Embed Size (px)

Citation preview

Innovation. Dedication. Knowledge. Purpose. Integrity. Vision. Talent. Results.

Bottom Line Driven Health Benefits Planning

Are You Going To Pay or Play?

September 18, 2013

Jeffery A. Schultz Phone: 262.207.1999 ext. 112

Email: [email protected]

Vice President, BeneCo of Wisconsin

-2- Are You Going to Pay or Play?

Are you Going to Pay or Play?

What we will cover: Impact on employer health plans Compliance implications

Cost implications

Micro and Macro views

Long term planning issues/thoughts

What employers need to do

How you can add value in the ACA discussion

-3- Are You Going to Pay or Play?

1300+ Pages of Regulations – REALLY?

-4- Are You Going to Pay or Play?

Ground rules

Some questions may fall under

Haven't read,

Haven't heard,

Guidance not released,

Just don’t know…

-5- Are You Going to Pay or Play?

As we start…

Beware Of All The Moving Parts

ACA introduces a wide variety of moving parts:

Mandates and plan tests

New concepts and paradigms

Inconsistent definitions

Adverse selection possibility / health risk pool

Industry wide taxes and fees

Penalties & Cadillac Plan Excise Tax

Additional Administrative complexities and costs

The moving parts interrelate – fixing one piece could introduce higher costs for another parts.

It is a very complicated mix, where decisions need to be based on facts and quality probability modeling.

-6- Are You Going to Pay or Play?

What is Delayed

The employer shared responsibility rule and accompanying

penalties, which also delays the requirement to offer

coverage to dependent children of full-time employees for

plans that had not previously extended that coverage.

The employer coverage informational reporting

requirements.

-7- Are You Going to Pay or Play?

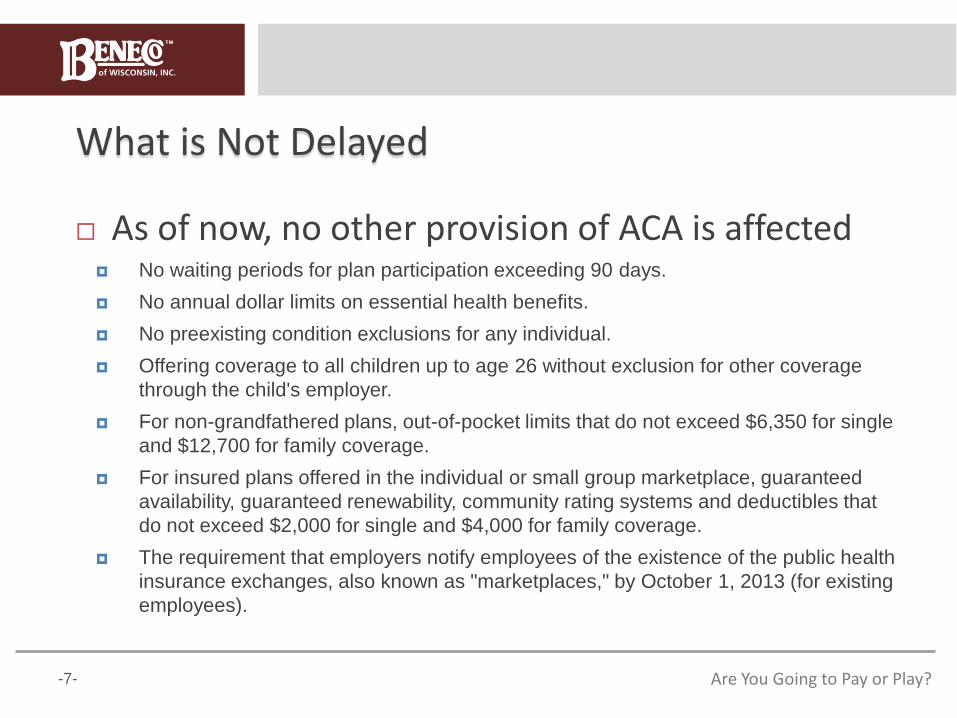

What is Not Delayed

As of now, no other provision of ACA is affected No waiting periods for plan participation exceeding 90 days.

No annual dollar limits on essential health benefits.

No preexisting condition exclusions for any individual.

Offering coverage to all children up to age 26 without exclusion for other coverage

through the child's employer.

For non-grandfathered plans, out-of-pocket limits that do not exceed $6,350 for single

and $12,700 for family coverage.

For insured plans offered in the individual or small group marketplace, guaranteed

availability, guaranteed renewability, community rating systems and deductibles that

do not exceed $2,000 for single and $4,000 for family coverage.

The requirement that employers notify employees of the existence of the public health

insurance exchanges, also known as "marketplaces," by October 1, 2013 (for existing

employees).

-8- Are You Going to Pay or Play?

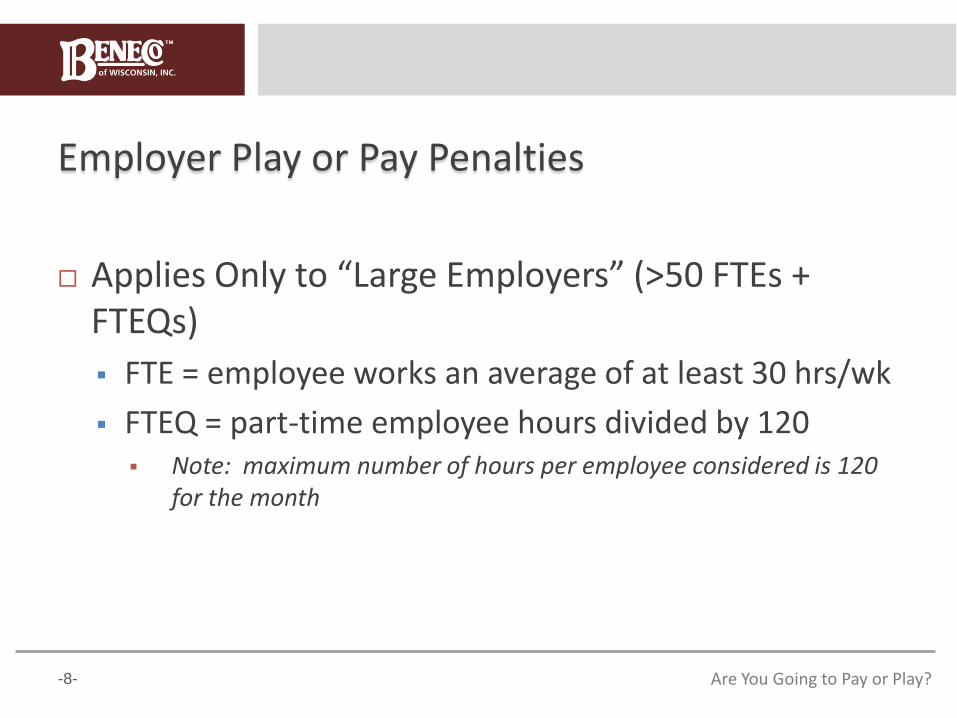

Employer Play or Pay Penalties

Applies Only to “Large Employers” (>50 FTEs + FTEQs)

FTE = employee works an average of at least 30 hrs/wk

FTEQ = part-time employee hours divided by 120 Note: maximum number of hours per employee considered is 120

for the month

-9- Are You Going to Pay or Play?

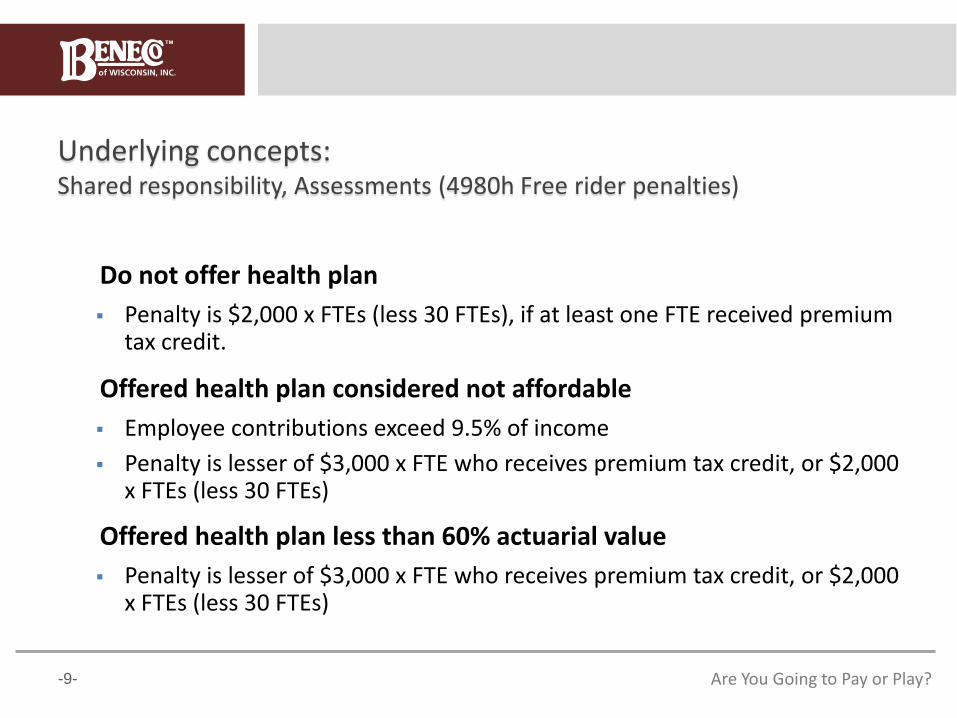

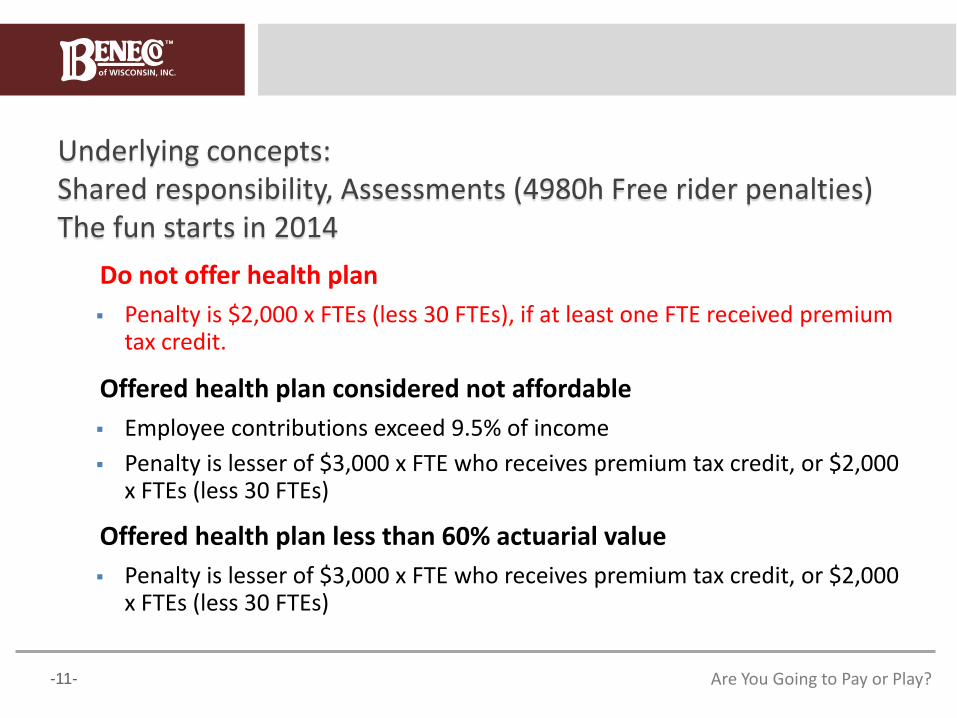

Underlying concepts: Shared responsibility, Assessments (4980h Free rider penalties)

Do not offer health plan

Penalty is $2,000 x FTEs (less 30 FTEs), if at least one FTE received premium tax credit.

Offered health plan considered not affordable

Employee contributions exceed 9.5% of income

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

Offered health plan less than 60% actuarial value

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

-10- Are You Going to Pay or Play?

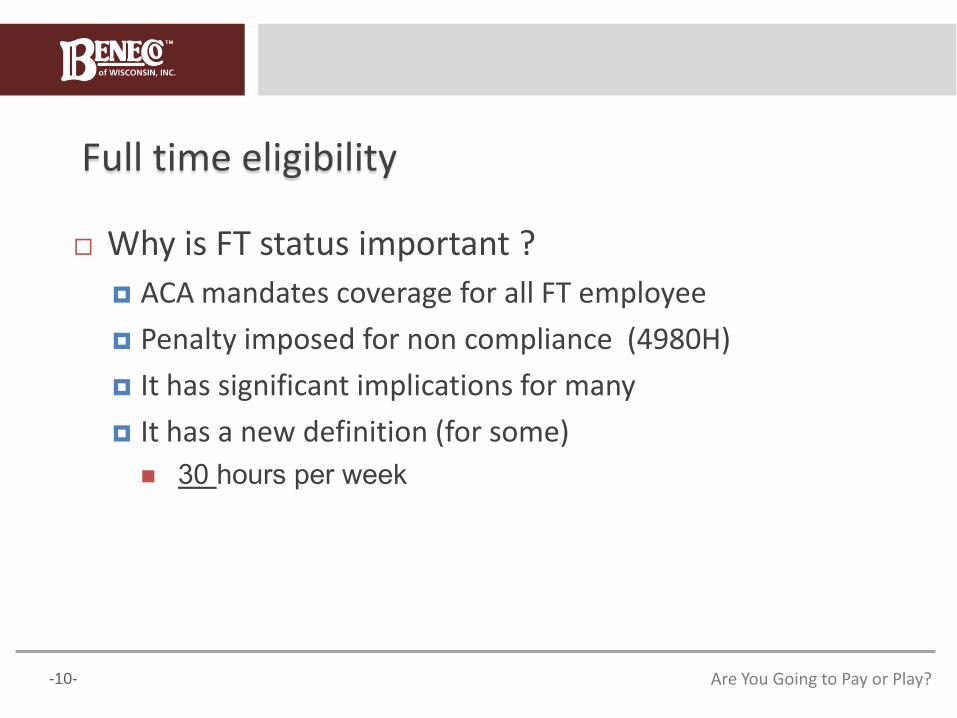

Full time eligibility

Why is FT status important ?

ACA mandates coverage for all FT employee

Penalty imposed for non compliance (4980H)

It has significant implications for many

It has a new definition (for some)

30 hours per week

-11- Are You Going to Pay or Play?

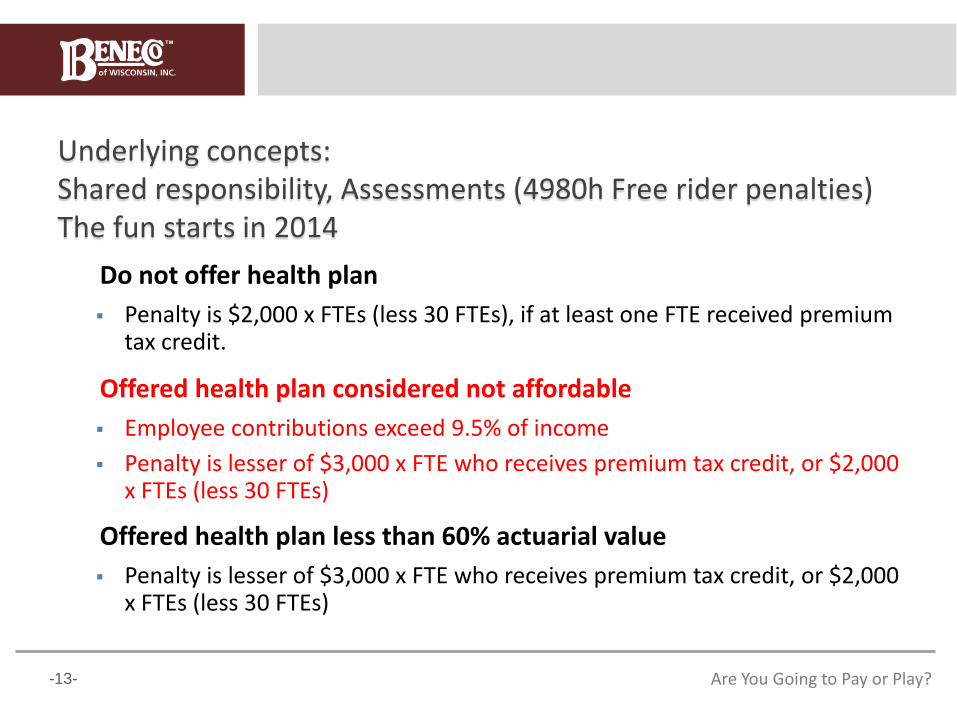

Underlying concepts: Shared responsibility, Assessments (4980h Free rider penalties) The fun starts in 2014

Do not offer health plan

Penalty is $2,000 x FTEs (less 30 FTEs), if at least one FTE received premium tax credit.

Offered health plan considered not affordable

Employee contributions exceed 9.5% of income

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

Offered health plan less than 60% actuarial value

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

-12- Are You Going to Pay or Play?

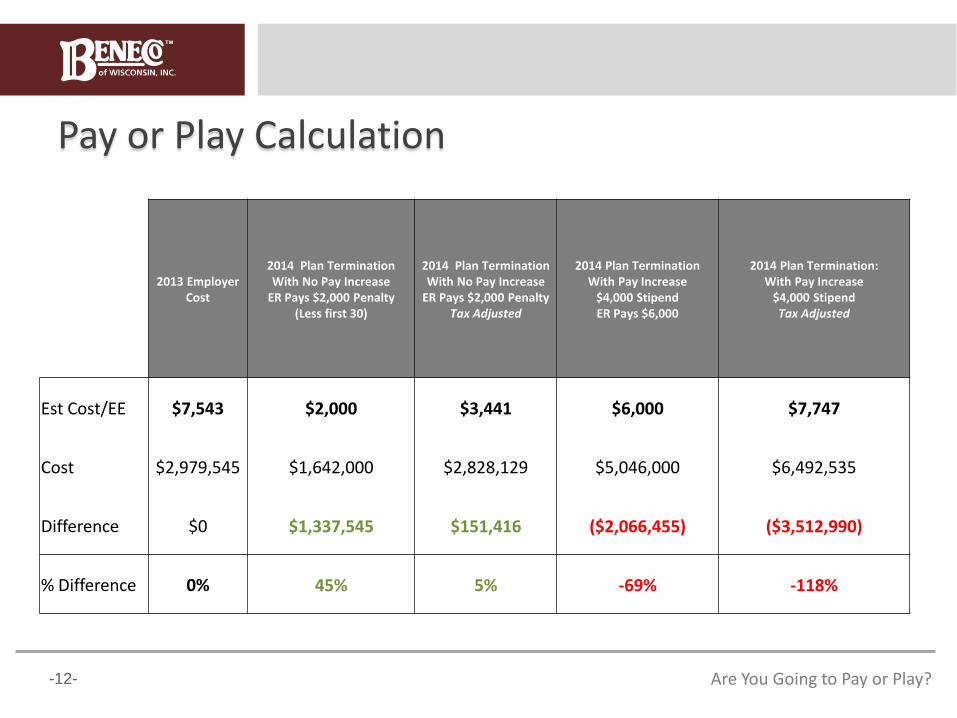

Pay or Play Calculation

2013 Employer Cost

2014 Plan Termination With No Pay Increase

ER Pays $2,000 Penalty (Less first 30)

2014 Plan Termination With No Pay Increase

ER Pays $2,000 Penalty Tax Adjusted

2014 Plan Termination With Pay Increase

$4,000 Stipend ER Pays $6,000

2014 Plan Termination: With Pay Increase

$4,000 Stipend Tax Adjusted

Est Cost/EE $7,543 $2,000 $3,441 $6,000 $7,747

Cost $2,979,545 $1,642,000 $2,828,129 $5,046,000 $6,492,535

Difference $0 $1,337,545 $151,416 ($2,066,455) ($3,512,990)

% Difference 0% 45% 5% -69% -118%

-13- Are You Going to Pay or Play?

Underlying concepts: Shared responsibility, Assessments (4980h Free rider penalties) The fun starts in 2014

Do not offer health plan

Penalty is $2,000 x FTEs (less 30 FTEs), if at least one FTE received premium tax credit.

Offered health plan considered not affordable

Employee contributions exceed 9.5% of income

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

Offered health plan less than 60% actuarial value

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

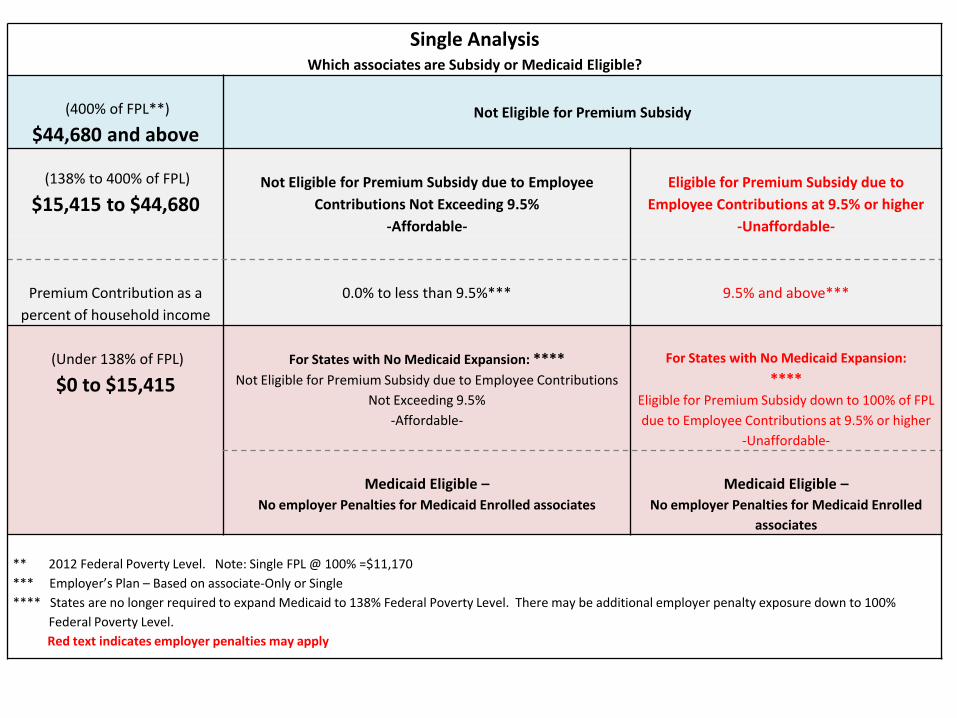

Single Analysis Which associates are Subsidy or Medicaid Eligible?

(400% of FPL**)

$44,680 and above Not Eligible for Premium Subsidy

(138% to 400% of FPL)

$15,415 to $44,680

Not Eligible for Premium Subsidy due to Employee

Contributions Not Exceeding 9.5%

-Affordable-

Eligible for Premium Subsidy due to

Employee Contributions at 9.5% or higher

-Unaffordable-

Premium Contribution as a

percent of household income

0.0% to less than 9.5%*** 9.5% and above***

(Under 138% of FPL)

$0 to $15,415

For States with No Medicaid Expansion: ****

Not Eligible for Premium Subsidy due to Employee Contributions

Not Exceeding 9.5%

-Affordable-

For States with No Medicaid Expansion:

****

Eligible for Premium Subsidy down to 100% of FPL

due to Employee Contributions at 9.5% or higher

-Unaffordable-

Medicaid Eligible –

No employer Penalties for Medicaid Enrolled associates

Medicaid Eligible –

No employer Penalties for Medicaid Enrolled

associates

** 2012 Federal Poverty Level. Note: Single FPL @ 100% =$11,170

*** Employer’s Plan – Based on associate-Only or Single

**** States are no longer required to expand Medicaid to 138% Federal Poverty Level. There may be additional employer penalty exposure down to 100%

Federal Poverty Level.

Red text indicates employer penalties may apply

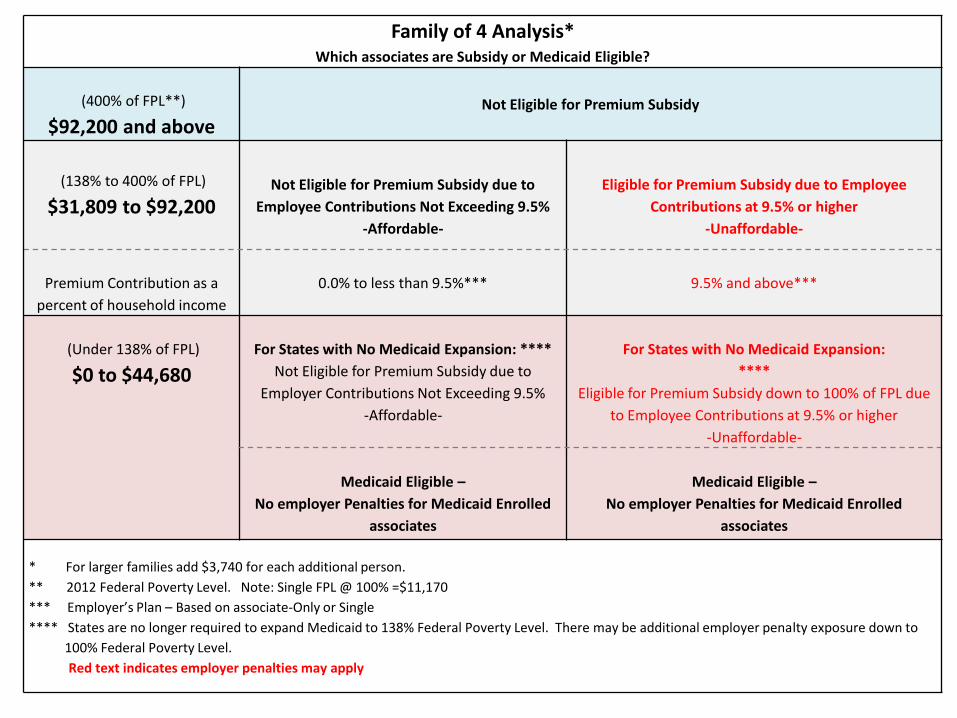

Family of 4 Analysis* Which associates are Subsidy or Medicaid Eligible?

(400% of FPL**)

$92,200 and above Not Eligible for Premium Subsidy

(138% to 400% of FPL)

$31,809 to $92,200

Not Eligible for Premium Subsidy due to

Employee Contributions Not Exceeding 9.5%

-Affordable-

Eligible for Premium Subsidy due to Employee

Contributions at 9.5% or higher

-Unaffordable-

Premium Contribution as a

percent of household income

0.0% to less than 9.5%*** 9.5% and above***

(Under 138% of FPL)

$0 to $44,680

For States with No Medicaid Expansion: ****

Not Eligible for Premium Subsidy due to

Employer Contributions Not Exceeding 9.5%

-Affordable-

For States with No Medicaid Expansion:

****

Eligible for Premium Subsidy down to 100% of FPL due

to Employee Contributions at 9.5% or higher

-Unaffordable-

Medicaid Eligible –

No employer Penalties for Medicaid Enrolled

associates

Medicaid Eligible –

No employer Penalties for Medicaid Enrolled

associates

* For larger families add $3,740 for each additional person.

** 2012 Federal Poverty Level. Note: Single FPL @ 100% =$11,170

*** Employer’s Plan – Based on associate-Only or Single

**** States are no longer required to expand Medicaid to 138% Federal Poverty Level. There may be additional employer penalty exposure down to

100% Federal Poverty Level.

Red text indicates employer penalties may apply

-16- Health Care Reform: 301 How to Determine if We Will Pay or Play

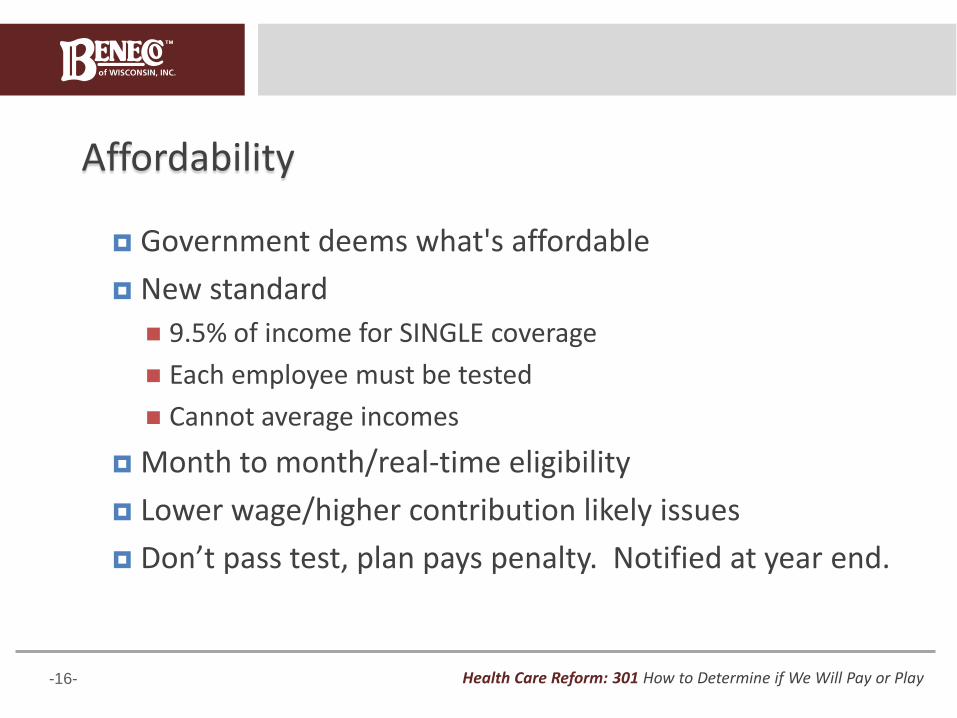

Affordability

Government deems what's affordable

New standard

9.5% of income for SINGLE coverage

Each employee must be tested

Cannot average incomes

Month to month/real-time eligibility

Lower wage/higher contribution likely issues

Don’t pass test, plan pays penalty. Notified at year end.

-17- Health Care Reform: 301 How to Determine if We Will Pay or Play

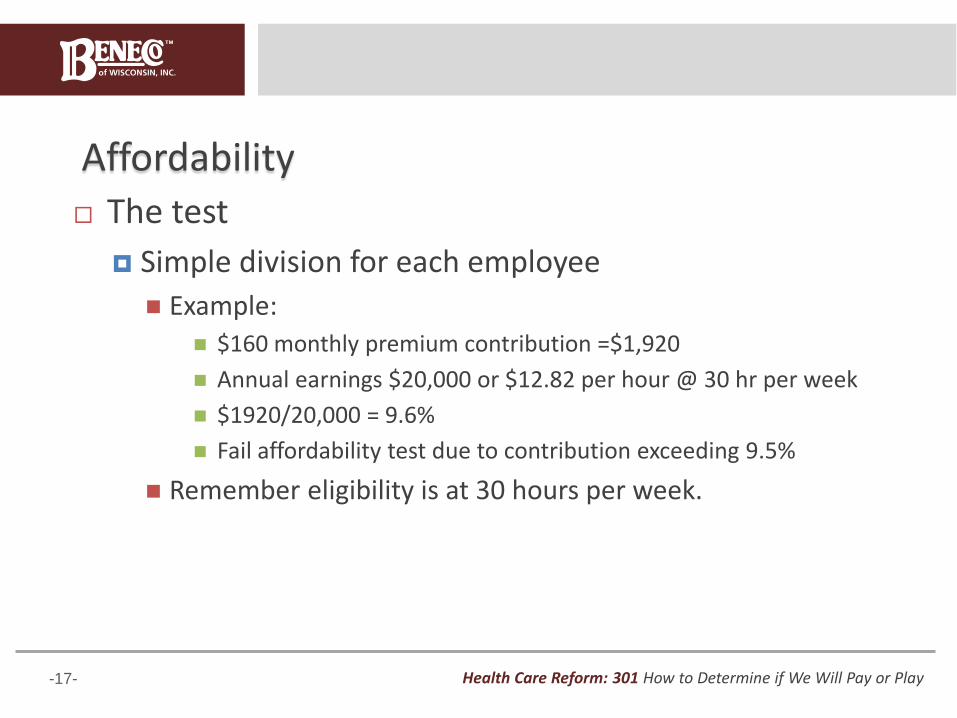

Affordability The test

Simple division for each employee

Example:

$160 monthly premium contribution =$1,920

Annual earnings $20,000 or $12.82 per hour @ 30 hr per week

$1920/20,000 = 9.6%

Fail affordability test due to contribution exceeding 9.5%

Remember eligibility is at 30 hours per week.

-18- Health Care Reform: 301 How to Determine if We Will Pay or Play

Affordability

The safe harbors

W-2 earnings (Box 1)

Rate of pay

FPL

-19- Health Care Reform: 301 How to Determine if We Will Pay or Play

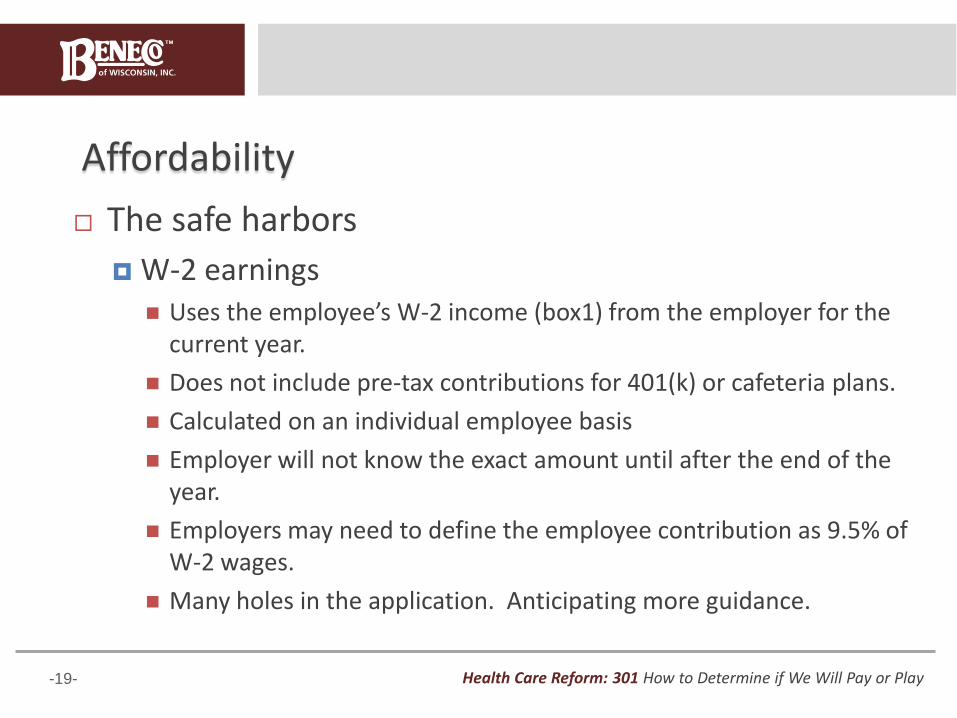

Affordability

The safe harbors

W-2 earnings Uses the employee’s W-2 income (box1) from the employer for the

current year.

Does not include pre-tax contributions for 401(k) or cafeteria plans.

Calculated on an individual employee basis

Employer will not know the exact amount until after the end of the year.

Employers may need to define the employee contribution as 9.5% of W-2 wages.

Many holes in the application. Anticipating more guidance.

-20- Health Care Reform: 301 How to Determine if We Will Pay or Play

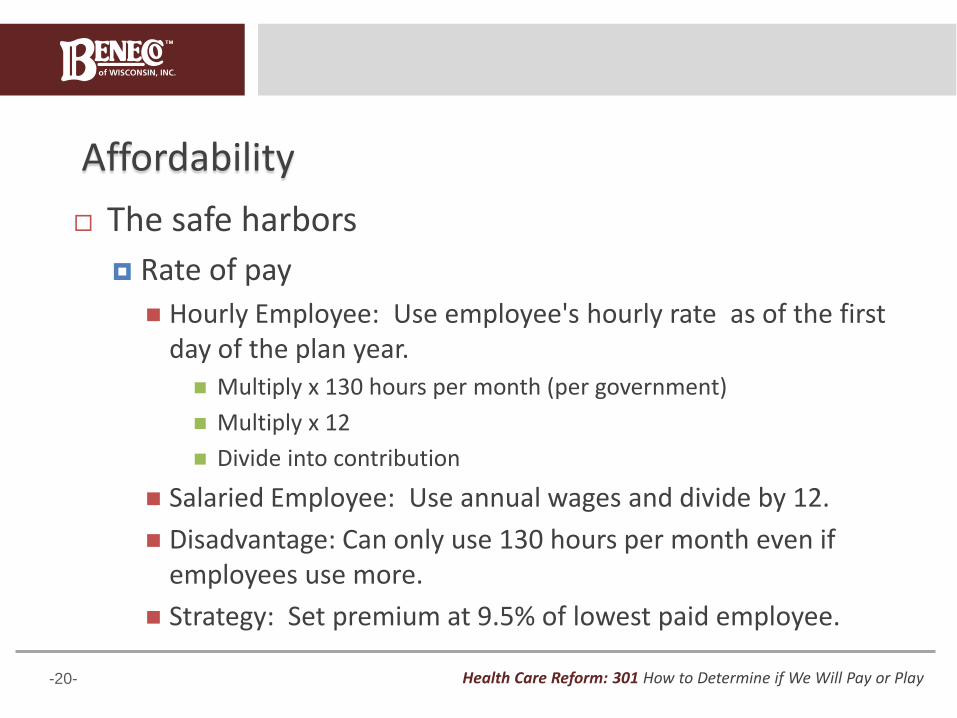

Affordability

The safe harbors

Rate of pay

Hourly Employee: Use employee's hourly rate as of the first day of the plan year.

Multiply x 130 hours per month (per government)

Multiply x 12

Divide into contribution

Salaried Employee: Use annual wages and divide by 12.

Disadvantage: Can only use 130 hours per month even if employees use more.

Strategy: Set premium at 9.5% of lowest paid employee.

-21- Health Care Reform: 301 How to Determine if We Will Pay or Play

Affordability

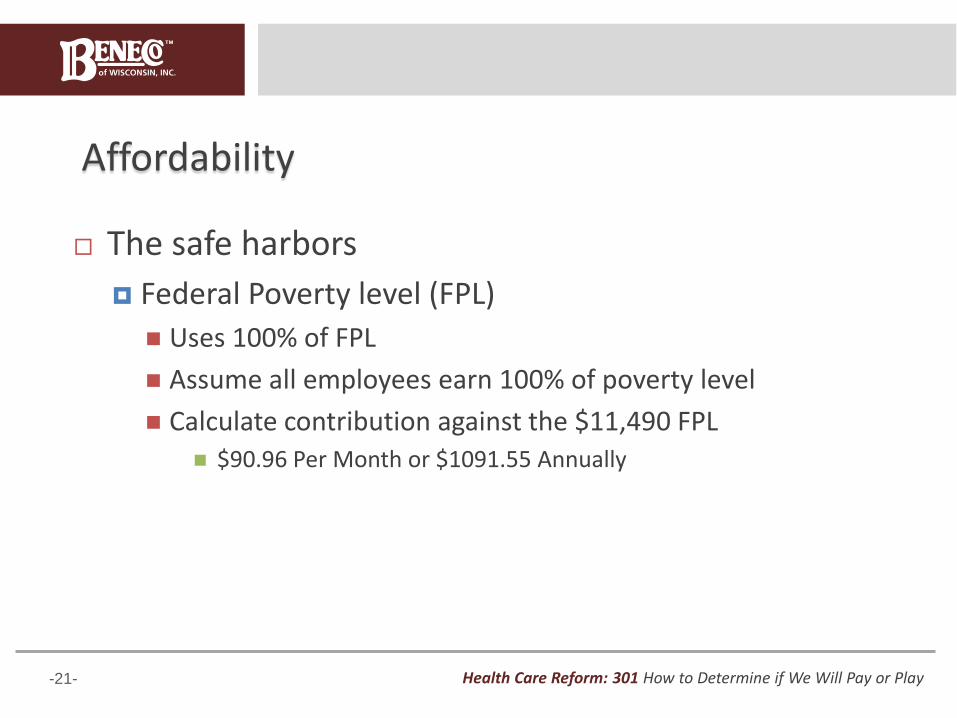

The safe harbors

Federal Poverty level (FPL)

Uses 100% of FPL

Assume all employees earn 100% of poverty level

Calculate contribution against the $11,490 FPL

$90.96 Per Month or $1091.55 Annually

-22- Health Care Reform: 301 How to Determine if We Will Pay or Play

Important Points on Affordability and Penalties

Less than a 9.5% of wage contribution immunizes plan from penalties

Employees may still be eligible for subsidies due to premium costs in excess of 9.5% of household earnings

Plan will be notified retrospectively

-23- Are You Going to Pay or Play?

What Should We Do Now?

Get educated.

Determine the subsidy eligible populations

Understand the position of states where employees reside.

Obtain assistance estimating in/out migration

Think about ways to leverage exchanges in your planning strategy. (i.e wellness)

Understand the complexity will not go away.

-24- Are You Going to Pay or Play?

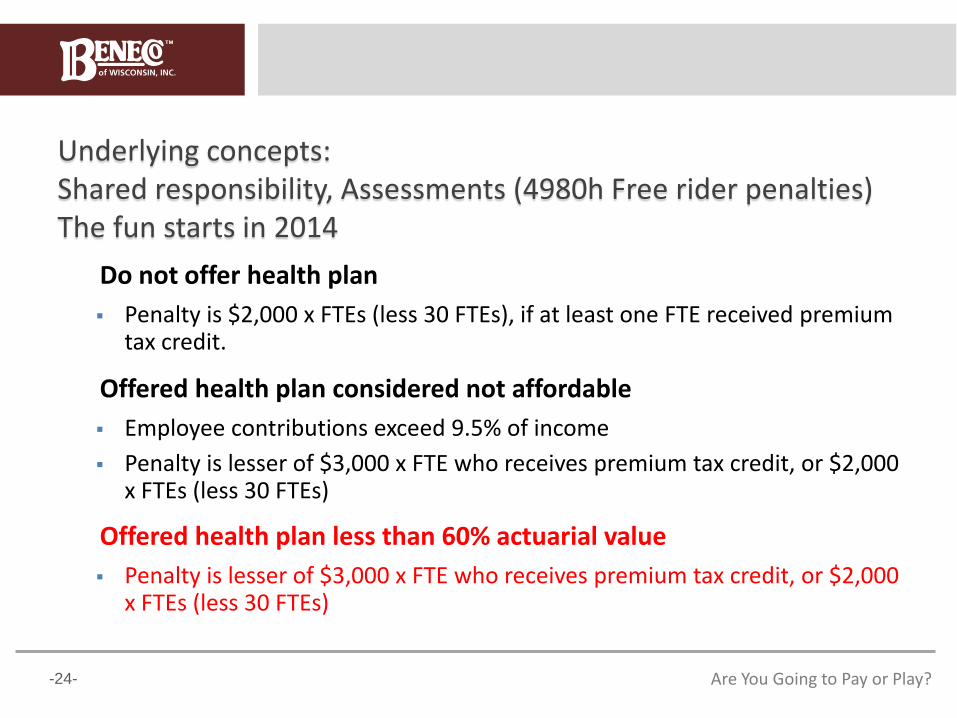

Underlying concepts: Shared responsibility, Assessments (4980h Free rider penalties) The fun starts in 2014

Do not offer health plan

Penalty is $2,000 x FTEs (less 30 FTEs), if at least one FTE received premium tax credit.

Offered health plan considered not affordable

Employee contributions exceed 9.5% of income

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

Offered health plan less than 60% actuarial value

Penalty is lesser of $3,000 x FTE who receives premium tax credit, or $2,000 x FTEs (less 30 FTEs)

-25- Are You Going to Pay or Play?

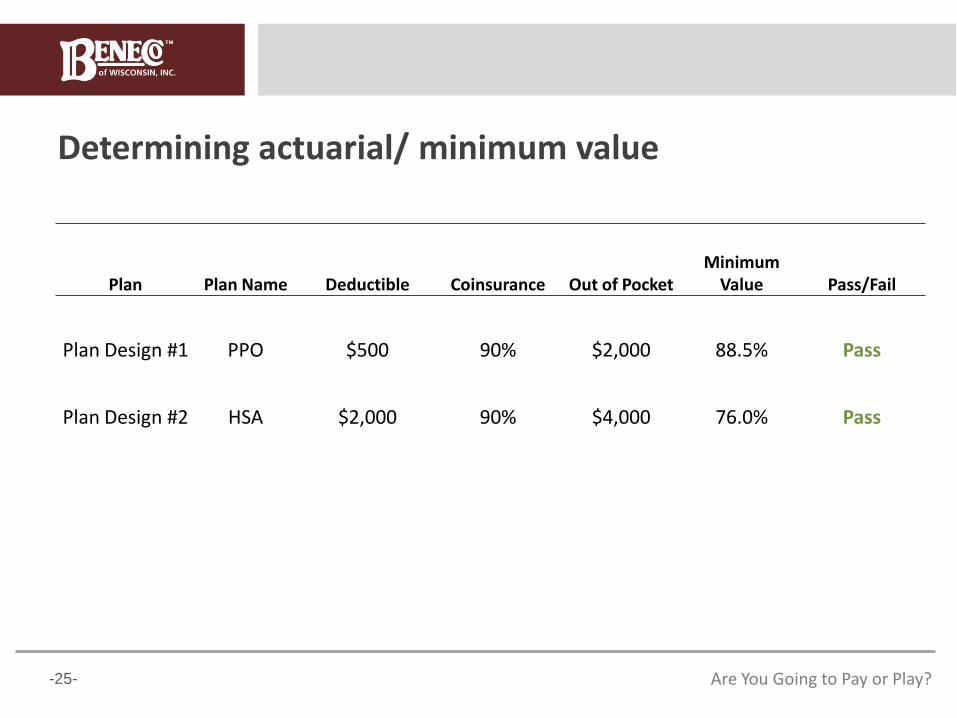

Determining actuarial/ minimum value

Plan Plan Name Deductible Coinsurance Out of Pocket Minimum

Value Pass/Fail

Plan Design #1 PPO $500 90% $2,000 88.5% Pass

Plan Design #2 HSA $2,000 90% $4,000 76.0% Pass

-26- Are You Going to Pay or Play?

What Should Employers Do?

Understand their plan’s Actuarial or Minimum value (may need actuarial help).

Examine plan pricing integrity and spreads

Re- evaluate the number of plans offered, coverage levels and price points

If employers to avoid penalties, consider offering a 60% (bronze) level plan

-27- Are You Going to Pay or Play?

ACA fees and taxes

Fully insured groups with other than January 1 renewal:

Will be a factor in the renewal

Expect line item on billing post renewal

Self insured groups

Will be paying the TPA or government directly

-28- Are You Going to Pay or Play?

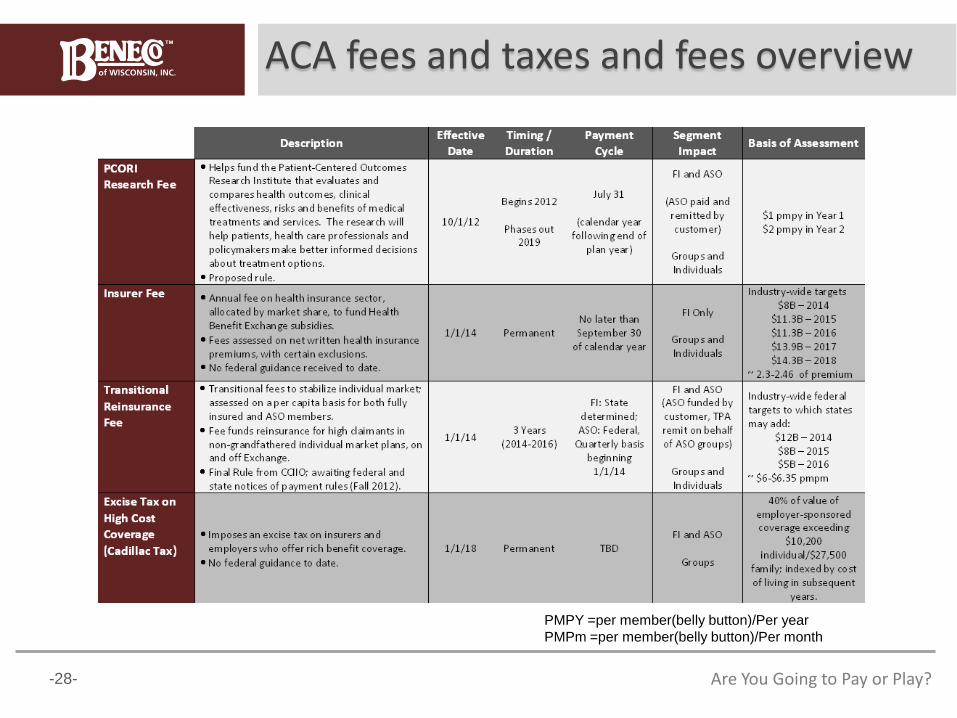

ACA fees and taxes and fees overview

PMPY =per member(belly button)/Per year

PMPm =per member(belly button)/Per month

-29- Are You Going to Pay or Play?

What Should Employers Do?

Get educated.

Ask your carrier /TPA for specific fee amounts.

Make sure to include all fees in budgets.

Communicate fees to employees

Include fees in total cost and contribution calculations

-30- Are You Going to Pay or Play?

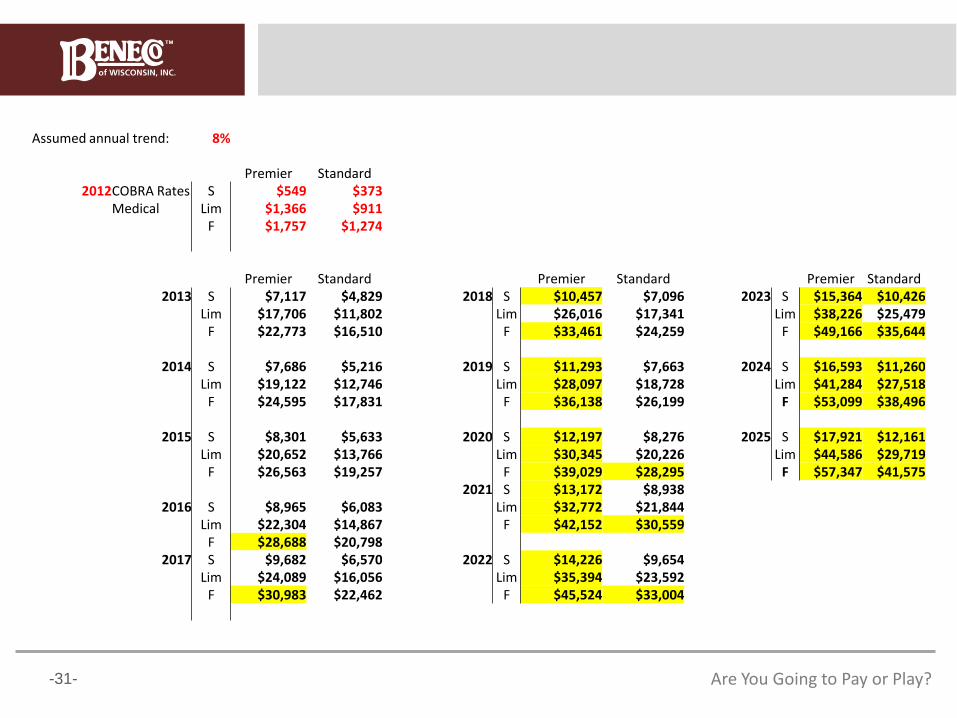

Assumed Annual Trend 8%

COMPLETE THE CADILLAC PLAN EXCISE TAX CALCULATIONS

Cadillac Tax

According to the current healthcare law, beginning in 2018, health plans that cost more than $10,200/single, $27,500 family will be taxed 40% on the amount over threshold. Stand-alone dental and vision plans are not included.

-31- Are You Going to Pay or Play?

Assumed annual trend: 8%

Premier Standard

2012 COBRA Rates S $549 $373 Medical Lim $1,366 $911 F $1,757 $1,274 Premier Standard Premier Standard Premier Standard 2013 S $7,117 $4,829 2018 S $10,457 $7,096 2023 S $15,364 $10,426 Lim $17,706 $11,802 Lim $26,016 $17,341 Lim $38,226 $25,479 F $22,773 $16,510 F $33,461 $24,259 F $49,166 $35,644 2014 S $7,686 $5,216 2019 S $11,293 $7,663 2024 S $16,593 $11,260 Lim $19,122 $12,746 Lim $28,097 $18,728 Lim $41,284 $27,518 F $24,595 $17,831 F $36,138 $26,199 F $53,099 $38,496 2015 S $8,301 $5,633 2020 S $12,197 $8,276 2025 S $17,921 $12,161 Lim $20,652 $13,766 Lim $30,345 $20,226 Lim $44,586 $29,719 F $26,563 $19,257 F $39,029 $28,295 F $57,347 $41,575 2021 S $13,172 $8,938 2016 S $8,965 $6,083 Lim $32,772 $21,844 Lim $22,304 $14,867 F $42,152 $30,559 F $28,688 $20,798 2017 S $9,682 $6,570 2022 S $14,226 $9,654 Lim $24,089 $16,056 Lim $35,394 $23,592 F $30,983 $22,462 F $45,524 $33,004

-32- Are You Going to Pay or Play?

Determining full time employee eligibility: The new frontier IRS notice 2012-58 & Proposed Treasury Regulations

Key issues: Eligibility is 30 hours per week in 2015 Employer selects measurement (look back) period in 2014 Employer selects beginning and ending points of periods FT status during Stability period NOT required Current FT status does not determine coverage eligibility Employee types: current, new, variable hour and limited duration Different measurement and stability periods can apply to

Union and non union; Hourly and salaried Other entities; Other states

-33- Are You Going to Pay or Play?

Determining full time employee eligibility: The new frontier

IRS notice 2012-58 & Proposed Treasury Regulations

Exciting new acronyms

IMP- Initial measurement period

SMP- Standard measurement period

SP- Stability period

SSP- Standard Stability period

AP – Administrative period

-34- Are You Going to Pay or Play?

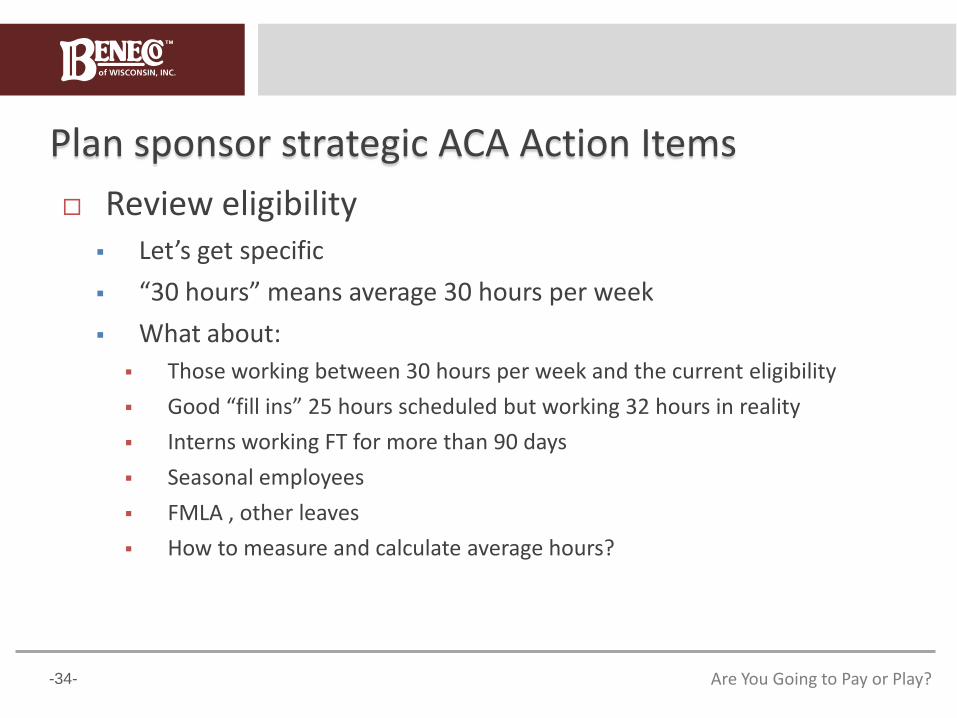

Plan sponsor strategic ACA Action Items

Review eligibility Let’s get specific

“30 hours” means average 30 hours per week

What about:

Those working between 30 hours per week and the current eligibility

Good “fill ins” 25 hours scheduled but working 32 hours in reality

Interns working FT for more than 90 days

Seasonal employees

FMLA , other leaves

How to measure and calculate average hours?

-35- Are You Going to Pay or Play?

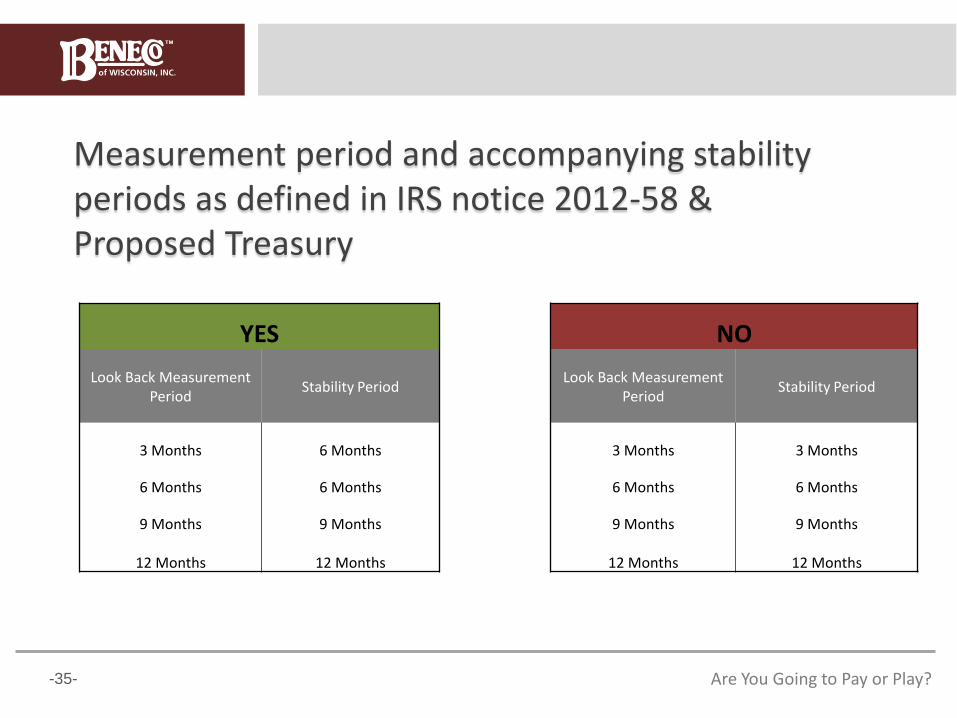

Measurement period and accompanying stability periods as defined in IRS notice 2012-58 & Proposed Treasury

YES NO

Look Back Measurement Period

Stability Period Look Back Measurement

Period Stability Period

3 Months 6 Months 3 Months 3 Months

6 Months 6 Months 6 Months 6 Months

9 Months 9 Months 9 Months 9 Months

12 Months 12 Months 12 Months 12 Months

-36- Are You Going to Pay or Play?

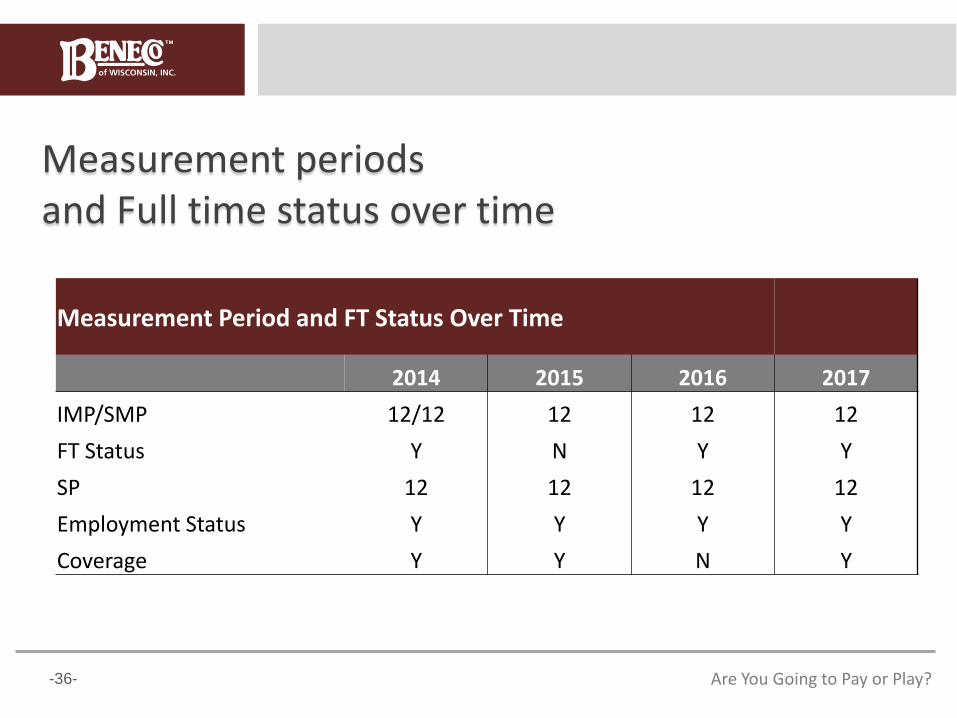

Measurement periods and Full time status over time

Measurement Period and FT Status Over Time

2014 2015 2016 2017

IMP/SMP 12/12 12 12 12

FT Status Y N Y Y

SP 12 12 12 12

Employment Status Y Y Y Y

Coverage Y Y N Y

-37- Are You Going to Pay or Play?

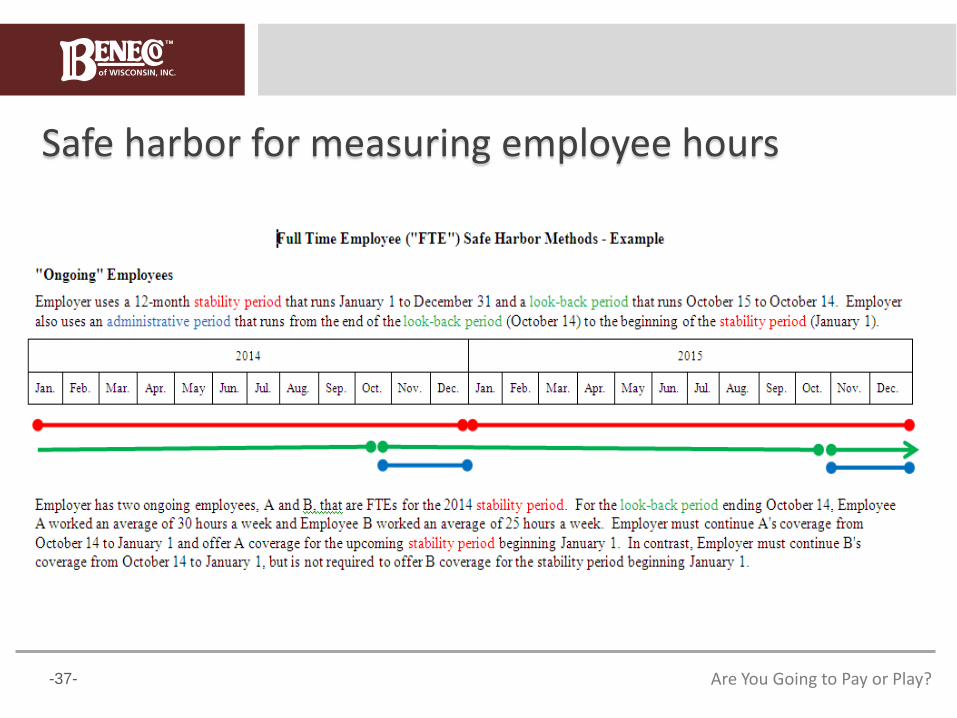

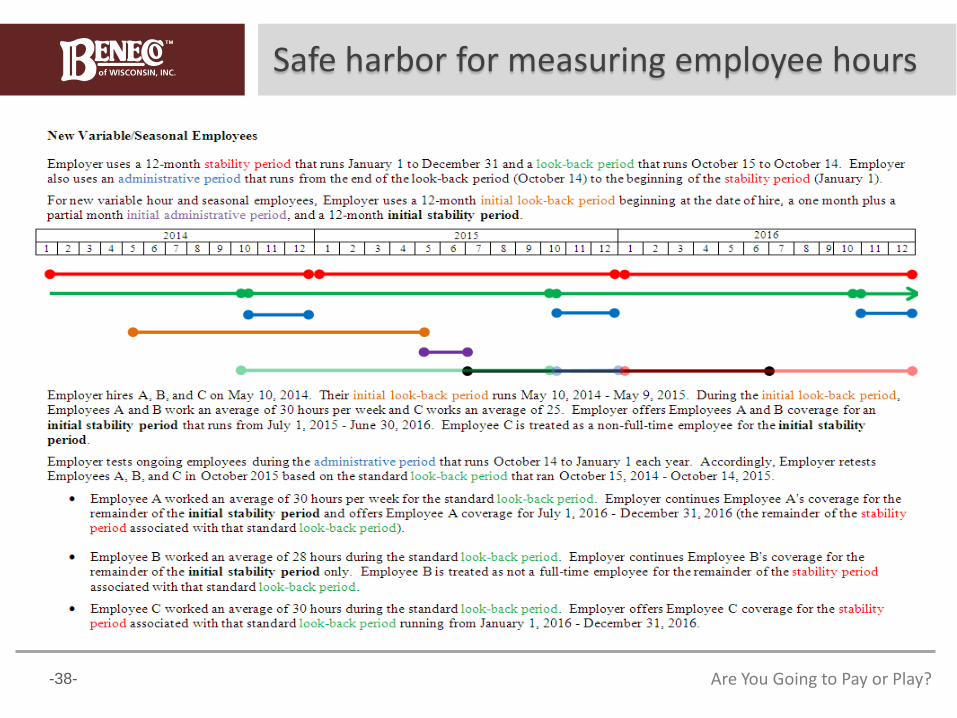

Safe harbor for measuring employee hours

-38- Are You Going to Pay or Play?

Safe harbor for measuring employee hours

-39- Are You Going to Pay or Play?

Determining full time employee eligibility: what should employers do?

Audit workforce eligibility

Determine employee classes

Assess IMP, SMP and SPs

Document

Continue to change the paradigm

Eligibility no longer real time

Complexities will continue

Safe harbors exist…use them

-40- Are You Going to Pay or Play?

The Play and pay Trap

Why wellness is more important than ever New options for coverage that never existed now

exist. Low wage earners migrate out of plan to Medicaid. Mid wage earners receive subsidy and go to

exchange. More tenured workforce remains on plan. Lower headcount and higher unit cost ($PEPY or

$PMPM) is possible.

-41- Are You Going to Pay or Play?

ACA and Wellness: The New Wellness Frontier

Plan sponsors will have to think like never before:

Go on the offense to retain attractive risk.

Possibly allow poor risk to leave.

Create strategy to enhance/maintain risk pool (defense to Medicaid eligible and subsidy eligible migration)

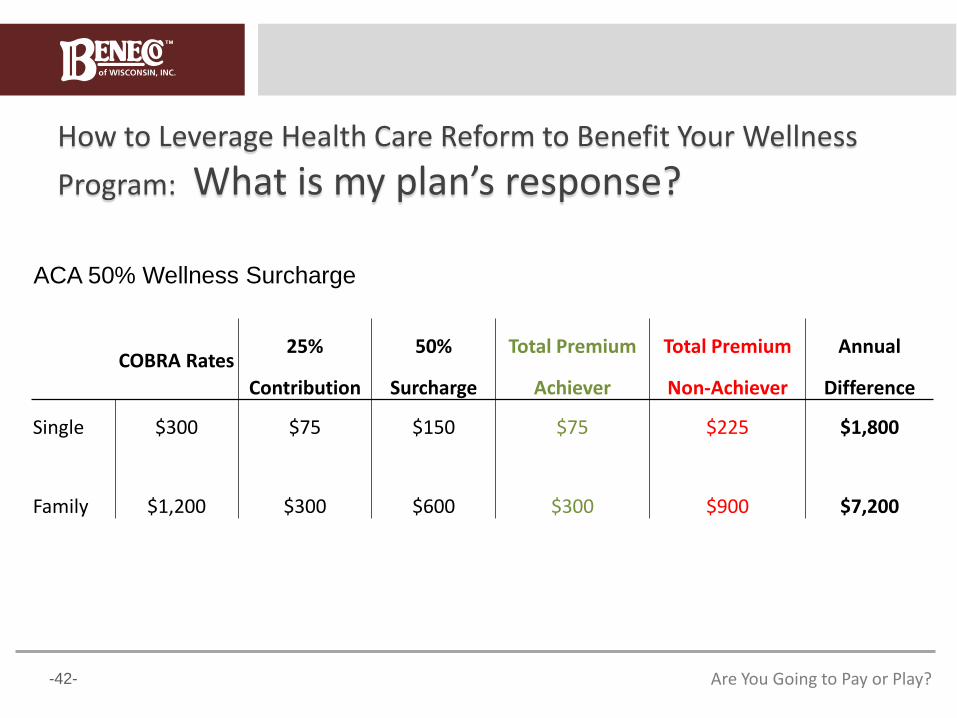

-42- Are You Going to Pay or Play?

How to Leverage Health Care Reform to Benefit Your Wellness

Program: What is my plan’s response?

COBRA Rates

25% 50% Total Premium Total Premium Annual

Contribution Surcharge Achiever Non-Achiever Difference

Single $300 $75 $150 $75 $225 $1,800

Family $1,200 $300 $600 $300 $900 $7,200

ACA 50% Wellness Surcharge

-43- Are You Going to Pay or Play?

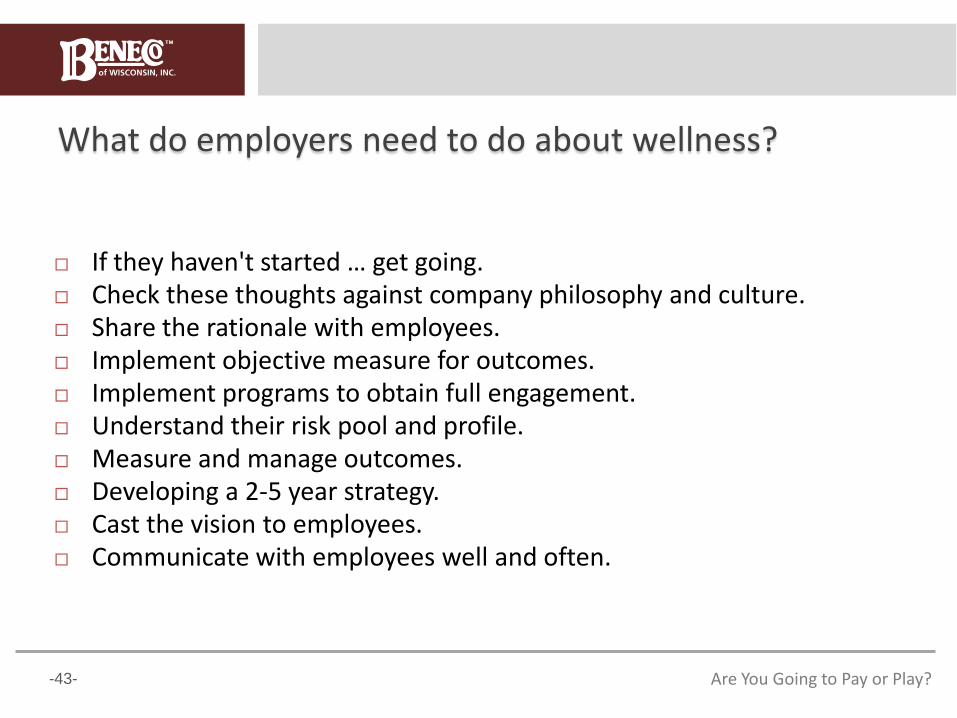

What do employers need to do about wellness? If they haven't started … get going. Check these thoughts against company philosophy and culture. Share the rationale with employees. Implement objective measure for outcomes. Implement programs to obtain full engagement. Understand their risk pool and profile. Measure and manage outcomes. Developing a 2-5 year strategy. Cast the vision to employees. Communicate with employees well and often.

-44- Are You Going to Pay or Play?

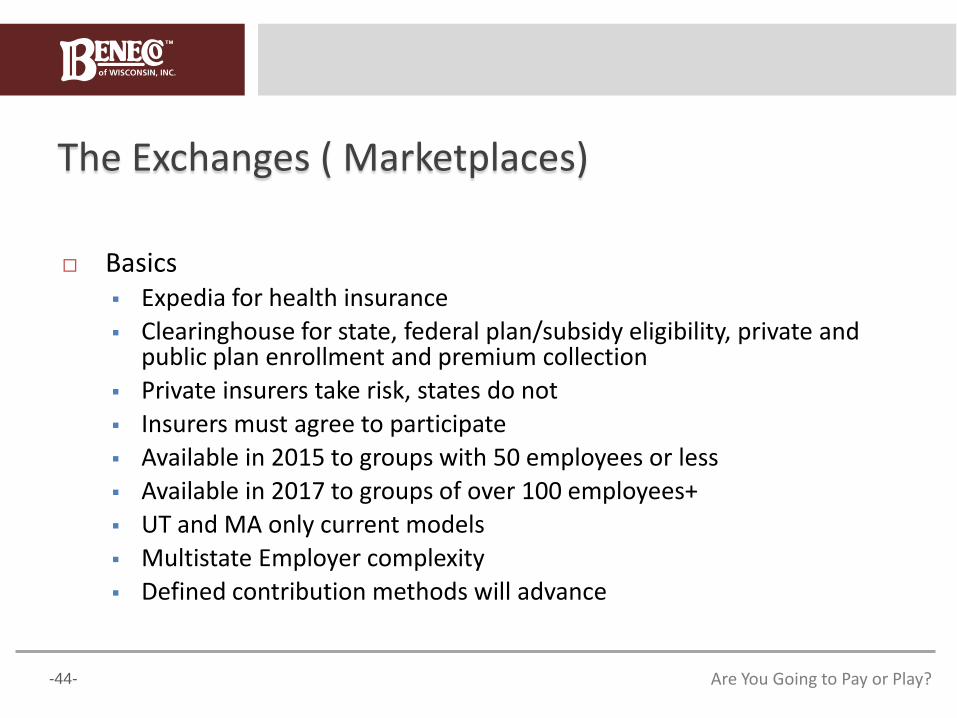

The Exchanges ( Marketplaces)

Basics Expedia for health insurance

Clearinghouse for state, federal plan/subsidy eligibility, private and public plan enrollment and premium collection

Private insurers take risk, states do not

Insurers must agree to participate

Available in 2015 to groups with 50 employees or less

Available in 2017 to groups of over 100 employees+

UT and MA only current models

Multistate Employer complexity

Defined contribution methods will advance

-45- Are You Going to Pay or Play?

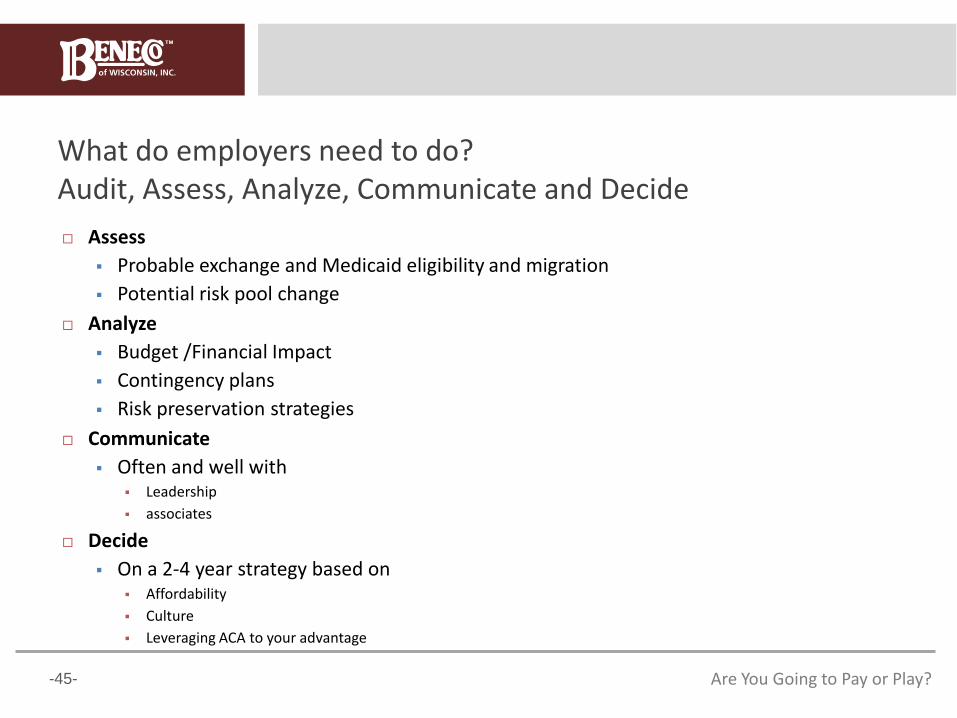

What do employers need to do? Audit, Assess, Analyze, Communicate and Decide

Assess

Probable exchange and Medicaid eligibility and migration

Potential risk pool change

Analyze

Budget /Financial Impact

Contingency plans

Risk preservation strategies

Communicate

Often and well with Leadership

associates

Decide

On a 2-4 year strategy based on Affordability

Culture

Leveraging ACA to your advantage

-46- Are You Going to Pay or Play?

What needs to be done? Be Tactical and Strategic Tactical

Be accurate and timely with compliance

Know the tasking and timelines

Enlist the appropriate resources

Strategic Know your group

Know your risk

Model probable scenarios

Create risk enhancement /preservation incentives

Understand the $$ involved in pay or play

Leverage ACA to your advantage

-47- Are You Going to Pay or Play?

How can payroll professionals add value in the ACA strategy conversation?

Know your system capabilities

Know your competitors capabilities

Know what employers need to do

W-2 reporting

Testing

To determine if an employer is an applicable large employer tests

Affordability and its testing nuances

-48- Are You Going to Pay or Play?

How can payroll professionals add value in the ACA strategy conversation?

Measurement:

Variable hour employees

Measurement - Look back period

Stability period

Administration:

Defined contribution

More product choices

Reporting:

For the employer on all of this stuff……..

To the government for attestation purposes

-50- Are You Going to Pay or Play?

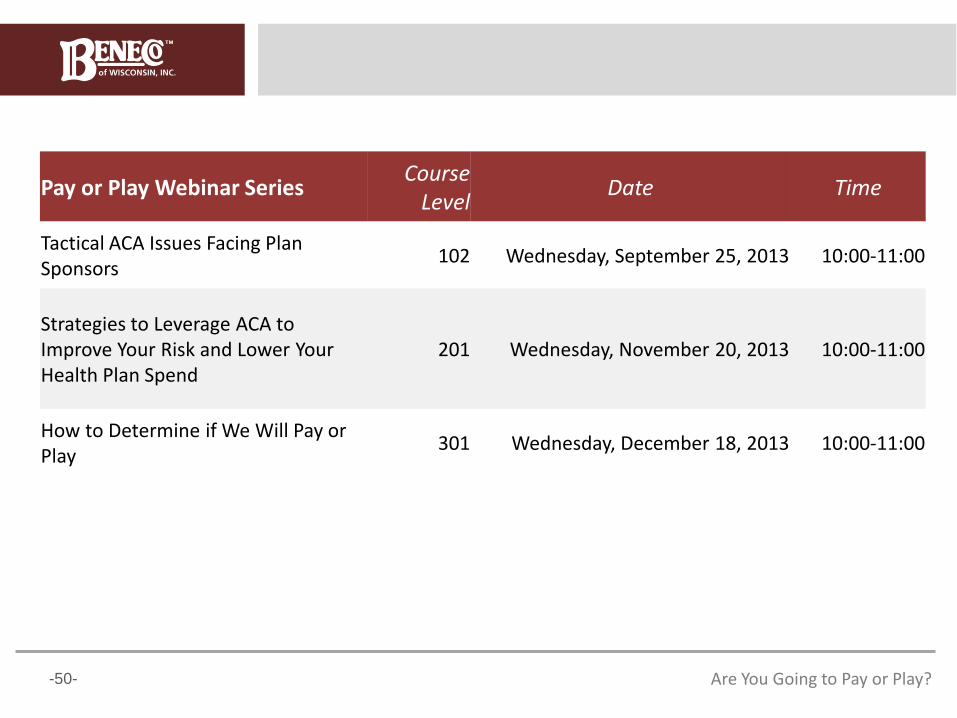

Pay or Play Webinar Series Course

Level Date Time

Tactical ACA Issues Facing Plan Sponsors

102 Wednesday, September 25, 2013 10:00-11:00

Strategies to Leverage ACA to Improve Your Risk and Lower Your Health Plan Spend

201 Wednesday, November 20, 2013 10:00-11:00

How to Determine if We Will Pay or Play

301 Wednesday, December 18, 2013 10:00-11:00

-51- Are You Going to Pay or Play?

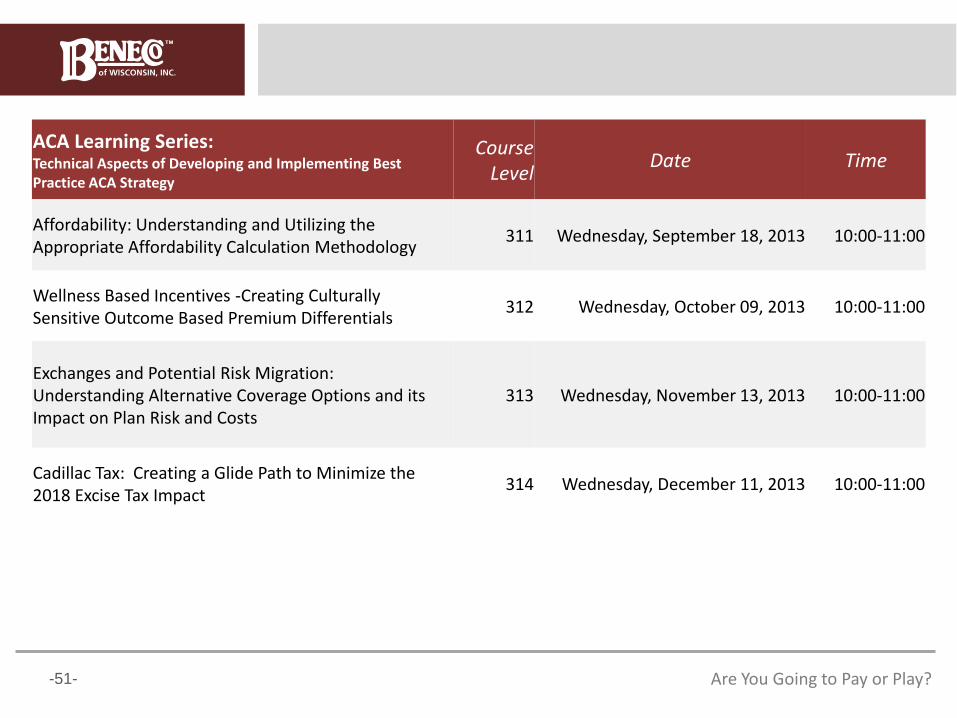

ACA Learning Series: Technical Aspects of Developing and Implementing Best Practice ACA Strategy

Course Level

Date Time

Affordability: Understanding and Utilizing the Appropriate Affordability Calculation Methodology

311 Wednesday, September 18, 2013 10:00-11:00

Wellness Based Incentives -Creating Culturally Sensitive Outcome Based Premium Differentials

312 Wednesday, October 09, 2013 10:00-11:00

Exchanges and Potential Risk Migration: Understanding Alternative Coverage Options and its Impact on Plan Risk and Costs

313 Wednesday, November 13, 2013 10:00-11:00

Cadillac Tax: Creating a Glide Path to Minimize the 2018 Excise Tax Impact

314 Wednesday, December 11, 2013 10:00-11:00

-52- Are You Going to Pay or Play?

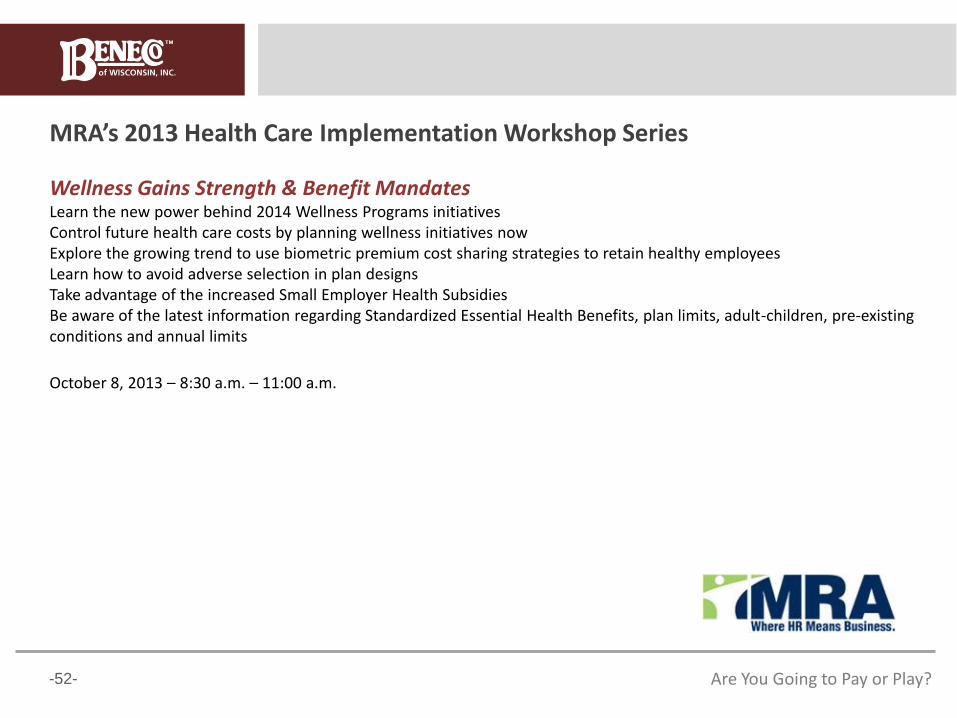

MRA’s 2013 Health Care Implementation Workshop Series

Wellness Gains Strength & Benefit Mandates Learn the new power behind 2014 Wellness Programs initiatives Control future health care costs by planning wellness initiatives now Explore the growing trend to use biometric premium cost sharing strategies to retain healthy employees Learn how to avoid adverse selection in plan designs Take advantage of the increased Small Employer Health Subsidies Be aware of the latest information regarding Standardized Essential Health Benefits, plan limits, adult-children, pre-existing conditions and annual limits

October 8, 2013 – 8:30 a.m. – 11:00 a.m.

-53- Are You Going to Pay or Play?

-54- Are You Going to Pay or Play?

Post-workshop questions or to get the links for upcoming webinars:

Jeff Schultz Vice President BeneCo of Wisconsin, Inc.

262-207-1999 x112 [email protected] www.beneco.co

![, If1L (Š61ubfe fibre) (élant-Sterds Stand Esters) Vit ...€¦ · r Portfolio Diet] 0 (Almond) 23 (Soy Protein 6.25 ft O Beneco 23 n N c F. p 90 Daily Values Not as based on a](https://img.pdfslide.net/doc/110x75/5f0a3a4b7e708231d42aa138/-if1l-61ubfe-fibre-lant-sterds-stand-esters-vit-r-portfolio-diet-0.jpg)