Embed Size (px)

DESCRIPTION

hello

Citation preview

Bracewell v. Court of Appeals G.R. No. 107427 January 25, 2000

JAMES R. BRACEWELL, petitioner, vs. HONORABLE COURT OF APPEALS and REPUBLIC OF THE PHILIPPINES, respondents.

Facts:

The controversy involves a total of nine thousand six hundred fifty-seven (9,657) square meters of land located in Las Piñas, Metro Manila.

In 1908, Maria Cailles, married to James Bracewell, Sr., who acquired the said parcels of land from the Dalandan and Jimenez families of Las Piñas; after which corresponding Tax Declarations were issued in the name of Maria Cailles.

On January 16, 1961, Maria Cailles sold the said parcels of land to her son, the petitioner, by virtue of a Deed of Sale which was duly annotated and registered with the Registry of Deeds of Pasig, Rizal. Tax Declarations were thereafter issued in the name of petitioner, canceling the previous Tax Declarations issued to Maria Cailles.

On September 19, 1963, petitioner filed before the then Court of First Instance of Pasig, Rizal an action for confirmation of imperfect title under Section 48 of Commonwealth Act No. 141.

The Director of Lands, represented by the Solicitor General, opposed petitioner's application on the grounds that neither he nor his predecessors-in-interest possessed sufficient title to the subject land nor have they been in open, continuous, exclusive and notorious possession and occupation of the same for at least thirty (30) years prior to the application, and that the subject land is part of the public domain.

On May 3, 1989, the lower court issued an Order granting the application of petitioner. The Solicitor General promptly appealed to respondent Court which, on June 29, 1992, reversed and set aside the lower court's Order. It also denied petitioner's Motion for Reconsideration in its Resolution of September 30, 1992.

Issues:

a) Whether the failure of the petitioner to prosecute his action for an unreasonable length of time?

b) Whether the tax declarations attached to the complaint do not constitute acquisition of the lands applied for?

Held:

The controversy is simple. On one hand, petitioner asserts his right of title to the subject land under Section 48 (b) of Commonwealth Act No. 141, having by himself and through his predecessors-in-interest been in open, continuous, exclusive and notorious possession and occupation of the subject parcels of land, under a bona fide claim of acquisition or ownership, since 1908. On the other hand, it is the respondents' position that since the subject parcels of land were only classified as alienable or disposable on March 27, 1972, petitioner did not have any title to confirm when he filed his application in 1963. Neither was the requisite thirty years possession met.

A similar situation in the case of Reyes v. Court of Appeals, where a homestead patent issued to the petitioners' predecessor-in-interest was cancelled on the ground that at the time it was issued, the subject land was still part of the public domain.

In the said case, this Court ruled as follows —

Under the Regalian doctrine, all lands of the public domain belong to the State, and that the State is the source of any asserted right to ownership in land and charged with the conservation of such patrimony. This same doctrine also states that all lands not otherwise appearing to be clearly within private ownership are presumed to belong to the State (Director of Lands vs. Intermediate Appellate Court, 219 SCRA 340).

Hence, the burden of proof in overcoming the presumption of State ownership of lands of the public domain is on the person applying for registration. The applicant must show that the land subject of the application is alienable or disposable. These petitioners failed to do.

The homestead patent was issued to petitioners' predecessor-in-interest, the subject land belong to the inalienable and undisposable portion of the public domain. Thus, any title issued in their name by mistake or oversight is void ab initio because at the time the homestead patent was issued to petitioners, as successors-in-interest of the original patent applicant, the Director of Lands was not then authorized to dispose of the same because the area was not yet classified as disposable public land. Consequently, the title issued to herein petitioners by the Bureau of Lands is void ab initio.

Neither has petitioner shown proof that the subject Forestry Administrative Order recognizes private or vested rights under which his case may fall. We only find on record the Indorsement of the Bureau of Forest Development from which no indication of such exemption may be gleaned.

Having found petitioner to have no cause of action for his application for confirmation of imperfect title, we see no need to discuss the other errors raised in this petition.

EN BANC

G.R. No. L-7670 March 28, 1914

CARMEN AYALA DE ROXAS, plaintiff-appellant, vs.

THE CITY OF MANILA, defendant-appellant.

Haussermann, Cohn & Fisher for appellant.City Attorney Nesmith for appellee.

MORELAND, J.:

Doña Carmen Ayala de Roxas, the plaintiff in this case, was in 1901, 1902, and 1903, and has since been, the owner of certain

property on the Escolta numbered 98-104, which was and is known and designated on the books and ta-roll of the city of

Manila as lot 3, block 35, district of Binondo. This property was assessed for taxation by the officials of the city of Manila for the

years 1901 and 1902 as follows:

Land ............................................................

P205,407.00

Improvements ..........................................…..

30,000.00

Total ..........................................……………..

235,407.00

the taxes levied during the two years pursuant to the assessment were duly paid by the plaintiff.

On the 8th of January, 1903, the Philippine Commission passed an Act, No. 581, for the purpose, expressed in the title, of creating a board of tax revision to revise the assessments of real estate and improvements in the city of Manila. The board therein created, in the performance of the

duty laid upon it by said Act, reassessed the plaintiff's property on April 4, 1903, fixing the value thereof at P120,534 for the land and P50,000 for the improvements, in all P170,534.

In February, 1903, plaintiff commenced the reconstruction of the improvements on said land at a costs of P25,000, and on April 4, 1903, when the commission appointed in pursuance of Act No.

581 made the reassessment of plaintiff's property, the latter was then in the act of reconstructing, altering and making additions to the improvements on said land.

On November 3, 1903, Act No. 975 was passed authorizing and requiring the Municipal Board "in all cases in which land assessed for taxation in the city of Manila for the years 1902 and 1902 was assessed at more than fifty per centum above the assessment" for 1903, as fixed by the board

of tax revision, to reduce the assessments for 1901 and 1902 to the amount fixed in the assessment for 1903. This Act then went on to provide:

SEC. 2. In all cases in which the money has been paid upon the excessive assessment as described in section one, either for one or two years, the city tax assessor and collector shall

allow the amount of such excess payment to be applied upon the taxes due nineteen hundred and three, or some subsequent year.

It is alleged in the amended complaint, admitted by the defendant, and found as a fact by the court that on December 10, 1903, the plaintiff made inquiry as to the amount of the 1903 taxes upon the premises in question; that she was informed by the city assessor and collector that the

tax for that year was P2,558.02, but that she was entitled to a refund under Act No. 975 of P2,121.80 arising from the excessive assessments of 1901, 1902, which assessments had been revised and reduced as aforesaid by the tax revision commission appointed under Act No. 581.

The plaintiff thereupon paid the difference between P2,558.02 and P2,121.80, or P436.22, taking a receipt in full for the sum of P2,558.02, the taxes for 1903.

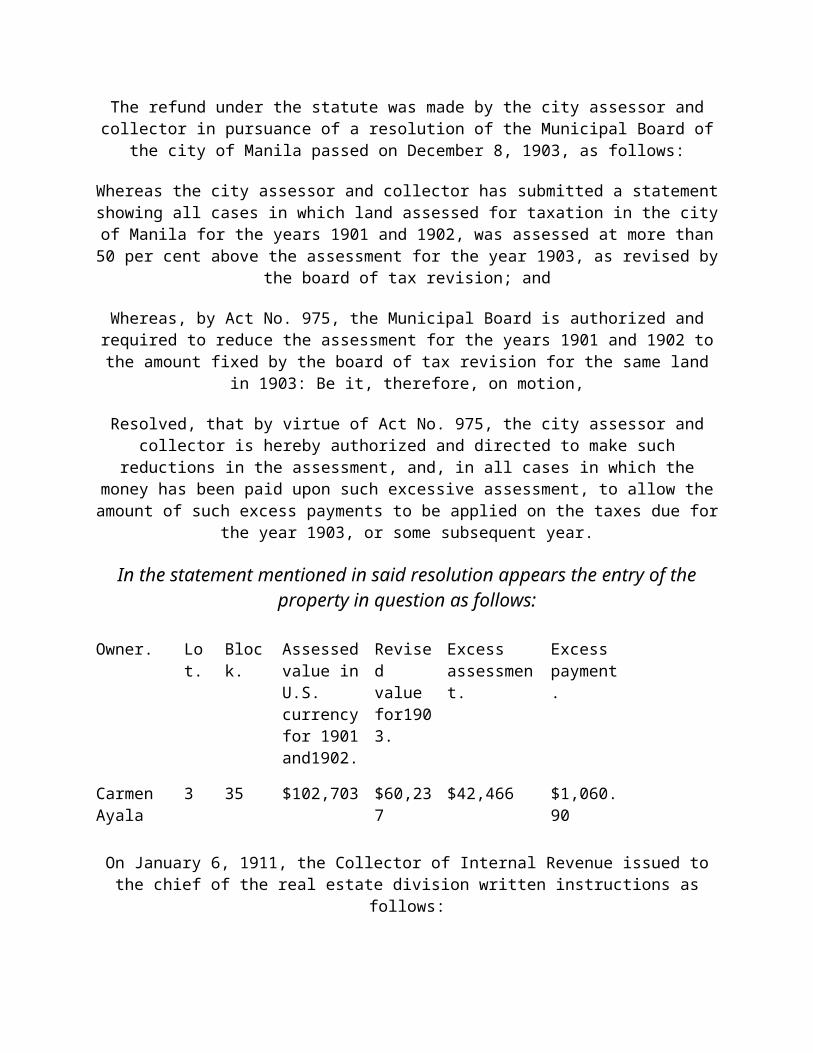

The refund under the statute was made by the city assessor and collector in pursuance of a resolution of the Municipal Board of the city of Manila passed on December 8, 1903, as follows:

Whereas the city assessor and collector has submitted a statement showing all cases in which land assessed for taxation in the city of Manila for the years 1901 and 1902, was assessed at more than 50 per cent above the assessment for the year 1903, as revised by the board of tax

revision; and

Whereas, by Act No. 975, the Municipal Board is authorized and required to reduce the assessment for the years 1901 and 1902 to the amount fixed by the board of tax revision for the

same land in 1903: Be it, therefore, on motion,

Resolved, that by virtue of Act No. 975, the city assessor and collector is hereby authorized and directed to make such reductions in the assessment, and, in all cases in which the money has

been paid upon such excessive assessment, to allow the amount of such excess payments to be applied on the taxes due for the year 1903, or some subsequent year.

In the statement mentioned in said resolution appears the entry of the property in question as follows:

Owner. Lot. Block. Assessed value in

Revised value

Excess assessment.

Excess payment.

U.S. currency for 1901 and1902.

for1903.

Carmen Ayala

3 35 $102,703 $60,237 $42,466 $1,060.90

On January 6, 1911, the Collector of Internal Revenue issued to the chief of the real estate division written instructions as follows:

Referring to the attached papers regarding the decision of the Supreme Court in cases involving the interpretation of Act No. 975, I desire to have this matter again tested in the courts by

collecting from a few large taxpayers the amounts refunded to them in 1903 under the interpretation of Act no. 975 by the city assessor and collector, which, according to the Supreme Court, was an erroneous interpretation. You will therefore arrange to enter on the 1903 tax rolls

back taxes for the year 1903 against the properties shown on the attached list in amounts equal to the refunds granted by the city assessor and collector under Act No. 975. notices regarding these entries should be forwarded to each of the taxpayers as per the attached form as soon as possible and at such time so as to enable the putting of such properties on the list for the next tax sale if

payments of these back taxes are not made.

Pursuant to these instructions the following letter was sent to and received by the plaintiff:

Subject: — Decision of the Supreme Court, re Act No. 975.

JANUARY 11, 1911.

MRS. CARMEN AYALA,No. 154 Malacañang, Manila.

MADAM: You are informed that the Supreme Court of these Islands has, in two decisions, one in the case of Felipe Zamora against the city of Manila, and the other in the case of Jose P.

Paterno against the city of Manila, held that the word `land' as used in section 1 of Act No. 975 of the Philippine Commission includes both the land and the buildings thereon. As construed by

the city assessor and collector the word `land,' as used in the above-mentioned Act, did not include the improvements upon the land, and therefore the credit of P2,121.80 allowed by the city assessor and collector on the tax lists for the year 1903 as a partial payment of the tax on

your property located at Nos. 98-104 Escolta, known as lot 3, block 35, district of Binondo, was erroneously applied according to the construction of the said Act by the Supreme Court in the cases above stated, since the total value of the property in question, as per assessment in 1901 and 1902, was not 50 per cent more than the value fixed by the board of tax revision, although

the value of the land was 50 per cent more than 1901 and 1902 than that fixed by the board of tax revision.

By direction of the Municipal Board of Manila, approved by His excellency, the Governor-General, the amount above stated which has been applied as a partial payment of your real estate tax for 1903 has been entered on the tax lists for 1903 and is a lien upon the said property, which

can only be removed by the payment of the proper amount.

By authority contained in a resolution adopted by the Municipal Board on December 10, 19010, the payment of the said sum, which is a delinquent tax for 1903, will be accepted without penalty

if made within twenty days from the date this communication is received by you.

Very respectfully,

(Sgd.) ELLIS CROMWELL,Collector of Internal Revenue,Ex Officio City Assessor and Collector.

To clear her property of this alleged encumbrance and to prevent the collector from carrying into effect his threat to sell the property at public sale, plaintiff, under protest, paid the city assessor

and collector the P2,121.80 demanded, which sum is now in special deposit in the Insular Treasury awaiting the outcome of this action.

This action was begun by the plaintiff to recover the said amount paid as aforesaid. The learned trial court dismissed the complaint on the merits and this appeal is taken from that judgment.

The defendant states its position in this controversy as follows:

From the figures set forth above, relating to plaintiff's property, it appears that the land alone was assessed during 1901 and 1902 at more than 50 per cent, in fact 70 per cent, above the valuation fixed for 1903, but that the land and improvements together were assessed during 1901 and 1902

at less than 50 per cent, in fact, only 38 per cent, above the valuation fixed for 1903. Consequently, if the word "land" as used in Act No. 975 were to be construed as "land only" then

plaintiff was entitled to a refund of a certain amount of excess paid, but if by "land" the legislature contemplated "land and improvements" or "real estate in general" then the plaintiff was not entitled to any refund. The city assessor and collector erroneously adopted the former construction as the correct one and estimated that the proper amount of refund of the excess

payment by the plaintiff for the years 1901 and 1902, as provided in Act No. 975, would be the sum of P2,121.80. . . .

Subsequent to this payment, however, the Supreme Court decided in the case of Felipe Zamora vs. City of Manila (7 Phil. Rep., 584) that the word "land" as used in Act No. 975 should not be

construed in a limited sense but that it was intended by the legislature to include not only the land as such but also the improvements thereon. The city assessor and collector, by direction of the municipal board approved by the Governor-General, then addressed a letter to the plaintiff explaining the mistake of the collector made in 1903, and stating that this amount of P2,121.80 had been entered upon the tax lists for 1903, and that it was a lien upon her property only to be

removed by payment of the proper amount, which if paid within a certain time would be received

without penalty. This the plaintiff then paid to the city assessor under protest and now brings this action for the recovery back of the P2,121.80 so paid.

From what has been said, it is clear that the basic contention of the city is that the city assessor and collector erroneously, and, therefore, unlawfully, refunded to the plaintiff herein, when she

paid her tax in 1903, the sum of P2,121.80, and that, having so wrongly and unlawfully refunded that sum by the proves, as the city council called it, of putting it on the lists for 1903. the reason

for claiming that this sum was unlawfully and erroneously refunded is that the word 'land,' as used in Act No. 975, was held by the Supreme Court in the case of Zamora vs. City of Manila (7 Phil. Rep., 584), to include the word "improvements," and that this Act requiring also, prior to

the right to refund in any given case, that the assessments for the years 1901 and 1902 should be more than 50 per cent higher than was the assessment of the same property in 1903, the basis on which the right rest does not exist, for, while the land itself was assessed in 1901 and 1902 about

70 per cent higher than it was in 1903, the improvements upon the land were assessed almost twice as high in 1903 as in 1901 and 1902, and while a rebate might be allowed upon the

assessment on the land if it had not been held by the Supreme Court to include improvements, no rebate can, in fact, be allowed, because the assessments of the land and improvements, under the

decision referred to, must be taken, that is, added, together; and that being the case, the assessments of both land and improvements for the years 1901 and 1902 were not, when added together, 50 per cent higher than the total of the two was in 1903. As a necessary result, says the

city, the refund was improper.

This contention may be answered in two ways. In the first place, section 46 No. 183 provides that "it shall be the duty of every owner of real estate in the city of Manila to prepare or cause to be prepared a statement of the amount of land and the improvements thereon which he owns."

This statement must be filed with the city assessor and collector and from it, primarily, he makes up the list of the taxable real estate in the city. Under the system established by this Act and by the practice which was adopted and has been consistently followed under it, the improvements are assessed separately fro the land even though both may be owned by the same person. This was the way the assessment was made in 1901, 1902 and 1903, and it is the manner in which assessments have been made since that time. This was the condition of assessments when the

remedial Act referred to was passed and presents the situation which the commission had before it. This being so, it might with propriety be contended that an owner of land might have been

entitled to the refund provided for in Act No. 975 with respect to the improvements. The fact that the Supreme Court held, in the case referred to, that, under the statute, land included

improvements, does not necessarily mean that the contention of the city is correct that the assessment for both land and improvements as made in 1901 and 1902 should have been added together and the sum of the two compared with the total assessments for land and improvements as made in 1903 before it could be determined whether the taxpayer was entitled to a refund. In the case referred to the plaintiff, as guardian for his minor children, brought suit against the city of Manila to recover the excess taxes paid to the city under the assessments of 1901 and 1902.

The assessments for that year were, land P7,000, and house P8,000. In 1903 the assessment was, land P4,476, and house P5,000. The plaintiff claimed a right to the refund on both the land and the house but the department of assessments and collections of the city allowed it on the land only, denying the benefits of the Act with regard to the improvements upon the theory that the

Act referred to land only. This court held in that case that, inasmuch as the statute was remedial,

the plaintiff was entitled, under the liberal construction given to that kind of statute, to a refund not only as to the taxes on the land but also as to those on the improvements. In that case the

assessments were treated separately, the one relating to the land and the other to the improvements, each one standing upon its own footing, the plaintiff evidently being permitted to

claim her right as to each apart from the other.

In the second place, it may be said, in answer to the city's contention that there was no reassessment made in 1903 of the improvements assessed in 1901 and 1902, and that, therefore, there was no basis from which it could be determined whether the improvements were assessed higher in 1901 and 1902 than they were in 1903 or vice versa. When the assessment was made by the commission in 1903 the taxpayer was engaged in making very extensive improvements

upon the premises, to a large extent rebuilding the buildings already thereon. It is undisputed that she was adding at least P25,000 worth of repairs to the premises at that time. It is very probable that, in making the assessment, the commission took into consideration these improvements and added their value to the improvements as they were assessed in 1901 and 1902. This appears to be so not only from the fact that it was that time impracticable to assess the improvements as

they existed in 1901 and 1902, but also from the fact that the assessed valuation of the improvements in 1903 was almost double what it was in 1901 and 1902. this latter fact is significant for the reason that the assessments in 1901 and 1902 were almost universally

excessive — so much so in fact that it led the Legislature in 1903, as we have seen, to pass a special Act for a reassessment of city property and the refunding of money paid as taxes under

the excessive assessments of those years. This being the case, it would be but fair to assume that, if the improvements as assessed in 1901 and 1902 had been assessed in 1903, the value thereof

would have been largely reduced. As a matter of fact, however, due undoubtedly to the extensive improvements that were then being made, the assessment of the improvements in 1903 was

almost double that in 1901 and 1902.

We believe it, therefore, a necessary conclusion that the city erred in adding the assessment of the improvements as made in 1903 to the land assessment of that year in order to determine

whether or not the plaintiff was entitled to the refund in question. As we have already intimated, the improvements as assessed in 1901 and 1902 no longer existed when the assessment of 1903

was made, and that, in reality and as a matter of fact, no assessment was made in 1903 of the improvements assessed in 1901 and 1902. As a necessary result, we have no basis from which we may compare the assessment of the improvements of 1903 with those of 1901 and 1902. If the plaintiff can gain nothing from this fact, she certainly should lose nothing from it. The land

assessed in 1901 and 1902 was the same land assessed in 1903 and upon that land alone she was entitled to the refund of P2,121.80, which was made to her when she paid her taxes in 1903. If

the improvements had been assessed in 1903 the same as they in 1901 and 1902, then the total of the assessments for 1901 and 1902 would have been more than 50 per cent higher than the total as assessed in 1903. It was only the addition in 1903 of about P20,000 to the assessed valuation of the improvements made in 1901 and 1902 that, even under the theory of the city, removed the plaintiff's claim from the provisions of the statute, the total assessments in 1901 and 1902, under

that theory, not being 50 per cent than the total assessment in 1903. It is clear, therefore, that plaintiff was entitled to the refund with respect to her 1903 taxes, that the refund was duly

authorized by a resolution of the municipal board, and that she received it as a credit upon her taxes pursuant to that resolution.

It is our opinion, therefore, that the taxes for 1903 were duly paid and the lien thereof fully discharged, and that the demand made by the defendant upon plaintiff that she again pay the

taxes for that year was without authority of law and unenforceable. Such demand placed upon the plaintiff no duty except that of selecting a legal method of contesting the validity of

defendant's claim. She selected the method of paying the sum demanded, under protest, and beginning an action to recover it, following the procedure prescribed in ordinary tax cases. In

doing that she was entirely justified, it appearing that the city claimed that the taxes for 1903 had not been paid, that they were a lien upon the plaintiff's property, and that, if they were not paid,

proceedings would be taken to seize and sell said lands by virtue thereof; and, particularly in view of that provision of the tax law which requires that, before the validity of a tax can be

attacked or a decision obtained therein in the courts, the tax must be paid under protest and an action begun for its recovery. It is unreasonable that a man who denies the legality of a tax should have a clear and certain remedy. the rule being established that, apart from special

circumstances, he cannot interfere by injunction with the state's collection of its revenues, an action at law to recover back what he has paid is the alternative left. Of course, we are speaking of those cases where the state is put to an action where the citizen refuses to pay. In these latter he can interpose his objections by way of defense, but when, as is common, the state has a more summary remedy, such as distress, and the party indicates by protest that he is yielding to what

he cannot prevent, courts have been a little too slow to recognize the implied duress under which the payment is made. But even if the state is driven to an action, if at the same time the citizen is put at a serious disadvantage in the assertion of his legal rights by defense in the suit, justice may require that he should be at liberty to avoid those disadvantages by paying promptly and bringing suit on his side. He is entitled to assert his supposed rights on reasonably equal terms. (Atchison

etc. Ry. Co. vs. O'Connor, 223 U. S., 280.)

The judgment appealed from is reversed, and the cause is remanded to the Court of First Instance whence it came with instructions to enter a judgment in favor of the plaintiff and against the defendant for the sum of P2,121.80 with interest thereon from the 26th of January, 1911. No

costs in this instance.

Arellano, C. J., Carson, Trent and Araullo, JJ., concur.

Judicial Notice, when mandatoryCity of Manila vs. Gerardo Garcia et.alFACTS:1. Plaintiff is the owner of certain parcels of land. Without the knowledge and consent of plaintiff, defendants occupied the property and built their houses.2. Having discovered, plaintiff through its mayor gave each defendant written permits, each labeled as “lease contract” to occupy specific areas. For their occupancy, defendants were charged nominal rentals.3. After sometime, plaintiff, through its treasurer, demanded payment of their rentals and vacate the premises for the Epifanio de los Santos Elementary School’s expansion.4. Despite the demand, defendants refused to vacate the said property. Hence, this case was filed for recovery of possession.5. The trial court ruled in favor of plaintiff taking judicial notice of Ordinance 4566 – appropriating P100k for the construction of additional building of Epifanio De Los Santos Elementary School.6. Defendants appealed.ISSUE: WoN the trial court properly found that the city needs the premises for school purposesHELD: YESThe trial court ruled out the admissibility of the documentary evidence presented by plaintiff – Certification of the Chairman, Committee on Appropriations of the Municipal Board which recites the amount of P100k had been set aside in Ordinance 4566 for the construction of additional building of the said school.But then the decision under review, the trial court revised his views. He there declared that there was a need for defendants to vacate the premises for school expansion; he cited the very document.Because of the court’s contradictory stance, defendants brought this case on appeal. However, the elimination of the certification as evidence would not profit defendants. For, in reversing his stand, the trial judge could well have taken — because he was duty bound to take — judicial notice 5of Ordinance 4566. The reason being that the city charter of Manila requires all courts sitting therein to take judicial notice of all ordinances passed by the municipal board of Manila.6

And, Ordinance 4566 itself confirms the certification aforesaid that an appropriation of P100,000.00 was set aside for the "construction of additional building" of the Epifanio de los Santos Elementary School.Further defendants’ entry to the said property is illeg

SECOND DIVISION

[G.R. No. 111088. June 13, 1997]

C & M TIMBER CORPORATION (CMTC), petitioner, vs. HON. ANGEL C. ALCALA, Secretary of the Department of Environment & Natural Resources, HON. ANTONIO T. CARPIO, Chief Presidential Legal Counsel, and HON. RENATO C. CORONA, Assistant Executive Secretary for Legal Affairs, respondents.

D E C I S I O N

MENDOZA, J.:

This is a petition for certiorari by which C & M Timber Corporation seeks the nullification of the order dated February 26, 1993 and the resolution dated June 7, 1993 of the Office of the President, declaring as of no force and effect Timber License Agreement (TLA) No. 106 issued to petitioner on June 30, 1972. TLA No. 106, with the expiry date June 30, 1997, covers 67,680 hectares of forest land in the municipalities of Dipaculao and Dinalongan in the Province of Aurora and the Municipality of Maddela in Quirino province.i[1]

It appears that in a letter dated July 20, 1984ii[2] to President Marcos, Filipinas Loggers Development Corporation (FLDC), through its president and general manager, requested a timber concession over the same area covered by petitioners TLA No. 106, alleging that the same had been cancelled pursuant to a presidential directive banning all forms of logging in the area. The request was granted in a note dated August 14, 1984 by President Marcos who wrote, as was his wont, on the margin of the letter of FLDC: Approved.iii[3]

Accordingly, on September 21, 1984, the Ministry of Natural Resources, as it was then called, issued TLA No. 360, with the expiry date September 30, 1994, to FLDC, covering the area subject of TLA No. 106. In 1985, FLDC began logging operations.

On June 26, 1986, then Minister of Natural Resources Ernesto M. Maceda suspended TLA No. 360 for FLDCs gross violation of the terms and conditions thereof, especially the reforestation and selective logging activities and in consonance with the national policy on forest conservation.iv[4] On July 26, 1986, Minister Maceda issued another order cancelling the license

iiiiii

of FLDC on the ground that in spite of the suspension order dated June 26, 1986, said concessionaire has continued logging operations in violation of forestry rules and regulations.v[5]

Learning of the cancellation of FLDCs TLA, petitioner, through its officer-in-charge, wrote Minister Maceda a letter dated October 10, 1986, requesting revalidation of its TLA No. 106.vi[6] As FLDC sought a reconsideration of the order cancelling its TLA, petitioner wrote another letter dated February 13, 1987,vii[7] alleging that because of the log ban imposed by the previous administration it had to stop its logging operations, but that when the ban was lifted on September 21, 1984, its concession area was awarded to FLDC as a result of [FLDCs] covetous maneuvers and unlawful machinations. (Petitioner was later to say that those behind FLDC, among them being the former Presidents sister, Mrs. Fortuna Barba, were very influential because of their very strong connections with the previous Marcos regime.)viii[8] Petitioner prayed that it be allowed to resume logging operations.

In his order dated May 2, 1988,ix[9] Secretary Fulgencio Factoran, Jr., of the DENR, declared petitioners TLA No. 106 as of no more force and effect and consequently denied the petition for its restoration, even as he denied FLDCs motion for reconsideration of the cancellation of TLA No. 360. Secretary Factoran, Jr. ruled that petitioners petition was barred by reason of laches, because petitioner did not file its opposition to the issuance of a TLA to FLDC until February 13, 1987, after FLDC had been logging under its license for almost two years. On the other hand, FLDCs motion for reconsideration was denied, since the findings on which the cancellation order had been based, notably gross violation of the terms and conditions of its license, such as reforestation and selective logging activities appear to be firmly grounded.

Both petitioner CMTC and FLDC appealed to the Office of the President. Petitioner denied that it was guilty of laches. It alleged that it had sent a letter to the then Minister of Natural Resources Rodolfo del Rosario dated September 24, 1984 protesting the grant of a TLA to FLDC over the area covered by its (petitioners) TLA and, for this reason, requesting nullification of FLDCs TLA.

In a decision dated March 21, 1991,x[10] the Office of the President, through then Executive Secretary Oscar Orbos, affirmed the DENRs order of May 2, 1988. Like the DENR it found petitioner guilty of laches, the alleged filing by petitioner of a protest on September 24, 1984 not having been duly proven. The decision of the Office of the President stated:xi[11]

ivvviviiviiiixxxi

As disclosed by the records, this Office, in a letter of June 1, 1989, had requested the DENR to issue a certification as to the authenticity/veracity of CMTCs aforesaid Annex A to enable it to resolve this case judiciously and expeditiously. Said letter-request pertinently reads:

x x x C & M Timber Corporation has attached to its Supplemental Petition For Review, dated June 1, 1988, a xerox copy of (Annex A) of its letter to the Minister of Natural Resources Rodolfo del Rosario, dated September 24, 1984, prepared by its counsel, Atty. Norberto J. Quisumbing, protesting against the award of the contested area to Filipinas Loggers Development Corporation and requesting that it be annulled and voided.

Considering that the aforementioned Annex A constitutes a vital defense to C & M Timber Corporation and could be a pivotal factor in the resolution by this Office of the instant appeal, may we request your good office for a certification as to the authenticity/veracity of said document (Annex A) to enable us to resolve the case judiciously and expeditiously.

In reply thereto, the DENR, thru Assistant Secretary for Legal Affairs Romulo D. San Juan, in a letter of July 7, 1989, informed this Office, thus:

x x x

Despite diligent efforts exerted to locate the alleged aforementioned Annex A, no such document could be found or is on file in this Office.

This Office, therefore, regrets that it can not issue the desired certification as to the authenticity/veracity of the document.

On September 10, 1990, this Office requested an updated comment of the DENR on (a) the duplicate original copy of Annex A; (b) a xerox copy of Page 164, entry No. 2233, of the MNRs logbook tending to show that the original copy of Annex A was received by the MNR; and (c) a xerox copy of Page 201 of the logbook of the BFD indicating that the original copy of Annex A was received by BFD from the MNR.

On October 26, 1990, DENR Assistant Secretary San Juan endorsed to this Office the updated comment of Director of Forest Management Bureau (FMB) in a 2nd endorsement of October 25, 1990, which pertinently reads as follows:

Please be informed that this Office is not the addressee and repository of the letter dated September 24, 1984 of Atty. Norberto Quisumbing. This Office was just directed by then Minister Rodolfo del Rosario to act on the purported letter of Atty. Quisumbing and as directed, we prepared a memorandum to the President which was duly complied with as shown by the entries in the logbook. Annex A, which is the main document of the letter-appeal of C & M Timber Corporation is presumed appended to the records when it was acted upon by the BFD (now FMB) and forwarded to the Secretary (then Minister). Therefore this Office is not in a position to certify as to the authenticity of Annex A.

Clearly therefore, CMTCs reliance on its Annex A is misplaced, the authenticity thereof not having been duly proven or established. Significantly, we note that in all the pleadings filed by CMTC in the office a quo, and during the hearing conducted, nothing is mentioned therein about its letter of September 24, 1984 (Annex A). Jurisprudence teaches that issues neither averred in the pleadings nor raised during the trial below cannot be raised for the first time on appeal (City of Manila vs. Ebay, 1 SCRA 1086, 1089); that issues of fact not adequately brought to the attention of the trial court need not be considered by a reviewing court, as they cannot be raised for the first time on appeal (Santos v. Intermediate Appellate Court, 145 SCRA 592, 595); and that parties, may not, on appeal, adopt a position inconsistent with what they sustained below (People v. Archilla, 1 SCRA 698, 700-701)

The Office of the President also declined to set aside the DENRs order of July 31, 1986, cancelling FLDCs TLA No. 360, after finding the same to be fully substantiated.

Petitioner and FLDC moved for reconsideration. In its order dated January 25, 1993,xii[12] the Office of the President, through Chief Presidential Legal Counsel Antonio T. Carpio, denied petitioners motion for reconsideration. It held that even assuming that CMTC did file regularly its letter-protest of September 24, 1984 with MNR on September 25, 1984, CMTC failed to protect its rights for more than two (2) years until it opposed reinstatement of FLDCs TLA on February 13, 1987. Within that two (2) year period, FLDC logged the area without any opposition from CMTC. In the same order, the Office of the President, however, directed the reinstatement of FLDCs TLA No. 360, in view of the favorable report of the Bureau of Forest Development dated March 23, 1987. Later, the Presidents office reconsidered its action after the Secretary of Environment and Natural Resources Angel C. Alcala, on February 15, 1993, expressed concern that reinstatement of FLDCs TLA No. 360 might negate efforts to enhance the conservation and protection of our forest resources. In a new order dated February 26, 1993,xiii

[13] the Office of the President reinstated its March 21, 1991 decision.

Petitioner again moved for a reconsideration of the decision dated March 21, 1991 and for its license to be revived/restored. Petitioners motion was, however, denied by the Office of the President on June 7, 1993xiv[14] in a resolution signed by Assistant Executive Secretary for Legal Affairs Renato C. Corona. The Presidents office ruled:

The above Order of February 26, 1993 was predicated, as stated therein, on a new policy consideration on forest conservation and protection, unmistakably implied from the Presidents handwritten instruction. Accordingly, this Order shall be taken not only as an affirmation of the March 21, 1991 decision, but also as a FINAL disposition of the case and ALL matters incident thereto, like CMTCs motion for reconsideration, dated April 16, 1991.

Hence, this petition. Petitioner contends that laches cannot be imputed to it because it did not incur delay in asserting its rights and even if there was delay, the delay did not work to the prejudice of other parties, particularly FLDC, because the cancellation of the FLDCs TLA was

xiixiiixiv

attributable only to its own actions. Petitioner also denies that its license had been suspended by reason of mediocre performance in reforestation by order of then Minister of Natural Resources Teodoro O. Pea. It says that it did not receive any order to this effect. Finally, petitioner claims that the denial of its petition, because of a new policy consideration on forest conservation and protection, unmistakably implied from the Presidents handwritten instruction, as stated in the resolution of June 7, 1993 of the Office of the President, would deny it the due process of law. Petitioner points out that there is no total log ban in the country; that Congress has yet to make a pronouncement on the issue; that any notice to this effect must be stated in good form, not implied; and that in any case, any new policy consideration should be prospective in application and cannot affect petitioners vested rights in its TLA No. 106.

We find the petition to be without merit.

First. As already stated, the DENR order of May 2, 1988, declaring petitioners TLA No. 106 as no longer of any force and effect, was based on its finding that although TLA No. 106s date of expiry was June 30, 1997 it had been suspended on June 3, 1983 because of CMTCs mediocre performance in reforestation and petitioners laches in failing to protest the subsequent award of the same area to FLDC. There is considerable dispute whether there was really an order dated June 3, 1983 suspending petitioners TLA because of mediocre performance in reforestation, just as there is a dispute whether there indeed was a letter written on September 24, 1984 on behalf of petitioner protesting the award of the concession covered by its TLA No. 106 to FLDC, so as to show that petitioner did not sleep on its rights.

The alleged order of June 3, 1983 cannot be produced. The Office of the Solicitor General was given until May 14, 1997 to secure a copy of the order but on May 7, 1997 the OSG manifested that the order in question could not be found in the records of this case in which the order might be.xv[15] Earlier, petitioner requested a copy of the order but the DENR, through Regional Executive Director Antonio G. Principe, said that based from our records there is no file copy of said alleged order.xvi[16]

On the other hand, the alleged letter of September 24, 1984 written by Atty. Norberto J. Quisumbing, protesting the award of the concession in question to FLDC cannot be found in the records of the DENR either. The Assistant Secretary for Legal Affairs of the DENR certified that Despite diligent efforts exerted to locate the alleged [letter], no such document could be found or is on file in this Office.xvii[17] In a later certification, however, Ofelia Castro Biron of the DENR, claimed that she was a receiving clerk at the Records and Documents Section of the Ministry of Natural Resources and that on September 25, 1984 she received the letter of Atty. Quisumbing and placed on all copies thereof the stamp of the MNR. She stated that the copy in the possession of petitioner was a faithful copy of the letter in question.xviii[18]

xvxvixviixviii

The difficulty of ascertaining the existence of the two documents is indeed a reflection on the sorry state of record keeping in an important office of the executive department. Yet these two documents are vital to the presentation of the evidence of both parties in this case. Fortunately, there are extant certain records from which it is possible to determine whether these documents even existed.

With respect to the alleged order of June 3, 1983 suspending petitioners TLA No. 106 for mediocre performance in reforestation, the Court will presume that there is such an order in accordance with the presumption of regularity in the performance of official functions inasmuch as such order is cited both in the order dated May 2, 1988 of the DENR, declaring as of no force and effect TLA No. 106, and in the decision dated March 21, 1991 of the Office of the President affirming the order of the DENR. It is improbable that so responsible officials as the Secretary of the DENR and the Executive Secretary would cite an order that did not exist.

On the other hand, with respect to the letter dated September 24, 1984, there are circumstances indicating that it existed. In addition to the aforesaid certification of Ofelia Castro Biron that she was the person who received the letter for the DENR, the logbook of the Ministry of Natural Resources contains entries indicating that the letter was received by the Bureau of Forest Development from the MNR.xix[19] DENR Assistant Secretary Romulo San Juan likewise informed the Office of the President that the Bureau of Forest Management prepared a memorandum on the aforesaid letter of September 24, 1984,xx[20] thereby implying that there was such a letter.

On the premise that there was an order dated June 3, 1983, we find that after suspending petitioners TLA for mediocre performance in reforestation under this order, the DENR cancelled the TLA, this time because of a Presidential directive imposing a log ban. The records of G.R. No. 76538, entitled Felipe Ysmael, Jr. & Co. v. Deputy Executive Secretary, the decision in which is reported in 190 SCRA 673 (1990), contain a copy of the memorandum of then Director Edmundo V. Cortes of the Bureau of Forest Development to the Regional Director of Region 2, in Tuguegarao, Cagayan, informing the latter that pursuant to the instruction of the President and the memorandum dated August 18, 1983 of then Minister Teodoro Q. Pea, the log ban previously declared included the concessions of the companies enumerated in Cortes memorandum, in consequence of which the concessions in question were deemed cancelled. The memorandum of Director Cortes stated:

MEMORANDUM ORDER

TO : The Regional DirectorRegion 2, Tuguegarao, Cagayan

FROM : The Director

DATE : 24 August 1983

xixxx

SUBJECT : Stopping of all logging operationsin Nueva Vizcaya and Quirino

REMARKS :

Following Presidential Instructions and Memorandum Order of Minister Teodoro Q. Pea dated 18 August 1983, and in connection with my previous radio message, please be informed that the coverage of the logging ban in Quirino and Nueva Vizcaya provinces include the following concessions which are deemed cancelled as of the date of the previous notice:

- Felipe Ysmael Co., Inc.- Industries Dev. Corp.- Luzon Loggers, Inc.- C & M Timber Corporation- Buzon Industrial Dev. Corporation- Dominion Forest Resources Corp.- FCA Timber Development Corp.- Kasibu Logging Corp.- RCC Timber Company

- Benjamin Cuaresma

You are hereby reminded to insure full compliance with this order to stop logging operations by all licensees above mentioned and submit a report on the pullout of equipment and inventory of logs within five days upon receipt hereof.

ACTIONDESIRED : For your immediate implementation.

EDMUNDO V. CORTES

(Emphasis added)

It thus appears that petitioners license had been cancelled way back in 1983, a year before its concession was awarded to FLDC. It is noteworthy that petitioner admits that at the time of the award to FLDC in 1984 petitioner was no longer operating its concession because of a log ban although it claims that the suspension of operations was only temporary. As a result of the log ban, the TLA of petitioner, along with those of other loggers in the region, were cancelled and petitioner and others were ordered to stop operations. Petitioner also admits that it received a telegram sent on August 24, 1983 by Director Cortes of the BFD, directing it to stop all logging operations to conserve our remaining forests.xxi[21] It is then not true, as Atty. Quisumbing stated in protesting the award of the concession to FLDC, that the logging ban did not cancel [petitioners] timber license agreement.

Now petitioner did not protest the cancellation of its TLA. Consequently, even if consideration is given to the fact that a year later, on September 24, 1984, its counsel protested the grant of the

xxi

concession to another party (FLDC), this failure of petitioner to contest first the suspension of its license on June 3, 1983 and later its cancellation on August 24, 1983 must be deemed fatal to its present action.

Second. Except for the letter of its counsel to the Minister of Natural Resources, which it reiterated in its letter to the President of the Philippines, petitioner took no legal steps to protect its interest. After receiving no favorable response to its two letters, petitioner could have brought the necessary action in court for the restoration of its license. It did not. Instead it waited until FLDCs concession was cancelled in 1986 by asking for the revalidation of its (petitioners) on TLA No. 106.

Petitioners excuse before the DENR is that it did not pursue its protest because its president, Ricardo C. Silverio, had been told by President Marcos that the area in question had been awarded to the Presidents sister, Mrs. Fortuna Barba, and petitioner was afraid to go against the wishes of the former President.xxii[22] This is a poor excuse for petitioners inaction. In Felipe Ysmael, Jr. & Co., Inc. v. Deputy Executive Secretary,xxiii[23] a similar excuse was given that Ysmael & Cos license had been cancelled and its concession awarded to entities controlled or owned by relatives or cronies of then President Marcos. For this reason, after the EDSA Revolution, Ysmael & Co. sought in 1986 the reinstatement of its timber license agreement and the revocation of those issued to the alleged presidential cronies. As its request was denied by the Office of the President, Ysmael & Co. filed a petition for certiorari with this Court. On the basis of the facts stated, this Court denied the petition: (1) because the August 25, 1983 order of the Bureau of Forest Development, cancelling petitioners timber license agreement had become final and executory. Although petitioner sent a letter dated September 19, 1983 to President Marcos seeking reconsideration of the 1983 order of cancellation of the BFD, the grounds stated there were different from those later relied upon by petitioner for seeking its reinstatement; (2) because the fact that petitioner failed to seasonably take judicial recourse to have the earlier administrative actions [cancelling its license and granting another one covering the same concession to respondent] reviewed by the court through a petition for certiorari is prejudicial to its cause. Such special civil action of certiorari should have been filed within a reasonable time. And since none was filed within such period, petitioners action was barred by laches; and (3) because executive evaluation of timber licenses and their consequent cancellation in the process of formulating policies with regard to the utilization of timber lands is a prerogative of the executive department and in the absence of evidence showing grave abuse of discretion courts will not interfere with the exercise of that discretion.

This case is governed by the decision in Felipe Ysmael, Jr. & Co., Inc. v. Deputy Executive Secretary.

Third. It is finally contended that any policy consideration on forest conservation and protection justifying the decision of the executive department not to reinstate petitioners license must be formally enunciated and cannot merely be implied from the Presidents instruction to his subordinates and that, at all events, the new policy cannot be applied to existing licenses such as petitioners.

xxiixxiii

The Presidents order reconsidering the resolution of the Presidential Legal Adviser (insofar as it reinstated the license of FLDC) was prompted by concerns expressed by the then Secretary of Environment and Natural Resources that said reinstatement [of FLDCs license] may negate our efforts to enhance conservation and protection of our forest resources. There was really no new policy but, as noted in Felipe Ysmael, Jr. & Co., Inc., a mere reiteration of a policy of conservation and protection. The policy is contained in Art. II, 16 of the Constitution which commands the State to protect and promote the right of the people to a balanced and healthful ecology in accord with the rhythm and harmony of nature. There is therefore no merit in petitioners contention that no new policy can be applied to existing licenses.

As to petitioners contention that the cancellation of its license constitutes an impairment of the obligation of its contract, suffice it for us to quote what we held in Felipe Ysmael, Jr. & Co. Inc. v. Deputy Executive Secretary:xxiv[24]

A cursory reading of the assailed orders issued by public respondent Minister Maceda of the MNR, which were affirmed by the Office of the President, will disclose public policy considerations which effectively forestall judicial interference in the case at bar.

Public respondents herein, upon whose shoulders rests the task of implementing the policy to develop and conserve the countrys natural resources, have indicated an ongoing department evaluation of all timber license agreements entered into, and permits or licenses issued, under the previous dispensation. . . .

The ongoing administrative reassessment is apparently in response to the renewed and growing global concern over the despoliation of forest lands and the utter disregard of their crucial role in sustaining a balanced ecological system. The legitimacy of such concern can hardly be disputed, most especially in this country. . . .

Thus, while the administration grapples with the complex and multifarious problems caused by unbridled exploitation of these resources, the judiciary will stand clear. . . . More so where, as in the present case, the interests of a private logging company are pitted against that of the public at large on the pressing public policy issue of forest conservation. . . . Timber licenses, permits and license agreements are the principal instruments by which the State regulates the utilization and disposition of forest resources to the end that public welfare is promoted. And it can hardly be gainsaid that they merely evidence a privilege granted by the State to qualified entities, and do not vest in the latter a permanent or irrevocable right to the particular concession area and the forest products therein. They may be validly amended, modified, replaced or rescinded by the Chief Executive when national interests so require. Thus, they are not deemed contracts within the purview of the due process of law clause [See Sections 3(33) and 20 of Pres. Decree No. 705, as amended. Also, Tan v. Director of Forestry, G.R. No. L-24548, October 27, 1983, 125 SCRA 302].

WHEREFORE, the petition is DISMISSED.

SO ORDERED.

xxiv