Embed Size (px)

Citation preview

SEQ 0023 JOB L47-001-008 PAGE-0003 COVER REVISED 28MAY96 AT 09:36 BY LR DEPTH: 66.04 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-001

3

Bulletin No. 1996–2January 8, 1996

HIGHLIGHTSOF THIS ISSUE

These synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Rev. Rul. 96–2, page 5.Insurance companies; interest rate tables. Prevailingstate assumed interest rates are provided for thedetermination of reserves under section 807 of theCode for contracts issued in 1995 and 1996. Rev. Rul.92–19 supplemented in part.

Rev. Rul. 96–6, page 8.Federal rates; adjusted federal rates; adjusted federallong-term rate, and the long-term exempt rate. Forpurposes of sections 1274, 1288, 382, and othersections of the Code, tables set forth the rates forJanuary 1996.

EMPLOYEE PLANS

Notice 96–2, page 15.Guidelines are set forth for determining for December1995, the weighted average interest rate and theresulting permissible range of interest rates used tocalculate current liability for purposes of the full fundinglimitation of section 412(c)(7) of the Code as amendedby the Omnibus Budget Reconciliation Act of 1987 andby the Uruguay Round Agreements Act (GATT).

EXEMPT ORGANIZATIONS

Announcement 96–3, page 57.A list is given of organizations now classified as privatefoundations.

Rev. Proc. 96–10, page 17.Information returns, organizations not required to file.This procedure lists a class of organizations, affiliatedwith a church or convention or association of churches,and exempt from federal income tax under section

501(c)(3) of the Internal Revenue Code, that is notrequired to file an annual information return Form 990,Return of Organizations Exempt from Income Tax.

ESTATE TAX

Rev. Rul. 96–3, page 14.Valuation of annuities. Interest for life or a term ofyears, and remainder and reversionary interests whenthe individual, who is the measuring life, is terminallyill. Rev. Ruls. 80–80 and 66–307 are obsoleteeffective December 14, 1995.

EXCISE TAXES

Announcement 96–2, page 57.A petition has been filed to add butyl benzyl phthalateto the list of taxable substances in section 4672(a)(3)of the Code.

ADMINISTRATIVE

Rev. Proc. 96–9, page 15.Early referral of unagreed issues from examination toappeals. This procedure describes the method by whicha taxpayer requests early referral of one or moreunagreed issues from Examination to Appeals.

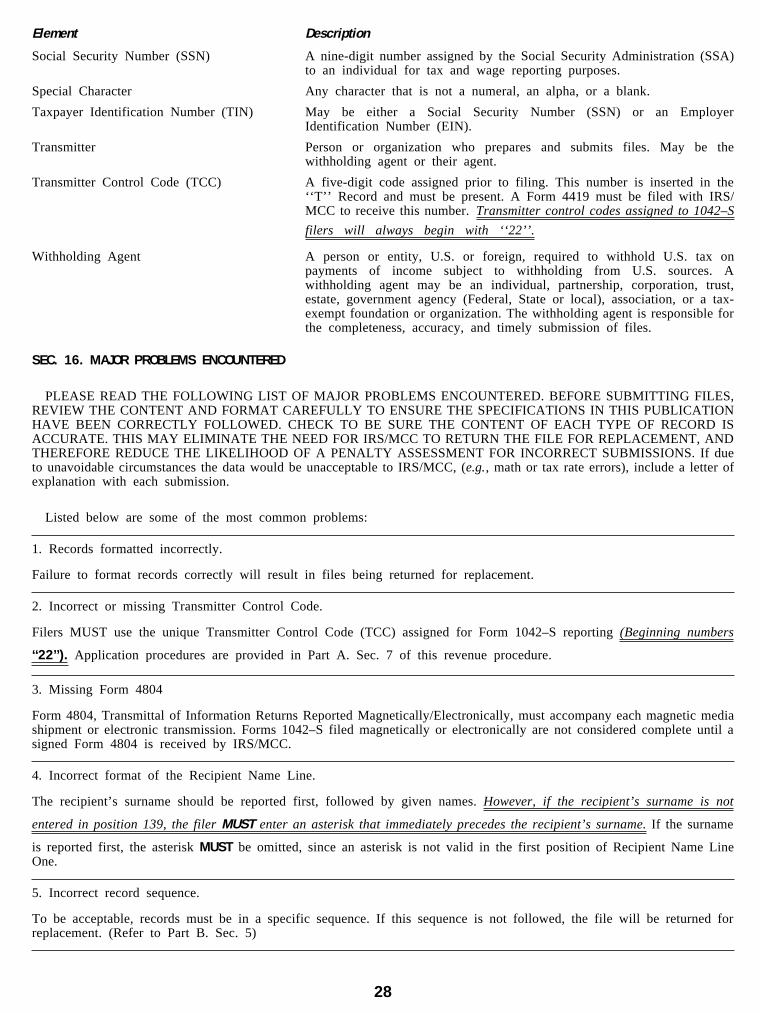

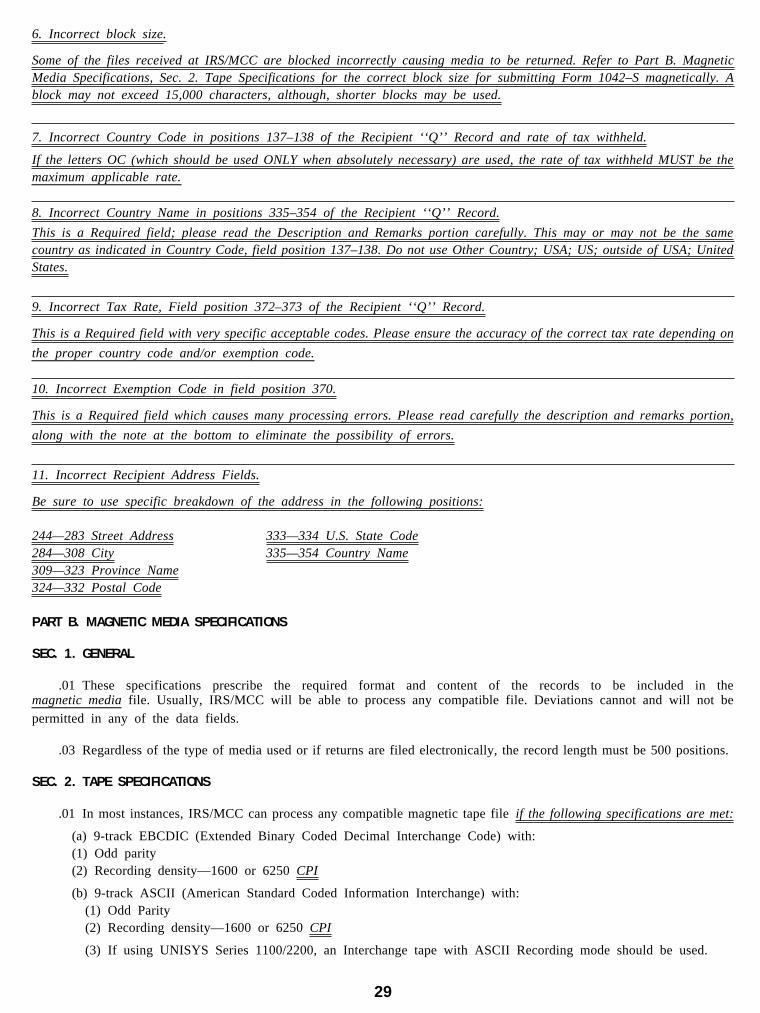

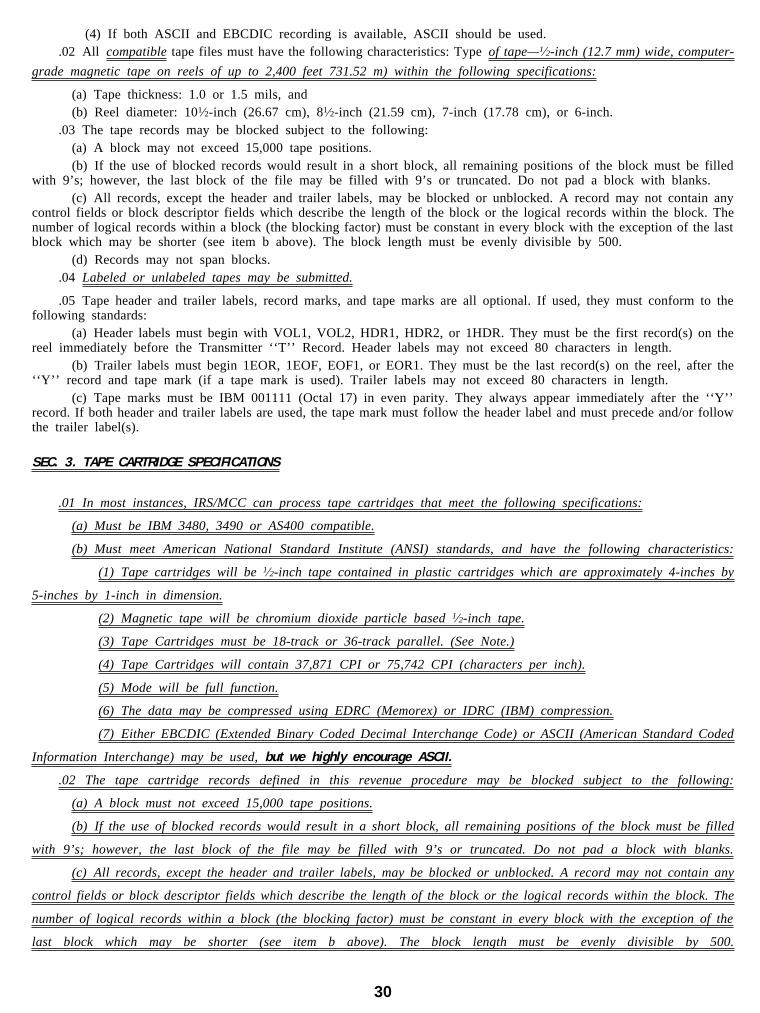

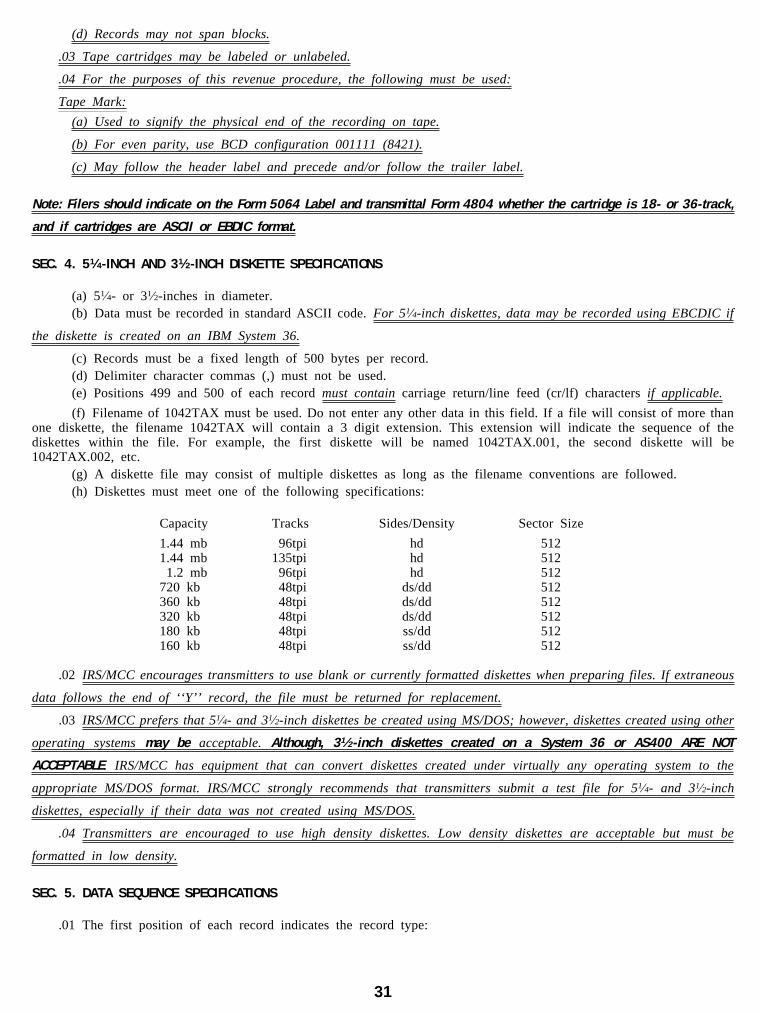

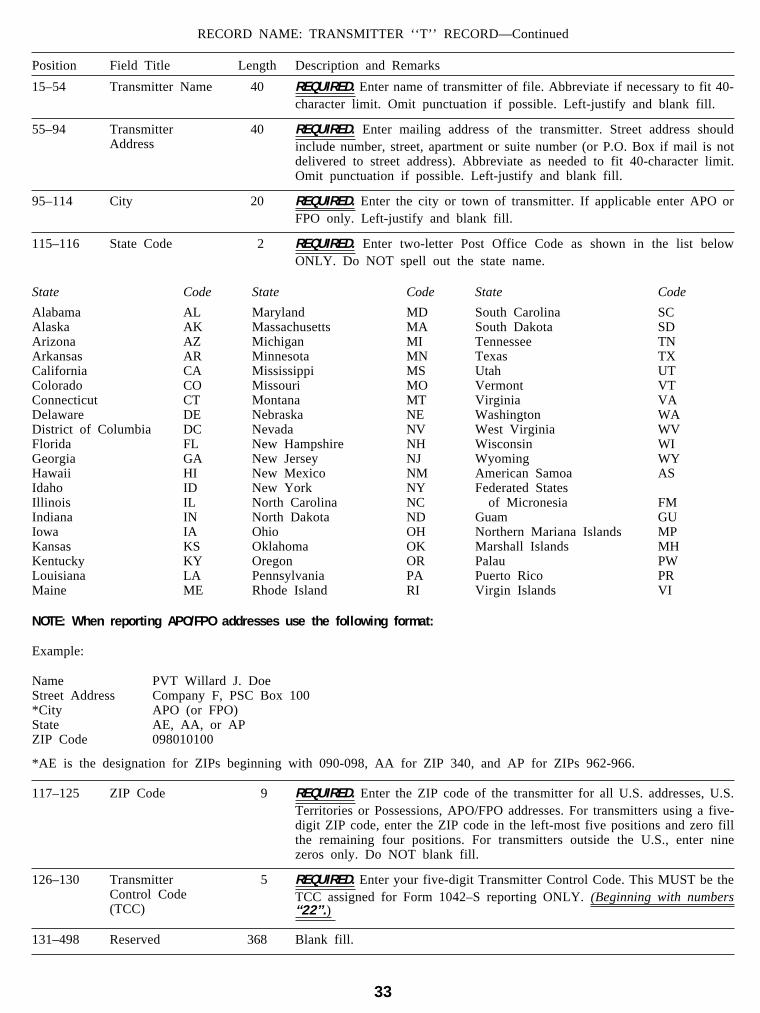

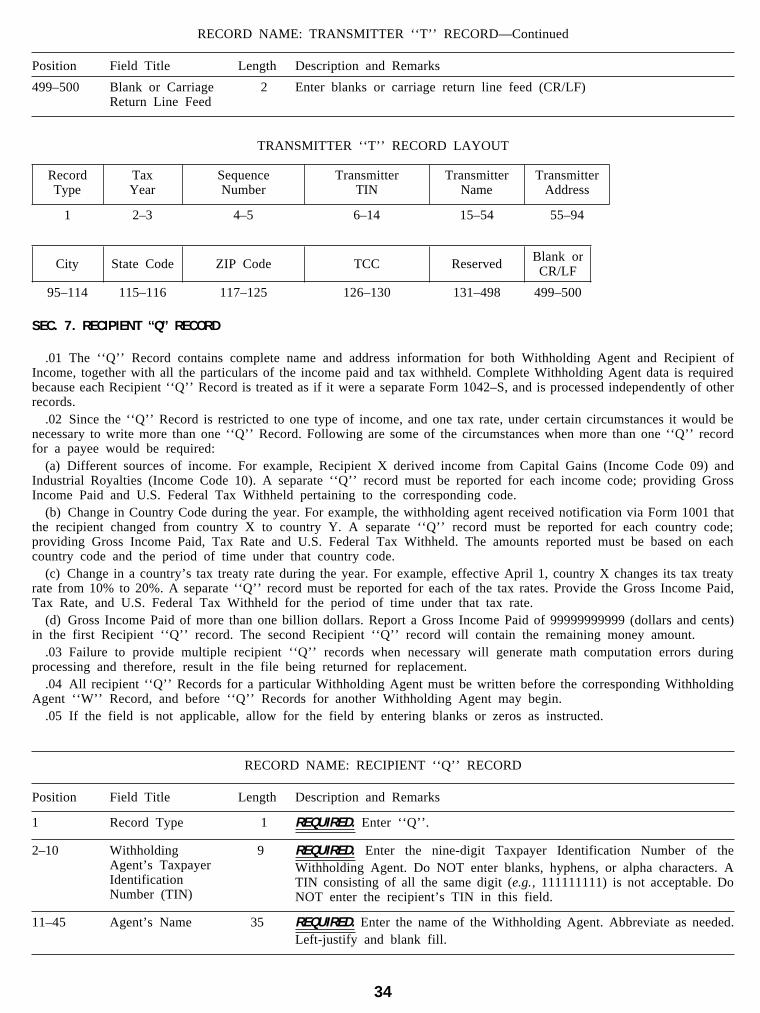

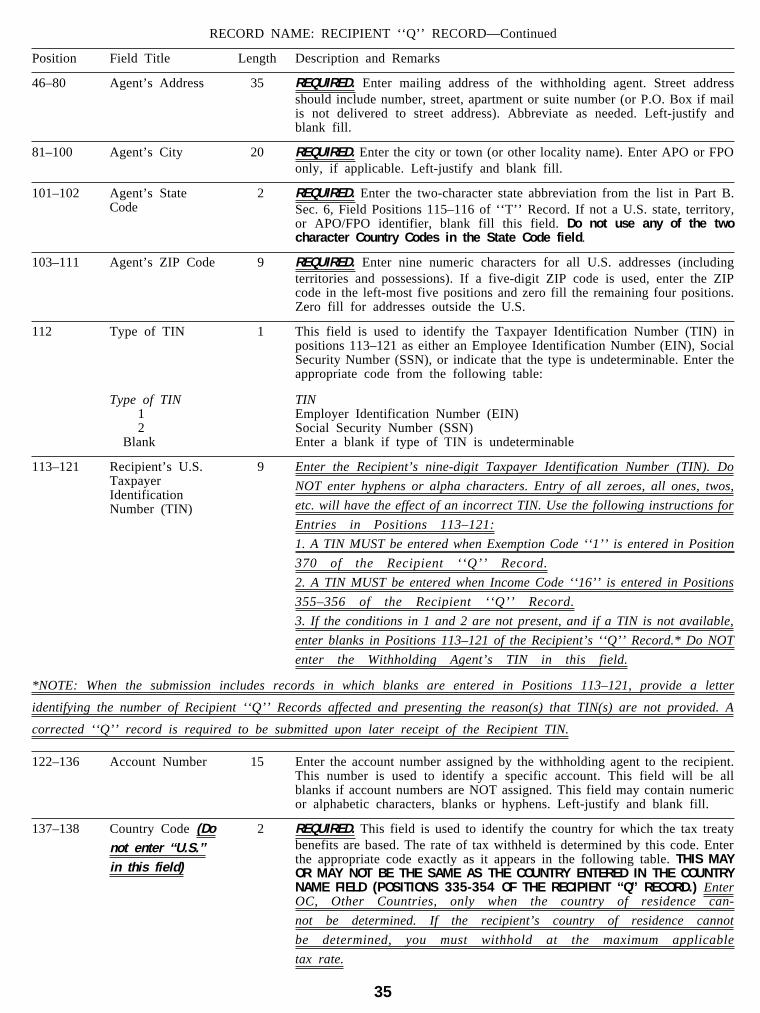

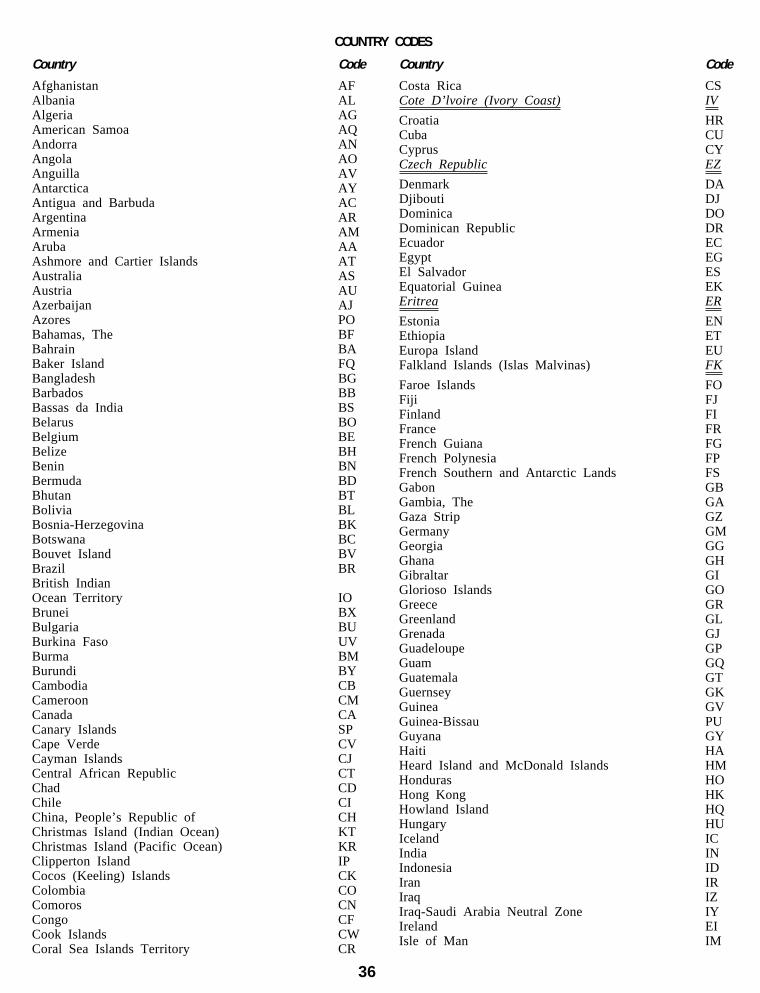

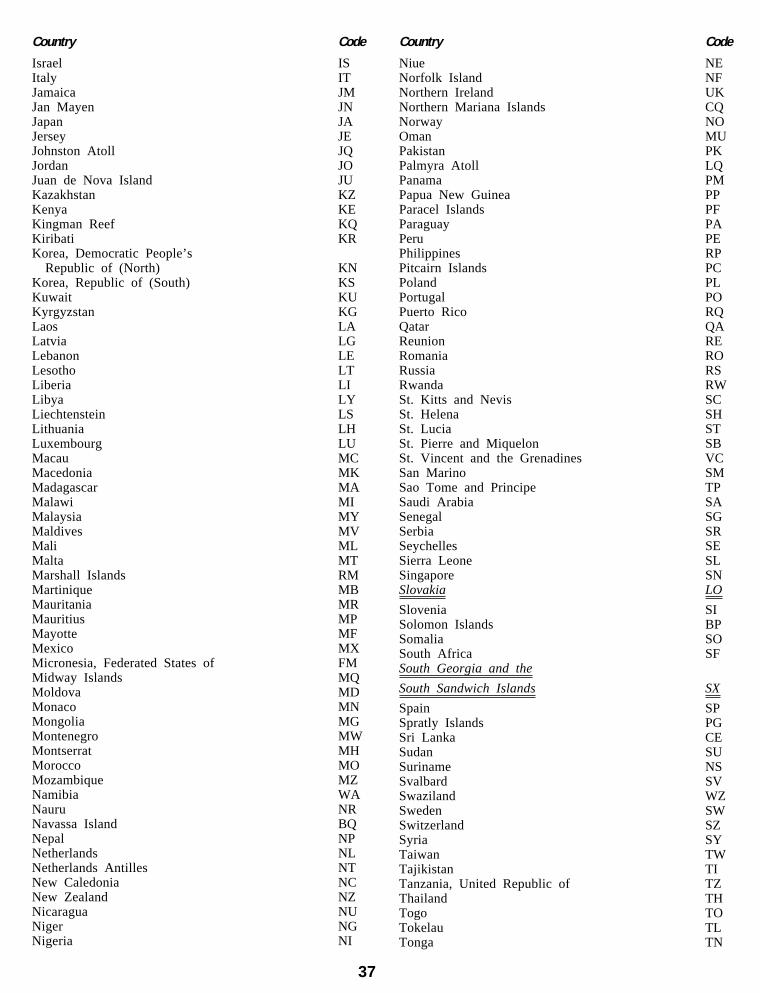

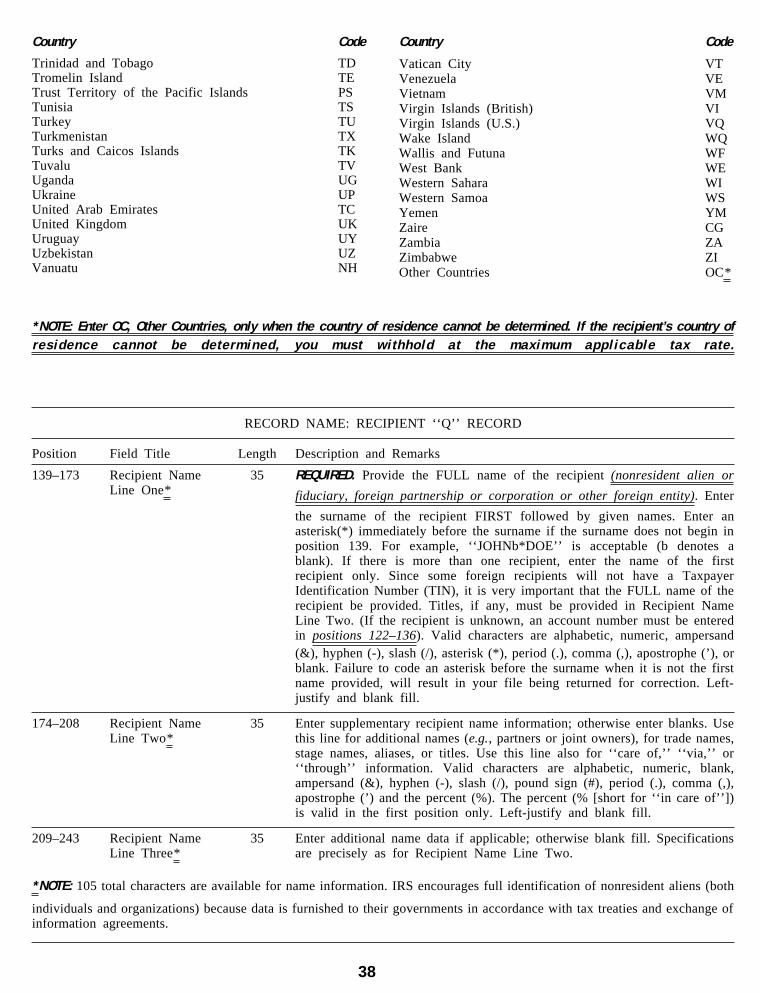

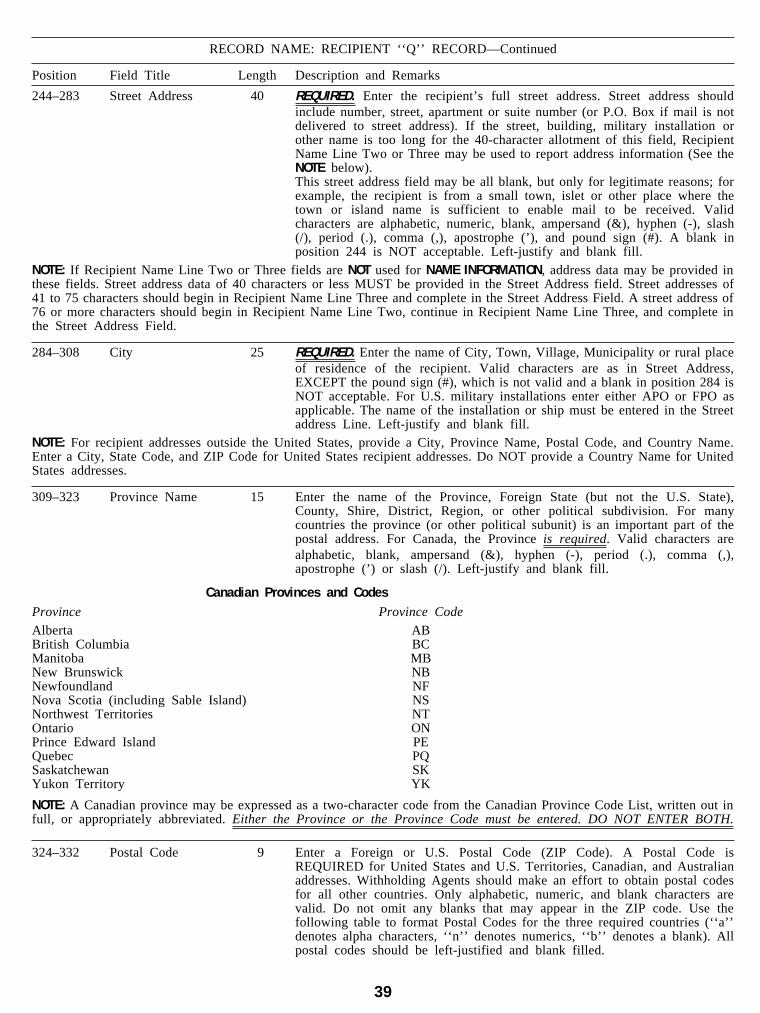

Rev. Proc. 96–11, page 18.Electronic filing; magnetic media; 1995 Form 1042Sspecifications. Specifications are set forth for themagnetic or electronic filing of 1995 From 1042–S. Theform may be filed with the Service using 1⁄2 inchmagnetic tape; IBM 3480/3490 or AS400 compatibletape cartridges; or 51⁄4-, 31⁄2-inch diskettes. Rev. Proc.93–16 superseded.

(Continued on page 4)

Finding Lists begin on page 60.

SEQ 0025 JOB L47-002-002 PAGE-0002 MISSION REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-002

2

Mission of the ServiceThe purpose of the Internal Revenue Service is tocollect the proper amount of tax revenue at the leastcost; serve the public by continually improving the

quality of our products and services; and perform in amanner warranting the highest degree of publicconfidence in our integrity, efficiency and fairness.

Statement of Principlesof Internal RevenueTax AdministrationThe function of the Internal Revenue Service is toadminister the Internal Revenue Code. Tax policyfor raising revenue is determined by Congress.

With this in mind, it is the duty of the Service tocarry out that policy by correctly applying the lawsenacted by Congress; to determine the reasonablemeaning of various Code provisions in light of theCongressional purpose in enacting them; and toperform this work in a fair and impartial manner,with neither a government nor a taxpayer point ofview.

At the heart of administration is interpretation of theCode. It is the responsibility of each person in theService, charged with the duty of interpreting thelaw, to try to find the true meaning of the statutoryprovision and not to adopt a strained construction inthe belief that he or she is ‘‘protecting the revenue.’’The revenue is properly protected only when we as-certain and apply the true meaning of the statute.

The Service also has the responsibility of applyingand administering the law in a reasonable,practical manner. Issues should only be raised byexamining officers when they have merit, neverarbitrarily or for trading purposes. At the sametime, the examining officer should never hesitateto raise a meritorious issue. It is also importantthat care be exercised not to raise an issue or toask a court to adopt a position inconsistent withan established Service position.

Administration should be both reasonable andvigorous. It should be conducted with as littledelay as possible and with great courtesy andconsiderateness. It should never try to overreach,and should be reasonable within the bounds of lawand sound administration. It should, however, bevigorous in requiring compliance with law and itshould be relentless in its attack on unreal taxdevices and fraud.

SEQ 0026 JOB L47-002-002 PAGE-0003 MISSION REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-002

3

IntroductionThe Internal Revenue Bulletin is the authoritativeinstrument of the Commissioner of Internal Revenue forannouncing official rulings and procedures of theInternal Revenue Service and for publishing TreasuryDecisions, Executive Orders, Tax Conventions, legisla-tion, court decisions, and other items of generalinterest. It is published weekly and may be obtainedfrom the Superintendent of Documents on a subscrip-tion basis. Bulletin contents of a permanent nature areconsolidated semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletinall substantive rulings necessary to promote a uniformapplication of the tax laws, including all rulings thatsupersede, revoke, modify, or amend any of thosepreviously published in the Bulletin. All publishedrulings apply retroactively unless otherwise indicated.Procedures relating solely to matters of internalmanagement are not published; however, statements ofinternal practices and procedures that affect the rightsand duties of taxpayers are published.

Revenue rulings represent the conclusions of theService on the application of the law to the pivotal factsstated in the revenue ruling. In those based onpositions taken in rulings to taxpayers or technicaladvice to Service field offices, identifying details andinformation of a confidential nature are deleted toprevent unwarranted invasions of privacy and to complywith statutory requirements.

Rulings and procedures reported in the Bulletin do nothave the force and effect of Treasury DepartmentRegulations, but they may be used as precedents.Unpublished rulings will not be relied on, used, or citedas precedents by Service personnel in the disposition ofother cases. In applying published rulings and proce-dures, the effect of subsequent legislation, regulations,court decisions, rulings, and procedures must beconsidered, and Service personnel and others con-cerned are cautioned against reaching the sameconclusions in other cases unless the facts andcircumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based onprovisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows:Subpart A, Tax Conventions, and Subpart B, Legislationand Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellanous.To the extent practicable, pertinent cross references tothese subjects are contained in the other Parts andSubparts. Also included in this part are Bank SecrecyAct Administrative Rulings. Bank Secrecy Act Admin-istrative Rulings are issued by the Department of theTreasury’s Office of the Assistant Secretary(Enforcement).

Part IV.—Items of General Interest.With the exception of the Notice of Proposed Rulemak-ing and the disbarment and suspension list included inthis part, none of these announcements are consoli-dated in the Cumulative Bulletins.

The first Bulletin for each month includes an index forthe matters published during the preceding month.These monthly indexes are cumulated on a quarterlyand semiannual basis, and are published in the firstBulletin of the succeeding quarterly and semi-annualperiod, respectively.

The Bulletin Index-Digest System, a research andreference service supplementing the Bulletin, may beobtained from the Superintendent of Documents on asubscription basis. It consists of four Services: ServiceNo. 1, Income Tax; Service No. 2, Estate and GiftTaxes; Service No. 3, Employment Taxes; Service No.4, Excise Taxes. Each Service consists of a basicvolume and a cumulative supplement that provides (1)finding lists of items published in the Bulletin, (2)digests of revenue rulings, revenue procedures, andother published items, and (3) indexes of Public Laws,Treasury Decisions, and Tax Conventions.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents U.S. Government Printing Office, Washington, D.C. 20402.

SEQ 0024 JOB L47-001-008 PAGE-0004 COVER REVISED 28MAY96 AT 09:36 BY LR DEPTH: 66.04 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-001

4

HIGHLIGHTSOF THIS ISSUE—Continued

ADMINISTRATIVE—Continued

T.D. 8640, page 10.Final regulations under section 6033 of the Code thatexempt certain integrated auxiliaries of churches fromfiling information returns.

Announcement 96–1, page 57.Executors and return preparers should continue to usethe August 1993 revision of Form 706, United StatesEstate (and Generation-Skipping Transfer) Tax Return,after December 31, 1995. The Service anticipates thata revised Form 706 will be available in early 1996.

SEQ 0027 JOB L47-003-008 PAGE-0005 PT 1 PGS 5- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-003

5

Part I. Rulings and Decisions Under the Internal Revenue Code of 1986

Section 42.—Low-Income HousingCredit

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

Section 170.—Charitable, etc.,contributions and gifts

26 CFR 1.170A–1: Charitable, etc.,contributions and gifts; allowance ofdeduction.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, page 14.

26 CFR 1.170A–6: Charitable contributions intrust.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which holds thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, page 14.

Section 280G.—Golden ParachutePayments

Federal short-term, mid-term, and long-termrates are set forth for the month of January 1996.See Rev. Rul. 96–6, page 8.

Section 382.—Limitation on NetOperating Loss Carryforwards andCertain Built-In Losses FollowingOwnership Change

The adjusted federal long-term rate is set forthfor the month of January 1996. See Rev. Rul.96–6, page 8.

Section 412.—Minimum FundingStandards

The adjusted applicable federal short-term,

mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

Section 467.—Certain Payments forthe Use of Property or Services

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

Section 468.—Special Rules forMining and Solid Waste Reclamationand Closing Costs

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

Section 483.—Interest on CertainDeferred Payments

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

Section 642.—Special rules forcredits and deductions

26 CFR 1.642(c)–6: Valuation of a remainderinterest in property transferred to a pooledincome fund after April 30, 1989.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, page 14.

Section 664.—Charitable remaindertrusts

26 CFR 1.664–1: Charitable remainder trusts.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time of

the transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, page 14.

Section 807.—Rules for CertainReserves

Insurance companies; interest ratetables. Prevailing state assumed inter-est rates are provided for the deter-mination of reserves under section 807of the Code for contracts issued in1995 and 1996. Rev. Rul. 92–19supplemented in part.

Rev. Rul. 96–2

For purposes of § 807(d)(4) of theInternal Revenue Code, for taxableyears beginning after December 31,1994, this ruling supplements theschedules of prevailing state assumedinterest rates set forth in Rev. Rul. 92–19, 1992–1 C.B. 227. This informationis to be used by insurance companies incomputing their reserves for (1) lifeinsurance and supplementary total andpermanent disability benefits, (2) indi-vidual annuities and pure endowments,and (3) group annuities and pureendowments. As § 807(d)(2)(B) re-quires that the interest rate used tocompute these reserves be the greaterof (1) the applicable federal interestrate, or (2) the prevailing state assumedinterest rate, the table of applicablefederal interest rates in Rev. Rul. 92–19 is also supplemented.

Following are supplements to sched-ules A, B, C, and D to Part III of Rev.Rul. 92–19, providing prevailing stateassumed interest rates for insuranceproducts with different features issuedin 1995 and 1996, and a supplement tothe table in Part IV of Rev. Rul. 92–19,providing the applicable federal interestrate under § 807(d) for 1995 and 1996.This ruling does not supplement Parts Iand II of Rev. Rul. 92–19.

This is the fourth supplement to theinterest rates provided in Rev. Rul. 92–19. Earlier supplements were publishedin Rev. Rul. 93–58, 1993–2 C.B. 241(interest rates for insurance productsissued in 1992 and 1993), Rev. Rul.94–11, 1994–1 C.B. 196 (1993 and1994), and Rev. Rul. 95–4, 1995–1C.B. 141 (1994 and 1995).

SEQ 0028 JOB L47-003-008 PAGE-0006 PT 1 PGS 5- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 41 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-003

6

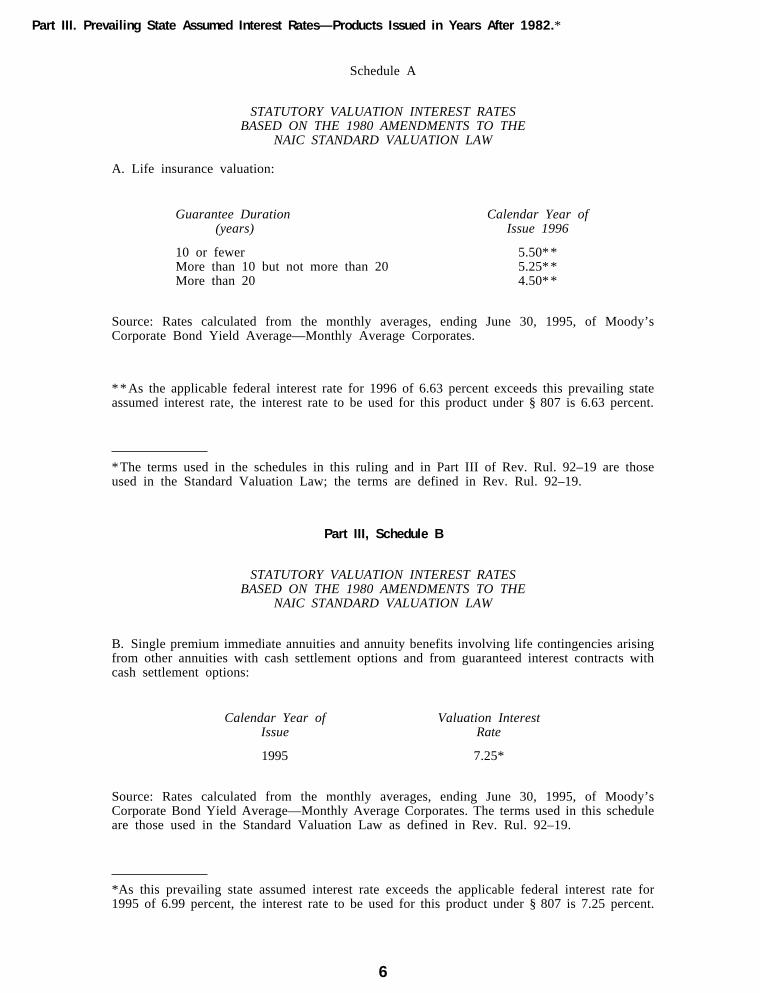

Part III. Prevailing State Assumed Interest Rates—Products Issued in Years After 1982.*

Schedule A

STATUTORY VALUATION INTEREST RATESBASED ON THE 1980 AMENDMENTS TO THE

NAIC STANDARD VALUATION LAW

A. Life insurance valuation:

Guarantee Duration(years)

Calendar Year ofIssue 1996

10 or fewer 5.50**More than 10 but not more than 20 5.25**More than 20 4.50**

Source: Rates calculated from the monthly averages, ending June 30, 1995, of Moody’sCorporate Bond Yield Average—Monthly Average Corporates.

**As the applicable federal interest rate for 1996 of 6.63 percent exceeds this prevailing stateassumed interest rate, the interest rate to be used for this product under § 807 is 6.63 percent.

*The terms used in the schedules in this ruling and in Part III of Rev. Rul. 92–19 are thoseused in the Standard Valuation Law; the terms are defined in Rev. Rul. 92–19.

Part III, Schedule B

STATUTORY VALUATION INTEREST RATESBASED ON THE 1980 AMENDMENTS TO THE

NAIC STANDARD VALUATION LAW

B. Single premium immediate annuities and annuity benefits involving life contingencies arisingfrom other annuities with cash settlement options and from guaranteed interest contracts withcash settlement options:

Calendar Year ofIssue

Valuation InterestRate

1995 7.25*

Source: Rates calculated from the monthly averages, ending June 30, 1995, of Moody’sCorporate Bond Yield Average—Monthly Average Corporates. The terms used in this scheduleare those used in the Standard Valuation Law as defined in Rev. Rul. 92–19.

*As this prevailing state assumed interest rate exceeds the applicable federal interest rate for1995 of 6.99 percent, the interest rate to be used for this product under § 807 is 7.25 percent.

SEQ 0029 JOB L47-003-008 PAGE-0007 PT 1 PGS 5- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-003

7

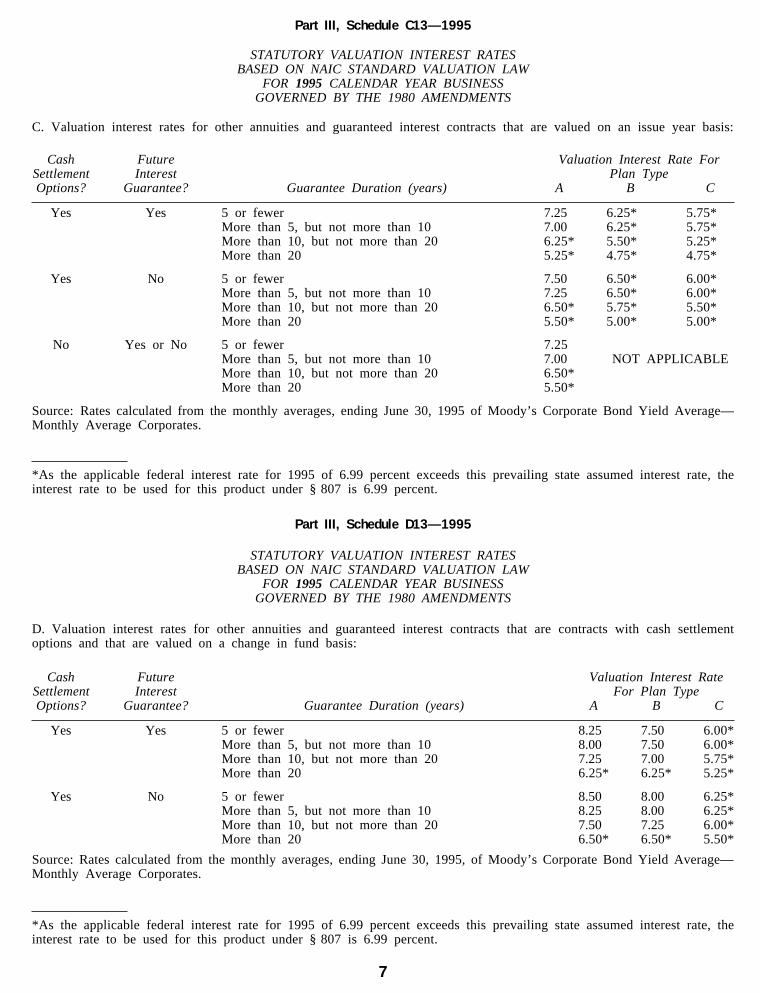

Part III, Schedule C13—1995

STATUTORY VALUATION INTEREST RATESBASED ON NAIC STANDARD VALUATION LAW

FOR 1995 CALENDAR YEAR BUSINESSGOVERNED BY THE 1980 AMENDMENTS

C. Valuation interest rates for other annuities and guaranteed interest contracts that are valued on an issue year basis:

CashSettlementOptions?

FutureInterest

Guarantee? Guarantee Duration (years)

Valuation Interest Rate ForPlan Type

A B C

Yes Yes 5 or fewer 7.25 6.25* 5.75*More than 5, but not more than 10 7.00 6.25* 5.75*More than 10, but not more than 20 6.25* 5.50* 5.25*More than 20 5.25* 4.75* 4.75*

Yes No 5 or fewer 7.50 6.50* 6.00*More than 5, but not more than 10 7.25 6.50* 6.00*More than 10, but not more than 20 6.50* 5.75* 5.50*More than 20 5.50* 5.00* 5.00*

No Yes or No 5 or fewer 7.25 More than 5, but not more than 10 7.00 NOT APPLICABLEMore than 10, but not more than 20 6.50*More than 20 5.50*

Source: Rates calculated from the monthly averages, ending June 30, 1995 of Moody’s Corporate Bond Yield Average—Monthly Average Corporates.

*As the applicable federal interest rate for 1995 of 6.99 percent exceeds this prevailing state assumed interest rate, theinterest rate to be used for this product under § 807 is 6.99 percent.

Part III, Schedule D13—1995

STATUTORY VALUATION INTEREST RATESBASED ON NAIC STANDARD VALUATION LAW

FOR 1995 CALENDAR YEAR BUSINESSGOVERNED BY THE 1980 AMENDMENTS

D. Valuation interest rates for other annuities and guaranteed interest contracts that are contracts with cash settlementoptions and that are valued on a change in fund basis:

CashSettlementOptions?

FutureInterest

Guarantee? Guarantee Duration (years)

Valuation Interest RateFor Plan Type

A B C

Yes Yes 5 or fewer 8.25 7.50 6.00*More than 5, but not more than 10 8.00 7.50 6.00*More than 10, but not more than 20 7.25 7.00 5.75*More than 20 6.25* 6.25* 5.25*

Yes No 5 or fewer 8.50 8.00 6.25*More than 5, but not more than 10 8.25 8.00 6.25*More than 10, but not more than 20 7.50 7.25 6.00*More than 20 6.50* 6.50* 5.50*

Source: Rates calculated from the monthly averages, ending June 30, 1995, of Moody’s Corporate Bond Yield Average—Monthly Average Corporates.

*As the applicable federal interest rate for 1995 of 6.99 percent exceeds this prevailing state assumed interest rate, theinterest rate to be used for this product under § 807 is 6.99 percent.

SEQ 0030 JOB L47-003-008 PAGE-0008 PT 1 PGS 5- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-003

8

Part IV. Applicable Federal Interest Rates.

TABLE OFAPPLICABLE FEDERAL INTEREST RATES

FOR PURPOSES OF § 807

Year Interest Rate

1995 6.991996 6.63

Sources: Rev. Rul. 94–73, 1994–2 C.B. 197 for the 1995 rate and Rev. Rul. 95–79, 1995–49I.R.B. 4 (at 6) for the 1996 rate.

EFFECT ON OTHER REVENUERULINGS

Rev. Rul. 92–19 is supplemented bythe addition to Part III of that ruling ofprevailing state assumed interest ratesunder § 807 for certain insurance prod-ucts issued in 1995 and 1996 and isfurther supplemented by an addition tothe table in Part IV of Rev. Rul. 92–19listing applicable federal interest rates.Parts I and II of Rev. Rul. 92–19 arenot affected by this ruling.

DRAFTING INFORMATION

The principal author of this revenueruling is Ann H. Logan of the Office ofAssistant Chief Counsel (Financial In-stitutions and Products). For furtherinformation regarding this revenue rul-ing contact her on (202) 622-3970 (nota toll-free call).

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 00.

Section 846.—Discounted UnpaidLosses Defined

The adjusted applicable federal short-term,mid-term, and long-term rates are set for themonth of January 1996. See Rev. Rul. 96–6,page 00.

Section 1274.—Determination ofIssue Price in the Case of CertainDebt Instruments Issued for Property

(Also Sections 42, 280G, 382, 412, 467, 468,483, 807, 846, 1288, 7520, 7872.)

Federal rates; adjusted federalrates; adjusted federal long-term rate,and the long-term exempt rate. Forpurposes of sections 1274, 1288, 382,and other sections of the Code, tablesset forth the rates for January 1996.

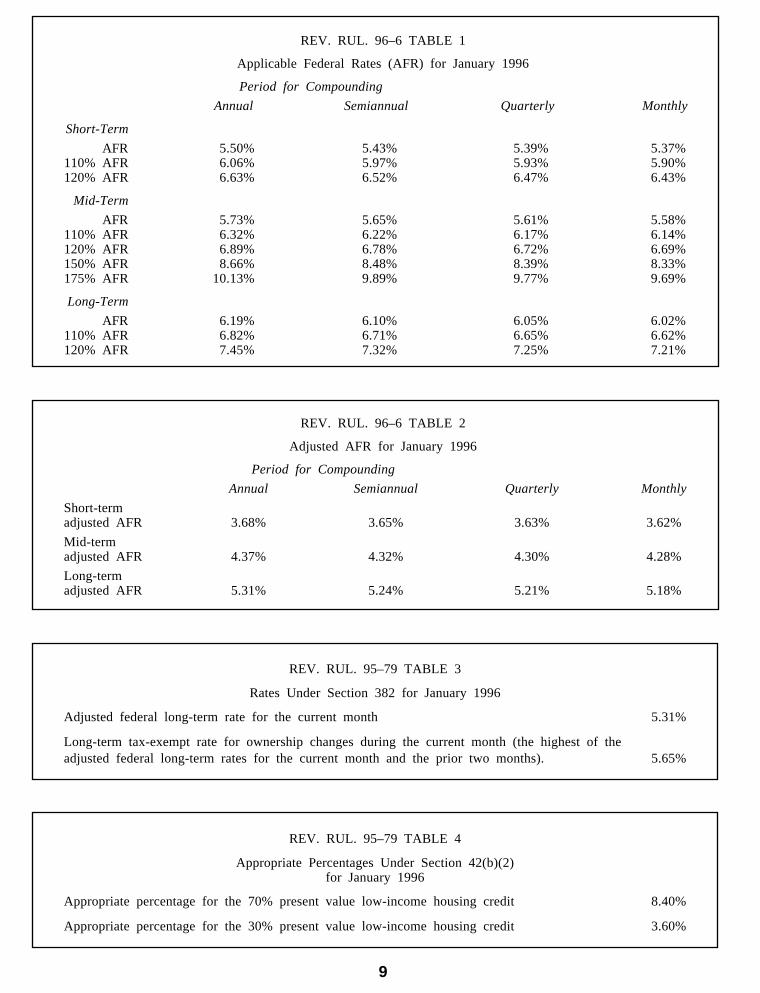

Rev. Rul. 96–6

This revenue ruling provides variousprescribed rates for federal income taxpurposes for January 1996 (the currentmonth). Table 1 contains the short-term, mid-term, and long-term applica-ble federal rates (AFR) for the current

month for purposes of section 1274(d)of the Internal Revenue Code. Table 2contains the short-term, mid-term, andlong-term adjusted applicable federalrates (adjusted AFR) for the currentmonth for purposes of section 1288(b).Table 3 sets forth the adjusted federallong-term rate and the long-term tax-exempt rate described in section 382(f).Table 4 contains the appropriate per-centages for determining the low-income housing credit described insection 42(b)(2) for buildings placed inservice during the current month. Fi-nally, Table 5 contains the federal ratefor determining the present value of anannuity, an interest for life or for aterm of years, or a remainder or areversionary interest for purposes ofsection 7520.

Rev. Rul. 95–79, 1995–49 I.R.B. 4,which set forth the applicable federalrates and various other rates for De-cember 1995, incorrectly provided inTable 1 that the Long-Term 120%Applicable Federal Rate based onannual compounding was 7.01%. Thecorrect percentage is 7.65%. This cor-rection will be made to Rev. Rul. 95–79 when it is published in issue 1995–2of the Cumulative Bulletin.

SEQ 0031 JOB L47-004-008 PAGE-0009 PT 1 PGS 9- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 45.01 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-004

9

REV. RUL. 96–6 TABLE 1

Applicable Federal Rates (AFR) for January 1996

Period for Compounding

Annual Semiannual Quarterly Monthly

Short-Term

AFR 5.50% 5.43% 5.39% 5.37%110% AFR 6.06% 5.97% 5.93% 5.90%120% AFR 6.63% 6.52% 6.47% 6.43%

Mid-Term

AFR 5.73% 5.65% 5.61% 5.58%110% AFR 6.32% 6.22% 6.17% 6.14%120% AFR 6.89% 6.78% 6.72% 6.69%150% AFR 8.66% 8.48% 8.39% 8.33%175% AFR 10.13% 9.89% 9.77% 9.69%

Long-Term

AFR 6.19% 6.10% 6.05% 6.02%110% AFR 6.82% 6.71% 6.65% 6.62%120% AFR 7.45% 7.32% 7.25% 7.21%

REV. RUL. 96–6 TABLE 2

Adjusted AFR for January 1996

Period for Compounding

Annual Semiannual Quarterly Monthly

Short-termadjusted AFR 3.68% 3.65% 3.63% 3.62%

Mid-termadjusted AFR 4.37% 4.32% 4.30% 4.28%

Long-termadjusted AFR 5.31% 5.24% 5.21% 5.18%

REV. RUL. 95–79 TABLE 3

Rates Under Section 382 for January 1996

Adjusted federal long-term rate for the current month 5.31%

Long-term tax-exempt rate for ownership changes during the current month (the highest of theadjusted federal long-term rates for the current month and the prior two months). 5.65%

REV. RUL. 95–79 TABLE 4

Appropriate Percentages Under Section 42(b)(2)for January 1996

Appropriate percentage for the 70% present value low-income housing credit 8.40%

Appropriate percentage for the 30% present value low-income housing credit 3.60%

SEQ 0032 JOB L47-004-008 PAGE-0010 PT 1 PGS 9- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-004

10

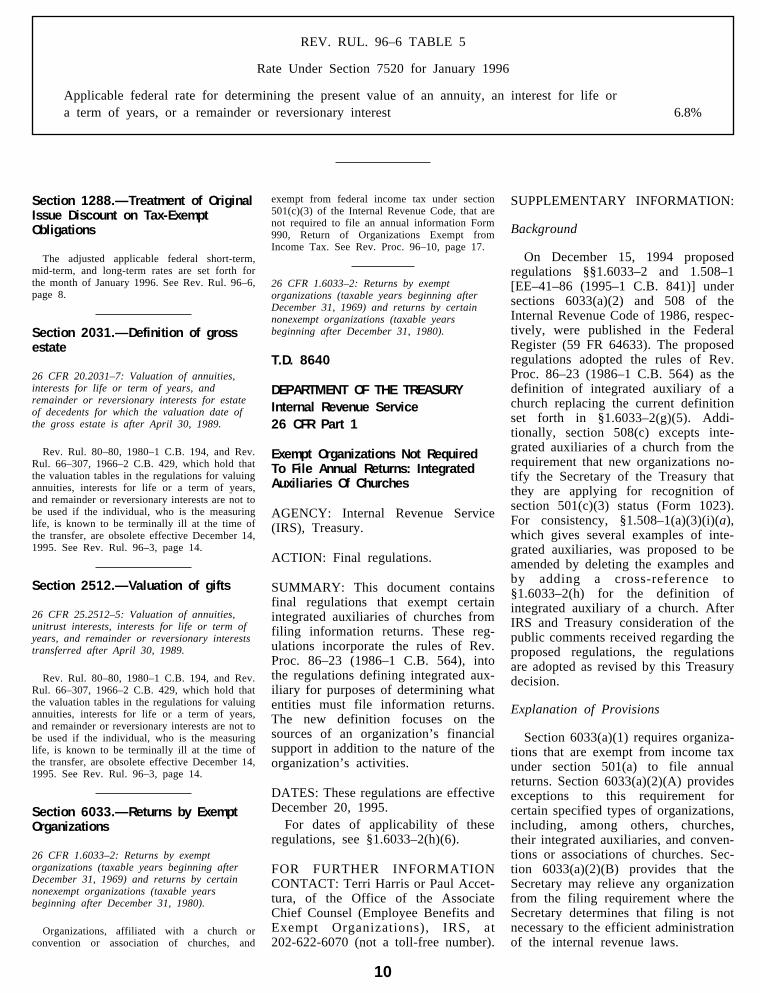

REV. RUL. 96–6 TABLE 5

Rate Under Section 7520 for January 1996

Applicable federal rate for determining the present value of an annuity, an interest for life ora term of years, or a remainder or reversionary interest 6.8%

Section 1288.—Treatment of OriginalIssue Discount on Tax-ExemptObligations

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

Section 2031.—Definition of grossestate

26 CFR 20.2031–7: Valuation of annuities,interests for life or term of years, andremainder or reversionary interests for estateof decedents for which the valuation date ofthe gross estate is after April 30, 1989.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, page 14.

Section 2512.—Valuation of gifts

26 CFR 25.2512–5: Valuation of annuities,unitrust interests, interests for life or term ofyears, and remainder or reversionary intereststransferred after April 30, 1989.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, page 14.

Section 6033.—Returns by ExemptOrganizations

26 CFR 1.6033–2: Returns by exemptorganizations (taxable years beginning afterDecember 31, 1969) and returns by certainnonexempt organizations (taxable yearsbeginning after December 31, 1980).

Organizations, affiliated with a church orconvention or association of churches, and

exempt from federal income tax under section501(c)(3) of the Internal Revenue Code, that arenot required to file an annual information Form990, Return of Organizations Exempt fromIncome Tax. See Rev. Proc. 96–10, page 17.

26 CFR 1.6033–2: Returns by exemptorganizations (taxable years beginning afterDecember 31, 1969) and returns by certainnonexempt organizations (taxable yearsbeginning after December 31, 1980).

T.D. 8640

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Exempt Organizations Not RequiredTo File Annual Returns: IntegratedAuxiliaries Of Churches

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document containsfinal regulations that exempt certainintegrated auxiliaries of churches fromfiling information returns. These reg-ulations incorporate the rules of Rev.Proc. 86–23 (1986–1 C.B. 564), intothe regulations defining integrated aux-iliary for purposes of determining whatentities must file information returns.The new definition focuses on thesources of an organization’s financialsupport in addition to the nature of theorganization’s activities.

DATES: These regulations are effectiveDecember 20, 1995.

For dates of applicability of theseregulations, see §1.6033–2(h)(6).

FOR FURTHER INFORMATIONCONTACT: Terri Harris or Paul Accet-tura, of the Office of the AssociateChief Counsel (Employee Benefits andExempt Organizations), IRS, at202-622-6070 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

Background

On December 15, 1994 proposedregulations §§1.6033–2 and 1.508–1[EE–41–86 (1995–1 C.B. 841)] undersections 6033(a)(2) and 508 of theInternal Revenue Code of 1986, respec-tively, were published in the FederalRegister (59 FR 64633). The proposedregulations adopted the rules of Rev.Proc. 86–23 (1986–1 C.B. 564) as thedefinition of integrated auxiliary of achurch replacing the current definitionset forth in §1.6033–2(g)(5). Addi-tionally, section 508(c) excepts inte-grated auxiliaries of a church from therequirement that new organizations no-tify the Secretary of the Treasury thatthey are applying for recognition ofsection 501(c)(3) status (Form 1023).For consistency, §1.508–1(a)(3)(i)(a),which gives several examples of inte-grated auxiliaries, was proposed to beamended by deleting the examples andby adding a cross-reference to§1.6033–2(h) for the definition ofintegrated auxiliary of a church. AfterIRS and Treasury consideration of thepublic comments received regarding theproposed regulations, the regulationsare adopted as revised by this Treasurydecision.

Explanation of Provisions

Section 6033(a)(1) requires organiza-tions that are exempt from income taxunder section 501(a) to file annualreturns. Section 6033(a)(2)(A) providesexceptions to this requirement forcertain specified types of organizations,including, among others, churches,their integrated auxiliaries, and conven-tions or associations of churches. Sec-tion 6033(a)(2)(B) provides that theSecretary may relieve any organizationfrom the filing requirement where theSecretary determines that filing is notnecessary to the efficient administrationof the internal revenue laws.

SEQ 0033 JOB L47-004-008 PAGE-0011 PT 1 PGS 9- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-004

11

Prior to this Treasury decision,§1.6033–2(g)(5)(i) defined the termintegrated auxiliary of a church as anorganization that is: (1) exempt fromtaxation as an organization described insection 501(c)(3); (2) affiliated with achurch (within the meaning of§1.6033–2(g)(5)(iii)); and (3) engagedin a principal activity that is ‘‘ex-clusively religious.’’ Section 1.6033–2(g)(5)(ii) provides that an organi-zation’s principal activity is not‘‘exclusively religious’’ if that activityis educational, literary, charitable, or ofanother nature (other than religious)that would serve as a basis forexemption under section 501(c)(3).

The ‘‘exclusively religious’’ elementof the definition was litigated inLutheran Social Service of Minnesotav. United States, 583 F. Supp. 1298 (D.Minn. 1984), rev’d 758 F.2d 1283 (8thCir. 1985), and Tennessee BaptistChildren’s Homes, Inc. v. UnitedStates, 604 F. Supp. 210 (M.D. Tenn.1984) aff’d, 790 F.2d 534 (6th Cir.1986). While the litigation over the‘‘exclusively religious’’ standard wasproceeding, Congress enacted section3121(w) of the Internal Revenue Code,Tax Reform Act of 1984, Pub. L. 98–369, section 2603(b), 98 Stat. 494,1128 (1984), which permits certainchurch-related organizations to electout of social security coverage if theymeet a standard based on the degree offinancial support they receive from achurch. In light of this litigation andthe enactment of section 3121(w), IRSpersonnel met with representatives ofvarious church organizations to en-courage voluntary compliance with thefiling requirements and to develop aless controversial and more objectivestandard for identifying an integratedauxiliary of a church.

Subsequent to these meetings theIRS published Rev. Proc. 86–23, whichprovides that, for tax years beginningafter December 31, 1975, an organiza-tion is not required to file Form 990 ifit is: (1) described in sections 501(c)(3)and 509(a)(1), (2), or (3); (2) affiliatedwith a church or a convention or as-sociation of churches; and (3) internallysupported. With respect to this lastcriterion, Rev. Proc. 86–23 sets forthan internal support standard that issimilar to the financial support standardin section 3121(w).

The proposed regulations adopted therules of Rev. Proc. 86–23 as thedefinition of the term integrated auxili-ary of a church replacing the currentdefinition set forth in §1.6033–2(g)(5).

The final regulations retain the defini-tion of an integrated auxiliary of achurch that is contained in the pro-posed regulations.

Under this Treasury decision, to bean integrated auxiliary of a church anorganization must first be described insection 501(c)(3) and section 509(a)(1),(2), or (3), and be affiliated with achurch in accordance with standards setforth in the regulations. An organiza-tion meeting those tests is an integratedauxiliary if it either: (1) does not offeradmissions, goods, services, or facili-ties for sale, other than on an incidentalbasis, to the general public; or (2)offers admissions, goods, services, orfacilities for sale, other than on anincidental basis, to the general publicand not more than 50 percent of itssupport comes from a combination ofgovernment sources, public solicitationof contributions, and receipts other thanthose from an unrelated trade orbusiness.

Some commentators have noted thatcertain church-related organizationsthat finance, fund and manage pensionprograms were originally excused fromfiling by Notice 84–2 (1984–1 C.B.331), which was issued pursuant to theCommissioner’s discretionary authorityunder section 6033(a)(2)(B). Rev. Proc.86–23 states that Notice 84–2 issuperseded by Rev. Proc. 86–23 be-cause the organizations excused fromfiling under the notice are excusedfrom filing by the revenue procedure.The commentators have expressed con-cern that the proposed regulations didnot relieve church pension plans de-scribed in Notice 84–2 from the filingrequirement. The organizations excusedfrom filing under Notice 84–2 do notnecessarily meet the definition of anintegrated auxiliary of a church underthese final regulations. Nevertheless,the proposed regulations were notintended to alter the exemption fromfiling provided in Notice 84–2 andreaffirmed in Rev. Proc. 86–23. Tomake this intent clear, the IRS isissuing Revenue Procedure 96–10 atthe same time that it issues these finalregulations. Rev. Proc. 96–10 carriesover the exemption from filing forchurch pension plan organizations thatwas set forth in Notice 84–2. Havingreaffirmed those parts of Rev. Proc.86–23 that were not incorporated intothese final regulations, Rev. Proc. 96–10 also obsoletes Rev. Proc. 86–23.

The IRS developed the internal sup-port test contained in the proposed

regulations based on its conclusion thatCongress intended that organizationsreceiving a majority of their supportfrom public and government sources, asopposed to those receiving a majorityof their support from church sources,should file annual information returnsin order that the public have a meansof inspecting the returns of theseorganizations. The annual informationreturn also was intended to serve as ameans by which the IRS could ex-amine, if necessary, those organizationsreceiving substantial non-churchsupport.

One commentator has suggested thatthe definition of an integrated auxiliaryof a church should consist of a church-related structural test rather than aninternal support test. The IRS and theTreasury Department believe that theuse of a structural test could lead toproblems similar to those caused by the‘‘exclusively religious’’ test. Addi-tionally, the suggested definition wouldfrustrate Congress’ intended objectiveof allowing ongoing public scrutiny oforganizations receiving the majoritytheir support from public and govern-ment sources.

A commentator has also suggestedthat by using the internal support testas part of the new definition of anintegrated auxiliary of a church, theIRS is attempting to ‘‘overrule’’ theholdings in the previously mentionedcourt cases (i.e. Tennessee BaptistChildren’s Home and Lutheran SocialService of Minnesota). The IRS and theTreasury Department believe that thecourts’ rulings questioned the validityof the ‘‘exclusively religious’’ activityrequirement contained in the formerregulation on the basis that it is notwithin the Service’s discretion to assessthe religious nature of a church’sactivities. Having eliminated the ‘‘ex-clusively religious’’ activity test fromthe definition of integrated auxiliary ofa church, the IRS and the TreasuryDepartment believe that the definitionin the final regulation is consistent withthe courts’ holdings as well as thestatute and the legislative history.

Some commentators have suggestedthat the first sentence of §1.6033–2(g)(5)(iv) of the regulations in effectprior to this Treasury decision shouldbe included in the final regulations.That sentence identified specific typesof organizations as integrated auxili-aries of churches in accordance withlegislative history. Although §1.6033–2(h) of the proposed regulations was

SEQ 0034 JOB L47-004-008 PAGE-0012 PT 1 PGS 9- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-004

12

intended to provide a general definitionthat could apply in all instances, theIRS and the Treasury Department agreethat, in order to be consistent with thelegislative history, parts of §1.6033–2(g)(5)(iv) of the regulations should beincluded in these final regulations.Therefore, these final regulations in-clude §1.6033–2(h)(5) that states that‘‘a men’s or women’s organization, aseminary, a mission society, or a youthgroup’’ is an integrated auxiliary of achurch regardless of whether it meetsthe internal support test in to §1.6033–2(h)(1)(iii). (The tests under §1.6033–2(h)(1)(i) and (ii) must still be met.)

Comments were received objectingthat Example 4 relating to seminariesdid not describe a realistic set of factsand, therefore, could lead to confusion.Accordingly, Example 4 has beeneliminated. Also, the treatment of semi-naries has been clarified by §1.6033–2(h)(5). We also note that, in additionto the exception for seminaries,§1.6033–2(g)(1)(vii) of the regulationsexcepts certain schools below collegelevel that are affiliated with a church oroperated by a religious order from thefiling requirements of section 6033.Except for a paragraph numberingchange contained in a cross-reference,§1.6033–2(g)(1)(vii) is unchanged bythese final regulations.

Several commentators have sug-gested that expanded definitions ofcertain terms used in the internalsupport test be included in this Treas-ury decision. The final regulations donot incorporate this suggestion. TheIRS and the Treasury Departmentintend for these final regulations toreissue the test published in Rev. Proc.86–23 as the new definition for anintegrated auxiliary of a church. Ifguidance is necessary on the applica-tion of the definition to specific cases,that guidance is more appropriatelyprovided in non-regulatory form, suchas through private letter rulings orrevenue rulings.

The amendment to §1.6033–2(g)(5)is effective with respect to returns filedfor taxable years beginning after De-cember 31, 1969. However, for returnsfiled for taxable years beginning afterDecember 31, 1969, but before Decem-ber 20, 1995, the exclusively religioustest contained in §1.6033–2(g)(5) priorto its amendment by these final regula-tions may, at the entity’s option, beused as an alternative to the financialsupport test in determining whether anentity is an integrated auxiliary of a

church. The remainder of the amend-ments are effective with respect toreturns for taxable years beginningafter December 31, 1969. Therefore,for returns filed for taxable yearsbeginning after December 20, 1995, thedefinition of integrated auxiliary of achurch contained in §1.6033–2(h) willbe used in determining whether anentity is an integrated auxiliary of achurch.

Special Analyses

It has been determined that thisTreasury decision is not a significantregulatory action as defined in EO12866. Therefore, a regulatory assess-ment is not required. It has also beendetermined that section 553(b) of theAdministrative Procedure Act (5 U.S.C.chapter 5) and the Regulatory Flex-ibility Act (5 U.S.C. chapter 6) do notapply to these regulations, and, there-fore, Regulatory Flexibility Analysis isnot required. Pursuant to section7805(f) of the Internal Revenue Code,the notice of proposed rulemakingpreceding these regulations was submit-ted to the Chief Counsel for Advocacyof the Small Business Administrationfor comment on its impact on smallbusiness.

Drafting Information

The principal author of this Treasurydecision is Terri Harris, Office of theAssociate Chief Counsel (EmployeeBenefits and Exempt Organizations),IRS. However, personnel from otheroffices of the IRS and the TreasuryDepartment participated in theirdevelopment.

* * * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 isamended as follows:

PART 1—INCOME TAXES

Paragraph l. The authority for part 1continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *Par. 2. Section 1.508–1 is amended

by revising paragraphs (a)(3)(i) intro-ductory text and (a)(3)(i)(a) to read asfollows:

§1.508–1 Notices.

(a) * * *(3) * * * (i) Paragraphs (a)(1) and

(2) of this section are inapplicable tothe following organizations:

(a) Churches, interchurch organiza-tions of local units of a church,conventions or associations ofchurches, or integrated auxiliaries of achurch. See §1.6033–2(h) regarding thedefinition of integrated auxiliary of achurch;

* * * * * *

Par. 3. Section 1.6033–2 is amendedas follows:

1. Paragraphs (g)(1)(i) and (g)(vii)are revised.

2. Paragraph (g)(5) is removed andreserved.

3. Paragraphs (h) through (j) areredesignated as paragraphs (i) through(k).

4. New paragraph (h) is added.The added and revised provisions

read as follows:

§1.6033–2 Returns by exemptorganizations (taxable yearsbeginning after December 31, 1969)and returns by certain nonexemptorganizations (taxable yearsbeginning after December 31, 1980).

* * * * * *

(g) * * * (1) * * * (i) A church, an interchurch organi-

zation of local units of a church, aconvention or association of churches,or an integrated auxiliary of a church(as defined in paragraph (h) of thissection);

* * * * * *

(vii) An educational organization(below college level) that is describedin section 170(b)(1)(A)(ii), that has aprogram of a general academic nature,and that is affiliated (within the mean-ing of paragraph (h)(2) of this section)with a church or operated by areligious order.

* * * * * *

(h) Integrated auxiliary—(1) In gen-eral. For purposes of this title, the termintegrated auxiliary of a church meansan organization that is—

(i) Described both in sections501(c)(3) and 509(a)(1), (2), or (3);

SEQ 0035 JOB L47-004-008 PAGE-0013 PT 1 PGS 9- REVISED 28MAY96 AT 09:36 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-004

13

(ii) Affiliated with a church or a con-vention or association of churches; and

(iii) Internally supported.(2) Affiliation. An organization is af-

filiated with a church or a convention orassociation of churches, for purposes ofparagraph (h)(1)(ii) of this section, if—

(i) The organization is covered by agroup exemption letter issued underapplicable administrative procedures,(such as Rev. Proc. 80–27 (1980–1C.B. 677); See §601.601(a)(2)(ii)(b)),to a church or a convention or associa-tion of churches;

(ii) The organization is operated,supervised, or controlled by or inconnection with (as defined in§1.509(a)–4) a church or a conventionor association of churches; or

(iii) Relevant facts and circumstancesshow that it is so affiliated.

(3) Facts and circumstances. Forpurposes of paragraph (h)(2)(iii) of thissection, relevant facts and circum-stances that indicate an organization isaffiliated with a church or a conventionor association of churches include thefollowing factors. However, the ab-sence of one or more of the followingfactors does not necessarily precludeclassification of an organization asbeing affiliated with a church or a con-vention or association of churches—

(i) The organization’s enabling in-strument (corporate charter, trust instru-ment, articles of association, constitu-tion or similar document) or by-lawsaffirm that the organization sharescommon religious doctrines, principles,disciplines, or practices with a churchor a convention or association ofchurches;

(ii) A church or a convention orassociation of churches has the au-thority to appoint or remove, or tocontrol the appointment or removal of,at least one of the organization’sofficers or directors;

(iii) The corporate name of theorganization indicates an institutionalrelationship with a church or a conven-tion or association of churches;

(iv) The organization reports at leastannually on its financial and generaloperations to a church or a conventionor association of churches;

(v) An institutional relationship be-tween the organization and a church ora convention or association of churchesis affirmed by the church, or conven-tion or association of churches, or adesignee thereof; and

(vi) In the event of dissolution, theorganization’s assets are required to bedistributed to a church or a conventionor association of churches, or to anaffiliate thereof within the meaning ofthis paragraph (h).

(4) Internal support. An organizationis internally supported, for purposes ofparagraph (h)(1)(iii) of this section,unless it both—

(i) Offers admissions, goods, serv-ices or facilities for sale, other than onan incidental basis, to the generalpublic (except goods, services, or facil-ities sold at a nominal charge or for aninsubstantial portion of the cost); and

(ii) Normally receives more than 50percent of its support from a combina-tion of governmental sources, publicsolicitation of contributions, and re-ceipts from the sale of admissions,goods, performance of services, orfurnishing of facilities in activities thatare not unrelated trades or businesses.

(5) Special rule . Men’s andwomen’s organizations, seminaries,mission societies, and youth groupsthat satisfy paragraphs (h)(1)(i) and (ii)of this section are integrated auxiliariesof a church regardless of whether suchan organization meets the internalsupport requirement under paragraph(h)(1)(iii) of this section.

(6) Effective date. This paragraph (h)applies for returns filed for taxableyears beginning after December 31,1969. For returns filed for taxableyears beginning after December 31,1969 but beginning before December20, 1995, the definition for the termintegrated auxiliary of a church setforth in §1.6033–2(g)(5) (as containedin the 26 CFR edition revised as ofApril 1, 1995) may be used as analternative definition to such term setforth in this paragraph (h).

(7) Examples of internal support.The internal support test of this para-graph (h) is illustrated by the followingexamples, in each of which it isassumed that the organization’s provi-sion of goods and services does notconstitute an unrelated trade orbusiness:

Example 1. Organization A is described insections 501(c)(3) and 509(a)(2) and is affiliated(within the meaning of this paragraph (h)) with achurch. Organization A publishes a weeklynewspaper as its only activity. On an incidentalbasis, some copies of Organization A’s publica-tion are sold to nonmembers of the church withwhich it is affiliated. Organization A advertisesfor subscriptions at places of worship of thechurch. Organization A is internally supported,

regardless of its sources of financial support,because it does not offer admissions, goods,services, or facilities for sale, other than on anincidental basis, to the general public. Organiza-tion A is an integrated auxiliary.

Example 2. Organization B is a retirementhome described in sections 501(c)(3) and509(a)(2). Organization B is affiliated (within themeaning of this paragraph (h)) with a church.Admission to Organization B is open to allmembers of the community for a fee. Organiza-tion B advertises in publications of generaldistribution appealing to the elderly and main-tains its name on non-denominational listings ofavailable retirement homes. Therefore, Organiza-tion B offers its services for sale to the generalpublic on more than an incidental basis. Organi-zation B receives a cash contribution of $50,000annually from the church. Fees received byOrganization B from its residents total $100,000annually. Organization B does not receive anygovernment support or contributions from thegeneral public. Total support is $150,000($100,000 + $50,000), and $100,000 of that totalis from receipts from the performance of services(66–2/3% of total support). Therefore, Organiza-tion B receives more than 50 percent of itssupport from receipts from the performance ofservices. Organization B is not internally sup-ported and is not an integrated auxiliary.

Example 3. Organization C is a hospital that isdescribed in sections 501(c)(3) and 509(a)(1).Organization C is affiliated (within the meaningof this paragraph (h)) with a church. Organiza-tion C is open to all persons in need of hospitalcare in the community, although most ofOrganization C’s patients are members of thesame denomination as the church with whichOrganization C is affiliated. Organization Cmaintains its name on hospital listings used bythe general public, and participating doctors areallowed to admit all patients. Therefore, Organi-zation C offers its services for sale to the generalpublic on more than an incidental basis. Organi-zation C annually receives $250,000 in supportfrom the church, $1,000,000 in payments frompatients and third party payors (including Medi-care, Medicaid and other insurers) for patientcare, $100,000 in contributions from the public,$100,000 in grants from the federal government(other than Medicare and Medicaid payments)and $50,000 in investment income. Total supportis $1,500,000 ($250,000 + $1,000,000 +$100,000 + $100,000 + $50,000), and $1,200,000($1,000,000 + $100,000 + $100,000) of that totalis support from receipts from the performance ofservices, government sources, and public contri-butions (80% of total support). Therefore,Organization C receives more than 50 percent ofits support from receipts from the performance ofservices, government sources, and public contri-butions. Organization C is not internally sup-ported and is not an integrated auxiliary.

* * * * * *

Margaret Milner Richardson,Commissioner of

Internal Revenue.

Approved November 27, 1995.

Leslie Samuels,Assistant Secretary of

the Treasury.

SEQ 0036 JOB L47-005-007 PAGE-0014 PT 1 PG 14 REVISED 28MAY96 AT 09:37 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-005

14

(Filed by the Office of the Federal Register onDecember 19, 1995, 8:45 a.m., and publishedin the issue of the Federal Register forDecember 20, 1995, 60 F.R. 65550)

Section 7121.—Closing Agreements

26 CFR 301.7121–1: Closing agreements.

What is the method by which a taxpayerrequests early referral of one or more unagreedissues from Examination to Appeals? See Rev.Proc. 96–9, page 15.

Section 7520.—Valuation Tables

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 8.

26 CFR 1.7520–3: Limitation on theapplication of section 7520.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, this page.

26 CFR 20.7520-3: Limitation on theapplication of section 7520.(Also §§ 170, 642, 664, 2031, 2512; 1.170A–1,1.170A–6, 1.642(c)–6, 1.664–1, 20.2031–7,25.2512–5, 1.7520–3, 25.7520–3.)

Valuation of annuities. Interest forlife or a term of years, and remainderand reversionary interests when theindividual, who is the measuring life, isterminally ill. Rev. Ruls. 80–80 and66–307 are obsolete effective Decem-ber 14, 1995.

Rev. Rul. 96–3

Rev. Rul. 80–80, 1980–1 C.B. 194,and Rev. Rul. 66–307, 1966–2 C.B.429, hold that the valuation tables in theregulations for valuing annuities, inter-ests for life or a term of years, andremainder or reversionary interests arenot to be used if the individual, who isthe measuring life, is known to beterminally ill at the time of the transfer.These revenue rulings have been super-seded by § 20.7520–3(b)(3) of theEstate Tax Regulations, effective withrespect to estates of decedents dyingafter December 13, 1995. Similar provi-sions are set forth in §§ 1.7520–3(b)(3)of the Income Tax Regulations and25.7520–3(b)(3) of the Gift Tax Regula-tions. Section 1.7520–3(b)(3) is effectivewith respect to transactions after De-cember 13, 1995 and § 25.7520–3(b)(3)is effective with respect to gifts madeafter December 13, 1995.

EFFECT ON OTHER REVENUERULINGS

Rev. Rul. 80–80, 1980–1 C.B. 194,

and Rev. Rul. 66–307, 1966–2 C.B.429 are obsolete effective December14, 1995.

DRAFTING INFORMATION

The principal author of this revenueruling is William L. Blodgett of theOffice of Assistant Chief Counsel(Passthroughs and Special Industries).For further information regarding thisrevenue ruling contact Mr. Blodgett on(202) 622-3090 (not a toll-free call).

26 CFR 25.7520–3: Limitation on theapplication of section 7520.

Rev. Rul. 80–80, 1980–1 C.B. 194, and Rev.Rul. 66–307, 1966–2 C.B. 429, which hold thatthe valuation tables in the regulations for valuingannuities, interests for life or a term of years,and remainder or reversionary interests are not tobe used if the individual, who is the measuringlife, is known to be terminally ill at the time ofthe transfer, are obsolete effective December 14,1995. See Rev. Rul. 96–3, this page.

Section 7872.—Treatment ofLoans with Below-MarketInterest Rates

The adjusted applicable federal short-term,mid-term, and long-term rates are set forth forthe month of January 1996. See Rev. Rul. 96–6,page 00.

SEQ 0037 JOB L47-006-011 PAGE-0015 PT 3 PGS 15- REVISED 28MAY96 AT 09:39 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-006

15

Part III. Administrative, Procedural, and Miscellaneous

Weighted Average Interest Rate Update

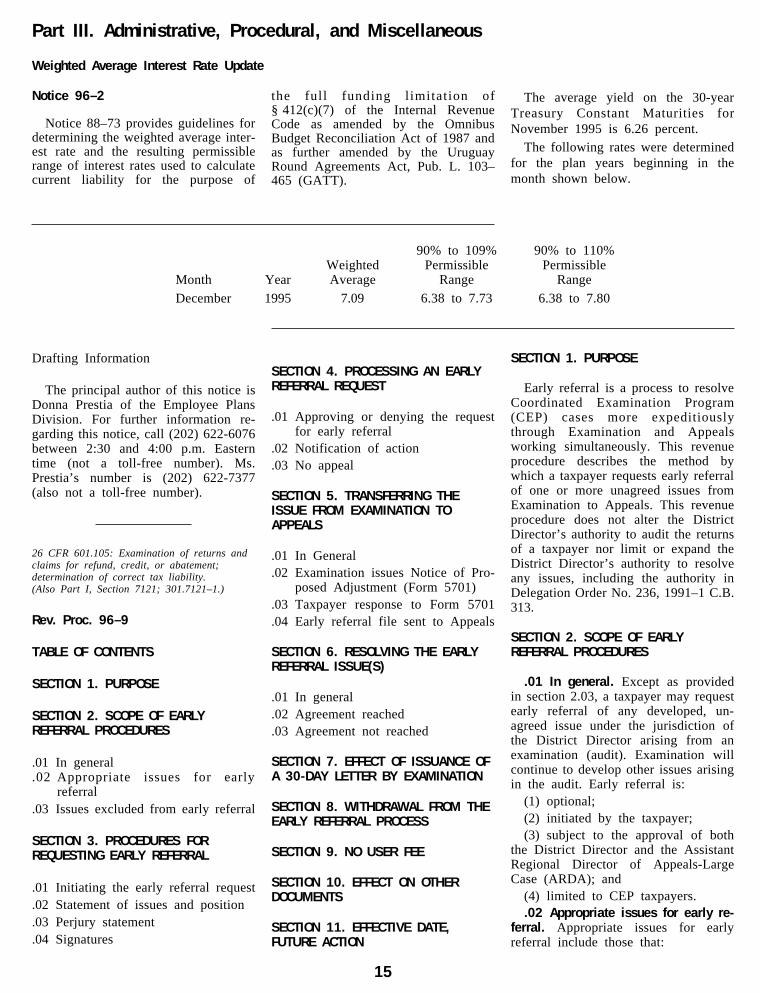

Notice 96–2

Notice 88–73 provides guidelines fordetermining the weighted average inter-est rate and the resulting permissiblerange of interest rates used to calculatecurrent liability for the purpose of

the full funding limitation of§ 412(c)(7) of the Internal RevenueCode as amended by the OmnibusBudget Reconciliation Act of 1987 andas further amended by the UruguayRound Agreements Act, Pub. L. 103–465 (GATT).

The average yield on the 30-yearTreasury Constant Maturities forNovember 1995 is 6.26 percent.

The following rates were determinedfor the plan years beginning in themonth shown below.

Month YearWeightedAverage

90% to 109%Permissible

Range

90% to 110%Permissible

Range

December 1995 7.09 6.38 to 7.73 6.38 to 7.80

Drafting Information

The principal author of this notice isDonna Prestia of the Employee PlansDivision. For further information re-garding this notice, call (202) 622-6076between 2:30 and 4:00 p.m. Easterntime (not a toll-free number). Ms.Prestia’s number is (202) 622-7377(also not a toll-free number).

26 CFR 601.105: Examination of returns andclaims for refund, credit, or abatement;determination of correct tax liability.(Also Part I, Section 7121; 301.7121–1.)

Rev. Proc. 96–9

TABLE OF CONTENTS

SECTION 1. PURPOSE

SECTION 2. SCOPE OF EARLYREFERRAL PROCEDURES

.01 In general

.02 Appropriate issues for earlyreferral

.03 Issues excluded from early referral

SECTION 3. PROCEDURES FORREQUESTING EARLY REFERRAL

.01 Initiating the early referral request

.02 Statement of issues and position

.03 Perjury statement

.04 Signatures

SECTION 4. PROCESSING AN EARLYREFERRAL REQUEST

.01 Approving or denying the requestfor early referral

.02 Notification of action

.03 No appeal

SECTION 5. TRANSFERRING THEISSUE FROM EXAMINATION TOAPPEALS

.01 In General

.02 Examination issues Notice of Pro-posed Adjustment (Form 5701)

.03 Taxpayer response to Form 5701

.04 Early referral file sent to Appeals

SECTION 6. RESOLVING THE EARLYREFERRAL ISSUE(S)

.01 In general

.02 Agreement reached

.03 Agreement not reached

SECTION 7. EFFECT OF ISSUANCE OFA 30-DAY LETTER BY EXAMINATION

SECTION 8. WITHDRAWAL FROM THEEARLY REFERRAL PROCESS

SECTION 9. NO USER FEE

SECTION 10. EFFECT ON OTHERDOCUMENTS

SECTION 11. EFFECTIVE DATE,FUTURE ACTION

SECTION 1. PURPOSE

Early referral is a process to resolveCoordinated Examination Program(CEP) cases more expeditiouslythrough Examination and Appealsworking simultaneously. This revenueprocedure describes the method bywhich a taxpayer requests early referralof one or more unagreed issues fromExamination to Appeals. This revenueprocedure does not alter the DistrictDirector’s authority to audit the returnsof a taxpayer nor limit or expand theDistrict Director’s authority to resolveany issues, including the authority inDelegation Order No. 236, 1991–1 C.B.313.

SECTION 2. SCOPE OF EARLYREFERRAL PROCEDURES

.01 In general. Except as providedin section 2.03, a taxpayer may requestearly referral of any developed, un-agreed issue under the jurisdiction ofthe District Director arising from anexamination (audit). Examination willcontinue to develop other issues arisingin the audit. Early referral is:

(1) optional; (2) initiated by the taxpayer; (3) subject to the approval of both

the District Director and the AssistantRegional Director of Appeals-LargeCase (ARDA); and

(4) limited to CEP taxpayers. .02 Appropriate issues for early re-

ferral. Appropriate issues for earlyreferral include those that:

SEQ 0038 JOB L47-006-011 PAGE-0016 PT 3 PGS 15- REVISED 28MAY96 AT 09:39 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-006

16

(1) if resolved, can reasonably beexpected to result in a quicker re-solution of the entire case; and

(2) both the taxpayer and the DistrictDirector agree should be referred toAppeals early.

Industry Specialization Program(ISP) and Appeals Coordinated Issues(ACIs) can be referred to Appeals forearly resolution under these early refer-ral procedures. ISP issues are listed inExhibit 8700–1 and ACIs are listed inExhibit 8700–4 of the Internal RevenueManual.

.03 Issues excluded from earlyreferral. Early referral does not applyto:

(1) an issue designated for litigationby the Office of Chief Counsel; or

(2) issues for which the taxpayer hasfiled a request for Competent Authorityassistance, or issues for which thetaxpayer intends to seek CompetentAuthority assistance. Taxpayers areencouraged to request the simultaneousAppeals/Competent Authority proce-dure described in section 8 of An-nouncement 95–9, 1995–7 I.R.B. 57 ora subsequent revenue procedure. If ataxpayer enters into a settlement withAppeals (including an Appeals settle-ment through the early referral proc-ess), and then requests CompetentAuthority assistance, the U.S. compe-tent authority will endeavor only toobtain a correlative adjustment with thetreaty country and will not take anyactions that would otherwise amend thesettlement. See section 7.05 of An-nouncement 95–9.

SECTION 3. PROCEDURES FORREQUESTING EARLY REFERRAL

.01 Initiating the early referral re-quest. A request for early referral mustbe submitted in writing by the CEPtaxpayer to the CEP case manager. TheCEP case manager may suggest that aCEP taxpayer make such a request.

.02 Statement of issues and posi-tion. An early referral request must:

(1) state the issues for which earlyreferral is requested;

(2) identify the taxpayer (and, whereapplicable, all related persons involvedin the issue(s)) and the tax period(s) towhich those issues relate; and

(3) describe the taxpayer’s and theService’s position with regard to therelevant early referral issues. This

statement must contain a brief dis-cussion of the material facts and ananalysis of the facts and law as theyapply to the early referral issues.

.03 Perjury Statement. The earlyreferral request, and any supplementalsubmission (including additional docu-ments), must include a declaration inthe following form:

Under penalties of perjury, Ideclare that I have examined thisrequest [or submission], includ-ing accompanying documents,and to the best of my knowledgeand belief, the facts presentedare true, correct, and complete.

This declaration must be signed by anyperson currently authorized to sign thetaxpayer’s federal income tax returns.

.04 Signatures. A request for earlyreferral must be signed by the taxpayeror the taxpayer’s authorized representa-tive. It is preferred that Form 2848,Power of Attorney and Declaration ofRepresentative, be used with regard toan early referral request under thisrevenue procedure.

SECTION 4. PROCESSING AN EARLYREFERRAL REQUEST

.01 Approving or denying the re-quest for early referral. An approval ofan early referral request requires theconcurrence of both the District Direc-tor and the ARDA. The early referralrequest will be processed as follows:

(1) The CEP case manager will sendthe taxpayer’s request for early referralto the District Director. The CEP casemanager also may include a recommen-dation that the early referral request beapproved or denied.

(2) The District Director will notethe district’s approval or denial andforward the request, whether approvedor denied, to the ARDA forconsideration.

(3) The ARDA will note his or herapproval or denial of the early referralrequest and will return the request tothe CEP case manager.

.02 Notification of action. The CEPcase manager will advise the taxpayerof the decision generally within 45days of receipt of the request. If anyissue is approved, the CEP case man-ager will forward the early referral filefor this issue to Appeals as describedin section 5 below. If the request forearly referral is denied with respect to

any issue, the taxpayer retains the rightto pursue the administrative appeal ofany proposed deficiency related to thatissue at a later time.

.03 No Appeal. There is no formaltaxpayer appeal if the early referralrequest is denied in whole or in part;however, the taxpayer can request aconference with the organization(s) thatdenied the early referral request.

SECTION 5. TRANSFERRING THEISSUE FROM EXAMINATION TOAPPEALS

.01 In General. Jurisdiction over theissues accepted will be transferred fromExamination to Appeals, and the proce-dures set forth in sections 5.02 through5.04 will apply.

.02 Examination issues Notice ofProposed Adjustment (Form 5701).Examination will complete a Notice ofProposed Adjustment (Form 5701), foreach approved early referral issue,generally within 30 days after the CEPcase manager advises the taxpayer ofthe approved early referral request.Examination will send the Form 5701to the taxpayer. The Form 5701 willdescribe the issue and explain Ex-amination’s proposed adjustment.

The issuance of the Form 5701 forthe early referral issue is not treated asthe first letter of proposed deficiencyfor purposes of computing increasedinterest under § 6621(c).

.03 Taxpayer response to Form5701. The taxpayer must respond inwriting to Examination’s proposed ad-justment to each issue set forth in theForm 5701. The response must containan explanation of the taxpayer’s posi-tion regarding the issues, similar to thatwhich would be provided in an Appealsprotest. The response shall be submit-ted to the CEP case manager within 30days (unless extended by the CEP casemanager) from the date that the pro-posed adjustment (Form 5701) is sentto the taxpayer. The procedural require-ments of sections 3.03 and 3.04 of thisrevenue procedure (perjury statementand signatures) also apply to thetaxpayer’s response to the Form 5701.If a response is not received for anyissue within the time provided, thetaxpayer’s early referral request will beconsidered withdrawn regarding thatparticular issue without prejudice to thetaxpayer’s right to an administrativeappeal at a later date. See section 8,Withdrawal from the Early Referral

SEQ 0039 JOB L47-006-011 PAGE-0017 PT 3 PGS 15- REVISED 28MAY96 AT 09:39 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-006

17

Process, regarding withdrawal afterAppeals has taken jurisdiction over anearly referral issue.

.04 Early referral file sent to Ap-peals. Once the taxpayer has respondedto the Form 5701, Examination willsend the early referral file to Appeals.Appeals will then take jurisdiction overthe issues accepted for early referral.All other issues in the case remain inExamination’s jurisdiction. The earlyreferral file should include copies of:

(1) applicable portions of tax returnsand workpapers;

(2) the approved early referralrequest;

(3) the Form 5701; (4) the taxpayer’s written response

to the Form 5701;(5) Examination’s response to the

taxpayer’s position, if any; and (6) an estimate of the potential tax

effect of the proposed adjustment.

SECTION 6. RESOLVING THE EARLYREFERRAL ISSUE

.01 In general. The taxpayer’s writ-ten response to the Form 5701 gener-ally serves the same purpose as anAppeals protest. Established Appealsprocedures, including those governingsubmissions and taxpayer conferences,apply to early referral issues. See§ 601.106 et seq of the Statement ofProcedural Rules.

.02 Agreement reached.(1) If an agreement is reached with

respect to an early referral issue, aspecific matters closing agreement(Form 906) will be prepared. See§ 7121 and also Rev. Proc. 68–16,1968–1 C.B. 770, which describes thepreparation of closing agreements. Theclosing agreement will be used tocompute the corrected tax as a partialagreement prior to or concurrently withthe resolution of any other issues in thecase.

(2) If an early referral issue resultsin a refund or credit requiring a reportdescribed in § 6405 that must besubmitted to the Joint Committee onTaxation, the report must include acopy of the proposed closing agreementsigned by or for the taxpayer, but notsigned by or on behalf of the Commis-sioner. The Service will not sign theproposed agreement until after reviewby the Joint Committee.

.03 Agreement not reached. If anagreement is not reached with respectto an early referral issue:

(1) Appeals will close the earlyreferral file and return jurisdiction overthe issue to Examination. Appeals willsend a copy of the Appeals CaseMemorandum for the issue to the CEPcase manager.

(2) Appeals will not reconsider anunagreed early referral issue if theentire case is later protested to Ap-peals, unless there has been a substan-tial change in the circumstances regard-ing the early referral issue.

SECTION 7. EFFECT OF CONCLUSIONOF EXAMINATION

If Examination issues a preliminarynotice of deficiency (‘‘30-day letter’’)with respect to any issue that is notaccepted for early referral, all unagreedissues, including any early referralissues that have not yet been settled byAppeals, will be combined in the 30-day letter. Likewise, if no issues in thecase remain unagreed except for theearly referral issues that are pending inAppeals, a 30-day letter will be issuedsolely with respect to the early referralissues. The issuance of the 30-dayletter generally will constitute the firstletter of proposed deficiency whichallows the taxpayer an opportunity foradministrative review for purposes ofthe increased underpayment rate forlarge corporate underpayments under§ 6621(c).

Except as provided in section6.03(2), once Appeals assumes jurisdic-tion over the case, all issues, includingall early referral issues that have notyet been settled by Appeals, will beconsidered under established Appealsprocedures.

If no issues in the case remainunagreed except for an early referralissue that could not be settled byAppeals and has been returned toExamination, no 30-day letter will beissued. Rather, a statutory notice ofdeficiency (‘‘90-day letter’’) will beissued, which will start the period forthe increased underpayment rate forlarge corporate underpayments under§ 6621(c).

SECTION 8. WITHDRAWAL FROM THEEARLY REFERRAL PROCESS

If the taxpayer withdraws its earlyreferral request with respect to one ormore of the early referral issues afterAppeals has taken jurisdiction over theissues, such withdrawal will be treated

in the same manner as if no agreementof those early referral issues wasreached. See section 6.03, Agreementnot reached. The withdrawal requestmust be communicated in writing to theARDA. See section 5.03, Taxpayerresponse to Form 5701, regarding awithdrawal without prejudice prior toAppeals taking jurisdiction over theissue(s).

SECTION 9. NO USER FEE

There is no user fee for an earlyreferral request.

SECTION 10. EFFECT ON OTHERDOCUMENTS

Announcement 94–41, 1994–12I.R.B. 7, is superseded.

SECTION 11. EFFECTIVE DATE,FUTURE ACTION

This revenue procedure is effectivefor requests for early referral filed afterJanuary 8, 1996, the date this revenueprocedure is published in the InternalRevenue Bulletin. Additional guidancemay be issued to supplement or modifythe procedures set forth in this revenueprocedure in order to extend the earlyreferral program.

DRAFTING INFORMATION

The principal author of this revenueprocedure is Thomas C. Louthan, Di-rector, Office of International, TEFRA,and Dispute Resolution Programs, Na-tional Office Appeals. For furtherinformation regarding this revenue pro-cedure, please contact Mr. Louthan at(202) 401-4098 (not a toll-freenumber).

26 CFR 601.602: Forms and instructions.(Also Part 1, Section 6033; 1.6033–2)

Rev. Proc. 96–10

SECTION 1. PURPOSE

The purpose of this revenue proce-dure is to list a class of organizations,affiliated with a church or conventionor association of churches and exemptfrom federal income tax under section501(c)(3) of the Internal RevenueCode, that is not required to file anannual information return on Form 990,

SEQ 0040 JOB L47-006-011 PAGE-0018 PT 3 PGS 15- REVISED 28MAY96 AT 09:39 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-006

18

Return of Organizations Exempt fromIncome Tax. This revenue proceduresupplements Rev. Proc. 83–23, 1983–1C.B. 687, and obsoletes Rev. Proc. 86–23, 1986–1 C.B. 564.

SEC. 2. BACKGROUND

.01 Section 6033(a)(1) of the Codegenerally requires all tax-exempt orga-nizations to file an annual informationreturn on Form 990.

.02 Section 6033(a)(2)(A) of theCode provides certain mandatory ex-ceptions to this filing requirement,specifically for churches, their inte-grated auxiliaries, and conventions orassociations of churches.

.03 Section 6033(a)(2)(B) of theCode provides discretionary exceptionsfrom filing such returns where theSecretary ‘‘determines such filing isnot necessary to the efficient admin-istration of the internal revenue laws.’’Section 1.6033–2(g)(6) of the IncomeTax Regulations delegates authority tothe Commissioner to excuse organiza-tions from the filing requirement. Itprovides that ‘‘the Commissioner mayrelieve any organization or class oforganizations from filing, in whole orin part, the annual information returnrequired by section 6033 where hedetermines that such returns are notnecessary for the efficient administra-tion of the internal revenue laws.’’

.04 Section 1.6033–2(g)(1) of theregulations provides a partial list oforganizations that are not required tofile annual returns either because theyare excepted by statute or because theCommissioner has exercised the au-thority referred to above in Sec. 2.03.A more complete list is contained inRev. Proc. 83–23, 1983–1 C.B. 687.

.05 A return filing exception forcertain church-affiliated organizationsengaged exclusively in managing fundsor maintaining retirement programs wasannounced originally in Notice 84–2,1984–1 C.B. 331. That exemption wascarried over into Rev. Proc. 86–23,which superseded Notice 84–2. Rev.Proc. 86–23 also defined what is anintegrated auxiliary of a church forpurposes of the filing exceptionprovided in section 6033(a)(2)(A).Treas. Reg. § 1.6033–2(h) now hasincorporated the definition of integratedauxiliary of a church, making Rev.Proc. 86–23 partially obsolete. Accord-ingly, this revenue procedure replacesRev. Proc. 86–23, preserving the filing

exemption that remains in effect forcertain church-affiliated organizationsthat manage funds and retirement pro-grams and deleting those portions ofRev. Proc. 86–23 that are now part ofthe regulations. Some organizationsexempted from filing by this revenueprocedure may also qualify as inte-grated auxiliaries exempt from filingunder section 6033(a)(2)(A).

SEC. 3. ORGANIZATIONSEXCUSED FROM FILING

.01 The following organizations willnot be required to file Form 990:

(1) An organization described insection 501(c)(3) that is operated,supervised, or controlled by one ormore churches, integrated auxiliaries,or conventions or associations ofchurches, and

(a) is engaged exclusively in financ-ing, funding the activities of, or manag-ing the funds of

(i) a church, integrated auxiliary, orconvention or association of churches,or

(ii) a group of organizations substan-tially all of which are described in(1)(a)(i), if substantially all of its assetsare provided by, or held for the benefitof, organizations described in (1)(a)(i);or

(b) maintains retirement insuranceprograms primarily for organizationsdescribed in (1)(a)(i), and

(i) more than 50 percent of theindividuals covered by the programsare directly employed by those organi-zations, or

(ii) more than 50 percent of theassets are contributed by, or held forthe benefit of, employees of thoseorganizations.

(2) An organization described insection 501(c)(3) that is operated,supervised or controlled by one ormore religious orders and is engaged infinancing, funding, or managing assetsused for exclusively religious activities.

.02 For purposes of this revenueprocedure, an integrated auxiliary is anorganization that meets the definitioncontained in Treas. Reg. § 1.6033–2(h).

SEC. 4. EFFECTIVE DATE

This revenue procedure is effectivefor tax years beginning after December20, 1995, the date of publication offinal Treas. Reg. § 1.6033–2(h) in theFederal Register.

SEC. 5. EFFECT ON OTHERDOCUMENTS

Rev. Proc. 83–23 is supplemented.Rev. Proc. 86–23 is rendered obsoleteas of the effective date set forth abovein Sec. 4.

DRAFTING INFORMATION

The principal author of this revenueprocedure is John Francis Reilly of theExempt Organizations Division. Forfurther information regarding this reve-nue procedure contact Mr. Reilly on(202) 622-7352 (not a toll-free call).

26 CFR 601.602: Tax forms and instructions.

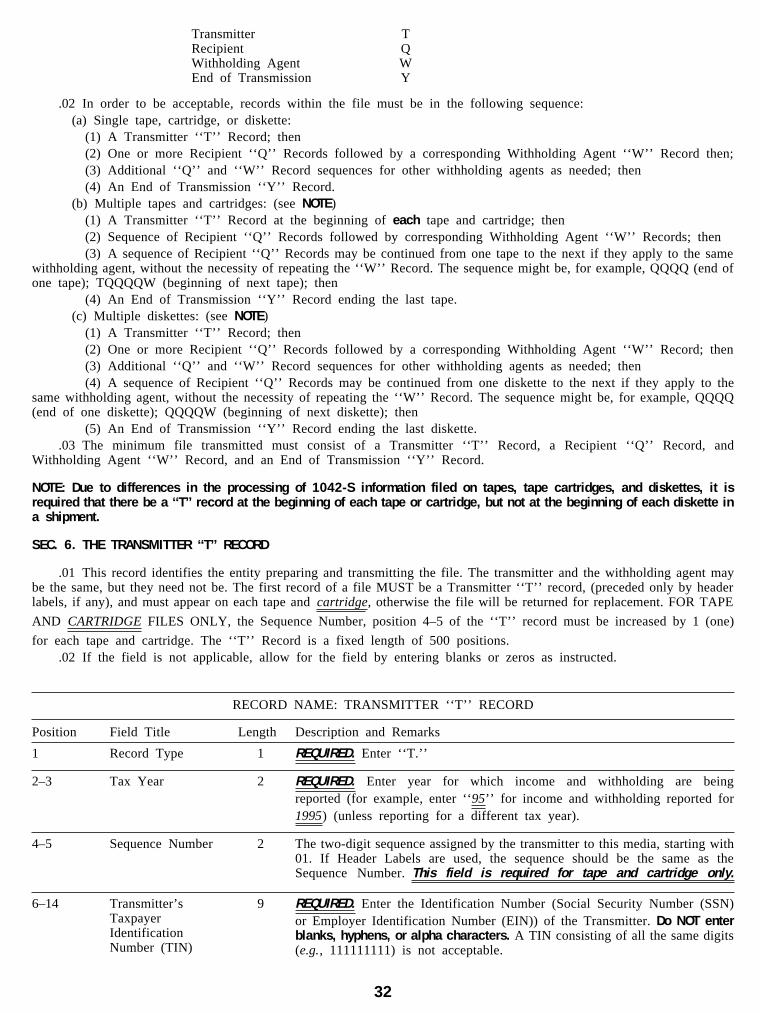

Rev. Proc. 96–11

NOTE: This revenue procedure may beused to prepare Tax Year 1995Form 1042–S for submission to Inter-nal Revenue Service (IRS) using any ofthe following:

Magnetic TapeTape Cartridge

51⁄4-inch Diskette31⁄2-inch DisketteElectronic Filing

*(Bisynchronous)

*(Asynchronous)

Please read this publication carefully.Persons required to file may be sub-ject to penalties for failure to file orfailure to include correct information ifthey do not follow the instructions inthis revenue procedure.

PLEASE NOTE:

ALL CHANGES IN THE PUBLI-C A T I O N , F O R M A T A N DEDITORIAL, HAVE BEEN HIGH-LIGHTED BY THE USE OF ITALICSAND DOUBLE UNDERLINES.

Contents

Part A. General

Section 1. PurposeSection 2. Nature of Changes—

Current year (Tax Year 1995 )

Section 3. Where to File and Howto Contact the IRS Mar-t insburg ComputingCenter (IRS/MCC)

SEQ 0041 JOB L47-007-015 PAGE-0019 PT 3 PGS 19- REVISED 28MAY96 AT 09:39 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/L47-007

19

Section 4. Filing RequirementsSection 5. Form 8508, Request

for Waiver from FilingInformation Returns onMagnetic Media

Section 6. Vendor List

Section 7. Form 4419, Applica-tion for Filing In-formation ReturnsMagnetically/Elec-tronically

Section 8. Test FilesSection 9. Filing of Form 1042–S

Magnetically/Electroni-cally and RetentionRequirements

Section 10. Due DatesSection 11. Extensions of Time to

FileSection 12. Processing of Form

1042–S Magnetically/Electronically

Section 13. Corrected ReturnsSection 14. Effect on Paper Docu-

mentsSection 15. Definition of TermsSection 16. Major Problems En-

countered

Part B. Magnetic Media Specifications

Section 1. GeneralSection 2. Tape SpecificationsSection 3. Tape Cartridge Specifi-

cations

Section 4. 51⁄4- and 31⁄2-Inch Dis-kette Specifications

Section 5. Data Sequence Specifi-cations

Section 6. The Transmitter ‘‘T’’Record

Section 7. Recipient ‘‘Q’’ RecordSection 8. Withholding Agent

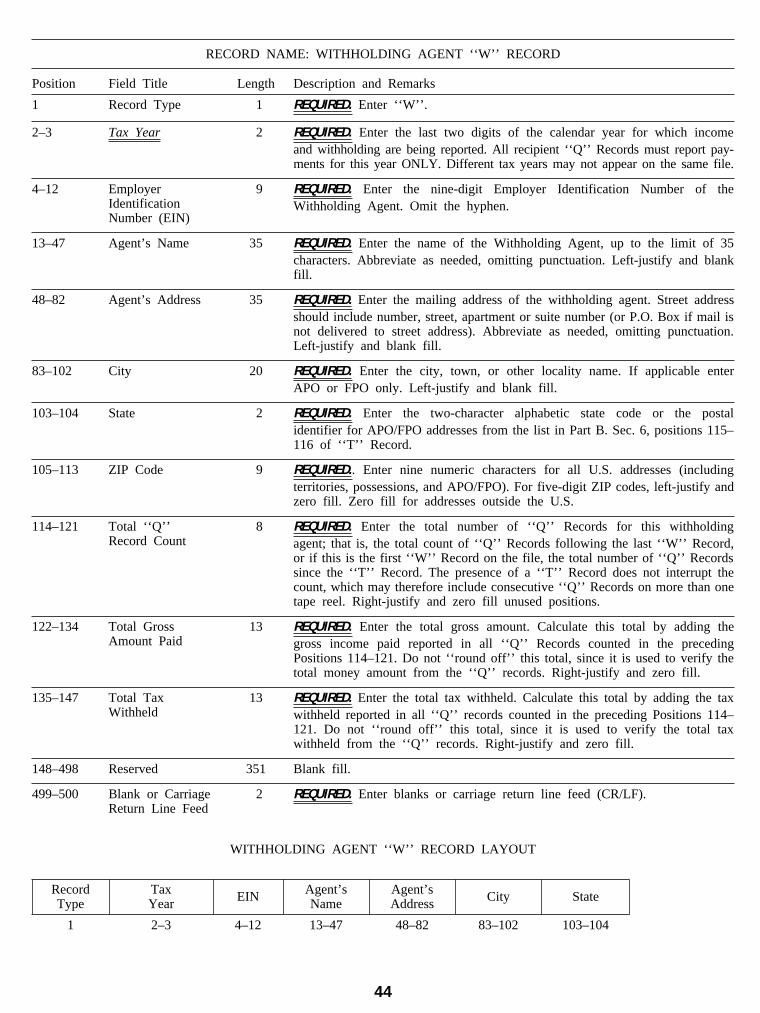

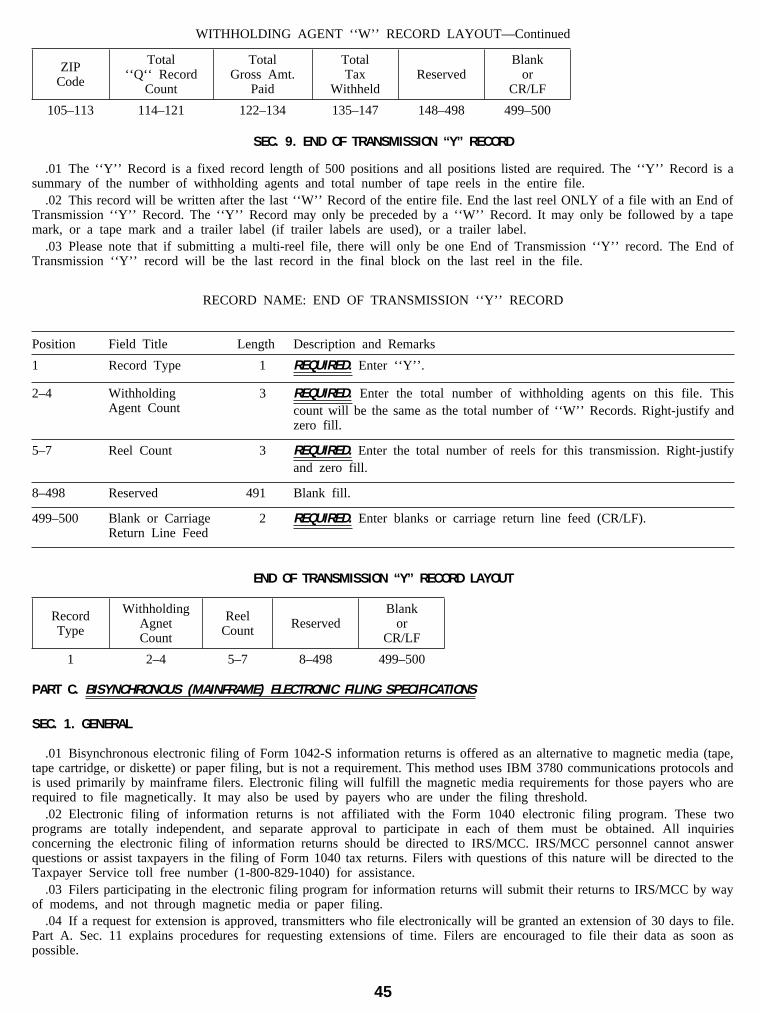

‘‘W’’ RecordSection 9. End of Transmission

‘‘Y’’ Record

Part C. Bisynchronous (Mainframe)

Electronic Filing Specifications

Section 1. General