Embed Size (px)

Citation preview

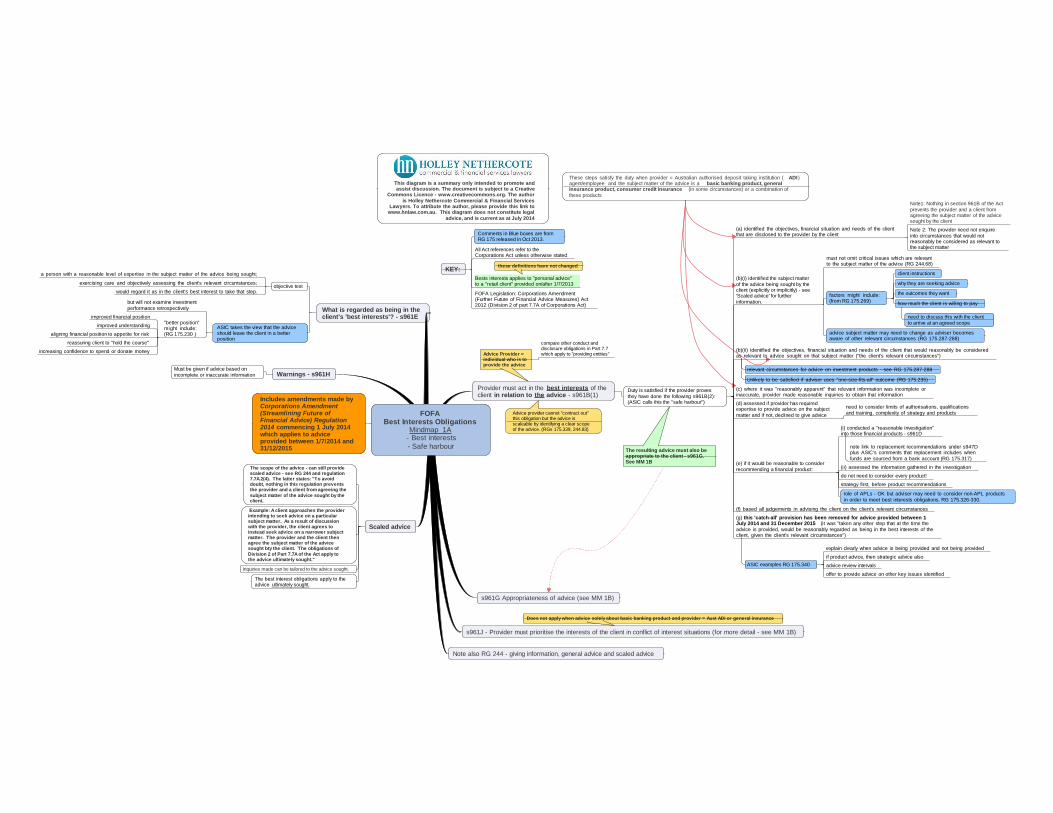

FOFABest Interests Obligations

Mindmap 1A - Best interests- Safe harbour

Provider must act in the best interests of theclient in relation to the advice - s961B(1)

Duty is satisfied if the provider provesthey have done the following s961B(2):(ASIC calls this the "safe harbour")

(a) identified the objectives, financial situation and needs of the clientthat are disclosed to the provider by the client

Note1: Nothing in section 961B of the Actprevents the provider and a client fromagreeing the subject matter of the advicesought by the client

Note 2: The provider need not enquireinto circumstances that would notreasonably be considered as relevant tothe subject matter

(b)(i) identified the subject matterof the advice being sought by theclient (explicitly or implicitly) - see'Scaled advice' for furtherinformation.

must not omit critical issues which are relevantto the subject matter of the advice (RG 244.68)

factors might include:(from RG 175.269)

client instructions

why they are seeking advice

the outcomes they want

how much the client is willing to pay

need to discuss this with the clientto arrive at an agreed scope

advice subject matter may need to change as adviser becomesaware of other relevant circumstances (RG 175.287-288)

(b)(ii) identified the objectives, financial situation and needs of the client that would reasonably be consideredas relevant to advice sought on that subject matter ("the client's relevant circumstances")

relevant circumstances for advice on investment products - see RG 175.287-288

Unlikely to be satisfied if adviser uses "one-size-fits-all" outcome (RG 175.235)

(c) where it was "reasonably apparent" that relevant information was incomplete orinaccurate, provider made reasonable inquiries to obtain that information

(d) assessed if provider has requiredexpertise to provide advice on the subjectmatter and if not, declined to give advice

need to consider limits of authorisations, qualificationsand training, complexity of strategy and products

(e) if it would be reasonable to considerrecommending a financial product:

(i) conducted a "reasonable investigation"into those financial products - s961D

note link to replacement recommendations under s947Dplus ASIC's comments that replacement includes whenfunds are sourced from a bank account (RG 175.317)

(ii) assessed the information gathered in the investigation

do not need to consider every product!

strategy first, before product recommendations

role of APLs - OK but adviser may need to consider non-APL productsin order to meet best interests obligations. RG 175.326-330.

(f) based all judgements in advising the client on the client's relevant circumstances

(g) this 'catch-all' provision has been removed for advice provided between 1July 2014 and 31 December 2015 (it was "taken any other step that at the time theadvice is provided, would be reasonably regarded as being in the best interests of theclient, given the client's relevant circumstances")

ASIC examples RG 175.340

explain clearly when advice is being provided and not being provided

if product advice, then strategic advice also

advice review intervals

offer to provide advice on other key issues identified

The resulting advice must also beappropriate to the client - s961G.See MM 1B

Advice Provider =individual who is toprovide the advice

compare other conduct anddisclosure obligations in Part 7.7which apply to "providing entities"

Advice provider cannot "contract out"this obligation but the advice isscaleable by identifying a clear scopeof the advice. (RGs 175.339, 244.83)

s961G Appropriateness of advice (see MM 1B)

s961J - Provider must prioritise the interests of the client in conflict of interest situations (for more detail - see MM 1B)

Does not apply when advice solely about basic banking product and provider = Aust ADI or general insurance

Note also RG 244 - giving information, general advice and scaled advice

Scaled advice

The scope of the advice - can still providescaled advice - see RG 244 and regulation7.7A.2(4). The latter states: "To avoiddoubt, nothing in this regulation preventsthe provider and a client from agreeing thesubject matter of the advice sought by theclient.

Example: A client approaches the providerintending to seek advice on a particularsubject matter. As a result of discussionwith the provider, the client agrees toinstead seek advice on a narrower subjectmatter. The provider and the client thenagree the subject matter of the advicesought bty the client. The obligations ofDivision 2 of Part 7.7A of the Act apply tothe advice ultimately sought."

Inquiries made can be tailored to the advice sought.

The best interest obligations apply to theadvice ultimately sought.

Includes amendments made byCorporations Amendment(Streamlining Future ofFinancial Advice) Regulation2014 commencing 1 July 2014which applies to adviceprovided between 1/7/2014 and31/12/2015

Warnings - s961HMust be given if advice based onincomplete or inaccurate information

What is regarded as being in theclient's 'best interests'? - s961E

objective test

a person with a reasonable level of expertise in the subject matter of the advice being sought;

exercising care and objectively assessing the client's relevant circumstances;

would regard it as in the client's best interest to take that step.

ASIC takes the view that the adviceshould leave the client in a betterposition

but will not examine investmentperformance retrospectively

"better position"might include:(RG 175.230 )

improved financial position

improved understanding

aligning financial position to appetite for risk

reassuring client to "hold the course"

increasing confidence to spend or donate money

This diagram is a summary only intended to promote andassist discussion. The document is subject to a Creative

Commons Licence - www.creativecommons.org. The authoris Holley Nethercote Commercial & Financial Services

Lawyers. To attribute the author, please provide this link towww.hnlaw.com.au. This diagram does not constitute legal

advice, and is current as at July 2014

KEY:

Comments in Blue boxes are fromRG 175 released in Oct 2013.

All Act references refer to theCorporations Act unless otherwise stated

Bests interests applies to "personal advice"to a "retail client" provided on/after 1/7/2013

these definitions have not changed

FOFA Legislation: Corporations Amendment(Further Future of Financial Advice Measures) Act2012 (Division 2 of part 7.7A of Corporations Act)

These steps satisfy the duty when provider = Australian authorised deposit taking institution ( ADI)agent/employee and the subject matter of the advice is a basic banking product, generalinsurance product, consumer credit insurance (in some circumstances) or a combination ofthese products