are to remain in stores before they are issued

for production.

The length of production cycle or work in process.

The length of sales cycle during which finished goods are to be kept waiting for sales.

The average period of credit allowed to customers.

The amount of cash required to make advance payment.

Optimization of working capital balance means minimizing the working capital requirements and

realizing maximum possible revenues. Efficient WCM increases firms’ free cash flow, which in

turn increases the firms’ growth opportunities and return to shareholders. Even though firms

traditionally are focused on long term capital budgeting and capital structure, the recent trend is

that many companies across different industries focus on WCM efficiency. An understanding of

9

Analysis of Working Capital requirements in Construction-Real Estate Sector

working capital is crucial to understanding and analyzing the financial position of construction

contractors.

1.3 Importance of Working Capital Management in the

Construction Industry

Traditionally construction business is a low margin business, where the margins can get wiped

out fairly fast if the projects are not executed on time and to requisite quality. Working capital

management is the cornerstone of the construction industry. The working capital requirements

flow from the fact that the contractor has to show considerable progress in project execution

before he can bill his client. And once the bill is raised, the client does get some time before he

has to pay up.

Construction contracts are of two types cost plus contract and fixed price contract. In a cost plus

contract, the contractor is reimbursed for permitted costs (permitted as per the construction

contract) plus a percentage of those costs or a fixed fee. These contracts are typically awarded

for projects in which it is very difficult for the owner of the project as well as the contractor to

estimate project costs upfront. This is typically the case for one‐off projects or projects where the

scope of work cannot be defined clearly upfront. In a fixed price contract, the contractor agrees

to a fixed contract price and bears the risk of cost over runs. Typically, these projects are

awarded by the owner by inviting a few chosen contractors to bid for constructing the project,

after clearly describing the scope of work, theexpected performance of the completed project etc.

Usually the owner awards the project for execution to the contractor who bids the lowest price.

Needless to say, considering the higher risks to the contractor than from fixed price contracts,

they yield higher margins if the project is executed flawlessly.

In a fixed price contract, once the contract is awarded, the contract price becomes sacrosanct and

few escalations are allowed. The contractor agrees to pay liquidated damages to the owner for

any delay in project execution. These damages could be structured as penalty per day’s delay,

with or without an upper cap on the extent of damages. Damages would also have to be paid

10

Analysis of Working Capital requirements in Construction-Real Estate Sector

should the delivered project fall short on performance grounds. Even at the bidding stage for a

project, the bidders would have to post bid bonds in the form of bank guarantees in favor of the

project owner. This is to assure the owner that the bidder is serious in his bid. If a contractor is

awarded the project,but tries to back out of entering into a firm contract, the project owner can

cash in the bid bond. Once a project is completed, before the contractor gets his final payment,

he has to post a performance guarantee bond in favor of the owner, which the owner can cash in

if the project does not perform to requisite specifications. As a part of their business, contractors

have to factor in bank guarantee expenses for bid bonds and performance bonds. Liquidated

damages and performance bonds create contingent liabilities for construction contractors.

Contractors typically have more receivables than inventory (as work in progress projects are

referred to in some parts of the world). Basically, the work in progress bit is the revenue the

company has booked in its income statement along with associated costs, but has not billed the

client for. The moment the contractor bills the client, the work‐in‐progress head gets converted

into receivables. The moment a project owner awards a project to a contractor, he pays the

contractor a certainamount as customer advance. This is recognized as a current liability under

the head customeradvances. As the contractor starts executing the project and recognizing

revenue, he writes down thecustomer advance. This can be an excellent source of financing for

the contractors at the early stageof a project.

Construction, like any other business, requires short term working capital for its existence. When

youstart a construction project, you will only have a limited amount of money. This money can

be thesavings from your previous project or the upfront money given by the client for this

project.Unfortunately, this money may not be enough to complete the project. You will have to

incuroverheads to run your business besides paying salaries to the people who work for you. A

majorexpense for you will be the procurement of raw materials like cement, structured steel and

nonferrousmetal to get on with the work. These materials can cost much more than what you

have andso it is important to have an alternate source of funding. So, what can one do to meet

theintermediate needs of construction projects? The best solution is to predict factors for

consideringand determining working capital requirement for construction projects.

11

Analysis of Working Capital requirements in Construction-Real Estate Sector

1.4 Profile of Companies under study

The Indian real estate sector has traditionally been an unorganized sector but it is slowly

evolving into a more organized one. The sector is embracing professional standards and

transparency with open arms. The major established domestic players in the sector are DLF,

Unitech, Hiranandani Constructions, Tata Housing, Godrej Properties, Omaxe, Parsvanath,

Raheja Developers, Ansal Properties and Infrastructure and Mahindra Lifespace Developers Ltd

to name a few. International players who have made a name for themselves in India include

Hines, Tishman Speyer, Emaar Properties, Ascendas, Capitaland, Portman Holdings and Homex.

DLF Ltd

DLF group is a leading real estate developer in India since 1946. DLF has been instrumental in

putting Gurgaon on the urban landscape of India. DLF has over 220 million sq. ft. of existing

development projects and 574 million sq. ft. of planned projects. DLF has so far developed 22

urban colonies, and an entire integrated 3,000-acre township - DLF City. DLF's development

projects across India span over 30 cities: Gurgaon, Ambala, Shimla, Amritsar, Jalandhar,

Ludhiana, Sonepat, Panipat, Chandigarh, Panchkula, Noida, New Delhi, Jaipur, Indore,

Ahemdabad, Baroda, Lucknow, Faridabad, Mumbai, Pune, Nagpur, Goa, Kochi, Kokkanad,

Chennai, Bangalore, Vytilla, Coimbatore, Hyderabad, Bhubhaneshwar and Kolkata.

UNITECH

Established in 1972, Unitech is India’s leading real estate developer in India. It is the first

developer to have been certified ISO 9001:2000 in North India. Project Spectrum: Unitech offers

diversified projects across residential, commercial/IT parks, retail, hotels, amusement parks and

SEZs segments. Unitech was the first real estate company to be part of the National Stock

Exchange’s NIFTY 50 Index. The company has over 600,000 shareholders. Unitech and Norway

based Telenor Group came together to build Uninor – a telecommunication services company

providing GSM services across India.

12

Analysis of Working Capital requirements in Construction-Real Estate Sector

ANSAL API

Established in 1967 as a family business, Ansal API today is clearly amongst the real estate

leaders of India. Having established itself very strongly in the NCR region, Ansal API is now

focusing on ventures in cities like Bhatinda, Mohali, Amritsar, Ludhiana, Jalandhar, Jaipur,

Jodhpur, Ajmer, Sonepat, Panipat, Karnal, Kurukshetra, Faridabad, Gurgaon, Greater Noida, and

Ghaziabad, Meerut, Agra, Lucknow, to name a few. Ansal API has till date, developed and

delivered more than 190 million sq ft. The company currently has a land reserve of about 9,335

acres. Project Spectrum: Integrated Townships, Condominiums, Group Housing, Malls,

Shopping Complex, Hotels, SEZs, IT Parks and Infrastructure and Utility Services

SOBHA DEVELOPERS LTD.

The Company was founded in 1995 by PNC Menon after he returned home from the Middle East

where he was acclaimed for quality interiors and construction since 1977. Today, this Rs10

billion plus company is one of the largest and only backward integrated company in the

construction arena. Its IPO in 2006 was oversubscribed by 126 times that created history, being

the first event of its kind in Indian capital markets. Till date, Sobha has completed 47 residential

projects, 13 commercial projects and 166contractual projects covering about 36 million sqft area

in 18 cities across India (as of 31 March 2010). The company currently has 21 ongoing

residential projects aggregating to 8.5 million sqft, while 4.24 million sqft of contractual projects

are under various stages of construction.

PARSVNATH DEVELOPERS LTD

Incorporated in July 1990 by Mr Jain in New Delhi, Parsvnath today has a substantial pan India

presence in over 45 cities across 16 states. The company has emerged as one of the most

progressive and multi faceted real estate and construction entities in India. Project spectrum:

Housing (premium, mid-market as well as affordable), office complexes, shopping malls &

hypermarkets, hotels, multiplexes, IT Parks and SEZs.

13

Analysis of Working Capital requirements in Construction-Real Estate Sector

2. LITERATURE REVIEWEvery business needs funds for two purposes basically; they are for establishment and to carry

day-to-day operations. Long term funds are required for establishment of the organization, it is

required for production facility through purchase of fixed assets and it needs fixed capital and the

funds which are needed for short term purposes for the purchase of raw materials, payment of

wages, payment of day to day expenses etc, the funds required for these are known as Working

Capital.

Working capital refers to that part of the firm's capital which is required for financing short term

or current assets such as cash, marketable securities, debtors and inventories. Funds, thus,

invested in current assets keep revolving fast and are being constantly converted into cash and

this cash flow out in exchange for other current assets. Hence it is also known as Circulating

capital or Revolving capital or Short term capital.

Agarwal (1988) devised the working capital decision as a goal programming problem, giving

primary importance to liquidity, by targeting the current ratio and quick ratio. The model

included three liquidity goals, two profitability goals, and, at a lower priority level, four current

asset sub-goals and a current liability sub-goal (for each component of working capital). In

particular, the profitability constraints were designed to capture the opportunity cost of excess

liquidity (in terms of reduced profitability).

Reddy (1995) in his study on “Management of working capital”, studies various issues related to

working capital management among selected (six companies) private large – scale companies in

the state of Andhra Pradesh during the period from 1977 to 1986 . The study revealed that

investment in current assets was more than that of fixed assets and inventories constituted

highest percentage of total current assets. Study also pointed out that the liquidity and solvency

position of sample units was found to be highly unsatisfactory. The study is based on his

findings, suggested the direct need for improvement of liquidity and solvency position of sample

companies failing which the situation would lead to serious liquidity crunch.

14

Analysis of Working Capital requirements in Construction-Real Estate Sector

According to Genestenberg

"Circulating capital means current assets of a company that are changed in the ordinary course of

business from one form to another, as for example, from cash to inventories, inventories to

receivables into cash."

Need for working capital cannot be over emphasized. Every business needs some amount of

working capital. The need of working capital arises due to the time gap between production and

realization of cash from sales. Thus, the working capital is needed for the following purposes:-

a) For the purchase of raw materials, components and spares.

b) To pay wages and salaries.

c) To incur day-to-day expenses and overhead costs such as fuel, power and office expenses etc.

d) To meet the selling costs as packing, advertising etc.

e) To provide credit facility to customers.

f) To maintain the inventories of raw material, work-in-progress, stores and spares and finished

stock.

For studying the need of working capital in a business, one has to study the business under

varying circumstances such as a new concern, as a going concern and as one which has attained

maturity. Many researchers have studied working capital from different views and in different

environments. The following ones were very interesting and useful for research

According to Ghosh and Maji, in 2003

In this paper made an attempt to examine the efficiency of working capital management of the

Indian cement companies during 1992 – 1993 to 2001 – 2002. For measuring the efficiency of

working capital management, performance, utilization, and overall efficiency indices were

calculated instead of using some common working capital management ratios. Setting industry

norms as target-efficiency levels of the individual firms, this paper also tested the speed of

achieving that target level of efficiency by an individual firm during the period of study.

Findings of the study indicated that the Indian Cement Industry as a whole did not perform

remarkably well during this period.

15

Analysis of Working Capital requirements in Construction-Real Estate Sector

Kenley and Wilson (1989) developed a model to forecast the net cash flow of construction

projects. The model is found to have an excellent fit for the data for 80% of the projects analyzed

and is useful for the post-examination of a construction project’s net cash flows. This model is

very flexible and capable of adapting to a wide degree of inter-project variability.

Kaka (1996) suggested that further variables be added to enhance the flexibility of the cash flow

produced and proposed a model designed to use more than 50 variables to calculate cash flow for

one individual contract. He also listed five disadvantages of the traditional cash flow model, but

the terms of payment being applied in his model do not suit the terms applied in India.

Singh and Pandey (2008) suggested that, for the successful working of any business

organization, fixed and current assets play a vital role, and that the management of working

capital is essential as it has a direct impact on profitability and liquidity. They studied the

working capital components and found a significant impact of working capital management on

profitability for Hindalco Industries Limited.

Niranjan Mandal and Dutta Smriti Mahavidyalaya, (2010) in their study makes an attempt to

provide an insight into the conceptual side of working capital and to assess the impact of

working capital management on liquidity, profitability and non-insurable risk of ONGC, a

leading public sector enterprise in India over a year period (i.e. from 1998-99 to 2006-07). It also

makes an endeavour to observe and test the liquidity and profitability position of the enterprise

and to study the correlation between liquidity and profitability as well as betweenprofitability

and risk. They may be concluded that working capital management is very muchuseful to ensure

better productive capacity, good profitability and sound liquidity of anenterprise, specifically the

PSE in India, for managerial decision making regarding the creationof sufficient surplus for its

growth and survival stability in the present competitive and complexenvironment.

Brahma (2011) conducted a study to examine and evaluate the importance of liquidity

management on profitability as a factor accountable for poor financial performance in the private

sector steel Industry in India.

16

Analysis of Working Capital requirements in Construction-Real Estate Sector

Article on ‘Working Capital Management in Projects – Case study on Indian Construction

Companies’ by Dr. Hiren Maniar (2011) In this study, it shows that Indian construction sector

is an integral part of the economy and conduit for a substantial part of India’s development

investment. Working capital management is the central issue of all short-term financial concerns.

Main purpose of this research is to establish relationship among the factors like inflation, labor

wages, material cost, construction equipment & machineries cost, subcontractor charges and

overhead cost that contributes to LWC requirements and presents a simple model that could be

used as a guide to estimate LWC for construction projects in India. An understanding of working

capital is crucial to understanding and analyzing the financial position of construction

contractors. The question posed in this subject are:

Why analyze working capital?

What is working capital?

How does it compare to current ratios?

What are the concerns of the surety and the banker?

How much working capital is enough, and how is that determined?

Is there such a thing as too much working capital?

How does company enhance working capital?

Main outcome of this paper is to establish the relationship among the factors responsible for

LWC requirements and presents a simple model that could be used as a guide to estimate the

LWC for Infrastructure projects in India.

17

Analysis of Working Capital requirements in Construction-Real Estate Sector

3. OBJECTIVE OF THE STUDY

Primary Objective:

To understand why there is need to analyze working capital of construction company

Secondary Objective:

To know How to improve working capital position of the company.

To examine the efficiency of working capital management practices of construction- real

estate sector.

To examine effective utilization of working capital.

To study the working capital management of DLF Ltd, Unitech, Ansal API, Sobha

developers and Parsvnath developers by analyzing liquidity position of the companies.

18

Analysis of Working Capital requirements in Construction-Real Estate Sector

4.RESEARCH METHODOLOGY

Data Source

The samples selected of five construction- real estate companies of Indian construction-

real estate sector namely, DLF Ltd, Unitech, Ansal API, Sobha Develpoers, Parsvanath

developers.. This study is based on secondary data. The study is based on the secondary

data obtained from the audited balance sheets and profit & loss accounts and also the

annual reports of the respective companies. Besides, the facts, figures and findings

advanced in similar earlier studies and the government publications are also used to

supplement the secondary data.

Study period

Study period is chosen from 2009-2013 i.e. 5 years.

Tools and techniques of data analysis

The data collected from the published annual reports of the selected company for the

eight years period have been suitably arranged, classified and tabulated as per

requirement for the study. Ratio analysis is used.

19

Analysis of Working Capital requirements in Construction-Real Estate Sector

5.DATA ANALYSIS OF 5 SELECTED COMPANIES

5.1 Ratio Analysis

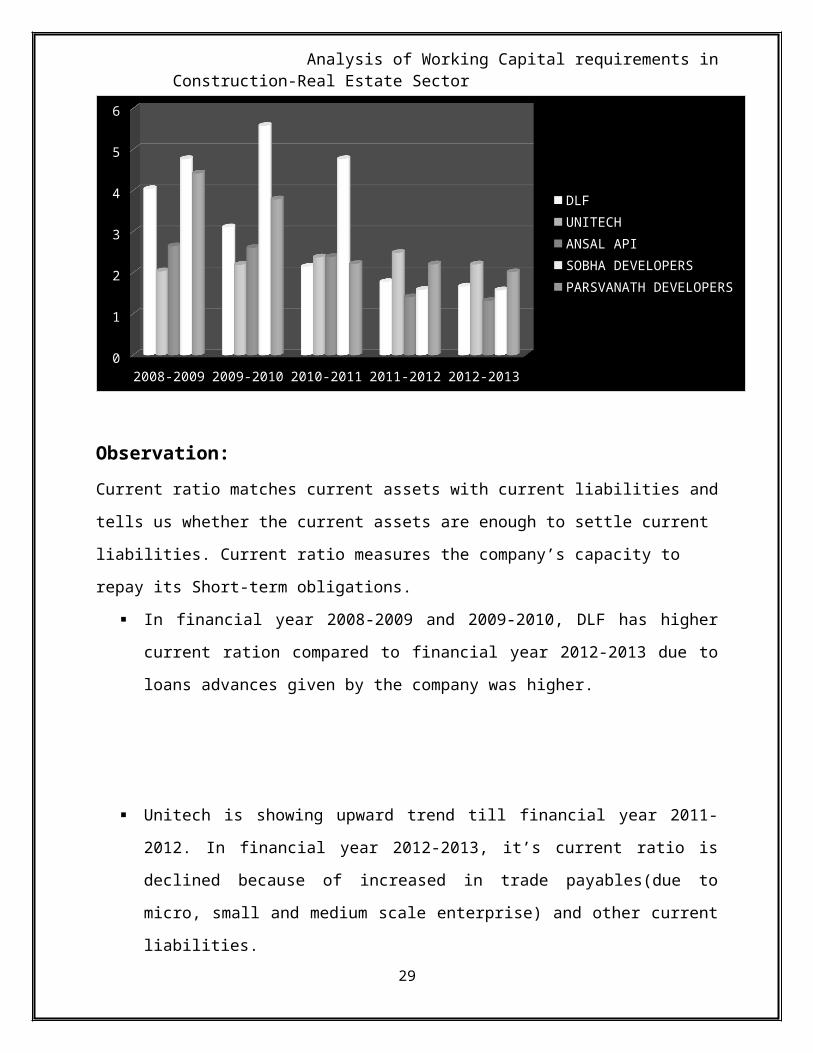

1. Current ratio

Company 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013DLF 4.04 3.11 2.15 1.78 1.67UNITECH 2.04 2.2 2.38 2.49 2.21ANSAL API 2.65 2.61 2.39 1.41 1.32SOBHA DEVELOPERS 4.77 5.58 4.77 1.59 1.58PARSVNATH DEVELOPERS 4.42 3.79 2.22 2.21 2.02

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

1

2

3

4

5

6

DLFUNITECHANSAL APISOBHA DEVELOPERSPARSVANATH DEVELOPERS

Observation:

Current ratio matches current assets with current liabilities and tells us whether the current assets

are enough to settle current liabilities. Current ratio measures the company’s capacity to repay its

Short-term obligations.

In financial year 2008-2009 and 2009-2010, DLF has higher current ration compared to

financial year 2012-2013 due to loans advances given by the company was higher.

20

Analysis of Working Capital requirements in Construction-Real Estate Sector

Unitech is showing upward trend till financial year 2011-2012. In financial year 2012-

2013, it’s current ratio is declined because of increased in trade payables(due to micro,

small and medium scale enterprise) and other current liabilities.

Ansal API’s current ratio trend is decreasing because it’s current liabilities such as

current maturities of long term debt and advances from customers against flats, shops,

houses and plots etc. increases without a corresponding increase in current assets.

In financial year 2008-2009, 2009-2010 and 2010-2011, Sobha Developers’ current ratio

is showing high because loans and advances were in large amount. This is mainly due to

increase in advance towards purchasing land at Rs.17,958 million (as on March 31, 2009)

from Rs. 16,248 million (as on March 31, 2008). Advances are primarily towards amount

paid in advance for value and services to be received in future. The Company considers

the advances/ deposit for land good as the advances have been given based on

arrangements/ Memoranda of Understanding executed by the Company and the

Company/ seller/ intermediary is in the course of obtaining clear and marketable titles

free from all encumbrances.. In this case deposits paid by the group to seller to seller was

right for development of land in exchange of constructed area are recognized as land

advance under loans and advances, unless they are non-refundable, wherein they are

transferred to work-in-progress on the launch of project. The current ratio is too high in

financial year 2009 to 2011, it means the company was not using its current assets or its

short-term financing facilities efficiently. This may also indicate problems in working

capital management. But, in financial year 2011-2012 and 2012-2013, company

recovered and maintained good current ratio.

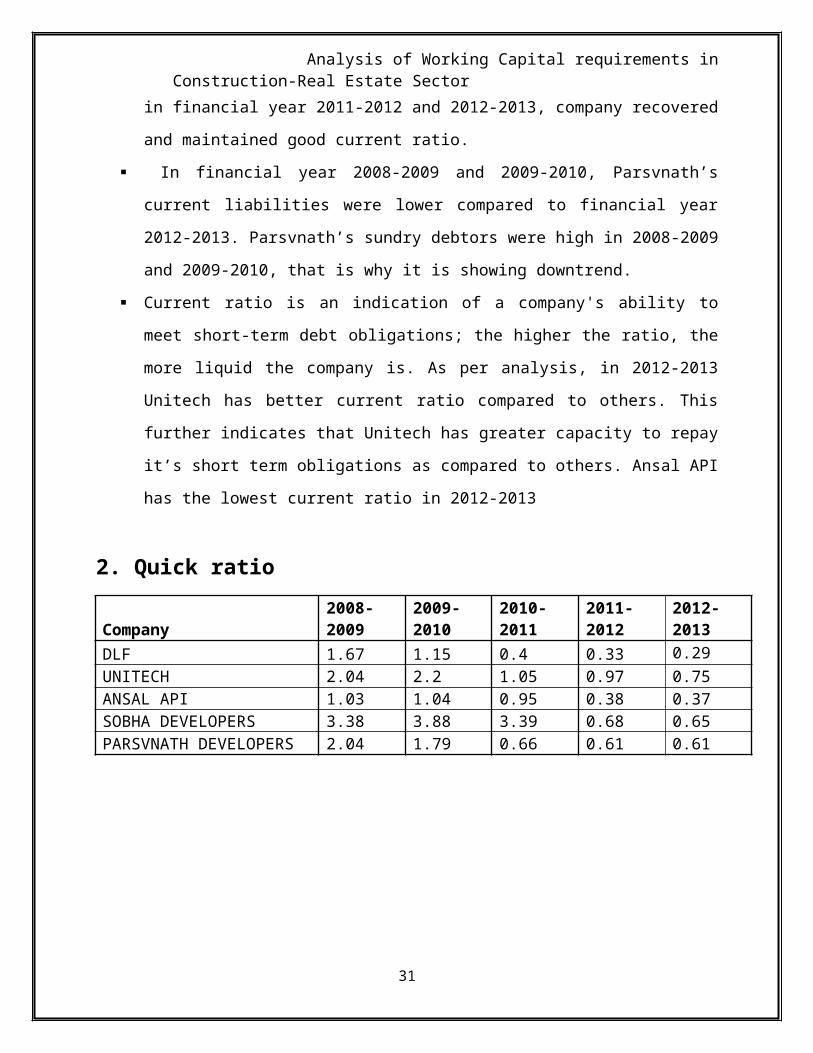

In financial year 2008-2009 and 2009-2010, Parsvnath’s current liabilities were lower

compared to financial year 2012-2013. Parsvnath’s sundry debtors were high in 2008-

2009 and 2009-2010, that is why it is showing downtrend.

Current ratio is an indication of a company's ability to meet short-term debt obligations;

the higher the ratio, the more liquid the company is. As per analysis, in 2012-2013

Unitech has better current ratio compared to others. This further indicates that Unitech

has greater capacity to repay it’s short term obligations as compared to others. Ansal API

has the lowest current ratio in 2012-2013

21

Analysis of Working Capital requirements in Construction-Real Estate Sector

2. Quick ratio

Company 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013

DLF 1.67 1.15 0.4 0.33 0.29

UNITECH 2.04 2.2 1.05 0.97 0.75ANSAL API 1.03 1.04 0.95 0.38 0.37SOBHA DEVELOPERS 3.38 3.88 3.39 0.68 0.65PARSVNATH DEVELOPERS 2.04 1.79 0.66 0.61 0.61

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

0.5

1

1.5

2

2.5

3

3.5

4

DLFUNITECHANSAL APISOBHA DEVELOPERSPARSVANATH DEVELOPERS

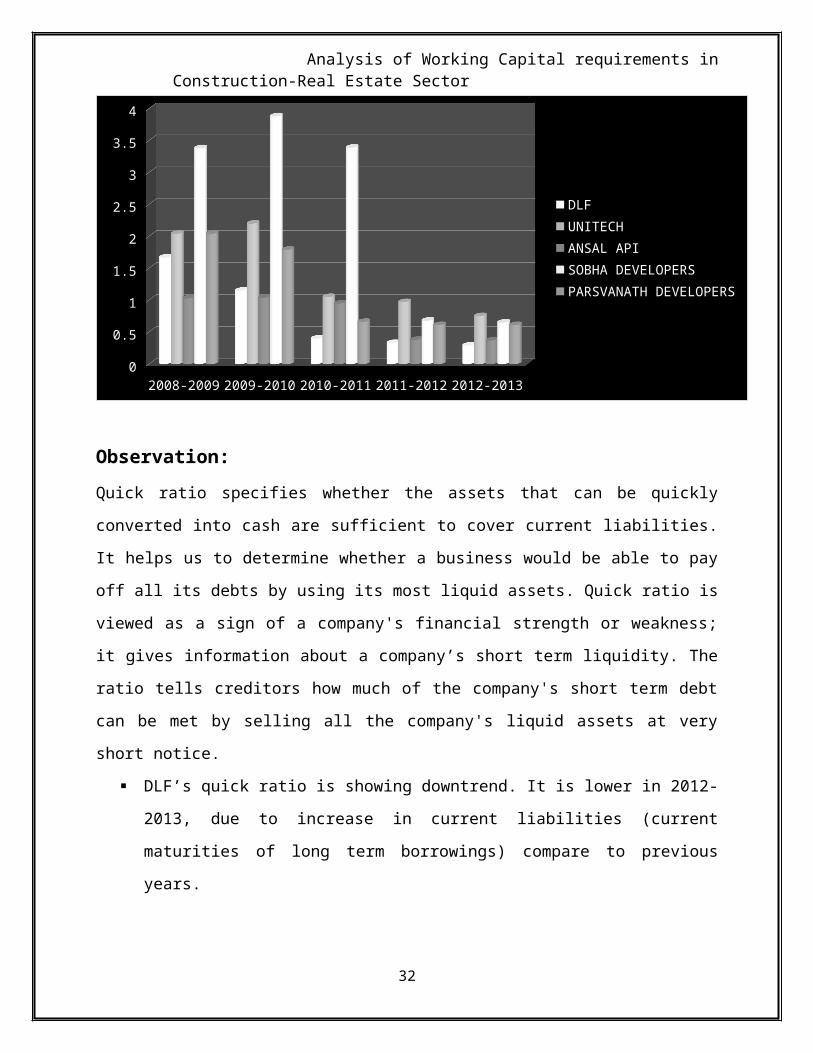

Observation:

Quick ratio specifies whether the assets that can be quickly converted into cash are sufficient to

cover current liabilities. It helps us to determine whether a business would be able to pay off all

its debts by using its most liquid assets. Quick ratio is viewed as a sign of a company's financial

strength or weakness; it gives information about a company’s short term liquidity. The ratio tells

creditors how much of the company's short term debt can be met by selling all the company's

liquid assets at very short notice.

DLF’s quick ratio is showing downtrend. It is lower in 2012-2013, due to increase in

current liabilities (current maturities of long term borrowings) compare to previous years.

22

Analysis of Working Capital requirements in Construction-Real Estate Sector

In 2012-2013, Unitech has better ability to meet it’s short term obligations.

Ansal API’s Liquid ratio is consistently going down due to increased in other current

liabilities such as current maturities of long term debt and advances from customers

against flats/shops/houses/plots etc.

In financial year 2008-2009, 2009-2010 and 2010-2011, Sobha Developers’ quick ratio is

showing high because loans and advances were in large amount. But in financial year

2012-2013, it’s ratio is looking better compared to previous years.

Parsvnath developer’s sundry debtors were large in amount and in financial year 2008-

2009 and 2009-2010 compared to financial year 2012-2013.

The quick ratio is more conservative than the current ratio because it excludes inventory

and other current assets, which are more difficult to turn into cash. Quick ratio is a

measure of a company's ability to settle its current liabilities on a very short notice.

Current ratio may provide a misleading indication of a company's liquidity position when

a considerable portion of its current assets is illiquid. Quick ratio is therefore a more

reliable measure of liquidity for construction firms that have relatively high levels of

inventory, work in progress and receivables. Therefore, a higher ratio means a more

liquid current position. In the above case Unitech has a better short term solvency

position whereas DLF’s quick ratio is lowest among all.

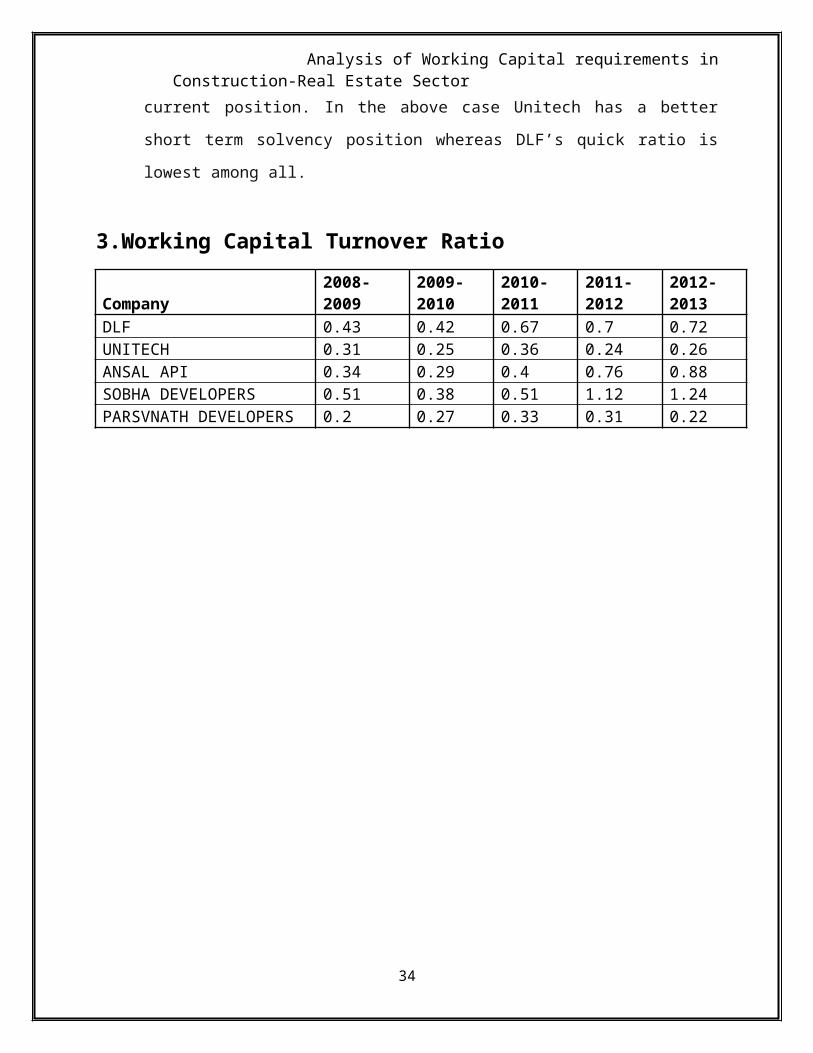

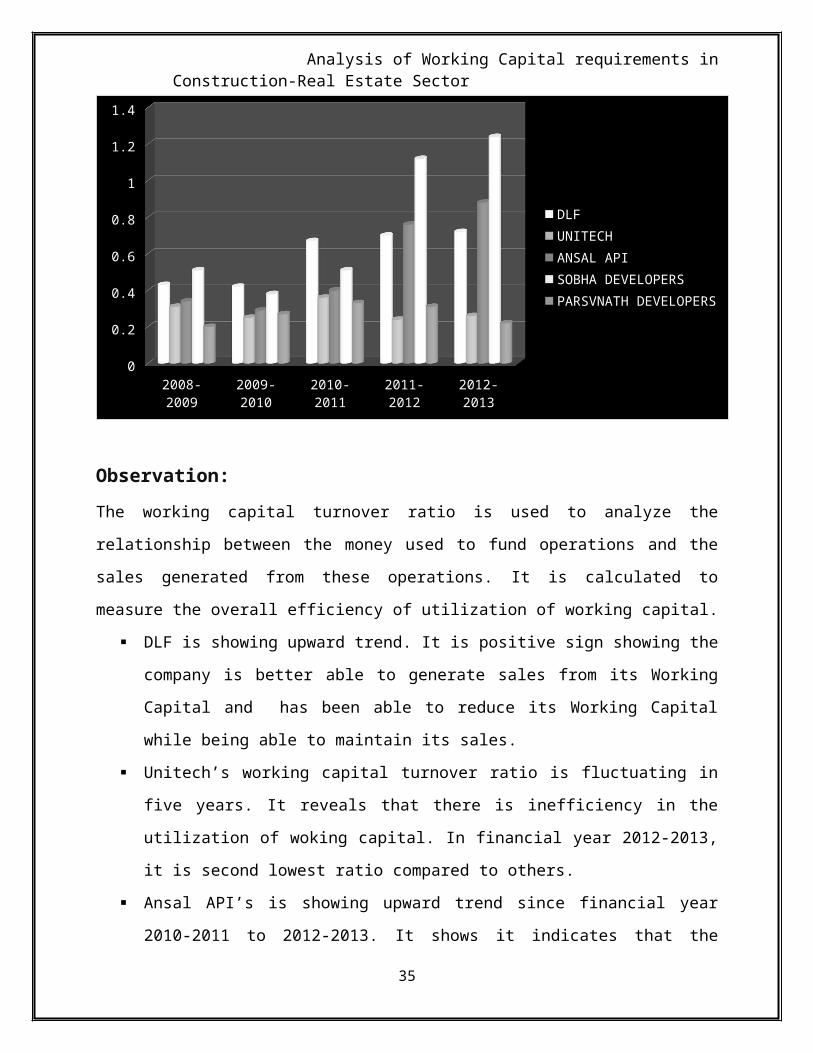

3.Working Capital Turnover Ratio

Company 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013DLF 0.43 0.42 0.67 0.7 0.72UNITECH 0.31 0.25 0.36 0.24 0.26ANSAL API 0.34 0.29 0.4 0.76 0.88 SOBHA DEVELOPERS 0.51 0.38 0.51 1.12 1.24PARSVNATH DEVELOPERS 0.2 0.27 0.33 0.31 0.22

23

Analysis of Working Capital requirements in Construction-Real Estate Sector

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

0.2

0.4

0.6

0.8

1

1.2

1.4

DLFUNITECHANSAL APISOBHA DEVELOPERSPARSVNATH DEVELOPERS

Observation:

The working capital turnover ratio is used to analyze the relationship between the money used to

fund operations and the sales generated from these operations. It is calculated to measure the

overall efficiency of utilization of working capital.

DLF is showing upward trend. It is positive sign showing the company is better able to

generate sales from its Working Capital and has been able to reduce its Working Capital

while being able to maintain its sales.

Unitech’s working capital turnover ratio is fluctuating in five years. It reveals that there is

inefficiency in the utilization of woking capital. In financial year 2012-2013, it is second

lowest ratio compared to others.

Ansal API’s is showing upward trend since financial year 2010-2011 to 2012-2013. It

shows it indicates that the company is generating good sales compared to the funds

invested in operations, i.e., the company is very efficient.

In a general sense, the higher the working capital turnover ratio is, the more efficient you

are in using working capital to generate sales. In this case, Sobha developer’s working

24

Analysis of Working Capital requirements in Construction-Real Estate Sector

capital turnover ratio is highest among all in financial year 2012-2013, it indicates the

company is generating a lot of sales compared to the money it uses to fund the sales.

In financial year 2012-2013, Parsvnath developers’ working capital ratio is lowest

compared to others. It indicates inefficient utilization of working capital.

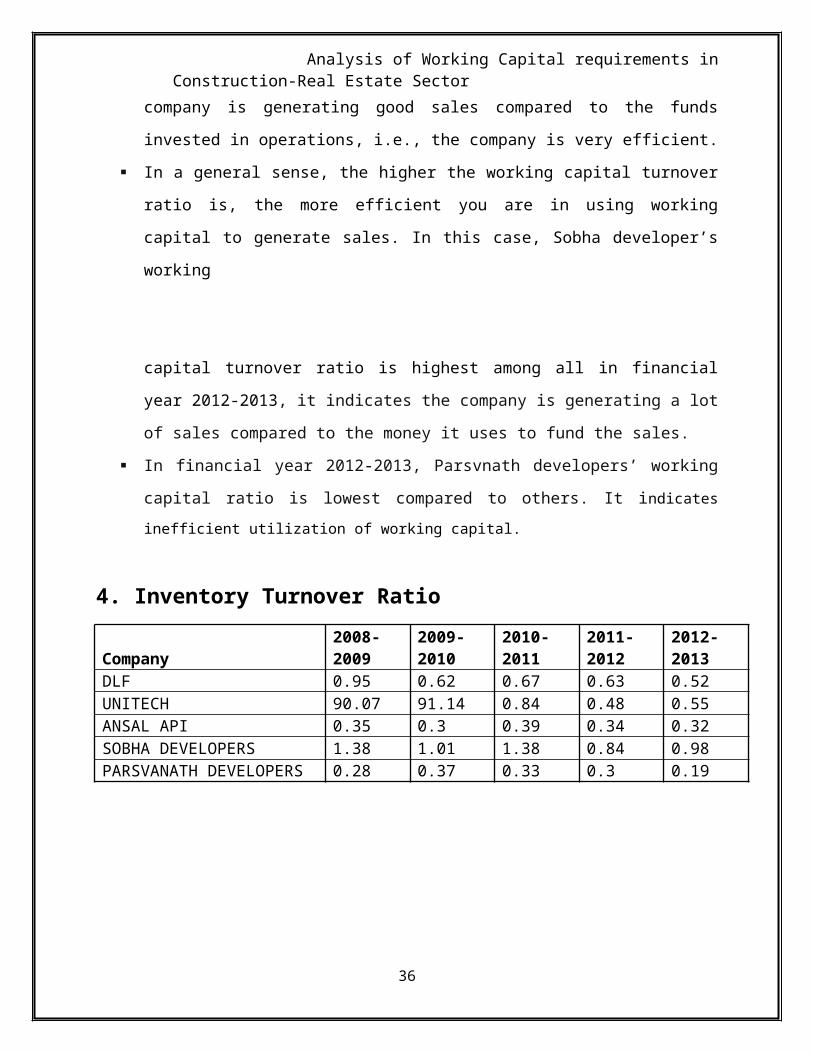

4. Inventory Turnover Ratio

Company 2008-2009 2009-2010 2010-2011 2011-2012 2012-2013DLF 0.95 0.62 0.67 0.63 0.52UNITECH 90.07 91.14 0.84 0.48 0.55ANSAL API 0.35 0.3 0.39 0.34 0.32SOBHA DEVELOPERS 1.38 1.01 1.38 0.84 0.98PARSVANATH DEVELOPERS 0.28 0.37 0.33 0.3 0.19

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

10

20

30

40

50

60

70

80

90

100

DLFUNITECHANSAL APISOBHA DEVELOPERSPARSVANATH DEVELOPERS

25

Analysis of Working Capital requirements in Construction-Real Estate Sector

Observation:

Inventory turnover ratio is used to measure the inventory management efficiency of a business. It

is an activity ratio that evaluates the liquidity of the inventories of a company. It measures how

many times the company has sold and replaced its inventory during a certain period. Higher ITR

shows higher efficiency of the management and vice versa.

DLF is showing downtrend, but for financial year 2012-2013 DLF’s inventory ratio is

good as per industry standards.

In financial year 2008-2009 and 2009-2010, Unitech is showing highest inventory

turnover ratio which indicates loss of sales due to inventory shortage. In short, it indicates

inadequate inventory that could lead to backorders and slow delivery to customers,

having eventually an adverse effect on sales. In financial year 2012-2013, Unitech’s

inventory turnover ratio is in good condition.

Ansal API’s inventory turnover ratio fluctuating in same range over the years. In

financial year 2012-2013, it has lower inventory ratio due to maintenance of excessive

inventories needlessly.

In 2012-2013, Sobha Developers ITR indicates better performance. It indicates fast

moving inventory. Whereas Parsvanath Developers lowest inventory ratio indicates over-

stocking which may pose risk of obsolescence and increased inventory holding costs. The

company should make necessary control measures with regard to management of

inventory.

5. Total assets turnover ratio

Company2008-2009

2009-2010

2010-2011

2011-2012

2012-2013

DLF 0.25 0.15 0.2 0.21 0.19UNITECH 0.2 0.18 0.17 0.19 0.2ANSAL API 0.42 0.35 0.45 0.65 0.6SOBHA DEVELOPERS 0.32 0.4 0.48 0.63 0.6PARSVANATH DEVELOPERS 0.15 0.2 0.18 0.17 0.13

26

Analysis of Working Capital requirements in Construction-Real Estate Sector

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

0.1

0.2

0.3

0.4

0.5

0.6

0.7

DLFUNITECHANSAL APISOBHA DEVELOPERSPARSVANATH DEVELOPERS

Observation:

The total asset turnover ratio measures the ability of a company to use its assets to efficiently

generate sales. This ratio considers all assets, current and fixed. Those assets include fixed assets,

like plant and equipment, as well as inventory, accounts receivable, as well as any other current

assets.

DLF’s total asset turnover ratio is showing downtrend over the years. But as per data

analysis it is showing that revenue is consistent it is a sign that DLF has "overinvested" in

assets. It means DLF has added capacity in fixed assets (like tangible and intangible fixed

assets and capital work in progress)- that isn't being used.

Unitech’s total assets turnover ratio is fluctuating in similar range over the years. It’s in

good condition.

In 2012-2013, Ansal API and Sobha developers ratio is highest and same. Total Asset

Turnover ratio reflects the effectiveness of the firm's use of its total asset base. It is an

indication to the firm's operation efficiency. It shows that both the companies are simply

27

Analysis of Working Capital requirements in Construction-Real Estate Sector

becoming efficient, and they are stretching their capacity to its limits and they need to

invest to grow.

Parsvnath developers total assets turnover ratio is fluctuating over the years. In financial

year 2012-2013, it’s ratio is lowest among all and it indicates inefficient utilization of

assets.

6. Fixed assets turnover ratio

Company2008-2009

2009-2010

2010-2011

2011-2012

2012-2013

DLF 1.2 0.42 0.48 0.45 0.4UNITECH 11.8 12.12 8.69 11.28 8.8ANSAL API 4.54 3.5 4.8 6.45 5.8SOBHA DEVELOPERS 3.45 4.01 4.5 3 3.8PARSVANATH DEVELOPERS 3.46 4.68 3.5 3.45 2.51

2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

2

4

6

8

10

12

14

DLFUNITECHANSAL APISOBHA DEVELOPERSPARSVANATH DEVELOPERS

28

Analysis of Working Capital requirements in Construction-Real Estate Sector

Observation:

Fixed asset turnover ratio compares the sales revenue a company to its fixed assets. This ratio

tells us how effectively and efficiently a company is using its fixed assets to generate revenues.

This ratio indicates the productivity of fixed assets in generating revenues. The fixed asset

turnover ratio measures the company's effectiveness in generating sales from its investments in

plant, property, and equipment. It is especially important for a manufacturing firm and

construction sector that uses a lot of plant and equipment in its operations to calculate this ratio.

DLF’s fixed assets turnover ratio is showing downtrend. For financial year 2012-2013, a

low turnover as compared to industry suggests that the fixed assets are being

underutilized or that there are more assets than can be effectively used.

Unitech’s fixed assets turnover ratio is showing high over the years due to business firm

is likely operating over capacity and needs to reduce its capacity.

If a company has a high fixed asset turnover ratio, it shows that the company is efficient

at managing its fixed assets. Fixed assets are important because they usually represent the

largest component of total assets. Ansal Api’s fixed assets turnover ratio is in good

condition over the years. From 2009 to 2011, Sobha developers and Ansal API has

increasing trend in fixed assets turnover ratio, it means the company has less money tied

up in fixed assets for each units of sales. In financial year 2012-2013, Ansal Api has

highest fixed asset turnover ratio, this means that its sales have exceeded the amount it

has invested in fixed assets, which is a positive sign for the company.

Parsvnath developers’ fixed assets turnover ratio is declining over the years. The turnover

ratio will be lower just after a significant amount of fixed asset is acquired to upgrade or

expand the plant facilities. A low asset turnover ratio may also suggest that a plant is

obsolete and needs to be upgraded, an undertaking that can negatively impact cash

reserves, the debt exposure, and cash flow for the medium to long term. Quite naturally,

it will take some time for these acquisitions to start making a positive impact on revenue

and, by extension, the asset turnover figures. But, as compared to industry average,

29

Analysis of Working Capital requirements in Construction-Real Estate Sector

Parsvnath developer’s fixed assets turnover ratio is showing positive sign in financial

year 2012-2013

5.2 Analysis of the liquidity position by Motaal’s comprehensive test

In this test the following ratios are taken into consideration:

i. Working capital (WC) to Current Asset Ratio = Working Capital*100 Current Assets

ii. Stock to current asset Ratio = Inventory or Stock*100 Current Assets

iii. Liquid Resources (LR) to Current Asset Ratio = Liquid Resources or Quick Assets*100Current Assets

The higher the value of both working capitals to current asset ratio and liquid resources to

current asset ratio, relatively the more favorable will be the liquidity position of a firm and vice-

versa. On the other hand, lower the value of stock to current assets ratio, relatively the more

favorable will be the liquidity position of the firm. The ranking of the above three ratios of a firm

over a period of time is done in their order of preferences. Finally, the ultimate ranking is done

on the basis of the principle that the lower the points score, the more favorable will be the

liquidity position and vice-versa

Motaal’s comprehensive test of liquidity for financial year 2012-2013Sl. No

Company WC to current asset ratio (%)

Rank Stock to Current Asset Ratio (%)

Rank Liquid Resources to Current Assets Ratio (%)

Rank Total rank

Ultimate rank

1 DLF LTD 0.4 3 0.56 3 0.17 5 13 42 UNITECH 0.54 1 0.25 1 0.34 2 4 13 ANSAL API 0.25 5 0.67 5 0.28 4 14 5

4 SOBHA DEVELOPERS

0.37 4 0.46 2 0.4 1 7 2

30

Analysis of Working Capital requirements in Construction-Real Estate Sector

5 PARSVNATH DEVELOPERS

0.5 2 0.58 4 0.3 3 9 3

Above table which shows Motaal’s Comprehensive Test of Liquidity reveals that on the basis of

Motaal’s ultimate rank test of Liquidity Unitech is awarded Rank – I, indicating the most liquid

company among the five. Sobha Developers has ranked - II, Parsvanath Developers- III, DLF

Ltd.- IV and Ansal API- V, indicates the most unfavorable liquidity position.

31

Analysis of Working Capital requirements in Construction-Real Estate Sector

6. LIMITATION OF THE STUDY

This study has been based on five construction- real estate sector companies as sample

but not considered all the companies. Hence it will reflect only a partial view of working

capital investing policies on firm’s profitability position of real estate sector companies

Study is solely based on secondary data and published financial statements of the selected

company, which may lead to some errors and assumptions.

Moreover, it is based on very short period of time i.e. 5 years (2009-2013), therefore, a

detailed analysis covering a lengthy period, which may give slightly different results has

not been made.

32

Analysis of Working Capital requirements in Construction-Real Estate Sector

7. CONCLUSIONWorking capital is an important liquidity indicator and historically it has been a major

benchmark for the profitability of construction contractors in infrastructure projects. A high

return on capital employed is an illusion if it is accompanied by inefficient or fraudulent working

capital management. If receivables or inventory keep going up disproportionately with growth in

sales, ever increasing amount of capital would have to be deployed for financing this working

capital requirement.

Current ratio of all the companies is near to industry average except Ansal API.

Therefore, performance of the companies except Ansal API in terms of current ratio is

satisfactory.

The performance of quick ratio of all companies is satisfactory except DLF in financial

year 2012-2013.

Inventory turnover ratio shows satisfactory performance during the study period.

In all the cases, growth of current assets are more than current liabilities, which in long

run will affect the working capital position of the company favorably ultimately affecting

the liquidity position of the companies. Hence, it is showing positive sign for all

companies.

Working capital turnover ratio, total assets turnover ratio and fixed assets turnover ratio

shows satisfactory position of the firms during the study period

Liquidity position of all the companies is satisfactory.

This Working capital management is, therefore, one of the important facets of firm’s

financial management effecting both liquidity and profitability. The working capital position of

33

Analysis of Working Capital requirements in Construction-Real Estate Sector

construction companies is deteriorating. Work-in-progress has been piling up due to delays in

obtaining certification of work from clients and disputes about work done. Receivables are also

increasing due to inadequately funded projects and disputes about escalation bills and changes in

the scope of projects. Delays in funding of equity for BOT (Build-operate-transfer) projects is

also likely to lead to stretched working capital at the parent level, who are also generally the EPC

(Engineering, procurement and construction) contractors for projects. This increase in working

capital is leading to a stretched liquidity position for construction companies, reflected in their

high use of working capital facilities. Working capital position will improve through faster

execution, which in turn may be due to a policy push from the government and also through an

improvement in funding availability.

That companies which have bid aggressively to build large order books have seen deterioration

in their financial positions and stressed liquidity. Unless availability of funds improve and pace

of execution increases, credit metrics are likely to deteriorate further. However, companies

which have demonstrated prudent growth policies by preferring quick execution over an increase

in order book, and hence bid less aggressively for projects, may see their financial positions

remaining stable or improving.

34

Analysis of Working Capital requirements in Construction-Real Estate Sector

8. BIBLIOGRAPHY

Books:

Financial Management : M.Y.Khan & P. K. Jain

Websites:

http://www.cii.in

http://www.business-standard.com

http://www.moneycontrol.com

www.iosrjournals.org

http://www.vsrdjournals.com

www.econicstimes.com

www.yahoofinance.com

35

Analysis of Working Capital requirements in Construction-Real Estate Sector

36