Embed Size (px)

DESCRIPTION

Business Magazine

Citation preview

1

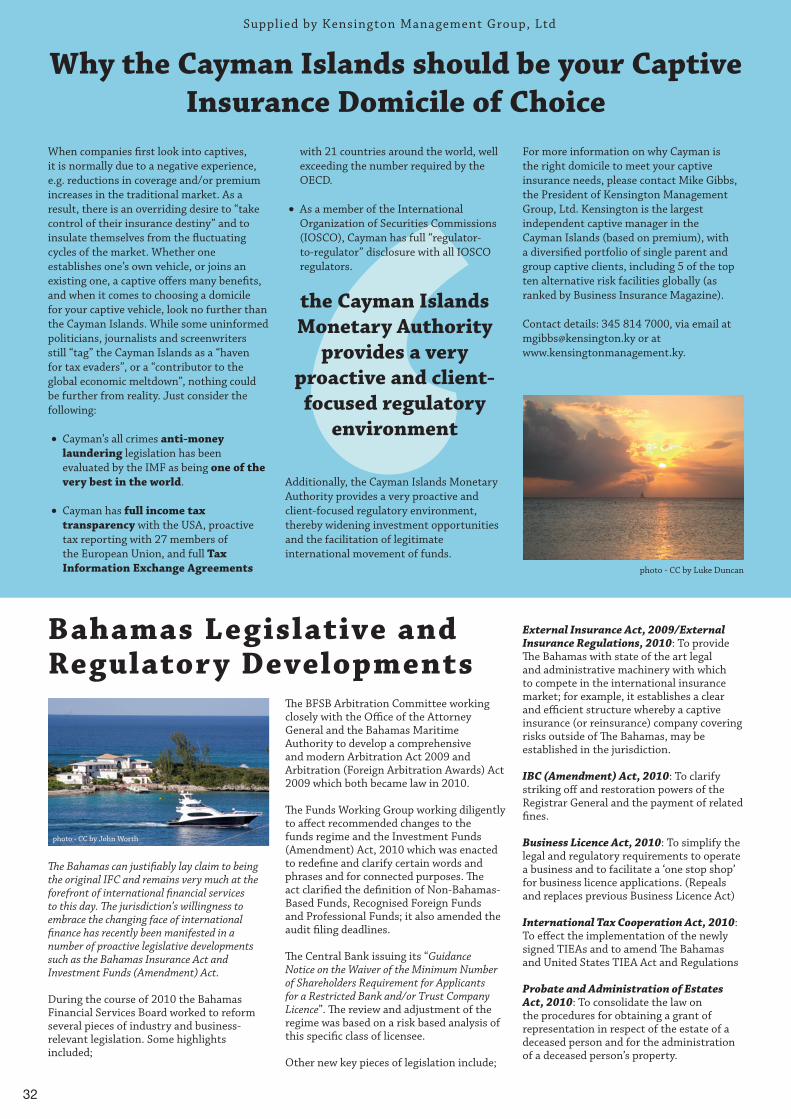

A New Dawn Beckons for International Finance

Beyond Tax Mitigation • Diversification In Defence of IFCs • Courting China • IFC Profiles

Offshore Guide2011/12www.offshoreguide.biz

3

A New Dawn Beckons for International Finance

International Financial Centres (IFCs) have had a tough time of it recently, but as the dust seems to be settling on the worst ravages of the global recession they have awoken to a new dawn, not only revitalised, but with a refined agenda and sense of purpose. This sees them proactively courting new HNWIs and UHNWIs from emerging markets such as China, and at the same time maintaining and consolidating their share of traditional US and European markets. Moreover, extensive legislative and regulatory reform across all jurisdictions constitutes evidence of a commendable willingness to embrace the prevailing international winds of the day.

No longer are IFCs solely synonymous with tax mitigation. Rather, with financial services infrastructures built up over many decades, they offer unrivalled expertise and an array of inspired and finely-tuned structures tailored to the requirements of their HNW clientele. These jurisdictions are driving growth and investment, not stifling it, and represent valuable conduits for investment capital into the developing world.

While it may be understandable that some G20 countries experiencing challenging fiscal conditions are looking to both top up their exchequers and appease their electorates by targeting IFCs, those same IFCs cannot be expected to self-destruct and drive away the very business that sustains and defines them in what can sometimes seem like a never-ending drive to comply with ever moving goalposts.

IFCs, like all jurisdictions have been forced to learn some tough lessons from the recession, but as the curtain rises on this new dawn they find that they remain essential cogs in the global financial machine, facilitating recovery, growth and ongoing stability.

_______________________________________________________

Editor: Richard Smith

Business Development: Dominic Hale, James Wilson

Production Manager: Claire Turner

Designer: Wallace Wainhouse

Editorial: Joanna Gray, Ken Shaw, Erik Herbert, Frances Law

All enquiries: [email protected]

W: www.offshoreguide.biz

________________________________________________________Disclaimer::The information contained in this publication has been obtained from sources the proprietors believe to be correct. However, the publishers cannot be held responsible for any errors or omissions. In no way does any of the content constitute legal advice and the publishers and staff accept no responsibility nor legal liability for any loss or damage caused by or arising from reliance on it. Persons are reminded that independent professional advice should be sought before any investment decisions are made.

Copyright: No part of this publication may be reproduced without the prior consent of the publisher. © Business Annual Offshore Guide. Unless otherwise stated all photographic content is licensed under the Creative Commons (cc) attribution license. To view a copy of this license visit http://creativecommons.org/licenses/by/3.0/

Cover Photo CC by Arturo Donate

Offshore Guide2011/12

4

Comment

6 The Chinese Example Prof. Jason Sharman looks at whether IFCs can foster development in poor countries

8 Financial Heavyweights Gather at AFF to Reshape Global Agenda Hong Kong strategy laid out at the Asian Financial Forum

9 Isle of Man Backed by Prominent UK MP Mark Field, UK MP, Cities of London and Westminster lends his support to the IFC

Jamaica to be a Centre for International Financial Services Legislation is passed to further this end

14 Crucial Consultants When geo-political events put extraordinary pressure on personnel, businesses and investors, the use of a consultancy becomes ever more vital, explains Joanna Gray

16 Offshore Diversification How IFCs are diversifying and expanding to stay ahead of the game, by Frances Law

18 Seek and Ye Shall Find: Swiss Banks and the Search for Dictators’ Assets by James Nason, Head of International Communications, Swiss Bankers’ Association

Profiles

22 Labuan25 Cook Islands26 Samoa

28 Cayman Islands: The Whole Package

32 Bahamas Legislative and Regulatory Developments

33 AIFMD Approval Boosts Fund Industry in BVI, Cayman and Jersey by the Walkers Group

34 Turks & Caicos Islands: ‘Transparency’, ‘Accountability’, ‘Responsibility’

35 Bermuda Insurance Market Retains Resilience in Another Challenging Year from the Bermuda Monetary Authority

36 Bermuda Set to Meet New EU Standards re: AIFM Directive37 BVI Signs 20th TIEA with Government of the Republic of India38 Anguilla

42 Guernsey Eyes Opportunities in the Emerging Markets by Peter Niven, Chief Executive, Guernsey Finance43 Jersey Remains the Leading Offshore Centre in the Latest GFCI from Jersey Finance 44 Future-oriented Strategy for the Liechtenstein Financial Centre: Quality, Stability and Sustainability from the Liechtenstein Bankers Association

46 Republic of the Seychelles49 Dubai: East-West Bridge50 Botswana52 Mauritius53 Liberia: Global Pioneers in the Offshore Corporate Services Industry

Comment

54 The Future of Asset Management Clusters from PWC’s ‘See the Future – Top Industry Clusters in 2040’ Report

55 Islamic Finance and Global Financial Stability Jointly published by the Islamic Financial Services Board (IFSB), the Islamic Development Bank (IDB) and the Islamic Research and Training Institute (IRTI)

56 Extinction or Evolution: The Future for Offshore Centres Reproduction of Anne Craine, Treasury Minister of the Isle of Man’s Sir Thomas Gresham Docklands Lecture from November 2010

60 The Global Forum on Transparency and Exchange of Information for Tax Purposes Extracts from an Organisation for Economic Co-operation and Development (OECD) background information brief, 18 February 2011

64 Position of Swiss Bankers Association (SBA) on Swiss Government’s Planned Revisions to Administrative Assistance in Tax Matters

65 Global Economic Outlook: Recovery is Gaining Pace and Confidence is Growing Report from the World Economic Forum 2011

66 Statement on Tax Avoidance Debate from the IFC Forum

C o n t e n t s

Asia-Pacific

Europe

Africa/Middle East

Caribbean/North Atlantic

Phot

o CC

by

Ian

Burt

6

Jason Sharman is Professor and Queen Elizabeth II Fellow at the Centre for Governance and Public Policy & Griffith Asia Institute, Griffith University.

Issues of poverty and economic under-development have, appropriately, got a great deal of attention from policy-makers and non-governmental organisations (NGOs) over the last few decades. But the relationship between International Financial Centres (IFCs) and economic growth and poverty alleviation in developing countries is largely unexplored. What little scrutiny this relationship has received has tended to portray IFCs as exerting a baleful influence on developing countries. In contrast, it is argued here that at least in the case of China, IFCs may actually assist economic development and poverty reduction. There is evidence that IFCs can make a positive contribution by helping foreign and domestic firms in developing countries access the kind of efficient institutions necessary to drive growth, but which are often unavailable locally.

Lowering costs

To put the case for this alternative perspective briefly, governance and institutions are now regarded as some of the key determinants of economic growth, and related poverty reduction. Efficient institutions promote growth by lowering transaction costs and thereby facilitating exchange. Transaction costs refer to the costs of fully specifying and enforcing economic exchanges. Because regulations and laws in developing countries are commonly confusing, rigid, obsolescent, politicised and poorly enforced, transaction costs at home are generally high, so local firms may seek efficient institutions abroad to make exchanges cheaper and easier.

IFCs can offer a natural complementarity for developing countries, as they provide an environment characterised by simple, flexible, modern, sophisticated and impartially-enforced regulations and laws that are readily accessible by foreigners. Small and medium-sized enterprises from

developing countries, the engines of job and income growth, may be able to access capital much more efficiently in or through IFCs than they can domestically. Judging from China’s experience, IFCs are seldom final destinations for capital from the developing world, which is commonly brought back and put to work in the country of origin.

Bizarre flows

The starting point for an investigation of the links between IFCs and China are what look to be some bizarre figures relating to capital flows. Why, for example, does the British Virgin Islands contribute more Foreign Direct Investment (FDI) to China than the United States, the European Union and Japan combined? How can it be that flows between China and Samoa or China and Barbados are bigger than flows between China and the United Kingdom? Why is there ten times more investment from China in the Cayman Islands than there is Chinese investment in the United States?

Those looking to account for these anomalous figures have so far relied on two answers: either that these flows represent criminal money flowing to IFCs, or a process of ‘round-tripping’, whereby locals send money out of the country, only to return it via IFCs to qualify for tax breaks. A closer look at the evidence, however, suggests that neither answer stands up.

As with any large flows of money across borders, it is almost certain that some proportion of the money flowing from developing countries to IFCs does indeed

represent plundered wealth. But there is no reason to suppose that the proportion of illicit wealth is any greater than that moving from developing countries to G20 financial centres. Indeed, G20 countries in many important cases provide a warm and secure welcome for the wealth of kleptocratic dictators. For example, in 2009 the NGO Global Witness published an expose showing how Teodorin Obiang, son of the president of Equatorial Guinea, has acquired a USD35 million mansion in Malibu, California, despite the US government’s judgment that the property was purchased with the proceeds of corruption. France has done nothing to stop corrupt heads of state and other senior public officials from Francophone Africa from owning luxury properties and maintaining their bank accounts in Paris. More broadly, my research has shown that OECD countries are much more likely to allow the formation of anonymous shell companies, invaluable in laundering corruption money, than are IFCs.1

What of the second answer, round-tripping? Here it is said that Chinese firms and individuals send money out of the country to an IFC, only to repatriate the same funds. The rationale is said to be the desire to capitalise on special tax breaks provided for foreigners: domestic money passed through IFC becomes foreign, and hence eligible for tax savings. If tax arbitrage through round-tripping explains the China-IFC link, then the real consequences for the Chinese economy would be slight, and probably negative as the government lost out on tax revenue it would otherwise be entitled to. But this view is highly incomplete.

If it were just the same funds being cycled between China and the Caribbean, the out-bound and in-bound flows would have to cancel out. In fact, however, flows from the Caribbean to China are more than twice as large as the equivalent flows in the other direction. Thus much, and probably a majority of the foreign investment through IFCs in China is indeed foreign, once again posing the question of why IFCs are such disproportionate contributors of foreign capital in developing economies like China.

The Chinese Example

IFCs are seldom final destinations for capital

from the developing world, which is

commonly brought back and put to work in the

country of origin

Comment

7

What of the money that is round-tripped? Here there are good reasons to think that there is a lot more going on than simple tax arbitrage. Fiscal reforms in China have meant that most tax concessions for foreign investors have now been withdrawn. And yet at the same time that the tax advantages of IFC-mediated investment have been reduced, investment from or through IFCs continues to increase.

The solution is to return to the subject of institutions and transaction costs introduced earlier. In China at least, and probably in other developing countries too, the reason why capital flows from IFCs are increasing as the tax rationale fades is because both local and foreign investors seek to combine the advantages of the economic dynamism of these markets, with the transparent, reliable and efficient institutions hosted by IFCs. Some examples illustrate how this logic applies in practice.

Small and medium-sized enterprises in China are the main engines of job creation, income growth and hence poverty alleviation. Yet these same firms find it very difficult to access adequate capital. The few large local banks have neither the capacity nor the inclination to come up with the risk models needed to assess the creditworthiness of disparate smaller firms, instead preferring to channel credit to large, state-owned enterprises.

To help address this problem, the Asian Development Bank (ADB) provided USD13 million to a Chinese loan guarantee company, COG, but was surprised to find the firm was incorporated in the Caymans. Asked to explain, the Bank’s response is highly illuminating:

‘The Cayman Islands’ legal system is based on British law, and therefore the legal concepts are familiar and acceptable to international investors... Most PRC [People’s Republic of China] companies seeking a listing on the Hong Kong Stock exchange incorporate their listed companies in the Cayman Islands. ADB’s external counsel and COG’s external counsel have confirmed that, in the present circumstances, a direct listing of COG as a

PRC company is not feasible, as listing would involve... a highly bureaucratic process, which is why PRC companies tend to use offshore jurisdictions... the Cayman Islands is generally considered desirable because (i) the legal requirements regarding capital reduction and the distribution of capital are less complicated than are those in Hong Kong, (ii) Hong Kong stamp duty is not chargeable for share transfers that take place prior to the IPO, and (iii) the Cayman Islands are FATF compliant and not on OECD’s tax haven blacklist (Asian Development Bank 2007: 5).2

As this legal opinion states, this is far from being a one-off situation. Ease of incorporation, the ability to reduce capital and issue different classes of shares, the reliance on tried and tested legal concepts and systems, the flexibility of corporate structures and the tax-neutral treatment of investment from different sources all argue in favour of using IFCs to invest in China. Thus Chinese technology and media firms have tended to form an IFC-based company that can list in New York, Hong Kong, or elsewhere depending on where the greatest amount of foreign capital can be raised. The IFC company then holds a wholly-owned Chinese operational subsidiary.

Joint Ventures may also choose to form companies or trusts in IFCs that then hold the underlying collaborative venture in China. Joint Venture firms in China must apply for permission from the government to change board members, re-adjust ownership shares, or change the focus of business. If underlying IFC vehicles are employed, however, partners may make all of these

changes quickly and easily. Disputes that arise between foreign partners can be settled in a familiar and credible legal setting using courts that have considerable expertise in solving complex commercial disputes.

In these and other examples, Chinese and foreign investors can profit from IFC-based institutions that allow contracting parties to both more accurately assess the value of exchanges, and be more confident that contracts will be upheld in an impartial and reliable manner. In an ideal world, of course, China and other developing countries would be able to provide the institutions that serve to lower measurement and governance transaction costs locally. Yet creating, for example, an expert and impartial court system is a long-term process. As Huang writes in his book Capitalism with Chinese Characteristics (Cambridge University Press, 2008), ‘China’s success has less to do with creating efficient institutions and more to do with permitting access to efficient institutions outside of China’. IFCs provide these efficient institutions. Given China’s unmatched success in lifting hundreds of millions of people out of poverty since 1978, we need to investigate whether other developing countries could also profit from closer relations with IFCs.

For a longer version of this paper, please see International Financial Centres Forum website: www.ifcforum.org.

1 For more on this research see ‘Onshore secrecy, offshore transparency’, STEP Journal Vol17 Iss7, p202 Asian Development Bank. 2007. Proposed Equity Investment in Credit. Orienwise Group. Project 38908. Manilla.

This article was first published in the STEP Journal (October 2010, Vol18 Iss9), the official magazine of the Society of Trust and Estate Practitioners (STEP). STEP is a unique professional body providing members with a local, national and international learning and business network focusing on the responsible stewardship of assets today and across the generations. Full members of STEP are the most experienced and senior practitioners in the field of trusts and estates. For further information please visit www.step.org

at the same time that the tax advantages

of IFC-mediated investment have been reduced, investment from or through IFCs continues to increase

Comment

8

Comment

More than 70 leading finance, business and regulatory players, as well as government officials from around the world gathered to exchange ideas on how to tap the opportunities of economic growth at the Asian Financial Forum in January 2011. The two-day forum was the fourth of its kind since September 2007, and offered a platform for more than 1,600 financial experts, officials and business leaders to look into Asia’s strategies and tactics for stable and balanced economic growth. Under the theme “Asia: Reshaping the Global Agenda”, the event was co-organised by the Hong Kong Special Administrative Region Government and the Hong Kong Trade Development Council, and held on January 17 and 18 at the Hong Kong Convention and Exhibition Centre in Wan Chai. The Chief Executive, Mr Donald Tsang, met many global financial leaders when delivering his opening address at the forum. “It is relatively safe to say Asia has weathered this crisis. Our economies are confidently moving ahead again,” he said. However, Mr Tsang reminded delegates that sovereign debt crises and high unemployment levels in regions such as the Euro-Zone and the United States would

doubtless have an impact on Asia. To conquer crises, Mr Tsang said that sound economic strategies and tactics, working hand-in-hand, had been the key to Asia’s early recovery.

Referring to the case of Hong Kong, he said that the main strategies were to maintain a stable financial sector, preserve jobs and support businesses through difficult times. Tactics, including a 100% deposit guarantee scheme and several rounds of stimulus measures, had supported the economy through the economic downturn.

Going forward, Mr Tsang said that Hong Kong’s strategies and tactics would focus on opening up opportunities for business in Asia and promoting greater transparency in financial markets. “In reshaping the global agenda, Hong Kong also has a leading role to play as China’s global financial centre,” he said. Mr Tsang said that many of Hong Kong’s extraordinary opportunities have been linked to the Mainland’s robust economic growth and rapid financial reform. “As we have seized these opportunities, so they have multiplied. This is especially the case for our role as our nation’s global financial centre,” he stressed. Mr Tsang noted that one of Hong Kong’s multiplying opportunities was the increased participation of Mainland companies in the stock market, which in turn attracted foreign investors for these companies as they complied with international standards. Foreign companies from Russia, France and Brazil listed in Hong Kong could also benefit from institutional money from the Mainland and other Asian investors. Another fast multiplying opportunity is Hong Kong’s role as a testing ground for the internationalisation of Renminbi.

“Since the Central Government expanded the Renminbi trade settlement scheme last July, Hong Kong has seen a sharp rise in activity,” Mr Tsang noted. He also cited the rapid expansion of Hong Kong’s Renminbi bond market, saying that local firms and global enterprises had tapped into Hong Kong’s “dim sum bonds” (the nickname given to bonds denominated in Renminbi and issued in Hong Kong) market. “As China’s global financial centre and as an international business hub with free flows of capital, information and talent, Hong Kong has been fully engaged in Asia’s full circle back to economic growth and prosperity,” Mr Tsang said. Speaking at the cocktail reception, the Financial Secretary, Mr John C Tsang, said “dim sum bonds” were born out of the necessity to internationalise Renminbi in the current climate of financial opening up and reform on the Mainland. “For us, ‘dim sum bonds’ represent more than just a new and appetising initiative for investors to expand their Renminbi portfolios. They also embody Hong Kong’s unique role in reshaping the global agenda through our positioning as China’s global financial centre,” Mr Tsang said.

©2011 GovHK (www.gov.hk)

Financial Heavyweights Gather at AFF to Reshape Global Financial Agenda

“It is relatively safe to say Asia has weathered

this crisis. Our economies are confidently moving

ahead again” – Mr. Donald Tsang,

CEO and President of the Executive Council of the

Government of Hong Kong

View from the Hong Kong Incline Tram Hong Kong Harbour

phot

o - C

C by

Ray

Dev

lin

phot

o - C

C by

Mat

thew

Hun

t

9

THE value of the Isle of Man’s contribution to the UK economy via the City of London was highlighted by UK MP Mark Field when he delivered the Chief Minister’s International Lecture on February 3, 2011.Speaking to invited guests at the Palace Hotel in Douglas, the MP for the Cities of London and Westminster urged the Island to continue promoting its positive role as a well-regulated small international financial centre (IFC) driving global business into London.

Mr Field said, ‘The Isle of Man adds enormous value to Britain’s international offering.’

He also praised the way the Island had diversified its economy into sectors such as shipping, aircraft registration, film and space. ‘They have meant that the Isle of Man brings into a British sphere of influence some very important strategic global business. And this is business that would otherwise have gone to Singapore, Hong Kong or the USA.”

Mr Field, whose lecture was entitled ‘Rebalancing the Debate Around International Financial Centres’, argued that

small IFCs had been caught up in public and political hostility to the financial services industry following the global banking crisis; but the debate about such centres was ‘totally one-eyed’ with no understanding of their benefits to the UK and global economy.He said, “Small IFCs such as the Isle of Man have repeatedly had to put up with unfair political attacks and misguided criticism.”

Mr Field went on to rebut what he called the ‘five myths’ about small IFCs: that they had a negative impact on global economic growth, that they had contributed to the global financial crisis, that they engaged in harmful tax practices, that they had a negative impact on transparency, regulation and

information exchange, and that they did not benefit developing countries. He concluded by stating that global competition was an opportunity for the Island.©2011 Crown Copyright

An Act to establish the Jamaica International Financial Services Authority for the promotion and development of Jamaica as a Centre for International Financial Services was passed in the House of Representatives on February 8 2011.

Minister of Industry, Investment and Commerce, Hon. Karl Samuda, who piloted the Jamaica International Financial Services Authority Act, noted that the Authority will be charged with ensuring that the necessary infrastructure for the creation of a viable and progressive financial service sector is designed.

He noted further that the financial services centre will create several economic opportunities for Jamaica, including significant employment for high skilled workers among the professional cadre, and create linkages with other domestic sectors, such as tourism.

“As a centre of excellence, Jamaica’s employment potential will be between ten and 25,000, government revenue can conservatively be estimated to range between US$400 million and US$800 million, and service provider revenue will be in the vicinity of US$1 billion-US$2 billion

dollars, on top of the obvious spin-offs that will flow from this investment,” Mr. Samuda said.

He also noted that the necessary studies and evaluations have been done, as to how to market the island as a new entrant and the type of services to be offered.

Opposition Spokesperson, Dr. Omar Davies, stated that the countries that would normally have interest in the proposed financial centre, particularly the United States and members of the European Union, have become much more vigilant about the operations of their firms externally.

“They have brought increasing pressure on some of the homes of the financial services

centres,” Dr. Davies said, while questioning the potential of the financial centre to employ up to 25,000 persons.

In his response, Mr. Samuda noted there “comes a time in every nation’s history when they must take bold creative decisions that carry with it an element of risk.”

“If you promote entrepreneurship as a necessary ingredient for growth, implicit in that is the need to take some risk. The rewards are greatest when the risk is greatest,” Mr. Samuda said.

The Jamaica International Financial Services Authority Act will next go to the Senate for its approval.

©2011 Latonya Linton (www.jis.gov.jm)

Isle of Man Backed by Prominent UK MP

“Small IFCs such as the Isle of Man have

repeatedly had to put up with unfair

political attacks and misguided criticism” –

Mark Field, UK MP Cities of London and

Westminster

Jamaica to be a Centre for International Financial Services

“If you promote entrepreneurship as a

necessary ingredient for growth, implicit in that is the need to take some risk” – Hon. Karl Samuda, Minister of

Industry, Investment and Commerce, Jamaica

Mark Field, UK MP, Cities of London and Westminster

Comment

Phot

o CC

by

drex

ston

12

The Republic of the Marshall Islands (RMI) consists of two parallel chains of atolls and islands that lie west of the International dateline in the Pacific Ocean, midway between Hawaii and the Philippines. A trust territory of the United Nations under United States administration following World War II, the RMI gained its independence as a sovereign nation in 1986. The Constitution is a blend of American and British models of government and the official language is English. In 1991, the RMI became a full member of the United Nations and maintains a politically stable, democratically elected parliamentary system of government.

The RMI operates the world’s third largest shipping registry, occupying white list positions with major post State control memorandums of understanding (MoUs). The success of the RMI Ship Registry has complimented the success of the RMI Corporate Registry, which has been the registry of choice for virtually all international shipping companies that have applied for initial public offerings (IPOs) on stock exchanges in New York, London and Singapore.

There are presently 36 RMI business entities publicly traded (32 corporations and 4 limited partnerships). There are 21 entities publicly traded on the New York Stock Exchange (NYSE), 13 on the National Association of Securities Dealers Automated Quotations (NASDAQ), one on the London Exchange, one on the Singapore Exchange (which is dual-listed on the NASDAQ), and one on the Plus Markets exchange. The continual increase of RMI publicly traded business entities demonstrates the worldwide acceptance of the RMI Corporate Registry and assists in raising the profile of the RMI.

International Registries, Inc. (IRI) and its affiliated companies administer the maritime and corporate programs of the RMI. IRI has been operating maritime and corporate registries for over 60 years and currently operates 21 offices worldwide with

a “decentralized” structure that enables clients to speak with maritime and corporate specialists in their own languages and in their own time zones. Each of the offices has the ability to incorporate a company, issue a certificate of good standing, register a vessel or yacht, record a mortgage and service clientele.

RMI Corporate Registry

The RMI Corporate Registry has experienced significant growth in recent years. Business professionals and financial advisors worldwide have hailed the RMI Corporate Registry for its innovative and flexible body of law, ease of business entity formation and superior customer service.

The RMI is a zero tax jurisdiction for all non-resident business entities. The RMI Associations Law, first enacted in 1990, and frequently updated to meet changing business needs, is largely modelled on the corporate laws of the United States state of Delaware. It includes the Business Corporations Act (BCA), Revised Partnership Act, Limited Partnership Act, and the Limited Liability Company (LLC) Act. The modernity of this legislation, which is commonly accepted by most major commercial centres, is essential; up-to-date legislation is more familiar to the banking and legal communities around the world, thereby enabling businesses to set up bank accounts and obtain financing once incorporated.

RMI corporations are low-cost, uniformly easy to form, and simple to administer. Standard Articles of Incorporation are available and, if utilised, a company can be formed in one business day. Articles of Incorporation may be customized and shelf corporations may be purchased through any IRI office. While it is necessary to file all documents in English, it is possible to accompany such filings with a foreign language translation. Additionally, unlike many other jurisdictions, the name of an RMI business entity can be in any language, with the condition that Roman characters must be used. Any recognized corporate suffix is acceptable.

Republic of the

Marshall Islands

The RMI Corporate Registry has experienced

significant growth in recent years

photo - CC by Matt Kieffer

Phot

o CC

by

Mat

t Kie

ffer

Republicof the

Marshall Islands

14

Comment

When geo-political events put extraordinary pressure on personnel, businesses and investors the use of a consultancy becomes ever more vital, explains Joanna Gray

In this age of social media, twitter, and such like, it is astonishing that geo-political events can still take us by surprise. They certainly have done in recent months. In 2010 nobody predicted the Arab Spring and the shocking earthquakes in New Zealand and Japan. British Foreign Secretary William Hague has already classed the uprisings in Tunisia, Egypt and Libya as coming, ‘In the top three most important events of the 21st century’, after the 9/11 terror attacks and the financial crash of 2008.

At times like this when international sands are shifting, the initial instinct can be to retreat inwards – return to your own village and leave the global one well alone. Markets have been unsure how to react, the price of crude is rising ever higher and those investing in nuclear are wondering if they’ll ever see good returns. Media, businesses and political voices alike have all been caught on the hop – ‘Nobody expected the Libyan War/ Arab Spring / Japanese earthquake,’ CEOs explain wide-eyed to angry shareholders.

It would be a foolish consultancy firm that is bold enough to stand up and announce, ‘Well actually we did see this coming,’ however it is almost certain that employing such firms helps to reduce risk, which during these uncertain times can often be reward

enough. This is particularly pertinent to the offshoring industry where bespoke approaches are needed for identifying opportunities and formulating fresh strategies across the globe.

At times when, ‘Events my dear boy, events,’ run away with themselves businesses can often feel left adrift: the stranded oil workers in Libya were a literal example of the exposure businesses and their personnel face. And when managing exposure to risk it is good to use statistics. IBM has 399,409 employees worldwide, and between them Accenture, Arvato and Capgemini have at least 1million consultants offering an

unrivalled pool of expertise, acumen and experience. To access accurate market analysis, strategic investment planning and equity research there is logic to working with consultants – they offer a service that even the smartest in-house CFO and diligent team couldn’t rival. The results speak for themselves: Accenture which operates in 200 cities in 53 countries with 211,000 employees has clients which include 94 of the Fortune Global 100 and more than three-quarters of the Fortune Global 500.

Indeed it is no longer the case that outsourcing is simply about cost reduction; risk management and discovering strategic investment opportunities are driving the success of BPO businesses. As Capgemini, which has over 108,000 staff operating in more than 40 countries, states regarding its work in the financial services sphere, ‘In the current financial services market, dramatic continuous change is the norm. Leadership is no longer about following the rules or applying traditional solutions to new challenges. The need to seize opportunity here and now requires innovative thinking to transform enterprises for the next level of performance.’

Indeed it is during times of acute geo-political anxieties when the best sort of businesses, backed with the best sort of consultants can thrive. And here a move away from raw statistics and pure bottom line profit to a focus on people can be an asset. Capgemini again underlines the key to a flourishing consultant/client relationship, ‘Business value cannot be achieved through technology alone. It starts with people: experts working together to get to the heart of your individual business objectives and develop the most adapted solutions to fit these requirements. We believe this human-centered approach to technology is what makes the difference for business...We aim to empower [businesses] to respond more quickly and intuitively to changing market dynamics.’

Crucial Consultants

it is no longer the case that outsourcing is simply about cost

reduction

phot

o - C

C by

Gen

erat

ion

Bass

CAPGEMEMINCOLLABORATION

OMMITTED TO RESU

DEDICATED TCAPGEMRKING TOGETHER

PEOPLE AT T

EW BRAND PROMI

A NEW SLOGAN…OLLABORATION

COMM

DEDIC

CAPGEMINIORKING TOGETHER

OPLE AT THE HEART

A NEW BRAND PROMISE,

LLABORATION

COMMITTED TO RESULTS

TED TO CLIENTS

CAPGEMI

WORKING TOGETHER

PEOPLE AT THE HEART

EW BRAND PROMISE, A NEW SLOGAN…

CO MMI TTE D TO RESU LTS

DEDICATED TO CLIENTSRKING TOGETHER

A N

For more information, please visit www.capgemini.com/bpo

We are the ones to transform your support functions to boost your business.We are Capgemini

We are the ones who helped more than 60 global companies to reduce operating costs substantially and supportedtheir business growth.

We are Capgemini Business Process Outsourcing.

“ “

C

M

Y

CM

MY

CY

CMY

K

Full Page Ad(Resized).pdf 1 3/9/2011 10:42:18 AM

16

Great opportunities lie in BRIC countries such as China

In order to stay ahead of the game...and the G20 and OECD, International Finance Centres are diversifying and expanding. Frances Law explores the trend.

The idea that offshoring is simply a way of increasing tax efficiency, as compared with its onshore equivalents, is long gone. As the G20, OECD and indeed Wikileaks attempt to probe, expose and scrutinise International Finance Centres, they in turn are not only becoming more transparent and accessible but more importantly, are diversifying and expanding into new territories and markets. Just as the general mercantile and financial sectors look to China and the other BRICs countries for opportunities, so too are competitive IFCs.

This interest in new markets can be viewed generally and specifically. In general, it is natural that as China and the other BRICs continue to power the world economy they will project increasing numbers of HNWIs and UHNWIs who are looking to grow their wealth effectively in manners that their own territories cannot accommodate. China, with 115 billionaires comes second on the recently announced 2011 Forbes billionaires list. This impressive number has doubled within a year from 2010’s 64, demonstrating the rapid rise and power of the Chinese economy. Russia comes in a close third with 101. In fact, it is telling that of the world’s 214 new billionaires half were from the BRICs nations and 101 from the Asian Pacific.

It is therefore no surprise that offshore legal specialists including Harneys, Walkers and

Thorp Alberga have recently consolidated or opened their first offices in Hong Kong, demonstrating the shifting of prospective business from old Europe to new Asia.

Vanuatu is determinedly courting the Chinese, but it is not alone. Samoa has recently opened an embassy in Beijing and the likes of the BVI, Bermuda, Jersey and the Cayman Islands are a constant presence at events on the Chinese mainland demonstrating their competitive financial service packages. Similarly, Liberia has offices and agents across the world in order to offer a 24/7 business construction. And the Chinese and their fellow BRICs nations are biting.

More specifically, IFCs are offering more in the way of financial services. Pertinent to the aforementioned HNWIs and UHNWIs, the Cook Islands, with more registered asset protection trusts than any other jurisdiction, is specifically targeting new markets/individuals. As the Financial Supervisory Commission of the Cook Islands states, ‘The Cook Islands was the first jurisdiction to legislate specifically for asset protection

trusts and the laws offer the strongest form of asset protection of any offshore jurisdiction.’ Indeed, the Cook Islands government is firmly behind the growth of this sector and with targeted approaches there is no reason to doubt further successful growth.

With HNWIs and UHNWIs bringing a continual stream of new business for traditional tax efficiency banking and asset protection, IFCs are also retrenching and growing their insurance sectors – in particular re-insurance and captive insurance. Recent natural disasters put the sector into sharp focus. Estimates from risk modelling agency AIR suggest that claims from the Japanese earthquake could reach up to US$35bn+, New Zealand’s earthquake could cost the industry over US$8bn and losses from the flooding in Australia could top US$6bn. The fact that most of the losses will be absorbed by global reinsurers will put enormous short term pressure and possibly long term opportunities on IFCs that have diversified into re-insurance. As the Association of Bermuda’s Insurers and Reinsurers states, “Today (Bermuda) is the home to more than 30 major international insurance and reinsurance firms. This market has grown up in the last 20 years in response to market needs for greater worldwide access to property and casualty insurance and reinsurance.” Bermuda is currently focussing a lot of energy into its reinsurance sector, and if recent events cause a long term increase in premiums, Bermuda’s industry, and similarly the Cayman Island’s captive insurance industry may benefit.

Offshore Diversification

of the world’s 214 new billionaires half were

from the BRICs nations and 101 from the Asian

Pacific

photo - CC by Marianna

Comment

LIBERIAN CORPORATE REGISTRYYOUR PARTNER IN THE PURSUIT OF CORPORATE FREEDOM

STABILITY SECURITY LONGEVITY INNOVATION

For more than half a century, Liberia has provided professional services to the world’s financial and investment communities. The Liberian Corporate Registry offers convenient, efficient and cost effective corporate structures to its clients worldwide. The Registry’s premier service is achieved through the stability of Liberia’s Corporate Program, as well as its commitment to quality service with continuous investments in advanced technology and experienced industry professionals.

Liberian corporations are at the core of private and public investments in all major financial sectors resulting in a significant percentage of global business activity being conducted through Liberian entities.

60+ YEAR HISTORY OF QUALITY SERVICE Commercially tested legal system• Accepted by all private and commercial financial institutions• 24/7 prompt customer support through a world-wide network of •full-service offices eCorp© - the world’s premier electronic corporate registry• Same day incorporation and document issuance - free apostilles •and acknowledgements Committed to protecting confidentiality• No annual reports or audits• Statutorily exempt from Liberian income and withholding taxes• Exclusive registered agent• Dual language filings • OECD white-listed•

Liberia is committed to providing prompt, efficient and quality service to meet the specific business needs of our clients. The Registry offers a variety of corporate services including the following:

CORPORATIONOne of the oldest and most popular types of entity for setting up a commercial enterprise. A corporation is a distinct legal entity which is separate from the individuals who own it. The corporation assumes liability for all debts undertaken on its behalf and limits the shareholder’s personal liability exposure to the sum of their investment. Liberian

Corporations are easy to form and administer and require no annual filing.

LIMITED LIABILITY COMPANY (LLC) A hybrid entity designed to provide the limited liability features of a corporation and the operational flexibility and efficiencies of a partnership. An LLC can be structured so that income generated by the LLC does not attach to the entity itself but flows directly through to its owners.

LIMITED PARTNERSHIPAn attractive form of entity for investors who seek limited liability and do not want to be involved in the daily operations of the business, but participate in profits generated by the entity. Limited Partnerships are often formed by business owners involved in real estate, manufacturing and other business ventures.

PRIVATE FOUNDATION This is a useful vehicle for individuals seeking to preserve the wealth-generating activities of a family, while making the income available to the beneficiaries in accordance with the donor’s wishes. The Private Foundation acts as a separate legal entity for assets transferred to it, usually in the form of a gift by a donor, and are designed to provide named beneficiaries, which might include the donor, with an income from the assets.

ADDITIONAL CORPORATE SERVICES:Voluntary filings•Re-domiciliation•Restructuring Options: Merger and Consolidation•Conversion•Foreign Maritime Entity (FME) •

For additional information regarding the Liberian Corporate Registry’s business entities and corporate services, please contact the Liberian Registry or visit our website.

VIRGINIA, USA I HAMBURG I HONG KONG I LONDON I MONROVIA I NEW YORK I PIRAEUS I TOKYO I ZURICH

[email protected] www.LiberianCorporations.com

18

by James Nason, Head of International Communications, Swiss Bankers Association

The pattern is well known: an authoritarian ruler, often long tolerated and courted by the West, falls from power and gets re-labelled as a ‘plundering dictator’. The race starts to find and freeze his assets and his country’s new leaders usually lodge requests for judicial assistance with a view to restituting any embezzled funds found abroad.

Eyes invariably turn to Switzerland – long

the world’s leader in international private banking - and the Swiss usually find something. Names such as Mobutu, Duvalier, Marcos, Abacha and, more recently, Ben Ali, Mubarak and Gaddafi become linked with plundered assets squirreled away at Swiss banks. Joe Public, taking his cue from James Bond films and tendentious media reports, remains convinced that any tin-pot dictator can turn up at a Swiss bank with crates of illicitly-obtained funds, politely raise his hat and open an account with no questions asked.

In reality, things work differently. Switzerland has long had a comprehensive range of legal instruments and measures in place for fending off assets of criminal origin and for identifying, freezing and returning them in the event that they should nonetheless find their way into its banks. Furthermore, Swiss banking secrecy has never been absolute – the rights to privacy can be suspended when a criminal investigation is underway – and it certainly does not impede existing protective and preventive measures in any way.

Seek and Ye Shall Find: Swiss Banks and the Search for Dictators’ Assets

Davos, Switzerland Photo by swiss-image.ch/Andy Mettler

Comment

19

On the shop floor, Swiss banks must adhere to strict regulations when opening accounts and they are required to report well-founded suspicions of money laundering and immediately freeze the relevant assets. In addition, special measures kick in if they decide to take on a client identified as a ‘politically-exposed person’ or ‘PEP’.

So how come the Swiss are so expert at sniffing out a dictator’s plundered assets, and why do such assets slip into Swiss banks in the first place?

The answer to the first question – and it’s a factor often overlooked by the media and commentators - is that Switzerland’s strict ‘know-your-customer’ rules force its banks to hold better quality information about their clients compared with banks in other countries. Swiss banks are required not only to verify the identity of the account holder but also to establish the identity of the beneficial owner of the assets. And the beneficial owner cannot be some construction in a far-flung Small IFC – the banks must get the name of a natural person. Furthermore, they must record details of all those holding power of attorney over the assets and also of any clients authorised to sign on behalf of companies. And all this information must be supported with documentation. The type of anonymity offered to beneficial owners by such vehicles as, for example, a UK trust or a Delaware shell company would be illegal under Swiss banking law.

So once Swiss banks are given names to search for they can set their computers whirring to look for any matches. At the time of writing, for example, they are busy entering the name ‘Gaddafi’. And also Gadhafi, Ghedaffi, Kadafi, Kadhafi and Qadhafi.

One interesting result of this is that funds of criminal origin can often be identified at banks in other countries with weak ‘know-your-customer’ rules simply because some of the transfers involved a Swiss bank which, thanks to the information it held about people connected with the assets, could supply a vital link in the paper trail.

The case of the late Nigerian dictator Sani Abacha is a classic example. The official Swiss report into the case revealed that a substantial proportion of Abacha’s plundered funds had first been laundered by banks in the US and UK before these banks transferred the money to Switzerland – not

in Abacha’s own name, of course. In March 2001, following the Swiss investigation, Britain’s Financial Services Authority sheepishly issued its own report which showed that between 1996 and 2000, a number of British banks were found to have ‘significant money laundering control weaknesses’ and were linked to some USD 1.3 billion of Abacha’s illicit assets. Nigeria’s ambassador to Switzerland, Mr. Ogbe Obande, told Swiss radio at the time: “I’m happy to say without equivocation that so far Switzerland has given the best cooperation to Nigeria in its quest to recover the looted property stashed in banks across Europe and the Americas.” Ten years later, Switzerland remains the only country in the world to have returned Abacha funds to Nigeria.

But how do dictators’ illicit assets get into Swiss banks in the first place?

First of all, money today is blips on a computer screen and criminal money is not colour-coded. It does not glow bright yellow. Secondly, identifying PEPs is only part of the story. Being a PEP does not automatically mean you are a criminal, but it does mean you pose a higher legal and reputational risk for the bank.

However, there is no universally-agreed definition of a PEP and neither is there any official international list of them. Furthermore, no plundering PEP opens a bank account in his own name. In fact they go to great lengths to disguise their beneficial ownership of assets. Very sophisticated databases exist listing heads of state, ministers and other important public officials, but these databases have their limits. While they may include the names of the PEP’s spouse, children and close relatives, they probably will not list his business cronies, lawyers, drivers, bodyguards, mistresses and favourite nurse. And such databases are useless unless kept up to date.

A bank cannot drop its guard even with a PEP from a supposedly ‘safe’ country. The Swiss bank whose Geneva airport branch had US National Security Council member Colonel Oliver North as a client in the 1980s when he was secretly funding anti-communist rebels in Nicaragua from the proceeds of illegal arms sales to Iran naïvely said it never imagined a high-ranking US government official would be involved in money laundering.

When a Swiss bank does break through a corrupt PEP’s camouflage and identifies illicit assets one would think it would be praised rather than criticised. It was only thanks to the vigilance of Swiss banks that

the criminal abuse of Switzerland’s banking system by, amongst others, Peru’s Vladimiro Montesinos and Taiwan’s former president, Chen Shui-bian, was detected and reported. Taiwan’s ‘China Post’ made the point in an August 2008 editorial: “If it had not been for the vigilance of banks based in Switzerland, we may never have learned of the dirty dealings of our former president. In the end, the self-policing carried out by Swiss financial institutions is what brought the consequences back to President Chen, rather than any effort at law enforcement in our own country.”

Some countries, however, are quite choosy about the information they want from Switzerland. Britain, for example, had no qualms when accepting confidential client data stolen from HSBC in Geneva. On the other hand it was not so keen to receive information throwing light on whether Swiss banks had been used by BAe Systems to launder bribes to individuals in Saudi Arabia to secure a multi-billion pound defence contract.

Seek and ye shall find – if you know what to look for and have the will to search.

James Nason, a former current affairs producer with the BBC World Service in London, has been Head of International Communications at the Swiss Bankers Association since 1999. This is not an official position paper of the Swiss Bankers Association.

money today is blips on a computer screen and criminal money is not

colour-coded

Swiss banking secrecy has never been absolute

no plundering PEP opens a bank account in his own

name

Comment

20

Comment

By Mike Grover, Tax Specialist, Labuan IBFC Inc. Sdn Bhd - www.LabuanIBFC.my

No businessman relishes the disruption caused by a tax audit. And yet, with the new mechanisms in place to exchange tax information and tax collectors now working together to aggressively challenge international tax structures, the risk of audit is increasing.

Sophisticated tax planning works on the assumption that tax collectors can pierce the corporate veil where hitherto secrecy rules may have thwarted them. This approach to ‘tax planning’ which relies solely on secrecy is flawed and will eventually fail. Consequently, the concept of ‘future proofing ’is fast finding favour.

In the context of international tax planning, future proofing anticipates the interest areas of tax collectors and with this knowledge attempts to create a tax structure which is sufficiently robust to withstand future enquiry, for instance, a probe by tax collectors into business purpose and operational substance.

As a general rule international tax structures lacking business purpose may be struck down. Operational substance, on the other hand is essentially about having the personnel and infrastructure in the right place, at the right time, doing the right things. Getting this ‘mix’ wrong can have unexpected and possibly unpleasant tax consequences.

Trading companies located in low tax locations attract tax collectors’ interest because the multiple activities a trading company undertakes, the cause and effect on profits such activities have and the possibility that the activities may be conducted in a number of locations gives rise to the possibility of ‘tax mischief”.

Businesses have to be mindful that as tax information begins to flow freely and

efficiently between tax authorities, future proofing of trading companies in low tax locations is paramount.

In this environment the Labuan Trading Company’s “star” is rising! As with many other possible locations, Labuan is highly suitable as a tax efficient ‘profit centre’ for trading companies. But Labuan is distinguished by a number of interesting and possibly unique features; its eight ‘Tax Treasures’ that should help trading companies navigate the new tax landscape.

Tax Treasure 1A trading company located a long distance from its market attracts the interest of tax collectors. If for instance the targeted market is in the Asia-Pacific region, a Labuan Trading company, being centrally located in the same region, makes practical sense and indicates business purpose.

Tax Treasure 2Labuan is part of Malaysia, an established trading nation ranked 24th worldwide and 9th within the Asia-Pacific region. As a result the infrastructure and services required to support the activities of a trading company, such as banking and insurance, are extremely well developed and available at competitive rates. Labuan is thus a credible trading company location with real functionality, both of which are indicators of business purpose.

Tax Treasure 3 Malaysia has a large network of ‘comprehensive’ tax treaties – those that create a reasonable balance between exchange of tax information and tax benefits - designed specifically to overcome tax ‘friction’ points that might impede its international trade flows.

On the one hand, a company that trades with another country is not generally subject to tax in the country it is trading with. On the other, a company that trades within a country may find itself taxed there.

Typically a tax treaty has rules in place concerning ‘safe harbour‘ activities in that other country, for instance, in relation to the holding of stock or the activities of employees or agents, without triggering a tax liability.

Without a specific tax treaty, there are no specific ‘safe harbour’ provisions and thus the final word on what constitutes trading within a country tends to lie with local tax collectors. This can result in some tough issues being faced, including the appropriate allocation of trading profits to their jurisdiction.

In contrast, a Labuan trading company may access Malaysia’s tax treaties and by doing so obtain a degree of protection not available to trading companies located in, for instance, the Caribbean, which typically have exchange of information type tax treaties, without the tax benefits and ‘safe harbour’ provisions.

Tax Treasure 4The conventional rules to determine the ‘source’ of trading profits’ are generally the bane of a trading company in ‘territorial’ type taxing systems.

Such rules, developed over time according to tax case law and the capricious practices of the tax collector create frequent disputes on whether the trading activities are ‘onshore ‘ and taxable, or ‘offshore’ and non-taxable.

Malaysia, Singapore and Hong Kong are all possible trading company locations in the Asia-Pacific and each employ a form of the conventional rules, but in a refreshing departure Labuan employs a very modern solution to this thorny issue – its tax provisions are neatly inscribed in an Act.

The Labuan Trading Company, your

‘Treasured Gateway’ to ‘Future Proofing’ and

Substance Creation

the concept of ‘future proofing’ is fast finding

favour

Advertorial

21

The Labuan Business Activity Tax Act 1990 encapsulates the jurisdiction’s tax structure and provides a yearly option for all Labuan registered trading companies to either incur a flat tax rate of RM20,000 per annum, or 3 percent of net profit.

To enjoy this tax structure a Labuan trading company merely has to demonstrate that it deals with non-Malaysians in a currency other than Malaysian Ringgit and does so in, from, or through Labuan.

This easily understood and simple to follow rule ensures a high level of certainty concerning the ability of a Labuan Trading Company to demonstrate its trading profits are generated within Labuan and hence will be efficiently taxed. Tax Treasure 5A Labuan Trading Company may, if it wishes, establish tax residency in Malaysia by demonstrating that its ‘highest level of control’ is exercised in Malaysia. This is desirable since a Labuan Trading Company can then assert that it is taxable according to Malaysian tax law.

The Malaysian Income Tax Act 1967 dictates a headline rate of 25% on domestically sourced income but does not tax foreign sourced income generated by a Malaysian company.

Clearly another ‘cherry on the pie’ is the fact that a Malaysian company has undeniable access to all 75 Malaysian tax treaties. Importantly, tax treaties include ‘tie-breaker’ clauses to resolve disputes between treaty partners relating to the tax residency of a company.

A Labuan Trading Company can achieve a ‘solid’ Malaysian tax residency by satisfying the ‘tie-breaker’ conditions of Malaysian tax treaties. In doing so, a Labuan Trading Company may avoid the ‘pitfall’ of being a dual-resident company and potentially taxable in two jurisdictions.

Tax Treasure 6The need for operational substance creates an enormous challenge on the location of a trading company’s functions. Fortunately, a Labuan Trading Company’s level of operational substance has no impact on its Labuan tax position. The same amount of tax is payable whether there is a ‘light’ presence in Labuan or a ‘substantial’ one.

Thus, businesses enjoy the flexibility of ‘housing’ in Labuan those activities causing contention in their home location and/or the targeted market.

In this regard, Labuan is clearly a sophisticated financial centre that ‘enables’ substance to be created in real terms. That is, a Labuan Trading Company has the ability to employ local staff, maintain a local office, and have access to local support services at a relatively low cost.

Placing the contentious activities in Labuan causes no adverse Labuan tax consequences and by corollary, helps to minimise international tax risks.

Tax Treasure 7Labuan’s tax efficient framework creates a level playing field for transactions no matter their nature. Transactions with uncertain tax outcomes may have to be reported for accounting purposes and tax collectors are known to leverage off the inherent level of comfort Company Directors have with the tax positions taken to encourage disclosure.

The source of trading income, whether profit is revenue (and taxable) or capital (and non taxable) and Islamic funding arrangements are examples of tax uncertain areas. There is no downside of conducting tax uncertain transactions via a Labuan Trading Company as the low tax system results in a minimal tax exposure whatever the outcome and therefore plays a useful tax risk management role.

Tax Treasure 8Labuan Trusts and Foundations have an unlimited ‘life’ and when employed as the shareholder of a Labuan Trading Company may navigate a way through transfer taxes and/or capital gains tax on the disposal and acquisition of shares between family members and additionally, avoid inheritance and wealth taxes.

One further interesting quality worth exploring is whether the holding of shares in the Labuan Trading Company by a Labuan Foundation or Trust might legitimately ‘side-step’ rules which seek to tax residents on the profits of foreign companies in which they hold controlling interests.

All for One and One for AllLabuan’s unique position in international tax planning is even more entrenched as

every single ‘treasure’ described above applies, with appropriate modifications; to ALL Labuan ‘business wrappers’ including the Labuan chargeable company, investment holding companies, banks, insurance entities, protected cell companies, limited partnerships, trusts and foundations. Across the board, these Labuan ‘wrappers’ are able to enjoy certainty in its tax liability, with the comfort of knowing that even the most stringent substance requirements can be met cost effectively in Labuan.

Over the last couple of years, the Labuan Financial Services Authority has embraced the idea that the Labuan framework; specifically it’s legal and tax structure, should not be limited to the confines of the island.

Indeed, the thinking is so long as the Labuan framework is utilized there should be no limitation of the actual physical location of the entity. Welcome to Abstract Labuan!

The ‘birth’ of abstract Labuan is personified with co location, which provides for Labuan entities to have a presence onshore in Kuala Lumpur or any other location within Malaysia. Clearly, Labuan is undergoing a paradigm shift.

A co located Labuan Holding company in Kuala Lumpur brings with it an array of practical benefits, for example Kuala Lumpur’s location within 6 hours flight time of all the largest markets in Asia is ideal for directors of a European headquartered Multinational Company seeking a holding company location in Asia.

In addition, consider Malaysia’s superb quality of life, its range of service providers, and its ever growing human resource pool, all of which are also big pull factors for holding companies to establish a co located Labuan company. The icing on the cake though, has to be Malaysia’s cost efficiency, at every turn and in every aspect, Malaysia provides better value for money than any other Asian jurisdiction instinctively considered.

Clearly, with the enhancements that Labuan IBFC is undergoing, there is no doubt it is fast becoming Asia’s jurisdiction of choice in the challenging world of cross border taxation.

The Labuan Trading Company, your

‘Treasured Gateway’ to ‘Future Proofing’ and

Substance Creation

Labuan is distinguished by…its eight ‘Tax

Treasures’ that should help trading companies

navigate the new tax landscape

22

Since 1990 Labuan, situated off NW Borneo has been Malaysia’s dedicated international financial services centre. In that time it has become something of a global hub for Islamic finance with the Labuan Islamic Financial Services and Securities Act 2010 (LIFSSA) constituting groundbreaking specific legislation relating to the sector. Investors also have access to Labuan International Business and Financial Centre (IBFC’s) own Shariah Advisory Council for endorsement and advice on the likes of Sukuk issuance and listing, takaful and re-takaful, syariah-compliant captive structures and Islamic trusts.

LIFSSA forms part of a raft of legislation and regulations that became effective in February 2010. These saw Labuan successfully white listed and heralded a host of new products across a range of sectors. These developments have further enhanced the jurisdiction’s reputation as a cost-effective, flexible and compliant location for foundations, limited liability partnerships, captive insurance, mutual funds, shipping operations, trusts and estate management.

The Labuan Business Activity Tax Act 1990 (LBATA) affords trading companies the option to pay 3% of audited profits, or alternatively a flat rate of MYR20,000 p.a. while non-trading companies pay no tax at all. Perhaps the most significant recent legislative development has been the amendment to it to introduce the option of receiving an advance tax ruling on any transaction or arrangement involving a Labuan entity, thus allowing for precision planning.

Other ground-breaking legislation has included the Labuan Financial Services and Securities Act (LFSSA). This has introduced Limited Liability Partnerships, Protected Cell Companies, the Labuan Private Trust Company and Labuan Managed Trust Company, while it has also effected the deregulation and redefinition of mutual and private funds.

Its new Foundations Act sees Labuan enter an elite club of jurisdictions offering both common law trusts as well as civil law foundations, while the Limited Partnerships and Limited Liability Partnerships Act allows for partnerships of those named types as well as Recognised Limited Liability Partnerships.

Malaysia has been proactive in complying with international standards in the updating of its Labuan Financial Services Authority Act 1996 such that the FSA has the capacity to gather and share information with other enforcement agencies where there is a compelling argument for wrongdoing. That said, Labuan very much subscribes to the principles of confidentiality, and ‘fishing’ expeditions’ are not tolerated.

Other legislative amendments that came to pass in February 2010 included those to the

cornerstone Labuan Companies Act 1990 which governs all Labuan Companies. Key of these involved the permitting of dealings between Malaysians and Labuan companies, and Labuan companies being able to take a controlling stake in domestic Malaysian companies.

Extensive updating to the Labuan Trusts Act 1996 has ushered in a new Trusts era for the jurisdiction. This not only allows for trusts to be ‘in perpetuity’, but where the Labuan Special Trust is concerned, shares may be held in a Labuan Holding Company which can itself own assets. This creates a clear distinction between the trustees’ custodian role and the directors’ fiduciary role in investing, where the trustee holds shares ‘on trust to retain,’ and is not responsible for handling the management of the assets, so reducing their exposure to liability.

Labuan’s location at the crossroads of Asia affords it natural status as an investment conduit into China, India and South Korea, not to mention Malaysia itself. Of particular note is its assumption of the role of a treaty intermediary between China and Taiwan.

Best Re’s and Nomura’s recent consolidation and expansion of their respective Labuan operations only serves to draw further attention to Labuan’s many merits, not least its status as having the most extensive DTA network in the world leading Asia Pacific region. All things considered, the jurisdiction is well placed to take advantage of renewed investment levels as the global economic recovery continues to take hold.

Labuan

Extensive updating to the Labuan Trusts Act has

ushered in a new trusts era for the jurisdiction

Asia-Pacific

24

A leading international finance center for nearly thirty years, the Cook Islands seeks to further modernize its services to enable continued standing as a prime choice for sophisticated international services for the most discerning wealthy clients and corporate entities. Located in the South Pacific northeast of New Zealand, east of Tahiti, and south of Hawaii, the country comprised of fifteen islands and 13,000 people boasts an ideal location and a global client reach for its legal and financial services. Part of the British Commonwealth, the Cook Islands has a stable Parliamentary system of democratic government. Popular with clients of countries with a Common Law legal system, the jurisdiction also attracts an increasing number of clients from Civil Law jurisdictions due to the country’s strong legislation related to international financial services. Close ties with New Zealand allow the Cook Islands access to the New Zealand judiciary from which it draws its judges in the High Court. This ensures a sophisticated and fair justice system providing confidence to the corporate entities and individuals who use the international financial services of the jurisdiction.

The first country to create legislation allowing for modern asset protection trusts, the Cook Islands is known for its innovative services and ability to respond quickly to changes in and demands from the global market. With the recent changes in the global banking environment, the Cook Islands finds itself ranked very highly for its

regulations and oversight of the financial industry. With a supportive government and proactive industry, the jurisdiction has been able to maintain its sophisticated legal and financial services at competitive prices and, most importantly, with an outstanding level of service. 2011-12 will see the advent of new and improved services to the jurisdiction:

Managed Trustee Companies•

Foundations•

Qualified Pension Scheme Administration •(QROPS/QNUPS)

Mutual Funds•

Segregated Cell Companies•

Amended International Companies Act•

Amended International Trusts Act•

Amended Insurance Act•

Known best for its trust legislation, the Cook Islands also offers corporate entity formation through International Companies, Limited Liability Companies, and International Partnerships. Legislation also allows for various insurance services and the jurisdiction maintains access to premium banking services through relationships with international banks. Trust companies also provide a wide array of

administrative services to allow centralized and efficient operation of client structures. The jurisdiction also has a strong Maritime Registry with representatives in countries all over the world, including China. As the client composition of the jurisdiction continues to diversify, the integration of multinational wealth and corporate services in an international best practices framework strengthens the quality of industry work.

Asset protection trusts were originally a focus of the US market. As wealth levels increase in other countries, such as China, the level of regulatory oversight increases and many countries are adopting US-style legislation to cope with the newly acquired wealth of its citizens. This has resulted in increased demand for wealth protection and preservation offered through Cook Islands entities. Cook Islands advisors work closely with clients’ existing advisors to create a structure that meets the regulations of the home country while at the same time providing clients with the means to grow, protect, and enjoy the results of their successes for many generations to come.

Conveniently located between the world’s two superpowers, the Cook Islands provides a full range of corporate, trust, and financial planning services in a globally advantageous business environment. Whether you represent large corporations, closely held businesses, family offices, or individuals, you will find everything you need in the Cook Islands. Stability. Innovation. Service.

photo - CC by Benedict Adam

25

The Cook Islands continues to represent a sound investment prospect with its cost-competitiveness, pedigree stretching back to 1981 and robust regulatory environment which includes strong anti-money laundering and counter terrorism financing measures. It has also nurtured over the years a highly skilled specialised workforce offering world leading expertise in certain areas and a commitment to international business best practice. Moreover, the jurisdiction offers excellent tax mitigation potential notwithstanding that we are now in an era of greater transparency and compliance.

The Cook Islands possesses the ideal marriage of a firm yet flexible legal and regulatory environment, as embodied in the activities of the FSC, with the government having earmarked international financial services as an essential key to the jurisdiction’s future prosperity. This in turn has fostered a strong public-private collective effort to further this end. For example, the Cook Islands Financial Services Development Authority (FSDA) works closely with the jurisdiction’s trust companies to both promote and grow the industry abroad, and to ensure that legislation reflects the prevailing winds of the day.

The Cook Islands’ location affords it natural status as an investment conduit into and out of the Asia-Pacific rim including the powerhouse that is China, and so it is well placed to take advantage of the exponential increase of HNWIs and UHNWIs coming out of the region, as well as to maintain and grow its share of more traditional markets such as the US.

The banking and insurance sectors are strong, and are regulated respectively by the Banking Act 2003 and Insurance Act 2008. As elsewhere, business entities take a number of forms to reflect varying requirements. These include the popular International Company and Limited Liability Partnership (LLC).

It is the Cook Islands’ global pre-eminence in the field of asset protection trusts that is perhaps most striking, however. This is linked to pioneering and much copied legislation in the form of the International Trusts Act 1984 (amended 1989) that affords the strongest form of asset protection from foreign courts anywhere in the world. By transferring assets to another individual or company who then acts as a trustee and holds the assets, it affords those with large liquid assets added protection in the event of litigation. It is also catered towards those with business or family interests in multiple jurisdictions looking for an opportunity to centralise assets.

Any party looking to access such assets must first exhaust all options in foreign courts before bringing the suit in the Cook Islands. Meanwhile, a statute of limitations requires

the claimant to bring the suit within two years, thereby providing further reassurance and an added layer of protection.

To ensure such trusts do not encourage criminal activity the Cook Islands has regulations in place that require trust companies to conduct stringent due diligence checks.

The Cook Islands is a mature jurisdiction with IFC traditions going back to the early 1980s, thereby reassuring any potential investors. It can also point to an advanced and extensive trust infrastructure, as well as to genuine proactive support from the government to promote international financial services. It’s small wonder then that the Cook Islands’ status as an IFC goes from strength to strength.

Cook Islands

It is the Cook Islands’ global pre-eminence in the field of asset

protection trusts that is perhaps most striking

photo - CC by Hector Garcia

photo - CC by Robert Engberg

Asia-Pacific

26

Samoa constitutes a reliable, conservative yet flexible option in uncertain times which has seen it described as the model Pacific state by the Asian Development Bank. It exhibits particular strength in the international trusts, insurance and banking sectors, but the cornerstone of the Samoan product offering is arguably the International Company (the equivalent of IBCs found elsewhere). This can be set up within 24 hours and has a fixed cost of just US$300, regardless of share capital. It requires only one director who need not be resident, but may be corporate. The International Companies Act 1987 to which it relates also allows for companies limited by shares, by guarantee or hybrids, and also limited life companies.

A highly developed trusts infrastructure has developed over the last couple of decades in Samoa bringing with it a full range of fiduciary services encompassing trust and corporate administration, investment management, custodian and secretarial services. Trusts are governed by the International Trusts Act 1987.

On the insurance front the International Insurance Act 1988 provides for four categories of licence; general, long term, reinsurance and captive.

The banking sector is governed by the International Banking Act 2005. This requires that all holders of international banking licences have an office in Samoa, at

least two individual directors and that they employ at least one person. Licences are granted subject to stringent international best banking practice standards.

In the matter of funds, the International Mutual Funds Act 2008 provides for three types of mutual funds; public, private and professional. They can be established as an international company, a partnership, a unit trust or other similar body formed or organised under the relevant legislation.