Embed Size (px)

Citation preview

STRICTLY PRIVATE & CONFIDENTIAL

ANALYST BRIEFING SEPT 2011ANALYST BRIEFING SEPT 2011

Page 2

CORPORATE INFORMATIONCORPORATE INFORMATION

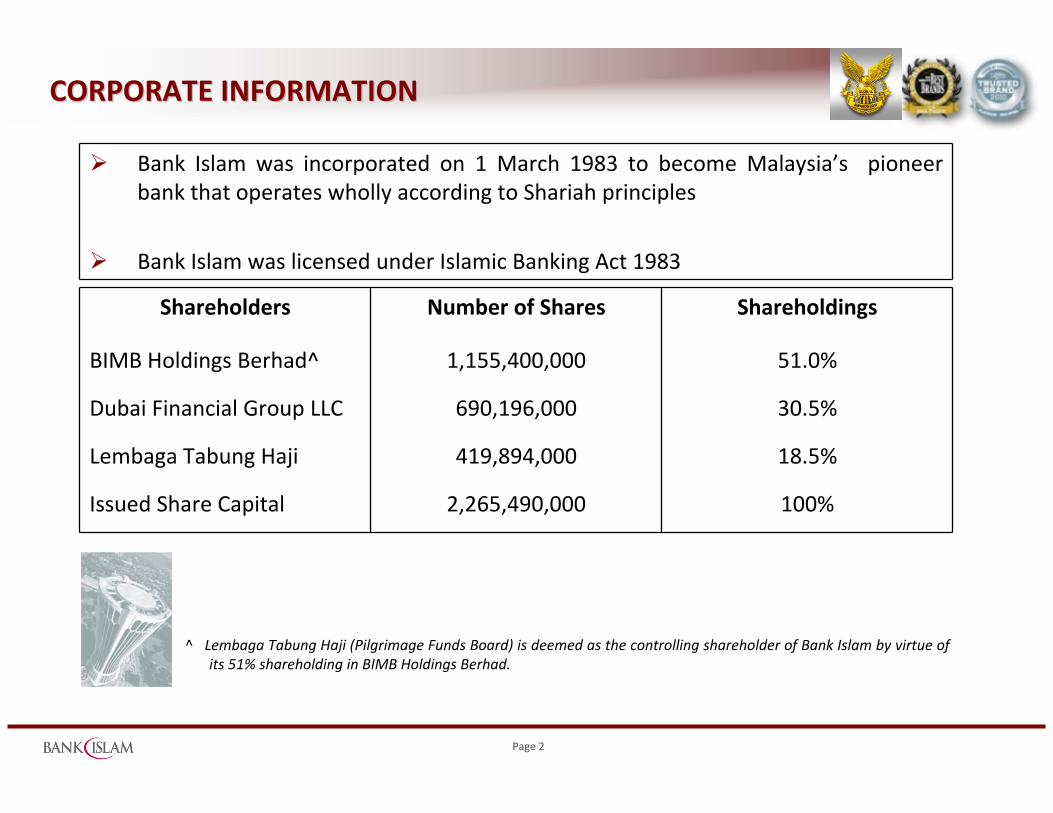

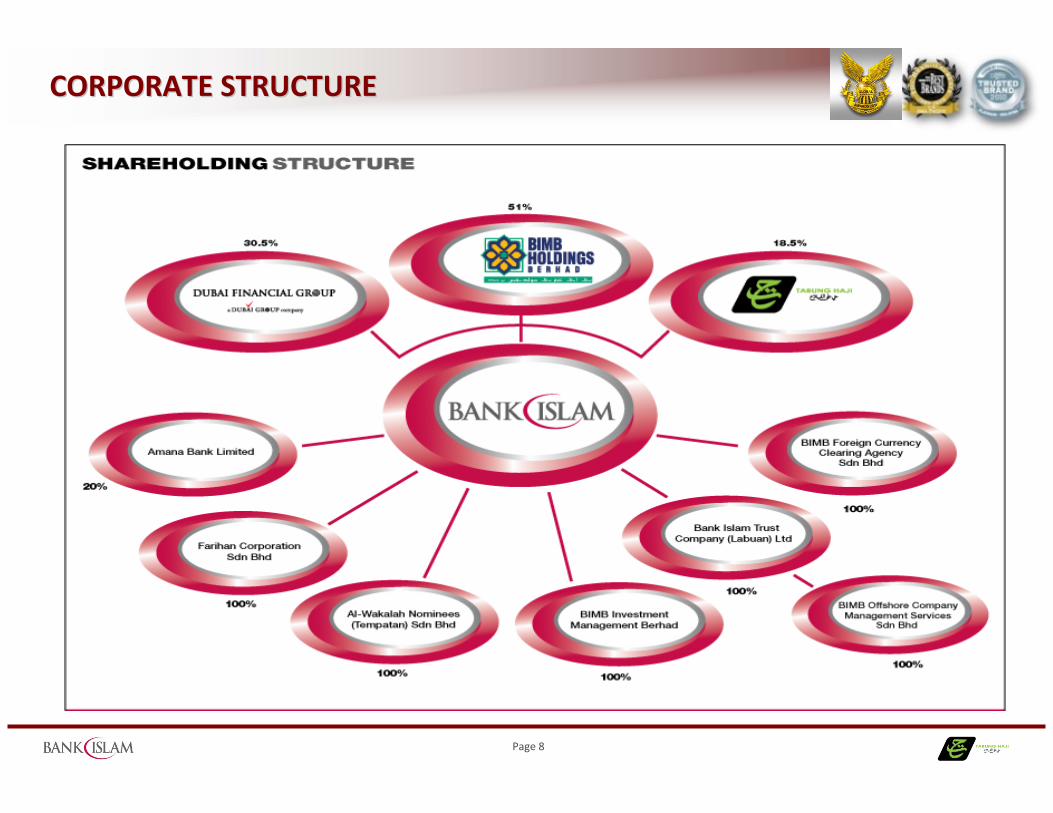

Shareholders Number of Shares Shareholdings

BIMB Holdings Berhad^ 1,155,400,000 51.0%

Dubai Financial Group LLC 690,196,000 30.5%

Lembaga Tabung Haji 419,894,000 18.5%

Issued Share Capital 2,265,490,000 100%

Bank Islam was incorporated on 1 March 1983 to become Malaysia’s pioneer bank that operates wholly according to Shariah principles

Bank Islam was licensed under Islamic Banking Act 1983

^ Lembaga Tabung Haji (Pilgrimage Funds Board) is deemed as the controlling shareholder of Bank Islam by virtue of its 51% shareholding in BIMB Holdings Berhad.

Page 3

OUR SHAREHOLDERSOUR SHAREHOLDERS

Lembaga Tabung Haji (18.5%)

Lembaga Tabung Haji (Pilgrim Fund Board) (TH) is a government controlled entity that was established mainly to assist Muslims in saving gradually for the purpose of pilgrimage. TH manages a fund size exceeding RM16 bil and invests in more than RM6 bil worth of shares on Bursa Malaysia. Currently, TH controls at least 6 listed companies in Bursa Malaysia that are involved in banking, Takaful, palm oil plantation, property development, construction and IT services. TH is highly determined to make each business and investment venture a roaring success at home and abroad. It has also made an impressive mark in its asset management as well as in facilitating various Islamic investment instruments such as sukuk/bonds, corporate notes, Government Investment Certificates, Mudharabah Bank Account and Bill of Acceptance.

BIMB Holdings Bhd (51%)BIMB Holdings Bhd (BHB) is an investment holding company which operates along Islamic principles. It holds broad appeal for investors and customers because of its strong commitment to upholding ethical practices. BHB was incorporated in Malaysia on 20 March 1997, and was listed on the Main Market of Bursa Malaysia Securities Berhad on 16 September in the same year. The authorized capital of BHB is RM2 billion while its paid‐up capital is approximately RM1.07 billion. The core subsidiaries of the BHB Group are pioneers in various Islamic financial services including banking, takaful, stockbroking, and other related services, namely Bank Islam Malaysia Berhad, Syarikat Takaful Malaysia Berhad, and BIMB Securities Sdn Bhd.

Dubai Financial Group LLC(30.5%)Dubai Banking Group is the global Shari’ah compliant investment company of Dubai Group. The company is established to tap the immense growth opportunities within the global Shari’ah compliant space, particularly in South East Asia, China and the Middle East. Its current investment portfolio includes: 100% ownership of Dubai Tadawul, a Dubai based private brokerage company, 70% ownership of Dubai Bank and 30% stake in Bank Islam, Malaysia’s oldest Islamic bank

Page 4

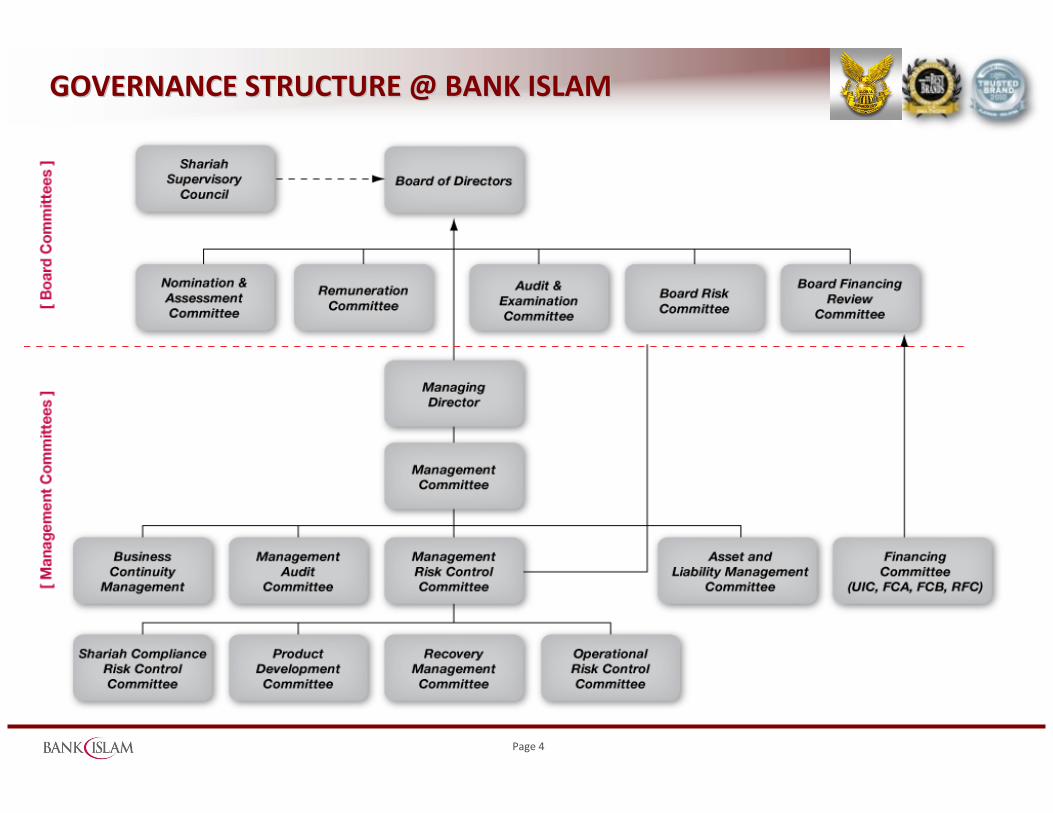

GOVERNANCE STRUCTURE @ BANK ISLAMGOVERNANCE STRUCTURE @ BANK ISLAM

Page 5

BOARD OF DIRECTORSBOARD OF DIRECTORS

Zaiton Mohd HassanChairman, Board Risk Committee

Mohamed Ridza bin Mohamed AbdullaIndependent Director

Zahari @ Mohd Zin IdrisChairman, Audit & Examination CommitteeChairman, Board Financing Review Committee

…INDEPENDENT DIRECTOR

Dato’ Zamani Abdul GhaniChairman

Page 6

BOARD OF DIRECTORSBOARD OF DIRECTORS……contcont

Dato’ Sri Zukri SamatManaging Director

Bank Islam Malaysia Bhd

Datuk Ismee IsmailGroup Managing DirectorLembaga Tabung Haji

Johan AbdullahGroup Managing Director

BIMB Holdings Bhd

… NON INDEPENDENT DIRECTOR

Abdullah AbdulRahman Abdullah Sharafi Board Member

Mohammed Abdul Ghafar HussainBoard Member

Page 7

MANAGEMENT TEAMMANAGEMENT TEAM

Page 8

CORPORATE STRUCTURECORPORATE STRUCTURE

Page 9

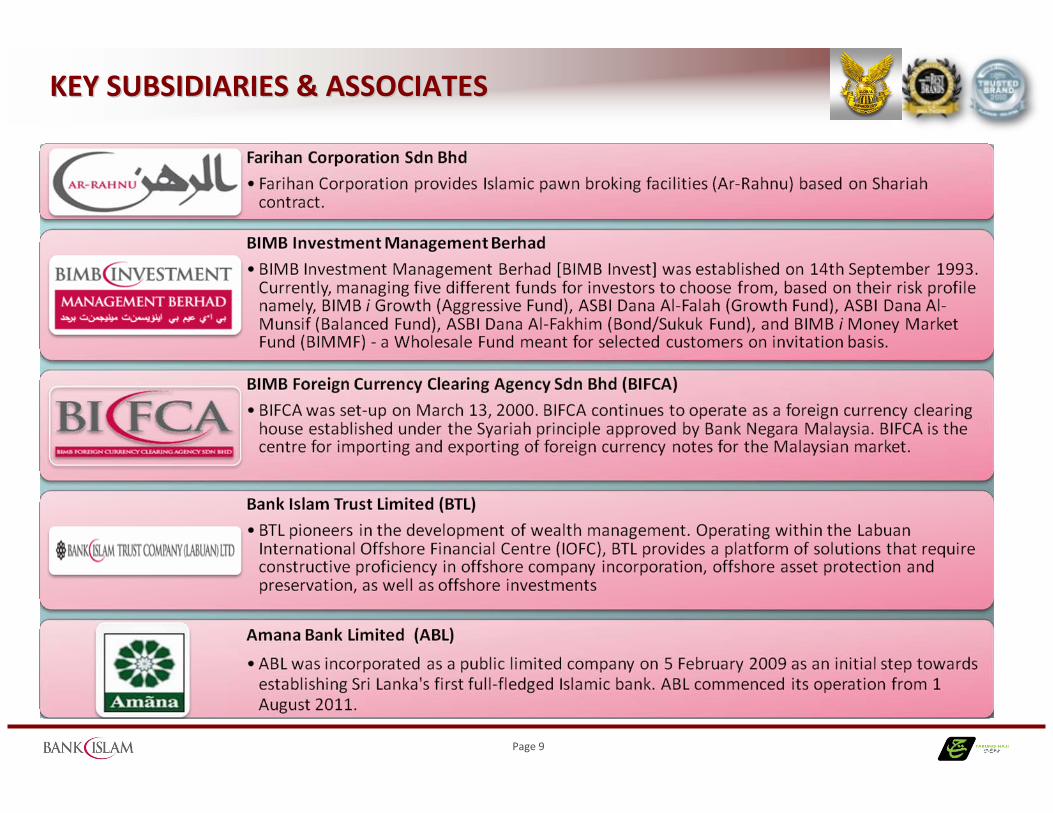

KEY SUBSIDIARIES & ASSOCIATESKEY SUBSIDIARIES & ASSOCIATES

Page 10

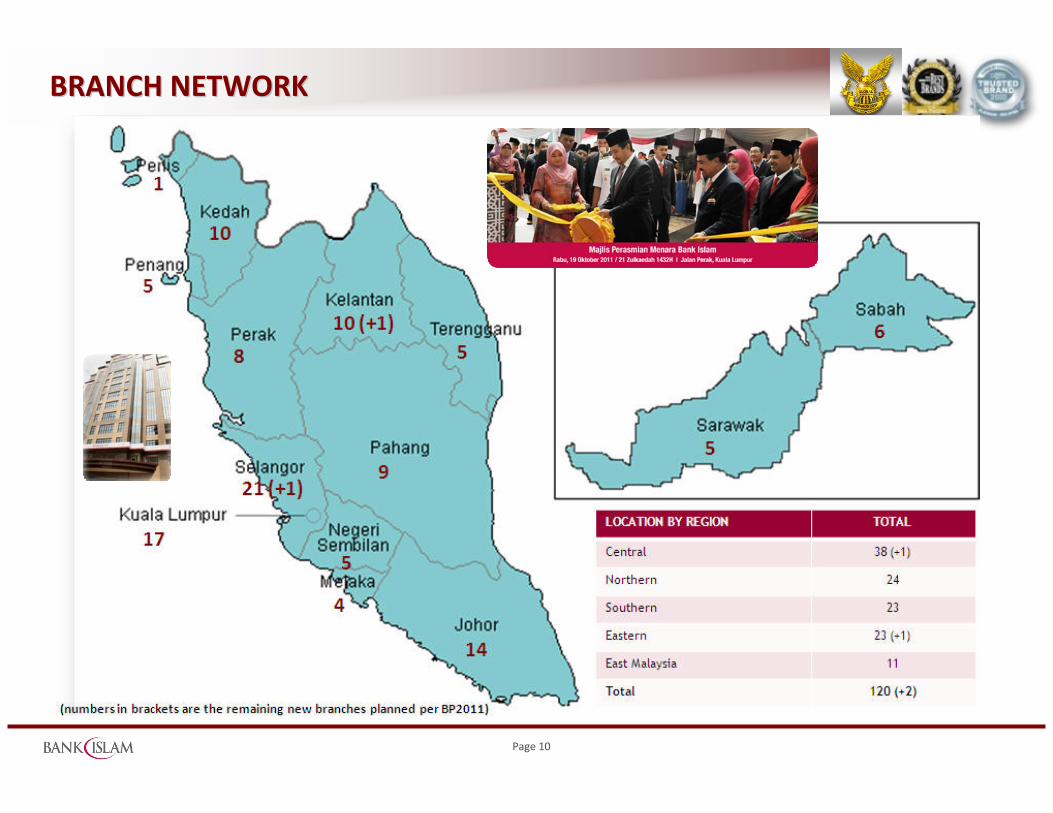

BRANCH NETWORKBRANCH NETWORK

Page 11

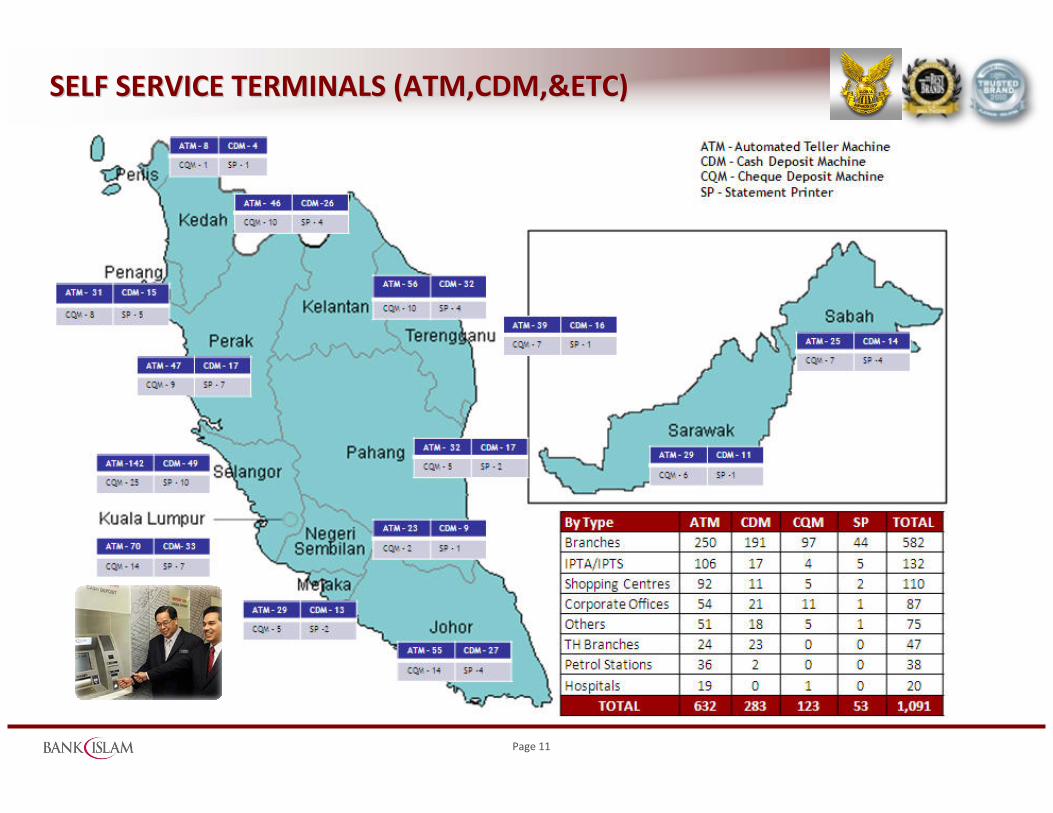

SELF SERVICE TERMINALS (ATM,CDM,&ETC)SELF SERVICE TERMINALS (ATM,CDM,&ETC)

Page 12

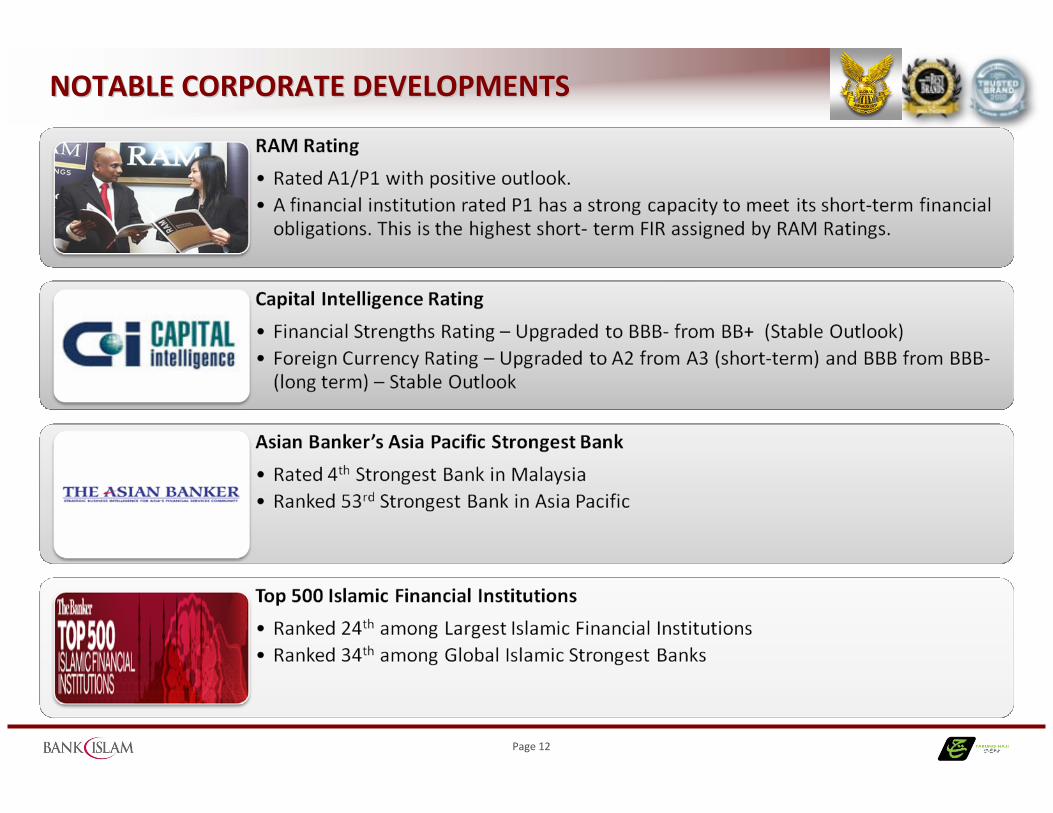

NOTABLE CORPORATE DEVELOPMENTSNOTABLE CORPORATE DEVELOPMENTS

Page 13

WINNING NOTABLE AWARDSWINNING NOTABLE AWARDS

Page 14

WINNING NOTABLE AWARDSWINNING NOTABLE AWARDS

Page 15

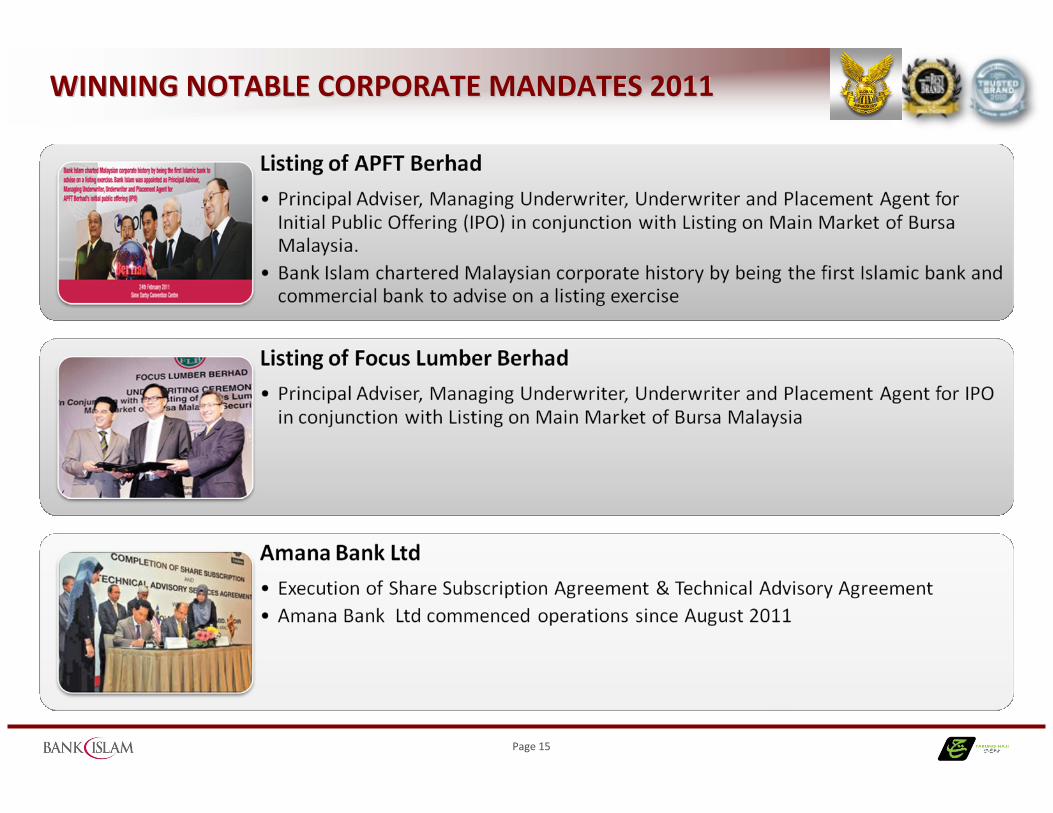

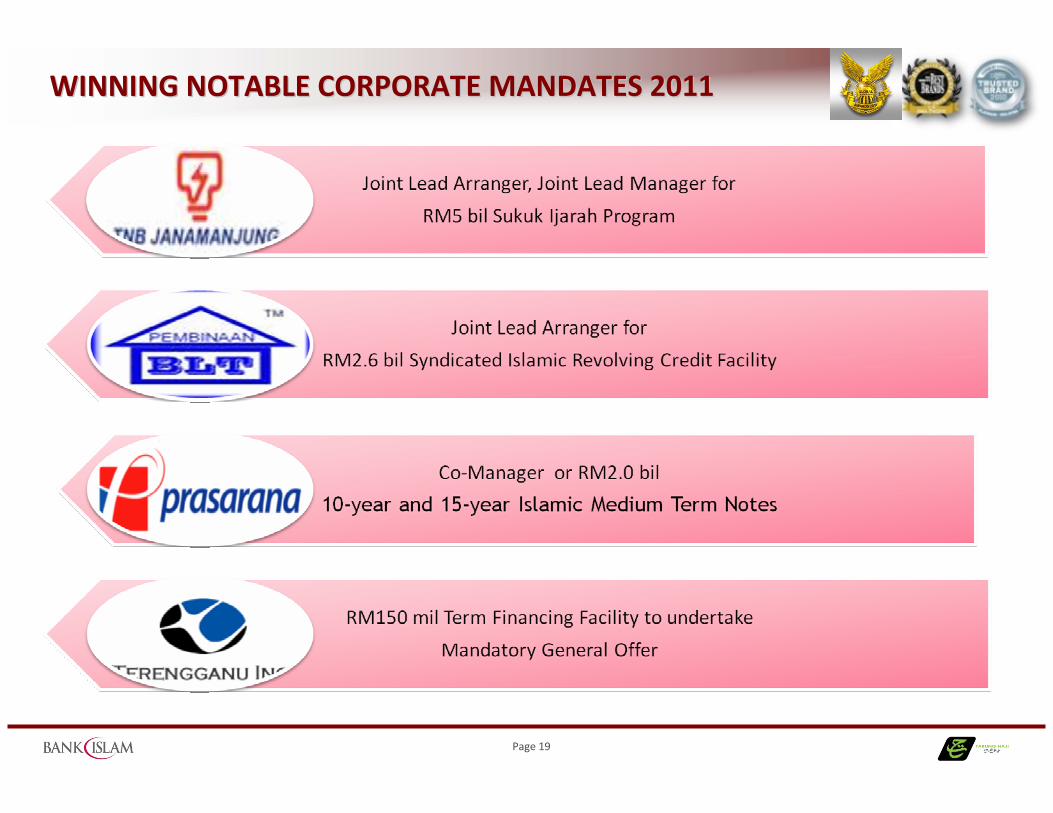

WINNING NOTABLE CORPORATE MANDATES 2011WINNING NOTABLE CORPORATE MANDATES 2011

Page 16

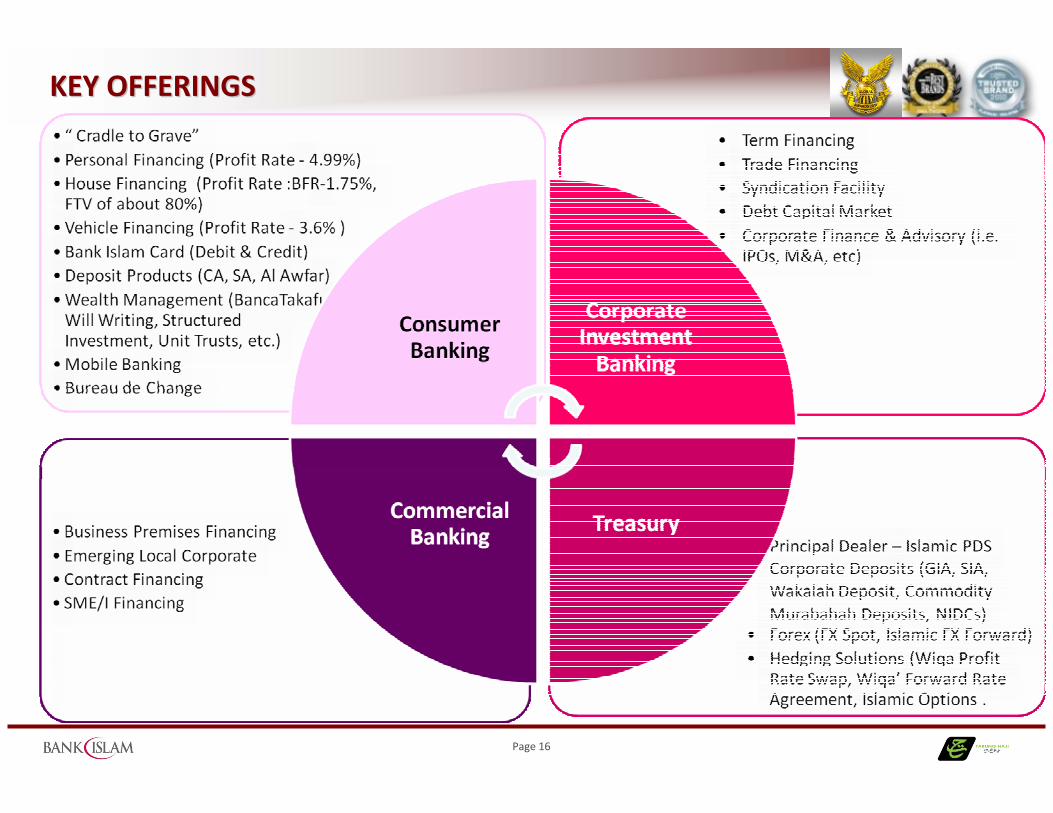

KEY OFFERINGSKEY OFFERINGS

Page 17

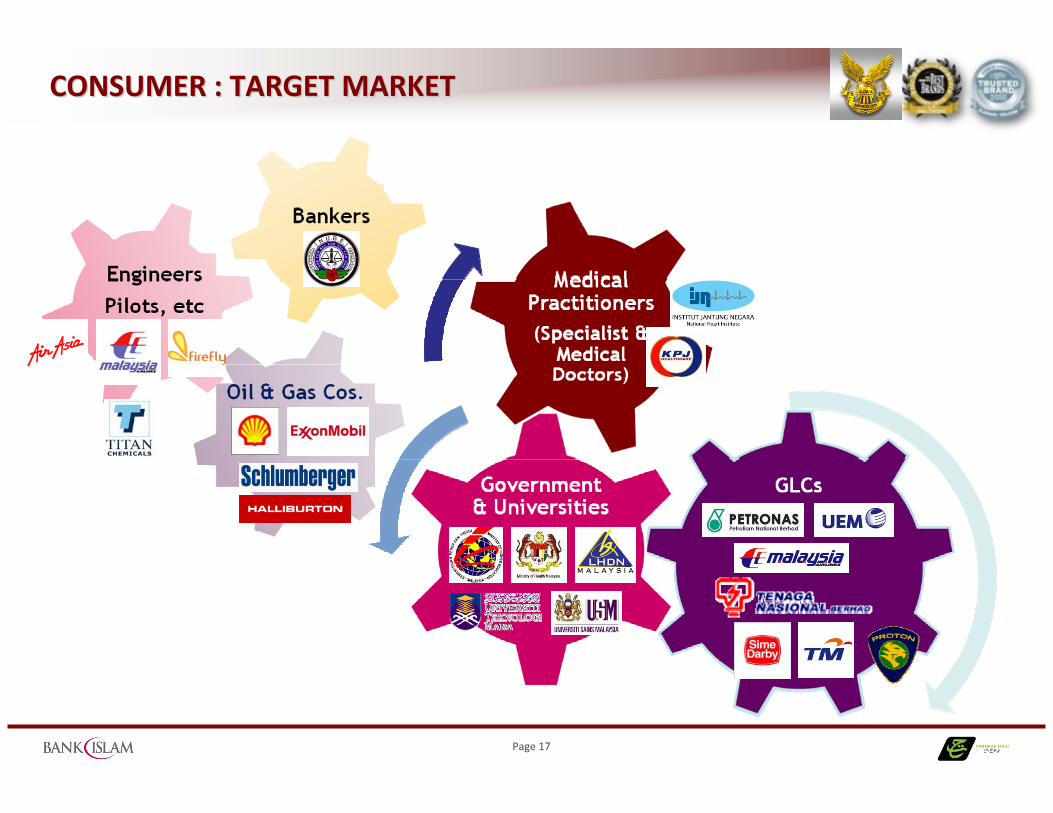

CONSUMER : TARGET MARKETCONSUMER : TARGET MARKET

Page 18

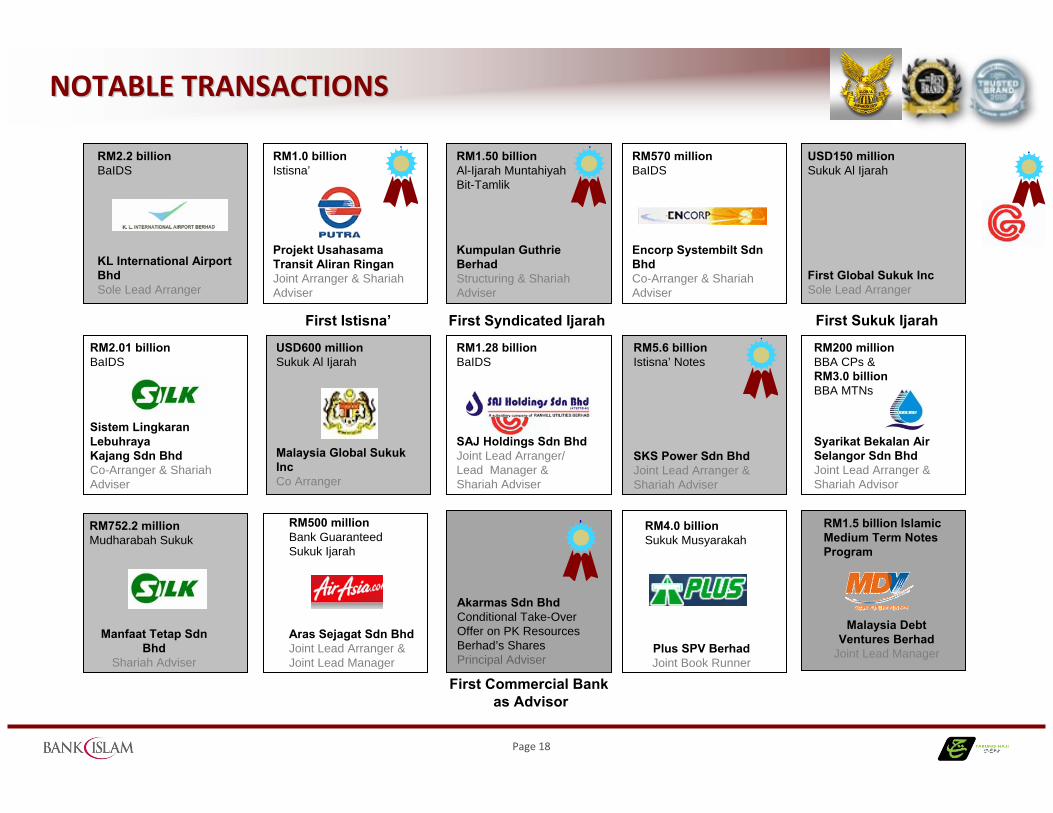

RM2.2 billionBaIDS

KL International Airport BhdSole Lead Arranger

RM1.0 billionIstisna’

Projekt Usahasama Transit Aliran RinganJoint Arranger & Shariah Adviser

First Istisna’ First Syndicated Ijarah

RM1.50 billionAl-Ijarah Muntahiyah Bit-Tamlik

Kumpulan Guthrie BerhadStructuring & Shariah Adviser

NOTABLE TRANSACTIONSNOTABLE TRANSACTIONS

RM570 millionBaIDS

Encorp Systembilt Sdn BhdCo-Arranger & Shariah Adviser

First Sukuk Ijarah

USD150 millionSukuk Al Ijarah

First Global Sukuk IncSole Lead Arranger

RM2.01 billionBaIDS

Sistem Lingkaran Lebuhraya Kajang Sdn BhdCo-Arranger & Shariah Adviser

USD600 millionSukuk Al Ijarah

Malaysia Global Sukuk IncCo Arranger

RM1.28 billionBaIDS

SAJ Holdings Sdn BhdJoint Lead Arranger/ Lead Manager & Shariah Adviser

RM5.6 billionIstisna’ Notes

SKS Power Sdn BhdJoint Lead Arranger & Shariah Adviser

RM200 millionBBA CPs &RM3.0 billion BBA MTNs

Syarikat Bekalan Air Selangor Sdn BhdJoint Lead Arranger &Shariah Advisor

RM500 millionBank Guaranteed Sukuk Ijarah

Aras Sejagat Sdn BhdJoint Lead Arranger &Joint Lead Manager

Akarmas Sdn BhdConditional Take-Over Offer on PK ResourcesBerhad’s SharesPrincipal Adviser

RM752.2 millionMudharabah Sukuk

Manfaat Tetap Sdn Bhd

Shariah Adviser

RM4.0 billionSukuk Musyarakah

Plus SPV BerhadJoint Book Runner

First Commercial Bank as Advisor

RM1.5 billion Islamic Medium Term Notes Program

Malaysia Debt Ventures Berhad

Joint Lead Manager

Page 19

WINNING NOTABLE CORPORATE MANDATES 2011WINNING NOTABLE CORPORATE MANDATES 2011

Page 20

ANCHORING INNOVATIONANCHORING INNOVATION

Page 21

ANNUAL CORPORATE AGENDAANNUAL CORPORATE AGENDA

Page 22

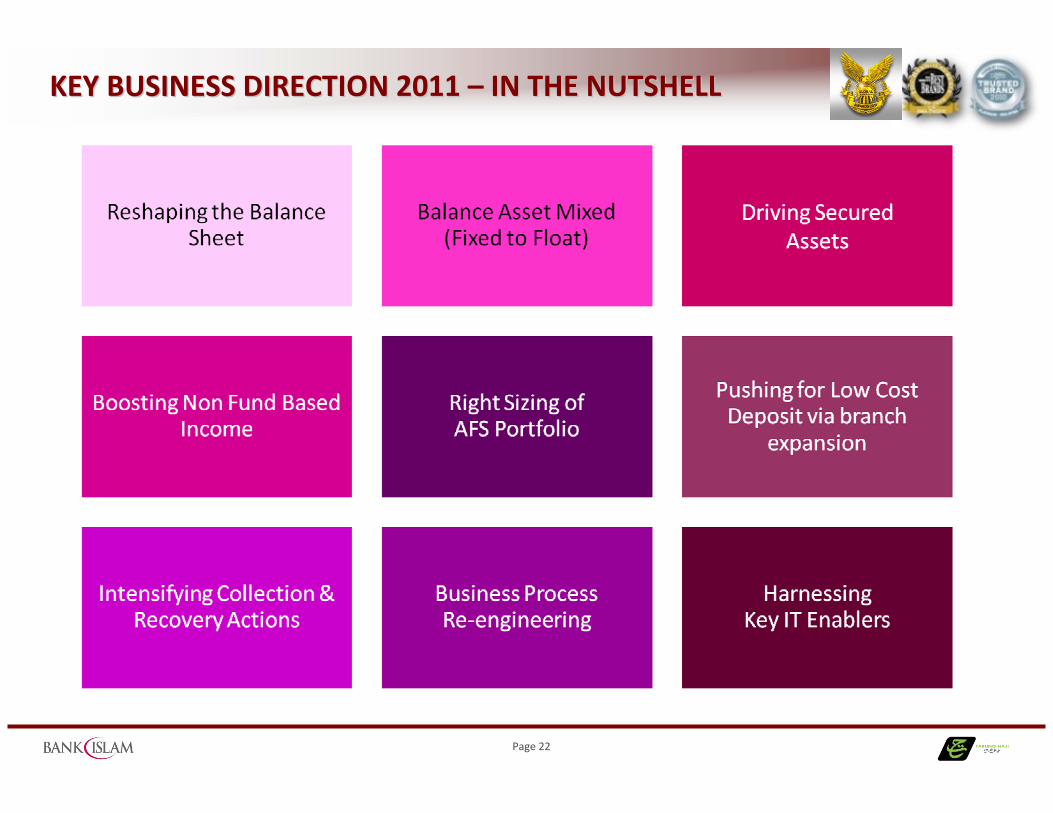

KEY BUSINESS DIRECTION 2011 KEY BUSINESS DIRECTION 2011 –– IN THE NUTSHELLIN THE NUTSHELL

Page 23

KEY RESULT AREAS (JAN 2011 KEY RESULT AREAS (JAN 2011 –– DEC 2013)DEC 2013)

Page 24

FINANCIAL HIGHLIGHTSFINANCIAL HIGHLIGHTS

Page 25

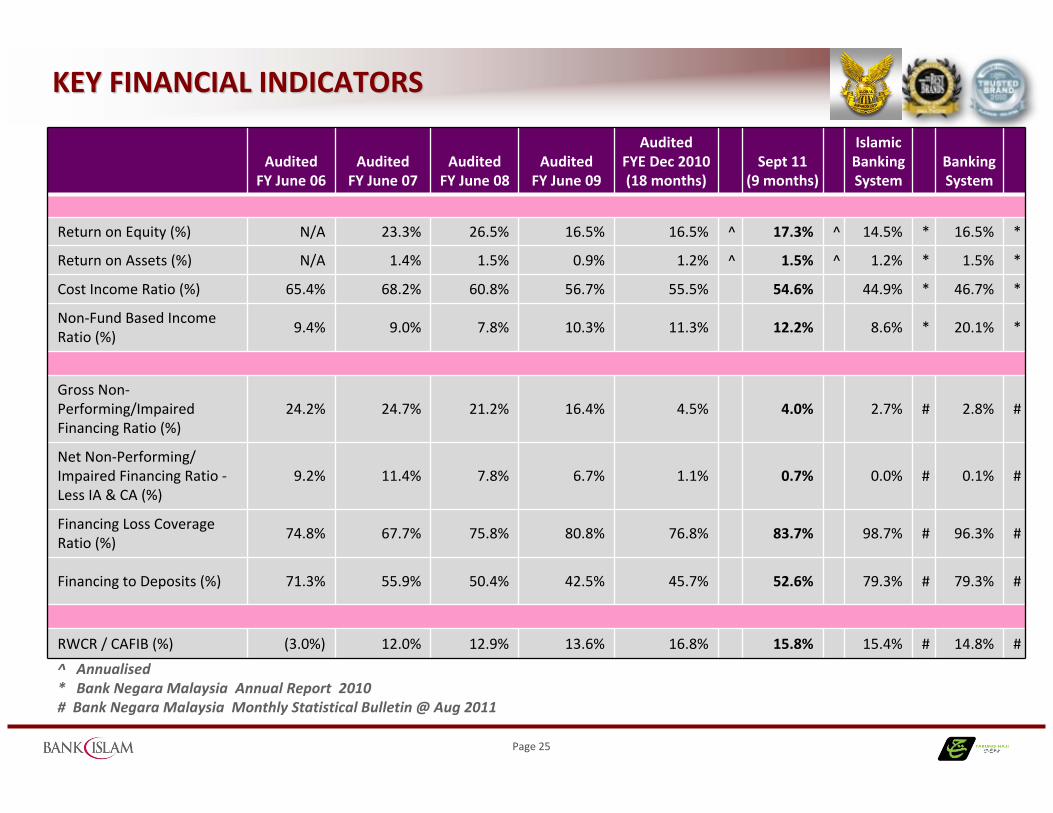

KEY FINANCIAL INDICATORSKEY FINANCIAL INDICATORS

^ Annualised* Bank Negara Malaysia Annual Report 2010 # Bank Negara Malaysia Monthly Statistical Bulletin @ Aug 2011

Audited FY June 06

AuditedFY June 07

AuditedFY June 08

Audited FY June 09

AuditedFYE Dec 2010(18 months)

Sept 11(9 months)

IslamicBanking System

Banking System

Return on Equity (%) N/A 23.3% 26.5% 16.5% 16.5% ^ 17.3% ^ 14.5% * 16.5% *

Return on Assets (%) N/A 1.4% 1.5% 0.9% 1.2% ^ 1.5% ^ 1.2% * 1.5% *

Cost Income Ratio (%) 65.4% 68.2% 60.8% 56.7% 55.5% 54.6% 44.9% * 46.7% *

Non‐Fund Based Income Ratio (%)

9.4% 9.0% 7.8% 10.3% 11.3% 12.2% 8.6% * 20.1% *

Gross Non‐Performing/Impaired Financing Ratio (%)

24.2% 24.7% 21.2% 16.4% 4.5% 4.0% 2.7% # 2.8% #

Net Non‐Performing/ Impaired Financing Ratio ‐Less IA & CA (%)

9.2% 11.4% 7.8% 6.7% 1.1% 0.7% 0.0% # 0.1% #

Financing Loss Coverage Ratio (%)

74.8% 67.7% 75.8% 80.8% 76.8% 83.7% 98.7% # 96.3% #

Financing to Deposits (%) 71.3% 55.9% 50.4% 42.5% 45.7% 52.6% 79.3% # 79.3% #

RWCR / CAFIB (%) (3.0%) 12.0% 12.9% 13.6% 16.8% 15.8% 15.4% # 14.8% #

Page 26

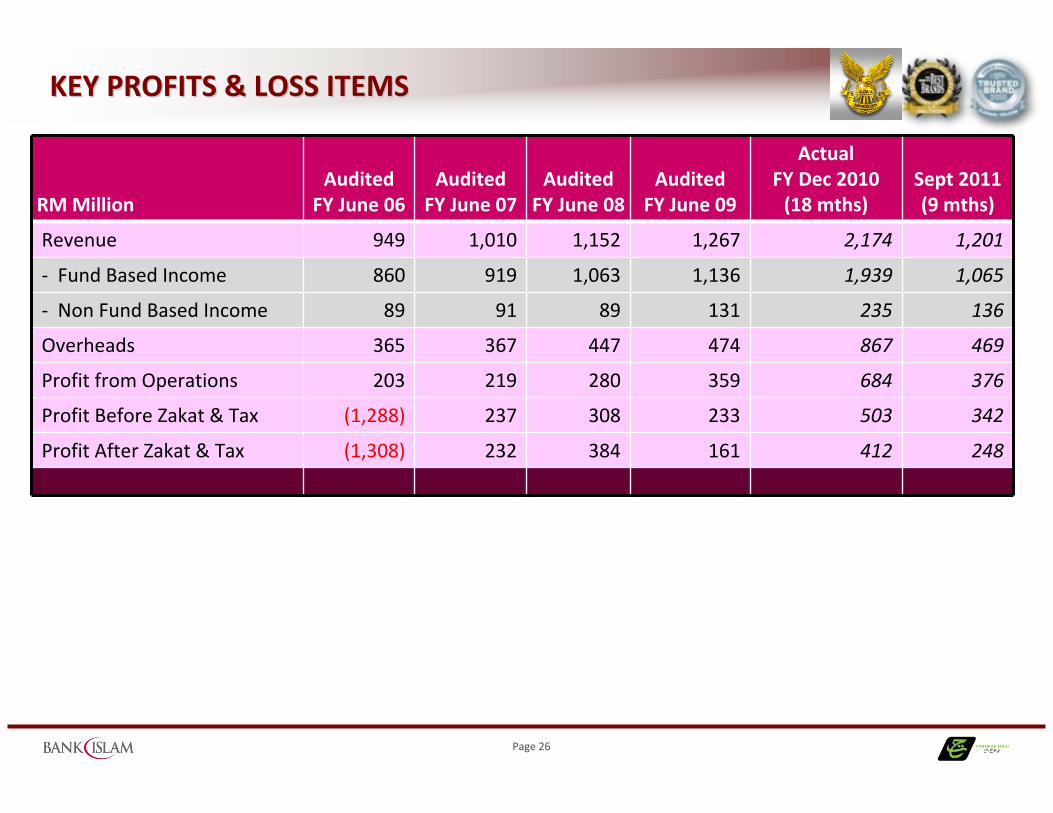

KEY PROFITS & LOSS ITEMS KEY PROFITS & LOSS ITEMS

RM MillionAudited

FY June 06Audited

FY June 07Audited

FY June 08Audited

FY June 09

Actual FY Dec 2010 (18 mths)

Sept 2011(9 mths)

Revenue 949 1,010 1,152 1,267 2,174 1,201

‐ Fund Based Income 860 919 1,063 1,136 1,939 1,065

‐ Non Fund Based Income 89 91 89 131 235 136

Overheads 365 367 447 474 867 469

Profit from Operations 203 219 280 359 684 376

Profit Before Zakat & Tax (1,288) 237 308 233 503 342

Profit After Zakat & Tax (1,308) 232 384 161 412 248

Page 27

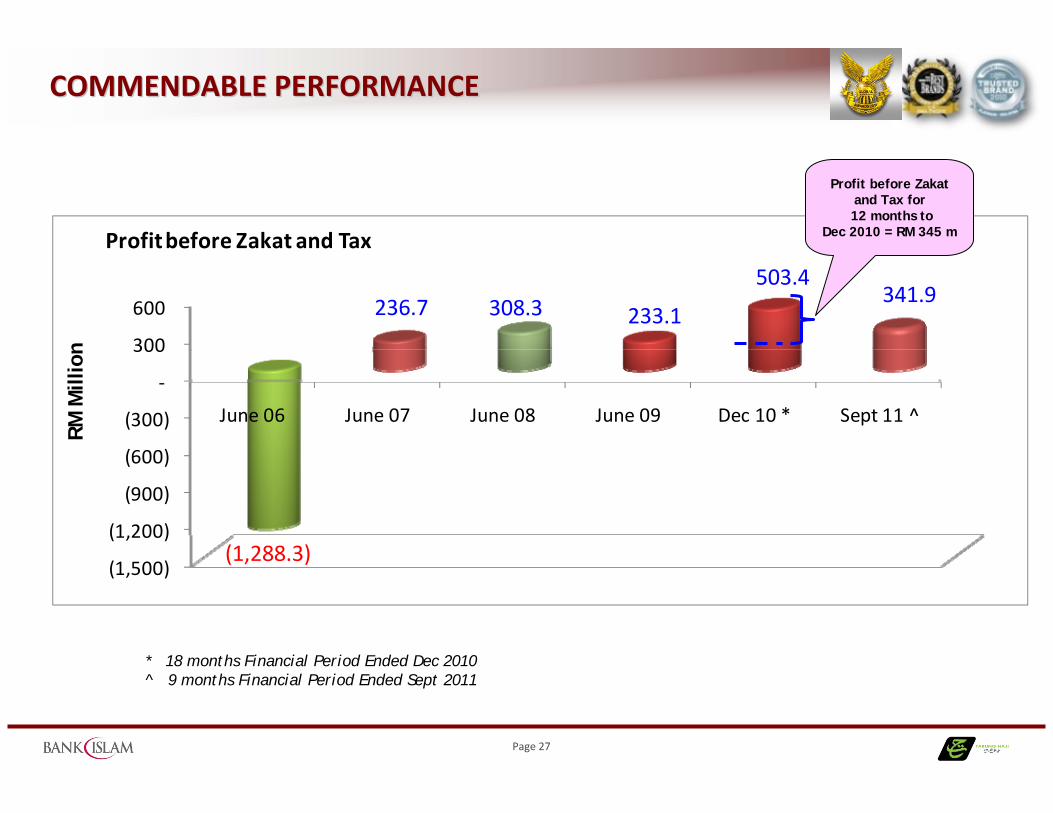

(1,500)

(1,200)

(900)

(600)

(300)

‐

300

600

June 06 June 07 June 08 June 09 Dec 10 * Sept 11 ^

(1,288.3)

236.7 308.3 233.1

503.4341.9

RM M

illio

n

Profit before Zakat and Tax

COMMENDABLE PERFORMANCECOMMENDABLE PERFORMANCE

* 18 months Financial Period Ended Dec 2010 ^ 9 months Financial Period Ended Sept 2011

Profit before Zakat and Tax for12 months to

Dec 2010 = RM 345 m

Page 28

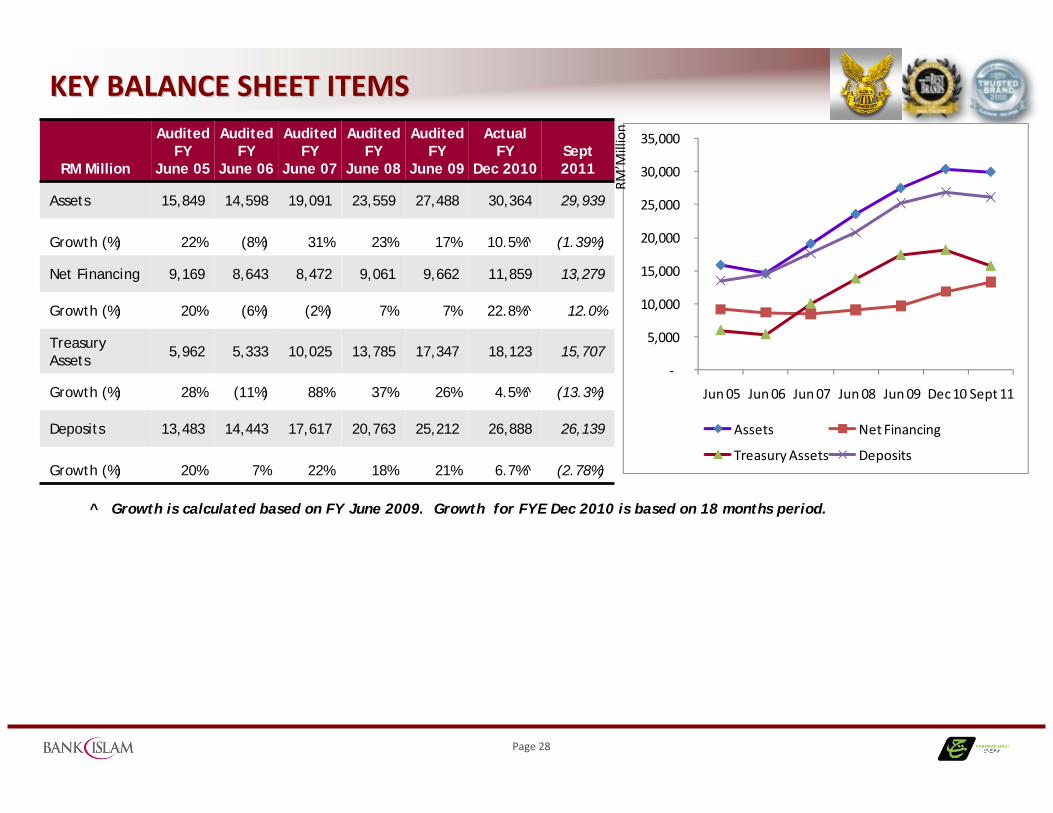

KEY BALANCE SHEET ITEMSKEY BALANCE SHEET ITEMS

RM Million

AuditedFY

June 05

AuditedFY

June 06

AuditedFY

June 07

AuditedFY

June 08

Audited FY

June 09

Actual FY

Dec 2010 Sept 2011

Assets 15,849 14,598 19,091 23,559 27,488 30,364 29,939

Growth (%) 22% (8%) 31% 23% 17% 10.5%^ (1.39%)

Net Financing 9,169 8,643 8,472 9,061 9,662 11,859 13,279

Growth (%) 20% (6%) (2%) 7% 7% 22.8%^ 12.0%

Treasury Assets

5,962 5,333 10,025 13,785 17,347 18,123 15,707

Growth (%) 28% (11%) 88% 37% 26% 4.5%^ (13.3%)

Deposits 13,483 14,443 17,617 20,763 25,212 26,888 26,139

Growth (%) 20% 7% 22% 18% 21% 6.7%^ (2.78%)

^ Growth is calculated based on FY June 2009. Growth for FYE Dec 2010 is based on 18 months period.

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jun 05 Jun 06 Jun 07 Jun 08 Jun 09 Dec 10 Sept 11

Assets Net Financing

Treasury Assets Deposits

RM’M

illion

Page 29

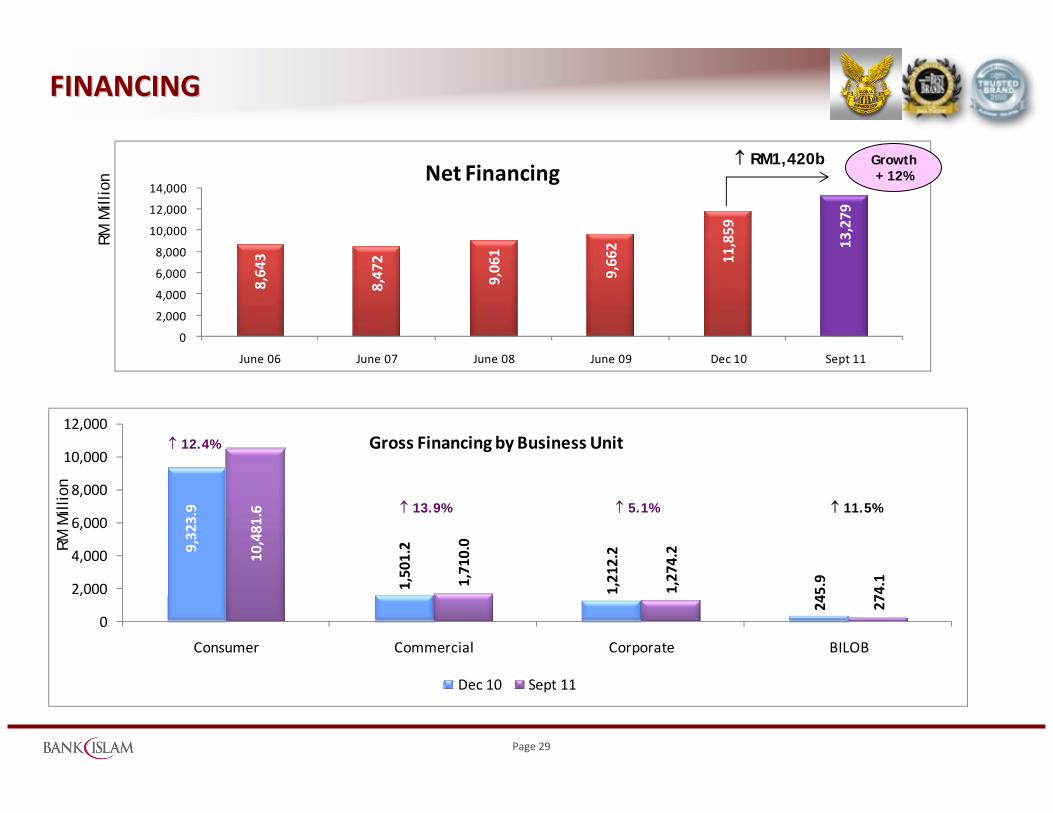

FINANCINGFINANCING

9,323.9

1,501.2

1,212.2

245.9

10,481.6

1,710.0

1,274.2

274.1

0

2,000

4,000

6,000

8,000

10,000

12,000

Consumer Commercial Corporate BILOB

Gross Financing by Business Unit

Dec 10 Sept 11

↑ 12.4%

↑ 13.9% ↑ 5.1% ↑ 11.5%

RM M

illio

n

RM M

illio

n

8,643

8,472

9,061

9,662

11,859

13,279

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

June 06 June 07 June 08 June 09 Dec 10 Sept 11

Net Financing↑ RM1,420b Growth

+ 12%

Page 30

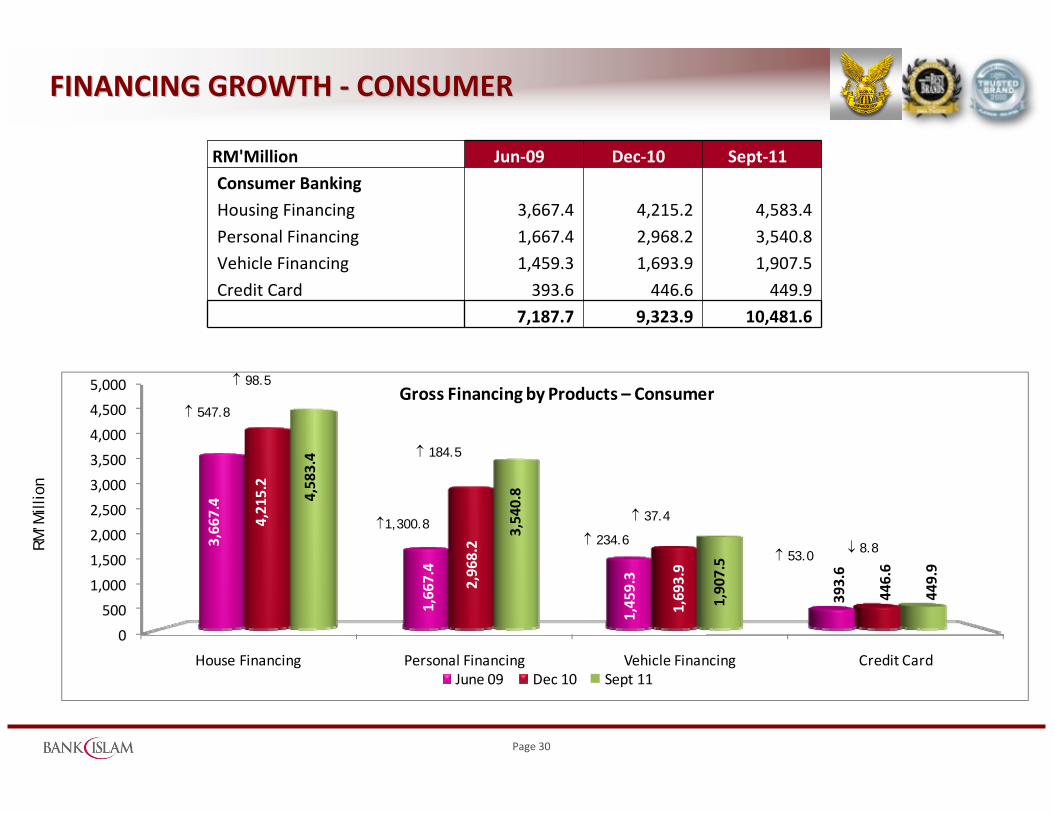

FINANCING GROWTH FINANCING GROWTH ‐‐ CONSUMERCONSUMER

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

House Financing Personal Financing Vehicle Financing Credit Card

3,667.4

1,667.4

1,459.3

393.6

4,215.2

2,968.2

1,693.9

446.6

4,583.4

3,540.8

1,907.5

449.9

Gross Financing by Products – Consumer

June 09 Dec 10 Sept 11

↑ 547.8

↑1,300.8↑ 234.6

↑ 53.0

RM’M

illio

n

RM'Million Jun‐09 Dec‐10 Sept‐11

Consumer Banking

Housing Financing 3,667.4 4,215.2 4,583.4

Personal Financing 1,667.4 2,968.2 3,540.8Vehicle Financing 1,459.3 1,693.9 1,907.5

Credit Card 393.6 446.6 449.97,187.7 9,323.9 10,481.6

↑ 98.5

↑ 37.4

↑ 184.5

↓ 8.8

Page 31

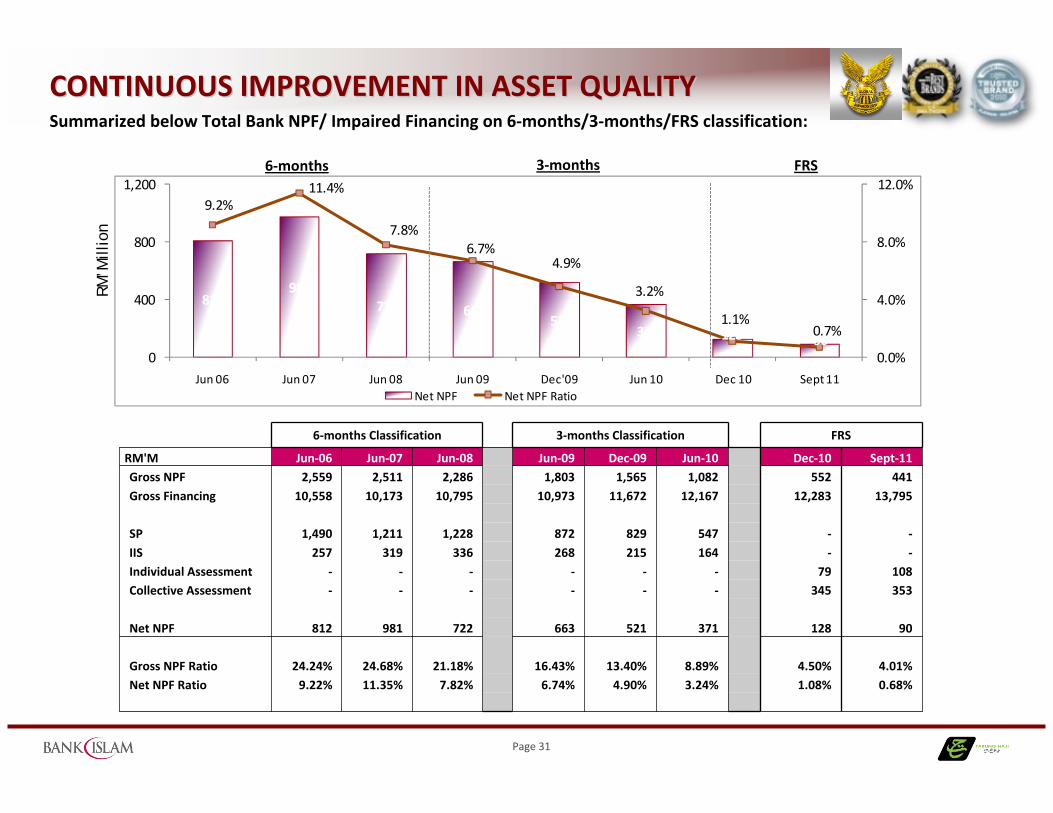

CONTINUOUS IMPROVEMENT IN ASSET QUALITYCONTINUOUS IMPROVEMENT IN ASSET QUALITYSummarized below Total Bank NPF/ Impaired Financing on 6‐months/3‐months/FRS classification:

6‐months Classification 3‐months Classification FRS

RM'M Jun‐06 Jun‐07 Jun‐08 Jun‐09 Dec‐09 Jun‐10 Dec‐10 Sept‐11Gross NPF 2,559 2,511 2,286 1,803 1,565 1,082 552 441Gross Financing 10,558 10,173 10,795 10,973 11,672 12,167 12,283 13,795

SP 1,490 1,211 1,228 872 829 547 ‐ ‐IIS 257 319 336 268 215 164 ‐ ‐Individual Assessment ‐ ‐ ‐ ‐ ‐ ‐ 79 108Collective Assessment ‐ ‐ ‐ ‐ ‐ ‐ 345 353

Net NPF 812 981 722 663 521 371 128 90

Gross NPF Ratio 24.24% 24.68% 21.18% 16.43% 13.40% 8.89% 4.50% 4.01%Net NPF Ratio 9.22% 11.35% 7.82% 6.74% 4.90% 3.24% 1.08% 0.68%

812981

722 663 521

371 128 90

9.2%11.4%

7.8%6.7%

4.9%

3.2%

1.1%0.7%

0.0%

4.0%

8.0%

12.0%

0

400

800

1,200

Jun 06 Jun 07 Jun 08 Jun 09 Dec'09 Jun 10 Dec 10 Sept 11Net NPF Net NPF Ratio

RM’M

illio

n

6‐months 3‐months FRS

Page 32

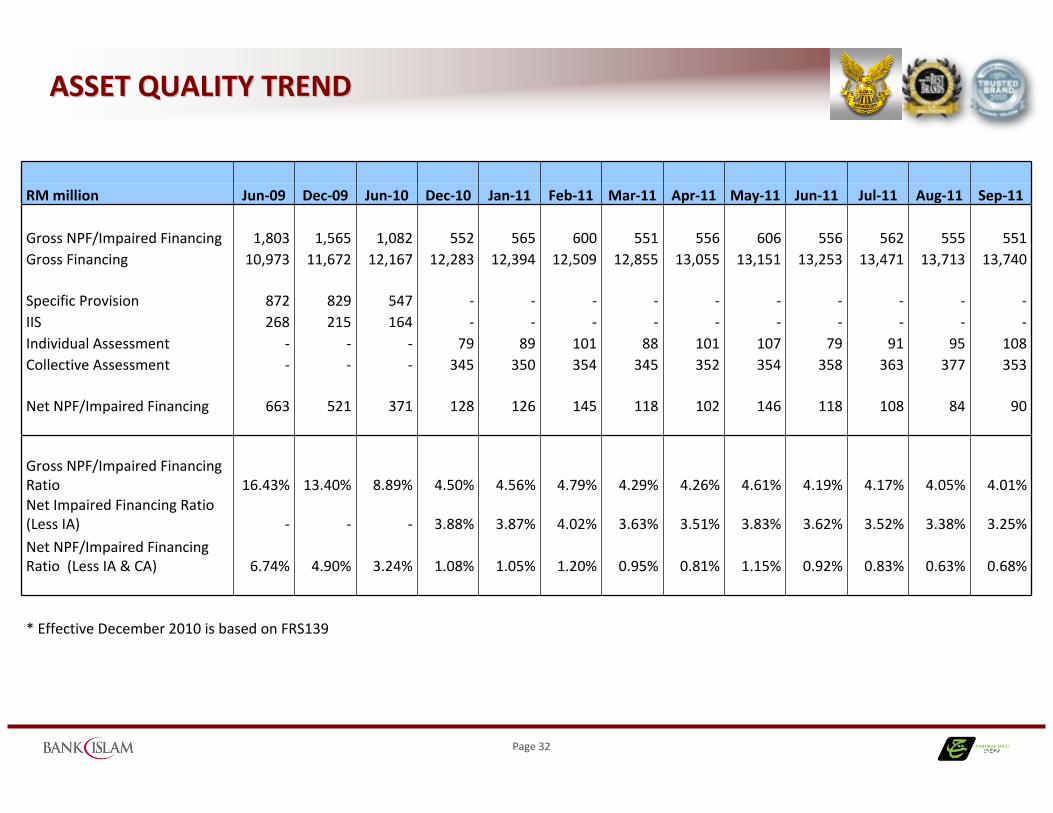

ASSET QUALITY TRENDASSET QUALITY TREND

RM million Jun‐09 Dec‐09 Jun‐10 Dec‐10 Jan‐11 Feb‐11 Mar‐11 Apr‐11 May‐11 Jun‐11 Jul‐11 Aug‐11 Sep‐11

Gross NPF/Impaired Financing 1,803 1,565 1,082 552 565 600 551 556 606 556 562 555 551Gross Financing 10,973 11,672 12,167 12,283 12,394 12,509 12,855 13,055 13,151 13,253 13,471 13,713 13,740

Specific Provision 872 829 547 ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐IIS 268 215 164 ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐Individual Assessment ‐ ‐ ‐ 79 89 101 88 101 107 79 91 95 108Collective Assessment ‐ ‐ ‐ 345 350 354 345 352 354 358 363 377 353

Net NPF/Impaired Financing 663 521 371 128 126 145 118 102 146 118 108 84 90

Gross NPF/Impaired Financing Ratio 16.43% 13.40% 8.89% 4.50% 4.56% 4.79% 4.29% 4.26% 4.61% 4.19% 4.17% 4.05% 4.01%Net Impaired Financing Ratio (Less IA) ‐ ‐ ‐ 3.88% 3.87% 4.02% 3.63% 3.51% 3.83% 3.62% 3.52% 3.38% 3.25%

Net NPF/Impaired Financing Ratio (Less IA & CA) 6.74% 4.90% 3.24% 1.08% 1.05% 1.20% 0.95% 0.81% 1.15% 0.92% 0.83% 0.63% 0.68%

* Effective December 2010 is based on FRS139

Page 33

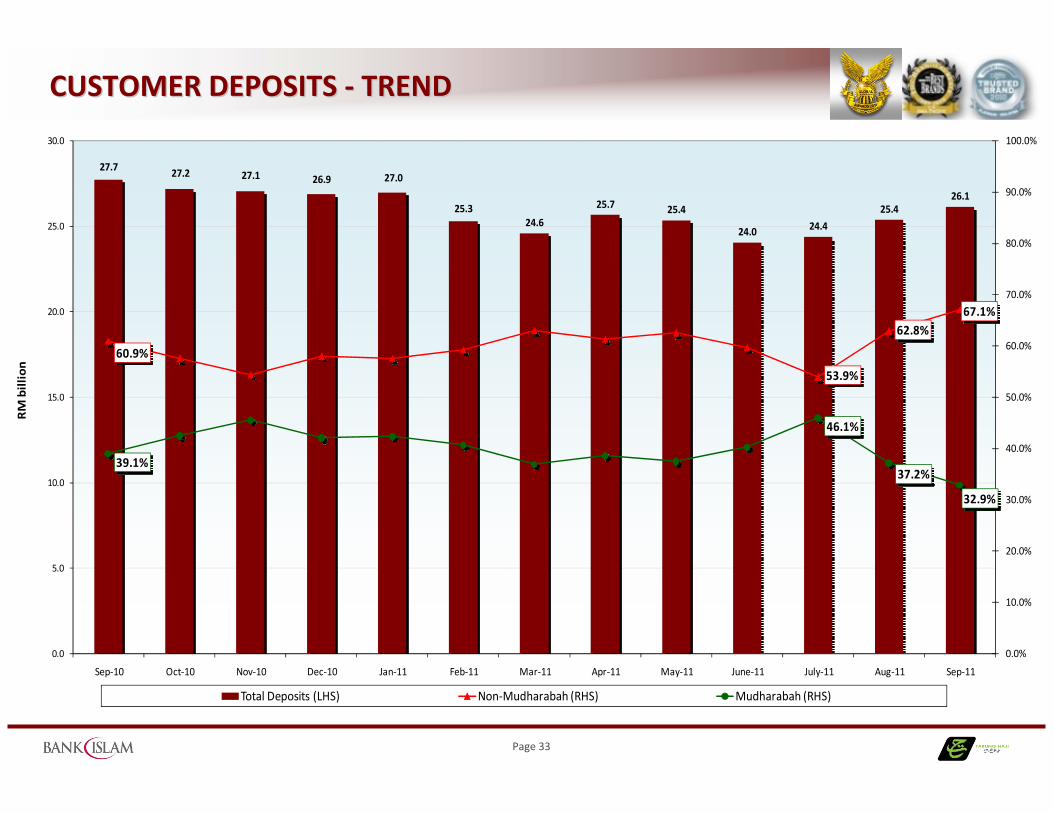

CUSTOMER DEPOSITS CUSTOMER DEPOSITS ‐‐ TRENDTREND

27.7 27.2 27.1 26.9 27.0

25.324.6

25.7 25.4

24.0 24.4

25.426.1

60.9%

53.9%

62.8%67.1%

39.1%

46.1%

37.2%

32.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Sep‐10 Oct‐10 Nov‐10 Dec‐10 Jan‐11 Feb‐11 Mar‐11 Apr‐11 May‐11 June‐11 July‐11 Aug‐11 Sep‐11

RM billion

Total Deposits (LHS) Non‐Mudharabah (RHS) Mudharabah (RHS)

Page 34

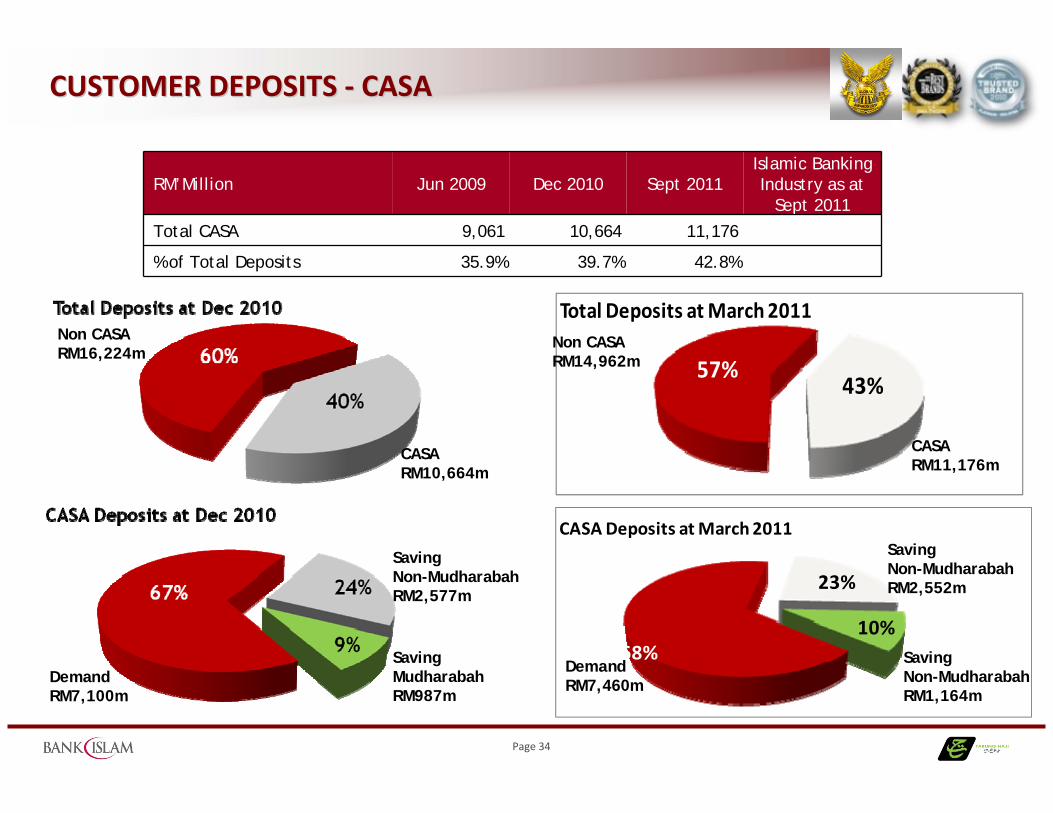

CUSTOMER DEPOSITS CUSTOMER DEPOSITS ‐‐ CASACASA

RM’Million Jun 2009 Dec 2010 Sept 2011Islamic Banking Industry as at

Sept 2011

Total CASA 9,061 10,664 11,176

% of Total Deposits 35.9% 39.7% 42.8%

CASA RM10,664m

Non CASA RM16,224m

Demand RM7,100m

Saving Mudharabah RM987m

Saving Non-Mudharabah RM2,577m

57%43%

Total Deposits at March 2011

68%

23%

10%

CASA Deposits at March 2011

Demand RM7,460m

Non CASA RM14,962m

CASA RM11,176m

Saving Non-Mudharabah RM2,552m

Saving Non-Mudharabah RM1,164m

Page 35

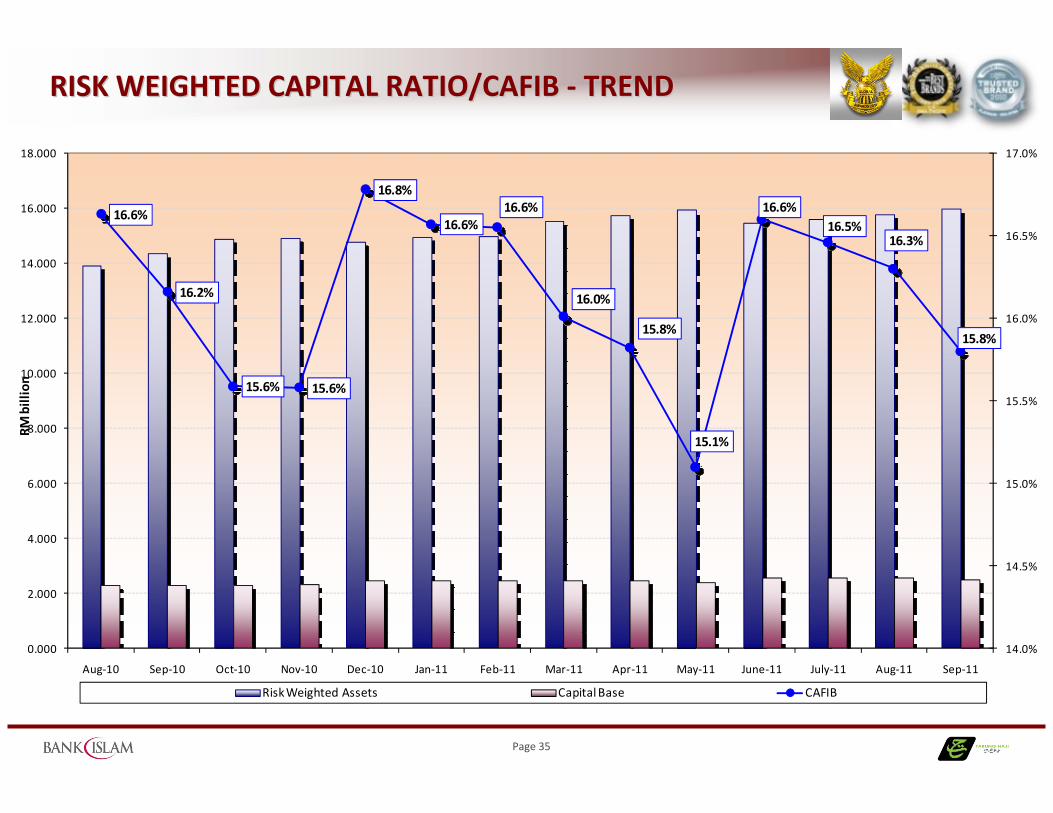

RISK WEIGHTED CAPITAL RATIO/CAFIB RISK WEIGHTED CAPITAL RATIO/CAFIB ‐‐ TRENDTREND

16.6%

16.2%

15.6% 15.6%

16.8%

16.6%16.6%

16.0%

15.8%

15.1%

16.6%16.5%

16.3%

15.8%

14.0%

14.5%

15.0%

15.5%

16.0%

16.5%

17.0%

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

Aug‐10 Sep‐10 Oct‐10 Nov‐10 Dec‐10 Jan‐11 Feb‐11 Mar‐11 Apr‐11 May‐11 June‐11 July‐11 Aug‐11 Sep‐11

RM billion

Risk Weighted Assets Capital Base CAFIB

Page 36

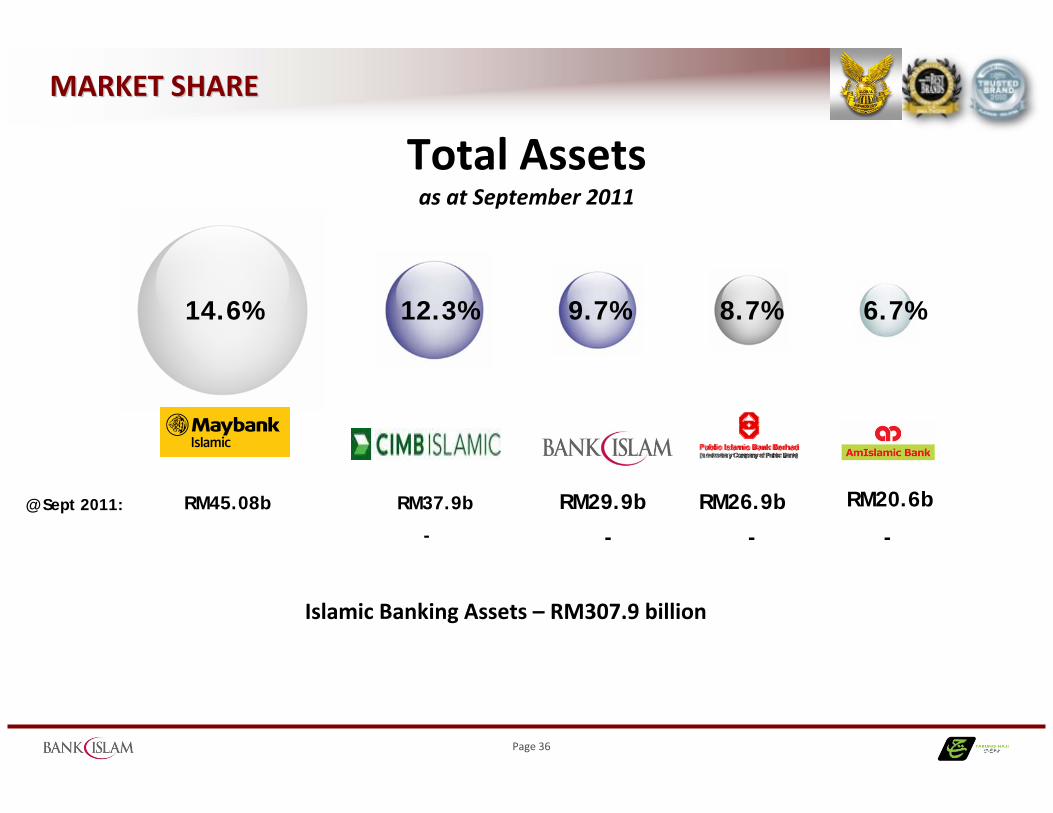

MARKET SHAREMARKET SHARE

14.6% 12.3% 9.7% 8.7% 6.7%

RM45.08b RM29.9bRM37.9b RM26.9b

Islamic Banking Assets – RM307.9 billion

@ Sept 2011:

-- -

RM20.6b

-

Total Assetsas at September 2011

Page 37

MARKET SHAREMARKET SHARE

18.6% 13.5% 10.0% 7.6% 7.1%

RM34.5b RM18.5bRM25.0b RM14.0b

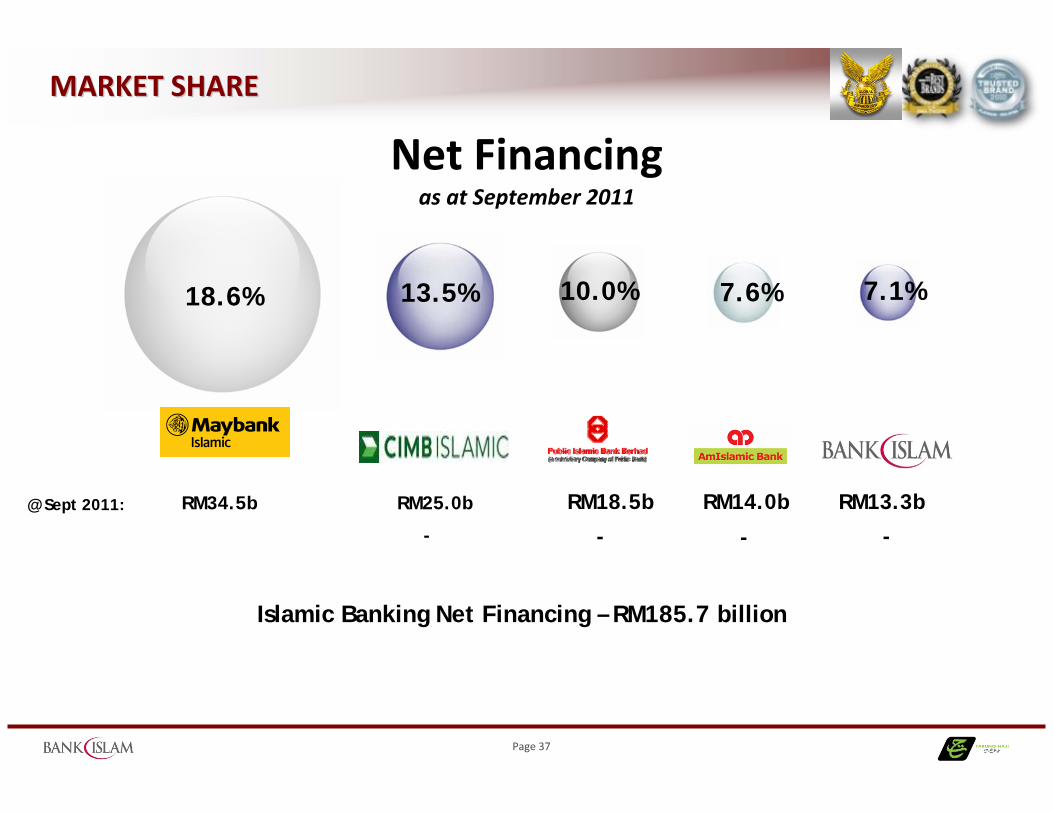

Islamic Banking Net Financing – RM185.7 billion

@ Sept 2011:

-- -

RM13.3b

-

Net Financingas at September 2011

Page 38

MARKET SHAREMARKET SHARE

14.3% 10.9% 10.4% 7.9% 6.2%

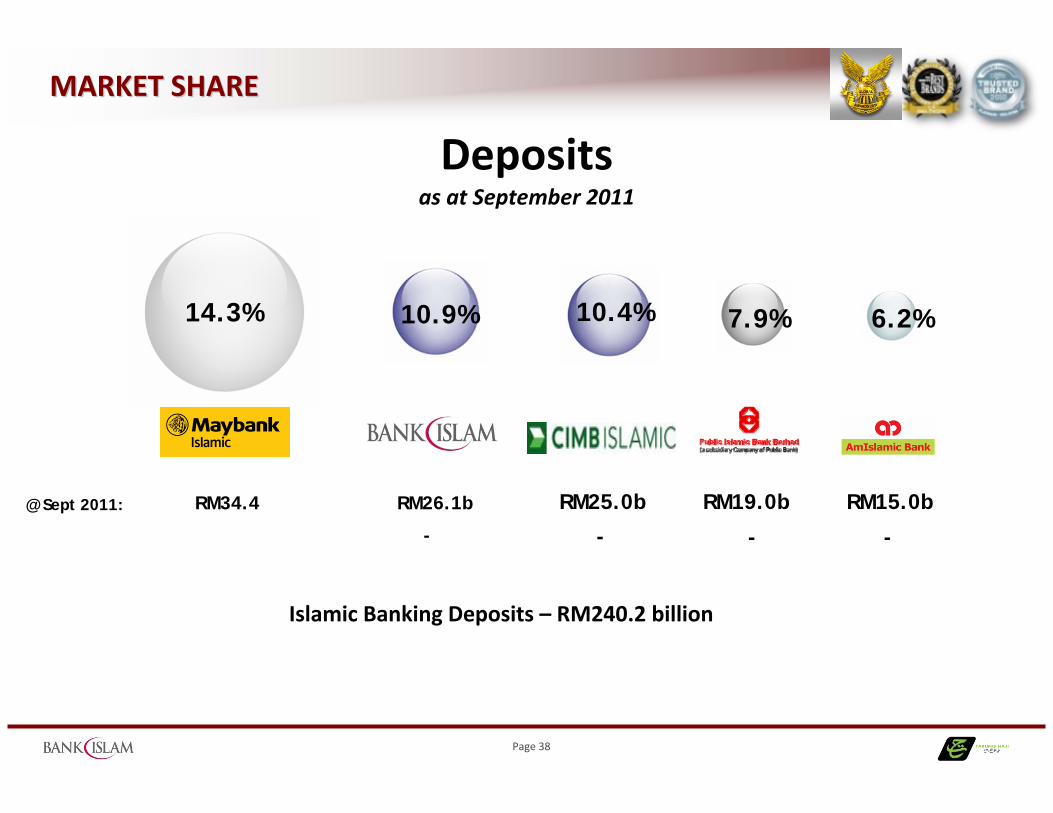

RM34.4 RM25.0bRM26.1b RM19.0b

Islamic Banking Deposits – RM240.2 billion

@ Sept 2011:

-- -

RM15.0b

-

Depositsas at September 2011

Page 39

MARKET SHAREMARKET SHARE

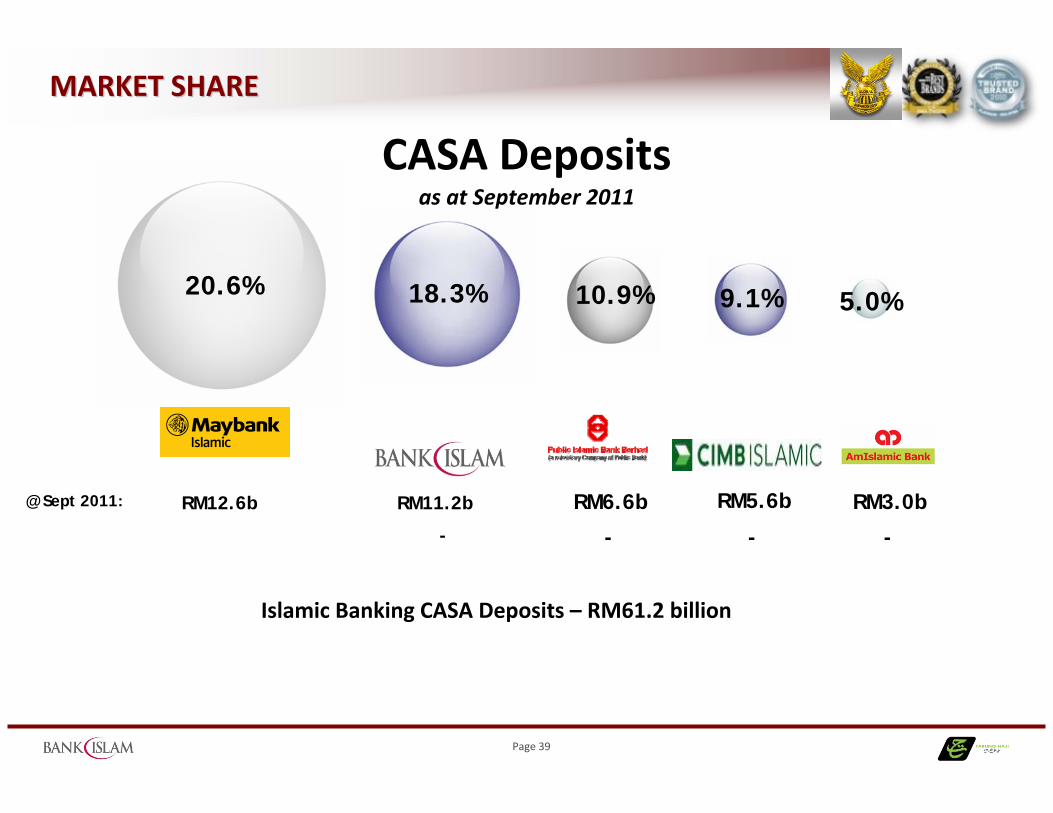

20.6% 18.3% 10.9% 9.1% 5.0%

RM12.6b RM6.6bRM11.2b RM5.6b

Islamic Banking CASA Deposits – RM61.2 billion

@ Sept 2011:

-- -

RM3.0b

-

CASA Depositsas at September 2011

Page 40

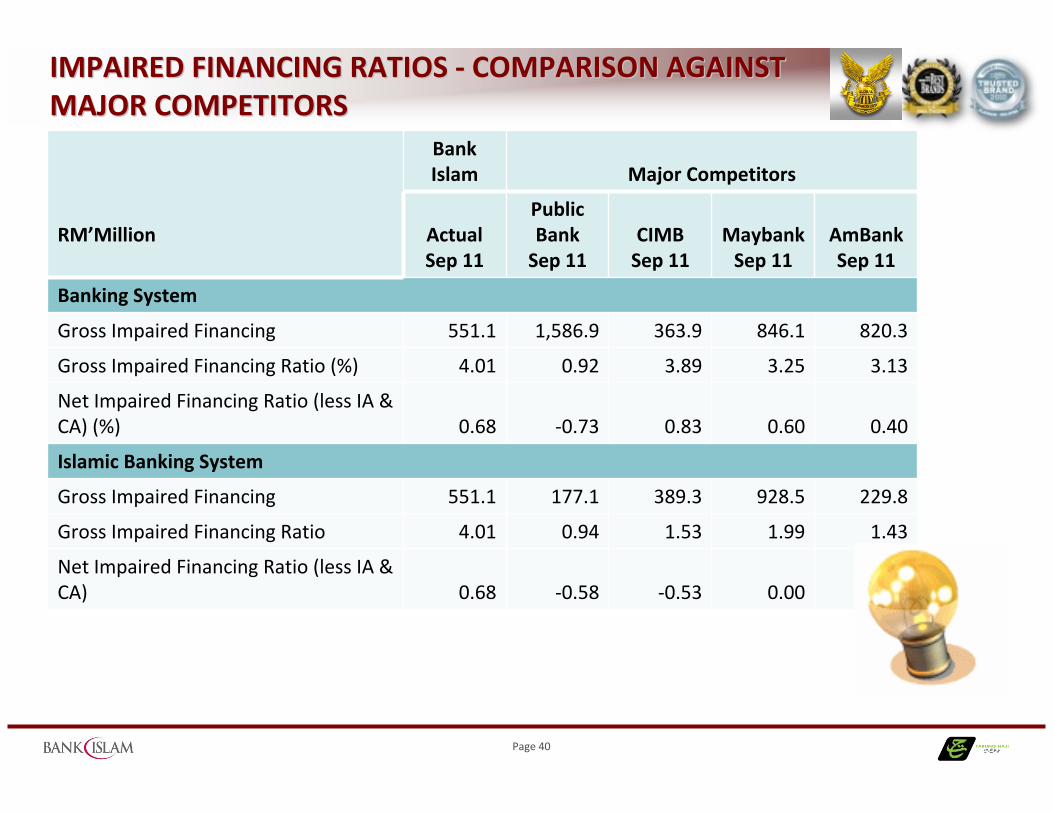

IMPAIRED FINANCING RATIOS IMPAIRED FINANCING RATIOS ‐‐ COMPARISON AGAINST COMPARISON AGAINST MAJOR COMPETITORS MAJOR COMPETITORS

RM’Million

Bank Islam Major Competitors

ActualSep 11

Public BankSep 11

CIMBSep 11

MaybankSep 11

AmBankSep 11

Banking System

Gross Impaired Financing 551.1 1,586.9 363.9 846.1 820.3

Gross Impaired Financing Ratio (%) 4.01 0.92 3.89 3.25 3.13

Net Impaired Financing Ratio (less IA & CA) (%) 0.68 ‐0.73 0.83 0.60 0.40

Islamic Banking System

Gross Impaired Financing 551.1 177.1 389.3 928.5 229.8

Gross Impaired Financing Ratio 4.01 0.94 1.53 1.99 1.43

Net Impaired Financing Ratio (less IA & CA) 0.68 ‐0.58 ‐0.53 0.00 ‐1.59

Page 41

شكراشكراوالسالوالسالجزيالجزيال

ممDisclaimer: This presentation material has been prepared by Bank Islam Malaysia Berhad (the Bank”) for information purposes only and does not purport to contain all the information that may be required to evaluate the Bank or its financial position. No representation or warranty, express r implied, is given by or on behalf of the Bank as to the accuracy of the information or opinions contained in this presentation. The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities , nor should it or any part of it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever. The Bank does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in connection therewith.

BANK ISLAM MALAYSIA BERHAD11th Floor, Wisma Bank IslamJalan Dungun, Bukit Damansara50490 Kuala LumpurTel: 603 2088 8222

www.bankislam.com.my

Malkit Singh MaanChief Financial OfficerContact: 602 2088 8118Email: [email protected]

Hizamuddin JamalluddinAGM, Strategic PlanningContact: 602 2088 8077Email: [email protected]