Embed Size (px)

Citation preview

BANKING IN CEE: adequate risk appetite crucial to win the upside

UniCredit Group CEE Strategic Analysis

Vienna, November 9, 2009

2

Executive Summary 1

World economic growth is recovering and this boosts prospects in CEE - 2010

will show a positive regional growth, though this will remain below

potential and subject to risks

Strong regional differentiation is confirmed, with Central Europe better

prepared to catch the international recovery. The performance of different

banks in the same market can widely differ

Markets are out of a “liquidity-crisis mood” – credit quality and risk appetite

are today’s key constraints for CEE banking

Medium term: “CEE convergence story” holds, but the banking model

has to be rebalanced

Financial penetration will continue, but the pace of growth will moderate,

with availability of funding (domestic or external) the main driver

Changing competition allows for leaner structure of costs

Cost of risk to stay high, representing a constraint for banking profitability

3

Executive Summary 2

The changing competitive environment means also opportunities

All CEE players have been affected by the crisis – access to funding,

credit quality, business/network diversification and strength the

determinants of future success

New entrants might take opportunities

Winners – new entrants or consolidated players, with appropriate risk

appetite for CEE, able to leverage on strong funding, capital and network

positioning and sound risk

UCG ready to take the upside – the Group can leverage on diversification,

a strong regional network and newly raised capital to strengthen and

optimize its positioning in the market

4

AGENDA

1. How the CEE banking landscape has changed in the short term

2. Banking through the crisis

3. International players - UniCredit ready to take the upside

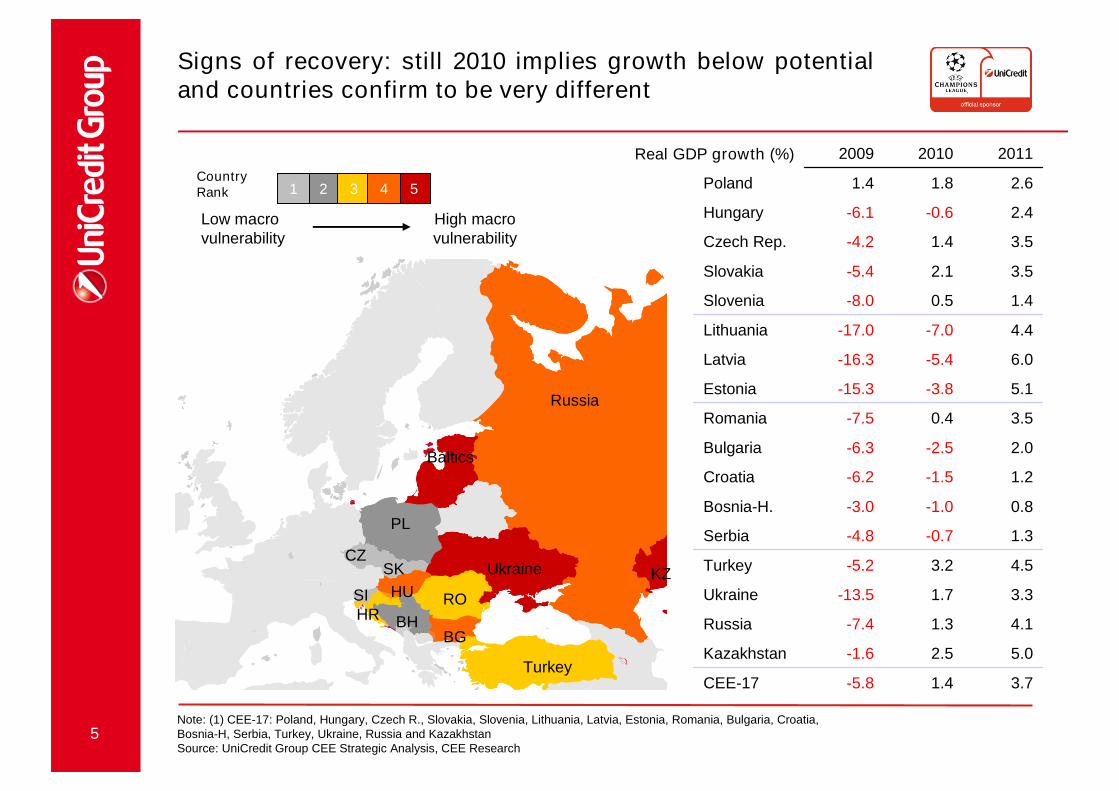

5Note: (1) CEE-17: Poland, Hungary, Czech R., Slovakia, Slovenia, Lithuania, Latvia, Estonia, Romania, Bulgaria, Croatia,Bosnia-H, Serbia, Turkey, Ukraine, Russia and KazakhstanSource: UniCredit Group CEE Strategic Analysis, CEE Research

Signs of recovery: still 2010 implies growth below potentialand countries confirm to be very different

Low macrovulnerability

2 5

High macrovulnerability

3 41CountryRank

PL

SK

Turkey

Russia

CZ

BG

Ukraine

ROHUKZ

Baltics

3.71.4-5.8CEE-17

5.02.5-1.6Kazakhstan

4.11.3-7.4Russia

3.31.7-13.5Ukraine

4.53.2-5.2Turkey

1.3-0.7-4.8Serbia

0.8-1.0-3.0Bosnia-H.

1.2-1.5-6.2Croatia

2.0-2.5-6.3Bulgaria

3.50.4-7.5Romania

5.1-3.8-15.3Estonia

6.0-5.4-16.3Latvia

4.4-7.0-17.0Lithuania

1.40.5-8.0Slovenia

3.52.1-5.4Slovakia

3.51.4-4.2Czech Rep.

2.4-0.6-6.1Hungary

2.61.81.4Poland

201120102009Real GDP growth (%)

HR BH

SI

6

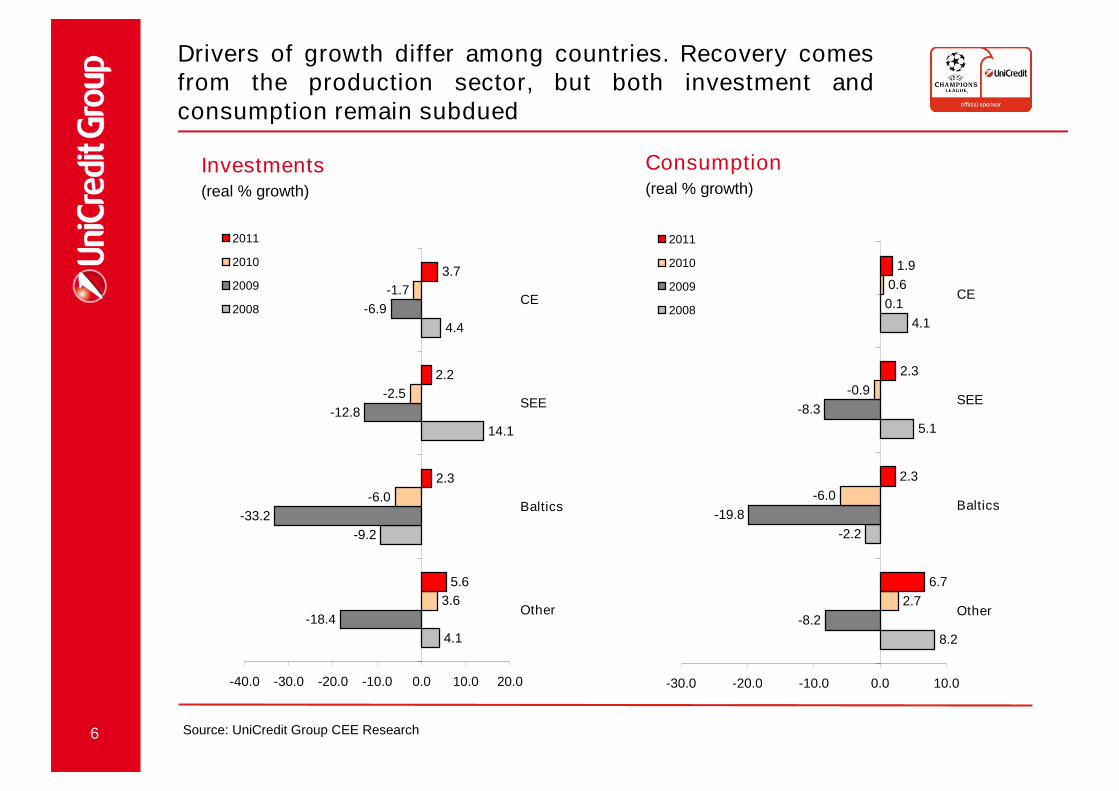

Drivers of growth differ among countries. Recovery comesfrom the production sector, but both investment andconsumption remain subdued

Source: UniCredit Group CEE Research

Investments(real % growth)

Consumption(real % growth)

4.1

-9.2

14.1

4.4

-18.4

-33.2

-12.8

-6.9

3.6

-6.0

-2.5

-1.7

5.6

2.3

2.2

3.7

-40.0 -30.0 -20.0 -10.0 0.0 10.0 20.0

Other

Baltics

SEE

CE

2011

2010

2009

2008

8.2

-2.2

5.1

4.1

-8.2

-19.8

-8.3

0.1

2.7

-6.0

-0.9

0.6

6.7

2.3

2.3

1.9

-30.0 -20.0 -10.0 0.0 10.0

Other

Baltics

SEE

CE

2011

2010

2009

2008

7

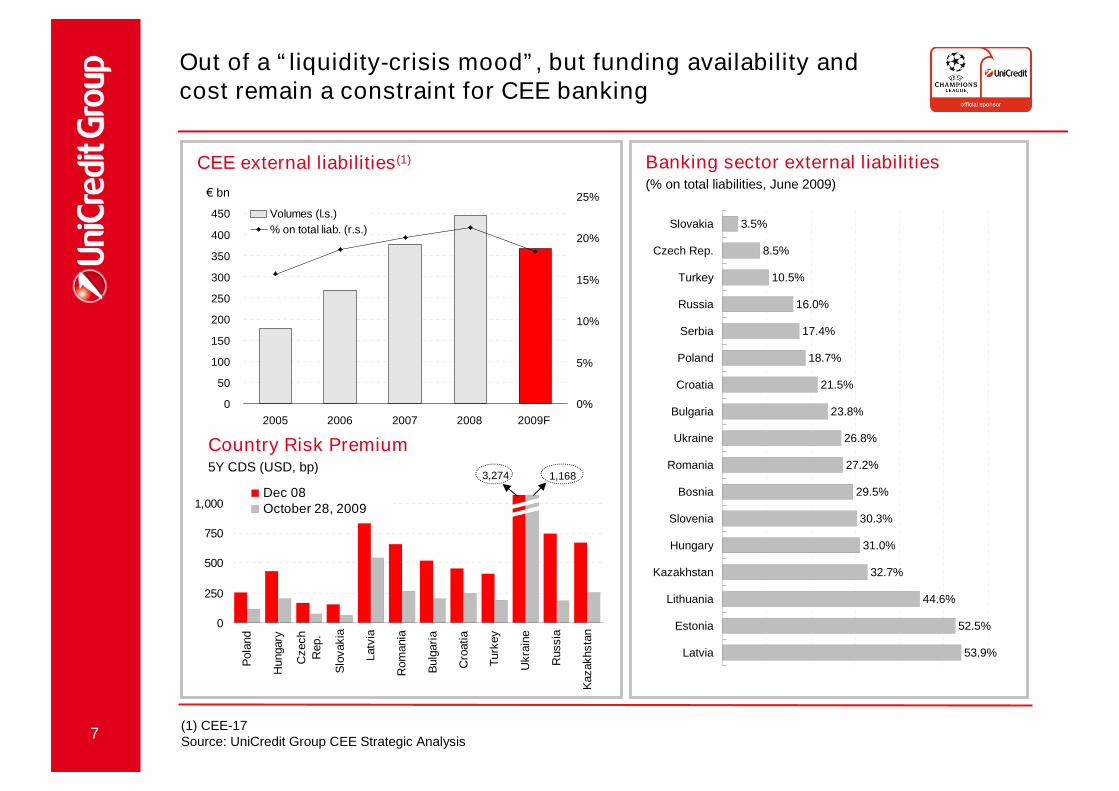

Out of a “liquidity-crisis mood”, but funding availability andcost remain a constraint for CEE banking

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009F

0%

5%

10%

15%

20%

25%

Volumes (l.s.)

% on total liab. (r.s.)

0

250

500

750

1,000

Pola

nd

Hungary

Czech

Rep.

Slo

vakia

Latv

ia

Rom

ania

Bulg

ari

a

Cro

atia

Turk

ey

Ukra

ine

Russia

Kazakhsta

n

Dec 08October 28, 2009

Country Risk Premium5Y CDS (USD, bp)

CEE external liabilities(1)

(1) CEE-17Source: UniCredit Group CEE Strategic Analysis

3,274 1,168

€ bn

Banking sector external liabilities(% on total liabilities, June 2009)

3.5%

8.5%

10.5%

16.0%

17.4%

18.7%

21.5%

23.8%

26.8%

27.2%

29.5%

30.3%

31.0%

32.7%

44.6%

52.5%

53.9%

Slovakia

Czech Rep.

Turkey

Russia

Serbia

Poland

Croatia

Bulgaria

Ukraine

Romania

Bosnia

Slovenia

Hungary

Kazakhstan

Lithuania

Estonia

Latvia

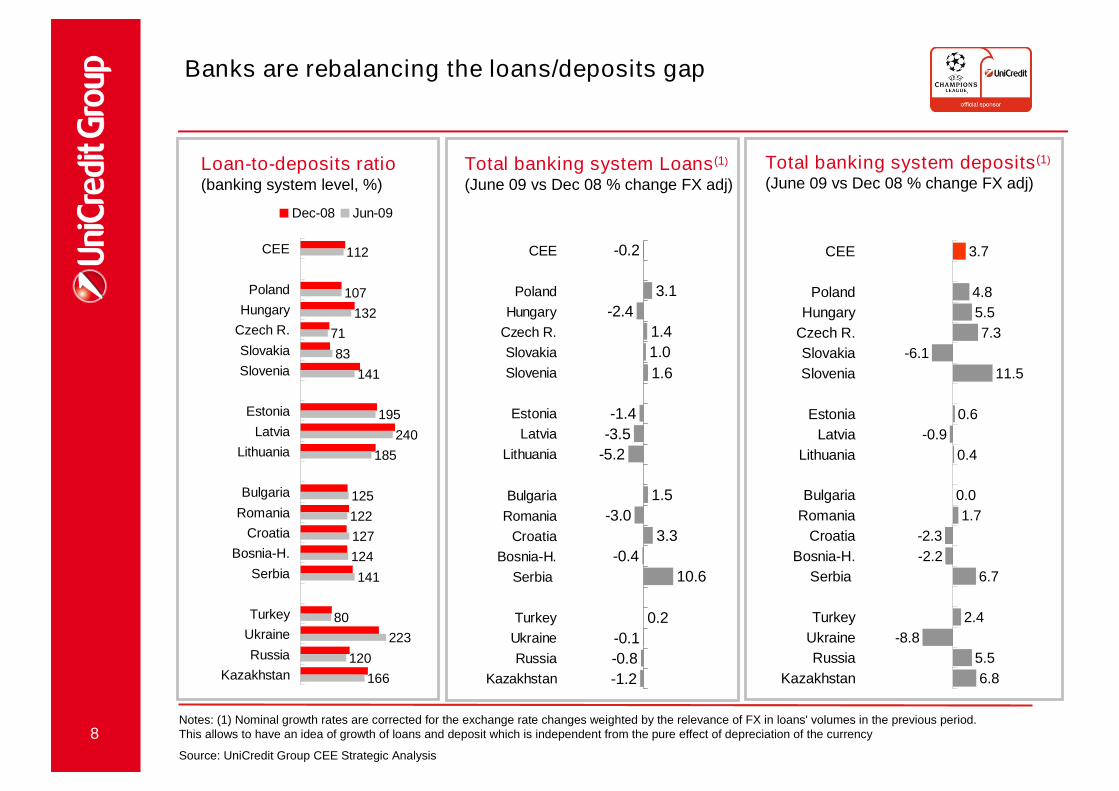

8Notes: (1) Nominal growth rates are corrected for the exchange rate changes weighted by the relevance of FX in loans' volumes in the previous period.This allows to have an idea of growth of loans and deposit which is independent from the pure effect of depreciation of the currency

Source: UniCredit Group CEE Strategic Analysis

Banks are rebalancing the loans/deposits gap

Total banking system deposits(1)

(June 09 vs Dec 08 % change FX adj)

-0.2

-2.4

1.4

1.0

1.6

-1.4

-5.2

1.5

-3.0

3.3

-0.4

0.2

-0.1

-0.8

-1.2

10.6

3.1

-3.5

CEE

Poland

Hungary

Czech R.

Slovakia

Slovenia

Estonia

Latvia

Lithuania

Bulgaria

Romania

Croatia

Bosnia-H.

Serbia

Turkey

Ukraine

Russia

Kazakhstan

112

107

132

71

83

141

195

240

185

125

122

127

124

141

80

223

120

166

CEE

Poland

Hungary

Czech R.

Slovakia

Slovenia

Estonia

Latvia

Lithuania

Bulgaria

Romania

Croatia

Bosnia-H.

Serbia

Turkey

Ukraine

Russia

Kazakhstan

Dec-08 Jun-09

Loan-to-deposits ratio(banking system level, %)

3.7

5.5

7.3

-6.1

11.5

0.6

0.4

0.0

1.7

-2.3

-2.2

6.7

2.4

-8.8

5.5

6.8

4.8

-0.9

CEE

Poland

Hungary

Czech R.

Slovakia

Slovenia

Estonia

Latvia

Lithuania

Bulgaria

Romania

Croatia

Bosnia-H.

Serbia

Turkey

Ukraine

Russia

Kazakhstan

Total banking system Loans(1)

(June 09 vs Dec 08 % change FX adj)

9

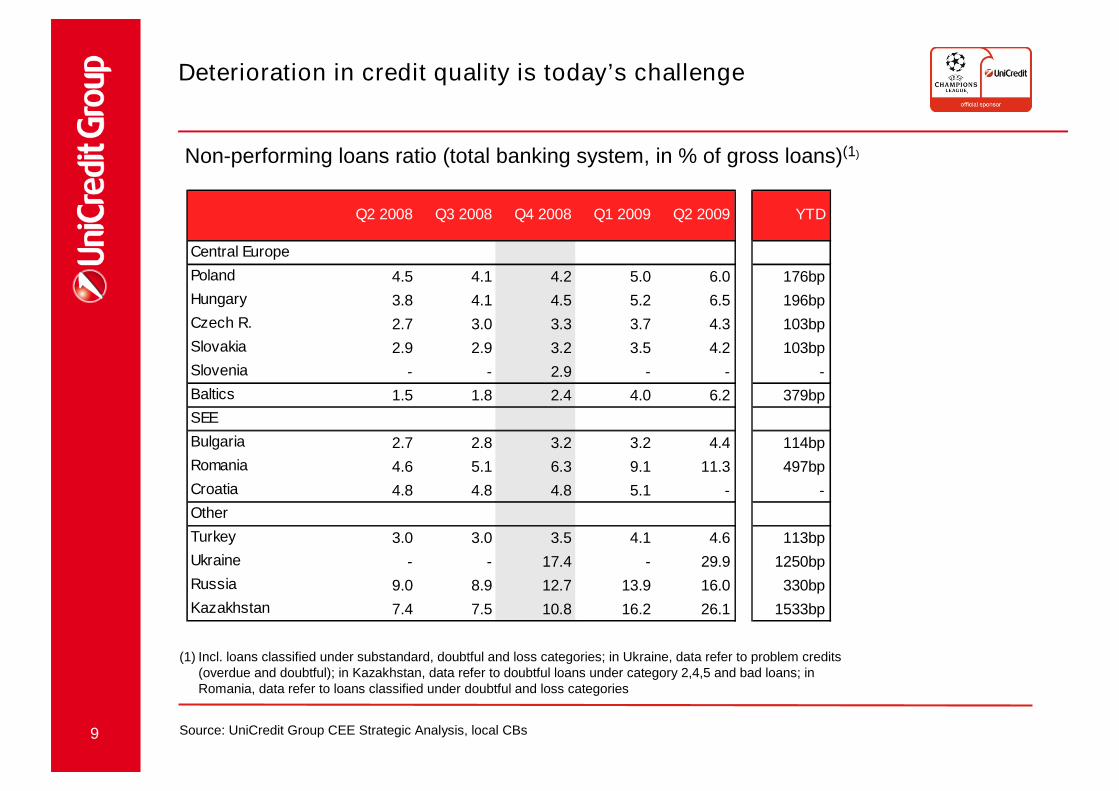

(1) Incl. loans classified under substandard, doubtful and loss categories; in Ukraine, data refer to problem credits(overdue and doubtful); in Kazakhstan, data refer to doubtful loans under category 2,4,5 and bad loans; inRomania, data refer to loans classified under doubtful and loss categories

Source: UniCredit Group CEE Strategic Analysis, local CBs

Non-performing loans ratio (total banking system, in % of gross loans)(1)

Deterioration in credit quality is today’s challenge

Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 YTD

Central Europe

Poland 4.5 4.1 4.2 5.0 6.0 176bp

Hungary 3.8 4.1 4.5 5.2 6.5 196bp

Czech R. 2.7 3.0 3.3 3.7 4.3 103bp

Slovakia 2.9 2.9 3.2 3.5 4.2 103bp

Slovenia - - 2.9 - - -

Baltics 1.5 1.8 2.4 4.0 6.2 379bp

SEE

Bulgaria 2.7 2.8 3.2 3.2 4.4 114bp

Romania 4.6 5.1 6.3 9.1 11.3 497bp

Croatia 4.8 4.8 4.8 5.1 - -

Other

Turkey 3.0 3.0 3.5 4.1 4.6 113bp

Ukraine - - 17.4 - 29.9 1250bp

Russia 9.0 8.9 12.7 13.9 16.0 330bp

Kazakhstan 7.4 7.5 10.8 16.2 26.1 1533bp

10

AGENDA

1. How the CEE banking landscape has changed in the short term

2. Banking through the crisis

3. International players - UniCredit ready to take the upside

11

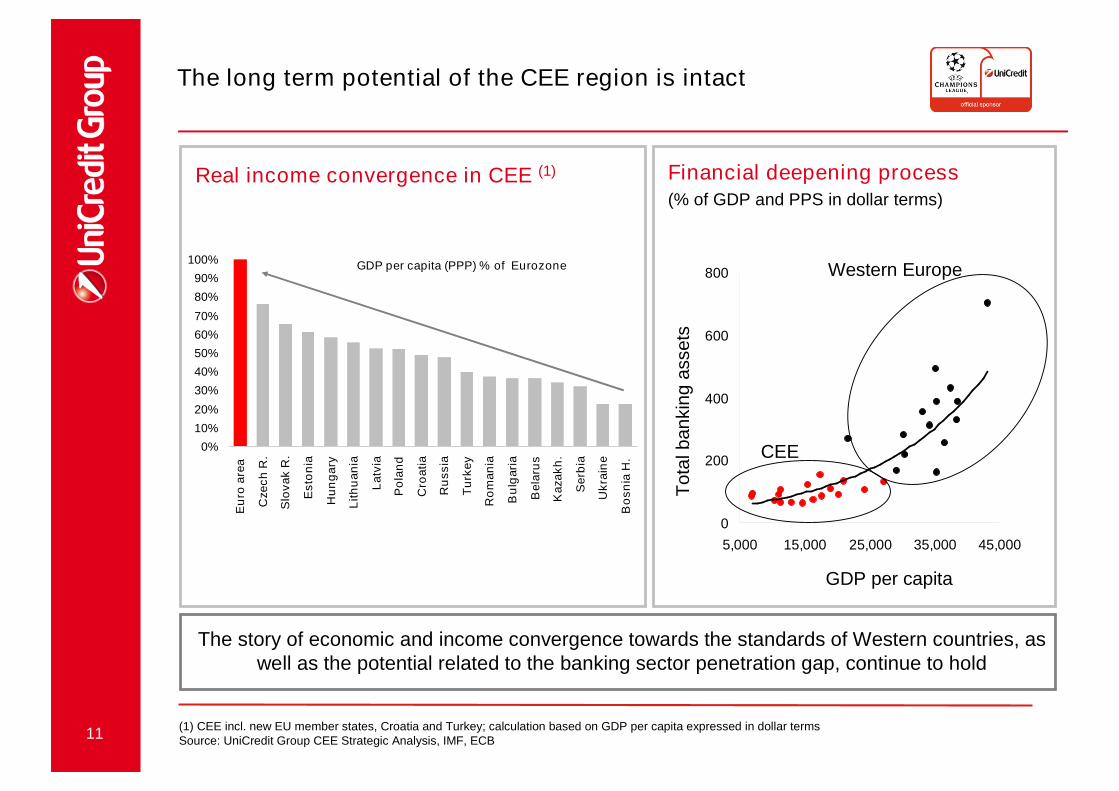

The long term potential of the CEE region is intact

Real income convergence in CEE (1)

(1) CEE incl. new EU member states, Croatia and Turkey; calculation based on GDP per capita expressed in dollar termsSource: UniCredit Group CEE Strategic Analysis, IMF, ECB

0

200

400

600

800

5,000 15,000 25,000 35,000 45,000

Financial deepening process(% of GDP and PPS in dollar terms)

GDP per capita

Tota

lbankin

gassets

Western Europe

CEE

The story of economic and income convergence towards the standards of Western countries, aswell as the potential related to the banking sector penetration gap, continue to hold

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eu

roa

rea

Cze

ch

R.

Slo

va

kR

.

Es

ton

ia

Hu

ng

ary

Lit

hu

an

ia

La

tvia

Po

lan

d

Cro

ati

a

Ru

ss

ia

Tu

rke

y

Ro

ma

nia

Bu

lgari

a

Be

laru

s

Ka

za

kh

.

Se

rbia

Uk

rain

e

Bo

sn

iaH

.

GDP per capita (PPP) % of Eurozone

12

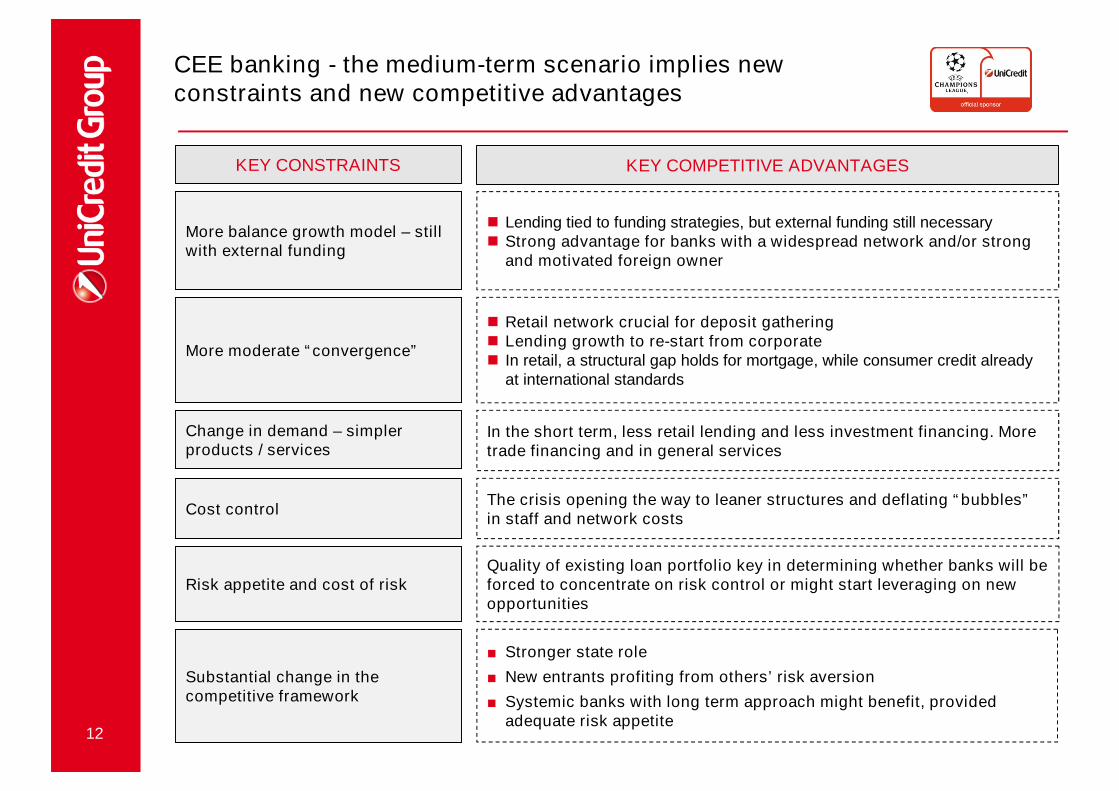

KEY COMPETITIVE ADVANTAGES

More balance growth model – stillwith external funding

Lending tied to funding strategies, but external funding still necessary Strong advantage for banks with a widespread network and/or strong

and motivated foreign owner

More moderate “convergence”

Retail network crucial for deposit gathering Lending growth to re-start from corporate In retail, a structural gap holds for mortgage, while consumer credit already

at international standards

Change in demand – simplerproducts / services

In the short term, less retail lending and less investment financing. Moretrade financing and in general services

Risk appetite and cost of riskQuality of existing loan portfolio key in determining whether banks will beforced to concentrate on risk control or might start leveraging on newopportunities

KEY CONSTRAINTS

CEE banking - the medium-term scenario implies newconstraints and new competitive advantages

Cost controlThe crisis opening the way to leaner structures and deflating “bubbles”in staff and network costs

Substantial change in thecompetitive framework

■ Stronger state role

■ New entrants profiting from others’ risk aversion

■ Systemic banks with long term approach might benefit, providedadequate risk appetite

13

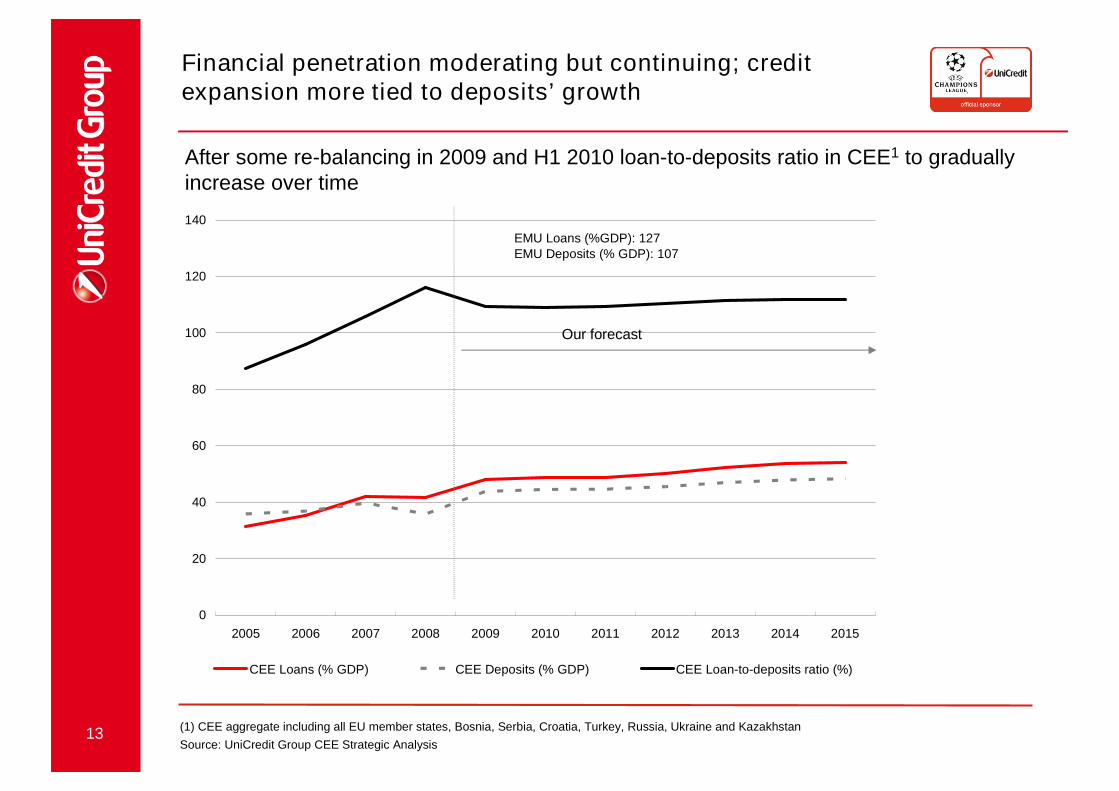

Financial penetration moderating but continuing; creditexpansion more tied to deposits’ growth

(1) CEE aggregate including all EU member states, Bosnia, Serbia, Croatia, Turkey, Russia, Ukraine and Kazakhstan

Source: UniCredit Group CEE Strategic Analysis

After some re-balancing in 2009 and H1 2010 loan-to-deposits ratio in CEE1 to graduallyincrease over time

0

20

40

60

80

100

120

140

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CEE Loans (% GDP) CEE Deposits (% GDP) CEE Loan-to-deposits ratio (%)

EMU Loans (%GDP): 127EMU Deposits (% GDP): 107

Our forecast

14

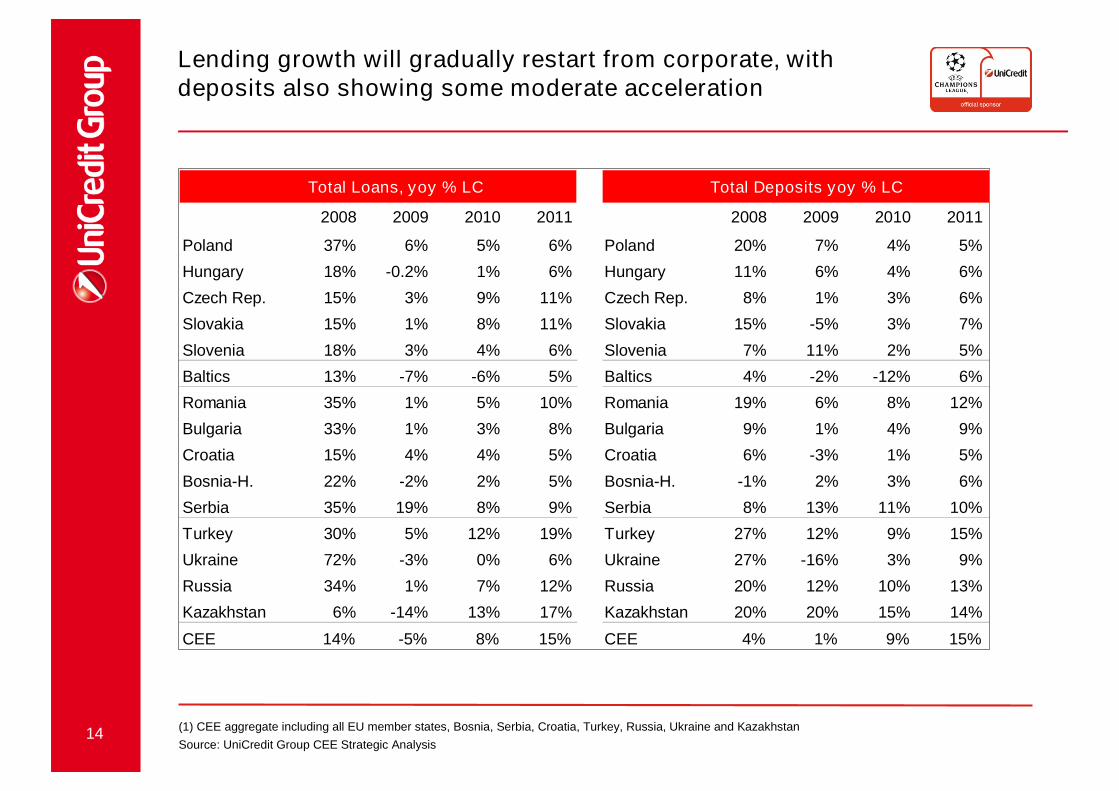

Lending growth will gradually restart from corporate, withdeposits also showing some moderate acceleration

(1) CEE aggregate including all EU member states, Bosnia, Serbia, Croatia, Turkey, Russia, Ukraine and Kazakhstan

Source: UniCredit Group CEE Strategic Analysis

Total Loans, yoy % LC Total Deposits yoy % LC

2008 2009 2010 2011 2008 2009 2010 2011

Poland 37% 6% 5% 6% Poland 20% 7% 4% 5%

Hungary 18% -0.2% 1% 6% Hungary 11% 6% 4% 6%

Czech Rep. 15% 3% 9% 11% Czech Rep. 8% 1% 3% 6%

Slovakia 15% 1% 8% 11% Slovakia 15% -5% 3% 7%

Slovenia 18% 3% 4% 6% Slovenia 7% 11% 2% 5%

Baltics 13% -7% -6% 5% Baltics 4% -2% -12% 6%

Romania 35% 1% 5% 10% Romania 19% 6% 8% 12%

Bulgaria 33% 1% 3% 8% Bulgaria 9% 1% 4% 9%

Croatia 15% 4% 4% 5% Croatia 6% -3% 1% 5%

Bosnia-H. 22% -2% 2% 5% Bosnia-H. -1% 2% 3% 6%

Serbia 35% 19% 8% 9% Serbia 8% 13% 11% 10%

Turkey 30% 5% 12% 19% Turkey 27% 12% 9% 15%

Ukraine 72% -3% 0% 6% Ukraine 27% -16% 3% 9%

Russia 34% 1% 7% 12% Russia 20% 12% 10% 13%

Kazakhstan 6% -14% 13% 17% Kazakhstan 20% 20% 15% 14%

CEE 14% -5% 8% 15% CEE 4% 1% 9% 15%

15

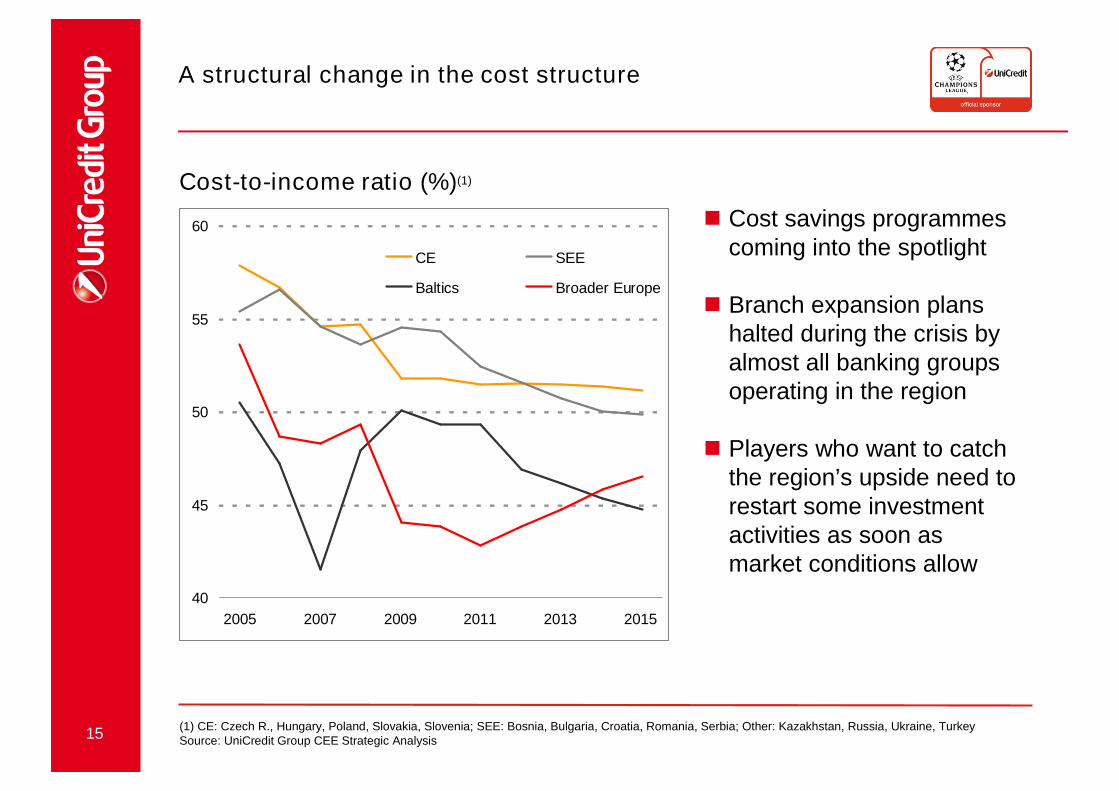

A structural change in the cost structure

Cost-to-income ratio (%)(1)

(1) CE: Czech R., Hungary, Poland, Slovakia, Slovenia; SEE: Bosnia, Bulgaria, Croatia, Romania, Serbia; Other: Kazakhstan, Russia, Ukraine, TurkeySource: UniCredit Group CEE Strategic Analysis

40

45

50

55

60

2005 2007 2009 2011 2013 2015

CE SEE

Baltics Broader Europe

Cost savings programmescoming into the spotlight

Branch expansion planshalted during the crisis byalmost all banking groupsoperating in the region

Players who want to catchthe region’s upside need torestart some investmentactivities as soon asmarket conditions allow

16

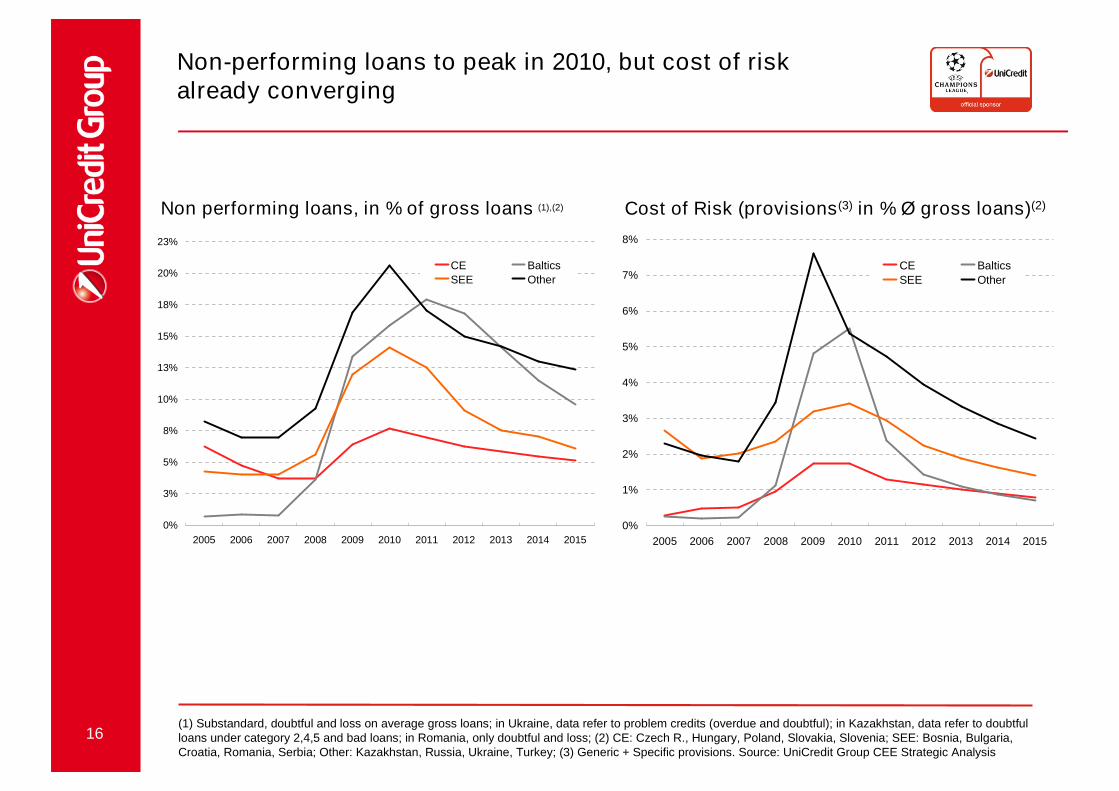

Non-performing loans to peak in 2010, but cost of riskalready converging

Non performing loans, in % of gross loans (1),(2)

(1) Substandard, doubtful and loss on average gross loans; in Ukraine, data refer to problem credits (overdue and doubtful); in Kazakhstan, data refer to doubtfulloans under category 2,4,5 and bad loans; in Romania, only doubtful and loss; (2) CE: Czech R., Hungary, Poland, Slovakia, Slovenia; SEE: Bosnia, Bulgaria,Croatia, Romania, Serbia; Other: Kazakhstan, Russia, Ukraine, Turkey; (3) Generic + Specific provisions. Source: UniCredit Group CEE Strategic Analysis

Cost of Risk (provisions(3) in % Ø gross loans)(2)

0%

3%

5%

8%

10%

13%

15%

18%

20%

23%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CE Baltics

SEE Other

0%

1%

2%

3%

4%

5%

6%

7%

8%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CE Baltics

SEE Other

18

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Central Europe Russia

SEE UA and KZ

Turkey Baltics

avg 2007-'08 avg 2010-'112009

Russia

TK

TK

TK

CESEE

Russia

Russia

SEE

SEE

Baltics

UA and KZ

CE

avg 2011-'15

Baltics

UA and KZ

CE

TK

UA and KZ

Baltics

Source: UniCredit Group CEE Strategic Analysis

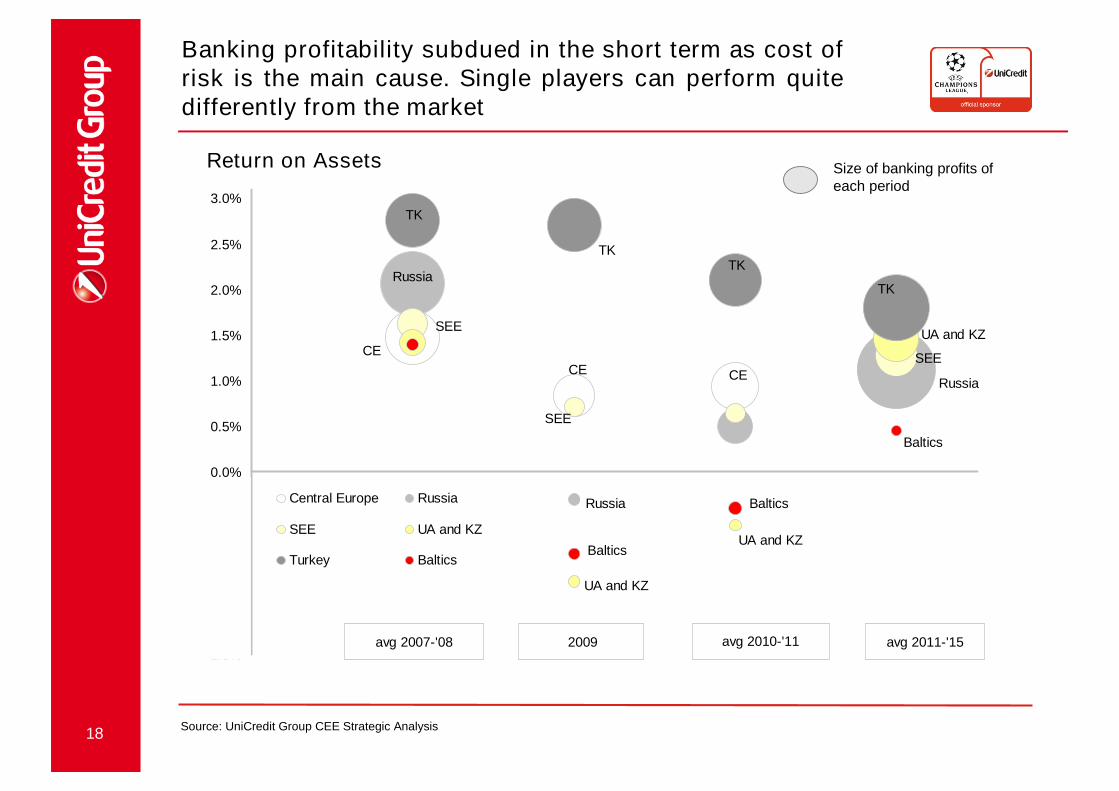

Size of banking profits ofeach period

Return on Assets

Banking profitability subdued in the short term as cost ofrisk is the main cause. Single players can perform quitedifferently from the market

19

AGENDA

1. How the CEE banking landscape has changed in the short term

2. Banking through the crisis

3. International players - UniCredit ready to take the upside

20

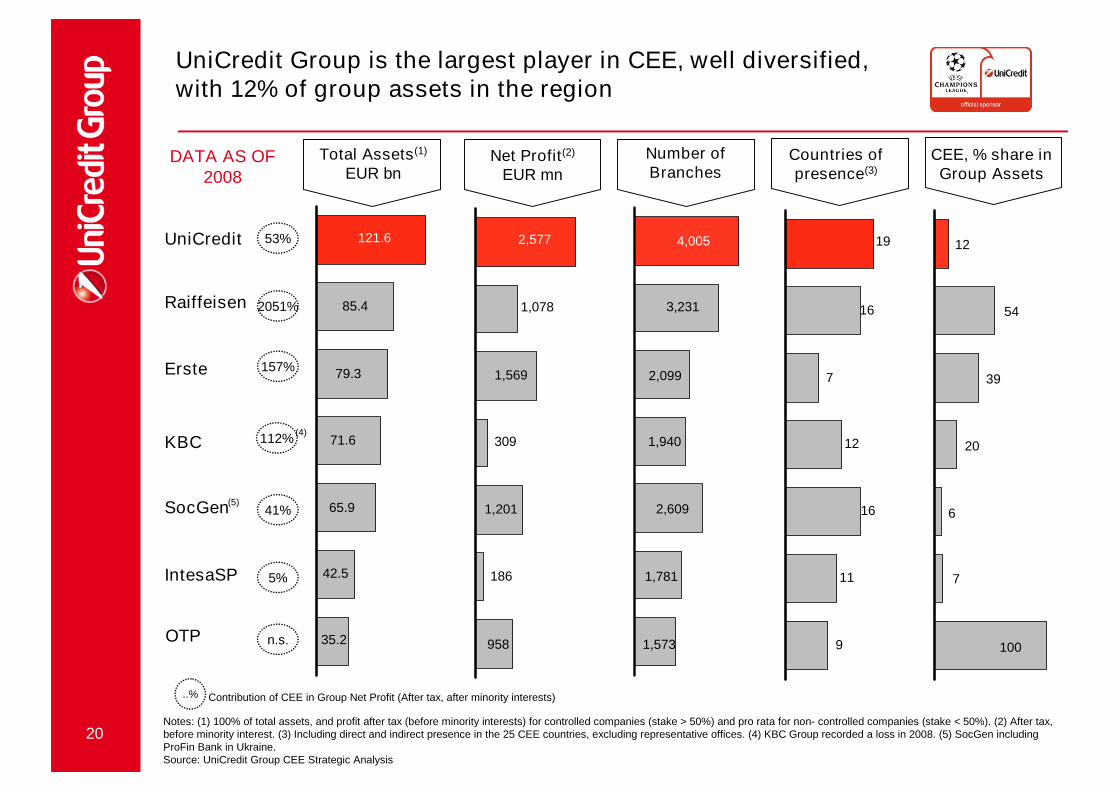

Total Assets(1)

EUR bnNet Profit(2)

EUR mn

Number ofBranches

Countries ofpresence(3)

OTP

KBC

Raiffeisen

Erste

UniCredit

IntesaSP

121.6 2,577

1,569

4,005

3,231

2,099

1,940

2,609

1,781

1,573

19

16

7

12

16

11

9

SocGen 1,201

112%

..% Contribution of CEE in Group Net Profit (After tax, after minority interests)

Notes: (1) 100% of total assets, and profit after tax (before minority interests) for controlled companies (stake > 50%) and pro rata for non- controlled companies (stake < 50%). (2) After tax,before minority interest. (3) Including direct and indirect presence in the 25 CEE countries, excluding representative offices. (4) KBC Group recorded a loss in 2008. (5) SocGen includingProFin Bank in Ukraine.Source: UniCredit Group CEE Strategic Analysis

1,078

958

(4)

53%

2051%

157%

41%

5%

n.s.

CEE, % share inGroup Assets

85.4

79.3

71.6

65.9

42.5

35.2

309

186

12

54

39

20

6

7

100

(5)

UniCredit Group is the largest player in CEE, well diversified,with 12% of group assets in the region

DATA AS OF2008

21

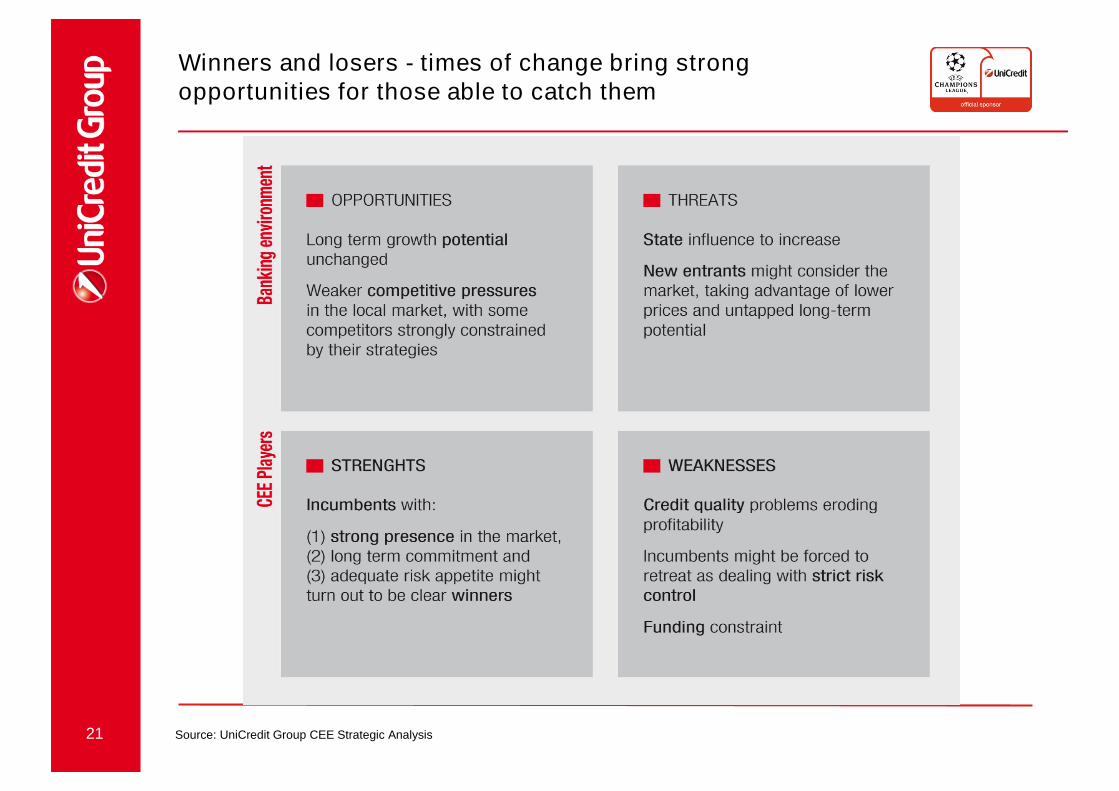

Winners and losers - times of change bring strongopportunities for those able to catch them

Source: UniCredit Group CEE Strategic Analysis

22

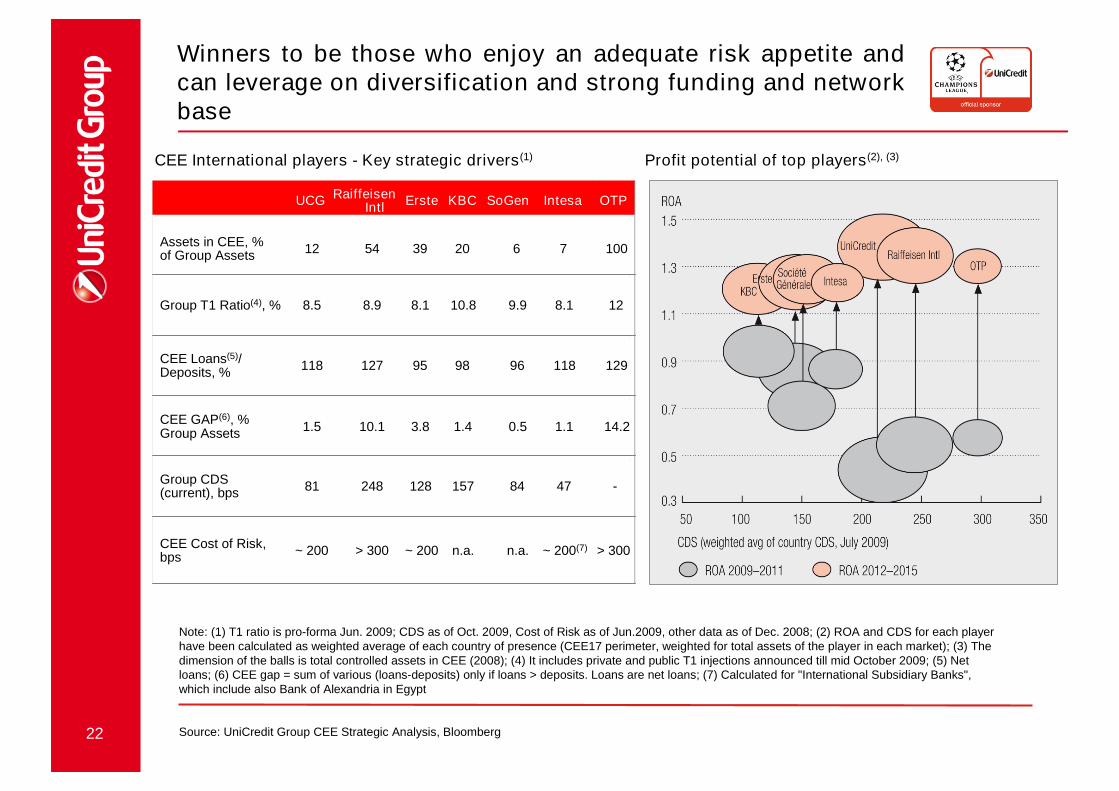

Note: (1) T1 ratio is pro-forma Jun. 2009; CDS as of Oct. 2009, Cost of Risk as of Jun.2009, other data as of Dec. 2008; (2) ROA and CDS for each playerhave been calculated as weighted average of each country of presence (CEE17 perimeter, weighted for total assets of the player in each market); (3) Thedimension of the balls is total controlled assets in CEE (2008); (4) It includes private and public T1 injections announced till mid October 2009; (5) Netloans; (6) CEE gap = sum of various (loans-deposits) only if loans > deposits. Loans are net loans; (7) Calculated for "International Subsidiary Banks",which include also Bank of Alexandria in Egypt

Source: UniCredit Group CEE Strategic Analysis, Bloomberg

CEE International players - Key strategic drivers(1) Profit potential of top players(2), (3)

Winners to be those who enjoy an adequate risk appetite andcan leverage on diversification and strong funding and networkbase

UCG RaiffeisenIntl

Erste KBC SoGen Intesa OTP

Assets in CEE, %of Group Assets

12 54 39 20 6 7 100

Group T1 Ratio(4), % 8.5 8.9 8.1 10.8 9.9 8.1 12

CEE Loans(5)/Deposits, %

118 127 95 98 96 118 129

CEE GAP(6), %Group Assets

1.5 10.1 3.8 1.4 0.5 1.1 14.2

Group CDS(current), bps

81 248 128 157 84 47 -

CEE Cost of Risk,bps

~ 200 > 300 ~ 200 n.a. n.a. ~ 200(7) > 300

23

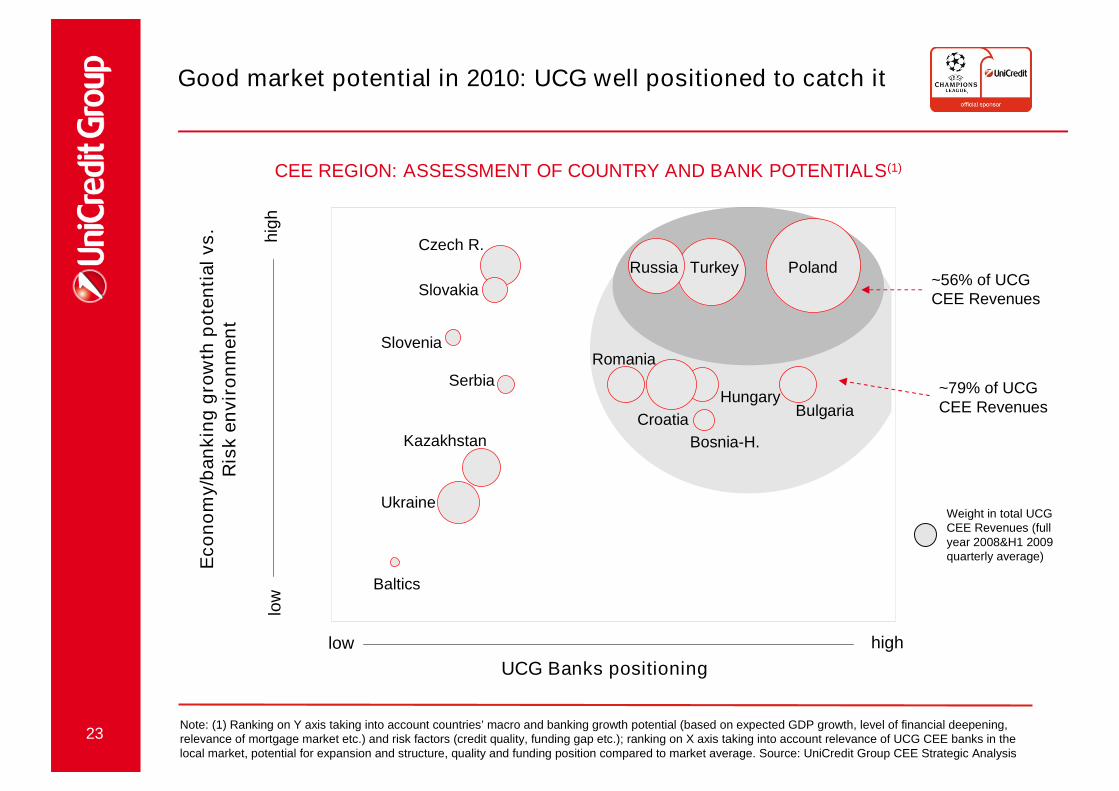

Good market potential in 2010: UCG well positioned to catch it

Note: (1) Ranking on Y axis taking into account countries’ macro and banking growth potential (based on expected GDP growth, level of financial deepening,relevance of mortgage market etc.) and risk factors (credit quality, funding gap etc.); ranking on X axis taking into account relevance of UCG CEE banks in thelocal market, potential for expansion and structure, quality and funding position compared to market average. Source: UniCredit Group CEE Strategic Analysis

UCG Banks positioning

Eco

no

my/b

an

kin

gg

row

thp

ote

nti

alvs.

Ris

ken

vir

on

men

t

low

hig

h

low high

CEE REGION: ASSESSMENT OF COUNTRY AND BANK POTENTIALS(1)

Romania

Croatia

Hungary

Bosnia-H.

Bulgaria

Baltics

Ukraine

Kazakhstan

Serbia

Slovenia

Slovakia

Czech R.

Weight in total UCGCEE Revenues (fullyear 2008&H1 2009quarterly average)

~56% of UCGCEE Revenues

~79% of UCGCEE Revenues

Russia PolandTurkey

24 Source: UniCredit Group CEE Strategic Analysis

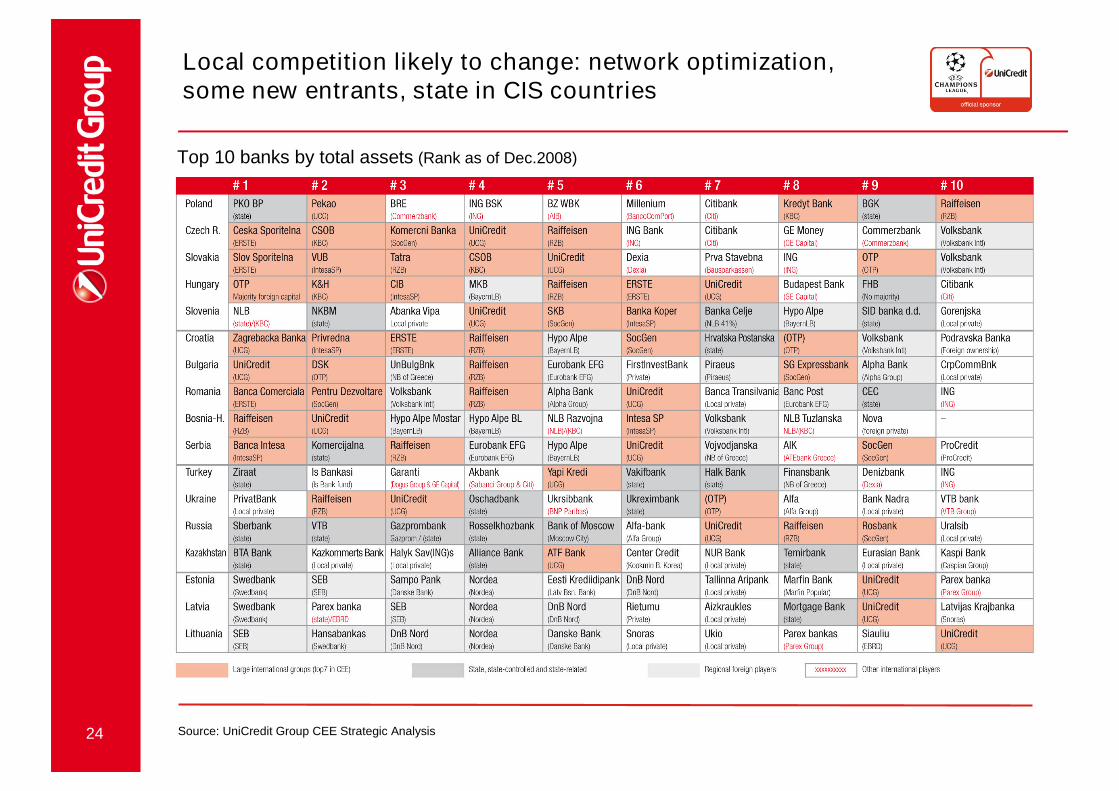

Top 10 banks by total assets (Rank as of Dec.2008)

Local competition likely to change: network optimization,some new entrants, state in CIS countries

25

Conclusions

Economic recovery, but risk and volatility remain. Strong regional

differentiation is confirmed

Credit quality and risk appetite today’s key constraints for CEE

banking

Medium term: “CEE convergence story” holds, but the banking

model has to be rebalanced

The changing competitive environment means also opportunities

Winners – new entrants or consolidated players, with appropriate

risk appetite for CEE, able to leverage on strong funding position

(both through a strong domestic network or through international

channels) and with sound risk

UCG ready to take the upside – can leverage on diversification,

strong regional network and newly raised capital to strengthen and

optimize its positioning in the market