Embed Size (px)

Citation preview

Building Integrated Photovoltaics: New trends and Challenges’

Prof. Hari M. Upadhyaya

Head, Energy Engineering Group Institute of Mechanical Process and Energy Engineering

School of Engineering & Physical Sciences, Heriot Watt University, Edinburgh- EH14 4AS

India-UK Collaboration in Solar Energy

Contents

1. Introduction: Global PV and BIPV scenario

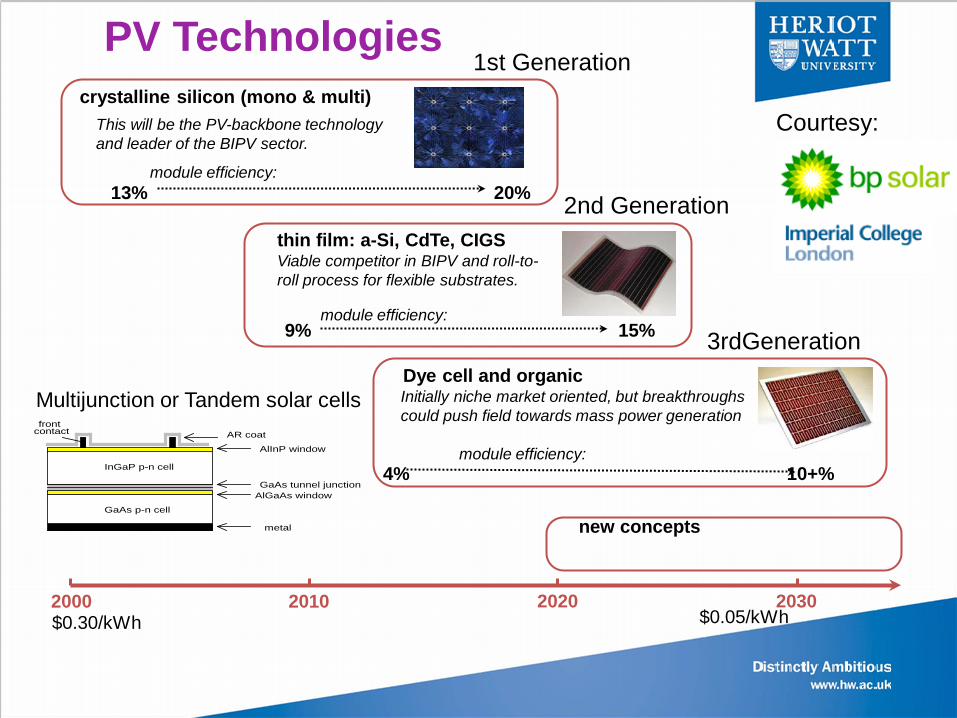

2.PV Technologies

3.New Developments 4. Future Trends 5. Summary and Conclusion

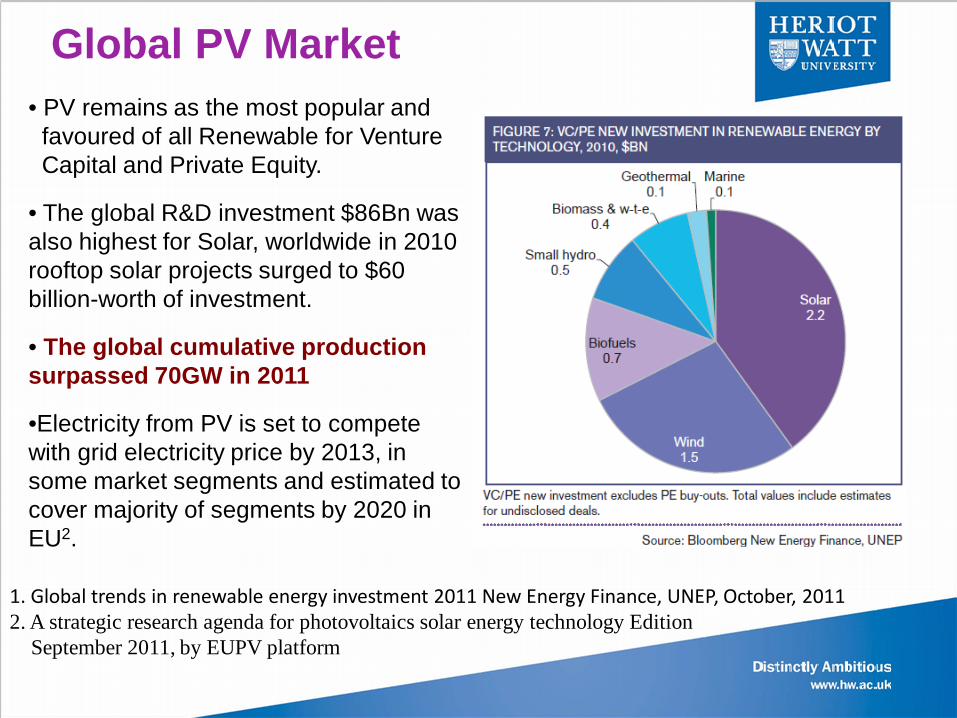

Global PV Market • PV remains as the most popular and favoured of all Renewable for Venture Capital and Private Equity.

• The global R&D investment $86Bn was also highest for Solar, worldwide in 2010 rooftop solar projects surged to $60 billion-worth of investment.

• The global cumulative production surpassed 70GW in 2011

•Electricity from PV is set to compete with grid electricity price by 2013, in some market segments and estimated to cover majority of segments by 2020 in EU2.

1. Global trends in renewable energy investment 2011 New Energy Finance, UNEP, October, 2011 2. A strategic research agenda for photovoltaics solar energy technology Edition September 2011, by EUPV platform

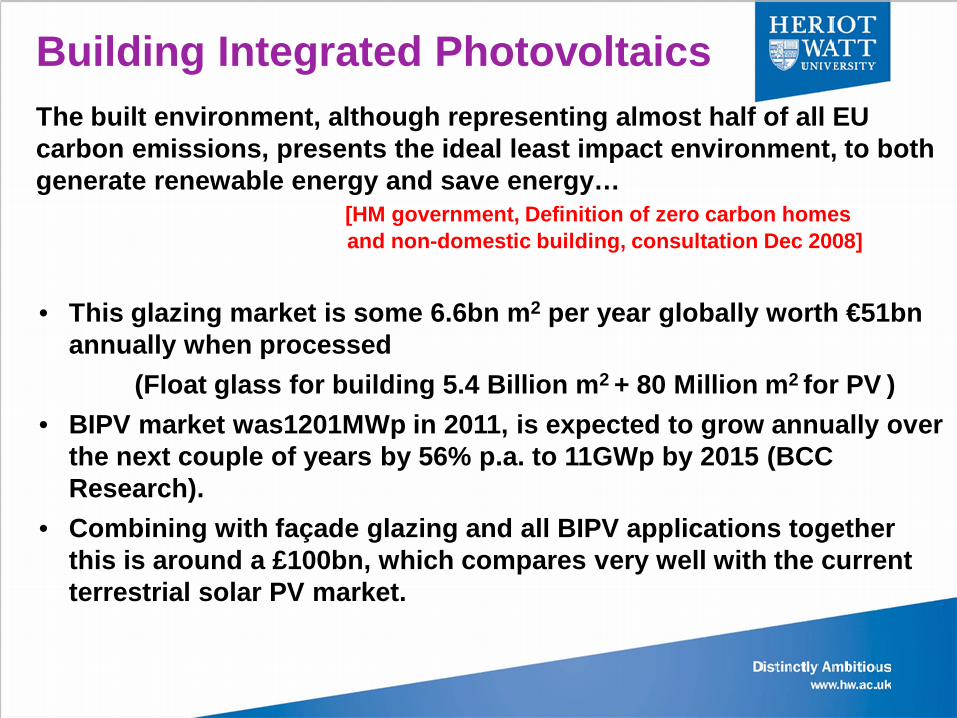

The built environment, although representing almost half of all EU carbon emissions, presents the ideal least impact environment, to both generate renewable energy and save energy… [HM government, Definition of zero carbon homes and non-domestic building, consultation Dec 2008]

Building Integrated Photovoltaics

• This glazing market is some 6.6bn m2 per year globally worth €51bn annually when processed

(Float glass for building 5.4 Billion m2 + 80 Million m2 for PV ) • BIPV market was1201MWp in 2011, is expected to grow annually over

the next couple of years by 56% p.a. to 11GWp by 2015 (BCC Research).

• Combining with façade glazing and all BIPV applications together this is around a £100bn, which compares very well with the current terrestrial solar PV market.

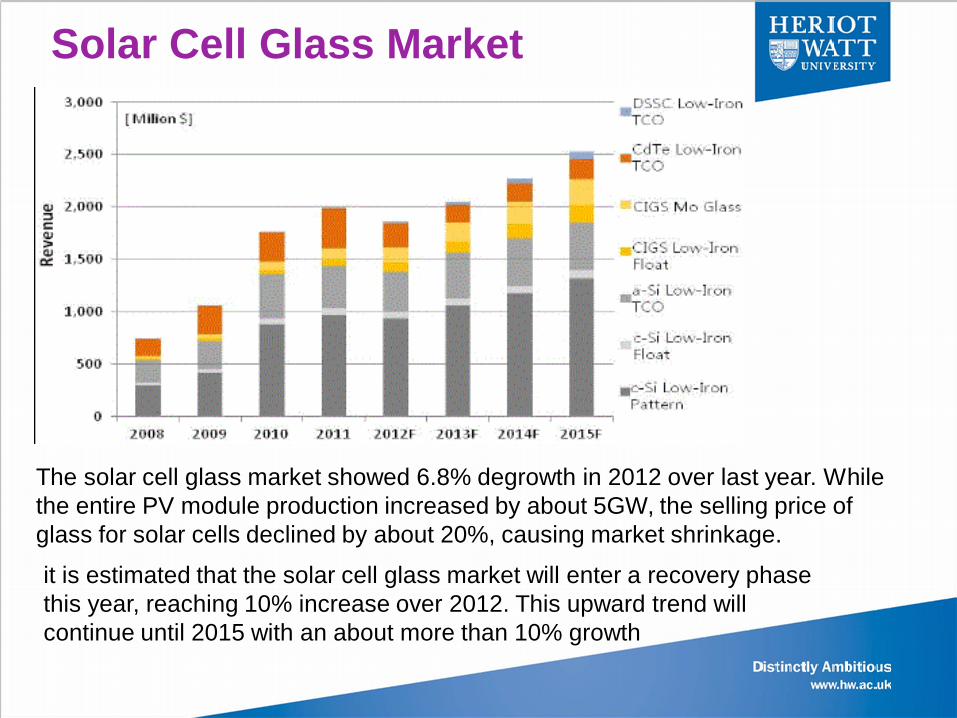

The solar cell glass market showed 6.8% degrowth in 2012 over last year. While the entire PV module production increased by about 5GW, the selling price of glass for solar cells declined by about 20%, causing market shrinkage.

it is estimated that the solar cell glass market will enter a recovery phase this year, reaching 10% increase over 2012. This upward trend will continue until 2015 with an about more than 10% growth

Solar Cell Glass Market

PV Technologies

2000 2030 2010 2020

crystalline silicon (mono & multi)

Dye cell and organic

thin film: a-Si, CdTe, CIGS

new concepts

This will be the PV-backbone technology and leader of the BIPV sector.

module efficiency:

Viable competitor in BIPV and roll-to-roll process for flexible substrates.

Initially niche market oriented, but breakthroughs could push field towards mass power generation module efficiency:

$0.30/kWh $0.05/kWh

13% 20%

9% 15% module efficiency:

4% 10+%

Courtesy:

metal

AlGaAs windowGaAs tunnel junction

AlInP window

AR coat

InGaP p-n cell

GaAs p-n cell

front contact

1st Generation

3rdGeneration

2nd Generation

Multijunction or Tandem solar cells

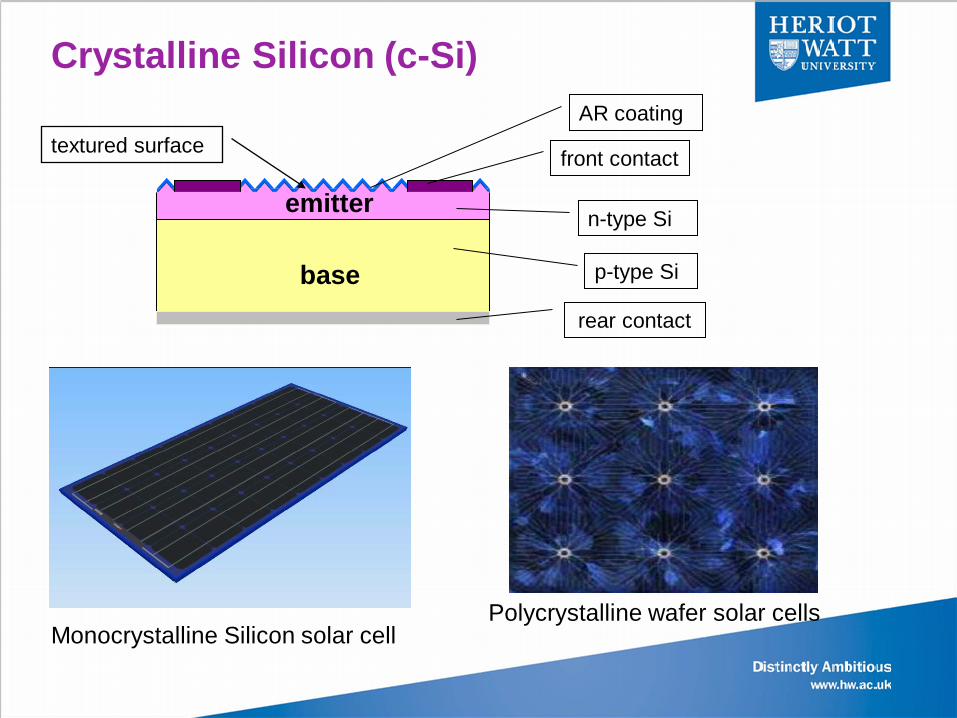

Crystalline Silicon (c-Si)

emitter

base rear contact

n-type Si

front contact textured surface AR coating

p-type Si

Monocrystalline Silicon solar cell Polycrystalline wafer solar cells

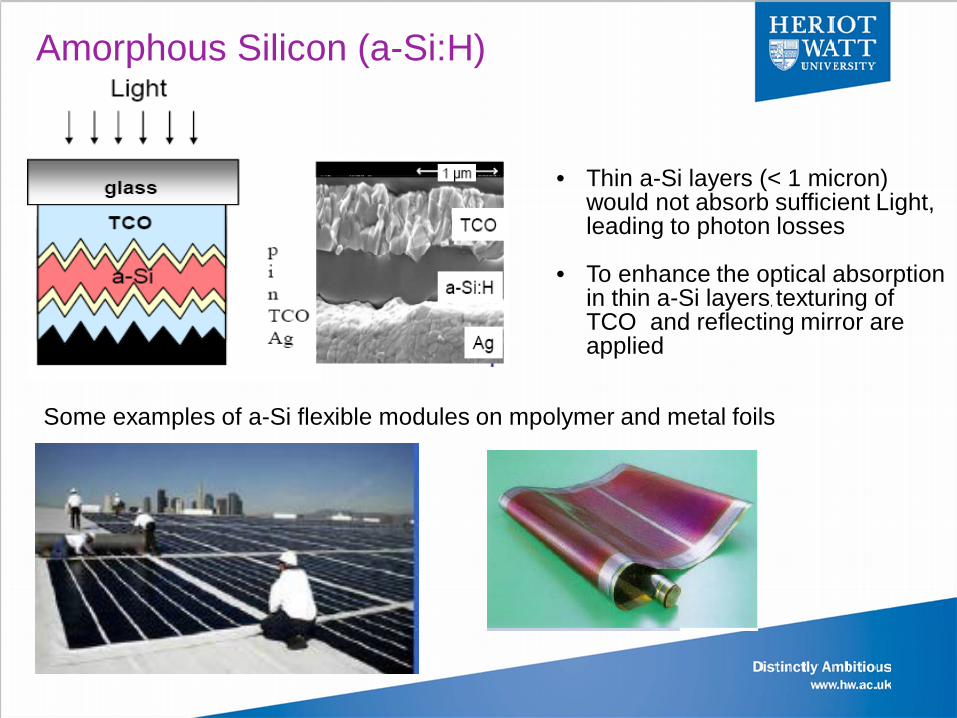

• Thin a-Si layers (< 1 micron) would not absorb sufficient Light, leading to photon losses

• To enhance the optical absorption in thin a-Si layers, texturing of TCO and reflecting mirror are applied

Amorphous Silicon (a-Si:H)

Some examples of a-Si flexible modules on mpolymer and metal foils

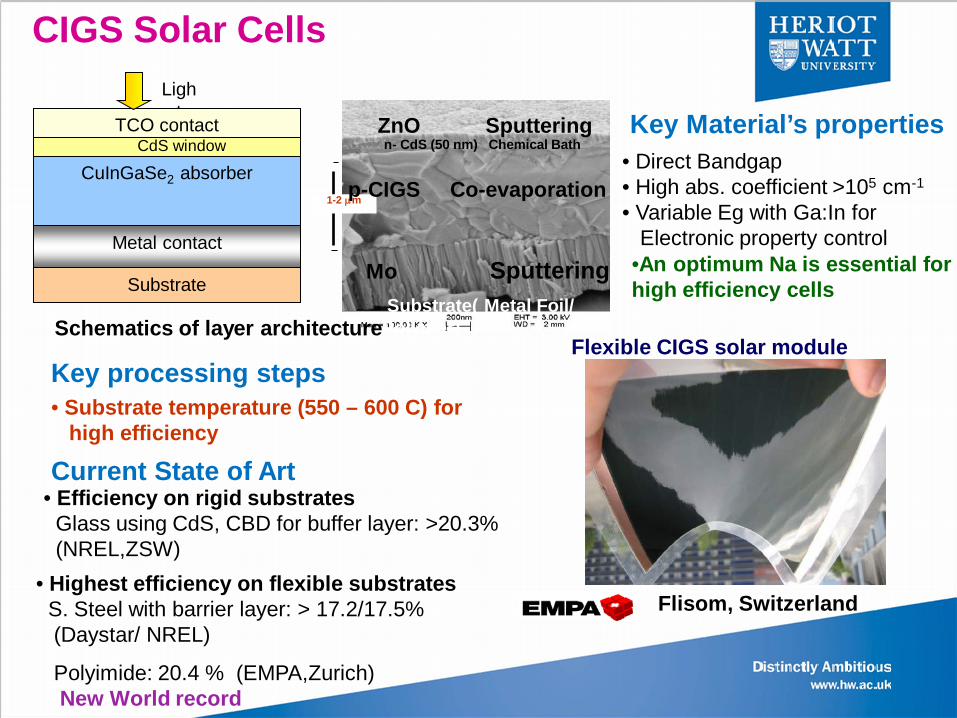

CIGS Solar Cells Ligh

t TCO contact

Substrate

Metal contact

CuInGaSe2 absorber CdS window

Sputtering

Mo Sputtering

1-2 µm

ZnO

Substrate( Metal Foil/ Polymer)

n- CdS (50 nm) Chemical Bath

p-CIGS Co-evaporation

Schematics of layer architecture

• Highest efficiency on flexible substrates S. Steel with barrier layer: > 17.2/17.5% (Daystar/ NREL)

Polyimide: 20.4 % (EMPA,Zurich) New World record

• Efficiency on rigid substrates Glass using CdS, CBD for buffer layer: >20.3% (NREL,ZSW)

Current State of Art

• Direct Bandgap • High abs. coefficient >105 cm-1 • Variable Eg with Ga:In for Electronic property control

• Substrate temperature (550 – 600 C) for high efficiency

Key Material’s properties

Key processing steps

Flisom, Switzerland

Flexible CIGS solar module

•An optimum Na is essential for high efficiency cells

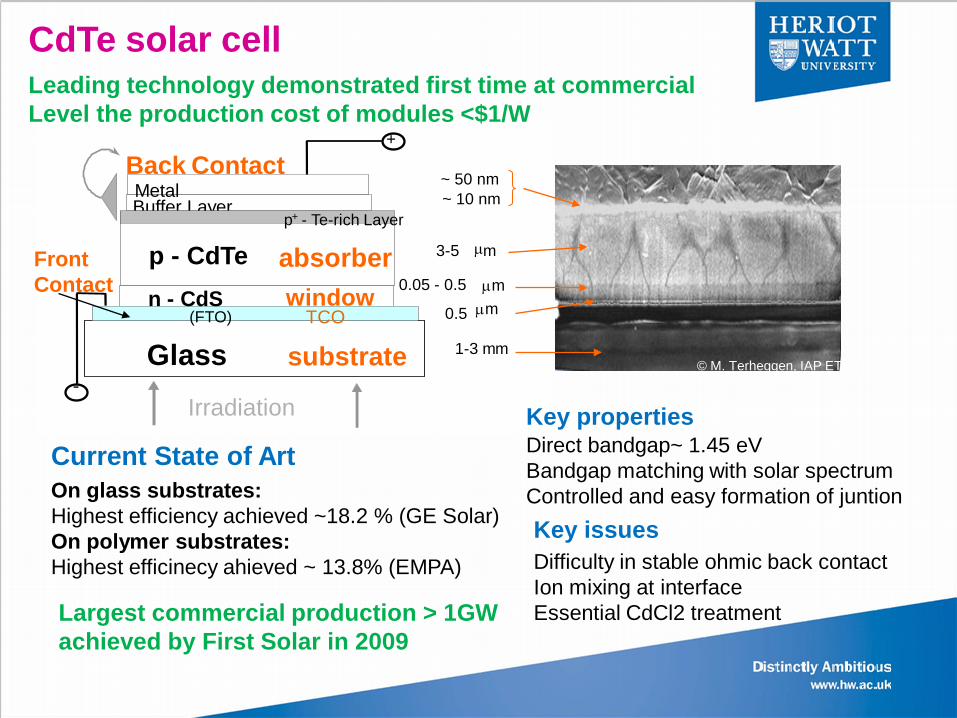

CdTe solar cell

3-5 µ m

Irradiation

- Glass

(FTO)

p - CdTe

~ 10 nm ~ 50 nm

Buffer Layer Metal

Back Contact

p + - Te-rich Layer

0.5

1-3 mm

n - CdS

+

absorber window

Front Contact

substrate © M. Terheggen, IAP ETHZ

0.05 - 0.5 µm µm TCO

Current State of Art On glass substrates: Highest efficiency achieved ~18.2 % (GE Solar) On polymer substrates: Highest efficinecy ahieved ~ 13.8% (EMPA)

Key properties Direct bandgap~ 1.45 eV Bandgap matching with solar spectrum Controlled and easy formation of juntion Key issues Difficulty in stable ohmic back contact Ion mixing at interface Essential CdCl2 treatment Largest commercial production > 1GW

achieved by First Solar in 2009

Leading technology demonstrated first time at commercial Level the production cost of modules <$1/W

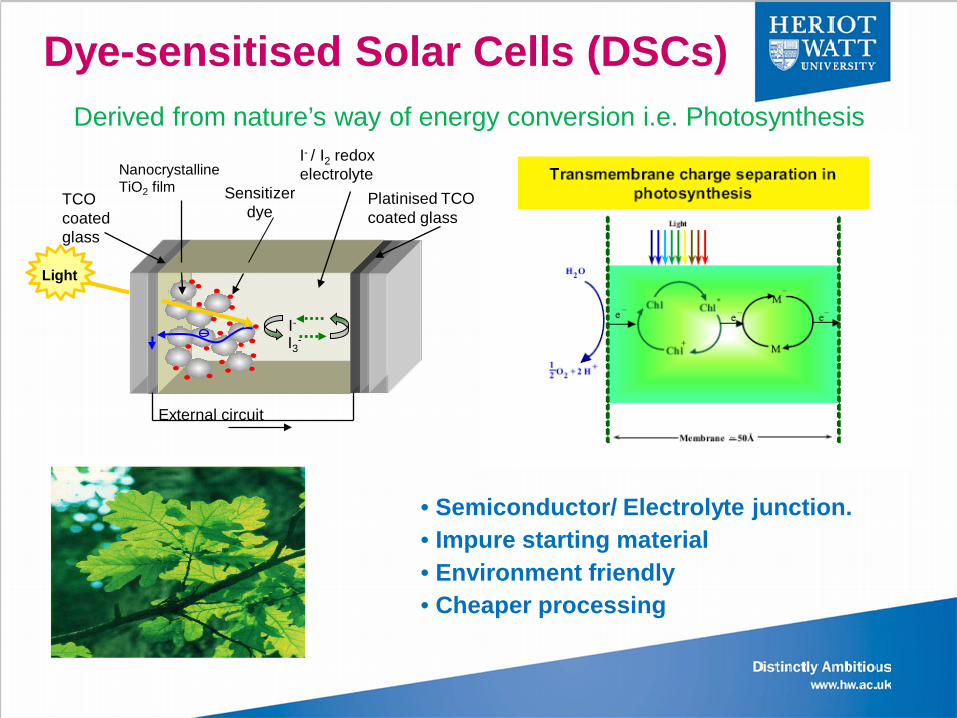

Platinised TCO coated glass

I- / I2 redox electrolyte

Light

External circuit

TCO coated glass

Nanocrystalline TiO2 film

I3- I-

Sensitizer dye

Derived from nature’s way of energy conversion i.e. Photosynthesis

Dye-sensitised Solar Cells (DSCs)

• Semiconductor/ Electrolyte junction. • Impure starting material • Environment friendly • Cheaper processing

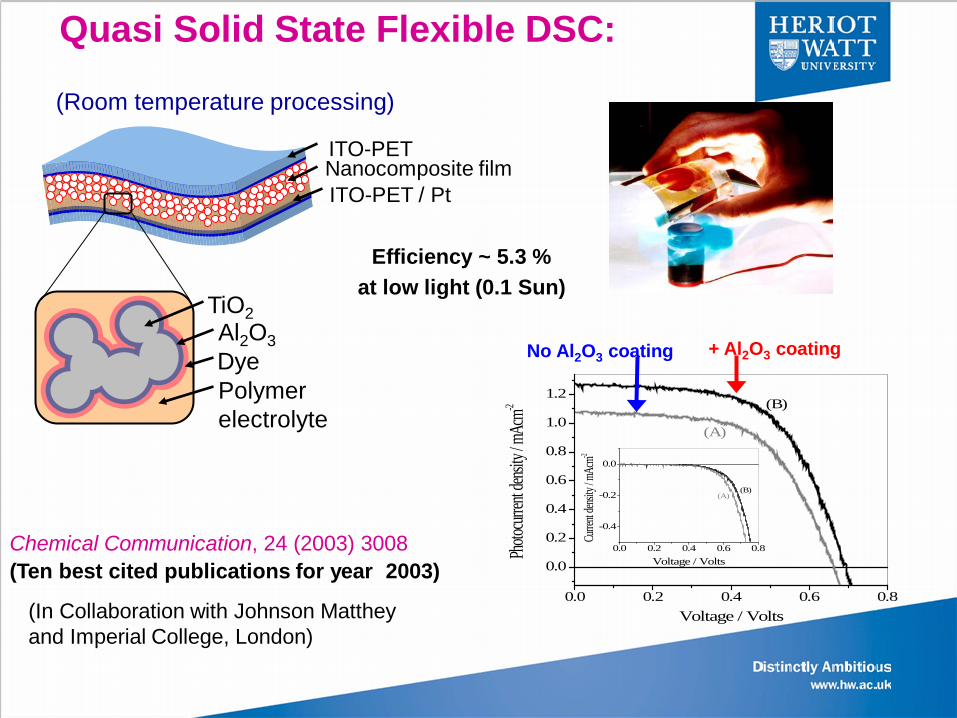

Quasi Solid State Flexible DSC:

ITO-PET Nanocomposite film ITO-PET / Pt

Dye

TiO2 Al2O3

Polymer electrolyte

Efficiency ~ 5.3 % at low light (0.1 Sun)

(Room temperature processing)

(Ten best cited publications for year 2003) Chemical Communication, 24 (2003) 3008

(In Collaboration with Johnson Matthey and Imperial College, London)

0.0 0.2 0.4 0.6 0.8

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0.0 0.2 0.4 0.6 0.8

-0.4

-0.2

0.0

(B)(A)

Curre

nt den

sity / m

Acm-2

Voltage / Volts

(B)

(A)

Photo

curren

t dens

ity / m

Acm-2

Voltage / Volts

+ Al2O3 coating No Al2O3 coating

13

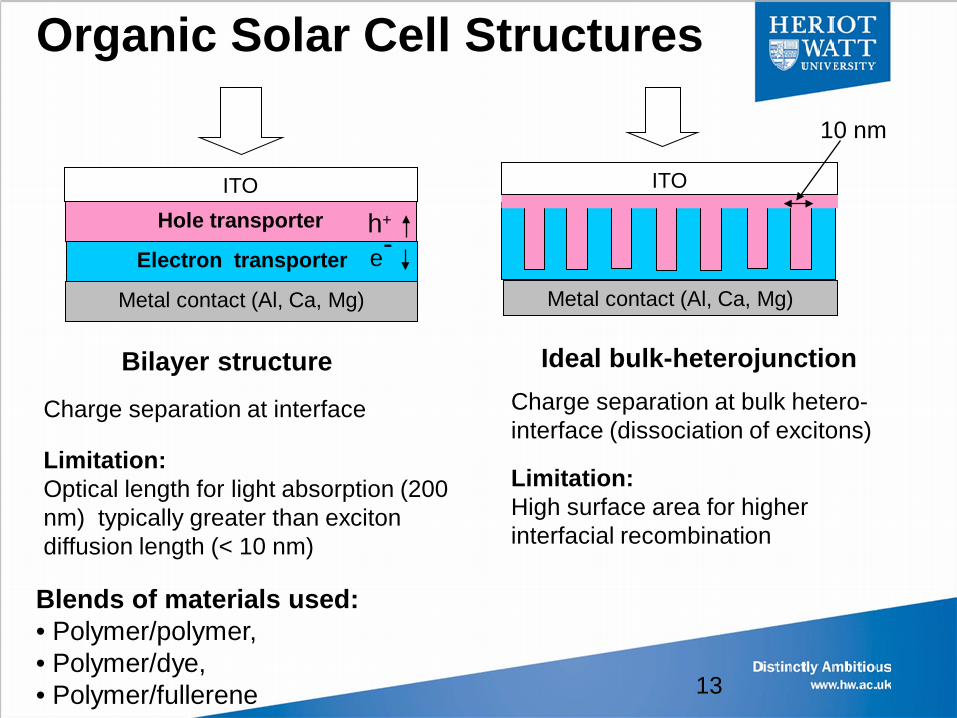

Organic Solar Cell Structures

ITO

Electron transporter

Metal contact (Al, Ca, Mg)

Hole transporter

e- h+

Charge separation at interface Limitation: Optical length for light absorption (200 nm) typically greater than exciton diffusion length (< 10 nm)

ITO

Metal contact (Al, Ca, Mg)

10 nm

Charge separation at bulk hetero- interface (dissociation of excitons) Limitation: High surface area for higher interfacial recombination

Bilayer structure Ideal bulk-heterojunction

Blends of materials used: • Polymer/polymer, • Polymer/dye, • Polymer/fullerene

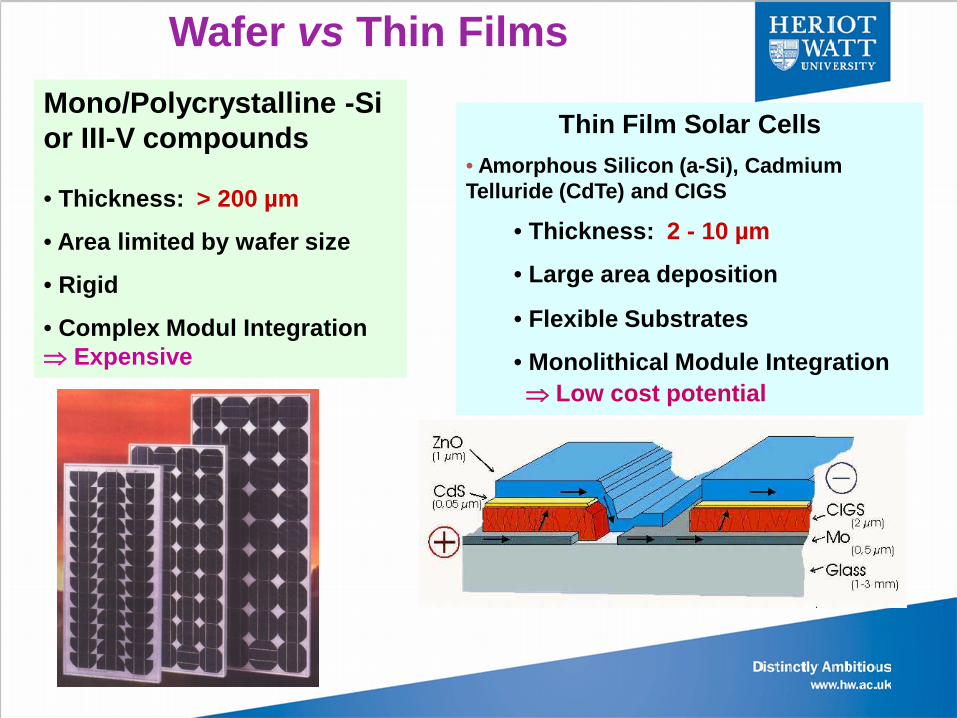

Wafer vs Thin Films Mono/Polycrystalline -Si or III-V compounds • Thickness: > 200 µm

• Area limited by wafer size

• Rigid

• Complex Modul Integration ⇒ Expensive

Thin Film Solar Cells

• Amorphous Silicon (a-Si), Cadmium Telluride (CdTe) and CIGS

• Thickness: 2 - 10 µm

• Large area deposition

• Flexible Substrates

• Monolithical Module Integration ⇒ Low cost potential

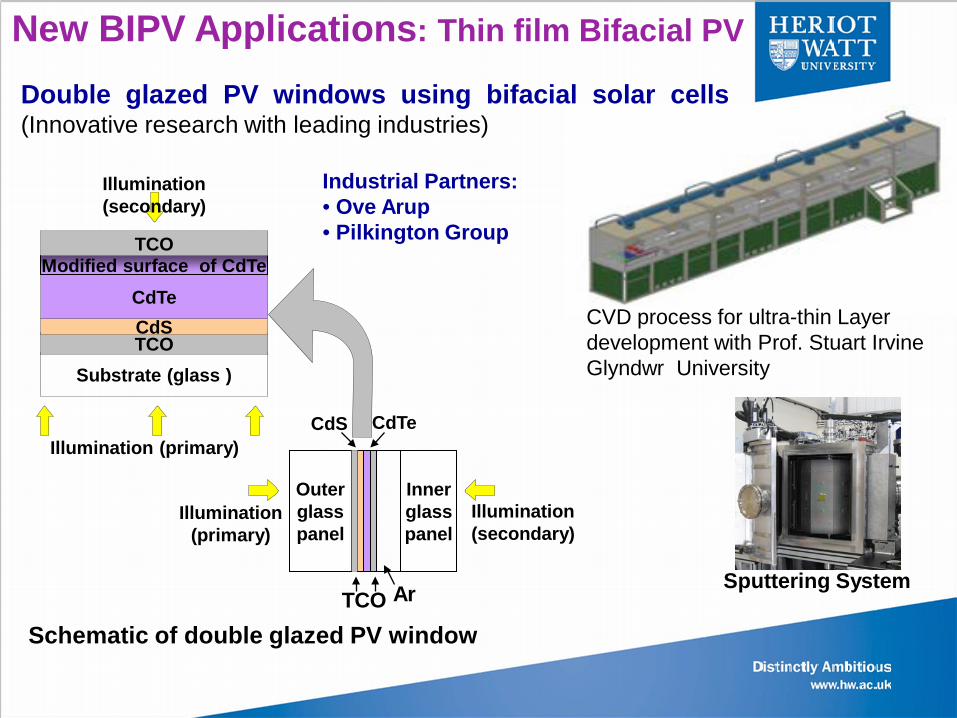

Industrial Partners: • Ove Arup • Pilkington Group

TCO

CdTe CdS

Ar

Outer glass panel

Inner glass panel

Illumination (secondary)

Illumination (primary)

Double glazed PV windows using bifacial solar cells (Innovative research with leading industries)

Schematic of double glazed PV window

Substrate (glass ) TCO CdS CdTe

Modified surface of CdTe TCO

Illumination (primary)

Illumination (secondary)

Sputtering System

CVD process for ultra-thin Layer development with Prof. Stuart Irvine Glyndwr University

New BIPV Applications: Thin film Bifacial PV

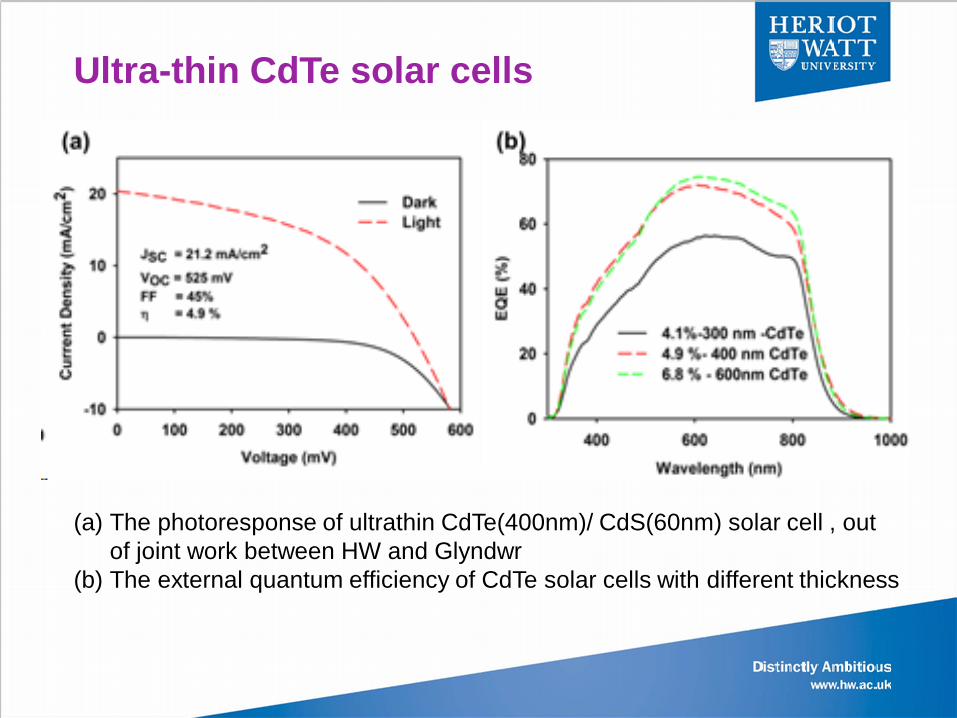

Ultra-thin CdTe solar cells

(a) The photoresponse of ultrathin CdTe(400nm)/ CdS(60nm) solar cell , out of joint work between HW and Glyndwr

(b) The external quantum efficiency of CdTe solar cells with different thickness

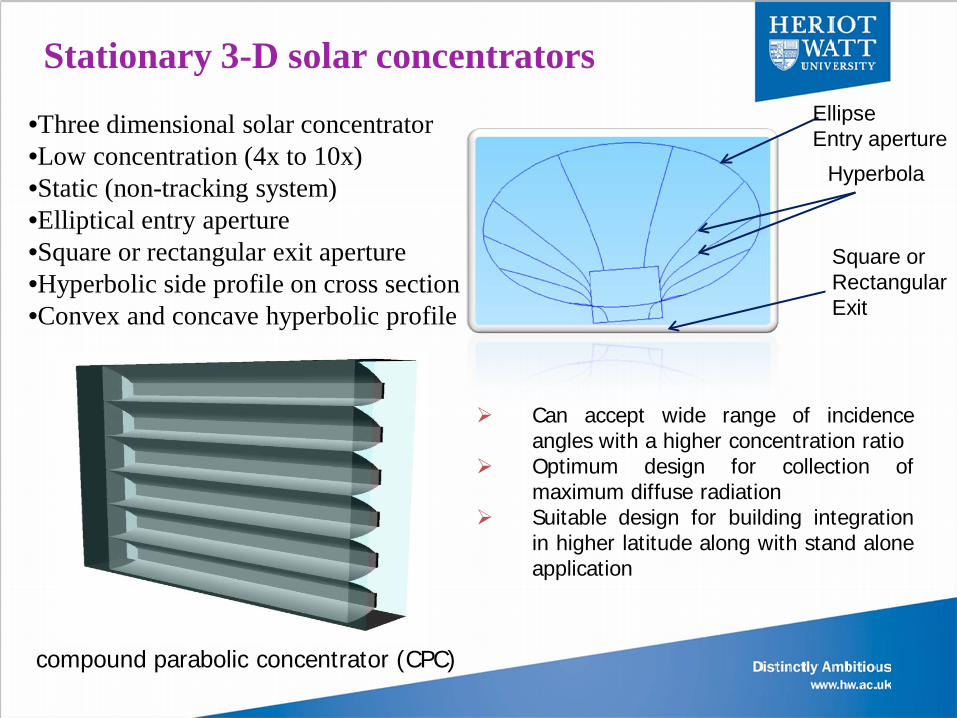

Stationary 3-D solar concentrators •Three dimensional solar concentrator •Low concentration (4x to 10x) •Static (non-tracking system) •Elliptical entry aperture •Square or rectangular exit aperture •Hyperbolic side profile on cross section •Convex and concave hyperbolic profile

Ellipse Entry aperture

Hyperbola

Square or Rectangular Exit

compound parabolic concentrator (CPC)

Can accept wide range of incidence angles with a higher concentration ratio

Optimum design for collection of maximum diffuse radiation

Suitable design for building integration in higher latitude along with stand alone application

Future Trends: The dis-advantages of c-Si viz. high materials cost, low

optical absorption, brittle, rigid, heavy, opaqueness will have to be overcome by flexible PV design

LARGE AREA, THIN, LIGHT WEIGHT AND FLEXIBE PRODUCTS

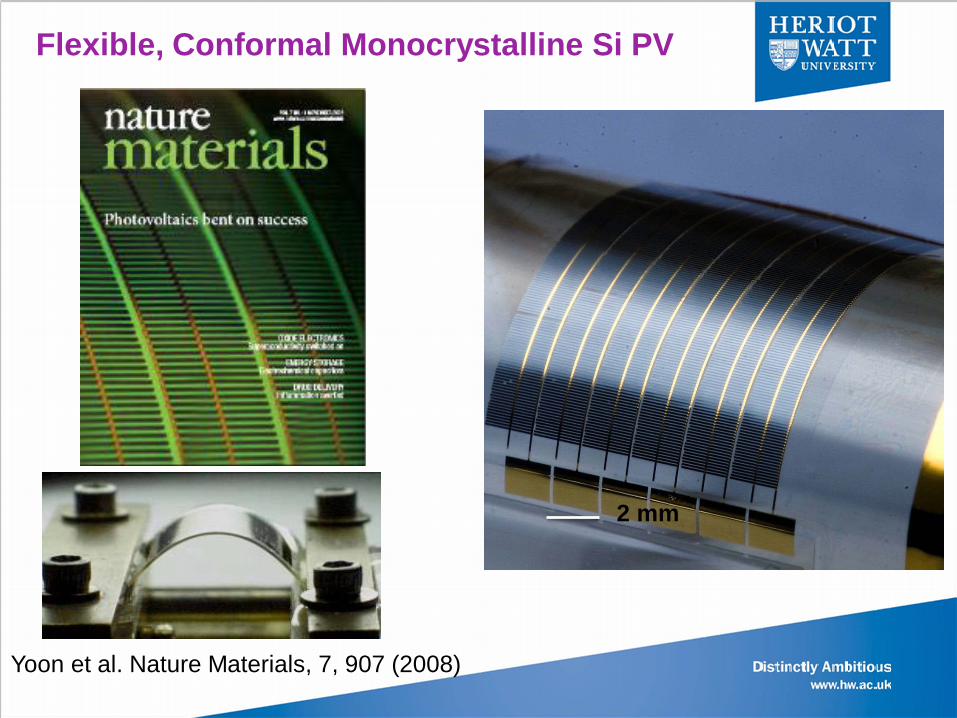

Yoon et al. Nature Materials, 7, 907 (2008)

2 mm

Flexible, Conformal Monocrystalline Si PV

The BIPV sector which is backed by an established glazing industry is set to grow over 50% rate in the future.

The dis-advantages of c-Si viz. high materials cost, low optical absorption, brittle, rigid, heavy, opaqueness will have to be overcome by flexible thin-film bifacial PV.

Thin-film modules allow greater freedom to select size and colour than c-Si module, e.g. module efficiency decreases as the temperature increases for mono and poly silicon cells but not for amorphous silicon cells.

The challenge lies with achieving the colour neutral glazing which is limited by a coloured tinge of the glass.

New concentrator PV designs combined with thermal integration will make it a viable industry in the future in a large number of countries.

Summary and Conclusions

Acknowledgements:

M. Graetzel, EPFL, Switzerland

Ayodhya Tiwari, ETH Zurich, Switzerland

Marc Kaelin, ETH Zurich, Switzerland

Prof. Tapas K. Mallick, Exeter University

Prof. Stuart Irvine, Glyndwr Univeristy

Thanks for your attention!