Embed Size (px)

Citation preview

BOND PRICE VOLATILITY

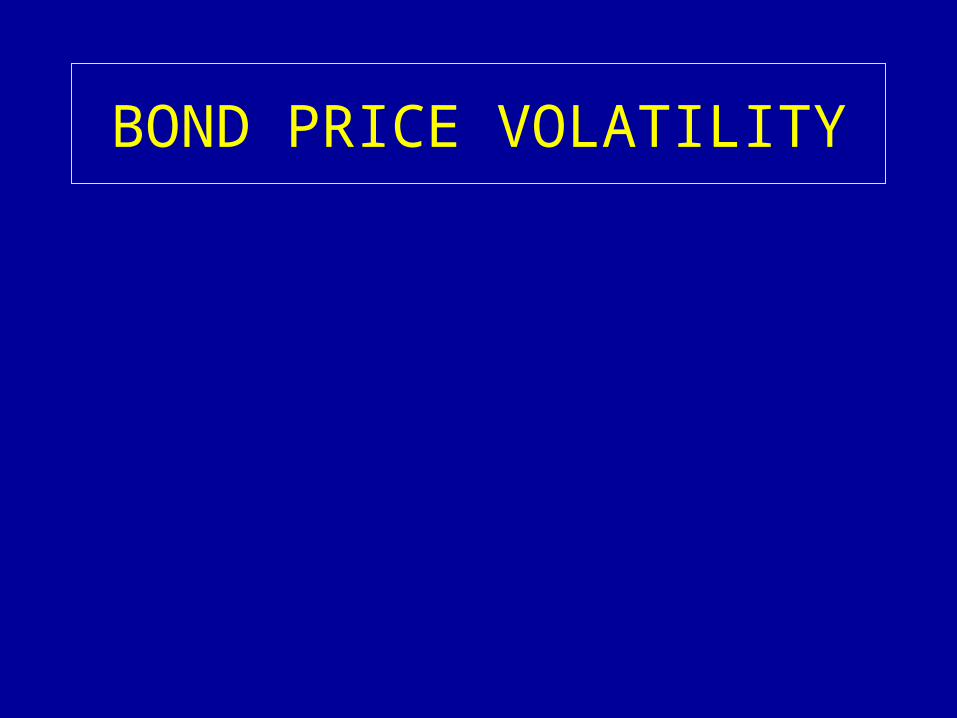

PR

ICE

YIELD

PRICE YIELD RELATIONSHIP

CONVEX SHAPE

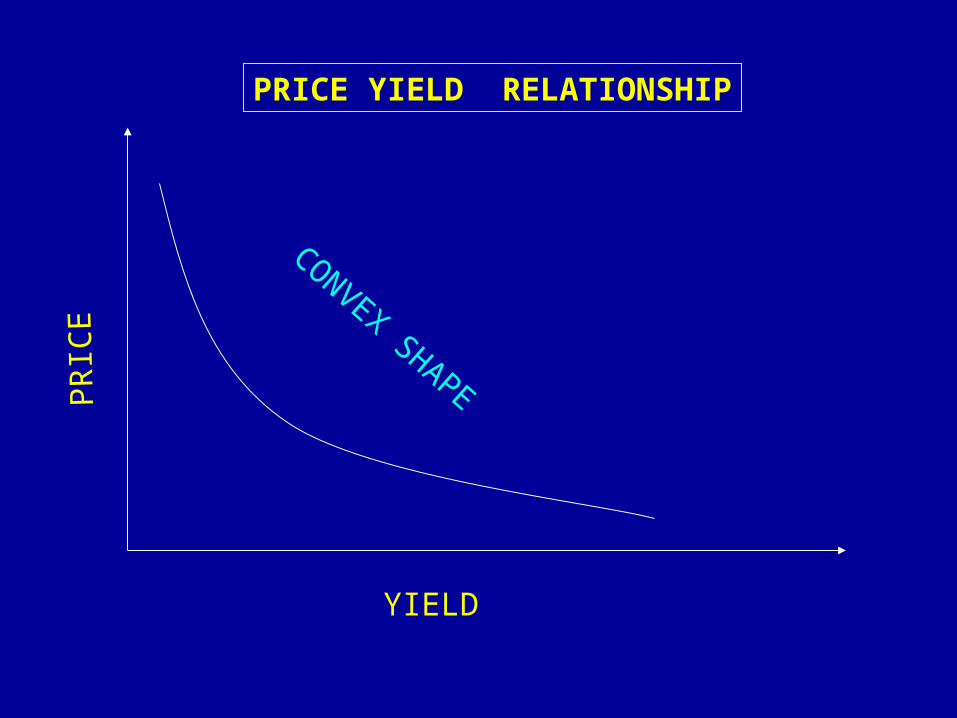

WHAT IS VOLATILITY ?

Volatility, a statistic similar to standard deviation, measures the uncertainty of the annualised underlying asset return.

More precisely, volatility is the annualized standard deviation of the natural logarithm of the underlying asset return.

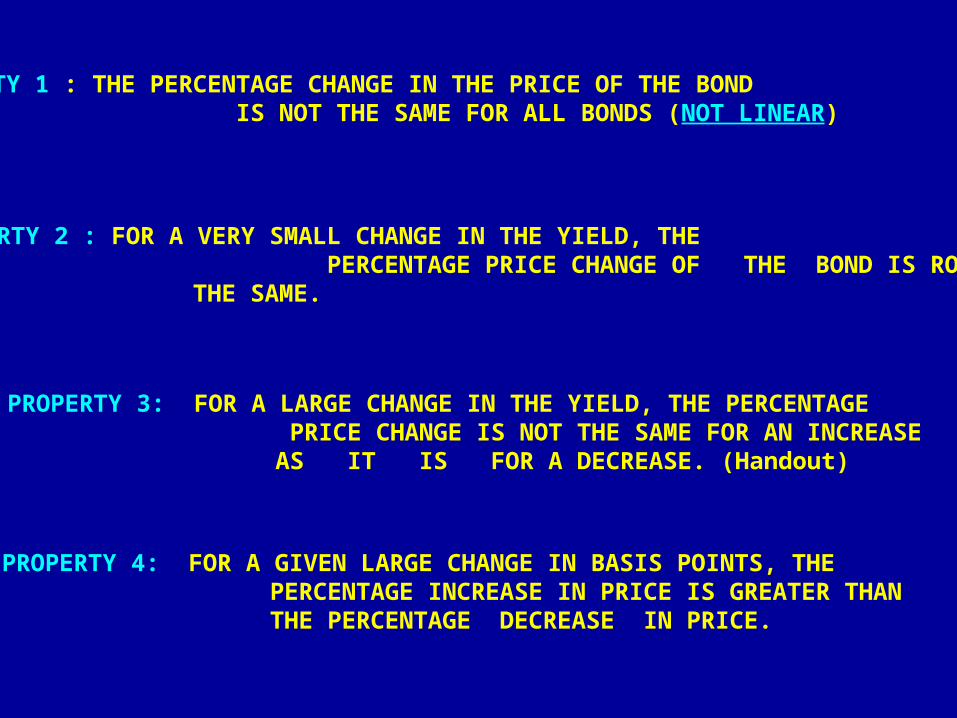

PROPERTY 1 : THE PERCENTAGE CHANGE IN THE PRICE OF THE BOND IS NOT THE SAME FOR ALL BONDS (NOT LINEAR)

PROPERTY 2 : FOR A VERY SMALL CHANGE IN THE YIELD, THE PERCENTAGE PRICE CHANGE OF THE BOND IS ROUGHLY

THE SAME.

PROPERTY 3: FOR A LARGE CHANGE IN THE YIELD, THE PERCENTAGE PRICE CHANGE IS NOT THE SAME FOR AN INCREASE AS IT IS FOR A DECREASE. (Handout)

PROPERTY 4: FOR A GIVEN LARGE CHANGE IN BASIS POINTS, THE PERCENTAGE INCREASE IN PRICE IS GREATER THAN THE PERCENTAGE DECREASE IN PRICE.

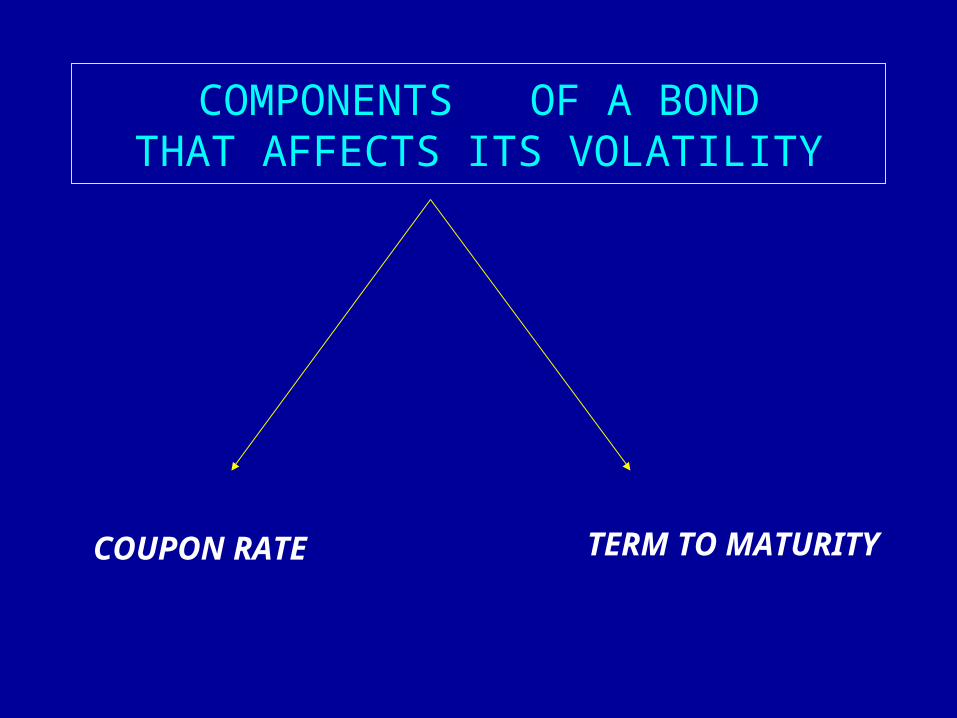

COMPONENTS OF A BONDTHAT AFFECTS ITS VOLATILITY

COUPON RATE TERM TO MATURITY

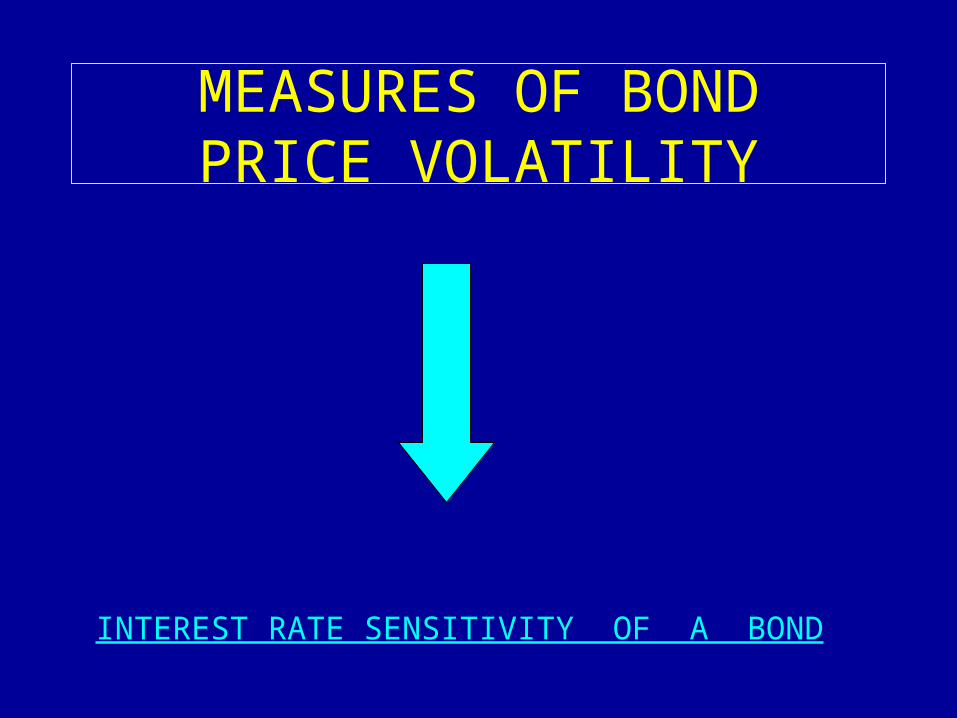

MEASURES OF BONDPRICE VOLATILITY

INTEREST RATE SENSITIVITY OF A BOND

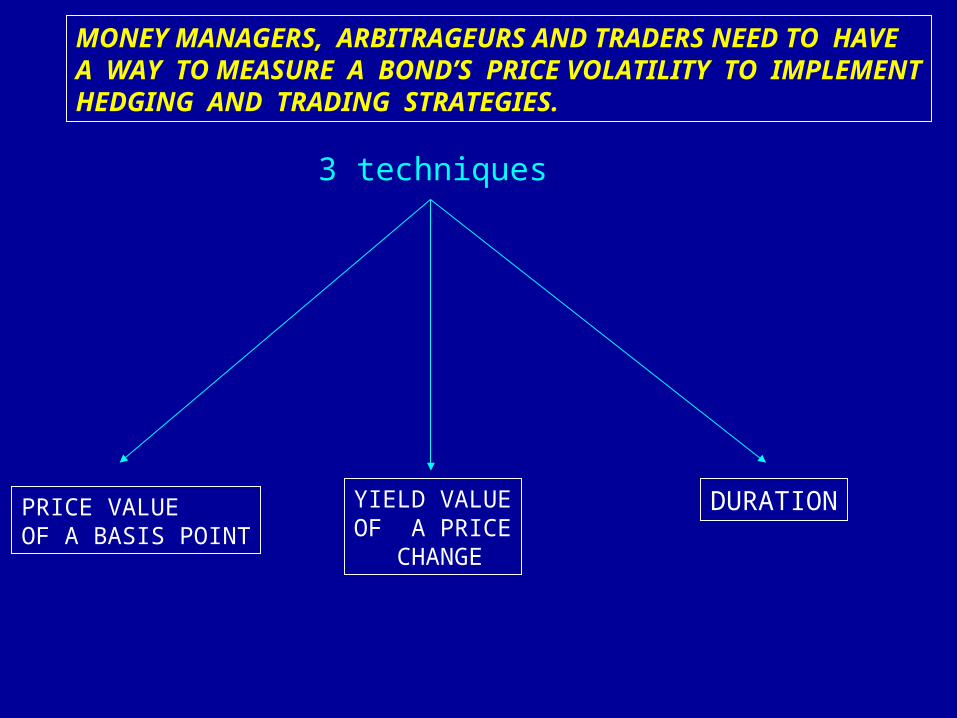

MONEY MANAGERS, ARBITRAGEURS AND TRADERS NEED TO HAVE A WAY TO MEASURE A BOND’S PRICE VOLATILITY TO IMPLEMENTHEDGING AND TRADING STRATEGIES.

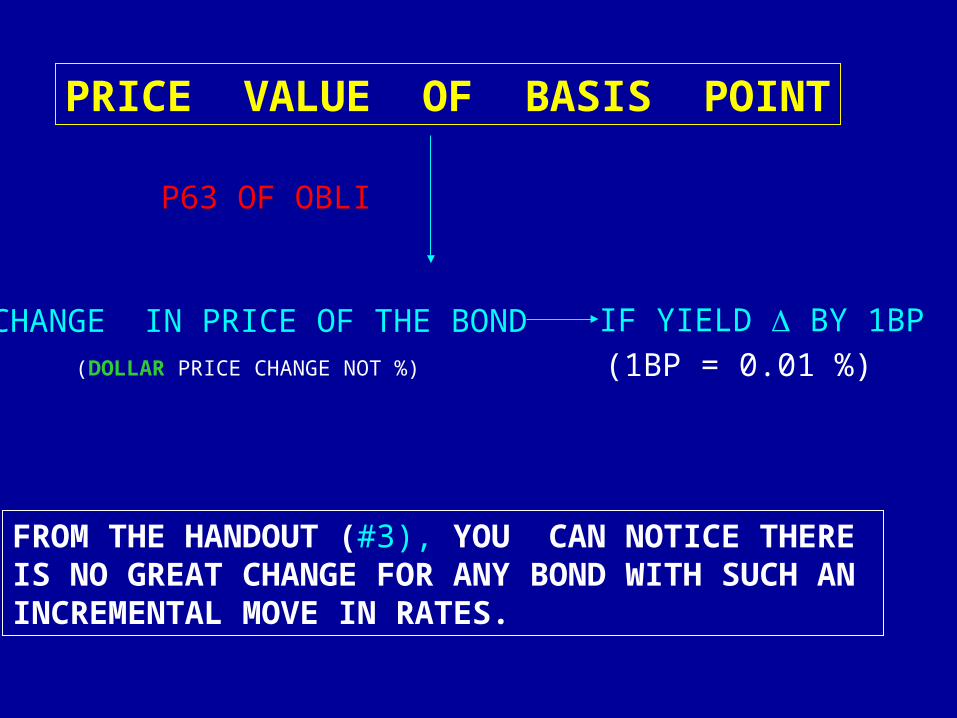

PRICE VALUEOF A BASIS POINT

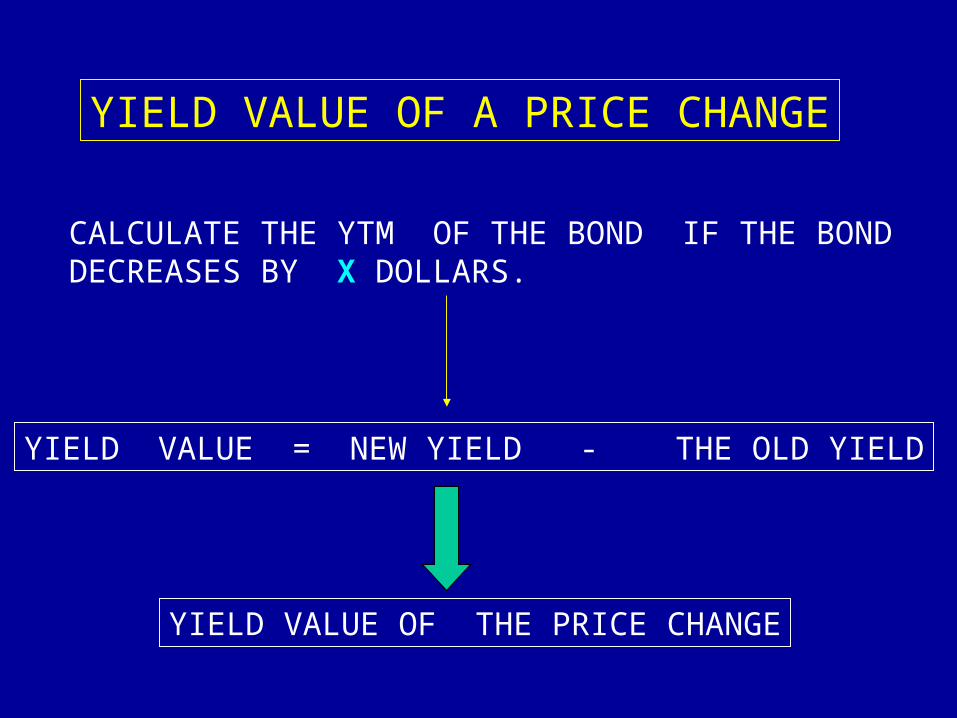

YIELD VALUEOF A PRICE CHANGE

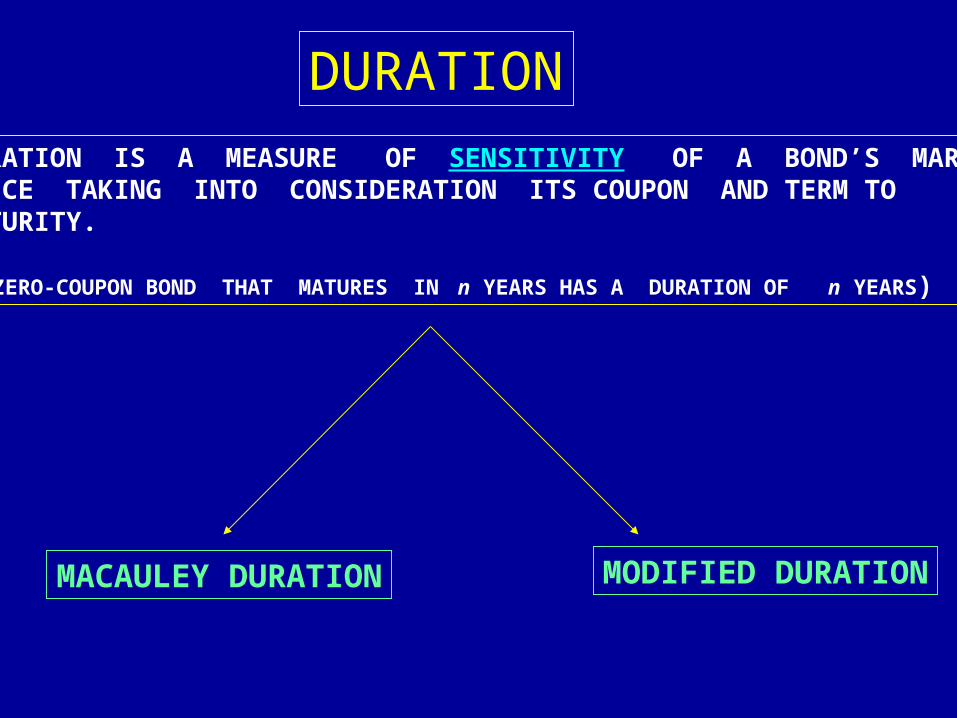

DURATION

3 techniques

PRICE VALUE OF BASIS POINT

CHANGE IN PRICE OF THE BOND IF YIELD BY 1BP

(DOLLAR PRICE CHANGE NOT %)

FROM THE HANDOUT (#3), YOU CAN NOTICE THERE IS NO GREAT CHANGE FOR ANY BOND WITH SUCH AN INCREMENTAL MOVE IN RATES.

(1BP = 0.01 %)

P63 OF OBLI

YIELD VALUE OF A PRICE CHANGE

CALCULATE THE YTM OF THE BOND IF THE BOND DECREASES BY X DOLLARS.

YIELD VALUE = NEW YIELD - THE OLD YIELD

YIELD VALUE OF THE PRICE CHANGE

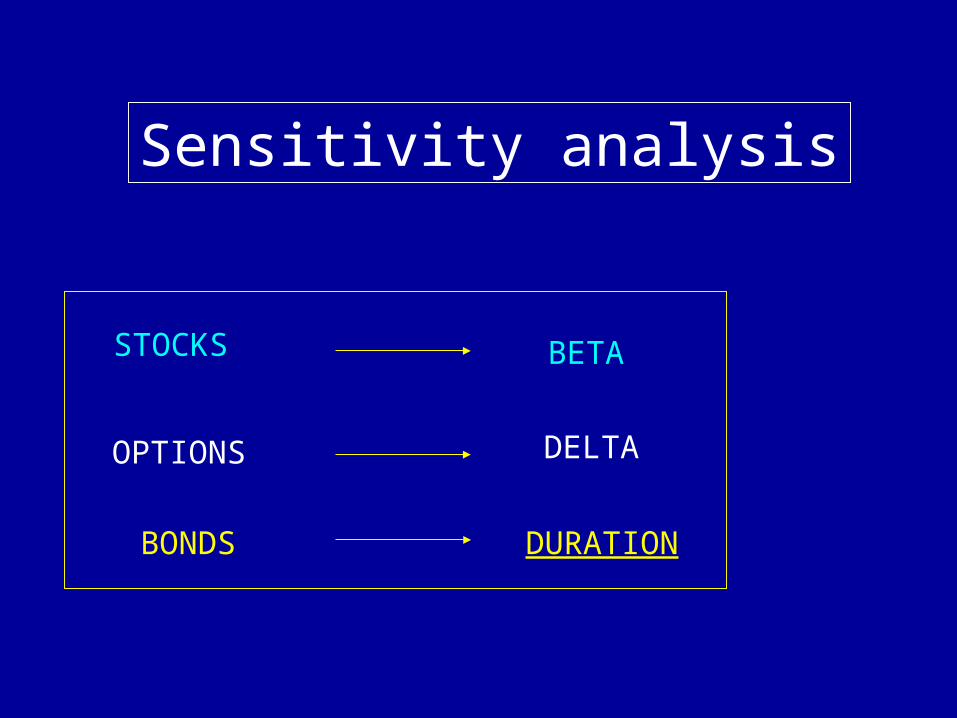

STOCKS BETA

BONDS DURATION

OPTIONS DELTA

Sensitivity analysis

DURATION

DURATION IS A MEASURE OF SENSITIVITY OF A BOND’S MARKETPRICE TAKING INTO CONSIDERATION ITS COUPON AND TERM TOMATURITY.

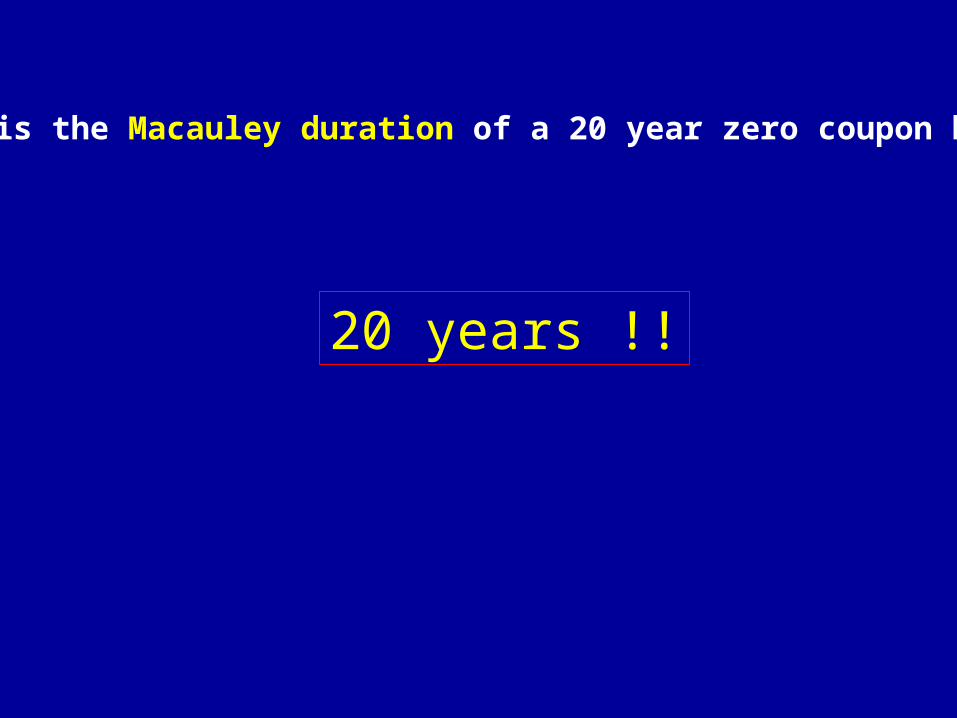

(A ZERO-COUPON BOND THAT MATURES IN n YEARS HAS A DURATION OF n YEARS)

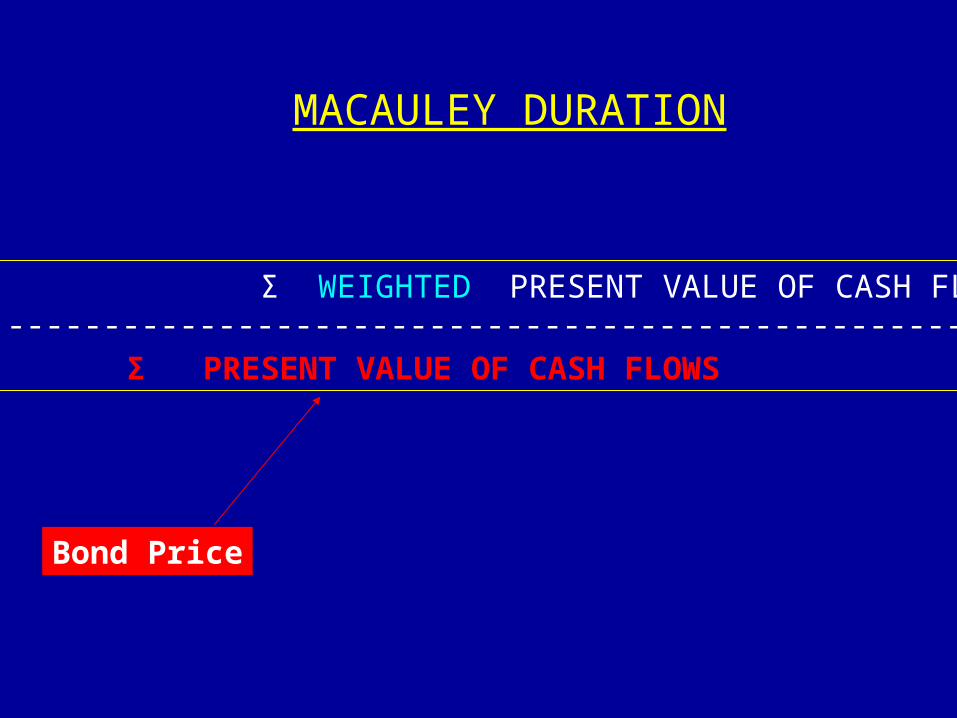

MACAULEY DURATION MODIFIED DURATION

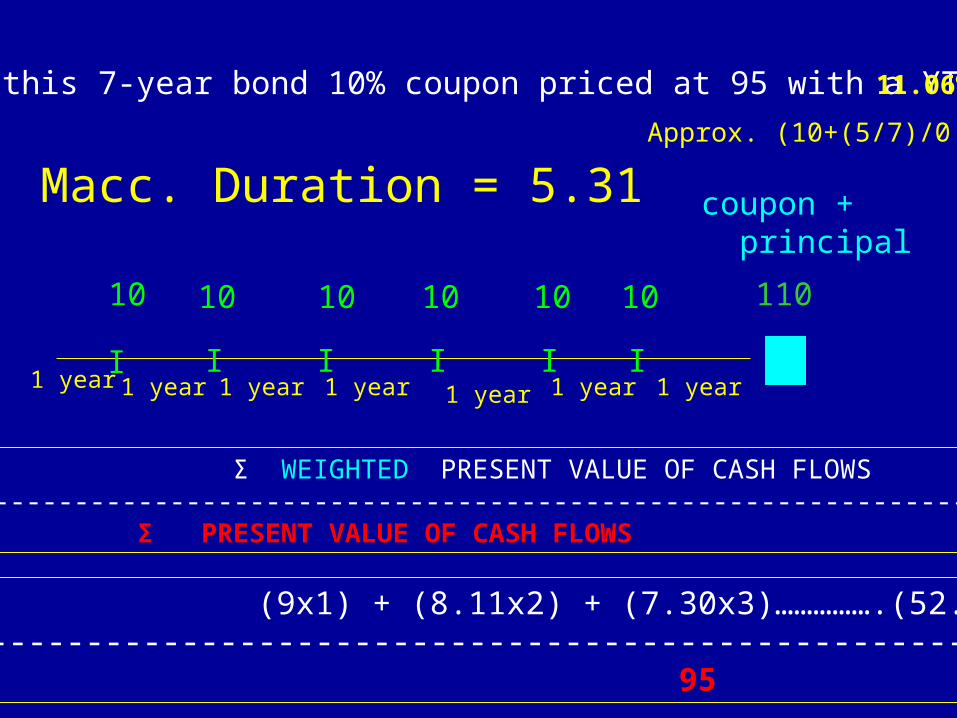

Σ WEIGHTED PRESENT VALUE OF CASH FLOWSDURATION mac= -----------------------------------------------------------------

Σ PRESENT VALUE OF CASH FLOWS

MACAULEY DURATION

Bond Price

I I I I I

10 10 10 10 10

coupon + principal

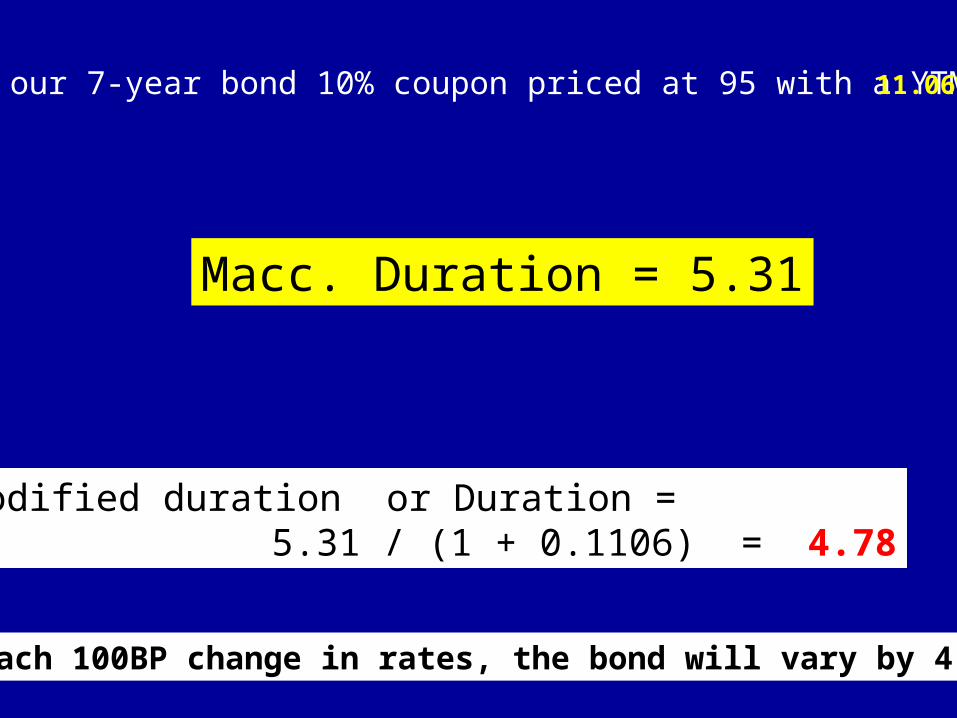

Consider this 7-year bond 10% coupon priced at 95 with a YTM of 11.06%

I

10

Approx. (10+(5/7)/0.95

1 year 1 year 1 year 1 year 1 year 1 year 1 year

110

Σ WEIGHTED PRESENT VALUE OF CASH FLOWSDURATION = -----------------------------------------------------------------

Σ PRESENT VALUE OF CASH FLOWS

(9x1) + (8.11x2) + (7.30x3)…………….(52.77x7)DURATION = -----------------------------------------------------------------

95

Macc. Duration = 5.31

What is the Macauley duration of a 20 year zero coupon bond ?

20 years !!

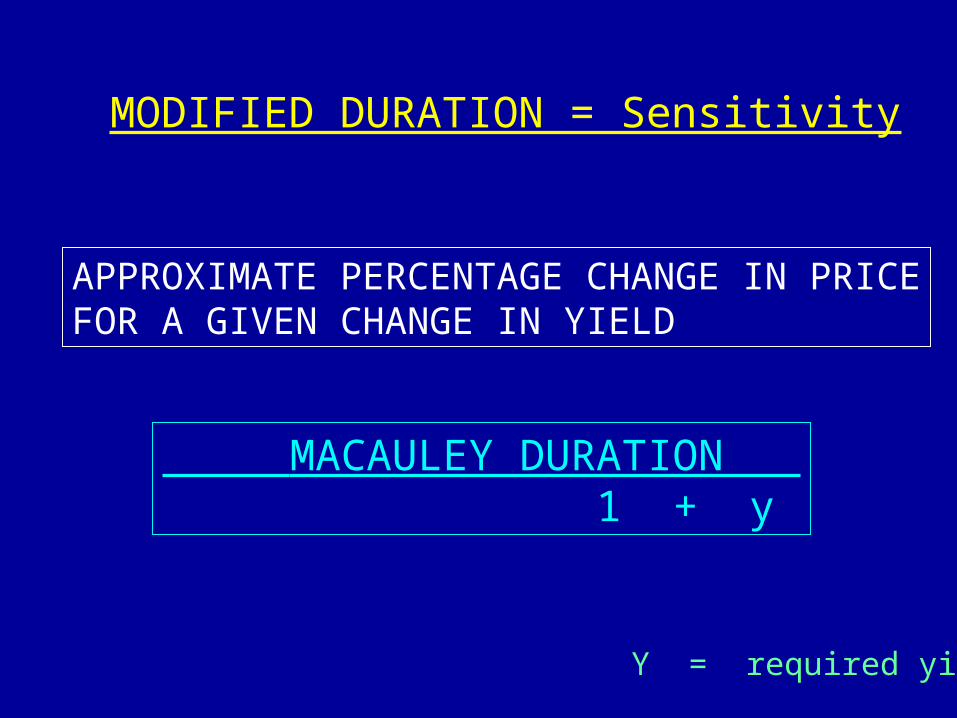

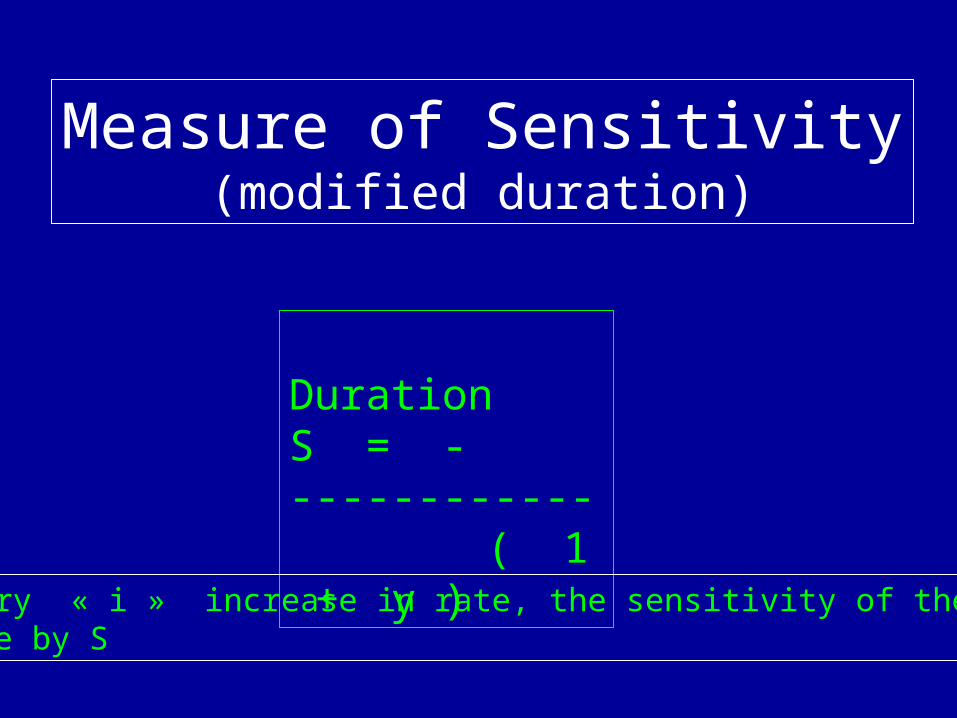

MODIFIED DURATION = Sensitivity

MACAULEY DURATION 1 + y

Y = required yield

APPROXIMATE PERCENTAGE CHANGE IN PRICEFOR A GIVEN CHANGE IN YIELD

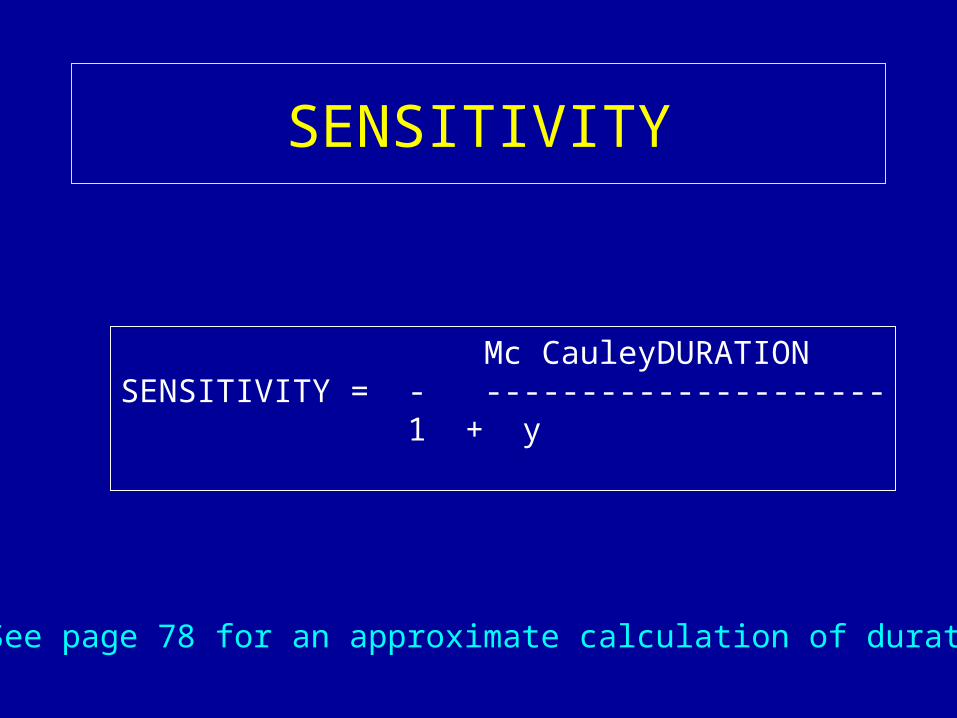

SENSITIVITY

Mc CauleyDURATIONSENSITIVITY = - ---------------------

1 + y

See page 78 for an approximate calculation of duration

DurationS = - ------------

( 1 + y )

Measure of Sensitivity(modified duration)

For every « i » increase in rate, the sensitivity of the bond willdecrease by S

Consider our 7-year bond 10% coupon priced at 95 with a YTM of

Macc. Duration = 5.31

11.06%

Modified duration or Duration = 5.31 / (1 + 0.1106) = 4.78

For each 100BP change in rates, the bond will vary by 4.78%

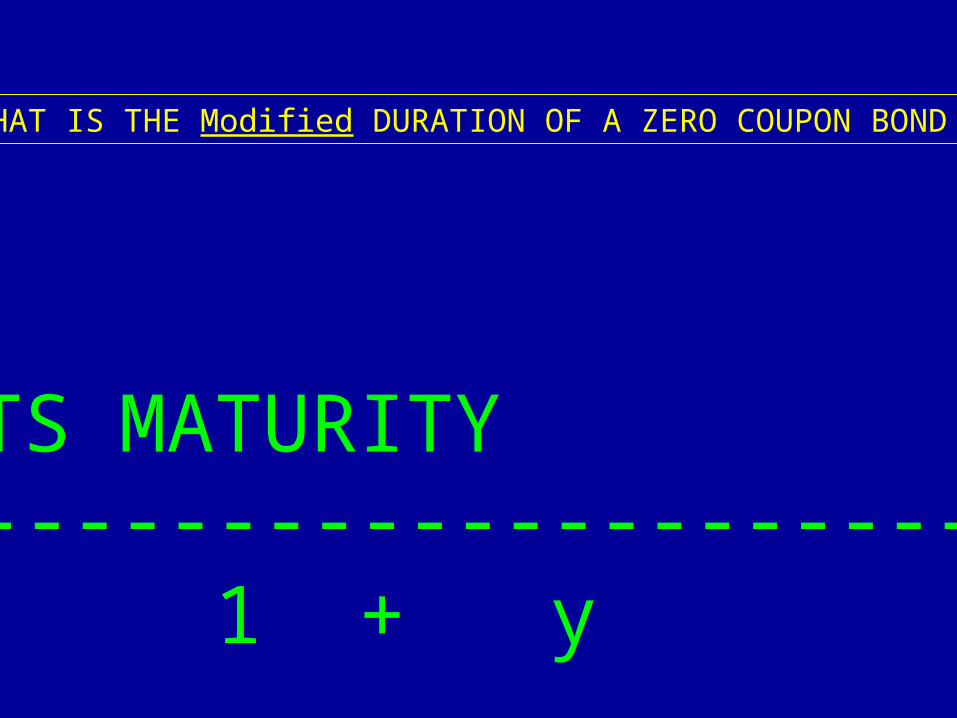

WHAT IS THE Modified DURATION OF A ZERO COUPON BOND ?

ITS MATURITY---------------------- 1 + y

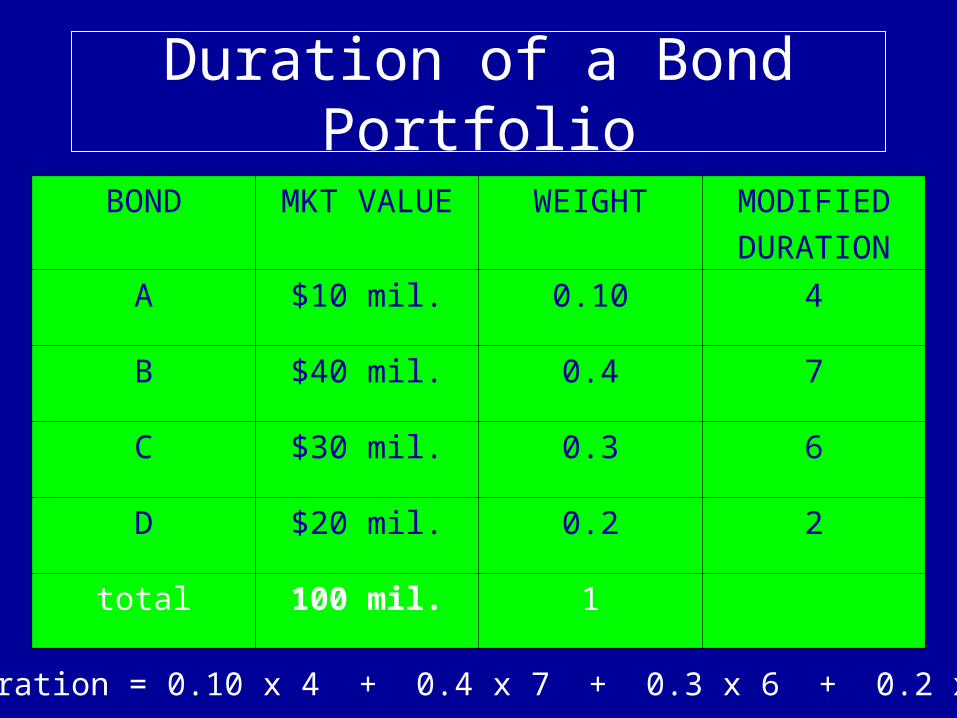

Duration of a Bond Portfolio

BOND MKT VALUE WEIGHT MODIFIED

DURATION

A $10 mil. 0.10 4

B $40 mil. 0.4 7

C $30 mil. 0.3 6

D $20 mil. 0.2 2

total 100 mil. 1

Portfolio duration = 0.10 x 4 + 0.4 x 7 + 0.3 x 6 + 0.2 x 2 = 5.4

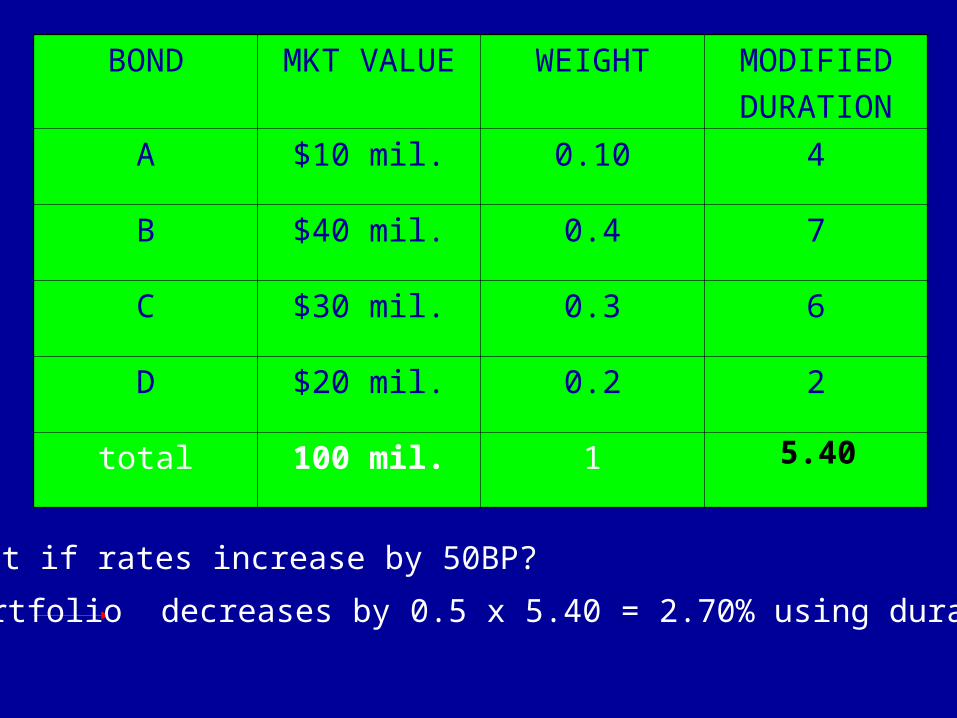

BOND MKT VALUE WEIGHT MODIFIED

DURATION

A $10 mil. 0.10 4

B $40 mil. 0.4 7

C $30 mil. 0.3 6

D $20 mil. 0.2 2

total 100 mil. 1

What if rates increase by 50BP?

Portfolio decreases by 0.5 x 5.40 = 2.70% using duration

5.40

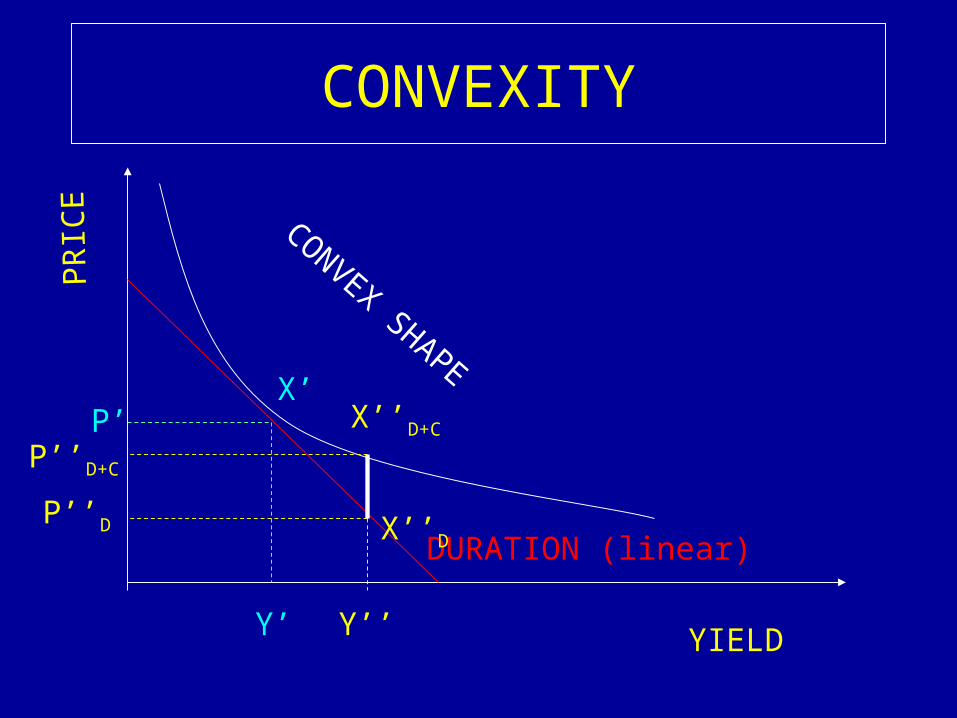

CONVEXITYP

RIC

E

YIELD

CONVEX SHAPE

DURATION (linear)

Y’

P’P’’D+C

Y’’

X’X’’D+C

P’’D X’’D

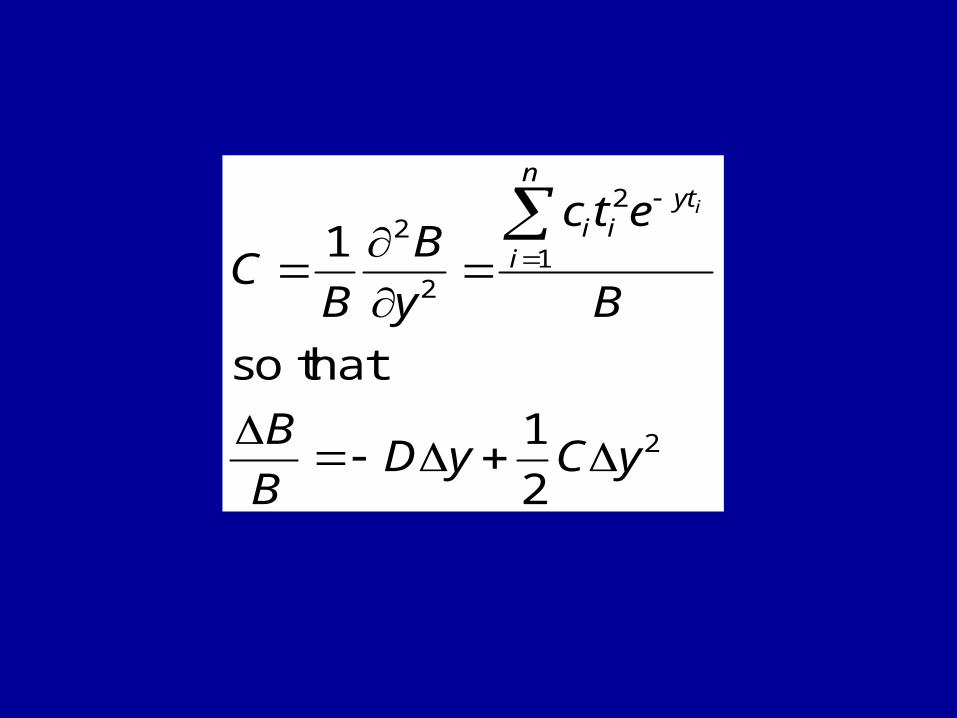

CB

B

y

c t e

B

B

BD y C y

i iyt

i

ni

1

1

2

2

2

2

1

2

so that

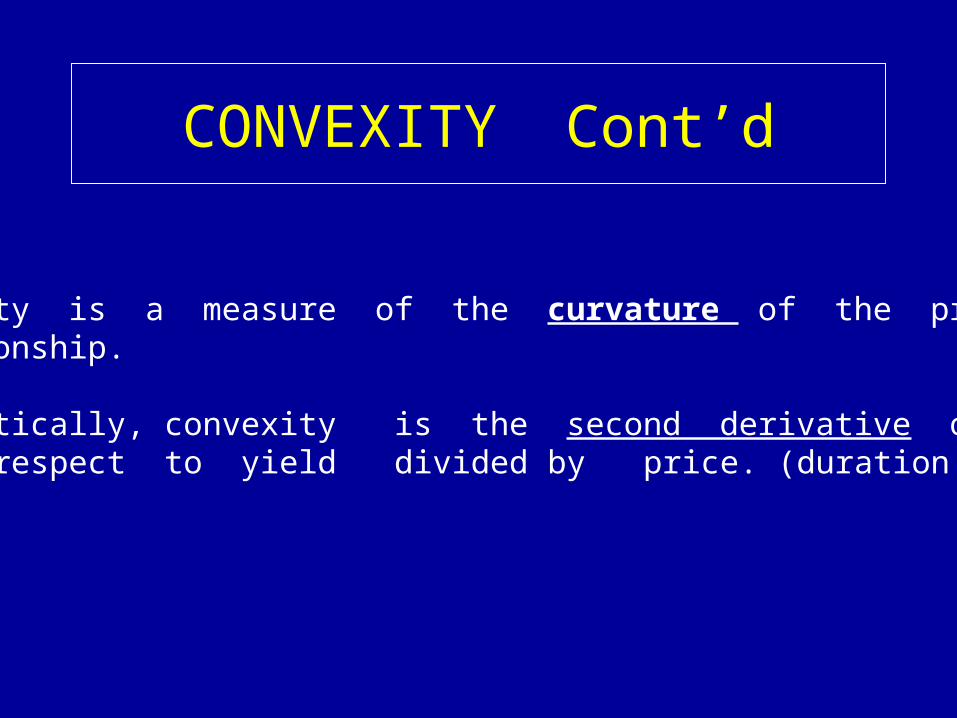

CONVEXITY Cont’d

•Convexity is a measure of the curvature of the price/yield relationship.

•Mathematically, convexity is the second derivative of price with respect to yield divided by price. (duration is first)

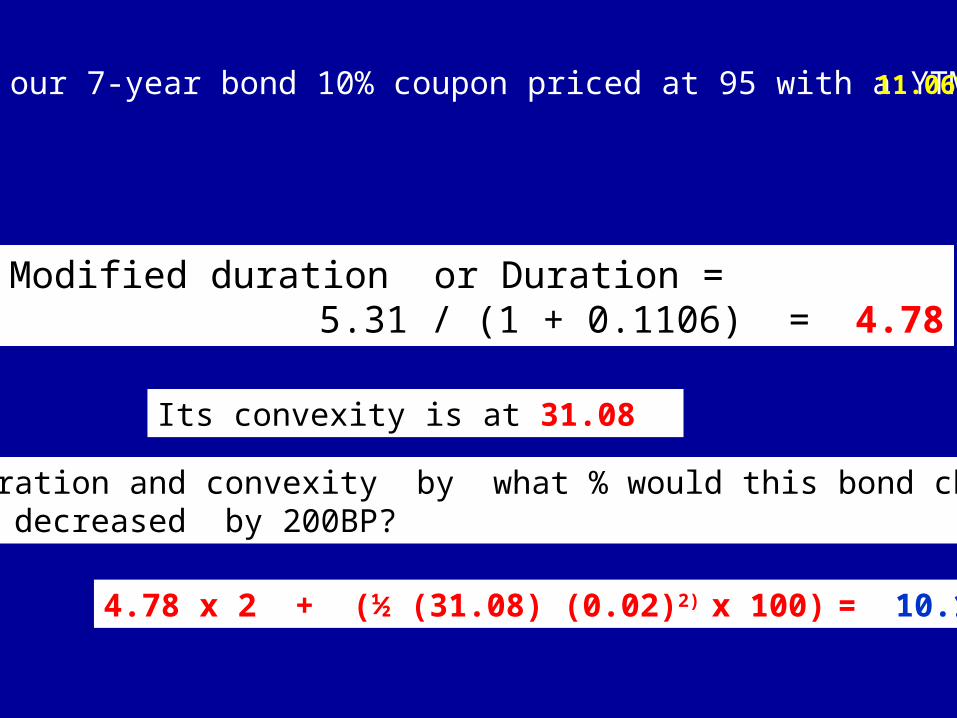

Consider our 7-year bond 10% coupon priced at 95 with a YTM of 11.06%

Modified duration or Duration = 5.31 / (1 + 0.1106) = 4.78

Its convexity is at 31.08

Using duration and convexity by what % would this bond change byIf rates decreased by 200BP?

4.78 x 2 + (½ (31.08) (0.02)2) x 100) = 10.18%

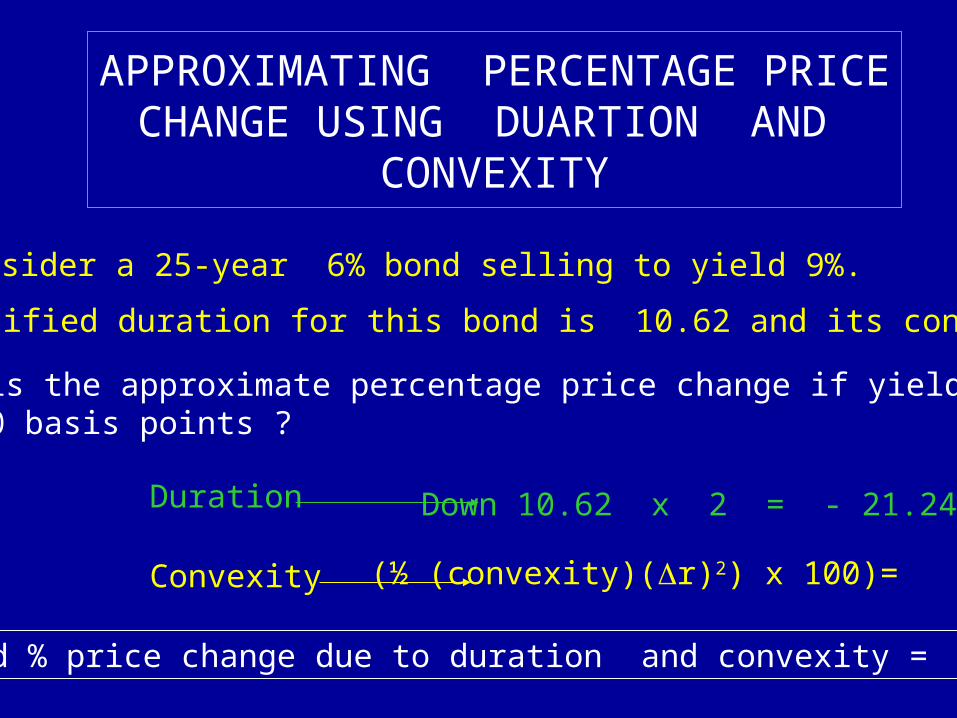

APPROXIMATING PERCENTAGE PRICE CHANGE USING DUARTION AND

CONVEXITY

•Consider a 25-year 6% bond selling to yield 9%.

•The modified duration for this bond is 10.62 and its convexity 183

What is the approximate percentage price change if yield rise by 200 basis points ?

Duration Down 10.62 x 2 = - 21.24%

Convexity (½ (convexity)(r)2) x 100)= +3.66%

Estimated % price change due to duration and convexity = -17.58%

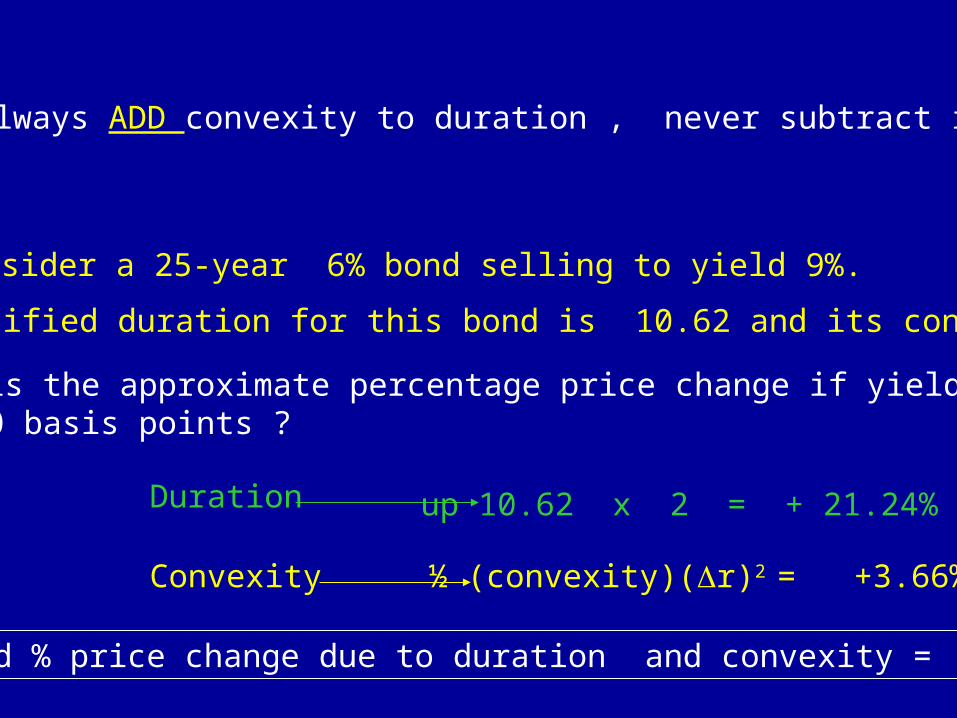

•You always ADD convexity to duration , never subtract it.

•Consider a 25-year 6% bond selling to yield 9%.

•The modified duration for this bond is 10.62 and its convexity 183

What is the approximate percentage price change if yield decreaseby 200 basis points ?

Duration up 10.62 x 2 = + 21.24%

Convexity ½ (convexity)(r)2 = +3.66%

Estimated % price change due to duration and convexity = +24.90%

THANK YOU AND

HAVE A GOODWEEK