Embed Size (px)

DESCRIPTION

Retail is booming in Thailand, and operators are modernising their business by going online and developing new shopping locations outside of central Bangkok. Consumer confidence was at a six-year high in the last quarter of 2012, thanks to a stable political situation and a year free from floods.

Citation preview

2011 / 2012

new Supply

RenTAlS

OccupAncy

ThAilAnd

www.colliers.co.th

Bangkok Retail MarketexecuTive SummARy

Q4 2012 | Retail

mARkeT indicATORS

Bangkok Retail MaRket RePoRt

Retail is booming in thailand, and operators are modernising their business by going online and developing new shopping locations outside of central Bangkok.

Consumer confidence was at a six-year high in the last quarter of 2012, thanks to a stable political situation and a year free from floods.

the growth of residential projects in suburban Bangkok has prompted retail developers to build new shopping malls and community malls to serve them. around 662,000 sq m of retail space was completed in Bangkok in 2012, the highest figure for the past six years.

More than 204,700 sq m of retail space is scheduled to be completed in Bangkok in 2013,

with approximately 128,000 sq m in community malls and the rest in shopping malls.

other cities in thailand are also increasingly attractive to retailers, especially in border provinces where consumers from neighbouring countries can easily cross in to thailand to shop.

online shopping is not yet as popular in thailand as it is in other asian countries, but it is the fastest-growing retail sector and every major retailer is expanding their business online.

COLLIERS INTERNATIONAL | P. 2

Bangkok Retail MaRket RePoRt | Q4 2012

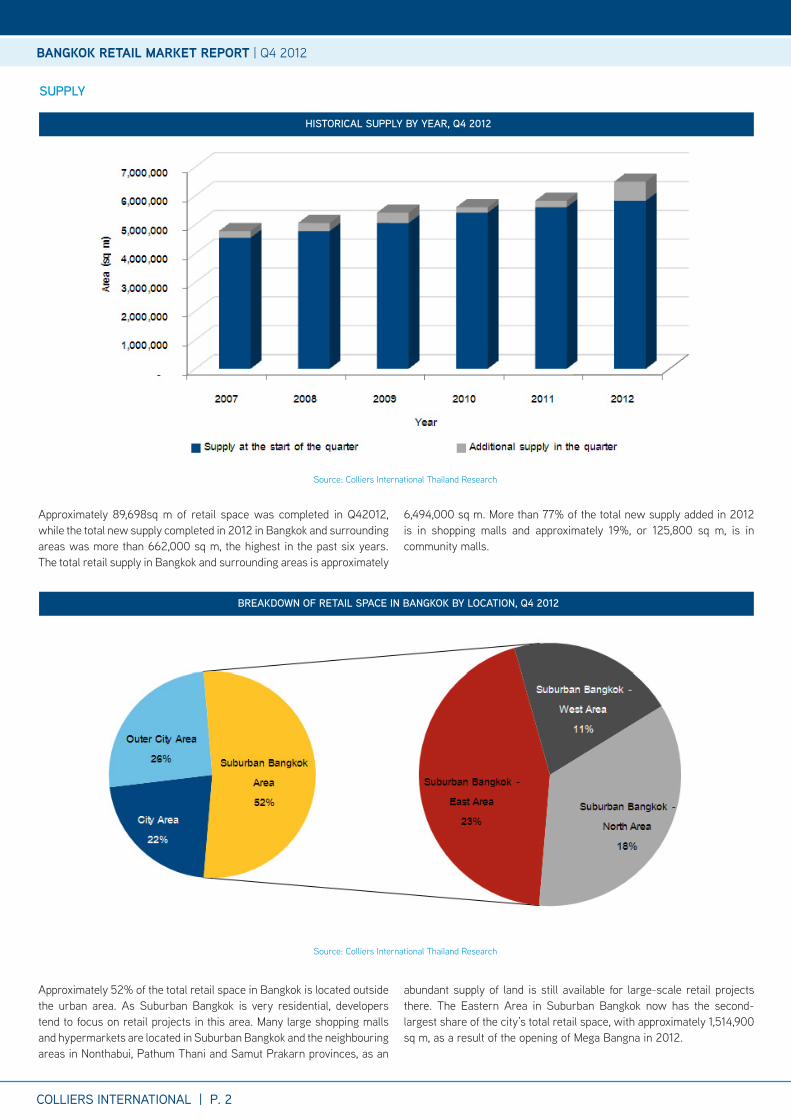

hiSTORicAl Supply by yeAR, Q4 2012

bReAkdOwn Of ReTAil SpAce in bAngkOk by lOcATiOn, Q4 2012

Source: Colliers international thailand Research

Source: Colliers international thailand Research

Approximately 89,698sq m of retail space was completed in Q42012, while the total new supply completed in 2012 in Bangkok and surrounding areas was more than 662,000 sq m, the highest in the past six years. The total retail supply in Bangkok and surrounding areas is approximately

6,494,000 sq m. More than 77% of the total new supply added in 2012 is in shopping malls and approximately 19%, or 125,800 sq m, is in community malls.

Approximately 52% of the total retail space in Bangkok is located outside the urban area. as Suburban Bangkok is very residential, developers tend to focus on retail projects in this area. Many large shopping malls and hypermarkets are located in Suburban Bangkok and the neighbouring areas in nonthabui, Pathum thani and Samut Prakarn provinces, as an

abundant supply of land is still available for large-scale retail projects there. The Eastern Area in Suburban Bangkok now has the second-largest share of the city’s total retail space, with approximately 1,514,900 sq m, as a result of the opening of Mega Bangna in 2012.

Supply

COLLIERS INTERNATIONAL | P. 3

Bangkok Retail MaRket RePoRt | Q4 2012

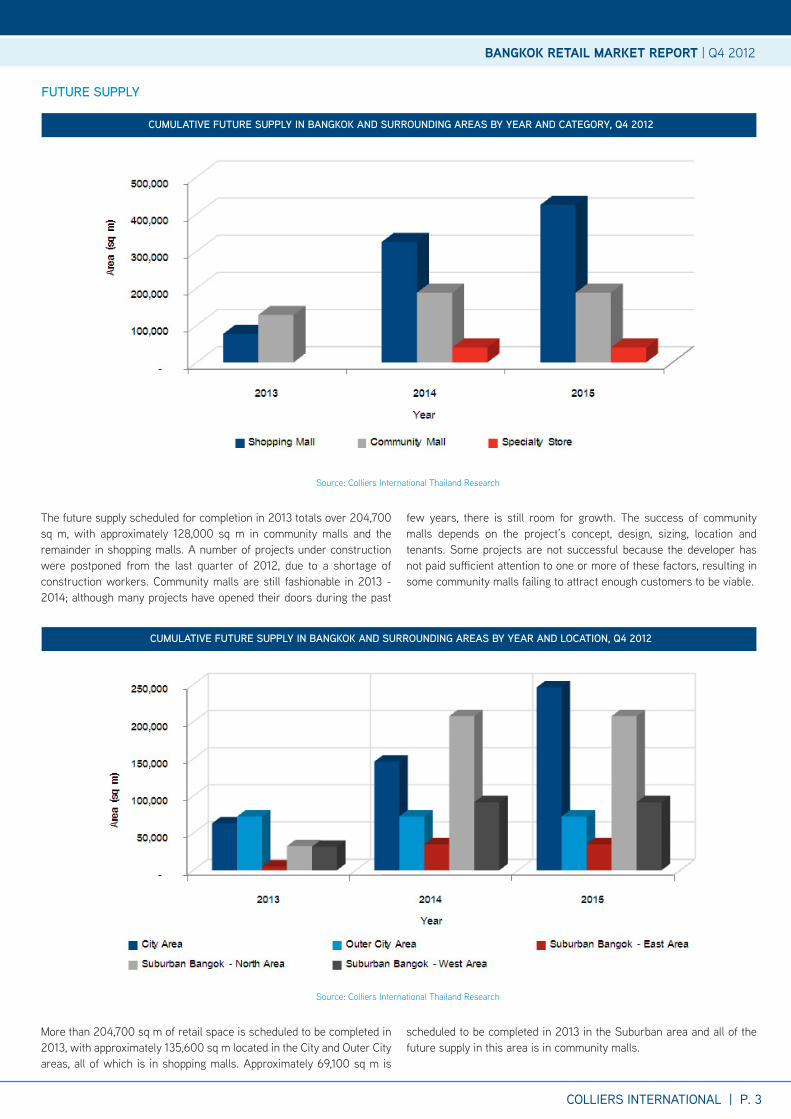

cumulATive fuTuRe Supply in bAngkOk And SuRROunding AReAS by yeAR And cATegORy, Q4 2012

cumulATive fuTuRe Supply in bAngkOk And SuRROunding AReAS by yeAR And lOcATiOn, Q4 2012

Source: Colliers international thailand Research

Source: Colliers international thailand Research

the future supply scheduled for completion in 2013 totals over 204,700 sq m, with approximately 128,000 sq m in community malls and the remainder in shopping malls. a number of projects under construction were postponed from the last quarter of 2012, due to a shortage of construction workers. Community malls are still fashionable in 2013 - 2014; although many projects have opened their doors during the past

few years, there is still room for growth. the success of community malls depends on the project’s concept, design, sizing, location and tenants. Some projects are not successful because the developer has not paid sufficient attention to one or more of these factors, resulting in some community malls failing to attract enough customers to be viable.

More than 204,700 sq m of retail space is scheduled to be completed in 2013, with approximately 135,600 sq m located in the City and Outer City areas, all of which is in shopping malls. Approximately 69,100 sq m is

scheduled to be completed in 2013 in the Suburban area and all of the future supply in this area is in community malls.

fuTuRe Supply

COLLIERS INTERNATIONAL | P. 4

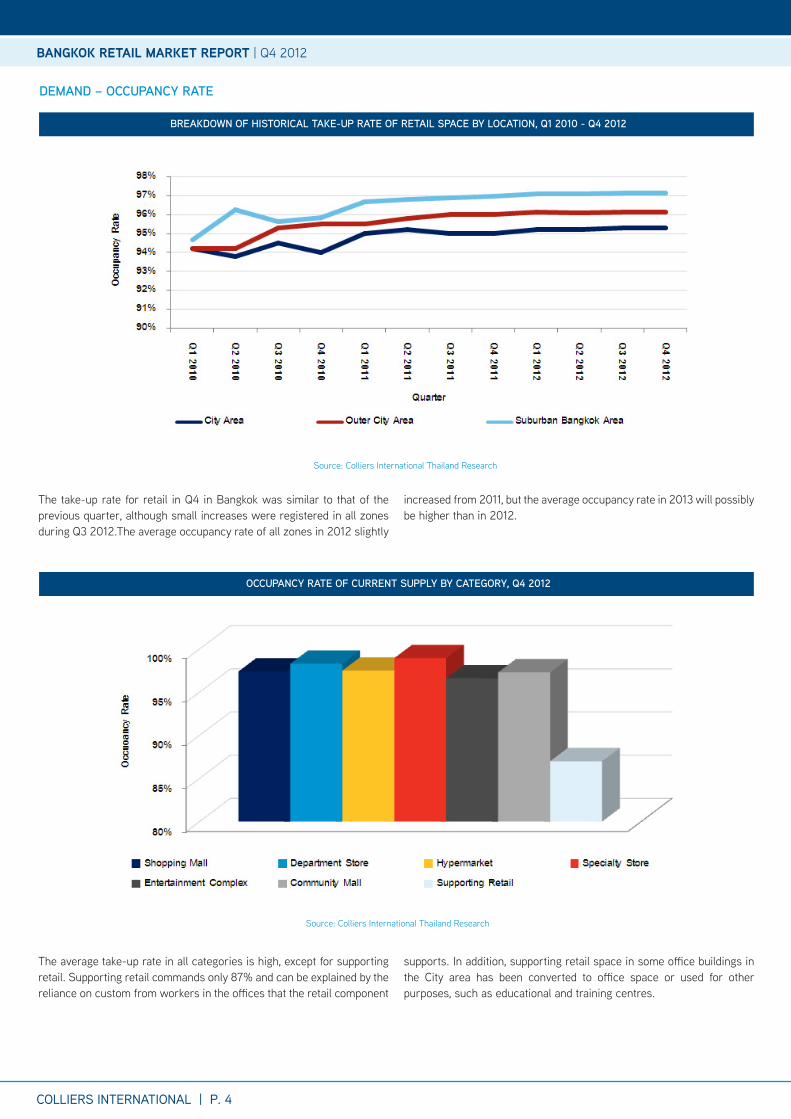

bReAkdOwn Of hiSTORicAl TAke-up RATe Of ReTAil SpAce by lOcATiOn, Q1 2010 - Q4 2012

OccupAncy RATe Of cuRRenT Supply by cATegORy, Q4 2012

Source: Colliers international thailand Research

Source: Colliers international thailand Research

The take-up rate for retail in Q4 in Bangkok was similar to that of the previous quarter, although small increases were registered in all zones during Q3 2012.the average occupancy rate of all zones in 2012 slightly

increased from 2011, but the average occupancy rate in 2013 will possibly be higher than in 2012.

The average take-up rate in all categories is high, except for supporting retail. Supporting retail commands only 87% and can be explained by the reliance on custom from workers in the offices that the retail component

supports. In addition, supporting retail space in some office buildings in the City area has been converted to office space or used for other purposes, such as educational and training centres.

demAnd – OccupAncy RATe

Bangkok Retail MaRket RePoRt | Q4 2012

COLLIERS INTERNATIONAL | P. 5

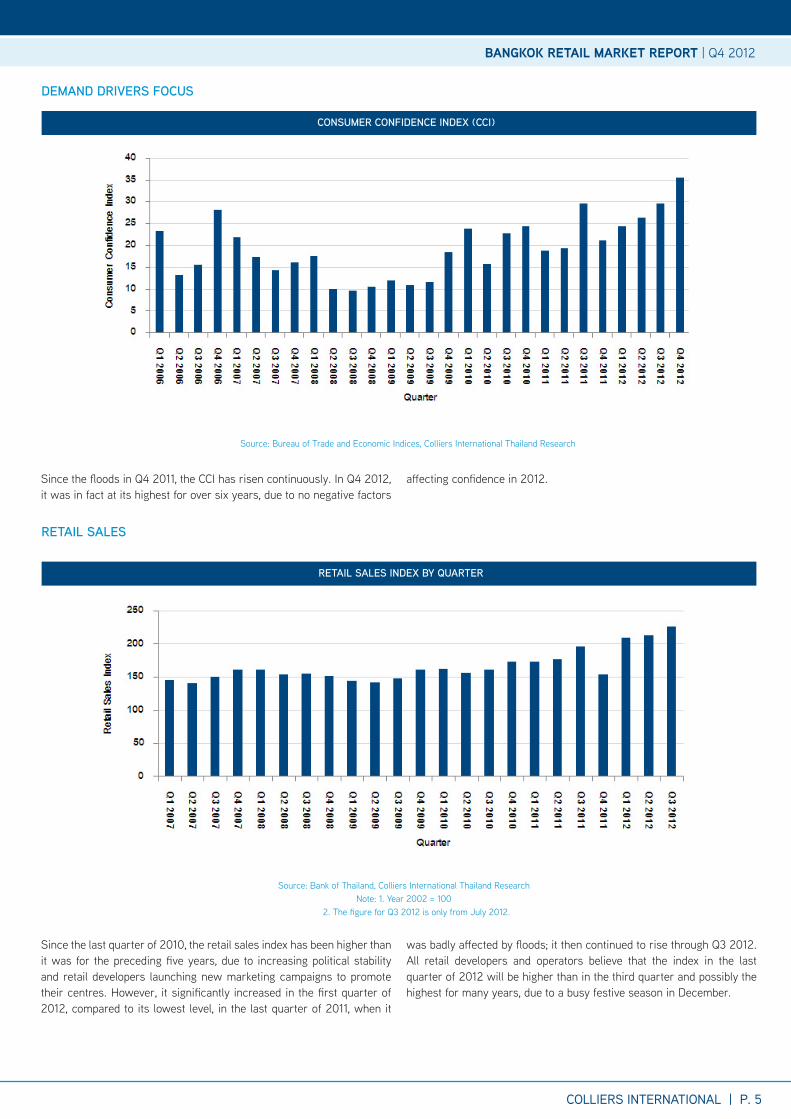

cOnSumeR cOnfidence index (cci)

ReTAil SAleS index by QuARTeR

Source: Bureau of trade and economic indices, Colliers international thailand Research

Source: Bank of thailand, Colliers international thailand Researchnote: 1. Year 2002 = 100

2. The figure for Q3 2012 is only from July 2012.

Since the floods in Q4 2011, the CCI has risen continuously. In Q4 2012, it was in fact at its highest for over six years, due to no negative factors

affecting confidence in 2012.

Since the last quarter of 2010, the retail sales index has been higher than it was for the preceding five years, due to increasing political stability and retail developers launching new marketing campaigns to promote their centres. However, it significantly increased in the first quarter of 2012, compared to its lowest level, in the last quarter of 2011, when it

was badly affected by floods; it then continued to rise through Q3 2012. All retail developers and operators believe that the index in the last quarter of 2012 will be higher than in the third quarter and possibly the highest for many years, due to a busy festive season in December.

demAnd dRiveRS fOcuS

ReTAil SAleS

Bangkok Retail MaRket RePoRt | Q4 2012

COLLIERS INTERNATIONAL | P. 6

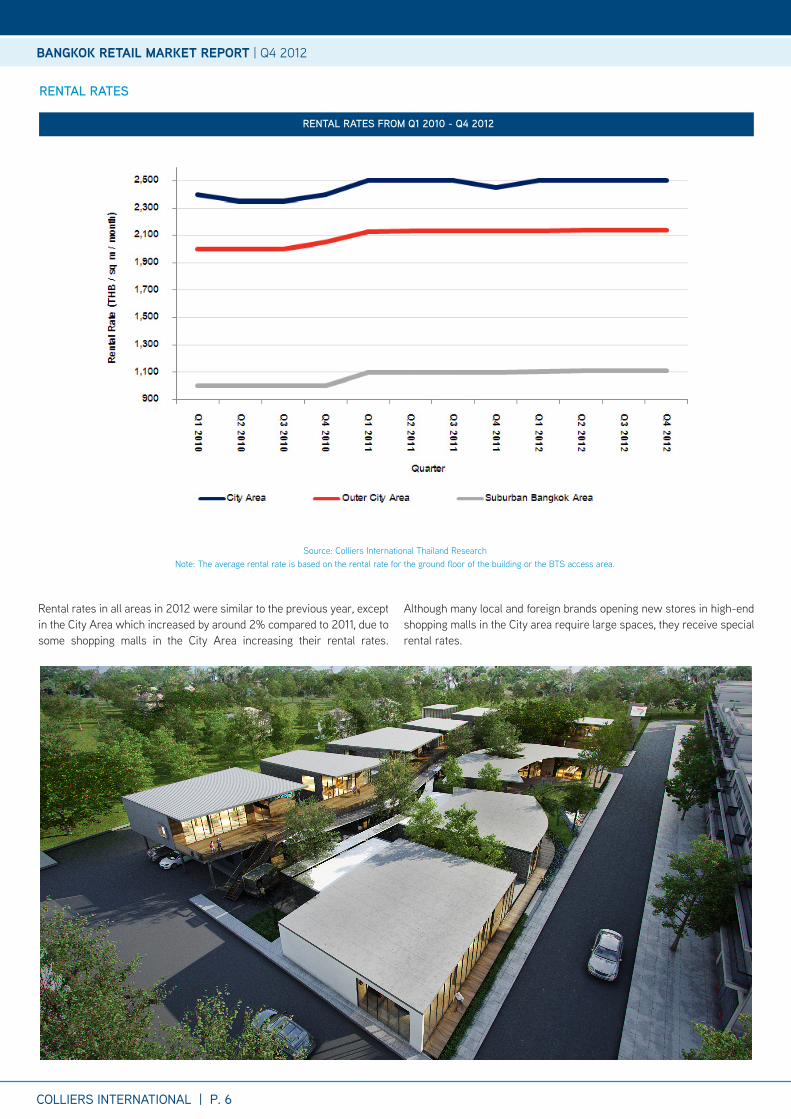

RenTAl RATeS fROm Q1 2010 - Q4 2012

Source: Colliers international thailand ResearchNote: The average rental rate is based on the rental rate for the ground floor of the building or the BTS access area.

Rental rates in all areas in 2012 were similar to the previous year, except in the City Area which increased by around 2% compared to 2011, due to some shopping malls in the City area increasing their rental rates.

Although many local and foreign brands opening new stores in high-end shopping malls in the City area require large spaces, they receive special rental rates.

RenTAl RATeS

Bangkok Retail MaRket RePoRt | Q4 2012

COLLIERS INTERNATIONAL | P. 7

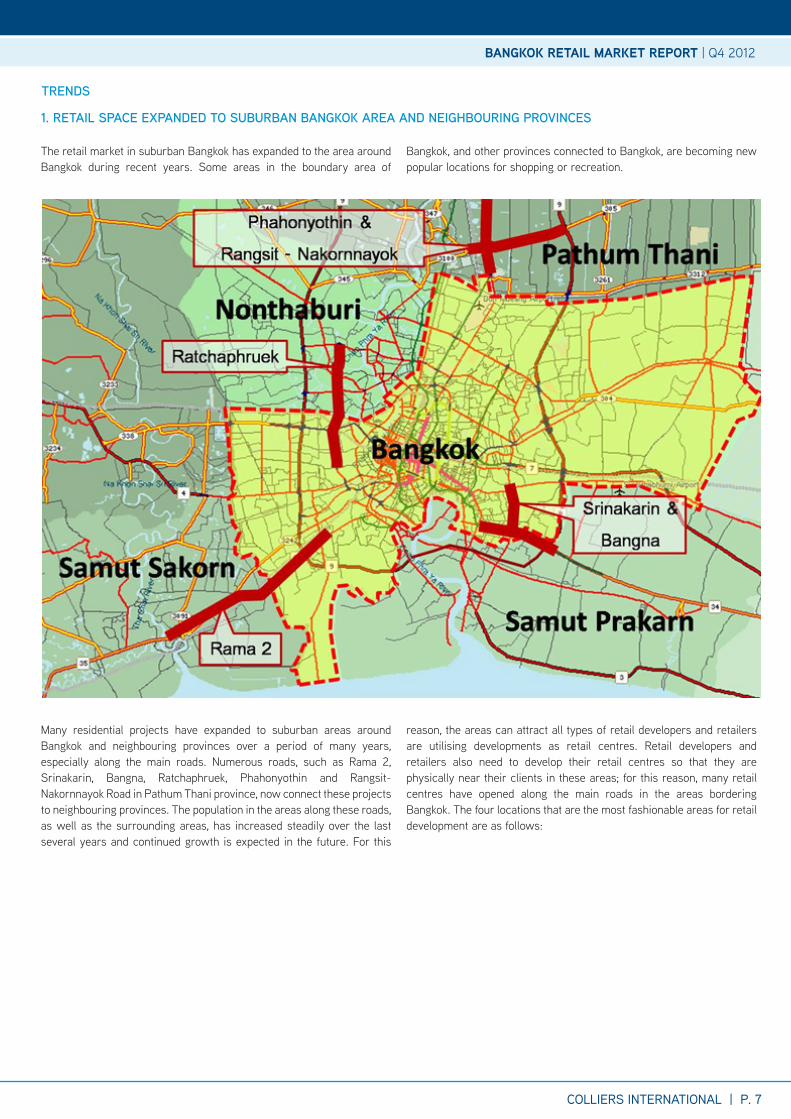

1. ReTAil SpAce expAnded TO SubuRbAn bAngkOk AReA And neighbOuRing pROvinceS

TRendS

Bangkok Retail MaRket RePoRt | Q4 2012

The retail market in suburban Bangkok has expanded to the area around Bangkok during recent years. Some areas in the boundary area of

Bangkok, and other provinces connected to Bangkok, are becoming new popular locations for shopping or recreation.

Many residential projects have expanded to suburban areas around Bangkok and neighbouring provinces over a period of many years, especially along the main roads. numerous roads, such as Rama 2, Srinakarin, Bangna, Ratchaphruek, Phahonyothin and Rangsit-nakornnayok Road in Pathum thani province, now connect these projects to neighbouring provinces. the population in the areas along these roads, as well as the surrounding areas, has increased steadily over the last several years and continued growth is expected in the future. For this

reason, the areas can attract all types of retail developers and retailers are utilising developments as retail centres. Retail developers and retailers also need to develop their retail centres so that they are physically near their clients in these areas; for this reason, many retail centres have opened along the main roads in the areas bordering Bangkok. the four locations that are the most fashionable areas for retail development are as follows:

COLLIERS INTERNATIONAL | P. 8

1.1 phAhOnyOThin And RAngSiT-nAkORnnAyOk ROAd The area along the Rangsit-Nakornnayok Road, and another small road connected to it, is a popular area for residential projects. although many residential projects were started in the area over ten years ago, room still exists for growth in the future.

Future Park Rangsit is the biggest shopping mall in the area and is located at the Phahonyothin and Rangsit-Nakornnayok Road intersection. During the past few years, the mall has shown continuous growth and has become the most attractive shopping mall in the area. another Future Park Rangsit shopping mall development is planned in the same area, with a total investment budget of approximately THB3 billion and a 2013 start date is expected.

Big C and tesco lotus’ hypermarket models also form part of the market. Most stores are located along Rangsit-Nakornnayok Road, with some stores located on Phahonyothin Road. tesco lotus has attempted to attract more customers by opening Tesco Lotus Express stores in surrounding community areas.

the owner of Zeer Rangsit has changed the business identity of the retail centre from a shopping mall to the largest it centre in Pathum thani province, and the former Merry king Rangsit was acquired by the owner of Bo Bae Tower ̶ the latter plans to re-develop the former Merry king Rangsit into Bo Bae Rangsit, a wholesale shopping mall concept that will be linked to Zeer Rangsit by an overpass. this area will become the new shopping area for the people of suburban Bangkok and Pathumthani province.

in addition, CPn bought a 616 rai plot of land on Phahonyothin Road, close to the Red Line of the BTS extension. CPN bought the land from Apex Riverside Co.Ltd, which had bought it from Thai Asset Management Corporation.CPN will joint-venture with Apex Riverside Co.Ltd. and are expected to develop this plot into a large-scale shopping mall, which will also have facilities outside for buses and other transport, with the concept being that it will function as a central point for transport from Bangkok to the north and northeast.

1.2 RATchAphRuek ROAdHaving opened in 2002, Ratchaphruek Road has now become a new location for residential projects, especially high-end and luxury housing projects. in addition, this road is connected to the Bangkok city area, suburban Bangkok and nonthaburi province, leading many developers to launch their housing projects along this road, and changing the green field area to a residential zone within a few years. The selling price of housing projects along this road start from tHB3 million and can rise above tHB100 million.

the high number of housing projects and the huge number of cars that pass over this road every day are a great attraction for retail developers, so some community malls have opened along this road. the Circle Ratchaphruek opened its doors in 2011 and became the new meeting place on Ratchaphruek Road, characterised by a european style and colourful buildings. the new lifestyle mall on this road is the Walk Ratchaphruek, by Index Living Mall Co.Ltd. The Walk has become the new social magnet along this road, with its Santa Monica Village style and many restaurants in a total area of more than 20,000 sq m, including the Index Living Mall.

in addition, Home Pro and Homeworks also opened stores on this road, and some housing developers have planned to develop a community mall in front of their housing projects, similar to Pure Place Ratchaphruek, which opened in May 2012. the retail centres along Ratchaphruek Road tend to consist of a greater number of high-end shops compared to other suburban areas, reflecting the relative affluence of residents in this area.

1.3 RAmA 2 ROAdthe other residential area in suburban Bangkok is the area along Rama 2 Road, an 18-lane road that connects Bangkok and the southern part of Thailand. In addition, Rama 2 Road is also connected to the expressway, thereby offering convenience to people who work in the Bangkok city area, as well as convenient access to nonthaburi, Pathum thani and Samut Prakarn via the outer link road. a lot of housing projects are located in the area along this road, and developers who started housing development projects along this road in the past ten years have observed the continual launching of new projects up until the present time. Most of the residential projects along this road are located in the small roads or sois connected to Rama 2 Road.

the largest shopping mall on this road is Central Plaza Rama 2, while Big C and tesco lotus, the two main hypermarket developers, have also opened stores along this road. in addition, supporting facilities, such as hospitals, schools, gas stations, car service centres and restaurants are located along this road. Many high-end housing projects are located around Central Plaza, Big C Supercenter and tesco lotus.

the area on the western side of the outer Ring Road is the newest area for residential projects; a large number of vacant plots of land remain available for new projects. the most recent lifestyle mall by D land Group, Porto Chino, is located on Rama 2 Road km 25, in front of the housing project. this project has received support from all of the area’s residents, as well as people who drive along Rama 2 Road.

1.4 SRinAkARin And bAngnA ROAd Both sides along Bangna Road include small roads and sois; these are large residential areas for Bangkok and Samut Prakarn province. Housing projects in the area start from lower than tHB1 million and can increase to more than tHB20 million, depending on location, the developers responsible and the quality of the project.

an area in the province of Samut Prakan, but adjacent to the Bangkok Metropolitan area, will be transformed into a shopping hub. in the eastern part of Bangkok, along Bangna Road, Mega Bangna, by Siam Future Development Plc and the big anchor partners̶ Major Cineplex, Home Pro, Big C, Robinson and IKEA̶ consists of a total area of approximately 400,000 sq m. as the newest retail centre attraction along this road, Meg Bangna will become the biggest shopping hub in thailand. in the vicinity there are other retail centres, such as SB Design Square, Index living Mall, tesco lotus,Big C, and Central Bangna.

Bangkok Retail MaRket RePoRt | Q4 2012

COLLIERS INTERNATIONAL | P. 9

in addition, Seacon Square and Paradise Park are located on Srinakarin Road. The total area of these two shopping malls is more than 250,000 sq m (leasable area) and even though Seacon Square has been open for more than 20 years, it still thrives as a modern retail centre. Siam Piwat and MBK Group acquired Seri Center and, following re-development of the entire centre, Paradise Park was launched in 2010.

However, the community mall remains the most fashionable retail model for the area’s community. thanya Shopping Park opened in november 2012 on Srinakarin Road, and more retail centres have been planned for Bangna Road, including the Mall shopping centre at the Bangna intersection. Srinakarin and Bangna Roads are expected to develop in to major shopping locations for Bangkok and the vicinity.

the Bangkok retail market has shown continual growth over several years and many new retail centres have been added to the market, especially community malls and lifestyle malls. Meanwhile, hypermarket and shopping mall developments are finding it difficult to expand in Bangkok, due to laws and regulations, as well as the increase in land prices over the last several years. Some retail developers are more focused on other provinces around thailand, especially major city centres and border provinces.

2. ShOpping Onlinethe total number of internet users in thailand has increased dramatically over the past several years and will continue to increase in the future. in addition, smart phones have become important devices for everyone. Major retail developers and operators in thailand are therefore looking at opportunities to expand their sales channels by opening their own online stores. However, fewer thais shop online than people in many asian countries.

2.1 The mAll gROup spent around THB80 - 100 million to set up their shopping website, and launched the “M online Department Store”, www.mods.co.th, on 8 December 2010. The website is frequently updated and has new items added to their online department store; the number of customers has also steadily increased.

2.2 cenTRAl gROup launched their own shopping online website, www.central.co.th, with more than 10,000 items on 15 October 2010, with tnt responsible for the logistics for all customers. in addition, tops Supermarket by Central Food Retail also launched their own online supermarket, www.tops.co.th,with more than 10,000 items.

2.3 big c also has a website for shopping online,“www.shoppingonline.bigc.co.th”;all buyers can choose to pick up the product by themselves or use the Big C delivery service. in addition, in the last quarter of 2012, Big C launched a new shopping experience at the Airport Rail Link Phayathai station, the “Big C Virtual Shelf”, which is 27-m long, open 24 hours and displays over 500 items. Airport Rail Link customers can use their smart phones to scan QR codes on the virtual shelf and place orders during their daily commutes without having to go to a Big C store. With purchasesover THB1,500 Big C will provide free delivery and accept payment at the delivery site.

2.4 SiAm piwAT the operator of Siam Center and Siam Discovery Center, launched their online shopping website,www.siamism.com, on 1 December 2012. Siamism is focused on limited editions and the latest collection products which are hard to find at the shopping mall.

2.5 TeScO lOTuS has a plan to launch their e-commerce service in thailand after its success in the Uk, ireland, Czech Republic and South korea. they will copy the format from South korea for the thailand market.

2.6 beRli JuckeR plans to launch its own virtual shopping system with the “BJC Smart Board: QR Code” in office buildings, mass transit stations and at Suvarnabhumi international airport. Products will be delivered free of charge within 24 hours for all bills over tHB1,000.

although shopping online is new for retail business in thailand, it has become the fastest growing trend over the past few years. Shopping experiences in retail centres with air-conditioning remain indispensable and most customers still prefer to go to a retail centre to shop. Shopping online is the newest marketing tool for retail developers and operators, and they cannot miss riding the e-commerce wave.

SummARy 2012 And fORecAST 2013all retail centres in Bangkok that are over 10 years old have plans for renovation or re-arrangement of their tenant mix as well as adding new brands to their retail centres. this is because several recently completed retail centres have impressive designs and tenants. Old-fashioned retail centres need to improve themselves to become competitive.

Retail operators in thailand are focusing more and more on online shopping, and big name players are developing their websites in support. They are also co-ordinating with commercial banks to encourage more spending from credit card users with cash rewards or points collection, as well as trying to increase the number of loyalty cards. Digital retail will grow in 2013 and beyond, due to convenience, low operation and management costs as well as suitability to the modern lifestyle.

Main provinces in other parts of thailand are becoming new targets for big names in the retail business, with some provinces along the thai border becoming especially attractive for all retail players. these include Chiang Mai province, for attracting shoppers from laos and Myanmar, Udonthani province for supporting clients from laos and Vietnam, and HatYai in Songkhla province for Malaysians. in addition, retailers are also expanding into some resort destinations and big cities around Thailand with different formats.

Convenience stores became the new competitive sector in the retail business after CRC took over Family Mart in Thailand. Although 7-Eleven has the biggest share in this sector, there is still room for growth. Many brands are focusing on convenience stores by increasing the number of branches throughout Thailand. Berli Jucker Plc. also plans to open its own chain of convenience stores, “BJC Smart Stores”, in early 2013.

Bangkok Retail MaRket RePoRt | Q4 2012

COLLIERS INTERNATIONAL | P. 10

Appendix

Bangkok Retail MaRket RePoRt | Q4 2012

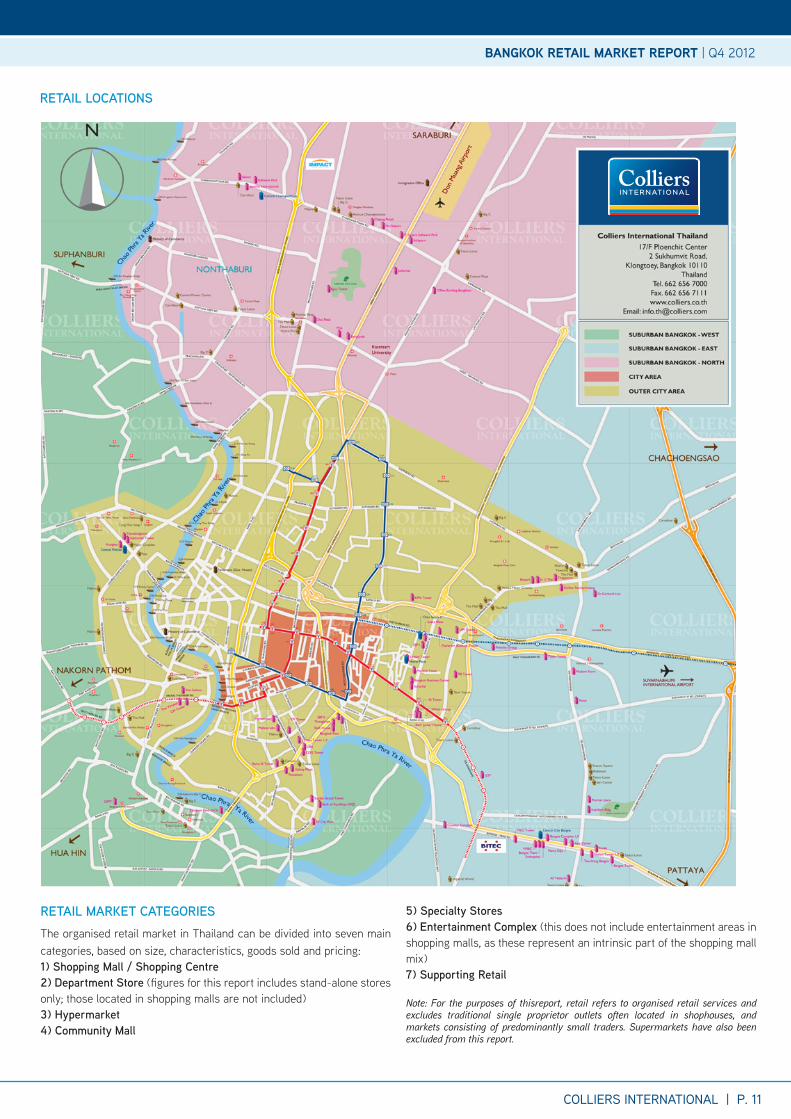

ReTAil lOcATiOnS

ReTAil mARkeT cATegORieSthe organised retail market in thailand can be divided into seven main categories, based on size, characteristics, goods sold and pricing:1) Shopping mall / Shopping centre2) department Store (figures for this report includes stand-alone stores only; those located in shopping malls are not included)3) hypermarket 4) community mall

5) Specialty Stores6) entertainment complex (this does not include entertainment areas in shopping malls, as these represent an intrinsic part of the shopping mall mix)7) Supporting Retail

Note: For the purposes of thisreport, retail refers to organised retail services and excludes traditional single proprietor outlets often located in shophouses, and markets consisting of predominantly small traders. Supermarkets have also been excluded from this report.

COLLIERS INTERNATIONAL | P. 11

Bangkok Retail MaRket RePoRt | Q4 2012

cOllieRS inTeRnATiOnAl ThAilAnd mAnAgemenT TeAm Retail SeRViCeSasharawan Wachananont | associate Director PROJECT SALES & MARKETINGMonchai orawongpaisan | associate Director RESIDENTIAL SALES & LEASINGnapaswan Chotephard | Manager ReSeaRCHSurachet kongcheep | Senior Manager

OFFICE SERVICESnattawan Radomyos | Senior Manager

inDUStRial SeRViCeSnarumon Rodsiravoraphat | associate Director aDViSoRY SeRViCeS | HoSPitalitY Jean Marc Garret | Director aDViSoRY SeRViCeSnapatr tienchutima | associate Director

Real eState ManageMent SeRViCeSthanasit tonsatcha | associate Director

inVeStMent SeRViCeSnukarn Suwatikul | associate Director Wasan Rattanakijjanukul | Senior Manager

VALUATION & ADVISORY SERVICESPhachsanun Phormthananunta | Director Wanida Suksuwan | associate Director PATTAYA OFFICEMark Bowling | Senior Sales ManagerSupannee Starojitski | Senior Business Development Manager / Office Manager

HUA HIN OFFICESunchai kooakachai | associate Director

ReSeARcheR:

thailandSurachet kongcheepSenior Manager | ResearchemAil [email protected]

522 offices in 62 countries on 6 continents

this report and other research materials may be found on our website at www.colliers.co.th. Questions related to information herein should be directed to the Research Department at the number indicated above. this document has been prepared by Colliers international for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reli-ability. any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties aris-ing out of this document and excludes all liability for loss and damages arising there from. Colliers Inter-national is a worldwide affiliation of independently owned and operated companies.

• a leader in real estate consultancy worldwide• 2nd most recognized commercial real estate brand globally

• 2nd largest property manager• 1.25 billion square feet under management• over 12,300 professionals

www.colliers.co.thwww.colliers.co.th

accelerating success.

Bangkok Retail MaRket RePoRt | Q4 2012

CollieRS inteRnational thailand:

Bangkok Office 17/F Ploenchit Center, 2 Sukhumvit Road, klongtoey,Bangkok 10110 thailandTel +662 656 7000fAx +662 656 7111 emAil [email protected] Pattaya Office 519/4-5, Pattaya Second Road (Opposite Central Festival Pattaya Beach), Nongprue, Banglamung, Chonburi 20150Tel +6638 427 771fAx +6638 427 772 emAil [email protected] Hua Hin Office 27/7, Petchakasem Road, Hua Hin, Prachuap khiri khan 77110 thailandTel +6632 530 177fAx +6632 530 677 emAil [email protected]