Embed Size (px)

Citation preview

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 1/13

Created by Sandeep 1

International Finance Economics and Forex Trade

PCL-I (Finance)

Section 9 and 10

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 2/13

Created by Sandeep 2

Topics covered in this secession:

1. Balance of Payment

2. Theory of purchasing Parity

3. Theory of interest rate Parity

4. Relation between nominal interest rates of inflation and future spot exchange

5. Method of forecasting exchange rate.

Balance of payment:

Balance of Payment (BOP) records commercial, financial and economic flows between a given

country and other countries of the world. BOP statement is kept in the form of credits and debits.

The major uses are:

. Imports of goods and services;

. Purchase of foreign financial assets;

. Foreign lendings and so on.

PRESENTATION OF BALANCE OF PAYMENTS

A BOP statement is divided into several intermediate accounts. The three major segments are:

(i) Current account,

(ii) Capital account, and

(iii) Official reserve:

Account Table 2.1 provides details of these accounts as shown in a typical BO] statement. The data

needed to prepare different accounts are collected from various sources. For instance, the data on

imports and exports are gathered from customs!

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 3/13

Created by Sandeep 3

Authorities whereas the financing of these transactions appears largely among the data on changes in

foreign assets and liabilities reported by financial.

institutions. That is why there is an additional account in the BOP Statement, 'namely Errors andOmissions. The succeeding paragraphs contain a brief description of various accounts] shown in the

BOP Statement.

The Current Account is a record of the trade in goods and services among countries. The trade in

goods is composed of exports (selling merchandize td foreigners) and imports (buying merchandize

from abroad). Exports are sources of funds and result in a decrease in real assets. On the other hand,

imports are a use of funds and result in an acquisition of real assets. The trade in services (also called

invisibles) includes interest, dividends tourism/travel expenses and financial charges, etc. Interest

and dividends measures the services that the country's capital renders abroad. Payments coming from

tourists measure the services that the country's shops and hotels provide to foreigners who visit the

country. Financial, insurance and shipping charges measure the services that the country's financialand shipping sectors render to foreigners. Receipts obtained by servicing foreigners on these counts

constitute, source of funds. On the other hand, when the country's residents receive the services from

foreign-owned assets, utilization of funds, takes place. .

Unilateral transfers consist of remittances by migrants to their kith and kin and gifts, donations and

subsidies received from abroad. Remittances so receive 1 are obviously sources; remittances made in

forms of gifts/donations, etc., b immigrants cause utilization of funds.

The Capital Account is divided into foreign direct investment (FDI), portfolio investment and private

short-term capital flows. FDIs are for relatively longer period of time and portfolio investments have

a maturity of more than one year. When they are made. The short-term capital flows mature in aperiod of less, than one year. The distinction between FDI and portfolio investment is made on the

basis of the degree of involvement in the management of the company (and not on the basis of the

extent of ownership) in which investment is made.

Table 2.1 Typical BOP Statement

Goods Accounts

Account Exports (+)

Imports (-)

Balance on Goods Account = A(1)

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 4/13

Created by Sandeep 4

Services Account

Receipts as interest are dividends, tourism receipts for travel and filarial charges (+) Payments as

interest and dividends, tourism payments for travel and financial charges (-)

Balance on Services Account = A(ll)

Unilateral Transfers

Gifts, donations, subsidies received from foreigners (+) Gifts, donations, subsidies made to

foreigners (-) Balance on Unilateral Transfers Account = A(llI) Current Account Balance: A(l) +

A(ll) + A(llI)

B. Long-term Capital Account

Foreign Direct Investment FDI.

Direct investment by foreigners (+) Direct investment abroad (-) Balance on Direct Foreign

Investment = B(1)

Portfolio Investment

Foreigner's investment in the securities of the country (+) Investment in securities abroad (-) Balance

on Portfolio Investment = B(ll) Balance on Long-term Capital Account = B(l) + B(ll)

Private Short-term Capital Flows

Foreigners' claim on the country (+) Short-term claim on foreigners (-) Balance on Short-term

Private Capital Account = B(llI) Overall Balance: [A(1) + A(ll) + A(ill) +. [B(1) + B(ll) + B(llI)]

C. Official Reserves Account decrease or increase in foreign exchange reserves.

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 5/13

Created by Sandeep 5

BALANCE OF PAYMENTS (BOP) AND EXCHANGE RATE

A deficit or surplus of certain segments in the BOP may also help to explain the level of exchange

rates as disequilibrium indicates the level of demand and supply of foreign currencies. Deficit

increases the demand of foreign exchange. This reduces, all other things being the same, the value of

national currency; on the contrary, surplus increases the value of national currency on the exchange

market

EXCHANGE RATE THEORIES

INTRODUCTION

The objective of this chapter is to explain forward rates theories, concerned with Determination of

exchange rates. The important factors affecting exchange rates are: (i) rate of inflation, (ii) interest

rates, and (iii) balance of payment the subject matter of this chapter is to describe two important

theories partly explain fluctuations in exchange rate:

(1) Purchasing Power Parity (PPP) (2) Interest Rate Parity

THEORY OF PURCHASING POWER PARITY (PPP)

This theory was enunciated by "Gustav Cassel. Purchasing power of a currency is determined by the

amount of goods and services that can be purchased with one unit of that currency. If there is more

than one currency, it is fair all equitable that the exchange rate between these currencies provides the

same purchasing power for each currency. This is referred to as purchasing POW. Parity.

It is ideal if the existing exchange rate is in tune with this cardinal principal of purchasing power

parity. On the contrary, if the existing exchange rates I such that purchasing power parity does not

exist in economic terms, it is f situation of disequilibrium. It is expected that the exchange rate

between the two currencies conforms eventually to purchasing power parity.

Likewise, if the rate of inflation is different in two countries, the floatin1 exchange rate should

accordingly vary to reflect that difference. Let us consider two countries, A and B. The rate of

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 6/13

Created by Sandeep 6

inflation in the country A is higher than that in the country B. As a result, imports of the country A

Increase since the prices of foreign goods tend to be lower. Similarly, exports from the country.

Criticism of the PPP Theory

Conceptually, this theory is sound. However, there are a nqruJ2.er of reed) factors that, prevent this

theory from determining exchange rates, in practice Some of the major factors in this regard are: (i)

Government intervention, directly in the exchange markets or indirectly through trade restrictions;

(ii) Speculation in the exchange market; (iii) structural changes in the economies of the countries (iv)

continuation of long-term flows in spite of the disequilibrium between purchasing power parity and

exchange rates. Another criticism levelled against this theory is that the rate of inflation or the

relevant price level indices are. Not weII defined. Questions pertaining to what constitutes an

appropriate sample and weight assigned to each commodity are not satisfactorily answered. For

example, should the sample represent goods, and services, or only those that are traded

internationally?' The theory takes into account only the movement of goods and not capital. In

operational terms, it is concerned only with the current account segment of the balance of payment

and not with the total BOP. , Above all, this theory ignores the fact that a currency may be an

instrument of payment by other countries (e.g. US dollar). In this situation, the exchange rate may

evolve in a manner that has nothing to do with the price levels of the country (i.e. the USA).

The ppp theory can be considered as an ideal theory to determine exchange rates in specific

situations, such as high inflation or monetary disturbances. In such situations, the response of

individuals to changes in value of real and monetary assets can be expected to be strong and the

exchange rate prediction by ppp theory may turn out to be realistic.

THEORY OF INTEREST RATE PARITY

This theory states that premium or discount of one currency against another should reflect the

interest differential between the two currencies. In a perfect market situation and where there is no

restriction on the flow of money, one should be able to gain the same real value on one's monetary

assets irrespective of the country where they are held.

Say, an investor has a sum of DM 1 today. The exchange rate is, say, f' $Co/DM. That is, he can

convert his DM 1 to get $Co if he so desires. Further, say, the net interest per dollar is t$ while per

DM it is tDM. The investor has two choices before him:

(i) He places his money in DM to receive 1 x (1 + tDM) after a period T;

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 7/13

Created by Sandeep 7

(ii) He converts his money into US dollar and places it in dollar market to receive Co x (1 + t$) at

the end of the period T.

In order that he be indifferent in placing his money either in DM or in US dollars, the two sums, atthe end of the period T, should be equal.

Co (1 + t$) dollars = 1 (1 + tDM) Deutschmark

or

DMI = $Co [(1 + t$)/(1 + tDM)] So, the rate of exchange after the period T is $CT/DM. So in

general, we can write:

CT = Co x (1+tD)/ (1+tE)

Where:

CT: forward rate;

Co: spot rate;

tD: domestic rate of interest;

tE: interest rate in foreign country.

This equation can be rearranged such that:

CT – Co/ Co = tD- tE/1+tE

If tE is considered very small compared to 1, then

CT'-CO/ Co = tD - tE

Thus, premium or discount should be almost equal to the difference between the rates of interest of

the two currencies.

Criticism of the Theory of Interest Rate Parity

The theory of interest rate parity is a very useful reference for explaining the differential between the

spot and future exchange rate, and international movement of capital. Accepting this theory implies

that international financial markets are perfectly competitive and function freely without any

constraints. However, reality is much more complex. Some of the major factors that inhibit the

theory from being put into practice are as follows:

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 8/13

Created by Sandeep 8

Availability of funds that can be used for arbitrage is not infinite. Further, the importance of capital

movements, when they are available, depends on the credit conditions practiced between the

financial places and on the freedom of actions of different operators as per the rules of the country in

vogue.

Exchange controls certainly place obstacles in the way of theory of interest rate parity. The same is

true about the indirect restrictions that can be placed on capital movements in short run.

Interest rate is only one factor affecting the attitude and the behaviour of arbitrageurs. In other words,

capital movements do not depend only on interest rates. Other important factors are concerned with

liquidity and the ease of placement.

Speculation is an equally important element. This becomes very significant during the crisis of

confidence in the future of a currency. The crisis manifests in tenns of abnormally high premium or

discount-much higher than what the interest rate parity can explain.

RELATION BETWEEN NOMINAL INTERFST RATES, RATES OF

INFLATION AND FUTURE SPOT EXCHANGE RATES

Variations of future spot rates should reflect:

. Difference of nominal interest rates;

. Difference of anticipated inflation.

As stated earlier, nominal interest rate difference, tE - tD, should be equal to premium or discount. If

the markets are efficient, the forward rate is an unbiased predictor of future spot exchange rate. For

example, if the nominal interest rate on US dollar is 4 per cent less than that on Indian rupee, this

difference of 4 per cent can be explained by the fact that an anticipated inflation rate is apprehended

to be 4 per cent higher in India than that in the USA. Consequently, this difference is expected to be

reflected in the future spot rate leading to a depreciation of the Indian rupee by 4 per cent.

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 9/13

Created by Sandeep 9

METHODS OF FORECASTING EXCHANGE RATES

Forecasting future exchange rates is virtually a necessity for a multinational enterprise, inter-alia, to

develop an international financial policy. In particular, it is useful when the international firn is to

borrow from or invest abroad.

Foreign investment decisions require forecast pertaining to future cash flows, which in turn, will

need input of host country's exchange rate. Above all, exchange rates are decisive in framing hedging

policy.

Forecasting the Exchange Rate in Short-term

Forecasting the exchange rate is one of the most difficult areas of international t finance. The

theories explaining exchange rate variations are not satisfactory to

Forecast how the rates are going to evolve. Under the circumstances, therefore,

Recourse is taken to less than perfect methods. The following three methods are generally employed

for the purpose.

(1) Method of advanced indicators

(2) Use of forward rate as a predictor of the future spot rate

(3) Graphical methods.

Method of Advanced Indicators

Several indicators are used for prediction of exchange rates. One important indicator widely used is

to determine the ratio of country's reserves to its imports.

The reserves consist of gold, foreign currencies and SDRs. The ratio indicates the number of months

(N) imports, covered by the reserves (R) (Eq. 6.4).

N = R/I x 12 (6.4)

Let us assume that annual imports of India cost Rs 80 billion and reserves are Rs 30 billion, the

number of months of imports covered by reserves is:

N = (30/80) x 12 = 4.5 months.

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 10/13

Created by Sandeep 10

The general rule that seems to be followed in this regard is that if amount of reserves is less than the

value of 3 months' imports, the currency is vulnerable and may face devaluation.

Use of Forward Rate as Predictor of Future Spot Rate

Some authors believe in the efficiency of markets and consider that forward rates are likely to be an

unbiased predictor of the future spot rate. If on 1 January of current year, the 6-month forward rate is

Rs 38/US$, the spot rate on 1 July should be Rs 38/US$. In other words, the rate of premium or

discount should be an unbiased predictor of the rate of appreciation or depreciation of a currency.

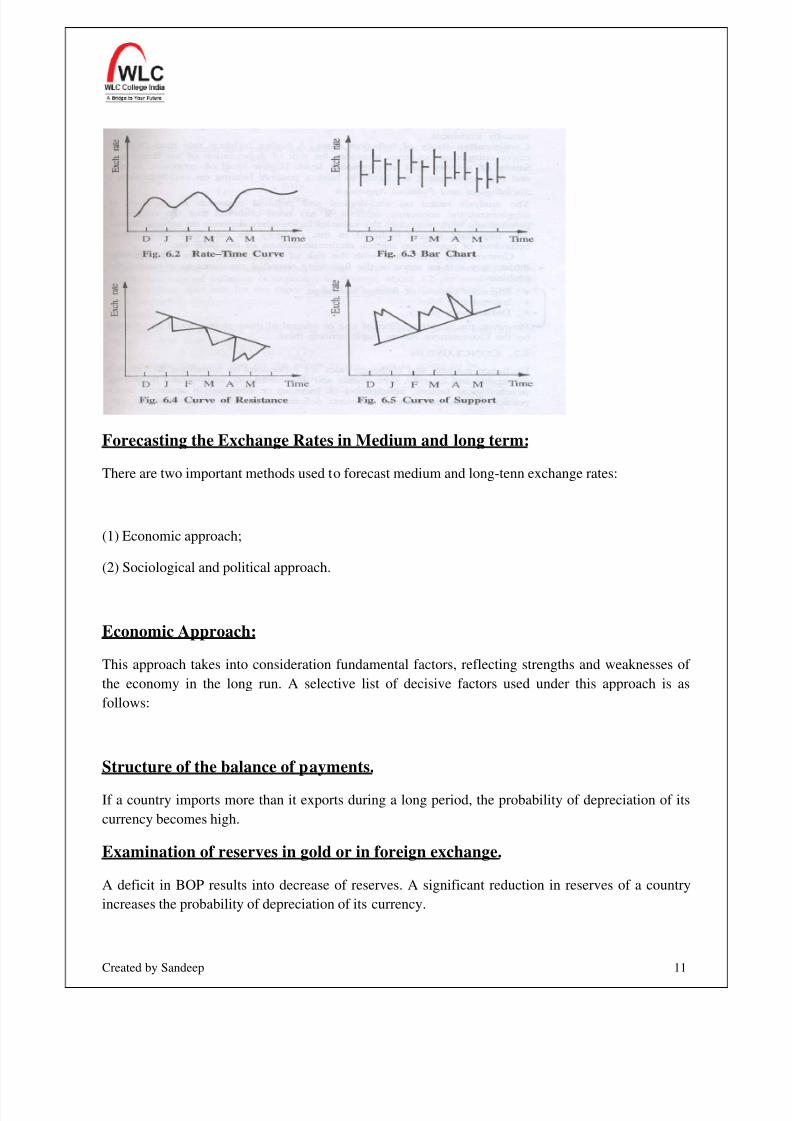

Graphical Methods

Since long, these methods have been used on exchange markets. The objective of making charts or

graphs is to gain insight into the trend of fluctuations' and forecast the moment when the trend is

likely to reverse. Technical analysts consider that the behaviour of operators remains stable over a

period. They identify certain configurations and then forecast rates.

One type of graph is in the form of a curve. Every day, the closing rate is marked on a vertical scale

while the horizontal scale is for time. Different points are linked to prepare a curve (Fig. 6.2).

Another type of graph can be in the form of bars. Every day or every week or every month, high and

low rates are indicated while closing rates are indicated by a small horizontal bar on the vertical line

joining high and low (Fig. 6.3).

Joining the points of high (also called resistance points), a curve of resistance (Fig. 6.4) is obtained.

On the other hand, by joining low points, a curve of support (Fig. 6.5) is obtained. The two curves

joining high and low points form a tunnel.

If rates become significantly distant from these curves, which indicate a change in: the market

behaviour.

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 11/13

Created by Sandeep 11

Forecasting the Exchange Rates in Medium and long term:

There are two important methods used to forecast medium and long-tenn exchange rates:

(1) Economic approach;

(2) Sociological and political approach.

Economic Approach:

This approach takes into consideration fundamental factors, reflecting strengths and weaknesses of

the economy in the long run. A selective list of decisive factors used under this approach is as

follows:

Structure of the balance of payments.

If a country imports more than it exports during a long period, the probability of depreciation of its

currency becomes high.

Examination of reserves in gold or in foreign exchange.

A deficit in BOP results into decrease of reserves. A significant reduction in reserves of a country

increases the probability of depreciation of its currency.

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 12/13

Created by Sandeep 12

Comparative examination of interest rates.

Relatively speaking, the higher interest rate (in comparison to other countries) is indicative of likely

depreciation of the currency. If higher rates persist for a long period, the devaluation is virtuallyimminent.

Comparative study of inflation rates.

A higher inflation rate than those of major competing countries increases the risk of depreciation of

the currency.

Study of activity and employment level.

Higher level of economic activity and full employment are likely to have a positive bearing on

exchange rates.

Sociological and Political Approach

The analysis based on sociological and political approach is important to supplement the economic

analysis. It has been observed that the attitude of government with respect to the value of its currency

depends on several factors.

The important factors included in-this category is proximity of elections, behaviour of opposition

parties, recommendations of the IMF, etc.

Government, confronted with the risk of depreciation of ' its currency may - initiate anyone or more

of the following remedial measures to overcome the problem.

• Rigorous control of foreign exchange

• Interest rate hike

• Deflationary policy.

However, the negative effect of one or several of these steps should be weighed by the Government

before implementing them.

CONCLUSION

8/8/2019 Business PCL I Fin Session 9&10 Techniques of Hedging

http://slidepdf.com/reader/full/business-pcl-i-fin-session-910-techniques-of-hedging 13/13

Created by Sandeep 13

Exchange markets and exchange rates are influenced by numerous factors such as exports and

imports, investments and disinvestrnents lending and borrowing, psychological factors, anticipation

of increase or decrease in reserves, sociopolitical factors, international payments deficits, and

stability of governments, etc.